RISK-ON AMID RETURN TO NORMALITY INVESTMENT ...

35

RISK-ON AMID RETURN TO NORMALITY SECOND QUARTER 2021 FLORENCE BARJOU JEANNE ASSERAF-BITTON CIO for Active Investment Strategies Global Head of Market Research JEAN-BAPTISTE BERTHON PHILIPPE FERREIRA Senior Strategist Senior Strategist VACCINATION TO DICTATE RETURN TO NORMALITY LOOMING U.S. BOOM EMU SLOW CATCH-UP CONDUCIVE POLICY BACKDROP O/W DM EQUITIES UNATTRACTIVE FIXED-INCOME FAVOR SHORT DURATION O/W U.S. BREAKEVEN TACTICAL BUY COMMIDITIES NEUTRAL CORPORATE CREDIT TACTICAL BUY EM O/W EVENT-DRIVEN U/W MARKET NEUTRAL L/S O/W CTA N GLOBAL MACRO INVESTMENT STRATEGY LYXOR CROSS ASSET RESEARCH

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of RISK-ON AMID RETURN TO NORMALITY INVESTMENT ...

R I S K- O N A M I D R E TU R N TO

N O R M A L ITY

S E C O N D Q U A R T E R 2 0 2 1

FLORENCE BARJOU JEANNE ASSERAF-BITTON

CIO for Active Investment Strategies Global Head of Market Research

JEAN-BAPTISTE BERTHON PHILIPPE FERREIRA

Senior Strategist Senior Strategist

VACCINATION TO DICTATE

RETURN TO NORMALITY

LOOMING U.S. BOOM

EMU SLOW CATCH-UP

CONDUCIVE POLICY BACKDROP

O/W DM EQUITIES

UNATTRACTIVE FIXED-INCOME FAVOR SHORT DURATION

O/W U.S. BREAKEVEN TACTICAL BUY COMMIDITIES

NEUTRAL CORPORATE CREDIT

TACTICAL BUY EM

O/W EVENT-DRIVEN U/W MARKET NEUTRAL L/S

O/W CTA N GLOBAL MACRO

I N V E ST M E N T ST RAT E G Y

LYXOR CROSS ASSET RESEARCH

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

Contact: [email protected] +33 (0) 1 42 13 31 31

Completed April 7th, 2021. Data as of March 31st, 2021 unless otherwise specified.

Important Notice: For investors in the European Economic Area, this material is intended for clients

(current or potential) who meet the definition of “Professional Counterparty” or “Eligible

Counterparty” under the Markets in Financial Instruments Directive (“MiFID”), and any products or

services described falling within the scope of the MiFID are only available to such clients. This

document is considered marketing communication within the meaning of the MiFID.

CONTENTS

EXECUTIVE SUMMARY 3

MACRO & MARKET VIEWS 4

Markets hesitating between Reflation and Inflation 4

Pandemic trends and policy response to continue dictate growth prospects 5

The looming U.S. economic boom 7

Will the U.S. economy overheat and yield unwanted inflation? 8

Fed, Taper, AIT and U.S. Yields 9

U.S. Fixed-income markets’ unattractive risk-return profile 10

Strong earnings prospects keep us O/W on U.S. Equities 10

Addressing U.S. Value and Growth themes through sectors 11

EURUSD, not a no-brainer! 12

Europe: near term challenges; mid-term opportunities 13

O/W EMU equities to leverage global growth; Neutral UK equities 15

EMU sectors: cyclicals vs. defensives 16

Japan Economy: The fundamental story remains intact 17

Japan Equities: Not taking profit yet (O/W) 18

EM Economies: Brightening outlook 19

EM Equities: Tactical Buy, but strategic Neutrality 20

EM HC Debt: Modest spread tightening in sight, but U.S. rates risk (N) 22

Commodities: Supercycle and sentivity to U.S. rates 23

Brent: Waltz in three-quarter time 23

Copper: shortage in 2021 (O/W) 25

Gold: Mixed fundamentals, tactical opportunity (N+) 25

ALTERNATIVE STRATEGIES 26

KEY VIEWS 26

UPGRADE CTA (O/W) AT THE EXPENSE OF GLOBAL MACRO (N) 27

DOWNGRADE L/S CREDIT TO NEUTRAL 27

STAY O/W EVENT-DRIVEN 28

L/S EQUITY: PREFER DIRECTIONAL TO MARKET NEUTRAL L/S (U/W) 28

Methodological appendix on Lyxor Alternative UCITs Peer Groups 29

DISCLAIMER 31

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

2

back to the top

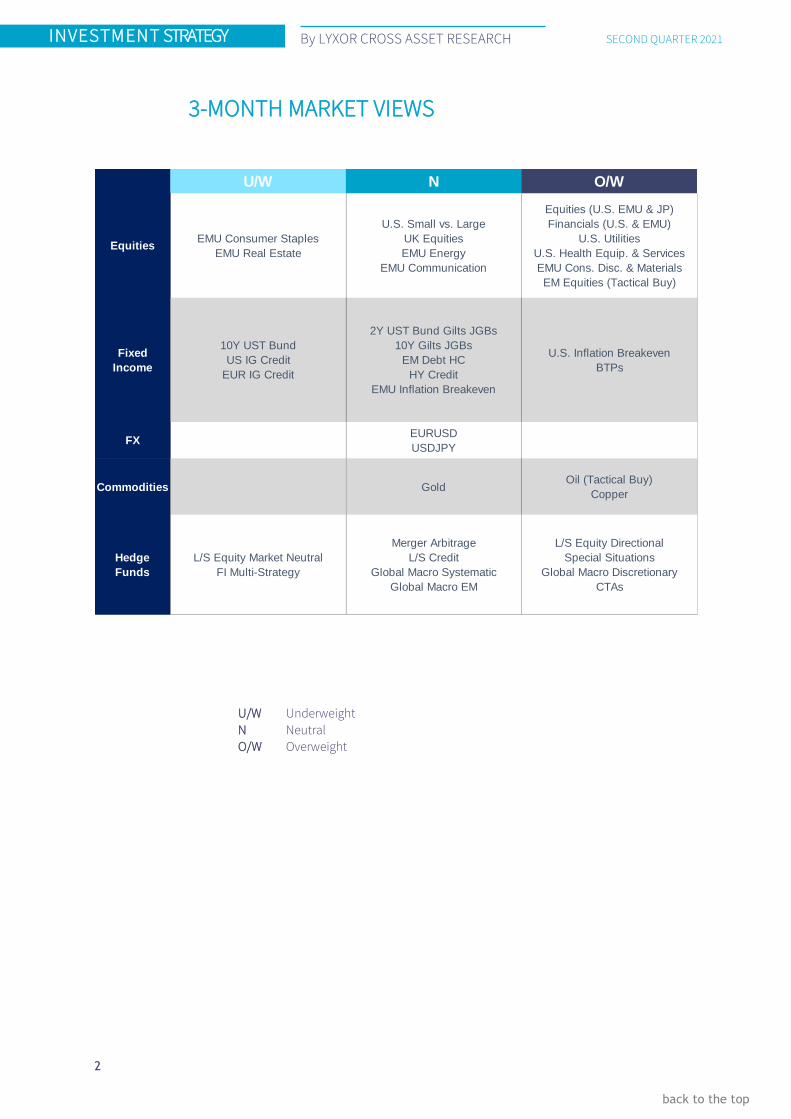

3-MONTH MARKET VIEWS

U/W Underweight

N Neutral

O/W Overweight

U/W N O/W

EquitiesEMU Consumer Staples

EMU Real Estate

U.S. Small vs. Large

UK Equities

EMU Energy

EMU Communication

Equities (U.S. EMU & JP)

Financials (U.S. & EMU)

U.S. Utilities

U.S. Health Equip. & Services

EMU Cons. Disc. & Materials

EM Equities (Tactical Buy)

Fixed

Income

10Y UST Bund

US IG Credit

EUR IG Credit

2Y UST Bund Gilts JGBs

10Y Gilts JGBs

EM Debt HC

HY Credit

EMU Inflation Breakeven

U.S. Inflation Breakeven

BTPs

FXEURUSD

USDJPY

Commodities GoldOil (Tactical Buy)

Copper

Hedge

Funds

L/S Equity Market Neutral

FI Multi-Strategy

Merger Arbitrage

L/S Credit

Global Macro Systematic

Global Macro EM

L/S Equity Directional

Special Situations

Global Macro Discretionary

CTAs

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

3

back to the top

EXECUTIVE SUMMARY

Macro & Market Views

The recovery is not over yet. The vaccination rollout and global stimulus point to a faster

recovery in H2, justifying a bullish bias on risky assets.

Yet, the recovery will likely be unequal and uneven. The U.S. would be a major global growth

driver, boosted by aggressive policy support. Chinese growth would moderate and remain

imbalanced. Europe could lag, slowed by renewed mobility restrictions. The path of the gradual

but steady Japanese recovery would depend on consumer confidence. The progress of EM

countries would remain uneven, a function of their access to vaccinations and exposure to U.S.

reflation.

The laborious services recovery still calls for continued fiscal and monetary support, inducing

recurrent inflation fears and rate volatility, amplified by intense supply-chain pressures. While

U.S. inflation has not reached its peak yet, other developed economies seem unlikely to

overheat. Inflation hedges would remain in demand, keeping us O/W on U.S. breakeven and

bullish on cyclical commodities - especially copper.

Highly abundant macro and market liquidity may result in trading anomalies, requiring tactical

monitoring. While Covid-19 developments should remain a significant market differentiator,

sequencing regional, sectors and factors recoveries would be challenging, unsettled by rate and

inflation uncertainties. Exposure to U.S. reflation will likely be a major theme in Q2, in particular

for Japan, UK, Germany, Asia and China, and Mexico.

We maintain our risk-on positioning. Our O/W on DM equities seeks to leverage on U.S. reflation,

on lagging valuations in Europe and on Japanese efforts to exit deflation. We combine value and

growth styles through sectors, looking for similar drivers. More affordable valuations in EM and

China open tactical opportunities. In contrast, we are U/W govies and have neutralized our

stance on HY credit.

Alternative Strategies

We have adjusted our views on alternative strategies given the changing environment discussed

above. In this context, carry strategies, on which we were constructive until now, are less

appealing with Treasury yields heading to 2-2.5%. We downgraded L/S Credit and EM Global

Macro to N. We don’t expect the conditions to be met for such strategies to outperform.

With regards to other strategies, we remain O/W Event-Driven and Neutral L/S Equity (Directional

L/S at O/W and Market Neutral L/S at U/W). Event-Driven strategies should continue to benefit

from robust corporate activity in the post-Covid world. Special Situations are more directional

than Merger Arbitrage and have a value bias which is likely to be rewarded. Merger Arbitrage

remains attractive as deal spreads fluctuate in the 6-7% range at present and SPACs have

become a new engine of performance. Finally, we upgraded CTAs to O/W. Their portfolios are

well-balanced and positioned for a cyclical upswing. Overall, we have a slight preference for

Event-Driven vs. L/S Equity and now favor CTAs to Global Macro strategies due to the EM bias of

the latter.

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

4

back to the top

MACRO & MARKET VIEWS

MARKETS HESITATING BETWEEN REFLATION

AND INFLATION

The quarter ended on a positive note for risk assets.

Improvement on the Covid-19 front, global growth

momentum gaining traction, the passing of a massive

policy stimulus bill in the U.S. and ample liquidity

pushed cyclical commodities and equity markets

higher. Oil (Brent generic first Future) and Copper (LME

generic first Future) led the way, surging +21.1% and

+13.3%, respectively. The MSCI World Index gained

+5.7% in local currency terms over the period.

While financial conditions (as measured by the Chicago

Fed ANFCI) continued to improve, risk asset volatility

remained elevated, signaling sustained investor

nervousness on the bumpy road to normality. Also,

markets started to show signs of froth. In the U.S., the

short squeeze on the video game retailer GameStop

triggered by Reddit users agitated markets. It only had a

transitory impact on financial stability but will likely lead

to new regulations to address the gamification of retail

investing. Other signs of frothiness include non or hardly

profitable companies (Tesla, Airbnb, etc.) trading at

extreme price to sales ratios. U.S. margin debt soared to

$814 bn by the end of February. Yet, relative to market

performance, this new record might be seen as a

recovery rather than a sign of uncontrolled speculation.

In China, asset bubbles in the stock and property

markets prompted the PBoC to adjust its monetary

policy, triggering a correction.

Better growth prospects triggered a sharp widespread

revival in inflation expectations. Inflation breakeven

jumped more than 60 bps (five-year maturity) in the U.S.

and United Kingdom. Implicit measures of Eurozone

inflation expectations rose as well, though the move was

shallower (+25 bps on five-year EUR inflation swap). The

U.S. 10-year government bond yield gained +83 bps,

ending March 2021 at 1.74%, thereby recouping its pre-

Covid level. Eurozone yields moved up as well, though

to a lesser extent.

Firmer USD and higher bond yields precipitated a major

Growth to Value rotation. In terms of geographies, the

shift favored Eurozone equities (EuroStoxx 300 +8.7%)

over U.S. equities (S&P 500 +5.8%) while hindering

emerging markets advance (MSCI EM +3.6%).

Typical safe-havens struggled in a period when reflation

trades occupied center stage. Gold prices lost about

10% as U.S. real yields gradually recovered from deeply

negative levels. Long-dated U.S. Treasuries and German

Bunds (Bloomberg-Barclays 7-10-year indices) yielded

Q1 2021 Asset Class Performance

Source: Macrobond, Lyxor AM

Persistent volatility

Source: Macrobond, Lyxor AM

U.S. Margin debt soaring

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

5

back to the top

negative returns of -5.7% and -1.6% returns,

respectively. Credit spread compression in the high yield

segment more than offset base yield increases, allowing

U.S. and Europe high-yield credit to offer thin but

positive total returns over the quarter.

Heading into Q2, pressing questions on investors’ minds

and ours include: do reflation trades continue to offer

attractive risk-return profiles? Will the economic

recovery affirm itself and spread to Europe? What are

the risks that U.S. growth overheats, leading to

unwanted inflation? When will central banks start

normalizing monetary policy?

PANDEMIC TRENDS AND POLICY RESPONSE

TO CONTINUE DICTATE GROWTH PROSPECTS

Global growth momentum improved in recent weeks as

suggested by the latest soft data on business

confidence. Purchasing manager indices are back at

levels coherent with a strong manufacturing activity in

most developed countries. However, Services are

lagging, notably in Europe where worrying Covid-19

trends prompted authorities to maintain or toughen

mobility restrictions.

Worldwide, a new wave of the pandemic is unfolding

with an acceleration of new cases above 600 000 per day

and a daily death toll remaining above 1 per million

people, on average over the last seven days. So far, at

least 2.7 million people have died from Covid-19.

The global outbreak picture hides large disparities

across geographies. Covid-19 trends result from a

combination of immunity from previous waves,

vaccination rollouts, adequacy of health system and

mobility restrictions.

Considering the seven-day average daily cases per

people (source NY Times), Africa or Asia seem relatively

spared from the current wave while the pandemic is still

raging in South America and Europe. Hot spots (new

cases above 30 per 100 000 and rising) include Brazil,

Argentina, Uruguay, Chile, Turkey, France, Italy, Sweden

and many Eastern European countries.

According to a recent poll from the journal Nature,

almost 90% of scientists surveyed think that the

coronavirus will become endemic. In other worlds, the

coronavirus and its many variants will likely continue to

circulate in pockets of the global population. However,

depending on the type of immunity acquired through

infection and vaccination, a return to normality remains

probable.

First, while there is still no cure, there is growing

evidence that some treatments are effective. Among

them, monoclonal antibodies appear able to stop

Covid-19 when administered at an early stage.

Strong ongoing manufacturing recovery …

Source: Macrobond, Lyxor AM

… but Services are lagging in many countries

Source: Macrobond, Lyxor AM

Covid-19: large disparities across geographies

Source: Macrobond, Lyxor AM

Covid-19 death toll remains elevated

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

6

back to the top

Unfortunately, they could lose their efficacy against new

variants, leading researchers to tailor them against

those variants. Second and more importantly in our

view, vaccination is key for a return to normality.

So far, accumulated evidence on available vaccines

suggest that they are less effective against new virus

variants, notably the so-called “United Kingdom”

variant that presents increased transmissibility. Also, it is

not yet clear whether vaccinated people could be

asymptomatic and contagious. However, on a more

positive note, most vaccines seem to prevent severe

symptoms from variants. Extended vaccination should

help preserve health systems and contain fatalities,

thereby allowing authorities to reopen economies.

While Covid-19 vaccine developments have been

acclaimed as unparalleled achievements, the

vaccination ramp-up looks hesitant and slow with only

3.5% of the world population fully vaccinated so far.

Overall, developed economies are more advanced than

most emerging countries but there are striking

differences. Despite logistics hurdles, the U.S.

vaccination rollout is accelerating, and already 16.2% of

the population are fully vaccinated and an additional

13.6% have received a first dose. The Eurozone is far

behind with vaccination levels at about a third of U.S.

ones. Despite newly released vaccine supply plans (with

an acceleration of deliveries in Q2 and Q3), Europe may

not succeed to provide full protection (2 doses) to 70%

of its population before September, probably few

months after the U.S.

The contrasting Covid-19 picture on both sides of the

Atlantic translates into contrasted policy response. In

the U.S., many states are already easing restrictions

whereas authorities in the Eurozone are maintaining or

strengthening anti-Covid-19 measures such as

lockdowns and curfews. Unsurprisingly, mobility

remains impaired in major Eurozone countries while it

is recovering quickly in the U.S.

We believe that the vaccination timeline will be critical

in assessing growth prospects. Over the last three

months, Bloomberg consensus on 2021 growth showed

continuous upward revisions for the U.S. and downward

revisions for the Eurozone. As detailed in later sections,

we think that risks remain skewed to the upside for the

U.S. and to the downside for Continental Europe.

As the pandemic enters its second year, many

epidemiologists doubt that herd immunity could be

achieved because of uneven and partial vaccination

efforts (children being left out), risks that vaccines may

not prevent transmission, the emergence of new

variants and the uncertainty over how long immunity

lasts (whether acquired through infection or

vaccination).

Yet, a new normal without herd immunity remains

probable when authorities reopen economies.

Pent-up demand combined with policy stimulus

would trigger a sharp rebound in activity. We believe

that the U.S. will return to normal over the coming

quarter while the Eurozone may have to wait until

Q3 2021.

Covid-19 Vaccination tracker

Source: Macrobond, Lyxor AM

Contrasted mobility trends…

Source: Macrobond, Lyxor AM

… should be pivotal for growth prospects

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

7

back to the top

THE LOOMING U.S. ECONOMIC BOOM

Recent soft and hard data suggest that the U.S.

economic reflation is already gaining traction. ISM

purchasing manager indices for manufacturing and

services are back to levels coherent with a strong

expansion. Our weekly GDP tracker designed to follow

U.S. macro momentum has picked up sharply over the

last few days. Based on consumer sentiment, rail

shipments, raw steel production and initial jobless

claims, the tracker that shows a strong correlation to

real GDP growth (R² above 80%) signaled that activity

was already accelerating mid-March. The latest update

of the Atlanta Fed’s GDPNow estimate points to 6%

annualized quarter-over-quarter real GDP growth in Q1,

above the current Bloomberg consensus of 4.7%.

Those estimates do not necessarily take into account

the new stimulus payments that Americans have started

to receive as part of the American Rescue Plan, a $1.9tn

stimulus bill signed into law by President Biden on

March 11, 2021. Key elements of the American Rescue

Plan include $300 per week supplement jobless benefits

until Labor Day, $1400 direct payments to individuals

and $350bn to help state and local governments

mitigate the Covid-19 related fiscal shock.

The minimum wage hike was left out but other

measures such as tax credits, subsidies and extended

health access will likely benefit low- and middle-income

households. The pace of support to consumers is

accelerating by about $1tn (annualized) in March and

Q2 compared to the previous six months.

Households have accumulated massive savings since

the start of the Covid-19 crisis resulting from both

lockdown measures preventing them from spending

and from stimulus checks and subsidies granted by the

government. Savings that jumped to 35% of personal

consumption in Q2 2020 and decreased to 15% in Q4

will likely firm-up to about 20% of personal spending

over the next two quarters.

Propensity to consume is typically a function of

confidence, which in turn depends on the employment

outlook. To that regard, consumer confidence is already

rebounding and March payroll data that showed over

900 000 job creations bodes well for the coming months.

To be sure, we do not expect that households will

immediately catch-up entirely on their consumption

and spend the total savings accumulated over the past

four quarters but part of it will likely be spent as the

economy reopens, boosting consumption and driving

Q2 real growth to double-digits levels.

U.S. activity is already gaining traction

Source: Macrobond, Lyxor AM

Massive savings waiting to be spent

Source: Macrobond, Lyxor AM

Consumer confidence rebounding

Source: Macrobond, Lyxor AM

Sizeable labor slack likely to contract quickly

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

8

back to the top

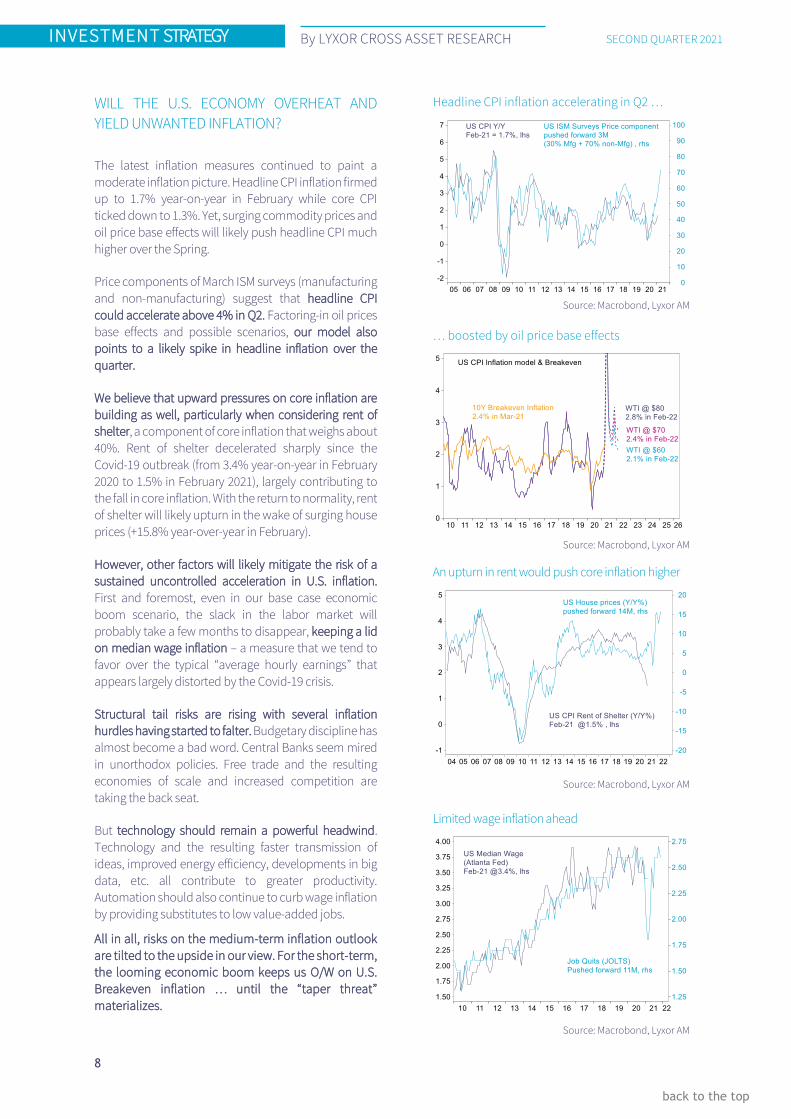

WILL THE U.S. ECONOMY OVERHEAT AND

YIELD UNWANTED INFLATION?

The latest inflation measures continued to paint a

moderate inflation picture. Headline CPI inflation firmed

up to 1.7% year-on-year in February while core CPI

ticked down to 1.3%. Yet, surging commodity prices and

oil price base effects will likely push headline CPI much

higher over the Spring.

Price components of March ISM surveys (manufacturing

and non-manufacturing) suggest that headline CPI

could accelerate above 4% in Q2. Factoring-in oil prices

base effects and possible scenarios, our model also

points to a likely spike in headline inflation over the

quarter.

We believe that upward pressures on core inflation are

building as well, particularly when considering rent of

shelter, a component of core inflation that weighs about

40%. Rent of shelter decelerated sharply since the

Covid-19 outbreak (from 3.4% year-on-year in February

2020 to 1.5% in February 2021), largely contributing to

the fall in core inflation. With the return to normality, rent

of shelter will likely upturn in the wake of surging house

prices (+15.8% year-over-year in February).

However, other factors will likely mitigate the risk of a

sustained uncontrolled acceleration in U.S. inflation.

First and foremost, even in our base case economic

boom scenario, the slack in the labor market will

probably take a few months to disappear, keeping a lid

on median wage inflation – a measure that we tend to

favor over the typical “average hourly earnings” that

appears largely distorted by the Covid-19 crisis.

Structural tail risks are rising with several inflation

hurdles having started to falter. Budgetary discipline has

almost become a bad word. Central Banks seem mired

in unorthodox policies. Free trade and the resulting

economies of scale and increased competition are

taking the back seat.

But technology should remain a powerful headwind.

Technology and the resulting faster transmission of

ideas, improved energy efficiency, developments in big

data, etc. all contribute to greater productivity.

Automation should also continue to curb wage inflation

by providing substitutes to low value-added jobs.

All in all, risks on the medium-term inflation outlook

are tilted to the upside in our view. For the short-term,

the looming economic boom keeps us O/W on U.S.

Breakeven inflation … until the “taper threat”

materializes.

Headline CPI inflation accelerating in Q2 …

Source: Macrobond, Lyxor AM

… boosted by oil price base effects

Source: Macrobond, Lyxor AM

An upturn in rent would push core inflation higher

Source: Macrobond, Lyxor AM

Limited wage inflation ahead

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

9

back to the top

FED, TAPER, AIT AND U.S. YIELDS

In early May 2013, the Federal Reserve alluded to a

possible tapering of its quantitative easing (‘QE’) that

was confirmed by Ben Bernanke on 19 June 2013.

Bond markets sold off in a move often referred to as

the “Taper Tantrum”. U.S. Treasury 10-year yields

spiked +85 bps over May-June 2013 buoyed by rising

term premiums (+60 bps) and higher average implicit

real short-term rates (+60 bps) that more than offset

the 35-bps compression in Breakeven inflation.

Notably, the recent “taperless” spike in yields was of

similar magnitude (+81 bps year-to-date) but was

primarily driven by rising inflation expectations and

higher term premiums. When the Fed will start

signaling a possible scaling down of its monthly QE

purchases (currently $80bn U.S. Treasuries and

$40bn MBS), a switch between implicit inflation and

real short-term rates will likely happen, abruptly

compressing breakevens. We believe that Fed’s QE

Taper is a major risk to our long call on U.S.

breakevens but not an immediate threat.

The latest FOMC meeting showed the Fed committed

to its average inflation targeting (‘AIT’) framework.

Fed Chair Jerome Powell insisted that the Fed will not

act preemptively and will react to actual data rather

than forecasts. A change in interest policy could be

considered when three features are met: 1) labor

conditions should be consistent with maximum

employment, 2) inflation should be at 2% and not on

a transitory basis and, 3) inflation should be on track

to exceed 2%. The Fed’s summary of economic

projections displayed no rate hike through 2023

despite higher growth and inflation estimates

showed few FOMC participants judging that

conditions for a rate hike would be met before the

end of 2023 and four of them considering a rate hike

was warranted before the end of next year.

The Fed seemed eager to maintain a strict control

over the short end of the yield curve (up to three

years) but does not seem overly concerned by the

recent rise in longer maturity yields. We concur that

10-year yields approaching 2% or even higher are

unlikely to derail the looming economic boom.

With nominal GDP growth likely to reach 10% in 2021,

fundamentals could call for much higher yields.

However, we think that the Fed’s dedication to

anchor short maturities will limit the normalization.

We revised up our forecasts and foresee a further

steepening of the two-to-ten-year slope towards 2%,

which would translate into 10-year yields rising to

1.90% over Q2 and 2.25% over the coming year. In our

opinion, risks are skewed to the upside.

Beware of the Taper threat for Breakevens

Source: Macrobond, Lyxor AM

The Fed revised up its macro projections …

Source: Macrobond, Lyxor AM

… but appeared committed to its AIT framework

Source: Macrobond, Lyxor AM

Further curve steepening ahead

Source: Macrobond, Lyxor AM

Change in bps YTDTaper Impact

May-June 2013

US 10YY 81 85

US 10Y Break-Even Inflation 38 -35

US 10YY Term Premium (Fed, Kim-Wright) 52 60

US 10Y Average Implicit Real ST Rate (K-W) -13 60

US 3YY 18 36

US 3Y Break-Even Inflation 65 -40

US 3YY Term Premium (Fed, Kim-Wright) 18 27

US 3Y Average Implicit Real ST Rate (K-W) -69 50

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

10

back to the top

U.S. FIXED-INCOME MARKETS’ UNATTRACTIVE

RISK-RETURN PROFILE

We continue to rank short-dated U.S. Treasuries at

Neutral for the next three months. The Fed’s

dedication to its AIT framework will likely keep a lid

on the short end of the curve for at least the coming

12 to 18 months.

Our new higher three-month and one-year targets on

U.S. 10-year yields of 1.90% and 2.25%, respectively,

translate into negative expected returns and prompt

us to prefer an U/W stance on long maturities.

Corporate spreads have fallen to historical lows,

leaving little room for further compression.

In the investment-grade (‘IG’) segment, spreads have

reached lows last seen in early 2018 or before 2008,

leaving little room for compression over the coming

quarter despite the booming economic outlook. We

find that IG risk-return profile has deteriorated and

we downgrade U.S investment grade to U/W.

We downgrade U.S. high-yield (‘HY’) credit to Neutral.

We estimate that the default probability implied in HY

current option adjusted spreads is 1.2% for next

November, about a fourth of Moody’s bottom-up

forecasts that have been revised down to reflect

improved macro prospects. Also, the recovery in oil

prices seems well advanced and is unlikely to

contribute much further to lowering default

probabilities in the HY energy segment. We find that

HY spreads are fully discounting our bullish macro

scenario at a time when base risks are increasing.

STRONG EARNINGS PROSPECTS KEEP US O/W

ON U.S. EQUITIES

After a milder contraction (-3%) in 2020 than

originally anticipated, Bloomberg bottom-up

consensus estimates point to a sharp rebound for

S&P 500 sales this year (+8%) and next (+6.7%).

Notably, our top-down model reaches similar results

when factoring-in nominal GDP forecasts from the

Congressional Budget Office, a stable dollar and WTI

prices at $65 per barrel for the next 18 months.

Moreover, if we factor in our base case scenario with

U.S. nominal GDP growth reaching 10% in 2021, we

find that sales growth could surprise on the upside.

Profit margins will likely benefit from the operating

leverage and stay firm at current high levels in 2021 or

even further recover. Combining booming sales

growth and solid profit margins should warrant eye-

catching EPS growth this year.

The Q1 earnings season is about to start, probably on

a strong footing, as suggested by the record-high

Corporate spreads at historical lows …

Source: Macrobond, Lyxor AM

… discounting a bullish macro scenario

Source: Macrobond, Lyxor AM

S&P 500 sales growth could surprise on the upside

Source: Macrobond, Lyxor AM

Margins likely to benefit from operating leverage

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

11

back to the top

number of S&P 500 companies having issued positive

sales and EPS guidance for the quarter.

Regarding 2021, I/B/E/S and Bloomberg bottom-up

consensus estimates for S&P 500 EPS have been

markedly revised up since the beginning of the year

and currently show EPS growth exceeding 25%.

Alongside Bloomberg top-down consensus, we reach

a similar conclusion and believe risks remain skewed

to the upside.

Prospects for 2022 are more moderate with about

10% expected EPS growth and more uncertain as U.S.

corporate profitability could be clouded by Biden’s

corporate tax agenda. We doubt that Democrats will

seek to raise the tax rate to 28%, a level proposed by

the candidate but exceeding the average OECD

corporate tax rate. A more modest phased-in

increase seems likely in our opinion, which may not

constitute a large drag on 2023 EPS.

U.S. Equity valuations look stretched on various

metrics. In Q4 2020, the Tobin’s Q that represents the

market value of equity related to the market value of

net worth for U.S. nonfinancial corporate business

staged a new 70-year record above 2.5. End of March,

the S&P 500 price to sales ratio stood at 2.8, a level

last seen during the Tech bubble. And the 12-month

forward PE ratio was still hovering at about two

standard deviations above its 30-year mean.

Yet, equity risk premia, a measure relative to U.S.

yields, remained close to its 30-year mean,

suggesting that valuations are supported by the Fed’s

unorthodox policies and its impact on the bond

market. Will the rise in yields compress equity

multiples and undermine the bull market?

As detailed in previous sections, we believe that the

U.S. return to normality will continue to pressure

yields higher but the Fed’s dedication to its AIT

framework should limit the potential upside over the

coming months. We anticipate that the acceleration

in macro and EPS growth will constitute a strong

tailwind for U.S. equities, prompting large inflows

(partly from stimulus payments) and dwarfing

valuation-related risks. We maintain an O/W stance

on U.S. equities.

ADDRESSING U.S. VALUE AND GROWTH

THEMES THROUGH SECTORS

Late February, we closed our O/W call on Small

versus Large caps initiated last November.

The impressive Small caps rally pushed their relative

valuations to overstretched territory, prompting us to

take some profits and to neutralize the size theme.

Strong S&P 500 EPS prospects

Source: Macrobond, Lyxor AM

Typical valuation metrics look stretched …

Source: Macrobond, Lyxor AM

… but not relative to the bond market

Source: Macrobond, Lyxor AM

Back to Neutral on Size

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

12

back to the top

While the Growth theme is usually represented by

similar definitions, the Value theme can be

interpreted quite differently depending on the

investor approach. Therefore, we prefer to address

the Growth versus Value rotation through sectors.

Considering the S&P 500 pure Value and pure Growth

indices, we find large differences concentrated in few

sectors. Growth is heavily weighted on 1) Information

Technology (45%) that we rank Neutral, 2) Media &

Entertainment (31%), a group dominated by

Facebook, Google, Netflix and Twitter, which calls for

a bottom-up approach in our view and, 3) Retailing

(12%), essentially representing Amazon, and

therefore also ranked Neutral from a top-down

perspective.

We favor three sectors, heavily weighted in the S&P

500 Pure Value index, and therefore O/W the Value

theme.

We remain O/W on U.S. Banks for their cyclicality and

attractive valuations. The sector should continue to

benefit from the yield curve steepening. We also favor

Healthcare Equipment and Services despite the

sector’s rich valuation. The Covid-19 crisis and

related policy response should lift earnings growth

potential in 2021 above current (+9%) expectations.

Finally, we are constructive on Utilities that will likely

be supported by green capex, offer about 3.5%

dividend yield and present little downside risks in the

early phases of a recovery.

EURUSD, NOT A NO-BRAINER!

Last quarter we refrained from joining the crowded

long EURUSD as we thought the pair would stay in a

narrow range around 1.20. Examining the main

drivers anew, we find conflicting forces and no strong

rationale for a long call on either side.

As of the end of March, short speculative positions on

USD have closed and long positions on EUR have

receded, leaving no major excesses to correct. Short-

term interest rate differentials are expected to

change little as the Fed and the ECB pledged to

maintain policy rates at current levels for the next 12

to 18 months. However, the more advanced reflation

in the U.S. could lead to a further widening of the

long-term yield gap between U.S. and Germany,

pressuring USD up. On the other side, the Eurozone is

expected to catch-up in terms of vaccination, return

to normality and macro momentum. Such a shift

would likely trigger renewed interest on Eurozone

assets, tilting risks on EUR to the upside.

On a longer-term horizon (1 to 3 years), we keep in

mind the U.S. ballooning twin deficits that could be

detrimental to the greenback.

S&P 500 Growth & Value Sector breakdowns

Source: Macrobond, Lyxor AM

S&P 500 Sector Rotation

Source: Macrobond, Lyxor AM

EURUSD under conflicting drivers

Source: Macrobond, Lyxor AM

Pure Growth Pure Value

Industry GroupsEnergy 0% 11%

Materials 0% 2%

Capital Goods 0% 6%

Commercial & Professional Serv 0% 0%

Transportation 0% 0%

Automobiles & Components 4% 2%

Consumer Durables & Apparel 0% 1%

Consumer Services 0% 0%

Retailing 12% 1%

Food & Staples Retailing 0% 4%

Food, Beverage & Tobacco 0% 2%

Household & Personal Products 0% 0%

Health Care Equipment & Servic 1% 7%

Pharmaceuticals, Biotechnology 3% 0%

Banks 0% 26%

Diversified Financials 1% 17%

Insurance 0% 7%

Real Estate 0% 1%

Software & Services 23% 0%

Technology Hardware & Equipmen 15% 2%

Semiconductors & Semiconductor 7% 0%

Telecommunication Services 0% 4%

Media & Entertainment 31% 4%

Utilities 0% 3%

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

13

back to the top

EUROPE: NEAR TERM CHALLENGES; MID-TERM

OPPORTUNITIES

The EMU recovery faces hurdles in the very near term.

France and Italy tightened mobility restrictions at the

turn of the quarter and the reopening will probably take

more time than what the consensus currently expects.

Vaccination campaigns in the EU continue to lag vs. the

U.S. and the U.K. and the difficulties faced by the

AstraZeneca vaccine could delay herd immunity.

A rebound in EMU activity looms nonetheless towards

late Q2 and Q3 as the economies reopen. Business and

consumer sentiment surveys improved in March despite

the Covid-19 headwinds and the industrial sector

bounced back markedly in recent months. Pent up

demand in services could show to be supportive, while

international firms are likely to be less constrained than

domestic ones thanks to their ability to capture external

growth.

The policy mix is supportive. The monetary stance is set

to remain highly accommodative as inflation stays

muted. Policy rates may remain unchanged in 2021/

2022 while the ECB announced asset purchases under

the Pandemic Emergency Purchase Program (“PEPP”)

will be frontloaded in Q2. The overall PEPP envelope

remains at EUR 1850bn until March 2022, of which

approximately half has already been purchased as of

end-March. In parallel, the ECB will also continue to

purchase EUR 20bn/ month under the Asset Purchase

Program (“APP”). The ECB will continue reinvesting

principal payments from maturing securities for “an

extended period of time” past the date when it starts

raising rates. Frequent refinancing operations

contribute to ample liquidity conditions. The ECB’s

January bank lending survey signaled a tightening of

credit standards for firms and households, related to

adverse economic prospects, and not with banks’ cost

of funds & balance sheet constraints.

On the other hand, the fiscal stance, albeit less

accommodative than in the U.S., will remain supportive.

EU fiscal rules have been suspended in 2021 and

possibly 2022, to prevent fiscal consolidation too early in

the cycle and allow for a reform of the framework. EU

fiscal rules are nonetheless unlikely to be reformed

before German (26/09) and possibly French (April 2022)

elections. Concurrently, fiscal stimulus at the level of the

EU is backloaded, the institutional set-up is complex,

and disbursements will only gain traction in 2022.

Our stance on EMU inflation breakevens stands at N.

Upside risks in service prices, which represent 40% of

the consumer price index, and potential spillovers from

higher inflation expectations in the U.S., suggest some

exposure to the asset class is deserved despite mixed

economic prospects and elevated unemployment

(8.1% in January according to Eurostat).

The expected shape of the European recovery

Bloomberg consensus forecasts. Source: Macrobond,

Bloomberg, Lyxor AM

Inflation pressures to remain muted in Europe,

with some upside risks

Source: Macrobond, Lyxor AM

The fiscal stance is less accommodative in

Europe than in the U.S.

General Government. Source: OECD, Macrobond, Lyxor AM

EU fiscal support is backloaded

Source: ECB, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

14

back to the top

In the UK, a strong recovery is likely to take shape as

early as Q2 on the back of the economic reopening, after

a sharp contraction in Q1-21 due to tight lockdowns.

The U.K. has started the gradual reopening of the

economy in March and will accelerate the pace of

normalization in April. We expect the BoE to stay put

over the next two years even if the vaccine rollout leads

to a stronger and earlier recovery than elsewhere in

Europe. On the fiscal front, support measures were

extended until the end of September 2021. Capex is

likely to get boosted by the two-year super-deduction

for capital allowances. The increase in the corporate tax

rate will start in FY 2023-24 (from 19% to 25%). Longer

term, the Brexit should also translate into welfare losses,

because of higher trade costs with the EU.

U/W Bunds and Guilts on spillovers from rising Treasury

yields. Elevated ECB purchases, which will result in

strongly negative net-net supply of mid-to-long term

sovereign bonds (c. EUR -350bn in the 10 largest

Eurozone countries until end-2021) and challenging

near term economic conditions will likely cap the rise in

German yields. But spillovers from higher Treasury

yields might push 10-year Bunds towards -20bps in Q2

and towards 0% in twelve months, in our view. We

estimate 10-year Bund yields rise 50bps when Treasury

yields rise 100bps, based on weekly data over the last

twenty years. Meanwhile, UK Gilts could be fueled by

their higher beta to U.S. Treasuries and by the faster

pace of economic reopening.

Concurrently, our stance on BTPs (Italy) remains at O/W.

Credit risks rose as public debt jumped significantly, but

near-term funding needs will be fully addressed by the

ECB. The new administration, under Prime Minister

Mario Draghi, benefits from a positive market

appreciation given the solid track record of the former

ECB governor during the euro zone sovereign crisis a

decade ago. Italian yields trade higher than peers

among large euro zone countries and, considering the

manageable risks, appear attractive. 10-year BTP yields

trade at 0.63%, almost 20bps above all-time lows

reached earlier in February 2021.

The upside in credit markets appears limited with Euro

Investment Grade (IG) and High Yield (HY) spreads below

pre-Covid-19 crisis levels. Risks are broadly neutral

thanks to state guarantee schemes which have been

extended until June 2021 in several European countries.

The French State-guaranteed loan is a one-year treasury

loan and will have a grace period over this period for

instance. In the medium term, there are question marks

over a potential rise in default rates. In the UK, IG

spreads, near 100 bps currently, are more attractive but

involve currency hedging costs that remove that

advantage. Overall, near the trough of the business cycle

we prefer getting exposure to equities over credit.

A strong rebound looms in the UK

Source: Macrobond, Lyxor AM

O/W Italy in Eurozone sovereign debt markets

Source: Macrobond, Lyxor AM

A slight preference for IG Credit (N) vs. Govies

Source: Macrobond, Lyxor AM

HY default rates are expected to have peaked

Source: Moody’s, Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

15

back to the top

O/W EMU EQUITIES TO LEVERAGE GLOBAL

GROWTH; NEUTRAL UK EQUITIES

At this preliminary stage of the business cycle and in

order to position portfolios for a global cyclical upswing,

we believe European equities are attractive. Domestic

fundamentals are unlikely to be highly supportive in the

very near term due to renewed mobility restrictions. But

large caps are in a good position to leverage global

growth, in a similar fashion than EMU equities delivered

upbeat returns in Q1 despite renewed lockdowns

domestically. Based on Bloomberg data we estimate

that more than half of the earnings (EBITDA) of

EuroStoxx 300 members is generated outside Europe, of

which half comes from the U.S. which is likely to

experience a healthy recovery.

The valuation of EMU equities is rich but less so than in

the U.S. The 12-months forward P/E ratio is near record

highs, at 17.8x. This is more than 20% above the average

valuation of the past five years. EMU equities are

nonetheless attractive vs. the U.S. market from a

valuation standpoint. U.S. equities trade at almost 23x

future earnings (25% above the 5-year average). Low

bond yields in the EMU reinforce the attractiveness of

equities, while upward revisions to earnings growth

expectations might temper rich valuations.

The expected (total) return of EMU equities, in the range

of 8-10% over the next twelve months, leads us to

upgrade our stance to O/W. Our model, based on lagged

industrial production, Brent oil prices and the consumer

price index helps to explain 75% of the sales p/ share

annual change over the past 15 years. Going forward, we

use our own forecasts and assume conservative profit

margin expansion (+200bps to 4.5%) and dividend yield

normalization (3.2%). Both would remain 50 bps below

the long-term average (5% profit margin and 3.7%

dividend yield) according to Bloomberg data.

Quantitative approaches are nonetheless challenged by

the huge disturbances caused by the Covid-19 in data

releases and must be handled with care. Having said

that, we believe our estimate is conservative.

Our stance on UK equities stands at N. From a valuation

standpoint, UK equities are more attractive than EMU

equities. The 12-months forward P/E ratio is below the

5-year average, at 13.3x, and below the valuation of U.S.

and EMU equity markets. Also, considering the vaccine

rollout, the recovery is likely to start earlier than in the

EMU. Yet, the composition of benchmarks such as the

FTSE 100 is quite defensive, resulting in a systematic

underperformance vs. the EuroStoxx 300 in expansion

cycles. The latter is biased towards Consumer

Discretionary stocks (16% weight) while the UK

benchmark is biased towards Consumer Staples (18%

weight) which underperform in recoveries. We expect

the underperformance of the FTSE 100 to continue.

Upward revisions to EPS expectations bode well

Source: I/B/E/S, Lyxor AM

Valuation is rich in the EMU compared to history

Source: Bloomberg, Macrobond, Lyxor AM

Our model explains 75% of sales p/share changes

Based on 3-months lagged EMU IP, current CPI and Brent oil

prices. R2: 75%. Source: Bloomberg, Macrobond, Lyxor AM

EMU outperformed UK equities in expansions

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

16

back to the top

EMU SECTORS: CYCLICALS VS. DEFENSIVES

From a top down perspective, our sector

recommendations are grounded in two

considerations. First, a recovery looms, which should

be supportive for cyclical sectors versus defensive

ones. In that regard, we maintain Consumer

Discretionary and Materials at O/W. Second, policy

risks eased and bond yields, albeit low, are set to

experience upward pressures. As a result, we upgrade

Financials to O/W. Concurrently, we downgrade Real

Estate and maintain Consumer Staples at U/W.

Financials are expected to benefit from three factors.

First, the looming recovery should be supportive for

value and cyclical stocks. The sector has been the

most attractively valued for some time. We expect

this value potential to be unlocked in the coming

quarters. Second, the sector should benefit from the

rise in bond yields. ECB purchases will put a cap on

yields but better economic prospects in the U.S.

should put upward pressure on Bund yields. Third,

the regulatory pressure is expected to have peaked

and dividend distribution should normalize partially.

One source of risk is the elevated volatility of the

sector and the possibility that bond yields remain

extremely low.

Consumer discretionary should benefit from the

economic reopening and pent-up demand for such

products. Dispersion is high within this sector and we

prefer Automobiles & Components and Consumer

Durables & Apparel at the industry group level (vs.

Consumer Services and Retailing). In terms of market

capitalization, they represent the bulk of the sector.

Meanwhile, Materials are expected to be bolstered by

increased infrastructure spending. Both sectors are

not particularly attractive from a valuation

perspective, but there is room for additional upward

revisions in earnings expectations.

U/W Real Estate and Consumer Staples. The former is

one of the most vulnerable sectors to the rise in bond

yields, along with Utilities. Over the past three years,

a 100bps rise in Bund yields has translated into a -

8.6% underperformance of the sector vs. the MSCI

EMU. Then, the valuation of Consumer Staples is

close to record highs. Its defensive features are less

appealing as we head towards a recovery and it is

also sensitive to rising bond yields.

Finally, we upgraded Communication Services to N.

Within the sector, Media & Entertainment are

expected to outperform. The environment for

Communication Services remains highly competitive

and regulations are tough. Elevated capex and

topline trends remain challenging. Pricing is

improving but continues to lag inflation.

EMU sectors: maintain a bias towards cyclicals

(+) upgrade; (-) downgrade vs. last quarter. Source: Lyxor AM

Cyclical sectors outperform during recoveries

Source: Macrobond, Lyxor AM

Upgrade Financials to O/W on valuation

Source: I/B/E/S, Macrobond, Lyxor AM

Real Estate and Consumer Staples are

vulnerable to rising bond yields

Source: Macrobond, Lyxor AM

U/W N O/W

Utilities

Consumer Staples Health CareConsumer

Discretionary

Real estate (-)Communication Services

(+)Materials

Energy Financials (+)

Industrials

IT

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

17

back to the top

JAPAN ECONOMY: THE FUNDAMENTAL STORY

REMAINS INTACT

Covid outperformance and cyclical exposure

We expect Japan to remain less impacted by the

pandemic than in the rest of the world. It is facing a

much milder fourth wave, even though some large cities

are instating some new mobility restrictions.

As a result, high frequency indicators of activity are close

to cruise level and outpacing most of its peers. Japan’s

relative isolation from the pandemic is all the more

remarkable that its vaccination is only beginning,

strongly lagging most DM countries.

Japan is also highly geared to external activity. Japan is

very sensitive to the economic pulse China, the U.S. and

the rest of Asia, which account for 80% of its exports.

These regions are leading in the way out of the

pandemic recession. Moreover, Japanese export

products tend to have an extra cyclical bias: machinery,

auto, tech, and cyclical services are their key exports.

Unsurprisingly, Japanese equity indices are sensitive to

foreign activity. About 40% of Topix stocks revenues are

generate abroad, 15/20% of which in the U.S. and China.

While Japanese exports face short-term downside risks

in the U.S., where tighter mobility restrictions are

probable, 2021 bodes well for Japan.

Meanwhile, we still see upside potential from Japanese

consumption, though progress remain slow for now.

The virus fear-factor was the last straw for consumer

confidence after a stream of shocks, including a major

typhoon and the rise in sales tax. Should confidence

revive in 2021, boosted by the end of the pandemic,

massive accumulated savings could boost household

spending.

In the medium-term, positive impacts from Suganomics

would also boost corporate demand through greater

investment on tech and M&A.

U.S. rate isolation but U.S. reflation exposure

Japanese long and short-term sovereign yields display a

low beta to U.S. rates (on average 0.1). Japanese

inflation trends are also softer than in the U.S.

reinforcing its isolation from U.S. rate volatility. A greater

sensitivity of Japanese assets to U.S. monetary policy is

through the currency. A weaker JPY due to a higher U.S.-

Japan rate differential would overall be supportive for

Japanese equities, which are highly exposed to foreign

revenues.

Meanwhile, Japan is primarily exposed to the U.S.

reflation. Through its exports of vehicle, chips,

machinery, services, Japan stand as a prime beneficiary

from a boom in U.S. consumption demand and greater

infrastructure spending.

Slow but steady economic progress

Japanese economic prints are steadily improving.

Orders remain driven by external demand, but pulse

in domestic orders is gaining traction. Orders are

pointing to increased manufacturing activity, amid

lows intermediary and finished goods inventories.

Unlike the U.S. and Europe, Japan is not facing

particularly severe supply chain disruptions, though

companies are struggling to fully pass higher

commodity prices. Hiring pressure is also improving

in the manufacturing sector.

Exports remain the main driver in Japan

Source: Bloomberg, Lyxor AM

The manufacturing recovery is not over yet

Source: Bloomberg, Lyxor AM

High Japanese exposure to the world recovery

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

18

back to the top

In nuance, the pulse looks weaker in services, which

remains in recovery mode, not being yet in full steam

expansion. It is evidencing progress yet to be achieved

in domestic demand.

The BoJ only a tad more hawkish

Japanese equities would also benefit from continued

monetary and fiscal support. The latest BoJ move, a tad

more hawkish, doesn’t question the highly

accommodative environment. It recently raised its daily

long-term rate trading range by 5bp to 25bp and

removed its explicit annual ETF purchase target (now

focusing on Topix instead of Nikkei underlying). We see

JPY remaining rangy.

JAPAN EQUITIES: NOT TAKING PROFIT YET

(O/W)

Japanese equities ranked amongst the top performers

in Q1, but we are not taking profits just yet.

We expect the asset class to remain supported by a

strong alignment of planets, benefitting from a deep

exposure to the U.S. reflation, a high gear to the world

recovery, especially through revenue exposure to

regions which are leading in the way out of the

pandemic recession.

With continued monetary and fiscal support, we expect

the slow but steady economic progress to translate into

greater domestic confidence and demand. The amount

of savings put back to work and renewed traction in

domestic investment will likely be pivotal for Japanese

equity returns.

The outperformance of Japanese equities has been

largely driven by export sensitive segments. So far

progress in domestic demand and prospects from

Suganomics are both loosely priced in, implying

significant re-rating potential.

The breakdown of Japanese total-return indices shows

that much of the performance year-to-date has been

driven by improving margins, not by valuation multiples

expansion.

We find that Japanese companies’ greatest room for

improvement lies with their gross margin, weaker than

in other developed markets. In contrast, years of

deflation have led Japanese companies to maintain

elevated control of their operational and non-operation

fixed costs. This leaves them with strong operational

leverage in this early cycle.

The profit backdrop for Q1 remains healthy, and

earnings are being firmly revised up.

Furthermore, despite the recent bull run, Japanese

stocks remain under-owned, while they can provide

diversification benefits. The tactical environment is

neutral, with technicals remaining stretched, but with

greater fundamental support.

Strong Japan exposure to the U.S. Reflation

Source: Macrobond, Lyxor AM

Consumption potential if confidence returns

Source: Macrobond, Lyxor AM

Continued fiscal and monetary support

Source: Macrobond, Lyxor AM

Japanese equities remain under-owned

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

19

back to the top

Key themes in this market include positioning around

companies’ U.S. reflation exposures (at the expense of

those rather exposed to Asia which already

outperformed). Value and cyclical stocks would remain

in demand. The worsening saturation global trade

would also be a positive for industrial and services

companies sensitive to shipping and naval

construction. The Japanese semi sector would remain

appealing, increasingly used as alternative amid supply

chain reshuffling.

We remain O/W for now.

EM ECONOMIES: BRIGHTENING OUTLOOK

A transitory and mild Q1 soft patch

New Covid-19 infections are picking up in several EM

countries, while vaccination programs are rolling out

at a much slower pace than in DM, making herd

immunity improbable until next year.

Yet, sensitivity of real activity in EM countries to

mobility restrictions has receded. The soft patch in

Q1 has been mild and high frequency indicators have

slowed less than in DM countries.

We expect EM countries to experience a meaningful

rebound in Q2, driven by the rebound in the rest of

the world and by the acceleration of the global

recovery. Eastern Europe, more sensitive to the pulse

in Western Europe, might lag other regions.

However, the EM economic upside would be capped

by the economic moderating in China as stimulus are

gradually unwound and as its manufacturing

recovery nears its completion. Moreover, we expect a

further erosion in the EM vs. DM growth differential

due to the ongoing deglobalization (which sees

concentrated supply chains, DM ageing, and more

protectionism) and due to EM countries’ uneven

ability to boost domestic consumption. Finally, a

heavy election calendar in EM countries would imply

a higher relative political risk. Main elections concern

Chile in April 11, Mexico in June 6, Iran in June 18,

Taiwan in August 28, Russia in September 19, the

Czech Republic in October 8, Iraq in October 10,

Argentina in October 24, Chile in November 21 and

Libya in December 24.

US Reflation becomes pivotal for EM, net positive

With its ambitious spending package, the U.S. will

likely be a key driver for global growth. The U.S.

buoyant economy will likely attract some investors’

flows at the expense of EM’s.

However, the US. Reflation will boost those most

connected to its supply chain. This includes China

and the largest Asia countries (including India, South

Korea, and Taiwan), as well as Mexico. In contrast,

EM and world trade recoveries are not over yet

Source: Bloomberg, Lyxor AM

Uneven EM recovery progress

Source: Markit, Lyxor AM

Uneven EM exposure to the U.S. reflation

Source: OECD, Lyxor AM

PMI Manuf

(SA) Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

US 49.9 51.0 51.5 52.2 52.5 51.7 50.8 49.2 36.9 39.8 49.6 51.3 53.6 53.5 53.3 56.7 56.5 59.1 58.5 59.0

Euro Area 47.0 45.7 45.9 46.9 46.3 47.9 49.2 44.5 33.4 39.4 47.4 51.8 51.7 53.7 54.8 53.8 55.2 54.8 57.9 62.5

Germany 43.5 41.7 42.1 44.1 43.7 45.3 48.0 45.4 34.5 36.6 45.2 51.0 52.2 56.4 58.2 57.8 58.3 57.1 60.7 66.6

France 51.1 50.1 50.7 51.7 50.4 51.1 49.8 43.2 31.5 40.6 52.3 52.4 49.8 51.2 51.3 49.6 51.1 51.6 56.1 59.3

Italy 48.7 47.8 47.7 47.6 46.2 48.9 48.7 40.3 31.1 45.4 47.5 51.9 53.1 53.2 53.8 51.5 52.8 55.1 56.9 59.8

Spain 48.8 47.7 46.8 47.5 47.4 48.5 50.4 45.7 30.8 38.3 49.0 53.5 49.9 50.8 52.5 49.8 51.0 49.3 52.9 56.9

UK 47.4 48.3 49.6 48.9 47.5 50.0 51.7 47.8 32.6 40.7 50.1 53.3 55.2 54.1 53.7 55.6 57.5 54.1 55.1 58.9

Japan 49.3 48.9 48.4 48.9 48.4 48.8 47.8 44.8 41.9 38.4 40.1 45.2 47.2 47.7 48.7 49.0 50.0 49.8 51.4 52.7

China 50.4 51.4 51.7 51.8 51.5 51.1 40.3 50.1 49.4 50.7 51.2 52.8 53.1 53.0 53.6 54.9 53.0 51.5 50.9 50.6

Asia ex-China & Japan49.6 49.6 49.2 49.9 50.8 51.6 51.0 46.6 33.4 36.1 44.8 46.8 50.0 51.7 52.8 53.1 53.7 54.4 54.2 54.1

India 51.4 51.4 50.6 51.2 52.7 55.3 54.5 51.8 27.4 30.8 47.2 46.0 52.0 56.8 58.9 56.3 56.4 57.7 57.5 55.4

South Korea 49.0 48.0 48.4 49.4 50.1 49.8 48.7 44.2 41.6 41.3 43.4 46.9 48.5 49.8 51.2 52.9 52.9 53.2 55.3 55.3

Taiwan 47.9 50.0 49.8 49.8 50.8 51.8 49.9 50.4 42.2 41.9 46.2 50.6 52.2 55.2 55.1 56.9 59.4 60.2 60.4 60.8

Indonesia 49.0 49.1 47.7 48.2 49.5 49.3 51.9 45.3 27.5 28.6 39.1 46.9 50.8 47.2 47.8 50.6 51.3 52.2 50.9 53.2

Malaysia 47.4 47.9 49.3 49.5 50.0 48.8 48.5 48.4 31.3 45.6 51.0 50.0 49.3 49.0 48.5 48.4 49.1 48.9 47.7 49.9

Philippines 51.9 51.8 52.1 51.4 51.7 52.1 52.3 39.7 31.6 40.1 49.7 48.4 47.3 50.1 48.5 49.9 49.2 52.5 52.5 52.2

Thailand 50.0 50.6 50.0 49.3 50.1 49.9 49.5 46.7 36.8 41.6 43.5 45.9 49.7 49.9 50.8 50.4 50.8 49.0 47.2 48.8

Vietnam 51.4 50.5 50.0 51.0 50.8 50.6 49.0 41.9 32.7 42.7 51.1 47.6 45.7 52.2 51.8 49.9 51.7 51.3 51.6 53.6

Brazil 52.5 53.4 52.2 52.9 50.2 51.0 52.3 48.4 36.0 38.3 51.6 58.2 64.7 64.9 66.7 64.0 61.5 56.5 58.4 52.8

Mexico 49.0 49.1 50.4 48.0 47.1 49.0 50.0 47.9 35.0 38.3 38.6 40.4 41.3 42.1 43.6 43.7 42.4 43.0 44.2 45.6

Russia 49.1 46.3 47.2 45.6 47.5 47.9 48.2 47.5 31.3 36.2 49.4 48.4 51.1 48.9 46.9 46.3 49.7 50.9 51.5 51.1

Poland 48.8 47.8 45.6 46.7 48.0 47.4 48.2 42.4 31.9 40.6 47.2 52.8 50.6 50.8 50.8 50.8 51.7 51.9 53.4 54.3

Czech Rep. 44.9 44.9 45.0 43.5 43.6 45.2 46.5 41.3 35.1 39.6 44.9 47.0 49.1 50.7 51.9 53.9 57.0 57.0 56.5 58.0

Turkey 48.0 50.0 49.0 49.5 49.5 51.3 52.4 48.1 33.4 40.9 53.9 56.9 54.3 52.8 53.9 51.4 50.8 54.4 51.7 52.6

2020 20212019

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

20

back to the top

Eastern European countries will be far less exposed

to rising U.S. spending in climate, infrastructure, and

housing.

Fundamental EM risks have receded

Heightened EM countries macro risk after several

years of trade war, global trade erosion, and the

pandemic, have now normalized. We also observe

that the countries that have structurally been the

most vulnerable to capital outflows, are more

dispersed.

This should limit risk contagion within the EM world.

Moreover, this should support greater investors’ risk

taking, who will rather focus on improving growth

and profit prospects as macro risks abate. Finally, this

would also help EM countries better navigate higher

US rate and USD volatility.

As a result, we expect the EM risk premium to return

to average.

Inflation (and the virus) remains the key risk

Inflation surprises are intensifying in many EM

countries. It is mainly due to soaring commodity

prices. In some countries, core CPI (which excludes

the most volatile inflation components) are catching

up with trends in headline inflation. These countries

look more at risk.

This will force several major central banks to tighten

their policy at an inopportune time, or to delay more

dovish policies. Turkey, Brazil, Russia, and to some

extent Mexico have or will soon have to alter their

policies.

EM EQUITIES: TACTICAL BUY, BUT STRATEGIC

NEUTRALITY

The correction is over, tactical buy

The stellar outperformance early this year has been

nearly erased during the correction that started by

mid-February. Over the process stretched technicals

and investors positioning along with overly rich

valuations have been clean up.

We believe this is opening a tactical window for a 5%

to 10% upside.

Brighter EM backdrop, but not brighter than the rest

of the world: strategically neutral EM

The EM equity backdrop has arguably improved.

Receding macro risk are allowing investors to focus

less on EM vulnerabilities, and more on growth and

profit prospects, which particularly opportune at

early cycle stage.

We also expect EM assets to navigate higher U.S.

rates as long as they remain driven by better

growth, not by a Fed policy shift.

Moreover, the ambitious U.S. reflation will provide

tailwind for a number of EM countries (especially

EM risk premium should converge to average

Source: Bloomber, Lyxor AM

EM countries prepare to hike rates next year

Source: Bloomberg, Lyxor AM

Multiple expansion is now more reasonable

Source: Macrobond, Lyxor AM

Target

Rate (%) CPI y/y M2 y/y

Target Rate Chg

Last 12M (bps)

Market-expected Rate

Chg Next 12M (bps)

China 2.2 -0.2 10.1 0 70

Sth Korea 0.5 1.5 10.1 -75 28

India 4.0 5.0 17.9 -40 69

Malaysia 1.8 0.1 5.5 -75 40

Philippines 2.0 4.5 10.8 -125 222

Thailand 0.5 -0.1 10.0 -37 29

Indonesia 3.5 1.4 11.4 -111 0

Brazil 2.8 5.2 27.1 -100 504

Mexico 4.0 3.8 12.8 -200 72

Chile 0.5 2.9 61.5 0 124

Russia 4.5 5.8 13.4 -100 138

Poland 0.1 3.2 16.6 -90 24

Hungary 0.6 3.1 20.8 -30 79

Turkey 19.0 16.2 29.8 871 -214

Sth Africa 3.5 2.9 13.1 -75 90

Aggr. (xTK) 2.6 2.9 15.5 -70 130

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

21

back to the top

China/Asia and Mexico), though some of the flow will

be diverted away from EM back into U.S. markets.

However, economic prospects have also improved in

DM countries, reducing the EM-DM differential. Also,

inflationary pressures will force several central banks

to hike rates or reduce their liquidity injection earlier

than in DM (in aggregate, about +130bps is priced for

the next 12M). Finally, the main EM growth driver

(China) is losing some traction as it tries to unwind

some of its stimulus.

So, beyond post-correction tactical opportunities, we

do not see a sustained period of EM outperformance

vs. DM equities.

EM countries’ sensitivity to higher inflation, to

commodity prices, and to the US reflation are likely to

be key differentiators in Q2. We also expect rotation

towards laggards to continue, though with volatility

until U.S. rates stabilize.

China: Tactical buying opportunity, strategically

neutral

The Chinese recovery is losing some traction, as

authorities unwind some of their stimulus, and is still

skewed towards the manufacturing sector. Questions

regarding the reliability of growth measures also start

to raise eyebrows.

We remain of the view that the USDCNY at 6.6 would

gradually rise towards 6.3, driven by a very solid

international position.

U.S. pressures have only changed in means. We

expect less initiatives on tariffs (though the existing

one are likely to remain for the foreseeable future),

more multilateral pressures, non-tariff barriers and a

focus on tech. The U.S.-China meeting in Alaska led to

limited change in this current stressed relationship. It

was likely more about setting the tone and aimed at

domestic and allies’ ears than to one another.

The steep correction confirmed our cautiousness in

the previous quarter. With excess valuation largely

cleaned up, we see tactical opportunity with a

+5/10% upside potential.

Brazil: Delayed recovery amid political mess (N)

A concerning rise in virus infections will likely lead to

new mobility restrictions. As a result, a longer soft

patch is probable, while inflationary trends are

delaying new stimulus packages.

Inflation is passing through to core CPI, leading the

central bank to tighten rate. An additional 25bp is

likely.

Moreover, President Bolsonaro’s eroding political

support would limit reforms.

The main current upside risk comes from low

absolute and relative valuations.

India: Strong U.S. reflation exposure (OW)

Reforms were validated and are boosting

sentiment, though the devil will be in the

implementation details.

India is undergoing a strong recovery. Its strong

exposure to the U.S. reflation provides powerful

tailwinds. Supply chain diversification also favors

India.

We remain O/W, though we acknowledge three

key downside risks. First, the rise in virus

infections is flagging orange and is leading several

states to set new mobility restrictions. Second,

elevated inflation could cap the leeway for

stimulus. Third, valuation is rich.

Russia: Capped recovery (N)

Rising inflation is anchoring in core CPI, calling for

tighter monetary policy.

Oil activity would gain further traction as output

normalizes amid firm oil prices. However, the rest

of the economy relies on still sluggish demand

and budget stimulus.

Chinese data smoothing?

Source: Bloomberg, Lyxor AM

Eroding Chinese stimulus

Source: Macrobond, Lyxor AM

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

22

back to the top

Western sanctions risk remains live but would not

substantially alter the current risk premium.

We are neutral. The main upside risk come from oil

prices creeping higher in 2021 and cheap relative

valuations.

Turkey: Monetary U-turn and political ambitions

(U/W)

The replacement of the central bank governor Ağbal

with Kavcioğlu, after only 5 months of a more hawkish

policy designed to tame the runaway inflation, is

shaking investors’ confidence. Since then, the Turkish

lira and equity markets dropped more than -10% and

sovereign CDS returned closer to their highs. After the

second dovish U-turn (governor Cetinkaya was fired

mid-2019 after hiking rates aggressively in 2018):

confidence might not return quickly.

The new governor, a loyal support of President

Erdogan and his unorthodox economic policies, will

have limited means to curb inflation without the lever

of higher rates. Capital control would also be tricky

given the elevated share of foreign debt.

We expect investor flows, which had returned since

mid-last year, to bleed again. Small FX reserves (only

7% of GDP), a current account deficit of more than

5%, and inflation showing no signs of moderation

(both for domestic and external reasons) will leave

the Lira highly vulnerable. It could also lead Turkey to

struggle meeting its more than $200bn funding needs

within the next 12 months. What the new central bank

managing team will do in its April and May meeting

(hold or rate cut?) will be closely monitored.

In perspective, the ruling party AKP came to power in

the early 2000’s, with the economic expansion by

then largely contributing to its popularity. By

encouraging an overheating economy, President

Erdogan might aim for more popular support to crush

a stronger opposition ahead of the 2023 elections,

unless he’s planning to gamble on early elections…

EM HC DEBT: MODEST SPREAD TIGHTENING IN

SIGHT, BUT U.S. RATES RISK (N)

Reasonable isolation from U.S. rates, but less than in

equities

The asset class has tended in line with DM credit year-

to-date, in line with our neutral positioning so far.

Historically, EM HC debt has managed to navigate

episodes of higher U.S. rates, provided the driver was

better growth, not a Fed policy shift. Weakness in the

asset class has so far been without panic.

However, correlation with U.S. rates and with the U.S.

dollar rose, pointing to higher volatility and risks.

Modest and selective spread tightening

opportunities

The macro backdrop has arguably improved, and

the asset class remains appealing to hold in

portfolios. EM macro risk have receded and there

are no pending major default situations –

Argentina and Turkey are the current weakest

links. The asset class also continues to offer

diversification within credit.

Inflation remains a downside risk in India

Source: Macrobond, Lyxor AM

Flows in Turkey will likely take another U-turn

Source: Macrobond, Lyxor AM

EM HC debt navigated episodes of higher U.S. rates

Source: Bloomberg, Lyxor AM

(in bps) (in % )

US rates

impact on EM

assets

US 10YUS Bkvn

10Y

US Real

10Y

Episodes of Rising

Yields

MSCI EM

Loc

EM HC

TR

EM Local

TR

JPM EM

FX

Sep20-Apr21 101 70 31 25.9 1.8 4.0 4.6

Mar20 43 -70 113 -22.2 -13.7 -8.1 -8.3

Sep17-Feb18 85 33 51 11.7 -0.7 3.1 -0.3

Jul-Dec16 121 46 75 3.8 -2.0 -4.8 -3.2

Jan-Jun15 73 26 48 0.5 1.6 -5.0 -2.5

May-Sep13 136 -22 159 -8.7 -7.9 -10.6 -8.6

Sep-Oct11 54 32 22 5.7 1.1 4.2 3.8

Oct-Dec10 113 39 75 1.2 -2.4 -3.2 -1.8

Dec08-Jun09 185 197 -13 41.6 17.5 4.3 -

Sep-Oct08 36 -90 126 -21.2 -16.0 -8.3 -

Mar-Jun08 80 9 71 3.7 0.2 - -

Mar-Jun07 76 14 62 17.3 -0.6 - -

Jan-Jun06 89 20 69 -7.0 -2.0 - -

Aug-Nov05 57 21 36 6.2 0.6 - -

Feb-Mar05 63 32 31 1.4 -1.7 - -

Mar-May04 109 38 71 -10.2 -7.8 - -

Jun-Sep03 144 51 93 15.1 -3.6 - -

-50 0 50 100 150 200

NominalYield

INVESTMENT STRATEGY INVESTMENT STRATEGY

By LYXOR CROSS ASSET RESEARCH SECOND QUARTER 2021

23

back to the top

Valuations of EM HC debt assets remain close to their

fair-value in aggregate with modest spread tightening

potential (around 20bps). Our models suggest

greater spread tightening opportunities in Brazil,

Russia, Indonesia and Philippines (around 40bps).

EM debt issuance is seasonally strong while flows to

this segment paused might cap prices.

We stay strategically neutral and expect lagging

higher yielders to be more sheltered from rate

volatility, provided risk aversion stays stable.

COMMODITIES: SUPERCYCLE AND SENTIVITY

TO U.S. RATES

A new “Supercycle”?

We expect cyclical commodity prices to remain firm

over the coming months.

The asset class benefits strong macro tailwinds, at

early cycle stage, amid major reflation policy, with