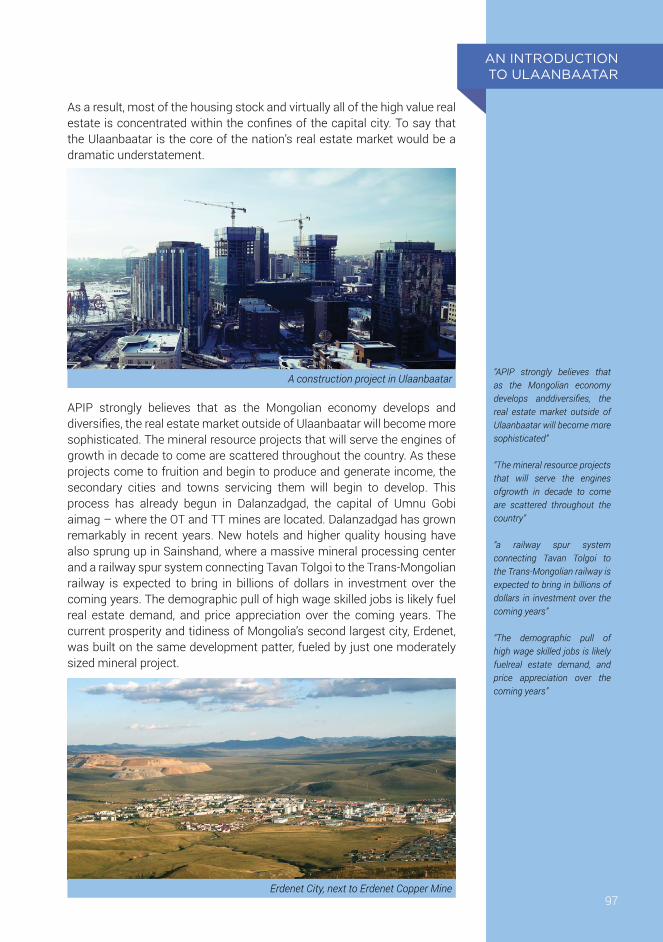

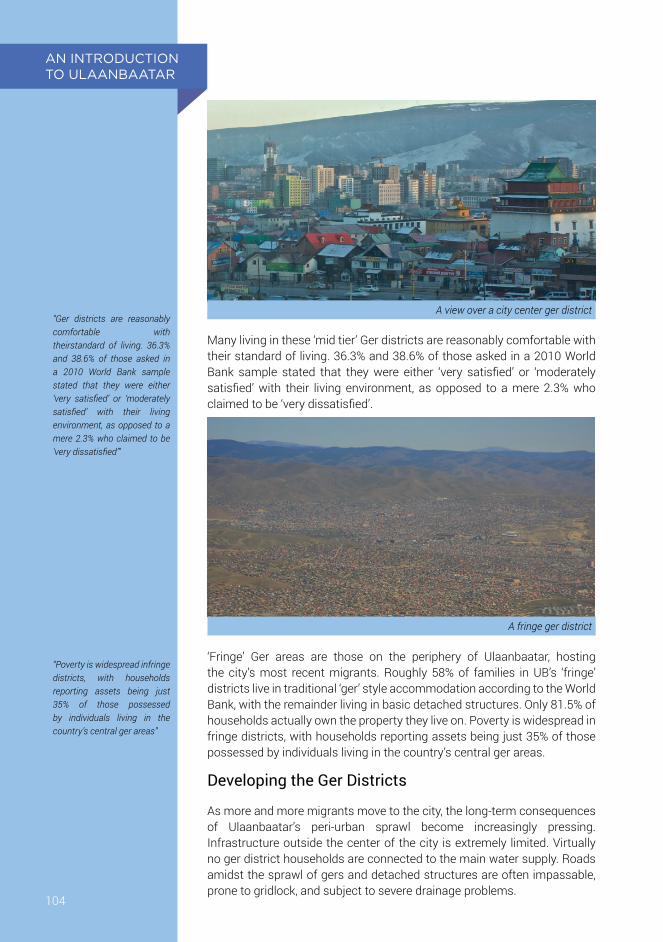

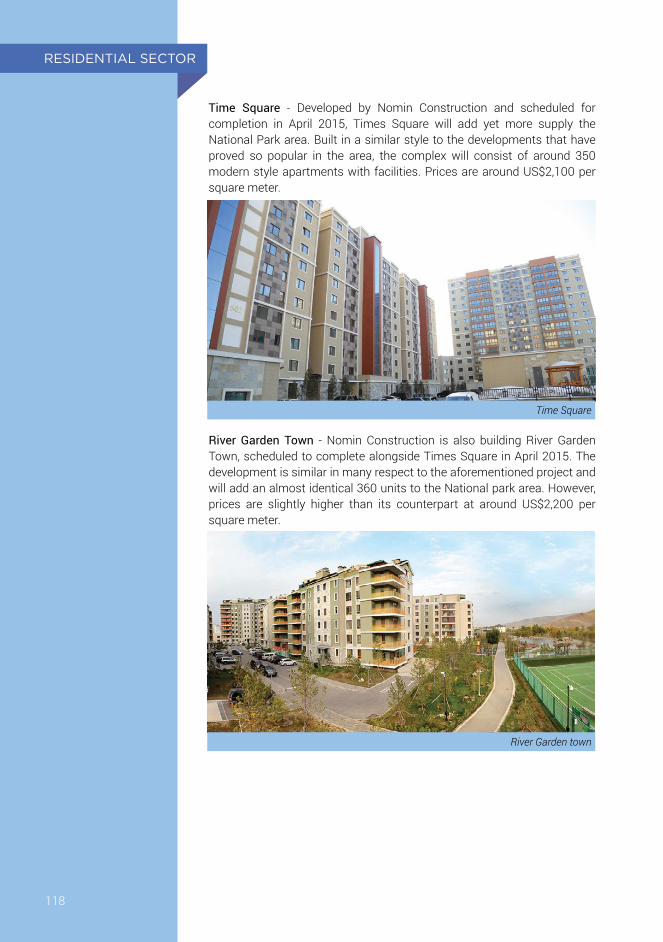

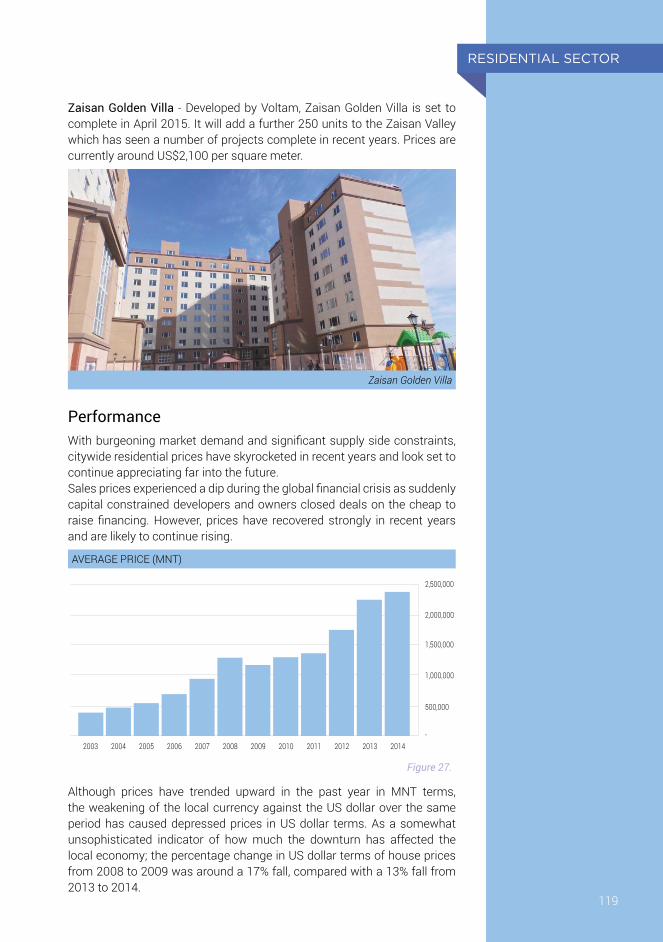

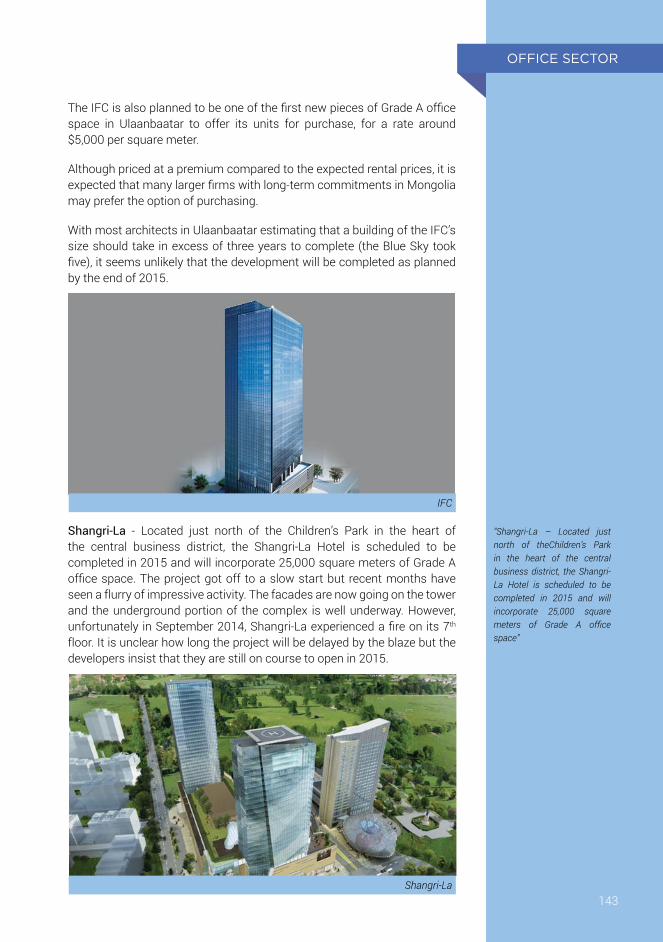

real-estate-report-2015.pdf - Mongolian Properties

256

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of real-estate-report-2015.pdf - Mongolian Properties

MONGOLIA

RUSSIA

CHINA

INDIA

NEPALBHUTAN

BANGLADESH

MYANMAR

THAILAND

LAOS

VIETNAM

Figure 1

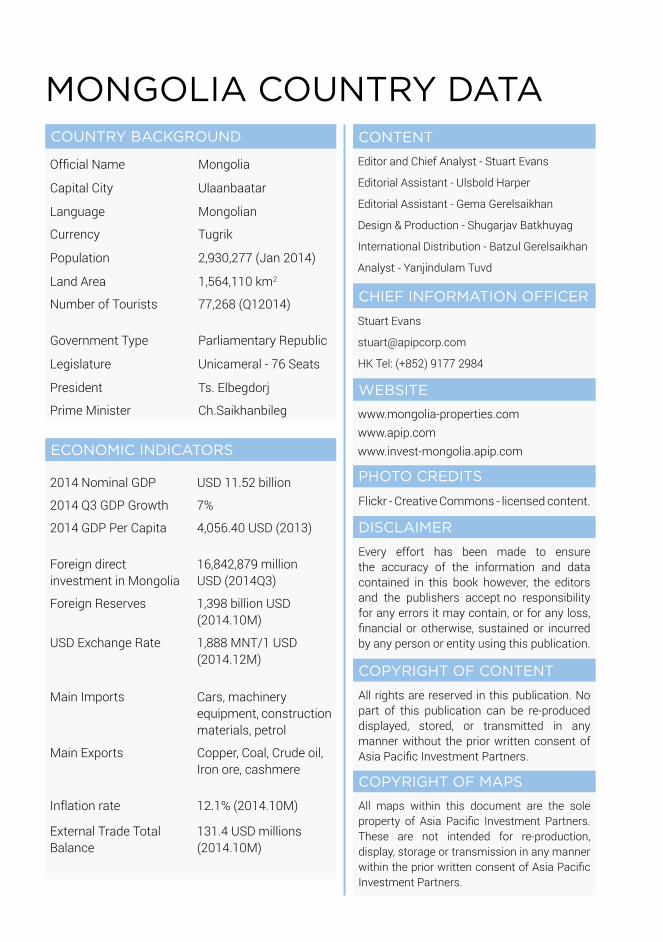

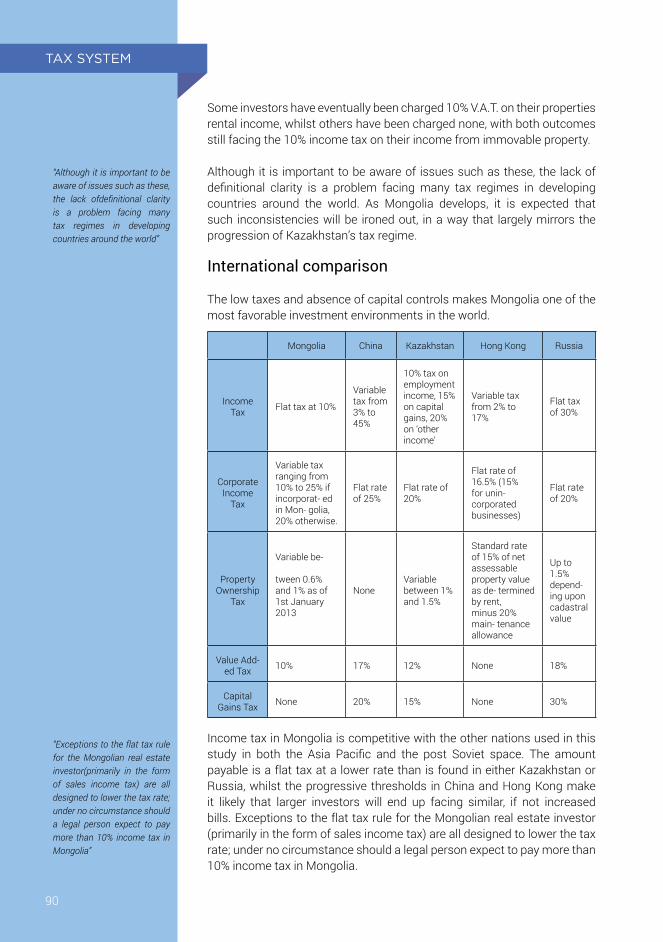

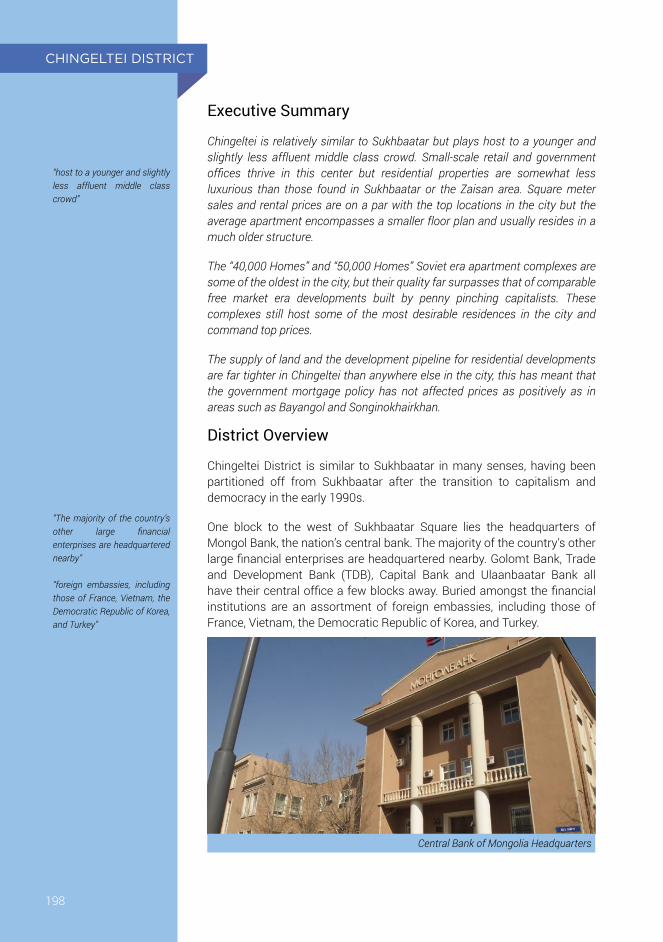

MONGOLIA COUNTRY DATACOUNTRY BACKGROUND

Official Name Mongolia

Capital City Ulaanbaatar

Language Mongolian

Currency Tugrik

Population 2,930,277 (Jan 2014)

Land Area 1,564,110 km2

Number of Tourists 77,268 (Q12014)

Government Type Parliamentary Republic

Legislature Unicameral - 76 Seats

President Ts. Elbegdorj

Prime Minister Ch.Saikhanbileg

ECONOMIC INDICATORS

2014 Nominal GDP USD 11.52 billion

2014 Q3 GDP Growth 7%

2014 GDP Per Capita 4,056.40 USD (2013)

Foreign direct investment in Mongolia

16,842,879 million USD (2014Q3)

Foreign Reserves 1,398 billion USD (2014.10M)

USD Exchange Rate 1,888 MNT/1 USD (2014.12M)

Main Imports Cars, machinery equipment, construction materials, petrol

Main Exports Copper, Coal, Crude oil, Iron ore, cashmere

Inflation rate 12.1% (2014.10M)

External Trade Total Balance

131.4 USD millions (2014.10M)

CONTENT

Editor and Chief Analyst - Stuart Evans

Editorial Assistant - Ulsbold Harper

Editorial Assistant - Gema Gerelsaikhan

Design & Production - Shugarjav Batkhuyag

International Distribution - Batzul Gerelsaikhan

Analyst - Yanjindulam Tuvd

CHIEF INFORMATION OFFICER

Stuart Evans

HK Tel: (+852) 9177 2984

WEBSITE

www.mongolia-properties.comwww.apip.comwww.invest-mongolia.apip.com

PHOTO CREDITS

Flickr - Creative Commons - licensed content.

DISCLAIMER

Every effort has been made to ensure the accuracy of the information and data contained in this book however, the editors and the publishers accept no responsibility for any errors it may contain, or for any loss, financial or otherwise, sustained or incurred by any person or entity using this publication.

COPYRIGHT OF CONTENT

All rights are reserved in this publication. No part of this publication can be re-produced displayed, stored, or transmitted in any manner without the prior written consent of Asia Pacific Investment Partners.

COPYRIGHT OF MAPS

All maps within this document are the sole property of Asia Pacific Investment Partners. These are not intended for re-production, display, storage or transmission in any manner within the prior written consent of Asia Pacific Investment Partners.

8

303256627484

9294

110126146170

178180194206216228236

Thoughts from the CEO

1. COUNTRY CONTEXT1.1. Macroeconomics1.2. History1.3. Politics1.4. Legal System1.5. Tax System

2. ULAANBAATAR REAL ESTATE – SECTORAL ANALYSIS2.1. An Introduction to Ulaanbaatar2.2. Residential Sector2.3. Office Sector2.4. Retail Sector2.5. Hospitality Sector

3. ULAANBAATAR REAL ESTATE – DISTRICT LEVEL ANALYSIS3.1. Sukhbaatar District3.2. Chingeltei District3.3. Bayangol District3.4. Bayanzurkh District3.5. Songinokhairkhan District3.6. Khan-Uul District

TABLE OF CONTENTS

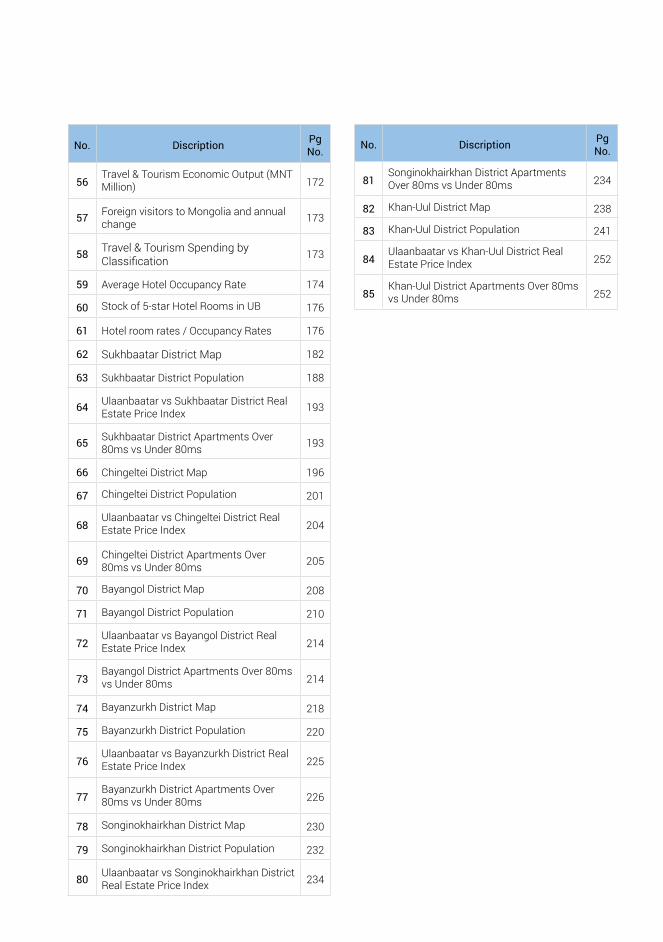

No. Discription Pg No.

1 World Map 3

2 Map of Ulaanbaatar Districts 26

3 Map of Ulaanbaatar’s Key Locations 28

4 Mongolia’s Explosive GDP Growth 36

5 Mongolia’s Diversifying Economy 37

6 Mongolia’s Experiencing Rapid Wage Growth 37

7 Mongolian Strategic Deposits 38

8 Oyu Tolgoi Ownership Structure 40

9 Oyu Tolgoi Mines 43

10 Mongolia Minerial Exports 45

11 Mongolian Imports 46

12 Mongolia’s Balance of Trade 47

13 Foreign Direct Investment Inflows 48

14 Mongolian Sovereign Bonds 51

15 Gross External Debt Position (USD Millions) 52

16 Mongolia Inflation rate 54

17 Mongolia Tugrik 54

18 Foreign Exchange Reserves (Billions MNT) 55

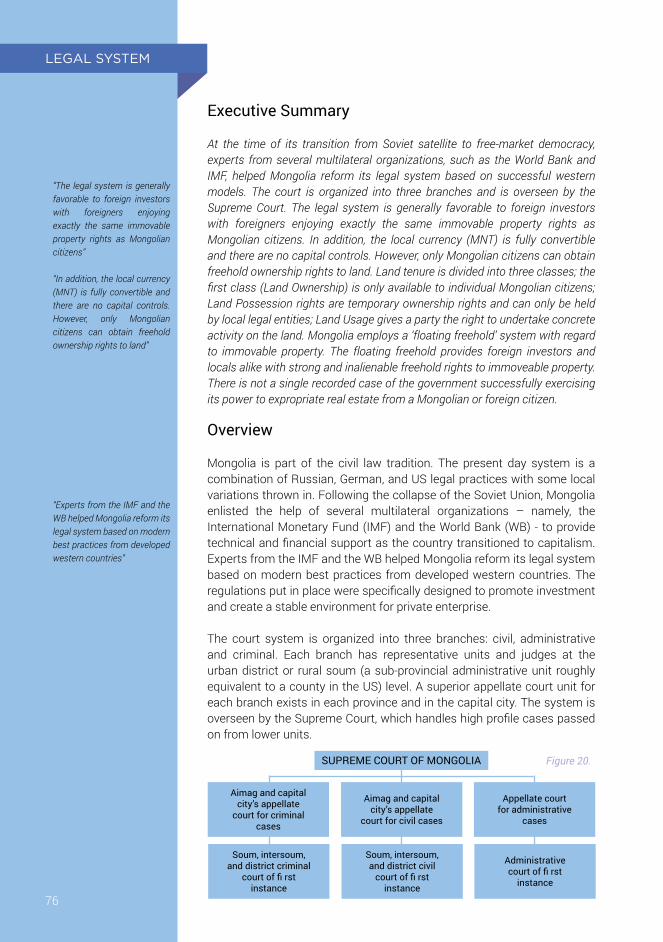

19 Total Outsanding Mortgage Loan and Year-on-year Growth Rate 55

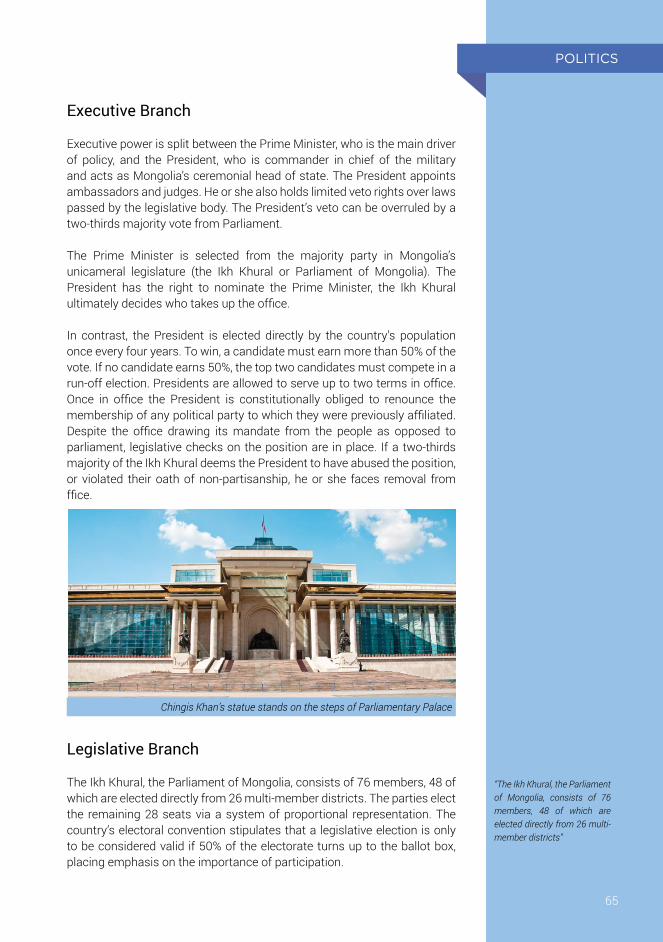

20 Supreme Court of Mongolia 76

21Average Monthly Temperature in Ulaanbaatar 98

22 Air Pollution in Ulaanbaatar 98

23 Residential Market 103

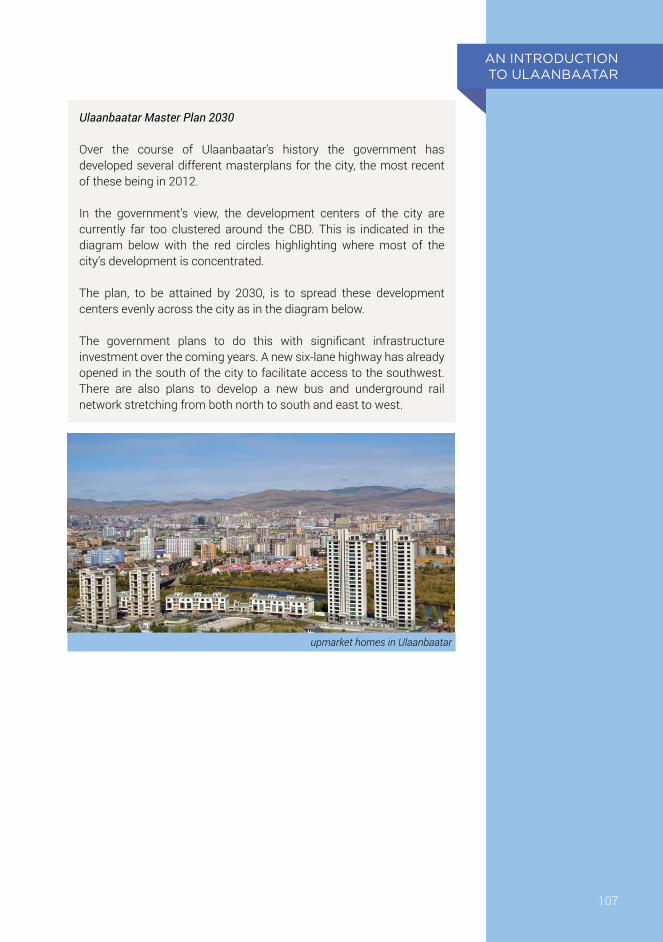

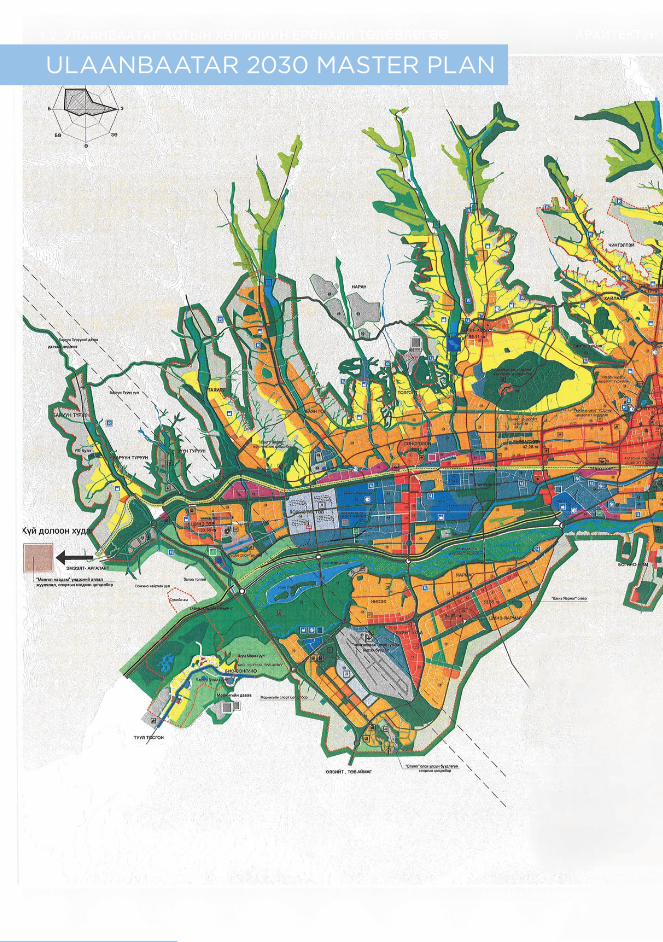

24 Ulaanbaatar 2030 Master Plan 108

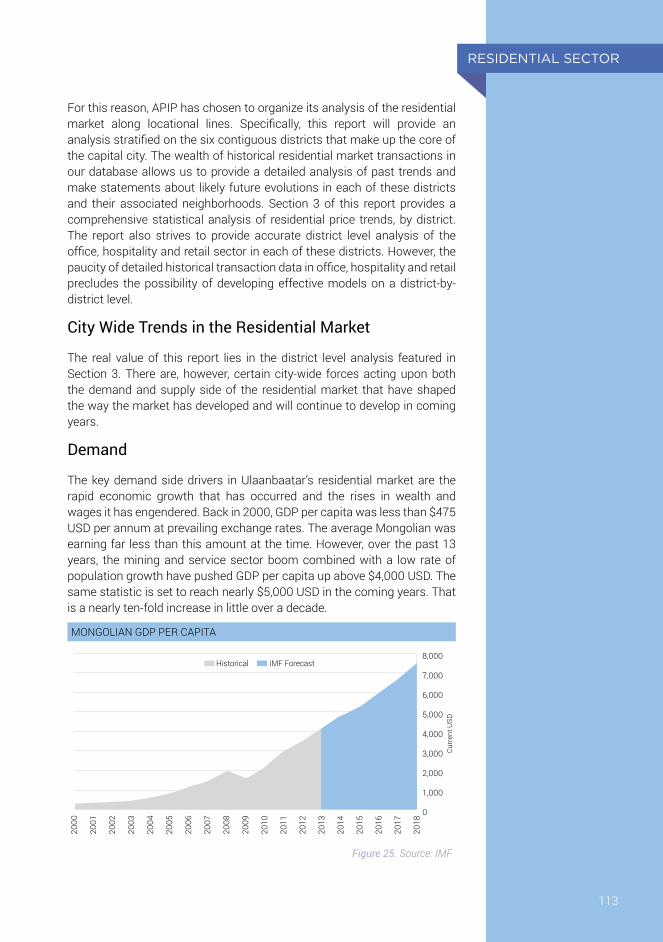

25 Mongolian GDP per Capita 113

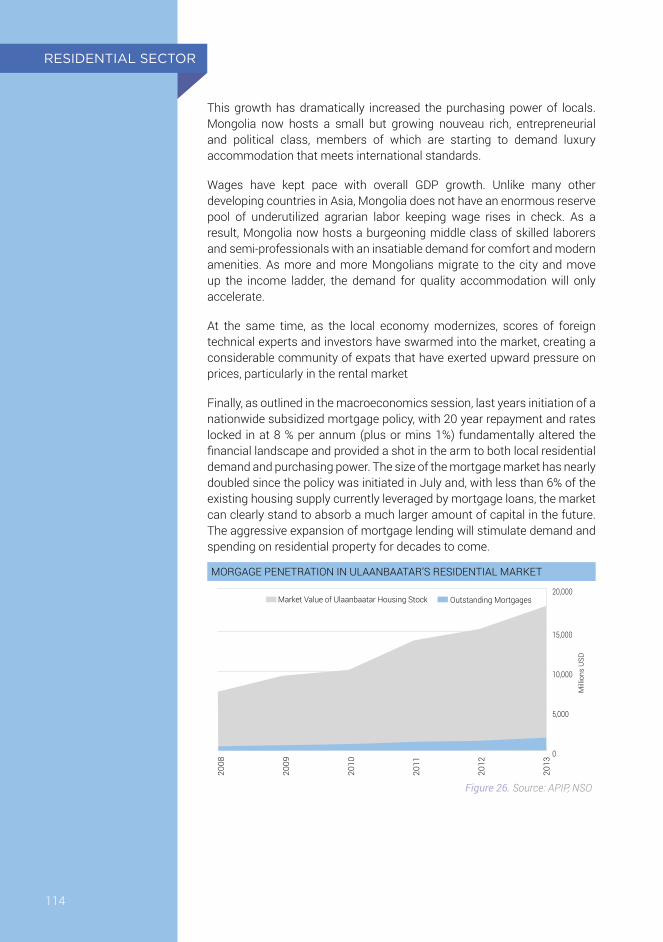

26 Morgage Penetration in Ulaanbaatar’s Residential Market 114

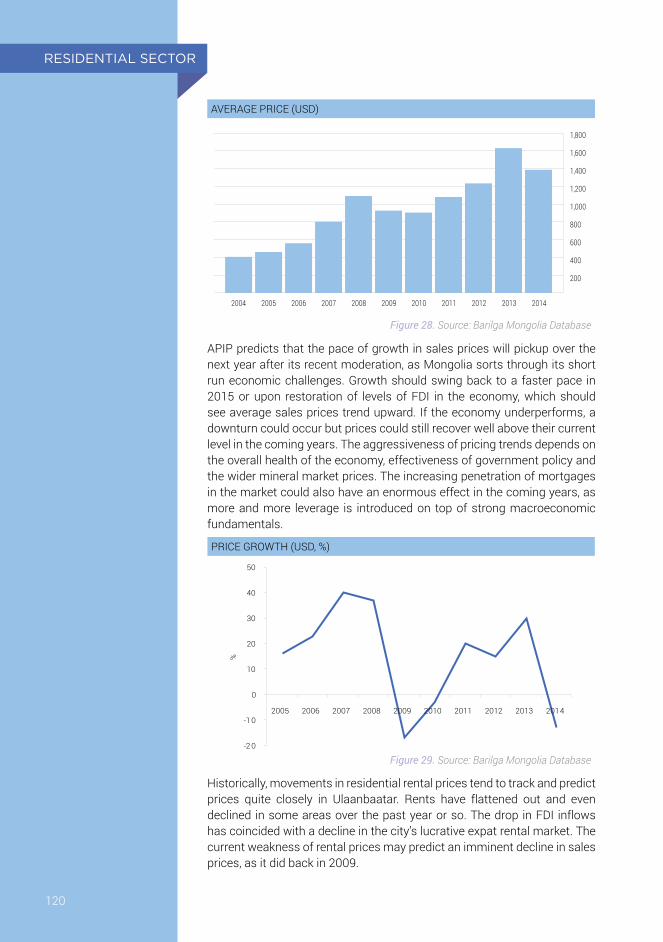

27 Average Price (MNT) 119

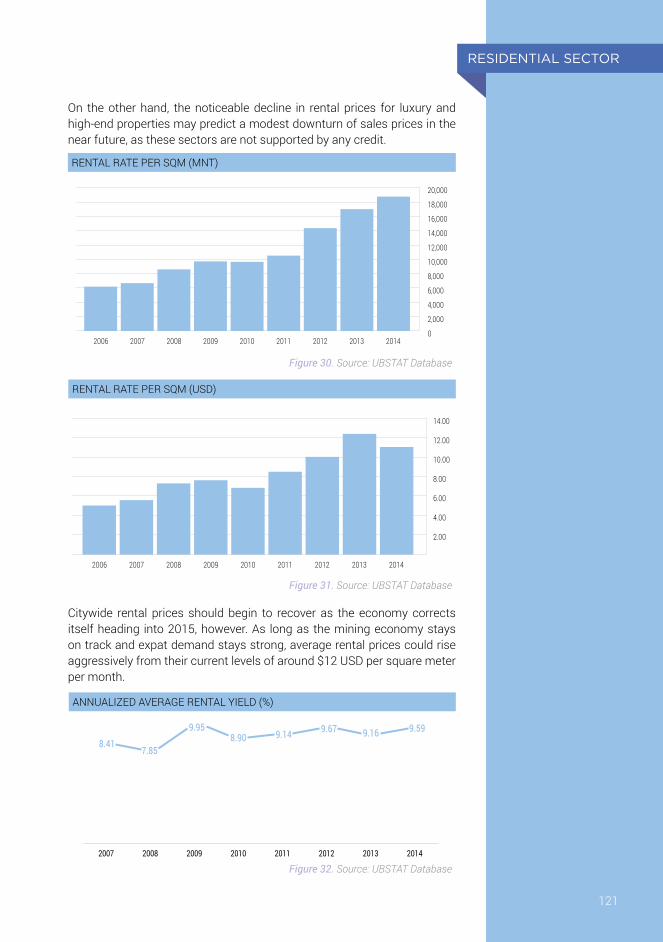

28 Average Price (USD) 120

29 Price Growth (USD, %) 120

No. Discription Pg No.

30 Rental Rate Per sqm (MNT) 121

31 Rental Rate Per sqm (USD) 121

32 Annualized Average Rental Yield (%) 121

33Newly Financed Mortgages vs. Refinanced Mortgages (in Million MNT) 122

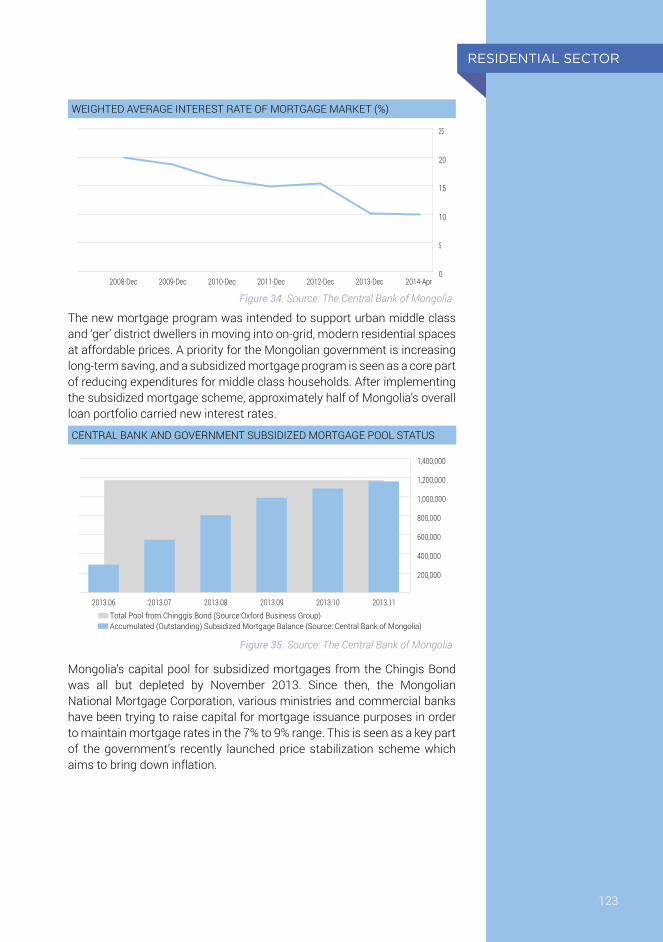

34 Weighted Average Interest Rate of Mortgage Market (%) 123

35 Central Bank and Government Subsidized Mortgage Pool Status 123

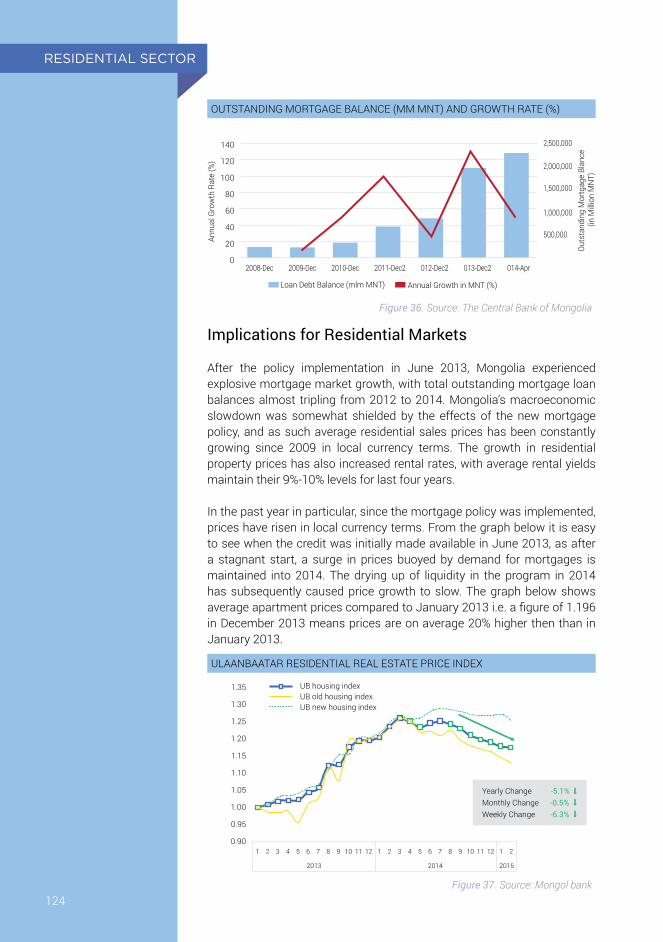

36 Outstanding Mortgage Balance (MM MNT) and growth rate (%) 124

37 Ulaanbaatar Residential Real Estate Price Index 124

38 Ulaanbaatar Office Map 128

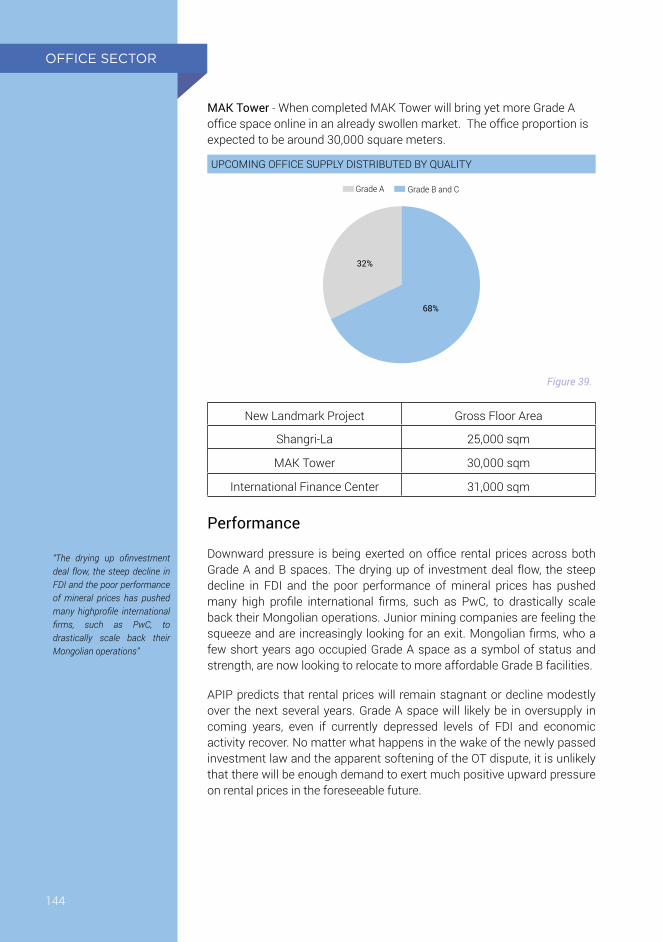

39Upcoming Office Supply Distributed by Quality 144

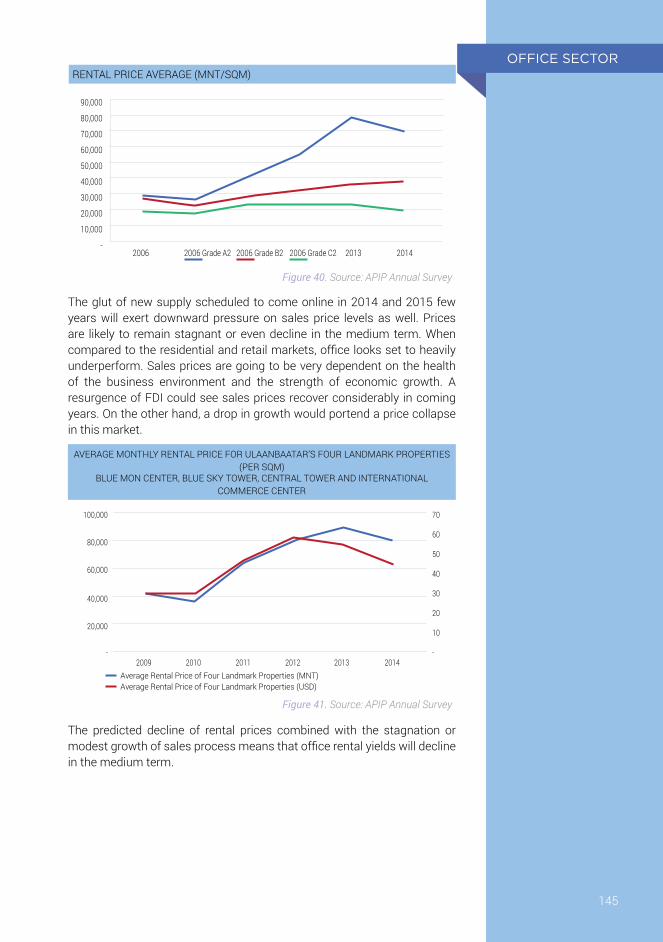

40 Rental Price Average (MNT/SQM) 145

41Average Rental Price of Four Landmark Properties 145

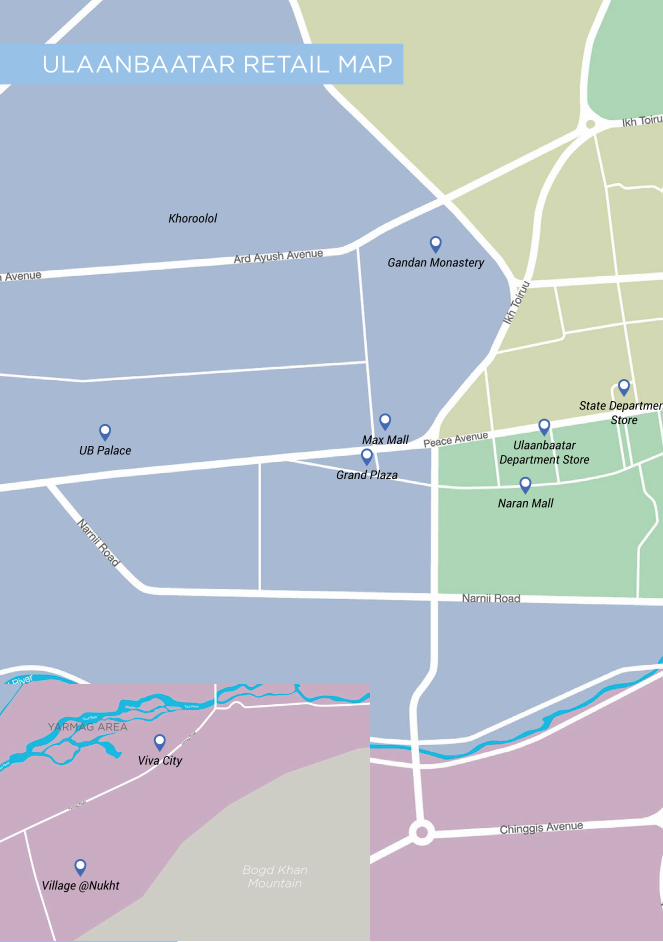

42 Ulaanbaatar Retail Map 148

43Rapidly Rising Wages for all income Categories 151

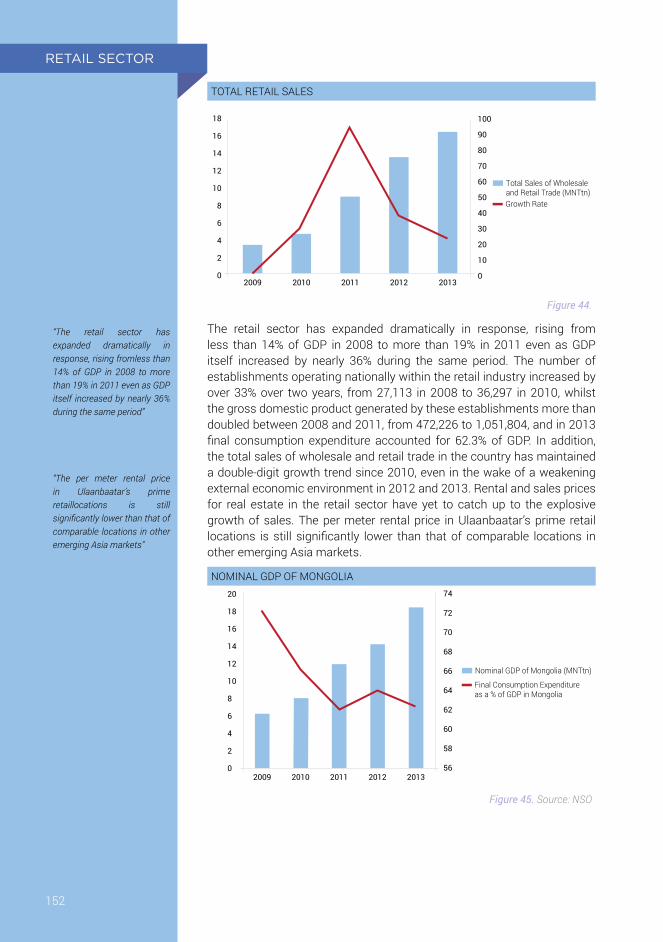

44 Total Retail Sales 152

45 Nominal GDO of Mongolia 152

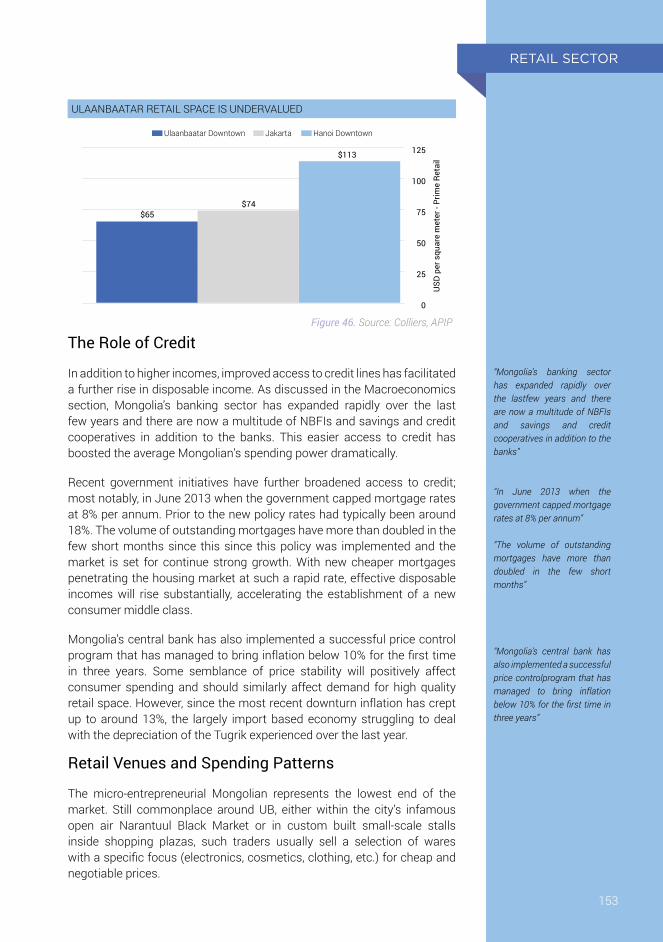

46 Ulaanbaatar Retail Space is Undervalued 153

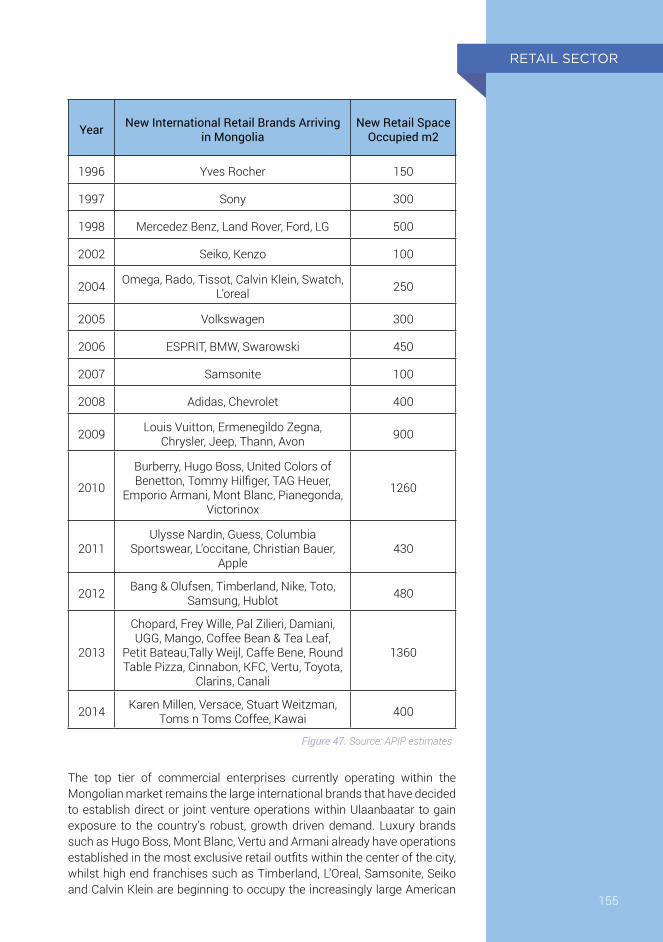

47 International Brands 155

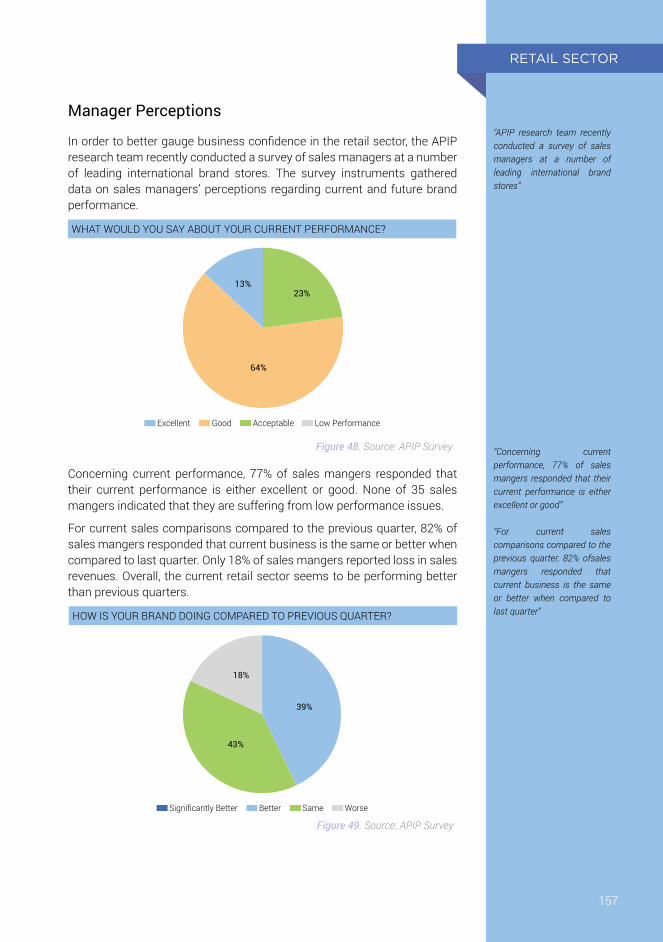

48What would you say about your current performance? 157

49How is your brand doing compared to previous quarter? 157

50 What’s your future outlook on sales? 158

51Are you thinking of expanding current retail space? 158

52 Are you thinking of increasing number of sales outlets? 158

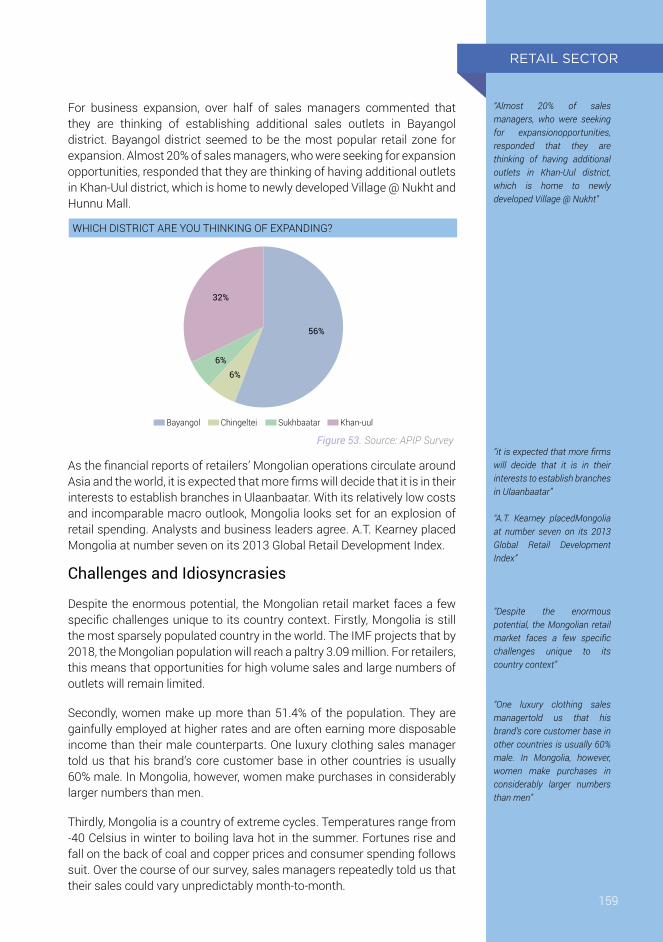

53 Which district are you thinking of expanding? 159

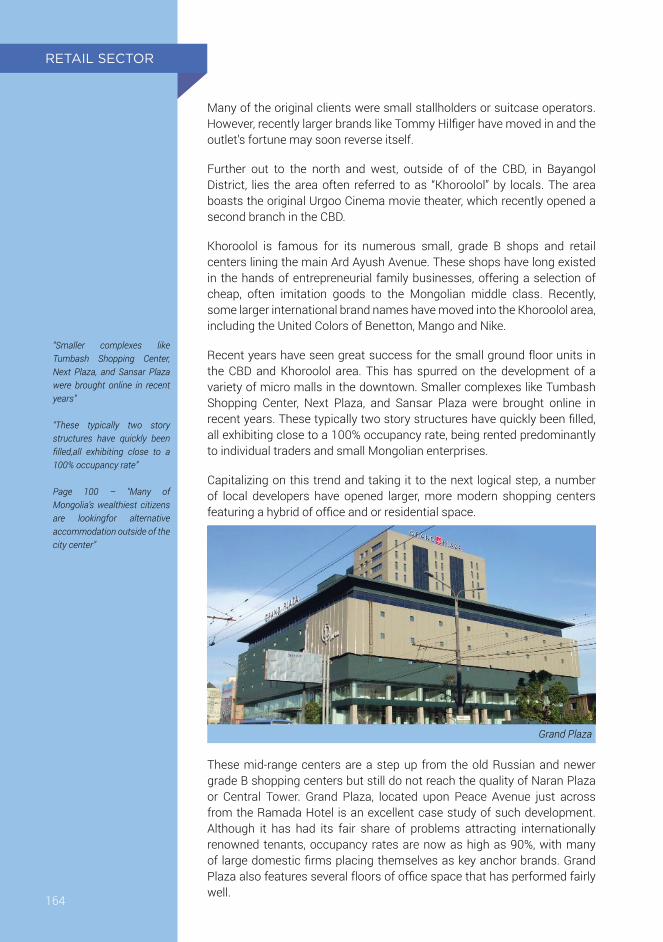

54 Prime Retail Space 162

55 Recent Developments 166

LIST OF FIGURES

No. Discription Pg No.

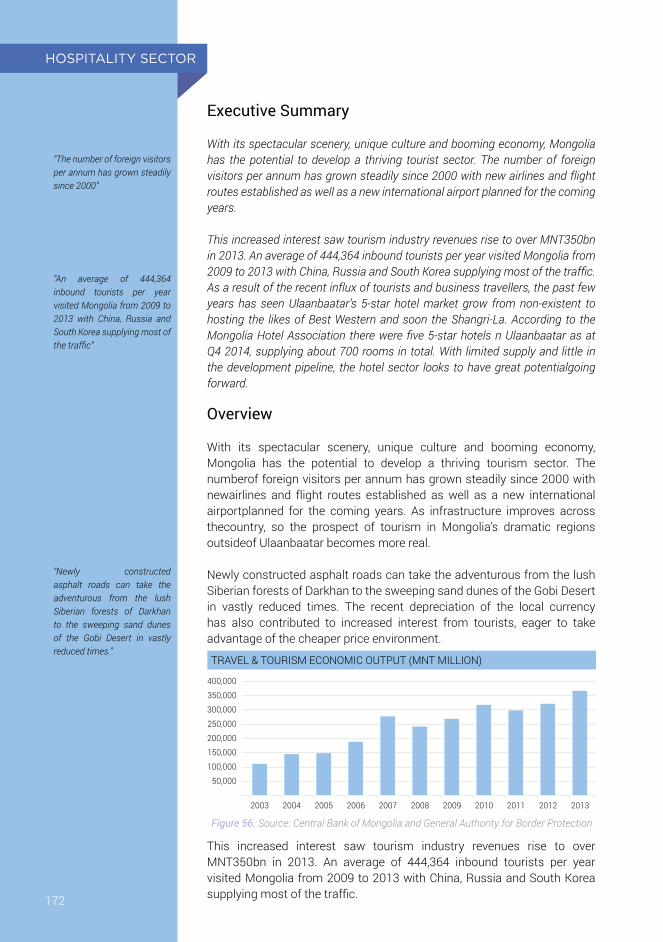

56Travel & Tourism Economic Output (MNT Million) 172

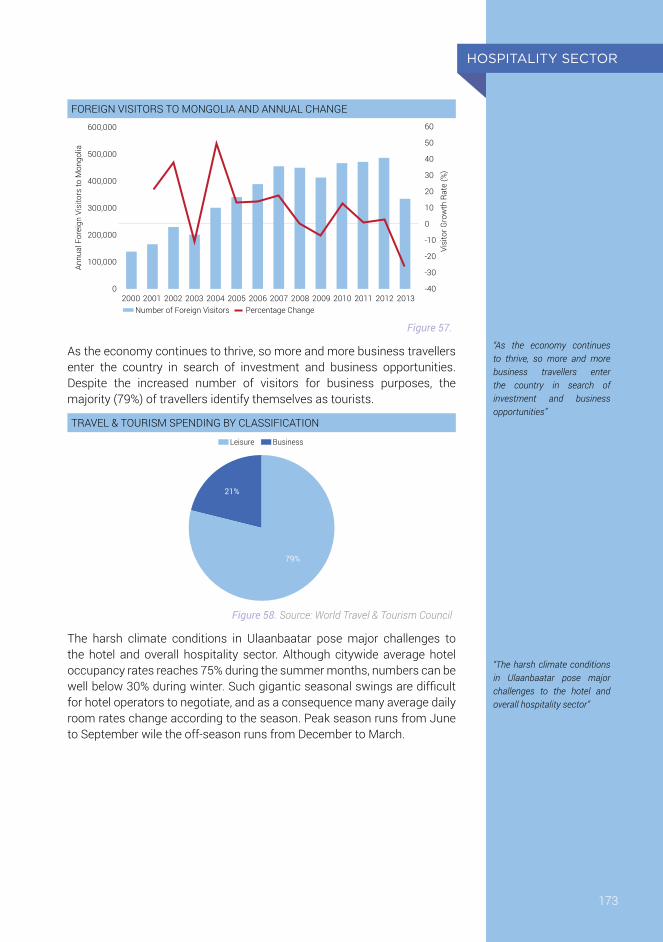

57 Foreign visitors to Mongolia and annual change 173

58 Travel & Tourism Spending by Classification 173

59 Average Hotel Occupancy Rate 174

60 Stock of 5-star Hotel Rooms in UB 176

61 Hotel room rates / Occupancy Rates 176

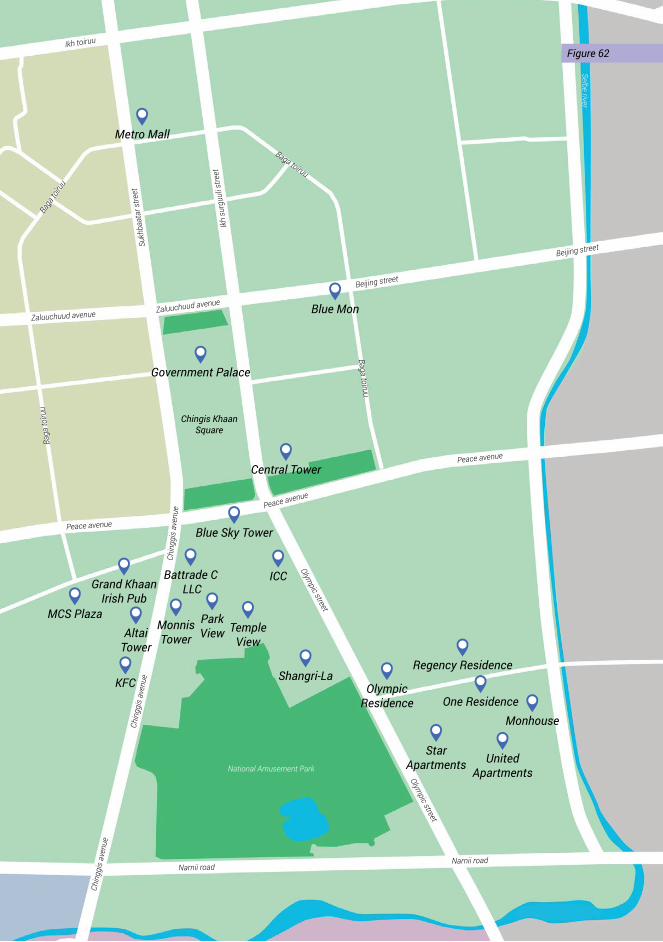

62 Sukhbaatar District Map 182

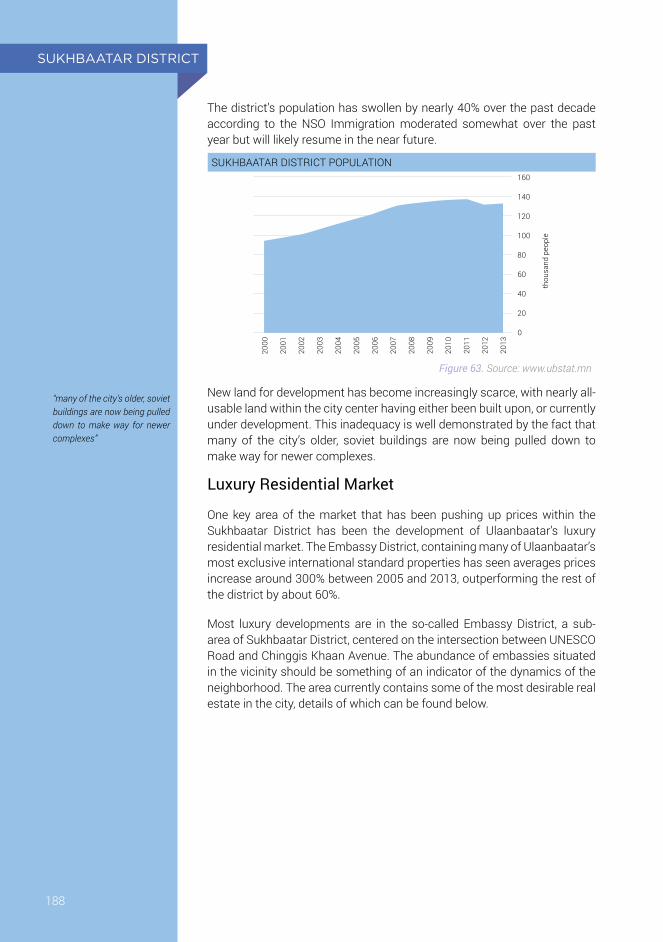

63 Sukhbaatar District Population 188

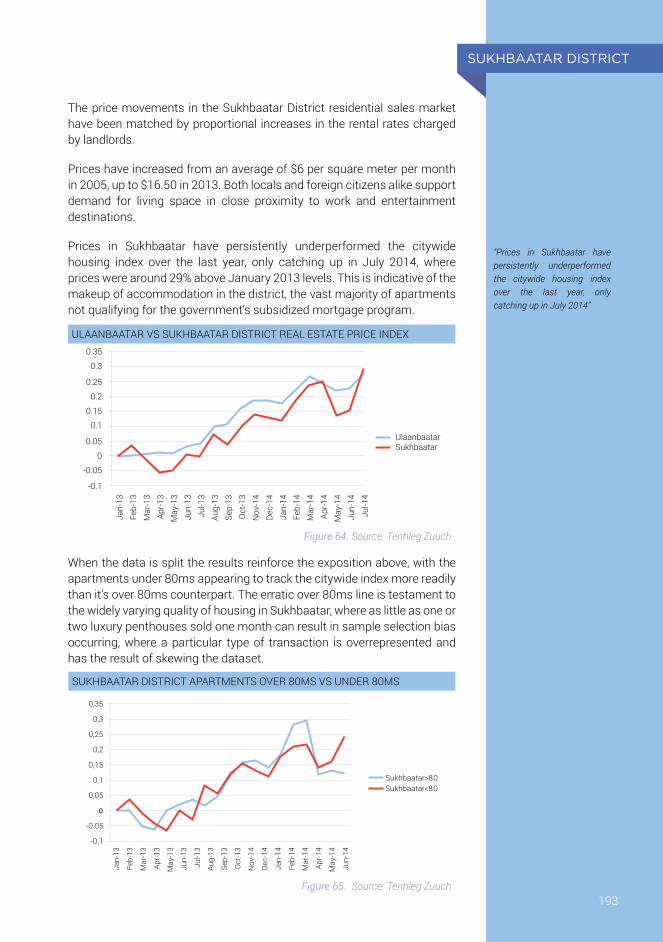

64 Ulaanbaatar vs Sukhbaatar District Real Estate Price Index 193

65 Sukhbaatar District Apartments Over 80ms vs Under 80ms 193

66 Chingeltei District Map 196

67 Chingeltei District Population 201

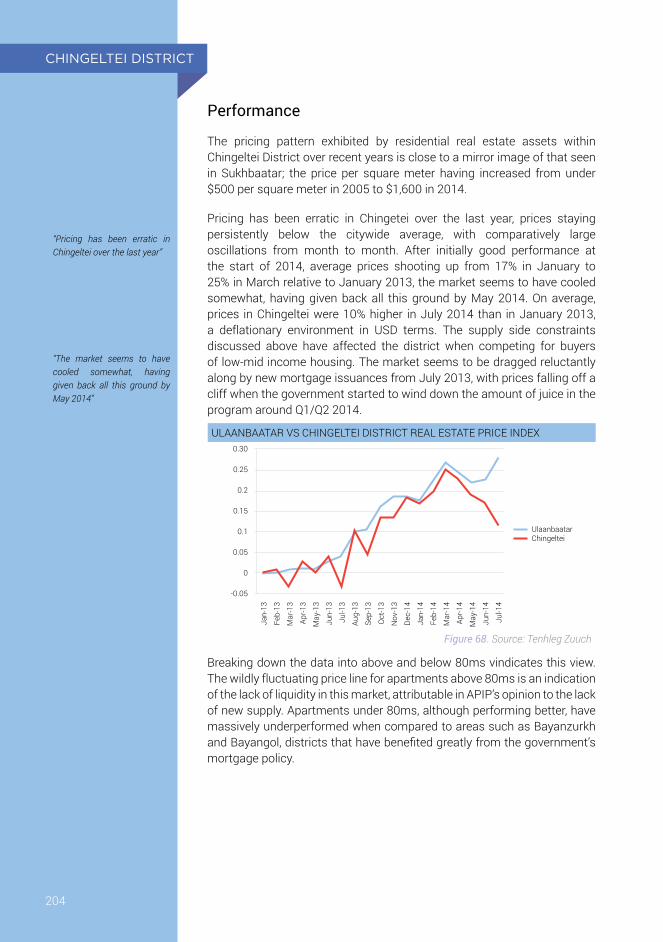

68Ulaanbaatar vs Chingeltei District Real Estate Price Index 204

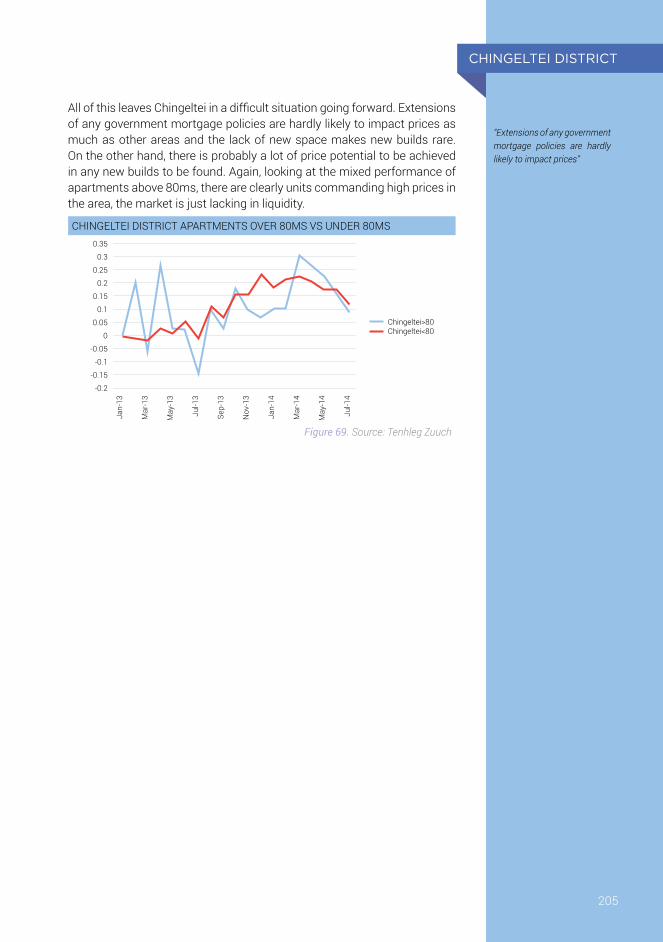

69 Chingeltei District Apartments Over 80ms vs Under 80ms 205

70 Bayangol District Map 208

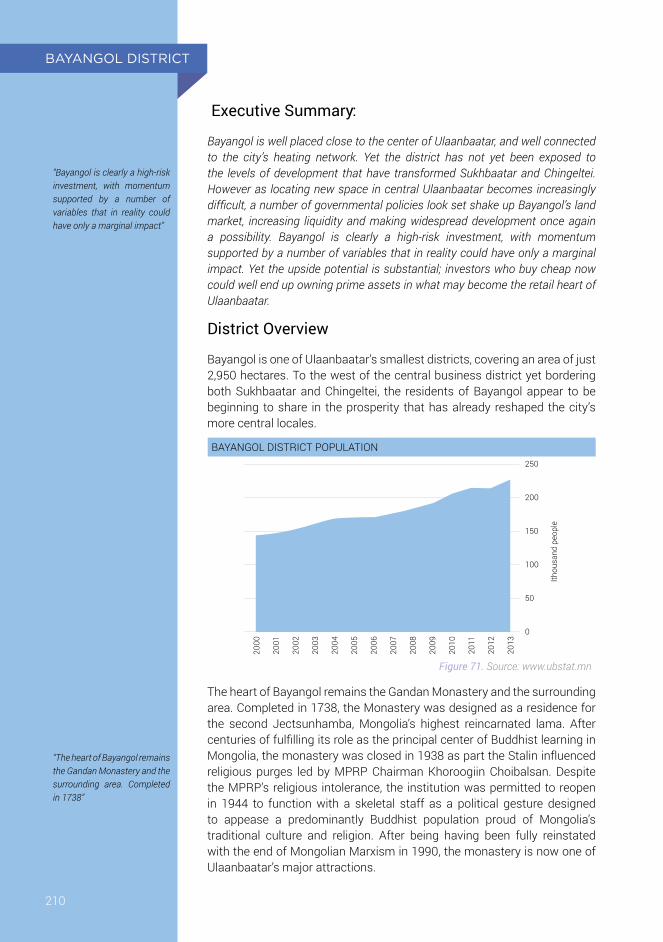

71 Bayangol District Population 210

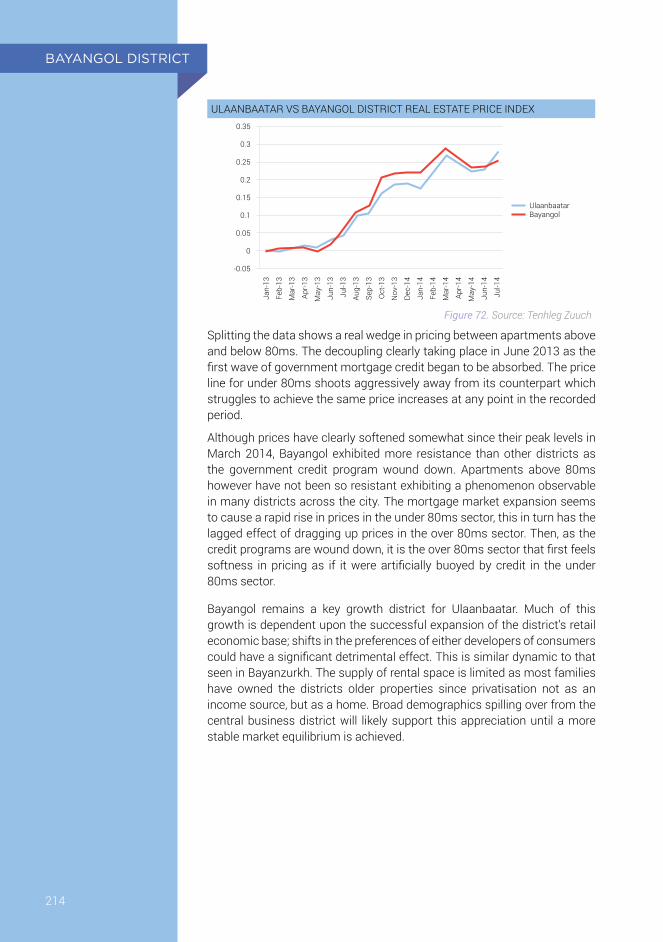

72Ulaanbaatar vs Bayangol District Real Estate Price Index 214

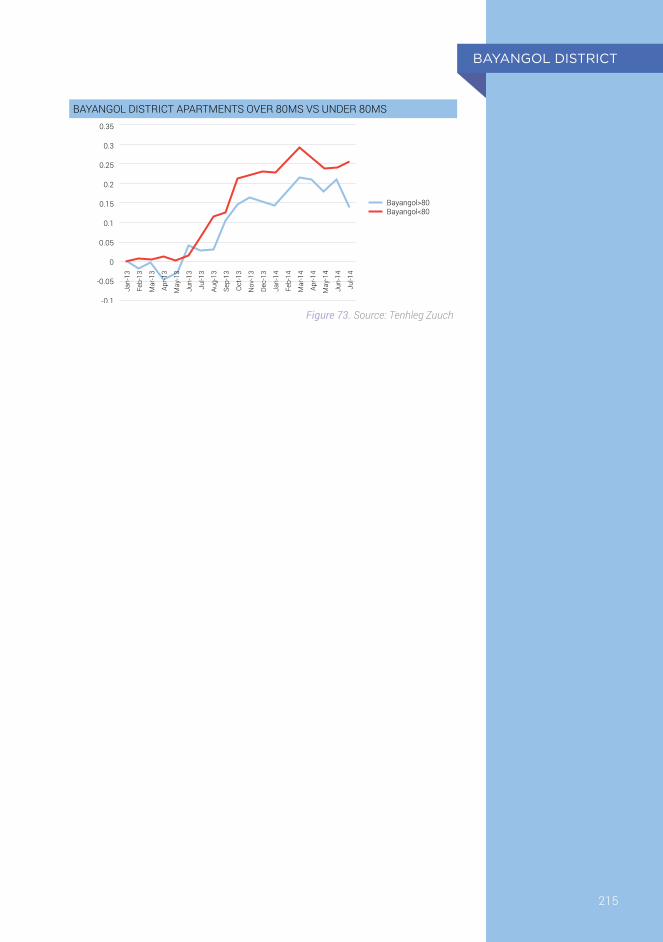

73Bayangol District Apartments Over 80ms vs Under 80ms 214

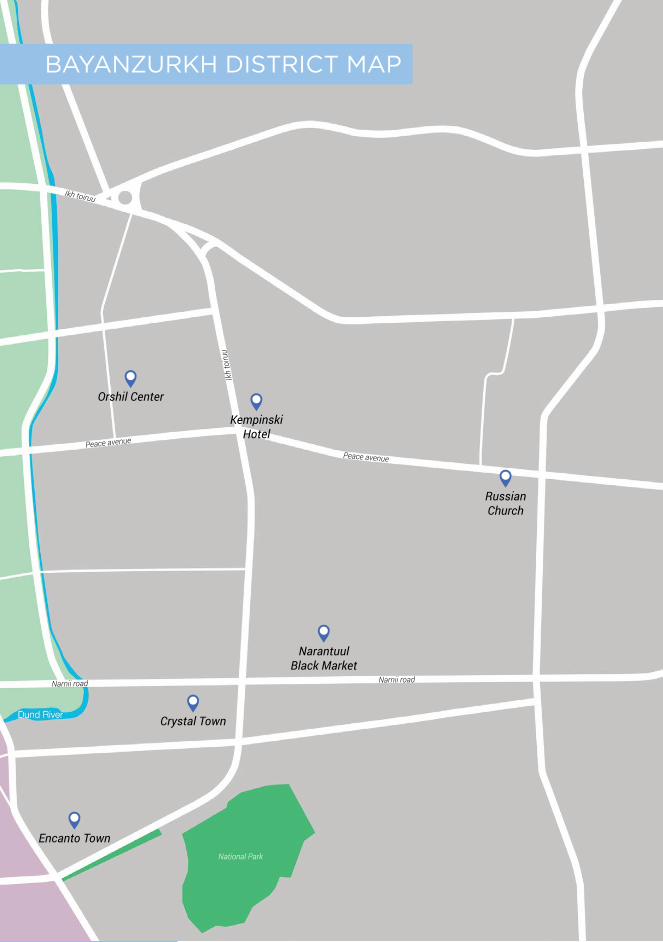

74 Bayanzurkh District Map 218

75 Bayanzurkh District Population 220

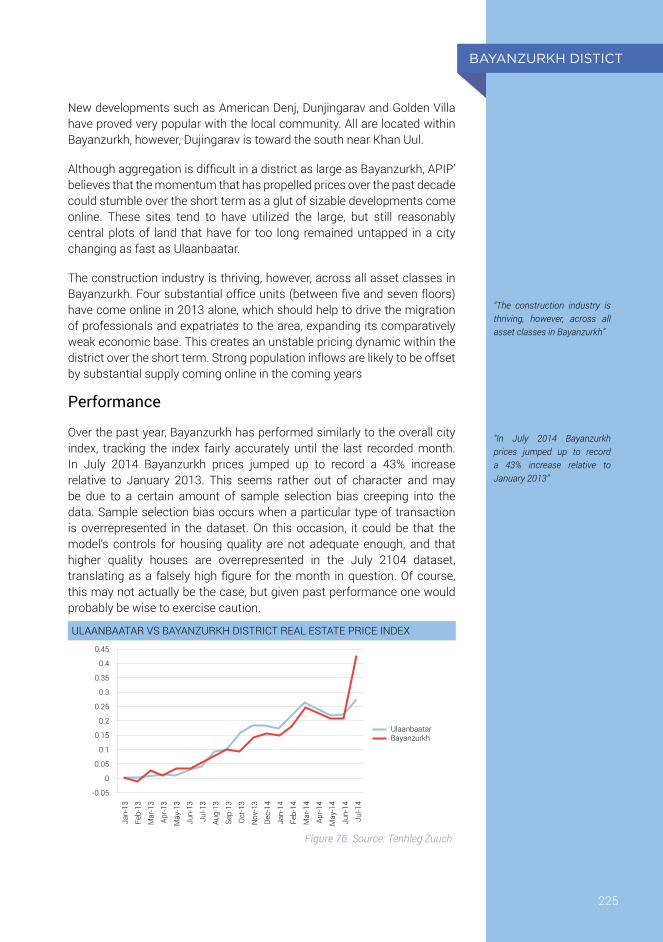

76Ulaanbaatar vs Bayanzurkh District Real Estate Price Index 225

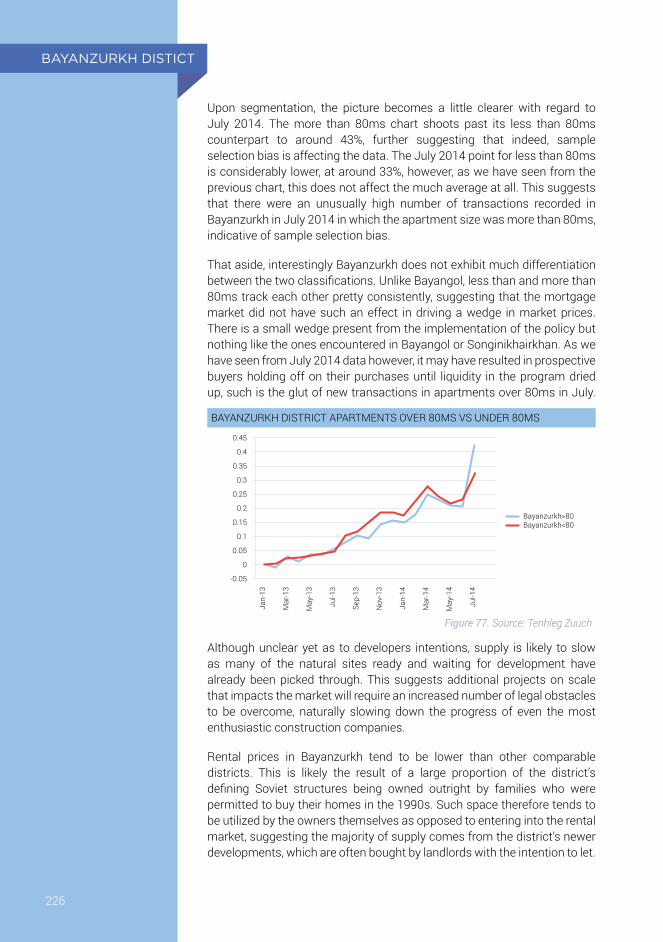

77Bayanzurkh District Apartments Over 80ms vs Under 80ms 226

78 Songinokhairkhan District Map 230

79 Songinokhairkhan District Population 232

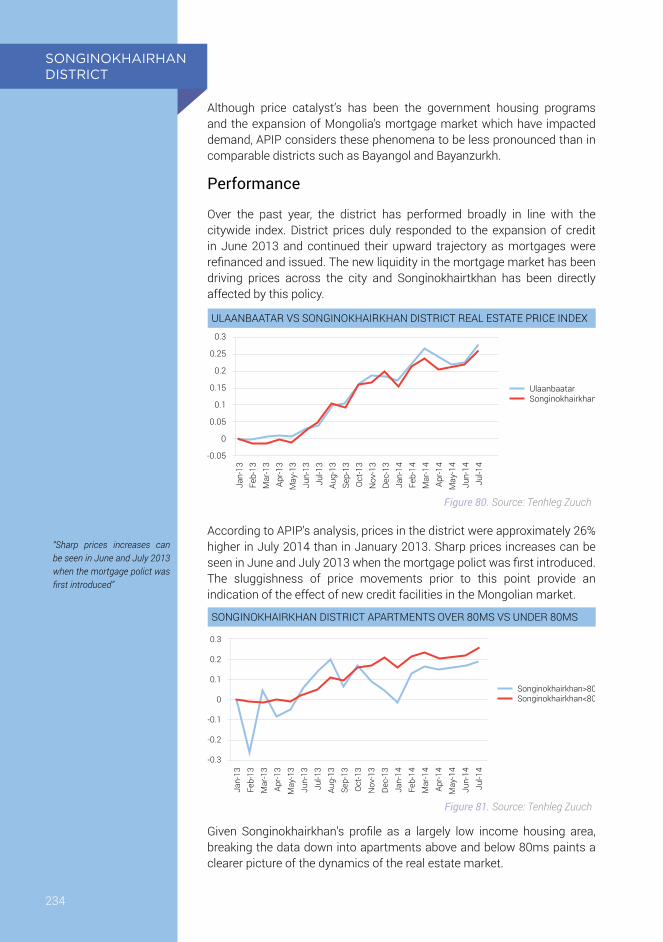

80 Ulaanbaatar vs Songinokhairkhan District Real Estate Price Index 234

No. Discription Pg No.

81Songinokhairkhan District Apartments Over 80ms vs Under 80ms 234

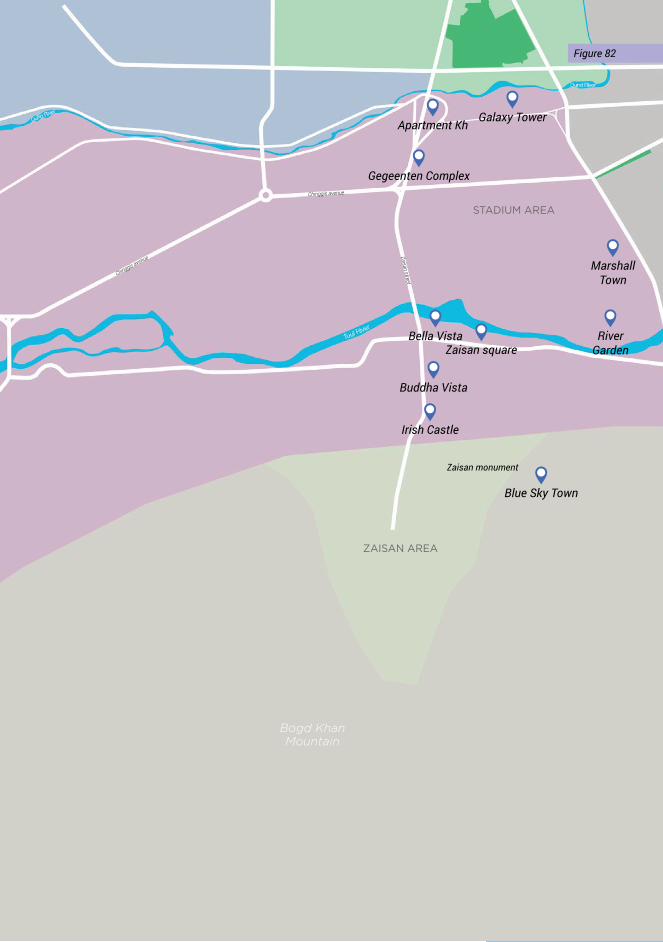

82 Khan-Uul District Map 238

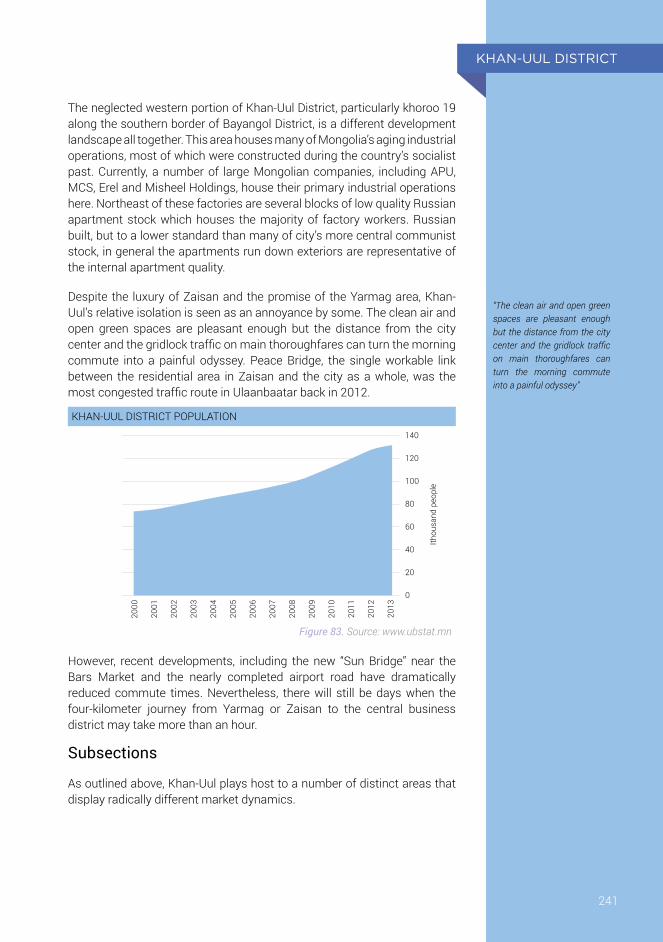

83 Khan-Uul District Population 241

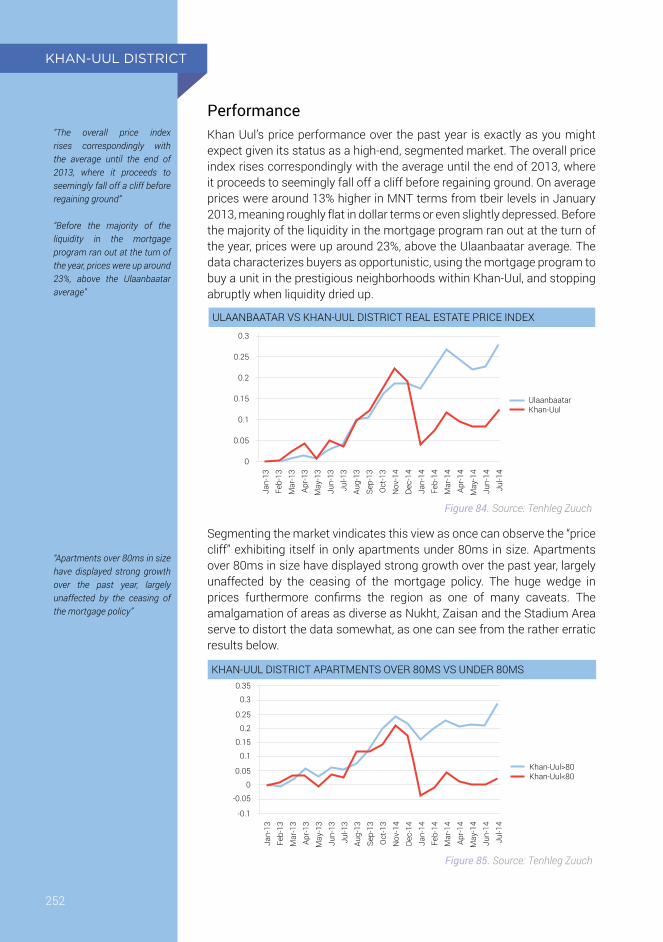

84Ulaanbaatar vs Khan-Uul District Real Estate Price Index 252

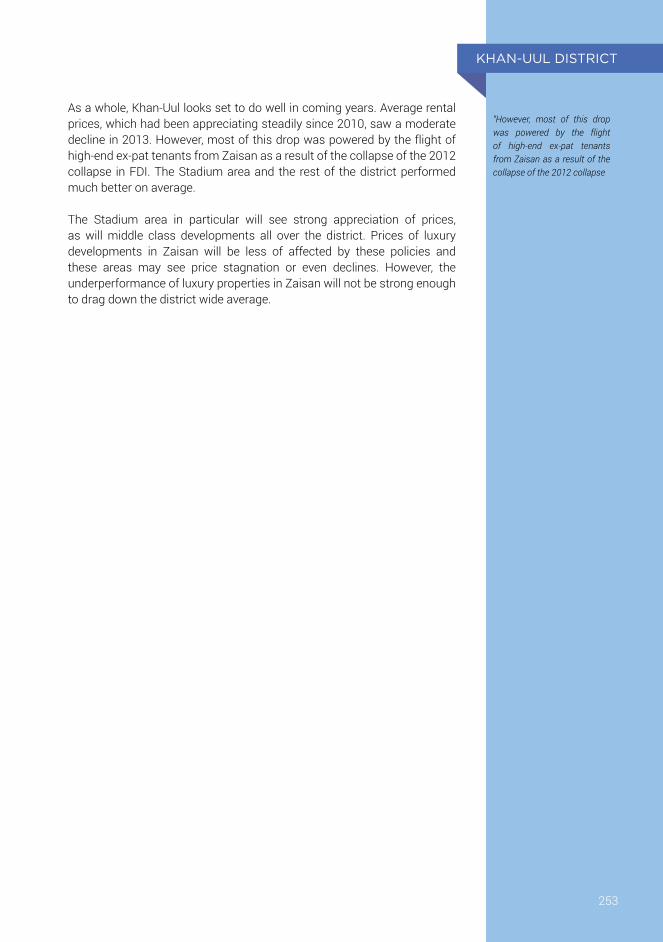

85Khan-Uul District Apartments Over 80ms vs Under 80ms 252

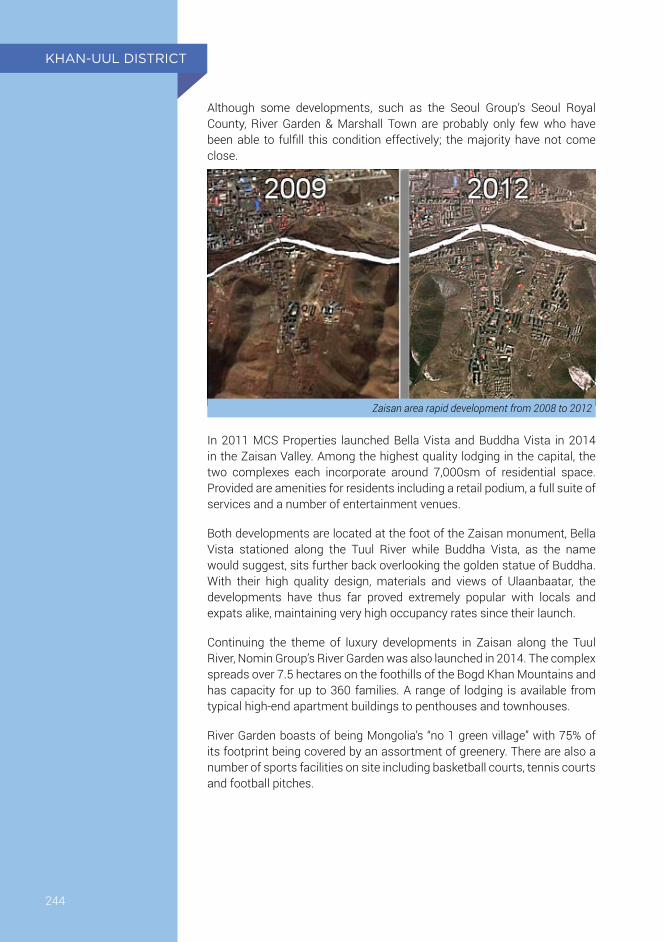

THOUGHTS FROM THE CEOThere is no getting around the fact that 2014 was a tough year for Mongolia and consequently, Ulaanbaatar’s real estate market.Despite this, Mongolian Properties continued to perform well, completing the Village @ Nukht and making great progress on the Olympic Residence. The coming year will see the Olympic completed and construction begin on our new project, the Oasis Residence. Looking forward to 2015 in the wider economy, there are plenty of reasons to be positive despite difficulties in 2014.

In December 2014, FDI had fallen offaround 80% y-o-y, GDP growth estimates slowed to around7% for 2014 from 17.5% in 2011, and the local currency depreciated substantially, barely a week passing by without it hitting new highs against the US dollar. All this was set against a backdrop of falling commodities prices and a long running dispute between Rio Tinto and the Government of Mongolia at OyuTolgoi, which continued to rumble on unabated.

A stubbornly high inflation rate and rapidly falling currency reserves in the first half of 2014 caused the government to raise interest rates twice to 13% from 10.5%, the latest rise coming in January 2015. Along with falling FDI, this has caused the local currency to depreciate by 14% since December 2013. Despite this, currency reserves in the second half of 2014 remained fairly stable at around US$1.35bn.

However, there are reasons to be positive. The 2014 balance of trade came in at a US$538m surplus, much better than expected. The total value of exports increased by 45% y-o-y in volume; translating to a 35% increase in US dollar terms and amounting to US$5.78bn. Copper made up the lions share of exports and saw its share of export value double to 45%,despite copper prices steadily dropping throughout the year. Mongolia’s dependence on coal exports was also greatly reduced with volumes only growing 7% y-o-y, falling in export value terms to 15% from 26% in 2013.

The government also increased the “debt ceiling” to 60% of total GDP, self-imposedjust last year at 40%. The revised debt ceiling will gradually taper back to 40% of GDP by 2018 in line with IMF recommendations, but allows the government to borrow now since it is currently below the threshold. The Bank of Mongolia also doubled its gold reserves in 2014 to 6.4 tonnes.

Last November saw former Prime Minister NorovAltankhuyag resign after a vote of no confidence. Two weeks later Mongolia’s Parliament approved a new Prime Minister, appointing acting Cabinet Secretary Saikhanbileg Chimed to the job. Saikhanbileg promised to boost the economy and bring political stability to the country. As part of his acceptance speech, Saikhanbileg stated that his top three priorities were “the economy, the economy and the economy”.

A few weeks later, the opposition party, the Mongolian People’s Party (“MPP”), accepted an offer by the new Prime Minister to join a coalition with the ruling Democratic Party (“DP”). Saikhanbileg urged all to end political divisions and concentrate on improving the economy. Members of both parties now hold various important positions in the cabinet making up what is perceived by most as a true coalition. The “Grand Coalition” should provide a solid foundation for tackling key economic issues, the business communitybenefiting from the added cohesion emanating from the government.

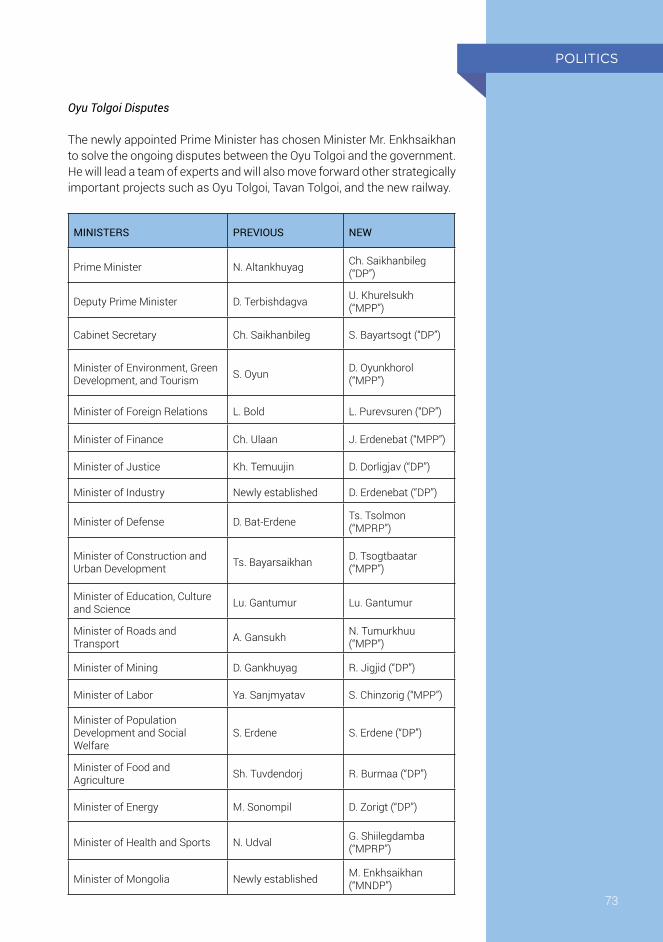

Along with the cabinet reshuffle, the new Prime Minister appointed Minister Enkhsaikhan to solve the ongoing dispute between Rio Tinto and the government. He now leads a team of experts in moving forward strategically important projects such as OyuTolgoi, TavanTolgoi, and the new railway, power plant and airport projects. Since his appointment, real progress has been made at TavanTolgoi, with a tender successfully awarded in January 2015 to China Shenhua, Sumitomo Corporation and Energy Resources, a subsidiary of Mongolian Mining Corporation, to develop the mine.

Progress has also been made at OyuTolgoi. In January 2015 Rio Tinto promised to drop their royalty demands by $1.6bn if the government approved the underground expansion phase of the mine. The recently resolved tax agreement, approval of afeasibility study, and securing of itspower supply are also positive noise for the project. Clear steps have been made on either side of the table to resolve the dispute and one can only hope that an agreement can be reached quickly.

The government’s recent actions demonstrate an increased amount of nuance and flexibility when negotiating with corporates and the international community. This was evident in February 2015 with the presidential pardoning of Justin Kapla and two other former executives at South Gobi Resources, whom hadformerly been imprisoned under questionable tax evasion charges.

Off the back of a state visit by Chinese Premier Xi Jinping in the summer of 2014, Mongoliaconsiderably strengthened it diplomatic relations with China. China signed an agreement with Mongolia giving them preferential terms of use of China’s northeastern seaports, including the use of the railways in which to access them. This is great news for Mongolia as it looks to diversify its revenue streams, with recent high-level state visits from Japan, Korea and Russia compounding its efforts. There is also a three-year RMB15bn currency swap line currently in place with the People’s Bank of China, which will strengthen Mongolia in times of duress.

The property market has remained relatively robust over the past year and was initiallypositively affected by government policy. Although prices dipped in the second half of 2014, the 2013 mortgage program supported prices through the first half of the year, and the speed at which the program’s liquidity dried up is a testament to the appetite for mortgages among residents. Consumption patterns indicate that the new wealth created by the mining boom has created a broader middle class, which will positively impact the real estate market in the long term. The commitment of the government to moving people out of the ger districts will also affect demand for housing.

The tough macroeconomic situation over the past couple of years has no doubt negatively impacted the real estate market and caused pain among the business community in general. However, positive developments in the mining sector and good steps made by the government are reasons for optimism in 2015. Assets are available at depressed prices at a time when exports are increasing and real progress is being made at OyuTolgoi.

Mongolia remains one of the most exciting places in the world to invest and real estate remains the best and safest way to gain exposure.

Lee Michael Cashell

Chief Executive OfficerMongolian Properties LLC

April 2015

OUR PROFESSIONALSANDREW McGregor

Chief Financial Officer Expertise: Real Estate Sales & Purchase, Project Finance, Corporate Finance and Private EquityE-mail: [email protected] Skype ID: andrew.apip1 MN Mobile: (+976) 9595 1899HK Mobile: (+852) 9866 5294 Fax: (+976) 7730 0880

BATGEREL Erdenebaatar

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: batgerel.mp Tel: (+976) 7011 1800Mobile: (+976) 9595 7510 Fax: (+976) 7011 8100

BATZUL Gerelsaikhan

Business Development Manager Expertise: Real estate sales & purchase, property consultancy & market research E-mail: [email protected] Skype ID: gbatzul HK Mobile: (+852) 9841 8871MN Mobile: (+976) 9917 8790 Fax: (+852) 2805 7801

BAYARSAIKHAN Purevsuren

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: bayarsaikhan.mp Tel: (+976) 1132 4545Mobile: (+976) 9907 5797 Fax: (+976) 7011 8100

DAVAADORJ Sukhbaatar

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: davaadorj.mp Tel: (+976) 7730 0660Mobile: (+976) 9908 6899 Fax: (+976) 7011 8100

DANIEL Hanson

Director of Property Development Expertise: MRICS, Project Delivery, Development Management, Shopping Centre Delivery, Commercial Leasing, Asset ManagementE-mail: [email protected] ID: daniel.apip12 Tel: (+976) 7730 0550Mobile: (+976) 9499 2030 Fax: (+976) 7730 0880

DANIEL Press

Deputy COO Expertise: Commercial Sales, Private Equity Real Estate, Mergers & Acquisition, Project ManagementE-mail: [email protected] ID: danny.apip Tel: (+44) 207495 6611Mobile: (+44) 7540550655

ENKHBAYAR Chimeddorj

Vice Director Expertise: Real estate sales & purchase, property consultancy & market researchE-mail: [email protected] ID: enkhbayar.mp Tel: (+976) 7730 0550Mobile: (+976) 9908 2757 Fax: (+976) 7730 0880

ENKHMUNGU Damdinbal

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: enkhmungu.mp Tel: (+976) 1132 4545Mobile: (+976) 9595 7400 Fax: (+976) 7011 8100

GERELMAA Gerelsaikhan

Sales & Marketing Manager Expertise: Real estate sales & purchase, property consultancy & market researchE-mail: [email protected] ID: gerelmaagerelsaikhan HK Mobile: (+852) 9547 1204SG Mobile: (+65) 8122 5180 Fax: (+852) 2805 5781

GERELCHIMEG Batsaikhan

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: gerelchimeg.mp Tel: (+976) 7011 1800Mobile: (+976) 9406 1017 Fax:(+976) 7011 8100

KHULAN Batgerel

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: khulan.mp Mobile: (+1) 425 623 6225

LEE MICHAEL Cashell

Chief Executive Officer Expertise: Commercial Sales, Private Equity Real Estate, Property Investment Strategy, ResearchE-mail: [email protected]

ORGIL Ariunbold

Sales and Marketing Manager Expertise: Real Estate Sales & Rentals, Property Tours and ConsultancyE-mail: [email protected] ID: orgil.mp Tel: (+976) 7730 0660Mobile: (+976) 9900 5969 Fax: (+976) 7730 0880

OTGONBAYAR Ganbayar

Senior Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: otgoo.mp Tel: (+976) 7011 1800Mobile: (+976) 9595 7540 Fax: (+976) 7011 8100

OYUNDARI Enkhbat

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: oyundari.mp Tel: (+976) 1132 4545Mobile: (+976) 9595 7580 Fax: (+976) 7011 8100

STUART Evans

Chief Information OfficerExpertise: Real Estate Sales & Purchase and Market ResearchE-mail: [email protected] Skype ID: stuart.evans89 Tel: (+852) 2805 7792HK Mobile: (+852) 9177 2984 Fax: (+852) 2805 7801

TSENDSUREN Bordukh

President Expertise: Commercial Sales, Mergers and Acquisition of Real Estate and Land, Project ManagementE-mail: [email protected]

TULGA Enkhbat

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] Skype ID: tulga.mp Tel: (+976) 1132 4545Mobile: (+976) 9595 7570 Fax: (+976) 7011 8100

UDVAL Tulga

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: udval.mp Tel: (+976) 7730 0660Mobile: (+976) 9595 7520 Fax: (+976) 7011 8100

ULSBOLD Harper

Associate - Business Development Expertise: Real Estate Sales & Purchase and Market ResearchE-mail: [email protected] ID: ulsbold.apip Tel: (+44) 207495 6611Mobile: (+44) 7501919392

UYANGA Tumurgan

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: uyanga.mp Tel: (+976) 1132 4545Mobile: (+976) 9595 7560 Fax: (+976) 70118100

URANGOO Narankhuu

Real Estate Agent Expertise: Real Estate Sales & Purchase and Long and short term rentalsE-mail: [email protected] ID: urangoo.mp Tel: (+976) 7011 1800Mobile: (+976) 9595 7530 Fax: (+976) 7011 8100

Real Estate Sales & Purchase AssistanceLong & Short Term RentalsProperty ManagementProperty ConsultancyArchitecture & Interior Design Advisory

Website: www.mongolia-properties.com, E-mail: [email protected]

HEAD OFFICE:Suite 202, Regency Residence16 Olympic Street, 1st Khoroo, Sukhbaatar DistrictUlaanbaatar 1422016, MONGOLIATel: (+976) 7730 0550Fax: (+976) 7730 0880

CIRCUS OFFICE:48/14 Seoul Street, 4th Khoroo Sukhbaatar DistrictUlaanbaatar 14250, MONGOLIA Tel: (+976) 1132 4545Fax: (+976) 7011 8100

TEMPLE VIEW OFFICE:1/F, Temple View Residence12 Jamyan Gun Street1st Khoroo, Sukhbaatar DistrictUlaanbaatar 14240 MONGOLIATel: (+976) 7011 1800Fax: (+976) 7011 8100

Real Estate & Market ResearchFurnishing ServicesOverseas Property TransactionsProperty ToursLegal ServicesRelocation Assistance

THE NUMBER #1 REAL ESTATE AGENCY IN MONGOLIA

HONG KONG OFFICE: Unit 301 Winsome House, 73 Wyndham Street, Central, Hong KongTel: (+852) 2805 7792Fax: +852 2805 7801E-mail: [email protected]

LONDON OFFICE: 47 Charles Street, MayfairLondon, W1J 5EL Tel: +44 207495 6611E-mail: [email protected]

THE OLYMPIC RESIDENCE WILL FEATURE:

• 97 luxury apartments, including penthouses• Four floors of prime retail• IRR in excess of 30% for the first 3 to 5 years• Projected rental yields of 14.2%A limited number of duplexes and penthouses are now available at a special rate.

If you are interested in the Olympic Residence, please feel free to contact us at the following:

Mobile: (+976) 9595 7570, 9908 9950, 9595 7580Tel: (+976) 1132 4545 & (+976) 7011 1800E-mail: [email protected]: www.theolympicresidence.com

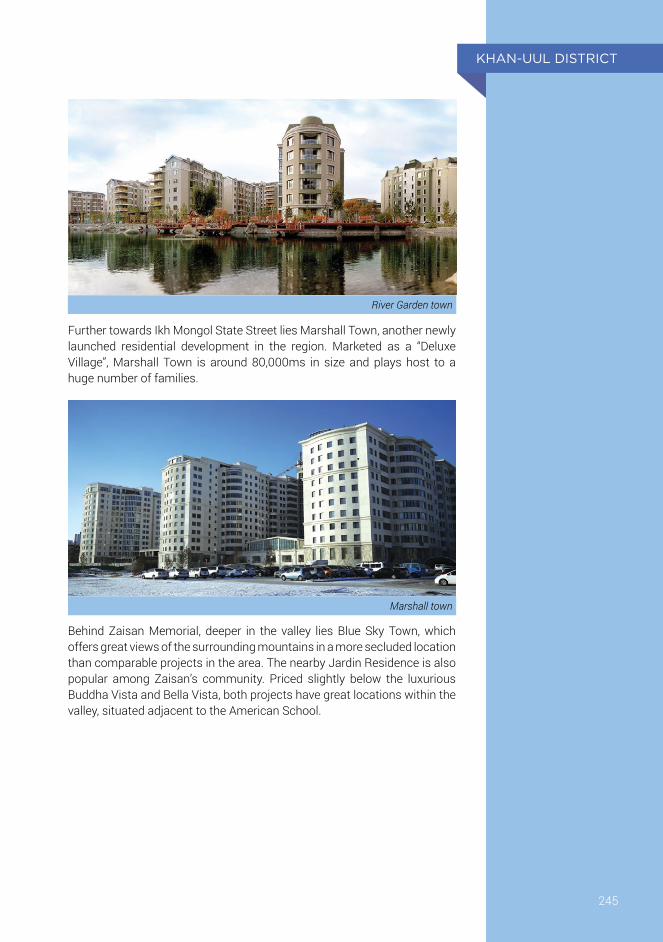

A LIMITED NUMBER OF DUPLEXES AND PENTHOUSES ARE NOW AVAILABLE AT A SPECIAL RATE.

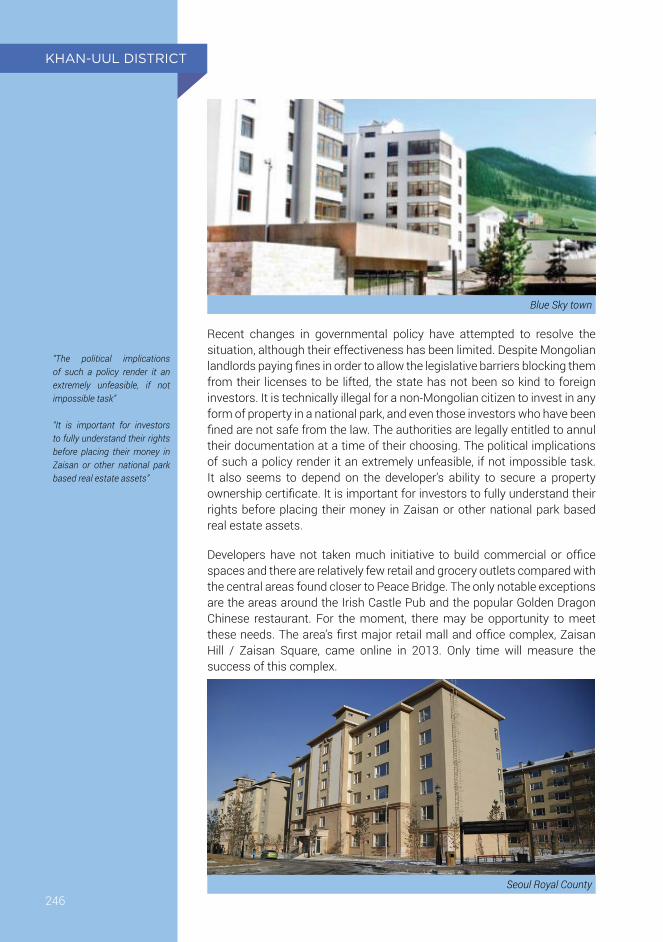

OLYMPIC RESIDENCE

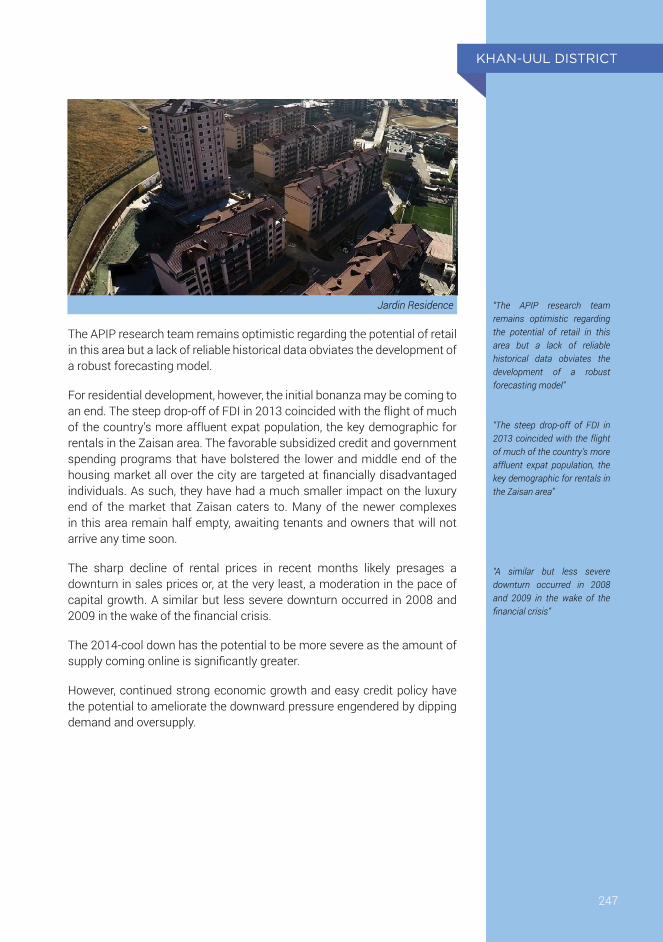

Government Palace

Central TowerUlaanbaatar Hotel

Regency Residence

DHL

Temple View

Monnis Tower

Blue Sky TowerState Department Store

Mongolian Properties

Naran Mall

Ulaanbaatar DepartmentStore

Central Post Office

National Amesument Park

Peace avenue

Olympi

c stre

et

Peace avenue

Peace avenue

Peace avenuePeace avenue

LOCATION

80%sold

VILLAGEThe

@ Nukht

The Village @ Nukht

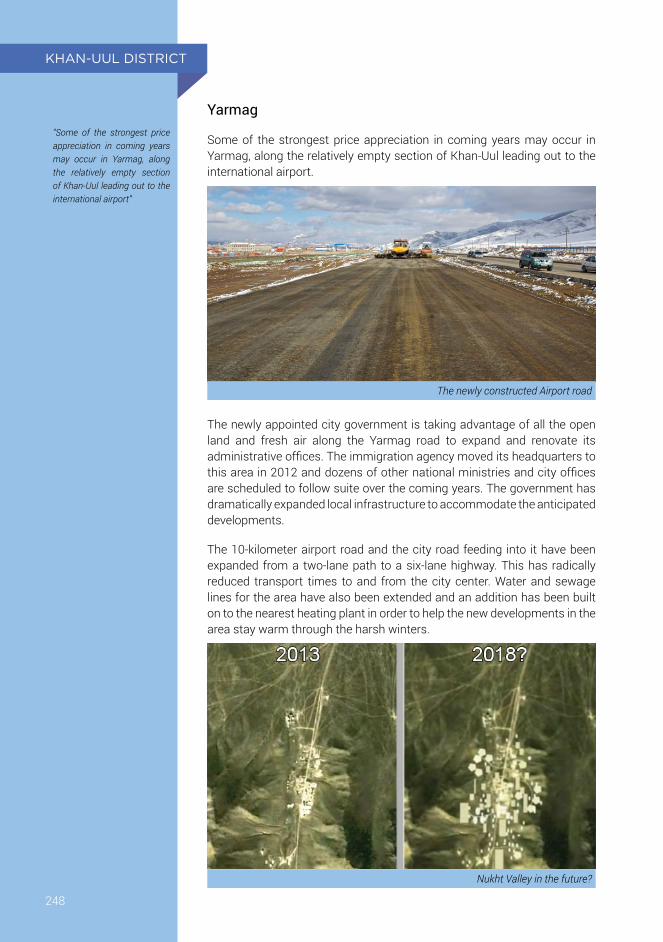

Located between Ulaanbaatar and Chinggis Khaan International Airport, the scheme nestles in a small valley adjacent to the Bogd Khaan Mountains.

Nukht has traditionally served as a holiday destination for former government officials and their families. In recent years, a number of prominent families and affluent Mongolian businessmen have relocated to the area and have built large, Western-style, single-family homes and condominiums.

In accordance with the city masterplan, Ulaanbaatar is growing out west along the Yarmag Road. The Nukht valley lies just off this road and thus has potential to become a new luxurious hub outside of the central business district.

NOW LEASING

The VILLAGE @ Nukht feature:• 8 penthouse suites• 7,500 sqm of mixed use retail space• Only commercial space at Nukht Valley• Leasing incentives available

If you are interested in the Village @ Nukht, please feel free to contact us at the following:

Mobile: (+976) 9595 7540, 9595 7560, 9595 7520Tel: (+976) 1132 4545 & (+976) 7011 1800 E-mail: [email protected] Website: www.village-nukht.com

Location:

VILLAGEThe

@ Nukht

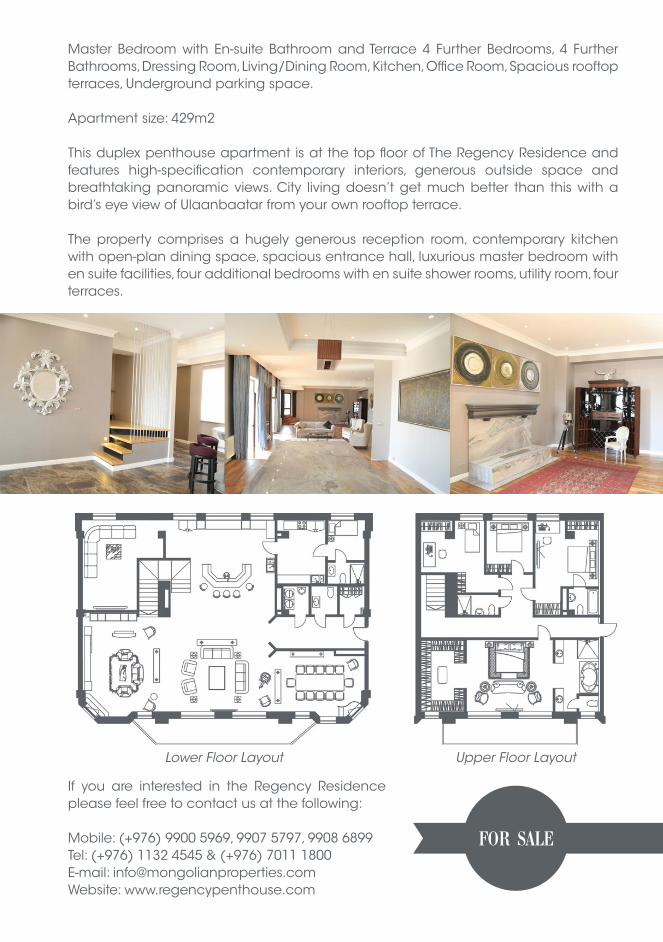

Duplex penthouse at THE REGENCY RESIDENCE

Master Bedroom with En-suite Bathroom and Terrace 4 Further Bedrooms, 4 Further Bathrooms, Dressing Room, Living/Dining Room, Kitchen, Office Room, Spacious rooftop terraces, Underground parking space.

Apartment size: 429m2

This duplex penthouse apartment is at the top floor of The Regency Residence and features high-specification contemporary interiors, generous outside space and breathtaking panoramic views. City living doesn’t get much better than this with a bird’s eye view of Ulaanbaatar from your own rooftop terrace.

The property comprises a hugely generous reception room, contemporary kitchen with open-plan dining space, spacious entrance hall, luxurious master bedroom with en suite facilities, four additional bedrooms with en suite shower rooms, utility room, four terraces.

If you are interested in the Regency Residence please feel free to contact us at the following:

Mobile: (+976) 9900 5969, 9907 5797, 9908 6899Tel: (+976) 1132 4545 & (+976) 7011 1800 E-mail: [email protected] Website: www.regencypenthouse.com

Lower Floor Layout Upper Floor Layout

FOR SALE

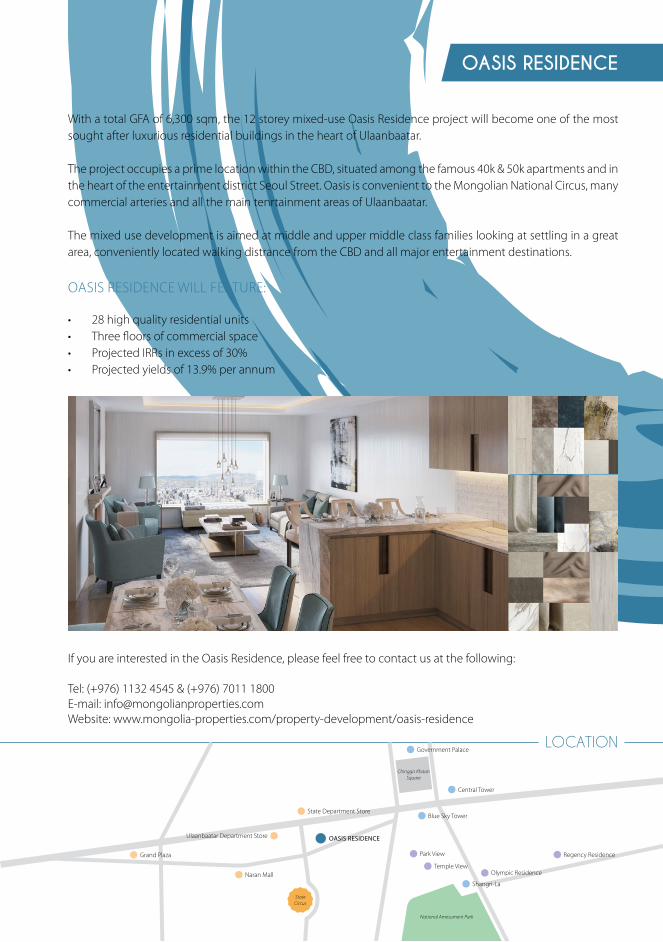

With a total GFA of 6,300 sqm, the 12 storey mixed-use Oasis Residence project will become one of the most sought after luxurious residential buildings in the heart of Ulaanbaatar.

The project occupies a prime location within the CBD, situated among the famous 40k & 50k apartments and in the heart of the entertainment district Seoul Street. Oasis is convenient to the Mongolian National Circus, many commercial arteries and all the main tenrtainment areas of Ulaanbaatar.

The mixed use development is aimed at middle and upper middle class families looking at settling in a great area, conveniently located walking distrance from the CBD and all major entertainment destinations.

OASIS RESIDENCE

OASIS RESIDENCE WILL FEATURE:

• 28 high quality residential units• Three floors of commercial space• Projected IRRs in excess of 30%• Projected yields of 13.9% per annum

If you are interested in the Oasis Residence, please feel free to contact us at the following:

Tel: (+976) 1132 4545 & (+976) 7011 1800E-mail: [email protected]: www.mongolia-properties.com/property-development/oasis-residence

LOCATION

Olympic Residence

Shangri-La

Temple View

Park View

State Department Store

Ulaanbaatar Department Store

Naran Mall

Grand Plaza

OASIS RESIDENCE

Blue Sky Tower

Government Palace

Central Tower

Regency Residence

Chinggis Khaan Square

State Circus

National Amesument Park

OFFICE SPACES, SERVICED APARTMENTS AND FUNCTION HOUSE.

FOR SALE AND

RENT

NORTH SPRING CAPITAL BLUE BUILDING

NSCB is a mixed-use building located along the Sun Road beside Traffic Police Headquarters.

Featuring : • Office Center located in Class A, semi-business district• Tall building in Ulaanbaatar. 13 story building with glass facade • Prime Office Suites: 7 floors of office space • Services Apartment: Luxury furnished 32 apartments • Convenience: Board meeting room, conference rooms, parking facilities • Recreation: Gym facilities, Entertainment lounge and roof top alfresco areas with

panoramic view of Ulaanbaatar city

If you are interested in the North Spring Capital Blue Building, please feel free to contact us at the following:

Tel: (+976) 1132 4545 & (+976) 7011 1800E-mail: [email protected]: www.mongolia-properties.com

Lobby

Office

SONGINOKHAIRKHAN DISTRICT

CHINGELTEI DISTRICT

SUKHBAATARDISTRICT

BAYANGOLDISTRICT

KHAN-UULDISTRICT

YARMAG AREA

ZAISAN AREA

STADIUM AREA

MAP OF ULAANBAATAR DISTRICTS

SUKHBAATARDISTRICT

BAYANZURKHDISTRICT

Bogd KhanMountain

ZAISAN AREA

STADIUM AREA

Figure 2

TBD Anduud

MAP OF ULAANBAATAR’S KEY LOCATIONS

Tengis MovieTheatre

Gandan Monastery

Bileg DefartmentStore

Urgoo MovieTheatre

UB PalaceMax Mall

Grand Plaza

Naran Mall

Ulaanbaatar Department Store

State Department Store

State Circus

Bogd Khan Museum

MongolianProperties

Viva City

Village @Nukht

YARMAG AREA

Bogd KhanMountain

Figure 3

Government Palace

IT Center

Blue Sky TowerState Department Store

State Circus

Chinggis Khaan Square

Central Tower

Bogd Khan Museum

MongolianProperties

Temple ViewAcademic Theatre of Drama

Bayangol Hotel

Naran Plaza

Shangri-LaOlympic Residence

Regency Residence

Mon House

BayanmongolKhoroolol

Chinggis Hotel

SOS Medical Ulaanbaatar

Wrestling Place

Park View

SECTION 1

COUNTRY CONTEXT

32

MACROECONOMICS

SECTION 1.1

33

MACROECONOMICS

MACROECONOMICS

34

MACROECONOMICS

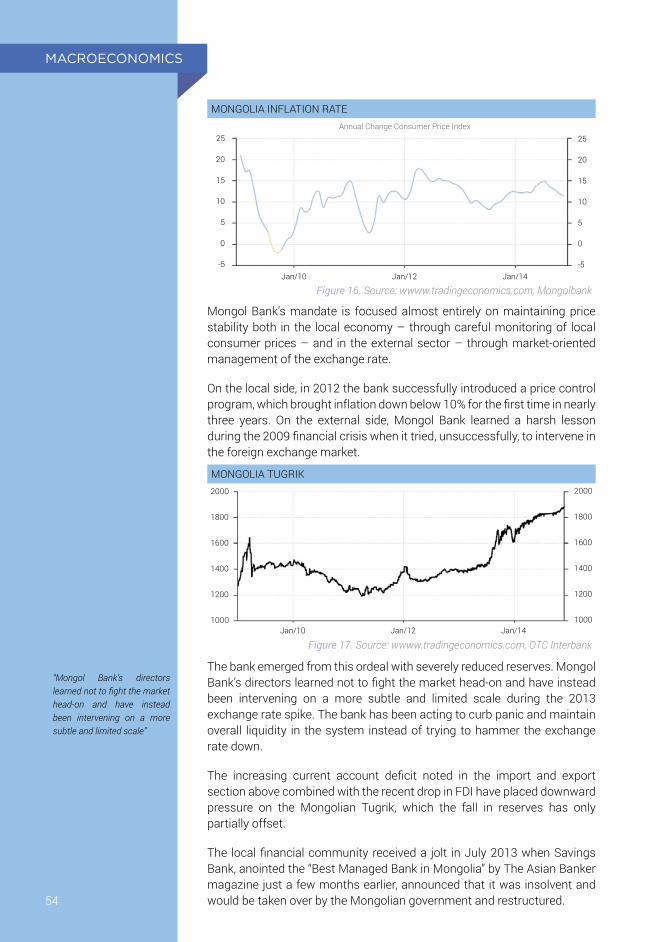

Executive Summary

Since 1992, Mongolia has adopted democratic ideals and free market principals, creating a stable business environment for the recent mining boom. As a result, the economy grew 17.5% in 2011, 12.4% in 2012, 11.7% in 2013 and is forecast to grow at a healthy pace for many years to come. Much of this growth has been powered by the huge copper/gold project at OyuTolgoi, owned by Rio Tinto and the Government of Mongolia. Ore extraction began at OyuTolgoi in February 2013, with commercial shipments beginning a few months later. However, progress has not been so straightforward.

Huge FDI inflows began to cool in 2012 with the introduction of a controversial foreign investment law. The drop off in FDI was exacerbated by poor commodities prices, a general retreat of capital from emerging markets, and the winding down of expenditures at OyuTolgoi. In October 2013, Parliament passed a new investment law much more open to foreign investment, revoking the old investment law in the process. But significant damage to investor sentiment was already done, with much of the investment community preferring to wait for progress at the OyuTolgoi mine, using the project as a litmus test for how the government would treat foreign investors in the future. Investors are still waiting for a resolution of the outstanding issues at the mine. Recent sounds and actions from the government have been positive, the newly appointed prime minister and his “grand coalition” making the delivery of stage II a priority.

By December 2014 FDI had fallen around 80% y-o-y. Despite this the 2014 balance of trade came in at a US$538m surplus, much better than expected. The total value of exports increased by 45% y-o-y in volume; translating to a 35% increase in US dollar terms and amounting to US$5.78bn. Copper made up the lions share of exports and saw its share of export value double to 45%, despite copper prices steadily dropping throughout the year.

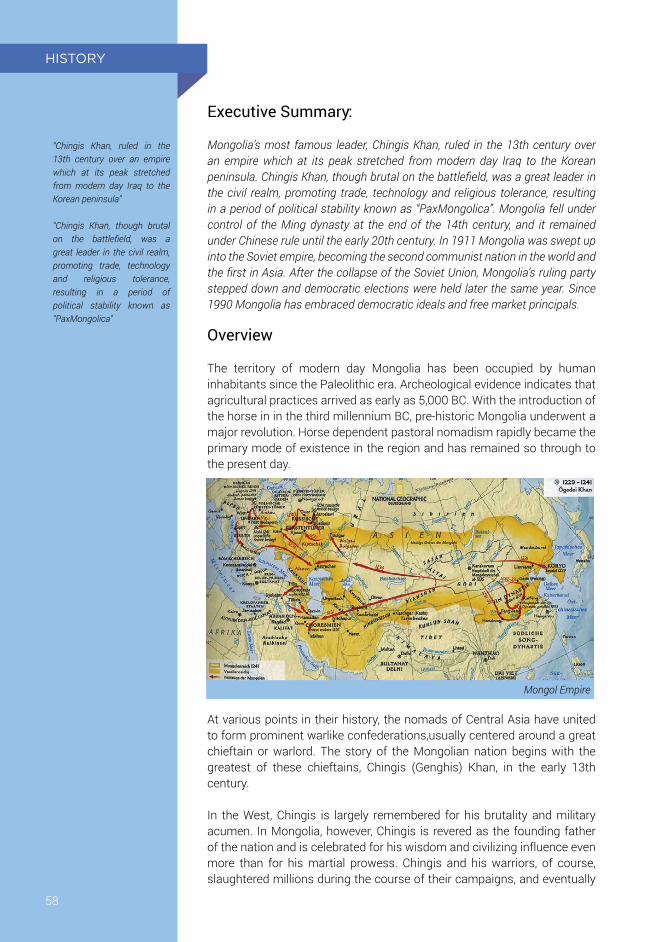

Overview

Since at least the second millennia B.C., nomadic pastoralism has constituted the primary mode of existence in Mongolia. Despite intervening centuries of conquests, political upheavals, and technological development, the traditional nomadic herding economy continues to shape Mongolia up to the present day.

This nomadic outlook has fostered a flexible and pragmatic mindset amongst Mongolians, perhaps most evident in the nation’s willingness to experiment with novel institutional forms. Mongolia was the first country in Asia to adopt communism and the first to abandon it in favor of capitalism.

Shortly after the fall of China’s Qing Dynasty in 1911, Mongolia declared its independence. However, the nascent Mongolian state was quickly put under pressure by resurgent Chinese republican forces and various Russian factions. In order to preserve the nation’s independence,

“The economy grew 17.5% in 2011, 12.4% in 2012, 11.7% in 2013 and is forecast to grow at a similar pace for many years to come”

“Huge FDI inflows began to cool in 2012 with the introduction of a controversial foreign investment law”

“In October 2013, Parliament passed a new investment law much more open to foreign investment, revoking the old investment law in the process”

“Mongolia was the first country in Asia to adopt communism and the first to abandon it in favor of capitalism”

35

MACROECONOMICS

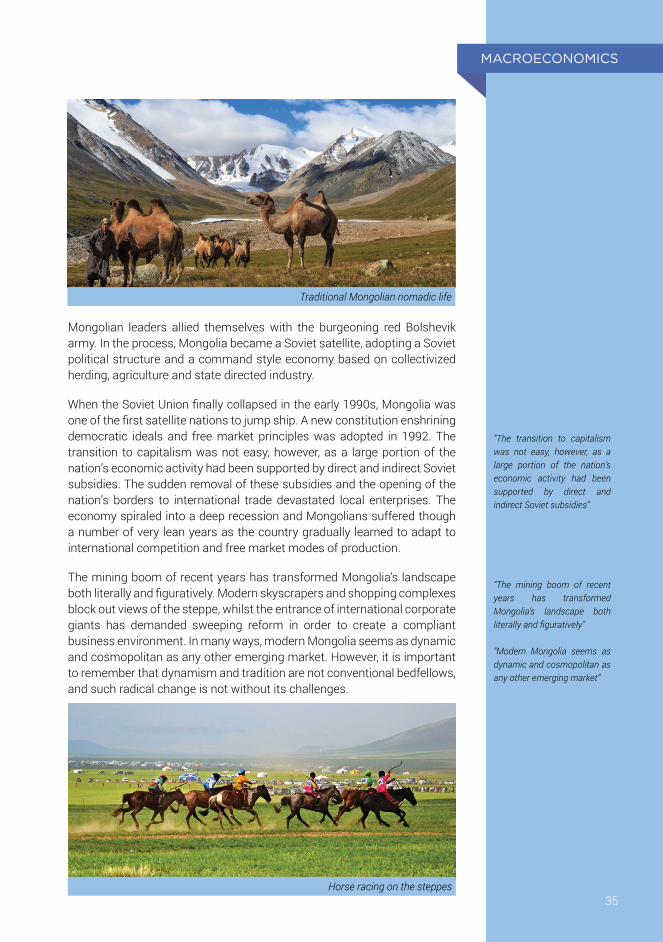

Mongolian leaders allied themselves with the burgeoning red Bolshevik army. In the process, Mongolia became a Soviet satellite, adopting a Soviet political structure and a command style economy based on collectivized herding, agriculture and state directed industry.

When the Soviet Union finally collapsed in the early 1990s, Mongolia was one of the first satellite nations to jump ship. A new constitution enshrining democratic ideals and free market principles was adopted in 1992. The transition to capitalism was not easy, however, as a large portion of the nation’s economic activity had been supported by direct and indirect Soviet subsidies. The sudden removal of these subsidies and the opening of the nation’s borders to international trade devastated local enterprises. The economy spiraled into a deep recession and Mongolians suffered though a number of very lean years as the country gradually learned to adapt to international competition and free market modes of production.

The mining boom of recent years has transformed Mongolia’s landscape both literally and figuratively. Modern skyscrapers and shopping complexes block out views of the steppe, whilst the entrance of international corporate giants has demanded sweeping reform in order to create a compliant business environment. In many ways, modern Mongolia seems as dynamic and cosmopolitan as any other emerging market. However, it is important to remember that dynamism and tradition are not conventional bedfellows, and such radical change is not without its challenges.

Traditional Mongolian nomadic life

Horse racing on the steppes

“The transition to capitalism was not easy, however, as a large portion of the nation’s economic activity had been supported by direct and indirect Soviet subsidies”

“The mining boom of recent years has transformed Mongolia’s landscape both literally and figuratively”

“Modern Mongolia seems as dynamic and cosmopolitan as any other emerging market”

36

MACROECONOMICS

Mongolia’s Growth Economy

Mongolia may never have registered on the radar of international investors if it was not for the explosive growth rates of the country’s gross domestic product (GDP) over the past several years. As the graph below demonstrates, Mongolia has been among the top economic performers in the world for most of the last decade and looks set to maintain its position as a growth powerhouse for many years to come.

The economy expanded at a staggering 17.5% pace in 2011. Growth has remained extremely strong if somewhat more moderate in subsequent years – 12.4% in 2012 and 11.7% for 2013. The growth rate for 2014 is projected to be 6.3% according to the World Bank, which reduced its forecast from around 9% in late 2014. The reason for the drastic reduction in growth rates over the past few years is largely due to political issues and an ongoing dispute between the government and Rio Tinto, explored in detail later in the chapter.

The 2012 election cycle gave rise to political conflicts and legal reforms that placed constraints on foreign investment in the minerals sector. 2012-13 also witnessed the beginning of a slowdown in China, which placed downward pressure on global commodity prices, thus limiting the profitability of Mongolian mineral exports. Despite these short run challenges, Mongolia remains one of the fastest growing economies in the world. With new investment promoting legislation and cost reducing infrastructure projects in the works, the potential is there for Mongolia to continue its unparalleled track record of growth for many years to come.

The country’s past and future performance is predicated upon significant discoveries in the mineral resource sector. Mongolia is now estimated to hold more than US $1.5 trillion in proven mineral reserves. The massive Oyu Tolgoi copper-gold mine in the southern Gobi Desert is alone is estimated to contain more than 37 million tonnes (81 billion pounds) of copper and more than 1,431 tonnes (46 million ounces) of gold.

10.6

7.38.6

10.28.9

-1 .3

6.4

17.5

12.4 11.7

6.3

-5 .0

0.0

5.0

10.0

15.0

20.0

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

GDP per capita (US$ current) Annual Growth %

Figure 4. Source: IMF

EXPLOSIVE GDP GROWTH

“Mongolia has been among the top economic performers in the world for most of the last decade”

“The economy expanded at a staggering 17.5% pace in 2011”

“Mongolia is now estimated to hold more than US $1.5 trillion in proven mineral reserves”

37

MACROECONOMICS

All this amazing mineral wealth has already been discovered with less than 30% of the country’s surface area explored. Initial investments in Mongolia’s mineral wealth propelled the economy forward at an explosive 17.5% growth rate in 2011. The development and exploitation of the deposits already uncovered are projected to keep the country’s growth locomotive moving forward at a double digit pace for the next several decades and the high probability of new discoveries in the future will only add fuel to the fire.

It would be a mistake to view Mongolia as a pure natural resource economy, however. Mining and corollary activities still make up less than 20% of gross domestic product and their predominance in the overall economy has actually fallen during the boom years. The mineral sector has served primarily as liquidity generating engine, which has spilled over, stimulating demand in other sectors of the economy. In fact, in recent years, the pace of expansion in the retail and financial sectors has been significantly faster than in the mining sector.

Despite perceptions of widening income equality, broad based economic expansion has trickled down to the general populace. Average monthly wages have more than doubled since 2009 and, with the exception of the financial crisis years, unemployment has fallen every year since it began to be recorded, in the mid 2000s.

This has led to the rise of a burgeoning consumer economy. Retail malls and exotic restaurants have sprung up alongside luxury housing developments and real estate prices have consequently soared.

0.0

5.0

10.0

15.0

20.0

25.0

2008 2009 2010 2011 2012 2013

AgricultureMiningManufacturingRetail

% o

f Tot

al G

DP

Figure 5. Source: NSO

MONGOLIA’S DIVERSIFYING ECONOMY

“All this amazing mineral wealth has already been discovered with less than 30% of the country’s surface area explored”

“the pace of expansion in the retail and financial sectors has been significantly faster than in the mining sector”

“Average monthly wages have more than doubled since 2009”

“Retail malls and exotic restaurants have sprung up alongside luxury housing developments and real estate prices have consequently soared”

1.000.0

800.0

600.0

400.0

200.0

0.0

20091/4

20093/4

20101/4

20103/4

20111/4

20113/4

20121/4

20123/4

20131/4

20143/4

Figure 6. Source: NSO

MONGOLIA IS EXPERIENCING RAPID WAGE GROWTH

38

MACROECONOMICS

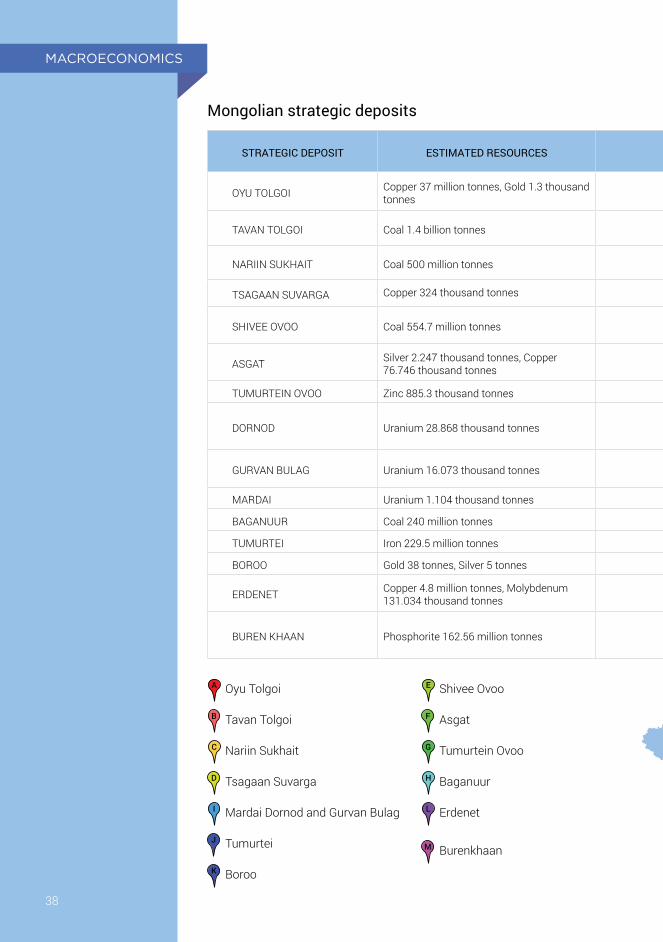

STRATEGIC DEPOSIT ESTIMATED RESOURCES LOCATION COMPANY STATE OR PRIVATE

OYU TOLGOI Copper 37 million tonnes, Gold 1.3 thousand tonnes Umnugobi, Khanbogd Turquoise Hill Resources, Rio Tinto,

Erdenes MGLState & Private

TAVAN TOLGOI Coal 1.4 billion tonnes Umnugobi, Tsogttsetsii Erdenes MGL, Erdenes TT, Energy Resource stock company

State & Private

NARIIN SUKHAIT Coal 500 million tonnes Umnugobi, GurvanTegs Qinhua-MAK-Nariin Sukhait LLC, South Gobi Energy Resources LLC Private

TSAGAAN SUVARGA Copper 324 thousand tonnes Dornogobi, Mandakh MAK Private

SHIVEE OVOO Coal 554.7 million tonnes Gobisumber, Shiveegobi Erdenes MGL, Shivee Ovoo JSC, State Grid Corporation of China

State & Private

ASGAT Silver 2.247 thousand tonnes, Copper 76.746 thousand tonnes BayanUlgii, Nogoon Nuur Mongolrostsvetmet LLC State

TUMURTEIN OVOO Zinc 885.3 thousand tonnes Sukhbaatar, Khuder Tsairt Mineral LLC Private

DORNOD Uranium 28.868 thousand tonnes Dornod, DashbalbarKhan Resources dispute Atom Mon and Russian state firm Atom Red Met Gold

Private

GURVAN BULAG Uranium 16.073 thousand tonnes Dornod, Dashbalbar CNNC China Private

MARDAI Uranium 1.104 thousand tonnes Dornod, Dashbalbar CNNC China Private

BAGANUUR Coal 240 million tonnes Ulaanbaatar, Baganuur Baganuur Joint Stock Company State

TUMURTEI Iron 229.5 million tonnes Sukhbaatar, Khuder Darkhan Black Iron Industry State

BOROO Gold 38 tonnes, Silver 5 tonnes Sukhbaatar, Bayangol Boroo Gold Private

ERDENET Copper 4.8 million tonnes, Molybdenum 131.034 thousand tonnes Orkhon, Bayan-Undur Erdenet Mining Corporation State

BUREN KHAAN Phosphorite 162.56 million tonnes Khuvsgul, Alag-ErdeneTalst Margad LLC, Tefas Mining LLC, Sutaikhentso LLC (China), Topruokhentso LLC (China)

Private

Mongolian strategic deposits

ABC DE FGI HJK LM Oyu Tolgoi ABC DE FGI HJK LM Shivee Ovoo

ABC DE FGI HJK LM Tavan Tolgoi ABC DE FGI HJK LM Asgat

ABC DE FGI HJK LM Nariin Sukhait ABC DE FGI HJK LM Tumurtein Ovoo

ABC DE FGI HJK LM Tsagaan Suvarga ABC DE FGI HJK LM Baganuur

ABC DE FGI HJK LM Mardai Dornod and Gurvan Bulag ABC DE FGI HJK LM Erdenet

ABC DE FGI HJK LM Tumurtei ABC DE FGI HJK LM BurenkhaanABC DE FGI HJK LM Boroo

39

MACROECONOMICS

STRATEGIC DEPOSIT ESTIMATED RESOURCES LOCATION COMPANY STATE OR PRIVATE

OYU TOLGOI Copper 37 million tonnes, Gold 1.3 thousand tonnes Umnugobi, Khanbogd Turquoise Hill Resources, Rio Tinto,

Erdenes MGLState & Private

TAVAN TOLGOI Coal 1.4 billion tonnes Umnugobi, Tsogttsetsii Erdenes MGL, Erdenes TT, Energy Resource stock company

State & Private

NARIIN SUKHAIT Coal 500 million tonnes Umnugobi, GurvanTegs Qinhua-MAK-Nariin Sukhait LLC, South Gobi Energy Resources LLC Private

TSAGAAN SUVARGA Copper 324 thousand tonnes Dornogobi, Mandakh MAK Private

SHIVEE OVOO Coal 554.7 million tonnes Gobisumber, Shiveegobi Erdenes MGL, Shivee Ovoo JSC, State Grid Corporation of China

State & Private

ASGAT Silver 2.247 thousand tonnes, Copper 76.746 thousand tonnes BayanUlgii, Nogoon Nuur Mongolrostsvetmet LLC State

TUMURTEIN OVOO Zinc 885.3 thousand tonnes Sukhbaatar, Khuder Tsairt Mineral LLC Private

DORNOD Uranium 28.868 thousand tonnes Dornod, DashbalbarKhan Resources dispute Atom Mon and Russian state firm Atom Red Met Gold

Private

GURVAN BULAG Uranium 16.073 thousand tonnes Dornod, Dashbalbar CNNC China Private

MARDAI Uranium 1.104 thousand tonnes Dornod, Dashbalbar CNNC China Private

BAGANUUR Coal 240 million tonnes Ulaanbaatar, Baganuur Baganuur Joint Stock Company State

TUMURTEI Iron 229.5 million tonnes Sukhbaatar, Khuder Darkhan Black Iron Industry State

BOROO Gold 38 tonnes, Silver 5 tonnes Sukhbaatar, Bayangol Boroo Gold Private

ERDENET Copper 4.8 million tonnes, Molybdenum 131.034 thousand tonnes Orkhon, Bayan-Undur Erdenet Mining Corporation State

BUREN KHAAN Phosphorite 162.56 million tonnes Khuvsgul, Alag-ErdeneTalst Margad LLC, Tefas Mining LLC, Sutaikhentso LLC (China), Topruokhentso LLC (China)

Private

Figure 7

40

MACROECONOMICS

Mineral Sector

During the Soviet era, Russian geologists were well aware of Mongolia’s vast mineral potential but for strategic reasons, few deposits aside from the Erdenet copper mine in the north of the country and a few coal occurrences near the capital were ever developed. Following the transition to capitalism, the sector began to develop gradually and organically, on a small and often informal artisanal level at first with ever larger and more organized interest entering the exploration field. Following the discovery of several world-class deposits in recent years, a number of large multinational corporate miners have entered the market. The result has been an explosion of foreign direct investment (FDI), which has made mineral exploration and extraction the new driving engine of the Mongolian economy.

To date, more than 1,170 mineral deposits and in excess of 7,654 mineral occurrences have been identified. It is estimated that Mongolia hosts more than $1.5 trillion USD in mineral reserves. This buried wealth includes deposits of copper, gold, silver, thermal and coking coal, iron, molybdenum, uranium, tungsten, tin, fluorspar, and the full suite of rare earths – to name just a few. The largest deposits discovered to date have been found in the southern Gobi desert region. However, less than 30% of the country’s surface area has been properly explored. Many more discoveries are expected in coming years, especially in the relatively underdeveloped western regions.

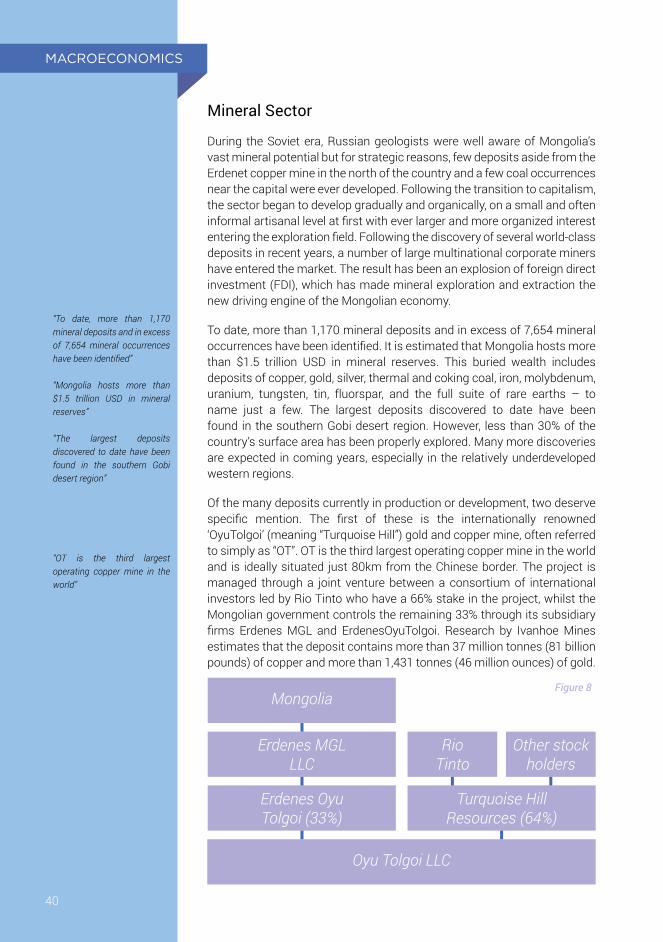

Of the many deposits currently in production or development, two deserve specific mention. The first of these is the internationally renowned ‘OyuTolgoi’ (meaning “Turquoise Hill”) gold and copper mine, often referred to simply as “OT”. OT is the third largest operating copper mine in the world and is ideally situated just 80km from the Chinese border. The project is managed through a joint venture between a consortium of international investors led by Rio Tinto who have a 66% stake in the project, whilst the Mongolian government controls the remaining 33% through its subsidiary firms Erdenes MGL and ErdenesOyuTolgoi. Research by Ivanhoe Mines estimates that the deposit contains more than 37 million tonnes (81 billion pounds) of copper and more than 1,431 tonnes (46 million ounces) of gold.

“To date, more than 1,170 mineral deposits and in excess of 7,654 mineral occurrences have been identified”

“Mongolia hosts more than $1.5 trillion USD in mineral reserves”

“The largest deposits discovered to date have been found in the southern Gobi desert region”

“OT is the third largest operating copper mine in the world”

Figure 8

Erdenes MGLLLC

Erdenes OyuTolgoi (33%)

Turquoise HillResources (64%)

RioTinto

Other stockholders

Oyu Tolgoi LLC

Mongolia

41

MACROECONOMICS

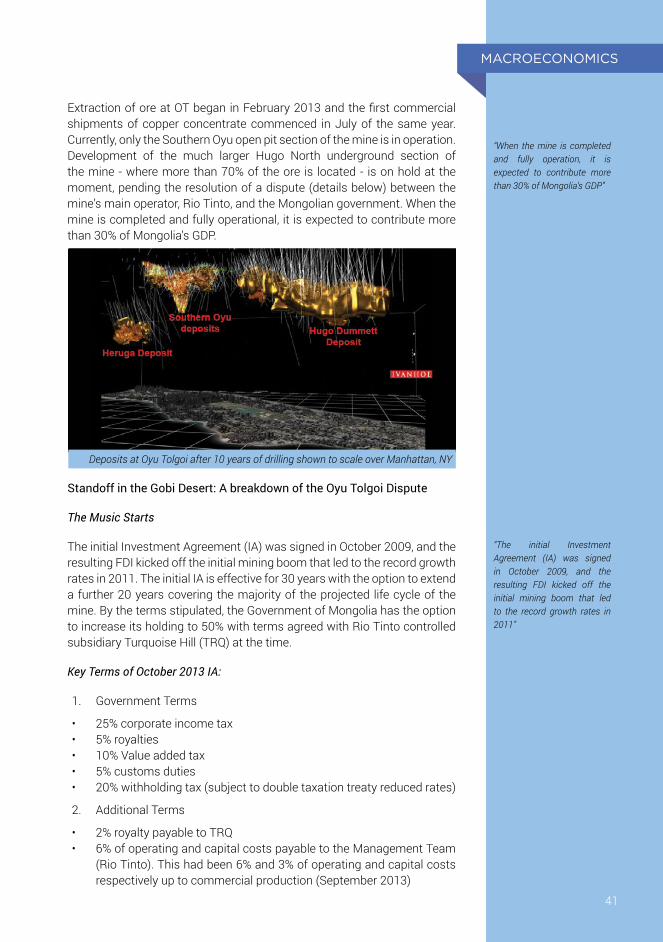

Extraction of ore at OT began in February 2013 and the first commercial shipments of copper concentrate commenced in July of the same year. Currently, only the Southern Oyu open pit section of the mine is in operation. Development of the much larger Hugo North underground section of the mine - where more than 70% of the ore is located - is on hold at the moment, pending the resolution of a dispute (details below) between the mine’s main operator, Rio Tinto, and the Mongolian government. When the mine is completed and fully operational, it is expected to contribute more than 30% of Mongolia’s GDP.

Standoff in the Gobi Desert: A breakdown of the Oyu Tolgoi Dispute

The Music Starts

The initial Investment Agreement (IA) was signed in October 2009, and the resulting FDI kicked off the initial mining boom that led to the record growth rates in 2011. The initial IA is effective for 30 years with the option to extend a further 20 years covering the majority of the projected life cycle of the mine. By the terms stipulated, the Government of Mongolia has the option to increase its holding to 50% with terms agreed with Rio Tinto controlled subsidiary Turquoise Hill (TRQ) at the time.

Key Terms of October 2013 IA:

1. Government Terms

• 25% corporate income tax• 5% royalties• 10% Value added tax• 5% customs duties• 20% withholding tax (subject to double taxation treaty reduced rates)

2. Additional Terms

• 2% royalty payable to TRQ• 6% of operating and capital costs payable to the Management Team

(Rio Tinto). This had been 6% and 3% of operating and capital costs respectively up to commercial production (September 2013)

Deposits at Oyu Tolgoi after 10 years of drilling shown to scale over Manhattan, NY

“When the mine is completed and fully operation, it is expected to contribute more than 30% of Mongolia’s GDP”

“The initial Investment Agreement (IA) was signed in October 2009, and the resulting FDI kicked off the initial mining boom that led to the record growth rates in 2011”

42

MACROECONOMICS

• The 34% funding provided by OT to the government will be repaid from the government’s share of cash flow accruing quarterly interest at LIBOR plus 6.5%

The Music Stops

The controversy started in 2011, at a time when Mongolia and the government were riding high on an economy stimulated by record levels of FDI. Parliamentary members demanded a renegotiation of the IA with Rio Tinto, requesting that royalty payments should be increased to 20% from the 5% initially stipulated in the agreement.

Phase I of the development was by this point well underway, and by September 2013 the mine came into commercial operation, triggering a clause in the 2009 IA relating to management pay as well as at last beginning to contribute to Mongolia’s current account in the form of exports. Although this was a huge milestone for the project, the vast majority (70%) of its resources lay in the underground portion of the mine, which would be financed in “Phase II”.

As the economy slowed in 2012 and 2013 amid legislation rashly passed by the government in response to a Chinese SOE takeover attempt of a key asset, the government’s challenges to Rio became more vociferous, culminating in Parliament submitting 22 points of dispute to Rio Tinto in July 2013. The main issues as seen by the government were:

• Cost of project financing (LIBOR + 6.5%) • Management Fee (6% of operating and capital and costs) • Phase I cost overrun from $4.1bn to $6.2bn • Disparities in pay between locals and expats • Repatriation of earnings and the structure of $5.1bn in funding

for phase two of the development • Unilateral cancellation of four dual taxation treaties in 2013,

including with the Netherlands (where OT is incorporated) • Amount due in taxation

Rio Tinto’s response to the points of dispute was to delay the financing of the more lucrative second phase of the project. In 2013, $4.1bn in project finance organized with the World Bank, US-EXIM and other commercial lenders was delayed. OyuTolgoi then paused its underground works and laid off 1,700 of its approximately 10,000 workers.

Fast forward into 2014 and still an agreement could not be reached. The furor at OT had observers in the foreign investment community waiting for a resolution before themselves committing capital, treating the project as a litmus test for how future investors would be treated by the government. As a result of this cautionary approach and stalled progress at the mine site, annual FDI had collapsed around 70% by September 2014.

“The controversy started in 2011, at a time when Mongolia and the government were riding high on an economy stimulated by record levels of FDI”

“Phase one of the development was by this point well underway, and by September 2013 the mine came into commercial operation”

“Rio Tinto’s response to the points of dispute was to stand firm and delay the financing of the more lucrative second phase of the project”

43

MACROECONOMICS

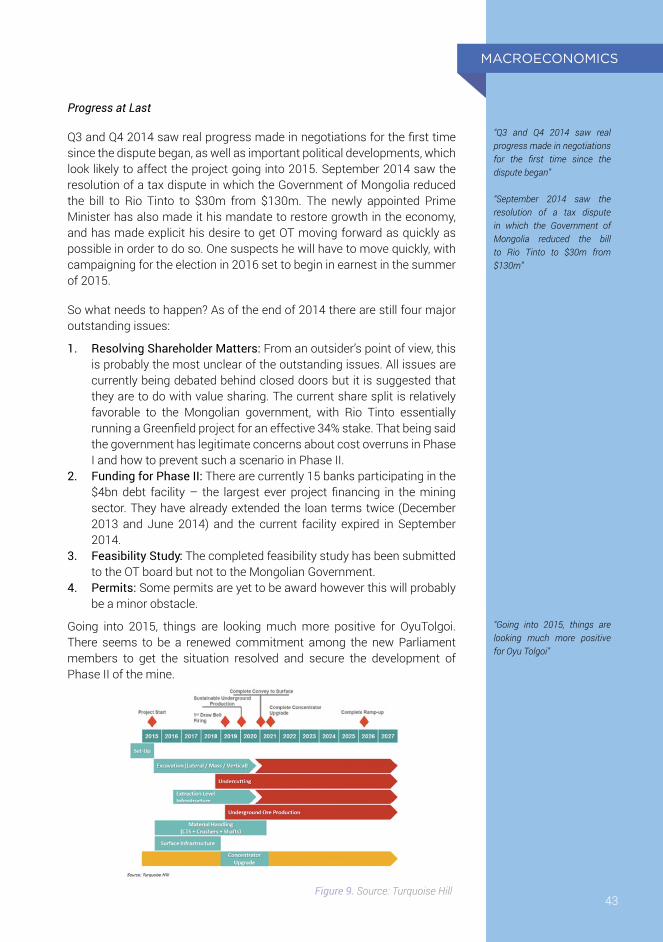

Progress at Last

Q3 and Q4 2014 saw real progress made in negotiations for the first time since the dispute began, as well as important political developments, which look likely to affect the project going into 2015. September 2014 saw the resolution of a tax dispute in which the Government of Mongolia reduced the bill to Rio Tinto to $30m from $130m. The newly appointed Prime Minister has also made it his mandate to restore growth in the economy, and has made explicit his desire to get OT moving forward as quickly as possible in order to do so. One suspects he will have to move quickly, with campaigning for the election in 2016 set to begin in earnest in the summer of 2015.

So what needs to happen? As of the end of 2014 there are still four major outstanding issues:

1. Resolving Shareholder Matters: From an outsider’s point of view, this is probably the most unclear of the outstanding issues. All issues are currently being debated behind closed doors but it is suggested that they are to do with value sharing. The current share split is relatively favorable to the Mongolian government, with Rio Tinto essentially running a Greenfield project for an effective 34% stake. That being said the government has legitimate concerns about cost overruns in Phase I and how to prevent such a scenario in Phase II.

2. Funding for Phase II: There are currently 15 banks participating in the $4bn debt facility – the largest ever project financing in the mining sector. They have already extended the loan terms twice (December 2013 and June 2014) and the current facility expired in September 2014.

3. Feasibility Study: The completed feasibility study has been submitted to the OT board but not to the Mongolian Government.

4. Permits: Some permits are yet to be award however this will probably be a minor obstacle.

Going into 2015, things are looking much more positive for OyuTolgoi. There seems to be a renewed commitment among the new Parliament members to get the situation resolved and secure the development of Phase II of the mine.

“Q3 and Q4 2014 saw real progress made in negotiations for the first time since the dispute began”

“September 2014 saw the resolution of a tax dispute in which the Government of Mongolia reduced the bill to Rio Tinto to $30m from $130m”

“Going into 2015, things are looking much more positive for Oyu Tolgoi”

Figure 9. Source: Turquoise Hill

44

MACROECONOMICS

Other Resources

Copper and gold have undoubtedly played a crucial role in the development of Mongolia’s mineral sector. However, it is likely that coal will be the country’s most important resource over the coming years. Mongolia possesses an estimated 163.2 billion tonnes of the mineral as opposed to just 77.3 million of copper.

The largest known deposit is at the ‘Tavan Tolgoi’ (meaning “Five Hills” in Mongolia) or “TT” site, located in the same southern province as OT, just 200 km from the Chinese border. The site is believed to be the second largest untapped reserve of coking coal in the world and contains more than 6.4 billion tons of the resource. Extraction of coal began as far back as 1960, but until recently, the mine has been functioning far below capacity and is subject to severe inefficiencies.

To develop the TT coalfield’s potential, the government has decided to split the project in two. The Eastern Tsankhi section it will develop alone, while the other “Western Tsankhi” branch will be opened up to foreign investment. The public sector operation is to be financed through a three way international equity IPO that will list shares in London, Hong Kong and Ulaanbaatar. Unfortunately, the much- vaunted IPO has been delayed several times. Political parties reportedly raided the companies coffers to help fund their 2012 election promises. The finances of TT are currently in rough shape and it does not seem likely that an IPO will occur before late 2015 at the earliest. In 2012, the government began courting international investors to fund the development of the private “West Tsankhi” venture. However, after carrying out an initial tender process, the government decided to backtrack and start over. The West Tsankhi branch is currently being mined on a short-term contract by a consortium of local Mongolian companies. A new international tender process to award long term operating rights to the western block commenced in late 2014.

With its vast mineral wealth and strategic location between Russia and China, Mongolia has the potential to supply the raw materials needed to sustain the development two of the largest BRIC growth economies.

“Mongolia possesses an estimated 163.2 billion tonnes of the mineral as opposed to just 77.3 million of copper”

“The largest known deposit is at the ‘Tavan Tolgoi’ (meaning “Five Hills” in Mongolia) or “TT” site”

“The public sector operation is to be financed through a three way international equity IPO that will list shares in London, Hong Kong and Ulaanbaatar”

“Unfortunately, the much- vaunted IPO has been delayed several times”

“The finances of TT are currently in rough shape and it does not seem likely that an IPO will occur before late 2015 at the earliest”

Work continues at OyuTolgoi

45

MACROECONOMICS

At the moment, China receives more than 90% of Mongolia’s exports. China’s monopsony is a constant cause for concern and consternation for Mongolian leaders. Resource revenue is perceived to be at the mercy of Chinese protectionism, infrastructural bottlenecks and imperfectly competitive price setting regimes. Mongolian leaders are eager to diversify their revenue base and export to new markets.

Even more than diversification, the Mongolian minerals industry desperately needs to develop its transportation infrastructure. To date, the majority of mineral ore exports are trundled to the Chinese border across miles of unpaved desert terrain in large trucks and lorries. Inefficient transport raises the price of Mongolian exports and limits the country’s ability to compete as a low cost producer in distant markets.

The government is undertaking rail and road network renewal projects in order to ease some of these concerns. Expanded service links to both China and the Trans- Siberian Railway will logistically connect OT and TT to the ports’ of Russia’s Pacific Coast. Access to naval trade through both of Mongolia’s neighbors is being negotiated and is expected to ensure a fair price is met for the country’s extracted minerals. The threat of Chinese monopsonistic abuse will be greatly reduced once these projects are realized. Competitive international commodity prices will allow Mongolia to convert its mineral exports into real tangible wealth that will benefit its people.

Imports and Exports

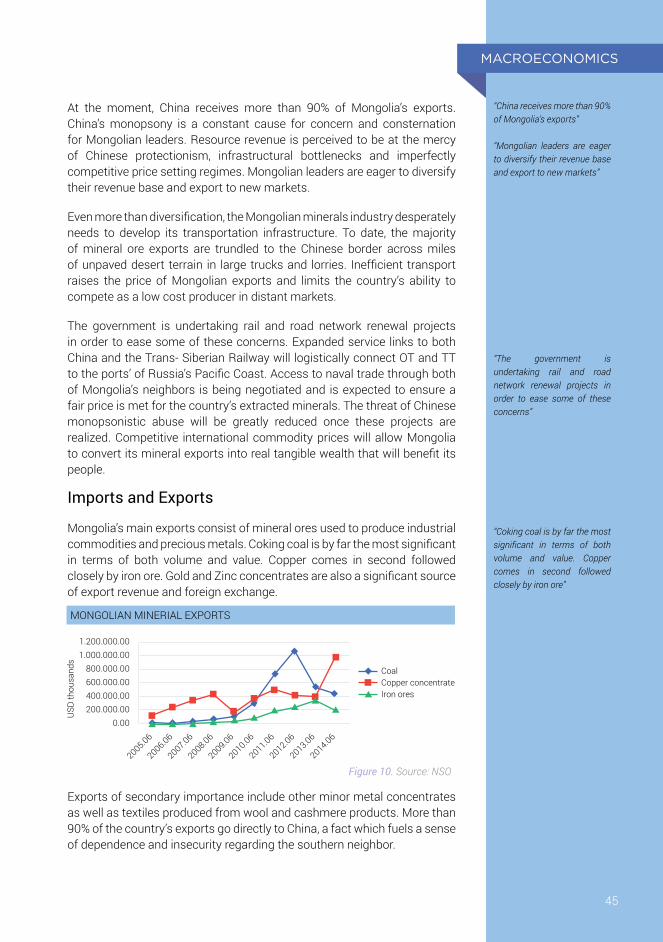

Mongolia’s main exports consist of mineral ores used to produce industrial commodities and precious metals. Coking coal is by far the most significant in terms of both volume and value. Copper comes in second followed closely by iron ore. Gold and Zinc concentrates are also a significant source of export revenue and foreign exchange.

Exports of secondary importance include other minor metal concentrates as well as textiles produced from wool and cashmere products. More than 90% of the country’s exports go directly to China, a fact which fuels a sense of dependence and insecurity regarding the southern neighbor.

“China receives more than 90% of Mongolia’s exports”

“Mongolian leaders are eager to diversify their revenue base and export to new markets”

“The government is undertaking rail and road network renewal projects in order to ease some of these concerns”

“Coking coal is by far the most significant in terms of both volume and value. Copper comes in second followed closely by iron ore”

0.00200.000.00400.000.00600.000.00800.000.00

1.000.000.001.200.000.00

2005.06

2006.06

2007.06

2008.06

2009.06

2010.06

2011.06

2012.06

2013.06

2014.06

USD

thou

sand

s

CoalCopper concentrateIron ores

Figure 10. Source: NSO

MONGOLIAN MINERIAL EXPORTS

46

MACROECONOMICS

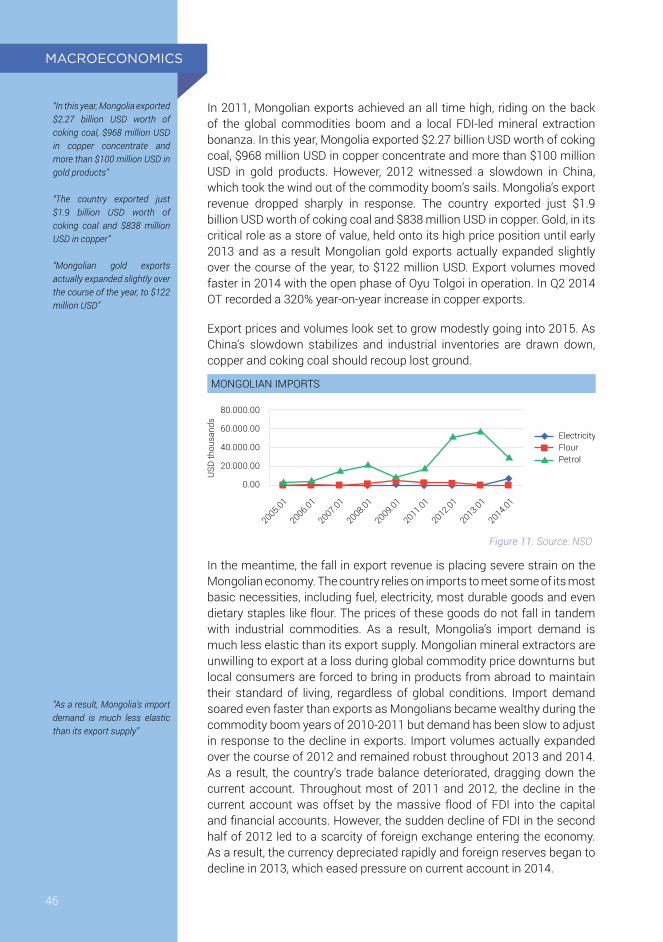

In 2011, Mongolian exports achieved an all time high, riding on the back of the global commodities boom and a local FDI-led mineral extraction bonanza. In this year, Mongolia exported $2.27 billion USD worth of coking coal, $968 million USD in copper concentrate and more than $100 million USD in gold products. However, 2012 witnessed a slowdown in China, which took the wind out of the commodity boom’s sails. Mongolia’s export revenue dropped sharply in response. The country exported just $1.9 billion USD worth of coking coal and $838 million USD in copper. Gold, in its critical role as a store of value, held onto its high price position until early 2013 and as a result Mongolian gold exports actually expanded slightly over the course of the year, to $122 million USD. Export volumes moved faster in 2014 with the open phase of Oyu Tolgoi in operation. In Q2 2014 OT recorded a 320% year-on-year increase in copper exports.

Export prices and volumes look set to grow modestly going into 2015. As China’s slowdown stabilizes and industrial inventories are drawn down, copper and coking coal should recoup lost ground.

In the meantime, the fall in export revenue is placing severe strain on the Mongolian economy. The country relies on imports to meet some of its most basic necessities, including fuel, electricity, most durable goods and even dietary staples like flour. The prices of these goods do not fall in tandem with industrial commodities. As a result, Mongolia’s import demand is much less elastic than its export supply. Mongolian mineral extractors are unwilling to export at a loss during global commodity price downturns but local consumers are forced to bring in products from abroad to maintain their standard of living, regardless of global conditions. Import demand soared even faster than exports as Mongolians became wealthy during the commodity boom years of 2010-2011 but demand has been slow to adjust in response to the decline in exports. Import volumes actually expanded over the course of 2012 and remained robust throughout 2013 and 2014. As a result, the country’s trade balance deteriorated, dragging down the current account. Throughout most of 2011 and 2012, the decline in the current account was offset by the massive flood of FDI into the capital and financial accounts. However, the sudden decline of FDI in the second half of 2012 led to a scarcity of foreign exchange entering the economy. As a result, the currency depreciated rapidly and foreign reserves began to decline in 2013, which eased pressure on current account in 2014.

“In this year, Mongolia exported $2.27 billion USD worth of coking coal, $968 million USD in copper concentrate and more than $100 million USD in gold products”

“The country exported just $1.9 billion USD worth of coking coal and $838 million USD in copper”

“Mongolian gold exports actually expanded slightly over the course of the year, to $122 million USD”

“As a result, Mongolia’s import demand is much less elastic than its export supply”

0.00

20.000.00

40.000.00

60.000.00

80.000.00

2005.01

2006.01

2007.01

2008.01

2009.01

2011.01

2012.01

2013.01

2014.01

USD

thou

sand

s

ElectricityFlourPetrol

Figure 11. Source: NSO

MONGOLIAN IMPORTS

47

MACROECONOMICS

The 2014 balance of trade came in at a US$538m surplus, much better than expected. The total value of exports increased by 45% y-o-y in volume; translating to a 35% increase in US dollar terms and amounting to US$5.78bn. Copper made up the lions share of exports and saw its share of export value double to 45%, despite copper prices steadily dropping throughout the year. Mongolia’s dependence on coal exports was also greatly reduced with volumes only growing 7% y-o-y, falling in export value terms to 15% from 26% in 2013.

Foreign Direct Investment

In many ways, foreign direct investment has been the real driver of growth over the past decade. Gross capital formation has expanded faster than any other form of economic expenditure and the majority (more than 70%) of the funds used to expand the capital stock have come from foreign sources.

Foreign investment has been directed primarily into the minerals sector but the rising tide of FDI has spread outward to contractors and service providers, lifting all sectors of the economy. Significant amounts of foreign capital have also been injected into the banking sector (e.g. Goldman Sachs in Trade and Development Bank), the telecom sector (Sumitomo Corporation in NewCom Group), and the real estate sector (Asia Pacific Investment Partners in Mongolian Properties).

The single largest foreign invested project, indeed the single largest project in Mongolia’s history, is the OT copper gold mine, described above. As the graph below illustrates, the OT project is responsible for a very large portion of the FDI that has entered the country over the past several years. The sudden decline of foreign investment in 2012 is due in large part to the winding down of expenditures related to the open pit first phase of OT’s construction. The global retreat of capital from emerging markets as developed economies recover is another factor that contributed to the fall in FDI. However, shifts in Mongolia’s domestic investment policy and local electoral politics also played an important role.

“Gross capital formation has expanded faster than any other form of economic expenditure”

“Foreign investment has been directed primarily into the minerals sector”

“Significant amounts of foreign capital have also been injected into the banking sector (e.g. Goldman Sachs in Trade and Development Bank), the real estate sector (Asia Pacific Investment Partners in Mongolian Properties)”

Figure 12. Source: www.tradingeconomics.com | Mongol bank

MONGOLIA’S BALANCE OF TRADE

48

MACROECONOMICS

As the politics section below discusses, Mongolia has had an uneasy and occasionally violent historical relationship with its large southern and northern neighbors. As recently as a century ago, Mongolia was a province of China’s Qing Empire. Mongolia has long feared that its southern neighbor’s hunger for resources would eventually drive it to re-assert control and violate the nation’s independence. This tense relationship with foreign powers combined with the new era of free market capitalism and FDI driven growth has triggered a wave of xenophobia. Locals, shocked by the flood of foreign investors buying up Mongolian assets, have become concerned that the nation’s resources are being unfairly exploited. Populist politicians have taken advantage of this sentiment to stir up fear in order to win elections and maintain power.

This sentiment came to a head in early 2012, when the Aluminum Corporation of China Limited (CHALCO), a Chinese state owned company, made a bid to acquire control of South Gobi Resources, a major local coal producer. China already buys more than 90% of the coal that Mongolia produces and Winsway Coking Coal, another Chinese company, is the biggest player in the purchasing and transportation market for Mongolian coal. Politicians stirred up fears that if Chinese companies obtained significant production stakes in addition to dominating sales and transport, they would control the entire supply chain of a very critical national industry. In the build-up to the 2012 parliamentary elections, most members of parliament were eager to show their nationalist credentials and score populist points in order to gain votes. As a result, the Chalco deal, which would have been a hot button issue at any point in time, started a political furor. In May of 2012, just a few weeks before the parliamentary elections, Mongolia passed the now infamous Strategic Entities Foreign Investment Law (SEFIL) by a wide margin. The law stated that any foreign investment of over $75 million USD or any foreign investment of any size that targets the mining sector or other sectors deemed “strategic” must be reviewed and approved by Parliament. The government simultaneously launched an aggressive legal campaign against South Gobi and several members of its foreign employees.

“China already buys more than 90% of the coal that Mongolia produces”

“Politicians stirred up fears that if Chinese companies obtained significant production stakes in addition to dominating sales and transport”

“The government simultaneously launched an aggressive legal campaign against South Gobi”

0

500

FDI has fallen even as exports have declined. The majority of the downturn is due to OT.

OT Investment Agreement Signed

SEFIL Passed

Total FDI Estimate of OT FDI Contribution

Q1-

2009

Q3-

2009

Q1-

2010

Q3-

2010

Q1-

2011

Q3-

2011

Q1-

2012

Q3-

2012

Q1-

2013

Mill

ions

USD

1,000

1,500

Figure 13. Source: Mongolbank, APIP Estimates

FOREIGN DIRECT INVESTMENT INFLOWS

49

MACROECONOMICS

Although its passage was motivated by valid concerns, the SEFIL’s ambiguous and aggressive provisions elicited a strong negative reaction from foreign investors. FDI inflows immediately began to cool.

In December of the same year, foreign investment received another blow when President Ts. Elbegdorj introduced a “Draft Law” designed to reform the nation’s mineral sector. The draft, though well intentioned, contained a number of provisions that investors found unpalatable, including binding production targets; the state’s right to take an ownership stake in many projects without contributing capital, and strict community approval guidelines.

A few months later, the President was on camera again, exhorting the government to pay more attention to development of the OyuTolgoi mine saying, “It is important that the government take the OyuTolgoi matter into its own hands.” The international press ran away with the story. Coming on top of the unfavorable laws passed earlier, the 2013 dispute with Rio Tinto and the other developers of the OyuTolgoi mine further soured the investment community’s sentiment on Mongolia.

“The draft, though well intentioned, contained a number of provisions that investors found unpalatable”

Parliament meets in the Great Khural

APIP

Foreign Invested Companies in Mongolia

50

MACROECONOMICS

In 2013 FDI dropped off more than 40% since year on year since the Chalco incident and, even on the passing of a new investment law in late 2013, FDI had dropped almost 70% year on year in late 2014.

However, the effect of the Chalco incident is greatly exaggerated. The most important exogenous factor is the simple fact that construction of the first open pit stage of the OT project began to wind down in mid 2012, around the same time as the Chalco controversy set off. Initial investments in OT accounted for a very large portion of the FDI upsurge in 2009-2011. The 2012 drop-off in expenditures was largely planned and had little connection to the ongoing political controversies. Delays in the second underground stage of the mine’s development are, however, directly related to domestic politics (discussed above).

Cognizant of the drop off in FDI and its dramatic negative impact on the economy, Mongolia’s Parliament called an emergency session in late September 2013. No regulations were passed during the session but a number of bipartisan proposals were floated regarding legislative changes that might help to lure capital back to Mongolia. During the first week of the regular fall session staring in October, parliament passed a new investment law designed to encourage FDI. The new law supersedes all prior investment laws, canceling the controversial SEFIL, and erases many of the former distinctions between foreign and local investors, limiting restrictions to foreign state owned firms. It is based on “stability agreements” that lock in tax rates, royalty payments and other regulations for investors of capital that pass predetermined thresholds.

The stability agreements delivered under the law provide investors with a guarantee that the profitability of their projects will not be subject to the whims of future elected regimes, thus significantly reducing sovereign risk. The exact length of the stability agreement guarantee depends on the amount of capital invested and the region where the project is developed, capital invested in Mongolia’s less developed provinces receiving preferential treatment. Its world-class mineral reserves hold incredible allure and will almost certainly be developed by one source of financing or another. However, if the country cannot maintain the confidence of large institutional investors from the developed world, it may be forced to turn to China for the capital required to develop its deposits. Ironically, by aggressively attempting to fend off advances from its southern neighbor, Mongolia may have played directly into its hands.

Pivot to the North and South

Against a backdrop of plummeting FDI, a local currency in free-fall and with negotiations stalled at Oyu Tolgoi, mid-late 2014 saw a number of high profile visits from neighboring heads of state. In August, Xi Jinping became the first Chinese President to visit Mongolia in more than a decade, pledging to double trade to $10bn by 2020 with a focus on infrastructure, transportation and financing requirements.

“In 2013 FDI dropped off more than 40% since year on year since the Chalco incident”

“FDI had dropped almost 70% year on year in late 2014”

“Delays in the second underground stage of the mine’s development are, however, directly related to domestic politics”

“The stability agreements delivered under the law provide investors with a guarantee that the profitability of their projects will not be subject to the whims of future elected regimes, thus significantly reducing sovereign risk”

“If the country cannot maintain the confidence of large institutional investors from the developed world, it may be forced to turn to China”

“In August, Xi Jinping became the first Chinese President to visit Mongolia in more than a decade, pledging to double trade to $10bn by 2020”

51

MACROECONOMICS

South Korean Foreign Minister Yun Byung-se followed with cooperation agreements on bilateral trade and national security, and Russia’s President Vladamir Putin visited in early September. Many hope that these visits, and a resolution at Oyu Tolgoi, will be enough to encourage foreign investment to return.

The Tugrik showed signs of stabilizing off the back of Xi Jinping’s visit, rallying for the first time in recent memory to around MNT1820 to the US dollar. The Chinese president increased the value of the currency swap agreement between the central banks from RMB10bn to RMB15bn, bolstering Mongolia’s weak external position. Hastened perhaps by western sanctions, Putin agreed to lift import duties on Mongolian meat, which should help develop the agricultural sector. There were also a number of trilateral agreements made with agreements on future infrastructure projects as part of China’s “new silk road” venture.

Fiscal Policy

With its booming resource sector, robust economic growth and moderate tax code, Mongolia has all the basic elements in place needed to achieve fiscal solvency and sustainable public finance. Unfortunately, in recent years, fiscal policy has deviated from its ideal path and public debt has started accumulating at a rapid rate.

In theory, public expenditure is meant to be countercyclical – with the government running surpluses when commodity prices are high and financing deficits from the saved funds when commodity prices are low. In reality, spending tends to be pro-cyclical and more closely related to the election cycle than the price of global commodities.

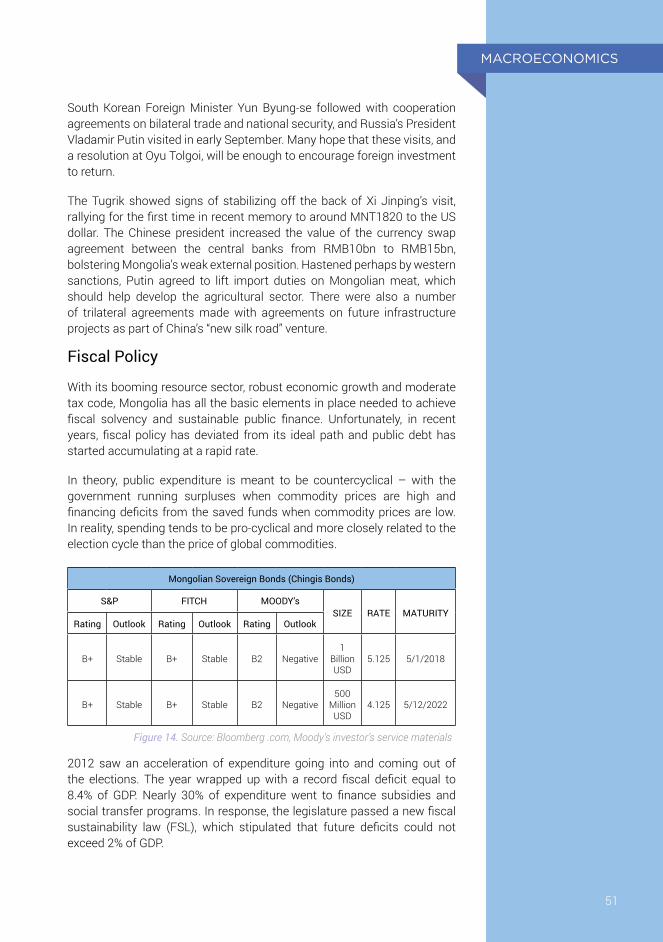

Mongolian Sovereign Bonds (Chingis Bonds)

S&P FITCH MOODY’sSIZE RATE MATURITY

Rating Outlook Rating Outlook Rating Outlook

B+ Stable B+ Stable B2 Negative1

Billion USD

5.125 5/1/2018

B+ Stable B+ Stable B2 Negative500

Million USD

4.125 5/12/2022

2012 saw an acceleration of expenditure going into and coming out of the elections. The year wrapped up with a record fiscal deficit equal to 8.4% of GDP. Nearly 30% of expenditure went to finance subsidies and social transfer programs. In response, the legislature passed a new fiscal sustainability law (FSL), which stipulated that future deficits could not exceed 2% of GDP.

Figure 14. Source: Bloomberg .com, Moody’s investor’s service materials

52

MACROECONOMICS

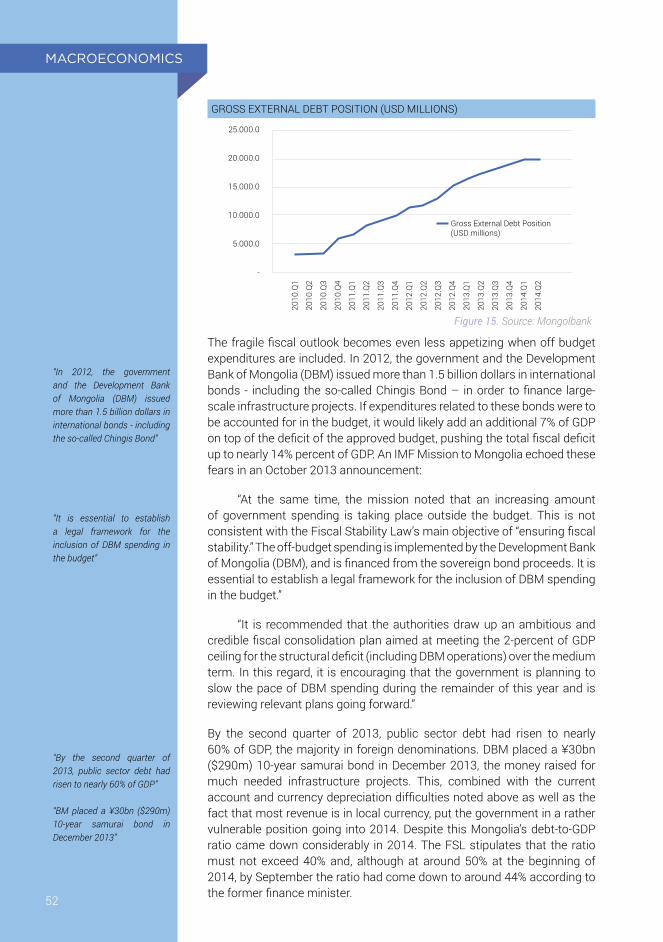

The fragile fiscal outlook becomes even less appetizing when off budget expenditures are included. In 2012, the government and the Development Bank of Mongolia (DBM) issued more than 1.5 billion dollars in international bonds - including the so-called Chingis Bond – in order to finance large-scale infrastructure projects. If expenditures related to these bonds were to be accounted for in the budget, it would likely add an additional 7% of GDP on top of the deficit of the approved budget, pushing the total fiscal deficit up to nearly 14% percent of GDP. An IMF Mission to Mongolia echoed these fears in an October 2013 announcement:

“At the same time, the mission noted that an increasing amount of government spending is taking place outside the budget. This is not consistent with the Fiscal Stability Law’s main objective of “ensuring fiscal stability.” The off-budget spending is implemented by the Development Bank of Mongolia (DBM), and is financed from the sovereign bond proceeds. It is essential to establish a legal framework for the inclusion of DBM spending in the budget.”

“It is recommended that the authorities draw up an ambitious and credible fiscal consolidation plan aimed at meeting the 2-percent of GDP ceiling for the structural deficit (including DBM operations) over the medium term. In this regard, it is encouraging that the government is planning to slow the pace of DBM spending during the remainder of this year and is reviewing relevant plans going forward.”

By the second quarter of 2013, public sector debt had risen to nearly 60% of GDP, the majority in foreign denominations. DBM placed a ¥30bn ($290m) 10-year samurai bond in December 2013, the money raised for much needed infrastructure projects. This, combined with the current account and currency depreciation difficulties noted above as well as the fact that most revenue is in local currency, put the government in a rather vulnerable position going into 2014. Despite this Mongolia’s debt-to-GDP ratio came down considerably in 2014. The FSL stipulates that the ratio must not exceed 40% and, although at around 50% at the beginning of 2014, by September the ratio had come down to around 44% according to the former finance minister.

“In 2012, the government and the Development Bank of Mongolia (DBM) issued more than 1.5 billion dollars in international bonds - including the so-called Chingis Bond”

“It is essential to establish a legal framework for the inclusion of DBM spending in the budget”

“By the second quarter of 2013, public sector debt had risen to nearly 60% of GDP”

“BM placed a ¥30bn ($290m) 10-year samurai bond in December 2013”

5.000.0

-

2010

.Q1

2010

.Q2

2010

.Q3

2010

.Q4

2011

.Q1

2011

.Q2

2011

.Q3

2011

.Q4

2012

.Q1

2012

.Q2

2012

.Q3

2012

.Q4

2013

.Q1

2013

.Q2

2013

.Q3

2013

.Q4

2014

.Q1

2014

.Q2

10.000.0

15.000.0

20.000.0

25.000.0