Research Monograph on Moblile Banking of Dhaka University Students

95

Page 5 Department of Public Administration University of Dhaka Research Monograph On Mobile Banking: A comprehensive study on the attitudes of the students of

Transcript of Research Monograph on Moblile Banking of Dhaka University Students

Page 5

Department of Public Administration University of Dhaka

Research Monograph

On

Mobile Banking: A comprehensive study on the attitudes of the students of

Page 5

science and social science faculty of Dhaka University towards mobile banking

Supervised by :Salahuddin M. Aminuzzaman

Professor,

Dept. of Public Administration.

University of Dhaka.

Presented by:

Md. Shahadat.

8th Semester 5th Batch

Reg. No. : H-5295

Session : 2009-10

Exam Roll: 4450

Group No. 03

Department of public administration

Page 5

University of Dhaka

Date of submission: Feb 4th ,2015

Chapter 01

Page 5

Introductory phase

Mobile Banking: A

comprehensive study on the

attitudes of the students

of science and social

Page 5

science faculty of Dhaka

University towards mobile

banking

Disclaimer

Page 5

The work I have presented hereby does not breach any extant copyright rules and regulations and no segment of this report iscopied from earlier work done for the same purpose and otherwise.

I further undertake to indemnify the Department of PublicAdministration against any loss and damage arising from theforgoing copyright obligation.

I do hereby solemnly declare that the work presented in thisreport has been carried out by me and has not been previouslysubmitted to any other University/ College/ Department/Institute/ Organization for Academic qualification /Certificate/Diploma or Degree.

Md.Shahadat

5th Batch, 8th Semester

Examination Roll: 4450

Reg. No.: H-5295 (Session: 2009-10)

Dept. of Public Administration

University of Dhaka

Page 5

Letter of Transmittal

31st January,2015

Dr. Saluddin M.Aminuzzaman

Professor

Department of Public Administration

University of Dhaka.

Dear Sir,

I have completed “Applied research In Public Administration” as anacademic course requirement of 8th Semester and would like to submitmy Study report as per your specifications. I would also like todraw your kind attention to the fact that I have tried my levelbest to gather and organize all the information needed for thisparticular report, and in doing so have tried my utmost to live upto your standards.

May I, therefore, wish and hope that you would be gracious enoughto accept my effort and oblige thereby.

Yours sincerely,

MD Shahadat | 01725630685 | _ _ _ _ _ _ _ __ _ _ _

Class roll: SS-66

5th Batch, 8th Semester

Page 5

Examination Roll: 4450

Reg. No.: H-5295 (Session: 2009-10)

Dept. of Public Administration

University of Dhaka

ACKNOWLEDGEMENT

hen people do something there do have some

stimulation which let him pursue to do so. For being

an academic requirement of 8th Semester of bachelor

degree on Public Administration “Applied research in Public

Administration” (under the Course Code of PA-423) dealing

with submitting a research monograph, we have been assigned

to study on “Mobile Banking: A comprehensive study on the attitudes of

the students of science and social science faculty of Dhaka University

towards mobile banking”. So I would like to take this

opportunity to extend my meekest solemn gratitude to my

W

Page 5

revered, venerated, esteemed, illustrious, extolled, exalted

sir Dr. Salauddin M. Aminuzzaman, Professor, Department of

Public Administration, University of Dhaka under whom we

have been instructed to prepare this report. It is useless

to say that without proper guidance and supervision of sir

it would not be possible to think to prepare this report.

I will also pull out my thanks to the respondents who have

given their moment to fill out the query chart as well as my

group members deserve most my appreciation for meeting,

discussing, scrutinizing, tabulating and finally presenting

the collecting data in well speculated manner.

Abstract : Nowadays Mobile Banking users are increasing day by day as of

late report depicts Mobile Banking clients now are approx.

25million people now use Mobile Banking meanwhile they transact

about 350 crore taka daily on average basis (Daily Prothom Alo,

January 26,2015). This report on Comprehensive study on the

attitude of Dhaka University students to using Mobile Banking

service focusing their belonging to different comparatively outer

districts and their fathers’ profession whether these factors

Page 5

influence them to adopt that or not in their daily necessary

money transaction activities instead of traditional banking

facilities aiming at less time consumption , hassle free, safe

and secure way of dealing, convenient service charge etc. our

whole respondents are two hundred amongst them top most 28 %

belong to greater Dhaka district then second highest 23% belong

to Khulna where Chittagong covers 17% of them then 13% and 11%

belong to Rajsahi and Rangpur respectively. Barishal and sylhet

become bottom of list having 7 % and 2% particularly.

Another salient aspect of our study is respondents’ fathers’

occupation. Where we see 33% students’ fathers’ profession is

business and 18% of them doing teaching. Among them 17%

students father belong to agriculture profession another 9% do

government service as well as 13% do private jobs. Doctor,

engineer, banker, advocate, driver cover 2%, 0.5%, 2%, 1%, 0.5%

respectively. Meanwhile 3.5 % are late. In this study we also

tried to give a balance between Science and Social science

faculty as well as gender i.e. male and female on the basis of

pro parta. Where 65% of them are male from each faculty and 35%

are female in lieu.

On the point of usage MB agents we have seen 61% (135) and 31%

(69) students use Bkash and BDBL while others belong to rest of

8%. 87% (174) students have a personal MB account and left 13%

(26) use agents’ account for operating Mobile transactions. On

the point of purpose of usage of Mb it is seen almost 87%

students from both faculty go to MB services to receive money

Page 5

from family which ultimately failed to reject our Hypothesis

beside that students use MB for shopping, paying bills and

recharging their mobile balances. We also have seen 58% students

of Pure Science have personal income most of which go to private

tuitions where only 26% students of Social Science have personal

which also belong to tuitions. It is observed that 77% student of

both faculties see MB as a convenient procedure where 18% say MB

is partially convenient and rest of 5% feel it inconvenient

system. Majority of students consider MB as a safe, secured, less

time consuming procedure and 59% opined that MB are available

while 30% commented it is found only at some places.

On the point of satisfaction 60% and 35% are satisfied and

partially satisfied respectively when other 4% are not satisfied

yet. In addition of multi facets of its prospects there have some

problems or risks as 22.5% students expressed network problem is

one of the risks, 18% saw it is less secured transaction for

large amount of money while 18% did not see any risks here yet.

Many felt password hacking, digital spoofing, fraudulent agents

and technical errors also risks.

Page 5

Table of contents

SL. No. CONTENTS Page

Number

Chapter 01

Introductory Phase 01-07

Page 5

Chapter 02 # part 01

Research topic: Mobile banking of DU Students

10-12

01

Introduction 11

02

Statement of problem 12

03

Background & significance of the study 12

04

Objective of the study 13

05

Statement of Hypothesis 13

Chapter 02 # part 02

Research Method and Design 15-23

06 Research methodology 15

07 Justification of selecting Survey method 15

08 Sources of data 16

09 Data collection method 16

10 Research questions 17

11 Sampling procedure 17

12 Variables 18

13 Study limitation 19

14 Statistical tools/treatment 19

15 Definition of terms

Page 5

19

Chapter 02 # part 03

Literature & Theory

25-29

16

Literature Review 25

17

Theoretical Framework 27

Chapter 03

Data analysis

31-54

18

Analysis of Empirical findings 27

19

Chart 01-20 27-54

Chapter 04

Concluding Phase 55-60

20 Conclusion 56

21 Recommendation for further study 56

22 Summary of the Study 57

Page 5

Chapter 04

Supplementary Phase 59-66

23 Appendix 59

24 Reference and bibliography 65

Page 5

Chapter 02 # Part 01

Research topic: Mobile banking of DUStudents

Introduction:“Nearly 13 million people in Bangladesh are getting financial

services, transferring money, paying in shops as bKash "exploited

ubiquity of cell phones to deliver a needed service”----- Bill

Page 5

Gates. (when interviewing with the Wall Street Journal (WSJ) on

01 Oct.,2014)

Mobile phones have become a tool for everyday use, which creates

an opportunity for the evolution of banking services to reach the

previously unbanked population through mobile banking. The use of

mobile banking can make basic financial services more accessible

to low-income people, minimizing time and distance to the nearest

retail bank branches (CGAP 2006). The outstanding growth of

mobile sector worldwide has created a unique opportunity to

provide social and financial services over the mobile network.

With over 4 billion mobile cellular subscriptions worldwide,

mobile network has the ability to immediately offer mobile

banking to 61% of the world population (Sultana 2009). But still

the usage of mobile banking is a debatable issue among the

educated persons and professional body because of the risk

involved in

Such transactions

Though many of such people argue that internet and other

technology based transaction is not safe, not practical and would

lead to fraud, a lot of people think it safer, flexible in time

and can be done anywhere and anytime (Chowdhury and Ahmmad 2011).

Cost and availability are the other factors which might influence

the usages of mobile banking. Thus, it is necessary to have an

in-depth analysis for the mobile banking service provider to

identify the factors influencing the usages of mobile banking. A

Page 5

clear understanding of these factors will enable mobile banking

service providers to develop suitable marketing strategies,

business models, processes, awareness programmes and pilot

projects (GSMA 2009).

This study has been conducted with the main objective of

identifying the factors that influence the usages of mobile

banking of the students of Dhaka University. We have tried to

find out factors and issues from the faculty basis (i.e. whether

students of Science faculty use mobile banking more or Social

Science students do that) for the purpose of sending money to

home or receiving in lieu basically who are far away from their

home depending on northern and southern districts of Bangladesh.

This paper has been divided in to several segments as first phase

has dealt with introductory discussion as usually done for any

social science research then second phase dealt with literature

review and research methodology of this report after that third

phase dealt with research findings as well as data analysis and

recommendation, conclusion with bibliography have been dealt with

least segment.

Statement of problem:This study seeks to explore the alluring factors that urge the

Students of University of Dhaka focusing Science and Social

Page 5

Science faculty at particular. This investigation has tried to

know the matters like Do the Students of Science faculty use

Mobile Banking more or Students of Social Science or Do the

Students who are from outer districts as Rangpur, Rajsahi,

Khulna, Chittagong depend on Mobile Banking much more. Meanwhile

this investigated the factors of fathers’ professions for using

Mobile Banking.

Background & significance of the study:

25million people now use Mobile Banking meanwhile they transact

about 350 crore taka daily on average basis (Daily Prothom Alo,

January 26, 2015). For the relevant causes Mobile Banking merits

much more heed to be paid to it. People being out of traditional

Bank to Bank financial transactions have been rushing to Mobile

based banking facilities. A recent study conducted by a Dr.

Salauddin M. Aminuzzaman sir (Department of Public Administration

University of Dhaka ) on the savings pattern and remittance back

to the village by rickshaw pullers in Dhaka has revealed some

interesting facts. It was found that of the 461 respondents who

took part in the study, 350 send money over mobile phones (76%).

With some 19 banks operating in the country that offer mobile

financial services, this sector has emerged as a major player in

the fast and safe means through which money can be transmitted to

intended recipients. With average weekly transfers averaging Tk.

981 per week, most of the surveyed Dhaka city rickshaw pullers

Page 5

come from the relatively less developed districts of Rangpur,

Kurigram, Jamalpur and Sirajganj char areas.

Taken all these issues we wanted to study on Dhaka University

students who are living here from outer districts of Dhaka where

they belong to, to examine whether they use Mobile Banking to

transact money form or to their family. As well as to know the

factors why they choose MB service despite innumerate Banks

serving hereby. Defining some Hypothesis we will try to show the

consistencies between Hypothesis and gathered information whether

it rejects Hypothesis or Fails to reject that.

Objective of the study:This study aimed at exploring the following issues-

To identify the factors that influence science and social

science faculty students of Dhaka University to adopt Mobile

Banking.

To know how Mobile Banking affects their life.

To know their different purposes of using mobile bank.

To identify which division’s students use mobile banking

most.

To find out how their parent’s occupation affect their using

of mobile banking.

Statement of Hypothesis:

Page 5

We hypothesize that the students of Dhaka University who usemobile banking are benefited from it. Money transfer with theirfamily is comfortable. It saves their time and money both. Thetheory leads us to predict that most users accept mobile bankingas beneficial for its less time consumption, affordability,convenience, trust, safety, comfortability. Since positive sideis more, we hypothesize that overall the students have a positiveattitude towards mobile banking. We also hypothesize that thestudents who live in Dhaka away from their family use mobilebanking more for transacting money with their family. Again thedegree of using mobile banking differs by the student’s parent’soccupation. It also varies by their geographical location. Thereare differences in purpose of using mobile banking betweenscience and social science faculty students.

Chapter 02 # Part 02

Page 5

Research Method and Design

Research Methodology:The research is concerned with the impact of factors of mobile

banking services on the students of science and social science

faculty of University of Dhaka. It will also look how the use of

mobile banking differs between science and social science faculty

students and their attitudes towards it. The study will be

Page 5

descriptive in design and empirical in nature where primary data

will be used to address the objectives. The descriptive design

will be applied because the study involves describing a

relationship that exists between a set of variables. The study

will aim at collecting information from target population on the

impact of factors that encourages using mobile banking services

and other relevant issues.

To conduct this research survey method will be used as research

methodology.

Survey Method

Survey is a research technique in which information is gathered

from a sample of people by use of a questionnaire or interview in

the light of specific research objectives. By following this

method we will get an overall picture of a given universe through

systematic collection of all available data on the subject. It is

a method of data collection based on communication with a

representative sample of individuals. In another words, survey

method provides a quantitative or numeric description of trends,

attitudes or opinions of a population by studying a sample of

that population. It involves cross sectional and longitudinal

studies using questionnaire or interview for data collection with

the intent of generalization. This method will be used to collect

basic information and observation over time and to identify the

variables and their relationships. We will able to describe the

ongoing state of practice and to interpret the findings

Page 5

rationally. By this we will contact to the respondents of our

research directly and be able to get more reliable data.

Justification of selecting Survey method:The main reasons why the survey method is preferred as follow in

the below:

Survey through sacrificing a certain details, enables quick

investigation of a large number case.

Survey entails much less cost

Sources of data:This study wholly has depended on primary source that meansinteractive feedback from respondents as who have been identifiedas sampling population by administering a structuredquestionnaire. As well as secondary sources in order to reviewthe earlier literature on this topic as Articles, Periodicals,Journals, research reports, daily news papers etc.

Data collection method:Here we have used Questionnaire method with a view to collectingadequate information to investigate the research query.

Questionnaire

It is an instrument to collect and aggregate primary data from

the basic sources. We will use questionnaire to obtain more

authentic data from selected participants. Respondents will be

Page 5

asked to fill up the questionnaire. Questionnaire will be

designed to capture demographic characteristics of respondents

and usage patterns in mobile banking; to capture information on

constructs affecting the mobile banking adoption, namely time

saving, security, responsiveness, affordability, customer trust,

convenience.

This technique is much more effective and will lead us to get

genuine data from the answers provided by the respondents.

Besides people feel interested and easy in responding the

questions of questionnaire. As our target population is DU

student community, it is difficult for them to give their

valuable time in helping us to carry out our survey. They find

questionnaire more comfortable to fill up quickly than other

available tools. We can easily reach our respondents by offering

questionnaire as it takes less time to fill up. We will use mixed

questionnaire to get numerical as well as descriptive data.

Mixed Questionnaire

This type of questionnaire is most commonly used in social

science research query. We will incorporate both open-ended and

closed questions in questionnaire to collect different types of

information. In order to find out descriptive information; open-

ended questions will be included where respondents are free to

express their views and ideas. These questions do not limit the

choice of respondents.

Page 5

On the other hand, we can gather categorized data through closed

questions. These questions offer respondents multiple choice

questions from which to choose the statement which most nearly

describes their response to an item. Respondents do not have much

liberty to express their own views thoroughly but to respond in

the light of the given responses.

Research questions:

What are the factors influencing the use of Mobile banking

among the students of science and social science faculty of

Dhaka University?

What are the different purposes of their using mobile

banking?

How their geographical location and parent’s occupation

affect their degree of using mobile banking?

Sampling procedure:In this research, target population is the students of science

and social science faculty of Dhaka University familiar with

mobile banking system; they may be resident or non-resident,

studying various disciplines in different sessions. Necessary

data will be sought from them who are enjoying mobile banking

services. They will be mobile subscriber using mobile banking

Page 5

because they are homogeneous in their use of services. We will

select them as they are supposed to evaluate the existing level

of services most accurately from their own point of view as

potential customer.

The sample size will be around 200 which refers to a total of 200

responses will be taken into account in collecting required data.

200 respondents with diverse backgrounds will be chosen

purposively. We will follow purposive sampling in selecting

sample as this method is seem more convenient in this regard. We

will try to make the selection of sample as representative as

possible and to pick out the most relevant sample from the

population.

Variables:We have defined Dependent variable as Mobile Banking of Dhaka

University students and independent variable as geographical

location that the outer districts where s/he belong to, fathers’

occupation, personal income sources, convenience, ubiquity of

Mobile Banking agents, time consumption and security particularly

as below illustrated diagram depicts.

Page 5

Study limitationIt is to admit that the study attempts only those aspects, which

are closely relevant to the purpose of the study. Facts and

figures, which otherwise might be equally important, but not

Page 5

having a direct bearing on the conclusions arrived at this study,

have been ignored. The most important limitation from which the

study suffers is the non-availability of information in a manner

required for analysis and lack of interactive communication to

the supervisor of this research monograph. As well as reluctance

from the respondents to fill up the questionnaire in a limited

extent. Another important limitation of the study is time and

political situation of country have been considered as a

constraint.

Statistical tools/treatment:

Upon the completion of this procedure, we have counted the entire

fill out questionnaire and divided them on the basis of faculty

s/he belongs to. We have tried to balance between male and female

as well as discipline studied at as stated earlier. After faculty

wise division of data we have added them on the basis of

“options” specified in the questionnaire and found out their

percentage to some extent faculty wised and somewhere in a gross.

After analyzed in percentage we have presented these tabulated

data in pie chart, column and table considering the easily

apprehending the presented data. Definition of terms:The conceptual framework for this study was based on the impacts

of mobile banking on the xstudents of Dhaka University. The study

Page 5

focuses on the factors that influence the lives of Dhaka

University students through the use of various mobile banking

facilities. The framework comprises of the internal and external

factors that affect the performance of Mobile banking.

The dependent variable in this study is the mobile banking. On

the other hand, in accordance with the Diffusion of Innovation

theory which we’ve selected to back our research, the independent

variables might be time, risk, security, responsiveness,

affordability, customer trust and convenience. We will also be

eager to find out whether the use of mobile banking is affected

within the students of University of Dhaka by the independent

variables like division (District), faculty, parents’

professions, residential status whether living in university’s

halls or dormitories.

Mobile Banking: Mobile banking is a system that allows customers

of a financial institution to conduct a number of financial

transactions through a mobile device such as a mobile phone or

personal digital assistant.

It means Electronic banking that uses mobile phone technology (or

other wireless devices) to deliver electronic financial services

to consumers. Mobile banking refers to the use of a smartphone or

other cellular device to perform online banking tasks while away

from your home computer, such as monitoring account balances,

transferring funds between accounts, bill payment and locating an

ATM.

Page 5

Present scenario of Mobile Banking in Bangladesh: At present

ninety banks are doing their Mobile Banking operation where

twenty eight banks have been given approval of operating Mobile

Banking Services following the Mobile Banking guide line provided

by Bangladesh Bank (BB) in 2009. Amongst these banks Brac Banks

which does in the brand name of Bkas, Dutch Bangla Bank Limited

Mobile Banking commonly familiar as DDBL Mobile Banking, M Cash

of Islami Bank, U Cash of United Commercial Bank at particular.

As latest information says that Mobile Banking Clients have

reached to nearby 25 million (Two and half crore) where they

transact three hundred fifty crore Taka on average at daily

basis.

Time Saving: Time saving refers to the time required to complete

a transaction. Lee (2009) found in his study that time plays an

important role in adopting mobile banking service by the users.

Mobile banking has to be dedicated to widening the net of

financial inclusion among the people by facilitating money

transfer through mobile phones. It has to provide Mobile

Financial Services allowing customers to send, receive, and pay

money from their mobile phones. It has to enable customers to

send money to anyone, using an advanced technology available on

others mobile phone. The recipient will receive money instantly,

no matter where s/he is. Payments through mobile banking also

should make life easier so that people do not have to go back

home or anywhere else to get money when someone need to buy

something and have run out of cash. Even if the customer don't

Page 5

have the required amount in the mobile bank Wallet, someone else

can easily send the amount in times of need.

Risk: It refers to the five facets of risk including performance

risk, security/privacy risk, time risk, social risk and financial

risk. According to Lee (2009) these five risks can be described

in case of mobile banking as follows:

1. Performance risk: refers to losses incurred by

deficiencies or malfunctions of mobile banking servers.

2. Security/privacy risk: is defined as a potential loss

due to fraud or a hacker compromising the security of a mobile

banking user.

3. Time/convenience risk: This refers to a loss of time and

any inconvenience incurred due to the delays of receiving

payments or the difficulty of navigation.

4. Social risk: refers to the possibility that using mobile

banking may result in disapproval by one’s friends/family/work

group.

5. Financial risk: is defined as the potential for monetary

loss due to transaction errors or bank account misuse.

Security: Security is the state of being free from danger or

threat. It can be also be defined as a thing deposited or pledged

as a guarantee of the fulfilment of an undertaking or the

repayment of a loan, to be forfeited in case of default.

Page 5

Security aspect is to be investigated as an important element

which influences the use of mobile banking. As an example, Soroor

(2005; 2006) focused on the security issue in mobile banking and

proposed some evaluation techniques which could be used to

improve the system.

First, the establishment of a secure channel to provide

data confidentiality and integrity between the client

and the bank service.

Secondly, the authentication of the client at the

beginning of a mobile banking session (e.g. entity

authentication, transaction authentication).

Responsiveness: Responsiveness is the willingness to help

customers and provide prompt service(Zeithaml et al, 2006). This

dimension is concerned with dealing with the customers’ requests,

questions and complaints promptly and attentively. Handling of

problems and returns through the site. A Bank is known to be

responsive when it communicates to its customers how long it

would take to get answers or have their problems dealt with. To

be successful, companies need to look at responsiveness from the

view point of the customer rather than the company’s perspective

(Zeithaml et al., 2006). Responsiveness also captures the notion

of flexibility and ability to customize the service to customers

need. Standard for speed and promptness that’sreflects the

companies view of process requirement may be very different from

the customer requirement. Responsiveness concerns the willingness

Page 5

or eagerness of employees for service provision. It involves

turnaround time of service actions like timely dispatch of a

receipt or quickly calling back the customer.

Affordability: Affordability means ability to afford something;

believed to be within one’s financial means. Customers of mobile

banking have to be able to send and receive money with minimal

effort and cost. Perceived cost Savings refer to the transaction

cost of conducting mobile banking transactions, including the

airtime and bank charges. Perceived cost is defined as the extent

to which a person believes that using mobile banking will cost

money (Luarn& Lin 2005). The cost may include the transactional

cost in the form of bank charges, mobile network charges for

sending communication traffic (including SMS or data) and mobile

device cost.

Mobile banking sectors should be able to provide the highest

benefits to its customers at an affordable cost, enabling

everyone to access the formal financial system of the economy.In

addition to eliminating initial monetary costs involved in

entering the banking system, mobile banking should be responsible

for greatly minimize opportunity costs such as time and effort

required to access such services. The service charges should be

minimal and there are no hidden costs involved.

Cost of opening a Mobile Bank Wallet on mobile phone should be

minimum and customers should not experience unexpected and

incidental costs. Perceived cost Savings refer to the transaction

Page 5

cost of conducting mobile banking transactions, including the

airtime and bank charges.

Customer Trust: Three dimensions of trust namely ability,

integrity and benevolence. This will be observed from three

perspectives: the bank, mobile network provider and wireless

infrastructure. Bhattacherjee (2002) defined these as:

Ability refers to the perception of the consumer about the

competency and salient knowledge of the mobile banking

service provider to deliver the expected service;

Integrity refers to users’ perceptions that the service

provider will be fair, honest and adhere to reasonable

conditions of transactions;

Benevolence refers to the extent to which a service provider

will demonstrate receptivity and empathy towards the user.

The service provider will make a good faith effort to

resolve users’ concerns and intends to do good to the users

beyond profit motives.

Convenience: It is defined as the extent to which mobile banking

can serve the users’ needs. It includes:

Perceived Usefulness: It refers to the degree to which a person

believes that using a particular system would enhance his or her

job performance. (Davis. F, 1989)

Page 5

Perceived Ease of Usefulness: It is defined as “the degree to

which a person believes that using a particular system would be

free of effort. (Davis. F, 1989)

Division: Students of the University of Dhaka comes from almost

all the districts or at least divisions of the country. We’ll try

to figure out whether the reason of their coming from different

regions of the country affects their use of mobile banking.

Faculty: Students from the science faculty are much more

habituated in doing tuition than the students of social science

faculty. They earn money through this. Thus they are also able to

send money to their families in times of need. We’re going to

seek out through our study, whether studying in one of the two

faculties affects the use of mobile banking within DU students.

Parents’ Occupation: We’ll be trying to figure out, whether the

difference in the occupation of the parents of the students of

Dhaka University affects their use of mobile banking.

Residents: University students live in various residential halls allocated for them. But, not all of them are accommodated in the halls. Some of them also resides in mess or by renting house. We hope to find out, whether the rate of using mobile banking withinthe hall students is higher or lower than the students living outside the hall.

Page 5

Chapter 02 # Part 03

Literature & theory

Page 5

Literature Review :Mobile Banking saves time compared to traditional banking,

majority customers use Mobile Banking for Air-time-top-up service

and it is costlier than traditional banking. The prospect of

mobile phone banking is high, although this concept is new in

Bangladesh.

Mobile banking is an application of m-commerce which enables

customers to access bank accounts through mobile devices to

conduct and complete bank-related transactions such as balancing

cheques, checking account statuses, transferring money and

selling stocks (Kim et al. 2009). Luo et.al (2010), defined

mobile banking as an innovative method for accessing banking

services via a channel whereby the customer interacts with a bank

using a mobile device.

In earlier studies in this regard have provided different results

as Wu and Wang (2005), in a study on middle class populations,

found that cost had minimal significant impact on the adoption of

mobile banking while perceived risk, compatibility and perceived

usefulness have significant influences. On the other hand Karnani

(2009) argues that cost plays important role in choosing mobile

banking.

Mattila (2010) identified that the most important attribute in

encouraging the use of mobile banking was related to the costs of

Page 5

conducting banking (mean 4.38, standard deviation 2.15). Wish of

faster data transmission accounted to the secondly highest

importance mean (mean 3.74, standard deviation 2.49).

Surprisingly, the third attribute mentioned to boost to mobile

banking adoption was authentication with mobile phone to Internet

bank (mean 3.67, standard deviation 2.60). Admittedly, the

response pattern along different attributes was pretty

homogenous. The distinctly most important reason for the trial of

mobile banking was the possibility to conduct banking truly

regardless of time and place (mean 5.09, standard deviation

1.62).

Cheah et.al (2011) argue that Factors such as perceived

usefulness (PU), perceived ease of use (PEOU), relative

advantages (RA) and personal innovativeness (PI) were found

positively related with the intention to adopt mobile banking

services. However, social norms (SN) were the only factor found

insignificant.

The outcomes of (Chian-Son, 2012) has revealed that individual

intention to accept Mobile Banking is significantly influenced by

social factors, perceived financial cost, performance expectancy,

and perceived credibility, in the order of their influencing

strength. According to Hasan et al. (2010), e-banking facilitates

to the Bangladeshi banking sector in various ways, however

Bangladeshi customers have lack of sound knowledge regarding e-

banking providing by banking industry in Bangladesh. Rahman et

al. (2012) have found in their study that the new challenges of

Page 5

E-banking in Bangladesh are to formulate and execute policy from

the perspectives of society, banks, regulatory authorities and

government as well. According to Ahmad et al. (2012),

Sharma (2011) has identified that banks have welcomed wireless

and mobile technology into their boardroom to offer their

customers the freedom to pay bills, planning payments while stuck

in traffic jams, to receive updates on the various marketing

efforts while present at a party to provide more personal and

intimate relationships. The main objective of her study is to

examine consumer adoption of a new electronic payment service as

Mobile Banking and the factors influencing the adoption of Mobile

Banking. Cheney (2008) has obtained that three relatively new

communication technologies – SMS text messaging, wireless

Internet access, and near field communication (NFC) that are

making important contributions to mobile financial services.

Online banking and contactless payments and consume’s experience

with them are also studied as building blocks to mobile financial

services. In addition, her analysis considers other factors that

are affecting adoption patterns, including financial inclusion

opportunities, data security problems, and coordination issues.

Together, the building blocks and these other factors will

influence how markets for mobile financial services develop.

Ismail and Masinge (2011) have found that customers in the BOP

will consider adopting Mobile Banking as long as it is perceived

to be useful and perceived to be easy to use. But the most

critical factor for the customer is cost; the service should be

Page 5

affordable. Furthermore, they also claimed that the Mobile

Banking service providers, both the banks and mobile network

providers, should be trusted. Trust was found to be significantly

negatively correlated to perceived risk. Trust therefore plays a

role in risk mitigation and in enhancing customer loyalty.

Klein and Mayer (2011) have discovered that by unbundling

payments services into its component parts, Mobile Banking

provides important lessons for the design of financial regulation

more generally in developed as well as developing economies.

Donner (2008) has emphasized the need for research focusing on

the context of m-banking/m-payments use. In his research he has

suggested that the challenges of linking studies of use to those

of adoption and impact reflect established dynamics within the

Information and Communication Technologies and Development (ICTD)

research community. Since much of literatures are not found

related to mobile banking in Bangladesh, this paper is an

endeavour to mitigate the research gap in this regard.

Since much of literatures are not found related to mobile banking

in Bangladesh, this paper is an endeavor to mitigate the research

gap in this regard. Thus on the basis of the above literatures

the paper aims at identifying the factors influencing the usage

of Mobile Banking of Dhaka University students focusing Science

and Social Science faculty.

Page 5

Theoritical Framework:We will prefer to back the independent variables of our work

through the study of the Diffusion of Innovation theory.

Diffusion of innovations is a theory that seeks to explain how,

why, and at what rate new ideas and technology spread

through cultures. Everett Rogers, a professor of communication

studies, popularized the theory in his book Diffusion of Innovations;

the book was first published in 1962, and is now in its fifth

edition (2003). A brief description of this theory is stated here

in below.

Diffusion of Innovations Theory:

Diffusion is the process by which an innovation is communicated

through certain channels over time among the members of a social

system. Diffusion is a special type of communication concerned

with the spread of messages that are perceived as new ideas.

An innovation, simply put, is “an idea perceived as new by the

individual.” An innovation is an idea, practice, or object that

is perceived as new by an individual or other unit of adoption.

The characteristics of an innovation, as perceived by the members

of a social system, determine its rate of adoption.

The four main elements in the diffusion of new ideas are:

(1) The innovation

Page 5

(2) Communication channels

(3) Time

(4) The social system (context)

1. The innovation: Why do certain innovations spread more quickly

than others? The innovation, to spread and be adopted should

show:

The characteristics which determine an innovation's rate of

adoption are:

(1) Relative advantage (2) Compatibility (3) Complexity (4) Trial

ability (5) Observability to those people within the social

system.

2. Communication: Communication is the process by which

participants create and share information with one another in

order to reach a mutual understanding. A communication channel is

the means by which messages get from one individual to another.

Mass media channels are more effective in creating knowledge of

innovations, whereas interpersonal channels are more effective in

forming and changing attitudes toward a new idea, and thus in

influencing the decision to adopt or reject a new idea. Most

individuals evaluate an innovation, not on the basis of

scientific research by experts, but through the subjective

evaluations of near-peers who have adopted the innovation.

3. Time: The time dimension is involved in diffusion in three

ways.

Page 5

3.1 - First, time is involved in the innovation-decision process.

The innovation- decision process is the mental process through

which an individual (or other decision- making unit) passes from

first knowledge of an innovation to forming an attitude toward

the innovation, to a decision to adopt or reject, to

implementation of the new idea, and to confirmation of this

decision.

3.2 - The second way in which time is involved in diffusion is in

the innovativeness of an individual or other unit of adoption.

Innovativeness is the degree to which an individual or other unit

of adoption is relatively earlier in adopting new ideas than

other members of a social system. There are five adopter

categories, or classifications of the members of a social system

on the basis on their innovativeness:

(1) Innovators – 2.5% (2) Early adopters – 13.5% (3) Early

majority – 34% (4) Late majority – 34% (5) Laggards – 16%

3.3 - The third way in which time is involved in diffusion is in

rate of adoption. The rate of adoption is the relative speed with

which an innovation is adopted by members of a social system.

4. The social system: The fourth main element in the diffusion of

new ideas is the social system. A social system is defined as a

set of interrelated units that are engaged in joint problem-

solving to accomplish a common goal. The members or units of a

social system may be individuals, informal groups, organizations,

and/or subsystems. The social system constitutes a boundary

within which an innovation diffuses.

Page 5

When any new innovation is introduced in a society, the people of

that society look out for the relative advantages of that

innovation all of at first. People like the flexibility to

observe the innovation very closely to seek out the complexity

and compatibility of it. They prefer the opportunity to give a

trial of it or a test run on it, just like trialing a new dress

to adopt the innovation.

A new idea or an innovation should be communicated throughout the

people of the social boundary, where it’s going to be initiated

or already been introduced. Time is also a very important element

in the path of acceptance of the idea or innovation by the

people. Acceptance of an idea depends on the adoption capacity of

the people. Some are early adopters some are slow. People of a

society who have got early adoption capability, can enjoy the

pros and perks of an innovation with ease.

So an innovation, being less complex and more compatible with the

social beliefs and norms and culture of the society and being

relatively much more advantageous to the people by saving their

time, taking risks on behalf of the people and providing adequate

security measures to protect the customers, is going to be

accepted and adopted by the people within a very short time. It’s

going to be diffused in the society with the smoothness of pure

non-alloy gold.

Page 5

Chapter 03

Empirical Findings

Page 5

Analysis of data/Empirical findings:

Science50%

Social Science50%

Total repondents

Chart: 01

Page 5

Interpretation:

The study on the mobile banking of Dhaka University students

brought two hundred students as a research sample. We have tried

to look up to the balance of number between Science and Social

Science faculty as well as balance between male and female.

Taking that in to account we have taken one hundred respondents

from each faculty (i.e. one hundred from Science and that of from

Social Science) among sixty five are male and rest thirty five

are female for both two faculties.

Illustrated tersely:

Science: 50% (total 100, 65 from Male and 35 from Female).

Social Science: 50% (total 100, 65 from Male and 35 from Female).Chart:02

Page 5

MaleFemale

0%

10%

20%

30%

40%

50%

60%

70%

65%

35%

Interpretation:

Among the total respondents we have dwelt on the gender issue. As

stated earlier interpretation we have tried to look up to the

balance of number between Pure Science and Social Science faculty

as well as balance between male and female. Taking that in to

account we have taken one hundred respondents from each faculty

(i.e. one hundred from Pure Science and that of from Social

Science) amongst them 65% (65) are male and rest 35% (35) are

female for both two faculties.

Illustrated tersely:

65% are Male which in numerical figure is 65 also.

35% are Female which numerical figure is 35 also.

Page 5

D Kh Chi Ra Ra Ba Sy

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

27.50%22.50%

16.50%13.00% 11.00%

6.50%1.50%

Interpretation:

First of all it is to say that our study on the mobile banking of

Dhaka University students aimed at region belongingness. If I

say in precise way that does the district where students come

from influence the usage of Mobile Banking here after and before

(MB)? Here we have analyzed division basis rather than districts.

After scrutinizing our collected data we have found that Dhaka

division has been topped in a ranking then Khulna, Chittagong,

Rajsahi and rangpur respectively. From this above illustrated pie

chart it is easily seen that 28% (i.e. total 55, from Pure

Science faculty 27 and 28 from Social Science) students are from

greater Dhaka division. When from Khulna division 23% students

Chart: 03

Page 5

(i.e. total 45, from Pure Science faculty 16 and 29 from Social

Science). Seen 17% students come from Chittagong division where

total students are 33, 15 from Science faculty and rest 28 from

Social Science. It shows 13% students from Rajsahi division (i.e.

total students are 28, 17 from Pure science 9 from Social

Science) and the Rangpur division belong to 11% students (i.e.

total students are 23, 17 from Pure science 5 from Social

Science). Here it is seen that 7% students from Barisal division

(i.e. total students are 13, 7 from science 6 from Social

Science) when the least division Sylhel falls in to the bottom of

rank bearing only 1% i.e. total 3, 1 from Pure Science and rest 2

from Social Science.

Illustrated tersely:

Dhaka : 28% ( total 55, 27 from Pure Science faculty and 28 from

Social Science).

Khulna : 23% ( total 45, 16 from Pure Science faculty and 29

from Social Science).

Chittagong : 17% ( total 33, 15 from Pure Science faculty and 28

from Social Science).

Rajsahi : 13% ( total 28, 17 from Pure Science faculty and 9

from Social Science).

Rangpur : 11% ( total 23, 17 from Pure Science faculty and 5

from Social Science).

Page 5

Barisal : 7% ( total 13, 7 from Pure Science faculty and 6 from

Social Science).

Sylhet : 1% ( total 3, 1 from Pure Science faculty and 2 from

Social Science).

Page 5

Interpretation:

Another salient quantum of our study was the students’ fathers’

occupation to examine whether fathers’ profession depend on using

the Mobile Banking service or not. Dwelling on this independent

variable we have scrutinized the administered data got from the

respondents. This table chart is depicting that business bar has

soared highest then teacher, agriculture, private service,

Business

Teacher

Agriculture

Pvt.Service

Govt. Service

Late

Banker

Retired

Doctor

Advocate

Engineer

Driver

32.50%

17.50%17.00%13.00%

8.50%3.50% 1.50% 1.50% 1.50% 1.00% 0.50% 0.50%

Fathers' profession

Page 5

Government service, Late, Banker, Retired, Doctor, Advocate,

Engineer and Driver bars have plunged down sequentially. With a

view to elucidating details it can be stated that business is the

maximum profession of students’ father we have meant by business

small or medium business in their respective locality. 32.5%

(total 65, 30 from Science and 35 from Social science) students’

profession is business. When 17.5% (total 35, 16 from Science and

19 from Social science) students’ fathers do the teaching

occupation. Fathers of 17% (total 34, 11 from Science and 23 from

Social science) are involved to agriculture. Meanwhile 13% (total

26, 15 from Science and 11 from Social science) and 8.5% (total

17, 12 from Science and 5 from Social science) students’ fathers

involve in private and government services respectively. When it

says 3.5% (total 7, 5 from Science and 2 from Social science) in

below area it is seen 2% (total 4, 2 from Science and 2 from

Social science) fathers are Banker when 1.5% are doctor and

retired person equally. At the least 0.5% portion go to both

Engineering and Driving profession.

In the study we had hypothesize that which students’ fathers are

farmers and small business men they avail Mobile Banking service

much more here it is apparent that maximum students’ father do

so. As well as there have sort of Private and govt. services

along with that nominal service of Banker, Advocate, Doctor and

Engineer. So it can be summed up whose fathers are insolvents

they use or depend on Mobile Banking facility despite the

traditional Banking services.

Page 5

Illustrated tersely:

Business: 32.5% (total 65, 30 from Pure Science and 35 from Social science).

Teaching: 17.5% (total 35, 16 from Pure Science and 19 from Social science).

Agriculture: 17% (total 34, 11 from Pure Science and 23 from Social science).

Pvt. Service: 13% (total 26, 15 from Pure Science and 11 from Social science).

Govt. Service: 8.5% (total 17, 12 from Pure Science and 5 from Social science).

Late: 3.5% (total 7, 5 from Pure Science and 2 from Social science).

Banker: 2% (total 4, 2 from Pure Science and 2 from Social science).

Retired: 1.5% (total 3, 2 from Pure Science and 1 from Social science).

Doctor: 1.5% (total 3, All from Pure Science).

Engineer: 0.5% (Only one from Pure Science).

Driver: 0.5% (Only one from Pure Science).Chart: 05

Page 5

Residential82%

Non Residential18%

Accommodation

Interpretation:

Living within the alma mater provided accommodation or outside of

that was one of the queries of our study on the concern topic.

Here before info graphics depicts that Majority of the students

live in the University hall and dormitories when only 18% have

kept their dwelling rented or own residences. As we see that many

studies and reports indicated erstwhile that majority of the

students live in university halls/ hostels/dormitories whose

financial situation comparatively low with some exception so we

can relate this information to our hypothesis which circuitously

says the matter of insolvencies of students’ fathers. As well as

who are out of University’s halls/dormitories they have rented or

own residences in Dhaka so they don’t dwell in here.

Illustrated tersely:

Page 5

Residential: 82% (total 157, 84 from Pure Science and 73 fromSocial science).

Non residential: 18% (total 43, 16 from Pure Science and 27 fromSocial science).

Bkash61%

DBBL31%

Ucash2%

Mcash3% Others

3%

MB Accounts

Interpretation:

In order to collecting our data we have kept a provision of

Mobile Banking (MB) service providing agents’ account in our

research questionnaire. Analyzing the whole data we have observed

as above illustrated chart portrays that almost 61% ( total

students are 135 where 66 from Science faculty and other 69 from

Social Science faculty) of Bkash which is BRACK Bank introduced

Chart:06

Page 5

Mobile Banking service then 31% ( total students are 69 where 33

from Science faculty and other 36 from Social Science faculty)

belong to Dutch Bangla Bank Limited commonly known as DBBL Mobile

Banking. Rest of 8% go to Ucash, Mcash and other MB services.

If also this data is not related to our research hypothesis but

for realizing the extant scenario of Mobile Banking service

providing agents of Bangladesh it was kept in the questionnaire.

As we would assume that many people use Bkash MB services

ultimately this has been come to the light by this data.

Illustrated tersely:

Bkash : 61% (total 135, 66 from Pure Science and 69 from Social

science).

DBBL: 31% (total 69, 33 from Pure Science and 36 from Social

science).

Mcash : 3% (total 6, 4 from Pure Science and 2 from Social

science).

Others: 3% (total 6, 1 from Pure Science and 5 from Social

science).

Ucash : 2% (total 5, 2 from Pure Science and 3 from Social

science).Chart:07

Page 5

Interpretation:

In order to collecting our data we have kept a provision of

personal Mobile Banking (MB) account in our research

questionnaire. Analyzing the whole data we have observed as above

illustrated chart gives a picture of having almost all 87%

students a self Mobile Banking account and rest of 13% have not

any own account but they complete the MB service through another

or agents’ accounts.

Illustrated tersely:

Yes: 87% (total 174, 89 from Pure Science and 85 from Social

science).

No: 13% (total 26, 11 from Pure Science and 15 from Social

science).

Yes87%

No13%

Personal Accounts

Page 5

Purposes of using mobile bank (multiple

answers)

Purposes Pure Science

faculty

Social science

faculty

Receiving money from family 87% 86%

Sending money to family 36% 23%

Shopping 15% 24%

Paying bills 12% 7%

Recharge mobile 49% 21%

Others 5% 5%

Interpretation:

With a pursue to investigating the intention of Mobile Banking

system of financial transaction we administered a query upon the

sample population of our study from both Pure Science and Social

Science faculty at particular. Most of the students from both

Pure Science and Social Science use MB to receive money from

their family that is 86% of Pure Science and 87% from Social

Science as we have hypothesized that many students have come from

many outer districts and they rely on MB verily for their money

Chart:08

Page 5

transaction from and to the family. I think by this information

this part of Hypothesis has been justified verily. As well as we

have said in the hypothesis that beside receiving money from

their respective family they also send back money to them whether

doing private tuition or part-time jobs and other miscellaneous

sources of income (i.e. Photography, freelancing, research

fellowship) as this table shows 36% from Pure Science and 23%

Social Science students also send back money to their homes.

Along with receiving and sending money they complete the

activities of Shopping, Paying utility bills and recharging

mobile balances as it is seen 15% and 24% from both faculties

respectively use MB for shopping, 12% and 7% from both faculties

sequentially pay their bills by MB while other 49% form Pure

Science and 21% from Social Science recharge their mobile

balances using Mobile Banking amenities. Meanwhile rest 5% form

both faculties use MB given facilities form varieties of

activities.

This should be here stated information is multiple choice basis

for that reason many ticked multi option filling up this section

of questionnaire.

Illustrated tersely:

Receiving money: 87% & 86% (87 from Pure Science and 86 from

Social science).

Page 5

Sending money: 36% & 23% (36 from Pure Science and 23 from

Social science).

Shopping: 15% & 24% (15 from Pure Science and 24 from Social

science).

Paying utility bills: 12% & 7% (12 from Pure Science and 7 from

Social science).

Recharging mobile balances: 49% & 21% (49 from Pure Science and

21 from Social science).

Other usages: 5% form both faculties being 5 students from each

faculty.Chart:09

Page 5

Once a week13%

Once a Month20%

Twice a Month 9%

Regualrly37%

Some times21%

Usage of MB (Pure Science)

Interpretation:

“How often do you use Mobile Banking?” incorporating this

question in the research questionnaire we wanted to know the

propensity of students towards MB usage from Science and Social

Science faculty particularly as this chart is depicting that

regularly use Mobile Banking service 37% (37) of science faculty

students then sometimes use 21% (21) when 20% use once a month

and 9% use twice a month at the least quantum portrays that 13%

use MB once a week.

From this it is can be easily judged that almost 70% students use

Mobile Banking services in a month.

Illustrated tersely:

Regularly: 37%

Page 5

Sometimes: 21%

Once a month: 20%

Twice a month: 9%

Once a week: 13%

Once a week15%

Once a month20%

Twice a month 17%

Regularly 29%

Sometimes18%

Usage of MB (Social Scince)

Interpretation:

Like previous chart we wanted to know the propensity of students

towards MB usage from Social Science faculty students by this

query “How often do you use Mobile Banking?” this chart also is

depicting the almost same quantity of MB usage as regularly use

Mobile Banking service 29% (29) then sometimes use 18% (18) when

Chart:10

Page 5

20% use once a month and 17% use twice a month at the least

quantum portrays that 15% use MB once a week.

From this it is can be easily judged that almost 70% students use

Mobile Banking services in a month.

Illustrated tersely:

Regularly: 29%

Sometimes: 18%

Once a month: 20%

Twice a month: 17%

Once a week: 15%

Income sources of Science faculty students

Chart:11

Page 5

Interpretation:

In order to know the students personal income sources we have

kept a provision of income source in the questionnaire from

science and social science faculty particularly as this chart

portrays that approx. half students have a personal income source

and other have not any income sources. 58% students who have a

income source almost majority goes to private tuition 89% where

4% to Photography, 3% work as research fellow and other 2% belong

to Freelancing and business respectively. Another 43% have not

any sources of income.

Tution 89%

Page 5

We hypothesized that students from Science faculty is more

involved in personal income i.e. private tuition basically. This

info graphics also gives that picture of.

Income sources of Science faculty students:

Interpretation:

Unlike Science faculty students only 26% Social science students

have a income of sources where 66% have not any sources of

income. Like science faculty students who have a income source

Chart:12

Page 5

almost majority goes to private tuition 92% where other 8% go

back to research fellow and Freelancing on equal basis. Another

66% have not any sources of income.

Convenient77%

Inconvenient

5%

Partially convenient18%

Users' Perception

Interpretation:

As we assumed hypothetically that many students use MB banking

for its multi facets of amenities this chart also says that. Here

it is seen that 77% (total 153, 73 from Science and 80 from

Social science) consider MB service is verily convenient than

traditional banking procedure. MB service is partially convenient

has been considered by 18% (total 37, 21 from Science and 16 from

Chart:13

Page 5

Social science) and too much tinny portion have found MB as

inconvenient they are only 5% (total 10, 6 from Science and 4

from Social science).

Illustrated tersely:

Convenient: 77% (total 153, 73 from Pure Science and 80 fromSocial science)

Partially convenient: 18% (total 37, 21 from Pure Science and 16from Social science)

Inconvenient: 5% (total 10, 6 from Pure Science and 4 from Social

science).

YesNo

89%

11%

Safe and Secure

Chart:14

Page 5

Interpretation:

It is verily apparent that many students use MB services for

being a safe and secure from any sort of hassle and uncertainty

as this table shows that almost all 89% (total 178, 88 from

Science and 90 from Social science) students use MB account and

its services contemplating safe and secure procedure for every

financial transactions. Only 11% consider MB service as not safe

or secured for many kinds of hassles like password forgetting,

password hacking, digital spoofing, stealling mobile at major

notion.

Illustrated tersely:

Safe and secure: 89% (total 178, 88 from Pure Science and 90 from

Social science).

Not safe and secure: 11% (total 17, 11 from Pure Science and 6

from Social science).Chart:15

Page 5

Yes 69.50%

No 29.50%

Interpretation:

Like previous query majority of students consider Mobile Banking

is a very cost effective that means Mobile Banking takes less

cost comparing to traditional banking procedure. As this pie

chart indicates that 70% students have found it as a cost

congenial service when rest of 30% have seen it as a high cost

consuming service.

Illustrated tersely:

Cost effective: 70% (total 140, 70 from Pure Science and 69 from

Social science)

Not cost effective: 30% (total 46, 27 from Pure Science and 29

from Social science)

Page 5

LowerSame as banking

Higher

85.00%

9.50%5.50%

Time consumption

Interpretation:

In the question of time consumption majority of students from

both science and social science faculty have expressed that MB

service is less time consuming procedure going out from extant

commercial banking service. as this tables shows that 85%

students it is lower time consuming banking services beside that

9.50% consider it same as banking and only 5.50% see it as a

higher time consuming service.

Illustrated tersely:

Lower time consumption: 85% (total 165, 79 from Pure Science and

86 from Social science).

Chart:16

Page 5

Same as banking: 9.5% (total 19, 11 from Pure Science and 8 from

Social science).

Higher: 5.5% (total 11, 6 from Pure Science and 5 from Social

science).

Yes59%

No 11%

Only some of them30%

Ubiquity of MB service

Interpretation:

On the point of availability of Mobile Banking facility many

students have considered it in a many ways. Above illustrated

chart depicts that more than half of the students think it is

available around them. In a percentage that is figured out as 59%

Chart:17

Page 5

(total 118, 50 from science and another 68 from social science).

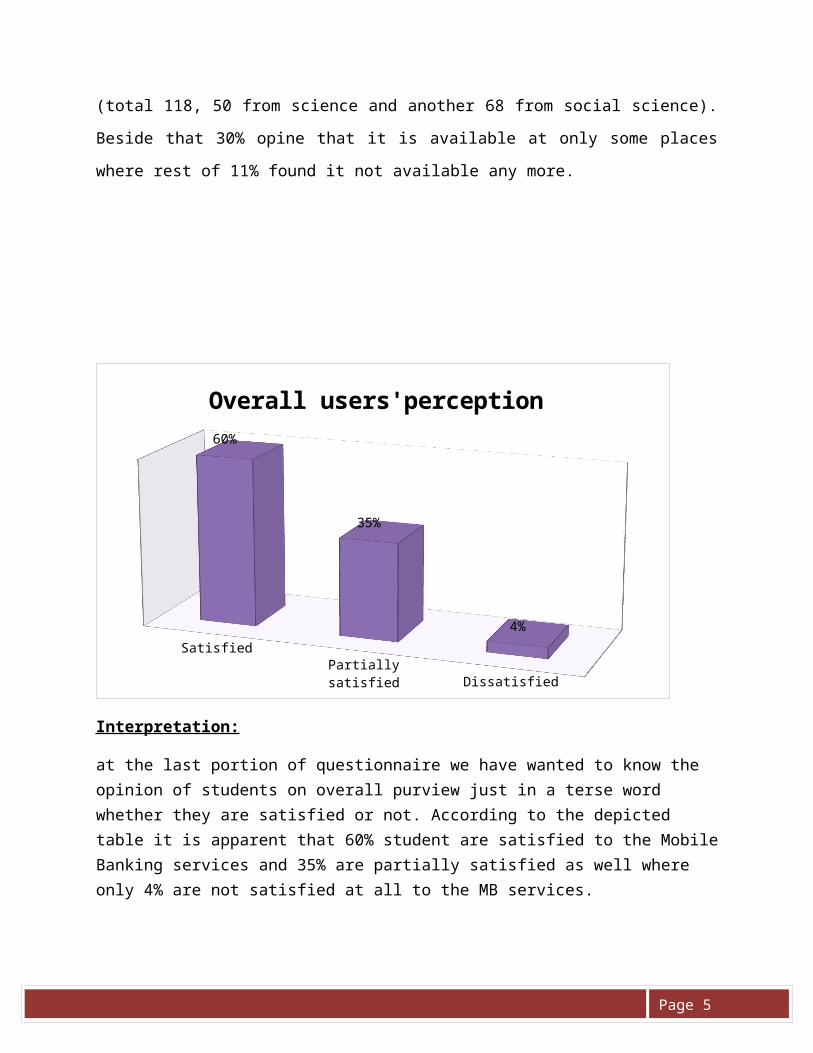

Beside that 30% opine that it is available at only some places

where rest of 11% found it not available any more.

SatisfiedPartially satisfied Dissatisfied

60%

35%

4%

Overall users'perception

Interpretation:

at the last portion of questionnaire we have wanted to know the opinion of students on overall purview just in a terse word whether they are satisfied or not. According to the depicted table it is apparent that 60% student are satisfied to the MobileBanking services and 35% are partially satisfied as well where only 4% are not satisfied at all to the MB services.

Chart:18

Page 5

Short time36%

No bank no queue1%Availability

27%

No need of ATM2%

Easy process22%

Safe8%

Cost effective4%

chance of deposite of money0%

How MB makes u flexible

Interpretation:

How Mobile Banking services make your daily tasks flexible and

easier? By this sort of query we have tried to know the factors

of making daily activities flexible. Responses to this question

have varied of multi type of issue like above chart shows the 35%

students consider MB service makes his daily activities or task

for taking short time to conduct the financial transaction and

Chart:19

Page 5

26% students consider availability of MB service makes him

flexible. Then some of them consider easier procedure of MB

transaction let him to be free and relaxed. When other people

find it as a safe, cost effective, provision of depositing money

as some agents have provided this amenities and no need of going

to ATM ( Automated Teller Machine) booths.

Illustrated tersely:

Availability: 27% (total 66 students, 27 from Pure Science and 39

from Social Science).

Shorter time: 36% (total 86 students, 31 from Pure Science and 57

from Social Science).

Easier procedure: 22% (total 53 students, 34 from Pure Science

and 19 from Social Science).

Safe and secured way: 7% (total 19 students, 6 from Pure Science

and 13 from Social Science).

Cost effective: 4% (total 9 students, all are from Social

Science).

Chance of depositing money: 0.5% only 01 from Pure Science.

No need going to ATM booth: 2% (total 6 students, all are from

Pure Science).

No need of queue like Banks: 1% (03 all are from Pure Science).

Page 5

No risk

Less secure

Password hacking

Network problem

dishonest agents

Cheating

Technical error

Complexity

Forgetting pas...

Mistransaction

High service c...

0%

5%

10%

15%

20%

25%

Risks of Mobile Banking

Interpretation:

Last query of our questionnaire wanted to seek the risks and

hazards of Mobile Banking after tabulating the collected data we

have found that some one found no risks yet in MB service beside

that someone saw password hacking, network problem and less

secure procedure are their major concerns. As above illuminated

info graphics indicates that 21% students feel no risks in the MB

services. While 22.5% found network problem is a risk of MB and

9.5% think pass word hacking also belongs to the risks of Mobile

Banking as well. 18% consider MB is less secured procedure

Chart: 20

Page 5

basically in transitioning large amount of money. Some students

found technical problem, swindling of MB agents and transitioning

to unintended persons also risks of Mobile Banking transaction. A

diminutive section of students as depicted 1% said forgetting

password also one kind of MB risks.

Illustrated tersely:

No risks: 21% (total 42 students, 28 from Pure Science and 14

from Social Science).

Less secure: 18% (total 37 students, 11 from Pure Science and 26

from Social Science).

Password hacking: 9.5% (total 19 students, 13 from Pure Science

and 6 from Social Science).

Network problem: 22.5% (total 45 students, 25 from Pure Science

and 20 from Social Science).

Technical/System error: 5% (total 14 students, 3 from Pure

Science and 11 from Social Science).

Cheating: 3.5% (total 9 students, 5 from Pure Science and 4 from

Social Science).

Complexity: 1.5% (All 5 are from Social Science).

Transaction to unintended persons: 1% (All 5 are from Pure

Science).

Page 5

Chapter 04

Concluding Phase

Page 5

Recommendation for further study :I would like to recommend for more deepest investigation on this

regard that as our Hypothesis has been failed to be rejected and

rejected to some point as well, who would like to pursue on this

field of study they should investigate on more broader scale as

sample size would be much more larger, analyzing step by step by

diving every possible sections of topics like on considering

fathers’ occupation how much use MB, how frequently use MB,

whether they receive money more from family or send to them from

his/her personal income etc. as well as taking Districts as a

point of analysis how much use MB form that particular

geographical region, why do not they take traditional banking,

why do they prefer MB etc.

Hopefully if it be scrutinized by this procedure there would comeout something more meaningful and exact.

Page 5

Conclusion:

I would like to draw the termination of this report by this we

tested our Hypothesis by that the students of Dhaka University

use Mobile Banking (MB) system for their financial transactions

with their family(i.e. from and to family) because it saves

their time and money both, it is secure, less hassle, convenient,

trustworthy and affordable as well. Along with that we have also

hypothesized that the students who live in Dhaka away from their

family use mobile banking more for transacting money with their

family. Again the degree of using mobile banking differs by the

student’s parents’ occupation. It also varies by their

geographical location. There are differences in purpose of using

mobile banking between science and social science faculty

students. If we look at the relation between Hypothesis and

gathered data then we find to some extent our proposed Hypothesis

has been rejected and some extent has failed to reject as well.

On the point of time consumption, convenience, affordability and

security of transitioning our Hypothesis has been failed to be

rejected I mean have been justified. As well as receiving or

sending (on extent of personal income provision) money to family

living at outer from Dhaka Hypothesis has been failed to be

overthrown. Unlike the first segment of Hypothesis second section

where it has been said in Hypothesis that who are far away from

Dhaka they use MB more but this has been rejected as our examined

Page 5

information says top most in the column 28% (55) use MB who

belong to Dhaka division if also 23% (45) and 17% (33) from

Khulna and Chittagong respectively which also proves Hypothesis a

bit.

On the point of fathers’ occupation we can see top most 32%students’ fathers’ profession is Business which meant as mediumor small business at their locality then 17.5% and 17% areteachers and farmers where teachers have been analyzed as Primary/not government / not registered or high school teachers. I thinkregarding “Bangladesh National Pay scale” teachers who are inthese level get relatively low salary which does not meet theirdaily expenses. So it can be judged that these scenario justifyour Hypothesis.

Summary:

I would like to bring the summary of our entire study here. We

have studied on Mobile Banking of Dhaka University Students (Pure

Science and Social Science faculty basis) that means what factors

pursue them to use Mobile Banking regarding their respective

geographical area from where s/he belong to, their fathers’

professions, personal income, convenience, time consumption,

security of transacting money at major. Our study goes to

qualitative research where I have collected our data by

questionnaire form two hundred students. We have analyzed our

Page 5

data by finding percentage of every segment out which we have

presented in pie chart, column and table.

We have found as follow in the below-

Chapter 05

Page 5

Supplementary phase

Appendix:

a . Research Questionnaire:

Research Questionnaire

Department of Public Administration, University

of Dhaka

I am a student of 8th semester in public Administration department, University of Dhaka. Irequest you to help me for collecting some information to make my research report on Mobile

Page 5

Banking. Your information will be used only for academic purpose. All kinds of cooperationfrom you will be highly appreciated.

Part A

* Name: …………………………………………………………………………………..

* Faculty: Science / Social science * Department:

……………………………..

* Year/ Semester: …………………….. * Gender: Male/Female

* Home district (division): ………………………...........

* Father’s occupation: ……………………………………………………………………..

* Mother’s occupation: …………………………………………………………………….

* Residential status (dormitory/hall): Residential/ Non-residential

Part B

1. Which mobile banking service do you use?

a. bkash b. DBBL c. U Cash d. M Cash

e. other ……………

2. Do you have your own mobile bank account?

a. Yes b. No

3. For what purpose do you use mobile banking? (Multiple response)

Page 5

a. receiving money from family

b. sending money to family

c. shopping

d. paying bills

e. recharge mobile

f. others……………………………………………

4. Do you have any income source? If yes, then mention what.

……………………………………………………………….

5. How often do you use mobile banking?

a. once a week

b. once a month

c. twice a month

d. regularly

e. sometimes