The Changing Face of the Tyre Industry and Implications for the Synthetic Rubber Industry APIC 2014...

38

©LMC International, 2013 1 26/05/2014 The Changing Face of the Tyre Industry and Implications for the Synthetic Rubber Industry APIC 2014 May 2014 Robert Simmons (Head of Tyre & Rubber Research) [email protected]

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of The Changing Face of the Tyre Industry and Implications for the Synthetic Rubber Industry APIC 2014...

©LMC International, 2013 1 26/05/2014

The Changing Face of the Tyre Industry and Implications for the Synthetic Rubber Industry

APIC 2014

May 2014

Robert Simmons (Head of Tyre & Rubber Research) [email protected]

©LMC International, 2013 2 26/05/2014

Overview

• Understanding the tyre market

• Vehicle sales (OE Tyre Sales)

• Replacement Tyre Sales

• Tyre Production

• Implications for the synthetic rubber industry

©LMC International, 2013 3 26/05/2014

Drivers of Tyre Demand

Vehicle Sales

Vehicle Production

Scrapping rate/vehicle lifecycle

Vehicle Parc

No. of Tyres per Vehicle Replacement Ratio

OE Tyre Demand (LV 28% MHCV 21%)

Replacement Tyre Demand (LV 72% MHCV 79%)

Total Tyre Demand

Trade in Tyres

Production of Tyres

©LMC International, 2013 4 26/05/2014

Tyre demand depends on vehicle ownership,

both for sales of new vehicles (OE tyre sales)

and replacement tyre sales. As incomes rise

so vehicle ownership increases.

IndiaIndonesia

China

Thailand

TurkeyBrazil

MexicoRussia Taiwan

Korea

Malaysia

UKJapan

Spain Germany

FranceItalyCanada

USA

0

100

200

300

400

500

600

700

800

900

1000

0 10,000 20,000 30,000 40,000 50,000 60,000

GDP per Capita

No o

f LV

per 1,0

00 p

op

ula

tion

©LMC International, 2013 5 26/05/2014

Strong growth in emerging market GDP during

the 2000s encouraged vehicle ownership.

Advance economies are picking up in 2014, but

emerging markets are weak

-4%

-2%

0%

2%

4%

6%

8%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

GD

P g

row

th

Advanced Emerging Advanced Emerging

©LMC International, 2013 6 26/05/2014

This can be seen in new vehicle sales

-10% -5% 0% 5% 10% 15% 20%

WORLD

Asean

China

East Asia

Eastern Europe

India

NAFTA

South America

EU-27

Annual % change in LV vehicle sales

2012 2013 2014

38%

©LMC International, 2013 7 26/05/2014

In the longer term, vehicle ownership levels

are low in the emerging markets

0

100

200

300

400

500

600

700

800

900

1,000

Nig

eria

India

Ph

ilipp

ines

Indo

nesia

Chin

aC

olo

mbia

Venezu

ela

Thaila

nd

WO

RLD

Turkey

Sou

th A

fric

aU

krain

eB

razil

Chile

Arg

entin

aR

om

an

iaM

exic

oTaiw

an

Russia

Hung

ary

Slo

vakia

Kore

aM

ala

ysia

Czech

Denm

ark

Sw

ed

en

Po

land

Belg

ium

/Lux

Neth

erla

nd

sIre

land

Po

rtug

al

Slo

venia

UK

Gre

ece

Sw

itzerla

nd

Jap

an

Sp

ain

Au

stria

Germ

any

Norw

ay

Fra

nce

Italy

Fin

lan

dC

an

ada

Au

stralia

New

Zeala

nd

USA

No. of LV

(p

er 1,0

00 p

op

ula

tion)

©LMC International, 2013 8 26/05/2014

The growth of vehicle density follows an S-

curve.

0

100

200

300

400

500

600

700

800

900

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Den

sity

(veh

icle

s p

er

1,0

00 p

op

ula

tion

)

Japan US UK

©LMC International, 2013 9 26/05/2014

The emerging markets are entering the rapid

growth stage, developed markets are

approaching stagnation.

0

50

100

150

200

250

300

350

400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Emer

ging

mar

ket d

ensi

ty

600

625

650

675

700

725

750

775

800

Western Europ

e Density

Brazil India Russia

China China (Urban) Western Europe

©LMC International, 2013 10 26/05/2014

The same is true within China

0

50

100

150

200

250

0 20,000 40,000 60,000 80,000 100,000

GDP per capita (RMB)

Car

den

sit

y p

er

1,0

00 p

op

ula

tio

n

Fujian

Jiangsu

Zhejiang

Beijing

Tianjin

Shandong

Guangdong

Jiangsu

Zhejiang

Beijing

Tianjin

Shanghai

Guizhou

Tibet

Gansu

Yunnan

©LMC International, 2013 11 26/05/2014

Growing incomes in emerging markets point to

strong emerging market demand for vehicles

(and OE tyres). Advanced market sales grow

modestly.

0

10

20

30

40

50

60

70

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Veh

icle

Sale

s (

mn

un

its)

Mature Emerging

©LMC International, 2013 12 26/05/2014

• Number of vehicles on the road (vehicle parc)

• Vehicle use (incomes, fuel prices, economic activity)

• Road and weather conditions

• Type of tyre fitted (dependent upon legislation, tyre

labelling, individual preference)

• Retreading (raw material prices, economic activity)

Replacement tyre sales (the largest

component of demand) are determined by:

©LMC International, 2013 13 26/05/2014

With growing vehicle sales, parc growth in recent years has been dominated by emerging markets.

0% 5% 10% 15% 20%

WORLD

ASEAN

Central Europe

China

East Asia

Eastern Europe

India

Middle East

NAFTA

Oceania

South America

Western Europe

Parc growth (5yr annual average)

LV MHCV

©LMC International, 2013 14 26/05/2014

Emerging market vehicle sales build parc.

Developed market sales are mainly for parc

replacement

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012

Veh

icle

sale

s (m

n u

nit

s)

-

50

100

150

200

250

Veh

icle P

arc (m

n u

nits)

USA China USA Parc China Parc

©LMC International, 2013 15 26/05/2014

Global replacement ratios began to recover

2013. However, the trend was not the same

across regions

90%

95%

100%

105%

110%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

LV

rep

lacem

en

t ra

tio

240%

260%

280%

300%

320%

MH

CV

rep

lacem

en

t ratio

LV MHCV

©LMC International, 2013 16 26/05/2014

The strongest growth was in Asia and the Americas.

-14% -12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

WORLD

ASEAN

China

East Asia

E Europe

India

NAFTA

S America

EU

2012 2013

©LMC International, 2013 17 26/05/2014

This reflects growth in the number of miles driven

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0.70

1.20

1.70

2.20

2.70

3.20

3.70

4.20

Gaso

line p

rices (S

/gallo

n)

US miles driven US miles driven US gasoline price

Dis

tan

ce t

ravell

ed

(12 m

th a

vera

ge (

bn

mil

es)

©LMC International, 2013 18 26/05/2014

85

90

95

100

105

110

115

120

125

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Dis

tan

ce d

riven

(2001 =

100)

UK (MHCV) UK (LV) France (All)

Miles driven are also picking up in Europe

©LMC International, 2013 19 26/05/2014

As the light vehicle parc increases so do

replacement tyre sales. Almost all growth is in

emerging markets.

0

100

200

300

400

500

600

700

800

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Re

pla

ce

me

nt

Sa

les

(m

n u

nit

s)

Advanced Emerging

©LMC International, 2013 20 26/05/2014

Emerging market demand is changing the tyre

industry as demand has risen strongly in these

markets

1,100

1,200

1,300

1,400

1,500

Wo

rld

Ch

ina

S.A

meric

a

AS

EA

N

Mid

dle

East

Ind

ia

E.E

uro

pe

Oth

er

E.A

sia

Eu

rop

e

N.A

meric

a

Wo

rldT

ota

l ty

res s

ale

s (

'000 u

nit

s)

Tyre sales growth 2004-13

©LMC International, 2013 21 26/05/2014

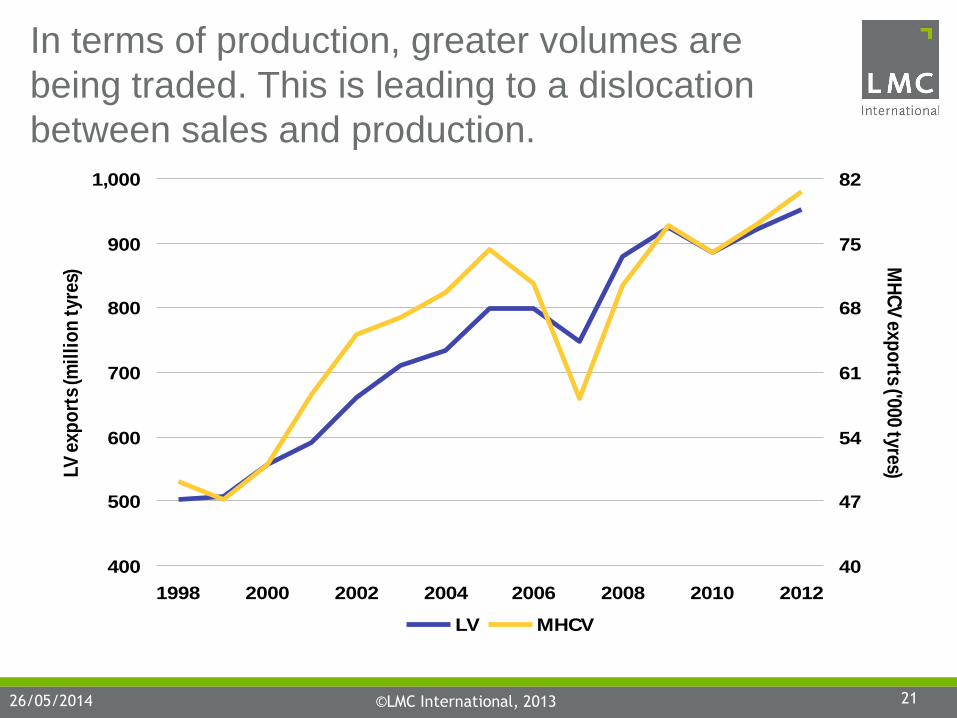

In terms of production, greater volumes are

being traded. This is leading to a dislocation

between sales and production.

400

500

600

700

800

900

1,000

1998 2000 2002 2004 2006 2008 2010 2012

LV

exp

ort

s (m

illi

on

tyre

s)

40

47

54

61

68

75

82

MH

CV

exp

orts ('0

00 ty

res)

LV MHCV

©LMC International, 2013 22 26/05/2014

North America and EU-27 are the largest net

importers …

-150

-125

-100

-75

-50

-25

0

25

50

75

100

125

NA

FTA

EU

-27

Oth

er E

uro

pe

E. A

sia

S. A

merica

M. E

ast

Oce

ania

ASEA

N

Chin

a

Ind

ia

Oth

er

LV

net Im

port

s (m

n u

nit

s)

Net Imports 2011 Net Imports 2000

©LMC International, 2013 23 26/05/2014

Imports are largely for the replacement market, these reached close to record levels in 2013

20%

30%

40%

50%

60%

70%

80%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Imp

ort

s %

of re

pla

cem

en

t sa

les

US LV Imports % replacement US MHCV Imports % replacement

EU LV Imports % replacement EU MHCV Imports % replacement

©LMC International, 2013 24 26/05/2014

Imports to the US grew strongly in 2013 with the ending of duties on Chinese imports

70

80

90

100

110

120

130

140

150

160

170

180

190

2001 2004 2007 2010 2013 2016

US L

igh

t V

eh

icle

Tyre

Im

po

rts (m

illi

on

s)

SAAR Moving Average Annual Forecast

©LMC International, 2013 25 26/05/2014

Imports are dominated by low cost producers. Chinese imports dropped between 2010 and 2012 with the introduction of an import duty, but grew strongly in 2013. Total imports did not fall.

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Ch

ina

(%)

US

LV

Tyre

Im

po

rts (

Mil

lio

ns)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Asean China East Asia Other NAFTA China %

©LMC International, 2013 26 26/05/2014

US trade values shows the difference in price between imports and a US produced (exported) tyre. An imported Chinese tyre is half the price of a US exported tyre.

0

20

40

60

80

100

120

140

Taiw

an

Ch

ina

Vie

tnam

Ind

on

esia

Th

aila

nd

Co

sta

Ric

a

Ch

ile

Mexic

o

Ph

ilipp

ines

Ko

rea

Slo

vakia

Can

ad

a

Jap

an

Ru

ssia

Ro

man

ia

Bra

zil

Fra

nce

Italy

Po

rtug

al

UK

Germ

an

y

Hu

ng

ary

Czech

Tyre

un

it p

rice (

$)

Import unit values export unit values

2013

©LMC International, 2013 27 26/05/2014

Combining sales with trade shows a strong increase in tyre production in emerging markets, while advanced market production has fallen

1,100

1,200

1,300

1,400

1,500

1,600

Wo

rld

Ch

ina

AS

EA

N

Ind

ia

E.A

sia

Mid

dle E

ast

E.E

uro

pe

S.A

merica

Oth

er

Eu

rop

e

N.A

merica

Wo

rldT

ota

l ty

res

sale

s ('0

00 u

nit

s)

Production growth 2004-13

©LMC International, 2013 28 26/05/2014

Implications for synthetic rubber: tyre production and weight determine demand. Tyre sizes and hence weights are increasing

6

8

10

12

14

16

18

20

2000 2002 2004 2006 2008 2010 2012

LV

tyre

weig

ht

(kg

) m

a

30

35

40

45

50

55

60

M/H

CV

tyre

weig

ht (k

g) m

a

Car LCV MHCV

©LMC International, 2013 29 26/05/2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013

To

tal

14 15 16 17 18

OE tyre sizes are increasing (for example: EU)

©LMC International, 2013 30 26/05/2014

As with the tyre industry, demand is growing strongly in emerging markets. Unlike in the tyre industry, much of this demand is met from advanced market exports

-800

-600

-400

-200

0

200

400

N A

meric

a

S A

meric

a

Eu

rop

e

E E

uro

pe

East A

sia

AS

EA

N

Ch

ina

Ind

ia

Oth

er

Net

imp

ort

s (

'000 t

on

nes)

SBR BR

©LMC International, 2013 31 26/05/2014

However, capacity is increasing in the emerging

markets. This is placing pressure on exporters

0

50

100

150

200

250

300

350

2003 2005 2007 2009 2011 2013

Pro

du

cti

on

/im

po

rts (

'000 t

on

nes)

66%

69%

72%

75%

78%

81%

84%

87%

Self-s

uffic

ien

cy (%

)

Imports SBR

China SBR

©LMC International, 2013 32 26/05/2014

For polybutadiene rubber, Chinese self

sufficiency is increasing, but capacity utilisation

has fallen

0

100

200

300

400

500

600

700

800

900

2000 2002 2004 2006 2008 2010 2012

Pro

du

cti

on

('0

00

to

nn

es

)

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

se

lf-su

fficie

nc

y/C

ap

ac

ity u

tilisa

tion

(%)

Production Capacity utilisation Self sufficiency

China BR

©LMC International, 2013 33 26/05/2014

New capacity has also been commissioned in

other net importing regions (India and ASEAN)

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Net

imp

ort

s (

'000 t

on

nes)

ASEAN India

Net SBR imports

©LMC International, 2013 34 26/05/2014

Changing raw materials:

pressure to reduce CO2 leads to demand for

low rolling resistance tyres. Starts with OE

80

100

120

140

160

180

200

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Gra

ms C

O2/k

m

EU average CO2 emissions

©LMC International, 2013 35 26/05/2014

Tyre labelling enhances this across the tyre

spectrum. Demand is not static moving towards

different raw materials (sSBR, enhanced

sSBR,etc.)

GCFEFCEEECEBCCCBCABCBBBA

0

20

40

60

80

100

120

140

Rating (Rolling Resistance/Wet Grip)

List

Pri

ce (€

)

Budget Quality Premium

195/65/15/H

©LMC International, 2013 36 26/05/2014

• The focus of vehicle and tyre demand growth is moving to the emerging markets

as incomes have risen.

• In 2014, demand from in many emerging markets has slowed, however, the

underlying story still holds. Demand is growing in the Advanced markets.

• In addition, tyre trade is increasing, with increasing volumes produced in low cost

countries and shipped to the advanced markets. This further encourages tyre

production in emerging markets.

• The focus of advanced market production is OE, the most technological advanced

tyres. Pressure to reduce CO2 emissions is leading to demand for new materials.

• Synthetic rubber capacity is increasing in emerging markets which is placing

pressure on exporters.

Conclusions

©LMC International, 2013 37 26/05/2014

Thank You www.lmc.co.uk

Acknowledgments:

©LMC International, 2013 38 26/05/2014

This presentation and its contents are to be held confidential by the client, and are not to be disclosed, in whole or in part, in

any manner, to a third party without the prior written consent of LMC International.

While LMC has endeavoured to ensure the accuracy of the data, estimates and forecasts contained in this presentation,

any decisions based on them (including those involving investment and planning) are at the client’s own risk.

LMC International can accept no liability regarding information analysis and forecasts contained in this presentation.

© LMC International, 2014

All rights reserved

New York

1841 Broadway

New York, NY 10023

USA

T +1 (212) 586-2427

F +1 (212) 397-4756

Oxford

4th Floor, Clarendon House

52 Cornmarket Street

Oxford OX1 3HJ

UK

T +44 1865 791737

F +44 1865 791739

Kuala Lumpur

B-03-19, Empire Soho

Empire Subang

Jalan SS16/1, SS16

47500 Subang Jaya

Selangor Darul Ehsan

Malaysia

T +603 5611 9337

Singapore

16 Collyer Quay #21-00

Singapore 049318

Singapore

Tel: +65 6818 9231