Review of High Performance Structure in Australian Women's ...

The Australian Economy and

PerformanceDecember 2014

The Australian Economy and Performance

Participants

Md. Ashrafuzzaman (ID: 11427049)

Faculty

Md. Shafayat Hossain

Assistant Professor , AIS

University of Dhaka

Australia is a Unique and Diverse country in every way- in culture, population,

climate, geography, history and economy as well. Australian culture is as broad and

varied as the county’s landscape. Australia is an island continent and the world’s sixth

largest country with an area of 7,682,300 sq km, with roughly 25.8 million people. As

of 2014 Index of Economic Freedom, Australia’s economic freedom score is 82, making

its economy the 3rd freest.

About Australian

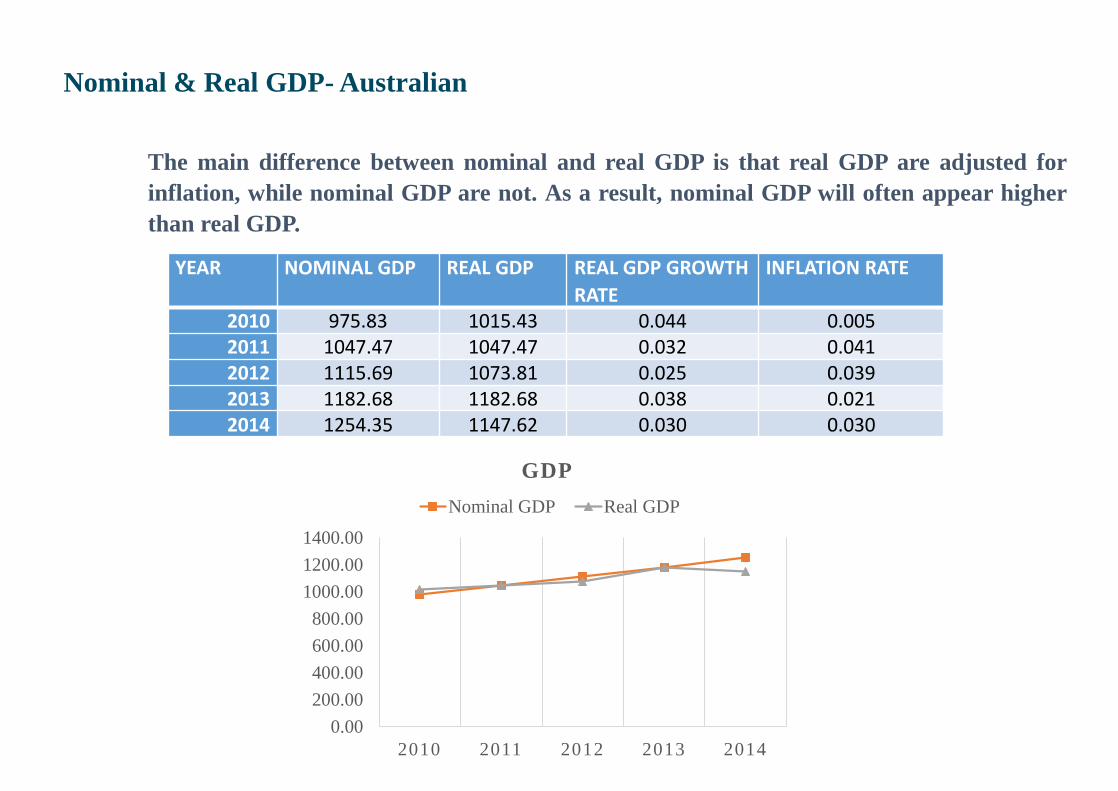

Nominal & Real GDP- Australian

The main difference between nominal and real GDP is that real GDP are adjusted for

inflation, while nominal GDP are not. As a result, nominal GDP will often appear higher

than real GDP.

YEAR NOMINAL GDP REAL GDP REAL GDP GROWTH

RATE

INFLATION RATE

2010 975.83 1015.43 0.044 0.0052011 1047.47 1047.47 0.032 0.0412012 1115.69 1073.81 0.025 0.0392013 1182.68 1182.68 0.038 0.0212014 1254.35 1147.62 0.030 0.030

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

2010 2011 2012 2013 2014

GDP

Nominal GDP Real GDP

Australian Economy

%

6

4

2

0

-2

-4 2002

GDP Growth - World Year-ended

Major trading partners*

World**

2006 2010

%

6

4

2

0

-2

-4

2014

Weighted using Australian export shares

** PPP-weighted; accounts for 87 per cent of world GDP

1994 1998

GDP Growth- Australia

Year-ended

Quarterly

2002 2006 2010

%

4

2

0

-2 2014

%

5

4

3

2

1

0

-1 1994

Consumer Price Inflation- Australia

Year-ended

Quarterly (seasonally adjusted)

1998 2002 2006 2010

%

5

4

3

2

1

0

-1 2014

Excluding interest charges prior to the September quarter 1998 and adjusted for the tax changes of 1999-2000

Inflation - East Asia Year-ended

% %

Middle-income*

8 8

4 4

0 High-income**

0

-4

2002 2005 2008

2011 2014

Indonesia, Malaysia, Philippines and Thailand; PPP-weighted Hong

Kong, Singapore, South Korea and Taiwan; PPP-weighted

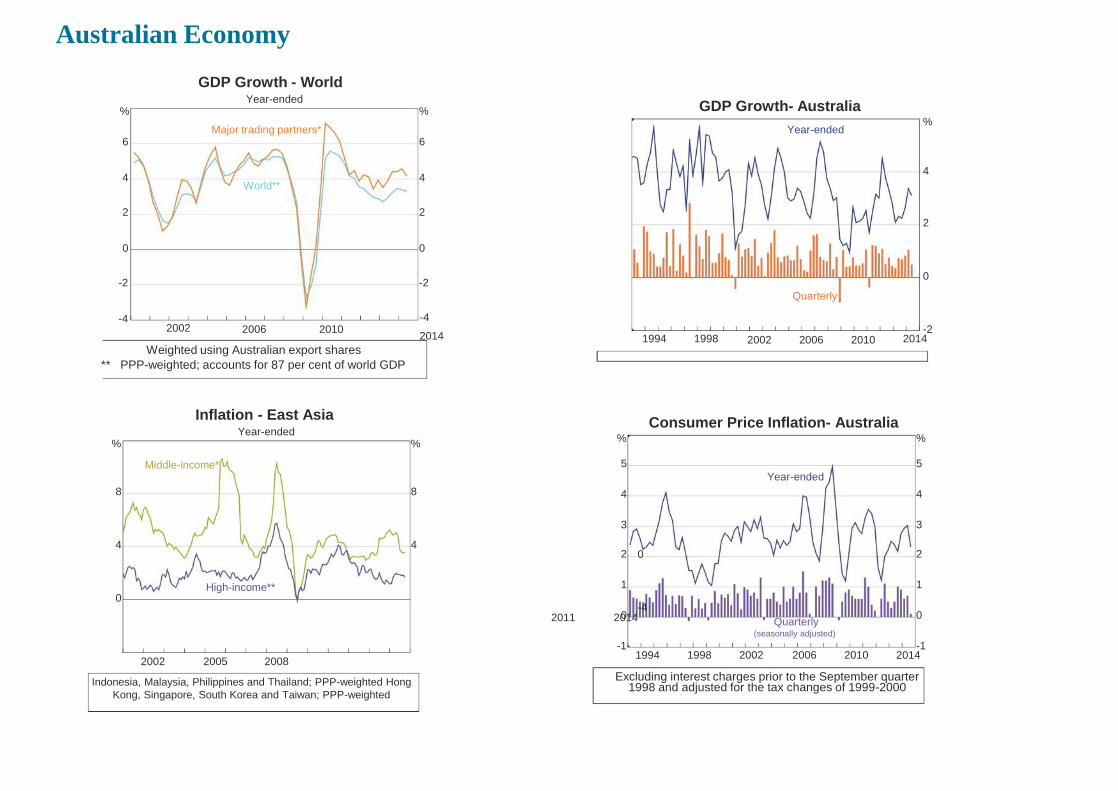

The Australian economy grew at 0.8% in Q4 despite a decline of 0.4% in hours

worked, largely in line with our expectations. Annual GDP growth of 2.8% is still

below the rate needed to prevent rising unemployment. The broad-based

inflation measures in the national accounts remain moderate: annual chain price

index inflation was 2.8% for private consumption and 2.2% for GDP.

Australian Economy

Sectorial Contribution (Household Sector)

Household Finances* Per cent of household disposable income

% Debt Interest paid %

150 14

125 12

100 10

75 8

50 6

25 4 1994 2004 2014 1994 2004 2014

Household sector excludes unincorporated enterprises; disposable income is after tax and before the deduction of

interest payments

Housing Prices $’000 $’000

750 750

Sydney 650 650

Canberra

Household Wealth and Liabilities* Per cent of annual household disposable income

% %

Net worth

600 600

Dwellings 450 450

300 300

Financial assets

150 150 Liabilities

0 0 1998 2002 2006 2010 2014

Household liabilities exclude the liabilities of unincorporated enterprises; disposable income is after tax and before the

deduction of interest payments

Housing Loan Approvals $b $b

Total 20 20

15 15 Perth

550

450

350

250 2006

Melbourne Australia

Brisbane Adelaide

Regional*

2010 2014 2010 2014

550

450

350

250

Owner-occupiers

10 10

5 5 Investors

0 0 2002 2005 2008 2011 2014

Excludes apartments; measured as areas outside of capital cities

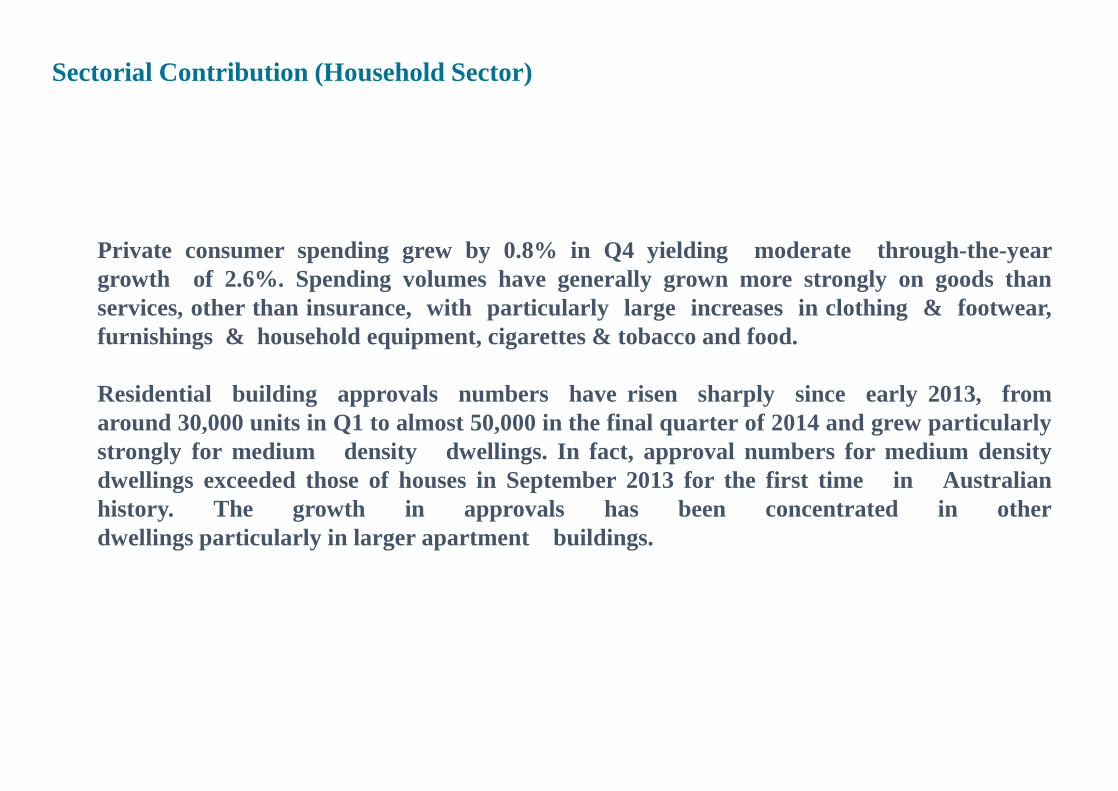

Private consumer spending grew by 0.8% in Q4 yielding moderate through-the-year

growth of 2.6%. Spending volumes have generally grown more strongly on goods than

services, other than insurance, with particularly large increases in clothing & footwear,

furnishings & household equipment, cigarettes & tobacco and food.

Residential building approvals numbers have risen sharply since early 2013, from

around 30,000 units in Q1 to almost 50,000 in the final quarter of 2014 and grew particularly

strongly for medium density dwellings. In fact, approval numbers for medium density

dwellings exceeded those of houses in September 2013 for the first time in Australian

history. The growth in approvals has been concentrated in other

dwellings particularly in larger apartment buildings.

Sectorial Contribution (Household Sector)

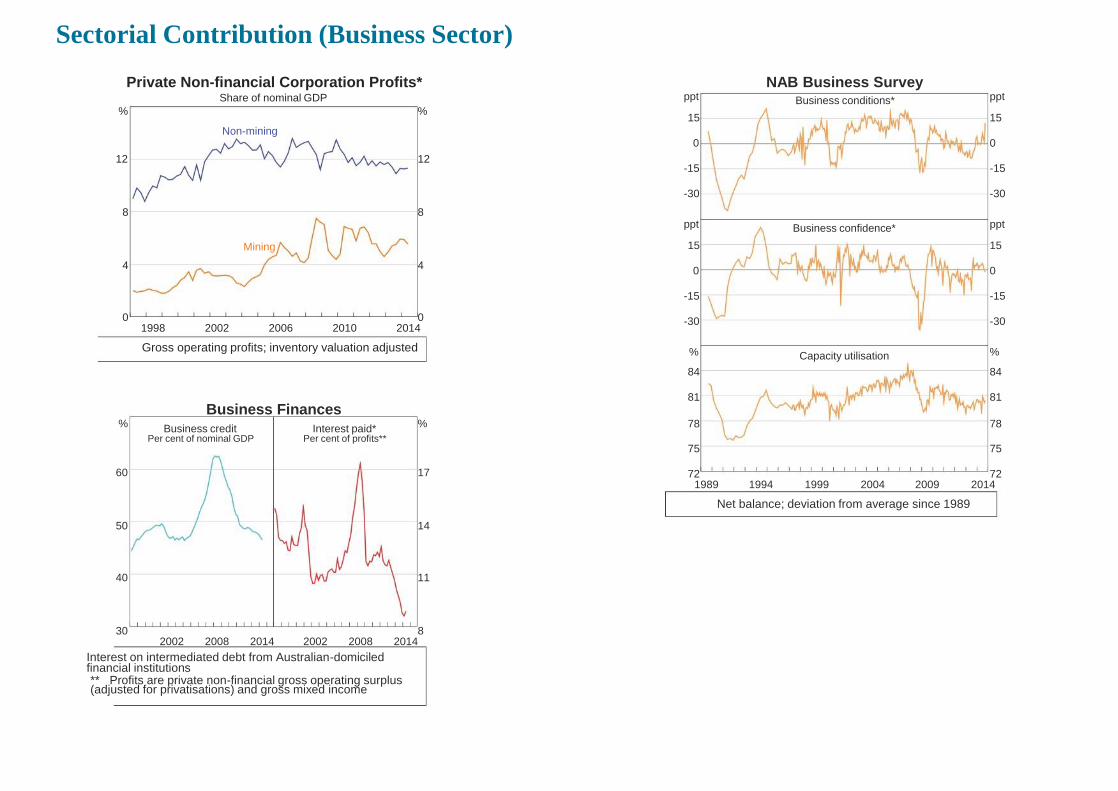

Sectorial Contribution (Business Sector)

Private Non-financial Corporation Profits* Share of nominal GDP

% %

Non-mining

12 12

8 8

Mining

4 4

0 0 1998 2002 2006 2010 2014

Gross operating profits; inventory valuation adjusted

Business Finances % %

ppt

15

0

-15

-30

ppt

15

0

-15

-30

%

84

81

78

NAB Business Survey Business conditions*

Business confidence*

Capacity utilisation

ppt

15

0

-15

-30

ppt

15

0

-15

-30

%

84

81

78 Business credit Interest paid*Per cent of nominal GDP Per cent of profits**

75 75

60 17 72 721989 1994 1999 2004 2009 2014

Net balance; deviation from average since 1989

50 14

40 11

30 82002 2008 2014 2002 2008 2014

Interest on intermediated debt from Australian-domiciled financial institutions ** Profits are private non-financial gross operating surplus (adjusted for privatisations) and gross mixed income

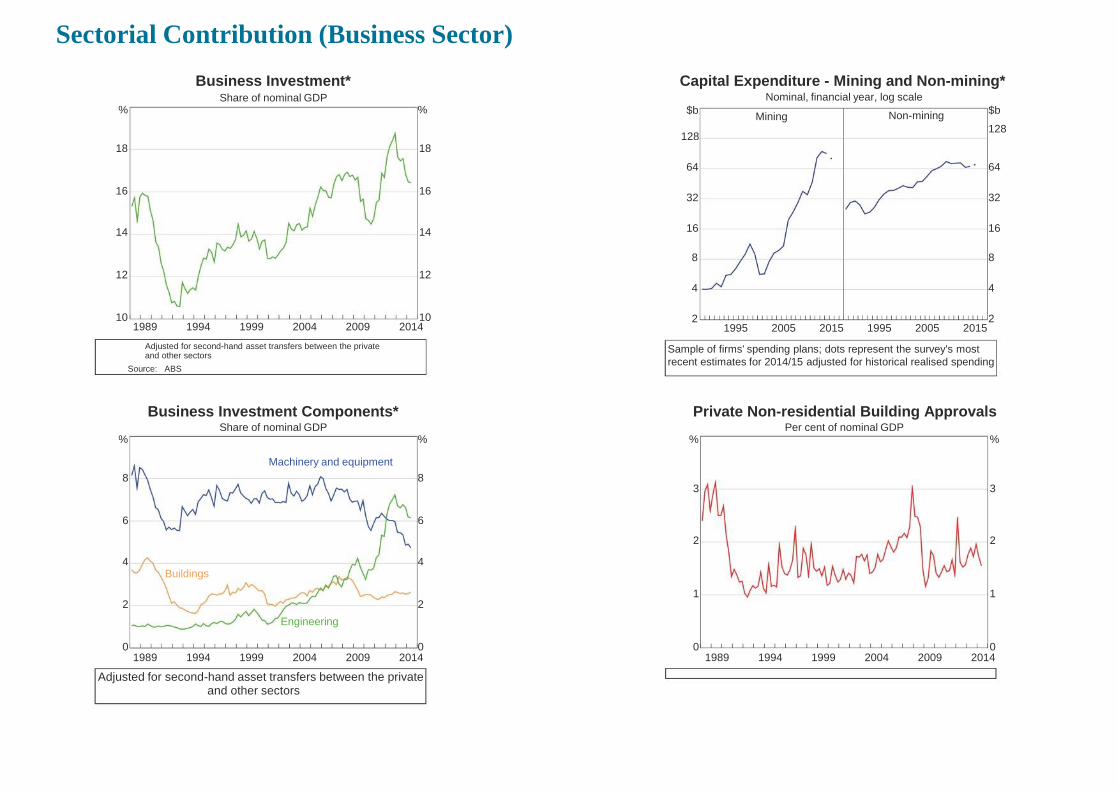

Sectorial Contribution (Business Sector)

Business Investment* Share of nominal GDP

% %

Capital Expenditure - Mining and Non-mining* Nominal, financial year, log scale

$b $b

18

16

14

12

10 1989 1994 1999

18

16

14

12

10 2004 2009 2014

Mining

128

64

32

16

8

4

2 1995 2005 2015

Non-mining

128

64

32

16

8

4

2 1995 2005 2015

Adjusted for second-hand asset transfers between the private Sample of firms' spending plans; dots represent the survey's most

recent estimates for 2014/15 adjusted for historical realised spendingand other sectors

Source: ABS

Business Investment Components* Private Non-residential Building ApprovalsShare of nominal GDP Per cent of nominal GDP

% % % %

Machinery and equipment

8 83 3

6 6

2 2

4 4Buildings

1 12 2

Engineering

0 0 0 01989 1994 1999 2004 2009 2014 1989 1994 1999 2004 2009 2014

Adjusted for second-hand asset transfers between the privateand other sectors

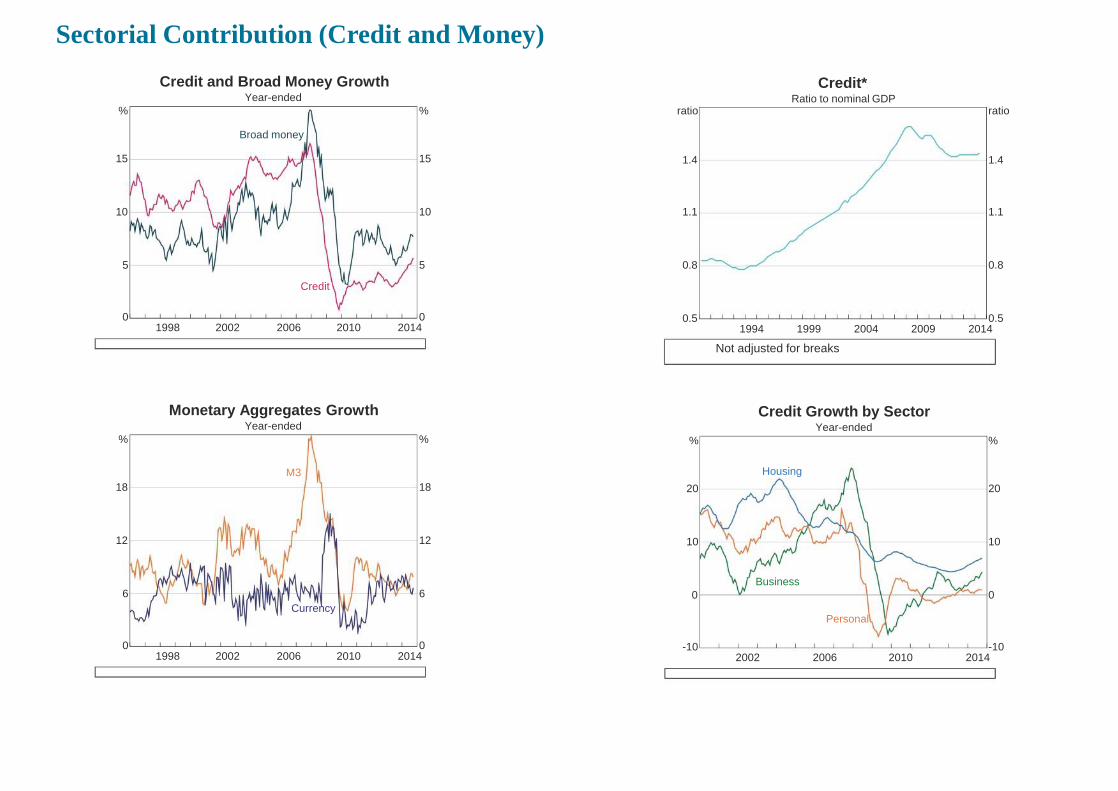

Sectorial Contribution (Credit and Money)

Credit and Broad Money Growth Credit*Year-ended Ratio to nominal GDP

% % ratio ratio

Broad money

15 15 1.4 1.4

10 10 1.1 1.1

5 5 0.8 0.8

Credit

0 0 0.5 0.51998 2002 2006 2010 2014 1994 1999 2004 2009 2014

Not adjusted for breaks

Monetary Aggregates Growth Credit Growth by SectorYear-ended Year-ended

% % % %

M3 Housing

18 18 20 20

12 12 10 10

Business6 6 0 0

CurrencyPersonal

0 0 -10 -101998 2002 2006 2010 2014 2002 2006 2010 2014

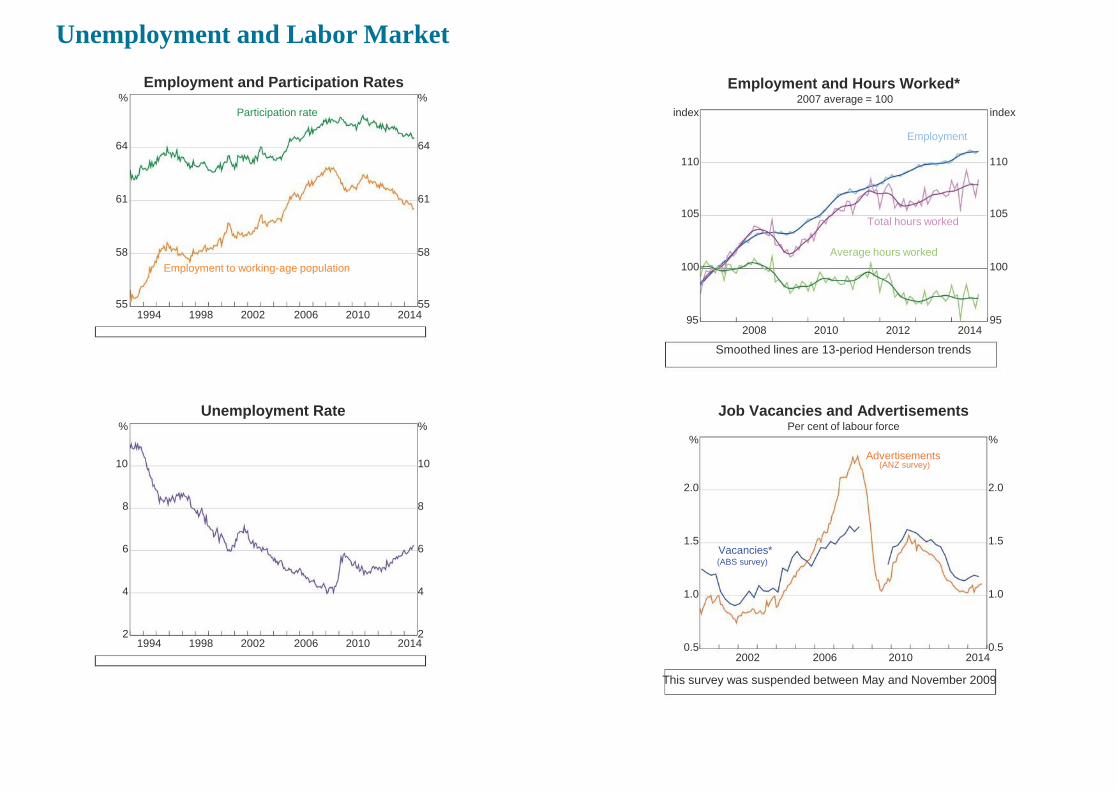

Unemployment and Labor Market

Employment and Participation Rates % %

Participation rate

64 64

61 61

58 58

Employment to working-age population

55 55 1994 1998 2002 2006 2010 2014

index

110

105

100

95

Employment and Hours Worked* 2007 average = 100

Employment

Total hours worked

Average hours worked

index

110

105

100

95 2008 2010 2012 2014

Smoothed lines are 13-period Henderson trends

Unemployment Rate % %

10 10

8 8

6 6

4 4

2 2 1994 1998 2002 2006 2010 2014

Job Vacancies and Advertisements Per cent of labour force

% %

Advertisements (ANZ survey)

2.0 2.0

1.5 1.5 Vacancies* (ABS survey)

1.0 1.0

0.5 0.5 2002 2006 2010 2014

This survey was suspended between May and November 2009

There have been mixed signals for the labor market since late 2013. Several key

indicators have pointed to improving conditions, or at least a slowing in the rate of

deterioration, including ANZ job ads, DEEWR internet vacancies and aggregate hours

worked (up 5.1%, 7.6% and1.3% respectively in January).

The labor adjustment task from the mining sector appears to have been magnified

by recent announcements of the end of automotive manufacturing and several

other high-profile operations as well as labor-shedding in aviation over the forecast

horizon. Our forecast profile for the unemployment rate is broadly unchanged until

2015, when we have slowed the rate of improvement marginally to be 6.1% by end-

2015(was 5.8%).

Unemployment and Labor Market

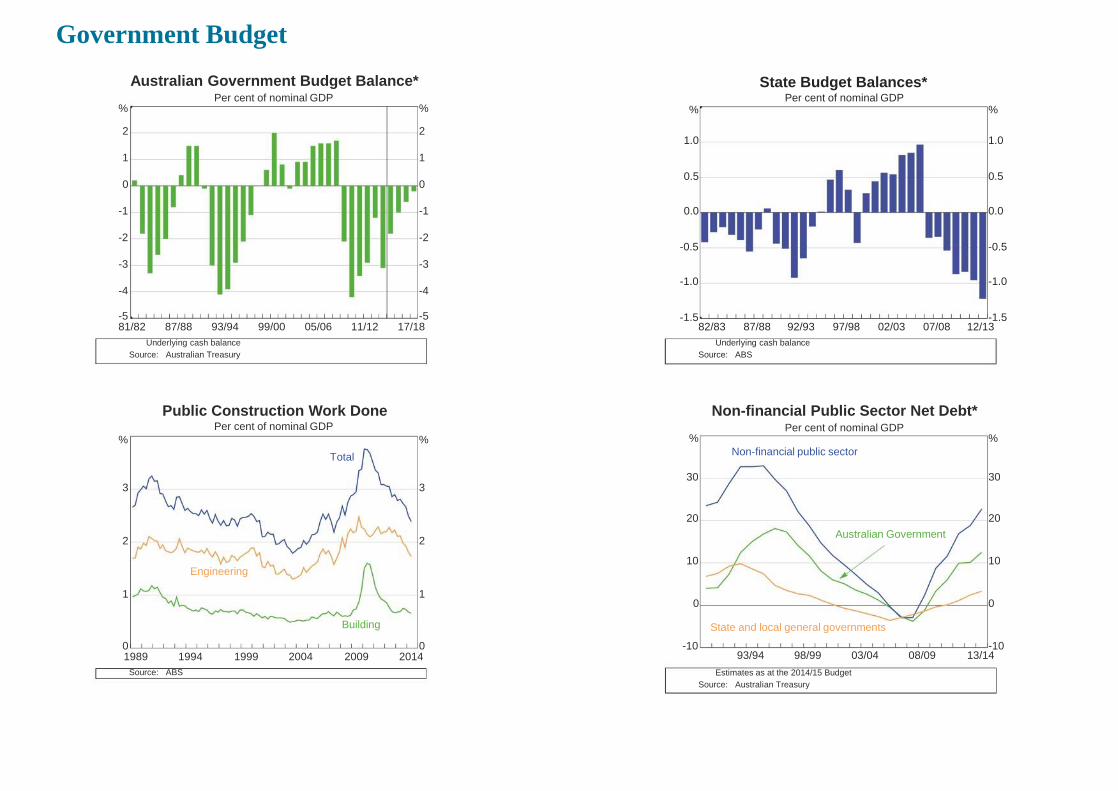

Government Budget

Australian Government Budget Balance* Per cent of nominal GDP

% %

2 2

1 1

0 0

-1 -1

-2 -2

-3 -3

-4 -4

-5 -5 81/82 87/88 93/94 99/00 05/06 11/12 17/18

Underlying cash balance

Source: Australian Treasury

Public Construction Work Done Per cent of nominal GDP

% %

Total

3 3

2 2

Engineering

1 1

Building

0 0 1989 1994 1999 2004 2009 2014

Source: ABS

State Budget Balances* Per cent of nominal GDP

% %

1.0 1.0

0.5 0.5

0.0 0.0

-0.5 -0.5

-1.0 -1.0

-1.5 -1.5 82/83 87/88 92/93 97/98 02/03 07/08 12/13

Underlying cash balance

Source: ABS

Non-financial Public Sector Net Debt* Per cent of nominal GDP

% %

Non-financial public sector

30 30

20 20

Australian Government

10 10

0 0

State and local general governments

-10 -10 93/94 98/99 03/04 08/09 13/14

Estimates as at the 2014/15 Budget

Source: Australian Treasury

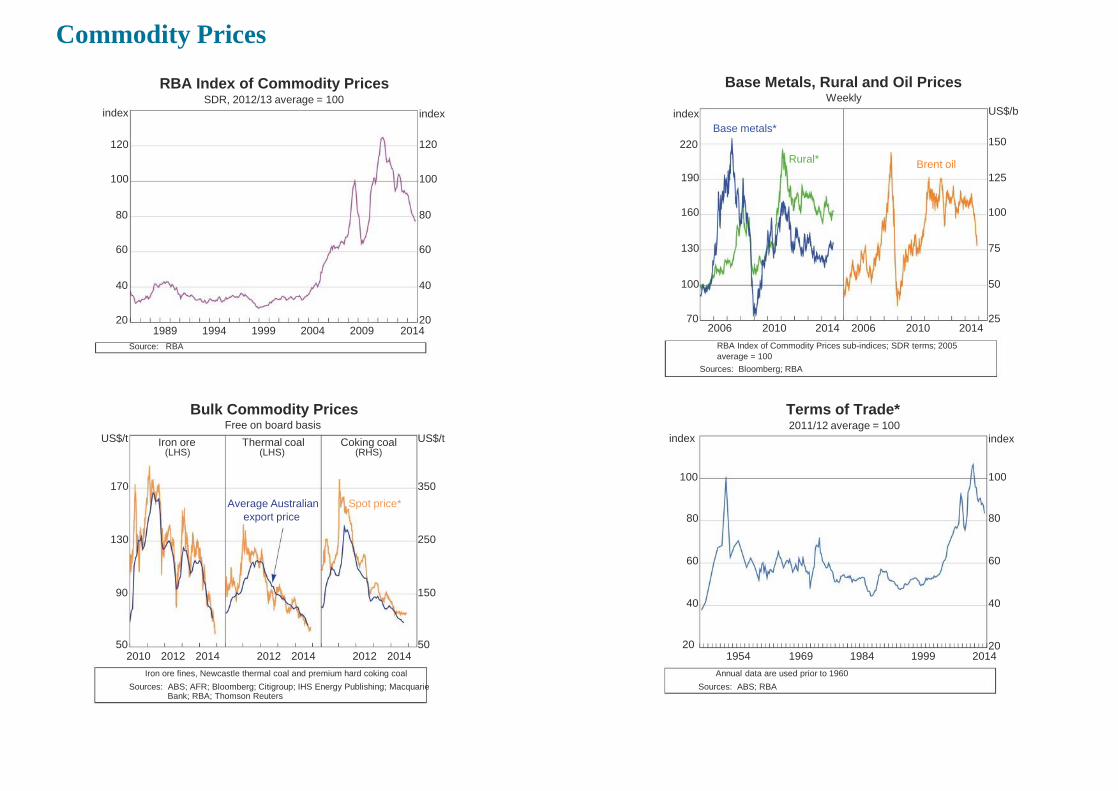

Commodity Prices

RBA Index of Commodity Prices SDR, 2012/13 average = 100

index

120

index index

120 220

Base Metals, Rural and Oil Prices Weekly

US$/b

Base metals*

150

100

80

60

40

20 1989 1994 1999

100

80

60

40

20 2004 2009 2014

Rural*

190

160

130

100

70 2006 2010 2014

Brent oil

125

100

75

50

25 2006 2010 2014

US$/t

170

130

90

50

Source: RBA

Bulk Commodity Prices Free on board basis

Iron ore Thermal coal Coking coal (LHS) (LHS) (RHS)

Average Australian Spot price*

export price

US$/t index

100 350

80

250

60

150 40

50 20

RBA Index of Commodity Prices sub-indices; SDR terms; 2005

average = 100

Sources: Bloomberg; RBA

Terms of Trade* 2011/12 average = 100

index

100

80

60

40

20 2010 2012 2014 2012 2014 2012 2014 1954 1969 1984 1999 2014

Iron ore fines, Newcastle thermal coal and premium hard coking coal Annual data are used prior to 1960

Sources: ABS; AFR; Bloomberg; Citigroup; IHS Energy Publishing; Macquarie Sources: ABS; RBABank; RBA; Thomson Reuters

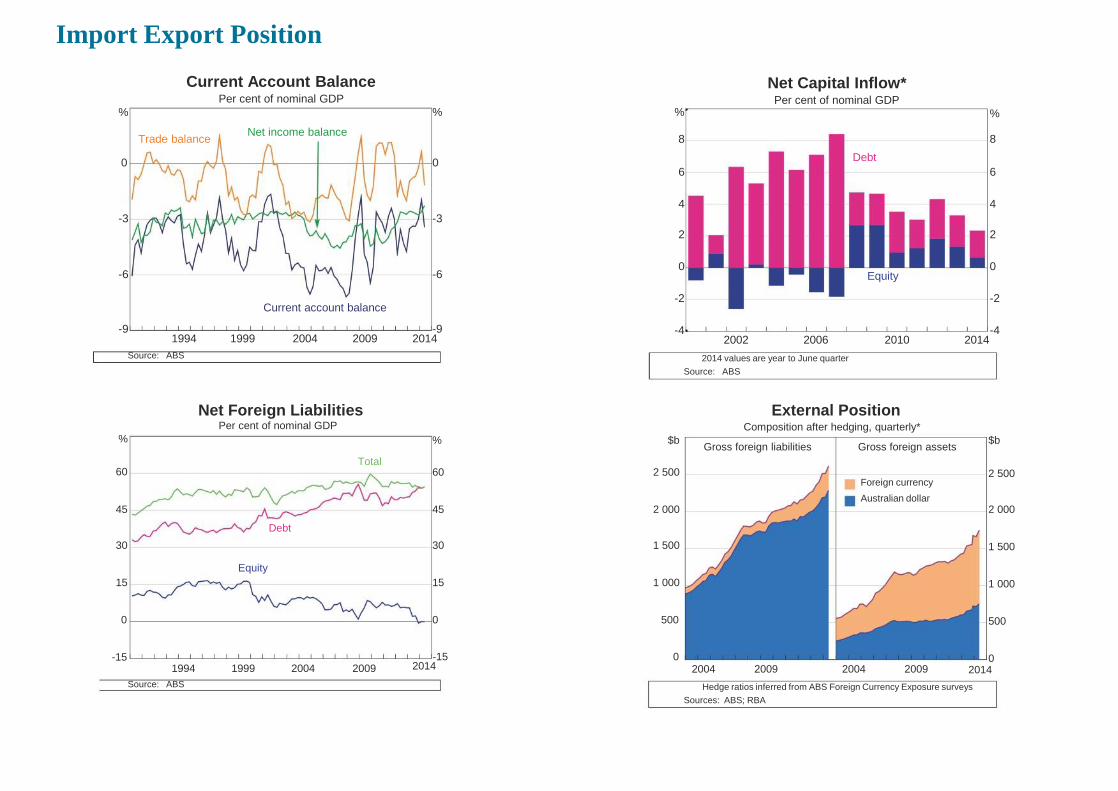

Import Export Position

Export Volumes Quarterly, 2011/12 prices, log scale

$b $b

Resources Services

40 12

Rural

20 6

Manufacturing

10 3 2000 2007 2014 2000 2007 2014

Mt

170

150

130

110

90

70

50

30 2004

Bulk Commodity Exports Quarterly

Iron ore Coal

2009 2014 2004 2009

Mt

110

100

90

80

70

60

50

40 2014

Sources: ABS; RBA

Import Volumes Quarterly, 2011/12 prices, log scale

$b

Intermediate

$b %

30

Sources: ABS; RBA

Exports by Destination Annual, share of total values

%

30 Consumption

16

8

Services

4

2 2000 2007 2014

16

8

Capital

4

2 2000 2007 2014

China

25 25

20 20 Japan

15 15

EU - 27

10 10 South Korea

5 5

India US

0 0 2001 2005 2009 2013

Source: ABS Source: ABS

Current Account Balance Per cent of nominal GDP

%

Net income balance

% %

Net Capital Inflow* Per cent of nominal GDP

%

Trade balance

0

-3

-6

-9 1994 1999

0

-3

-6

Current account balance

-9 2004 2009 2014

8

6

4

2

0

-2

-4 2002 2006

8

Debt

6

4

2

0 Equity

-2

-4 2010 2014

Source: ABS

Net Foreign Liabilities Per cent of nominal GDP

%

Total 60

45

Debt

30

Equity

15

0

-15 1994 1999 2004 2009

% $b

60 2 500

45 2 000

30 1 500

15 1 000

0 500

-15 0 2014

2014 values are year to June quarter

Source: ABS

External Position Composition after hedging, quarterly*

Gross foreign liabilities Gross foreign assets

Foreign currency

Australian dollar

2004 2009 2004 2009

$b

2 500

2 000

1 500

1 000

500

0 2014

Source: ABS Hedge ratios inferred from ABS Foreign Currency Exposure surveys

Sources: ABS; RBA

Import Export Position

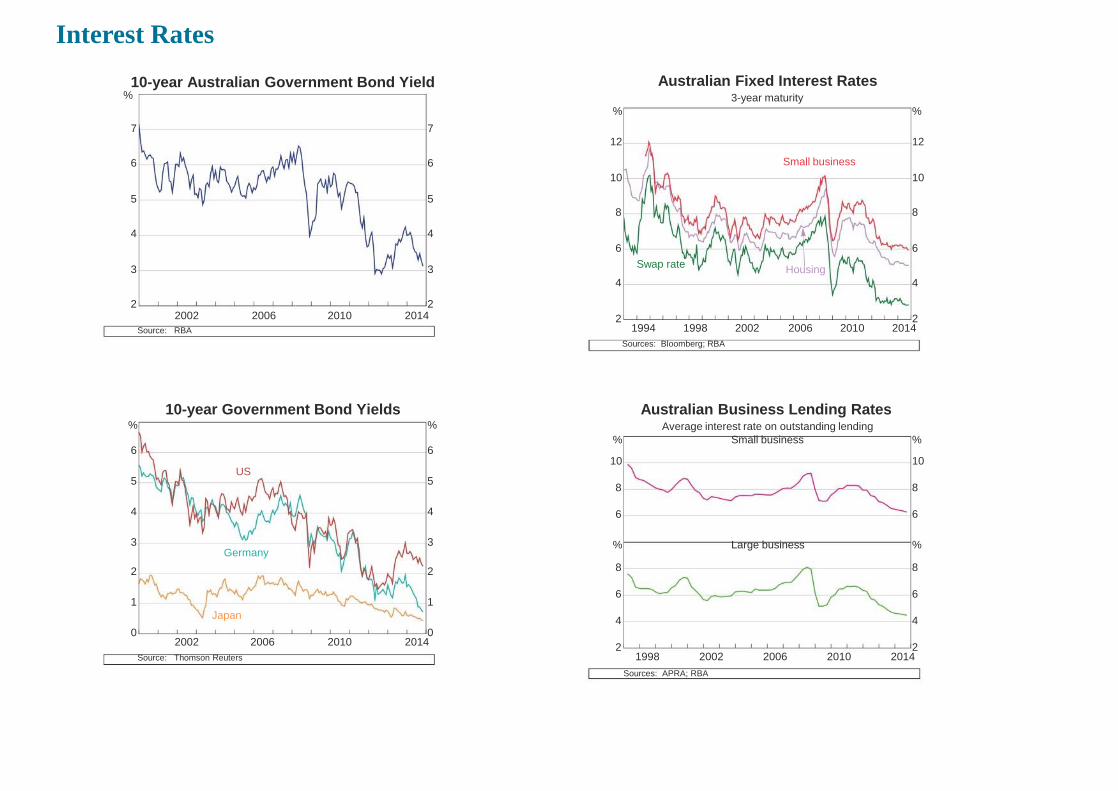

Interest Rates

10-year Australian Government Bond Yield %

7 7

6 6

5 5

4 4

3 3

2 2 2002 2006 2010 2014

Source: RBA

10-year Government Bond Yields %

6

%

6

US 5 5

4 4

3 3 Germany

2 2

1 1

Japan

0 0 2002 2006 2010 2014

Source: Thomson Reuters

Australian Fixed Interest Rates 3-year maturity

% %

12 12

Small business

10 10

8 8

6 6

Swap rate

4

2 1994 1998 2002

Housing

4

2 2006 2010 2014

Sources: Bloomberg; RBA

Australian Business Lending Rates Average interest rate on outstanding lending

% Small business %

10 10

8 8

6 6

% Large business %

8 8

6 6

4 4

2 2 1998 2002 2006 2010 2014

Sources: APRA; RBA

The Australia continues to maintain a watching brief on he flow of economic data,

having left the cash rate unchanged at 2.5% since July 2013. In our view, there are

three conditions that all need to be satisfied before another rate cut becomes likely:

rising unemployment, stabilization of asset prices and low inflation (well into the

bottom half of the target range). The first of these is in place, there are increasing signs

that the second is occurring and we expect that weak cost growth should bring about

the third by the end of the year.

Interest Rates

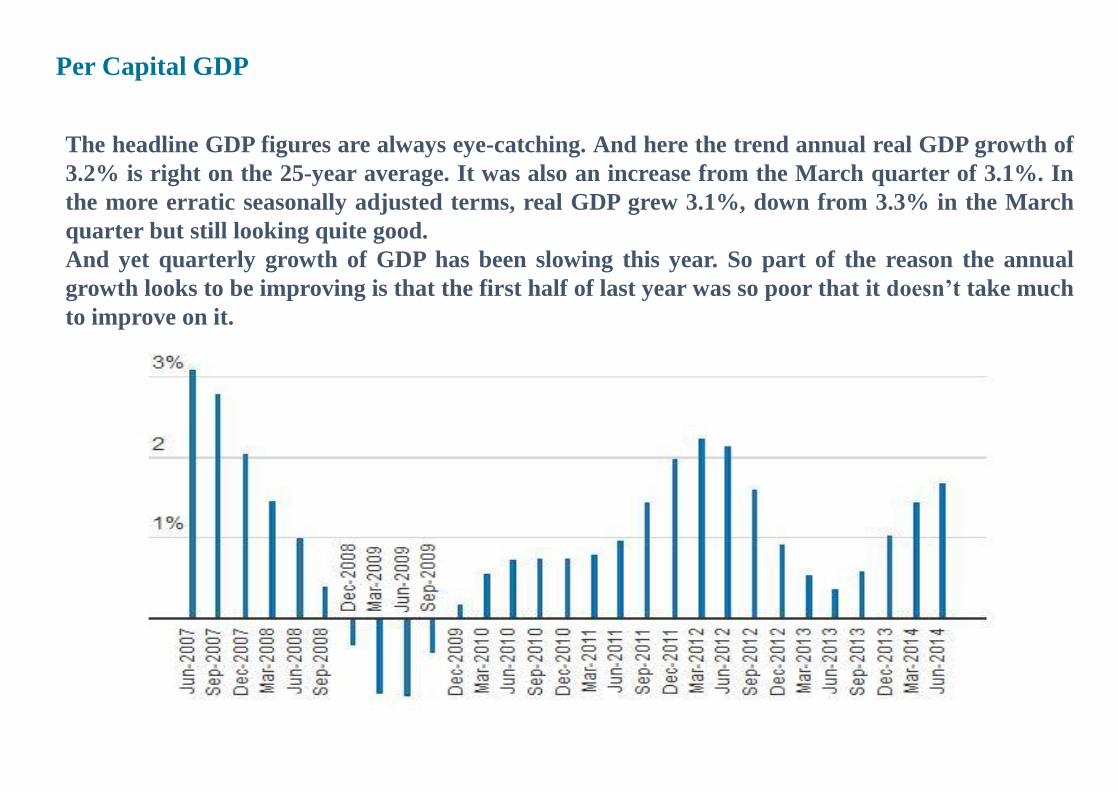

Per Capital GDP

The headline GDP figures are always eye-catching. And here the trend annual real GDP growth of

3.2% is right on the 25-year average. It was also an increase from the March quarter of 3.1%. In

the more erratic seasonally adjusted terms, real GDP grew 3.1%, down from 3.3% in the March

quarter but still looking quite good.

And yet quarterly growth of GDP has been slowing this year. So part of the reason the annual

growth looks to be improving is that the first half of last year was so poor that it doesn’t take much

to improve on it.

THANK YOU

Copyright © 2022 FDOKUMEN