Sri Lanka: Multimodal Transport Project

223

Technical Assistance Consultant’s Report This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design. Project Number: 41249-022 June 2012 Sri Lanka: Multimodal Transport Project (Financed by the Japan Fund for Poverty Reduction) Main Report Volume 2 – Costs, Revenue, Financial Analysis, Economic Appraisal Prepared by Roughton International Ltd., in association with Nippon Koei Co., Ltd. and Engineering Consultants Ltd. United Kingdom For Ministry of Transport

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Sri Lanka: Multimodal Transport Project

Technical Assistance Consultant’s Report

This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design.

Project Number: 41249-022 June 2012

Sri Lanka: Multimodal Transport Project (Financed by the Japan Fund for Poverty Reduction)

Main Report Volume 2 – Costs, Revenue, Financial Analysis, Economic Appraisal

Prepared by Roughton International Ltd., in association with Nippon Koei Co., Ltd. and Engineering Consultants Ltd.

United Kingdom

For Ministry of Transport

The Asian Development Bank The Democratic Socialist

Republic of Sri Lanka

7600SRI: Multimodal Transport Project

Final Report – Main Report Volume 2

Costs, Revenue, Financial Analysis, Economic Appraisal

June 2012

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 1

SRI LANKA MULTIMODAL TRANSPORT PROJECT

FINAL REPORT – VOLUME 2

CONTENTS

8 Project costs 148

8.1 Railway costs 148

8.2 Cost components of each project 152

8.3 Port railhead – 3 track and 4 track options 153

8.4 Sedwatta link 157

8.5 Veyangoda ICD site and Daraluwa Bemmulla Loop 158

8.6 Enderamulla ICD site 159

8.7 Peliyagoda/Telangapata ICD site 160

8.8 Ratmalana ICD site 161

8.9 Total project costs 162

9 Forecast gross revenue 167

9.1 Results 167

9.2 Key determinants 169

10 Applicable forms of Procurement Contracts 171

10.1 Responsibility for Procurement 171

10.2 Selecting a Delivery Model 172

10.3 Procurement under BOO/BOT, Concessions etc. 179

10.4 Packaging of Procurement and Bidding Strategy 179

11 Procurement Strategy under PPP and Public Finance 187

11.1 Introduction 187

11.2 Procurement Approach from Public Finance to Private Finance 188

11.3 Evaluation Approach of Public Finance and PPP Options 189

11.4 Identification of Procurement Options 190

11.5 Risk Assessment 196

11.6 Proposed Sensitivity Cases for Sensitivity Testing 203

12 Financial evaluation and recommendations 204

12.1 Basic Assumptions for the Financial Analysis 204

12.2 Revenue and Costs 205

12.3 Base Case Analysis for Public Financing 209

12.4 Base Case Analysis for PPP 210

12.5 Sensitivity Analysis for PPP Options 229

12.6 Further Sensitivity Analysis for PPP Options 231

12.7 Summary of Sensitivity Testing on PPP Options 233

12.8 Recommended Procurement Options and Implementation Plan 234

12.9 Summary and Recommendations 237

13 Summary of environmental, resettlement & social reports 241

13.1 Initial Environmental Examination (IEE) 241

13.2 Resettlement plans of ICD sites 242

13.3 Poverty and Social Assessment Report 250

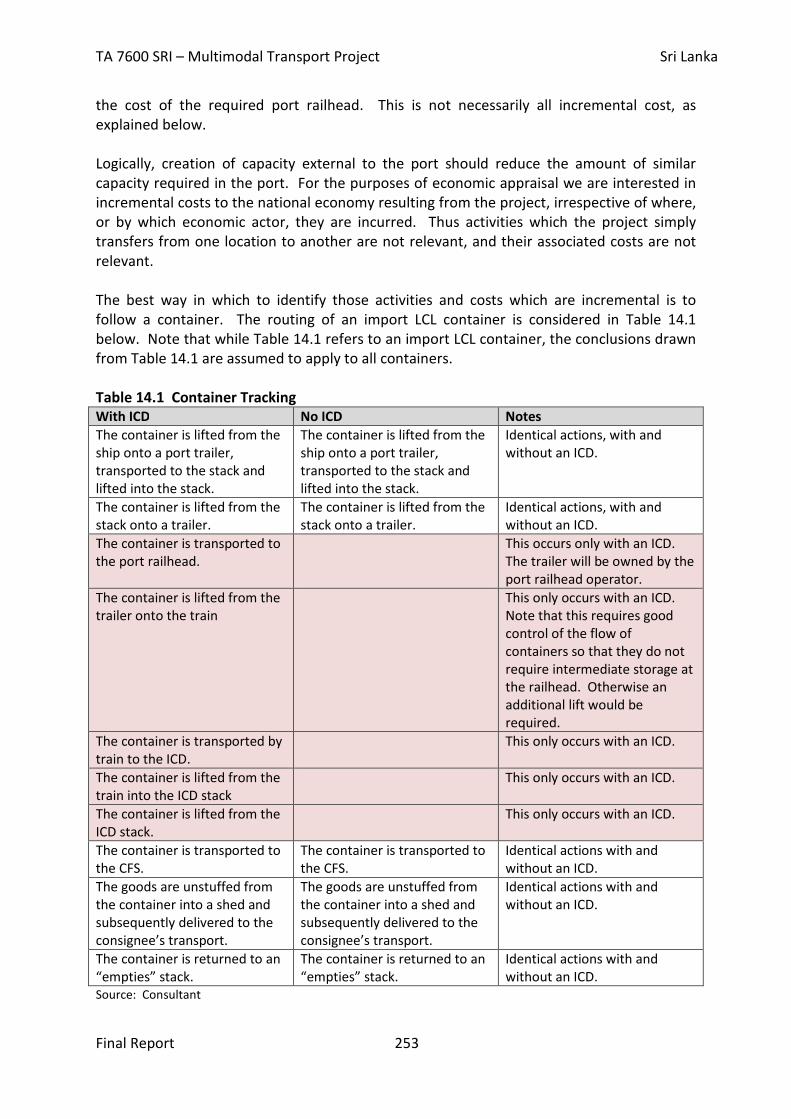

14 Economic evaluation methodology 252

14.1 The “Without Project” Case 252

14.2 Opportunity Costs 252

14.3 Incremental Capital Costs 252

14.4 Shadow Pricing 255

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 2

15 Economic appraisal 268

15.1 Land Values 268

15.2 Incremental Capital Costs 270

15.3 Recurrent Costs 276

15.4 Traffic Impacts and Decongestion Benefits 282

15.5 Results 283

15.6 Interpretation 290

15.7 Risk and Sensitivity 292

15.8 Poverty and Benefits Distribution 294

15.9 Reductions in Noxious Emissions 302

15.10 Other Benefits 304

16 Traffic modeling and decongestion benefits 305

16.1 Introduction 305

16.2 Types of transport model 305

16.3 Short term Do Nothing analysis 306

16.4 The University of Moratuwa traffic model 308

16.5 Future year scenarios 312

16.6 Traffic model output 313

16.7 Vehicle Categories and Unit Cost Savings 320

16.8 Decongestion benefits 331

17 Project impact monitoring 333

17.1 Project Impact Monitoring Framework 333

17.2 Baseline data and monitoring approach 335

18 Conclusions 337

Tables

Table 8.1 Cost of container transport by rail from the port each ICD

Table 8.2 Components of project costs

Table 8.3 Summary of costs at the port railhead (3 track version for one ICD site)

Table 8.4 Summary of costs at the port railhead (4 track version for two ICD sites)

Table 8.5 Summary of costs at the new Sedawatta link

Table 8.6 Summary of costs at Veyangoda ICD site and Daraluwa Bemmulla Loop

Table 8.7 Summary of costs at Enderamulla ICD site

Table 8.8 Summary of costs at Peliyagoda/Telangapata ICD site

Table 8.9 Summary of costs at Ratmalana ICD site

Table 9.1 Forecast gross revenue (Rs Million) between 2015 and 2034

Table 9.2 Calculation of transport & cranage revenue and stuffing/destuffing revenue

Table 10.1 Sample Procurement Plan, Procurement of Goods and Works by ICB/NCB

Table 10.2 Sample Procurement Plan, Procurement Services

Table 11.1 ICD Sites and Facility Requirements

Table 11.2 General Procurement Options from Preliminary Evaluation

Table 11.3 Risk Score Structure

Table 11.4 Evaluated Risks for ICD Service Project

Table 11.5 Sensitivity Testing Scenarios

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 3

Table 12.1 Revenue Projection for the ICD and ICD Combinations (Rs m)

Table 12.2 Estimate of the Starting Project Costs (Rs m)

Table 12.3 CAPEX during Concession Period 2015-2034 (Rs m)

Table 12.4 Operation and maintenance Cost Summary (Rs m)

Table 12.5 Project IRR under Public Fundings

Table 12.6 The Weighted Average Costs of Capital for each ICD

Table 12.7 FIRR of Veyangoda ICD under different PPP options

Table 12.8 FIRR of Enderamulla ICD under different PPP options

Table 12.9 FIRR of Peliyagoda/Telangapata ICD under different PPP options

Table 12.10 FIRR of Ratmalana ICD under different PPP options

Table 12.11 FIRR of Veyangoda + Ratmalana ICDs under different PPP options

Table 12.12 FIRR of Enderamulla + Ratmalana ICD under different PPP options

Table 12.13 FIRR of Peliyagoda/Telangapata + Ratmalana ICDs under different PPP options

Table 12.14 ICD Base Case Summary

Table 12.15 ICD Base Case Cash Flow Summary (Rs m)

Table 12.16 Financial projections: FIRR sensitivities to revenue

Table 12.17 Financial projections: FIRR sensitivities to construction and M&E costs

Table 12.18 Financial projections: FIRR sensitivities to O&M costs

Table 12.19 Veyangoda ICD FIRR Sensitivities

Table 12.20 Enderamulla ICD FIRR Sensitivities

Table 12.21 Peliyagoda/Telangapata ICD FIRR Sensitivities

Table 12.22 Ratmalana ICD FIRR Sensitivities

Table 12.23 Veyangoda + Ratmalana ICD FIRR Sensitivities

Table 12.24 Enderamulla+ Ratmalana ICD FIRR Sensitivities

Table 12.25 Peliyagoda/Telangapata + Ratmalana ICD FIRR Sensitivities

Table 12.26 FIRR sensitivity Summary

Table 12.27 Recommended ICD PPP Equity Structure

Table 12.28 ICD PPP Implementation

Table 13.1 Summary of resettlement costs

Table 14.1 Container Tracking

Table 14.2 Government Tax Revenues, 2008 -2011 (Rs’000)

Table 14.3 Nominal Rate vs Tax Take, Cement, 2011

Table 14.4 Selected Tax Rates, 2011

Table 14.5 Calculation of Total Taxes on Imports, Excluding Fuels, 2011

Table 14.6 Taxes on Vehicle Imports (Rs. per 100 Rs. CIF value)

Table 14.7 International Fuel Prices, 2nd half of September 2011

Table 14.8 Taxes/Subsidies and Shadow Prices, September 2011 (Rs)

Table 14.9 Sri Lanka Trade Performance in Jan-Dec 2010

Table 14.10 Minimum Wages vs Average Earnings 2003 – 2009 (Rs/day)

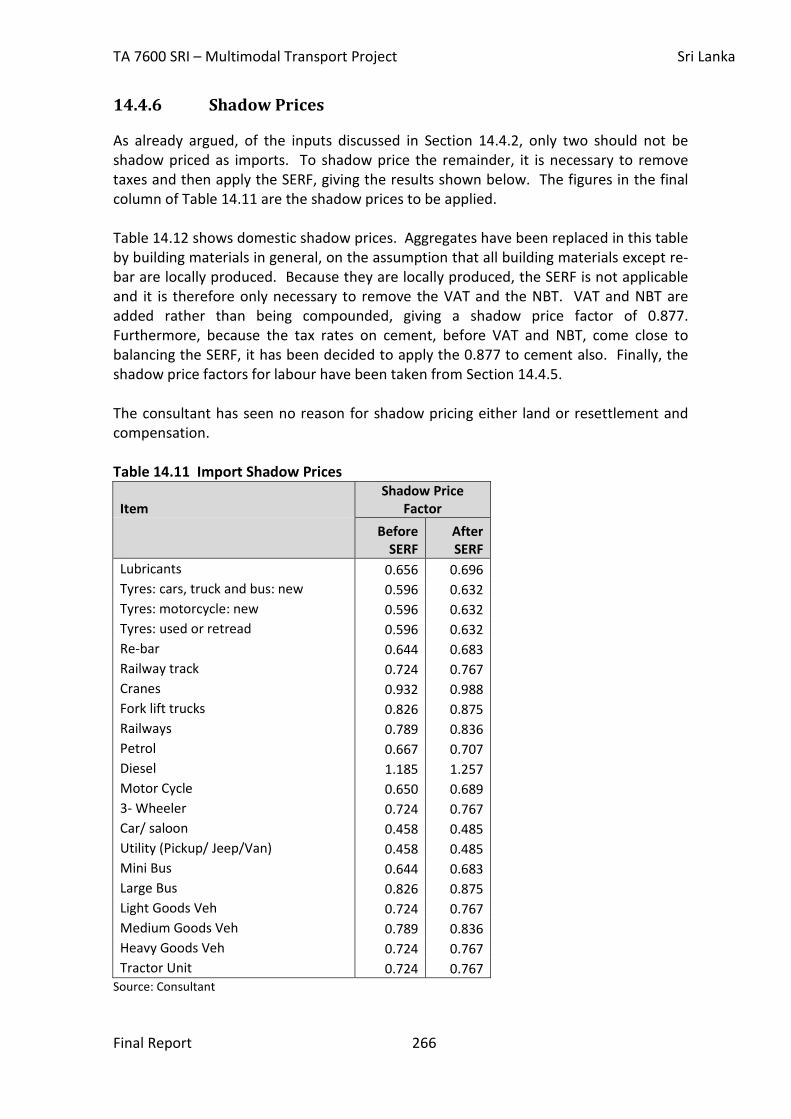

Table 14.11 Import Shadow Prices

Table 14.12 Domestic Shadow Prices

Table 15.1 Opportunity Cost of Land

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 4

Table 15.2 Economic Costs of Land and Civil Works (Rs million)

Table 15.3A Economic Capital Costs of Rolling Stock & Cargo Handling Equipment:

Veyangoda (Rs million)

Table 15.3B Economic Capital Costs of Rolling Stock & Cargo Handling Equipment:

Enderamulla (Rs million)

Table 15.3C Economic Capital Costs of Rolling Stock & Cargo Handling Equipment:

Peliyagoda/Telangapata (Rs million)

Table 15.3D Economic Capital Costs of Rolling Stock & Cargo Handling Equipment:

Ratmalana (Rs million)

Table 15.4 Veyangoda Railway Recurrent Costs Breakdown 2015

Table 15.5A Economic Recurrent Costs of Railways and ICD for Veyangoda (Rs million)

Table 15.5B Economic Recurrent Costs of Railways and ICD for Enderamulla (Rs million)

Table 15.5C Economic Recurrent Costs of Railways and ICD for Peliyagoda/Telangapata (Rs

million)

Table 15.5D Economic Recurrent Costs of Railways and ICD for Ratmalana (Rs million)

Table 15.6 Annual Transport and Congestion Savings (Rs. million/yr)

Table 15.7 Veyangoda: Economic Costs and Benefits (Rs. Million)

Table 15.8 Enderamulla: Economic Costs and Benefits (Rs. Million)

Table 15.9 Peliyagoda/Telangapata: Economic Costs and Benefits (Rs. Million)

Table 15.10 Ratmalana: Economic Costs and Benefits (Rs. Million)

Table 15.11 Veyangoda + Ratmalana: Economic Costs and Benefits (Rs. Million)

Table 15.12 Enderamulla + Ratmalana: Economic Costs and Benefits (Rs. Million)

Table 15.13 PelTel + Ratmalana: Economic Costs and Benefits (Rs. Million)

Table 15.14 Results Summary - 1

Table 15.15 Results Summary - 2

Table 15.16 Project Ranking

Table 15.17A Sensitivity Results for Veyangoda

Table 15.17B Sensitivity Results for Enderamulla

Table 15.17C Sensitivity Results for Peliyagoda/Telangapata

Table 15.18 Poverty Headcount Ratio by District

Table 15.19 Percentage of Poor Households Based on the Official Poverty Line by District

Table 15.20 Distribution of Benefits: Veyangoda (Rs million)

Table 15.21 Distribution of Benefits: Enderamulla (Rs million)

Table 15.22 Distribution of Benefits: Peliyagoda/Telangapata (Rs million)

Table 15.23 Fuel Balance for Enderamulla, 2015

Table 15.24 Emissions by Engine Type (g/l)

Table 16.1 Times of day of police control at Ingunkade junction

Table 16.2 Typical green times and cycle times when not under police control

Table 16.3 Incidence of no queue on the Port Access Road approach

Table 16.4 Transport and congestion savings 2015

Table 16.5 Transport and congestion savings 2024

Table 16.6 Transport and congestion savings 2034

Table 16.7 Principal highways for congestion savings

Table 16.8 Breakdown of veh-kms and veh-hrs savings by highway corridor

Table 16.9 ADT data vehicle classes

Table 16.10 HDM4 data vehicle classes

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 5

Table 16.11 Vehicle distributions

Table 16.12 Expansion of TransPlan vehicle population

Table 16.13 Central road user costs (Rs/km)

Table 16.14 Weighted average values per truck km saved (Rs./km)

Table 16.15 Weighted average values per vehicle hour saved (Rs./hr)

Table 16.16 Daily transport and congestion savings (Rs. million)

Table 16.17 Annual transport and congestion savings (Rs. million)

Table 17.1: Project Impact Monitoring Framework

Figures

Figure 8.1 Annual expenditure profile for the Veyangoda project (SLR millions)

Figure 8.2 Annual expenditure profile for the Enderamulla project (SLR millions)

Figure 8.3 Annual expenditure profile for the PelTel project (SLR millions)

Figure 8.4 Annual expenditure profile for the Ratmalana project (SLR millions)

Figure 8.5 Annual expenditure profile for Veyangoda + Ratmalana (SLR millions)

Figure 8.6 Annual expenditure profile for Enderamulla + Ratmalana (SLR millions)

Figure 8.7 Annual expenditure profile for PelTel + Ratmalana (SLR millions)

Figure 9.1 Forecast gross revenue at Veyangoda ICD site

Figure 9.2 Forecast gross revenue at Enderamulla ICD site

Figure 9.3 Forecast gross revenue at Peliyagoda/Telangapata ICD site

Figure 9.4 Forecast gross revenue at Ratmalana ICD site

Figure 11.1 Overview of Procurement Approaches

Figure 11.2 Evaluation Process Chart

Figure 11.3 Public Finance Model

Figure 11.4 PPP Basic Option

Figure 11.5 PPP Alternative Option

Figure 11.6 The ICD Risk Assessment Procedure

Figure 11.7 Major Risk Constituents for ICD Projects

Figure 12.1 Veyangoda ICD - Project Revenue and Costs

Figure 12.2 Relationship between Government Grant and FIRR for Veyangoda ICD

Figure 12.3 Veyangoda ICD - Cash Flow from PPP Option 5

Figure 12.4 2020 Expansion Costs being Redistributed for Four Years

Figure 12.5 Enderamulla ICD: Project Revenue and Costs

Figure 12.6 Enderamulla ICD - Cash Flow from PPP Option 1

Figure 12.7 2020 Expansion Costs being Redistributed for Four Years

Figure 12.8 Peliyagoda/Telangapata ICD: Project Revenue and Costs

Figure 12.9 Peliyagoda/Telangapata ICD - Cash Flow for PPP Option 3

Figure 12.10 Ratmalana ICD: Project Revenue and Costs

Figure 12.11 Ratmalana ICD - Cash Flow from PPP Option 2

Figure 12.12 Veyangoda + Ratmalana ICDs: Project Revenue and Costs

Figure 12.13 Relationship between Govt Grant and FIRR for Veyangoda+Ratmalana ICDs

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 6

Figure 12.14 Veyangoda + Ratmalana ICDs - Cash Flow from PPP Option 5

Figure 12.15 Enderamulla + Ratmalana ICDs: Project Revenue and Costs

Figure 12.16 Enderamulla + Ratmalana ICDs - Cash Flow from PPP Option 3

Figure 12.17 Peliyagoda/Telangapata + Ratmalana ICD: Project Revenue and Costs

Figure 12.18 Peliyagoda/Telangapata + Ratmalana ICDs - Cash Flow from PPP Option 5

Figure 16.1 Traffic flow on Port Access Road approach to Ingurukade junction

Figure 16.2A Veyangoda decongestion corridor

Figure 16.2B Enderamulla decongestion corridor

Figure 16.2C Peliyagoda/Telangapata decongestion corridor

Figure 16.2D Ratmalana decongestion corridor

Figure 16.3 Road haulage price model derived from regression of ACT data

Figure 16.4 Road user costs: articulated truck

Figure 16.5 Road user costs: car

Appendices

Appendix A SLPA’s Peliyagoda scheme and complementary long term options

Appendix B Responses to comments on the Draft Final Report

Appendix C Terms of Reference

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 7

FINAL REPORT

EXECUTIVE SUMMARY

See Volume 1

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 148

FINAL REPORT

8 Project costs There are many elements of project costs, firstly by category and location:

• Capital expenditure (capex) at ICD sites;

• O & M expenditure at ICD sites;

• Capex at the New Port railhead;

• O & M expenditure at the New Port railhead;

• Capex on the Sedawatta link and the rest of the connecting railway; and

• O & M expenditure on the Sedawatta link and the rest of the connecting railway.

Both capex and O&M are broken down by item type, examples being equipment purchases

and fuel consumption. We begin with a detailed examination of railway costs; these exclude

all lifting equipment costs.

8.1 Railway costs

The unit costs of rail transport can be shown to decline with increasing distance and with

increasing transport unit capacity and with increasing transport volume. This results from

the fact that (a) there is a high level of fixed cost associated with railway operation and (b)

that rail carrying capacity cannot be adjusted easily to match the level of transport demand.

The costs of operating container trains of various sizes, over various distances and for

various levels of ICD throughput were assessed for the purposes of:

• Providing a basis for comparison with road container haulage charges, to determine

the scope for setting a competitive level of rail container haulage tariff in future;

• Demonstrating the extent to which costs will vary with train size (and hence

container carrying capacity), distance and transport volume.

A point-to-point train costing model was adapted to generate the cost estimates for this

assessment.

8.1.1 Cost model adaptation

Train operating costs were estimated for future railway services to the ICDs under

consideration – Veyangoda, Enderamulla, Peliyagoda/Telengapata and Ratmalana.

For this purpose, the unit rates for individual items of cost were obtained from the Sri Lanka

Railways and other sources, for inputting to the model. The relevant items of cost are as

follows:

Variable costs

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 149

• Train crews

• Fuel consumption

• Locomotive maintenance

• Wagon maintenance

• Variable track maintenance

Fixed costs

• Fixed cost of infrastructure maintenance

(track and bridges, buildings and signalling)

• Station operations

Administrative overhead

Incremental capital costs

• Locomotive capital

• Wagon capital

• Infrastructure capital

(i) Variable costs

(a) Train crews. The total annual cost of train crews in the Sri Lanka Railway system

was calculated from personnel data which showed that there were 460 drivers,

460 assistant drivers and 600 guards and assistant guards in the system, each

with a monthly wage, including overtime and benefits of Rs. 75,000.1 The

resulting cost of Rs. 1.368 billion was distributed over an estimated 411,756 train

hours in 2010 (both passenger and freight), to derive an average crew cost of Rs.

3,332 per train hour.

(b) Fuel consumption. Based on the rate of fuel consumption per engine km2 for M8

locomotives, the rate of fuel consumption was calculated at 4.2 litres per gross

trailing tonne-km. For the more modern 3,500 HP locomotives, a fuel

consumption rate of 3.9 litres per gross trailing tonne-km was applied. The

current price of Rs. 80 per litre paid by Sri Lanka Railways for diesel fuel was used

to estimate the fuel consumption cost.

(c) Locomotive maintenance. The cost of overhaul for M8 locomotives was given as

Rs. 40 million per unit.3 Since these overhauls are undertaken every 360,000 km,

the average cost per locomotive km is Rs. 111.11. To this cost was added 10% to

cover the cost of running repairs and servicing, giving an all-up estimate of Rs.

122.2 per locomotive-km.

1 Meeting with Commercial Superintendent and Principal Costing Officer, Sri Lanka Railways, 20 May 2011. 2 FT Study – ADB 07/07/2011, prepared by former Sri LaMnka Railways staff. 3 Chief Mechanical Engineer, Sri Lanka Railways, 11 August 2011.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 150

(d) Wagon maintenance. The cost of scheduled overhaul of wagons (based on the

Bogie Low Sided, or BLS, wagon) was given as Rs. 2 million every 4 years.4 Based

on an average of 50,000 km per wagon per year in future, the average cost per

wagon-km was estimated at Rs. 10 per wagon-km. With the addition of 10% to

cover running maintenance, all-up maintenance was estimated to cost Rs. 11 per

wagon-km.

(e) Variable track maintenance. The cost of maintaining track (including bridges,

culverts, tunnels and other track structures) may be divided into variable and

fixed portions. The variable portion is that which varies directly with the level of

traffic (measured in gross tonne-km) passing over the track, while the fixed

portion is invariant with the level of traffic. Advice was given that the fixed

portion would represent approximately 90% of the total track maintenance cost

in Sri Lanka.5 This largely reflects the effects of a tropical climate, where time-

related maintenance activities such as vegetation control or ballast tamping in

areas of high rainfall would account for a high proportion of track maintenance.

The system-wide cost of track maintenance was given as Rs. 740 million in 2010.6

The variable portion of this amount was estimated at Rs. 74 million, which when

distributed over the 5,248 million GTK estimated for the Sri Lanka Railway system

in 2010, gave an average rate of Rs. 0.0141 per gross tonne-km.

(ii) Fixed costs

(a) Fixed cost of infrastructure maintenance. This comprises 90% of the cost of track

maintenance, as indicated above, plus the costs of buildings and signalling

system maintenance, both of which categories are invariant with traffic. The

total fixed cost of infrastructure maintenance was estimated as Rs. 1.09 billion in

2010. When distributed over the total track length of the Sri Lanka Railways

system (1,569 km), this gave an average cost of Rs. 694,779 per track-km per

year. The model distributes this cost between container and other trains in direct

proportion to the numbers of each operated. On the Main Line to Enderamulla,

container trains would represent only 12% of the total number of trains on the

line in 2034, so would bear only 12% of the fixed maintenance cost, or Rs.

83,373 per track-km.

(b) Station operations. The number of station staff for 329 stations in Sri Lanka (i.e.

all excluding Colombo Fort) was reported as 3950, or an average of 12 staff per

station.7 Application of the average monthly wage, including overtime and

benefits, of Rs. 50,000 per person gives an average annual cost per station of Rs.

7,203,647. The model allocates some station costs to container trains, since the

station staff have a safe-working function in addition to their passenger handling

functions. The allocation is in direct proportion to the share of freight trains in

the total number of trains operated on the system in 2010. This share was

4 Ibid 5 Mr P De Silva, former GM Sri Lanka Railways 6 Chief Engineer (Track and Bridges) Sri Lanka Railways. 7 Op cit. Commercial Superintendent Sri Lanka Railways

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 151

calculated at 6%, so that container trains would bear a cost of 0.06 x Rs. 7.2

million = Rs. 400,000 per station per year.

(iii) Administrative overhead

An administrative overhead rate of 20% was applied to the total of the variable

and fixed costs attributable to the container traffic to provide an estimate of the

administrative overhead cost of this traffic.

(iv) Incremental capital cost

(a) Locomotive capital. Based on the number of container trains estimated to be

operated per day and the train cycle time for a single trip, the required number

of train sets may be calculated. This gives the incremental number of

locomotives to be purchased to support the traffic. The purchased quantity is

then valued at the assumed purchase price for a 3,500 HP locomotive of Rs. 320

million and the resulting capital cost is depreciated over an assumed life of 25

years to obtain the annual cost of the locomotive purchases.

(b) Wagon capital. The number of train sets calculated by the above method

multiplied by the number of wagons per train set gives the incremental number

of wagons to be purchased to support the traffic. The purchased quantity is then

valued at the assumed purchase price for a 3-TEU wagon of Rs. 6.78 million and

the resulting capital cost is depreciated over an assumed life of 20 years to

obtain the annual cost of the wagon purchases.

(c) Infrastructure capital. Calculation of the incremental infrastructure capital cost is

based on the assessed need for construction of the following trackage:

• Construction of loading/unloading tracks in the New Port and in the

proposed ICDs;

• Reconstruction of the existing port access line;

• Construction of a “Y” short-cut track at Sedawatta to connect the port

access line to the Main Line;

• Construction of access tracks from the Main and Coast lines to connect

with ICDs.

For train costing purposes, the cost for construction of fully signalled embedded track in the

port and the ICD’s was assumed to be US$ 2.0 million per km (Rs. 218.5 million), while the

cost for construction of fully signalled ballasted track outside of the terminals was assumed

to be US$ 1.0 per km (Rs. 109.3 million). The annual cost of the incremental infrastructure is

calculated by depreciating the total capital cost over an assumed track life of 50 years.

8.1.2 Cost results

This section contains the results generated by the railway cost model, excluding the

incremental capital costs, which are summarized later.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 152

(i) Estimates of railway operating costs for transportation of containers to/from

ICD’s

Table 8.1 gives the estimated cost per TEU and per TEU-km of container transport by rail

from the port to the various ICDs in 2015, 2020, 2021 and 2034. Distances from the port

railhead to the ICDs are given in the table headings. At Veyangoda, short trains – 15 x 3 TEU

wagons (shaded green) – are used in all years. At the other ICDs, short trains are used until

2020, after which long trains – 35 x 3 TEU wagons (shaded yellow) – are used.

Table 8.1: Cost of container transport by rail from the port each ICD

Year Veyangoda

(42.5 km)

Enderamulla

(16.3 km)

PelTel

(14.3 km)

Ratmalana

(27.0 km)

Rs per

TEU

Rs per

TEU-km

Rs per

TEU

Rs per

TEU-km

Rs per

TEU

Rs per

TEU-km

Rs per

TEU

Rs per

TEU-km

2015 1072 25.26 517 31.79 478 33.51 797 29.47

2020 501 30.79 466 32.65 761 28.11

2021 351 21.59 389 27.27 648 23.96

2034 991 23.35 334 20.56 372 26.10 599 22.12 Source: SLMMT train cost model

During a visit to the ICD of Aitken Spence at Wattala, the project team was informed that

the prevailing rate for road haulage of a laden 20 ft container to the port is US$ 50 (Rs.

5,500). The distance involved is about 8 km, giving a unit cost of Rs. 687.5 per TEU-km. This

is considerably more than the rail unit costs in Table 8.1 but the road haulage unit cost

includes truck replacement costs, whereas locomotive and wagon replacement costs are

additional to the Figures in Table 8.1, as are lifting equipment costs.

8.2 Cost components of each project

Each alternative project consists of one or two ICD sites, a compatible railhead at the New

Port and works on the connecting railway. Table 8.2 shows the components of project costs.

If there are two ICD sites, four tracks are needed at the port railhead. If there is only one ICD

site, three tracks suffice. Reinstatement of the Sedawatta link is necessary for all three

northern ICD sites but not for Ratmalana on its own.

Table 8.2 Components of project costs

Project description

Component

Port

Rail-

head

4 tracks

Port

Rail-

head

3 tracks

Seda-

watta

Link

Veyan-

goda

ICD

Endera-

mulla

ICD

PelTel

ICD

Ratma-

lana

ICD

Veyangoda Include Include Include

Enderamulla Include Include Include

Peliyagoda/Telangapata Include Include Include

Ratmalana Include Include

Veyangoda + Ratmalana Include Include Include Include

Enderamulla + Ratmalana Include Include Include Include

PelTel + Ratmalana Include Include Include Include

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 153

8.3 Port railhead – 3 track and 4 track options

Table 8.3 summarises costs at the port railhead for the 3 track option (if one ICD site is

chosen). Table 8.4 summarises costs at the port railhead for the 4 track option (if two ICD

sites are chosen).

Both tables shows key results from detailed spreadsheets compiled by Roughton

International from local, international, government, commercial and internet sources. In

both tables, item descriptions indicate which ICD(s) the railhead is connected to.

‘Operations staff – Veyangoda’ denotes expenditure on operations staff at the 3 track

railhead if Veyangoda is the ICD. ‘Equipment + container control system maintenance –

Enderamulla + Ratmalana’ denotes expenditure on such maintenance at the 4 track railhead

if Enderamulla and Ratmalana are the ICDs.

As may be expected, within the infrastructure capital expenditure railway construction costs

are higher for the 4 track railhead than for the 3 track railhead.

Equipment required at the railhead consists of rubber tyred gantries (RTGs) and tractor-

trailer units. The former load and unload the containers at the railhead and the number of

RTGs required is related to the number of TEUs per train and the number of trains to be

loaded and unloaded at once. Each RTG can move between 28 and 30 TEU/hr. Each

incoming train must be unloaded and loaded in 105 minutes. Veyangoda can handle only

short trains (45 TEU); the other ICDs will handle long trains (105 TEU) from 2021. The

number of RTGs required by 2034 varies from 3 if Veyangoda is the only ICD to 10 if

Enderamulla + Ratmalana or Peliyagoda/Telengapata + Ratmalana are the ICDs selected.

The unit price is 175.5 SLR millions.

Tractor-trailer units will transfer containers between the railhead and the New Port. The

number required is related to the anticipated daily TEU throughput. Each tractor-trailer unit

can make 4 round trips per hour, carrying 12 TEU/hr. The number of units required by 2034

varies from 3 if Ratmalana is the only ICD to 11 if Enderamulla + Ratmalana or

Peliyagoda/Telengapata + Ratmalana are the ICDs selected. The unit price per tractor-trailer

is 19.0 SLR millions.

A management information system is required for the control of containers. The server and

software would be located at the railhead, with monitors at the ICDs. One system has been

investigated. There is a purchase cost and an annual maintenance and support charge. The

purchase cost is greater if the system has to monitor containers at two ICDs rather than one.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 154

Table 8.3 Summary of costs at the port railhead (3 track version for one ICD site)

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 0.45 49 0.45 49

Land acquisition N/A

Resettlement N/A

Deck preparation 1.88 207 1.88 207

Circulation N/A

Access road 0.06 7 0.06 7

Boundary wall N/A

CFS buildings N/A

Other buildings 0.62 68 0.62 68

Sub-total civil & building works 3.01 331 3.01 331

Railway track & buildings 8.38 922 8.38 922

Level crossings & signaling 4.03 443 4.03 443

Sub-total railways works 12.41 1,365 12.41 1,365

Rubber tyred gantries 4.79 527 4.79 527

Trucks & trailers 0.35 38 0.35 38 0.69 76

Container control system 0.26 29 0.26 29

Sub-total equipment + container control

system capex – Veyangoda

5.40 594 0.35 38 5.74 632

Rubber tyred gantries 4.79 527 4.78 526 9.57 1,053

Trucks & trailers 0.69 76 0.86 95 1.55 171

Container control system 0.26 29 0.26 29

Sub-total equipment + container control

system capex – Enderamulla

5.74 632 5.64 621 11.38 1,253

Rubber tyred gantries 4.79 527 4.78 526 9.57 1,053

Trucks & trailers 0.69 76 0.86 95 1.55 171

Container control system 0.26 29 0.26 29

Sub-total equipment + container control

system capex – PelTel

5.74 632 5.64 621 11.38 1,253

Rubber tyred gantries 4.79 527 4.78 526 9.57 1,053

Trucks & trailers 0.35 38 0.17 19 0.52 57

Container control system 0.26 29 0.26 29

Sub-total equipment + container control

system capex – Ratmalana

5.40 594 4.95 545 10.35 1,139

Capex sub-total – Veyangoda 20.82 2,290 0.35 38 21.16 2,328

Capex sub-total – Enderamulla 21.16 2,328 5.64 621 26.80 2,948

Capex sub-total – Peliyagoda 21.16 2,328 5.64 621 26.80 2,948

Capex sub-total – Ratmalana 20.82 2,290 4.95 545 25.77 2,835

Operations staff – Veyangoda 4.16 458

Operations staff – Enderamulla 8.21 903

Operations staff – PelTel 8.21 903

Operations staff – Ratmalana 5.94 653

Other staff 4.50 495

Energy 22.37 2,461

Equipment + container control system

maintenance – Veyangoda

7.03 773

Equipment + container control system

maintenance – Enderamulla

11.25 1,238

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 155

Equipment + container control system

maintenance – PelTel

11.25 1,238

Equipment + container control system

maintenance – Ratmalana

9.03 993

O&M sub-total – Veyangoda 38.06 4,187

O&M sub-total – Enderamulla 46.33 5,096

O&M sub-total – PelTel 46.33 5,096

O&M sub-total – Ratmalana 41.84 4,602

Overall total – Veyangoda 59.22 6,515

Overall total – Enderamulla 73.13 8,044

Overall total – PelTel 73.13 8,044

Overall total – Ratmalana 67.61 7,437 Sources: Government of Sri Lanka, commercial sources, internet sources, Consultant’s calculations

Table 8.4 Summary of costs at the port railhead (4 track version for 2 ICD sites)

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 0.45 49 0.45 49

Land acquisition N/A

Resettlement N/A

Deck preparation 1.88 207 1.88 207

Circulation N/A

Access road 0.06 7 0.06 7

Boundary wall N/A

CFS buildings N/A

Other buildings 0.62 68 0.62 68

Sub-total civil & building works 3.01 331 3.01 331

Railway track & buildings 9.94 1,093 9.94 1,093

Level crossings & signaling 4.03 443 4.03 443

Sub-total railways works 13.97 1,537 13.97 1,537

Rubber tyred gantries 7.98 878 4.78 526 12.76 1,404

Trucks & trailers 0.52 57 0.52 57 1.04 114

Container control system 0.34 38 0.34 38

Equipment + container control system –

Veyangoda + Ratmalana

8.85 973 5.30 583 14.14 1,556

Rubber tyred gantries 7.98 878 7.97 877 15.96 1,755

Trucks & trailers 0.86 95 1.04 114 1.90 209

Container control system 0.34 38 0.34 38

Equipment + container control system –

Enderamulla + Ratmalana

9.18 1,011 9.01 991 18.20 2,002

Rubber tyred gantries 7.98 878 7.97 877 15.96 1,755

Trucks & trailers 0.86 95 1.04 114 1.90 209

Container control system 0.34 38 0.34 38

Equipment + container control system –

PelTel + Ratmalana

9.18 1,011 9.01 991 18.20 2,002

Capex sub-total – V + R 25.83 2,841 5.30 583 31.12 3,424

Capex sub-total – E + R 26.16 2,879 9.01 991 35.18 3,870

Capex sub-total – P + R 26.16 2,879 9.01 991 35.18 3,870

Operations staff – 8.69 956

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 156

Veyangoda + Ratmalana

Operations staff –

Enderamulla + Ratmalana

11.85 1,304

Operations staff – PelTel + Ratmalana 11.85 1,304

Other staff 4.50 495

Energy 34.97 3,847

Equipment + container control system

maintenance – Veyangoda + Ratmalana

12.55 1,380

Equipment + container control system

maintenance – Enderamulla + Ratmalana

15.98 1,758

Equipment + container control system

maintenance – PelTel + Ratmalana

15.98 1,758

O&M s/t – Veyangoda + Ratmalana 60.71 6,678

O&M s/t – Enderamulla + Ratmalana 67.31 7,404

O&M s/t – PelTel + Ratmalana 67.31 7,404

Overall total – Veyangoda + Ratmalana 91.83 10,102

Overall total – Enderamulla + Ratmalana 102.49 11,274

Overall total – PelTel + Ratmalana 102.49 11,274 Sources: Government of Sri Lanka, commercial sources, internet sources, Consultant’s calculations

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 157

8.4 Sedwatta link

The Sedawatta link is the missing arm of a ‘Y’ rail junction located near Orugodawatta. In its

absence, trains travelling between the port and northern locations have to divert to the

south and reverse the engine at sidings before proceeding northwards. This wastes an hour

and restoration of the link is essential for efficient operation. The site has been surveyed

and an alignment selected so as to minimize the need for resettlement. Construction of a

trough span bridge is needed and a signaling upgrade is needed to control trains travelling

along the restored ‘Y’ link.

Table 8.5 Summary of costs at the new Sedawatta link

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 0.10 11 0.10 11

Land acquisition 0.00 0 0.00 0

Resettlement 1.44 158 1.44 158

Deck preparation 1.60 176 1.60 176

Circulation N/A

Access road N/A

Boundary wall N/A

CFS buildings N/A

Other buildings N/A

Sub-total civil & building wks 3.14 345 3.14 345

Railway track & buildings 4.40 484 4.40 484

Level crossings & signaling 0.90 99 0.90 99

Sub-total railway works 5.30 583 5.30 583

Locomotives and wagons N/A

Rubber tyred gantries N/A

Trucks & trailers N/A

Forklift trucks N/A

Sub-total equipment capex 0.00 0 0.00 0

Capex sub-total 8.44 928 8.44 928

Transport costs N/A

Operations staff N/A

Other staff N/A

Energy N/A

Equipment maintenance N/A

Infrastructure maintenance N/A

O&M sub-total 0.00 0 0.00 0

Total 8.44 928 8.44 928

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 158

8.5 Veyangoda ICD site and Daraluwa Bemmulla Loop

At the Veyangoda site, expenditure falls naturally into three categories:

• Infrastructure capex, with most expenditure occurring in either 2014 (stage 1) or

2020 (stage 2); stage 2 expenditure is mainly on additional CFS building capacity and

associated works;

• Equipment capex, in which equipment is bought as required. ‘Stage 1’ refers to

equipment to be purchased between 2014 and 2019. ‘Stage 2’ refers to equipment

bought in 2020 onwards; and

• Operations and maintenance costs, where expenditure occurs in every year and is

generally on a rising trend, as TEU throughput increase.

There are significant resettlement costs. Deck preparation costs of 1,225 SLR millions

include 749 SLR millions for demolition of existing structures. Within infra buildings, the

building of CFS stations will cost 570 SLR millions in 2014, 719 SLR millions in 2020. By 2034,

equipment purchase needs will be 4 locomotives, 56 wagons, 7 RTGs, 14 tractor-trailers and

22 forklift trucks.

Table 8.6 Summary of costs at Veyangoda ICD site and Daraluwa Bemmulla Loop

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 0.91 100 0.91 100

Land acquisition 0.00 0 0.00 0

Resettlement 9.67 1,064 9.67 1,064

Deck preparation 11.14 1,225 2.16 238 13.30 1,463

Circulation 0.32 35 0.36 40 0.68 75

Access road 0.28 31 0.28 31

Boundary wall 0.74 81 0.74 81

CFS buildings 5.70 627 6.54 719 12.24 1,346

Other buildings 5.11 562 5.11 562

Sub-total civil & building wks 33.87 3,726 9.06 997 42.93 4,722

Railway works on ICD site 5.51 606 5.51 606

Daraluwa Bemmulla loop 1.25 137 1.25 137

Sub-total railway works 6.76 743 6.76 743

Locomotives and wagons 1.48 163 9.25 1,017 10.73 1,180

Rubber tyred gantries 7.97 877 1.60 176 9.57 1,053

Trucks & trailers 1.73 190 0.69 76 2.42 266

Forklift trucks 0.25 28 0.25 27 0.50 55

Sub-total equipment capex 11.43 1,258 11.78 1,296 23.22 2,554

Capex sub-total 52.06 5,727 20.84 2,293 72.91 8,020

Transport costs 37.32 4,105

Operations staff 54.67 6,014

Other staff 16.45 1,810

Energy 22.37 2,461

Equipment maintenance 15.01 1,651

Infrastructure maintenance 3.52 387

O&M sub-total 149.34 16,427

Overall total 222.25 24,447

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 159

8.6 Enderamulla ICD site

At the Enderamulla site, expenditure falls naturally into three categories:

• Infrastructure capex, with most expenditure occurring in either 2014 (stage 1) or

2020 (stage 2); stage 2 expenditure is mainly on additional CFS building capacity and

associated works;

• Equipment capex, in which equipment is bought as required. ‘Stage 1’ refers to

equipment to be purchased between 2014 and 2019. ‘Stage 2’ refers to equipment

bought in 2020 onwards; and

• Operations and maintenance costs, where expenditure occurs in every year and is

generally on a rising trend, as TEU throughput increase.

Deck preparation costs of 2,763 SLR millions include 2,072 SLR millions of costs incurred by

building on marshy land. Within infra buildings, the building of CFS stations will cost 1,452

SLR millions in 2014, 1,665 SLR millions in 2020. By 2034, equipment purchase needs will be

4 locomotives, 131 wagons, 14 RTGs, 30 tractor-trailers and 54 forklift trucks.

Table 8.7 Summary of costs at Enderamulla ICD site

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 1.36 150 1.36 150

Land acquisition 1.51 166 1.51 166

Resettlement 1.71 188 1.71 188

Deck preparation 25.12 2,763 4.16 458 29.28 3,221

Circulation 0.62 68 0.64 70 1.26 138

Access road 1.04 114 1.04 114

Boundary wall 1.33 146 1.33 146

CFS buildings 14.52 1,597 16.65 1,832 31.17 3,429

Other buildings 12.10 1,331 12.10 1,331

Sub-tot civil & building works 59.31 6,524 21.45 2,360 80.76 8,883

Railway track & buildings 3.59 395 3.59 395

Level crossings & signalling 2.02 222 2.02 222

Sub-total railway works 5.61 617 5.61 617

Locomotives and wagons 3.45 380 15.55 1,710 19.00 2,090

Rubber tyred gantries 11.16 1,228 11.17 1,229 22.34 2,457

Trucks & trailers 3.11 342 2.07 228 5.18 570

Forklift trucks 0.59 65 0.64 70 1.23 135

Sub-total equipment capex 18.31 2,014 29.43 3,237 47.74 5,252

Capex sub-total 83.23 9,155 50.88 5,597 134.12 14,753

Transport costs 34.86 3,835

Operations staff 133.68 14,705

Other staff 16.45 1,810

Energy 48.08 5,289

Equipment maintenance 28.50 3,135

Infrastructure maintenance 6.97 767

O&M sub-total 268.55 29,541

Overall total 402.67 44,294

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 160

8.7 Peliyagoda/Telangapata ICD site

At the Peliyagoda/Telangapata site, expenditure falls naturally into three categories:

• Infrastructure capex, with most expenditure occurring in either 2014 (stage 1) or

2020 (stage 2); stage 2 expenditure is mainly on additional CFS building capacity and

associated works;

• Equipment capex, in which equipment is bought as required. ‘Stage 1’ refers to

equipment to be purchased between 2014 and 2019. ‘Stage 2’ refers to equipment

bought in 2020 onwards; and

• Operations and maintenance costs, where expenditure occurs in every year and is

generally on a rising trend, as TEU throughput increase.

There will be high resettlement costs on the Thelangapata side, particularly in 2020. Within

infra buildings, the building of CFS stations will cost 1,452 SLR millions in 2014, 1,665 SLR

millions in 2020. By 2034, equipment purchase needs will be 4 locomotives, 131 wagons, 14

RTGs, 30 tractor-trailers and 54 forklift trucks.

Table 8.8 Summary of costs at Peliyagoda/Telangapata ICD site

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 1.36 150 1.36 150

Land acquisition 0.00 0 0.00 0 0.00 0

Resettlement 22.81 2,509 68.00 7,480 90.81 9,989

Deck preparation 21.48 2,363 4.32 475 25.80 2,838

Circulation 0.64 70 0.55 61 1.19 131

Access road 0.67 74 0.67 74

Boundary wall 0.79 87 0.42 46 1.21 133

CFS buildings 14.52 1,597 16.65 1,832 31.17 3,429

Other buildings 12.10 1,331 0.02 2 12.12 1,333

Sub-tot civil & building works 74.37 8,181 89.96 9,896 164.33 18,077

Railway track & buildings 2.88 317 1.45 160 4.33 477

Level crossings & signalling 1.72 189 0.20 22 1.92 211

Sub-total railway works 4.60 506 1.65 182 6.25 688

Locomotives and wagons 3.45 380 15.55 1,710 19.00 2,090

Rubber tyred gantries 11.16 1,228 11.17 1,229 22.34 2,457

Trucks & trailers 3.11 342 2.07 228 5.18 570

Forklift trucks 0.59 65 0.64 70 1.23 135

Sub-total equipment capex 18.31 2,015 29.43 3,237 47.75 5,252

Capex sub-total 97.28 10,702 121.04 13,315 218.33 24,017

Transport costs 37.35 4,109

Operations staff 133.68 14,705

Other staff 16.45 1,810

Energy 48.08 5,289

Equipment maintenance 28.50 3,135

Infrastructure maintenance 6.55 721

O&M sub-total 270.62 29,768

Overall total 488.95 53,785

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 161

8.8 Ratmalana ICD site

At the Ratmalana site, expenditure falls naturally into three categories:

• Infrastructure capex, with most expenditure occurring in either 2014 (stage 1) or

2020 (stage 2); stage 2 expenditure is mainly on additional CFS building capacity and

associated works;

• Equipment capex, in which equipment is bought as required. ‘Stage 1’ refers to

equipment to be purchased between 2014 and 2019. ‘Stage 2’ refers to equipment

bought in 2020 onwards; and

• Operations and maintenance costs, where expenditure occurs in every year and is

generally on a rising trend, as TEU throughput increase.

There will be high resettlement costs in 2014. Within infra buildings, the building of CFS

stations will cost 433 SLR millions in 2014, 496 SLR millions in 2020. By 2034, equipment

purchase needs will be 1 locomotive, 44 wagons, 7 RTGs, 14 tractor-trailers and 17 forklift

trucks.

Table 8.9 Summary of costs at Ratmalana ICD site

Item Stage 1 Stage 2 Total

(1 US$ = 110 SLR) US$ m SLR m US$ m SLR m US$ m SLR m

Preliminaries 0.82 90 0.82 90

Land acquisition 0.00 0 0.00 0

Resettlement 14.98 1,648 14.98 1,648

Deck preparation 2.49 274 0.91 100 3.40 374

Circulation 0.18 20 0.21 23 0.39 43

Access road 0.13 14 0.13 14

Boundary wall 0.75 83 0.75 83

CFS buildings 4.32 475 4.96 546 9.28 1,021

Other buildings 4.19 461 4.19 461

Sub-total civil & building wks 27.86 3,065 6.08 669 33.94 3,734

Railway track & buildings 2.83 311 2.83 311

Level crossings & signalling 1.35 149 1.35 149

Sub-total railway works 4.18 460 4.18 460

Locomotives and wagons 1.17 129 5.18 570 6.35 699

Rubber tyred gantries 9.57 1,053 9.57 1,053 19.14 2,106

Trucks & trailers 1.73 190 2.07 228 3.80 418

Forklift trucks 0.20 22 0.19 21 0.39 43

Sub-total equipment capex 12.67 1,394 17.01 1,872 29.68 3,266

Capex sub-total 44.71 4,919 23.10 2,541 67.81 7,459

Transport costs 17.98 1,978

Operations staff 51.69 5,686

Other staff 16.45 1,810

Energy 18.35 2,019

Equipment maintenance 23.65 2,601

Infrastructure maintenance 1.63 179

O&M sub-total 129.76 14,274

Overall total 197.57 21,733

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 162

8.9 Total project costs

All the projects consist of works at one or two ICD sites, at the railhead by the New Port and,

in the case of any project containing a northern ICD site (all ICD sites except Ratmalana), the

Sedawatta link. All involve major expenditure in 2014 and a second wave of expenditure in

2020. Amounts vary and main features are highlighted for each project.

8.9.1 Veyangoda project

Veyangoda is the most remote northern site, with an anticipated annual throughput of

109,909 TEU per annum in 2015, rising to 318,781 in 2034. The Veyangoda project consists

of Veyangoda ICD + a 3-track New Port railhead + Sedawatta link. The expected expenditure

profile is shown in Figure 8.1. Some aspects of O&M costs increase with throughput. The

ratio of expenditure in 2020 to that in 2014 is less than at other sites because Veyangoda

runs short trains throughout; larger, more expensive locomotives are unnecessary.

Figure 8.1 Annual expenditure profile for the Veyangoda project (SLR millions)

8.9.2 Enderamulla project

Enderamulla is a large northern site located just south of Ragama, with an anticipated

annual throughput of 279,904 TEU per annum in 2015, rising to 811,838 in 2034. The

Enderamulla project consists of Enderamulla ICD + a 3-track New Port railhead + Sedawatta

link. The expected expenditure profile is shown in Figure 8.2. Some aspects of O&M costs

increase with throughput. Expenditure in 2014 includes a high site preparation cost.

Expenditure in 2020 includes the costs of 3 powerful SD-50 locomotives and additional CFS

buildings.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

Veyangoda project costsOperation & maintenance

Equipment capex

Railway works

Civil & building works

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 163

Figure 8.2 Annual expenditure profile for the Enderamulla project (SLR millions)

8.9.3 Peliyagoda/Telangapata project

Peliyagoda/Telangapate (PelTel) is a large northern site located across the Kelania river from

Colombo, with an anticipated annual throughput of 279,904 TEU per annum in 2015, rising

to 811,838 in 2034. The PelTel project consists of PelTel ICD + a 3-track New Port railhead +

Sedawatta link. The expected expenditure profile is shown in Figure 8.3. Some aspects of

O&M costs increase with throughput. Expenditure in 2014 includes a high land acquisition

cost. Expenditure in 2020 includes high resettlement and compensation costs.

Figure 8.3 Annual expenditure profile for the PelTel project (SLR millions)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,0002

01

4

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

Enderamulla project costs

Operation & maintenance

Equipment capex

Railway works

Civil & building works

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

PelTel project costs

Operation & maintenance

Equipment capex

Railway works

Civil & building works

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 164

8.9.4 Ratmalana project

Ratmalana is the only ICD site south of Colombo, located on the southern railway, with an

anticipated annual throughput of 83,356 TEU per annum in 2015, rising to 241,767 in 2034.

The Ratmalana project consists of Ratmalana ICD + a 3-track New Port railhead. The

expected expenditure profile is shown in Figure 8.4. Some aspects of O&M costs increase

with throughput. Expenditure in 2014 includes high land and resettlement costs.

Expenditure in 2020 includes the costs of one powerful SD-50 locomotives and additional

CFS buildings.

Figure 8.4 Annual expenditure profile for the Ratmalana project (SLR millions)

8.9.5 Veyangoda + Ratmalana project

The Veyangoda + Ratmalana project consists of Veyangoda ICD + Ratmalana ICD + a 4-track

New Port railhead + Sedawatta link. Anticipated annual throughput at the New Port railhead

would be 193,265 TEU per annum in 2015, rising to 560,548 in 2034. The expected

expenditure profile is shown in Figure 8.5. Costs would be less than the sum of Veyangoda

project and Ratmalana project costs because two 3-track railheads in the New Port would

be replaced by one 4-track railhead.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

Ratmalana project costsOperation & maintenance

Equipment capex

Railway works

Civil & building works

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 165

Figure 8.5 Annual expenditure profile for Veyangoda + Ratmalana (SLR millions)

8.9.6 Enderamulla + Ratmalana project

The Enderamulla + Ratmalana project consists of Enderamulla ICD + Ratmalana ICD + a 4-

track New Port railhead + Sedawatta link. Anticipated annual throughput at the New Port

railhead would be 363,260 TEU per annum in 2015, rising to 1,053,605 in 2034.The expected

expenditure profile is shown in Figure 8.6. Costs would be less than the sum of Enderamulla

project and Ratmalana project costs because two 3-track railheads in the New Port would

be replaced by one 4-track railhead.

Figure 8.6 Annual expenditure profile for Enderamulla + Ratmalana (SLR millions)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,0002

01

4

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

Veyangoda + Ratmalana costs

Operation & maintenance

Equipment capex

Railway works

Civil & building works

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

Enderamulla + Ratmalana costsOperation & maintenance

Equipment capex

Railway works

Civil & building works

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 166

8.9.7 Peliyagoda/Telangapata + Ratmalana project

The Peliyagoda/Telangapata (PelTel) + Ratmalana project consists of PelTel ICD + Ratmalana

ICD + a 4-track New Port railhead + Sedawatta link. Anticipated annual throughput at the

New Port railhead would be 363,260 TEU per annum in 2015, rising to 1,053,605 in

2034.The expected expenditure profile is shown in Figure 8.7. Costs would be less than the

sum of Enderamulla project and Ratmalana project costs because two 3-track railheads in

the New Port would be replaced by one 4-track railhead.

Figure 8.7 Annual expenditure profile for PelTel + Ratmalana (SLR millions)

0

5,000

10,000

15,000

20,000

25,000

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

SLR

mil

lio

ns

PelTel + Ratmalana costs

Operation & maintenance

Equipment capex

Railway works

Civil & building works

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 167

9 Forecast gross revenue

9.1 Results

Chapter 3 presented the demand forecast, including TEU throughput at each ICD site, the

proportion of TEU expected to be stuffed / destuffed, and the charges for rail transport

needed to achieve these targets. Table 9.1 summarises the forecast gross revenue. Note

that revenue accrues only at the ICD sites, not at the port railhead. Figures 9.1 to 9.4 show

the forecast gross revenue streams for each site, subdivided into five categories.

For the two ICD projects – Venyangoda + Ratmalana, Enderamulla + Ratmalana, PelTel +

Ratmalama – the revenue is the sum of the revenues at the two individual ICD sites.

Table 9.1 Forecast gross revenue (Rs Million) between 2015 and 2034

Revenue item Veyangoda Enderamulla Peliyagoda /

Telangapata

Ratmalana

Transport charges 28,770 51,057 47,739 13,195

Stuffing & destuffing 17,827 45,400 44,946 13,520

Container storage 1,764 4,493 4,493 1,338

Warehousing & inventory 1,470 3,744 3,744 1,115

Office rentals 2,341 5,962 5,962 1,775

Total 52,172 110,657 106,884 30,944

Figure 9.1 Forecast gross revenue at Veyangoda ICD site

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

An

nu

al r

ev

en

ue

(R

s m

illi

on

)

Veyangoda gross revenue

Office rentals

Warehouing & inventory

Container storage

Stuffing & destuffing

Transport charges

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 168

Figure 9.2 Forecast gross revenue at Enderamulla ICD site

Figure 9.3 Forecast gross revenue at PelTel ICD site

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,0002

01

5

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

An

nu

al r

ev

en

ue

(R

s m

illi

on

)

Enderamulla gross revenue

Office rentals

Warehousing & inventory

Container storage

Stuffing & destuffing

Transport charges

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

An

nu

al r

ev

en

ue

(R

s m

illi

on

)

Peliyagoda/Telangapata gross revenue

Office rentals

Warehousing & inventory

Container storage

Stuffing & destuffing

Transport charges

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 169

Figure 9.4 Forecast gross revenue at Ratmalana ICD site

9.2 Key determinants

As indicated, the principal revenue earners would be transport and cranage charges and

charges for stuffing and destuffing, accounting for more than 85% of all revenue. The key

unit charges and annual revenues are indicated in Table 9.2 below.

Table 9.2 Calculation of transport & cranage revenue and stuffing/destuffing revenue

Item Unit Veyangoda Enderamulla Peliyagoda /

Telangapata

Ratmalana

Year 2015

Annual TEU throughput TEU 109,909 279,904 279,904 83,356

Transport & cranage

charge/trip

Rs / TEU 7,175 5,000 4,675 4,339

Annual transport &

cranage revenue

Rs million 789 1,400 1,309 362

CFS throughput TEU 36,636 93,301 92,368 17,785

Stuffing/destuffing charge Rs / TEU 13,338 13,338 13,338 13,338

Annual stuffing/destuffing

revenue

Rs million 489 1,244 1,232 371

Year 2034

Annual TEU throughput TEU 318,781 811,838 811,838 241,767

Transport & cranage

charge/trip

Rs / TEU 7,175 5,000 4,675 4,339

Annual transport &

cranage revenue

Rs million 2,287 4,059 3,795 1,049

CFS throughput TEU 106,260 270,613 267,906 80,589

Stuffing/destuffing charge Rs / TEU 13,338 13,338 13,338 13,338

Annual stuffing/destuffing

revenue

Rs million 1,417 3,609 3,573 1,075

0

500

1,000

1,500

2,000

2,500

3,0002

01

5

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

An

nu

al r

ev

en

ue

(R

s m

illi

on

)

Ratmalana gross revenue

Office rentals

Warehousing & inventory

Container storage

Stuffing & destuffing

Transport charges

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 170

The forecast of annual revenue is crucially dependent on the two unit charge rates – for

transport and cranage and for stuffing / destuffing. Derivation of the transport and cranage

charges to/from each ICD has been presented in Chapter 4.

The Rs 13,338 per TEU is a composite. Prices for stuffing & destuffing 20ft, 40 ft and 45 ft

containers were obtained from 3 sources, SLPA and two commercial sources. The middle of

the 3 data sets, those of a leading consolidator, were used. These were Rs 16,500 for 20 ft

containers, Rs 11,000 per TEU for 40ft and 45 ft containers. The numbers of laden 20ft, 40 ft

and 45 ft passing through Colombo Port in 2010 were used as the basis for forming the

composite rate.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 171

10 Applicable forms of Procurement Contracts

10.1 Responsibility for Procurement

The responsibility for the implementation of the project, and therefore for the payment of

goods, works, and services under this Project, rests solely with the borrower. ADB, for its

part, is required by its Charter to ensure that funds are paid from ADB financing only as

expenditures are incurred. Disbursements are made only at the borrower’s request.

Supporting evidence that the funds are used in accordance with the financing agreement

and/or the procurement plan shall be submitted with the borrower’s withdrawal

application.

Payment may be made (a) to reimburse the borrower for payment(s) already made from its

own resources, (b) directly to a third party (usually to a supplier or contractor), or (c) to a

commercial bank for expenditures against a Commitment Letter covering a commercial

bank’s letter of credit. The borrower is legally responsible for the procurement. It invites,

receives, and evaluates bids, and awards the contract. The contract is between the

borrower and the supplier or contractor. ADB is not a party to the contract.

ADB’s Role

ADB reviews the procurement procedures, documents, bid evaluations, award

recommendations, and the contract to ensure that the process is carried out in accordance

with agreed procedures, as required in the financing agreement. In the case of major

contracts, the documents are reviewed by ADB prior to their issue.

ADB, for its part, has the obligation to ensure that the proceeds of its financing are used

with due attention to considerations of economy and efficiency.

If, at any time in the procurement process (even after the award of contract), ADB

concludes that the agreed procedures were not followed in any material respect, ADB may

declare misprocurement. However, if a borrower has awarded a contract after obtaining

ADB’s “no objection,” ADB will declare misprocurement only if the “no objection” was

issued on the basis of incomplete, inaccurate, or misleading information furnished by the

borrower. Furthermore, if ADB determines that corrupt or fraudulent practices were

engaged in by representatives of the borrower or of the bidder, ADB may impose applicable

sanctions.

Bidder’s Role

Once a bidder receives the prequalification or bidding document, the bidder should study

the documents carefully to decide if it can meet the technical, commercial, and contractual

conditions, and if so, proceed to prepare its bid. The bidder should then critically review the

documents to see if there is any ambiguity, omission, or internal contradiction, or any

feature of specifications or other conditions which are unclear or appear discriminatory or

restrictive; if so, it should seek clarification from the borrower, in writing, within the time

period specified in the bidding documents for seeking clarifications.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 172

The criteria and methodology for selection of the successful bidder are outlined in the

bidding documents, generally under Instructions to Bidders and Specifications. If these are

not clear, clarification should be similarly sought from the borrower.

ADB's Procurement Guidelines require that borrowers must use the appropriate standard

procurement documents issued by ADB for International Competitive Bidding.

ADB's standard procurement documents for the procurement of goods, and for the

procurement of works (large contracts) are based on Master Procurement Documents

prepared jointly by multilateral development banks and other public international financing

institutions.

Roughton International has considered and will recommend the use of these documents for

this Project, an important feature of the documents is that they can be used with minimum

changes, as they do not contain explanations, footnotes or examples.

The rights and obligations of the borrower and the providers of goods and works for the

project are governed by the bidding documents, and by the contracts signed by the

borrower with the providers of goods and works.

On a large project, there may be a number of different contracts and delivery models.

Roughton International wish to emphasise that the ADB will review the borrower’s

procurement procedures, documents, bid evaluations, award recommendations, and

contracts to ensure that the procurement process is carried out in accordance with the

agreed procedures. The procurement plan approved by ADB shall specify the extent to

which these review procedures shall apply in respect of the different categories of goods

and works to be financed, in whole or in part by ADB.

10.2 Selecting a Delivery Model

10.2.1 The Choice

Determining the procurement method is a critical step in the project delivery process. It is

important to consider which method will best balance the control of project cost and risk

against achieving project objectives and outcomes. The key issue is which form of project

delivery provides the best value for money in meeting the client's service objectives.

The vast majority of investment in Sri Lankan public services has been, and will continue to

be, procured through traditional means. However, other innovative approaches, PPPs

(Public Private Partnerships)8 in particular, must be considered to be used to deliver some

of the country's most complex and significant public sector infrastructure projects.

Major infrastructure projects require detailed and careful planning and it is important that a

robust, value for money assessment is made when choosing the procurement option.

8

Refer Chapters 11 & 12 of this Report

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 173

Open competition is the basis for efficient public procurement. Borrowers need to select the

most appropriate method for the specific procurement. In most cases, international

competitive bidding (ICB), properly administered, and with the allowance for preferences

for domestically manufactured goods and, where appropriate, for domestic contractors for

works under prescribed conditions is the most appropriate method. In most cases,

therefore, ADB requires its borrowers to obtain goods, works and services through ICB open

to eligible suppliers and contractors.

10.2.2 Procurement Plan

As part of the preparation of the project the borrower must prepare and, before loan

negotiations, furnish to ADB for its approval, a Procurement Plan acceptable to ADB setting

forth: (a) the particular contracts for the goods, works, and/or services required to carry out

the project during the initial period of at least 18 months; (b) the proposed methods for

procurement of such contracts that are permitted under the financing agreement, and (c)

the related ADB review procedures. The borrower must update the Procurement Plan

annually or as needed throughout the duration of the project. The borrower must

implement the Procurement Plan in the manner in which it has been approved by ADB.

The Procurement Plan for this Project can be found later in this Chapter of this report.

10.2.3 International Competitive Bidding

The objective of International Competitive Bidding (ICB) is to provide all eligible prospective

bidders with timely and adequate notification of a borrower’s requirements and an equal

opportunity to bid for the required goods and works.

The bidding documents clearly state the type of contract to be entered into and contain the

proposed contract provisions appropriate therefore. The most common types of contracts

provide for payments on the basis of a lump sum or unit prices, or combinations thereof.

The size and scope of individual contracts depend on the magnitude, nature, and location of

the project. For projects requiring a variety of goods and works, separate contracts generally

will be awarded for the supply and/or installation of different items of equipment and plant

and for the works.

On this Project, International Competitive Bidding (ICB) procedures will be used for works

contracts valued above $3 million and goods valued above $500,000, National competitive

bidding for works and goods beneath that stated for ICB. Shopping will be used for contracts

for procurement of works and equipment worth less than $100,000.

When and if any National Competitive Bidding (NCB) is proposed, before starting any

procurement, ADB and the Government will review the public procurement laws of the

central and state governments to ensure consistency with ADB’s Procurement Guidelines.

TA 7600 SRI – Multimodal Transport Project Sri Lanka

Final Report 174

Two-Stage Bidding

For certain packages of this Project, for example, for the construction of the Inland

Container Depots, Roughton International are recommending two-envelope bidding

procedures. With these procedures, bids with separate envelopes for technical and financial

proposals are submitted simultaneously. Such procedures are also recommended for the

procurement of goods. The borrower uses the two-envelope procedure with single-stage

bidding. In this procedure, the technical proposal is opened first and reviewed to determine

responsiveness to the bidding documents. Only the financial proposals of bidders with

responsive technical proposals are opened for evaluation and comparison. The financial

proposals of bidders whose technical proposals are not responsive shall be returned

unopened. The use of these procedures must be agreed upon by ADB and the borrower.

10.2.4 National Competitive Bidding

General

National competitive bidding shall conform to the provisions for "National Competitive

Bidding" as prescribed in the Procurement Guidelines 2006 for Goods and Works issued in

January 2006 by the National Procurement Agency, and the specific procedures prescribed

by the Procurement Manual issued on March 2006, with the clarifications and modifications

described in the following paragraphs required for compliance with the provisions of the

ADB Procurement Guidelines.

Registration

(i) Bidding shall not be restricted to pre-registered firms under the national

registration system of the Institute for Construction, Training and Development

(ICTAD), and such registration shall not be a condition for the submission of bids

in the bidding process.

(ii) Where registration is required prior to award of contract, bidders: (i) shall be

allowed a reasonable time to complete the ICTAD registration process; and (ii)

shall not be denied registration for reasons unrelated to their capability and

resources to successfully perform the contract, which shall be verified through

post-qualification.

(iii) National sanction lists or blacklists may be applied only with prior approval of

ADB.

10.2.5 Notification and Advertising

Timely notification of bidding opportunities is essential in competitive bidding. For this

Project the borrower will be required to prepare and submit to ADB a draft general

procurement notice. ADB will arrange for its publication. The notice shall contain