Report Summers Birla Sunlife Copy

116

WELINGKAR INSTITUTE OF MANAGEMENT DEVELOPMENT & RESEARCH SUMMER PROJECT ON “PORTFOLIO ANALYSIS & MANAGEMENT” BY ALEKH VAGRECHA PGDM 2010 – 12 TRIMESTER IV SPECIALISATION: FINANCE ROLL NO: 138 1

Transcript of Report Summers Birla Sunlife Copy

WELINGKAR INSTITUTE OF MANAGEMENT DEVELOPMENT & RESEARCH

SUMMER PROJECT

ON

“PORTFOLIO ANALYSIS & MANAGEMENT”

BY

ALEKH VAGRECHA

PGDM 2010 – 12 TRIMESTER IV

SPECIALISATION: FINANCE

ROLL NO: 138

1

ACKOWLEDGEMENT

It is my great pleasure and privilege to acknowledge the valuable

guidance and support; I received in the preparation of this

project report.

I wish to express my sincere gratitude and thankfulness to Mr.

Vinod Subramanian, Business Partner, Birla Sun Life Insurance

Company Ltd. Who obliged me a chance to complete my summer

training at this esteemed Organization.

I am extremely thankful to the officers and staff of Birla Sun

Life Insurance Company Ltd. For their Kind Cooperation and

immense help, without their support and valuable guidance my

project would have never seen the light of the day.

This note of thanks would be incomplete if I do not thank my co-

trainees from Welingkar, K.C.College & Fr.Agnel College with whom

I have worked in groups during the project and advisors of Birla

Sunlife Insurance with whom I have worked during last stage of

the project & has learned valuable things from them and Academic

2

Development Cell (ADC) & faculty members, who always encourage us

to do challenging tasks.

I am deeply indebted to my parents and friends for providing me

all necessary help in completing my project.

3

INDEX

SR.NO DESCRIPTION PAGENO.

1. ABOUT BIRLA SUNLIFE INSURANCE 42. INTRODUCTION TO INDIAN INSURANCE INDUSTRY

2.1 HISTORY 52.2 PLAYERS IN THE INDIAN INSURANCE SECTOR 62.3 ROLE OF IRDA 82.4 TYPE OF INSURANCE POLICIES 82.5 INTRODUCTION TO ULIPS 10

3. EXECUTIVE SUMMARY 124. RESEARCH METHODOLOGY 135. PORTFOLIO ANALYSIS & MANAGEMENT 16

5.1 WHAT IS PORTFOLIO MANAGEMENT 165.2 MAGNIFIER FUND 185.3 MAXIMISER FUND 19

6. SECURITY ANALYSIS 206.1 Larsen & Toubro6.1.1 ABOUT THE COMPANY 226.1.2 KEY FUNDAMENTALS 246.1.3 TREND ANALYSIS 276.1.4 BALANCE SHEET ANALYSIS 366.2 AXIS BANK6.2.1 ABOUT THE COMPANY 386.2.2 KEY FUNDAMENTALS 396.2.3 TREND ANALYSIS 426.3 BALANCE SHEET ANALYSIS 50

7. COMPETITOR ANALYSIS (ULIPs COMPARISION)7.1 INTRODUCTION TO BSIL CLASSIC LIFE PLAN 527.2 COMPARISION WITH COMPETITION 547.3 INTRODUCTION TO BSIL PLATINUM ADVANTAGE PLAN 67

4

7.4 COMPARISION WITH COMPETITION 688. ULIPs Vs MUTUAL FUNDS

8.1 INTRODUCTION TO BSIL FORESIGHT PLAN 768.2 RETURNS COMPARISION OF FORESIGHT Vs. MUTUAL FUND

79

9. SUMMARY & CONCLUSIONS 8210. RECOMMENDATIONS 8311. REFERENCES & BIBILOGRAPHY 84

1.ABOUT BIRLA SUNLIFE INSURANCE

Established in 2000, Birla Sun Life Insurance Company Limited

(BSLI) is a joint venture between the Aditya Birla Group, A

US $30 billion corporation, anchored by an extraordinary force

of 130,000 employees, belonging to 40 different nationalities

operating in 27 countries across six continents and Sun Life

Financial Inc, leading international financial services

organization from Canada. The local knowledge of the Aditya

Birla Group combined with the domain expertise of Sun Life

Financial Inc., offers a formidable protection for its

customers' future. With an experience of over 10 years, BSLI

has contributed significantly to the growth and development of

the life insurance industry in India and currently ranks

amongst the top 6 private life insurance companies in the

country.

Known for its innovation and creating industry benchmarks,

BSLI has several firsts to its credit. It was the first Indian

Insurance Company to introduce "Free Look Period" and the same

5

was made mandatory by IRDA for all other life insurance

companies. Additionally, BSLI pioneered the launch of Unit

Linked Life Insurance plans amongst the private players in

India. To establish credibility and further transparency, BSLI

also enjoys the prestige to be the originator of practice to

disclose portfolio on monthly basis. BSLI offer the complete

bouquet of insurance products viz. pure term plan, life stage

products, health plan, retirement plan & Unit Linked Insurance

Plans (ULIPs) etc.

Add to this, the extensive reach through its network of 600

branches and 1, 47,900 empanelled advisors. This impressive

combination of domain expertise, product range, reach and ears

on ground, helped BSLI cover more than 2.4 million lives since

it commenced operations and establish a customer base spread

across more than 1500 towns and cities in India. BSLI has

ensured that it has lowest outstanding claims ratio of 0.00%

for FY 2010-11.. Such services are well supported by sound

financials that the Company has. The AUM of BSLI stood at

19725 crs as on April 30, 2011, while the company has a robust

capital base of Rs. 2450 crs.

2. INTRODUCTION TO INDIAN INSURANCE INDUSTRY2.1 HISTORY

Insurance in India has its history dating back till 1818, when

Oriental Life Insurance Company was started by Europeans in

6

Kolkata to cater to the needs of European community. Pre-

independent era in India saw discrimination among the life of

foreigners and Indians with higher premiums being charged for

the latter. It was only in the year 1870, Bombay Mutual Life

Assurance Society, the first Indian insurance company covered

Indian lives at normal rates.

At the dawn of the twentieth century, insurance companies

started mushrooming up. In the year 1912, the Life Insurance

Companies Act, and the Provident Fund Act were passed to

regulate the insurance business. The Life Insurance Companies

Act, 1912 made it necessary that the premium rate tables and

periodical valuations of companies should be certified by an

actuary. However, discrimination still existed between Indian

and foreign companies. The oldest existing insurance company

in India is National Insurance Company Ltd, which was founded

in 1906 and is doing business even today. The Insurance

industry earlier consisted of only two state insurers: Life

Insurers i.e. Life Insurance Corporation of India and General

Insurers i.e. General Insurance Corporation of India.

This millennium has seen insurance come a full circle in a

journey extending to nearly 200 years. The process of re-

opening of the sector had begun in the early 1990s and the

last decade and more has seen it been opened up substantially.

In 1993, the Government set up a committee under the

chairmanship of RN Malhotra, former Governor of RBI, to

propose recommendations for reforms in the insurance sector.

7

The objective was to complement the reforms initiated in the

financial sector. The committee submitted its report in 1994

wherein, among other things, it recommended that the private

sector be permitted to enter the insurance industry. They

stated that foreign companies be allowed to enter by floating

Indian companies, preferably a joint venture with Indian

partners.

Following the recommendations of the Malhotra Committee

report, in 1999, the Insurance Regulatory and Development

Authority (IRDA) was constituted as an autonomous body to

regulate and develop the insurance industry. The IRDA was

incorporated as a statutory body in April, 2000. The key

objectives of the IRDA include promotion of competition so as

to enhance customer satisfaction through increased consumer

choice and lower premiums, while ensuring the financial

security of the insurance market.

The IRDA opened up the market in August 2000 with the

invitation for application for registrations. Foreign

companies were allowed ownership of up to 26%. The Authority

has the power to frame regulations under Section 114A of the

Insurance Act, 1938 and has from 2000 onwards framed various

regulations ranging from registration of companies for

carrying on insurance business to protection of policyholders’

interests. In December, 2000, the subsidiaries of the General

Insurance Corporation of India were restructured as

8

independent companies and at the same time GIC was converted

into a national re-insurer. Parliament passed a bill de-

linking the four subsidiaries from GIC in July, 2002.

The insurance sector is a colossal one and is growing at a speedy

rate of 15-20%. Together with banking services, insurance services

add about 7% to the country’s GDP. A well-developed and evolved

insurance sector is a boon for economic development as it provides

long- term funds for infrastructure development at the same time

strengthening the risk taking ability of the country.

2.2 PLAYERS IN THE INDIAN INSURANCE SECTOR

Today there are 24 general insurance companies including the

ECGC and Agriculture Insurance Corporation of India and

23 life insurance companies operating in the country.

1. Bajaj Allianz Life Insurance Company Limited2. Birla Sun Life Insurance Co. Ltd 3. HDFC Standard Life Insurance Co. Ltd 4. ICICI Prudential Life Insurance Co. Ltd 5. ING Vysya Life Insurance Company Ltd.6. Life Insurance Corporation of India7. Max New York Life Insurance Co. Ltd 8. Met Life India Insurance Company Ltd.9. Kotak Mahindra Old Mutual Life Insurance Limited10. SBI Life Insurance Co. Ltd 11. Tata AIG Life Insurance Company Limited 12. Reliance Life Insurance Company Limited.13. Aviva Life Insurance Company India Limited14. Sahara India Life Insurance Co, Ltd.15. Shriram Life Insurance Co, Ltd.

9

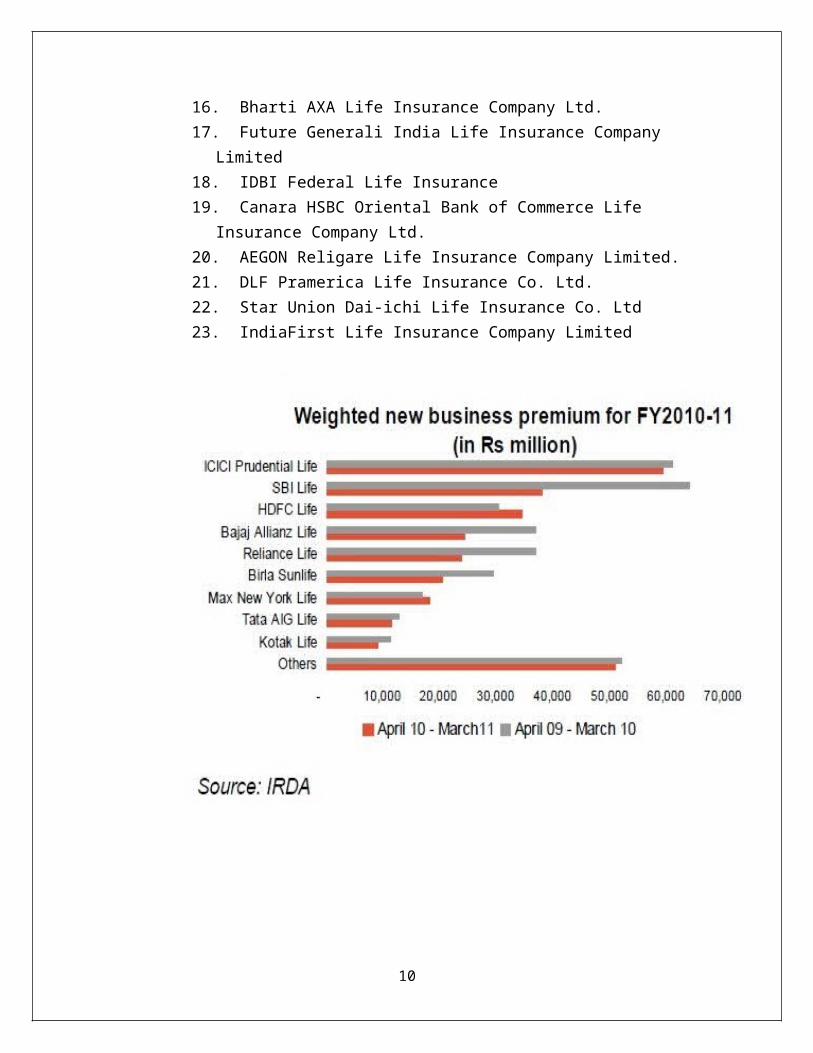

16. Bharti AXA Life Insurance Company Ltd. 17. Future Generali India Life Insurance Company

Limited 18. IDBI Federal Life Insurance19. Canara HSBC Oriental Bank of Commerce Life

Insurance Company Ltd. 20. AEGON Religare Life Insurance Company Limited. 21. DLF Pramerica Life Insurance Co. Ltd.22. Star Union Dai-ichi Life Insurance Co. Ltd23. IndiaFirst Life Insurance Company Limited

10

2.3 ROLE OF IRDA

The Insurance Regulatory and Development Authority Act of 1999

brought about several crucial policy changes in the insurance

sector of India. It led to the formation of the Insurance

Regulatory and Development Authority (IRDA) in 2000.

The goals of the IRDA are to safeguard the interests of

insurance policyholders, as well as to initiate different

policy measures to help sustain growth in the Indian insurance

sector.

IRDA has notified Protection of Policyholders Interest

Regulations 2001 to provide for: policy proposal documents in

easily understandable language; claims procedure in both life

and non-life; setting up of grievance redressal machinery;

speedy settlement of claims; and policyholders' servicing. The

Regulation also provides for payment of interest by insurers

for the delay in settlement of claim.

The insurers are required to maintain solvency margins so that

they are in a position to meet their obligations towards

policyholders with regard to payment of claims. It is

obligatory on the part of the insurance companies to disclose

clearly the benefits, terms and conditions under the policy.

The advertisements issued by the insurers should not mislead

the insuring public. All insurers are required to set up

proper grievance redress machinery in their head office and at

11

their other offices. The Authority takes up with the insurers

any complaint received from the policyholders in connection

with services provided by them under the insurance contract.

2.4 TYPES OF INSURANCE POLICIES

Taking out a life insurance policy covers the risk of dying

early, by providing for your family in the event of your

death. It also manages the risk of retirement providing an

income for you in non-earning years. Choosing the right policy

type with the coverage that is right for you therefore becomes

critical.

There are a variety of policies available in the market,

ranging from Term Endowment and Whole Life Insurance, to Money

Back Policies, ULIPs, and Pension plans. Let's see what each

of these is about, so that you can consider the one that best

suits you.

Term Insurance

Term Insurance, as the name implies, is for a specific period,

and has the lowest possible premium among all insurance plans.

You can select the length of the term for which you would like

coverage, up to 35 years.

Payments are fixed and do not increase during your term

period. In case of an untimely death, your dependents will

receive the benefit amount specified in the term life

12

insurance agreement. You can customize Term life insurance

with the addition of riders, such as Child, Waiver of Premium,

or Accidental Death.

Endowment Insurance

Endowment Insurance is ideal if you have a short career path,

and hope to enjoy the benefits of the plan (the original sum

and the accumulated bonus) in your life time.

Endowment plans are especially useful when you retire; by

buying an annuity policy with the sum received, it generates a

monthly pension for the rest of your life.

Whole Life Insurance

Whole Life Policies have no fixed end date for the policy;

only the death benefit exists and is paid to the named

beneficiary. The policy holder is not entitled to any money

during his or her own lifetime, i.e., there is no survival

benefit. This plan is ideal in the case of leaving behind an

estate.

Primary advantages of Whole Life Insurance are guaranteed

death benefits, guaranteed cash values, and fixed and known

annual premiums.

Money-Back Plan

In a Money-Back plan, you regularly receive a percentage of

the sum assured during the lifetime of the policy. Money-Back

13

plans are ideal for those who are looking for a product that

provides both - insurance cover and savings.

It creates a long-term savings opportunity with a reasonable

rate of return, especially since the payout is considered

exempt from tax except under specified situations.

ULIP

Unit-linked Insurance Plans (ULIPs), introduced by the private

players, are hugely popular, because they combine the benefits

of life insurance policies with mutual funds. A certain part

of the premium is invested in listed equities/debt

funds/bonds, and the balance is used to provide for life

insurance and fund management expenses.

Pension Plan

Insurance companies offer two kinds of pension plans -

endowment and unit linked. Endowment plans invest in fixed

income products, so the rates of return are very low.

Unit-linked plans are more flexible. You can stop contributing

after 10 years and the fund will keep compounding your corpus

till the vesting date. You can opt for higher exposure in the

stock market for your plan if your risk appetite allows it.

Lower risk options like balanced funds are also offered.

Riders: Comprehensive coverage

14

In addition to the insurance plan of your choice, you might

want to consider additional risk covers, in which case you can

you can opt for riders: additional benefits that can be

purchased with an insurance policy.

Examples of riders include the Term rider, the Accidental

Death Benefit rider, and the Critical Illness rider. Choosing

the right set of riders ensures a comprehensive insurance

cover.

2.5 INTRODUCTION TO ULIPS (UNIT LINKED INSURANCE PLANS)

The introduction of Unit Linked Insurance Plans has possibly

been the single largest innovation in the field of life

insurance .It has addressed and overcome many difficulties and

concerns that customers had about life insurance – liquidity,

flexibility, and transparency. These benefits are possible

because ULIPs are differently structured products and leave

many choices to the policyholder. They are structured such

that the protection (insurance) element and the savings

element (investment) can be distinguish and hence managed

according to one’s specific needs, offering flexibility and

transparency. Thus we can say it is such a product that takes

care of multiple needs. ULIPs are also called as “Bundled

Policies”.

There were some factors which gave entry for ULIPs in the

insurance market: - Firstly was the arrival of private of

private players, and ULIPs were the most significant

15

innovation done by them, and secondly was the decline of

assured returns in endowment plans. Early the market of ULIPs

was taken up Birla Sun Life as they were the first to

introduce such product in the market. These are the insurance

plans which are attached to Units. The premium amount received

in this policy, some part is used in investment of funds and

remaining is used for insurance cover.

ULIPs are remarkably similar to, mutual fund in terms of

structure and functioning: premium payments are converted into

units and net asset value (NAV) is declared regularly.

Investors have an option of choosing their fund according to

their risk taking ability. They disclose all the material

facts most frequent and consistent (often quarterly or half-

yearly) .Also investor has a fairly good idea about expenses.

The expenses which are considered are as follows:-

1) Mortality Rate: - These are charged by the life insurance

company to cover the risk of an eventuality to the

individual.

2) Administration, sales/marketing Charges: - All life insurance

companies incur certain expenses on regular basis. Agent’s

commission, sales & marketing expenses and overhead costs

incurred to run the day to day basis are some examples.

3) Fund Management Charges: - These charges are levied by the

insurance company to cover the expenses incurred by them on

managing Ulip monies.

16

4) Ulip-fund Switch Charges: - These charges are borne by the

individuals when they decide to switch their, money from one

type of fund to another.

5) Top-up Charges: A certain percentage is deducted from the top-up

amount to recover the expenses incurred on managing the same.

ULIPs are very different from the traditional policies because

they are based on some fundamentals of Mutual funds as

different types of funds which are created wherein the

premiums which are received on the policy these are invested

in these funds basically these funds are of following types:-

a) Equity (Aggressive/Growth) Funds:-Such funds invest a major

portion in equity markets. They are therefore considered to

be high on risk parameter.

b) Debt Funds: - These types of funds invest the premium

money in debt instruments like g-secs, bonds and AAA rated

securities. Such funds are low risk in nature.

c) Balanced Funds: - This fund is combination of growth &

debt fund. This means its portfolio consists of both

equities and debt instruments. The risk for this fund is

moderate.

d) Money Market/Liquid Funds:- Such a fund invests the premium

money in short term liquid instruments like bank deposits

and money market instruments.

17

The features of ULIPs are as follows:-

a) Flexibility: - Flexibility in choosing your own funds how you

would like to invest your own money.

b) Transparency: - It discloses all your material facts, i.e.

you know where your money is been invested.

c) Liquidity: - Here you can withdraw certain amount from your

Units which have been collected.

d) Tax Benefits: - tax benefits are available under Section

80C subject to a maximum limit of Rs 100,000.

The other features of ULIPs are like, life protection which

can be adjustable, many investment options, benefits like

disability, critical illness, surgeries, and also financial

planning etc.

3 EXECUTIVE SUMMARY

The project on Portfolio Management and analysis was carried out

with BSLI. The objective of this project was to primarily

understand the various funds of Birla Sunlife & analyzing the 18

performance of various scrip involved in the portfolio & to

suggest whether the company is missing out on any performing

company as an investment option. The project also helped us in

understanding the past performance of the companies & the impact

companies had during recession. After going through the balance

sheet we also tried to analyze whether the company is able to

survive any recession in near future & what will be the impact on

them.

In the second part of the project dealt with ULIP comparison of

various players. For this product brochures of different life

insurance companies were referred. Also the company website was

used to find out the performance of the various funds. Fund

comparison was done to find out why a particular fund has

performed better than the other. This part was done was going

through each company in the portfolio & it’s since inception

returns & decrease in stock price during recession & increase of

stock price after the recession. In this part we also compared

highest NAV products of major competitors & tried to analyze the

NAV pattern of all the mutual funds as well as insurance funds.

Highest NAV products performance was evaluated as compared to

mutual funds. IRR calculation & analysis of each product based on

IRR was done.

In the third part of the project we analyzed the different

investment options available and to compare them with the mutual

19

fund investments. For the purpose of analyzing the investment

pattern and selecting effective and beneficial schemes of mutual

funds different available schemes were thoroughly analyze &

insurance can be used as an investment option was proved.

4 RESEARCH METHODOLOGY

4.1 Research Brief:

The first stage involved initial discussion between the various

team members and the company in order to identify the research

objectives (Rationale of the research), which is the most

difficult step in the research process.

4.2 Research Design:

Research design is the arrangement of condition for collection

and analysis of data in a manner that aims to combine relevance

to the research purpose with the economy in procedure. It is the

blueprints for collection, measurement and analysis of data.

4.2.1 Type of Research: Analytical Research

20

Under the analytical research, the researcher has to use facts or

information already available and analyze the facts and

information to make a critical evaluation of the material. The

research is designed to study the performance of insurance

companies in the post-liberalization era. Under this type the

researcher has to use the facts and information already available

and analyze them to make evaluation of the market. In analytical

research the researcher has to use the facts already available,

and analyse these to make the critical evaluation data of the

material.

The methodology followed for research is as following:

1. Survey of concerned literature

2. Collecting data:

Quantitative

Qualitative

3. After the collection of data the raw data is processed through

editing, loading, classification and tabulation to make analysis

of the data of information

After the analysis the finding are drawn and

recommendations/conclusion are made.

The research design which help to answer the following questions:

Why the study is being made?

From where the data needed can be collected?

21

4.2.2 Data Collection:

1. Primary Data:

These include the survey or questionnaire method, telephonic

interview as well as the personal interview methods of data

collection

2. Secondary Data:

The secondary data as it has always been important for the

completion of any report provides a reliable, suitable, adequate

and specific knowledge.

Secondary data is a data, which is collected from various

sources. Secondary data is not a fresh data so it has its own

limitations like: Time Constraints, Accuracy and Applicability.

The sample size for measuring the performance for life insurance

companies is as follows:

This study is based on analysis the performance of different life

insurance company in India, LIC is the major player in the

market, there are 23 other life insurance companies operating in

the country. Thus the size of the universe is 24.

Out of these 16 companies, 4 companies are selected; in these one

is Public Company and other Three are Private Companies:

Birla Sunlife insurance

Life Insurance Corporation of India

Bajaj Allianz life insurance

ING Vysya life insurance

Analysis pattern

22

After the data is collected and editing, the next job of the

researcher is to present it systematically. The collected data is

so large, complex and unarranged that it can’t be processed

without arranging it according to same characteristics.

The following statistical and analytical tools have been used:

Graph:

Various plans offered by the companies.

Net Asset Value of Companies major Plans.

Market Share of the companies.

Data has been collected from the Fact sheet of the various

insurance funds & mutual fund schemes & used those data s

for the research. In fact sheet past returns were given of

different funds.

5 PORTFOLIO ANALYSIS & MANAGEMENT

5.1 What is Portfolio Management?

An investor considering in securities is faced with the

problem of choosing from among a large number of securities.

His choice depends upon the risk return characteristics of

individual securities. He would attempt to choose the most

desirable securities and like to allocate his funds over this

group of securities. Again he is faced with problem of

deciding which securities to hold and how much to invest in

each. The investor faces an infinite number of possible

portfolios or groups of securities. The risk and return

characteristics of portfolios differ from those of individual

23

securities combining to form a portfolio. The investor tries

to choose the optimal portfolio taking into consideration the

risk return characteristics of all possible portfolios

The first phase of the project involved analyzing the existing

fund portfolios underlying different insurance products

offered by Birla Sun life Insurance. The analysis involved

analyzing the performance of the funds (portfolios)

considering parameters such as asset size, asset allocation,

returns generated over specific time periods w.r.t. Benchmark

Index etc.

Phases of Portfolio Management

1. Security Analysis

2. Portfolio Analysis

3. Portfolio Selection

4. Portfolio Revision

5. Portfolio Evaluation

1. Security Analysis

(a) Fundamental analysis: This analysis concentrates on the

fundamental factors affecting the company such as EPS (Earning

per share) of the company, the dividend payout ratio,

competition faced by the company, market share, quality of

management etc.

(b) Technical analysis: The past movement in the prices of

shares is studied to identify trends and patterns and then

tries to predict the future price movement. Current market

24

price is compared with the future predicted price to determine

the mispricing. Technical analysis concentrates on price

movements and ignores the fundamentals of the shares.

(c) Efficient market hypothesis: This is comparatively more

recent approach. This approach holds that market prices

instantaneously and fully reflect all relevant available

information. It means that the market prices will always be

equal to the intrinsic value.

2. Portfolio Analysis

A portfolio is a group of securities held together as

investment. It is an attempt to spread the risk all over. The

return & risk of each portfolio has to be calculated

mathematically and expressed quantitatively. Portfolio

analysis phase of portfolio management consists of identifying

the range of possible portfolios that can be constituted from

a given set of securities and calculating their risk for

further analysis.

3. Portfolio Selection

The goal of portfolio construction is to generate a portfolio

that provides the highest returns at a given level of risk.

Harry Markowitzh portfolio theory provides both the conceptual

framework and the analytical tools for determining the optimal

portfolio in a disciplined and objective way.

4. Portfolio Revision

25

The investor/portfolio manager has to constantly monitor the

portfolio to ensure that it continues to be optimal. As the

economy and financial markets are highly volatile dynamic

changes take place almost daily. As time passes securities

which were once attractive may cease to be so. New securities

with anticipation of high returns and low risk may emerge.

5. Portfolio Evaluation

Portfolio evaluation is the process, which is concerned with

assessing the performance of the portfolio over a selected

period of time in terms of return & risk. The evaluation

provides the necessary feedback for better designing of

portfolio the next time around.

6. Measurement of risk

Risk refers to the possibility that the actual outcome of an

investment will differ from the expected outcome. In other

words we can say that risk refers to variability or

dispersion. Whenever we calculate the mean returns of an

investment we also need to calculate the variability in the

returns.

The first phase of the project involved analyzing the existing

fund portfolios underlying different insurance products

offered by Birla Sun life Insurance. The analysis involved

analyzing the performance of the funds (portfolios)

considering parameters such as asset size, asset allocation,

returns generated over specific time periods w.r.t. Benchmark

Index etc.

26

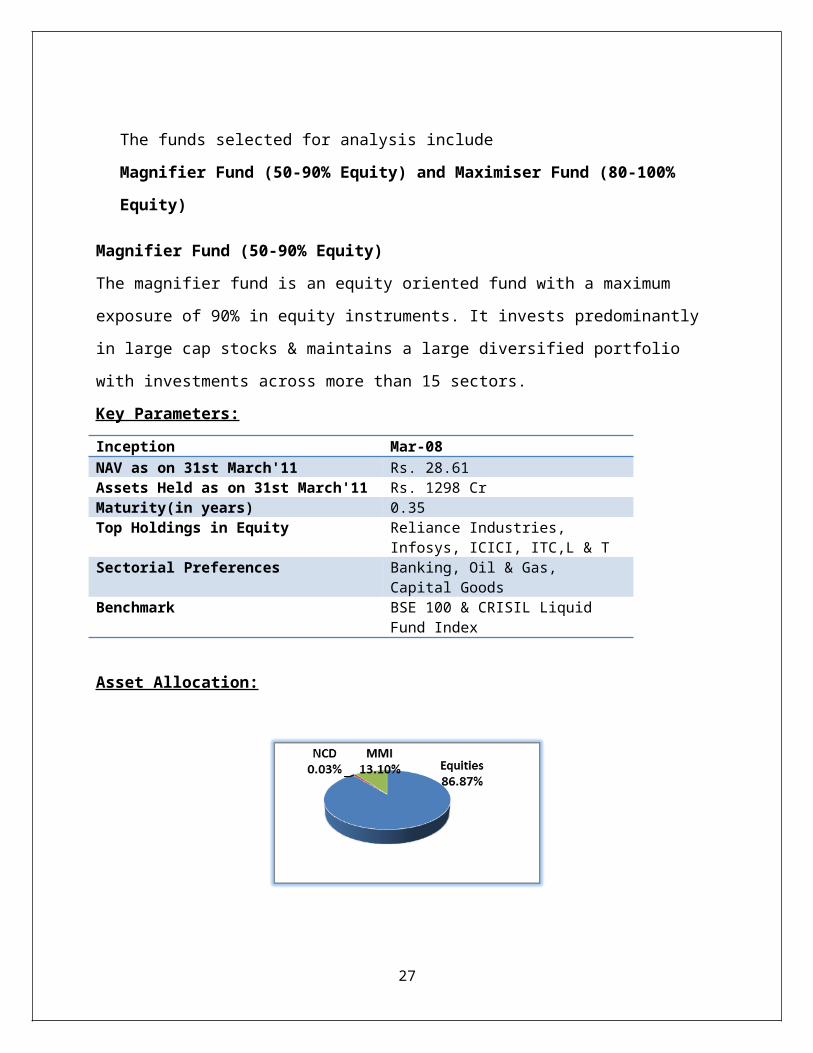

The funds selected for analysis include

Magnifier Fund (50-90% Equity) and Maximiser Fund (80-100%

Equity)

Magnifier Fund (50-90% Equity)

The magnifier fund is an equity oriented fund with a maximum

exposure of 90% in equity instruments. It invests predominantly

in large cap stocks & maintains a large diversified portfolio

with investments across more than 15 sectors.

Key Parameters:

Inception Mar-08NAV as on 31st March'11 Rs. 28.61Assets Held as on 31st March'11 Rs. 1298 CrMaturity(in years) 0.35Top Holdings in Equity Reliance Industries,

Infosys, ICICI, ITC,L & TSectorial Preferences Banking, Oil & Gas,

Capital GoodsBenchmark BSE 100 & CRISIL Liquid

Fund Index

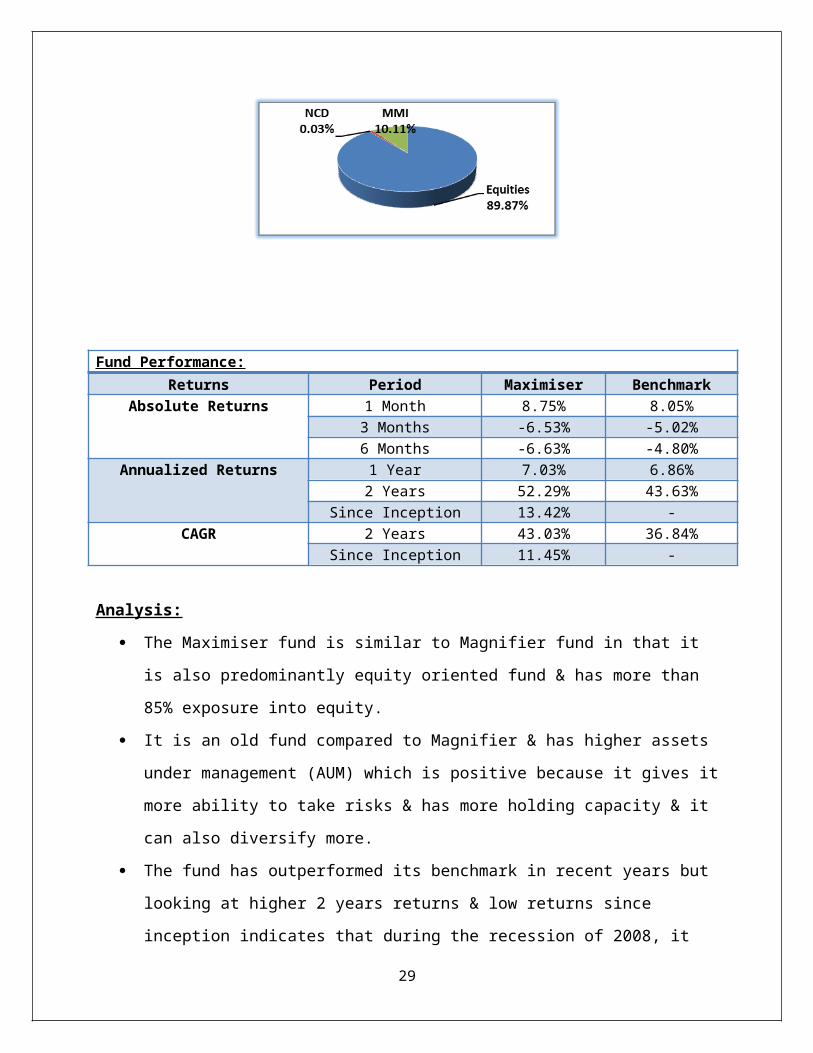

Asset Allocation:

27

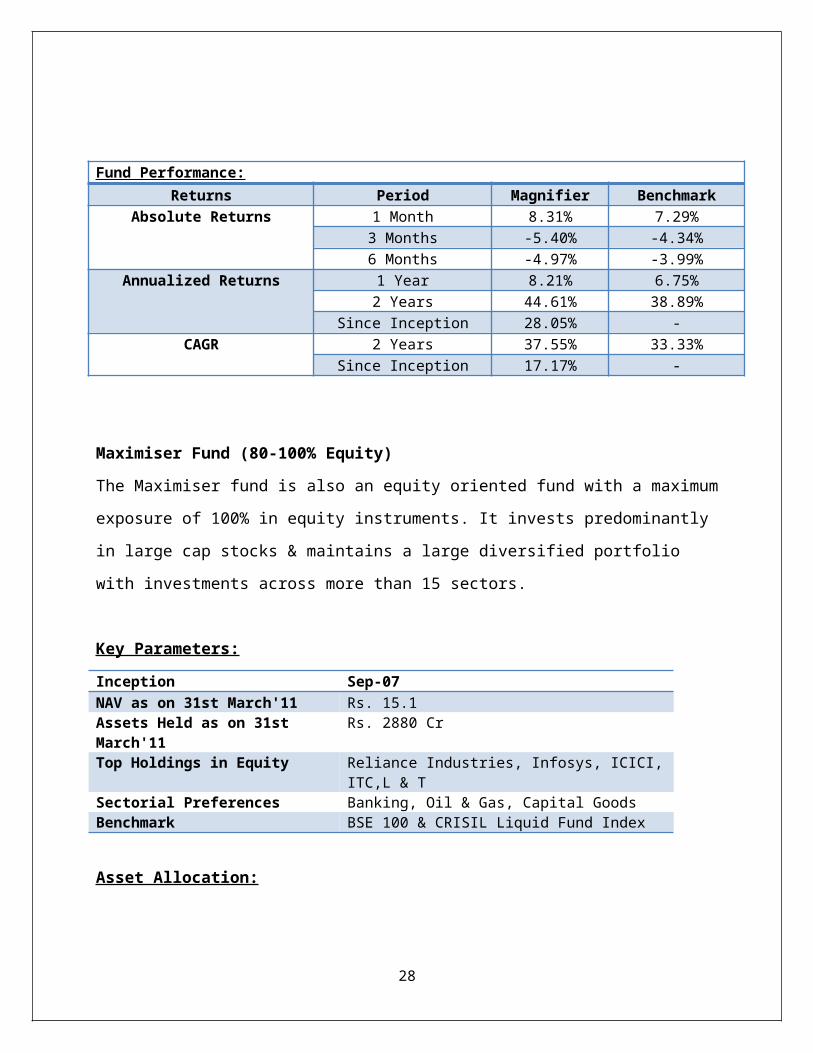

Fund Performance:Returns Period Magnifier Benchmark

Absolute Returns 1 Month 8.31% 7.29%3 Months -5.40% -4.34%6 Months -4.97% -3.99%

Annualized Returns 1 Year 8.21% 6.75%2 Years 44.61% 38.89%

Since Inception 28.05% -CAGR 2 Years 37.55% 33.33%

Since Inception 17.17% -

Maximiser Fund (80-100% Equity)

The Maximiser fund is also an equity oriented fund with a maximum

exposure of 100% in equity instruments. It invests predominantly

in large cap stocks & maintains a large diversified portfolio

with investments across more than 15 sectors.

Key Parameters:

Inception Sep-07NAV as on 31st March'11 Rs. 15.1Assets Held as on 31st March'11

Rs. 2880 Cr

Top Holdings in Equity Reliance Industries, Infosys, ICICI,ITC,L & T

Sectorial Preferences Banking, Oil & Gas, Capital GoodsBenchmark BSE 100 & CRISIL Liquid Fund Index

Asset Allocation:

28

Fund Performance:Returns Period Maximiser Benchmark

Absolute Returns 1 Month 8.75% 8.05%3 Months -6.53% -5.02%6 Months -6.63% -4.80%

Annualized Returns 1 Year 7.03% 6.86%2 Years 52.29% 43.63%

Since Inception 13.42% -CAGR 2 Years 43.03% 36.84%

Since Inception 11.45% -

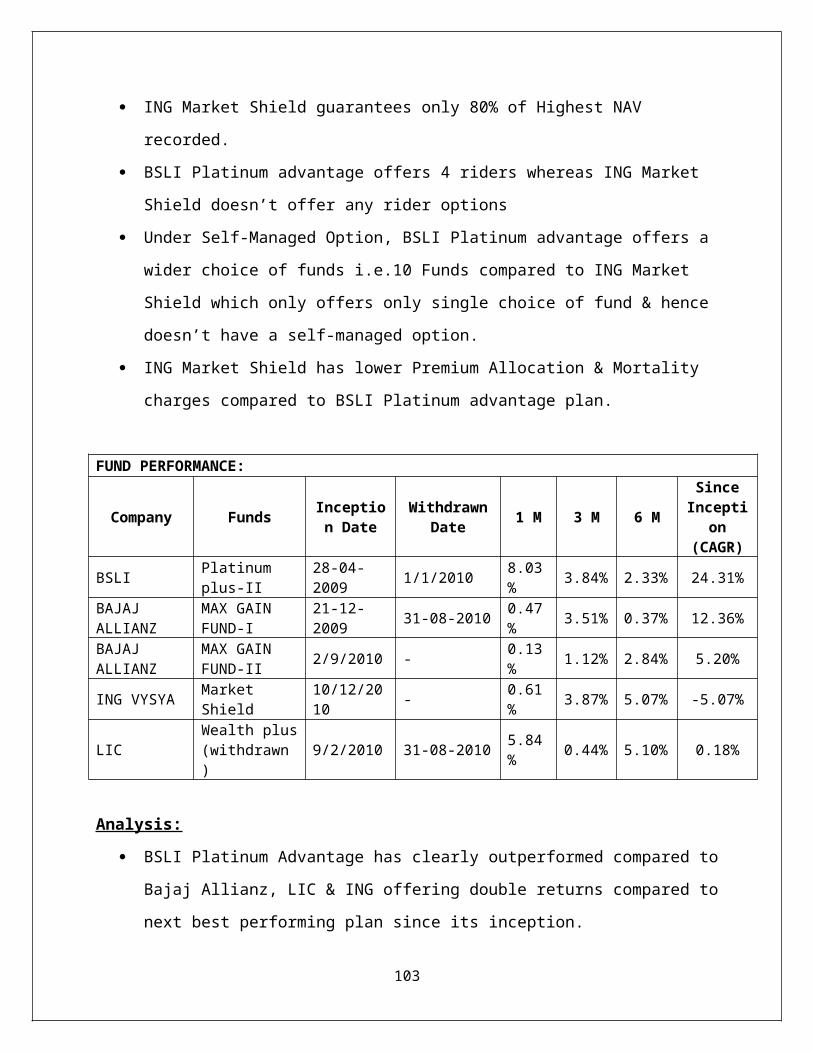

Analysis:

The Maximiser fund is similar to Magnifier fund in that it

is also predominantly equity oriented fund & has more than

85% exposure into equity.

It is an old fund compared to Magnifier & has higher assets

under management (AUM) which is positive because it gives it

more ability to take risks & has more holding capacity & it

can also diversify more.

The fund has outperformed its benchmark in recent years but

looking at higher 2 years returns & low returns since

inception indicates that during the recession of 2008, it

29

has underperformed by a wider margin but has recovered

quickly in the past 2 years.

Its CAGR return since launch is lower than Magnifier & but

has given higher returns compared to Magnifier in the past

two years indicating that the fund is more volatile compared

to Magnifier.

6 SECURITY ANALYSIS

After analyzing the fund portfolios 2 sectors & scrip in that

sector which was (or could be) the part of the existing

portfolios were analyzed in details to review the performance

of the sector & scrip over past 3 years.

The basic concept of analyzing the company & understanding was

to get these following details:

What factors affected the company which resulted in increase

or decrease in its stock price?

Which sectors were impacted during recession?

30

In which companies we should increase the exposure & why?

Performance of the company & growth of stock price in three

years

Find the recovery period of companies after recession

Finding the stock fluctuation in past three years

Balance sheet analysis of the company

Which companies can survive another recession if double dip

occurs in near future?

The following data was collected & analyzed in detail.

The everyday Open, High, Low & Close price, Volume traded

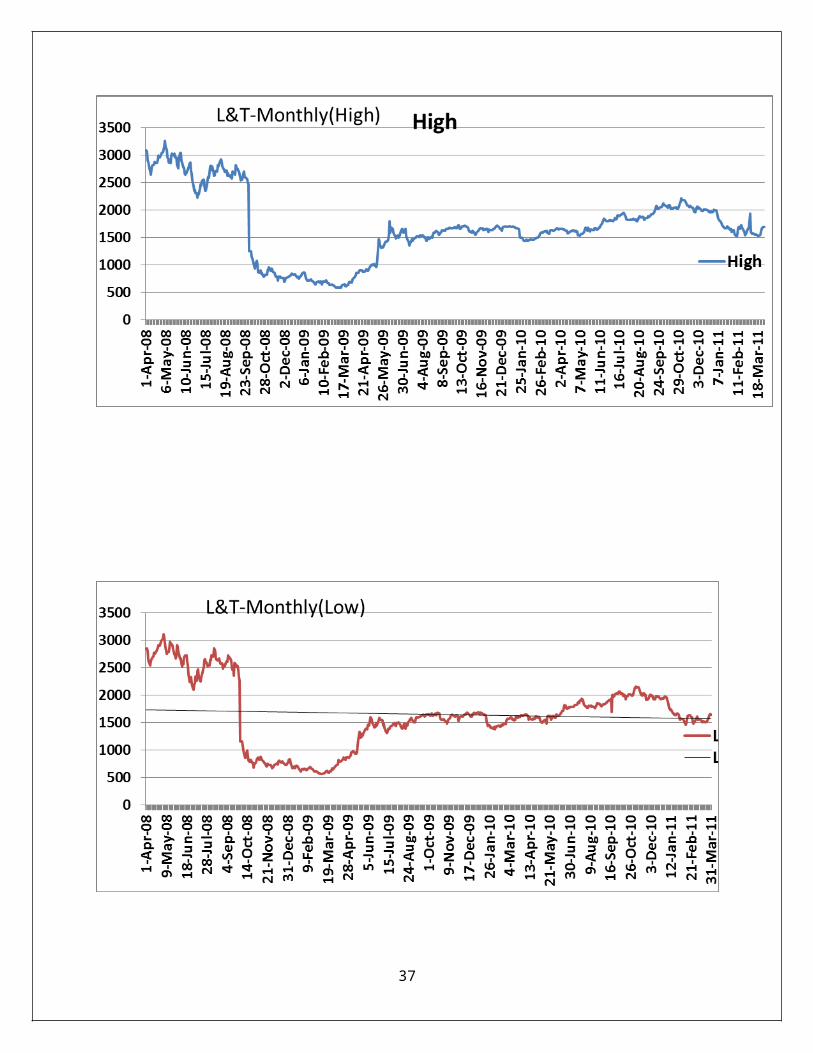

of the scrip from 1st April 2008 to 31st March 2011

recorded on the stock exchanges was collected.

The Weekly, Fortnightly, Monthly, Quarterly, Semi-

Annually, Annually averages were then calculated in the

excel sheet.

The data was also plotted on a line graph to analyze the

trend in the stock over the three year period

The All-time High & All-time low of the stock over a

three year period was found out & probable reasons behind

the same were explored.

Also any significant rise or downfall in the stock was

found & probable reasons were explored.

31

Every Pyramid (Rise & subsequent fall) & Inverted Pyramid

(fall & subsequent rise) pattern on the plotted graph

were highlighted & also analyzed.

Also the recovery period of the stock in days was

calculated i.e. the time stock took to recover the global

recession of 2008.

The detailed Balance Sheet analysis of the stock was

carried out to judge whether the company under analysis

will be able to recover another recession in the future

if it were to happen.

The Sectors & Scrip under the sector selected for study was:

SECTOR SCRIP

Banking Axis BankCapital Goods Larsen & toubro

6.1.1 L&T:

About the Company:

L&T Ltd. is an $11.7 B company, providing a range of

engineering solutions to the energy and environment sectors.

32

Larsen & Toubro Limited (L&T) is a technology, engineering,

construction and manufacturing company. It is one of the

largest and most respected companies in India's private

sector.

More than seven decades of a strong, customer-focused

approach and the continuous quest for world-class quality

have enabled it to attain and sustain leadership in all its

major lines of business.

L&T has an international presence, with a global spread of

offices. A thrust on international business has seen

overseas earnings grow significantly. It continues to grow

its overseas manufacturing footprint, with facilities in

China and the Gulf region.

L&T believes that progress must be achieved in harmony with

the environment. A commitment to community welfare and

environmental protection are an integral part of the

corporate vision. L&T has diversified business portfolio and it operates through

its different operating divisions

which include:

Engineering & Construction Projects

EPC Power

Heavy Engineering

Engineering, Construction & Contracts33

Electrical & Electronics

Machinery & Industrial Products

IT and Integrated Engineering Services

Financial Services

L&T, one of the India’s largest Engineering Companies, was

incorporated in February 1946. It

was converted into a public limited company in 1950. L&T, along

with its group companies,

provides integrated design, engineering, procurement,

construction and project management

services to various sectors. The company is present in multiple

operating segments such as

Engineering & Construction (E&C), Electrical & Electronics (E&E),

Machinery & Industrial

Products (MIP) and others. It has exposure to infrastructure BOT

projects in roads, ports and

real estate. Through its subsidiaries like L&T Finance, L&T

Infrastructure Finance and L&T

Infotech, L&T has also diversified into financial services and

the IT/ITeS sector. The E&C

division of L&T undertakes engineering design and construction of

buildings, factories,

infrastructure, industrial and power transmission & distribution,

while the E&E segment is

34

engaged in manufacturing of electrical standard products, systems

and equipment. The MIP

division of L&T is focused on manufacturing industrial valves,

construction and hydraulic

equipment, machinery for mining, paper and rubber processing

industry.

L&T is regarded as the preeminent infrastructure major – often

referred to as the ‘builder of

the India of the 21st century’. Its achievements across sectors

include:

Hydrocarbon projects executed in India, the Middle East and

South East Asia

Power projects executed in India, the Gulf and Sri Lanka.

The world’s largest coal gasifier made in India and exported

to China

The world’s biggest EO Reactor for a petrochemical complex

in the Gulf

The world’s largest FCC (Fluid Catalytic Cracker)

Regenerator for a refinery

Asia’s highest viaduct

Infrastructure projects in Jordan, U.A.E. and South East

Asia

The world’s longest limestone conveyor

India’s widest range of switchgear

A wide range of construction and mining equipment

35

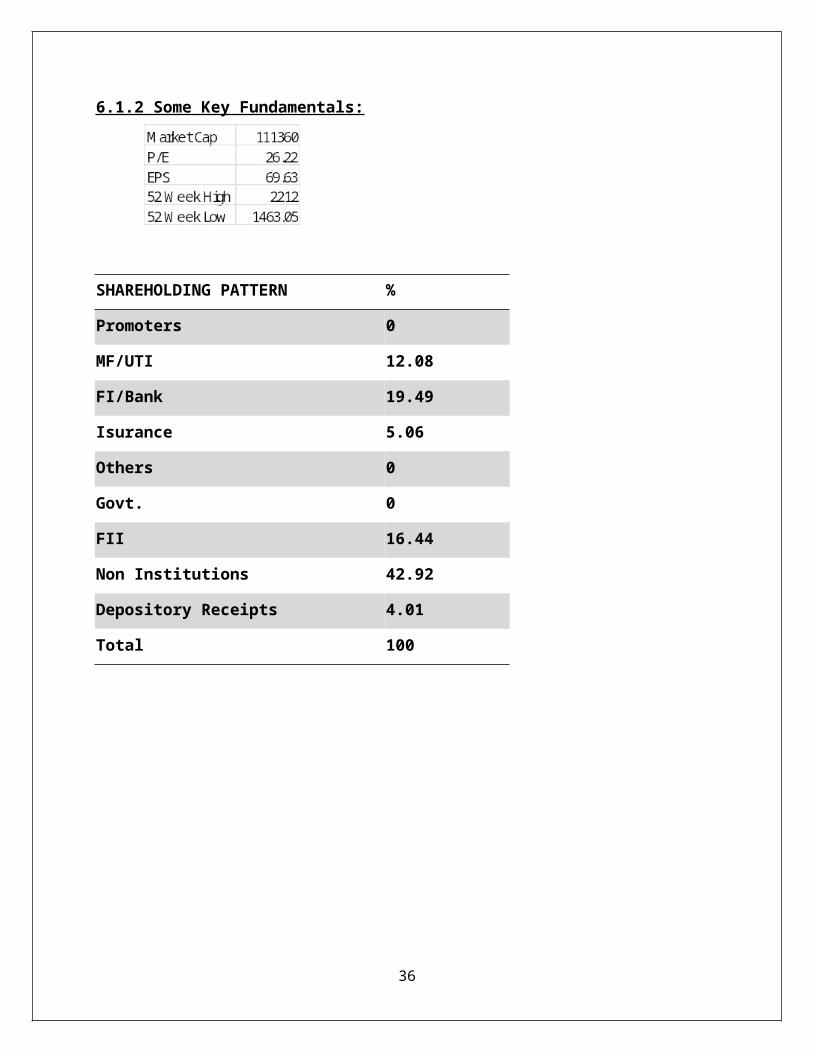

6.1.2 Some Key Fundamentals:

36

SHAREHOLDING PATTERN %

Promoters 0

MF/UTI 12.08

FI/Bank 19.49

Isurance 5.06

Others 0

Govt. 0

FII 16.44

Non Institutions 42.92

Depository Receipts 4.01

Total 100

37

38

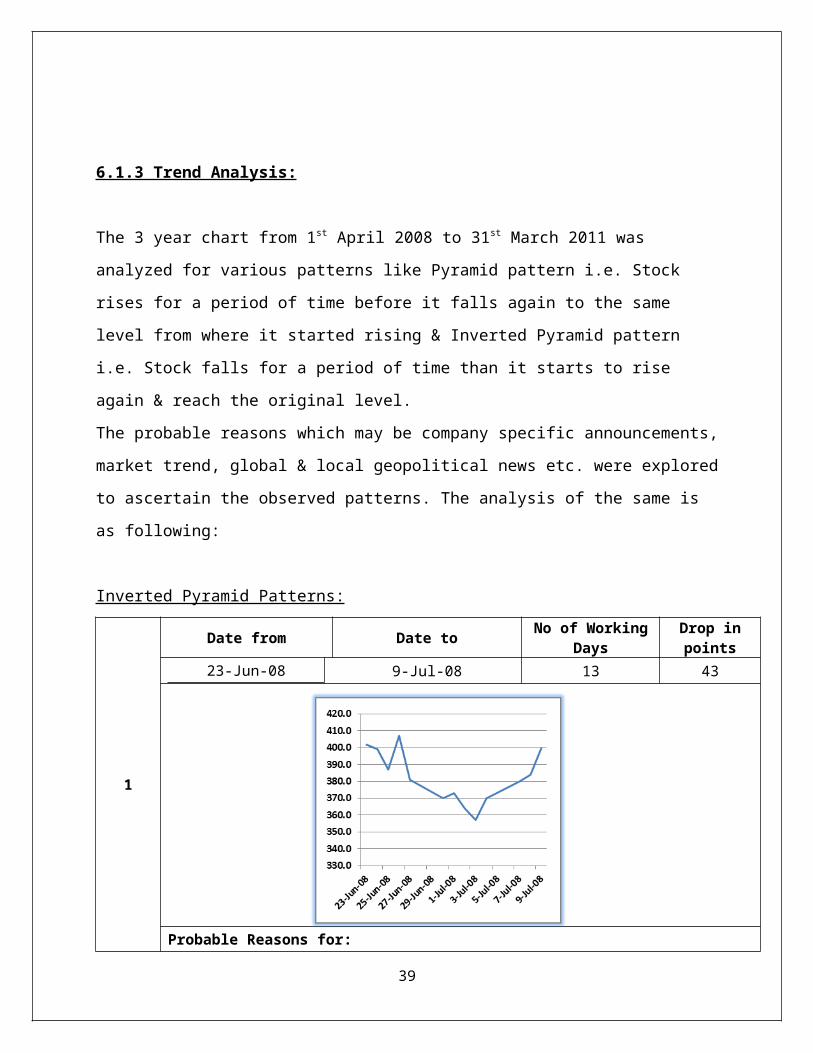

6.1.3 Trend Analysis:

The 3 year chart from 1st April 2008 to 31st March 2011 was

analyzed for various patterns like Pyramid pattern i.e. Stock

rises for a period of time before it falls again to the same

level from where it started rising & Inverted Pyramid pattern

i.e. Stock falls for a period of time than it starts to rise

again & reach the original level.

The probable reasons which may be company specific announcements,

market trend, global & local geopolitical news etc. were explored

to ascertain the observed patterns. The analysis of the same is

as following:

Inverted Pyramid Patterns:

1

Date from Date to No of WorkingDays

Drop inpoints

23-Jun-08 9-Jul-08 13 43

Probable Reasons for:

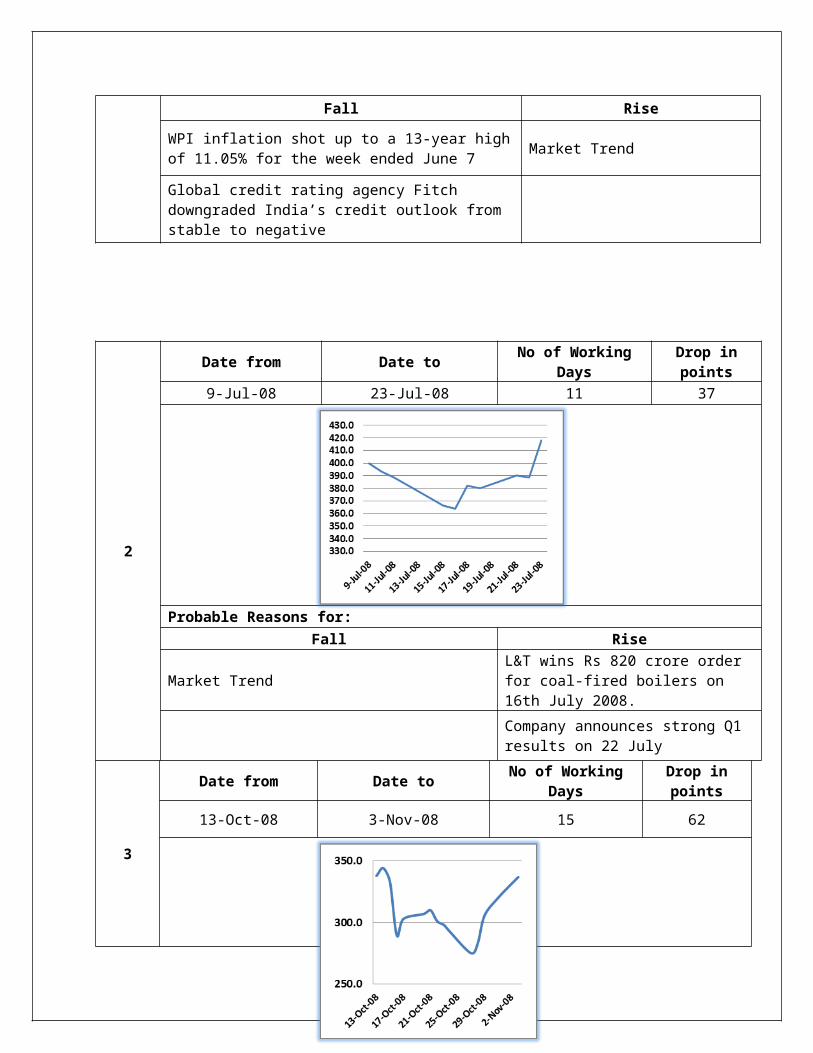

39

Fall Rise

WPI inflation shot up to a 13-year highof 11.05% for the week ended June 7 Market Trend

Global credit rating agency Fitch downgraded India’s credit outlook from stable to negative

2

Date from Date to No of WorkingDays

Drop inpoints

9-Jul-08 23-Jul-08 11 37

Probable Reasons for:Fall Rise

Market TrendL&T wins Rs 820 crore order for coal-fired boilers on 16th July 2008.

Company announces strong Q1 results on 22 July

3

Date from Date to No of WorkingDays

Drop inpoints

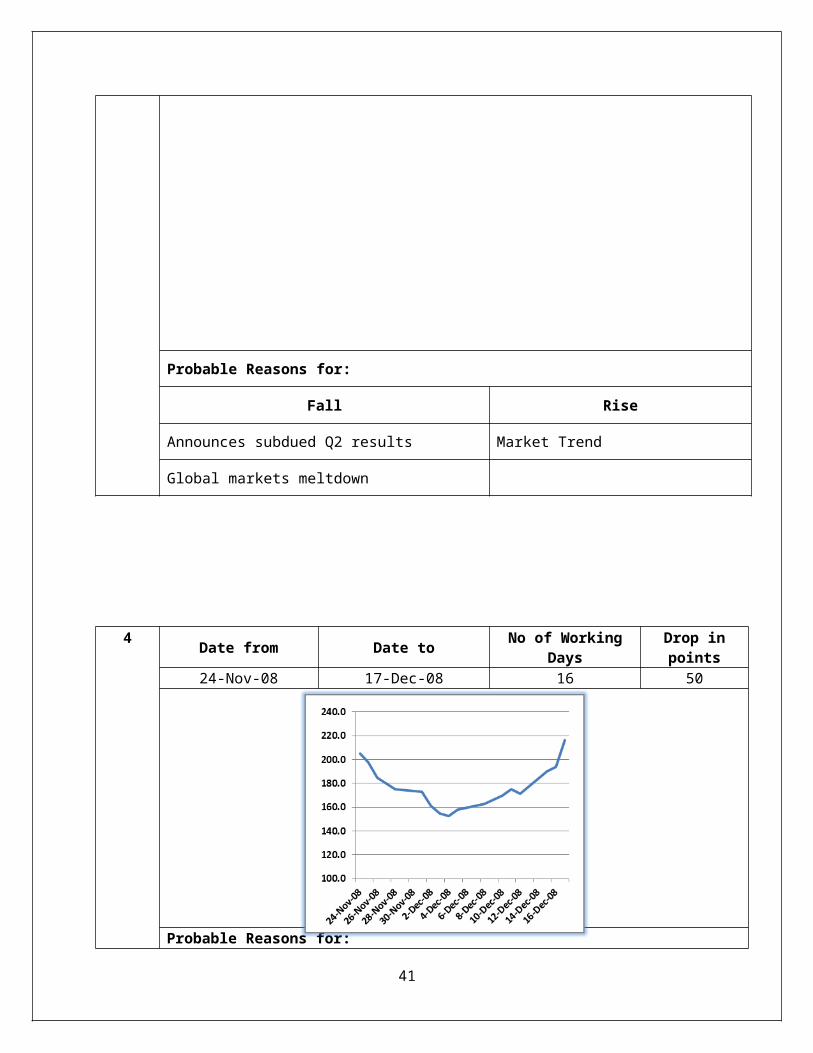

13-Oct-08 3-Nov-08 15 62

40

Probable Reasons for:

Fall Rise

Announces subdued Q2 results Market Trend

Global markets meltdown

4 Date from Date to No of WorkingDays

Drop inpoints

24-Nov-08 17-Dec-08 16 50

Probable Reasons for:

41

Fall RiseManagement concerns over orders not flowing in Market Trend

Market Trend

5

Date from Date to No of WorkingDays

Drop inpoints

21-May-09 2-Jun-09 9 39

Probable Reasons for:Fall Rise

Market Trend Market Trend

6

Date from Date to No of WorkingDays

Drop inpoints

11-Dec-09 24-Dec-09 10 25

42

Probable Reasons for:Fall Rise

Various Analysts concernsovervaluation of the stock Market Trend

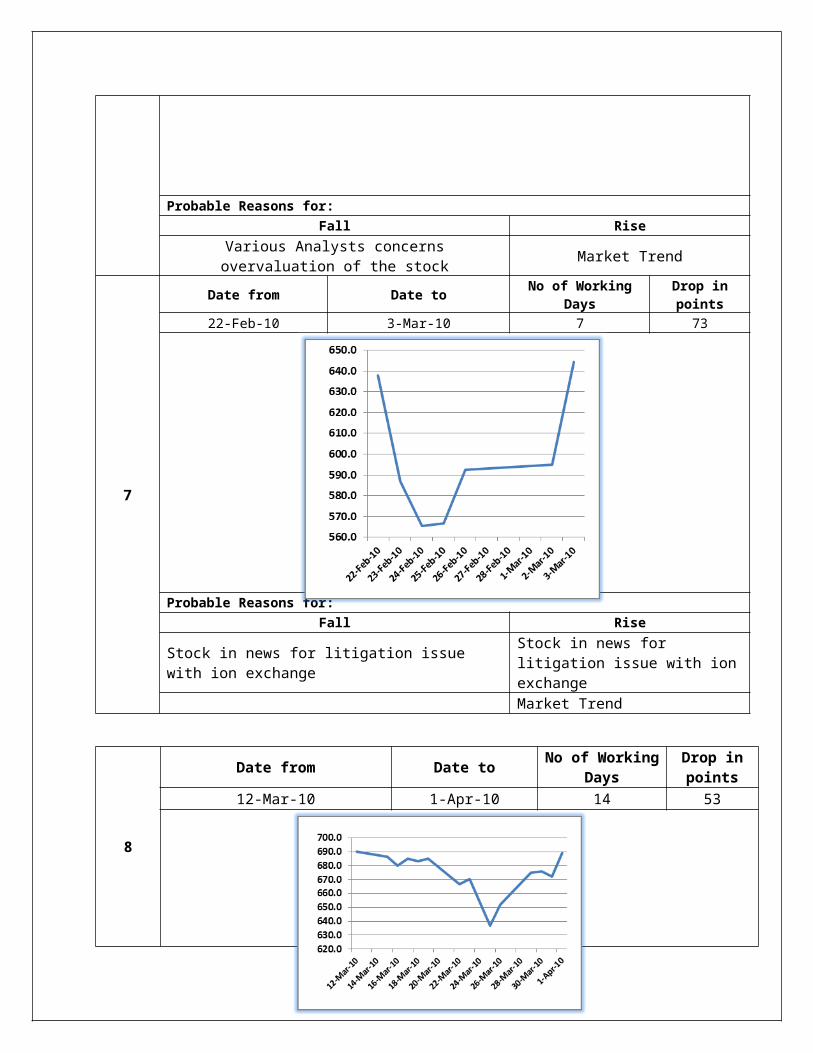

7

Date from Date to No of WorkingDays

Drop inpoints

22-Feb-10 3-Mar-10 7 73

Probable Reasons for:Fall Rise

Stock in news for litigation issue with ion exchange

Stock in news for litigation issue with ionexchange

Market Trend

8

Date from Date to No of WorkingDays

Drop inpoints

12-Mar-10 1-Apr-10 14 53

43

Probable Reasons for:Fall Rise

Market Trend Strong IIP Nos

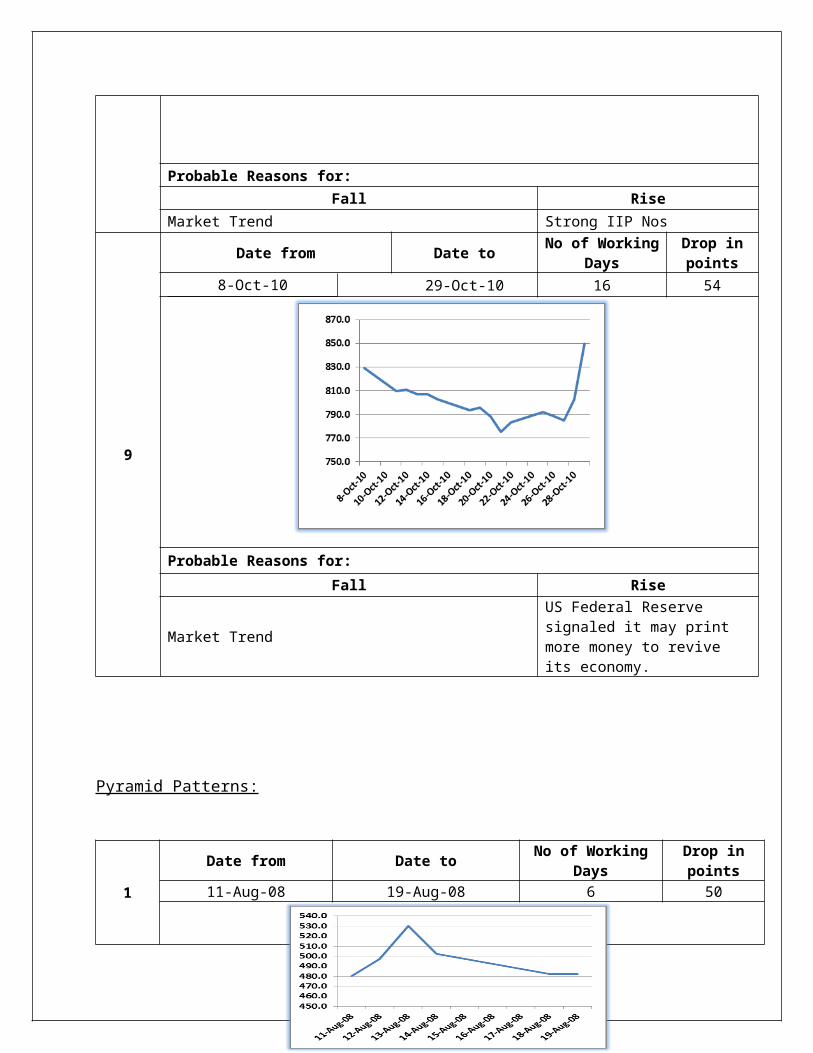

9

Date from Date to No of WorkingDays

Drop inpoints

8-Oct-10 29-Oct-10 16 54

Probable Reasons for:Fall Rise

Market Trend

US Federal Reserve signaled it may print more money to revive its economy.

Pyramid Patterns:

1

Date from Date to No of WorkingDays

Drop inpoints

11-Aug-08 19-Aug-08 6 50

44

Probable Reasons for:Rise Fall

Market Trend Market Trend

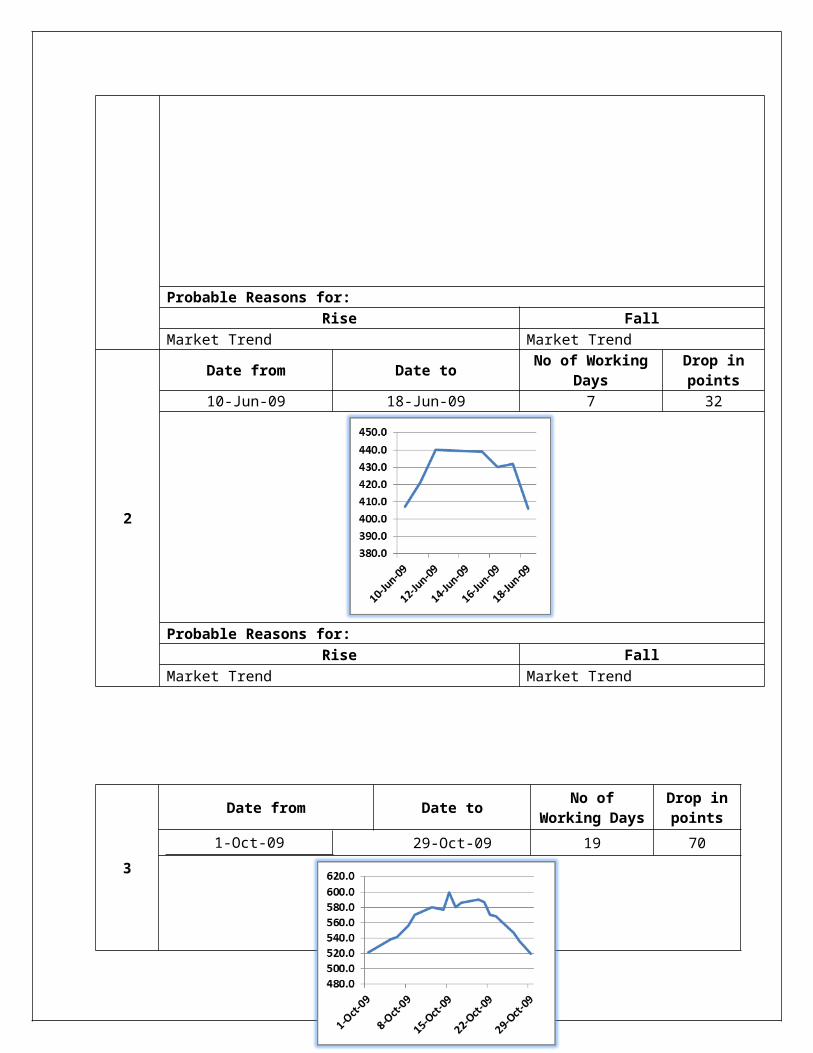

2

Date from Date to No of WorkingDays

Drop inpoints

10-Jun-09 18-Jun-09 7 32

Probable Reasons for:Rise Fall

Market Trend Market Trend

3

Date from Date to No ofWorking Days

Drop inpoints

1-Oct-09 29-Oct-09 19 70

45

Probable Reasons for:Rise Fall

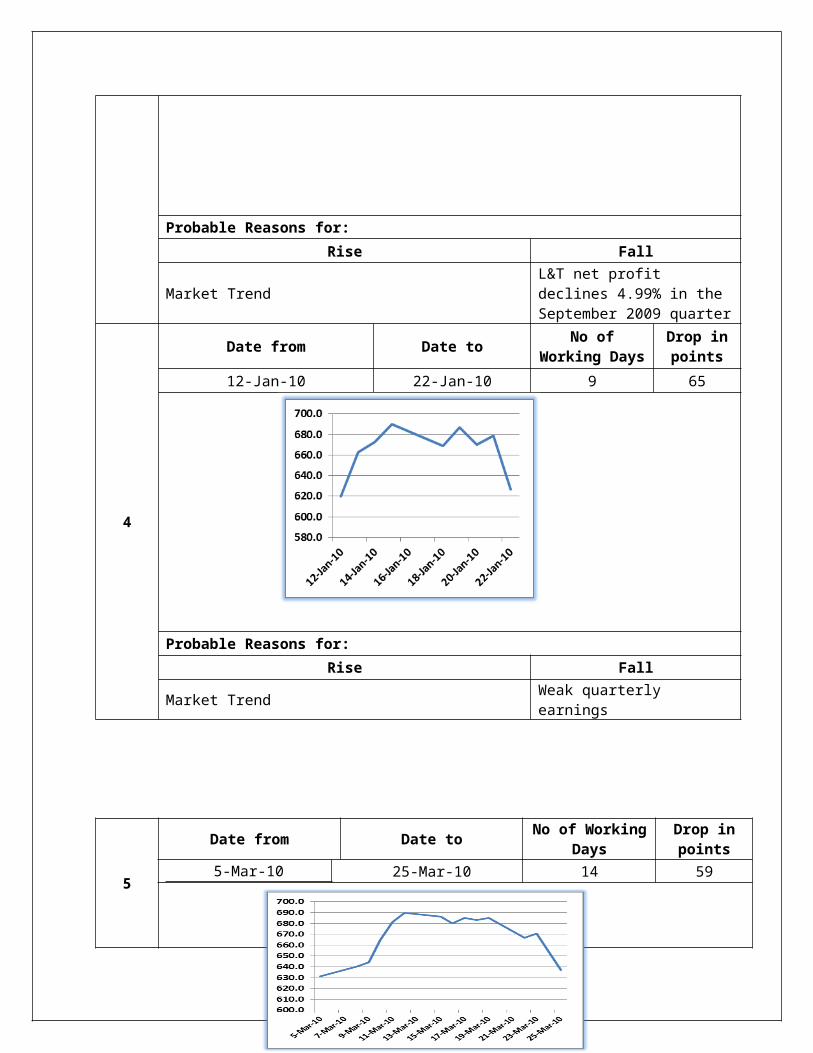

Market TrendL&T net profit declines 4.99% in the September 2009 quarter

4

Date from Date to No ofWorking Days

Drop inpoints

12-Jan-10 22-Jan-10 9 65

Probable Reasons for:Rise Fall

Market Trend Weak quarterly earnings

5

Date from Date to No of WorkingDays

Drop inpoints

5-Mar-10 25-Mar-10 14 59

46

Probable Reasons for:Rise Fall

L&T - Babcock & Wilcox Joint Venture for Supercritical Boilers: Offers higher efficiency of power generation in India's mega projects(10 March)

Market Trend

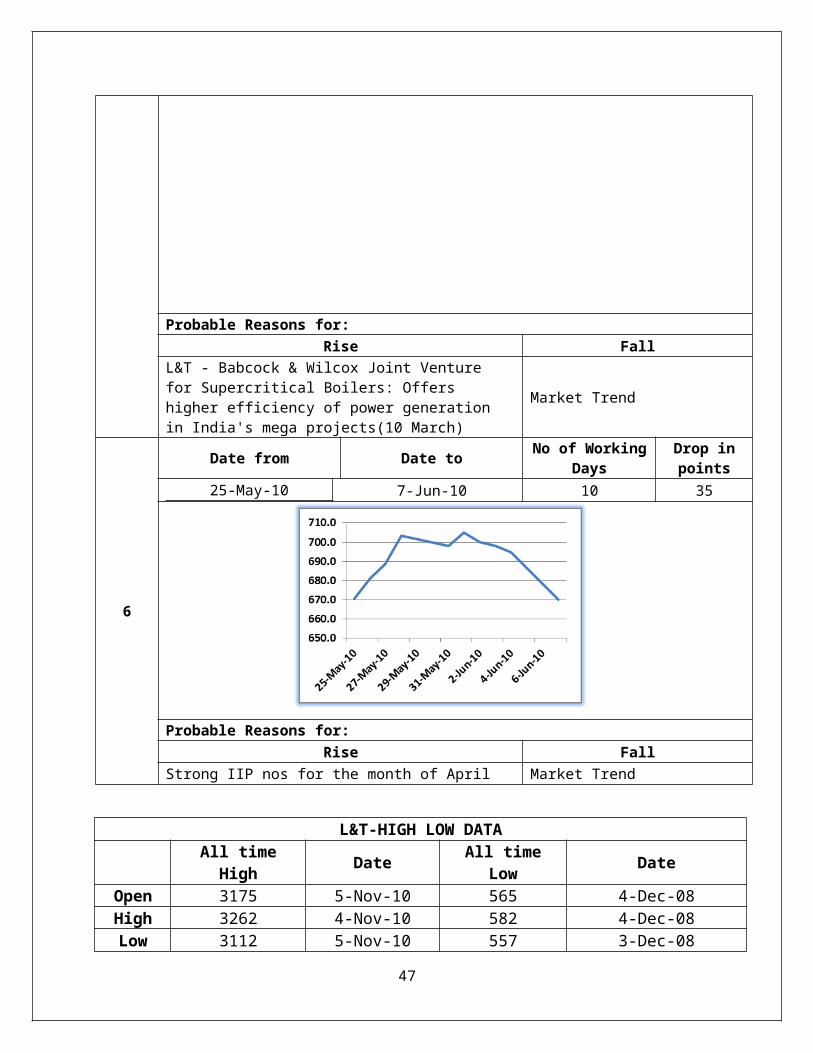

6

Date from Date to No of WorkingDays

Drop inpoints

25-May-10 7-Jun-10 10 35

Probable Reasons for:Rise Fall

Strong IIP nos for the month of April Market Trend

L&T-HIGH LOW DATA

All time

High Date All timeLow Date

Open 3175 5-Nov-10 565 4-Dec-08High 3262 4-Nov-10 582 4-Dec-08Low 3112 5-Nov-10 557 3-Dec-08

47

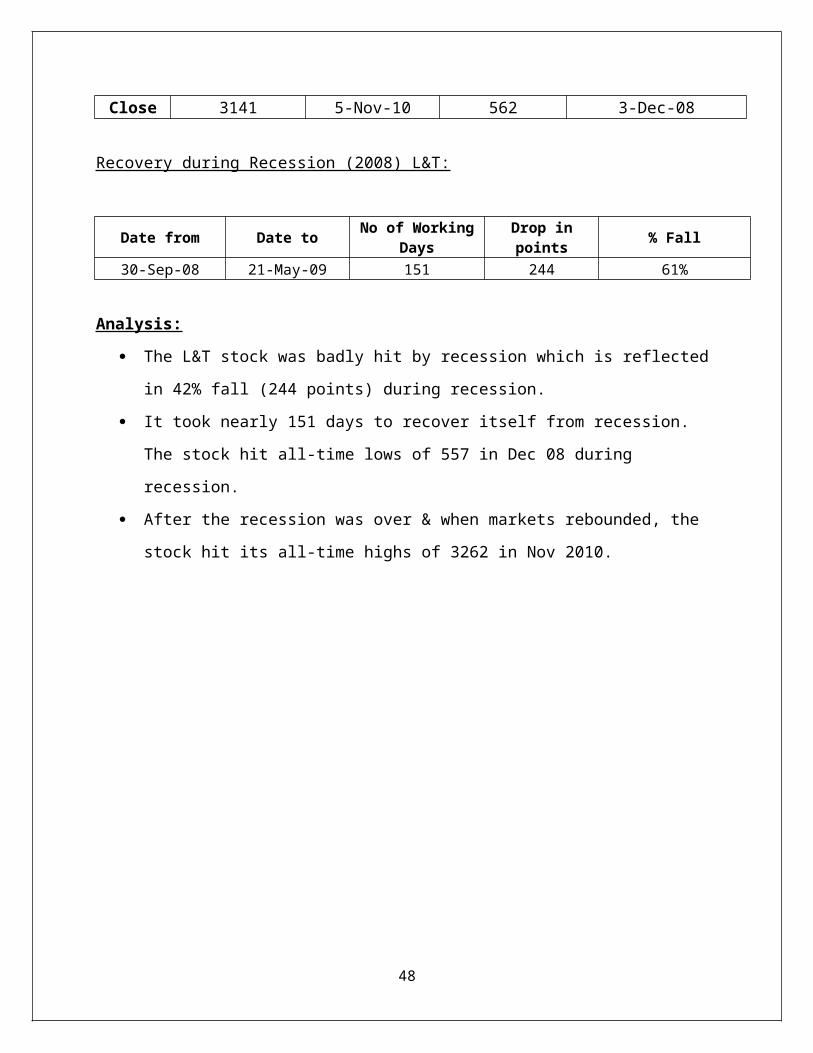

Close 3141 5-Nov-10 562 3-Dec-08

Recovery during Recession (2008) L&T:

Date from Date to No of WorkingDays

Drop inpoints % Fall

30-Sep-08 21-May-09 151 244 61%

Analysis:

The L&T stock was badly hit by recession which is reflected

in 42% fall (244 points) during recession.

It took nearly 151 days to recover itself from recession.

The stock hit all-time lows of 557 in Dec 08 during

recession.

After the recession was over & when markets rebounded, the

stock hit its all-time highs of 3262 in Nov 2010.

48

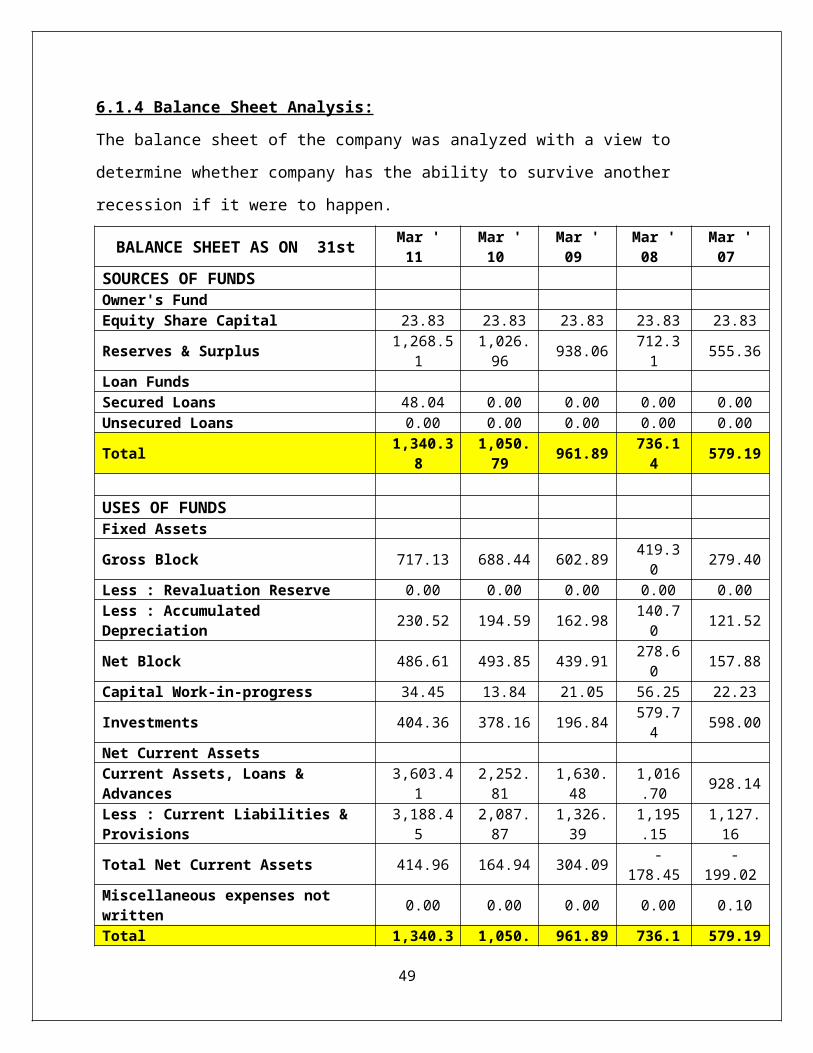

6.1.4 Balance Sheet Analysis:

The balance sheet of the company was analyzed with a view to

determine whether company has the ability to survive another

recession if it were to happen.

BALANCE SHEET AS ON 31st Mar '11

Mar '10

Mar '09

Mar '08

Mar '07

SOURCES OF FUNDS Owner's Fund Equity Share Capital 23.83 23.83 23.83 23.83 23.83

Reserves & Surplus 1,268.51

1,026.96 938.06 712.3

1 555.36

Loan Funds Secured Loans 48.04 0.00 0.00 0.00 0.00Unsecured Loans 0.00 0.00 0.00 0.00 0.00

Total 1,340.38

1,050.79 961.89 736.1

4 579.19

USES OF FUNDS Fixed Assets

Gross Block 717.13 688.44 602.89 419.30 279.40

Less : Revaluation Reserve 0.00 0.00 0.00 0.00 0.00Less : Accumulated Depreciation 230.52 194.59 162.98 140.7

0 121.52

Net Block 486.61 493.85 439.91 278.60 157.88

Capital Work-in-progress 34.45 13.84 21.05 56.25 22.23

Investments 404.36 378.16 196.84 579.74 598.00

Net Current Assets Current Assets, Loans & Advances

3,603.41

2,252.81

1,630.48

1,016.70 928.14

Less : Current Liabilities & Provisions

3,188.45

2,087.87

1,326.39

1,195.15

1,127.16

Total Net Current Assets 414.96 164.94 304.09 -178.45

-199.02

Miscellaneous expenses not written 0.00 0.00 0.00 0.00 0.10

Total 1,340.3 1,050. 961.89 736.1 579.19

49

8 79 4Note : Number of Equity shares outstanding (in Lacs)

1,191.56

1,191.56

1,191.56

1,191.56

1,191.56

Mar '11

Mar '10

Mar '09

Mar '08 Mar ' 07

Sales 4,883.23

3,185.47

3,264.35

3,204.17 2,173.03

Operating Profit 566.09 384.11 414.42 409.58 279.08Net Profit / Loss 382.42 141.44 287.29 280.78 187.80EPS (in Rs.) 32.09 11.87 24.11 23.57 15.76

KEY RATIOS Mar '11

Mar '10

Mar '09

Mar '08

Mar '07

PROFITABILITY RATIOS Operating Margin (%) 10.79 11.12 15.93 12.50 13.63Gross Profit Margin (%) 9.88 9.80 14.89 11.81 12.73Net Profit Margin (%) 7.87 4.46 9.09 8.69 8.80Reported Return On Net Worth (%) 29.59 13.46 29.86 38.14 32.43

LEVERAGE RATIOS Long Term Debt / Equity 0.00 0.00 0.00 0.00 0.00Total Debt/Equity 0.03 0.00 0.00 0.00 0.00Owners fund as % of total Source 96.41 100.00 100.00 100.00 100.00

Fixed Assets Turnover Ratio 6.88 4.59 5.29 7.78 7.57

LIQUIDITY RATIOS Current Ratio 1.13 1.08 1.23 0.85 0.82Quick Ratio 1.03 0.94 1.01 0.67 0.57Inventory Turnover Ratio 17.77 12.95 12.20 16.81 8.10

Analysis:

50

It is almost a debt free company with strong operating

performance over the years. Its net sales have grown @CAGR

of 18% & its Net profit & EPS has grown @ CAGR of 15% over

the last five years.

It has been able to maintain its profit margin even during

times of recession due to prudent cost management

initiatives taken by the company.

It has been able to generate strong positive operating cash

flows even during the time of the recession.

It also has high inventory turnover ratio compared to

industry which indicates that company is able to generate

sales quickly.

It has provided high ROCE compared to its peers indicating

the strong management capabilities to generate return on the

capital employed.

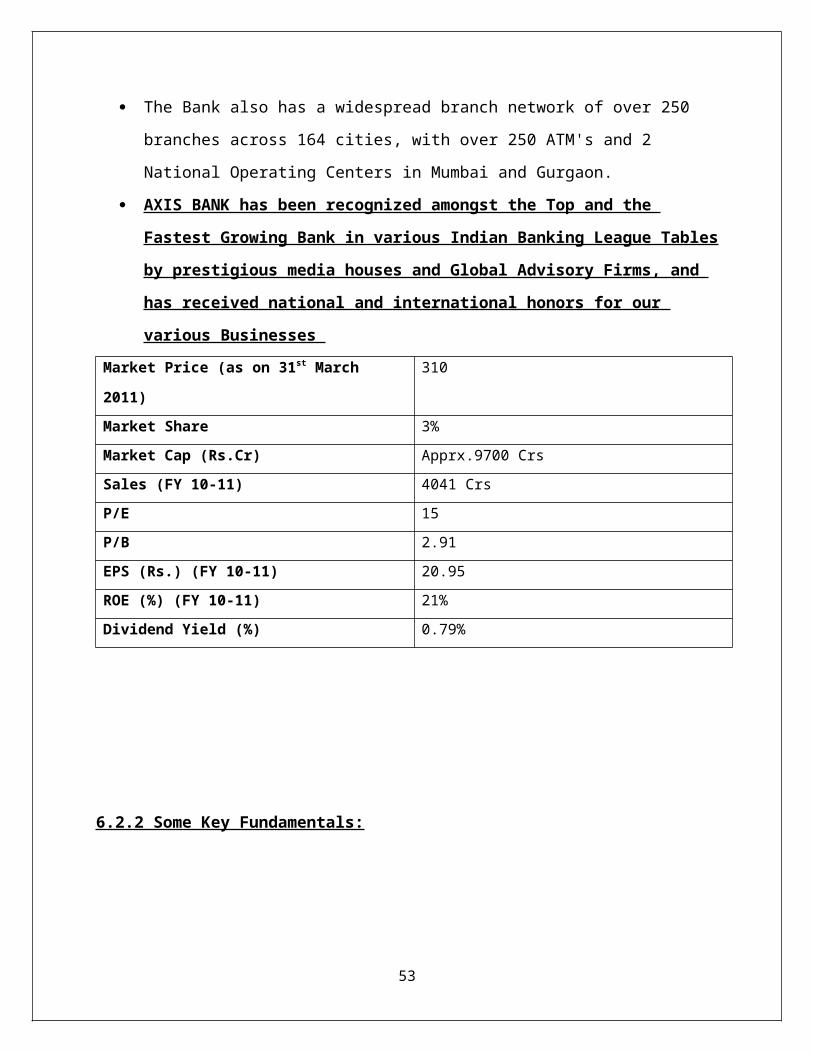

6.2 AXIS BANK:

6.2.1 About the Company:

51

AXIS BANK is a state-of-the-art high quality, customer

centric, service driven, private Indian Bank catering to the

“Future Businesses of India”

Since inception, AXIS BANK has tried to play a catalytic

role in bridging the infrastructure and knowledge gap in

various Sunrise sectors of the economy. As part of the

differentiated strategy, AXIS BANK has had a strong focus on

Development Banking, as is evident from the cutting-edge

work that the Bank has done in the area of Food &

Agribusiness, Infrastructure, Microfinance, and

Sustainability which in most cases has been first-of-its

kind in India.

In a short span of 6 years, AXIS BANK has fructified into a

‘“Full Service Commercial Bank” that has steadily built

Corporate and Institutional Banking, Financial Markets,

Investment Banking, Corporate Finance, Branch Banking,

Business and Transaction Banking, and Wealth Management

business lines across the country, and is well equipped to

offer a range of products and services to corporate and

retail customers.

AXIS BANK offers a full-range of client-focused corporate

banking services, including working capital finance,

specialized corporate finance, trade and transactional

services, treasury risk management services, investment

banking solutions and liquidity management solutions among

others to a highly focused client base.

52

The Bank also has a widespread branch network of over 250

branches across 164 cities, with over 250 ATM's and 2

National Operating Centers in Mumbai and Gurgaon.

AXIS BANK has been recognized amongst the Top and the

Fastest Growing Bank in various Indian Banking League Tables

by prestigious media houses and Global Advisory Firms, and

has received national and international honors for our

various Businesses Market Price (as on 31st March

2011)

310

Market Share 3%Market Cap (Rs.Cr) Apprx.9700 CrsSales (FY 10-11) 4041 CrsP/E 15P/B 2.91EPS (Rs.) (FY 10-11) 20.95ROE (%) (FY 10-11) 21%Dividend Yield (%) 0.79%

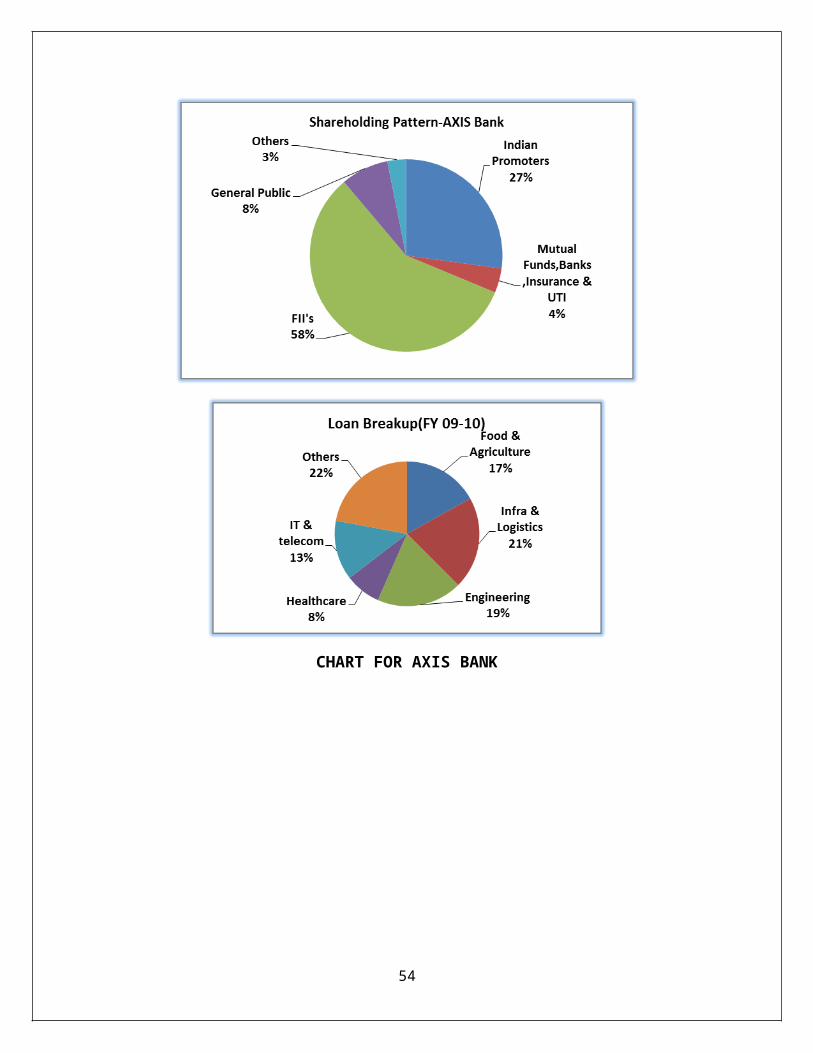

6.2.2 Some Key Fundamentals:

53

CHART FOR AXIS BANK

54

CHART FOR AXIS BANK

55

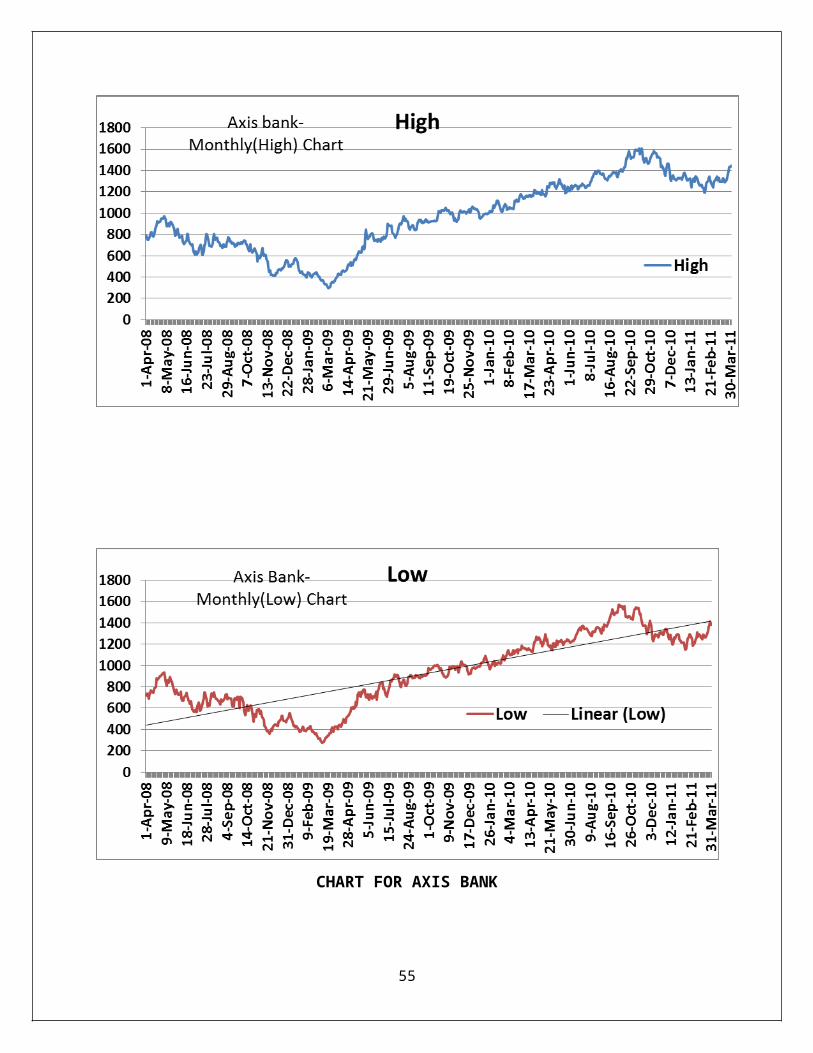

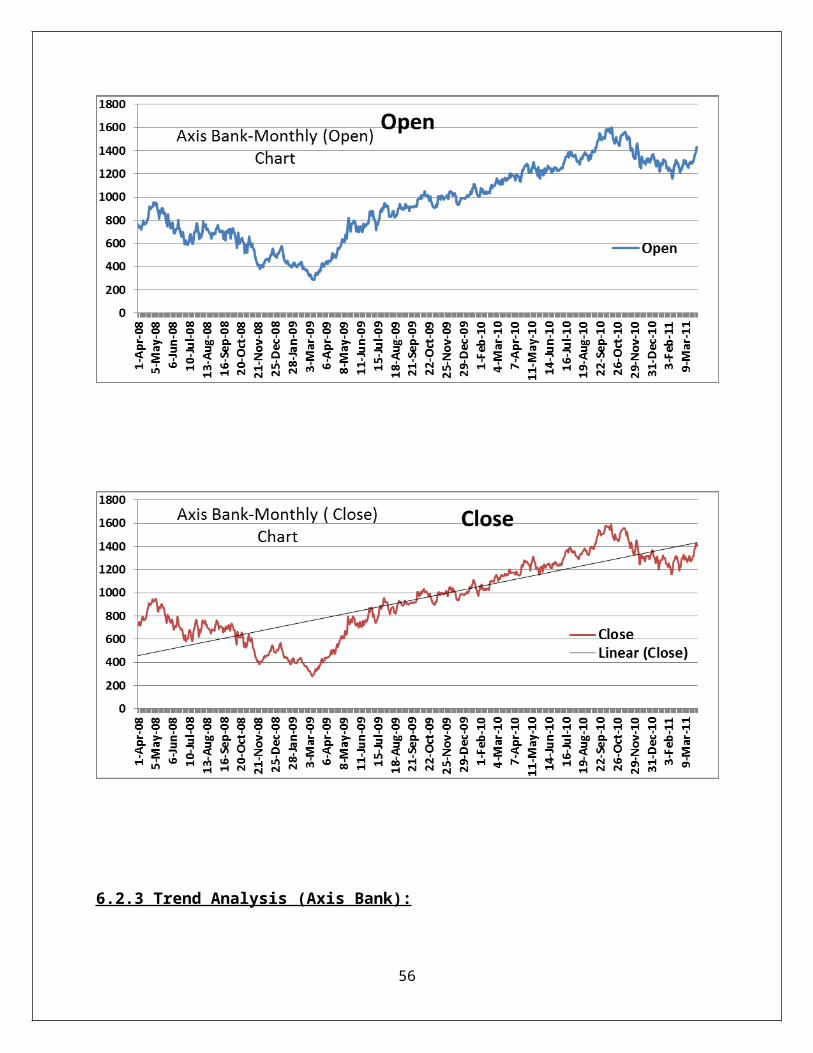

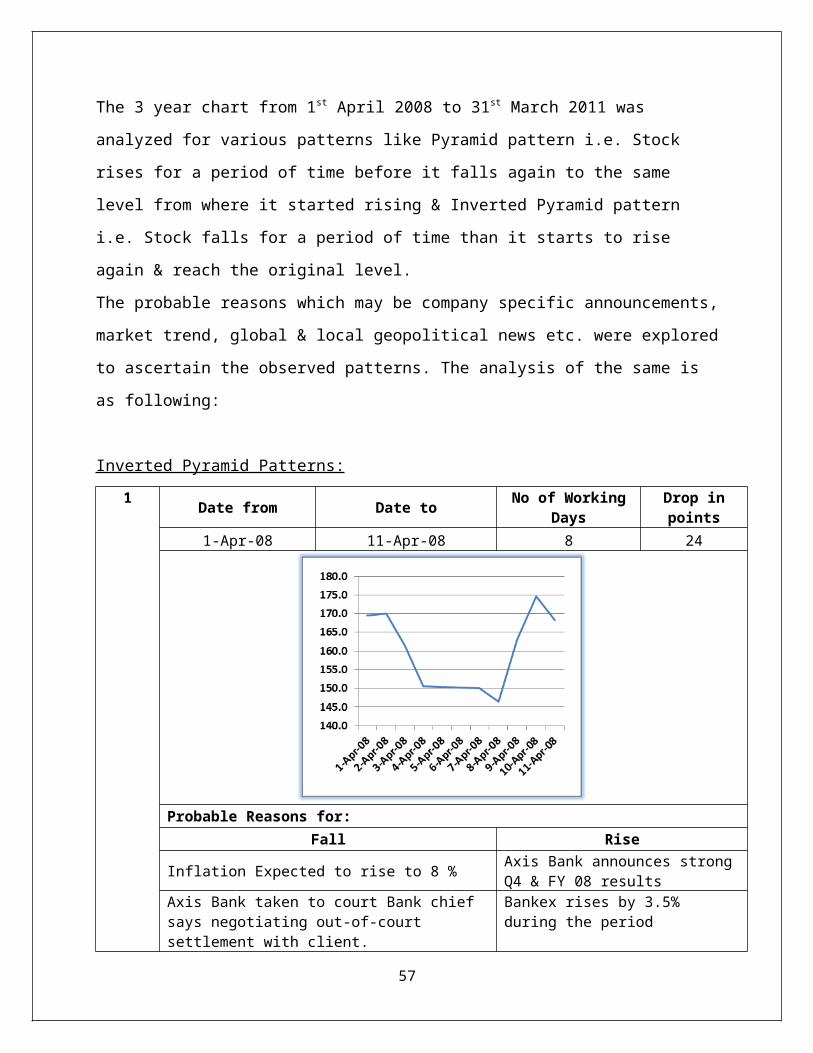

6.2.3 Trend Analysis (Axis Bank):

56

The 3 year chart from 1st April 2008 to 31st March 2011 was

analyzed for various patterns like Pyramid pattern i.e. Stock

rises for a period of time before it falls again to the same

level from where it started rising & Inverted Pyramid pattern

i.e. Stock falls for a period of time than it starts to rise

again & reach the original level.

The probable reasons which may be company specific announcements,

market trend, global & local geopolitical news etc. were explored

to ascertain the observed patterns. The analysis of the same is

as following:

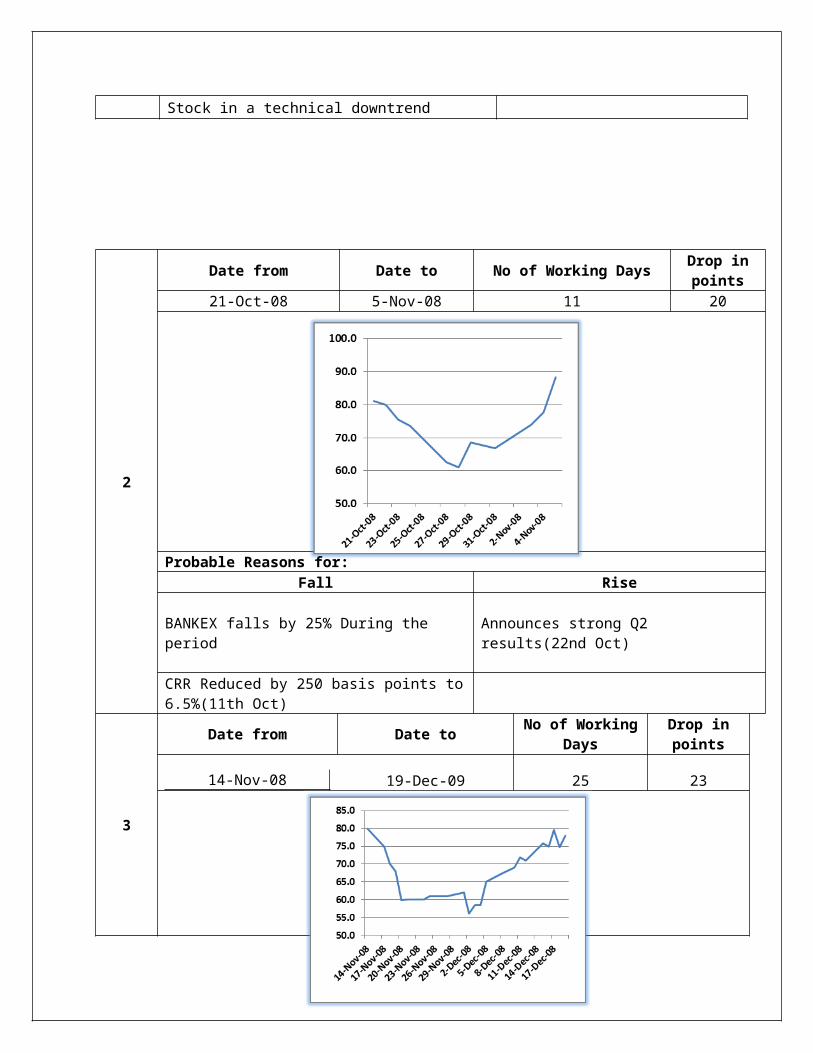

Inverted Pyramid Patterns:1 Date from Date to No of Working

DaysDrop inpoints

1-Apr-08 11-Apr-08 8 24

Probable Reasons for:Fall Rise

Inflation Expected to rise to 8 % Axis Bank announces strongQ4 & FY 08 results

Axis Bank taken to court Bank chief says negotiating out-of-court settlement with client.

Bankex rises by 3.5% during the period

57

Stock in a technical downtrend

2

Date from Date to No of Working Days Drop inpoints

21-Oct-08 5-Nov-08 11 20

Probable Reasons for:Fall Rise

BANKEX falls by 25% During the period

Announces strong Q2 results(22nd Oct)

CRR Reduced by 250 basis points to6.5%(11th Oct)

3

Date from Date to No of WorkingDays

Drop inpoints

14-Nov-08 19-Dec-09 25 23

58

Probable Reasons for:

Fall Rise

Axis Bank non-exe chairman died in Mumbai terror at Taj Hotel

Repo & RR reduced by 100 basis points each to 6.5%& 5% resp

4

Date from Date to No of WorkingDays

Drop inpoints

6-Jul-09 16-Jul-09 9 18

Probable Reasons for:Fall Rise

59

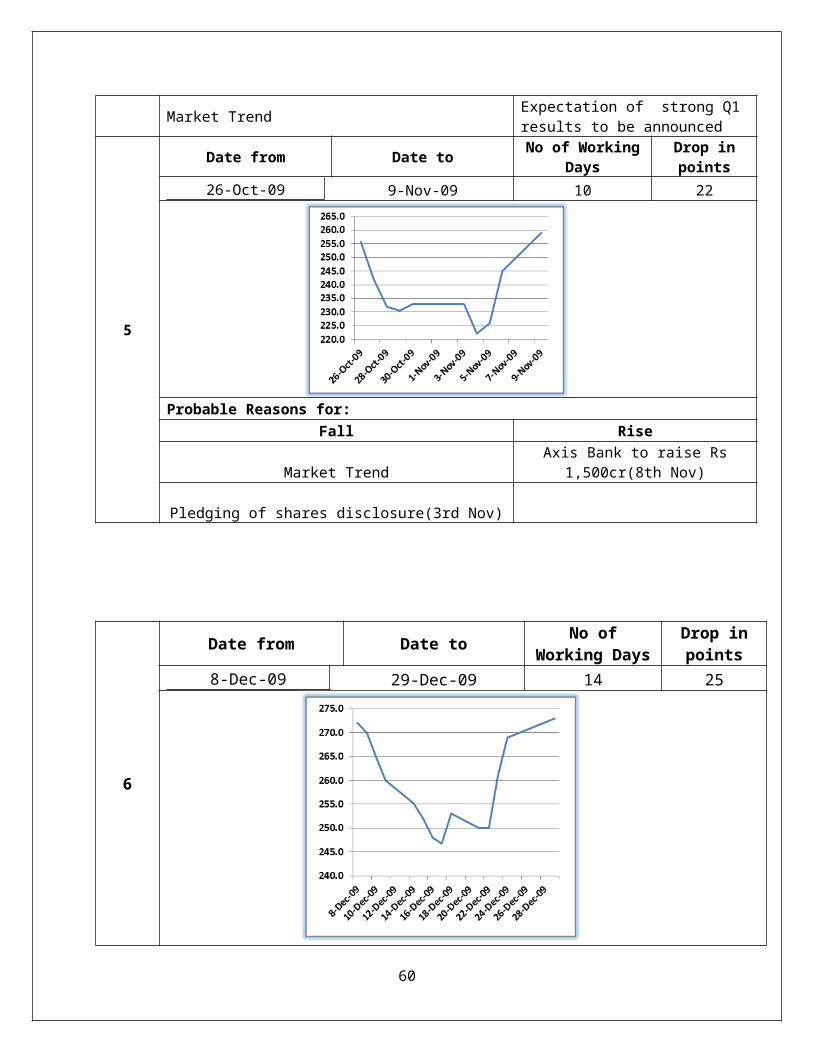

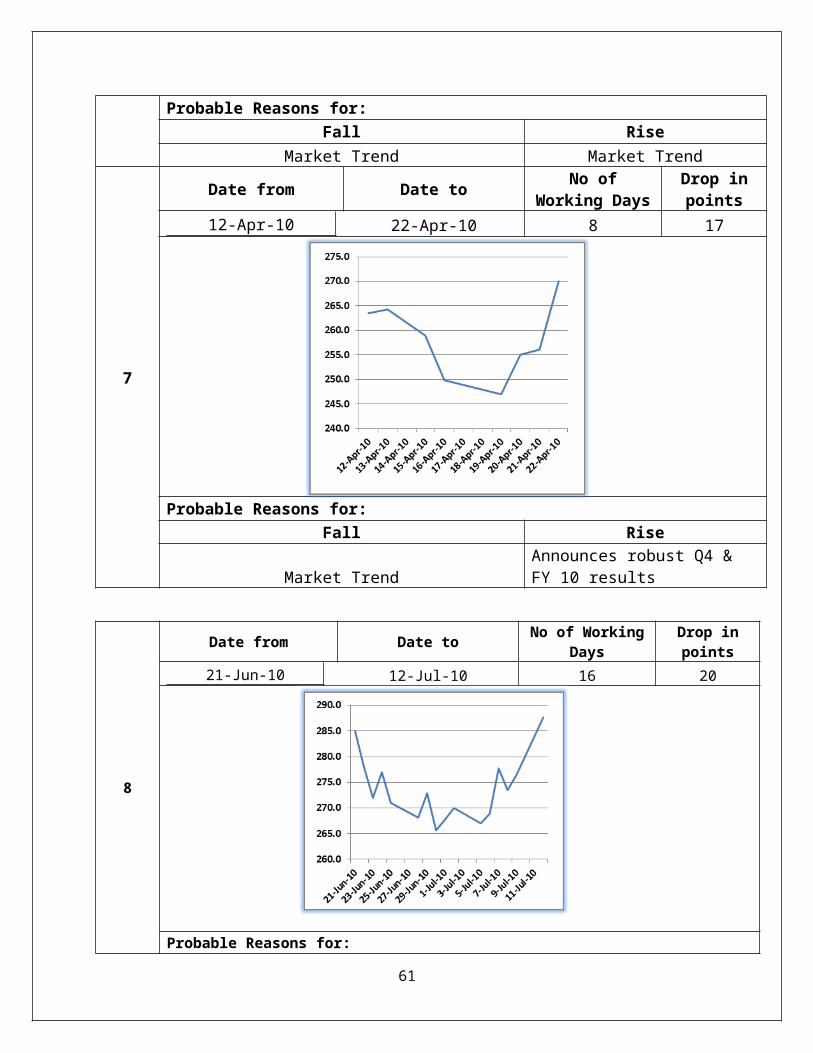

Market Trend Expectation of strong Q1 results to be announced

5

Date from Date to No of WorkingDays

Drop inpoints

26-Oct-09 9-Nov-09 10 22

Probable Reasons for:Fall Rise

Market TrendAxis Bank to raise Rs

1,500cr(8th Nov)

Pledging of shares disclosure(3rd Nov)

6

Date from Date to No ofWorking Days

Drop inpoints

8-Dec-09 29-Dec-09 14 25

60

Probable Reasons for:Fall Rise

Market Trend Market Trend

7

Date from Date to No ofWorking Days

Drop inpoints

12-Apr-10 22-Apr-10 8 17

Probable Reasons for:Fall Rise

Market TrendAnnounces robust Q4 & FY 10 results

8

Date from Date to No of WorkingDays

Drop inpoints

21-Jun-10 12-Jul-10 16 20

Probable Reasons for:

61

Fall Rise

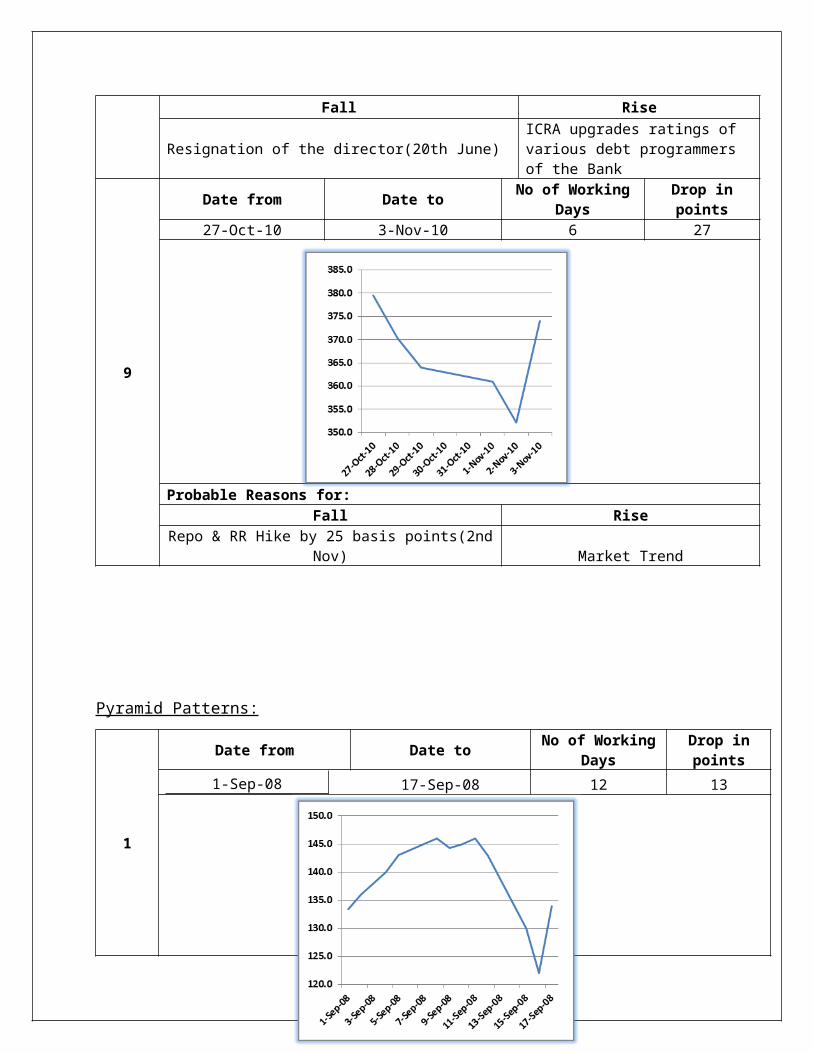

Resignation of the director(20th June)ICRA upgrades ratings of various debt programmers of the Bank

9

Date from Date to No of WorkingDays

Drop inpoints

27-Oct-10 3-Nov-10 6 27

Probable Reasons for:Fall Rise

Repo & RR Hike by 25 basis points(2ndNov) Market Trend

Pyramid Patterns:

1

Date from Date to No of WorkingDays

Drop inpoints

1-Sep-08 17-Sep-08 12 13

62

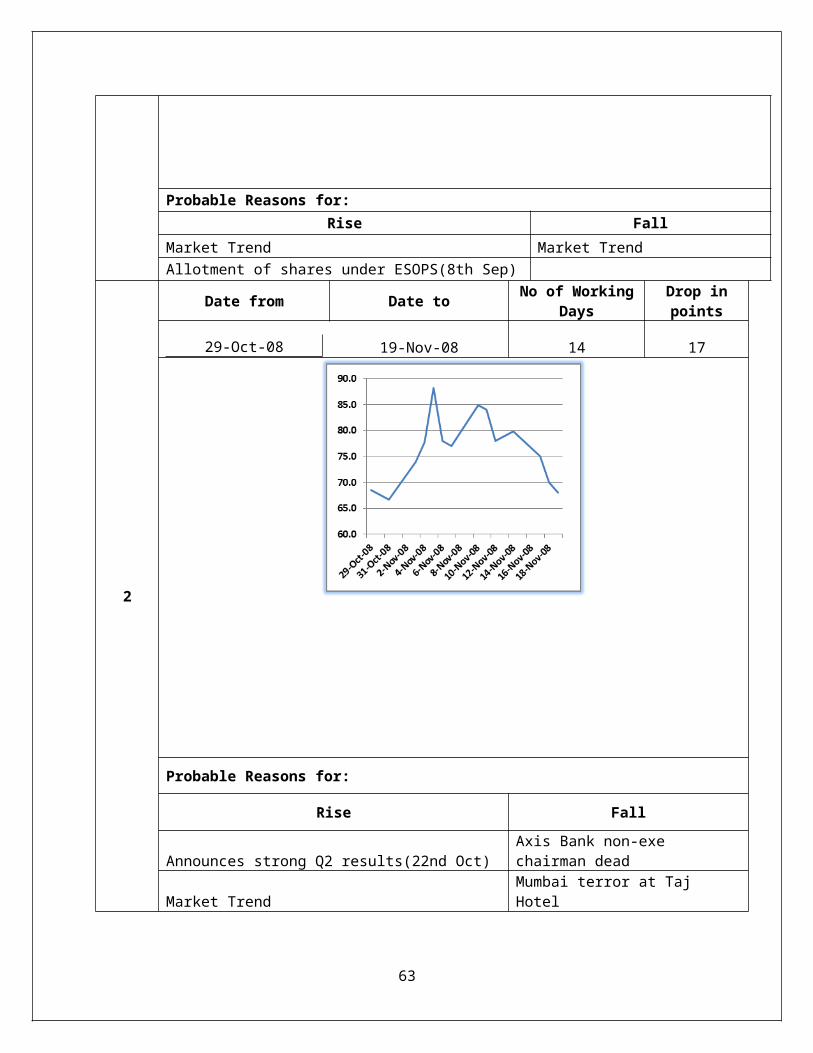

Probable Reasons for:Rise Fall

Market Trend Market TrendAllotment of shares under ESOPS(8th Sep)

2

Date from Date to No of WorkingDays

Drop inpoints

29-Oct-08 19-Nov-08 14 17

Probable Reasons for:

Rise Fall

Announces strong Q2 results(22nd Oct)Axis Bank non-exe chairman dead

Market TrendMumbai terror at Taj Hotel

63

3

Date from Date to No of WorkingDays

Drop inpoints

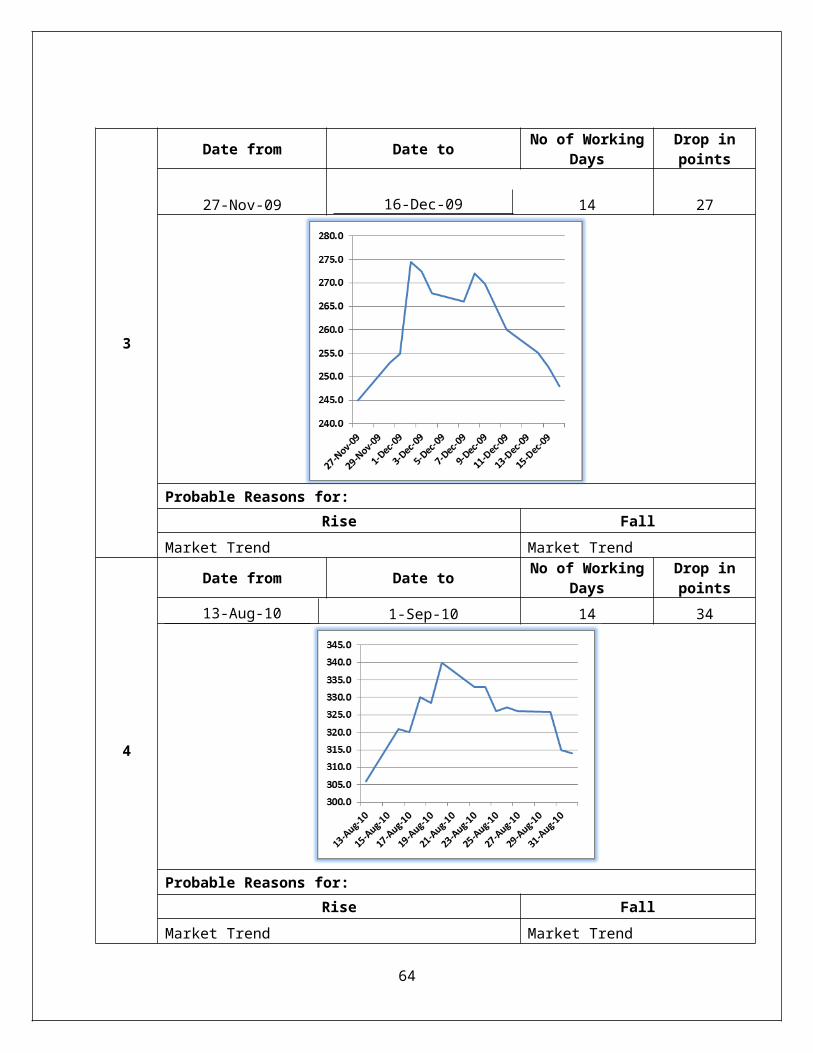

27-Nov-09 16-Dec-09 14 27

Probable Reasons for:Rise Fall

Market Trend Market Trend

4

Date from Date to No of WorkingDays

Drop inpoints

13-Aug-10 1-Sep-10 14 34

Probable Reasons for:Rise Fall

Market Trend Market Trend

64

5

Date from Date to No of WorkingDays

Drop inpoints

20-Oct-10 2-Nov-10 10 29

Probable Reasons for:

Rise Fall

Strong Q2 results on 20th OctRepo & RR Hike by 25 basispoints(2nd Nov)

AXIS BankAll timeHigh Date

All-timeLow Date

Open 1600 27-Oct-10 287 9-Mar-09High 1608 1-Nov-10 296 9-Mar-09Low 1571 5-Nov-10 278 9-Mar-09Close 1588 26-Oct-10 281 9-Mar-09

Recovery Period during Recession (2008):

Date from Date to No of WorkingDays

Drop inpoints % Fall

22-Sep-08 20-May-09 155 100 71%

65

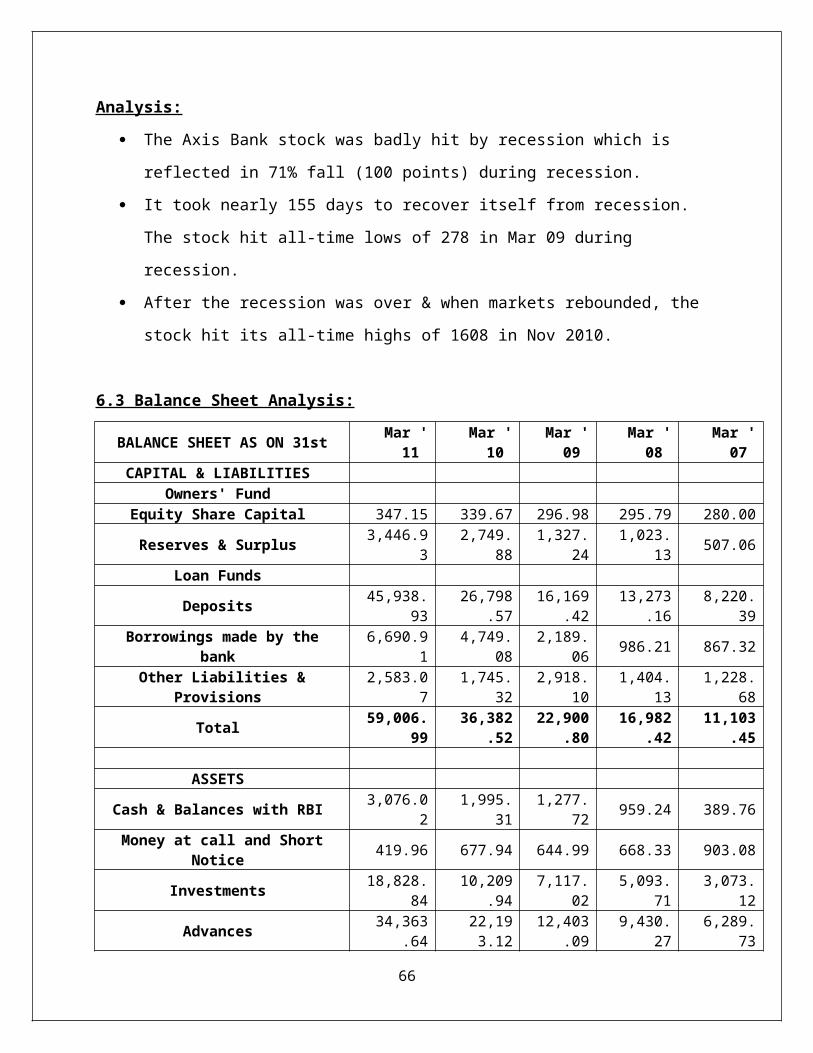

Analysis:

The Axis Bank stock was badly hit by recession which is

reflected in 71% fall (100 points) during recession.

It took nearly 155 days to recover itself from recession.

The stock hit all-time lows of 278 in Mar 09 during

recession.

After the recession was over & when markets rebounded, the

stock hit its all-time highs of 1608 in Nov 2010.

6.3 Balance Sheet Analysis:

BALANCE SHEET AS ON 31st Mar '11

Mar '10

Mar '09

Mar '08

Mar '07

CAPITAL & LIABILITIES Owners' Fund

Equity Share Capital 347.15 339.67 296.98 295.79 280.00

Reserves & Surplus 3,446.93

2,749.88

1,327.24

1,023.13 507.06

Loan Funds

Deposits 45,938.93

26,798.57

16,169.42

13,273.16

8,220.39

Borrowings made by thebank

6,690.91

4,749.08

2,189.06 986.21 867.32

Other Liabilities &Provisions

2,583.07

1,745.32

2,918.10

1,404.13

1,228.68

Total 59,006.99

36,382.52

22,900.80

16,982.42

11,103.45

ASSETS

Cash & Balances with RBI 3,076.02

1,995.31

1,277.72 959.24 389.76

Money at call and ShortNotice 419.96 677.94 644.99 668.33 903.08

Investments 18,828.84

10,209.94

7,117.02

5,093.71

3,073.12

Advances 34,363.64

22,193.12

12,403.09

9,430.27

6,289.73

66

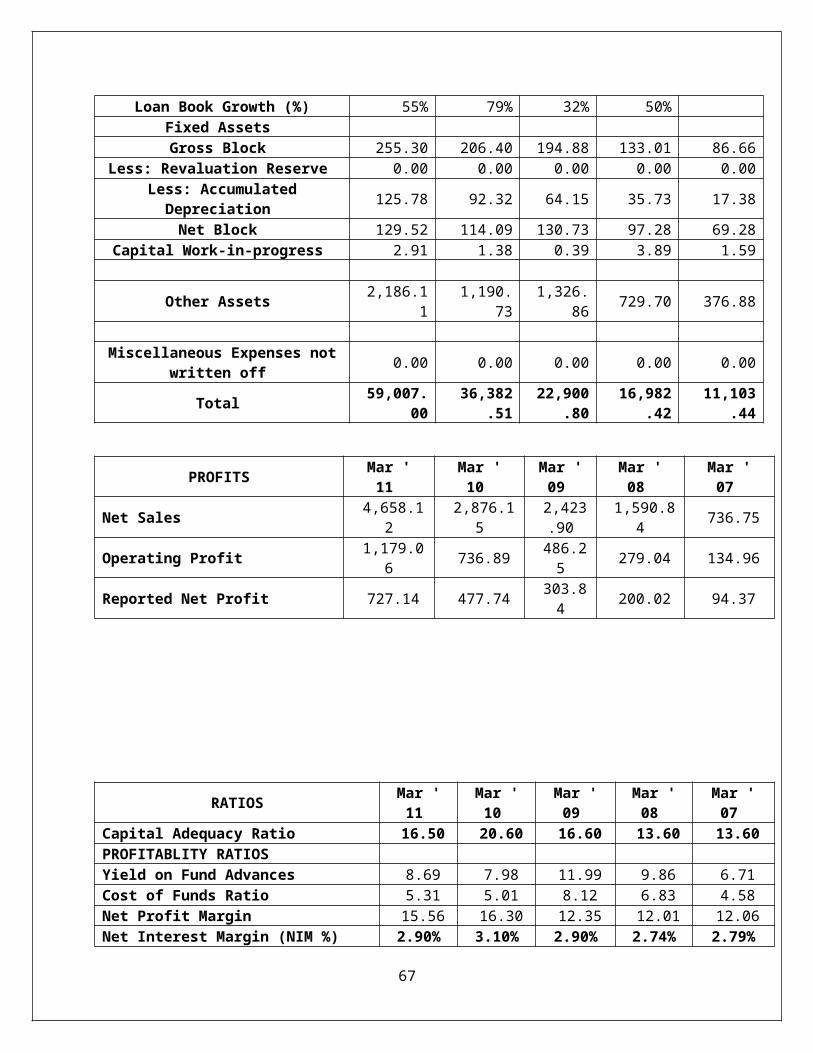

Loan Book Growth (%) 55% 79% 32% 50% Fixed Assets Gross Block 255.30 206.40 194.88 133.01 86.66

Less: Revaluation Reserve 0.00 0.00 0.00 0.00 0.00Less: AccumulatedDepreciation 125.78 92.32 64.15 35.73 17.38

Net Block 129.52 114.09 130.73 97.28 69.28Capital Work-in-progress 2.91 1.38 0.39 3.89 1.59

Other Assets 2,186.11

1,190.73

1,326.86 729.70 376.88

Miscellaneous Expenses not

written off 0.00 0.00 0.00 0.00 0.00

Total 59,007.00

36,382.51

22,900.80

16,982.42

11,103.44

PROFITS Mar '11

Mar '10

Mar '09

Mar '08

Mar '07

Net Sales 4,658.12

2,876.15

2,423.90

1,590.84 736.75

Operating Profit 1,179.06 736.89 486.2

5 279.04 134.96

Reported Net Profit 727.14 477.74 303.84 200.02 94.37

RATIOS Mar '11

Mar '10

Mar '09

Mar '08

Mar '07

Capital Adequacy Ratio 16.50 20.60 16.60 13.60 13.60PROFITABLITY RATIOS Yield on Fund Advances 8.69 7.98 11.99 9.86 6.71Cost of Funds Ratio 5.31 5.01 8.12 6.83 4.58Net Profit Margin 15.56 16.30 12.35 12.01 12.06Net Interest Margin (NIM %) 2.90% 3.10% 2.90% 2.74% 2.79%

67

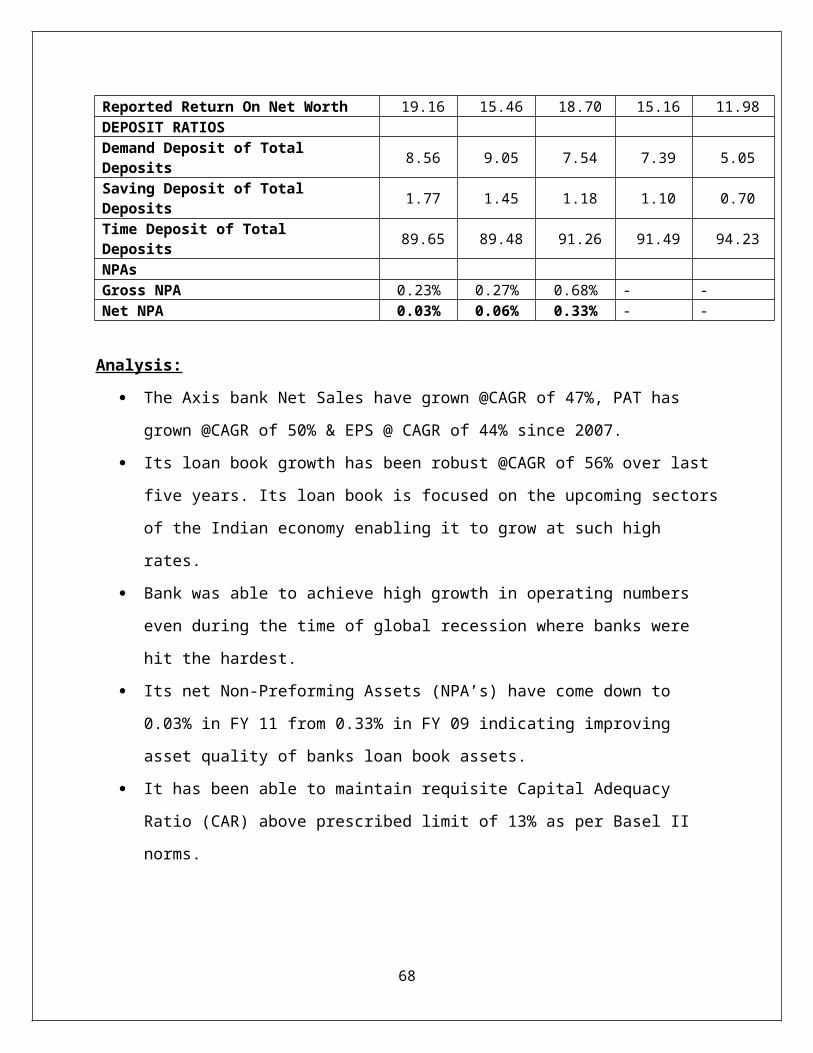

Reported Return On Net Worth 19.16 15.46 18.70 15.16 11.98DEPOSIT RATIOS Demand Deposit of Total Deposits 8.56 9.05 7.54 7.39 5.05

Saving Deposit of Total Deposits 1.77 1.45 1.18 1.10 0.70

Time Deposit of Total Deposits 89.65 89.48 91.26 91.49 94.23

NPAs Gross NPA 0.23% 0.27% 0.68% - -Net NPA 0.03% 0.06% 0.33% - -

Analysis:

The Axis bank Net Sales have grown @CAGR of 47%, PAT has

grown @CAGR of 50% & EPS @ CAGR of 44% since 2007.

Its loan book growth has been robust @CAGR of 56% over last

five years. Its loan book is focused on the upcoming sectors

of the Indian economy enabling it to grow at such high

rates.

Bank was able to achieve high growth in operating numbers

even during the time of global recession where banks were

hit the hardest.

Its net Non-Preforming Assets (NPA’s) have come down to

0.03% in FY 11 from 0.33% in FY 09 indicating improving

asset quality of banks loan book assets.

It has been able to maintain requisite Capital Adequacy

Ratio (CAR) above prescribed limit of 13% as per Basel II

norms.

68

The bank has achieved various accolades for his superior

performance over the past few years which put the bank in

the league of high quality private banks in India.

Conclusion:

Based on the above analysis we can conclude that if another

recession were to happen considering the superior operating

performance on key parameters which bank has demonstrated in

the recent years, it will be able to survive another

recession.

69

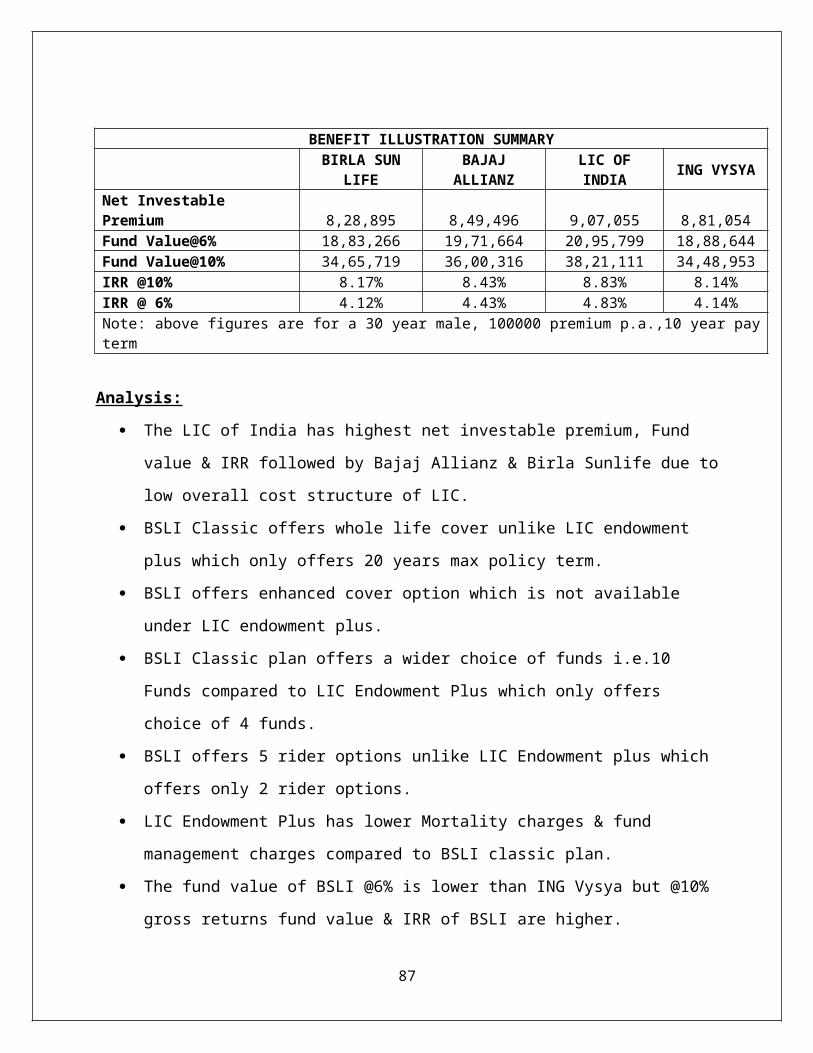

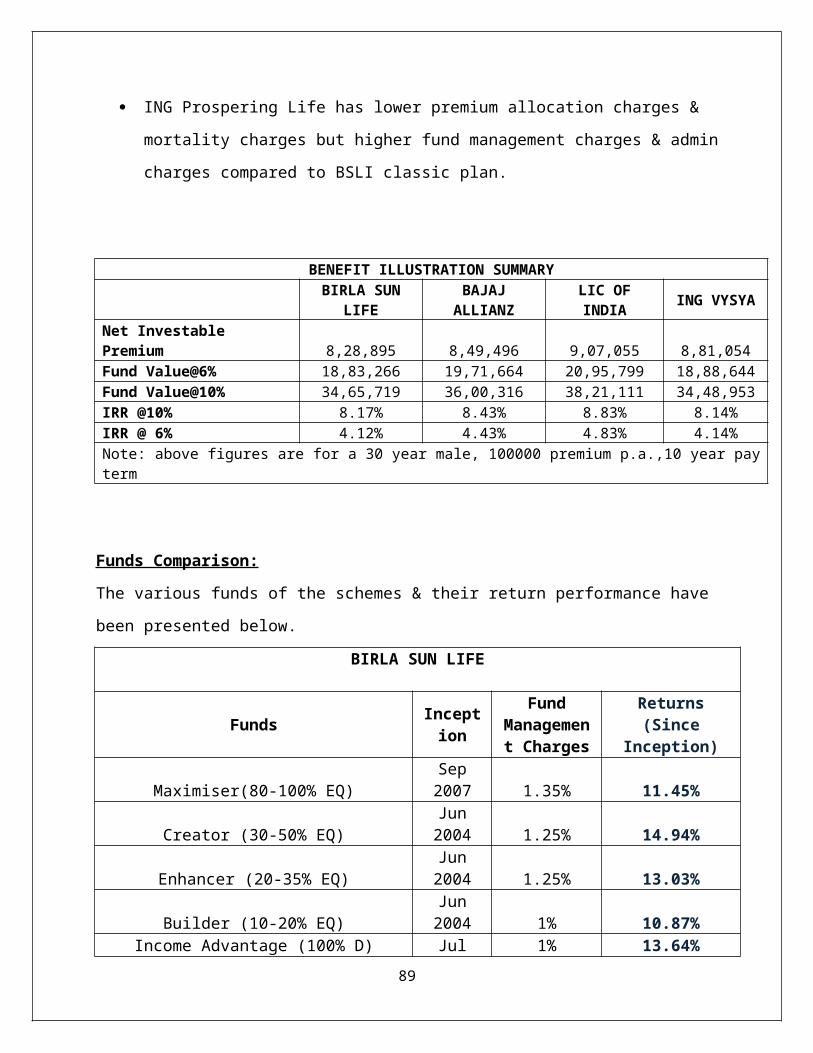

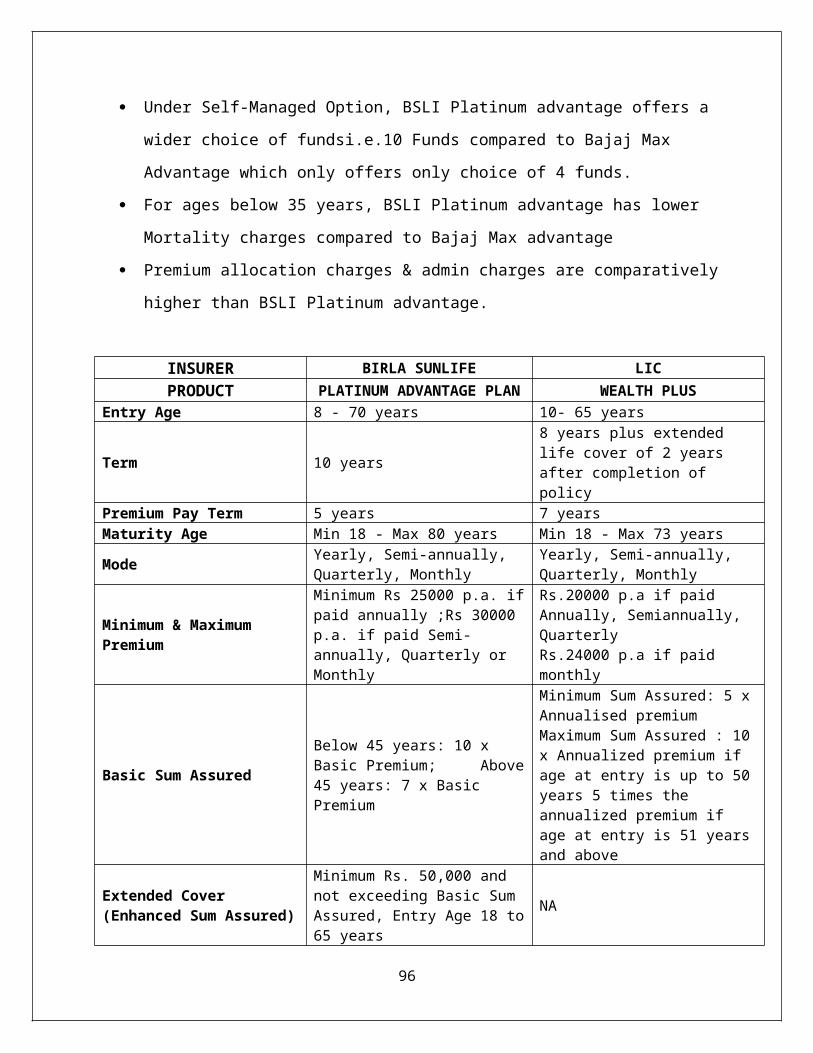

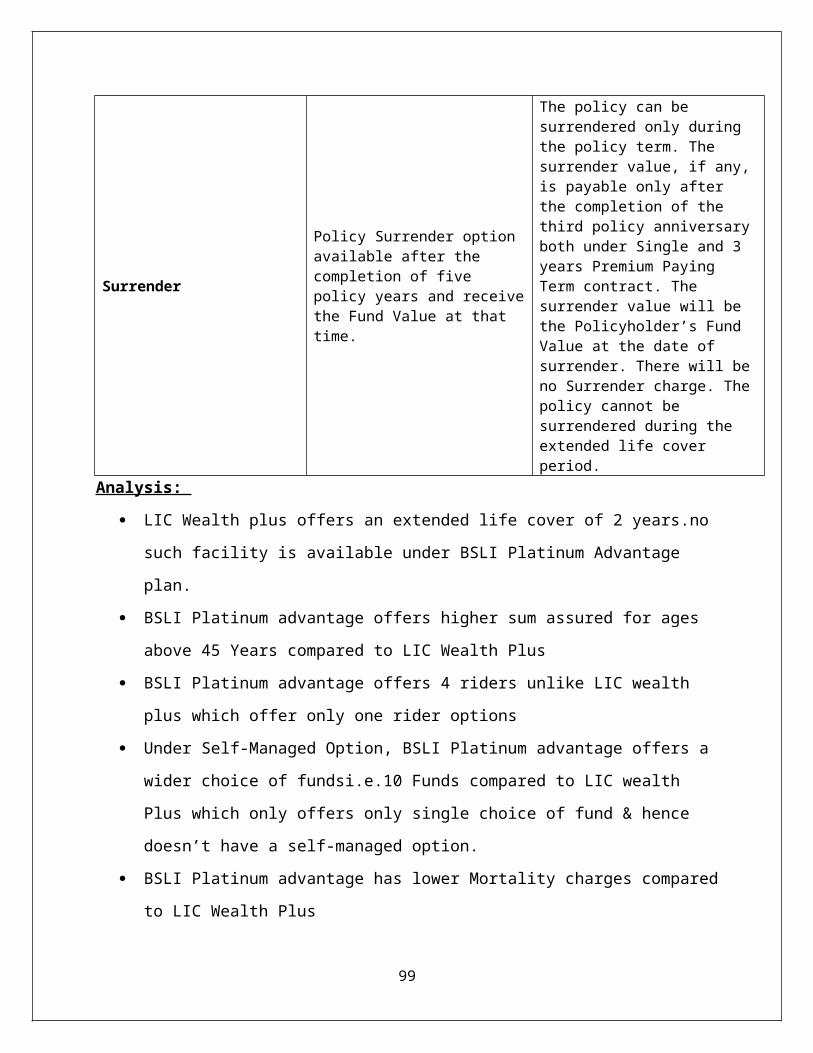

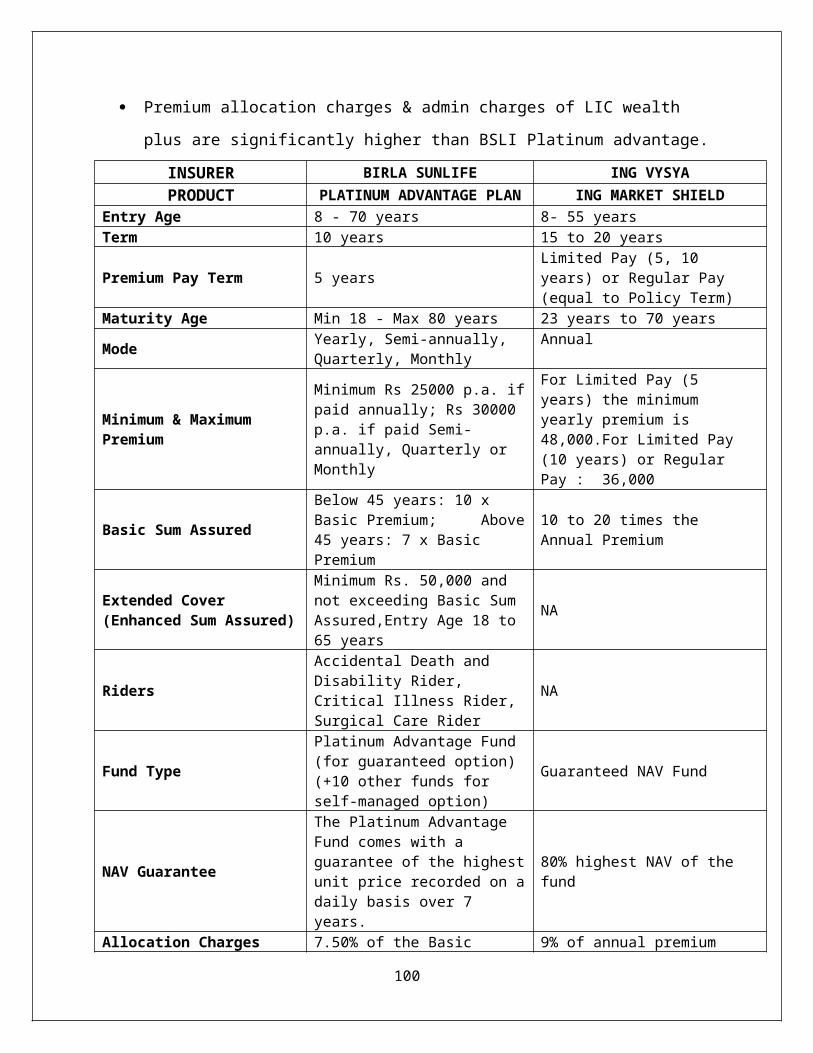

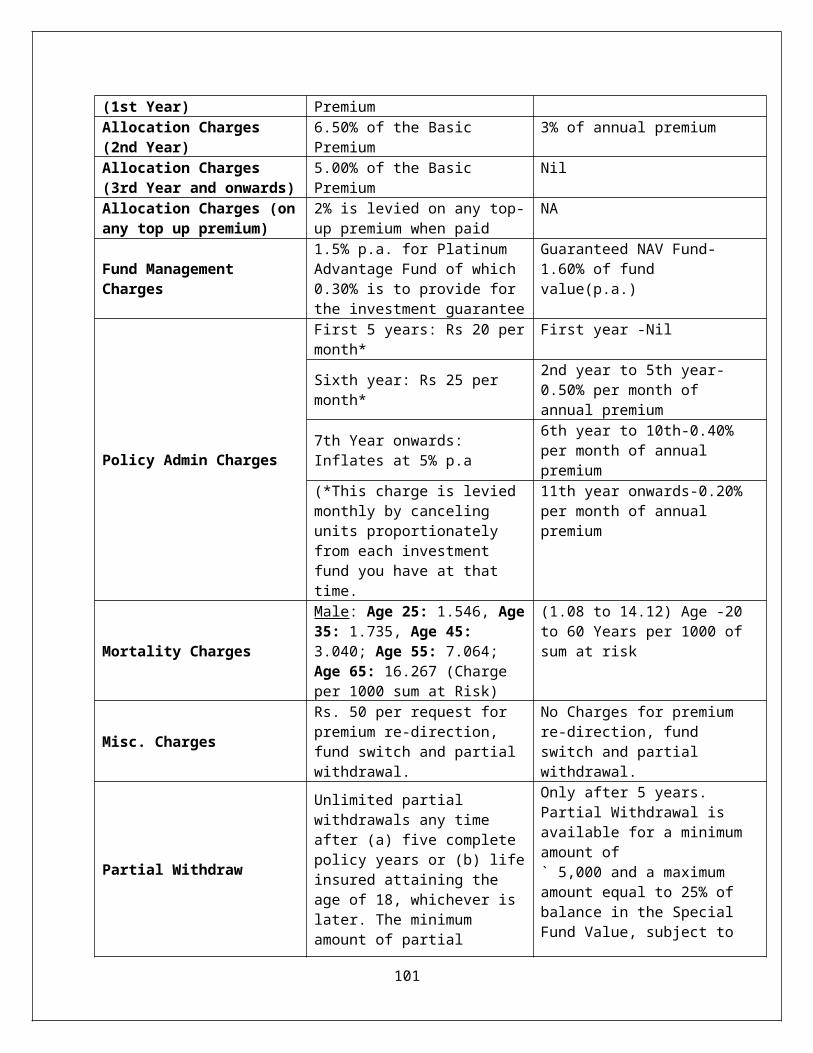

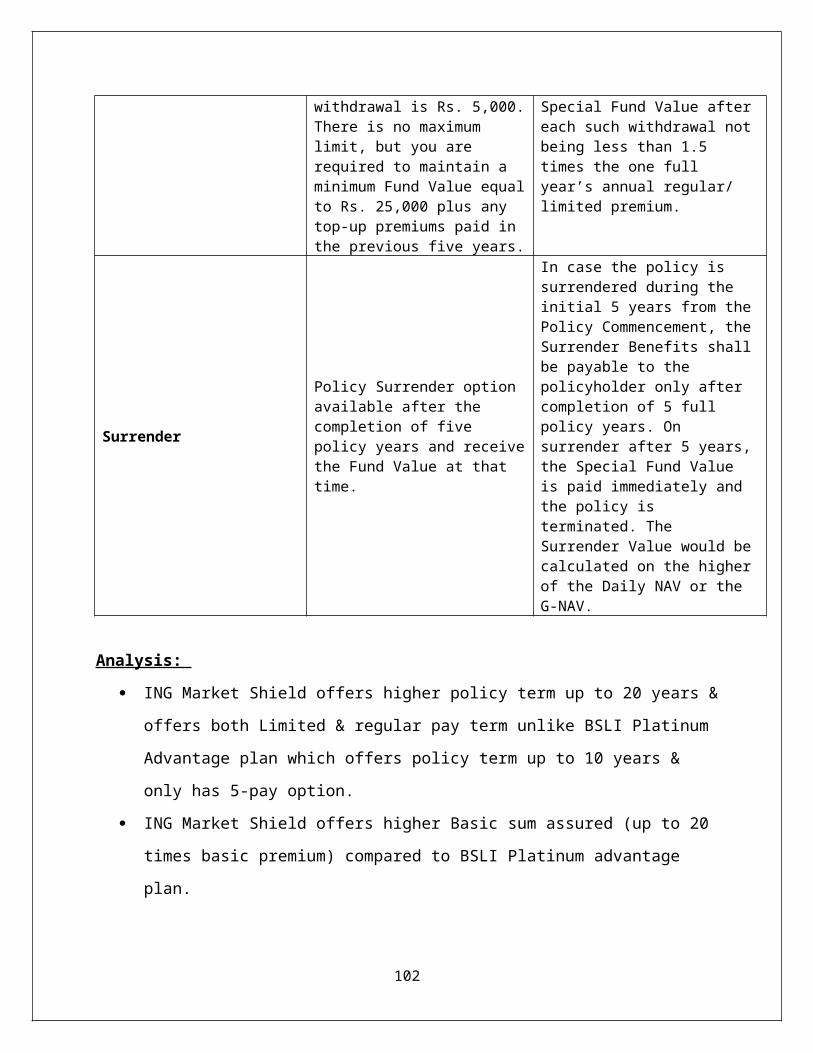

7 COMPETITORS ANALYSIS (ULIPs COMPARISION):

This phase of the project involved comparing one of the most successful ULIP product under BSLI i.e. BSLI Classic Life Planstable with the existing similar products of competitors in the marketplace.

After identifying the similar product of competitors & collection of relevant data, the detail comparison was carriedconsidering all the parameters mentioned above. The competitors selected for the study included LIC, Baja Allianz & ING Vysya.

7.1 INTRODUCTION TO BSLI CLASSIC WHOLE LIFE PLAN

While one works hard towards achieving ambitions, one also

wishes to save for a comfortable retirement. And want a plan

that gives you the flexibility to manage your savings. The

BSLI Classic Life Plan gives complete control over the

investments by directing premiums to range of 10 Investment

Funds along with a range of rider options to give the security

of financial protection.

This plan offers:

Flexibility of directing your savings in 10 Investment

Funds, as per risk appetite

Choice of Pay Term

Whole life cover

Enhanced financial security for loved ones

70

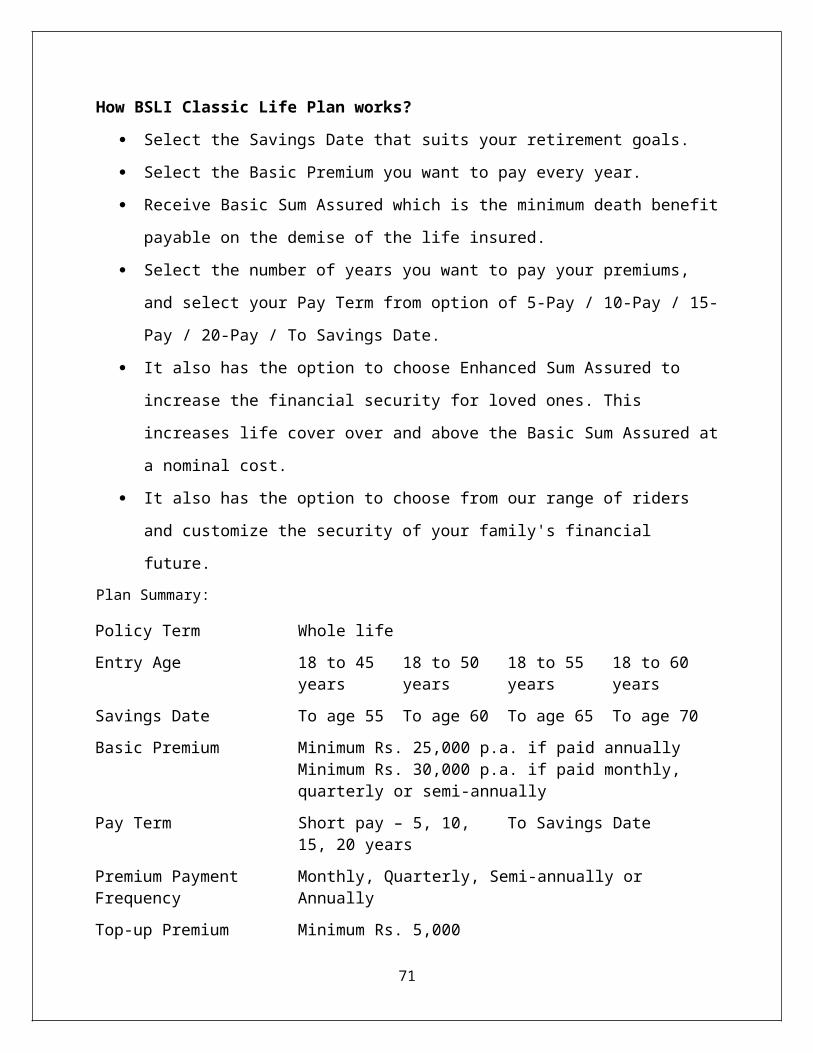

How BSLI Classic Life Plan works?

Select the Savings Date that suits your retirement goals.

Select the Basic Premium you want to pay every year.

Receive Basic Sum Assured which is the minimum death benefit

payable on the demise of the life insured.

Select the number of years you want to pay your premiums,

and select your Pay Term from option of 5-Pay / 10-Pay / 15-

Pay / 20-Pay / To Savings Date.

It also has the option to choose Enhanced Sum Assured to

increase the financial security for loved ones. This

increases life cover over and above the Basic Sum Assured at

a nominal cost.

It also has the option to choose from our range of riders

and customize the security of your family's financial

future.Plan Summary:

Policy Term Whole lifeEntry Age 18 to 45

years18 to 50 years

18 to 55 years

18 to 60 years

Savings Date To age 55 To age 60 To age 65 To age 70Basic Premium Minimum Rs. 25,000 p.a. if paid annually

Minimum Rs. 30,000 p.a. if paid monthly, quarterly or semi-annually

Pay Term Short pay – 5, 10, 15, 20 years

To Savings Date

Premium Payment Frequency

Monthly, Quarterly, Semi-annually or Annually

Top-up Premium Minimum Rs. 5,000

71

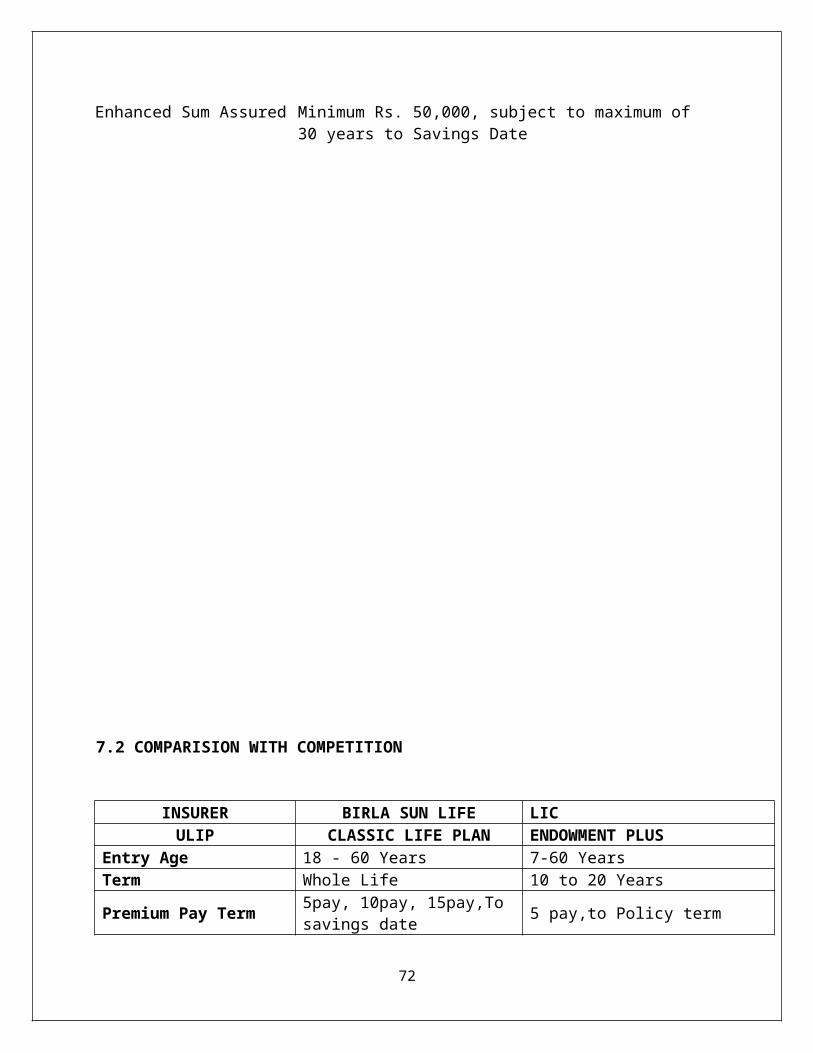

Enhanced Sum Assured Minimum Rs. 50,000, subject to maximum of 30 years to Savings Date

7.2 COMPARISION WITH COMPETITION

INSURER BIRLA SUN LIFE LICULIP CLASSIC LIFE PLAN ENDOWMENT PLUS

Entry Age 18 - 60 Years 7-60 YearsTerm Whole Life 10 to 20 Years

Premium Pay Term 5pay, 10pay, 15pay,To savings date 5 pay,to Policy term

72

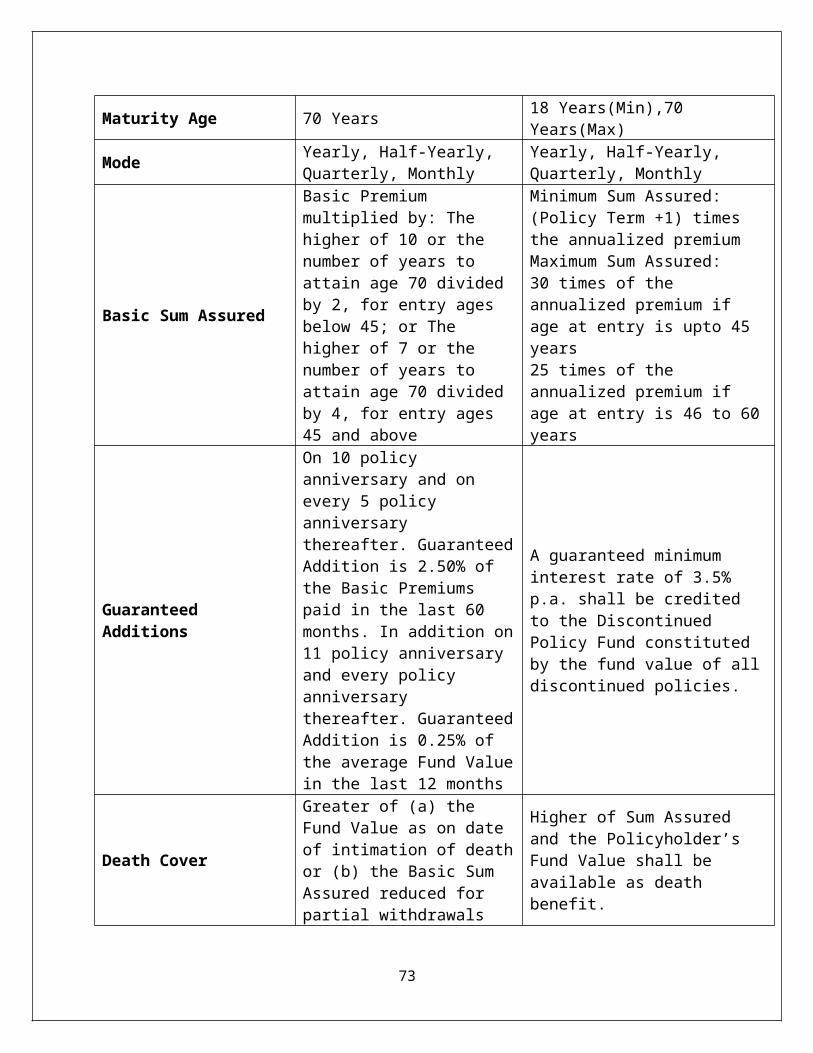

Maturity Age 70 Years 18 Years(Min),70 Years(Max)

Mode Yearly, Half-Yearly, Quarterly, Monthly

Yearly, Half-Yearly, Quarterly, Monthly

Basic Sum Assured

Basic Premium multiplied by: The higher of 10 or the number of years to attain age 70 divided by 2, for entry ages below 45; or The higher of 7 or the number of years to attain age 70 divided by 4, for entry ages45 and above

Minimum Sum Assured: (Policy Term +1) times the annualized premium Maximum Sum Assured:30 times of the annualized premium if age at entry is upto 45 years25 times of the annualized premium if age at entry is 46 to 60years

Guaranteed Additions

On 10 policy anniversary and on every 5 policy anniversary thereafter. GuaranteedAddition is 2.50% of the Basic Premiums paid in the last 60 months. In addition on11 policy anniversary and every policy anniversary thereafter. GuaranteedAddition is 0.25% of the average Fund Valuein the last 12 months

A guaranteed minimum interest rate of 3.5% p.a. shall be credited to the Discontinued Policy Fund constituted by the fund value of alldiscontinued policies.

Death Cover

Greater of (a) the Fund Value as on date of intimation of deathor (b) the Basic Sum Assured reduced for partial withdrawals

Higher of Sum Assured and the Policyholder’s Fund Value shall be available as death benefit.

73

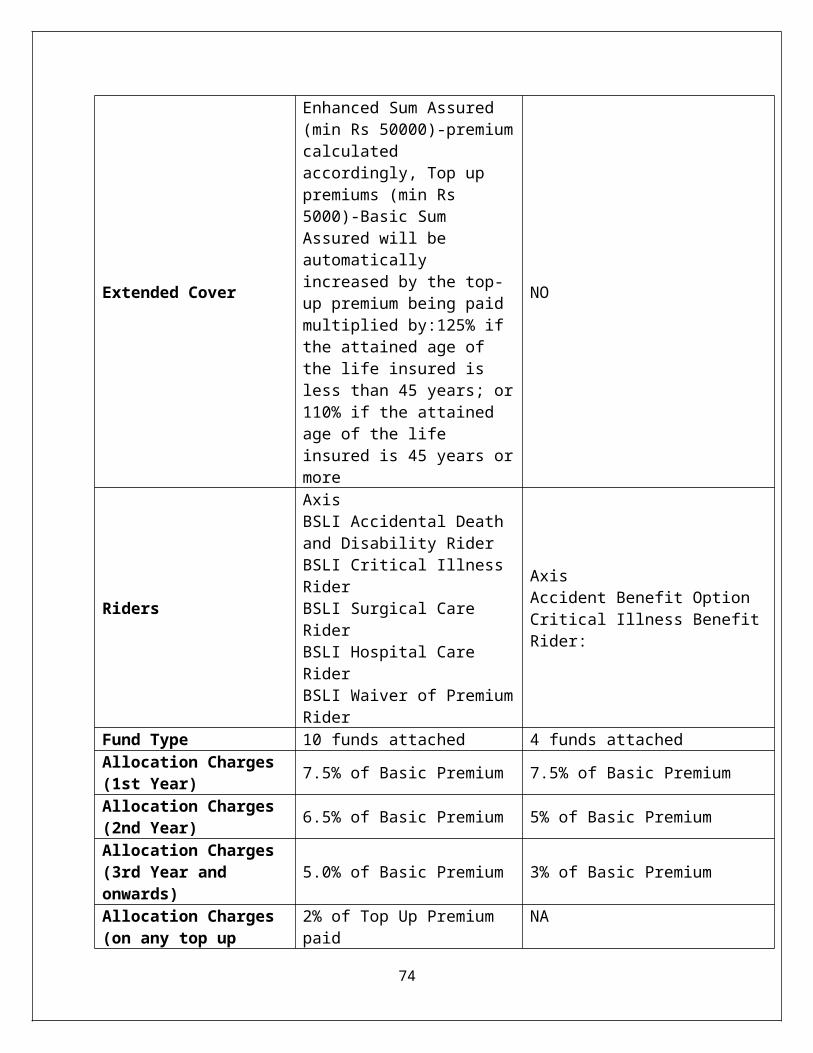

Extended Cover

Enhanced Sum Assured (min Rs 50000)-premiumcalculated accordingly, Top up premiums (min Rs 5000)-Basic Sum Assured will be automatically increased by the top-up premium being paid multiplied by:125% if the attained age of the life insured is less than 45 years; or110% if the attained age of the life insured is 45 years ormore

NO

Riders

Axis BSLI Accidental Death and Disability RiderBSLI Critical Illness RiderBSLI Surgical Care RiderBSLI Hospital Care RiderBSLI Waiver of PremiumRider

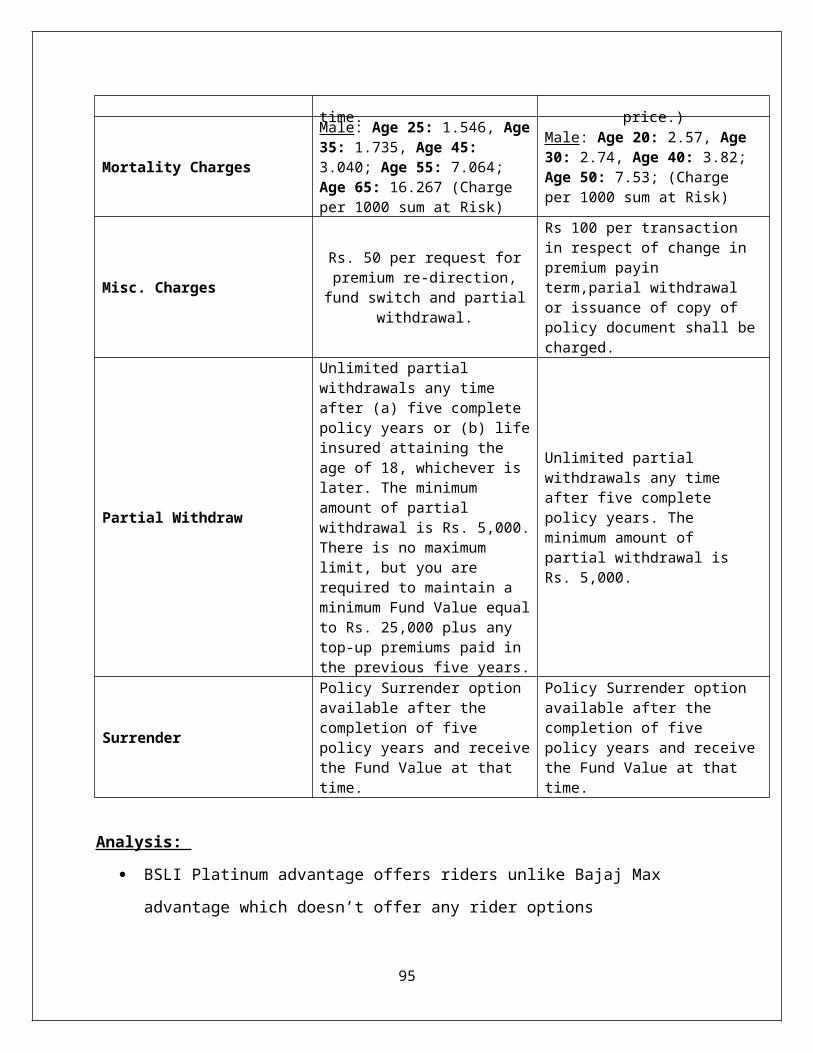

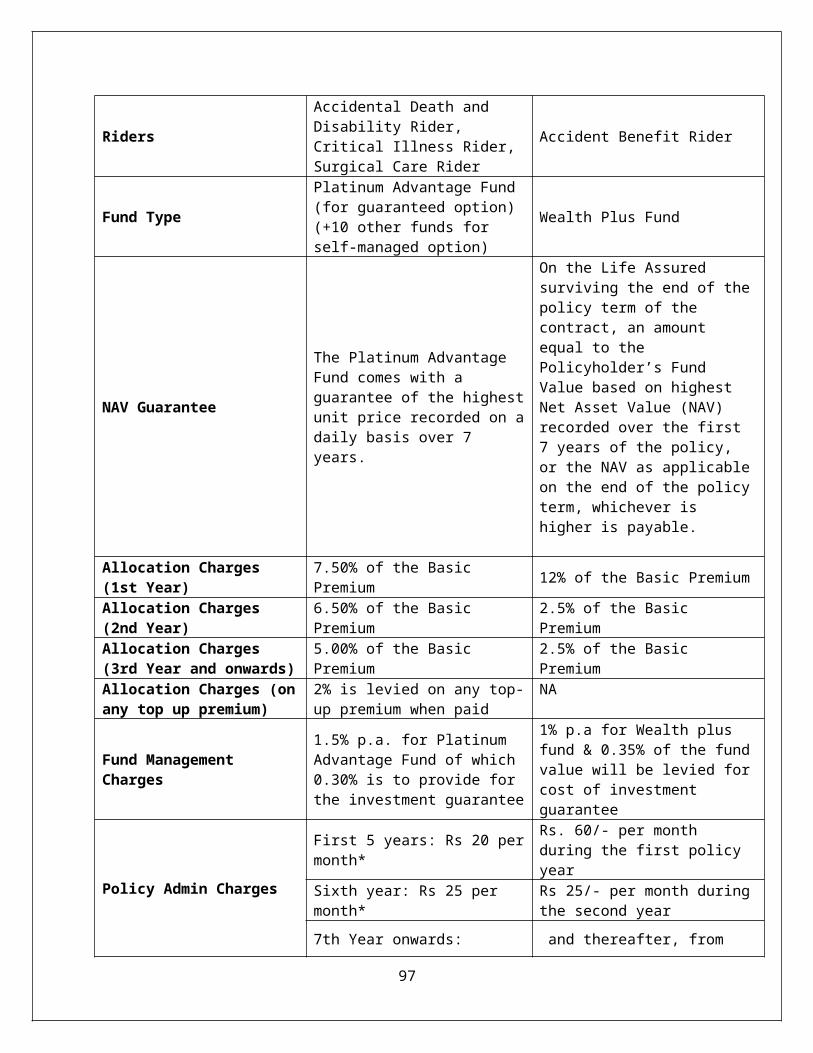

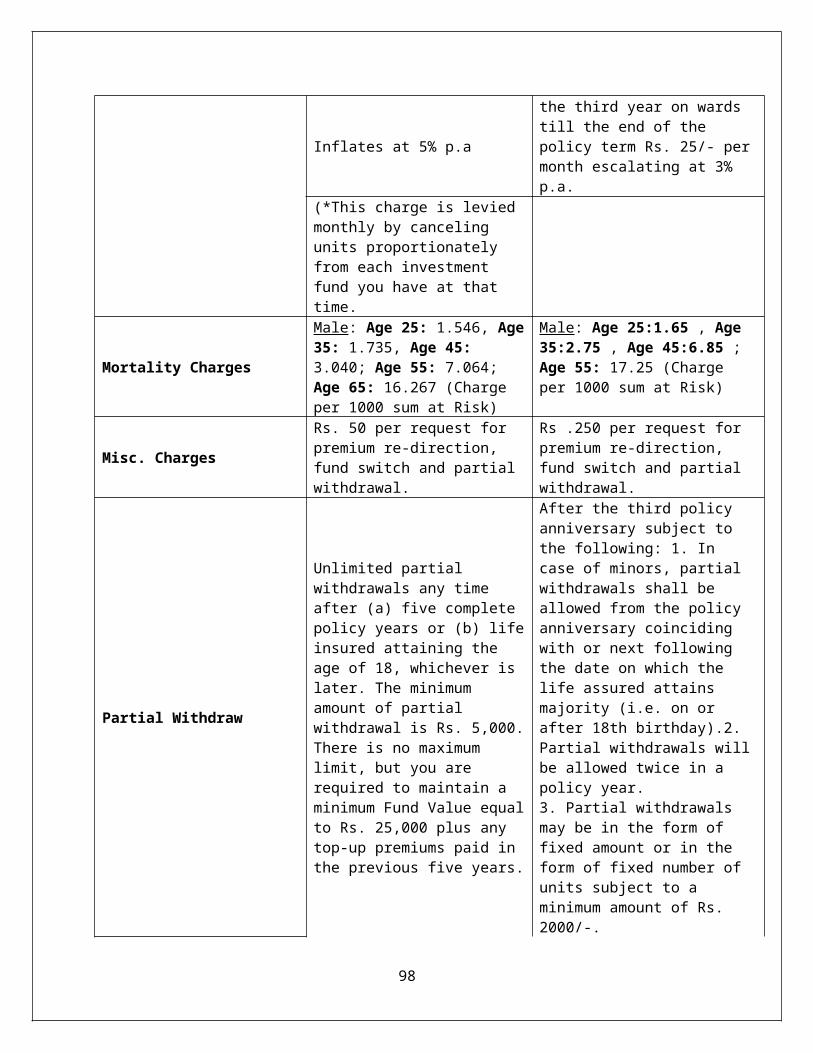

Axis Accident Benefit Option Critical Illness BenefitRider:

Fund Type 10 funds attached 4 funds attachedAllocation Charges (1st Year) 7.5% of Basic Premium 7.5% of Basic Premium

Allocation Charges (2nd Year) 6.5% of Basic Premium 5% of Basic Premium

Allocation Charges (3rd Year and onwards)

5.0% of Basic Premium 3% of Basic Premium

Allocation Charges (on any top up

2% of Top Up Premium paid

NA

74

premium)

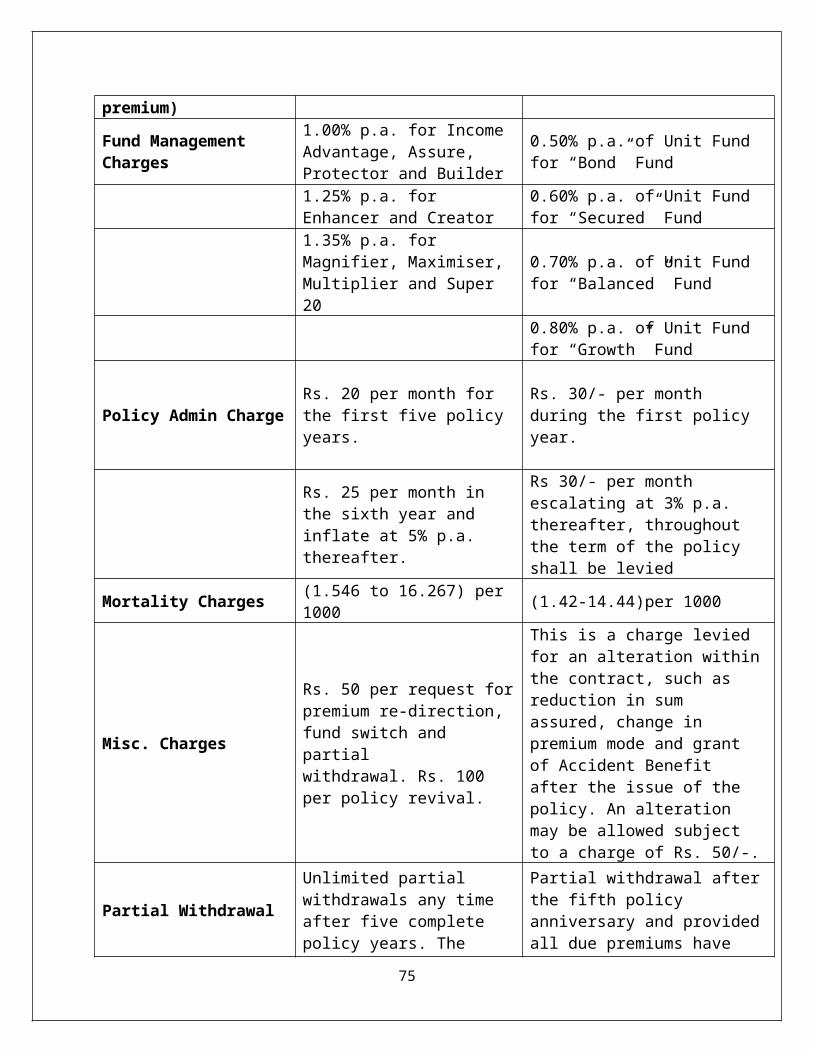

Fund Management Charges

1.00% p.a. for Income Advantage, Assure, Protector and Builder

0.50% p.a. of Unit Fund for “Bond” Fund

1.25% p.a. for Enhancer and Creator

0.60% p.a. of Unit Fund for “Secured” Fund

1.35% p.a. for Magnifier, Maximiser, Multiplier and Super 20

0.70% p.a. of Unit Fund for “Balanced” Fund

0.80% p.a. of Unit Fund for “Growth” Fund

Policy Admin ChargeRs. 20 per month for the first five policy years.

Rs. 30/- per month during the first policy year.

Rs. 25 per month in the sixth year and inflate at 5% p.a. thereafter.

Rs 30/- per month escalating at 3% p.a. thereafter, throughout the term of the policy shall be levied

Mortality Charges (1.546 to 16.267) per 1000 (1.42-14.44)per 1000

Misc. Charges

Rs. 50 per request forpremium re-direction, fund switch and partialwithdrawal. Rs. 100 per policy revival.

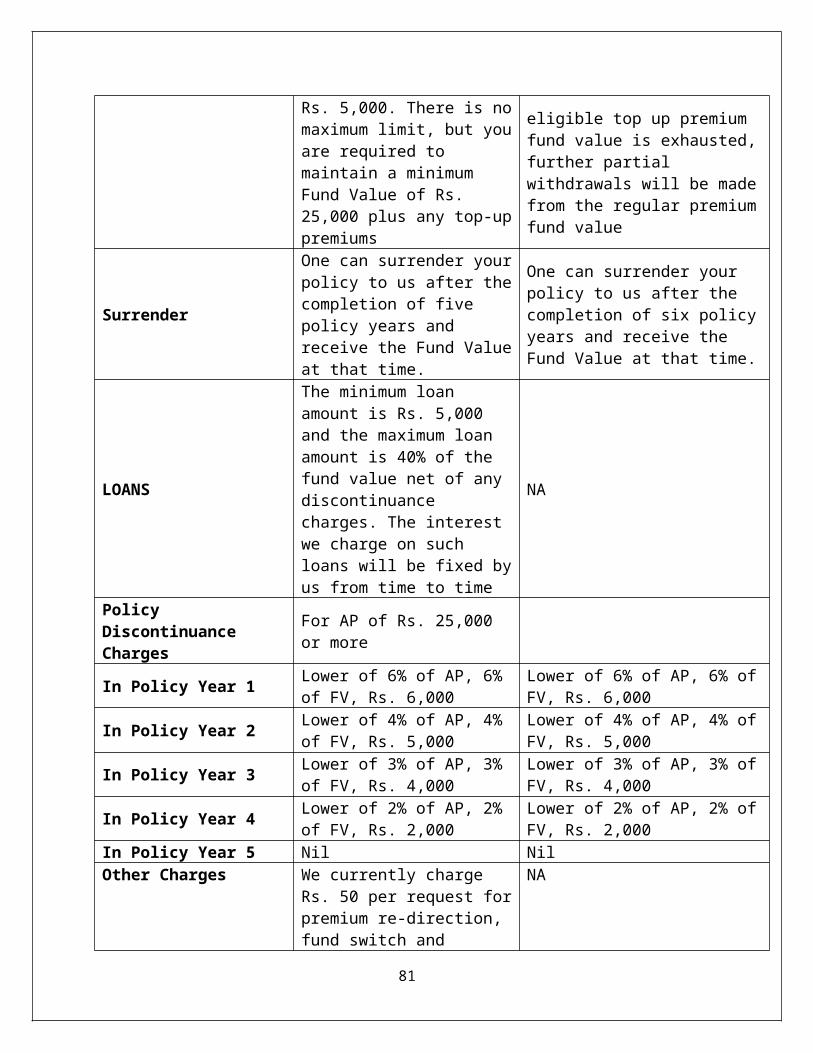

This is a charge levied for an alteration withinthe contract, such as reduction in sum assured, change in premium mode and grant of Accident Benefit after the issue of the policy. An alteration may be allowed subject to a charge of Rs. 50/-.

Partial Withdrawal

Unlimited partial withdrawals any time after five complete policy years. The

Partial withdrawal afterthe fifth policy anniversary and providedall due premiums have

75

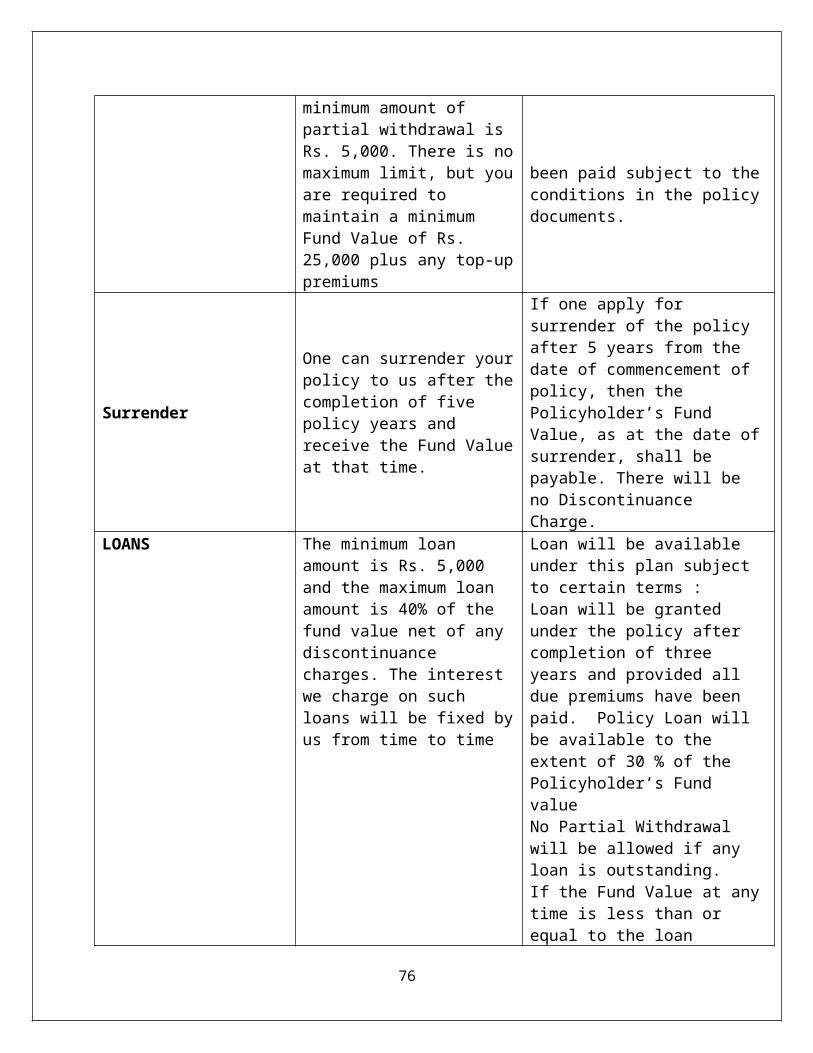

minimum amount of partial withdrawal is Rs. 5,000. There is nomaximum limit, but youare required to maintain a minimum Fund Value of Rs. 25,000 plus any top-uppremiums

been paid subject to theconditions in the policydocuments.

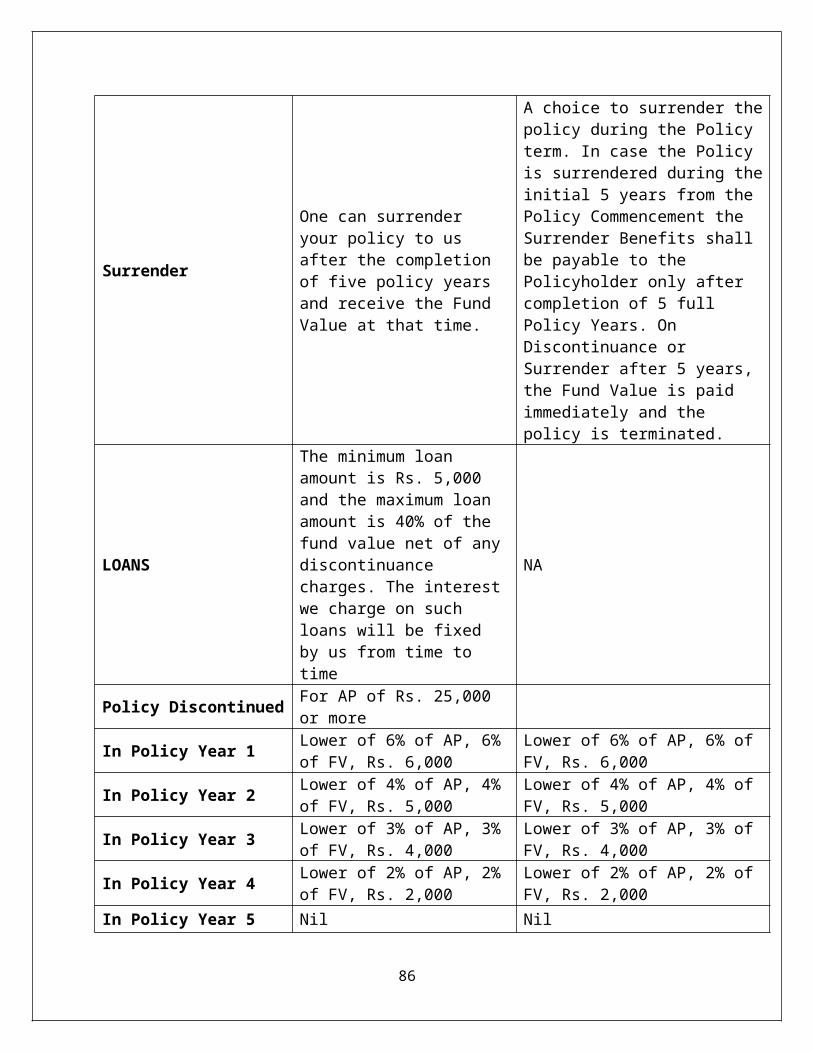

Surrender

One can surrender yourpolicy to us after thecompletion of five policy years and receive the Fund Valueat that time.

If one apply for surrender of the policy after 5 years from the date of commencement of policy, then the Policyholder’s Fund Value, as at the date ofsurrender, shall be payable. There will be no Discontinuance Charge.

LOANS The minimum loan amount is Rs. 5,000 and the maximum loan amount is 40% of the fund value net of any discontinuance charges. The interest we charge on such loans will be fixed byus from time to time

Loan will be available under this plan subject to certain terms : Loan will be granted under the policy after completion of three years and provided all due premiums have been paid. Policy Loan will be available to the extent of 30 % of the Policyholder’s Fund value No Partial Withdrawal will be allowed if any loan is outstanding. If the Fund Value at anytime is less than or equal to the loan

76

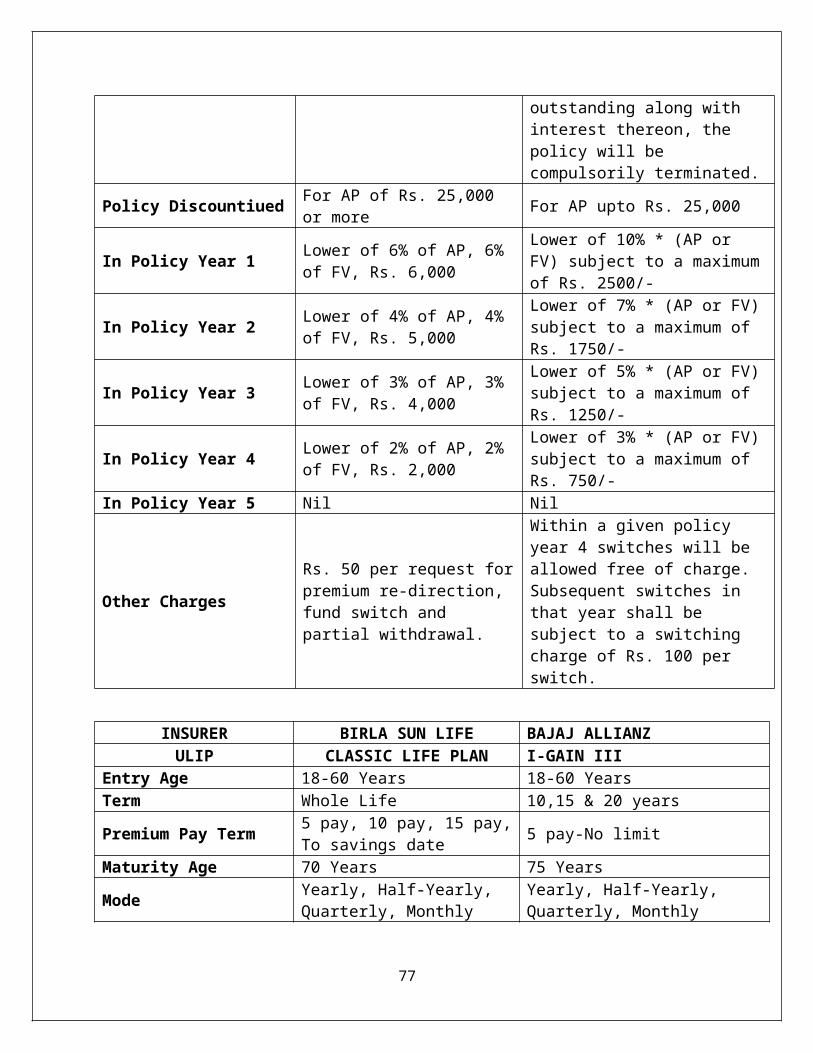

outstanding along with interest thereon, the policy will be compulsorily terminated.

Policy Discountiued For AP of Rs. 25,000 or more For AP upto Rs. 25,000

In Policy Year 1 Lower of 6% of AP, 6% of FV, Rs. 6,000

Lower of 10% * (AP or FV) subject to a maximumof Rs. 2500/-

In Policy Year 2 Lower of 4% of AP, 4% of FV, Rs. 5,000

Lower of 7% * (AP or FV)subject to a maximum of Rs. 1750/-

In Policy Year 3 Lower of 3% of AP, 3% of FV, Rs. 4,000

Lower of 5% * (AP or FV)subject to a maximum of Rs. 1250/-

In Policy Year 4 Lower of 2% of AP, 2% of FV, Rs. 2,000

Lower of 3% * (AP or FV)subject to a maximum of Rs. 750/-

In Policy Year 5 Nil Nil

Other Charges

Rs. 50 per request forpremium re-direction, fund switch and partial withdrawal.

Within a given policy year 4 switches will be allowed free of charge. Subsequent switches in that year shall be subject to a switching charge of Rs. 100 per switch.

INSURER BIRLA SUN LIFE BAJAJ ALLIANZULIP CLASSIC LIFE PLAN I-GAIN III

Entry Age 18-60 Years 18-60 YearsTerm Whole Life 10,15 & 20 years

Premium Pay Term 5 pay, 10 pay, 15 pay,To savings date 5 pay-No limit

Maturity Age 70 Years 75 Years

Mode Yearly, Half-Yearly, Quarterly, Monthly

Yearly, Half-Yearly, Quarterly, Monthly

77

Basic Sum Assured

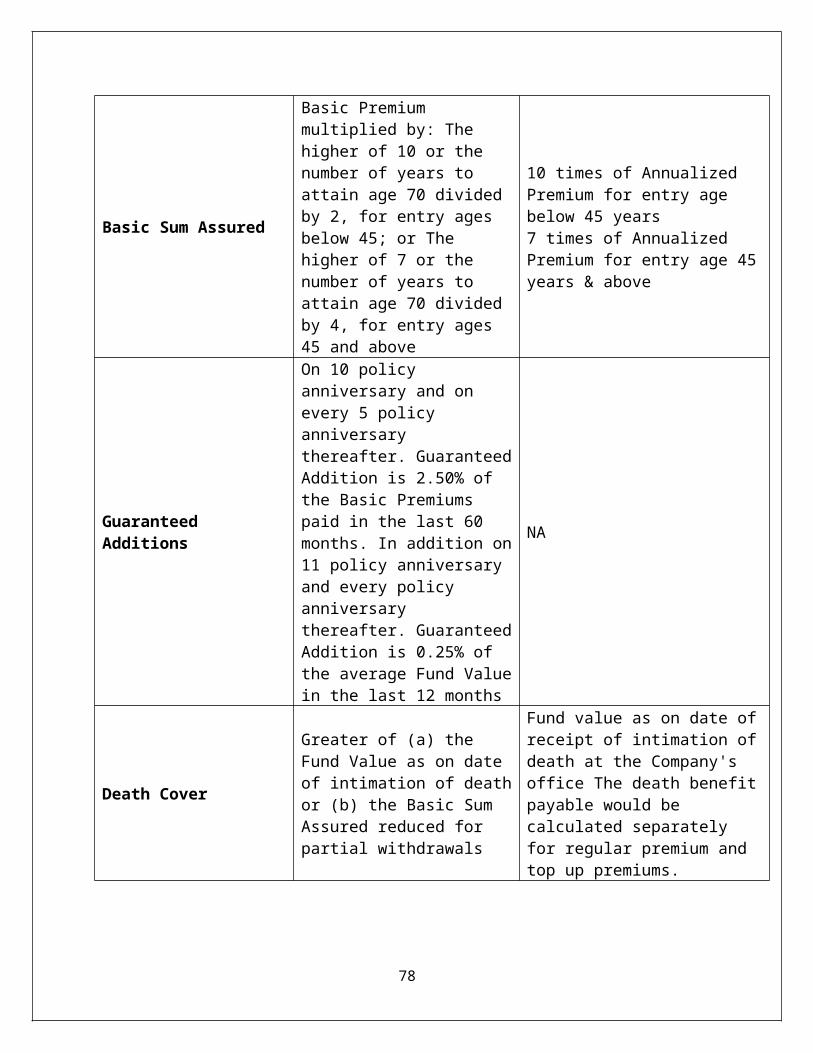

Basic Premium multiplied by: The higher of 10 or the number of years to attain age 70 divided by 2, for entry ages below 45; or The higher of 7 or the number of years to attain age 70 divided by 4, for entry ages45 and above

10 times of Annualized Premium for entry age below 45 years7 times of Annualized Premium for entry age 45years & above

Guaranteed Additions

On 10 policy anniversary and on every 5 policy anniversary thereafter. GuaranteedAddition is 2.50% of the Basic Premiums paid in the last 60 months. In addition on11 policy anniversary and every policy anniversary thereafter. GuaranteedAddition is 0.25% of the average Fund Valuein the last 12 months

NA

Death Cover

Greater of (a) the Fund Value as on date of intimation of deathor (b) the Basic Sum Assured reduced for partial withdrawals

Fund value as on date ofreceipt of intimation ofdeath at the Company's office The death benefitpayable would be calculated separately for regular premium and top up premiums.

78

Extended Cover

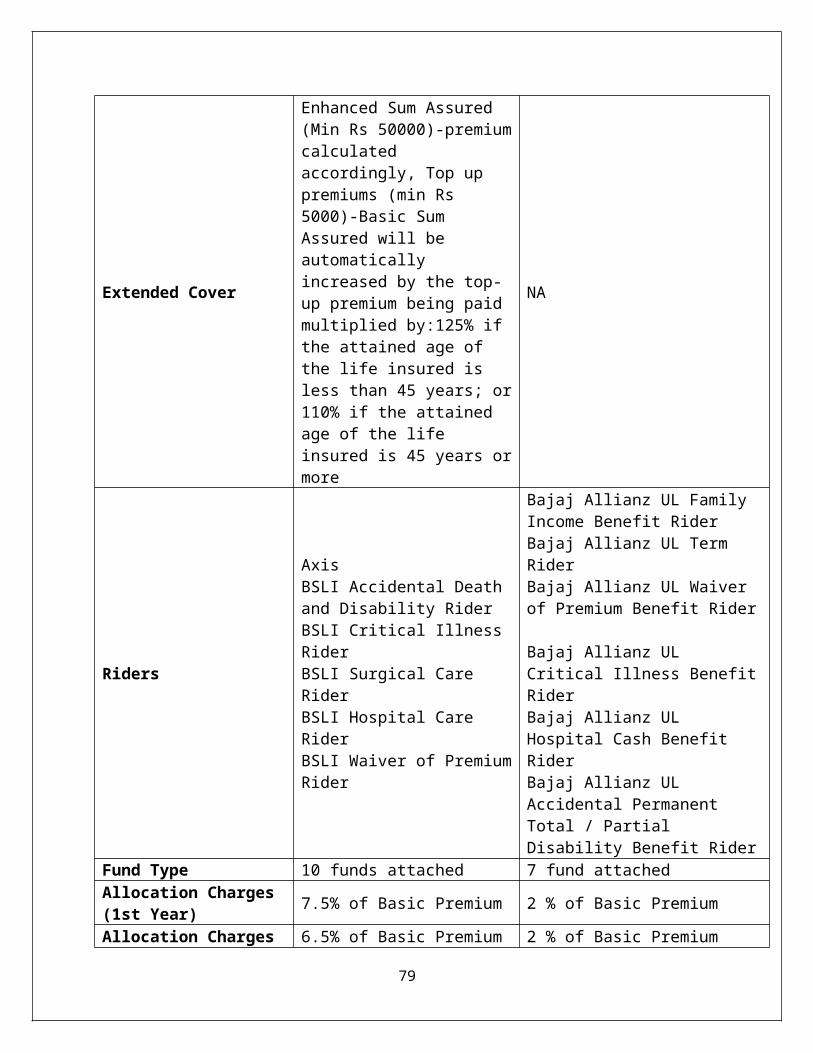

Enhanced Sum Assured (Min Rs 50000)-premiumcalculated accordingly, Top up premiums (min Rs 5000)-Basic Sum Assured will be automatically increased by the top-up premium being paid multiplied by:125% if the attained age of the life insured is less than 45 years; or110% if the attained age of the life insured is 45 years ormore

NA

Riders

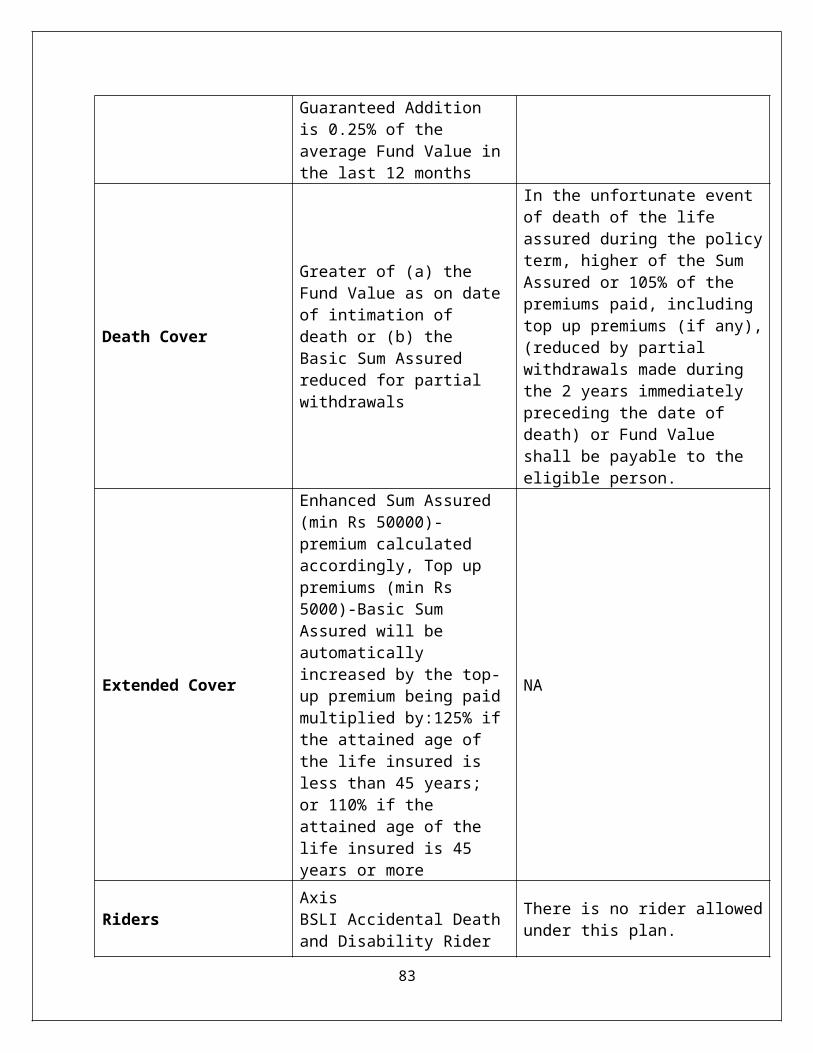

Axis BSLI Accidental Death and Disability RiderBSLI Critical Illness RiderBSLI Surgical Care RiderBSLI Hospital Care RiderBSLI Waiver of PremiumRider

Bajaj Allianz UL Family Income Benefit RiderBajaj Allianz UL Term RiderBajaj Allianz UL Waiver of Premium Benefit Rider

Bajaj Allianz UL Critical Illness BenefitRider Bajaj Allianz UL Hospital Cash Benefit Rider Bajaj Allianz UL Accidental Permanent Total / Partial Disability Benefit Rider

Fund Type 10 funds attached 7 fund attachedAllocation Charges (1st Year) 7.5% of Basic Premium 2 % of Basic Premium

Allocation Charges 6.5% of Basic Premium 2 % of Basic Premium

79

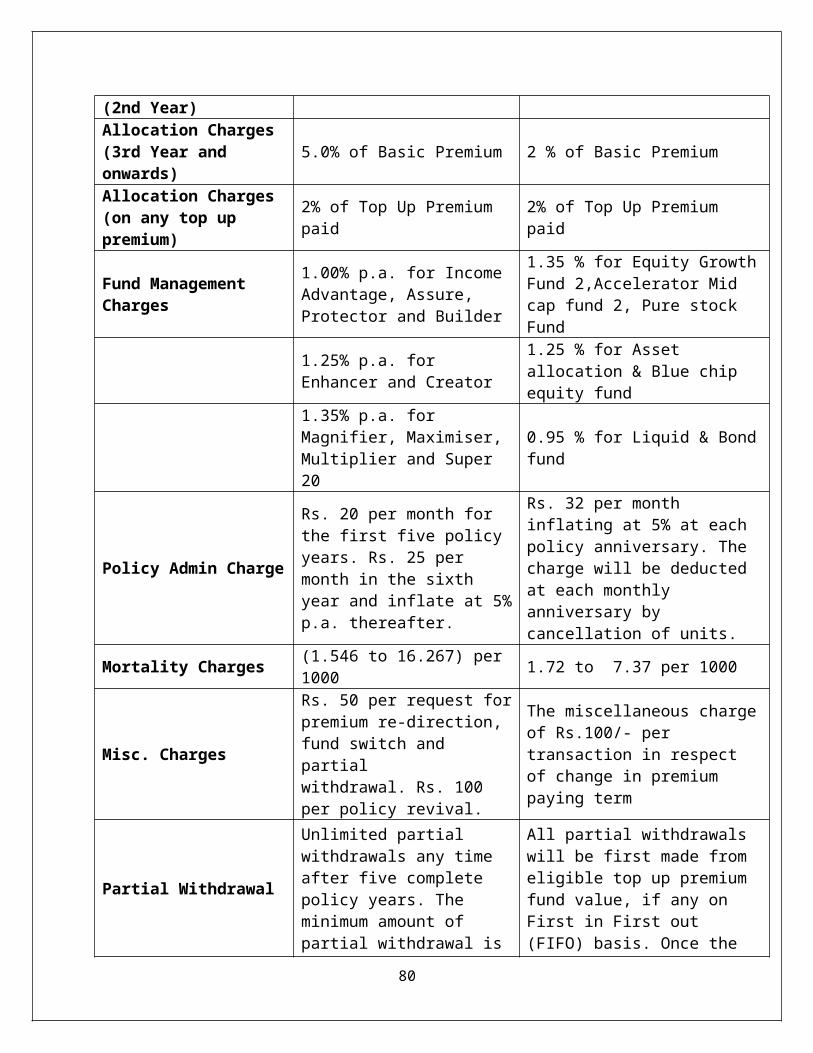

(2nd Year)Allocation Charges (3rd Year and onwards)

5.0% of Basic Premium 2 % of Basic Premium

Allocation Charges (on any top up premium)

2% of Top Up Premium paid

2% of Top Up Premium paid

Fund Management Charges

1.00% p.a. for Income Advantage, Assure, Protector and Builder

1.35 % for Equity GrowthFund 2,Accelerator Mid cap fund 2, Pure stock Fund

1.25% p.a. for Enhancer and Creator

1.25 % for Asset allocation & Blue chip equity fund

1.35% p.a. for Magnifier, Maximiser, Multiplier and Super 20

0.95 % for Liquid & Bondfund

Policy Admin Charge

Rs. 20 per month for the first five policy years. Rs. 25 per month in the sixth year and inflate at 5%p.a. thereafter.

Rs. 32 per month inflating at 5% at each policy anniversary. The charge will be deducted at each monthly anniversary by cancellation of units.

Mortality Charges (1.546 to 16.267) per 1000 1.72 to 7.37 per 1000

Misc. Charges

Rs. 50 per request forpremium re-direction, fund switch and partialwithdrawal. Rs. 100 per policy revival.

The miscellaneous chargeof Rs.100/- per transaction in respect of change in premium paying term

Partial Withdrawal

Unlimited partial withdrawals any time after five complete policy years. The minimum amount of partial withdrawal is

All partial withdrawals will be first made from eligible top up premium fund value, if any on First in First out (FIFO) basis. Once the

80

Rs. 5,000. There is nomaximum limit, but youare required to maintain a minimum Fund Value of Rs. 25,000 plus any top-uppremiums

eligible top up premium fund value is exhausted,further partial withdrawals will be madefrom the regular premiumfund value

Surrender

One can surrender yourpolicy to us after thecompletion of five policy years and receive the Fund Valueat that time.

One can surrender your policy to us after the completion of six policyyears and receive the Fund Value at that time.

LOANS

The minimum loan amount is Rs. 5,000 and the maximum loan amount is 40% of the fund value net of any discontinuance charges. The interest we charge on such loans will be fixed byus from time to time

NA

Policy Discontinuance Charges

For AP of Rs. 25,000 or more

In Policy Year 1 Lower of 6% of AP, 6% of FV, Rs. 6,000

Lower of 6% of AP, 6% ofFV, Rs. 6,000

In Policy Year 2 Lower of 4% of AP, 4% of FV, Rs. 5,000

Lower of 4% of AP, 4% ofFV, Rs. 5,000

In Policy Year 3 Lower of 3% of AP, 3% of FV, Rs. 4,000

Lower of 3% of AP, 3% ofFV, Rs. 4,000

In Policy Year 4 Lower of 2% of AP, 2% of FV, Rs. 2,000

Lower of 2% of AP, 2% ofFV, Rs. 2,000

In Policy Year 5 Nil NilOther Charges We currently charge

Rs. 50 per request forpremium re-direction, fund switch and

NA

81

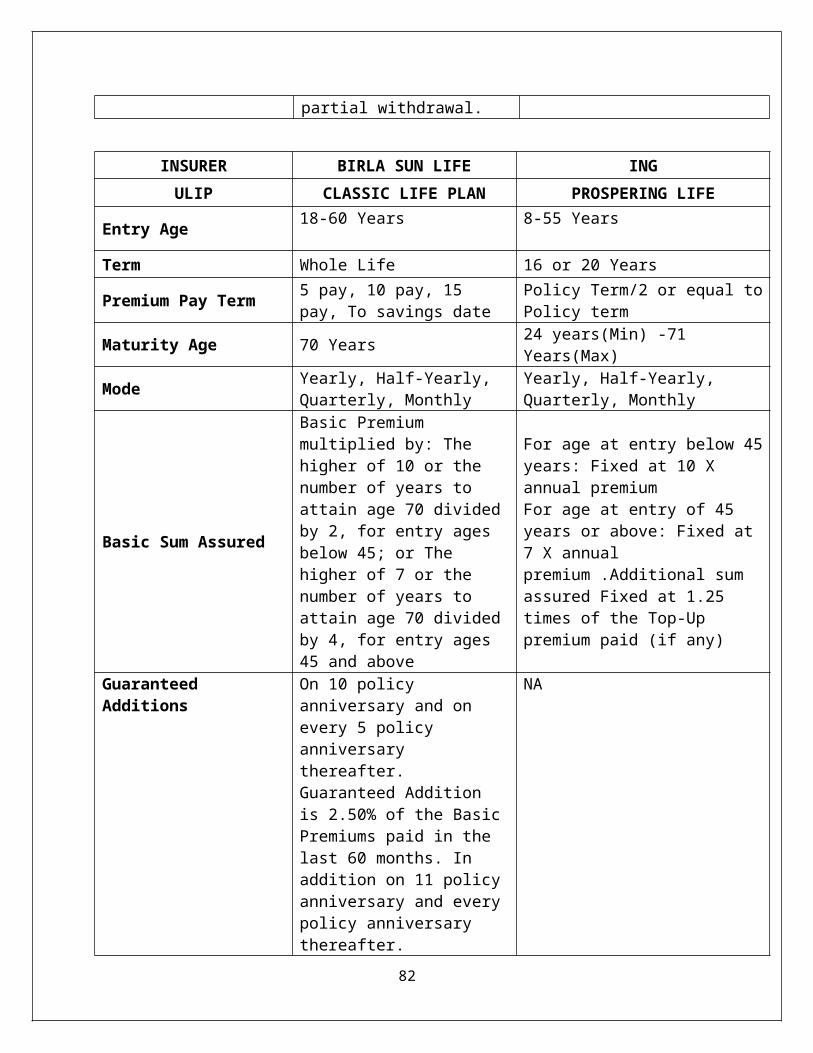

partial withdrawal.

INSURER BIRLA SUN LIFE INGULIP CLASSIC LIFE PLAN PROSPERING LIFE

Entry Age 18-60 Years 8-55 Years

Term Whole Life 16 or 20 Years

Premium Pay Term 5 pay, 10 pay, 15 pay, To savings date

Policy Term/2 or equal toPolicy term

Maturity Age 70 Years 24 years(Min) -71 Years(Max)

Mode Yearly, Half-Yearly, Quarterly, Monthly

Yearly, Half-Yearly, Quarterly, Monthly

Basic Sum Assured

Basic Premium multiplied by: The higher of 10 or the number of years to attain age 70 dividedby 2, for entry ages below 45; or The higher of 7 or the number of years to attain age 70 dividedby 4, for entry ages45 and above

For age at entry below 45years: Fixed at 10 X annual premiumFor age at entry of 45 years or above: Fixed at 7 X annual premium .Additional sum assured Fixed at 1.25 times of the Top-Up premium paid (if any)

Guaranteed Additions

On 10 policy anniversary and on every 5 policy anniversary thereafter. Guaranteed Addition is 2.50% of the BasicPremiums paid in the last 60 months. In addition on 11 policyanniversary and everypolicy anniversary thereafter.

NA

82

Guaranteed Addition is 0.25% of the average Fund Value inthe last 12 months

Death Cover

Greater of (a) the Fund Value as on dateof intimation of death or (b) the Basic Sum Assured reduced for partial withdrawals

In the unfortunate event of death of the life assured during the policyterm, higher of the Sum Assured or 105% of the premiums paid, including top up premiums (if any),(reduced by partial withdrawals made during the 2 years immediately preceding the date of death) or Fund Value shall be payable to the eligible person.

Extended Cover

Enhanced Sum Assured (min Rs 50000)-premium calculated accordingly, Top up premiums (min Rs 5000)-Basic Sum Assured will be automatically increased by the top-up premium being paidmultiplied by:125% ifthe attained age of the life insured is less than 45 years; or 110% if the attained age of the life insured is 45 years or more

NA

RidersAxis BSLI Accidental Deathand Disability Rider

There is no rider allowedunder this plan.

83

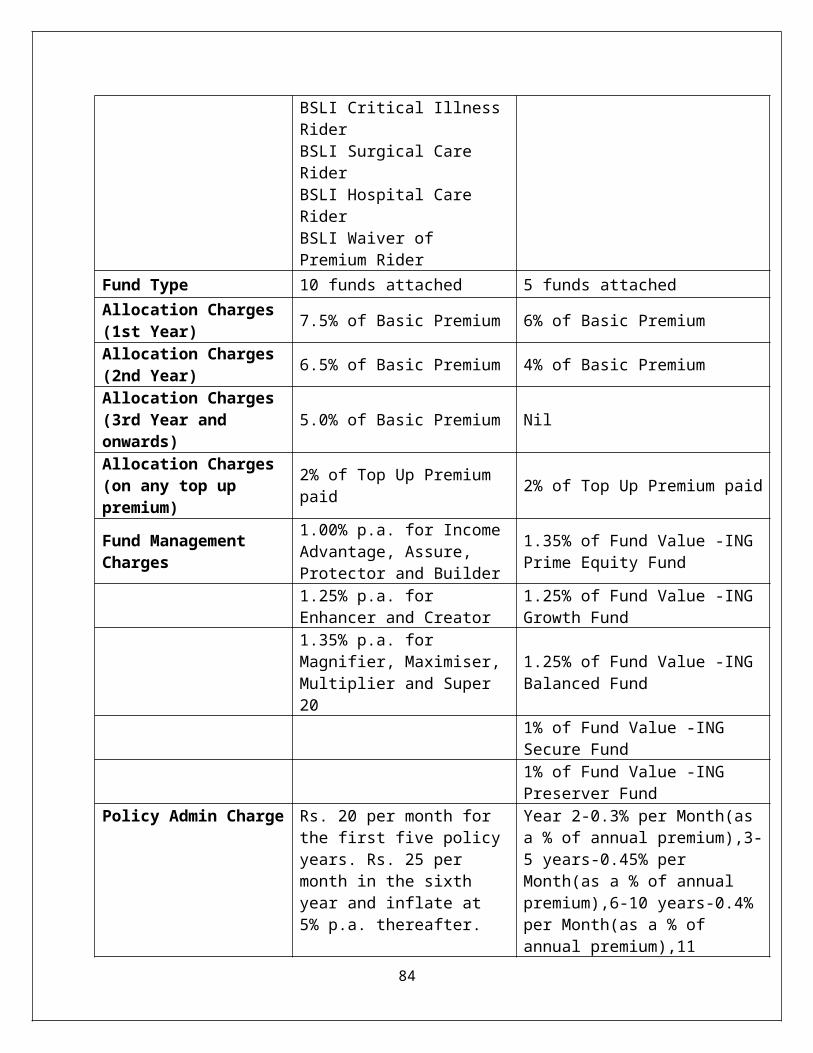

BSLI Critical IllnessRiderBSLI Surgical Care RiderBSLI Hospital Care RiderBSLI Waiver of Premium Rider

Fund Type 10 funds attached 5 funds attachedAllocation Charges (1st Year) 7.5% of Basic Premium 6% of Basic Premium

Allocation Charges (2nd Year) 6.5% of Basic Premium 4% of Basic Premium

Allocation Charges (3rd Year and onwards)

5.0% of Basic Premium Nil

Allocation Charges (on any top up premium)

2% of Top Up Premium paid 2% of Top Up Premium paid

Fund Management Charges

1.00% p.a. for IncomeAdvantage, Assure, Protector and Builder

1.35% of Fund Value -ING Prime Equity Fund

1.25% p.a. for Enhancer and Creator

1.25% of Fund Value -ING Growth Fund

1.35% p.a. for Magnifier, Maximiser,Multiplier and Super 20

1.25% of Fund Value -ING Balanced Fund

1% of Fund Value -ING Secure Fund

1% of Fund Value -ING Preserver Fund

Policy Admin Charge Rs. 20 per month for the first five policyyears. Rs. 25 per month in the sixth year and inflate at 5% p.a. thereafter.

Year 2-0.3% per Month(as a % of annual premium),3-5 years-0.45% per Month(as a % of annual premium),6-10 years-0.4% per Month(as a % of annual premium),11

84

onwards-0.3% per month

Mortality Charges (1.546 to 16.267) per1000

(1.08 to 14.12) Age -20 to 60 Years per 1000 of sum at risk

Misc. Charges

Rs. 50 per request for premium re-direction, fund switch and partialwithdrawal. Rs. 100 per policy revival.

No charges for premium re-direction, fund switchand partialwithdrawal.

Partial Withdrawal

Unlimited partial withdrawals any time after five complete policy years. The minimum amount of partial withdrawal isRs. 5,000. There is no maximum limit, butyou are required to maintain a minimum Fund Value of Rs. 25,000 plus any top-up premiums

The Partial Withdrawal Benefit is available for a minimum amount of Rs. 5,000 and a maximum amount equal to 25% of the Fund Value, subject to Fund Value after each such withdrawal not beingless than 1.5 times the one full years’ annual regular premium. The policyholder will be allowed to make any partial withdrawals from the Top-up contributions only after completion of 5 years from the date of remittance/realization ofTop-up contribution. The Partial Withdrawals made during the 24 months preceding the date of death, shall be reduced from the Sum Assured payableunder the policy.

85

Surrender