RGE Sleptsova Ukraine's perfect storm

10

EMERGING EUROPE AND CIS 1 Page | 1 www.roubini.com NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent. December 16, 2013 Ukraine’s Perfect Storm: Stay Clear While Political Crisis Persists By Evghenia Sleptsova Ukraine’s last-minute U-turn, bowing to Russian pressure and suspending preparations for an Association Agreement with the EU, was an attempt to achieve short-term economic stability at the cost of medium-term development. However, the strategy misfired and triggered a political crisis, with over 500,000 protesters taking to the streets, demanding the President step down. Bottom line: We believe the risk of a currency crisis and default has increased significantly: 40%, versus our earlier estimate of 25%. Previously, we thought Ukraine could “muddle through” and avoid a debt restructuring in the next 12 months. However, the government’s efforts to avoid a default at all costs (given the upcoming 2015 presidential election), the stand-off with Russia and lack of agreement with the IMF, and the civil unrest, increase the odds of at least a partial debt restructuring, which is unlikely to be orderly. We see a 70%+ chance of Ukraine proceeding with closer integration with Russia in the short term, eschewing the European path. Within this, there is a 50/50 chance of the political crisis escalating and causing a disorderly devaluation and partial debt restructuring, or an uneasy calm facilitating a “muddle through.” We see a 30% chance of Ukraine signing the EU Association Agreement and reaching an IMF deal, in which event the external debt burden will gradually stabilize toward 2017. Market implications: Avoid Ukrainian assets as long as political risk persists. Although we do not expect Ukraine to default on its debts, external debt spreads may widen further in the near term as reserves deplete. Thereafter, signs of the civil unrest subsiding will provide opportunities to enter external debt. Avoid UAH, which is poised for a 15% step devaluation; moreover, the risk of a disorderly and larger (30%) devaluation persists. Figure 1: Key Scenarios for Ukraine’s Political and Financial Impasse Source: RGE Scenario 1A Scenario 1B Scenario 2 Closer integration with Russia, exacerbating political crisis (35%) Closer integration with Russia; political crisis overcome (35%) Association Agreement with EU signed (30%) No Russia-related current account shock No current account shock Russia-related current account shock, of up to 2% of GDP Political crisis escalates Protests subside into uneasy calm on broad support for EU integration, deteriorating in 2015 election Political crisis overcome Run on FX deposits and disorderly devaluation of 30% No run on FX deposits, no devaluation Managed 10-15% devaluation Russian bailout is insufficient to compensate for sharp devaluation Bailout from Russia sufficient to avoid debt restructuring IMF bailout External debt spikes to 115% of GDP in 2014, increasing risk of coercive debt restructuring Interest rates stay high on persisting imbalances and ongoing political uncertainty, ext. debt reaches 89% by 2017 Interest rates decline (8% on average over 2014- 17); debt initially rises to 86% of GDP, but stabilizes at 76% by 2017

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of RGE Sleptsova Ukraine's perfect storm

EMERGING EUROPE AND CIS

1

Page | 1

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

December 16, 2013

Ukraine’s Perfect Storm: Stay Clear While Political

Crisis Persists By Evghenia Sleptsova

Ukraine’s last-minute U-turn, bowing to Russian pressure and suspending preparations for an

Association Agreement with the EU, was an attempt to achieve short-term economic stability at the

cost of medium-term development. However, the strategy misfired and triggered a political crisis,

with over 500,000 protesters taking to the streets, demanding the President step down.

Bottom line: We believe the risk of a currency crisis and default has increased significantly: 40%,

versus our earlier estimate of 25%. Previously, we thought Ukraine could “muddle through” and

avoid a debt restructuring in the next 12 months. However, the government’s efforts to avoid a

default at all costs (given the upcoming 2015 presidential election), the stand-off with Russia and lack

of agreement with the IMF, and the civil unrest, increase the odds of at least a partial debt

restructuring, which is unlikely to be orderly.

We see a 70%+ chance of Ukraine proceeding with closer integration with Russia in the short term,

eschewing the European path. Within this, there is a 50/50 chance of the political crisis escalating and

causing a disorderly devaluation and partial debt restructuring, or an uneasy calm facilitating a

“muddle through.” We see a 30% chance of Ukraine signing the EU Association Agreement and

reaching an IMF deal, in which event the external debt burden will gradually stabilize toward 2017.

Market implications: Avoid Ukrainian assets as long as political risk persists. Although we do not

expect Ukraine to default on its debts, external debt spreads may widen further in the near term as

reserves deplete. Thereafter, signs of the civil unrest subsiding will provide opportunities to enter

external debt. Avoid UAH, which is poised for a 15% step devaluation; moreover, the risk of a

disorderly and larger (30%) devaluation persists.

Figure 1: Key Scenarios for Ukraine’s Political and Financial Impasse

Source: RGE

Scenario 1A Scenario 1B Scenario 2

Closer integration with Russia, exacerbating

political crisis (35%)

Closer integration with Russia; political crisis

overcome (35%)Association Agreement with EU signed (30%)

No Russia-related current account shock No current account shock Russia-related current account shock, of up to

2% of GDP

Political crisis escalates Protests subside into uneasy calm on broad

support for EU integration, deteriorating in

2015 election

Political crisis overcome

Run on FX deposits and disorderly devaluation

of 30%

No run on FX deposits, no devaluation Managed 10-15% devaluation

Russian bailout is insufficient to compensate

for sharp devaluation

Bailout from Russia sufficient to avoid debt

restructuring

IMF bailout

External debt spikes to 115% of GDP in 2014,

increasing risk of coercive debt restructuring

Interest rates stay high on persisting imbalances

and ongoing political uncertainty, ext. debt

reaches 89% by 2017

Interest rates decline (8% on average over 2014-

17); debt initially rises to 86% of GDP, but

stabilizes at 76% by 2017

EMERGING EUROPE AND CIS

2

Page | 2

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

After years of failing to resolve either its macroeconomic or geopolitical challenges, Ukraine seems to have

reached a day of reckoning. Having made a last-minute U-turn away from the EU, bowing to Russia’s political and

economic pressure, the government is still trying to maintain the status quo in its relations with Russia and the EU.

But this strategy has instead left Ukraine between a rock and hard place. The magnitude of the public protests

does not let Ukraine proceed easily with closer integration with Russia, and the latter will resist offering significant

financial assistance or cheaper gas without first securing Ukraine’s commitment to closer cooperation.

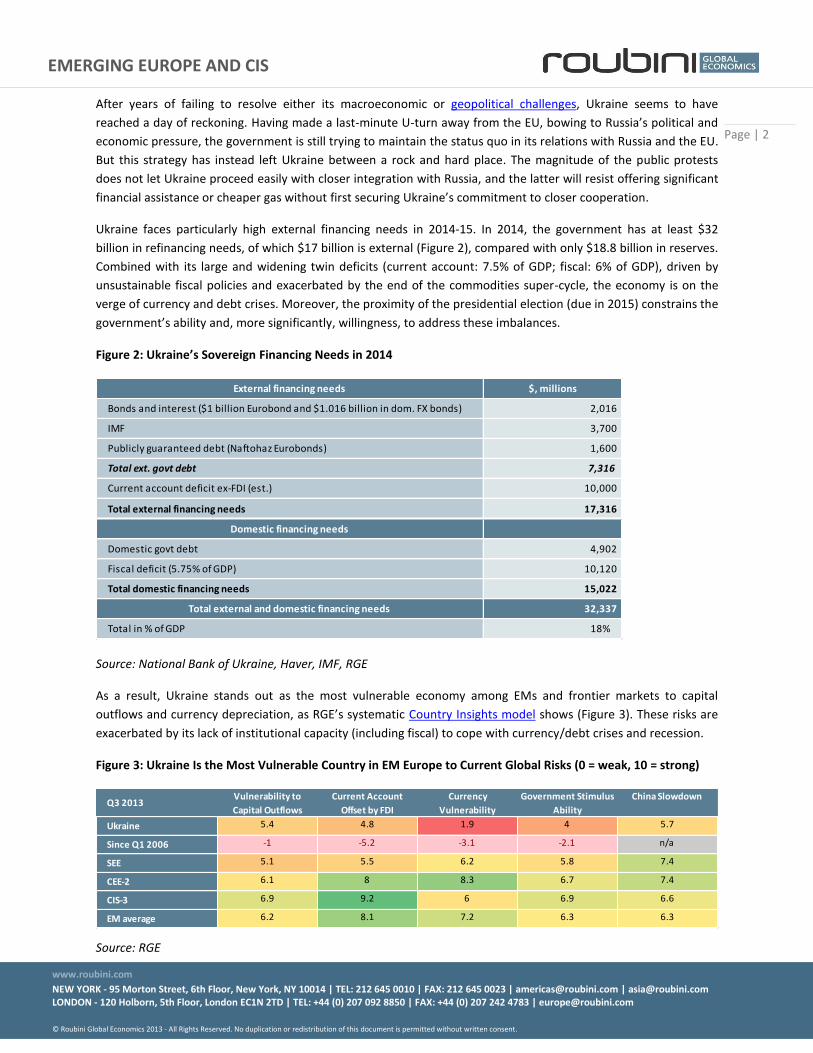

Ukraine faces particularly high external financing needs in 2014-15. In 2014, the government has at least $32

billion in refinancing needs, of which $17 billion is external (Figure 2), compared with only $18.8 billion in reserves.

Combined with its large and widening twin deficits (current account: 7.5% of GDP; fiscal: 6% of GDP), driven by

unsustainable fiscal policies and exacerbated by the end of the commodities super-cycle, the economy is on the

verge of currency and debt crises. Moreover, the proximity of the presidential election (due in 2015) constrains the

government’s ability and, more significantly, willingness, to address these imbalances.

Figure 2: Ukraine’s Sovereign Financing Needs in 2014

Source: National Bank of Ukraine, Haver, IMF, RGE

As a result, Ukraine stands out as the most vulnerable economy among EMs and frontier markets to capital

outflows and currency depreciation, as RGE’s systematic Country Insights model shows (Figure 3). These risks are

exacerbated by its lack of institutional capacity (including fiscal) to cope with currency/debt crises and recession.

Figure 3: Ukraine Is the Most Vulnerable Country in EM Europe to Current Global Risks (0 = weak, 10 = strong)

Source: RGE

External financing needs $, millions

Bonds and interest ($1 billion Eurobond and $1.016 billion in dom. FX bonds) 2,016

IMF 3,700

Publicly guaranteed debt (Naftohaz Eurobonds) 1,600

Total ext. govt debt 7,316

Current account deficit ex-FDI (est.) 10,000

Total external financing needs 17,316

Domestic financing needs

Domestic govt debt 4,902

Fiscal deficit (5.75% of GDP) 10,120

Total domestic financing needs 15,022

Total external and domestic financing needs 32,337

Total in % of GDP 18%

Q3 2013 Vulnerability to

Capital Outflows

Current Account

Offset by FDI

Currency

Vulnerability

Government Stimulus

Ability

China Slowdown

Ukraine 5.4 4.8 1.9 4 5.7

Since Q1 2006 -1 -5.2 -3.1 -2.1 n/a

SEE 5.1 5.5 6.2 5.8 7.4

CEE-2 6.1 8 8.3 6.7 7.4

CIS-3 6.9 9.2 6 6.9 6.6

EM average 6.2 8.1 7.2 6.3 6.3

EMERGING EUROPE AND CIS

3

Page | 3

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

Currency Peg Strains Already Overstretched External Balances

Ukraine is highly dependent on exports of industrial metals, and economic growth has slowed sharply and

macroeconomic imbalances have widened as the commodities super-cycle has neared its end. Steel exports fell by

nearly 20% in 2012 in value terms and 7% in volume terms, and growth stalled at 0.2% in 2012 (Figure 4) and we

expect it to contract by 1.5% in 2013. As a result of unfavorable terms of trade, and partly due to the overvalued

currency, the current account balance weakened to -8% in 2012 from +2.9% in 2005, and will remain at around -7%

in 2013, with slowing demand for imports failing to compensate for the low commodity prices. FDI fell by 20% y/y

in H1 2013 (extending the 6% decline in 2012) to only $3 billion (1.7% of GDP), meaning Ukraine is increasingly

reliant on financial inflows to finance the remaining current account deficit ($8 billion or 4.6% of GDP in 2013 and

$10 billion or 4.4% of GDP in 2014). Given the FX depreciation of key trading partners (particularly RUB, but also

TRY, EGP, INR) and worsening terms of trade (high gas import prices and falling metal export prices), a de facto

fixed exchange rate and lack of productivity gains are eroding the competitiveness of Ukrainian exports, putting

increasing strain on the collapsing current account.

Figure 4: Falling Steel Exports Hit Growth

Source: Haver, UN Comtrade

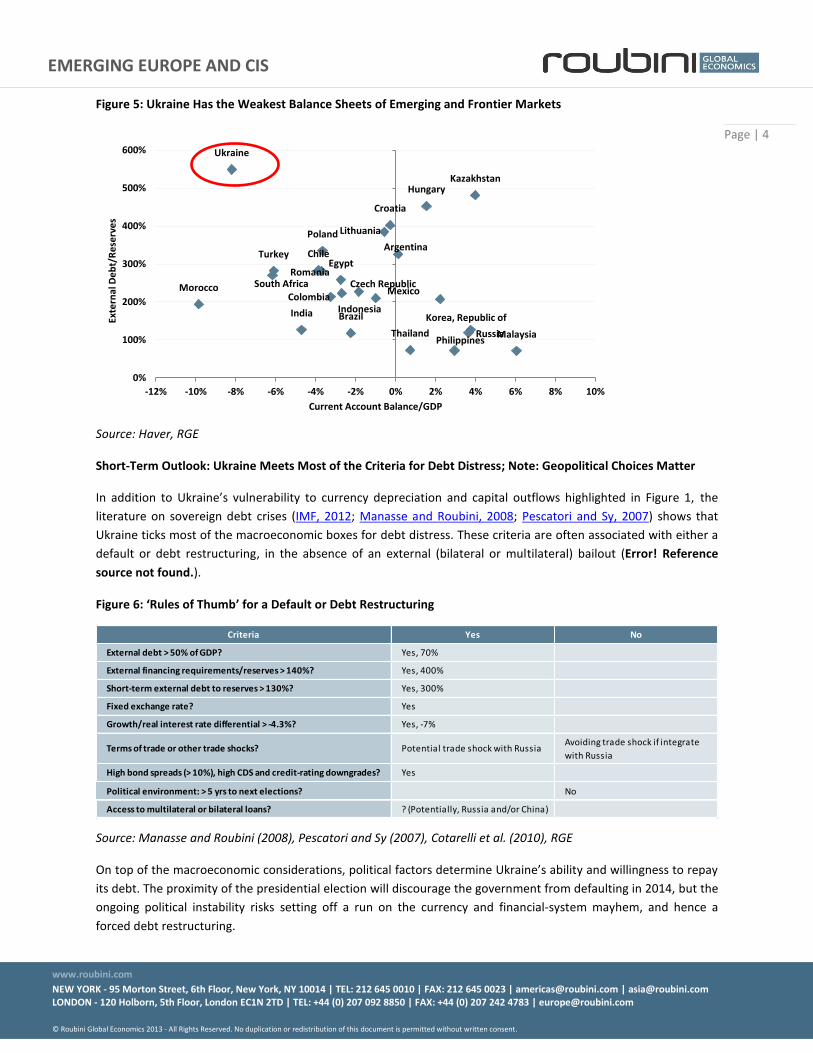

FX interventions and the financing of the current account are depleting Ukraine’s FX reserves, which had fallen to

$18.8 billion (less than two months of imports) by the end of November. Ukraine’s debt-to-reserves ratio and

current account deficit are the highest among EMs (Figure 5). A gradual devaluation of UAH by 10-15% or more

would be needed to bring the currency in line with the current account and, in turn, narrow the current account

deficit. However, a sharp devaluation would inflate the local currency value of Ukraine’s ballooning external debt,

while a sharp correction of the fiscal and current account deficits would hurt growth even more in the short term.

The recent popular unrest has already come close to triggering a run on the currency. At the time of writing, the

pressure has subsided, but the risk of a UAH run remains as long as the protests persist and the government fails

to find a solution to the stand-off.

-60

-40

-20

0

20

40

60

80

-20

-15

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Ukraine real GDP growth, % y/y Ukraine exports of steel, $bn, % y/y (right axis)

EMERGING EUROPE AND CIS

4

Page | 4

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

Figure 5: Ukraine Has the Weakest Balance Sheets of Emerging and Frontier Markets

Source: Haver, RGE

Short-Term Outlook: Ukraine Meets Most of the Criteria for Debt Distress; Note: Geopolitical Choices Matter

In addition to Ukraine’s vulnerability to currency depreciation and capital outflows highlighted in Figure 1, the

literature on sovereign debt crises (IMF, 2012; Manasse and Roubini, 2008; Pescatori and Sy, 2007) shows that

Ukraine ticks most of the macroeconomic boxes for debt distress. These criteria are often associated with either a

default or debt restructuring, in the absence of an external (bilateral or multilateral) bailout (Error! Reference

source not found.).

Figure 6: ‘Rules of Thumb’ for a Default or Debt Restructuring

Source: Manasse and Roubini (2008), Pescatori and Sy (2007), Cotarelli et al. (2010), RGE

On top of the macroeconomic considerations, political factors determine Ukraine’s ability and willingness to repay

its debt. The proximity of the presidential election will discourage the government from defaulting in 2014, but the

ongoing political instability risks setting off a run on the currency and financial-system mayhem, and hence a

forced debt restructuring.

Argentina

Brazil

Chile

Colombia

Croatia

Czech Republic

Egypt

Hungary

India Indonesia

Kazakhstan

Korea, Republic of

Lithuania

Malaysia

Mexico Morocco

Philippines

Poland

Romania

Russia

South Africa

Thailand

Turkey

Ukraine

0%

100%

200%

300%

400%

500%

600%

-12% -10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

Exte

rnal

De

bt/

Re

serv

es

Current Account Balance/GDP

Criteria Yes No

External debt > 50% of GDP? Yes, 70%

External financing requirements/reserves > 140%? Yes, 400%

Short-term external debt to reserves > 130%? Yes, 300%

Fixed exchange rate? Yes

Growth/real interest rate differential > -4.3%? Yes, -7%

Terms of trade or other trade shocks? Potential trade shock with RussiaAvoiding trade shock if integrate

with Russia

High bond spreads (> 10%), high CDS and credit-rating downgrades? Yes

Political environment: > 5 yrs to next elections? No

Access to multilateral or bilateral loans? ? (Potentially, Russia and/or China)

EMERGING EUROPE AND CIS

5

Page | 5

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

Ukraine’s geopolitical choices have implications for both the restoration of public order and for external debt

refinancing options. The EU option comes with medium-term gains, but short-term losses from the inevitable

Russian trade and economic retaliation. The Ukrainian government was hoping that the EU would also help it strike

a more favorable deal with the IMF, avoiding or moderating the most politically sensitive condition—phasing out

gas-price subsidies for households. Despite the EU’s attempts (with no formal mandate), the IMF did not change its

conditions, which, according to Ukrainian Prime Minister Nikolay Azarov, was one of the reasons why Ukraine

suspended talks with the EU and chose the “pragmatic short-term option” of reconciliation with Russia.

However, by suspending EU negotiations, the government miscalculated the scale of the public response. After

massive protests broke out across the country, reignited by the use of force, the government found itself cornered.

The option of realigning with Russia may now turn out to be politically more costly than the consequences of

signing up to the Association Agreement or an IMF deal, yet the short-term costs of a trade war with Russia still

appear prohibitively high. Despite mounting pressure from the streets, at the time of writing the authorities

appeared to be continuing to bargain with both Russia and the EU, sending delegations to Brussels and Moscow.

Short-Term Scenarios: Refinancing Options and Debt Sustainability

Although the situation is highly unpredictable, we see the following key scenarios unfolding over the next months.

These have implications for Ukraine’s longer-term debt sustainability, which we assess using the IMF External Debt

Sustainability framework. In all of these scenarios, the risks of a currency crisis and default remain very high in the

short term, should the political uncertainty persist.

Although closer integration with Russia is our base case for the short term (next one-to-two years), in the longer

term overwhelming public support for EU integration will make this option unsustainable. We believe that this or

the next government will eventually return to the European path.

Scenario 1: Reconciliation With Russia, Despite Popular Protests (70% Probability)

Apart from being a major trade partner (accounting for 25% of Ukraine’s merchandise exports), Russia is Ukraine’s

major creditor: Ukraine’s Naftogaz is consistently late on its payments to Russia’s Gazprom for gas imports ($2

billion debt is outstanding for August-November); and Russian banks account for 12% of Ukrainian banking-sector

assets. Ukraine has little room for maneuver, given its debt-burdened economy, lack of market access (and

unwillingness to accept the IMF’s conditions) and the risk of a trade shock from Russia.

By bowing to Russian pressure, the government is trying to extract as many concessions as possible (loans, cheaper

gas), while ceding as little sovereignty as it can. The public protests make a formal Ukrainian commitment to

Russia’s Customs Union unlikely, at least prior to the 2015 election. But the government is likely to commit to

some form of closer integration with Russia, trying to defuse the protests by continuing negotiations with the EU

and the opposition, and potentially reshuffling the cabinet.

Scenario 1A (35%): This sub-scenario would see a return to the use of force and/or an outright commitment to

Russia’s Customs Union. This would cause political instability to rise and could trigger a run on foreign currency

deposits and a disorderly currency devaluation, and might force the government or quasi-sovereign corporates

into debt restructuring.

In the case of a disorderly 30% UAH depreciation and a spike in long-term interest rates to at least 16% (staying

elevated at 10% thereafter) and no current account shock, the external debt burden would hit 115% of GDP in

2013-14, increasing the risk of a coercive debt restructuring (Figure 7, 1A).

EMERGING EUROPE AND CIS

6

Page | 6

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

Scenario 1B (35%): A “muddle through” sub-scenario is equally possible: The government would reach an

agreement with Russia on a deal that is short of the Customs Union; the opposition would be weak; the legal case

for the dissolution of the government would be missing; and the protests might fade in cold weather. Political risk

would subside until the election, giving room for spread compression. However, integration with Russia would

remove incentives for structural and institutional reforms (as opposed to EU integration), imbalances would

persist, borrowing costs would remain high (at around 9%) and external debt would ultimately be unsustainable,

but might avoid an immediate adjustment, reaching 89% by 2017 (Figure 7, Scenario 1B).

Figure 7: Debt-Sustainability Scenarios (external debt as % of GDP)

Source: IMF External Debt Sustainability Analysis, RGE

Scenario 2: Ukraine Signs Association Agreement With EU (30% Probability)

Although it is not our short-term baseline, and recent news from Brussels makes it unlikely. Ukraine might still sign

the Association Agreement, with the EU-Ukraine summit in March 2014 likely to be the next opportunity.

Having realized the fiasco of its negotiation tactics in the run up to the EU Eastern Partnership Summit in Vilnius on

November 28-29, the EU initially tried to change its approach by offering Ukraine more “carrots” (i.e., financial

support for the implementation of the Association Agreement and more support in Ukraine’s negotiations with the

IMF), while potentially downplaying the “sticks” (the demand that Ukraine should free former prime minister Yulia

Tymoshenko from jail). However, EU officials were unable to increase funding very much.

Moreover, oligarchs are a major political force in Ukraine (as we have discussed), and many of them would still

favor European integration over the Russian-led Customs Union for pragmatic reasons (i.e., ensuring their property

rights and access to broader global markets). For now, Ukraine’s President, Viktor Yanukovych, has neutralized the

initial signs that these oligarchs might side with the opposition, but the risk remains. In 2004, most oligarchs

supported the then-President Leonid Kuchma and his successor Yanukovych but, when protests reached 1 million

people, several oligarchs switched sides, changing the course of the revolution. Should political risks escalate this

time, a split among Ukraine’s business elites could see the country return to the negotiating table with the EU.

77

89

67

119

130

85

76

40

50

60

70

80

90

100

110

120

130

140

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Gro

ss E

xte

rnal

De

bt

as %

of

GD

P

Rapprochement with Russia, muddle-through (35% probability)

Rapprochement with Russia, sharp deval. (35% probability)

AA signed, CAB shock (30% probability)

Historical

EMERGING EUROPE AND CIS

7

Page | 7

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

In this scenario, we assume that Ukraine would face a current account shock in 2014 from falling trade with Russia,

of around 2% of GDP, and undergo a managed UAH depreciation of 10% under an IMF program. Growth would

initially stagnate at 1% in 2014, but would then recover to 2.5% in 2015. At the same time, Ukraine would benefit

from declining interest rates on long-term external debt (on average 8% in 2014-17) and higher FDI (up from 1.7%

in 2013 to 3% in 2014 and 5% from 2015 onward), which would reduce its debt-service burden and current

account financing needs. In this event, external debt would initially spike to around 84% of GDP in 2014, but would

then be on a consistent declining trajectory, stabilizing at 76% by 2017 (Figure 7, Scenario 2).

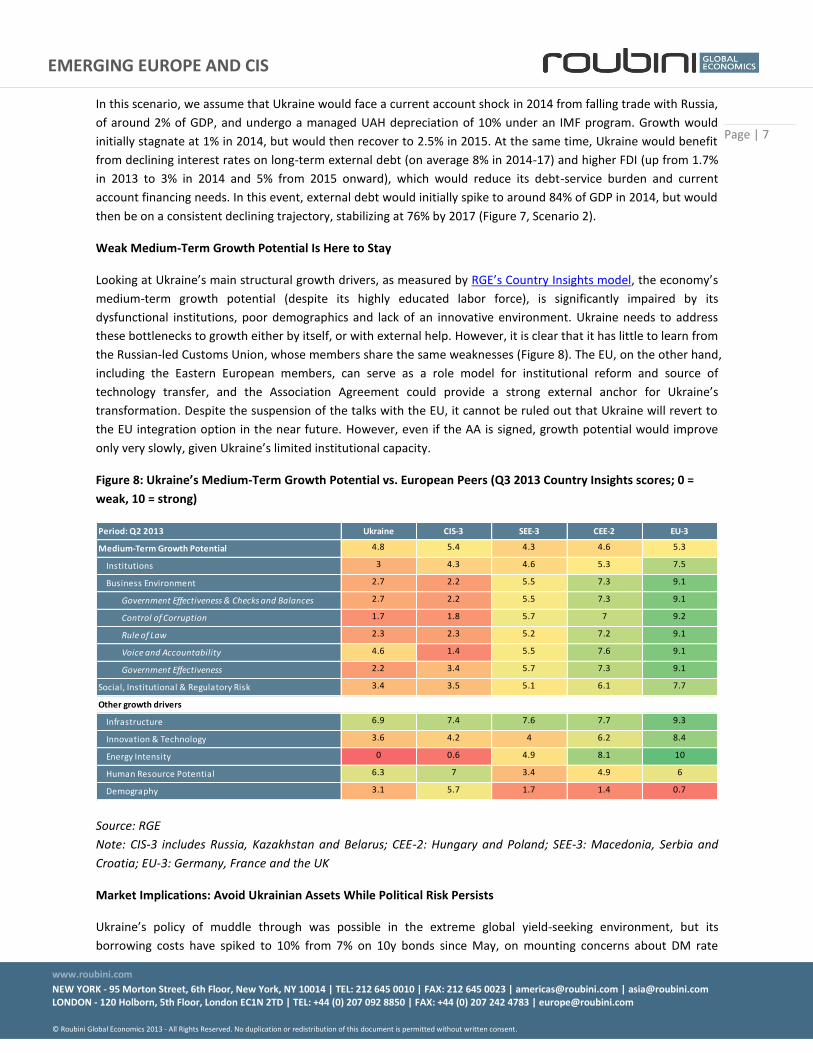

Weak Medium-Term Growth Potential Is Here to Stay

Looking at Ukraine’s main structural growth drivers, as measured by RGE’s Country Insights model, the economy’s

medium-term growth potential (despite its highly educated labor force), is significantly impaired by its

dysfunctional institutions, poor demographics and lack of an innovative environment. Ukraine needs to address

these bottlenecks to growth either by itself, or with external help. However, it is clear that it has little to learn from

the Russian-led Customs Union, whose members share the same weaknesses (Figure 8). The EU, on the other hand,

including the Eastern European members, can serve as a role model for institutional reform and source of

technology transfer, and the Association Agreement could provide a strong external anchor for Ukraine’s

transformation. Despite the suspension of the talks with the EU, it cannot be ruled out that Ukraine will revert to

the EU integration option in the near future. However, even if the AA is signed, growth potential would improve

only very slowly, given Ukraine’s limited institutional capacity.

Figure 8: Ukraine’s Medium-Term Growth Potential vs. European Peers (Q3 2013 Country Insights scores; 0 =

weak, 10 = strong)

Source: RGE

Note: CIS-3 includes Russia, Kazakhstan and Belarus; CEE-2: Hungary and Poland; SEE-3: Macedonia, Serbia and

Croatia; EU-3: Germany, France and the UK

Market Implications: Avoid Ukrainian Assets While Political Risk Persists

Ukraine’s policy of muddle through was possible in the extreme global yield-seeking environment, but its

borrowing costs have spiked to 10% from 7% on 10y bonds since May, on mounting concerns about DM rate

Period: Q2 2013 Ukraine CIS-3 SEE-3 CEE-2 EU-3

Medium-Term Growth Potential 4.8 5.4 4.3 4.6 5.3

Institutions 3 4.3 4.6 5.3 7.5

Business Environment 2.7 2.2 5.5 7.3 9.1

Government Effectiveness & Checks and Balances 2.7 2.2 5.5 7.3 9.1

Control of Corruption 1.7 1.8 5.7 7 9.2

Rule of Law 2.3 2.3 5.2 7.2 9.1

Voice and Accountability 4.6 1.4 5.5 7.6 9.1

Government Effectiveness 2.2 3.4 5.7 7.3 9.1

Social, Institutional & Regulatory Risk 3.4 3.5 5.1 6.1 7.7

Other growth drivers

Infrastructure 6.9 7.4 7.6 7.7 9.3

Innovation & Technology 3.6 4.2 4 6.2 8.4

Energy Intensity 0 0.6 4.9 8.1 10

Human Resource Potential 6.3 7 3.4 4.9 6

Demography 3.1 5.7 1.7 1.4 0.7

EMERGING EUROPE AND CIS

8

Page | 8

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

normalization. As a result, issuance came to a halt as investors first focused on deficit-country risks in general and

then Ukraine’s idiosyncratic risks. Even ignoring the rise in political risk, Ukraine’s fundamentals look weaker than

even those of three other high-yield credits—Venezuela, Argentina and Belarus— and have worsened the most in

that group since 2005 (Figure 9). Despite Ukraine’s downgrades from all three major agencies (Figure 12), the

significant spike in spreads and CDS (260 and 600, respectively) and the steeply inverted yield curve (Figure 11),

markets do not appear to have fully priced in risks in the CDS space (partly due to limited liquidity), as Ukraine still

fares better than the same three high-yield economies. External debt spreads are more in line with fundamentals

(except vis-à-vis those of Venezuela), but we believe they do not fully price in the current political risk.

Figure 9: Ukraine’s Fundamentals Weakest Among EMs, Justifying Higher CDS

Source: RGE

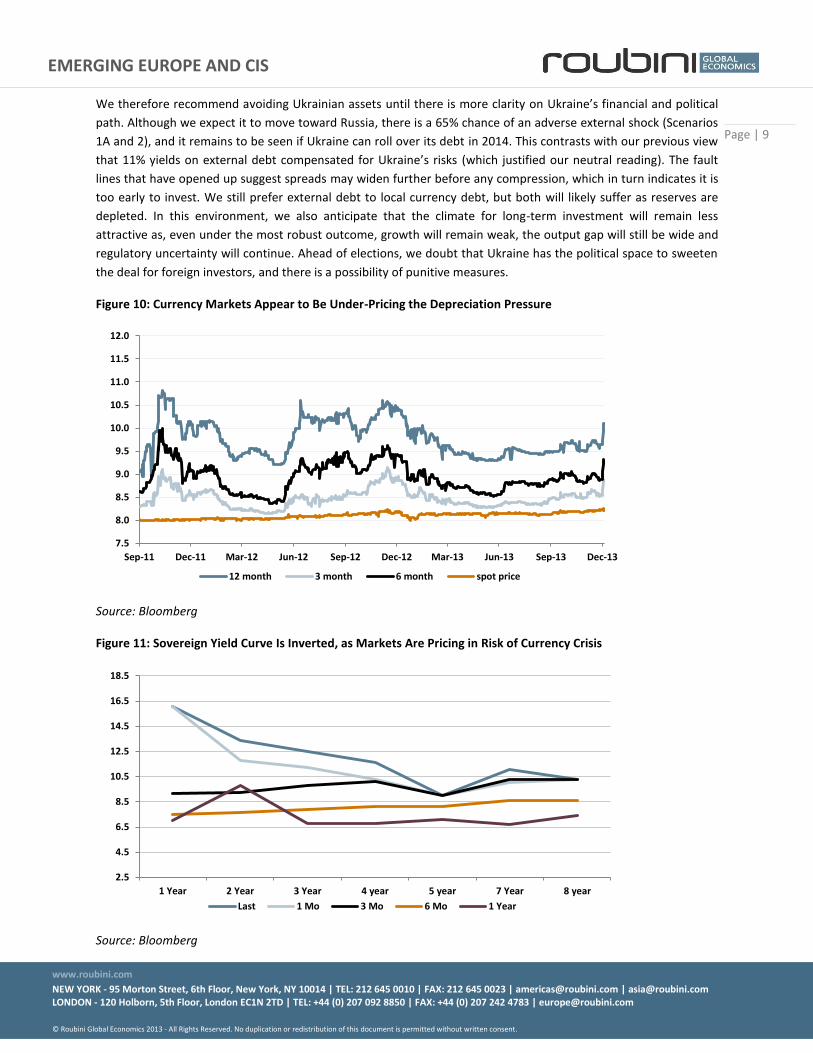

As we have already highlighted, Ukrainian currency non-deliverable forwards (NDFs) have somewhat spiked on the

back of civil unrest, and are now pricing in a devaluation of 8% in three months, and 22% in 12 months, which is

largely in line with our base case of 15% over-valuation. But the risk of a disorderly devaluation (by 30% or more,

which we estimate is around 40%) still appears to be under-priced, as reflected in the much lower level of NDFs

than in late 2012. Household complacency about the continuous pressure on the hryvnia (largely due to 20%

interest rates on UAH deposits), as well as the high costs of hedging FX risk for corporates, are significant support

factors for the Ukrainian currency. However, a reversal in retail-depositor sentiment could increase the demand

for cash FX and trigger a disorderly devaluation in a matter of days. In this event, the government would still be

incentivized not to default, given the upcoming election; but the combination of a stand-off with Russia and lack of

agreement with the IMF, magnified by civil unrest, might prompt a partial default.

UKR VEN ARG BLR UKR VEN ARG BEL

Sovereign Risk Index 5.2 5.3 6.6 5.4 -1.5 -1.3 1.1 -0.1

Vulnerability to

Capital Outflows

4.8 5 5.4 5.8 -1.8 -1.8 -0.2 0.3

Medium-Term

Growth Potential

4.6 4.5 4.7 5.1 0.1 0.5 0.3 1.3

Current Account

Balance

2 7.8 5.7 4.7 -8 -2.2 -2.2 0.9

Fiscal Policy (deficit

and debt)

7.3 3.9 7.6 10 -0.3 -6.1 3.4 -

Inflation 1.8 0 0.2 0 - - -7 -

Total Indebtedness 8.5 9 8.9 8.9 -0.9 -0.9 4.2 -0.8

Banking Sector

Vulnerability

5.9 6.7 8.3 7.3 -1.7 -1.6 2.6 0.1

Banking Sector 5.7 6.5 8.8 6.6 - -3.3 2.4 0.8

Current Account

Balance

2 7.8 5.7 4.7 -8 -2.2 -2.2 0.9

Macrofinancial

Adjustment Capacity

3 2.2 5.5 6.8 -4.4 0.3 1.9 0.4

Total Indebtedness 8.5 9 8.9 8.9 -0.9 -0.9 4.2 -0.8

Current Account

Offset by FDI

4.6 10 9.7 5.7 -5.4 - -0.3 -0.3

CDS 1098 1270 1870 n/a

EMBIG Spread 1013 1200 780 861

Score, Q3 2013 (0 = weak, 10 = strong) Change from 2005

Period: Q3 2013 to

Q3 2005

EMERGING EUROPE AND CIS

9

Page | 9

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

We therefore recommend avoiding Ukrainian assets until there is more clarity on Ukraine’s financial and political

path. Although we expect it to move toward Russia, there is a 65% chance of an adverse external shock (Scenarios

1A and 2), and it remains to be seen if Ukraine can roll over its debt in 2014. This contrasts with our previous view

that 11% yields on external debt compensated for Ukraine’s risks (which justified our neutral reading). The fault

lines that have opened up suggest spreads may widen further before any compression, which in turn indicates it is

too early to invest. We still prefer external debt to local currency debt, but both will likely suffer as reserves are

depleted. In this environment, we also anticipate that the climate for long-term investment will remain less

attractive as, even under the most robust outcome, growth will remain weak, the output gap will still be wide and

regulatory uncertainty will continue. Ahead of elections, we doubt that Ukraine has the political space to sweeten

the deal for foreign investors, and there is a possibility of punitive measures.

Figure 10: Currency Markets Appear to Be Under-Pricing the Depreciation Pressure

Source: Bloomberg

Figure 11: Sovereign Yield Curve Is Inverted, as Markets Are Pricing in Risk of Currency Crisis

Source: Bloomberg

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

12 month 3 month 6 month spot price

2.5

4.5

6.5

8.5

10.5

12.5

14.5

16.5

18.5

1 Year 2 Year 3 Year 4 year 5 year 7 Year 8 year

Last 1 Mo 3 Mo 6 Mo 1 Year

EMERGING EUROPE AND CIS

10

Page | 10

www.roubini.com

NEW YORK - 95 Morton Street, 6th Floor, New York, NY 10014 | TEL: 212 645 0010 | FAX: 212 645 0023 | [email protected] | [email protected] LONDON - 120 Holborn, 5th Floor, London EC1N 2TD | TEL: +44 (0) 207 092 8850 | FAX: +44 (0) 207 242 4783 | [email protected] © Roubini Global Economics 2013 - All Rights Reserved. No duplication or redistribution of this document is permitted without written consent.

Figure 12: Among the Lowest, Credit Rating Is Broadly in Line With Fundamentals (0 = weak, 10 = strong)

Source: Moody’s, RGE

Rachel Ziemba, Director of Global Emerging Markets, contributed to this piece.

Contact the author

The above content is offered for the exclusive use of RGE's clients. No forwarding, reprinting, republication or any other redistribution of this content is permissible

without expressed consent of Roubini Global Economics, LLC. All rights reserved. If you have received access to this content in error, RGE reserves the right to enforce

its copyright and pursue other redress. RGE is not a certified investment advisory service and aims to create an intellectual framework for informed financial

decisions by its clients. This content is for informational purposes only and does not constitute, and may not be relied on as, investment advice or a recommendation

of any investment or trading strategy. This information is intended for sophisticated professional investors who will exercise their own judgment and will

independently evaluate factors bearing on the suitability of any investment or trading strategy. Information and views, including any changes or updates, may be

made available first to certain RGE clients and others at RGE's discretion. Roubini Global Economics, LLC is not an investment adviser.

For questions about reprints or permission to excerpt or redistribute RGE content, or for a PDF version, clients should contact their RGE account representative.

ARG BLR

BRA

BGR

CHL

CHN

COL

DOM

ECU

GAB

GHA

HUN IDN

KAZ

MYS

MEX

NGA

PAK

PER

PHL

POL

ROU

RUS

SEN

ZAF

LKA

TUR

UKR

VEN VNM

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

5.0 5.5 6.0 6.5 7.0 7.5

Ave

rage

of

thre

e c

red

it r

atin

gs

Country Insights Investment Attractiveness Index, September 2013