Sara Lee by Mark Susor

24

Sara Lee 1 Running head: SARA LEE Sara Lee Mark D. Susor Strategic Management MBA 671-D5B4 Benedictine University June 8, 2014

Transcript of Sara Lee by Mark Susor

Sara Lee 1

Running head: SARA LEE

Sara Lee

Mark D. Susor

Strategic Management MBA 671-D5B4

Benedictine University

June 8, 2014

Sara Lee 2

Abstract

Sara Lee’s CEO (Chief Operating Officer) in 2000 decided to

narrow the focus of the global organization believing that the

company’ broad diversification and geographically scattered

operations had become too difficult to manage effectively.

Evidence of this was reflected by a flattening of the

organization’s revenues at the $20 billion level achieved during

1998 to 1999. The case discusses Sara Lee’s retrenchment

diversification strategy and it impact on the organization and

shareholders.

Sara Lee 3

Introduction

“The origins of Sara Lee Corporation date “back to 1939, when

Nathan Cummins acquired C.D. Kenny Company, a small wholesale

distributor of sugar, coffee, and tea that had net sales of $24

million. The purchase of Sprague, Warner & Company in 1942

prompted a name change to Sprague Warner-Kenny Corporation and a

shift in the headquarters location from Baltimore to Chicago; the

company’s shares began trading on the New York Stock Exchange in

1946” (Gamble, Peteraf, Strickland & Thompson, 2012, p. C-244).

In 1954, the company changed its name to Consolidate Foods

Corporation to emphasize the company’s diversified role in food

processing, packaging, and distribution. The company continued

to acquire numerous companies over the next 40 years and

eventually changed its name to the Sara Lee Corporation in 1985.

(Gamble et al, 2012, pp. C-244 – C-245).

What is Sara Lee's corporate strategy?

Sara Lee’s corporate strategy is to narrow its focus to a

“smaller number of global branded consumer packaged-goods

segments—Food and Beverage, Intimates and Underwear, and

Household Products” (Gamble et al, 2012, p. C-245). The idea

Sara Lee 4

behind the strategy was to “concentrate its financial and

managerial resources on a smaller number of business segments in

which market prospects were promising and Sara Lee’s brands were

well positioned” (Gamble et al, 2012, p. C-243). The company set

financial goals that stated that they would grow revenues to $14

billion by fiscal 2010 and would also improve operating profit

margin from 8.1 percent in 2004 to at least 12 percent by 2010.

(Gamble et al, 2012, p. C-243). Sara Lee planned to achieve

these financial objectives by developing three competitive

capabilities in its remaining business units. The first

capability is to develop “competitive pricing, innovative new

products, and brand-building capabilities” (Gamble et al, 2012,

p. C-250); all of which are essential to pleasing consumers. The

second capability is category management leveraged through size

to win accounts with supermarkets and discount store customers.

The third key element is operational excellence, which was

critical to competitive pricing. (Gamble et al, 2012, p. C-250).

How has its retrenchment strategy changed the nature of its business lineup?

The retrenchment strategy significantly changed the nature of

Sara Lee’s business lineup. The implementation of the strategy

Sara Lee 5

began in 2005 with the divestiture of weak-performing businesses

and product categories worth $7.2 billion in revenue or 37

percent of their annual revenue. The efforts focused on

divesting 8 business units which included: Direct Selling, US

(United States) Retail Coffee, European Apparel, European Nuts &

Snacks, European Rice, US Meat Snacks, European Meats, and Sara

Lee Branded Apparel. (Gamble et al, 2012, pp. C-246 – C-250).

Once the divestiture was complete the strategy was to drive

growth via initiatives to boost sales, market shares, and

profitability of the key remaining brands. These brands included

“Sara Lee breads, bakery products, Ball Park meats, Douwe Egberts

coffees, Hillshire Farm meats, Jimmy Dean sausage, and Senseo

single-serve coffee products” (Gamble et al, 2012, p. C-243).

In 2011, after Brenda Barnes, Sara Lee CEO, stepped down

after suffering a stroke in May 2010; her interim replacement,

Marcel Smits restated the organizations strategy by stating that

the company would focus on three areas: increasing share in the

company’s most powerful brands, pursuing attractive geographic

markets, and fully capturing the benefits of Project Accelerate.

Project Accelerate was a company-wide initiatives launched in

Sara Lee 6

2008 that focused on outsourcing, supply chain efficiencies, and

overhead reduction. The project had provided $180 million in

savings as of 2010 and was expected to provide $350 to $400

million in cumulative savings by the end of fiscal 2012. Gamble

et al, 2012, p. C-241).

What is your assessment of the long-term attractiveness of the

industries represented in Sara Lee Corp.'s business portfolio?

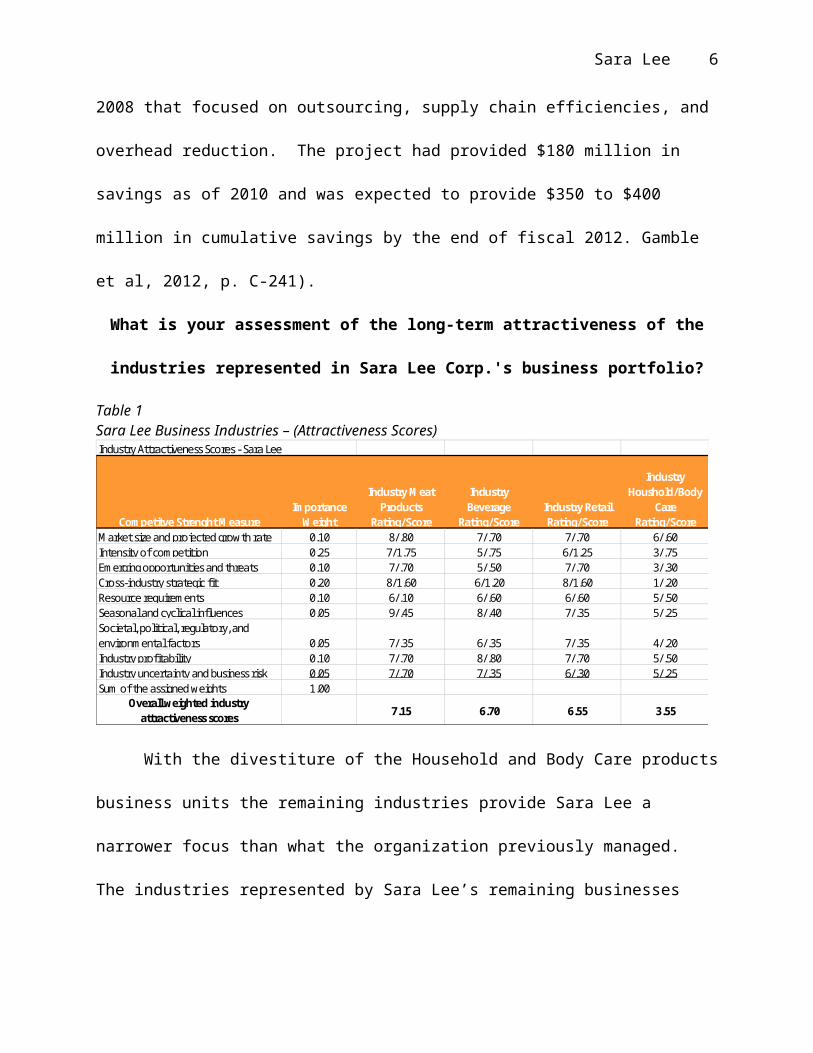

Table 1Sara Lee Business Industries – (Attractiveness Scores)Industry Attractiveness Scores - Sara Lee

M arket size and projected growth rate 0.10 8/.80 7/.70 7/.70 6/.60Intensity of competition 0.25 7/1.75 5/.75 6/1.25 3/.75Emerging opportunities and threats 0.10 7/.70 5/.50 7/.70 3/.30Cross-industry strategic fit 0.20 8/1.60 6/1.20 8/1.60 1/.20Resource requirements 0.10 6/.10 6/.60 6/.60 5/.50Seasonal and cyclical influences 0.05 9/.45 8/.40 7/.35 5/.25Societal, political, regulatory, and environm ental factors 0.05 7/.35 6/.35 7/.35 4/.20Industry profitability 0.10 7/.70 8/.80 7/.70 5/.50Industry uncertainty and business risk 0.05 7/.70 7/.35 6/.30 5/.25Sum of the assigned weights 1.00

Overall weighted industry attractiveness scores 7.15 6.70 6.55 3.55

Industry Houshold/Body

Care Rating/ScoreCom petitve Strenght M easure

Im portance W eight

Industry M eat Products

Rating/Score

Industry Beverage

Rating/ScoreIndustry Retail Rating/Score

With the divestiture of the Household and Body Care products

business units the remaining industries provide Sara Lee a

narrower focus than what the organization previously managed.

The industries represented by Sara Lee’s remaining businesses

Sara Lee 7

allow the management team to compete with products that are top

producers and maintain strong market share positions.

The meat products industry is providing Sara Lee the

opportunity to market higher margin and faster growth products

than that of its industry competitors. The industry is currently

providing Sara Lee operating profit margins of 12.3 percent as of

2010 and the company should be able to further improve its

margins when it opens a state-of-the art meat-slicing plant in

2011; enhancing its current competitive advantage.

In the beverage industry the global retail coffee market is

expecting strong growth, increasing from $51 billion in 2009 to

$62 billion in 2013; instant coffee from $19.6 billion to $23.6

billion; espresso from $4.3 billion to $9.9 billion, and single-

serve coffee pods from $2.9 to $5.3 billion. (Gamble et al, 2012,

p. C-255).

The Food service industry is a considerable growth

opportunity as Americans continue to eat a higher percentage of

meals away from home. This trend should continue as declines due

to recession impacts begin to fade. (Gamble et al, 2012, p. C-

254).

Sara Lee 8

What is your assessment of the competitive strength of Sara Lee

Corp.'s different business units?

After the divestiture of the 8 business units, Sara Lee

reorganized their businesses into six divisions. They included:

North American Retail division (lunch meats, breakfast sausage,

smoked sausage, frozen desserts, and single-serve coffee sold in

supermarkets and discount stores); North American Fresh Bakery

division (Breads, Buns, and Bagels sold in supermarkets); North

American Foodservice division (meat, bakery, coffee and tea sold

to food service accounts); International Beverage division

(coffee and tea products in Europe); International Bakery

division (baked goods in Europe); and the International Household

and Body Care division (insecticides, personal hygiene products,

cleaning brands sold outside the US).

Sara Lee 9

Table 2Sara Lee Business Units – (Competitive strength scores)Competitive Strenght Scores for Sara Lee's Business Units

Relative market share 0.15 8/1.05 9/1.20 8/1.05 8/1.05 4/.55 6/.75Cost's relative to competitor's costs 0.20 6/1.20 7/1.40 6/1.20 6/1.20 5/1.00 5/1.00Ability to m atch or beat rivals on key product attributes 0.05 6/.30 8/.40 7/.35 6/.30 6/.30 6/.30Ability to benefit from strategic fit with com pany's other businesses 0.20 7/1.40 9/1.80 9/1.80 7/1.40 6/1.20 0/.00Bargaining leverage with suppliers/buyers; caliber of alliances 0.05 10/.50 10/.50 10/.50 8/.40 4/.20 2/.10Brand image and reputation 0.10 8/.80 9/.90 9/.90 7/.70 6/.60 7/.70Competively valuable capabilities 0.15 7/1.05 7/1.05 7/1.05 6/.90 4/.60 4/.60Profitability relative to competitors 0.10 7/.70 7/.70 6/.60 7/.70 4/.40 5/.50Sum of the assigned weights 1.00Overall weighted com petive strength

scores 7.00 8.95 7.45 6.50 4.85 3.95

International Bakery

International Beverage

North Am erican Foodservice

International Household and Body CareCom petitve Strenght M easure

Im portance W eight

North Am erican Retail

North Am erican Fresh Bakery

The North American Retail business unit products are growing

faster than the industry and continues to show that consumers

prefer branded versus private-label brands. The businesses

market-leading brands maintained market shares that range from 14

in lunch meat to 55 percent in single-serve coffee. The division

operating profit margin improved from 9.2 percent in 2009 to 12.3

percent in 2010 and reflects the overall strength of this

business unit. (Gamble et al, 2012, p. C-251).

The North American Fresh Bakery division has shown very

strong growth increasing revenues from $91 million in 2003 to

$2.1 billion in 2008. The division owns 8.3 percent of the US

packaged bread market, highly rated brands, and considerable

Sara Lee 10

leverage with buyers and thereby the ability to exploit its

distribution channels. (Gamble et al, 2012, p. C-251).

North American Foodservice sells products to supermarkets,

food service distributors, and national restaurant chains. While

the business unit has been impacted by the recession it has been

able to maintain strong market positions in liquid coffee – 65

percent; pies – 52 percent; cakes – 19 percent; and refrigerated

dough sold to food service customers – 20 percent. The division

has also benefited from innovations developed by Sara lee’s

retail division that provide convenience for today’s busy

lifestyles. (Gamble et al, 2012, pp. C-254 to C- 255).

International Beverage also reflects considerable strength as

a Sara Lee business unit. The company’s coffee brands are highly

ranked in European and US markets. The retail coffee, instant

coffee, espresso and single-serve coffee pods market growth is

expected to remain extremely strong over the next 5 years. The

business unit’s single-serve coffee makers own 40 percent of the

European market and coffee pod sales had increased from 15,000

tons in 2004 to 28,000 tons in 2009. The business unit espresso

capsules also owned 27 percent of the Europe market in 2009.

Sara Lee 11

The International Bakery division which consisted of bread

products sold in primarily in Spain, France and Australia

accounted for 63 percent of the fresh bread sold in Spain and 12

percent of the division sales were its frozen bread product sold

in Australia. The division also generated 25 percent of its

sales from its refrigerated bread sold in France, and owned 37

percent of Spain’s packaged bread market. The division had

experienced sales declines and operating losses due to the long-

term economic recession in Spain. It had only limited success

expanding into other European countries because of the consumer’s

preference for fresh. Sara Lee was looking to turn the business

unit around by introducing new products and improving operating

efficiencies. (Gamble et al, 2012, p. C-255).

The following table provides a synopsis of the remaining

business unit’s sales an operating profit from 2008 to 2010:

Table 3Sara Lee Business Units – (Net Sales, Sales CAGR % 2008-2010, Operating Profits, Op. Profit CAGR % 2008-2010) ($ millions)

Sara Lee Corporation’s Business Units

Net Sales2008-2010

Net SalesCAGR %

2008-2010

Operating

Profits2008-2010

OperatingProfitsCAGR %

2008-2010

Sara Lee 12

North American Retail

$8,198 3.85% $748 52.39%

North American FreshBakery

North American Foodservice

$6,356

$6,151

2.44%

-7.44%

$125

-$163

-10.56%

*$224.50/Yr.

International Beverage

International Bakery

Total business segments

$9,521

$2,514

$32,624

-0.26%

-8.32%

0.11%

$1,636

-$554

$1,707

3.65%

*$166/Yr.

258.59%

*Due to negative values; utilized raw $ improvement per year.

Each of the remaining business units have shown steady sales

during the recession and all but North American Fresh bakery have

shown improvement in operating profit, with the strongest

operating profit improvement reflected by North American

Foodservice, followed by International Bakery and then North

American Retail.

What does a 9-cell industry attractiveness/business strength

matrix displaying Sara Lee's business units look like?

Table 4Sara Lee Industry attractiveness/business strength matrix

Sara Lee 13

High

M edium

Low

Industry A

rractiveness

Com petitive Strenght/M arket Position

Sara Lee 9-Cell Industry Attractiveness-Com petitive Strength M atrix

Strong Average W eak

N.A. Fresh Bakery

N.A. Foodservice

N.A. Retail

Intr'lBeverage

Intr'lBakery

Intr'lhousehold and Body Care

Does Sara Lee's portfolio exhibit good strategic fit?

Sara Lee’s portfolio exhibits a good strategic fit and it

improves with the announcement of the International Household &

Body Care divesture in 2010. The remaining portfolio of packaged

food, bakery, meat and beverage products offers numerous

opportunities to generate cost savings, cross-business transfer

Sara Lee 14

of skills, technology, or intellectual capital. There is also

the ability to transfer Sara Lee’s potent brand name to the

products offered by other business units.

What value-chain match-ups do you see?

With the corporations narrowed focus (Packaged food, meat,

bakery, and Beverage products) there are value-chain match-ups

that include opportunities to combine purchasing activities and

gain more leverage with suppliers and realize supply chain

economies. There is also the opportunity to share technology,

transfer technical skills, and combine R&D (Research &

Development. The remaining business units also offer the ability

to combine sales and marketing activities, use common

distribution channels, leverage the Sara Lee brand name, and/or

combine after sale service activities. In the manufacturing

operations and marketing there will be ample opportunity to

create new competitive capabilities and innovative products

through collaboration across the business units.

What opportunities for skills transfer, cost sharing, or brand sharing do you see?

The primary opportunities for skills transfer, cost sharing,

or brand sharing in the areas of production and marketing. By

Sara Lee 15

sharing production best practices the business units can improve

efficiencies and thereby reduce operating expense. There may

also be opportunities to consolidate production, increase plant

utilization, look for outsourcing opportunities, reduce

inventories, and improve delivery times with enhanced

transportation and logistics coordination. On the marketing side

there will be an opportunity to transfer product development

ideas and improve the innovativeness necessary to maintain

customer loyalty. There will also be an ability to share

advertisement and leverage the Sara Lee brand across each

business unit, thus further growing the brand in the marketplace

and the ability to grow in a profitable manner.

What is your assessment of Sara Lee's financial and operating

performance in fiscal years 2008-2010, the period following the

divestitures that were the core of Sara Lee's retrenchment

strategy?

The following two charts provide a financial analysis of

Sara Lee’s (Hillshire Brands Co.) for the years of the case 2007

to 2010 and an update that reflects the years 2011 to 2013.

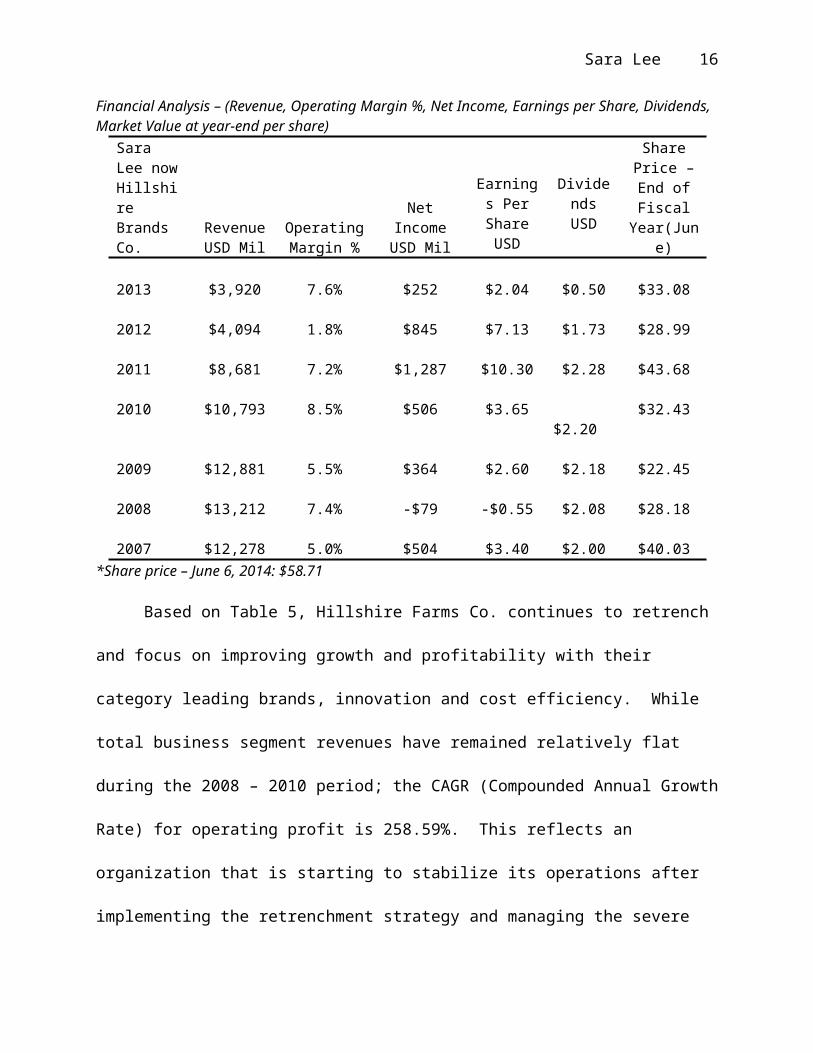

Table 5

Sara Lee 16

Financial Analysis – (Revenue, Operating Margin %, Net Income, Earnings per Share, Dividends, Market Value at year-end per share)

Sara Lee nowHillshire Brands Co.

RevenueUSD Mil

OperatingMargin %

NetIncomeUSD Mil

Earnings PerShareUSD

DividendsUSD

SharePrice –End ofFiscal

Year(June)

2013 $3,920 7.6% $252 $2.04 $0.50 $33.08

2012 $4,094 1.8% $845 $7.13 $1.73 $28.99

2011 $8,681 7.2% $1,287 $10.30 $2.28 $43.68

2010 $10,793 8.5% $506 $3.65 $2.20

$32.43

2009 $12,881 5.5% $364 $2.60 $2.18 $22.45

2008 $13,212 7.4% -$79 -$0.55 $2.08 $28.18

2007 $12,278 5.0% $504 $3.40 $2.00 $40.03*Share price – June 6, 2014: $58.71

Based on Table 5, Hillshire Farms Co. continues to retrench

and focus on improving growth and profitability with their

category leading brands, innovation and cost efficiency. While

total business segment revenues have remained relatively flat

during the 2008 – 2010 period; the CAGR (Compounded Annual Growth

Rate) for operating profit is 258.59%. This reflects an

organization that is starting to stabilize its operations after

implementing the retrenchment strategy and managing the severe

Sara Lee 17

economic downturn as a result of the Great Recession. While

operating margins remained below plan at 8.5 percent, EPS

(Earnings per Share) improved to $3.65 in 2010, above the $3.40

EPS posted in 2007. The company has also increased its operating

margins to high of 35.3% in 2012, followed by a 28.7% in 2013.

The operating margins indicate pricing strength and the ability

to control operating expenditures and other related operational

costs. Net income improved from -$79.0 million in 2008 to $506

million in 2010, reflecting pre-retrenchment levels of $504

million in 2007. Another indication of financial strength is

reflected by the company’s ability to maintain a dividend

throughout the restructuring at or above $2.00 per share.

As an addendum to the case, the period following 2010

reflected additional restructuring and retrenchment on the part

of Sara Lee. In fiscal 2012, the company completed a spin-off of

its international coffee and tea business into an independent,

publicly traded Dutch company named D.E. Master Blenders 1753

N.V.; after the spin-off, Sara Lee changed its name to The

Hillshire Brands Company. The company also divested North

American refrigerated dough business, North American Foodservice

Sara Lee 18

Coffee business, Spanish Bakery and French refrigerated dough

business, and completed the sale of the North American Bakery

business. This narrowed The Hillshire Brands Company to a meat-

centric foods company. (The Hillshire Brands, 2011). Since this

further retrenchment, the company has been able to increase its

share price to $58.71 as of June 6, 2014, reflecting a 13% growth

CAGR since posting a $28.18 per share price at the end of fiscal

2008.

Table 6Key Ratios – (Net Margin %, Asset Turnover (Average), Return on Assets %, Return on Equity %, Return on Invested Capital %, Interest Coverage)

Sara Lee nowHillshire Farms Co.

NetMargin

%

AssetTurnover(Average)

Return onAssets %(ROA)

Returnon

Equity% (ROE)

Returnon

Invested

Capital %

Interest

Coverage

2013 6.43% 1.61 10.32% 70.10% 21.92% 6.33

2012 20.64% 0.68 14.10% 77.52% 31.02% 0.52

2011 14.83% 0.95 14.01% 75.00% 30.89% 5.16

2010 4.69% 1.18 5.54% 28.73% 13.69% 6.41

2009 2.83% 1.27 3.60% 15.02% 8.65% 4.46

2008 -0.60% 1.15 -0.69% -2.91% 0.66% --

2007 4.10% 0.92 3.77% 19.91% 10.00% --

Sara Lee 19

In Table 5 we see that Hillshire Farms Co. has effectively

leveraged its assets with a net margin that has increased from

single digits to a high of 20.64% in 2012, while slipping back to

6.43% in 2013 which still exceeds the net margin recorded from

2007 to 2010. Asset turnover continues to average well over 1,

with the TTM (Trailing Twelve Months) reflecting a strong 1.59.

Improved asset utilization is reflected in an ROA of 14% in 2011

and 2012, and a 10.32% in 2013; this is significantly improved

versus single digit returns that date back as far as 2004. ROE

has improved to 70+ percent in 2011 and 2012 and remains strong

at 70.10% in 2013; again this is considerably higher than the 22

percent returns experienced during the preceding 7 years. These

financial ratios indicate a company that has gone through

significant restructuring, the great recession and is now

starting to focus its remaining operations on generating long-

term value for its shareholders.

What is your overall evaluation of Sara Lee's retrenchment plan?

My overall evaluation of the Sara Lee retrenchment strategy

is that at the end of 2010 the profitability of the remaining

Sara Lee 20

business units was beginning to show promise. Improvement in

income from continuing operations before income taxes was showing

tremendous improvement in all business units with a combined

operating segment income CAGR (Compounded Annual Growth Rate) of

258.59% for the period 2008 to 2010.

The problem with assessing the organization during this time

period is that there was significant outside variable impacts as

the world was experiencing the Great Recession brought on by the

financial crisis that took place in 2008.

What evidence and/or reasons support a conclusion that Sara Lee's shareholders have

or have not benefitted from the company's retrenchment strategy?

The original retrenchment plan goal called for proceeds of

$3 billion to be generated from the selloff of the targeted

business units, $14 billion in revenues by fiscal 2010, and

operating profit margins of at least 12 percent by 2010 versus

8.1 percent in 2004. The actual results reflected $1.3 billion

in proceeds without the $2.4 billion dividend paid by the

Hanesbrands spin-off. Revenues came in at $10.73 billion versus

the $14 billion target and operating profit margin reflected

8.5%, not 12%.

Sara Lee 21

While these goals were not attained it is again difficult to

attribute the short-fall to company performance without taking

the recession into consideration. What can be stated is that the

shareowners have continued to receive a dividend payment

throughout the implementation of the retrenchment strategy and

that share price for Sara Lee (now Hillshire Farms) has shown a

13.01% CAGR for the last 6 years 2008 to 2014; increasing from

$28.18 at the fiscal end of 2008 to the current share price of

$58.71 as of June 6, 2014. (Morningstar, 2014). The company

has also provided shareholders a 70%+ ROE over the last three

years.

What actions do you recommend that Sara Lee management take

to improve the company's performance and boost shareholder value?

At the end of 2010, I would recommend that Sara Lee focus on

leveraging the resource fit in its remaining business units to

reduce operating costs, provide innovative products to the

marketplace, and leverage the Sara Lee brand. By focusing the

management team the organization can ensure that it has well

developed strategies that allow the business to grow in a

profitable manner.

Sara Lee 22

I would also recommend that the company make a decision to

devote additional resources to its International bakery Division

or divest. The company, based in Spain could present obstacles

going forward and takes company’s resources away from more

profitable opportunities.

In the Foodservice division, I would recommend additional

sharing of ideas take place with Sara Lee’s retail division and

other business to develop innovative products that can generate

growth opportunities with supermarkets, food service

distributors, and national restaurant chains. Idea sharing

between the remaining business units can lead to a competitive

advantage when it comes to bringing innovative products to the

market place.

Another recommendation would be to continue with the efforts

and initiatives started with Project Accelerate. In order to

improve operating margins and thereby provide competitive

pricing, the company will need to look for further outsourcing

opportunities, operating segment restructuring throw the sharing

of generalized services, supply chain efficiencies, and

reductions in corporate overhead. The company must make lean

Sara Lee 23

manufacturing an everyday way of life and expand the competitive

advantage they have established in the North American Retail

division when it comes to operating efficiency.

The lean manufacturing efforts will also allow the firm to

maintain competitive pricing within the US, its primary market,

and thereby establish barriers to entry in its core businesses.

By creating innovative products and improving operating

efficiencies in its remaining business units, Sara Lee can

provide long-term competitive returns to its shareholders.

Sara Lee 24

References

Gamble, J. E., Peteraf, M. A., Strickland III, A. J., & Thompson,

A. A. (2012). Crafting & executing strategy. (18th. ed.),

New York, NY: McGraw-Hill.

Morningstar, Inc. (2014, June 6). Hillshire Brands Co HSH.

Retrieved from

http://financials.morningstar.com/ratios/r.html?

ops=clear&t=HSH®ion=usa&culture=en-US

The Hillshire Brands Co. (2011). SEC Form 10-K for the Year Ended

December 31, 2011. Retrieved from

http://www.annualreports.com/Company/4341