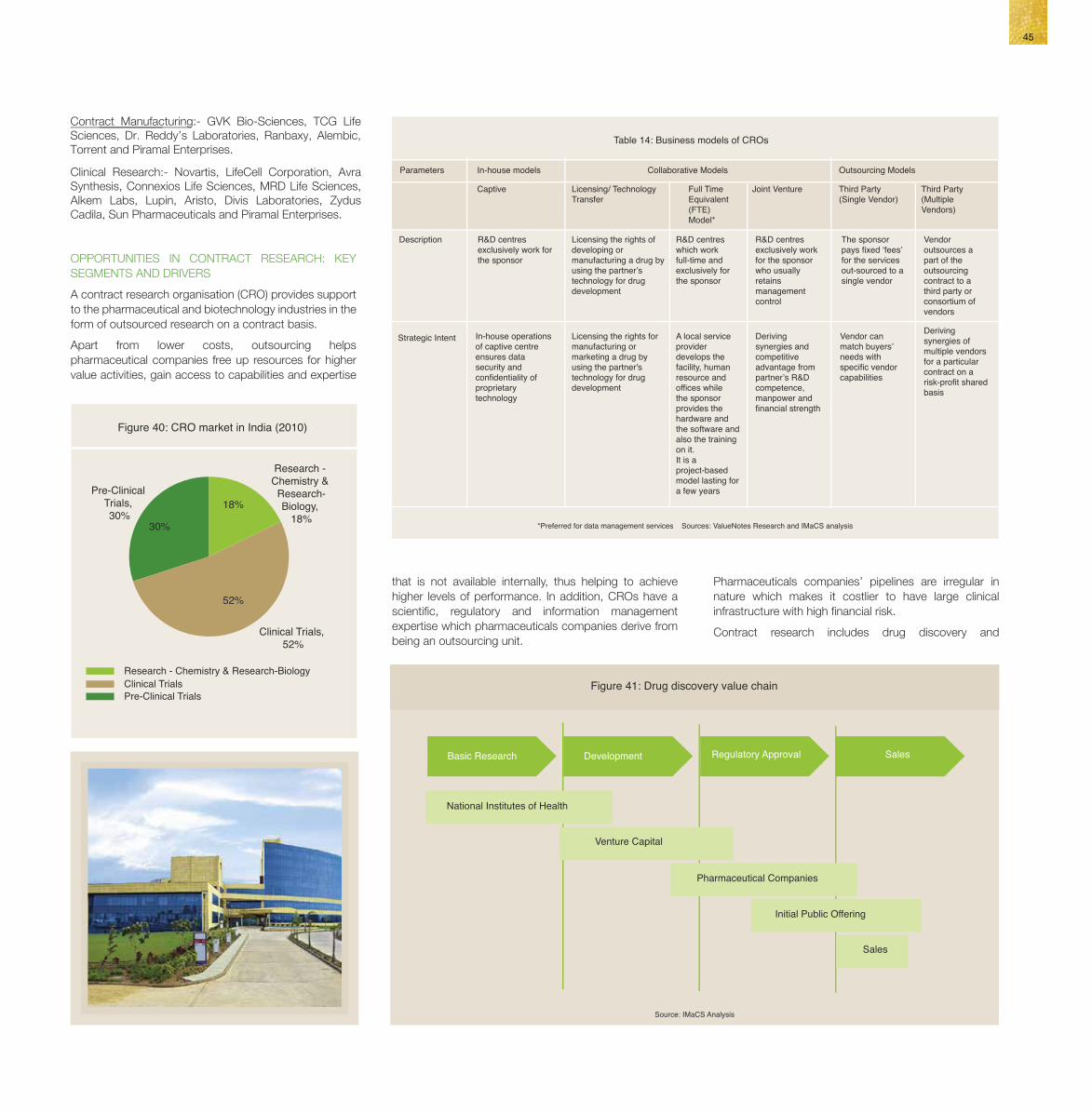

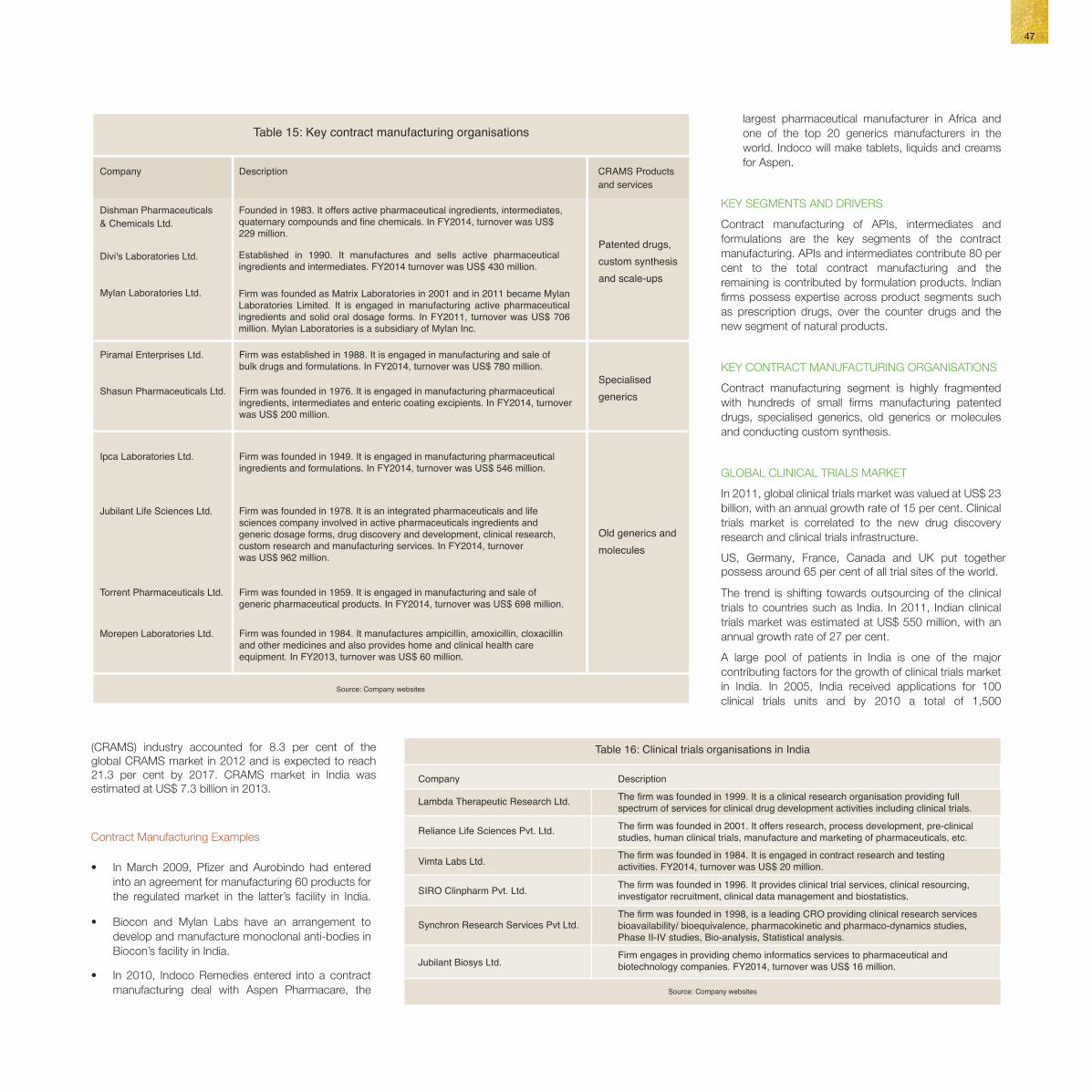

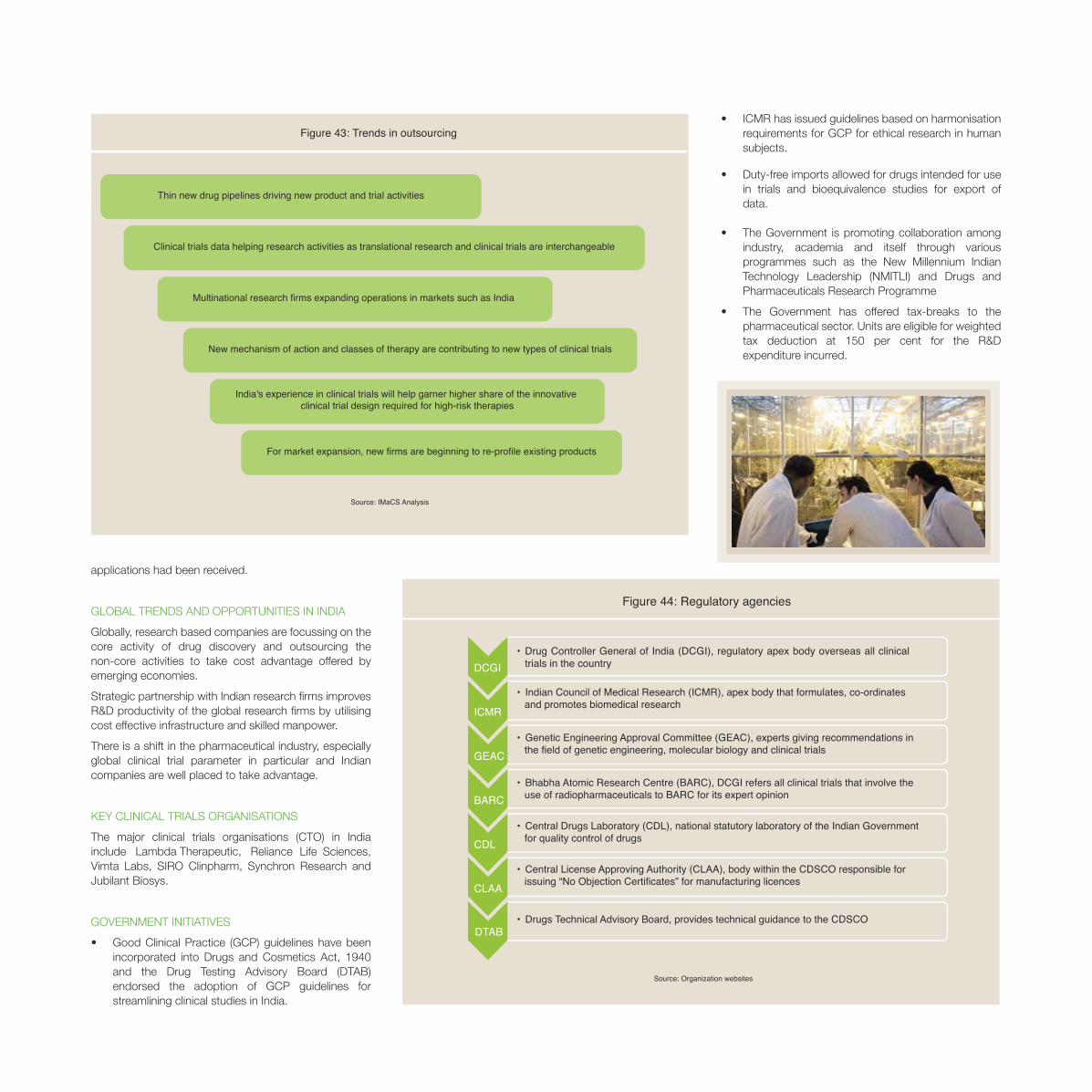

The Best of India in Pharmaceuticals.pdf - IBEF

72

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of The Best of India in Pharmaceuticals.pdf - IBEF

India Brand Equity FoundationApparel House, # 519-22, 5th Floor

Sector 44, Gurgaon 122003Haryana, India

Tel: +91 124 449 9601Fax: +91 124 449 9615

Email: [email protected]

Web: www.ibef.orgwww.brandindiapharma.in

India Brand Equity Foundation (IBEF) is a Trust established by the

Ministry of Commerce, Government of India. IBEF’s

primary objective is to promote and create international

awareness of the Made in India label in markets overseas and to

facilitate the dissemination of knowledge of Indian products

and services. Towards this objective, IBEF works closely with stakeholders across government

and industry.

AN INTRODUCTION

The Indian pharmaceutical industry has been consistently advancing rapidly, expanding on a global scale. Pharmaceutical exports from India have grown at a CAGR of 21 per cent over the last decade. India today ranks amongst the top global generic formulation exporters in volume terms and accounts for about 10 per cent of the global pharmaceutical industry in volume terms. A producer of high quality and affordable pharma products, India today is aptly described as the Pharmacy of the World.

Indian pharmaceutical manufactures comply with global regulatory standards.

India accounts for 36.9 per cent (3,411) of the 9,296 Drug Master Files (DMFs) filed with the USA, which is the highest outside of the USA (as on December 31, 2013) and is home to about 1,400 WHO GMP approved manufacturing units. India has been accredited with approximately 1,105 CEPs, more than 950 TGA approvals and 584 sites approved by the USFDA. India has gained significant strengths in the area of biopharmaceuticals, generics, over-the-counter (OTC) drugs, drug delivery mechanisms, alternative medicine, contract research and manufacturing.

A major growth driver for generics globally, the Indian pharma industry is spearheaded by a strong talent base and manufacturing excellence. The capability of the Indian pharma industry to produce high quality products at reasonable prices offers solutions to many countries to manage health expenses for their increasing populace.

The Best of India in Pharmaceuticals showcases the strengths and successes of the Indian pharmaceutical industry, which make India a Responsible Healthcare provider.

AN INTRODUCTION

The Indian pharmaceutical industry has been consistently advancing rapidly, expanding on a global scale. Pharmaceutical exports from India have grown at a CAGR of 21 per cent over the last decade. India today ranks amongst the top global generic formulation exporters in volume terms and accounts for about 10 per cent of the global pharmaceutical industry in volume terms. A producer of high quality and affordable pharma products, India today is aptly described as the Pharmacy of the World.

Indian pharmaceutical manufactures comply with global regulatory standards.

India accounts for 36.9 per cent (3,411) of the 9,296 Drug Master Files (DMFs) filed with the USA, which is the highest outside of the USA (as on December 31, 2013) and is home to about 1,400 WHO GMP approved manufacturing units. India has been accredited with approximately 1,105 CEPs, more than 950 TGA approvals and 584 sites approved by the USFDA. India has gained significant strengths in the area of biopharmaceuticals, generics, over-the-counter (OTC) drugs, drug delivery mechanisms, alternative medicine, contract research and manufacturing.

A major growth driver for generics globally, the Indian pharma industry is spearheaded by a strong talent base and manufacturing excellence. The capability of the Indian pharma industry to produce high quality products at reasonable prices offers solutions to many countries to manage health expenses for their increasing populace.

The Best of India in Pharmaceuticals showcases the strengths and successes of the Indian pharmaceutical industry, which make India a Responsible Healthcare provider.

T

Figure 3: State-wise share of pharmaceuticals

manufacturing formulations.

Sources: Department of Pharmaceuticals Annual Report 2010-11, IMaCS Analysis

Company Annual sales Achievements (US$, million)

pharmaceuticals company.

-lowering molecule

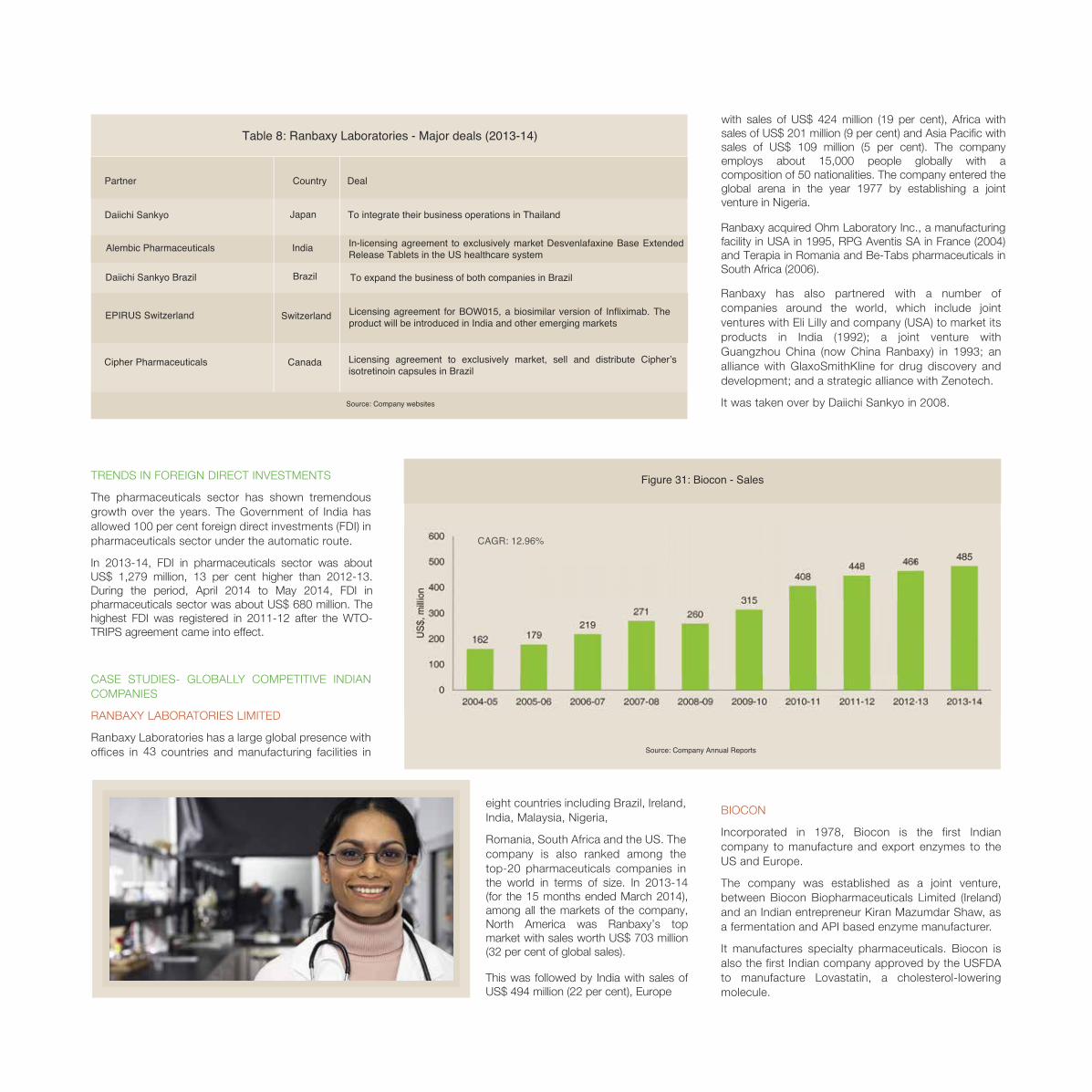

industry in India was valued at about US$ 27.83 billion in2012-13.

13.2314.60

Anti-infective medicines contribute 17.2 per cent to thetotal therapeutic needs of the country. Other majortherapeutic segments are: cardiac (11.4 per cent),gastro-intestinal (10.9 per cent), respiratory (8.7 percent) and analgesics (8.6 per cent).

Lupin Limited, Aurobindo Pharma, Piramal Enterprises,Sun Pharmaceuticals Industries, GlaxoSmithklinePharmaceuticals, Zydus Cadila, Novartis India, SanofiIndia Limited, Abbott India and Biocon.

industry is valued at about US$ 2.5 billion.

1,520.53

2223.72*

2,645.72

2,184.98

1,328.89 One of the largest API manufacturer with USFDA approved facilities

484.90

Sources: Company websites, Annual Reports, Note: *Data is for 15 months

Source: Department of Pharmaceuticals, Annual Report 2011-12

of 10.03 per cent between 2006-07 and 2012-13.

Domesticmarket 48%

Exports 52%

Sources: Pharmexcil, CII-PwC report: 'India Pharma Inc; Changing Landscapeof Indian Pharma Industry'

Figure 1: Indian pharmaceuticals market (2012-13)

Figure 2: Growth in Indian pharmaceutical industry (US$ Billion)

Sources: Department of Pharmaceuticals, Pharmexcil, CII-PwC report: 'India Pharma Inc;Changing Landscape of Indian Pharma Industry'

manufacturing units

Source: Department of Pharmaceuticals, Annual Report 2011-12

T

Figure 3: State-wise share of pharmaceuticals

manufacturing formulations.

Sources: Department of Pharmaceuticals Annual Report 2010-11, IMaCS Analysis

Company Annual sales Achievements (US$, million)

pharmaceuticals company.

-lowering molecule

industry in India was valued at about US$ 27.83 billion in2012-13.

13.2314.60

Anti-infective medicines contribute 17.2 per cent to thetotal therapeutic needs of the country. Other majortherapeutic segments are: cardiac (11.4 per cent),gastro-intestinal (10.9 per cent), respiratory (8.7 percent) and analgesics (8.6 per cent).

Lupin Limited, Aurobindo Pharma, Piramal Enterprises,Sun Pharmaceuticals Industries, GlaxoSmithklinePharmaceuticals, Zydus Cadila, Novartis India, SanofiIndia Limited, Abbott India and Biocon.

industry is valued at about US$ 2.5 billion.

1,520.53

2223.72*

2,645.72

2,184.98

1,328.89 One of the largest API manufacturer with USFDA approved facilities

484.90

Sources: Company websites, Annual Reports, Note: *Data is for 15 months

Source: Department of Pharmaceuticals, Annual Report 2011-12

of 10.03 per cent between 2006-07 and 2012-13.

Domesticmarket 48%

Exports 52%

Sources: Pharmexcil, CII-PwC report: 'India Pharma Inc; Changing Landscapeof Indian Pharma Industry'

Figure 1: Indian pharmaceuticals market (2012-13)

Figure 2: Growth in Indian pharmaceutical industry (US$ Billion)

Sources: Department of Pharmaceuticals, Pharmexcil, CII-PwC report: 'India Pharma Inc;Changing Landscape of Indian Pharma Industry'

manufacturing units

Source: Department of Pharmaceuticals, Annual Report 2011-12

05

%

%

%

%

%

%%

%

%

%

T

Figure 3: State-wise share of pharmaceuticals

manufacturing formulations.

Sources: Department of Pharmaceuticals Annual Report 2010-11, IMaCS Analysis

Company Annual sales Achievements (US$, million)

pharmaceuticals company.

-lowering molecule

industry in India was valued at about US$ 27.83 billion in2012-13.

13.2314.60

Anti-infective medicines contribute 17.2 per cent to thetotal therapeutic needs of the country. Other majortherapeutic segments are: cardiac (11.4 per cent),gastro-intestinal (10.9 per cent), respiratory (8.7 percent) and analgesics (8.6 per cent).

Lupin Limited, Aurobindo Pharma, Piramal Enterprises,Sun Pharmaceuticals Industries, GlaxoSmithklinePharmaceuticals, Zydus Cadila, Novartis India, SanofiIndia Limited, Abbott India and Biocon.

industry is valued at about US$ 2.5 billion.

1,520.53

2223.72*

2,645.72

2,184.98

1,328.89 One of the largest API manufacturer with USFDA approved facilities

484.90

Sources: Company websites, Annual Reports, Note: *Data is for 15 months

Source: Department of Pharmaceuticals, Annual Report 2011-12

of 10.03 per cent between 2006-07 and 2012-13.

Domesticmarket 48%

Exports 52%

Sources: Pharmexcil, CII-PwC report: 'India Pharma Inc; Changing Landscapeof Indian Pharma Industry'

Figure 1: Indian pharmaceuticals market (2012-13)

Figure 2: Growth in Indian pharmaceutical industry (US$ Billion)

Sources: Department of Pharmaceuticals, Pharmexcil, CII-PwC report: 'India Pharma Inc;Changing Landscape of Indian Pharma Industry'

manufacturing units

Source: Department of Pharmaceuticals, Annual Report 2011-12

T

Figure 3: State-wise share of pharmaceuticals

manufacturing formulations.

Sources: Department of Pharmaceuticals Annual Report 2010-11, IMaCS Analysis

Company Annual sales Achievements (US$, million)

pharmaceuticals company.

-lowering molecule

industry in India was valued at about US$ 27.83 billion in2012-13.

13.2314.60

Anti-infective medicines contribute 17.2 per cent to thetotal therapeutic needs of the country. Other majortherapeutic segments are: cardiac (11.4 per cent),gastro-intestinal (10.9 per cent), respiratory (8.7 percent) and analgesics (8.6 per cent).

Lupin Limited, Aurobindo Pharma, Piramal Enterprises,Sun Pharmaceuticals Industries, GlaxoSmithklinePharmaceuticals, Zydus Cadila, Novartis India, SanofiIndia Limited, Abbott India and Biocon.

industry is valued at about US$ 2.5 billion.

1,520.53

2223.72*

2,645.72

2,184.98

1,328.89 One of the largest API manufacturer with USFDA approved facilities

484.90

Sources: Company websites, Annual Reports, Note: *Data is for 15 months

Source: Department of Pharmaceuticals, Annual Report 2011-12

of 10.03 per cent between 2006-07 and 2012-13.

Domesticmarket 48%

Exports 52%

Sources: Pharmexcil, CII-PwC report: 'India Pharma Inc; Changing Landscapeof Indian Pharma Industry'

Figure 1: Indian pharmaceuticals market (2012-13)

Figure 2: Growth in Indian pharmaceutical industry (US$ Billion)

Sources: Department of Pharmaceuticals, Pharmexcil, CII-PwC report: 'India Pharma Inc;Changing Landscape of Indian Pharma Industry'

manufacturing units

Source: Department of Pharmaceuticals, Annual Report 2011-12

05

%

%

%

%

%

%%

%

%

%

Figure 5: Major industry growth drivers

Increase in

income

Rise inhealthcareawareness

Growinghealth

insurancemarket

Growth ofpopulation

Rising prevalenceof chronicdiseases

Improvementin medicalfacilities

MajorGrowthDrivers

Source: IMaCS Analysis

Skilled manpower

Financial capability

Infrastructure

R&D

networks overseas.

existing infrastructure and facilities.

segments.

Region Percentage of total exports North America European Union

Figure 8: Imports of pharmaceuticals to India

Figure 9: Major demand drivers for exports

Source: IMaCS Analysis

Increasingcertificationfrom WHO,USFDA,

MHRA. etc.

Complexsynthesis

Cost effective drugs,

exports market

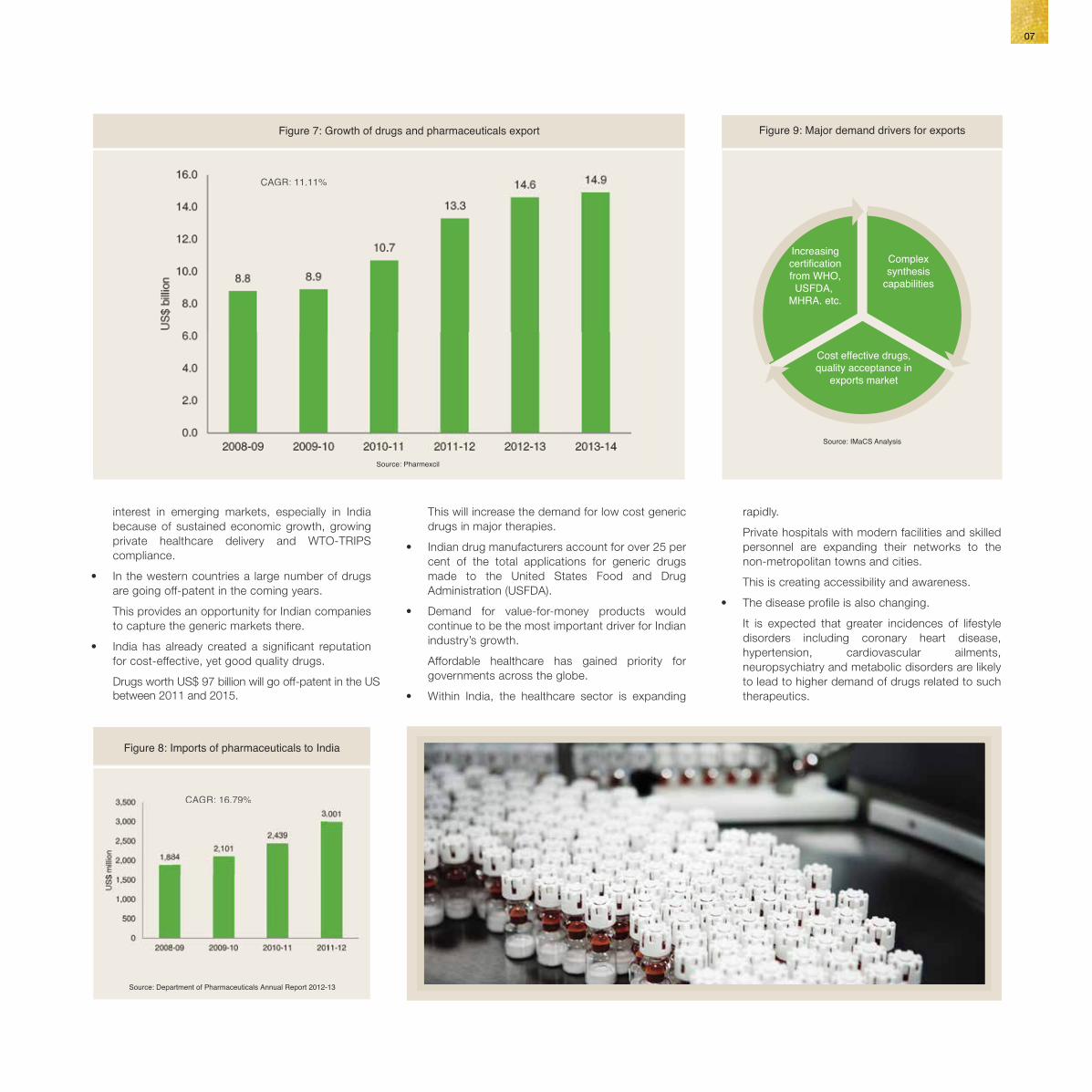

Over 50 per cent of pharmaceuticals produced in Indiaare exported.

The exports of drugs and pharmaceuticals were valued atUS$ 14.9 billion in 2013-14, growing at a CAGR of 11.11per cent.

Destinations for exports cover over 200 countries aroundthe globe, the major ones being the US, Russia, the UK,Germany and South Africa.

As per the Department of Pharmaceuticals, imports in2011-12 were valued at around US$ 3.0 billion and havebeen growing at a CAGR of 16.79 per cent.

10,563 pharmaceuticals manufacturing units in the organised sector; 370 USFDA approved plants.

Average R&D expenditure by companies increased by 19.6 per cent in 2011-12.

Sources: Department of Pharmaceuticals Annual Report 2011-12, Pharmexcil

Drugs worth US$ 97 billion will go off-patent in the USbetween 2011 and 2015.

Source: Department of Pharmaceuticals Annual Report 2012-13

67

Association of Southeast AsianNations (ASEAN)Latin AmericaCommonwealth ofIndependent States (CIS)Asia (Excluding MiddleEast)

South Asia

28%

18%16%Africa

7%Middle East

7%

6%

6%

4%

4%

Source: Pharmaceuticals Export Promotion Council (Pharmexcil)

from India (2012-13)

Source: Pharmexcil

CAGR: 16.79%

CAGR: 11.11%

Figure 7: Growth of drugs and pharmaceuticals export

CAGR: 16.79%

CAGR: 11.11%

07

Figure 5: Major industry growth drivers

Increase in

income

Rise inhealthcareawareness

Growinghealth

insurancemarket

Growth ofpopulation

Rising prevalenceof chronicdiseases

Improvementin medicalfacilities

MajorGrowthDrivers

Source: IMaCS Analysis

Skilled manpower

Financial capability

Infrastructure

R&D

networks overseas.

existing infrastructure and facilities.

segments.

Region Percentage of total exports North America European Union

Figure 8: Imports of pharmaceuticals to India

Figure 9: Major demand drivers for exports

Source: IMaCS Analysis

Increasingcertificationfrom WHO,USFDA,

MHRA. etc.

Complexsynthesis

Cost effective drugs,

exports market

Over 50 per cent of pharmaceuticals produced in Indiaare exported.

The exports of drugs and pharmaceuticals were valued atUS$ 14.9 billion in 2013-14, growing at a CAGR of 11.11per cent.

Destinations for exports cover over 200 countries aroundthe globe, the major ones being the US, Russia, the UK,Germany and South Africa.

As per the Department of Pharmaceuticals, imports in2011-12 were valued at around US$ 3.0 billion and havebeen growing at a CAGR of 16.79 per cent.

10,563 pharmaceuticals manufacturing units in the organised sector; 370 USFDA approved plants.

Average R&D expenditure by companies increased by 19.6 per cent in 2011-12.

Sources: Department of Pharmaceuticals Annual Report 2011-12, Pharmexcil

Drugs worth US$ 97 billion will go off-patent in the USbetween 2011 and 2015.

Source: Department of Pharmaceuticals Annual Report 2012-13

67

Association of Southeast AsianNations (ASEAN)Latin AmericaCommonwealth ofIndependent States (CIS)Asia (Excluding MiddleEast)

South Asia

28%

18%16%Africa

7%Middle East

7%

6%

6%

4%

4%

Source: Pharmaceuticals Export Promotion Council (Pharmexcil)

from India (2012-13)

Source: Pharmexcil

CAGR: 16.79%

CAGR: 11.11%

Figure 7: Growth of drugs and pharmaceuticals export

CAGR: 16.79%

CAGR: 11.11%

07

Figure 10: Measures to improve export performance

Sources: Strategy for increasing exports of Pharmaceutical products - Report of the task force, Ministry of Commerce, 2008, IMaCS Analysis

trained professionals

Promoting AYUSHeducationCreating national

Service tax exemptions

Investing in outsourcing Simplifying approvalprocedures

Enhancing

PromotingCRAMS, drugdiscovery andclinical trials

PromotingIndian systemof medicine

such as AYUSH

Acceleratinggrowth ofgenericsindustry

26

09

Figure 10: Measures to improve export performance

Sources: Strategy for increasing exports of Pharmaceutical products - Report of the task force, Ministry of Commerce, 2008, IMaCS Analysis

trained professionals

Promoting AYUSHeducationCreating national

Service tax exemptions

Investing in outsourcing Simplifying approvalprocedures

Enhancing

PromotingCRAMS, drugdiscovery andclinical trials

PromotingIndian systemof medicine

such as AYUSH

Acceleratinggrowth ofgenericsindustry

26

09

25070

registered revenue of US$ 1.83 billion in FY2013-14with 48 per cent of exports to the advanced marketsand 27 per cent to emerging markets.

1961.

2014, Sun Pharma has announced to acquire Ranbaxyfor US$ 4 billion from Daiichi Sankyo.

In April

France, Jordan and Sri Lanka.

25

Alendronate Sodium, Budesonide and Carvedilol.

Torrent Pharmaceuticals was established in 1970. It isengaged in the business of branded formulations. In theBrazilian market, the company has 15 products with 4products in the cardiovascular segment, 5 products inthe central nervous system (CNS) segment and 3products in the oral anti-diabetic segment and 3products in other segments.

38 new products. In 2013, the company entered into adefinitive binding agreement with Elder PharmaceuticalsLimited to acquire its branded domestic formulationsbusiness in India and Nepal ("India Business") for aconsideration of about US$ 330.63 million. TorrentPharma exports products to over 50 countries.

11

25070

registered revenue of US$ 1.83 billion in FY2013-14with 48 per cent of exports to the advanced marketsand 27 per cent to emerging markets.

1961.

2014, Sun Pharma has announced to acquire Ranbaxyfor US$ 4 billion from Daiichi Sankyo.

In April

France, Jordan and Sri Lanka.

25

Alendronate Sodium, Budesonide and Carvedilol.

Torrent Pharmaceuticals was established in 1970. It isengaged in the business of branded formulations. In theBrazilian market, the company has 15 products with 4products in the cardiovascular segment, 5 products inthe central nervous system (CNS) segment and 3products in the oral anti-diabetic segment and 3products in other segments.

38 new products. In 2013, the company entered into adefinitive binding agreement with Elder PharmaceuticalsLimited to acquire its branded domestic formulationsbusiness in India and Nepal ("India Business") for aconsideration of about US$ 330.63 million. TorrentPharma exports products to over 50 countries.

11

Figure 11: Pharmaceuticals distribution chain

Retail/Chemist

Customer

Institution

Manufacturer

Central Warehouse

Super Stockist

Hospitals

Stockist

Wholesaler

Source: IMaCS analysis

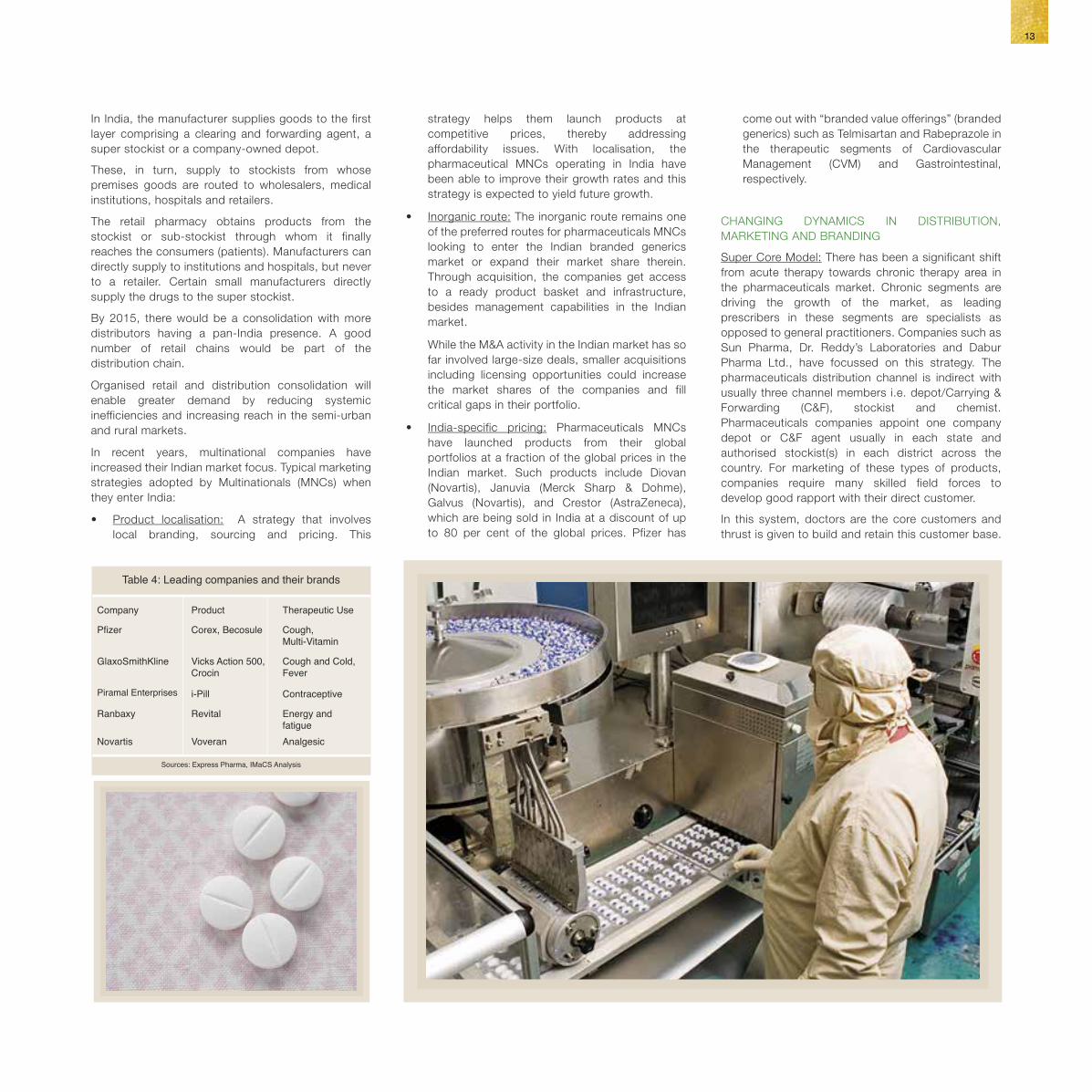

Table 4: Leading companies and their brands

Company Product Therapeutic Use

Pfizer Corex, Becosule Cough, Multi-Vitamin

GlaxoSmithKline Vicks Action 500, Cough and Cold, Crocin Fever

i-Pill Contraceptive

Ranbaxy Revital Energy and fatigueNovartis Voveran Analgesic

Sources: Express Pharma, IMaCS Analysis

In January 2014, Aurobindo Pharma signed anagreement with Actavis to acquire its personnel,commercial infrastructure, products, marketingauthorisations and dossier licence rights in sevenEuropean countries for €30 million.

Cipla bought Yemen-based drug distributor for US$21 million. The company acquired 51 per cent stakein pharmaceuticals manufacturing and distributionbusiness in Yemen.

Videocon Industries is set to acquire Dr DatsonsLabs Ltd (DTL) at an enterprise value of US$ 57.8million.

Torrent Pharma entered into a definitive bindingagreement with Elder Pharmaceuticals Limited toacquire its branded domestic formulations businessin India and Nepal ("India Business") for aconsideration of about US$ 330.63 millionCadila Pharmaceuticals Ltd signed a joint licensingagreement with the UK-based antibiotics discoverycompany Helperby Therapeutics on antibiotic drugresistance research and development.

Zydus Cadila and Germany-based Pieris AGannounced an alliance for development andcommercialisation of multiple novel Anticalin-basedprotein therapeutics.

Lupin has acquired 100 per cent equity stake inLaboratorios Grin, S.A. De C.V., Mexico, subject tocertain closing conditions, for an unspecifiedamount. The acquisition marks Lupin's entry into thehigh-growth Mexican and the larger Latin Americanpharmaceuticals market.

In April 2014, Sun Pharma announced to acquireRanbaxy for US$ 4 billion from Daiichi Sankyo.

Biocon Ltd and Quark Pharmaceuticals Inc haveentered into a tie-up for the discovery anddevelopment of small interfering RNA (siRNA)-basedmedicines. This collaboration will enable Biocon toco-develop, manufacture and commercialiseQPI-1007, a novel siRNA drug candidate forophthalmic conditions, for India and other markets,according to a company statement.

Cipla acquired a majority stake in Uganda's QualityChemical Industries (QCIL), with the acquisition ofan additional 14.5 per cent stake for US$ 15 millionthrough its subsidiary, Meditab Holdings Ltd (MHL).

Sun Pharmaceutical Industries acquired DUSA, aUS-based dermatology company, in an all-cashtransaction of US$ 230 million.

Lupin acquired Dutch firm Nanomi to enter complexinjectables market. Piramal Enterprises

13

Figure 11: Pharmaceuticals distribution chain

Retail/Chemist

Customer

Institution

Manufacturer

Central Warehouse

Super Stockist

Hospitals

Stockist

Wholesaler

Source: IMaCS analysis

Table 4: Leading companies and their brands

Company Product Therapeutic Use

Pfizer Corex, Becosule Cough, Multi-Vitamin

GlaxoSmithKline Vicks Action 500, Cough and Cold, Crocin Fever

i-Pill Contraceptive

Ranbaxy Revital Energy and fatigueNovartis Voveran Analgesic

Sources: Express Pharma, IMaCS Analysis

In January 2014, Aurobindo Pharma signed anagreement with Actavis to acquire its personnel,commercial infrastructure, products, marketingauthorisations and dossier licence rights in sevenEuropean countries for €30 million.

Cipla bought Yemen-based drug distributor for US$21 million. The company acquired 51 per cent stakein pharmaceuticals manufacturing and distributionbusiness in Yemen.

Videocon Industries is set to acquire Dr DatsonsLabs Ltd (DTL) at an enterprise value of US$ 57.8million.

Torrent Pharma entered into a definitive bindingagreement with Elder Pharmaceuticals Limited toacquire its branded domestic formulations businessin India and Nepal ("India Business") for aconsideration of about US$ 330.63 millionCadila Pharmaceuticals Ltd signed a joint licensingagreement with the UK-based antibiotics discoverycompany Helperby Therapeutics on antibiotic drugresistance research and development.

Zydus Cadila and Germany-based Pieris AGannounced an alliance for development andcommercialisation of multiple novel Anticalin-basedprotein therapeutics.

Lupin has acquired 100 per cent equity stake inLaboratorios Grin, S.A. De C.V., Mexico, subject tocertain closing conditions, for an unspecifiedamount. The acquisition marks Lupin's entry into thehigh-growth Mexican and the larger Latin Americanpharmaceuticals market.

In April 2014, Sun Pharma announced to acquireRanbaxy for US$ 4 billion from Daiichi Sankyo.

Biocon Ltd and Quark Pharmaceuticals Inc haveentered into a tie-up for the discovery anddevelopment of small interfering RNA (siRNA)-basedmedicines. This collaboration will enable Biocon toco-develop, manufacture and commercialiseQPI-1007, a novel siRNA drug candidate forophthalmic conditions, for India and other markets,according to a company statement.

Cipla acquired a majority stake in Uganda's QualityChemical Industries (QCIL), with the acquisition ofan additional 14.5 per cent stake for US$ 15 millionthrough its subsidiary, Meditab Holdings Ltd (MHL).

Sun Pharmaceutical Industries acquired DUSA, aUS-based dermatology company, in an all-cashtransaction of US$ 230 million.

Lupin acquired Dutch firm Nanomi to enter complexinjectables market. Piramal Enterprises

13

Figure 12: Drug discovery and development process

Sources: Pharmaceutical Research and Manufacturers of America, Pharmaceutical Industry Profile 2011 (Washington, DC: PhRMA, April 2011; IMaCS Analysis)

USFDA Review(Up to 2 years)

Large ScaleManufacturing

Manufacturingand sales

COMPOUNDS: 5VOLUNTEERS:Phase I: 20-100Phase II: 100-500Phase III: 1,000-5,000

USFDA APPROVAL:One drug approved

COMPOUNDS:-Stage I: 5,000-10,000Stage II: 250

Stage I - Drug Discovery+Stage II - Preclinical

(3-6 years)

Stage III - Clinical Trials(6-7years)

Figure 13: ANDA approvals for Indian pharmaceuticals

around US$ 984.38 million in 2012-13, an increase of5.38 per cent over previous year.

Average R&D spending of top Indian pharmaceuticalscompanies in 2012-13 is 7-8 per cent of the total sales, up

370

In 2013, of the total 400 ANDAs and 86 tentativeapprovals, Indian companies received 154 approvals forthe ANDAs and 38 tentative approvals. This gives leadingIndian companies’ dominance in US generic drug market.

Source: Pharmabiz - January 22, 2014

companies (2013)

Global R&D spending in the life sciences industry wasaround US$ 195.3 billion in 2013. The biopharmaceuticalsector accounts for around 85 per cent of all R&Dexpenditures in the life sciences industry.

141

annual handling capacity of 30,000 tonnes.

15

Figure 12: Drug discovery and development process

Sources: Pharmaceutical Research and Manufacturers of America, Pharmaceutical Industry Profile 2011 (Washington, DC: PhRMA, April 2011; IMaCS Analysis)

USFDA Review(Up to 2 years)

Large ScaleManufacturing

Manufacturingand sales

COMPOUNDS: 5VOLUNTEERS:Phase I: 20-100Phase II: 100-500Phase III: 1,000-5,000

USFDA APPROVAL:One drug approved

COMPOUNDS:-Stage I: 5,000-10,000Stage II: 250

Stage I - Drug Discovery+Stage II - Preclinical

(3-6 years)

Stage III - Clinical Trials(6-7years)

Figure 13: ANDA approvals for Indian pharmaceuticals

around US$ 984.38 million in 2012-13, an increase of5.38 per cent over previous year.

Average R&D spending of top Indian pharmaceuticalscompanies in 2012-13 is 7-8 per cent of the total sales, up

370

In 2013, of the total 400 ANDAs and 86 tentativeapprovals, Indian companies received 154 approvals forthe ANDAs and 38 tentative approvals. This gives leadingIndian companies’ dominance in US generic drug market.

Source: Pharmabiz - January 22, 2014

companies (2013)

Global R&D spending in the life sciences industry wasaround US$ 195.3 billion in 2013. The biopharmaceuticalsector accounts for around 85 per cent of all R&Dexpenditures in the life sciences industry.

141

annual handling capacity of 30,000 tonnes.

15

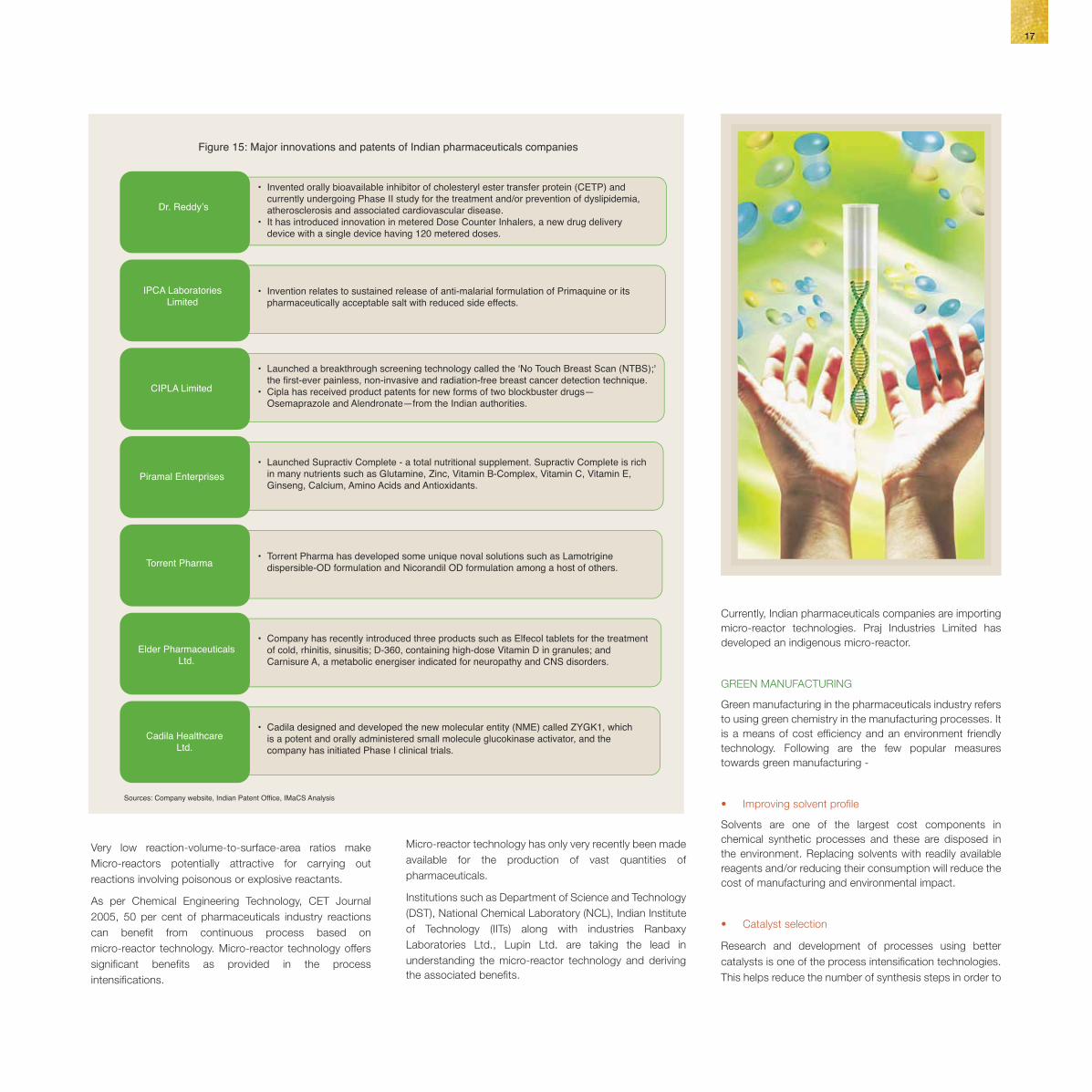

Dr. Reddy’s currently undergoing Phase II study for the treatment and/or prevention of dyslipidemia, atherosclerosis and associated cardiovascular disease.

device with a single device having 120 metered doses.

IPCA LaboratoriesLimited

CIPLA Limited

Torrent Pharma

Elder PharmaceuticalsLtd.

Cadila HealthcareLtd.

Figure 15: Major innovations and patents of Indian pharmaceuticals companies

pharmaceutically acceptable salt with reduced side effects.

dispersible-OD formulation and Nicorandil OD formulation among a host of others.

of cold, rhinitis, sinusitis; D-360, containing high-dose Vitamin D in granules; and Carnisure A, a metabolic energiser indicated for neuropathy and CNS disorders.

is a potent and orally administered small molecule glucokinase activator, and the company has initiated Phase I clinical trials.

Sources: Company website, Indian Patent Office, IMaCS Analysis

CASE STUDIES – MAJOR INNOVATIONS

Figure 14: Pharmaceutical product patents granted3672012,in India (2005-2012)

Source: Controller General of Patents, Designs, and Trade Marks, India

Currently, India holds 76th rank in Global Innovation Index(GII), study conducted by the Confederation of IndianIndustry (CII), INSEAD and World Intellectual Property

Organisation (WIPO).

Piramal Enterprises

17

Dr. Reddy’s currently undergoing Phase II study for the treatment and/or prevention of dyslipidemia, atherosclerosis and associated cardiovascular disease.

device with a single device having 120 metered doses.

IPCA LaboratoriesLimited

CIPLA Limited

Torrent Pharma

Elder PharmaceuticalsLtd.

Cadila HealthcareLtd.

Figure 15: Major innovations and patents of Indian pharmaceuticals companies

pharmaceutically acceptable salt with reduced side effects.

dispersible-OD formulation and Nicorandil OD formulation among a host of others.

of cold, rhinitis, sinusitis; D-360, containing high-dose Vitamin D in granules; and Carnisure A, a metabolic energiser indicated for neuropathy and CNS disorders.

is a potent and orally administered small molecule glucokinase activator, and the company has initiated Phase I clinical trials.

Sources: Company website, Indian Patent Office, IMaCS Analysis

CASE STUDIES – MAJOR INNOVATIONS

Figure 14: Pharmaceutical product patents granted3672012,in India (2005-2012)

Source: Controller General of Patents, Designs, and Trade Marks, India

Currently, India holds 76th rank in Global Innovation Index(GII), study conducted by the Confederation of IndianIndustry (CII), INSEAD and World Intellectual Property

Organisation (WIPO).

Piramal Enterprises

17

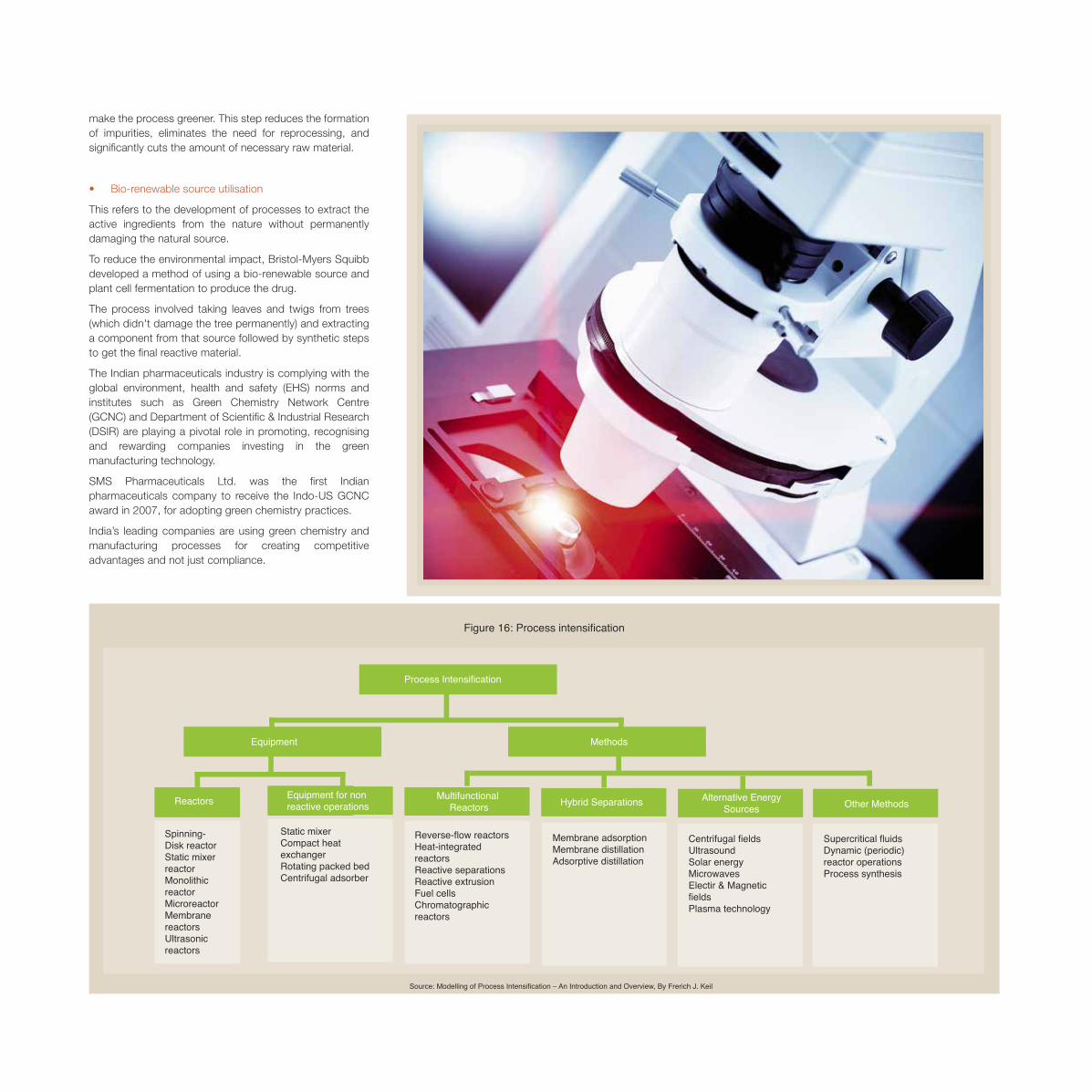

Figure 16: Process intensification

Process Intensification

Reactors reactive operationsMultifunctional

Reactors Hybrid Separations Alternative EnergySources

Spinning-Disk reactor

reactorMonolithicreactor MicroreactorMembranereactors Ultrasonicreactors

Compact heat

Rotating packed bed Centrifugal adsorber

Reverse-flow reactors Heat-integrated reactors Reactive separations

Fuel cellsChromatographicreactors

Membrane adsorptionMembrane distillationAdsorptive distillation

Centrifugal fieldsUltrasound Solar energy Microwaves Electir & Magneticfields Plasma technology

Other Methods

Supercritical fluids Dynamic (periodic)reactor operationsProcess synthesis

Methods

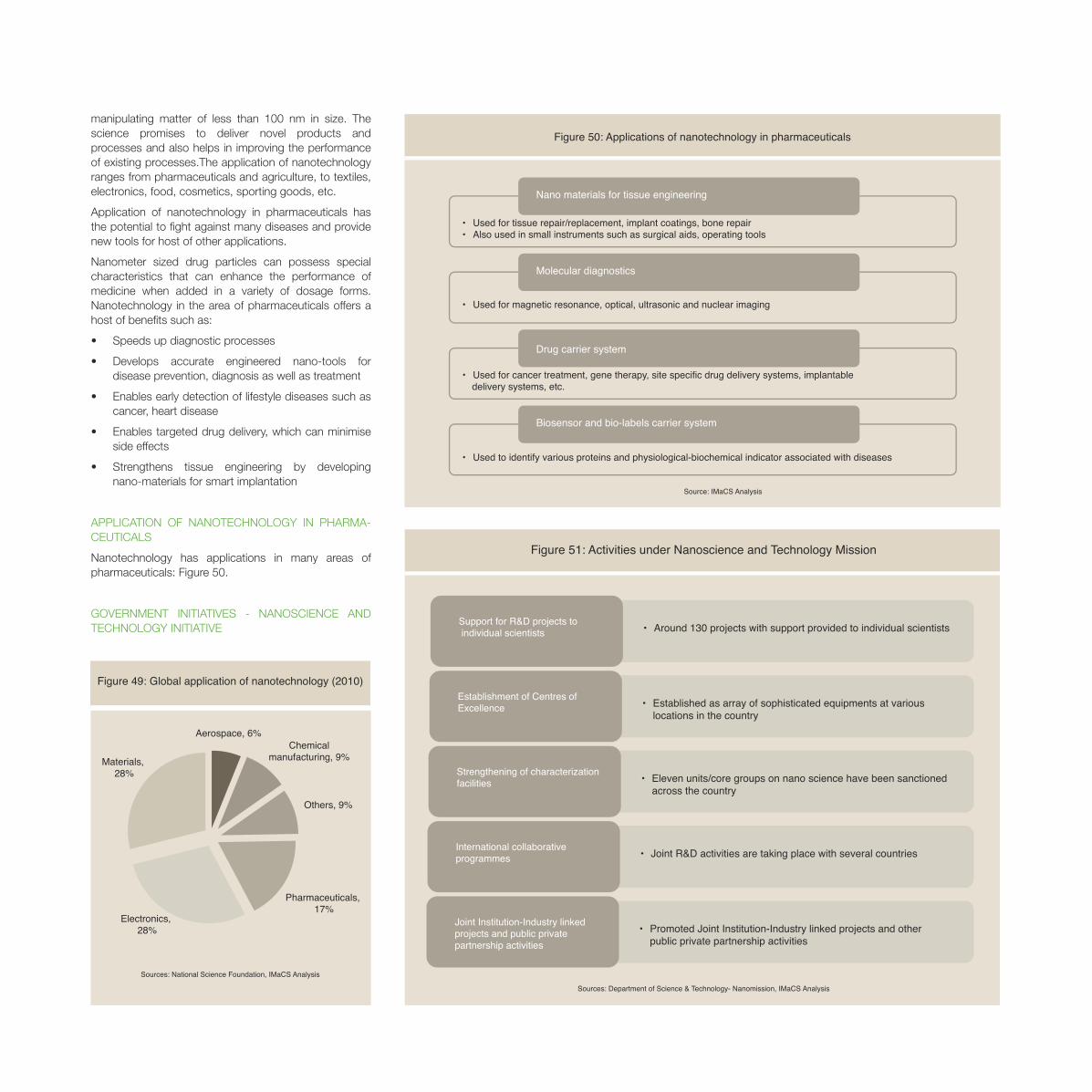

The global market for nanotechnology in medicalapplications was estimated at approximately US$ 1.7 billionin 2009.

19

Figure 16: Process intensification

Process Intensification

Reactors reactive operationsMultifunctional

Reactors Hybrid Separations Alternative EnergySources

Spinning-Disk reactor

reactorMonolithicreactor MicroreactorMembranereactors Ultrasonicreactors

Compact heat

Rotating packed bed Centrifugal adsorber

Reverse-flow reactors Heat-integrated reactors Reactive separations

Fuel cellsChromatographicreactors

Membrane adsorptionMembrane distillationAdsorptive distillation

Centrifugal fieldsUltrasound Solar energy Microwaves Electir & Magneticfields Plasma technology

Other Methods

Supercritical fluids Dynamic (periodic)reactor operationsProcess synthesis

Methods

The global market for nanotechnology in medicalapplications was estimated at approximately US$ 1.7 billionin 2009.

19

Public Expenditure Private Expenditure

Figure 17: Evolution of government policies - Indian healthcare sector

1946, PHC conceptualisation

1952-1977, Integrated health service and medical education

1978, Health for all by 2000 AD

1983, National Health Policy I

2000, National Population Policy (NPP)

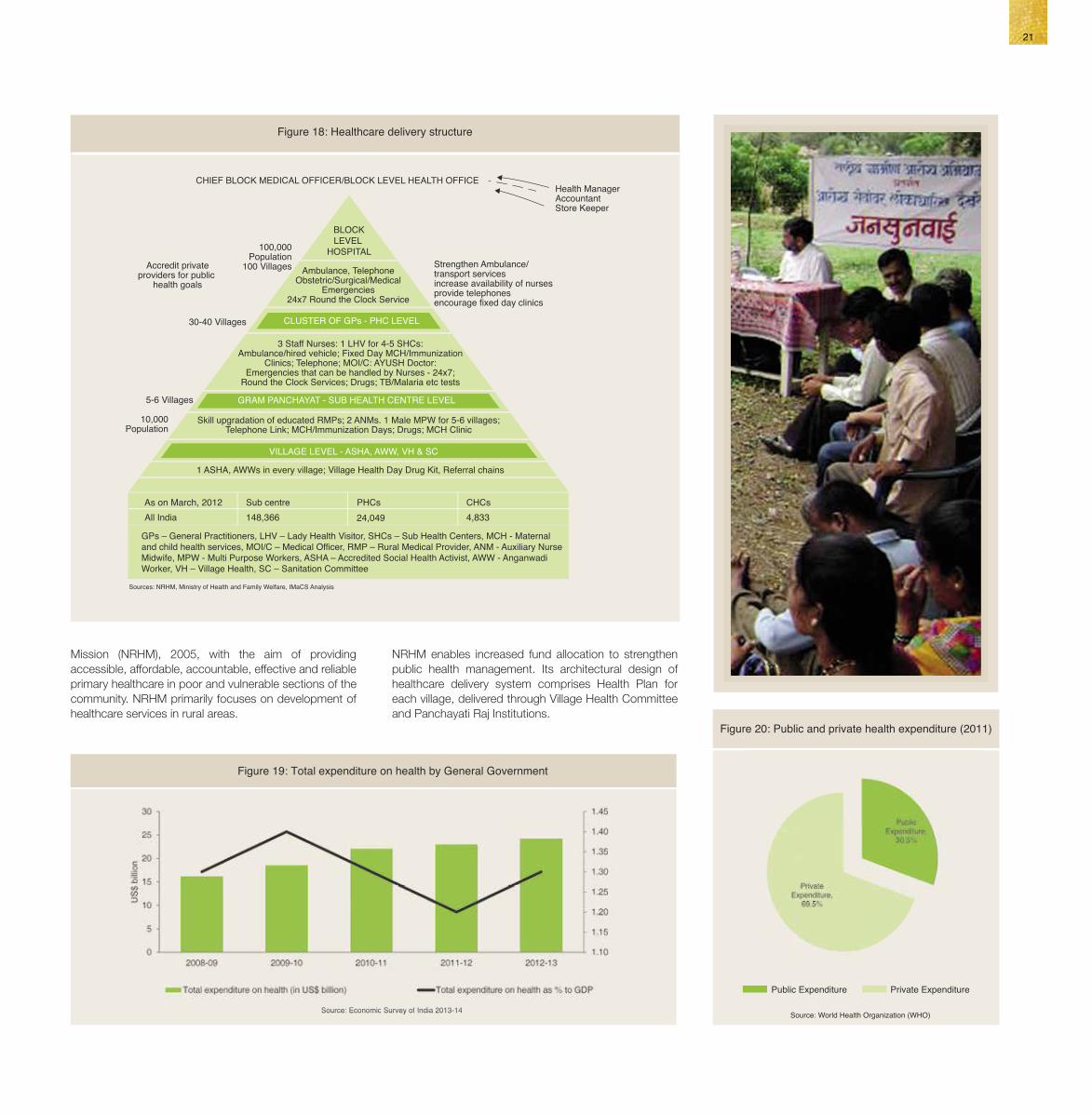

Figure 18: Healthcare delivery structure

Ambulance, TelephoneObstetric/Surgical/Medical

Emergencies24x7 Round the Clock Service

Accredit privateproviders for public

health goals

Strengthen Ambulance/transport servicesincrease availability of nursesprovide telephonesencourage fixed day clinics

100,000Population

100 Villages

30-40 Villages

5-6 Villages

10,000Population

Health ManagerAccountantStore Keeper

3 Staff Nurses: 1 LHV for 4-5 SHCs:Ambulance/hired vehicle; Fixed Day MCH/Immunization

Clinics; Telephone; MOI/C: AYUSH Doctor:Emergencies that can be handled by Nurses - 24x7;

Round the Clock Services; Drugs; TB/Malaria etc tests

Skill upgradation of educated RMPs; 2 ANMs. 1 Male MPW for 5-6 villages;Telephone Link; MCH/Immunization Days; Drugs; MCH Clinic

1 ASHA, AWWs in every village; Village Health Day Drug Kit, Referral chains

BLOCKLEVEL

HOSPITAL

CHIEF BLOCK MEDICAL OFFICER/BLOCK LEVEL HEALTH OFFICE

CLUSTER OF GPs - PHC LEVEL

GRAM PANCHAYAT - SUB HEALTH CENTRE LEVEL

VILLAGE LEVEL - ASHA, AWW, VH & SC

Sources: NRHM, Ministry of Health and Family Welfare, IMaCS Analysis

Sub centre PHCs CHCs All India

GPs – General Practitioners, LHV – Lady Health Visitor, SHCs – Sub Health Centers, MCH - Maternal and child health services, MOI/C – Medical Officer, RMP – Rural Medical Provider, ANM - Auxiliary Nurse Midwife, MPW - Multi Purpose Workers, ASHA – Accredited Social Health Activist, AWW - Anganwadi Worker, VH – Village Health, SC – Sanitation Committee

As on March, 2012148,366 24,049 4,833

Figure 20: Public and private health expenditure (2011)

Source: World Health Organization (WHO)Source: Economic Survey of India 2013-14

Figure 19: Total expenditure on health by General Government

Source: Economic Survey of India 2013-14

2005, National Rural Health Mission (NRHM)

2013, National Health Mission (NHM)Sources: Ministry of Health and Family Welfare,Planning Commission, Government of India

21

Healthcare And Diagnostic Sector In India

Chapter 4

Mission (NRHM), 2005, with the aim of providing accessible, affordable, accountable, effective and reliable primary healthcare in poor and vulnerable sections of the community. NRHM primarily focuses on development of healthcare services in rural areas.

NRHM enables increased fund allocation to strengthen public health management. Its architectural design of healthcare delivery system comprises Health Plan for each village, delivered through Village Health Committee and Panchayati Raj Institutions.

EVOLUTION AND OVERVIEW OF INDIAN HEALTHCARE SECTOR

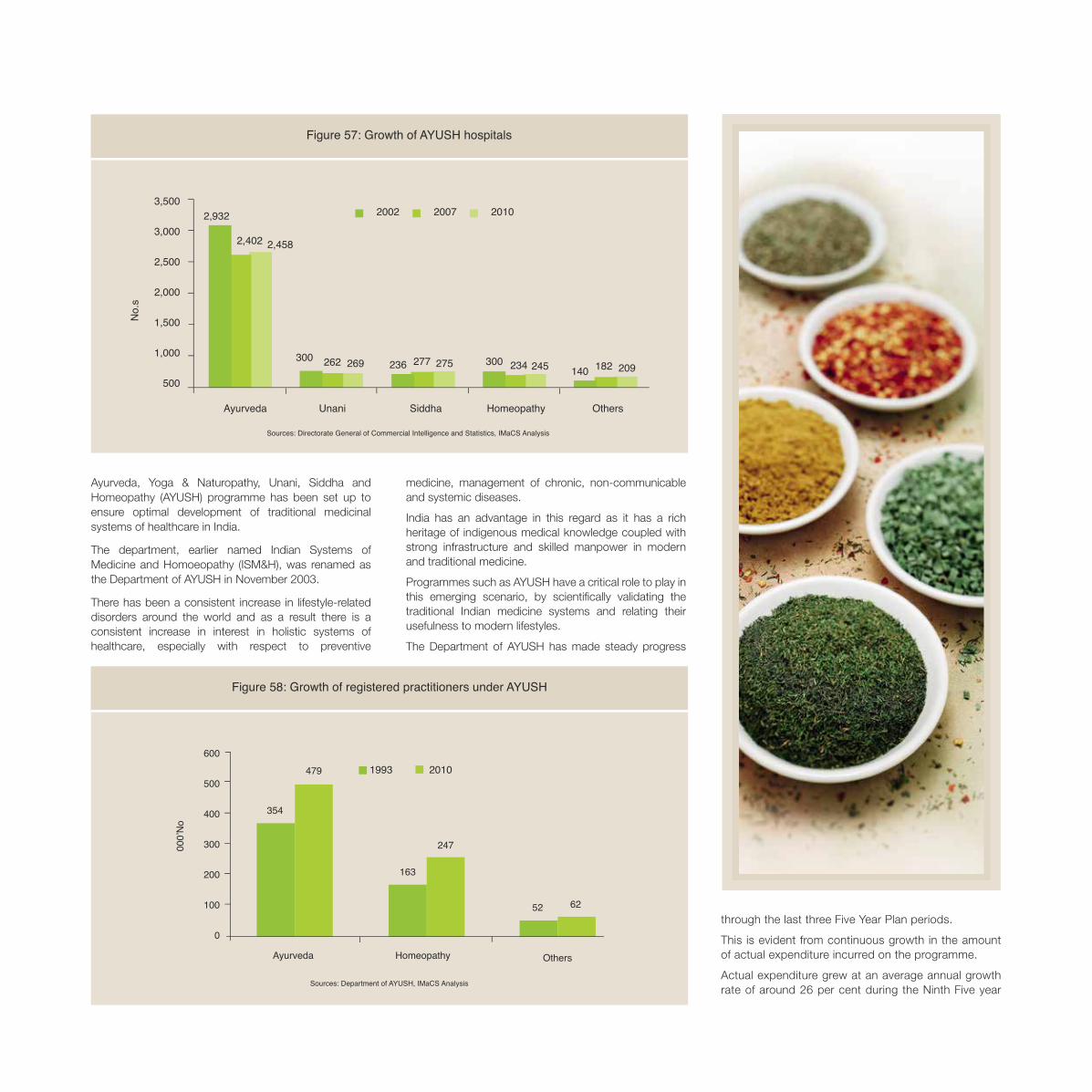

India is among the first countries to have recognised the importance of primary health care (PHC) approach. Conceptualised in 1946, PHC approach emphasised social orientation of medical practices and high level of public participation.

The period up to the first National Health Policy (NHP) in 1983 was dedicated to a concerted effort towards building programmes covering: health and sanitation through establishment of PHCs and sub-centres, health survey and planning, integrated health services, inclusion of larger population, building medical and support workforce, linking medical colleges and health centres.

Thereafter, policy improvements and evolution of industry have increased private sector participation.

The Government of India’s commitment to health for all led to the formulation of India’s first NHP. The period 1986-1996 was one of substantial growth in the private sector investments and it surpassed the public sector by a wide margin.

Private sector gained significance as the more preferred choice.

The Government of India launched National Rural Health

• Diagnostics industry is highly competitive and fragmented

The Indian diagnostics services industry, including pathological laboratories services, has grown at 20 per cent CAGR for the period 2006-2010.

Pathological laboratories services constitute over 52 per cent of the diagnostic market.With the increasing number of organised players in the segment, diagnostic services industry is likely to expand at more than this growth rate.

GOVERNMENT INITIATIVES - INDIAN HEALTHCARE SECTOR

In the Union Budget 2010-11, the Government increased total allocation for healthcare to US$ 5,240 million, more than an 11 per cent increase over 2009-10.

In the Union Budget 2012-13, the Government increased total allocation for healthcare to US$ 6,400 million, about 14 per cent higher than 2011-12. NRHM has been a successful scheme, launched to make the quality healthcare accessible and affordable.

GOVERNMENT INCENTIVES

The Government is encouraging private sector and investments in the healthcare sector through several

incentives and policy initiatives:

• New hospitals with 100 beds or more will be subject to 100 per cent tax holiday for the initial period of five years of operation.

• To attract investments in the healthcare infrastructure, 100 per cent FDI is permitted for health and medical services under the automatic route.

• Life-saving equipment is exempted from countervailing duty. Custom duty has been reduced to 5 per cent from 25 per cent.

• Multiplicity of customs duty on medical equipment is being done away with and basic customs duty reduced to 5 per cent from 7.5 per cent.

• Hospitals and dispensaries providing health travel facilities and attracting medical tourists are eligible for tax holidays and incentives.

IMPACT OF HEALTHCARE GROWTH ON PHARMACEUTICALS SECTOR

• Expanding overall market

Growth in the healthcare industry is based on the inclusive business model and incorporates a range of activities such as infrastructure development, services penetration, enhancement in training and education.

Consequently, it helps expand the whole healthcare market including pharmaceuticals. Historically, pharmaceuticals sector growth has tracked increase in healthcare expenditure.

• New healthcare players will influence reforms in healthcare industry including pharmaceuticals

Local and international players bring in new ideas and lead to systemic reforms, which in turn foster a streamlined, transparent, and better-regulated healthcare and hospital financing environment for the industry.

This trend will help increase demand for innovative drugs and hence support the long-term sustainable growth of the pharmaceutical sector.

• Industry wide collaboration will help innovate and maximise benefit

The healthcare scenario is ever evolving and the Government is planning to increase the public provisioning of healthcare. As per World Health Organisation (WHO), total expenditure on health increased from US$ 22.42 billion in 2001 to US$ 59.5 billion in 2010.

INDIAN HEALTHCARE SECTOR: MARKET SIZE

Domestic healthcare sector sales recorded a 17 per cent

CAGR during 2005-2010 to reach US$ 59.5 billion a year. The healthcare sector employs about 4.5 million people directly or indirectly and is the largest service sector employer in the country after retail. According to the Investment Commission of India, the healthcare sector is projected to grow at 15 per cent CAGR and reach the market value of US$ 79 billion by 2012 and US$ 280 billion by 2020.

Key segments and growth drivers

Hospital and pharmaceuticals are the largest segments of the sector in India, combined revenue from these segments are estimated to contribute 79 per cent of the total healthcare market by 2012.

• Demand driving healthcare infrastructure investments

For the distribution of healthcare across all demographic segments, 2.8 million additional beds are required by 2025, according to the WHO. Investments of US$ 100 billion are required.

• Flourishing medical tourism attracting growth

Medical tourists in India are expected to increase from

0.8 million in 2010 to 1.6 million by 2015.

India is expected to be a medical tourist hub and likely to contribute 3 per cent of the US$ 100 billion global medical tourism industry by 2013.

• Healthcare information and communication technology (ICT) spend is playing a significant role in healthcare delivery

Information and communication technology (ICT) including electronic medical records requirement of the healthcare industry was around US$ 270 million in 2010.

With the growth in the healthcare infrastructure and telemedicine, it is estimated to grow at 22 per cent CAGR until 2013.

• Pharmaceutical industry is poised for growth on back of affordability, increasing disposable income

The pharmaceuticals industry in India was valued at about US$ 21.73 billion in 2010.

Sustained economic growth, healthcare reforms and patent-related legislation are key drivers for average estimated growth of 12 to 15 per cent CAGR for next 10 years.

• Immense potential in medical equipment and consumables

The medical equipment market is heavily dependent on imports.

Domestic manufacturers such as Anand Medicaids, Carewell Mediproducts, Dental Products of India, Hindustan Syringes and Medical Devices, Lifeline Systems, Relisys Medical Devices Ltd, Surya Surgical Industries, etc., contribute to 25 per cent of the market.

In 2011, the Indian medical equipment market was estimated at US$ 2.64 billion and it is expected to reach US$ 4.95 billion by 2016, according to the Department of Health.

• Health insurance penetration will augment the overall healthcare market

In 2010, 15 per cent of the Indian population were covered through health insurance and 80 per cent of the healthcare expenditure was financed out-of-pocket.

The health insurance market is growing. It was valued at US$ 1.73 billion in 2010, with a 39 per cent CAGR from 2006-2010.

The insurance market is expected to grow to over 4 billion by 2013.

at US$ 345 million in 2010-11, contributing over 70 per cent of the total diagnostics services market and is expected to grow at 15-20 per cent year on year.

The largest segments are blood screening and infectious diseases. The fastest growing segments are genetic diseases, oncology and pharmacogenomics. Tulip Group, Transasia Biomedicals, RFCL (Diagnova), Span Diagnostics and Trivitron are the leading Indian players in this space.

GOVERNMENT INITIATIVES - DIAGNOSTIC INDUSTRY

The Indian diagnostic market is highly regulated for maintaining quality standards and the safety of the patients.

All the diagnostic laboratories need to register and get the license from Central Licensing Approving Authority (CLAA), accreditation from National Accreditation Board for Testing & Calibration of Laboratories (NABL), and imaging centres have to be approved by Bhabha Atomic Research Centre (BARC) or Atomic Energy Regulatory Board (AERB). Central Drugs Standard Control Organization (CDSCO) regulates the manufacture and marketing of drugs, diagnostics, devices, and cosmetics in the Indian market.

In 2010-11, the Indian Government announced fiscal incentives for the diagnostic sector to make it more affordable and accessible.

For the domestic medical device industry, a uniform concessional duty of 5 per cent is levied and assistive devices, rehabilitation aid, etc., are fully exempted.

Import/customs duty on 24 medical equipments including X-ray, goniometer, tele-therapy simulator machines were reduced to 5 per cent. The Government is also promoting domestic device manufacturers by establishing R&D centres and reducing prices of the critical equipment.

TECHNOLOGY TRENDS IN INDIAN DIAGNOSTIC INDUSTRY

Amid government regulations and awareness among physicians and patients, the Indian diagnostic industry is encouraged to provide high quality and technological advanced medical devices, equipments and therapy.

• Technology transfer and outsourcing trend

Due to heavy dependence on imported products, foreign players are attracted to the Indian market for localising high-end products by setting up manufacturing facilities or outsourcing to local players.

• Emerging hub and spoke model

With the development of easy to use and handle devices, corporate players are able to service the tier II and III markets by establishing collection centres and satellite

labs near patients. These centres are networked to the central laboratory.

• Self-diagnosis test market in India

Preference of the patients to conduct self-diagnosis test or tests at home is increasing. Around 10 per cent of the patients opt for the tests at home.

In the last 15 years, several products in the therapeutic devices, monitoring devices, interventional devices, X-rays, ultrasound, electrocardiogram (ECG), pathological tests category have been developed for the self-diagnosis test market

• ICT in healthcare for deep rural penetration

Large ICT players are developing systems for inclusive healthcare services through telemedicine. The industry is

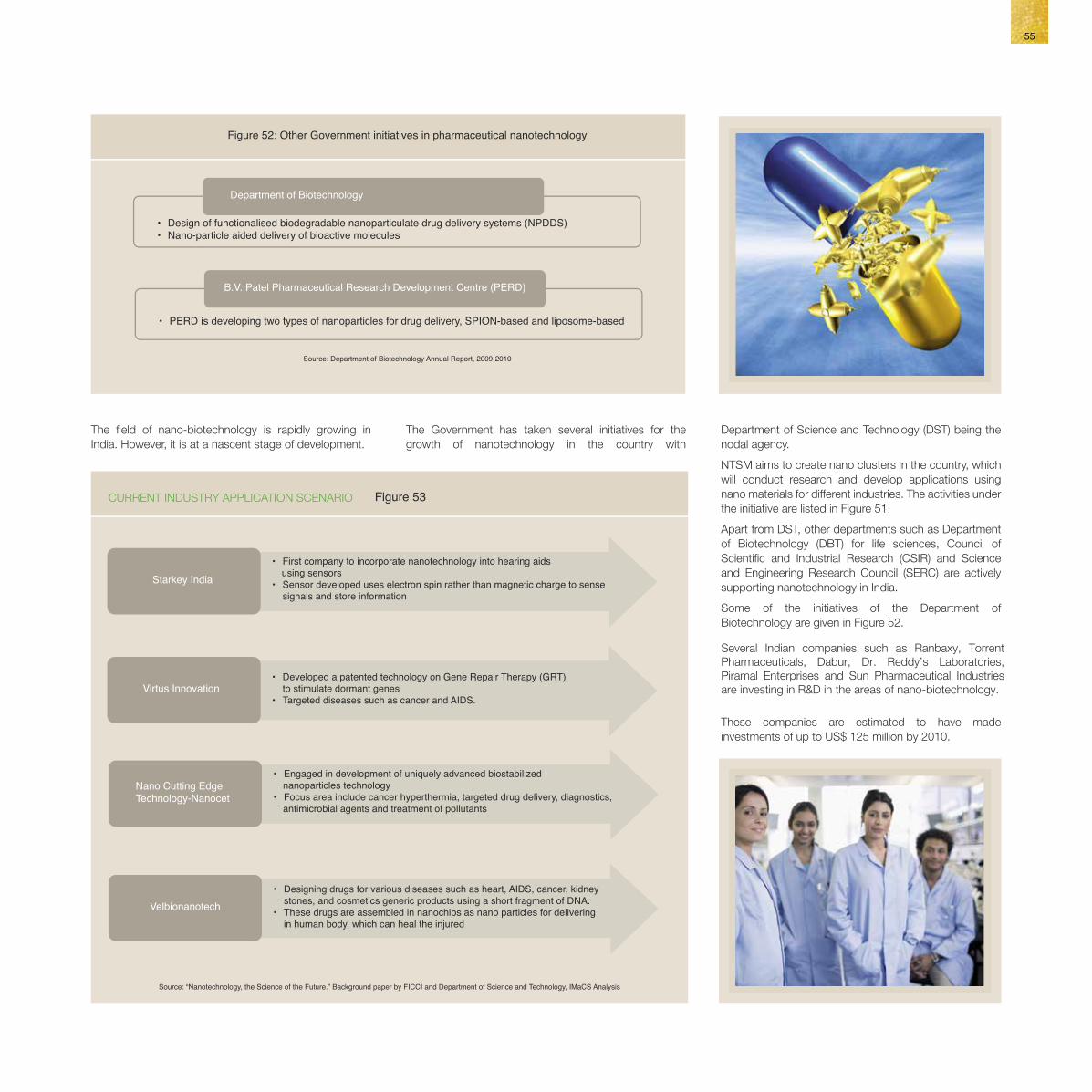

undertaking research programmes to develop affordable technology platforms such as molecular diagnostic, nanotechnology, micro-fluids to make healthcare accessible to rural India.

• Customer relationship management (CRM) resulting in preventive care technology

Database of patients helps in two ways, by offering preventive care to the patients and also transmitting patient’s data to the research firms for developing novel drugs and medical devices. CRM is a key tool for such use.

• Outsourcing laboratory management

Emerging organised players in diagnostic services are building on their expertise and collaborating with hospitals to manage laboratories effectively.

Collaboration within the healthcare industry segments such as – healthcare delivery, pharmaceuticals and medical equipment – can play significant role in making the innovation partnerships successful.

• Government scheme for inclusive healthcare services will benefit affordability

Government schemes encouraging health insurance penetration will bridge the urban-rural gap and make the healthcare services including pharmaceutical market more accessible and affordable.

• Improved margins and profitability

Access to technology and cost efficiency in the healthcare services will lead to higher profit margin for the pharmaceutical industry

DIAGNOSTIC INDUSTRY OVERVIEW

The Indian diagnostic industry comprises of pathological

services and devices. In 2010, total diagnostic market was valued at US$ 1.57 billion.

By 2015, the market is likely to grow to US$ 5.3 billion at 28 per cent CAGR on the back of rising demand from health consciousness and increasing disposable income in the country. In 2010, the diagnostic imaging estimated market was valued at US$ 731 million.

The size of the ultrasound product and services, clinical chemistry, immunology, hematology and molecular diagnostics segments was US$ 120 million, US$ 112 million, US$ 132 million, US$ 47 million and US$ 300 million respectively for the year 2010.

Domestic industry serves 25 per cent of the diagnostic imaging market and the remaining is comprised of imports mainly from the USA, Germany, Japan and China.

Pathological services contribute more than 52 per cent of the total diagnostic market; there are over 40,000 pathology labs in the country servicing around 1-1.25 million patients per day.

Pathological services industry is highly competitive, fragmented and price driven, however it is experiencing increased investments from organised players such as Super Religare Laboratories, Dr. Lal Pathlabs, Metropolis, Thyrocare Quest Diagnostics and Medinova.

In-vitro diagnostics including the analysing body fluids or tissue samples segments account for a significant 25 per cent of total diagnostic services market, remaining is contributed by biochemistry, immunology and haematology, coagulation, molecular diagnostics and critical.

Molecular diagnostic

Molecular diagnostics takes DNA, RNA and genes as

base for diagnostic tests

It plays a crucial role in the early detection of diseases, including identification of predisposition, and comprehensive analysis of pathogens, qualitative, quantitative and detection of resistance mechanisms to pathogens.

The Indian molecular diagnostics market was estimated

Public Expenditure Private Expenditure

Figure 17: Evolution of government policies - Indian healthcare sector

1946, PHC conceptualisation

1952-1977, Integrated health service and medical education

1978, Health for all by 2000 AD

1983, National Health Policy I

2000, National population policy (NPP)

Figure 18: Healthcare delivery structure

Ambulance, TelephoneObstetric/Surgical/Medical

Emergencies24x7 Round the Clock Service

Accredit privateproviders for public

health goals

Strengthen Ambulance/transport servicesincrease availability of nursesprovide telephonesencourage fixed day clinics

100,000Population

100 Villages

30-40 Villages

5-6 Villages

10,000Population

Health ManagerAccountantStore Keeper

3 Staff Nurses: 1 LHV for 4-5 SHCs:Ambulance/hired vehicle; Fixed Day MCH/Immunization

Clinics; Telephone; MOI/C: AYUSH Doctor:Emergencies that can be handled by Nurses - 24x7;

Round the Clock Services; Drugs; TB/Malaria etc tests

Skill upgradation of educated RMPs; 2 ANMs. 1 Male MPW for 5-6 villages;Telephone Link; MCH/Immunization Days; Drugs; MCH Clinic

1 ASHA, AWWs in every village; Village Health Day Drug Kit, Referral chains

BLOCKLEVEL

HOSPITAL

CHIEF BLOCK MEDICAL OFFICER/BLOCK LEVEL HEALTH OFFICE

CLUSTER OF GPs - PHC LEVEL

GRAM PANCHAYAT - SUB HEALTH CENTRE LEVEL

VILLAGE LEVEL - ASHA, AWW, VH & SC

Sources: NRHM, Ministry of Health and Family Welfare, IMaCS Analysis

Sub centre PHCs CHCs All India

GPs – General Practitioners, LHV – Lady Health Visitor, SHCs – Sub Health Centers, MCH - Maternal and child health services, MOI/C – Medical Officer, RMP – Rural Medical Provider, ANM - Auxiliary Nurse Midwife, MPW - Multi Purpose Workers, ASHA – Accredited Social Health Activist, AWW - Anganwadi Worker, VH – Village Health, SC – Sanitation Committee

21

21206529_20_25.pdf 1 25/09/12 7:19 PM

Public Expenditure Private Expenditure

Figure 17: Evolution of government policies - Indian healthcare sector

1946, PHC conceptualisation

1952-1977, Integrated health service and medical education

1978, Health for all by 2000 AD

1983, National Health Policy I

2000, National Population Policy (NPP)

Figure 18: Healthcare delivery structure

Ambulance, TelephoneObstetric/Surgical/Medical

Emergencies24x7 Round the Clock Service

Accredit privateproviders for public

health goals

Strengthen Ambulance/transport servicesincrease availability of nursesprovide telephonesencourage fixed day clinics

100,000Population

100 Villages

30-40 Villages

5-6 Villages

10,000Population

Health ManagerAccountantStore Keeper

3 Staff Nurses: 1 LHV for 4-5 SHCs:Ambulance/hired vehicle; Fixed Day MCH/Immunization

Clinics; Telephone; MOI/C: AYUSH Doctor:Emergencies that can be handled by Nurses - 24x7;

Round the Clock Services; Drugs; TB/Malaria etc tests

Skill upgradation of educated RMPs; 2 ANMs. 1 Male MPW for 5-6 villages;Telephone Link; MCH/Immunization Days; Drugs; MCH Clinic

1 ASHA, AWWs in every village; Village Health Day Drug Kit, Referral chains

BLOCKLEVEL

HOSPITAL

CHIEF BLOCK MEDICAL OFFICER/BLOCK LEVEL HEALTH OFFICE

CLUSTER OF GPs - PHC LEVEL

GRAM PANCHAYAT - SUB HEALTH CENTRE LEVEL

VILLAGE LEVEL - ASHA, AWW, VH & SC

Sources: NRHM, Ministry of Health and Family Welfare, IMaCS Analysis

Sub centre PHCs CHCs All India

GPs – General Practitioners, LHV – Lady Health Visitor, SHCs – Sub Health Centers, MCH - Maternal and child health services, MOI/C – Medical Officer, RMP – Rural Medical Provider, ANM - Auxiliary Nurse Midwife, MPW - Multi Purpose Workers, ASHA – Accredited Social Health Activist, AWW - Anganwadi Worker, VH – Village Health, SC – Sanitation Committee

As on March, 2012148,366 24,049 4,833

Figure 20: Public and private health expenditure (2011)

Source: World Health Organization (WHO)Source: Economic Survey of India 2013-14

Figure 19: Total expenditure on health by General Government

Source: Economic Survey of India 2013-14

2005, National Rural Health Mission (NRHM)

2013, National Health Mission (NHM)Sources: Ministry of Health and Family Welfare,Planning Commission, Government of India

21

Healthcare And Diagnostic Sector In India

Chapter 4

Mission (NRHM), 2005, with the aim of providing accessible, affordable, accountable, effective and reliable primary healthcare in poor and vulnerable sections of the community. NRHM primarily focuses on development of healthcare services in rural areas.

NRHM enables increased fund allocation to strengthen public health management. Its architectural design of healthcare delivery system comprises Health Plan for each village, delivered through Village Health Committee and Panchayati Raj Institutions.

EVOLUTION AND OVERVIEW OF INDIAN HEALTHCARE SECTOR

India is among the first countries to have recognised the importance of primary health care (PHC) approach. Conceptualised in 1946, PHC approach emphasised social orientation of medical practices and high level of public participation.

The period up to the first National Health Policy (NHP) in 1983 was dedicated to a concerted effort towards building programmes covering: health and sanitation through establishment of PHCs and sub-centres, health survey and planning, integrated health services, inclusion of larger population, building medical and support workforce, linking medical colleges and health centres.

Thereafter, policy improvements and evolution of industry have increased private sector participation.

The Government of India’s commitment to health for all led to the formulation of India’s first NHP. The period 1986-1996 was one of substantial growth in the private sector investments and it surpassed the public sector by a wide margin.

Private sector gained significance as the more preferred choice.

The Government of India launched National Rural Health

• Diagnostics industry is highly competitive and fragmented

The Indian diagnostics services industry, including pathological laboratories services, has grown at 20 per cent CAGR for the period 2006-2010.

Pathological laboratories services constitute over 52 per cent of the diagnostic market.With the increasing number of organised players in the segment, diagnostic services industry is likely to expand at more than this growth rate.

GOVERNMENT INITIATIVES - INDIAN HEALTHCARE SECTOR

In the Union Budget 2010-11, the Government increased total allocation for healthcare to US$ 5,240 million, more than an 11 per cent increase over 2009-10.

In the Union Budget 2012-13, the Government increased total allocation for healthcare to US$ 6,400 million, about 14 per cent higher than 2011-12. NRHM has been a successful scheme, launched to make the quality healthcare accessible and affordable.

GOVERNMENT INCENTIVES

The Government is encouraging private sector and investments in the healthcare sector through several

incentives and policy initiatives:

• New hospitals with 100 beds or more will be subject to 100 per cent tax holiday for the initial period of five years of operation.

• To attract investments in the healthcare infrastructure, 100 per cent FDI is permitted for health and medical services under the automatic route.

• Life-saving equipment is exempted from countervailing duty. Custom duty has been reduced to 5 per cent from 25 per cent.

• Multiplicity of customs duty on medical equipment is being done away with and basic customs duty reduced to 5 per cent from 7.5 per cent.

• Hospitals and dispensaries providing health travel facilities and attracting medical tourists are eligible for tax holidays and incentives.

IMPACT OF HEALTHCARE GROWTH ON PHARMACEUTICALS SECTOR

• Expanding overall market

Growth in the healthcare industry is based on the inclusive business model and incorporates a range of activities such as infrastructure development, services penetration, enhancement in training and education.

Consequently, it helps expand the whole healthcare market including pharmaceuticals. Historically, pharmaceuticals sector growth has tracked increase in healthcare expenditure.

• New healthcare players will influence reforms in healthcare industry including pharmaceuticals

Local and international players bring in new ideas and lead to systemic reforms, which in turn foster a streamlined, transparent, and better-regulated healthcare and hospital financing environment for the industry.

This trend will help increase demand for innovative drugs and hence support the long-term sustainable growth of the pharmaceutical sector.

• Industry wide collaboration will help innovate and maximise benefit

The healthcare scenario is ever evolving and the Government is planning to increase the public provisioning of healthcare. As per World Health Organisation (WHO), total expenditure on health increased from US$ 22.42 billion in 2001 to US$ 59.5 billion in 2010.

INDIAN HEALTHCARE SECTOR: MARKET SIZE

Domestic healthcare sector sales recorded a 17 per cent

CAGR during 2005-2010 to reach US$ 59.5 billion a year. The healthcare sector employs about 4.5 million people directly or indirectly and is the largest service sector employer in the country after retail. According to the Investment Commission of India, the healthcare sector is projected to grow at 15 per cent CAGR and reach the market value of US$ 79 billion by 2012 and US$ 280 billion by 2020.

Key segments and growth drivers

Hospital and pharmaceuticals are the largest segments of the sector in India, combined revenue from these segments are estimated to contribute 79 per cent of the total healthcare market by 2012.

• Demand driving healthcare infrastructure investments

For the distribution of healthcare across all demographic segments, 2.8 million additional beds are required by 2025, according to the WHO. Investments of US$ 100 billion are required.

• Flourishing medical tourism attracting growth

Medical tourists in India are expected to increase from

0.8 million in 2010 to 1.6 million by 2015.

India is expected to be a medical tourist hub and likely to contribute 3 per cent of the US$ 100 billion global medical tourism industry by 2013.

• Healthcare information and communication technology (ICT) spend is playing a significant role in healthcare delivery

Information and communication technology (ICT) including electronic medical records requirement of the healthcare industry was around US$ 270 million in 2010.

With the growth in the healthcare infrastructure and telemedicine, it is estimated to grow at 22 per cent CAGR until 2013.

• Pharmaceutical industry is poised for growth on back of affordability, increasing disposable income

The pharmaceuticals industry in India was valued at about US$ 21.73 billion in 2010.

Sustained economic growth, healthcare reforms and patent-related legislation are key drivers for average estimated growth of 12 to 15 per cent CAGR for next 10 years.

• Immense potential in medical equipment and consumables

The medical equipment market is heavily dependent on imports.

Domestic manufacturers such as Anand Medicaids, Carewell Mediproducts, Dental Products of India, Hindustan Syringes and Medical Devices, Lifeline Systems, Relisys Medical Devices Ltd, Surya Surgical Industries, etc., contribute to 25 per cent of the market.

In 2011, the Indian medical equipment market was estimated at US$ 2.64 billion and it is expected to reach US$ 4.95 billion by 2016, according to the Department of Health.

• Health insurance penetration will augment the overall healthcare market

In 2010, 15 per cent of the Indian population were covered through health insurance and 80 per cent of the healthcare expenditure was financed out-of-pocket.

The health insurance market is growing. It was valued at US$ 1.73 billion in 2010, with a 39 per cent CAGR from 2006-2010.

The insurance market is expected to grow to over 4 billion by 2013.

at US$ 345 million in 2010-11, contributing over 70 per cent of the total diagnostics services market and is expected to grow at 15-20 per cent year on year.

The largest segments are blood screening and infectious diseases. The fastest growing segments are genetic diseases, oncology and pharmacogenomics. Tulip Group, Transasia Biomedicals, RFCL (Diagnova), Span Diagnostics and Trivitron are the leading Indian players in this space.

GOVERNMENT INITIATIVES - DIAGNOSTIC INDUSTRY

The Indian diagnostic market is highly regulated for maintaining quality standards and the safety of the patients.

All the diagnostic laboratories need to register and get the license from Central Licensing Approving Authority (CLAA), accreditation from National Accreditation Board for Testing & Calibration of Laboratories (NABL), and imaging centres have to be approved by Bhabha Atomic Research Centre (BARC) or Atomic Energy Regulatory Board (AERB). Central Drugs Standard Control Organization (CDSCO) regulates the manufacture and marketing of drugs, diagnostics, devices, and cosmetics in the Indian market.

In 2010-11, the Indian Government announced fiscal incentives for the diagnostic sector to make it more affordable and accessible.

For the domestic medical device industry, a uniform concessional duty of 5 per cent is levied and assistive devices, rehabilitation aid, etc., are fully exempted.

Import/customs duty on 24 medical equipments including X-ray, goniometer, tele-therapy simulator machines were reduced to 5 per cent. The Government is also promoting domestic device manufacturers by establishing R&D centres and reducing prices of the critical equipment.

TECHNOLOGY TRENDS IN INDIAN DIAGNOSTIC INDUSTRY

Amid government regulations and awareness among physicians and patients, the Indian diagnostic industry is encouraged to provide high quality and technological advanced medical devices, equipments and therapy.

• Technology transfer and outsourcing trend

Due to heavy dependence on imported products, foreign players are attracted to the Indian market for localising high-end products by setting up manufacturing facilities or outsourcing to local players.

• Emerging hub and spoke model

With the development of easy to use and handle devices, corporate players are able to service the tier II and III markets by establishing collection centres and satellite

labs near patients. These centres are networked to the central laboratory.

• Self-diagnosis test market in India

Preference of the patients to conduct self-diagnosis test or tests at home is increasing. Around 10 per cent of the patients opt for the tests at home.

In the last 15 years, several products in the therapeutic devices, monitoring devices, interventional devices, X-rays, ultrasound, electrocardiogram (ECG), pathological tests category have been developed for the self-diagnosis test market

• ICT in healthcare for deep rural penetration

Large ICT players are developing systems for inclusive healthcare services through telemedicine. The industry is

undertaking research programmes to develop affordable technology platforms such as molecular diagnostic, nanotechnology, micro-fluids to make healthcare accessible to rural India.

• Customer relationship management (CRM) resulting in preventive care technology

Database of patients helps in two ways, by offering preventive care to the patients and also transmitting patient’s data to the research firms for developing novel drugs and medical devices. CRM is a key tool for such use.

• Outsourcing laboratory management

Emerging organised players in diagnostic services are building on their expertise and collaborating with hospitals to manage laboratories effectively.

Collaboration within the healthcare industry segments such as – healthcare delivery, pharmaceuticals and medical equipment – can play significant role in making the innovation partnerships successful.

• Government scheme for inclusive healthcare services will benefit affordability

Government schemes encouraging health insurance penetration will bridge the urban-rural gap and make the healthcare services including pharmaceutical market more accessible and affordable.

• Improved margins and profitability

Access to technology and cost efficiency in the healthcare services will lead to higher profit margin for the pharmaceutical industry

DIAGNOSTIC INDUSTRY OVERVIEW

The Indian diagnostic industry comprises of pathological

services and devices. In 2010, total diagnostic market was valued at US$ 1.57 billion.

By 2015, the market is likely to grow to US$ 5.3 billion at 28 per cent CAGR on the back of rising demand from health consciousness and increasing disposable income in the country. In 2010, the diagnostic imaging estimated market was valued at US$ 731 million.

The size of the ultrasound product and services, clinical chemistry, immunology, hematology and molecular diagnostics segments was US$ 120 million, US$ 112 million, US$ 132 million, US$ 47 million and US$ 300 million respectively for the year 2010.

Domestic industry serves 25 per cent of the diagnostic imaging market and the remaining is comprised of imports mainly from the USA, Germany, Japan and China.

Pathological services contribute more than 52 per cent of the total diagnostic market; there are over 40,000 pathology labs in the country servicing around 1-1.25 million patients per day.

Pathological services industry is highly competitive, fragmented and price driven, however it is experiencing increased investments from organised players such as Super Religare Laboratories, Dr. Lal Pathlabs, Metropolis, Thyrocare Quest Diagnostics and Medinova.

In-vitro diagnostics including the analysing body fluids or tissue samples segments account for a significant 25 per cent of total diagnostic services market, remaining is contributed by biochemistry, immunology and haematology, coagulation, molecular diagnostics and critical.

Molecular diagnostic

Molecular diagnostics takes DNA, RNA and genes as

base for diagnostic tests

It plays a crucial role in the early detection of diseases, including identification of predisposition, and comprehensive analysis of pathogens, qualitative, quantitative and detection of resistance mechanisms to pathogens.

The Indian molecular diagnostics market was estimated

Public Expenditure Private Expenditure

Figure 17: Evolution of government policies - Indian healthcare sector

1946, PHC conceptualisation

1952-1977, Integrated health service and medical education

1978, Health for all by 2000 AD

1983, National Health Policy I

2000, National population policy (NPP)

Figure 18: Healthcare delivery structure

Ambulance, TelephoneObstetric/Surgical/Medical

Emergencies24x7 Round the Clock Service

Accredit privateproviders for public

health goals

Strengthen Ambulance/transport servicesincrease availability of nursesprovide telephonesencourage fixed day clinics

100,000Population

100 Villages

30-40 Villages

5-6 Villages

10,000Population

Health ManagerAccountantStore Keeper

3 Staff Nurses: 1 LHV for 4-5 SHCs:Ambulance/hired vehicle; Fixed Day MCH/Immunization

Clinics; Telephone; MOI/C: AYUSH Doctor:Emergencies that can be handled by Nurses - 24x7;

Round the Clock Services; Drugs; TB/Malaria etc tests

Skill upgradation of educated RMPs; 2 ANMs. 1 Male MPW for 5-6 villages;Telephone Link; MCH/Immunization Days; Drugs; MCH Clinic

1 ASHA, AWWs in every village; Village Health Day Drug Kit, Referral chains

BLOCKLEVEL

HOSPITAL

CHIEF BLOCK MEDICAL OFFICER/BLOCK LEVEL HEALTH OFFICE

CLUSTER OF GPs - PHC LEVEL

GRAM PANCHAYAT - SUB HEALTH CENTRE LEVEL

VILLAGE LEVEL - ASHA, AWW, VH & SC

Sources: NRHM, Ministry of Health and Family Welfare, IMaCS Analysis

Sub centre PHCs CHCs All India

GPs – General Practitioners, LHV – Lady Health Visitor, SHCs – Sub Health Centers, MCH - Maternal and child health services, MOI/C – Medical Officer, RMP – Rural Medical Provider, ANM - Auxiliary Nurse Midwife, MPW - Multi Purpose Workers, ASHA – Accredited Social Health Activist, AWW - Anganwadi Worker, VH – Village Health, SC – Sanitation Committee

21

21206529_20_25.pdf 1 25/09/12 7:19 PM

Figure 21: Segment-wise Revenue (2012)E

Sources: The Business World, IMaCS Analysis. E = Estimated.

Health Insurance, 5%

Diagnostics, 3%

Training and Education, 3%

Healthcare Delivery63%

Pharmaceuticals16%

Medical Equipment& Consumables

10%

Figure 22: Key segments of Indian healthcare sector

Indi

an H

ealth

care

Sec

tor

Healthcare Delivery

Public Healthcare System - healthcare centres, district hospitals and general hospitals

Private Healthcare System - clinics, nursing homes, specialty and superspecialty hospitals

Drug discovery, NDDS and manufacture of APIs and Bulk Drugs

Manufacturing medical devices and equipments and consumablesdesigned to aid in the diagnosis, monitoring or treatment

of medical conditions

Insurance covering the risk of incurring medical expenses among individuals

Serving to Identify and analyse the body for a possible disease

Institutions teaching and training medical practitioners

Pharmaceuticals

Medical Equipmentsand Consumables

Health Insurance

Diagnostics

Training and Education

Sources: The Business World, IMaCS Analysis

For the prevention and cure of diseasessuch as cancer , diabetes, heart ailmentsand stroke

to US$ 158.2 billion in 2017. The healthcare sectoremploys about 4.5 million people directly or indirectlyand is the largest service sector employer in the countryafter retail. The healthcare sector is growing at a 15 percent CAGR and increased from US$ 45 billion in 2008 toUS$ 78.6 billion in 2012. The country's healthcaresystem is developing rapidly and it continues to expandits coverage in both the public as well as private sectors.

Domestic healthcare sector in India is expected to grow

India is emerging as a medical tourist hub. It contributedaround 3 per cent of the US$ 100 billion global medicaltourism industry in 2013.

The pharmaceutical industry in India was valued atabout US$ 27.83 billion in 2012-13.

In 2013, the Indian medical electronics market wasvalued at US$ 6.5 billion and it is expected to grow at acompound annual growth rate of 16 per cent to reachUS$ 11.7 billion by 2017.

In 2013, 15 per cent of the Indian population werecovered through health insurance and 61 per cent of thehealthcare expenditure was financed out-of-pocket.

The health insurance market is growing. It was valued atUS$ 2.88 billion in 2012-13.

The health insurance market is expected to grow toaround US$ 4.95 billion by 2015.

The Indian diagnostics services industry, includingpathological laboratories services, is growing at a CAGRof 15 per cent.

In the Union Budget 2012-13, the Governmentincreased total allocation for healthcare to US$ 6,400million, about 14 per cent increase over 2011-12.

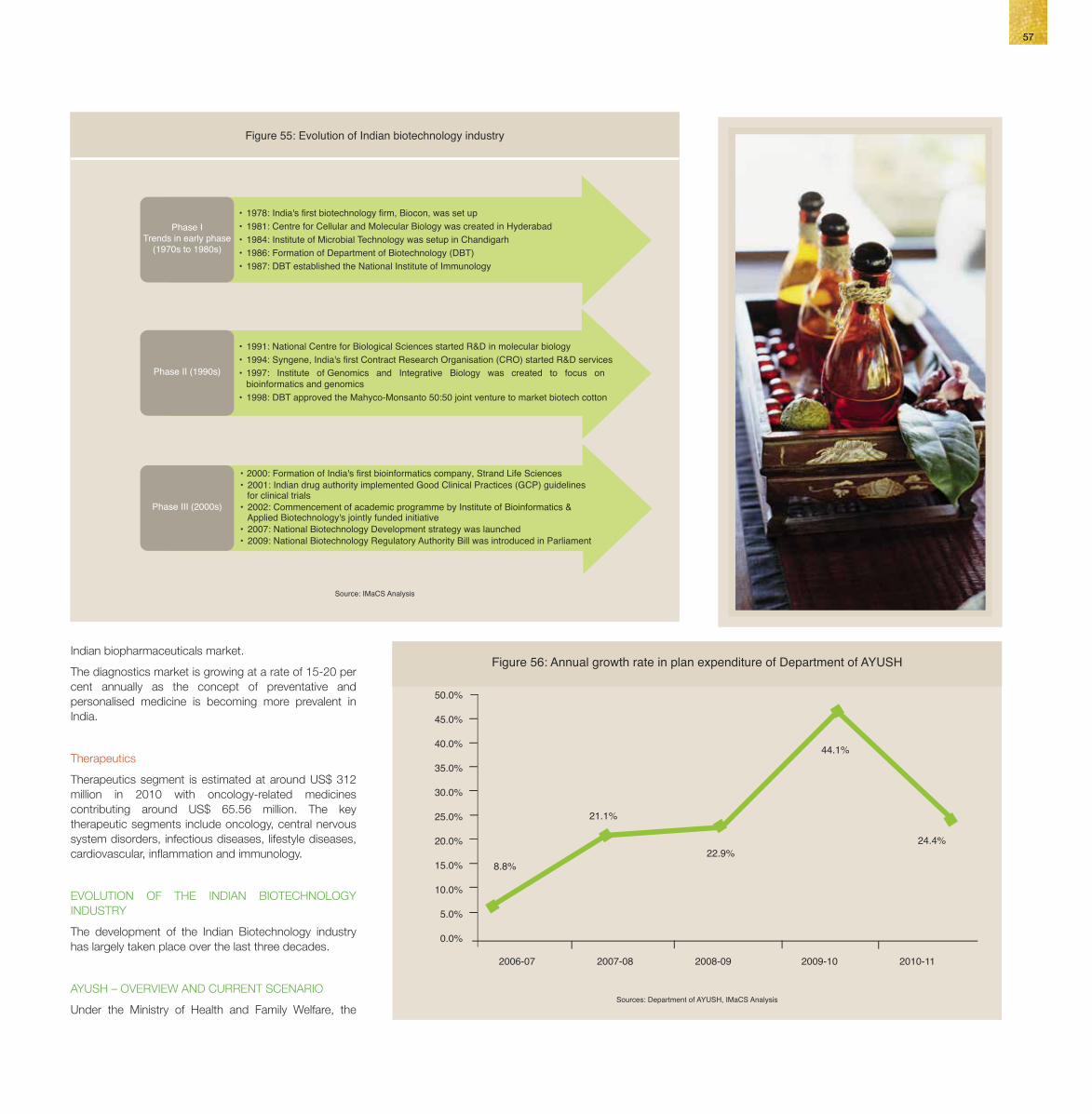

In the Union Budget 2014-15, the Government hasallocated US$ 5,813 million for healthcare. NRHM hasbeen a successful scheme, launched to make the qualityhealthcare accessible and affordable.

NHM

provisioning of healthcare. As per Economic Survey ofIndia 2013-14, total expenditure on health by generalgovernment has increased from US$ 16.17 billion in2008-09 to US$ 24.26 billion in 2012-13.

In 2012, the telemedicine market in India was valued atUS$ 7.5 million, and is expected to rise at a CAGR of 20per cent to US$ 18.7 million by 2017.

Figure 23: Government schemes and planned outlay (2013-14)

US$ 3,103million

To enable access to equitable,affordable, and quality health careservices

Medical Education Training& Research

US$ 755million

For medical education training &research, and to establish AIIMS typeSuper Speciality Hospitals

National Program for Preventionand Control of Cancer, Diabetes,

Cardiovascular Diseses and StrokeUS$ 53million

Health Care for the Elderly US$ 14million

Preventive and promotive care,management of illness, health manpowerdevelopment for geriatric services

National Program for Control ofBlindness

US$ 10million

Reduction of prevalence of blindness to0.3 per cent by 2020 by providingcomprehensive eye care services

Sources: Economic Survey of India 2013-14, Ministry of Health & Family Welfare

23

Figure 21: Segment-wise Revenue (2012)E

Sources: The Business World, IMaCS Analysis. E = Estimated.

Health Insurance, 5%

Diagnostics, 3%

Training and Education, 3%

Healthcare Delivery63%

Pharmaceuticals16%

Medical Equipment& Consumables

10%

Figure 22: Key segments of Indian healthcare sector

Indi

an H

ealth

care

Sec

tor

Healthcare Delivery

Public Healthcare System - healthcare centres, district hospitals and general hospitals

Private Healthcare System - clinics, nursing homes, specialty and superspecialty hospitals

Drug discovery, NDDS and manufacture of APIs and Bulk Drugs

Manufacturing medical devices and equipments and consumablesdesigned to aid in the diagnosis, monitoring or treatment

of medical conditions

Insurance covering the risk of incurring medical expenses among individuals

Serving to Identify and analyse the body for a possible disease

Institutions teaching and training medical practitioners

Pharmaceuticals

Medical Equipmentsand Consumables

Health Insurance

Diagnostics

Training and Education

Sources: The Business World, IMaCS Analysis

For the prevention and cure of diseasessuch as cancer , diabetes, heart ailmentsand stroke

to US$ 158.2 billion in 2017. The healthcare sectoremploys about 4.5 million people directly or indirectlyand is the largest service sector employer in the countryafter retail. The healthcare sector is growing at a 15 percent CAGR and increased from US$ 45 billion in 2008 toUS$ 78.6 billion in 2012. The country's healthcaresystem is developing rapidly and it continues to expandits coverage in both the public as well as private sectors.

Domestic healthcare sector in India is expected to grow

India is emerging as a medical tourist hub. It contributedaround 3 per cent of the US$ 100 billion global medicaltourism industry in 2013.

The pharmaceutical industry in India was valued atabout US$ 27.83 billion in 2012-13.

In 2013, the Indian medical electronics market wasvalued at US$ 6.5 billion and it is expected to grow at acompound annual growth rate of 16 per cent to reachUS$ 11.7 billion by 2017.

In 2013, 15 per cent of the Indian population werecovered through health insurance and 61 per cent of thehealthcare expenditure was financed out-of-pocket.

The health insurance market is growing. It was valued atUS$ 2.88 billion in 2012-13.

The health insurance market is expected to grow toaround US$ 4.95 billion by 2015.

The Indian diagnostics services industry, includingpathological laboratories services, is growing at a CAGRof 15 per cent.

In the Union Budget 2012-13, the Governmentincreased total allocation for healthcare to US$ 6,400million, about 14 per cent increase over 2011-12.

In the Union Budget 2014-15, the Government hasallocated US$ 5,813 million for healthcare. NRHM hasbeen a successful scheme, launched to make the qualityhealthcare accessible and affordable.

NHM

provisioning of healthcare. As per Economic Survey ofIndia 2013-14, total expenditure on health by generalgovernment has increased from US$ 16.17 billion in2008-09 to US$ 24.26 billion in 2012-13.

In 2012, the telemedicine market in India was valued atUS$ 7.5 million, and is expected to rise at a CAGR of 20per cent to US$ 18.7 million by 2017.

Figure 23: Government schemes and planned outlay (2013-14)

US$ 3,103million

To enable access to equitable,affordable, and quality health careservices

Medical Education Training& Research

US$ 755million

For medical education training &research, and to establish AIIMS typeSuper Speciality Hospitals

National Program for Preventionand Control of Cancer, Diabetes,

Cardiovascular Diseses and StrokeUS$ 53million

Health Care for the Elderly US$ 14million

Preventive and promotive care,management of illness, health manpowerdevelopment for geriatric services

National Program for Control ofBlindness

US$ 10million

Reduction of prevalence of blindness to0.3 per cent by 2020 by providingcomprehensive eye care services

Sources: Economic Survey of India 2013-14, Ministry of Health & Family Welfare

23

Figure 24: Regulation and fiscal initiatives in diagnostic industry (2010-11)

Government regulatory initiatives indiagnostic industry

Government fiscal initiatives in diagnostic industry

Regulatory, licensing and monitoring authority under Clinical Establishment Act Accreditation

Indian FDA CDSCO CLAANABL,BARC/AERB

Taxes and duties for medicaldevices

Investment

Uniformconcessionon exciseduty of 4%

Full exemption to assistive

devices

Import andcustom dutyreduced to

5%

US$ 69million

Sources: “Excellence in diagnostic care” by KPMG, Expresshealthcare, IMaCS Analysis

CASE STUDY: INTEGRATED HEALTHCARE COMPANIES

APOLLO HOSPITALS ENTERPRISE LTD. (APOLLO)

services and devices. In 2010, total diagnostic marketwas valued at US$ 1.57 billion.

SRL Limited, Dr. Lal Pathlabs, Metropolis, Thyrocare,Quest Diagnostics and Medinova.