Tata mind rover 2014

41

MINDROVER 3.0 Team Name- KUNG FU PANDA TEAM MEMBERS- ABHISHEK TWARI DHIRAJ KUMAR College- Masters in International Business(DSE)

Transcript of Tata mind rover 2014

MINDROVER 3.0Team Name- KUNG FU PANDA

TEAM MEMBERS- ABHISHEK TWARI DHIRAJ

KUMARCollege- Masters in International

Business(DSE)

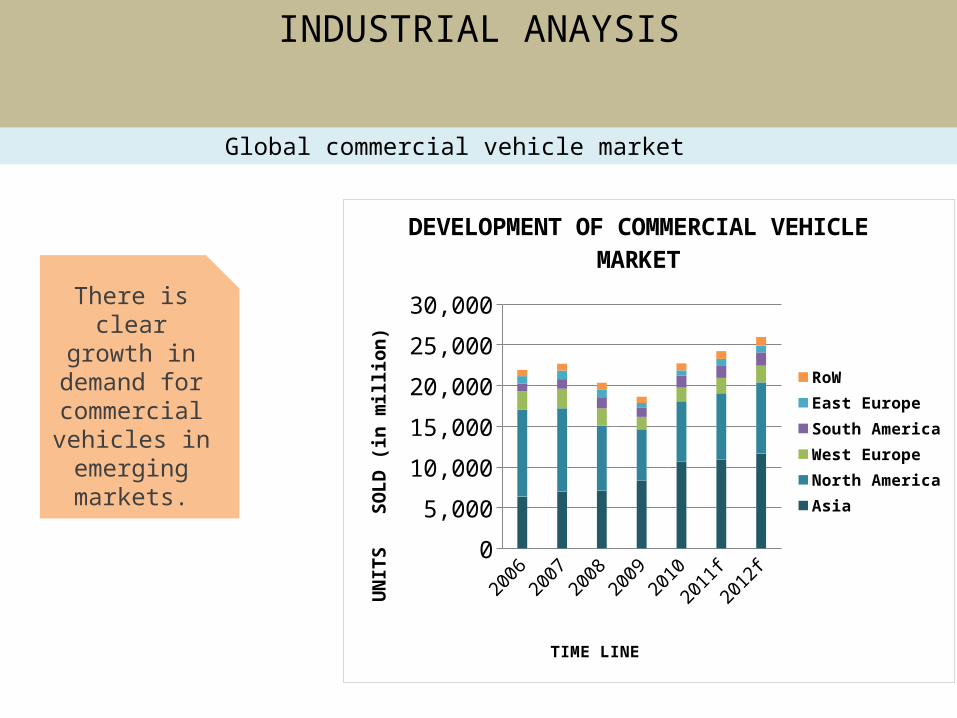

2006

2007

2008

2009

20102011f2012f

05,00010,00015,00020,00025,00030,000

DEVELOPMENT OF COMMERCIAL VEHICLE MARKET

RoWEast EuropeSouth AmericaWest EuropeNorth AmericaAsia

TIME LINE

UNITS SOLD (in million)

Global commercial vehicle market

There is clear

growth in demand for commercial vehicles in emerging markets.

INDUSTRIAL ANAYSIS

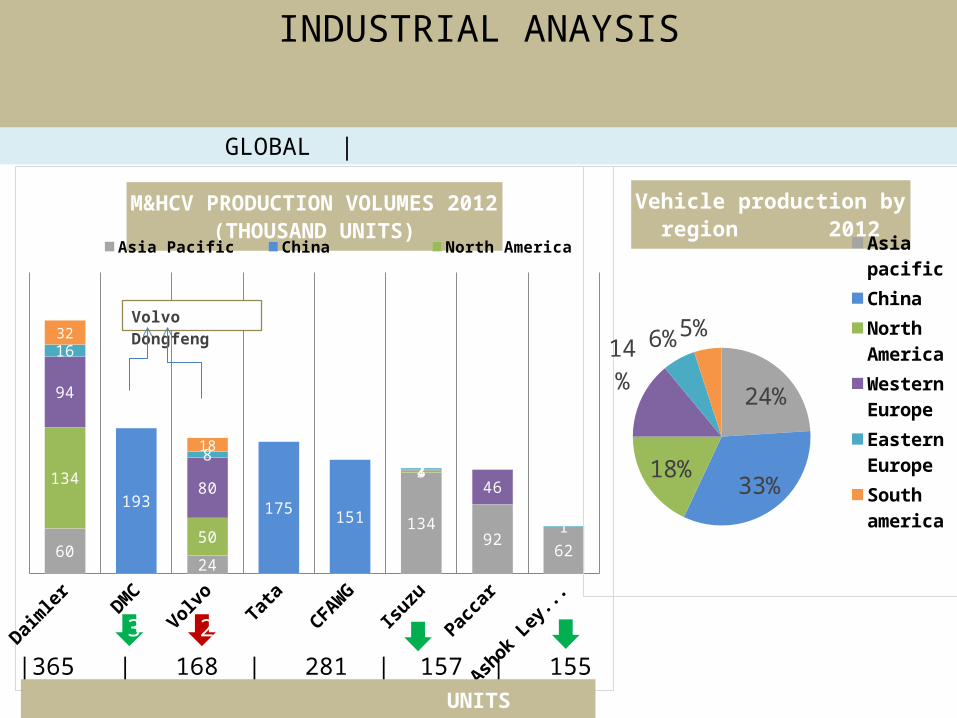

6024

13492 62

134

50

3

94

801

46

16

82

1

32

18

193 175 151

M&HCV PRODUCTION VOLUMES 2012 (THOUSAND UNITS)

Asia Pacific China North America

Volvo Dongfeng

24%

33%18%

14%

6%5%

Vehicle production by region 2012Asia

pacificChinaNorth AmericaWestern EuropeEastern EuropeSouth america

|365 | 168 | 281 | 157 | 155 | 140 | 123 | 51 | UNITS PRODUCED IN 2008

3 2

GLOBAL |

INDUSTRIAL ANAYSIS

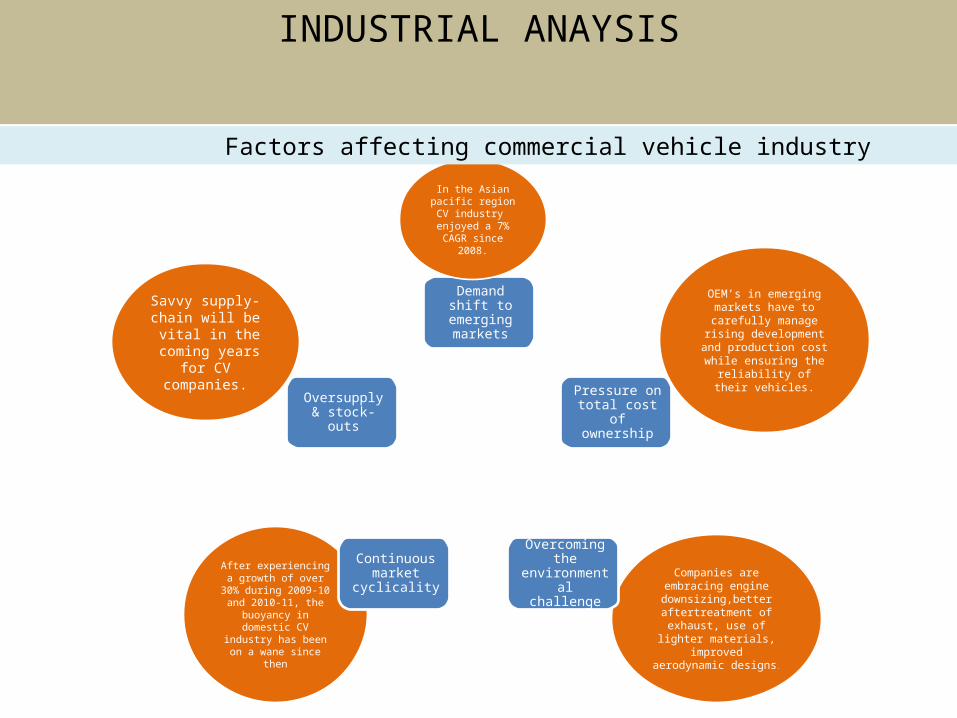

After experiencing a growth of over 30% during 2009-10 and 2010-11, the

buoyancy in domestic CV

industry has been on a wane since

then

Companies are embracing engine downsizing,better aftertreatment of exhaust, use of

lighter materials, improved

aerodynamic designs.

OEM’s in emerging markets have to carefully manage rising development and production cost while ensuring the reliability of their vehicles.

Savvy supply- chain will be vital in the coming years

for CV companies.

Demand shift to emerging markets

Pressure on total cost

of ownership

Overcoming the

environmental

challenge

Continuous market

cyclicality

Oversupply & stock-outs

In the Asian pacific region CV industry enjoyed a 7% CAGR since

2008.

Factors affecting commercial vehicle industry

INDUSTRIAL ANAYSIS

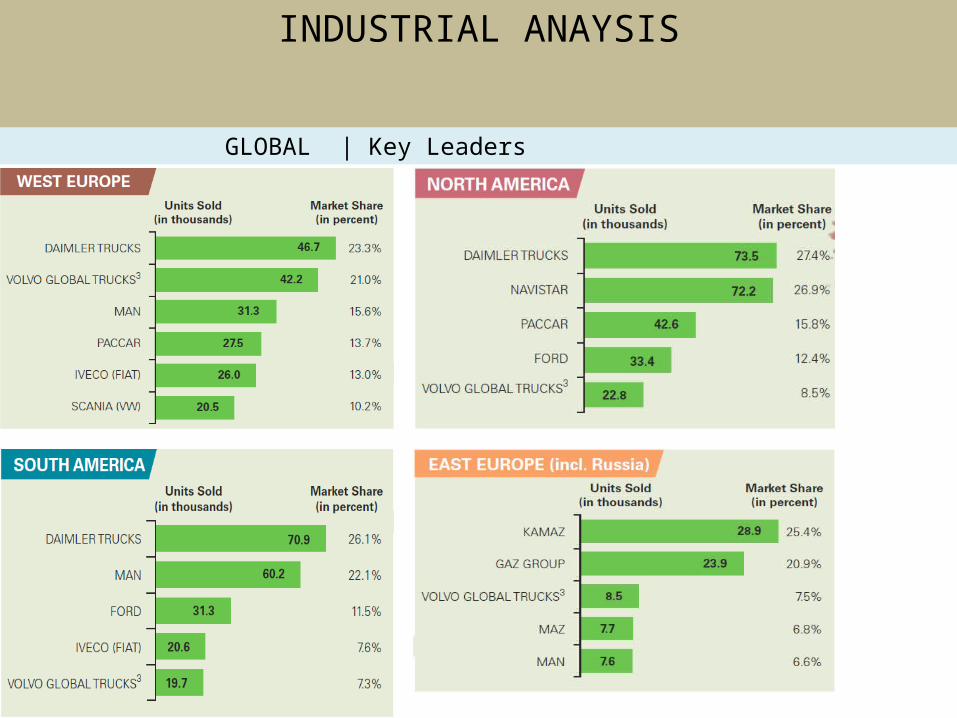

GLOBAL | Key Leaders

INDUSTRIAL ANAYSIS

GLOBAL | Key Leaders

INDUSTRIAL ANAYSIS

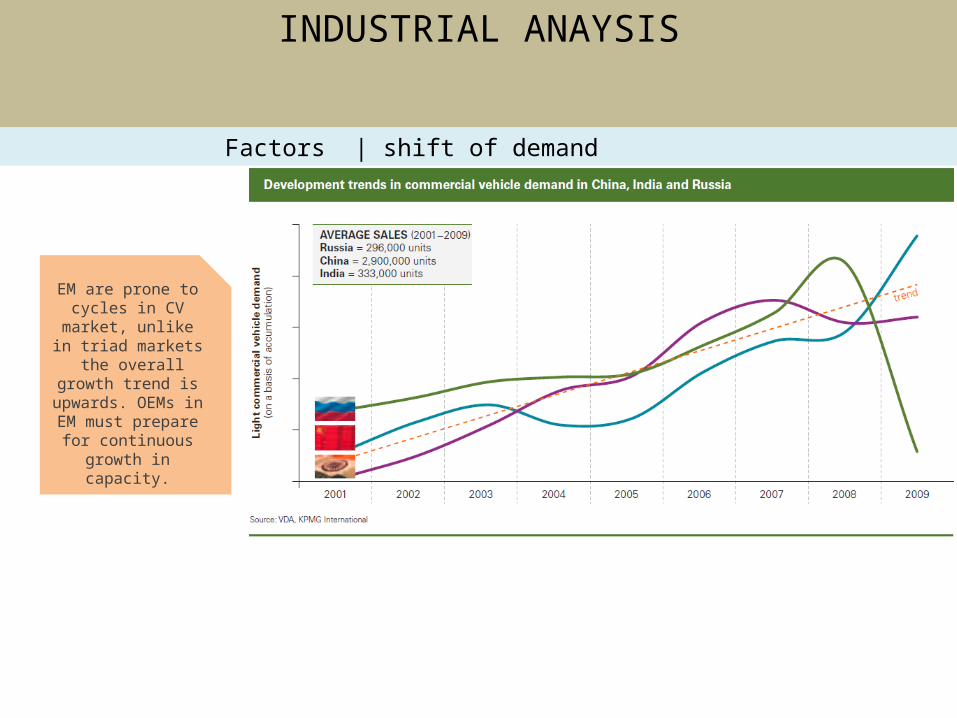

EM are prone to cycles in CV market, unlike in triad markets the overall

growth trend is upwards. OEMs in EM must prepare for continuous

growth in capacity.

Factors | shift of demand

INDUSTRIAL ANAYSIS

Dependency on overall economic

development : commercial

vehicle sales usually trail behind changes

in GDP.

INDUSTRIAL ANAYSIS

FACTORS | cyclicality

STRENGTHDiverse product/customer

centered productMarket leader

Brand Association

WEAKNESSLimited customer baseLesser modification

Lower adaptability to market

OPPORTUNITIESExport to other emerging

markets.M&A options availableEco-friendly products.

THREATSRising oil prices

Weak investment sentiments.Slowing industrial activity

Entry of global players

SWOT ANALYSIS

INDUSTRIAL ANAYSISM&HCV SEGMENT

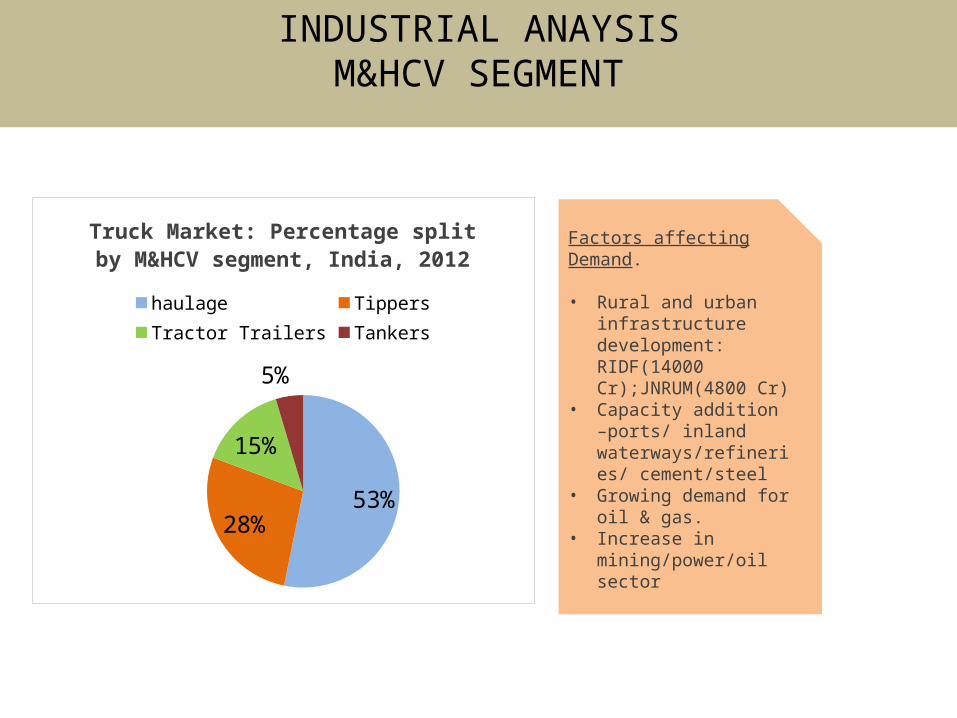

53%28%

15%

5%

Truck Market: Percentage split by M&HCV segment, India, 2012

haulage TippersTractor Trailers Tankers

Factors affecting Demand.

• Rural and urban infrastructure development: RIDF(14000 Cr);JNRUM(4800 Cr)

• Capacity addition –ports/ inland waterways/refineries/ cement/steel

• Growing demand for oil & gas.

• Increase in mining/power/oil sector

INDUSTRIAL ANAYSISM&HCV SEGMENT

61%28%

5%7%

Total Industry Market in 2012-13

(164295 units)

Tata Motors Ashoka LeylandsEicher Others

Tata Motors

Ashoka Leyl...

Eicher

Industry

-5

0

5

10

15Growth over the years 2007-2013

Growth over the years 2007-2013

INDUSTRIAL ANAYSISM&HCV SEGMENT

4P’s

PRODUCT•Regionalized technology and product management

•Standardize component manufacturing –giving a cool look

PRICE

PLACING

PROMOTION

•Expansion of the Value chain.

• Improve distribution channel

• Business unit wise dealership

•Promoted as investor friendly

•Tyre insurance for 10-tyre trucks.

•Easy insurance by tying up with banks.

INDUSTRIAL ANAYSISM&HCV SEGMENT

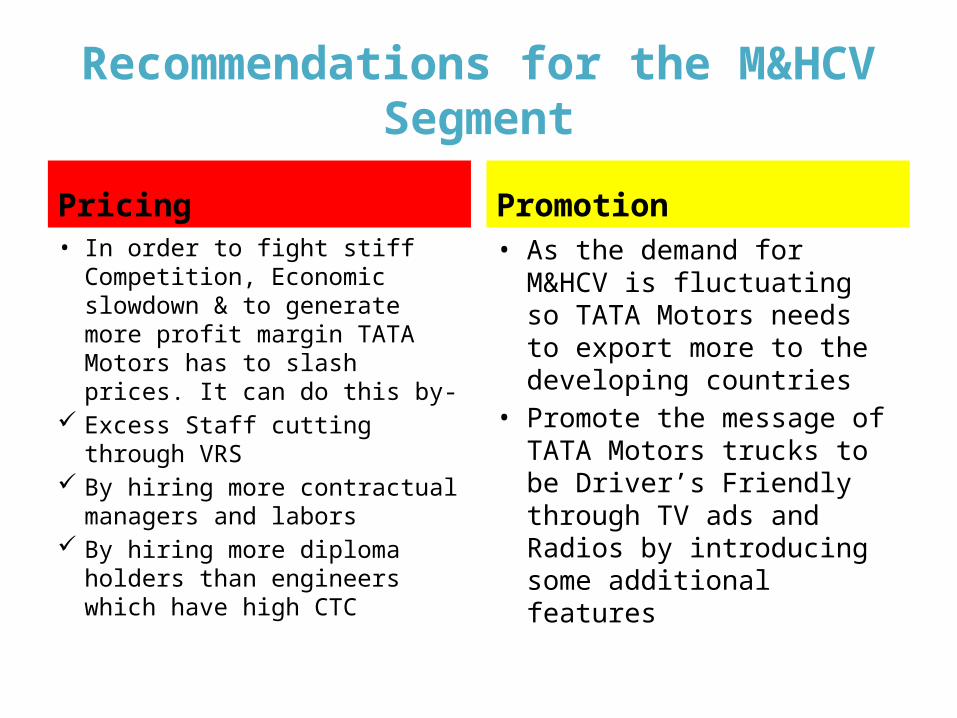

Recommendations for the M&HCV Segment

Pricing• In order to fight stiff Competition, Economic slowdown & to generate more profit margin TATA Motors has to slash prices. It can do this by-

Excess Staff cutting through VRS

By hiring more contractual managers and labors

By hiring more diploma holders than engineers which have high CTC

Promotion• As the demand for M&HCV is fluctuating so TATA Motors needs to export more to the developing countries

• Promote the message of TATA Motors trucks to be Driver’s Friendly through TV ads and Radios by introducing some additional features

STRENGTHDiverse product/customer

centered productProducts considered as Sturdier & ReliableBrand Association

WEAKNESSLimited customer baseLesser modification

Lower adaptability to market

OPPORTUNITIESExport to other emerging

markets.M&A options availableEco-friendly products

Penetration into the Southern Market

THREATSRising oil prices

Weak investment sentiments.Slowing industrial activity

Entry of global players

SWOT ANALYSIS

SWOT of both LCV & ICV truck segment

INDUSTRIAL ANAYSISLCV & ICV TRUCK SEGMENT

68%11%

13%8%

Total Industry Market in 2012-13

(38891 units)

Tata MotorsMahindra & MahindraEicherOthers

Tata Motors

Mahindra& Mahindra

Eicher

Industry

-4-20246810

Growth over the years 2007-2013

Growth over the years 2007-2013

INDUSTRIAL ANAYSISLCV TRUCK SEGMENT

42%

11%

40%

6%

Total Industry Market in 2012-13

(57416 units)

Tata Motors Ashoka LeylandsEicher Others

0

10

20

30

40

50

Growth over the years 2007-2013

Growth over the years 2007-2013

INDUSTRIAL ANAYSISICV TRUCK SEGMENT

4P’s

PRODUCT•Regionalized technology and product management

•Standardize component manufacturing –giving a cool look

PRICE

PLACING

PROMOTION

•Reducing cost by

Cutting Staff

By providing VRS to Staff

• Improve distribution channel

• Business unit wise dealership

•Promoted as investor friendly

•Export promotion in major developing countries

•Promote it as a driver friendly truck

•Easy insurance to FTUs

Strategies for both LCV & ICV truck Segment

INDUSTRIAL ANAYSISLCV & ICV TRUCK SEGMENT

STRENGTHDiverse product/customer centered product

Market leaderBrand Association

First Mover advantageProvides 5S’s (Stability, Safety, Speed,

Space, Style)

WEAKNESSLimited customer baseLesser modification

Comfortableness of driver is lowLower adaptability to market

OPPORTUNITIESExport to other emerging markets

Rural PenetrationGrowing demand for LMPTs

FTUs increasingM&A options available

Retail Sector growth is a booster

THREATSRising oil prices

Weak investment sentiments.Slowing industrial activity

Rising Competition both nationally & Internationally

SWOT ANALYSIS

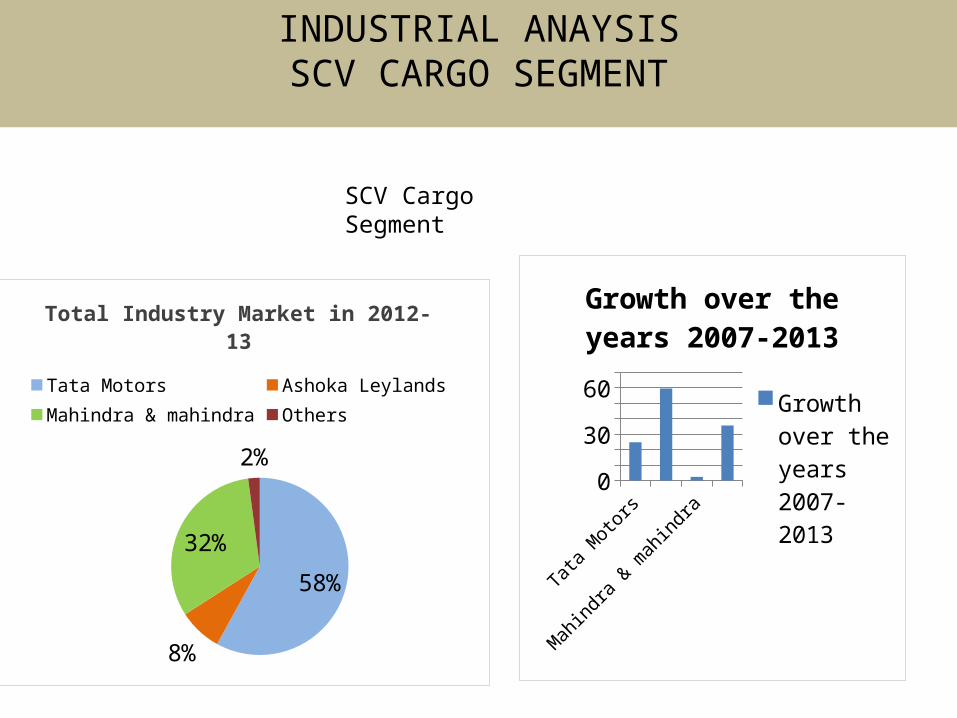

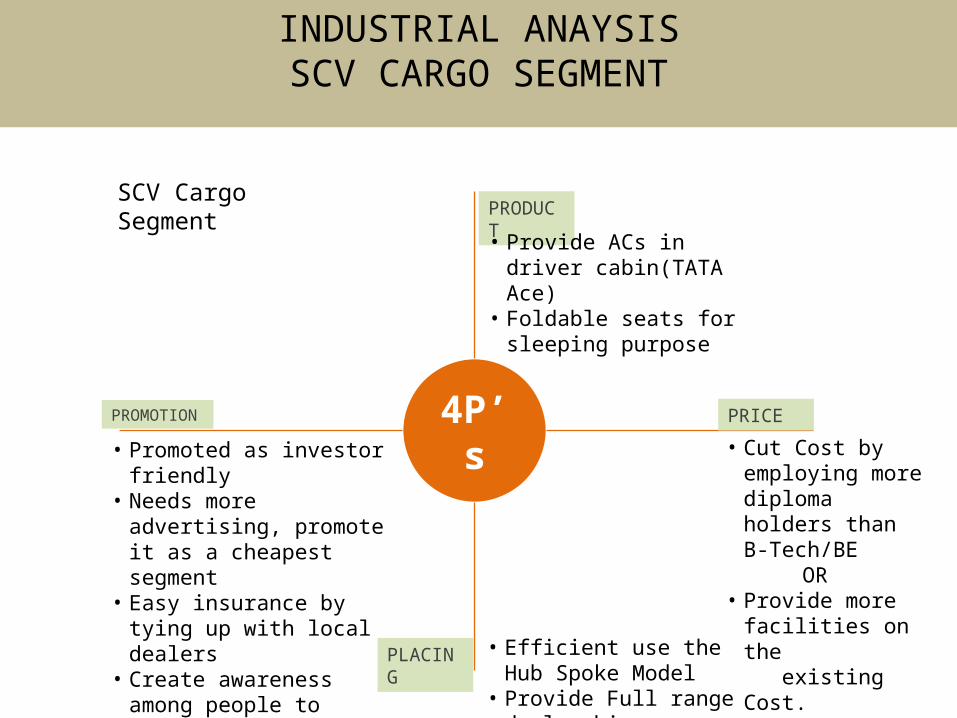

SCV Cargo Segment

INDUSTRIAL ANAYSISSCV CARGO SEGMENT

58%

8%

32%

2%

Total Industry Market in 2012-13

Tata Motors Ashoka LeylandsMahindra & mahindra Others

Tata Motors

Mahindra & mahindra

03060

Growth over the years 2007-2013

Growth over the years 2007-2013

SCV Cargo Segment

INDUSTRIAL ANAYSISSCV CARGO SEGMENT

4P’s

PRODUCT• Provide ACs in driver cabin(TATA Ace)

• Foldable seats for sleeping purpose

PRICE

PLACING

PROMOTION

• Cut Cost by employing more diploma holders than B-Tech/BE

OR • Provide more facilities on the existing Cost.

• Efficient use the Hub Spoke Model

• Provide Full range dealership

• Promoted as investor friendly

• Needs more advertising, promote it as a cheapest segment

• Easy insurance by tying up with local dealers

• Create awareness among people to convert from drivers to owners to Entrepreneurs

SCV Cargo Segment

INDUSTRIAL ANAYSISSCV CARGO SEGMENT

Recommendations in Promotion of SCVs

• Promote drivers & FTUs to be entrepreneurs by proving them easy insurance

• With opening up of big retails brands such as TESCO and Wal-Mart, the use of SCVs will increase

• Come-up with a Vehicle in this segment and promote it as the cheapest SCVs for the poor in India

Recommendations- Value Product

Today’s

Driver

Needs

Comfort

ability

Safety

Reliability

Performance

PRIMARY RESEARCH- Driver’s preference

Another comfort ability factor they demanded were a proper place to rest/ Sleep which can be in the

form of foldable seats.

AC should be provided in TATA Ace cabin , the primary research showed that

drivers now prefer to have the comfort while driving Especially in a county

like India where the temp are too high during summers.

With the competitors already marching ahead in this segment TATA Motors need to come up with a product which

would satisfy the needs of the customer

STRENGTHBetter comfort ability than 3Ws segment

Market leaderBrand Association

First Mover advantageProvides 5S’s (Stability, Safety, Speed,

Space, Style)

WEAKNESSLimited Product availability

Lesser modificationChallenging established market of the

3Ws Segment

OPPORTUNITIESExport to other emerging markets

Rural PenetrationGrowing demand for LMPTs

Increasing demand for public transportation

Collaborate with Schools to provide VANs by modifying the safety elements

THREATSRising oil prices

Weak investment sentiments.Slowing industrial activity

Rising Competition both nationally & Internationally

SWOT ANALYSIS

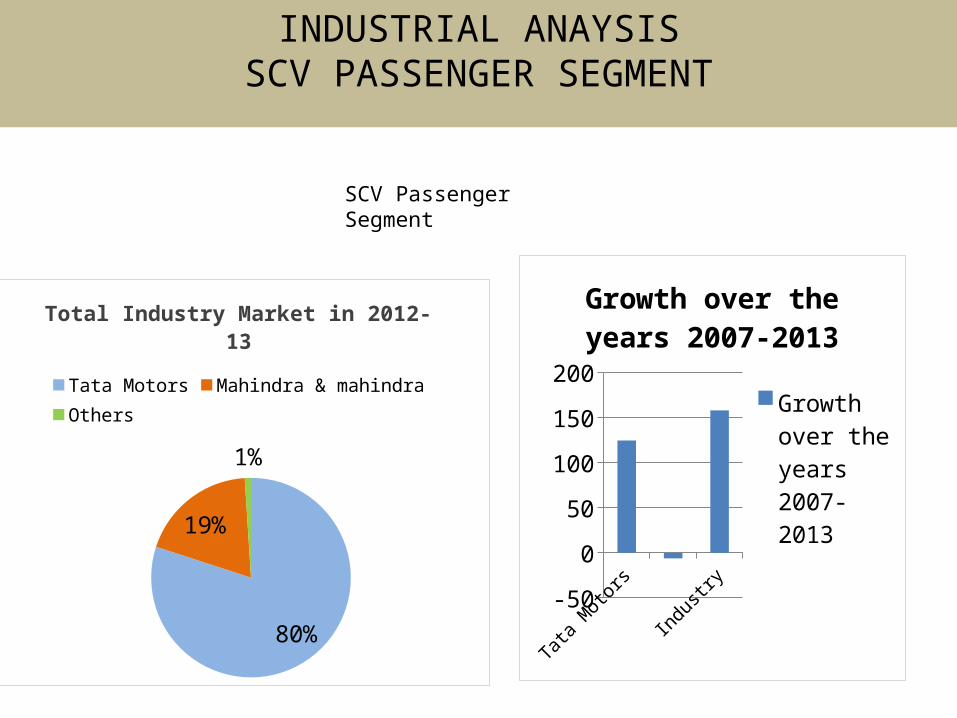

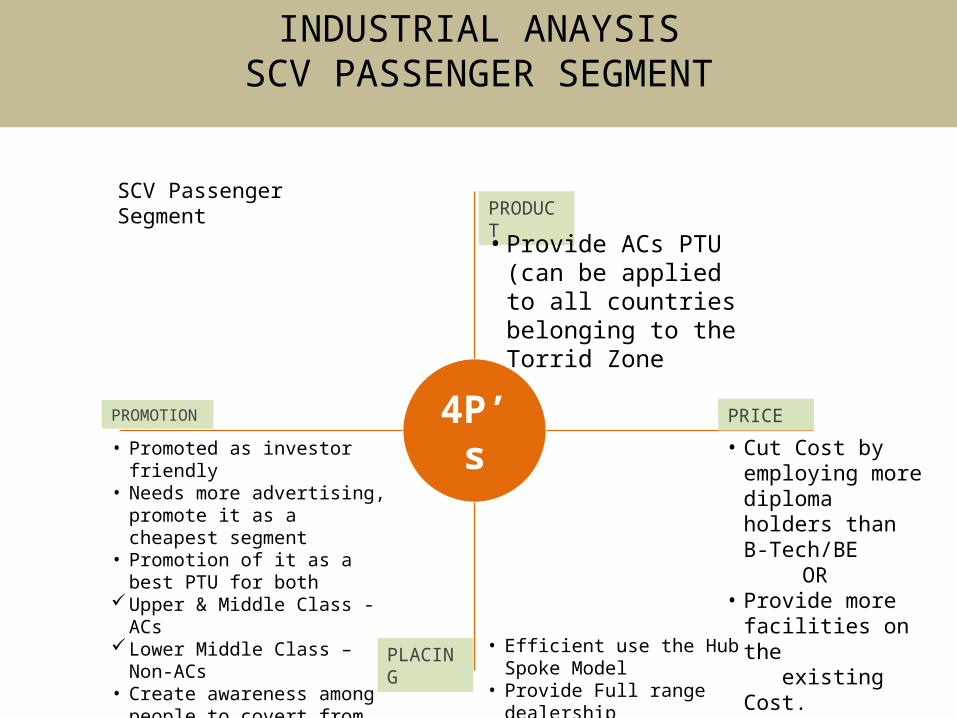

SCV Passenger Segment

INDUSTRIAL ANAYSISSCV PASSENGER SEGMENT

80%

19%

1%

Total Industry Market in 2012-13

Tata Motors Mahindra & mahindraOthers

Tata Motors

Industry-50

050100150200

Growth over the years 2007-2013

Growth over the years 2007-2013

SCV Passenger Segment

INDUSTRIAL ANAYSISSCV PASSENGER SEGMENT

4P’s

PRODUCT•Provide ACs PTU (can be applied to all countries belonging to the Torrid Zone

PRICE

PLACING

PROMOTION

• Cut Cost by employing more diploma holders than B-Tech/BE

OR • Provide more facilities on the existing Cost.

• Efficient use the Hub Spoke Model

• Provide Full range dealership

• Promoted as investor friendly

• Needs more advertising, promote it as a cheapest segment

• Promotion of it as a best PTU for both

Upper & Middle Class - ACs

Lower Middle Class – Non-ACs

• Create awareness among people to covert from drivers to owners to Entrepreneurs

• Associate with Bollywood Stars

SCV Passenger Segment

INDUSTRIAL ANAYSISSCV PASSENGER SEGMENT

SCV passenger segment – Our Strategy(Primary Research)

Sample Size – 100 people from diverse backgrounds ,Location – Near Metro Stations & Bus Stands of New Delhi

Would you prefer PTUs like AC Tata Magic /

Iris/ Vans than Conventional Non-AC

vehiclesi.e Shell out extra money for the same

NO27%

Don’t

Know4%

YES69%

Change in the taste of the customer- People now prefer comfort ability factor more than the price

The strategy is best suited for the metro cities in the initial phase

STRENGTHMarket leader

Brand AssociationHigh Capita

WEAKNESSLimited Product availability

Products not competitive against competitors

OPPORTUNITIESGovernment tender

Help Government as CSR to promote PTS

THREATSRising oil prices

Weak investment sentiments.Slowing industrial activity

Rising Competition both nationally & Internationally

SWOT ANALYSIS

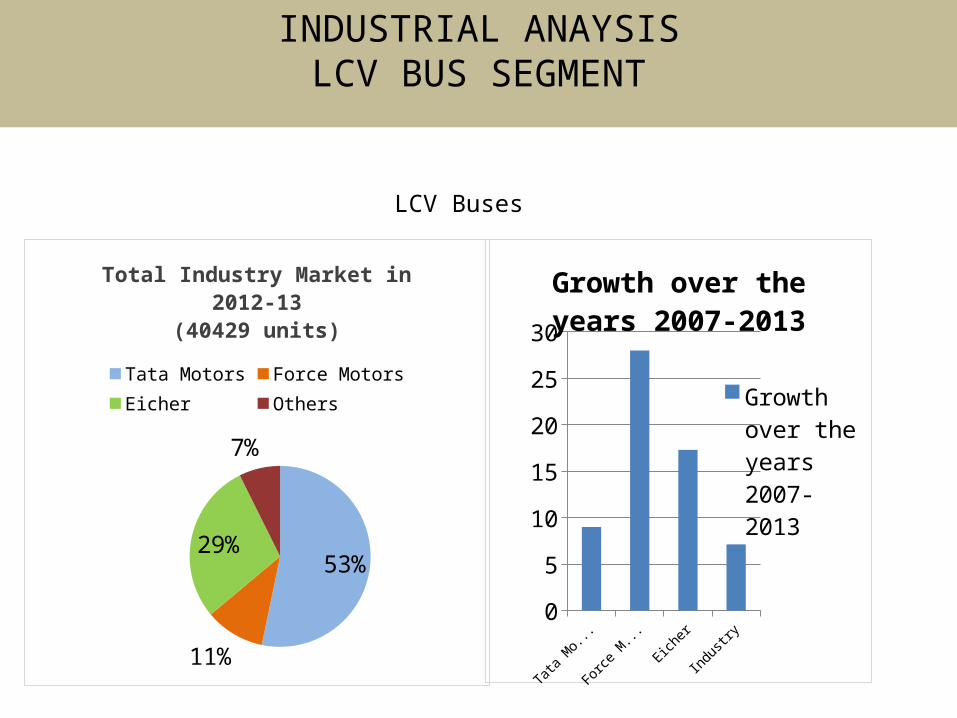

INDUSTRIAL ANAYSISLCV, ICV & MCV BUS SEGMENT

53%

11%

29%

7%

Total Industry Market in 2012-13

(40429 units)

Tata Motors Force MotorsEicher Others

051015202530

Growth over the years 2007-2013

Growth over the years 2007-2013

LCV Buses

INDUSTRIAL ANAYSISLCV BUS SEGMENT

39%

18%19%

23%

1%

Total Industry Market in 2012-13

(16914 units)

Tata Motors Ashoka LeylandsEicher Swaraj MazdaOthers

010203040506070

Growth over the years 2007-2013

Growth over the years 2007-2013

ICV Buses

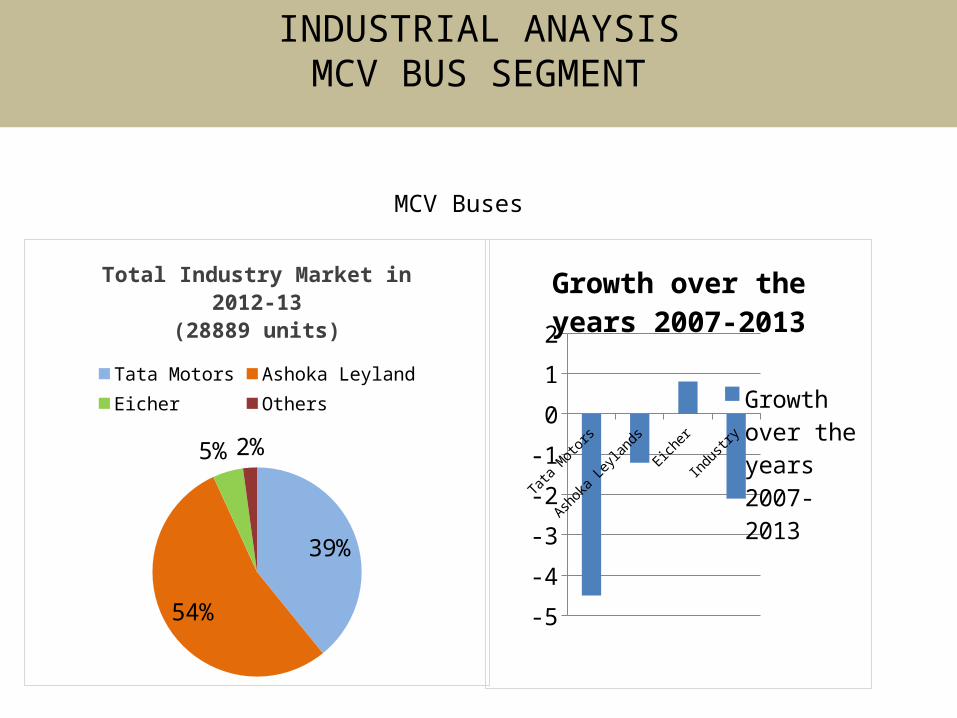

INDUSTRIAL ANAYSISICV BUS SEGMENT

39%

54%

5% 2%

Total Industry Market in 2012-13

(28889 units)

Tata Motors Ashoka LeylandEicher Others

Tata Motors

Ashoka L

eyland

sEic

her

Industry

-5-4-3-2-1012

Growth over the years 2007-2013

Growth over the years 2007-2013

MCV Buses

INDUSTRIAL ANAYSISMCV BUS SEGMENT

4P’s

PRODUCT• Provide ACs PTU (can be applied to all countries belonging to the Torrid Zone)

• Product modifications such as for school Buses & luxury segment-

Installation of fire resistant, electronic event recorder that will function like black box o aircrafts

Introduce smoke detectors More breakable windows Radium stickers for easy exit during emergency

PRICE

PLACING

PROMOTION• Cut Cost by employing more diploma holders than B-Tech/BE

OR • Provide more facilities on the existing Cost.

• Increase price of Luxury Segment & provide quality Products

• Efficient use the Hub Spoke Model

• Provide Full range dealership including all three segments i.e. LCV, ICV & MCV

• Promoted as investor friendly

• Promotion of it as a best PTU for both

Upper & Middle Class - ACs

Lower Middle Class – Non-ACs

• Tenders of STUs for MCV segment

• Collaborating with Schools to insure safety of students by product enhancement

LCV , ICV & MCV Bus Segment

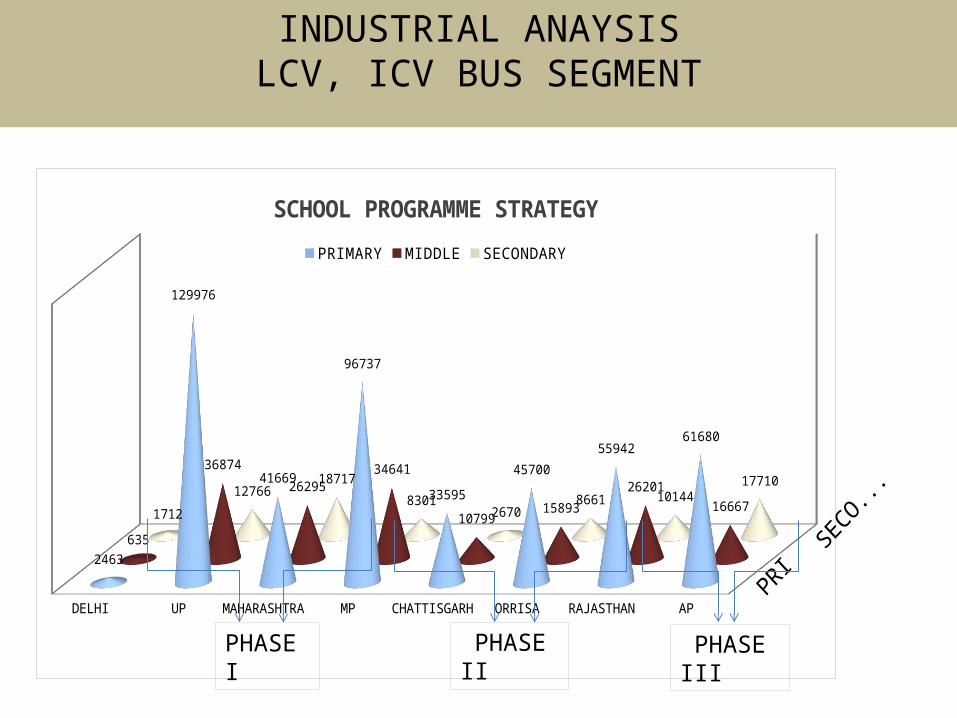

INDUSTRIAL ANAYSISLCV, ICV & MCV BUS SEGMENT

DELHI UP MAHARASHTRA MP CHATTISGARH ORRISA RAJASTHAN AP

2463

129976

41669

96737

3359545700

5594261680

635

3687426295

34641

10799 1589326201

16667171212766

187178301

26708661 10144

17710

SCHOOL PROGRAMME STRATEGYPRIMARY MIDDLE SECONDARY

PHASE I

PHASE II

PHASE III

INDUSTRIAL ANAYSISLCV, ICV BUS SEGMENT

The School Concept Contd.• We have divided our plan into 3 phases

Phase I- Covers Schools of Delhi, Uttar Pradesh, Maharashtra Phase II- Covers Schools of Rajasthan & Andhra Pradesh Phase III- Covers Schools of MP, Chhattisgarh, Orissa• The Idea is to make buses more safe for children and promote them in

the same way. The sales team has the prime role in the idea• If we can just cover 20% of the market at each level of primary,

Middle and High School level , the market share can be increased by a very large amount

• If each School has minimum 4 buses the total sales in the year will be 573140 units

• The same plan is applicable for the School Vans sector too.

TATA should add some additional features in its school buses, some measure are suggested in the above slides

Sales Team Promotes TATA buses as more

safe for children both to the school authorities and parents by some

promotional campaigns

Regular follow up with the schools and

improvements thereafter.

ACTION PLAN to increase sales to whooping numbers

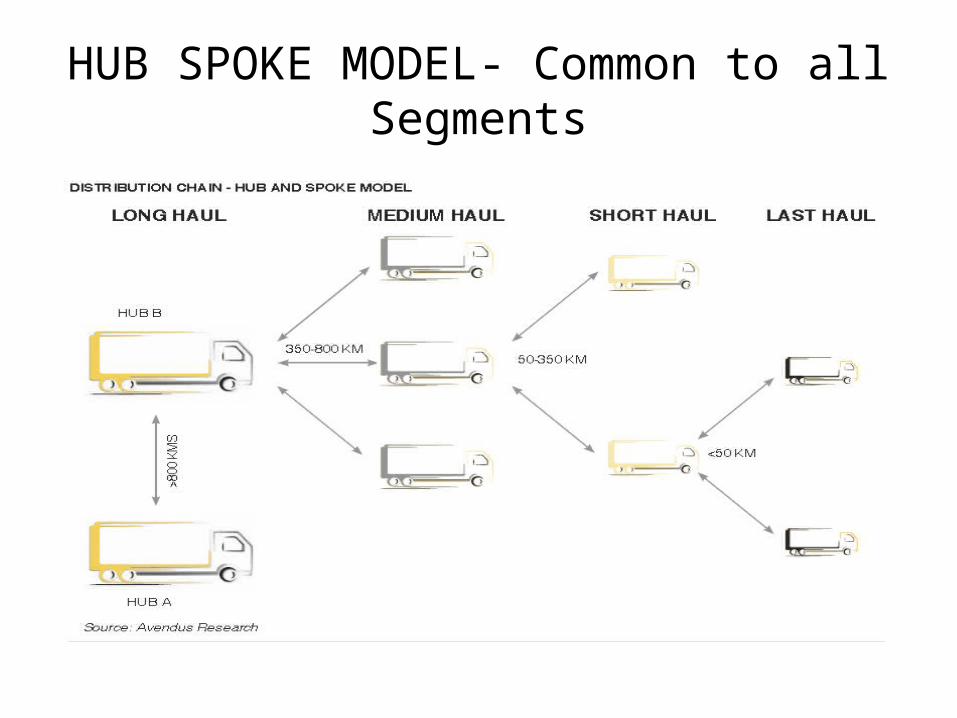

HUB SPOKE MODEL- Common to all Segments

Advantage of Hub Spoke Model

• Saves time• Saves Extra Inventory Cost• Saves overall Cost• On Time delivery of vehicles• It should be used effectively and efficiently by the coherent work of both dealers and distributors.

• Distribution network Outsourcing to some specific can cut cost due to rise in petrol/diesel prices and weak economy

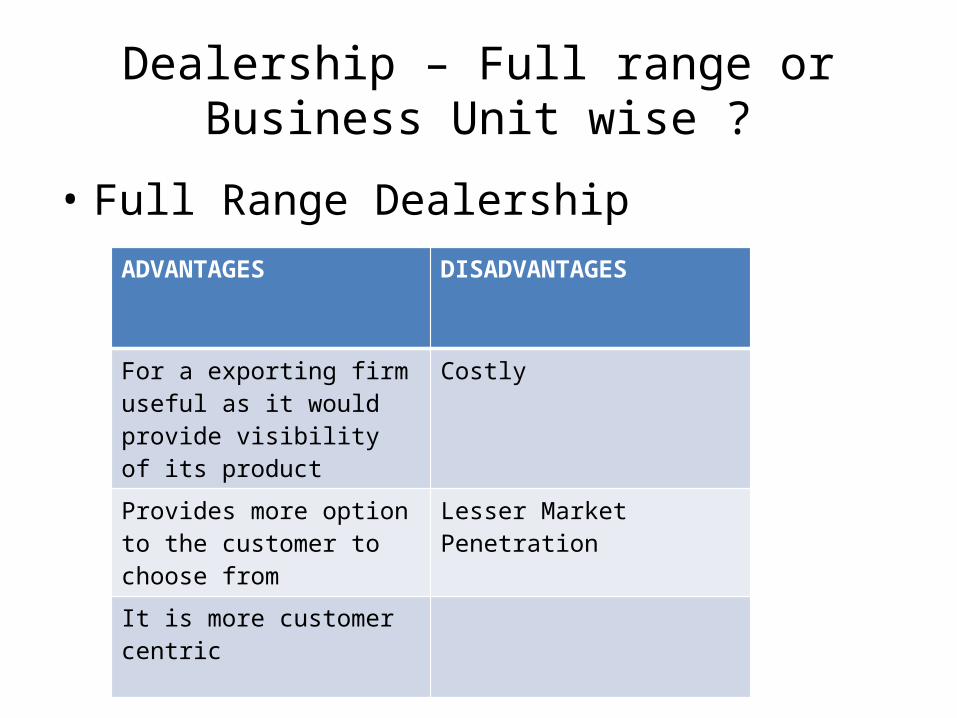

Dealership – Full range or Business Unit wise ?

• Full Range DealershipADVANTAGES DISADVANTAGES

For a exporting firm useful as it would provide visibility of its product

Costly

Provides more option to the customer to choose from

Lesser Market Penetration

It is more customer centric

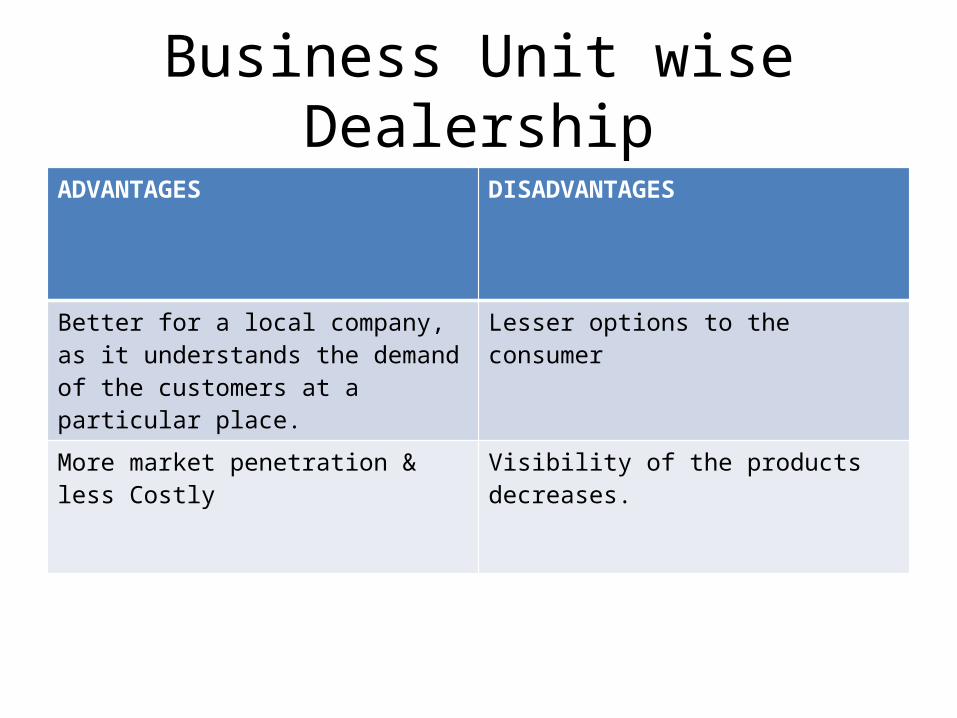

Business Unit wise Dealership

ADVANTAGES DISADVANTAGES

Better for a local company, as it understands the demand of the customers at a particular place.

Lesser options to the consumer

More market penetration & less Costly

Visibility of the products decreases.

WHAT SHOULD BE TATA MOTORS DEALERSHIP STRATEGY

• For the Heavy & Medium Segments TATA Motors should go for Business Unit wise Dealership as the demand of such segment is niche

• For other categories the Dealership model should be full range dealership model.

Rising interest rates in the economy is a

cause of concern as it dampens both

capital investments and

softens the domestic demand.

Positives: The cash flow from

operations has grown 11 times

compared to last year despite a huge

CAPEX. Tata Ace single handedly

raised the market share of Tata Motors in LCV

segment by 5%. The operating leverage for Tata Motors is higher due to the

high fixed costs of CAPEX. But still

the overall financial leverage of Tata Motors is well under control when compared to Ashok Leyland.

Excess debt has led to a high Debt to Equity

ratio and this is not good news as the company plans to go for further

capital expansion. Also the percentage of cash flow used for CAPEX is increasing.

FINANCIAL ANAYSIS & SUGGESTED STRATEGIES

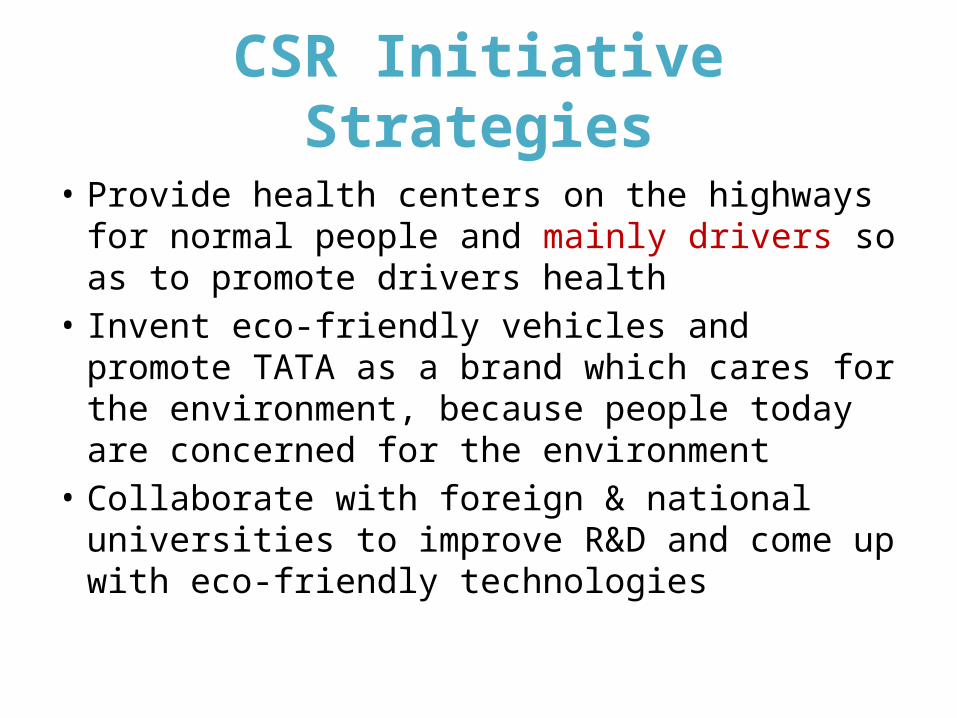

CSR Initiative Strategies

• Provide health centers on the highways for normal people and mainly drivers so as to promote drivers health

• Invent eco-friendly vehicles and promote TATA as a brand which cares for the environment, because people today are concerned for the environment

• Collaborate with foreign & national universities to improve R&D and come up with eco-friendly technologies

THANK YOU