Taking Stock: Transitional Justice and Market Effects in Latin America

39

Electronic copy available at: http://ssrn.com/abstract=1666892 Taking Stock: Transitional Justice and Market Effects Tricia D. Olsen PhD Candidate University of Wisconsin-Madison [email protected] Andrew G. Reiter PhD Candidate University of Wisconsin-Madison [email protected] Eric Wiebelhaus-Brahm Senior Research Fellow International Human Rights Law Institute, DePaul University [email protected] Paper prepared for the 2010 Midwest Political Science Association Annual Meeting, April 22-25, 2010, Chicago, IL Abstract The relationship between transitional justice and economic development has recently attracted the attention of academics and policymakers. An emerging literature highlights the tension between the forward-looking economic goals of growth, development, and investment, and the backward-looking trials and truth commissions. Current research focuses on states’ ability to compete for international assistance or on underdeveloped countries’ efforts toward economic reconstruction following periods of civil war and authoritarianism. This paper broadens the scope of the study of the political economy of transitional justice by examining the effect of transitional justice mechanisms (trials, truth commissions, and amnesties) on the perceptions of private investors. Specifically, using time-series data for Argentina, Chile, Brazil, and Spain, we explore how stock markets have responded to efforts to uncover information about past human rights abuses and to prosecute those responsible. The paper draws on a range of data on transitional justice events, and utilizes daily stock market data. 1

Transcript of Taking Stock: Transitional Justice and Market Effects in Latin America

Electronic copy available at: http://ssrn.com/abstract=1666892

Taking Stock: Transitional Justice and Market Effects

Tricia D. Olsen PhD Candidate

University of Wisconsin-Madison [email protected]

Andrew G. Reiter PhD Candidate

University of Wisconsin-Madison [email protected]

Eric Wiebelhaus-Brahm Senior Research Fellow

International Human Rights Law Institute, DePaul University [email protected]

Paper prepared for the 2010 Midwest Political Science Association Annual Meeting, April 22-25, 2010, Chicago, IL

Abstract

The relationship between transitional justice and economic development has recently attracted the attention of academics and policymakers. An emerging literature highlights the tension between the forward-looking economic goals of growth, development, and investment, and the backward-looking trials and truth commissions. Current research focuses on states’ ability to compete for international assistance or on underdeveloped countries’ efforts toward economic reconstruction following periods of civil war and authoritarianism. This paper broadens the scope of the study of the political economy of transitional justice by examining the effect of transitional justice mechanisms (trials, truth commissions, and amnesties) on the perceptions of private investors. Specifically, using time-series data for Argentina, Chile, Brazil, and Spain, we explore how stock markets have responded to efforts to uncover information about past human rights abuses and to prosecute those responsible. The paper draws on a range of data on transitional justice events, and utilizes daily stock market data.

1

Electronic copy available at: http://ssrn.com/abstract=1666892

Introduction

Until recently, discussions of transitional justice often occurred in isolation from the

economic development needs of transitional societies. Historically, transitional justice

has typically focused on violations of civil and political rights, to the neglect of socio-

economic rights. As such, the picture of past violence that emerges often overlooks the

structural violence and economic inequality that gave rise to human rights abuses, as well

as the suffering caused by economic mismanagement. Similarly, there is little focus on

how post-conflict development plans may exacerbate tensions in societies still healing

from periods of conflict and authoritarianism.

Fortunately, the gulf between economic development and transitional justice has

begun to shrink. The International Journal of Transitional Justice devoted an issue to

the topic, and the International Center for Transitional Justice has produced an edited

volume on the subject.1 These pieces, and others, have drawn attention to the need for

greater collaboration between these two fields and have offered theoretical and practical

suggestions for doing so. Moreover, official development agencies are seeking similar

synergies.2 They are increasingly recognizing that states must design development

projects so as not to reproduce the socio-economic conditions that gave rise to the

conflict in the first place.

The literature to date is limited, however, in at least two ways. First, existing

work remains largely conceptual and theoretical; there are few empirical studies of the

relationship between transitional justice and economic development. Thus far, scholars

are more concerned with exploring potential points of complementarity between the two

1 International Journal of Transitional Justice 2(3) (2008); De Grieff and Duthie 2009. 2 Alexander 2003.

2

goals rather than exploring empirical relationships. The dialogue is embryonic. Second,

the literature tends to define development in the narrow sense of development assistance.

Scholars focus their attention primarily on state-to-state assistance and the role of

development nongovernmental organizations (NGOs). While this is an important area of

study, economic development is more expansive. In this paper, we seek to broaden the

discussion by examining how private investors respond to transitional justice initiatives.

Private investors are important components in the development equation. Indeed,

international financial organizations react slowly and often they condition their support

on the fulfillment of specific requirements. By contrast, private investors can inject

capital quickly into emerging markets to help them recover quickly from economic

hardship. Therefore, how these actors respond to transitional justice initiatives has

potentially significant development consequences.

This paper addresses this question in four parts. The first section discusses the

complex intersection between transitional justice and development, highlighting the key

advances in the field. It concludes that scholarship has identified a number of important

relationships between development and transitional justice, but to date, has failed to

evaluate the effect of private investors. The following section thus draws upon the

existing literatures on transitional justice and the political economy of financial markets

to theorize the relationship between private investors and transitional justice. It

highlights the importance of these actors for economic development in societies

recovering from authoritarianism and mass atrocity. We then derive several hypotheses

about the impact of transitional justice on the behavior of private investors. In the next

section, we empirically test these hypotheses in four post-authoritarian cases in which

3

transitional justice has played a prominent role: Argentina, Chile, Brazil, and Spain. The

analysis relies on a range of data on transitional justice events, and utilizes daily stock

market data. We examine the impact of other macroeconomic events and utilize

anecdotal evidence on investor decision-making in our analysis. We conclude with a

discussion of the policy implications of our findings, and provide suggestions for future

research.

Transitional Justice and Development

Scholars, activists, and policymakers of transitional justice and economic development

have increasingly recognized that the failure of each to account for the other has rendered

the post-conflict work of each less effective than it might otherwise be. Several

criticisms have emerged from the growing dialogue between the two fields. For example,

activists often accuse transitional justice of being blind to socio-economic issues.

Observers have criticized transitional justice for ignoring social inequality as a cause of

violence and repression. Moreover, they contend that transitional justice has frequently

ignored economic crimes in favor of dealing with gross violations of human rights.3 Yet

they point out that economic mismanagement and its legacies typically affect far more

people.4 While authoritarian regimes, at times, are able to generate growth, it is usually

due to excessive borrowing and increased state expenditure, rather than by promoting

industry or trade. Transitional justice mechanisms, theoretically, address the negative

effects of a fragile economy. Some scholars, for example, conceive of transitional justice

broadly as tools to encourage “social integration,” of which development efforts are

3 Miller 2008. 4 Carranza 2008.

4

critical part.5 Some scholars suggest that transitional justice and development might also

complement one another. By addressing the structural and institutional factors that lead

to socioeconomic injustice, new democratic leaders and citizens can achieve societal

transformation and, ultimately, reconciliation.6

An alternative perspective suggests that transitional justice and economic

development work at cross-purposes. Transitional justice and development projects,

scholars often contend, compete for the same resources. New democracies—faced with

economic instability—may choose to address more forward-looking needs rather than

addressing the past. Jon Elster is one of the few researchers examining the tradeoff

between transitional justice and more immediate, pressing economic concerns.7 More

recently, Peter Boettke and Christopher Coyne also acknowledge such a tradeoff. As

they state, “it is important to realize that investing resources in the administration of

justice means that those resources are diverted away from other transition activities that

can also yield a future stream of benefits. In other words, there is an opportunity cost to

investing resources in the administration of justice.”8

Though research on the relationship between transitional justice and development

is just beginning to emerge, there has been little attention to how private investors might

perceive transitional justice. The literature typically focuses on official development

assistance (ODA) and the work of international development NGOs. Yet attracting

private investment is essential for economic development following authoritarianism. To

date, the literature focuses on initial aid and reconstruction, and misses the long-term

5 De Greiff 2009. 6 Mani 2002. 7 Elster 2006. 8 Boettke and Coyne 2007, p. 57.

5

necessity of developing a dynamic economy that attracts foreign investment and capital.

Furthermore, given the fact that states can delay transitional justice initiatives and these

mechanisms can last for many years, they may still be active when a post-conflict country

is attempting to attract private investment more concertedly. As such, private investors’

views on transitional justice have potential implications for post-transition economic

development.

Transitional Justice and Private Investors

To date, there has been neither a theoretical nor an empirical exploration of the

relationship between transitional justice and investment patterns. There is significant

debate on whether transitional justice promotes peace or instability, but the question has

not been satisfactorily resolved.9 Studies have explored how victims, perpetrators, and

the public10 react to transitional justice initiatives, but scholars have not explored the

views of other groups, such as investors. While the impact of transitional justice on

transitional societies remains an open question, examining the behavior of investors, who

make their living by calculating risk, can reveal important insights.

Although none focus on transitional justice, the political economy literature has

devoted considerable attention to the behavior of financial markets. In particular, there is

a significant literature on stock market reaction to political events.11 Generally, the

literature emphasizes the role of either institutions12 or partisanship13 in shaping investor

9 See, for example, Kim and Sikkink forthcoming; Lie et al. 2007; Olsen et al. 2010; Sikkink and Walling 2007; and Wiebelhaus-Brahm 2010. 10 See Backer 2006; Stover and Weinstein 2004; and Gibson 2004. 11 See for example Herron 2000; Mcgillivray 2003; and Jensen and Schmith 2005. 12 See for example Bachman 1992; Freeman et al. 2000; and Lobo and Tufte 1998.

6

perceptions of future returns. One branch of the institutional literature emphasizes the

importance of institutions that insulate economic policymaking from political

interference, which leads to greater policy stability. Others focus on electoral

institutions, arguing that proportional representation systems are more attractive to

investors. Because coalitions are typically necessary in order to form a government, they

are less prone to dramatic policy swings. In the partisanship literature, there is some

consensus that investors generally prefer parties on the right, which tend to prefer price

stability and fiscal balance. Overall, recent studies suggest that uncertainty is as

important, if not more so, than partisan politics in influencing investors’ preferences.14

Uncertainty makes it difficult for investors to predict future returns.

Despite the relative size of the literature, there are several limitations in its utility

for predicting investor reaction to transitional justice initiatives. First, most research

focuses on developed country stock markets. This is sensible given that these stock

exchanges are the largest in the world and have operating for long time. However, with

notable exceptions, these countries have not been active in terms of transitional justice.

Second, the literature has focused largely on investor reactions to elections and their

potential to result in significant change in economic policy. Yet investor concerns in

other policy areas have attracted little attention. As such, the literature provides us with

only general guidance on what we might expect to find.

Nonetheless, stock markets are an attractive means of assessing investor

sentiment for several reasons. Many studies of stock market behavior employ the

13 See for example Alesina and Rosenthal 1995; Alesina et al. 1993; Alt and Crystal 1983; Franzese 2002; Hibbs 1987; and Leblang and Mukherjee 2005. 14 Bernhard and Leblang 2002; Bernhard and Leblang 2006; Benton 2008; and Jensen and Schmith 2005.

7

efficient market hypothesis.15 The efficient market hypothesis assumes that asset prices

are a reflection of all relevant information that market actors have available to them.

Further, it assumes that actors respond instantaneously to any new information that

becomes available. Investors continually reevaluate their prognosis for future earnings

based upon new information. As such, the movement of asset prices reflects investor

expectations of the effect of new political and economic information on their future

returns.

Investor behavior is not a simple matter of stimulus and response. In some

instances, investors may not react to events that appear significant. Investors may not

view political rhetoric as credible and, therefore, may discount talk in terms of assessing

their returns.16 Investors might also react only to good news. Investors follow political

events over the long term and, being risk-averse, they price the market in light of

potentially worse case scenarios.17 As a result, investors may respond to positive

developments rather than negative news. In addition, the literature also suggests that

markets may not react to political events because investors have anticipated them, and

have already incorporated the likelihood of the events occurring into prices. In short,

stock prices react may not only to actual events, but also to the probability of particular

events occurring.18

Extrapolating from the literature on the political economy of stock market activity

yields theoretical reasons for contrary hypotheses regarding private investors’ preferences

15 Fama 1991. 16 Benton 2008. 17 Benton 2008. 18 Measuring investors’ opinions about the probability of certain events, however, is very difficult to do. As such, we are only able to measure the reaction to particular events or announcements of such events.

8

with respect to transitional justice. On the one hand, investors prefer stability. Some

scholars are critical of at least more punitive transitional justice measures for fomenting

instability in fragile transitional states.19 The risk of prosecution may lead those accused

to protect themselves through violence or a coup. For example, in Chile, in response to

Patricio Aylwin’s pro-transitional justice rhetoric during the 1989 presidential campaign,

Pinochet countered: “the day they touch any one of my men, the state of law is ended.”20

There is some anecdotal evidence to suggest that investors are concerned about the

destabilizing potential of transitional justice. Rama Mani, for example, finds that, in the

Democratic Republic of the Congo, the World Bank, and International Monetary Fund

are concerned that transitional justice may scare off investors.21 Furthermore, trials and

vetting programs can eliminate individuals with expertise that might create an

environment less conducive to investment. Iraqi reconstruction was long-delayed by the

punitive de-Baathification process, which stripped the Iraqi army and police of expertise

needed to fight the insurgency and promote order. Investors might see reparations and

other compensation programs as wasteful, capricious, or rapacious, and raise fears about

increased taxes or the security of property rights. Finally, amnesties may lead to popular

uproar, which could also be detrimental for investment.

Investors may also react negatively to transitional justice because they were

complicit in past abuses. South Africa’s Truth and Reconciliation Commission (TRC),

for example, held hearings on the role of the business community in apartheid-era abuses.

In its final report, the TRC recommended a one-time tax on businesses to fund

19 Snyder and Vinjamuri 2003. 20 La Epoca, October 11, 1989, 13. 21 Mani 2008, 258.

9

development programs.22 Moreover, South Africans seeking damages for exploitation

under apartheid have sued several MNCs in US courts.23 Thus, whether by being a direct

target of transitional justice or because of perceived instability due to transitional justice,

private investors may flee from such initiatives.

By contrast, there are theoretical reasons to expect transitional justice to help

promote an investment-friendly environment. Transitional justice, by addressing past

abuses, providing accountability, and promoting reconciliation, may be a boon to

development.24 In particular, many have promoted trials and truth commissions

explicitly for their ability to encourage the development of the rule of law, which is

important for investment.25 Furthermore, if a new regime is able to try perpetrators with

little disruption, it could signal to investors that the new democracy is stable and it will

not be overthrown. This may even be preferable to a situation in which a dictator is

sitting in the wings protected by an amnesty and able to overthrown the regime at

anytime. Truth commissions might also encourage investment by producing reform

recommendations that strengthen the rule of law, rebuild infrastructure and institutions,

and promote trust.26 Furthermore, programs that compensate for loss or damage of

property may resolve lingering property rights issues thereby reducing uncertainty.27

Given that investors want consistent enforcement of laws and contracts, they may

welcome such measures. Finally, investors might approve of amnesties because, even if

unjust, they believe such measures will promote stability. More generally, Pablo de

22 The government has thus far rejected the recommendation. 23 Forde 2010. 24 Alexander 2003. 25 De Greiff 2009, 59-60. 26 De Greiff 2006. 27 Boettke and Coyne 2007.

10

Grieff postulates that transitional justice might promote development by supporting

positive norms of social interaction, and by encouraging the development of civic trust.28

While investors may or may not be part of the transitional society, he argues that

transitional justice might promote a more general trust in others and in government

institutions.

A third hypothesis is that transitional justice has little influence on investment

decisions. Some observers are skeptical that transitional justice has any measurable

effect on a transitional society’s economy.29 Economic factors, such as the country’s

growth prospects, levels of taxation, and exchange rate policies may all play a much more

significant role in influencing investment decisions. In addition, investors may have

already anticipated the possibility of transitional justice and their perceptions figured in

their decision whether or not to invest in the country in the first place. Therefore,

transitional justice developments may not generate much reaction.

In sum, the literature provides a wealth of potential hypotheses to explain investor

reaction to transitional justice initiatives. In fact, investors are unlikely to react in the

same way in different transitional situations. Perceptions of transitional justice may

change as such initiatives become further chronologically removed from a political

transition. The presence of multiple transitional justice mechanisms may complicate

investor calculations. A country’s possession of rare natural resources may trump any

concerns about transitional justice or the lack thereof.

28 De Greiff 2009, 42-48; see also de Greiff 2006. 29 Duthie 2008, 294; and de Greiff 2009, 39.

11

Empirical Analysis

To test these hypotheses, we focus on four countries in which transitional justice has

played a prominent role in the post-authoritarian democracy: Chile, Argentina, Brazil,

and Spain. In addition, each country is a relatively developed country where investors

are likely to play a greater role than in a country like Rwanda where the emphasis is on

humanitarian aid rather than investment. We use data from each country’s major stock

market index. Argentina’s MERVAL (Mercado de Valores) Index is a price-weighted

index of stocks traded on the Buenos Aires Stock Exchange. Stocks are selected based

on market share, trading volume, and stock price. Brazil’s Índice Bovespa (Bolsa de

Valores do Estado de São Paulo) is composed of the stocks that account for 80 percent of

trading volume in the past year. It is typically composed of about 50 stocks, and daily

data are available since 1988. In Chile, the IPSA (Índice de Precio Selectivo de

Acciones) has been calculated since 1977, and daily data are available since 1988. IPSA

is composed of the 40 stocks with the highest average annual trading volume in the

previous year. The IBEX 35 is Spain’s main benchmark index. It is market

capitalization weighted so larger companies are more influential in its rise and fall. The

35 companies that make up the IBEX 35 are selected by the Technical Advisory

Committee, which reviews their choice biannually. Drawn from Spain’s four major stock

exchanges, the movement of the IBEX 35 provides a general sense of investor sentiment

in the country. The index was launched in 1992, though it is possible to calculate the

IBEX 35’s value back to 1987.

In creating timelines of key transitional events in each of our four cases, we relied

on a variety of resources, including the Transitional Justice Data Base, the New York

12

Times, and other secondary sources. We code major arrests, indictments, and convictions

of those involved in the design and carrying out of state terror. In terms of truth

commissions, we note formal proposals, the passage of legislation or issuance of

executive orders establishing one, and the release of a commission report. We also

include major truth revelations, whereby a report is released or confessions are made that

reveal previously unknown details about the authoritarian past. In addition, we include

proposals and approval of amnesties and pardons, as well as repeals of such laws. We

also track reparations programs from proposal to implementation. Finally, we also note

major domestic reactions to transitional justice events, such as protests and riots. This is

particularly important in analyzing investor reactions since they are likely most interested

in the domestic impact of transitional justice rather than the events themselves. Overall,

we find six amnesties, nine repeals of amnesties, seven truth commission events, 22

warrants/arrests/charges and three convictions, and seven instances in which trials were

dropped or prohibited. Across the four cases, there were also four events in which

reparations were furthered, eight instances of major revelations about the past, and five

events coded as domestic unrest related to transitional justice. During the period for

which stock market data are available, we find just four transitional justice events in

Spain, all related to the Law of Historical Memory, and just seven in Brazil. We identify

24 transitional justice events in Argentina and 35 in Chile. A full listing of events is

provided in the appendix.

We go further than to identify correlations between transitional justice events and

movements of stock market indices. First, we calculated the daily percent change in the

stock indices between the day of and the day following a significant transitional justice

13

event. Next, we compared the daily percent change with the average daily percent

change over the previous year to determine if the magnitude of the change is unusual.

Second, we control for other influences on the movement of the respective stock market

index. One element of this is a news search of major national economic and political

events, such as devaluations, loan defaults, elections, or resignations that are theoretically

likely to influence the market. To do so, we examined Facts on File’s World News

Digest for all news entries from each country for a full two weeks prior to each

transitional justice event. Furthermore, local stock markets are also influenced by global

events. As a result, we compared the daily movement of the local stock market index

with that of the Dow Jones Industrial Average (DJIA), a bellwether of global investor

sentiment. Below, we examine each case in turn by outlining the general transitional

justice proceedings and their effect on investment, if any.

Argentina

Argentina has been wrestling with military-era abuses for nearly three decades.

In the aftermath of the democratic transition in 1983, the prospect of accountability for

human rights abuses seemed probable. Within a few years, however, military unrest and

economic crisis temporarily slowed progress in terms of transitional justice. Nonetheless,

by the mid-1990s, the past was back, as new revelations and innovative legal strategies

put human rights violations back in the spotlight. Under President Nestor Kirchner’s

administration (2003-2007), Argentina’s amnesty laws were swept away. As a result,

Argentina’s courts are actively engaged in trials for crimes committed during military

rule.

14

In 1976, the Argentine military seized power and established a three-man junta

composed of the leaders of the three branches of the armed forces. In the aftermath of the

coup, the military began a brutal campaign to repress any opposition. By the time the

military relinquished power to a democratically elected government in 1983, an estimated

30,000 people had been killed or disappeared by the military government.30 The junta’s

ultimate downfall was its poor handling of the economy and the misguided Falklands

War. In the wake of growing discontent, it consented to return power to civilians.

Shortly after winning the 1983 presidential election, Raul Alfonsín established the

National Commission for the Disappearance of Persons (CONADEP) to uncover

information regarding human rights abuses committed during military rule. In total, it

collected information on nearly 9,000 disappearance cases. CONADEP’s final report

was turned over to the Alfonsín administration in September 1984 and, when publicly

released shortly thereafter, became a best seller. The government viewed CONADEP as

a prelude to prosecuting human rights abuses. Alfonsín had planned to pursue only the

junta leaders, but the CONADEP report, entitled Nunca Más, generated pressure to

broaden the judicial net.31 The number of court cases exploded. Following the

conviction of five former junta members, cases were brought against some 2,000 other

military officers.32

Growing military unease led to a series of uprisings. While they were quelled, the

government grew increasingly cautious. It passed the Full Stop Law, which put a

deadline on bringing new cases regarding military-era human rights violations. When the

courts were flooded with cases to beat the deadline, the prospect of a military coup 30 Barrionuevo 2008. 31 Amstutz 2005. 32 Acuna and Smulovitz.

15

appeared to increase further. The government responded by passing the Due Obedience

Law, which granted amnesty to all military personnel at the rank of lieutenant colonel

and below. After replacing Alfonsín, President Carlos Menem went one step further and

pardoned the generals not covered by the Due Obedience Law.

The past did not reemerge as a major issue again until the mid-1990s. Retired

naval captain Adolfo Scilingo and others began to publicly confess to their roles in

human rights violations. Around the same time, courts in Europe were becoming more

active in seeking the extradition of Latin American officials in relation to the deaths and

disappearances of their nationals. Although Pinochet is the most well known, former

Argentine officials were the target of several cases. Finally, in the late 1990s, victims

groups in Argentina began using innovative legal strategies to subvert the amnesty such

as seeking charges related to kidnapping and baby theft.

All of this culminated in the election of President Nestor Kirchner. He vowed to

repeal the Due Obedience Law, which Congress did in 2003. Two years later, the

Supreme Court struck down the Full Stop and Due Obedience Laws as unconstitutional.

Since then, hundreds of former and current police, military, and intelligence officials

have faced trial for their role in past human rights abuses. Human rights groups have

estimated the upwards of 1,000 individuals may eventually be subject to prosecution.33

Although sentiment has shifted over time, investors in Argentina have displayed a

distinct preference for sweeping the past under the rug. While Alfonsín was personally

popular, his handling of the economy was found wanting. In the mid-1980s, Argentina

was in the midst of a deep economic crisis. The government’s foreign debt approached

USD 50 billion and the annual inflation rate reached 800 percent. To be sure, some 33 Rohter 2006.

16

investors were probably more scared off by record levels of hyperinflation than by the

prospect of transitional justice. However, in such an environment, the pursuit of

transitional justice was an unwelcome distraction that riled the military and raised fears

of another coup.

The pardons under Menem were indirectly linked to investment promotion.

Menem pursued an aggressive liberalization program that included privatization schemes

and fiscal austerity in order to restore macroeconomic stability and once again attract

investment to Argentina. While these policies were paramount in influencing investor

sentiment, creating political stability by foregoing prosecutions certainly contributed.

The Menem administration sought to distance itself from Alfonsín’s transitional

justice policy from the very start. On June 11, 1989, the incoming Defense Minister,

Italo Luder, called for an end to human rights trials. Investors greeted the news with a

nearly 8 percent jump in the MERVAL. The next day, Alfonsín abruptly resigned six

months prior to the end of his term. The MERVAL rose over 6 percent on September 17,

1989 as Menem formally announced his intention to pardon the military officers who had

been convicted of past human rights abuses or of leading earlier rebellions against the

Alfonsín government. The following month, Luder offered an economic defense of the

pardon. “If the military issue is not solved quickly,” he said, “it's hardly likely that any

(foreign) investments will come to the country.”34 Investors agreed. Media tycoon,

Robert Maxwell, for example, described the pardon as a “courageous political

decision.”35

34 Reuters. 1989. “Officers pardoned for roles in dirty war” The Globe and Mail. October 9. 35 Morgan, Jeremy. 1989. “Maxwell to Invest 63m Pounds in Argentina.” The Guardian October 21.

17

Strangely, investor sentiment appeared to be shifting at roughly this time.

Menem’s announcements of over 200 individual pardons on October 7, 1989 and an

additional 100 more on October 10 were greeted with declines of 5.8 percent and 1.3

percent respectively. Following the early December 1990 army uprising, the view that

the pardons had emboldened the military gained credence.36 Even the government’s

Economy Minister, German Gonzalez, wondered whether the rebellion would

demonstrate to foreign investors that Argentina was not yet a stable democracy.37

Fears about the destabilizing potential of trials remained the norm, however, and

persisted through the 1990s. Scilingo’s March 2, 1995 admissions were accompanied by

a 5.5 percent drop in the MERVAL. Menem continued to contend that “the examination

of the past a distraction from the task of reforming the economy and making Argentina an

investment paradise.”38 In late 1997, political consultant Felipe Noguera presciently

warned that many Argentines feared digging up the past would “provoke[e] the military

and jeopardize[e] Argentina's fledgling democracy and recent economic gains.”39 When

former Argentine President General Videla was arrested on child kidnapping charges on

June 10, 1998, the MERVAL dropped 3 percent. The December 28, 1998 arrest of

retired Admiral Ruben Franco on the same charges (the ninth officer to be detained for

child kidnapping) led to a 2.6 percent decline.

36 Bonasegna, Christina. 1990. “Argentine Revolt Reveals Lingering Army Tensions” Christian Science Monitor. December 5. 37 Christian, Shirley. 1990. “Argentine Army Revolt Is Crushed Days Before Planned Bush Arrival” The New York Times. December 4. 38 Scott, Noll. 1995. “Argentina’s Dark, Dirty Past Refuses to Lie Down and Die.” The Guardian May 23. 39 Epstein, Jack. 1997. “Argentina's 'Dirty War' Laundry May Get a Public Airing.” Christian Science Monitor December 4.

18

Even twenty years after the military returned power to civilians, the fear of

instability persisted. Nestor Kirchner’s efforts to promote accountability for human

rights abuses under military rule have largely been greeted negatively by investors. On

July 25, 2003, he revoked a government edict prohibiting handing over current and

former government officials to face trial in foreign counties; the MERVAL fell 1.6

percent. When the Senate followed the Chamber of Deputies in approving a repeal of the

Due Obedience Law on August 21, 2003, the MERVAL dropped 2 percent. In the

aftermath, Ruben Pasquali, an Argentine stock trader, commented that some people

“wonder if Kirchner is spending his energy and political capital on the right thing.”40

Only in the past few years have the instability fears perhaps begun to permanently

fade. The MERVAL rose nearly 1 percent on June 15, 2005, the day Argentina’s

Supreme Court struck down the Full Stop and Due Obedience Laws. Similarly, the

market seemed to shrug off late May 2006 Army Day protests by military officers and

exhibited strong gains. Following Argentina’s most recent economic crisis, investors

have returned to the country. As court cases and convictions multiply and the military

remains largely quiet, investors appear to be learning that transitional justice need not be

threatening.

Chile

On September 11, 1973, General Augusto Pinochet led the armed forces in a coup

against the regime of democratically elected Salvador Allende. Pinochet quickly

consolidated his power and ushered in an era of repressive rule. It is estimated that

between 1973 and 1977 more than 130,000 people were jailed, with at least 3,000 40 Winter, Brian. 2003. “Argentines confronting nation's violent past” USA Today September 18.

19

disappeared.41 Thousands more fled the country in exile during this period. On April 19,

1978, Pinochet passed an amnesty law covering all crimes committed between September

11, 1973 and March 10, 1978.

The 1980s were characterized by increased opposition to Pinochet’s regime, due

to both political and economic factors. In accordance with the constitution written by the

military regime in 1980, a plebiscite was held in 1988 to vote on another eight-year term

for Pinochet. It was assumed by most that this would merely reaffirm his rule. The

opposition, however, seized the political opening and mounted a strong campaign against

Pinochet. Despite some intimidation and voter fraud, the plebiscite held on October 5,

1988 was reasonably fair and the “No” vote won (55% to 43%). This paved the way for

democratic elections in December 1989, where Christian Democrat Patricio Aylwin won,

beating Pinochet’s candidate, Hernán Büchi. Despite this electoral defeat, Pinochet was

able to relinquish power in all other respects under this own terms. He remained the

commander-in-chief and appointed himself as senator for life (thereby ensuring his own

immunity to prosecution). In addition, the military was granted privileged status within

the government by the 1980 constitution. Pinochet also handpicked many of the senators

and Supreme Court justices.

Despite these challenges, Aylwin attempted to investigate the crimes of the past.

On April 25, 1990, he formed the Commission on Truth and Reconciliation, popularly

known as the Rettig Commission after its chair, to uncover the human rights abuses

committed by the former regime. After nine months of work, the commission produced

the Rettig Report in an attempt to establish the truth about the past. This was followed by

41 Pion-Berlin 1993.

20

an official apology by Aylwin and the establishment of a comprehensive reparations

program. The amnesty law of 1978, however, remained intact.

The mid-1990s marked a period of uncertainty with respect to transitional justice

in Chile. Judges became bolder in their interpretation of the amnesty law and in their

efforts to prosecute violators of human rights abuses.42 Most notably, in 1993, an arrest

warrant was issued for an active high-ranking officer, Colonel Fernando Laureani. But in

response, Pinochet ordered the military to readiness, and troops lined the streets in full

combat gear as a show of force, and despite Aylwin’s statement on March 6, 1991, that

amnesty can only be applied after a case is decided, most judges still chose to simply

closed cases once it was confirmed that a crime was committed. By 1997, however,

judgers finally stopped this practice, and in the late 1990s, courts began a renewed effort

to try perpetrators of human rights violations.43

The impetus for the recent surge in domestic court action in Chile can be partially

attributed to the arrest of Pinochet in London in 1998 on charges brought against him in a

Spanish court.44 Pinochet was eventually sent back to Chile, but the series of events had

an indirect, political impact on Chilean judges. David Pion-Berlin argues that the courts

were shamed and now felt the need to show that they were capable of taking their own

actions.45 In a crucial legal breakthrough, on June 8, 1999, Judge Juan Guzmán, an

appellate court judge, ruled that the amnesty law did not apply to disappearances; they

would be categorized as aggravated kidnappings instead since there was no body or proof

of death presented by the former regime. Later that summer, the Santiago Appellate

42 Sutil 1997, 140-1 43 Arceneaux and Pion-Berlin 2005, 129 44 Roht-Arriaza 2005; Woodhouse 2000; and Wilson 1999. 45 Pion-Berlin 2004.

21

Court and the Chilean Supreme Court upheld his decision.46 In late 1999, courts stripped

Pinochet of his immunity.47 From then until his death in 2006, Pinochet found himself

indicted many times and spent most of his final days under house arrest. During the same

time, many other members of the Chilean military have been tried and convicted. In

addition, from August 21, 1999 to June 13, 2000, the Mesa de Diálogo (Human Rights

Round-Table Dialogue) was held, and in 2003, the government created a new truth

commission—the National Commission on Political Prison and Torture—to examine

abuses not covered by previous commissions. It issues a final report in November 2004

based on over 35,000 testimonies.

Overall, investor reactions to transitional justice were more muted in Chile than

they were in Argentina, and they were more in favor of accountability for past human

rights abuses. Chile had the advantage of being on relatively strong economic footing

when it emerged from authoritarian rule. While Pinochet’s regime was heavily criticized

for human rights violations, even its opponents noted Chile’s economic success brought

on by the unique bureaucratic-authoritarian system. Pinochet’s military regime provided

the stability necessary for his “Chicago Boys” to successfully implement free-market

principles. Indeed, Chile was one of only a handful of Latin American countries to avoid

the 1980s debt crises that rocked the region throughout what known as the “lost decade.”

Investors in Chile also had the advantage of already witnessing the effects of

transitional justice in Argentina and elsewhere in the region. Thus, there has been a clear

trend in investor behavior towards wanting Chile to move quickly to consolidate its

democracy by holding trials for human rights violations. Aylwin immediately issued

46 Arceneaux and Pion-Berlin 2005, 138-9. 47 Arceneaux and Pion-Berlin 2005, 139.

22

pardons for past abuses when he took office, but this decision was greeted with a drop of

1.33 percent in the IPSA. A year later, however, the release of the truth commission

report resulted in a nearly 2 percent increase.

Investor sentiment became more apparent in the mid-1990s, when the new

democracy began to issue arrest warrants and attempt to hold perpetrators accountable for

the first time. Investors watched the interaction between democratic actors and members

of the military closely. In particular, the case of General Manuel Contreras, former head

of Chile’s secret police, served as bellwether for investors. The Supreme Court

sentenced him to seven years in jail in early 1995, but he subsequently refused to

acknowledge the verdict as legitimate, took refuge in the south, then in a military

regiment, and later in a military hospital where he declared himself unfit to go to jail.

Many in the military during this period shielded him and verbally challenged the decision

of the court. Investors viewed this series of events as a serious threat to Chile’s economic

success, and noted “President Frei’s reluctance to force Contreras’s hand reflects the

ruling coalition’s reluctance to rattle the skeletons of the Pinochet era.”48

It was also during this time that Chile was in discussions to join NAFTA, and

investors openly argued that this should not happen until Chile’s democratic reforms

were complete. They warned about the impact of expanding NAFTA to “another country

with dangerously weak democratic institutions.”49 There was a strong sense that a

democratic victory over the military on the Contreras issue would be an important sign

that Chile’s democracy was strengthening. When the military finally turned over

Contreras, the Journal of Commerce noted: “The arrest set an important precedent. It

48 Taylor 1995. 49 Reding 1995.

23

showed that Chile’s military, which enjoys special privileges, nonetheless is willing to

respect the rule of law. That bodes well for the nation's future as a full-fledged

democracy, free of the long shadow of its 17-year military dictatorship.”50 Not

surprisingly, the IPSA rose by 1.38 percent the day the military announced Contreras

would be turned over, and nearly another half percent when he finally went to jail.

Investors have continued to react positively to further trials. When authorities arrested

two retired generals and 14 other former military officers on charges of kidnapping and

murder in 1999, the IPSA rose nearly 2 percent. The stock market rose nearly 1 percent

when a high-ranking general was forced to retire in 2002 after charges that he obstructed

human rights investigations – perhaps a final sign that democratic actors were now well

in charge of the military.

The most prominent transitional justice efforts in Chile have been the legal

developments with Pinochet himself. Here too, investors have reacted positively to

accountability. Interestingly, however, this only happened with domestic events. Despite

the political circus surrounding Pinochet’s arrest in London and possible extradition to

Spain, those events show very little effect on investors in Chile. When he returned to

Chile, however, this changed dramatically. When Chilean courts stripped him of his

immunity in August 2000, the IPSA rose 2.44 percent. In recent years, now that

democracy is firmly consolidated in Chile, investor reaction to the myriad of smaller

transitional justice events has been largely undetectable.

50 Journal of Commerce 2005.

24

Brazil

Though Brazil’s military rule was actually longer than that of its neighbors, there

has been relatively very little transitional justice activity. Brazilians seem intent upon

leaving the past behind after its slow, cautious transition to democracy. With immunity

granted to both sides—left-wing activists and the military—neither side pursued trials.

Since the democratic transition, government officials have officially recognized past

abuses and launched informal truth-seeking bodies that have released detailed reports on

the past. Yet the amnesty law remains untouched. Even so, current debates surrounding

transitional justice occupy the political sphere as the government is considering holding

an official truth commission.

In 1964, Brazilian military leaders ousted President João Goulart in a bloodless

coup with hopes of bringing a new era to Brazilian politics. Though the military led

Brazil for over the next two decades, they were—relatively—less violent than

neighboring military dictatorships. Victims in Brazil numbered in the hundreds rather

than the tens of thousands who were “disappeared” in Argentina and Chile. The total

number of victims remained relatively low, widely reported only to be in the hundreds.

Amid growing unrest and calls for a return to democracy, General Ernesto Geisel

became president and introduced a number of reforms in the mid-1970s. These reforms

allow citizens to take part in political activity and elections, initiating a period known as

the “opening” or abertura. While citizens became increasingly active, the next military

president, João Figueiredo, sent an amnesty law to Congress in 1979. The law granted

immunity for all political crimes committed between September 2, 1961 and August 15,

1979. The amnesty covered crimes committed by both leftist groups and members of the

25

military government and armed services in an effort to promote an era of forgiveness and

ensure the success of the democratic transition.

In 1985, the election of the first civilian in 21 years marked the beginning of

democratic rule. One year later, the Archdiocese of São Paulo published a report, Brasil:

Nunca Mais, which consisted of 2,700 pages of testimony from military trial transcripts

recorded between 1964 and 1979. Their work documents close to three hundred forms of

torture and identifies 17,000 victims.51 While the report gained widespread attention

internationally, additional action in Brazil did not take place until a decade later. In 1995,

the government officially recognized military-era wrongdoings and initiated a reparations

program for 135 victims’ families. At the time, Cardoso also created the National

Commission on Political Deaths and Disappearances to investigate those who were killed

or “disappeared” by state security forces between 1961 and 1988. The commission,

however, produced a report, The Right to Memory and to Truth, 11 years later noting that

they were unable to confirm many details since they were not granted access to key

archives.

In 2008, following the 2007 publication of The Right to Memory and to Truth, the

Office of the Prosecutor in São Paulo brought a civil suit against two former officials of

Brazil’s military and the central government. It is the first of its kind in that it challenges

the validity of the 1979 amnesty. In fact, human rights activists had expected a sea

change in Brazil’s transitional justice policy following the election of the leftist PT

candidate, Luiz Inácio “Lula” da Silva, in 2003. Yet there have been relatively few

advances under Lula, and he has supported the status quo more than most expected.

Lula’s government argues that the 1979 amnesty should be respected and that the two 51 Archdiocese of São Paulo 1986.

26

individuals in question are immune from their alleged acts.52 Despite opposing views

within his cabinet, Lula discouraged recent efforts to investigate the past: “Whenever we

talk of the dead students, of the dead workers, we claim after those who killed them,

when we should understand this martyrdom will not end if we don't learn to make our

dead heroes, and not victims.”53

The explicit discouragement of transitional justice and the tacit acceptance of past

abuses is a great disappointment to advocates of human rights. Nonetheless, the past has

refused to stay buried under Lula. In 2004, Correio Braziliense published pictures of

what appeared to be well-known journalist Vladimir Herzog, who was murdered by

Brazil’s military regime in 1975. The pictures unleashed a firestorm. The army public

affairs office issued a statement, that was quickly withdrawn, that sought to justify human

rights violations as a necessary evil to fight communism. The statement said, in part,

“[t]he measures taken by legally constituted forces were a legitimate response to the

violence of those who rejected dialogue and opted for radicalism” and were conducted

“in response to a public clamor” for a tough stand against extremists and subversives.54

The government reprimanded the army commander, but the defense minister also left his

post decrying “the persistence of authoritarian thinking” in the armed forces.55

Indeed, when Lula finally signed a decree calling for an official truth commission

in December 2009, he was faced with the threatened resignation of the heads of the three

armed forces along with his defense minister. Lula promised to review the matter and

retracted his support for the truth commission. As of this writing, this issue has not been 52 http://www.ictj.org/en/news/features/2116.html. 53 http://en.mercopress.com/2008/08/13/lula-openly-confirms-1979-amnesty-bill-and-silences-ministers. 54 Rohter 2004. 55 Economist 2004.

27

settled. Others in Lula’s cabinet, some of whom were detained and tortured during the

military dictatorship, continue to push for the truth commission. Some military officials

say they would support the truth commission if it were to investigate crimes committed

by both sides, alluding to possible investigations of the Worker’s Party’s 2010

presidential candidate, Dilma Rousseff, who was a leftist activist in the 1970s.56

Investors appear to have some concerns about the destabilizing potential of

transitional justice in the mid-1990s but have reacted only modestly to more recent

accountability mechanisms. Cardoso’s announcement in January 1995 of the National

Commission on Political Deaths and Disappearances, which was created specifically to

investigate crimes committed by the military dictatorship from 1961-1988, was met with

nearly a six percent dip in Brazil’s market, BOVESPA. When Lula released the report

from the commission in August, 2007, the market dropped again (2.7 percent), though

this also coincides with the downturn in the international economy.

Likewise, investors showed early skepticism about reparations efforts. When

Cardoso officially recognized the deaths during the military dictatorship and granted

victims’ families reparations, BOVESPA reported a small drop (0.75 percent). When

reparations efforts were extended to political acts prior to the military regime in 2002, the

market took an even larger fall (1.67 percent). Investor sentiment shifted, however, with

later reparation efforts. In 2003, the market rose nearly three percent (2.79 percent) when

Lula established the Inter-ministerial Commission and means to pay political reparations.

When the government announced the extended period to apply for preparations, investors

greeted this policy with a nearly five percent jump (4.84 percent). Positive reactions to

transitional justice decisions may imply that investors are confident that the government 56 Economist 2010.

28

is only truly committed to pursuing reparations. This is somewhat unsurprising, given

possibly destabilizing mechanisms—like trials and truth commissions—are not a real

concern for investors, given the government’s lukewarm attitude toward those

mechanisms.

Spain

In Spain, transitional justice has been a long time coming. Following Franco’s

1936 coup, hundreds of thousands of people are believed to have been victims of human

rights abuses at the hands of the military government. Most of the victims suffered

during Spain’s 1936-1939 civil war. After Franco’s death in 1975, other members of

Franco’s government and the opposition reached an agreement on a 1977 amnesty to

facilitate the democratic transition. Several officials who were part of the negotiations in

the 1970s remain in positions of authority and are loathe to jeopardize their positions.

The attempted military coup in 1981 has been repeatedly put forward as a warning

against digging up the past. Decades later, in many circles Spain’s past remains a taboo

subject.

However, in the wake of the controversy regarding Spanish Judge Baltasar

Garzon’s attempt to try Pinochet for past human rights abuses, Spain’s own troubled past

has been the subject of growing activism. By the early 2000s, the Franco era had become

the subject of art exhibitions and popular books, television, and film. A range of

transitional justice initiatives have been discussed, with a few implemented. Frustrated

with the lack of progress, in 2002, relatives of the disappeared asked the United Nations

working group on disappearances to press the Spanish government to uncover mass

29

graves.57 Informal exhumations beginning in the late 1990s had begun to uncover

forensic evidence of past human rights abuses. The calls of victims and their families for

a truth commission, however, have found little support within the Spanish government.

The proposal remains largely a matter for civil society discussion. During its reign, the

Popular Party government, which has pro-Franco origins, only went so far as to pass a

resolution in the fall of 2002 condemning Franco’s 1936 coup and recognized victims of

the civil war-era violence. In July 2006, the new Socialist Party government proposed a

Law for the Recovery of Historical Memory that would provide reparations to individuals

who lost property of suffered personal hard under the Franco regime. The legislation also

called for removing public symbols exalting Franco and encouraged local governments to

conduct efforts to exhume bodies. The law passed in late 2007, but it has not been put

into practice by the state or courts.

By and large, investors in Spain do not appear concerned about transitional

justice. Movements in the DJIA mirror the IBEX on most days with significant

transitional justice activity and likely are a greater influence. If anything, the IBEX

tended to move in concert with pro-accountability initiatives. The index closed nearly

one percent higher on December 14, 2006, the day on which parliament began debating

the Law on Historical Memory. In addition, on October 31, 2007, when the Congress of

Deputies approved the law, IBEX managed a .3 percent rise while the DJIA was down .6

percent.58 The importance of transitional justice in investor sentiment should not be

overstated, however. Thus far, transitional justice initiatives in Spain have been modest.

57 Tremlett 2002. 58 On the same day, a Spanish court acquitted Rabei Osman Sayed Ahmed, the accused Egyptian mastermind of the March 2004 terrorist attacks in Madrid. Three other main suspects were convicted of murder. It is unclear how the market would respond, if at all, to a mixed verdict.

30

In addition, although the past remains a source of tension, events are in the relatively

distant past. While many alleged perpetrators remain politically powerful, their numbers

fall with each passing year. The activities of Basque separatists likely weigh more

heavily in the minds of investors. Perhaps most important in explaining investor reaction

in Spain is that the country is firmly entwined within the European Union, which

provides stability and security.

Conclusion

The purpose of this paper is to explore the role of transitional justice and development.

While our research illustrates that investors react to transitional justice decisions, how

they react varies considerably. The Chilean case closely aligns with the expectations in

the transitional justice literature; investors reacted positively to trials. This supports the

general ideal that investors may view trials as a strong signal that a country is stable and

is prepared to respect the rule of law. While this reasoning explains the patterns in Chile,

investors in Argentina were content with forgetting the past. There, they repeatedly

showed their aversion to the destabilizing potential of trials. Certainly, the attempted

1985 coup shook investor sentiment about what trials might do for political and economic

stability. Yet investors continued to be wary of trials as late as 1998 with the arrests of

Argentina President General Videla and Admiral Ruben Franco. We might then

conclude more generally that when stability is threatened, investors prefer to avoid

dealing with the past. Investors tended to react positively to amnesty laws in Argentina

and Menem’s outright acknowledgement that he hoped amnesty would bring the political

stability that was necessary to attract investment. In sum, we contend that investors

31

prefer trials over other transitional justice mechanisms, but only when they pose no

significant threat to political and economic stability.

Though preliminary, our analysis supports the hypothesis that transitional justice

decisions affect investor sentiment. There are at least three potential areas of future

research that are worth pursuing to further explore the causal mechanisms at play.

First, additional work should look beyond the transitional justice mechanism

alone and aim to understand how investors perceive various characteristics of these

particular mechanisms and their effect on political stability. Maybe it is the scope of

mechanisms—in terms of who is involved—that affects perceptions about stability.

Widespread accountability efforts may concern investors while trials of a few, key

individuals will not. Our research also highlights the importance of the context in which

transitional justice occurs. Perhaps the timing of transitional justice, relative to

democratic transition, plays a role in investor sentiment. In addition, stability, as we have

noted, is key. It is thus possible that investors react differently to transitional justice

mechanisms depending on the relative stability of the wider political environment—

whether authoritarian or democratic.

Second, future work could investigate timing. First, we might think about timing

of investment. Understanding how long investors shy away from investment could shed

light on the extent to which transitional justice affects investment in the long-run.

Second, we might also think about timing of transitional justice mechanisms. While

investors—especially in the Brazilian case—reacted strongly to early transitional justice

efforts, their reaction was more modest as time passed. Perhaps once investors feel

32

confident that democratic stability will not be threatened, they are less likely to react

negatively to accountability efforts. A cumulative investor effect could be at play.

In sum, investors are paying attention to transitional justice choices. Thus, the

transitional justice literature is right to seriously consider how domestic actors will weigh

particular mechanisms in light of economic ramifications. Future research, however,

should be careful not to assume investors will react homogeneously to a particular

mechanism. Mechanisms and the contexts in which they take place vary. Paying close

attention to this variation—as domestic leadership and investors do—will also strengthen

the theoretical work surrounding transitional justice and development.

33

Bibliography

Alesina, Alberto and Howard Rosenthal. 1995. Partisan Politics, Divided Government, and the Economy. New York: Cambridge University Press.

Alesina, Alberto, Nouriel Roubini, and Gerald Cohen. 1993. “Electoral Business Cycles in Industrial Democracies.” European Journal of Political Economy 23: 1-25.

Alexander, Jane. 2003. “A Scoping Study of Transitional Justice and Poverty Reduction.” London: Department for International Development (DFID).

Alt, James and Alec Crystal. 1983. Political Economics. Berkeley: University of California Press.

Amstutz, Mark R. 2005. The Healing of Nations: The Promise and Limits of Political Forgiveness. Lanham, MD: Rowman & Littlefield Publishers.

Arceneaux, Craig and David Pion Berlin. 2005. Transforming Latin America: The International and Domestic Origins of Change. Pittsburgh, PA: University of Pittsburgh Press.

Archdiocese of São Paulo. 1986. Torture in Brazil: A Report (English translation of Brasil: Nunca Mais) Translated by Jaime Wright. New York: Vintage Books.

Bachman, Daniel. 1992. “The Effect of Political Risk on the Forward Exchange Bias: The Case of Elections.” Journal of International Money and Finance 11: 208-219.

Backer, David. 2006. “Victims’ Responses to Truth Commissions: Evidence from South Africa,” in Muna Ndulo ed., Security, Reconciliation and Reconstruction: When the Wars End. London: University College of London Press.

Barrionuevo, Alexei. 2008. “Argentine Ex-Army Chief Gets Life Sentence in ‘Dirty War’ Crimes.” The New York Times July 25.

Benton, Allyson Lucinda. 2008. “Do Investors Assess the Credibility of Campaign Commitments?: The Case of Mexico’s 2006 Presidential Race.” Political Research Quarterly 61(3): 403-418.

Bernhard, William and David Leblang. 2002. “Political Parties and Monetary Commitments.” International Organization 56: 803-31.

Bernhard, William and David Leblang. 2006. Democratic Processes and Financial Markets: Pricing Politics, Cambridge University Press.

Boettke, Peter J., and Christopher J. Coyne. 2007. “Political Economy of Forgiveness.” Society 44(2).

Carranza, Ruben. 2008. “Plunder and Pain: Should Transitional Justice Engage with Corruption and Economic Crimes?” International Journal of Transitional Justice 2(3): 310-330.

De Greiff, Pablo. 2006. “Truth-Telling and the Rule of Law.” In Telling the Truths: Truth Telling and Peacebuilding in Post-Conflict Societies, edited by T. A. Borer. South Bend: University of Notre Dame Press.

De Greiff, Pablo. 2009. “Articulating the Links Between Transitional Justice and Development: Justice and Social Integration.” In Transitional Justice and Development: Making Connections, edited by P. De Greiff and R. Duthie. New York: Social Science Research Council: Distributed by Columbia University Press.

34

De Greiff, Pablo, and Roger Duthie, eds. 2009. Transitional Justice and Development: Making Connections. New York: Social Science Research Council: Distributed by Columbia University Press.

Duthie, Roger. 2008. “Toward a Development-Sensitive Approach to Transitional Justice.” International Journal of Transitional Justice 2(3): 292-309.

Economist. 2004. “Resurrecting the Right to History.” The Economist, November 25. Economist. 2010. “Don’t Look Back; Lula and the Generals.” The Economist, January 9. Elster, Jon. 2006. Retribution and Reparation in the Transition to Democracy.

Cambridge, UK: Cambridge University Press. Fama, Eugene. 1991. “Efficient Capital Markets II.” Journal of Finance 46: 1575-1618. Forde, Fiona. 2010. “Apartheid Reparations Case Back in US Court.” The Sunday

Independent (South Africa) January 3. Franzese, Robert. 2002. “Electoral and Partisan Cycles in Economic Policies and

Outcomes.” Annual Review of Political Science 5: 369-421. Freeman, John R., Jude C. Hays, and Helmut Stix. 2000. “Democracy and Markets: The

Case of Exchange Rates.” American Journal of Political Science 44(3): 449-468. Gibson, James L. 2004. “Does Truth Lead to Reconciliation? Testing the Causal

Assumptions of the South African Truth and Reconciliation Process.” American Journal of Political Science 48(2): 201-217.

Herron, Michael. 2000. “Estimating the Economic Impact of Political Party Competition in the 1992 British Election. American Journal of Political Science 44(3): 326-337.

Hibbs, Douglas A. 1987. The Political Economy of Industrial Democracies. Cambridge, MA: Harvard University Press.

Jensen, Nathan M. and Scott Schmith. 2005. “Market Responses to Politics: The Rise of Lula and the Decline of the Brazilian Stock Market.” Comparative Political Studies 38: 1245-1270.

Journal of Commerce. 1995. “Showdown in Chile.” Journal of Commerce, June 22. Kim, Hunjoon, and Kathryn Sikkink. Forthcoming. “Explaining the Deterrence Effect of

Human Rights Prosecutions.” International Studies Quarterly. Leblang, David and Bumba Mukherjee. 2005. Government Partisanship, Elections, and

the Stock Market: Examining American and British Stock Returns, 1930–2000. American Journal of Political Science 49(4): 780-802.

Lie, Tove Grete, Helga Malmin Binningsbø, and Scott Gates. 2007. “Post-Conflict Justice and Sustainable Peace.” World Bank Policy Research Working Paper 4191, Post-Conflict Transitions Working Paper No. 5.

Lobo, Bento and David Tufte. 1998. “Exchange Rate Volatility: Does Politics Matter?” Journal of Macroeconomics 20: 351-365.

Mani, Rama. 2002. Beyond Retribution: Seeking Justice in the Shadows of War. Cambridge: Polity/Blackwell.

Mani, Rama. 2008. “Dilemmas of Expanding Transitional Justice, or Forging the Nexus between Transitional Justice and Development.” International Journal of Transitional Justice 2(3): 253-265.

McGillivray, Fiona. 2003. Coalition Formation and Stock Price Volatility. Manuscript: New York University.

35

Miller, Zinaida. 2008. “Effects of Invisibility: In Search of the ‘Economic’ in Transitional Justice.” International Journal of Transitional Justice 2(3): 266-291.

Olsen, Tricia D., Leigh A. Payne, and Andrew G. Reiter. Forthcoming. Transitional Justice in Balance: Comparing Processes, Weighing Efficacy. Washington DC: United States Institute of Peace Press.

Pion-Berlin, David. 2004. “The Pinochet Case and Human Rights Progress in Chile: Was Europe a Catalyst, Cause or Inconsequential?” Journal of Latin American Studies 36(3): 479-505.

Pion-Berlin, David. 1993. “To Prosecute or to Pardon? Human Rights Decisions in the Latin American Southern Cone.” Human Rights Quarterly 15(1): 105-130.

Reding, Andrew A. 1995. “Chile: Reforms First, then NAFTA.” Journal of Commerce, August 31.

Roht-Arriaza, Naomi. 2005. The Pinochet Effect: Transnational Justice in the Age of Human Rights. Philadelphia, PA: University of Pennsylvania Press.

Rohter, Larry. 2004. “Exhuming a Political Killing Reopens Old Wounds in Brazil.” The New York Times, October 24.

Rohter, Larry. 2006. “Argentine Leader’s Bid to Rein In Military Leads to Clash.” The New York Times, June 4.

Sikkink, Kathryn, and Carrie Booth Walling. 2007. “The Impact of Human Rights Trials in Latin America.” Journal of Peace Research 44(4): 427-445.

Snyder, Jack L., and Leslie Vinjamuri. 2003. “Trials and Errors: Principle and Pragmatism in Strategies of International Justice.” International Security 28(3): 5-44.

Stover, Eric, and Harvey M. Weinstein, eds. 2004. My Neighbor, My Enemy: Justice and Community in the Aftermath of Mass Atrocity. Cambridge, UK: Cambridge University Press.

Sutil, Jorge Correa. 1992. “Dealing with Past Human Rights Violations: The Chilean Case after Dictatorship.” Notre Dame Law Review 67(5): 1455-1485.

Taylor, Robert. 1995. “Chile: Too Good to be True - Latin Countries Stand in Awe of the Turnaround that Chile’s Banks have Achieved since the 1980s.” The Banker, November 1.

Tremlett, Giles. 2002. “Franco’s Secrets Haunt Spain.” The Guardian, October 21. Wiebelhaus-Brahm, Eric. 2009. Truth Commissions and Transitional Societies: The

Impact on Human Rights and Democracy. New York: Routledge. Wilson, Richard J. 1999. “Prosecuting Pinochet: International Crimes in Spanish

Domestic Law.” Human Rights Quarterly 21(4): 927-979. Woodhouse, Diana, ed. 2000. The Pinochet Case: A Legal and Constitutional Analysis.

Oxford, UK: Hart.

36

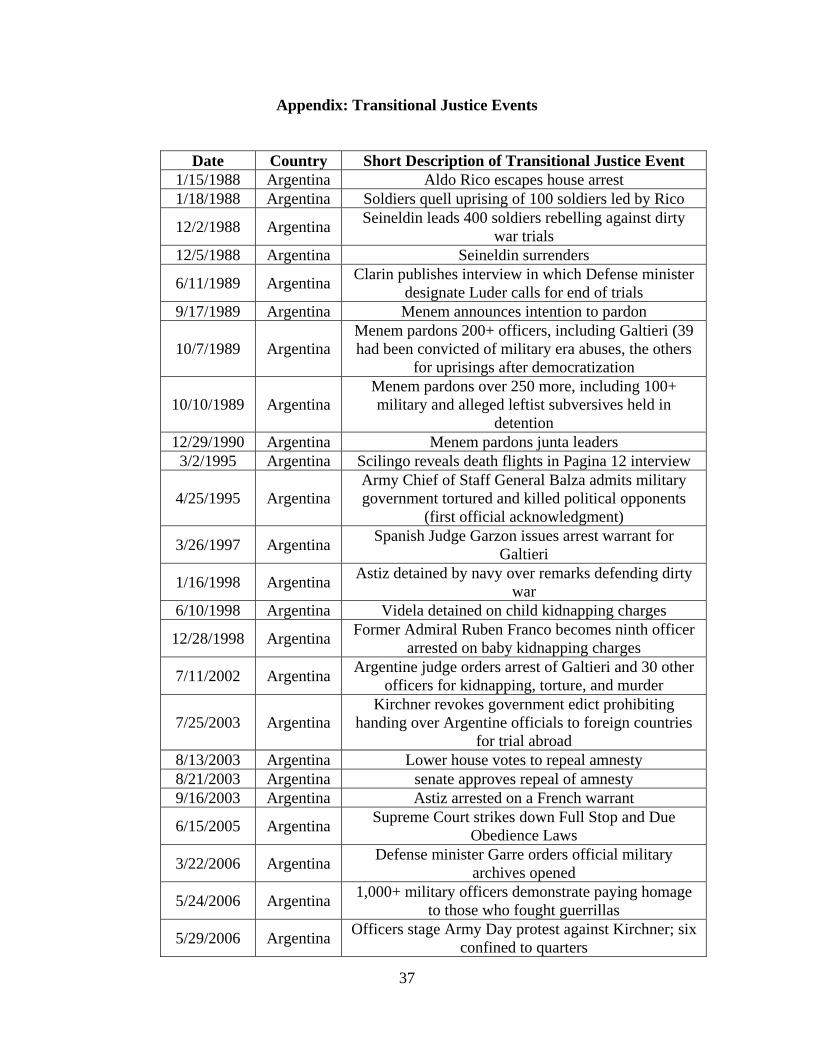

Appendix: Transitional Justice Events

Date Country Short Description of Transitional Justice Event 1/15/1988 Argentina Aldo Rico escapes house arrest 1/18/1988 Argentina Soldiers quell uprising of 100 soldiers led by Rico

12/2/1988 Argentina Seineldin leads 400 soldiers rebelling against dirty war trials

12/5/1988 Argentina Seineldin surrenders

6/11/1989 Argentina Clarin publishes interview in which Defense minister designate Luder calls for end of trials

9/17/1989 Argentina Menem announces intention to pardon

10/7/1989 Argentina Menem pardons 200+ officers, including Galtieri (39 had been convicted of military era abuses, the others

for uprisings after democratization

10/10/1989 Argentina Menem pardons over 250 more, including 100+ military and alleged leftist subversives held in

detention 12/29/1990 Argentina Menem pardons junta leaders 3/2/1995 Argentina Scilingo reveals death flights in Pagina 12 interview

4/25/1995 Argentina Army Chief of Staff General Balza admits military government tortured and killed political opponents

(first official acknowledgment)

3/26/1997 Argentina Spanish Judge Garzon issues arrest warrant for Galtieri

1/16/1998 Argentina Astiz detained by navy over remarks defending dirty war

6/10/1998 Argentina Videla detained on child kidnapping charges

12/28/1998 Argentina Former Admiral Ruben Franco becomes ninth officer arrested on baby kidnapping charges

7/11/2002 Argentina Argentine judge orders arrest of Galtieri and 30 other officers for kidnapping, torture, and murder

7/25/2003 Argentina Kirchner revokes government edict prohibiting

handing over Argentine officials to foreign countries for trial abroad

8/13/2003 Argentina Lower house votes to repeal amnesty 8/21/2003 Argentina senate approves repeal of amnesty 9/16/2003 Argentina Astiz arrested on a French warrant

6/15/2005 Argentina Supreme Court strikes down Full Stop and Due Obedience Laws

3/22/2006 Argentina Defense minister Garre orders official military archives opened

5/24/2006 Argentina 1,000+ military officers demonstrate paying homage to those who fought guerrillas

5/29/2006 Argentina Officers stage Army Day protest against Kirchner; six confined to quarters

37

7/26/2006 Spain Government unveils proposed Law on Historical Memory

12/14/2006 Spain Parliament begins debate on Law on Historical Memory

10/31/2007 Spain Lower house of parliament passes Law on Historical Memory

10/16/2008 Spain

Judge Garzon orders opening of 19 mass graves from civil war, opens criminal investigation on crimes against humanity charges against Franco and 34

former generals and ministers 11/18/2008 Spain Garzon drops crimes against humanity case

10/5/2007 Chile Chilean Court Orders Arrests of Pinochet's Kin and Close Allies

11/25/2005 Chile Judge Indicts Pinochet on Human Rights Charges 11/24/2005 Chile Pinochet Held on Charges Linked to Bank Accounts

8/11/2005 Chile Police in Chile Detain Pinochet's Wife and Son in Fraud Inquiry

3/12/2005 Chile Fugitive Leader of Chilean Sect Is Captured in Argentina

12/14/2004 Chile Pinochet Fit to Stand Trial, Judge Rules in Chile 11/28/2004 Chile Torture Report Given to President Lagos

11/6/2004 Chile Chile's Army Accepts Blame for Rights Abuses in the Pinochet Era

9/27/2004 Chile Judge Questions Pinochet About Killings Under His Rule

8/27/2004 Chile Chile's Top Court Strips Pinochet of Immunity

5/29/2004 Chile Chilean Court Revokes Pinochet's Immunity From Prosecution

9/26/2003 Chile Creation of Torture Commission

5/16/2003 Chile Former Chief of Secret Police Is Indicted by Judge in Chile

10/14/2002 Chile Chile General Quits In Wake of Charges of Obstruction Human Rights Investigation

7/10/2001 Chile Chile Court Bars Trials of Pinochet

1/30/2001 Chile Judge Reinstates Pinochet Case With New Order for House Arrest

12/21/2000 Chile High Court Voids Charges For Pinochet; Sets New Date

12/2/2000 Chile Pinochet’s Arrest Ordered by Judge 8/9/2000 Chile Pinochet Ruled No Longer Immune From Prosecution

8/2/2000 Chile Pinochet Reportedly Stripped of Immunity in Secret Court Vote

6/14/2000 Chile Chile Military Agrees To Search For Victims Of Its Rule

6/13/2000 Chile Human Rights Roundtable Finishes its Work

38

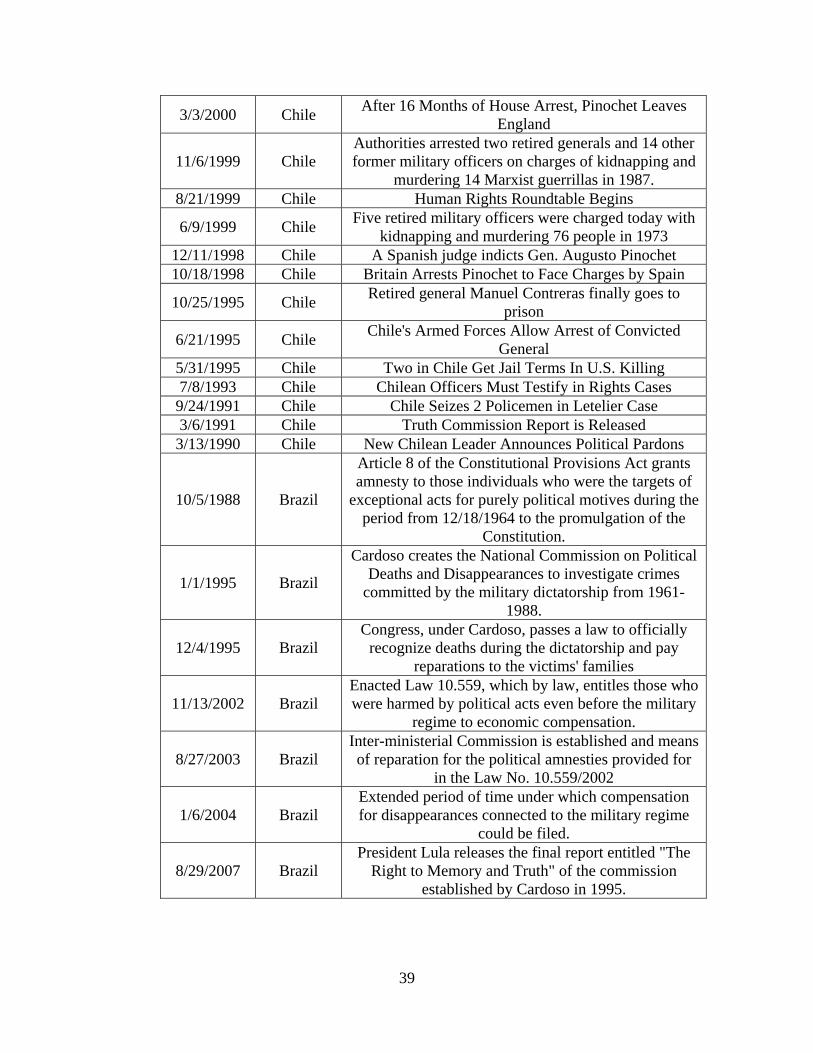

39

3/3/2000 Chile After 16 Months of House Arrest, Pinochet Leaves England

11/6/1999 Chile Authorities arrested two retired generals and 14 other former military officers on charges of kidnapping and

murdering 14 Marxist guerrillas in 1987. 8/21/1999 Chile Human Rights Roundtable Begins

6/9/1999 Chile Five retired military officers were charged today with kidnapping and murdering 76 people in 1973

12/11/1998 Chile A Spanish judge indicts Gen. Augusto Pinochet 10/18/1998 Chile Britain Arrests Pinochet to Face Charges by Spain

10/25/1995 Chile Retired general Manuel Contreras finally goes to prison

6/21/1995 Chile Chile's Armed Forces Allow Arrest of Convicted General