the challenges facing saving and credit cooperative

87

THE CHALLENGES FACING SAVING AND CREDIT COOPERATIVE SOCIETIES IN SUPPORTING SMALL ENTERPRISES IN TANZANIA: A CASE OF TEMEKE MUNICIPALITY.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of the challenges facing saving and credit cooperative

THE CHALLENGES FACING SAVING AND CREDIT COOPERATIVE

SOCIETIES IN SUPPORTING SMALL ENTERPRISES IN TANZANIA:

A CASE OF TEMEKE MUNICIPALITY.

THE CHALLENGES FACING SAVING AND CREDIT COOPERATIVE

SOCIETIES IN SUPPORTING SMALL ENTERPRISES IN TANZANIA:

A CASE OF TEMEKE MUNICIPALITY

By

Felister Maliaki Kipuyo

A Dissertation Submitted to Mzumbe University, in Partial Fulfilment of the

Requirements for an Award of the Degree of Master of Business Administration

in Corporate Management (MBA-CM) of Mzumbe university

2013

i

CERTIFICATION

We, the undersigned, certify that we have read and hereby recommend for

acceptance by the Mzumbe University, a dissertation entitled Challenges facing

saving and Credit cooperative societies in supporting Small and Medium Sized

Enterprises in Tanzania: A case of Temeke Municipality, in partial fulfillment of the

requirements for the degree of Master of Business Administration of Mzumbe

University.

___________________________

Major Supervisor

__________________________

Internal Examiner

__________________________

External Examiner

Accepted for the Board of Dar-es-Salaam Business School

_______________________________________________

DEAN DIRECTOR /FACULTY/DOCTORATE/SCHOOL/BOARD

ii

DECLARATION

I, Felister Maliaki Kipuyo, declare that this dissertation is my own original work

except where stated and that it has not been presented and will not be presented to

any other university for a similar or any other degree or academic award.

Signature _______________________

Date _________________________

iii

COPYRIGHT

© 2013

This dissertation is a copyright material protected under the Berne Convention, the

Copyright Act, 1999 and other international and national enactments, in that behalf,

on intellectual property. It may not be reproduced by any means in full or in part,

except for short extracts in fair dealings, for research or private study, critical

scholarly review or discourse with an acknowledgement, without the prior written

permission of the Chief Academic Officer on behalf of both the author and the

Mzumbe University, on the behalf of the author.

iv

ACKNOWLEDGEMENT

First of all I sincerely give thanks to Almighty God for his Grace, love, mercy and

blessing in my life. He has always been with me during the preparation of this work.

I praise and glorify his Holy name.

I also extend my humble acknowledgement to my Supervisor Dr. Bony Mgonja for

his support, guidance and concern during the time of writing and conducting this

research.

Honestly I also thank my beloved parents, mother and my late father, brothers, sisters

who encouraged, supported and sponsored me on this program, indeed they made

me to continue smoothly in my studies. May God continue to bless them.

I also thanks and appreciate the support from Cooperatives officers of Temeke

Municipality, SACCOS staffs and SMEs owners who shared with me their

experiences concerning the challenges which facing them towards their economic

development.

Lastly I also thanks every person who is not mention here for positive response and

contribution in numerous ways in the accomplishment of this work. May God bless

you all.

v

DEDICATION

I dedicate this work to the living God who helped and enable me to accomplish it. I

honor and glorify his Holy name. I also dedicate it to my beloved parents for their

love, care, courage and support to attain my goals. May God bless you now and

forever

vi

ABBREVIATION

CBOs - Community Based Organizations

CGAP - Consultative Group to Assist the Poorest

CRDB - Cooperative and Rural Development Bank

FINCA - Foundation for International Community Assistance

FGD - Focus Group Discussion

GOT - Government of Tanzania

ILO - International Labour Organization

KFWT - Kenya Finance Women Trust

MFIs - Microfinance Institutions

MSEs - Micro and Small Medium Enterprises

NBC - National Bank of Commerce

NGOs - Non Government Organizations

PRIDE - Promotion of Rural Initiatives Development Ent

ROSCAs - Rotating Saving and Credit Associations

SACAS - Savings and Credit Associations

SACCOS - Savings and Credit Co-operative Societies

SCCULT - Savings and Credit Cooperatives Union League

SMEs - Small and Medium sized Enterprises

URT - United Republic of Tanzania

vii

ABSTRACT

The Tanzania cooperative sector plays a significant role in the Tanzania financial

sector. SACCOs is a now predominant form of external financing for small and

micro enterprises in most of the developing counties. Despite of the role played by

SACCOs in supporting SMEs SACCOs is still facing with a lot of challenges which

hindering them to meet the demand of their clients. Considering their support, this

paper aims to unveil the constraints which hinder SACCOs development in

supporting SMEs in Tanzania. The study was carried in Temeke municipality

whereby three SACCOs were involved. The sample size of this study was 40

respondents. The questionnaires were administered and distributed to respective

respondents which include line managers of SACCOs and the entire members of the

SACCOs.

The study objectives were to examine the operation capital of SACCOs in supporting

the Small Enterprises, determine the extent in which the management of SACCOs is

supporting SMEs, and assess the extent in which SACCOs have contributed to the

development and growth of SMEs in Tanzania.

The findings of this study revealed that SACCOs has been contributed to the

economy of individual and national level. Despite of some challenges facing

SACCOs such as delay in payment of the loan; poor management of database

system; lack of enough capital, insufficient debt and equity funds to pass to the poor,

poor computerized system; and delaying of presentation of financial reports to

clients/ members, still yet SMEs operate their business but with small initiatives from

the government.

viii

TABLE OF CONTENT

CERTIFICATION ......................................................................................................... I

DECLARATION .......................................................................................................... II

COPYRIGHT .............................................................................................................. III

ACKNOWLEDGEMENT .......................................................................................... IV

DEDICATION ............................................................................................................. V

ABBREVIATION ....................................................................................................... VI

ABSTRACT ............................................................................................................... VII

LIST OF TABLES ...................................................................................................... XI

LIST OF FIGURES ................................................................................................... XII

CHAPTER ONE ......................................................................................................... 2

INTRODUCTION AND BACKGROUND ............................................................... 2

1.1 Introduction ........................................................................................................ 2

1.2 Background Information .................................................................................... 2

1.3 Statement of the Research Problem. .................................................................. 6

1.4 Research Objectives ........................................................................................... 7

1.4.1 General Objective............................................................................................... 7

1.4.2 Specific Objective .............................................................................................. 7

1.5 Research Questions ............................................................................................ 8

1.6 Significance of the Study ................................................................................... 8

1.7 Scope of the Study ............................................................................................. 8

1.8 Limitation of the Study ....................................................................................... 9

1.9 Definition of Key Terms .................................................................................... 9

CHAPTER TWO ...................................................................................................... 12

LITERATURE REVIEW ......................................................................................... 12

2.1 Introduction ...................................................................................................... 12

2.2 Theoretical Literature ....................................................................................... 12

2.2.1 Theory for group formation ............................................................................. 12

ix

2.2.2 Challenge on operation capital of SACCOS in Supporting SMEs .................. 14

2.2.3 Financial Challenges facing SACCOS in supporting SMEs ........................... 15

2.2.4 Challenges on the Management of Saccos in supporting SMEs ...................... 17

2.2.5 The extent in which Saccos have Contributed in supporting SMEs ................ 20

2.2.6 SMEs Growth and Development ..................................................................... 21

2.2.7 Empirical Literature Review ............................................................................ 23

2.2.8 Research Gap .................................................................................................. 26

2.2.9 Conceptual Framework .................................................................................... 26

CHAPTER THREE .................................................................................................. 29

RESEARCH METHODOLOGY ............................................................................ 29

3.1 Introduction ...................................................................................................... 29

3.1.1 Study Area ........................................................................................................ 29

3.1.2 Research Design ............................................................................................... 29

3.1.4 Population ........................................................................................................ 30

3.1.5 Sample and Sampling Procedures .................................................................... 30

3.1.6 Data Collection Techniques ............................................................................. 31

3.1.7 Primary source of information ......................................................................... 31

3.1.8 Interviews ......................................................................................................... 32

3.1.9 Focus Group Discussion (FGD) ....................................................................... 32

3.1.10 Secondary source of information ..................................................................... 33

3.1.11 Documentary Review ....................................................................................... 33

3.2 Data Collection Instruments ............................................................................. 33

3.2.1 Interview guides ............................................................................................... 34

3.2.2 Questionnaires .................................................................................................. 34

3.2.4 Documentary Reviews ..................................................................................... 34

3.3 Data Analysis Plan ........................................................................................... 35

x

CHAPTER FOUR ..................................................................................................... 36

PRESENTATION AND DISCUSSION OF FINDINGS ....................................... 36

4.1 Introduction ...................................................................................................... 36

4.2 Demographic Profile of Respondents .............................................................. 37

4.2.1 Gender of the Respondents .............................................................................. 37

4.2.2 Age of the Respondents .................................................................................. 38

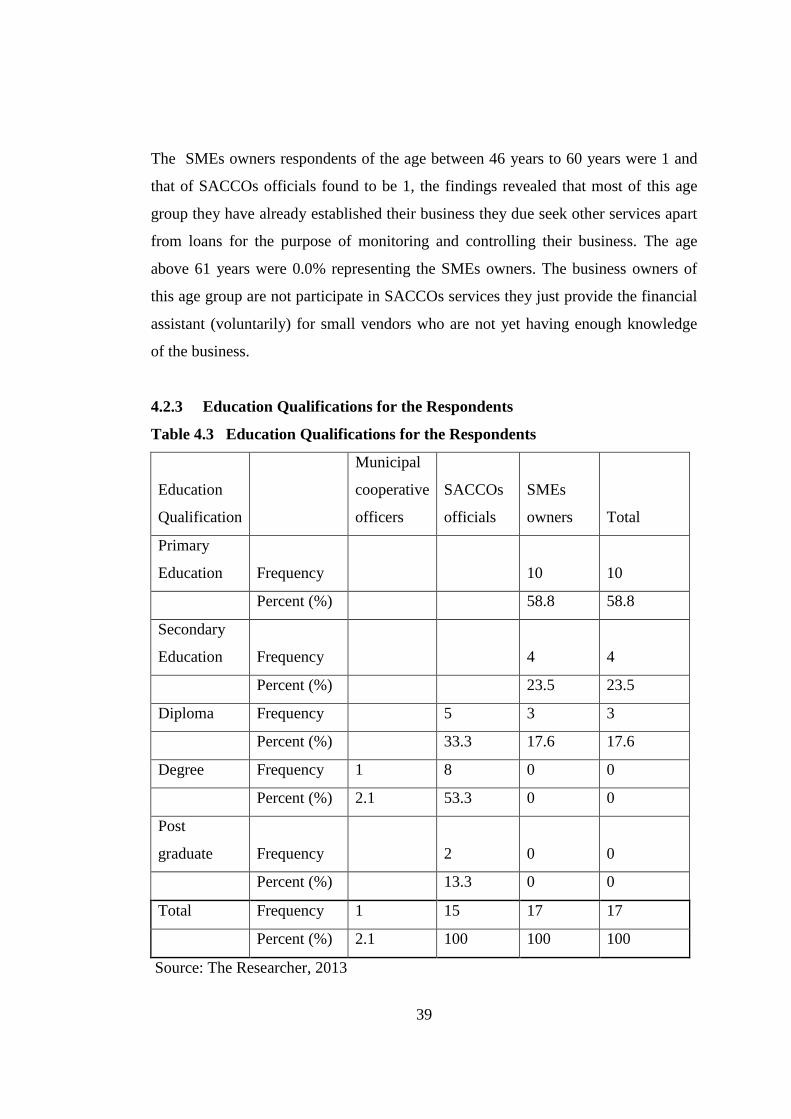

4.2.3 Education Qualifications for the Respondents ................................................ 39

4.2.4 The Status of the Studied Businesses ............................................................... 40

4.2.5 Sources of Business Capital ............................................................................. 41

4.2.6 Contribution of SACCOs in the development of SMEs .................................. 42

4.2.7 Operation Capital of SACCOs in supporting SMEs. ...................................... 43

4.2.8 Challenges facing SACCOS in Supporting the SMEs .................................... 44

4.2.9 Operation capital of SACCOS in Supporting SMEs ...................................... 45

4.2.10 Capital in Saving Products ........................................................................... 45

4.3 Capital in Loan Products/ Services ................................................................. 46

4.3.1 Diversification of Technical Advices Services ................................................ 47

4.3.2 The extent in which the Management of SACCOS is Supporting SMEs ....... 48

4.3.3 challenges and contribution of saccos to the economic development of SMEs50

CHAPTER FIVE ....................................................................................................... 55

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS .......................... 55

5.1 Introduction ......................................................................................................... 55

5.2 Summary of the key Findings ............................................................................. 55

5.3 Conclusions ........................................................................................................ 56

5.4 Recommendations .............................................................................................. 57

5.5 Implications for Further Studies.......................................................................... 59

REFERENCES ............................................................................................................ 60

APPENDICES ............................................................................................................ 68

APPENDIX 1: Questionnaires for small business owners ......................................... 68

APPENDIX 2: Questionnaires for saving and credit co-operative societies .............. 71

xi

LIST OF TABLES

Table 1.1: Categories of SMEs in Tanzania ............................................................ 6

Table 4.1 Genders of the Respondents ..................................................................... 37

Table 4.2 Ages of the Respondents ............................................................................ 38

Table 4.3 Education Qualifications for the Respondents ......................................... 39

Table 4.4 The Status of the Studied Businesses ....................................................... 40

Table 4.5 Duration of Business for Respondents .................................................... 41

Table 4.6 Sources of Business Capital for the Respondents .................................... 41

Table 4.7 Awareness of the Contribution of SACCOs in meeting Business Needs 42

Table 4.8 Borrowed Capital ..................................................................................... 43

Table 4.9 Summary of challenges facing SACCOs. .............................................. 44

xii

LIST OF FIGURES

Pages

Figure 2.1 Challenges facing SACCOs in supporting SMEs ..................................... 27

2

CHAPTER ONE

INTRODUCTION AND BACKGROUND

1.1 Introduction

Tanzania’s networks of Savings and Credit Cooperative Societies (SACCOs) are

grass-roots financial institutions which have stood the test of time as effective micro

financial institutions, offering members a convenient home for their savings and an

access point for loans. For many people, membership of their SACCOs is an

invaluable safeguard against unexpected illness, accident or family death. Workers in

the informal economy have increasingly looked to SACCOs in recent years to meet

their needs. Savings and Credit Cooperative Societies (SACCOs) are said to be the

alternative sources of finance for entrepreneurs and the provision of financial and

banking services to Small and Medium Enterprises (SMEs) who for economic

reasons cannot be covered by the activities of formal banks and financial institutions.

SACCOs are established under the cooperative societies Act and are important form

of financial intermediary, which over the years played vital role in the provision of

financial services to their members. The societies accept monthly payment for shares

from which members may borrow any amount equivalent to two or three times their

own savings if they can get other members to guarantee them. SACCOs societies

have developed to meet the fundamental human need to find a way of saving and

borrowing methods without taking risks and without handling over too much power

to money lender. SACCOs are established in Tanzania with the aim of supporting

people with low income earners such as SMEs and other groups by create a source of

capital to its members. Therefore this study aims at assessing challenges facing

Saving and Credit Cooperative Society in supporting SMEs in Tanzania.

1.2 Background Information

In the early 1950s there was the emergence of financial co-operatives (SACCOs)

promoted mainly by Roman Catholic Missionaries who had studied in United States.

In Tanzania SACCOs spread quickly to Bukoba, Kilimanjaro and Dar-es-salaam in

3

the period of 1960’s.In 1963 the SACCOs movement established the Savings and

Credit Cooperative Union League of Tanzania (SCCULT) as their apex (Mlowe and

Kalesh, 2006).

SACCOs performs major functions in relations to its members and general economic

development of the country. In particular, these functions are collecting savings from

members, giving loans to the members, education, training, and giving financial and

non-financial advice to the members. In some cases, some government and private

institutions may also give financial assistance to SACCOs in order to enable them

(SACCOs) give loans to more SACCOs members. In turn members of SACCOs are

expected to use the borrowed funds for the intended projects.

Members of SACCOs used loans for different activities such as trade, agriculture

,small scale manufacturing industries, service sectors such as saloon etc and in few

cases; some SACCOs members borrow SACCOs loans to finance their non-

economic activities.Since members borrow SACCOs funds to finance their

respective micro investments, it is important that there should be a close cooperation

between SACCOs borrowers and professional experts in various fields such as

banking, marketing, commerce, economics, finance, agriculture, trade, engineering

etc. These professionals will provide valuable advice to SACCOs members on how

to run their micro projects financed by micro loans borrowed by members. At the

same time, the government is also expected to establish a conducive monetary

policy, fiscal policy, trade investment policy, wage-income redistribution policy, etc

which will in general facilitate better performance of SACCOs member’s and micro

projects financed by SACCOs loans.

Specifically, SACCOs institution provide a broad range of services which include

deposits, loans, payment services, money transfer and insurance to the poor/low-

income households, SMEs and their enterprises .SACCOs is supporting SMEs in

urban and rural areas in Tanzania. SACCOs as a Micro finance Institution (MFIs) is

facing with a lot of challenge in supporting SMEs in Tanzania. Due to these

4

challenges many SACCOs have been formed and collapsed so they failed to meet

their objectives of saving the poor.

To meet unsatisfied demand for financial services, a variety of MFIs has emerged

over time in Africa. Some of these institutions concentrate only on providing credit,

others are engaged in providing both deposit and credit facilities, and some are

involved only in deposit collection.

The concept of SMEs has no any universal accepted definition. Thus, there is no

clear definition of SMEs. People in different countries defined SMEs in different

ways. For example, Frank (1999) defines SMEs on the basis of number of

employees, turnover and other essential characteristics of the small firms. Different

countries use different measurement techniques to determine SMEs and it depend on

their purposes (Kirby, 2003; Ngasongwa, 2002).

SMEs are used to mean micro, small and medium enterprises. It is sometimes

referred to as micro, small and medium enterprises (MSMEs).

SMEs are estimated to contribute 30-35% of the gross domestic product. The sector

consists of more than 1 million business activities engaging 3-4 million persons, that

is, about 20 -30% of the labor force. There has been an expansion of SMEs for

income and employment generation between 1990 to 1996 following the adoption of

economic reforms creating some space for the self-employment and private sector

activities. This growth would have been higher if the business environment and

Government policies had provided deliberate incentives to the development of this

sector.

Also, URT (2002) has reported that the SMEs mostly cover non-farm economic

activities mainly manufacturing, mining, commerce and services. There is no

universally accepted definition of SMEs. Different countries use various measures of

5

size depending on their level of development. The commonly used yardsticks are

total number of employees, total investment and sales turnover.

SMEs play a fundamental role in utilizing and adding value to local resources. In

addition, development of SMEs facilitates distribution of economic activities within

the economy and thus fosters equitable income distribution. Furthermore, SMEs

technologies are easier to acquire, transfer and adopt. Also, SMEs are better

positioned to satisfy limited demands brought about by small and localized markets

due to their lower overheads and fixed costs. Moreover, SMEs owners tend to show

greater resilience in the face of recessions by holding on to their businesses, as they

are prepared to temporarily accept lower compensation.

Through business linkages, partnerships and subcontracting relationships, SMEs

have great potential to complement large industries requirements. A strong and

productive industrial structure can only be achieved where SMEs and large

enterprises not only coexist but also function in a symbiotic relationship. In addition,

SMEs serve as a training ground for entrepreneurship and managerial development

and enable motivated individuals to find new avenues for investment and expanding

their operations (Olomi, 2006).

In the context of Tanzania, micro enterprises are those engaging up to 4 people, in

most cases family members or employing capital amounting up to Tshs.5.0 million.

The majority of micro enterprises fall under the informal sector. Small enterprises are

mostly formalized undertakings engaging between 5 and 49 employees or with

capital investment from Tshs.5 million to Tshs.200 million. Medium enterprises

employ between 50 and 99 people or use capital investment from Tshs.200 million to

Tshs.800 million. This is illustrated in the table below:

6

Table 1.1: Categories of SMEs in Tanzania

Category Category Employees Capital Investment in Machinery

(Tshs.)

Micro enterprise 1 – 4 Up to 5 mil.

Small enterprise 5 – 49 Above 5 mil. to 200 mil.

Medium enterprise 50 – 99 Above 200mil.to 800 mil.

Large enterprise 100 + Above 800 mil.

Source: SME policy 2002 at http://www.tanzania.go.tz/pdf/smepolicy.pdf.

SMEs sector plays an important role in economies of most of the developing

countries. Over half of Tanzania’s national output comes from small business sector

and a third of urban labour force is employed in this sector (Planning Commission,

1999). There are various researchers advocating the importance of small business on

the economy and people all together. Yunus (1984) for example, argues that people

who live in developing countries could improve their living standards by becoming

micro- entrepreneurs if financial institutions could support their initiatives with small

loans.

1.3 Statement of the research problem.

In Tanzania, there are a number of MFIs such as SACCOs, NGOs which are there

purposefully for reducing the income gap between the low and high income earners

as well as sustaining and developing SMEs in Tanzania. The aim of forming this

group, is to develop and support SMEs. In Tanzania among the major MFIs which

are known by the SMEs in order to give them support are SACCOs units.

According to (URT,2002),Tanzania has considerable number of formal, semi- formal

and informal Microfinance Institutions which are there purposefully for reducing the

income gap between the low and high income earners as well as sustaining SMEs

development. But the contribution of these MFIs in general has not been evident in

supporting those SMEs apart from the good intention shown by the Government of

putting in place the SMEs policy in order to; promote the Small and medium sized

7

Enterprises, improving the performance and competitiveness of the existing ones,

still the sector is operating under low level.

Therefore this study focuses on the analysis of challenges facing SACCOs in

supporting SMEs in Tanzania. The study explains how and why SACCOs are not

succeeding to support SMEs as intended by the government. A key stand point of

this study is that in reality SACCOs were seen as vehicles for reaching the SMEs and

therefore being unique from other microfinance institutions. The government

approach of channeling micro credit funds for the SMEs through SACCOs was

viewed as a viable approach undermining the complexity surrounding the SMEs and

their willingness to join SACCOs, access and use of credit. Micro credit through

SACCOS would be effective in benefiting SMEs in supporting them financially.

It is true that despite of the efforts made by SACCOs to make conducive

environment and access of funds to SMEs, there is lower development in the sector

than what is expected, and this is due to various challenges facing many SACCOs in

supporting SMEs in Tanzania.

1.4 Research objectives

1.4.1 General objective

The general Objective of the study is to investigate on the challenges facing

SACCOs in supporting Small and Medium sized Enterprises in Tanzania.

1.4.2 Specific objective

Specifically the study intended to:

i. To identify the operation capital of SACCOs in supporting Small and

Medium sized enterprises in Tanzania

ii. Examine the extent in which the management of SACCOs is supporting

Small and Medium sized Enterprises

iii. Assess the extent to which SACCOs have contributed to the development and

growth of SMEs in Tanzania.

8

1.5 Research Questions

The study used the following specific research questions;

(i) What are the type of capital do the SACCOs provide in supporting SMEs?

(ii) How does the management of SACCOs help to overcome challenges associated

with supporting SMEs?

(iii)What are the contribution of SACCOs to the development and growth of SMEs?

1.6 Significance of the study

The study will be significant to different people at different levels:-

At the level of the researcher, it will help them to advance knowledge and gaining

skills by thinking logically and organizing the idea in a proper manner. The study

will help other researchers to identify viable areas for further researches. This study

also will help different people such as SMEs and members of SACCOs inoder to

solve challenges which are facing them in their activities.

The study will identify the major challenges facing SACCOs in supporting SMEs

and how to overcome those challenges.

At the level of the institute, it will have data and information, which will add into an

institute data bank.

At the level of policy makers within the Organization, the study findings may help to

improve the organization’s employee’s motivation and designing intervention

strategies.

At the level of SMEs owners, of SMEs will benefit from outcome through assessing

suitable information and gaining knowledge for the good business performance.

At the level of other researchers, they will utilize the gathered information as

baseline data for those who want to venture into the similar field.

1.7 Scope of the Study

This study was conducted in Temeke district in Dar es Salaam region at selected

SACCOs. Temeke district, with latitude of 39. 42 (39° 25' 0 E), is an administrative

region (second-order administrative division) located in Tanzania that is a part of

9

Africa. The location is situated 498 kilometres east (102°) of the approximate centre

of Tanzania and 20 kilometres south east (131°) of Dar es Salaam.

A 100 square kilometres area around Temeke District has an approximate population

of 5,760,080 (0.057601 persons per square meter) and an average elevation of 36

meters above the sea

(http://www.traveljournals.net/explore/tanzania/map/m3542334/temeke_district.html

ret. The selection of study area considered the following fact; it is because the

researcher is living in Dar es Salaam and is a bit familiar with the mentioned District

(Temeke).

1.8 Limitation of the Study

The study was focused on assessing the challenges facing SACCOs in supporting

Small and medium sized Enterprises (SMEs) in Tanzania. In every kind of study,

limits are inescapable. Being aware of limitations helps the researcher to avoid or to

minimize the pitfalls, over expectation, and frustrations in the course of study (Keya

et al., 1989).

In conducting this study the researcher had been limited in terms of language, budget

constraints and the time available for conducting the research, as the researcher at the

same time she was working in her officer, so only few SACCOs and SMEs were

visited during the time of which the collection of data was done. Also there were

challenges on data inaccessibility as some respondents were refusing to give the

researcher correct information.

1.9 Definition of Key Terms

SACCO:

SACCO is the acronym for Savings And Credit Co-operative. There is no difference

between a credit union and a SACCO. The term “credit union” is generally not used

in Africa

10

(www.saccol.org.za). And the acronym SACCOs stands for Savings and Credit

Cooperative Societies.

A SACCOs is a democratic, unique member driven, self co-operative. It is owned,

governed and managed by its members who have the same common bond: working

for the same employer, belonging to the same church, labour union, social fraternity

or living/ working in the same community. A SACCOs membership is open to all

who belong to the group, regardless of race, religion, colour, creed and gender or job

status.

These members agree to save their money together in the SACCOs and to make

loans to each other at reasonable rates of interest. Interest is charged on loans, to

cover the interest cost on savings and the cost of administration. There is no payment

or profit to outside interest or internal owners. The members are the owners and they

the members decide how their money will be used for the benefits of each other

(http://www.saccol.org.za/what_is_sacco.).

Savings

Savings mobilization in microfinance is a very controversial issue. They have been

increase awareness among policy makers and practitioners on the vast number of

informal savings schemes. MFIs such as credit union organizations around the world

have been very successful in rallying clients to save (Paxton, 1996a, p.8).

Credit/ Loan

These are borrowed funds with specified terms for repayment. People borrow when

there are insufficient accumulated savings to finance a business. They also take into

consideration if the return on borrowed funds exceeds the interest rate charged on the

loan and if it is advantageous to borrow rather than to postpone the business

operations until when it is possible to accumulate sufficient savings, assuming the

capacity to service the debt is certain (Waterfield & Duval, 1996). Loans are usually

acquired for productivity reasons; that is to generate revenue within a business.

11

SMEs:

SME is the acronym of Small and medium sized Enterprises and we term these as

small businesses. The term SME covers a wide range of definitions and measures,

varying from country to country and between the sources reporting SMEs statistics.

Among them the most common definitional basis used is employees because of the

comparatively ease of collecting information and here again there is variation in

defining the upper and lower size limit of an SME. In developing countries the

number of employees and size of asses or turnover for SMEs tend to be much smaller

compared to their counterparts in developed countries due to their relative size of

business entities and economies. At current there is no universal acceptable

definition of small- scale business (ibid).

URT (2006) defines Micro, Small and Medium Enterprises as; Micro enterprises are

those undertakings engaging up to 4 employees, Small enterprises are those

undertakings between 5 and 49 employees, and Medium enterprise employ between

50 and 99 people. It should be noted that even when the number of employees is used

as a measure of size, the upper limit of a small is not universal across time and space.

In Tanzania, micro-enterprises are those engaging up to 4 people, in most cases

family members or employing capital amounting up to Tshs. 5.0 million.

The majority of micro-enterprises fall under the informal sector. Small enterprises

(small businesses) are mostly formalized and engaging between 5 to 49 employees or

with capital investment from above Tshs.5 millions. Medium enterprises employ

between 50 and 99 people or use capital investments above Tshs. 200 millions to 800

million (URT, 2003,

12

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter focuses on some of the concepts of Saving and Credit Cooperative

society and the role they play in the development of SMEs. The concepts chosen are

those that are in relation with the area of this thesis.

This chapter opens with an overview of Saving and Credit cooperative Society

available in Tanzania and the services they provide to SMEs. This shows various

policies available in Tanzania and the effects of these policies to the development of

SMEs in Tanzania. It is the part of the research which provides the information or the

explanation of other researchers, writers, authors and authorities relating to the topic

or research problem at hand.

This chapter tells what others have said or written concerning the similar topic which

a researcher is dealing with. The objective here is to enhance our understanding of

the theory of SACCOs and their modes of operation, discussing the empirical

literature etc.

Literature review enables the researcher to study different theories related to the

identified topic, in order to incorporate other people’s idea in the study.

2.2 Theoretical Literature

2.2.1 Theory for Group Formation

Komives (1998) and Tuckman (1977) identified 6 stages in group formation that are

relevant to process through which SACCOs are operating at community level.

SACCOs are examples of groups at community level and the processes they go

through are assessed using the group formation theory.Tuckman and Jensen draw on

the movement known as group dynamics, which is concerned with why groups

behave in particular ways. This offers various suggestions for how groups are formed

and how they develop over time. The formation of some groups can be represented

13

as a spiral; other groups form15 with sudden movements forward and then have

periods with no change. Whatever variant of formation each group exhibits, they

suggest that all groups pass through six sequential stages of development. These

stages may be longer or shorter for each group, or for individual members of the

group, but all groups will need to experience them. They are forming, storming,

norming, and performing.

a. Forming

This is the initial stage when the group comes together and members begin to

develop their relationship with one another and learn what is expected of them. This

is the stage when the team building begins and trust starts to develop. Group

members will start establishing limits on acceptable behavior through

experimentation. Other member’s reactions will determine if a behaviour will be

repeated. This is also the time when tasks of the group and the members will be

decided. When a group is forming, participants can feel anxious not knowing how

the group will work or what exactly will be required of them.

b. Storming

During this stage of group development, interpersonal conflicts arise and differences

in opinions about the group and its goals will surface. If the group is unable to clearly

state its purposes and goals or if it cannot agree on shared goals, the group may

collapse at this point. It is important to work through the conflict and establish clear

goals. It is necessary for there to be discussion so everyone feels heard and can come

to an agreement on the direction the group is to move in. Storming, as the word

suggests, is when things may get stormy.Conflict can emerge, individual differences

are expressed and the leader's role may be challenged. The value and the feasibility

of the task may also be challenged.

c. Norming

Once the group resolves its conflicts, it can now establish patterns of how to get its

work done. Expectations of another are clearly articulated and accepted by members

14

of the group Formal and informal procedures are established in delegating tasks,

responding to questions and in the process by which the group functions. Members

of the group come to understand how the group as a whole operates.

d. Performing

Under this stage, issues related to roles, expectations and norms are no longer of

major importance. The group is more focused on its task, working intentionally and

effectively to accomplish its goals. The group will find that it can celebrate its

accomplishments and members will be learning new skills and sharing roles. He

again argues that after the group enters the performing stage, it is unrealistic to

expect it to remain there permanently. When new members join or some people

leave, there will be a new process of forming, storming and norming engaged as

everyone learns about one another. External events may lead to conflicts within the

group, to remain health; the groups will go through all of these processes in a

continuous loop.

When conflict arises in the group, do not try to silence the conflict or to run from it.

Let the conflict come out into the open so people can discuss it. If the conflict is kept

under the surface, members will not be able to build trusting relationships and this

could harm the group’s effectiveness. If handled properly, the group will come out of

the conflict with a stronger sense of cohesiveness than before. When the group retires

or adjourns, much learning happens through informal chat and feedback about the

group performance. Tuckman and Jenson recognise that when groups dismantle

themselves and the loose endsare all tied up, participants often go through a stage of

mourning or grieving.

2.2.2 Challenge on Operation capital of SACCOs in supporting SMEs

SACCOs have the greatest potential to reach out to rural areas, but they have weak

institutional and financial bases and their inability to operate strictly on commercial

principles further minimized their chances of becoming sustainable.

15

There are many SACCOs which did not access credit because they were weak and

could not fulfill the requirement .At the same time, within a SACCOs itself there

were many individual who did not access credit/loan. Adequate capital for

cooperative societies and cooperators can be obtained through modernization of

SACCOs procedures and guidelines, as well as strengthening the capital base of

Cooperative banks. Part of the modernization process of SACCOs procedures entails

having new rules and regulations, having in place responsible leadership, employing

competent personnel, and adopting “Best Practices” in the provision of financial

services to members. In strengthening the SACCOs capital base, members will be

sensitized to fully pay for their shares and to invest the generated capital rationally.

Through a SACCOs network mechanism, a system of interlending between SACCOs

will be developed i.e. to link SACCOs which have surplus funds with those with a

deficit. Measures will be instituted to strengthen the capital base of Cooperative

Banks already in place and those which may be established.

To strengthen the overall availability of capital to cooperatives (for production,

processing, marketing), a nationwide Cooperative bank will be established whose

base capital will originate from the cooperative movement itself and relevant

stakeholders (within and outside the country).

Nevertheless sustainable financing of Cooperative Societies can be attained by

reducing the burden of indebtedness on the cooperatives due to past loans (mostly

channeled to agriculture). To this end the Government will be requested to consider

the indebtedness situation of cooperatives and come up with a solution which will

facilitate the transformation process envisaged.

2.2.3 Financial Challenges Facing SACCOS in supporting SMEs

Low-income men and women have a serious hindrance in gaining access to finance

from formal financial institutions. Ordinary financial intermediation is not more

often than not enough to help them participate, and therefore SACCOs have to adopt

tools to bridge the gaps created by poverty, gender, illiteracy and remoteness. The

16

clients also need to be trained so as to have the skills for specific production and

business management as well as better access to markets so as to make profitable use

of the financial resource they receive (Bennett, 1994).

In providing effective financial services to the poor requires social intermediation.

This is “the process of creating social capital as a support to sustainable financial

intermediation with poor and disadvantaged groups or individuals” (Bennett, 1997).

SACCOs Institution comprise of financial sustainability, outreach to the poor, and

institutional impact. There are costs to be incurred when reaching out to the poor and

most especially with small loans (Christabell, 2009). The financial institutions

always try to keep this cost as minimum as possible and when the poor are in a

dispersed and vast geographical area, the cost of outreach increases. The provision of

financial services to the poor is expensive and to make the financial institutions

sustainable requires patience and attention to avoid excessive cost and risks (Adam

& Piscke, 1992).

The deliveries of micro-finance products and services have transaction cost

consequences in order to have greater outreach. Some microfinance institutions visit

their clients instead of them to come to the institution thereby reducing the cost that

clients may suffer from (FAO, 2005). For MFIs to be sustainable, it is important for

them to have break-even interest rates. This interest rates need to be much higher so

that the financial institution’s revenue can cover the total expenditure (Hulme &

Mosley, 1996a). The break-even rate which is higher than the market rate is defined

as the difference between the cost of supply and the cost of demand of the products

and services. The loan interest rates are often subsidised (Robinson, 2003).

The loans demanded by smaller enterprises are smaller than those requested by larger

ones but the interest rates remain the same. This indicates that, per unit cost is high

for MFIs targeting customers with very small loans and possessing small savings

accounts (Robinson, 2003). Even though the interest rate is high for applicants

17

requesting very small loans, they are able to repay and even seek repeatedly for new

loans.

The social benefits that are gained by clients of MFIs supersede the high interest

charged (Rosenberg, 1996). The high interest rate is also as a means to tackle the

problem of adverse selection where a choice is made between risky and non risky

projects. The good clients suffer at the expense of the bad ones (Graham et al., 1997).

2.2.4 Challenges on the Management of SACCOS in supporting SMEs

SACCOs do not differ much from other MFIs in terms of credit management. They

charge interest to member’s equivalent to 2% per month, give a repayment period of

6months and in some cases require collaterals securities. The difference emerges on

the management where the board and management comes from members and set

their own decision as a group. Some Cooperatives scholars are of the view that

although the SACCOs movement is growing very fast.

Although the importance of SACCOs in the process of poverty eradication is

realized, it faces multiple challenges. This is because offering credit to the

disadvantaged group is a complicated process and the sector is still in its

experimental stage. The following are the major challenges facing the management

of SACCOs and other MFIs.

a. Perceived High Risk of Micro Entrepreneurship and Small Businesses

Micro entrepreneurs usually have no collateral to offer to micro-finance providers

against loans, they usually lack an alternate source of income, and have little, if any,

formal education or training in the area of their business. Msemwa (2007) has

concluded that, as a result, commercial banks attribute a high credit risk to micro

entrepreneurs and steer clear of this sector. SACCOs are compelled to compensate

for this risk by charging interest rates on loans so as to cover; cost of funds, operating

expense, tax expenses, credit rating of client, inflation levels, higher competition,

other factors impacting the interest rate. Fortunately, the challenge can be resolved

18

through the idea of group lending (social collateral against loans) which ensures

good repayment rates.

b. High Costs Involved in Small Transactions/Micro-Lending

The small size of micro enterprises increases the transaction cost for MFIs because

they cannot process loans in bulk. This denies MFIs the benefit of economies of

scale; hence, they are forced to cover their costs through high interest rates on loans.

According to a study conducted by Asian Development Bank, microfinance

providers in the Asia-Pacific region charge interest rates on micro-sized loans

ranging from 30 to 70% a year, which is much higher than rates offered by

commercial banks (Fernando, 2006). However, there are instances where the interest

rates charged were too low for the MFIs’ sustainability. There is, however, a way to

overcome this; their operational costs can be significantly lowered and efficiencies

may be gained during automated loan processing.

c. Lack of Debt and Equity Funds for MFIs to Pass on to the Poor

Capital availability for SACCOs is hardly a problem owing to the rapid growth in the

micro-finance sector, which has been fuelled by attention from the media and

development agencies. Likewise, Descrochers and Lamberte (2002) have added that

even though there are plenty of financing options available for MFIs, there is an

emerging shortage of money because of the current financial crisis across the globe.

Another reason for this shortfall is the lack of awareness of funding sources by

SACCOs managers.

d. Difficulty in Measuring the Social Performance of MFIs

Microfinance is delivering the economic returns its proponents promised, but there

are only a handful of tools available that measure the social return of loan programs

for the poor. To add to the problem, the tools use proxies to estimate the amount of

poverty and social change surrounding micro entrepreneurs. This makes the

19

gathering of funds a challenge because donors may question the actual impact made

my microfinance (Cassimon, 1997).

e. Lack of Customized Solutions for the Poor

Inappropriate targeting of poor households by micro-finance programs is a common

problem because MFIs in particular SACCOSs fail to understand the varied needs of

micro entrepreneurs. MFIs must spend time in the field with their clients and his/her

business, and then use this research to develop customized microfinance tools for

each micro entrepreneur. Generalized solutions may work for large companies

dealing with large homogeneous customer groups, but micro-finance providers need

to serve the varied needs of individuals in each micro market segments (Fernando,

ibid).

f. Lack of Micro-Finance Training For Human Resource in MFIs

Working in the microfinance sector is a different ball game compared to the

traditional financial sector. For instance, micro-finance officers and volunteers need

to talk a different language, build lasting relationships with individual micro

entrepreneurs, understand the unique needs of the poor, evaluate the borrower’s

sustainability, and grasp the cultural nuances of the borrower’s communities. Of

course, all this needs to be done by large financial firms as well, but the needs and

characteristics of the two markets are very different. It’s no surprise microfinance

providers need special training to ensure they avoid problems such as intimidating or

under-serving clients.

g. Poor Distribution system of SACCOs and lack of Information about

Microfinance Investment Opportunities

There are over 10,000 MFIs across the world, but their reach is only 4% of the

potential market (World Bank, 2001). Firstly, micro-finance providers may be

complacent with their client base in certain cities and feel no economic need

(ignoring the social need to eradicate poverty) to spread out their distribution system

to cater to the poorest of households. Secondly, micro entrepreneurs are sprawled

20

over large geographical areas, often in remote places, which often make them

inaccessible to MFIs. This is a slight problem because even though there are over

10,000 MFIs around the world, they may not know about the existence and All these

challenges can broadly fall into both financial and operational in nature; and we can

therefore see that they should not be impossible to solve as the micro-finance sector

moves towards its optimal performance level in the next several years. In other

words, despite these challenges, the prospects of micro-finance are quite bright.

2.2.5 The Extent in which SACCOs have contributed in supporting SMEs

Several MFIs such as SACCOs have shown that they can profitably serve large

numbers of relatively poor households, micro-enterprises, and small businesses.

Although the client base is typically in peri-urban markets or in off-farm business

activities in rural markets, those experiences have renewed interest in the feasibility

of reorienting rural finance and MFIs.

There is a growing list of MFIs that have moved beyond their initial urban client base

to tailor their products to rural clients, including the Equity Building Society in

Kenya, CrediAmigo, a bank-affiliated MFIs in Brazil and the Development Bank of

Brazil (BNDES), MiBanco in Peru, Financiera Calpia in El Salvador, and Basix

India Ltd, a micro–credit institution serving the rural poor in India. The experiences

of these MFIs point toward the possibilities of adaptation and replication by other

MFIs operating in predominantly rural markets

(http://www.imf.org/external/pubs/ft/fsa/eng/pdf/ch07

In a few countries, agricultural development banks have succeeded in transforming

themselves into more-sustainable institutions by offering demand-driven financial

services, building credible lending contracts, and using full-cost recovery interest

rates. The experiences of Thailand’s Bank for Agriculture and Agricultural

Cooperatives (BAAC),Bank Rakyat Indonesia’s (BRI) village units in its micro-

banking system (Yaron &Charitonenko, 1999; Zeller, 2003).

21

The revival and restructuring for privatization of Mongolia’s Agricultural Bank

(Boomgar et al., 2003) and of Tanzania’s National Microfinance Bank have

demonstrated that state-owned banks can be transformed into dynamic, profitable,

and successful rural-oriented financial intermediaries with business-oriented

management reforms. As supported by Zeller (2003) that such transformation of state

owned banks can be achieved only with firm political commitment, ownership of

reforms, management autonomy, and incentives.

Micro-finance operators in Tanzania function within the framework of the

Government’s National Micro Finance Policy of 2000. The objectives of this policy

are to provide the basis for the evolution of an efficient and effective micro-finance

system to serve the low segment of society and contribute to economic growth and

poverty reduction.

The policy establishes a framework within which micro-finance operators will

develop, lays out the principles to guide operations of the system, defines roles and

responsibilities of actors, and provides guidelines for coordinating mechanisms

(URT, 2000, p. 5). The Central Bank was given the mandate to coordinate

implementation of the policy. It is interesting to note that the Micro Finance Policy

includes “saving the poor” as a best practice in developing the SMEs.

2.2.6 SMEs Growth and Development

The purpose or goal of any business or firm is to make profit and growth. A firm is

defined as an administrative organisation whose legal entity or frame work may

expand in time with the collection of both physical resources, tangible or resources

that are human nature (Penrose, 1995). The term growth in this context can be

defined as an increase in size or other objects that can be quantified or a process of

changes or improvements.

The firm size is the result of firm growth over a period of time and it should be noted

that firm growth is a process while firm size is a state (ibid). The growth of a firm

22

can be determined by supply of capital, labour and appropriate management and

opportunities for investments that are profitable. The determining factor for a firm’s

growth is the availability of resources to the firm (Ghoshal, Halm & Moran, 2002).

According to Ledgerwood (1999) enterprise development services or business

development services or nonfinancial services are provided by some MFIs adopting

the integrated approach. The services provided by nonfinancial MFIs services are;

marketing and technology services, business training, production training and sub

sector analysis and interventions. Enterprise development services can be sorted out

into two categories.

The first is enterprise formation which is the offering of training to persons to

acquire skills in a specific sector such as weaving and as well as persons who want to

start up their own business. The second category of enterprise development service

rendered to its clients is the enterprise transformation program which is the provision

of technical assistance, training and technology in order to enable existing SMEs to

advance in terms of production and marketing. Enterprise development services are

not a prerequisite for obtaining financial services and they are not offered free of

charge (ibid).

These charges are subsidized by the government or an external party since to recover

the full cost in providing the services will be impossible by the MFIs. The enterprise

development services may be very meaningful to businesses but the impact and

knowledge that is gained cannot be measured since it does not usually involve any

quantifiable commodity. It has been observed that there is little or no difference

between enterprises that receive credit alone and those that receive both credit

packages and integrated enterprise development services (Ledgerwood, ibid).

Although the importance of SACCOs in the process of poverty eradication is

realized, it faces multiple challenges. This is because offering credit to the

23

disadvantaged group is a complicated process and the sector is still in its

experimental stage.

2.2.7 Empirical Literature Review

Similar studies related to the study at hand have been done in Cameroon, Sierra-

Leone, Ghana, Zambia, Malawi, Rwanda, Kenya, Uganda and Tanzania. In Ghana

Oti-Boateng and Dawoe (2005) carried out the study that revealed that, good

practices that could lead to the technological growth of SMEs. They identified good

practices as homogeneous group formation, capacity building, timely disbursement

of credit, development of collaboration, linkages and Networks among technology

developers, Government and NGOs; advocacy at all levels and creation of enabling

environment, and monitoring and evaluation of loans.

According to Dowson (1997) and ILO (1999), small scale entrepreneurs often have

difficulty gaining access to credit. In some cases this is due to the small loans

requested by the entrepreneurs which are not profitable for financial institutions.

Kitine (1980) has noted that 60% of small industries had difficulties in obtaining

loans from the commercial banks, and this has caused difficulties for sector to install

modern technology machines and purchase of raw material.

A 2002 study by the Bank of Tanzania (BOT) established that 82% of households

were saving in their homes. Almost all of these (79%) were ready to save in

financial institutions if these were there. The study also showed that 94% were

willing to borrow more if resources and appropriate methodologies were available.

Access to finance remains a serious problem in rural areas.

In Kenya (Kabecha, 2005) carried a study which found to encourage the

technological growth of SMEs. The study discovered that MFI loan products were

broadly classified into four categories: group-based minimalist credit, individual

credit with collateral, individual credit with training, and asset financing and the

provision of working sheds. Similar findings and practices were identified in the

24

other countries (Aikins, 2005; Asman & Diyamett, 2005; Jalloh et al., 2005; and

Ruzibuka, 2005).

Byaruhanga (2005) conducted a study on policy impact on small scale enterprises in

Uganda. In his study he found that MFI interest rates ranged from 28%-48%. Most of

MFIs sourced capital for on-lending from Commercial Banks at rates ranging 18%-

22% and had to double the interest rates to SMEs borrowers in order to break even

and make same profit. The purpose of the loans was mainly for working capital. The

amounts were small and the payback period was not more than six months with

repayment being made weekly. Although the loans were fairly easy to access there

were no grace periods.

There were individual loans in some MFIs although most practiced the group landing

system. Some MFIs have plans for technology funding to SMEs but were restricted

by the Micro Deposit Taking Act of 2003 the Ugandan MDI policy, which restricts

loans to 24 months and defines MFI as one fiving loans that are not more than 24

months duration. According to Byaruhanga (ibid) MFIs could cut the interest rates if

they had alternative sources of cheaper capital.

However, SACCOs had large contribution to SMEs growth and development due to

the fact that most of SMEs cannot access credit from formal banks. The good

practices identified were that some SACCOs were funding technology driven SMEs,

reduction interest rates, giving longer loan repayment and grace periods to clients.

Others include the use of special schemes such as asset leasing, making information

about their product and services available to clients, and the use of Information

Communication Technology (ICT) by MFIs to reduce costs (ibid).

Furthermore, Byaruhanga has added that it is limited by the long distances to

financial institutions, delivery models which are unsuitable to rural sparsely

populated and seasonal income earners and small loans sizes. Banks are now

entering the micro-finance industry and some of them have started micro finance

25

windows. However, except for wholesale lending to rural Savings and Credit Co-

operative Societies (SACCOs), the outreach of the banks remains urban areas.

SACCOs have the greatest potential to reach out to rural areas, but they have weak

institutional and financial bases and their inability to operate strictly on commercial

principles further minimized their chances of becoming sustainable. They have to

charge very high interest rates to sustain their operations. In 2004, one of the

relatively well established SACCOs in Tukuyu was charging an interest rate of 5%

per month, which translated to 60% per annum. Management was considering

proposing a revision to 3% per month.

In Moshi Rural, an IFAD supported project for building capacity of SACCOs

realized that members were not borrowing because they did not see viable

investment opportunities in the villages. As a result, the project started supporting

economic projects, including mushroom farming. NGOs - MFIs offer credit ranging

from Tshs. 50,000 (US $50) to Tshs. 2,000,000 (US $ 2,000), but the terms and

conditions make them inaccessible to rural sparsely populated areas with few

economically active populations. A study by Sathyamoorth and Mburu, (2002)

indicated that 78% of SMEs surveyed were the opinion that it was not at all easy to

obtain financial assistance from financial institution and Government. Only 25% felt

that it was easy to get the kind of financial help they need.

Despite the finance sector in Tanzania going a number of development phases

growing small business appear to be still constrained in terms of credit accessibility.

After independence, Tanzania implemented pro-state financing of targeted sectors

including small business and farmers. Likewise, Schaedler (1968, 1976) has noted

that during this period about 95% of all small businesses in Tanzania sourced their

capital from personal savings. As 2002 report of (BOT) shows that 94% were willing

to borrow more if resources and appropriate methodologies were available but access

to finance were still a serious problem in rural areas.

26

The study conducted by Rutasitara on three Regions of Ruvuma, Mwanza and

Dodoma in 1989 also revealed that, despite of different policies on poverty

alleviation in Tanzania, there are extreme poverty in rural area.

Diagne and Zeller (2001) in their study in Malawi suggest that micro-finance do not

have any significant effect in household income meaning no effect on SMEs

development. Investing in SME activities will have no effect in raising household

income because the infrastructure and market is not developed. A study of thirteen

MFIs in seven countries carried out by Mosley and Hulme (1998) has concluded that

household income tends to increase at a decreasing rate as the income and asset

position of the debtors is improve.

2.2.8 Research Gap

Based on the empirical literature (above) it is evident that extensive study similar to

this study has been done. Furthermore, researcher’s experience on this study supports

this. However, there is no documented or published evidence which indicates that the

same study has been done or was done at Temeke municipality which this study tries

to explore. After looking at the framework, the next chapter presents on the

methodology that is applied in conducting the research. Therefore findings from this

study, conclusion and recommendations will cover the gap.

2.2.9 Conceptual Framework

A frame work is asset principles or ideas used as a basis for one’s judgment,

decisions and so on (Oxford Advanced Learners’ [OAL], 1996). Commencing the

study from theoretical perspective may have certain advantages, for it will link the

study into the existing body of knowledge in the subject area and help get started and

provide an initial analytical framework. In order to devise a theoretical framework,

one has to identify main variables, components, themes and issues in the research

project and predict or presume relationship between them.

27

The conceptual framework is developed after extensively reviewing literature about

SACCOs and be able to narrow the relationship between SACCOs and SMEs growth

and development. Hence, the challenges on SMEs development can objectively be

analyzed. The study on hand, which includes an assessment of the challenges facing

SACCOs to development of small enterprises, needs a conceptual framework which

investigates the objectives and the methodology of the study to get quality data. In

this case a model

Figure 2.1 Challenges facing SACCOs in supporting SMEs

Independent variables Dependent variables

Researcher constructs 2013

According to the above diagram, SACCOs have been faced with a lot of challenges

which hindering their support to SMEs in Tanzania. SACCOs have the greatest

potential to reach out SMEs and rural areas but they have been facing with the

problems of lack of capital, poor management, employees, defaulters and weak

institutional and financial bases.

Capital Adequacy

Liquidity management

Lack of knowledge

Governance

Successful Implementation

Key challenges facing SACCOs SMEs support

28

SACCOs are organizations with a goal to serve the needs of un-served or

underserved markets as a means of meeting development objectives. Some SACCOs

provide services such as skills training, marketing, bookkeeping, and production to

develop small enterprises. The problem of capital has been hindering many SACCOs

in Tanzania. Large numbers of SMEs are depending on SACCOs as it is important to

note that, small enterprises are hardly facing with the problem of accessing loan from

formal financial institutions like banks because of terms and conditions which are

employed.

Poor governance and weak institutional base is among the problem which hindering

SACCOs toward support to SMEs.

The SACCOs movement in Tanzania has faced a number of challenges that need to

be addressed inoder to improve their support to SMEs in Tanzania. The major

challenges inherent in the cooperative movement in Tanzania include; poor

governance, lack of capacity in management, and weak capital base and

infrastructure.

For successful implementation on different policies which have been set by

cooperative societies in Tanzania, SACCOs need to improve on soundness, stability,

efficiency, corporate governance as well as integration to the formal system inoder to

support SMEs in Tanzania.

29

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This is the part which describes procedures which were used in conducting the study.

By “methodology” we mean the philosophy of the research process (Bailey, 1994).

This includes the assumptions and values that serve as a rationale for research and

standards or criteria the researcher use for interpreting data and researching

conclusions (ibid). This chapter is organized under the following sub- sections; study

area, research design, population, sample and sampling procedures/techniques, data

collection techniques, data collection instruments and data analysis plan.

3.1.1 Study Area

This study was conducted in Temeke district in Dar es Salaam region where

researcher selected a few SACCOs as units of analysis.

3.1.2 Research Design

A research design is an arrangement of conditions for collection and analysis of data

in a manner that aims to combine relevance to the research purpose with economy in

procedure (Kothari, 2004). The research design is well devised and acts as a general

guideline or blue print for the investigation. This guides the investigator to see

his/her way more clear (Frankfort – Nachmias, 1996). It is a plan outlined how

information is to be gathered. There are three research designs of interests, which are

the case study, survey and experimental design. However, this study was conducted

under the case study design.

The case study design is the research design which usually involves the in depth

study of a particular milieu (village, association, organization, institution) rather than

of individuals drawn more widely (Bulmer & Warwick, 1983).

30

The study adopt the case study research design because of its flexibility in data

collection and analysis as it is less expensive than other research designs like survey

design.

Therefore, this study was conducted at a selected SACCOs in Dar es Salaam region

specifically in Temeke District as the researchers’ case study, for the purpose of

undertaking the in-depth study on the assessment of the challenges facing SACCOs

in supporting SMEs in Tanzania.

3.1.4 Population

Population may be defined as the target group which the researcher wants to know

about by studying one or more of its samples (Tripathi, 1991). In sampling, the

population may refer to the units, from which the sample is drawn. The term “unit” is

used, as in a business research process; samples are not necessarily people all the

time. A population of interest may be the universe of nations or cities.

Therefore, population, contrary to its general notion as a nation’s entire population

has a much broader meaning in sampling. “N” represents the size of the population.

The population of this study comprised of the Municipal Cooperatives Officers

dealing with semi-formal business sector, heads of SACCOs/ loan or credit officers

and SMEs owners who were chosen as samples were traced so as to be interviewed.

3.1.5 Sample and Sampling Procedures

A sample, as the name implies, is a smaller representation of a larger whole

(Population). (Goode & Hatt, 1981). In statistics, a sample is a subset of a population

that is used to represent the entire group as a whole. When doing research, it is often

impractical to survey every member of a particular population because the sheer

number of people is simply too large. Moore (2004, pg, 178) defines sample as a part

that we actually examine in order to gather information. Also Ennon (1995, p.13)

defines sampling techniques as the process of drawing a sample from a larger

population.

31

In this study the researcher used a probability sampling. Probability is that each

sampling unit of the population, you can specify that unit will be included in the

sample (Nachimias & Nachimias, 1996, p.86). In probability sampling the researche

use simple random sampling technique, each member will be chosen by chance. The

selected SACCOs and SMEs owners will be chosen by simple random sampling

technique by throwing pieces of papers with the names of each (active) SMEs in the

municipality.

The SACCOs staffs and municipal cooperative officers was selected by using

purposive sampling technique. As claimed by Rwegoshora (2005: 120) that in this

sampling, also known as judgmental sampling, the researcher choose a person who,

in his judgment about some appropriate characteristics required of the sample

members, is relevant to the research topic and easily available to him/ her.

Additionally, SACCOs staffs who have an experience ranging from 2 to 10 working

years of SACCOs was interviewed. The goal is to obtain a sample that is

representative of the larger population.

The sample of this study consists of 40 respondents with the following distributions:

(18) SACCOs officials, (20) SMEs owners and (2) municipality Cooperative

officers.

3.1.6 Data Collection Techniques

Data collection refers to the gathering of information to prove some facts. In research

the term data collection refers to the gathering of specific information aimed at

providing some facts (Kombo& Tromp, 2006, p.99). The researcher used both

Primary and Secondary sources of information. The researcher use interviews, Focus

Group Discussion (FGD) and documentary sources as methods for data collection.

3.1.7 Primary Source of Information

According to White (2002:31) primary data is information gathered directly from

respondents, it involves creating new data. The researcher used questionnaires,

32

interviews and FGD in collecting data. A primary source is document, speech, or

other sort of evidence written, created or otherwise produced during the time under

study.

The researcher used questionnaires which were administered to SACCOs staffs and

SME’s owners; and FGD to small business owners as well as interview questions

which help in obtaining the information.

3.1.8 Interviews

The interview is of course merely one of the many ways in which two people talk to

each other (Bulmer, 1977). The unstructured or informal interviews used to get the

required information. This is because it might not be easy to get the specific

respondents even if the appointment was made as this would lead to the shortage of

time and increased the impossibility for arranging the structured interviews with the

particular respondents.

The researcher interviewed different respondents such as Municipal Cooperatives

Officers, heads of SACCOs and SMEs owners. Face to face, conversation between