Securities Analysis - Union Medical Healthcare (2138 HK)

34

7 Dec 2017 Securities Analysis PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE BUY (Initiation) Target Price HK$4.76 Up/downside +31.8% Current price HK$3.61 Amy Ge Tel: (852) 3761 8778 Email: [email protected] Cyrus Ng, CFA Tel:(852) 3761 8780 Email:[email protected] China Healthcare Sector Mkt. Cap. (HK$mn) 3,541 Avg. 3mths t/o (HK$mn) 4.04 52W High/Low (HK$) Total Issued Shares (mn) 4.35/2.36 980.9 Source: Bloomberg Shareholding Structure Management 74.46% Free float 25.54% Source: Bloomberg Share performance Absolute Relative 1-mth 14.2% 13.3% 3-mth 47.3% 41.0% 6-mth 49.0% 34.3% Source: Bloomberg 12-mth price performance Source: Bloomberg Auditor: KPMG Web-site: www.umhgp.com 2.0 2.5 3.0 3.5 4.0 4.5 Nov 16 Jan 17 Mar 17May 17 Jul 17 Sep 17 Nov 17 HK$ Union Medical Healthcare (2138 HK) Top pick among HK aesthetic service providers The leading aesthetic medical service provider expanding into multiple medical fields. UMH was the largest aesthetic medical service provider in Hong Kong in terms of revenue in 2016, according to Frost & Sullivan. UMH has gradually transformed itself from a purely aesthetic medical player to a comprehensive medical service provider through self-launched services and acquisitions. It provides a broad range of services, including aesthetic medical services, traditional beauty services, dental services, physical examination services, chiropractic therapy, health management services and sales of skincare products. New medical services to bring additional growth momentum. We believe the new business divisions, including physical examination, acquired chiropractic business and dental services, could enjoy strong growth momentum from cross selling activities among the large and loyal customer base of the Company. Potential acquisitions in other medical fields such as dermatology, ophthalmology, ENT and gynecology would add additional growth momentum for the Company. Booming medical tourism to boost growth. In FY2017, revenue from PRC clients was HK$241.2mn and accounted for 25% of total revenue (vs. 14% in FY16). As of 1H FY18, revenue from PRC clients had increased to HK220.4mn and generated 35.7% of overall revenue (vs.17.7% in 1H FY17). Medical tourism has become a major growth driver for the Company. In addition, the PRC clinics will play a key role on client referral and can refer some clients to Hong Kong for services not offered by PRC clinics. The Company expected the proportion of revenue from PRC clients to increase to around 30%-40% in FY2018. We forecast 26.4% core net profit CAGR in FY17-FY20E. We forecast core net profit to grow 34.6% /23.0% /21.9% YoY in FY18/FY19/FY20E with a core NPM of 20.4% /20.1% /20.6%. Initiation coverage with TP of HK$4.76. We believe the Company would continue to strengthen its leading position in aesthetic medical industry and to grow other medical services which would complement each other. Given the robust growth, better profitability over peers and not demanding valuation (trading at 13.8x/11.2x FY18/FY19E PER), we initiate coverage on UMH with BUY rating and target price of HK$4.76, which is based on our DCF model (WACC:13.5%, terminal growth rate:3%). Our target price implies 18.2x/14.8x FY18/FY19E PER, with upside potential of 31.8%. Earnings summary (YE Mar 31) FY16A FY17A FY18E FY19E FY20E Turnover (HK$ mn) 705 965 1,256 1,563 1,861 Core net income (HK$ mn) 177 190 256 315 384 Core EPS (HK$) 0.24 0.20 0.26 0.32 0.39 Core EPS CHG (%) -1.7 -16.7 32.4 23.0 21.9 PE (x) 15.3 18.3 13.8 11.2 9.2 PB (x) 4.8 4.5 4.4 3.6 2.8 Yield (%) 5.3 5.7 5.8 2.7 3.3 ROE (%) 20.3 25.8 32.5 32.4 30.7 Net gearing (%) Net cash Net cash Net cash Net cash Net cash Source: Company, CMBIS

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Securities Analysis - Union Medical Healthcare (2138 HK)

7 Dec 2017

Securities Analysis

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE

BUY (Initiation)

Target Price HK$4.76 Up/downside +31.8% Current price HK$3.61

Amy Ge Tel: (852) 3761 8778

Email: [email protected]

Cyrus Ng, CFA Tel:(852) 3761 8780

Email:[email protected]

China Healthcare Sector Mkt. Cap. (HK$mn) 3,541 Avg. 3mths t/o (HK$mn) 4.04 52W High/Low (HK$) Total Issued Shares (mn)

4.35/2.36 980.9

Source: Bloomberg

Shareholding Structure Management 74.46% Free float 25.54% Source: Bloomberg

Share performance Absolute Relative 1-mth 14.2% 13.3% 3-mth 47.3% 41.0% 6-mth 49.0% 34.3% Source: Bloomberg

12-mth price performance

Source: Bloomberg

Auditor: KPMG Web-site: www.umhgp.com

2.0

2.5

3.0

3.5

4.0

4.5

Nov 16 Jan 17 Mar 17May 17 Jul 17 Sep 17 Nov 17

HK$

Union Medical Healthcare (2138 HK)

Top pick among HK aesthetic service providers

The leading aesthetic medical service provider expanding into multiple

medical fields. UMH was the largest aesthetic medical service provider in Hong Kong in terms of revenue in 2016, according to Frost & Sullivan. UMH has gradually transformed itself from a purely aesthetic medical player to a comprehensive medical service provider through self-launched services and acquisitions. It provides a broad range of services, including aesthetic medical services, traditional beauty services, dental services, physical examination services, chiropractic therapy, health management services and sales of skincare products.

New medical services to bring additional growth momentum. We believe the new business divisions, including physical examination, acquired chiropractic business and dental services, could enjoy strong growth momentum from cross selling activities among the large and loyal customer base of the Company. Potential acquisitions in other medical fields such as dermatology, ophthalmology, ENT and gynecology would add additional growth momentum for the Company.

Booming medical tourism to boost growth. In FY2017, revenue from PRC clients was HK$241.2mn and accounted for 25% of total revenue (vs. 14% in FY16). As of 1H FY18, revenue from PRC clients had increased to HK220.4mn and generated 35.7% of overall revenue (vs.17.7% in 1H FY17). Medical tourism has become a major growth driver for the Company. In addition, the PRC clinics will play a key role on client referral and can refer some clients to Hong Kong for services not offered by PRC clinics. The Company expected the proportion of revenue from PRC clients to increase to around 30%-40% in FY2018.

We forecast 26.4% core net profit CAGR in FY17-FY20E. We forecast core net profit to grow 34.6% /23.0% /21.9% YoY in FY18/FY19/FY20E with a core NPM of 20.4% /20.1% /20.6%.

Initiation coverage with TP of HK$4.76. We believe the Company would continue to strengthen its leading position in aesthetic medical industry and to grow other medical services which would complement each other. Given the robust growth, better profitability over peers and not demanding valuation (trading at 13.8x/11.2x FY18/FY19E PER), we initiate coverage on UMH with BUY rating and target price of HK$4.76, which is based on our DCF model (WACC:13.5%, terminal growth rate:3%). Our target price implies 18.2x/14.8x FY18/FY19E PER, with upside potential of 31.8%.

Earnings summary

(YE Mar 31) FY16A FY17A FY18E FY19E FY20E

Turnover (HK$ mn) 705 965 1,256 1,563 1,861

Core net income (HK$ mn) 177 190 256 315 384

Core EPS (HK$) 0.24 0.20 0.26 0.32 0.39

Core EPS CHG (%) -1.7 -16.7 32.4 23.0 21.9

PE (x) 15.3 18.3 13.8 11.2 9.2

PB (x) 4.8 4.5 4.4 3.6 2.8

Yield (%) 5.3 5.7 5.8 2.7 3.3

ROE (%) 20.3 25.8 32.5 32.4 30.7

Net gearing (%) Net cash Net cash Net cash Net cash Net cash

Source: Company, CMBIS

7 Dec 2017

Table of content

INVESTMENT SUMMARY ............................................................................. 3

THE LARGEST AESTHETIC MEDICAL SERVICE PROVIDERS IN

HONG KONG WITH STRONG BRAND RECOGNITION ......................... 5

BECOMING A DIVERSIFIED MEDICAL SERVICE PROVIDER .......... 16

POTENTIAL M&A TO PROPEL REVENUE GROWTH ........................ 20

FINANCIALS .................................................................................................. 21

FINANCIAL STATEMENTS ........................................................................ 26

VALUATION .................................................................................................. 28

KEY INVESTMENT RISKS .......................................................................... 30

APPENDIX 1: COMPANY BACKGROUND ............................................. 32

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 3

Investment summary

The Company is the largest aesthetic medical service provider in Hong Kong in terms of

revenue in 2016, according to Frost & Sullivan. The Company provides a broad range of

services, including aesthetic medical service, dental service, physical examination,

chiropractic therapy, health management service and sales of skincare products. We believe

revenue growth of the Company will mainly be driven by 1) fast growing aesthetic medical

industry and increasing penetration; 2) the Company’s network expansion in Hong Kong and

the PRC; 3) booming medical tourism and referral programme from PRC clinics; 4) mature

cross-selling between different business segments; 5) potential M&As.

The largest aesthetic medical service provider in Hong Kong with strong

brand recognition

Surfing on the fast growing aesthetic medical industry. According to Frost & Sullivan, Hong

Kong aesthetic medical market reached HK$4.2bn in 2015 (CAGR of 12.5% in 2011-2015) and

is expected to increase to HK$8.1bn in 2020E, delivering a CAGR of 13.9% in 2016-2020E.

Growth of aesthetic medical market will be driven by1) increasing penetration, and 2) growing

expenditure per client on aesthetic services.

Network expansion in Hong Kong to add growth momentum. By far, the Company has 33

chains in Hong Kong, 2 in Macau and 3 self-operating aesthetic medical clinics in China. The

utilization rate of Hong Kong chains has reached 60%-70%. The Company planned to open

two new shops in Causeway Bay and Mongkok in 1H2018. We expect the total GFA to increase

25%/22%/19% to 200k sq ft/240k sq ft/280k sq ft in FY18E/FY19E/FY20E, with GFA in

Hong Kong to increase 21%/17%/15% to 158k sq ft /186k sq ft/214k sq ft. We believe the

expansion should help the Company in catering the increasing demand of medical aesthetic

service in Hong Kong.

Medical tourism to become a main growth driver. In FY2017, UMH’s revenue from PRC

clients was HK$241.2mn and accounted for 25% of total revenue (vs. 14% in FY16), among

which 92% (HK$222.1mn) came from medical tourists to Hong Kong and 8% (HK$19.1mn)

derived from PRC clinics. The revenue from PRC medical tourists increased from HK$90mn in

FY16 to HK$222.1mn in FY17. As per Management, medical tourism has become a major

growth driver for the Company and expects the proportion of revenue from PRC clients to

increase to 30%-40% in FY2018.

The PRC market is promising and supports referral business. According to Deloitte

research, the aesthetic medical market in China reached US$7.4bn in 2015 and is expected to

deliver a CAGR of 22.7% in 2015-2020E. UMH’s two new clinics in Shenzhen and Chongqing

are expected to commence operation in 1H2018. Management plans to establish 1-2 aesthetic

medical clinics each year in first or second tier cities in China and prefers forming JVs with

local established aesthetic medical players. In the short run, we believe the PRC clinics will

mainly contribute by referring more clients to Hong Kong and in the long run, we expect the

PRC clinics to become a major growth engine of the Company.

Developing into an one-stop medical service provider

While continuing growing its aesthetic medical business, the Company also expanded into

other medical services, such as dental services, physical examination and chiropractic services.

The Company aimed to leverage their client base and raise client spending as well as attract

new clients by offering a wide range of high quality medical services. The average contracted

sales per client were HK$24,355/HK$20,891/HK$18,491 in FY15/FY16/FY17. The ASP

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 4

decline was due to the relatively lower package price of new business when comparing to

aesthetic medical service.

Fast growing health management business. The Company established its health

management center “re:HEALTH” in May 2016. It contributed HK$51mn revenue in FY2017

with around 10 months of operation since its debut and recorded a revenue of HK$51.2mn in

1H18. We believe it was a successful attempt to launch the health management service and the

new business ramped up very quickly. The health management business will maintain a high

growth rate in the next few years, in our view, driven mainly by medical tourism from the PRC.

We expect the health management business to grow 80%/20%/20% in FY18/FY19/FY20E.

To expand dental service business in Hong Kong through acquisitions. The dental service

business delivered a strong growth with a CAGR of 31.6% in FY15-FY17. Management aimed

to enlarge the dental business scale and currently is in negotiation to acquire a dental chain

with multiple dental centers in Hong Kong, according to an announcement published on 14

Nov 2017. Given the low base and future acquisition potential, we believe the dental business

will maintain robust growth.

Potential M&As propel revenue growth.

Apart from dental services, the Company will continue to explore M&A potentials in other

medical fields, such as cardiac angiography, gastroscopy, dermatology, ophthalmology, ENT

and gynecology. We believe future M&As would broaden the type of services offered and

propel the total revenue growth. The Company had a strong cash flow of HK$333.1mn and low

gearing ratio of 13.8% in 1H18, which we believe is healthy and would support future M&As.

We forecast 26.4% core net profit CAGR in 2017-2020E

Revenue is expected to grow 30.2%/24.4%/19.1% in FY18/FY19/FY20E. Driven by 1)

aesthetic medical clinic expansions, 2) newly acquired business ramp up, and 3) increasing

medical tourism, total revenue is expected to grow 30.2%/24.4%/19.1% to HK$1,256.3mn

/HK$1,562.9mn /HK$1,860.9mn in FY18 /FY19 /FY20E with a CAGR of 24.5% in 2017-20E.

We forecast core net profit to grow 34.6%/23%/21.9% in FY18/FY19/FY20E. Supported

by revenue ramp up, effective integration and utilization improvement, we forecast core

net profit to grow 34.6%/23.0%/21.9% to HK$256mn /HK$314.8mn /HK$383.9mn in

FY18/FY19/FY20E.

Initiation coverage with BUY rating and target price of HK$4.76

We initiate coverage on UMH with BUY rating and target price of HK$4.76 based on DCF model

(WACC: 13.5%, terminal growth rate: 3%). Our target price implies 18.2x/14.8x 2018E/19E

PER, with upside potential of 31.8%.

Key investment risks 1) Highly dependent on the strength of brand image and reputation.

2) Change in clients’ behavior in utilization of prepaid packages may impact the Company’s

revenue growth.

3) Dependent on skilled and competent Registered Practitioners and may not be able to retain

and attract suitable candidates.

4) Failure to replicate the success business models in Hong Kong to the PRC.

5) The Hong Kong aesthetic medical tourism industry sector faces intense competition from

other market, including Japan and Korea.

6) Fail to identify or execute acquisition opportunities.

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 5

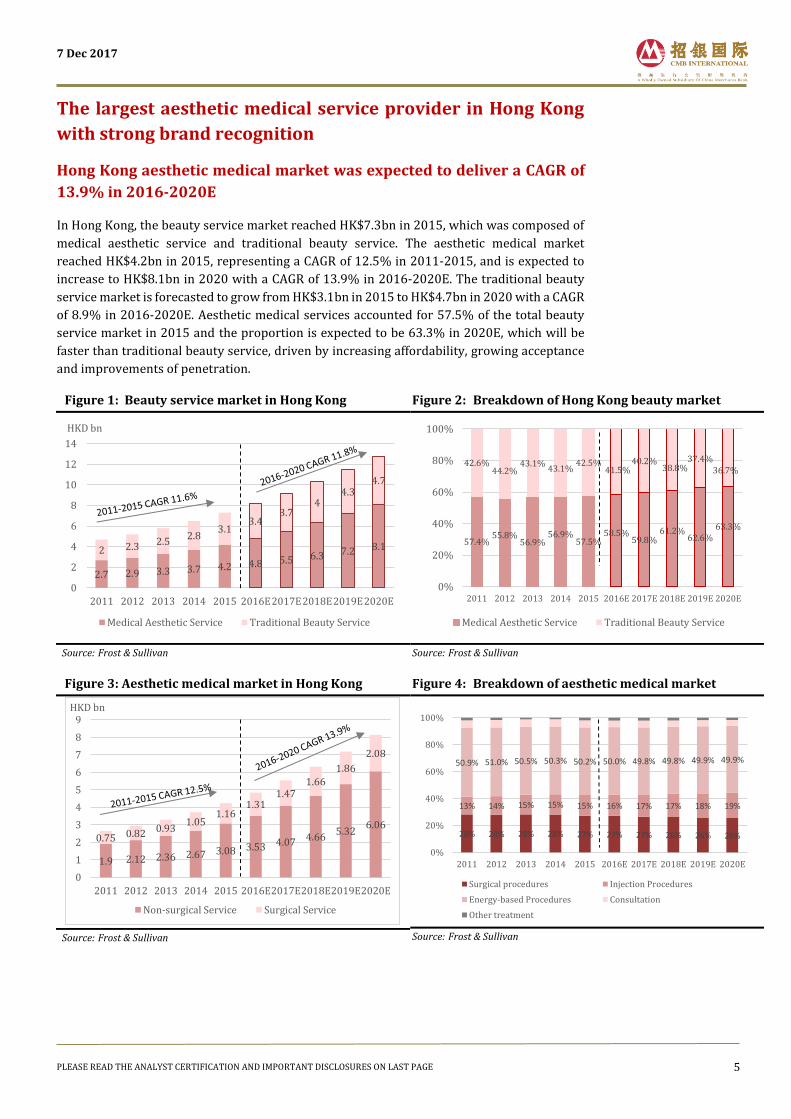

The largest aesthetic medical service provider in Hong Kong

with strong brand recognition

Hong Kong aesthetic medical market was expected to deliver a CAGR of

13.9% in 2016-2020E

In Hong Kong, the beauty service market reached HK$7.3bn in 2015, which was composed of

medical aesthetic service and traditional beauty service. The aesthetic medical market

reached HK$4.2bn in 2015, representing a CAGR of 12.5% in 2011-2015, and is expected to

increase to HK$8.1bn in 2020 with a CAGR of 13.9% in 2016-2020E. The traditional beauty

service market is forecasted to grow from HK$3.1bn in 2015 to HK$4.7bn in 2020 with a CAGR

of 8.9% in 2016-2020E. Aesthetic medical services accounted for 57.5% of the total beauty

service market in 2015 and the proportion is expected to be 63.3% in 2020E, which will be

faster than traditional beauty service, driven by increasing affordability, growing acceptance

and improvements of penetration.

Figure 1: Beauty service market in Hong Kong

Source: Frost & Sullivan

Figure 2: Breakdown of Hong Kong beauty market

Source: Frost & Sullivan

Figure 3: Aesthetic medical market in Hong Kong

Source: Frost & Sullivan

Figure 4: Breakdown of aesthetic medical market

Source: Frost & Sullivan

2.7 2.9 3.3 3.7 4.2 4.8 5.5 6.3 7.2 8.12 2.3 2.52.8

3.13.4

3.74

4.34.7

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015 2016E2017E2018E2019E2020E

HKD bn

Medical Aesthetic Service Traditional Beauty Service

57.4%55.8%

56.9%56.9%

57.5%58.5%

59.8%61.2%

62.6%63.3%

42.6%44.2%

43.1%43.1%

42.5%41.5%

40.2%38.8%

37.4%36.7%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Medical Aesthetic Service Traditional Beauty Service

1.9 2.12 2.36 2.67 3.08 3.53 4.07 4.665.32

6.060.75 0.82 0.93

1.051.16

1.311.47

1.661.86

2.08

0

1

2

3

4

5

6

7

8

9

2011 2012 2013 2014 2015 2016E2017E2018E2019E2020E

HKD bn

Non-surgical Service Surgical Service

28% 28% 28% 28% 27% 27% 27% 26% 26% 26%

13% 14% 15% 15% 15% 16% 17% 17% 18% 19%

50.9% 51.0% 50.5% 50.3% 50.2% 50.0% 49.8% 49.8% 49.9% 49.9%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Surgical procedures Injection Procedures

Energy-based Procedures Consultation

Other treatment

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 6

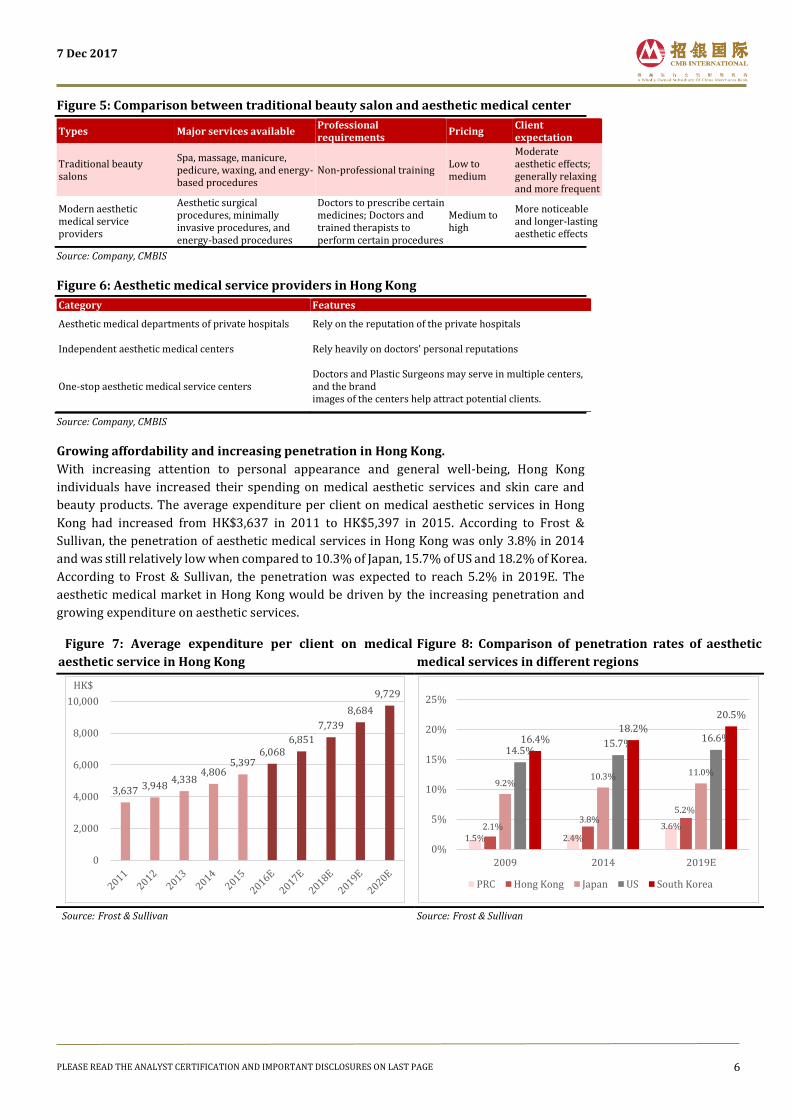

Figure 5: Comparison between traditional beauty salon and aesthetic medical center

Types Major services available Professional requirements

Pricing Client expectation

Traditional beauty salons

Spa, massage, manicure, pedicure, waxing, and energy-based procedures

Non-professional training Low to medium

Moderate aesthetic effects; generally relaxing and more frequent

Modern aesthetic medical service providers

Aesthetic surgical procedures, minimally invasive procedures, and energy-based procedures

Doctors to prescribe certain medicines; Doctors and trained therapists to perform certain procedures

Medium to high

More noticeable and longer-lasting aesthetic effects

Source: Company, CMBIS

Figure 6: Aesthetic medical service providers in Hong Kong

Category Features

Aesthetic medical departments of private hospitals Rely on the reputation of the private hospitals

Independent aesthetic medical centers Rely heavily on doctors' personal reputations

One-stop aesthetic medical service centers Doctors and Plastic Surgeons may serve in multiple centers, and the brand images of the centers help attract potential clients.

Source: Company, CMBIS

Growing affordability and increasing penetration in Hong Kong.

With increasing attention to personal appearance and general well-being, Hong Kong

individuals have increased their spending on medical aesthetic services and skin care and

beauty products. The average expenditure per client on medical aesthetic services in Hong

Kong had increased from HK$3,637 in 2011 to HK$5,397 in 2015. According to Frost &

Sullivan, the penetration of aesthetic medical services in Hong Kong was only 3.8% in 2014

and was still relatively low when compared to 10.3% of Japan, 15.7% of US and 18.2% of Korea.

According to Frost & Sullivan, the penetration was expected to reach 5.2% in 2019E. The

aesthetic medical market in Hong Kong would be driven by the increasing penetration and

growing expenditure on aesthetic services.

Figure 7: Average expenditure per client on medical

aesthetic service in Hong Kong

Source: Frost & Sullivan

Figure 8: Comparison of penetration rates of aesthetic

medical services in different regions

Source: Frost & Sullivan

3,637 3,948 4,338

4,806 5,397

6,068 6,851

7,739

8,684

9,729

0

2,000

4,000

6,000

8,000

10,000

HK$

1.5% 2.4%

3.6%2.1%3.8%

5.2%

9.2%10.3% 11.0%

14.5%15.7%

16.6%16.4%18.2%

20.5%

0%

5%

10%

15%

20%

25%

2009 2014 2019E

PRC Hong Kong Japan US South Korea

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 7

UMH is the largest aesthetic medical service providers in Hong Kong with

strong brand recognition

The aesthetic medical market in Hong Kong is highly fragmented. According to Frost & Sullivan,

the top five players only accounted for 18.6% of total aesthetic medical market in 2014, while

the other smaller ones occupied the remaining market. UMH ranked first with a market share

of 6.84% in terms of revenue in 2014. Therefore, the Company still has great room to expand

its market share in the future.

Figure 9: Aesthetic medical market share in Hong Kong in 2014

Source: Frost & Sullivan

According to the Frost & Sullivan, the Company ranked first in Hong Kong in terms of: 1) The

number of aesthetic injection procedures performed involving utilization of the top-six

revenue-generating aesthetic medications in Hong Kong, including Botox, Dysport, Sculptra,

Restylane, Juvedem and Teosyal in 2016. 2) The number of breast augmentation, liposuction

and double-eyelid surgery procedure performed, which are the top-tree revenue-generating

aesthetic surgical procedures in Hong Kong in 2014.

The Company operates its aesthetic medical business under the well-recognized brand “DR

REBORN”. According to a consumer survey conducted by Frost & Sullivan in 2015, “DR

REBORN” ranked first in brand preference among consumers when choosing one-stop

aesthetic medical service center. The Company aimed to build up a premier aesthetic medical

brand, focusing on high-end aesthetic medical services, high standards of safety, professionals

and client satisfactions.

6.84%5.72%

2.40%1.89%

1.78%

81.40%

UMH Player A Player B Player C Player D Others

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 8

Figure 10: Awards and recognition in Hong Kong

Brand Type Achievements

Botox

Botulinum Toxin A Highest Sales Achievement for Consecutive 7 Years from 2010 to 2016 within Hong Kong

Dysport

Botulinum Toxin A Highest Sales Achievement for Consecutive 9 Years from 2008 to 2016 within Hong Kong

Juvederm

Dermal Fillar Highest Sales Achievement for Consecutive 7 Years from 2010 to 2016 within Hong Kong

Restylane

Hyaluronic acid Highest Sales Achievement for Consecutive 7 Years from 2010 to 2016 within Hong Kong

Sculptra

Poly-l-lactic Acid Highest Sales Achievement for Consecutive 7 Years from 2010 to 2016 within Hong Kong

Teosyal

Hyaluronic acid Highest Sales Achievement for Consecutive 6 Years from 2011 to 2016 within Hong Kong

Source: company, CMBIS

One-stop aesthetic service provider, focusing on aesthetic medical

service, supplemented by traditional beauty service

The Company provides a broad range of aesthetic medical services and traditional beauty

services with treatments performed by doctors or trained therapists and operates it aesthetic

medical business under the well-recognized brand “DR REBORN” and some sub-brands

(“Dermagic”, “Young Aesthetics”). Aesthetic medical service is divided into surgical

procedures and non-surgical procedures. Aesthetic surgical procedures of the Company

comprise treatments of eyelid and nose related procedures, breast augmentation and

liposuction. Non-surgical procedures include minimally invasive procedures and energy-

based procedures performed by doctors,

The aesthetic surgical business accounted for 1.6% of total revenue in FY2017 and was not

expected to deliver high growth in the future, due to the limited plastic surgeon resource and

operating rooms. The minimally invasive service involves treatments of injection procedures,

such as Botulinum Toxin A, Dermal Fillers, Hyaluronic acid and Poly-L-lactic acid. The

minimally invasive business boosted by 81.7% YoY to HK$324mn in FY2017 and generated

33.6% of total revenue (Ranked first among all procedures). Revenue from energy-based

procedures performed by doctors and quasi-medical services (Energy-based procedures

performed by trained therapists) increased by 104.5% / 30.2% YoY to HK$83.2mn/

HK$96.4mn and accounted for 8.5%/10% of total revenue in FY2017.

The Company offers non-medical and non-invasive traditional beauty services, which

complement medical and quasi-medical services. Traditional beauty services include body and

facial procedures, such as Guinot Hydrafermie, Moisturizing Facials, Robolex and Aromatic

Massages. Revenue from traditional beauty increased by 169.6% YoY to HK$175.4mn and

contributed 18% of total revenue. Besides, the Company also offers skincare products,

including self-owned brands (PRODERMA LAB and Suissebeaute), which generated a revenue

of HK$61.9mn in FY2017. Furthermore, the company invested in 5 “Mulan” beauty salons and

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 9

integrated a haircare chain “Tony & Guy” in Hong Kong in Sep 2017, which would supplement

to existing beauty service business.

The market concerned about the high ratios of unutilized prepaid packages may damage the

reputation of the Company. However, the proportion of revenue recognized from unutilized

prepaid packages has declined from 35.8% in FY2016 to 8.1% of total revenue in FY2017, due

to the KPI mechanism. The Company had regarded the utilization of prepaid package as a KPI

for its client relationship managers and had taken various measures to encourage its clients

to make reservations.

Figure 11: Aesthetic service procedures

Categories Sub-categories Major procedures

Aesthetic medical service

Aesthetic surgical procedures

Eye and nose related surgery/ breast augmentation/ liposuction

Minimally invasive procedures

Injection procedures: Botulinum Toxin A / Dermal Fillers/ Hyaluronic acid/ Poly-L-lactic acid

Energy-based procedures performed by doctors

Cryolyposis/ lasers/ radio frequency/ HIFU/ intense pulsed light

Quasi-medical Energy-based procedures performed by Trained Therapists

Energy-based procedures performed by Trained Therapists

Traditional beauty

Facial Guinot Hydrafermie/ moisturising facials

Massages, other non-invasive procedures

Robolex/ aromatic massages

Sales of products Skincare, healthcare and beauty product

self-owned brands ( PRODERMA LAD, Swissline) / third party bands

Source: Company, CMBIS

Figure 12: Total revenue breakdown in FY2017

Source: Company, CMBIS

Figure 13: DR REBORN clinic (Langham Place)

Source: Company, CMBIS

Figure 14: PRODERMA LAB and Swiss line products

Source: Company, CMBIS

Network expansion in Hong Kong to add growth momentum

The Company takes prudent expansion strategy. By far, the Company has 33 chains in Hong Kong, 2 in Macau (1 aesthetic medical clinic and 1 beauty service center) and 11 shops in China (3 self-operating aesthetic medical clinics and 8 acquired beauty salons). The gross service floor areas had been expanded by 49.4% YoY to 160k sq.ft in FY2017 and reached 183k sq ft in 1H FY18. We expect the gross floor to expand to 200k sq ft in FY2018E according to the Company’s expansion plan. The Company established the first medical aesthetic center “DR REBORN” in 2005. By far, the

Company has 14 aesthetic chains (2 flagships and 12 aesthetic medical centers) in Hong Kong.

Quasi-medical 10%

Traditional beauty

18%

Skincare products

6%

Health management

5%

Revenue from unutilised packages

8%

Aesthetic surgical

2%

Minimally invasive

34%Energy-based

services by doctors

9%

Dental 6%

Chiropractic 2%

Aesthetic medical

53%

7 Dec 2017

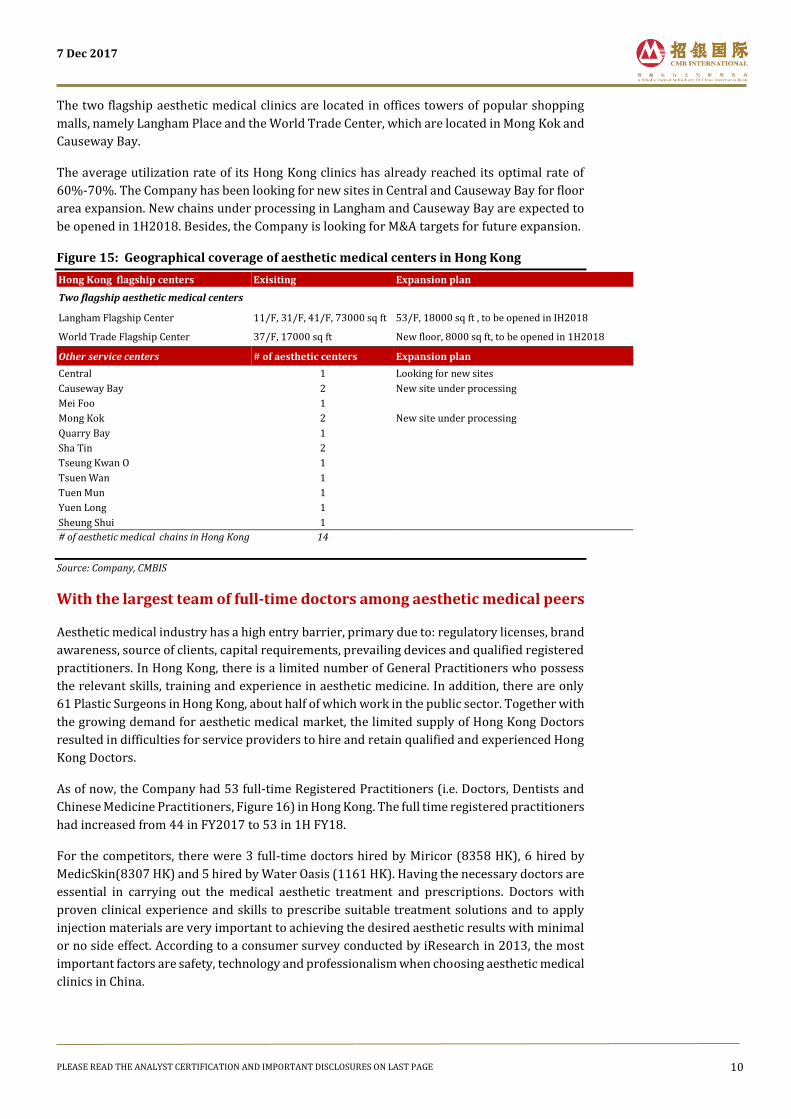

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 10

The two flagship aesthetic medical clinics are located in offices towers of popular shopping

malls, namely Langham Place and the World Trade Center, which are located in Mong Kok and

Causeway Bay.

The average utilization rate of its Hong Kong clinics has already reached its optimal rate of

60%-70%. The Company has been looking for new sites in Central and Causeway Bay for floor

area expansion. New chains under processing in Langham and Causeway Bay are expected to

be opened in 1H2018. Besides, the Company is looking for M&A targets for future expansion.

Figure 15: Geographical coverage of aesthetic medical centers in Hong Kong

Hong Kong flagship centers Exisiting Expansion plan

Two flagship aesthetic medical centers

Langham Flagship Center 11/F, 31/F, 41/F, 73000 sq ft 53/F, 18000 sq ft , to be opened in IH2018

World Trade Flagship Center 37/F, 17000 sq ft New floor, 8000 sq ft, to be opened in 1H2018

Other service centers # of aesthetic centers Expansion plan

Central 1 Looking for new sites

Causeway Bay 2 New site under processing

Mei Foo 1

Mong Kok 2 New site under processing

Quarry Bay 1

Sha Tin 2

Tseung Kwan O 1

Tsuen Wan 1

Tuen Mun 1

Yuen Long 1

Sheung Shui 1

# of aesthetic medical chains in Hong Kong 14

Source: Company, CMBIS

With the largest team of full-time doctors among aesthetic medical peers

Aesthetic medical industry has a high entry barrier, primary due to: regulatory licenses, brand

awareness, source of clients, capital requirements, prevailing devices and qualified registered

practitioners. In Hong Kong, there is a limited number of General Practitioners who possess

the relevant skills, training and experience in aesthetic medicine. In addition, there are only

61 Plastic Surgeons in Hong Kong, about half of which work in the public sector. Together with

the growing demand for aesthetic medical market, the limited supply of Hong Kong Doctors

resulted in difficulties for service providers to hire and retain qualified and experienced Hong

Kong Doctors.

As of now, the Company had 53 full-time Registered Practitioners (i.e. Doctors, Dentists and

Chinese Medicine Practitioners, Figure 16) in Hong Kong. The full time registered practitioners

had increased from 44 in FY2017 to 53 in 1H FY18.

For the competitors, there were 3 full-time doctors hired by Miricor (8358 HK), 6 hired by

MedicSkin(8307 HK) and 5 hired by Water Oasis (1161 HK). Having the necessary doctors are

essential in carrying out the medical aesthetic treatment and prescriptions. Doctors with

proven clinical experience and skills to prescribe suitable treatment solutions and to apply

injection materials are very important to achieving the desired aesthetic results with minimal

or no side effect. According to a consumer survey conducted by iResearch in 2013, the most

important factors are safety, technology and professionalism when choosing aesthetic medical

clinics in China.

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 11

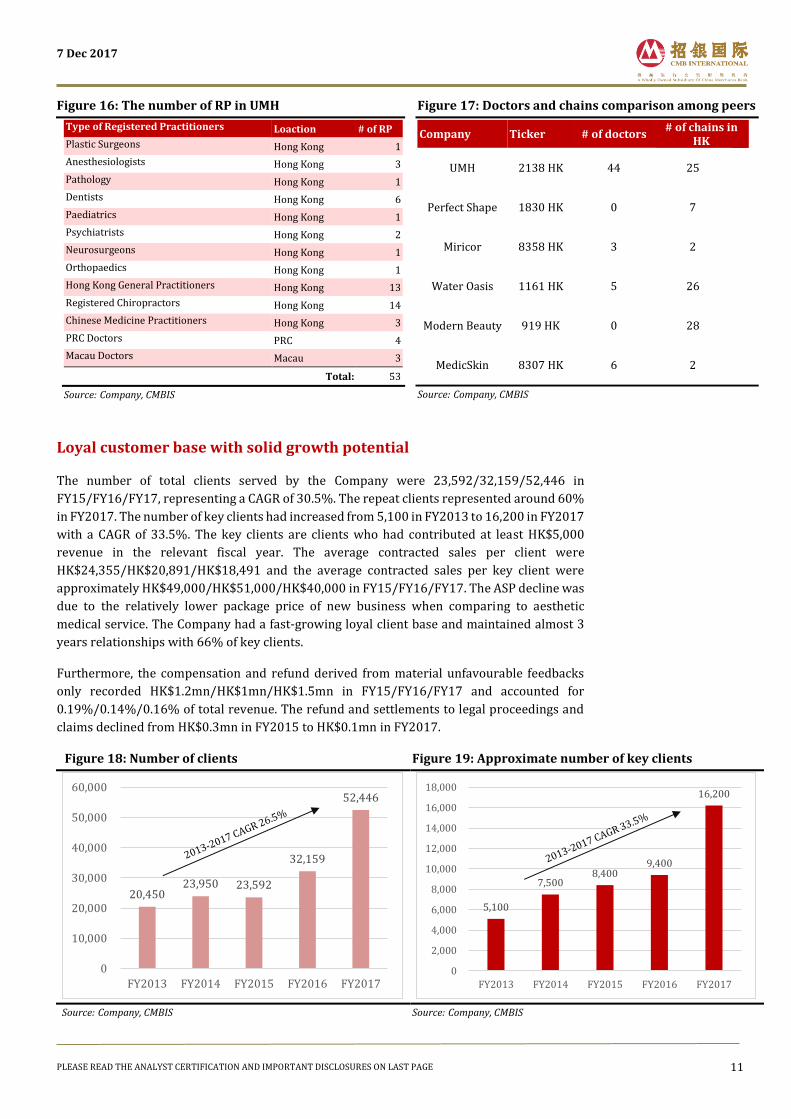

Figure 16: The number of RP in UMH

Type of Registered Practitioners Loaction # of RP

Plastic Surgeons Hong Kong 1

Anesthesiologists Hong Kong 3

Pathology Hong Kong 1

Dentists Hong Kong 6

Paediatrics Hong Kong 1

Psychiatrists Hong Kong 2

Neurosurgeons Hong Kong 1

Orthopaedics Hong Kong 1

Hong Kong General Practitioners Hong Kong 13

Registered Chiropractors Hong Kong 14

Chinese Medicine Practitioners Hong Kong 3

PRC Doctors PRC 4

Macau Doctors Macau 3

Total: 53

Source: Company, CMBIS

Figure 17: Doctors and chains comparison among peers

Company Ticker # of doctors # of chains in

HK

UMH 2138 HK 44 25

Perfect Shape 1830 HK 0 7

Miricor 8358 HK 3 2

Water Oasis 1161 HK 5 26

Modern Beauty 919 HK 0 28

MedicSkin 8307 HK 6 2

Source: Company, CMBIS

Loyal customer base with solid growth potential

The number of total clients served by the Company were 23,592/32,159/52,446 in

FY15/FY16/FY17, representing a CAGR of 30.5%. The repeat clients represented around 60%

in FY2017. The number of key clients had increased from 5,100 in FY2013 to 16,200 in FY2017

with a CAGR of 33.5%. The key clients are clients who had contributed at least HK$5,000

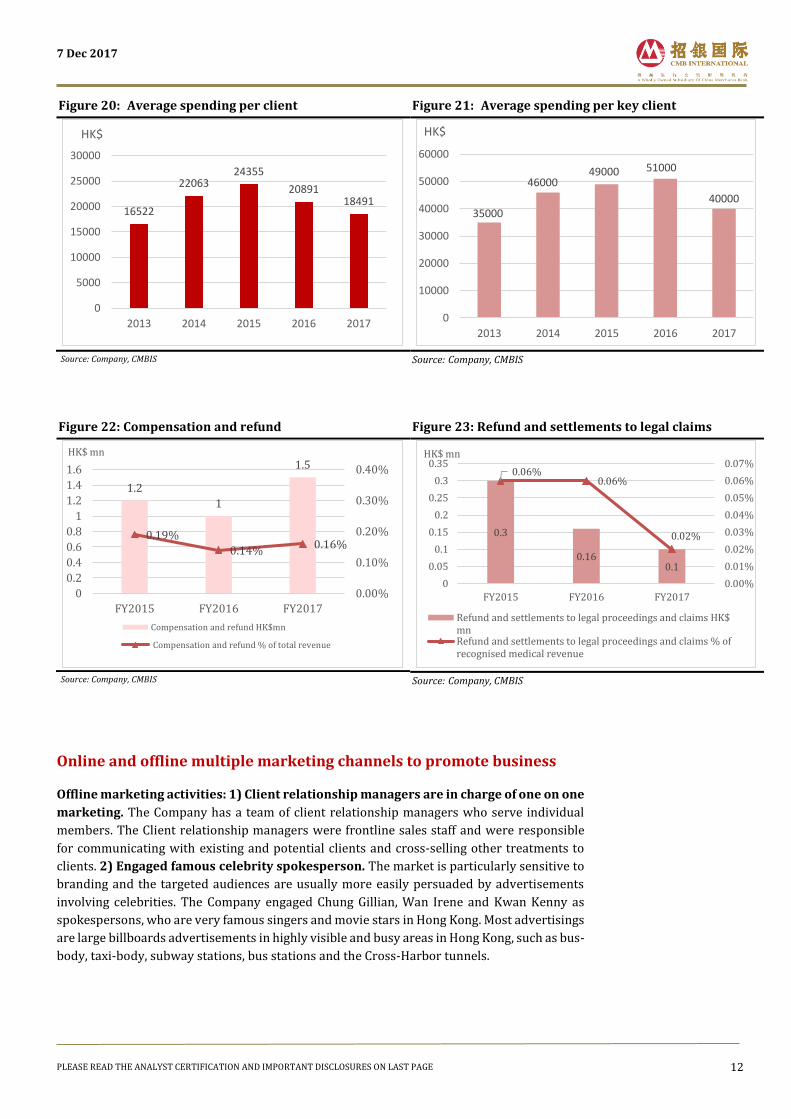

revenue in the relevant fiscal year. The average contracted sales per client were

HK$24,355/HK$20,891/HK$18,491 and the average contracted sales per key client were

approximately HK$49,000/HK$51,000/HK$40,000 in FY15/FY16/FY17. The ASP decline was

due to the relatively lower package price of new business when comparing to aesthetic

medical service. The Company had a fast-growing loyal client base and maintained almost 3

years relationships with 66% of key clients.

Furthermore, the compensation and refund derived from material unfavourable feedbacks

only recorded HK$1.2mn/HK$1mn/HK$1.5mn in FY15/FY16/FY17 and accounted for

0.19%/0.14%/0.16% of total revenue. The refund and settlements to legal proceedings and

claims declined from HK$0.3mn in FY2015 to HK$0.1mn in FY2017.

Figure 18: Number of clients

Source: Company, CMBIS

Figure 19: Approximate number of key clients

Source: Company, CMBIS

20,450 23,950 23,592

32,159

52,446

0

10,000

20,000

30,000

40,000

50,000

60,000

FY2013 FY2014 FY2015 FY2016 FY2017

5,100

7,500 8,400

9,400

16,200

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FY2013 FY2014 FY2015 FY2016 FY2017

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 12

Figure 20: Average spending per client

Source: Company, CMBIS

Figure 21: Average spending per key client

Source: Company, CMBIS

Figure 22: Compensation and refund

Source: Company, CMBIS

Figure 23: Refund and settlements to legal claims

Source: Company, CMBIS

Online and offline multiple marketing channels to promote business

Offline marketing activities: 1) Client relationship managers are in charge of one on one

marketing. The Company has a team of client relationship managers who serve individual

members. The Client relationship managers were frontline sales staff and were responsible

for communicating with existing and potential clients and cross-selling other treatments to

clients. 2) Engaged famous celebrity spokesperson. The market is particularly sensitive to

branding and the targeted audiences are usually more easily persuaded by advertisements

involving celebrities. The Company engaged Chung Gillian, Wan Irene and Kwan Kenny as

spokespersons, who are very famous singers and movie stars in Hong Kong. Most advertisings

are large billboards advertisements in highly visible and busy areas in Hong Kong, such as bus-

body, taxi-body, subway stations, bus stations and the Cross-Harbor tunnels.

16522

2206324355

2089118491

0

5000

10000

15000

20000

25000

30000

2013 2014 2015 2016 2017

HK$

35000

4600049000 51000

40000

0

10000

20000

30000

40000

50000

60000

2013 2014 2015 2016 2017

HK$

1.2

1

1.5

0.19%

0.14%0.16%

0.00%

0.10%

0.20%

0.30%

0.40%

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

FY2015 FY2016 FY2017

HK$ mn

Compensation and refund HK$mn

Compensation and refund % of total revenue

0.3

0.160.1

0.06%0.06%

0.02%

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

0.06%

0.07%

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

FY2015 FY2016 FY2017

HK$ mn

Refund and settlements to legal proceedings and claims HK$mnRefund and settlements to legal proceedings and claims % ofrecognised medical revenue

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 13

Online marketing activities: social network advertising

The Company was also actively on social network and engaged some web celebrity (aesthetic

medical KOL) to promote their business. The Company invited some web celebrities from

Hong Kong and mainland China to try their services. Those web celebrities would post the pics

and reviews on their social media accounts, which attracted the attentions of their followers.

The Company adjusted their spokesperson strategy from very famous stars to aesthetic

medical KOL.

The Company adjusted its marketing effort from time to time in response to the business

development and market changes. It had two main categories of advertising (fixed-budget and

flexible-budget) and made budget based on the returns generated from different marketing

channels. The marketing expenses ratios were 3.9%/5.4%/7.1% for FY15/FY16/ FY17,

respectively. In FY2017, the marketing and advertising expenses had increased by 80.1% to

HK$68.5mn, due to the increasing aesthetic services and new business promotions.

Management aimed to control the marketing expenses ratio below 10% in the future.

Figure 24: Marketing channels of UMH

Source: Company, CMBIS

Medical tourism to become a main growth driver

The Hong Kong medical aesthetic service market is professionally managed by qualified

personnel. This professional reputation has been consistently attracting clients from the PRC

to seek for treatments in Hong Kong, especially for non-surgical aesthetic treatments like

injection or facial laser which do not require a long recovery time. Hong Kong is usually

preferred over Japan and Korea for those medical tourists thanks to easy travel arrangement

and use of same language. It is expected that Hong Kong medical tourism trend will continue

to stay in the coming years.

In Nov 2016, the Company acquired a travel agent (Window-Discovery Tour Ltd), which was

principally engaged in the provision of travelling packages, accommodation and other travel-

related services. Through the acquisition, the Company set up its own in-house travel agent to

attract and assist more medical tourists from the PRC.

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 14

Revenue from PRC clients accounted for 9%/14%/25% of total revenue in FY15/FY16/FY17.

In FY2017, PRC clients contributed a revenue of HK$241.2mn, among which 92%

(HK$222.1mn) came from medical tourists to Hong Kong and 8% (HK$19.1mn) derived from

PRC clinics. The revenue from PRC medical tourists increased from HK$90mn in FY16 to

HK$222.1mn in FY17. As per Management, medical tourism has become a major growth driver

for the Company. In 1H FY2018, PRC clients generated a revenue of HK$220.4mn and

accounted for 35.7% of overall revenue and we expected the revenue proportion from PRC

clients to be around 30%-40% in FY2018.

Promising PRC market supports medical tourism referral

The fast-growing aesthetic medical market in China

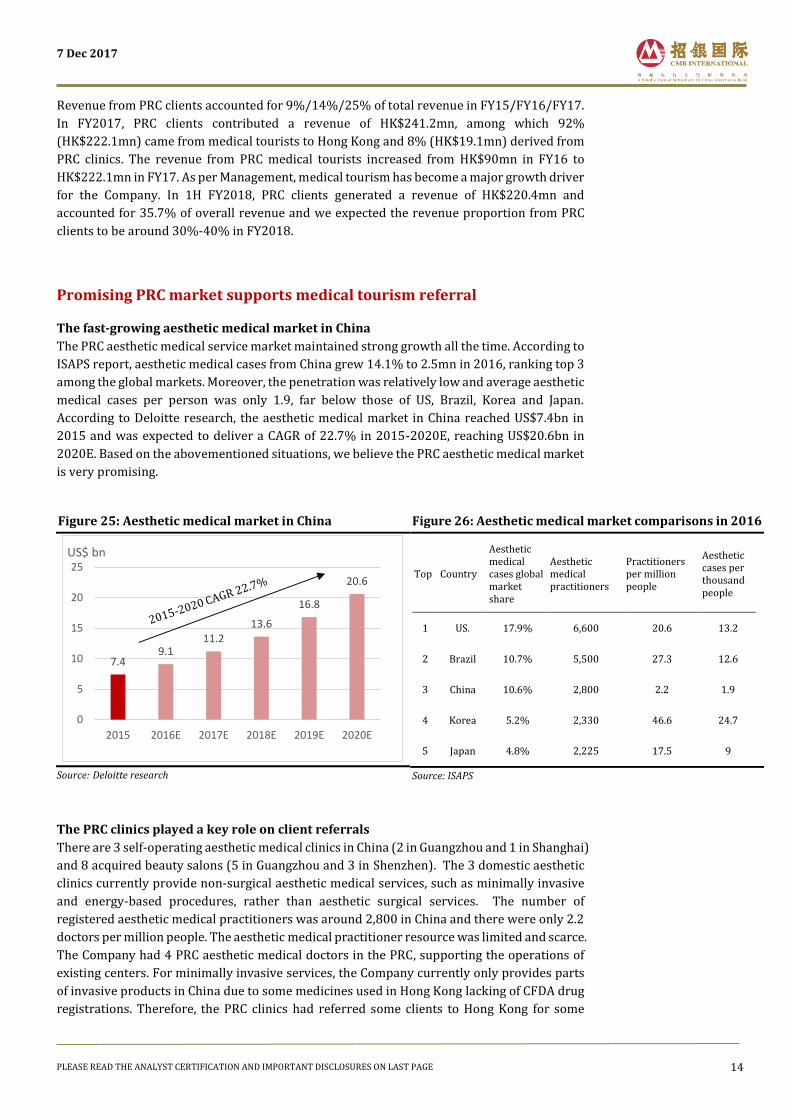

The PRC aesthetic medical service market maintained strong growth all the time. According to

ISAPS report, aesthetic medical cases from China grew 14.1% to 2.5mn in 2016, ranking top 3

among the global markets. Moreover, the penetration was relatively low and average aesthetic

medical cases per person was only 1.9, far below those of US, Brazil, Korea and Japan.

According to Deloitte research, the aesthetic medical market in China reached US$7.4bn in

2015 and was expected to deliver a CAGR of 22.7% in 2015-2020E, reaching US$20.6bn in

2020E. Based on the abovementioned situations, we believe the PRC aesthetic medical market

is very promising.

Figure 25: Aesthetic medical market in China

Source: Deloitte research

Figure 26: Aesthetic medical market comparisons in 2016

Top Country

Aesthetic medical cases global market share

Aesthetic medical practitioners

Practitioners per million people

Aesthetic cases per thousand people

1 US. 17.9% 6,600 20.6 13.2

2 Brazil 10.7% 5,500 27.3 12.6

3 China 10.6% 2,800 2.2 1.9

4 Korea 5.2% 2,330 46.6 24.7

5 Japan 4.8% 2,225 17.5 9

Source: ISAPS

The PRC clinics played a key role on client referrals

There are 3 self-operating aesthetic medical clinics in China (2 in Guangzhou and 1 in Shanghai)

and 8 acquired beauty salons (5 in Guangzhou and 3 in Shenzhen). The 3 domestic aesthetic

clinics currently provide non-surgical aesthetic medical services, such as minimally invasive

and energy-based procedures, rather than aesthetic surgical services. The number of

registered aesthetic medical practitioners was around 2,800 in China and there were only 2.2

doctors per million people. The aesthetic medical practitioner resource was limited and scarce.

The Company had 4 PRC aesthetic medical doctors in the PRC, supporting the operations of

existing centers. For minimally invasive services, the Company currently only provides parts

of invasive products in China due to some medicines used in Hong Kong lacking of CFDA drug

registrations. Therefore, the PRC clinics had referred some clients to Hong Kong for some

7.49.1

11.213.6

16.8

20.6

0

5

10

15

20

25

2015 2016E 2017E 2018E 2019E 2020E

US$ bn

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 15

services not offered by PRC clinics. The Company also intends to establish programmes where

PRC clients would be referred to Hong Kong service centers.

Prudent aesthetic medical clinics expansion plan for the PRC market

For the PRC market, the first aesthetic medical clinic in Guangzhou was established in Jun 2015.

The capex of Guangzhou clinic was HK$3.1mn and the cashflow breakeven period was 8

months. The Company set up the second clinic in Guangzhou in Sep 2016 after the first one

had reached breakeven point. The Shanghai clinic was launched in Mar 2017. For the PRC

expansion plan, clinics in Shenzhen (self-operating) and Chongqing (JV with a local player) are

in the process of being established and will commence operation in 1H2018. According to

Management, the Company plans to establish 1-2 aesthetic medical clinics each year in first

and second tier cities in China and prefers forming JVs with local established aesthetic medical

players with customer base and licenses. Unlike other aesthetic medical players in China, the

Company takes a more careful expansion strategy. We believe, it would be an adoptable

strategy before establishing its own brand image in China.

The PRC market is very promising and supports referral business

Revenue from the PRC clinics was HK$8.9mn/HK$19mn in FY2016/FY2017, accounting

for1.3%/2% of total revenue. In the near term, the PRC clinics played a key role on client

referrals. The Company tries to leverage its brand image in the PRC, establishes a referral

programme and captures the opportunities of growing medical tourism on reliable and quality

medical service. In the long term, the Company will accelerate the domestic expansion once it

has built a well-known branding in the PRC. The Company is committed to expanding its

presence in the PRC through setting up self-owned clinics or JVs with local players.

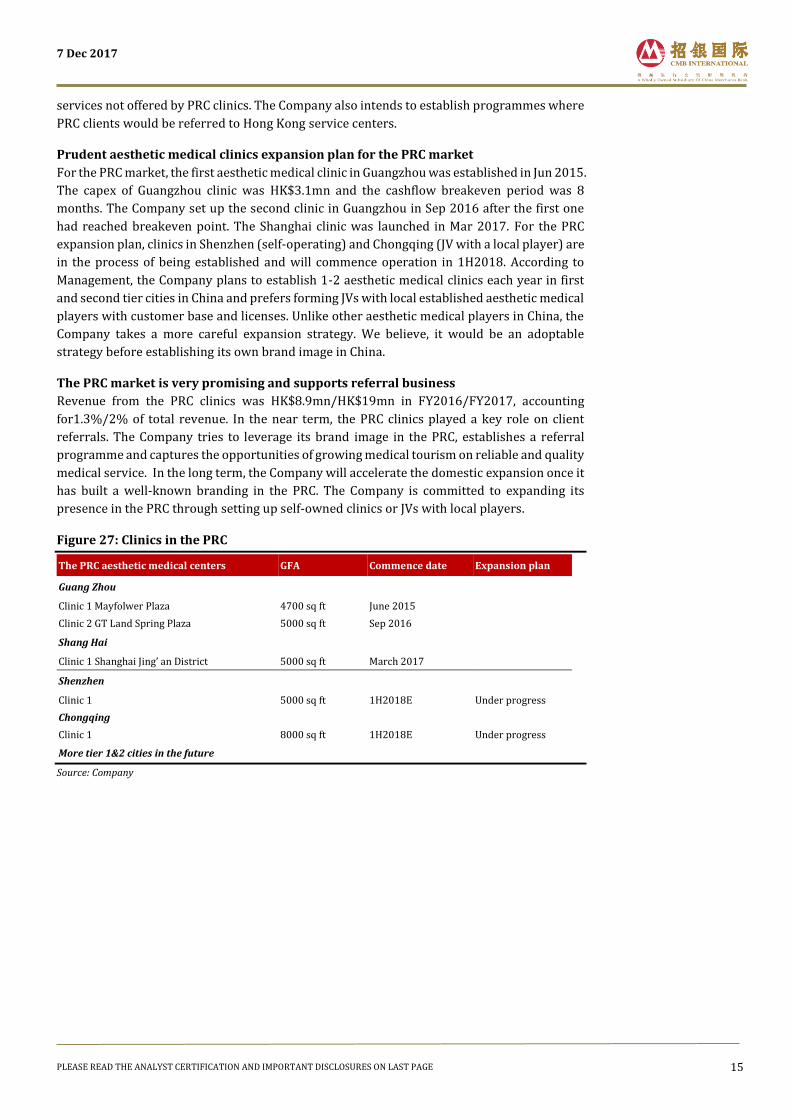

Figure 27: Clinics in the PRC

The PRC aesthetic medical centers GFA Commence date Expansion plan

Guang Zhou

Clinic 1 Mayfolwer Plaza 4700 sq ft June 2015

Clinic 2 GT Land Spring Plaza 5000 sq ft Sep 2016

Shang Hai

Clinic 1 Shanghai Jing’ an District 5000 sq ft March 2017

Shenzhen

Clinic 1 5000 sq ft 1H2018E Under progress

Chongqing

Clinic 1 8000 sq ft 1H2018E Under progress

More tier 1&2 cities in the future

Source: Company

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 16

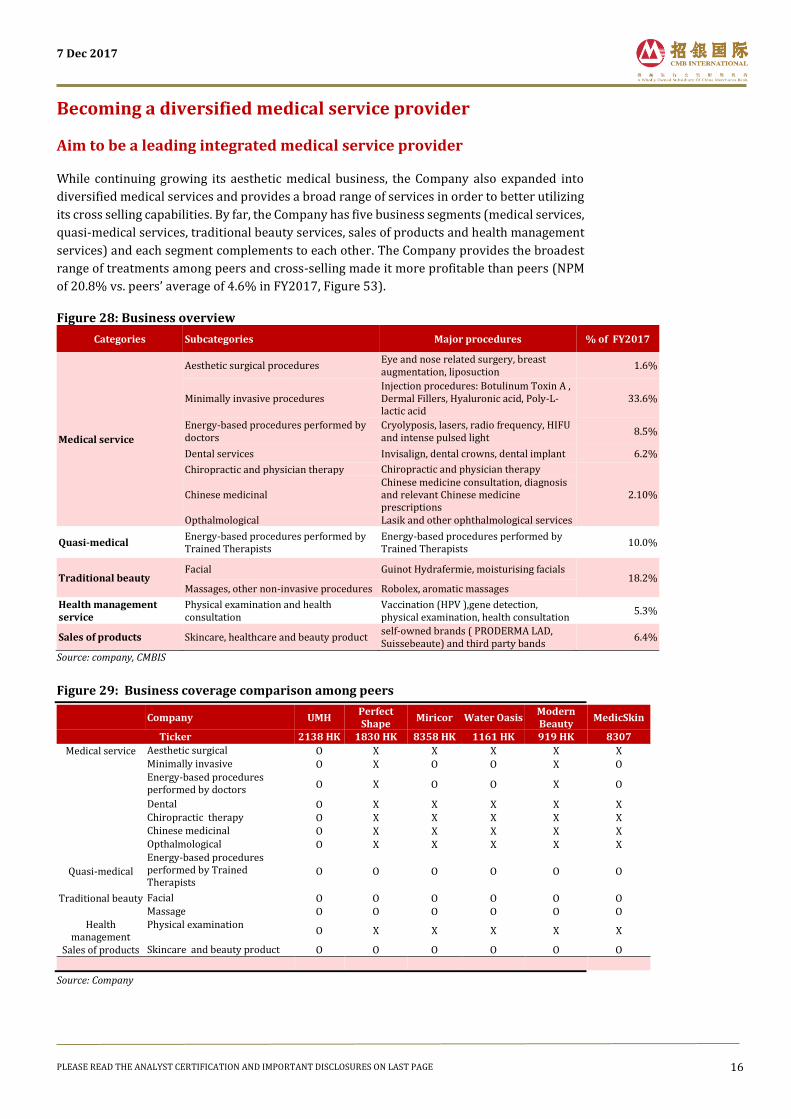

Becoming a diversified medical service provider

Aim to be a leading integrated medical service provider

While continuing growing its aesthetic medical business, the Company also expanded into

diversified medical services and provides a broad range of services in order to better utilizing

its cross selling capabilities. By far, the Company has five business segments (medical services,

quasi-medical services, traditional beauty services, sales of products and health management

services) and each segment complements to each other. The Company provides the broadest

range of treatments among peers and cross-selling made it more profitable than peers (NPM

of 20.8% vs. peers’ average of 4.6% in FY2017, Figure 53).

Figure 28: Business overview

Categories Subcategories Major procedures % of FY2017

Medical service

Aesthetic surgical procedures Eye and nose related surgery, breast augmentation, liposuction

1.6%

Minimally invasive procedures Injection procedures: Botulinum Toxin A , Dermal Fillers, Hyaluronic acid, Poly-L-lactic acid

33.6%

Energy-based procedures performed by doctors

Cryolyposis, lasers, radio frequency, HIFU and intense pulsed light

8.5%

Dental services Invisalign, dental crowns, dental implant 6.2%

Chiropractic and physician therapy Chiropractic and physician therapy

2.10% Chinese medicinal Chinese medicine consultation, diagnosis and relevant Chinese medicine prescriptions

Opthalmological Lasik and other ophthalmological services

Quasi-medical Energy-based procedures performed by Trained Therapists

Energy-based procedures performed by Trained Therapists

10.0%

Traditional beauty Facial Guinot Hydrafermie, moisturising facials

18.2% Massages, other non-invasive procedures Robolex, aromatic massages

Health management service

Physical examination and health consultation

Vaccination (HPV ),gene detection, physical examination, health consultation

5.3%

Sales of products Skincare, healthcare and beauty product self-owned brands ( PRODERMA LAD, Suissebeaute) and third party bands

6.4%

Source: company, CMBIS Figure 29: Business coverage comparison among peers

Company UMH Perfect Shape

Miricor Water Oasis Modern Beauty

MedicSkin

Ticker 2138 HK 1830 HK 8358 HK 1161 HK 919 HK 8307

Medical service Aesthetic surgical O X X X X X

Minimally invasive O X O O X O

Energy-based procedures performed by doctors O X O O X O

Dental O X X X X X Chiropractic therapy O X X X X X

Chinese medicinal O X X X X X

Opthalmological O X X X X X

Quasi-medical

Energy-based procedures performed by Trained Therapists

O O O O O O

Traditional beauty Facial O O O O O O Massage O O O O O O

Health management

Physical examination O X X X X X

Sales of products Skincare and beauty product O O O O O O

Source: Company

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 17

The Company operates it aesthetic service business under the main brand “DR REBORN”, and sub-brands (“Young Aesthetic” and “DERMAGIC”), health management under the brand “re:HEALTH”, dental services under the brand” ONE DENTAL” and chiropractic therapy under the brand “NYMG” and “SPINE Central”. The Company currently provides comprehensive medical services through multiple brands in Hong Kong. We believe it will take the advantage of its cross-selling opportunities and refer more clients to each business segment.

Figure 30: Multi-brands of Union Medical

Source: Company, CMBIS

Successful launch of health management business

The Company established the health management center under the brand of “re:HEALTH” in

May 2016 and expanded its business into physical examination field. The health management

center was located in 11/F (GFA: 18,000 sq ft), Langham Place (the same building with the

flagship center), one of the most popular shopping mall with a high visitors flow and

convenient transportation. The health management center provides vaccinations (HPV), gene

detection, physical examination and health consultation. It was equipped with in-house

clinical lab and advanced medical report system (reports can be available within one hour

after test). The quick access to body check reports was efficient and attractive, attracting more

PRC medical tourists. Moreover, the Company cooperated with insurance companies in Hong

Kong, which would refer their clients to “re:HEALTH” for body check and vaccinations.

During June 2016 to May 2017, the health management business recorded a client visits of

over 5,5000, completed over 6,000 full health screening and served around 700 clients per

day. It contributed around HK$51mn to total revenue in FY2017 since launch (10 months

operation) and recorded a revenue of HK$51.2mn in 1H FY18 (vs. HK$13mn in 1H FY17). We

believe it was a very successful attempt to launch health management services and the new

business ramped up very quickly.

The expiration period of the health check pre-paid packages is 6 months and the revenue will

be recognized once the pre-paid package expired. We expect the health management sector to

maintain a high growth rate in the next few years, due to the booming PRC medical tourists.

We expect the health check business to grow 80%/20%/20% in FY18/FY19/FY20E.

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 18

Figure 31: re:HEALTH clinic ( Langham Place )

Source: Company, CMBIS

Figure 32: re:HEALTH website landscape

Source: Company, CMBIS

Newly acquired chiropractic business bring additional growth engine

The Company entered into chiropractic business fields through acquisition. It operated

chiropractic business under the brand “NYMG” and “SPINE Central”.

In Sep 2016, the Company acquired 51% stake of New York Medical Group which provides

chiropractic and physiotherapy services. New York Medical Group was one of the largest

group of chiropractors, physiotherapists and other health professionals in Hong Kong, which

specialized in the musculoskeletal and nervous systems. To further integrating chiropractic

service chains, it further acquired a chiropractic center in Central, Hong Kong.

It had 8 chiropractic operating centers (NYMG Central, NYMG Wan Chai, NYMG North Point,

NYMG Quarry Bay, NYMG Tsim Sha Tsui, NYMG Shatin, NYMG Tsuen Wan and SPINE Central)

and 13 full-time registered chiropractors.

The chiropractic and physiotherapy business contributed a revenue of HK$20.2mn and a net

profit of HK$6mn in FY2017 as a result of consolidation. New York Medical recorded a total

revenue of HK$40.9mn and the net profit margin was around 20%. Pursuant to the acquisition

agreement, the sellers guaranteed the next three years net profit of HK$6.9mn/ HK$7.4mn

/HK$7.9mn for FY17/FY18/FY19. Otherwise, the seller has to pay back the Company an

amount equivalent to 10 time of the shortfall between the target net profits and actual net

profits. We expect chiropractic business to grow 120%/15%/13.3% for FY18/19/20E,

considering subsequent well integration, cross-selling effects and increasing utilization.

According to Management, it commenced to offer a one-stop solution to pain management in

the multi-service flagship store in Langham Place, Mong Kok, Hong Kong, from August 2017

onwards. We believe the chiropractic business integration would bring additional growth

engine to the Company.

To expand dental service business in Hong Kong through acquisitions.

According to Frost & Sullivan, the total market of aesthetic dental service in Hong Kong

increased from HK$240.7mn in 2009 to HK$430.2mn in 2014, representing a CAGR of 12.3%,

and is expected to reach HK$803mn in 2019 at a CAGR of 13.3% in 2015-2019E.

The Company established the first dental service center in Hong Kong in 2013 and further

acquired Kevinsdental & Vision Dental in July 2014. It operated the dental services under the

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 19

brands “ONE DENTAL” and “ONE DENTAL PLUS”. The Company offered a full range of dental

services for both aesthetic and general dental health purposes, such as prosthetic dentistry,

orthodontics, cosmetic dentistry and dental implants. The top revenue-generating dental

services are Invisalign, dental crowning and dental implanting. Expect for routine dental

cleaning performed by dental hygienists, other services are performed by dentists.

By far, the Company had 2 dental centers and 6 full-time dentists. The 2 dental centers located

in Langham Place and World Trade Center, the same building with the two flagship aesthetic

centers. Management aimed to enlarge the scope of dental service. It is said that the Company

is in negotiation to acquire a dental chain which is principally engaged in dental services via

multiple dental centers in Hong Kong, according to the announcement published on 14 Nov

2017. The completion of the acquisition is expected to take place by 31 Dec 2017.

The dental business maintained a strong growth recent years and recorded a revenue of

HK$34.8mn/HK$41.6mn/HK$60.3mn for FY15/FY16/FY17, with a CAGR of 31.6%. Given the

low base and organic growth, we expect dental business to grow 20%/15%/15% for

FY18/FY19/FY20E.

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 20

Potential M&As to propel revenue growth

Expand into diversified medical service fields through M&A

The Company acquired 100% stake of Kevinsdetnal& Vison Dental in July 2014 and enlarged

its dental business. In Sep 2016, the Company acquired 51% equity interest of New York

Medical Group and further acquired a chiropractic center in Central, which integrated the

chiropractic service chains. In Nov 2016, it invested in “Good Union”, a distributor which

distributes internationally renowned medical products. In Sep 2017, the Company integrated

a haircare chain “TONI&GUY” and invested in “Mulan” beauty service chain, which operated 5

beauty service centers in Hong Kong.

Potential M&A to propel revenue growth

On 14 Nov 2017, the Company announced that it was in negotiation to acquire a dental chain

which is engaged in the provision of dental services via multiple dental centers in Hong Kong.

The completion of this acquisition is expected to take place by 31 Dec 2017.

The Company aimed to build up a one-stop integrated medical service group, leverage its

client base and raise client spending as well as attract new clients by broadening the types of

services offered. Management guided that they had been actively seeking for new M&A targets

on the medical service fields of cardiac angiography, gastroscopy, dermatology,

ophthalmology, ENT and gynecology in Hong Kong and aesthetic services in the PRC. We

believe future M&A would have a synergistic effect with existing business and propel the total

revenue growth.

Figure 33: Proven M&A track records

Date Event Brand

Oct-10 Acquired Be A Lady and expanded into traditional beauty services in Hong Kong

Apr-13 Acquired all equity interest of Blue Ocean and All Angles (2 centers in Macau)

Jul-14 Acquired 100% stake of Kevinsdental & Vision Dental

Sep-16

Acquired 51% equity interest of New York Medical Group at the consideration of HKD32.8mn; further acquired Spine Central, a chiropractic center in Central.

Nov-16 Acquired 50% equity interest of Good Union at the consideration of HKD25.2mn and launched of medcial products distribution business

Nov-16

Acquired 97% stake of a travel agent (Window-Discovery Tour Ltd.,), which engaged in provision of travelling packages, accommodation and other related issues.

2017

Acquired beauty salons in China; In Sep, invested in TONY & GUY in Hong Kong franchises; In Oct, invested in Mulan beauty salons in Hong Kong; Acquired beauty product (Swissline) franchise in Hong Kong and Macau

Source: Company

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 21

Financials

We forecast a core net profit CAGR of 26.4% in 2017-2020E

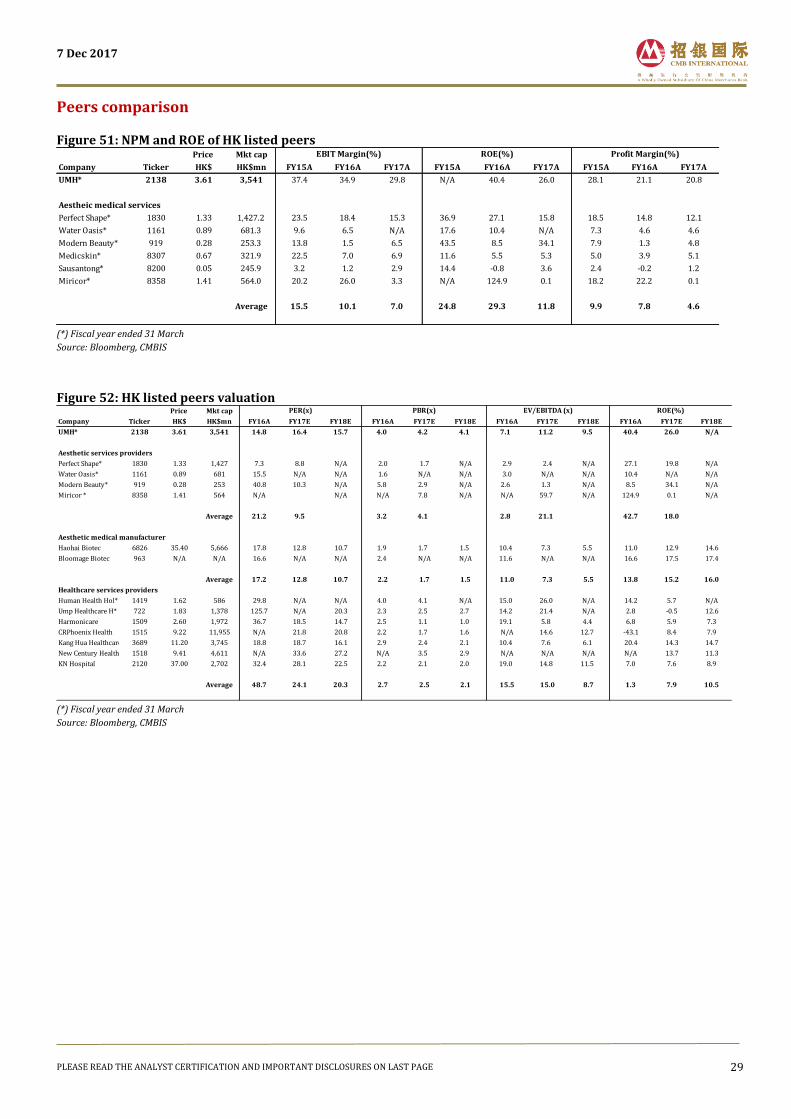

Historically, the Company had a higher profitability over peers. It maintained a net profit

margin and ROE above 20% for recent fiscal years with a NPM of 28.1%/21.1%/20.8%

FY15/FY16/FY17 and a ROE of 20.3%/25.4% in FY16/FY17.

We forecast a core net profit CAGR of 26.4% for the Company in 2017-2020E, driven by

revenue ramp up, effective integration and utilization improvement. We expect core net profit

to grow 34.6%/23%/21.9% to HK$256mn/HK$314.8mn /HK$383.9mn in FY18 /FY19

/FY20E respectively.

Figure 34: Core profit projections

Source: Company, CMBIS

Figure 35: Core net profit margin projections

Source: Company, CMBIS

Figure 36: ROE comparison among peers

Source: Company, CMBIS

Figure 37: Net Profit Margin comparison among peers

Source: Company, CMBIS

177.0 177.3 190.2

256.0

314.8

383.9

-

50

100

150

200

250

300

350

400

450

FY2015 FY2016 FY2017 2018E 2019E 2020E

HKD mn

28.5%

25.2%

19.7% 20.4% 20.1% 20.6%

5%

10%

15%

20%

25%

30%

35%

40%

FY2015 FY2016 FY2017 2018E 2019E 2020E

20.3%25.4%

27%

16%

10%

14%

27%

6%

5%

-1% 4%

-5%

0%

5%

10%

15%

20%

25%

30%

FY2016 FY2017

UMH (2138) Perfect Shape(1830)Water Oasis(1161) Modern Beauty (919)Medicskin(8307) Sausantong(8200)

28.1%

21.1% 20.8%

18.5%14.8%

12.1%

18.20%

22%

17.9%

-10%

0%

10%

20%

30%

FY2015 FY2016 FY2017

UMH (2138) Perfect Shape(1830)

Water Oasis(1161) Modern Beauty (919)

Medicskin(8307) Sausantong(8200)

Miricor (8358)

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 22

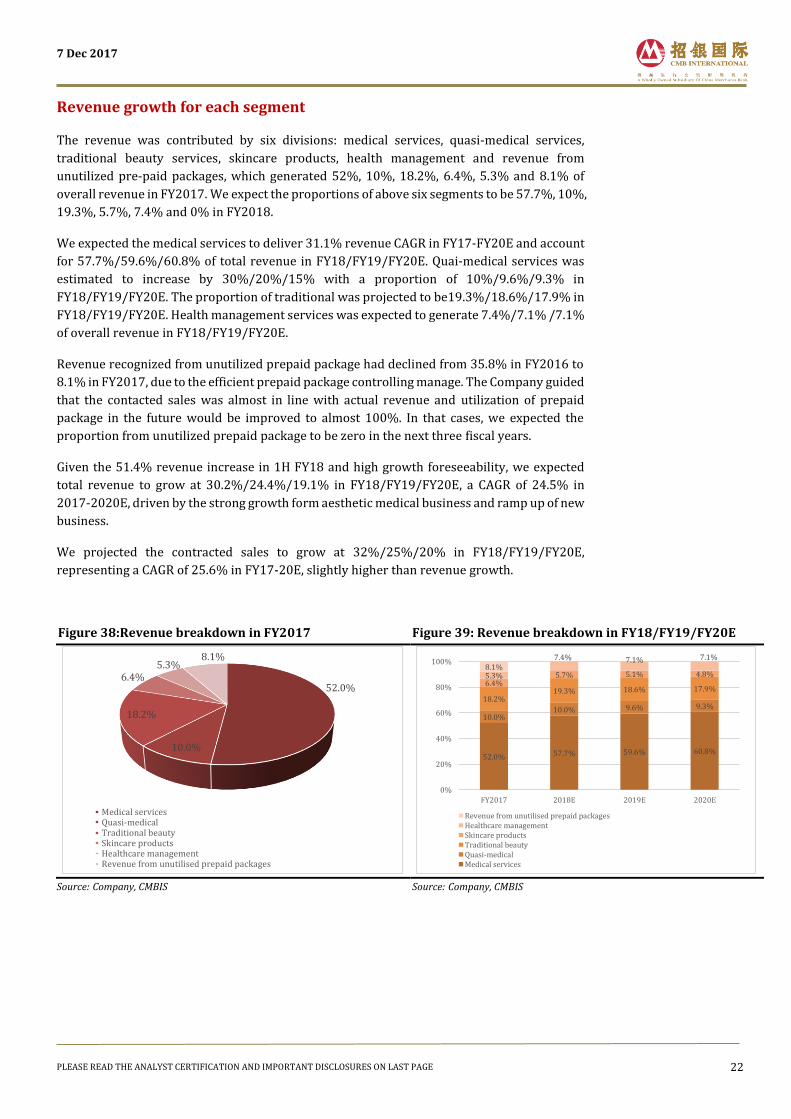

Revenue growth for each segment

The revenue was contributed by six divisions: medical services, quasi-medical services,

traditional beauty services, skincare products, health management and revenue from

unutilized pre-paid packages, which generated 52%, 10%, 18.2%, 6.4%, 5.3% and 8.1% of

overall revenue in FY2017. We expect the proportions of above six segments to be 57.7%, 10%,

19.3%, 5.7%, 7.4% and 0% in FY2018.

We expected the medical services to deliver 31.1% revenue CAGR in FY17-FY20E and account

for 57.7%/59.6%/60.8% of total revenue in FY18/FY19/FY20E. Quai-medical services was

estimated to increase by 30%/20%/15% with a proportion of 10%/9.6%/9.3% in

FY18/FY19/FY20E. The proportion of traditional was projected to be19.3%/18.6%/17.9% in

FY18/FY19/FY20E. Health management services was expected to generate 7.4%/7.1% /7.1%

of overall revenue in FY18/FY19/FY20E.

Revenue recognized from unutilized prepaid package had declined from 35.8% in FY2016 to

8.1% in FY2017, due to the efficient prepaid package controlling manage. The Company guided

that the contacted sales was almost in line with actual revenue and utilization of prepaid

package in the future would be improved to almost 100%. In that cases, we expected the

proportion from unutilized prepaid package to be zero in the next three fiscal years.

Given the 51.4% revenue increase in 1H FY18 and high growth foreseeability, we expected

total revenue to grow at 30.2%/24.4%/19.1% in FY18/FY19/FY20E, a CAGR of 24.5% in

2017-2020E, driven by the strong growth form aesthetic medical business and ramp up of new

business.

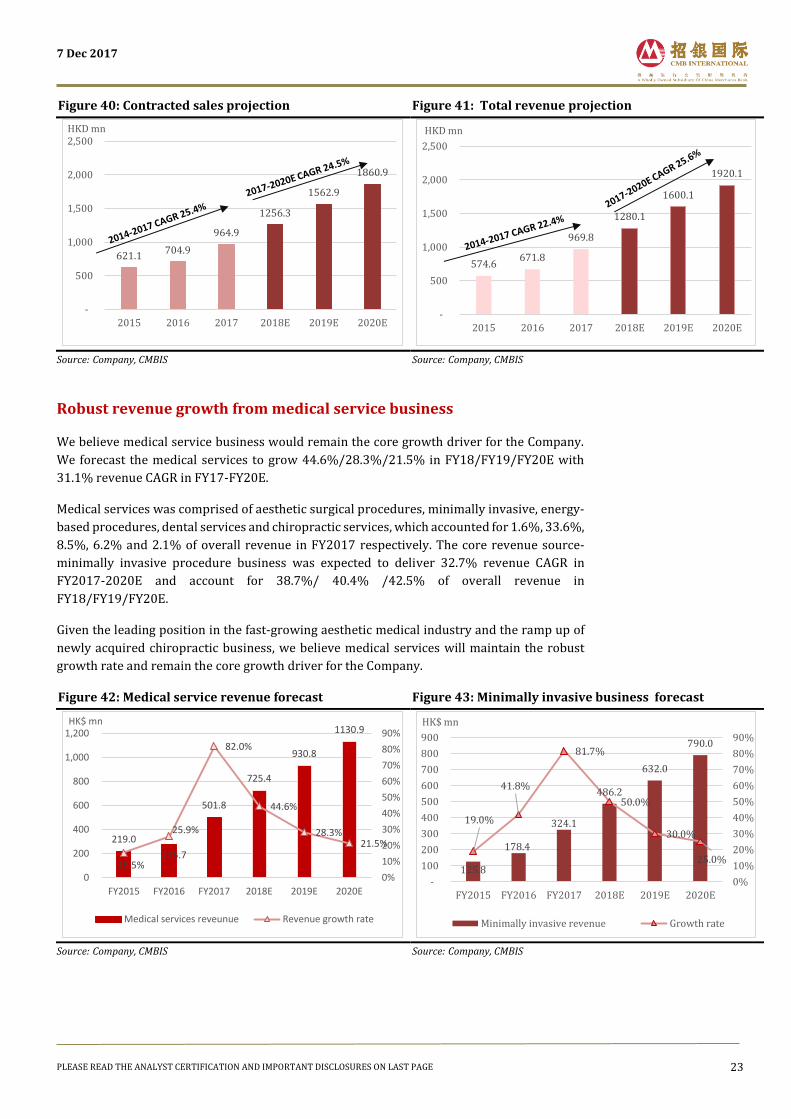

We projected the contracted sales to grow at 32%/25%/20% in FY18/FY19/FY20E,

representing a CAGR of 25.6% in FY17-20E, slightly higher than revenue growth.

Figure 38:Revenue breakdown in FY2017

Source: Company, CMBIS

Figure 39: Revenue breakdown in FY18/FY19/FY20E

Source: Company, CMBIS

52.0%

10.0%

18.2%

6.4%5.3%

8.1%

Medical servicesQuasi-medicalTraditional beautySkincare productsHealthcare managementRevenue from unutilised prepaid packages

52.0% 57.7% 59.6% 60.8%

10.0%10.0% 9.6% 9.3%

18.2%19.3% 18.6% 17.9%

6.4%5.7% 5.1% 4.8%5.3%

7.4% 7.1% 7.1%8.1%

0%

20%

40%

60%

80%

100%

FY2017 2018E 2019E 2020E

Revenue from unutilised prepaid packagesHealthcare managementSkincare productsTraditional beautyQuasi-medicalMedical services

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 23

Figure 40: Contracted sales projection

Source: Company, CMBIS

Figure 41: Total revenue projection

Source: Company, CMBIS

Robust revenue growth from medical service business

We believe medical service business would remain the core growth driver for the Company.

We forecast the medical services to grow 44.6%/28.3%/21.5% in FY18/FY19/FY20E with

31.1% revenue CAGR in FY17-FY20E.

Medical services was comprised of aesthetic surgical procedures, minimally invasive, energy-

based procedures, dental services and chiropractic services, which accounted for 1.6%, 33.6%,

8.5%, 6.2% and 2.1% of overall revenue in FY2017 respectively. The core revenue source-

minimally invasive procedure business was expected to deliver 32.7% revenue CAGR in

FY2017-2020E and account for 38.7%/ 40.4% /42.5% of overall revenue in

FY18/FY19/FY20E.

Given the leading position in the fast-growing aesthetic medical industry and the ramp up of

newly acquired chiropractic business, we believe medical services will maintain the robust

growth rate and remain the core growth driver for the Company.

Figure 42: Medical service revenue forecast

Source: Company, CMBIS

Figure 43: Minimally invasive business forecast

Source: Company, CMBIS

621.1704.9

964.9

1256.3

1562.9

1860.9

-

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018E 2019E 2020E

HKD mn

574.6671.8

969.8

1280.1

1600.1

1920.1

-

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018E 2019E 2020E

HKD mn

219.0

275.7

501.8

725.4

930.8

1130.9

15.5%

25.9%

82.0%

44.6%

28.3%21.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

FY2015 FY2016 FY2017 2018E 2019E 2020E

HK$ mn

Medical services reveunue Revenue growth rate

125.8

178.4

324.1

486.2

632.0

790.0

19.0%

41.8%

81.7%

50.0%

30.0%

25.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

100

200

300

400

500

600

700

800

900

FY2015 FY2016 FY2017 2018E 2019E 2020E

HK$ mn

Minimally invasive revenue Growth rate

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 24

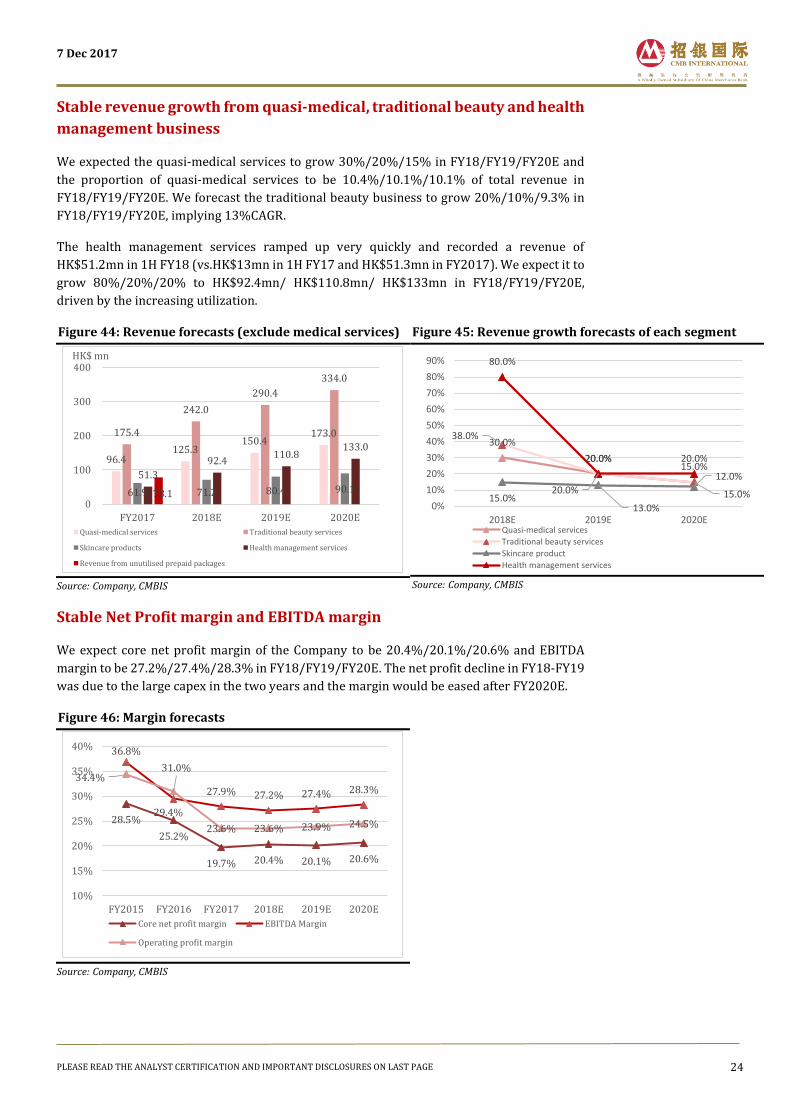

Stable revenue growth from quasi-medical, traditional beauty and health

management business

We expected the quasi-medical services to grow 30%/20%/15% in FY18/FY19/FY20E and

the proportion of quasi-medical services to be 10.4%/10.1%/10.1% of total revenue in

FY18/FY19/FY20E. We forecast the traditional beauty business to grow 20%/10%/9.3% in

FY18/FY19/FY20E, implying 13%CAGR.

The health management services ramped up very quickly and recorded a revenue of

HK$51.2mn in 1H FY18 (vs.HK$13mn in 1H FY17 and HK$51.3mn in FY2017). We expect it to

grow 80%/20%/20% to HK$92.4mn/ HK$110.8mn/ HK$133mn in FY18/FY19/FY20E,

driven by the increasing utilization.

Figure 44: Revenue forecasts (exclude medical services)

Source: Company, CMBIS

Figure 45: Revenue growth forecasts of each segment

Source: Company, CMBIS

Stable Net Profit margin and EBITDA margin

We expect core net profit margin of the Company to be 20.4%/20.1%/20.6% and EBITDA

margin to be 27.2%/27.4%/28.3% in FY18/FY19/FY20E. The net profit decline in FY18-FY19

was due to the large capex in the two years and the margin would be eased after FY2020E.

96.4125.3

150.4173.0175.4

242.0

290.4

334.0

61.9 71.2 80.4 90.1

51.3

92.4110.8

133.0

78.10

100

200

300

400

FY2017 2018E 2019E 2020E

HK$ mn

Quasi-medical services Traditional beauty services

Skincare products Health management services

Revenue from unutilised prepaid packages

30.0%

20.0%15.0%

38.0%

20.0% 15.0%15.0%13.0%

12.0%

80.0%

20.0% 20.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2018E 2019E 2020EQuasi-medical services

Traditional beauty services

Skincare product

Health management services

Figure 46: Margin forecasts

Source: Company, CMBIS

28.5%

25.2%

19.7% 20.4% 20.1% 20.6%

36.8%

29.4%

27.9% 27.2% 27.4% 28.3%34.4%

31.0%

23.6% 23.6% 23.9% 24.5%

10%

15%

20%

25%

30%

35%

40%

FY2015 FY2016 FY2017 2018E 2019E 2020E

Core net profit margin EBITDA Margin

Operating profit margin

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 25

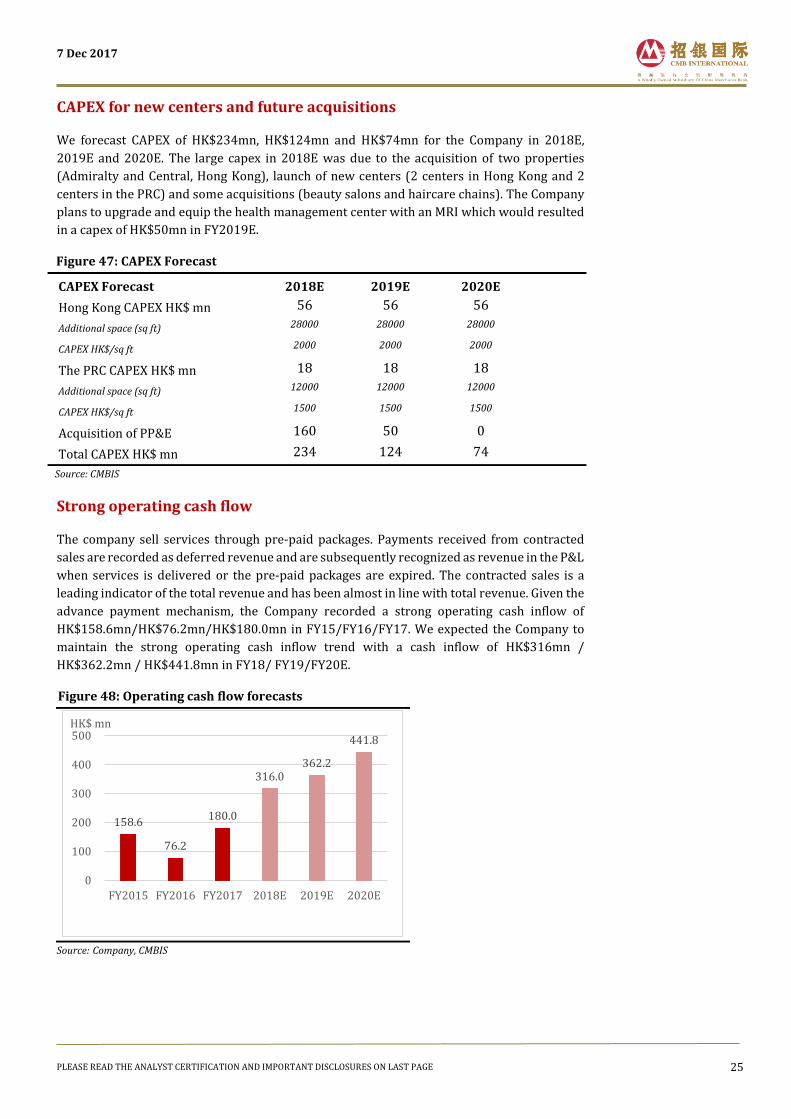

CAPEX for new centers and future acquisitions

We forecast CAPEX of HK$234mn, HK$124mn and HK$74mn for the Company in 2018E,

2019E and 2020E. The large capex in 2018E was due to the acquisition of two properties

(Admiralty and Central, Hong Kong), launch of new centers (2 centers in Hong Kong and 2

centers in the PRC) and some acquisitions (beauty salons and haircare chains). The Company

plans to upgrade and equip the health management center with an MRI which would resulted

in a capex of HK$50mn in FY2019E.

Figure 47: CAPEX Forecast

CAPEX Forecast 2018E 2019E 2020E

Hong Kong CAPEX HK$ mn 56 56 56

Additional space (sq ft) 28000 28000 28000

CAPEX HK$/sq ft 2000 2000 2000

The PRC CAPEX HK$ mn 18 18 18

Additional space (sq ft) 12000 12000 12000

CAPEX HK$/sq ft 1500 1500 1500

Acquisition of PP&E 160 50 0

Total CAPEX HK$ mn 234 124 74

Source: CMBIS

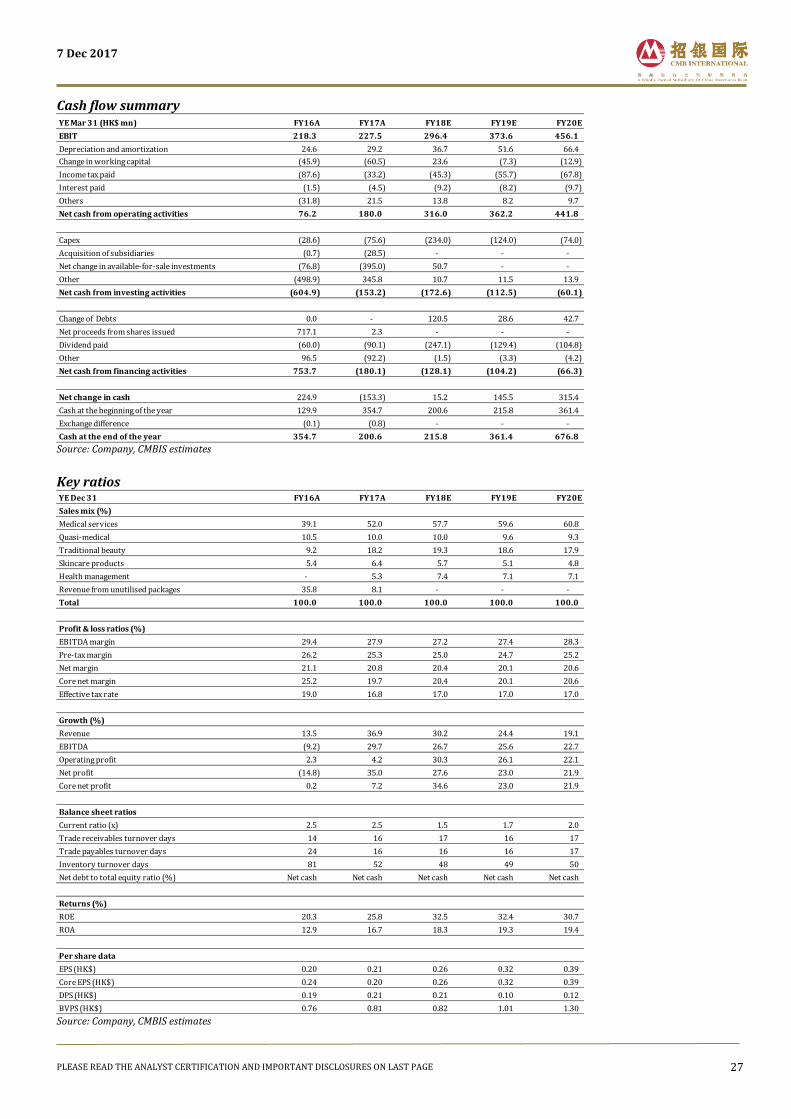

Strong operating cash flow

The company sell services through pre-paid packages. Payments received from contracted

sales are recorded as deferred revenue and are subsequently recognized as revenue in the P&L

when services is delivered or the pre-paid packages are expired. The contracted sales is a

leading indicator of the total revenue and has been almost in line with total revenue. Given the

advance payment mechanism, the Company recorded a strong operating cash inflow of

HK$158.6mn/HK$76.2mn/HK$180.0mn in FY15/FY16/FY17. We expected the Company to

maintain the strong operating cash inflow trend with a cash inflow of HK$316mn /

HK$362.2mn / HK$441.8mn in FY18/ FY19/FY20E.

Figure 48: Operating cash flow forecasts

Source: Company, CMBIS

158.6

76.2

180.0

316.0362.2

441.8

0

100

200

300

400

500

FY2015 FY2016 FY2017 2018E 2019E 2020E

HK$ mn

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 26

Financial statements

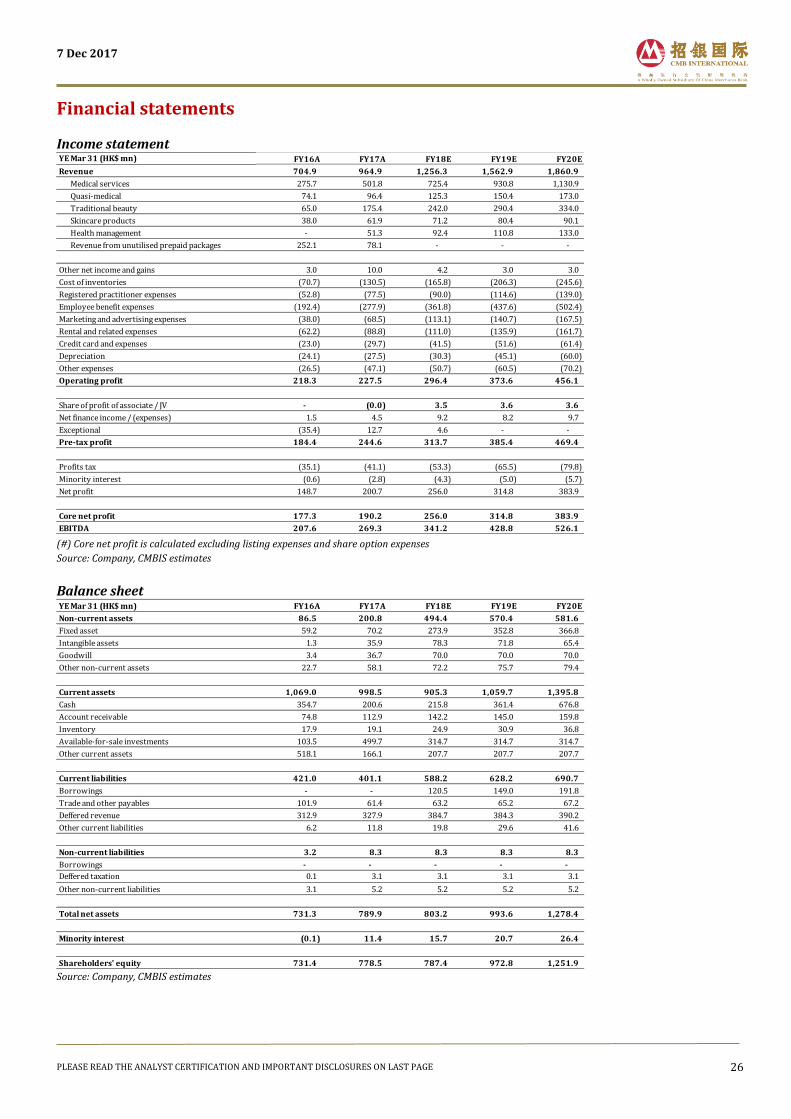

Income statement

(#) Core net profit is calculated excluding listing expenses and share option expenses

Source: Company, CMBIS estimates

Balance sheet

Source: Company, CMBIS estimates

YE Mar 31 (HK$ mn) FY16A FY17A FY18E FY19E FY20E

Revenue 704.9 964.9 1,256.3 1,562.9 1,860.9

Medical services 275.7 501.8 725.4 930.8 1,130.9

Quasi-medical 74.1 96.4 125.3 150.4 173.0

Traditional beauty 65.0 175.4 242.0 290.4 334.0

Skincare products 38.0 61.9 71.2 80.4 90.1

Health management - 51.3 92.4 110.8 133.0

Revenue from unutilised prepaid packages 252.1 78.1 - - -

Other net income and gains 3.0 10.0 4.2 3.0 3.0

Cost of inventories (70.7) (130.5) (165.8) (206.3) (245.6)

Registered practitioner expenses (52.8) (77.5) (90.0) (114.6) (139.0)

Employee benefit expenses (192.4) (277.9) (361.8) (437.6) (502.4)

Marketing and advertising expenses (38.0) (68.5) (113.1) (140.7) (167.5)

Rental and related expenses (62.2) (88.8) (111.0) (135.9) (161.7)

Credit card and expenses (23.0) (29.7) (41.5) (51.6) (61.4)

Depreciation (24.1) (27.5) (30.3) (45.1) (60.0)

Other expenses (26.5) (47.1) (50.7) (60.5) (70.2)

Operating profit 218.3 227.5 296.4 373.6 456.1

Share of profit of associate / JV - (0.0) 3.5 3.6 3.6

Net finance income / (expenses) 1.5 4.5 9.2 8.2 9.7

Exceptional (35.4) 12.7 4.6 - -

Pre-tax profit 184.4 244.6 313.7 385.4 469.4

Profits tax (35.1) (41.1) (53.3) (65.5) (79.8)

Minority interest (0.6) (2.8) (4.3) (5.0) (5.7)

Net profit 148.7 200.7 256.0 314.8 383.9

Core net profit 177.3 190.2 256.0 314.8 383.9

EBITDA 207.6 269.3 341.2 428.8 526.1

YE Mar 31 (HK$ mn) FY16A FY17A FY18E FY19E FY20E

Non-current assets 86.5 200.8 494.4 570.4 581.6

Fixed asset 59.2 70.2 273.9 352.8 366.8

Intangible assets 1.3 35.9 78.3 71.8 65.4

Goodwill 3.4 36.7 70.0 70.0 70.0

Other non-current assets 22.7 58.1 72.2 75.7 79.4

Current assets 1,069.0 998.5 905.3 1,059.7 1,395.8

Cash 354.7 200.6 215.8 361.4 676.8

Account receivable 74.8 112.9 142.2 145.0 159.8

Inventory 17.9 19.1 24.9 30.9 36.8

Available-for-sale investments 103.5 499.7 314.7 314.7 314.7

Other current assets 518.1 166.1 207.7 207.7 207.7

Current liabilities 421.0 401.1 588.2 628.2 690.7

Borrowings - - 120.5 149.0 191.8

Trade and other payables 101.9 61.4 63.2 65.2 67.2

Deffered revenue 312.9 327.9 384.7 384.3 390.2

Other current liabilities 6.2 11.8 19.8 29.6 41.6

Non-current liabilities 3.2 8.3 8.3 8.3 8.3

Borrowings - - - - -

Deffered taxation 0.1 3.1 3.1 3.1 3.1

Other non-current liabilities 3.1 5.2 5.2 5.2 5.2

Total net assets 731.3 789.9 803.2 993.6 1,278.4

Minority interest (0.1) 11.4 15.7 20.7 26.4

Shareholders' equity 731.4 778.5 787.4 972.8 1,251.9

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 27

Cash flow summary

Source: Company, CMBIS estimates

Key ratios

Source: Company, CMBIS estimates

YE Mar 31 (HK$ mn) FY16A FY17A FY18E FY19E FY20E

EBIT 218.3 227.5 296.4 373.6 456.1

Depreciation and amortization 24.6 29.2 36.7 51.6 66.4

Change in working capital (45.9) (60.5) 23.6 (7.3) (12.9)

Income tax paid (87.6) (33.2) (45.3) (55.7) (67.8)

Interest paid (1.5) (4.5) (9.2) (8.2) (9.7)

Others (31.8) 21.5 13.8 8.2 9.7

Net cash from operating activities 76.2 180.0 316.0 362.2 441.8

Capex (28.6) (75.6) (234.0) (124.0) (74.0)

Acquisition of subsidiaries (0.7) (28.5) - - -

Net change in available-for-sale investments (76.8) (395.0) 50.7 - -

Other (498.9) 345.8 10.7 11.5 13.9

Net cash from investing activities (604.9) (153.2) (172.6) (112.5) (60.1)

Change of Debts 0.0 - 120.5 28.6 42.7

Net proceeds from shares issued 717.1 2.3 - - -

Dividend paid (60.0) (90.1) (247.1) (129.4) (104.8)

Other 96.5 (92.2) (1.5) (3.3) (4.2)

Net cash from financing activities 753.7 (180.1) (128.1) (104.2) (66.3)

Net change in cash 224.9 (153.3) 15.2 145.5 315.4

Cash at the beginning of the year 129.9 354.7 200.6 215.8 361.4

Exchange difference (0.1) (0.8) - - -

Cash at the end of the year 354.7 200.6 215.8 361.4 676.8

YE Dec 31 FY16A FY17A FY18E FY19E FY20E

Sales mix (%)

Medical services 39.1 52.0 57.7 59.6 60.8

Quasi-medical 10.5 10.0 10.0 9.6 9.3

Traditional beauty 9.2 18.2 19.3 18.6 17.9

Skincare products 5.4 6.4 5.7 5.1 4.8

Health management - 5.3 7.4 7.1 7.1

Revenue from unutilised packages 35.8 8.1 - - -

Total 100.0 100.0 100.0 100.0 100.0

Profit & loss ratios (%)

EBITDA margin 29.4 27.9 27.2 27.4 28.3

Pre-tax margin 26.2 25.3 25.0 24.7 25.2

Net margin 21.1 20.8 20.4 20.1 20.6

Core net margin 25.2 19.7 20.4 20.1 20.6

Effective tax rate 19.0 16.8 17.0 17.0 17.0

Growth (%)

Revenue 13.5 36.9 30.2 24.4 19.1

EBITDA (9.2) 29.7 26.7 25.6 22.7

Operating profit 2.3 4.2 30.3 26.1 22.1

Net profit (14.8) 35.0 27.6 23.0 21.9

Core net profit 0.2 7.2 34.6 23.0 21.9

Balance sheet ratios

Current ratio (x) 2.5 2.5 1.5 1.7 2.0

Trade receivables turnover days 14 16 17 16 17

Trade payables turnover days 24 16 16 16 17

Inventory turnover days 81 52 48 49 50

Net debt to total equity ratio (%) Net cash Net cash Net cash Net cash Net cash

Returns (%)

ROE 20.3 25.8 32.5 32.4 30.7

ROA 12.9 16.7 18.3 19.3 19.4

Per share data

EPS (HK$) 0.20 0.21 0.26 0.32 0.39

Core EPS (HK$) 0.24 0.20 0.26 0.32 0.39

DPS (HK$) 0.19 0.21 0.21 0.10 0.12

BVPS (HK$) 0.76 0.81 0.82 1.01 1.30

7 Dec 2017

PLEASE READ THE ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ON LAST PAGE 28

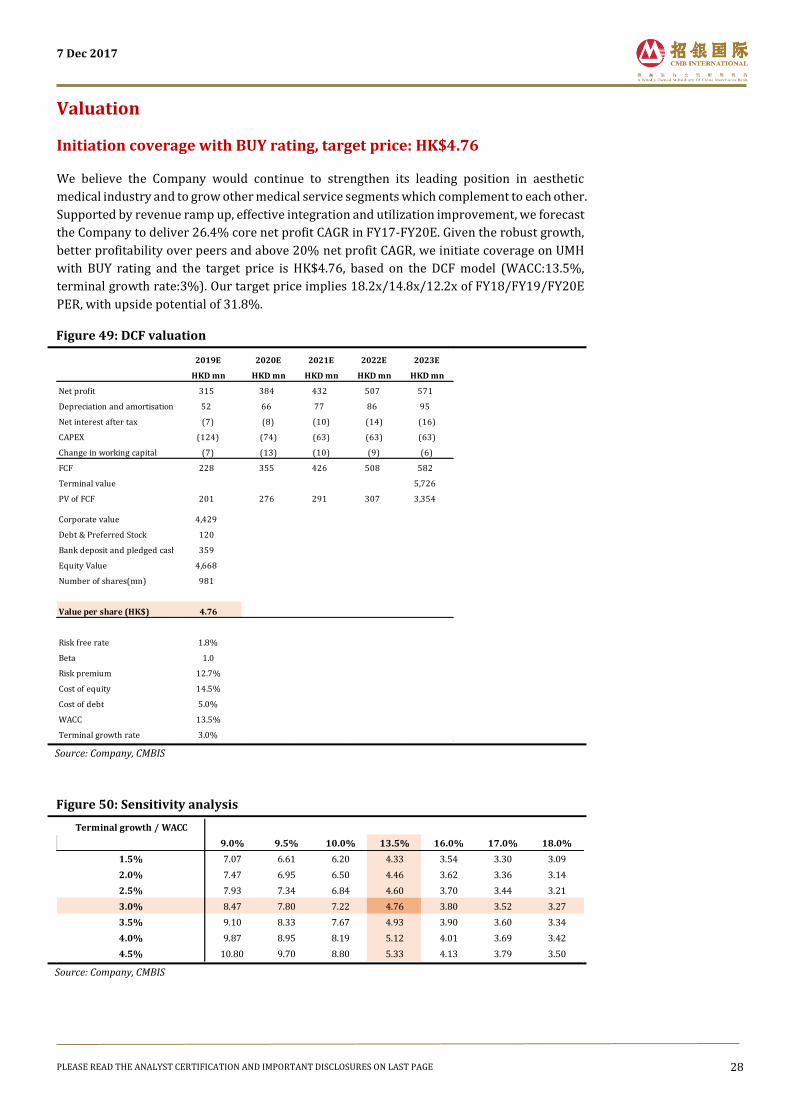

Valuation

Initiation coverage with BUY rating, target price: HK$4.76

We believe the Company would continue to strengthen its leading position in aesthetic

medical industry and to grow other medical service segments which complement to each other.

Supported by revenue ramp up, effective integration and utilization improvement, we forecast

the Company to deliver 26.4% core net profit CAGR in FY17-FY20E. Given the robust growth,

better profitability over peers and above 20% net profit CAGR, we initiate coverage on UMH

with BUY rating and the target price is HK$4.76, based on the DCF model (WACC:13.5%,

terminal growth rate:3%). Our target price implies 18.2x/14.8x/12.2x of FY18/FY19/FY20E

PER, with upside potential of 31.8%.

Figure 49: DCF valuation

Source: Company, CMBIS

Figure 50: Sensitivity analysis

Source: Company, CMBIS

2019E 2020E 2021E 2022E 2023E

HKD mn HKD mn HKD mn HKD mn HKD mn

Net profit 315 384 432 507 571

Depreciation and amortisation 52 66 77 86 95

Net interest after tax (7) (8) (10) (14) (16)

CAPEX (124) (74) (63) (63) (63)

Change in working capital (7) (13) (10) (9) (6)

FCF 228 355 426 508 582

Terminal value 5,726

PV of FCF 201 276 291 307 3,354

Corporate value 4,429

Debt & Preferred Stock 120

Bank deposit and pledged cash 359

Equity Value 4,668