Terms Paper of Marine Insurance

29

1 JATIYA KABI KAZI NAZRUL ISLAM UNIVERSITY DEPARTMENT OF FINANCE AND BANKING FACULTY OF BUSINESS ADMINISTRATION JATIYA KABI KAZI NAZRUL ISLAM UNIVERSITY

Transcript of Terms Paper of Marine Insurance

1

JATIYA KABI KAZI NAZRUL ISLAM

UNIVERSITY

DEPARTMENT OF FINANCE AND BANKING FACULTY OF BUSINESS ADMINISTRATION JATIYA KABI KAZI NAZRUL ISLAM UNIVERSITY

2

ASSIGNMENT ON

(DETAILS OF MARINE INSURANCE)

COURSE TITLE: INSURANCE AND RISK MANAGEMENT

COURSE CODE: F-303

Date of Submission: January 28, 2014

Submitted To: Prahallad Chandra Das Lecturer, Department of Accounting & Information Systems Jatiya Kabi Kazi Nazrul Islam University

Submitted By: Group No: 02

Session: 2010-2011 3rd Year, 1st Semester Department of Finance and Banking Jatiya Kabi Kazi Nazrul Islam University

3

Name of the Group members along with ID

Serial No. Name ID

01 Muminunnessa Shwuly 11132611

02 Iqbal Hossain 11132612

03 Naima Afrin 11132613

04 Neger Sultana Nipa 11132614

05 Jannatul Fardousi 11132615

06 Sabbir Ahamed 11132617

07 Sultan Mahmud 11132618

08 Mst. Kawsari Akter 11132619

09 Md. Towhiduzzaman 11132620

4

Letter of Transmittal

January 28, 2014.

Prahallad Chandra Das

Lecturer,

Course: INSURANCE AND RISK MANAGEMENT

Subject: Prayer for the Submission of Assignment.

Dear Sir,

We are very pleased to submit the assignment as you assigned us. Through the procedure of preparing

the assignment, We have collected and used necessary data from our text book & class lecture.We hope

the assignment has attained its purpose to a considerable extent.

For your perusal and kind consideration. It will be pleasure to us if you kindly accept our assignment.

Special thanks to you for your valuable advice and co-operation.

If you need any more information related to our assignment, please let us inform.

Thanks.

Sincerely yours,

…………………………….

(Md. Towhiduzzaman)

On behalf of Group 02

5

Table of Contents

Serial Number

Topics Page number

01. Definition of Marine Insurance 06 of 06

02. Principles and Elements of Marine Insurance 06 of 12

03. Classification of Marine Insurance 12 of 14

04. Types of Marine policies 14 of 16

05. Causes of Marine Losses 16 of 17

06. Types of Marine Losses 18 of 20

07. Claims and Settlement 20 of 20

08. Mathematical Problems & Solutions 21 of 29

6

DETAILS OF MARINE INSURANCE

Definition of marine insurance:

Marine insurance has been defined as a contract between insurer and insured whereby insurer undertakes to indemnify the insured in a manner and to the interest thereby agreed, against marine losses incident to marine adventure.

Elements and principles of marine insurance

1. Features of general contract 2. Insurable interest 3. Utmost good faith 4. Doctrine of indemnity 5. Subrogation 6. Warranties 7. Proximate cause 8. Assignment and nomination 9. Return of policy

Feature of general contract

1.Proposal: The broker will prepare a slip upon receipt of instructions to insure from ship owner , merchants or other proposers. Proposal form is so common in any branches of insurance, are unknown in the marine insurance and only the slip so called is used for the proposal. 2. Acceptance: The original slip is presented to the LLOyd’s or other insurer or to the lead of the insurer, who initial the slip and proposal is formally accepted. But contract cannot be legally enforced until a policy is issued. The slip is evidence that the underwriter has accepted the insurance and that he has agreed subsequently to sign a policy on the terms and conditions indicated on the sleep. 3. Consideration: The premium is determined on assessment of the proposal and is paid at the time of the contract .The premium is called consideration to the contract. 4. Issue of policy: Having effected the insurance, the broker will now send his client a cover note advising the terms and conditions, on which the insurance has been placed.

7

Insurable interest Section7, 8 and 9 to 16 provide for insurable interest .An insured person will have insurable interest in the subject matter where he stands in any legal or equitable relation to the subject matter in such a way that he may be benefited by the safety or due arrival of insurable property may be prejudice by its losses or by damage thereto or by the detention thereof or may incur liability in respect thereof. Exception: There are two exceptions of the rules in marine insurance

1. lost or not lost: A person can also purchases policy in subject matter in which it was known whether the matter was lost or not. In such cues the assured and the underwriter are ignorant about the safety or otherwise of the goods and complete reliance was placed on the principle of good faith.

2. P.P.I policy:

The subject matter can be insured in the usual manner by p.p.i (policy proof interest).i.e interest proof interest. It means that in event of claim underwrites dispenses with all proof of insurable interest. The insurable interest in marine insurance can be following forms: a .According to ownership: The owner has insurable interest up to the full value of the subject matter. The owners are of different types according to the subject matter. b. In case of ship: The ship owner or any person who has purchase it on charter basis can insure the ship up to the full price of it. c. In case of cargo: The cargo owner can purchase policy up to the full price of the cargo. If he has paid the freight in advanced, he can take the policy for the full price of the goods plus amount of freight plus expenses of insurance. d. In case of freight : The receiver of the freight can insure up to the amount of freight to be received by him

Utmost good faith Section 19, 20, 21, and 22 of the marine insurance Act 1963 explained doctrine of utmost good faith .The doctrine of caveat emptor applies to commercial contracts, but insurance contract are based upon the legal principle of subprime fides .If this is not observed by either of the parties, the contract can be avoided by the other party.

8

The duty of utmost good faith applies to the insurer .He may mot urge the proposal to affect an insurance which he knows is not legal or has run off safely. The assured therefore, must disclose all the material information which may influence the decision of the contract. Any non-discloser was intentional or inadvertent .The assured is expected to know every circumstance which in the ordinary courses of business ought to know by him .He cannot rely on his own inefficiency or neglect. The duty of discloser of all material facts falls even more heavily on the broker. He must disclose every material fact which the assured ought to disclose and also every material which he knows. The broker is expected to know or inquire from the assured all the material fact. Exceptions:

I. Facts of common knowledge II. Facts which are known should be known to the insurer

III. Facts which are not required by the insurer IV. Facts which the insurer ought reasonably to have inferred from details given to

him V. Facts of public knowledge

Doctrine of indemnity

Under section 3 of the act is provided ‘A contract of marine insurance is an agreement whereby the insurer undertakes to indemnify the assured in a manner and the extent agreed upon. The contract of marine insurance is of indemnity. Under no circumstances an assured is allowed to make a profit. The insurer agreed to indemnify the assured only in the manner and only to the extent agreed. Marine insurance fails to provide a complete indemnity due to large and varied nature of the marine nature of the voyage. The basis of indemnity is always cash basis as underwriter cannot replace the lost ship and cargo and the basis of indemnification is the value of subject matter. This value may be either insured or insurable value. If the value of the subject matter Is determined at the time of taking the policy is called insured value. Exceptions:

1. Profits allowed: Actually the doctrine says that the market price of the loss should be indemnified and no profit should be permitted, but in marine insurance a certain profit margin is always allowed.

2. Insured value: The doctrine of indemnity is based on the insurable value, whereas the

marine insurance is mostly based on insured value. The purpose of the valuation is to be predetermined in the worth of insured.

9

Doctrine of subrogation

Section 79 of the act explains the doctrine of subrogation. The aim of doctrine of subrogation is that insured should not get more than the actual loss or damage. After payment to the loss, the insurer gets the right to receive the compensation or any sum from the third part from whom the assured is liable to get the amount of compensations. The main characteristics of subrogation are as follows:

1. The insurer subrogates all the remedies rights and liabilities of the insured alter payments of the compensation.

2. The insurer has the right to pay the amount of loss after reducing the sum received by the

insured from the third party. But in marine insurance the right of subrogation arises only after payment has been paid, and it is not customary as in fire and accident insurance.

3. After indemnification, the insurer gets all the rights of the insured on the third parties, but

insurer can’t file suit in his name. Therefore, the insured must assist the insured for receiving money from the third party.

Warranties

A warranty is that by which the assured undertakes that some particular thing shall or shall not be done, or that some conditions shall be fulfilled or whereby he affirms or negatives the existences of a particular state of facts. Warranties are the statement according to which insured person promises to do or not to do a particular thing or to fulfill or not to fulfill a certain conditions. Warranties are of two types:

1. Express warranties 2. Implied warranties Express warranties: Express warranties are those warranties which are expressly included or incorporated in the policy by reference. Implied warranties: These are not mentioned in the policy at all but are tactically understand by the parties to the contract and are as fully binding as express warranties. In marine insurance, implied warranties are important. These are:

a) Seaworthiness of ship b) Legality of venture c) Non- deviation

10

a. Seaworthiness of ship: The warranty implies that the ship should be seaworthy at the

commencement of the voyage , or if the voyage is carried out in the stage at the commencement of each stage. This warranty implies only to voyage policy, through such policy may be of ship, cargo, freight or any other interest.

b. Legality of the venture: This warranty implies that the adventure insured shall be lawful

and that so far as the assured can control the matter it shall be carried out in a lawful manner of the country. Illegality must not be confused with the illegal conduct of the third party e.g. barratry, theft, pirates, rovers .The waiver of this warranty is not permitted as it is against public policy.

Other implied warranties: a. No change in voyage: When the destination of the voyage is changed intentionally

after the beginning of the risk, this is called change in voyage. In absence of any warranty contrary to this one.

b. No delay in voyage: This warranty applies only to voyage policies. There should not be delay in starting of voyage and laziness or delay during the course of the journey. This is implied condition that venture must start within the reasonable time.

c. Non deviation: The liability of the insurer ends in deviation of journey Deviation means removal of the common route or path. When the ship deviates from the fixed passage without any legal reason.

Proximate cause

According to section 55(1) marine insurance act , ‘subject to the provision of the act and unless the policy otherwise provides the insurer is liable for any loss proximately caused by a peril insured against , but subject to as aforesaid he is not liable for any loss which is not proximately caused by any peril insured against .’Section 55(20 ensures the losses which are not payable are (a)misconduct of the assured(b) delay although the delay be caused by a peril or proximately caused by rates or vermin or any injury to machinery not proximately caused by maritime perils.

1. The insurer is not liable for any loss attributed to the willful misconduct of the assured, but, unless the policy otherwise provide, he is liable for any loss proximately caused by a peril insured against. 2. The insurer will not be liable for any loss caused by delay unless otherwise provide.

11

3. The insurer will not be liable for ordinary wear and tear, ordinary leakage and breakage, inherent vice and or nature of subject matter insured. Dover says…….`` The cause proximate of a loss is the cause of the loss , proximate to the loss , not necessarily in time , but in efficiency .While remote causes may be disregarded in determining the causes of loss , the doctrine must be interpreted with good sense .So as to uphold and not defeat the intention of the parties to the contract.

Assignment

A marine policy is assignable unless it contains terms expressly prohibiting assignment. It may be assigned either before or after loss. A marine policy maybe assigned by endorsement thereon or on other customary manner. A marine policy is freely assignable unless assignment is express prohibited. A marine policy is not an incident of sale. So, if there is intention to assign a policy when interest passes. There must be an agreement to this effect. Section 53 of marine insurance act 1963-states.Where the assured has parted with or loss his interest kin subject matter insured and has no, before or at the time of so doing, expressly or impliedly agreed to assign the policy.

Classification of marine insurance:

1. Hull insurance

2. Cargo insurance

3. Freight insurance

4. Liability insurance

Hull insurance

Insurance of vessel and its equipment are included under hull insurance. There are a number of classification of vessel such as ocean steamers, sailing vessel, builders, risks fleet policies and so on. It is concerned with the insurance of hull and machinery of ocean going and other vessels like tankers fishing and sailing vessel. The ship is to be measured with GTR (gross register tonnage)and NTR(net register tonnage)GTR is calculated by dividing the volume in cubic feet of the ship hull bellow to tonnage dock , plus all spaces above the deck with permanent means of closing.Thehull insurance is further sub classified into:

a) General cargo vessel b) Dry bulk carriers c) Liquid bulk carriers d) Passenger vessels

12

e) Others vessels Cargo insurance

Cargo insurance is covered under risk policy or floating policies. The cargo may be of any description, for example wares, merchandise, property, goods, and so on. Transit clause of ICC (A), (B), and (C) describes the duration of risks as attaching from the time the goods leave the warehouse or any other place of storage at the placement in the policy for commencement of transit. The risks then continues during the ordinary courses of transit to terminate on delivery. Cargo insurance has coverage of losses or damage caused by war, civil war, revolution, rebellion, insurrection or civil strife or any hostile act, capture, seizure, arrest, restraint detainment, general average and salvage charges, strikes, riots, etc. Risk covered: All risk clauses covers inland Transit risks also for the cargo insurance. Losses or damages are covered if risks occurred due to:

Fire Lighting Exploitation Riot, strikes, malicious damage Impact by rail\road vehicle Storm, cyclone, flood, inundation Earth quack, burglary Accidental physical loss or damage

A special declaration policy is a form of floating policy issued to insure who have a large turnover with many and frequent dispatches of goods anywhere within the country by rail or road or in water wrap.

Freight insurance Freight is to be payable for carriage of cargo or if vessel, is chartered, the money is to be paid for the vessel use of the vessel. The carriage is unable to earn freight if the goods or properties are not safely transported. Pre-paid freight payable in advanced is at the risk of the cargo owner who includes it in the value of the goods insured under cargo policy. But freight payable only on delivery of the goods at the destination is at the risk of the ship owner who has insurable interest in it and therefore can insure it. Time charter hire is payable to the ship owner for the use of his ship for carriage of goods for specific period of time. If any events occur such as break down of machinery , damage to the vessel etc. which prevents the operation of the vessel for more than 24 consecutive hours of the payment hire shall cease until the ship become operational .this freight is at the risk of the ship owner

13

Liability insurance The marine insurance policy may include liability hazard such as collision or running down. Insurance can also be taken for the expenses involved in noncompliance of rules and regulation without any intention to device. It should be clear here that the marine perils insurance covers not only the ‘ocean but also the inland perils’, The perils to be included in the policy are clearly defined and the insurer will be liable only for insured perils. Forms of liability:

There are two types of liabilities: cross liability and single liability

Exclusion: a. Removal or disposal of obstruction wreaks b. Any real or personal property c. Cargo or other property d. Loss of life, personal injury

Classification of the policies

The marine insurance policy is issued only when the contract has been finalized and it would be the legal document of the contract. The form of marine insurance has been taken from the pretty old time. There has been a slight change in the wording of the policy. The standard policy has been contained the following information:

I. Name of the insured or his agent II. Subject matter insured .It may be ship, cargo or freight.

III. Risks insured against. IV. Name of the vessel and officers. V. Description of the voyage or period of insurance.

VI. Amount and term of insurance VII. Premium

There are various clauses which are suitably inserted according to the nature and type of policies. Hull cargo and freight policies have different standard clauses. In case of hull insurance, the clauses provided that if the insured vessel at the expiration of the policy is at sea, or at a port of refuge .Generally the ship may be covered until arrival at port of destination.

14

Different classes of policies are used in marine insurance. These are given below:

1. Voyage policies: The policy is issued to be covered a particular voyage from one port to another port and from one place to another place. The policy mentions the port of departure and port of destination between which the policy are generally underwritten. This policy is not suitable for hull insurance as a ship usually does not operate over a particular rote only.

This policy is used in case of cargo insurance. The goods remain covered even when the ship halts at intermediate port.

2. Time policies: Under this policy, the subject matter is insured for a definite period of

time. e.g from 6 pm of 1st journey ,1997 to 6 pm of 1st journey ,1999.The policy is generally taken for one year although it may be for less than one year.

3. Voyage and time policy or maxed: In this policy, the elements of voyage or time policy are combined in under policy. The reference is made certain period after completion of voyage. For example, 24 hours after arrival. It may be beneficial to hull as well as to cargo insurance.

4. Valued policy: Under this policy the value of loss to be compensated is fixed and remained constant throughout the risk except where there is fraud and excess over valuation. The value of subject matter is agreed between the insurer and the assured at the time of taking the insurance. It is also called insured value or agreed value.

5. Unvalued policy: When the value of the policy is not determined at the time of commencement of risk but is left to be valued when the loss takes place. The value thus decided later on is called the insurable value or valuable policy. In deciding the value, the invoice cost, freight, shipping and insurable charges are included and no margin for anticipated profit is added.

6. Floating policy: this policy describes the general terms and leaves the amount of cash and other particulars to be declared on it. The declaration is made in order of dispatch of shipment

7. Blanket policy: The policy is taken to cover losses within the particular time and place. The policy is taken for a certain amount and premium is paid on the whole of it in the beginning of the policy and readjusted at the end of the policy according to the actual amount at risk.

8. Named policy: Under this policy, the name of the ship and the amount of insured cargo are mentioned these policies are specific policy.

15

9. Single vessel fleet policy: A ship or a fleet of is insured in a single policy. When a one policy is assured, it is called single vessel policy and when a fleet of a ship is insured is called fleet policy.

10. Block policy: This policy insures incidental island risk, too, along with marine perils. For example; cotton is insured from time of processing to the time when it was delivered at the point of destination.

11. Currency policies: Policies insured for foreign currency is called currency policy, where the sum assured is stated in foreign currency. This policy avoids the foreign currencies because the claim amount is determined in the foreign currency and the fluctuations in the exchange of the inland.

12. P.P.I policy: The policy is issued to avoid the complication of the principle of insurable interest. This is called`` policy proof of interest’ and are honored by the insurer even in absence of insurable interest .This policy is based on mutual understanding, so it is called honored policy.

13. Special declaration policy: A special declaration policy is a floating policy issued to clients who have large turnover with many and frequent dispatches of goods. The minimum annual estimates dispatches shall be RS.3 crores for individual company.

Causes of Marine Losses/ Marine perils

The perils insured against are mentioned in the policy and the underwriter shall be liable for damages caused by the insured perils.

“Marine perils means the perils consequent”, or incidental to the navigation of the sea, that is to say, perils of the sea, fire , war perils, pirates, rovers, thieves, captures, seizures, restraints and determine of princes and people, jettisons, barratry and other perils, either of the like kind or which may be designated by the policy.

1) Perils of Sea: Under perils of Sea, ordinary action of the winds and waves, ordinary wear and tear to the vessel, inherent risk of the cargo are not included. Perils of the sea refers to fortuitous accidents or casualties of the sea. If the loss arising out of any of the perils of the sea insured is attributable to the fraud or willful misconduct of the assured, the underwriter is acquitted from the liability under the policy.

2) Fire: In older times fire was the biggest maritime perils, but recently it has been under control to a greater extent. Damage resulting from the fire and smoke is included under fire-peril. The water used for extinguishing fire may cause damage to the insured goods. So, this peril is also insurable.

3) Man-of-War: This is the vessel which is authorized by nations for the purpose of defense or attack in the event of hostilities. Any damage to the goods or ships arising out of collision against a man-of-war is insurable.

16

4) Enemies: The ship belonging to the foe (enemy) may cause to the insured and is re-underwritten by the marine policy. This policy extends to all the persons of the enemy country and to their hostile acts provided such acts form part of enemy action.

5) Pirates, Rovers, Thieves: The perils on account of pirates, rovers and thieves were common in olden times, but it has been reduced considerably these days. These acts are generally committed for the pursuit of individual gain by the persons beyond the jurisdiction of a state. The term ‘thieves’ does not mean clandestine theft or a theft committed by anyone of the crew or officers or passengers.

Jettison: Jettison means voluntary throwing away of the cargo or part of a vessel’s equipment for the lightening or relieving the ship for common safety. The aim of the intentional throwing away of the goods or property is to relieve the vessel from some imminent peril. Accidental falling of things does not constitute jettison. The own inherent- vice of cargo is also not included in the jettison.

Barratry: Barratry includes every wrongful act willfully committed by the master or crew the prejudice of the owner. The act of barratry must be committed without the knowledge of the owner. The insurer, if barratry insured, is liable for losses arising out of barratry.

Restraints and Detainments: The prevention to fee as of a port by the government of the country is called restraints. It may cause interruption and possible loss of voyages involving such ports and sacrifice of cargo. The term ‘detainments’ covers losses resulting from the detention of a vessel its cargo by blockage or possible quarantine regulation or other interference by the policy power of a nation while a vessel is in part.

The Free of Capture and Seizure Clause (F.C & S. Clause): The policy generally covers war perils. But, to include perils of sudden declaration of war, the war clause or free of capture and seizure clause is added to relive war perils.

Explosion: The risk of explosion has greatly increased. The explosion on board of a vessel damaging hull or cargo or both could be constructed as a peril on a sea. An explosion on shore might damage a ship or its cargo.

Strikes, Riots and Civil Commotion Clause: The marine insurance on cargo is extended to cover from warehouse to warehouse or otherwise insures the goods on shore prior to shipment and after discharge; the damage of underwriters being held liable for losses, resulting from the unlawful acts of strikers from riots or civil commotions is materially enhanced.

All Other Perils: Loss occurred by salt water of the sea, actions of worms on timber, cattle dying due to want of fodder as a result of lengthy voyage constitute sea perils. There may be other damage due to oil, sweat, heat, which are insured under other perils.

17

Types of Marine Losses

If the loss takes place on account of any of the perils insured against with the insurer, the insurer will be liable for it and shall have to make good the losses to the assured. If the peril is insured, the insurer will indemnify the assured, otherwise not.

There are two types of marine losses

i) Total loss

ii) Partial loss or average loss

Total Loss: According to S. 57(1) of the Marine Insurance Act, there is an actual total loss where the subject matter insured is destroyed or so damaged as to cease to be a thing of the kind insured or where the assured is irretrievable deprived thereof. In case of total loss, the insured stands to lose to the extent of the value of the property provided the policy amount was to that limit.

1) Actual Total Loss: Actual total loss is a materials and physical loss of the subject-matter insured. Where the subject-matter insured is destroyed or so damaged as to cease to be a thing of the kind insured, or where the insured is irretrievable deprived thereof, there is an actual total loss. When a vessel is foundered or when merchandise is so damaged as to be valueless or when ship is missing it will be an actual total loss.

The actual total loss occurs in the following cases:

i) The subject-matter is destroyed, e.g. a ship is entirely destroyed by fire.

ii) The subject-matter is so destroyed as to cease to be a thing of the kind insured. Here the subject-matter is not totally destroyed but damaged to such as extent as the result of the mishap; it is no longer of the same specie as originally insured.

iii) The insured is irretrievably deprived of the ownership of goods even they are in physical existence as in the case of capture by enemy, stealth by thief or fraudulent disposal by the captain or crew.

iv) The subject-matter is lost. For Example- where a ship is missing for a very longtime and no news of her is received after the lapse of a reasonable time. An actual total loss is presumed unless there is some other proof to show against it.

2) Constructive Total Loss: Section 60 of the Act defines constructive Total loss. Where the subject-matter is not actually lost in the above matter, but is reasonably abandoned when its actual total loss is unavoidable or when it is cannot be preserved from total loss without involving expenditure which would exceed the value of the subject matter.

18

The constrictive total loss will be were--

i) The subject-matter insured is reasonably abandoned on account of its actual total loss appearing to be unavoidable.

ii) The subject matter could not be preserved from actual total loss without an expenditure which would exceed its repaired and recovered value.

Partial Loss: Section 56 of the Act provides that any loss other than a total loss is a partial loss. Partial loss is there where only part of the property insured is lost or destroyed or damaged. Partial losses, in contradiction from total losses, include (a) Particular Average losses, i.e., damage, or total loss of a part, (b) General Average losses i.e., the sacrifice expenditure, etc., done for common safety of subject matter insured, (c) Particular or Special Charges i.e., expenses incurred in special circumstances, and (d) Salvage Charges

a) Particular Average loss: Section 64 of the Act defines Particular Average loss as ‘a partial loss’ of the subject-matter insured caused by a peril insured and is not a general average loss. The general average loss or expenses is voluntarily done for the common safety of all the parties insured. But, the particular average loss is fortuitous or accidental.

The particular average loss must fulfill the following conditions

i) Particular Average loss is a partial loss or damage to any particular interest caused to that interest only by a peril insured against.

ii) The loss should be accidental and not intentional.

iii) The loss should be of the particular subject-matter only.

iv) It should be the loss of a part of the subject-matter or damage thereto or both. The distinguishing feature in this matter is that where the properties insured are all of the same description, kind and quality and they are valued as a whole in the policy, the total loss of a part of this whole is a particular loss, but where the properties insured are not all of the same description, kind and quality and they are separately valued in the policy, the loss of an apportion able part of the interest is a total loss.

b) General Average loss: Section 66 of the Act defines General Average as a loss caused by or directly consequential on a general average act which includes a general average expenditure as well as a general average sacrifices. The following elements are involved in general average loss.

i) The loss must be extra ordinary in nature. The sacrifices or expenditure must not be related to the performance of routine work.

19

ii) The whole adventure must be imperiled. The peril should be something more than the ordinary perils of the sea. It should be imminent and real.

iii) The General Average loss must be voluntary and intentional accidental loss or damage is excluded.

iv) The loss must be direct result of a general average act. Indirect losses such as demurrage and market losses are not allowed as general average.

v) General average must not be due to same default on the part of the person whose interest has been sacrificed.

Types of General average loss

The general average losses are divided into two classes

General Average Sacrifices The general average sacrifices are made for common safety. For example- Jettison, which means throwing away of the cargo in order to lighten the ship.

General Average Expenditure: The general average act involves expenditure. In this case extra expenditures are involved for common safety.

c) Particular or Special Charges: Where the policy contains a “ Sue and Labour” clause, the engagement thereby entered into is deemed to be supplementary to the contract of insurance and the assured may recover from the insurer any expenses properly incurred pursuant to the clause.

i) The expenses must be incurred for the benefit of the subject matter insured. The expenses incurred for the common benefit will be a part of general average.

ii) The expenses must be reasonable and be incurred by “the assured” his factors, his servants or assigns” and this provision effectively excludes salvage charges.

iii) They are recoverable only when incurred to avert or minimize a loss from a peril covered by the policy.

Sue and Labour: Sue and Labour charge are a types of particular charges. They are incurred short of destination i. e. reconditioning costs and follow upon loss or damage.

Extra Charges: Extra charges are the expenses of proving a claim e. g. survey fee. These are payable only if the loss is payable under the policy.

d) Salvage Charges: Section 65 of the Act defines Salvage Charges as those recoverable under maritime law by a salvor independent of contract. It is the remuneration or reward

20

payable according to maritime law of salvors who voluntarily and independently of contract render services it recuse or save property at sea i. e. hull, cargo and freight. No reward for services or payments for loss or expenses can be claimed by salvors where the services were unsuccessful and the property was totally lost.

Claims and Settlement

Notice of claim: A prompt notice of claim by the insured is required . The received of notice or approval of the course of action taken by the insured does not mean that the liability of any loss is acknowledged. The damage notice must be given prior to survey by insurer’s representative and the survey report signed by him.

Documents Required for Claim: The following documents are required at the time of claim.

1) Policy or certificate of insurance.

2) Bill of lading. It determines the scope of the contract of carriage.

3) Invoice or bill stating term and condition of sale.

4) Copy of protest. In the event of stranding of or accident to the vessel, the master of the ship notes ‘protest’ before a counsel or notary public. The protest state that everything was done to bring safety the ship and cargo and loss or damage was not due to lack of diligence on the part of the master or crew.

5) Certificate of survey. This is necessary to find out whether the necessary franchise is reached or not in the case of particular average.

6) Account sales or bill of sale. Similar documents where goods have been sold. The difference between gross sound value and proceeds as per account sales might be accepted as amount of loss.

7) Letter of Subrogation. It gives the underwriters to sue and recover compensation from third parties where the same is due.

Mathematical Problems and Solution

21

Problem-1: A Cargo consisting of 10,000 bags was insured for Tk. 2, 00,000. But 4,000 bags were damaged and would realize Tk. 4 per bag. The following expenses also incurred by the insured 2% Commission, Tk. 40 as Survey fee and Tk. 100 as sales expenses.

Requirements:

i) To prepare a particular Average Statement assuming that goods would have realized Tk. 22 per bag in their undamaged condition and the policy is valued.

ii) To prepare a particular Average Statement assuming that goods would have realized Tk. 16 per bag in their undamaged condition and the policy is valued.

iii) To state what would be the extent of claim in each of the above two cases if the policy is unvalued.

Requirement solution (i)

Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.) Insured value 10,000 bags------------------------------------------

In undamaged market value of 4000 bags----------------------

In damage condition value of 4000 bags------------------------

Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 88,000 loss is Tk. 72,000 Out of Tk. 1 loss is Tk. 72,000 Tk. 88,000 Out of Tk. 80,000 loss is Tk. 72,000 × Tk. 80, 000 Tk. 88,000 Add Extra Expenses: Sales Commission @2% (4,000*4)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

20

22

4

2, 00,000

65,454.54

460

88,000 16,000

72,000

320 40

100

65, 914.54

22

Requirement solution (ii) Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.)

Insured value 10,000 bags------------------------------------------

In undamaged market value of 4,000 bags----------------------

In damage condition value of 4,000 bags------------------------ Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 64,000 loss is Tk. 48,000 Out of Tk. 1 loss is Tk. 48,000 Tk. 64,000 Out of Tk. 80,000 loss is Tk. 48,000 × Tk. 80, 000 Tk. 64,000 Add Extra Expenses: Sales Commission @2% (4,000*4)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

20

16

4

2, 00,000

60,000

460

64,000 16,000

48,000

320 40

100

60, 460

Requirement solution (iii) If the policy is unvalued in both of the above causes, the extant of claim will be calculated as follows. In case of unvalued policy the amount of loss needs no adjustment. In that case, with the actual losses will be added with the actual expenditure and that will be the actual amount of claim. The claim in the first case will be Tk. 72,000 + Tk. 460 = Tk. 72,460 The claim in the second case will be Tk. 48,000 + Tk. 460 = Tk. 48,460

23

Problem-2: A Cargo consisting of 8,000 bags was insured for Tk. 80,000. But 1,500 bags of cargo were damaged and would realize Tk. 3.00 per bag. The following expenses also incurred by the insured Sales Commission 2%, Survey fee Tk. 4,000 and Sales expenses Tk. 900.

Requirements:

i) To prepare a particular Average Statement assuming that goods would have realized Tk. 11.50 per bag in their undamaged condition and the policy is valued.

ii) To prepare a particular Average Statement assuming that goods would have realized Tk. 7.50 per bag in their undamaged condition and the policy is valued.

iii) State what would be the extent of claim in each of the above two cases if the policy is unvalued.

Requirement solution (i)

Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.) Insured value 8,000 bags------------------------------------------

In undamaged market value of 1,500 bags----------------------

In damage condition value of 1,500 bags------------------------

Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 17,250 loss is Tk. 12,750 Out of Tk. 1 loss is Tk. 12,750 Tk. 17,250 Out of Tk. 15,000 loss is Tk. 12,750 × Tk. 15, 000 Tk. 17,250 Add Extra Expenses: Sales Commission @2% (1,500*3)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

10

11.50

3.00

80,000

11,086.96

4,990

17,250 4,500

12,750

90

4,000 900

16, 076.96

24

Requirement solution (ii)

Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.) Insured value 8,000 bags------------------------------------------

In undamaged market value of 1,500 bags----------------------

In damage condition value of 1,500 bags------------------------

Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 11,250 loss is Tk. 6,750 Out of Tk. 1 loss is Tk. 6,750 Tk. 11,250 Out of Tk. 15,000 loss is Tk. 6,750 × Tk. 15, 000 Tk. 11,250 Add Extra Expenses: Sales Commission @2% (1,500*3)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

10

7.50

3.00

80,000

9,000

4,990

11,250 4,500

6,750

90

4,000 900

13,990

Requirement solution (iii) If the policy is unvalued in both of the above causes, the extant of claim will be calculated as follows. In case of unvalued policy the amount of loss needs no adjustment. In that case, with the actual losses will be added with the actual expenditure and that will be the actual amount of claim. The claim in the first case will be Tk. 12,750 + Tk. 4,990 = Tk. 17,740 The claim in the second case will be Tk. 6,750 + Tk. 4,990 = Tk. 11,740

25

Problem-3: Following are information relating to Mr. Karim and sons ltd. a) Cement 15,000 bags b) Amount of insurance Tk. 4,50,000 c) Partial damaged bag sold Tk. 5 per bag d) Number of partial damaged bags 3,000 e) Related expenditure,

Commission--- 3% Survey fee Tk. 400 Selling expense Tk. 1,000

Requirements: i) Partial average loss statement when the market value of cement per bag is Tk. 32 ii) Partial average loss statement when the market value of cement per bag is Tk. 28

and iii) If the policy is unvalued, what will be claim for the above two situation.

Requirement solution (i)

Statement regarding the particular average statement of claim Particulars Rate Amount (tk.) Amount (tk.)

Insured value 15,000 bags------------------------------------------

In undamaged market value of 3,000 bags----------------------

In damage condition value of 3,000 bags------------------------ Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 96,000 loss is Tk. 81,000 Out of Tk. 1 loss is Tk. 81,000 Tk. 96,000 Out of Tk. 90,000 loss is Tk. 81,000 × Tk. 90, 000 Tk. 96,000 Add Extra Expenses: Sales Commission @3% (3,000*5)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

30

32

5

4, 50,000

75,937.5

1,850

96,000 15,000

81,000

450 400

1,000

77,787.5

26

Requirement solution (ii)

Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.) Insured value 15,000 bags------------------------------------------

In undamaged market value of 3,000 bags----------------------

In damage condition value of 3,000 bags------------------------

Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 84,000 loss is Tk. 69,000 Out of Tk. 1 loss is Tk. 69,000 Tk. 84,000 Out of Tk. 90,000 loss is Tk. 69,000 × Tk. 90, 000 Tk. 84,000 Add Extra Expenses: Sales Commission @3% (3,000*5)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

30

28

5

4, 50,000

73,928.57

1,850

84,000 15,000

69,000

450 400

1,000

75,778.57

Requirement solution (iii) If the policy is unvalued in both of the above causes, the extant of claim will be calculated as follows. In case of unvalued policy the amount of loss needs no adjustment. In that case, with the actual losses will be added with the actual expenditure and that will be the actual amount of claim. The claim in the first case will be Tk. 81,000 + Tk. 1,850 = Tk. 82,850 The claim in the second case will be Tk. 69,000 + Tk. 1,850 = Tk. 70,850

27

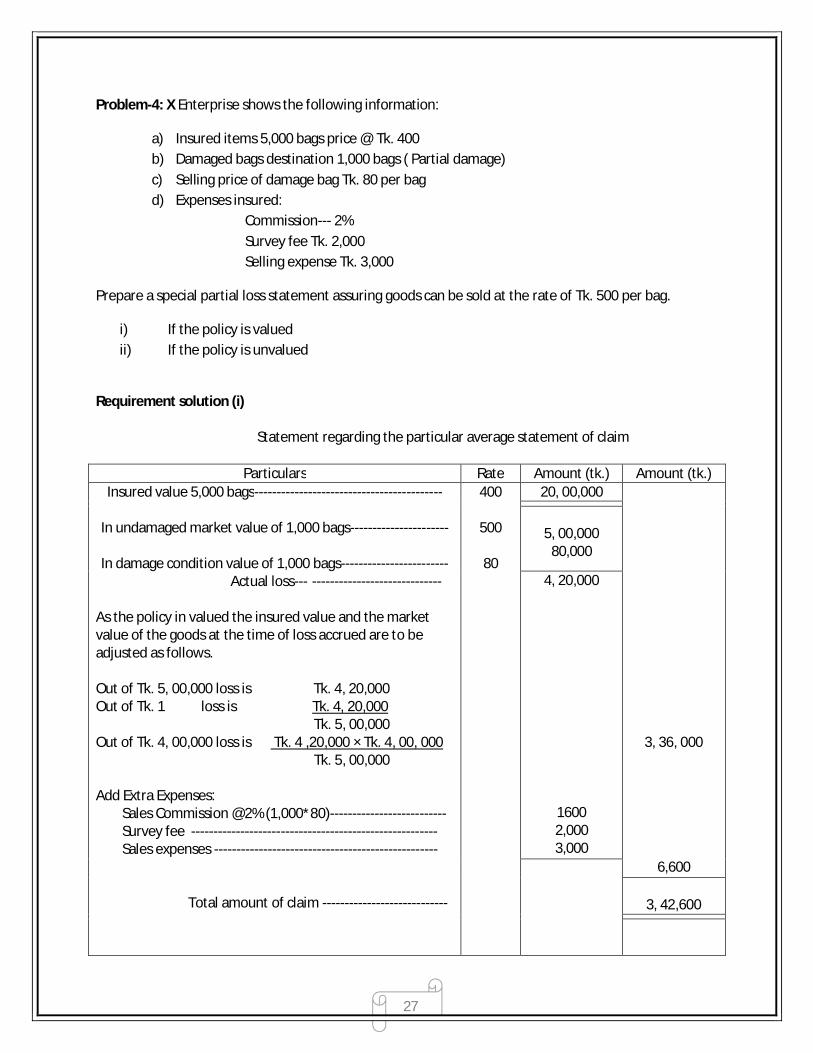

Problem-4: X Enterprise shows the following information:

a) Insured items 5,000 bags price @ Tk. 400 b) Damaged bags destination 1,000 bags ( Partial damage) c) Selling price of damage bag Tk. 80 per bag d) Expenses insured:

Commission--- 2% Survey fee Tk. 2,000 Selling expense Tk. 3,000

Prepare a special partial loss statement assuring goods can be sold at the rate of Tk. 500 per bag.

i) If the policy is valued ii) If the policy is unvalued

Requirement solution (i)

Statement regarding the particular average statement of claim

Particulars Rate Amount (tk.) Amount (tk.)

Insured value 5,000 bags------------------------------------------

In undamaged market value of 1,000 bags----------------------

In damage condition value of 1,000 bags------------------------ Actual loss--- ----------------------------- As the policy in valued the insured value and the market value of the goods at the time of loss accrued are to be adjusted as follows. Out of Tk. 5, 00,000 loss is Tk. 4, 20,000 Out of Tk. 1 loss is Tk. 4, 20,000 Tk. 5, 00,000 Out of Tk. 4, 00,000 loss is Tk. 4 ,20,000 × Tk. 4, 00, 000 Tk. 5, 00,000 Add Extra Expenses: Sales Commission @2% (1,000*80)-------------------------- Survey fee ------------------------------------------------------- Sales expenses -------------------------------------------------- Total amount of claim ----------------------------

400

500

80

20, 00,000

3, 36, 000

6,600

5, 00,000

80,000

4, 20,000

1600 2,000 3,000

3, 42,600

28

Requirement solution (ii) If the policy is unvalued of the above causes, the extant of claim will be calculated as follows. In case of unvalued policy the amount of loss needs no adjustment. In that case, with the actual losses will be added with the actual expenditure and that will be the actual amount of claim. The claim in the case will be Tk. 4, 20,000 + Tk. 6,600 = Tk. 4, 26,600 Problem-5: A ship is cullieded against hidden rock Under Sea Water. A part of cargo was dropped in the Sea to set the ship. However, the ship was managed to drag to the safe zone. The ship was partially damaged. Prepare a general average statement and show the adjustment of loss to various partners involved. From the following information Original value of Ship ---------- Tk. 1, 00, 00,000 Original value of Cargo ------- Tk. 60, 00,000 Original value of Freight ------ Tk. 10, 00,000 Partial loss and expenditures: Damage of Ship Tk. 40, 00,000; Cargo dropped Tk. 8, 00,000; Freight loss Tk. 7, 00,000; Dragging expenses Tk. 6, 00,000. Solution: Total loss of expenditure= Tk. 40, 00,000 + Tk. 8, 00,000 + Tk. 7, 00,000 + Tk. 6, 00,000 = Tk. 61, 00,000

Items Original value Total loss Value after loss Calculation of loss

Ship Cargo Freight

1, 00, 00,000

60, 00,000

10, 00,000

40, 00,000

8, 00,000

7, 00,000

60, 00,000

52, 00,000

3, 00,000

61, 00,000 × 60, 00,000 1, 15, 00,000 61, 00,000 × 52, 00,000 1, 15, 00,000 61, 00,000 × 3, 00,000 1, 15, 00,000

31, 82,608.696

27, 58,260.87

1, 59,190.434

Total 1, 70, 00,000 1, 15, 00,000 61, 00,000

29

Problem-6: A Ship was caught by a cyclone in the Sea. A part of the Cargo was dropped in the Sea and the Ship was damaged manually to the safe zone. The Ship was however, partly damaged. The partial loss and expenditures in this connection are given below. Prepare a statement showing general average loss and its adjustments to various partners involved. Partial loss and other expenditures:

Damage of Ship ---------- Tk. 20,000 Dragging Expenditures Tk. 50,000 Cargo dropped ----------- Tk. 20,000 Freight loss ---------------- Tk. 10,000

Other information: Ship (Original Value) ------- Tk. 6, 50,000 Goods (Original Value) -----Tk. 4, 00,000 Freight (Original Value) --- Tk. 31,000 Solution: Total loss of expenditure= Tk. 20,000 + Tk. 50,000 + Tk. 20,000 + Tk. 10,000 = Tk. 1, 00,000

Items Original value Total loss Value after loss Calculation of loss

Ship Goods Freight

6, 50,000

4, 00,000

31,000

20,000

20,000

10,000

6, 30,000

3, 80,000

21,000

1, 00,000 × 6, 30,000 10, 31,000 1, 00,000 × 3, 80,000 10, 31,000 1, 00,000 × 21,000 10, 31,000

61,105.7226

36,857.41998

2,036.85742

Total 10, 81,000 10, 31,000 1, 00,000