The Analysis of Consumption Theories In the Ethiopian Economy

78

ANALYSIS OF CONSUMPTION THEORIES IN THE ETHIOPIAN ECONOMY A SENIOR ESSAY SUBMITTED TO THE DEPARTEMENT OF ECONOMICS IN PARTIAL FULLFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF BACHELOR OF ARTS IN ECONOMICS ESSAY ADVISOR:-ATLAW ALEMU (ATO) ADDIS ABABA UNVERSITY FACULTY OF BUSINESS AND ECONOMICS DEPARTEMENT OF ECONOMICS BY-YOSEPH CHALA

-

Upload

addisababa -

Category

Documents

-

view

0 -

download

0

Transcript of The Analysis of Consumption Theories In the Ethiopian Economy

ANALYSIS OF CONSUMPTION THEORIES

IN THE ETHIOPIAN ECONOMY

A SENIOR ESSAY SUBMITTED TO THE DEPARTEMENT OF ECONOMICS IN PARTIAL FULLFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF BACHELOR OF ARTS IN

ECONOMICS

ESSAY ADVISOR:-ATLAW ALEMU (ATO)

ADDIS ABABA UNVERSITY FACULTY OF BUSINESS AND ECONOMICS

DEPARTEMENT OF ECONOMICS

BY-YOSEPH CHALA

i

ACKNOLGEMENTS

HANK GOD!!! AFTER ALL THOSE DAYS, FINALLY, IT COMES TO AN END.

When I am writing this, I feel the ups-and-downs that I have been through for the

past years. But, JESUS is LORD. Those days are now passed only because of HIM. HE

has been the anchor of my life since my birth and I believe HE will be so forever. Oh!

I am living at HIS mercy. GLORY TO GOD!!

When I come to the individuals who were with me during my days at AAU,

definitely family comes first. My father, my sister and my brothers were all with me

and I am glad to thank them, at this time, for every thing they have done for me. You

were all with me for every walk that I walk. Never would I forget that. But, special

thanks should be reserved to my dearest sister, Genet Chala and her husband

Abateneh Mulugeta. I have no word to express the financial contribution and

generosity they have extended to me. Bless You. I am grateful to you. Without your

support, I doubt where I would become at this time. And, it will be totally unfair not

to mention the advice and the contribution that I have been receiving from my

brother, Ephrem Chala. He was an ardent supporter of my higher education from its

conception. I am so indebted to you.

This paper would not come to realization as the form as it is now without a

valuable advice and follow up of my essay adviser, Ato Atlaw Alemu. He is always

open to discussions and ready to supply materials, even at his own expense. I sincerely

appreciate his approach towards his advisees. Thanks a lot.

Next to that friends certainly come. In that case, I am not bold enough to forget

the support from Melaku Taddesse, a grad student at AAU, Mengistu Emo, a senior

alumnus, Ermias Tefera, fellow student at AAU and, of course, Sisay Birru, Loan

Officer at DBE, Nekemte Branch. They were all helping me by providing books,

materials and by extending valuable suggestions in the preparation of this paper.

Besides, I would like to thank all my classmates, particularly Abiot S. of the CBE,

T

ii

Matias A., Sisay K., Mulugeta B., Demssew T. and others who make my stay at AAU

so much enjoyable. I do believe that the memories of those days will last with me.

Yoseph Chala

August, 2008

iii

Table of contents

PAGE

AKNOLGEMENTS----------------------------------------------------------------------i

ABSTRACT----------------------------------------------------------------------------- v

CHPTER ONE

INTODUCTION------------------------------------------------------------------------ 1

1.1 BACKGROUND--------------------------------------------------------------1

1.2 STATEMENT OF THE PROBLEM-------------------------------------------5

1.3 OBJECTIVE OF THE STUDY------------------------------------------------ 5

1.4 SIGNIFICANCE OF THE STUDY-------------------------------------------- 5

1.5 WORKING HYPOTHESIS-------------------------------------------------- 6

1.6 SCOPE AND LIMITATIONS OF THE STUDY-------------------------------6

1.7 ORGANIZATION OF THE STUDY----------------------------------------- 7

CHAPTER TWO

REVIEW OF LITERATURE------------------------------------------------------------ 9

2.1. DEFINITIONS: CONSUMPTION AND CONSUMPTION

EXPENDITUE-------------------------------------------------------- 10

2.2. THEORIES OF CONSUMPTION EXPENDITURE------------------------11

2.2.1. THE CLASSICAL BACKGROUND------------------------------- 11

2.2.2 THE ABSOLUTE INCOME HYPOTHESIS-----------------------12

2.2.3 THE LIFE-CYCLE HYPOTHESIS-------------------------------- 17

2.2.4. THE PERMANENT INCOME HYPOTHESIS--------------------23

2.3. THE ETHIOPIAN CASE--------------------------------------------------34

CHAPTER THREE

DATA, METHODS OF DATA ANALYSIS AND EMPIRICAL ESTIMATION-------39

3.1 SOURCE AND NATURE OF DATA --------------------------------------- 40

3.1.1. AUTOCORELATION----------------------------------------------41

iv

3.1.2. NONSTATIONARITY------------------------------------------------ 42

3.1.3. COINTEGRATION--------------------------------------------------- 43

3.2. MODEL ANALYSIS AND METHODOLOGY--------------------------------44

3.3. EMPIRICAL ESTIMATIONS AND PRESENTATION OF RESULTS------- 46

3.3.1. TESTING FOR UNIT ROOT----------------------------------------- 46

3.3.2. EMPIRICAL ESTIMATION-THE AIH-------------------------------47

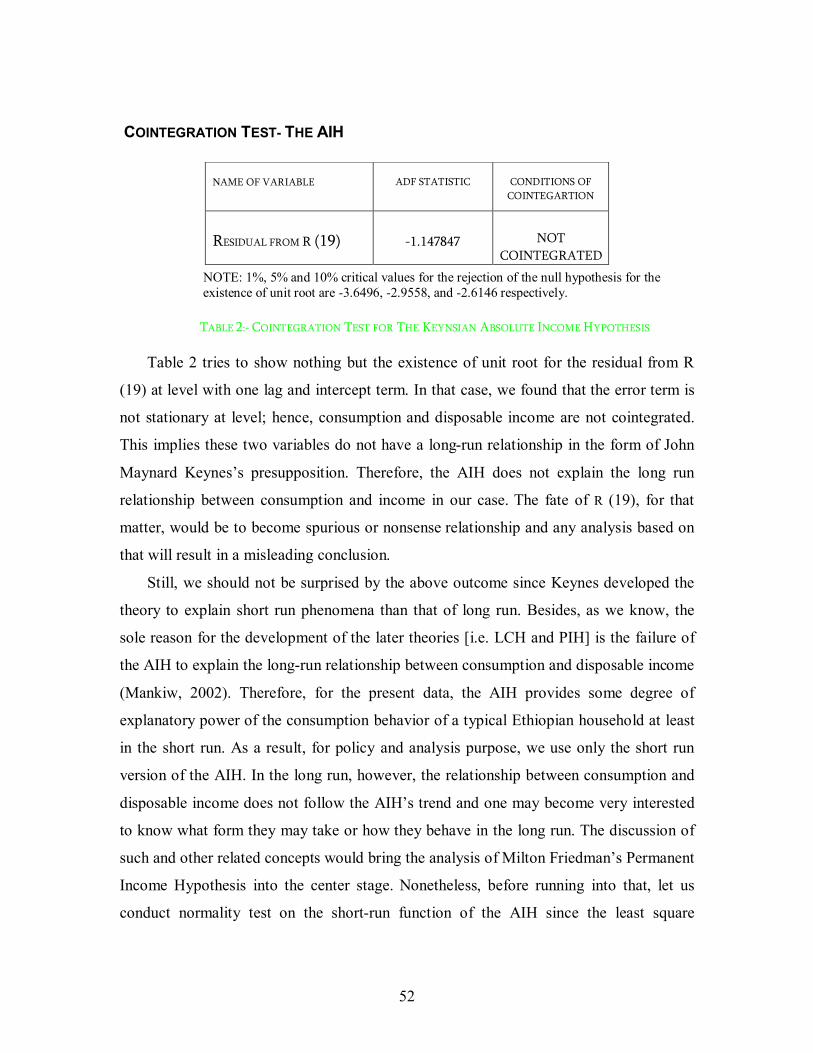

- COINTEGRATION TEST-THE AIH------------------------------ 52

- NORMALITY TEST ON THE AIH--------------------------------- 53

3.3.3. EMPIRICAL ESTIMATION-THE PIH------------------------------- 54

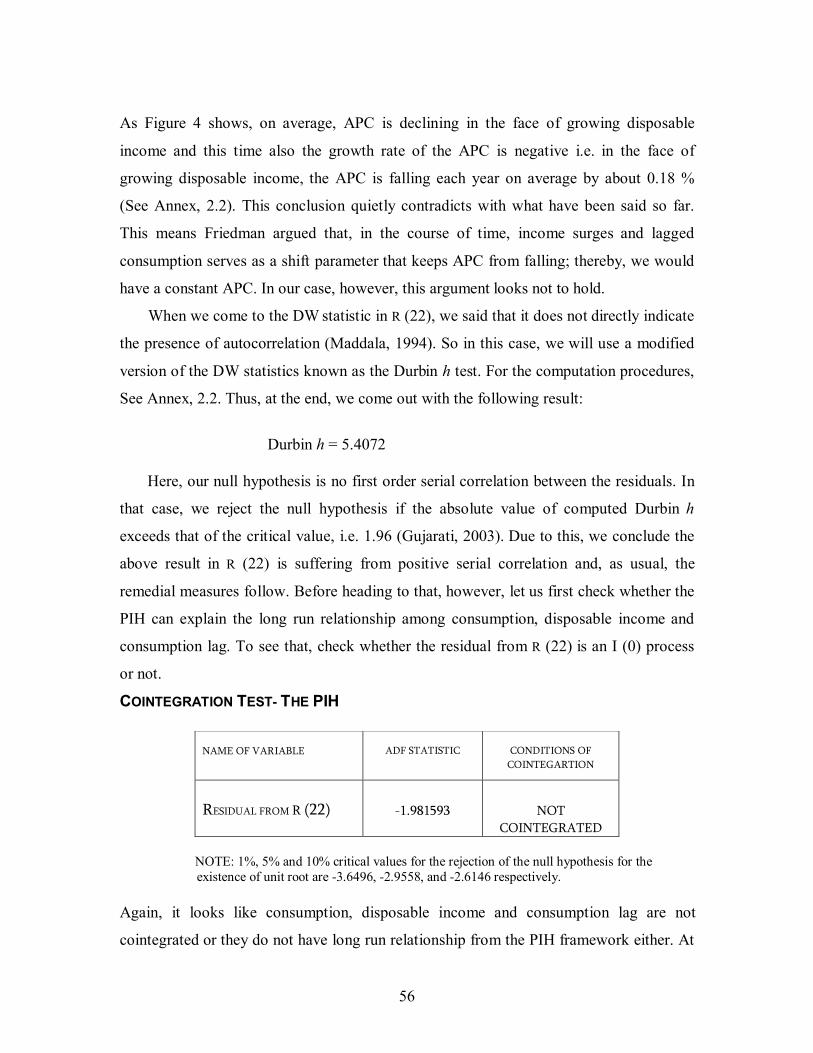

- COINTEGRATION TEST-THE PIH------------------------------- 56

3.4. WHY THE PIH HAS FAILED TO EXPLAIN OUR DATA? ------ --------- 57

CHAPTER FOUR

CONCLUSION AND RECOMMENDATIONS------------------------------------------60

4.1. CONCLUSION--------------------------------------------------------------- 60

4.2. POLICY PRESCRIPTIONS-------------------------------------------------- 60

4.2.1. ON UNEMPLOYMENT----------------------------------------------60

4.2.2. ON INFLATION------------------------------------------------------61

BIBILOGRAPHY----------------------------------------------------------------------- 63

ANNEX ONE-REGRESSION OUTPUTS---------------------------------------------- 67

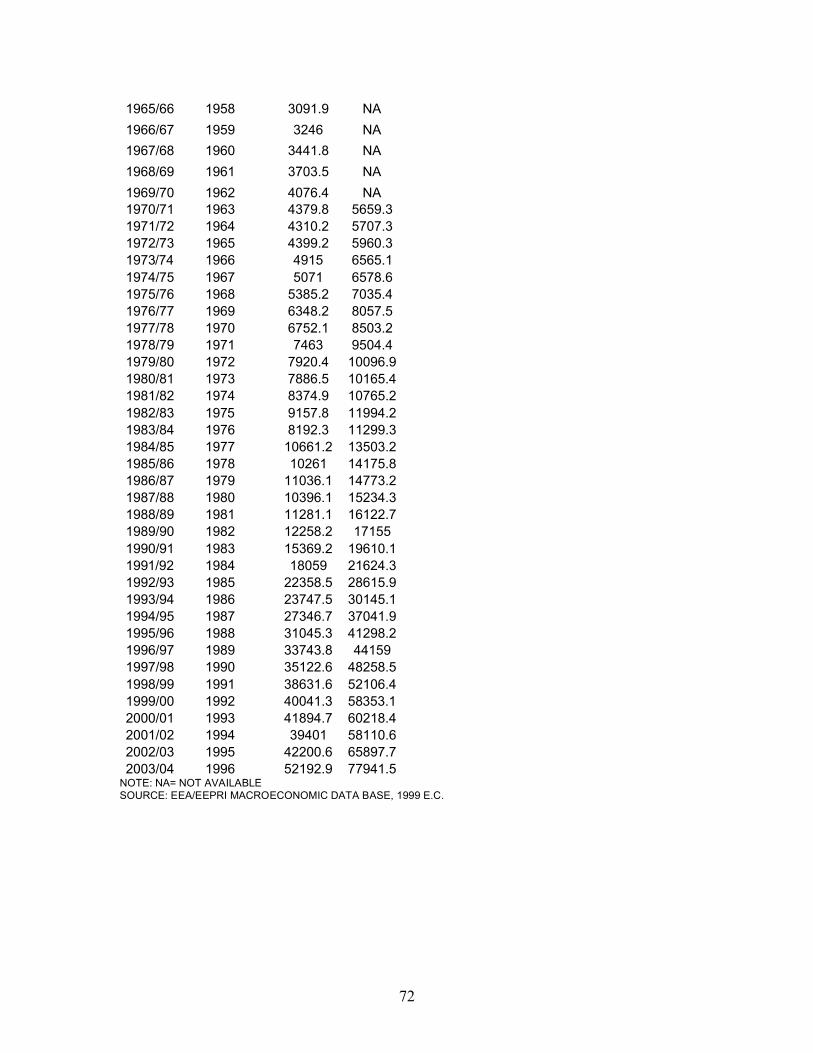

ANNEX TWO- DATA------------------------------------------------------------------71

v

ABSTRACT

In an effort to investigate the dynamic link between consumption and income, this

paper tries to test the validity of the Absolute Income Hypothesis of John Maynard

Keynes and the Permanent Income Hypothesis of Milton Friedman using country

level aggregate time series data. In that case, we found that consumption is not to be a

martingale process i.e., it follows the AIH’s presuppositions. But, that is only in the

short run. In the long run, neither of these theories were able to explain the data at

hand. That is primarily because of the nature of the theory on the AIH’s side and, the

assumptions it rests on and the quality of the data can be mentioned as reasonable

sources of failures for that of the PIH’s. In that essence, the paper concludes by

suggesting some short run policy prescriptions that are in line with Keynes’s

argument.

1

Chapter one

Introduction

1.1 BACKGROUND According to the eighteenth century Scottish classical economist Adam Smith, the

large international variations in income and standards of living over time and across

countries is not primarily because of other factors but due to the transformative effect

of the division of labor. After a century, David Ricardo, another classical economist

from Great Britain, came and accentuated the importance of trade for such differences

in affluence. Still, in the mid-twenty century, an American born neoclassical

economist Robert Solow came up with his highly influential and sophisticated growth

theory that gives emphasis on the importance of technological progress as the source

of such huge differences in income among nations across the globe. This means for

Solow sustained economic growth depends largely on technological advancement and

this innovation determines the country’s steady-state capital stock, a capital stock that

represents the long run equilibrium of the economy. Therefore, if a nation devotes a

large fraction of its income to invest in R&D and in higher educations, the major

sources of technological outlets; it will have a higher level steady-state capital stock,

thereby a higher level of income (Vaish, 1980, Dornbush et al, 1982, Todaro and

Smith, 2003).

In this area, empirical literatures so far produced based on the experiences of

both developed and underdeveloped countries seem to support the validity of Solow’s

argument1 (Barro and Sala-i-Martin, 2004).As the member of the later group,

Ethiopia’s case is not very far from what has been said in the theory. But, this does

not mean that the dire conditions of the country are entirely attributed to the luck of

such investments. Though officials from the government bloc are tireless to persuade

the skeptic public about the current boom the economy has been enjoying for the past

four or five years, both the public and the government know that Ethiopia is one of

1 Actually, Solow was not the first to provide a growth theory for country’s economy but his

theory is “the best known and it is the basic reference point for the literature on growth and

development” (See Todaro and Smith,2003)

2

the poorest country on earth with low level of per capita income ($160, World Bank,

2007), poverty is ubiquitous throughout the nation and the danger of this social unjust

will surely be remained as the major wrestling ground of all stakeholders and the

government at large in the coming years. If we agree on this issue and decide that the

key to reduce the extent of poverty is to register fast and consecutive growth, as the

theory suggests, the major task that should be done is to expand investment in R&D

and in higher education. As various literatures acknowledges, this kind of investment

is essential particularly for the agricultural sector (Mulat Demeke, 2003) and we

know that it depends largely on the amount of the country’s national income that is

saved.

The Ethiopian saving rate, however, was enjoying its good years during the last

days of the imperial regime. In those periods, Gross Domestic Saving (GDS) as a

percent of Gross Domestic Product (GDP) reached 13pc; the highest so far mobilized

(Befekadu Degefe and Berhanu Nega,1999/2000).Since then, as figures show, on

average, it has been fluctuating between 7.2pc in the last days of the military junta

and 4.1pc for the years 1993/94-2004/05, (EEA, Annual Report, 2005/06).This shows

the fact that GDS as the percent of GDP has been very low in Ethiopia both from a

historical perspective and relative to similar economies and it has not been , in it

history, around the usual recommended rates of saving and investment that ranges

from 12pc to 15pc and even as high as 25pc in some cases.

Economists provide a number of explanations for the existence of such kind of

traditionally low saving rate in developing countries and if we consider these

arguments seriously for us, we can easily understand why we are on such trend all

those periods. First of all, the concept of saving is directly related to income and as

mentioned earlier our country is among one of the world’s low income countries. So

such low income forces her to reduce her saving, that is, whatever earned is

consumed. Second, the spread of financial institutions in the country also has a

significant effect on the saving behavior the population. Alas, we all know that we are

unlucky in this respect too. Furthermore, the consumption behavior of the population

clearly determines the fate of the country’s saving rate. In this case, as studies show,

during the imperial era one of the challenges of the development was “to make such

3

transformation as the process involves changes in the traditional consumption

pattern” (Befekadu Degefe and Berhanu Nega: 1999/2000) and in the same report

these academics refer the consumption pattern of the then feudalist society as

“conspicuous consumption”, the famous phrase first used by an early twenty century

American economist and social scientist Veblen to refer the extravagant spending

behavior of Americans of his time( Mitchell,1947).If we also consider the periods of

post revolution , the policies of the Derge regime and its immediate heir are unable to

switch the public from the practice of such large wasteful behaviors. Thus, due to

such and other reasons, we are not enjoying higher saving rate and hence higher

investment and higher growth. As a result, we have become low income earners at

least from the crude arguments of low saving –low investment in R&D and in higher

education in so doing low growth approach.

Nevertheless, in the above discussion we have said so much about saving not

because we are interested in it but it gives a close insight to another important

economic variable what economists call consumption expenditure, the flip side of

saving.

The most important single fact about saving and consumption is that they are two

opposite sides of disposable income, income after tax and any transfers. This shows

that saving means abstaining from present consumption in order to provide for larger

future consumption. In the same way, today’s larger consumption results in low level

of saving and hence lower level of consumption in the future. As a result, every

explanation forwarded in favor of the former implicitly explains the later and vice

versa. Therefore, we would not be mistaken if we assume that the low saving

behavior of the country forwarded earlier is basically due to the fact that the high

consumption behavior of its citizens as the latest report of Ethiopian Economic

Association (EEA) clearly puts:

“this [low saving] is partly due to the subsistence nature of the economy in which total

consumption constitutes a significant share of domestic output” (EEA, 2005/06)

However, data clearly shows that, of this total consumption, private aggregate

consumption usually takes in the lion’s share. For instance, during the years of the

4

military rule, out of the total consumption 92.8pc of the domestic total consumption,

on average, private consumption absorbs 76.2pc; leaving only about 7.2pc for average

GDS.The same is true for the current government, that is, the data collected for the

periods 1993/94 to 2004/05 depicted that out of the 96.1pc of the total consumption,

private consumption again engrosses 78.7pc of the national output to make GDS at its

historically lower level of 4.1pc(EEA, 2005/2006).This and the above facts about

saving and consumption reveal important points about the economy under

investigation. These are we are in the historically low saving trend and

simultaneously we are consuming whatever produced in the economy. Therefore, at

this stage at least we can say something about private consumption expenditure, that

is, it exhausts the largest part of domestic output and it should deserve a close

understanding of how it operates in the economy.

Similarly, according to the Keynesian conventional four sector economy model,

aggregate output is the sum of personal consumption expenditure, total gross

investment, government purchase of goods and services and, of course, net export. Of

these, consumption expenditure is the largest macro variable irrespective of the size

and nature of the economy. In the words of Venieris and Sebold:

“depending on the country in question, expenditures on consumption amount to any where from two-

thirds to four-fifths of net national product.”(Venieris and Sebold, 1977)

Empirical findings in the literature also support the above conclusion.Branson

(2006) shows that 65pc of GNP in the US is absorbed by consumption expenditure.

Similarly, Mankiw (2002) implies that household consumption expenditure makes up

two-thirds of GDP. In the case of Ethiopia, as one can easily guess from the above

discussions, consumption expenditure makes about three-fourth of our total spending

(Oman, 2006).This shows that not only long run growth of the economy but short run

fluctuation of aggregate demand is also highly susceptible to what is going on in the

hands of consumers.

5

1.2 STATEMENT OF THE PROBLEM

As the nature of behavior underlying consumption is extremely important from

the standpoint of economic theory and policy, economists and theoreticians for the

past years have made every effort to examine the consumption behavior of an

economy and to come up with a more credible theory of consumption function. In this

perspective, based on the data on income and aggregate private consumption, many

economists have suggested a number of competing theories. Among these, we here

consider the three most influential and most important works of, Absolute Income

Hypothesis (Keynes, 1936), Life Cycle Hypothesis (Modigliani et al, 1950s) and

Permanent Income Hypothesis (Friedman, 1957).But, the problem is which one is

superior? That is a nearly century old debate for other economies, though we can not

indicate the exact time in our case. Anyway to put it clearly, which of these

outstanding works best reflect the consumption behavior of the Ethiopian economy?

1.3 OBJECTIVE OF THE STUDY

A thorough understanding of the consumption behavior of an economy helps

policy makers, practitioners and the government’s think tanks in general to make a

timely and appropriate policy prescription towards aggregate private spending.

Having this in mind:

- the major objective of this study is to find out the theory that governs the

consumption behavior of the Ethiopian economy and to create a general

understanding of the concept of consumption and its related issues like how it works

in the economy.

1.4 SIGNIFICACE OF THE STUDY

To gauge the effectiveness of alternative economic policies, both economists and

policy makers use the IS-LM model of the economy and from our macroeconomics

background we know that such model is partly based on the country’s Marginal

Prpensity to Consume (MPC) developed on the basis of the consumption behavior of

the economy .As a result, a clear understanding of the impact of any economic policy,

6

whether it is fiscal or monetary , requires a comprehensive understanding of the

concept of MPC which is “an ingredient in determining the response of the economy

to changes in the values of the policy variables” (Venieris and Sebold,

1977).Therefore , the perception of consumption function helps us to determine the

scenario of many public policies.

1.5 WORKING HYPOTHESIS

As said earlier, this paper is neither trying to discover the major determinants of

consumption expenditure in the Ethiopian economy nor aim to model the

consumption behavior of the economy using its own macro variables.Rather, it limits

itself to what has been said in the theories and attempts to test which one of the above

three theories that best represents the consumption behavior of typical Ethiopian

consumers. Consequently, we have the following two theories to work with:

According to Absolute Income Hypothesis:

Consumption is primarily determined by current income.

According to Permanent Income Hypothesis:

Consumption should depend primarily on permanent income.

For this reason, this study hypothesizes that consumption is dependent on permanent

income.

1.6 SCOPE AND LIMITATIONS OF THE STUDY

The scope of this study is not at household level but it is at a national level. This

is only because of the following two reasons. First, there is difficulty of obtaining

household data on consumption and disposable income. But, aggregate data are

readily available from the publication of any one of the government institutions.

Second, if household data are yet to be found, there are still problems of aggregation

and computation due to time and resource constraints. On the contrary, aggregate data

are usually free from these problems.

7

The strength of this study is that it tries simultaneously to discuss the seminal

works of the three giant economists in the fields of consumption. Certainly, this

provides the reader an opportunity to debate over three perspectives at a time.

However, it has the following obvious limitations .The first and most serious

limitation of this study traces with the Life Cycle Hypothesis of Franco Modigliani

and his collaborators. Because as we shall see in the coming discussions, this

hypothesis rests on the assumption that private consumption expenditure at any

period‘t’ is dependent on individuals’ income as well as wealth. Hence, to test the

explanatory power of Modigliani’s theory, one must have time series data on income

and wealth. But, as Modigliani himself acknowledged, generally in the developing

countries aggregate data on wealth is almost nonexistent (Modigliani, 1986) and as

local studies show our country’s case is not different from the above conclusion

(Solomon, 1999, Oman, 2006). In this context, the study becomes unable to analyze

the relationship between income and consumption from the perspective of the Life

Cycle framework. The second serious limitation of this study is that it is subject to the

basic assumptions of the theories. This means when the economists develop their

theories they made some bold assumptions based on the empirical evidences of the

developed world. Unfortunately, some of these assumptions are almost nonexistent in

the context of LDCs like Ethiopia. For instance, as we shall see in the coming

chapters, the latter two theories are based on Irving Fisher’s theory of consumer

behavior which implicitly assumes that there is no borrowing and saving constraints

but as Mankiw puts it “for many such borrowing is impossible”(Mankiw,2002).

The last limitation that should be mentioned here is that the study is limited in the

time span of the available data. So in this case, we will fail to catch the influence of

some missing observations in our analysis.

1.7 ORGANIZATION OF THE STUDY

The paper is organized in the following four major chapters. The first chapter is

an introductory part. The second chapter will provide a detailed analysis of the

consumption theories forwarded in the previous discussions by reviewing a number

of literatures in this respect. Based on that notion, it also formulates the mathematical

8

version of each theory for ease of estimation. The third chapter, the most important

chapter, will have two parts. In the first part, we will briefly discuss the nature and

sources of data and consider some methodological concepts to be used in the study.

The second part will entirely devoted to the process of empirical verification. Chapter

four, the last chapter, will conclude the research findings and recommend some policy

prescriptions

9

Chapter Two

Review of Literatures

In the previous chapter, it was said that aggregate private consumption expenditure or

simply consumption expenditure is the largest component of aggregate demand

irrespective of the nature and type of economy and due to this fact it has become the

major of concern of government policy makers and independent [nonpartisan] researchers

who are interested in policy issues. As a result of this and other factors, macroeconomists

devote much of their precious time to study the behavior of this macro variable in greater

detail and in the literature we can find a number of perspectives on such issue. According

to these literatures economists generally divide determinants of consumption expenditure

into two categories:-objective and subjective determinants (Kurihara, 1957). Objective

determinants include income, the distribution of income, corporate financial policies,

consumers’ liquid assets, the rate of interest and so forth. Contrarily, subjective factors

are security motives, ‘keeping up with the Joneses’, the desire for improvement, financial

prudence et cetera. As a result of this, there are a number of theories or hypotheses in this

field. In this section [generally in this study], however, we only focus on those which are

based on the dynamic relation between consumption and income and we try to

comprehend the essence of the theories forwarded in the introductory part of this paper

with a brief reviews of the classical writings since that helps us to understand the nature

and originality of Keynes’s idea and the subsequent works of those giant economists.

But, before doing that I believe that it is necessary to say some thing about the economic

concepts of consumption and consumption expenditure because economists, chiefly those

interested in the study of household behavior, usually use these concepts in different

contexts. Though it seems we generally have a clear understanding of these

terminologies, as we see in later discussions, one of the serious problems that arise in the

applications of these consumption theories is the luck of clear understanding about such

basic issues. Hence, we should devote some time to deal with those concepts. After that,

we will run into the theoretical debates that attract economists from all around for the

past years.

10

2.1 DEFINITIONS: CONSUMPTION AND CONSUMPTION EXPENDITURE

According to Seldon and Pennance1, consumption is “the process of deriving utility

from a commodity or service. More generally, it describes the business of acquiring

commodities and services in order to obtain satisfaction directly from them; or indicates

the amount of expenditure on them.” Additionally, they argued that consumption dose not

necessary indicate the destruction of the commodity consumed because, for instance,

food is consumed in the same way other objects like movies are also consumed though

the latter action does not include the destruction of the commodity, movie. Thus, in this

concept consumption is not necessarily a tangible process. Similarly, other literatures

argued that consumption should be defined in terms of ‘the use of goods rather than the

expenditure on it in any period’ (Branson, 2006). In general, economists use the word

‘consumption’ to mean the process of acquiring goods and services and the amount of

expenditure on them where the objective is to derive utility. But the problem, in this case,

is that the above definition is not clear about the nature of these commodities to be

consumed. Because we know that in economics consumer goods are generally divided

into two categories: durables and non durables. So, the above definition is no help.

Therefore, we should consider the following explanation. “Consumption expenditures by

household are personal consumption expenditures to national accounts. It includes

expenditures by households on durable consumer goods [automobiles, refrigerators, and

video recorders], nondurable consumer goods [bread, milk, vitamins pencils, shirts,

toothpaste] and consumer expenditure for services [of lawyers, doctors, mechanics,

barbers.]” (McConnell and Brue, 1994 pp.123-124). In this context, households allocate

their income between consumer durables, non durables and services. Though Keynes

agrees with this kind of understanding on consumption expenditure or simply

consumption (Keynes, 1949, pp.61), Modigliani’s Life Cycle Hypothesis (LCH) would

like to take a different perspective as the following definition asserts: “total consumption

consists of current outlays for nondurable goods [bread, milk] and services [net of

changes if any in the stock of nondurable] plus the rental value of stock of service –

yielding consumer durable goods (Ando and Modigliani, 1963). As clearly seen from this

1 Everyman’s Dictionary of Economics,1969, J. M. Dent & Sons Ltd, pp. 88

11

perception, the LCH or Modigliani dose not want to include the expenditure on durable

goods as consumption expenditure by the households while Keynes dose so. But we

know that any ‘careful’ studies on consumption should distinguish between the

investment and consumption activities of consumers or the households by not

incorporating expenditure on consumer durables- investment-in their analysis and the

results of such study are sensitive to the definition they assigned to consumption

expenditure (Houthakker, 1958, Hall, 1978, Flavin, 1981). In other perspective,

Friedman, for his part, assumes that consumption should not incorporate the ‘purchase

price of durables but it should include their use value’ (Houthakker, 1958). Here, such

acquisition of consumer durables is regarded as saving and the use value of the

commodity is measured by ‘depreciation and interest cost rather than expenditure on

them (Branson, 2006). This clearly shows that consumption for Permanent Income

Hypothesis considers only expenditure on nondurable goods, services and the use value

of durables. Understanding these concepts is very helpful for the coming discussions and

when we discuss the central points of the respective theories, the reader should be remind

these different definitions assigned by the respective theories to the variable under study.

Having this in mind, the point to be underscore here is that, in this paper, unless noted

otherwise, though we said that they refer different concepts, the terms consumption and

consumption expenditure are used interchangeably to refer the same thing.

2.2 THEORIES OF CONSUMPTION EXPENDITURE

2.2.1 THE CLASSICAL BACKGROUND

As it is clear largely for economics students, the term “classical economics”, as first

coined by German political philosopher and revolutionary Karl Marx, refers primarily to

Ricardo and his intellectual predecessor, Adam Smith (Dillard, 1979) and similarly John

Maynard Keynes used the term to refer to the disciples of Ricardo, “those, that is so say,

who adopted and perfected the theory of Ricardian economics, including …. John S.

Mill, Alfred Marshall, Edgeworth and Prof. Pigou” (Keynes, 1949)2.As a result of this,

2 In this case, Keynes uses the term ‘classical’ in unusual way because history of economic thought

categorizes F. Y. Edgeworth as the proponent of marginlist school but Keynes considers him as classical

for his own analytical purpose. See Dillard, 1979, pp.14

12

we here use the latter perception of the classical economics, that is, the traditional works

of all the abovementioned thinkers since the time of Ricardo. In so doing, as we clearly

know that during the periods of theses economists, there was hardly any theory or

function that relates consumption and income. This is because of the fact that the

classical theory rests on the assumption of full employment of resources so that out of a

constant full employment of real income the decision of people how much to consume

today and how much to save for the future and vice versa was influenced by changes in

the interest rate (Vaish, 1980).This means that a higher interest rate induced or

encourages the consumers to save more by postponing current consumption while a lower

interest rate discourages saving. Therefore, for the classicists, consumption is a negative

function of interest rate and it is not a function of income for the simple reason that

income is not a variable or income dose not vary in their economy [i.e. it is assumed to be

fixed in a fully employed economy] and this assumption prohibit any possibility of

increase in the equilibrium aggregate income in the short period in the economy. Hence,

we can conclude that for the classical school, consumption is a function of the rate of

interest and the relationship is negative:

Ct = f (i)

where Ct and i represent real consumption expenditure at time‘t’ and the rate of interest

for the same period in the given economy respectively. And the relation between the two

variables is indirect or opposite; that is, as interest rate rises consumption declines and

vice versa.

2.2.2 THE ABSOLUTE INCOME HYPOTHESIS-KEYNES. The 1930’s marked the most important turning point for the economic ideology.

Because the Great Depression (1929-1940) and its aftermaths brought an end to the

traditional economic principles of laissez faire that had been dominating the mind set

almost for two centuries. This means the then conviction was not enough to cope up with

the realities on the ground and as a result of this, many economists, practitioners, policy

makers and pundits were trying to diagnose the economy in order to forward the best

13

prescription. Among these, the point man was Cambridge lecturer John Maynard Keynes

who took the center stage in the wake of the great downturn of the economy of many

industrialized nations of West Europe and US. According to the accounts of many

writers, the Great Depression is still considered as one of the greatest economic

catastrophe of western nations. It saw rapid declines in the production and sale of goods

and a sudden, severe rise in unemployment. For instance, at the worst point in the

depression, more than 15 million Americans-one –quarter of the nation’s workforce-were

unemployed (Blanchard,1997). Given all these factors, the ultimate goal of Keynes

analysis was to discover the factors that determine the volume of employment in any

economy (Keynes, 1949, Dillard, 1979).Thus, as he discussed in his General Theory, the

volume of employment is determined at the equilibrium point of the aggregate supply

function with that of the aggregate demand and the latter relates any given level of

employment to the income which that level of employment is expected to realize. And,

such aggregate demand is further decomposed into- consumption expenditure and

investment expenditure. Consumption expenditure, which is of our interest, becomes his

stepping stone for his analysis of the theory economic fluctuations. Thus, he attempted to

investigate the determinants and the behavior of consumption expenditure when

employment is at a given level and his findings can be summarized as follows.

First, based on the psychological law, experience and facts he said that “men are

disposed, as a rule and on the average, to increase their consumption as their income

increase, but not by as much as the increase in their income.”(Keynes, 1949).This is to

state that the amount of consumption out of income has the same sign as change in

income but smaller in amount. Economists relate this classical guess with the concept of

marginal propensity to consume – a variable that measures additional consumption out of

additional income-and hence, according to Keynes’s intellectual conjecture, marginal

propensity to consume is positive and less than one. Therefore, when a person or an

individual receives an additional birr, he/she spends some of it and saves the rest.

Second, he hypothesized that the ratio of consumption to income decrease as income

rises, i.e. in his own words “a rising income will often be accompanied by increased

saving, and a falling income by decreased saving, on a greater scale at first than

14

subsequently” (Ibid., pp.97). This means the average propensity to consume declines as

income rises and generally the economy will tend to save more and more of its income as

it gets prosperous. From this we can see, it is natural to conclude that as the average

propensity to consume falls, the marginal propensity to consume would do so but only at

a faster rate; hence, marginal propensity to consume is less than average propensity to

consume.

Third and most important of the three, he argued that real consumption is a fairly

stable function of real income i.e. “consumption is obviously much more a function of …

real income than of money-income” (Ibid.). Clearly, this point is a direct attack to the

then governing doctrine of the classical principle that rests its argument based on full

employment and that assumes real consumption is a function of real interest rate. But for

Keynes, who had already ruled out the assumption of full employment, “the short period

influence of the rate of interest on individual spending out of a given income is secondary

and relatively unimportant” (Ibid.).

These three hypotheses are the corner stones of Keynes analysis of economic

fluctuations in particular and the Keynesian economics in general and based on these

conjectures economists put the following mathematical version of the Absolute Income

Hypothesis(AIH) (Wonnacott, 1978 , Ando and Modigliani, 1963):

Ct = + Yt

d (1)

Where C, Yd

, and represent real consumption expenditure, real disposable

income, the height at which the consumption function meets the vertical axis and the

marginal propensity to consume out of disposable income respectively3.

As we have said earlier, this consumption function is the foundation of the early

Keynesian economists and fulfills Keynes’s three hypotheses because

3 For the moment, we ignore the stochastic disturbance term to make things not too complicated and we

shall proceed with this manner throughout this chapter.

15

- first Keynes assumed that the marginal propensity to consume ‘c’ obeys that

double restrictions between zero and unity.

- second he said that the average propensity to consume (APC) declines as the

society gets richer i.e. in our case APC is

APC = Consumption Expenditure/Disposable Income

= C/Yd

= [ + Yd]/ Yd

= [ /Yd

+ Yd/Y

d]

= [ / Yd + ]

Therefore, as clearly seen from this relation, as income rises the ratio C/Yd

,

the average propensity to consume declines hence the second conjecture

satisfied. This implies saving is a luxury good, that is, it increase with the

rise in income (Mankiw, 2002).

- third he postulated that income is the primary determinate of consumption

and interest rate has no role in influencing the short period spending

behavior of the society. As a result, the above equation doses not incorporate the

effect of interest rate on consumption expenditure.

So for the Keynesian theory of consumption, the relation between consumption and

income is non-proportional and it linearly relates the short run consumption expenditure

to only current income, that is, in this function consumption is determined solely by

current income [both measured in real terms].

On saving, the AIH is believed to explain the saving behavior of the poor countries.

The reason is that people in low income countries are not able to save at their working or

younger ages for future consumption because they receive low income which is not even

sufficient to cover consumption at that period. Hence, they become unable to make

intertemporal transfer of resources, the basic assumption of the Life Cycle and Permanent

16

Income theories of consumer’s behavior [We will consider that later on]. So in that

context, consumption is likely to follow only current disposable income (Modigliani and

Cao, 2004). This is exactly what Keynes says.

Hence, after Keynes proposed his consumption function, economists and researchers

soon tried to verify the validity of this function by using both time series and cross-

sectional data and as summarized by Branson, in both cases the results were quite

supporting the theory of John Maynard Keynes or Absolute Income Hypothesis (AIH)

(Branson, 2006). However, according to various literatures, those early empirical success

of the AIH started to loose with the truth on the ground in the mid- 1940s.This is

primarily because of the fact that based on the second conjecture some economists

forecasted that as income rises consumption declines and hence saving rises. So first they

reasoned that there will not be enough aggregate consumption demand to goods and

services and second there will also be no enough investment to absorb such huge

accumulation of saving or capital. Hence, in one way or another, they argued that the

economy will dive into what they called ‘stagnation’. In the literatures, these economists

and their ‘school’ that advocated such kind of conviction is known as ‘stagnationst

school’ (Modigliani, 1986). But, in those days what really happened was contrary to what

the ‘stagnationst’ forecasted based on the AIH (Branson, 2006). This made economists

speculate the validity of Keynes’ arguments. The other most important discovery that

brought stark evidence against the AIH’s basic tenets is that the findings of the 1971

Noble Prize-winning economist Simon Kuznets. In his influential work, Kuznets

collected data on consumption and saving dating back to the 1860s (Mankiw, 2002) and

he found that in the long run there was near proportionality between income and

consumption. This means the value of the intercept “” in equation (1) should be zero

(Dornbush et al, 1982). On top of this, Kuznets argued in the long run there was little

variation in the average propensity to consume or the average propensity to consume was

almost constant for the period under investigation, that is, as income rises, the society did

not decrease its consumption as the theory suggests (Wonnacott, 1978). Thus, these two

results also brought the weaknesses of the AIH to light.

17

Similarly, other economists argued that the above simple consumption function

should by no means be ‘a fundamental law of human nature’ (Gilboy, 1938). In her

paper, Gilboy criticized the simple Keynesian consumption function for not incorporating

the effects of income distribution, working conditions [like farm and non farm families],

and working places [city and village] on its analysis and she clearly provides a detailed

statistical analysis for her argument. In other cases, even these days several economists

used the AIH to forecast the behavior of the consumers in the economy. For instance,

Dornbush, Fisher and Sparks in their 1982 book used the 1926-1940 data for the Canada

economy to test the validity of the AIH. Their finding was satisfactory for those periods

but when they tried to forecast the marginal propensity to consume for the year 1982, it

becomes something devastating, that is, it is far from reality.

Therefore, these phenomena particularly the first two, the ‘stagnation’ doctrine and

the works Kuznets, presented what is known in economics as consumption puzzle among

the then economists and motivated the search for a more sophisticated and dynamic

consumption function that could reconcile such long run – short run discrepancies. This is

the main reason that the contemporary theories of consumption function focus primarily

on this reconciliation effort. Anyway, in doing so, some economists finally arrived at

their own version of consumption function and in the literature we can find a mountain of

debates on this issue but in this study a focus is made only on those works of Modigliani

et al. and Friedman that were proposed in the 1950s when the intellectual debate over

what really determines consumption arrived at its peak point.

2.2.3 THE LIFE-CYCLE HYPOTHESIS-MODIGLIANI-ANDO-BRUMBERG.

In the introductory chapter, it was said that the analysis of the Life-Cycle Hypothesis

(LCH) of consumption expenditure is highly constrained by the nonexistent of time series

data on net worth and that problem is generally acknowledge by a number of economists

including the mastermind, Modigliani. When we consider that case from developing

countries perspectives, as one clearly guesses, the problem becomes very series.

Notwithstanding, in the presence of such problem, Abebe (2005) made an interesting

study that attempts to verify the explanatory power of the LCH in the Ethiopian context.

18

Hence, for that and other theoretical reasons, in this section, we will devote little time for

a brief discussion of the LCH.

As frankly acknowledged by Franco Modigliani, the LCH of consumption and

saving behavior made its departing point on the works of an early twentieth century

American economist Irving Fisher’s theory of Intertemporal Utility Maximization which

argued that rational, utility-maximizing consumers will optimally allocate their resources

to consumption over their life time (Modigliani, 1986).Hence, based on this notion

Franco Modigliani, Albert Ando and Richard Brumberg tried to study the consumer

behavior of the households as well as the economy very carefully(Mankiw,2002). The

main purposes of these three individuals were to explain the determinants of consumption

in the given economy and to solve the long run-short run puzzle that arose when the AIH

came to data. So, contrary to what have been said in the Absolute Income Hypothesis

(AIH) of Keynes, the LCH argued that for a representative consumer who lives for two

periods-present and future -with finite life time at any age‘t’, the consumption decision

depends “not at all on income accruing currently but only on his life resource [the present

value of labour income plus bequests received if any]” (Modigliani, 1986). In other

words, they argued that at any time‘t’, the total consumption of an individual age T will

be proportional to the present value of total resources available to him (Ando and

Modigliani, 1963). Besides this, the LCH observed that an individual consumer has an

income stream that is relatively low at the beginning [at this time the consumer is a net

borrower] and end [here he dissaves] of his life (Branson, 2006). The major reason for

this systematic variation in income throughout the life-cycle of the individual is maturing,

retiring and family size. Hence, saving, for the LCH, is primarily done for the purpose of

financing consumption at the retirement age. To progress further with their theory,

Modigliani and his colleagues made further assumptions. These are income is constant

until retirement, zero thereafter; no interest rate, constant or smooth consumption over

life, no bequest and perfect capital market. These assumptions clearly imply that

“consumption is geared not to current income which is zero during retirement, but rather

to lifetime income” (Dornbush and Fischer, 1994). Following that assumptions, the

Ando-Modigliani version of consumption function for the representative consumer at any

age T, can be written as follows:

19

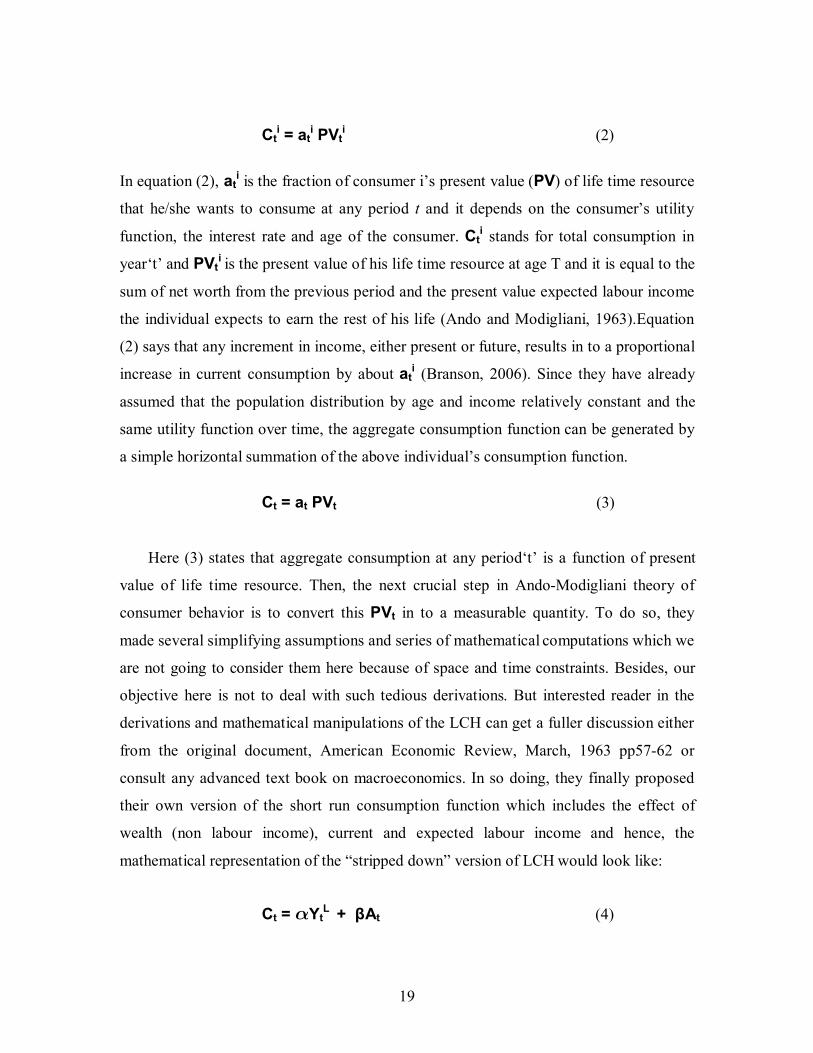

Cti = at

i PVti (2)

In equation (2), ati is the fraction of consumer i’s present value (PV) of life time resource

that he/she wants to consume at any period t and it depends on the consumer’s utility

function, the interest rate and age of the consumer. Cti stands for total consumption in

year‘t’ and PVti is the present value of his life time resource at age T and it is equal to the

sum of net worth from the previous period and the present value expected labour income

the individual expects to earn the rest of his life (Ando and Modigliani, 1963).Equation

(2) says that any increment in income, either present or future, results in to a proportional

increase in current consumption by about ati (Branson, 2006). Since they have already

assumed that the population distribution by age and income relatively constant and the

same utility function over time, the aggregate consumption function can be generated by

a simple horizontal summation of the above individual’s consumption function.

Ct = at PVt (3)

Here (3) states that aggregate consumption at any period‘t’ is a function of present

value of life time resource. Then, the next crucial step in Ando-Modigliani theory of

consumer behavior is to convert this PVt in to a measurable quantity. To do so, they

made several simplifying assumptions and series of mathematical computations which we

are not going to consider them here because of space and time constraints. Besides, our

objective here is not to deal with such tedious derivations. But interested reader in the

derivations and mathematical manipulations of the LCH can get a fuller discussion either

from the original document, American Economic Review, March, 1963 pp57-62 or

consult any advanced text book on macroeconomics. In so doing, they finally proposed

their own version of the short run consumption function which includes the effect of

wealth (non labour income), current and expected labour income and hence, the

mathematical representation of the “stripped down” version of LCH would look like:

Ct = YtL

+ βAt (4)

20

Equation (4) states that aggregate consumption in any given period‘t’ depends on current

labour [non property] income, YtL and assets [non labour income or net worth], At and the

parameters and β measure the marginal propensity to consume out of labour income

and wealth (net) respectively. Beware that in the above equation the parameter

measures the marginal propensity to consume out of both current and expected future

incomes and the latter is, by naïve assumption, the same as current income with ‘possible

scale factor’ (Ando and Modigliani, 1963). Such kind of expectation in economics is

known as naïve expectation (Maddala, 1992). Here, people generally use only current

information of a variable to determine its future values, that is, in our case, they assume

that next period income will be exactly the same as income in the current period and such

assumption gives due emphasis to current income in determining current consumption.

But, as various authors clearly put such kind of assumption has got its own drawbacks

(Wonnacott, 1978) and faced series critics from economists like Robert. E .Hall of

Stanford University. We will see that soon. To return to our discussions, as it is clear

from the above relation in the short run wealth is constant so βAt is the intercept and it is

clearly greater than zero and hence the LCH’ s consumption function looks like its AIH

counterpart. But in the long run, we should assume that there exists economic growth i.e.

income grows and through saving wealth increase. Then, βAt continually shifts up ward

so does the consumption function for each period. In that case, if we join each period

income with its respective new consumption curves and connect the intersection points of

period one’s income with its consumption curve and period two’s income with its

respective consumption curve and so on, we can get the long run consumption function

that passes through these intersection points and hence through the origin. As clearly

stated in the above discussions, these results are exactly the same as what Kuznets found

in his empirical study.

When we come to empirical verifications for the Life-Cycle Hypothesis, we find that

the process is extremely difficult for Modigliani and Brumberg (Modigliani, 1986) and

some kind of indirect even for the US economy, the place where the theory primarily

developed for. This was predominantly because of the lack of aggregate time series data

21

on annual private net worth. But, decades later, the availability of data on net worth

became possible and Ando and Modigliani tested equation (4) for the US economy using

time series data for the period 1929-59 excluding the periods of 1941-1946. And as

Modigliani discussed this in his Nobel Lecture, the result was ‘quite well’ and from those

periods on ward the LCH is considered by the US policy makers , econometric-model

builders and forecasters as the major intellectual contributions that used to analyze and

forecast the behavior of consumers in particular and the economy in general. However,

when we come to other recent efforts of verification, we can see that the realities are still

similar to US’s condition some fifty years ago. For instance, four years ago, by using the

LCH framework, Modigliani and Cao tried to analyze not the consumption but its

flipside, the saving behavior of one of the world’s fastest growing economy, China. In

that case, they encountered the same problem as Modigliani and Brumberg did some fifty

years ago (Modigliani and Cao, 2004). Yet, by using some kind of indirect method, they

tested the theoretical implication of the LCH and they found that the theory has a

remarkable explanatory power. This and similar other incidents indicate that the

empirical verification of the LCH is exceedingly difficult even for developed nations and

the cases of underdeveloped nations are not different. For our country’s case, as we put

earlier, the conditions are worse than other country’s case and any attempt to verify the

applicability of this theory is constrained by the non existent of time series data on net

worth (Solomon, 1999, Oman, 2006). Therefore, for that matter, we are not, here,

privileged to analyze Ethiopia’s case from the perspective of Life-Cycle theory.

Well, as we have seen the Modigliani et al.’s theory of consumer behavior is a

significant departure from the Keynesian approach which assumes consumption in any

period‘t’ is only a function of income earned in that period or current income. And for

LCH individuals always make the best use of the resources at hand to maximize life time

utility other than the simple current utility. For that reason, we see that the LCH relates

consumption to the present value of life resource. But at this time it is necessary to ask

the fate of any windfall gains or transitory deviations from this life time resource. First,

Modigliani argued that such transitory deviations of income are usually responsive to

saving motives rather than consumption (Modigliani, 1986) and hence those parts of

society which are characterized by a large amount of transitory income than their life

22

time income, for instance farmers, save a significant portion of their income than those

with lower transitory income and higher life time income, government employers.

Second, he showed that this saving rate is highly influenced by the long run growth rate

of the economy than the simple per capita income. Consider these arguments for our

country, particularly that of the first. We know that farmers comprise eighty five percent

of the population and as the theory suggests, they are characterized by a huge transitory

income, that is, rural household depend on seasonal agricultural income for their

consumption and this conviction is supported by various empirical findings (Nigussie,

2006). Though they are not detailed and small sample size, his [Nigussie] findings

suggest that such huge transitory income and consumption patters are uncorrelated. This

means consumption (only on food) style is similar or stable throughout the period despite

income fluctuations. Therefore, we can say that if farmers try to smooth consumption in

the face of this erratic income, those periods with high incomes are characterized by high

saving for financing consumption in low income periods. This indicates an important

implication, that is; farmers could also decide the fate of the country’s saving rate if there

is effective policy by the government or other stakeholders to exploit it. We shall fully

discuss this point in the coming chapter.

Other application of the LCH is that it considers the impact population distribution

on aggregate consumption. In this case, though it is subject to debate (Farrell, 1959),

Modigliani and his collaborates argued that saving is primarily done for financing future

consumption, thus the population dominated by many middle age earners is characterized

by high saving ratio. In contrast, if the community is dominated by young folk, like our

country (Befekadu Degefe and Berhanu Nega, 1999/2000 pp.62) and aging population,

the majority of the people are engaged in dissaving, that is, saving rate would be low.

Thus, from this concept, such demographic characteristic might be one of the main

reasons for the existence of low saving trend that we have seen earlier. Clearly, this

finding is contrary to the AIH which simply assumes that the saving rate of the economy

is determined solely by the rate of the growth of the economy. In addition, the theory

under discussion provides a much more powerful estimate of monetary policy than its

competitors (Wonnacott, 1978). This is simply because of the fact that the LCH

incorporates the effect of wealth in its analysis. The above discussions and several other

23

implications of the LC theory point out that the theory being discussed generally provides

a through understanding of the society’s consumption–saving behavior and its analysis of

the variable under investigation is far reaching than the simple theory of Keynes’s ‘rule

of thumb’ or the AIH.

As we have said in the earlier chapter, the application of the LCH is highly limited

by its basic assumptions. In this case, we can raise at least the following points. First,

consider the role of liquidity constraints. Modigliani clearly puts that due to liquidity

constraints consumers failed to maximize their inter-temporal utility and hence their

consumption path become forced to track their current disposable income like the simple

Keynesian consumption model. Hence, such relaxation of the ‘stripped down’ version of

the LCH will result in a different implication of the hypothesis, particularly if the

liquidity constraint is significant. Second, the assumptions about family size, interest rate,

the length of working and retired years, bequests and bequest motives and the case of

myopia etc. pose problems in empirical analysis, though Modigliani argued such

relaxation would not change the validity of the basic hypothesis (1986).

The other point of limitation that should be considered here is that of the assumption

of naïve expectation. The LCH hypothesizes that consumption at any period‘t’ depends

on wealth, current income and expected future income. We know that the latter is the

same as its current value with possible scale factor. Nonetheless, this kind of naïve

expectation brought several controversies in the literature and due to this fact economists

dissatisfied with this concept propounded their own version of expectation known in

literature as rational expectation. Yet, this argument is advanced not only against the

LCH but also to Friedman’s Permanent Income Hypothesis (PIH). So for the sake of

better understanding I believe we should deal with such discussion after a brief review of

the PIH of Milton Friedman.

2.2.4 THE PERMANENT - INCOME HYPOTHESIS-FRIEDMAN In the 1950s, an American economist Milton Friedman tried to study the behavior of

consumers in detail in order to propose the theory that could reconcile the short run –

long run discrepancies of the AIH that arose as a result of the outstanding works of

Kuznets and late in that decade he came up with his own version of consumption

24

expenditure known in literature as Permanent Income Hypothesis (PIH). According to

various literatures, the PIH is considered as one of the most widely studied theory of

consumer behavior (Singh and Drost, 1971). In this work, like Modigliani et al, Friedman

first assumed that households prefer stable consumption path over unstable one

throughout their life, that is, they tend to smooth consumption over time (Sachs and

Larrain B., 1993) and he argued that both measured consumption and income include

‘permanent’ and ‘transitory’ components (Branson, 2006, Vernis and Sebold, 1977). As a

result of this, at any time‘t’, the measured values of consumption(C) and income(Y) for

cross-section and time series aggregate data could be written as:

Ct= Ctp

+ Ctt (5)

Yt = Yt

p + Ytt (6)

In equations (5) and (6)4 both Ct

t and Ytt respectively measure the transitory components

of consumption and income at any period‘t’. Similarly, Cpt and Yp

t respectively represent

the permanent components of both consumption and income in the same period‘t’. The

decomposition of both consumption and income into transitory and permanent is based

on the concept of consumption which Friedman argued that “observed consumption

expenditures do not always reflect real consumption.” (Veranis and Sebold, 1977,

pp377). This means the use of some durable goods such as a refrigerator or VCR is

distributed over life time while there expenditure the consumer incurs has only a one

period effect. This indicates that the consumption of some consumer goods is

characterized by their permanent nature, though the expenditure on them has only

transitory or a one period effect. Equally, consumers do not always follow the same

consumption track or behavior over time, as a result they sometimes are forced to

‘deviate’ from their normal behavior and in this case their consumption, in the Friedman

context, is regarded as transitory (Ibid.).

Thus, the distinction between permanent and transitory income is the existence of

windfall gains or losses made by consumers. That is transitory components are made up

of unforeseen gains or losses to income and they are supposed to cancel out in the long

4 From now on, we will be using the superscript‘t’ to indicate the transitory component of the respective

variable where as the subscript ‘t’ to refer the time period ‘t’.

25

run (Houthakker, 1958). Thus, the PIH considers permanent income as part of current or

measured income that people expects to persist in their future or a kind of average of

present and future income and transitory income is that part they expect to not hold in the

future or any random deviation from the permanent income (Mankiw, 2002, Sachs and

Larrain B.,1993 ). Besides, Friedman argued based on the evaluation of their labour and

non labour income, each consuming unit has an implicit notion of its permanent income.

Relying on this understanding of the permanent and transitory components of income

and consumption, the PIH made three important assumptions known as- permanent

income and transitory income are independent, permanent consumption and transitory

consumption are independent and transitory consumption and transitory income are

independent. This means the co-variances between permanent income and transitory

income, permanent consumption and transitory consumption and transitory consumption

and transitory income are zero (Branson, 2006).

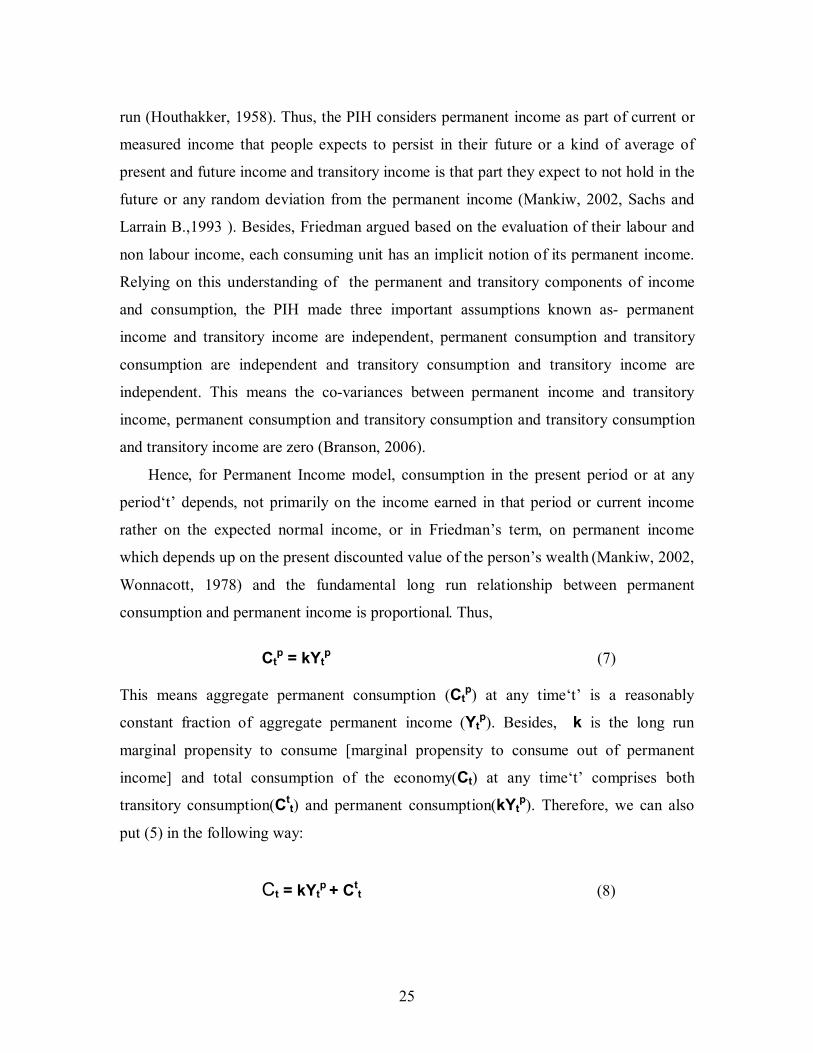

Hence, for Permanent Income model, consumption in the present period or at any

period‘t’ depends, not primarily on the income earned in that period or current income

rather on the expected normal income, or in Friedman’s term, on permanent income

which depends up on the present discounted value of the person’s wealth (Mankiw, 2002,

Wonnacott, 1978) and the fundamental long run relationship between permanent

consumption and permanent income is proportional. Thus,

Ct

p = kYtp (7)

This means aggregate permanent consumption (Ctp) at any time‘t’ is a reasonably

constant fraction of aggregate permanent income (Ytp). Besides, k is the long run

marginal propensity to consume [marginal propensity to consume out of permanent

income] and total consumption of the economy(Ct) at any time‘t’ comprises both

transitory consumption(Ctt) and permanent consumption(kYt

p). Therefore, we can also

put (5) in the following way:

Ct = kYtp + Ct

t (8)

26

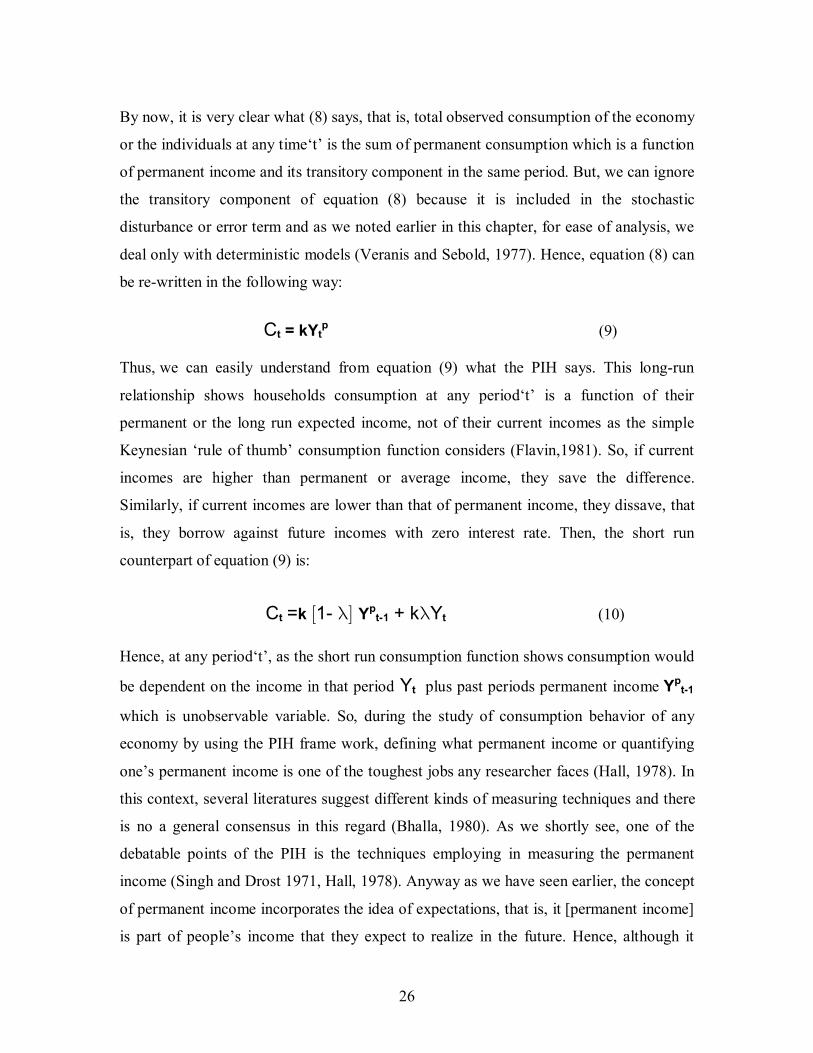

By now, it is very clear what (8) says, that is, total observed consumption of the economy

or the individuals at any time‘t’ is the sum of permanent consumption which is a function

of permanent income and its transitory component in the same period. But, we can ignore

the transitory component of equation (8) because it is included in the stochastic

disturbance or error term and as we noted earlier in this chapter, for ease of analysis, we

deal only with deterministic models (Veranis and Sebold, 1977). Hence, equation (8) can

be re-written in the following way:

Ct = kYtp (9)

Thus, we can easily understand from equation (9) what the PIH says. This long-run

relationship shows households consumption at any period‘t’ is a function of their

permanent or the long run expected income, not of their current incomes as the simple

Keynesian ‘rule of thumb’ consumption function considers (Flavin,1981). So, if current

incomes are higher than permanent or average income, they save the difference.

Similarly, if current incomes are lower than that of permanent income, they dissave, that

is, they borrow against future incomes with zero interest rate. Then, the short run

counterpart of equation (9) is:

Ct =k 1- Ypt-1 + kYt (10)

Hence, at any period‘t’, as the short run consumption function shows consumption would

be dependent on the income in that period Yt plus past periods permanent income Ypt-1

which is unobservable variable. So, during the study of consumption behavior of any

economy by using the PIH frame work, defining what permanent income or quantifying

one’s permanent income is one of the toughest jobs any researcher faces (Hall, 1978). In

this context, several literatures suggest different kinds of measuring techniques and there

is no a general consensus in this regard (Bhalla, 1980). As we shortly see, one of the

debatable points of the PIH is the techniques employing in measuring the permanent

income (Singh and Drost 1971, Hall, 1978). Anyway as we have seen earlier, the concept

of permanent income incorporates the idea of expectations, that is, it [permanent income]

is part of people’s income that they expect to realize in the future. Hence, although it

27

exposes Friedman and the PIH to serious critics [we will consider that below], he

assumed that expectation is “adaptive”. This means households readjust or ‘adapt’ their

estimates of the permanent income each period based on their past estimates of actual or

observed incomes and he suggests that the permanent income of the economy or the

household can best be approximated by the weighted sum of current and past values of

observed (current) incomes (Venieris and Sebold, 1977, Branson, 2006) and this

approach is the most conventional one( Bhalla, 1980).Thus, using this concept of

adaptive expectation, Friedman’s permanent income for an infinite horizon at any year‘t’

follows the following pattern:

Yt

p = Yt + (1- ) Yp

t-1 (11)

Alternatively, (11) can be described in the following way

Yt

p = Yt+ (1- ) Yt-1+ (1- ) 2 Yt-2+……+ (1- ) n Yt-n+ … (12)

These two equations are the same in a sense that if we lag (12) by one period, multiply it

by (1- ) and subtract the final result from the original equation, we can easily get (11).

This kind of formulation of the permanent income, despite the controversies it faces

(Singh and Drost, 1971), is very common and it was first used by Friedman himself.

Since then it is extensively used by many researchers (Bhalla, 1980). In equation (11), Yt

is the current or measured income in time period‘t’ and ‘’ is the coefficient of

expectation and it is between zero and one. In this process of approximating permanent

income, Friedman uses a converging geometric series for weighing the consumers past

and current values. And this method is extensively used in empirical researches because

of its ease of manipulation. To appreciate the central point of (11) let us see it in greater

detail. Equation (11) or (12) implies regarding income people use their past experience

to expect or guess what is coming in the future and in this process they are generally

assumed to learn from their mistakes (Gujarati, 2003). In so doing, expectations about

incomes are revised period by period by a fraction of and if this coefficient of

28

expectation is equal to 1, expectations are realized immediately and fully, that is, in the

same period. But, if it is 0, expectations become static, that is, future expected conditions

will be the same as today i.e. expectations become naïve (Gujarati, 2003, Maddala,

1992). Then, to progress further, first lag (12) by one period and substitute this result in

equation (10), then the resulting equation would look like this:

Ct=k1-Yt-1+(1-)Yt-2+(1-)2Yt-3+…+(1-)nYt-n-1+.. + kYt (13)

This is another short-run version of equation (9) and models like (13) in economics

are known as distributed-lag models. As we shall see in the coming discussions, they

have their own peculiar features (Gujarati, 2003) and the existence of such lagged

variables in consumption function have become important at least since the time of

Brown (1952).Following this, the PIH engages into a series of mathematical formulations

which, as traditionally, we are not going to deal with it at this time so we skip them. But,

any interested reader can consult any advanced macroeconomic text books for a fuller

discussion. Here, it is clear that equation (13) can not be estimated by the celebrated

simple least square procedure since it has both non linear and infinite parameters. As a

result of this, he tried to quantify this ‘inherently non measurable’ variable i.e. permanent

income and hence to transform or convert equation (13) in to a more measurable term. To

do so we have number of alternatives in the literature. Few of these are Koyck Approach,

Adaptive Expectation Approach, Partial Adjustment Approach and the combination of

the latter two, that is, Adaptive Expectation and Partial Adjustment Approaches (see

Gujarati, 2003 or any other econometric book). Bear in mind that the Koyck and

Adaptive approaches use the same procedures and result in identical outcomes, however,

they differ in their theoretical foundations, assumptions about the consumers’ behavior

and their treatment of the stochastic disturbance term. Anyway, we have already seen that

Friedman chose the concept of Adaptive Expectation for his analysis. The central theme

of this concept is people use their entire past experience to predict their future income

and they are assumed to learn from their mistakes, i.e. expectations about incomes are

revised (upward or downward) based on the most recent error. In our case, since the latter

part of equation (13) is not observable, we use the following transformation methods of

29

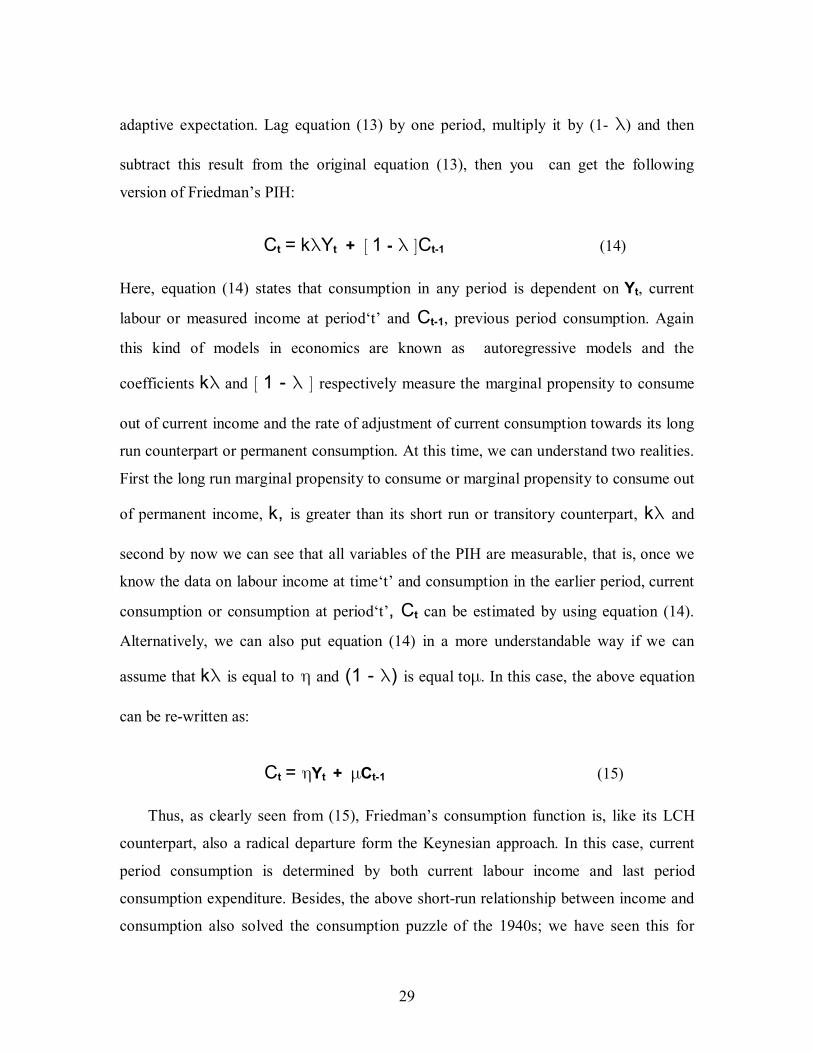

adaptive expectation. Lag equation (13) by one period, multiply it by (1- ) and then

subtract this result from the original equation (13), then you can get the following

version of Friedman’s PIH:

Ct = kYt + 1 - Ct-1 (14)

Here, equation (14) states that consumption in any period is dependent on Yt, current

labour or measured income at period‘t’ and Ct-1, previous period consumption. Again

this kind of models in economics are known as autoregressive models and the

coefficients k and 1 - respectively measure the marginal propensity to consume

out of current income and the rate of adjustment of current consumption towards its long

run counterpart or permanent consumption. At this time, we can understand two realities.

First the long run marginal propensity to consume or marginal propensity to consume out

of permanent income, k, is greater than its short run or transitory counterpart, k and

second by now we can see that all variables of the PIH are measurable, that is, once we

know the data on labour income at time‘t’ and consumption in the earlier period, current

consumption or consumption at period‘t’, Ct can be estimated by using equation (14).

Alternatively, we can also put equation (14) in a more understandable way if we can

assume that k is equal to and (1 - ) is equal to. In this case, the above equation

can be re-written as:

Ct = Yt + Ct-1 (15)

Thus, as clearly seen from (15), Friedman’s consumption function is, like its LCH

counterpart, also a radical departure form the Keynesian approach. In this case, current

period consumption is determined by both current labour income and last period

consumption expenditure. Besides, the above short-run relationship between income and

consumption also solved the consumption puzzle of the 1940s; we have seen this for

30

LCH. For PIH’s part, Friedman assumes that past period consumption acts as a shift

parameter and in the long run, as income rises successively the later part of the above

equation also shifts upward to keep up with the new levels of current incomes. Then, if

we try to connect the intersection points of the new current incomes with the new levels

of lagged values of consumption, we would get the long run consumption function that

passes through the origin. As we have put above, it was this kind of consumption

function that Kuznets had proposed in the mid 1940s. Hence, Milton Friedman, in his

own way, solved one of the problems the Keynesian consumption function.

When we come to the empirical analysis of the PIH, Friedman tested equation (15) or

its counterpart (13) for the US economy for the periods 1905-1951 excluding the war

years. In his groundbreaking book, he put the result as follows k=0.88, = 0.33 and 0.67

for. So, the marginal propensities for the US economy for the specified period can

easily found by multiplying k and , that is equal to, is 0.299 (Wonnacott, 1978) This

means an average US citizen consume only 0.29 cents of labour income from each

additional dollar for the specified period, of course, keeping all other factors unchanged.

This was just what was expected from the theory (Sachs and Larrain B., 1993). Other test

by other individuals show that the permanent income theory generally provides a slightly

better explanation of consumer behavior than a very simple hypothesis based on current

income, though this margin of superiority is “ small and not consistently maintained” (

Friend and Kravis, 1957). Similarly, Singh and Drost (1971) by themselves test the

applicability of the PIH for eleven countries and they conclude that the theory ‘offers a

valid explanation of the consumption behavior of countries with different economic

structures.’ But note that though the theoretical underpinning is the same, they use their

own method of testing techniques that is different form the one we have seen above or

proposed by Friedman.

However, the above success stories of the PIH were forced to face other

contradictory results by different individuals. As reported by Singh and Drost (1971),

economists like Choudhury and Laumans found a significant marginal propensities to

31

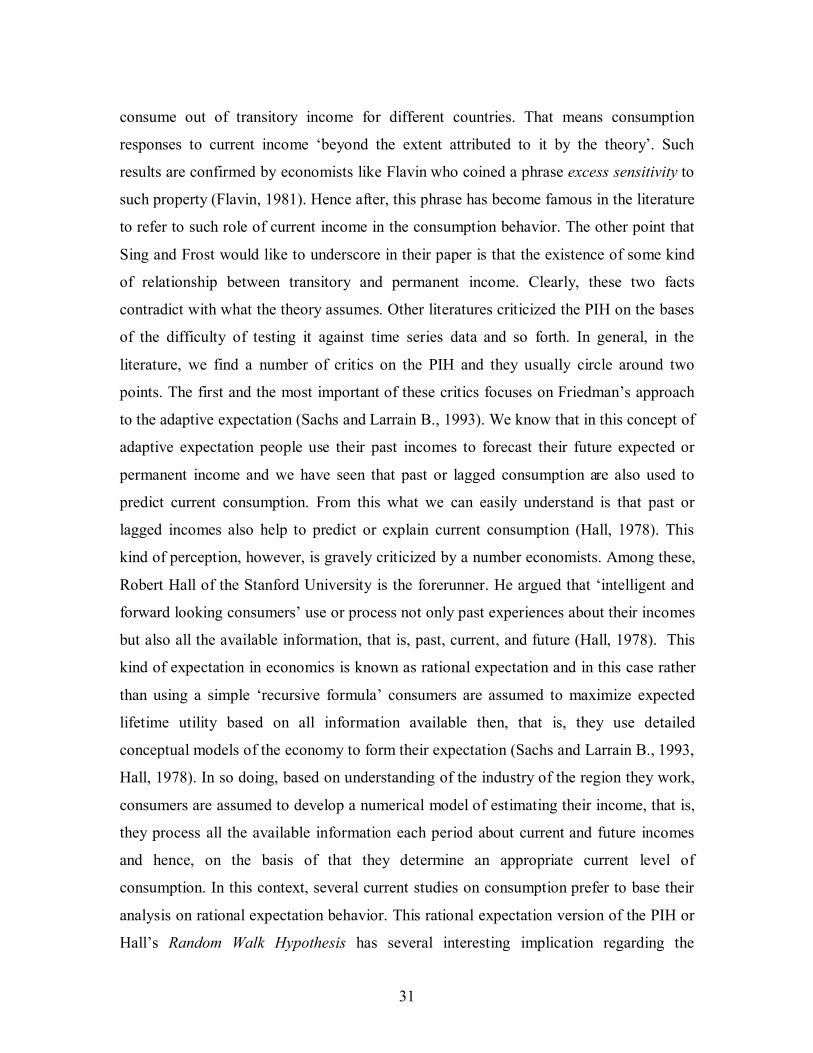

consume out of transitory income for different countries. That means consumption

responses to current income ‘beyond the extent attributed to it by the theory’. Such

results are confirmed by economists like Flavin who coined a phrase excess sensitivity to

such property (Flavin, 1981). Hence after, this phrase has become famous in the literature

to refer to such role of current income in the consumption behavior. The other point that

Sing and Frost would like to underscore in their paper is that the existence of some kind

of relationship between transitory and permanent income. Clearly, these two facts

contradict with what the theory assumes. Other literatures criticized the PIH on the bases

of the difficulty of testing it against time series data and so forth. In general, in the

literature, we find a number of critics on the PIH and they usually circle around two