Just Do It: Schopenhauer and Peirce on the Immediacy of Agency

Organizational Behavior and Human Decision Processes 96 (2005) 104–118

www.elsevier.com/locate/obhdp

The combined eVects of risk and time on choice:Does uncertainty eliminate the immediacy eVect?

Does delay eliminate the certainty eVect? �

Bethany J. Weber ¤, Gretchen B. Chapman

Psychology Department, Rutgers University, 152 Frelinghuysen Road, Piscataway, NJ 08854-8020, USA

Received 2 February 2004

Abstract

Researchers have noted parallels between decisions under uncertainty and over time. Three experiments evaluated the theory thatuncertainty and time aVect choice via a common underlying dimension, such that delaying an outcome is equivalent to making ituncertain. To test this account we asked whether adding uncertainty to outcomes would eliminate the immediacy eVect bias. We alsoasked whether adding time delay to outcomes would eliminate the certainty eVect bias. The answer to both questions was yes, pro-vided the prospects were presented singly rather than jointly. In single evaluation uncertainly eliminated the immediacy eVect anddelay eliminated one form of the certainty eVect, while in joint evaluation, these eVects did not occur. These Wndings suggest that atleast in some contexts decision makers may equate risk and delay. Other explanations are possible, however, demonstrating that theinteraction between risk and delay is complex and not easily understood. 2005 Elsevier Inc. All rights reserved.

Keywords: Risk; Time; Choice; IndiVerence points; Allais Paradox; Certainty eVect; Common ratio eVect; Immediacy eVect; Delay; Preference rever-sals; Joint evaluation

Sometimes decisions are risky: we don’t know whatthe outcome of the selected option will be. At othertimes, the outcomes of our decisions are delayed: weknow what is going to happen, but we must wait for theWnal result. Frequently decision outcomes are both riskyand delayed. Not only is the result uncertain, but it willnot occur for some time to come.

Although delay and risk initially appear quite diVer-ent, there are a number of apparent parallels betweenthe biases people show when making risky decisionsand when making decisions with delayed outcomes.The purpose of this paper is to explore one particularapparent parallel: that between the certainty eVect and

� This research was supported by an NSF graduate fellowship to theWrst author and NSF grant SES 99-75083 to the second author.

¤ Corresponding author. Fax: +1 732 445 2263.E-mail address: [email protected] (B.J. Weber).

0749-5978/$ - see front matter 2005 Elsevier Inc. All rights reserved.doi:10.1016/j.obhdp.2005.01.001

the immediacy eVect. Do the immediacy eVect and thecertainty eVect draw on the same underlying mecha-nism? An identity relationship between the two biasesis predicted by the view (Keren & Roelofsma, 1995)that uncertainty and time delay aVect decisions via asingle common dimension, where delaying an outcomehas the same eVect as making it (more) uncertain. Wetested this account in three experiments that assessedwhether adding uncertainty to outcomes would elimi-nate the immediacy eVect just as adding time delaydoes, and whether adding time delay to outcomeswould eliminate the certainty eVect just as addinguncertainty does. The Wrst experiment followed closelythe procedure used by Keren and Roelofsma (1995) butdid not replicate their results. Consequently, our sec-ond and third experiments used more sensitive tech-niques to try to detect an identity relationship betweenthe two biases.

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 105

The certainty eVect

The certainty eVect describes decision-makers’ ten-dencies to place a disproportionate weight on certainoutcomes. For example, given the choice between $30 forsure and $45 with 80% probability, people will tend tochoose $30 for sure. However, when choosing between$30 with 25% probability and $45 with 20% probability,most people choose the $45 option, despite the fact thatthe second set of options is the same as the Wrst with allprobabilities reduced by a factor of 4 (Kahneman &Tversky, 1979). Normatively, this common ratio trans-formation should not change the rank ordering of thetwo options.

Perhaps the most famous example of the certaintyeVect is the Allais Paradox. For example, decision-mak-ers usually prefer $2700 for certain to a gamble thatoVers a 33% chance of $3000 and a 66% chance of $2700(with a corresponding 1% chance of $0), passing up thepossibility of an extra $300 to avoid the 1% chance ofgetting nothing that the second option entails. Given thechoice between a 34% chance of $2700 and a 33% chanceof $3000, however, most people prefer the latter option.This is not normative, as the second set of options isobtained from the Wrst set by removing the commonconsequence, a 66% chance of winning $2700. The 1%chance of receiving nothing instead of $2700 that lookedso large when moving from 100% probability to 99% isapparently negligible when moving from 34 to 33%(Allais, 1953).

The certainty eVect is explained descriptively by anon-linear probability weighting function: in the AllaisParadox example above, the diVerence between 100 and99% is given more weight in the decision than the diVer-ence between 34 and 33%. Kahneman & Tversky (1979;Tversky & Kahneman, 1992) call this non-linear weight-ing function the � function. The � function is concavefor higher values of probability and increases very rap-idly near certainty, so that small actual deviations fromcertainty have a large inXuence on the decision-makingprocess. Because the � function is steepest very near cer-tainty, decision biases connected to the � function arelargest when one of the choices involves certainty, hencethe name, “certainty eVect.”

The immediacy eVect

In the immediacy eVect, decision-makers place a dis-proportionate weight on immediate outcomes. Forexample, people prefer $30 immediately to $45 in 1 year,but prefer $45 in 2 years to $30 in one, despite the factthat the diVerence in time delay between the options isthe same in both sets (Kirby & Herrnstein, 1995).

The standard explanation for time-variant prefer-ences in decisions with delayed outcomes is the hyper-

bolic discount function (Ainslie, 1975; Kirby &Marakovic, 1995; Loewenstein & Prelec, 1992). The dis-count function describes the present value of a delayedoutcome—that is, how much a decision-maker valuesthe delayed outcome at the present time. Normatively,the value of a delayed outcome is described by an expo-nential function. Exponential discount functions fordiVerent outcomes do not cross each other—if the deci-sion-maker considers one delayed option to be morevaluable now, that option should also be consideredmore valuable by the decision-maker at every point inthe future as well. However, the hyperbolic discountfunctions for two outcomes may cross each other. In theexample above, the present values of $30 and $45 at var-ious time delays would each form a hyperbola. Thesetwo hyperbolas cross each other, so that while $30 nowis more valuable than $45 in 1 year, $45 in 2 years ismore valuable than $30 in one year. Because the hyper-bolic function is steepest very near immediacy, decisionbiases connected to the hyperbolic function are are larg-est when one of the choices involves immediacy, hencethe name “immediacy eVect.”

Possible parallel

If certainty is analogous to immediacy, then the cer-tainty and immediacy eVects are related. Both biasesinvolve a change in preference from the smaller mone-tary outcome to the larger one as both outcomes becomemore risky or more distant in time. Several possibleexplanations have been put forward to explain this pos-sible parallel between risky and intertemporal choice.Rachlin and colleagues have proposed that delay is thefundamental factor, and that the eVect of uncertainty onchoice is due to an eVect of delay, arguing that overrepeated gambles, a higher risk translates into a longerdelay before the decision maker can expect a pay oV

(Rachlin, Raineri, & Cross, 1991; Rachlin, Logue, Gib-bon, & Frankel, 1986). On the other hard, Keren andRoelofsma (1995) suggest that uncertainty is fundamen-tal and delay aVects our decisions only to the extent thatdelay entails uncertainty.

Keren and Roelofsma’s view is a very appealing one,because any delay in the outcome of a decision must ofnecessity entail uncertainty about what the outcome willactually be. If nothing else, the decision-maker could gethit by a truck on the way home and never have a chanceto enjoy the fruits of the decision. Keren and Roelofsmapropose that all delay eVects are actually eVects of theuncertainty implicit in the delay. The immediacy eVect/certainty eVect parallel arises naturally from this theory:they are actually the same eVect. When asked to considertwo outcomes, one immediate and one delayed, the deci-sion-maker responds to the implicit uncertainty, not thedelay. The immediate outcome entails no uncertainty

106 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

and therefore is perceived as a certain outcome, whereasthe delayed outcome is treated as an uncertain outcome.However, when the same implicit risk is added to bothoutcomes, in the form of adding a common time delay,the decision maker prefers the more delayed (implicitlyriskier) outcome. Adding the common delay is equiva-lent to reducing the implicit uncertainty by a commonfactor.

Reducing all the probabilities of a certainty eVectproblem should reduce or eliminate the eVect: the �function is not nearly as steep in the middle of the func-tion as it is near certainty. If the immediacy eVect is sim-ply the certainty eVect in disguise, adding uncertainty toit should accomplish the same thing as it would in a truecertainty eVect problem. Likewise, if delay is simplyanother form of risk, than adding delay to a certaintyeVect problem should have the same eVect as adding riskto one. The size of the certainty eVect should decrease,and if the risk being added is large enough, the eVectshould be altogether eliminated.

Thus, Keren and Roelofsma (1995) propose that riskand delay produce the same phenomena, with risk beingthe more psychologically fundamental construct. That is,what look like delay eVects are actually eVects of the riskinherent in delay—the delay itself does not inXuencejudgments and decisions. In two separate experiments,Keren and Roelofsma tested the eVect of adding uncer-tainty to the immediacy eVect and of adding delay to thecertainty eVect. They found that reducing the probabili-ties involved from 100 to 50% eliminated the immediacyeVect, as their theory predicts. However, they found thatadding a 1-year delay to all the Allais Paradox outcomesdid not eliminate or even reduce the certainty eVect. Thispattern of results seems puzzling in light of their theory,which postulates that delay aVects decision making byintroducing uncertainty. Making a certain outcomedelayed should make the outcome seem no longer cer-tain, thus removing its appeal and reducing or eliminat-ing the certainty eVect. The 1-year delay used in Kerenand Roelofsma’s study should be suYcient to removethe special appeal of a certain outcome, since this samedelay was suYcient to remove the appeal of the immedi-ate outcome in their study on the immediacy eVect.

Thus, Keren and Roelofsma found that uncertaintyeliminated the immediacy eVect, but delay does not elim-inate the certainty eVect. They propose that this asym-metry is due to the fact that risk is the more fundamentalof the two properties, but it is not clear whether thisassertion solves the problem. If delay implies risk, thenrisk should have the same eVects as delay—the two areinterchangeable. Thus, the failure to eliminate the cer-tainty eVect with the addition of delay cannot beexplained by postulating that one property is more fun-damental than the other. Rather, it seems possible thatthe 1-year delay was simply not large enough to elimi-nate the Allais Paradox.

The purpose of the present research was to examinefurther the potential equivalence of risk and delay as anexplanation for the parallels between the immediacy andcertainty eVects. The current experiments examinedwhether the addition of risk would reduce or eliminatethe immediacy eVect and whether the addition of delaywould reduce or eliminate the Allais Paradox. Experi-ment 1 used choice methodology and is essentially a rep-lication of Keren and Roelofsma (1995) whereasExperiments 2 elicited indiVerence points to the gambles.Experiment 3 used both choice and indiVerence pointelicitation techniques.

Experiment 1: Choice

The purpose of Experiment 1 was to test whetheradding delay reduced the Allais Paradox and whetheradding risk reduced the immediacy eVect, by replicatingKeren and Roelofsma’s (1995) two studies in a singleexperiment. Because the 1-year delay used by Keren andRoelofsma might have been too short to reduce or elimi-nate the Allais Paradox, we tested both 1- and 25-yeardelays.

Method

ParticipantsFour hundred and forty-six undergraduates partici-

pated in the experiment as part of a class requirementfor an introductory psychology class.

DesignEach subject was presented with two questions: one

Allais Paradox question and one immediacy eVect ques-tion. Each question was a binary choice in which sub-jects chose one of two options.

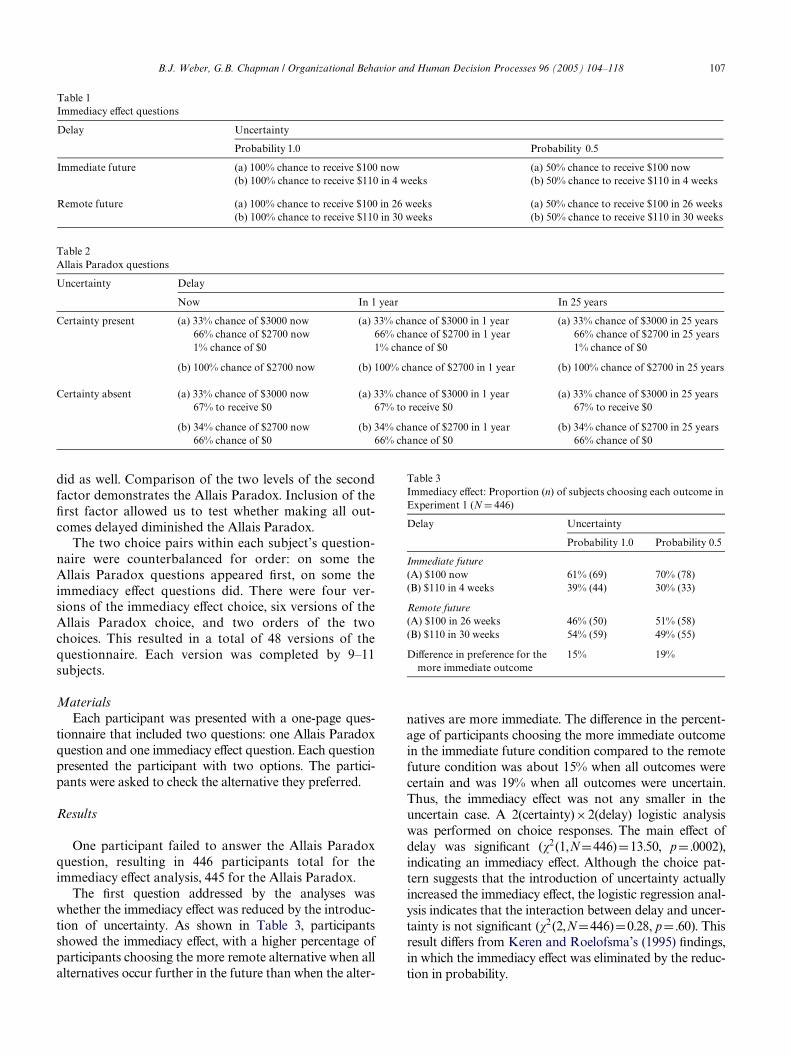

Four versions of the immediacy eVect choices resultedfrom a 2 £ 2 between-subjects design (see Table 1). First,the question involved either outcomes that were certainor outcomes that occurred with 50% probability. Sec-ond, each choice pair involved either a short time delay(the nearer outcome was immediate) or a long one (thenearer outcome occurred in 26 weeks). Comparison ofthe two levels of the second factor demonstrates theimmediacy eVect. Inclusion of the Wrst factor allowed usto test whether making all outcomes uncertain dimin-ished the immediacy eVect.

Six versions of the Allais Paradox choices resultedfrom a 3 £ 2 between-subjects design (see Table 2). First,questions involved either immediate outcomes or out-comes delayed by 1 or 25 years. Second, like the immedi-acy eVect questions, the Allais Paradox questions hadtwo levels: one that contained a certain outcome and onethat did not. Because Keren and Roelofsma used theAllais Paradox to demonstrate the certainty eVect, we

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 107

did as well. Comparison of the two levels of the secondfactor demonstrates the Allais Paradox. Inclusion of theWrst factor allowed us to test whether making all out-comes delayed diminished the Allais Paradox.

The two choice pairs within each subject’s question-naire were counterbalanced for order: on some theAllais Paradox questions appeared Wrst, on some theimmediacy eVect questions did. There were four ver-sions of the immediacy eVect choice, six versions of theAllais Paradox choice, and two orders of the twochoices. This resulted in a total of 48 versions of thequestionnaire. Each version was completed by 9–11subjects.

MaterialsEach participant was presented with a one-page ques-

tionnaire that included two questions: one Allais Paradoxquestion and one immediacy eVect question. Each questionpresented the participant with two options. The partici-pants were asked to check the alternative they preferred.

Results

One participant failed to answer the Allais Paradoxquestion, resulting in 446 participants total for theimmediacy eVect analysis, 445 for the Allais Paradox.

The Wrst question addressed by the analyses waswhether the immediacy eVect was reduced by the introduc-tion of uncertainty. As shown in Table 3, participantsshowed the immediacy eVect, with a higher percentage ofparticipants choosing the more remote alternative when allalternatives occur further in the future than when the alter-

natives are more immediate. The diVerence in the percent-age of participants choosing the more immediate outcomein the immediate future condition compared to the remotefuture condition was about 15% when all outcomes werecertain and was 19% when all outcomes were uncertain.Thus, the immediacy eVect was not any smaller in theuncertain case. A 2(certainty)£2(delay) logistic analysiswas performed on choice responses. The main eVect ofdelay was signiWcant (�2(1,ND446)D13.50, pD .0002),indicating an immediacy eVect. Although the choice pat-tern suggests that the introduction of uncertainty actuallyincreased the immediacy eVect, the logistic regression anal-ysis indicates that the interaction between delay and uncer-tainty is not signiWcant (�2(2,ND446)D0.28, pD .60). Thisresult diVers from Keren and Roelofsma’s (1995) Wndings,in which the immediacy eVect was eliminated by the reduc-tion in probability.

Table 3Immediacy eVect: Proportion (n) of subjects choosing each outcome inExperiment 1 (N D 446)

Delay Uncertainty

Probability 1.0 Probability 0.5

Immediate future(A) $100 now 61% (69) 70% (78)(B) $110 in 4 weeks 39% (44) 30% (33)

Remote future(A) $100 in 26 weeks 46% (50) 51% (58)(B) $110 in 30 weeks 54% (59) 49% (55)

DiVerence in preference for the more immediate outcome

15% 19%

Table 1Immediacy eVect questions

Delay Uncertainty

Probability 1.0 Probability 0.5

Immediate future (a) 100% chance to receive $100 now (a) 50% chance to receive $100 now(b) 100% chance to receive $110 in 4 weeks (b) 50% chance to receive $110 in 4 weeks

Remote future (a) 100% chance to receive $100 in 26 weeks (a) 50% chance to receive $100 in 26 weeks(b) 100% chance to receive $110 in 30 weeks (b) 50% chance to receive $110 in 30 weeks

Table 2Allais Paradox questions

Uncertainty Delay

Now In 1 year In 25 years

Certainty present (a) 33% chance of $3000 now (a) 33% chance of $3000 in 1 year (a) 33% chance of $3000 in 25 years 66% chance of $2700 now 66% chance of $2700 in 1 year 66% chance of $2700 in 25 years 1% chance of $0 1% chance of $0 1% chance of $0

(b) 100% chance of $2700 now (b) 100% chance of $2700 in 1 year (b) 100% chance of $2700 in 25 years

Certainty absent (a) 33% chance of $3000 now (a) 33% chance of $3000 in 1 year (a) 33% chance of $3000 in 25 years 67% to receive $0 67% to receive $0 67% to receive $0

(b) 34% chance of $2700 now (b) 34% chance of $2700 in 1 year (b) 34% chance of $2700 in 25 years 66% chance of $0 66% chance of $0 66% chance of $0

108 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

We next examined whether the introduction of delayaltered the Allais Paradox. As shown in Table 4,participants demonstrated the Allais Paradox across allthree levels of delay, with a higher percentage ofparticipants choosing the safer (B) option when cer-tainty was present than when certainty was absent. A2 (certainty) £ 3 (delay) logistic analysis showed a maineVect of certainty (�2 (1, N D 445) D 66.83, p < .0001),indicating a Allais Paradox. However, there was nointeraction between certainty and delay (�2 (2, ND 445) D 0.59, p D .74). Thus, the Allais Paradox was notreduced by making all outcomes delayed. This result isconsistent with the results from Keren and Roelofsma(1995) who also found no change in the Allais Paradoxwith a 1-year delay.

Discussion

In Experiment 1 we found that the immediacy eVectdid not diminish with the addition of uncertainty. Theseresults are inconsistent with Keren and Roelofsma’s(1995) Wndings that the immediacy eVect was eliminatedwith the addition of uncertainty. We also found that theAllais Paradox did not diminish with the addition ofdelay. This result does agree with Keren and Roelofsma(1995), who also found that the Allais Paradox was noteliminated by delay. However, this Wnding does not seemto support their theory. According to this theory, delayeVects are due to the delay’s inherent uncertainty. There-fore, it is the addition of a 26-week delay’s worth ofuncertainty that removes the appeal of the immediate/certain outcome, producing the immediacy eVect. If evena 25-year delay does not entail enough uncertainty tocause a signiWcant reduction in the certainty eVect, thenit seems unlikely that a 26-week delay could causeenough to explain the immediacy eVect.

Table 4Certainty eVect: Proportion (n) of subjects choosing each outcome inExperiment 1 (N D 445)

Uncertainty Delay

Now In 1 year In 25 years

Certainty present(A) $3000 with p D .33 15% (11) 24% (17) 18% (14)

$2700 with p D .66 $0 with p D .01

(B) $2700 with p D 1.0 85% (61) 76% (55) 82% (65)

Certainty absent(A) $3000 with p D .33 58% (41) 60% (43) 57% (45)

$0 with p D .67

(B) $2700 with p D .66 42% (30) 40% (29) 43% (34) $0 with p D .34

DiVerence in preferencefor outcome B

43% 36% 39%

Although the results of Experiment 1 suggest thatrisk and delay are not psychologically equivalent, thereare other possible accounts of the Wndings. One alterna-tive account is that the choice response mode wasinsuYciently sensitive to detect changes in the size ofthe immediacy eVect or Allais Paradox when risk ordelay was added. To examine this possibility, we con-ducted a follow-up study (not reported) that used a rat-ing response mode. Rather than choosing betweenoptions as in Experiment 1, participants divided 100points between the two options in each condition toexpress their level of preference for each option. Theresults were identical to those of Experiment 1, suggest-ing that the insensitivity of the choice response modewas not responsible for the failure of risk to eliminatethe immediacy eVect or of delay to eliminate the AllaisParadox.

Another alternative account of Experiment 1 is thatparticipants may simply have ignored informationthat was common to both options as being unimportantfor the task of choosing between them. Both addingrisk to the immediacy eVect and delay to the AllaisParadox involved adding a probability or delay that wasthe same in both options presented to the partici-pant. If the participants edited this information out, itwould appear that the addition did not alter the eVect,when in fact the participant had simply ignored theaddition.

To determine if participant insensitivity to proba-bility or delay information common to both optionswas responsible for the lack of reduction in the imme-diacy and certainty eVects in Experiment 1, in Experi-ment 2 subjects provided indiVerence points to singleoptions rather than jointly evaluating pairs ofoptions.

Experiment 2: IndiVerence points

In Experiment 2 participants evaluated single optionsby specifying the amount of money to be received imme-diately and for certain that would be just as attractive asthe delayed, uncertain amount presented. As a conse-quence, it was necessary for them to consider all threeattributes of the option to be evaluated (monetaryamount, delay, and probability). This design allowed usto conWrm that participants’ evaluations were sensitiveto both uncertainty and delay and that they were notediting out one dimension.

Method

ParticipantsThree hundred and twenty-seven undergraduates par-

ticipated in the experiment as part of a class requirementfor an introductory psychology class.

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 109

DesignBoth previous experience and pilot studies suggested

that subjects have diYculty providing indiVerence pointsvia a traditional matching task for problems dealingwith both uncertainty and delay. Therefore, Experiment2 was conducted on the computer where indiVerencepoints could be elicited through a series of choices with abisection algorithm, as discussed below.

This change in format necessitated some changes indesign. To reduce confusion to subjects and to simplifyprogramming, each subject saw only Allais Paradoxquestions or immediacy eVect questions, instead of oneof each as in Experiment 1. To reduce the length of theexperiment, the 1-year delay was eliminated from theAllais Paradox questions. Lastly, no counterbalancingwas needed for Experiment 2 because the computerallowed the questions to be presented in a diVerent ran-dom order for every subject.

The net results of these changes were 2 £ 2 within-subject designs for both the Allais Paradox and immedi-acy eVects.

The questions also diVered slightly from those of pre-vious versions. Because the goal of Experiment 2 was toavoid confronting participants with two outcomes fea-turing identical probability or delay information, onlyone outcome for each outcome pair was presented at atime. The participant was asked to give a present cer-tainty equivalent to this outcome. That is, they wereasked to identify the monetary amount, payable immedi-ately and for certain, that would make them indiVerentbetween that amount and the presented outcome.Because only one option was presented at a time, andbecause no delay or uncertainty was added to the out-comes provided by the participants, there was no chancethat that they could simply ignore the probability ordelay as common to both options.

Because it seemed nonsensical to ask the subjects fora certainty equivalent to a 100% chance of $2700, or forthe present value of $100 payable immediately, we didnot elicit present certainty equivalents for these options.For purposes of analysis, we assumed them to be $2700and $100, respectively. Thus, each subject was presentedwith seven prospects and an indiVerence point was elic-ited for each.

Obtaining indiVerence pointsFor each question we identiWed the subject’s indiVer-

ence point: the amount of money, payable immediatelyand for certain, that was just as good as the delayed and/or risky gamble.

To do this we used a choice titration procedure wherethe subject made a repeated series of choices betweentwo options: the risky or delayed outcome for whichwe wished to obtain an indiVerence point and a certain,immediate outcome. The amount of the certain,immediate outcome was adjusted towards the subject’s

indiVerence point in response to the subject’s previouschoices using a bisection algorithm until the indiVerencepoint was obtained to the desired degree of accuracy.For example, consider a question requiring the partici-pant to give an indiVerence point to a 10% chance ofwinning $3000. The Wrst choice presented to the subjectwould be between a 10% chance of winning $3000 and a100% chance of $1500 (1500 being the midpoint of 0 and3000). If the subject chose the 100% chance of $1500, itindicated that $1500 was too high to be the correctindiVerence point. The second choice presented to thesubject would be between the gamble and $750 for cer-tain (750 being the midpoint of 0 and 1500). If, however,the subject had chosen the gamble on the Wrst choice,that would indicate that $1500 was too low to be the cor-rect indiVerence point. The second choice presented tothe subject would be between the gamble and $2250 forsure (2250 being the midpoint of 1500 and 3000). Thesecond choice would then indicate whether the certain,immediate amount used (either $750 or $2250) washigher or lower than the subject’s indiVerence point, andthe certain, immediate amount used in the third choicewould be adjusted accordingly. For example, if the sub-ject’s second choice was between $750 and the 10%chance of winning $3000, then the certain amount usedin the subject’s third choice would be $375—the mid-point of (0, 750)—if the subject chose $750 for certain. Itwould be $1125—the midpoint of (750,1500) if the sub-ject preferred the gamble. (We already know the sub-ject’s indiVerence point is less than $1500 in this examplebecause they indicated they preferred $1500 to the gam-ble in the Wrst choice of the sequence.)

The process continued until the interval was $25 orsmaller for the Allais Paradox questions, $3 or smallerfor the immediacy eVect questions. At this point, themidpoint of the interval was considered the indiVerencepoint of the subject.

One modiWcation was made to the straight bisectionmethod described above for use in the present experi-ment. Using a straight bisection method, the Wrst choicepresented to the subjects for any given gamble woulddepend upon the payout of the gamble. For example, forthe Allais Paradox gambles where the maximum payoutwas $3000, the Wrst choice would be between the gambleand $1500 for certain. For the Allais Paradox gambleswhere the maximum payout was $2700,the Wrst choicewould be between the gamble and $1350 for certain.Using diVerent initial choices for the indiVerence pointsfor diVerent gambles introduces the possibility ofanchoring eVects. To avoid this possibility, we used amodiWed bisection algorithm in which the Wrst certainamount in each series of choices was always the sameregardless of the payout size of the gamble under evalua-tion. For Allais Paradox questions, the Wrst certainamount was always $1500, whether the maximum pay-out of the gamble was $3000 or $2700. For immediacy

110 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

eVect questions it was always $50, regardless of whetherthe delayed amount was $100 or $110. After the Wrstchoice the bisection method proceeded as describedabove. (e.g., for the Allais Paradox questions, the certainamount used in the second choice bisected the portion ofthe interval above or below $1500, depending onwhether the subject preferred the certain $1500 or thegamble. If the subject chose the $1500 the second certainamount was the midpoint of (0,1500). If the subjectchose the gamble, then the second amount was the mid-point of either (1500, 3000) or (1500,2700) depending onthe maximum value of the gamble.)

Check choicesTo eliminate incorrect indiVerence points caused by

subject inattention or an incorrect choice, the subjectwas presented with two check choices after their indiVer-ence point was obtained. One check choice presented acertain, immediate amount slightly higher than theinferred indiVerence point—$25 higher for Allais Para-dox questions, $8 higher for immediacy eVect questions.The other presented an amount either $25 or $8 lowerthan the inferred indiVerence point. The order of the twocheck choices was randomized, and they were not distin-guished from other choices in the series in any way. If aparticipant’s response to either check choice was incon-sistent with the estimated indiVerence point, a messagebox was displayed informing the subject that they hadresponded inconsistently, and the series of choices waspresented again from the beginning. Each question wasrepeated until the participant produced a consistentseries of responses or until the question had been pre-sented three times. Questions for which subjects failed togive a consistent series of responses after three repeti-tions were not used in the analysis.

After an indiVerence point had been successfullyobtained, a pop-up window appeared asking the subjectwhich of the two probabilities (for the immediacy eVect)or delays (for the Allais Paradox) used in the experimenthad been presented in the last series of choices. If thesubject answered correctly, a message was displayed andthe next randomly selected question began. If not, a mes-sage urging subjects to pay more attention to the proba-bility or delay in the future was presented and thequestion was repeated at a random time later in theexperiment. This step was added to further encourageattention to the delays and probabilities that were addedto the certainty and immediacy eVect. Questionsrepeated for this reason were repeated indeWnitely untilthe subject responded with the correct delay.

MaterialsQuestions were presented to the subjects on the sub-

ject’s own computer via the World Wide Web. Subjectsread through a series of instruction pages before startingthe experiment. The choices were presented one at a time

in a separate window. The instructions were available tothe subjects at all times during the experiment.

Results

One hundred and eighty-nine subjects were givenAllais Paradox questions and 138 were shown immedi-acy eVect questions. Subjects who failed to report thecorrect delay or probability for the preceding question(as described above) for 10 questions or more were elim-inated from the analysis. (Although there were only 7diVerent questions, because questions were repeated upto three times when subjects failed a check question, orindeWnitely when they failed the delay question, subjectscould potentially fail arbitrarily many times.) Four sub-jects were eliminated from the Allais Paradox analysisfor this reason, and four subjects were eliminated fromthe immediacy eVect analysis.

Subjects apparently found the choice titration task tobe more diYcult than the choice task used in Experiment1, as a number of responses violated dominance. For theAllais Paradox items, subjects had three opportunities todemonstrate violations of dominance: by pricing the(33% chance of $3000; 67% chance of $0) gamble as highas or higher than the (33% chance of $3000; 66% chanceof $2700; 1% chance of $0) gamble, by showing the samepattern when the two gambles were delayed by 25 years,and by pricing the 25-year delayed (34% chance of$2700; 66% chance of $0) gamble as high or higher thanthe delayed (100% chance of $2700) gamble. (The choicetitration algorithm used does not permit any gamble tobe priced as high as or higher than the payout of thegamble. Therefore subjects could not violate dominanceby pricing the immediate (34% chance of $2700; 66%chance of $0) as high as or higher than $2700.) Twenty-four of the 25 Allais Paradox subjects (13.8% of total)who showed all three of these violations were eliminatedfrom the analysis (one had already been eliminated forfailing to report the correct delay more than 10 times).Subjects who showed 0, 1 or 2 dominance violationswere retained in the analysis.

For the immediacy eVect questions, subjects also hadthree opportunities to violate dominance: by pricing the50% chance of receiving $110 in 4 months, $110 in 30months, or $100 in 26 months higher than the 100%chance of receiving same. The 10 immediacy eVect sub-jects (7.2% of total) who showed all three violations ofdominance were eliminated from the analysis. Again,subjects showing 0, 1, or 2 dominance violations wereretained in the analysis.

Thus, a total of 28 Allais Paradox subjects and 14immediacy eVect subjects were eliminated, leaving 161Allais Paradox subjects and 124 immediacy eVect subjectsin the analyses. Although these percentages may seemhigh, they are not excessive for studies involving bothrisky and delayed gambles (Ahlbrecht & Weber, 1997).

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 111

Analysis of the immediacy eVect

The immediacy eVect can be detected by inferringchoices from the indiVerence points given by the sub-jects. For each subject we compared the indiVerencepoints for $100 at 26 weeks and $110 at 30 weeks. If oneindiVerence point was higher than the other, the subjectwas inferred to have preferred that option. If the indiVer-ence points were equal, or if one of the two indiVerencepoints was missing (due to check question failure), thenthe choice was not used in the analysis. Each subject’sindiVerence point for $110 in 4 weeks was also comparedto $100 using the same procedure.

A choice can only be inferred for a subject if bothindiVerence points are known and if one is larger thanthe other. Out of 496 indiVerence pairs (124 subjects x 4choices), 83 were ties, with 3 subjects showing 3 ties, 16showing 2 ties, and 42 showing 1 tie. Ties were least fre-quent for the immediate future, certain pair (where theindiVerence point for one prospect was set at $100) andmost frequent for the remote future, uncertain pair. FourindiVerence pairs had an unknown indiVerence point forone or both prospects because the subject failed thecheck questions three times. No subject had more thanone such pair. Both the mean indiVerence points and thechoices inferred for the subjects are found in Table 5.

A 2 (delay) £ 2 (risk) logistic regression analysis on theinferred choices revealed that the main eVect of delaywas signiWcant (�2 (1, N D 124) D 21.01, p < .0001), indi-cating the presence of an immediacy eVect. The interac-tion between delay and uncertainty was also signiWcant(�2 (1, N D 124) D 14.91, p < .0001), indicating that the sizeof the immediacy eVect was reduced by the addition ofuncertainty. These results diVer from those of Experi-ment 1, in which the size of the immediacy eVect was notreduced by risk.

We next asked whether the uncertainty manipulationeliminated or just reduced the immediacy eVect. Toaddress this question we examined whether the uncertain(probability D 50%) condition yielded a signiWcantimmediacy eVect. The logistic regression analysis onchoices inferred from present values limited to theprobability D 50% gambles indicates that the main eVect

of delay is not signiWcant (�2 (1, N D 124) D 0.61, p D 0.44).Thus, the addition of risk rendered the immediacy eVectno longer detectable. This suggests that that the immedi-acy eVect may have been completely eliminated by theaddition of probability. Again, these results diVer fromthose of Experiment 1.

We hypothesized that subjects in Experiment 1 mayhave ignored the probability information in the outcomepairs as being common to both options. We hoped thatsubjects would attend to both delay and probability infor-mation when the outcomes were presented individually.This seems to have been the case: A 2(delay: immediatevs. remote future)£2(risk: 100% or 50%)£2(immediacy:0 or 4 weeks) ANOVA on the indiVerence points showedsigniWcant main eVects of both delay (F (1,123) D290.89,p< .0001) and risk (F(1,123)D476.98, p< .0001). This con-Wrms that subjects did attend to both risk and delay whenproviding their indiVerence points.

Analysis of the Allais Paradox

Like the immediacy eVect data, the Allais Paradoxdata were analyzed by inferring choices from the sub-jects’ indiVerence points. This was done in the samemanner reported for the immediacy eVect above. Boththe mean indiVerence points and the choices inferred forthe subjects are found in Table 6. Again, no choice couldbe inferred when the subject had the same indiVerencepoints for both options to be compared, or if the indiVer-ence point could not be determined because the subjecthad failed the relevant the check questions three times.Three subjects had 2 ties and 5 showed 1 tie. Two sub-jects were missing two choices due to missing data, 8more missed 1 choice for that reason.

A 2 (delay) £ 2 (risk) logistic regression analysisshowed that the main eVect of risk was signiWcant(�2 (1, N D 161) D 5.09, p D .02), indicating the presence ofthe Allais Paradox. However, the interaction betweenrisk and delay was not signiWcant (�2 (1, N D 161) D 1.52,p D .22), suggesting that unlike the immediacy eVect, thesize of the Allais Paradox was not diminished by delay.This agrees with the results of Experiment 1, which alsofound that the Allais Paradox was not eliminated by the

Table 5Immediacy eVect: Mean indiVerence points and proportion (n) of subjects choosing each outcome (inferred from indiVerence points) in Experiment 2(N D 124)

Delay Mean present value Percent choice

Probability 1.0 Probability 0.5 Probability 1.0 Probability 0.5

Immediate future$100 immediately ($100) 38.32 76% (94) 57% (58)$110 in 4 weeks 70.52 35.46 24% (29) 43% (44)

Remote future$100 in 26 weeks 41.11 23.34 34% (33) 51% (44)$110 in 30 weeks 47.85 23.75 66% (65) 49% (42)

DiVerence in preference (immediate outcome) 42% 6%

112 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

addition of delay. As with the immediacy eVect, a between two gambles, where subjects tend to focus on

Table 6Certainty eVect: Mean indiVerence points and proportion (n) of subjects choosing each outcome (inferred from indiVerence points) in Experiment 2(N D 161)

Uncertainty Mean certainty equivalent Percent choice

Now In 25 years Now In 25 years

Certainty present$3000 with p D .33 1611.32 893.65 32% (51) 45 % (70)$2700 with p D .66$0 with p D .01

$2700 with p D 1.0 (2700) 998.05 68% (107) 55% (86)

Certainty absent$3000 with p D .33 535.00 362.01 62% (93) 66 % (103)$0 with p D .67

$2700 with p D .34 461.58 329.77 38% (57) 34% (54)$0 with p D .66

DiVerence in preference (smaller outcome) 30% 21%

2 (certainty: present or absent) £ 2 (risk: more risky,higher payout option, or less risky, lower payoutoption) £ 2 (delay: 0 or 25 years) ANOVA on theindiVerence points showed signiWcant main eVects ofboth delay (F(1,160) D 340.93, p < .0001) and certainty(F(1,160) D 936.19, p < .0001), indicating that subjectswere attending to the delays and probabilities whenmaking their responses.

Discussion

The purpose of Experiment 2 was to test an alterna-tive hypothesis for the results of Experiment 1: that par-ticipants were ignoring the probabilities or time delayscommon to both outcomes when choosing or distribut-ing points between them. The results suggest that this is apossibility. Unlike Experiment 1, in Experiment 2, theaddition of uncertainty eliminated the immediacy eVect,although the addition of delay did not eliminate theAllais Paradox. These Wndings agree with Keren andRoelofsma (1995), who also found that risk eliminatedthe immediacy eVect, but delay did not eliminate theAllais Paradox. However, Keren and Roelofsma used achoice response like that used in Experiment 1, ratherthan eliciting indiVerence points.

It is a common Wnding that subjects display diVerentpreferences when choosing between options comparedto when they give indiVerence points via matching (e.g.,Lichtenstein & Slovic, 1971; Tversky, Sattath, & Slovic,1988; Tversky, Slovic, & Kahneman, 1990). However, itis not clear that this diVerence can explain the presentresults. The standard explanation of these preferencereversals is the principle of scale compatibility (Tverskyet al., 1990). Subjects giving monetary matchingresponses to single gambles tend to focus more on thepayout of the gamble than subjects making choices

the probability. It is not clear whether these consider-ations apply when indiVerence points are elicited viachoice titration, rather than via a bidding or matchingresponse (Bostic, Herrnstein, & Luce, 1990; Tversky etal., 1988). Additionally, a greater tendency to favor theoption with the higher payout would tend to eliminateboth the Allais Paradox and the immediacy eVect, butthere seems to be no reason why this compatibility eVectwould be larger for the risky/delayed pairs than for thestandard pairs. In any case, it remains unclear whyKeren and Roelofsma (1995) found the immediacy eVectwas eliminated by uncertainty using a choice responsewhile the present experiment found that a responsemode that did not present the options together was nec-essary to eliminate the immediacy eVect.

The certainty eVect

Keren and Roelofsma (1995) found that uncertaintyeliminated the immediacy eVect but delay did not elim-inate the Allais Paradox. They hypothesized that thisindicated that risk was more fundamental than delay.

As already discussed in the introduction, if delay andrisk are psychologically equivalent, then the eVectsshould be symmetrical: delay should eliminate the cer-tainty eVect as easily as risk eliminates the immediacyeVect. However, the results of Experiment 2 are in agree-ment with the argument and results of Keren and Roe-lofsma (1995): that adding risk reduces or eliminates theimmediacy eVect, but adding delay does not eliminatethe Allais Paradox. Even an extreme time delay of 25years did not reduce the size of the Allais Paradox inExperiment 2. If the two eVects are symmetrical, it is apuzzle why one is eliminated and not the other.

The Allais Paradox and the immediacy eVect aresimilar in that both are believed to result from a specialemphasis on an immediate or certain outcome.

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 113

If immediacy and certainty are in some sense parallel,then so are the immediacy eVect and the Allais Paradox.However, eVects that are parallel in some ways are notnecessarily parallel in all ways. The immediacy eVect andthe Allais Paradox may have similar causes, but theydiVer considerably in structure: the immediacy eVectinvolves the addition of a common delay to both options,whereas the Allais Paradox involves the removal of anoutcome from both options in the choice set.

One possibility is that the Allais Paradox may simplybe much more robust to changes in probability anddelay than the immediacy eVect is. In Experiments 1 and2 we hypothesized that if risk and delay are equivalent,then adding delay should eliminate the Allais Paradoxbecause it is the equivalent to adding additional risk—that is, reducing the probabilities of all outcomes. How-ever, this presupposes that adding additional risk to theAllais Paradox would eliminate it as well. If adding riskto the Allais Paradox does not eliminate the eVect, thenthe failure of delay to eliminate the Allais Paradox inExperiments 1 and 2 and Keren and Roelofsma (1995)are unproblematic for the theory that risk and time arepsychologically equivalent. If risk and time are equiva-lent and adding risk does not eliminate the Allais Para-dox, then there is no reason to expect delay to, either.

An additional study (Weber, Marks, & Chapman,2003) suggested that this is indeed the case. Adding riskto the Allais Paradox by reducing all the probabilities inthe Allais Paradox presentation used in Experiment 1 by50% did not eliminate the paradox. (Although it didreduce the size of the paradox somewhat, the reductionwas only marginally signiWcant.)

This result suggests that the failure of delay to elimi-nate the Allais Paradox is not as problematic for the the-ory of risk and delay equivalence as originally supposed,as neither adding delay nor adding risk eliminates theAllais Paradox. Moreover, the Allais Paradox may notbe as parallel to the immediacy eVect as we originallysupposed. In the same additional study (data not shown)we found that increasing all delays in the immediacyeVect by 22 weeks did eliminate the immediacy eVect,just as adding risk did. In fact, given that the Allais Para-dox still occurred even when no choice options oVered acertain outcome, the Allais Paradox may well not be anexample of the certainty eVect at all.

The possibility that the Allais Paradox does not con-stitute a certainty eVect suggests that we ought to exam-ine a decision bias that clearly does constitute a certaintyeVect. The common ratio eVect is a form of the certaintyeVect that is produced by reducing the probabilities oftwo outcomes by a common ratio. Repeating the exampleabove, given the choice between $30 for sure and $45with 80% probability, people will tend to choose $30 forsure. However, when choosing between $30 with 25%probability and $45 with 20% probability, most peoplechoose the $45 option, despite the fact that the second set

of options is the same as the Wrst with all probabilitiesreduced by a factor of 4 (Kahneman & Tversky, 1979).

Notice that the common ratio formulation is moresimilar in structure to the immediacy eVect problem thanis the Allais Paradox used in Experiments 1–2 and Kerenand Roelofsma (1995). In both formulations, all pros-pects have a single non-zero outcome and the diVerencebetween the delays to the outcomes or the ratio betweenthe probabilities to win, respectively, are maintained forboth sets of options. This is quite diVerent from theAllais Paradox, in which the gambles do not all have asingle non-zero outcome and the ratio between probabil-ities to win is not maintained between the certainty pres-ent and certainty absent conditions. It is possible that thecertainty eVect would be eliminated by delay if the com-mon ratio eVect form of the paradox were used, ratherthan the Allais Paradox, which may well not be a cer-tainty eVect at all.

Experiment 3: The common ratio eVect

The purpose of Experiment 3 was to test whether thecommon ratio form of the certainty eVect would show apattern of elimination symmetric to that of the immediacyeVect. SpeciWcally, we predicted that the common ratioeVect would be eliminated by the addition of delay in acomputerized indiVerent point task like that used in Exper-iment 2, but would not be aVected by the addition of delayin a simple choice task like that used in Experiment 1.

Method

ParticipantsNintey-one undergraduates participated in the pencil-

and-paper choice condition and 225 undergraduatesparticipated in the computerized indiVerence point con-dition. All students participated as part of a classrequirement for an introductory psychology class.

DesignThe experiment was conducted in two parts: comput-

erized indiVerence point elicitation and pencil-and-paperchoice. The computerized portion was identical to thecertainty eVect condition of Experiment 2, except thatthe common ratio certainty eVect was used in the ques-tions instead of the Allais Paradox.

Although the choice portion of Experiment 3 wassimilar to Experiment 1, it diVered in several ways. As inExperiment 2, only two delays (0 and 25 years) wereused, resulting in a 2 £ 2 design. As no immediacy eVectquestions were presented in Experiment 3, subjects werenot shown both an immediacy and certainty eVectquestion as they were in Experiment 1. Instead, each sub-ject saw two certainty eVect questions, the Wrst diVeringfrom the second both in level of risk and in level of delay.

114 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

The common ratio questions used in Experiment 3are presented in Table 7. The dollar amounts and proba-bilities used in the questions were selected to be similarto those used in the Allais Paradox questions posed inExperiments 1–3.

MaterialsMaterials for the choice condition were like those

used in Experiment 1: Each participant was presentedwith a one-page questionnaire that included two ques-tions. Each question presented the participant with twooptions. The participants were asked to check the alter-native they preferred. There were four versions of thecertainty eVect choice, of which each subject saw two. Inaddition, there were two orders of the two choices,resulting in a total of four versions of the questionnaire.Each version was completed by 21–24 subjects.

Materials for the indiVerence point condition werelike those used in Experiment 2. Questions were pre-sented to the subjects on the subject’s own computer viathe World Wide Web. Subjects read through a series ofinstruction pages before starting the experiment. Thechoices were presented one at a time in a separate win-dow, and indiVerence points obtained via the same mod-iWed bisection algorithm used in Experiment 2. Theinstructions were available to the subjects at all timesduring the experiment.

Results and discussion

As in Experiment 2, subjects in the indiVerence pointcondition were asked to report the delay of the proceed-ing question in the indiVerence point condition. No sub-jects failed to report the correct delay 10 times or more,and therefore none was eliminated from the analysis forthis reason.

In the indiVerence point condition subjects had threeopportunities to violate dominance in the present experi-ment, as they did in Experiment 2: by pricing the (18%chance of $3000) gamble as high or higher than the (90%chance of $3000) gamble, by showing the same patternwhen the two gambles were delayed by 25 years, and bypricing the 25-year delayed (20% chance of $2700)gamble as high or higher than the delayed (100% chanceof $2700) gamble. (As in Experiment 2, subjects were notasked to provide an indiVerence point to the immediate

(100% chance of $2700) gamble; it was assumed to be$2700.) The 17 subjects who showed all three of theseviolations were eliminated from the analysis. Again, sub-jects showing 0, 1, or 2 dominance violations wereretained in the analysis, leaving 208 subjects in theindiVerence point analysis.

In the choice condition, 1 subject failed to answer aquestion in the certainty present, 0-year delay condition,leaving 90 subjects in this condition.

Analysis of choice

The percentage of subjects choosing each option isshown in Table 8. A 2(certainty) £ 2(delay) logisticregression analysis indicates that the main eVect ofcertainty is signiWcant (�2 (1,N D 90) D 15.71, p < .0001).This indicates that subjects displayed the certainty eVect,showing a far greater preference for the less risky optionwhen that option was certain than when the probabilitieshad been reduced by 5. The interaction between certaintyand delay is not signiWcant. (�2 (1,N D 90) D 2.12,p D 0.15), implying that the certainty eVect was notaltered by the addition of delay.1 This result agrees withthe Allais Paradox result in Experiment 1 and is

1 Due to the design of the experiment, both of the main eVects of thelogistic regression analysis are within-subjects eVects. However, the in-teraction is between-subjects.

Table 8Certainty eVect—common ratio choice: Proportion (n) of subjectschoosing each outcome in Experiment 3 (N D 91)

Note. Each subject was presented with two conditions: either the cer-tainty present/now and certainty absent/25 years conditions, or thecertainty present/25 years and the certainty absent/now conditions.

Uncertainty Delay

Now In 25 years

Certainty present(A) $3000 with p D .90 10% (5) 2% (1)(B) $2700 with p D 1.0 90% (43) 98% (42)

Certainty absent(A) $3000 with p D .18 31% (13) 29% (14)(B) $2700 with p D .20 69% (29) 71% (34)

DiVerence in preference for themore immediate outcome

20% 27%

Table 7Common ratio certainty eVect questions used in Experiment 3

Uncertainty Delay

Now In 25 years

Certainty present (a) 90% chance of $3000 now (a) 90% chance of $3000 in 25 years(b) 100% chance of $2700 now (b) 100% chance of $2700 in 25 years

Certainty absent (a) 18% chance of $3000 now (a) 18% chance of $3000 in 25 years(b) 20% chance of $2700 now (b) 20% chance of $2700 in 25 years

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 115

symmetric to the Wndings for the immediacy eVect inExperiment 1.

Analysis of indiVerence points

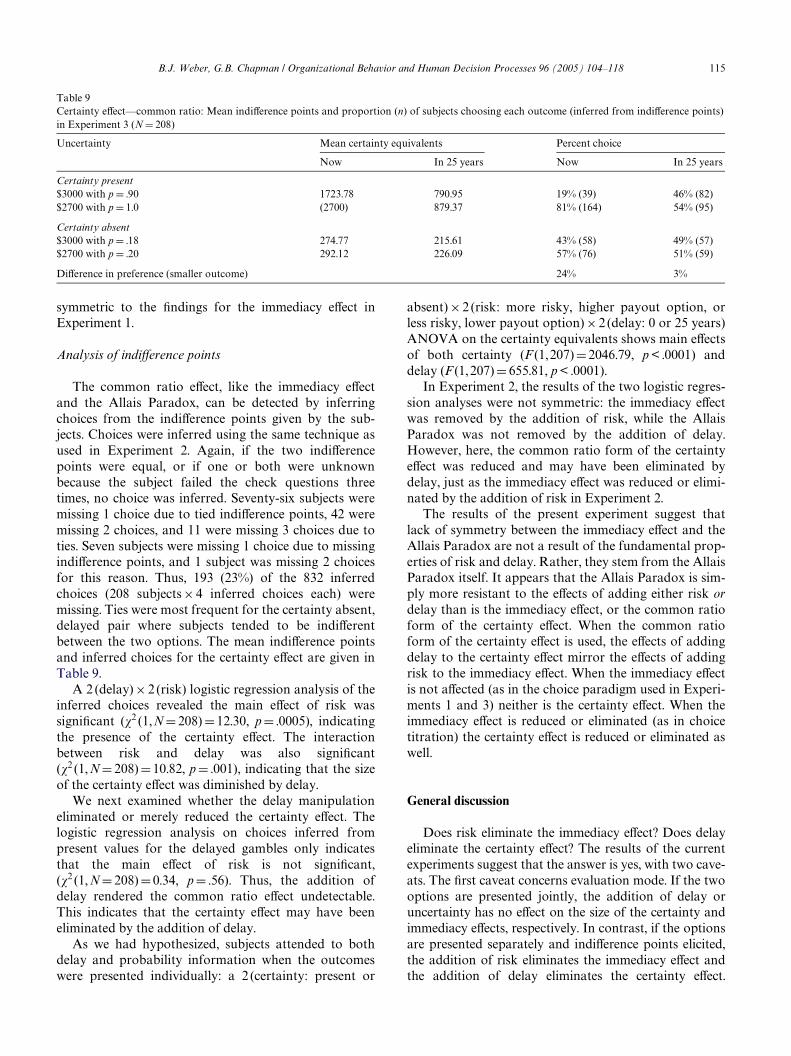

The common ratio eVect, like the immediacy eVectand the Allais Paradox, can be detected by inferringchoices from the indiVerence points given by the sub-jects. Choices were inferred using the same technique asused in Experiment 2. Again, if the two indiVerencepoints were equal, or if one or both were unknownbecause the subject failed the check questions threetimes, no choice was inferred. Seventy-six subjects weremissing 1 choice due to tied indiVerence points, 42 weremissing 2 choices, and 11 were missing 3 choices due toties. Seven subjects were missing 1 choice due to missingindiVerence points, and 1 subject was missing 2 choicesfor this reason. Thus, 193 (23%) of the 832 inferredchoices (208 subjects £ 4 inferred choices each) weremissing. Ties were most frequent for the certainty absent,delayed pair where subjects tended to be indiVerentbetween the two options. The mean indiVerence pointsand inferred choices for the certainty eVect are given inTable 9.

A 2 (delay) £ 2 (risk) logistic regression analysis of theinferred choices revealed the main eVect of risk wassigniWcant (�2 (1,N D 208) D 12.30, p D .0005), indicatingthe presence of the certainty eVect. The interactionbetween risk and delay was also signiWcant(�2 (1, N D 208) D 10.82, p D .001), indicating that the sizeof the certainty eVect was diminished by delay.

We next examined whether the delay manipulationeliminated or merely reduced the certainty eVect. Thelogistic regression analysis on choices inferred frompresent values for the delayed gambles only indicatesthat the main eVect of risk is not signiWcant,(�2 (1, N D 208) D 0.34, p D .56). Thus, the addition ofdelay rendered the common ratio eVect undetectable.This indicates that the certainty eVect may have beeneliminated by the addition of delay.

As we had hypothesized, subjects attended to bothdelay and probability information when the outcomeswere presented individually: a 2 (certainty: present or

absent) £ 2 (risk: more risky, higher payout option, orless risky, lower payout option) £ 2 (delay: 0 or 25 years)ANOVA on the certainty equivalents shows main eVectsof both certainty (F (1,207) D 2046.79, p < .0001) anddelay (F (1, 207) D 655.81, p < .0001).

In Experiment 2, the results of the two logistic regres-sion analyses were not symmetric: the immediacy eVectwas removed by the addition of risk, while the AllaisParadox was not removed by the addition of delay.However, here, the common ratio form of the certaintyeVect was reduced and may have been eliminated bydelay, just as the immediacy eVect was reduced or elimi-nated by the addition of risk in Experiment 2.

The results of the present experiment suggest thatlack of symmetry between the immediacy eVect and theAllais Paradox are not a result of the fundamental prop-erties of risk and delay. Rather, they stem from the AllaisParadox itself. It appears that the Allais Paradox is sim-ply more resistant to the eVects of adding either risk ordelay than is the immediacy eVect, or the common ratioform of the certainty eVect. When the common ratioform of the certainty eVect is used, the eVects of addingdelay to the certainty eVect mirror the eVects of addingrisk to the immediacy eVect. When the immediacy eVectis not aVected (as in the choice paradigm used in Experi-ments 1 and 3) neither is the certainty eVect. When theimmediacy eVect is reduced or eliminated (as in choicetitration) the certainty eVect is reduced or eliminated aswell.

General discussion

Does risk eliminate the immediacy eVect? Does delayeliminate the certainty eVect? The results of the currentexperiments suggest that the answer is yes, with two cave-ats. The Wrst caveat concerns evaluation mode. If the twooptions are presented jointly, the addition of delay oruncertainty has no eVect on the size of the certainty andimmediacy eVects, respectively. In contrast, if the optionsare presented separately and indiVerence points elicited,the addition of risk eliminates the immediacy eVect andthe addition of delay eliminates the certainty eVect.

Table 9Certainty eVect—common ratio: Mean indiVerence points and proportion (n) of subjects choosing each outcome (inferred from indiVerence points)in Experiment 3 (N D 208)

Uncertainty Mean certainty equivalents Percent choice

Now In 25 years Now In 25 years

Certainty present$3000 with p D .90 1723.78 790.95 19% (39) 46% (82)$2700 with p D 1.0 (2700) 879.37 81% (164) 54% (95)

Certainty absent$3000 with p D .18 274.77 215.61 43% (58) 49% (57)$2700 with p D .20 292.12 226.09 57% (76) 51% (59)

DiVerence in preference (smaller outcome) 24% 3%

116 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

The second caveat concerns the form of the certaintyeVect. The Allais Paradox appears to be diYcult to elimi-nate by any means, including via delaying the outcomes,and may well not be an example of the certainty eVectafter all. The common ratio eVect, in contrast, parallelsthe immediacy eVect both in form and results. These twoparadoxes share a common fate—either both are elimi-nated (with separate evaluation), or neither is (with jointevaluation). Each of these caveats is considered in turn.Finally, we consider the implications of the currentresults for the thesis that a common underlying dimen-sion is responsible for the eVects of both delay and risk.

Evaluation mode

Why does the evaluation mode make a diVerence?Previous research has shown that evaluating two optionsjointly can lead to a diVerent preference order than eval-uating each option separately (e.g., Hsee, 1996). Work byHsee and colleagues has demonstrated that diYcult-to-evaluate attributes are given more weight in joint evalua-tion than in separate evaluation. The present results,however, do not show that the weight of one attributechanges with evaluation mode. Instead, an interactionbetween two attributes (risk and delay) is found for sep-arate but not joint evaluation. Thus, the eVect of evalua-tion mode in the current studies likely requires adiVerent explanation.

The explanation for the current Wnding may simply bethat subjects disregard the attribute that has a commonvalue for the two options shown together. Thus, if twogambles are both delayed by 25 years, the delay attributedoes not discriminate between the two gambles and istherefore ignored or edited out when making a choice orrating. Likewise, if two delayed outcomes both have a50% probability of occurring, the options are equivalenton the risk attribute, and so that attribute is ignored. Ifthe common attribute is edited out of the decision, thenthe delay and uncertainty manipulations used in Experi-ment 1 would have no eVect. In contrast, elicitingindiVerence points to separate prospects, as in Experi-ments 2 and 3, forces subjects to attend to all three attri-butes: risk, delay, and monetary amount. Indeed, theANOVAs performed in those experiments found maineVects for both risk and delay, indicating that both ofthese attributes were incorporated into evaluations.

An example of editing that is particularly relevant tothe present experiments is the psuedocertainty eVect(Kahneman & Tversky, 1984). In this study, subjectswere asked to imagine a game with two stages in whichthe subjects have a 25% chance to progress to the secondstage. If they get to the second stage they then receiveeither a 100% chance of $30 or an 80% chance of $45.Subjects have to decide what option they prefer toreceive in the second stage before they learn whetherthey will proceed to the second stage or not.

This decision is logically equivalent to a single-stagegame with a choice between a 25% chance of $30 and a20% chance of $45. However, subjects respond to thetwo-stage game quite diVerently than they do to this sin-gle-stage game. Instead, they respond to the two-stagegame in the same manner as they do for a one-stagegame with a choice between a 100% chance of $30 andan 80% chance of $45—that is, they show a strong pref-erence for the certain outcome (even though, in the two-stage game the “certain” outcome is only certain condi-tional on getting to the second stage—that is, it ispseudocertain). Evidentially the segmentation of the riskinto two parts in the two-stage game encourages subjectsto disregard the 25% chance of reaching the second stageof the gamble when making a choice, since the 25%chance is common to both outcomes. They proceed tochoose as though the Wrst stage of the game did not exist.This result is similar to the behavior shown in the choiceresponses of Experiments 1 and 3, in which subjectschose as though the delays or uncertainties common toboth outcomes were not present.

The existence of the psuedocertainty eVect illustratesthat the mere fact subjects edit out the common risk ordelay does not imply that risk and delay are not psycho-logically equivalent. In psudeocertainty, the risk in theWrst stage is edited out even though this risk is obviouslyon the same dimension as the risk in the second stage(that is, both are risks expressed on a probability scale).By analogy, risk and delay might be segmented in partic-ular situations even if both can be placed on the samepsychological dimension.

Allais Paradox and the common ratio eVect

The current studies examined two biases commonlythought to constitute the certainty eVect: the Allais Para-dox and the common ratio eVect. In the Allais Paradox,a choice between a certain outcome and a gamble istransformed into a choice between two gambles byremoving the common consequence. In the commonratio eVect, a choice between a certain outcome and agamble is transformed into a choice between two gam-bles by reducing the probabilities to win by a commonratio. Both biases are commonly explained in terms ofoverweighting certain outcomes and thus have the samedescriptive account, according to Prospect Theory.

However, the current experiments suggest that thereare important diVerences between these two decisionbiases. The Allais Paradox was not eliminated by intro-ducing delay in the current Experiments 1 and 2. Simi-larly, Keren and Roelofsma (1995) also found no eVectof delaying the outcomes. In contrast, in the currentExperiment 3 the common ratio eVect was eliminatedwhen the gambles were delayed.

The results for the common ratio eVect were exactlyparallel to those for the immediacy eVect: both were

B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118 117

eliminated when a delay or uncertainty manipulationwas introduced, respectively. Furthermore, in both casesthis elimination occurred only with the separate indiVer-ent point evaluation mode and not with the joint choiceevaluation mode.

As discussed in the introduction to Experiment 3, thecommon ratio and common diVerence eVects are parallelin structure, while the Allais Paradox is not. Moreover,in an additional study (Weber et al., 2003), we found thatthe Allais Paradox is not eliminated by reducing allprobabilities by 50%. This means that the failure of delayto eliminate the Allais Paradox is compatible with thetheory that risk and delay are equivalent, as risk anddelay do not behave diVerently in this situation: neithereliminates the Allais Paradox. Although the enigmassurrounding the Allais Paradox must await futureresearch, the fact that even a probability manipulationwas not successful in eliminating the Allais Paradoxindicates that the failure of a delay manipulation to elim-inate it has more implications for the nature of the AllaisParadox than it does for understanding interactionsbetween risk and delay.

Delay D Risk?

Keeping the two caveats in mind, the current resultsindicate that risk does eliminate the immediacy eVect,and delay does eliminate the certainty eVect, providedthat the decision maker attends to all attributes pre-sented. This result is compatible with the theory that riskand delay have their eVects via a single underlyingdimension. Moreover, the results of the present experi-ments solve a problem posed by Keren and Roelofsma’s(1995) original Wnding of an the asymmetry between thebehavior of the immediacy eVect and the Allais Paradox.As mentioned above, the present experiments suggestthat this asymmetry occurred because the Allais Paradoxmay not be an example of the certainty eVect.

Keren and Roelofsma (1995) propose that the inter-action between risk and delay occurs because risk anddelay act via a single underlying function. According totheir argument, decision makers surmise that delayentails a certain amount of risk: the longer it is until youget your outcome, the more likely it is you’ll be hit by atruck (or be otherwise unable to collect). That is, risk isthe psychologically primary concept, and delay aVectsevaluation because of the risk that it entails. A relatedpossibility (Rachlin et al., 1991) is that delay is the psy-chologically primary concept, and risk aVects evaluationbecause low probability prospects must be played outmany times on average before they yield an outcome.Another possibility is that decision makers view risk anddelay as psychologically distinct concepts, but that themechanism by which they are incorporated into deci-sions entails a common underlying dimension. The cur-rent results do not discriminate among these possibilities

(indeed, it is not clear that any data could). They are allequivalent in that all these views posit that risk anddelay are psychologically interchangeable in the waythey inXuence preference.

Although the current results are consistent with theview that risk and delay are psychologically equivalent,they do not necessitate this view. We consider two otherconclusions that might be reached. One possibility is thatdecision makers view delay as entailing risk in addition toputting oV the outcome. If this is the case, risk and delayare not treated in the same fashion psychologically.Although delay entails risk, it also has additional psy-chological eVects that do not arise from the risk itentails. According to this view, the immediacy eVectmust be due to the risk entailed by delay, rather than bydelay proper. Otherwise the introduction of explicit riskwould not have eliminated the immediacy eVect.

A second alternative conclusion is that parallelsbetween risk and delay apply only to the immediacy andcertainty eVects and not to risk and delay more broadly.According to this view, the usual descriptions ofthe immediacy and certainty eVects are incomplete. Theimmediacy eVect is usually described as arising from thespecial appeal of immediate outcomes, and the certaintyeVect from the appeal of certain outcomes. However,demonstrations of the immediacy eVect do not normallyinvolve risk, and demonstrations of the certainty eVectdo not normally involve delay. Thus, it is possible that itis actually the combination of immediacy and certaintythat has a special attraction, and not simply immediacyor certainty alone. If this were the case, then making animmediate outcome uncertain or a certain outcomedelayed would remove the special appeal of that out-come and thus eliminate the eVect. This would explainthe removal of the certainty/immediacy eVect by theaddition of delay/risk without requiring that risk anddelay be psychologically equivalent. Instead, accordingto this view, the combined eVects of both risk and delayare needed to produce the certainty/immediacy eVect.

The existence of multiple alternative accounts indi-cates that the interaction between risk and delay is notwell understood. Risk and delay need not work via thesame psychological mechanism to interact. Furtherresearch is clearly needed.

Whatever the relationship between risk and delay, thefact that they interact at all has implications for descrip-tive theories of risky and intertemporal decision making.If some of the apparent eVects of delay are actuallyeVects of risk entailed by delay, then the hyperbolic dis-count function normally found for delayed outcomesmay not reXect merely the eVects of delay, but mayincorporate the eVects of risk as well. The actual timediscount function—that is, one which incorporates onlyeVects of time, not of time plus implicit risk—may lookquite diVerent. If the special emphasis normally assumedto be placed on immediacy and on certainty is actually

118 B.J. Weber, G.B. Chapman / Organizational Behavior and Human Decision Processes 96 (2005) 104–118

placed only on the combination of immediacy and cer-tainty, then the usual explanation for this emphasis maynot be correct. The emphasis decision makers place oncertainty and immediacy is usually said to result fromthe steepness of the � and hyperbolic discount functionsat certainty and immediacy respectively, but if this is thecase then the combination of immediacy and certaintyshould not be necessary to produce this emphasis—either one or the other should be suYcient. Of course, ifrisk and delay do indeed prove to be psychologicallyequivalent, as Keren and Roelofsma (1995) suggested,then this has very strong implications for descriptive the-ories of risk and delay, as it implies that any correctdescriptive theory of risk must be mathematically equiv-alent to the correct descriptive theory of delay and viceversa.

Given that many real-world decisions are made aboutoutcomes that are both risky and delayed, understand-ing the way risk and delay interact would be a valuablestep towards understanding human decision making.The results of the present experiment suggest that riskand delay do not combine in a straightforward manner.When either time or delay can be edited out of consider-ation, the two dimensions may not interact at all. Whendecision makers are forced to consider the combinedinXuence of risk and delay, parallels between the twoemerge. These parallels are consistent with the idea thatrisk and delay are psychologically equivalent, althoughalternate interpretations are possible. It is clear, how-ever, that outcomes that occur immediately and for cer-tain have special appeal to decision makers.

References

Ahlbrecht, M., & Weber, M. (1997). An empirical study on intertempo-ral decision making under risk. Management Science, 43, 813–826.

Ainslie, G. (1975). Specious reward: A behavior theory of impulsive-ness and impulse control. Psychological Bulletin, 82, 463–509.

Allais, M. (1953). Le comportement de l’homme rationnel devant le ris-que: Critique le postulats et axioms de L’École Américaine. Eco-nometrica, 21, 503–546.

Bostic, R., Herrnstein, R. J., & Luce, R. D. (1990). The eVect on thepreference-reversal phenomenon of using choice indiVerence. Jour-nal of Economic Behavior and Organization, 13, 193–212.

Hsee, C. (1996). The evaluability hypothesis: An explanation for pref-erence reversals between joint and separate evaluations of alterna-tives. Organizational Behavior and Human Decision Processes,67(3), 247–257.

Kahneman, D., & Tversky, A. (1979). Prospect Theory: An analysis ofdecision under risk. Econometrica, 47, 263–291.

Kahneman, D., & Tversky, A. (1984). Choices, values, and frames.American Psychologist, 39(4), 341–350.

Keren, G., & Roelofsma, P. (1995). Immediacy and certainty in inter-temporal choice. Organizational Behavior and Human Decision Pro-cesses, 63, 287–297.

Kirby, K. N., & Herrnstein, R. J. (1995). Preference reversals due tomyopic discounting of delayed reward. Psychological Science, 6,83–89.

Kirby, K. N., & Marakovic, N. N. (1995). Modeling myopic decisions:Evidence for hyperbolic delay-discounting within subjects andamounts. Organizational Behavior and Human Decision Processes,64, 22–30.

Lichtenstein, S., & Slovic, P. (1971). Reversal of preferences betweenbids and choices in gambling decisions. Journal of ExperimentalPsychology, 89, 46–55.

Loewenstein, G., & Prelec, D. (1992). Anomalies in intertemporalchoice: Evidence and interpretation. Quarterly Journal of Econom-ics, 107, 573–597.

Rachlin, H., Logue, A. W., Gibbon, J., & Frankel, M. (1986). Cognitionand behavior in studies of choice. Psychological Review, 93(1), 33–45.

Rachlin, H., Raineri, A., & Cross, D. (1991). Subjective probability anddelay. Journal of Experimental Analysis of Behavior, 55(2), 233–244.

Tversky, A., & Kahneman, D. (1992). Advances in Prospect Theory:Cumulative representation of uncertainty. Journal of Risk andUncertainty, 5, 297–323.

Tversky, A., Sattath, S., & Slovic, P. (1988). Contingent weighting injudgment and choice. Psychological Review, 95, 371–384.

Tversky, A., Slovic, P., & Kahneman, D. (1990). The causes of prefer-ence reversals. The American Economic Review, 80, 204–217.

Weber, B. J., Marks, M., & Chapman, G. B. (2003). Variants on theAllais paradox: Testing the certainty eVect account. Poster presentedat the November, 2003 meeting of the Society for Judgment andDecision Making, Vancouver.

Copyright © 2022 FDOKUMEN