solutions - Worthy & James Publishing

36

SOLUTIONS Learning Goal 4 Multiple Choice 1. b 2. c $500 cash received comes from a revenue recorded in a prior period—June. 3. b Because cash is paid for a future expense. 4. a Because this is a payment for a previously accrued expense. (b involves unearned revenue; c involves supplies which are really an expense that is prepaid; d involves unearned revenue) 5. d 6. c 7. b 8. d 9. b If you have difficulty, try a simple example using the accounting equation: Assume assets are $10, liabilities are $3, and stockholders’ equity is $7. Now assume the amount of the adjustment is $1. Before adjustment: A $10 = L $3 + SE $7 en, the adjustment: A $10 = L $2 ↓ + SE $8 (↑ revenue) You can see that if you failed to make the adjustment, liabilities would be higher at $3, and stockholders’ equity would be lower at $7 because of less revenue. You can use this method for the next four questions as well. 10. a 11. d 12. c 13. d 14. a Unadjusted net income is $8,000. en subtract: $4,700 insurance expense + $2,000 insurance expense + $3,500 rent expense. 15. a 16. b 17. a 18. b 19. c 20. b 21. a 22. d Adjusting entries are never done in cash basis accounting because adjusting entries only recognize noncash revenues and noncash expenses. Cash basis accounting, therefore, would never record adjustments. 23. d 24. c Discussion Questions and Brief Exercises 1. e two important principles are the revenue recognition principle and the matching principle.e revenue recognition principle requires that revenues be recorded in the period in which they were earned. e matching principle requires that expenses be matched against (meaning “subtracted from”) the revenues they helped to create. e matching is done by direct tracing or by identifying the period(s) in which benefits were received from the expense item. Adjusting entries record revenue and expense items that had not yet been recorded into the correct accounting periods. 2. Adjusting entries are recorded at the end of period aſter all transactions are completed for the period. erefore, any event during the period that creates the need for an adjusting entry can be identified. In this way, as discussed in #1 above, all the revenues and expenses are recorded into the correct periods. Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S1 Mostyn-Vol 2_SG4.indd 1 12/2/16 4:56 PM

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of solutions - Worthy & James Publishing

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S1

SOLUTIONS Learning Goal 4

Multiple Choice

1. b2. c $500 cash received comes from a revenue recorded in a prior period—June.3. b Because cash is paid for a future expense.4. a Because this is a payment for a previously accrued expense. (b involves unearned revenue;

c involves supplies which are really an expense that is prepaid; d involves unearned revenue)5. d6. c7. b8. d9. b If you have difficulty, try a simple example using the accounting equation: Assume assets are

$10, liabilities are $3, and stockholders’ equity is $7. Now assume the amount of the adjustment is $1. Before adjustment: A $10 = L $3 + SE $7 Then, the adjustment: A $10 = L $2 ↓ + SE $8 (↑ revenue) You can see that if you failed to make the adjustment, liabilities would be higher at $3, and

stockholders’ equity would be lower at $7 because of less revenue. You can use this method for the next four questions as well.

10. a11. d12. c13. d14. a Unadjusted net income is $8,000. Then subtract: $4,700 insurance expense + $2,000

insurance expense + $3,500 rent expense.15. a16. b17. a18. b19. c20. b21. a22. d Adjusting entries are never done in cash basis accounting because adjusting entries only

recognize noncash revenues and noncash expenses. Cash basis accounting, therefore, would never record adjustments.

23. d24. c

Discussion Questions and Brief Exercises

1. The two important principles are the revenue recognition principle and the matching principle.The revenue recognition principle requires that revenues be recorded in the period in which they were earned. The matching principle requires that expenses be matched against (meaning “subtracted from”) the revenues they helped to create. The matching is done by direct tracing or by identifying the period(s) in which benefits were received from the expense item. Adjusting entries record revenue and expense items that had not yet been recorded into the correct accounting periods.

2. Adjusting entries are recorded at the end of period after all transactions are completed for the period. Therefore, any event during the period that creates the need for an adjusting entry can be identified. In this way, as discussed in #1 above, all the revenues and expenses are recorded into the correct periods.

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S1

Mostyn-Vol 2_SG4.indd 1 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S2 Section I · Adjusting the Accounts

3. An unearned revenue adjustment will be needed. Unearned revenue is debited, and a revenue is credited.

4. A prepaid expense adjustment will be needed. An expense is debited, and short-term asset is credited.

5. A depreciation expense adjustment will be needed. Depreciation expense is debited, and accumulated depreciation is credited.

6. An accrued revenue adjustment will be needed. A receivable is debited, and a revenue is credited.

7. An accrued expense adjustment will be needed. An expense is debited, and a liability is credited. 8. The purpose of a Depreciation Expense account is to record the estimated amount of plant and

equipment cost that has been used up and has become an expense. Depreciation Expense has a normal debit balance. It appears on the income statement as an operating expense.The purpose of an Accumulated Depreciation account is to record the cumulative amount of depreciation that has been calculated for a plant and equipment asset. Accumulated depreciation a contra-asset account, which means that it acts as an offset to the balance in a plant and equipment asset account. An accumulated depreciation account has a normal credit balance. The amount of accumulated depreciation appears on the balance sheet as a subtraction from its related plant and equipment asset. An example of a common balance sheet format is:Equipment $100,000Less: Accumulated depreciation 22,000

78,000 9. The total wages expense is $29,000 + $3,500 = $32,500. To show a wages payable liability of

$3,500, wages expense of the same amount is also recorded. 10. Consulting Expense 10,000

Accounts Payable 10,000 11. Accounts Receivable 10,000

Consulting Revenue 10,000 12. The equality of the totals on a trial balance only means that debits equal credits; in other words,

the accounting equation is in balance. Although this is important, it does not mean that all the individual account balances are correct. Adjusting entries may still be needed to correctly record revenues and expenses.

13. Accounts Payable 1,000Repairs Expense 2,800

Cash 3,800 14. Net income would be understated by $200 in the current period and overstated by $200 in the

next period when cash is received for the revenue and paid for the expense. 15. Adjusting entries involve revenues and expenses. Revenues and expenses always affect both the

income statement and the balance sheet. Mary is correct. 16. Yes. One month of interest expense is owing and unpaid since the last payment on December 1.

A December 31 entry that debits Interest Expense and credits Interest Payable is required. 17. This is incorrect. For accounting and financial purposes the word “depreciation” does not refer

to loss of value. It means the process of allocating the cost of a plant and equipment asset into expense, as the asset provides benefits during its estimated useful life. This is unrelated to whatever the asset might sell for.

18. a. credit Accumulated Depreciationb. debit Office Supplies Expensec. debit Accounts Receivable or debit Unearned Revenued. credit Rent Payable or credit Prepaid Rente. credit a revenue

Mostyn-Vol 2_SG4.indd 2 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S3

Learning Goal 4, continued

Reinforcement Problems

LG 4-1.

SituationAdjusting for what?

Adjusting accounts at end of period

a. On May 1, Holyoke Company paid $12,000 for a three- year insurance policy. Holyoke Company has a June 30 year end.

prepaid expense

Dr. Insurance Expense Cr. Prepaid Insurance

b. In November, Middlesex Company earned one-fourth of the amount that had been advanced by a customer in September.

unearned revenue

Dr. Unearned Revenue Cr. Revenue

c. An inventory count shows $520 of office supplies on hand at year end. The beginning balance was $1,000.

prepaid expense

Dr. Supplies Expense Cr. Supplies

d. Cape Cod Enterprises performed $7,000 of services for customers during December that remained unrecognized at year end.

accrued revenue

Dr. Accounts Receivable Cr. Revenue

e. Burdett Enterprises shows $15,000 of Office Equipment and $105,000 of Automotive Equipment on the balance sheet.

depreciation expense

Dr. Depreciation Expense Cr. Accumulated Depreciation

f. This year, Massasoit Company paid for 18 months of magazine subscriptions, and at year end seven months’ worth is still in force.

prepaid expense

Dr. Subscription Expense Cr. Prepaid Subscriptions

g. Kinyon Company records show utility expenses unrecorded and unpaid of $350.

accrued expense

Dr. Utility Expense Cr. Accounts Payable

h. Campbell Corporation paid a utility bill that was owing in the amount of $240.

Not an adjusting entry. This is a payment of a previously accrued expense.

i. In June, Springfield Company completed negotiations, signed a contract, and received $25,000 in advance. By year end, the company had performed $5,500 of services on the contract.

unearned revenue

Dr. Unearned Revenue Cr. Revenue

j. North Shore Inc. has a six-day workweek and pays employees weekly, each Saturday. June 30, year end, is on a Tuesday.

accrued expense

Dr. Wages Expense Cr. Wages Payable

k. Bristol Enterprises signed a contract to perform $30,000 of future services.

No entry required. Just signing a contract does not affect the accounting equation.

l. The Supplies account of Northern Essex Enterprises shows a beginning balance of $700 and purchases of $1,200. The ending inventory shows $150 still unused.

prepaid expense

Dr. Supplies Expense Cr. Supplies

m. Three Rivers Corporation received a $50,000 advance from a customer for 2,500 switching devices, all at the same fixed price. By year end, 520 of the switches had been shipped.

unearned revenue

Dr. Unearned Revenue Cr. Revenue

Mostyn-Vol 2_SG4.indd 3 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S4 Section I · Adjusting the Accounts

LG 4-1, continued

SituationAdjusting for what?

Adjusting accounts at end of period

n. In April, Manchester Company made an $8,500 deposit with a security services company. At year end on September 30, there were $7,200 of charges against the deposit.

prepaid expense

Dr. Security Expense Cr. Prepaid Security Service

o. The trial balance of Hartford and Hartford Partnership shows a note payable of $10,000. Principle and interest is not payable until next year.

accrued expense

Dr. Interest Expense Cr. Interest Payable

p. The trial balance of Mitchell Company shows Unearned Fees of $11,000. Fees still unearned at the end of the period are $2,200.

unearned revenue

Dr. Unearned Revenue Cr. Revenue

q. In April, Naugatuck Services, Inc., received an advance from a client for 10 months’ services at a monthly fee of $1,000. The date of the trial balance is December 31.

unearned revenue

Dr. Unearned Revenue Cr. Revenue

r. At year end, a tenant of the Bridgeport Company owes two months of unpaid rent, which has not been recorded.

accrued revenue

Dr. Accounts Receivable Cr. Revenue

s. In September, Housatonic Company prepaid for 500 hours of computer maintenance services. At December 31, year end, 390 hours would be used in the following year.

prepaid expense

Dr. Maintenance Expense Cr. Prepaid Maintenance

t. Northaven Company has $1,500 of advertising expense incurred but unpaid at year end.

accrued expense

Dr. Advertising Expense Cr. Accounts Payable

u. Waterbury Company has $440 of earned but uncol- lected service revenue at year end.

accrued revenue

Dr. Accounts Receivable Cr. Revenue

v. The trial balance of Boston Company shows a balance of $1,800 in Prepaid Insurance.

prepaid expense

Dr. Insurance Expense Cr. Prepaid Insurance

w. The Norwich Company makes semiannual insurance payments. At year end, the Prepaid Insurance account shows debits of: beginning bal. of $900, and March 1 and Sept. 1, $1,800 each.

prepaid expense

Dr. Insurance Expense Cr. Prepaid Insurance

x. A corporation calculates at year end that it owes $100,000 of income tax.

accrued expense

Dr. Income Tax Expense Cr. Income Tax Payable

Mostyn-Vol 2_SG4.indd 4 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S5

LG 4-2.

Journal Entry ItemWhat kind of

adjustment is it?What is the

adjustment recording?

Dr. Cr.a. Utilities Expense 820

Accounts Payable 820

accrued expense a utilities expense that is unpaid

Dr. Cr.b. Accounts Receivable 1,100

Fees Earned 1,100

accrued revenue revenue that is earned but not yet paid by the customer

Dr. Cr.c. Unearned Revenue 200

Subscriptions Revenue 200

unearned revenue revenue for which cash was received in advance and recorded as a liability

Dr. Cr.d. Depreciation Expense 2,500

Accumulated Depreciation—Truck 2,500

depreciation expense the using up of plant and equipment assets

Dr. Cr.e. Cash 1,100

Accounts Receivable 1,100

Not an adjustment (Clue: adjusting entries never involve the cash account.) This

is a receipt of cash for a previously accrued revenue.

Dr. Cr.f. Rent Expense 500

Prepaid Rent 500

prepaid expense rent expense that was paid in advance and recorded as an asset

Dr. Cr.g. Rent Expense 500

Rent Payable 500

accrued expense rent expense that is unpaid

Dr. Cr.h. Accounts Receivable 950

Service Revenue 950

accrued revenue revenue that is earned but not yet paid by the customer

Dr. Cr.i. Unearned Revenue 950

Service Revenue 950

unearned revenue revenue for which cash was received in advance and recorded as a liability

Dr. Cr.j. Supplies Expense 200

Supplies 200

prepaid expense supplies expense that was paid in advance and recorded as an asset (supplies)

Dr. Cr.k. Supplies 200

Accounts Payable 200

Not an adjusting entry. No unrecorded revenue or expense.This entry is a purchase of supplies on account.

Dr. Cr.l. Advertising Expense 3,000

Accounts Payable 3,000

accrued expense advertising expense that is unpaid

Dr. Cr.m. Wages Expense 10,000

Wages Payable 10,000

accrued expense wages expense that is unpaid

Mostyn-Vol 2_SG4.indd 5 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S6 Section I · Adjusting the Accounts

LG 4-2, continued

Journal Entry ItemWhat kind of adjustment is it?

What is the adjustment recording?

Dr.n. Insurance Expense 700

Prepaid Insurance

Cr.

700

prepaid expense insurance expense that was paid in advance and recorded as an asset (prepare insurance.)

Dr. o. Unearned Sales Revenue 2,000

Sales Revenue

Cr.

2,000

unearned revenue revenue for which cash was received in advance and recorded as a liability

LG 4-3.

a. $3,260. The formula that calculates the balance of any account is: Beginning Balance + Increases − Decreases = Ending Balance

The supplies used are decreases in the Supplies account. So in this case: 150 + 3,530 − x = 420. So, x = 3,260.

You could also visualize the Supplies account to help you solve the problem:

b. Other asset accounts analysis:

ItemPrepaid

InsurancePrepaid

RentPrepaid Travel

Prepaid Subscriptions

Beginning balance $1,000 $3,750 $5,000 $300

Payments/purchases made $5,050 $ 850 $3,000 $550

Expense for the period $5,350 $4,100 $3,250 $750

Ending balance $ 700 $ 500 $4,750 $100

c. $13,250 d. $110,100

Supplies

Bal. 1503,530 x

Bal. 420

Mostyn-Vol 2_SG4.indd 6 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S7

LG 4-4.

June 30 Supplies Expense 6,040a. Supplies 6,040

($4,950 + $2,800 − $1,710 = $6,040)

Wages Expense 6,180b. Wages Payable 6,180

($10,300 × 3/5 = $6,180)

Unearned Revenue 20,250c. Services Revenue 20,250

[$2,750 + ($25,000 × .7)] = $20,250

Depreciation Expense 5,100d. Accumulated Depreciation − Office Equipment 2,250

Accumulated Depreciation − Auto. Equipment 2,850($9,000/4 = $2,250; $11,400/4 = $2,850)

Accounts Receivable 3,100e. Service Revenue 3,100

Advertising Expense 800f. Accounts Payable 800

Insurance Expense 5,250 g. Prepaid Insurance 5,250

$1875 + ($9,000 × 3/8) = $5,250

Mostyn-Vol 2_SG4.indd 7 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S8 Section I · Adjusting the Accounts

Learning Goal 4, continuedSOLUTIONS

LG 4-5.

Sept. 30a. Wages Expense 14,000

Wages Payable 14,000($35,000 × 2/5 = $14,000)

Dec. 31 Repairs Expense 3,800b. Accounts Payable 3,800

Dec. 31 Depreciation Expense 7,111c. Accumulated Depreciation − Equipment 7,111

($128,000 − 0)/12 = $10,666.67. $10,666.67 × 8/12 = $7,111.11 Depreciation is for a partial year beginning May 1.

July 31 Unearned Revenue 10,800d. Materials Revenue 10,800

($18,000 /500 = $36/lb. $36 × 300 = $10,800)

Sept. 30 Insurance Expense 10,000e. Prepaid Insurance 10,000

[$18,000 − ($12,000 × 8/12) ] = $10,0008 months remain on the policy still in force.

f. No accounting transaction

Jan. 31 Cash 45,000g. Accounts Receivable 20,000

Revenue 25,000

Mostyn-Vol 2_SG4.indd 8 12/2/16 4:56 PM

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S9

SOLUTIONS Learning Goal 4, continued

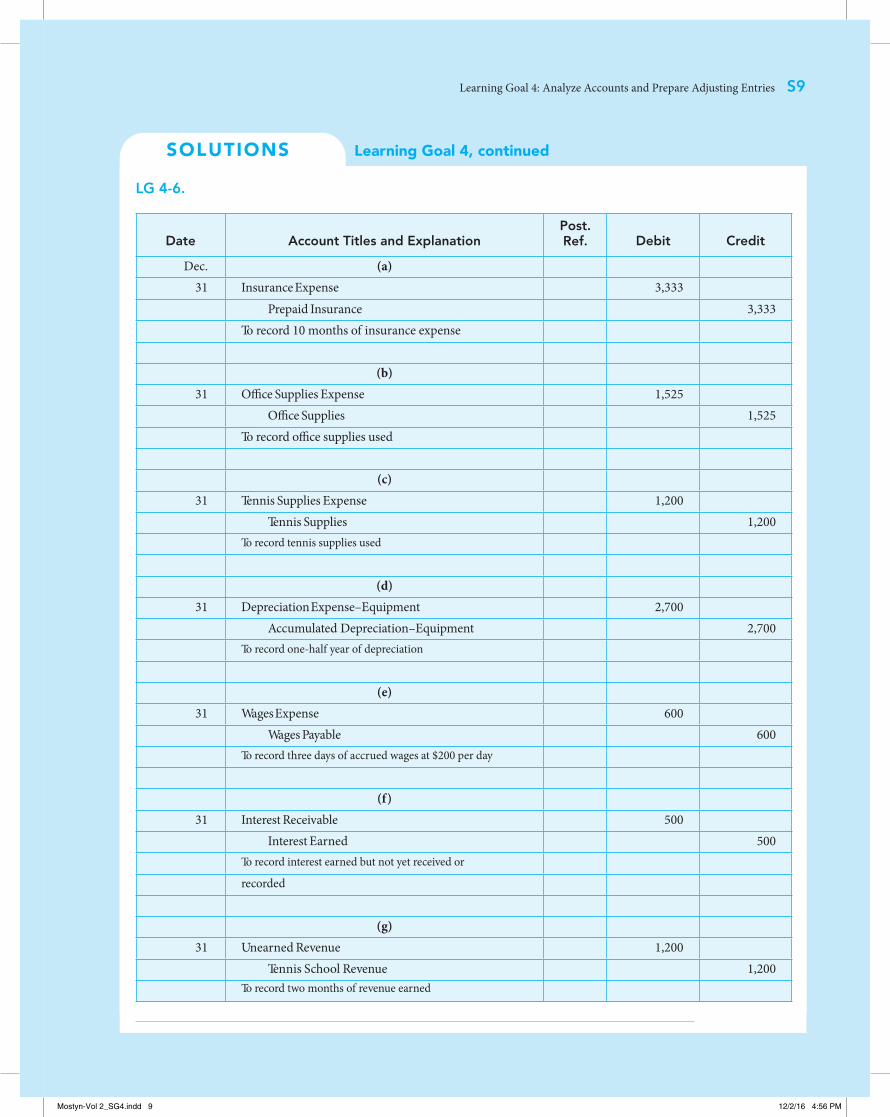

LG 4-6.

Date Account Titles and ExplanationPost. Ref. Debit Credit

Dec. (a)31 Insurance Expense 3,333

Prepaid Insurance 3,333To record 10 months of insurance expense

(b)31 Office Supplies Expense 1,525

Office Supplies 1,525To record office supplies used

(c)31 Tennis Supplies Expense 1,200

Tennis Supplies 1,200To record tennis supplies used

(d)31 Depreciation Expense–Equipment 2,700

Accumulated Depreciation–Equipment 2,700To record one-half year of depreciation

(e)31 Wages Expense 600

Wages Payable 600To record three days of accrued wages at $200 per day

(f)31 Interest Receivable 500

Interest Earned 500To record interest earned but not yet received or

recorded

(g)31 Unearned Revenue 1,200

Tennis School Revenue 1,200To record two months of revenue earned

Mostyn-Vol 2_SG4.indd 9 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S10 Section I · Adjusting the Accounts

LG 4-7.

Date Account Titles and ExplanationPost. Ref. Debit Credit

June (a)30 Accounts Receivable 4,500

Consulting Fees Revenue 4,500To accrue revenue from Megawatt Industries

(b)30 Supplies 150

Supplies Expense 150To adjust overstated expense

(c)

30 Utilities Expense 900Accounts Payable 900

To accrue utilities expense

(d)30 Insurance Expense 1,900

Prepaid Insurance 1,900To record usage of prepaid item

(e)30 Unearned Revenue 2,500

Research Revenue 2,500To record two months of revenue earned

(f )30 Depreciation Expense 5,000

Accumulated Depreciation 5,000To record current year depreciation

Note on adjustment B: This is an unusual adjustment because too much supplies expense was recorded. The expense was overstated by $150 because the actual supplies on hand were $650, not $500. The asset must be adjusted up, so this is the opposite of the usual entry.

Mostyn-Vol 2_SG4.indd 10 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S11

LG 4-7, continued

2. Classification, valuation, and timing elements of each adjusting entry:

Item Classification Valuation Timing

a Accounts Receivable and Consulting Revenue both increase.

The amount to record is $4,500.

The revenue was earned in the current year ending June 30, so it must be recorded in this period instead of recording it when the cash is received next period.

b Supplies increases and Supplies Expense decreases.

The expense is overstated by $150.

The correct amount of supplies expense must be matched against the current year’s revenue for the year that ends on June 30.

c Accounts Payable and Utilities Expense both increase.

The amount of service consumed was $900.

The correct amount of utilities expense must be matched against the current year’s revenue instead of being recorded when the expense is paid next period.

d Prepaid Insurance decreases and Insurance Expense increases.

The amount of the asset consumed was $1,900. $500 remains to be consumed next year.

The correct insurance expense must be matched against the revenues in each of the periods that receive a benefit. These are the current year ending June 30 and the next period beginning July 1.

e Unearned Revenue decreases and Research Revenue increases.

The amount of the liability earned was $2,500.$12,500 remains to be earned next year.

Some revenue was earned in the current year ending June 30. The revenue must be recorded as earned, instead of recording all the revenue when the cash was received.

f Accumulated Deprecia- tion and Depreciation Expense both increase.

Based on a straight-line depreciation calculation,$5,000 of the asset cost is estimated to be used up.

The depreciation expense must be matched against the revenues in each of the years that receive a benefit during the estimated useful life of the asset.

Mostyn-Vol 2_SG4.indd 11 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S12 Section I · Adjusting the Accounts

LG 4-8.

Date Account Titles and ExplanationPost. Ref. Debit Credit

June (a)

30 Unearned Charter Revenue 18,870

Charter Service Revenue 18,870To record revenue earned ($5,250 + $13,620)

(b)

30 Depreciation Expense—Aircraft 48,000

Accumulated Depreciation—Aircraft 48,000

To record one year of depreciation

(c)

30 Wages Expense 840

Wages Payable 840To accrue two days unpaid wages at $420 per day

(d)

30 Insurance Expense 1,175

Prepaid Insurance 1,175To record prepaid insurance expired

(R173 $400 + JRX22 $775)

(e)

30 Equipment Rental Expense 4,400

Accounts Payable 4,400

To record accrued rental charges

(f )

30 Office Supplies Expense 650

Aircraft Supplies Expense 18,050

Office Supplies 650

Aircraft Supplies 18,050

To record use of supplies

Mostyn-Vol 2_SG4.indd 12 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

Learning Goal 4: Analyze Accounts and Prepare Adjusting Entries S13

LG 4-8, continued

2. Net income after adjustments:

Total revenue $221,000Total expense (55,050)Net income before adjustments 165,950 Revenue adjustment 18,870Expense adjustments:Depreciation $48,000Wages 840Insurance 1,175Rental 4,400Office supplies 650Aircraft supplies 18,050 Total expense adjustments (73,115)Net income after adjustments $111,705

3. Cash basis would not have any prepaid items, unearned items, or revenue and expense receivables or payables. There would be no adjusting entries. In effect, cash basis is simply ‘money in and money out’, with the exception of long-term assets such as equipment (called a “modified cash basis”.)

Net income on a cash basis:

Total revenue $221,000Total expense (55,050)Net income before adjustments 165,950The following would have been recorded as expenses:Prepaid insurance $4,900Office supplies 1,150Aircraft supplies 37,950The following would have been recorded as revenue:

(44,000)

Unearned charter revenue: 47,700Cash basis income $169,650

Mostyn-Vol 2_SG4.indd 13 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONS

S14 Section I · Adjusting the Accounts

LG 4-9.

a. $12,000 × 2/36 = $667b. The amount of the customer advance is missing. This should be divided by 4.c. The amount of purchases is missing. Assuming that all uses are recorded with a single

adjustment at ear end, the calculation would be: $1,000 + purchases − $520 = amount used.d. No calculation is required. The amount needed for the adjustment is given.e. The years of estimated useful life for each asset is missing. Details of depreciation

calculation methods are in Learning Goal 19.f. The amount paid is missing. The calculation for adjustment would be: $ paid × 11/18 =

amount used. (Or, $ paid/18 × 11)g. No calculation is required. The amount needed for the adjustment is given.h. This does not involve an adjusting entry. It is the payment of a liability.

Adjusting entries will always involve either a revenue or expense.i. No calculation is required. The amount needed for the adjustment ($5,500)

is given.j. The amount of the weekly wages is missing. The calculation for adjustment

would be: $ weekly wages × 2/6 = 2 days of wages expense.

k. This event does not require an adjusting entry. A contract has been signed, but no services have been performed yet, so no revenue has been earned.

l. Assuming that supplies expense for the period is recorded with a single adjustment: $700 + $1,200 – $150 = $1,750.

m. $50,000/2,500 = $20 per switch. $20 × 520 = $10,400.n. No calculation is required. The amount for security services expense

($7,200) is given.o. The amount of any interest expense incurred but not yet paid is missing.

This should be accrued.

p. $11,000 – $2,200 = $8,800.q. $10,000 × 9/10 = $9,000. (counting April)r. The monthly rent amount is missing. The calculation for adjustment would

be: $ monthly × 2s. The amount of the prepayment is missing. The current expense calculation

would be: ($ paid/500) × 110

t. No calculation is required. The amount of the expense is given.u. No calculation is required. The amount of the revenue is given.v. The amount of the prepayment and the periods prepaid are missing. The

calculation for adjustment would be: $ prepaid/periods prepaid × periods used in current accounting period.

w. $900 + $1,800 + ($1,800 × 4/6) = $3,900.x. No calculation is required. The amount of the tax expense is given.

Mostyn-Vol 2_SG4.indd 14 12/2/16 4:56 PM

SOLUTIONS Appendix Solutions

Multiple Choice Appendix I and II

1. b To record the supplies used up.2. d To record the amount of revenue earned as time passes.3. d4. d Debit an expense, credit Prepaid Expense.5. c Because the asset Prepaid Expense should have been reduced. Also, Insurance Expense should have

been increased, so expenses are too low, which overstates net income.6. a Because the liability Unearned Revenue should have been reduced. Also, revenue should have been

increased, so revenue is too low, which understates net income.7. d8. c

Multiple Choice Appendix III

1. d All the names are used. In this book, we use “plant and equipment” most often.2. b Note: Some textbooks do not use separate Depreciation Expense accounts. That is, all the

depreciation expense is recorded in only one expense account called “Depreciation Expense.”3. a4. d No such account! There is Depreciation Expense and there is Accumulated Depreciation.

Be precise here.5. c Total assets are decreased because the credit balance in Accumulated Depreciation increases.

Net income is decreased because Depreciation Expense increases total expenses.6. d Total assets would be overstated because accumulated depreciation would be too small. Net

income would be overstated because total expenses would be understated—not enough depreciation expense.

7. c8. a (17,500 – 3,500) + 100,000 = 114,0009. b The credit balance of the Accumulated Depreciation account offsets the debit balance in the

asset account. This is called a contra-asset account.10. c The most difficult situation in which to apply the matching principle is when some item

must be allocated between two or more accounting periods and the item does not have an exactly predictable usage. This forces accountants to estimate the usage. The only item here that requires an estimate of usage (useful life) is item (c). Item (d) is the easiest because the transaction only affects one period.

11. b12. c ($27,000/5) × 9/12 (the asset was owned for nine months in the fiscal year) = $4,050.

Note: What the asset normally sells for is irrelevant. Only actual cost is used for depreciation.

Multiple Choice Appendix IV and V

1. c Choice “a” is a deferral—cash has been paid before the expense. There is no expense with “b”—an asset is purchased.

2. d 3. a 4. c 5. b Accounts receivable are understated. Revenue is also understated, which understates net

income. 6. a Accounts payable (or similar payables) are understated. Expense is also understated, which

overstates net income. 7. c 8. a 9. d ($3,300)

Learning Goal 4 Appendix Solutions S15

Mostyn-Vol 2_SG4.indd 15 12/2/16 4:56 PM

S16 Section I · Adjusting the Accounts

SOLUTIONS Learning Goal 4 Appendices I-V Solutions

Reinforcement Problems

LG A 4-1.

Information Example

The key information type is . . .

To determine the cost used up, you need to . . .

1. On April 1, Madison Company prepaid $1,750 for five service repair calls. On June 30, the trial balance shows a balance of $1,750 in the Prepaid Repairs account, after three repair jobs have been done.

the cost per unit of the asset (five service jobs)

calculate the cost per unit of the asset (in units of jobs)

2. The balance of the Spare Parts Supplies account on the trial balance is $14,550. A physical count shows $1,500 of the supplies remaining at year end.

the asset cost remaining

subtract the asset cost remaining from the unadjusted balance of the Prepaid Expense account

3. On October 1, Fox Valley Company purchased a 12-month fire insurance policy for $9,000. The year-end trial balance on January 31 shows $9,000 of Prepaid Fire Insurance. The trial balance also shows $2,500 of Insurance Expense, which does not include the cost of any fire insurance.

the cost per unit of the asset(12 months)

calculate the cost per unit of the asset (units of time)

4. Wisconsin Grand Hotel provides each guest with a complimentary bar of soap. The unadjusted trial balance shows $17,500 of soap supplies at year end. At year end, a physical count shows $3,500 of soap supplies actually remaining. (Soap Expense is recorded only at year end.)

the asset cost remaining

subtract the asset cost remaining from the unadjusted balance of the Prepaid Expense account

5. Blue Mountain Corporation has a December 31 year end. On December 31, year end, an analysis of the unadjusted balance of the Prepaid Insurance shows:

Policy Type Date Purchased AmountFire July 10 $5,000Liability May 1 $2,100Flood Oct. 20 $7,500

The insurance agent verifies that $900 worth of the fire policy is still in force, as well as $1,000 of the liability policy and $2,750 of the flood policy.

the asset cost actually remaining

subtract the asset cost remaining from the unadjusted balance of the Prepaid Expense account

6. On June 30, year end, the trial balance of Milwaukee Company showed an ending balance of $2,110 in the Prepaid Rent account. This represents the rent for May and June. $10,550 of rent expense is showing in the final trial balance.

the asset cost used up

interpret the statement to determine the portion that is used up

Mostyn-Vol 2_SG4.indd 16 12/2/16 4:56 PM

SOLUTIONS Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S17

Reinforcement Problems, continued

LG A 4-1, continued

Information Example

The key information type is . . .

To determine the cost used up, you need to . . .

7. On December 31, year end, the Prepaid Insurance account of Moraine Park Company shows:

The beginning balance is the unexpired part of a one-year policy purchased in the prior year. The October amount is for a three-year policy.

Combination: cost used up and cost per unit ■ One-year policy

was bought last year, so it will be completely used up in this year.

■ Three months of the Oct. 1 payment have been used up.

■ 100% of the first policy

■ Calculate the expense per month.

Note: You could also see this as a “portion” of 3/12.

8. At the beginning of the year, the Prepaid Rent account had a balance of $1,300, and during the year $10,700 of additional prepayments were made. The amount of Prepaid Rent in force at year end is $3,000.

The asset cost remaining

Subtract the asset cost remaining from the unadjusted balance of the Prepaid Expense account.

9. At year end, the Prepaid Rent account balance shows as $12,000. 75% of this balance expired during the year. The remaining 25% will be used next year.

The asset cost used up

Determine portion (75%) used up.

10. The June 30 trial balance of Waukesha Company shows prepaid interest of $5,000 for money borrowed on June 1. Interest expense is incurred at $1,500 per month. No interest expense has been recorded.

The cost per unit of the asset (units of time)

Use the cost per unit of the asset. ($1,500 per month is already calculated for you.)

11. Springfield Company, which has a December 31 year end, shows the following in the Prepaid Advertising account:

The advertising is purchased and consumed semiannually.

Combination: cost used up and cost per unit ■ Six-month

prepayments from Jan. 1 and May 1 are fully used up by December 31.

■ Cost per unit (month) of Nov. 1 prepayment

By interpreting the “purchased semiannually” information, the amounts used up are: ■ All of the

beginning balance ■ All of the May 1

purchase ■ Two months of the

Nov. 1 purchase

Note: You could also see this as a “portion” of 2/12.

Prepaid Insurance

Beg. Bal. Jan. 1 2,500Oct. 1 9,000

Prepaid Advertising

Jan. 1 2,000May 1 4,500Nov. 1 4,500

Mostyn-Vol 2_SG4.indd 17 12/2/16 4:56 PM

SOLUTIONS

S18 Section I · Adjusting the Accounts

Reinforcement Problems, continued

LG A 4-2. Do the adjustment and verify new account balances:

1.

Calculate the Amount of the Adjustment Make the Journal Entry

Cost per month:$1,750/5 = $350/per service call

Amount used up:$350 × 3 mo. = $1,050

June30 Repairs Expense 1,050

Prepaid Repairs 1,050

A ↓ = L + SE ↓Prepaid RepairsRepairs Expense−1,050 +1,050

Determine the New Balances of the Accounts Affected

Prepaid Repairs Repairs Expense

1,750 −0−1,050 1,050

700 1,050

2.

Calculate the Amount of the Adjustment Make the Journal Entry

Spare parts cost on trial balance: Actual spare parts on hand cost: Spare parts used up:

$14,550 $1,500$13,050

Parts ExpenseSpare Parts

13,05013,050

A ↓ Spare Parts−13,050

= L + SE ↓ Parts Expense+13,050

Determine the New Balances of the Accounts Affected

Spare Parts Parts Expense

14,550 −0−13,050 13,050

1,500 13,050

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 18 12/2/16 4:56 PM

SOLUTIONS Learning Goal 4 Appendices I-V Solutions

Reinforcement Problems, continued

LG A 4-2, continued

3.

Calculate the Amount of the Adjustment Make the Journal Entry

Cost per month:$9,000/12 month = $750/mo.

Amount used up:$750 × 4 mo. = $3,000(Oct., Nov., Dec., and Jan. = 4 months in the current accounting period until January 31, date of the trial balance.)

January31 Insurance Expense 3,000

Prepaid Insurance 3,000

A ↓ = L + SE ↓Prepaid InsuranceInsurance Expense−3,000 +3,000

Determine the New Balances of the Accounts Affected

Prepaid Insurance Insurance Expense9,000 2,500

3,000 3,0006,000 5,500

Note: $2,500 of insurance expense has come from other transactions. Other policies must have been used up.

4.

Calculate the Amount of the Adjustment Make the Journal Entry

Unadjusted balance at year end: Actual soap on hand at year end: Soap cost used up:

$17,500 $3,500$14,000

Soap ExpenseSoap Supplies

14,00014,000

A ↓ Soap Supplies−14,000

= L + SE ↓ SoapExpense+14,000

Determine the New Balances of the Accounts Affected

Soap Supplies Soap Expense17,500 −0−

14,000 14,0003,500 14,000

Learning Goal 4 Appendix Solutions S19

Mostyn-Vol 2_SG4.indd 19 12/2/16 4:56 PM

SOLUTIONS

S20 Section I · Adjusting the Accounts

Reinforcement Problems, continued

LG A 4-2, continued

5.

Calculate the Amount of the Adjustment Make the Journal Entry

Prepaid insurance cost on trial balance: $14,600Actual prepaid insurance remaining: $ 4,650Prepaid insurance used up: $ 9,950

Insurance Expense 9,950Prepaid Insurance 9,950

A ↓ = L + SE ↓Prepaid InsuranceInsurance Expense−9,950 +9,950

Determine the New Balances of the Accounts Affected

Prepaid Insurance Insurance Expense

14,600 −0−9,950 9,950

4,650 9,950

6.

Calculate the Amount of the Adjustment Make the Journal Entry

Cost used up:You are told that the $2,110 is for the months of May and June. So the Prepaid Rent had been fully used up as of June 30. The full$2,110 is the amount of the adjustment.

Rent ExpensePrepaid Rent

2,1102,110

A ↓ Prepaid Rent−2,110

= L + SE ↓ Rent Expense+2,110

Determine the New Balances of the Accounts Affected

Prepaid Rent Rent Expense

2,110 10,5502,110 2,110

−0− 12,660

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 20 12/2/16 4:56 PM

SOLUTIONS

Reinforcement Problems, continued

LG A 4-2, continued

7.

Calculate the Amount of the Adjustment Make the Journal Entry

January 1 balance: All of this amount is used up in the current year (purchased in the prior year,so less than 1 year is left): $2,500

October 1 purchase:Amount per month:$9,000/36 = $250 per month × 3 $750Total Prepaid Insurance used up: $3,250

Insurance Expense 3,250Prepaid Insurance 3,250

A ↓ = L + SE ↓Prepaid InsuranceInsurance Expense−3,250 +3,250

Determine the New Balances of the Accounts Affected

Prepaid Insurance Insurance Expense11,500 −0−

3,250 3,2508,250 3,250

8.

Calculate the Amount of the Adjustment Make the Journal Entry

Unadjusted balance at year end: (1,300 + 10,700 − 0) = $12,000Prepaid Rent in force at year end: $ 3,000Prepaid Rent used up: $ 9,000

Rent ExpensePrepaid Rent

9,0009,000

A ↓ Prepaid Rent−9,000

= L + SE ↓ Rent Expense+9,000

Determine the New Balances of the Accounts Affected

Prepaid Rent Rent Expense

12,000 −0−9,000 9,000

3,000 9,000

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S21

Mostyn-Vol 2_SG4.indd 21 12/2/16 4:56 PM

SOLUTIONS

S22 Section I · Adjusting the Accounts

Reinforcement Problems, continued

LG A 4-2, continued

9.

Calculate the Amount of the Adjustment Make the Journal Entry

You can calculate that $9,000 is the cost of Prepaid Rent that has been consumed. This is the amount of the adjustment.$12,000 × .75 = $9,000

Rent Expense 9,000Prepaid Rent 9,000

A ↓ = L + SE ↓Prepaid RentRent Expense−9,000 +9,000

Determine the New Balances of the Accounts Affected

Prepaid Rent Rent Expense

12,000 −0−9,000 9,000

3,000 9,000

10.

Calculate the Amount of the Adjustment Make the Journal Entry

Cost per month:$1,500 per month is already calculated for you

Amount used up:$1,500 × 1 mo. = $1,500 total expense(June 1–June 30 is 1 month in the current accounting period that ends on June 30.)

June30 Interest Expense 1,500

Prepaid Interest 1,500

A ↓ Prepaid Interest−1,500

= L + SE ↓ Interest Expense+1,500

Determine the New Balances of the Accounts Affected

Prepaid Interest Interest Expense

5,000 −0−1,500 1,500

3,500 1,500

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 22 12/2/16 4:56 PM

SOLUTIONS

Reinforcement Problems, continued

LG A 4-2, continued

11.

Calculate the Amount of the Adjustment Make the Journal Entry

January 1 balanceBecause we know that a contract lasts 6 months, we know that any balance purchased in the prior year expires in the current year. (Also, we do not know the original cost of the prior year purchase, so we cannot calculate its cost per unit, that is, per month.)

Amount used up from prior year purchase: $2,000

May 1 purchaseAmount used up is:Full 6 months is used up: $4,500

November 1 purchaseAmount per month:$4,500/6 = $750/month × 2 = $1,500

Total Prepaid Advertising used up: $8,000

Dec.31 Advertising Expense 8,000

Prepaid Advertising 8,000

A ↓ = L + SE ↓Prepaid AdvertisingAdvertising Expense−8,000 +8,000

Determine the New Balances of the Accounts Affected

Prepaid Advertising Advertising Expense

11,000 −0−8,000 8,000

3,000 8,000

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S23

Mostyn-Vol 2_SG4.indd 23 12/2/16 4:56 PM

SOLUTIONS

S24 Section I · Adjusting the Accounts

Reinforcement Problems

LG A 4-3.

Information Example

The key information type is . . .

and to determine the total revenue earned to decrease the liability . . .

1. On April 1, Adirondack Rental Company received $1,750 for five months of equipment rental. The June 30 trial balance shows a balance of $1,750 in the Unearned Rent Revenue account.

the unearned revenue per unit,

■ calculate the unearned revenue per unit (per month)

■ multiply by the number of units provided

2. The trial balance of Manhattan Company shows the balance in the Unearned Sales account as $4,040. A review of sales invoices shows that 75% of these orders was shipped.

the unearned revenue that was earned,

■ use percent given to determine the portion earned

3. On October 1, Erie Insurance, Inc. received a $9,000 payment for a 12-month insurance policy. The year- end trial balance on January 31 shows $9,000 of Unearned Revenue.

the unearned revenue per unit,

■ calculate the unearned revenue per unit (per month)

■ multiply by the number of units provided

4. The ledger of La Guardia Enterprises showed $25,000 of Unearned Service Revenue as a beginning balance. This is a balance from the prior year for six months of services. During this year, La Guardia received $52,000 of advance payments and earned $40,000 of them.

the unearned revenue that was earned,

■ $25,000 beginning balance fully earned in the current period

■ $40,000 earned from current receipts

5. The Nassau Company sells computer service contracts. Each $1,500 contract is good for 10 service repairs calls. All contracts sold are recorded as Unearned Revenue. During the quarter ended September 30, Nassau Company made 710 service calls.

the unearned revenue per unit,

■ calculate the unearned revenue per unit (per service call)

■ multiply by the number of units provided

6. Suffolk Printing Partnership received a $10,000 advance payment on February 1 to print 5,000 calendars. By December 31, year end, 3,500 calendars were supplied to customers who made the prepayment.

the unearned revenue per unit,

■ calculate the unearned revenue per unit (per calendar)

■ multiply by the number of units provided

7. Queensborough Corporation’s Unearned Revenue account showed an $8,000 balance at year end. $7,000 of the amount is for the last seven months’ rent. The remainder is a deposit for the last month’s rent of a rental agreement that expires next year.

the unearned revenue that was earned,

■ $7,000 is the amount earned during the last seven months of the current period

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 24 12/2/16 4:56 PM

SOLUTIONS

LG A 4-3, continued

Information Example

The key information type is . . .

and to determine the total revenue earned to decrease the liability . . .

8. On September 1, Kingsborough Banking Company made a loan that required the customer to prepay six months’ interest in the amount of $9,000. On December 31, year end, the Kingsborough ledger showed:

the unearned revenue per unit (per month),

■ calculate the unearned revenue per month

■ multiply by the number of months earned

9. On March 22, Suny Consulting Company received a $14,000 advance payment from a client. By June 30, year end, $1,500 of the advance was still not earned.

the unearned revenue actually remaining,

subtract the amount remaining from the unadjusted trial balance amount

10. On March 22, Suny Consulting Company received a $14,000 advance payment from a client. By June 30, year end, $12,500 of the advance had been earned.

the unearned revenue that was earned,

use the dollar amount given

11. At year end, Hudson Valley Test Labs, Inc. has a Deferred Revenue account that shows a beginning balance of $50,000 from a prior year’s five-month service contract. During the current year, the company received an advance payment of $200,000 to test 1,000 units. This was also recorded in Deferred Revenue. The company tested 212 units.

Combination: ■ the unearned

revenue that was earned,

■ the unearned revenue per unit,

■ the beginning balance was fully earned.

■ calculate the unearned revenue per unit (per test) and multiply by the number of units

Deferred Interest Revenue

9,000

Interest Revenue

200,000

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S25

Mostyn-Vol 2_SG4.indd 25 12/2/16 4:56 PM

SOLUTIONS

S26 Section I · Adjusting the Accounts

LG A 4-4.

1.

Calculate the Amount of the Adjustment Make the Journal Entry

Unearned revenue per month:$1,750/5 mo. = $350/mo.

Amount earned:$350 × 3 mo. = $1,050(April, May, and June = 3 months in the current accounting period until June 30, the date of the trial balance)

June30 Unearned Revenue 1,050

Rent Revenue 1,050

A = L ↓ + SE ↑Unearned RentRevenue Revenue−1,050 +1,050

Determine the New Balances of the Accounts Affected

Unearned Revenue Rent Revenue

1,750 −0−1,050 1,050

700 1,050

2.

Calculate the Amount of the Adjustment Make the Journal Entry

Amount earned:$4,040 × .75 = $3,030

Unearned RevenueSales Revenue

3,0303,030

A = L ↓ +Unearned Revenue −3,030

SE ↑Sales Revenue +3,030

Determine the New Balances of the Accounts Affected

Unearned Revenue Sales Revenue

4,040 −0−3,030 3,030

1,010 3,030

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 26 12/2/16 4:56 PM

SOLUTIONS

LG A 4-4, continued

3.

Calculate the Amount of the Adjustment Make the Journal Entry

Unearned revenue per month:$9,000/12 mo. = $750/mo.

Jan. 31 Unearned Revenue 3,000

Insurance Revenue 3,000

Amount earned:$750 × 4 mo. = $3,000(Oct., Nov., Dec., and Jan. = 4 months in the current accounting period until Jan. 31, the date of the trial balance)

A = L ↓Unearned Revenue−3,000

+ SE ↑ Insurance Revenue+3,000

Determine the New Balances of the Accounts Affected

Unearned Revenue Insurance Revenue

9,000 −0−3,000 3,000

6,000 3,000

4.

Calculate the Amount of the Adjustment Make the Journal Entry

Beginning account balance: $25,000(fully earned because we know 6 months from last year does not extend beyond the current year)

Unearned RevenueService Revenue

65,00065,000

Earned during the year: 40,000 A = L ↓ + SE ↑UnearnedRevenue−65,000

ServiceRevenue+65,000

Total: $65,000

Determine the New Balances of the Accounts Affected

Unearned Revenue Service Revenue

77,000 −0−65,000 65,000

12,000 65,000

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S27

Mostyn-Vol 2_SG4.indd 27 12/2/16 4:56 PM

SOLUTIONS

S28 Section I · Adjusting the Accounts

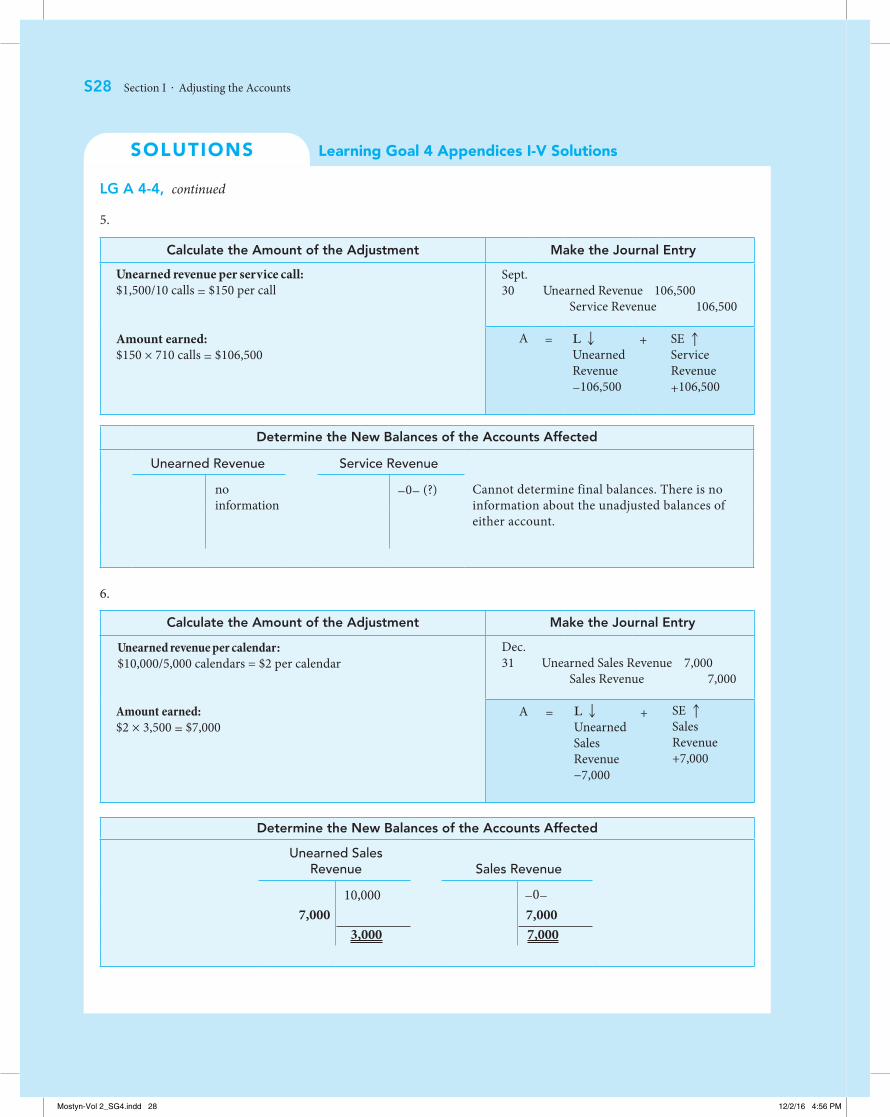

LG A 4-4, continued

5.

Calculate the Amount of the Adjustment Make the Journal Entry

Unearned revenue per service call:$1,500/10 calls = $150 per call

Sept. 30 Unearned Revenue 106,500

Service Revenue 106,500

Amount earned:$150 × 710 calls = $106,500

A = L ↓Unearned Revenue−106,500

+ SE ↑ Service Revenue+106,500

Determine the New Balances of the Accounts Affected

Unearned Revenue Service Revenue

no information

−0− (?) Cannot determine final balances. There is no information about the unadjusted balances of either account.

6.

Calculate the Amount of the Adjustment Make the Journal Entry

Unearned revenue per calendar:$10,000/5,000 calendars = $2 per calendar

Dec. 31 Unearned Sales Revenue 7,000

Sales Revenue 7,000

Amount earned:$2 × 3,500 = $7,000

A = L ↓Unearned Sales Revenue−7,000

+ SE ↑SalesRevenue+7,000

Determine the New Balances of the Accounts Affected

Unearned SalesRevenue Sales Revenue

10,000 −0−7,000 7,000

3,000 7,000

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 28 12/2/16 4:56 PM

SOLUTIONS

LG A 4-4, continued

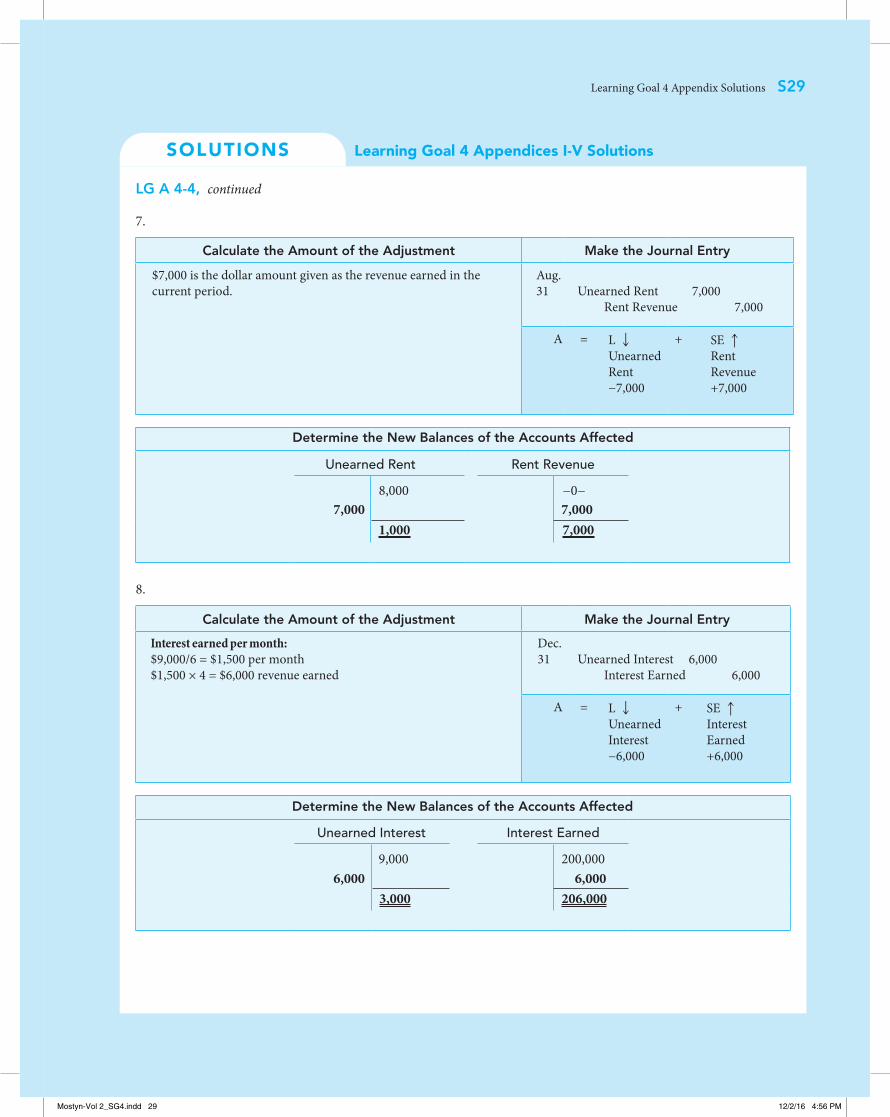

7.

Calculate the Amount of the Adjustment Make the Journal Entry

$7,000 is the dollar amount given as the revenue earned in the current period.

Aug. 31 Unearned Rent

Rent Revenue7,000

7,000

A = L ↓Unearned Rent−7,000

+ SE ↑RentRevenue+7,000

Determine the New Balances of the Accounts Affected

Unearned Rent Rent Revenue

8,000 −0−7,000 7,000

1,000 7,000

8.

Calculate the Amount of the Adjustment Make the Journal Entry

Interest earned per month:$9,000/6 = $1,500 per month$1,500 × 4 = $6,000 revenue earned

Dec. 31 Unearned Interest 6,000

Interest Earned 6,000

A = L ↓Unearned Interest−6,000

+ SE ↑InterestEarned+6,000

Determine the New Balances of the Accounts Affected

Unearned Interest Interest Earned

9,000 200,0006,000 6,000

3,000 206,000

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S29

Mostyn-Vol 2_SG4.indd 29 12/2/16 4:56 PM

S30 Section I · Adjusting the Accounts

SOLUTIONS

LG A 4-4, continued

9.

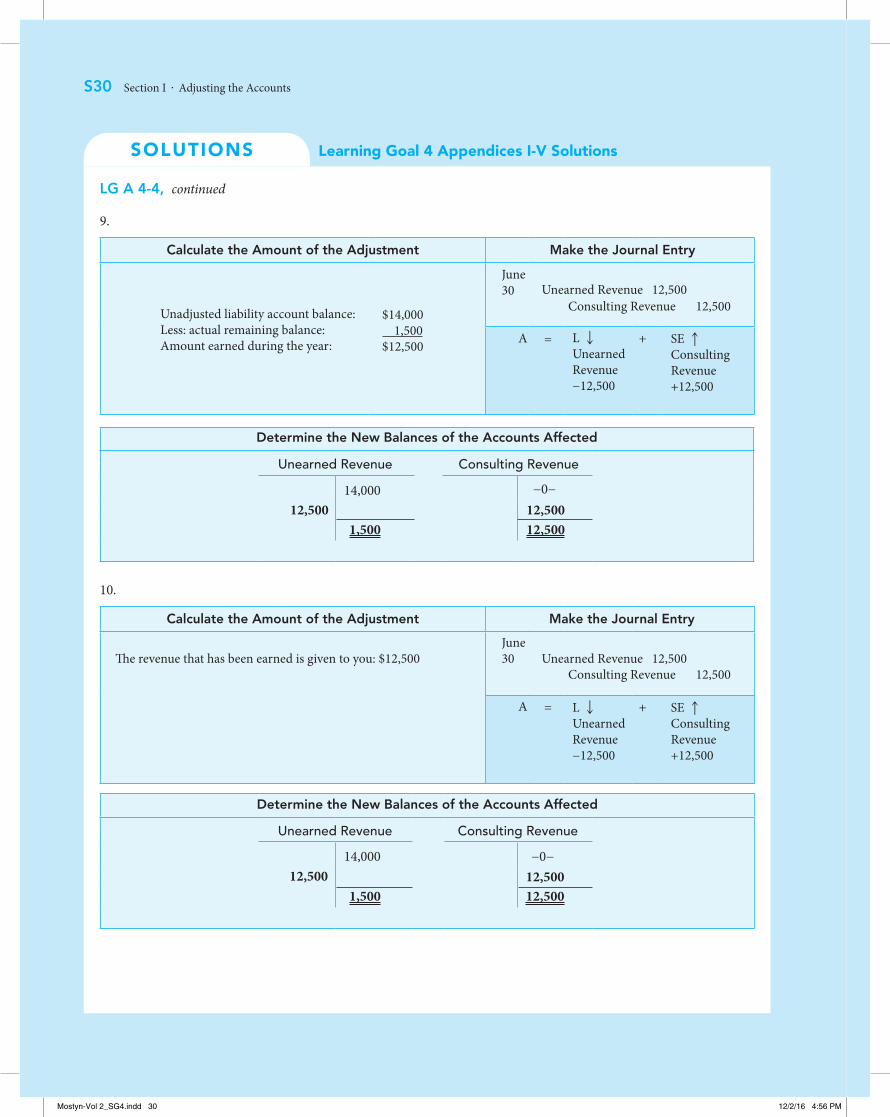

Calculate the Amount of the Adjustment Make the Journal Entry

Unadjusted liability account balance: Less: actual remaining balance: Amount earned during the year:

$14,000 1,500$12,500

June 30 Unearned Revenue 12,500

Consulting Revenue 12,500

A = L ↓Unearned Revenue−12,500

+ SE ↑Consulting Revenue+12,500

Determine the New Balances of the Accounts Affected

Unearned Revenue Consulting Revenue

14,000 −0−12,500 12,500

1,500 12,500

10.

Calculate the Amount of the Adjustment Make the Journal Entry

The revenue that has been earned is given to you: $12,500June 30 Unearned Revenue 12,500

Consulting Revenue 12,500

A = L ↓Unearned Revenue−12,500

+ SE ↑Consulting Revenue+12,500

Determine the New Balances of the Accounts Affected

Unearned Revenue Consulting Revenue

14,000 −0−12,500 12,500

1,500 12,500

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 30 12/2/16 4:56 PM

SOLUTIONS

LG A 4-4, continued

11.

Calculate the Amount of the Adjustment Make the Journal Entry

Unearned Revenue earned: $50,000

Unearned Revenue per test:$200,000/1,000 units = $200 per unit

Dec. 31 Deferred Revenue 92,400

Testing Revenue 92,400

$200 per unit × 212 units =Total earned

$42,400 A = L ↓DeferredRevenue−92,400

+ SE ↑TestingRevenue+92,400

$92,400

Determine the New Balances of the Accounts Affected

Deferred Revenue Testing Revenue

250,000 −0−92,400 92,400

157,600 92,400

Reinforcement Problems

LG A 4-5. Accumulated depreciation is a contra asset account and has a normal credit balance. It appears with the asset accounts on the balance sheet. Depreciation expense is an expense account and has a normal debit balance. It appears with the expenses on the income statement.

LG A 4-6. By using the Accumulated Depreciation account, credit entries in the asset account are only for reductions or disposals of the asset. Secondly, the use of an Accumulated Depreciation account allows us to quickly and easily see the total accumulated depreciation that has been recorded for each plant and equipment asset (or group).

LG A 4-7. Depreciation Expense—Office Equipment 1,500 Accumulated Depreciation—Office Equipment 1,500

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S31

Mostyn-Vol 2_SG4.indd 31 12/2/16 4:56 PM

Learning Goal 4, continuedSOLUTIONSSOLUTIONS

LG A 4-8.

Date Account Titles and ExplanationPost. Ref. Debit Credit

Dec. (a)31 Depreciation Expense—Computer 2,450

Accumulated Depreciation—Computer 2,450To record one year of depreciation expense: 12,250/5

(b)Dec. Depreciation Expense–Drilling Equipment

31 Accumulated Depreciation—Drilling Equipment 2,550To record nine months of depreciation expense: 2,550Calculated as (35,000 – 1,000/10) × (9/12)

June (c)30 Depreciation Expense–Truck 5,400

Accumulated Depreciation—Truck 5,400To record six months of depreciation expense:(54,000/5) × (6/12)

LG A 4-9. $480,000. Use the formula for 10-year straight-line depreciation [cost (x) – residual value (0)]/useful life (10): [(x – 0)/10] × 3/12 = 12,000. 1/10 x = 48,000 x = 480,000

The $12,000 in the accumulated depreciation account is the current period depreciation expense (for three months) because this is the first year the asset is owned.

Learning Goal 4 Appendices I-V Solutions

S32 Section I · Adjusting the Accounts

Mostyn-Vol 2_SG4.indd 32 12/2/16 4:56 PM

SOLUTIONS

Reinforcement Problems

LG A 4-10.

Item

Accrued . . .Not an accrualRevenue Expense

a. Dutchess Company owes employee wages in the amount of $15,000 that are not recorded.

✔

b. Finger Lakes Tourist Company has fees earned but unbilled of $7,500.

✔

c. Niagra Company received the December telephone bill in early January.

✔

d. On June 30, fiscal year end for Corning, Inc. $10,000 of wages expense accrued since the last payday.

✔

e. Briarcliffe Company collected $4,500 from accounts receivable.

There is no revenue here—just collecting cash owed by customers.

✔

f. Services provided but unbilled are $9,800. ✔

g. Utica Partnership has $3,000 of rent still due from tenants at year end.

✔

h. Westchester Company earned $2,500 of a customer advance that had been credited to unearned revenue.

This revenue has already been prepaid by the customer—a deferral.

✔

i. On December 31, year end, Jefferson Company records show $1,500 of interest on money borrowed unpaid and not due until January 15.

✔

j. On March 3, Rockaway Operations Co. signed a contract to provide $12,000 of consulting services.

Signing a contract does not immediately affect the accounting equation.

✔

k. Accounts Receivable 700 Fees Earned 700

✔

l. Unearned Rent 700 Fees Earned 700

We are reducing the Unearned Revenue, so the customer must have already paid us.

✔

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S33

Mostyn-Vol 2_SG4.indd 33 12/2/16 4:56 PM

SOLUTIONS

S34 Section I · Adjusting the Accounts

LG A 4-10, continued

Item

Accrued . . .Not an accrualRevenue Expense

m. Rent Expense 8,000 Rent Payable 8,000

✔

n. Rent Expense 8,000 Prepaid Rent 8,000

We are reducing the Prepaid Rent, so the item was already prepaid.

✔

o. The trial balance shows a balance of $2,500 in the Prepaid Rent account.

✔

p. The trial balance shows a balance of $4,000 in the Unearned Service Revenue account.

✔

LG A 4-11.

Date Account Titles and ExplanationPost. Ref. Debit Credit

Sept. 30 Wages Expense 5,000Wages Payable 5,000

To accrue wages

30 Accounts Receivable 4,400Fees Earned 4,400

To accrue fees earned

30 Interest Expense 2,500Interest Payable 2,500

To accrue interest expense

30 Accounts Receivable 800

Service Revenue 800

To accrue service revenue

30 Accounts Receivable 2,000Consulting Revenue 2,000

To accrue unbilled consulting revenue: 3,000 × 2/3 = 2,000

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 34 12/2/16 4:56 PM

SOLUTIONS

LG A 4-11, continued

Date Account Titles and ExplanationPost. Ref. Debit Credit

30 Rent Expense 4,000Rent Payable 4,000

To accrue rent owing but unpaid

30 Wages Expense 3,600Wages Payable 3,600

To accrue four days of wages to Sept. 30 at $900 per day

Note on last item: First, you calculate the rate per day: $4,500/5 = $900 per day. Second, you count backwards from Oct. 4 to find what day of the week September 30 was on! If October 4 is a Monday, then September 30 must have been a Thursday. Therefore, at the end of business on September 30, there must have been four days of accrued wages: Monday, Tuesday, Wednesday, and Thursday: 4 × $900/day = $3,600.

LG A 4-12.

Date AccountPost. Ref. Debit Credit

December (a)31 Accounts Receivable 7,600

Financial Service Revenue 7,600(b)

31 Internet Service Expense 4,500Accounts Payable 4,500

(c)31 Wages Expense 12,600

Wages Payable 12,600(d)

31 Computer Lease Expense 1,250Accounts Payable 1,250

(e)31 Interest Receivable 180

Interest Revenue 180

Learning Goal 4 Appendices I-V Solutions

Learning Goal 4 Appendix Solutions S35

Mostyn-Vol 2_SG4.indd 35 12/2/16 4:56 PM

SOLUTIONS

S36 Section I · Adjusting the Accounts

LG A 4-12, continued

Date AccountPost. Ref. Debit Credit

(f )31 Franchise Expense 34,200

Prepaid Franchise Expense 12,000Accounts Payable 22,200

January (g)9 Wages Payable 12,600

Wages Expense 16,800Cash 29,400

(h)11 Cash 38,000

Accounts Receivable 7,600Financial Service Revenue 30,400

a. $38,000 × .2 = $7,600b. Accrue the amount given.c. $2,100 × 6 = $12,600 (6 days expense as of December 31).d. $1,550 × 25/31 = $1,250 (or $1,550/31 × 25 = $1,250).e. One month of (December) interest has accrued, payable on January 1.f. $136,800 × .25 = $34,200 of expense, of which $12,000 has been prepaid. The balance is still

payable. The prepayment is used up and becomes an expense. The rest of the franchise expense is an accrued expense.

g. Total cash to pay is $2,100 × 14 = $29,400. Eight days of this expense for January is $2,100 × 8 = $16,800.

h. The total revenue is $38,000 for the job, of which $7,600 was earned and accrued last year.

Learning Goal 4 Appendices I-V Solutions

Mostyn-Vol 2_SG4.indd 36 12/2/16 4:56 PM