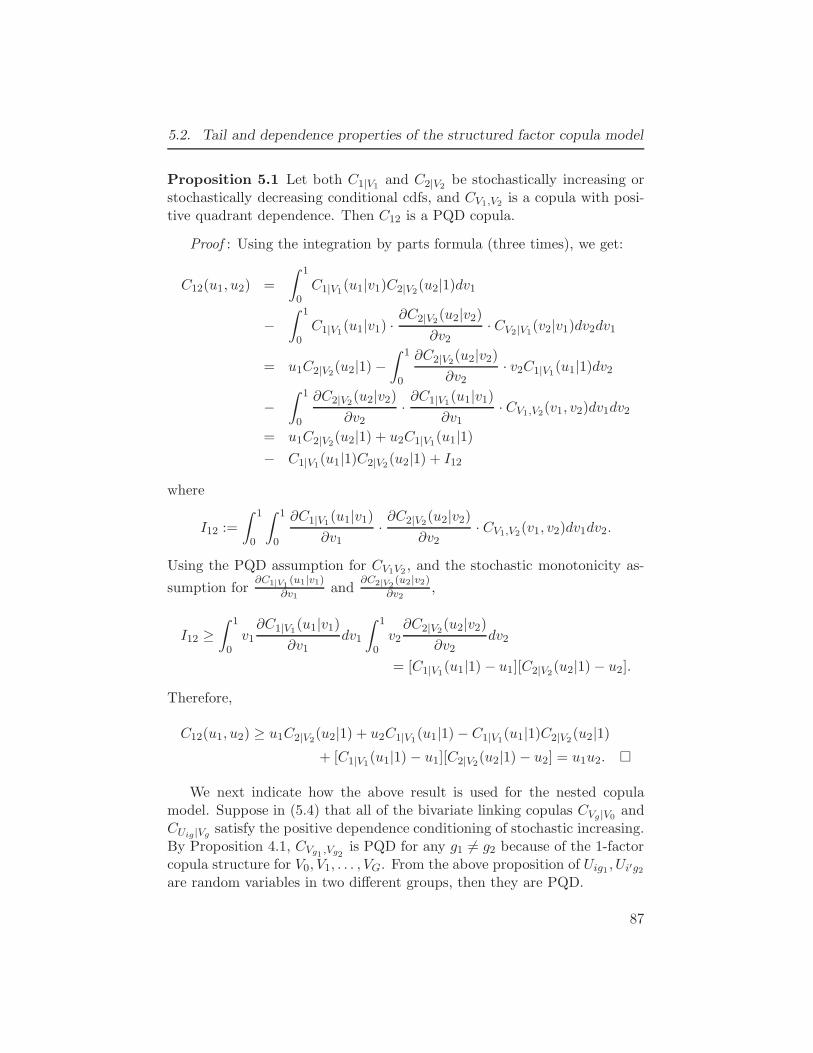

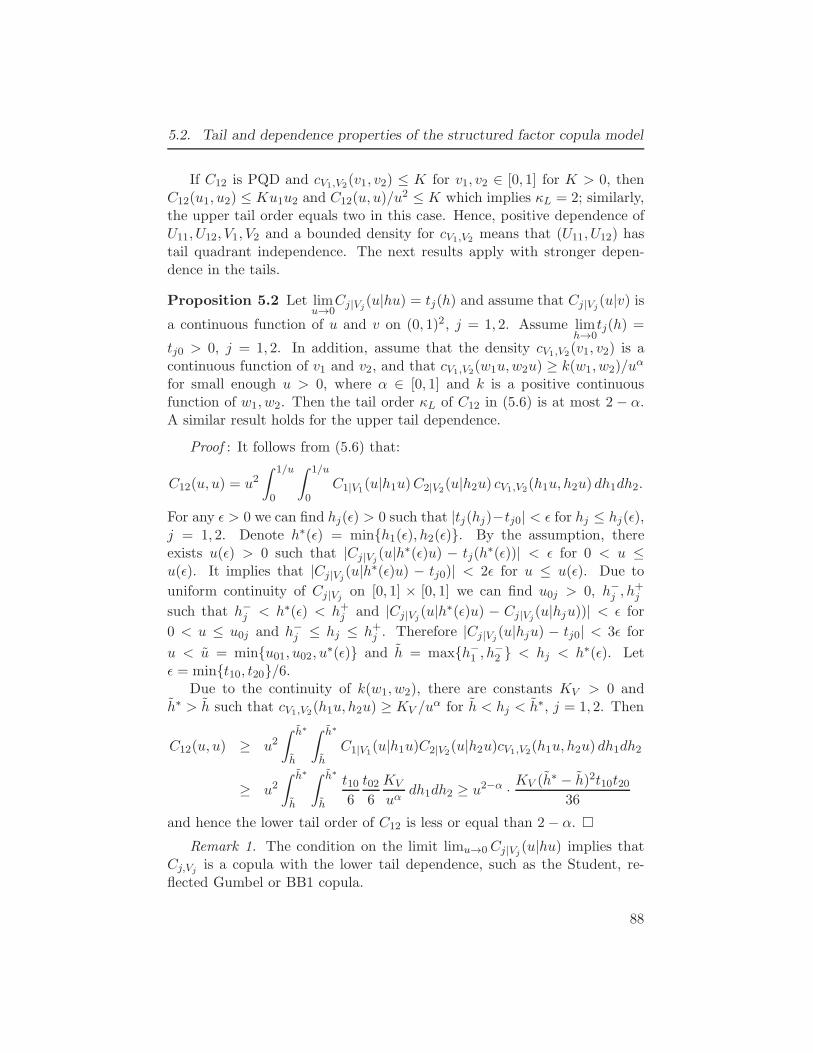

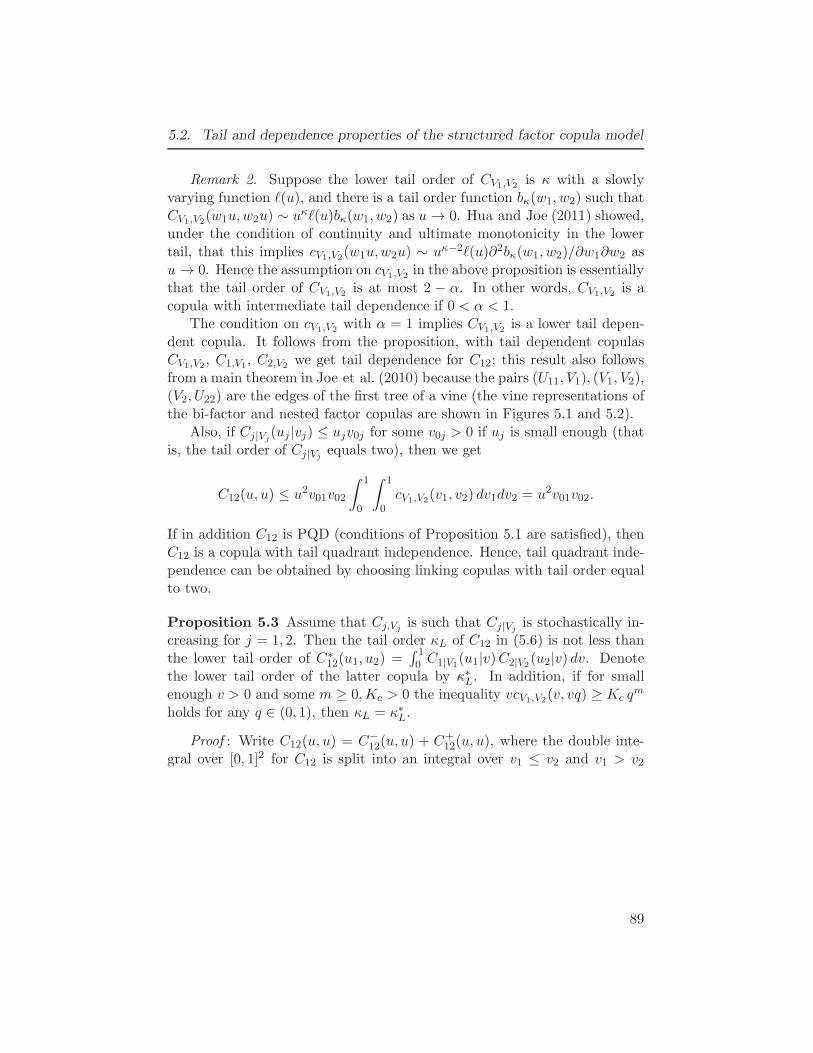

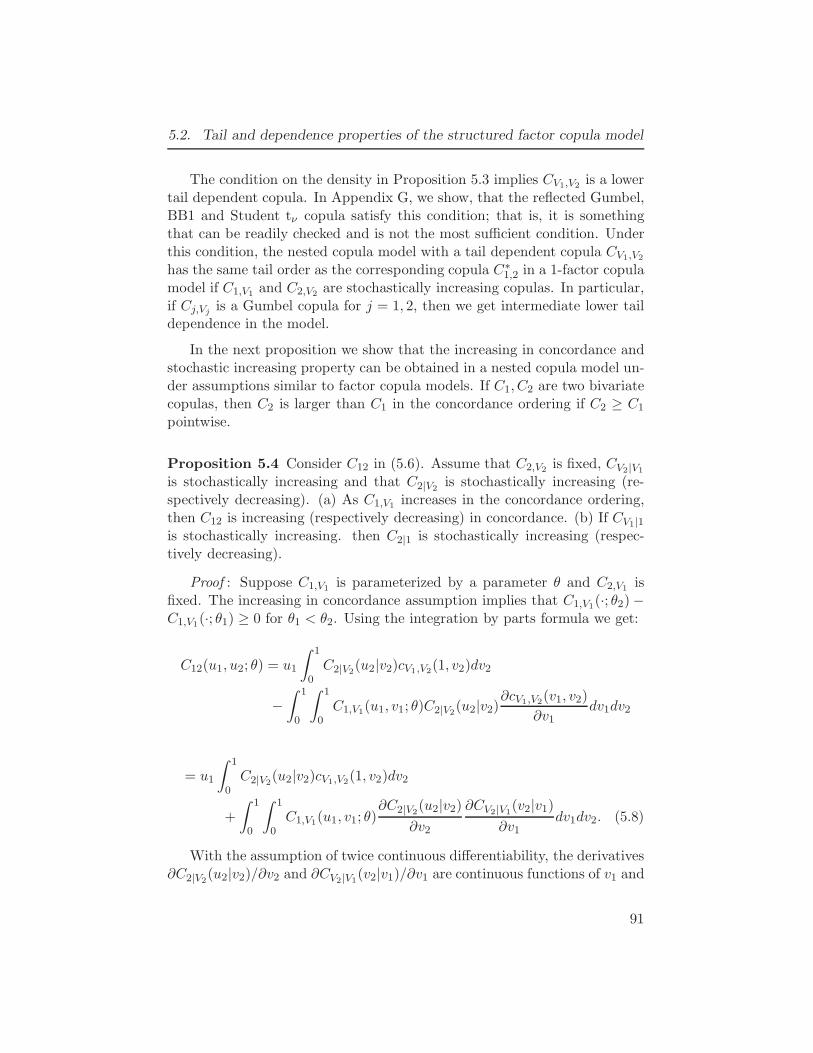

STRUCTURED FACTOR COPULAS AND TAIL INFERENCE

172

STRUCTURED FACTOR COPULAS AND TAIL INFERENCE by Pavel Krupskii B.Sc., Moscow State University, Moscow, Russia, 2006 M.Sc., New Economic School, Moscow, Russia, 2009 A THESIS SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY in The Faculty of Graduate and Postdoctoral Studies (Statistics) THE UNIVERSITY OF BRITISH COLUMBIA (Vancouver) July 2014 c Pavel Krupskii 2014

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of STRUCTURED FACTOR COPULAS AND TAIL INFERENCE

STRUCTURED FACTOR COPULAS

AND TAIL INFERENCE

by

Pavel Krupskii

B.Sc., Moscow State University, Moscow, Russia, 2006M.Sc., New Economic School, Moscow, Russia, 2009

A THESIS SUBMITTED IN PARTIAL FULFILLMENT OFTHE REQUIREMENTS FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY

in

The Faculty of Graduate and Postdoctoral Studies

(Statistics)

THE UNIVERSITY OF BRITISH COLUMBIA

(Vancouver)

July 2014

c© Pavel Krupskii 2014

Abstract

In this dissertation we propose factor copula models where dependence ismodeled via one or several common factors. These are general conditionalindependence models for d observed variables, in terms of p latent variablesand the classical multivariate normal model with a correlation matrix hav-ing a factor structure is a special case. We also propose and investigatedependence properties of the extended models that we call structured fac-tor copula models. The extended models are suitable for modeling largedata sets when variables can be split into non-overlapping groups such thatthere is homogeneous dependence within each group. The models allowfor different types of dependence structure including tail dependence andasymmetry. With appropriate numerical methods, efficient estimation ofdependence parameters is possible for data sets with over 100 variables.

The choice of copula is essential in the models to get correct inferencesin the tails. We propose lower and upper tail-weighted bivariate measuresof dependence as additional scalar measures to distinguish bivariate copulaswith roughly the same overall monotone dependence. These measures allowthe efficient estimation of strength of dependence in the joint tails and canbe used as a guide for selection of bivariate linking copulas in factor copulamodels as well as for assessing the adequacy of fit of multivariate copulamodels.

We apply the structured factor copula models to analyze financial datasets, and compare with other copula models for tail inference. Using model-based interval estimates, we find that some commonly used risk measuresmay not be well discriminated by copula models, but tail-weighted depen-dence measures can discriminate copula models with different dependenceand tail properties.

ii

Preface

This dissertation was prepared under the supervision of professor Harry Joeand it is mainly based on three papers coauthored with Harry Joe. One ofthe papers has been published and the other two are currently under review.

Chapter 2 is based on the submitted paper Krupskii and Joe (2014b),Tail-weighted measures of dependence. The idea of using a weighting func-tion to get a measure of dependence in the tails that can perform bettercomparing to semicorrelations of normal scores came from the supervisor.Some good choices of the weighting function were proposed by the author ofthis dissertation. The author also proved asymptotic results and wrote thefirst version of the manuscript followed by the revisions proposed by HarryJoe.

Chapter 3 contains material which is not published or submitted any-where yet. The author of the dissertation uses the concept of tail weightingthat was originally motivated by the supervisor and construct some measuresof asymmetry. Asymptotic results and empirical study was conducted by theauthor. Harry Joe made some useful suggestions on improving the presenta-tion of material in this Chapter and using the 1-factor gamma convolutionmodel to compare the performance of different measures of asymmetry.

Chapter 4 is mostly based on the published paper Krupskii and Joe(2013), Factor copula models for multivariate data, published in Journalof Multivariate Analysis. The idea of using factor copula models came fromthe supervisor. The author completed most of the proofs in this Chapterand implemented fast algorithm based on a modified Newton-Raphson al-gorithm with an adjustment to a positive definite Hessian for estimatingparameters in the model. Some parts of the code were written in Fortran90 to speed up computational process and the author used templates forderivatives of the log-likelihoods that were proposed by the supervisor. Theauthor also provided details on estimating the multivariate Student modelwith a factor correlation structure, including simple formulas for the inverseand determinant of the correlation matrix; this part of research is not in-cluded in the paper. The first version of the manuscript was written by theauthor followed by the revisions proposed by Harry Joe.

iii

Preface

Chapter 5 is mostly based on the submitted paper Krupskii and Joe(2014a), Structural factor copula models: theory, inference and computa-tion. The supervisor proposed to use the bi-factor copula model, which isan extension of the factor copula model, to handle data with a group struc-ture. The author of this dissertation proposed an alternative model, thenested copula model, and completed most of the proofs in this Chapter. Healso adjusted the modified Newton-Raphson algorithm from the previousChapter to estimate parameters in the models proposed in this Chapter.The author also provided details on estimating the multivariate Studentmodel with a bi-factor correlation structure, including simple formulas forthe inverse and determinant of the correlation matrix; this part of researchis not included in the paper. The first version of the manuscript was writtenby the author followed by the revisions proposed by Harry Joe.

In addition to the aforementioned contributions of the supervisor, profes-sor Harry Joe made lots of suggestions regarding the presentation of materialin this dissertation, relevant literature and motivation of the research. Healso checked all the proofs and made some changes in the writing to improvethe flow of ideas in the dissertation and papers.

iv

Table of Contents

Abstract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Table of Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xi

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . xii

Dedication . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiii

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.1 Copula notation . . . . . . . . . . . . . . . . . . . . . . . . . 51.2 Some commonly used parametric copula families and their

properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2 Tail-weighted measures of dependence . . . . . . . . . . . . 112.1 Tail-weighted measures of dependence: definition and prop-

erties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.2 Empirical versions of tail-weighted measures and the choice

of the weighting function . . . . . . . . . . . . . . . . . . . . 152.3 Normal scores plots and tail-weighted measures of dependence 22

3 Measures of asymmetry based on the empirical copula pro-cess . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263.1 Measures of reflection asymmetry . . . . . . . . . . . . . . . 273.2 Measures of bivariate permutation asymmetry . . . . . . . . 303.3 The power of tests based on the measures of asymmetry . . . 333.4 Preliminary diagnostics using measures of asymmetry . . . . 36

v

Table of Contents

4 Factor copula models for multivariate data . . . . . . . . . 394.1 Factor copula models . . . . . . . . . . . . . . . . . . . . . . 40

4.1.1 One and two-factor copula models . . . . . . . . . . . 414.1.2 Models with p > 2 factors . . . . . . . . . . . . . . . . 44

4.2 p-factor structure in LT-Archimedean copulas . . . . . . . . 474.3 Properties of 1- and 2-factor copula models . . . . . . . . . . 49

4.3.1 Dependence properties . . . . . . . . . . . . . . . . . 504.3.2 Tail properties . . . . . . . . . . . . . . . . . . . . . . 53

4.4 Computational details . . . . . . . . . . . . . . . . . . . . . . 584.4.1 Numerical integration and likelihood optimization . . 584.4.2 Multivariate Student model with a p-factor correlation

structure . . . . . . . . . . . . . . . . . . . . . . . . . 604.5 Empirical results for simulated and financial data sets . . . . 65

4.5.1 Choice of bivariate linking copulas . . . . . . . . . . . 654.5.2 Dependence measures . . . . . . . . . . . . . . . . . . 654.5.3 Simulation results . . . . . . . . . . . . . . . . . . . . 664.5.4 Financial return data . . . . . . . . . . . . . . . . . . 68

5 Structured factor copula models . . . . . . . . . . . . . . . . 755.1 Two extensions of factor copula models for data clustered in

groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 775.1.1 Bi-factor copula model . . . . . . . . . . . . . . . . . 785.1.2 Nested copula model . . . . . . . . . . . . . . . . . . 805.1.3 Special case of Gaussian copulas . . . . . . . . . . . . 81

5.2 Tail and dependence properties of the structured factor cop-ula model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

5.3 Computational details for factor copula models . . . . . . . . 935.3.1 Log-likelihood maximization in factor copula models . 935.3.2 Multivariate Student model with bi-factor correlation

structure . . . . . . . . . . . . . . . . . . . . . . . . . 965.3.3 Multivariate Student model with tri-factor correlation

structure . . . . . . . . . . . . . . . . . . . . . . . . . 985.3.4 Asymptotic covariance matrix of 2-stage copula-GARCH

parameter estimates . . . . . . . . . . . . . . . . . . . 995.4 Interval estimation of VaR, CTE for copula-GARCH model . 1005.5 Empirical study . . . . . . . . . . . . . . . . . . . . . . . . . 103

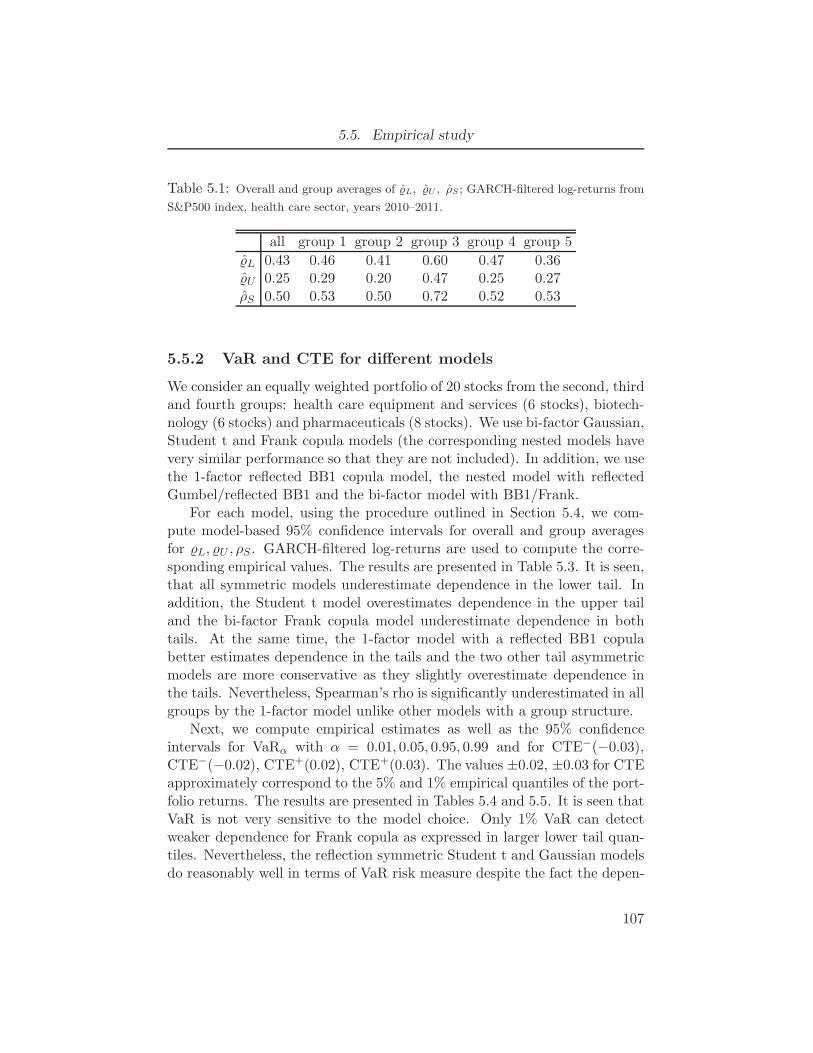

5.5.1 Assessing the strength of dependence in the tails . . . 1055.5.2 VaR and CTE for different models . . . . . . . . . . . 1075.5.3 Comparing performance of nested copula models . . . 109

vi

Table of Contents

6 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . 118

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

Appendices

A Proof of Proposition 2.1, Section 2.2 . . . . . . . . . . . . . . 127

B Proof of Proposition 2.2, Section 2.2 . . . . . . . . . . . . . . 131

C Proof of Proposition 4.5, Section 4.3.2 . . . . . . . . . . . . 133

D Proof of Proposition 4.6, Section 4.3.2 . . . . . . . . . . . . 134

E Proof of Proposition 4.7, Section 4.3.2 . . . . . . . . . . . . 136

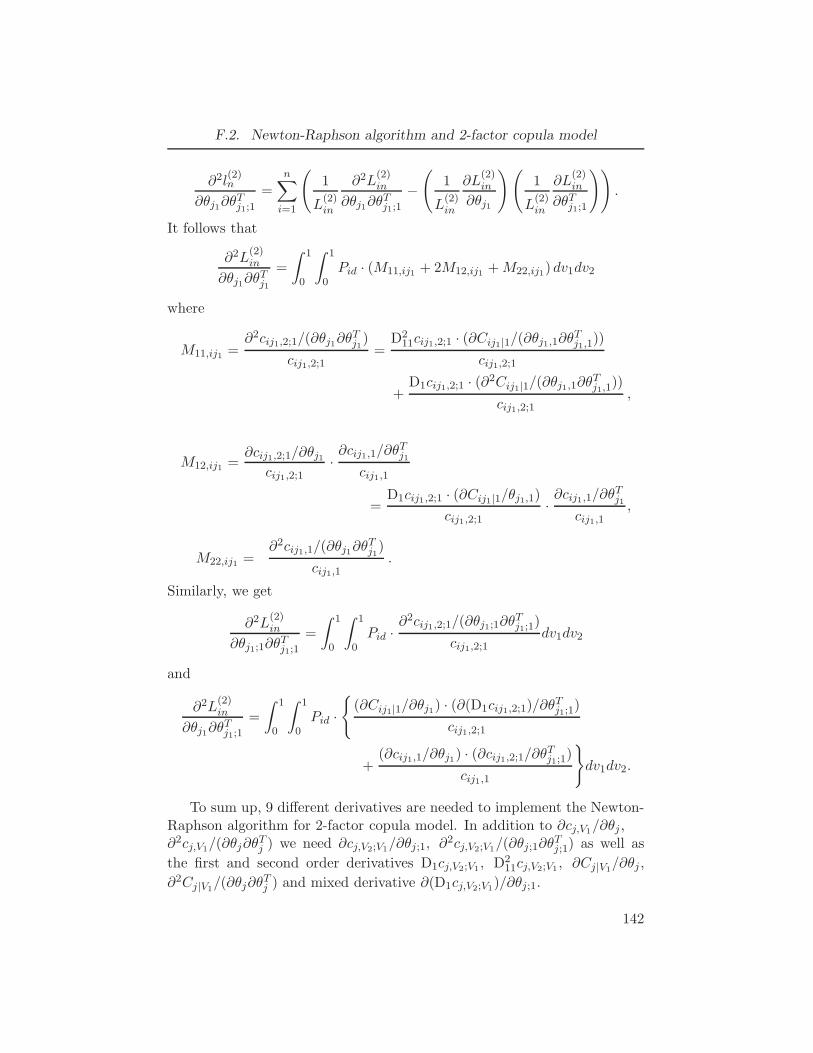

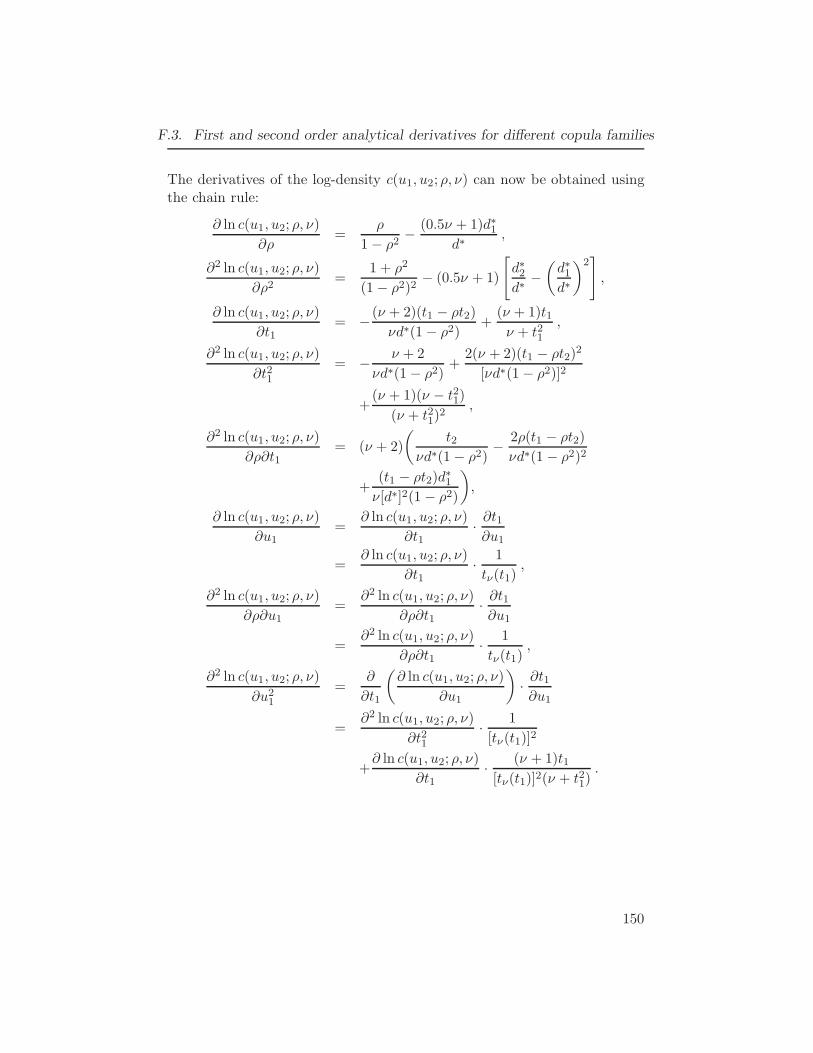

F Parameter estimation in factor copula models . . . . . . . 139F.1 Newton-Raphson algorithm and 1-factor copula model . . . . 139F.2 Newton-Raphson algorithm and 2-factor copula model . . . . 141F.3 First and second order analytical derivatives for different cop-

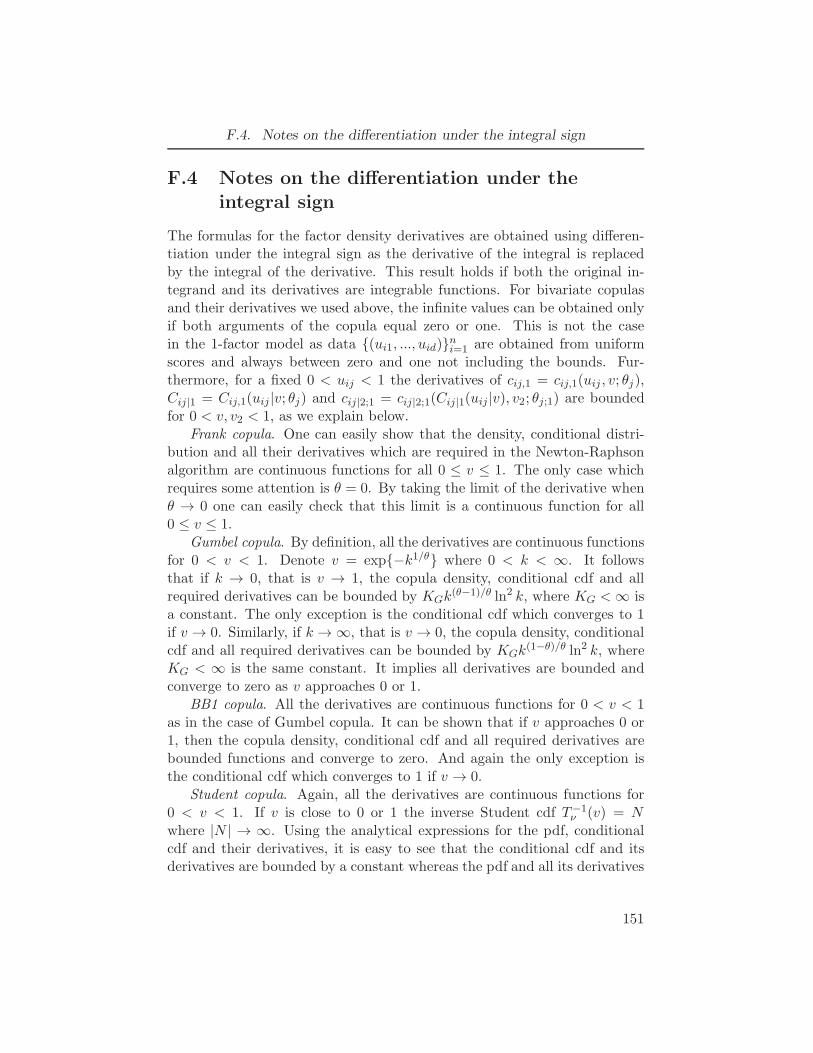

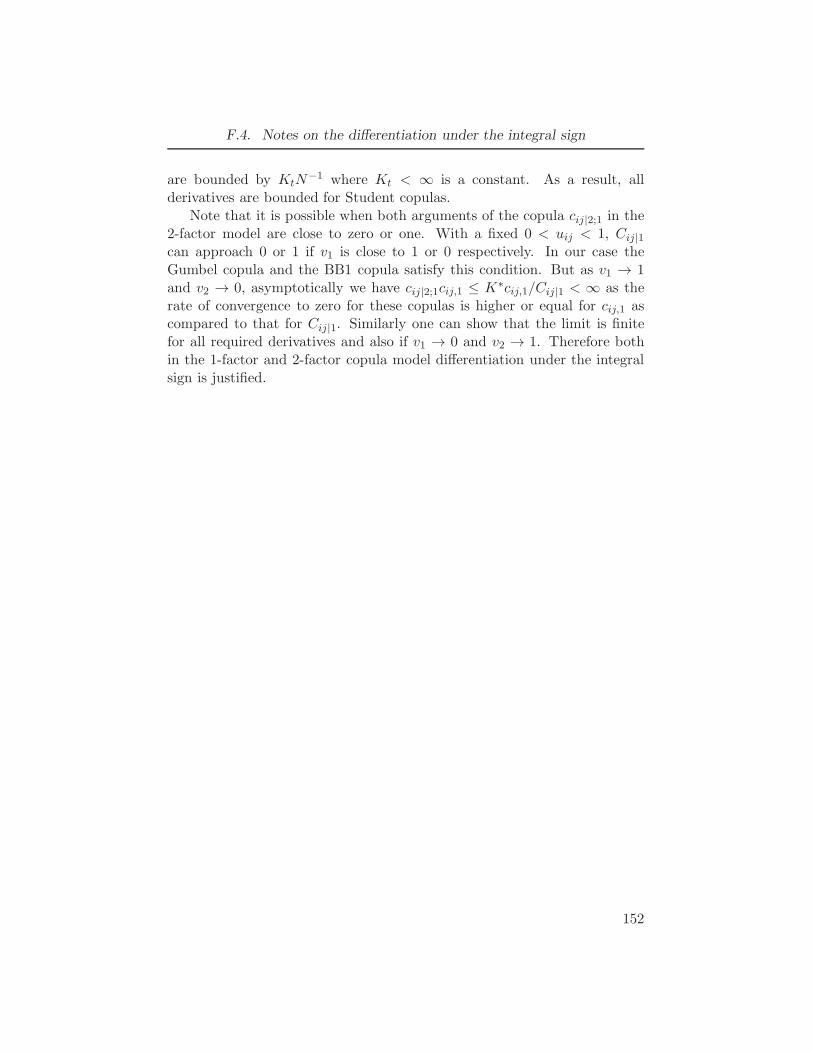

ula families . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143F.4 Notes on the differentiation under the integral sign . . . . . . 151

G Bivariate copulas satisfying assumptions of Proposition 5.3 153

H Derivatives of bivariate linking copulas . . . . . . . . . . . . 155

I Correlation matrix inverse and determinant in the struc-tured factor Gaussian model . . . . . . . . . . . . . . . . . . . 156

vii

List of Tables

1.1 Some copula notation used throughout this dissertation . . . 61.2 The values λL, λU , κL and κU for some bivariate copulas; ql = −

√(ν+1)(1−ρ)

(1+ρ). 9

2.1 Tail-weighted dependence measures for bivariate copulas with Spear-

man’s rho = 0.7: Spearman rho on quadrants, semicorrelations of normal

scores, TR with a(u) = u5 and p = 0.5 and RT with a(u) = u6 and

p = 0.5; for the definitions see (2.7), (2.4), (2.5) . . . . . . . . . . . . 152.2 Tail-weighted dependence measures: ρL and ρU (conditional Spearman’s

rhos), ρ−N and ρ+N (semi-correlations), and RTL , RT

U with a(u) = u6,

p = 0.5, for different bivariate copulas with Spearman’s rho equals 0.7;

for the definitions see (2.7), (2.4), (2.5) . . . . . . . . . . . . . . . . 202.3 The values ∆(a, p = 0.5;C1, C2) for different pairs of copulas with ρS =

0.5, 0.7, based on 20000 samples of size 400; asymptotic standard er-

rors for the sample size 400 are shown in brackets. The values that are

significantly positive at the 5% significance level are shown in bold font . 212.4 The values RT

L (a, p;C) for Gaussian and reflected Gumbel copula with

different Spearman’s rho, based on 20000 samples of size 400; asymptotic

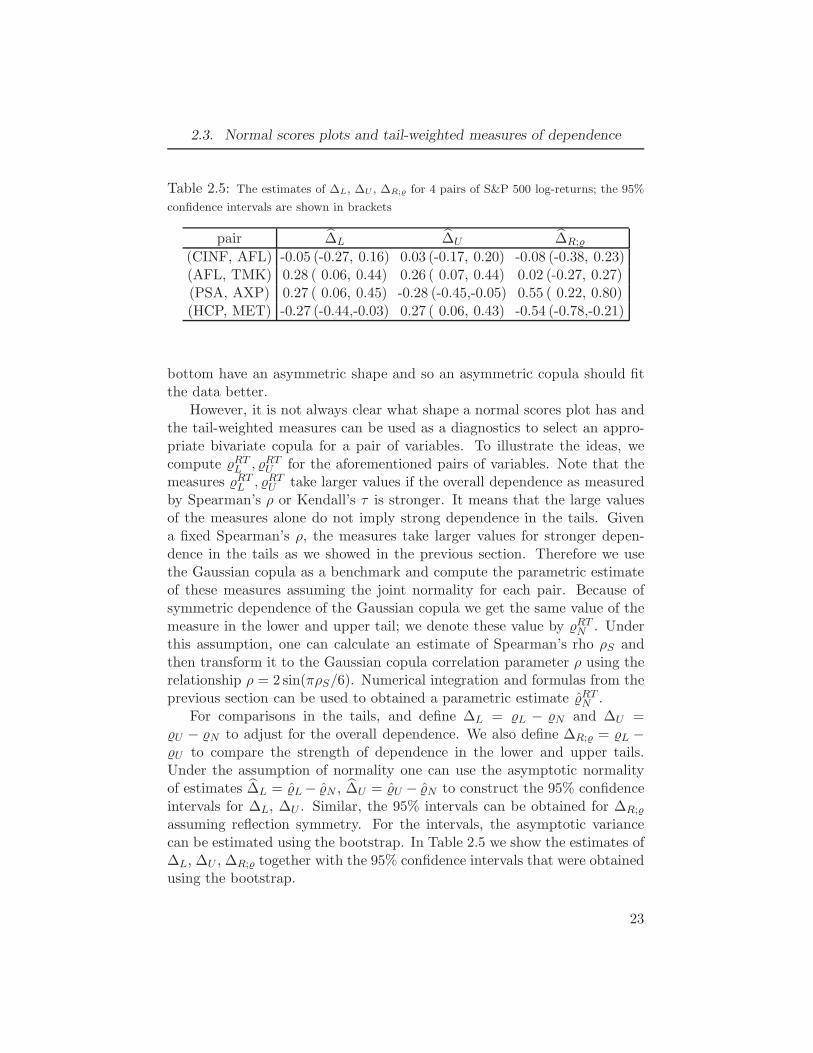

standard errors for the sample size 400 are shown in brackets . . . . . . 222.5 The estimates of ∆L, ∆U , ∆R; for 4 pairs of S&P 500 log-returns; the

95% confidence intervals are shown in brackets . . . . . . . . . . . . 23

3.1 The power of the three tests for reflection asymmetry. Test 1 is based on

the measure ∆R;C,; Test 2 is based on the measure ζ2(R;C, p = 0.05);

Test 3 is based on the measure G(∆R; k = 5). . . . . . . . . . . . . . 343.2 The power of the two tests for permutation asymmetry. Model 1: 1-factor

convolution gamma distribution, θ = (1.75, 0.5, 1); Model 2: Gumbel

copula, θ = 2. Test 1 is based on the measure ζ2(R;C, p = 0.05); Test 2

is based on the measure G∗(∆P ; k = 0.2). . . . . . . . . . . . . . . . 353.3 The estimated values of M1 = 42

√N · G(∆R; k = 5), M2 = 2.64

√N ·

G∗(∆P ; k = 0.2) for 4 pairs of S&P 500 log-returns; N = 252, standard

errors are shown in brackets . . . . . . . . . . . . . . . . . . . . . 36

viii

List of Tables

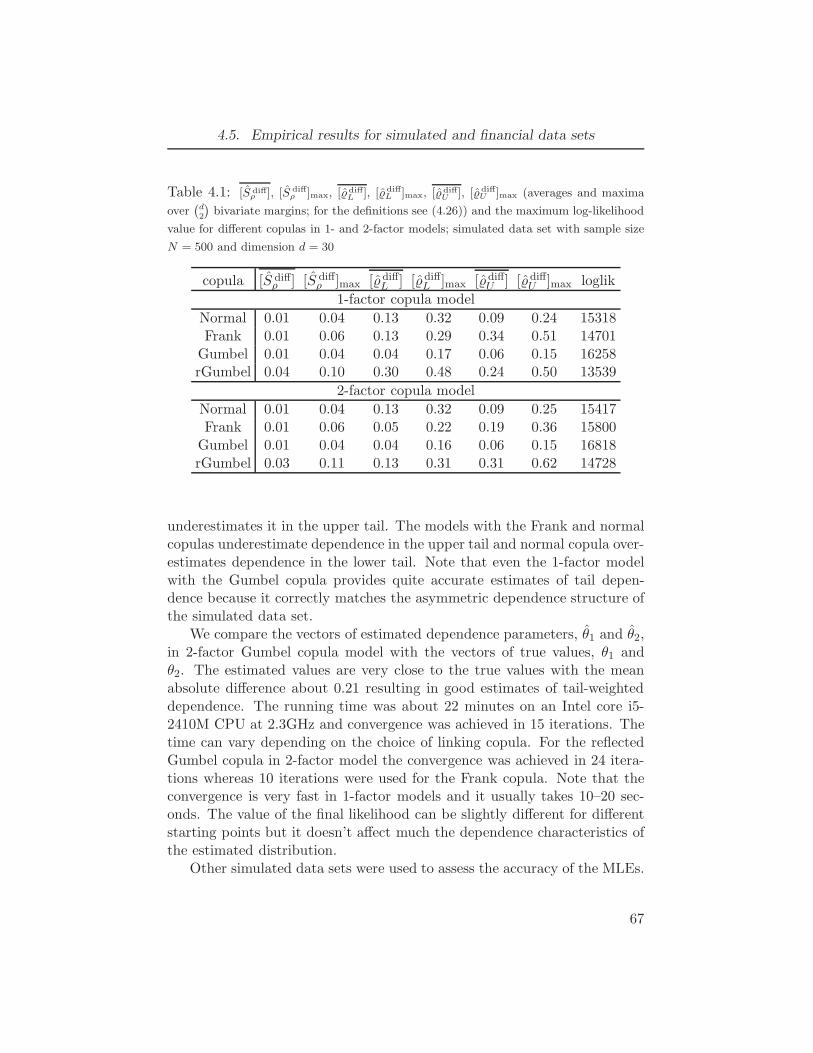

4.1 [S diffρ ], [S diff

ρ ]max, [ ˆdiffL ], [ ˆdiff

L ]max, [ ˆdiffU ], [ ˆdiff

U ]max (averages and max-

ima over(d2

)bivariate margins; for the definitions see (4.26)) and the

maximum log-likelihood value for different copulas in 1- and 2-factor

models; simulated data set with sample size N = 500 and dimension

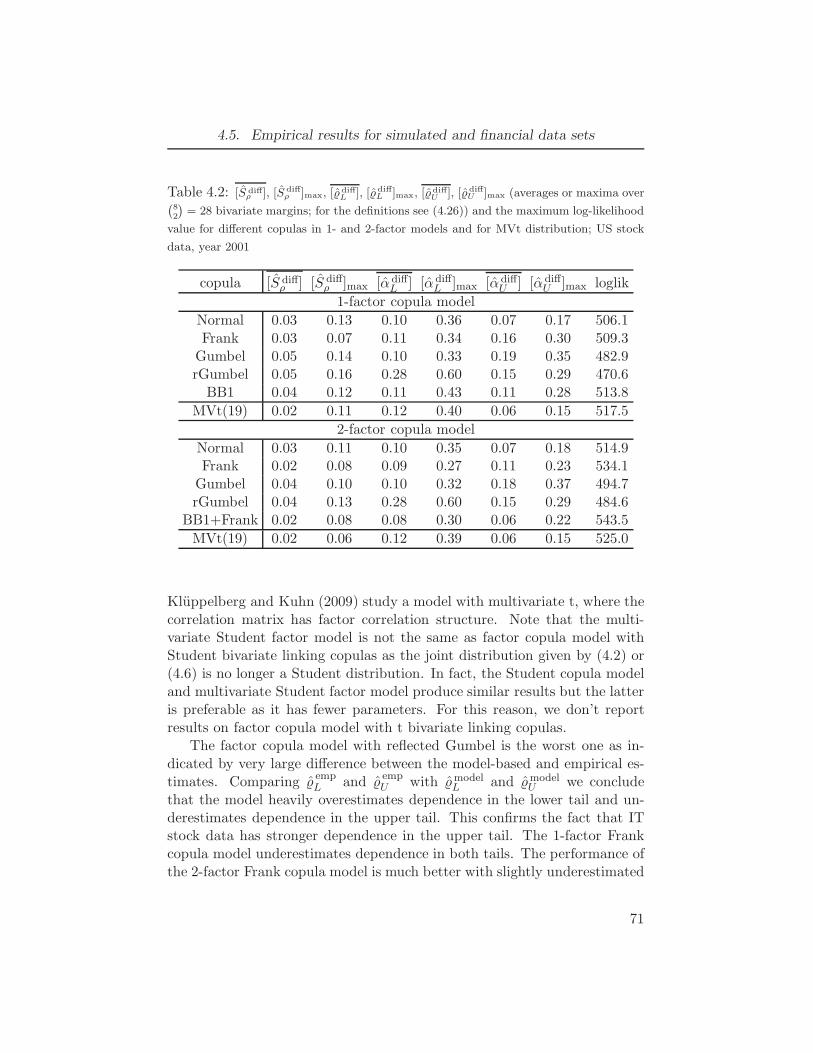

d = 30 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 674.2 [S diff

ρ ], [S diffρ ]max, [ ˆdiff

L ], [ ˆdiffL ]max, [ ˆdiff

U ], [ ˆdiffU ]max (averages or maxima

over(82

)= 28 bivariate margins; for the definitions see (4.26)) and the

maximum log-likelihood value for different copulas in 1- and 2-factor

models and for MVt distribution; US stock data, year 2001 . . . . . . 714.3 MLEs for parameters of linking copula families in 1-factor models, US IT

stock data, year 2001; variables 1=INTC, 2=CSCO, 3=NOVL, 4=MOT,

5=AAPL, 6=MSFT, 7=DELL, 8=ADBE. . . . . . . . . . . . . . . . 724.4 MLEs for parameters of linking copula families in 2-factor models, US IT

stock data, year 2001; variables 1=INTC, 2=CSCO, 3=NOVL, 4=MOT,

5=AAPL, 6=MSFT, 7=DELL, 8=ADBE. . . . . . . . . . . . . . . . 734.5 Log-likelihoods for different models, US data, year 2001; number of de-

pendence parameters for each model is shown in parentheses . . . . . 744.6 Log-likelihoods for truncated R-vine models: US data, year 2001. . . . . 74

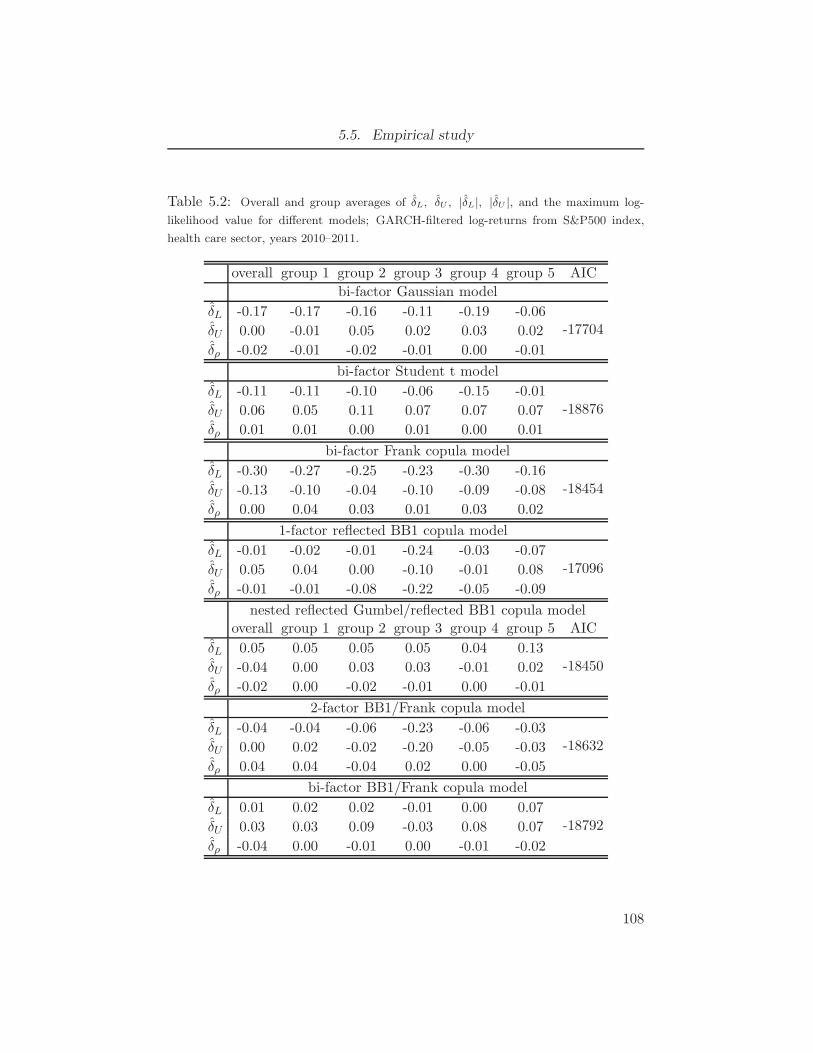

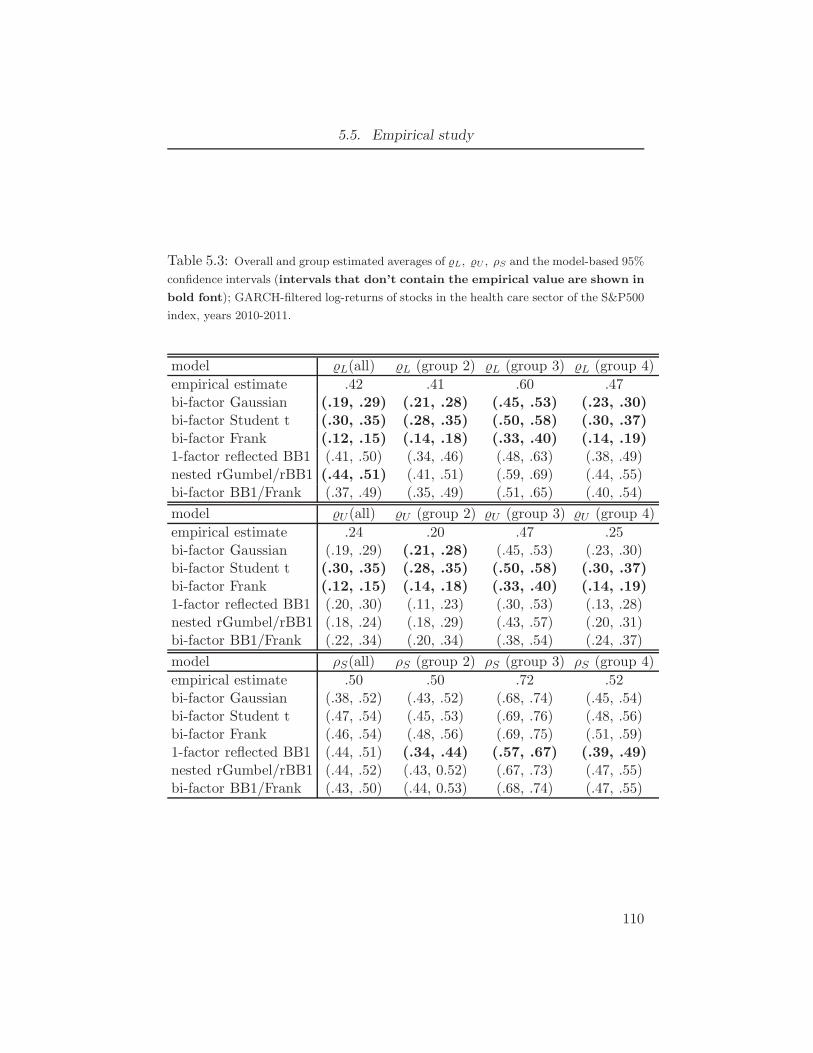

5.1 Overall and group averages of ˆL, ˆU , ρS; GARCH-filtered log-returns

from S&P500 index, health care sector, years 2010–2011. . . . . . . . . 1075.2 Overall and group averages of δL, δU , |δL|, |δU |, and the maximum log-

likelihood value for different models; GARCH-filtered log-returns from

S&P500 index, health care sector, years 2010–2011. . . . . . . . . . . 1085.3 Overall and group estimated averages of L, U , ρS and the model-based

95% confidence intervals (intervals that don’t contain the empirical

value are shown in bold font); GARCH-filtered log-returns of stocks

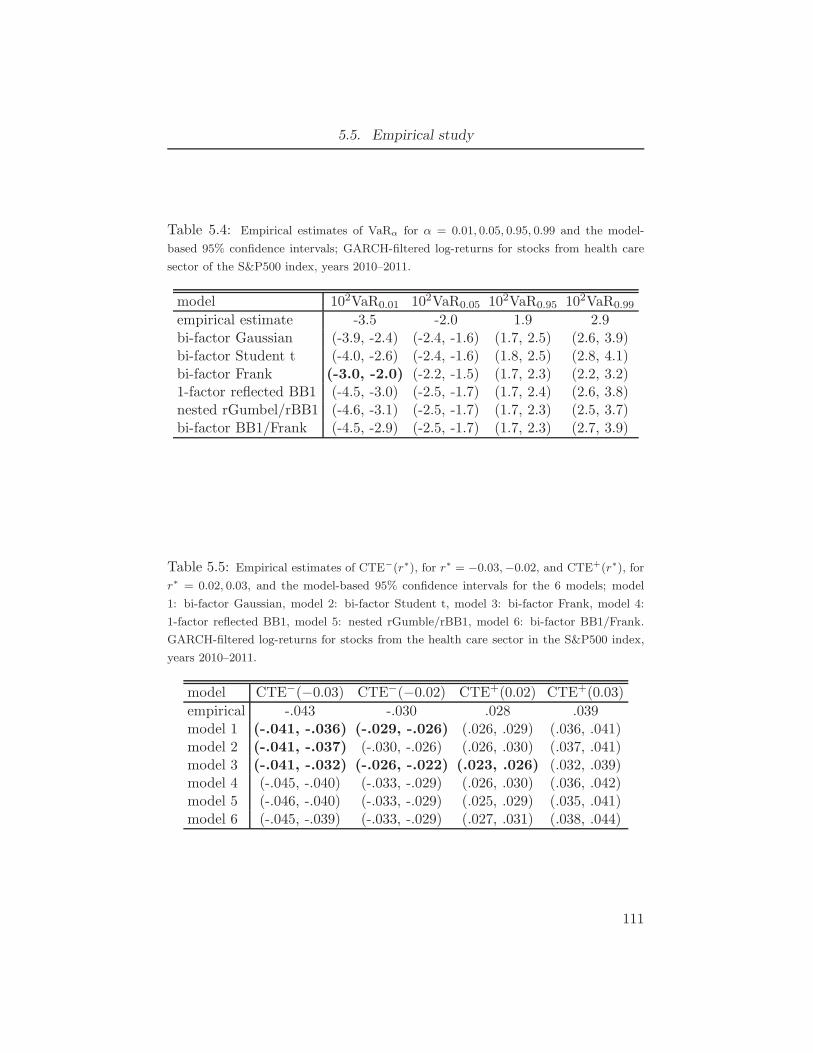

in the health care sector of the S&P500 index, years 2010-2011. . . . . 1105.4 Empirical estimates of VaRα for α = 0.01, 0.05, 0.95, 0.99 and the model-

based 95% confidence intervals; GARCH-filtered log-returns for stocks

from health care sector of the S&P500 index, years 2010–2011. . . . . . 1115.5 Empirical estimates of CTE−(r∗), for r∗ = −0.03,−0.02, and CTE+(r∗),

for r∗ = 0.02, 0.03, and the model-based 95% confidence intervals for the

6 models; model 1: bi-factor Gaussian, model 2: bi-factor Student t,

model 3: bi-factor Frank, model 4: 1-factor reflected BB1, model 5:

nested rGumble/rBB1, model 6: bi-factor BB1/Frank. GARCH-filtered

log-returns for stocks from the health care sector in the S&P500 index,

years 2010–2011. . . . . . . . . . . . . . . . . . . . . . . . . . . . 1115.6 Empirical Spearman’s ρS for GARCH-filtered log return data . . . . . 112

ix

List of Tables

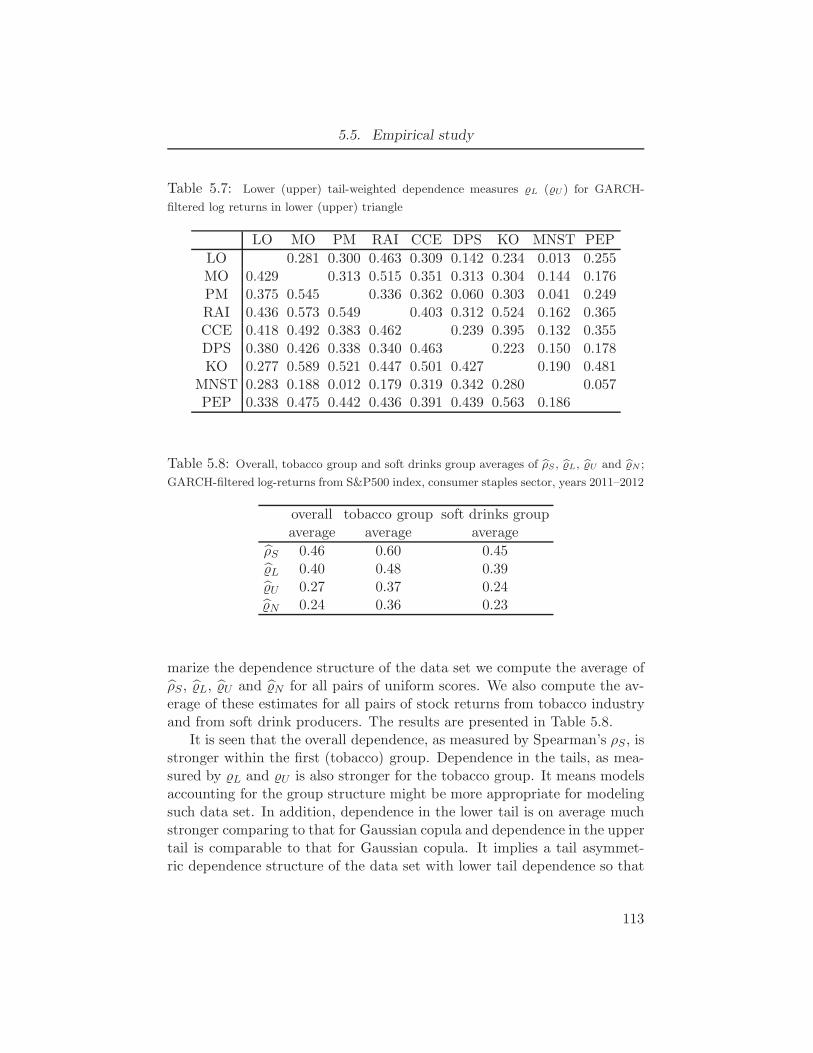

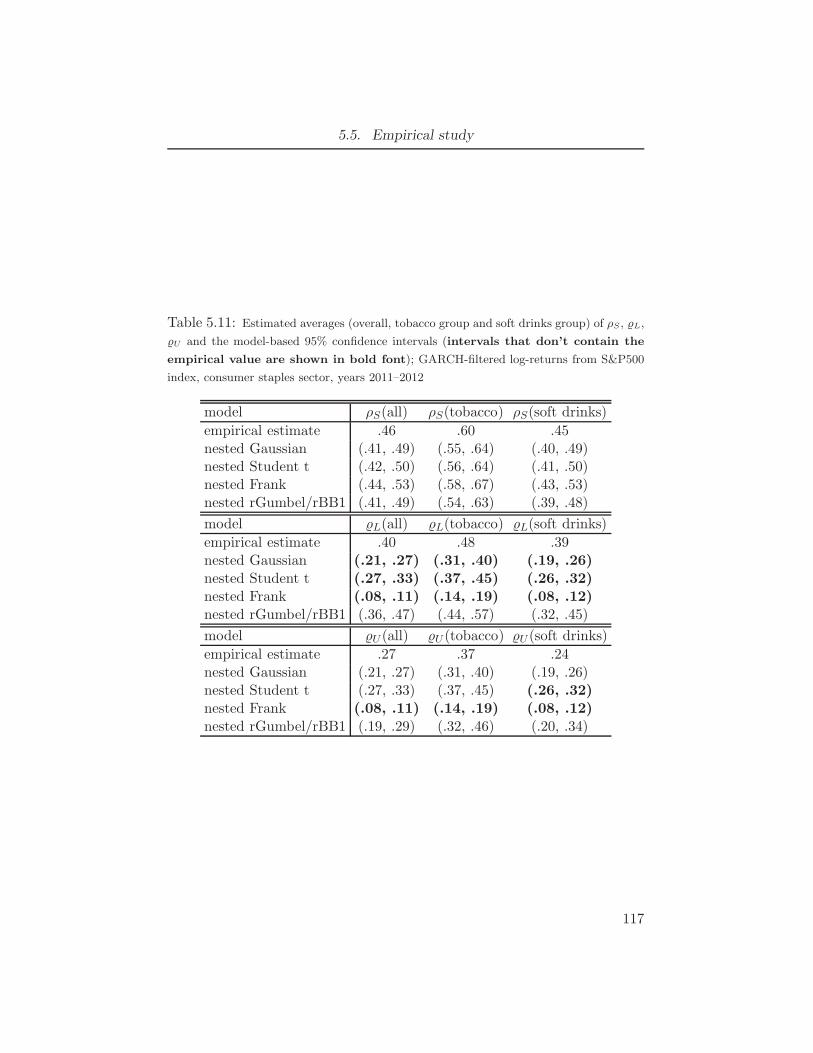

5.7 Lower (upper) tail-weighted dependence measures L (U ) for GARCH-

filtered log returns in lower (upper) triangle . . . . . . . . . . . . . . 1135.8 Overall, tobacco group and soft drinks group averages of ρS, L, U and

N ; GARCH-filtered log-returns from S&P500 index, consumer staples

sector, years 2011–2012 . . . . . . . . . . . . . . . . . . . . . . . 1135.9 Negative log-likelihood and AIC values for copula models applied to

GARCH-filtered log returns; AIC is 2 times the negative log-likelihood

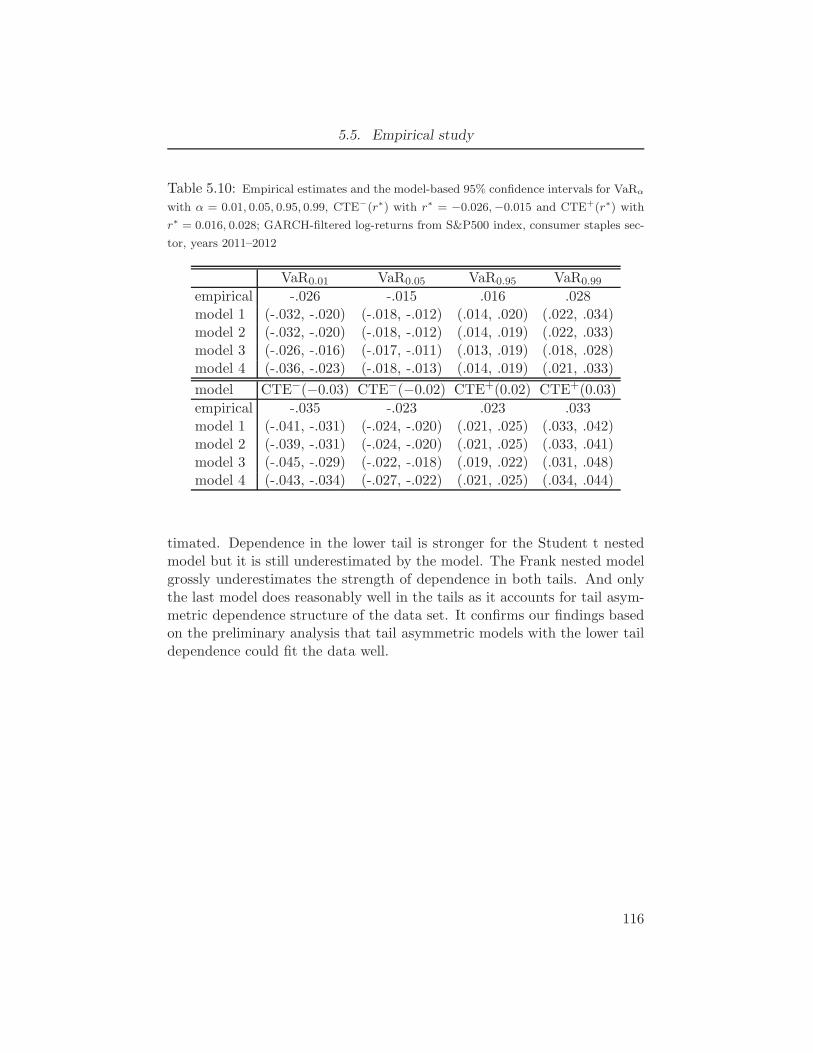

+ 2 times #parameters . . . . . . . . . . . . . . . . . . . . . . . 1155.10 Empirical estimates and the model-based 95% confidence intervals for

VaRα with α = 0.01, 0.05, 0.95, 0.99, CTE−(r∗) with r∗ = −0.026,−0.015

and CTE+(r∗) with r∗ = 0.016, 0.028; GARCH-filtered log-returns from

S&P500 index, consumer staples sector, years 2011–2012 . . . . . . . 1165.11 Estimated averages (overall, tobacco group and soft drinks group) of

ρS, L, U and the model-based 95% confidence intervals (intervals

that don’t contain the empirical value are shown in bold font);

GARCH-filtered log-returns from S&P500 index, consumer staples sec-

tor, years 2011–2012 . . . . . . . . . . . . . . . . . . . . . . . . . 117

x

List of Figures

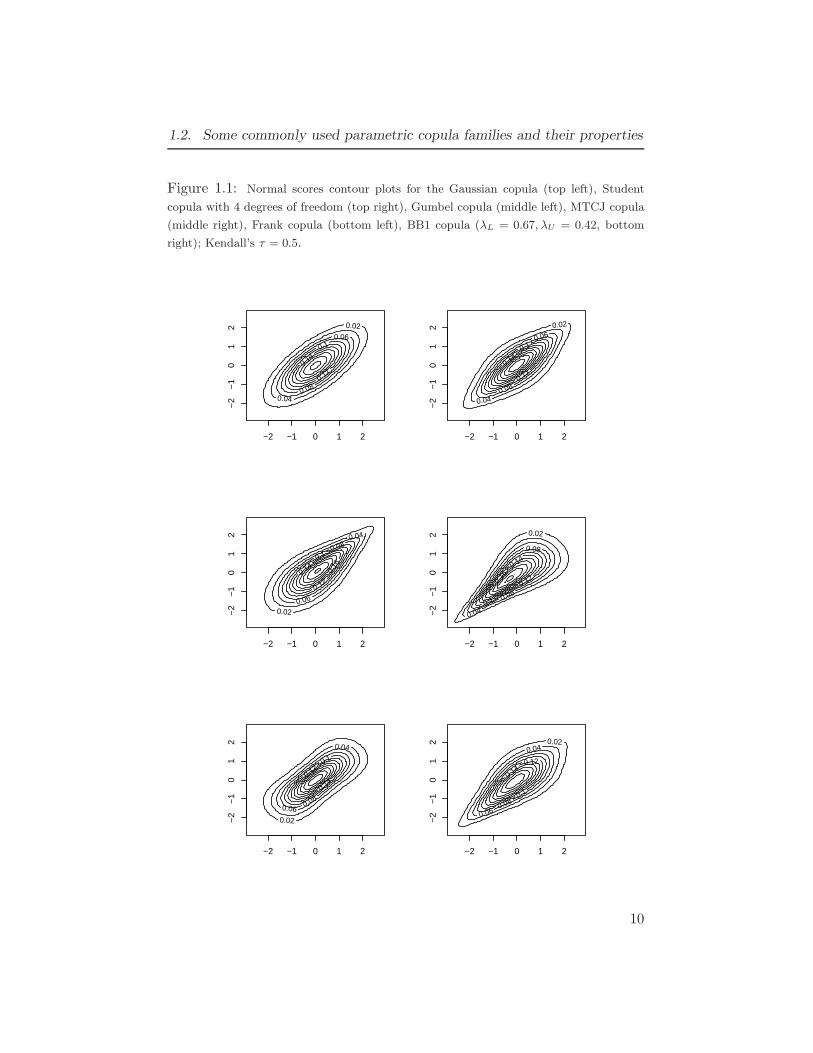

1.1 Normal scores contour plots for the Gaussian copula (top left), Student

copula with 4 degrees of freedom (top right), Gumbel copula (middle

left), MTCJ copula (middle right), Frank copula (bottom left), BB1

copula (λL = 0.67, λU = 0.42, bottom right); Kendall’s τ = 0.5. . . . . 10

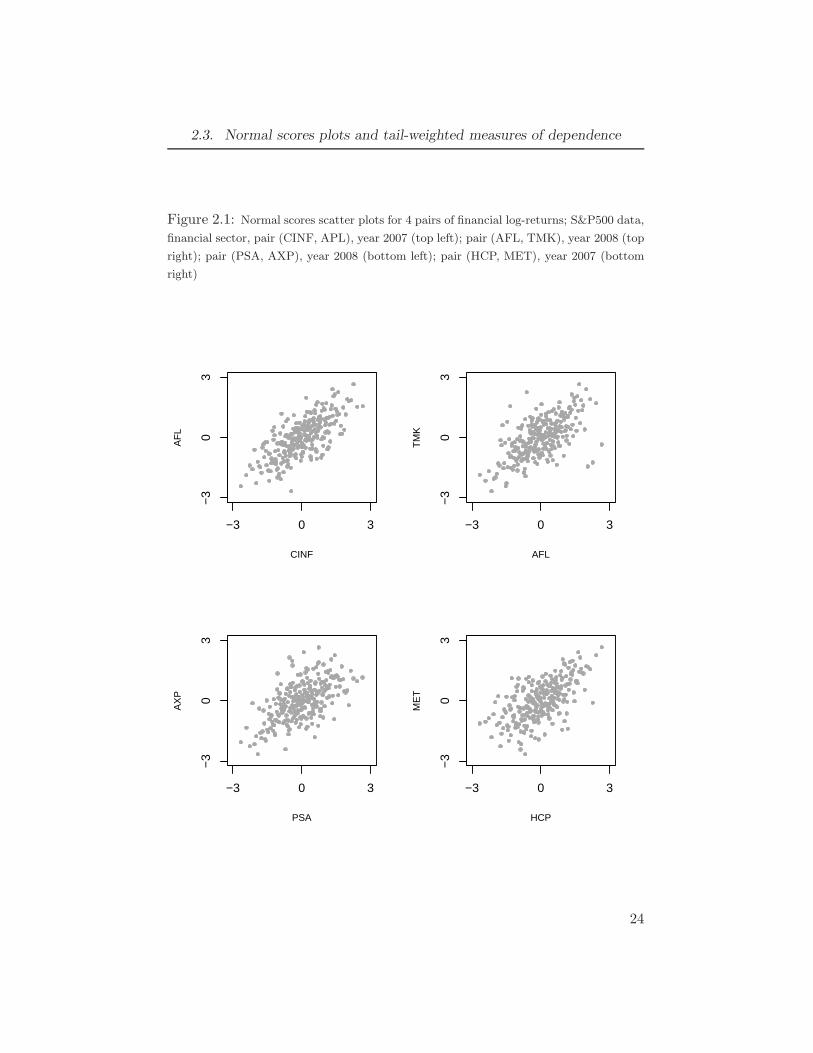

2.1 Normal scores scatter plots for 4 pairs of financial log-returns; S&P500

data, financial sector, pair (CINF, APL), year 2007 (top left); pair (AFL,

TMK), year 2008 (top right); pair (PSA, AXP), year 2008 (bottom left);

pair (HCP, MET), year 2007 (bottom right) . . . . . . . . . . . . . 24

3.1 Uniform scores scatter plots for data generated from the 1-factor convo-

lution gamma distribution with Kendall’s τ = 0.5: no asymmetry (right,

θ0 = 2.2, θ1 = θ2 = 1); moderate asymmetry (middle, θ0 = 1.75, θ1 =

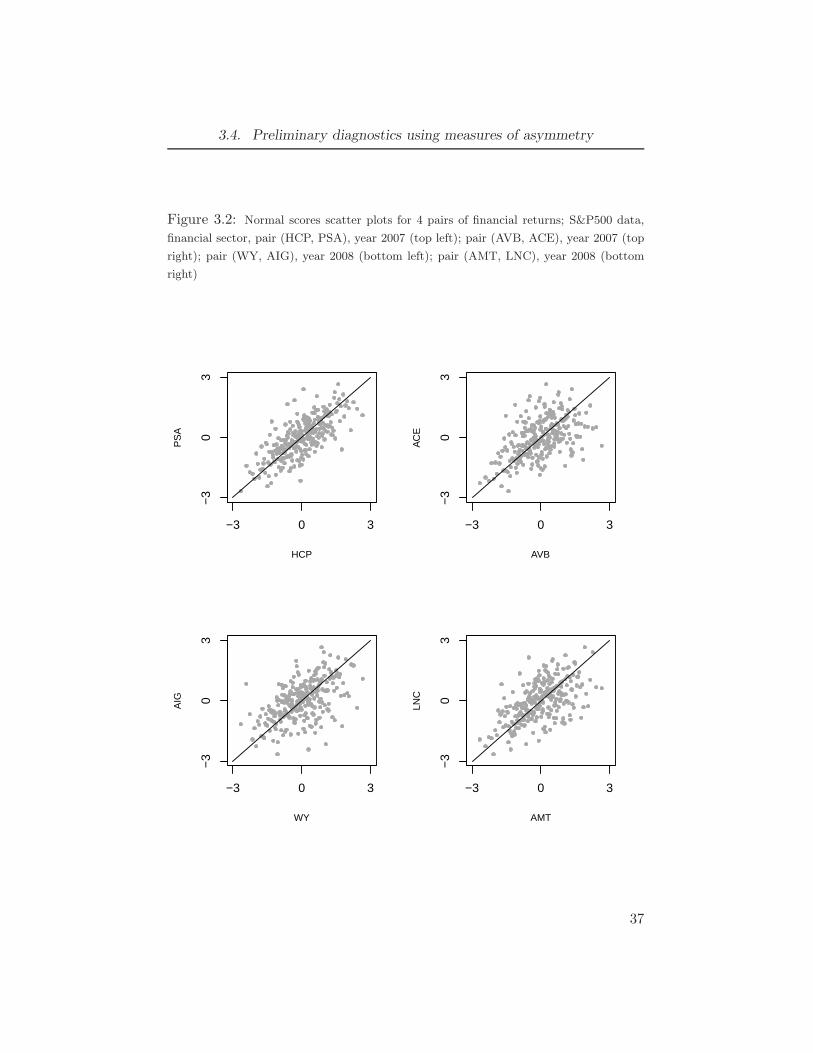

0.5, θ2 = 1); strong asymmetry (left, θ0 = 1.3, θ1 = 0.2, θ2 = 1) . . . . . 333.2 Normal scores scatter plots for 4 pairs of financial returns; S&P500 data,

financial sector, pair (HCP, PSA), year 2007 (top left); pair (AVB, ACE),

year 2007 (top right); pair (WY, AIG), year 2008 (bottom left); pair

(AMT, LNC), year 2008 (bottom right) . . . . . . . . . . . . . . . 37

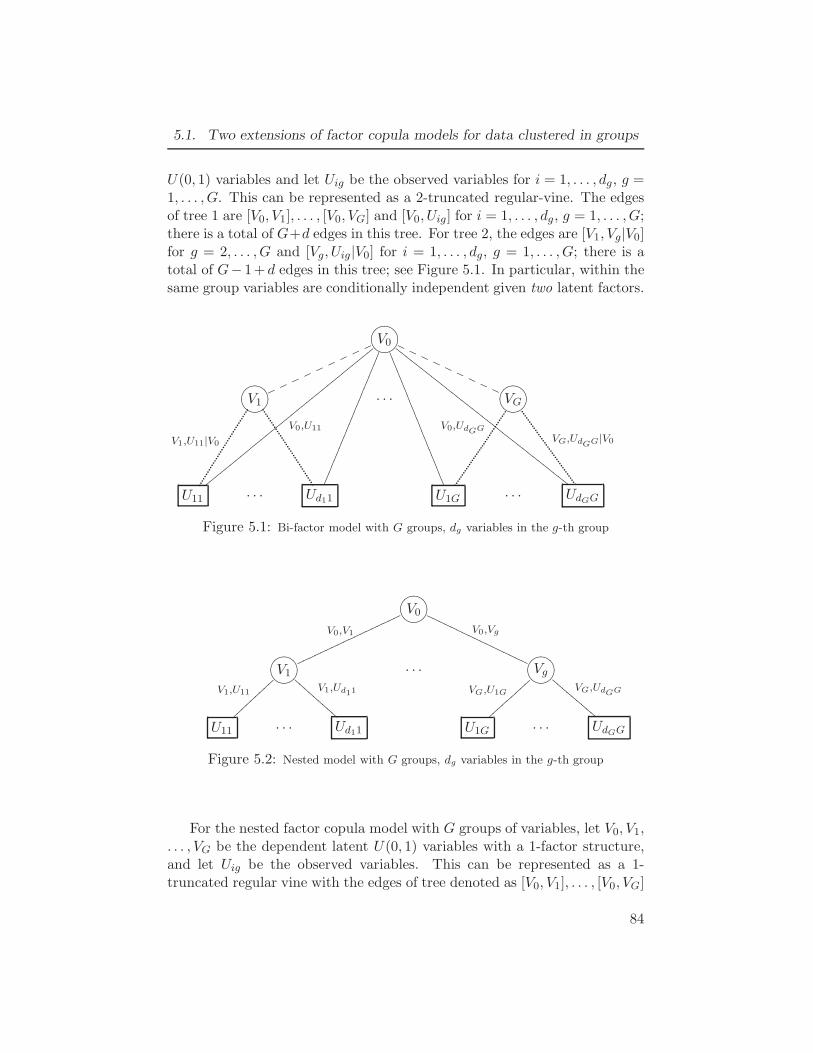

5.1 Bi-factor model with G groups, dg variables in the g-th group . . . . . 845.2 Nested model with G groups, dg variables in the g-th group . . . . . . 84

xi

Acknowledgements

This research has been supported by an NSERC Discovery Grant. I wouldlike to thank my supervisor, professor Harry Joe, for his help and sup-port during my graduate work. I am grateful to the supervisory committeemembers, Natalia Nolde and Haijun Li, and external examiner AlexanderMcNeil for the valuable comments and suggestions that helped to improvepresentation in this dissertation.

xii

TO MY PARENTS

xiii

Chapter 1

Introduction

The multivariate normality assumption is widely used to model the joint dis-tribution of high-dimensional data. The univariate margins are transformedto normality and then the multivariate normal distribution is fitted to thetransformed data. In this case, the dependence structure is completely de-fined by the correlation matrix and different models on the correlation struc-ture can be used to reduce the number of dependence parameters from O(d2)to O(d), where d is the multivariate dimension or number of variables. TheseGaussian models, however, may not be appropriate for modeling data thathave very strong dependence in the tails. In many applications, variablesin a multidimensional data set tend to take very large negative or positivevalues simultaneously much more often than it is predicted by the Gaussianmodel. Typical examples include financial return data or insurance claimsdata. In addition to strong dependence in the tails, asymmetric dependencecan not be handled by the Gaussian models.

To overcome these difficulties, different models that use a copula functionto model the joint distribution become more popular in different applica-tions. The copula is a function linking univariate margins into the jointdistribution. Let X = (X1, . . . ,Xd) be a random d-dimensional vector withthe joint cumulative distribution function (cdf) FX. Let FXj be the marginalcdf of Xj for j = 1, . . . , d. The copula CX, corresponding to FX, is a multi-variate uniform cdf such that FX(x1, . . . , xd) = CX(FX1(x1), . . . , FXd

(xd)).By Sklar (1959), there exists a unique copula CX if FX is continuous. Cop-ulas are suitable for modeling non-Gaussian data such as financial asset re-turns or insurance data; see Patton (2006), McNeil et al. (2005) and others.The superiority of non-normal copulas over the normal copula in modelingfinancial and insurance data has been discussed in Embrechts (2009).

In a copula model, univariate data are fitted first and the variables arethen transformed to uniform data to obtain estimates of the copula de-pendence parameters. This approach allows modeling in two steps withestimation of parameters for univariate marginals and then for the copulacdf. This greatly simplifies the estimation procedure for high-dimensionaldata. Simple multivariate copula families, such as Archimedean, however,

1

Chapter 1. Introduction

do not have flexible dependence structure. To get flexibility, a popularapproach is to use a sequence of algebraically independent bivariate copu-las applied to either marginal or univariate conditional distributions. Ap-proaches that use a sequence of bivariate copulas include vine pair-copulaconstructions (Kurowicka and Joe (2011)). These classes of copulas havebeen used for finance and other applications because they can cover a widerange of dependence and tail behavior; see for example, Aas et al. (2009),Nikoloulopoulos et al. (2012), Brechmann et al. (2012). More papers onvine copulas can be found at the web site http://vine-copula.org.

In many multivariate applications, the dependence in observed vari-ables can be explained through latent variables; in multivariate item re-sponse in psychology applications, latent variables are related to the ab-stract variable being measured through items, and in finance applications,latent variables are related to economic factors. Classical factor analysis as-sumes (after transforms) that all observed and latent random variables arejointly multivariate normal. Books on multivariate analysis (see for example,Johnson and Wichern (2002)) often have examples with factor analysis andfinancial returns. In this dissertation we propose and study the propertiesof the copula version of multivariate Gaussian models with a factor corre-lation structure. The models, which we will call factor copula models, arespecial cases of vine models with latent variables. The factor copula mod-els keep the interpretability of the Gaussian factor models while allowingfor different types of dependence structure including strong tail dependenceand dependence asymmetry.

A special case of factor copula models is models with conditionally in-dependent and identically distributed random variables. Due to de Finettitheorem (see Loeve (1963)) these models are equivalent to exchangeable ran-dom variables. The latter class of models is not flexible enough for appli-cations; it includes Archimedean copulas. In the general case, factor copulamodels proposed in this dissertation have different conditional margins andexchangeability does not hold.

These common factor copula models implicitly require a homogeneousdependence structure with the assumption of conditional independence givenseveral common factors. In data sets with a large number of variables, datacan come from different sources or be clustered in different groups, for ex-ample, stock returns from different sectors or grouped item response datain psychometrics; thus dependence within each group and among differentgroups can be different. In psychometrics, sometimes a bi-factor correlationstructure is used when variables or items can be split into non-overlappinggroups; see for example Gibbons and Hedeker (1992) and

2

Chapter 1. Introduction

Holzinger and Swineford (1937). In a Gaussian bi-factor model, there is onecommon Gaussian factor which defines dependence among different groups,and one or several independent group-specific Gaussian factors which definedependence within each group. An alternative way to model dependencefor grouped data is a nested model where the dependence in groups is mod-eled via dependent group-specific factors and the observed variables are as-sumed to be conditionally independent given these group-specific factors.The nested model is similar to Gaussian models with multilevel covariancestructure; see Muthen (1994). In this dissertation, we propose copula ex-tensions for the bi-factor and nested Gaussian models. We will call theseextensions as structured factor copula models. The proposed models con-tain 1- and 2-factor copula models as special cases, while allowing flexibledependence structure both for within group and between group dependence.As a result, the models can be suitable for modeling high-dimensional datasets consisting of several groups of variables with homogeneous dependencein each group.

The main advantage of factor copula models is that they can be nicelyinterpreted when used in some applications. In finance applications, for ex-ample, the group latent factors may represent the current state of a financesector and the common latent factor may represent the current state of thewhole economy. In vine copula models the structure of the joint distributioncan be quite complicated and is usually chosen to maximize the likelihoodvalue and a simple interpretation of the model is thus quite difficult. Themain disadvantage of the factor models is that numerical integration is re-quired to compute the likelihood whereas in vine models the joint copuladensity is given in a simple form. It implies the computation can takelonger compared to vine models. However, factor models are closed underthe marginalization, and data can be divided into smaller subsets and pa-rameters can be estimated for each subset independently. This significantlyreduces computational time and the estimates obtained in this way can thenbe used as starting points when all parameters in the model are estimatedsimultaneously. With good starting points, estimation becomes much fasteras quite a small number of iterations is usually required for convergence.

Appropriate choices of bivariate copulas used in the vine and factor cop-ula models are very important. Inappropriate choices can cause the modelto provide incorrect inference on joint tail probabilities. This is crucial inmany applications such as quantitative risk analysis in finance and insur-ance where good estimates of joint tail probabilities are essential. We pro-pose tail-weighted measures of dependence which can be used to distinguishdifferent bivariate copula families through their strength of dependence in

3

Chapter 1. Introduction

the joint tails. The tail-weighted measures provide additional informationto commonly used monotone dependence measures such as Kendall’s τ andSpearman’s ρS , because a single dependence measure, which is dominated bythe copula density in the center part of the unit square, cannot summarizeall of the important dependence and tail properties of the copula.

Bivariate tail-weighted measures of dependence that we propose are de-fined as correlations of transformed variables; they have easily-computedsample versions. The measures can be applied to each pair of variables in amultidimensional data set. These measures put more weight in the tails andthus can efficiently estimate the strength of dependence in the tail even if thesample size is not very large. We also propose some tail-weighted measuresof asymmetry and introduce diagnostic procedures. These procedures canbe used to detect possible departures from normality and help to select moresuitable copula for the data set. What is more important, the measures andprocedures can be used for assessing the adequacy of the chosen model inthe tails. Therefore these measures can be employed in factor copula modelsand in vine models (and other copula models), and we use empirical studiesto illustrate these ideas.

Note that the purpose of these tail-weighted measures of dependenceto assess models is quite different in aim than copula goodness-of-fit proce-dures; Huang and Prokhorov (2014) and Schepsmeier (2014) have developedlikelihood-based copula goodness-of-fit tests and Genest et al. (2009) havean overview of bivariate goodness-of-fit tests for copulas. However these pre-viously proposed goodness-of-fit procedures are not diagnostic in suggestingimproved models when the P-values are small. For preliminary data anal-ysis, the tail-weighted measures of dependence can provide a guide to thechoice of bivariate copulas to use in vine and factor models. After fittingcompeting copula models, the comparison of empirical and model-based es-timates is a method to assess whether the best-fitting copula models basedon AIC or BIC are adequate for tail inference or whether alternative modelsshould be considered. Different copula models with a similar dependencestructure can typically perform similarly in the comparison of empirical ver-sus model-based measure of monotone association such Spearman’s rho, butthey can differ more for tail inference. This is because while the dependencestructure, which is based mostly on the middle of the data, dominates thelog-likelihood of parametric copula models, a secondary contribution to thelog-likelihood is based on the quality of fit in the tails. Most parametriccopula families, including Gaussian, have densities that asymptote to infin-ity at one or more corners of the hypercube, and hence parametric copulafamilies with different strength of dependence in the tails (or different rates

4

1.1. Copula notation

of asymptotes to infinity) can perform quite differently when assessed bytail-weighted dependence measures.

The rest of the dissertation is organized as follows. We define somebasic copula notation and dependence properties in Sections 1.1, 1.2. Thetail-weighted measures of dependence and their properties are presented inChapter 2. We also propose some measures of asymmetry based on theempirical copula function in Chapter 3. The measures perform better com-paring to some other dependence measures that are used in applications.Factor copula models, their dependence and tail properties, and details onparameter estimation are presented in Chapter 4. Extensions of the fac-tor models, structured copula models, are defined in Chapter 5. We derivedependence and tail properties for the structured models and show thatdifferent types of dependence structure can be obtained depending on thechoice of bivariate linking copulas. We apply the models to estimate depen-dence structure of some data sets of financial returns and find that with agood choice of linking copulas the structured copula models fit data quitewell. We find that, unlike the tail-weighted measures of dependence, somerisk measures used in applications in finance are not very sensitive to modelswith different tail behavior. More details are provided for a special case ofthe Gaussian linking copulas. The estimation is much faster in this case asthe log-likelihood function can be obtained in a simple form. Concludingremarks and topics for the future research are presented in Chapter 6 whilethe proofs for some results and more details on numerical computation ofparameters are given in the Appendix.

1.1 Copula notation

We define some general notation that we will use throughout this disserta-tion. Let θ be a dependence parameter (the parameter can be a scalar ora vector). If this parameter is not important it can be suppressed in somenotation. We summarized the copula notation in Table 1.1.

In addition, we will be using the concept of the reflected C copula, or thesurvival copula. If (U1, U2) ∼ C, it follows that (1−U1, 1−U2) ∼ CR, whereCR(u1, u2) := −1+u1 +u2 +C(1−u1, 1− u2). The copula CR is called thereflected C copula. It also implies that C(u1, u2) := 1− u1 − u2 +C(u1, u2)is the survival function for the pair (U1, U2). The function C(1− u1, 1−u2)is usually called the survival copula.

5

1.2. Some commonly used parametric copula families and their properties

Table 1.1: Some copula notation used throughout this dissertation

Notation Definition

C(u1, ..., ud; θ) the cdf of a d-variate copula C withdependence parameter θ

c(u1, ..., ud; θ) the pdf of a d-variate copula C withdependence parameter θ

C1|2(u1|u2; θ) := ∂C(u1, u2; θ)/∂u2 the conditional cdf of the first variable

given the second variable

C2|1(u2|u1; θ) := ∂C(u1, u2; θ)/∂u1 the conditional cdf of the second variable

given the first variable

CU1,U2(u1, u2) the joint cdf of a pair (U1, U2)

cU1,U2(u1, u2) the joint pdf of a pair (U1, U2)

CU1|U2(u1|u2) the conditional cdf of U1 given U2

1.2 Some commonly used parametric copula

families and their properties

In this section, we list some copulas that are widely used in applications andgive their basic properties. There are many other parametric copula families(see Joe (1997)), but the ones listed here show a variety of tail properties,and flexible vine and factor copulas can be built from them.

• Normal (Gaussian) copula:C(u1, ..., ud; Σ) = Φd(Φ

−1(u1), ...,Φ−1(ud); Σ) where, Φd is the cdf of a

multivariate normal random variable with a correlation matrix Σ andΦ−1 is the inverse univariate standard normal cdf.

• Student t copula:C(u1, ..., ud; Σ, ν) = Td(T

−1(u1; ν), ..., T−1(ud; ν); Σ, ν) where Td is the

cdf of a multivariate Student random variable with a correlation matrixΣ and ν degrees of freedom and T−1(·; ν) is the inverse univariateStudent cdf with ν degrees of freedom.

• Frank copula (Frank (1979)):

C(u1, ..., ud; θ) = −1θ log

(1 +

∏dj=1(e

−θuj−1)

(e−θ−1)d−1

), θ 6= 0.

6

1.2. Some commonly used parametric copula families and their properties

• Gumbel copula (Gumbel (1960)):C(u1, ..., ud; θ) = exp{−(uθ1+...+u

θd)

1/θ}, where θ > 1 and ui = − lnui,i = 1, ..., d.

• MTCJ copula (Mardia (1962), Takahashi (1965), Cook and Johnson(1981)):C(u1, ..., ud; θ) = (u−θ1 + ...+u−θd −d+1)−1/θ, θ > 0. For the bivariatecase, this is also known as the Clayton copula (Clayton (1978)).

• BB1 copula (Joe and Hu (1996), Joe (1997)):C(u1, u2; θ, δ) = {1 + [(u−θ1 − 1)δ + (u−θ2 − 1)δ ]1/δ}−1/θ, θ > 0, δ > 1.

In this dissertation, we will be mainly using bivariate versions of theabove copulas. The densities and conditional cdfs for this copulas for d = 2can be found in Section F.3. Below we define some basic properties forbivariate copulas.

Symmetric copulas

A bivariate copula C is said to be permutation symmetric ifC(u1, u2) = C(u2, u1) for any u1, u2 ∈ (0, 1). If (U1, U2) ∼ C, the permu-tation symmetry implies (U2, U1) ∼ C. It is easy to see that all copulaspresented above are permutation symmetric copulas.

A bivariate copula C is said to be reflection symmetric if C(u1, u2) =CR(u1, u2) for any u1, u2 ∈ (0, 1). If (U1, U2) ∼ C, the reflection symmetryimplies (1 − U1, 1 − U2) ∼ C. The normal, Student and Frank copulas arereflection symmetric copulas and the Gumbel, MTCJ and BB1 copulas arenot.

Dependence properties

A bivariate copula C is said to have positive quadrant dependence(PQD) if C(u1, u2) ≥ u1u2 for any u1, u2 ∈ (0, 1). The normal and Studentcopula with ρ > 0, Frank copula with θ > 0, Gumbel, MTCJ and BB1copula are copulas with positive quadrant dependence. For these copulasdependence is stronger in the first and third quadrants of a unit square.

A bivariate copula C is said to have negative quadrant dependence(NQD) if C(u1, u2) ≤ u1u2 for any u1, u2 ∈ (0, 1). The normal and Studentcopula with ρ < 0, Frank copula with θ < 0 are copulas with negativedependence. For these copulas dependence is stronger in the second andfourth quadrants of a unit square.

The conditional cdf C1|2 of the copula C is stochastically increasing,SI (decreasing) if C1|2(u1|u2) is a decreasing (increasing) function of u2. It

7

1.2. Some commonly used parametric copula families and their properties

implies that the second variable is more likely to take larger (smaller) valueas the first variable increases. The Normal copula with ρ > 0, Frank copulawith θ > 0, Gumbel, MTCJ and BB1 copulas are stochastically increasingcopulas and the Normal copula with ρ < 0, Frank copula with θ < 0 arestochastically decreasing copulas.

The copula C increases (decreases) in concordance ordering ifC(u1, u2; θ) is an increasing (decreasing) function of θ with any fixed 0 <u1, u2 < 1. All copulas that are listed above increase in concordance order-ing. In other words, dependence becomes stronger as dependence parameterincreases. The Student copula does not increase in concordance orderingwith respect to the number of degrees of freedom parameter.

The detailed overview of these dependence concepts are given in Chapter2 of Joe (1997).

Tail properties

Standard measures of tail dependence used in the literature are tail de-pendence coefficients. Assuming the limits exist, the coefficients are definedas follows:

λL = limu↓0

C(u, u)

u, λU = lim

u↓0C(1− u, 1− u)

u. (1.1)

The copula C is said to be lower (upper) tail dependent if the lower(upper) tail dependence coefficient λL (λU ) is positive.

Hua and Joe (2011) assess tail dependence and asymmetry based on therates with which C(u, u) and C(1− u, 1− u) go to 0 as u→ 0. They definethe tail order as the reciprocal of a quantity used in Ledford and Tawn(1996) and Heffernan (2000). It measures the strength of dependence inthe joint lower and upper tails. If C(u, u) ∼ ℓL(u)u

κL as u → 0, whereℓL(u) is a slowly varying function, then we say that the lower tail order isκL. Similarly if C(1 − u, 1 − u) ∼ ℓU (u)u

κU as u → 0, where ℓU (u) is aslowly varying function, then the upper tail order is κU . If 1 < κL < 2or 1 < κU < 2 then λL = 0 (λU = 0 respectively), and this is termedintermediate tail dependence in Hua and Joe (2011). A smaller value ofthe tail order corresponds to more tail dependence (more probability in thecorner). Then, the strongest dependence in the tail corresponds to κL = 1or κU = 1. The tail order can be used to assess tail dependence strength iftail dependence coefficient is zero.

In Table 1.2 the values λL, λU together with κL and κU are presented forbivariate versions of copulas listed in the beginning of this section. It is seenthat the normal copula has intermediate lower and upper tail dependenceand the Student copula is a tail dependent copula. At the same time the

8

1.2. Some commonly used parametric copula families and their properties

Table 1.2: The values λL, λU , κL and κU for some bivariate copulas; ql = −√

(ν+1)(1−ρ)(1+ρ)

.

copula λL λU κL κUNormal 0 0 2

1+ρ2

1+ρ

Student 2Tν+1 (ql) 2Tν+1 (ql) 1 1Frank 0 0 2 2

Gumbel 0 2− 21/θ 21/θ 1

MTCJ 2−1/θ 0 1 2

BB1 2−1/θδ 2− 21/δ 1 1

tail order of a normal copula is close to 1 if the correlation parameter ρis large and therefore the normal and Student copulas have very similartail behavior in this case. The Frank copula is a tail quadrant independentcopula with tail order equal two in both tails. The Gumbel copula hasasymmetric tail dependence with intermediate dependence in the lower tailand tail dependence in the upper tail. The MTCJ copula is a lower taildependent copula with upper tail quadrant independence. Finally, the BB1copula is a copula with asymmetric tail dependence and lower and uppertail dependence. There are other parametric copula families in Joe (1997)with tail properties similar to those in Table 1.2.

To visualize different types of dependence structures, one can use normalscores contour plots when bivariate distributions with univariate marginstransformed to the standard normal distribution are plotted for differentbivariate copulas; see Figure 1.1 for contour plots for some bivariate copulas.In case of the Gaussian copula we get a bivariate normal distribution withelliptical shape. For copulas with lower (upper) tail dependence contourplots have sharper lower (upper) tails and for copulas with tail quadrantindependence (the Frank copula, upper tail of the MTCJ copula) counterplots have more rounded tails. Asymmetric copulas with tail dependence inboth tails (for example, BB1 copula) have contour plots with sharper lower(upper) tail if dependence in the lower (upper) tail is stronger.

9

1.2. Some commonly used parametric copula families and their properties

Figure 1.1: Normal scores contour plots for the Gaussian copula (top left), Student

copula with 4 degrees of freedom (top right), Gumbel copula (middle left), MTCJ copula

(middle right), Frank copula (bottom left), BB1 copula (λL = 0.67, λU = 0.42, bottom

right); Kendall’s τ = 0.5.

0.02

0.04

0.06

0.08

0.1

0.12 0.14

−2 −1 0 1 2

−2

−1

01

2 0.02

0.04

0.06

0.08

0.1

0.12 0.14

−2 −1 0 1 2−

2−

10

12

0.02

0.04

0.06

0.08

0.1

0.12 0.14

0.1

6

−2 −1 0 1 2

−2

−1

01

2 0.02

0.04 0.06

0.08

0.1

0.12 0.14

0.1

6

−2 −1 0 1 2

−2

−1

01

2

0.02

0.04

0.06 0.08

0.1

0.12

0.14

−2 −1 0 1 2

−2

−1

01

2 0.02 0.04

0.06 0.08 0.1

0.12

0.14

−2 −1 0 1 2

−2

−1

01

2

10

Chapter 2

Tail-weighted measures of

dependence

In this chapter we define some measures of dependence for bivariate copulasthat put more weight in the tails and thus allow to estimate dependence inthe tails more efficiently. The measures are defined for continuous variablesand they are not applicable for discrete variables. These types of measuresare important because there are no exact counterparts to the tail dependencecoefficients and tail orders which are defined through limits. The measurescan be used as a diagnostic tool to detect possible departures from the nor-mal copula, such as stronger dependence in the tails or tail asymmetry. Fora bivariate copula C, we denote theoretical values of dependence measuresin the lower (upper) tail by L(C) (U (C), respectively). There will be twoclasses of such measures. Then we consider

L(C)− U (C) (2.1)

as a tail-weighted measure of asymmetry,

L(C)− L(CN (·; ρ)) (2.2)

as a lower tail-weighted measure of departure from the bivariate normalcopula CN (·; ρ) with ρ chosen as the correlation of normal scores (see (2.6)below) based on C, and

U (C)− U (CN (·; ρ)) (2.3)

as an upper tail-weighted measure of departure from the bivariate normalcopula. For data which are assumed to be realizations of a random sample,we use the sample version of these measures, where C is replaced by anempirical copula and ρ by the sample correlation of normal scores.

We will define tail-weighted measures that depend on a weighting func-tion and a truncation level. We expect a good tail-weighted measure of de-pendence to discriminate data from the normal and Student t copulas. The

11

2.1. Tail-weighted measures of dependence: definition and properties

sample versions of the measures L, U are then the correlation of rankeddata transformed using a weighting function. In other words, the originaldata are converted to uniform ranks and the ranks are then transformed us-ing a monotone function. Since we define our measures for truncated data,there are two versions of L, U . The first version is obtained when theoriginal data truncated in the lower (upper) tail first and then the trun-cated data converted to uniform ranks. For the second version, the originaldata are converted to uniform ranks and the ranks are then truncated in thelower (upper) tail.

Details are given in Section 2.1 for the probabilistic version and Section2.2 for the sample version. Included is a demonstration of how tail-weighteddependence measures can distinguish different copula families with the sameoverall dependence measures such as Kendall’s tau or Spearman’s rho.

2.1 Tail-weighted measures of dependence:

definition and properties

Let a(·) : [0, 1] → (0,∞) be a continuous and strictly increasing functionand let p be a truncation level satisfying 0 < p ≤ 0.5. For a bivariatecopula C, let (U1, U2) ∼ C and let (V1, V2) be distributed with the copulaCp corresponding to conditional distribution of (U1, U2|U1 < p,U2 < p). Forthe lower tail, define

TRL (C, a, p) = cor(a(1− V1), a(1 − V2))

=E[a(1 − V1) a(1− V2)]− E[a(1− V1)]E[a(1 − V2)]

{Var[a(1 − V1)] ·Var[a(1− V2)]}1/2,

RTL (C, a, p) = cor(a(1− U1/p), a(1 − U2/p) | U1 < p,U2 < p)

=Cov[a(1− U1/p), a(1 − U2/p)|U1 < p,U2 < p]

{Var[a(1− U1)|U1 < p,U2 < p] · Var[a(1 − U2/p)|U1 < p,U2 < p]}1/2 .

(2.4)

The notation TRL = TRL (C, a, p) and RTL = RTL (C, a, p) indicates the mea-sure depends on the bivariate copula C, weighting function a(·) and trun-cation level p. The superscript TR (RT) means that truncation is donebefore ranking (after ranking, respectively). For the brevity of notation wewill write TRL and RTL unless we want to indicate a particular copula C,weighting function a(·) or truncation level p.

12

2.1. Tail-weighted measures of dependence: definition and properties

The measure TRU (RTU ) is defined as TRL (RTL , respectively) with thesame weighting function a(·) and truncation level p, applied to univariatemargins of the negative of the variable. Equivalently, the measures areapplied to CR, where the copula CR(u1, u2) = −1+u1+u2+C(1−u1, 1−u2)is the distribution of (U1, U2) = (1 − U1, 1 − U2) when (U1, U2) ∼ C. Let(W1,W2) be a bivariate vector distributed with copula CRp corresponding

to the conditional distribution of (U1, U2|U1 < p, U2 < p), then

TRU (C, a, p) = cor(a(1−W1), a(1 −W2)),

RTU (C, a, p) = cor(a(1− U1/p), a(1 − U2/p) | U1 < p, U2 < p). (2.5)

Special cases of the measures defined above have been proposed previ-ously. Schmid and Schmidt (2007) define a conditional Spearman rho thatcorresponds to TRL and TRU with a(u) = u and 0 < p ≤ 0.5. Letting Φbe the standard normal cdf, if we take a(u) = Φ−1(0.5(1 + u)) and p = 0.5for RTL , we get the semicorrelation of normal scores, that is, the correlationof data in the lower tail, transformed using inverse normal cdf. Semicor-relations were employed in some publications to study the comovementsof financial assets; see for example Ang and Chen (2002) and Gabbi (2005).These semicorrelations of normal scores naturally follow as a diagnostic fromNikoloulopoulos et al (2012), where it is advocated to plot pairs of variablesafter a normal score transform in order to check for deviations from theelliptical shape scatterplot expected for the bivariate normal copula.

When a(u) = Φ−1(0.5(1 + u)), we use the following notation for RTL .If (Z1, Z2) ∼ C(Φ,Φ) and (U1, U2) ∼ C, we define the correlation of thenormal scores as

ρN (C) = cor[Φ−1(U1),Φ−1(U2)] = cor(Z1, Z2), (2.6)

and the upper and lower semi-correlations (of normal scores) are defined as

ρ+N (C) = cor[Z1, Z2|Z1 > 0, Z2 > 0],

ρ−N (C) = cor[Z1, Z2|Z1 < 0, Z2 < 0]. (2.7)

When C = CN (·; ρ) is the bivariate normal copula with parameter ρ, thenρN = ρ and using results in Shah and Parikh (1964),

+N (CN ) = −N (CN ) =v1,1(ρ)− v21,0(ρ)

v2,0(ρ)− v21,0(ρ),

where v1,0(ρ) = (1+ ρ)/[2β0√2π ], v2,0(ρ) = 1+ ρ

√1− ρ2 /[2πβ0], v1,1(ρ) =

ρ+√

1− ρ2 /[2πβ0], β0(ρ) =1

4+ (2π)−1 arcsin(ρ).

13

2.1. Tail-weighted measures of dependence: definition and properties

However, ρ−N , ρ+N and the conditional Spearman rho might not be suffi-

ciently sensitive to the dependence in the tail. We aim to find better choicesof the combination of a transformation function a(·) and truncation levelp. We expect a good measure of dependence in the lower tail based on theweighting function a(·) should have the following properties:

i a(·) is an increasing function: a(1− u) is larger if u is closer to zero.

ii∫ 10 a

4(u)du < ∞: the existence of the fourth moment ensures asymp-totic normality of the sample versions of TRL , RTL .

The following properties follow from i, ii:

iii V1 = V2 (given that U1 < p, U2 < p) or U1 = U2 if and only if TRL = 1or RTL = 1 respectively (comonotonic in the tail).

iv V1 = 1 − V2 (given that U1 < p, U2 < p) or U1 = p − U2 if and onlyif TRL = −1 or RTL = −1 respectively (countermonotonic in the tail).

v If V1, V2 or U1, U2 are independent, then TRL = 0 or RTL = 0 respec-tively (independence in the tail).

Monotonicity of the weighting function is important to guarantee thatthe maximum (minimum) value of the measure can only be achieved whenthere is perfect comonotonic (countermonotonic, respectively) dependencein the tail (properties iii and iv). Then we expect large (small) positive val-ues of L(a, p) and U (a, p) to indicate that dependence in the tails of C isstrong (weak, respectively). However these tail-weighted dependence mea-sures (and likewise the tail dependence parameters) do not satisfy some prop-erties of positive dependence measures as given in Kimeldorf and Sampson(1989); for example, they are not defined for some copulas such as the coun-termonotonic copula that has zero probability on the set U1 < p,U2 < p for0 < p < 0.5. The criterion of tail weighting is to provide information notavailable from the commonly used positive dependence measures.

We next show that the tail-weighted measures of dependence can distin-guish members of common parametric copula families that have the sameSpearman’s rho. We will use 6 copula families to make comparisons in thisdissertation: Gaussian, Student, Gumbel, Frank, MTCJ and BB1 copulas.

In Section 2.2, we provide some theory and computations that suggestgood choices are a(u) = u5 with p = 0.5 for TRL , TRU , and a(u) = u6 withp = 0.5 for RTL , RTU . To demonstrate that these measures can discriminatethe tails of different common bivariate copula families, we show some valuesof ρ−S (C), ρ+S (C) (conditional Spearman rho in lower and upper quadrants),ρ−N (C), ρ−N (C), TRL (C), TRU (C), RTL (C), RTU (C) for some copulas C with

14

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

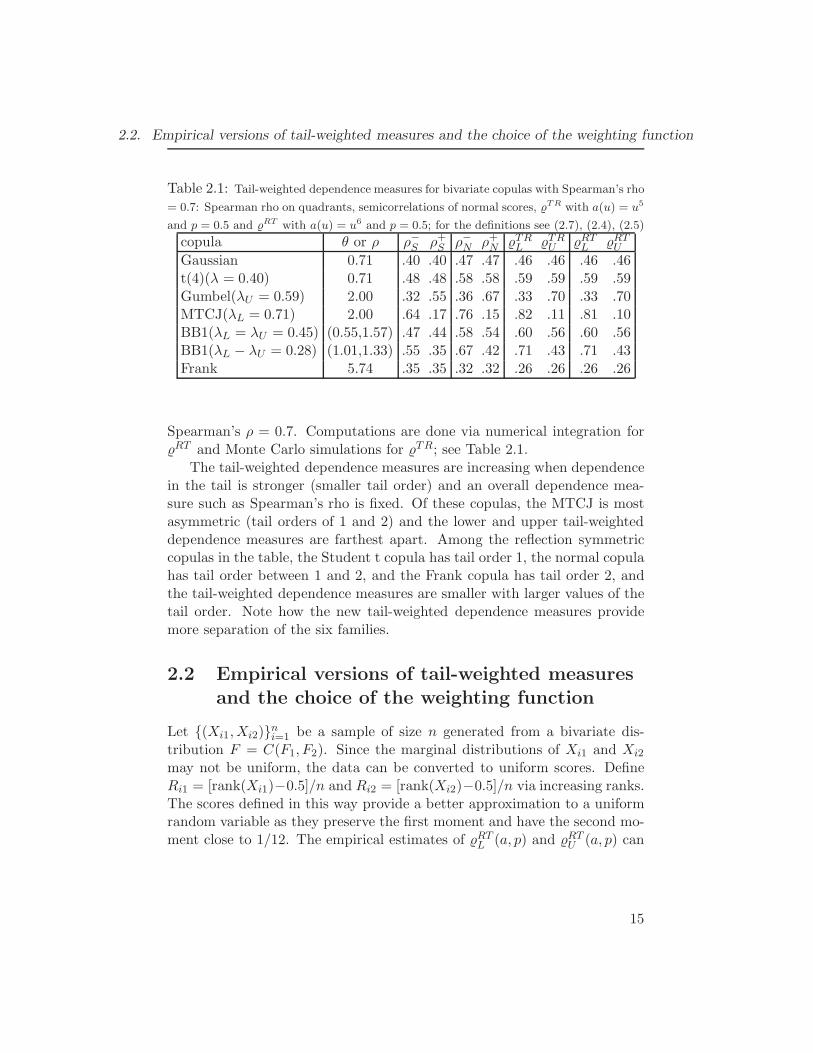

Table 2.1: Tail-weighted dependence measures for bivariate copulas with Spearman’s rho

= 0.7: Spearman rho on quadrants, semicorrelations of normal scores, TR with a(u) = u5

and p = 0.5 and RT with a(u) = u6 and p = 0.5; for the definitions see (2.7), (2.4), (2.5)

copula θ or ρ ρ−S ρ+S ρ−N ρ+N TRL TRU RTL RTUGaussian 0.71 .40 .40 .47 .47 .46 .46 .46 .46t(4)(λ = 0.40) 0.71 .48 .48 .58 .58 .59 .59 .59 .59Gumbel(λU = 0.59) 2.00 .32 .55 .36 .67 .33 .70 .33 .70MTCJ(λL = 0.71) 2.00 .64 .17 .76 .15 .82 .11 .81 .10BB1(λL = λU = 0.45) (0.55,1.57) .47 .44 .58 .54 .60 .56 .60 .56BB1(λL − λU = 0.28) (1.01,1.33) .55 .35 .67 .42 .71 .43 .71 .43Frank 5.74 .35 .35 .32 .32 .26 .26 .26 .26

Spearman’s ρ = 0.7. Computations are done via numerical integration forRT and Monte Carlo simulations for TR; see Table 2.1.

The tail-weighted dependence measures are increasing when dependencein the tail is stronger (smaller tail order) and an overall dependence mea-sure such as Spearman’s rho is fixed. Of these copulas, the MTCJ is mostasymmetric (tail orders of 1 and 2) and the lower and upper tail-weighteddependence measures are farthest apart. Among the reflection symmetriccopulas in the table, the Student t copula has tail order 1, the normal copulahas tail order between 1 and 2, and the Frank copula has tail order 2, andthe tail-weighted dependence measures are smaller with larger values of thetail order. Note how the new tail-weighted dependence measures providemore separation of the six families.

2.2 Empirical versions of tail-weighted measures

and the choice of the weighting function

Let {(Xi1,Xi2)}ni=1 be a sample of size n generated from a bivariate dis-tribution F = C(F1, F2). Since the marginal distributions of Xi1 and Xi2

may not be uniform, the data can be converted to uniform scores. DefineRi1 = [rank(Xi1)−0.5]/n and Ri2 = [rank(Xi2)−0.5]/n via increasing ranks.The scores defined in this way provide a better approximation to a uniformrandom variable as they preserve the first moment and have the second mo-ment close to 1/12. The empirical estimates of RTL (a, p) and RTU (a, p) can

15

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

be defined as the sample correlations of the ranked data:

RTL (a, p) = Cor

[a

(1− Ri1

p

), a

(1− Ri2

p

) ∣∣∣∣Ri1 < p, Ri2 < p

],

RTU (a, p) = Cor

[a

(1− Ri1

p

), a

(1− Ri2

p

) ∣∣∣∣Ri1 < p, Ri2 < p

],

where Rij = 1−Rij, j = 1, 2, and the notation Cor[yi1, yi2|(yi1, yi2) ∈ B] isthe shorthand for

∑i∈JB yi1yi2 − n−1

B

∑i∈JB yi1

∑i∈JB yi2[∑

i∈JB y2i1 − n−1

B

(∑i∈JB yi1

)2]1/2[∑i∈JB y

2i2 − n−1

B

(∑i∈JB yi2

)2]1/2 ,

with JB = {i : (yi1, yi2) ∈ B} and nB is the cardinality of JB .To obtain the empirical estimates of TRL (a, p) and TRU (a, p) we define the

uniform scores of data truncated in the tails: R−i1 = [rank(Vi1) − 0.5]/nL,

R+i1 = [rank(Wi1) − 0.5]/nU , where {(Vi1, Vi2)}nL

i=1 = {(Ri1, Ri2) : Ri1 <p,Ri2 < p, i = 1, ..., n}, {(Wi1,Wi2)}nU

i=1 = {(Ri1, Ri2) : Ri1 > p,Ri2 >p, i = 1, ..., n}. The estimates can then be defined as the sample correlations:

TRL (a, p) = Cor[a(1−R−

i1

), a(1−R−

i2

)],

TRU (a, p) = Cor[a(R+i1

), a(R+i2

)].

Under mild conditions on the weighting function a(·), the empirical esti-mates for both versions of the measures are asymptotically normal as statednext.

Proposition 2.1 Let a(·) be a continuously differentiable function on [0, 1]such that a(0) = 0 and let C be a bivariate copula cdf with continuouspartial derivatives of the first order. Then TRL (a, p), TRU (a, p) and RTL (a, p),RTU (a, p) are asymptotically normal as the sample size n→ ∞.

Proof: See Appendix A.

A good choice of the truncation level p and the weighting function a(·) isimportant for the measure to discriminate well copula families with differenttail properties. Without loss of generality, we now restrict our attentionto the lower tail. More formally, assume that we have two samples frombivariate copulas C1 and C2 with the same value of Spearman’s ρS but withdifferent tail properties. We want the difference

∆(a, p;C1, C2) = L(a, p;C1)− L(a, p;C2) (2.8)

16

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

to be large in absolute value and the variance σ2(∆) of the estimate∆(a, p;C1, C2) = L(a, p;C1) − L(a, p;C2) to be small so that the largeabsolute value of ∆(a, p;C1, C2) does not have a big standard error. Thisis also important for assessing how different copula models fit data in thetails. When likelihood maximization is used to estimate copula parameters,the model-based estimates of Spearman’s ρS or other measure of overallmonotone dependence can be about the same for different models. Thereason is that the overall dependence characteristics such as Spearman’s ρSare often estimated fairly well by the likelihood regardless of the copulachoice but tail characteristics can be estimated very poorly.

It is seen that in the case of copula C+ with comonotonic dependencein the lower tail, we get TRL (a, p;C+) = RTL (a, p;C+) = 1 and the varianceof the sampling distribution is σ2(TRL ) = σ2(RTL ) = 0. With the indepen-dence copula C⊥(u, v) = uv, we get TRL (a, p;C⊥) = RTL (a, p;C⊥) = 0 andσ2(TRL ) = σ2(RTL ) = 1/p2 as follows from the next result.

Proposition 2.2 Let a(·) be a weighting function satisfying the conditionsof Proposition 1 and C⊥ be bivariate independence copula. It follows thatthe asymptotic variance σ2(TRL (a, p;C⊥)) = σ2(RTL (a, p;C⊥)) = 1/p2.

Proof: See Appendix B.

This result implies that with weak to moderate overall dependence asmeasured by Spearman’s ρS or Kendall’s τ , it is preferable to use largervalue of the truncation level p as the standard errors of the estimates for Lare smaller and the weighting function can be chosen to make the difference∆(a, p;C1, C2) large in absolute value for C1, C2 with different lower tailproperties. This is especially important if the sample size is small so thatsmaller values of p result in a very small truncated sample size to estimateL.

To illustrate these ideas, we consider the power weighting functionsa(u) = uk with k = 1, 2, . . .. The power weighting functions satisfy allconditions of Proposition 2.1 and, with larger k, more weight is put in thejoint tail, whereas with small values of k even those points far from the tailreceive quite large weights. To compute L(a, p;C) for a given bivariatecopula C, one can use the formula:

TRL (a, p;C) =

∫ 1

0

∫ 1

0a′(1− u1)a

′(1− u2)C(p)L (u1, u2) du1du2,

where C(p)L (u1, u2) is the copula corresponding to the cdf F (u1, u2) =

17

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

C(u1, u2)/C(p, p), u1 < p, u2 < p of data truncated in the lower tail, and

RTL (a, p;C) =C(p, p)m12 −m1m2

[{C(p, p)m11 −m21}{C(p, p)m22 −m2

2}]1/2,

where

m12 =1

p2

∫ p

0

∫ p

0a′(1− u1/p) a

′(1− u2/p)C(u1, u2) du1du2,

m1 =1

p

∫ p

0a′(1−u1/p)C(u1, p) du1, m2 =

1

p

∫ p

0a′(1−u2/p)C(p, u2) du2,

m11 =1

p

∫ p

02a(1− u1/p) a

′(1− u1/p)C(u1, p) du1,

m22 =1

p

∫ p

02a(1− u2/p) a

′(1− u2/p)C(p, u2) du2;

see the proof of Proposition 2.1 for details. All integrands here are boundedfunctions so that numerical integration should be fast and stable for RTL . To

compute the measure TRL , the copula C(p)L (u1, u2) is needed and therefore

the inverse functions for C(u1, p)/C(p, p) and C(p, u2)/C(p, p) are required.Computation of these inverse functions can be time-consuming and there-fore computation of the measure RTL is faster. With some other weightingfunctions, such as the semi-correlations of normal scores, the integrands areunbounded so that numerical integration can be slower for both measures.This is especially important if one wants to compute the model-based esti-mates of the measures for each pair of variables in a multidimensional dataset.

In practice using copulas with intermediate dependence (tail order 1 <κ < 2 based on Hua and Joe (2011)) or tail quadrant independence (κ = 2and the slowly varying function is a constant) can lead to incorrect inferencesin the tails if the true copula is tail dependent. It means that a good mea-sure of tail-weighted dependence should discriminate well copulas with taildependence and copulas that are not tail dependent. We use the followingbivariate parametric copula families for comparisons in the tails.

• Student t copula with 4 degrees of freedom: This is a reflection sym-metric tail dependent copula.

• Gaussian copula: This is a reflection symmetric copula with interme-diate dependence for 0 < ρ < 1. The tail order is κL = 2/(1 + ρ) andit gets closer to 1 as ρ increases. Therefore it is harder to discriminatethe Student t and Gaussian copulas if the overall dependence is strong.

18

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

• Gumbel copula: This is a tail asymmetric copula with intermediatelower tail dependence; the tail order is κL = 21/θ where θ > 1 is thecopula dependence parameter.

• Reflected Gumbel (rGumbel) copula: This is a tail asymmetric copulawith lower tail dependence.

• Frank copula: This is a reflection symmetric copula with tail quadrantindependence.

• BB1 copula: This is a tail asymmetric and tail dependent copula.

More details on these copulas can be found in Joe (1997) and Nelsen(2006). Results on how tail properties of the bivariate linking copulas af-fect the tail properties of the bivariate margins of vine models are given inJoe et al. (2010). The various tail-weighted dependence measures can dis-criminate strength of dependence in the tail somewhat like the (limiting)tail order, since the t4 and BB1 copulas have lower and upper tail order of1, the Gaussian copula has lower and upper tail order in (1, 2) for 0 < ρ < 1,the Gumbel copula has κU = 1 and κL ∈ (1, 2) and the Frank copula hasκL = κU = 2; see Table 2.2. Note that the conditional Spearman’s rhos andthe normal scores semi-correlations are less sensitive (especially the former,as seen in Table 2.2) to stronger dependence in the tails and tail asymmetry.

Assuming the Spearman’s ρ is constant, the tail-weighted measures takelarger values for copulas with stronger dependence in the tails. Comparingto copulas with intermediate dependence, the values RTL , RTU are largerfor copulas with tail dependence (the Student, BB1 copulas) and smallerfor copulas with tail quadrant independence (the Frank copula). For taildependent copulas the values RTL , RTU are larger for copulas with larger taildependence coefficients λL and λU . For example, for the tail dependent BB1copula, the tail-weighted dependence measures L and U discriminate wellthree different cases when dependence in the lower tail is about equal (withquite close values of the tail-weighted measures), weaker (with RTL < RTU )or stronger (with RTL > RTU ) than dependence in the upper tail.

The next step is a comparison of a(·) functions that can be used for thetail-weighted dependence measures; we use power functions for a(·) as theresulting measures are fast to compute. We start with the measures RTL ,RTU .

In Table 2.3, we compute ∆(a, p = 0.5;C1, C2) in (2.8) for two copulasC1, C2 with the same value of Spearman’s ρS such that C1 is a tail depen-dent copula and C2 is not; also asymptotic standard errors are included.

19

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

Table 2.2: Tail-weighted dependence measures: ρL and ρU (conditional Spearman’s

rhos), ρ−N and ρ+N (semi-correlations), and RTL , RT

U with a(u) = u6, p = 0.5, for different

bivariate copulas with Spearman’s rho equals 0.7; for the definitions see (2.7), (2.4), (2.5)

copula (λL, λU ) (κL, κU ) ρL ρU ρ−N ρ+N RTL RTUGaussian (.00, .00) (1.17, 1.17) .40 .40 .47 .47 .46 .46t(4) (.40, .40) (1.00, 1.00) .48 .48 .58 .58 .59 .59BB1 (.45, .45) (1.00, 1.00) .47 .44 .58 .54 .60 .56BB1 (.08, .55) (1.00, 1.00) .37 .52 .45 .64 .43 .66BB1 (.66, .20) (1.00, 1.00) .59 .27 .71 .34 .76 .31Gumbel (.00, .59) (1.41, 1.00) .32 .55 .36 .67 .33 .70Frank (.00, .00) (2.00, 2.00) .35 .35 .32 .32 .26 .26

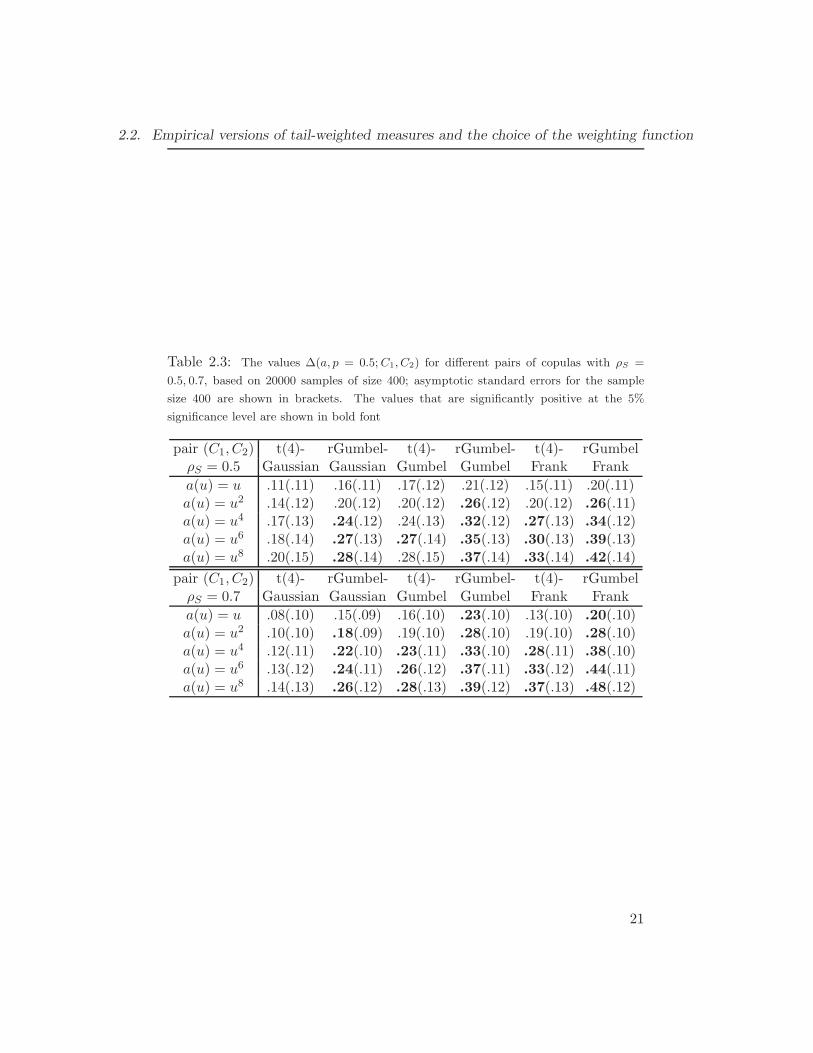

Spearman’s ρS equals 0.5 in the top part of the table and 0.7 in the bot-tom part. Standard errors with the sample size equals 400 are computedusing Monte-Carlo simulations. An alternative way is to use delta-methodto obtain the formula for σ(∆(a, p;C1, C2)) and then use numerical integra-tion. It is seen, that a higher power k results in a larger absolute difference|∆(a, p;C1, C2)|. The main difference between the tail dependent copula C1

and the copula C2 with intermediate dependence or tail quadrant indepen-dence can be found in the tail. The power function with large k puts moreweight in the tail and thus makes the difference ∆(a, p;C1, C2) larger. Thestandard errors of the empirical version increase slowly unless the power kis very large. The ratio ∆/σ(∆) attains its maximum at k in the interval 6to 8 for all pairs of copulas considered in Table 2.3. It implies that k = 6can be a good choice when the absolute difference |∆(a, p;C1, C2)| is quitelarge and the asymptotic variance is reasonably small.

The values |∆(a, p;C1, C2)| can be slightly larger for p smaller than 0.5but the asymptotic variance increases significantly so that there is no im-provement. To illustrate this, we compute RTL (a, p;C) with a(u) = u6 forGaussian copula and reflected Gumbel copula with different ρS and differenttruncation levels p; see Table 2.4. Similar results can be obtained for otherpairs of copulas. With ρS = 0 we have L = 0 and the asymptotic varianceequals 1/p2. With larger ρS the variance can increase slightly but eventuallyit goes to zero as ρS goes to 1. It is seen that with smaller p < 0.5, the stan-dard errors are larger whereas the values of the tail-weighted measures donot change much. As a result, we propose to use p = 0.5 and a(u) = u6 forthe tail-weighted measures of dependence RTL (a, p) and RTU (a, p) in section

20

2.2. Empirical versions of tail-weighted measures and the choice of the weighting function

Table 2.3: The values ∆(a, p = 0.5;C1, C2) for different pairs of copulas with ρS =

0.5, 0.7, based on 20000 samples of size 400; asymptotic standard errors for the sample

size 400 are shown in brackets. The values that are significantly positive at the 5%

significance level are shown in bold font

pair (C1, C2) t(4)- rGumbel- t(4)- rGumbel- t(4)- rGumbelρS = 0.5 Gaussian Gaussian Gumbel Gumbel Frank Frank

a(u) = u .11(.11) .16(.11) .17(.12) .21(.12) .15(.11) .20(.11)a(u) = u2 .14(.12) .20(.12) .20(.12) .26(.12) .20(.12) .26(.11)a(u) = u4 .17(.13) .24(.12) .24(.13) .32(.12) .27(.13) .34(.12)a(u) = u6 .18(.14) .27(.13) .27(.14) .35(.13) .30(.13) .39(.13)a(u) = u8 .20(.15) .28(.14) .28(.15) .37(.14) .33(.14) .42(.14)

pair (C1, C2) t(4)- rGumbel- t(4)- rGumbel- t(4)- rGumbelρS = 0.7 Gaussian Gaussian Gumbel Gumbel Frank Frank

a(u) = u .08(.10) .15(.09) .16(.10) .23(.10) .13(.10) .20(.10)a(u) = u2 .10(.10) .18(.09) .19(.10) .28(.10) .19(.10) .28(.10)a(u) = u4 .12(.11) .22(.10) .23(.11) .33(.10) .28(.11) .38(.10)a(u) = u6 .13(.12) .24(.11) .26(.12) .37(.11) .33(.12) .44(.11)a(u) = u8 .14(.13) .26(.12) .28(.13) .39(.12) .37(.13) .48(.12)

21

2.3. Normal scores plots and tail-weighted measures of dependence

Table 2.4: The values RTL (a, p;C) for Gaussian and reflected Gumbel copula with

different Spearman’s rho, based on 20000 samples of size 400; asymptotic standard errors

for the sample size 400 are shown in brackets

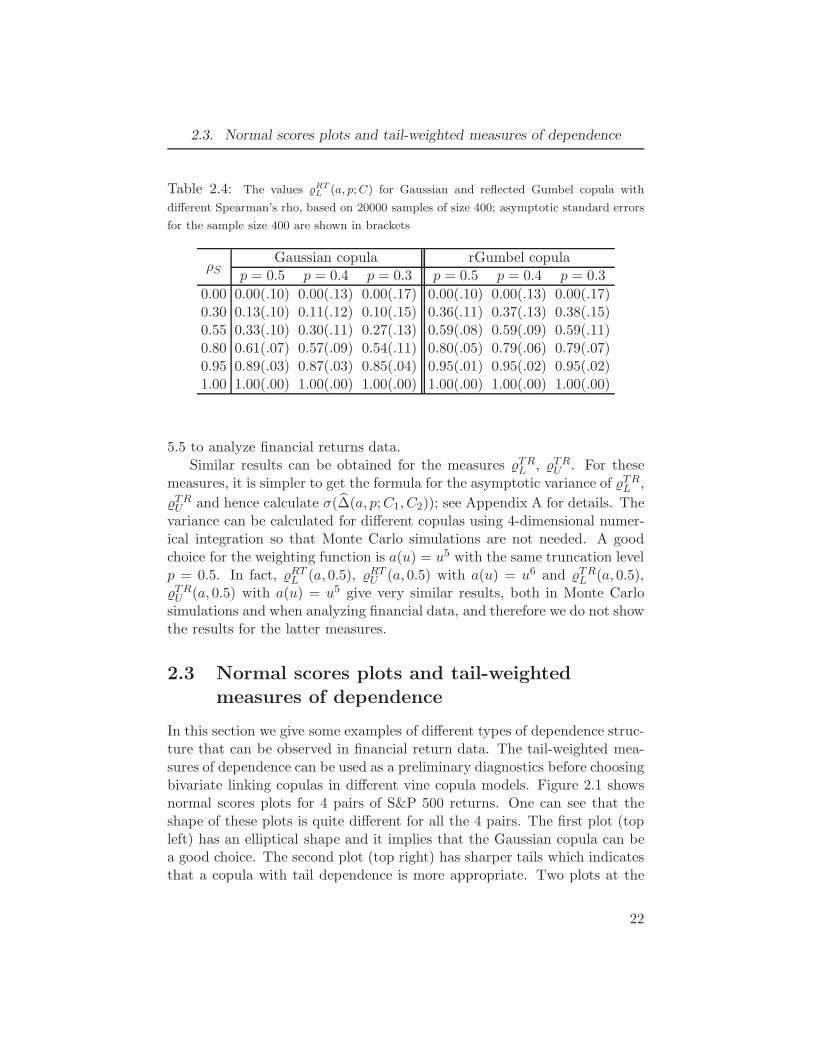

ρSGaussian copula rGumbel copula

p = 0.5 p = 0.4 p = 0.3 p = 0.5 p = 0.4 p = 0.3

0.00 0.00(.10) 0.00(.13) 0.00(.17) 0.00(.10) 0.00(.13) 0.00(.17)0.30 0.13(.10) 0.11(.12) 0.10(.15) 0.36(.11) 0.37(.13) 0.38(.15)0.55 0.33(.10) 0.30(.11) 0.27(.13) 0.59(.08) 0.59(.09) 0.59(.11)0.80 0.61(.07) 0.57(.09) 0.54(.11) 0.80(.05) 0.79(.06) 0.79(.07)0.95 0.89(.03) 0.87(.03) 0.85(.04) 0.95(.01) 0.95(.02) 0.95(.02)1.00 1.00(.00) 1.00(.00) 1.00(.00) 1.00(.00) 1.00(.00) 1.00(.00)

5.5 to analyze financial returns data.Similar results can be obtained for the measures TRL , TRU . For these

measures, it is simpler to get the formula for the asymptotic variance of TRL ,

TRU and hence calculate σ(∆(a, p;C1, C2)); see Appendix A for details. Thevariance can be calculated for different copulas using 4-dimensional numer-ical integration so that Monte Carlo simulations are not needed. A goodchoice for the weighting function is a(u) = u5 with the same truncation levelp = 0.5. In fact, RTL (a, 0.5), RTU (a, 0.5) with a(u) = u6 and TRL (a, 0.5),TRU (a, 0.5) with a(u) = u5 give very similar results, both in Monte Carlosimulations and when analyzing financial data, and therefore we do not showthe results for the latter measures.

2.3 Normal scores plots and tail-weighted

measures of dependence

In this section we give some examples of different types of dependence struc-ture that can be observed in financial return data. The tail-weighted mea-sures of dependence can be used as a preliminary diagnostics before choosingbivariate linking copulas in different vine copula models. Figure 2.1 showsnormal scores plots for 4 pairs of S&P 500 returns. One can see that theshape of these plots is quite different for all the 4 pairs. The first plot (topleft) has an elliptical shape and it implies that the Gaussian copula can bea good choice. The second plot (top right) has sharper tails which indicatesthat a copula with tail dependence is more appropriate. Two plots at the

22

2.3. Normal scores plots and tail-weighted measures of dependence

Table 2.5: The estimates of ∆L, ∆U , ∆R; for 4 pairs of S&P 500 log-returns; the 95%

confidence intervals are shown in brackets

pair ∆L ∆U ∆R;

(CINF, AFL) -0.05 (-0.27, 0.16) 0.03 (-0.17, 0.20) -0.08 (-0.38, 0.23)(AFL, TMK) 0.28 ( 0.06, 0.44) 0.26 ( 0.07, 0.44) 0.02 (-0.27, 0.27)(PSA, AXP) 0.27 ( 0.06, 0.45) -0.28 (-0.45,-0.05) 0.55 ( 0.22, 0.80)(HCP, MET) -0.27 (-0.44,-0.03) 0.27 ( 0.06, 0.43) -0.54 (-0.78,-0.21)

bottom have an asymmetric shape and so an asymmetric copula should fitthe data better.

However, it is not always clear what shape a normal scores plot has andthe tail-weighted measures can be used as a diagnostics to select an appro-priate bivariate copula for a pair of variables. To illustrate the ideas, wecompute RTL , RTU for the aforementioned pairs of variables. Note that themeasures RTL , RTU take larger values if the overall dependence as measuredby Spearman’s ρ or Kendall’s τ is stronger. It means that the large valuesof the measures alone do not imply strong dependence in the tails. Givena fixed Spearman’s ρ, the measures take larger values for stronger depen-dence in the tails as we showed in the previous section. Therefore we usethe Gaussian copula as a benchmark and compute the parametric estimateof these measures assuming the joint normality for each pair. Because ofsymmetric dependence of the Gaussian copula we get the same value of themeasure in the lower and upper tail; we denote these value by RTN . Underthis assumption, one can calculate an estimate of Spearman’s rho ρS andthen transform it to the Gaussian copula correlation parameter ρ using therelationship ρ = 2 sin(πρS/6). Numerical integration and formulas from theprevious section can be used to obtained a parametric estimate ˆRTN .

For comparisons in the tails, and define ∆L = L − N and ∆U =U − N to adjust for the overall dependence. We also define ∆R; = L −U to compare the strength of dependence in the lower and upper tails.Under the assumption of normality one can use the asymptotic normalityof estimates ∆L = ˆL− ˆN , ∆U = ˆU − ˆN to construct the 95% confidenceintervals for ∆L, ∆U . Similar, the 95% intervals can be obtained for ∆R;

assuming reflection symmetry. For the intervals, the asymptotic variancecan be estimated using the bootstrap. In Table 2.5 we show the estimates of∆L, ∆U , ∆R; together with the 95% confidence intervals that were obtainedusing the bootstrap.

23

2.3. Normal scores plots and tail-weighted measures of dependence

Figure 2.1: Normal scores scatter plots for 4 pairs of financial log-returns; S&P500 data,

financial sector, pair (CINF, APL), year 2007 (top left); pair (AFL, TMK), year 2008 (top

right); pair (PSA, AXP), year 2008 (bottom left); pair (HCP, MET), year 2007 (bottom

right)

−3 0 3

−30

3

CINF

AF

L

−3 0 3

−30

3

AFL

TM

K

−3 0 3

−30

3

PSA

AX

P

−3 0 3

−30

3

HCP

ME

T

24

2.3. Normal scores plots and tail-weighted measures of dependence

For the pair (CINF, AFL) all the three confidence intervals contain zeroso that there are no significant departures from normality. For the pair(AFL, TMK), the lower bound of the first two confidence intervals is greaterthan zero and this indicates that dependence in both tails is significantlystronger comparing to the Gaussian copula. At the same time, there is noevidence of tail asymmetry. It means a symmetric copula with tail depen-dence is a better choice for this pair. The last two pairs, (PSA, AXP) and(HCP, MET), has an asymmetric dependence as the third confidence intervaldoes not contain zero. The first of these two pairs has stronger dependencein the lower tail and weaker dependence in the upper tail, comparing to theGaussian copula. And the second pair has stronger dependence in the uppertail and weaker dependence in the lower tail. It implies that an asymmetriccopula with tail dependence in one tail is needed for these pairs.

Note that because of a large variability, especially if the sample size isnot very large, the 95% confidence intervals can be quite wide and containthe estimates ∆L, ∆U , ∆R; despite the large values for these estimates. Wesuggest using non-Gaussian copula if the estimates are close to the lower orupper boundaries of the confidence intervals. The choice of the copula willthen depend on the sign of these estimates. The primary goal of the mea-sures is not testing against normality but rather providing some guidancein choosing more appropriate bivariate copula depending on the estimatedstrength of dependence in the tails, especially if consistent tail asymmetry orstronger dependence than that for bivariate Gaussian tails is seen in manypairs of variables.

25

Chapter 3

Measures of asymmetry

based on the empirical

copula process

In this chapter we introduce some other measures of dependence asymmetryfor two variables for multivariate data, these can be applied to each pair.Two types of asymmetry will be considered: reflection asymmetry and per-mutation asymmetry. For each of these types of asymmetry, we proposemeasures that are based on the empirical copula process. This approachuse all data unlike the measures proposed in Section 2.2 where only datatruncated in the tails are used. Unlike the measures L, U , the measuresproposed in this chapter use data from the middle of the distribution aswell and this allows to detect possible asymmetric dependence structurein the middle of the distribution and not in the tails (especially for per-mutation asymmetry). When combined with the tail-weighted measures ofdependence, the measures of asymmetry can provide useful summaries ofthe dependence structure. This can help to select suitable bivariate linkingcopulas at the first level of vine or factor copula models.

Assume that (U1, U2) ∼ C where C is a bivariate copula. Throughoutthis section, we will assume that C satisfies the regularity conditions ofProposition 2.1 in Section 2.2. If C is a reflection symmetric copula then∆R := C(u1, u2) − CR(u1, u2) = 0 for all u1, u2 ∈ [0, 1]. Similarly, if C isa permutation symmetric copula, we get ∆P := C(u1, u2) − C(u2, u1) = 0for all u1, u2 ∈ [0, 1]. The idea is to find a functional G(∆) : R2 → R for∆ = ∆R (∆ = ∆P ) such that G(∆) = 0 if and only if the copula C is areflection (respectively, permutation) symmetric copula.

Typical choices for G include the integral of ∆2 or supremum of |∆| overthe unit square: G(∆) =

∫ ∫[0,1]2 ∆

2(u1, u2)du1du2, G(∆) =

sup[0,1]2 |∆(u1, u2)|. Tests of permutation symmetry based on these twofunctionals are proposed in Genest et al. (2012). However the exact distri-bution of the corresponding test statistic under the null hypothesis: H0 :

26

3.1. Measures of reflection asymmetry

∆P ≡ 0 is unknown and depends on the copula C so the authors designa method to get bootstrap replicates of the test statistic and compute P-values. It makes this method of testing relatively slow especially when oneneeds to measure asymmetry for each pair of multidimensional data set. Alsothis functional does not provide information on the direction of asymmetry.The power of the proposed tests may not be very high unless permutationasymmetry is quite strong.

At the same time, any non-degenerate linear transformation of ∆ resultsin a statistic with asymptotic normal distribution. In other words, if wedefine the functional G as follows:

G(∆) =

∫ 1

0

∫ 1

0w(u1, u2)∆(u1, u2)du1du2, (3.1)

the asymptotic distribution of G(∆) = G(∆) will be normal where ∆ is anestimate of ∆ obtained from a sample and w(u1, u2) is a weighting function.It is important that this function does not depend on data and hence thecopula C. The simplest choice w(u1, u2) = 1 results in the degeneratetransformation ∆(G) ≡ 0 since ∆P (u1, u2) = −∆P (u1, u2) and ∆R(u1, u2) =−∆R(1 − u1, 1 − u2) so that the resulting integral equals zero. Thereforemore careful choice of the weighting function w is required. Below we providesome choices for w that work well for ∆R and ∆P .

3.1 Measures of reflection asymmetry