Montreal Camera Club Introduction to Astrophotography By ...

Risky Spaces :The Montreal Fire Insurance Company, 1817-

20.

MONTREAL FIRE INSURANCE COMPANY In conformity to the articles ofassociation of the MONTREAL FIRE INSURANCECOMPANY, the stock holders are herebyrequired by the subscribing Directors tomeet at the Office of the said Company inthis city, on the FIRST MONDAY in FEBRUARY nextensuing at ELEVEN o’clock in the forenoon forthe purpose of dissolving the said COMPANY. A statement of the affairs of theInstitution may be seen by the stockholderson application to the Secretary.Benjn. Hall, Prest. Turton Penn, Ralph Taylor.John Frothingham V.P.

J.T. Barrett, Hiram Nicols,

Chs. Bowman, Jh.Roy, A. Laframboise,

Thomas Phillipps, Olivier Berthelet,

John Brown.

By-order of the President and Directors.Montreal, July 18th, 1820.

J. BLEAKLEY, Secy

This advertisement first ran in the Montreal Gazette on July 26th 1820. It appeared another five times in English over the ensuing three months.1 In marked contrast to the Gazette’s reaction to a recent fire that destroyed 22 homes in St Joseph suburb,2 no editorial comment on the failure of the firm was made. This 1. The Gazette was then a bilingual weekly and normally advertisements appeared in both languages. An advertiser had to specifically request a unilingual advertisement for it to run only in English.

silence surprises, given what people would have known of this company from the public record. Thomas Doige mentioned the Montreal Fire in both the November 18193 and the May 18204 editions of the city directory he compiled. Montreal Fire was oneof three fire insurance companies Doige identified as operating in the city.5 The laconic entry for 1819 has Montreal Fire sharing the same address as the Directory’s own offices, at 105 Notre Dame, just east of the Chateau de Ramezay, but the 1820 listing for Montreal Fire was more befitting a local company withan advertised capitalization of £250,000 current.6 It proudly displayed the names of seventeen directors, five officers and even the firm’s messenger, Louis Asselin.Between the directory in May and the advertisement in July, the firm’s leadership changed significantly. In May, the President was Austin Cuvillier an auctioneer in Marie-Claire Cuvillier & Co, while John Molson, Sr. the brewer and steam-boat proprietor was Vice-President.7 Neither Cuvillier, nor Molson, nor six of their fellow directors signed the call to dissolve the company inJuly. Instead, Benjamin Hall, a merchant, and John Frothingham, ahardware merchant headed up the group of twelve directors, four of whom were new since May, who subscribed to the call.

2. “We are sorry to find proprietors of houses so blind to their interest as to neglect insuring against losses by fire especially as the rates of insurance are at present low and reasonable” Montreal Gazette, May 10, 1820.3. Robert C.H. Sweeny, An Alphabetical List of the Merchants, Traders and Housekeepers residing in Montreal, to which is prefixed a descriptive account of the town by Thomas Doige. St John’s, MUN, 1997-2002. 4. Robert C.H. Sweeny, An Alphabetical List of the Merchants, Traders and Housekeepers residing in Montreal. Second Edition by Thomas Doige. St John’s, MUN, 1999-2002.5. The other two were the Phoenix Fire Assurance Company of London, England and the Quebec Fire Insurance Company of Québec City.6. All pounds, shillings and pence in this article are expressed in the currency of account of the Canadas, the pound current. Equal to four dollars or 24 livres tournois, the pound current was worth 1/10th less than the pound sterling. Kelly’s Cambrist Volume 1, London, 1826, p.59. There are 20 shillings in apound current and 12 pence in a shilling. 7. The occupational information on directors is drawn from Sweeny, Doige 1820 and checked against Robert C.H. Sweeny, Monetary Protests of the Bank of Montreal, 1820-27, St John’s, MUN 1998-2002 and Robert C.H. Sweeny, Monetary Protests of the Bank ofCanada, 1820-24, St John’s, MUN, 1999-2002.

Who had left the board and who had joined it? Two of the city’s leading merchants, the Hon. James Irvine of Irvine, Leslie & Co. and John Forsyth Esq. of Forsyth & Richardson, the latter like Cuvillier a Bank of Montreal director, left, as did hardware merchant William Peddie, merchant Ezekiel Hart of Trois Rivières,miller Samuel Hatt of Chambly and Jean B. Raymond. They were replaced by Olivier Berthelet leather merchant, Turton Penn auctioneer, Ralph Taylor commission merchant and Thomas Phillips grocer.

Such a significant change in direction would not have gone unnoticed. This smaller and clearly less powerful board’s relationship to other financial intermediaries might well explainthe Montreal Gazette’s editorial discretion. In May, directors of Montreal Fire held nine seats on the boards of local banks,8 by July this was down to seven. No longer represented on the board of the Bank of Montreal, Montreal Fire maintained its close relationship to the Bank of Canada. Four directors sat on this bank’s board, whose President, Thomas Andrew Turner, owned the Montreal Gazette.

The February stock holders’ meeting proved to be a non-event, because of a board decision made on October 21, 1820 behind the closed doors of Nicolas Benjamin Doucet, Notary Public. There, directors signed an unusual deed. It transferred ownership of allof the company’s policies to a new director, Adam L. MacNider, acting as attorney for and on behalf of the Quebec Fire InsuranceCompany.9 Macnider, an auctioneer and Bank of Canada director, had been the Montréal agent for Quebec Fire for at least two years. The first takeover of a financial intermediary in Canadianhistory went unnoticed in the pages of the Gazette.

8. By 1820, Montreal had three banks. The Bank of Montreal opened in the fall of 1817, had a subscribed capital of £250,000 in May of 1820 and thirteen maledirectors. The Bank of Canada was a year younger, had a paid up capital of £90,000 and eleven male directors. The Montreal Savings Bank was formed in 1819 as a joint venture by these two chartered banks and boasted a board of directors of twenty-nine men.9. Transfer By The President & Directors of the Montreal Fire Insurance Co to A.L. Macnider, No 8018 Greffe de N.B. Doucet, Archives Nationales du Québec à Montréal. Apparently, Macnider replaced Taylor.

Whatever the reasons for the poor press coverage, clearly, the Montreal Fire Insurance Company was a singular failure. Indeed, the firm had to pay Quebec Fire an indemnity of £590 for assumingthe risk of taking over their policies. The historical question is why did this firm fail? Was it because of insufficient resources? Was the competition too stiff? Was management incompetent? Did they not know how to evaluate risk properly? Or did the market not yet exist for their line of insurance? In this article I assess the firm’s business practices and conclude that it was the social constraints of the market that made Montreal such a risky place to do business. So, I argue, the fateof this short-lived venture has quite a lot to tell us about the nature of capitalist development in pre-industrial Canada.

The deed of transfer contained two appendices compiled for a meeting of the directors held before notaries public on October 3, 1820. Both described insurance in force at the end of September 1820. The first listed summary information on policies sold by company agents in Trois Rivières and Upper Canada covering 70 assets held by 48 clients. The second was a much moredetailed, 51 page, listing of 664 assets held by 274 clients. These two appendices constitute the principal sources for this article. Extracts drawn from the appendices illustrate the strengths and weaknesses of each.

Table 1Extract from Appendix One of the Deed of Transfer

Risks at Three RiversOn a Wooden house in the bay de Levre F. Cottrel Nov’r 10 760 household furniture 200 Goods 850 On a Store Behind 200On a Wooden house Jos. Turcott Oct’r 21 11/

6600

On a Stone house in Three Rivers E. Durette Nov’r 10 7/5 400On a Stone Wood house in do J.G. Detonnencour Dec’r 15 11/ 400On do do do do. “ 11/ 300On a Wooden house do. “ 11/ 100On furniture in Wooden house do. “ 11/ 300On a Store & Wooden house in bay de Levre

Jean Rollett “ 22 12/ 450

Household furniture do. “ “ “ 140 Books in Back Store do. “ “ 17/ 60On a Stone house Cov’d with Wood in Three Rivers – Goods

H.F. huges May 8 7/5 800

On a Stone house Cov’d with Wood in Three Rivers on Goods

Sautell & Co. “ 12 7/11

1800

£ 7350

This extract from the manuscript shows sales by IsaacValentine, the firm’s agent in Trois Rivières. It consists ofa brief description of the property, the name of the policyholder, the date coverage commenced, the cost of the premiumexpressed in shillings and pence per hundred pounds ofcoverage and the monetary value of the policy in poundscurrent. The symbols “ and do both mean ‘the same as above’.

These appendices are the sole records of the firm to have survived, but they only detail the firm’s business at the end of its short life. To reconstruct Montreal Fire’s history and business practices requires careful listening to what these sources have to tell us, including their eloquent silences.

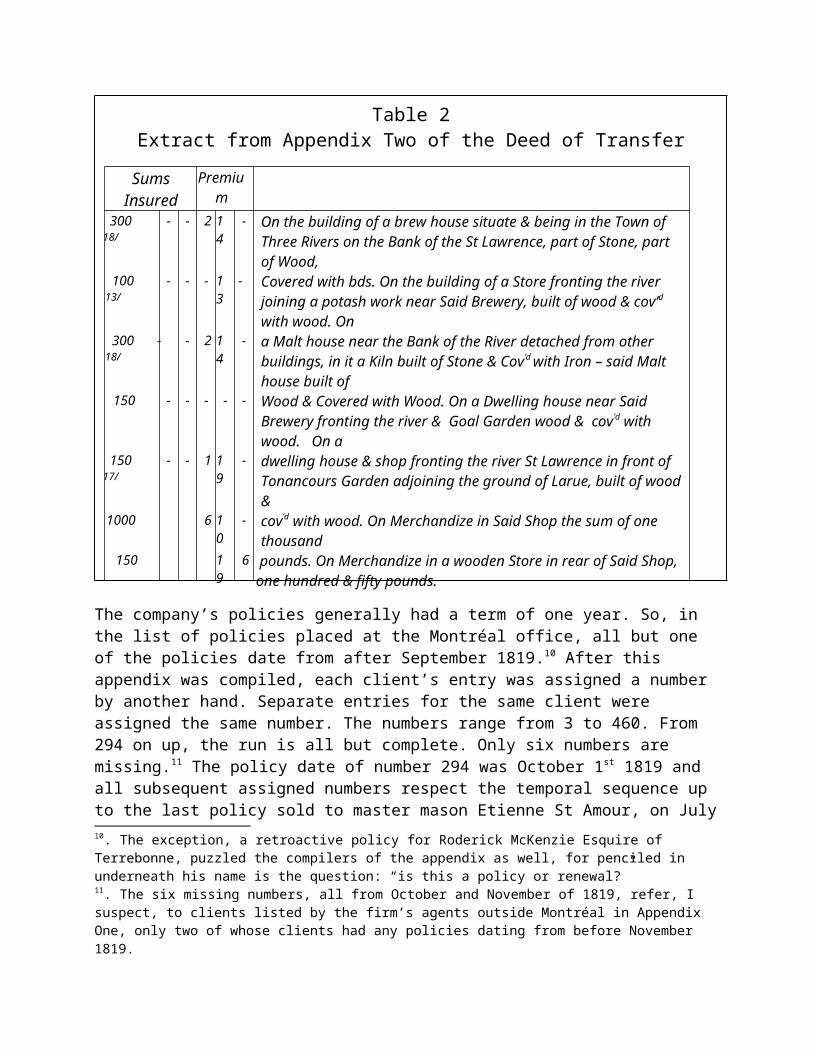

Table 2Extract from Appendix Two of the Deed of Transfer

SumsInsured

Premium

300 18/

- - 2 14

- On the building of a brew house situate & being in the Town of Three Rivers on the Bank of the St Lawrence, part of Stone, part of Wood,

100 13/

- - - 13

- Covered with bds. On the building of a Store fronting the river joining a potash work near Said Brewery, built of wood & cov’d

with wood. On 300 18/

- - 2 14

- a Malt house near the Bank of the River detached from other buildings, in it a Kiln built of Stone & Cov’d with Iron – said Malt house built of

150 - - - - - Wood & Covered with Wood. On a Dwelling house near Said Brewery fronting the river & Goal Garden wood & cov’d with wood. On a

150 17/

- - 1 19

- dwelling house & shop fronting the river St Lawrence in front of Tonancours Garden adjoining the ground of Larue, built of wood&

1000 6 10

- cov’d with wood. On Merchandize in Said Shop the sum of one thousand

150 19

6 pounds. On Merchandize in a wooden Store in rear of Said Shop, one hundred & fifty pounds.

The company’s policies generally had a term of one year. So, in the list of policies placed at the Montréal office, all but one of the policies date from after September 1819.10 After this appendix was compiled, each client’s entry was assigned a number by another hand. Separate entries for the same client were assigned the same number. The numbers range from 3 to 460. From 294 on up, the run is all but complete. Only six numbers are missing.11 The policy date of number 294 was October 1st 1819 and all subsequent assigned numbers respect the temporal sequence up to the last policy sold to master mason Etienne St Amour, on July10. The exception, a retroactive policy for Roderick McKenzie Esquire of Terrebonne, puzzled the compilers of the appendix as well, for penciled in underneath his name is the question: “is this a policy or renewal?”11. The six missing numbers, all from October and November of 1819, refer, I suspect, to clients listed by the firm’s agents outside Montréal in Appendix One, only two of whose clients had any policies dating from before November 1819.

13th 1820. That is less than a week before the call to dissolve the company was made. Clearly then, these numbers were not created after the appendix was compiled, but were how the companyhad kept track of its policy holders.

Clients with numbers lower than 294 were therefore renewals. There are two differing sequences of renewals. Those from 3 to 92are almost without exception dated in December or very early January12. Starting from number 93, Forsyth & Richardson, through to 238 the dates progress through the calendar year up to July, but then there is a major gap through to September, for numbers 239 to 293. These patterns suggest three things. First, the firm started business in December 1817 and initially sold coverage by the calendar year. Second, after a full year of operations and possibly in response to the demands of a very influential mercantile firm,13 Montreal Fire began selling policies with flexible starting dates. Third, clients were not allowed to renewtheir policies even for short periods after the decision was madeto dissolve the firm.

Client turnover was high. Only 114 of the 238 clients who could have been with the firm for more than a year were still on the books at the end of September 1820: 46 of the 92 clients from thefirst year of operations and 68 of the 145 from the first six anda half months of 1819. As these figures suggest, however, although retention was a problem it was partially assuaged by rapid growth. In the last nine and half months of full operation,from October 1819 to mid-July 1820, the firm signed up 200 new clients with £220,948 worth of insurance. So why did the firm fail?

12. I attribute the exceptions to clients who changed the property they had insured. 13. The largest firm in Montréal, Forsyth & Richardson was the Canadian branch of Phyn, Ellice & Inglis.

Spatial considerations are crucial for fire insurance companies. A properly managed company spreads its risks out over as wide a territory as administratively feasible. As Map 1 shows, Montreal Fire was quite successful at developing business outside Montreal. Just slightly less than a third of all of insured assets (31%) were located in the smaller villages and towns of western Lower Canada and in selected settlements of Upper Canada.The map clearly highlights the significance of the Richelieu valley to the east of the city, as well as settlements along the Ottawa to the west and the back river to the north. Business outside the city strongly reflected the tight commercial relations between Montréal and the surrounding countryside. In addition, the firm had agents in York, Kingston, Amherstburg and Trois Rivières, but in each case more than 40% of the business byvalue in these towns was sold directly by the Montréal office. Agents relied more heavily on domestic than commercial business,14

14. In this late pre-industrial society, the division between workplace and domestic space was not very advanced, many dwellings would have been used for commercial purposes within the formal economy. The language used in describingthe property was, however, unambiguous. On the one hand were dwelling houses

76% compared to 63% for polices in Montréal and only 56% for policies sold by the Montréal office outside the city. Penetration of these small town markets followed well worn commercial paths.

Graph 1The value and number of detailed

clauses,according to the rate paid in shillings per

£100 pounds coverage. £’000

Shillings

Perhaps the problem lay with an inability to assess risks. Graph 1 plots the value and number of those detailed clauses from appendix two where the premium rate was less than one percent.15 It shows that Montreal Fire maintained a wide range of rates in a

and household furniture, china , glass, plate, bed and table linen and wearingapparel, while on the other were shops, stores, stock in trade, merchandize and explicitly commercial buildings and equipment.

series of quite distinctive clusters. Most paid rates of 8/9d or more but that was because assets located outside the city were charged quite disproportionately these higher rates. While 58% ofthe assets in Montréal were charged the lower rates, 84% of assets outside the city were charged the higher rates. Meanwhile the firm faced its greatest potential losses on the almost exclusively Montréal based assets that were charged less than 5/9d per £100. Almost 45% of all insurance in force generated a premium of only a quarter of one per cent or less. So was this just another example of merchants egregiously exploiting their hinterland?

Table 3Premium Rate Characteristics of the Building

3 shillings 9penceto

5 shillings 6pence

occupied dwelling house, store or vaultstone buildingtin roofiron covered doors and shutters18 inch gables through the roof

6 to 8shillings

occupied dwelling house, store or warehousestone or brickwooden or shingled roofwooden shutters

8 shillings 9pence to

11 shillings 6pence

occupied dwelling house, store or warehousewooden buildingwooden roof

12 to 15shillings

unoccupied wooden structures: stores, shops, barns, sheds, stablesor workshopsmills, manufactories or isolated

15. In only six cases did the company charge a pound or more per £100 coverage.In four of these six cases, it charged its highest rate of 42 shillings, or 2.1%, reserved for steam engines installed in manufactories.

16 to 42shillings

unoccupied structuresongoing construction, steam power orother hazardous activities

Well, no. Montreal clients paid lower premiums because so many oftheir assets were considered low risks. To each cluster on Graph 1 there corresponds a quite clear set of criteria directly linkedto a risk assessment based primarily on building type. The logic of this system is sketched out in Table 3. Within each of these broad categories there were quite fine gradations, however, overall rates for business placed at the Montréal office were determined by the specific blend of building materials and the nature of the site, not by geographic location. Agents did chargehigher rates, generally at the top end of the Montréal office’s range for apparently similar buildings or at most a couple of shillings more. Presumably this mark-up covered their commission,although it does not explain the anomalous situation in York, where the agent charged 1% or more on seven of the ten policies.16

Taken as whole, one can understand why the Montreal Gazette considered fire insurance rates to be “low,” but what about theirclaim that they were also “reasonable”? Two sources detail the nature of the built environment in Montréal for 1825. John Adams’ map distinguishes between dwellings and outbuilding buildings, while Jacques Viger’s statistical tables provide the numbers of occupied stone and wooden buildings.17 Applying

16. To be sure, these included stables, taverns, a brew house and a malt house,however, the owner of two wooden houses on the premises of Government House paid £40 to get £4000 in coverage.17. Robert C.H. Sweeny, A Map of the City and Suburbs of Montreal by John Adams. St John`s, MUN, 1996-2003 and “Les Tablettes Statistiques du Comté de Montréal” in Groupe de recherche sur la société montréalaise au 19ième siècle, Rapports de recherche 1972-75. Montréal, UQAM, 1975. I applied the GRSM’s estimate, that the city’s population increased 22.25% between 1820 and 1825, (GRSM, Tableaux. Montréal UQAM, 1973) to both Adams` and Viger`s figures. Rapid suburban growth probablydid not surpass that of the town centre, due to a building boom resulting fromthe development of the Récollet (1818) and Garrison Hill (1821) properties and the completion of the demolition of the city walls (1817) . All of which created 230 new building lots in the town centre. The surviving tax information for 1825 suggests only 57 vacant lots were left, for a growth rateof 28%. Robert C.H. Sweeny, A Reconstituted Tax Roll for the City of Montréal, 1825. St

Montreal Fire’s level of exposure to these sources suggests that fires would have had to consume completely a Montreal stable or shed daily, two wooden homes a week and a stone building every seven weeks in order for the company’s rates to be a losing proposition. Period newspapers do not report fires at anything like this frequency, but of course a single fire could destroy numerous properties. So once again I turn to the question of risky spaces.

With 97% of Montréal`s occupied wooden buildings and 75% of the city’s outbuildings, the suburbs were the riskiest of urban spaces. Montreal Fire appears to be have been quite selective in their insurance of suburban property. Two out of five suburban buildings insured by Montreal Fire were made of stone, whereas five out six occupied suburban buildings were made of wood. To be sure, few of the insured buildings met the high standards of iron shutters, tin roofs and full gables characteristic of thetown centre, but policies almost always noted how close the buildings were to any wooden structures. Apparently, a distance of at least twenty feet (6 metres) was required for it not to affect the rate charged on the stone building.

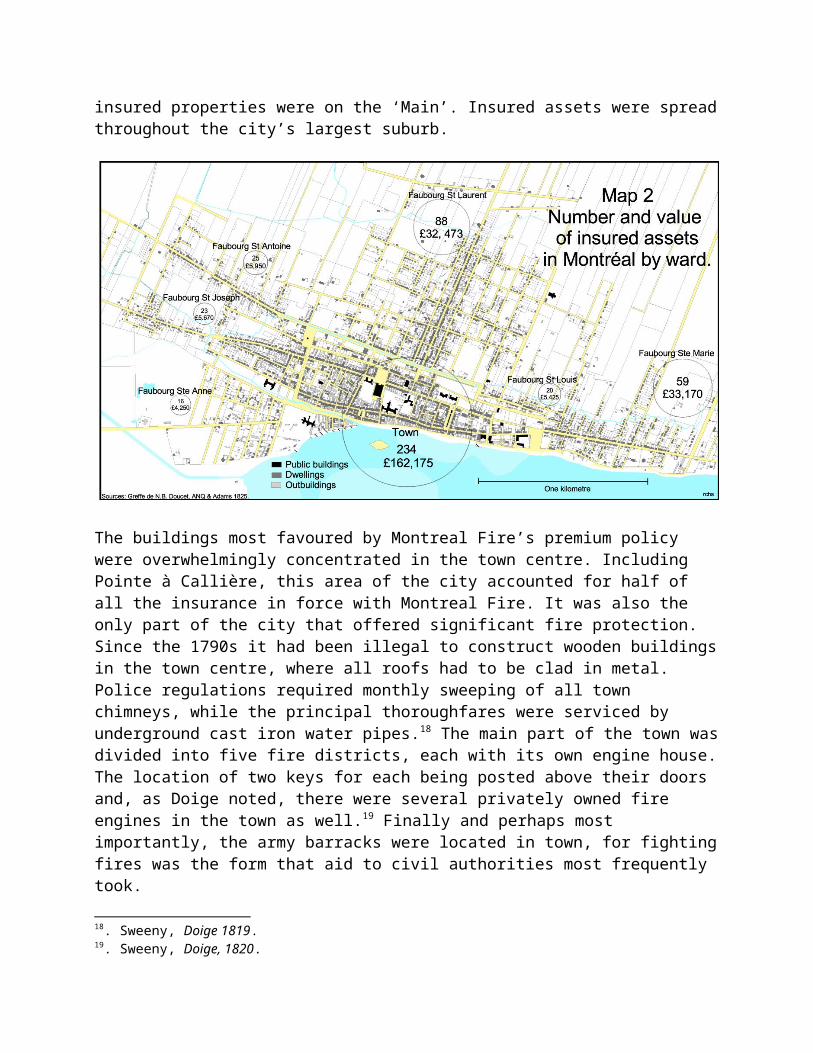

As Map 2 shows, Montreal Fire had quite limited exposure in four of the city’s six suburban wards. Only in St Laurent and Ste Marie had the company insured numerous, relatively expensive properties. Indeed, at an average asset value of £562, Ste Marie was not that far behind the town centre’s average of £693. These surprisingly high values in one of the poorest wards in the city stemmed, in large measure, from the company’s coverage of two large manufacturing complexes. Adjacent to the town centre were the 11 risks, seven of them dwellings, insured for £12,550 that made up John Pickel Jr.’s property. It included a tobacco manufactory and a bake house. At the far end of Ste Marie was Molson’s brewery, with 14 risks, five of them dwellings, insured for £12,400. Two thirds of the remaining insured properties were along the 1.4 kilometre of suburban main street that joined thesetwo sites. By contrast, in St Laurent fewer than a third of

John`s, MUN, 1997-2002.

insured properties were on the ‘Main’. Insured assets were spreadthroughout the city’s largest suburb.

The buildings most favoured by Montreal Fire’s premium policy were overwhelmingly concentrated in the town centre. Including Pointe à Callière, this area of the city accounted for half of all the insurance in force with Montreal Fire. It was also the only part of the city that offered significant fire protection. Since the 1790s it had been illegal to construct wooden buildingsin the town centre, where all roofs had to be clad in metal. Police regulations required monthly sweeping of all town chimneys, while the principal thoroughfares were serviced by underground cast iron water pipes.18 The main part of the town wasdivided into five fire districts, each with its own engine house.The location of two keys for each being posted above their doors and, as Doige noted, there were several privately owned fire engines in the town as well.19 Finally and perhaps most importantly, the army barracks were located in town, for fightingfires was the form that aid to civil authorities most frequently took.

18. Sweeny, Doige 1819.19. Sweeny, Doige, 1820.

Map 3 shows the location of 162 of the insured buildings in the town centre.20 At first glance, it seems that the properties are fairly widely distributed throughout the town, although clearly the company was not pushing its insurance among the property owners in the manufacturing district to the south west of Place d’Armes. Commercial properties, near the wharfs of Pointe à Callière and adjacent to the Old and New Markets, were important for the company. But just over half of all the buildings insured for more than a £1000 were residences and these 34 homes were on eleven different streets.21

20. The property of Samuel Gerrard, a stone house with furnishings, a store andstables, insured for £3,500 are the only ones not shown. They were demolished in 1823 to make room for the new parish church on Place d’Armes .21. The amount of insurance on the 165 buildings in the town centre broke down as follows: 23 insured for more than £2000, 41 for more than £1000, 46 for more than £500, 34 for more than £250 and 31for less than £250. A craft familyearned approximately £50 a year.

So it does appear that the company did its best to minimise risk.Nevertheless, 79 of the 162 insured buildings shared a common wall with another insured building. A moderate size fire in any number of different parts of the town centre could easily wipe out all the firm’s accumulated premiums, while a single large fire would bankrupt the firm. Hence the substantial compensation demanded by Quebec Fire, equivalent to almost half the annual income of the subsumed firm.22 If this clarifies the nature of theproblem that the directors of Montreal Fire found insurmountable by the summer of 1820, it still leaves us with a question. Why did Montreal Fire accept to insure so many adjacent properties?

The short answer is the social constraints structuring property relations in late pre-industrial Montréal left them little choice. At the time of the transfer to Quebec Fire, 186 people orfirms had insured 456 assets in the city with Montreal Fire. These assets consisted of 217 dwellings, furnishings for 90 households, the stock in trade of 70 stores or manufactories, 52 outbuildings and 29 commercial buildings. Of these 186 proprietors, 55 owned at least two insured dwellings.23 So, slightly more than one in four clients (29%) were to use the vocabulary of the day rentiers. They accounted, however, for halfof the insured assets and the distribution of these assets is quite revealing. Rentiers owned 159 (73%) of the insured dwellings and 23 (79%) of the insured commercial buildings. They had just under half of the outbuildings, yet only a fifth of the stock in trade and a mere eighth of the furnishings. Both Austin Cuvillier with thirteen properties and John Molson Sr. with seven, respectively former President and Vice-President of Montreal Fire, figured prominently among the rentiers, while directors John Brown and Joseph Roy counted among their ranks.

The assets insured by the 131 people or firms who, according to their insurance policies, were not rentiers revealed strikingly different profiles. Thirty-three insured just their own home,

22. The premium income for all business detailed in Appendix Two totalled £1280. 23. I restricted the selection to dwellings so as not to count as rentiers people who insured their dwelling and a separate place of work, such as store.

while a further 18 including Hiram Nichols, director, and Josiah Bleakley, Secretary, insured both home and household furnishings.A clear majority, however, insured only movables: 37 were like director Turton Penn and insured just household furnishings; 17 were like Benjamin Hall, the new President, and Alexis Laframboise, director, and insured only their stock in trade; while another 17 were like Joseph Frothingham, the new Vice-President, and Charles Bowman, director, and insured both stock in trade and household furnishings. The other nine had varying combinations of insured assets, the director Joseph T. Barrett, for instance insured his furnishings, stock in trade and store.

There were three fire insurance companies operating in the city and it was possible to have policies with two or three companies at the same time. Four policies in Appendix Two specifically mention that a particular asset or a related property was insuredwith another company. It is not possible to know if they were theonly ones, although it was certainly in Montreal Fire’s interest to keep track of multiple policies.24 So some clients, only insuring movables, might have been like the firm’s last President, Benjamin Hall, whose store on the Main in St Laurent was insured by Quebec Fire. Others may have considered that theirmodest real estate holdings were not worth insuring. Nevertheless, it seems more than likely that most insured only movables because they had no immovables to insure. Furthermore, this seems to be the situation for the majority of directors who signed the call to dissolve the company.25

These differing profiles are highly suggestive of the types of tensions that must have racked the board of directors as it changed directions in the late spring of 1820, then announced thefirm’s closure in July and finally agreed to a costly takeover in

24. Newspaper reports of fires always identified by firm the amount of insured losses, so it does not seem to have been considered confidential information. 25. Thomas Phillips was co-proprietor of a stone house on the Main in St Laurent with Joseph Chevalier who owned three other dwellings. Neither OlivierBerthelet, nor Ralph Taylor appear in either appendix. It is surprising that adirector would not do any business with the firm, but they may have been amongthose clients whose policies came up for renewal between July and September 1820 and therefore did not appear in these compilations.

October. These tensions were probably not new, for rentiers had always been important for the firm. Twenty seven of the 45 policyholders still with the firm from 1817-18, the first year of operations, qualified as rentiers in September 1820. They frequently insured a mixed portfolio of assets that were by no means all located in the same area. The problem threatening the viability of the firm was not one, two or even ten rentiers. It was the cumulative effect of a large number operating in a constrained space.

So the greatest risk facing the company was primarily social in nature. It was a product of prevailing property relations and theextant records of Montreal Fire tell us some intriguing things about those relations. First, ownership of urban property was highly concentrated. Second, many people prominent in business owned no real property. Third, movables were an important form ofwealth. Fourth, the market is historically a social construction.These are significant points, that challenge established ways of understanding the development of capitalism in British North America.

In Canada, there are two relevant historiographical traditions: the long dominant staples approach26 and a more progressive paradigm used in labour history.27 The staple historians applied Adam Smith’s characterization of colonies of settlement as the inverse of Europe; in British North America land was plentiful and labour scarce. Basing themselves on the pioneering work of H.Claire Pentland, most labour historians have tended to consider that the large scale immigration from the British Isles, peaking in the 1830s and 1840s, laid the basis for the subsequent development of capitalism. In differing ways, the suggestion thatcontrol of the built environment of Montréal was already concentrated in relatively few hands as early as 1820 undermines both of these meta-narratives. By the end of the Napoleonic wars,26.Robert C.H. Sweeny, “The Staples as the Significant Past: A case study in historical theory and method.” In Canada: Theoretical Discourse /Discours théoriques. Edited by Jane Greenlaw, Terry Goldie, Carmen Lambert & Rowland Lorimer. Montréal: Association of Canadian Studies, 1994, 327-49. 27. For a discussion of the problems and successes of this approach see the 50th

anniversary issue of Labour/Le Travail, Fall/Automne 2002.

land was no longer plentiful in Lower Canada and immigrants arrived in cities that were already strongly marked by unequal property relations.

The corollary to such inequality was that many people and firms, whom we might reasonably consider as prominent members of the business community, owned no real property. Their material wealthwas in personal belongings or stock in trade and not in land or buildings. The insured stock in trade of the commercial tenant was not infrequently held on commission and almost invariably on credit, hence the significance of insurance on inventories, that most ephemeral form of wealth. A common thread running through the many studies of merchant capital in British North America is the recognition that the commercial world was highly volatile. One might insure against fire, but how could one ensure not to beswept away in the maniacal swings of the trade cycle? Devastatingcommercial crises punctuate the period like so many decennial exclamation marks: 1825! 1836! 1847! 1857! Explanations have varied from the ethnic stereotypes of an older scholarship, through an over dependence on staple production, the weakness of foreign markets, excessive spending on transportation infrastructure, to the need to extend credit in a competitive market and the long time needed to realise one’s advances in a highly seasonal and still largely agricultural economy. No one, however, has suggested that so many merchants simply stood on fragile feet of clay. To be washed away in the first collapse of prices and, of course, in these British colonies every boom climaxed in a frenzy of imperial dumping.

Jacques A. Cartier was a prosperous Richelieu valley merchant, who kept two rooms in town at Joseph Perrault’s stone dwelling onSt Vincent. His policy does not describe the rooms, but in what Iassume were a sitting room and a bedroom he had “household furniture, printed Books and wearing apparel” insured for £200. That was four times the annual income of a skilled craft family. The average value of a policy on household furniture in Montréal was an astounding £430. Currency conversions across centuries arehighly problematic, but surely it is significant that an average policy on household furnishings was worth close to the total

income for an entire decade of a craft family engaged in independent commodity production. The relative value of movables was clearly many times greater than it is now.28 This has a numberof implications for the way we think about this society. Foremostis the enhanced significance it gives to the movable property that most women brought with them into marriage. Second, it underscores the substantial status distinctions within this society. Third, it highlights the importance of variable capital for family businesses.

For economic and business historians the most salutary lesson these records have to teach us concerns the demystification of the market. In advanced capitalist societies the market has of late attained an ideological hegemony that brokers no opposition.In these records, however, instead of being a paradigmatic natural force, the market appears as a limiting, yet circumscribed and historically grounded, social construction. Clearly, the mere existence of large numbers of assets that needed to be insured and the relatively sophisticated risk management strategies and business practices of Montreal Fire were not enough. Success required the prior existence of a relatively broadly-based system of property ownership. In the absence of such a social distribution, the only solution was a wider geographic distribution.

Socially constrained markets still characterize most of the world’s societies, as they did all societies before the maturation of capitalism. Industrialisation radically transformedcertain of these markets by creating new social relations, which through a complex process dramatically lowered the value of movable property and reconfigured the importance of real property. This dual change in the nature of property profoundly altered gender relations along increasingly patriarchal lines neatly symbolized by the creation of a market for life insurance,a field where Montréal firms set new standards.

28. A conversion using the average income of households with at least two adults in Canada in 2000 gives the average value of insured household furnishings a present day value of $591,079. Statistics Canada, Cansim II, table 202-0102, Ottawa 2002.

AppendixText of the Deed of Transfer

No. 801821 Oct’r 1820Transfer by the President & Directors of the Montreal Fire Insurance Co. ToA.L. Macnider

On the twenty first day of October in the year of our Lord one thousand Eight hundred and twenty in the after noon Before the undersigned public notaries duly admitted and sworn in and for the Province of Lower Canada residing at the city of Montreal Personally Came and appeared Benjamin Hall [President] of Montreal aforesaid President; John Frothingham Vice President; Hiram Nichols; Charles Bowman; Turton Penn; Joseph T. Barrett; John Brown; Olivier Berthelet; Adam L. Macnider; Thomas Phillips; Alexis Laframboise of the same Place, Directors of the Montreal Fire insurance Company acting for themselves and for and on behalf of their Associates Carrying on the business of Insurance against damage by fire in the said City of Montreal under the name, style and title of the President, Directors and Proprietors of the Montreal Fire Insurance Company of the one part

And Adam Lynburner Macnider of the city of Montreal aforesaid in the Said Province Merchant, Attorney duly appointed by John Macnider of the City of Quebec in the said Province President, Michel Berthelot Vice President, François Blanchet; Charles Hunter, James Hunt; Joseph Jones; Thomas Wilson; & Benjamin Lemoine Directors of the Quebec Fire Insurance Company acting for themselves and for and in behalf of their associates carrying on the business of Insurance against damage by Fire in the City of Quebec aforesaid under the name, style and Tytle of the President, Directors and Proprietors of the Quebec Fire insurance Company of the other part. {As appeared by their power of att’y executed (...) }

Which said Adam Lynburner McNider in his Said Capacity of Attorney of them the said President, Director and Proprietors of the said Quebec Fire insurance Company and in the name and in the behalf of the said [for them jointly and severally] President Directors and Proprietors of the Quebec Fire Insurance Company in consideration the Sum of five hundred and eighty pounds Currency to him in hand paid {by the said President and directors of the Said Montreal Fire insurance Company} the receipt whereof being hereby acknowledged [the] did assume and take up as their own all the risks and Policies of Insurance according to the terms and conditions therein which have

been undertaken and prevailed previous to the thirtieth day of September last past by the persons associated and Carrying on the business of Insurance against Damage by fire in the City of Montreal under the name of the President Directors and Proprietors of the Montreal Fire insurance company {according to the three schedules herein annexed and after having been signed by the parties (…)} and [that they the Said President] and further have agreed and covenanted and promised in the name and behalf aforesaid that they the said President, Directors and Proprietor of the said Quebec Fire insurance Company will indemnify and save harmless the Said President, Directors and Proprietorsof the said Montreal Fire Insurance Company of and From all Claims for loss or damage by fire which might or could be made under and by reason of any risks and polices now in force and which have been undertaken and granted by the said Montreal Fire Insurance Company prior to the said thirtieth day of September one thousand eight hundred and twenty. Thus done and passed at the City of Montreal at the day and year first above written and the parties have signed with us the said Notaries these presents having been first duly read in their presence

Signatures H.Nichols John Frothingham V.P.Chas Bowman Olivier BertheletTurton Penn Adam L. Macnider

P.Lukin N.P. J.T. Barrett Benj’n Hall, Pres’tJohn Brown Thomas Phillips

Alexis Laframboise N.B. Doucet N.P.

Please note the text in square brackets […] was crossed in the original, while text in brackets with curlicues {…} appeared in the margins of the deed. Both changes were made when the text wasread out to the parties, prior to signing.

Risks in YorkOn a Wooden house Stable in York C. Wedner Nov’r 4 20/ 430On a Wooden house in port hope G. S. Bolton “ 1

015/ 600

On a Wooden house in York A.Mcdonnell Dec’r 22

16/ 1200

On a Wooden house in York as a tavern Jos’h Schass “ 30

20/ 600

On a Wooden house in York hon. J.McGill Jan’y 1820 8 18/ 300On a Wooden house in York a tavern John Burke “ 2

220/ 500

On a Brew house in York Joseph Shaw “ 28

25/ 125

On a dwelling house do. “ “ 18/ 150On a Shed do. “ “ 22/6 50On a Malt house do. “ “ 25/ 50On a Stable do. “ “ 22/6 25On a Wooden house in York S. Smith or h.

coffin“ 1

820/ 400

On a Wooden house in York G. Willard feb'y 1 20/ 3000On a Wooden house in York Same premises

Gov’t houseJuly 6 20 1000

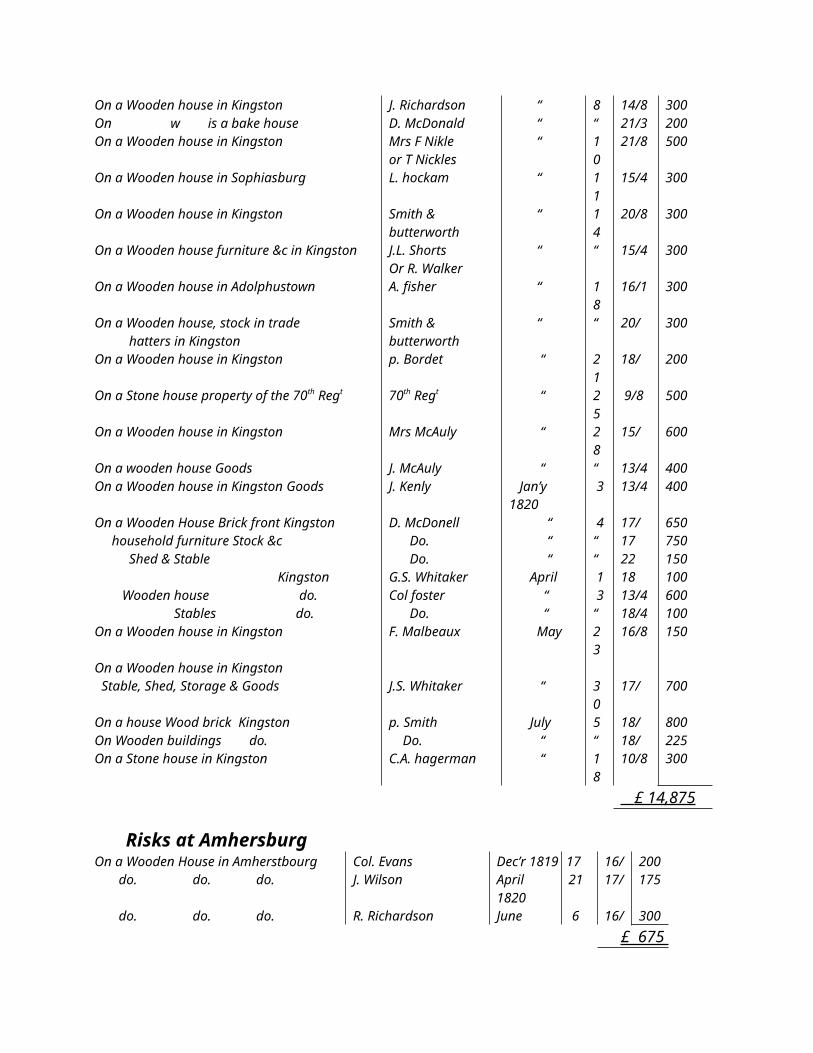

£8430

Risks in KingstonOn a Stone house cov’d with wood inKingston

Sam’l Cheasby April 21

10/6 360

On a Brick house cov’d with shingles C.A. Hangerman Oct’r 9 9/8 1350Books do. “ “ 12/6 60On an office do. “ “ 10/8 150On furniture, drugs &c. in a Wooden house in Kingston

Dr. Marshall Novem’r 9 19/4 500

On a Wooden house in Kingston Robert Walker “ 11

15/4 350

On a Stone house in the village of Bath Jas. Hawkin “ 24

9/11 800

On a Wooden house in Kingston R. Richardson “ “ 13/4 300On Merchandise do. “ “ 18 500On a Wooden house in Kingston on apparatus W.C.Thompson Dec’r 1

817/10

300

Furniture do. “ “ 14/4 200On a Stone house covered with woodin Kingston

John Strage “ 19

9/8 200

On a Stone house cov’d with wood at pointe frederik in Kingston

Ed Lewis “ 28

9/11 400

On a Wooden house in Kingston p. Smith Jan’y 1820 7 8/2 300

On a Wooden house in Kingston J. Richardson “ 8 14/8 300On w is a bake house D. McDonald “ “ 21/3 200On a Wooden house in Kingston Mrs F Nikle

or T Nickles “ 1

021/8 500

On a Wooden house in Sophiasburg L. hockam “ 11

15/4 300

On a Wooden house in Kingston Smith & butterworth

“ 14

20/8 300

On a Wooden house furniture &c in Kingston J.L. ShortsOr R. Walker

“ “ 15/4 300

On a Wooden house in Adolphustown A. fisher “ 18

16/1 300

On a Wooden house, stock in trade hatters in Kingston

Smith & butterworth

“ “ 20/ 300

On a Wooden house in Kingston p. Bordet “ 21

18/ 200

On a Stone house property of the 70th Regt 70th Regt “ 25

9/8 500

On a Wooden house in Kingston Mrs McAuly “ 28

15/ 600

On a wooden house Goods J. McAuly “ “ 13/4 400On a Wooden house in Kingston Goods J. Kenly Jan’y

1820 3 13/4 400

On a Wooden House Brick front Kingston D. McDonell “ 4 17/ 650 household furniture Stock &c Do. “ “ 17 750 Shed & Stable Do. “ “ 22 150 Kingston G.S. Whitaker April 1 18 100 Wooden house do. Col foster “ 3 13/4 600 Stables do. Do. “ “ 18/4 100On a Wooden house in Kingston F. Malbeaux May 2

316/8 150

On a Wooden house in Kingston Stable, Shed, Storage & Goods J.S. Whitaker

“ 3

017/ 700

On a house Wood brick Kingston p. Smith July 5 18/ 800On Wooden buildings do. Do. “ “ 18/ 225On a Stone house in Kingston C.A. hagerman “ 1

810/8 300

£ 14,875

Risks at AmhersburgOn a Wooden House in Amherstbourg Col. Evans Dec’r 1819 17 16/ 200 do. do. do. J. Wilson April

182021 17/ 175

do. do. do. R. Richardson June 6 16/ 300 £ 675

Risks at Three RiversOn a Wooden house in the bay de Levre F. Cottrel Nov’r 10 760 household furniture 200 Goods 850 On a Store Behind 200On a Wooden house Jos. Turcott Oct’r 21 11/

6600

On a Stone house in Three Rivers E. Durette Nov’r 10 7/5 400On a Stone Wood house in do. J.G. Detonnencour Dec’r 15 11/ 400On do. do. do. Do. “ 11/ 300On a Wooden house Do. “ 11/ 100On furniture in Wooden house Do. “ 11/ 300On a Store & Wooden house in bay de Levre

Jean Rollett “ 22 12/ 450

Household furniture Do. “ “ “ 140 Books in Back Store Do. “ “ 17/ 60On a Stone house Cov’d with Wood in Three Rivers – Goods

H.F. huges May 8 7/5 800

On a Stone house Cov’d with Wood in Three Rivers on Goods

Sautell & Co. “ 12 7/11

1800

£ 7350

Montreal fire office 3rd October 1820 We the undersigned directors of the Montreal fire insurance Company do hereby certify that the foregoing schedule contains a statement of all the Risks now unexpired taken by the agents of this company in upper Canada and at Three Rivers.

Signatures H Nichols John Frothinham VPThomas Phillips Benjamin Hall Pres.Turton Penn Olivier BertheletJ. T. Barrett Chs BowmanJohn Brown Alexis Laframboise

J.H. Roy P. Lukin NP N.B. Doucet NP

Copyright © 2022 FDOKUMEN