SANDHAR TECHNOLOGIES LIMITED

536

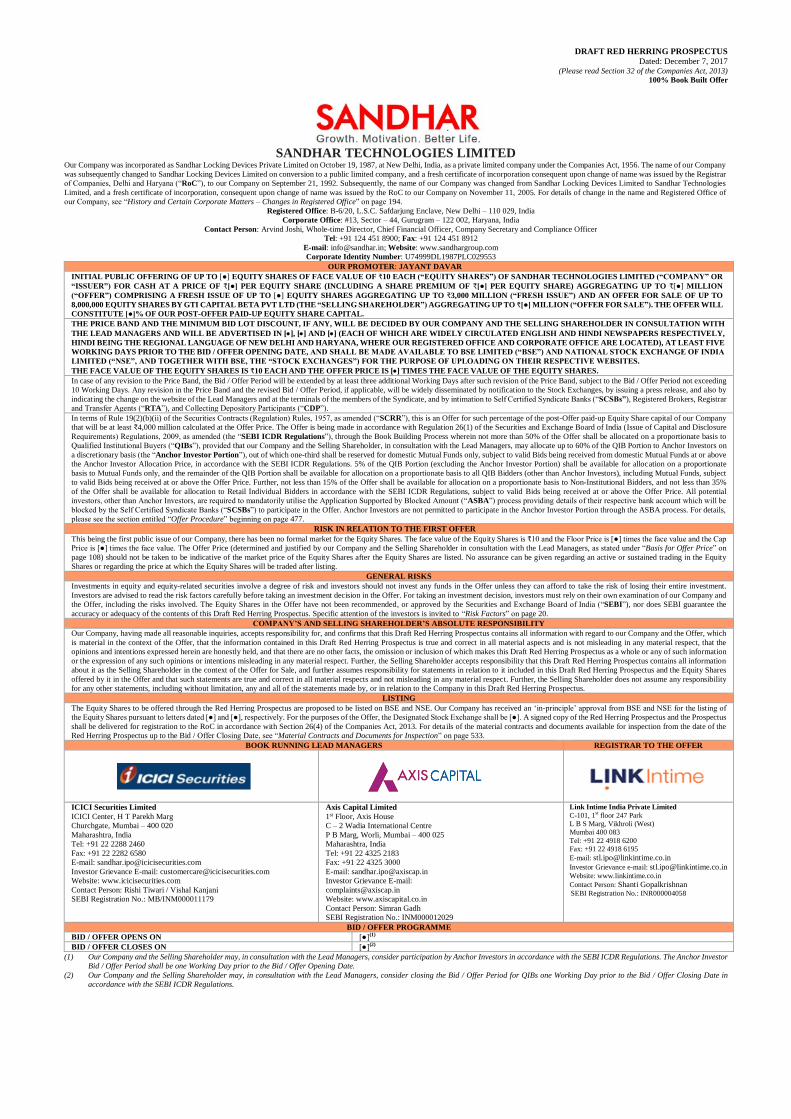

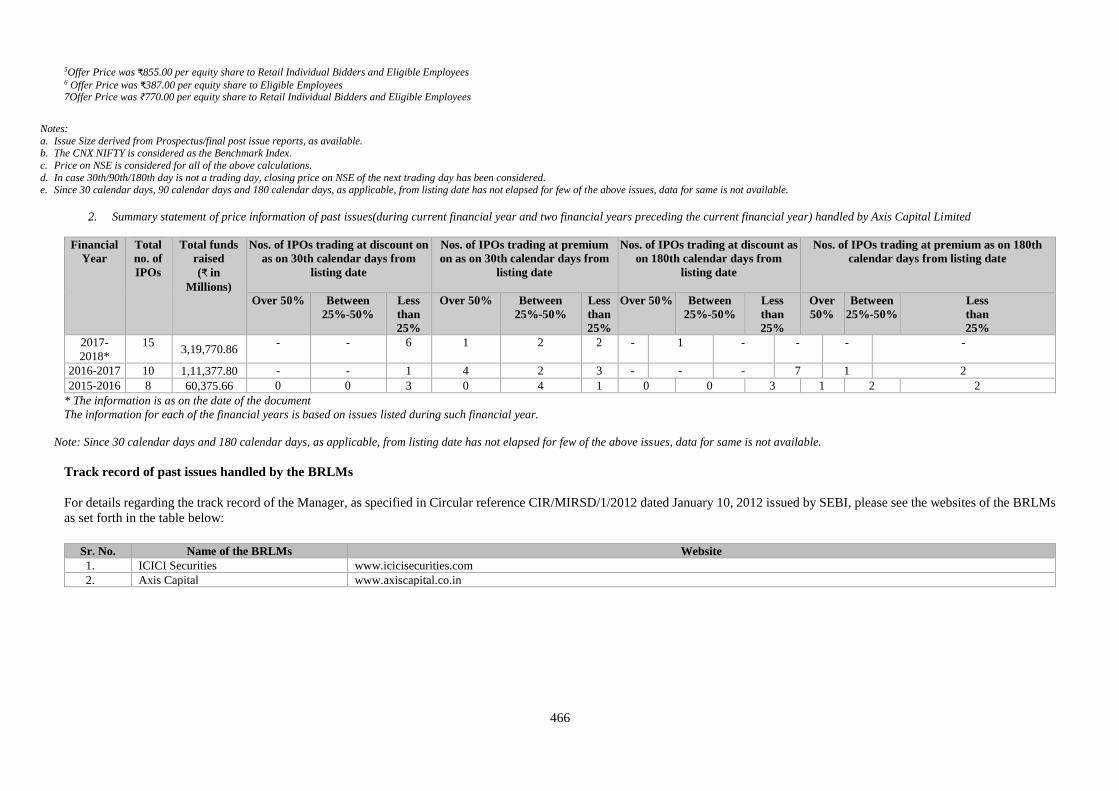

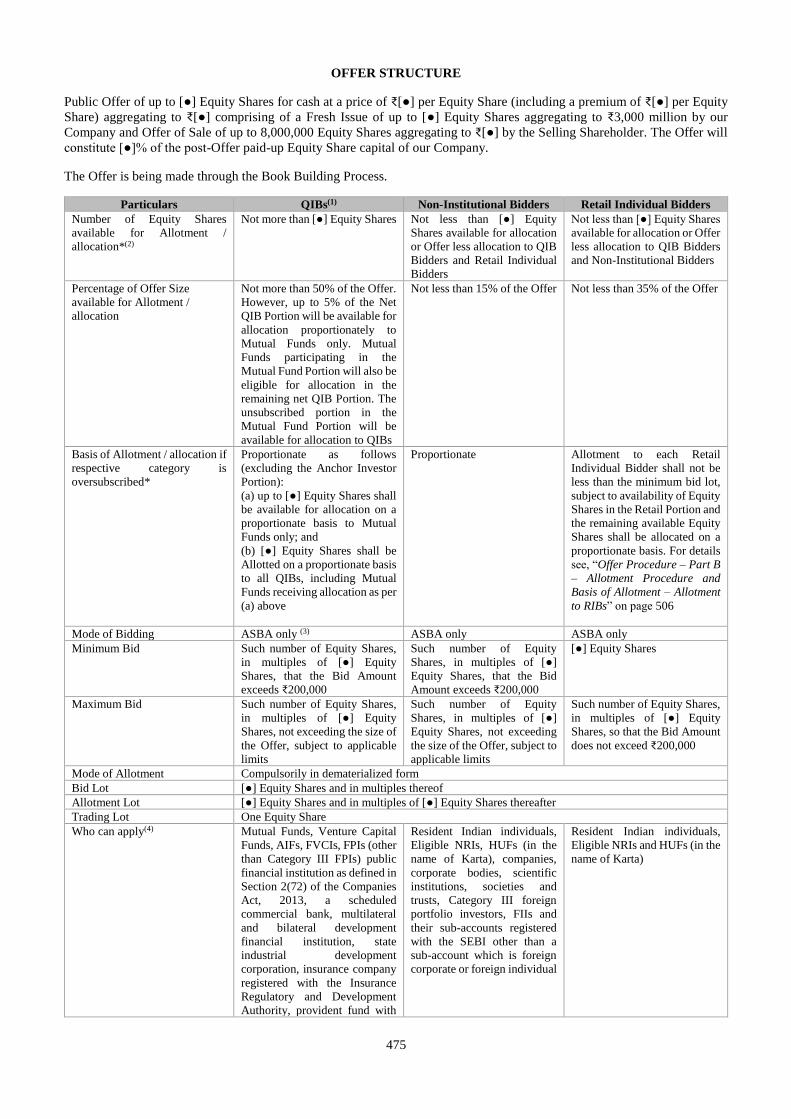

DRAFT RED HERRING PROSPECTUS Dated: December 7, 2017 (Please read Section 32 of the Companies Act, 2013) 100% Book Built Offer SANDHAR TECHNOLOGIES LIMITED Our Company was incorporated as Sandhar Locking Devices Private Limited on October 19, 1987, at New Delhi, India, as a private limited company under the Companies Act, 1956. The name of our Company was subsequently changed to Sandhar Locking Devices Limited on conversion to a public limited company, and a fresh certificate of incorporation consequent upon change of name was issued by the Registrar of Companies, Delhi and Haryana (“RoC”), to our Company on September 21, 1992. Subsequently, the name of our Company was changed from Sandhar Locking Devices Limited to Sandhar Technologies Limited, and a fresh certificate of incorporation, consequent upon change of name was issued by the RoC to our Company on November 11, 2005. For details of change in the name and Registered Office of our Company, see “History and Certain Corporate Matters – Changes in Registered Office” on page 194. Registered Office: B-6/20, L.S.C. Safdarjung Enclave, New Delhi – 110 029, India Corporate Office: #13, Sector – 44, Gurugram – 122 002, Haryana, India Contact Person: Arvind Joshi, Whole-time Director, Chief Financial Officer, Company Secretary and Compliance Officer Tel: +91 124 451 8900; Fax: +91 124 451 8912 E-mail: [email protected]; Website: www.sandhargroup.com Corporate Identity Number: U74999DL1987PLC029553 OUR PROMOTER: JAYANT DAVAR INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹10 EACH (“EQUITY SHARES”) OF SANDHAR TECHNOLOGIES LIMITED (“COMPANY” OR “ISSUER”) FOR CASH AT A PRICE OF ₹[●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹[●] PER EQUITY SHARE) AGGREGATING UP TO ₹[●] MILLION (“OFFER”) COMPRISING A FRESH ISSUE OF UP TO [●] EQUITY SHARES AGGREGATING UP TO ₹3,000 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO 8,000,000 EQUITY SHARES BY GTI CAPITAL BETA PVT LTD (THE “SELLING SHAREHOLDER”) AGGREGATING UP TO ₹[●] MILLION (“OFFER FOR SALE”). THE OFFER WILL CONSTITUTE [●]% OF OUR POST-OFFER PAID-UP EQUITY SHARE CAPITAL. THE PRICE BAND AND THE MINIMUM BID LOT DISCOUNT, IF ANY, WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDER IN CONSULTATION WITH THE LEAD MANAGERS AND WILL BE ADVERTISED IN [•], [•] AND [•] (EACH OF WHICH ARE WIDELY CIRCULATED ENGLISH AND HINDI NEWSPAPERS RESPECTIVELY, HINDI BEING THE REGIONAL LANGUAGE OF NEW DELHI AND HARYANA, WHERE OUR REGISTERED OFFICE AND CORPORATE OFFICE ARE LOCATED), AT LEAST FIVE WORKING DAYS PRIOR TO THE BID / OFFER OPENING DATE, AND SHALL BE MADE AVAILABLE TO BSE LIMITED (“BSE”) AND NATIONAL STOCK EXCHANGE OF INDIA LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR THE PURPOSE OF UPLOADING ON THEIR RESPECTIVE WEBSITES. THE FACE VALUE OF THE EQUITY SHARES IS ₹10 EACH AND THE OFFER PRICE IS [•] TIMES THE FACE VALUE OF THE EQUITY SHARES. In case of any revision to the Price Band, the Bid / Offer Period will be extended by at least three additional Working Days after such revision of the Price Band, subject to the Bid / Offer Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid / Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by indicating the change on the website of the Lead Managers and at the terminals of the members of the Syndicate, and by intimation to Self Certified Syndicate Banks (“SCSBs”), Registered Brokers, Registrar and Transfer Agents (“RTA”), and Collecting Depository Participants (“CDP”). In terms of Rule 19(2)(b)(ii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Offer for such percentage of the post-Offer paid-up Equity Share capital of our Company that will be at least ₹4,000 million calculated at the Offer Price. The Offer is being made in accordance with Regulation 26(1) of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”), through the Book Building Process wherein not more than 50% of the Offer shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIBs”), provided that our Company and the Selling Shareholder, in consultation with the Lead Managers, may allocate up to 60% of the QIB Portion to Anchor Investors on a discretionary basis (the “Anchor Investor Portion”), out of which one-third shall be reserved for domestic Mutual Funds only, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price, in accordance with the SEBI ICDR Regulations. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional Bidders, and not less than 35% of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All potential investors, other than Anchor Investors, are required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”) to participate in the Offer. Anchor Investors are not permitted to participate in the Anchor Investor Portion through the ASBA process. For details, please see the section entitled “Offer Procedure” beginning on page 477. RISK IN RELATION TO THE FIRST OFFER This being the first public issue of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹10 and the Floor Price is [●] times the face value and the Cap Price is [●] times the face value. The Offer Price (determined and justified by our Company and the Selling Shareholder in consultation with the Lead Managers, as stated under “Basis for Offer Price” on page 108) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended, or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 20. COMPANY’S AND SELLING SHAREHOLDER’S ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for, and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held, and that there are no other facts, the omission or inclusion of which makes this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Further, the Selling Shareholder accepts responsibility that this Draft Red Herring Prospectus contains all information about it as the Selling Shareholder in the context of the Offer for Sale, and further assumes responsibility for statements in relation to it included in this Draft Red Herring Prospectus and the Equity Shares offered by it in the Offer and that such statements are true and correct in all material respects and not misleading in any material respect. Further, the Selling Shareholder does not assume any responsibility for any other statements, including without limitation, any and all of the statements made by, or in relation to the Company in this Draft Red Herring Prospectus. LISTING The Equity Shares to be offered through the Red Herring Prospectus are proposed to be listed on BSE and NSE. Our Company has received an ‘in-principle’ approval from BSE and NSE for the listing of the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A signed copy of the Red Herring Prospectus and the Prospectus shall be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of the Red Herring Prospectus up to the Bid / Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 533. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER ICICI Securities Limited ICICI Center, H T Parekh Marg Churchgate, Mumbai – 400 020 Maharashtra, India Tel: +91 22 2288 2460 Fax: +91 22 2282 6580 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.icicisecurities.com Contact Person: Rishi Tiwari / Vishal Kanjani SEBI Registration No.: MB/INM000011179 Axis Capital Limited 1 st Floor, Axis House C – 2 Wadia International Centre P B Marg, Worli, Mumbai – 400 025 Maharashtra, India Tel: +91 22 4325 2183 Fax: +91 22 4325 3000 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.axiscapital.co.in Contact Person: Simran Gadh SEBI Registration No.: INM000012029 Link Intime India Private Limited C-101, 1 st floor 247 Park L B S Marg, Vikhroli (West) Mumbai 400 083 Tel: +91 22 4918 6200 Fax: +91 22 4918 6195 E-mail: [email protected] Investor Grievance e-mail: [email protected] Website: www.linkintime.co.in Contact Person: Shanti Gopalkrishnan SEBI Registration No.: INR000004058 BID / OFFER PROGRAMME BID / OFFER OPENS ON [●] (1) BID / OFFER CLOSES ON [●] (2) (1) Our Company and the Selling Shareholder may, in consultation with the Lead Managers, consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor Bid / Offer Period shall be one Working Day prior to the Bid / Offer Opening Date. (2) Our Company and the Selling Shareholder may, in consultation with the Lead Managers, consider closing the Bid / Offer Period for QIBs one Working Day prior to the Bid / Offer Closing Date in accordance with the SEBI ICDR Regulations.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SANDHAR TECHNOLOGIES LIMITED

DRAFT RED HERRING PROSPECTUS

Dated: December 7, 2017 (Please read Section 32 of the Companies Act, 2013)

100% Book Built Offer

SANDHAR TECHNOLOGIES LIMITED

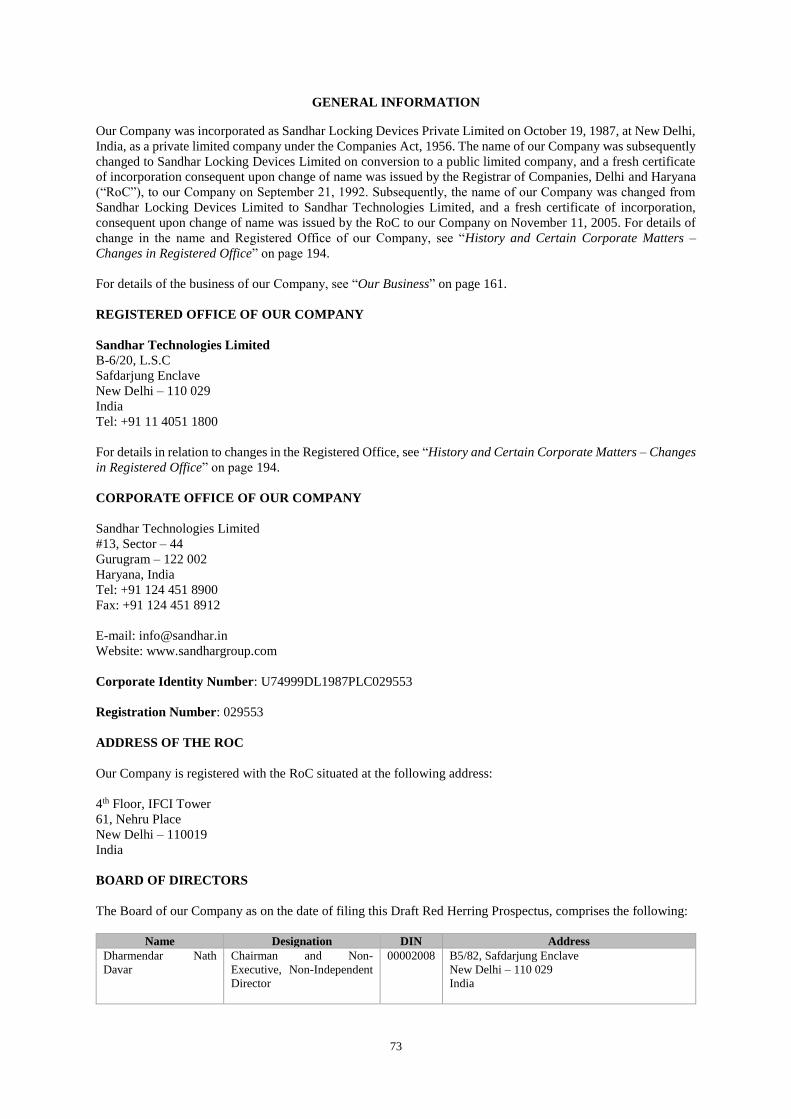

Our Company was incorporated as Sandhar Locking Devices Private Limited on October 19, 1987, at New Delhi, India, as a private limited company under the Companies Act, 1956. The name of our Company

was subsequently changed to Sandhar Locking Devices Limited on conversion to a public limited company, and a fresh certificate of incorporation consequent upon change of name was issued by the Registrar

of Companies, Delhi and Haryana (“RoC”), to our Company on September 21, 1992. Subsequently, the name of our Company was changed from Sandhar Locking Devices Limited to Sandhar Technologies

Limited, and a fresh certificate of incorporation, consequent upon change of name was issued by the RoC to our Company on November 11, 2005. For details of change in the name and Registered Office of

our Company, see “History and Certain Corporate Matters – Changes in Registered Office” on page 194.

Registered Office: B-6/20, L.S.C. Safdarjung Enclave, New Delhi – 110 029, India

Corporate Office: #13, Sector – 44, Gurugram – 122 002, Haryana, India

Contact Person: Arvind Joshi, Whole-time Director, Chief Financial Officer, Company Secretary and Compliance Officer

Tel: +91 124 451 8900; Fax: +91 124 451 8912

E-mail: [email protected]; Website: www.sandhargroup.com

Corporate Identity Number: U74999DL1987PLC029553

OUR PROMOTER: JAYANT DAVAR

INITIAL PUBLIC OFFERING OF UP TO [●] EQUITY SHARES OF FACE VALUE OF ₹10 EACH (“EQUITY SHARES”) OF SANDHAR TECHNOLOGIES LIMITED (“COMPANY” OR

“ISSUER”) FOR CASH AT A PRICE OF ₹[●] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹[●] PER EQUITY SHARE) AGGREGATING UP TO ₹[●] MILLION

(“OFFER”) COMPRISING A FRESH ISSUE OF UP TO [●] EQUITY SHARES AGGREGATING UP TO ₹3,000 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF UP TO

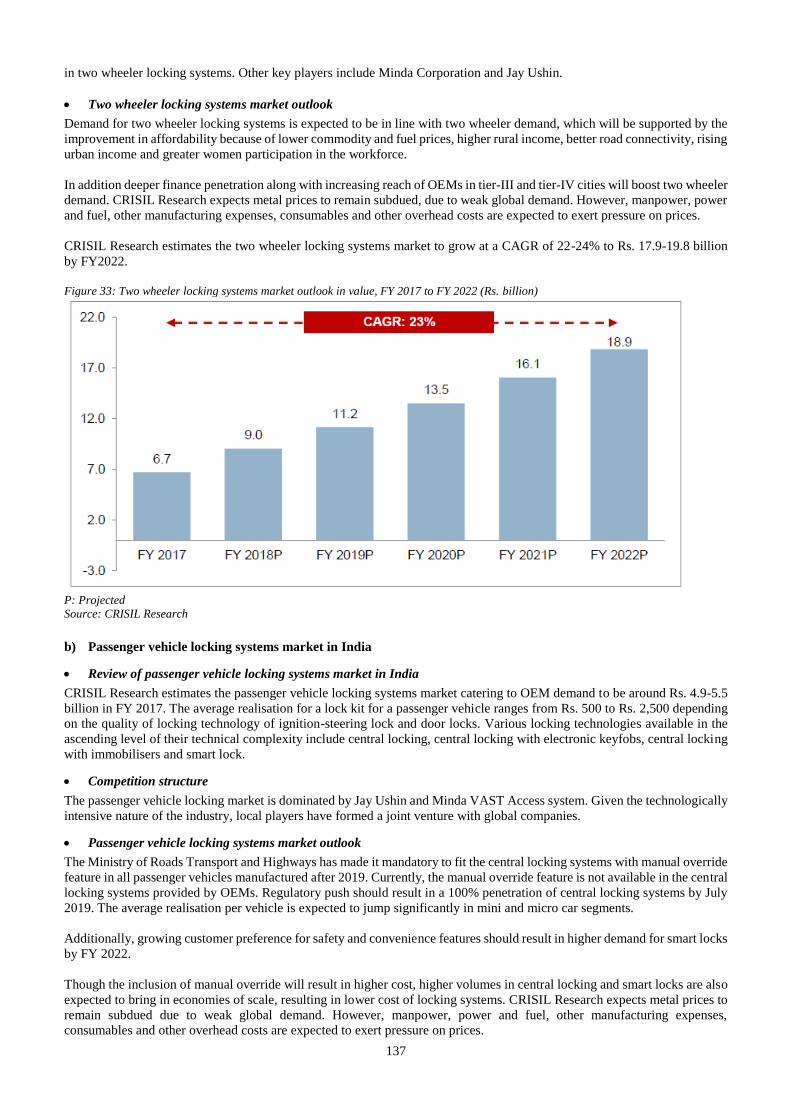

8,000,000 EQUITY SHARES BY GTI CAPITAL BETA PVT LTD (THE “SELLING SHAREHOLDER”) AGGREGATING UP TO ₹[●] MILLION (“OFFER FOR SALE”). THE OFFER WILL

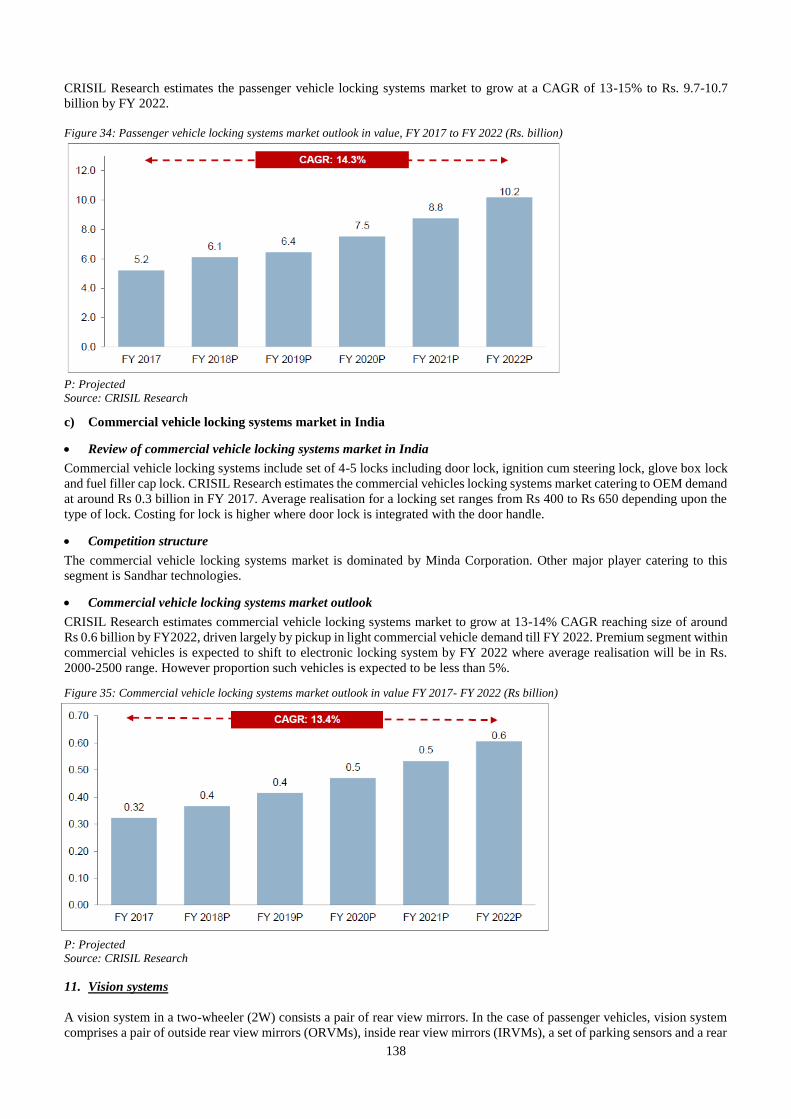

CONSTITUTE [●]% OF OUR POST-OFFER PAID-UP EQUITY SHARE CAPITAL.

THE PRICE BAND AND THE MINIMUM BID LOT DISCOUNT, IF ANY, WILL BE DECIDED BY OUR COMPANY AND THE SELLING SHAREHOLDER IN CONSULTATION WITH

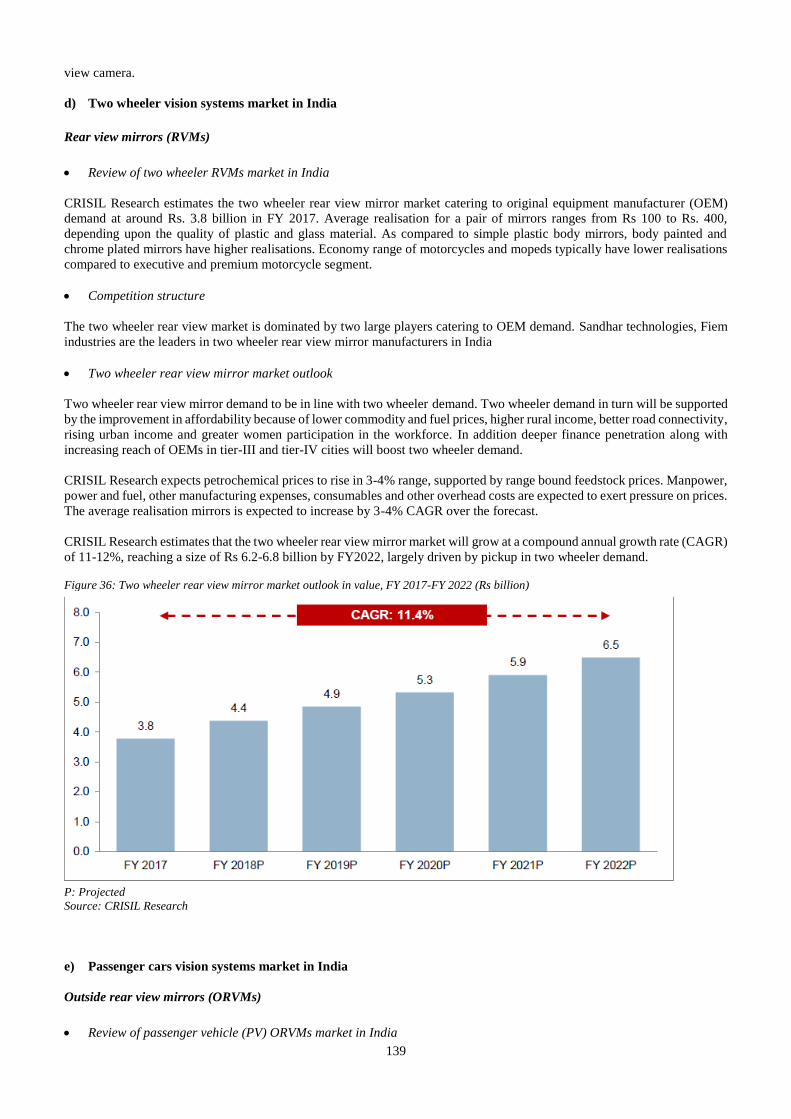

THE LEAD MANAGERS AND WILL BE ADVERTISED IN [•], [•] AND [•] (EACH OF WHICH ARE WIDELY CIRCULATED ENGLISH AND HINDI NEWSPAPERS RESPECTIVELY,

HINDI BEING THE REGIONAL LANGUAGE OF NEW DELHI AND HARYANA, WHERE OUR REGISTERED OFFICE AND CORPORATE OFFICE ARE LOCATED), AT LEAST FIVE

WORKING DAYS PRIOR TO THE BID / OFFER OPENING DATE, AND SHALL BE MADE AVAILABLE TO BSE LIMITED (“BSE”) AND NATIONAL STOCK EXCHANGE OF INDIA

LIMITED (“NSE”, AND TOGETHER WITH BSE, THE “STOCK EXCHANGES”) FOR THE PURPOSE OF UPLOADING ON THEIR RESPECTIVE WEBSITES.

THE FACE VALUE OF THE EQUITY SHARES IS ₹10 EACH AND THE OFFER PRICE IS [•] TIMES THE FACE VALUE OF THE EQUITY SHARES.

In case of any revision to the Price Band, the Bid / Offer Period will be extended by at least three additional Working Days after such revision of the Price Band, subject to the Bid / Offer Period not exceeding

10 Working Days. Any revision in the Price Band and the revised Bid / Offer Period, if applicable, will be widely disseminated by notification to the Stock Exchanges, by issuing a press release, and also by

indicating the change on the website of the Lead Managers and at the terminals of the members of the Syndicate, and by intimation to Self Certified Syndicate Banks (“SCSBs”), Registered Brokers, Registrar

and Transfer Agents (“RTA”), and Collecting Depository Participants (“CDP”).

In terms of Rule 19(2)(b)(ii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Offer for such percentage of the post-Offer paid-up Equity Share capital of our Company

that will be at least ₹4,000 million calculated at the Offer Price. The Offer is being made in accordance with Regulation 26(1) of the Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009, as amended (the “SEBI ICDR Regulations”), through the Book Building Process wherein not more than 50% of the Offer shall be allocated on a proportionate basis to

Qualified Institutional Buyers (“QIBs”), provided that our Company and the Selling Shareholder, in consultation with the Lead Managers, may allocate up to 60% of the QIB Portion to Anchor Investors on

a discretionary basis (the “Anchor Investor Portion”), out of which one-third shall be reserved for domestic Mutual Funds only, subject to valid Bids being received from domestic Mutual Funds at or above

the Anchor Investor Allocation Price, in accordance with the SEBI ICDR Regulations. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate

basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject

to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Offer shall be available for allocation on a proportionate basis to Non-Institutional Bidders, and not less than 35%

of the Offer shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All potential

investors, other than Anchor Investors, are required to mandatorily utilise the Application Supported by Blocked Amount (“ASBA”) process providing details of their respective bank account which will be

blocked by the Self Certified Syndicate Banks (“SCSBs”) to participate in the Offer. Anchor Investors are not permitted to participate in the Anchor Investor Portion through the ASBA process. For details,

please see the section entitled “Offer Procedure” beginning on page 477.

RISK IN RELATION TO THE FIRST OFFER

This being the first public issue of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹10 and the Floor Price is [●] times the face value and the Cap

Price is [●] times the face value. The Offer Price (determined and justified by our Company and the Selling Shareholder in consultation with the Lead Managers, as stated under “Basis for Offer Price” on

page 108) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity

Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Offer unless they can afford to take the risk of losing their entire investment.

Investors are advised to read the risk factors carefully before taking an investment decision in the Offer. For taking an investment decision, investors must rely on their own examination of our Company and

the Offer, including the risks involved. The Equity Shares in the Offer have not been recommended, or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the

accuracy or adequacy of the contents of this Draft Red Herring Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 20.

COMPANY’S AND SELLING SHAREHOLDER’S ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for, and confirms that this Draft Red Herring Prospectus contains all information with regard to our Company and the Offer, which

is material in the context of the Offer, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the

opinions and intentions expressed herein are honestly held, and that there are no other facts, the omission or inclusion of which makes this Draft Red Herring Prospectus as a whole or any of such information

or the expression of any such opinions or intentions misleading in any material respect. Further, the Selling Shareholder accepts responsibility that this Draft Red Herring Prospectus contains all information

about it as the Selling Shareholder in the context of the Offer for Sale, and further assumes responsibility for statements in relation to it included in this Draft Red Herring Prospectus and the Equity Shares

offered by it in the Offer and that such statements are true and correct in all material respects and not misleading in any material respect. Further, the Selling Shareholder does not assume any responsibility

for any other statements, including without limitation, any and all of the statements made by, or in relation to the Company in this Draft Red Herring Prospectus.

LISTING

The Equity Shares to be offered through the Red Herring Prospectus are proposed to be listed on BSE and NSE. Our Company has received an ‘in-principle’ approval from BSE and NSE for the listing of

the Equity Shares pursuant to letters dated [●] and [●], respectively. For the purposes of the Offer, the Designated Stock Exchange shall be [●]. A signed copy of the Red Herring Prospectus and the Prospectus

shall be delivered for registration to the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents available for inspection from the date of the

Red Herring Prospectus up to the Bid / Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 533.

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER

ICICI Securities Limited

ICICI Center, H T Parekh Marg

Churchgate, Mumbai – 400 020

Maharashtra, India

Tel: +91 22 2288 2460

Fax: +91 22 2282 6580

E-mail: [email protected]

Investor Grievance E-mail: [email protected]

Website: www.icicisecurities.com

Contact Person: Rishi Tiwari / Vishal Kanjani

SEBI Registration No.: MB/INM000011179

Axis Capital Limited

1st Floor, Axis House

C – 2 Wadia International Centre

P B Marg, Worli, Mumbai – 400 025

Maharashtra, India

Tel: +91 22 4325 2183

Fax: +91 22 4325 3000

E-mail: [email protected]

Investor Grievance E-mail:

Website: www.axiscapital.co.in

Contact Person: Simran Gadh

SEBI Registration No.: INM000012029

Link Intime India Private Limited

C-101, 1st floor 247 Park

L B S Marg, Vikhroli (West)

Mumbai 400 083

Tel: +91 22 4918 6200 Fax: +91 22 4918 6195

E-mail: [email protected]

Investor Grievance e-mail: [email protected]

Website: www.linkintime.co.in

Contact Person: Shanti Gopalkrishnan

SEBI Registration No.: INR000004058

BID / OFFER PROGRAMME

BID / OFFER OPENS ON [●](1)

BID / OFFER CLOSES ON [●](2)

(1) Our Company and the Selling Shareholder may, in consultation with the Lead Managers, consider participation by Anchor Investors in accordance with the SEBI ICDR Regulations. The Anchor Investor

Bid / Offer Period shall be one Working Day prior to the Bid / Offer Opening Date.

(2) Our Company and the Selling Shareholder may, in consultation with the Lead Managers, consider closing the Bid / Offer Period for QIBs one Working Day prior to the Bid / Offer Closing Date in

accordance with the SEBI ICDR Regulations.

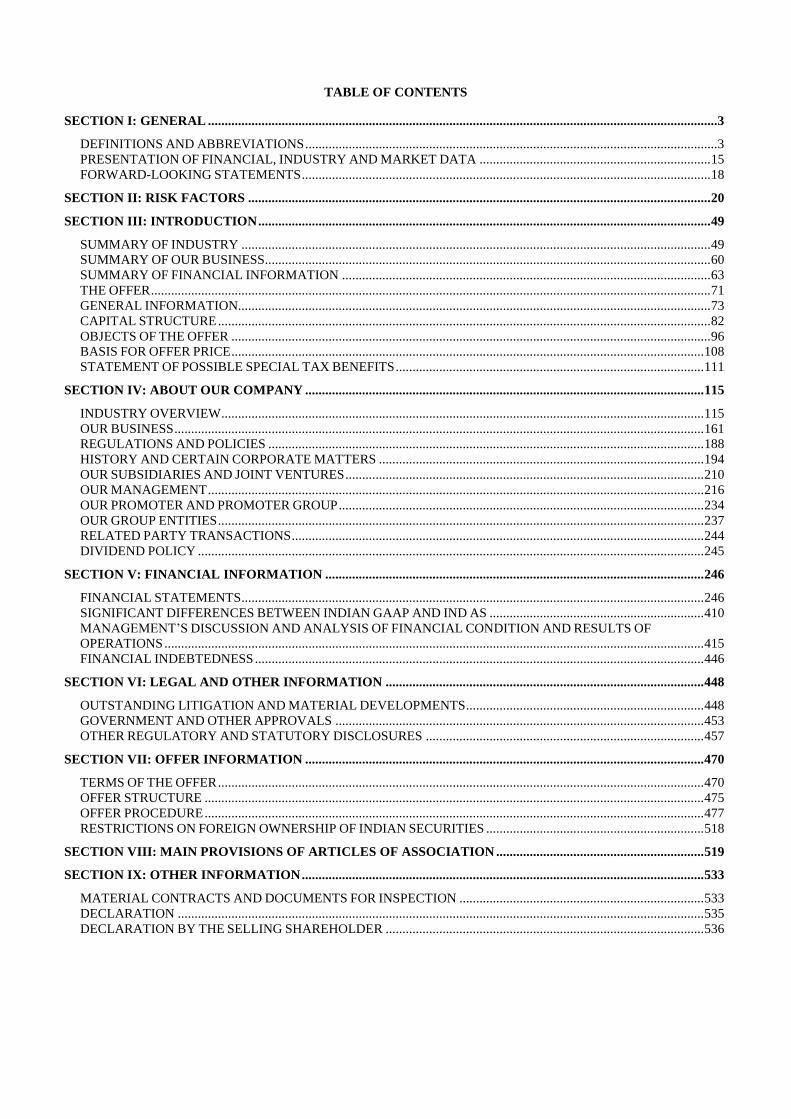

TABLE OF CONTENTS

SECTION I: GENERAL ........................................................................................................................................................ 3

DEFINITIONS AND ABBREVIATIONS ........................................................................................................................... 3 PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA ..................................................................... 15 FORWARD-LOOKING STATEMENTS .......................................................................................................................... 18

SECTION II: RISK FACTORS .......................................................................................................................................... 20

SECTION III: INTRODUCTION ....................................................................................................................................... 49

SUMMARY OF INDUSTRY ............................................................................................................................................ 49 SUMMARY OF OUR BUSINESS..................................................................................................................................... 60 SUMMARY OF FINANCIAL INFORMATION .............................................................................................................. 63 THE OFFER ....................................................................................................................................................................... 71 GENERAL INFORMATION............................................................................................................................................. 73 CAPITAL STRUCTURE ................................................................................................................................................... 82 OBJECTS OF THE OFFER ............................................................................................................................................... 96 BASIS FOR OFFER PRICE ............................................................................................................................................. 108 STATEMENT OF POSSIBLE SPECIAL TAX BENEFITS ............................................................................................ 111

SECTION IV: ABOUT OUR COMPANY ....................................................................................................................... 115

INDUSTRY OVERVIEW ................................................................................................................................................ 115 OUR BUSINESS .............................................................................................................................................................. 161 REGULATIONS AND POLICIES .................................................................................................................................. 188 HISTORY AND CERTAIN CORPORATE MATTERS ................................................................................................. 194 OUR SUBSIDIARIES AND JOINT VENTURES ........................................................................................................... 210 OUR MANAGEMENT .................................................................................................................................................... 216 OUR PROMOTER AND PROMOTER GROUP ............................................................................................................. 234 OUR GROUP ENTITIES ................................................................................................................................................. 237 RELATED PARTY TRANSACTIONS ........................................................................................................................... 244 DIVIDEND POLICY ....................................................................................................................................................... 245

SECTION V: FINANCIAL INFORMATION ................................................................................................................. 246

FINANCIAL STATEMENTS .......................................................................................................................................... 246 SIGNIFICANT DIFFERENCES BETWEEN INDIAN GAAP AND IND AS ................................................................ 410 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

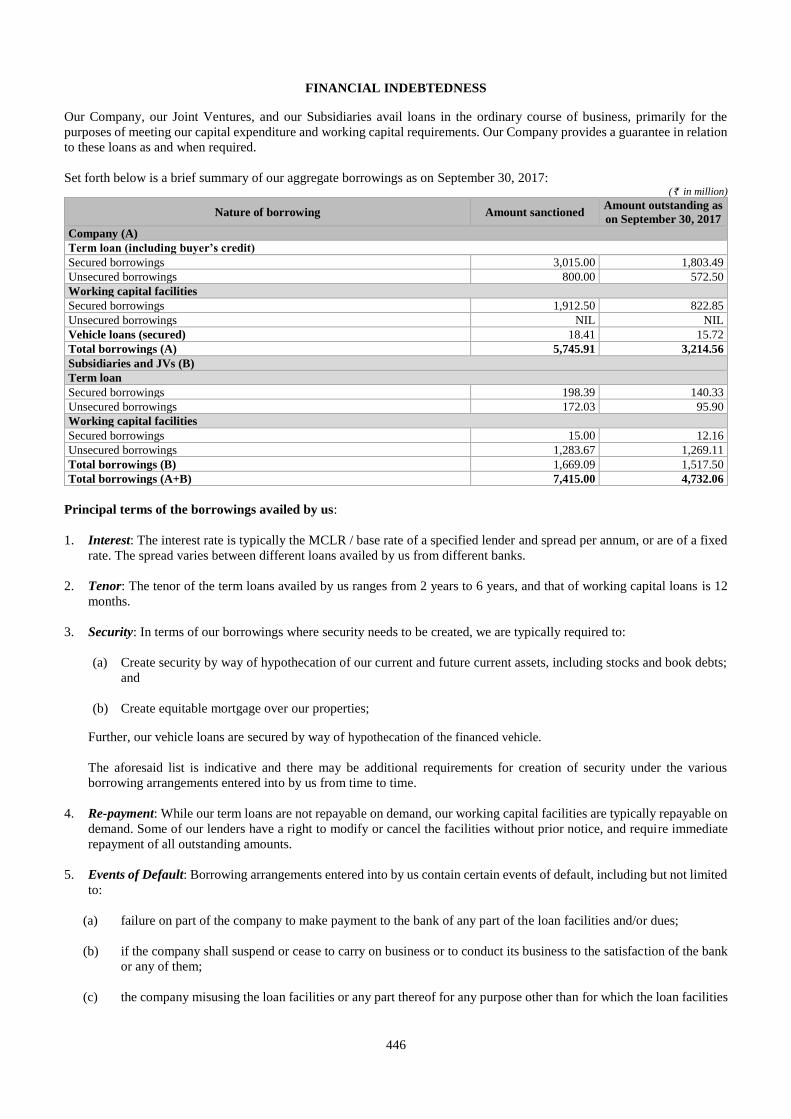

OPERATIONS ................................................................................................................................................................. 415 FINANCIAL INDEBTEDNESS ...................................................................................................................................... 446

SECTION VI: LEGAL AND OTHER INFORMATION ............................................................................................... 448

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ....................................................................... 448 GOVERNMENT AND OTHER APPROVALS .............................................................................................................. 453 OTHER REGULATORY AND STATUTORY DISCLOSURES ................................................................................... 457

SECTION VII: OFFER INFORMATION ....................................................................................................................... 470

TERMS OF THE OFFER ................................................................................................................................................. 470 OFFER STRUCTURE ..................................................................................................................................................... 475 OFFER PROCEDURE ..................................................................................................................................................... 477 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ................................................................. 518

SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION .............................................................. 519

SECTION IX: OTHER INFORMATION ........................................................................................................................ 533

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ......................................................................... 533 DECLARATION ............................................................................................................................................................. 535 DECLARATION BY THE SELLING SHAREHOLDER ............................................................................................... 536

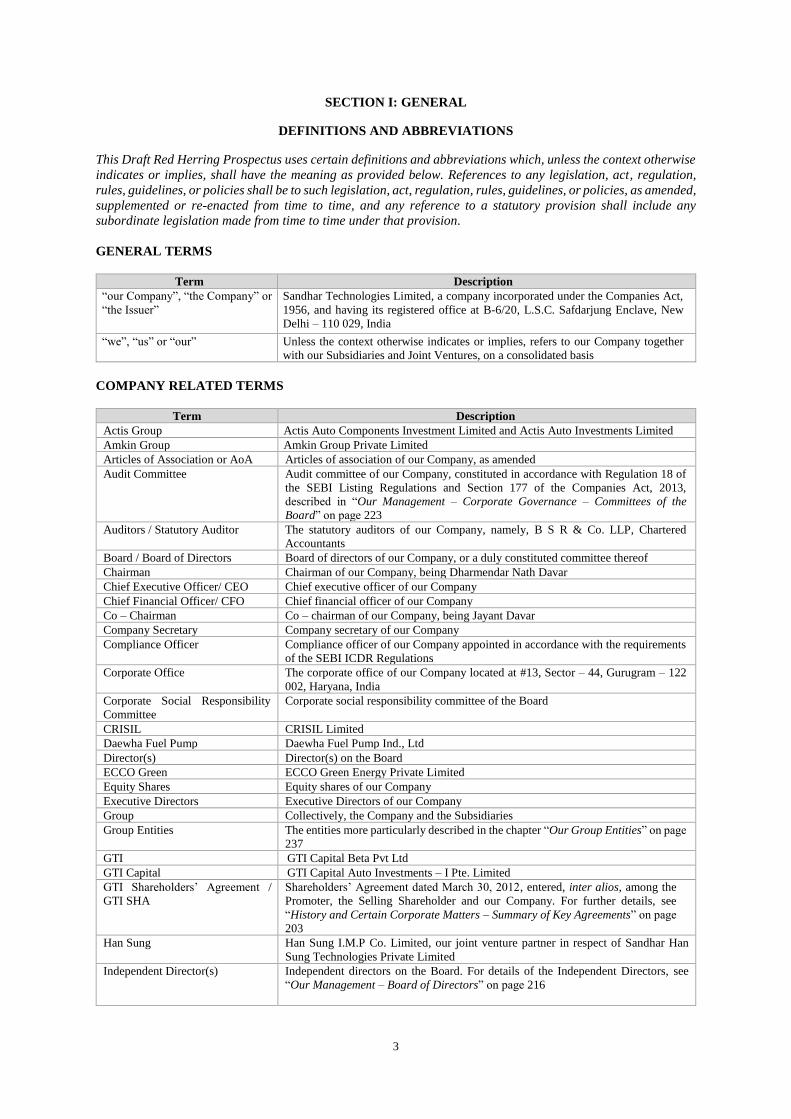

3

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

This Draft Red Herring Prospectus uses certain definitions and abbreviations which, unless the context otherwise

indicates or implies, shall have the meaning as provided below. References to any legislation, act, regulation,

rules, guidelines, or policies shall be to such legislation, act, regulation, rules, guidelines, or policies, as amended,

supplemented or re-enacted from time to time, and any reference to a statutory provision shall include any

subordinate legislation made from time to time under that provision.

GENERAL TERMS

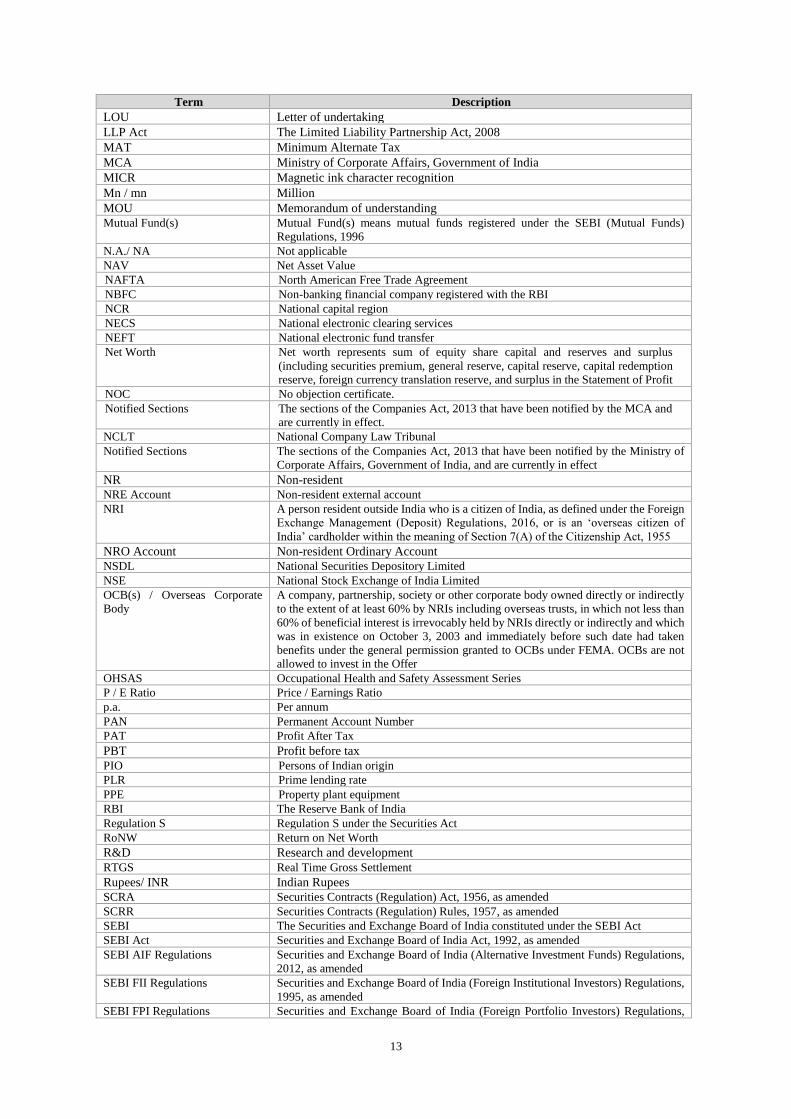

Term Description

“our Company”, “the Company” or

“the Issuer”

Sandhar Technologies Limited, a company incorporated under the Companies Act,

1956, and having its registered office at B-6/20, L.S.C. Safdarjung Enclave, New

Delhi – 110 029, India

“we”, “us” or “our” Unless the context otherwise indicates or implies, refers to our Company together

with our Subsidiaries and Joint Ventures, on a consolidated basis

COMPANY RELATED TERMS

Term Description

Actis Group Actis Auto Components Investment Limited and Actis Auto Investments Limited

Amkin Group Amkin Group Private Limited

Articles of Association or AoA Articles of association of our Company, as amended

Audit Committee Audit committee of our Company, constituted in accordance with Regulation 18 of

the SEBI Listing Regulations and Section 177 of the Companies Act, 2013,

described in “Our Management – Corporate Governance – Committees of the

Board” on page 223

Auditors / Statutory Auditor The statutory auditors of our Company, namely, B S R & Co. LLP, Chartered

Accountants

Board / Board of Directors Board of directors of our Company, or a duly constituted committee thereof

Chairman Chairman of our Company, being Dharmendar Nath Davar

Chief Executive Officer/ CEO Chief executive officer of our Company

Chief Financial Officer/ CFO Chief financial officer of our Company

Co – Chairman Co – chairman of our Company, being Jayant Davar

Company Secretary Company secretary of our Company

Compliance Officer Compliance officer of our Company appointed in accordance with the requirements

of the SEBI ICDR Regulations

Corporate Office The corporate office of our Company located at #13, Sector – 44, Gurugram – 122

002, Haryana, India

Corporate Social Responsibility

Committee

Corporate social responsibility committee of the Board

CRISIL CRISIL Limited

Daewha Fuel Pump Daewha Fuel Pump Ind., Ltd

Director(s) Director(s) on the Board

ECCO Green ECCO Green Energy Private Limited

Equity Shares Equity shares of our Company

Executive Directors Executive Directors of our Company

Group Collectively, the Company and the Subsidiaries

Group Entities The entities more particularly described in the chapter “Our Group Entities” on page

237

GTI GTI Capital Beta Pvt Ltd

GTI Capital GTI Capital Auto Investments – I Pte. Limited

GTI Shareholders’ Agreement /

GTI SHA

Shareholders’ Agreement dated March 30, 2012, entered, inter alios, among the

Promoter, the Selling Shareholder and our Company. For further details, see

“History and Certain Corporate Matters – Summary of Key Agreements” on page

203

Han Sung Han Sung I.M.P Co. Limited, our joint venture partner in respect of Sandhar Han

Sung Technologies Private Limited

Independent Director(s) Independent directors on the Board. For details of the Independent Directors, see

“Our Management – Board of Directors” on page 216

4

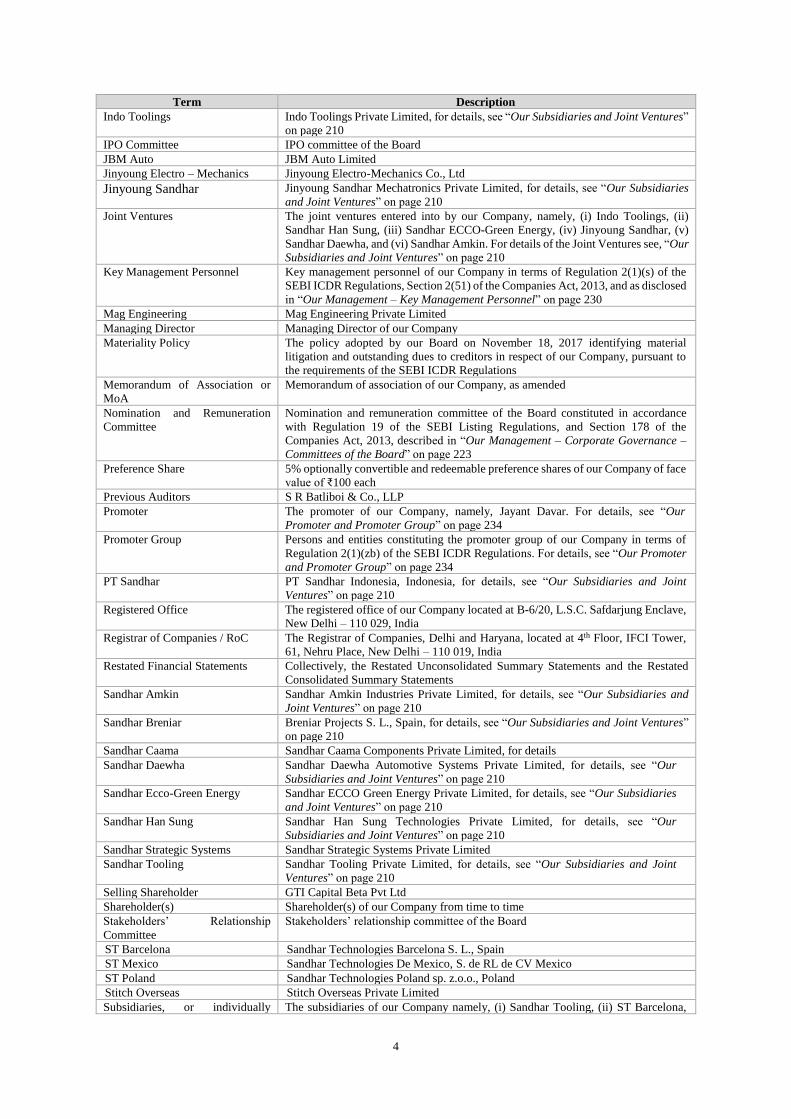

Term Description

Indo Toolings Indo Toolings Private Limited, for details, see “Our Subsidiaries and Joint Ventures”

on page 210

IPO Committee IPO committee of the Board

JBM Auto JBM Auto Limited

Jinyoung Electro – Mechanics Jinyoung Electro-Mechanics Co., Ltd

Jinyoung Sandhar Jinyoung Sandhar Mechatronics Private Limited, for details, see “Our Subsidiaries

and Joint Ventures” on page 210

Joint Ventures The joint ventures entered into by our Company, namely, (i) Indo Toolings, (ii)

Sandhar Han Sung, (iii) Sandhar ECCO-Green Energy, (iv) Jinyoung Sandhar, (v)

Sandhar Daewha, and (vi) Sandhar Amkin. For details of the Joint Ventures see, “Our

Subsidiaries and Joint Ventures” on page 210

Key Management Personnel Key management personnel of our Company in terms of Regulation 2(1)(s) of the

SEBI ICDR Regulations, Section 2(51) of the Companies Act, 2013, and as disclosed

in “Our Management – Key Management Personnel” on page 230

Mag Engineering Mag Engineering Private Limited

Managing Director Managing Director of our Company

Materiality Policy The policy adopted by our Board on November 18, 2017 identifying material

litigation and outstanding dues to creditors in respect of our Company, pursuant to

the requirements of the SEBI ICDR Regulations

Memorandum of Association or

MoA

Memorandum of association of our Company, as amended

Nomination and Remuneration

Committee

Nomination and remuneration committee of the Board constituted in accordance

with Regulation 19 of the SEBI Listing Regulations, and Section 178 of the

Companies Act, 2013, described in “Our Management – Corporate Governance –

Committees of the Board” on page 223

Preference Share 5% optionally convertible and redeemable preference shares of our Company of face

value of ₹100 each

Previous Auditors S R Batliboi & Co., LLP

Promoter The promoter of our Company, namely, Jayant Davar. For details, see “Our

Promoter and Promoter Group” on page 234

Promoter Group Persons and entities constituting the promoter group of our Company in terms of

Regulation 2(1)(zb) of the SEBI ICDR Regulations. For details, see “Our Promoter

and Promoter Group” on page 234

PT Sandhar PT Sandhar Indonesia, Indonesia, for details, see “Our Subsidiaries and Joint

Ventures” on page 210

Registered Office The registered office of our Company located at B-6/20, L.S.C. Safdarjung Enclave,

New Delhi – 110 029, India

Registrar of Companies / RoC The Registrar of Companies, Delhi and Haryana, located at 4th Floor, IFCI Tower,

61, Nehru Place, New Delhi – 110 019, India

Restated Financial Statements Collectively, the Restated Unconsolidated Summary Statements and the Restated

Consolidated Summary Statements

Sandhar Amkin Sandhar Amkin Industries Private Limited, for details, see “Our Subsidiaries and

Joint Ventures” on page 210

Sandhar Breniar Breniar Projects S. L., Spain, for details, see “Our Subsidiaries and Joint Ventures”

on page 210

Sandhar Caama Sandhar Caama Components Private Limited, for details

Sandhar Daewha Sandhar Daewha Automotive Systems Private Limited, for details, see “Our

Subsidiaries and Joint Ventures” on page 210

Sandhar Ecco-Green Energy Sandhar ECCO Green Energy Private Limited, for details, see “Our Subsidiaries

and Joint Ventures” on page 210

Sandhar Han Sung Sandhar Han Sung Technologies Private Limited, for details, see “Our

Subsidiaries and Joint Ventures” on page 210

Sandhar Strategic Systems Sandhar Strategic Systems Private Limited

Sandhar Tooling Sandhar Tooling Private Limited, for details, see “Our Subsidiaries and Joint

Ventures” on page 210

Selling Shareholder GTI Capital Beta Pvt Ltd

Shareholder(s) Shareholder(s) of our Company from time to time

Stakeholders’ Relationship

Committee

Stakeholders’ relationship committee of the Board

ST Barcelona Sandhar Technologies Barcelona S. L., Spain

ST Mexico Sandhar Technologies De Mexico, S. de RL de CV Mexico

ST Poland Sandhar Technologies Poland sp. z.o.o., Poland

Stitch Overseas Stitch Overseas Private Limited

Subsidiaries, or individually The subsidiaries of our Company namely, (i) Sandhar Tooling, (ii) ST Barcelona,

5

Term Description

known as Subsidiary (iii) PT Sandhar, (iv) ST Poland, (v) ST Mexico, and (vi) Sandhar Breniar. For details

of the Subsidiaries, see “Our Subsidiaries and Joint Ventures” on page 210

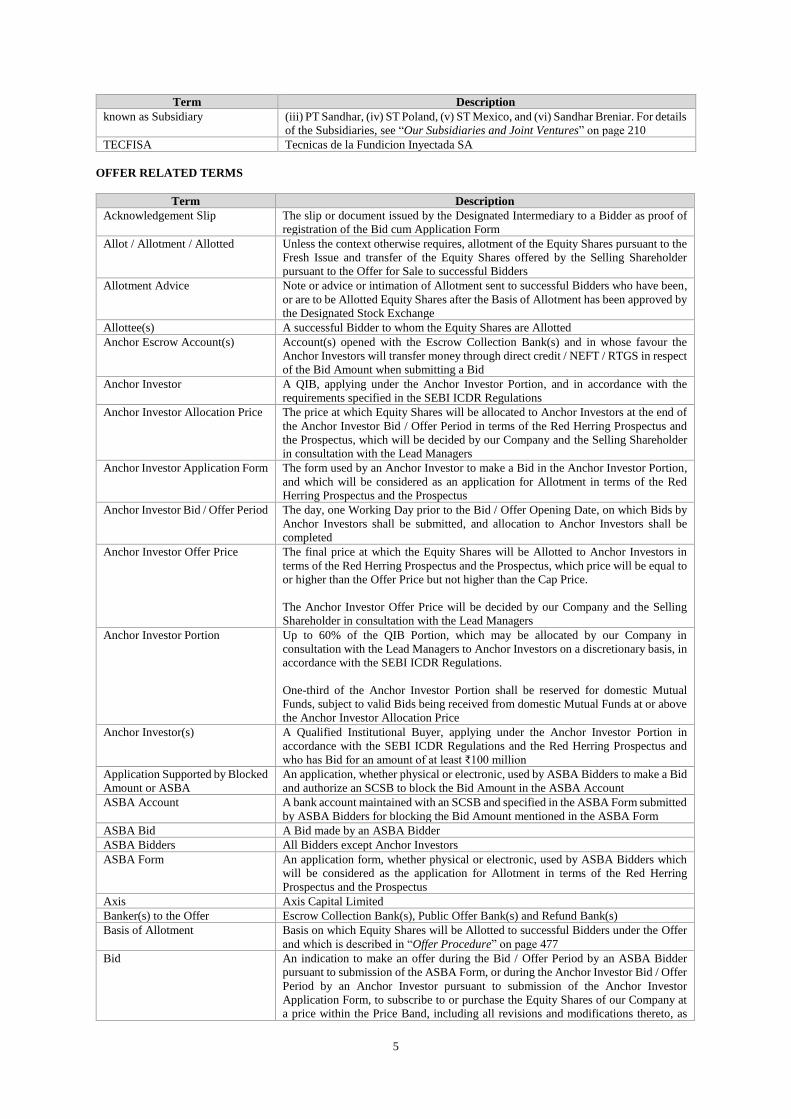

TECFISA Tecnicas de la Fundicion Inyectada SA

OFFER RELATED TERMS

Term Description

Acknowledgement Slip The slip or document issued by the Designated Intermediary to a Bidder as proof of

registration of the Bid cum Application Form

Allot / Allotment / Allotted Unless the context otherwise requires, allotment of the Equity Shares pursuant to the

Fresh Issue and transfer of the Equity Shares offered by the Selling Shareholder

pursuant to the Offer for Sale to successful Bidders

Allotment Advice Note or advice or intimation of Allotment sent to successful Bidders who have been,

or are to be Allotted Equity Shares after the Basis of Allotment has been approved by

the Designated Stock Exchange

Allottee(s) A successful Bidder to whom the Equity Shares are Allotted

Anchor Escrow Account(s) Account(s) opened with the Escrow Collection Bank(s) and in whose favour the

Anchor Investors will transfer money through direct credit / NEFT / RTGS in respect

of the Bid Amount when submitting a Bid

Anchor Investor A QIB, applying under the Anchor Investor Portion, and in accordance with the

requirements specified in the SEBI ICDR Regulations

Anchor Investor Allocation Price The price at which Equity Shares will be allocated to Anchor Investors at the end of

the Anchor Investor Bid / Offer Period in terms of the Red Herring Prospectus and

the Prospectus, which will be decided by our Company and the Selling Shareholder

in consultation with the Lead Managers

Anchor Investor Application Form The form used by an Anchor Investor to make a Bid in the Anchor Investor Portion,

and which will be considered as an application for Allotment in terms of the Red

Herring Prospectus and the Prospectus

Anchor Investor Bid / Offer Period The day, one Working Day prior to the Bid / Offer Opening Date, on which Bids by

Anchor Investors shall be submitted, and allocation to Anchor Investors shall be

completed

Anchor Investor Offer Price The final price at which the Equity Shares will be Allotted to Anchor Investors in

terms of the Red Herring Prospectus and the Prospectus, which price will be equal to

or higher than the Offer Price but not higher than the Cap Price.

The Anchor Investor Offer Price will be decided by our Company and the Selling

Shareholder in consultation with the Lead Managers

Anchor Investor Portion Up to 60% of the QIB Portion, which may be allocated by our Company in

consultation with the Lead Managers to Anchor Investors on a discretionary basis, in

accordance with the SEBI ICDR Regulations.

One-third of the Anchor Investor Portion shall be reserved for domestic Mutual

Funds, subject to valid Bids being received from domestic Mutual Funds at or above

the Anchor Investor Allocation Price

Anchor Investor(s) A Qualified Institutional Buyer, applying under the Anchor Investor Portion in

accordance with the SEBI ICDR Regulations and the Red Herring Prospectus and

who has Bid for an amount of at least ₹100 million

Application Supported by Blocked

Amount or ASBA

An application, whether physical or electronic, used by ASBA Bidders to make a Bid

and authorize an SCSB to block the Bid Amount in the ASBA Account

ASBA Account A bank account maintained with an SCSB and specified in the ASBA Form submitted

by ASBA Bidders for blocking the Bid Amount mentioned in the ASBA Form

ASBA Bid A Bid made by an ASBA Bidder

ASBA Bidders All Bidders except Anchor Investors

ASBA Form An application form, whether physical or electronic, used by ASBA Bidders which

will be considered as the application for Allotment in terms of the Red Herring

Prospectus and the Prospectus

Axis Axis Capital Limited

Banker(s) to the Offer Escrow Collection Bank(s), Public Offer Bank(s) and Refund Bank(s)

Basis of Allotment Basis on which Equity Shares will be Allotted to successful Bidders under the Offer

and which is described in “Offer Procedure” on page 477

Bid An indication to make an offer during the Bid / Offer Period by an ASBA Bidder

pursuant to submission of the ASBA Form, or during the Anchor Investor Bid / Offer

Period by an Anchor Investor pursuant to submission of the Anchor Investor

Application Form, to subscribe to or purchase the Equity Shares of our Company at

a price within the Price Band, including all revisions and modifications thereto, as

6

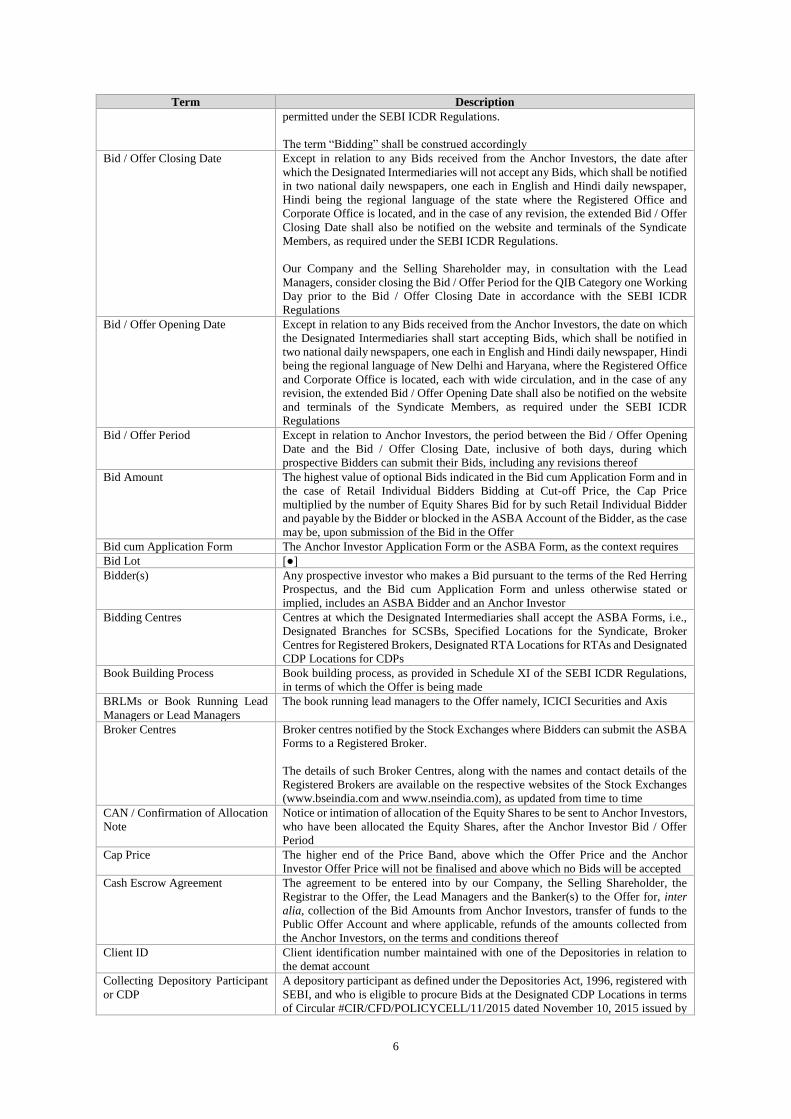

Term Description

permitted under the SEBI ICDR Regulations.

The term “Bidding” shall be construed accordingly

Bid / Offer Closing Date Except in relation to any Bids received from the Anchor Investors, the date after

which the Designated Intermediaries will not accept any Bids, which shall be notified

in two national daily newspapers, one each in English and Hindi daily newspaper,

Hindi being the regional language of the state where the Registered Office and

Corporate Office is located, and in the case of any revision, the extended Bid / Offer

Closing Date shall also be notified on the website and terminals of the Syndicate

Members, as required under the SEBI ICDR Regulations.

Our Company and the Selling Shareholder may, in consultation with the Lead

Managers, consider closing the Bid / Offer Period for the QIB Category one Working

Day prior to the Bid / Offer Closing Date in accordance with the SEBI ICDR

Regulations

Bid / Offer Opening Date Except in relation to any Bids received from the Anchor Investors, the date on which

the Designated Intermediaries shall start accepting Bids, which shall be notified in

two national daily newspapers, one each in English and Hindi daily newspaper, Hindi

being the regional language of New Delhi and Haryana, where the Registered Office

and Corporate Office is located, each with wide circulation, and in the case of any

revision, the extended Bid / Offer Opening Date shall also be notified on the website

and terminals of the Syndicate Members, as required under the SEBI ICDR

Regulations

Bid / Offer Period Except in relation to Anchor Investors, the period between the Bid / Offer Opening

Date and the Bid / Offer Closing Date, inclusive of both days, during which

prospective Bidders can submit their Bids, including any revisions thereof

Bid Amount The highest value of optional Bids indicated in the Bid cum Application Form and in

the case of Retail Individual Bidders Bidding at Cut-off Price, the Cap Price

multiplied by the number of Equity Shares Bid for by such Retail Individual Bidder

and payable by the Bidder or blocked in the ASBA Account of the Bidder, as the case

may be, upon submission of the Bid in the Offer

Bid cum Application Form The Anchor Investor Application Form or the ASBA Form, as the context requires

Bid Lot [●]

Bidder(s) Any prospective investor who makes a Bid pursuant to the terms of the Red Herring

Prospectus, and the Bid cum Application Form and unless otherwise stated or

implied, includes an ASBA Bidder and an Anchor Investor

Bidding Centres Centres at which the Designated Intermediaries shall accept the ASBA Forms, i.e.,

Designated Branches for SCSBs, Specified Locations for the Syndicate, Broker

Centres for Registered Brokers, Designated RTA Locations for RTAs and Designated

CDP Locations for CDPs

Book Building Process Book building process, as provided in Schedule XI of the SEBI ICDR Regulations,

in terms of which the Offer is being made

BRLMs or Book Running Lead

Managers or Lead Managers

The book running lead managers to the Offer namely, ICICI Securities and Axis

Broker Centres Broker centres notified by the Stock Exchanges where Bidders can submit the ASBA

Forms to a Registered Broker.

The details of such Broker Centres, along with the names and contact details of the

Registered Brokers are available on the respective websites of the Stock Exchanges

(www.bseindia.com and www.nseindia.com), as updated from time to time

CAN / Confirmation of Allocation

Note

Notice or intimation of allocation of the Equity Shares to be sent to Anchor Investors,

who have been allocated the Equity Shares, after the Anchor Investor Bid / Offer

Period

Cap Price The higher end of the Price Band, above which the Offer Price and the Anchor

Investor Offer Price will not be finalised and above which no Bids will be accepted

Cash Escrow Agreement The agreement to be entered into by our Company, the Selling Shareholder, the

Registrar to the Offer, the Lead Managers and the Banker(s) to the Offer for, inter

alia, collection of the Bid Amounts from Anchor Investors, transfer of funds to the

Public Offer Account and where applicable, refunds of the amounts collected from

the Anchor Investors, on the terms and conditions thereof

Client ID Client identification number maintained with one of the Depositories in relation to

the demat account

Collecting Depository Participant

or CDP

A depository participant as defined under the Depositories Act, 1996, registered with

SEBI, and who is eligible to procure Bids at the Designated CDP Locations in terms

of Circular #CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by

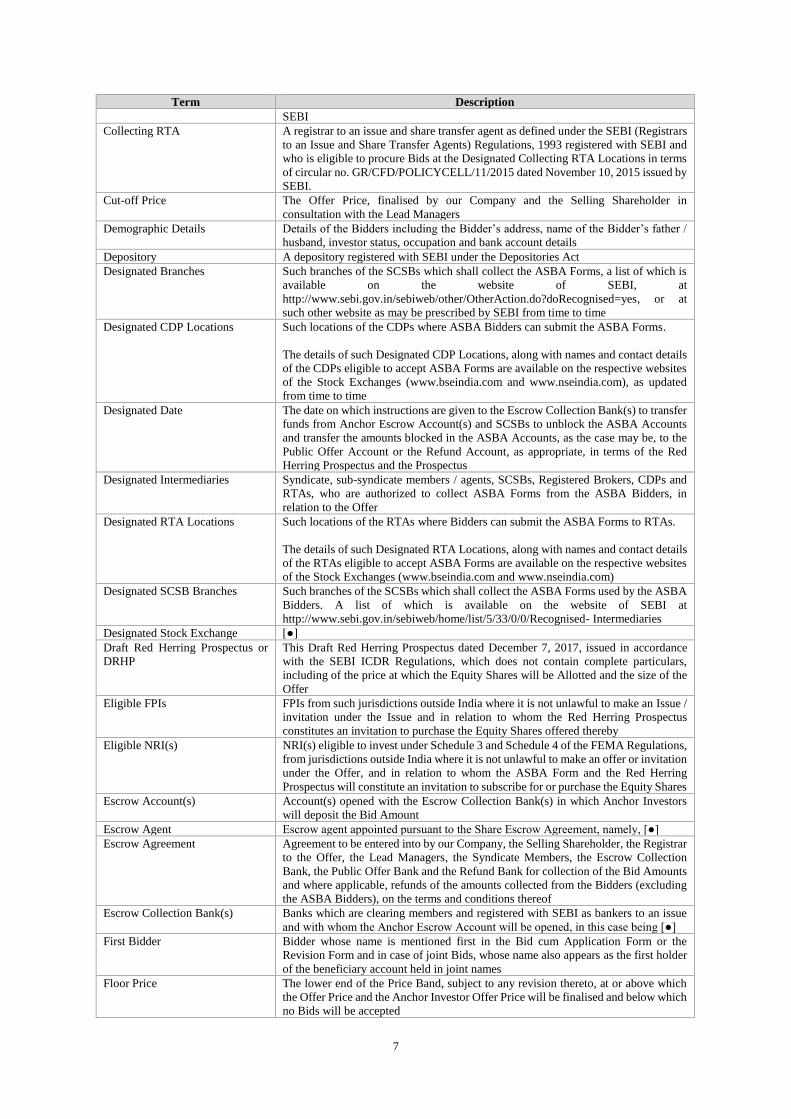

7

Term Description

SEBI

Collecting RTA A registrar to an issue and share transfer agent as defined under the SEBI (Registrars

to an Issue and Share Transfer Agents) Regulations, 1993 registered with SEBI and

who is eligible to procure Bids at the Designated Collecting RTA Locations in terms

of circular no. GR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by

SEBI.

Cut-off Price The Offer Price, finalised by our Company and the Selling Shareholder in

consultation with the Lead Managers

Demographic Details Details of the Bidders including the Bidder’s address, name of the Bidder’s father /

husband, investor status, occupation and bank account details

Depository A depository registered with SEBI under the Depositories Act

Designated Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which is

available on the website of SEBI, at

http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes, or at

such other website as may be prescribed by SEBI from time to time

Designated CDP Locations Such locations of the CDPs where ASBA Bidders can submit the ASBA Forms.

The details of such Designated CDP Locations, along with names and contact details

of the CDPs eligible to accept ASBA Forms are available on the respective websites

of the Stock Exchanges (www.bseindia.com and www.nseindia.com), as updated

from time to time

Designated Date The date on which instructions are given to the Escrow Collection Bank(s) to transfer

funds from Anchor Escrow Account(s) and SCSBs to unblock the ASBA Accounts

and transfer the amounts blocked in the ASBA Accounts, as the case may be, to the

Public Offer Account or the Refund Account, as appropriate, in terms of the Red

Herring Prospectus and the Prospectus

Designated Intermediaries Syndicate, sub-syndicate members / agents, SCSBs, Registered Brokers, CDPs and

RTAs, who are authorized to collect ASBA Forms from the ASBA Bidders, in

relation to the Offer

Designated RTA Locations Such locations of the RTAs where Bidders can submit the ASBA Forms to RTAs.

The details of such Designated RTA Locations, along with names and contact details

of the RTAs eligible to accept ASBA Forms are available on the respective websites

of the Stock Exchanges (www.bseindia.com and www.nseindia.com)

Designated SCSB Branches Such branches of the SCSBs which shall collect the ASBA Forms used by the ASBA

Bidders. A list of which is available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/home/list/5/33/0/0/Recognised- Intermediaries

Designated Stock Exchange [●]

Draft Red Herring Prospectus or

DRHP

This Draft Red Herring Prospectus dated December 7, 2017, issued in accordance

with the SEBI ICDR Regulations, which does not contain complete particulars,

including of the price at which the Equity Shares will be Allotted and the size of the

Offer

Eligible FPIs FPIs from such jurisdictions outside India where it is not unlawful to make an Issue /

invitation under the Issue and in relation to whom the Red Herring Prospectus

constitutes an invitation to purchase the Equity Shares offered thereby

Eligible NRI(s) NRI(s) eligible to invest under Schedule 3 and Schedule 4 of the FEMA Regulations,

from jurisdictions outside India where it is not unlawful to make an offer or invitation

under the Offer, and in relation to whom the ASBA Form and the Red Herring

Prospectus will constitute an invitation to subscribe for or purchase the Equity Shares

Escrow Account(s) Account(s) opened with the Escrow Collection Bank(s) in which Anchor Investors

will deposit the Bid Amount

Escrow Agent Escrow agent appointed pursuant to the Share Escrow Agreement, namely, [●]

Escrow Agreement Agreement to be entered into by our Company, the Selling Shareholder, the Registrar

to the Offer, the Lead Managers, the Syndicate Members, the Escrow Collection

Bank, the Public Offer Bank and the Refund Bank for collection of the Bid Amounts

and where applicable, refunds of the amounts collected from the Bidders (excluding

the ASBA Bidders), on the terms and conditions thereof

Escrow Collection Bank(s) Banks which are clearing members and registered with SEBI as bankers to an issue

and with whom the Anchor Escrow Account will be opened, in this case being [●]

First Bidder Bidder whose name is mentioned first in the Bid cum Application Form or the

Revision Form and in case of joint Bids, whose name also appears as the first holder

of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, subject to any revision thereto, at or above which

the Offer Price and the Anchor Investor Offer Price will be finalised and below which

no Bids will be accepted

8

Term Description

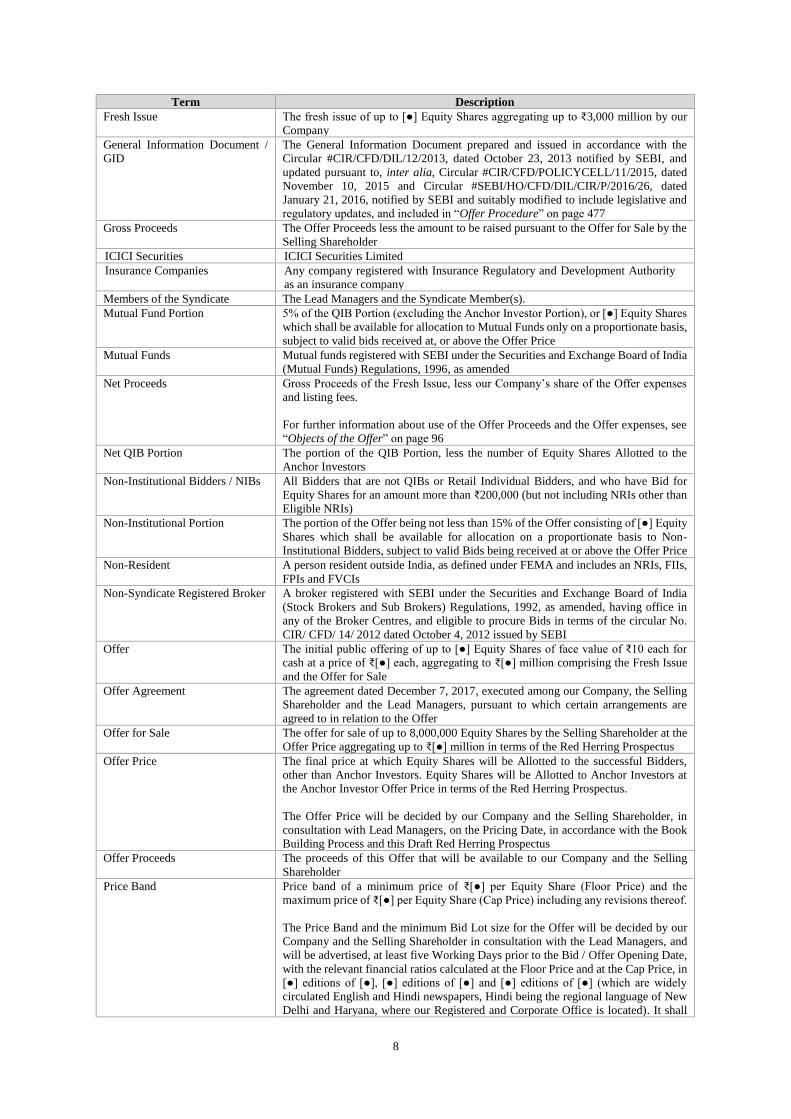

Fresh Issue The fresh issue of up to [●] Equity Shares aggregating up to ₹3,000 million by our

Company

General Information Document /

GID

The General Information Document prepared and issued in accordance with the

Circular #CIR/CFD/DIL/12/2013, dated October 23, 2013 notified by SEBI, and

updated pursuant to, inter alia, Circular #CIR/CFD/POLICYCELL/11/2015, dated

November 10, 2015 and Circular #SEBI/HO/CFD/DIL/CIR/P/2016/26, dated

January 21, 2016, notified by SEBI and suitably modified to include legislative and

regulatory updates, and included in “Offer Procedure” on page 477

Gross Proceeds The Offer Proceeds less the amount to be raised pursuant to the Offer for Sale by the

Selling Shareholder

ICICI Securities ICICI Securities Limited

Insurance Companies Any company registered with Insurance Regulatory and Development Authority

as an insurance company

Members of the Syndicate The Lead Managers and the Syndicate Member(s).

Mutual Fund Portion 5% of the QIB Portion (excluding the Anchor Investor Portion), or [●] Equity Shares

which shall be available for allocation to Mutual Funds only on a proportionate basis,

subject to valid bids received at, or above the Offer Price

Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of India

(Mutual Funds) Regulations, 1996, as amended

Net Proceeds Gross Proceeds of the Fresh Issue, less our Company’s share of the Offer expenses

and listing fees.

For further information about use of the Offer Proceeds and the Offer expenses, see

“Objects of the Offer” on page 96

Net QIB Portion The portion of the QIB Portion, less the number of Equity Shares Allotted to the

Anchor Investors

Non-Institutional Bidders / NIBs All Bidders that are not QIBs or Retail Individual Bidders, and who have Bid for

Equity Shares for an amount more than ₹200,000 (but not including NRIs other than

Eligible NRIs)

Non-Institutional Portion The portion of the Offer being not less than 15% of the Offer consisting of [●] Equity

Shares which shall be available for allocation on a proportionate basis to Non-

Institutional Bidders, subject to valid Bids being received at or above the Offer Price

Non-Resident A person resident outside India, as defined under FEMA and includes an NRIs, FIIs,

FPIs and FVCIs

Non-Syndicate Registered Broker A broker registered with SEBI under the Securities and Exchange Board of India

(Stock Brokers and Sub Brokers) Regulations, 1992, as amended, having office in

any of the Broker Centres, and eligible to procure Bids in terms of the circular No.

CIR/ CFD/ 14/ 2012 dated October 4, 2012 issued by SEBI

Offer The initial public offering of up to [●] Equity Shares of face value of ₹10 each for

cash at a price of ₹[●] each, aggregating to ₹[●] million comprising the Fresh Issue

and the Offer for Sale

Offer Agreement The agreement dated December 7, 2017, executed among our Company, the Selling

Shareholder and the Lead Managers, pursuant to which certain arrangements are

agreed to in relation to the Offer

Offer for Sale The offer for sale of up to 8,000,000 Equity Shares by the Selling Shareholder at the

Offer Price aggregating up to ₹[●] million in terms of the Red Herring Prospectus

Offer Price The final price at which Equity Shares will be Allotted to the successful Bidders,

other than Anchor Investors. Equity Shares will be Allotted to Anchor Investors at

the Anchor Investor Offer Price in terms of the Red Herring Prospectus.

The Offer Price will be decided by our Company and the Selling Shareholder, in

consultation with Lead Managers, on the Pricing Date, in accordance with the Book

Building Process and this Draft Red Herring Prospectus

Offer Proceeds The proceeds of this Offer that will be available to our Company and the Selling

Shareholder

Price Band Price band of a minimum price of ₹[●] per Equity Share (Floor Price) and the

maximum price of ₹[●] per Equity Share (Cap Price) including any revisions thereof.

The Price Band and the minimum Bid Lot size for the Offer will be decided by our

Company and the Selling Shareholder in consultation with the Lead Managers, and

will be advertised, at least five Working Days prior to the Bid / Offer Opening Date,

with the relevant financial ratios calculated at the Floor Price and at the Cap Price, in

[●] editions of [●], [●] editions of [●] and [●] editions of [●] (which are widely

circulated English and Hindi newspapers, Hindi being the regional language of New

Delhi and Haryana, where our Registered and Corporate Office is located). It shall

9

Term Description

also be made available to the Stock Exchanges for the purpose of uploading on their

websites

Pricing Date The date on which our Company and the Selling Shareholder in consultation with

Lead Managers, will finalise the Offer Price

Prospectus The Prospectus to be filed with the RoC, on or after the Pricing Date in accordance

with Section 26 of the Companies Act, 2013, and the SEBI ICDR Regulations,

containing, inter alia, the Offer Price that is determined at the end of the Book

Building Process, the size of the Offer and certain other information, including any

addenda or corrigenda thereto

Public Offer Account Bank The Banker(s) to the Offer with whom the Public Offer Account(s) shall be

maintained, in this case being [●]

Public Offer Account(s) Bank account opened under Section 40(3) of the Companies Act, 2013 to receive

monies from the Anchor Escrow Account(s) and ASBA Accounts on the Designated

Date

QIB Category / QIB Portion The portion of the Offer (including the Anchor Investor Portion) being not more than

50% of the Offer or [●] Equity Shares, available for allocation to QIBs (including

Anchor Investors) on a proportionate basis (in which allocation shall be on a

discretionary basis, as determined by our Company, in consultation with the Lead

Managers), subject to valid Bids being received at our above the Offer Price

Qualified Institutional Buyer(s) or

QIBs or QIB Bidders

Qualified institutional buyer(s) as defined under Regulation 2(1)(zd) of the SEBI

ICDR Regulations

Red Herring Prospectus or RHP The Red Herring Prospectus to be issued in accordance with Section 32 of the

Companies Act, 2013 and the provisions of the SEBI ICDR Regulations, which will

not have complete particulars of the price at which the Equity Shares will be offered

and the size of the Offer including any addenda or corrigenda thereto.

The Red Herring Prospectus will be registered with the RoC at least three days before

the Bid / Offer Opening Date and will become the Prospectus upon filing with the

RoC after the Pricing Date

Refund Account(s) The account opened with the Refund Bank(s), from which refunds, if any, of the

whole or part of the Bid Amount to the Anchor Investors shall be made

Refund Bank(s) The Bankers to the Offer with which the Refund Account(s) will be opened, in this

case being [●]

Refunds through electronic

transfer of funds

Refunds through electronic transfer of funds means refunds through NECS, Direct

Credit, NEFT or RTGS, as applicable

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other

than the BRLMs and the Syndicate Members who are eligible to procure Bids in terms

of Circular #CIR/CFD/14/2012 dated October 4, 2012 issued by SEBI

Registrar Agreement Registrar agreement dated December 5, 2017, amongst our Company, the Selling

Shareholder and the Registrar to the Offer

Registrar and Share Transfer

Agents or RTAs

Registrars to an issue and share transfer agents registered with SEBI and eligible to

procure Bids at the Designated RTA Locations in terms of Circular

#CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Registrar to the Offer or Registrar Link Intime India Private Limited

Retail Discount Our Company and the Selling Shareholder, in consultation with the Lead Managers,

may decide to offer a discount of [●]% to the Floor Price, i.e., ₹[●] to Retail

Individual Investors and which shall be announced at least five Working Days prior

to the Bid / Issue Opening Date

Resident Indian A person resident in India, as defined under FEMA

Retail Individual Bidder(s) /

RIB(s)

Individual Bidders who have Bid for the Equity Shares for an amount of not more

than ₹200,000 in any of the bidding options in the Offer (including HUFs applying

through their karta and Eligible NRIs)

Retail Portion The portion of the Offer being not less than 35% of the Offer consisting of [●] Equity

Shares which shall be available for allocation to Retail Individual Bidder(s) in

accordance with the SEBI ICDR Regulations, subject to valid Bids being received at

or above the Offer Price

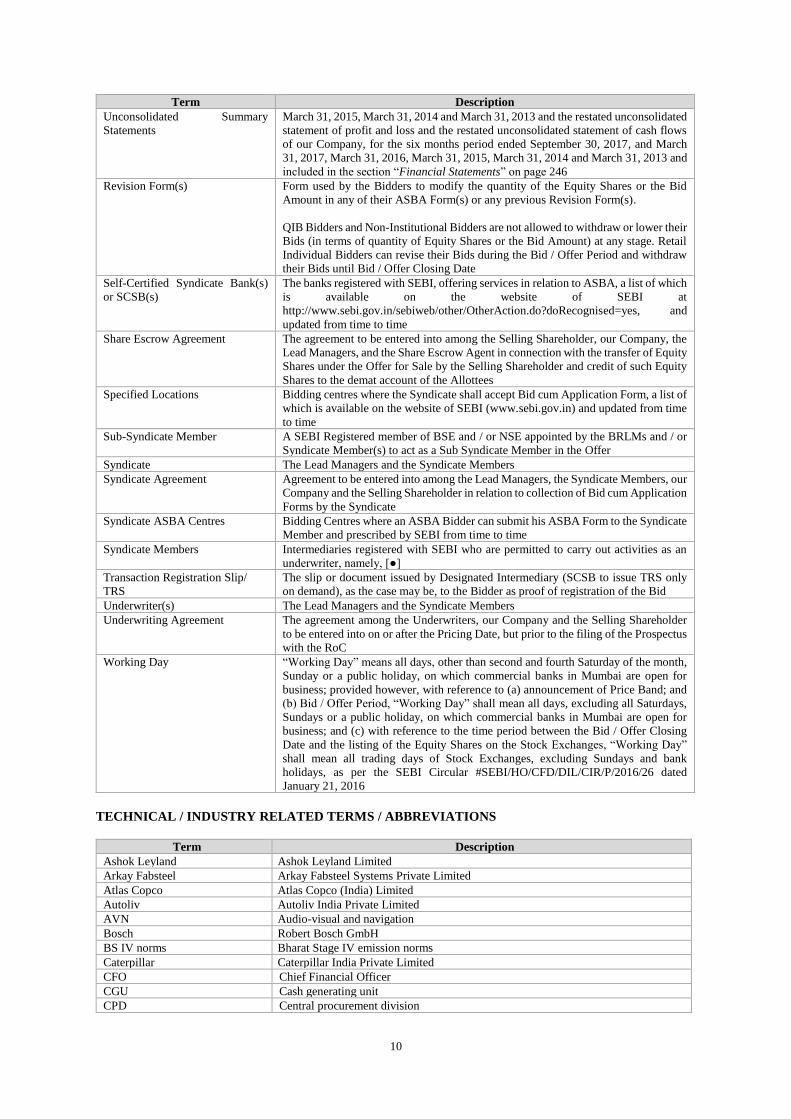

Restated Consolidated Financial

Information / Restated

Consolidated Summary

Statements

Restated consolidated statement of assets and liabilities of our Company as at the six

months period ended September 30, 2017, and March 31, 2017, March 31, 2016,

March 31, 2015, March 31, 2014 and March 31, 2013, and the restated consolidated

statement of profit and loss and the restated consolidated statement of cash flows of

our Company, for the six months period ended September 30, 2017, and March 31,

2017, March 31, 2016, March 31, 2015, March 31, 2014 and March 31, 2013 and

included in the section “Financial Statements” on page 246

Restated Standalone Financial

Information / Restated

Restated unconsolidated statement of assets and liabilities of our Company as at the

six months period ended September 30, 2017, and March 31, 2017, March 31, 2016,

10

Term Description

Unconsolidated Summary

Statements

March 31, 2015, March 31, 2014 and March 31, 2013 and the restated unconsolidated

statement of profit and loss and the restated unconsolidated statement of cash flows

of our Company, for the six months period ended September 30, 2017, and March

31, 2017, March 31, 2016, March 31, 2015, March 31, 2014 and March 31, 2013 and

included in the section “Financial Statements” on page 246

Revision Form(s) Form used by the Bidders to modify the quantity of the Equity Shares or the Bid

Amount in any of their ASBA Form(s) or any previous Revision Form(s).

QIB Bidders and Non-Institutional Bidders are not allowed to withdraw or lower their

Bids (in terms of quantity of Equity Shares or the Bid Amount) at any stage. Retail

Individual Bidders can revise their Bids during the Bid / Offer Period and withdraw

their Bids until Bid / Offer Closing Date

Self-Certified Syndicate Bank(s)

or SCSB(s)

The banks registered with SEBI, offering services in relation to ASBA, a list of which

is available on the website of SEBI at

http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes, and

updated from time to time

Share Escrow Agreement The agreement to be entered into among the Selling Shareholder, our Company, the

Lead Managers, and the Share Escrow Agent in connection with the transfer of Equity

Shares under the Offer for Sale by the Selling Shareholder and credit of such Equity

Shares to the demat account of the Allottees

Specified Locations Bidding centres where the Syndicate shall accept Bid cum Application Form, a list of

which is available on the website of SEBI (www.sebi.gov.in) and updated from time

to time

Sub-Syndicate Member A SEBI Registered member of BSE and / or NSE appointed by the BRLMs and / or

Syndicate Member(s) to act as a Sub Syndicate Member in the Offer

Syndicate The Lead Managers and the Syndicate Members

Syndicate Agreement Agreement to be entered into among the Lead Managers, the Syndicate Members, our

Company and the Selling Shareholder in relation to collection of Bid cum Application

Forms by the Syndicate

Syndicate ASBA Centres Bidding Centres where an ASBA Bidder can submit his ASBA Form to the Syndicate

Member and prescribed by SEBI from time to time

Syndicate Members Intermediaries registered with SEBI who are permitted to carry out activities as an

underwriter, namely, [●]

Transaction Registration Slip/

TRS

The slip or document issued by Designated Intermediary (SCSB to issue TRS only

on demand), as the case may be, to the Bidder as proof of registration of the Bid

Underwriter(s) The Lead Managers and the Syndicate Members

Underwriting Agreement The agreement among the Underwriters, our Company and the Selling Shareholder

to be entered into on or after the Pricing Date, but prior to the filing of the Prospectus

with the RoC

Working Day “Working Day” means all days, other than second and fourth Saturday of the month,

Sunday or a public holiday, on which commercial banks in Mumbai are open for

business; provided however, with reference to (a) announcement of Price Band; and

(b) Bid / Offer Period, “Working Day” shall mean all days, excluding all Saturdays,

Sundays or a public holiday, on which commercial banks in Mumbai are open for

business; and (c) with reference to the time period between the Bid / Offer Closing

Date and the listing of the Equity Shares on the Stock Exchanges, “Working Day”

shall mean all trading days of Stock Exchanges, excluding Sundays and bank

holidays, as per the SEBI Circular #SEBI/HO/CFD/DIL/CIR/P/2016/26 dated

January 21, 2016

TECHNICAL / INDUSTRY RELATED TERMS / ABBREVIATIONS

Term Description

Ashok Leyland Ashok Leyland Limited

Arkay Fabsteel Arkay Fabsteel Systems Private Limited

Atlas Copco Atlas Copco (India) Limited

Autoliv Autoliv India Private Limited

AVN Audio-visual and navigation

Bosch Robert Bosch GmbH

BS IV norms Bharat Stage IV emission norms

Caterpillar Caterpillar India Private Limited

CFO Chief Financial Officer

CGU Cash generating unit

CPD Central procurement division

11

Term Description

CTS Together, CTS India Private Limited and, CTS Corporation

DMRG DMRG Investment Private Limited

Doosan Bobcat Doosan Bobcat India Private Limited

Escorts Escorts Limited

EVAP Evaporative Emission Control System

Hero Hero MotorCorp Limited

Honda Cars Honda Cars India Limited

Honda Lock Honda Lock Manufacturing Company Limited

HSIIDC Haryana State Industrial & Infrastructure Development Corporation Limited

Hyundai Construction Hyundai Construction Equipment India Private Limited

IDC Industrial development corporation

International Tractors International Tractors Limited

JCB JCB India Limited

JEM Techno JEM Techno Co. Limited, Korea

Kobelco Kobelco Construction Equipment India Private Limited

Komatsu Komatsu India Private Limited

LeeBoy India LeeBoy India Construction Equipment (P) Limited

Mahindra & Mahindra Mahindra and Mahindra Limited

MIDC Maharashtra Industrial Development Corporation

OEM Original Equipment Manufacturer

OHV Off-highway vehicle

Potain India Potain India Private Limited

RIICO Rajasthan State Industrial Development and Investment Corporation

Royal Enfield Royal Enfield, a unit of Eicher Motors Group

Scania Scania Commercial Vehicles India Private Limited

SCID Sandhar Centre for Innovation and Development, Gurugram

SML Isuzu SML Isuzu Limited

Steady Stream Steady Stream Business Limited, Taiwan

Suzuki Suzuki Motorcycle India Private Limited

Tata Motors Tata Motors Limited

TAFE Tractors and Farm Equipment Limited

TVS TVS Motor Company Limited

UM Lohia UM Lohia Two Wheelers Private Limited

Volvo Volvo Group India Private Limited

Yamaha India Yamaha Motor Private Limited

CONVENTIONAL AND GENERAL TERMS OR ABBREVIATIONS

Term Description

₹ / Rs. / Rupees / INR Indian Rupees

AGM Annual general meeting

AIF Alternative Investment Fund as defined in and registered with SEBI under the SEBI

AIF Regulations

AS / Accounting Standards Accounting Standards issued by the ICAI under the provisions of the Companies Act

AY Assessment year

BPLR Bank prime lending rate

BG Bank guarantee

BR Base rate

BSE BSE Limited

Bn / bn Billion

CAGR Compounded annual growth rate being the annualised average year-on-year growth

rate over a specific period of time which is calculated using the formula as below:

{[V(t_n)/V(t_0)]^(1/(t_n-t_0)]} – 1*

* V(t_0): start value, V(t_n): finish value, t_n-t_0: number of years

CC Cash credit

Category I Foreign Portfolio

Investors

FPIs who are registered as “Category I foreign portfolio investors” under the SEBI

FPI Regulations

Category II Foreign Portfolio

Investors

FPIs who are registered as “Category II foreign portfolio investors” under the SEBI

FPI Regulations

Category III Foreign Portfolio

Investors

FPIs who are registered as “Category III foreign portfolio investors” under the SEBI

FPI Regulations which shall include investors who are not eligible under Category I

12

Term Description

and II foreign portfolio investors such as endowments, charitable societies, charitable

trusts, foundations, corporate bodies, trusts, individuals and family offices

CDSL Central Depository Services Limited

CII Confederation of Indian Industry

CIN Corporate Identity Number

Companies Act Companies Act, 1956 and / or the Companies Act, 2013, as applicable

Companies Act, 1956 Companies Act, 1956, and the rules thereunder (without reference to the provisions

thereof that have ceased to have effect upon the notification of the Notified Sections)

Companies Act, 2013 The Companies Act, 2013, and the rules and clarifications issued thereunder to the

extent in force pursuant to the notification of the Notified Sections

Consolidated FDI Policy Consolidated FDI Policy, effective from August 28, 2017, issued by the DIPP

including any modifications thereto or substitutions thereof

CSR Corporate social responsibility

CST Central sales tax

CST Act Central Sales Tax Act, 1956

CWIP Capital work in progress

Depositories NSDL and CDSL

Depositories Act Depositories Act, 1996

DIN Director Identification Number

DIPP Department of Industrial Policy and Promotion, Ministry of Commerce and Industry,

Government of India

DP / Depository Participant A depository participant as defined under the Depositories Act

DP ID Depository Participant’s Identification

EBITDA Earnings Before Interest Taxes Depreciation and Amortisation

EGM Extraordinary general meeting

EPS Earnings Per Share

ERP Enterprise resource planning

EUR Euro

FCNR Account Foreign currency non-resident account

FDI Foreign direct investment

FEMA Foreign Exchange Management Act, 1999, and the rules and regulations thereunder

FEMA Regulations FEMA (Transfer or Issue of Security by a Person Resident Outside India) Regulations,

2000, as amended

FG Finished goods

FII(s) Foreign institutional investors as defined under the SEBI FPI Regulations investing

under the portfolio investment scheme under Schedule 2 of the FEMA Regulations

Finance Act Chapter V of the Finance Act, 1994

Financial Year / Fiscal(s) / FY Unless stated otherwise, the period of 12 months ending March 31 of that particular

year

FIPB Foreign Investment Promotion Board

FLC Foreign letter of credit

FPI(s) Foreign portfolio investors as defined under the SEBI FPI Regulations investing under

the portfolio investment scheme under Schedule 2A of the FEMA Regulations

FVCI Foreign venture capital investors as defined and registered under the SEBI FVCI

Regulations

GDP Gross domestic product

GoI, Government of India,

Central Government

Government of India

GST Goods and service tax

HNI High Net worth Individual

ICAI The Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

India Republic of India

Indian GAAP Generally Accepted Accounting Principles in India

Insider Trading Regulations The Securities and Exchange Board of India (Prohibition of Insider Trading)

Regulations, 2015, as amended

IPO Initial public offering

IRDAI Insurance Regulatory and Development Authority of India

ISO International Organisation for Standardisation

I.T. Act Income Tax Act, 1961

LEED Leadership in Energy and Environmental Design

LER Loan equivalent risk

LOC Letters of credit

13

Term Description

LOU Letter of undertaking

LLP Act The Limited Liability Partnership Act, 2008

MAT Minimum Alternate Tax

MCA Ministry of Corporate Affairs, Government of India

MICR Magnetic ink character recognition

Mn / mn Million

MOU Memorandum of understanding

Mutual Fund(s) Mutual Fund(s) means mutual funds registered under the SEBI (Mutual Funds)

Regulations, 1996

N.A./ NA Not applicable

NAV Net Asset Value

NAFTA North American Free Trade Agreement

NBFC Non-banking financial company registered with the RBI

NCR National capital region

NECS National electronic clearing services

NEFT National electronic fund transfer

Net Worth Net worth represents sum of equity share capital and reserves and surplus

(including securities premium, general reserve, capital reserve, capital redemption

reserve, foreign currency translation reserve, and surplus in the Statement of Profit

NOC No objection certificate.

Notified Sections The sections of the Companies Act, 2013 that have been notified by the MCA and

are currently in effect.

NCLT National Company Law Tribunal

Notified Sections The sections of the Companies Act, 2013 that have been notified by the Ministry of

Corporate Affairs, Government of India, and are currently in effect

NR Non-resident

NRE Account Non-resident external account

NRI A person resident outside India who is a citizen of India, as defined under the Foreign

Exchange Management (Deposit) Regulations, 2016, or is an ‘overseas citizen of

India’ cardholder within the meaning of Section 7(A) of the Citizenship Act, 1955

NRO Account Non-resident Ordinary Account

NSDL National Securities Depository Limited

NSE National Stock Exchange of India Limited

OCB(s) / Overseas Corporate

Body

A company, partnership, society or other corporate body owned directly or indirectly

to the extent of at least 60% by NRIs including overseas trusts, in which not less than

60% of beneficial interest is irrevocably held by NRIs directly or indirectly and which

was in existence on October 3, 2003 and immediately before such date had taken

benefits under the general permission granted to OCBs under FEMA. OCBs are not

allowed to invest in the Offer

OHSAS Occupational Health and Safety Assessment Series

P / E Ratio Price / Earnings Ratio

p.a. Per annum

PAN Permanent Account Number

PAT Profit After Tax

PBT Profit before tax

PIO Persons of Indian origin

PLR Prime lending rate

PPE Property plant equipment

RBI The Reserve Bank of India

Regulation S Regulation S under the Securities Act

RoNW Return on Net Worth

R&D Research and development

RTGS Real Time Gross Settlement

Rupees/ INR Indian Rupees

SCRA Securities Contracts (Regulation) Act, 1956, as amended

SCRR Securities Contracts (Regulation) Rules, 1957, as amended

SEBI The Securities and Exchange Board of India constituted under the SEBI Act

SEBI Act Securities and Exchange Board of India Act, 1992, as amended

SEBI AIF Regulations Securities and Exchange Board of India (Alternative Investment Funds) Regulations,

2012, as amended

SEBI FII Regulations Securities and Exchange Board of India (Foreign Institutional Investors) Regulations,

1995, as amended

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations,

14

Term Description

2014, as amended

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investors)

Regulations, 2000, as amended

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure

Requirements) Regulations, 2009, as amended

SEBI Listing Regulations Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015, as amended

SEBI VCF Regulations Securities and Exchange Board of India (Venture Capital Fund) Regulations, 1996, as

amended

Securities Act U. S. Securities Act of 1933, as amended

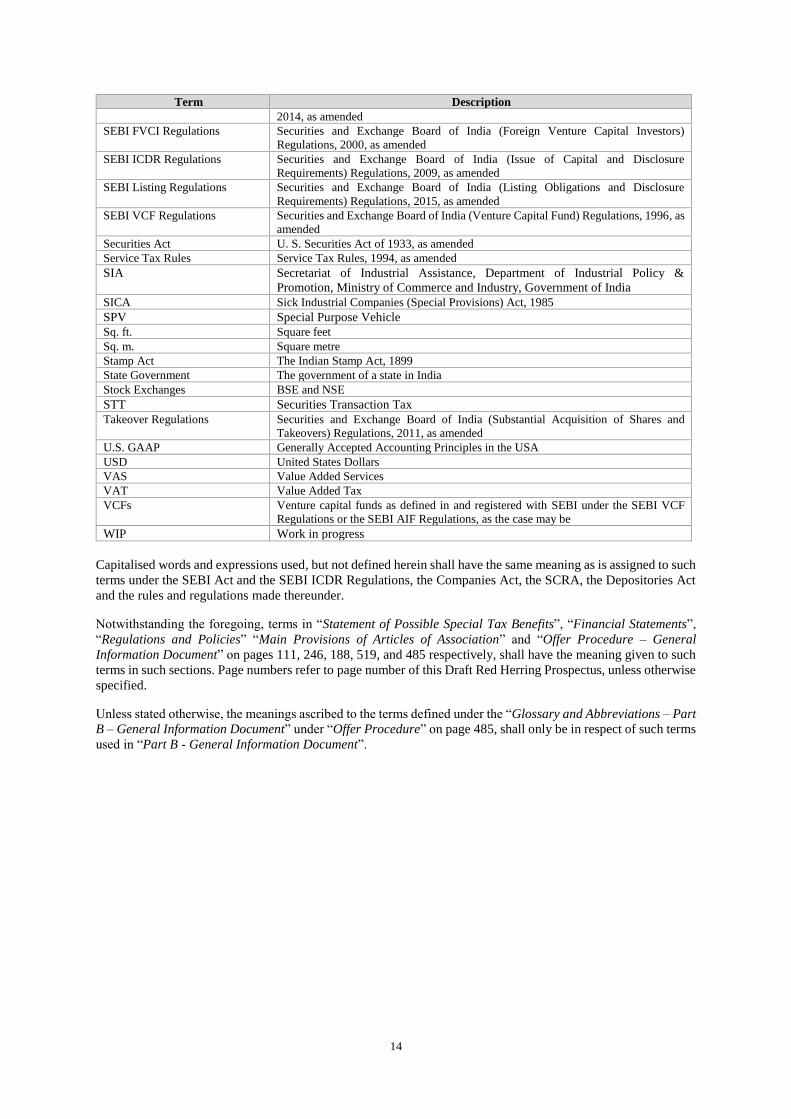

Service Tax Rules Service Tax Rules, 1994, as amended