Meat System in Cologne – ART JOURNAL 74, no. 1 (Spring 2015)

Upload

independentCategory

view

0download

0

Student Script

Module 20.4 – Media Finance

Financial Management of Media Firms – Key Issues, Theories, and Case Evidence

Prof.Dr. Paul Murschetz, MSc.

Cologne Business School GmbH

May 1, 2006

Media Finance

1 May 2011 2

Acknowledgements

This report was prepared by Paul Murschetz on behalf of Cologne Business School GmbH.

Rights Restrictions

Material from this report can be freely used and reproduced but not commercially resold and, if quoted, the exact

source must be clearly acknowledged.

Cologne, May 2006

3 15 May 2011

Table of Contents

Executive Summary ................................................................................................................................ 4

1 Introduction to Financial Management of the Media .................................................................... 6

Study objectives and research questions ................................................................................ 9

Methodology and study organization ................................................................................... 10

2 Financial Management of Media Organizations – Key Issues .................................................... 12

2.1 General issues – The impact of competition on firm performance .......................... 12

2.2 Specific issues of financial media management ......................................................... 19

2.3 Further theoretical approaches to financial media management ............................ 33

2.4 Financial indicators and measures of firm performance ......................................... 35

2.5 Strategic responses of media companies .................................................................... 38

3 Financial Management in Media Practice – Case Evidence ....................................................... 46

Case Study A: http://DerStandard.at – The Internet success for quality news publishing

........................................................................................................................................ 46

Case Study B: ORF – The Austrian Broadcasting Corporation exploiting cross-media

financial strategies ........................................................................................................ 51

4 Conclusions ................................................................................................................................. 56

Media Finance

1 May 2011 4

Executive Summary

Research background and objective

The research study project “Financial Management of Media Firms – Key Issues, Theories, and Case

Evidence” (in the following abbreviated as „the study‟) will research and analyse key issues of

financial economics and financial management of the media sector. It will introduce fundamental

concepts of financial economics and financial management of the media sector, present the vocabulary

of financial economics and financial management and as applied to the media sector, present key

issues and main principles of financial management of media organizations, and offer analytical

reasoning for the impacts of general socio-economic forces on firm performance in the media sector.

Further, this study will present two best-practice case studies in the media sector in order to test

theoretical issues discussed against empirical evidence.

The study must be regarded as an exploratory pilot study of mapping thematic issues regarding

financial management in general and the media in particular. Main objective is to introduce key

theoretical issues of financial economics and financial management of the media sector and to test

these issues against two selected best-practice case studies in the media sector. By this, this study

provides theoretical and empirical analysis of financial economics and financial management of the

media sector in order to understand the following multi-levelled key issues in more detail:

(a) Impacts of competition on media firm performance as viewed from an Industrial Organisation

theory perspective

(b) Potential behavioural responses of media firms as viewed from a media economics perspective

(c) Sources of finance of off-line and online media firms in selected industry sectors as possible

responses to require sufficient funding for their operations

(d) Specific theoretical issues of financial media management

(e) Background theories to explain issues of financial media economics and media management

(f) Indicators and measures of firm performance as adapted for the media sector, and

(g) Issues of strategic management in general and marketing management in particular

Results

This study defines financial management in a broad sense. This means that while financial

management theory in general is concerned with the “acquisition, financing, and management of

assets with some overall goal in mind” (Van Horne & Wachowicz 2001, p. 2), this study proposes the

view that financial management of media firms needs to be defined more broadly. A proper definition

needs to include issues of governance, marketing, and competitive strategy. This said, the decision

function of financial management can not only be broken down into three major areas: the investment,

financing, and asset management decisions, but, following the American Marketing Association, may

view financial management in a broader way as an “organizational function and a set of processes for

creating, communicating, and delivering value to customers and for managing customer relationships

5 15 May 2011

in ways that benefit the organization and its stakeholders” (American Marketing Association,

website).

Only few scholars in media economics and media management research offer analytical reasoning and

explanations for issues of investment, financing, asset management, governance and firm value

creation processes for media firms. This study has laid the groundwork for analysing theoretical issues

in financial media management. It looked into the theoretical offers of the theory of the firm and the

Industrial Organisation model of competition to set-up a theoretical framework for effects of financial

media management on competition. Further, it identified a set of other theoretical approaches well

applicable to the field of financial media management such as theories of ownership control and its

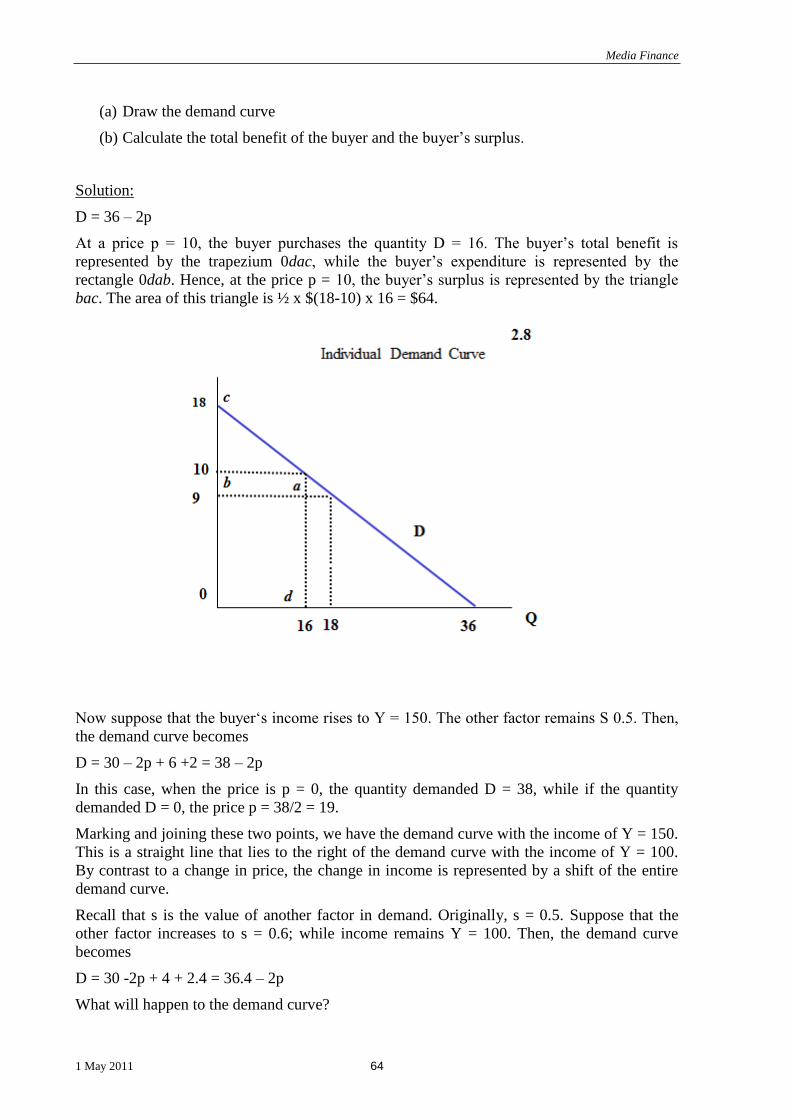

effects on media performance, financial commitment and financial control, resource dependence

theory, and corporate governance theory. Case studies on the financial management practices of

mass media firms revealed that, in fact, print and broadcasting media apply various sets of

management and marketing practices to become economically and financially viable

organizations.

This study showed that able to show that the Internet‟s impact on the content utilization chains of a

traditional print media publisher manifests itself in various ways. It identified a set of new revenue-

generation practices, whereby the media firm studied exploited its content wealth and unique selling

propositions (USPs) for its online representations. As for the second best-practice case study, the

ORF‟s positive economics is mainly accounted for by well accepted informational programming,

programming of low-cost US-feature films and series, exclusive sports transmissions and an overall

successful „Austrification‟ of programmes. Further, Internet strategies, cross-media marketing

strategies, and digitization as innovation strategy make for a strong Public Service Broadcaster in the

future.

Media Finance

1 May 2011 6

1 Introduction to Financial Management of the Media

Chapter overview

The following chapter will:

Introduce fundamental concepts of financial economics and financial management of the media

sector.

Present the vocabulary of financial economics and financial management and as applied to the

media sector.

Define objectives and selected methods for the present study.

Offer a set of research questions which will guide this study and will be answered in the concluding

chapter.

Give a brief overview of the organisation of this present study.

The economics and financing of media companies is a central issue in media management research

and practice. According to Picard (2002, p. xi), “the economics and financing of media companies are

the foundations upon which all media activity takes place. Regardless of cultural, political, and social

roles and expectations for media, media must cover their costs and create returns, just as any other

business, or they will wither and disappear. The forces that require effective operation are the same

for both private media and non-commercial media such as public service broadcasting”.

The financial requirements of varying types of media operations affect the forms and structures of

media firms, as do the scale and scope of their operations (see, Picard 2002, p. 2-3). The three most

common legal forms of business organization are sole proprietorship, the partnerships, and the

corporation. Sole proprietorship is a form of business owned by one person and operated for his or her

own profit. A partnership is a business owned by two or more people and operated for profit. A

corporation is an artificial being created by law (often called a “legal entity”) (see, Gitman 2003).

Because the needs of media differ and because of the organizational requirements to create media

goods and services vary depending upon their markets, the sizes of media organizations cover the

range from small to large.

Media organizations are guided by specific goals-sets. These goals include cultural goals, as well as

economic goals such as efficiency, effective organization of resources and processes, profit

maximization, economic growth, and economic stability.

Profit maximization as primary firms goal: The traditional „Theory of the Firm‟ which studies the

behaviour of firms with respect to the inputs they buy, the production techniques they adopt, the

quantity they produce, and the price at which they sell their output, asserts that the development and

operations of firms is guided by the primary goal of maximizing profit and the value of the firm

(Coase 1937, Crew 1975, Jensen & Meckling 1973). The purpose of the creation and operation of

commercial media firms is thus to produce the most profit and the highest value for the firm. The

former tends to be a short-term annual perspective, while the latter is a longer-term goal. If resources

7 15 May 2011

and the processes by which they are transformed into goods and services are efficiently and effectively

organized and managed, the ability to achieve these goals becomes possible.1

What is profit? Profit is a primary goal of firms. Profit is defined as a “measure of surplus by a

company from some activity or project over some time period” (Bannock et al. 2002). Bannock et al.

(2002, p. 293) continue as follows: “While simple at first sight, profit has a number of definitions, and

is far from simple in practice. In an accounting sense of the term, two important concepts of profit are:

(a) net profit before tax (or pretax profit), which is the residual after reduction of all money costs, i.e.

sales revenue minus wages, salaries, rent, raw materials, interest payments on loan, and depreciation,

and (b) gross profit, which is net profit before depreciation and interest. In other words, economic

profits are equal to total revenue minus total cost”. Thus, a profit-maximizing firm chooses to produce

at an output level or price that maximizes the difference between total revenue and total cost (Hoskins

et al. 2004).

For commercial firms, profit creates the money available to pay their owners or investors, make

capital expenditures, and pay debts. For non-commercial media, ownership/investor do not receive the

profit, but it provides funds to improve the company through capital investments, make additional

expenditures on content and other items, and pay debts (Picard 2002). To investors, revenue is less

important than profit (which in US business, somewhat confusingly, often is called income), which is

the amount of money the business has earned after deducting all the business‟s expenses.

There is a difference between economic profit and accounting profit. Economic profit is different from

the profit that a business might declare in its accounts, which might typically exist of some economic

rent plus normal profit, i.e. a return that just compensates the producer for the opportunity cost of the

capital and entrepreneurship that it provides.2

The role of profit: Profit measures the return to risk when making an investment. The role of profit in

capital investment decisions is explained by the risk theory of profit (Knight 1921). This argues that

the potential for high economic profits is necessary to induce investment, especially in industries with

higher risk. As a result, firms operating in these industries require above-average returns, or the capital

will move to other more profitable investments (Picard 2002).

The role of profit in the media sector: The media sector is not “naturally” profit-driven. Some

industries in the sector are regulated by law to operate as not-for-profit firms. For example,

broadcasting law imposes specific income restrictions on media companies. In addition, media

companies have to pursue other goals than profit maximisation such as cultural and social goals as part

of their public remit.

Financial economics: Financial economics is the branch of economics studying the interrelation of

financial variables, such as prices, interest rates and shares as opposed to those concerning the real

economy. Besides studying financial market and instruments, financial economics is concerned with

issues of asset valuation, i.e. the determination of the fair value of firm assets (cash, bank deposits,

bills receivable; land buildings, plant, machinery; intangible assets such as patents, goodwill). This

asset valuation involves questions such as: „How risky is the asset?‟ (identification of the asset

appropriate discount rate), „What cash flows will it produce?‟ (discounting of relevant cash flows),

1 Some critics of this theory have argued that the rise of modern corporations and the separation of management and

ownership may lead to objectives other than profit maximization such as firm growth, or management utility (Klein 1998). 2 Opportunity cost is a ubiquitous concept and can be translated as the value that has to be given up – a lost opportunity – as a

result of a decision. It ensures that the price of every input to production is charged at the price equal to its value in its best

alternative use.

Media Finance

1 May 2011 8

„How does the market price compare to similar assets?‟ (relative valuation), and „Are the cash flows

dependent on some other asset or event?‟ (derivatives, contingent claim valuation).

Financial management: Financial management is concerned with the acquisition, financing, and

management of assets with some overall goal in mind (Van Horne & Wachowitz 1997). According to

Picard (2002), “financing involves meeting the monetary needs of a firm so that it may be established,

operated, and developed. Issues of financing range from creating sufficient funds to establish a firm,

to obtaining money to pay for operations, to gathering funds to fund growth” (p. 154). The essential

objective of financial management can be categorized into two broad functional categories: recurring

finance functions and non-recurring or episodic finance functions, defining the functional role of a

financial manager. This time-perspective gives financing issues a specific note: they need to

understand the financial flow in the firm. In this context, critical issues are cash flow management,

credit management, investment decisions, and financing decisions (Alexander et al. 1993).

According to Bradley (cited in: Gitman 1999, p. 8), “financial management is the area of business

management, devoted to a judicious use of capital and a careful selection of sources of capital, in

order to enable a spending unit to move in the direction of reaching its goals”. This definition points

to the four essential aspects of financial management:

Financial management is a distinct area of business management, i.e. financial manager has a

key role in overall business management.

Prudent or rational use of capital resources, i.e. proper allocation and utilization of funds.

Careful selection of the source of capital, i.e. determining the debt equity ratio and designing a

proper capital structure for the corporate.

Goal achievement, i.e. ensuring the achievement of business objectives viz. wealth or profit

maximization.

Academic reasoning in financial management for the media is sparse. Discipline development could

be undertaken alongside traditional topic heading such as (Van Horne & Wachowitz 1997):

Introduction to financial management for the media

Valuation of assets

Tools of financial analysis and planning of media operations

Working capital management

Investment in capital assets

The cost of capital, capital structure, and dividend policy

Intermediate and long-term financing of media operations

Special areas of financial management for the media

The role of a financial manager: The role of a financial manager can be best understood by

analyzing the definition of financial management. Following (Gitman 2003, p. 3), “financial managers

actively manage the financial affairs of any type of businesses – financial and non-financial, private

and public, large and small, profit-seeking and not-for-profit. They perform such varied financial

tasks as planning, extending credit to customers, evaluating proposed large expenditures, and raising

money to fund the firm‟s operations. In recent years, the changing economic and regulatory

9 15 May 2011

environments have increased the importance and complexity of the financial manager‟s duties. As a

result, many top executives have come from the finance area”.

Treasurer and controller: Corporate organizations differ between treasurer and controller. The

treasurer is the firm‟s chief financial manager, who is responsible for the firm‟s financial activities,

such as financial planning and fund raising, making capital expenditure decisions, and managing cash,

credit, the pension fund, and foreign exchange. The controller is the firm‟s chief accountant, who is

responsible for the firm‟s accounting activities such as corporate accounting, tax management,

financial accounting, and cost accounting.

Relationship to accounting: The firm‟s finance (treasurer) and accounting (controller) activities are

closely related and generally overlap. Indeed, managerial finance and accounting are not often easily

distinguishable. In small firms the controller often carries out the finance function, and in large firms

many accountants are closely involved in various finance activities. However, there is one major

difference between finance and accounting: the accountant‟s primary function is to develop and report

data for measuring the performance of the firm, and the financial manager‟s primary function is to

evaluate the accounting statements and make decisions on the basis of their assessment of the

associated returns and risks.

The financial manager must understand the economic environment and relies heavily on the economic

principle of marginal analysis to make financial decisions. The marginal analysis is a principle in

economics that states that financial decisions should be made and actions taken only when the added

benefits exceed the added costs. Financial managers use accounting but concentrate on cash flows and

decision making.

In addition, managerial finance involves separate further types of positions and functions within a

business firm: (a) the financial analyst, who primarily prepares the firm‟s financial plan‟s and budgets.

Other duties include financial forecasting, performing financial comparisons, and working closely

with accounting; (b) the capital expenditures manager, who evaluates and recommends proposed asset

investments and may be involved in the financial aspects of implementing approved investments; (c)

the project finance manager, who arranges financing for approved asset investments, coordinates

consultants, investment bankers, and legal counsel in large firms; (d) the cash manager, who maintains

and controls the firm‟s daily cash balances; (e) the credit analyst, who administers the firm‟s credit

policy and evaluates credit applications, extending credit, and monitoring and collecting accounts

receivable; (f) the pension fund manager, who oversees or manages the assets and liabilities of the

employees‟ pension fund; and (g) the foreign exchange manager, who manages specific foreign

operations and the firm‟s exposure to fluctuations in exchange rates (Gitman 2003).

Study objectives and research questions

Main objective: Main objective of this study is to introduce key theoretical issues of financial

economics and financial management of the media sector and to test these theoretical issues against

two selected best-practice case studies in the media sector.

By this, this study provides theoretical and empirical analysis of financial economics and financial

management of the media sector in order to understand the following multi-levelled key issues in more

detail:

Media Finance

1 May 2011 10

(h) Impacts of competition on media firm performance as viewed from an Industrial Organisation

theory perspective

(i) Potential behavioural responses of media firms as viewed from a media economics perspective

(j) Sources of finance of off-line and online media firms in selected industry sectors as possible

responses to require sufficient funding for their operations

(k) Specific theoretical issues of financial media management

(l) Background theories to explain issues of financial media economics and media management

(m) Indicators and measures of firm performance as adapted for the media sector, and

(n) Issues of strategic management in general and marketing management in particular

Research Questions: The following general research questions guide this study:

1. RQ1: Which socio-economic forces influence firm performance in the media sector?

2. RQ2: Do new information and communication technologies have an impact on firm

performance?

3. RQ 3: Which sources of finance are vital for viability and sustainability of operations?

4. RQ4: Which specific fields may guarantee financial viability and sustainability?

5. RQ4: What background theories do explain the relations between structure, firm conduct, and

performance of firms in the media sector and the impact of these factors on financial

management?

6. RQ 5: Which indicators and measures are used to show the financial performance of media

firms?

7. RQ6: What role does strategy play in market positioning of firms in the media sector?

8. RQ7: What role does marketing strategy play in strengthening the financial position of firms

in the media sector?

Methodology and study organization

Selected research methods: The analysis will apply a set of theoretical and empirical methods:

scientific literature review, study of business reports and industry data, and case study research.

Literature review: We apply a scientific literature review, i.e. a documentation of a

comprehensive review of the published academic and practitioner‟s work from secondary

sources of data in the areas of interest.

Study of other written material: We will study other data sources to include published and

unpublished documents, expert reports, industry data, company reports, memos, letters, and

newspaper articles.

11 15 May 2011

Case Study research: We explore particular cases by applying the case study method.

Single-case studies of financial management in media organization are analyzed as an

empirical validation of our approach.

Study organisation: This study is organized alongside the following three main chapters, according

sub-chapters, and a reference section:

Chapter 1 Introduction – Fundamentals, study objective, methodology

Chapter 2 Financial Management of Media Organisations – Key issues

Chapter 3 Financial Management of Media Organisations – Case Evidence

Appendix References

Media Finance

1 May 2011 12

2 Financial Management of Media Organizations – Key

Issues

Chapter overview

The following chapter will:

Present key issues and main principles of financial management of media organizations.

Offer analytical reasoning for the impacts of general socio-economic forces on firm performance

in the media sector including competition, market forces, cost forces, regulatory forces, and

barriers to entry and mobility.

Analyse specific issues of financial media management such as sources of revenue, start-up

financing management, cash flow and credit management, and investment management

Discuss background theories of financial media management, and

Present key indicators and measure of firm performance

Introduce theories and key issues of strategic responses of firms to market challenges and

opportunities, and

Depict marketing strategies as specific firm responses to market pressures

2.1 General issues – The impact of competition on firm performance

According to Picard (2002), four major drivers of change are affecting media operations and put

pressure on choices of managers of media firms to develop appropriate responses to them: (1) market

forces, (2) cost forces, (3) regulatory forces, and (4) barriers to entry and mobility. Picard (2002, p. 48)

defines “market forces as external forces based on structures and choices in the marketplace. Cost

forces are internal pressures based on operating expenses of firms. Regulatory forces represent the

legal, political, and self-regulatory forces that constrain and direct operations of media firms.

Barriers represent factors that make it difficult for new firms to enter and successfully compete in a

market”.

In the following paragraph, these four categories of market forces will be described and impacts for

financial media management will be introduced and discussed. Additionally, this chapter will

introduce the impact of technology as main driver of market changes and its potential impacts in

financial management of the media.

Market forces

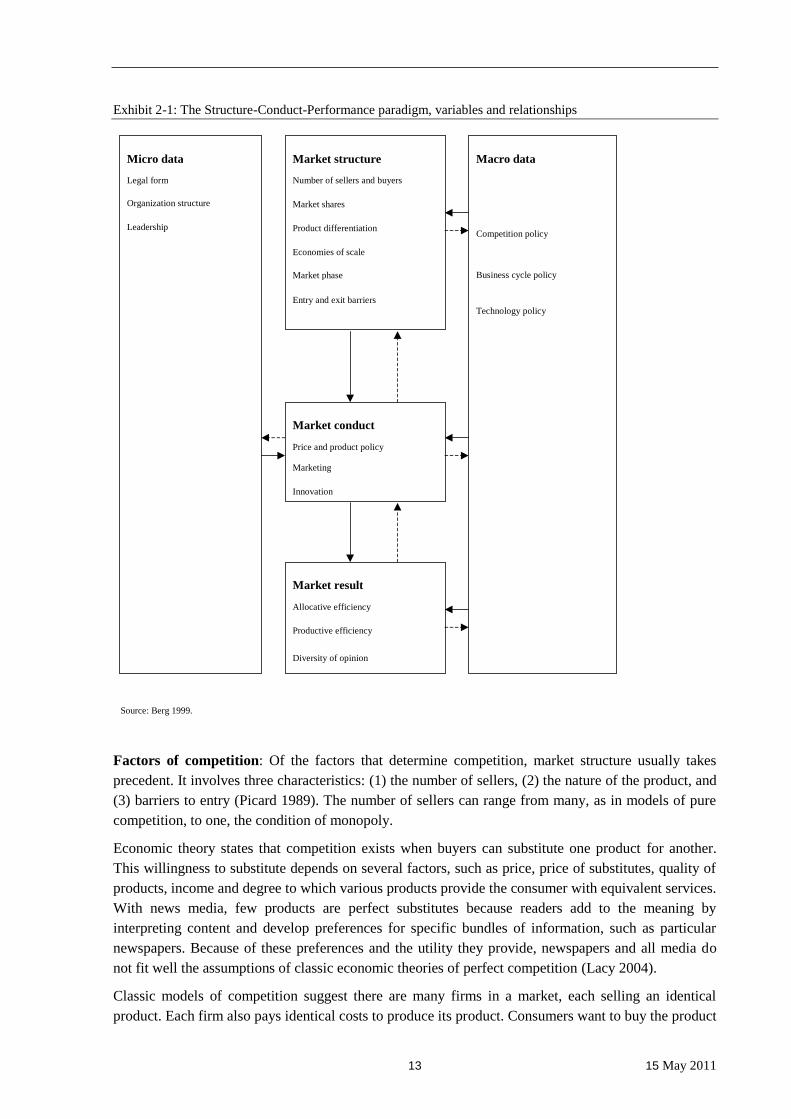

Competition: The theory of the firm forms the basis of the industrial organization (IO) model that

provides an analytical framework for examining competition in the media and other industries. Most

media economics texts follow the IO model using the SCP-paradigm. This paradigm posits a causal

relationship between market structure, conduct and performance. Market structure determines the

conduct of firms, which in turn determines industry performance.

13 15 May 2011

Exhibit 2-1: The Structure-Conduct-Performance paradigm, variables and relationships

Factors of competition: Of the factors that determine competition, market structure usually takes

precedent. It involves three characteristics: (1) the number of sellers, (2) the nature of the product, and

(3) barriers to entry (Picard 1989). The number of sellers can range from many, as in models of pure

competition, to one, the condition of monopoly.

Economic theory states that competition exists when buyers can substitute one product for another.

This willingness to substitute depends on several factors, such as price, price of substitutes, quality of

products, income and degree to which various products provide the consumer with equivalent services.

With news media, few products are perfect substitutes because readers add to the meaning by

interpreting content and develop preferences for specific bundles of information, such as particular

newspapers. Because of these preferences and the utility they provide, newspapers and all media do

not fit well the assumptions of classic economic theories of perfect competition (Lacy 2004).

Classic models of competition suggest there are many firms in a market, each selling an identical

product. Each firm also pays identical costs to produce its product. Consumers want to buy the product

Micro data

Legal form

Organization structure

Leadership

Market structure

Number of sellers and buyers

Market shares

Product differentiation

Economies of scale

Entry and exit barriers

Market phase

Market conduct

Price and product policy

Marketing

Innovation

Market result

Allocative efficiency

Productive efficiency

Diversity of opinion

Macro data

Competition policy

Business cycle policy

Technology policy

Source: Berg 1999.

Media Finance

1 May 2011 14

at the lowest possible price, and it doesn‟t matter which firm produces the product. Any firm that

increases its price loses customers who switch to another firm selling the same product at a lower

price. Each firm‟s product is a perfect substitute for any other firm‟s product. Firms cannot influence

competitors and are forced to sell at a price that just covers their costs. Market conditions must change

before firms can increase prices without losing all of their customers. If only a few firms compete,

each individual firm‟s actions will influence the response from other firms. In oligopolistic markets

firms might agree to raise prices above production costs, earning excess profits. Explicit pricing

agreements are illegal, so oligopolists must depend on tacit understandings to maintain pricing

discipline. However, such agreements are unstable, and individual firms will violate these

understandings if they believe they can gain an advantage.

Newspaper markets tend to be either oligopolistic or monopolistically competitive. The nature of the

product refers to its substitutability. While products under pure competition differ only in price,

competition under monopolistic competition is based on product differentiation and advertising.

Barriers to entry can take on several forms, from technology to regulation to illegal behavior of firms.

Lacy (2004) has studied the relationhsip of competition, circulation, and advertising on the

performance of daily newspapers. According to Lacy, economic theory and research provide evidence

that intense newspaper competition among newspapers will result in increases in newsroom budget,

changes in content and decreases in advertising cost per thousand. However, empirical evidence is less

storng that competition decreases subscription prices. Considerable variations across newspapers can

be found with all these relationships, which represent a variety of managerial decisions.

However, the following general statements are supported by Lacy‟s (2004) research:

Intense newspaper competition increases expenditures in the newsroom and improves

journalism performance.

The increased expenditure and performance translates into changes in content and

improvements in quality aimed at attracting readers.

The relationship between these content changes and circulation growth is not perfect.

However, evidence suggests quality content can attract readers and that failure to provide

acceptable levels of quality and content will lead to declines in circulation and penetration.

Competition for advertising decreases the cost per thousand that advertisers pay newspapers

for at least some forms of advertising. At least some advertisers see other media as substitutes

for some forms of newspaper advertising, especially retail advertising. The number of

advertisers who accept this seems to be growing. At some point, rising cost per thousand

probably leads to businesses moving their advertising to other media, although this is just one

factor in the substitution.

Clustering reduces competition and affects content and advertising prices.

As a result, market performance is impacted by these relationships and dynamics. As put forward by

Lacy (2004, p. 33), “as readership declines and the cost per thousand increases, advertisers will be

more likely to switch to imperfect substitutes. If ad lineage declines, newspapers that want to maintain

profit margins will either have to increase ad prices or maintain revenue or cut newsroom and other

expenses to control costs. In the former case, the probability of advertisers‟ seeking substitutes

increases. In the latter, quality declines will cause readers to leave, increasing the cost per thousand.

As cost per thousand increases, businesses are more likely to substitute other forms of advertising”.

15 15 May 2011

Lacy (2004, p. 34) continues as follows: “Newspapers often take advantage of declining competition

to enhance short-term profits. However, this is a strategic choice. According to economic theory,

businesses that cut quality and pursue aggressive pricing policies can invite competition. A recent

study of the relationship between type of daily ownership and existence of weekly competition in a

county found that counties with publicly owned dailies or no dailies averaged about one more weekly

newspaper than did counties with privately owned dailies. Because publicly owned dailies tend to cut

newsroom budgets and price aggressively, this exploratory study suggests that dailies might be

inviting weekly competition through short-run pricing and content strategies”.

Changes in consumer demand: There is a multitude of factors for change in consumer demand in

printed products. Lifestyle changes and the focus individuals place on their leisure time have changed.

There has also been a reduction in the number of younger people reading newspapers as new

communications channels continue to proliferate. Individual working patterns continue to change

either. Further, there are visible demands for higher performance from media products, through higher

quality, personalisation of services or other means. To leverage consumer trust, media publishers are

advised to build on their potential strengths in branding and customer relationship management in

print and new online markets.

Changes in the value chain: The media publishing value chain is informed by a variety of different

market players who contribute to adding value to information-based products and services under

specific competitive and environmental conditions. A set of new access, service and technology

providers have entered the scene in the media sector. These new providers put pressure on incumbents,

some forward-integrate their businesses and thus increase horizontal supplier market power while

others become vertically integrated and differentiate-out into key specialists in niche markets. On the

other hand, these challenges open ways for new supply chain partnerships.

Changes in customer relations: Today, a new business model is emerging: electronic networks and

markets allow the break-up of what previously thought to be firmly controlled value chains. The value

chain looses its chain attributes, and is replaced by flexible relations, so-called „value webs‟

(Reichwald et al. 2004). By integrating customers into market research and product development

activities, companies can get efficient support to improve products for more customer satisfaction as

well as to identify new sources of revenue. Equally, the role of the customer is changing from a pure

consumer of products or services to a coequal partner in a process of adding value - consumers are

becoming co-producers and co-designers. Both e-business partners are tied together in these value

webs. Mass customisation as pre-condition of customer integration may result in economies of

integration which may lead to product innovation, lower transaction costs, more precise information

about market demands, and increase in brand loyalty by directly interacting with each customer. In

practice, the Publishing and Printing industry sector needs to improve supplier-customer relations in

order to strengthen market position in an increasingly dynamic market environment. Individualisation,

personalisation, and customer integration are achieved by integration of CRM-system solutions and

direct marketing tools.

Competitive pressures: Publishers are facing increased pressures from competition through market

players within the sector (e.g., in publishing through the increasing number of „free sheets‟ in major

cities) and from other sectors moving into the industry. These new competitors apply new ICTs to

enter core publishing fields to distribute their content. To counter customer churn, branding is an

effective counter measure and strengthens customer loyalty. Additionally, the general macro-economic

situation greatly affects the media industry (Picard 2002). A bad economic situation triggers a

decrease on advertising spend on print products as well as on direct consumer sales and the level of

Media Finance

1 May 2011 16

circulation. Particularly the job, housing, and car advertisement markets are increasingly read online

and mostly for free. Overall, there is potentially increased competition in shrinking markets.

Cost forces

A variety of forces related to the costs of operations play important roles in the economics of media.

These include input costs such as costs for newsprint or personnel, production costs, and distribution,

marketing and advertising costs of media goods and services. Total costs of production can be divided

into fixed and variable costs, the former being those costs that are incurred regardless of the volume of

production, the latter varying with output. As Picard (2002, p. 56) has put it: “Television stations have

basic expenses for facilities, studios, and transmitters that do change significantly whether the station

broadcast sixteen hours per day or twenty-four hours a day”. And: “A magazine that increases its

press run from 100,000 to 125,000 will incur additional variable cost for paper, ink, production time,

and distribution because of the added production. Conversely, if it reduces its press run, those costs

will be reduced” (ibid.). Transaction cost theory would assume that a major source of market failure is

found in the fact that transactions which would need to occur for the sake of economic efficiency

simply do not occur because transaction costs interfere with or discourage the process of transacting.

Examples include the cost of writing contracts, or the cost of finding partners with whom to trade. The

costs of enforcing agreements, and the costs of bargaining (Coase 1937, Coase 1960, Williamson

1985).

Economies of scale and scope: As with other business functions, large enterprises tend to profit from

economies of scale, i.e. cost savings to cause the average cost of producing a commodity to fall as

output of the commodity rises. This generally results from technological factors which ensure optimal

size of production is large. With high fixed costs in plant and machinery, the larger the production the

lower the costs per unit of the fixed inputs. Large companies can afford to implement

disproportionately more powerful IT solutions in printing and publishing and achieve higher EoS.

Economies of scope are cost savings that make it cheaper to produce a range of related products by

one single firm than to produce each of the individual products by a single firm. In addition, larger

companies need to employ relatively fewer IT people (measured as % of the total staff) than small

enterprises, even if the architecture of their ICT networks is much more complex. SMEs face barriers

to entry into new markets which result from a lack of EoS, limitations in access to high-quality

printing, an inability to offer suitable packages to advertisers and an inability to obtain finance at rates

available to larger publishers.

Regulatory forces

According to Picard (2002, p. 69), “regulatory forces involve approvals for media operations or

requirements placed on media to avoid or to behave in certain ways”. Regulatory forces may differ in

degree, object, goal, and effects of regulation.

Market failure: Market failure or market imperfections are viewed as a necessary but not sufficient

condition for government intervention. Hoskins et al. (2004) discussed theories of government

intervention as applicable to the media industries: public interest theory (Posner 1974) and capture

theory (Stigler 1971). The public interest theory of regulation explains, in general terms, that

regulation seeks the protection and benefit of the public at large. This will maximize wealth and,

hence, the size of the pie to be shared. The capture theory is that government intervention is provided

17 15 May 2011

to further the economic interests of specific groups, such as producers and labour unions. The theory

has been particularly applied to intervention in the form of regulation, where it claims regulators are

“captured” by the industry they are regulating and intervene in ways demanded by industry.

Additionally, the regulatory game involves information asymmetry. Since the state does not run the

firm, it does not have the full information on how well or badly the firm is performing.

Government failure: Government failure is the case when intervention is undertaken when the costs

of intervention are greater than the benefits. This type of failure may occur because it is too costly to

set up and operate the subsidy scheme, regulation, or other form of intervention proposed.

Barriers to entry and mobility

Barriers are defined as factors that make it possible for established firms in an industry to enjoy supra-

normal profits without attracting new entry (McAfee et al. 2004, Bain, 1956). Without entry barriers

there can be no long-run market power (Schmalensee 1988). Additionally, industrial organization (IO)

theory has identified strategic behaviours working as entry barriers such as exclusive dealing and long-

term contracts with retailers (Tirole 1988). Further, government regulation, patents, predatory pricing,

economies of scale, customer loyalty, and investment requirements can act as barriers to entry too.

The movie industry is a best-practice example for the existence of barriers to entry. There, the most

obvious barrier for independents to entry is the high cost of acquisition. Larger studios owe their

survival to ample resources, which afford them the ability to weather box office disasters. Small

studios would not necessarily be able to survive box office failures. Major studios also have an

advantage in their ability to maintain distribution networks across the country and in foreign markets.

This ensures that their films get to theatres and television screens. Further, barriers to entry exist in

huge marketing expenditures in opening a film in several theatres simultaneously, particularly on a

national or world-wide basis. Importantly, intellectual property rights create apparently strong barriers

to entry.

Mobility barriers, on the other hand, are factors which impede the ability of firms to exit an industry,

or to move from one segment of an industry to another.

The following Exhibit 2-2 shows a typical industry analysis and the factors impacting on the industry

competitors as conceptualized by Harvard Business Professor Michael Porter (1980).

Media Finance

1 May 2011 18

Exhibit 2-2: Industry Analysis following Michael Porter (1980)

Source: Porter 1980

As shown in exhibit 2-2 above, Porter (1980) identifies five forces that drive competition within an

industry:

(1) The threat of entry by new competitors.

(2) The intensity of rivalry among existing competitors.

(3) Pressure from substitute products.

(4) The bargaining power of buyers.

(5) The bargaining power of suppliers.

One obvious application of all this is to would-be entrants and the problem of entering new markets.

Another is to the current competitors and the ongoing task of staying competitive in markets where

they already operate. Perhaps the most important thing to keep in mind is the inverse relationship

between profit margins or returns and the intensity of competition: as the intensity of competition goes

19 15 May 2011

up, margins and returns are driven down. This can require changes in competitive strategy to remain

in an industry and, under some circumstances, it can occasion the decision to exit a business or an

industry (Nichols 2000).

Technology as market driver

Digitization is currently having sustainable impact on the media industry sector. The sector is

undergoing structural changes both in terms of organizational processes and with respect to the type of

products and services which are produced, delivered, and consumed.

Publishing has become a complex, multi-channel, rich-media content delivery business. Adoption and

use of Internet-based and other ICTs causes companies to embrace new strategies, platforms, and

infrastructure and value chains. Publishers can place their strategic development and business

modelling on content as their core competence. However, to fulfil changing customer expectations and

requirements, Internet offers need to be more complex as opposed to the printed version and offer

value added to consumers. The „content‟-business model can be supplemented by the „community‟-

business model whose viability is based on user loyalty. Further, publishers have been able to develop

innovative business models for financing their Internet presence and other online activities, thus

strengthening the third pillar of business modelling „commerce‟. As shown in one of our case studies,

traditional publishers can benefit from the Internet business model. Online advertising and online

classifieds can be a definite business opportunity for newspaper publishers.

Investment in information technology (IT): There is a sizeable stream of research examining the

domain of the business value of IT investments (Melville et al. 2004). Early studies failed to find the

expected link between enormous increases in IT capital investments on the one hand and productivity

improvement on the other, leading to the so-called “productivity paradox” (Brynjolfsson 1993).

However, subsequent studies established that, in general, investments in IT capital do produce net

efficiency benefits, although this varies depending on other factors such as management practices, and

organizational and industry structure (Bresnahan et al. 2002). Also there is no assurance the investing

firm, rather than customers or competitors, will capture the value of those efficiency improvements

(Hitt & Brynjolfsson 1996).

2.2 Specific issues of financial media management

Definition of Media Finance

All forms of internal & external procurement of capital

Media finance studies how and with what effect media industries, media companies, media

content, and media products/services (i.e. the production and selling) are refinanced

There is a wide variety of media finance methods. This owes to the fact that there are many

types of media itself: Print, audio-visual, Online etc. All have their specific media finance

models.

A business model describes the rationale of how an organization creates, delivers, and

captures value - economic, social, or other forms of value.

Media Finance

1 May 2011 20

Most generally, media firms collect revenues from sales in circulation of items sold or from

sales in advertising space.

Circulation is defined as the number of copies issued of an advertising medium in print; by

extension, the audience reached by advertising media, outdoor posters, radio, and television

programs. Circulation sales in the print media can be made on the basis of single-copy sales or

on the basis of subscription. Single-copy sales are “newsstand sales” sold to customers at

retail. Print media can also be sold on a subscription basis. Most single-copy sales are made in

supermarkets and other mass retail outlets.

As for advertising sales, media companies such as TV channels, cable networks or radio

stations collect most of their revenues from selling “eye-balls” through advertisement space

during various programmes.

Similarly, print media companies sell advertising space to be filled in their outlets to readers

and, accordingly, advertisers.

Sources of finance

Sources of finance: Most generally, media firms collect revenues from sales in circulation of items

sold or from sales in advertising space. Circulation is defined as the number of copies issued of an

advertising medium in print; by extension, the audience reached by other advertising media, outdoor

posters, radio, and television programs. Circulation sales in the print media can be made on the basis

of single-copy sales or on the basis of subscription. Single-copy sales are “newsstand sales” sold to

customers at retail. Print media can also be sold on a subscription basis. Most single-copy sales are

made in supermarkets and other mass retail outlets. Many publishers also distribute through specialty

stores.

As for advertising sales, media companies such as TV channels, cable networks or radio stations

collect most of their revenues from selling “eye-balls” through advertisement space during various

programmes. Similarly, print media companies sell advertising space to be filled in their outlets to

readers and, accordingly, advertisers. Media work on dual markets: information/ideas markets and

advertising markets (Picard 1989). How these two markets are interlinked is explained by the theory of

the circulation spiral, originally proposed by the media scholar Lars Furhoff (1973). The main point of

this theory as applied to newspaper competition is well synthesized by the following quotation by

Gustafsson (1978, p. 1): “The larger of two competing newspapers is favoured by a process of mutual

reinforcement between circulation and advertising, as a larger circulation attracts advertisements,

which in turn attracts more advertising and again more readers. In contrast, the smaller of two

competing newspapers is caught in a vicious circle; its circulation has less appeal for the advertisers,

and it loses readers if the newspaper does not contain attractive advertising. A decreasing circulation

again aggravates the problems of selling advertising space, so that finally the smaller newspaper will

have to close down”.

Under this perspective, the key objective of the media revenue management problem is to optimally

allocate advertising space across upfront and scatter markets to hedge against audience uncertainty,

honor client contracts and maximize short-term profits. Scatter markets are the remnants of TV

network markets of unsold commercial time that remain after preseason upfront buying has been

completed.

21 15 May 2011

Direct types of media finance

Media content directly funded or finances by user = User-financed

This means that media content is directly funded by users with the purchase of media content

(similar to other markets for other products). Here, the principle of consumer sovereignty is

crucial: demand for content and media forms determines supply. Such one-off direct payments

also exist in media markets

Direct payment – single copy sales of carrier media (i.e. carrying content);

advantage: price discrimination becomes possible between premium users and

commodity users

Ex: books, mags, newspapers, music CDs, digital files (iTunes), video tapes

Revenues from sound files sold: downloadable MP3 files

Sales of ringtone services (would that be selling media?)

Revenues from games sold (online or offline)

Subcription payments (Abonnement)

E.g.: newspapers, magazines, pay TV

Rental: e.g. video or DVD, pay TV?

Directly funded media content can be usage-dependent or non-usage dependent.

Usage dependent:

One-off transactions: volume or duration of usage (e.g. single VoD film

download of Premiere for duration of 24 hours)

Non-usage dependent:

One-off:

Access charges to basic cable service (e.g. Kabelanschlussgebühr)

Periodical:

Broadcast licence fee (Grundgebühr GEZ) to be payable for TV and

radio sets that may receive PSB programming

Subscription to basic cable or sat service (e.g. pay TV)

What are rentals?

EC law: Renting of carrier media is exclusively dealt with by author and artist

Ban on renting music carriers (1996), no commercial book renting; but video renting is

important

“Sell-Through” – In the home video business, movies that are sold to consumers rather than

rented to them; there is (still) a market for video and DVD

Media Finance

1 May 2011 22

Film Rental: What the theater owner pays the distributor for the right to show the movie. As a

rough rule of thumb, this usually amounts to about half of the box office gross; normally the

revenue split is 50/50 between cinema and distributor.

Direct payment - Single Copy Sales

Distribution via retailers

Chain stores, shops, discounters, garages, etc.

Internet as distribution channel (B2C is business to customer)

Pros & Cons:

Direct connection to acquisition and consumption of good through user.

Principle of consumer sovereignty is fulfilled, i.e. the consumer takes out the things

s/he prefers

Carrier media like CD or book allow for durable and unlimited use of content

Paid content is an example of SCS (music files on iTunes)

With purchase users gain rights for unlimited use

Indicators: Sales volumes by country

DE: www.ivw.de

Ad info portal in general: www.warc.com

Direct payment – Subscription revenues

Distribution via retailers

Similar to single copy sales, but makes buyer-seller relation durable. This is important for

customer retention; otherwise they switch to another provider

This decreases information problems for buyers and reduces high costs of retailing and avoids

costs of remissions

This allows for greater bargaining security as money is paid in advance

But: No ad effectiveness of goods in retailing is achieved

And: Market entry barriers are higher, as seller needs to undertake a lot of customer research

and advertising in consumer and what they wish to purchase (and how their lifestyles are in

general); customer loyalty has to be achieved

For the ad market, subscription is better, as subscriber data improves target marketing (higher

prices can be charged!)

Ex: Newspapers, mags, but also Music CD, Pay-TV (without carrier medium, only right to

access and watch program).

23 15 May 2011

Newspapers: Most important means of delivery is subscription revs, but majority of revs are

made through ad and supplements. Just consider Sunday editions of newspapers, how heavy

they are and how many pages they include; in addition, they carry a lot of supplements (in the

UK this is drastic; there will be a lots of product samples in newspaper to tease new

consumers. Consumer industry wants to prove the product quality and raise attention for new

products; they are all for free as well.

Pay-TV subscription is most popular in USA; strongest players in EU are Canal+ and BSkyB;

Premiere is small comparatively; 3.5 m subscribers in 2008.

Subscribers receive basic cable services and premium channels (when paying an extra fee)

Indirect types of media finance

Media content that is also indirectly funded or financed

Indirect media finance accrues from advertising and third parties as well as through sales of

products & services.

Advertising finance

3rd party financed or product / services financed (i.e. not directly through the media content

offered but through additional products or services offered; e.g. when you watch teleshopping

on RTL Shop, you do not pay for it directly but you pay for it by calling into the show to

purchase some consumer goods (or nice tiger-patterned dresses for real ladies!)

Indirect types of media finance - Advertising

Advertising is sometimes not to be differentiated to be either informative, entertaining,

exaggerated, untruthful, … but so much is non-advertising content

Advertising is protected by public law in D (Grundrecht auf Meinungsfreiheit)

Advertising promotes other goods but is not in itself object of consumer demand

“TV stations are in the business of producing audiences. These audiences, or means of access

to them, are sold to advertisers” (Owen, Beebe & Manning 1974, p. 4)

Advertising finance is attractive as financing media content through other means may be

difficult! Why, because perhaps the topography in a country does not allow for broadcasting

TV signals (there are many mountains in Switzerland); the provider must convince the

advertiser to pay for the broadcasts (which will be difficult because he wants to access

consumers); or the volume of consumers is too small to finance full-scale PSB (such as in

Austria because the country is too small; and only advertising can finance all the programming

on Österreichischer Rundfunk; it is a 50/50 % split of revenues, which is unique in the world;

the BBC, by contrast is financed exclusively by fees. And then, the ORF programs are bad

which dissatisfies viewers, and, as a result, … advertisers = the vicious circle!

This is because it is technically very costly to charge monetary prices for radio and TV; or

media content is not dividable, thus charging prices for use is impossible

Ex: newspaper content consumer pay the same price whether they are reading much business

news or not; similar to pay-TV. In theory this means, that no price discrimination is possible

Media Finance

1 May 2011 24

and that makes consumers dissatisfied and angry; and providers do not like that either because

they cannot skim-off all WTP (willingness to pay) from premium customers, for example. As

a result, they are losing producer surplus.

Advertising finance make it possible to link payments to use intensity (just as with use-

dependent monetary consumer payments)

Advertising is subject to regulation: consumer and youth

Ban on product advertising (tobacco in D); user mis-lead; specific targets (children); ad

messages mixed with content; we know advertorials (these have to be marked as such)

Ban on TV ad: Total time of ad breaks, time distance of ad breaks is important too; naturally

there are time laps of 20min between 2 min breaks.

PSB is subject to tight regulation

TV in Germany: Ad ban on political, Ideological, and religious kind (§ 7 Abs 7

Rundfunkstaatsvertrag)

When are ads most effective (dependent on content)

For advertisers: Not only price but also effectiveness of contacts is important

Effectiveness is dependent on:

(a) Qualitative consistency of recipients;

(b) Image of media content;

(c) Technical adequacy of medium.

Consistency of recipients:

Local / regional media: Geographic concentration, socio-demographic characteristics

Goal: To attract homogeneous and attractive group of recipients (= higher prices for average

contact)

Practically speaking: would you advertise alcohol during a children‟s programming; or

alcohol and car adverts?

Young recipients are most attractive target group: brand loyalty is not pronounced (e.g. CPT

prices for ZDF viewers under 50 years 4 times as high)

Image of media content: program context and ad spot need to be homogeneous (e.g. car

producer should not advertise with sportive cars when context program content on car

accidents was aired)

Technical problems: Ad in books is difficult. They are sold to one common language area,

reception takes a long time, i.e. regional and current ad can hardly be communicated

Newspaper and magazines are much more flexible: socio-demographic targeting (mags) and

geographic targeting is highly effective

TV ad: flexible and target-effective, but more emotional, suggestive

25 15 May 2011

Problem overall: How to measure effectiveness? Media-Analyses: factual media consumption

remains unclear

Consumer aversion to advertising: ad is annoying; gross utility of use of TV program is

reduced

Media content thus can get devalued to a point where its consumption is just more attractive

than other consumption opportunities; people switch to outdoor activities for example or meet

friends; but – on the other hand – overall media consumption time gets larger.

Ad aversion is also empirically evident: EMNID surveys.

But, there is lower aversion to print media advertising than TV ad

Overall: advertisers look for high purchasing power of consumers and low brand affinity

And: Direct funding of content may be more effective than indirect ad finance (e.g. even if

PPV channels charge such a high price for top-sport events that excludes 90% of viewers, the

remaining 10% may bring revenues which are much higher than ad revenues

TV spots

Political TV advertising (social advertising)

Infomercials

Product placement (e.g., cars in James Bond movies)

Promo (television program): “Dauerwerbesendung” (at least 90sec); it is legal if the ad

character is explicitly presented; they must also be signed as such.

Sponsorship

Merchandizing

The sale of products that are thematically related to TV or movie productions. Typical

merchandising products include accompanying books, video cassettes and audio cassettes.

Merchandising also refers to the sale of licensing rights, meaning the rights to use programs

and trademark-protected brand names, symbols, figures or logos.

A term of many varied and not generally adopted meanings. It can (1) relate to the

promotional activities of manufacturers that bring about in-store displays, or (2) identify the

product and product line decisions of retailers.

An indirect finance instrument for media content

Media-related merchandising: special variation of merchandize. This shall enhance the level

of awareness of the media-reated programs, titles, persons on TV, artists, in order to promote

sales of the media content.

E.g.: Tokyo Hotel: Magazines, DVD, CDs, Baseball caps, scarfs, etc.

E.g.: DVD of DSDS; T-shirts, caps

Media Finance

1 May 2011 26

“We love” collection worn by the contestants of Germany‟s next top model

Sponsoring

A cooperative arrangement, usually between advertisers and the media. In television,

sponsoring is a special advertising form, an independent way of directly or indirectly

financing a broadcast. At the beginning and / or end of every sponsored broadcast, a mention

of financing by the sponsor must be presented for a reasonable length of time [for example,

"This show brought to you by"]. Unlike other special advertising forms, sponsoring is subject

to no time limits under German broadcast regulations. But program sponsoring is subject to its

own set of regulations under the State Broadcasting Treaty and the Advertising Guidelines of

the State Regulatory Agencies for Broadcasting. Cooperation between advertiser and media

firm.

Within TV, sponsoring is a special ad form of direct and indirect financing of content or

programs. At the beginning or at the end of a TV show sponsoring needs to be explicitly

mentioned (“Die Sendung wird Ihnen präsentiert von …”).

Sponsoring (by companies): e.g. Krombacher presents the games of the German national

soccer team on ARD.

In contrast to other special ad forms, sponsoring is not subject to time restriction in Germany.

However, program sponsoring is bound to specific ad regulation (Rundfunkstaatsvertrag and

Werberichtlinien der Landesmedienanstalten).

Teleshopping & testimonials

Commission revenues from teleshopping (e.g. RTL Shop, HSE, QVC)

Viewers of a teleshopping program are given the opportunity to order the offered products by

telephone or fax during the program. The EU Television Directive, as amended in June 1997,

provides specific rules for teleshopping. Teleshopping spots continue to be subject to the

hourly advertising time limits [Advertising Guidelines], but teleshopping windows, on the

other hand, are permitted up to a maximum of three hours and eight windows per day, and

each window must be at least 15 minutes long. Under the new directive, moreover, pure

teleshopping channels are permitted without any advertising time restrictions at all.

Testimonials: Advertising format in which the product message is conveyed by personal

experience reports, either those of well-known personalities [celebrity testimonials] or normal

consumers [real-people testimonials].

Placement of brand-name products, services or known company logos in TV and movie

productions for commercial purposes. In Germany, the State Broadcasting Treaty prohibits

product placement both by the public television broadcasters and the privately-owned

broadcasting stations. According to the Advertising Guidelines, the presentation of products in

the editorial sections of the program is not considered to be a product placement if the

products and services are presented mainly for artistic or dramatic reasons or to fulfill

information duties.

27 15 May 2011

Product placement

Product placement is a type of advertising, in which promotional advertisements placed by

marketers using real commercial products and services in media, where the presence of a

particular brand is the result of an economic exchange. When featuring a product is not part of

an economic exchange, it is called a product plug. Product placement appears in plays, film,

television series, music videos, video games and books. It became more common starting in

the 1980s, but can be traced back to at least 1949. Product placement occurs with the inclusion

of a brand's logo in shot, or a favorable mention or appearance of a product in shot. This is

done without disclosure, and under the premise that it is a natural part of the work. Most major

movie releases today contain product placements. The most common form is movie and

television placements and more recently computer and video games. Recently, websites have

experimented with in-site product placement as a revenue model.

Product placement of brand-name products, services or known company logos in TV and

movie productions for commercial purposes. In Germany, the State Broadcasting Treaty

prohibits product placement both by the public television broadcasters and the privately-

owned broadcasting stations. According to the Advertising Guidelines, the presentation of

products in the editorial sections of the program is not considered to be a product placement if

the products and services are presented mainly for artistic or dramatic reasons or to

fulfill information duties (wow! Consider Raab‟s WOK WM, is this true?)

A telepromotion is a form of extended-length commercial. It is an advertisement for goods or

services that is editorially designed to resemble a television program. The rules applicable to

extended-length commercials must be observed.

Direct Response TV, a special form of advertising, refers to advertising spots in which

viewers are invited to contact the product supplier by fax or telephone. Unlike teleshopping,

DRTV spots are not designed to collect direct product orders, but to give viewers an

opportunity to learn more about the products being offered. Unless they are set up as

extended-length commercials, DRTV spots are subject to the commercial time-per-hour

restrictions applicable to spot advertising. Furthermore, DRTV spots are subject to the

maximum allowable advertising times for special advertising forms.

Direct Response Television, or DRTV for short, includes any TV advertising that asks

consumers to respond directly to the company --- usually either by calling an 800 number or

by visiting a web site. This is a form of direct response marketing. When it first appeared,

DRTV was used to market goods and services directly from the manufacturer or wholesaler to

the consumer, bypassing retail. Over time, it has also become used as a more general

advertising medium and is now used by a wide range of companies --- often to support retail

distribution.

Call-in media: Ad and marketing for products and services, which are fulfilled via tele VAS

(0190 / 0900/ 013X), mobile phone networks (call media SMS) or the Internet; services used

are erotic services, votes, polls, games, consulting and general information services).

Media Finance

1 May 2011 28

Syndication

In broadcasting, syndication is the sale of the right to broadcast radio shows and television

shows to multiple individual stations, without going through a broadcast network. It is

common in countries where television is organized around networks with local affiliates,

notably the United States. In the rest of the world, however, countries have mainly centralized

networks without local affiliates and syndication is less common. Shows can also be

syndicated internationally.

Syndication and program sales (e.g., reselling programs to other broadcasters; very popular in

USA).

first-run syndication refers to programming that is broadcast for the first time as a

syndicated show (not any one particular network), or at least first so offered in a given

country (programs originally created and broadcast outside of the United States, first

presented on a network in their country of origin, have often been syndicated in the

U.S. and in some other countries);

off-network syndication involves the sale of a program that was originally run on

network television: a rerun;

Public-broadcasting syndication has arisen in the U.S. as a parallel service to stations

in the PBS service and the handful of independent public stations.

Opening snapshot of The Muppet Show, with Kermit The Frog in the O, one of the

most successful (and successfully) syndicated TV series in the U.S. during the 1970s,

and shown worldwide for decades since (see, Cover page).

Licensing

Lisensing revenues: such as Music licensing is the licensed use of copyrighted music. Music

licensing is intended to ensure that the creators of musical works get paid for their work. A purchaser

of recorded music owns the media on which the music is stored, not the music itself. A purchaser has

limited rights to use and reproduce the recorded work

Other revenue models

Yes, many more; this list above was not exhaustive.

Just consider hardware sales: e.g. through selling set-top-boxes by Premiere (BSkyB in the

UK has given them away for free which made achieve such a big market share)

Premiere Hotel (also a revenue source for Premiere)

Handelsblatt archive articles from the print copy to be purchase online

In economics, a subsidy is a form of financial assistance paid, usually by the government, to

keep prices below what they would be in a free market, or to keep alive businesses that would

otherwise go bust, or to encourage activities that would otherwise not take place.

Subsidies can be a regarded as a form of protectionism or trade barrier by making domestic

goods and services artificially competitive against imports. Subsidies often distort markets,

and can impose large economic costs.

29 15 May 2011

The term subsidy may also refer to assistance granted by others, such as individuals or non-

government institutions, although this is more commonly described as charity.

New ICTs and e-business solutions have introduced a variety of new online business models which are

well applicable to newspaper publishers. Prof. Rappa from North Carolina State University has

systematized online business models as follows (see, http://digitalenterprise.org/models/models.html):

Brokerage: Brokers are market-makers: they bring buyers and sellers together and

facilitate transactions. Brokers play a frequent role in business-to-business (B2B),

business-to-consumer (B2C), or consumer-to-consumer (C2C) markets. Usually a broker

charges a fee or commission for each transaction it enables. The formula for fees can vary.

Advertising: The web advertising model is an extension of the traditional media

broadcast model. The broadcaster, in this case, a web site, provides content (usually, but

not necessarily, for free) and services (like e-mail, chat, forums) mixed with advertising

messages in the form of banner ads. The banner ads may be the major or sole source of

revenue for the broadcaster. The broadcaster may be a content creator or a distributor of

content created elsewhere. The advertising model only works when the volume of viewer

traffic is large or highly specialized.

Infomediary: Data about consumers and their consumption habits are valuable, especially

when that information is carefully analyzed and used to target marketing campaigns.

Independently collected data about producers and their products are useful to consumers

when considering a purchase. Some firms function as infomediaries (information

intermediaries) assisting buyers and/or sellers understand a given market.

Merchant: Wholesalers and retailers of goods and services. Sales may be made based on

list prices or through auction.

Manufacturer: The manufacturer or „direct model‟, it is predicated on the power of the

web to allow a manufacturer (i.e., a company that creates a product or service) to reach

buyers directly and thereby compress the distribution channel. The manufacturer model

can be based on efficiency, improved customer service, and a better understanding of

customer preferences.

Affiliate: In contrast to the generalized portal, which seeks to drive a high volume of

traffic to one site, the affiliate model provides purchase opportunities wherever people

may be surfing. It does this by offering financial incentives (in the form of a percentage of

revenue) to affiliated partner sites. The affiliates provide purchase-point click-through to

the merchant. It is a pay-for-performance model -- if an affiliate does not generate sales, it

represents no cost to the merchant. The affiliate model is inherently well-suited to the

web, which explains its popularity. Variations include banner exchange, pay-per-click,

and revenue sharing programs.

Community: The viability of the community model is based on user loyalty. Users have a

high investment in both time and emotion. Revenue can be based on the sale of ancillary

products and services or voluntary contributions.

Subscription: Users are charged a periodic - daily, monthly or annual - fee to subscribe to

a service. It is not uncommon for sites to combine free content with „premium‟ (i.e.,

Media Finance

1 May 2011 30

subscriber- or member-only) content. Subscription fees are incurred irrespective of actual

usage rates. Subscription and advertising models are frequently combined.

Utility: The utility or „on-demand‟ model is based on metering usage, or a „pay as you go‟

approach. Unlike subscriber services, metered services are based on actual usage rates.

Traditionally, metering has been used for essential services (e.g., electricity water, long-