SECTION 1 - VIETDATA

28

Domestic Electrical Appliances - Vietnam Euromonitor International : Country Market Insight June 2009

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of SECTION 1 - VIETDATA

Domestic Electrical Appliances - Vietnam Euromonitor International : Country Market Insight June 2009

Domestic electrical appliances Vietnam

Euromonitor International Page i

List of Contents and Tables

Executive Summary ................................................................................................................................................ 1 Growth Rates Slump Due To Economic Downturn ................................................................................................... 1 Foreign Companies Expand Their Business in Vietnam ........................................................................................... 1 Many New Launches in 2008 .................................................................................................................................... 1 Energy-saving Products Are the New Trend ............................................................................................................. 1 Panasonic Remains Top Player ................................................................................................................................ 1 Key Trends and Developments .............................................................................................................................. 1 Consumers Postpone Spending Due To Economic Downturn ................................................................................... 1 Prices of Domestic Electrical Appliances Continue To Fall ..................................................................................... 2 Emerging Trend of A Shift To Higher Quality Products ........................................................................................... 3 Foreign Retailers Consider Entering the Vietnamese Dea Market ........................................................................... 4 Power Saving Products Are Increasingly Preferred ................................................................................................. 4 Cooking Appliances Have A Bigger Appeal .............................................................................................................. 5 Rural Market Yet To Be Fully Tapped ...................................................................................................................... 6 Market Indicators ................................................................................................................................................... 7

Table 1 Household Penetration of Selected Total Stock Domestic Electrical Appliances by Sector/Subsector 2003-2008 ...................................................................... 7

Table 2 Replacement Cycles of Domestic Electrical Appliances by Sector 2008 .......................... 7 Market Data ............................................................................................................................................................ 8

Table 3 Sales of Domestic Electrical Appliances by Sector: Volume 2003-2008 .......................... 8 Table 4 Sales of Domestic Electrical Appliances by Sector: Value 2003-2008 ............................. 8 Table 5 Sales of Domestic Electrical Appliances by Sector: % Volume Growth 2003-

2008 ................................................................................................................................... 8 Table 6 Sales of Domestic Electrical Appliances by Sector: % Value Growth 2003-

2008 ................................................................................................................................... 8 Table 7 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: Volume 2003-2008 .................................................................................................. 8 Table 8 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: Value 2003-2008 .....................................................................................................10 Table 9 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: % Volume Growth 2003-2008 ................................................................................11 Table 10 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: % Value Growth 2003-2008 ...................................................................................12 Table 11 Company Shares of Large Kitchen Appliances 2004-2008 ..............................................13 Table 12 Brand Shares of Large Kitchen Appliances 2005-2008 ....................................................13 Table 13 Company Shares of Small Kitchen Appliances (Non-cooking) 2004-2008 ......................14 Table 14 Brand Shares of Small Kitchen Appliances (Non-cooking) 2005-2008 ...........................14 Table 15 Large Kitchen Appliances by Distribution Format: % Breakdown 2003-2008 ................15 Table 16 Forecast Sales of Domestic Electrical Appliances by Sector: Volume 2008-

2013 ..................................................................................................................................15 Table 17 Forecast Sales of Domestic Electrical Appliances by Sector: Value 2008-

2013 ..................................................................................................................................15 Table 18 Forecast Sales of Domestic Electrical Appliances by Sector: % Volume

Growth 2008-2013............................................................................................................16 Table 19 Forecast Sales of Domestic Electrical Appliances by Sector: % Value

Growth 2008-2013............................................................................................................16 Table 20 Forecast Sales of Large Kitchen Appliances by Sector and by Built-

in/Freestanding Split: Volume 2008-2013 ........................................................................16 Table 21 Forecast Sales of Large Kitchen Appliances by Sector and by Built-

in/Freestanding Split: Value 2008-2013 ...........................................................................17

Domestic electrical appliances Vietnam

Euromonitor International Page ii

Table 22 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: % Volume Growth 2008-2013 ......................................................19

Table 23 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: % Value Growth 2008-2013 ..........................................................20

Definitions ...............................................................................................................................................................21 Summary 1 Research Sources ..............................................................................................................24

Domestic electrical appliances Vietnam

Euromonitor International Page 1

DOMESTIC ELECTRICAL APPLIANCES IN VIETNAM EXECUTIVE SUMMARY Growth Rates Slump Due To Economic Downturn In the latter half of 2008 until 2009, the Vietnam’s economy plunged into a downturn due to the global economic crisis. According to established business press, Moneyweek, Vietnam witnessed slowest GDP growth rate for a decade in 2008 – 6.8%. There were massive layoffs and consumer confidence has dropped. The economy is expected to perform even worse in 2009. Demand for domestic electrical appliances is still growing but growth rates of most DEA segments in 2008 were lower than in previous years. Sales only picked up prior to Lunar New Year, a traditional buying and sale season. Foreign Companies Expand Their Business in Vietnam In manufacturing, foreigners such as Toshiba and Sanyo established new factories in Vietnam during 2008. In retailing, many major foreign retailers have either entered Vietnam market or expressed their interest. Japanese retail giant, Best Denki, has joined forces with a domestic retailer to open three new electrical appliances outlets in 2008. Korea’s GS Retail and US’s Best Buy are seeking to enter the market. In the forecast period, foreign investors are expected to co-operate with domestic retailers to start building up their network in Vietnam. Many New Launches in 2008 Despite a fall in demand for domestic electrical appliances, home appliances leading manufacturers have launched many new advanced products in 2008. Philips and Panasonic, the two leading brands in small home appliances, launched new steam irons with automatic functions. Samsung introduced three new air treatment product lines Vivace, Forte and Neo Forte. LG Electronics Vietnam also launched their new product lines of air conditioners named Jet Cool, Neo Plasma and Art Cool. In November 2008, Panasonic launched its new air conditioners named Envio I2 and P2. Established manufacturers believe that the number of middle and high-income consumers is increasing and they are competing by launching new products that target these consumers. Energy-saving Products Are the New Trend Consumer awareness about saving energy has greatly increased partly due to the country’s current power shortage problem and also due to the government’s effort to encourage people to save electricity. As a result, most consumers have started to seek for energy saving products. Aware of this new trend, manufacturers have also launched new products with energy-saving features. LG’s Ecosave washing machines and Inverter air conditioners and Panasonic’s Envio air conditioners are typical examples of new power saving products in 2008. Panasonic Remains Top Player Panasonic is the famous brand of the home appliances produced by Matsushita Home Appliances Co Ltd, a subsidiary of Japan’s Panasonic Corp. The company has maintained its number one position in Vietnam’s domestic electrical appliances since 2001 although it has slightly lost share. In 2008, Matsushita’s value-share was 15%, down from 16% in 2001. Matsushita is the leader in small electrical appliances and is among the top five in large appliances such as refrigerators and washing machines. KEY TRENDS AND DEVELOPMENTS Consumers Postpone Spending Due To Economic Downturn Affected by the global economic crisis, Vietnam has suffered from an economic downturn since the later half of 2008. According to Moneyweek, Vietnam witnessed the slowest GDP growth rate for a decade at 6.8%. Half a million workers lost their jobs in 2008. According to the Prime Minister, the economy is expected to get even worse in 2009. Electronic goods exports fell 13.7% in the first two months of 2009. A further 400,000 jobs are

Domestic electrical appliances Vietnam

Euromonitor International Page 2

expected to go in 2009. Foreign investors are slow to disburse their investment projects and tourism has also suffered from falls in numbers. The economic downturn has led consumers to cut back on their consumption of durable goods including domestic electrical appliances. Current Impact A severe reduction in consumption of consumer goods and durable goods occurred in November and December 2008. Concern about the country’s economic prospects illustrated by layoffs, gasoline and electricity price hikes have made consumers postpone their spending. According to the General Statistical Office, national retail sales had a year-on-year 6% increase between 2007-2008, the lowest increase in the review period. To entice demand for domestic appliances, manufacturers and retailers have lowered prices and offered numerous promotions. In December 2008, Nguyen Kim, Thien Hoa and HCHomeCenter also known as Cho Lon had sales with reductions of around 20 to 50% for a variety of domestic electrical appliances such as refrigerators, washing machines, cooling fans, vacuum cleaners. However, sales did not pick up very much until the period before Lunar New Year 2009. Vietnamese consumers have a long-standing habit of purchasing new things before Lunar New Year as they want their houses to look new and fresh in the New Year. Outlook Since the beginning of 2009, there were more employment redundancies. Gas prices are not likely to rise again in 2009, as crude oil prices were slow in the midst of global recession. As the economy is likely to suffer even more in 2009, consumers are expected to continue to cut back on their consumption in 2009 and only purchase when prices are lowered. Therefore, retailers are likely to continue offering large-scale sale-offs, promotions and improved post-sales services to entice demand, particularly at year-end and in festive seasons such as Christmas and Lunar New Year. Leading manufacturers such as Sanyo and Panasonic always have promotions prior to Lunar New Year. Consumption of domestic electrical appliances will thus rise especially during festive seasons but the increase in retail sale volume will be much lower than the past years. Future Impact The government has imposed tax cuts and loaned out to enterprises to stimulate the economy. This has enabled manufacturers and retailers to reduce prices and hence attract consumers. Low import prices of household appliances from countries like Thailand, Singapore, Malaysia and low tax rates have also enabled manufacturers and retailers to lower prices and therefore entice purchase. Consumers gained in terms of prices, new advanced products and better services. Hence, the market for domestic electrical appliances will continue to grow healthily in the long term. In general, all segments in the domestic electrical appliances market will grow. Products that are still new and unfamiliar with Vietnamese consumers such as dishwashers, microwaves will start to gain share as income rises and consumers will have more sophisticated demand. Prices of Domestic Electrical Appliances Continue To Fall As consumers are cutting back on their consumption of durable goods due to the economic downturn, prices of all domestic electrical appliances continued to fall in 2008 and 2009. Major retailers such as Nguyen Kim, Thien Hoa, facing a significant drop in demand, negotiated with producers to lower prices to entice consumption. Furthermore, at year-end, manufacturers and retailers tend to launch large-scale sale-offs of the old inventories to make way for new products coming in. Current Impact Domestic manufacturers and retailers in 2008 continued to lower the price of all domestic appliances in order to counteract the falling demand for durable goods and get rid of their mounted inventories so that they can launch new advanced products to compete with foreign producers. Hence, 2008 was an eventful year in terms of sale-offs and promotions in electrical chain stores. Retailers offered 20 to 30% discounts on rice cookers, gas cookers, irons and cooking appliances. Manufacturers such as Electrolux, Panasonic, LG and Toshiba also reduced prices by 13 to 18%. During the peak sale season, small cooking appliances such as cookers, food processors dropped to around VND100,000 per product.

Domestic electrical appliances Vietnam

Euromonitor International Page 3

Outlook As the economic downturn will continue into 2009, domestic consumption will fall which will result in falling prices of domestic electrical appliances. Furthermore, since Vietnam has become a member of WTO, Vietnam has opened its markets to foreign investors as well as reduced tariffs which created a highly competitive environment for the retail industry including sales of domestic electrical appliances. This will lead to more price competition between existing players and new foreign players. The Association of Southeast Asian Nations (ASEAN) is planning to implement ASEAN economic integration which will take place from 2010 to 2015. The ASEAN Free Trade Agreement (AFTA), tariffs and non-tariff barriers in 12 product lines will be eliminated by 2010. Electronics are one of these 12 product lines. At the end of 2008, ASEAN airlines had started to facilitate transportation of goods between ASEAN members. Future Impact Prices are expected to continue falling in 2009. The extent of the price decrease will depend on the penetration of foreign players as well as the competition between existing manufacturers and retailers. With lower prices of imported products and lower import taxes, prices of new products will also fall. New products introduced in 2008 had lower prices than ones introduced a year ago. Consumers benefit from this trend, as they are now able to buy advanced products at a lower price. Retailers can also enjoy higher sales volume due to low prices. When WTO and AFTA agreements come into force from 2009 onwards, tariffs for domestic electrical appliances will be cut further and this will reduce the import price. Manufacturers are likely to shift to importing products made in other Asian countries into Vietnam. Vietnamese consumers largely prefer imported products, as they believe these products to be of higher quality. Emerging Trend of A Shift To Higher Quality Products Since January 2008, the government raised the minimum salary range to VND620,000 for domestic enterprises, a rise of 38% and VND1,000,000 for foreign invested enterprises a rise of 15%. As income and living standards rise, Vietnamese consumers can now afford more domestic electrical appliances. In addition, due to a busier lifestyle, people have started to value convenience. Hence, products with intelligent functions and greater convenience became more attractive despite their higher prices. Cordless irons, wireless vacuum cleaners or side-by-side fridge freezer are typical examples of popular products with intelligent functions. Current Impact The trend towards products with premium features has affected virtually all domestic electrical appliances. In many product lines such as home laundry appliances, irons and air conditioners, modern products have gained in value-share while traditional products have lost in terms of share. Many leading manufacturers such as Matsushita Home Appliances, LG Electronics, Samsung VINA launched plenty of new advanced products with intelligent functions in 2007 and 2008. In 2008, LG launched its new product line of washing machines named Spirit. In 2008, Samsung launched new models of washing machines that targeted low-end to high-end consumers. Matsushita launched its new air conditioners named Envio I2 and P2. Furthermore there were several incidents of faulty and fake products in 2008 which raised consumer concern. Consumers now choose to shop for electrical appliances in large retail stores rather than small shops. They have also switched towards famous Japanese and Korean brands despite their higher prices rather than cheap Chinese brands. Outlook This shift towards high-quality fully featured products will continue in the medium and long term despite the economic downturn. Although consumers became more hesitant about purchasing new durable goods, they will buy lower-priced products offered during sale seasons. Furthermore, consumers are now more aware of quality issues after several accidents caused by faulty products which were brought to light in 2007. Hence, they will go for high-quality products despite their high prices.

Domestic electrical appliances Vietnam

Euromonitor International Page 4

With lower import prices and lower import taxes, there will be more advanced foreign products in the market. Also, manufacturers are attracting consumers towards their new product lines. These factors will contribute to higher retail volumes of quality products. Future Impact The increasing consumer demand for intelligent and convenient products is a potential field to exploit in the forecast period. LG has so far succeeded in exploiting this trend with its new series of washing machines (Tromm and Spirit) and air conditioners (Jet Cool, Neo Plasma and Art Cool) which are establishing the company as a leading brand of quality products. Samsung VINA, Sony Vietnam and LG have said that they plan to import more high quality products into Vietnam in the future. Best Denki, the popular Japanese retailer of high quality, highly intelligent products has entered the segment. In the forecast period, it is expected that other foreign retailers such as Korea’s GS Retail and US’s Best Buy will bring to Vietnam a large supply of advanced products Foreign Retailers Consider Entering the Vietnamese Dea Market Vietnam became the 150th official member of the World Trade Organisation in November 2006. Starting from1st January 2009, Vietnam’s retail segment was opened up to foreign investors. WTO agreements allow foreign retailers to set up wholly foreign invested distribution channels and stores in Vietnam. Current Impact Foreign retail giants have increasingly expressed interest in the Vietnamese domestic electrical appliances market and a number entered since the end of 2006. Japan's leading retailer, Best Denki , entered into partnership with local retailer Ben Thanh Trading and Marketing Company to set up two electrical superstores in Hanoi and Can Tho under the name Best Carings in early 2008. South Korea's GS Retail and Best Buy from the US are preparing to open their chain stores across Vietnam. The South Korean retail chain Lotte has one floor in its supermarket which was opened in December 2008, for home appliances, with the priority given to products from South Korea. Lotte aims to set up 30 outlets in Vietnam in the next 15 years. As domestic retailers are going to face stiff competition from foreign players, major domestic retailers are seeking to expand rapidly in the large cities like Hanoi and Ho Chi Minh as well as smaller cities and provinces. HCHomeCenter (also known as Cho Lon) set up 20 outlets nationwide. Nguyen Kim aims to open 9 retail stores in 2009 and have one retail store in every province. Outlook Although foreign retailers may have difficulty in obtaining licenses to open chain stores, industry insiders warn that only 20% of domestic retailers will survive. Major domestic players such as Nguyen Kim and Cho Lon are likely to lose value-share to their foreign competitors. However, the impacts may not be seen in 2009 and in the medium term foreign investors will mainly focus on importing and distributing their imported goods through existing networks. Foreign retailers such as GS Retail and Best Buy are likely to officially enter the market when the economic downturn has alleviated and consumers are more generous in their spending. Future Impact With the presence of foreign retail giants in the market, strong domestic players will push forward their plans to expand in various parts of the country especially in small cities (such as Hai Phong, Hue, Can Tho) and provinces (such as Dong Nai, Ba Ria Vung Tau, Vinh Long). Competition will force every retailer to improve their services and lower prices. Manufacturers will also be under pressure to produce more advanced products. In the forecast period, domestic retailers are likely to lose share to foreign retailers as consumers tend to rely more on foreign brands. Foreign players are likely to partner with domestic distributors to gradually expand their retail channels, like the joint venture of Ben Thanh Trading and Marketing Co and Japan’s Best Denki. Power Saving Products Are Increasingly Preferred

Domestic electrical appliances Vietnam

Euromonitor International Page 5

Vietnam has suffered from power shortages since 2007 that have caused numerous problems to people and manufacturers, including domestic electrical appliances producers. The power shortage becomes particularly severe during the dry season as most of the country’s electricity comes from hydroelectric plants. The electricity industry is running out of capacity to meet demand. As living standard rise and businesses are expanding, demand for electricity has risen sharply. People now enjoy using air conditioners rather than cooling fans or vacuum cleaners rather than brooms. In addition to the power shortage problem, electricity and gas prices also increased between 2007-2008. This has raised awareness among consumers to save energy and switch to power saving products. Current Impact The government has launched an energy-saving campaign among households and businesses since 2008. This campaign is carried out though television programmes as well as popular newspapers. According to a survey in 2008 by the Energy Conservation Centre, 8,000 households, businesses and agencies in Ho Chi Minh City and neighbouring provinces, Can Tho and Binh Duong, showed a remarkable change in energy-saving awareness. Consumers are now more aware of energy when buying electrical products and choose to buy power saving products. Some popular energy-saving products are LG’s Ecosave washing machines and Inverter air conditioners. In 2008, Matsushita launched its new air conditioners named Envio I2 and P2 which claim to save up to 50% of the energy consumed. Outlook The government has announced many new electricity plants projects with an aim to make Vietnam self-sufficient in electricity and even export to neighbouring countries. The government also aims to establish the country’s electricity industry as the chief driver of economic development by 2020. The government aims to build many more electricity generators all over the country to achieve an output of 201 to 250 billion kWh and export electricity to other countries by 2020. However, in the forecast period, consumers will still go for power saving products and producers of power savings products will also gain better reputation in the industry. Future Impact This trend in energy-saving products will continue in the medium and longer term, particularly in 2009 when the economy is still in a mild recession and consumers have to save. Therefore, manufacturers will focus on producing more power saving products to meet this demand. This trend will lead to a rise in value-share of certain products with energy-saving functions across all large appliances such as refrigerators, washing machines, air conditioners as they tend to consume a large amount of electricity. Small appliances such as irons will also feature energy saving functions. Cooking Appliances Have A Bigger Appeal The kitchen plays a crucial role in family life in Vietnam and is used for family gatherings every day as well as during traditional occasions such as Lunar New Year. Cooking is therefore considered an essential part in daily life. Vietnamese women believe that good cooking is the best way to bond their families. As living standards have improved and apartment dwelling becomes increasingly common, Vietnamese families are paying more attention to their kitchens and cooking appliances to bring convenience and quality cooking. Modern kitchens with advanced cooking appliances are becoming more popular among Vietnamese households since these products were introduced three years ago. Vietnamese households can now afford to own a Western-styled kitchen with numerous electrical appliances as well as cooking and food preparation appliances. Current Impact Influenced by the media, Vietnamese housewives and young women now have a keen interest in cooking, baking and preparing food and drinks by themselves. Therefore, they became increasingly interested in cooking appliances with special functions which allow them to cook not only Vietnamese cuisine but also Western and other countries cuisines. The retail volume growth rate of kitchenware appliances has been high over the recent years such as microwaves, food processors, toasters and toaster ovens.

Domestic electrical appliances Vietnam

Euromonitor International Page 6

Outlook There are more young consumers living in apartments who want to learn and improve their cooking skills, so demand for electrical appliances and cooking appliances will increase over the forecast period. Manufacturers of cooking appliances have launched new marketing activities to win value-share in this segment. In 2007, LG introduced a new high quality kitchenware product line that included microwaves, ovens and freezers. This product line offers different types of products and prices to cater to all consumers. These products also appeal to middle-income to high-income consumers as they can buy a whole set of high quality products with similar designs which will make their kitchens look more beautiful. Future Impact As demand for cooking and food preparation appliances has risen, this will be an ideal segment for manufacturers and retailers to expand in the forecast period. An increasing number of Vietnamese high-income households will be interested in buying an entire suite of electrical appliances, cooking appliances and kitchenware to enhance the look of their kitchens. This trend will benefit sectors such as refrigerators, cookers, hobs and microwaves. Cooking appliances and kitchenware are likely to see strong growth, particularly when the economy recovers. Rural Market Yet To Be Fully Tapped Some 77% of the Vietnamese population live in rural areas and 63% of Vietnam’s GDP is generated in rural areas. However, the rural market has not been tapped by manufacturers and retailers of domestic electrical appliances. Although many new retailers appear in the market recently, they still focus on urban areas rather than rural areas. Current Impact According to the Saigon Businessmen, one of the leading business newspapers in Vietnam, more than 90% of rural households can afford electric and gas hobs and 30% want to own a refrigerator. The number of consumers in rural areas is three times the number of urban consumers and the number of households who can afford domestic electrical appliances is increasing rapidly. However, this market remains untapped as retailers and manufacturers are competing only in large cities such as Ho Chi Minh, Hanoi, Can Tho, Da Nang. Among the retailers of domestic electrical appliances, only HCHomeCenter (also known as Cho Lon) has many outlets in rural provinces and cities such as Quy Nhon, Phan Thiet, My Tho, Vinh Long. Across all segments of domestic electrical appliances, gas hobs, fridges and washing machines are currently the most demanded in rural areas. Outlook As the retailing industry has been opened for foreign investors since January 2009, domestic retailers are expected to expand to rural areas as they have local knowledge and can more easily set up their network in these areas. Nguyen Kim is seeking to open nine more outlets in 2009 and aims to have one outlet in every province. In urban areas, domestic retailers are expected to lose share to foreign players. One typical example is Best Caring, a joint venture of Ben Thanh Trading and Marketing Company and Japan’s Best Denki which has successfully expanded into three outlets in Hanoi, Can Tho and Ho Chi Minh in just one year. Future Impact Rural demand will be exploited by domestic manufacturers and retailers in the forecast period, as this is their most important strategy to remain in the market and earn revenue in the presence of foreign competitors. Foreign investors are expected to form partnerships and joint ventures with domestic players in order to make use of their local knowledge and expand in urban areas first and then rural cities. It is expected that domestic retailers will lose value-share to foreign retailers in urban areas as consumer income in urban areas are relatively high and they pay more attention to foreign products and services. Large cooking appliances, refrigerators and washing machines are most likely to have the biggest growth as a result of the rural penetration.

Domestic electrical appliances Vietnam

Euromonitor International Page 7

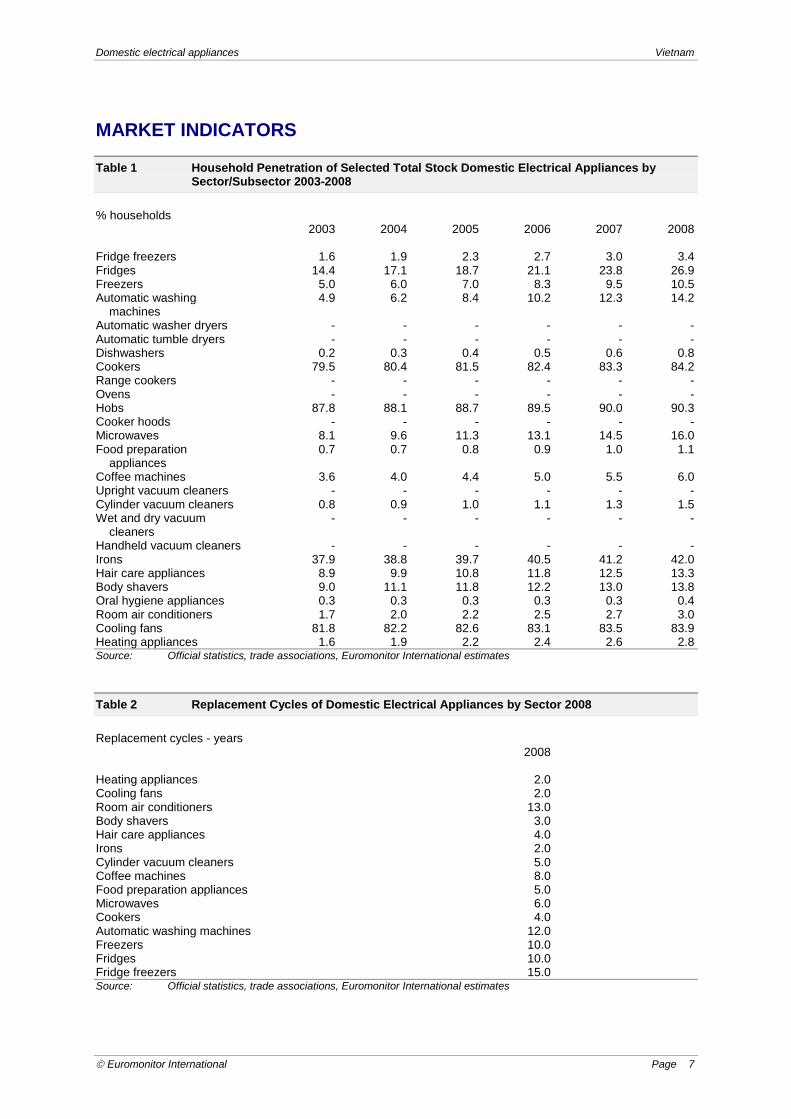

MARKET INDICATORS Table 1 Household Penetration of Selected Total Stock Domestic Electrical Appliances by

Sector/Subsector 2003-2008 % households 2003 2004 2005 2006 2007 2008 Fridge freezers 1.6 1.9 2.3 2.7 3.0 3.4 Fridges 14.4 17.1 18.7 21.1 23.8 26.9 Freezers 5.0 6.0 7.0 8.3 9.5 10.5 Automatic washing 4.9 6.2 8.4 10.2 12.3 14.2 machines Automatic washer dryers - - - - - - Automatic tumble dryers - - - - - - Dishwashers 0.2 0.3 0.4 0.5 0.6 0.8 Cookers 79.5 80.4 81.5 82.4 83.3 84.2 Range cookers - - - - - - Ovens - - - - - - Hobs 87.8 88.1 88.7 89.5 90.0 90.3 Cooker hoods - - - - - - Microwaves 8.1 9.6 11.3 13.1 14.5 16.0 Food preparation 0.7 0.7 0.8 0.9 1.0 1.1 appliances Coffee machines 3.6 4.0 4.4 5.0 5.5 6.0 Upright vacuum cleaners - - - - - - Cylinder vacuum cleaners 0.8 0.9 1.0 1.1 1.3 1.5 Wet and dry vacuum - - - - - - cleaners Handheld vacuum cleaners - - - - - - Irons 37.9 38.8 39.7 40.5 41.2 42.0 Hair care appliances 8.9 9.9 10.8 11.8 12.5 13.3 Body shavers 9.0 11.1 11.8 12.2 13.0 13.8 Oral hygiene appliances 0.3 0.3 0.3 0.3 0.3 0.4 Room air conditioners 1.7 2.0 2.2 2.5 2.7 3.0 Cooling fans 81.8 82.2 82.6 83.1 83.5 83.9 Heating appliances 1.6 1.9 2.2 2.4 2.6 2.8 Source: Official statistics, trade associations, Euromonitor International estimates Table 2 Replacement Cycles of Domestic Electrical Appliances by Sector 2008 Replacement cycles - years 2008 Heating appliances 2.0 Cooling fans 2.0 Room air conditioners 13.0 Body shavers 3.0 Hair care appliances 4.0 Irons 2.0 Cylinder vacuum cleaners 5.0 Coffee machines 8.0 Food preparation appliances 5.0 Microwaves 6.0 Cookers 4.0 Automatic washing machines 12.0 Freezers 10.0 Fridges 10.0 Fridge freezers 15.0 Source: Official statistics, trade associations, Euromonitor International estimates

Domestic electrical appliances Vietnam

Euromonitor International Page 8

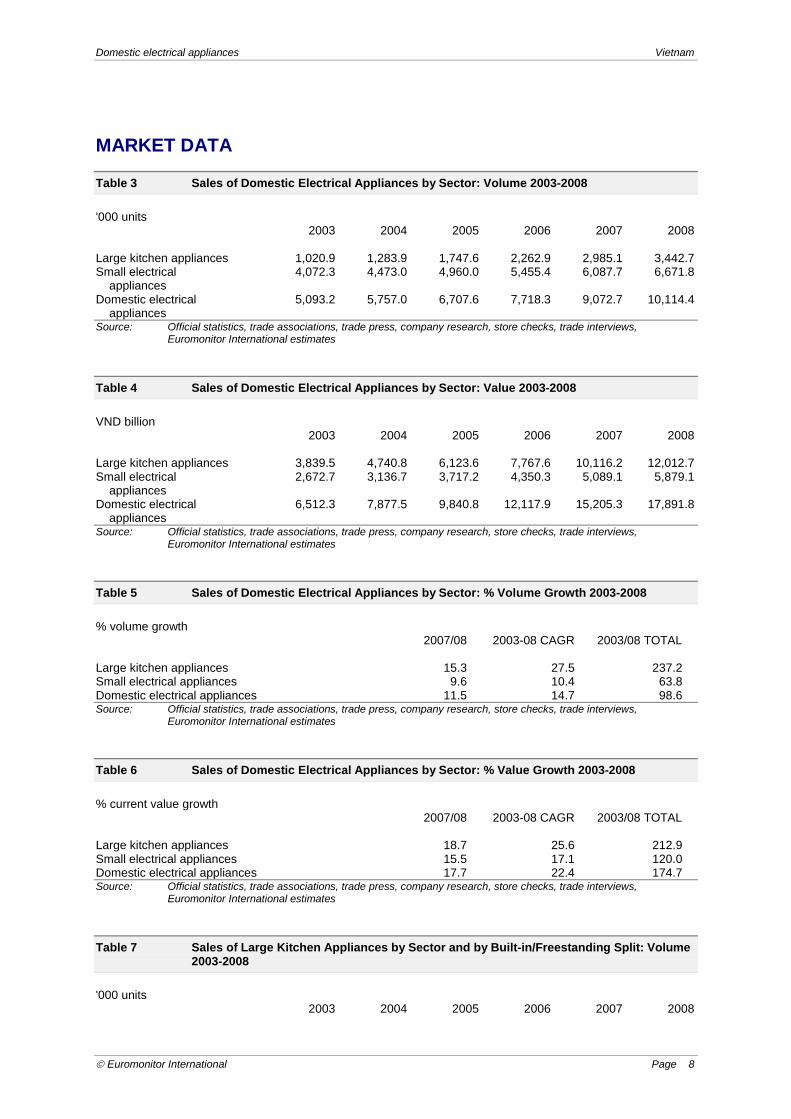

MARKET DATA Table 3 Sales of Domestic Electrical Appliances by Sector: Volume 2003-2008 '000 units 2003 2004 2005 2006 2007 2008 Large kitchen appliances 1,020.9 1,283.9 1,747.6 2,262.9 2,985.1 3,442.7 Small electrical 4,072.3 4,473.0 4,960.0 5,455.4 6,087.7 6,671.8 appliances Domestic electrical 5,093.2 5,757.0 6,707.6 7,718.3 9,072.7 10,114.4 appliances Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 4 Sales of Domestic Electrical Appliances by Sector: Value 2003-2008 VND billion 2003 2004 2005 2006 2007 2008 Large kitchen appliances 3,839.5 4,740.8 6,123.6 7,767.6 10,116.2 12,012.7 Small electrical 2,672.7 3,136.7 3,717.2 4,350.3 5,089.1 5,879.1 appliances Domestic electrical 6,512.3 7,877.5 9,840.8 12,117.9 15,205.3 17,891.8 appliances Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 5 Sales of Domestic Electrical Appliances by Sector: % Volume Growth 2003-2008 % volume growth 2007/08 2003-08 CAGR 2003/08 TOTAL Large kitchen appliances 15.3 27.5 237.2 Small electrical appliances 9.6 10.4 63.8 Domestic electrical appliances 11.5 14.7 98.6 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 6 Sales of Domestic Electrical Appliances by Sector: % Value Growth 2003-2008 % current value growth 2007/08 2003-08 CAGR 2003/08 TOTAL Large kitchen appliances 18.7 25.6 212.9 Small electrical appliances 15.5 17.1 120.0 Domestic electrical appliances 17.7 22.4 174.7 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

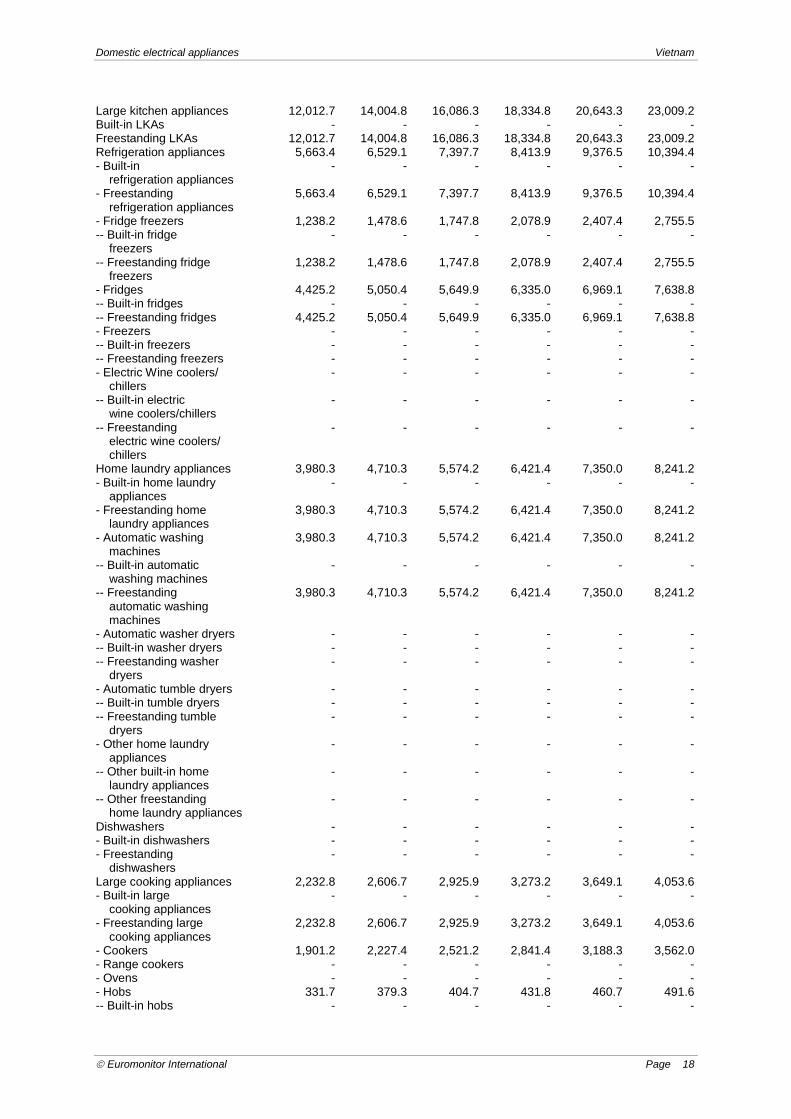

Euromonitor International estimates Table 7 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: Volume

2003-2008 '000 units 2003 2004 2005 2006 2007 2008

Domestic electrical appliances Vietnam

Euromonitor International Page 9

Large kitchen appliances 1,020.9 1,283.9 1,747.6 2,262.9 2,985.1 3,442.7 Built-in LKAs - - - - - - Freestanding LKAs 1,020.9 1,283.9 1,747.6 2,262.9 2,985.1 3,442.7 Refrigeration appliances 438.8 633.5 877.6 1,142.9 1,500.2 1,692.5 - Built-in - - - - - - refrigeration appliances - Freestanding 438.8 633.5 877.6 1,142.9 1,500.2 1,692.5 refrigeration appliances - Fridge freezers 37.4 46.3 64.6 99.4 154.0 184.8 -- Built-in fridge - - - - - - freezers -- Freestanding fridge 37.4 46.3 64.6 99.4 154.0 184.8 freezers - Fridges 401.4 587.2 813.1 1,043.5 1,346.2 1,507.7 -- Built-in fridges - - - - - - -- Freestanding fridges 401.4 587.2 813.1 1,043.5 1,346.2 1,507.7 - Freezers - - - - - - -- Built-in freezers - - - - - - -- Freestanding freezers - - - - - - - Electric Wine coolers/ - - - - - - chillers -- Built-in electric - - - - - - wine coolers/chillers -- Freestanding - - - - - - electric wine coolers/ chillers Home laundry appliances 251.0 285.2 462.1 656.1 944.7 1,133.7 - Built-in home laundry - - - - - - appliances - Freestanding home 251.0 285.2 462.1 656.1 944.7 1,133.7 laundry appliances - Automatic washing 251.0 285.2 462.1 656.1 944.7 1,133.7 machines -- Built-in automatic - - - - - - washing machines -- Freestanding 251.0 285.2 462.1 656.1 944.7 1,133.7 automatic washing machines - Automatic washer dryers - - - - - - -- Built-in washer dryers - - - - - - -- Freestanding washer - - - - - - dryers - Automatic tumble dryers - - - - - - -- Built-in tumble dryers - - - - - - -- Freestanding tumble - - - - - - dryers - Other home laundry - - - - - - appliances -- Other built-in home - - - - - - laundry appliances -- Other freestanding - - - - - - home laundry appliances Dishwashers - - - - - - - Built-in dishwashers - - - - - - - Freestanding - - - - - - dishwashers Large cooking appliances 310.2 339.0 374.9 423.6 491.7 558.4 - Built-in large - - - - - - cooking appliances - Freestanding large 310.2 339.0 374.9 423.6 491.7 558.4 cooking appliances - Cookers 90.5 99.5 111.5 125.9 152.4 178.3 - Range cookers - - - - - - - Ovens - - - - - - - Hobs 219.7 239.5 263.4 297.7 339.3 380.1

Domestic electrical appliances Vietnam

Euromonitor International Page 10

-- Built-in hobs - - - - - - -- Freestanding hobs 219.7 239.5 263.4 297.7 339.3 380.1 - Cooker hoods - - - - - - -- Built-in cooker hoods - - - - - - -- Freestanding cooker - - - - - - hoods Microwaves 21.0 26.3 33.1 40.4 48.4 58.1 - Built-in microwaves - - - - - - - Freestanding microwaves 21.0 26.3 33.1 40.4 48.4 58.1 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

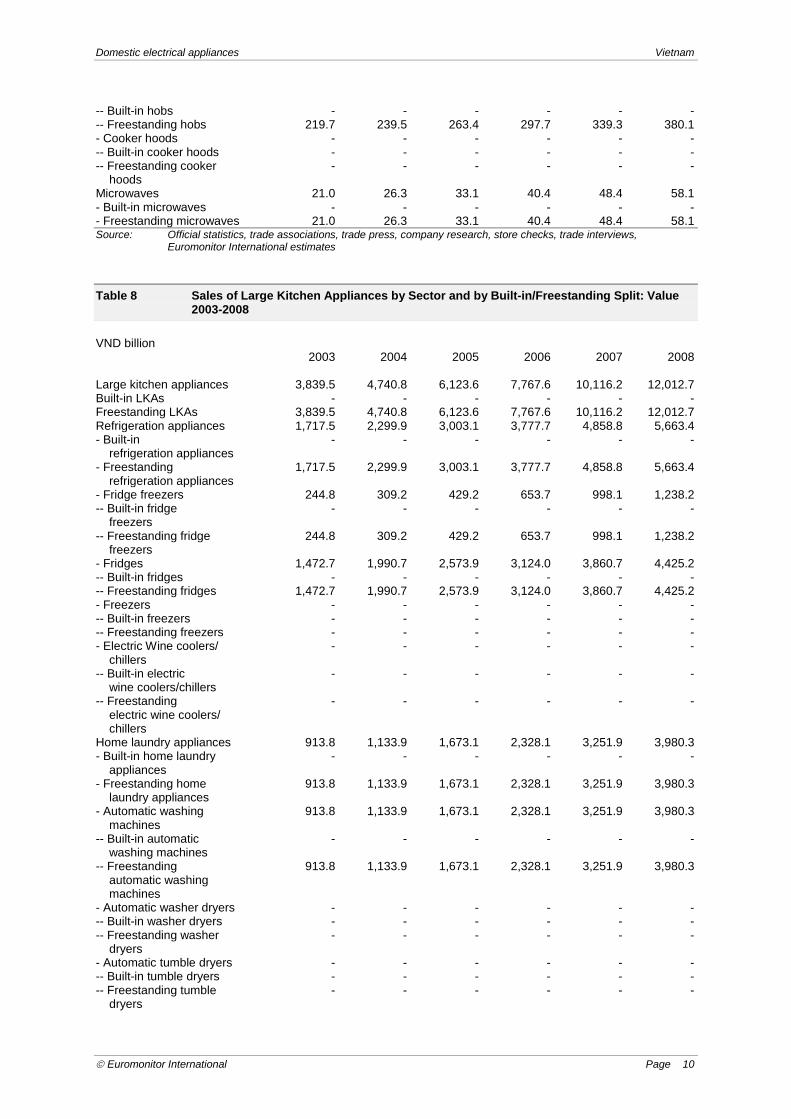

Euromonitor International estimates Table 8 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: Value

2003-2008 VND billion 2003 2004 2005 2006 2007 2008 Large kitchen appliances 3,839.5 4,740.8 6,123.6 7,767.6 10,116.2 12,012.7 Built-in LKAs - - - - - - Freestanding LKAs 3,839.5 4,740.8 6,123.6 7,767.6 10,116.2 12,012.7 Refrigeration appliances 1,717.5 2,299.9 3,003.1 3,777.7 4,858.8 5,663.4 - Built-in - - - - - - refrigeration appliances - Freestanding 1,717.5 2,299.9 3,003.1 3,777.7 4,858.8 5,663.4 refrigeration appliances - Fridge freezers 244.8 309.2 429.2 653.7 998.1 1,238.2 -- Built-in fridge - - - - - - freezers -- Freestanding fridge 244.8 309.2 429.2 653.7 998.1 1,238.2 freezers - Fridges 1,472.7 1,990.7 2,573.9 3,124.0 3,860.7 4,425.2 -- Built-in fridges - - - - - - -- Freestanding fridges 1,472.7 1,990.7 2,573.9 3,124.0 3,860.7 4,425.2 - Freezers - - - - - - -- Built-in freezers - - - - - - -- Freestanding freezers - - - - - - - Electric Wine coolers/ - - - - - - chillers -- Built-in electric - - - - - - wine coolers/chillers -- Freestanding - - - - - - electric wine coolers/ chillers Home laundry appliances 913.8 1,133.9 1,673.1 2,328.1 3,251.9 3,980.3 - Built-in home laundry - - - - - - appliances - Freestanding home 913.8 1,133.9 1,673.1 2,328.1 3,251.9 3,980.3 laundry appliances - Automatic washing 913.8 1,133.9 1,673.1 2,328.1 3,251.9 3,980.3 machines -- Built-in automatic - - - - - - washing machines -- Freestanding 913.8 1,133.9 1,673.1 2,328.1 3,251.9 3,980.3 automatic washing machines - Automatic washer dryers - - - - - - -- Built-in washer dryers - - - - - - -- Freestanding washer - - - - - - dryers - Automatic tumble dryers - - - - - - -- Built-in tumble dryers - - - - - - -- Freestanding tumble - - - - - - dryers

Domestic electrical appliances Vietnam

Euromonitor International Page 11

- Other home laundry - - - - - - appliances -- Other built-in home - - - - - - laundry appliances -- Other freestanding - - - - - - home laundry appliances Dishwashers - - - - - - - Built-in dishwashers - - - - - - - Freestanding - - - - - - dishwashers Large cooking appliances 1,148.6 1,234.6 1,359.4 1,557.4 1,886.3 2,232.8 - Built-in large - - - - - - cooking appliances - Freestanding large 1,148.6 1,234.6 1,359.4 1,557.4 1,886.3 2,232.8 cooking appliances - Cookers 935.4 1,007.1 1,114.4 1,289.5 1,593.1 1,901.2 - Range cookers - - - - - - - Ovens - - - - - - - Hobs 213.1 227.5 245.0 267.9 293.2 331.7 -- Built-in hobs - - - - - - -- Freestanding hobs 213.1 227.5 245.0 267.9 293.2 331.7 - Cooker hoods - - - - - - -- Built-in cooker hoods - - - - - - -- Freestanding cooker - - - - - - hoods Microwaves 59.7 72.4 88.0 104.4 119.3 136.1 - Built-in microwaves - - - - - - - Freestanding microwaves 59.7 72.4 88.0 104.4 119.3 136.1 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 9 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: %

Volume Growth 2003-2008 % volume growth 2007/08 2003-08 CAGR 2003/08 TOTAL Large kitchen appliances 15.3 27.5 237.2 Built-in LKAs - - - Freestanding LKAs 15.3 27.5 237.2 Refrigeration appliances 12.8 31.0 285.8 - Built-in refrigeration appliances - - - - Freestanding refrigeration appliances 12.8 31.0 285.8 - Fridge freezers 20.0 37.7 394.3 -- Built-in fridge freezers - - - -- Freestanding fridge freezers 20.0 37.7 394.3 - Fridges 12.0 30.3 275.6 -- Built-in fridges - - - -- Freestanding fridges 12.0 30.3 275.6 - Freezers - - - -- Built-in freezers - - - -- Freestanding freezers - - - - Electric Wine coolers/chillers - - - -- Built-in electric wine coolers/ - - - chillers -- Freestanding electric wine coolers/ - - - chillers Home laundry appliances 20.0 35.2 351.7 - Built-in home laundry appliances - - - - Freestanding home laundry appliances 20.0 35.2 351.7 - Automatic washing machines 20.0 35.2 351.7 -- Built-in automatic washing machines - - - -- Freestanding automatic washing 20.0 35.2 351.7 machines

Domestic electrical appliances Vietnam

Euromonitor International Page 12

- Automatic washer dryers - - - -- Built-in washer dryers - - - -- Freestanding washer dryers - - - - Automatic tumble dryers - - - -- Built-in tumble dryers - - - -- Freestanding tumble dryers - - - - Other home laundry appliances - - - -- Other built-in home laundry - - - appliances -- Other freestanding home laundry - - - appliances Dishwashers - - - - Built-in dishwashers - - - - Freestanding dishwashers - - - Large cooking appliances 13.5 12.5 80.0 - Built-in large cooking appliances - - - - Freestanding large cooking appliances 13.5 12.5 80.0 - Cookers 17.0 14.5 97.1 - Range cookers - - - - Ovens - - - - Hobs 12.0 11.6 73.0 -- Built-in hobs - - - -- Freestanding hobs 12.0 11.6 73.0 - Cooker hoods - - - -- Built-in cooker hoods - - - -- Freestanding cooker hoods - - - Microwaves 20.0 22.6 176.7 - Built-in microwaves - - - - Freestanding microwaves 20.0 22.6 176.7 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

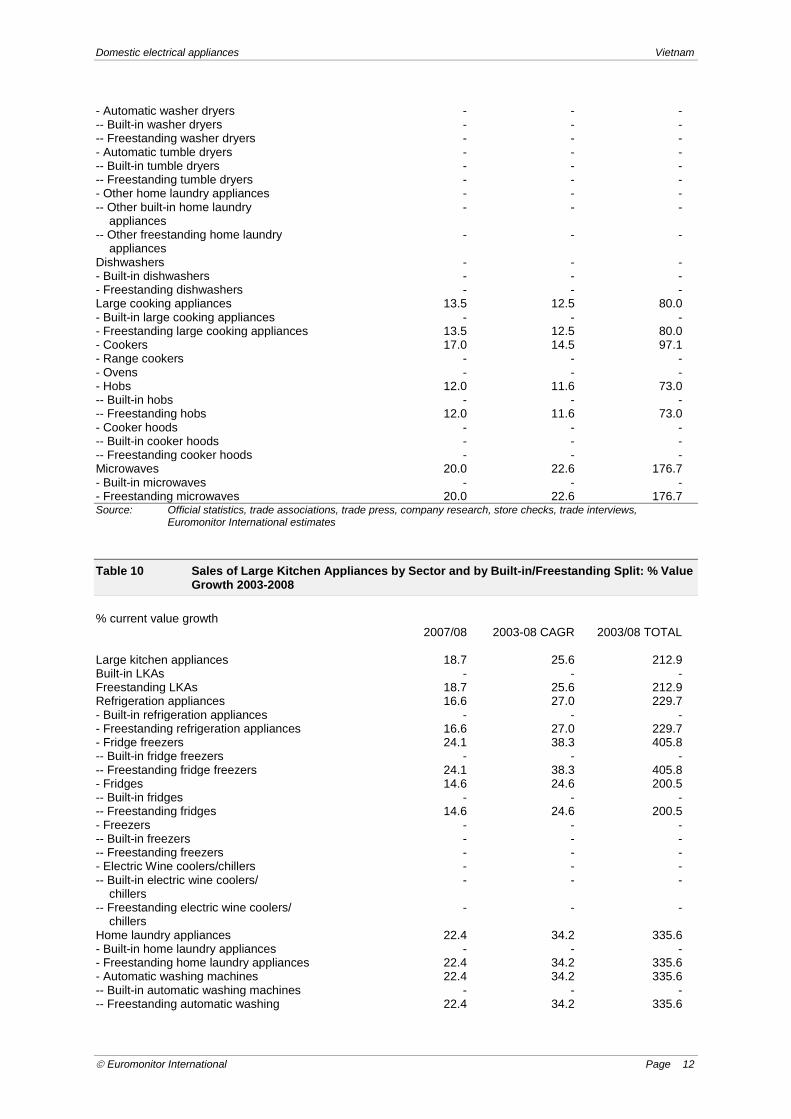

Euromonitor International estimates Table 10 Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding Split: % Value

Growth 2003-2008 % current value growth 2007/08 2003-08 CAGR 2003/08 TOTAL Large kitchen appliances 18.7 25.6 212.9 Built-in LKAs - - - Freestanding LKAs 18.7 25.6 212.9 Refrigeration appliances 16.6 27.0 229.7 - Built-in refrigeration appliances - - - - Freestanding refrigeration appliances 16.6 27.0 229.7 - Fridge freezers 24.1 38.3 405.8 -- Built-in fridge freezers - - - -- Freestanding fridge freezers 24.1 38.3 405.8 - Fridges 14.6 24.6 200.5 -- Built-in fridges - - - -- Freestanding fridges 14.6 24.6 200.5 - Freezers - - - -- Built-in freezers - - - -- Freestanding freezers - - - - Electric Wine coolers/chillers - - - -- Built-in electric wine coolers/ - - - chillers -- Freestanding electric wine coolers/ - - - chillers Home laundry appliances 22.4 34.2 335.6 - Built-in home laundry appliances - - - - Freestanding home laundry appliances 22.4 34.2 335.6 - Automatic washing machines 22.4 34.2 335.6 -- Built-in automatic washing machines - - - -- Freestanding automatic washing 22.4 34.2 335.6

Domestic electrical appliances Vietnam

Euromonitor International Page 13

machines - Automatic washer dryers - - - -- Built-in washer dryers - - - -- Freestanding washer dryers - - - - Automatic tumble dryers - - - -- Built-in tumble dryers - - - -- Freestanding tumble dryers - - - - Other home laundry appliances - - - -- Other built-in home laundry - - - appliances -- Other freestanding home laundry - - - appliances Dishwashers - - - - Built-in dishwashers - - - - Freestanding dishwashers - - - Large cooking appliances 18.4 14.2 94.4 - Built-in large cooking appliances - - - - Freestanding large cooking appliances 18.4 14.2 94.4 - Cookers 19.3 15.2 103.2 - Range cookers - - - - Ovens - - - - Hobs 13.1 9.2 55.6 -- Built-in hobs - - - -- Freestanding hobs 13.1 9.2 55.6 - Cooker hoods - - - -- Built-in cooker hoods - - - -- Freestanding cooker hoods - - - Microwaves 14.1 17.9 128.1 - Built-in microwaves - - - - Freestanding microwaves 14.1 17.9 128.1 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

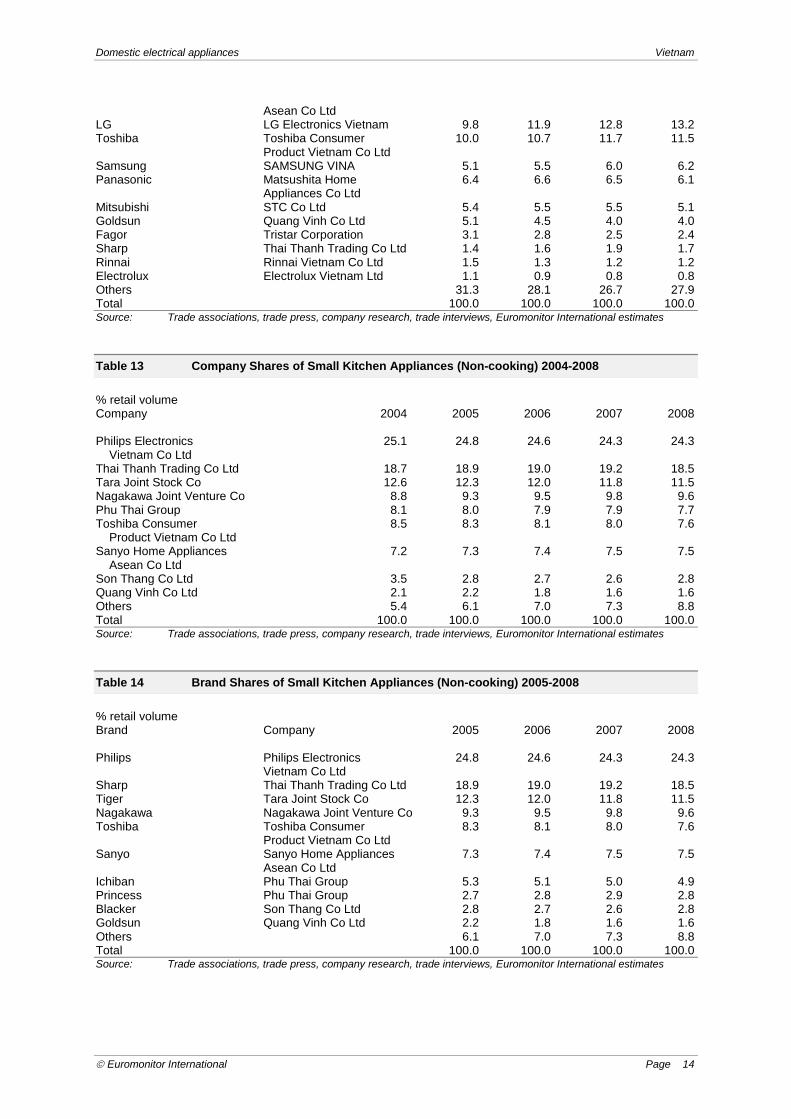

Euromonitor International estimates Table 11 Company Shares of Large Kitchen Appliances 2004-2008 % retail volume Company 2004 2005 2006 2007 2008 Sanyo Home Appliances 18.8 19.9 20.5 20.5 20.0 Asean Co Ltd LG Electronics Vietnam 7.8 9.8 11.9 12.8 13.2 Toshiba Consumer 9.4 10.0 10.7 11.7 11.5 Product Vietnam Co Ltd SAMSUNG VINA 4.3 5.1 5.5 6.0 6.2 Matsushita Home 6.2 6.4 6.6 6.5 6.1 Appliances Co Ltd STC Co Ltd 5.1 5.4 5.5 5.5 5.1 Quang Vinh Co Ltd 6.2 5.1 4.5 4.0 4.0 Tristar Corporation 3.7 3.1 2.8 2.5 2.4 Thai Thanh Trading Co Ltd 1.1 1.4 1.6 1.9 1.7 Rinnai Vietnam Co Ltd 1.9 1.5 1.3 1.2 1.2 Electrolux Vietnam Ltd 1.4 1.1 0.9 0.8 0.8 Others 34.1 31.3 28.1 26.7 27.9 Total 100.0 100.0 100.0 100.0 100.0 Source: Trade associations, trade press, company research, trade interviews, Euromonitor International estimates Table 12 Brand Shares of Large Kitchen Appliances 2005-2008 % retail volume Brand Company 2005 2006 2007 2008 Sanyo Sanyo Home Appliances 19.9 20.5 20.5 20.0

Domestic electrical appliances Vietnam

Euromonitor International Page 14

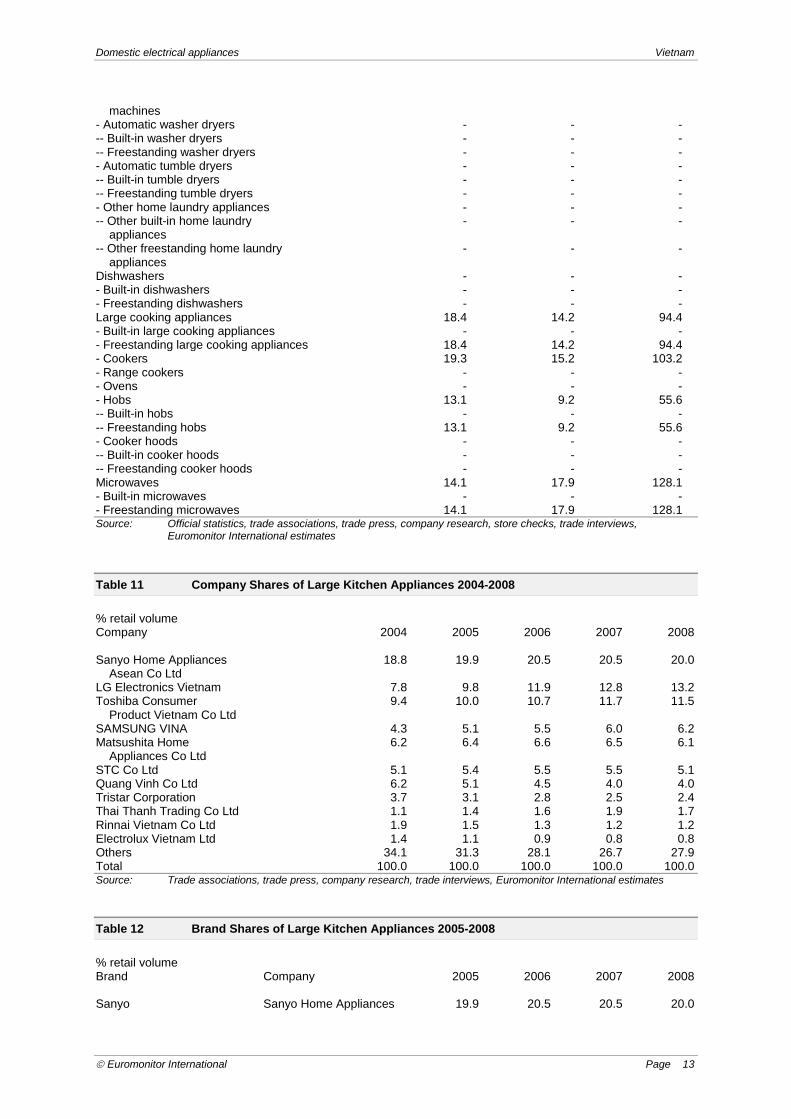

Asean Co Ltd LG LG Electronics Vietnam 9.8 11.9 12.8 13.2 Toshiba Toshiba Consumer 10.0 10.7 11.7 11.5 Product Vietnam Co Ltd Samsung SAMSUNG VINA 5.1 5.5 6.0 6.2 Panasonic Matsushita Home 6.4 6.6 6.5 6.1 Appliances Co Ltd Mitsubishi STC Co Ltd 5.4 5.5 5.5 5.1 Goldsun Quang Vinh Co Ltd 5.1 4.5 4.0 4.0 Fagor Tristar Corporation 3.1 2.8 2.5 2.4 Sharp Thai Thanh Trading Co Ltd 1.4 1.6 1.9 1.7 Rinnai Rinnai Vietnam Co Ltd 1.5 1.3 1.2 1.2 Electrolux Electrolux Vietnam Ltd 1.1 0.9 0.8 0.8 Others 31.3 28.1 26.7 27.9 Total 100.0 100.0 100.0 100.0 Source: Trade associations, trade press, company research, trade interviews, Euromonitor International estimates Table 13 Company Shares of Small Kitchen Appliances (Non-cooking) 2004-2008 % retail volume Company 2004 2005 2006 2007 2008 Philips Electronics 25.1 24.8 24.6 24.3 24.3 Vietnam Co Ltd Thai Thanh Trading Co Ltd 18.7 18.9 19.0 19.2 18.5 Tara Joint Stock Co 12.6 12.3 12.0 11.8 11.5 Nagakawa Joint Venture Co 8.8 9.3 9.5 9.8 9.6 Phu Thai Group 8.1 8.0 7.9 7.9 7.7 Toshiba Consumer 8.5 8.3 8.1 8.0 7.6 Product Vietnam Co Ltd Sanyo Home Appliances 7.2 7.3 7.4 7.5 7.5 Asean Co Ltd Son Thang Co Ltd 3.5 2.8 2.7 2.6 2.8 Quang Vinh Co Ltd 2.1 2.2 1.8 1.6 1.6 Others 5.4 6.1 7.0 7.3 8.8 Total 100.0 100.0 100.0 100.0 100.0 Source: Trade associations, trade press, company research, trade interviews, Euromonitor International estimates Table 14 Brand Shares of Small Kitchen Appliances (Non-cooking) 2005-2008 % retail volume Brand Company 2005 2006 2007 2008 Philips Philips Electronics 24.8 24.6 24.3 24.3 Vietnam Co Ltd Sharp Thai Thanh Trading Co Ltd 18.9 19.0 19.2 18.5 Tiger Tara Joint Stock Co 12.3 12.0 11.8 11.5 Nagakawa Nagakawa Joint Venture Co 9.3 9.5 9.8 9.6 Toshiba Toshiba Consumer 8.3 8.1 8.0 7.6 Product Vietnam Co Ltd Sanyo Sanyo Home Appliances 7.3 7.4 7.5 7.5 Asean Co Ltd Ichiban Phu Thai Group 5.3 5.1 5.0 4.9 Princess Phu Thai Group 2.7 2.8 2.9 2.8 Blacker Son Thang Co Ltd 2.8 2.7 2.6 2.8 Goldsun Quang Vinh Co Ltd 2.2 1.8 1.6 1.6 Others 6.1 7.0 7.3 8.8 Total 100.0 100.0 100.0 100.0 Source: Trade associations, trade press, company research, trade interviews, Euromonitor International estimates

Domestic electrical appliances Vietnam

Euromonitor International Page 15

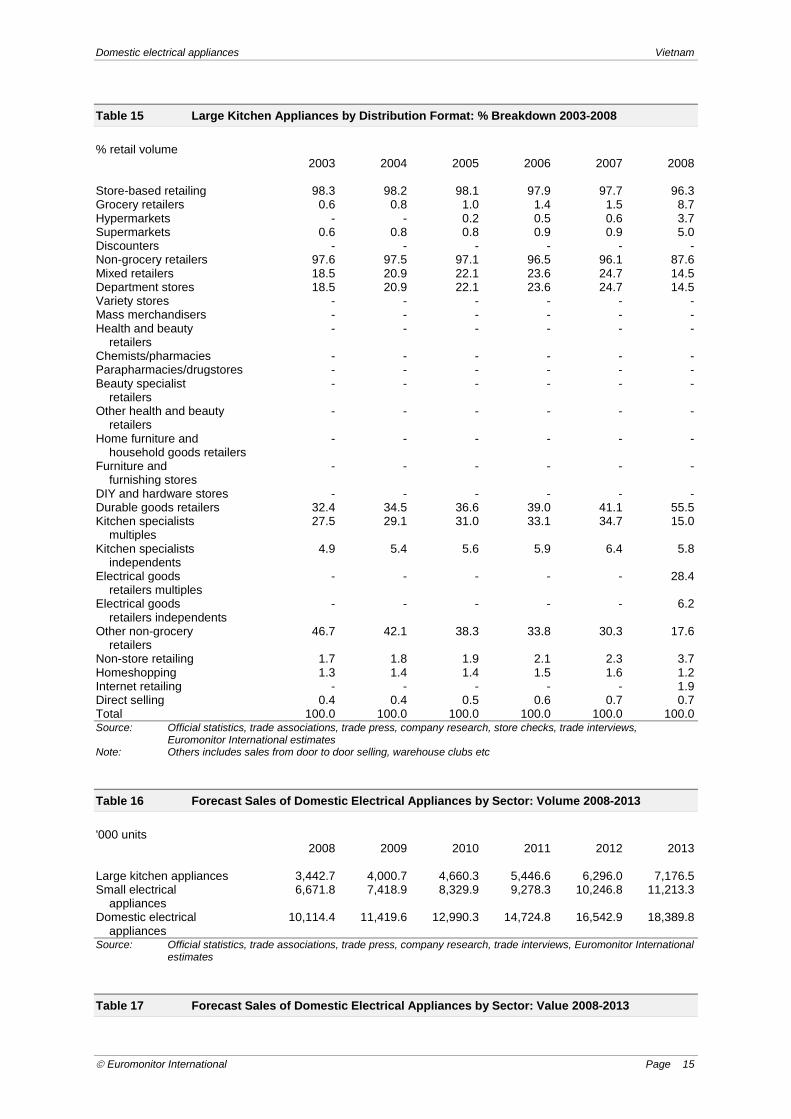

Table 15 Large Kitchen Appliances by Distribution Format: % Breakdown 2003-2008 % retail volume 2003 2004 2005 2006 2007 2008 Store-based retailing 98.3 98.2 98.1 97.9 97.7 96.3 Grocery retailers 0.6 0.8 1.0 1.4 1.5 8.7 Hypermarkets - - 0.2 0.5 0.6 3.7 Supermarkets 0.6 0.8 0.8 0.9 0.9 5.0 Discounters - - - - - - Non-grocery retailers 97.6 97.5 97.1 96.5 96.1 87.6 Mixed retailers 18.5 20.9 22.1 23.6 24.7 14.5 Department stores 18.5 20.9 22.1 23.6 24.7 14.5 Variety stores - - - - - - Mass merchandisers - - - - - - Health and beauty - - - - - - retailers Chemists/pharmacies - - - - - - Parapharmacies/drugstores - - - - - - Beauty specialist - - - - - - retailers Other health and beauty - - - - - - retailers Home furniture and - - - - - - household goods retailers Furniture and - - - - - - furnishing stores DIY and hardware stores - - - - - - Durable goods retailers 32.4 34.5 36.6 39.0 41.1 55.5 Kitchen specialists 27.5 29.1 31.0 33.1 34.7 15.0 multiples Kitchen specialists 4.9 5.4 5.6 5.9 6.4 5.8 independents Electrical goods - - - - - 28.4 retailers multiples Electrical goods - - - - - 6.2 retailers independents Other non-grocery 46.7 42.1 38.3 33.8 30.3 17.6 retailers Non-store retailing 1.7 1.8 1.9 2.1 2.3 3.7 Homeshopping 1.3 1.4 1.4 1.5 1.6 1.2 Internet retailing - - - - - 1.9 Direct selling 0.4 0.4 0.5 0.6 0.7 0.7 Total 100.0 100.0 100.0 100.0 100.0 100.0 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Note: Others includes sales from door to door selling, warehouse clubs etc Table 16 Forecast Sales of Domestic Electrical Appliances by Sector: Volume 2008-2013 '000 units 2008 2009 2010 2011 2012 2013 Large kitchen appliances 3,442.7 4,000.7 4,660.3 5,446.6 6,296.0 7,176.5 Small electrical 6,671.8 7,418.9 8,329.9 9,278.3 10,246.8 11,213.3 appliances Domestic electrical 10,114.4 11,419.6 12,990.3 14,724.8 16,542.9 18,389.8 appliances Source: Official statistics, trade associations, trade press, company research, trade interviews, Euromonitor International

estimates Table 17 Forecast Sales of Domestic Electrical Appliances by Sector: Value 2008-2013

Domestic electrical appliances Vietnam

Euromonitor International Page 16

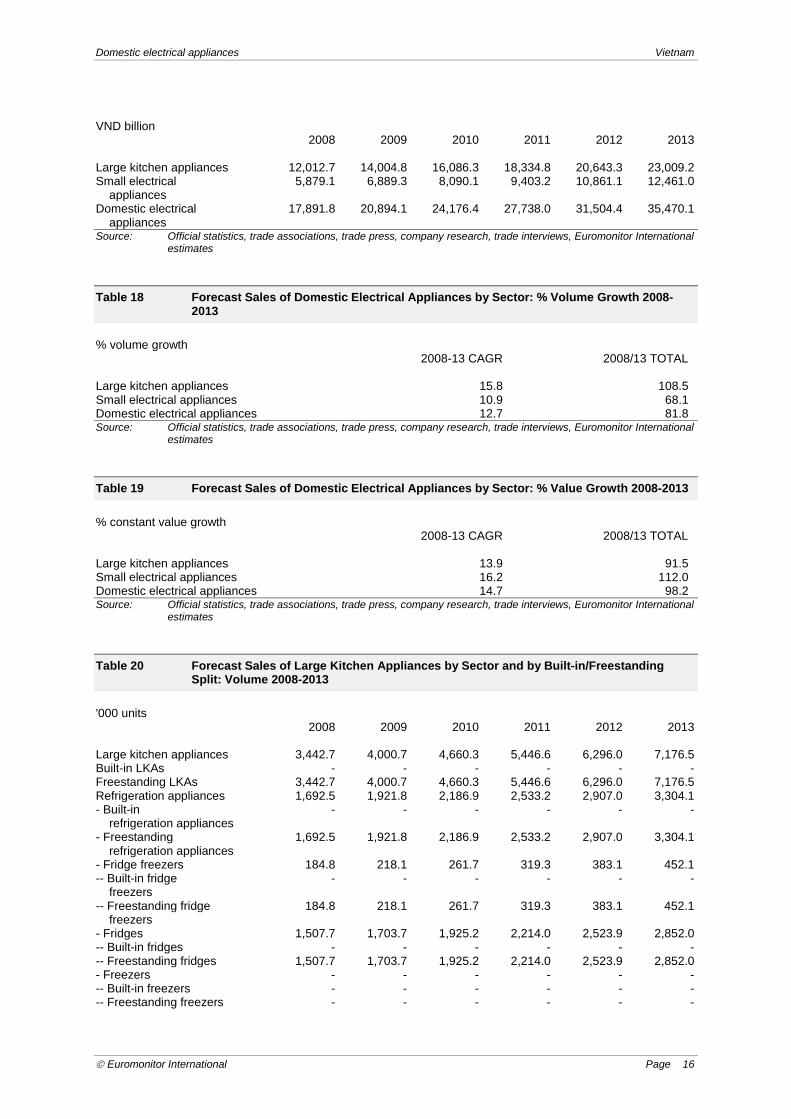

VND billion 2008 2009 2010 2011 2012 2013 Large kitchen appliances 12,012.7 14,004.8 16,086.3 18,334.8 20,643.3 23,009.2 Small electrical 5,879.1 6,889.3 8,090.1 9,403.2 10,861.1 12,461.0 appliances Domestic electrical 17,891.8 20,894.1 24,176.4 27,738.0 31,504.4 35,470.1 appliances Source: Official statistics, trade associations, trade press, company research, trade interviews, Euromonitor International

estimates Table 18 Forecast Sales of Domestic Electrical Appliances by Sector: % Volume Growth 2008-

2013 % volume growth 2008-13 CAGR 2008/13 TOTAL Large kitchen appliances 15.8 108.5 Small electrical appliances 10.9 68.1 Domestic electrical appliances 12.7 81.8 Source: Official statistics, trade associations, trade press, company research, trade interviews, Euromonitor International

estimates Table 19 Forecast Sales of Domestic Electrical Appliances by Sector: % Value Growth 2008-2013 % constant value growth 2008-13 CAGR 2008/13 TOTAL Large kitchen appliances 13.9 91.5 Small electrical appliances 16.2 112.0 Domestic electrical appliances 14.7 98.2 Source: Official statistics, trade associations, trade press, company research, trade interviews, Euromonitor International

estimates Table 20 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: Volume 2008-2013 '000 units 2008 2009 2010 2011 2012 2013 Large kitchen appliances 3,442.7 4,000.7 4,660.3 5,446.6 6,296.0 7,176.5 Built-in LKAs - - - - - - Freestanding LKAs 3,442.7 4,000.7 4,660.3 5,446.6 6,296.0 7,176.5 Refrigeration appliances 1,692.5 1,921.8 2,186.9 2,533.2 2,907.0 3,304.1 - Built-in - - - - - - refrigeration appliances - Freestanding 1,692.5 1,921.8 2,186.9 2,533.2 2,907.0 3,304.1 refrigeration appliances - Fridge freezers 184.8 218.1 261.7 319.3 383.1 452.1 -- Built-in fridge - - - - - - freezers -- Freestanding fridge 184.8 218.1 261.7 319.3 383.1 452.1 freezers - Fridges 1,507.7 1,703.7 1,925.2 2,214.0 2,523.9 2,852.0 -- Built-in fridges - - - - - - -- Freestanding fridges 1,507.7 1,703.7 1,925.2 2,214.0 2,523.9 2,852.0 - Freezers - - - - - - -- Built-in freezers - - - - - - -- Freestanding freezers - - - - - -

Domestic electrical appliances Vietnam

Euromonitor International Page 17

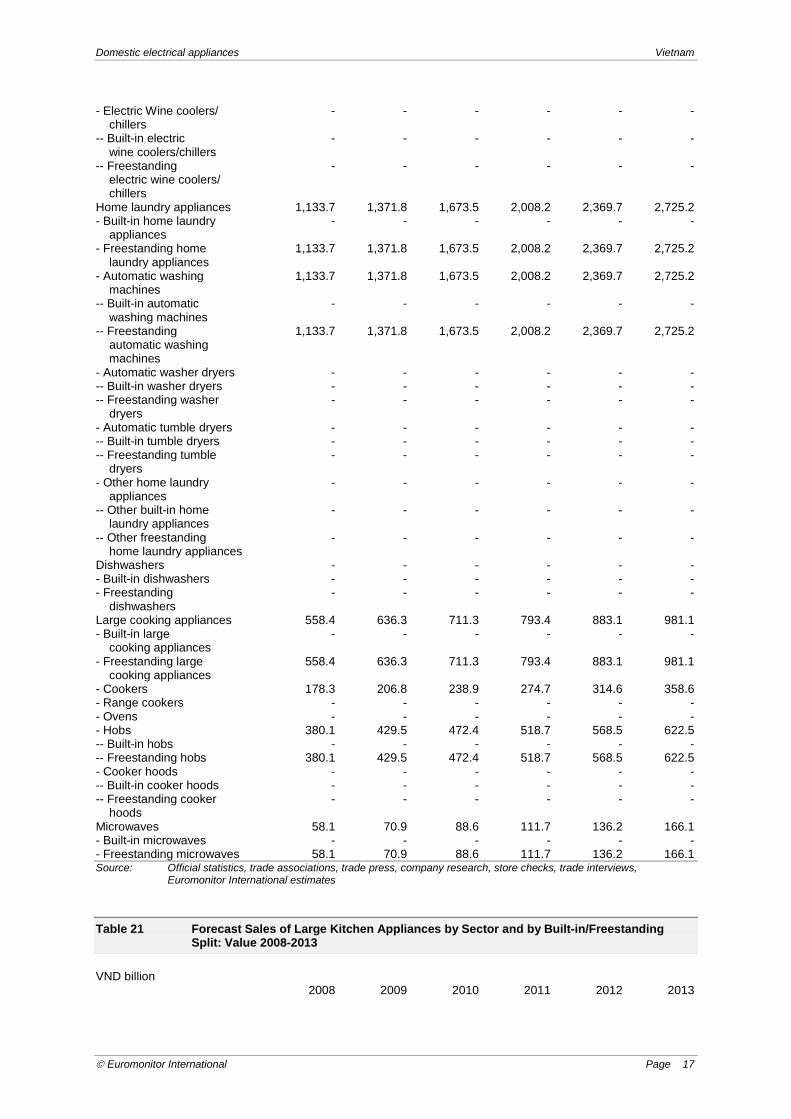

- Electric Wine coolers/ - - - - - - chillers -- Built-in electric - - - - - - wine coolers/chillers -- Freestanding - - - - - - electric wine coolers/ chillers Home laundry appliances 1,133.7 1,371.8 1,673.5 2,008.2 2,369.7 2,725.2 - Built-in home laundry - - - - - - appliances - Freestanding home 1,133.7 1,371.8 1,673.5 2,008.2 2,369.7 2,725.2 laundry appliances - Automatic washing 1,133.7 1,371.8 1,673.5 2,008.2 2,369.7 2,725.2 machines -- Built-in automatic - - - - - - washing machines -- Freestanding 1,133.7 1,371.8 1,673.5 2,008.2 2,369.7 2,725.2 automatic washing machines - Automatic washer dryers - - - - - - -- Built-in washer dryers - - - - - - -- Freestanding washer - - - - - - dryers - Automatic tumble dryers - - - - - - -- Built-in tumble dryers - - - - - - -- Freestanding tumble - - - - - - dryers - Other home laundry - - - - - - appliances -- Other built-in home - - - - - - laundry appliances -- Other freestanding - - - - - - home laundry appliances Dishwashers - - - - - - - Built-in dishwashers - - - - - - - Freestanding - - - - - - dishwashers Large cooking appliances 558.4 636.3 711.3 793.4 883.1 981.1 - Built-in large - - - - - - cooking appliances - Freestanding large 558.4 636.3 711.3 793.4 883.1 981.1 cooking appliances - Cookers 178.3 206.8 238.9 274.7 314.6 358.6 - Range cookers - - - - - - - Ovens - - - - - - - Hobs 380.1 429.5 472.4 518.7 568.5 622.5 -- Built-in hobs - - - - - - -- Freestanding hobs 380.1 429.5 472.4 518.7 568.5 622.5 - Cooker hoods - - - - - - -- Built-in cooker hoods - - - - - - -- Freestanding cooker - - - - - - hoods Microwaves 58.1 70.9 88.6 111.7 136.2 166.1 - Built-in microwaves - - - - - - - Freestanding microwaves 58.1 70.9 88.6 111.7 136.2 166.1 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 21 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: Value 2008-2013 VND billion 2008 2009 2010 2011 2012 2013

Domestic electrical appliances Vietnam

Euromonitor International Page 18

Large kitchen appliances 12,012.7 14,004.8 16,086.3 18,334.8 20,643.3 23,009.2 Built-in LKAs - - - - - - Freestanding LKAs 12,012.7 14,004.8 16,086.3 18,334.8 20,643.3 23,009.2 Refrigeration appliances 5,663.4 6,529.1 7,397.7 8,413.9 9,376.5 10,394.4 - Built-in - - - - - - refrigeration appliances - Freestanding 5,663.4 6,529.1 7,397.7 8,413.9 9,376.5 10,394.4 refrigeration appliances - Fridge freezers 1,238.2 1,478.6 1,747.8 2,078.9 2,407.4 2,755.5 -- Built-in fridge - - - - - - freezers -- Freestanding fridge 1,238.2 1,478.6 1,747.8 2,078.9 2,407.4 2,755.5 freezers - Fridges 4,425.2 5,050.4 5,649.9 6,335.0 6,969.1 7,638.8 -- Built-in fridges - - - - - - -- Freestanding fridges 4,425.2 5,050.4 5,649.9 6,335.0 6,969.1 7,638.8 - Freezers - - - - - - -- Built-in freezers - - - - - - -- Freestanding freezers - - - - - - - Electric Wine coolers/ - - - - - - chillers -- Built-in electric - - - - - - wine coolers/chillers -- Freestanding - - - - - - electric wine coolers/ chillers Home laundry appliances 3,980.3 4,710.3 5,574.2 6,421.4 7,350.0 8,241.2 - Built-in home laundry - - - - - - appliances - Freestanding home 3,980.3 4,710.3 5,574.2 6,421.4 7,350.0 8,241.2 laundry appliances - Automatic washing 3,980.3 4,710.3 5,574.2 6,421.4 7,350.0 8,241.2 machines -- Built-in automatic - - - - - - washing machines -- Freestanding 3,980.3 4,710.3 5,574.2 6,421.4 7,350.0 8,241.2 automatic washing machines - Automatic washer dryers - - - - - - -- Built-in washer dryers - - - - - - -- Freestanding washer - - - - - - dryers - Automatic tumble dryers - - - - - - -- Built-in tumble dryers - - - - - - -- Freestanding tumble - - - - - - dryers - Other home laundry - - - - - - appliances -- Other built-in home - - - - - - laundry appliances -- Other freestanding - - - - - - home laundry appliances Dishwashers - - - - - - - Built-in dishwashers - - - - - - - Freestanding - - - - - - dishwashers Large cooking appliances 2,232.8 2,606.7 2,925.9 3,273.2 3,649.1 4,053.6 - Built-in large - - - - - - cooking appliances - Freestanding large 2,232.8 2,606.7 2,925.9 3,273.2 3,649.1 4,053.6 cooking appliances - Cookers 1,901.2 2,227.4 2,521.2 2,841.4 3,188.3 3,562.0 - Range cookers - - - - - - - Ovens - - - - - - - Hobs 331.7 379.3 404.7 431.8 460.7 491.6 -- Built-in hobs - - - - - -

Domestic electrical appliances Vietnam

Euromonitor International Page 19

-- Freestanding hobs 331.7 379.3 404.7 431.8 460.7 491.6 - Cooker hoods - - - - - - -- Built-in cooker hoods - - - - - - -- Freestanding cooker - - - - - - hoods Microwaves 136.1 158.7 188.5 226.3 267.8 320.0 - Built-in microwaves - - - - - - - Freestanding microwaves 136.1 158.7 188.5 226.3 267.8 320.0 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

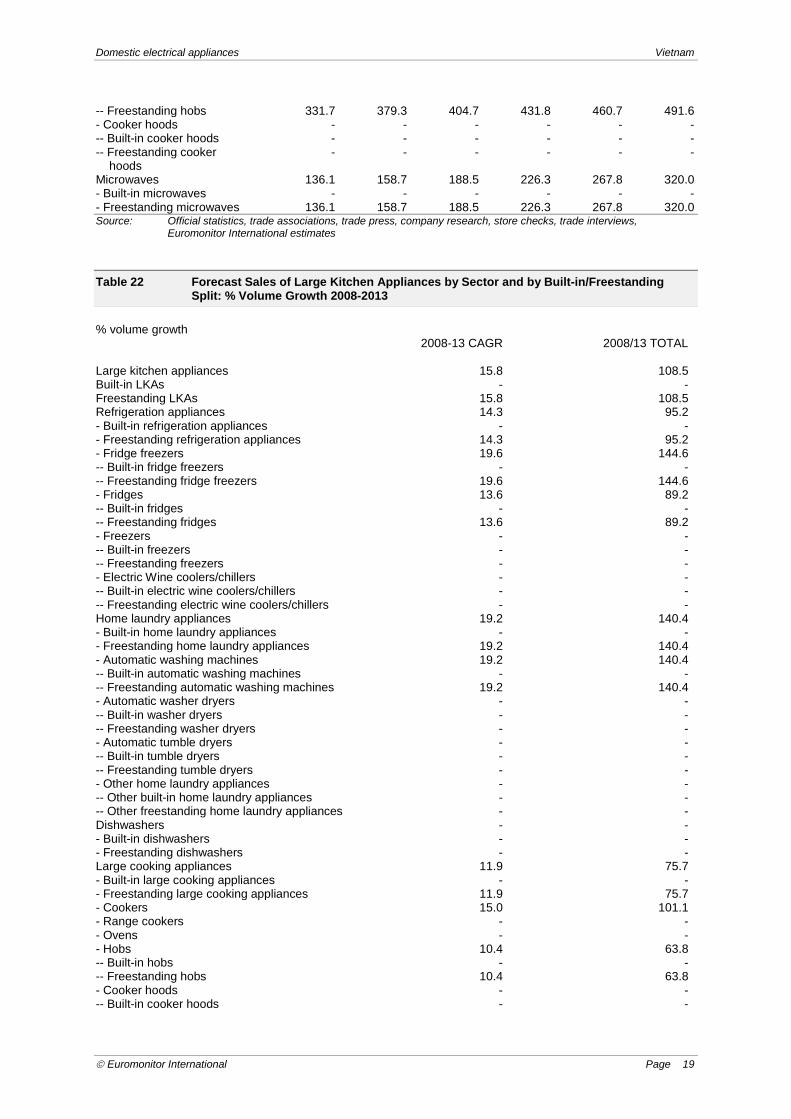

Euromonitor International estimates Table 22 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: % Volume Growth 2008-2013 % volume growth 2008-13 CAGR 2008/13 TOTAL Large kitchen appliances 15.8 108.5 Built-in LKAs - - Freestanding LKAs 15.8 108.5 Refrigeration appliances 14.3 95.2 - Built-in refrigeration appliances - - - Freestanding refrigeration appliances 14.3 95.2 - Fridge freezers 19.6 144.6 -- Built-in fridge freezers - - -- Freestanding fridge freezers 19.6 144.6 - Fridges 13.6 89.2 -- Built-in fridges - - -- Freestanding fridges 13.6 89.2 - Freezers - - -- Built-in freezers - - -- Freestanding freezers - - - Electric Wine coolers/chillers - - -- Built-in electric wine coolers/chillers - - -- Freestanding electric wine coolers/chillers - - Home laundry appliances 19.2 140.4 - Built-in home laundry appliances - - - Freestanding home laundry appliances 19.2 140.4 - Automatic washing machines 19.2 140.4 -- Built-in automatic washing machines - - -- Freestanding automatic washing machines 19.2 140.4 - Automatic washer dryers - - -- Built-in washer dryers - - -- Freestanding washer dryers - - - Automatic tumble dryers - - -- Built-in tumble dryers - - -- Freestanding tumble dryers - - - Other home laundry appliances - - -- Other built-in home laundry appliances - - -- Other freestanding home laundry appliances - - Dishwashers - - - Built-in dishwashers - - - Freestanding dishwashers - - Large cooking appliances 11.9 75.7 - Built-in large cooking appliances - - - Freestanding large cooking appliances 11.9 75.7 - Cookers 15.0 101.1 - Range cookers - - - Ovens - - - Hobs 10.4 63.8 -- Built-in hobs - - -- Freestanding hobs 10.4 63.8 - Cooker hoods - - -- Built-in cooker hoods - -

Domestic electrical appliances Vietnam

Euromonitor International Page 20

-- Freestanding cooker hoods - - Microwaves 23.4 185.9 - Built-in microwaves - - - Freestanding microwaves 23.4 185.9 Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews,

Euromonitor International estimates Table 23 Forecast Sales of Large Kitchen Appliances by Sector and by Built-in/Freestanding

Split: % Value Growth 2008-2013 % constant value growth 2008-13 CAGR 2008/13 TOTAL Large kitchen appliances 13.9 91.5 Built-in LKAs - - Freestanding LKAs 13.9 91.5 Refrigeration appliances 12.9 83.5 - Built-in refrigeration appliances - - - Freestanding refrigeration appliances 12.9 83.5 - Fridge freezers 17.3 122.5 -- Built-in fridge freezers - - -- Freestanding fridge freezers 17.3 122.5 - Fridges 11.5 72.6 -- Built-in fridges - - -- Freestanding fridges 11.5 72.6 - Freezers - - -- Built-in freezers - - -- Freestanding freezers - - - Electric Wine coolers/chillers - - -- Built-in electric wine coolers/chillers - - -- Freestanding electric wine coolers/chillers - - Home laundry appliances 15.7 107.0 - Built-in home laundry appliances - - - Freestanding home laundry appliances 15.7 107.0 - Automatic washing machines 15.7 107.0 -- Built-in automatic washing machines - - -- Freestanding automatic washing machines 15.7 107.0 - Automatic washer dryers - - -- Built-in washer dryers - - -- Freestanding washer dryers - - - Automatic tumble dryers - - -- Built-in tumble dryers - - -- Freestanding tumble dryers - - - Other home laundry appliances - - -- Other built-in home laundry appliances - - -- Other freestanding home laundry appliances - - Dishwashers - - - Built-in dishwashers - - - Freestanding dishwashers - - Large cooking appliances 12.7 81.5 - Built-in large cooking appliances - - - Freestanding large cooking appliances 12.7 81.5 - Cookers 13.4 87.4 - Range cookers - - - Ovens - - - Hobs 8.2 48.2 -- Built-in hobs - - -- Freestanding hobs 8.2 48.2 - Cooker hoods - - -- Built-in cooker hoods - - -- Freestanding cooker hoods - - Microwaves 18.6 135.1 - Built-in microwaves - - - Freestanding microwaves 18.6 135.1

Domestic electrical appliances Vietnam

Euromonitor International Page 21

Source: Official statistics, trade associations, trade press, company research, store checks, trade interviews, Euromonitor International estimates

DEFINITIONS This report analyses the market for Domestic Electrical Appliances in Vietnam. For the purposes of the study, the market has been defined as follows:

• Refrigeration appliances

• Home laundry appliances

• Dishwashers

• Large cooking appliances

• Microwaves

• Food preparation appliances

• Small cooking appliances

• Small kitchen appliances (Non-cooking)

• Vacuum cleaners

• Irons

• Personal care appliances

• Heating

• Air treatment The market is measured in terms of retail sales. Retail sales of domestic electrical appliances include both replacement sales and new sales, ie repurchases of the same product and first-time buyer sales. Retail sales also include sales of fitted appliances through fitted kitchen sales and sales to the building industry for installation in new housing units. Sales to industrial and foodservice users are excluded, in addition to second-hand sales. Sector and subsector definitions Refrigeration appliances The refrigeration appliances sector includes freestanding, upright refrigerators, table top refrigerators and built-in refrigerators, which can be frost free or standard. The subsector breakdown is as follows:

• Fridge freezers: usually 2- or 3-door appliances with separate units for refrigeration and freezing operations

• Fridges: standard fridges and larder fridges, which come with or without a small icebox

• Freezers: separate freezers Breakdowns are given for built-in and freestanding appliances by subsector. Additional product sub-subsectorisation is provided for:

• Fridge freezers by double door freezer bottom/double door freezer top/side by side

• Fridges by upright/tables top/compact

• Freezers by upright/table top/chest split A further subsector breakdown is provided where available, eg static/frost free split for fridge freezers and fridges.

Domestic electrical appliances Vietnam

Euromonitor International Page 22

Home laundry appliances The home laundry appliances sector includes freestanding and built-in units. The breakdown between built-in and freestanding is provided at overall sector level. The subsector breakdown is as follows:

• Automatic washing machines: automatic washing machines are pre-programmable and incorporate a spin-dryer

• Automatic washer dryers: washer dryers combine both washing machine and tumble dryer functions

• Automatic tumble dryers: automatic tumble dryers use the action of a rotating drum and heat to dry the laundry

• Others: includes spin-dryers (spin-dryers are cylindrical with top loading), twin tubs etc Additional product sub-subsectorisation is provided for:

• Automatic washing machines: by front loading/top loading split A further subsector breakdown is provided where available, eg washing machines by pulsator/agitator/tumble split. Dishwashers The dishwashers sector includes both freestanding, portable and built-in units. The breakdown between built-in and freestanding is provided at overall sector level. A further subsector breakdown is provided where available, eg built-in dishwashers by semi-integrated/fully integrated split. Large cooking appliances The large cooking appliances sector includes gas or electric, freestanding or built-in cookers, ovens, hobs and cooker hoods. The subsector breakdown is as follows:

• Cookers: Western-style cookers are normally floor-standing appliances with oven, grill and hot plate facilities

• Ovens: usually double ovens with two cavities, some circulate heat with a fan, ie a fan oven

• Hobs: a hotplate with four areas for heating saucepans and other vessels, sold as a separate item not attached to a cooker

• Cooker hoods: includes canopy, standard, integrated, telescopic and chimney hoods; includes vents Breakdowns are given for built-in and freestanding appliances by subsector. Additional product sub-subsectorisation is provided for:

• Cookers by gas/electric split

• Ovens by standard/multifunction split

• Hobs by gas/standard electric/mixed/vitroceramic/induction split A further subsector breakdown is provided where available, eg ovens by single oven/double oven split. Microwaves The microwaves sector encompasses standard microwaves, combination microwaves (combines full microwave and conventional oven facilities) and microwave grills (with radiant grill function). Food preparation appliances

Domestic electrical appliances Vietnam

Euromonitor International Page 23

Food preparation appliances include food processors, table top blenders and mixers and hand-held blenders and mixers and other food preparation appliances including items, such as liquidisers, smoothie makers and juicers. Small cooking appliances Small cooking appliances cover coffee machines, toasters, deep-fat fryers and table top steamers, and other small cooking appliances including items, such as raclettes, fondue appliances, waffles irons, electrical woks and slow cookers. Small kitchen appliances Other small kitchen appliances include kettles and others including electric coffee mills, can openers, knife sharpeners and food slicers. Vacuum cleaners Vacuum cleaners break down into the following subsectors:

• Upright

• Cylinder

• Wet and dry

• Hand-held Irons The irons sector encompasses the following subsectors:

• Steam

• Dry

• Travel

• Steam generator Personal care appliances

• Hair care appliances: includes hairdryers, hair styling appliances, and hair and beard trimmers. A further subsector breakdown is provided where available.

• Body shavers: includes men's shavers, women's shavers and depilators. A further subsector breakdown is provided where available.

• Oral hygiene appliances: electric toothbrushes, and others, such as electric plaque removers.

• Other personal care appliances: includes waxers, facial saunas, facial solarium, food spa, facial massagers and body toners.

Air treatment The air treatment appliance sector encompasses the following subsectors:

• Air conditioners, which is split into room air conditioners and mini splits

• Cooling fans, which is split into desk and standing fans

• Ceiling fans

• Dehumidifirs

• Humidifiers

• Air coolers

Domestic electrical appliances Vietnam

Euromonitor International Page 24

• Air purifiers Heating appliances The heating and cooling appliances sector encompasses the following subsectors:

• Oil filled radiator

• Electric fires

• Convector heaters

• Panel heaters

• Fan heaters

• Electric blankets

• Other heating appliances Distribution definitions

• Specialist multiples: or chains that specialise in electrical household appliances. A chain is defined by operating 10 or more outlets.

• Specialist independents: independent retailers specialising in the sale of domestic electrical appliances. Independents are defined by operating less than 10 outlets.

• Kitchen specialists: sell built-in appliances and specialise in building industry sales for installation in housing units.

• Grocery multiples: include hypermarkets, supermarkets, and voluntary chains that sell a variety of food and non-food products.

• Department/variety stores: sell mainly non-food merchandise and at least five lines in different departments. They are usually arranged over several floors. Variety stores are usually located on one floor and offer a limited assortment of fast-moving goods on a self-service basis.

• DIY sheds: large retail outlets specialising in the sale of products for the purposes of home maintenance, improvement, modernisation and new construction.

• Catalogue showrooms: products are viewed in a catalogue and purchases are ordered in the showroom.

• Mail order: the purchase of goods through the postal system, either in direct response to an advertisement or mail item, or via a catalogue.

• The internet: the purchase of goods over the internet.

• Other: includes sales from door-to-door selling; mass merchandisers, warehouse clubs etc. Units of measurement

• Market volume is measured in terms of the number of units sold through retail outlets.

• Market value is measured at current retail prices in local currency, ie the market value is measured in terms of the actual spending by consumers in retail outlets.

• Brand and market shares are based on retail volume sales.

• Retail distribution is measured in volume sales through retail outlets. Sources used during research include the following: Summary 1 Research Sources

Official Sources National Statistics Office

Trade Press Appliance Magazine

Domestic electrical appliances Vietnam

Euromonitor International Page 25

VNA Source: Euromonitor International