Sino-Ocean Group Holding Limited (3377.HK)

31

2020 ANNUAL RESULTS Sino-Ocean Group Holding Limited (3377.HK) March 2021

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Sino-Ocean Group Holding Limited (3377.HK)

2020 ANNUAL RESULTS

Sino-Ocean Group Holding Limited (3377.HK)

March 2021

BUSINESS

REVIEW

Contracted sales: Total sales RMB131.04 bn, a slight YoY growth.

GFA sold: 7.06 mn sqm, up 11% YoY.

ASP: RMB18,600/sqm, a drop of 9% YoY, mainly attributable to regional distribution and product structure.

Cash proceeds: RMB88.8 bn, up 13% YoY, a record high; cash collection rate* reached 93%.

3.52 3.009.00 8.03 8.21

10.08 9.04 9.12

16.03 16.11 16.10

22.8

167 143459 440 454 523 483 493

692894 892

1,423

21,100 21,00019,600

18,300 18,10019,300 18,700 18,500

23,200

18,000 18,000 16,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Contracted sales (RMB bn) GFA sold ('000 sqm) ASP (RMB/sqm)

Monthly contracted sales in 2020 Cash collection

( RMB bn)

68.078.6

88.8

87% 89%93%

2018 2019 2020

Cash proceeds Cash collection rate

*Cash collection rate = cash proceeds/ attributable sales

Contracted sales

Contracted sales (cont.)

Beijing Region30%

Bohai Rim Region

19%

Eastern Region

15%

Central Region

11%

Western Region7%

Southern Region

18%

Distribution (by amount)

Sales distribution: By regions, sales focused on 6 major core regions, of which Beijing Region 30%, Bohai

Rim Region 19%, Eastern Region 15%, Southern Region 18%, Central and Western Region 18%; by city tiers,

T1&2 cities reached 94%, of which T1 35%, T2 59%.

Sales highlights: various projects in core cities topped sales chart, such as Oriental World View (Wuhan), Xixi

Mansion (Hangzhou), Ocean Palace (Shenzhen) and Sino-Ocean Royal Landscape (Xi'an), etc.

Sales highlights

Oriental World View (Wuhan)

No. 1 in Wuhan by sales amount

Xixi Mansion (Hangzhou)

No. 3 by regional sales amount

Sino-Ocean Royal Landscape (Xi'an)

No. 2 by regional sales amount

Ocean Palace (Shenzhen)

100% sell-through ratio

By region By city tier*

Tier 135%

Tier 259%

Tier 3 & 46%

Note: According to CBN2020 city classification standard

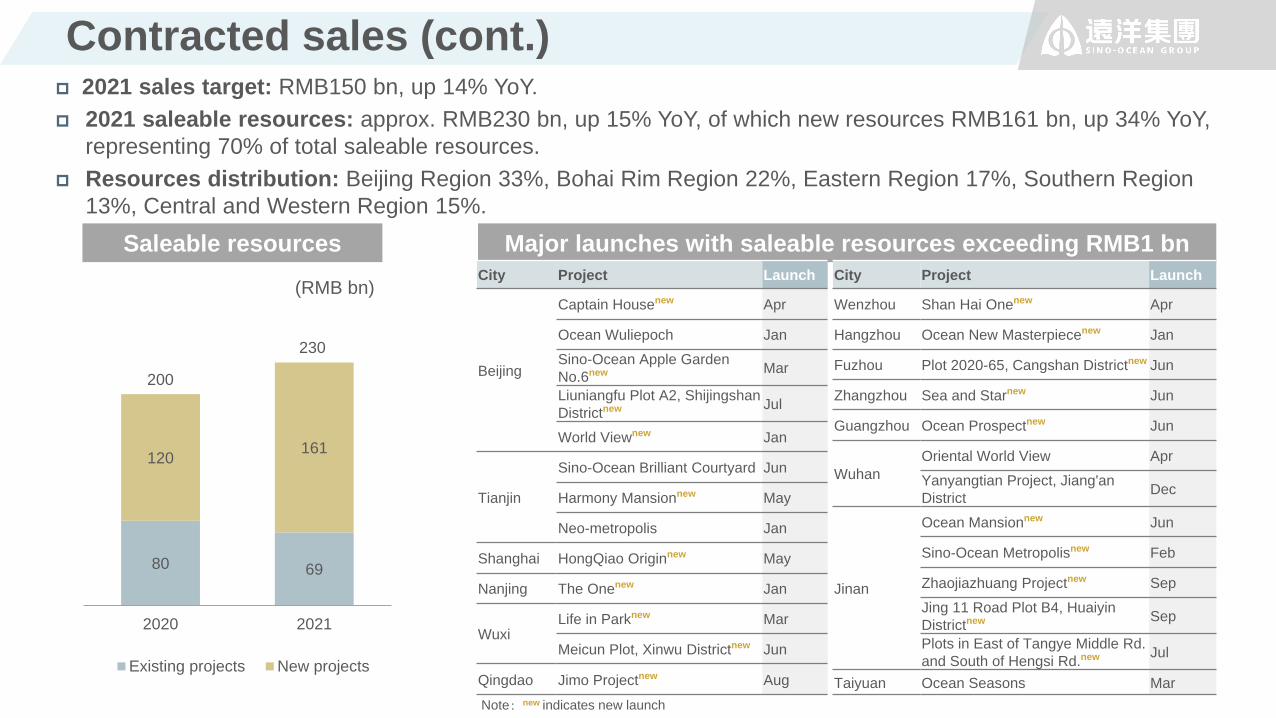

Contracted sales (cont.) 2021 sales target: RMB150 bn, up 14% YoY.

2021 saleable resources: approx. RMB230 bn, up 15% YoY, of which new resources RMB161 bn, up 34% YoY,

representing 70% of total saleable resources.

Resources distribution: Beijing Region 33%, Bohai Rim Region 22%, Eastern Region 17%, Southern Region

13%, Central and Western Region 15%.

Saleable resources

80 69

120161

2020 2021

Existing projects New projects

230

(RMB bn)

200

Major launches with saleable resources exceeding RMB1 bn

City Project Launch

Beijing

Captain Housenew Apr

Ocean Wuliepoch Jan

Sino-Ocean Apple Garden

No.6new Mar

Liuniangfu Plot A2, Shijingshan

Districtnew Jul

World Viewnew Jan

Tianjin

Sino-Ocean Brilliant Courtyard Jun

Harmony Mansionnew May

Neo-metropolis Jan

Shanghai HongQiao Originnew May

Nanjing The Onenew Jan

WuxiLife in Parknew Mar

Meicun Plot, Xinwu Districtnew Jun

Qingdao Jimo Projectnew Aug

City Project Launch

Wenzhou Shan Hai Onenew Apr

Hangzhou Ocean New Masterpiecenew Jan

Fuzhou Plot 2020-65, Cangshan Districtnew Jun

Zhangzhou Sea and Starnew Jun

Guangzhou Ocean Prospectnew Jun

Wuhan

Oriental World View Apr

Yanyangtian Project, Jiang'an

District Dec

Jinan

Ocean Mansionnew Jun

Sino-Ocean Metropolisnew Feb

Zhaojiazhuang Projectnew Sep

Jing 11 Road Plot B4, Huaiyin

Districtnew Sep

Plots in East of Tangye Middle Rd.

and South of Hengsi Rd.new Jul

Taiyuan Ocean Seasons Mar

Note:new indicates new launch

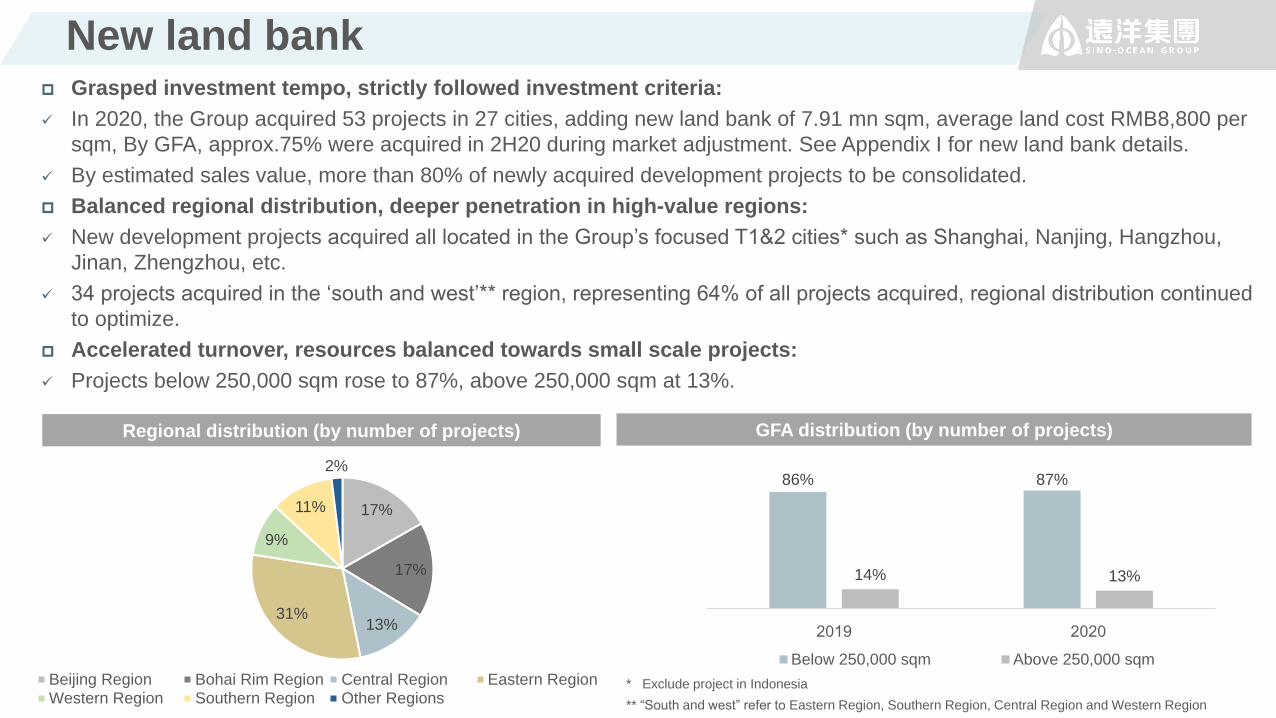

New land bank Grasped investment tempo, strictly followed investment criteria:

In 2020, the Group acquired 53 projects in 27 cities, adding new land bank of 7.91 mn sqm, average land cost RMB8,800 per

sqm, By GFA, approx.75% were acquired in 2H20 during market adjustment. See Appendix I for new land bank details.

By estimated sales value, more than 80% of newly acquired development projects to be consolidated.

Balanced regional distribution, deeper penetration in high-value regions:

New development projects acquired all located in the Group’s focused T1&2 cities* such as Shanghai, Nanjing, Hangzhou,

Jinan, Zhengzhou, etc.

34 projects acquired in the ‘south and west’** region, representing 64% of all projects acquired, regional distribution continued

to optimize.

Accelerated turnover, resources balanced towards small scale projects:

Projects below 250,000 sqm rose to 87%, above 250,000 sqm at 13%.

* Exclude project in Indonesia

GFA distribution (by number of projects)

** “South and west” refer to Eastern Region, Southern Region, Central Region and Western Region

Regional distribution (by number of projects)

17%

17%

13%31%

9%

11%

2%

Beijing Region Bohai Rim Region Central Region Eastern Region

Western Region Southern Region Other Regions

86% 87%

14% 13%

2019 2020

Below 250,000 sqm Above 250,000 sqm

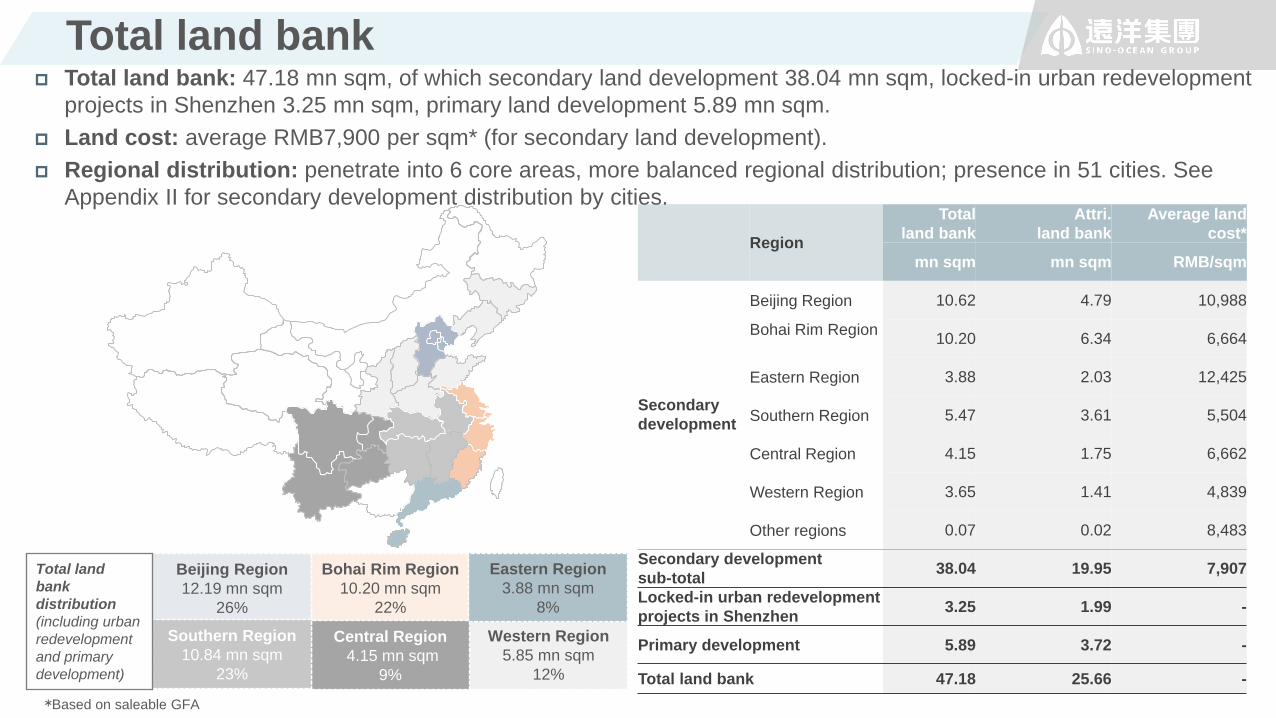

Total land bank

7*Based on saleable GFA

Western Region

5.85 mn sqm

12%

Beijing Region

12.19 mn sqm

26%

Bohai Rim Region

10.20 mn sqm

22%

Eastern Region

3.88 mn sqm

8%

Central Region

4.15 mn sqm

9%

Southern Region

10.84 mn sqm

23%

Total land

bank

distribution

(including urban

redevelopment

and primary

development)

Region

Total

land bank

Attri.

land bank

Average land

cost*

mn sqm mn sqm RMB/sqm

Secondary

development

Beijing Region 10.62 4.79 10,988

Bohai Rim Region10.20 6.34 6,664

Eastern Region 3.88 2.03 12,425

Southern Region 5.47 3.61 5,504

Central Region 4.15 1.75 6,662

Western Region 3.65 1.41 4,839

Other regions 0.07 0.02 8,483

Secondary development

sub-total38.04 19.95 7,907

Locked-in urban redevelopment

projects in Shenzhen3.25 1.99 -

Primary development 5.89 3.72 -

Total land bank 47.18 25.66 -

Total land bank: 47.18 mn sqm, of which secondary land development 38.04 mn sqm, locked-in urban redevelopment

projects in Shenzhen 3.25 mn sqm, primary land development 5.89 mn sqm.

Land cost: average RMB7,900 per sqm* (for secondary land development).

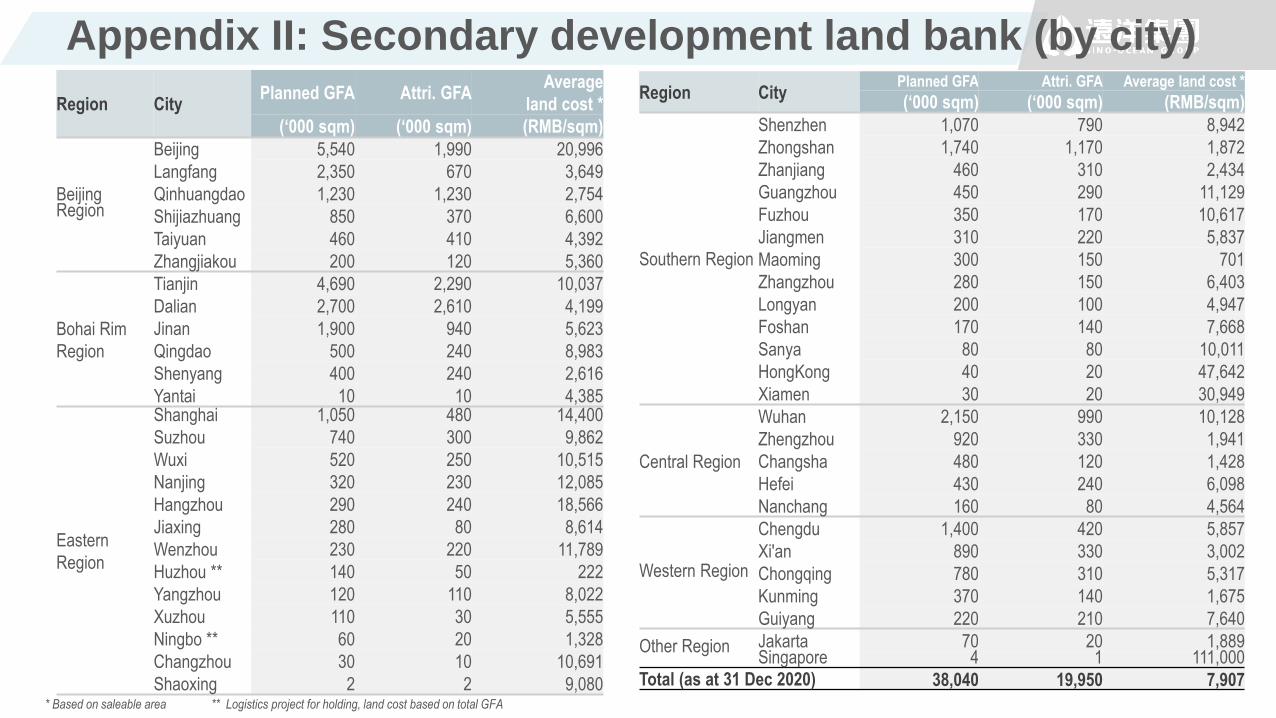

Regional distribution: penetrate into 6 core areas, more balanced regional distribution; presence in 51 cities. See

Appendix II for secondary development distribution by cities.

88

Project reserve: 4.32 mn sqm, of which 6 projects are acquired, with land bank of 1.07 mn sqm; another 5 projects

are locked in, with GFA of 3.25 mn sqm. In 1H20 newly locked in Pingxi Project in Longgang District, with GFA of

97,000 sqm.

Launch schedule: 4 projects in sale for 2020, including 2 brand new projects of Ocean Palace and Ocean Seafront

Towers, generating sales of RMB11.9 bn, nearly 100% sell-through ratio; Lishan Project, De’ai and Pingxi Project are

estimated to be launched in 2022.

De’ai Project Shanxia Project Sino-Ocean Dream Land

Ocean Express

Dapeng Project

Nanyuan Village Project

Ocean Palace

远洋滨海大厦

Lishan Project

Honghualing Project

Acquired Project

Locked-in Project

Pingxi Project

Ocean Seafront Towers

Project Status Location TypeAttri.

interest

GFA

‘000 sqm

Launch

schedule

Sino-Ocean Dream Land AcquiredLonggang

DistrictUrban complex 100% 10 In sale

Ocean Express AcquiredLonggang

DistrictUrban complex 85% 145 In sale

Ocean Seafront Towers AcquiredNanshan

DistrictUrban complex 60% 77 In sale

Ocean Palace AcquiredNanshan

DistrictResidential 63% 148 In sale

Lishan Project AcquiredNanshan

DistrictResidential 60% 156 2022

De’ai Industrial Park AcquiredLonghua

DistrictUrban complex 80% 533 2022

Land bank Subtotal 1,069

Pingxi Projectnew Locked-inLonggang

DistrictResidential 100% 97 2022

Shanxia Project Locked-inLonggang

District

Urban

complex55% 941 2023

Honghualing Industrial

District ProjectLocked-in

Nanshan

District

Urban

complex51% 838 2024

Dapeng Project Locked-inDapeng New

DistrictResidential 65% 230 2024

Nanyuan Village Project Locked-inNanshan

District

Urban

complex70% 1,147 2026

Locked-in Subtotal 3,253

Total 4,322

Total land bank (cont.)-urban redevelopment projects in Shenzhen

FINANCIAL

REVIEW

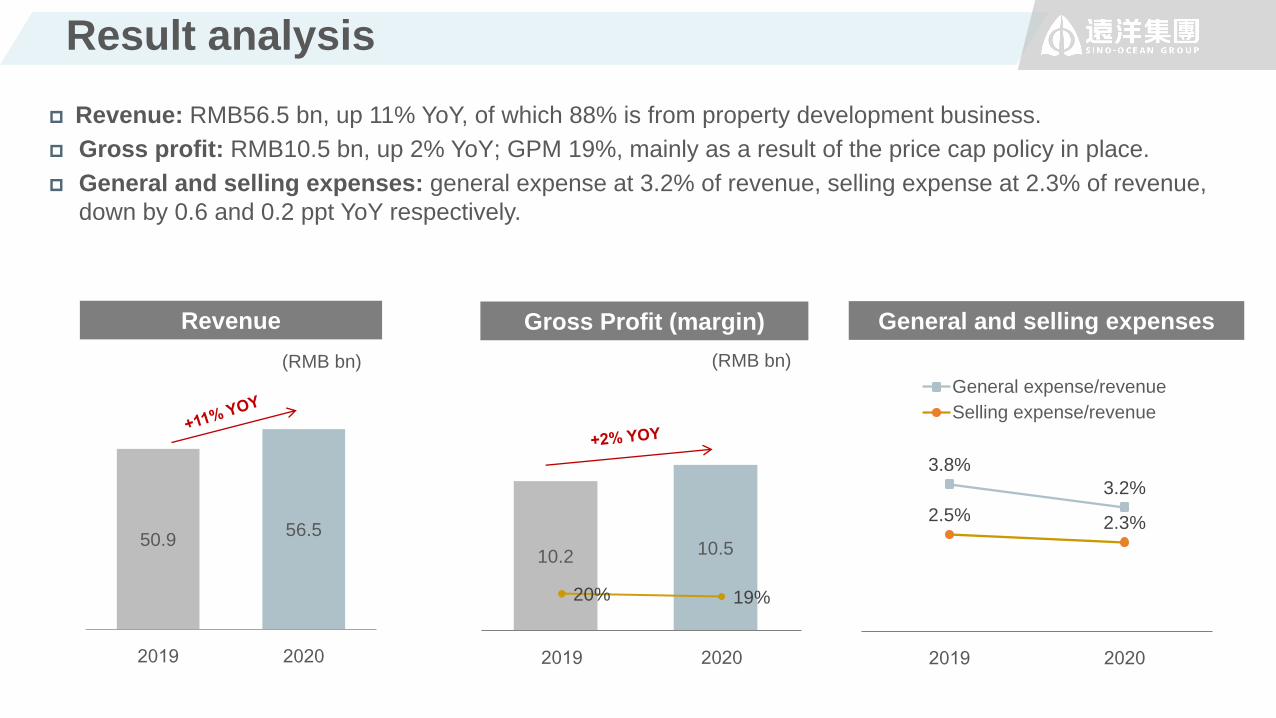

Result analysis

Revenue: RMB56.5 bn, up 11% YoY, of which 88% is from property development business.

Gross profit: RMB10.5 bn, up 2% YoY; GPM 19%, mainly as a result of the price cap policy in place.

General and selling expenses: general expense at 3.2% of revenue, selling expense at 2.3% of revenue,

down by 0.6 and 0.2 ppt YoY respectively.

3.8%

3.2%

2.5% 2.3%

2019 2020

General expense/revenue

Selling expense/revenue

Revenue

(RMB bn)

Gross Profit (margin)

(RMB bn)

General and selling expenses

10.2 10.5

20% 19%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

80

85

90

95

100

105

110

2019 2020

50.956.5

2019 2020

Result analysis (cont.)

Net profit: RMB2.87 bn, up by

8% YoY, as a result of

tightened SG&A and finance

expenses control and lower

tax expenses.

Core net profit: RMB2.23 bn,

up by 7% YoY.

Dividend: RMB0.131/share,

dividend payout ratio at 35% of

net profit. Dividend yield of 9%

based on 23 Mar closing price.

(RMB mn) 2020 2019 YoY Change

Revenue 56,511 50,926 11%

Gross Profit 10,457 10,222 2%

Other income 2,394 2,771

SG&A and finance expenses -5,220 -5,583

Fair value gains -156 373

Other gains 1,335 699

Losses and gains of JCEs 1,241 1,935

Profit before tax 10,050 10,416 -4%

LAT and income tax -5,367 -6,250

Profit for the year 4,683 4,166 12%

Non-controlling interests -1,817 -1,510

Profit attributable to owners

of the company2,866 2,656 8%

Basic EPS (RMB cents) 37.6 34.9

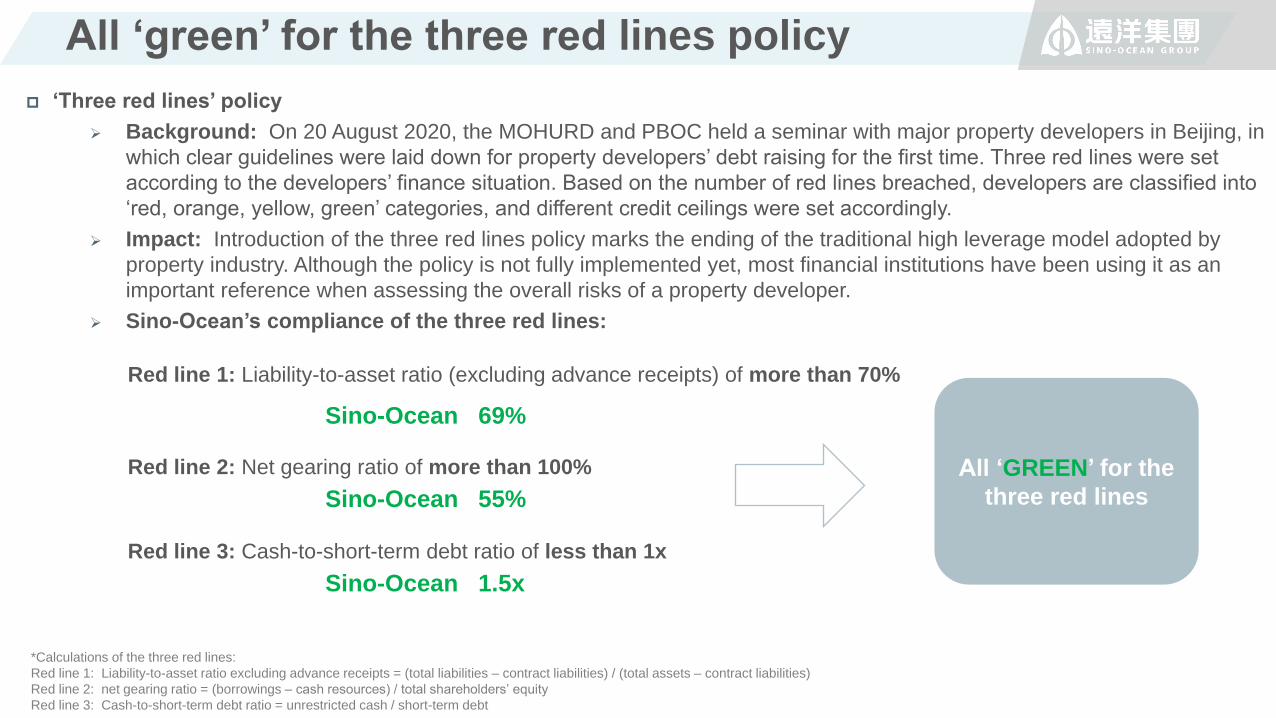

All ‘green’ for the three red lines policy

Red line 2: Net gearing ratio of more than 100%

Sino-Ocean 55%

‘Three red lines’ policy

Background: On 20 August 2020, the MOHURD and PBOC held a seminar with major property developers in Beijing, in

which clear guidelines were laid down for property developers’ debt raising for the first time. Three red lines were set

according to the developers’ finance situation. Based on the number of red lines breached, developers are classified into

‘red, orange, yellow, green’ categories, and different credit ceilings were set accordingly.

Impact: Introduction of the three red lines policy marks the ending of the traditional high leverage model adopted by

property industry. Although the policy is not fully implemented yet, most financial institutions have been using it as an

important reference when assessing the overall risks of a property developer.

Sino-Ocean’s compliance of the three red lines:

Red line 1: Liability-to-asset ratio (excluding advance receipts) of more than 70%

Sino-Ocean 69%

Red line 3: Cash-to-short-term debt ratio of less than 1x

Sino-Ocean 1.5x

All ‘GREEN’ for the

three red lines

*Calculations of the three red lines:

Red line 1: Liability-to-asset ratio excluding advance receipts = (total liabilities – contract liabilities) / (total assets – contract liabilities)

Red line 2: net gearing ratio = (borrowings – cash resources) / total shareholders’ equity

Red line 3: Cash-to-short-term debt ratio = unrestricted cash / short-term debt

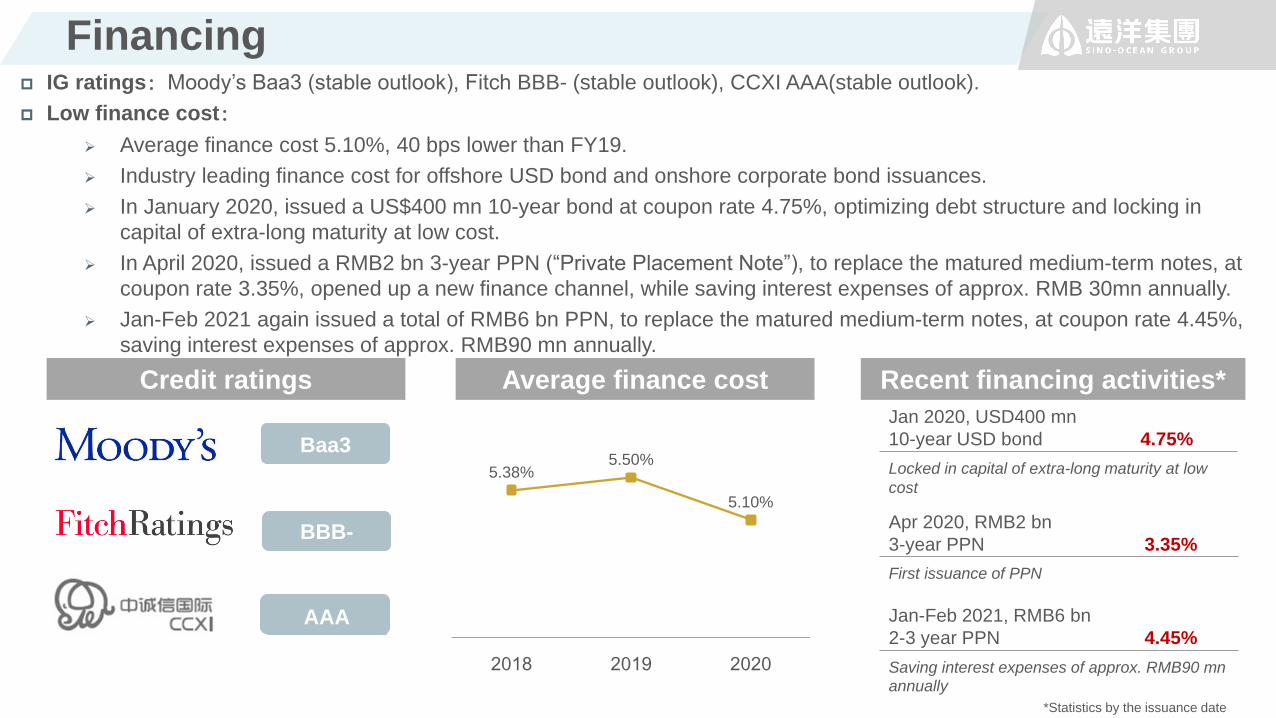

Financing IG ratings:Moody’s Baa3 (stable outlook), Fitch BBB- (stable outlook), CCXI AAA(stable outlook).

Low finance cost:

Average finance cost 5.10%, 40 bps lower than FY19.

Industry leading finance cost for offshore USD bond and onshore corporate bond issuances.

In January 2020, issued a US$400 mn 10-year bond at coupon rate 4.75%, optimizing debt structure and locking in

capital of extra-long maturity at low cost.

In April 2020, issued a RMB2 bn 3-year PPN (“Private Placement Note”), to replace the matured medium-term notes, at

coupon rate 3.35%, opened up a new finance channel, while saving interest expenses of approx. RMB 30mn annually.

Jan-Feb 2021 again issued a total of RMB6 bn PPN, to replace the matured medium-term notes, at coupon rate 4.45%,

saving interest expenses of approx. RMB90 mn annually.

Average finance costCredit ratings

Baa3

AAA

Recent financing activities*

Jan 2020, USD400 mn

10-year USD bond 4.75%

Locked in capital of extra-long maturity at low

cost

Apr 2020, RMB2 bn

3-year PPN 3.35%

First issuance of PPN

Baa3

BBB-

Jan-Feb 2021, RMB6 bn

2-3 year PPN 4.45%

Saving interest expenses of approx. RMB90 mnannually

*Statistics by the issuance date

5.38%5.50%

5.10%

2018 2019 2020

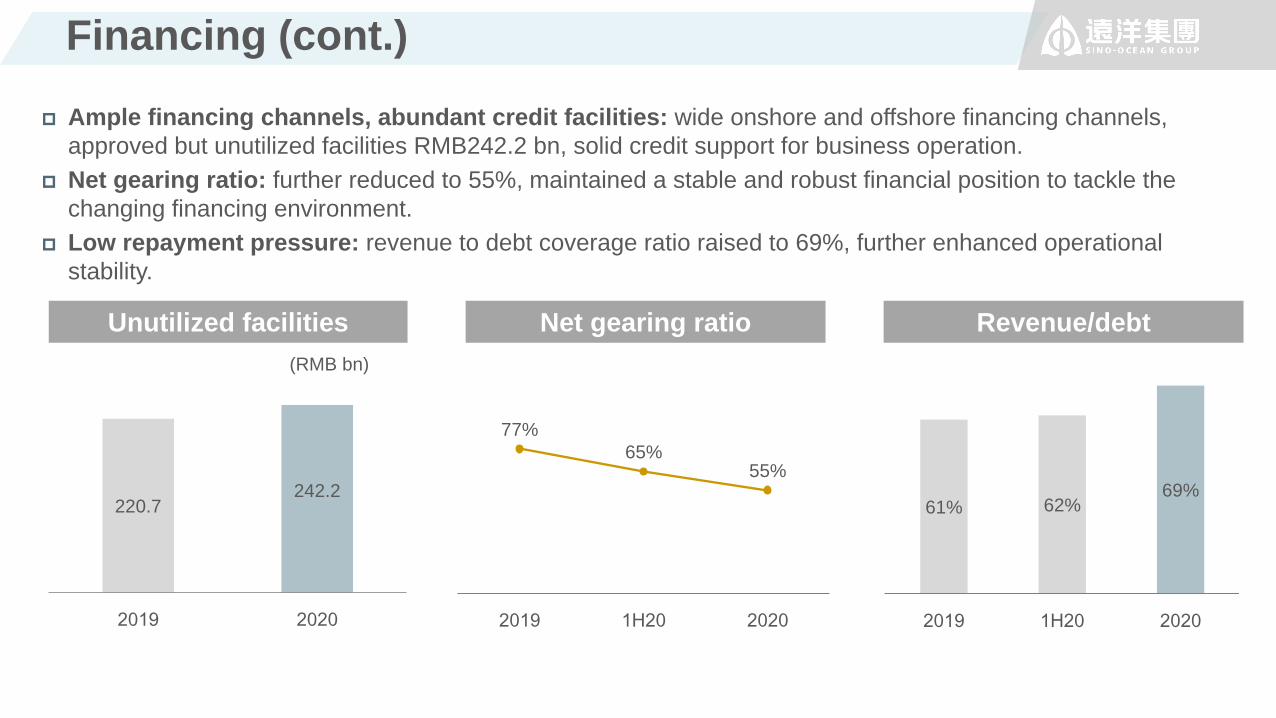

Financing (cont.)

Ample financing channels, abundant credit facilities: wide onshore and offshore financing channels,

approved but unutilized facilities RMB242.2 bn, solid credit support for business operation.

Net gearing ratio: further reduced to 55%, maintained a stable and robust financial position to tackle the

changing financing environment.

Low repayment pressure: revenue to debt coverage ratio raised to 69%, further enhanced operational

stability.

220.7242.2

2019 2020

Unutilized facilities Revenue/debtNet gearing ratio

61% 62%69%

2019 1H20 2020

(RMB bn)

77%

65%55%

2019 1H20 2020

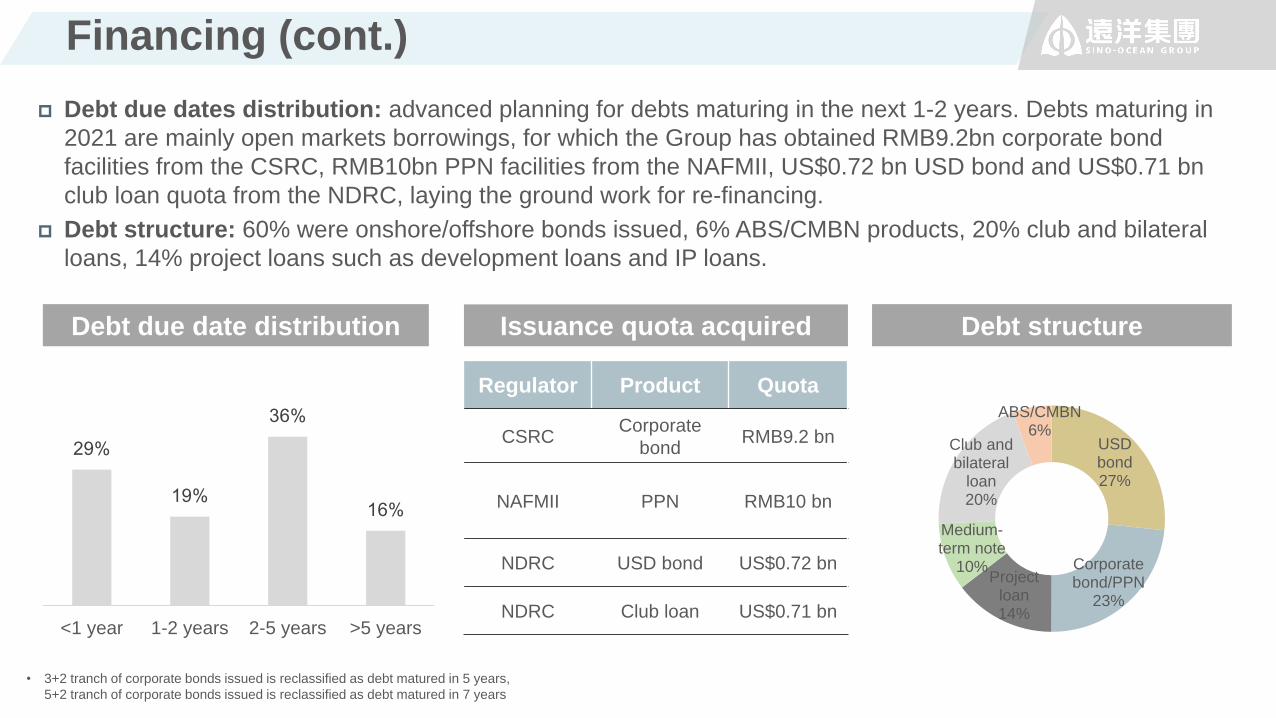

Financing (cont.)

Debt due date distribution Issuance quota acquired Debt structure

USD bond27%

Corporate bond/PPN

23%

Project loan14%

Medium-term note

10%

Club and bilateral

loan20%

ABS/CMBN6%

29%

19%

36%

16%

<1 year 1-2 years 2-5 years >5 years

Debt due dates distribution: advanced planning for debts maturing in the next 1-2 years. Debts maturing in

2021 are mainly open markets borrowings, for which the Group has obtained RMB9.2bn corporate bond

facilities from the CSRC, RMB10bn PPN facilities from the NAFMII, US$0.72 bn USD bond and US$0.71 bn

club loan quota from the NDRC, laying the ground work for re-financing.

Debt structure: 60% were onshore/offshore bonds issued, 6% ABS/CMBN products, 20% club and bilateral

loans, 14% project loans such as development loans and IP loans.

Regulator Product Quota

CSRCCorporate

bondRMB9.2 bn

NAFMII PPN RMB10 bn

NDRC USD bond US$0.72 bn

NDRC Club loan US$0.71 bn

• 3+2 tranch of corporate bonds issued is reclassified as debt matured in 5 years,

5+2 tranch of corporate bonds issued is reclassified as debt matured in 7 years

INVESTMENT

PROPERTY

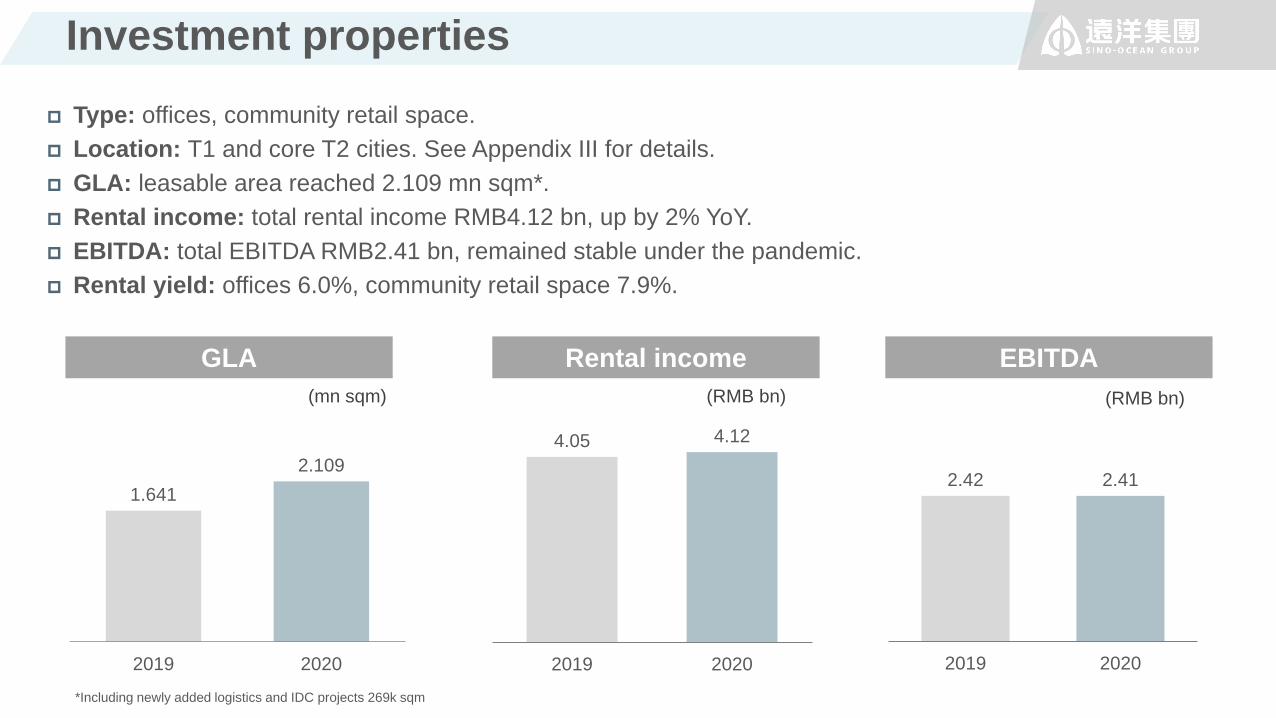

Investment properties

Type: offices, community retail space.

Location: T1 and core T2 cities. See Appendix III for details.

GLA: leasable area reached 2.109 mn sqm*.

Rental income: total rental income RMB4.12 bn, up by 2% YoY.

EBITDA: total EBITDA RMB2.41 bn, remained stable under the pandemic.

Rental yield: offices 6.0%, community retail space 7.9%.

Rental income

(RMB bn)

EBITDA

(RMB bn)(mn sqm)

GLA

1.641

2.109

2019 2020

4.05 4.12

2019 2020

2.42 2.41

2019 2020

*Including newly added logistics and IDC projects 269k sqm

Investment properties (in operation)

Retail spaceOffice

High end offices in core districts were more resistant to risks,

with occupancy rate remained stable at high level. The

pandemic caused a slight fall in rental income but overall

operation was stable.

Retail properties in core T1 & T2 cities. Strong operation recovery

recorded in 2H, with occupancy maintained stable at high level

and sales volume bounced back quickly to a YoY increase .

Rental and occupancy

Rental and occupancy

北京

远洋大厦Ocean Plaza

北京

远洋国际中心二期Ocean International Center Phase II

成都

成都远洋太古里Sino-Ocean Taikoo Li Chengdu

杭州

远洋乐堤港Grand Canal Place

(RMB mn)

186 182

98%91%

2019 2020

Rental Occupancy

(RMB mn) Operating Performance

Occupancy 95%

Sales volume +6%

Operation Highlight

Sales in August, October and

November 2020 recorded new

highs since opening, up by 35%,

39% and 38% YoY respectively.

Operating Performance

Occupancy 92%

Sales volume +14%

Operation Highlight

69 new shops opened in 2020,

newly added 13K sqm in operation;

monthly average sales per square

foot up by 13% YoY.

121 116

90% 86%

2019 2020

Rental Occupancy

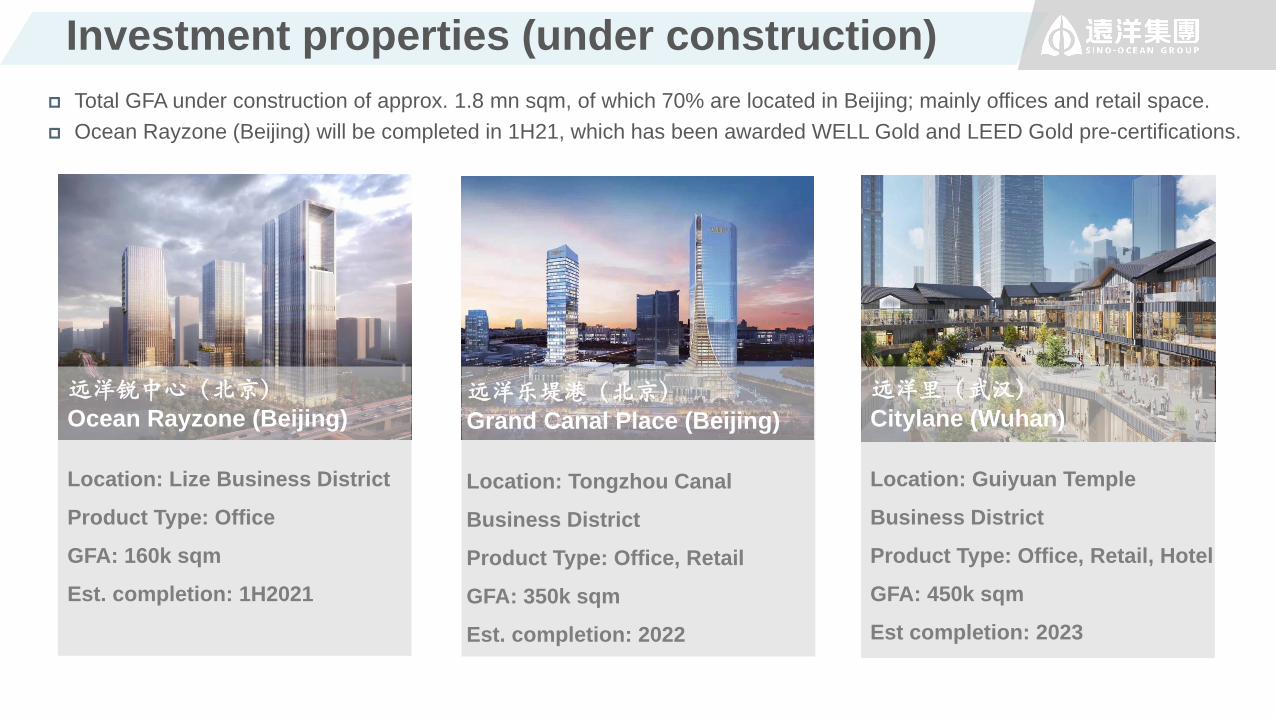

Investment properties (under construction)

远洋锐中心(北京)

Ocean Rayzone (Beijing)

Location: Lize Business District

Product Type: Office

GFA: 160k sqm

Est. completion: 1H2021

Total GFA under construction of approx. 1.8 mn sqm, of which 70% are located in Beijing; mainly offices and retail space.

Ocean Rayzone (Beijing) will be completed in 1H21, which has been awarded WELL Gold and LEED Gold pre-certifications.

远洋里(武汉)

Citylane (Wuhan)

Location: Guiyuan Temple

Business District

Product Type: Office, Retail, Hotel

GFA: 450k sqm

Est completion: 2023

远洋乐堤港(北京)

Grand Canal Place (Beijing)

Location: Tongzhou Canal

Business District

Product Type: Office, Retail

GFA: 350k sqm

Est. completion: 2022

Investment properties (under construction) (cont.)

Construction of CBD Plot Z6 (Beijing) commenced in Oct 2020. Construction of INDIGO II (Beijing) commenced in 2H20,

the third joint-venture project with Swire Properties after INDIGO (Beijing) and Sino-Ocean Taikoo Li (Chengdu).

As pipeline projects gradually complete and commence operation, rental income will maintain a steady growth.

艳阳天(武汉)Yanyangtian Project (Wuhan)

Location: Inner ring core

districts in Jiang'an District

Product Type: Office, Retail

GFA: 110k sqm

Est. completion: 2023

Z6项目(北京)CBD Plot Z6 (Beijing)

Location: CBD

Product Type: Office

GFA: 170k sqm

Est. completion: 2025

颐堤港二期(北京)INDIGO II (Beijing)

Location: Jiuxianqiao Business

District

Product Type: Office, Retail, Hotel

GFA: 590k sqm

Est. completion: 2025

PROPERTY

MANAGEMENT

Property management

↑35%

↑20%

Outstanding capability in

high-end commercial properties

33%

17.6

27%

31%

↑ 36%

↑4ppts

↑ 25%

↑1.4ppts

↑ 11%

↑10.6x 80%↑ 44%

↑2.9ppts

Sino-Ocean Service (6677.HK) was successfully listed on the Main Board of HKEX

on 17 December 2020, aiming to be a leading comprehensive property manager

with commercial edge.

Performance highlights in 2020:

Business scale: parent company’s business grew steadily, actively developed

business from third parties.

Specialized in commercial properties: both volume and fees of existing

premises rose, potential operating services injection.

Profitability: increased continually, exploring the value of VAS.

Continued to develop business with the property portfolios of parent company Sino-

Ocean Group, and its shareholders China Life and Dajia Insurance Group, laying a

solid foundation for rapid growth.

Reserved GFA

25.63 mn sqm

Contracted GFA

71.08 mn sqm

Third-party projects as %

of contracted GFA

Management fee

(RMB/ month/ sqm)

As % of total revenue

2017-2020 Contracted GFA

CAGR

Gross profit RMB510 mn

GPM 25%

Net profit RMB260 mn

NPM 12.7%

Revenue

RMB2.02 bn

Third-party bidding

9.1 mn sqm

As % of non-residential

properties revenue

Core net profit RMB250mn

Core NPM 12.4%

Rapid business expansion Consistently rising profitability

SHAREHOLDERS’

SUPPORT

On 24 Feb 2021, China Life and Sino-Ocean Group signed a strategic

cooperation agreement, to further strengthen capital ties and promote

comprehensive cooperation in areas such as financial products, insurance,

investment property, property management and senior living, etc.

Capital support: China Life commits to maintain the single largest

shareholder position

Financial products: priority in subscription of financial products issued by

Sino-Ocean, support in credit ratings, etc.

IP: joint development of IP projects; Sino-Ocean could provide

commissioned construction services for China Life’s projects, etc.

Property management: Sino-Ocean could provide property management

services and VAS to China Life’s existing and future projects, etc.

Senior living: equity cooperation and joint investment, explore the

combination of social insurance and community senior living services, etc.

China Life

Dajia Insurance Group

Sino-Ocean Service provides property management services to Dajia Insurance Group including its headquarters in Beijing and residential projects in Wenzhou.

Shareholder cooperation continues to intensify

APPENDIX

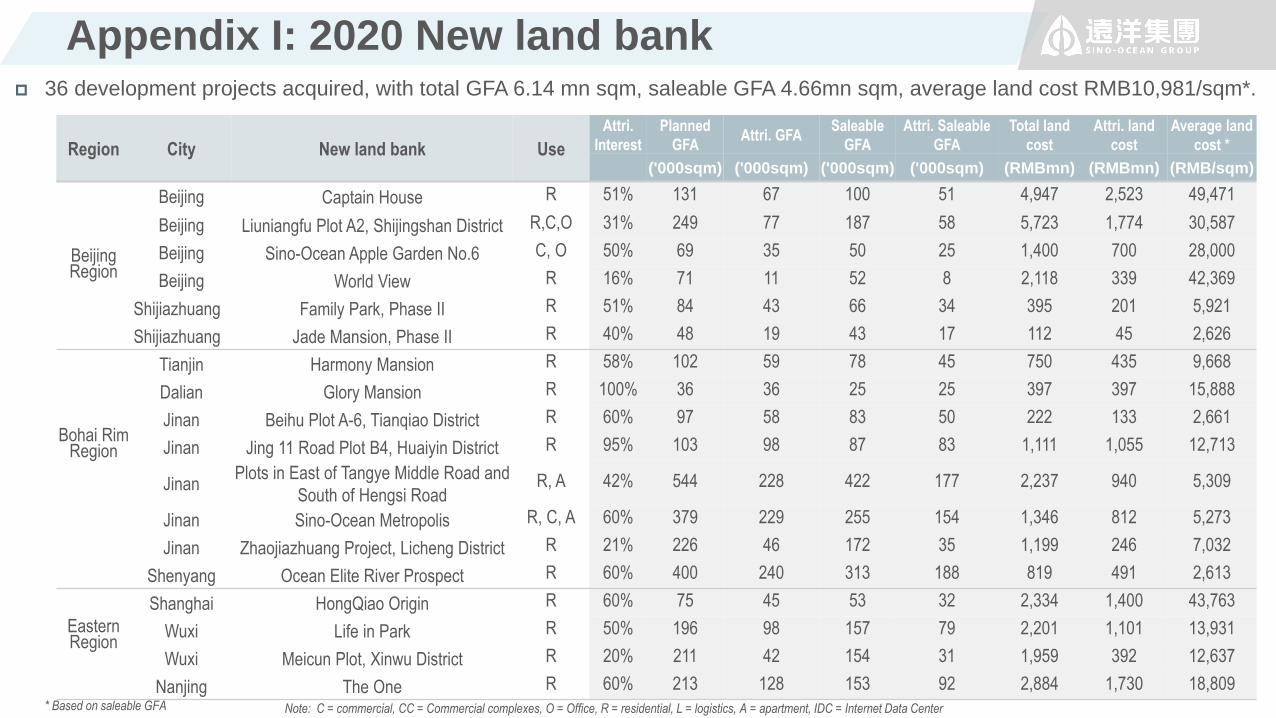

Appendix I: 2020 New land bank

Region City New land bank Use

Attri.

Interest

Planned

GFAAttri. GFA

Saleable

GFA

Attri. Saleable

GFA

Total land

cost

Attri. land

cost

Average land

cost *

('000sqm) ('000sqm) ('000sqm) ('000sqm) (RMBmn) (RMBmn) (RMB/sqm)

Beijing Region

Beijing Captain House R 51% 131 67 100 51 4,947 2,523 49,471

Beijing Liuniangfu Plot A2, Shijingshan District R,C,O 31% 249 77 187 58 5,723 1,774 30,587

Beijing Sino-Ocean Apple Garden No.6 C, O 50% 69 35 50 25 1,400 700 28,000

Beijing World View R 16% 71 11 52 8 2,118 339 42,369

Shijiazhuang Family Park, Phase II R 51% 84 43 66 34 395 201 5,921

Shijiazhuang Jade Mansion, Phase II R 40% 48 19 43 17 112 45 2,626

Bohai Rim Region

Tianjin Harmony Mansion R 58% 102 59 78 45 750 435 9,668

Dalian Glory Mansion R 100% 36 36 25 25 397 397 15,888

Jinan Beihu Plot A-6, Tianqiao District R 60% 97 58 83 50 222 133 2,661

Jinan Jing 11 Road Plot B4, Huaiyin District R 95% 103 98 87 83 1,111 1,055 12,713

JinanPlots in East of Tangye Middle Road and

South of Hengsi RoadR, A 42% 544 228 422 177 2,237 940 5,309

Jinan Sino-Ocean Metropolis R, C, A 60% 379 229 255 154 1,346 812 5,273

Jinan Zhaojiazhuang Project, Licheng District R 21% 226 46 172 35 1,199 246 7,032

Shenyang Ocean Elite River Prospect R 60% 400 240 313 188 819 491 2,613

Eastern Region

Shanghai HongQiao Origin R 60% 75 45 53 32 2,334 1,400 43,763

Wuxi Life in Park R 50% 196 98 157 79 2,201 1,101 13,931

Wuxi Meicun Plot, Xinwu District R 20% 211 42 154 31 1,959 392 12,637

Nanjing The One R 60% 213 128 153 92 2,884 1,730 18,809

36 development projects acquired, with total GFA 6.14 mn sqm, saleable GFA 4.66mn sqm, average land cost RMB10,981/sqm*.

* Based on saleable GFA Note: C = commercial, CC = Commercial complexes, O = Office, R = residential, L = logistics, A = apartment, IDC = Internet Data Center

Appendix I: 2020 New land bank (cont.)

Region City New land bank Use

Attri.

Interest

Planned

GFAAttri. GFA

Saleable

GFA

Attri. Saleable

GFA

Total land

cost

Attri. land

cost

Average land

cost *

('000sqm) ('000sqm) ('000sqm) ('000sqm) (RMBmn) (RMBmn) (RMB/sqm)

Eastern Region

Hangzhou Ocean New Masterpiece R 51% 44 22 33 17 930 474 27,888

Hangzhou Xixi Mansion R 100% 395 395 285 285 4,900 4,900 17,193

Wenzhou Harbor Heart R 85% 87 74 66 56 877 743 13,263

Wenzhou Shan Hai One R 100% 123 123 100 100 1,119 1,119 11,186

Yangzhou Sino-Ocean Grand Canal Milestone R 100% 63 63 47 47 397 397 8,445

Southern Region

Guangzhou Ocean Prospect R 100% 133 133 96 96 1,093 1,093 11,380

Fuzhou East Bay Upgrade R 34% 51 17 42 14 313 105 7,495

Fuzhou Plot 2020-65, Cangshan District R 51% 128 65 97 49 1,561 796 16,243

Jiangmen Cloud Mansion R 51% 176 90 133 68 737 376 5,528

Jiangmen Top Mansion R 100% 131 131 101 101 610 610 6,036

Zhangzhou Sea and Star R 51% 266 136 210 107 1,439 734 6,857

Central Region

Zhengzhou Fontaine Polaris R 25% 176 43 141 35 293 72 2,052

Zhengzhou Grand Apartment A 28% 172 49 133 38 220 62 1,634

Zhengzhou Ocean Landscape Courtyard R 55% 204 112 150 83 145 80 958

Zhengzhou Rong Fu R 18% 156 28 101 18 130 23 1,287

Changsha Special Mansion R 25% 482 118 384 94 548 134 1,429Western Region Chongqing Tanzikou Plot, Jiulongpo District R 34% 52 18 37 13 365 124 9,548Other

Region Jarkata Alam Sutera Project R 28% 66 18 57 16 108 30 1,884

Total 6,139 3,194 4,663 2,421 47,936 26,585 10,981

* Based on saleable GFA Note: C = commercial, CC = Commercial complexes, O = Office, R = residential, L = logistics, A = apartment, IDC = Internet Data Center

Appendix I: 2020 New land bank (cont.)

Region City New land bank Use

Attri.

Interest

Planned

GFAAttri. GFA Total land cost Attri. land cost

Average land

cost **

('000sqm) ('000sqm) (RMBmn) (RMBmn) (RMB/sqm)

Eastern RegionShanghai H88 Yuehong Plaza O, C 24% 62 15 2,002 488 32,512

Suzhou Wangting Logistics Project L 49% 66 32 335 164 5,130

Total 128 47 2,337 652 13,869

1 investment project acquired, with total GFA 570k sqm, average land cost RMB20,306/sqm.

Note: C = commercial, CC = Commercial complexes, O = Office, R = residential, L = logistics, A = apartment, IDC = Internet Data Center* * Based on total GFA

Region City New land bank Use

Attri.

Interest

Planned

GFAAttri. GFA Total land cost Attri. land cost

Average land

cost **

('000sqm) ('000sqm) (RMBmn) (RMBmn) (RMB/sqm)

Beijing Region Beijing INDIGO II CC 65% 565 366 11,471 7,432 20,306

Total 565 366 11,471 7,432 20,306

2 mature projects acquired, with total GFA 128k sqm, average land cost RMB13,869/sqm.

14 logistics and IDC projects acquired, with total GFA 1.08 mn sqm, average land cost RMB722/sqm.

Region CityPlanned GFA Attri. GFA

Average

land cost *

(‘000 sqm) (‘000 sqm) (RMB/sqm)

Beijing Region

Beijing 5,540 1,990 20,996

Langfang 2,350 670 3,649

Qinhuangdao 1,230 1,230 2,754

Shijiazhuang 850 370 6,600

Taiyuan 460 410 4,392

Zhangjiakou 200 120 5,360

Bohai Rim

Region

Tianjin 4,690 2,290 10,037

Dalian 2,700 2,610 4,199

Jinan 1,900 940 5,623

Qingdao 500 240 8,983

Shenyang 400 240 2,616

Yantai 10 10 4,385

Eastern

Region

Shanghai 1,050 480 14,400

Suzhou 740 300 9,862

Wuxi 520 250 10,515

Nanjing 320 230 12,085

Hangzhou 290 240 18,566

Jiaxing 280 80 8,614

Wenzhou 230 220 11,789

Huzhou ** 140 50 222

Yangzhou 120 110 8,022

Xuzhou 110 30 5,555

Ningbo ** 60 20 1,328

Changzhou 30 10 10,691

Shaoxing 2 2 9,080

Region CityPlanned GFA Attri. GFA Average land cost *

(‘000 sqm) (‘000 sqm) (RMB/sqm)

Southern Region

Shenzhen 1,070 790 8,942

Zhongshan 1,740 1,170 1,872

Zhanjiang 460 310 2,434

Guangzhou 450 290 11,129

Fuzhou 350 170 10,617

Jiangmen 310 220 5,837

Maoming 300 150 701

Zhangzhou 280 150 6,403

Longyan 200 100 4,947

Foshan 170 140 7,668

Sanya 80 80 10,011

HongKong 40 20 47,642

Xiamen 30 20 30,949

Central Region

Wuhan 2,150 990 10,128

Zhengzhou 920 330 1,941

Changsha 480 120 1,428

Hefei 430 240 6,098

Nanchang 160 80 4,564

Western Region

Chengdu 1,400 420 5,857

Xi'an 890 330 3,002

Chongqing 780 310 5,317

Kunming 370 140 1,675

Guiyang 220 210 7,640

Other Region Jakarta 70 20 1,889Singapore 4 1 111,000

Total (as at 31 Dec 2020) 38,040 19,950 7,907

Appendix II: Secondary development land bank (by city)

* Based on saleable area ** Logistics project for holding, land cost based on total GFA

Type City ProjectAttri.

interest

GLA

( sqm)

2020

Rental income

(RMB mn)

Occupancy

as at 31 Dec 2020

Grade-A offices

Beijing Ocean Plaza 72% 30,000 182 91%

Beijing Ocean International Center 100% 103,000 195 82%

Beijing Ocean International Center Phase II 35% 51,000 116 86%

Beijing Ocean Office Park 50% 107,000 302 88%

Beijing China Life Financial Center 10% 111,000 164 48%

Tianjin Ocean International Center 69% 53,000 33 70%

Shanghai Sino-Ocean Tower 15% 64,000 83 81%

Self-owned brand

retail

Beijing Ocean We-Life Plaza 64% 31,000 75 97%

Beijing Ocean We-Life 35% 19,000 25 89%

Beijing Ocean Landscape We-Life 64% 25,000 30 100%

Tianjin Ocean We-Life Plaza 64% 42,000 38 97%

Tianjin Ocean We-Life 100% 28,000 15 91%

Dalian Ocean Worldview Retail Street 100% 35,000 17 91%

Commercial

complexes

Beijing INDIGO 50% 181,000 478 O 70% R 98%

Chengdu Sino-Ocean Taikoo Li Chengdu 50% 174,000 1,075 95%

Hangzhou Grand Canal Plaza 60% 69,000 73 92%

Note: O = Office, R = retail

Appendix III: Major investment properties (in operation)

These materials have been prepared by Sino-Ocean Group Holding Limited (the “Company”) solely for

informational use during its presentation to prospective and existing investors for introduction of the

Company and to provide an update on the business performance and development of the Company. These

material may not be taken away, reproduced, redistributed or passed on, directly or indirectly, to any other

person (whether within or outside your organization/firm) or published, in whole or in part, for any purpose.

By attending this presentation, you are agreeing to be bound by the foregoing restrictions.

The information contained in these materials has not been independently verified. No representation or

warranty express or implied is made as to, and no reliance should be placed on, the fairness, accuracy,

completeness or correctness of the information or opinions contained herein. It is not the intention to

provide, and you may not rely on these materials as providing, a complete or comprehensive analysis of the

Company’s financial or trading position or prospects. The information contained in these materials should be

considered in the context of the circumstances prevailing at the time and is subject to change without notice

and has not been, and will not be, updated to reflect material developments which may occur after the date

of the presentation. None of the Company nor any of its respective directors, officers, employees, affiliates,

advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss or

damage howsoever arising from any use of these materials or their contents or otherwise arising in

connection with these materials.

Certain statements contained in these materials constitute “forward-looking statements”. Such forward-

looking statements involve risks, uncertainties and other factors that may cause the actual results,

performance or achievements of the Company to be materially different from those expressed by, or implied

by the forward-looking statements in these materials. There can be no assurance that the results and events

contemplated by the forward-looking statements contained in these materials will in fact occur.

This document does not constitute an offer or invitation to purchase or subscribe for any securities of the

Company or any holding company or any of its subsidiaries or an inducement to enter into any investment

activity. No part of these materials, or the fact of its distribution or use, shall form the basis of or be relied

upon in connection with any contract, commitment or investment decision in relation thereto.

DISCLAIMER