global marine insurance report 2017

55

GLOBAL MARINE INSURANCE REPORT 2017 Astrid Seltmann Analyst/Actuary, The Nordic Association of Marine Insurers (Cefor) Vice chair of IUMI’s Facts & Figures Committee

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of global marine insurance report 2017

GLOBAL MARINE INSURANCE REPORT 2017

Astrid Seltmann Analyst/Actuary, The Nordic Association of Marine Insurers (Cefor)Vice chair of IUMI’s Facts & Figures Committee

2

Warning!

Figures reflect the 2017 state of reporting/ estimates and will change retrospectively!

For comparison purposes, do NOT compare figures in this report to last year’s report, but check updated premiums and loss ratios for the last ten years at www.iumi.com !

Global Marine Insurance report

• Global Marine Insurance – Overview

• Cargo – Market & Results

• Hull – Market & Results

• Offshore Energy – Market & Results

______________________________________For for download at www.iumi.com:

• Marine premiums by country

• Loss ratios triangulations: Hull, Cargo, Energy3

Focus/New in 2017

• New: Loss ratios Asia & Latin America (Cargo & Hull, accounting year)

• Cargo: Recent deterioration.

• Hull: Vessel value & claims trends. Major versus serious casualties.

• Offshore energy: Survival training?

• Hurricanes are back, too.

4

Global Marine Insurance report

• Global Marine Insurance – Overview

• Cargo – Market & Results

• Hull – Market & Results

• Offshore Energy – Market & Results

5

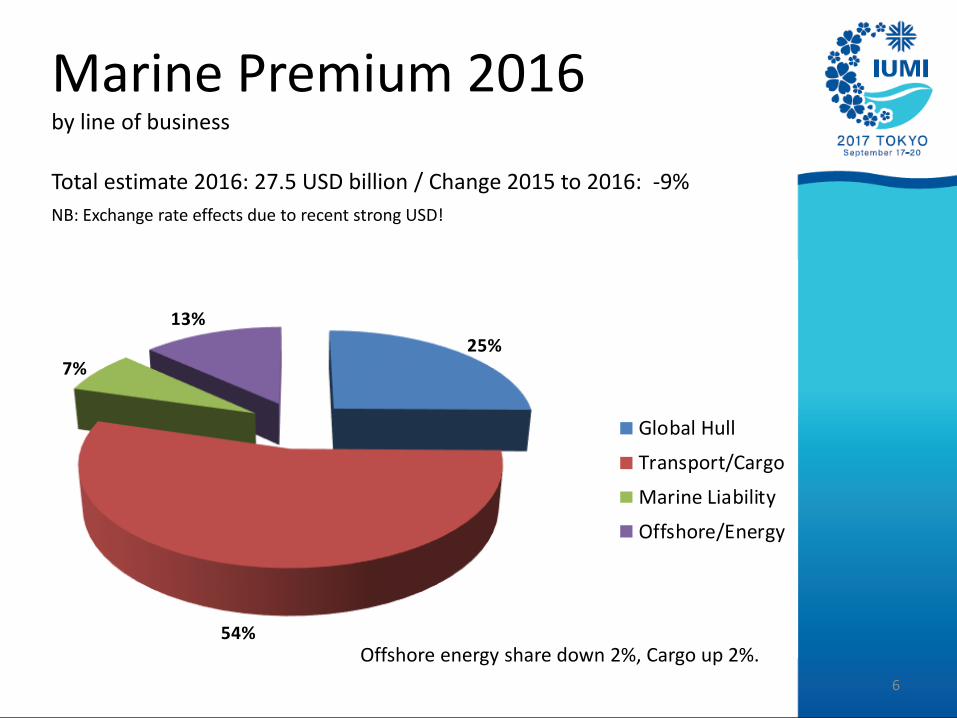

25%

54%

7%

13%

2016

Global Hull

Transport/Cargo

Marine Liability

Offshore/Energy

Marine Premium 2016by line of business

Total estimate 2016: 27.5 USD billion / Change 2015 to 2016: -9%

NB: Exchange rate effects due to recent strong USD!

Offshore energy share down 2%, Cargo up 2%.

6

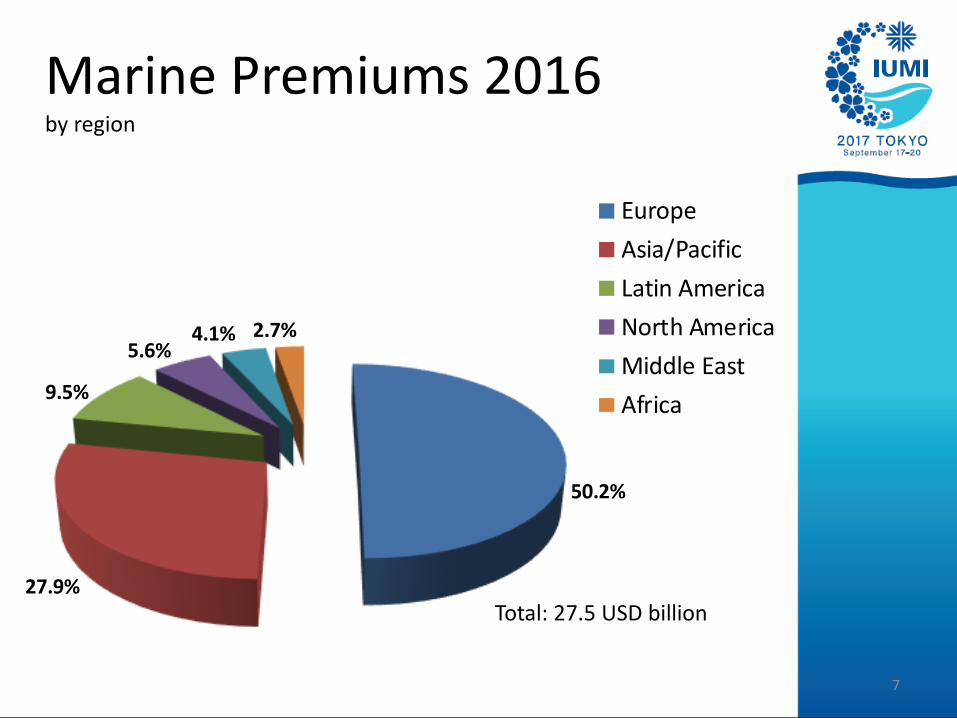

50.2%

27.9%

9.5%

5.6%4.1% 2.7%

2016Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

Total: 27.5 USD billion

Marine Premiums 2016by region

7

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

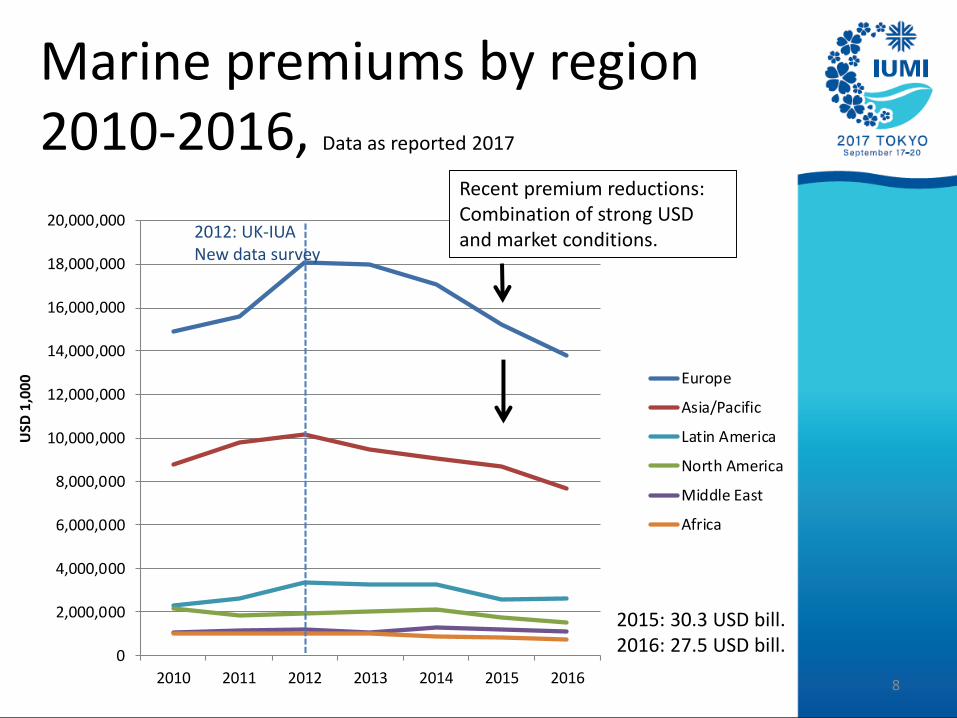

2010 2011 2012 2013 2014 2015 2016

Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

8

Marine premiums by region2010-2016, Data as reported 2017

2012: UK-IUANew data survey

2015: 30.3 USD bill. 2016: 27.5 USD bill.

Recent premium reductions: Combination of strong USD and market conditions.

50%

70%

90%

110%

130%

150%

170%

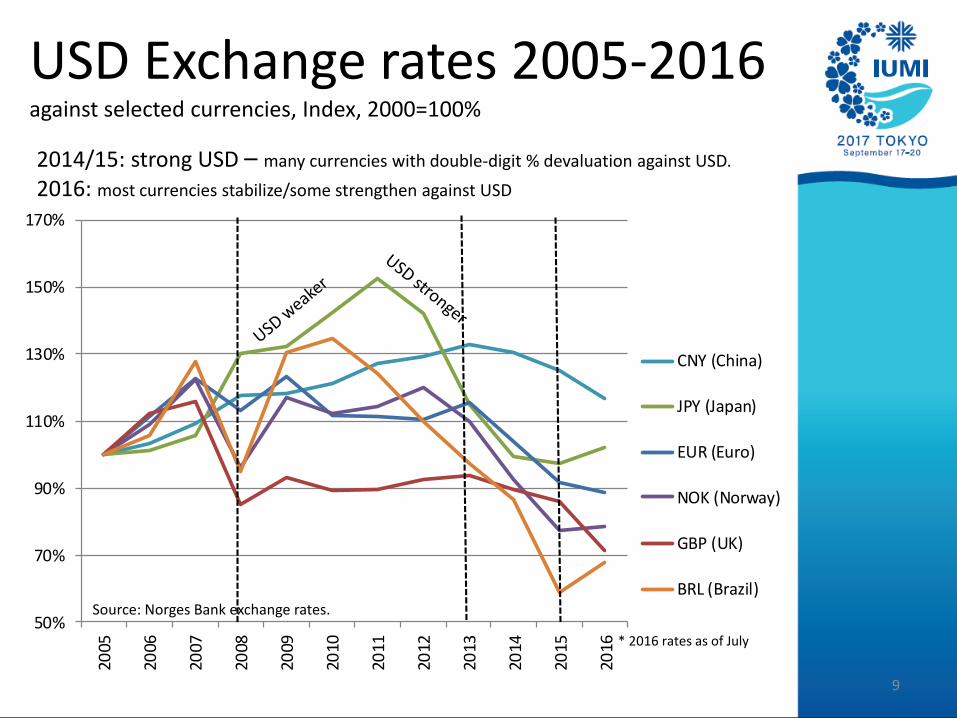

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

CNY (China)

JPY (Japan)

EUR (Euro)

NOK (Norway)

GBP (UK)

BRL (Brazil)

* 2016 rates as of July

Source: Norges Bank exchange rates.

USD Exchange rates 2005-2016against selected currencies, Index, 2000=100%

9

2014/15: strong USD – many currencies with double-digit % devaluation against USD.

2016: most currencies stabilize/some strengthen against USD

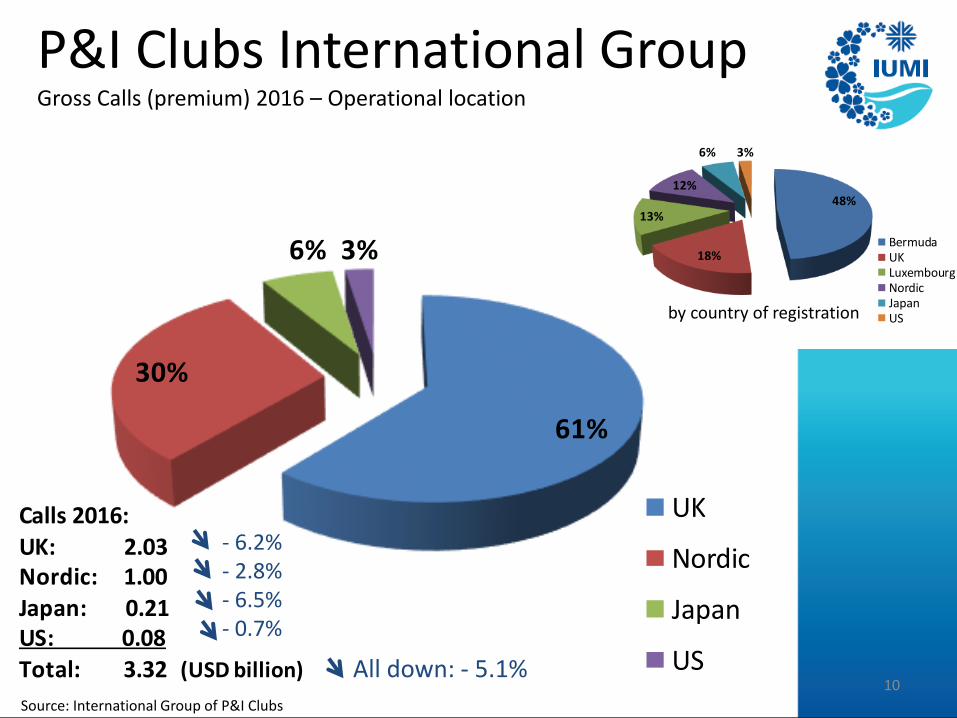

61%

30%

6% 3%

UK

Nordic

Japan

US

Calls 2016:UK: 2.03 Nordic: 1.00Japan: 0.21US: 0.08

Total: 3.32 (USD billion)

48%

18%

13%

12%

6% 3%

BermudaUKLuxembourgNordicJapanUS

P&I Clubs International Group Gross Calls (premium) 2016 – Operational location

All down: - 5.1%

by country of registration

10

- 6.2%- 2.8%- 6.5%- 0.7%

Source: International Group of P&I Clubs

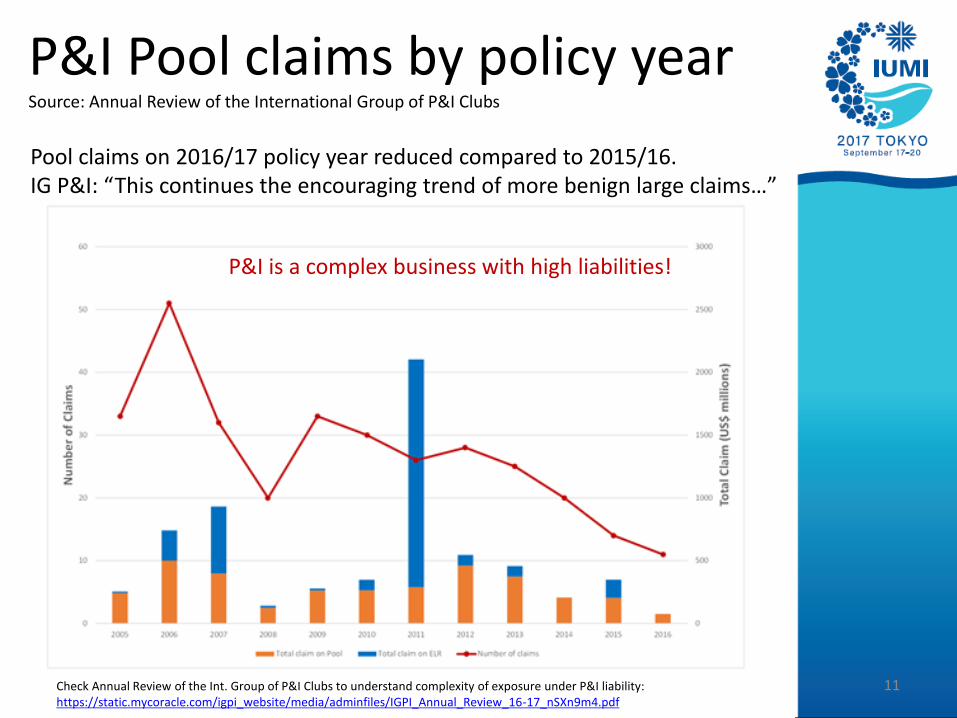

P&I Pool claims by policy yearSource: Annual Review of the International Group of P&I Clubs

11Check Annual Review of the Int. Group of P&I Clubs to understand complexity of exposure under P&I liability: https://static.mycoracle.com/igpi_website/media/adminfiles/IGPI_Annual_Review_16-17_nSXn9m4.pdf

Pool claims on 2016/17 policy year reduced compared to 2015/16.IG P&I: “This continues the encouraging trend of more benign large claims…”

P&I is a complex business with high liabilities!

Global Marine Insurance report

• Global Marine Insurance – Overview

• Cargo – Market & Results

• Hull – Market & Results

• Offshore Energy – Market & Results

12

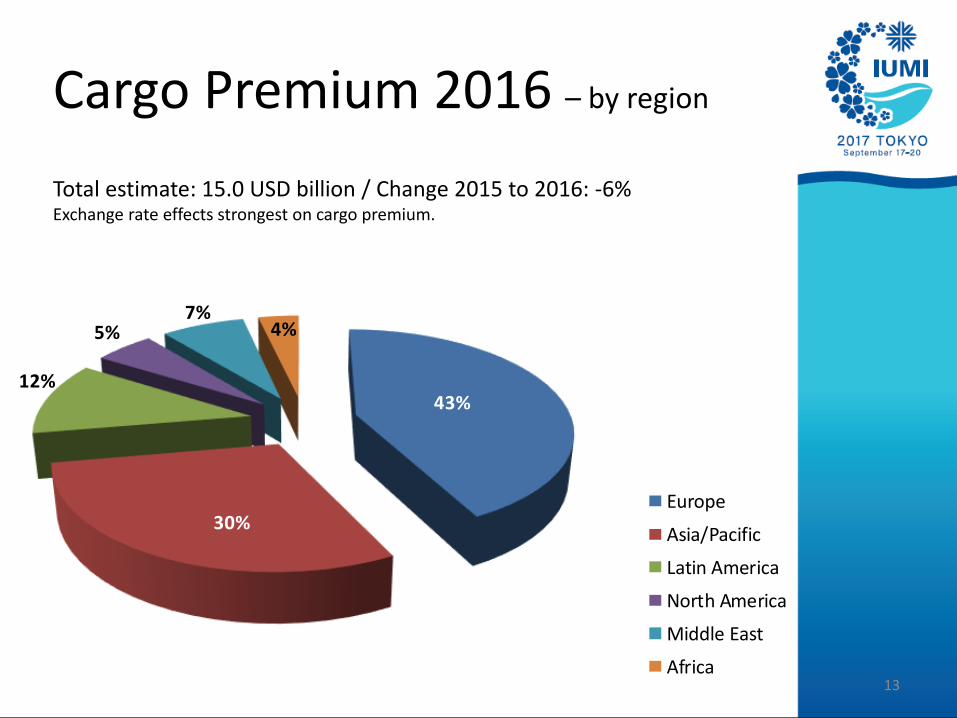

Cargo Premium 2016 – by region

Total estimate: 15.0 USD billion / Change 2015 to 2016: -6%Exchange rate effects strongest on cargo premium.

13

43%

30%

12%

5%7%

4%2016

Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

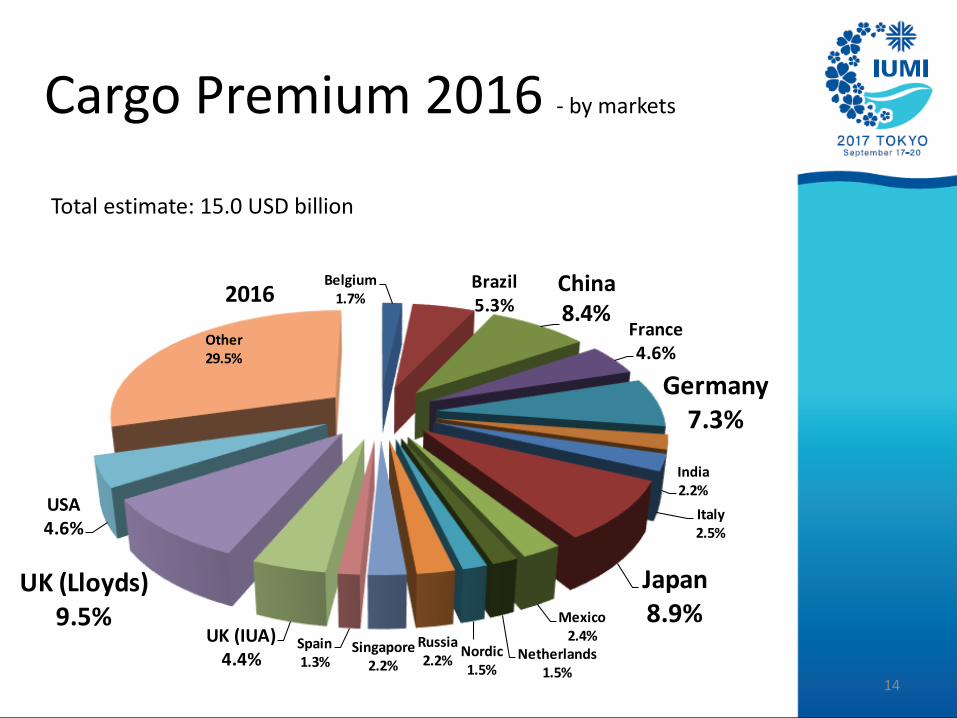

Cargo Premium 2016 - by markets

Total estimate: 15.0 USD billion

14

Belgium1.7%

Brazil5.3%

China8.4%

France4.6%

Germany7.3%

India2.2%

Italy2.5%

Japan8.9%Mexico

2.4%Netherlands

1.5%

Nordic1.5%

Russia2.2%

Singapore2.2%

Spain1.3%

UK (IUA)4.4%

UK (Lloyds)9.5%

USA4.6%

Other29.5%

2016

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

China

UK (Lloyds)

Japan

Germany

USA

Brazil

France

UK (IUA)

India

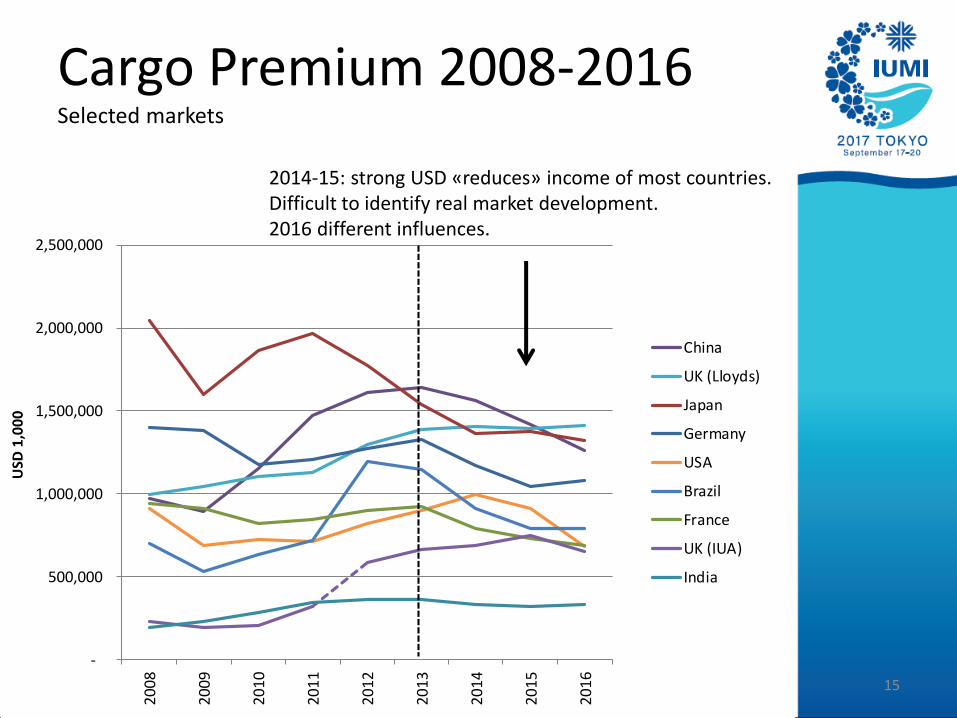

Cargo Premium 2008-2016Selected markets

2014-15: strong USD «reduces» income of most countries. Difficult to identify real market development.2016 different influences.

15

0%

50%

100%

150%

200%

250%

300%

350%

400%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

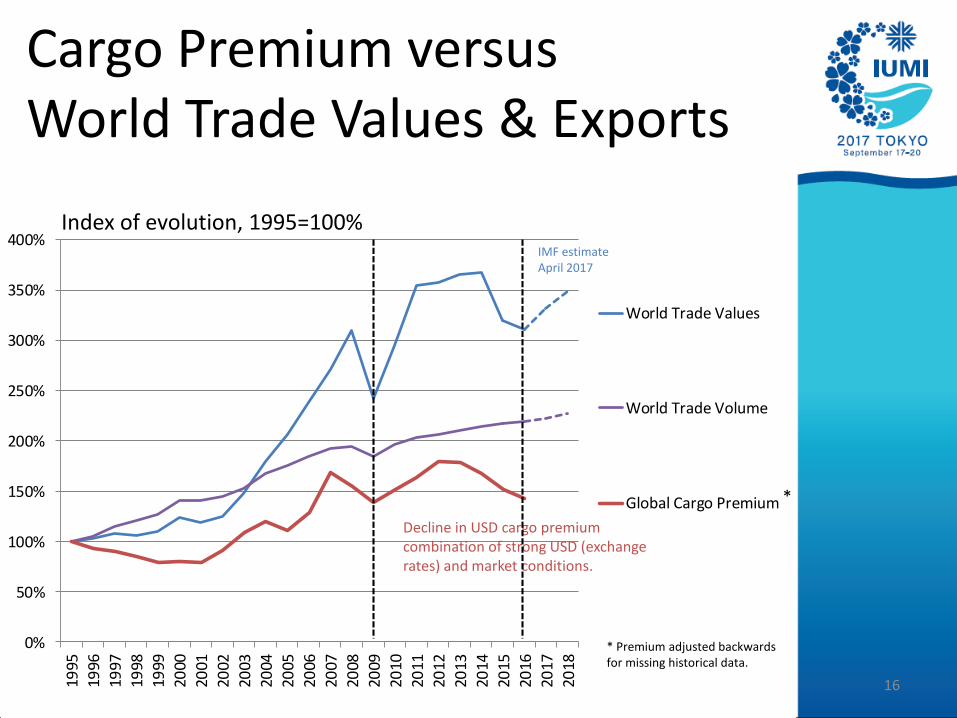

World Trade Values

World Trade Volume

Global Cargo Premium

Cargo Premium versus World Trade Values & Exports

Decline in USD cargo premiumcombination of strong USD (exchangerates) and market conditions.

Index of evolution, 1995=100%IMF estimateApril 2017

16

* Premium adjusted backwards for missing historical data.

*

50%

60%

70%

80%

90%

1 2 3 4 5

2009

2010

2011

2012

2013

2014

2015

2016

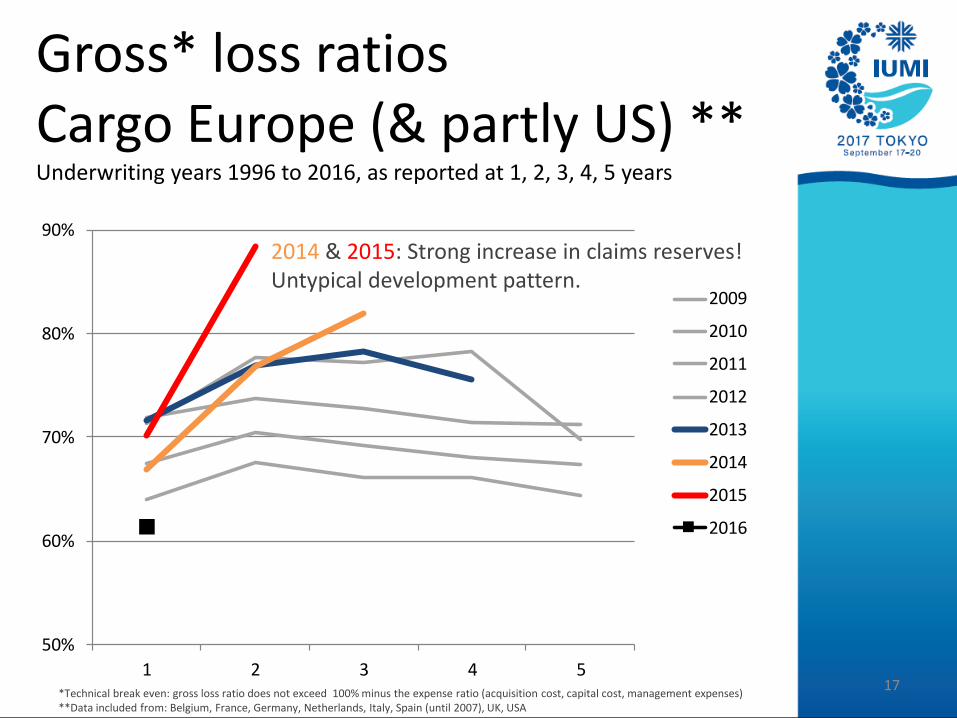

2014 & 2015: Strong increase in claims reserves! Untypical development pattern.

17*Technical break even: gross loss ratio does not exceed 100% minus the expense ratio (acquisition cost, capital cost, management expenses)**Data included from: Belgium, France, Germany, Netherlands, Italy, Spain (until 2007), UK, USA

Gross* loss ratiosCargo Europe (& partly US) **Underwriting years 1996 to 2016, as reported at 1, 2, 3, 4, 5 years

0%

20%

40%

60%

80%

100%

120%

140%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

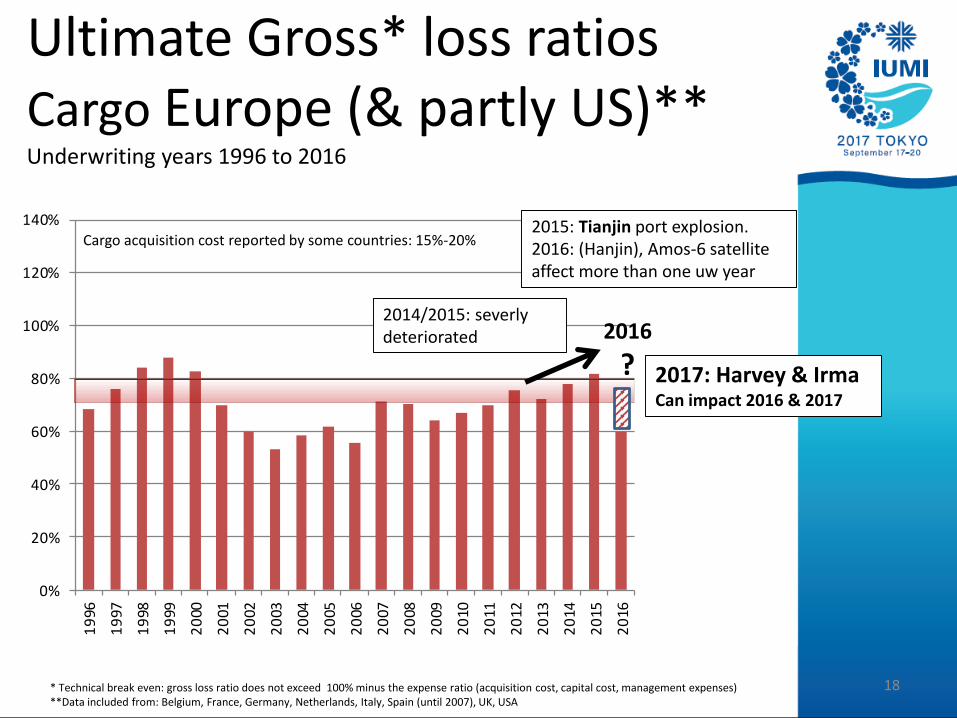

* Technical break even: gross loss ratio does not exceed 100% minus the expense ratio (acquisition cost, capital cost, management expenses)**Data included from: Belgium, France, Germany, Netherlands, Italy, Spain (until 2007), UK, USA

Ultimate Gross* loss ratiosCargo Europe (& partly US)** Underwriting years 1996 to 2016

18

2015: Tianjin port explosion. 2016: (Hanjin), Amos-6 satelliteaffect more than one uw year

Cargo acquisition cost reported by some countries: 15%-20%

2016

?

2014/2015: severlydeteriorated

2017: Harvey & IrmaCan impact 2016 & 2017

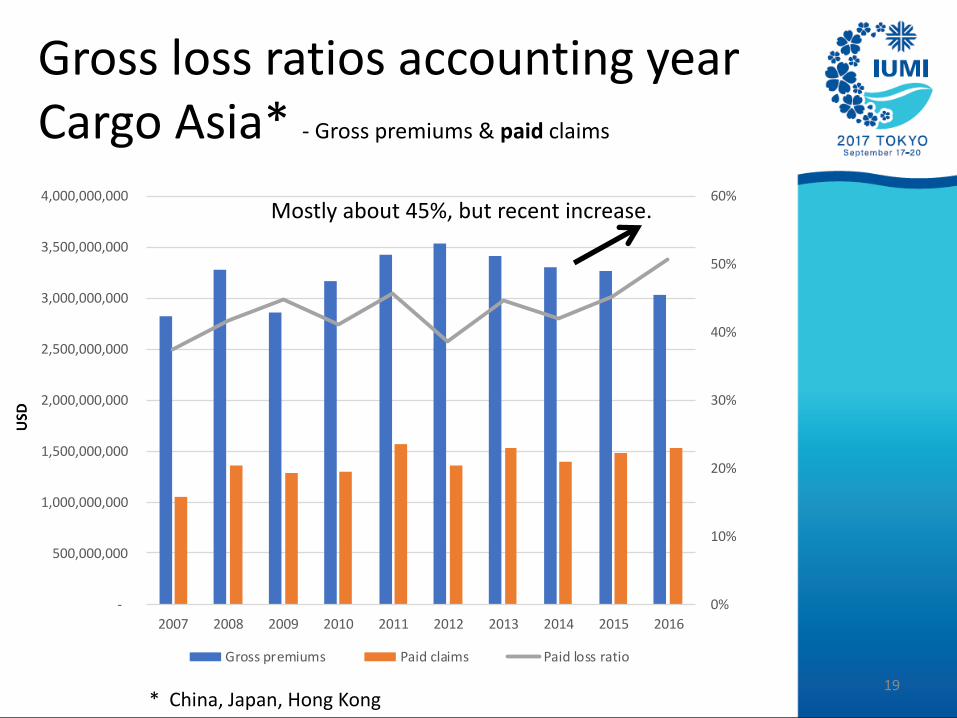

Gross loss ratios accounting yearCargo Asia* - Gross premiums & paid claims

19

0%

10%

20%

30%

40%

50%

60%

-

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

3,000,000,000

3,500,000,000

4,000,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross premiums Paid claims Paid loss ratio

* China, Japan, Hong Kong

Mostly about 45%, but recent increase.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

-

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

3,000,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross premiums Paid claims Paid loss ratio

Gross loss ratios accounting yearCargo Latin America*- Gross premiums & paid claims

20

Average 50-55%, but peak in 2015.

*Figures included from: Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Guatemala, Honduras, Mexico, Panama, Paraguay, Peru, Venezuela.

Cargo Key points

• USD premium influenced by combination of market conditions and exchange rates (strong USD).

• Market change and results differ by region.

• 2014 & 2015 Results severely deteriorated (Tianjin).Uncertain how 2016 will develop (Amos-6, Harvey, Irma).

• Risk of even larger event claims: Climate (NatCat) & Increasing value accumulation on single sites

• Premiums represent increasingly stock exposure rather than transit exposure

• Despite some increase in trade, changing economic and political environment adds to uncertainty.

21

Global Marine Insurance report

• Global Marine Insurance – Overview

• Cargo – Market & Results

• Hull – Market & Results

• Offshore Energy – Market & Results

22

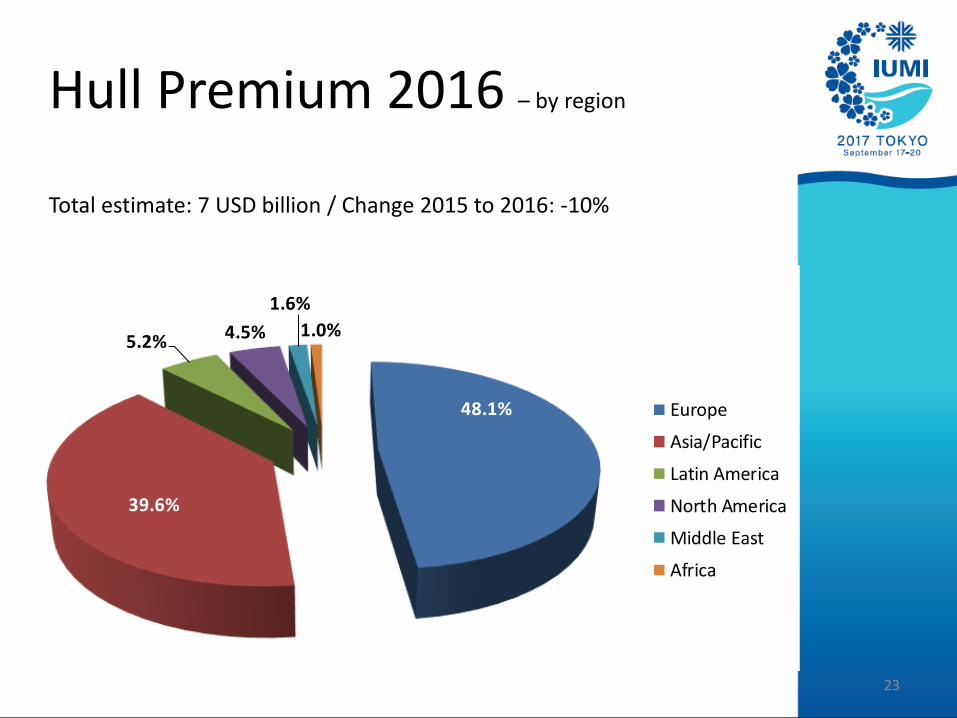

48.1%

39.6%

5.2% 4.5%

1.6%

1.0%2016

Europe

Asia/Pacific

Latin America

North America

Middle East

Africa

Hull Premium 2016 – by region

Total estimate: 7 USD billion / Change 2015 to 2016: -10%

23

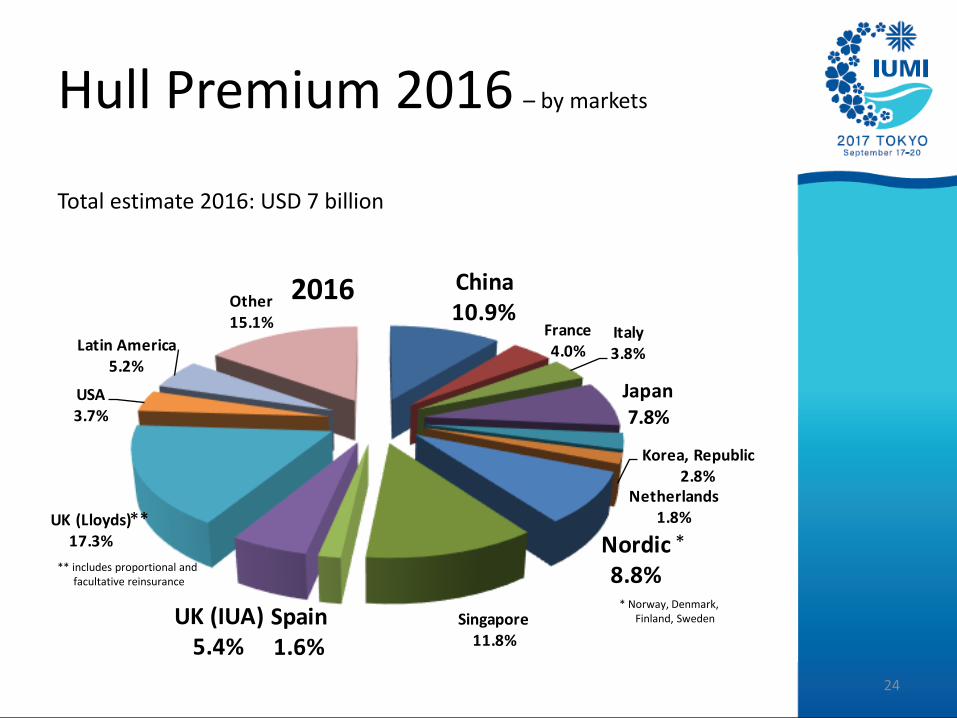

China10.9%

France4.0%

Italy3.8%

Japan

7.8%

Korea, Republic2.8%

Netherlands1.8%

Nordic8.8%

Singapore11.8%

Spain1.6%

UK (IUA)5.4%

UK (Lloyds)17.3%

USA3.7%

Latin America5.2%

Other15.1%

2016

Hull Premium 2016 – by markets

24

Total estimate 2016: USD 7 billion

*

* Norway, Denmark, Finland, Sweden

**

** includes proportional andfacultative reinsurance

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

20

10

20

11

20

12

20

13

20

14

20

15

20

16

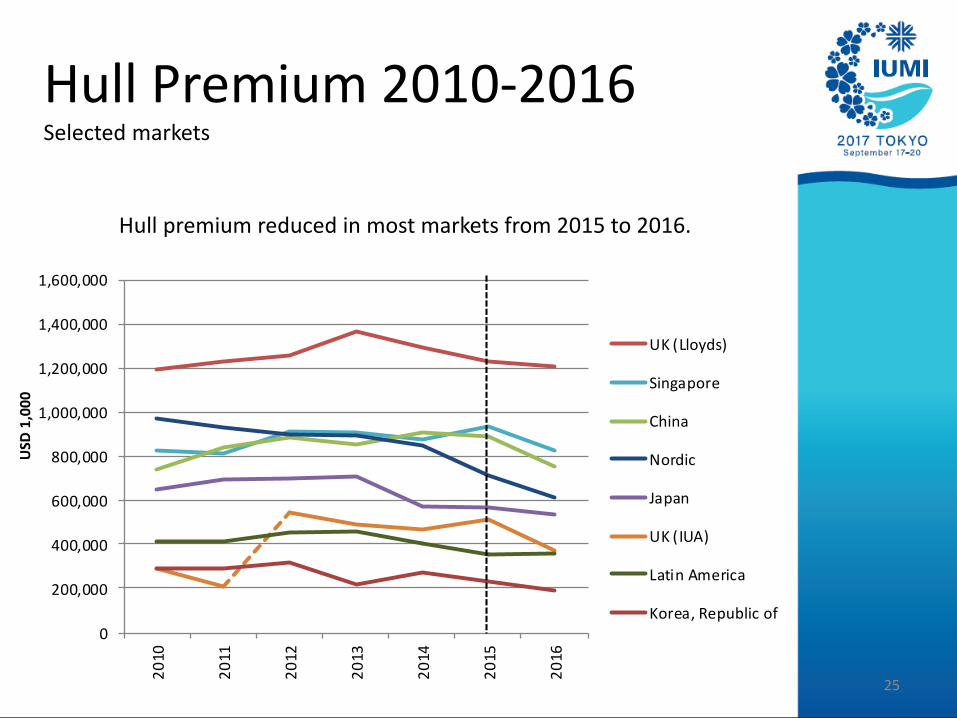

UK (Lloyds)

Singapore

China

Nordic

Japan

UK (IUA)

Latin America

Korea, Republic of

25

Hull Premium 2010-2016Selected markets

Hull premium reduced in most markets from 2015 to 2016.

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

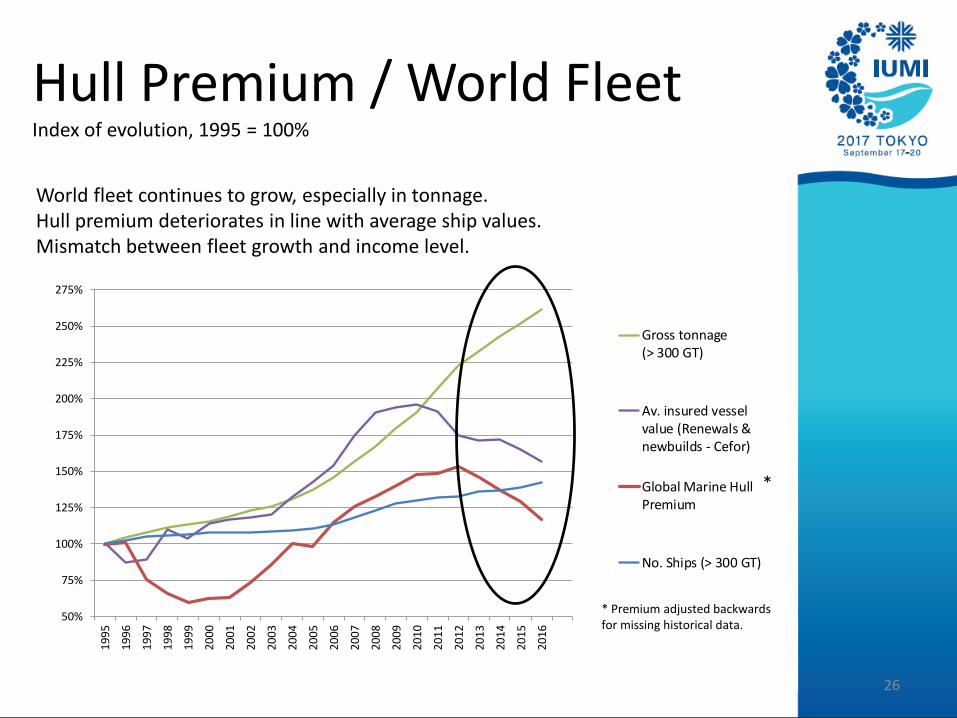

Gross tonnage(> 300 GT)

Av. insured vesselvalue (Renewals &newbuilds - Cefor)

Global Marine HullPremium

No. Ships (> 300 GT)

Hull Premium / World Fleet Index of evolution, 1995 = 100%

World fleet continues to grow, especially in tonnage. Hull premium deteriorates in line with average ship values.Mismatch between fleet growth and income level.

26

*

* Premium adjusted backwards for missing historical data.

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5

2010

2011

2012

2013

2014

2015

2016

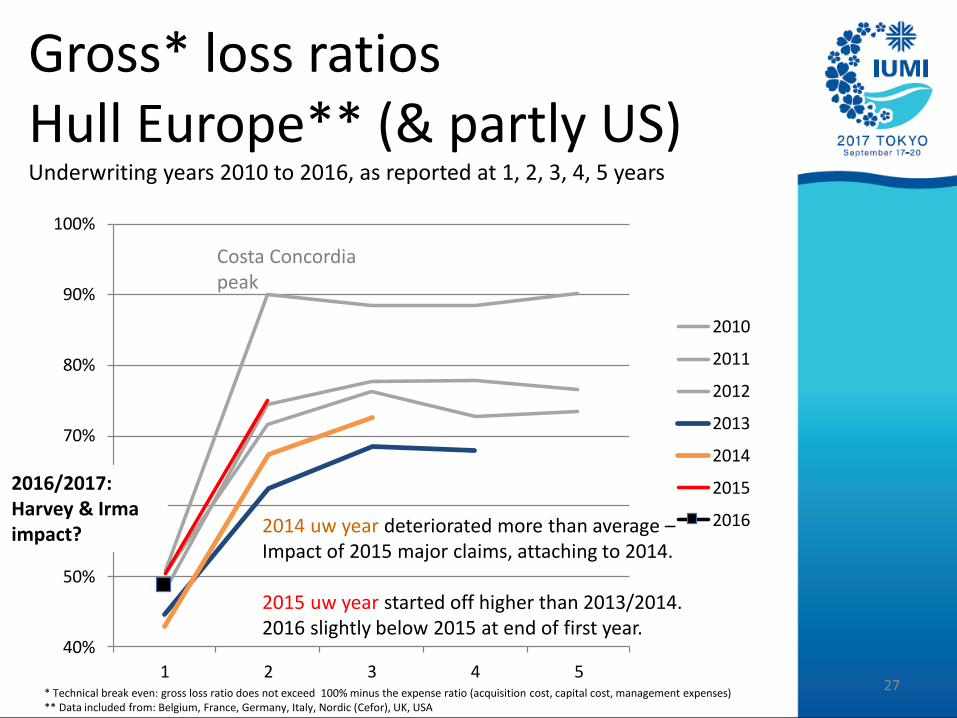

* Technical break even: gross loss ratio does not exceed 100% minus the expense ratio (acquisition cost, capital cost, management expenses)** Data included from: Belgium, France, Germany, Italy, Nordic (Cefor), UK, USA

Costa Concordia peak

27

2014 uw year deteriorated more than average –Impact of 2015 major claims, attaching to 2014.

2015 uw year started off higher than 2013/2014. 2016 slightly below 2015 at end of first year.

Gross* loss ratiosHull Europe** (& partly US)Underwriting years 2010 to 2016, as reported at 1, 2, 3, 4, 5 years

2016/2017: Harvey & Irma impact?

0%

20%

40%

60%

80%

100%

120%

140%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

*Technical break even: gross loss ratio does not exceed 100% minus the expense ratio (acquisition cost, capital cost, management expenses)** Data included from: Belgium, France, Germany, Italy, Nordic (Cefor), Spain (until 2007), UK, USA

28

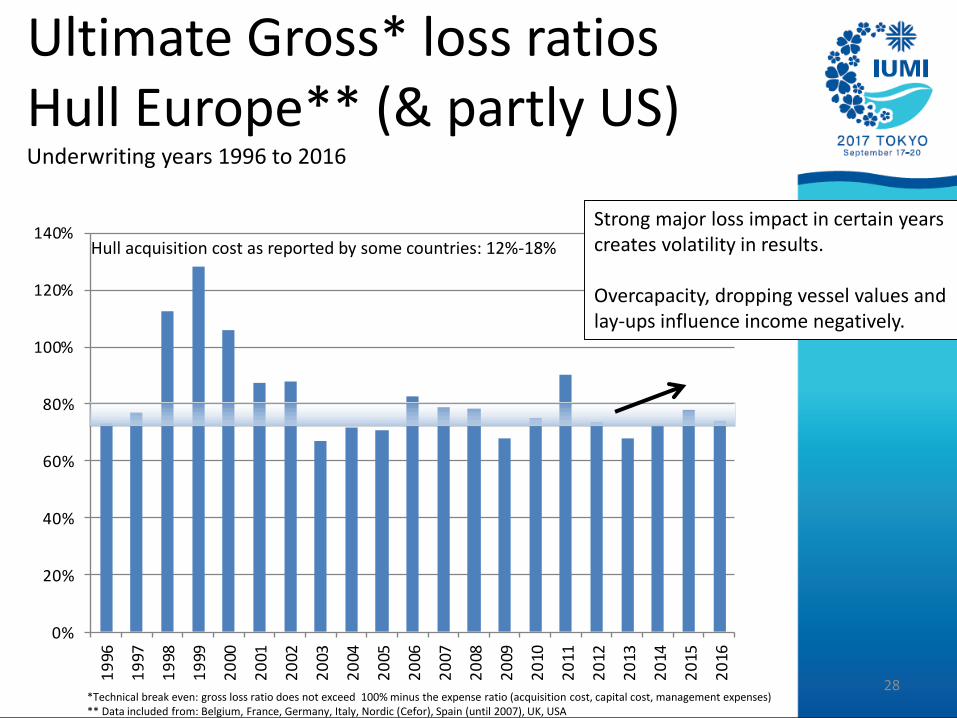

Hull acquisition cost as reported by some countries: 12%-18%

Strong major loss impact in certain yearscreates volatility in results.

Overcapacity, dropping vessel values and lay-ups influence income negatively.

Ultimate Gross* loss ratiosHull Europe** (& partly US)Underwriting years 1996 to 2016

29

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

-

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross premiums Paid claims Loss ratio - paid claims

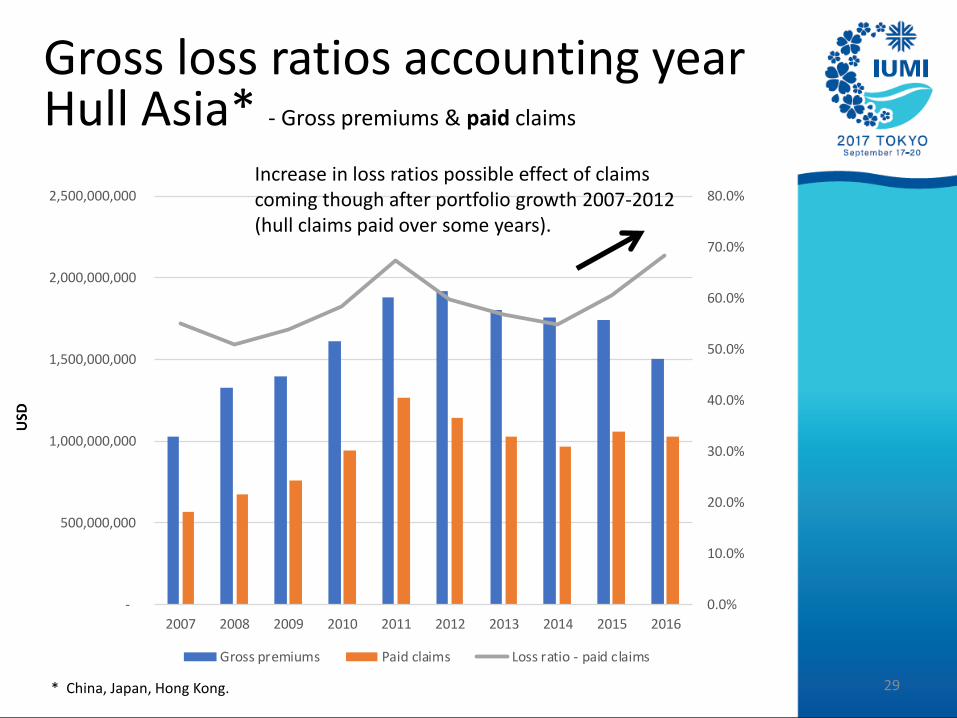

Gross loss ratios accounting yearHull Asia* - Gross premiums & paid claims

* China, Japan, Hong Kong.

Increase in loss ratios possible effect of claims coming though after portfolio growth 2007-2012 (hull claims paid over some years).

30

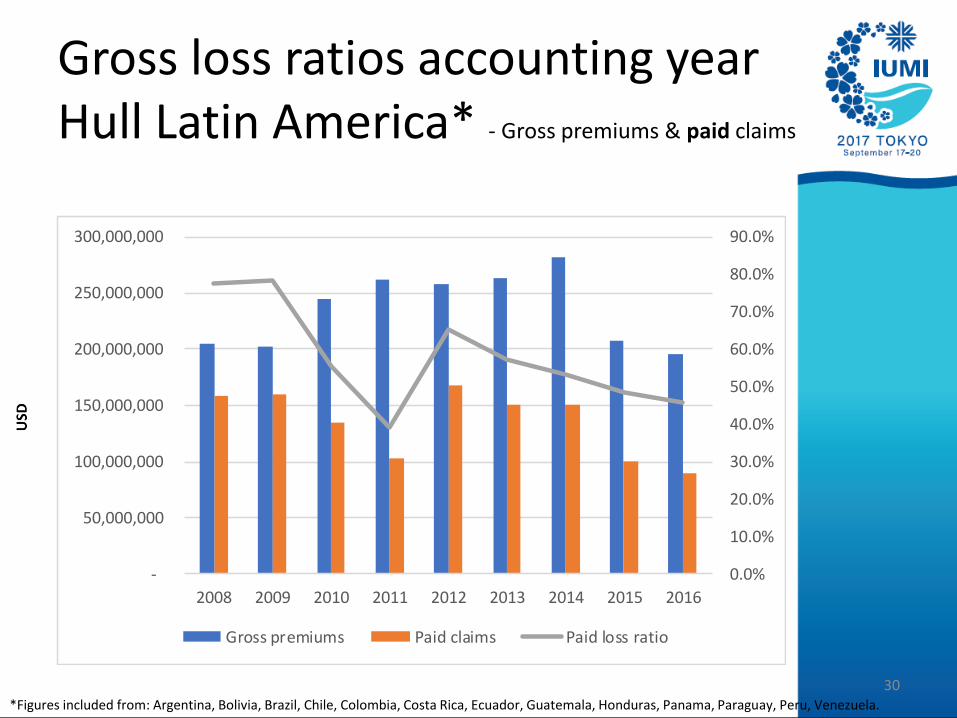

Gross loss ratios accounting yearHull Latin America* - Gross premiums & paid claims

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Gross premiums Paid claims Paid loss ratio

*Figures included from: Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, Ecuador, Guatemala, Honduras, Panama, Paraguay, Peru, Venezuela.

Global Marine Insurance report

• Global Marine Insurance Overview

• Cargo – Market & results

• Hull – Focus:

– Portfolio & Claims trends

– ‘Serious’ versus ‘major’ casualties

• Offshore Energy – Market & results

31

Hull Portfolio trends

32

© Astrid Seltmann

Some reduction expected due to aging of vessels, but from 2015 vessel

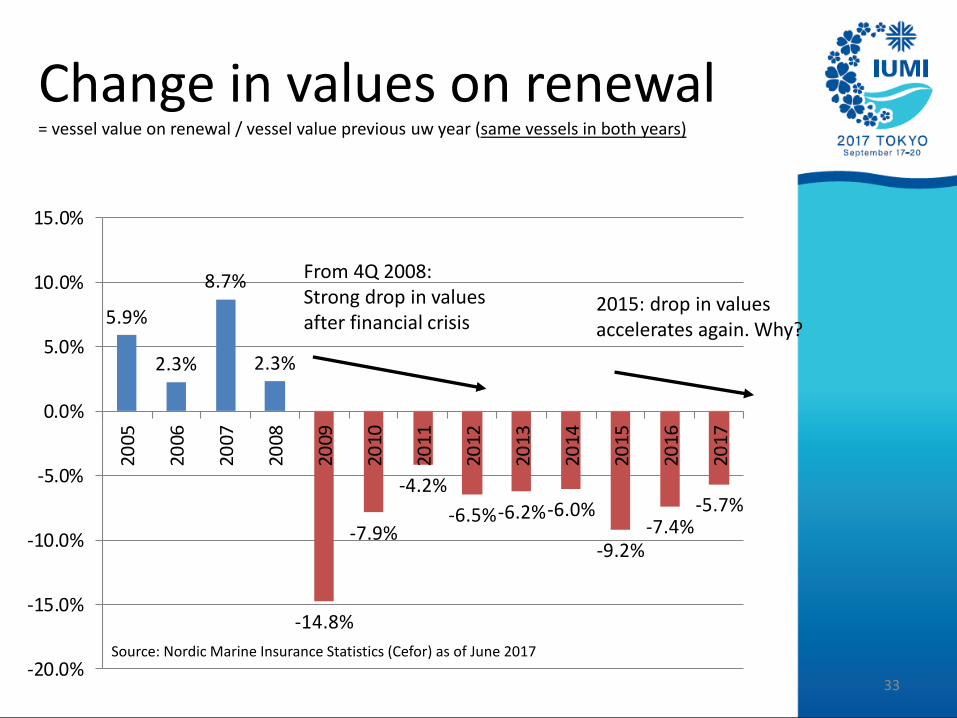

Change in values on renewal = vessel value on renewal / vessel value previous uw year (same vessels in both years)

Financial crisis effect

33

5.9%

2.3%

8.7%

2.3%

-14.8%

-7.9%

-4.2%

-6.5%-6.2%-6.0%

-9.2%-7.4%

-5.7%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Source: Nordic Marine Insurance Statistics (Cefor) as of June 2017

From 4Q 2008:Strong drop in values after financial crisis

2015: drop in values accelerates again. Why?

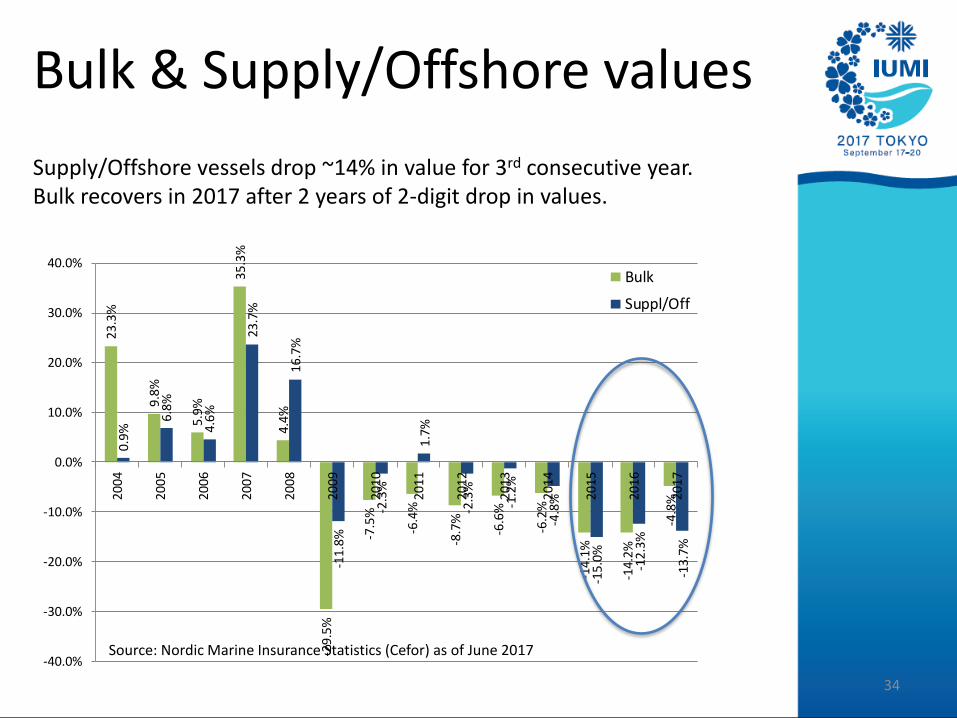

Bulk & Supply/Offshore values23

.3%

9.8%

5.9%

35.3

%

4.4%

-29.

5%

-7.5

%

-6.4

%

-8.7

%

-6.6

%

-6.2

%

-14.

1%

-14.

2%

-4.8

%

0.9

%

6.8%

4.6%

23.7

%

16.7

%

-11.

8%

-2.3

%

1.7%

-2.3

%

-1.2

%

-4.8

%

-15

.0%

-12.

3%

-13.

7%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

2004

20

05

2006

2007

20

08

20

09

2010

2011

20

12

2013

2014

20

15

20

16

2017

Bulk

Suppl/Off

Source: Nordic Marine Insurance Statistics (Cefor) as of June 2017

34

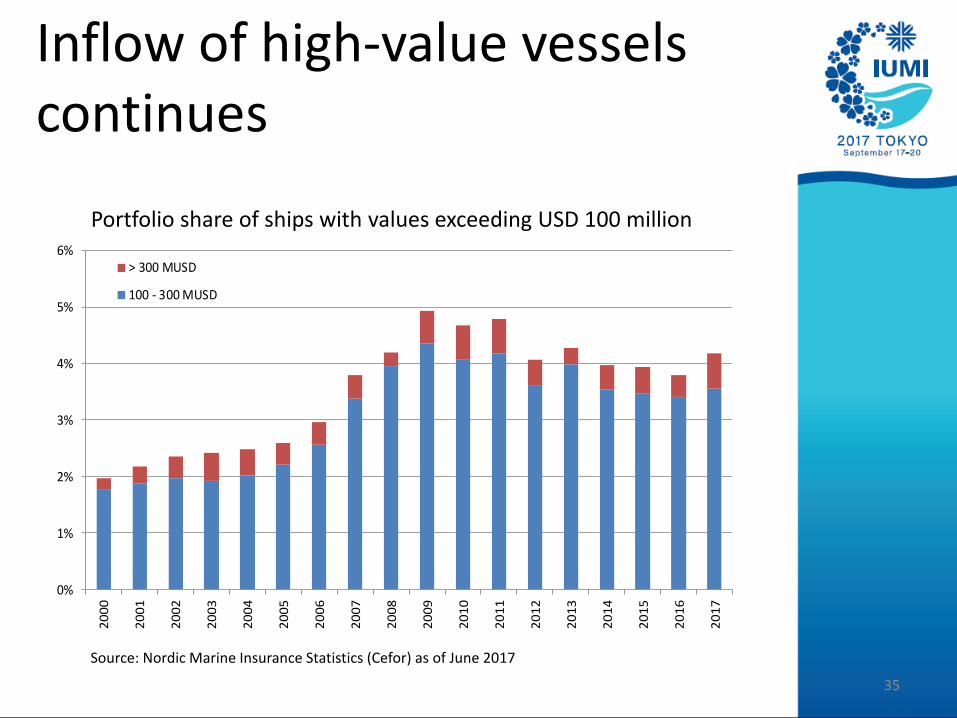

Supply/Offshore vessels drop ~14% in value for 3rd consecutive year.Bulk recovers in 2017 after 2 years of 2-digit drop in values.

0%

1%

2%

3%

4%

5%

6%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

> 300 MUSD

100 - 300 MUSD

Source: Nordic Marine Insurance Statistics (Cefor) as of June 2017

Inflow of high-value vesselscontinues

Portfolio share of ships with values exceeding USD 100 million

35

Hull claims trends

36

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

partial claims <75% SI (left axis) TLO claims >75% SI (right axis)

Source: Nordic Marine Insurance Statistics (Cefor) as of June 2017

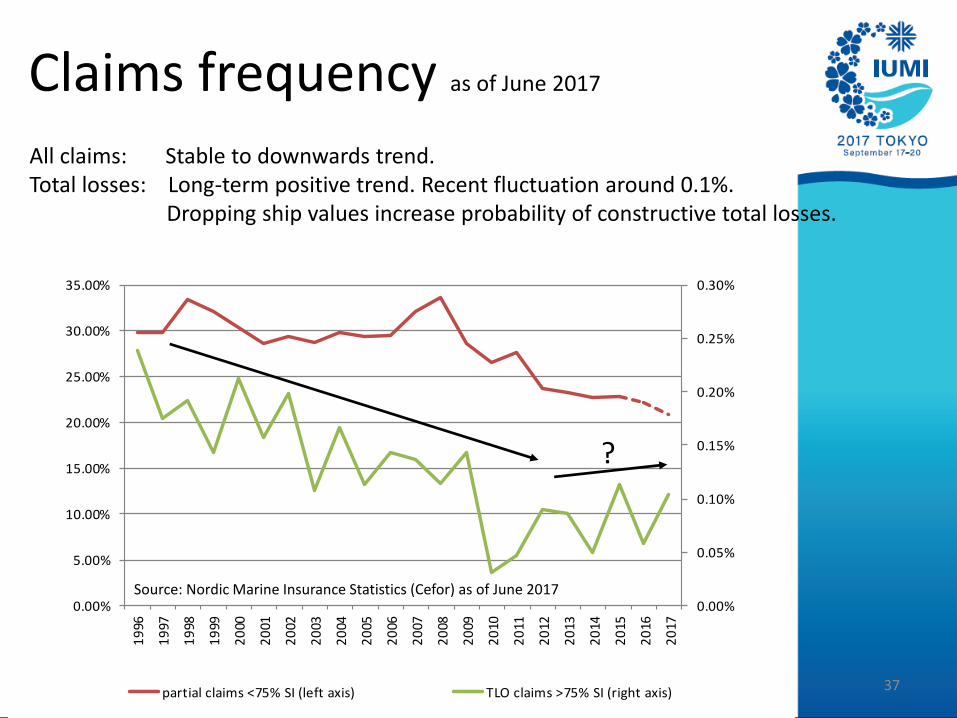

Claims frequency as of June 2017

37

All claims: Stable to downwards trend.Total losses: Long-term positive trend. Recent fluctuation around 0.1%.

Dropping ship values increase probability of constructive total losses.

?

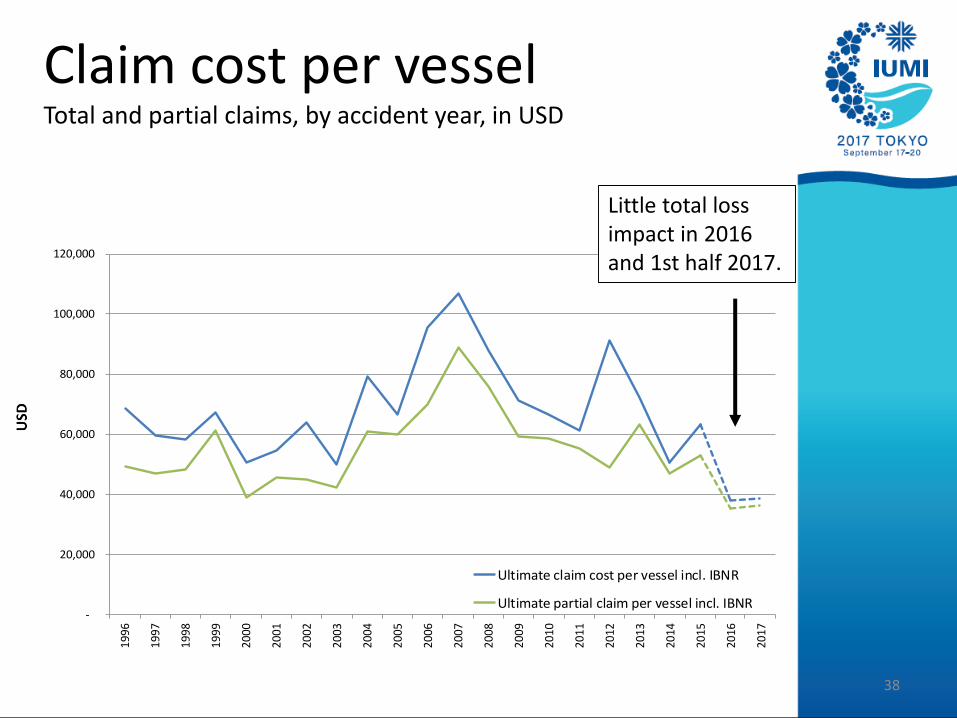

Claim cost per vesselTotal and partial claims, by accident year, in USD

38

-

20,000

40,000

60,000

80,000

100,000

120,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Ultimate claim cost per vessel incl. IBNR

Ultimate partial claim per vessel incl. IBNR

Little total loss impact in 2016 and 1st half 2017.

0

20,000

40,000

60,000

80,000

100,000

120,000

19

961

997

19

981

999

20

002

001

20

022

003

20

042

005

20

062

007

20

082

009

20

102

011

20

122

013

20

142

015

20

162

017

> 50 MUSD

30 <= 50 MUSD

10 <= 30 MUSD

5 <= 10 MUSD

1 <= 5 MUSD

<= 1 MUSD

IBNR

Source: Nordic Marine Insurance Statistics (Cefor) as of June 2017

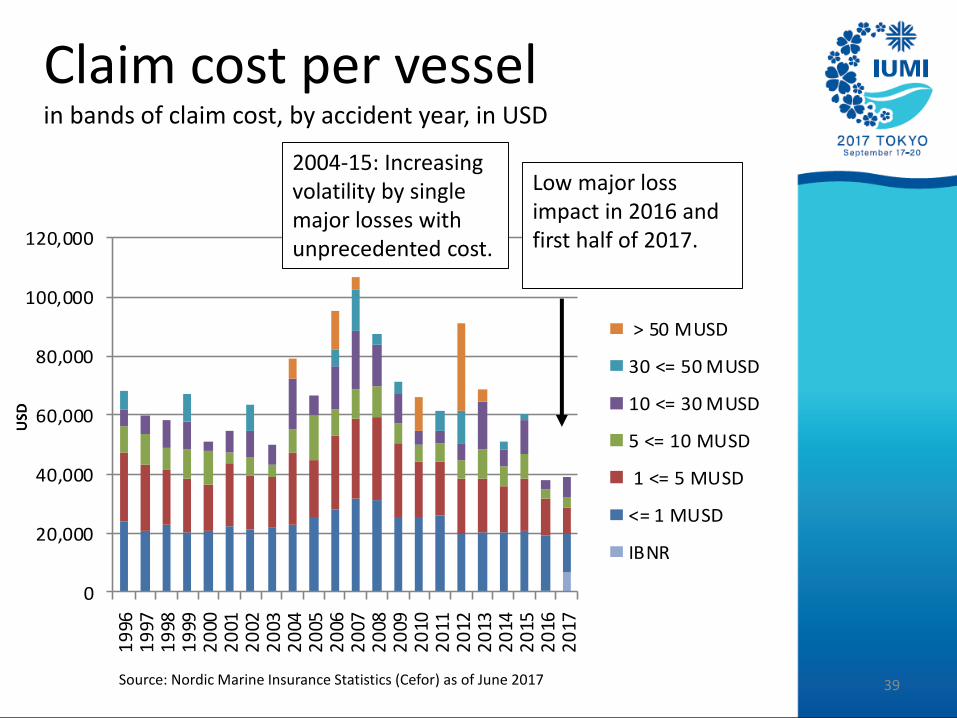

Claim cost per vesselin bands of claim cost, by accident year, in USD

39

Low major loss impact in 2016 and first half of 2017.

2004-15: Increasingvolatility by single major losses withunprecedented cost.

‘Serious’ versus ‘major’ casualtiesAn excursion into terminology

‘Major claims’ (=extraordinary costly claims)strongly impact marine insurers results.

Marine bodies such as IMO and providers of maritime data (LLI, IHS, Clarkson,…) categorize casualties as ‘serious’ / ‘non-serious’*.

‘Serious’ is related to the nature of the event.

Causality:Major losses usually result from serious casualties.But the majority of serious casualties is not costly.

* Complete definitions (IMO, LLI) at end of presentation. 40

41

-

20

40

60

80

100

120

140

160

180

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Non-serious / <= 5 MUSD

Serious / <= 5 MUSD

Serious / > 5 MUSD

Non-serious / > 5 MUSD

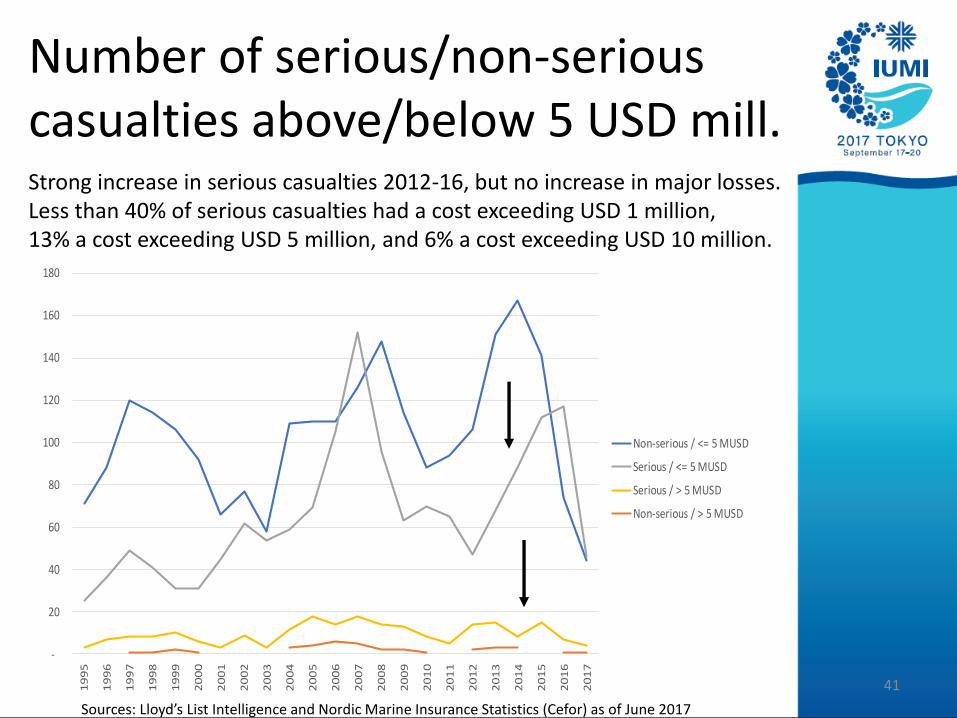

Number of serious/non-serious casualties above/below 5 USD mill.

Sources: Lloyd’s List Intelligence and Nordic Marine Insurance Statistics (Cefor) as of June 2017

Strong increase in serious casualties 2012-16, but no increase in major losses.Less than 40% of serious casualties had a cost exceeding USD 1 million, 13% a cost exceeding USD 5 million, and 6% a cost exceeding USD 10 million.

Hull Key pointsExposure• Values Supply/offshore v. drop ~14% for 3rd year.

Bulk v. show some recovery in 2017. Inflow of high-value vessels continues.

• Premiums deteriorate in line with values (or inactivity), while fleet continues to grow.

• Increasing single-risk exposure.

Claims• Claim cost per vessel: Stable to downward trend.• Total losses: long-term downward trend, but came to a

halt with recent fluctuation around 0.1%.• Major losses: Strong impact in 2015, few in 2016.

Volatility in recent results mainly driven by major losses.

For Sustainability all risk aspects must be taken into account! Current income levels do not cater for major losses. 42

Issues to monitor

High-value risks

Arctic risks

Dagfinn Bakke, Foto by Astrid Seltmann

© Astrid Seltmann

© Astrid Seltmann

Navigation

Oil price, fuel quality

New technology

Climate change

Changes in regulation (liabilities)

Human factor/Qualification

Dagfinn Bakke. Foto by Astrid Seltmann)

Value accumulation

Cyber risk

Fire on RoRo & Container vessels

Internet of things/complex technologies

Global Marine Insurance report

• Global Marine Insurance – Overview

• Cargo – Market & results

• Hull – Market & results

• Offshore Energy – Market & results

44

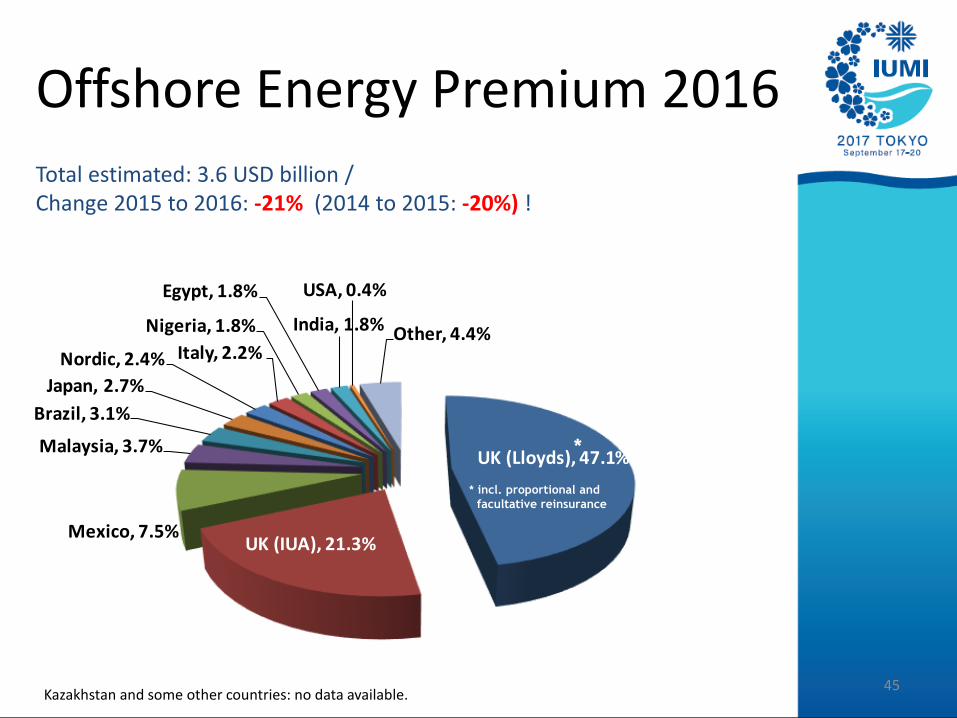

Offshore Energy Premium 2016

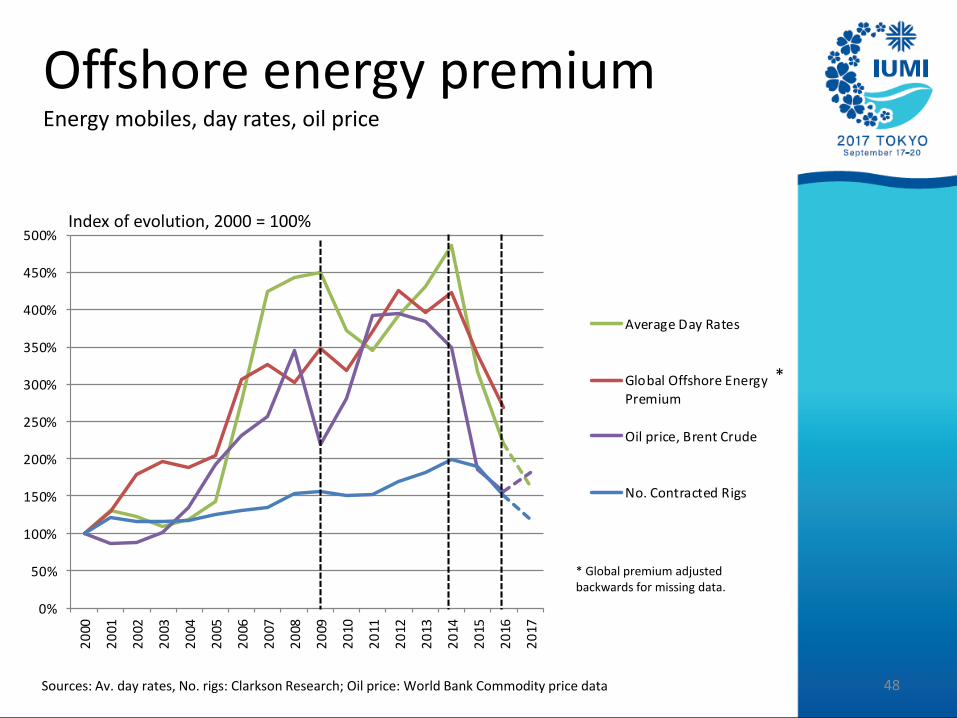

Total estimated: 3.6 USD billion / Change 2015 to 2016: -21% (2014 to 2015: -20%) !

45

UK (Lloyds), 47.1%

UK (IUA), 21.3%Mexico, 7.5%

Malaysia, 3.7%

Brazil, 3.1%

Japan, 2.7%

Nordic, 2.4% Italy, 2.2%

Nigeria, 1.8%

Egypt, 1.8%

India, 1.8%

USA, 0.4%

Other, 4.4%

2016

*

* incl. proportional and

facultative reinsurance

Kazakhstan and some other countries: no data available.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2012

2013

2014

2015

2016

Other

USA

Nordic

Nigeria

Mexico

Malaysia

Japan

Italy

India

Brazil

UK-IUA (2012)

UK-Lloyds

Willis estimatedupstream premium

Offshore Energy Premium 2012 – 2016

Kazakhstan and some other countries: no data available. 46

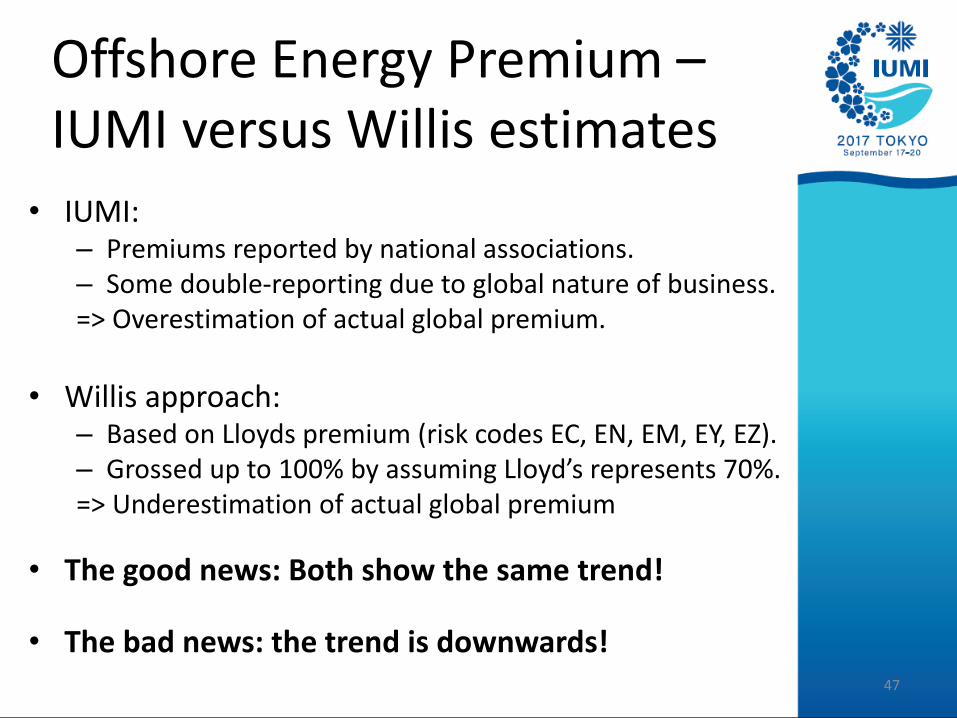

Offshore Energy Premium –IUMI versus Willis estimates

• IUMI:– Premiums reported by national associations.– Some double-reporting due to global nature of business.=> Overestimation of actual global premium.

• Willis approach:– Based on Lloyds premium (risk codes EC, EN, EM, EY, EZ).– Grossed up to 100% by assuming Lloyd’s represents 70%.=> Underestimation of actual global premium

• The good news: Both show the same trend!

• The bad news: the trend is downwards!47

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

500%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Average Day Rates

Global Offshore Energy

Premium

Oil price, Brent Crude

No. Contracted Rigs

Offshore energy premiumEnergy mobiles, day rates, oil price

Index of evolution, 2000 = 100%

Sources: Av. day rates, No. rigs: Clarkson Research; Oil price: World Bank Commodity price data 48

* Global premium adjusted backwards for missing data.

*

0%

50%

100%

150%

200%

250%

300%

350%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

outstanding

paid 10th year

paid 9th year

paid 8th year

paid 7th year

paid 6th year

paid 5th year

paid 4th year

paid 3rd year

paid 2nd year

paid 1st year

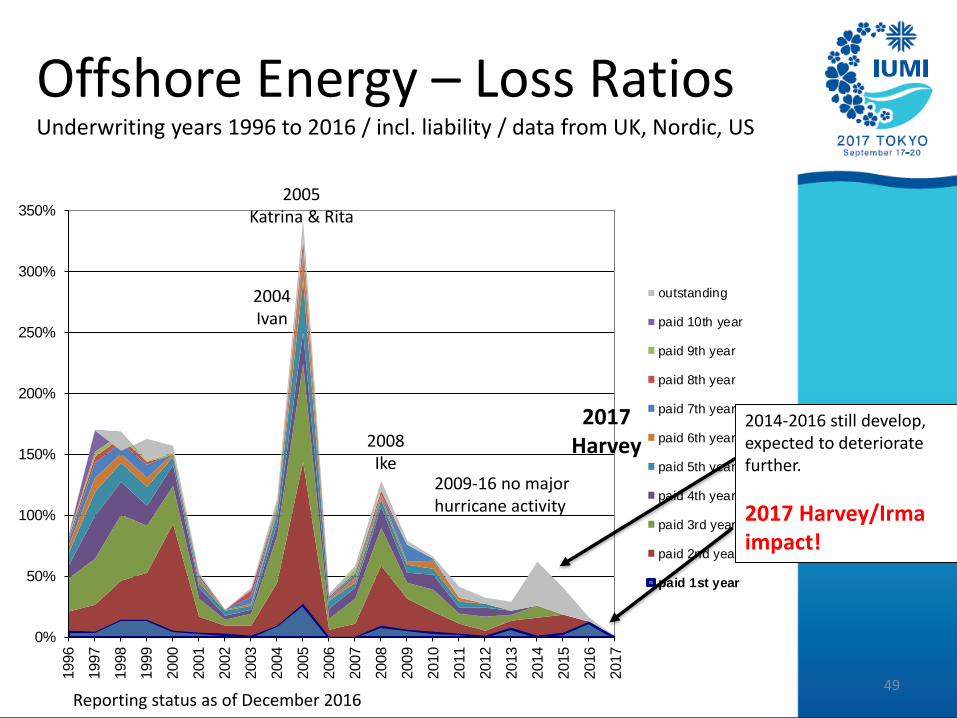

2005Katrina & Rita

2004Ivan

2008Ike

2009-16 no major hurricane activity

Offshore Energy – Loss RatiosUnderwriting years 1996 to 2016 / incl. liability / data from UK, Nordic, US

Reporting status as of December 201649

2014-2016 still develop, expected to deteriorate further.

2017 Harvey/Irma impact!

2017Harvey

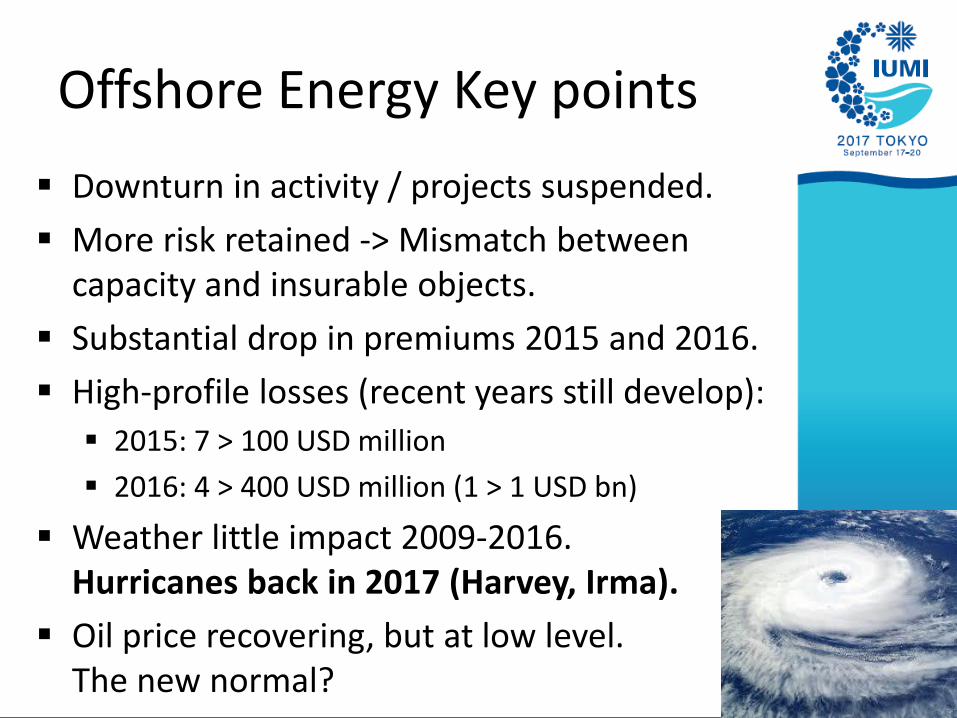

Offshore Energy Key points

▪ Downturn in activity / projects suspended.

▪ More risk retained -> Mismatch betweencapacity and insurable objects.

▪ Substantial drop in premiums 2015 and 2016.

▪ High-profile losses (recent years still develop):

▪ 2015: 7 > 100 USD million

▪ 2016: 4 > 400 USD million (1 > 1 USD bn)

▪ Weather little impact 2009-2016.Hurricanes back in 2017 (Harvey, Irma).

▪ Oil price recovering, but at low level. The new normal? 50

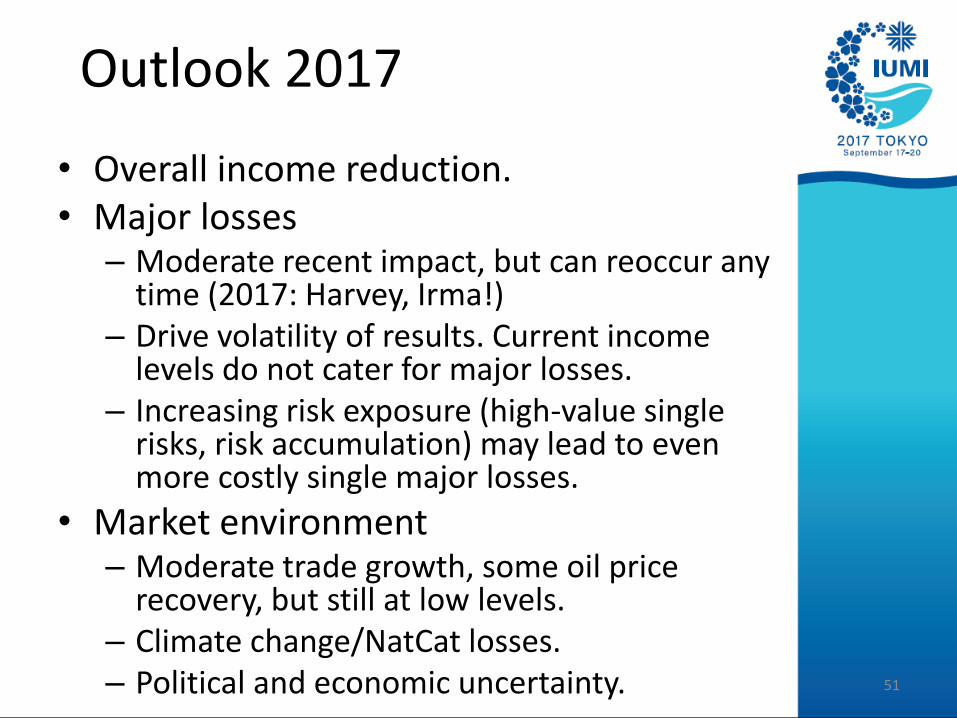

• Overall income reduction. • Major losses

– Moderate recent impact, but can reoccur any time (2017: Harvey, Irma!)

– Drive volatility of results. Current income levels do not cater for major losses.

– Increasing risk exposure (high-value single risks, risk accumulation) may lead to even more costly single major losses.

• Market environment– Moderate trade growth, some oil price

recovery, but still at low levels.– Climate change/NatCat losses. – Political and economic uncertainty. 51

Outlook 2017

52

Astrid SeltmannAnalyst/Actuary

The Nordic Association of Marine Insurers (Cefor)[email protected]

53

Astrid SeltmannAnalyst/Actuary

The Nordic Association of Marine Insurers (Cefor)[email protected]

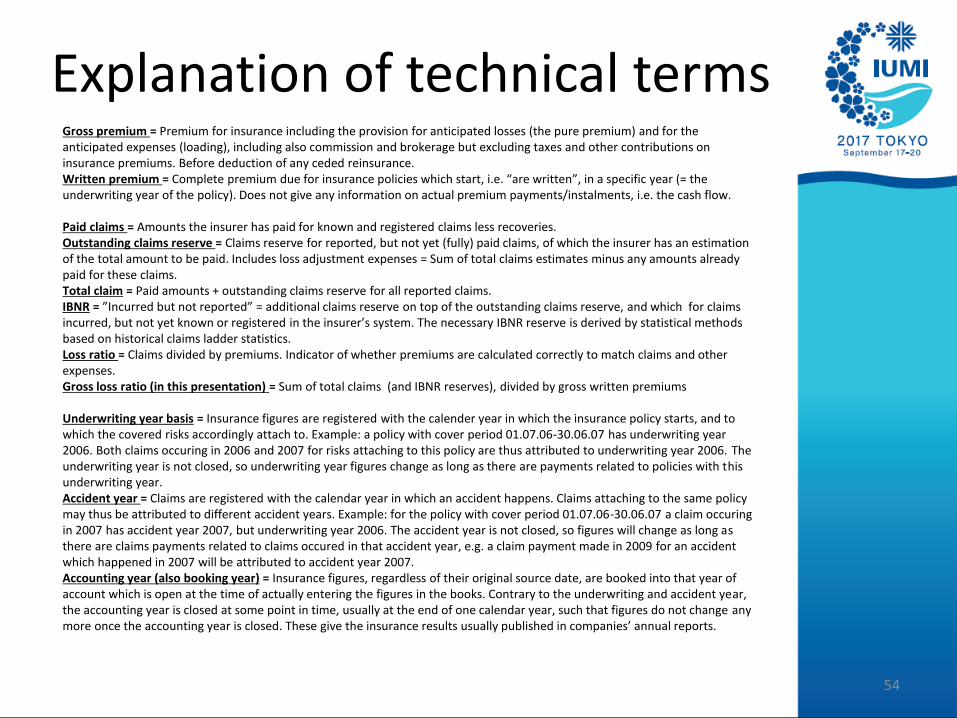

Gross premium = Premium for insurance including the provision for anticipated losses (the pure premium) and for the anticipated expenses (loading), including also commission and brokerage but excluding taxes and other contributions on insurance premiums. Before deduction of any ceded reinsurance.Written premium = Complete premium due for insurance policies which start, i.e. “are written”, in a specific year (= the underwriting year of the policy). Does not give any information on actual premium payments/instalments, i.e. the cash flow.

Paid claims = Amounts the insurer has paid for known and registered claims less recoveries.Outstanding claims reserve = Claims reserve for reported, but not yet (fully) paid claims, of which the insurer has an estimation of the total amount to be paid. Includes loss adjustment expenses = Sum of total claims estimates minus any amounts already paid for these claims. Total claim = Paid amounts + outstanding claims reserve for all reported claims.IBNR = ”Incurred but not reported” = additional claims reserve on top of the outstanding claims reserve, and which for claims incurred, but not yet known or registered in the insurer’s system. The necessary IBNR reserve is derived by statistical methods based on historical claims ladder statistics.Loss ratio = Claims divided by premiums. Indicator of whether premiums are calculated correctly to match claims and other expenses.Gross loss ratio (in this presentation) = Sum of total claims (and IBNR reserves), divided by gross written premiums

Underwriting year basis = Insurance figures are registered with the calender year in which the insurance policy starts, and to which the covered risks accordingly attach to. Example: a policy with cover period 01.07.06-30.06.07 has underwriting year 2006. Both claims occuring in 2006 and 2007 for risks attaching to this policy are thus attributed to underwriting year 2006. The underwriting year is not closed, so underwriting year figures change as long as there are payments related to policies with thisunderwriting year.Accident year = Claims are registered with the calendar year in which an accident happens. Claims attaching to the same policy may thus be attributed to different accident years. Example: for the policy with cover period 01.07.06-30.06.07 a claim occuringin 2007 has accident year 2007, but underwriting year 2006. The accident year is not closed, so figures will change as long as there are claims payments related to claims occured in that accident year, e.g. a claim payment made in 2009 for an accident which happened in 2007 will be attributed to accident year 2007.Accounting year (also booking year) = Insurance figures, regardless of their original source date, are booked into that year of account which is open at the time of actually entering the figures in the books. Contrary to the underwriting and accident year,the accounting year is closed at some point in time, usually at the end of one calendar year, such that figures do not change any more once the accounting year is closed. These give the insurance results usually published in companies’ annual reports.

Explanation of technical terms

54

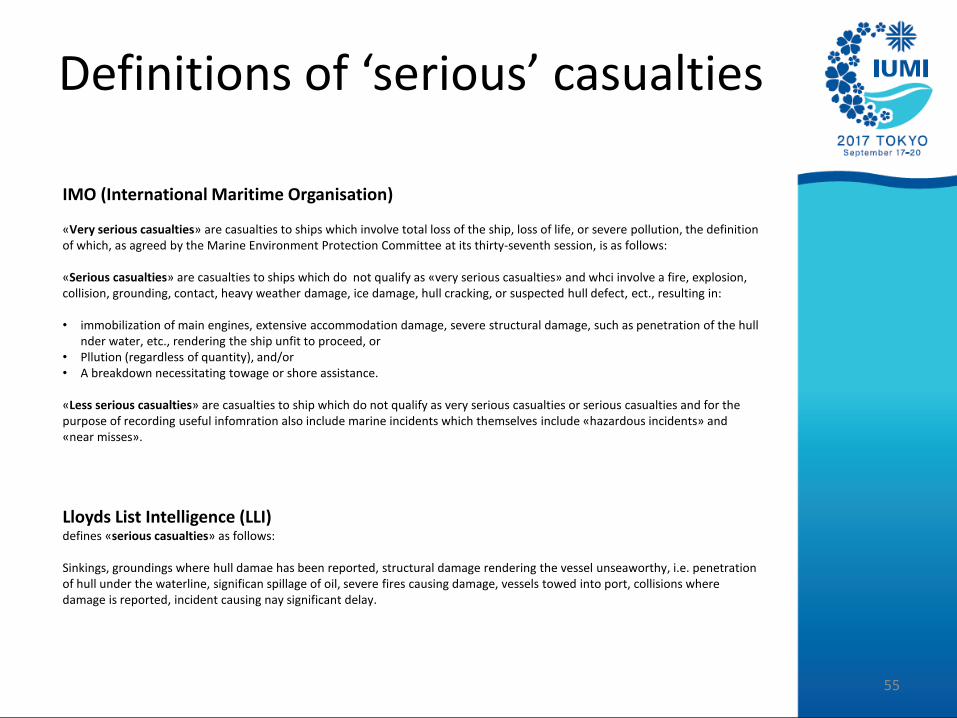

IMO (International Maritime Organisation)

«Very serious casualties» are casualties to ships which involve total loss of the ship, loss of life, or severe pollution, the definitionof which, as agreed by the Marine Environment Protection Committee at its thirty-seventh session, is as follows:

«Serious casualties» are casualties to ships which do not qualify as «very serious casualties» and whci involve a fire, explosion, collision, grounding, contact, heavy weather damage, ice damage, hull cracking, or suspected hull defect, ect., resulting in:

• immobilization of main engines, extensive accommodation damage, severe structural damage, such as penetration of the hull nder water, etc., rendering the ship unfit to proceed, or

• Pllution (regardless of quantity), and/or• A breakdown necessitating towage or shore assistance.

«Less serious casualties» are casualties to ship which do not qualify as very serious casualties or serious casualties and for thepurpose of recording useful infomration also include marine incidents which themselves include «hazardous incidents» and «near misses».

Lloyds List Intelligence (LLI) defines «serious casualties» as follows:

Sinkings, groundings where hull damae has been reported, structural damage rendering the vessel unseaworthy, i.e. penetrationof hull under the waterline, significan spillage of oil, severe fires causing damage, vessels towed into port, collisions wheredamage is reported, incident causing nay significant delay.

Definitions of ‘serious’ casualties

55