SuperviSion AnnuAl report - Banka e Shqipërisë

108

2 0 0 7 B a n k o f A l b a n i a SUPERVISION ANNUAL REPORT

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SuperviSion AnnuAl report - Banka e Shqipërisë

Supervision Annual Report Supervision Annual Report2007 2007

PB Bank of Albania Bank of Albania �

2 0 0 7

B a n k o f A l b a n i a

SuperviSion AnnuAl report

Supervision Annual Report Supervision Annual Report2007 2007

2 Bank of Albania Bank of Albania �

Supervision Annual Report Supervision Annual Report2007 2007

2 Bank of Albania Bank of Albania �

If you use data from this publication, you are requested to cite the source.Published by : Bank of Albania, Sheshi “Skënderbej”, No.�, Tirana, AlbaniaTel : �55-4-22222�0; 22�5568; 22�5569;Fax : �55-4-222�558

For enquiries relating to this publication, please contact:Publications Section, Foreign Relations, European Integration and Communication Departmente-mail: [email protected]

Printed in: �000 copies

www.bankofalbania.org

Supervision Annual Report Supervision Annual Report2007 2007

2 Bank of Albania Bank of Albania �

Supervision Annual Report Supervision Annual Report2007 2007

2 Bank of Albania Bank of Albania �

C o n t e n t S

A. DOCUMENT “ON SUPERVISION MISSION” 7

B. REGULATORY FRAMEWORK AND LICENSING PROCESS 9�. Legal and regulatory framework 92. Licensing ��

C. ON-SITE SUPERVISION �7�. Activity of the on-site supervision function �72. Cooperation with other authorities �7�. Problems observed during the examinations �8

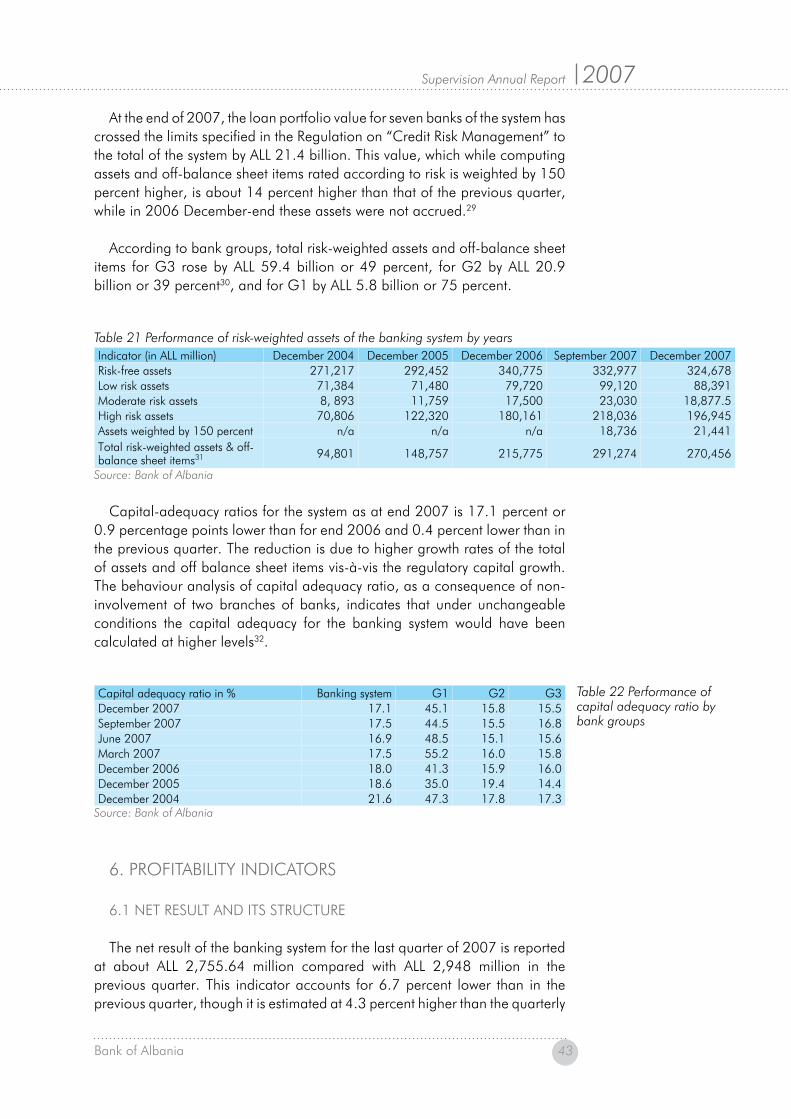

D. BANKING SYSTEN AND NON-BANK DEVELOPMENTS 22�. Economic environment 222. Main banking system highlights 24�. Banking system structure 264. Managing banking activity risk ��5. Capital adequacy 406. Profitability indicators 4�7. Non-bank financial institutions 49

E. CREDIT REGISTRY 52�. Overview 522. Main characteristics of the Credit Registry 5��. Reports and information designed by the Credit Registry 54

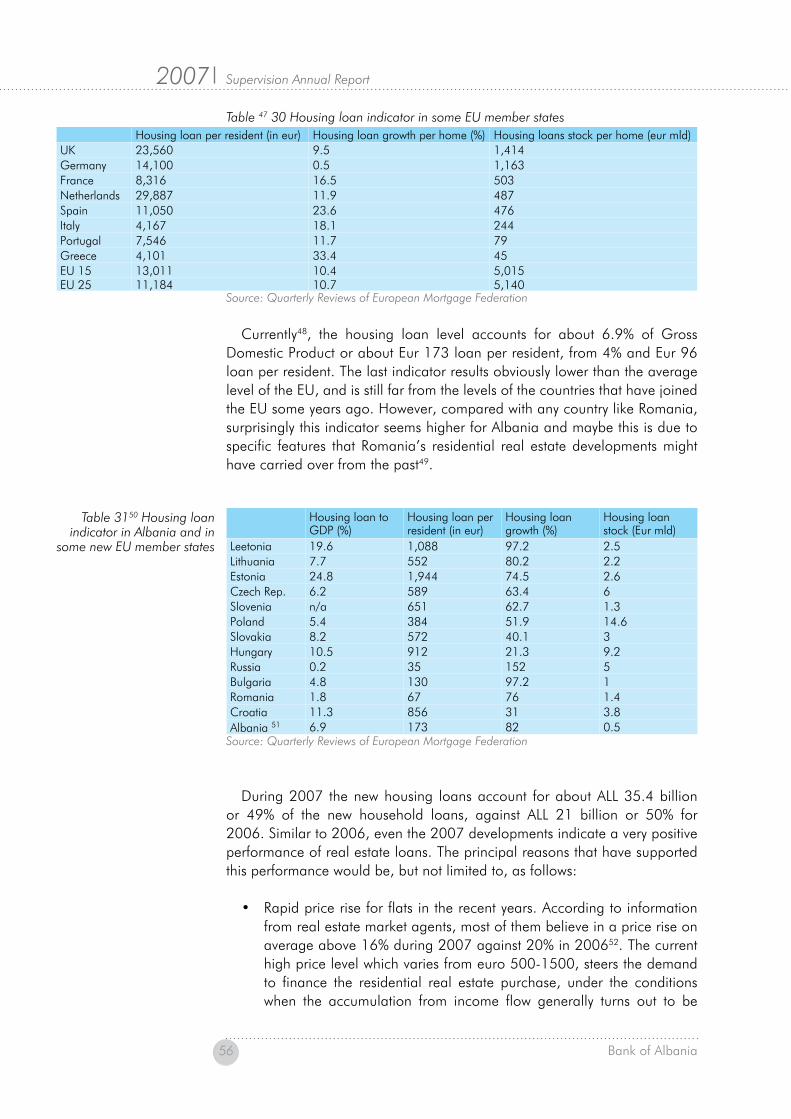

F. OTHER 55�. Housing loans. Financial stability implications 552. Albanian banking system position related to IFRS 60

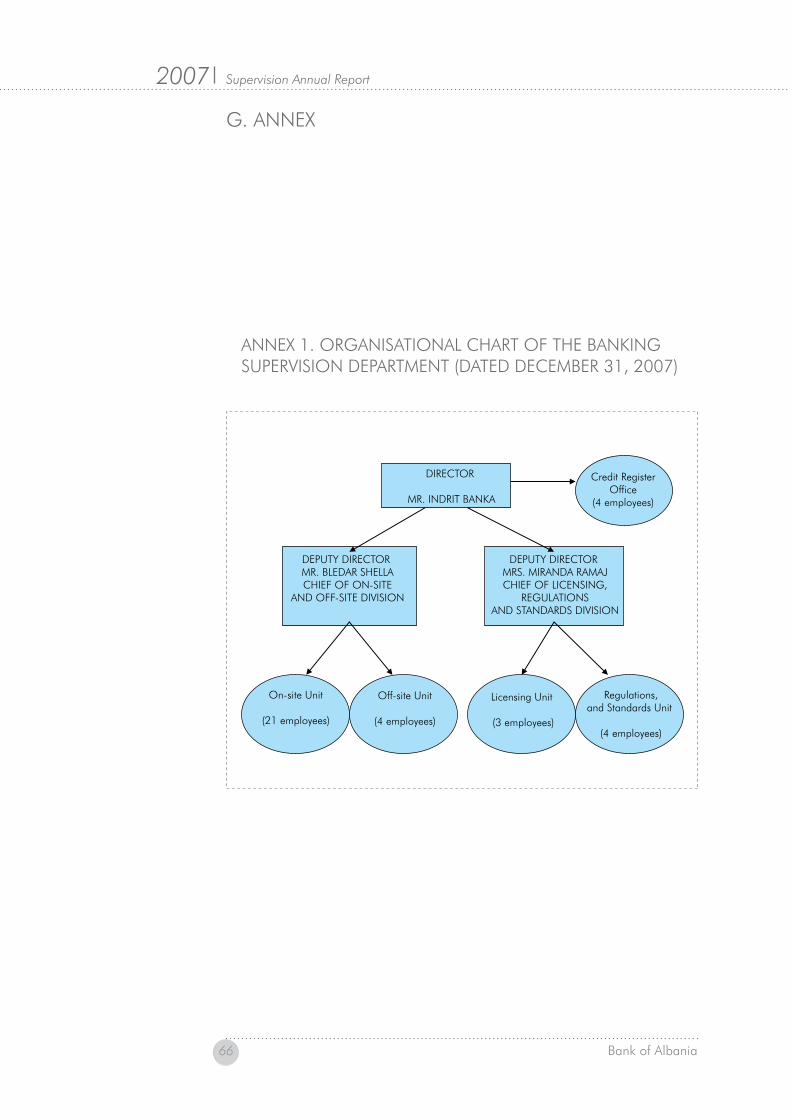

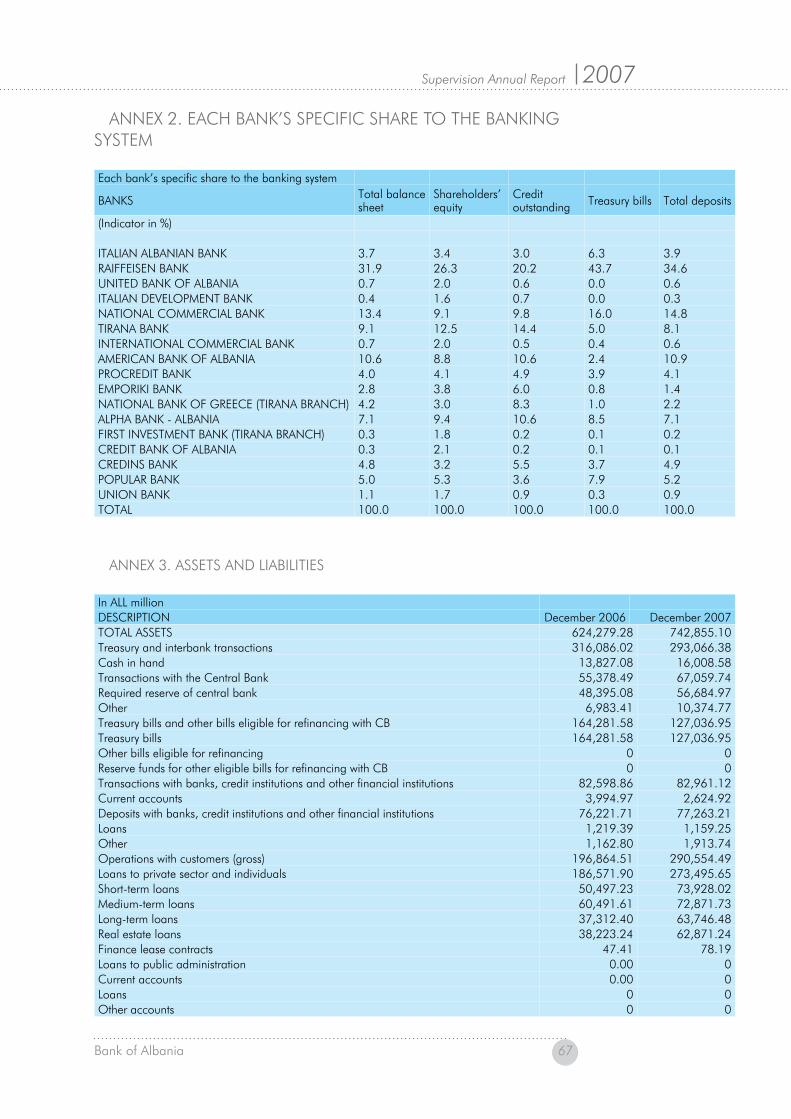

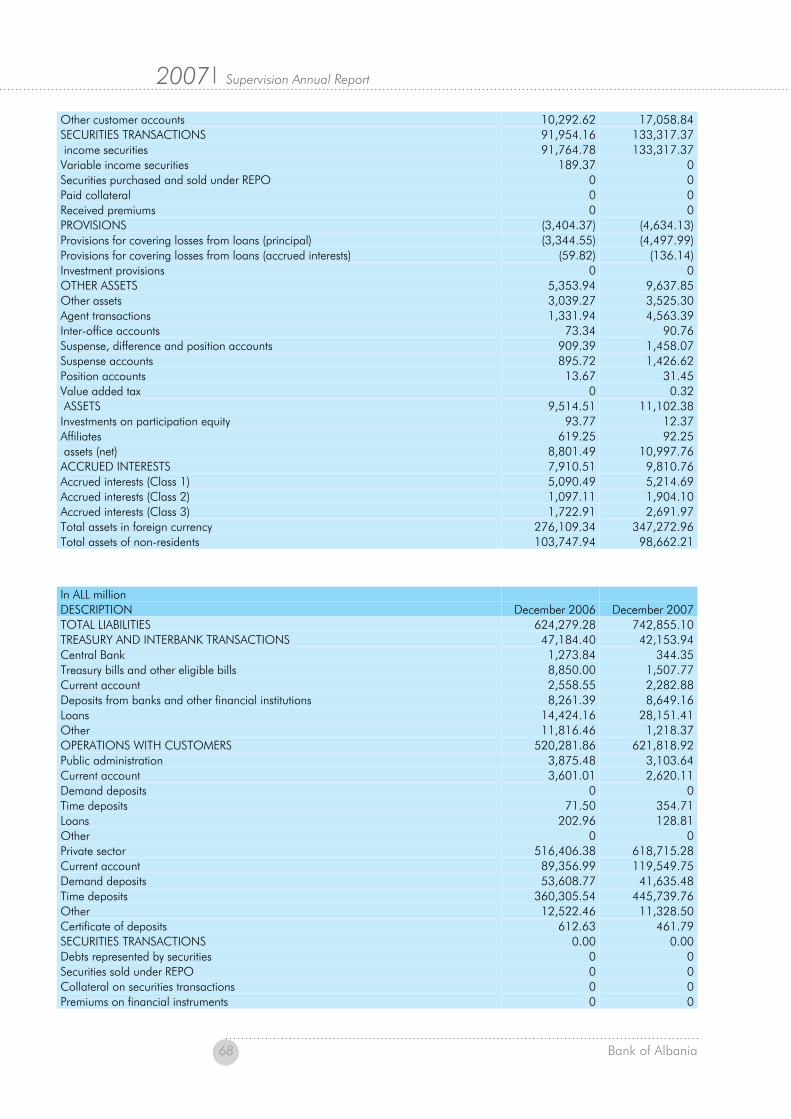

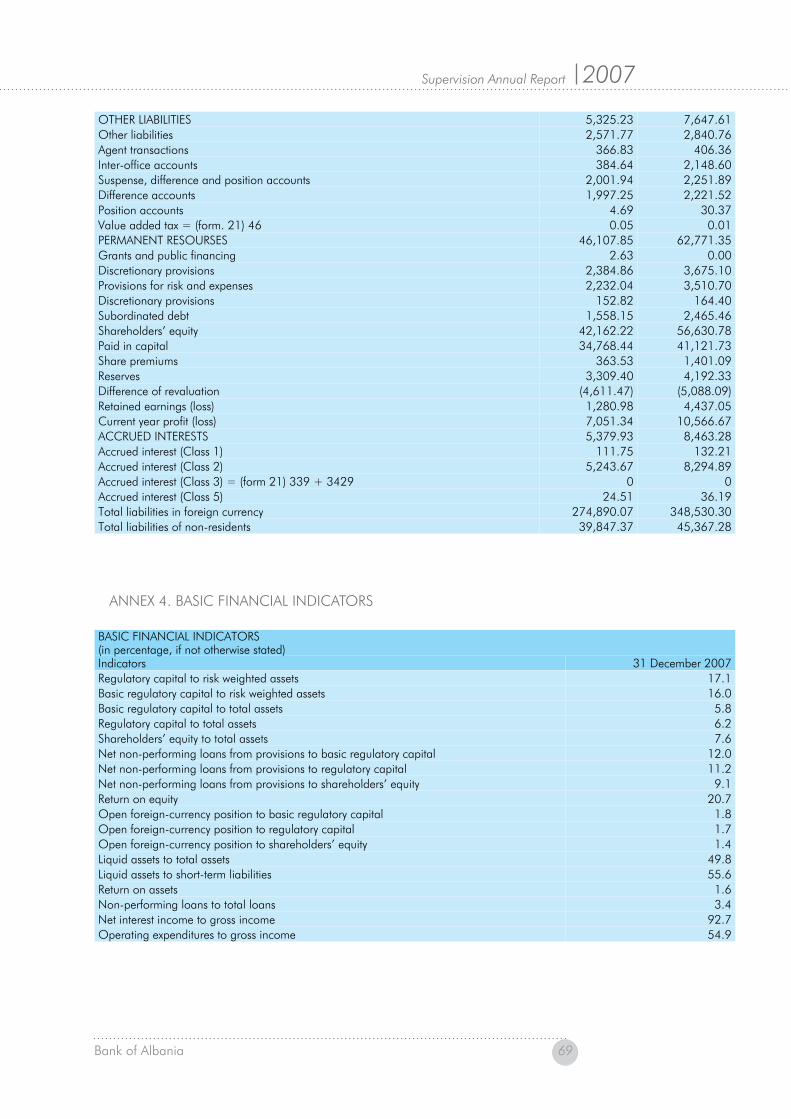

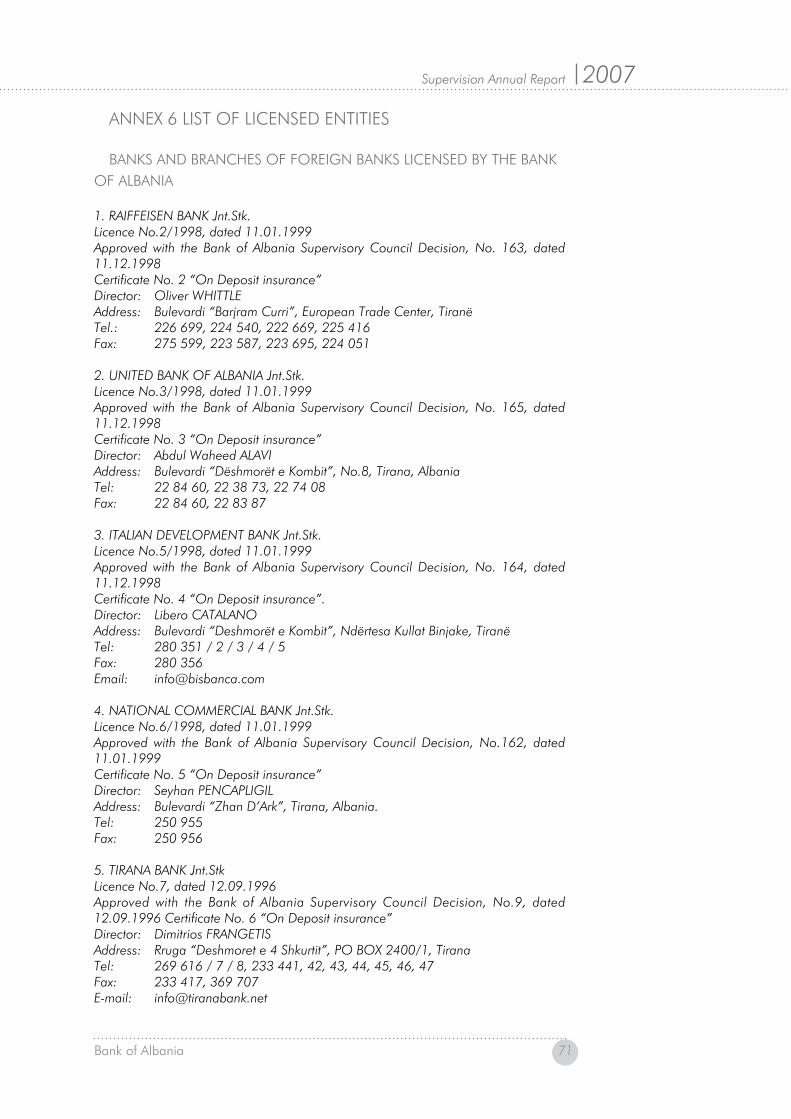

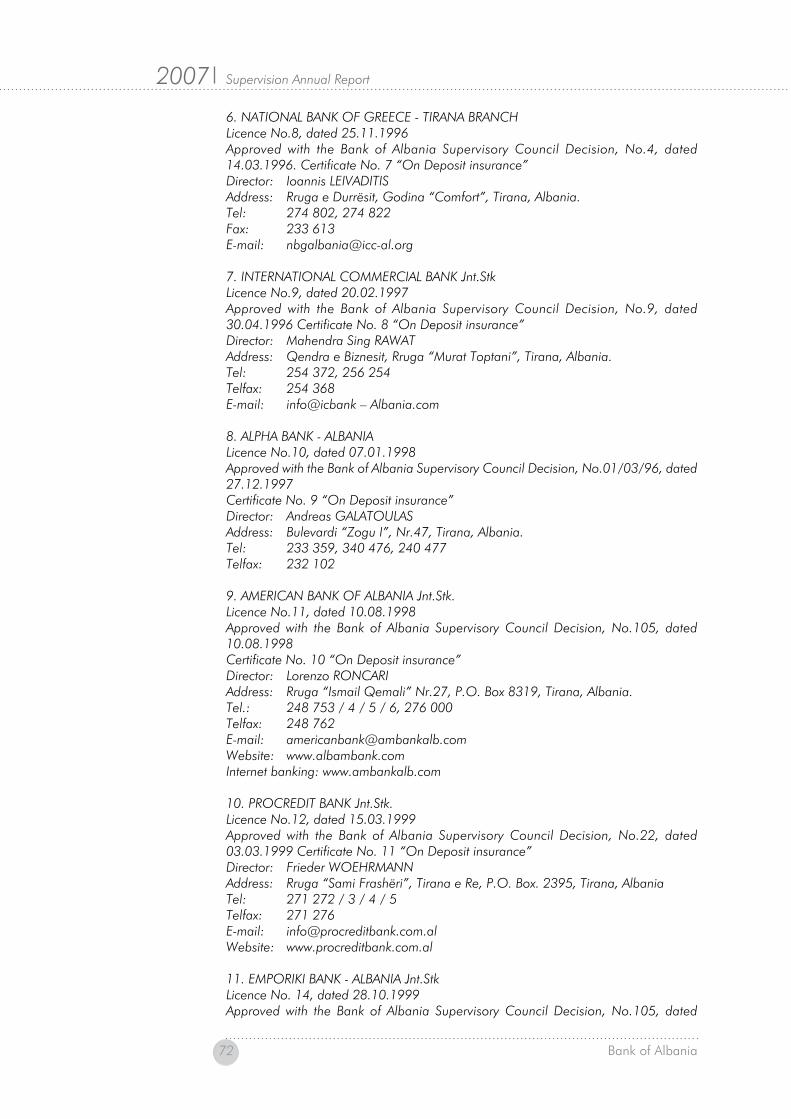

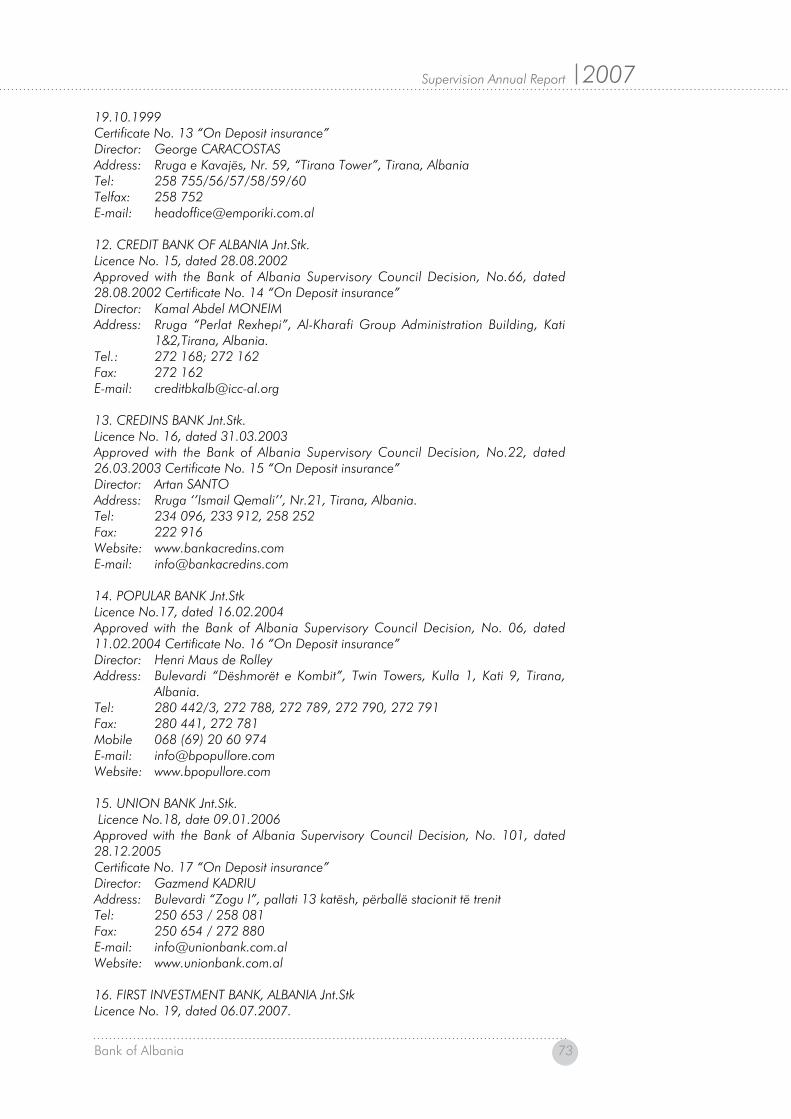

G. ANNEx 66Annex �. Organisational chart of the Banking Supervision Department (dated December ��, 2007) 66Annex 2. Each bank’s specific share to the banking system 67Annex �. Assets and liabilities 67Annex 4. Basic financial indicators 69Annex 5. Bank network extention indicators as at end 2007 and the number of employees 70Annex 6 List of licensed entities 7�Annex 7 List of Banking Supervision Regulations and Guidelines in force as of July 2008 �0�

ENDNOTES �06

Supervision Annual Report Supervision Annual Report2007 2007

4 Bank of Albania Bank of Albania 5

Supervision Annual Report Supervision Annual Report2007 2007

4 Bank of Albania Bank of Albania 5

T A B L E S

B. regulatory framework and licensing processTable � Electronic products supplied by banks, December 2007 �4Table 2 Number of cases of administrators approved according to these categories �5Table � List of entities licensed by the Bank of Albania in years �5Table 4 Geographical distribution of banking branches and agencies as at end 2007 �6

C. on-site supervisionTable 5 Examinations performed over 2007 �8

D. Banking systen and non-bank developments Table 6 Banking network extension indicator as at end 2007 28Table 7 Coverage with banking services 28Table 8 Total asset share of the banking system to GDP 29Table 9 Performance of main asset items of the banking system �0Table �0 Performance of main banking system liability items �0Table �� H (Herfindahl) index of assets, deposits and loans concentration ��Table �2 Credit outstanding structure by terms, in percentage �2Table �� Credit outstanding structure by currencies (in %) ��Table �4 The share of foreign currency credit unhedged against foreign exchange risk (in percent) ��Table �5 Credit rating in % to credit outstanding �4Table �6 Region developments on lending quality �6Table �7 Performance of short-term assets to short-term liabilities of the banking system �7Table �8 Monthly and quarterly maturity gap of the banking system �8Table �9 Shareholders’ equity structure of the system and its components performance in years 4�Table 20 Performance of net overdues to regulatory capital ratio (in %) 42Table 2� Performance of risk-weighted assets of the banking system by years 4�Table 22 Performance of capital adequacy ratio by bank groups 4�Table 2� Performance of core elements of net result (non-cumulative) in ALL million 44Table 24 Core profitability indicators in percentage (cumulative) 45Table 25 Indicators of profitability from core activity in percentage (cumulative) 47Table 26 Average indicators of profitability in ALL million (quarterly average) 48Table 27 Efficiency indicator (non-cumulative) in ALL million 49Table 29 Assets quality 50Table 28 Asset structure 50

F. otherTable �0 Housing loan indicator in some EU member states 56Table �� Housing loan indicator in Albania and in some new EU member states 56

Supervision Annual Report Supervision Annual Report2007 2007

4 Bank of Albania Bank of Albania 5

Supervision Annual Report Supervision Annual Report2007 2007

4 Bank of Albania Bank of Albania 5

C H A R T S

B. regulatory framework and licensing process Chart � Number of branches/agencies (in per cent) by peer groups �6

D. Banking systen and non-bank developments Chart 2 Paid in capital structure of the system by origin 27Chart � Capital origin by peer groups, December 2007 27Chart 4 Number of employees (in per cent) by peer groups 27Chart 5 Share of peer groups to the system by total assets �0Chart 6 Share of peer groups to total credit outstanding of the banking system (in %) �2Chart 7 Credit outstanding to enterprises and households (in % to total credit outstanding) �2Chart 8 Credit outstanding volume by terms, in ALL billion ��Chart 9 Credit outstanding volume by currencies, in ALL bn. ��Chart �0 Performance of non-performing credit outstanding of the banking system �4Chart �� Non-performing loans to credit outstanding of the previous year (in %) �4Chart �2 Provisions for non-performing loans �5Chart �� Non-performing credit outstanding by sectors �5Chart �4 Non-performing credit outstanding by currencies �5Chart �5 Performance of liquid asset composition in years �7Chart �6 Asset liability structure by residual maturity (in ALL billion) �7Chart �7 Performance of total deposits (in ALL million) and their growth rate (in percentage) during 2002-2007 �8Chart �8 Deposit structure by availability �8Chart �9 Deposit structure by final maturity �9Chart 20 Performance of deposit share in ALL and in foreign currency to total deposits (in percentage) �9

Supervision Annual Report Supervision Annual Report2007 2007

6 Bank of Albania Bank of Albania 7

Supervision Annual Report Supervision Annual Report2007 2007

6 Bank of Albania Bank of Albania 7

Supervision Annual Report Supervision Annual Report2007 2007

6 Bank of Albania Bank of Albania 7

Supervision Annual Report Supervision Annual Report2007 2007

6 Bank of Albania Bank of Albania 7

A. DoCuMent “on SuperviSion MiSSion”

Supervision function is carried out by the Bank of Albania, which comprises the central bank of the country, pursuant to the law “on the Bank of Albania”, no. 8269 of 23.12.1997 and the law “on Banks in the republic of Albania”, no. 8365 of 02.07.1998.

Supervision mission

the Bank of Albania, in line with its legal responsibilities, as the supervisory authority of banks and other financial institutions licensed by it, is committed to:

• ensuring a sound banking activity that is in good harmony with the Bank of Albania laws, rules and regulations, in order to protect depositors and prevent financial crises;

• Safeguarding the banking system stability and even broader, by monitoring the market developments and recommending adequate measures, so that banks adapt to these developments and are continuously managed according to best principles;

• Strengthening the banking system credibility and promoting a healthier market discipline, by requiring higher transparency in the system;

• providing a fair competition in the banking system and beyond, and ensuring equal treatment of licensed entities and their clients;

• providing continuous and professional communication with financial market operators and other institutions which influence the activity of the Bank of Albania, in the framework of enhancing the functioning of the financial market and its operators.

the Bank of Albania will carry out its supervisory function through:

a) Continuous establishment and improvement of the supervisory regulatory framework, so that it is in harmony with the best international principals and applicable in practice;

b) on-site and off-site examinations of licensed institutions indices, as well as through corrective measures taken for sorting out various problems.

c) orientation of supervisory process towards risk identification the licensed institutions are faced with, recommending proper solutions.

d) implementation of policies which focus toward a development-oriented

Supervision Annual Report Supervision Annual Report2007 2007

8 Bank of Albania Bank of Albania 9

Supervision Annual Report Supervision Annual Report2007 2007

8 Bank of Albania Bank of Albania 9

banking system;e) Co-operation with financial institutions under supervision and with other

domestic financial institutions, as well as with international supervisory authorities;

f) ongoing improvement of the supervisory capacities.

the Bank of Albania, in compliance with the requirements of the supervisory function, strives for the highest levels of integrity, professionalism, efficiency and transparency.

Supervision Annual Report Supervision Annual Report2007 2007

8 Bank of Albania Bank of Albania 9

Supervision Annual Report Supervision Annual Report2007 2007

8 Bank of Albania Bank of Albania 9

B. reGulAtorY FrAMeWorK AnD liCenSinG proCeSS

1. leGAl AnD reGulAtorY FrAMeWorK

2007 challenges and priorities, the new law “on Banks in the republic of Albania” and the regulatory framework were comprehensive processes in progress of the work for reviewing and drafting regulatory acts that regulate the activity of entities licensed and supervised by the Bank of Albania.

the Bank of Albania, in order to precede the process of adapting the regulatory framework to new requirements of the law “on Banks in the republic of Albania”, to the Directives of the european Council, to the Basle Committee principles for effective supervision and to the new Capital Accord concepts, even during 2007 aimed to complete the draft regulations. they have effectively reflected the banking industry thought, subject of implementing the requirements of regulatory acts and have also taken into account the recent developments of the Albanian banking market.

1.1 neW reGulAtorY ACtS

2007 finalised the drafting of two new regulations and witnessed changes to some banking supervision regulations.

Decision no. 57 of 15.10.2007 adopted the regulation “on operational risk management at branches of foreign banks”. the regulation was drafted in implementation of the new banking law and in the framework of the national strategy for legal harmonization with the european union Directives. the regulation considers the observance of the Basle principles, Minimum Standards of the Basle Committee, as well as other countries` experience with regard to regulating the activities of foreign bank branches. exclusion of the branch from the obligation to complete some standard bank regulatory acts evidently creates the genuine profile of real supervision of foreign bank branches.

the regulation establishes the regulatory supervisory base for foreign bank branches, including therein as very important documents, the memorandum of understanding with the supervisory authorities of the bank and the memoranda of understanding with the parent bank itself. the regulation anticipates that

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

the branch activity is administratively dependent on and authorized by the parent bank, while the entirety of risks and exposure to them is a responsibility of the parent bank and shall be analyzed in the framework of the whole bank. So, the financial position and risk profile shall be monitored by the parent bank.

the regulation sets out the instruments aimed at ensuring a safe and sound activity of the foreign bank branch licensed to carry out banking and financial activity in the republic of Albania. An important instrument to this end is the Capital equivalency Deposit (CeD), which is equal to a part of the minimum initial capital granted to open a bank. CeD, comprising its “obligatory” investment in unencumbered assets, is aimed at ensuring financial position sustainability of the branch, depositors` protection and in the event of liquidation, rapid return being considered as a minimum investment level. the regulation sets out the CeD amount, functions, investment criteria, its reporting and supervision.

Decision no. 58 of 15.10.2007 adopted the “unified reporting System – urS for foreign bank branches”. the unified reporting system for foreign bank branches stipulates the entirety of financial data and prudential indicators that a foreign bank branch should report to the Bank of Albania. this system was drafted in cooperation with the Statistics Department, pursuant to and in implementation of the regulation “on operational risk management at branches of foreign banks”.

Decision no. 31of 06.06.2007 adopted the regulation “on licensing, organization, activity and supervision of foreign exchange bureaus”. the regulation was drafted in response to the requirement for formalizing the foreign exchange market. it is a total revising of the existing regulation and is presented as more complete. it encompasses also requirements for integration, transparency to clients, document holding manner, additions to activity and capital level according to these activities, reporting manner, supervision, etc. Also, the regulation provides for a reduction of capital requirements for entities operating as foreign exchange bureaus, this being a right to be recognized only to trading legal entities organized under the law “on trade Associations” that have included even foreign exchange business in their statutes. From the conceptual viewpoint, the regulation has been broadened even with stipulations on foreign exchange bureau organization, on additional activities permitted to be carried out by the bureau as an agent for a nonbank entity about money transfer, supervision and penalties, obligation and about transaction reporting form, as well as about measures to be taken for money laundering prevention.

1.2 reGulAtorY ChAnGeS

Decision no. 7 of 31.01.2007 adopted a change to the regulation “on capital-adequacy ratio”. this change is related to the addition for weighting bank assets at a 150 % weighting ratio. the change to the regulation arose

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

as a logical necessity from the recent changes to the regulation “on credit risk management”. According to stipulations of the latter one, banks under the phase of a significant growth of portfolios or their quality deterioration should accrue even larger risky undertaking, deriving from this activity. in order to prevent banks’ and the system’s failure from this process, the Bank of Albania takes into consideration some indicators related to credit risk management, presented in detail under Article 22/2 on “risk management operations” of the respective regulation. the banks weight a part of performing credit and/or of non-performing credit to a higher risk factor, in the event some prudential indicator limits are exceeded, as specified under the regulation. So, the part of assets weighted at a 150 percent weighting rate is added to the part of risk-weighted assets, as an element of capital adequacy calculation. this will enable a fairer allocation and calculation of bank capital requirements, for every (counterparty) credit risk level or degree. Capital-adequacy ratio (CAr), which is calculated as a ratio of bank’s regulatory capital to risk-weighted assets and off-balance sheet items, denominated in percentage, will consider more effective economic needs of the bank for capital, in the monitoring process of risks, mainly of (counterparty) credit risk.

Decision no. 73, dated 27.11.2007 adopted some changes to the regulation “on licensing, organization, activity and supervision of foreign exchange bureaus”. these changes relate to specifying some moments in licensing and operating process of foreign exchange bureaus; specifying the organ – national registration Centre (nrC) – that presently holds the trading register and defines a unique number for the association; specifying the possibilities of the entity in the quality of the trade association, to carry out other operations besides those permitted in the licence by the Bank of Albania. this is so, provided these operations can not be carried out in the bureau, i.e., in the premises, which under the regulation have been destined only for carrying out foreign exchange activity and money transfer in agent’s role. other changes relate to specifying the required capital level for carrying out foreign exchange activity and the agent’s role. it also specifies that the licensed entity may carry out its activity in one or more than one bureau, without creating the obligation of existence of two offices.

2. liCenSinG

2.1 GrAntinG A liCenCe, ApprovAlS

During 2007, the banking system underwent important qualitative and quantitative developments, mainly due to structural changes taking place in banks because of the consolidation process encompassing the banking system and the tasks arising from the implementation of the law “on Banks on the republic of Albania”, which provided its effects over the second half of the year. under more concrete terms:

Structural changes in commercial bank’s ownership

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

• As an outcome of consolidation of the American Bank of Albania’s position in the banking system, in early June 2007 the acquisition of 80 percent of the shares of the American Bank of Albania by the intesa Sanpaolo Bank was approved. the impact of this group on the Albanian banking market will not only contribute to enhancing the competition but will also become a positive factor for the country’s economic growth.

• Decision no. 43 of the Supervisory Council of the Bank of Albania of August 29, 2007 adopted the ownership transfer of 76.129 percent of the shares of the shareholders’ equity of the italian Albanian Bank Jnt.Stk., from the shareholder Sanpaolo iMi S.p.A. italy to the shareholder intesa Sanpaolo S.p.A., italy. this transfer results from the merger of Sanpaolo iMi S.p.A. and Banca intesa S.p.A.

• on December 2007 the merger of the italian Albanian Bank and the American Bank of Albania was approved. the integrating banking environment that associated many banks in europe along the year, involved even the Albanian banking market through the integration of these two banks of the Albanian banking system. Bank merger practice was applied for the first time by the Bank of Albania and the effects of this merger commenced on January 2008.

• Further to the growth process of foreign capital participation, there was granted approval to the entry of the Société Général Bank (of French capital) into the Albanian banking system, for the first time in early July 2007, through the acquisition of 75.006 percent of the shareholders’ equity of the Banka popullore (popular Bank). the Société Général group is specialized mainly in investment and corporation and over the long run it is expected to contribute even to banking industry stability in the country.

• Aiming at restructuring and optimizing the management of shares owned by the raiffeisen Bank, on December, at indirect shareholder’s request, the transfer of indirect qualifying holding was approved for 70 percent of the shareholders’ equity of the raiffeisen Bank to Cembra Beteilingugs GMBh, Austria. But, in essence, the economic structure of the raiffeisen Bank’s shareholders did not change.

• on January 2007 the sale of 14.67 percent of the shares of the Credins Bank shareholders’ equity was adopted, from the shareholder Muhamet Malo to the shareholder renis tërshana.

• the proposed shareholder BFSe holding Bv, netherland, requested its stake in Credins Bank, by acquiring the bank’s existing shares and by underwriting new shares, at 22.17 percent of the shareholding of this bank. the approval of this new shareholder of the Credins Bank was granted on February 2008.

• proCredit holding AG, Germany requested to increase its stake in proCredit Bank Albania, by acquiring the shares from iFC and FeFAD foundation. Following this transaction, proCredit holding AG holds 80 percent stake in proCredit. the approval on changing the participating equity in proCredit Bank Jnt.Stk., was made on January 2008.

• italian Development Bank had decided on changing the structure of its shareholders through acquisition of the shares of Francesco Mariano Mariano by nereo Finance S.A., luxemburg (37 percent), Cerere S.r.l.,

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

italy (18 percent + 2 shares), Assicurazioni Generali S.p.A., italy (10 percent – 1 share) and Banka podravska d.d., Croatia (10 percent – 1 share). under the process of looking into the request and documentation, the main shareholder of the iDB notified the Bank of Albania that he resigned from the offer submitted by the proposed shareholders as above stated. As a result of this notification, the practice was closed.

in the meantime, the company veneto Banca holding soc.coop., italy has expressed the interest in and has notified of the signing of Agreement for acquiring 75.1 percent of the shares of the italian Development Bank. this practice is under the process of providing the documentation and assessing the potential shareholder of this bank.

licensing new banks

• June 2007 witnessed the transformation and licensing process as a bank of the First investment Bank - tirana Branch. the process initiated since 2006 went on even in early 2007, with the preparation of material for postponing the bank’s licensing term, because of some conditions created for the implementation of new legislation on capital requirements (Basle ii) in Bulgaria, for the parent bank. As a new practice, the transformation process from a foreign bank branch into a subsidiary was solved by preparing and later on making an agreement for transferring the banking activity from the branch into a new bank. the process was completed with the decision of the Supervisory Council of the Bank of Albania for licensing the First investment Bank, Albania.

revoking bank licence

• Decision of the Supervisory Council of the Bank of Albania of 12. 03. 2008, no. 22, revoked the italian Albanian Bank’s licence. the revoking of this licence was supported by the request of the italian Albanian Bank, following the merging of the italian Albanian Bank (the merged company) with the American Bank of Albania (the merger).

• Decision of the Supervisory Council of the Bank of Albania of 09.04.2008, no. 28, revoked the licence to the First investment Bank -tirana Branch. the revoking of this licence was carried out because of the voluntary liquidation of the First investment Bank - tirana Branch, after the completion of the agreement on transformation into the First investment Bank, Albania.

Due to above-mentioned changes, the number of banks in our banking system as at April 2008 went to 16.

the new law “on Banks in the republic of Albania” adds the cases when banks must not operate without the initial approval of the Bank of Albania, such as initial approval for changes to banks’ statutes; approval for internal audit managers, considering them as bank administrators. it also stipulates clearly the steps and procedures to be followed for prior approval on bank network extension within the country.

Supervision Annual Report Supervision Annual Report2007 2007

�4 Bank of Albania Bank of Albania �5

Supervision Annual Report Supervision Annual Report2007 2007

�4 Bank of Albania Bank of Albania �5

the provisions of the law “on Banks in the republic of Albania” for sanctions applied against unlicensed activity and the administrative action of relevant bodies for closing the informal foreign exchange market over the first semi-annual of 2007 made necessary changes to the regulation on licensing foreign exchange bureaus and led to replacing of the previous regulation. the new regulation “on licensing, organization, activity and supervision of foreign exchange bureaus” eased the capital requirement for performing foreign exchange business, from All 2,500,000 to All 1,500,000; regulated the agent’s activity of money transfer and cut the licensing process commissions. Due to these operations, 59 foreign exchange bureaus were licensed during 2007, against 9 foreign exchange bureaus licensed in the preceding year. the joint commitment of the State police structures, the prosecution and the Bank of Albania to market formalization has been at maximum. the licensing process of foreign exchange bureaus was accompanied not only with treatment, completion and assessment of submitted documentation, but also with explanatory meetings. this practice was applied for coming to entities’ assistance, in order to cut cost and time needed for their definitive licensing.

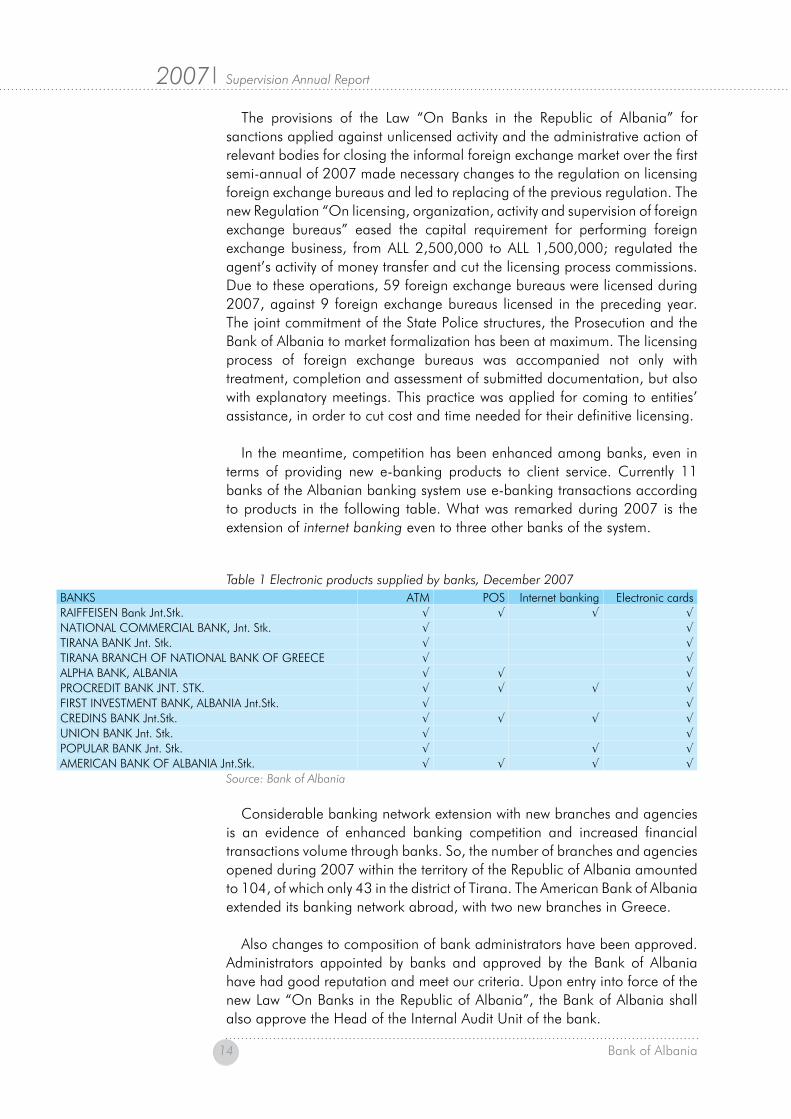

in the meantime, competition has been enhanced among banks, even in terms of providing new e-banking products to client service. Currently 11 banks of the Albanian banking system use e-banking transactions according to products in the following table. What was remarked during 2007 is the extension of internet banking even to three other banks of the system.

Table � Electronic products supplied by banks, December 2007 BAnKS AtM poS internet banking electronic cardsrAiFFeiSen Bank Jnt.Stk. √ √ √ √nAtionAl CoMMerCiAl BAnK, Jnt. Stk. √ √tirAnA BAnK Jnt. Stk. √ √tirAnA BrAnCh oF nAtionAl BAnK oF GreeCe √ √AlphA BAnK, AlBAniA √ √ √proCreDit BAnK Jnt. StK. √ √ √ √FirSt inveStMent BAnK, AlBAniA Jnt.Stk. √ √CreDinS BAnK Jnt.Stk. √ √ √ √union BAnK Jnt. Stk. √ √populAr BAnK Jnt. Stk. √ √ √AMeriCAn BAnK oF AlBAniA Jnt.Stk. √ √ √ √

Source: Bank of Albania

Considerable banking network extension with new branches and agencies is an evidence of enhanced banking competition and increased financial transactions volume through banks. So, the number of branches and agencies opened during 2007 within the territory of the republic of Albania amounted to 104, of which only 43 in the district of tirana. the American Bank of Albania extended its banking network abroad, with two new branches in Greece.

Also changes to composition of bank administrators have been approved. Administrators appointed by banks and approved by the Bank of Albania have had good reputation and meet our criteria. upon entry into force of the new law “on Banks in the republic of Albania”, the Bank of Albania shall also approve the head of the internal Audit unit of the bank.

Supervision Annual Report Supervision Annual Report2007 2007

�4 Bank of Albania Bank of Albania �5

Supervision Annual Report Supervision Annual Report2007 2007

�4 Bank of Albania Bank of Albania �5

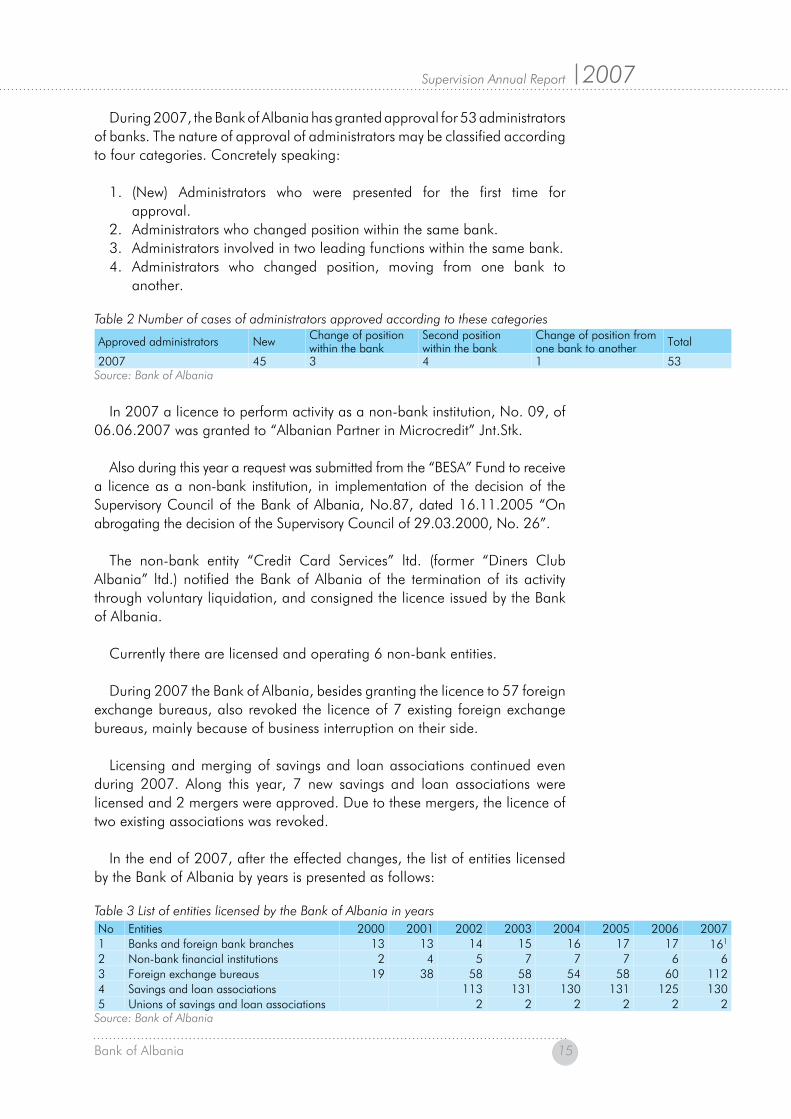

During 2007, the Bank of Albania has granted approval for 53 administrators of banks. the nature of approval of administrators may be classified according to four categories. Concretely speaking:

1. (new) Administrators who were presented for the first time for approval.

2. Administrators who changed position within the same bank.3. Administrators involved in two leading functions within the same bank.4. Administrators who changed position, moving from one bank to

another.

Table 2 Number of cases of administrators approved according to these categories

Approved administrators new Change of position within the bank

Second position within the bank

Change of position from one bank to another total

2007 45 3 4 1 53Source: Bank of Albania

in 2007 a licence to perform activity as a non-bank institution, no. 09, of 06.06.2007 was granted to “Albanian partner in Microcredit” Jnt.Stk.

Also during this year a request was submitted from the “BeSA” Fund to receive a licence as a non-bank institution, in implementation of the decision of the Supervisory Council of the Bank of Albania, no.87, dated 16.11.2005 “on abrogating the decision of the Supervisory Council of 29.03.2000, no. 26”.

the non-bank entity “Credit Card Services” ltd. (former “Diners Club Albania” ltd.) notified the Bank of Albania of the termination of its activity through voluntary liquidation, and consigned the licence issued by the Bank of Albania.

Currently there are licensed and operating 6 non-bank entities.

During 2007 the Bank of Albania, besides granting the licence to 57 foreign exchange bureaus, also revoked the licence of 7 existing foreign exchange bureaus, mainly because of business interruption on their side.

licensing and merging of savings and loan associations continued even during 2007. Along this year, 7 new savings and loan associations were licensed and 2 mergers were approved. Due to these mergers, the licence of two existing associations was revoked.

in the end of 2007, after the effected changes, the list of entities licensed by the Bank of Albania by years is presented as follows:

Table � List of entities licensed by the Bank of Albania in years no entities 2000 2001 2002 2003 2004 2005 2006 20071 Banks and foreign bank branches 13 13 14 15 16 17 17 161

2 non-bank financial institutions 2 4 5 7 7 7 6 63 Foreign exchange bureaus 19 38 58 58 54 58 60 1124 Savings and loan associations 113 131 130 131 125 1305 unions of savings and loan associations 2 2 2 2 2 2

Source: Bank of Albania

Supervision Annual Report Supervision Annual Report2007 2007

�6 Bank of Albania Bank of Albania �7

Supervision Annual Report Supervision Annual Report2007 2007

�6 Bank of Albania Bank of Albania �7

Chart 1 Number of branches/agencies(in per cent) by peer groups

6%

19%

75%

16%

18%

66%

10%

31%

59%

11%

35%

54%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007

G1 G2

Source: Bank of Albania

G3

2.2 BrAnCheS

As concerns the banking network extension, a great number of requests and projects for opening branches and agencies have been dealt with. in accordance with the law, a different approval process was applied, dividing the licensing into two phases. the first phase has to do with assessment of the extending capability of the bank and the granting of initial approval of a licence. the second phase has to do with examination of technical conditions and the granting of a licence to conduct banking business. So, based on this practice, 100 initial approvals for opening bank branches and agencies have been granted, of which 60 have acquired the licence to commence business.

virtually all banks have opened new branches and agencies during 2007. the largest share to 2007 network extension is occupied by medium-sized banks (G2 peer group), with 49 new branches and agencies.

no. Districts totAl no. Districts totAl1 tiranë 144 26 Gramsh 22 Sarandë 10 27 librazhd 32

3 Kavajë 7 28 peshkopi 34 Bilisht 5 29 Koplik 25 Durrës 27 30 Shijak 36 Fier 16 31 Delvinë 37 elbasan 14 32 Divjakë 28 Korcë 93 33 rrëshen 39 Shkodër 13 34 Krujë 310 vlorë 17 35 laç 611 lezhë 8 36 tepelenë 24

12 pogradec 10 37 Bajram Curri 113 Berat 8 38 Bulqizë 114 Gjirokastër 9 39 Çorovodë 15

15 lushnje 10 40 ersekë 116 Kukës 4 41 Krumë 117 Burrel 3 42 pukë 16

18 himarë 2 43 peqin 119 Kakavijë (Customs) 4 44 Fushë Krujë 320 Kuçovë 3 45 Athinë 321 Kamëz 4 46 Selanik 122 Shëngjin 3 47 Shkup 123 Kapshticë (Customs) 324 përmet 37

25 Ballsh 2 t o t A l 404Source: Bank of Albania

Table 4 Geographical distribution of banking

branches and agencies as at end 2007

Supervision Annual Report Supervision Annual Report2007 2007

�6 Bank of Albania Bank of Albania �7

Supervision Annual Report Supervision Annual Report2007 2007

�6 Bank of Albania Bank of Albania �7

C. on-Site SuperviSion

1. ACtivitY oF the on-Site SuperviSion FunCtion

During 2007 the on-site supervision worked in view of fulfilling the rights assigned by the legal and regulatory framework. the supervisory cycle defined by the operational supervision policy serves as a basis for carrying out this function. Being an important link of accomplishing Bank of Albania’s mission, it has carried out its tasks, adhering to the supervisory principles, clarifying, broadening and observing them. the presence in the financial system not only has guaranteed an orientation of the banking activity towards standard observance, but has also increased its specific weight in order to preserve the stability.

the use of supervisory instruments has been intensified, giving priority to nature of problems and type of entity and constantly keeping their use at a minimum satisfactory level. Special attention has been paid to the objective of working to prevent phenomena rather than addressing them after the appearance of weaknesses. to this end, possible impacts of certain risk positions have been taken into account and awareness of certain phenomena has been made, aiming at taking proper measures in due time.

it is aimed at achieving a fair objective behaviour of market actors in service to clients. this issue having to do with bank transparency has been an innovation of 2007 on-site supervision. observance of effective legal and regulatory framework has been taken into special consideration and other assessments on market operators’ behaviour have been taken into account to identify problems and to succeed in providing adequate and comparative information.

2. CooperAtion With other AuthoritieS

taking into consideration the financial market developments, increased importance of extended banks’ presence in different countries of the region, as well as banking supervision challenges, the cooperation with other supervisory authorities has been increased. this cooperation has been mainly with countries where the capital of banks carrying out their activity in Albania comes from.

Supervision Annual Report Supervision Annual Report2007 2007

�8 Bank of Albania Bank of Albania �9

Supervision Annual Report Supervision Annual Report2007 2007

�8 Bank of Albania Bank of Albania �9

A multi-lateral cooperation agreement was signed over the last year with six countries of the region, to promote a structured coordination in banking supervision area.

Cooperation with the Bank of Greece, the banking supervisory authority in that country, has been strengthened and a joint examination has been carried out to one of the banks having the capital origin from Greece, a subsidiary of a bank founded in Greece.

Strong bridges of cooperation with the supervisory authorities of Austria and italy have been set up. the capital originating from these countries comprises an important structural share and development to the domestic market. At the same time, these links have been developed, aiming at final signing of a cooperation agreement with the supervisory authorities of these countries.

During 2007 joint examinations with other authorities were also carried out. in cooperation with the responsible Anti-Money laundering Authority, examinations were carried out over all banks of the system, about issues that are subject to the law on money laundering prevention.

Based on a memorandum of cooperation signed between the Bank of Albania and the Financial Supervision Authority, a joint examination with this authority has been carried out on some banks concerning bank - insurance company relations in Albania.

A sound cooperation practice has been established with the Central Banking Authority of Kosovo. Joint trainings have been carried out, mainly in tirana.

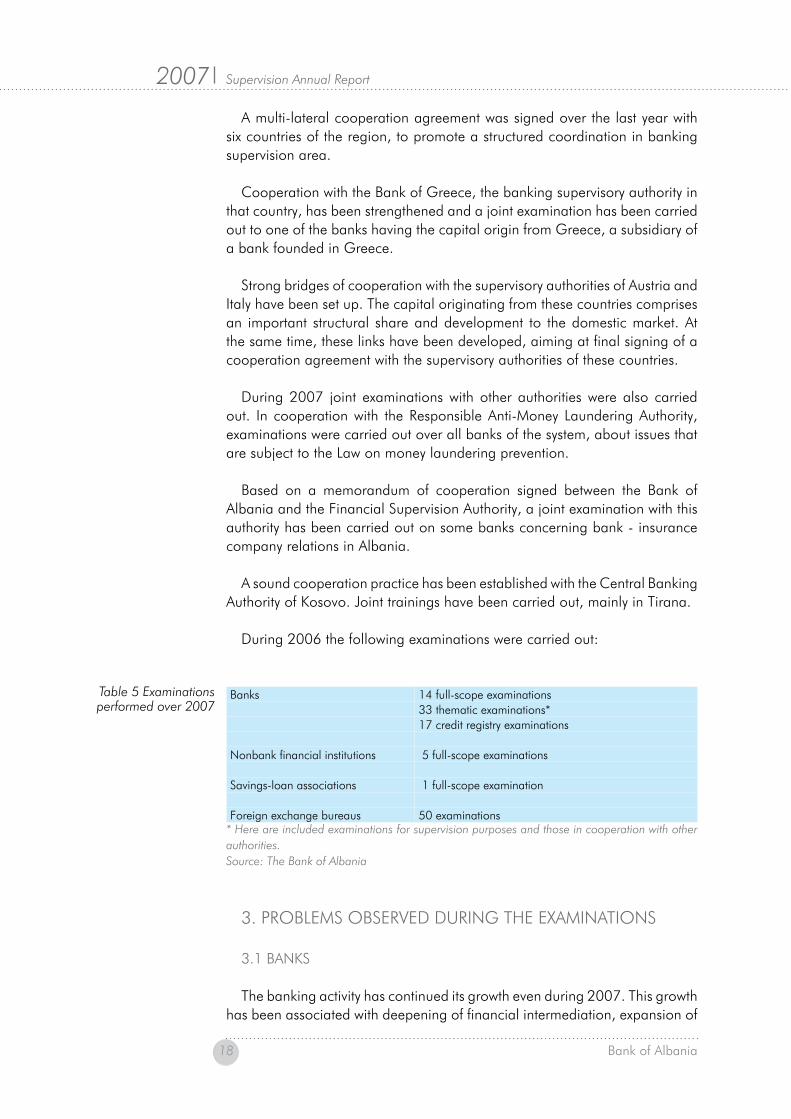

During 2006 the following examinations were carried out:

Banks 14 full-scope examinations33 thematic examinations*17 credit registry examinations

nonbank financial institutions 5 full-scope examinations

Savings-loan associations 1 full-scope examination

Foreign exchange bureaus 50 examinations* Here are included examinations for supervision purposes and those in cooperation with other authorities.Source: The Bank of Albania

3. proBleMS oBServeD DurinG the exAMinAtionS

3.1 BAnKS

the banking activity has continued its growth even during 2007. this growth has been associated with deepening of financial intermediation, expansion of

Table 5 Examinations performed over 2007

Supervision Annual Report Supervision Annual Report2007 2007

�8 Bank of Albania Bank of Albania �9

Supervision Annual Report Supervision Annual Report2007 2007

�8 Bank of Albania Bank of Albania �9

supplied products, and extension of services geographically, coverage of ever larger parts of the country’s territory and broadening of client base, both in existing locations and in new districts. A constant effort of banking operators to ensure a large client base has been noticed, enhancing the competition for all banking products supplied. no banks of special scope of activity have been pointed out, thus the same activity specifics have been maintained. even during this year the lending activity in particular draws attention. it continues to grow significantly in absolute value, while the growth rate in relative terms has decreased. lending has continued to support the economy, raising its specific share to liabilities, total assets and gross domestic product. this activity constitutes one of the most important activities of banks and has constantly had attention of the on-site supervision.

Generally, various bank behaviours have been noticed as concerns their internal development. A differentiated reaction of banks has been noted about different issues. expansion of activity and type of products has brought about internal needs for change in some aspect, such as in structure, task allocation, development support with manuals and policies and coverage with personnel. Further development of lending activity has influenced on other structures and operations. the increased use of lending funds source has presented the need for a total revision of the investment nature. this phenomenon has undergone dynamic developments, putting banks in an active position, aiming at management of liquidity and realization of activity expectations. Shareholders’ pressures for profit maximization have encouraged banks to undertake more risk. So, besides lending, there have been largely used possibilities of profiting from foreign exchanges or diversifying investments in securities, compared with traditional choices of investing in low return placements.

entrance of large banks with expanded international presence has brought about new developments in terms of management nature. parent bank relations have been expanded from both, the financial viewpoint and the orientation of bank operations. local banks have taken constant support in terms of observance of more developed standards of the banking activity, through trainings and making use of practices set up in home countries.

Deficiencies pointed out during on-site examination are summarized in structures adjustment to bank development, meaning the creation of new units, delegation of work authorities and their support by means of operational policies and work procedures. Some deficiencies have been noted in internal audit systems. the need to improve work quality, cover the whole activity and address and follow up problems has been noticed in internal audit unit. priority has been constantly given to the attention of management in the direction of activity, in cases when it has not been sufficient.

on-site supervision has paid special attention to banks’ capitalization level. Along with the situation analysis, there is also required a rigorous observance of regulatory limits and forecasting of needs for capital and for finding sources. Client base enlargement related to both, obligations and lending, has been

Supervision Annual Report Supervision Annual Report2007 2007

20 Bank of Albania Bank of Albania 2�

Supervision Annual Report Supervision Annual Report2007 2007

20 Bank of Albania Bank of Albania 2�

required, in order to reduce concentration risk. Credit risk diversification in various branches of the economy has also been part of recommendations issued.

Problems related to implementation of regulations. Generally good observance of the regulatory framework has been observed. Deficiencies have been present, but in most cases they have not had any material impact on risks exposure situation.

violations are mostly noticed in the following regulations:

• the banking law: violations have been observed especially in terms of exposure to connected persons and to significant risks. this is so due to changed limits in the new law, since banks had undertaken the exposure prior to entry into force of the law.

• regulation “on credit risk management”: risk level to borrowers has been constantly examined and in some cases, incorrect observance of this regulation has been noticed. Completion of documents in accordance with its requirements has been constantly required, following the ascertainment.

• regulation “on open foreign-currency positions”: Some sporadic cases of non-observance of this regulation were pointed out. however, they have been temporary situations, which have been improved rapidly.

• regulation “on capital adequacy”. non-observances have been mainly of technical nature and of interpretation of requirements.

• regulation “on foreign exchange operations”: remarks on implementation of this regulation relate mainly with the purpose of transfers or the supporting documents.

• regulation “on Money laundering prevention”: Deficiencies are related to prevention of suspicious transactions, establishment and observance of structures, staff training, and establishment of a database.

• regulation “on using the communication and information technology at entities licensed by the Bank of Albania”: violations of this regulation are more frequent than the above-mentioned ones. this indicates the need of banks for more investment in improving the information and technology systems. these improvements should be made in terms of assessing the system, ensuring physical security, drafting an operational plan, documenting the activity and making a disaster recovery plan. Also, control on communication and information and technology systems by specialized companies has been constantly recommended.

• regulation “on supervision of e-banking transactions”: Deficiencies in terms of this regulation have to do with completion of necessary documentation and its term of delivery to the Bank of Albania.

• Guideline “on transparency of banking services and operations”: non-observance has to do mainly with giving timely information on the change of working conditions in respect of contracts.

Supervision Annual Report Supervision Annual Report2007 2007

20 Bank of Albania Bank of Albania 2�

Supervision Annual Report Supervision Annual Report2007 2007

20 Bank of Albania Bank of Albania 2�

3.2 nonBAnK FinAnCiAl inStitutionS AnD SAvinGS AnD loAn ASSoCiAtionS

this grouping includes two types of entities, non-bank financial institutions and savings and loan associations. the first may not collect deposits from the public, whereas the second may collect deposits as stipulated under the relevant law. Among the most frequent problems confronted during the examinations is the observance of prudential rates specified in the regulations drafted for their functioning. these prudential rates are mainly related to lending exposure levels and liquidity situation.

Another evidenced problem is the non-observance of accounting principles in accounting registers. their periodical reporting has not always been accurate, containing inaccuracies even concerning entities’ data. in some cases, non-observance of legal requirements on account holding or with respect to the licence has been pointed out. Account holding has gone beyond the licensed activities, while lending has not been an object of the licence, or there are exceeded the lending thresholds required by law.

An important issue raised during examinations is the quality improvement of internal auditor’s work or its positioning in line with the functioning purpose. pronounced deficiencies were noted in investment in communication and information technology, and in observance of the corresponding regulation. Some of those entities do not make use of a computer system for data recording or the existing one does not cover the work needs. in such cases, keeping of data manually has been frequently noticed.

During examinations, fulfilment of functioning structures based on written manuals or procedures is recommended, since incomplete application of the existing ones was noticed.

other recommendations have aimed at enhancing measures to monitor and hedge against operational risk, fight against money laundering, improve the structure and the internal regulatory framework, implement rigorously the regulation “on foreign exchange operations”, “on credit risk management”, “on money laundering prevention” “on reporting foreign exchange operations”.

3.3 ForeiGn exChAnGe BureAuS

there are carried out 50 examinations on these entities. Deficiencies in their work are recurrent and consist in lack of reporting, data inaccuracy, non-provision of foreign exchange invoices to clients; non-keeping of accounting or deficiencies in documentation required under the regulation on their operation. Sanctions have been imposed on problematic entities.

Supervision Annual Report Supervision Annual Report2007 2007

22 Bank of Albania Bank of Albania 2�

Supervision Annual Report Supervision Annual Report2007 2007

22 Bank of Albania Bank of Albania 2�

D. BAnKinG SYSten AnD non-BAnK DevelopMentS

1. eConoMiC environMent

1.1 WorlD eConoMY

the world economy underwent a lower growth rate, following some-year extension. World economy performance risks have increased mainly over the second half of 2007. the basis of these risks stands in the deterioration of the financial position in Western markets, mainly in the American one. the American economy and some industrialised countries reflect slowdown signs, while the large economies of developing countries continued to play the main role in the world economy growth. high growth in China, india and Middle east has offset the uS economic slowdown effect.

the uS economy saw a decline of the economic growth rate during 2007, after a good performance over some consecutive years. this performance was impacted mainly by housing market situation and by the deterioration of residential investment trend. house price drop provided implications in contracting credit and liquidity in the economy. in the meantime, the economic activity of the euro area continued to expand at a moderate pace during 2007, compared with the previous year. Gross Domestic product grew by 2.7 percent in 2007, from 2.8 percent in 2006, according to the latest estimates of the european Commission. During this year there is noted a slowdown in industrial output, an increase in the services sector and an improvement in labour market conditions.

rise of oil price and of some agricultural products has impacted on the real economy demand, as a result of purchase power reduction. the world oil demand has increased by about 1.4 percent against the previous year. in the meantime, the international market oil price almost doubled. the agro-food product prices have gone up as a result of the dry weather. on the demand side, prices may have gone up also as a result of the use of some agricultural products in the energy generating industry.

1.2 reGion CountrieS

During 2007 the economic growth of Greece is estimated at 4 percent. Greece has had a relatively high economic growth and a dropping of unemployment against the economy of the euro area.

Supervision Annual Report Supervision Annual Report2007 2007

22 Bank of Albania Bank of Albania 2�

Supervision Annual Report Supervision Annual Report2007 2007

22 Bank of Albania Bank of Albania 2�

italy’s economy has been characterised by a lower performance than in the previous year and a reduction of investments and unemployment. the economic growth resulted slower than in the first half of 2007, as a consequence of a lower exports rise. the foreign demand has been influenced by the euro’s appreciation. unemployment fell slightly at the year start and maintained this trend even during the second half of the year.

the economy of Former Yugoslavia republic of Macedonia has recorded a better economic growth compared with 2006. this has been associated with increased inflationary pressures along the year and labour market improvement. the annual average inflation rate was 2.3 percent during 2007.

the economic activity of turkey grew by a lower rate compared with last two years, in the presence of annual inflate rate reduction, whereas the fiscal situation has been deteriorated. Gross domestic product grew by 5.1 percent during 2007. the tightening monetary policy and the deterioration of lending worldwide have limited the domestic demand increase.

1.3 eConoMiC environMent oF AlBAniA

in 2007 the Bank of Albania implemented its monetary policy in a stable macroeconomic environment, with relatively high economic growth rates and accommodating monetary conditions. they ensured upward but still favourable interest rates, exchange rate stability and financial resources for the economy. the average annual inflation rate resulted to 2.9%. Core inflation recorded an annual increase by 2.6%, about 1.2 percentage points more than the average of four last years. until July 2007, the annual inflation recorded rates within the lower half of the tolerance band, about 2-3%. in two following quarters of the year the annual inflation increased obviously, amounting to considerable rates of above 3%. this growth was due to the world crisis of foodstuff price hikes. risks to price stability over a medium term horizon were assessed to have had an upward trend. these risks included: further rise of raw prices, mainly of foodstuffs; application of the expected energy price rise; constant and fast wage rise, not fully backed by productivity growth; concentration of budget spending at year-end; constant increased aggregate demand; deterioration of consumer and business expectations on inflation, as well as materialization of second round effects on wages and price setting, as a consequence of high raw prices and high inflation rates.

the economic growth for 2007 is estimated at 6.0 percent. likewise in the previous years, the economic growth is ensured by upward performance of the sector of services, industry, transport and telecommunication. in the meantime, according to latest assessments, construction sector continues to be characterised by different problems, leading to a slowdown of production in this sector.

Domestic demand remained high during 2007, being reflected mostly in consumer loan enlargement and increased imports (more particularly rising

Supervision Annual Report Supervision Annual Report2007 2007

24 Bank of Albania Bank of Albania 25

Supervision Annual Report Supervision Annual Report2007 2007

24 Bank of Albania Bank of Albania 25

imports for machinery and equipment). the whole economic activity of the country has been developed under the conditions of an environment with inflation under control, in spite of difficulties fuelled by the uninterrupted foodstuff price movements in the international market. Grain prices rose considerably, while the same performance was recorded by foodstuff items in general. Fiscal policy has positively contributed to the overall economy performance of 2007. Generally the fiscal policy may be regarded as tightening, highlighting a lower budget deficit than the planned one.

the sales index for the industry sector has recorded a growth of 25% during 2007, against 17% of the previous year. the highest annual growth was recorded in the extractive industry subsector (50.6%). Considerable growth has been also recorded by “energy, gas, steam and water” subsector (37%) against 2006 (0.6%).

the annual sales increase in construction sector during 2007 has been about two times lower than the annual growth over 2004 - 2006. the sales level in this sector has recorded its lower value over the last quarter (4.6%) or about 11 times lower than the annual increase of sales during the same period of 2006 (52%). the overall construction volume has been decreasing, while the new construction volume accounts for the highest decline during the last quarter of 2007, by 23.3%.

Gross Domestic product for 2007 grew by 1.5%. Agriculture sub-branch output, accounting for 74% of the overall agricultural product, increased by 0.8% or about four times less than in the preceding year. the main contribution to product growth has been rendered by animal husbandry, unlike in 2006 when the main impact on the growth was given by high fruit production.

on a per annual basis, the transport sales sector fell slightly by 1.2%. During the fourth quarter of 2007, the transport and telecommunication sales sector declined by 11% compared with the preceding quarter. reduction of this sector’s activity was influenced by reduction of sales in “post and communication” branch (14%) and in ‘transport’ branch (6.3 %).

2007 coincided with important reforms in the economy. Among them we highlight the credit registry completion, re-organisation and strengthening of financial sector supervision, better management of taxes and public spending, privatisation of Albtelecom, improvement of business climate through establishment of the national registration Centre, and further reduction of customs duties on a number of products, in compliance with the obligations deriving from the free trade agreement with the european union.

2. MAin BAnKinG SYSteM hiGhliGhtS

2007 continues with generally positive and steady developments in the banking system. During this year, the banking system underwent striking changes in shareholders’ structure. Some banks of good reputation in the

Supervision Annual Report Supervision Annual Report2007 2007

24 Bank of Albania Bank of Albania 25

Supervision Annual Report Supervision Annual Report2007 2007

24 Bank of Albania Bank of Albania 25

international arena are present even in Albania, enhancing the prospects for a more competitive and efficient development of the banking system, and for a larger and safer capital support. this view, along with the appearance for the first time of bank consolidation phenomenon through mergers, makes headway to optimizing synergies of the system. these integrating developments might have increased and strengthened even the Albanian banking system interdependence on global market dynamics. As a consequence, all in all we estimate that there is noticed a tendency towards smaller frequencies but with a larger impact of possible financial, regional or global crises on our banking system. in this light, we assess that the financial crisis springing mainly from subprime housing loans8, whose wave has not been soothed yet, has not impacted at all on our banking system. the banks operating in Albania are regarded as institutions, which have not had any direct exposure to American house loan market of low quality, while the impact from their possible indirect exposures seems to be totally non-material or non-existent.

the financial position of the banking system is assessed as a good one and reflects the following highlights:

• high levels and generally steady growth of profitability indicators. roAA is estimated at 1.57 percent against 1.36 percent at end of 2006. niM is estimated at 4.35 percent, against 4.22 percent;

• net indicator sustainability of the loan portfolio quality (1.8 percent to 1.7 in the previous year) and an insignificant deterioration of gross indicator, due to more rapid increase of non-performing loans to total loans (3.4 percent, to 3.1 percent);

• Stability of loan portfolio weight, when there is noncompliance between the loan currency and the currency in which the borrowers generate their income. nonetheless, there are not yet signals for any concerning levels of non-performing loans for this portfolio, particularly under the conditions when the exchange rate has been steady;

• Deterioration of the banking sector capabilities of covering with capital the possible losses from loans, assessing this from an obvious increase of net non-performing loans/regulatory capital ratio, from 6.8 percent to 11.2 percent. Anyways, the coverage capability is still at benign levels;

• Capital adequacy above the minimum level defined by the Bank of Albania and the downward trend as a result of ever larger orientation of the system to risky assets (from 18 percent to 17.1 percent);

• lower debt level against own equity and in consequence, a lower financial leverage level, from 14.8 percent to 13.2 percent;

• limited market risks level;• increased activity in foreign currency, as an expression of a greater

increase of liabilities/deposits in foreign currency and the loan portfolio;

• increased depth of the banking intermediation in the optics of increased ratio of loan portfolio to total assets and increased total assets to GDp;

• Constant extension of the banking activity volume, as an expression of

Supervision Annual Report Supervision Annual Report2007 2007

26 Bank of Albania Bank of Albania 27

Supervision Annual Report Supervision Annual Report2007 2007

26 Bank of Albania Bank of Albania 27

gradual increase of total assets, operating expenses, operating income, banks’ network, etc;

• increased new banking products to absorb inactive resources as much as possible and to increase the lending intensity;

• Better liquidity situation, as an expression of benign levels of liquidity ratios and increased deposits volume;

• Gradual reduction of assets and deposits concentration, even though their levels continue to remain far from the optimum level estimated according to herfindahl index;

• improvement of banking system efficiency compared with other economy sectors, as an expression of increased net share to GDp, from 0.8 percent to 1.1 percent.

these developments, along with increased paid in capital and increased net result, have offset the increased risk-weighted assets and have created a sufficient framework for maintaining banking system stability during 2007.

3. BAnKinG SYSteM StruCture

3.1 nuMBer oF BAnKS

over 2007 the number of banks operating in the banking system was 17 (same as in the previous year). But, during this year the first bank merger occurred in the Albanian banking market. the merger of Sanpaolo iMi from Banka intesa, italy, which brought about the establishment of the intesa Sanpaolo banking group, had as a consequence the merger of the italian Albanian Bank with the American Bank of Albania, having intesa Sanpaolo as their main shareholder. the financial merging effects started on January 1, 2008. So, from this date on the number of banks operating in Albania is down to 16.

Also, the change in the legal status of the First investment Bank - tirana Branch into an incorporated bank in Albania reduced the number of foreign bank branches operating in Albania compared to the increased number of subsidiaries. At the end of 2007, the number of foreign bank branches in Albania is two, the number of subsidiaries of foreign banks and of foreign financial groups was nine, the number of domestically-owned capital banks is two, whereas four banks are owned by other shareholders, physical persons, legal ones or banks.

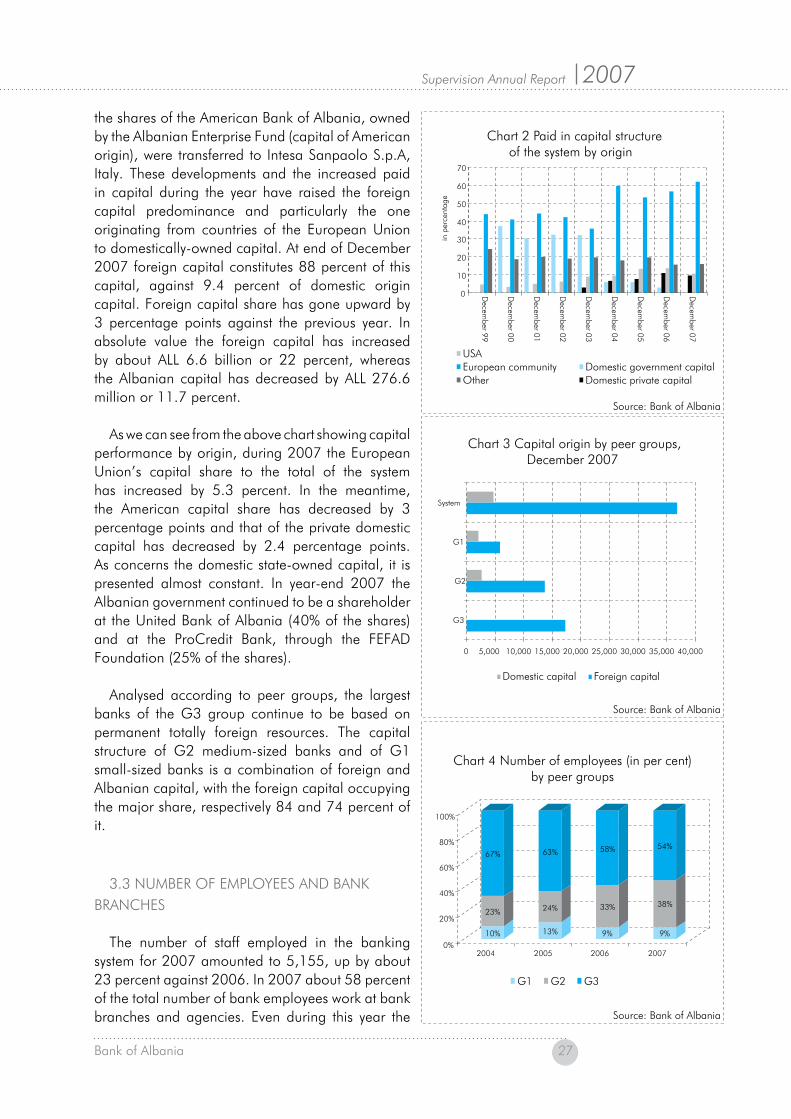

3.2 oWnerShip StruCture BY CApitAl oriGin

During 2007 some important changed occurred in shareholders’ equity structure by capital origin. So, in July 2007, the Société Général group acquired 75 percent of the popular Bank’s shares, which until that moment was a totally private domestically-owned bank. on June 2007, 80 percent of

Supervision Annual Report Supervision Annual Report2007 2007

26 Bank of Albania Bank of Albania 27

Supervision Annual Report Supervision Annual Report2007 2007

26 Bank of Albania Bank of Albania 27

the shares of the American Bank of Albania, owned by the Albanian enterprise Fund (capital of American origin), were transferred to intesa Sanpaolo S.p.A, italy. these developments and the increased paid in capital during the year have raised the foreign capital predominance and particularly the one originating from countries of the european union to domestically-owned capital. At end of December 2007 foreign capital constitutes 88 percent of this capital, against 9.4 percent of domestic origin capital. Foreign capital share has gone upward by 3 percentage points against the previous year. in absolute value the foreign capital has increased by about All 6.6 billion or 22 percent, whereas the Albanian capital has decreased by All 276.6 million or 11.7 percent.

As we can see from the above chart showing capital performance by origin, during 2007 the european union’s capital share to the total of the system has increased by 5.3 percent. in the meantime, the American capital share has decreased by 3 percentage points and that of the private domestic capital has decreased by 2.4 percentage points. As concerns the domestic state-owned capital, it is presented almost constant. in year-end 2007 the Albanian government continued to be a shareholder at the united Bank of Albania (40% of the shares) and at the proCredit Bank, through the FeFAD Foundation (25% of the shares).

Analysed according to peer groups, the largest banks of the G3 group continue to be based on permanent totally foreign resources. the capital structure of G2 medium-sized banks and of G1 small-sized banks is a combination of foreign and Albanian capital, with the foreign capital occupying the major share, respectively 84 and 74 percent of it.

3.3 nuMBer oF eMploYeeS AnD BAnK BrAnCheS

the number of staff employed in the banking system for 2007 amounted to 5,155, up by about 23 percent against 2006. in 2007 about 58 percent of the total number of bank employees work at bank branches and agencies. even during this year the

0

10

20

30

40

50

60

70

in p

erce

ntag

e

Domestic government capitalDomestic private capital

USAEuropean communityOther

Decem

ber 07

Decem

ber 06

Decem

ber 05

Decem

ber 04

Decem

ber 03

Decem

ber 02

Decem

ber 01

Decem

ber 00

Decem

ber 99

Source: Bank of Albania

Chart 2 Paid in capital structureof the system by origin

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

G3

G2

G1

System

Domestic capital Foreign capital

Source: Bank of Albania

Chart 3 Capital origin by peer groups,December 2007

Chart 4 Number of employees (in per cent)by peer groups

10%

23%

67%

13%

24%

63%

9%

33%

58%

9%

38%

54%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007

G1 G2 G3

Source: Bank of Albania

Supervision Annual Report Supervision Annual Report2007 2007

28 Bank of Albania Bank of Albania 29

Supervision Annual Report Supervision Annual Report2007 2007

28 Bank of Albania Bank of Albania 29

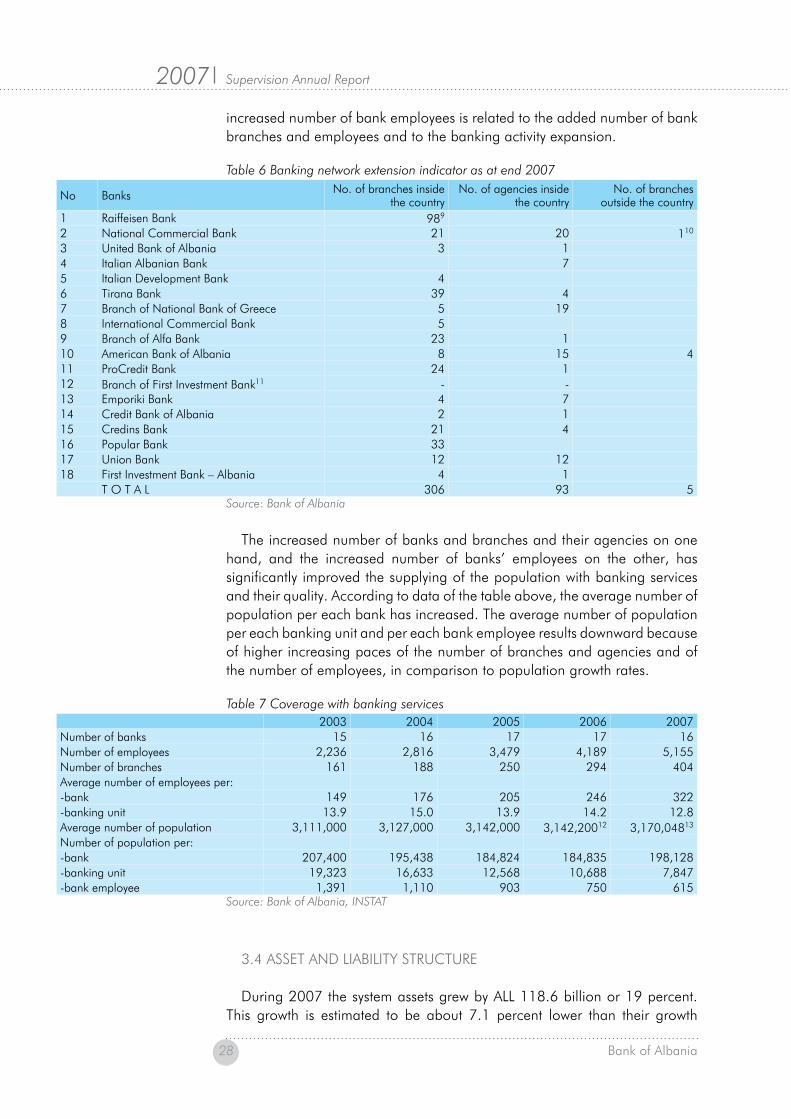

increased number of bank employees is related to the added number of bank branches and employees and to the banking activity expansion.

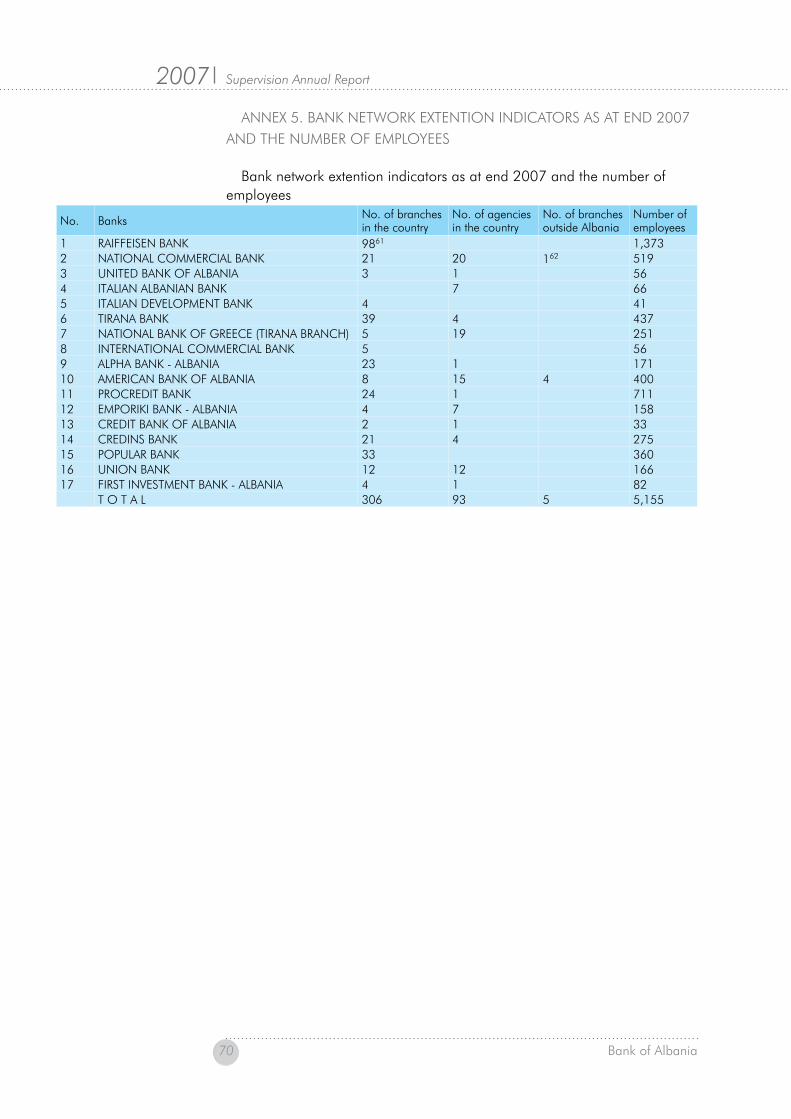

Table 6 Banking network extension indicator as at end 2007

no Banks no. of branches inside the country

no. of agencies inside the country

no. of branches outside the country

1 raiffeisen Bank 989

2 national Commercial Bank 21 20 110

3 united Bank of Albania 3 14 italian Albanian Bank 75 italian Development Bank 46 tirana Bank 39 47 Branch of national Bank of Greece 5 198 international Commercial Bank 59 Branch of Alfa Bank 23 110 American Bank of Albania 8 15 411 proCredit Bank 24 112 Branch of First investment Bank11 - -13 emporiki Bank 4 714 Credit Bank of Albania 2 115 Credins Bank 21 416 popular Bank 3317 union Bank 12 1218 First investment Bank – Albania 4 1

t o t A l 306 93 5Source: Bank of Albania

the increased number of banks and branches and their agencies on one hand, and the increased number of banks’ employees on the other, has significantly improved the supplying of the population with banking services and their quality. According to data of the table above, the average number of population per each bank has increased. the average number of population per each banking unit and per each bank employee results downward because of higher increasing paces of the number of branches and agencies and of the number of employees, in comparison to population growth rates.

Table 7 Coverage with banking services 2003 2004 2005 2006 2007number of banks 15 16 17 17 16number of employees 2,236 2,816 3,479 4,189 5,155number of branches 161 188 250 294 404Average number of employees per:-bank 149 176 205 246 322-banking unit 13.9 15.0 13.9 14.2 12.8Average number of population 3,111,000 3,127,000 3,142,000 3,142,20012 3,170,04813 number of population per:-bank 207,400 195,438 184,824 184,835 198,128-banking unit 19,323 16,633 12,568 10,688 7,847-bank employee 1,391 1,110 903 750 615

Source: Bank of Albania, INSTAT

3.4 ASSet AnD liABilitY StruCture

During 2007 the system assets grew by All 118.6 billion or 19 percent. this growth is estimated to be about 7.1 percent lower than their growth

Supervision Annual Report Supervision Annual Report2007 2007

28 Bank of Albania Bank of Albania 29

Supervision Annual Report Supervision Annual Report2007 2007

28 Bank of Albania Bank of Albania 29

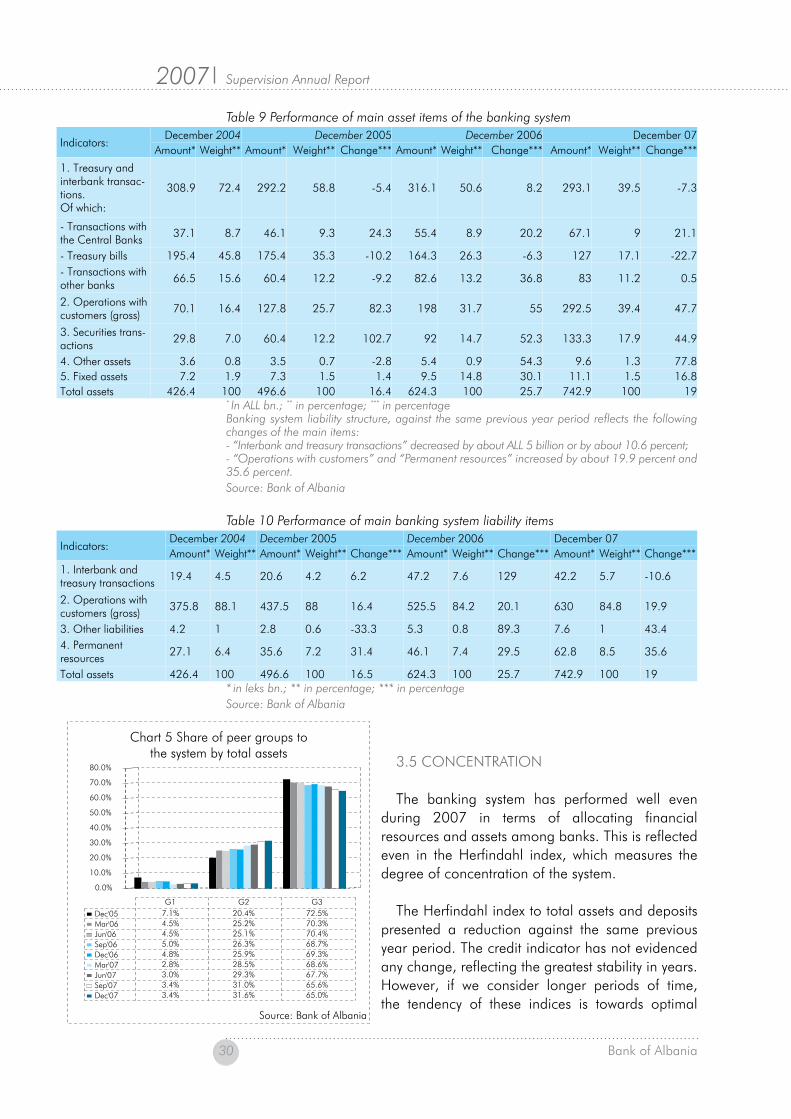

during 2006. the bank groups’ performance dynamics during 2007 was reflected in their weight to the total of the system. At the end of 2007 their evidenced weights are 3.4, 31.6 and 65 percent, respectively for G1, G2 and G3, against 4.8, 25.9 and 69.3 percent in the previous year.

only during the last quarter, the banking system assets grew by All 42.8 billion or about 6 percent, from All 33.1 billion or 5 percent in the third quarter. the upward trend of the banking activity is explained by high increasing paces of G3 banks, G1 banks and the majority of G2 banks over this period.

the share of assets to Gross Domestic product (GDp) and that of the loan portfolio to GDp for 2007 has increased, amounting to 75.9 percent and 29.9 percent respectively. the positive performance of these indicators was determined by the highest growth rates of assets of the system (December ’07 - December ’06 by 19 percent), against the growth of annual GDp (December ’07 - December ’06, by 8.9 percent). increased indicators speak for increased intermediation in the banking sector and larger presence of this sector in the economic growth.

Table 8 Total asset share of the banking system to GDPindicators in All bn. Dec ‘00 Dec ‘01 Dec ‘02 Dec ‘03 Dec ‘04 Dec ‘05 Dec ‘06 Dec ‘07total assets 270.8 318.5 339.3 373.6 426.4 496.6 624.3 742.9total assets/GDp 50.2 53.5 51.6 50.2 51.9 59.3 69.4 75.9total loans/GDp 5.3 4.7 5.9 6.8 8.5 15.3 22.0 29.9

Source: Bank of Albania, INSTAT

the banking system asset structure, against the same previous year period, has reflected the following changes:

• reduction in Albanian Government treasury bill investments, by about All 37 billion or 22.7 percent;

• increase in lending by All 94.5 billion or 47.7 percent, and;• increase in securities investment, Albanian Government treasury bills

excluded, by All 41.4 billion or 45 percent. investments in other securities include a significant share of Albanian Government bonds by 90.6 percent, followed by foreign government bonds by 3.9 percent, foreign banks and foreign financial institutions by 3.7 percent and 1.7 percent respectively. Compared with the previous year, there is highlighted the tendency to invest in Albanian government bonds, while the weight of this item at year-end 2006 constituted 82.5 percent. the other items have decreased in absolute value and in the weight to the total of this portfolio. the analysis of this portfolio indicates that virtually all banks have securities portfolio in lek and only three banks have portfolio in foreign currency. the weight of investments in foreign currency bonds (non-residents) is evidenced, on December ’07, at about 9.4 percent of fixed and variable income securities portfolio, from 17.5 percent at end 2006. Most of these securities are estimated as of low credit risk by international rating agencies. in the meantime, given the data on the type of currency in which they are issued14 and their residual term to maturity15, we assess that they do not constitute any significant risk in the framework of market risk.

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

Table 9 Performance of main asset items of the banking system

indicators:December 2004 December 2005 December 2006 December 07

Amount* Weight** Amount* Weight** Change*** Amount* Weight** Change*** Amount* Weight** Change***

1. treasury and interbank transac-tions.of which:

308.9 72.4 292.2 58.8 -5.4 316.1 50.6 8.2 293.1 39.5 -7.3

- transactions with the Central Banks 37.1 8.7 46.1 9.3 24.3 55.4 8.9 20.2 67.1 9 21.1

- treasury bills 195.4 45.8 175.4 35.3 -10.2 164.3 26.3 -6.3 127 17.1 -22.7- transactions with other banks 66.5 15.6 60.4 12.2 -9.2 82.6 13.2 36.8 83 11.2 0.5

2. operations with customers (gross) 70.1 16.4 127.8 25.7 82.3 198 31.7 55 292.5 39.4 47.7

3. Securities trans-actions 29.8 7.0 60.4 12.2 102.7 92 14.7 52.3 133.3 17.9 44.9

4. other assets 3.6 0.8 3.5 0.7 -2.8 5.4 0.9 54.3 9.6 1.3 77.85. Fixed assets 7.2 1.9 7.3 1.5 1.4 9.5 14.8 30.1 11.1 1.5 16.8total assets 426.4 100 496.6 100 16.4 624.3 100 25.7 742.9 100 19

* In ALL bn.; ** in percentage; *** in percentageBanking system liability structure, against the same previous year period reflects the following changes of the main items:- “Interbank and treasury transactions” decreased by about ALL 5 billion or by about �0.6 percent; - “Operations with customers” and “Permanent resources” increased by about �9.9 percent and �5.6 percent. Source: Bank of Albania

Table �0 Performance of main banking system liability items

indicators:December 2004 December 2005 December 2006 December 07Amount* Weight** Amount* Weight** Change*** Amount* Weight** Change*** Amount* Weight** Change***

1. interbank and treasury transactions 19.4 4.5 20.6 4.2 6.2 47.2 7.6 129 42.2 5.7 -10.6

2. operations with customers (gross) 375.8 88.1 437.5 88 16.4 525.5 84.2 20.1 630 84.8 19.9

3. other liabilities 4.2 1 2.8 0.6 -33.3 5.3 0.8 89.3 7.6 1 43.44. permanent resources 27.1 6.4 35.6 7.2 31.4 46.1 7.4 29.5 62.8 8.5 35.6

total assets 426.4 100 496.6 100 16.5 624.3 100 25.7 742.9 100 19* in leks bn.; ** in percentage; *** in percentageSource: Bank of Albania

3.5 ConCentrAtion

the banking system has performed well even during 2007 in terms of allocating financial resources and assets among banks. this is reflected even in the herfindahl index, which measures the degree of concentration of the system.

the herfindahl index to total assets and deposits presented a reduction against the same previous year period. the credit indicator has not evidenced any change, reflecting the greatest stability in years. however, if we consider longer periods of time, the tendency of these indices is towards optimal

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Dec'05 7.1% 20.4% 72.5%Mar'06 4.5% 25.2% 70.3%Jun'06 4.5% 25.1% 70.4%Sep'06 5.0% 26.3% 68.7%Dec'06 4.8% 25.9% 69.3%Mar'07 2.8% 28.5% 68.6%Jun'07 3.0% 29.3% 67.7%Sep'07 3.4% 31.0% 65.6%Dec'07 3.4% 31.6% 65.0%

G1 G2 G3

Source: Bank of Albania

Chart 5 Share of peer groups tothe system by total assets

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�0 Bank of Albania Bank of Albania ��

concentration level, though the latter one is still far from being achieved. reduced banking system concentration level is attributed to reorganisation of this sector. Banks of G2 peer group are benefiting from loss of terrain of large banks of G3 peer group. this is testified also by the reduced share of the latter one to total assets of the system in the last two years16.

Table �� H (Herfindahl) index of assets, deposits and loans concentration December’02

December’03

December’04

December’05

December ’06

September ’07

December’07

h index (assets) 0.32 0.30 0.27 0.21 0.18 0.16 0.15h index (deposits) 0.37 0.35 0.31 0.24 0.20 0.17 0.17h index (credit) 0.17 0.15 0.11 0.10 0.11 0.11 0.11

Source: Bank of Albania

4. MAnAGinG BAnKinG ACtivitY riSK

4.1 CreDit riSK

4.1.1 lending activity

During the fourth quarter the banking system credit outstanding increased by about All 32.6 billion or 12.6 percent, from All 20.6 billion or 8.6 percent in the previous quarter. over one year, the credit outstanding increased by All 94.5 billion or 47.7 percent (against the same previous year period). the main contribution to this increase has been rendered by seven banks of the system, which have evidenced credit increase by All 79.8 billion, constituting 84.4 percent of credit outstanding growth for the whole system. During the fourth quarter credit in All increased by All 5.3 billion or 7.1 percent, whereas credit in foreign currency recorded a growth of All 27.3 billion or about 14.8 percent.

Compared with the same previous year period, loan portfolio by currency increased by All 24.7 billion (44.3 percent) and All 69.8 billion (49.1 percent) respectively for credit in lek and credit in foreign currency. the largest contribution to credit outstanding growth during 2007 was rendered by G2 banks, followed by G3 banks, by All 50.8 billion (70.6 percent) and All 49.8 billion (44.9 percent) respectively. the large growth of credit outstanding of banks of G2 peer group is attributed even to the passing of one bank from G1 to G217.

in the meantime, credit outstanding growth for the fourth quarter highlights the peer groups of G2, G3 followed by G1, respectively by All 17.2 billion (16.3 percent), All 14.4 billion (9.9 percent) and All 1 billion (12.1 percent), from All 8.3 billion (8.5 percent), All 11.4 billion (8.4 percent) and All 367 million (5.2 percent) in the preceding quarter.

notwithstanding the increased share of banks of G2 peer group to total credit outstanding of the system over last two years, the banks of G3 peer group continue to have the largest share to this portfolio.

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

Supervision Annual Report Supervision Annual Report2007 2007

�2 Bank of Albania Bank of Albania ��

0.0

10.0

20.0

30.0

40.0

50.0

60.0

G1 13.1 13.1 7.7 7.9 7.6 2.7 2.9 2.9 3.0

G2 34.0 42.9 38.8 37.6 36.4 40.5 40.7 40.7 42.0

G3 52.9 44.0 53.5 54.5 56.0 56.8 56.4 56.4 55.0

Dec'05 Mar'06 Jun'06 Sep'06 Dec'06 Mar'07 Jun'07 Sep’07 Dec'07

Source: Bank of Albania

Chart 6 Share of peer groups to total creditoutstanding of the banking system (in %)

Dynamics analysis of loan portfolio structure highlights a higher growth rate for the loan portfolio extended to enterprises, by about 12.2 percent, against household loan portfolio growth by 10.7 percent18. in the meantime, 2007 highlights the contrary of what is revealed by the panorama of this quarter. Actually the loan portfolio to enterprises has increased 38.1 percent, against 58.9 percent increase of the household loan portfolio. however, notwithstanding the positive developments in terms of increasing loans to households, influencing on the increased share of this portfolio to total loans of the system, from 33 percent at year-end 2006 to 35.5 percent at year-end 2007, loans to enterprises constitute the most favourable segment, accounting for 62.5 percent of the loan portfolio as at year-end 2007.

the fourth quarter has presented increased credit extended to the public sector by All 2.4 billion or 71 percent. Credit portfolio for this sector is reported at All 5.8 billion, from about All 0.2 billion in 2006 and has a very high concentration level.