Tazania Basic Economic Report - World Bank Documents

198

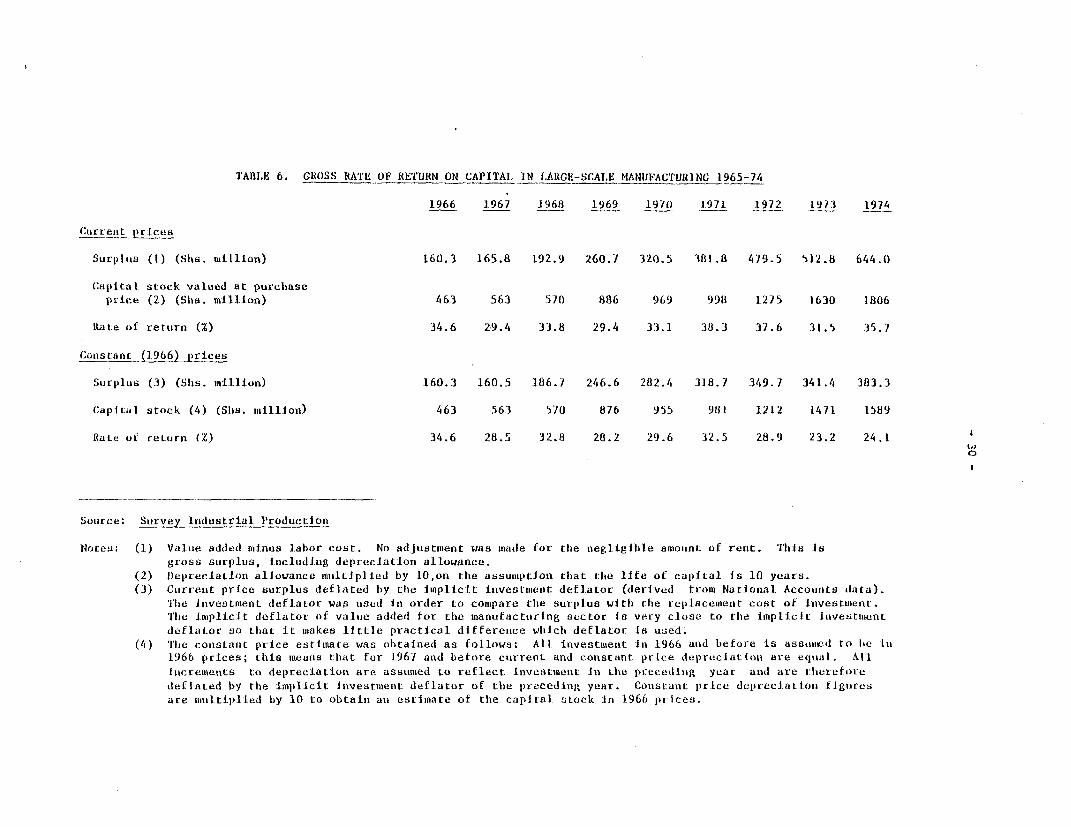

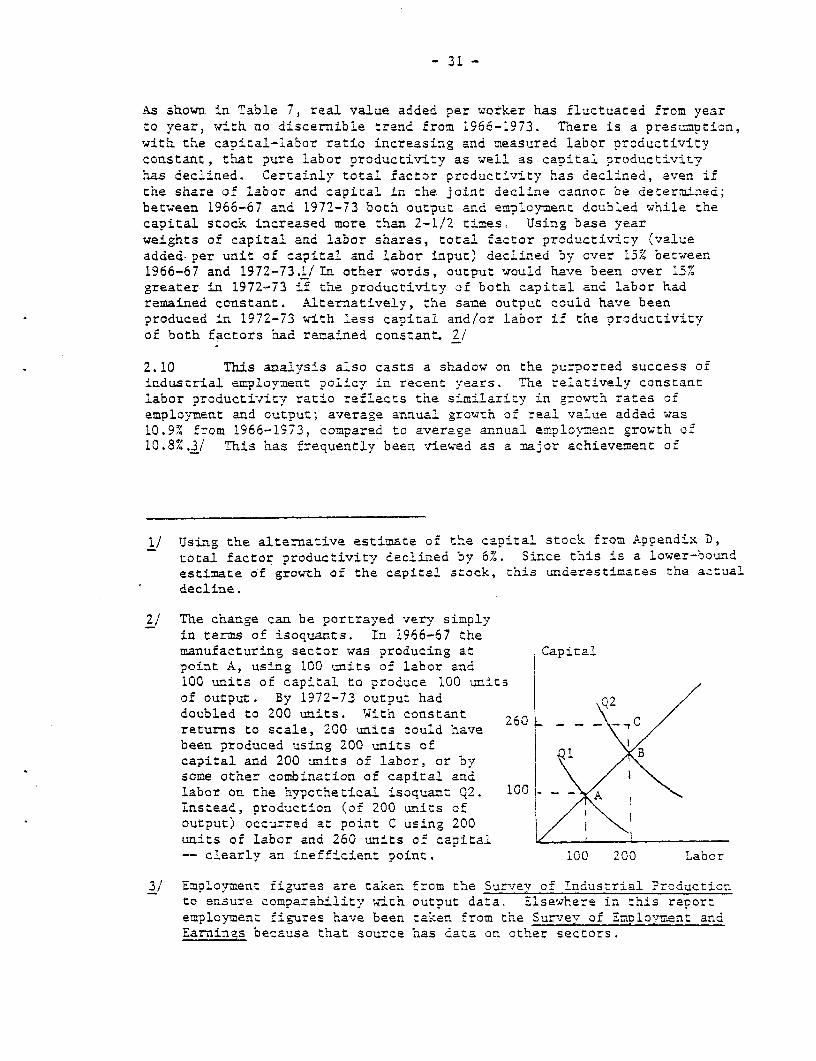

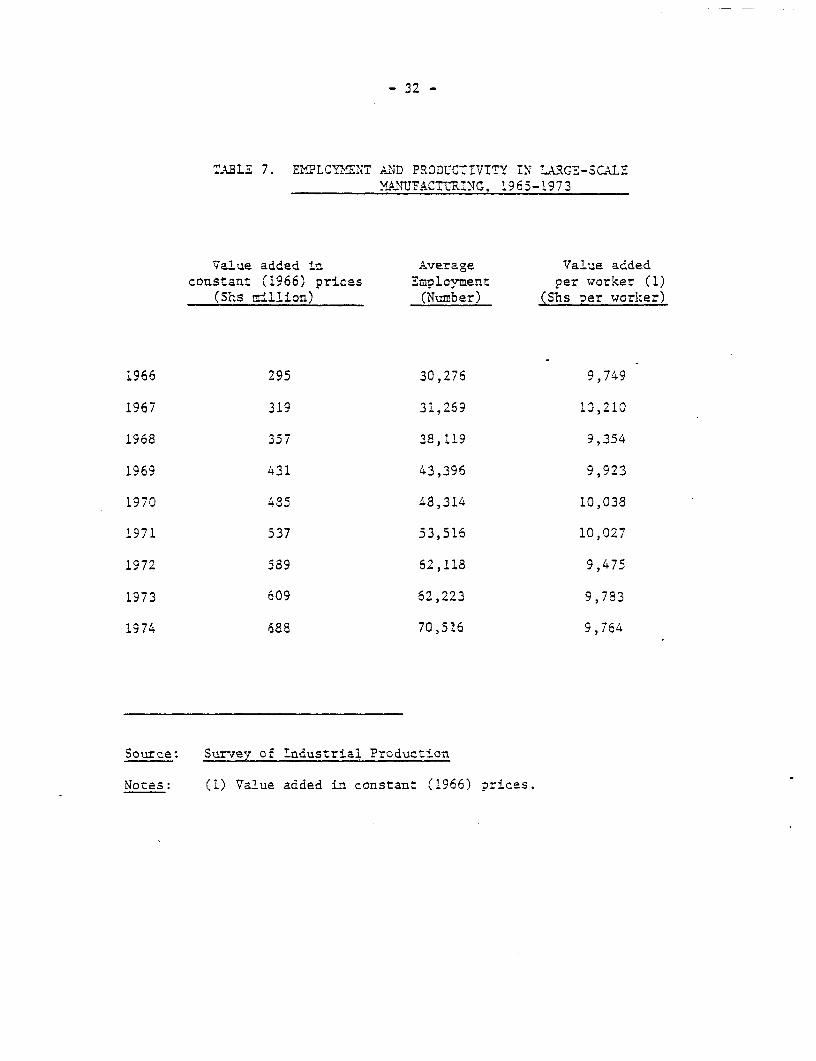

Report No. 1616-TA Tazania BasicEconomic Report LE COPY Annex V-Industry: Perspective and Strategic Choices December 1977 Eastern A.nca Country Prograrrs I FOR OFfICIAL USE ONLY Document of the Worid Bank This document has a restricted distnbut-on andmaybe used by rec!pients orlv in the pe-forrnance of their offic!ai dut:es Itscontents -nay not otherfwise be disclosed without vVofd BanK authonzatkno Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

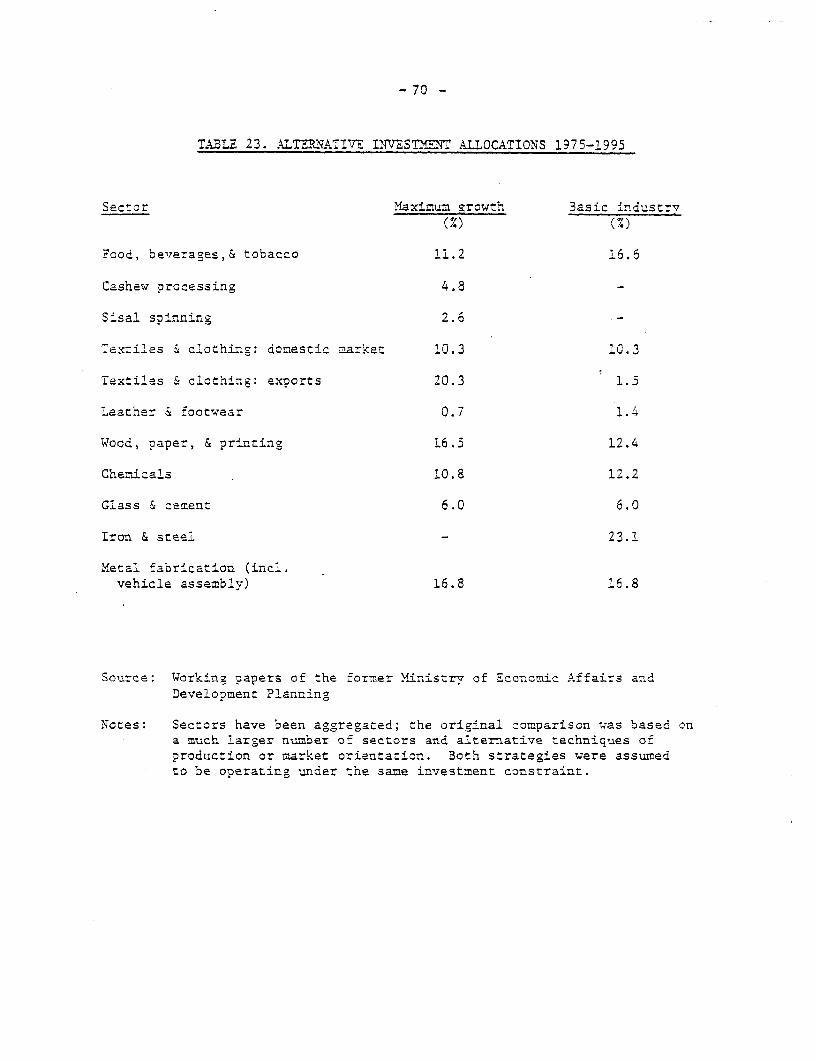

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Tazania Basic Economic Report - World Bank Documents

Report No. 1616-TA

Tazania Basic Economic Report LE COPYAnnex V-Industry: Perspective and Strategic Choices

December 1977

Eastern A.nca Country Prograrrs I

FOR OFfICIAL USE ONLY

Document of the Worid Bank

This document has a restricted distnbut-on and may be used by rec!pientsorlv in the pe-forrnance of their offic!ai dut:es Its contents -nay nototherfwise be disclosed without vVofd BanK authonzatkno

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

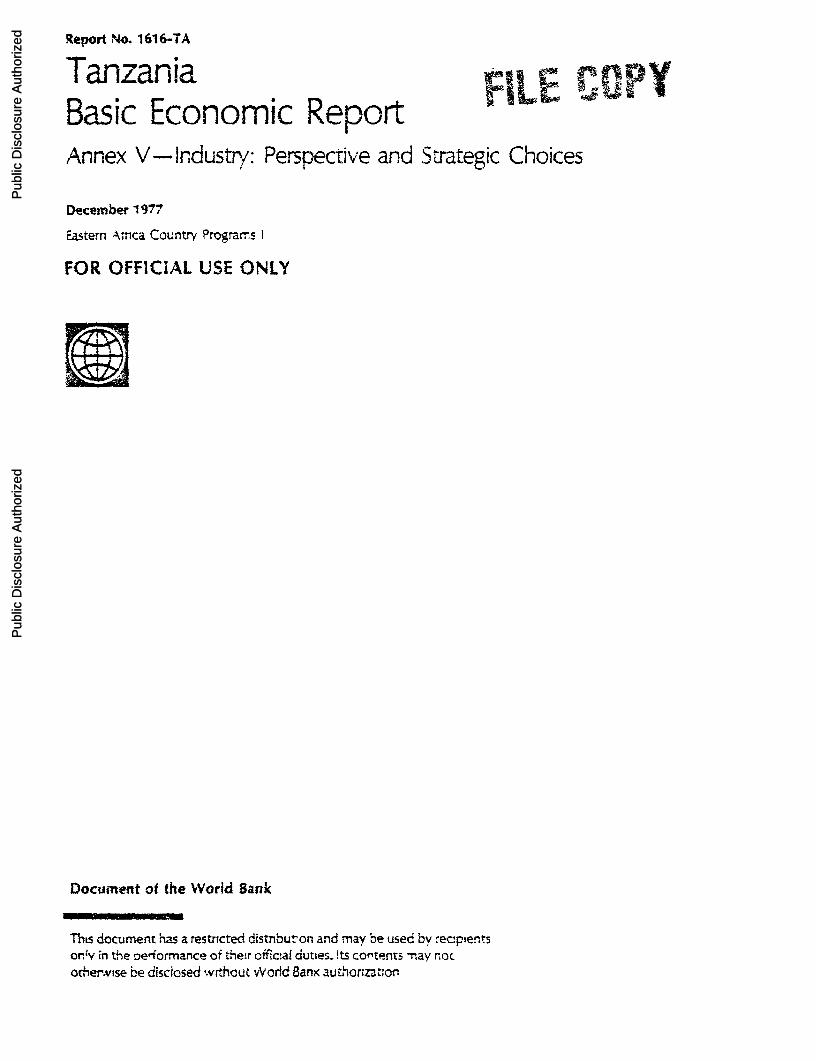

CVM.ECY EQUIVALENTS I1

SDR. 1. 00 Tarnzania Shilling (T.Sh.) 9.66US$ 1.00 - Tanzania Shilling (T.Sh.) 8.30T:Sh. 1.00 :US$0.12

TANZANIA FTSCAL TEAB..

July lst -June 30th

I/1 in 0ctober- 1975 the- Talnzanian Shilling was pegged to thevalue of the Special Drawing Rights (SDR) of the InternationalMonetary Fund. The US Dollar/Tanzania Shilling exchange rateis therefore subject to change.

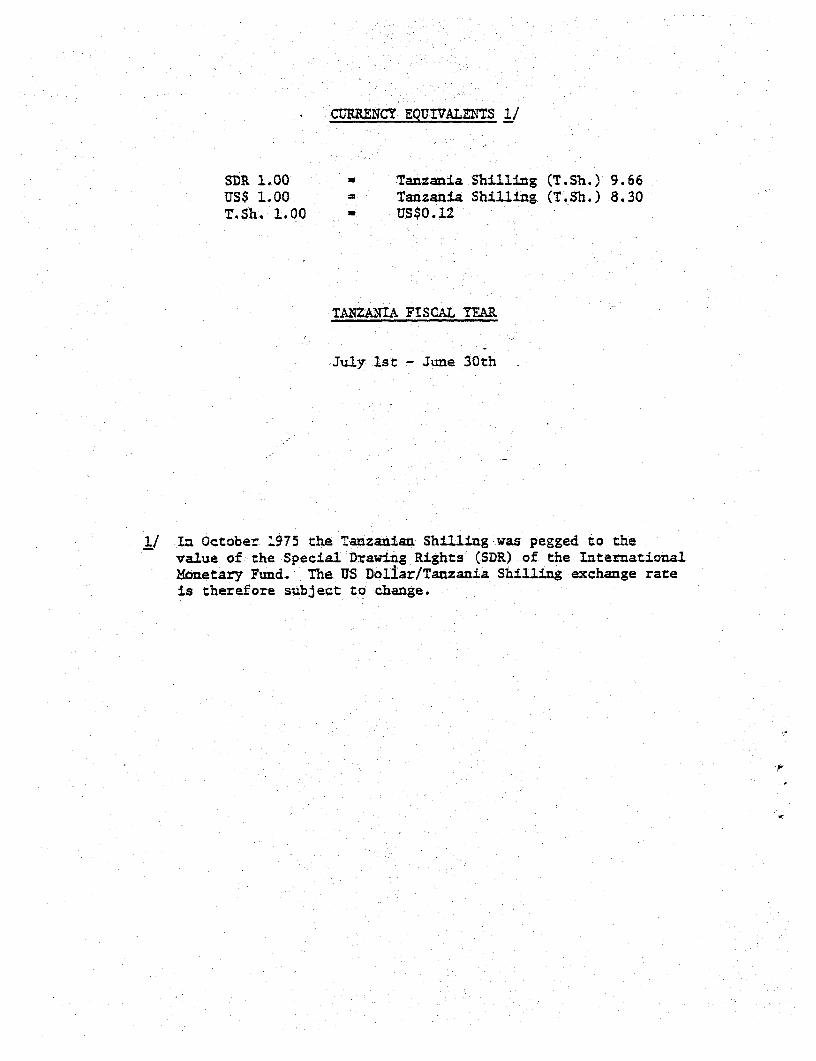

FOR OFFICIAL USE ONLY

TANZANIA - BASIC ECONOMIC REPORT

ANNEX V

INDUSTRY: PERSPECTIVE A-YD STRATEGIC CHOICES

Prepared by

Mr. Gene Tidrick

The full report consists of the following separately boundvolumes:

Main ReportAnnex I - Domestic Finance and Resource UseAnnex II - Fiscal Implications of Universal Primary

Education and Universal Rural Water SupplyAnnex III - Labor Market Allocation and Income

DistributionAnnex IV - Income Distribution and Growth: A Simulation

ModelAnnex V - Industry: Perspective and Strategic CnoicasAnnex VI - Key Issues in Agriculture and Rural DevelopmentAnnex VII - Appropriaze Technology in Tanzanian

Agriculture: Some Empirical and PolicyConsiderations

This document ha!b Artntrycteddistribufion and riay :eoused by recipients oniy 1%1 I P f omace of their oinciai duties. itscontents iuy not othtrwi.e be dlbciosed without World BLnk -uthorization .

(i)

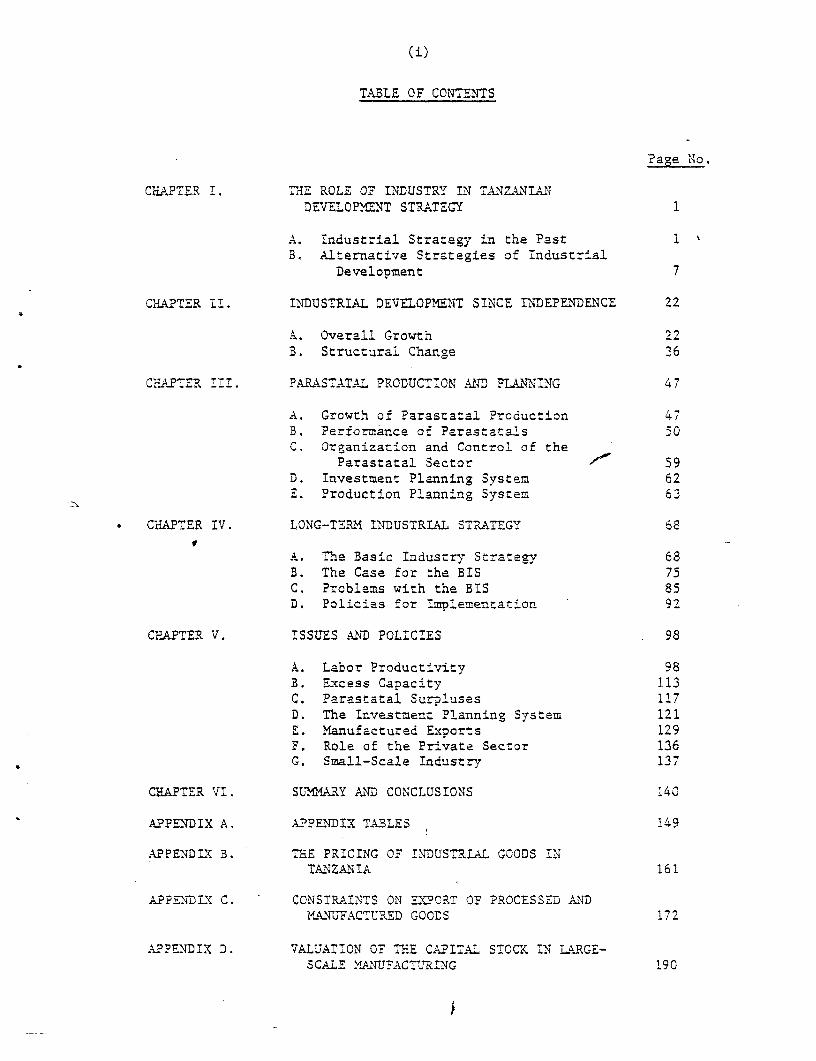

TABLE OF CONTENTS

2a.,e No,

CHAPTER I. THE ROLE OF INDUSTRY IN TANZANIANDEVELOPMEENT STRATEGY 1

A. Industrial Strategy in the Past 1B. Alternative Strategies of Industrial

Development 7

CHAPTER II. INDUSTRIAL DEVELOPEtENT SINCE INDEPENDENCE 22

A. Overall Growth 22B. Structural Change 36

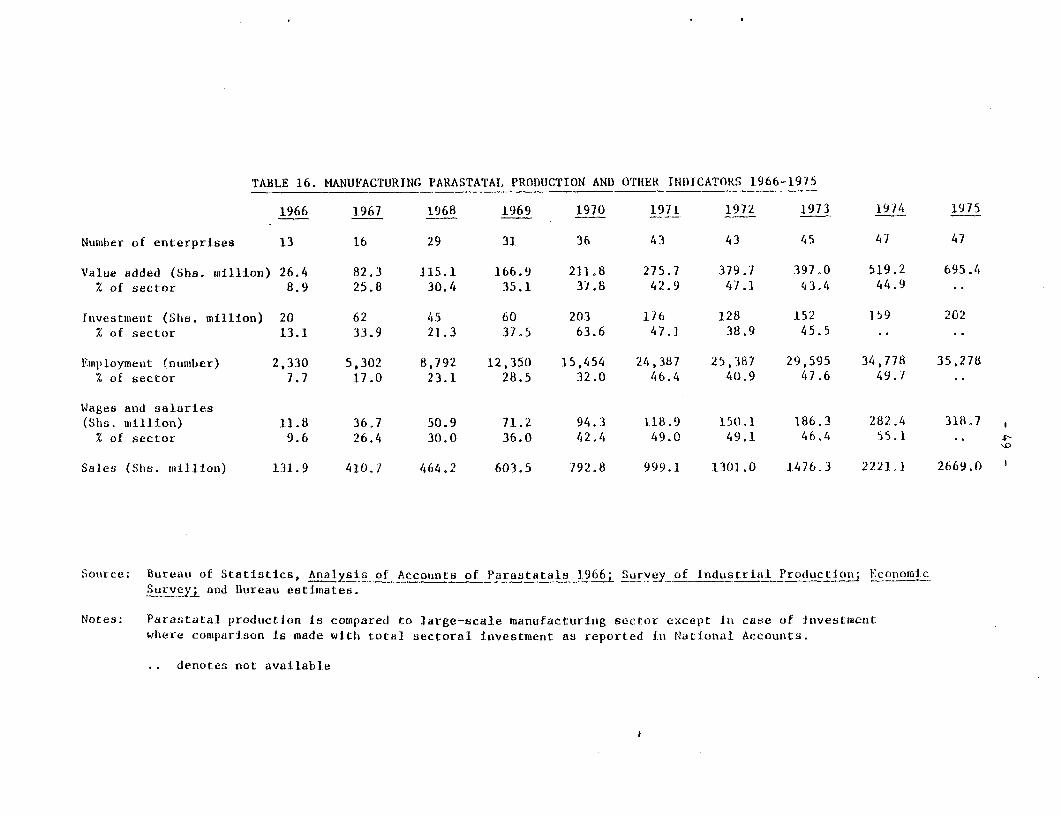

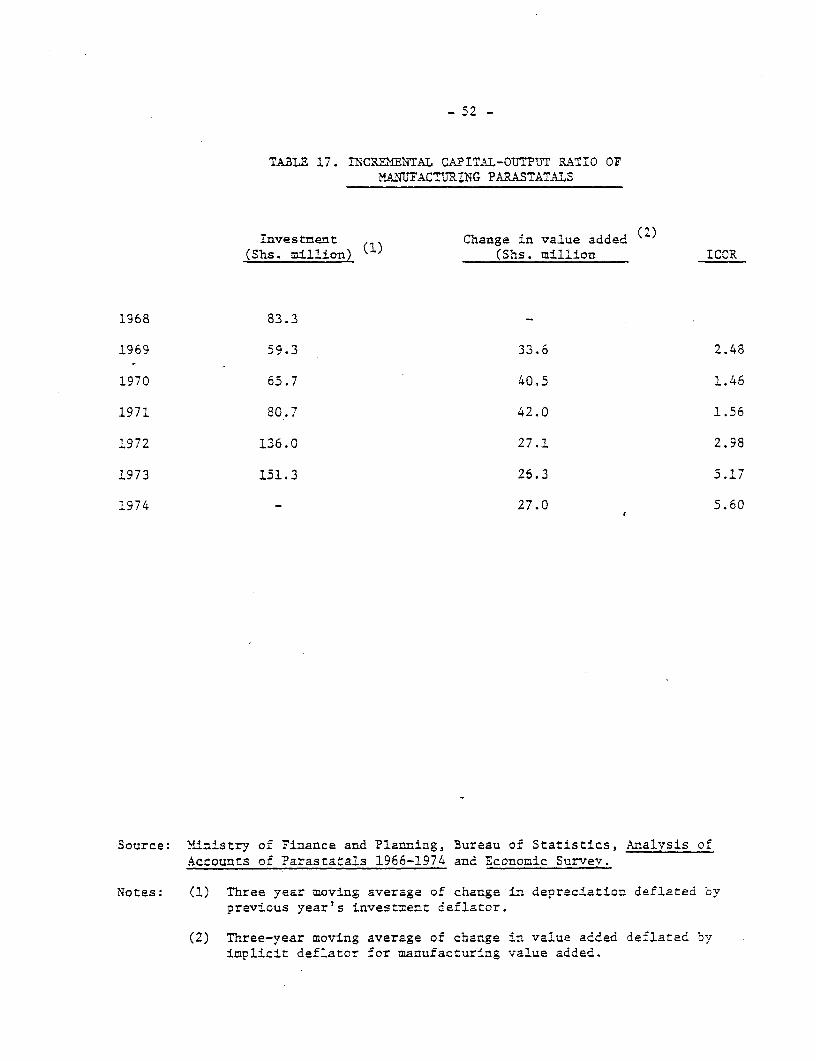

CHAPTER III. PARAST'ATAL PRODUCTION AND PLA2NNING 47

A. Growth of Parastatal Production 47B. Performance of Parastatals 5OC. Organization and Control of the

Parastatal Sector 59D. Investment Planning System 62E. Production Planning System 63

CHAPTER IV. LONG-TEPM INDUSTRIAL STRATEGY 68

A. The Basic Industry Strategy 68B. The Case Lor the BIS 75C. Problems with the BIS 85D. Policies for Implementation 92

CHAPTER V. ISSUES AND POLICIES 98

A. Labor Productivity 98B. Excess Capacity 113C. Parastatal Surpluses 117D. The Investment Planning System 121E. Manufactured Exports 129F. Role of the Private Sector 136G. Small-Scale Industry 137

CHAPTER VI. SUMMARY AND CONCLUSIONS 140

APPENDIX A. APPENDIX TABLES 149

APPENDIX B. THE PRICING OF INDUSTRIAL GOODS INTANZANIA 161

APPENDIX C. CONSTRAINTS ON EXPORT OF PROCESSED ANDMANUFACTURED GOODS 172

APPENDIX D. VALUATION OF THE CAPITAL STOCK IN LiLRGE-SCALE MAINUFACTURING i90

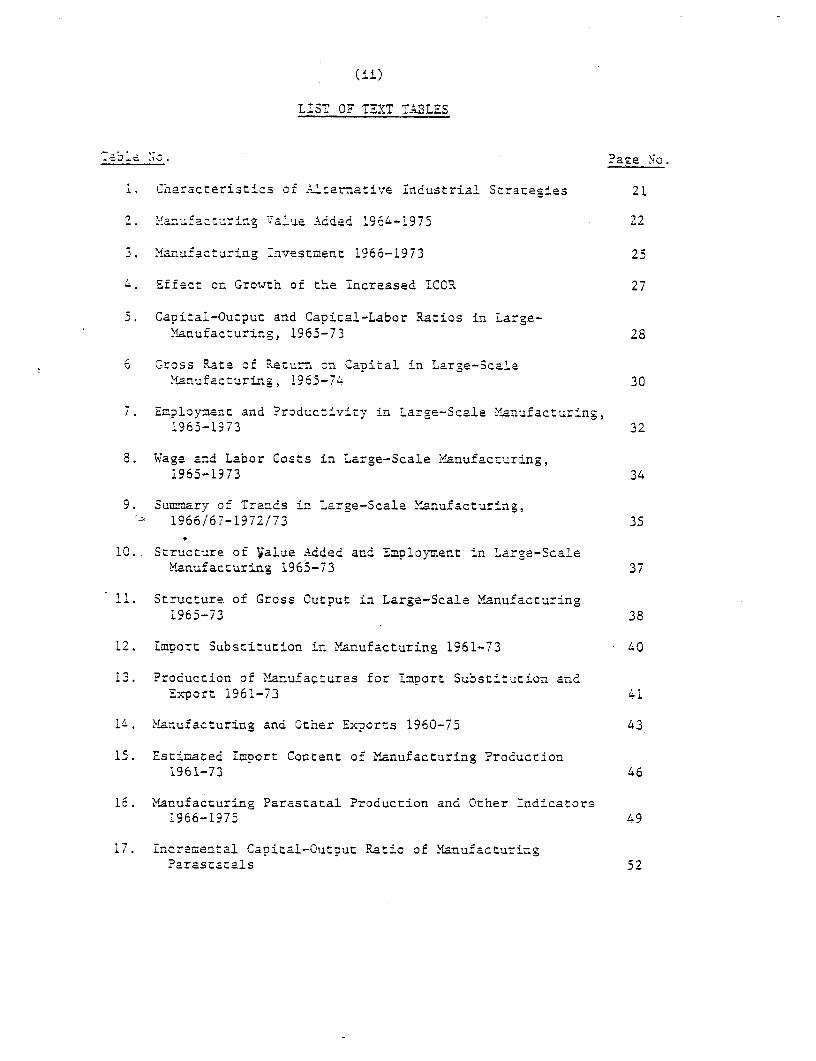

( ii.)

LIST OF TEXT T-ULES

-_'a c. -?aze Mc.

1 Characterist4cs of :ernative Industrial Strategies 21

2. 'Ma-.fa turi-.g V~a ue cAdded 1964-1975 22

3. Manufacturing investment 1966-1973 25

4. Ef`ect on Growth of the Ircreased ICOR 27

3. CaDital-Output and Capital-Labor Ratios in Large-Manufacturing, 1963-73 28

6 C-ross Rate of Returm on CaDital in Large-ScalaYanufacturing, 196i-74 30

7. Employment and Productivity in Large-Scale Manufacturing,1963-1973 32

8. Wage and Labor Costs in Large-Scale Manufacturing,1965-1973 34

9. Summary of Trends in Large-Scale Manufacturing,1966/67-1972/73 35

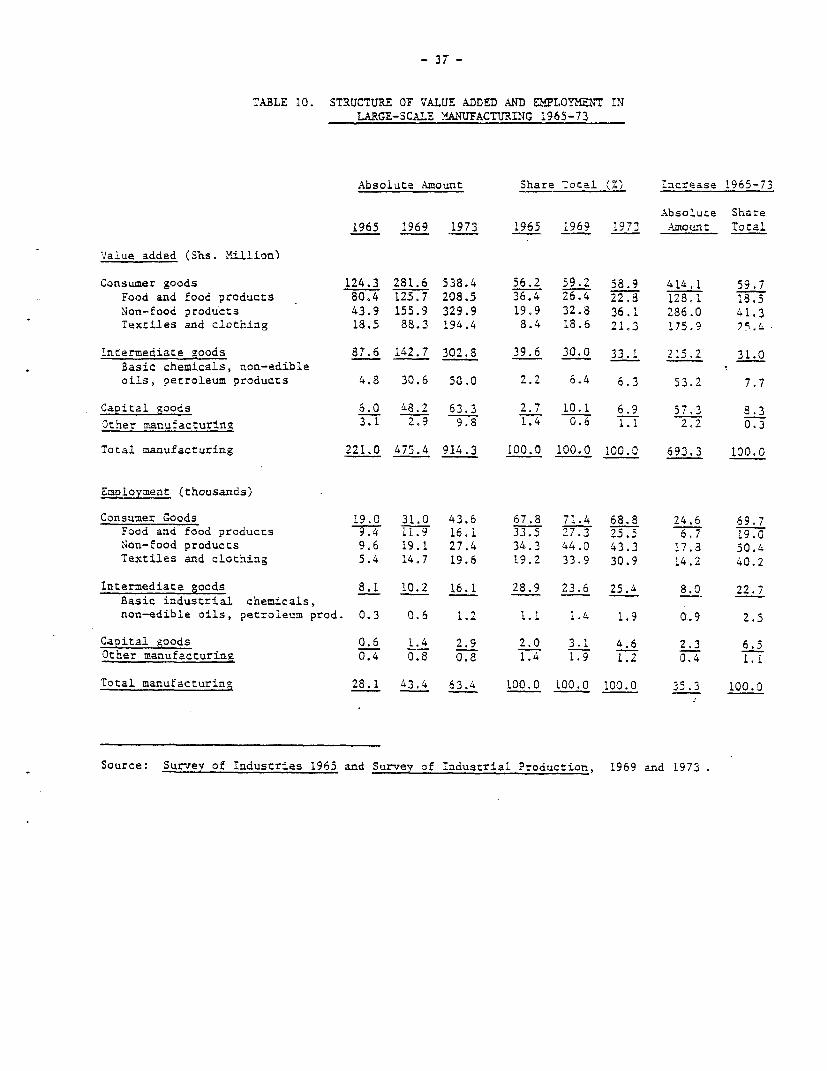

10. Structure of Value Added and Employment in Large-ScaleManufacturing 1965-73 37

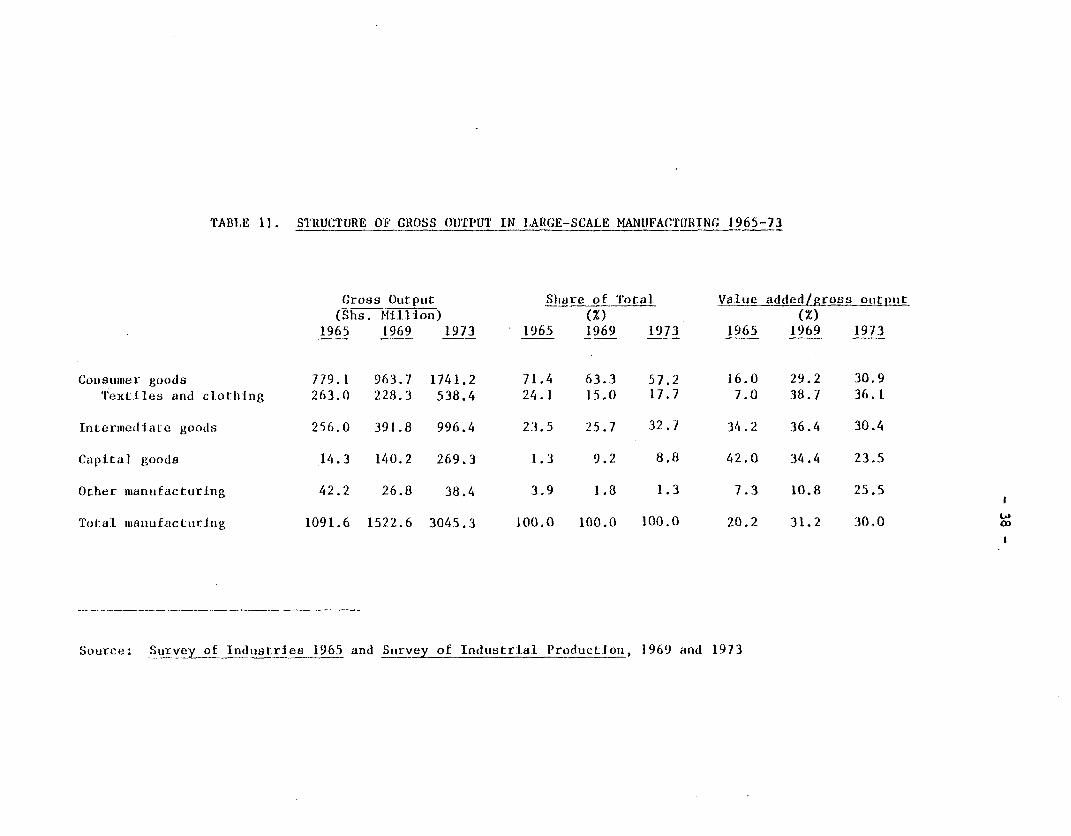

11. Structure of Gross Output in Large-Scale Manufacturing1965-73 38

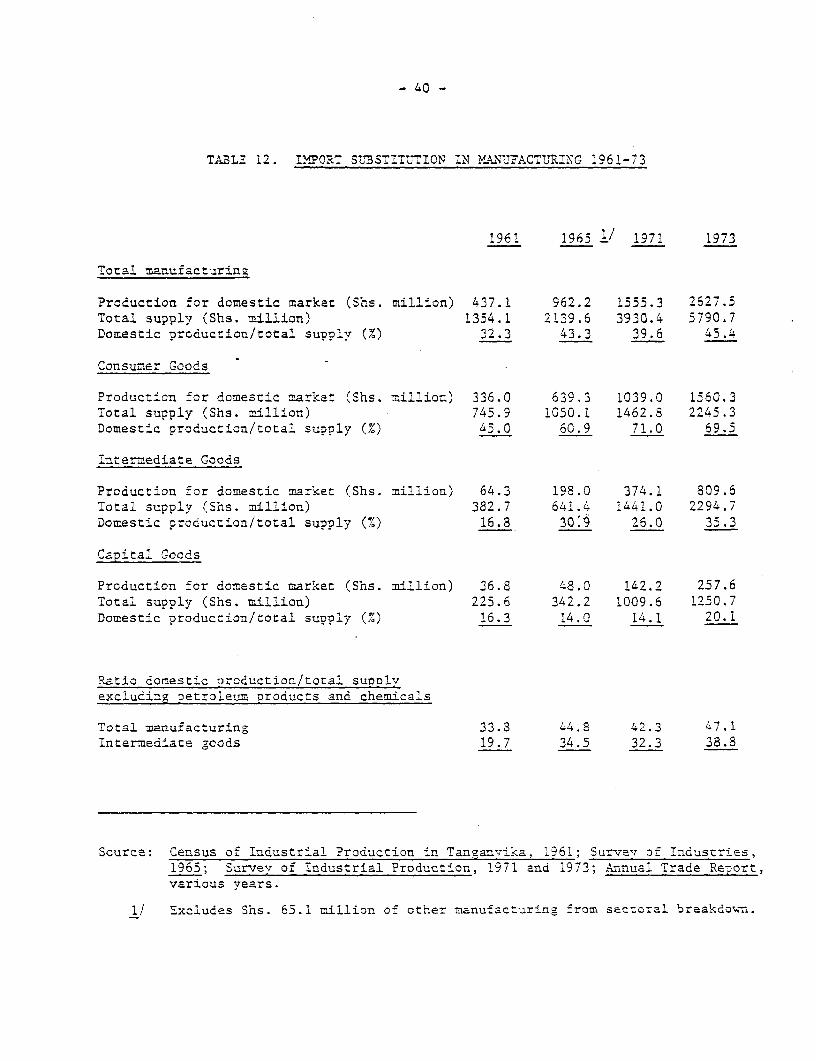

12. tmmort Substitution in Manufacturing 1961-73 40

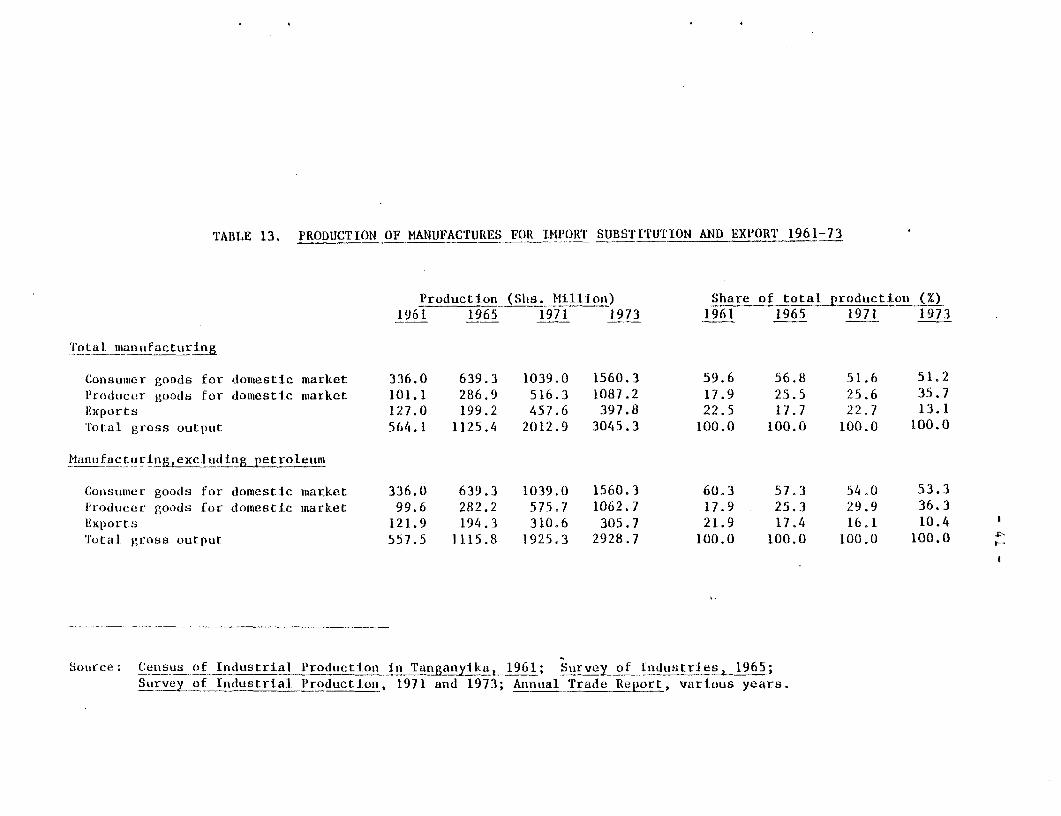

13. Production of Manufacturas for Import Substitution andExport 1961-73 41

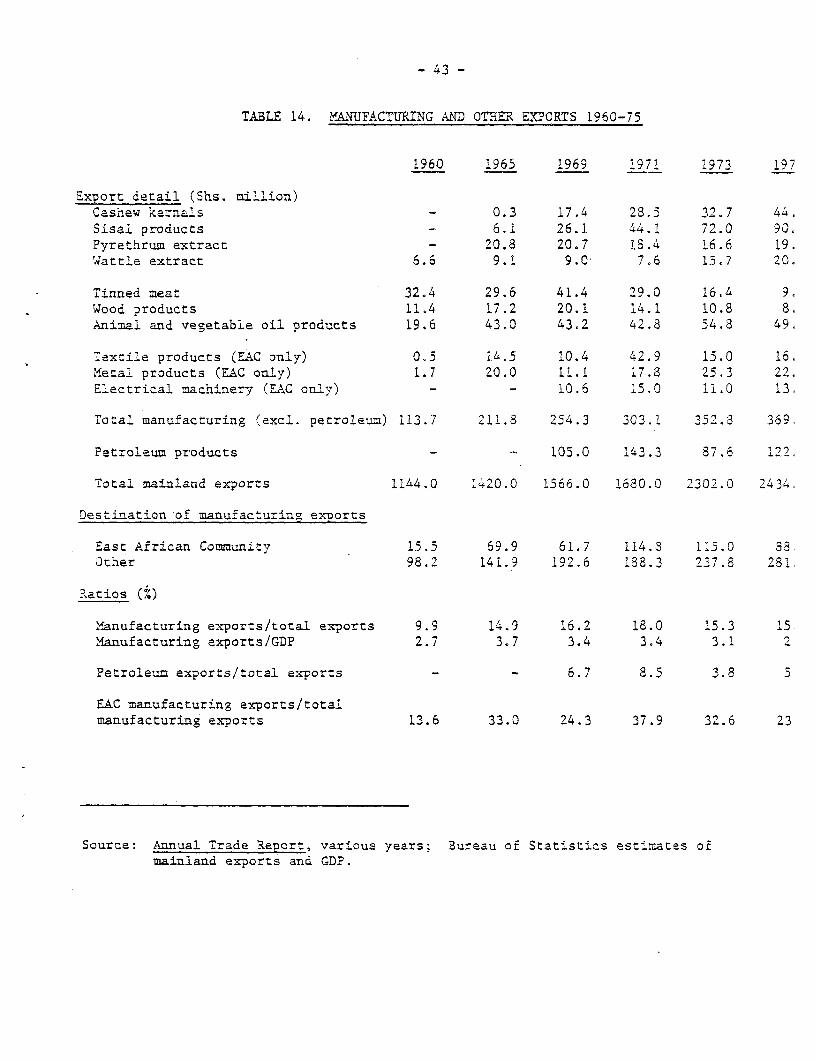

14. Manufacturing and Other Exports 1960-75 43

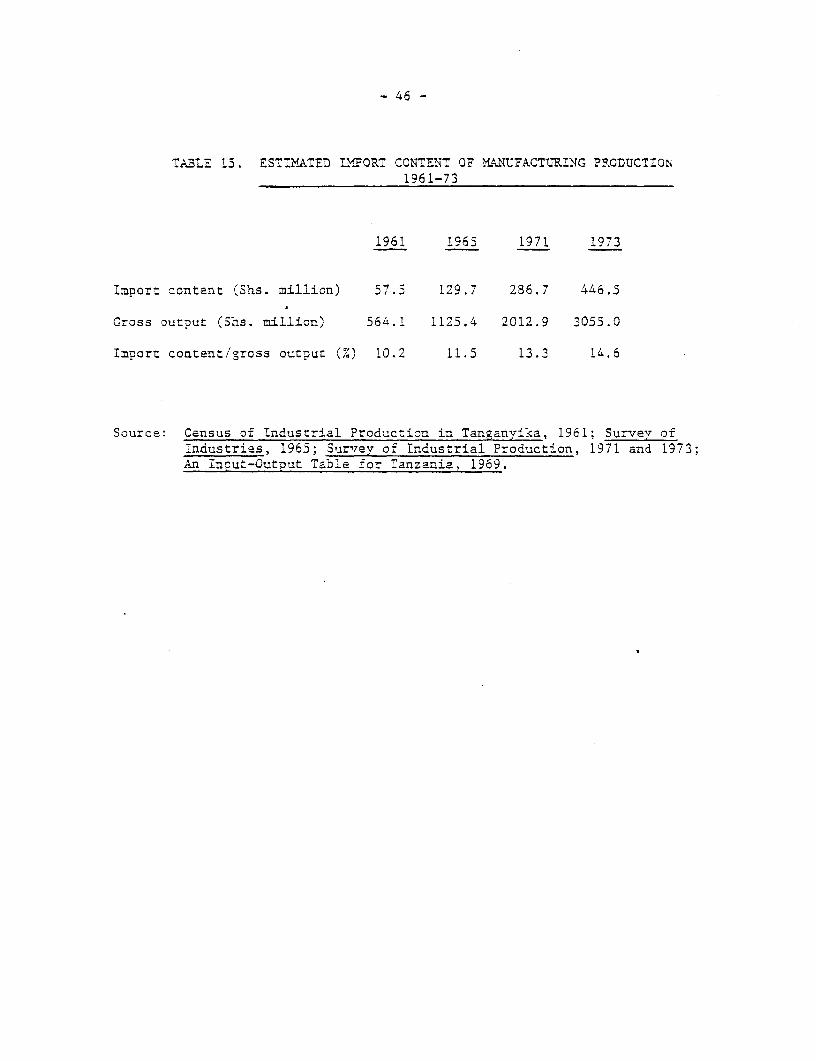

15. Estimated Import Content of Manufacturing Production1961-73 46

16. Manufacturing Parastatal Production and Other Indicators1966-1975 49

17. Incremental Capital-Output Ratio of ManufacturingParastatals 52

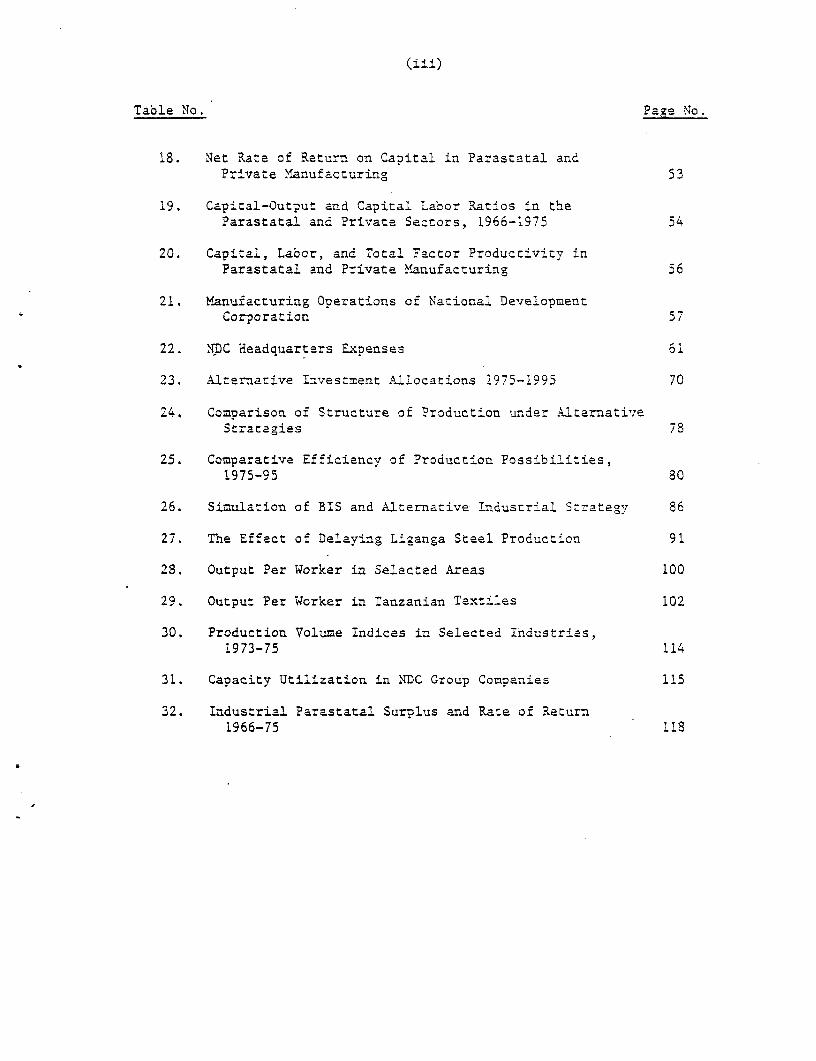

(ii i)

Table No. Page No.

18. Net Rate of Return on Capital in Parastatal andPrivate Mbanufacturing 53

19. Capital-Output and Capital Labor Ratios in theParastatal and Private Sectors, 1966-1975 54

20. Capital, Labor, and Total Factor Productivity inParastatal and Private Manufacturing 56

21. iManufacturing Operations of National DevelopmentCorporation 57

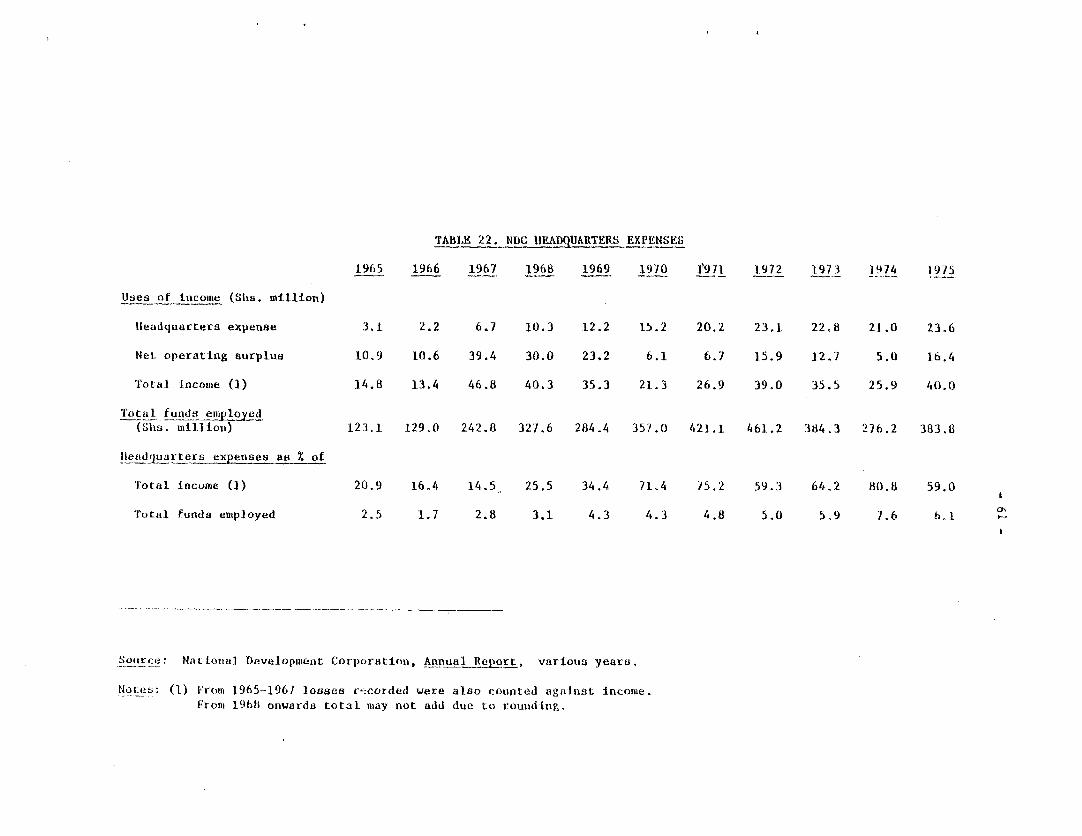

22. MC Headquarters Expenses 61

23. Alternative Investment Allocations 1975-1995 70

24. Comparison of Structure of Production under AlternativeStrategies 78

25. Comparative Efficiency of Production Possibilities,1975-95 80

26. Simulation of BIS and Alternative Industrial Strate-y 86

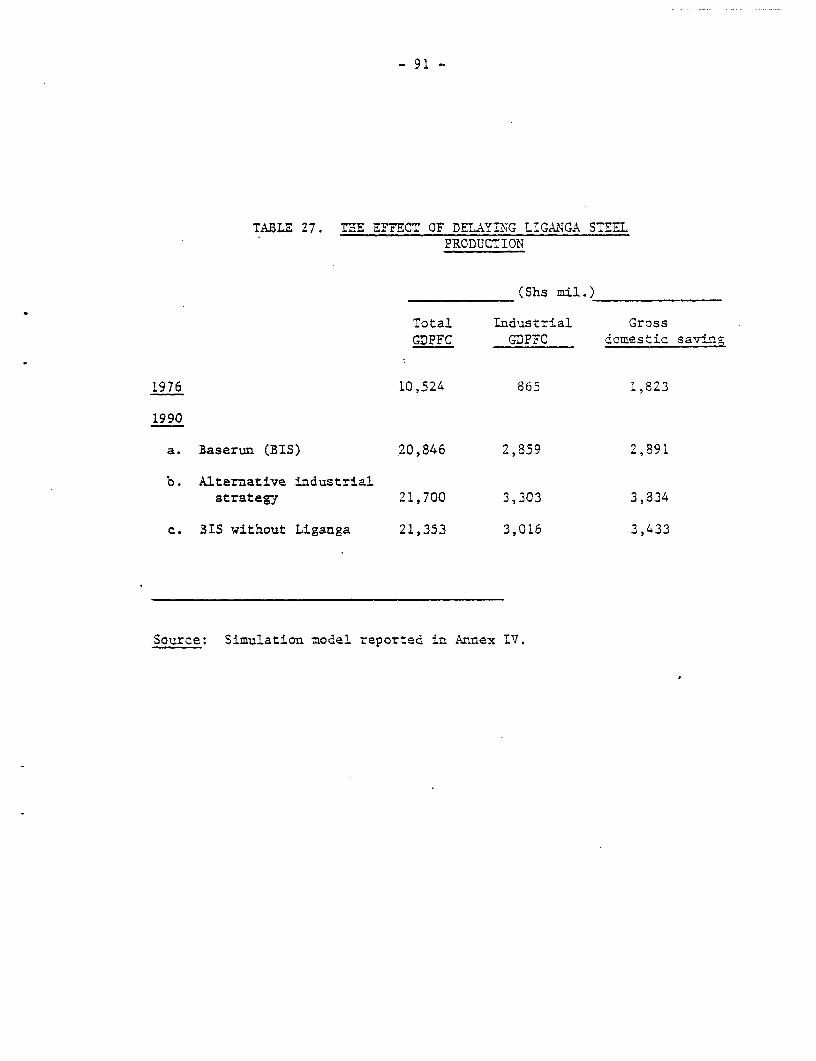

27. The Effect of Delaying Liganga Steel Production 91

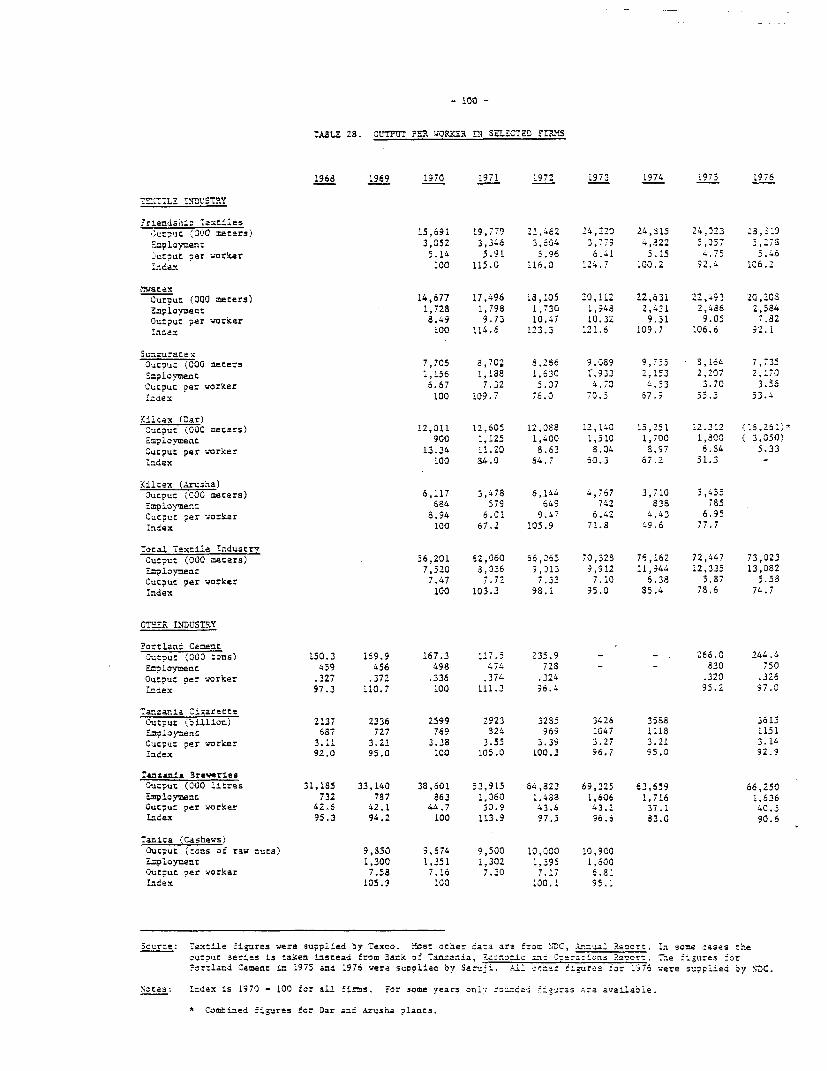

28. Output Per Worker in Selected A-reas 100

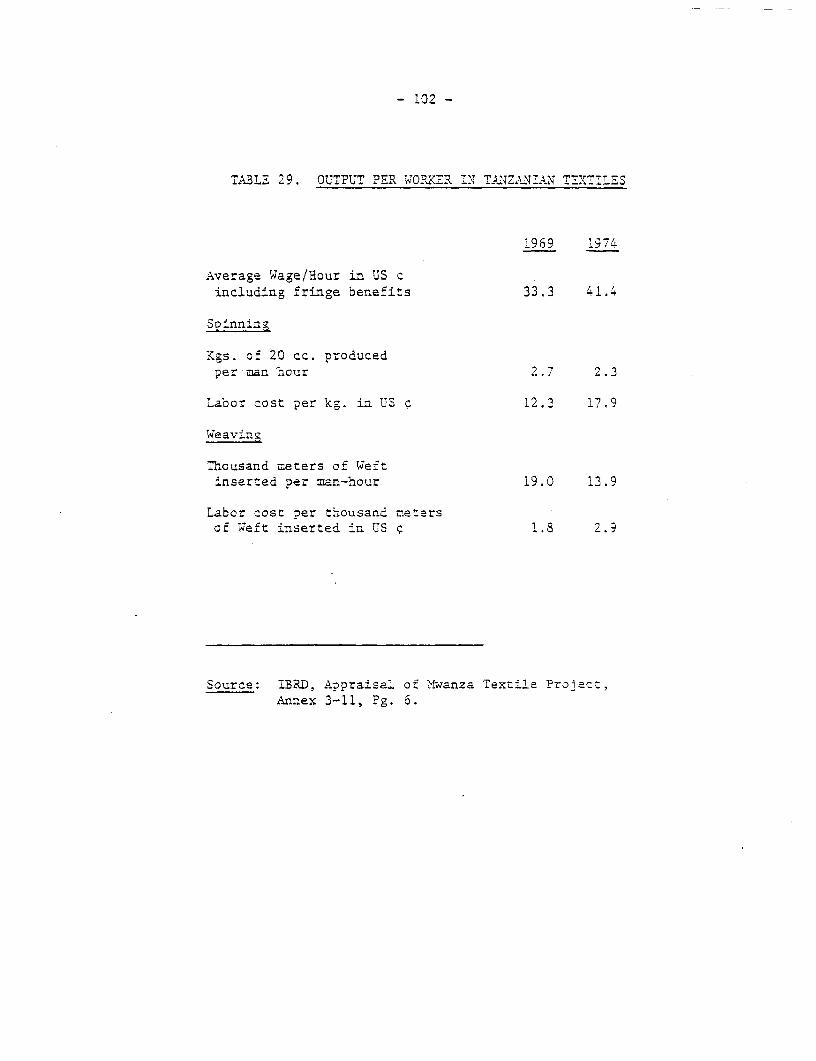

29. Output Per Worker in Tanzanian Textiles 102

30. Production Volume Indices in Selected Industrias,1973-75 114

31. Capacity Utilization in 'DC Group Companies 115

32. Industrial Parastatal Surplus and Rate of Return1966-75 118

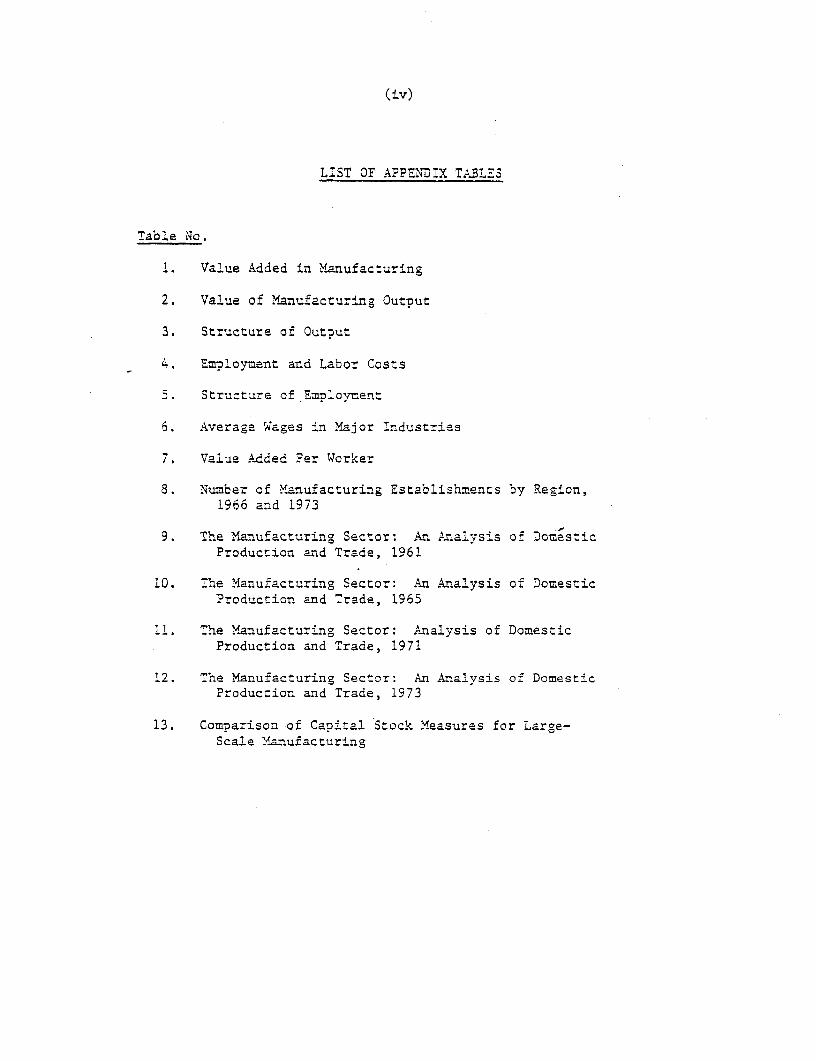

(iv)

LIST OF APPENDIX TABLiES

Table No.

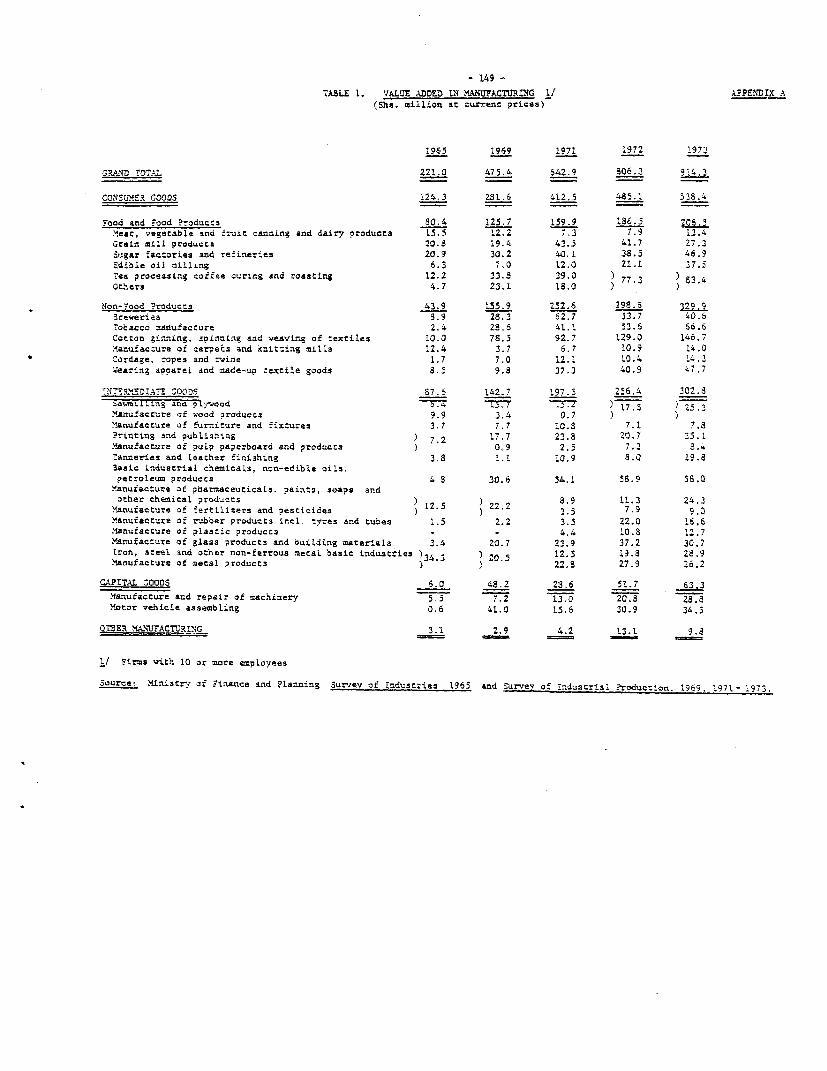

1. Value Added in Manufacturing

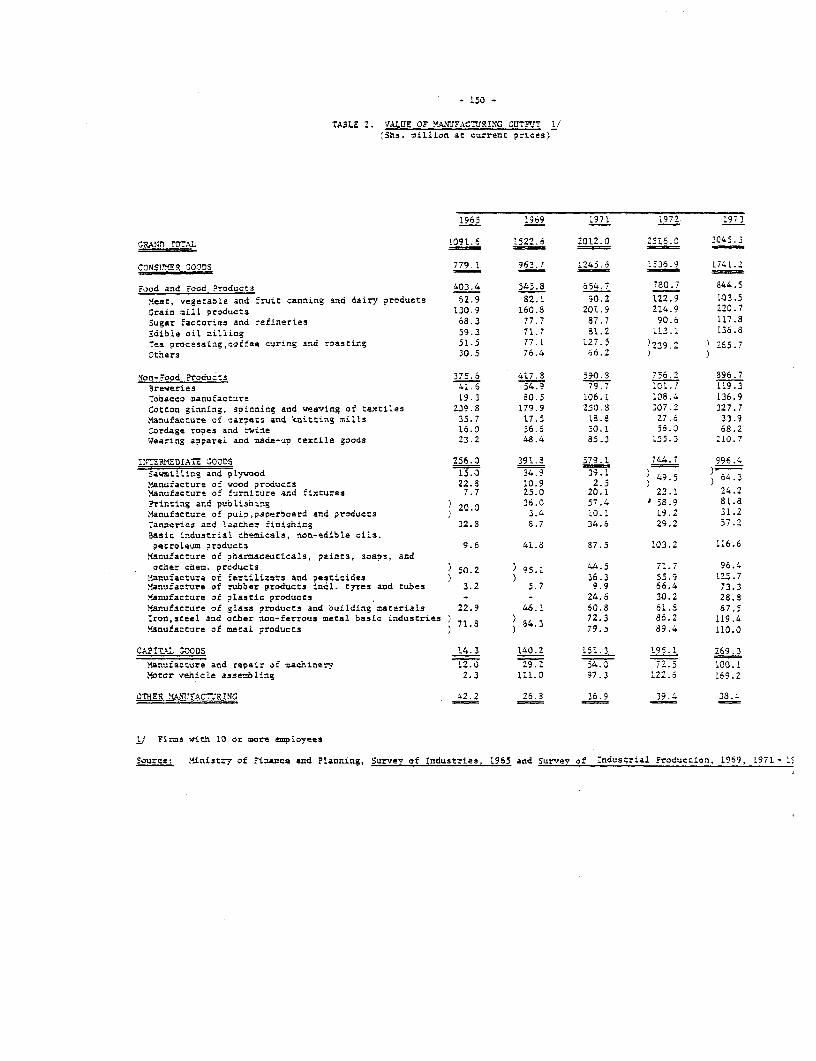

2. Value of Manufacturing Output

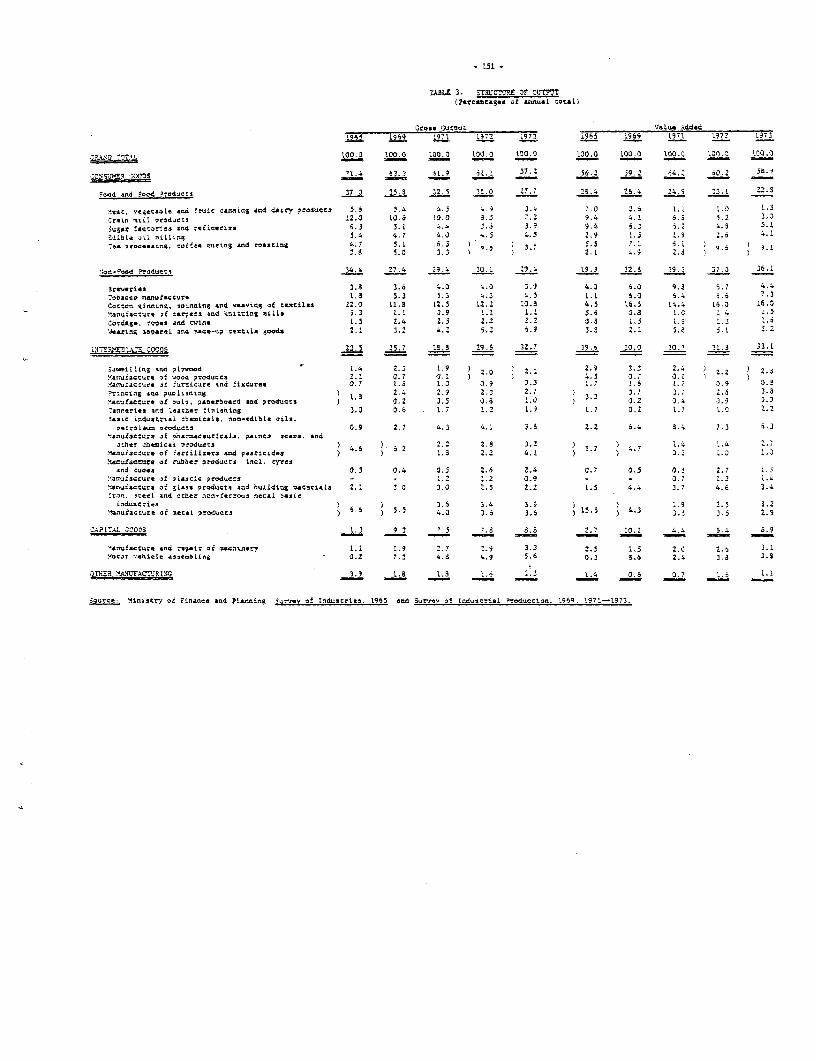

3. Structure of Output

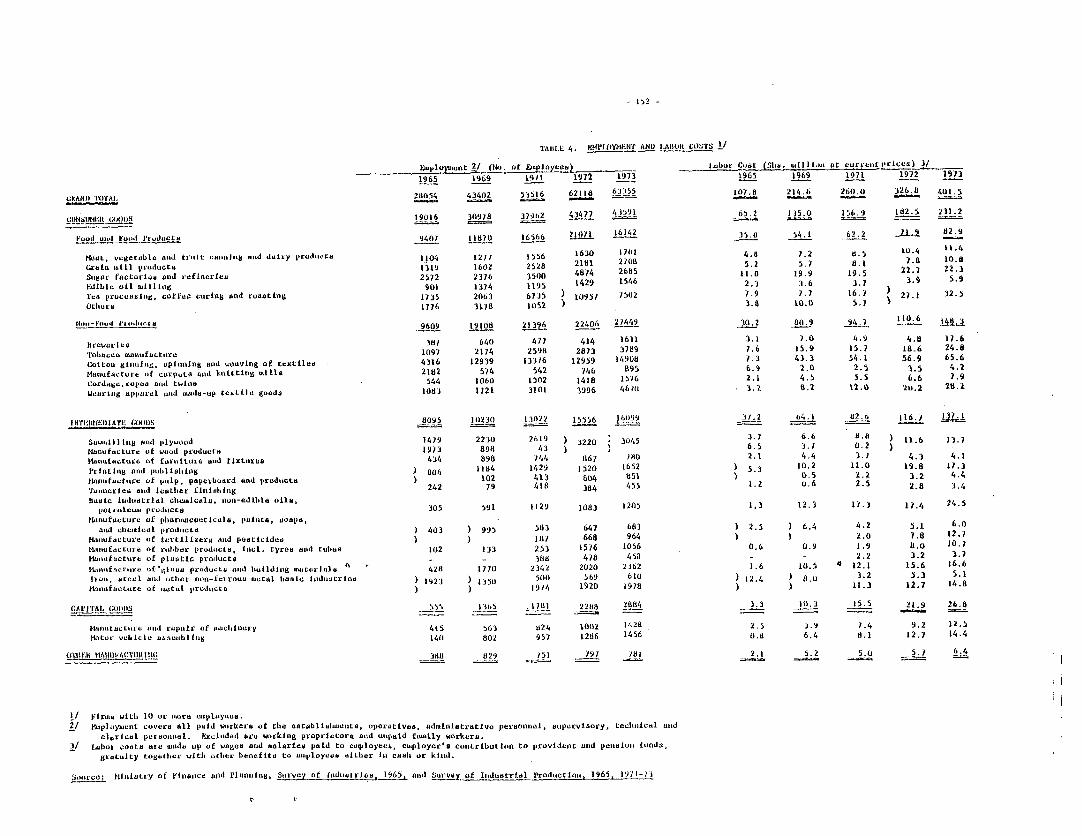

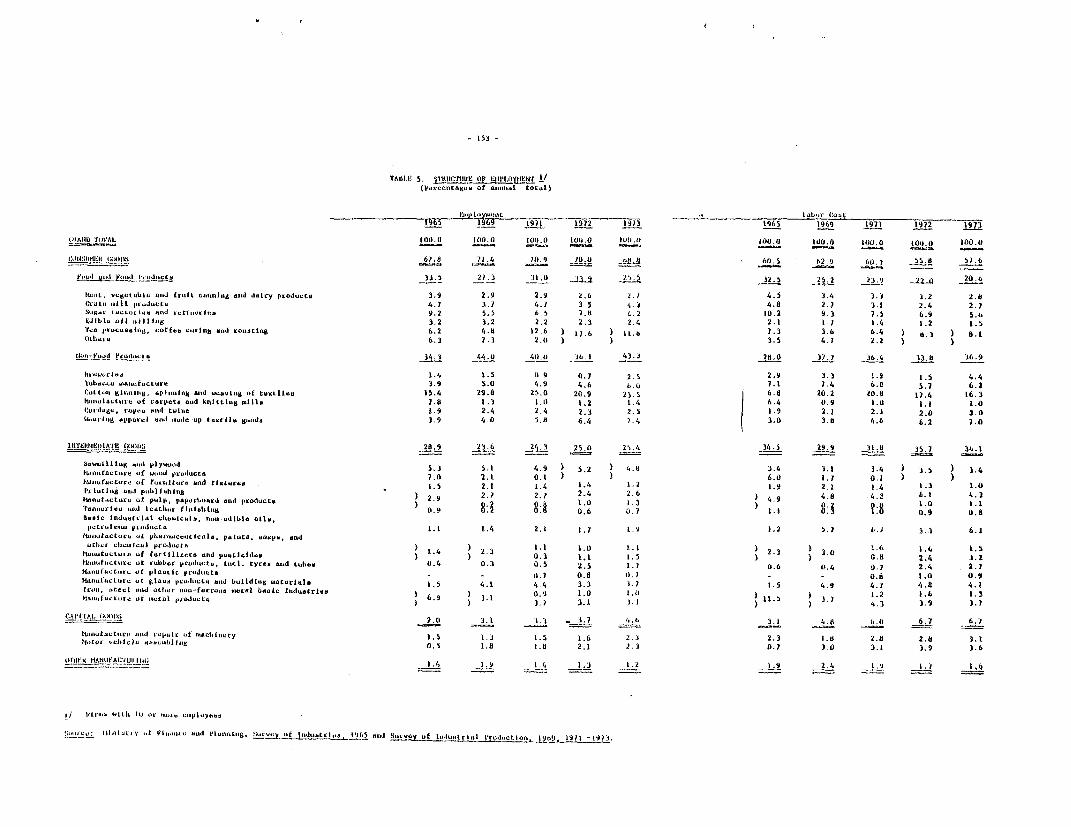

4. Employment and Labor Costs

5. Structure of Employment

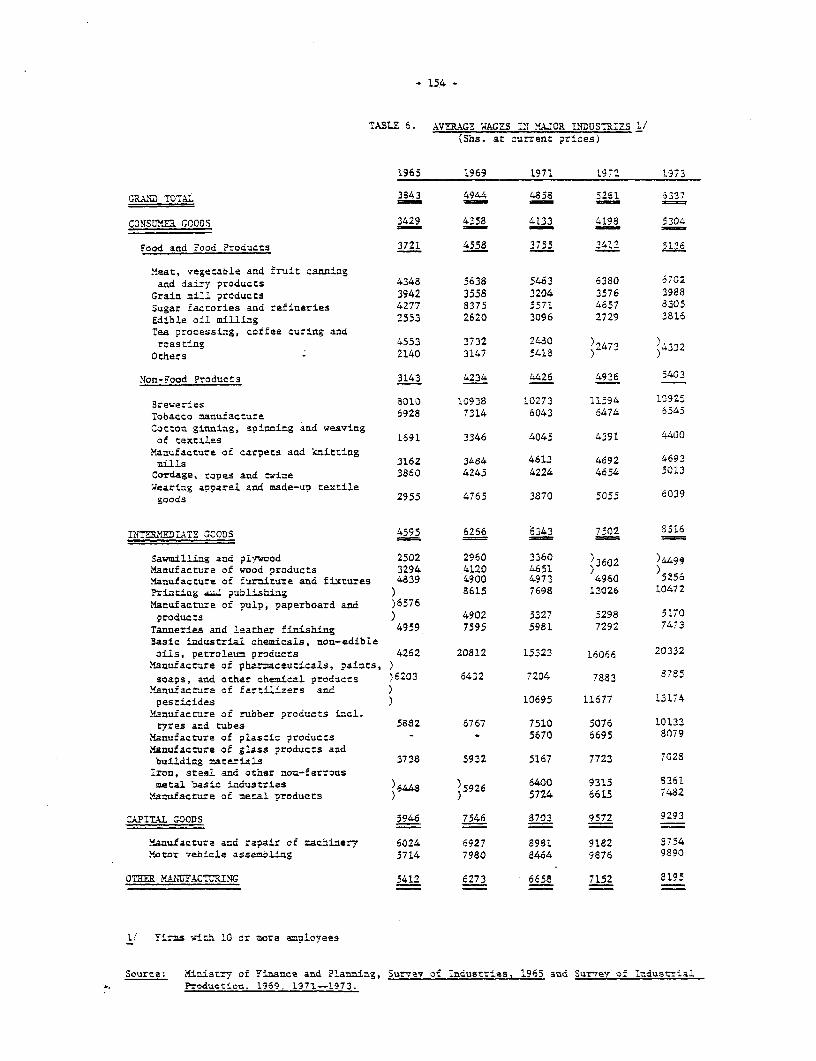

6. Average Wages in Major Industries

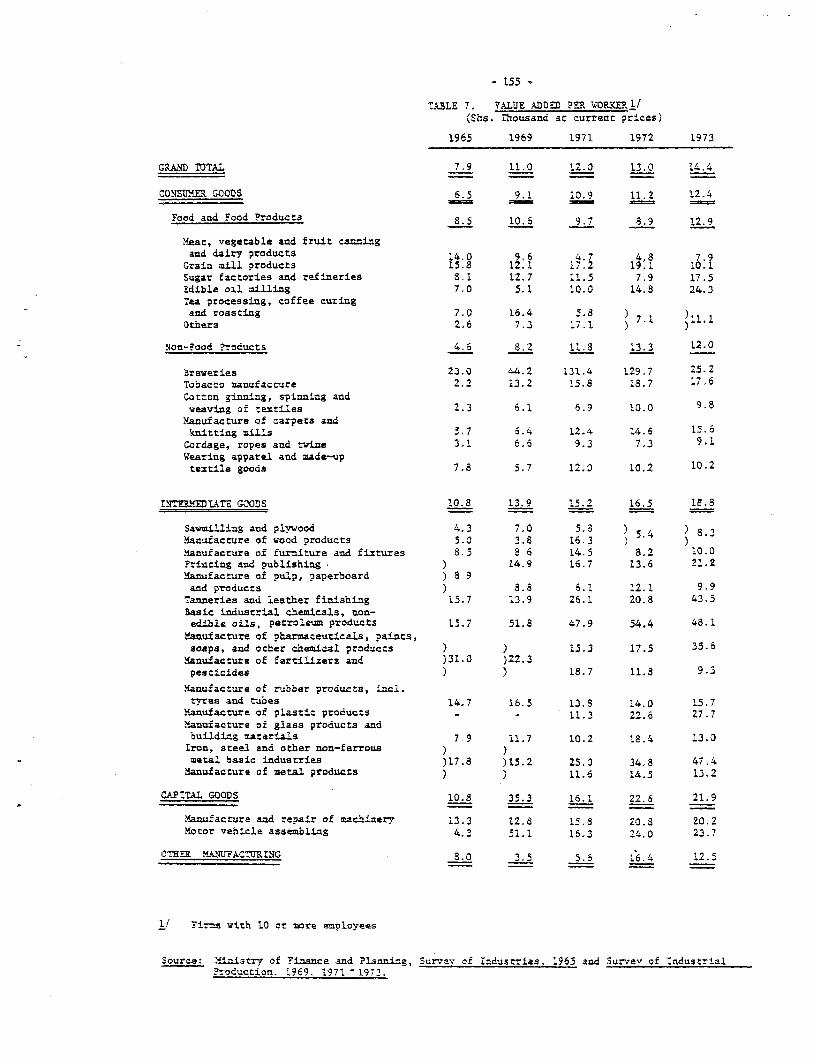

7. Value Added Per 'Worker

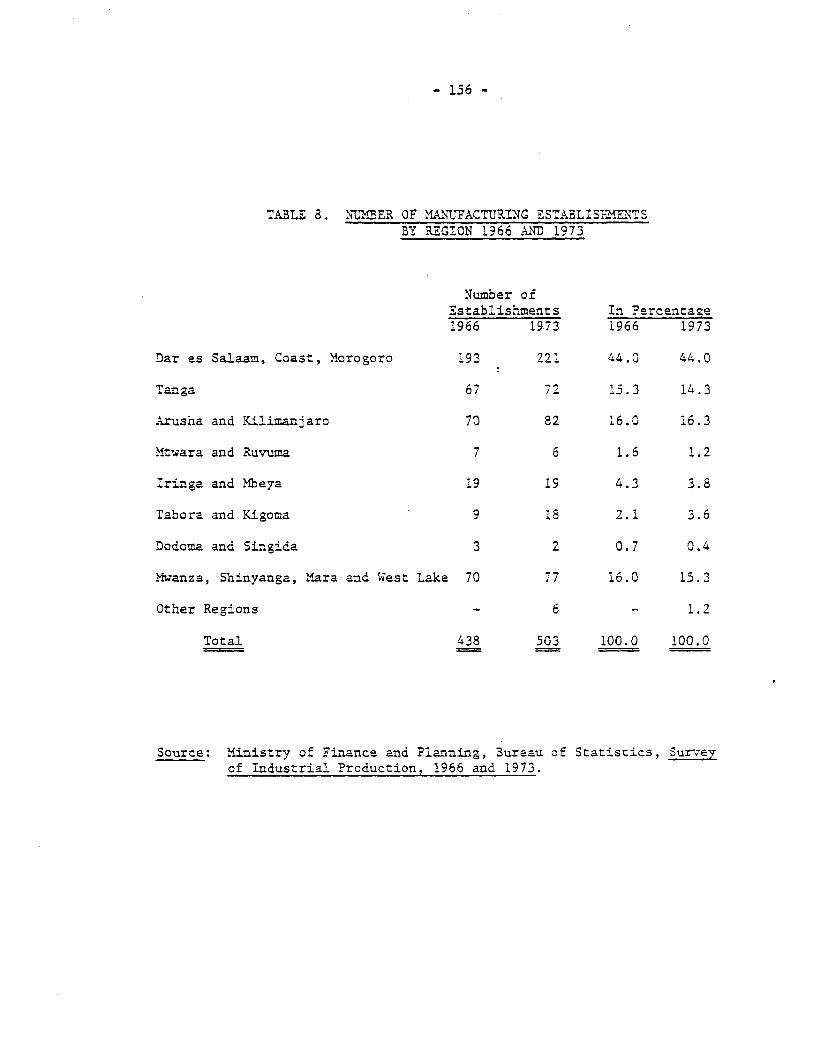

8. Number of Manufacturing Establishments by Region,1966 ard 1973

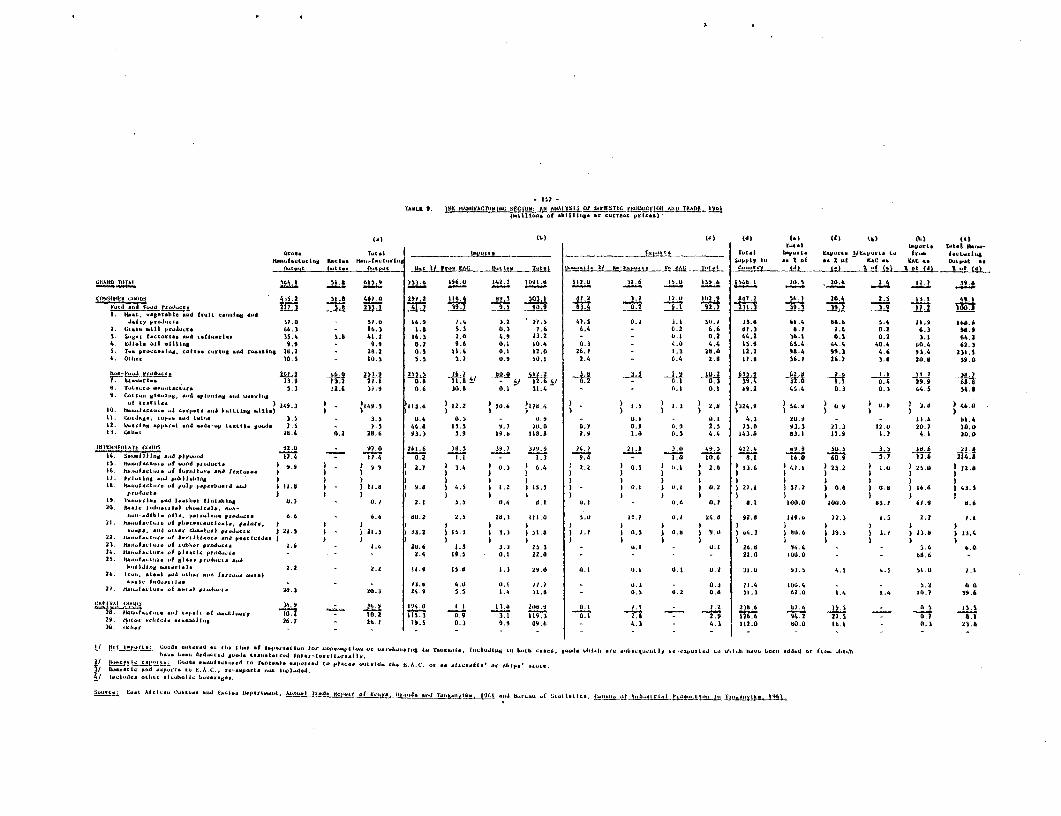

9. The MaLnufacturing Sector: An Analysis of DomesticProduction and Trade, 1961

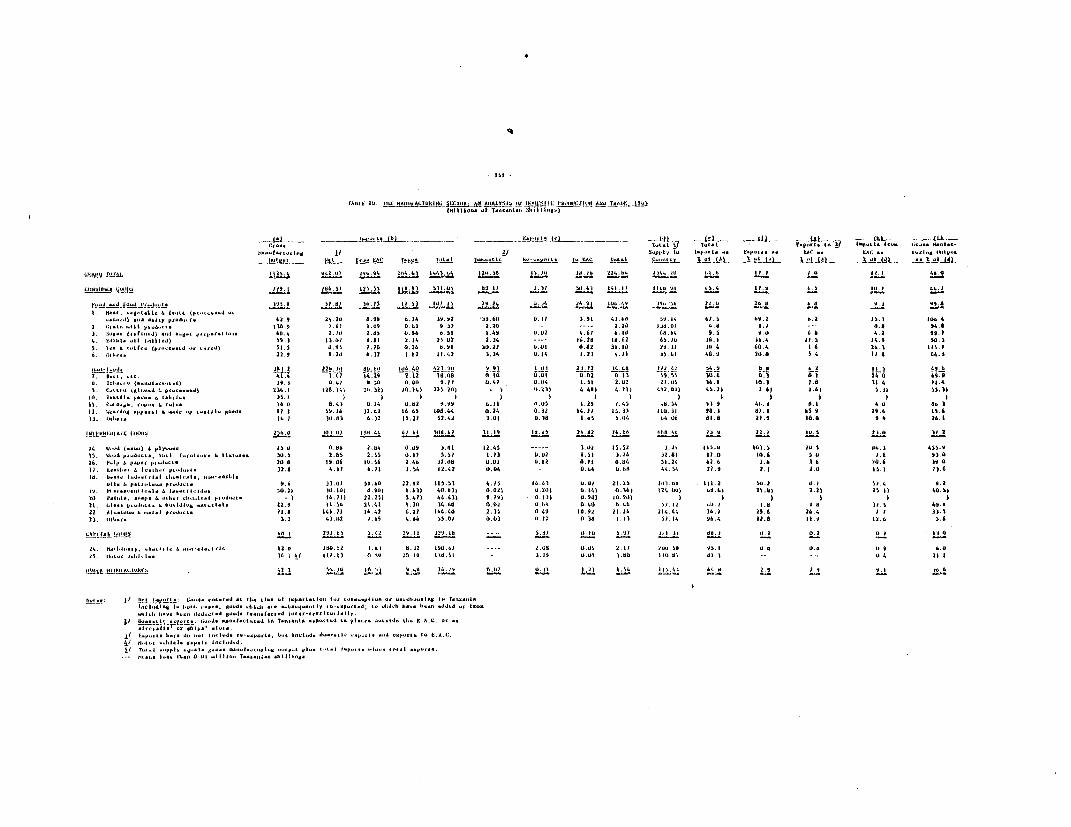

10. The Manufacturing Sector: An Analysis of DomesticProduction and Trade, 1965

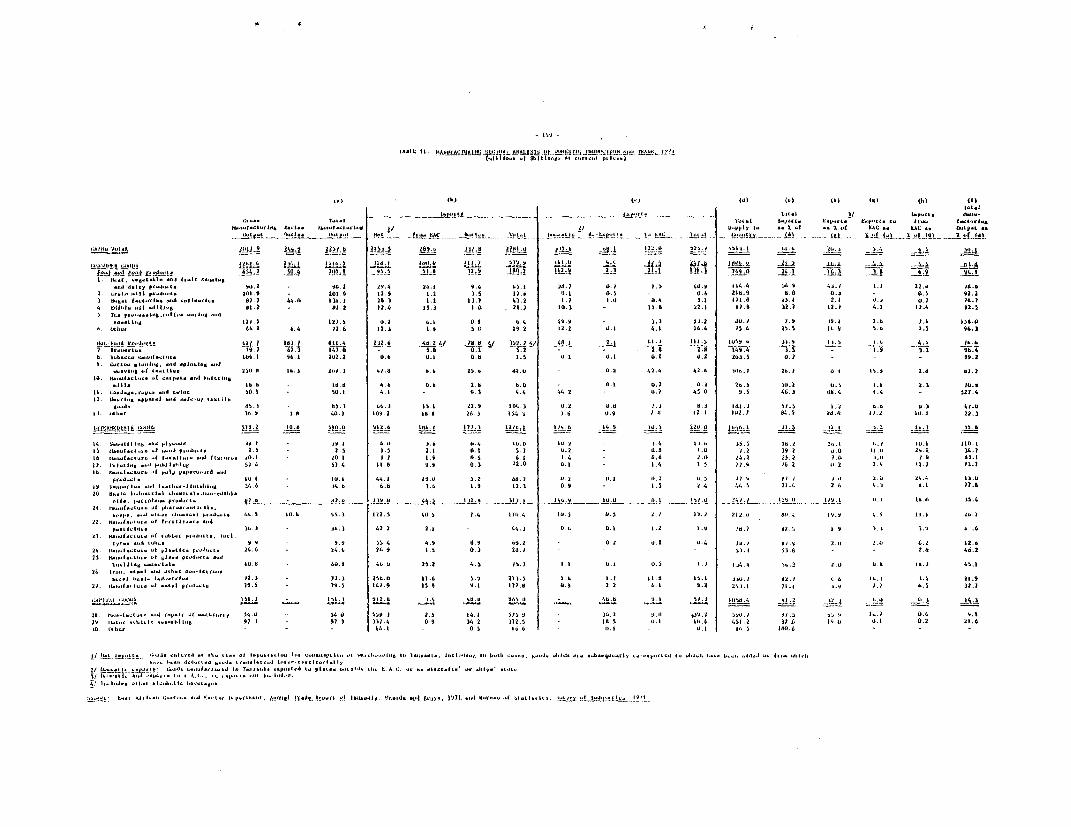

11. The Manufacturing Sector: Analysis of DomesticProduction and Trade, 1971

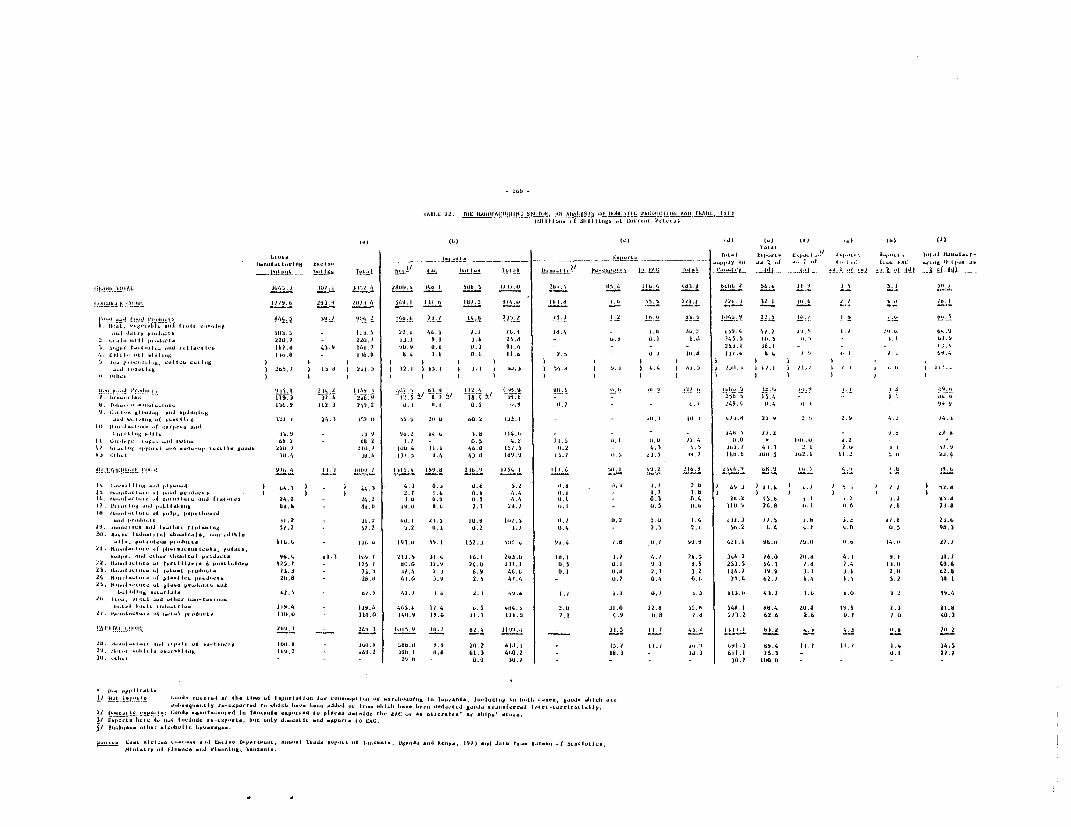

12. The Manufacturing Sector: An Analysis of DomesticProduction and Trade, 1973

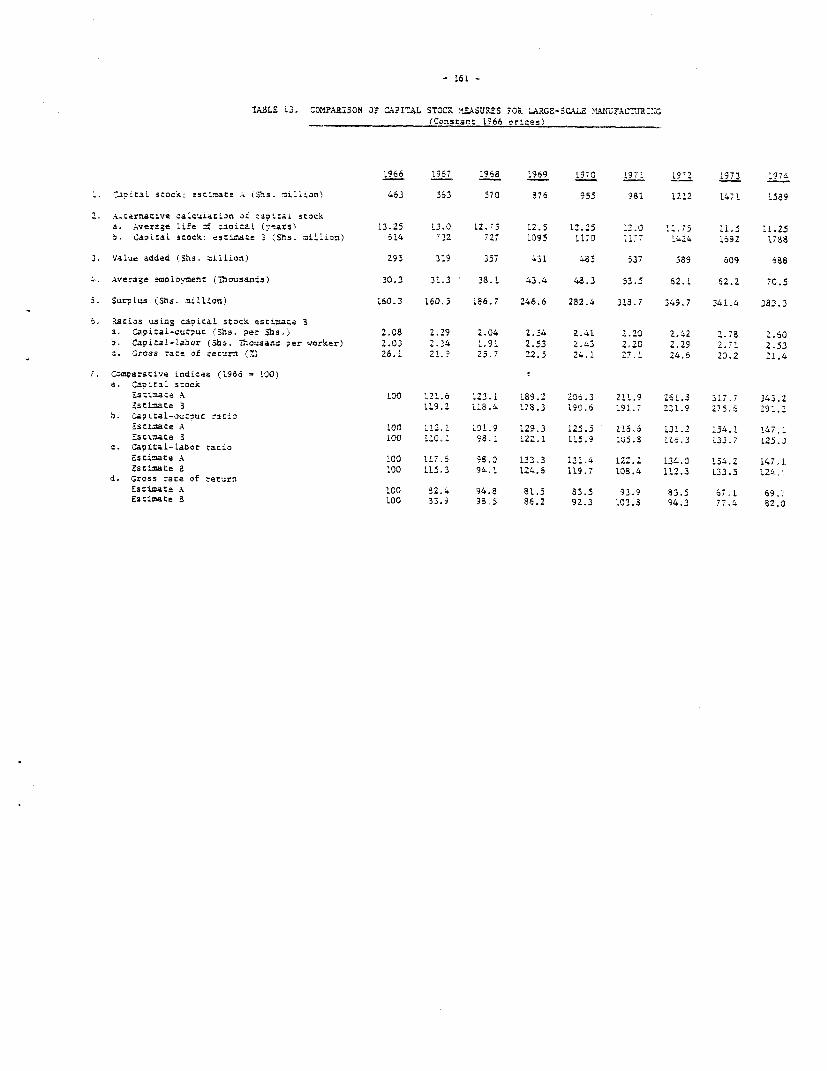

13. Comparison of Capital Stock Measures for Large-Scale Manufacturing

CHAPTER I. RE ROLE OF INDUSTRY IN TANZAINIANDEVELOPF_UT STRITEGY

A. Industrial Strategy in the Past

Strategy After Independence

1.1 At the time of indenendence in late 1961, Tanzania had only arudimentary industrial structure. The largest single manufacturing sub-sector was cotton ginning. There was no factory production of textiles,shoes, cement, or cigarettes. Beer and sugar were produced but did notmeet domestic demand. The only export industries were canned meat andwattle extract. There were numerous small establishments producingclothing, bread, bricks, footwear, and the like, mostly owned by Asians.Total manufacturing employment was about 20,000 out of a total populationof around 10 million and manufacturing and handicrafts contributed lessthan 5% of GDP.

1.2 The newly-independent Government inherited an industrialstrategy based upon reports by Arthur D. Little and the World Bank. 1/This strategy was to encourage private investors (mostly foreign) toproduce a few simple goods for the domestic market. Processing of localraw materials for export was seen as a longer-term possibility, but forthe moment the most promising prospect was to substitute domestic produc-tion for the import of cotton textiles, cigarettes, shoes, beer, sugar,cement, and tires. The World Bank's sober assessment was that thisprogram of import substitution, while large in relation to existingcapacity, would add only 3% to existing GDP.

1.3 The First Five-Year Plan (22X2)2/ published in 1964, proposeda more ambitious program of industrial development without changing thebroad outline of the inherited strategy. The analysis underlying theFFYP strategy was that industrialization was limited by two factors: theavailability of capital and the extent of the market. The capitalconstraint could only be overcome by reliance on private, including foreign

1/ Arthur D. Little, Inc., Tanganyika Industrial Develovment (Dar esSalaam: 1961); IBRD, Economic Development of Tanganyika (Baltimore:John Hopkins Press, 1961). See also Government of Tanganyika,DeveloDment Plan for Tanganyika, 1961-1962, 1963-1964 (Dar es Salaam,Government Prircer, 1961)

2/ The United Republic of Tanganyika and Zanzibar, Tanganyika Five-YearPlan for Economic and Social Development 1st July, 1964 - 30th June1969 (Dar es Salaam: Government Printer, 1964)

- 2 -

investment. .hree-cuarters of total industrial invest-ent during theFir-st Plarn oeriod was to come from the private sector. The Governmentwas preparad to participate in financing through its Tanganyika evelop-menc Corporation, but the ain policy instr=ments to achieve ind.ustrialinvestment targets were to be accelerated deoreciation allowances, tariffprotection, and guarantees for the repatriation of capital.

1.4 Thne market constraint was to be loosened bv a charge ir therules of the East African Common Market. The Common Market with Ugandaand Kenya had been in force since 1927 and was widely regarded as anobstacle to Tanzanian industrial development. Kenya, with a largerexisting industrial base, attracted a disproportionate share of industrialinvestment. Under the relativ-ely unrestricted customs union which existedat the time of indenendence, Tanzania not only had little hope of attract-ting industries which would produce for the entire Common Market, but alsohad difficulty in setting up industries to substitute for imports ofKenyan manufactures. President Nyerere had attempted to achieve Politicalfederaticn which would have preserved a full customs union, but when thatfailed Tanzania sought greater scope to pursue an independent industrialpolicy. The result of these efforts was the Kampala Agreement of 1964which modified the rules of the Common Market and widened the potentialmarket for Tanzanian industry in two ways. First, it permitted Tanzaniato impose restrictions on some partner state imports, thereby givingprotection to local import substitution irdustries. Second, it set up alicensing procedure which reserved to each of the partner states theproduction of several industries which depended on the entire regiornalmarket. Tanzania was allocated aluminum rolling, tires, and radioassembly. Although Kenya never ratified the Kampala Agreement and laterset up some of these same industries, production was started in Tanzaniain the expectation cf obtaining the entire Common Market.l/

1.5 The First Five-Year Plan did move beyond the Three Year Planin some ways. It proposed a wider range of import substitute investmentsfor the domestic market, including rolled steel, oil refining, andfertilizer. it also proposed that processing of sisal and cashews forexport be initiated on a modest scale. Finally, it extended the conceptof import substitution to embrace the entire East African Common Market.Nevertheless, industrial strategy remained broadly consistent from thetime of independence until the Arusha Declaration. rne aim was toincrease the rate of economic growth by exploiting some obvious opportu-nities for industrial investment. The fact that most of these opportunitieswere for the import substitution of simple consumer goods or buildingmaterials was inC4dental; no signiflcance was attached to the nature of

1/ J.F. Rweyemamu, Underdevelooment and Industrialization in Tanzanria(Nairobi: Oxford University Press, 1973), p. 119. Chapters 2 and 4of this book give a detailed analysis and c-iti'ue of Tanzanianindustrial strategy through 1971.

-3-

either the product or of the market. There did not even appear to be anyparticular significance attached to industrialization as such; manufactu-ring output was valued largely for its potential contribution to GDPrather than for its linkage effects, external economies, or role instructural transformation. The early industrial strategy also paid littleattention to three other aspects of industrial structure: pattern ofownership, choice of technique, and comparative advantage. The Tanzanianleadership would probably have preferred public, or at least local,ownership of industry, but this was not viewed as a serious possibilitygiven the capital and managerial requirements of the industrial program.There is little evidence that much thought was given to the choice oftechnique; increased employment was a professed aim of industrializationbut there seems to have been little consideration of the possibility ofsystematically promoting labor-intensive techniques or sectors, nor tothe likely effect on employment growth of promotional policies such asaccelerated depreciation allowances. Comparative advantage and productioncost considerations were also neglected. Tariffs were usually establishedthrough negotiations with investors and tariff levels varied amongstindustries. If the level of protection proved to be too low, the tariffmight be raised again as happened in the case of radio assembly. Nominalrates of protection for new industries usually ranged between 33% and50%, but effective rates of protection ranged from negative to over 500%.1/

Post-Arusha Industrial Strategy

1.6 The Arusha Declaration charted a completely new course forTanzania based upon socialism and self-reliance. It reversed a basicprinciple of previous industrial strategy; dependence on foreign invest-ment as the major instrument of industrial development. Henceforth, mostmajor industries would be publicly owned and most new investment could bemade by the public sector. Foreign investment could no longer be theprincipal agent of industrial development, first, because the requisiteamounts of foreign capital were not forthcoming and, second, becausedependence on foreign investment would not be consistent with politicalindependence, self-reliance, or socialism. As the Declaration put it,"Th.e policy of inviting a chain of capitalists to come and establishindustries in our country might succeed in giving us all the industrieswe need, but it would also succeed in preventing the establishment ofsocialism unless we believe that without first building capitalism, wecannot build socialism".2/

1/ See Rweyemamu, pp. 130-137, and D. Kessel, "Effec-ive Protection inTanzania", East African Economic Review, (June, 1968).

2/ Julius K. Nyerere, "The Arusha Declaration," reprinted in UJamaa -

Essays on Socialism (New Y7ork: Oxford UnTriversity t ress, 1968),p.26.

-4-

1.7 A second consequence of the policy changes following the ArushaDeclaration was increased attention to employment creation in industry.One concern which led up to the Declaration was the rapid growth of wages,particularly in large-scale industry. This was believed to be respcnsiblefor growing inequality between urban' workers and peasants and for thestagnation of overall employment growth. A new incomes policy based uponan ILO report was introduced to reverse these trends.l/ The wage guide-lines establi shed by the new incomes policy set an upper limit of 5% forannual wage increases.

1.8 The Arusha Declaration also attempted to define the role ofindustry within the overall strategy of economic and social development.A major theme of the document was that too much emphasis had been put onindustry in the past. Tanzaria could no:t establish very much industrybecause it had neither the =oney nor the expertise to do so, and depend-ence on foreigners was no.t acceptable because it jeopardized self-relianceand socialism. More fundamentally, reliance on industrialization as theprimary agent of development was to confuse means and ends. Industry,like money, was a consequence rather than a cause of development."Industries will come and money will come but their foundation is the?eople and hard work, especially in AGRIC'ULTURE. This is the meaning ofself-reliance." 1/

1.9 This stress on agriculture and rural development and thedisparagement of the importance of industry created in some minds anexpectation that Tanzanials industrial program would be'drastically cutback. It is doubtful if that was ever the intention. The intention wasto exhort people to greater effort - to persuade them that developmentdid not mean having what developed countries have (a l'ot of money andmodern industries) but that it meant acquiring the skills and attitudeswhich would enable Tanzanians to be as productive as people in developedcountries. Development was seen as the development of people, not asincome growth or structural change. But since the development of peopleis not primarily a matter of investment, this did not mean that investmentin industry would be greatly changed. The Arusha Declaration made noconnection between the structure of production and its underlying conceptof development. It therefore had almost no implications for the structure

1/ International Labour Organization, Report to the Government of theUnited Republic of Tanzania on Wages, Incomes and Prices Policy,Government Paper No. 3, (Dar es Salaam: Government Printer, 1967).This is frequently called the Turner Report after its authorProfessor H.A. Turner. The Government's response was contained inUnited Republic of Tanzania, Wages, Incomes Rural Development,Investment and Price Policy, Government Paper No. 4, (Dar es Salaam:Government Printer, 1967).

2/ Nyerere, "The Azrusha Declaration", p. 33 .Iiphasis in. the original.

of production and investment, though it did of course imply a betterdistribution of income between urban and rural areas. In the absence ofany link between the production structure and development, as implici lydefined in the Arusha Declaration, investment in industry was to continuemuch as before, except that now it would be undertaken by public enter-prise.

1.10 This interpretation of the strategic implications for industryof the Arusha Declaration is supported by subsequent development plans.The Second Five-Year Plan (SFYP),1/ published two years after the ArushaDeclaration, set a target rate of growth for manufacturing of 13.0%,exactly double the target rate of 6.5% for total GDP. This differedlittle from the First FY? (which had also declared agriculture to be thefoundation of development) with a planned rate of industrial developmentof 14.8% and a target rate for total GDP of 6.7%. President Nyerereendorsed the new industrial growth targets in a speech introducing theSecond FE?.

1.11 In addition to being ambiguous on the size of industrial program,the Arusha Declaration gave no positive guidance on the content. Thisuncertainty about the appropriate content of industrial investment, andthe basic continuity with previous industrial strategy, are reflected inPresident Nyerere's sul-Azry of industrialization plans for the SecondFive-Year Plan period.

"We shall continue to expand simple manufacturing, the process-ing of primary commodities, and the provision of basic constr-uction materials; but we have now reached the stage where wemust think seriously about the next and more difficult phase ofindustrialization. For it is comparatively easy to produceyour own textiles, cement, and similar goods; beginning toproduce your own capital goods, and goods which are used onlyin the production of other things, is a more complex operatior.and demands a more sophisticated degree of economic planning.Yet such a move is essential for long-term growth; an importanttask which will be undertaken early in the Second Plan periodis the preparation of a long-term in.dustrialization ?lan, takinginto account the possibilities of the East African CommonMarket and of exports. The aim is that we should be ready toembark on this kind of work at the very beginning of the ThirdPlan.

Let me just add one further point. Although mass productionis the best and cheapest way of meeting the needs of our people

1/ United Renublic of Tanzania, Tanzania Second Five-Year Plan forEconomic and Social Develosment 1st July, 1969 - 30th june. 1974(Dar es Salaam: Government Printer, 1969).

-6-

for certain types of goods, there are many others where the needscan be best met by labour intensive, small-scale industriesand craft workshops. Obvious examples of this are furniture,which can be made locally from local materials without theproblem of transportation over long distances; ready-madeclothes, and local food preservation. It is vital that weshould increase our efforts in this matter, for such activitieshave the further advantage that they require very littlecapital investment, and they can be carried on in the villagesand small towns of our country, thus improving the quality andvariety of life in the rural areas."I/

!.12 The industry chapter of the Plan extended the range of possibi-lities. In addition to producing simple import substitution goods,intermediate and capital goods (later), manufactures for exports,manufactures for the East African market, and simple manufactures fromsmall-scale industries, the Plan provided that industry was to bedecentralized, labor-intensive techniques were to be encouraged, socialcost-benefit analysis was to be used to evaluate all industrial investmentsconsistently, and cost reduction was to be enforced through reducingtariffs over time. A case could be made for each of these proposals onits own, but taken as a group, they did not add up to a coherent industrialstrategy. The industrial section of the Plan as it finally emerged waslittle more than a list of 385 projects of which 70% were expected to becompleted.

1.13 The Arusha Declaration changed the ownership pattern of industryand, through the new incomes policy, sought to increase the rate ofemployment growth and to improve the distribution of income between urbanand rural areas. Fowever, it did not appreciably affect industrialstrategy in any other way. There was increasing concern about whatindustrial products should be produced, the market orientation of industry,the cost of production, and linkages with other sectors, but no guidingdoctrine emerged nor was there any visibly coherent pattern of policywith respect to these aspects of industrial strategy. The definition ofa long-term industrial strategy was left as an exercise to prepare for theThird Five-Year Plan.

1/ United Republic of Tanzania, Tanzania Second Five-Year Plan, Vol. 1,p. xiii.

B. Alternative Strategies of SocialistIndustrial Development

1.14 After the Arusha Declaration there was general agreement thatTanzania must pursue a socialist industrial strategy. Hiowever, apartfrom the implication that the role of the private sector would be limiced,there was little agreement about what constituted a truly socialiststrategy. While not everyone concerned with Tanzania industrial policy had afully-articulated strategy, most subscribed, either implicitly or explicitly, toone of four main models of socialist industrial development: a maximumgrowth strategy, a processing strategy, a basic industry strategy, or asmall-scale industry strategy. As presented below, the distinctionsbetween these alternative models are heightened and individual variationsare minimized in order to keep the discussion within manageable bounds.While no single individual might agree with every aspect of the idealtypes which are presented, the mcdels do give a fair summary of therange of conflicting views of the role of industry in socialist develop-ment.1/

Maximum Growth Strategy

1.15 Perhaps the dominant model of industrial development duringthe late 1960's and early 1970's was the maximum growth strategy. Inthis strategy industrialization is seen as the main engine of growth cfthe economy. Industry is valued for its contribution to GDP andindustrial projects are selected on the basis of their rate of return.No importance is attached to what, how or for what market a product isproduced; it matters only whether a product is in demand and can be.produced at a cost which gives an acceptable rate of return. In practice,cost considerations tend to favor light industrial products for importsubstitution or the processing of local raw materials for export, andthe use of relatively labor-intensive techniques of production, but thisis an incidental result of the search for projects which would maximizethe growth of GDP.

1.16 There are two main streams of thought within the group ofmaximum growth strategists. The first, and most influential, is the"state capitalist" school. This was best exemplified in the late 1960'sby the National Development Corporation which became the princiDalindustrial development institution after the Arusha Declaration. TheNDC model of development depended on the establishment of independent,state-owned firms (parastatals) which would act as profit maximizers.

1/ Much of the discussion in this section is based upon an unpublishedpaper by M. Roemer, "Models of Socialist Industrial Development",(Dar es Salaam: mimeo, September, 1972).

NDC's role was to identify the most profitable investment opportunities(with some allowances made for employment and foreign exchange benefits)and then to set up a subsidiary company to produce the goods. Thesubsidiary parastatal was then supposed to operate much like a capitalistfirm, seeking out the most profitable product lines and searching forways to reduce costs of productior.. The parastatal sector did not havethe resources to produce all the manufactured goods possible, of course,so a sizeable amount of residual manufacturing would be left to theprivate sector. Cooperatives would be encouraged to compete with theprivate sector wherever possible and the parastatal sector would graduallyexpand its share of manufacturing production.

1.17 Since the Arusha Declaration did nct have a clearly statedindustrial strategy, the state capitalist version of the maximum growthstrategy became the actual Tanzanian strategy by default. However, thestrategy has not worked in practice quite as intended. AJthough parastatalproduction has expanded rapidly and with little regard to the type ofproduct vroduced, the technique of production, cr to market orientation,the parastatal sector has not been as cost-conscious as the ideal set bythe maximum growth model. Ideally, a parastatal considering productionof a new product would ask, "Can it be produced efficiently?" Tanzanianparastatals have tended to ask only, "Can it be Droduced?" In bothinvestment and production decisions the parastatal sector has not respondedwell to market signals which indicate that costs are too high., Whenmarket signals have impinged upon parastatal thinking - for example, whenlosses are being made - the response has frequently been to try to removethe market cnnstraint by securing a higher product price or by convertingloans to ecuity, rather than to try to reduce costs. In spite of thislapse, the ideal of the state capitalism model remains for independentstate enterorises to maxi'mize profits (and reduce costs) subject to theconstraints of existing market prices.

1.18 The second variant of the maxiJum growth strategy is the"market socialism" model. This has been advocated largely by professionaleconomists (frequently foreign) and is based on the well-known Lange-Lerner model.I/ Yugoslavia is probably the closest working model ofmarket socialism, thiough the Yugoslav economy differs significantly fromthe Lange-Lerner ideal. The market socialism model pays more attentionto the policy framework within which parastatals operate than does thestate capitalism model. Independent state-owned firms (worker-managedfirms in Yugoslavia) would still seek to maxi.mize profits, but decisionswould be based uvon social costs and benefits rather than commercial costsand benefits as in the state capitalism model. Investment decisions, forexample, would be based upon social cost-benefit analysis using shadow

I/ 0. Lange, On the Economic Theory of Socialism, (Minneapol4s: Univer-sity of Minnesota Press, 1938); and A.P. Lerner, The Economics ofControl,(New York: Macmillan, 1944).

- 9 -

prices or, better yet, market prices would be brought into line withshadow prices. Since the social cost (shadow price) of foreign exchangeand capital is higher than the market price and the social cost of labor(shadow wage) lower than the market wage in Tanzania, a market socialismstrategy would tend to favor labor-intensive production techniques andprojects bringing quick foreign exchange returns even more than the statecapitalism model. As in the state capitalism variant, however, thestructure of production which results is due to the attention paid tocomparative advantage and the cost of production rather than to any dogmathat labor-intensive, export-oriented industries are always better.

1.19 A maximum growth strategy of either the state capitalist ormarket socialist variety has several drawbacks. First, it may be diffi-cult to reconcile maximum growth with certain socialist objectives suchas minimizing the use of material incentives or increasing worker parti-cipation.l/ The difficulties encountered by some parastatals in ea-rningthe profits expected of them is partly due to an incentive structurewhich inadequately focuses the attention of planners, managers, and workerson efficiency and profit maximization. The problem of devising anincentive structure which adequately reconciles growth-efficiency withequity-participation objectives is discussed in more detail in a latezsection.

1.20 A second drawback is that the strategy may not be effective inmeeting its own major goal of maximum growth in the long run. Commercialcost-benefit analysis, orn which the state capitalism strategy is based,does not adequately take account of linkages or training effects whichcreate external economies for other industries. Social cost-benefitanalysis, on which the market socialism strategy is based, takes accountof these benefits in principle, but in practice frequently ignores thedifferential training effects of alternative projects because they aredifficult to quantify. This means that the maximum growth strategy mayignore infant industries with high long-term growth potential. In thelong run, the non-quantifiable benefits of certain industries may outweighthe gains of maximizing short-term comparative advantage.

1.21 A third criticism of the maximum growth strategy is that it basesdecisions on distorted market prices. On the production side, alternativeproduction structures will generate different sets of future pricestructures (in spite of international trade) owing to linkages amongindustries and to differential productivity growth from learning by doing.On the consumption side, relative prices and profitability reflect thepresent inegalitarian income distribution. The state capitalism model

1/ For a discussion of the way in which worker-managed firms may bebiased against growth see J. Meade, "The Theory of Labour-ManagedFirms and Profit-Sharing," Economic Journal, Vol. 82, No. 325supplement (March, 1972), pp. 402-428.

- 10 -

bases ali production and investmenr decisions on these distorted prices,n or bcialysm a-1 distortions could be corrected by the use

c: ie-; orzl'care- s-acow p but as a oract-ical matter, manz of thediscoroSrzls rwoull Se Le _ .Z-ected because of the scarcityr of o'u-li_iedproject analysts and the zressures to make timely investment decisions.

I1. 22J A^. final criticism of the maximum growth strategy is tnat it ismarginal_st. The method of analysis is based on small (marginal) ch:angesand therefore is frequently biased against major structural change. Itis not just that the strategy may reject a particular structural changebecause its cost in terms of foregone growth would be high. It is alsothat the maximum growth strategy may not even envision possible structuralchange which would be perfectly consistent with high growth. This iscue to the short-cern rocus and deceatralized decision-making characteristicof the planning mechanism under thle strategy. Most projects are proposedby parastatals which tend to propose only marginal changes ±n the existingeconomic structure; rroects are appraised as they are generated and areapproved or rewecr_ed according to whether they meet some acceptable=inimum rate of return and fit within the short-term budget. Withoutsome more purposeful vision, a maximum growth strategy is unlikely torestructure the economy in a major way.

Processing Strate2y

1.23 A second strategy frequently proposed in the post-Arusha periodis a processing strategy. Emphasis is placed on processing major rawmaterials - cotto.., cashews, sisal, h'des and skins - before exportingthem. To a lesser extent, the strategy also stresses substituting processeddomestic materials for manufactures produced from imported raw materials:for example, using tile rather cor-rugated iron sheet roofing, bricks ratherthan cement, cotton textiles rather than blended fabrics, and leatherrather than rubber or plastic shoes and sandals. In 1974 the Governmentendorsed an investmenc program heavily inf-luenced by the processing strategy.(Ironically, this occurred just as the Planning Commission was pre?aringa report to,recommend a long-term industrial strategy based on the basicindustry strategy which is largely incompatible with a processing strategy).The Economic Committee of the Cabinet (ECC) approved sectoral investmentplans which provided for processing of all hides and skins into leather,processing of about half the cashew crop, processing of three-fourths or-ore of sisal production, and a tripling of cotton textile production, allby 1980. At the same time, official statements called for sharply increa-sed brick production to substitute for imports of cement and for processingof 60% of the cotton crop, which implied arn even larger expansion oftextile production than approved by the ECC.

1.24 Although the ECC approval was only an endorsement in principleand hence subject to later reversal or modification, it showed the appealto Tanzanians of a processing strategy of industrial develooment. Externalfinancing of a substantial portion of the cashew and leather processingproposals by the World Bank and others suggested that a processing strategyapoealed to ex-ternal donors as well. In the case of outside agencies,the appeal probably stemmed from a oresunvticn that Tanzania has a

- 11 -

comparative advantage in processing. For Tanzanian planners, the appeal ismore complex. Some support a processing strategy because they also believethat Tanzania's comparative advantage, and best growth prospects, lie inincreased processing for export. For others, a processing strategy is aconvenient tool for identifying the next step in industrializaticn; it peformsthe same identification function as the imoort substitution strategy and isbased on a similar premise that any investment is desirable so long as itproduces incremental value added. For yet others, processing for export isthe most obvious way to earn much-needed foreign exchange. Finally, theprocessing strategy also appeals to a large number of people because it wouldbreak the colonial tra2:a pattern of exporting raw materials and therebvreduce dependency, improve the terms or trade, and end the exploitationincnerent in producing raw materials for otners to manufacture.

1.25 The main criticism of the processing strategy is that it maynot perform any of the roles expected of it. The presumption that Tanzaniahas a comparative advantage in processing for export is brought intoquestion by industry studies prepared for the long-term industrial strategyexercise in preparation for the Third Five-Year Plar../ Cashew processingin Tanzania has never been profitable at commercial prices; despite somenatural transport protection, neither hand nor machine urocessing inTanzania has been competitive with Indian hand processing. It was onlymarginally efficient at shadow prices in 1973; since that time capitalcosts of machine srocessing have tripled, wages have risen by about 60%,and the processing margin (the difference between the value of a ton ofraw nuts and the value of a raw nut ton-equivalent of kernels) has decreasedby 5%.2/. It is also questionable whether Tanzania has a comparative advantage

1/ The studies were done during 1973-74 by a group of foreign economistsLrom the Harvard Institute for International Development in collabora-tion with Tanzanian colleagues in the former Ministry of EconomicAffairs and Development Planning (Devplan). A si=ary is given inM. Roemer, G. Tidrick, and D. Williams, "The Range of Strategic Choicein Tanzanian Industry," Journal of Develoment Economics 3(1976),pp. 257-275.

2/ Based on the 1973 and 1975 export statistics and assuming a 22.5%outturn of kernels per ton of raw nuts, the margin between a raw nutton-equivalent of kernels and a ton of raw nuts fell from Shs 699 in1973 to Shs 665 in 1975. Fortunately for the rate of return onprocessing (though not for the economy as a whole), the processingmargin increased in 1976 to Shs 1586 according to preliminary estimates,This may reflect one of three things: a lag in the response of raw nutprices to increased kernel prices, the skillful exercise of bargainingpower by the Indian state trading company which purchases all ofTanzania's raw nuts, or an increase in the cost of hand processing inIndia. If it is the last, then Tanzania's comparative advantage haschazged. If it is the second reason, there may be a case forinvestment in the industry on strategic grounds.

- 12 -

in processing h4ider into finished leather; the capital and labor cost inshadow prices of leather production in 1973 was calculated to be 20%above value added at world orices.l/ Ir textiles Tanzania would havegreat difficulty in exporting profitably at current productivity levels.Even if productivity improved, it is hard to imagine Tanzania competingin the world market for standardized products such as crey cloth vithAsian economies having one-third the Tanzanian wage level. However, -heremight be scope for exporting fine-count yarns based on the local hign-quality cotton, or of exporting finished textiles to nearby markets.Finally, Tanzania does have a clear-cut cost advantage over Europeancompetitors ir. the production of sisal twine, but the future of theindustry itself is in question.

1.26 The foreign exchange benefits of a -rocessing strategy mayalso be d±sa-pointing. Processing should always increase net foreignexchange earnings, even after deducting the cost of additional importsused in processing. The key questicn, however, is whether Processingwould increase net foreign exchange earnin gs more -.ar. would an alter-native use of the same domestic resources. The background _ndustrystudies for the long-term industrial strategy showed that many processingindustries had relatively high domestic resource costs Der unit of foreignexchange earned. At the extreme, mechanical processing of cashews in1973 had a domestic resource cost of Shs 1,74 for each shilling of netforeign exchange earnings. This was weil above the shadow exchangerate of 1.30 and implies that there were other i-ndustries where the samedomestic resources would have saved or earned more foreign excliange.

1.27 Finally, it is questionable whether processing raw materialsbefore exporting them actually reduces dependency or imprcves terms oftrade prospects. In the case of sisal, for example, where technologicalchange threatens a drastic reduction in the demand for sisal twine,investment in t-wine production may make Tanzania even more dependent onexternal events than when exoorting raw sisal. Although it is possiblethat processing most of its sisal into twine will enable Tanzania to obtaina sufficiently large share of the world market to stabilize the price oftwine, and thus help preserve demand for it, it is equally possible thatdemand for twine will decline anywav. With heavy investment in process-ing Tanzania would have much more at risk. The terms of trade argumentfor a processing strategy is similarly questionable. Processing might

1/ On this measure of efficiency, the production of leather for expor:ranked fourth from the bottom in a comparison of 38 industrialproduction possibilities in 1973. See Roemer, et a', ̀The Range ofStrategic Choice", pp 262-3.

- 13 -

help iron out fluctuations in export prices in some case, but in thehighly competitive industries which Tanzania has proposed entering it ishard to imagine that the prospective price trends would be mcre favorablefor processed products than raw materials.l/

1.28 None of the above criticism is meant to imply that Tanzaniahas ncthing to gain from processing any product for exrort. It would besurprising if na good possibilities existed. However, it is essentialto go beyond identification to analysis of prospects on a case by casebasis. A large margin in price between finished good and raw materialdoes not establish a case for processing. In spite of its limitations,cost-benefit analysis is a necessary step in appraising whether benefitsare commensurate with costs.

3asic Industry Strategy v

1.29 The most fully articulated, and recently the most influential,model of socialist industzial development for Tanzania is the basicindustry strategy. There are two main sources for this strategy:J.F. Rweyemamu, whose aim is to remedy the deficiencies of the ArushaDeclaration with respect to industrial strategy, and C.Y. Thomas, whodeveloped a theory of transformation based largely on Tanzanian experience.2/No attem=t is made in this summAry to give a full exposition of eithersource or to distinguish differences between the two. Although manv ofthe sVecific features of the basic industry strategy as applied to Tanzaniaare new, the model is similar to the Mahalanobis model of developmenrt forIndia and to the strategy of industrialization pursued by the SovietUnion since the late 1920's. 3/

1.30 The goal of the basic industry strategy is to restructureproduction and eliminate dependence on outside forces; industry is seenas the principal agent of structural transformation and self-reliance.The colonial pattern of trade fostered dependence; it resulted in aneconomic struacture in which Tanzania produced what it didn't consume andconsumed what it did not produce. The structure brought about by amaximum growth or a processing stratagy is little better according tobasic industry proponents; a decade after the Arusha Declaration Tanzania's

1/ To take extreme examples, for the past two years the price of sisaltwine has frecuently been below the price of an ecuivalent amount orfiber; and in 1974 and 1975 the price for raw hides and skins exceededthat of wet blue leather. On the latter see Indecentre, "Leather andLeather Goods Industries" (Dar es Salaam: mimeo, April, 1976).

2/ Rweyemamu, Underdeveloament and Industrialization in Tanzaria; andC.Y. Thomas, Dependence and Transformation: The Economics of theTransition to Socialism, (New York: Monthly Review Press, 1974).

3/ The term "basic industry strategy" focuses attention on the structureof production, but the strategy is also concerned with the structureof consumption. In this sense the strategy is closer to the basicneeds approach recently emphasized by the ILO and others.

- 14 -

e 0no''c tsruc-ure still lar"l7 reflects the inherited colonial trade---::r-. a-.¢ ;:ne economy is sill dependent on the world cazitalist systemn_ 'bo.h markets and sup>'-_sof basic consumer and nroducer goods. The

_a -dustr st.ateg~ rcuit transform tihe structure of the economy bybringing prcduction and consur.tion into line. A recur'ring theme in thisstrate2v is the use of "domestic resources for domestic needs". The basicneeds of food, shelter, cloth4ng, health services, transportation, andco a oil goods would all be procduced using domestic resources as 'ar aspossibl a.

1.31 There are major features which distinguish the basic industrys^rategy from other industrial strategies advocated in. Tanzania. First,t'ne strategy emplhasizes the producticn of producer goods. Wherever7possible, of course, producer gocas must use domestic resources, but,he major producer goods with high potential linkages in a modern eccnomy(sceel and other metals, chemicals, glass, rubber, etc.) should beproduced using imported raw materials if necessary. Capital gocdsindustries are oarticularly important because they have high linkagesand externalities, permit the adaptation of production techniques to localconditions, and produce higher growth in the long run. The emphasis ison the production of goods with high linkages; the basic industry strategyuses an input-output matrix of a developed industrial economy to identifypriority investments in the way an import substitution strategy uses_moort dem.and statistics or a processing strategy uses export statistics.

1.32 A second distinguishing feacure of the basic industry strategyis its limitation of consumer preferences in the interest of- restructuringoroduction and using domestic resources. The basic minimal needs of allconsumers, rather than market demand, determine production prioritiesfor consumer goods. A skewed income distribution should not be allowed,o distort production priorities, nor should irrational preference forgoods based on imported raw materials determine production when goodsusing local raw materials can be produced to meet the same aeeds of..utrition, shelter, clothing, etc.

1.33 A third feature of this strategy is i'ts goal of reducing thesnare O-f inte .ational trade in production - the willingness to foregoshort-term gains o' specialization in the interest of reducing dependence.The aim is not complete autarky. It is recognized that Tanzania will bedependent on trade for a long time to come and that this trade willlargely reflect the existing economic structure. In the long run, tradewill be needed to secure advanced technology, some raw materials, andother goods which could be produced only at prohibitive cost. Trade willalso Drov±de a useful vent for surplus production of basic industriesestablished or a larger scale than the domestic market can initiallyabsorb. The direction of policy is clear, however. The strategy has animport-substitution bias for both agriculture and industry. Backward-linkage import substitution, in particular, is strongly preferred overprocessing for export.

- 15 -

1.34 The final distinguishing characteristic of the basic industrystracegy is that costs and comparative advantage do not guide investmentor production decisions. Market prices (including world trade prices)are not regarded as a mean±ngful measure of song-run opportunity costs.Very high comnarative costs of production may impose some constraints;for example, the need to achieve minimum economies of scale may delayproduction. However, it is argued chat the importance of scale economiesis exaggerated and that medium-sized ecoromies l Tke anzania can takeadvantage of recent techinological advances such as relatively small-scalesteel mills which Droduce at competitive prices. But even if rates ofreturn are relatively low, the strategy would still direct investmenttoward industries defined as basic. This might conflict with short-termgrowth, but in the long run it is argued that there is no conflict;only a structure in which production and consumption are congruent canproduce a high and sustainable growth rate in the long run.

1.35 Since the basic industry strategy has influenced plans for thelon'g term industrial strategy, a detailed examination of its strengthsand weakn,esses will be deferred unt-il a later section on cucure strategy.In summary the main drawbacks of the basic industry strategy are that:it has very high requirements for some of the scarcest resources - capital.foreign exchange, and planniLng capacity; cost coasiderations are moreimportant than the strategy acknowledges; and the supposed benefits ofwme basic industries may be illusory.

Smnall-Scale Industry Strategy

1.36 A fourth distinctive strategy sometimes advocated for Tanzaniais a rural-based, small-scale industry strategy. Its advocates maintainthat such a strategy is the most consistent vith socialism, particularlyTanzania's distinctive ujamaa policy, for several reasons. First, itextends the principle of self-reliance to the local level. Each communitywould produce many of its own consumption goods and tools, with productionbased as much as possible on local raw materials. The strategy would alsohelp national self-reliance by reducing the need f4or imports of rawmaterials and advanced equipment. Second, a small-scale industry strategywould promote worker participation in a way which couldn't be done withlarge-scale industry. 'Workers would be using a technology they couldunderstand and would be producing on a scale which lends itself to workermanagement. Third, the strategy promotes equality by bringing industryto the countryside. This helps eliminate the biggest source of inequalitv- the urban-rural gap - and reduces the incentive to migrate to urbanareas. Finally, because it encourages the use of simpler .and more labor-intensive technology, the small-scale industry strategy helps develop theskills of a much larger number of workers. The employment effect of thestrategy thus permits more widespread participation in the direct benefitsof industrialization than other strategies. These direct benefits tosocialist development should not obscure the fact that industry as a wholewould be de-emphasized under the rural based, small-scale industry strategy.Fewer resources would be devoted to industry than under alternativestrategies and industry would not be expected to be the or4mary egent of

- 16 -

development. The main role of industry under the small-scale strategyis as an adjunct to u,amaa. Indus:rv would lend support to agriculturaldevelopment and the la-rgely social and oolitical aims of ujamaa.

1.37 The emphasis of the strate-gy is or. small-scale productioncsing mostly local resources. As =any industrial activities as possiblewould be left to the individual village or to groups of villages workingtogether. Village production would typically incluce mtany consumer goods,building materials, and farm implements. There would still be trade bothbetween villages and with national markets and suppliers, but the emphasiswould be on productionr for local consumption. In this respect, the small-scale strategy is a village-level version of the basic industry strategy.In order to make small-scale oroduction possible, it might be necessaryto override consumer preferences for standardized mass-produced products.The strate-y also implies that cost considerations will be subordinatedwhen these conflict with the goals of small-scale production.

1.38 The most ardent advocates of a rural-based, small-scale industrystrategy are usually foreigners who see this as the logical consequenceof President Nverere's emphasis on rural development and ujamaa socialism.l/In its pure form, where small-scale industry is virtually the only industryand manufacturing is relegated to a very subordinate role, there is noworking model of a small-scale industry strategy. However, a variant ofthe model which is sometimes oroposed is based on Chinese industrialstrategy. In this variant, each village or district would be expectedto be self-sufficient in the production of a large number of simpleconsumer goods, building materials, and farm implements using small-scalemethods of production, but there would -still be national or regionalproduction of heavy industrial products and some consumer goods. Industrywould still play a leading role in development under this variant, butsmall-scale production would be strongly promoted because of its inherentvirtues and in order to save capital and foreign exchange for investmentin essential large-scale industry.

1.39 Most Tanzanian leaders have at some time or oth-er give general-expressions of support for-small-scale industry. Even. the Working ?art7,n Long-Term Industrial Stategy endorsed a program similar to theChinese variant of the small-scale industry: the large-scale zationalsector would be oriented toward basic industry, but small-scale productionwould be encouraged over a substantial range of industries. However,there has been less evidence of meaningful support for a small-scaleindustry strategy in most Government policy actions. The major parastatals

1/ It is doubtful whether President Nyerere himself holds this view.Based on statements such as that quoted earlier from nis introductionto the Second Five Year Plar it would acsear that- hie would not favorliniting industrial develoo-ent tc small-scale village industry, noreven to giving preferenc_ to 'high-cost, small-scale industry.

- 17 -

(with Governmrent approval) have consistent-ly pre-empted opportuni-ties forsmall-scale oroduction by building large factories for mass production ofgoods in which there are small-scale alternatives. Moreover, the Govern-ment has beer. unwilling to override consumer preferences for goodsproduced in large-scale factories,

1.40 This ambi,valence toward sm-all-scale industry reflects, in Dart,the 1i=itacions of th,e strategy itself. lny strategy relying heavily onsmall-scale industry faces formidable obstacles. The first obstacle isthat the scope for small-scale production at a cost approaching that ofmass production may be very limited. The most obvious candidates fo-small-scale ptoductior are: garments, soap, canned food, simple tools,hand-made bricks and tiles, sugar, shoes, and milled grain. Beyond this,few suggestions have been advanced. It is sometimes suggested t;hatChina could provide technical assistance to establish a much broaderrange of small-scale industries. It is crue that the typical Chinesecountry or district produces 'ertilizer, cement, machinery, iron andsteel and energy, but these are not really on a scale suitable for aTanzanian district. The average C'hinese country or district is aboutthe size of tne average Tanzanian region.i/

1.41 The second obstacle to a strategy emphasizin, small-scaleproduction is that consumers have an aversion to many of the possibilitieswhich have been identified because of the cost or quality of the products.Leather sandals, for example, genera2ly cost more than factory-producedrubber or plastic sandals. Small-scale production therefore may conflictwith the goal of providing low-cost footwear to the mass of the population.There is a similar conflict between tiles and galvanized iron roofing;because tiles require much more timber to support them they are sometimesmore expensive roofing material than factory-produced galvanized ironsheets. Ever. bricks may be more expensive than cement in areas wherefirewcod is scarce. Consumers also frequently prefer goods produced ona large scale even if they cost more. For example, one significantpossibility for village industry is the use of hammer mills to grindmaize. However, consumers almost universally prefer the higher-cost, butfiner (and nutritionally inferior), product of large-scale roller mills.There is no evidence tha. the Tanzanian Government is w;illing to overrideconsumer preferences 4n suICa cases in the interest of smal--;^aleproduction.2/

1/ For a brief descriotio. of Chinese industrial policy see D.3. Keesing,"Eccnomic Lessons from China," Journal of Development Economics2(1975) prp 1-32.

2/ However, consumer preferences have been overridden for ot.er reasons.See page 75.

- 18 -

1.42 A final difficulty is that it requires a great deal of planningto integrate small-scale with large-scale production in a socialist economy.Although small -scale oroduction conserves scarce high-level managementresources at the production level, it requires a lot of higah-level r.anpowerat the coordination level. At the very least it is necessary to coordinateplans sufficiently to prevent the ore-em=tion of small-scale opportunities.A serious effort to promote village industry in several sectors wouldrequire the acquisition and dissemination of information on small-scaleproduction techniques, physical controls or market intervention in orderto protect small-scale industry from competition from large-scale productionor imports, and detailed plans for tne integration of small-scale productionof components with large-scale assembly.

Comparison of Strategies

1.43 The four major strategies of industrial development proposedfor Tanzania differ in several ways. The major difference, from whichmany other differences stem, is the conception of industry's role insocialist economic development. For advocates of the maximum growthstrategy, the role of industry is to promote economic developmentthrough rapid growth cf output, foreigr. exchange earnings (or savings),and employment. The focus is on economic development rather than socialism,though the strategy is not necessarily incompatible with socialism;-ndustrial organization, pricing, and incomes policy can help ensureconsistency betweenA Tanzania's broad socialist goals and the efficiencyrequirements of the strategy. The role of industry in both the basicand the small-scale industry strategies is determined by a vision of anideal socialist society. Advocates of the basic industry strategyenvision the possibility of a future Tanzanian economy which is self-reliant and indenendent of the world canitalist system; a particularform of industrial development is required to restructure the economy tomeet this aim. Advocates of the small-scale industry strategy see afuture economy in which small communities work together cooperativelyto produce most of their basic needs; small-scale industry can play animportant auxiliary role in the development of the village socialisteconomv. Supporters of the processing strategy have differing views onthe role of industry, ranging from the promotion of growth to thereduction of dependence. It is doubtful whether a strategy based largelyon processing for export would be effective in promoting either of thesegoals, however.

1.44 A second difference among the strategies is the factors consideredto be most important in choosing what to produce and how to produce it.This follows directly from the different conceptions of the role ofindustry. The maximum growth strategy attaches primary importance to thecost of production because low production costs are the key to profit-ability and economic growth. The basic industry strategy stresses thenature of the product because the productio-n of certain cozmodities isnecessary to achieve desired structural change. The small-scale industrystrategy places most importance on the process of production becausesmall-scale production is essential for worker control and rural self-reliance and equity. Finally, the processing strategy regards the sourceof raw material as the most important ractor in choosing what to produce

-19-

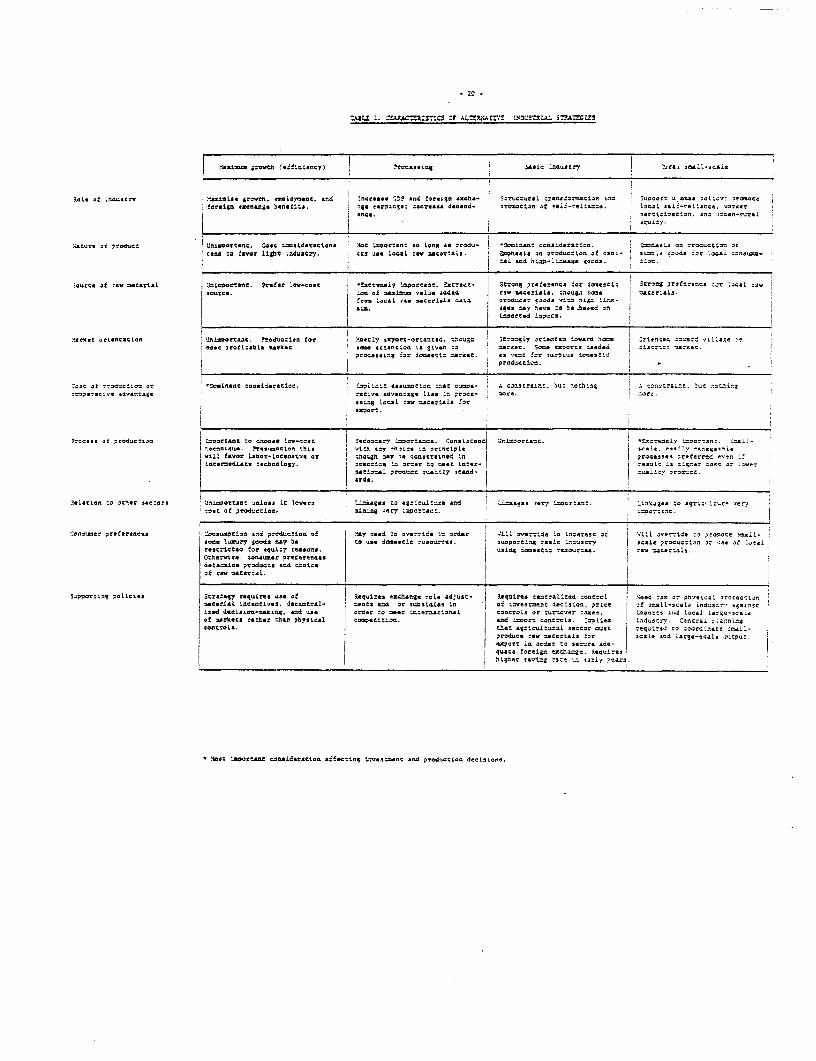

because extraction of maximum value added is perceived as the best way tomaximize growth, prevent exploitation by foreigners, and reduce deoendenceon external markets. Table 1 summarizes additional differences amongststrategies. The summary table highlights differences among "pure" strategies;innumerable variations and differences in emphasis are possible.

1.45 In spite of the conflicting premises upon which the alternativestrategies are based, there is a substantial overlap in the outcomes ofthe different strategies. It is probably fair to say that 80% of theadvocates of contending stragegies would agree on 80% of the products,processes of production, and supporting policies over the next 20 years.There is a large core of products which would be produced under anystrategy (with the partial exception of the pure small-scale industrystrategy): sugar, other processed foods, cotton textiles, beer, tobacco,clothing, wood products, pulp and paper, printing and publishing, PVCplastics, plastic products, fertilizer, paints, glass, cement, metalfabrication, and assembly of trucks and buses. The essential differencesamong the strategies with regard to what is produced are two: timing andemphasis. The shorter the planning horizon the greater are the differencesin investment choices. Over a twenty-year planning horizon, for example,the processing, maximum growth, and basic industry strategies would allinclude additional investment in sugar, cotton textiles, and iron andsteel. However, the processing strategy would sequence investments asfollows: sugar and textiles (including production for export) followedby iron and steel; the basic industry strategy would reverse the sequenceby building a smaller-scale (and higher-cost) steel mill immediately;and the maximum growth strategy would delay investment in iron and steelfor several years until a larger-scale and lower cost plant could beconstructed. Both the maximum growth and basic industry strategieswould probably restrict production of sugar and textiles to the domesticmarket, though for different reasons. At the margin each of the strategieswould emphasize different industries, but there would still be a largenumber of industries and production processes common to all strategies.It was because of this substantial overlap that agreement on a long termindustrial strategy was possible in spite of apparently irreconcilabledifferences in the premises on which the conflicting strategies werebased. A detailed examination of the proposed long-term strategy isundertaken in a later section.

-iJ2 1. 'AAC-Z2tI1C J AL-3J;ArI' 2 lp.IA1. SA r!c;s

| .tLoa grswch (sfialcecy) a rcssLo 34aac inustoy '.r.1 saui l-cala

.L. Pi L.ndustr.C ....... .owt.h ouoLapsP *nd d? rse 0th.- -5rs Lccu ro far-tian and S!oonetr: oss :oL:c7; -e-C! forign xaegse;. oa-sefte. | earning; d..:.... tdalnd- ' arneatlon of caij-es.oc. local eeit-rnllanne Macca

uc-?5 of 7rdunc! 'niacetnt. Coat cracsidsr.iono I .St I.ocrtnt so Lang aX a rodu- 3-ir.nc c nsidasz:ila. pfehash an orodutcian or-and .O !Svor light lzduacry. uces ot l'ocl rav ac*rilis. &IphasiL on .rad'c:lan of :o.L- -sLI. ;a..da far Las ranos

j I :aL sad~~~~co hian-lza.ga goon.. tIn

z-urc a raw mcartel Jnaoortsce. frfl r low-cas !.n ty Ilpertanc. Ucract- Strng p?refrersca for ISaustic Screng preference for L cal Iawsaute.. :neof at n L-, addscd re c na rici _ J :h or. erai..

ala. L;c- L: v Y;wrt L =e L | ages =xy have o be t ..sed an

Ysnasc ari-nattSton | Crolaparca . Prduction tan Meetcly exyrpor-erlan:ca Ohuh ongf ;rvLy ortatccnd togard Marcc j naactd :004,5 otUago Mrjase prafLtablo nekac i ottanntica L. S- .:. .c... San -len: :s adad 1iuc:- rte:

{ | ~~~~~~~~PronaesLc% far docastlc :mrktht ' s rent far surplus :ausstt

.one ad rroda: o, or LcJ. %si ad.r.ln ImaidcLt *.nton:; -0-: uoaec- A b.nonatr: Mu: natas i S: t _c a:: ::Lrgc= rsv advantage [ j rle±ve advontcgs lisa In .. a.a- acts. Pr.re.!

j ^sal3ing al ra v tr±orala for!

_ .- _ fa

prone. a prO. antcoa I rcpr-:ant to alOe.. Ins-cast i Ocendsry Iinas:nnta. CaIaLu..nt Untncarsn cinaroOclY zccrcan: Sr i.-r eoneique. Presainottor :inta c7tch ay onates to principle arjnie.k eastLy eranaeacia

I v.11 favor i oar.Ltoansh or Ihno gn 3. se anacrtaled LIn praos.. urederrod -e.n fincarin.dLazt :.nhosLsgy. Practice In ardr to neat lnter- j r.auL S hIgher :c.. ar Lacer

patealn L renue qatitcystand. 3 | qu.i0y srsdsac.ards. [ tj

felotIao ta cher nr:a -agro sunles iC Lpre -.aaes Ia sgres l.tars and .LL=k.gaa racy inpat:aoc. Iinsaa :a agr:aalr.re .eryn ost a produetie. l 0407 -orcc. !Lar:atI

Cans--er prefer.e.e. !acaUnetcis and praductian of SAY ... t to aorrita in u:der Will override in ... erest o S dtil override :0 -rtee naIL-ce. iSurY SOods at7 a ca u-. do-iscn rsaurnet. esiporciog ba.ia '-n-usry -a.ia oroductIon Mr M -of Lcul

rlocrtetsd for equiTy reasons, oscag iceactiz rcaaurtoa rig nartaicOrthes . .. .o s-r presr suce dts=teea produt *. end h;I'f rest nataniaUL.' °

Saapponr:ig colicies Str.--:e rquir.. of legumeahang. -. La dfast- Rsquirt. calrid croa . r. a...

macctal ltc.uetl . taneetr. i- ents .td or s-idLes i j of Inveatneet icIsioa, price of rnll-saclo ied:srr'a- str-cIo d dsiai -ain. nd us order :eatc iaternantass.e anetrais or :.rnavcr caars pcrco and lan -argn-aeaoaf nras.ca rather tahe physical I Po.pecita. and aotr: :a-tri. L.:o IatAatr. Cun.r.. - ain.n..

c -.ris. cst: ag:Iasalturil "ctr oCust -equ-ret ta acuriino:t Snail-prods tav materIal, far scalaend Larg.-.eais outec.BtPcrt in ord.r no s-cure cd-4rotto forecgn 'ccran as .- legue

higt o-ing Ite Aoo ta*-1 7nde.

oMost tnprtast w"nid.acti.a.efetn to-ecan and produ-tiondoiias

- 21 -

CHAPTER II. INDUSTRIAL DEVELOPMENT SINCE INDEPENDENCE

A. Overall Growth

The Data Base

2.1 This section attempts to describe what has happened to aggregatemanufacturing output during the period from the mid-60's through 1975,and to analyze why the sector has performed as it has. It is possible toobtain a fairly good picture of what has happened to manufacturingoutput over the period, but statistics for the sector are no: sufficientlycomprehensive, accurate, or comparable.to establish with certainty whyoutput has grown as it has. National accounts statistics give estimatesof total manufacturing and handicrafts value added in both current andconstant prices for 1964-75.1/The same source provides estimates of invest-ment by sector in current prices for 1966-73 and total investment incurrent and constant prices for 1964-75. The annual SurveV Of TndustrialProduction provides estimates of gross output, value added, and severalother variables (not including investment) in current prices for thelarge-scale manufacturing sector (firms employing ten or more workers)for the period 1965-73. However, coverage and the response rate of thissurvey vary slightly from year to year and some of the individual firmreturns are unreliable. In spite of these data limitations some ir.er-ences have been drawn about the performance of the manufacturing sector,but these should be regarded as a set of hypotheses rather than establishedfact. In later sections scattered evidence on the performance of indivi-dual firms or sub-sectors will be presented in an attempt to clarifyfurther what has been happening in the manufacturing sector.

1/ The implicit GDP deflator for industry has some limitations. In someindustries, employment is used as a proxy for quantity of output andthe quantity indices fail to take account of backward or forwardintegration in some industries. This tends to understate the growthof real output and overstate price increases. An opposite biasprobably occurs as a result of the inclusion of new industries sincethe base year of 1966; these new industries are likely to have a higherratio of value added in domestic prices to value added in world pricesthus overstating the real growth of output in world prices resultingfrom the addition of new industries. In spite of these limitations andbecause of offsetting biases the implicit GDP deflator for industryseems to be a reasonably reliable index. A comparison with other priceindices over the period 1966 -75 shows that the implicit GDP deflatorfor industry is very much in line with comparable indices. The 1975indices (1966 = 100) for several price measures are as follows: implicitGDP deflator for industry 194.1; implicit total GDP deflator 175.8;implicit equipment price index 202.5; World Bank international inflationindex (SITC sections 5-8 of industrialized countries exports in U.S,dollars) IU.t.

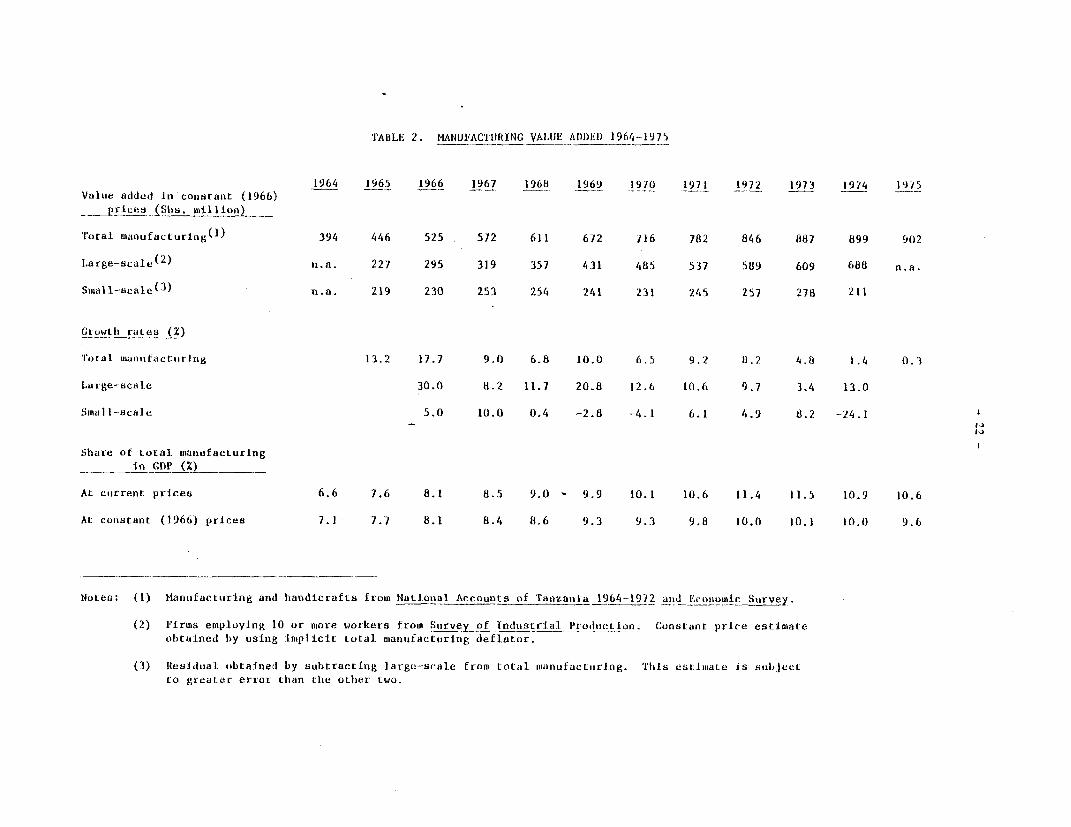

TABLE 2. MANUFACT1RING VALUE ADDED 1964-1975

1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975

Value added in constant (1966)pricea S. million)_

i'otal inanufacturing(l) 394 446 525 572 611 672 716 782 846 887 899 902

Large-scale(2) n.a. 227 295 319 357 431 485 537 589 609 688 n.a.

Small-scale(3) - .a. 219 230 253 254 241 231 245 257 278 211

Growth rates (2)

'I'otal manuftacturlig 13.2 17.7 9.0 6.8 10.0 6.5 9.2 8.2 4.8 1.4 0. 3

Lavge-scale 30.0 8.2 11.7 20.8 12.6 10.6 9.7 3.4 13.0

Small-scale 5.0 10.0 0.4 -2.8 -4.1 6.1 4.9 8.2 -24.1

Share of total manufacturing_ in GDP (2)

At current prices 6.6 7.6 8.1 8.5 9.0 - 9.9 10.1 10.6 11.4 11.5 10.9 10.6

At constanL (1966) prices 7.1 7.7 8.1 8.4 8.6 9.3 9.3 9.8 10.0 10.1 10.0 9.6

Notes: (1) Mantifacturing and handicrafts from National Accounts of Tanizania 1964-1972 a_d Econonmtx_c Survey.

(2) Firms employing 10 or miore workers from Survey_of Indtistrial Production. Constant price estimate

obtained by using impi icit total maniufacttiring deflator.

(3) Residual obtained by subtracting large-scale from total maniufactuiring. Tils estimiate is subject

to greater error than the otiher two.

- 23 -

Output

2.2 Manufacturing output has more than doubled since the early post-independence period, the average annual ra-e of real growth in manufactu-ring 1964-75 was 7.8% compared to an average growth ra.e of 4.o% of totalGDP. Growth was even more vigorous prior to the economic crisis of 1974-75;-rom. 1964-73 the annual aterage rate cf growh of manufacturing was 9.4%compared to an average growth of 5.1% for the entire economy. The shareof manufacturing in total output increased from 6.6% in 1964 to 11.5% in1973, buc has slipped back. to 10.6% in 1975 as a result of the stagnationcf industr4al output during 1974 and 1975.1/

2.3 Large-scala manufacturing has expanded particularly fast -- by13.1% per year from 1965-73 compared to 9.0% for total manufacturing.Small-scale manufacturing and handicrafts appear to have grown more slowly(3.0% average annual growth 1965-73), but this is an estimate subject toa higher degree of error._/_

1/ Thais is the share of manufacturing in current 4rices. As Table 2 shosmanufacturing as a percentage of total GDP in cornstant prices increasedby less - from 7.1% in 1964 to 10.1% in 1973. This means that Oar. ofthe increased share of manufacturing output in current prices was dueto an increase in the relative price of manufactured coods. This mayreflect either an increased level of protection for the manufacturingsector during the period or a change in relative world prices, probablyboth.

2/ According to the Ministry of Industries there has been a decli'ne irn theresponse rate of small-scale industries to surveys in recent years withthe result chat small-scale production may be underestimated. TheSmall-Scale Industry Development Organization (SIDO) is conducting aninventory of all small-scale firms and believes there may be around4,000 firms operating in 1977. Assuming that there were 4,000 small-scale firms in 1973, that each firm employed 10 workers, and that valueadded per worker was Shs. 14,400 (the equivalent of VA per worker inlarge-scale enterprises), then value added in current prices from thesmall-scale sector in 1973 would have been Shs. 576 million. This is38% higher than the actual estimate derived from official statistics.However the assumptions used to estimate the higher figure are undoubtedlybiased upward so that it is not clear that the official statisticsunderestimate small-scale industrial production much, i' at all, urtil1974.

-4- t; -

2.4 Although t'ne a-rae a aca 3: g 0ro7th has been high, t-e rate o'growth has been sloSng r -'s ese-4' 4 > mar;ted ln 197' and 1975when manufacturing output irtla'7 san-ted. Capacity continued toexpand in 1974 and 1975. but ,-_.. :an u-nceruzi ized capacitv emerged.This was largely due ro s^_ no- I - c ..S rc:cer thnan to a decline indemand. There was e:xcess _c._c r fz'-us-il goods but productionwas not forthcoming for a s: e, asonsh: s:r:ages of lccally-oroduced raw materials o';_g t_h :r ig- and azriculcurai oroductlonproblems; di'ficulties in obra-'ni *-:-:ate _ :nol es of ut l-ities,particularly water and elae'ri nd; dashOr tage o f spare parts, rawmaterials and transport, owing in part to th severe import restrictionsintroduced to deal with the foreign Zx<change cris:s.

2.5 Of more concern th.an _he recent stagnation is the apparentdecline in growth of industrial utou. t orno to 1974. Table 2 shows chatthe annual rate of growth in larrge-scale anu-rac:uring declined each yearfrom 1969-73. Splitting the 8-vear -er-' 1965-73 -r half, the averageannual growth rate of large-scai manu:acturi-n was 9.0Y from 1965through 1969, but only 9.0% f'rom the end off 1969 through 1973. To someextent this may reFlect the ver-- lcw oase __m wnhich growth started in1965. However, it is worrving that the growth race had declined to only3.4% bv 1973. Analvsis of investmen-t and eno1m,iaent trends revealsthat the slowing rate of growth of ranufacturnig outout bet77een 1969 and1973 reflects something m.ore than an enl2ared 'ndustrial base.

Investment

2.6 Table 3 shows investment (fixed cacital for-ation) inmanufacturing from 1966-1973. The absolute amount of investment inmanufacturing in real terms increased sharply in 1970 and 1971 and thendeclined again in 1972 and 1973; avera,e inr.estment in real terms inmanufacturing rose from Shs 173 m4illiorn in 18-69 to Shs 297 millionin 1970-71, before falling back to Shs 32 -million in 1972-73. Sectoralinvestment Figures are not available for 1,974 an.d 1975, though we cnonwthat substantial parastatal investment in manufacturing continued tobe made while total invescment in t'ae economy increased sl4ghtly overthe 1973 level. Manufacturing investment as a share of total investmentbegan to decline a year before the decline in the absolute amount;manufacturing's share peaked at 1.4% in 1970, decliring to 11.7% in1973.

2.7 The decline in manufacturing investment is onl- a small ?art ofthe reason for the decline in the growth rate of manuracturing output,however. In the first place, the h iav investment of 1970 and 1971should have yielded increased out-ut ir. .971-1973, the very years thatthe growth rate was decli--nin. ianufactur lng vestmeac -s a pcrcentage

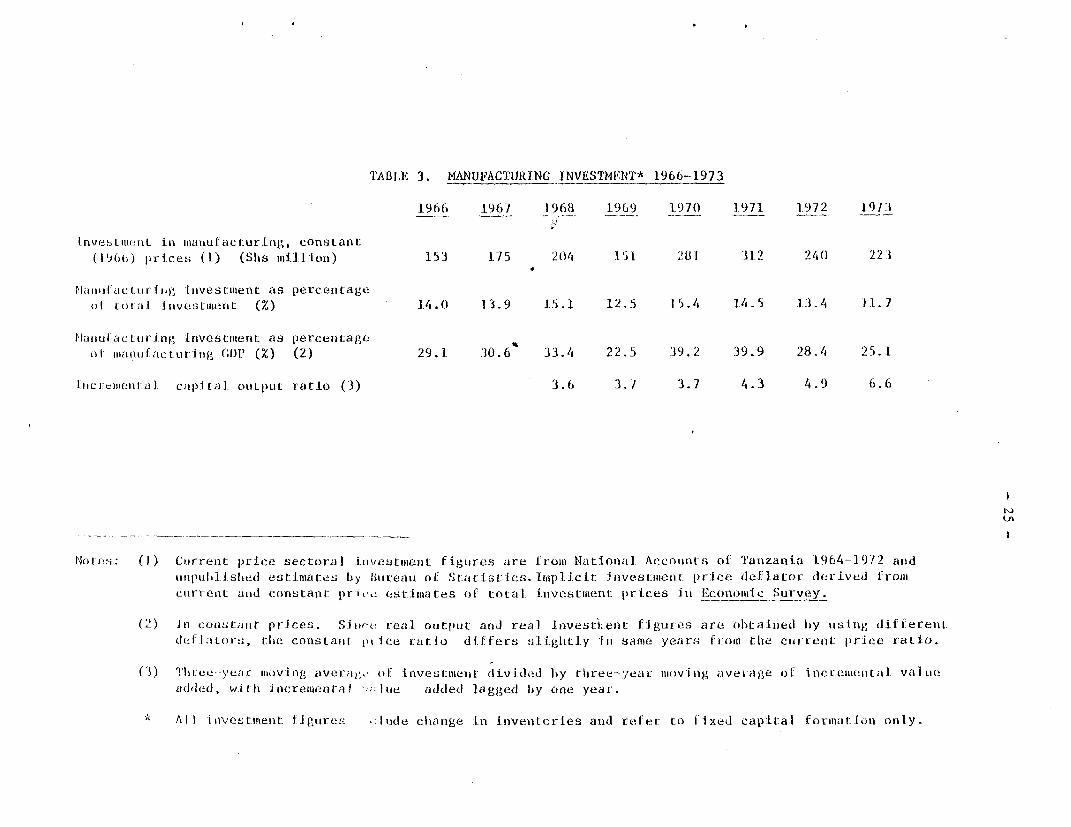

TABlE 3. MANUFACTURING TNVESTMENT* 1966-1973

1966 1967 1-9668 1969' 197( 1971 1.972 19 73.

lnvesLmtnt in mantiufacturing, constant(I.9)(1) prices (1) (Slun mIlli.on1) 153 175 204 151 281 112 240 2 23

Mamifiiac hrio)- investment as percentageOf tLotl ilvestment (%) 14.0 13.9 15.1 12.5 15.4 I/ .5 13.4 11.7

Hamn-ufactmri ng investment as percentageof manufacturing (;CP (%) (2) 29.1 30.6 33.4 22.5 39.2 39.9 28.4 25.1

IncremljentaJ. capi tal outputit ratio (3) 3.6 3.7 3.7 4.3 4.9 6.6

Notes: (I) Culrrent price sectoral im)\'estment figures are Ifronm National Accounts of Tanzania 1964-1972 and

uinpublJ1ished estfliiates by llureati of SltcistcLcs. impli.cit lnvesutllent price (leflator (lerived frolil

current antd constant -rir estilmates of total iLnvestment prices ill Economic Survey.

(2) In coOstauIt: prices. Siw (t real output and real investit-ent figures are obttained by using dif ferenii

de f .Itorts, tlhe constant olice ratio difffers slightliLy In sanme years from the cutrrent price rati.o.

(3 ) Three-year moving averal (if investtineLn divided by thiree-year mioving average of increlmkental valune

aidded, wit:h incrementa I u I tie added lagiged by o)ne year.

' Al I investimient figures .:lude change in invenitci-ies and refer to Ifixed capital formatiJon only.

- 26 -

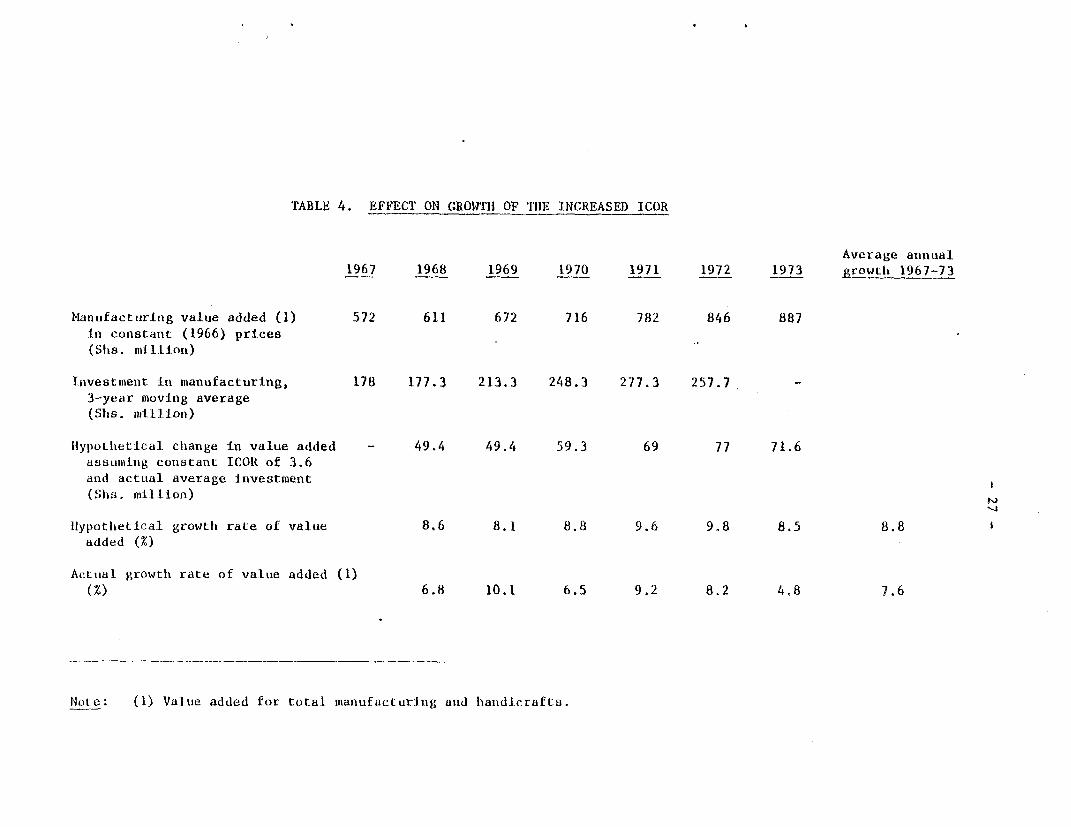

of manufacturi.ng value added was nearly 40% in 1970 and 1971 comnared toonly about 30% in 1966 and 1967.1/ A more important bit of evidence onthe reason for the decline in the growth. of manufacturing output comes-rom an anal-vss of the incremental cait-al-outvut ratio (ICOR). This isshown in the last line of Table 3. Lr order to obtain tie trend, athree vear moving averaze of investment and incremental value added wascalculated, with incremental value added lagged one year to reflect thedelay between the time of investment and the time when additional outoutcomes on stream. Even if we ignore the 1973 ICOR because it oartiallyreflects the output stagnation of 1974, there is a clear upward trend inthe ICOR - from 3.6 in 1968 to 4.9 in 1972. An increased ICOR implies alower rate of growth for a given rate of investment. For example, if aconstant one-third of manufacturing value-added were invested each year,the annual growth race would be 6.8% with an ICOR of 4.9 compared to agrowth rate of 9.3% with an ICOR of 3.6. The effect of the increasedICOR can be seen by comparing the actual growth rate of manufacturingvalue added with the hypochetical growth rate which would have resultedif actual investment had remained the same but the 1COR had remainedconstant at the 3.6 level of 1968 (see Table 4). Not only would theaverage growth rate have been higher (8.8% per year versus an accual 7.6%),but the trend would have been different as well: the growth rate wouldhave risen continuously from 1969-72 and have fallen off only slightly in1973 to 8.5% instead of the actual 4.8%. The conclusion is that thedeclining rate of industrial growth in Tanzania has not been due to adrop in investment.

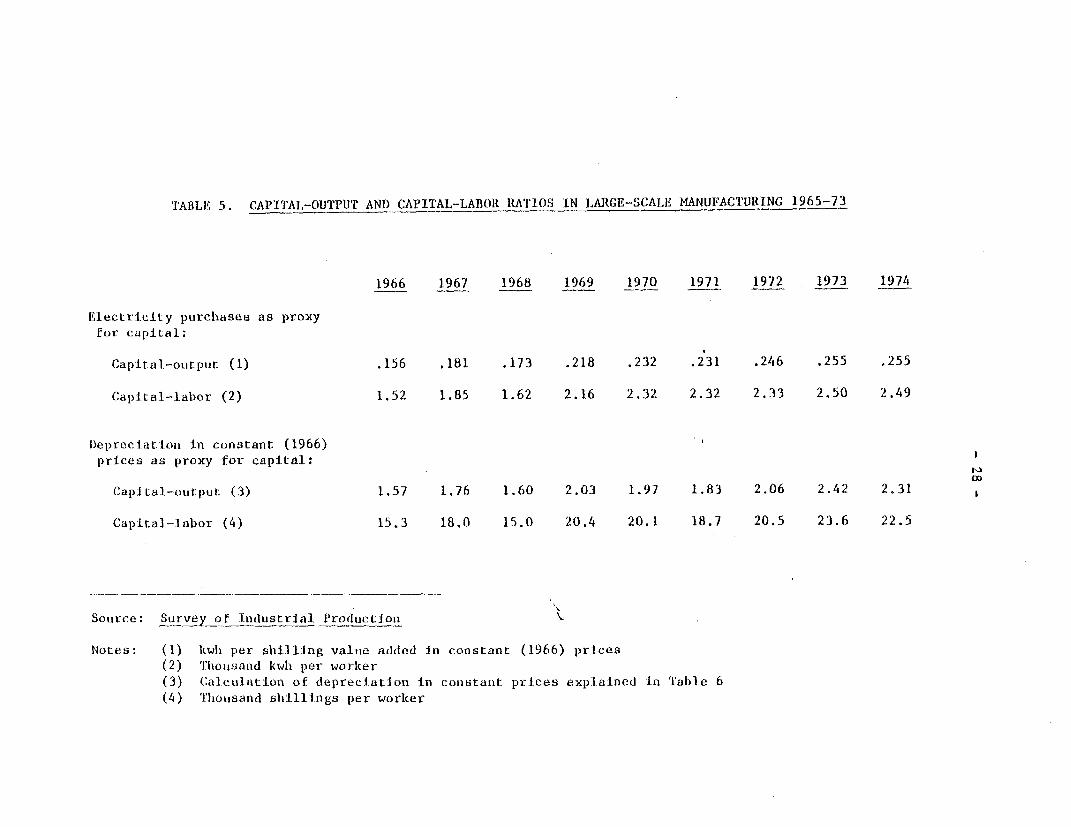

2.8 An increase in the incremental capital-output ratio may reflecteither a shift toward more capital-intensive investment or a decline inthe productivity of capital-; the available evidence suggests that bothmay have occurred. Table 5 presents estimates of capital intensity inthe manufacturing sector, using electricity purchases and depreciation

1/ This suggests that there is verv l41tle to the argument that thehigher growth rate of 1965-69 was due to the smaller industrial basein the early years; with a higher proportion of investment to outputin later years, the growth rate should have been higher in lateryears as well. We do not have in.vestment figures for 1965 or earlier,