Form di Visual Basic. 1. Membuat Report dengan menggunakan Seagate Crystal Report

Chapter One

1 | P a g e

Introduction

Every bank deals with different vital division such as:

General Banking Division

Loans and Advance Division

Foreign Exchange Division.

Among these three divisions general banking is the core and

leading division. General banking division is the most

important point of all activates. It is the storage point of

all kinds of transactions of foreign exchange division,

loans and advice division, other relevant events. Except

General Banking functions a bank cannot sustain for long.

With the technological advancement this sector is growing

tremendously. As a fast growing bank BASIC Bank actively

realizing that development and trying to conform to the

changing environment.

2 | P a g e

Introduction

1.1 Origin of the Report

Banking is one of the most important sectors for country’s

wealth building activities. Commercial banks are certainly

profit making Financial Institutions. These institutions

play great role in the money market of every economy.

Due to recent financial crisis (Particularly in U.S.A,

G.B,EU,Japan) globalization, technological innovation and

deregulation in the banking system all over the world has

been changing rapidly. Now a day’s banks have to compete in

the market place not only with local institutions but also

with foreign financial institutions.

The course under BBA program is designed with an excellent

combination of theoretical and practical aspects. The whole

course is divided into twelve semesters of 4 months each.

After completion of 11th semester consisting of theoretical

exposure, the student are sent to different organization to

3 | P a g e

obtain some practical exposure in different sectors which

would help them in taking up more professional courses in

BBA.as a student of BBA,I have assigned to BASIC Bank

Limited, Karwan Bazar Branch for my practical orientation. I

have mainly focused on General Banking Activities of BASIC

Bank Limited.

1.2 Objective of the study

General objective

The study is intended for providing me invaluable

practical knowledge about banking operation in

Bangladesh. The general objective is to prepare the

4 | P a g e

report to acquire practical knowledge of the Banking

Sector.

Specific objective

To accomplish the partial requisite of BBA Program and

to achieve of good judgment with theoretical base.

To have a revelation on the banking environment in

Bangladesh.

To examine the extent of Foreign exchange earnings as

compared to total earning, interest income and, non-

interest income.

To understand the general banking activities of any

banks.

To evaluate Overall performance indicators of BASIC

Bank Ltd.

To make myself more confident and active in future to

finger my job.

5 | P a g e

1.3 Limitation of the Study

In collecting information, there is some problem

because of the excessive nature confidentiality

maintained by the officials of BASIC.

Learning all the banking functions within 90 days

really tough.

The bank authority was very busy, so they did not

give me enough time for discussion on various

problems.

This is my first experience on job, so there may

arise some faults though I have tried my level best.

6 | P a g e

Chapter Two

7 | P a g e

Literature Review

Islam (2003) states that the monetary authority determines

the exchange rate policy aiming to achieve two main

objectives. First, the “domestic target”, which includes

restraining inflation rate, credit growth in the public and

private sector, and the growth of liquidity and broad money.

Secondly, the „external target‟, which includes promotion in

international reserves level, reduce the current account

gap, control trends of exchange rate changes in the local

inter-bank foreign exchange market, and adjust the trends in

the exchange rates of neighboring trade partners: India,

Pakistan and Sri Lanka.

8 | P a g e

2. Literature Review

It is also emphasized by King (2001) that the many

descriptions today haveh no exactness of meaning. There is

no point in giving labels to credits unless the labels are

of universal application and are reasonably descriptive of

the credit to which they are attached.

Proactive fraud prevention has to be conducted, and it

covers good division of responsibilities, supervision of

staff, monitoring work performance, and all those measures

intended to ensure dishonest people cannot access the

system, or even if the systemis accessed that a proper

control is in place (COSO, 2004). Further factors that help

to prevent fraud can be anti-fraud policies, procedures,

training and fraud awareness (Naill, 2006). Nevertheless,

It can be criticised as being impractical for banks to check

the authenticity of any documents or the signatures on such

documents, due to the large number of shipping companies and

agents in the world and the vast number of documents

presented to banks in L/C transactions. but it may not be

possible to determine whether the goods were loaded on that

ship and the nature or quality of the goods (UNCTAD Report,

1983). Thus, it was further suggested that banks carry out

investigations on some documents on an ad hoc basis; but

9 | P a g e

such an approach did not seem to be a satisfactory answer

(UNCTAD Report, 1983).

Chapter Three

10 | P a g e

Methodology

3.1 Methodology

To prepare this report all the data and information have

been collected through primary and secondary sources. I

have applied both qualitative and quantitative method.

During my study I followed the following two broad

sources to collect all necessary data and information:

Sources of Information and data:

The sources of information are:

11 | P a g e

1. Primary sources: It includes interviews and

conversation with officers and executives of the

Bank of different divisions and Departments.

2. Secondary Sources: It includes annual report,

investment manual, general banking manual,

selected books, journals and other publication.

Study Place:

I have worked BASIC Bank Limited (Karwan Bazar Branch) at

Latif Tower 47,Karwan Bazar,Dhaka-1215

Study Period:

I have worked BASIC Bank Limited (Karwan Bazar Branch) for 3

month (From 5th February-2014 to 28st April 2014).

3.2 Data Analysis:To make this report successful one researcher will analyze

the data as follows:

12 | P a g e

The analysis of this report is qualitative. In

qualitative analysis researcher will cover the foreign

Exchange Operation under commercial banking system.

This research will also show some financial performance

analysis for making comparisons among some previous

years of this bank.

Statistical comparison among three month of this branch

will be described by some graphical presentation

analysis.

13 | P a g e

Chapter Four

4.1 Historical Background:14 | P a g e

Overview of the Company

4. Profile of the Bank

Bank of Small Industries and Commerce Bangladesh Limited

(BASIC) is a banking company registered under the Companies

Act 1913. It was incorporated under this Act on the 2nd of

August, 1988. The bank started its operation from the 21st

of January, 1989. It is governed by the banking Companies

Act 1991. The bank was established as the policy makers of

the country felt the urgency for a bank in the private

sector for financing Small Scale Industries (SSIs). At the

outset, the bank started as a joint venture enterprise of

the BCC Foundation with 70 percent shares and the government

of Bangladesh (GOB) with the remaining 30 percent shares.

The BCC Foundation being nonfunctional following the closure

of the BCCI, the government of Bangladesh took over 100

percent ownership of BASIC on 4th June 1992. Thus the bank is

state-owned. However the Bank is not nationalized; it

operates like a private bank as before.

BASIC is unique in its objectives. It is a blend of

development and commercial banks. The Memorandum and

Articles of Association of the Bank stipulate that 50

percent of loan able funds shall be invested in small and

cottage industries sector.

Steady growth in client base and their high retention rate

since Bank’s inception testify to the immense confidence

they repose on its services. Diversified products and

15 | P a g e

particularly a wide range of lending products related to

development of small industries and micro enterprise and

commercial sector are trading activities attract

entrepreneurs from varied economics fields. Along with

promotion of products, special importance is given to

individual clients through providing personalized services.

In fact individuals matter in this Bank. This motto has been

followed for development of clientele as well as human

resources of the Bank.

BASIC Bank is operated by a team of skilled highly

qualified, experienced and enthusiastic working forces

headed by the well conversant Managing Director of the Bank

who has about three decades prolong close attachment in

different horizon of Banking.

4.2 Functions:

The Bank Offers:

Term loans to industries especially to small-scale

enterprises.

Full-fledged commercial banking service including

collection of deposit, short term trade finance,

working capital finance in processing and manufacturing

units and financing and facilitating international

trade.

16 | P a g e

Technical support to Small Scale Industries (SSIs) in

order to enable them to run their enterprises

successfully.

Micro credit to the urban poor through linkage with

Non- Government Organizations (NGOs) with a view to

facilitating their access to the formal financial

market for the mobilization of resources.

In order to perform the above tasks, BASIC Bank works

closely with its clients, the regulatory authorities, the

shareholders (GOB), banks and other financial institutions.

4.3 Organization Strategy

17 | P a g e

Financing establishment of small units of industries and

business and facilitate their growth Small Balance Sheet

size composed of quality assets.

Steady and sustainable growth.

Investment in a cautious way.

Adoption of new banking technology.

To employ funds for profitable purposes in various

fields with special emphasis on small scale industries.

To undertake project promotion on identify profitable

areas of investment.

To search for newer avenues for investment and develop

new products to suit such needs.

To establish linkage with other institutions which are

engaged in financing micro enterprises.

To cooperate and collaborate with institutions

entrusted with the responsibility of promoting and

aiding SSI sector.

4.4 Objectives of the BASIC Bank:

18 | P a g e

As mentioned earlier, BASIC’s priority is in promoting

and financing development of small and cottage

industries.

Besides, the Bank is to provide full range of

commercial banking services including collection of

deposits, such as current, savings, STD, and FDR;

short term trade finance, handling of import and

export business.

BASIC offers Micro credit to the urban poor through

linkage with NGO’s with a view to facilitating their

access to the formal financial market.

4.5 Organization Goals:

BASIC Bank is always ready to maintain the highest quality

of services by upgrading banking technology prudence in

management and by applying high standard of business ethics

through its established commitment and heritage. Among many

goals of BASIC Bank, one of them is to maximize profit

through optimum utilization of resources by providing best

customers service.

4.6 Organization Mission & Vision:

Mission:

19 | P a g e

To provide best development and commercial banking services

to the common people of Bangladesh. And to provide special

support to the small-scale business enterprises so that,

they can play an important role in the economic development

of the country.

Vision:

To be a bank of choice by interwining excellence in customer

service experience, optimum profitability with efficiency,

imitable corporate culture in terms of complints banking

activitiesand efficient & motivated human resource and

endless quest for becoming the best corporate citizen &

serving peaple for progress.

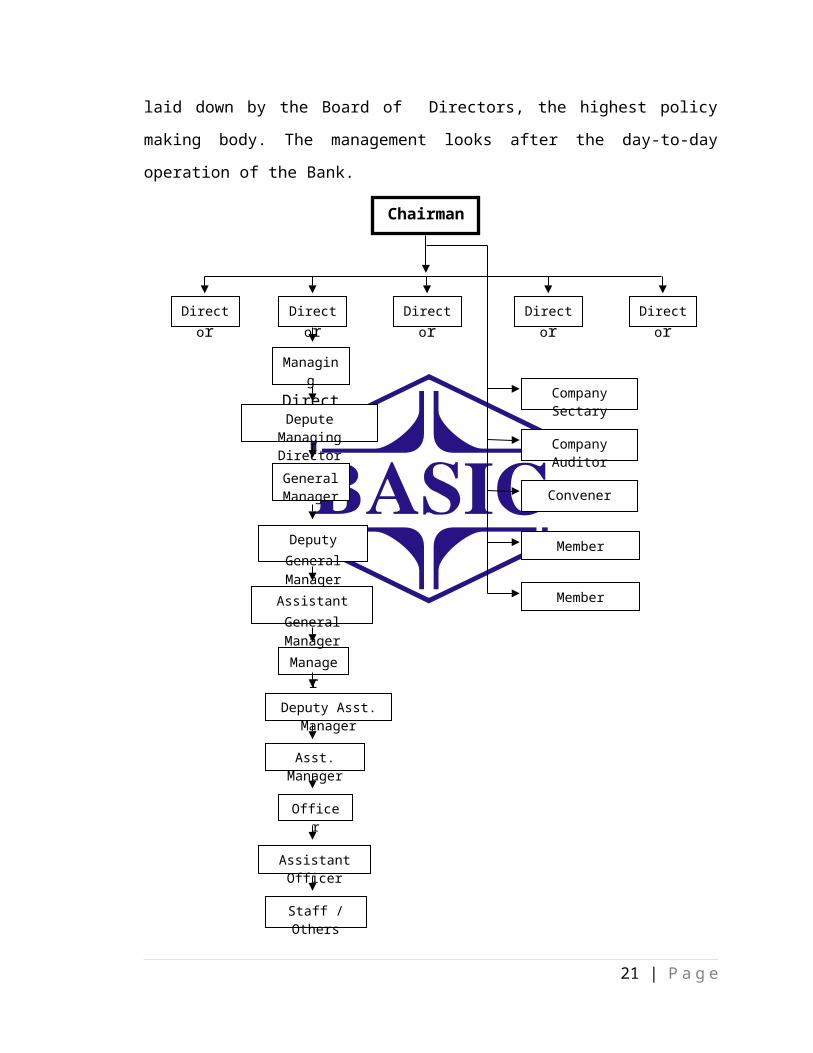

4.7 Organization StructureTo achieve its organizational goals, the bank conducts its

operations in accordance with the major policy guidelines

20 | P a g e

laid down by the Board of Directors, the highest policy

making body. The management looks after the day-to-day

operation of the Bank.

21 | P a g e

Company Sectary

Company Auditor

Member

Convener

Member

Managing

Director

Deputy General Manager

Manager

Officer

Assistant Officer

Asst. Manager

Staff / Others

Chairman

Director

Director

Director

Director

Director

General Manager

Assistant General Manager

Depute Managing Director

Deputy Asst. Manager

Chapter FIVE

22 | P a g e

General Banking

Activities of BASIC Bank LTD

[5.1] GENERAL BANKING:

General Banking is the most important and common part of anybank. Cause majority transaction is held in this section.This section has four (4) parts as follows:

The structure of General Banking as follows :

23 | P a g e

GENERALBANKING

ACTIVITIES

[5.1.1] CASH:Cash section demonstrates liquidity strength of a bank.It also sensitive as it deals with liquid money. Maximumconcentration is given while working on this section. Asfar as safety is concerned special precaution is alsotaken. Tense situation prevails if there is any imbalancein the case account.

CASH SECTION: The function of this unit is to receive and payment of cash.The vault limit cash limit of the branch is TK.15000000 andTK.1000000 respectively. The head teller is allowed to encash check up to TK.100000 with her own signature. Ifadditional cash is required then the second man of thebranch makes arrangement on request. There are one chiefofficer, one senior officer, and two Banking officers inthis department.

Operation of this section begins at the banking hour. Cashofficer begins her/his transaction with taking money fromthe vault, known as the opening cash balance. Vault is keptin a much secured room. Keys to the room are kept under

24 | P a g e

CASHRECEIVE

& PAYMENT

ACCOUNTOPEN

PROCEDURE

CLEARINGHOUSE

CUSTOMERSERVICEDD,TT, &

control of cash officer and branch in charge. The amount ofopening cash balance is entered into registered. After wholedays’ transaction, the surplus money remains in the cashcounter is put back in the vault and known as the closingbalance. Money is received and paid in this section.

CASH RECEIPT:

At first the depositor fills up the Deposit inthe Slip. For saving account and currentaccount same Deposit in Slip is used in thisBranch.

After filling the required deposit in slip,depositor deposits the money.

Officers at the cash counter receives themoney, count it, enter the amount of money inthe register kept at the counter, seal thedeposit in slip and sign on it with date andkeep the bank’s part of the slip. Other part isgiven to the depositor.

All deposit slip of saving; Current and STD A/Care maintained in accounts section.

CASH PAYMENT:

Cash payment of different instruments is made in the

cash section. Procedure of cash payment against check is

discussed below elaborately. Cash payment of check

includes few steps.

First of the entire client comes to the counter withthe check and give it to the officer in charge there.The officer checks whether there are two signatures

25 | P a g e

on the back of the check and checks his balance inthe computer. After that the officer will give it tothe cash in charge.

Then the cash in charge verifies the signature fromthe signature card and permits the officer incomputer to debit the client’s account by givingposting. A posted seal with teller number is given.

If the signature matches with the one givenpreviously then the teller will make payment keepingthe paying check with him while writing thedenomination on the back of the check.

Cash paid seal is given on the check and make entryin the payment register.

There are few things that shall be scrutinized and checkedbefore making payments.

Name of the drawer. Account number. Specimen signature. The validity of the check and make it sure that

it is not postdated or undated. The amount in words and figures are same.

CASH BALANCE CALCULATION:

The officer in charge of cash section does the calculationand then Sub-manager or authorized officer will check thebalance and sign in the cash balance book. The balance ismaintained in the balance book. Opening balance of currentday is the closing balance of the previous day. Totalreceive of the current day is added with the opening balanceand total payment is deducted for calculating the closingbalance or cash balance.

26 | P a g e

BANK VAULT: All cash, instruments (P.O.D.D. check) and othervaluables are kept in the vault is insured up to Tk. 10crore with a local insurance company. If cash stock goesbeyond its limit of Tk. 10 crore, the excess money istransferred to Bangladesh Bank if there is shortage ofcash during transaction period money is transferred todrawn from the central bank. There are three keys of thevault, which are given to three seniors most officers.Daily, an estimated amount of cash is brought out fromthe vault, for transaction purpose. No more than Tk. 4Crore brought at once from the vault, on a single day.

CASH PACKING AND HANDLING: Cash packing and handling needs a lot of care as anymistake may lead to disaster. Packing after banking hourwhen the counter is closed, cash are packed according todenomination. Notes are counted several times and packedin bundle, stetted and stumped with initial.

TELLER CUSTOMER RELATIONSHIP: In a bank a person who delivers and receives cash fromthe cash counter is known as teller, a customer meetsmost of the time in a bank with a teller on the counter.So teller should hold certain quality.

Should be friendly.

Provide prompt service.

Be accurate in his task.

Be carefully.

To have endless patience.

Be smart.

27 | P a g e

In short a teller should be efficient otherwise he hasto pay.

[5.1.2] TYPES OF ACCOUNT: Keeping an eye on the needs of the customers and to ensure theirfull satisfaction BASIC Bank has a full range of depositproducts.

There are mainly five types of Accounts are as follows:-

1. Savings Deposit (SB) 2. Current Deposit (CD) 3. Short Notice Term Deposit (STD) 4. Fixed Term Deposit (FTD) 5. Bearer Certificate of Deposit (BCD)

1. SAVINGS BANK DEPOSIT ACCOUNTS (S.B):

Savings Bank Deposit account may be opened in the nameof adult individual or jointly in the names of two ormore persons payable either or both or all them orto the survivor with total satisfaction of Bank.

These are interest bearing deposit accounts. (Presentinterest rate 5.00% in BASIC Bank Ltd.

Savings Bank Account shall not be allowed to beoverdrawn.

Saving Bank Account must not be allowed to be conductedas Current Account.

The drawings are restricted in respect of both theamount of withdrawal and the frequency thereof so thatthe payment of interest does not become non-compensating for the banker.

No interest will be paid in a Savings Bank Account forthe month in which withdrawals have been made more than

28 | P a g e

twice a week or over 25% of the balance of his/heraccounts without notice. For withdrawal of sumexceeding 25% of the balance, 7 days notice in writingshould be given to the bank.

Interest shall be calculated on the minimum balance atthe credit of an account between the close of the 5th

day and the last day of the month. Interest will be applied half yearly on 30th June &

31st December at the prescribed rates as advised byHead Office

These accounts intended for individual savings and arenot suitable for business concerns that requirefrequent withdrawals.

Bank may however refuse without assigning any reasonsto open savings account by any body.

The Bank reserves the right to close any Savings BankDeposit account with prior notice.

29 | P a g e

2. CURRENT DEPOSIT ACCOUNT (C.D):

A Current Deposit Account may be opened in the name ofperson(s) having contractual capacities. Anyindividuals, firm, company, club, association, andcorporate body may open a Current Account.

Drawings are allowed on demand from such an accountwithout any restriction within the funds available inits credits.

No interest is payable on the balance of currentaccounts.

Bank may however refuse without assigning any reasonsto open current account by anybody.

The Bank reserves the right to close any currentaccount with prior notice.

3. SHORT TERM DEPOSIT ACCOUNTS (STD):

Short Term Deposit Account (STD) is opened usually byCorporations, Banks and Financial Institutes etc.

These deposits are withdrawn able on 7 days’ notice bythe account holder(s). Withdrawal is allowed after theexpiry of notice period.

Interest on such deposits are payable at the ratedetermined by Head Office from time to time. (Presentinterest rate on STD A/C is 3.00% in BASIC Bank Ltd.)

Interest shall be calculated on daily product basis andapplied half yearly at end of June and December or whenan account is closed.

4. FIXED TERM DEPOSITS (FTD):

Fixed Deposits may be opened by one adult individualsingly or by more than one adult individual jointly orby any Government/Private /Autonomous or otherorganization.

30 | P a g e

These deposits shall be opened for a fixed periodranging from three months to two years.

Interest on FDR shall be payable only after maturity ofthe FDR along with the principal.

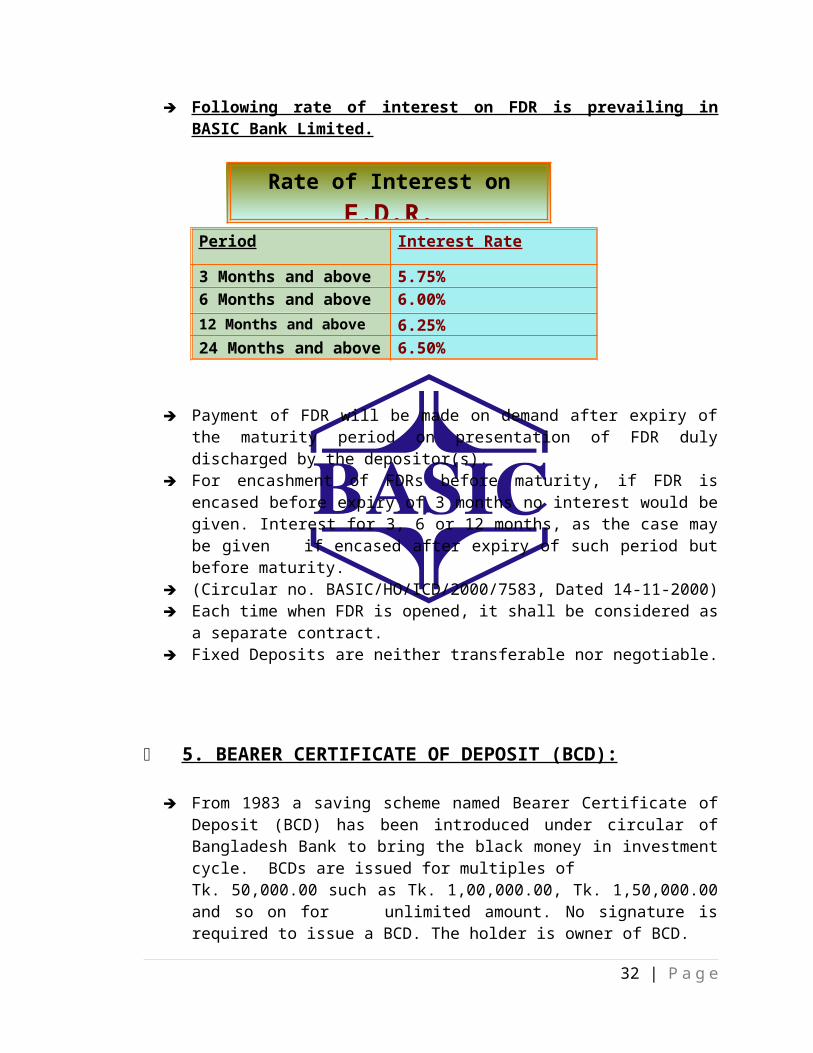

Following rate of interest on FDR is prevailing inBASIC Bank Limited.

31 | P a g e

Following rate of interest on FDR is prevailing in BASIC Bank Limited.

Period Interest Rate

3 Months and above 5.75%6 Months and above 6.00%12 Months and above 6.25%24 Months and above 6.50%

Payment of FDR will be made on demand after expiry ofthe maturity period on presentation of FDR dulydischarged by the depositor(s).

For encashment of FDRs before maturity, if FDR isencased before expiry of 3 months no interest would begiven. Interest for 3, 6 or 12 months, as the case maybe given if encased after expiry of such period butbefore maturity.

(Circular no. BASIC/HO/ICD/2000/7583, Dated 14-11-2000) Each time when FDR is opened, it shall be considered as

a separate contract. Fixed Deposits are neither transferable nor negotiable.

5. BEARER CERTIFICATE OF DEPOSIT (BCD):

From 1983 a saving scheme named Bearer Certificate ofDeposit (BCD) has been introduced under circular ofBangladesh Bank to bring the black money in investmentcycle. BCDs are issued for multiples of Tk. 50,000.00 such as Tk. 1,00,000.00, Tk. 1,50,000.00and so on for unlimited amount. No signature isrequired to issue a BCD. The holder is owner of BCD.

32 | P a g e

Rate of Interest on F.D.R.

Who can get it issued: Any individual withoutdisclosing his/her identity and without Opening anyaccount.

Period: These deposits shall be opened for a fixedperiod ranging from three months to two years.

33 | P a g e

Interest: Interest rate is 1% below as that of FDR. i.e.

Following rate of interest on BCD is prevailing inBASIC Bank Limited.

Period Interest Rate

3 Months andabove

5.75%

6 Months andabove

6.00%

12 Months and above 6.25%24 Months andabove

6.50%

BCD Calculation: The value after the maturity is theface value of BCD. Calculation is as under:

PV=FV / (1+i) Where PV =Present value, FV = Future value i =Interest Rate, n = year

EXAMPLE : -

To issue a BCD for Tk.1 .00 lac for the period of 1year

PV = 1, 00,000.00 / (1+0.0625) = 94,117.65

10 % Income Tax on interest = Tk.625.0034 | P a g e

Rate of Interest on B.C.D.

Excise Duty = Tk.120

So required deposit = PV + Income tax on interest+Excise Duty

= Tk. 94,117.65 +Tk. 625.00 + Tk.120 = Tk.94, 862.65

Present Status: As per BRPD Circular No.08 dated 25-07-2000& BRPD Circular No.09 dated 20-10-2002 BCD cannot be issued or renewedfurther.

[5.1.3] Papers /Documents required for opening of INDIVIDUAL/JOINT, PROPRITORSHIP, &PARTNERSHIP ACCOUNTS:

INDIVIDUAL /JOINT:

Two copies of passport size photograph of theAccount holder(s) or Person(s) who will operatethe Account duly attested by acceptableintroducer,

Passport, Introductory Certificate from Employer, Introductory Certificate from renowned person of

the society acceptable to Bank/FinancialInstitutions, and

TIN Number (If applicable).

CAUTIONS:

In Account opening form Name, Present &Permanent address, Date of birth, Age ofaccount holder, Father’s Name, Mother’s Name,

35 | P a g e

Husband’s Name in case of married lady must befilled up properly in Account opening form.(Money Laundering Circular no.02 of Bangladesh Bank,

Dated 17-07-2002 & Circular no.03 Dated 10-12-2002)

The Introducer of the proposed new account mustbe maintained an account with the branch forat least one year and the account must havegood transactions over the last year.

(Circular no. BASIC/HO/Gen/2000/14, Dated 18-10-2000)

The details of the identity, address andbusiness of the new account holder must beverified and the branch In Charge should besatisfied about the person/firm/company’scredibility. (Circular no. BASIC/HO/Gen/2000/14, Dated 18-10-2000)

A letter of thanks shall be sent to theintroducer and to the account holder onBank’s Standard Form.

36 | P a g e

PROPRIETORSHIP FIRM:

Two copies of passport size photograph of theAccount holder(s) or person(s) who will operatethe Account duly attested by the introducer.

Certified copy of valid Trade License from theMunicipality/ City Corporation/Union Parishad.

Passport/ Introductory Certificate from Employer/Introductory Certificate from renowned personof the society acceptable to Bank/FinancialInstitutions.

TIN Number (If applicable).

CAUTIONS: Same as Joint/Individual Account.

PARTNERSHIP FIRM:

Two copies of passport size photograph of theAccount holder(s) or person(s) who will operatethe Account duly attested by the introducer.

Certified copy of valid Trade License from theMunicipality/ City Corporation/Union Parishad.

Certified copy of the Registration Certificateof Partnership Deed duly attested by NotaryPublic in case of registered firm.

Partnership Account Agreement.

Resolution signed by all partners to open theA/C.

Passport/ Introductory Certificate from Employer/Introductory Certificate from renowned person

37 | P a g e

of the society acceptable to Bank/FinancialInstitutions.

TIN Number (If applicable).

CAUTIONS: Same as Joint/Individual Account.

[5.1.4] Papers /Documents required for opening of LIMITED COMPANIES ACCOUNTS:

LIMITED COMPANY:

Two copies of passport size photograph of theAccount holder(s) / person(s) who will operatethe Account duly attested by the introducer.

Certified copy of Memorandum & Articles ofAssociation by RJSC.

Certified copy of Certificate of Incorporationby RJSC.

Certified copy of Certificate of Commencement of

Business (in case of Public Limited Company).

Up to date list of Directors.

Certified copy of Resolution of the Board ofDirectors for opening & operation of theAccount.

38 | P a g e

Passport/ Introductory Certificate from Employer/Introductory Certificate from renowned personof the society acceptable to Bank/FinancialInstitutions.

TIN Number (If applicable).

CAUTIONS: Same as Joint/Individual Account.

TRUST:

Two copies of passport size photograph of theAccount holder(s) / person(s) who will operatethe Account duly attested by the introducer.

Up to date list of Members of the Trustee Board.

Certified copy of Deed of Trust certified by theChairman/Secretary of Trustee Board.

Certified copy of Resolution of the TrusteeBoard for opening & operation of the Account.

CAUTIONS: Same as Joint/Individual Account.

39 | P a g e

[5.1.5] Papers /Documents required for opening ofEXECUTORSHIPS ACCOUNTS:

EXECUTOR:

An executor is a person appointed by a testator forexecution of the last will leave by him. Upon production ofprobate of the will the executor should be allowed to closethe deceased’s account and deal with the credit balance asper terms and conditions of the will, affecting the account.

In case of credit balance of the deceased’s account, it ispreferable for the banker that the executor opens therequired account as an executorships account instead of anaccount in the personal name of the executor.

Required Paper for an executorships account: -

Two copies of passport size photograph of the executor/ person(s) who will operate the Account duly attestedby appointed by the testator for execution of the lastwill leave by him.

Will deed executed by a testator for execution of thelast will leave by him in the front of 02 male or 01male & 02 female to operate the account.

Will probate accepted by Court.

Power of Attorney executed by a testator for executionof the last will leave by him favoring the executor inthe front of 02 male or 01 male & 02 female to operatethe account.

CAUTIONS:

40 | P a g e

Same as Joint/Individual Account.

The banker should not allow any transfer of thedeceased’s assets. The banker should not allowany transfer of the deceased’s funds to thepersonal account of the executor nor should heallow the executor to raise any personal loanagainst security of the deceased’s property.

Otherwise, he will be held liable for the misuse.

[5.1.6] Papers /Documents required for opening ofADMINISTRATOR & CLUB/SOCIETY/SCHOOL/COLLEGE ACCOUNTS:

ADMINISTRATOR:

An administrator is appointed under the authority of a courtof competent jurisdiction where the deceased appointing anexecutor leaves no will. The administrator has substantiallythe same duties and powers as those of the executor; theydiffer mainly in the manner of their appointment. While theexecutor derives his authority from the will immediatelyafter the testator’s death, the administrator derives hisauthority from the letters of administration, which heproduces to the banker for inspection as an executorproduces probate of the will for the purpose of a bankaccount. The administrator is also the legal representativeof the deceased with powers to sue, recover debts and incurexpenses. But he may not mortgage, charge or transfer anyproperty without prior permission of the court granting theletters of administration. On the death of an administratorthe surviving administrator, if any, acts, but on the deathof the last administrator fresh letter of administrator isnecessary.

41 | P a g e

CLUB/ SOCIETY/SCHOOL/COLLEGE ETC:

Two copies of passport size photograph of theAccount holder(s) or person(s) who will operate theAccount duly attested by the introducer.

Memorandum & Articles of Association duly certifiedby the Chairman/Secretary.

Bye Laws & Regulation/ constitution duly certifiedby the Chairman or Secretary.

In case of cooperative society Bye Laws &Regulation/ constitution.

Duly certified by Cooperative Officer. Resolution of Management Committee/ Executive

Committee for opening & operation of the Account. Up to date list of Office Bearers/ Governing Body/

Managing Committee duly certified by the Chairman/Secretary.

Government approval in case of registeredClub/society.

CAUTIONS: Same as Joint/Individual Account.

42 | P a g e

[5.1.7] Papers /Documents required for opening of NGO, JOINT VENTURE, & AIRLINES ACCOUNTS:

NGO: Two copies of passport size photograph of the

Account holder(s) / person(s) who will operate theAccount duly attested by the introducer.

Certified copy of Bye Laws & Regulation/constitution duly certified by the Chairman/Secretary.

Certified copy of Resolution of ManagementCommittee/ Executive Committee for opening &operation of the Account.

Up to date list of Office Bearers/ Governing Body/Managing Committee duly certified by the Chairman/Secretary.

Permission from NGO Bureau. Permission from Head Office.

(Circular no. BASIC/HO/Gen/2000/14, Dated 18-10-2000)

CAUTIONS: Same as Joint/Individual Account.

JOIN VENTURE COMPANY (BANGLADESHI + FOREIGNER):

Two copies of passport size photograph of theAccount holder(s) or person(s) who will operate theAccount duly attested by the introducer.

Copies of passports of A/C operators (1st 6 pages +visa pages for foreigners).

List of Directors Resolution of the Board of directors for opening &

operation of the 43 | P a g e

Account Permission from Board of Investment. Joint Venture agreement attested by Notary public Certified copies of the Memorandum and Articles of

Association Certified copies of incorporation.

CAUTIONS: Same as Joint/Individual Account.

44 | P a g e

ACCOUNTS OF MUNICIPAL CORPORATIONS, LOCAL

AUTHORITIES, DISTRICT COUNCILS, OTHER PUBLICBODIES:

Before opening the account of any Government or Semi-Government Organization or a Local Body, a certified copy ofthe Statute or any other law by which the body is createdand governed shall be obtained.

Two copies of passport size photograph of the Accountholder(s) or person(s) who will operate the Accountduly attested.

Resolution of the Board of Directors for opening &operation of the Account.

The Name, Address, Signature and Power of the accountoperator should be mentioned in mandate.

If the account operator is transferred then postingorder and joining report of newly posted employee arerequired and the previous person verified the newlyposted employee’s signature.

[5.1.8] SPECIAL CASES IN ACCOUNT OPENING:

MINOR ACCOUNT:

Who is Minor?

A person who has not completed his 18th year of age isconsidered to be a minor.

Minor is not owner of deposited money in minor account:

CAUTIONS:

45 | P a g e

Banker has to take special care so that nooverdraft can be made on minor account. Minorcannot be liable for any loan as minor has noright to sign a contract.

Minor should not provide cheque books. But she/hecan use cheque leaf. Minor will sign an only aloose cheque leaf in front of Branch In Charge sothat he/she cannot draw excess amount of money.In any case, when there is the least doubt, properidentification must be obtained & banker shouldinform the Guardian of minor.

No cheque, bill should not receive in minoraccount. If any dispute arises minor cannot beliable for any contract.

46 | P a g e

Minor is owner of deposited money in minor account:

In that case minor cannot withdraw money from this accountbefore being adult.

CAUTIONS:

Date of birth of minor and the date ofattaining majority should be noted at the topof the Account Opening Form and in thecomputer. So that he/she can withdraw moneyafter being major.

The Guardian who opened the account in theminor’s name will introduce the minor afterbecoming adult to bank. In this introduction arenowned person should be present as a witness.

How ever the minor’s account can be opened in his own name and minor himself can operate the accountin the following way:

I. Minor who is 12 years or above may beallowed to maintain deposit account with us.

II. Normal procedure of introduction and otherformalities shall be observed.

III. The account shall be non-borrowing innature. Under no circumstances there shallbe any overdraft in this account.

IV. Minor can draw a cheque. If there iswrongful dishonor of such cheque minorcan sue Bank for damage and for wrongful

47 | P a g e

dishonor. If there is a wrongful paymentto the minor, Bank will not be able torecover such payment. So Branch should bevery cautious for any payment to the minor.

V. In case of death of the minor, his legalheirs would be the beneficiaries of theAccount.

[5.1.9] SPECIAL CASES IN ACCOUNT SURVIVOR:

JOINT ACCOUNT:

In case of accounts to be opened in two or morenames, “Either or Survivor” containing clear andspecific instructions regarding operations of theaccounts. These instructions shall be obtainedunder the signatures of all of them.

“EITHER OR SURVIVOR”

If in the account opening form contains theInstruction “Either or Survivor”, in case of deathof any joint account holders the balance will bepayable to the survivor with total satisfaction ofBank.

48 | P a g e

In absences of the instruction “Either or Survivor”

In the absence of specific instructions inthe Form “ Either or Survivor” balance ofthe joint account will be payable to thesurvivors and the legal representatives ofthe deceased joint account holder.

CAUTIONS:

In the event of death of any account holders, thesurvivor shall be requested to close the oldaccount and open a new account in the name of thesurviving account holder

No overdraft shall be allowed in a Joint Account,unless all the parties to the account operate itjointly, and charge documents in respect of theadvance are also signed by all of them.

[5.1.10] SPECIAL CASES IN ACCOUNT DECEASED /STOP PAYMENT:

DECEASED ACCOUNT:

49 | P a g e

In case of death of an individual accountholder, alloperations in his account shall be stopped for with. A“Caution mark: Deceased account” shall be drawn just belowthe balance of the account.

As soon as the information is received either throughnewspaper or some reliable source about the death of aconstituent, the date of death and source of informationshall be noted in the Computer against the relevant account.Interest on the account of the Deceased shall not be paid asdeath terminates the contract with the Bank.

CAUTIONS:

i) The credit balance of the deceasedcustomer shall not be paid to any personunless a probate or letter of administrationor succession certificate issued by acompetent court is produced to the Bank andthe Bank is satisfied about the bona fides ofthe beneficiary.

ii) In special circumstances, Head Office maywaived the above requirement where the Bankis satisfied about the bona fides of thesuccessors subject to their submitting anindemnity duly executed on a non-judicialstamp paper along with two suretiesacceptable to the Bank.

iii) The account of a deceased shall not beallowed to be operated on or transferredunder the instructions of any Executor orAdministrator or any claimant under Indemnityletter or otherwise.

50 | P a g e

51 | P a g e

STOP PAYMENT ORDER:

Instructions of stopping payment of any Chequeshall be obtained from the account holders inwriting.

If such instructions are received on telephoneor by telegram, a provisional note in respectthereof shall be made in the Computer pendingreceipt of written instructions from the accountholder. Should the Cheque be presented in themeantime, the same should be returned with theobjection “Drawer’s Confirmation Required”

The date and time on which those instructionsare received shall be marked on the letter andinitiated by an Authorized Officer.

The signature of the account holder shall beverified on the letter.

The instruction shall be passed on the ComputerOfficer to check the respective account toascertain whether that particular Cheque hasalready been paid or not.

The Stop Payment instruction should be recordedin the Computer instantly.

The Stop Payment letters received from theparties shall be kept in the “Stop PaymentFile”.

52 | P a g e

[5.1.11] ACCOUNTS CLOSING:

To close an account, parties may be requested to send anapplication along with the unused leaves of the Cheque Booksissued to them.

On receipt of the application, the following will bedone:

The signature of the account holder shall be verified. The number of unused Cheque Leaves shall be noted

there on. Before the account is closed the Branch In-Charge

shall approve the application after asserting theliability, if any, and incidental charges to bedebited to the account.

After debiting the incidental charges to the account,the account holder shall be advised to draw theremaining balance from his account.

The “Account Closed” stamp shall be affixed on theAccount Opening Form and Specimen Signature Cards.

The application shall be posted with the accountOpening Form and the Specimen Signature Cards shall bekept separately under lock and key.

An Authorized Officer shall destroy the unused Chequeleaves.

53 | P a g e

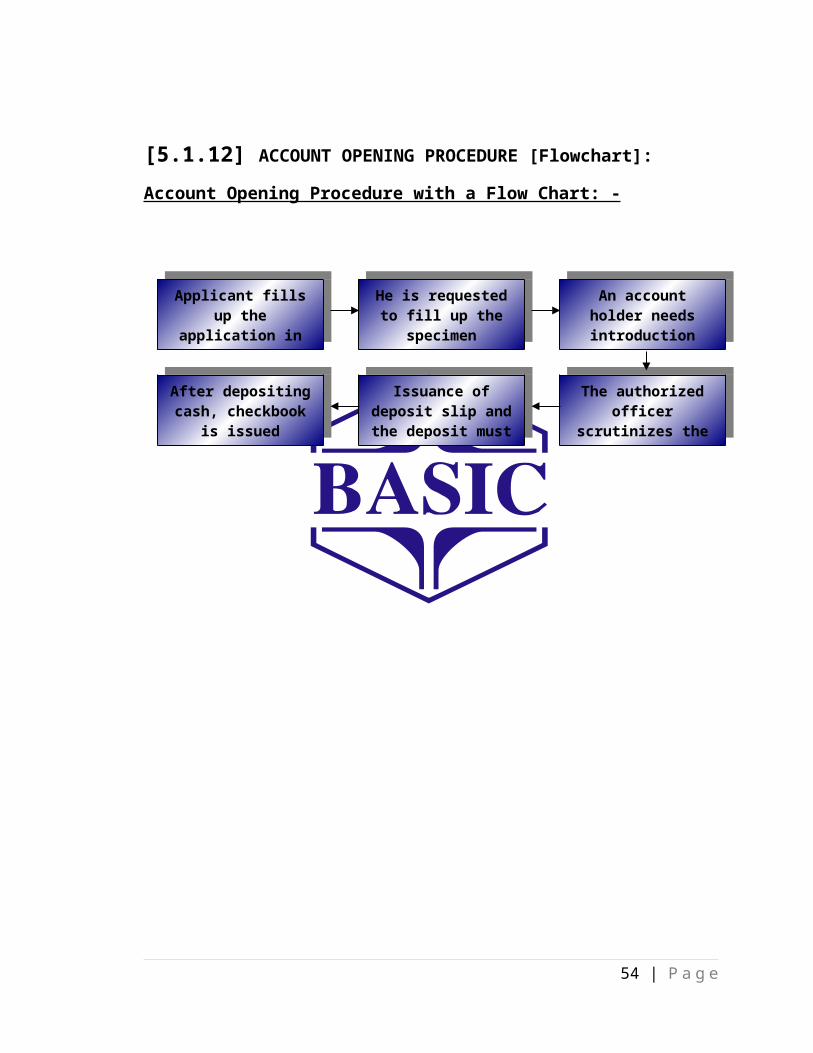

[5.1.12] ACCOUNT OPENING PROCEDURE [Flowchart]:Account Opening Procedure with a Flow Chart: -

54 | P a g e

Applicant fillsup the

application in

He is requestedto fill up the

specimen

An accountholder needsintroduction

After depositingcash, checkbook

is issued

Issuance ofdeposit slip andthe deposit must

The authorizedofficer

scrutinizes the

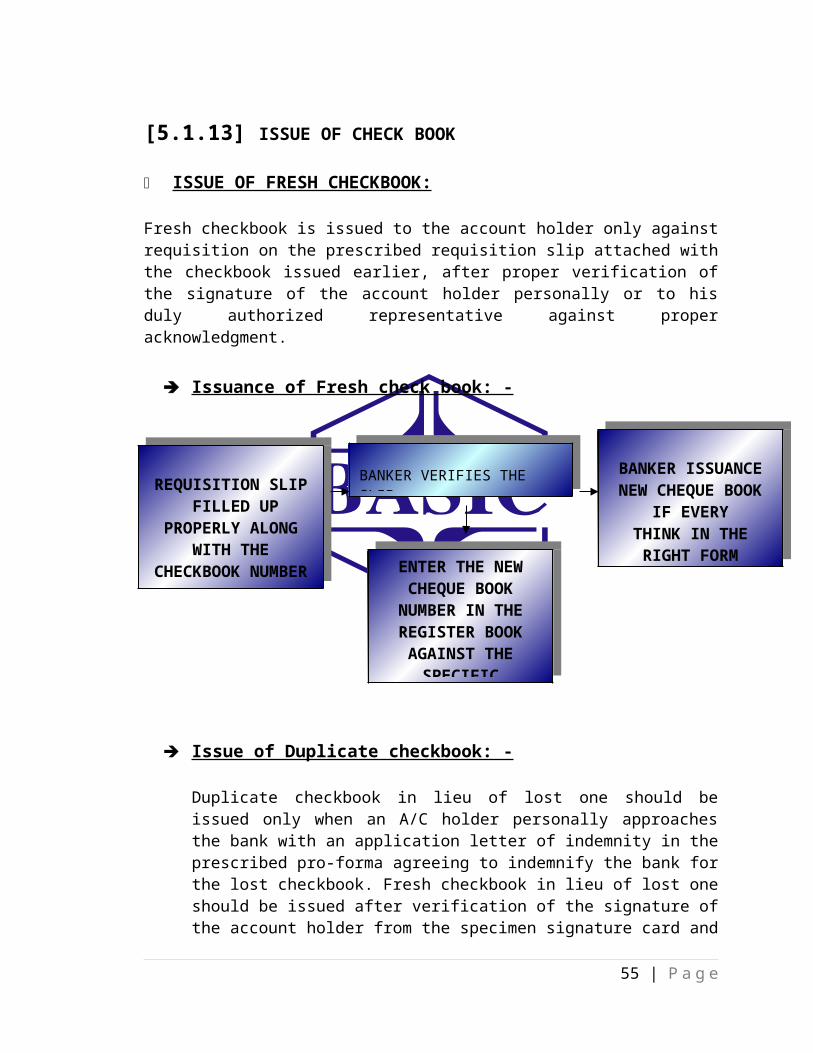

[5.1.13] ISSUE OF CHECK BOOK

ISSUE OF FRESH CHECKBOOK:

Fresh checkbook is issued to the account holder only againstrequisition on the prescribed requisition slip attached withthe checkbook issued earlier, after proper verification ofthe signature of the account holder personally or to hisduly authorized representative against properacknowledgment.

Issuance of Fresh check book: -

Issue of Duplicate checkbook: -

Duplicate checkbook in lieu of lost one should beissued only when an A/C holder personally approachesthe bank with an application letter of indemnity in theprescribed pro-forma agreeing to indemnify the bank forthe lost checkbook. Fresh checkbook in lieu of lost oneshould be issued after verification of the signature ofthe account holder from the specimen signature card and

55 | P a g e

REQUISITION SLIP FILLED UP

PROPERLY ALONGWITH THE

CHECKBOOK NUMBER ENTER THE NEWCHEQUE BOOK

NUMBER IN THEREGISTER BOOKAGAINST THESPECIFIC

BANKER ISSUANCENEW CHEQUE BOOK

IF EVERY THINK IN THERIGHT FORM

BANKER VERIFIES THE SLIP

on realization of required exercise duty only withprior approval of manager of the branch. Check seriesnumber of the new checkbook should be recorded inledger card signature card as usual. Series number oflost checkbook should be recorded in the stop paymentregister and caution should be exercised to guardagainst fraudulent payment.

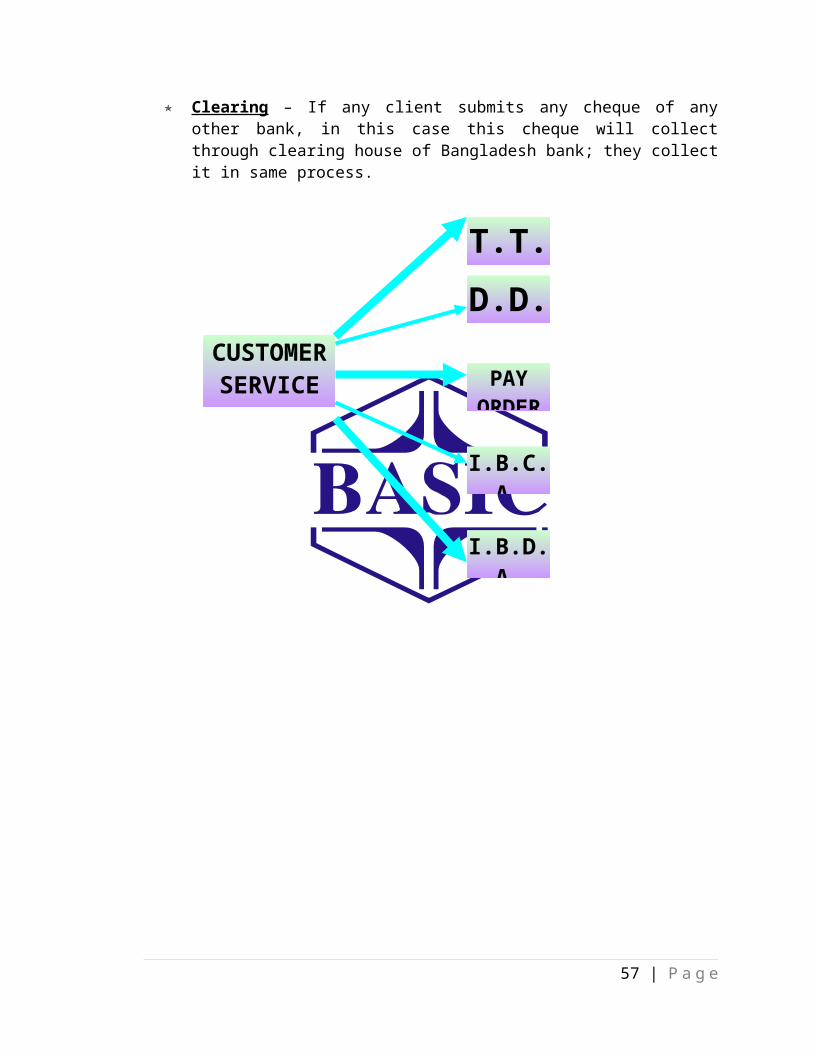

[5.2] CUSTOMER SERVICES:

Through this section customers can do D.D, T.T, PAYORDER, I.B.C.A, & I.B.D.A.

PROCEDURES OF D.D, T.T, PAY ORDER, I.BCA, & I.B.D.A:

There are three types of transaction can do through D.D,T.T, & Pay Order as follows:

Cash – Receive cash and send pay order to anotherbranch.

Accounts to Accounts – One can transfer his accounts toanother branch through D.D, & T.T.

56 | P a g e

Clearing – If any client submits any cheque of anyother bank, in this case this cheque will collectthrough clearing house of Bangladesh bank; they collectit in same process.

57 | P a g e

CUSTOMERSERVICE

D.D.

I.B.D.A.

T.T.

I.B.C.A.

PAYORDER

[5.2.1] T.T. – TELEGRAPHIC TRANSFER:These are two types. One is inward T.T & another is outwardT.T. In this procedure one can transfer money from one placeto another place. For this reason money carrying risk isreduced. As well as time also save.

This procedure is only applicable for in this bank & itsother branches. No one can do T.T. from in this bank toanother bank. Cause for any T.T. clients must have accountsin this bank.

PROCEDURE OF INWARD T.T:

This means any client of our branch want to does T.T. thenhe inform his branch and from that branch inform to mainbranch through telephone.

In this case bank must see some important things as follows:-

T.T. control number. Payee name and account number. By order. Test number. [For any amount of money this number

must be needed] Amount in ward. Amount in figure.

After getting this T.T. bank check that T.T. andregister it in register book according to that branch.In this case most important things are test number.Cause it maintained for client’s security. If the testnumber doses not match with the register book, thenbank inform it to that branch and bank does not paythat money. But usually this type of mistake does nothappen.

58 | P a g e

After register T.T. banks make an advice, which hasfour parts. Bank indicates clearly the date, the amountof T.T. inward and in amount.

In this advice bank dose customer accounts debit andhead office account credit and write test number.

Two copies send to that branch, one to the head officeaccount and one is attach with voucher.

59 | P a g e

PROCEDURE OF OUTWARD T.T: This is like reverse of inward T.T. In

this case if any client wants totransfer money or account, he informsbank. Bank informs that branch wherethe client wants to transfer hisamount. In this case, bankcommunicates with that branch throughtelephone.

Bank must inform the payee name, by

order, amount of money, advice number.

Same as inward T.T. procedure thatbranch makes advice against thisbranch.

For an example if any client of ourbranch wants to T.T. to Chittagongthen he must fill up the form of T.T.where he writes all information as perT.T. form. Then bank check allinformation and charge commission, vatand telex charge.

For any amount of T.T. test number isneeded.

Charge for T.T. as follows:

CHARGES PERCENTAGECommission Minimum 150TK. Or 0.1% (Which one

greater).

VAT 15%.Telex Charge 50TK. (Fixed)

60 | P a g e

Note: Inward & Outward T.T.’s copy enclose in appendix.

[5.2.2] D.D. – DEMAND DRAFT:Demand Draft is another way to pay money or transfer accountone branch to another branch. In this case one can pay moneyto his client to any place of Bangladesh. In this caseclient does need account in this bank.

These are two types. One is in ward D.D. and another isoutward D.D. In this procedure one can transfer money fromone place to another place. For this reason money carryingrisk is reduced. As well as time also save.

PROCEDURE OF OUTWARD D.D:

In this case transferee fills up the formwhere he must write the drawer name andaccount number and the bank name where branchoffice collects the money.

In D.D. there must have important information as follows:

D.D. Number. Control number.

61 | P a g e

Payee name and account number. Amount in ward and amount in figure. Branch code of from and to. Test number. Signature of applicant.

For an example if any client of our branch wantsto D.D. to Sylhet then he must fill up the formof D.D. where he writes all information as perD.D. form. Then bank check all information andcharge commission, VAT and postage charge.

For D.D. (1 to 49,999) Tk. There is no testnumber is needed. Greater than 49,999 Tk. D.D.needs test number.

62 | P a g e

Charges for D.D. as follows:

CHARGES PERCENTAGECommission Minimum 50Tk. Or 0.1% (Which one

greater).

VAT 15%.Postage Charge 25Tk. (Fixed)

Then register D.D. in register book. Where bankwrites control number, test number, amount inword and figure, payee name and the branch namewhere it sends.

The bank makes an advice, which has four parts. Twocopies send to the payee’s branch, one copy sends tothe head office and the rest one in this banksvoucher.

PROCEDURE OF INWARD D.D:

When D.D. from any branch, then we register it in registerbook, in this case bank must see the previous serialnumber. If it is correct, than bank register it inregister book. Where bank entry date on the D.D., D.D.number, payee name, amount, and serial number.

For an example if any D.D. comes from Rajshahi. Then bankdoes:

Head Office A/c (Rajshahi Br) Dr.D.D. Payable A/c Cr.

63 | P a g e

CHARGES ON

When branch gets that money from head office then bank does:

D.D. payable A/C Dr.Customer A/C Cr.

Branch office maintain a with head office which is calledHead Office Account.

Note: Inward D.D.’s copy enclose in appendix.

[5.2.3] PAY ORDER:Pay orders are the safest way of making payments, as theyare drawn on the bank issuing them. So, there is no scope offraudulent or cheque bouncing. A pay order is issued onlywithin the members of the Bangladesh Bank clearing house(Dhaka Metro). It can be issued in favor of a customerholding an account, by debiting his account and creditingbills payable account. In case of a non-customer, cashequivalent of the payment plus order charges is received incash and held in the daily suspense account until thepayment is made through clearing.

It is another facility for client to transfer his money toanother place. In this he must has an account in this bank.If he has no account in this bank, he can deposit money inthis bank and does Pay Order. But in this case he must needa person how knows him. He can deposit check, which isconfirmed, by Bangladesh bank’s clearinghouse. If it iscorrect than bank does this Pay Order.

Application must fill up the Pay Order form, where Pay Ordernumber, Payee name, Amount in figure and in wards.

64 | P a g e

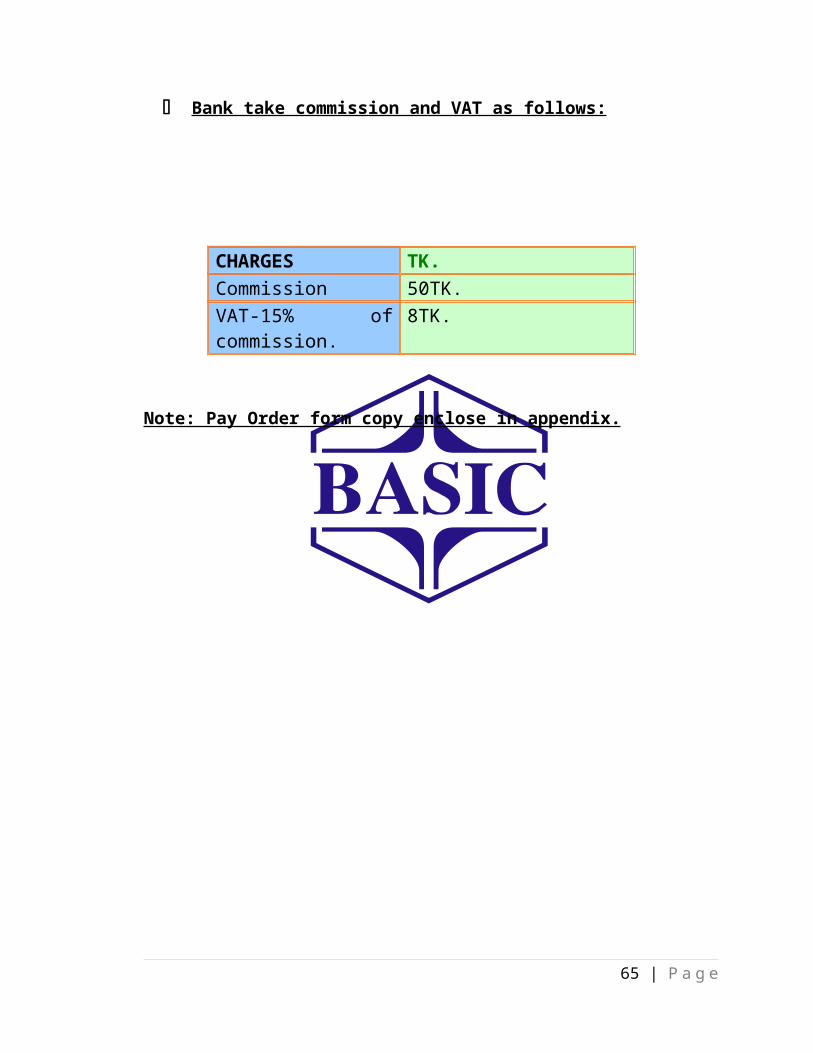

Bank take commission and VAT as follows:

CHARGES TK.Commission 50TK.VAT-15% ofcommission.

8TK.

Note: Pay Order form copy enclose in appendix.

65 | P a g e

REFUND OF PAY ORDER:

The following procedure should be followed for refund of payorder by cancellation: -

1. The purchase should submit a writtenrequest for refund of pay order bycancellation attaching therewith theoriginal pay order.

2. The signature of the purchaser will haveto be verified from the originalapplication form on record.

3. Manager/ sub-manager's prior permissionis to be obtained before refunding theamount of pay order cancellation.

4. Prescribed cancellation charge is to berecovered from the applicant and only theamount of the pay order less cancellationcharge should be refunded. Commissionrecorded for issuing the pay order shouldnot be refunded.

5. The pay order should be affixed with astamp ''Cancelled'' under properauthentication and the authorizedofficer's signature of the pay ordershould also be cancelled with red ink butin no case should be torn. The cancelledpay order should be kept with therelevant ticket.

6. The original entries are to be reversedwith proper narration.

66 | P a g e

7. Cancellation of the pay order should alsobe recorded in the pay order issueregister.

[5.2.4] I.B.C.A. & I.B.D.A: [Inter Bank Credit Advice & Inter Bank Debit Advice]

Check comes from different bank. If these checks come fromwithin Dhaka city then it goes to clearing house. If thesecome from outside the city then bank do OBC (Outward Billsfor Collection) against that bank to collect that amount ofmoney. After receiving the checks and crossing on thatcheck, then put OBC sill on that checks, then putendorsement sill backside of these check and register it inthe register book.

Then bank makes advice against that bank where the checkcomes. If the bank request for OBC to any branch of its,then bank advice to send I.B.C.A. then Bank make a liabilityvoucher, where: -

Customer Liability Dr.Bankers Liability Cr.

After collection money bank does: -67 | P a g e

Bankers Liability Dr.Customer Liability Cr.

On the credit voucher bank write the OBC number, Date, inadvice, Bank name and amount.If the bank requests it’s any branch to collect the amountof money where it needs to collect, then bank must write thename of the bank where it will be collected. If bankcollects in directly from any bank, in that case bank writesDrawn Yourself.

I.B.C.A. PROCEDURE:

When any branch send I.B.C.A. to this bank, then bankregister it into register book. Where bank write the date,branch name, check number, date on the check, name of thebank, and amount. Then it is place for clearing and afterrealization of that check, and then bank makes a voucher.Where bank does-

Misc. A/c Dr.Branch A/c Cr.

Then Bank registers it in OBC register book.

68 | P a g e

[5.3] CLEARING HOUSE:

ORIGIN OF BANKS’ CLEARING HOUSE:

Before introduction of the present concept ofClearing House, the representatives of the bankshad to collect the proceeds of the instrumentsin Cash from the drawee banks, which involverisk, time and money. Mr., Arbin first thoughtabout Clearing House to solve those problems andon the basis of his revolutionary thought Banks’Clearing House was initially established in 1775in London as “London Clearing”.

CLEARING HOUSE:

Clearing House is mechanisms for expeditioussettlement of inter bank claims arising out oftheir constituent’s negotiable instruments inpresence of representatives of all member banks.In Bangladesh, Clearing arrangements exist inthe office of the Bangladesh Bank, at otherplaces in the office of Sonali Bank whereBangladesh Bank has no Office.

TYPES OF CLEARING HOUSE:

There are two types of clearing System in Bangladesh. They are: –

Inter-Branch Clearing, and Inter-Bank Clearing.

Under the system of Inter-Branch Clearing,inter-branch claims of a particular bank withinthe City or town area are settled through theirMain Office or Local Office.

69 | P a g e

But under the system of Inter Bank Clearing, theclaims among the members of the clearing houseof different Banks within the area of clearinghouse are settled under the direct supervisionand control of Bangladesh Bank and each memberbank of the Clearing House has to maintain theiraccount with Bangladesh Bank.

USEFULNESS OF CLEARING HOUSE:

Clearing House is essential for adjustment of adeveloped Banking System. It makes easysettlement of inter-bank claims and it saveshuge cash transactions and consequent danger ofloss in transit and the necessity of holding byevery bank of a huge cash balances for thepurpose. The Clearing House is of incalculablebenefit as a time, labor, risk and currencysaver.

FUNCTION OF CLEARING HOUSE:

Entire function of Clearing House may be divided into 3 parts:

Operational procedure at Branch Level, Internal or Inter-Branch Clearing procedure,

and Main Clearing House or Inter-Bank procedure.

[5.3.1] OPERATIONAL PROCEDURE AT BRANCH LEVEL:

There are two types of clearing activities at BranchLevel:

Outward Clearing, Inward Clearing.

70 | P a g e

OUTWARD CLEARING:

Under this system negotiable instruments drawn on otherbanks are presented in the respective bank through ClearingHouse for receiving payment and after receiving the proceedsof the cheque / instruments the accounts of the respectiveclients are credited.

INWARD CLEARING:

Under this system negotiable instruments of different bankspresented in the Clearing House are received by therepresentative of the respective bank and bring theinstruments of their branches for making payment.

Procedural activities of Outward Clearing System:

Outward Clearing System includes the following activities:

Scrutinizing the correctness of the instruments thatreceived for clearing.

Affixing the branch crossing seal on the face of theinstrument.

Affixing branch clearing seal on the deposit slips andon the face of the instruments.

Making necessary endorsement on the back of theinstruments.

71 | P a g e

Encoding the necessary information of the instrumentsin the diskette.

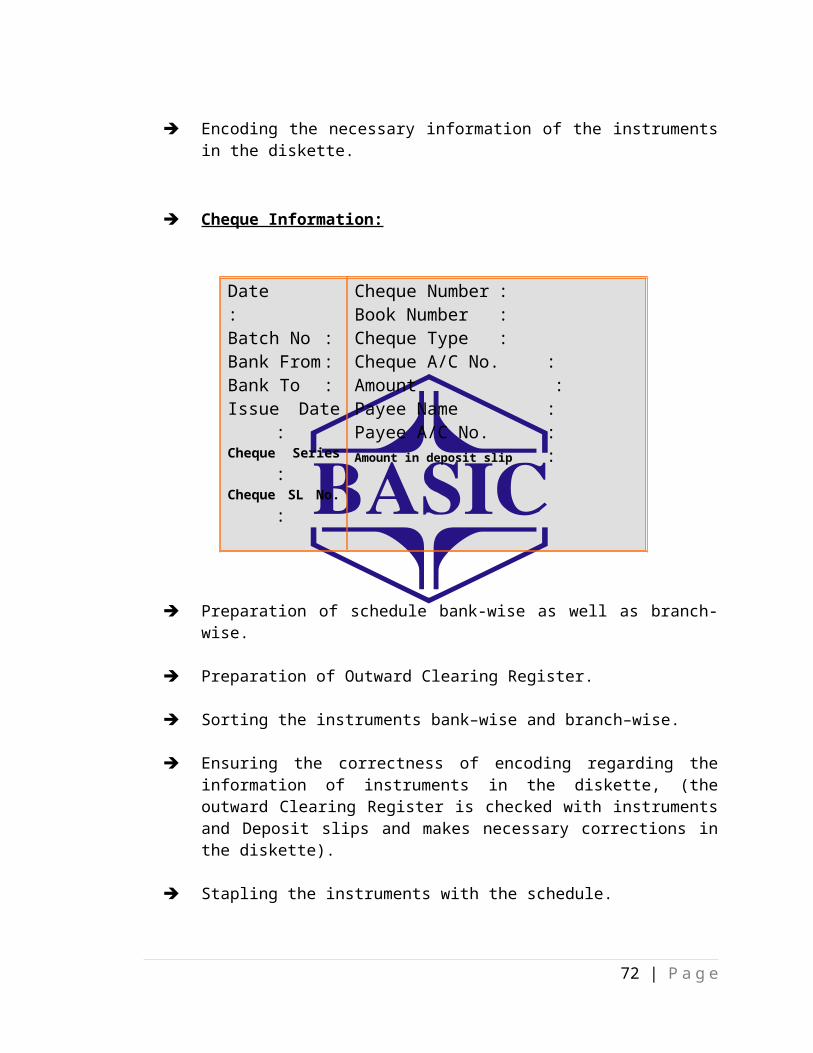

Cheque Information:

Date:Batch No :Bank From:Bank To :Issue Date

:Cheque Series

:Cheque SL No.

:

Cheque Number :Book Number :Cheque Type :Cheque A/C No. :Amount :Payee Name :Payee A/C No. :Amount in deposit slip :

Preparation of schedule bank-wise as well as branch-wise.

Preparation of Outward Clearing Register.

Sorting the instruments bank–wise and branch–wise.

Ensuring the correctness of encoding regarding theinformation of instruments in the diskette, (theoutward Clearing Register is checked with instrumentsand Deposit slips and makes necessary corrections inthe diskette).

Stapling the instruments with the schedule.

72 | P a g e

Sending the instruments along with diskette to theMain Branch or Local Office for clearing.

Passing the entries at the time of sending clearinginstruments is as under: For branch other than Main Branch / Local Office:

Debit : Head Office A/C (Main Branch)Credit : Sundry Clients A/C / other A/Cs

Activities of Internal Clearing House at Main Branch:

Receiving the diskettes containing theinformation of negotiable instruments along withinstruments supported by its clearing schedulesand necessary Inter Branch Debit Advice (IBDA)from the representatives of branches.

The diskettes received from the branches aremerged and transferred to a diskette, which is tobe presented in the Clearing House at BangladeshBank.

Preparation of Summary Schedule and House Sheet.

Sorting the instruments Bank-wise as well asBranch-wise and stapling the instruments with theschedules accordingly.

Preparation of summary Outward Clearing Register.

Passing the entries by Main Branch at the time ofsending the instruments to Bangladesh BankClearing House are as under:

For Main Branch/ Local Office:

73 | P a g e

Debit : Suspense A/C – Clearing Receivable.Credit : Sundry Clients A/C / other A/Cs.Credit : Head Office A/C (Responding the IBDA ofBranches)

[5.3.2] ACTIVITIES OF INTER BANK CLEARING HOUSEAT BANGLADESH BANK:

Handing over the diskette and House sheet to theComputer Section of the Clearing House.

Handing over the bank-wise sorted instruments tothe representatives of the respective Bank.

Diskettes received from different Banks aremerged in the Computer Section of Clearing Houseand summary House Sheets of all Banks areprepared separately.

Handing over the summary House Sheet of the Bankto the respective representative of the Bank.All instruments received and delivered are

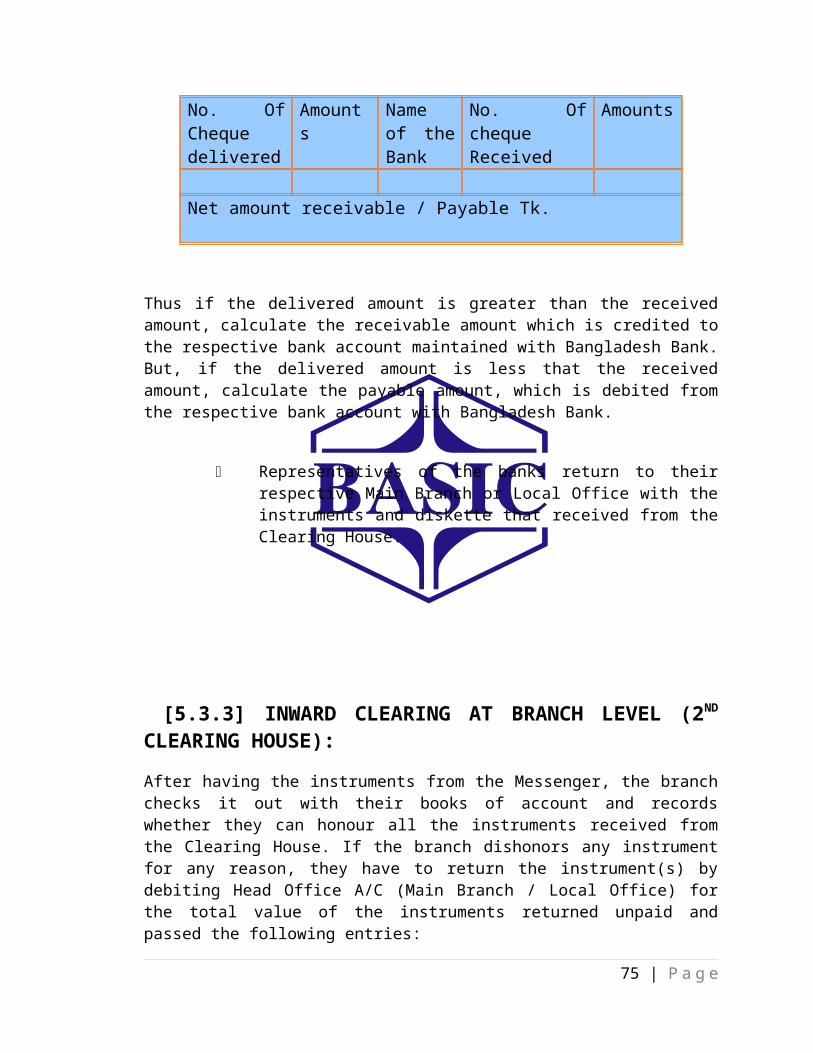

Printed in the Summary House Sheet, which is asunder:

BASIC Bank Limited1st Clearing, Dhaka Date: …………

74 | P a g e

No. OfChequedelivered

Amounts

Nameof theBank

No. OfchequeReceived

Amounts

Net amount receivable / Payable Tk.

Thus if the delivered amount is greater than the receivedamount, calculate the receivable amount which is credited tothe respective bank account maintained with Bangladesh Bank.But, if the delivered amount is less that the receivedamount, calculate the payable amount, which is debited fromthe respective bank account with Bangladesh Bank.

Representatives of the banks return to theirrespective Main Branch or Local Office with theinstruments and diskette that received from theClearing House.

[5.3.3] INWARD CLEARING AT BRANCH LEVEL (2ND

CLEARING HOUSE):After having the instruments from the Messenger, the branchchecks it out with their books of account and recordswhether they can honour all the instruments received fromthe Clearing House. If the branch dishonors any instrumentfor any reason, they have to return the instrument(s) bydebiting Head Office A/C (Main Branch / Local Office) forthe total value of the instruments returned unpaid andpassed the following entries:

75 | P a g e

Debit: SB / CD / CC / STD A/C of the clients, PayOrder A/C / D.D. Payable A/C / Draftpaid without Advice A/C etc.

Debit: Head Office A/C (Main Branch) for the amountof dishonoured instrument(s) if any.

Credit: Head Office A/C (Responding the IBDA of MainBranch).

The branch then prepares the return Memo for each returnedinstrument that contains instrument No., Amount and reasonfor its dishonor and recorded it in the Cheque ReturnRegister. Now the instruments are enclosed with the ReturnMemos and are sent to the Main Branch / Local Office withInter Branch Debit Advice (IBDA).After receiving the returned instruments from the branches,instruments are encoded in the diskette at Main Branch /Local Office and perform the following activities:

Preparation of schedule,

Preparation of outward clearing return register,

Sorting the instrument bank-wise as well as branch-wise,

Stapling the instrument(s) with the schedule.

76 | P a g e

Chapter SIX

77 | P a g e

Data Analysis & Findings

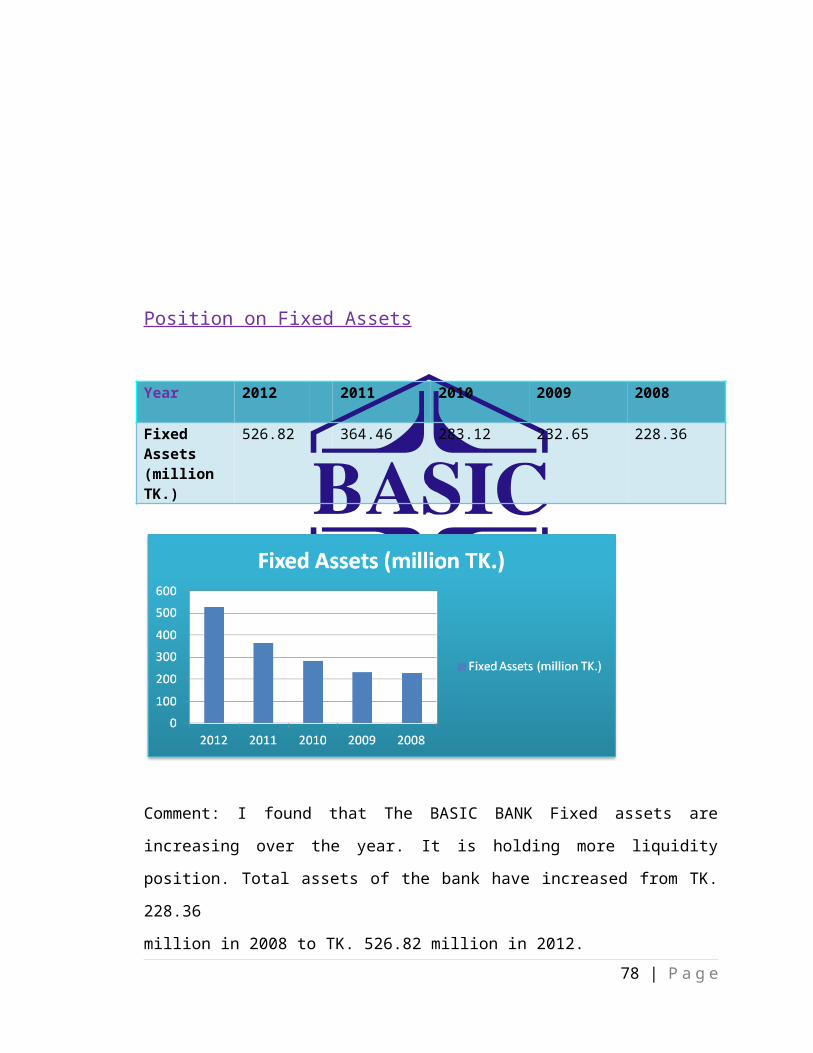

Position on Fixed Assets

Year 2012 2011 2010 2009 2008

FixedAssets(millionTK.)

526.82 364.46 283.12 232.65 228.36

Comment: I found that The BASIC BANK Fixed assets are

increasing over the year. It is holding more liquidity

position. Total assets of the bank have increased from TK.

228.36

million in 2008 to TK. 526.82 million in 2012.78 | P a g e

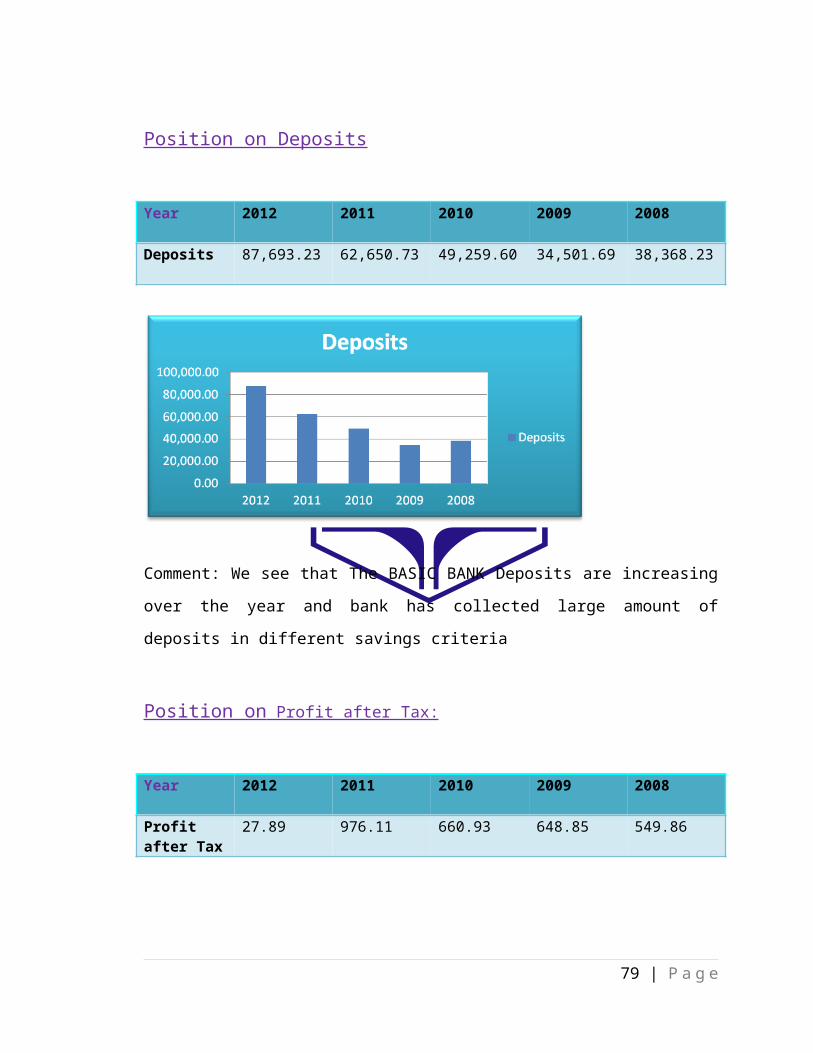

Position on Deposits

Year 2012 2011 2010 2009 2008

Deposits 87,693.23 62,650.73 49,259.60 34,501.69 38,368.23

Comment: We see that The BASIC BANK Deposits are increasing

over the year and bank has collected large amount of

deposits in different savings criteria

Position on Profit after Tax:

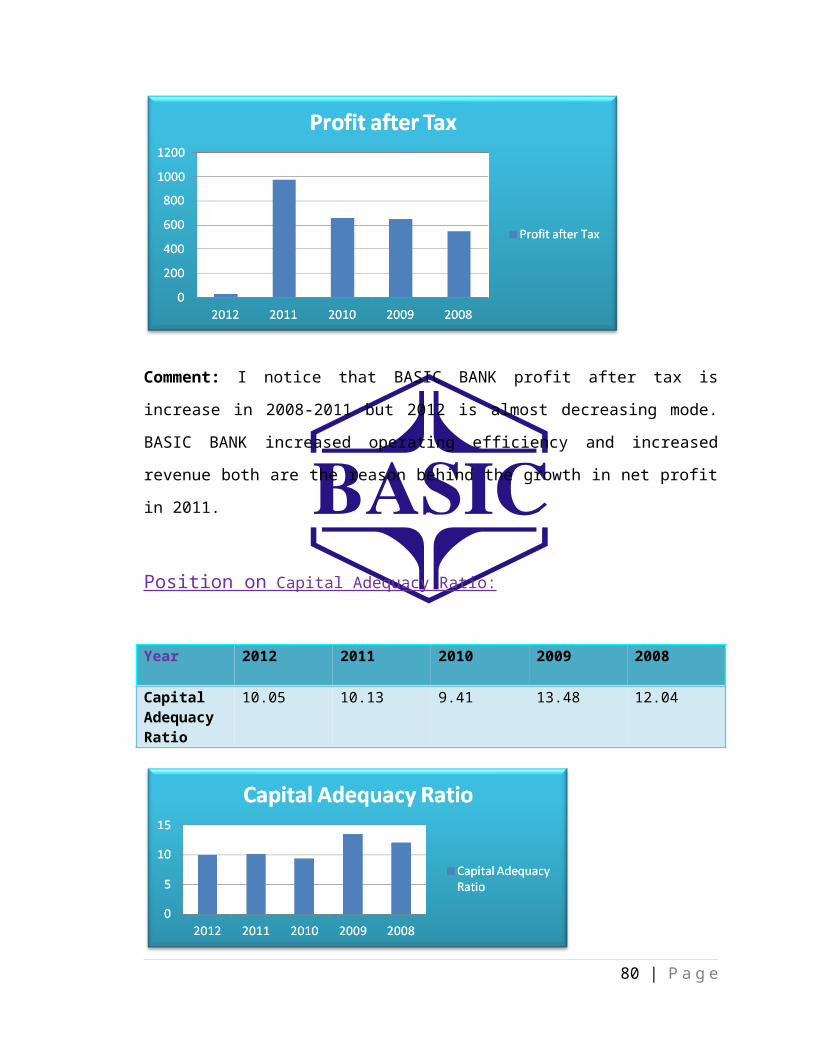

Year 2012 2011 2010 2009 2008

Profitafter Tax

27.89 976.11 660.93 648.85 549.86

79 | P a g e

Comment: I notice that BASIC BANK profit after tax is

increase in 2008-2011 but 2012 is almost decreasing mode.

BASIC BANK increased operating efficiency and increased

revenue both are the reason behind the growth in net profit

in 2011.

Position on Capital Adequacy Ratio:

Year 2012 2011 2010 2009 2008

CapitalAdequacyRatio

10.05 10.13 9.41 13.48 12.04

80 | P a g e

Comment: From this trend analysis we have seen that the

Capital Adequacy Ratio of BASIC BANK has Increasing mode in

2009 & after 2010. But, bank also decreased significantly

during 2010 & 2012.

Findings

The employees of the branch are not much smart and

active in rendering customer service.

The bank has limited branch.

81 | P a g e

Each and every section of the general banking

department has not computerized.

Number of officers in the general banking department

has not sufficient

The bank has no social service.

The bank has not sufficient products based on the

market demand.

The minimum balance is so high to attract more

customers.

The department of bank has not been efficient to make

profit by satisfying customers.

BBL has not attractive promotional activities.

Very few number of ATM booths.

ATM network of BBL is not efficient.

There is no separate team for the marketing of their

services who might inform the customers about their

different services of the bank.

82 | P a g e

Chapter SEVEN

83 | P a g e

Conclusion & Recommendations

Conclusion

The Banking arena in recent time is one of the most

competitive business fields in Bangladesh. As Bangladesh is

a developing country, a strong banking sector can change the

socio economic structure of the country. So, we can say, the

whole economy of the country is linked up with its banking

system. There are 54 banks in Bangladesh in which 38 are

indigenous commercial Banks. BASIC Bank Ltd. is a state-

owned scheduled Bank as well as a potential and promising

bank in the banking sector in Bangladesh. As desired, its

functions and activities in the economy are being aligned

with the objectives set by the Government of Bangladesh

since its inception. This bank performs hundreds of

important activities both for the public and for the

government as a whole. It has an outstanding bearing to

thrive our business sector. It has strong performance on

General Banking, Loans & Advances, Industrial credit and

foreign Exchange. By using limited technology and having

limited of branches at home it is increasing the volume of

export-import business including homebound remittances. The

84 | P a g e

effective and efficient Foreign Exchange Business of the

Bank helps in the continuous growth and progress of national

economy.

BASIC Bank Limited is, no doubt, playing a vital role in the

economic sector of Bangladesh. I hope, the successful

walkway of BASIC Bank Limited will remain continuous for a

long time and become a role model in the banking sector in

our country.

BASIC Bank Ltd is redefining the traditional banking

concepts and transforming it into relationship banking.

BASIC considers the borrower as clients. The mutual

relationship is the essence of long term success in the

banking industry. The ever increasing competitive nature of

banking business determines the direction of the bank.

Sustainability in better performance is the prime focus in

BASIC Bank.

Recommendation

85 | P a g e

To increase the efficiency in customer service the BASIC

Bank should develop its process of providing services. To

get a perfect process of delivering services, the customers

should be asked. The other suggestions are as follows:

The employees of the branch should be more smart and

active in rendering customer service.

The bank can open more branches to reach to more

customers.

Each and every section of the general banking

department should be fully computerized for rendering

better service.

Number of officers in the general banking department

should be increased.

The bank should be more profit concerned as well as to

take part in the social service.

The bank should introduce more products based on the

market demand.

The bank should reduce their minimum balance to attract

more customers.

86 | P a g e

The department of bank more efficient to make profit by

satisfying customers.

BBL shall take more attractive promotional activities.

Increase number of ATM booths.

Ensure smooth network to ensure uninterrupted ATM

service.

The software used by BBL for their operations shall be

improved.

Bank should introduce separate team for the marketing

of their services who might inform the customers about

their different services of the bank.

References

Annual report, 2008 – 20012 “BASIC Bank Ltd”

Bishop, E. (2004), Finance of International Trade, Elsevier

Butterworth-Heinemann, Burlington, MA.

87 | P a g e

COSO (2004), Enterprise Risk Management – Integrated

Framework: Application Techniques, The Committee of

Sponsoring Organizations of the Treadway Commission,

Jersey City, NJ, pp. 93-104.

General Banking Guidelines of BASIC Bank Ltd.

King, R. (2001), Gutteridge and Megrah’s Law of Bankers’

Commercial Credits, Europe

Publications, London.

Madura, Jeff. (2002-2003) “Financial Markets & Institutions”. 7th

Edition, Thomson South Western.

www.basicbanklimited.com . [Accessed 15 March 2014]

88 | P a g e

Copyright © 2022 FDOKUMEN