1 Insurance Claim

10

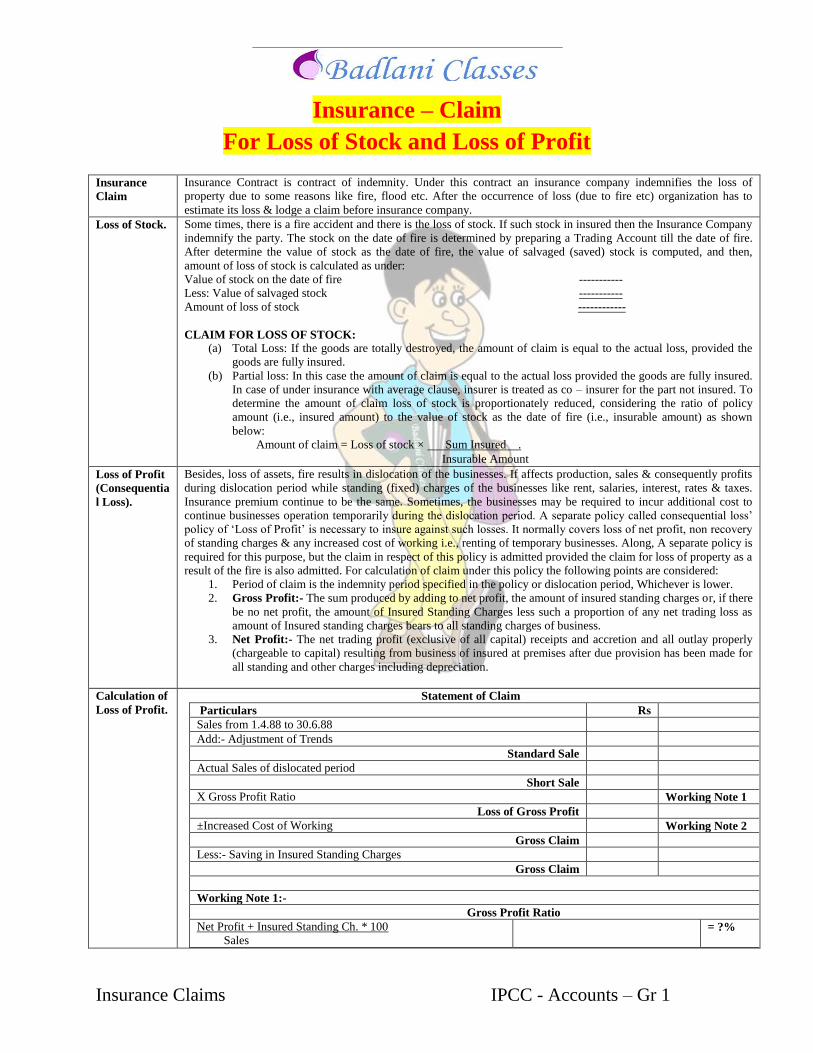

Insurance Claims IPCC - Accounts – Gr 1 Insurance – Claim For Loss of Stock and Loss of Profit Insurance Claim Insurance Contract is contract of indemnity. Under this contract an insurance company indemnifies the loss of property due to some reasons like fire, flood etc. After the occurrence of loss (due to fire etc) organization has to estimate its loss & lodge a claim before insurance company. Loss of Stock. Some times, there is a fire accident and there is the loss of stock. If such stock in insured then the Insurance Company indemnify the party. The stock on the date of fire is determined by preparing a Trading Account till the date of fire. After determine the value of stock as the date of fire, the value of salvaged (saved) stock is computed, and then, amount of loss of stock is calculated as under: Value of stock on the date of fire ----------- Less: Value of salvaged stock ----------- Amount of loss of stock ------------ CLAIM FOR LOSS OF STOCK: (a) Total Loss: If the goods are totally destroyed, the amount of claim is equal to the actual loss, provided the goods are fully insured. (b) Partial loss: In this case the amount of claim is equal to the actual loss provided the goods are fully insured. In case of under insurance with average clause, insurer is treated as co – insurer for the part not insured. To determine the amount of claim loss of stock is proportionately reduced, considering the ratio of policy amount (i.e., insured amount) to the value of stock as the date of fire (i.e., insurable amount) as shown below: Amount of claim = Loss of stock × Sum Insured . Insurable Amount Loss of Profit (Consequentia l Loss). Besides, loss of assets, fire results in dislocation of the businesses. If affects production, sales & consequently profits during dislocation period while standing (fixed) charges of the businesses like rent, salaries, interest, rates & taxes. Insurance premium continue to be the same. Sometimes, the businesses may be required to incur additional cost to continue businesses operation temporarily during the dislocation period. A separate policy called consequential loss‟ policy of „Loss of Profit‟ is necessary to insure against such losses. It normally covers loss of net profit, non recovery of standing charges & any increased cost of working i.e., renting of temporary businesses. Along, A separate policy is required for this purpose, but the claim in respect of this policy is admitted provided the claim for loss of property as a result of the fire is also admitted. For calculation of claim under this policy the following points are considered: 1. Period of claim is the indemnity period specified in the policy or dislocation period, Whichever is lower. 2. Gross Profit:- The sum produced by adding to net profit, the amount of insured standing charges or, if there be no net profit, the amount of Insured Standing Charges less such a proportion of any net trading loss as amount of Insured standing charges bears to all standing charges of business. 3. Net Profit:- The net trading profit (exclusive of all capital) receipts and accretion and all outlay properly (chargeable to capital) resulting from business of insured at premises after due provision has been made for all standing and other charges including depreciation. Calculation of Loss of Profit. Statement of Claim Particulars Rs Sales from 1.4.88 to 30.6.88 Add:- Adjustment of Trends Standard Sale Actual Sales of dislocated period Short Sale X Gross Profit Ratio Working Note 1 Loss of Gross Profit ±Increased Cost of Working Working Note 2 Gross Claim Less:- Saving in Insured Standing Charges Gross Claim Working Note 1:- Gross Profit Ratio Net Profit + Insured Standing Ch. * 100 Sales = ?%

-

Upload

badlanionline -

Category

Documents

-

view

0 -

download

0

Transcript of 1 Insurance Claim

Insurance Claims IPCC - Accounts – Gr 1

Insurance – Claim

For Loss of Stock and Loss of Profit

Insurance

Claim

Insurance Contract is contract of indemnity. Under this contract an insurance company indemnifies the loss of

property due to some reasons like fire, flood etc. After the occurrence of loss (due to fire etc) organization has to

estimate its loss & lodge a claim before insurance company.

Loss of Stock. Some times, there is a fire accident and there is the loss of stock. If such stock in insured then the Insurance Company

indemnify the party. The stock on the date of fire is determined by preparing a Trading Account till the date of fire.

After determine the value of stock as the date of fire, the value of salvaged (saved) stock is computed, and then,

amount of loss of stock is calculated as under:

Value of stock on the date of fire -----------

Less: Value of salvaged stock -----------

Amount of loss of stock ------------

CLAIM FOR LOSS OF STOCK:

(a) Total Loss: If the goods are totally destroyed, the amount of claim is equal to the actual loss, provided the

goods are fully insured.

(b) Partial loss: In this case the amount of claim is equal to the actual loss provided the goods are fully insured.

In case of under insurance with average clause, insurer is treated as co – insurer for the part not insured. To

determine the amount of claim loss of stock is proportionately reduced, considering the ratio of policy

amount (i.e., insured amount) to the value of stock as the date of fire (i.e., insurable amount) as shown

below:

Amount of claim = Loss of stock × Sum Insured .

Insurable Amount

Loss of Profit

(Consequentia

l Loss).

Besides, loss of assets, fire results in dislocation of the businesses. If affects production, sales & consequently profits

during dislocation period while standing (fixed) charges of the businesses like rent, salaries, interest, rates & taxes.

Insurance premium continue to be the same. Sometimes, the businesses may be required to incur additional cost to

continue businesses operation temporarily during the dislocation period. A separate policy called consequential loss‟

policy of „Loss of Profit‟ is necessary to insure against such losses. It normally covers loss of net profit, non recovery

of standing charges & any increased cost of working i.e., renting of temporary businesses. Along, A separate policy is

required for this purpose, but the claim in respect of this policy is admitted provided the claim for loss of property as a

result of the fire is also admitted. For calculation of claim under this policy the following points are considered:

1. Period of claim is the indemnity period specified in the policy or dislocation period, Whichever is lower.

2. Gross Profit:- The sum produced by adding to net profit, the amount of insured standing charges or, if there

be no net profit, the amount of Insured Standing Charges less such a proportion of any net trading loss as

amount of Insured standing charges bears to all standing charges of business.

3. Net Profit:- The net trading profit (exclusive of all capital) receipts and accretion and all outlay properly

(chargeable to capital) resulting from business of insured at premises after due provision has been made for

all standing and other charges including depreciation.

Calculation of

Loss of Profit.

Statement of Claim

Particulars Rs

Sales from 1.4.88 to 30.6.88

Add:- Adjustment of Trends

Standard Sale

Actual Sales of dislocated period

Short Sale

X Gross Profit Ratio Working Note 1

Loss of Gross Profit

±Increased Cost of Working Working Note 2

Gross Claim

Less:- Saving in Insured Standing Charges

Gross Claim

Working Note 1:-

Gross Profit Ratio

Net Profit + Insured Standing Ch. * 100

Sales

= ?%

Insurance Claims IPCC - Accounts – Gr 1

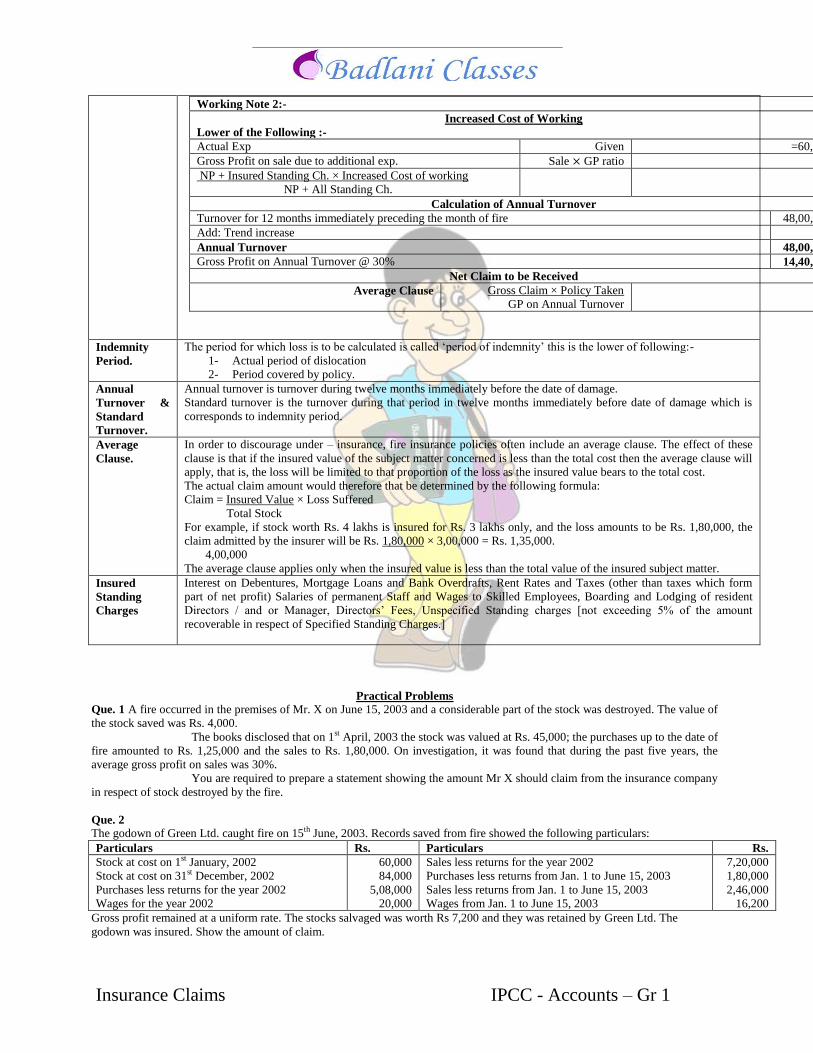

Working Note 2:-

Increased Cost of Working

Lower of the Following :-

Actual Exp Given =60,000

Gross Profit on sale due to additional exp. Sale × GP ratio

NP + Insured Standing Ch. × Increased Cost of working

NP + All Standing Ch.

Calculation of Annual Turnover

Turnover for 12 months immediately preceding the month of fire 48,00,000

Add: Trend increase Nil

Annual Turnover 48,00,000

Gross Profit on Annual Turnover @ 30% 14,40,000

Net Claim to be Received

Average Clause Gross Claim × Policy Taken

GP on Annual Turnover

Indemnity

Period.

The period for which loss is to be calculated is called „period of indemnity‟ this is the lower of following:-

1- Actual period of dislocation

2- Period covered by policy.

Annual

Turnover &

Standard

Turnover.

Annual turnover is turnover during twelve months immediately before the date of damage.

Standard turnover is the turnover during that period in twelve months immediately before date of damage which is

corresponds to indemnity period.

Average

Clause.

In order to discourage under – insurance, fire insurance policies often include an average clause. The effect of these

clause is that if the insured value of the subject matter concerned is less than the total cost then the average clause will

apply, that is, the loss will be limited to that proportion of the loss as the insured value bears to the total cost.

The actual claim amount would therefore that be determined by the following formula:

Claim = Insured Value × Loss Suffered

Total Stock

For example, if stock worth Rs. 4 lakhs is insured for Rs. 3 lakhs only, and the loss amounts to be Rs. 1,80,000, the

claim admitted by the insurer will be Rs. 1,80,000 × 3,00,000 = Rs. 1,35,000.

4,00,000

The average clause applies only when the insured value is less than the total value of the insured subject matter.

Insured

Standing

Charges

Interest on Debentures, Mortgage Loans and Bank Overdrafts, Rent Rates and Taxes (other than taxes which form

part of net profit) Salaries of permanent Staff and Wages to Skilled Employees, Boarding and Lodging of resident

Directors / and or Manager, Directors‟ Fees, Unspecified Standing charges [not exceeding 5% of the amount

recoverable in respect of Specified Standing Charges.]

Practical Problems

Que. 1 A fire occurred in the premises of Mr. X on June 15, 2003 and a considerable part of the stock was destroyed. The value of

the stock saved was Rs. 4,000.

The books disclosed that on 1st April, 2003 the stock was valued at Rs. 45,000; the purchases up to the date of

fire amounted to Rs. 1,25,000 and the sales to Rs. 1,80,000. On investigation, it was found that during the past five years, the

average gross profit on sales was 30%.

You are required to prepare a statement showing the amount Mr X should claim from the insurance company

in respect of stock destroyed by the fire.

Que. 2

The godown of Green Ltd. caught fire on 15th June, 2003. Records saved from fire showed the following particulars:

Particulars Rs. Particulars Rs.

Stock at cost on 1st January, 2002

Stock at cost on 31st December, 2002

Purchases less returns for the year 2002

Wages for the year 2002

60,000

84,000

5,08,000

20,000

Sales less returns for the year 2002

Purchases less returns from Jan. 1 to June 15, 2003

Sales less returns from Jan. 1 to June 15, 2003

Wages from Jan. 1 to June 15, 2003

7,20,000

1,80,000

2,46,000

16,200

Gross profit remained at a uniform rate. The stocks salvaged was worth Rs 7,200 and they was retained by Green Ltd. The

godown was insured. Show the amount of claim.

Insurance Claims IPCC - Accounts – Gr 1

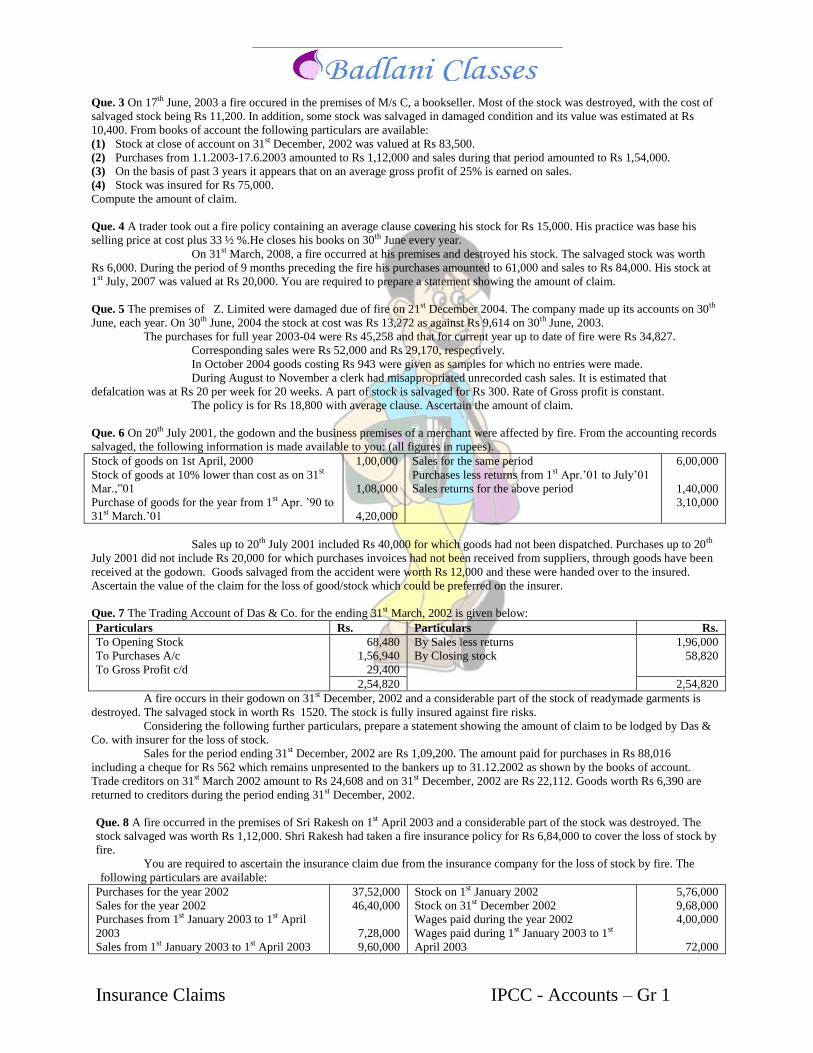

Que. 3 On 17th June, 2003 a fire occured in the premises of M/s C, a bookseller. Most of the stock was destroyed, with the cost of

salvaged stock being Rs 11,200. In addition, some stock was salvaged in damaged condition and its value was estimated at Rs

10,400. From books of account the following particulars are available:

(1) Stock at close of account on 31st December, 2002 was valued at Rs 83,500.

(2) Purchases from 1.1.2003-17.6.2003 amounted to Rs 1,12,000 and sales during that period amounted to Rs 1,54,000.

(3) On the basis of past 3 years it appears that on an average gross profit of 25% is earned on sales.

(4) Stock was insured for Rs 75,000.

Compute the amount of claim.

Que. 4 A trader took out a fire policy containing an average clause covering his stock for Rs 15,000. His practice was base his

selling price at cost plus 33 ½ %.He closes his books on 30th June every year.

On 31st March, 2008, a fire occurred at his premises and destroyed his stock. The salvaged stock was worth

Rs 6,000. During the period of 9 months preceding the fire his purchases amounted to 61,000 and sales to Rs 84,000. His stock at

1st July, 2007 was valued at Rs 20,000. You are required to prepare a statement showing the amount of claim.

Que. 5 The premises of Z. Limited were damaged due of fire on 21st December 2004. The company made up its accounts on 30th

June, each year. On 30th June, 2004 the stock at cost was Rs 13,272 as against Rs 9,614 on 30th June, 2003.

The purchases for full year 2003-04 were Rs 45,258 and that for current year up to date of fire were Rs 34,827.

Corresponding sales were Rs 52,000 and Rs 29,170, respectively.

In October 2004 goods costing Rs 943 were given as samples for which no entries were made.

During August to November a clerk had misappropriated unrecorded cash sales. It is estimated that

defalcation was at Rs 20 per week for 20 weeks. A part of stock is salvaged for Rs 300. Rate of Gross profit is constant.

The policy is for Rs 18,800 with average clause. Ascertain the amount of claim.

Que. 6 On 20th July 2001, the godown and the business premises of a merchant were affected by fire. From the accounting records

salvaged, the following information is made available to you: (all figures in rupees).

Stock of goods on 1st April, 2000

Stock of goods at 10% lower than cost as on 31st

Mar.,”01

Purchase of goods for the year from 1st Apr. ‟90 to

31st March.‟01

1,00,000

1,08,000

4,20,000

Sales for the same period

Purchases less returns from 1st Apr.‟01 to July‟01

Sales returns for the above period

6,00,000

1,40,000

3,10,000

Sales up to 20th July 2001 included Rs 40,000 for which goods had not been dispatched. Purchases up to 20th

July 2001 did not include Rs 20,000 for which purchases invoices had not been received from suppliers, through goods have been

received at the godown. Goods salvaged from the accident were worth Rs 12,000 and these were handed over to the insured.

Ascertain the value of the claim for the loss of good/stock which could be preferred on the insurer.

Que. 7 The Trading Account of Das & Co. for the ending 31st March, 2002 is given below:

Particulars Rs. Particulars Rs.

To Opening Stock

To Purchases A/c

To Gross Profit c/d

68,480

1,56,940

29,400

By Sales less returns

By Closing stock

1,96,000

58,820

2,54,820 2,54,820

A fire occurs in their godown on 31st December, 2002 and a considerable part of the stock of readymade garments is

destroyed. The salvaged stock in worth Rs 1520. The stock is fully insured against fire risks.

Considering the following further particulars, prepare a statement showing the amount of claim to be lodged by Das &

Co. with insurer for the loss of stock.

Sales for the period ending 31st December, 2002 are Rs 1,09,200. The amount paid for purchases in Rs 88,016

including a cheque for Rs 562 which remains unpresented to the bankers up to 31.12.2002 as shown by the books of account.

Trade creditors on 31st March 2002 amount to Rs 24,608 and on 31st December, 2002 are Rs 22,112. Goods worth Rs 6,390 are

returned to creditors during the period ending 31st December, 2002.

Que. 8 A fire occurred in the premises of Sri Rakesh on 1st April 2003 and a considerable part of the stock was destroyed. The

stock salvaged was worth Rs 1,12,000. Shri Rakesh had taken a fire insurance policy for Rs 6,84,000 to cover the loss of stock by

fire.

You are required to ascertain the insurance claim due from the insurance company for the loss of stock by fire. The

following particulars are available:

Purchases for the year 2002

Sales for the year 2002

Purchases from 1st January 2003 to 1st April

2003

Sales from 1st January 2003 to 1st April 2003

37,52,000

46,40,000

7,28,000

9,60,000

Stock on 1st January 2002

Stock on 31st December 2002

Wages paid during the year 2002

Wages paid during 1st January 2003 to 1st

April 2003

5,76,000

9,68,000

4,00,000

72,000

Insurance Claims IPCC - Accounts – Gr 1

Shri Rakesh had in June 2002 consigned goods worth Rs 2,00,000 which were lost in an accident. As there was no

insurance the loss was borne by him in full. Stocks at end of each year for and till the end of calendar year 2001 had been valued

at cost less 10%. From 2002 however, there was a change in the valuation of closing stock which was ascertained by adding

10% to its cost.

Que. 9 A fire occurred on 1st October, 2001 in the premises of Amit Co. Ltd. From the following figures, calculate the amount

for claim to be lodged with the insurance company for loss of stock:

Stock at cost on 1.1.2000

Stock at cost on 1.1.2001

Purchases during 2000

90,000

70,000

4,00,000

Purchases from 1.1.2001 to 30.9.2001

Sales during 2000

Sales from 1.1.2001 to 30.9.2001

6,00,000

6,00,000

8,80,000

You are informed that: (a) In 2001 the cost of purchases has risen by 20% over the levels prevailing in 2000; (b) In

2001 the selling prices have gone up by 10% over the levels prevailing in 2000; and (c) Salvaged value is Rs 5,000.

Que. 10 On 1st April 2008, the godown of India Ltd. was destroyed by fire. From the books of account, the following particulars

are gathered: (all figures in rupees)

Stock at cost on 1st January 2007

Stock as per Balance Sheet at 31st December 2007

Purchases during 2007

Purchases from 1st January 2008 to 31st March 2008

27,570

51,120

2,71,350

75,000

Sales during 2007

Sales from 1st January 2008 to 31st March 2008

Value of goods salvaged

3,51,000

91,500

6,300

Goods of which original cost was Rs 3,600 had been valued at Rs 1,500 on 31st December 2007. These were sold in

March 2008 for Rs 2,700. Except this transaction, the rate of gross profit has remained constant.

On 31st March 2008 goods worth Rs 15,000 had been received by the godown keeper, but had not been entered in the

purchase Account. Calculate the value of goods destroyed by fire.

Que. 11 On 15th June 2009, the business house of Monica & Co. was destroyed by fire. The following particulars are given to

you;

Stock at cost 1st January 2008

Stock at cost 31st December 2008

Purchases less returns year ended 31.12.2008

4,41,000

4,77,600

23,88,000

Sales less returns year ended 31.12.2008

Purchases less returns Jan. 1-15th June 2009

Sales less returns Jan 1-15th June 2009

29,22,000

9,72,000

13,87,200

In valuing stock for Balance Sheet at 31.12.2008, Rs 13,800 had been written-off on certain stock which was a poor selling line,

having cost Rs 41,400. A portion of these goods was sold in March 2009 at a loss of Rs 1,500 on the original cost of Rs 20,700.

The remainder of this stock is now estimated to be worth the original cost. Subject to the above exception, Gross profit remained

at a uniform rate throughout. The stock salvaged from fire was valued at Rs 34,800. You are to ascertain the amount of claim to be

placed.

Que. 12 On 1st April 2009, the stock of Shri Dheeraj was destroyed by fire but sufficient records were saved from which

following particulars were ascertained: (all figures in rupees)

Stock at cost 1st January 2008

Stock at cost 31st December 2008

Purchases for the year ended 31.12.2008

73,500

79,600

3,98,000

Sales for the year ended 31.12.2008

Purchases from Jan. 1 to March 31 2009

Sales less returns Jan 1 to March 31 2009

4,87,000

1,62,000

2,31,200

In valuing the stock for the Balance Sheet at 31st December 2008, Rs 2,300 had been written-off on certain stock which

was a poor selling line having cost Rs 6,900. A portion of these goods was sold in March 2009 at a loss of Rs 250 on the original

cost of Rs 3,450. The remainder of this stock is now estimated to be worth its original cost. Subject to the above exception, gross

profit had remained at a uniform rate throughout the year.

The value of stock salvaged was Rs 5,800. The insurance policy was for Rs 50,000 and was subject to the average

clause. Work out the amount of the claim of loss by fire.

Q.13. Mr. „A‟ prepares accounts on 30th September each year, but on 31st December, 2001 fire destroyed the greater part of his

stock. Following information was collected from his books:

Stock as on 1.10.2001

Purchases from 1.10.2001 to 31.12.2001

Wages from 1.10.2001 to 31.12.2001

Sales from 1.10.2001 to 31.12.2001

Rs.

29,700

75,000

33,000

1,40,000

The rate of Gross Profit is 33.33% on cost. Stock to the value of Rs. 3,000 was salvaged, Insurance policy was for Rs. 25,000 and

claim was subject to average clause.

Additional Information:

(i) Stock in the beginning was calculated at 10% less than cost.

(ii) A Plant was installed by firm‟s own worker. He was paid Rs. 500, which was included in wages.

(iii) Purchases include the purchase of the plant for Rs. 5,000.

Insurance Claims IPCC - Accounts – Gr 1

You are required to calculate the claim for the loss of Stock.

Q.14. A fire occurred in the workshop of Mr. A on 31st March, 2006 where a large part of the stock was destroyed. Scrap realized

Rs. 7,500. Mr. A gives you the following information for the period of 1st January to 31st March, 2006:

(i) Purchases

(ii) Sales

(iii) Goods costing Rs. 1,000 were taken by Mr. A for personal use.

(iv) Cost price of stock on 1st January, 2006 was Rs.20,000.

(v) Over the past few years, Mr. A has been selling goods at a consistent gross profit margin of 30%.

(vi) The Insurance policy was for Rs. 25,000. It included an average clause. Prepare a statement of claim

to be made on the Insurance Company by Mr. A.

Rs.

42,500

45,000

Que. 15 On 1st July 2003, a fire took place in the godown of Shyam which destroyed the stock. Calculate the amount of insurance

claim for stock from the following details:

Sales in 2001

Gross Profit in 2001

Sales in 2002

Gross Profit in 2002

2,00,000

60,000

3,00,000

60,000

Stock as on 1.1.2003

Purchases from 1.1.2003 to 30.6.2003

Sales from 1.1.2003 to 30.6.2003

2,70,000

4,00,000

7,20,000

The following are also to be taken into consideration:

1. Stock as on 31st December 2002 has been undervalued by 10%.

2. A stock taking conducted in March 2003 had revealed that stock costing Rs 80,000 was lying in a damaged condition

50% of this stock was sold in May 2003 at 50% of cost and the balance was expected to be sold at 40% of cost.

Que. 16 On 30th September 2003 the stock of Mr Dilip was lost in a fire accident. From the records, the following information is

made available to enable you to prepare a statement of claim on the insurers:

Stock at cost on 1st April 2002

Stock at cost on 31st March 2003

Purchases less returns for the year ended 31st

March 2003

37,500

52,000

2,53,750

Sales less returns for the year ended 31st

March 2003

Purchases less return up to 30th September

2003

Sales less returns up to 30th September 2003

3,15,000

1,45,000

1,84,050

In valuing the stock on 31st March 2003, due to obsolescence 50% of the value of the stock which originally cost Rs 6,000 has

been written-off. In May 2003, three-fourths of this stock had been sold at 90% of the original cost and it is now expected that the

balance of the obsolete stock is also expected to realize the same price. Subject to the above, gross profit had remained uniform

throughout. The stock salvaged was worth Rs 7,200.

Que 17 Bharat Co. suffered a loss of stock due of fire on 31.3.2001. From the following information, prepare a statement

showing claim for the loss to be submitted:

Stock on 1.1.2000

Purchases during the year 2000

Sales during the year 2000

76,800

3,20,000

4,05,200

Closing Stock on 31.12.2000

Purchases from 1.1.91 to 31.3.2001

Sales from 1.1.2001

63,600

1,08,000

1,22,800

An item of goods purchased in 1999 at a cost of Rs 20,000 were valued at Rs 12,000 on 31.12.1999. Half of these goods were

sold for Rs 5,200 during 2000, and the remaining stock was valued at Rs 4,800 on 31.12.90 2/4 of the original stock was sold for

Rs 2,800 in February 2001 and the remaining was valued at 60% of the original cost. With this exception of this item, the rate of

gross profit remained uniform. There was an average clause in the insurance policy which was for Rs 3,00,000. The stock

salvaged was Rs 24,000.

Que. 18 The premises of Fireproof Ltd. were destroyed by fire on 30.6.2003. The following figures were ascertained:

2000 2001 2002 1.1.03 to 30.6.03

Opening Stock Rs. 2,000 2,200 1,180 3,402

Purchases Rs. 16,000 14,.500 17,000 3,500

Sales Rs. 20,000 19,850 18,750 2,.600

Carriage Inwards Rs. 500 300 500 100

Freight Outwards Rs. 600 700 300 25

In 2000, while valuing closing stock, some defective goods costing Rs 500 were valued at Rs 400. These were sold for Rs 450 in

2001.

In 2001, an item costing Rs 600 was wrongly valued at Rs 700. This was sold for Rs 550 in 2002.

In 2002, items costing Rs 1,200 were valued at Rs 1,000. 50% of these items was sold in June 2003 for Rs 600.

Subject to this, the gross profit rate is more or less uniform. Value of salvage was Rs 800.

Insurance Claims IPCC - Accounts – Gr 1

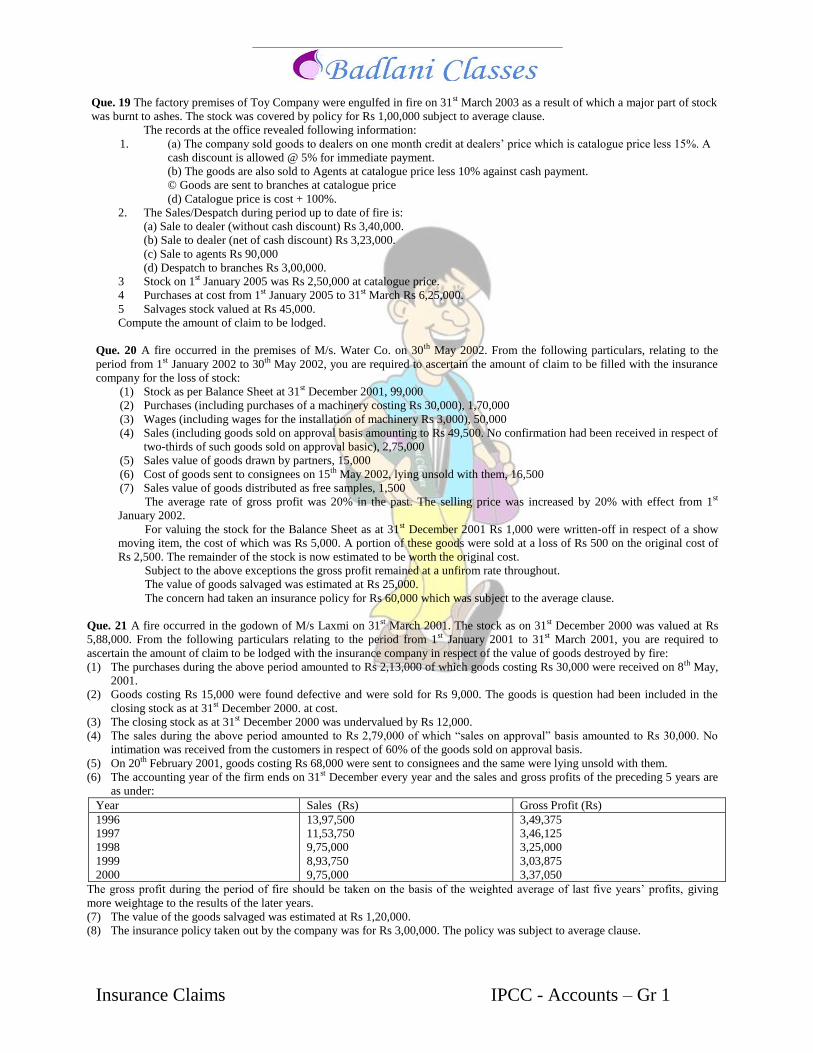

Que. 19 The factory premises of Toy Company were engulfed in fire on 31st March 2003 as a result of which a major part of stock

was burnt to ashes. The stock was covered by policy for Rs 1,00,000 subject to average clause.

The records at the office revealed following information:

1. (a) The company sold goods to dealers on one month credit at dealers‟ price which is catalogue price less 15%. A

cash discount is allowed @ 5% for immediate payment.

(b) The goods are also sold to Agents at catalogue price less 10% against cash payment.

© Goods are sent to branches at catalogue price

(d) Catalogue price is cost + 100%.

2. The Sales/Despatch during period up to date of fire is:

(a) Sale to dealer (without cash discount) Rs 3,40,000.

(b) Sale to dealer (net of cash discount) Rs 3,23,000.

(c) Sale to agents Rs 90,000

(d) Despatch to branches Rs 3,00,000.

3 Stock on 1st January 2005 was Rs 2,50,000 at catalogue price.

4 Purchases at cost from 1st January 2005 to 31st March Rs 6,25,000.

5 Salvages stock valued at Rs 45,000.

Compute the amount of claim to be lodged.

Que. 20 A fire occurred in the premises of M/s. Water Co. on 30th May 2002. From the following particulars, relating to the

period from 1st January 2002 to 30th May 2002, you are required to ascertain the amount of claim to be filled with the insurance

company for the loss of stock:

(1) Stock as per Balance Sheet at 31st December 2001, 99,000

(2) Purchases (including purchases of a machinery costing Rs 30,000), 1,70,000

(3) Wages (including wages for the installation of machinery Rs 3,000), 50,000

(4) Sales (including goods sold on approval basis amounting to Rs 49,500. No confirmation had been received in respect of

two-thirds of such goods sold on approval basic), 2,75,000

(5) Sales value of goods drawn by partners, 15,000

(6) Cost of goods sent to consignees on 15th May 2002, lying unsold with them, 16,500

(7) Sales value of goods distributed as free samples, 1,500

The average rate of gross profit was 20% in the past. The selling price was increased by 20% with effect from 1st

January 2002.

For valuing the stock for the Balance Sheet as at 31st December 2001 Rs 1,000 were written-off in respect of a show

moving item, the cost of which was Rs 5,000. A portion of these goods were sold at a loss of Rs 500 on the original cost of

Rs 2,500. The remainder of the stock is now estimated to be worth the original cost.

Subject to the above exceptions the gross profit remained at a unfirom rate throughout.

The value of goods salvaged was estimated at Rs 25,000.

The concern had taken an insurance policy for Rs 60,000 which was subject to the average clause.

Que. 21 A fire occurred in the godown of M/s Laxmi on 31st March 2001. The stock as on 31st December 2000 was valued at Rs

5,88,000. From the following particulars relating to the period from 1st January 2001 to 31st March 2001, you are required to

ascertain the amount of claim to be lodged with the insurance company in respect of the value of goods destroyed by fire:

(1) The purchases during the above period amounted to Rs 2,13,000 of which goods costing Rs 30,000 were received on 8th May,

2001.

(2) Goods costing Rs 15,000 were found defective and were sold for Rs 9,000. The goods is question had been included in the

closing stock as at 31st December 2000. at cost.

(3) The closing stock as at 31st December 2000 was undervalued by Rs 12,000.

(4) The sales during the above period amounted to Rs 2,79,000 of which “sales on approval” basis amounted to Rs 30,000. No

intimation was received from the customers in respect of 60% of the goods sold on approval basis.

(5) On 20th February 2001, goods costing Rs 68,000 were sent to consignees and the same were lying unsold with them.

(6) The accounting year of the firm ends on 31st December every year and the sales and gross profits of the preceding 5 years are

as under:

Year Sales (Rs) Gross Profit (Rs)

1996

1997

1998

1999

2000

13,97,500

11,53,750

9,75,000

8,93,750

9,75,000

3,49,375

3,46,125

3,25,000

3,03,875

3,37,050

The gross profit during the period of fire should be taken on the basis of the weighted average of last five years‟ profits, giving

more weightage to the results of the later years.

(7) The value of the goods salvaged was estimated at Rs 1,20,000.

(8) The insurance policy taken out by the company was for Rs 3,00,000. The policy was subject to average clause.

Insurance Claims IPCC - Accounts – Gr 1

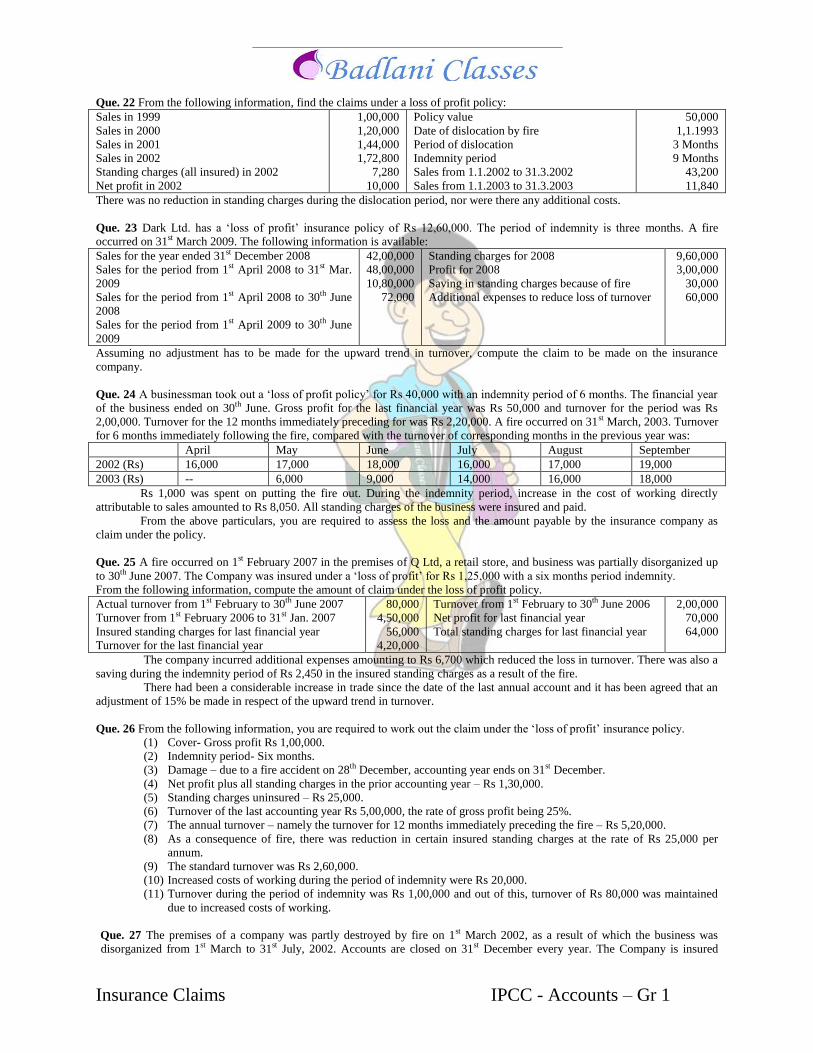

Que. 22 From the following information, find the claims under a loss of profit policy:

Sales in 1999

Sales in 2000

Sales in 2001

Sales in 2002

Standing charges (all insured) in 2002

Net profit in 2002

1,00,000

1,20,000

1,44,000

1,72,800

7,280

10,000

Policy value

Date of dislocation by fire

Period of dislocation

Indemnity period

Sales from 1.1.2002 to 31.3.2002

Sales from 1.1.2003 to 31.3.2003

50,000

1,1.1993

3 Months

9 Months

43,200

11,840

There was no reduction in standing charges during the dislocation period, nor were there any additional costs.

Que. 23 Dark Ltd. has a „loss of profit‟ insurance policy of Rs 12,60,000. The period of indemnity is three months. A fire

occurred on 31st March 2009. The following information is available:

Sales for the year ended 31st December 2008

Sales for the period from 1st April 2008 to 31st Mar.

2009

Sales for the period from 1st April 2008 to 30th June

2008

Sales for the period from 1st April 2009 to 30th June

2009

42,00,000

48,00,000

10,80,000

72,000

Standing charges for 2008

Profit for 2008

Saving in standing charges because of fire

Additional expenses to reduce loss of turnover

9,60,000

3,00,000

30,000

60,000

Assuming no adjustment has to be made for the upward trend in turnover, compute the claim to be made on the insurance

company.

Que. 24 A businessman took out a „loss of profit policy‟ for Rs 40,000 with an indemnity period of 6 months. The financial year

of the business ended on 30th June. Gross profit for the last financial year was Rs 50,000 and turnover for the period was Rs

2,00,000. Turnover for the 12 months immediately preceding for was Rs 2,20,000. A fire occurred on 31st March, 2003. Turnover

for 6 months immediately following the fire, compared with the turnover of corresponding months in the previous year was:

April May June July August September

2002 (Rs) 16,000 17,000 18,000 16,000 17,000 19,000

2003 (Rs) -- 6,000 9,000 14,000 16,000 18,000

Rs 1,000 was spent on putting the fire out. During the indemnity period, increase in the cost of working directly

attributable to sales amounted to Rs 8,050. All standing charges of the business were insured and paid.

From the above particulars, you are required to assess the loss and the amount payable by the insurance company as

claim under the policy.

Que. 25 A fire occurred on 1st February 2007 in the premises of Q Ltd, a retail store, and business was partially disorganized up

to 30th June 2007. The Company was insured under a „loss of profit‟ for Rs 1,25,000 with a six months period indemnity.

From the following information, compute the amount of claim under the loss of profit policy.

Actual turnover from 1st February to 30th June 2007

Turnover from 1st February 2006 to 31st Jan. 2007

Insured standing charges for last financial year

Turnover for the last financial year

80,000

4,50,000

56,000

4,20,000

Turnover from 1st February to 30th June 2006

Net profit for last financial year

Total standing charges for last financial year

2,00,000

70,000

64,000

The company incurred additional expenses amounting to Rs 6,700 which reduced the loss in turnover. There was also a

saving during the indemnity period of Rs 2,450 in the insured standing charges as a result of the fire.

There had been a considerable increase in trade since the date of the last annual account and it has been agreed that an

adjustment of 15% be made in respect of the upward trend in turnover.

Que. 26 From the following information, you are required to work out the claim under the „loss of profit‟ insurance policy.

(1) Cover- Gross profit Rs 1,00,000.

(2) Indemnity period- Six months.

(3) Damage – due to a fire accident on 28th December, accounting year ends on 31st December.

(4) Net profit plus all standing charges in the prior accounting year – Rs 1,30,000.

(5) Standing charges uninsured – Rs 25,000.

(6) Turnover of the last accounting year Rs 5,00,000, the rate of gross profit being 25%.

(7) The annual turnover – namely the turnover for 12 months immediately preceding the fire – Rs 5,20,000.

(8) As a consequence of fire, there was reduction in certain insured standing charges at the rate of Rs 25,000 per

annum.

(9) The standard turnover was Rs 2,60,000.

(10) Increased costs of working during the period of indemnity were Rs 20,000.

(11) Turnover during the period of indemnity was Rs 1,00,000 and out of this, turnover of Rs 80,000 was maintained

due to increased costs of working.

Que. 27 The premises of a company was partly destroyed by fire on 1st March 2002, as a result of which the business was

disorganized from 1st March to 31st July, 2002. Accounts are closed on 31st December every year. The Company is insured

Insurance Claims IPCC - Accounts – Gr 1

under a „loss of profit‟ policy for Rs 7,50,000. The period of indemnity specified in the policy is 6th months. From the following

information, you are required to compute the amount of claim under the loss of profit policy.

Turnover for the year 2001

Net profit for the year 2001

Insured standing charges

Uninsured standing charges

Turnover during the period of dislocation i.e. from

1.3.02 to 31.7.02

Savings in insured standing charges

40,00,000

2,40,000

4,80,000

80,000

8,00,000

30,000

Standard turnover for the corresponding period in the

preceding year i.e. from 1.3.90 to 31.7.01

Annual turnover for the year immediately preceding

the fire i.e. from 1.3.01 to 29.2.02

Increased cost of working

Reduction in turnover avoided through

Increase in working cost

20,00,000

44,00,000

1,50,000

4,00,000

Owing to reasons acceptable to the insurer, the “Special circumstances clause” stipulates for: (a) Increase of turnover (standard

and annual ) by 10% and (b) Increase of rate of gross profit by 2%.

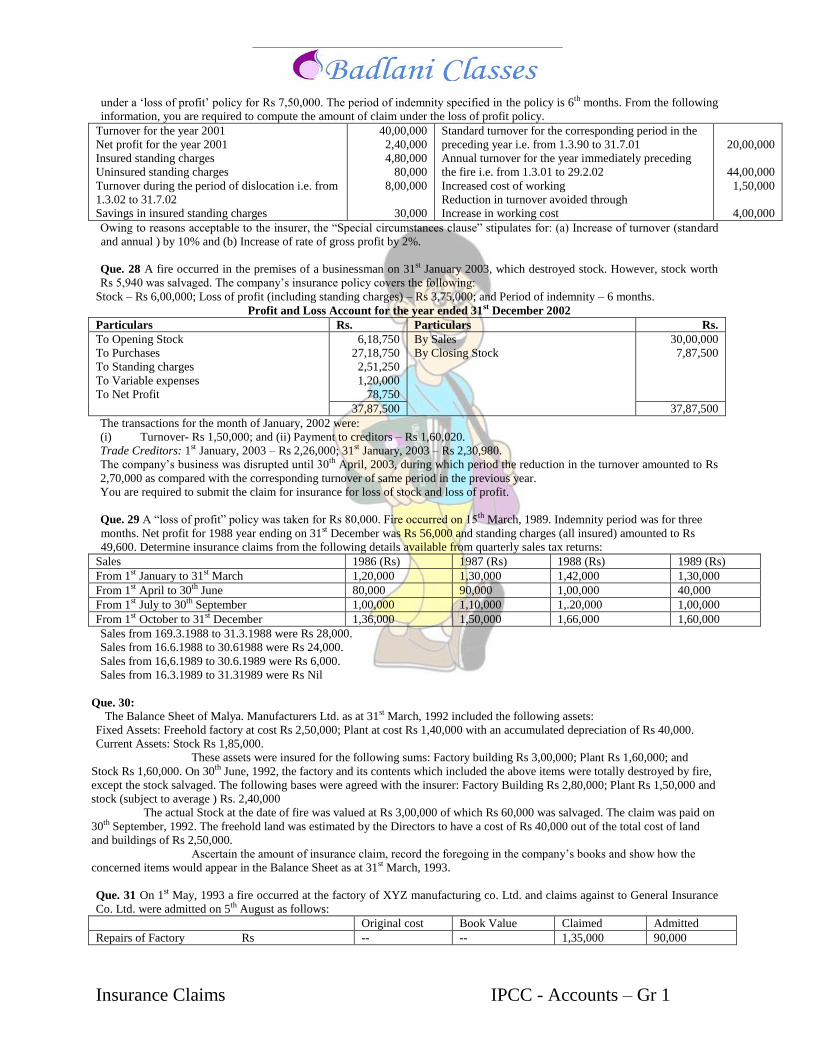

Que. 28 A fire occurred in the premises of a businessman on 31st January 2003, which destroyed stock. However, stock worth

Rs 5,940 was salvaged. The company‟s insurance policy covers the following:

Stock – Rs 6,00,000; Loss of profit (including standing charges) – Rs 3,75,000; and Period of indemnity – 6 months.

Profit and Loss Account for the year ended 31st December 2002

Particulars Rs. Particulars Rs.

To Opening Stock

To Purchases

To Standing charges

To Variable expenses

To Net Profit

6,18,750

27,18,750

2,51,250

1,20,000

78,750

By Sales

By Closing Stock

30,00,000

7,87,500

37,87,500 37,87,500

The transactions for the month of January, 2002 were:

(i) Turnover- Rs 1,50,000; and (ii) Payment to creditors – Rs 1,60,020.

Trade Creditors: 1st January, 2003 – Rs 2,26,000; 31st January, 2003 – Rs 2,30,980.

The company‟s business was disrupted until 30th April, 2003, during which period the reduction in the turnover amounted to Rs

2,70,000 as compared with the corresponding turnover of same period in the previous year.

You are required to submit the claim for insurance for loss of stock and loss of profit.

Que. 29 A “loss of profit” policy was taken for Rs 80,000. Fire occurred on 15th March, 1989. Indemnity period was for three

months. Net profit for 1988 year ending on 31st December was Rs 56,000 and standing charges (all insured) amounted to Rs

49,600. Determine insurance claims from the following details available from quarterly sales tax returns:

Sales 1986 (Rs) 1987 (Rs) 1988 (Rs) 1989 (Rs)

From 1st January to 31st March 1,20,000 1,30,000 1,42,000 1,30,000

From 1st April to 30th June 80,000 90,000 1,00,000 40,000

From 1st July to 30th September 1,00,000 1,10,000 1,.20,000 1,00,000

From 1st October to 31st December 1,36,000 1,50,000 1,66,000 1,60,000

Sales from 169.3.1988 to 31.3.1988 were Rs 28,000.

Sales from 16.6.1988 to 30.61988 were Rs 24,000.

Sales from 16,6.1989 to 30.6.1989 were Rs 6,000.

Sales from 16.3.1989 to 31.31989 were Rs Nil

Que. 30:

The Balance Sheet of Malya. Manufacturers Ltd. as at 31st March, 1992 included the following assets:

Fixed Assets: Freehold factory at cost Rs 2,50,000; Plant at cost Rs 1,40,000 with an accumulated depreciation of Rs 40,000.

Current Assets: Stock Rs 1,85,000.

These assets were insured for the following sums: Factory building Rs 3,00,000; Plant Rs 1,60,000; and

Stock Rs 1,60,000. On 30th June, 1992, the factory and its contents which included the above items were totally destroyed by fire,

except the stock salvaged. The following bases were agreed with the insurer: Factory Building Rs 2,80,000; Plant Rs 1,50,000 and

stock (subject to average ) Rs. 2,40,000

The actual Stock at the date of fire was valued at Rs 3,00,000 of which Rs 60,000 was salvaged. The claim was paid on

30th September, 1992. The freehold land was estimated by the Directors to have a cost of Rs 40,000 out of the total cost of land

and buildings of Rs 2,50,000.

Ascertain the amount of insurance claim, record the foregoing in the company‟s books and show how the

concerned items would appear in the Balance Sheet as at 31st March, 1993.

Que. 31 On 1st May, 1993 a fire occurred at the factory of XYZ manufacturing co. Ltd. and claims against to General Insurance

Co. Ltd. were admitted on 5th August as follows:

Original cost Book Value Claimed Admitted

Repairs of Factory Rs -- -- 1,35,000 90,000

Insurance Claims IPCC - Accounts – Gr 1

Plant destroyed Rs 3,60,000 2,25,000 3,15,000 2,70,000

Repairs to Plant Rs -- -- 27,000 22,500

Stock destroyed Rs 4,50,000 -- 4,50,000 3,87,000

Stock damaged Rs -- -- 45,000 36,000

Loss of Profit Rs -- -- 90,000 45,000

Fire Brigade Charges Rs -- -- 7,000 6,300

The amounts claimed for repairs to factory and plant and the fire brigade charges were paid by the company.

Give journal entries in the company‟s books and state how the final differences, if any, should be treated in the company‟s

Accounts including the profit or loss on account of insurance.

Question 32.

S Ltd., which operates a wholesale warehouse, had a fire in the premises on Jan. 31, 2009 which destroyed most of the building,

although stock of the value of Rs.396 was salvaged.

The company has an insurance policy covering the stock for Rs. 60,000, the building for Rs. 80,000 and loss of profits

including standing charges for Rs. 25,000 with six month period of indemnity.

The company‟s last annual accounts for the year ended Dec. 31, 2009 showed the following position:

Rs. Rs.

To Opening Stock 41,250

Add: Purchases 1,81,250

2,22,500

Less: Closing Stock 52,500

Add: Gross profit

1,70,000

30,000

By Sales 2,00,000

2,00,000 2,00,000

To Variable Expenses

To Standing Charges

To Net Profit

8,000

16,750

5,250

By Gross Profit 30,000

30,000 30,000

The company‟s records show that the turnover for Jan. 2009 had been the same as for the corresponding month in the

previous year at Rs. 10,000, payments made in Jan. 2009 to trade creditors were Rs. 10,668 and at the end of the that month the

balance owing to trade creditors had increased by Rs. 332.

The company‟s business was disrupted until the end of April, during which period the turnover fell by Rs. 18,000

compared with the same period in the previous year.

It was agreed that three-quarters of the value of the building had been lost and that the time of the fire it had been worth

Rs. 1,00,000.

You are required to prepare statements showing the amount to be claimed by the company from its insurers for (a) Loss

of Stock: (b) the building and (c) Loss of Profits.

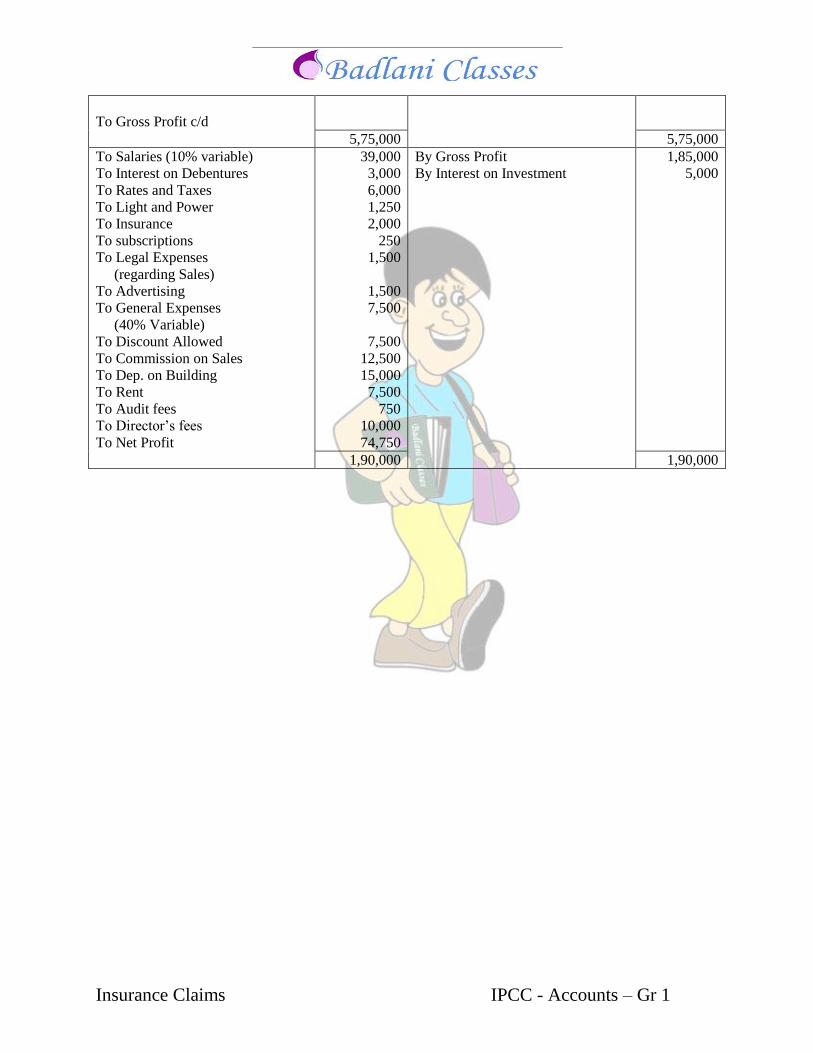

Question 33.

From the following Trading and Profit and Loss account of S Ltd. for the year ended 30th June

2009. Compute the sum for insurance under a loss of profits policy. It is desired that all standing charges

be issued.

S Ltd.

Trading and Profit and Loss Account

Dr. for the year ended 30th June 2009

Cr.

Rs Rs

To Opening Stock

To Purchases

To Wages:

Skilled

10,000

Unskilled

30,000

1,00,000

2,50,000

40,000

1,85,000

By Sales

By Closing Stock

4,50,000

1,25,000

Insurance Claims IPCC - Accounts – Gr 1

To Gross Profit c/d

5,75,000 5,75,000

To Salaries (10% variable)

To Interest on Debentures

To Rates and Taxes

To Light and Power

To Insurance

To subscriptions

To Legal Expenses

(regarding Sales)

To Advertising

To General Expenses

(40% Variable)

To Discount Allowed

To Commission on Sales

To Dep. on Building

To Rent

To Audit fees

To Director‟s fees

To Net Profit

39,000

3,000

6,000

1,250

2,000

250

1,500

1,500

7,500

7,500

12,500

15,000

7,500

750

10,000

74,750

By Gross Profit

By Interest on Investment

1,85,000

5,000

1,90,000 1,90,000