Qualifying the Competitiveness of Solar Photovoltaic ...

157

Wesleyan University The Honors College 50 States and 50 Markets: Qualifying the Competitiveness of Solar Photovoltaic Electricity in the United States by Alexander Speiser Class of 2013 A thesis submitted to the faculty of Wesleyan University in partial fulfillment of the requirements for the Degree of Bachelor of Arts with Departmental Honors from the College of Social Studies Middletown, Connecticut April, 2013

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Qualifying the Competitiveness of Solar Photovoltaic ...

Wesleyan University The Honors College

50 States and 50 Markets: Qualifying the Competitiveness of Solar Photovoltaic Electricity in the

United States

by

Alexander Speiser Class of 2013

A thesis submitted to the faculty of Wesleyan University

in partial fulfillment of the requirements for the Degree of Bachelor of Arts

with Departmental Honors from the College of Social Studies Middletown, Connecticut April, 2013

1

Table of Contents Acknowledgements…...…..………………………………………………………….2

Figures………………………………………………………………………………...3

Introduction……....…..………………………………………………………..……..4

Background………………………………………………………………………4 Policy Specifics…………………………………………………………………..8 Chapter Roadmaps……………………………………………………………...11 Review of Existing Literature………………………………………………......16

I. PV’s Topsy-Turvy Road to Development………………………………………19

The Federal Government’s Sporadic Support of PV……………………………19 The Current Status of the American PV Industry…………...…….……………32 Room for Improvement and Regulation………………………………….……..45

II. The Relics of Electricity Regulation and the Inhibitors of PV Markets….….48

Regulation’s Role in the Electrification of the U.S……………………….…….48 Defining PV Cost-Competitiveness…….……………………………….……...52 Modern Electricity Market Inefficiencies….………………………….………..58 Market Inhibitors to PV Development….………………………….….………..61 Towards More Efficient Electricity Markets……………………….….……….69

III. Net Metering: A 21st Century Policy for a 20th Century Relationship.….….73

Accounting for Solar PV’s Unique Production Cycle….……………………….73 Policy Specifics and Experiences….………………….…………….…………..79 Reforms to Complement Demand-Side Priorities………………………………85 Automation and Optimizing Net Metering………………………….……….…92 Conclusion………………………………………………………………………97

IV. Realizing Cooperation rather than Collision………………...…..…..……...102

Background…………………….…….…….….………………………………102 The Design of Deliberate PV Promotion Through RPS………………………106 Assessing SREC Markets Through the Experience of the Garden State……...111 Connecticut’s National Model for Renewable Portfolio Standards…………...118 Conclusion: A Fiscally Practical Solution to Deliberate PV Promotion………125

V. Conclusion……………………………...………………………………………129

2

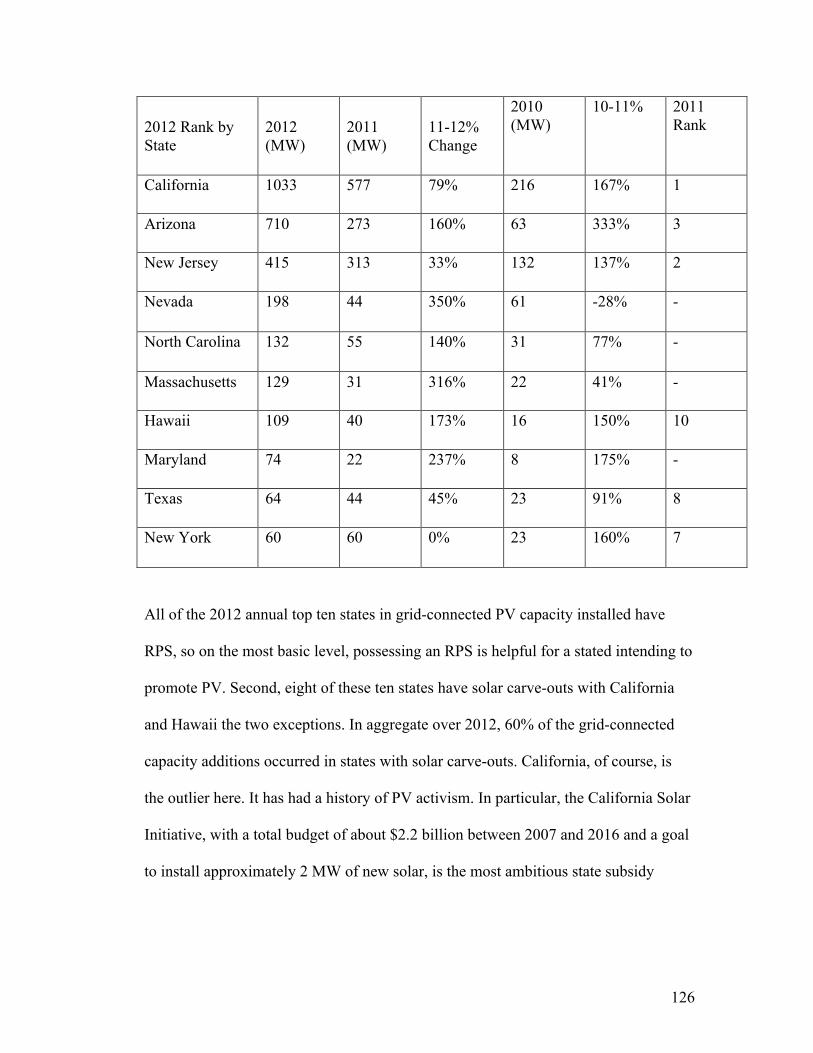

Figures Figure 1. Renewable Energy Consumption in the nation’s energy supply, 2011……6 Figure 2: Framework for policy stacking……………………………………………10 Figure 3. Basic Schematic of a PV Module……………………………….………...15 Figure 4. Example of Standard Residential Photovoltaic System……….…..….…..16 Figure 5. Number of State Renewable Portfolio Standards Since 1997…….……....29 Figure 6. Federal Clean Technology Policy Support is Falling off a Cliff….………31 Figure 7. Data Sample Compared to Total U.S. Grid-Connected PV Capacity.……33 Figure 8. Installed Price of Residential & Commercial PV over Time…….………..34 Figure 9: Case Studies of Residential Solar Power in Five U.S. cities…….………..35 Figure 10. The Steady Fall of Solar Panel Prices……………….…………………...37 Figure 11. Balance of System Costs for Silicon and Cadmium PV Systems………..42 Figure 12. Vertical Third Party Financing Model………………….………………..43 Figure 13. Broadway and St. John before and after Regulated Electricity………......51 Figure 14. Photovoltaic Solar Resource of the United States………………….…….55 Figure 15. Load and Generation Mix………………………………………………..57 Figure 16. Customer Acquisition Costs in Germany vs. U.S………………………..64 Figure 17. The Basics of a Rooftop Net Metered System…………………………...74 Figure 18. The Phases of PV System Operation……………………………………..75 Figure 19. Net Metering Policy Grades in the United States as of April 2013….…...79 Figure 20. Net Metering Landscape as of March 2013………………..….….……...82 Figure 21. PV’s influence on Tiered Electricity Prices……………………………...86 Figure 22. The Traditional Electricity Meter and the Smart Meter……………...…..93 Figure 23. RPS Policies with Solar and Distributed Generation Requirements.…...107 Figure 24. The General Schema of RPS……………………..……………………..108 Figure 25. Mid-Atlantic SREC Market Trends………………….……….…………113 Figure 26. NJ Solar Carve-Out: PV Megawatt Obligations Prior Vs. S. 1925……..114 Tables Table 1. Mean Cumulative Capacity per FTG Net Metering Grade Group…..…..…80 Table 2. Results from May, 2012 ZREC Auctions……………..…………………..120 Table 3. 2012 Top Ten States: Ranked by Grid-Connected PV Capacity (2012),,,,,125

3

Acronyms Alternative Compliance Payment ACP Balance of Systems BOS Commercial Property Assessed Clean Energy C-PACE Clean Energy Finance and Investment Authority CEFIA Chlorofluorocarbon CFC Connecticut Light & Power CL&P Carbon Dioxide CO2 California Public Utilities Commission CPUC Concentrated Solar Power CSP Federal Energy Regulatory Commission FERC Feed-In Tariff FIT Freeing The Grid FTG Greenhouse Gas GHG Kilowatt-Hour kWh Levelized Cost of Electricity LCOE Low-Emission Renewable Energy Credit LREC Master Limited Partnership MLP Megawatt MW Photovoltaic PV Research & Development R&D Renewable Energy RE Renewable Energy Credit REC Real Estate Investment Trusts REITS Renewable Portfolio Standard RPS Solar Alternative Compliance Payment SACP Solar Renewable Energy Credit SREC Time of Use TOU United Illuminating Company UI

Zero Emission Renewable Energy Credit ZREC

4

Acknowledgements This would be more fun if it were for a wedding speech, maybe even a quinceanera. With that said, I hope that years from now I can be at some sort of event with everyone I acknowledge here and this project comes up, so that I can tell them once more how grateful I will forever be for their contributions to my thesis. First of all, my deepest and most sincere thanks goes to my advisor, Professor Gary Yohe. Without your reassuring guidance and insight, I would have never come this far.

I would also like to express my wholehearted gratitude to everybody who helped me grow as a thinker during the thesis process: Professor Gilbert Skillman, for taking me “out of the clouds” over countless hours of challenging my ideals and then my arguments; Professor Cecilia Miller, for her candor and constructive criticism, which I much needed and appreciated; Professor Michael Dorsey, for challenging me to ask for what I want; Barry Chernoff for his devotion to the COE, which I am so glad was apart of my Wesleyan experience. I’d like to extend my further thanks to Prof. Richard Elphick, Prof. Brian Fay, and Prof. Don Moon, who were formative in my development as a student in the CSS. I owe a great deal to those who generously worked to proofread and provided feedback on this work, especially Grace Kuipers, Max Bevilacqua, and Ilana Bondell. Additionally, to my buddies, who allowed themselves to also be coaxed into my editing process: Yosh Kule, Adam Hirschberg, and especially Sam Walker, with whom I look forward to joining forces and taking over the solar industry. Thanks also to members of the solar and renewables industries, who took the time to speak to a lowly student and offer more than their two-cents to my questions: Ben Higgins, Rhone Resch, Richard Kaufman, Alec Guettel, Joshua Paradise, Alan Bernheimer, Kerinia Kusick, Joachim Seel, Larry Sherwood, Sloane Morgan, Mike Jacobs, Chris Lotspeech, Mike Hill, Omay Elphick, Gary Sheehan, Andrew McKenna, Ryan Gilchrist, John Nordeman, and Kate Gerlach. To my partners in crime in CSS, Michael Zazzaro and Luke Wherry. These last three years would have been a whole lot harder without you. If it were not for Luke, the thesis process would have been to quote our friend, Alvy Singer, “full of misery, loneliness, and suffering.” To my roommates at 53 Home, my Horace Mann boys, my mom, and my brother, you will not read this (it is 3:52 PM)—I love you. -ABS

5

Introduction

[T]he question of the relation of the States to the federal government is the cardinal question of our constitutional system. At every turn of our national development, we have been brought face to face with it, and no definition either of statesmen or of judges has ever quieted or decided it. It cannot, indeed, be settled by the opinion of any one generation, because it is a question of growth, and every successive stage of our political and economic development gives it a new aspect, makes it a new question.

-Woodrow Wilson1

I. Background

A dire reality confronts the electrical apparatus underpinning modern

civilization: climate change. To be more specific, close to 40 percent of the United

States’ carbon dioxide emissions come from the production of electricity used in

homes, factories, stores, and offices.2 The global climate is changing as a result of the

buildup of atmospheric greenhouse gases (GHGs) such as carbon dioxide (CO2),

methane, nitrous, and chlorofluorocarbons (CFCs), which in the United States come

1Woodrow Wilson, Constitutional Government in the United States. (New York: Columbia Univ. Pr., 1921),173. 2"Carbon Dioxide Emissions," Environmental Protection Agency, accessed November 29, 2012, http://www.epa.gov/climatechange/ghgemissions/gases/co2.html.

Précis: The story of solar photovoltaic electricity (PV) in the United States is one of auspicious potential curtailed by inconsistent policies. The public sector’s support is essential for PV to compete with conventional forms of electricity. Yet, the role of federal and state policymaking on PV has, alas, amounted to negligible contributions to the American energy system. Mindful of the public sector’s budget belt tightening, this thesis focuses on how regulatory measures, not financial incentives, affect PV's cost competitiveness and market development. First, this Introduction provides necessary background on PV, the American Energy System, and climate change. Second, the Introduction transitions into a brief survey of the policies that will be assessed in this thesis. Finally, it concludes with a statement of the thesis’ structure, goals, and sources.

6

primarily from the combustion of fossil fuels used to power our industrial, residential,

and commercial systems. The work of globally renowned scientific bodies such as the

United Nation’s Intergovernmental Panel on Climate Change confirms the urgency to

slash emissions,3 as do farmland bakes from historic droughts and subway floods

from surging seas.4 Public policies promoting renewable energy (hereafter

“renewable(s)” or RE) address this link between conventional electricity production

and climate change. RE, especially solar and wind electricity, have the potential to

play a crucial role in mitigating climate change.5 Unlike fossil fuels, renewables

provide desired energy services with little or no emissions.6 They offer the possibility

of continuous supplies of energy in perpetuity that are many orders of magnitude

greater than humanity’s entire use of energy.7 The promise of REs, however, is

diminished by their inability to compete with conventional electricity in the majority

3Through the use of climate models and analysis of past climate variations from the impact science of painstaking studies published in the world’s leading peer-reviewed journals, the IPCC expects that significant climate changes will occur in the coming decades and beyond due to the accumulation of GHGs in the atmosphere. In the absence of measures restricting the emission of GHGs, particularly

CO2, it is projected that global surface temperature will rise over this century between 1.1–6.4◦C, precipitation and evaporation will increase, and sea levels will rise 10-90 cm. (S Solomon, D. Qin, M. Manning, Z. Chen, M. Marquis, K.B. Averyt, M. Tignor and H.L. Miller, Climate Change 2007: The Physical Basis of Climate Change-Contribution of Working Group I to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change (Cambridge: Cambridge University Press, 2007) 4While climate change regulation is generally beyond the scope of this paper, the pages that follow do identify ways in which renewable energy regulation, specifically of solar electric power, can be fine-tuned to achieve climate change mitigation objectives. 5The IPCC defines a renewable energy as “any form of energy from solar, geophysical or biological sources that is replenished by natural processes at a rate that equals or exceeds its rate of use.” (O. Edenhofer, R. Pichs-Madruga, Y. Sokona, K. Seyboth, P. Matschoss, S., T. Zwickel, P. Eickemeier, G. Hansen, S. Schloemer, C. von Stechow, Renewable Energy Sources and Climate Change Mitigation, (Cambridge: Cambridge University Press, 2011), 164). 6Ibid, 164 7For instance, the amount of sunlight reaching the earth is over 10,000 times greater than the total human direct use of energy. (Ramez Naam, "Smaller, cheaper, faster: Does Moore’s law apply to solar cells?," Scientific America, (March 2011) Accessed 11/02/12: http://blogs.scientificamerican.com/guest-blog/2011/03/16/smaller-cheaper-faster-does-moores-law-apply-to-solar-cells/)

7

of states. Indeed, renewables contribute a relatively slim portion to the overall

American energy system, as shown in Figure 1.

Figure 1. Renewable Energy Consumption in the nation’s energy supply, 20118

Though renewable sources have experienced significant growth in the last decade,

they contribute to a very small portion of total electricity generation today due to their

high direct costs.

In contrast to the telecommunications and computing industries, where

incumbents saw potential opportunities and threats of new technologies and therefore

took it upon themselves to innovate, most utilities have not deviated from the status

quo of conventional generation. Unlike innovations in cellphones or laptops, a

premium is not placed on a kilowatt hour (kWh) of renewable electricity because the

cost of conventional power does not include the environmental, health, and other

social costs of GHG emissions.9 “Investors are most concerned with a positive returns

on their investment,” Joshua Paradise, Director of Research at the Renewable Energy

8 One BTU (British Thermal Unit) is the amount of energy required to raise the temperature of one pound of water by one degree Fahrenheit. One quadrillion BTUs is equivalent to the annual energy consumption of ten million U.S. households: U.S. Department of Energy, Energy Information Administration, Annual Energy Review 2011, 2012, accessed December 01, 2012, http://www.eia.gov/totalenergy/data/annual/pdf/aer.pdf. 9Utilities charge their customers in terms of kilowatt-hours (kWh). A kWh is the unit of energy equal to 1000 watts of power used over the course of an hour. It is also the energy required to run a 100 watt light bulb for 10 hours.

8

Consulting Firm, PHOTON, remarked. “Other factors like environmental attributes

are secondary.”10 Paradise’s comment touches on the problem of placing a cost on

environmental externalities. Since Arthur Pigou’s seminal work in 1920 on the topic,

11 economists have understood that pricing externalities is likely to be the best way to

move consumer and producer behavior towards market efficiency. In the context of

electricity, this means placing a price on fossil fuels’ GHG emissions through taxes or a

tradable permits system.12 By placing a price on carbon, the social costs of emissions

would be embedded in the price of related goods. Such mechanisms would provoke

fundamental changes in the electricity behavior of millions of American people and

businesses, who would now have to account for the damages resulting from

conventional electricity generation. However, carbon-pricing policies have been

eschewed by Congress and only implemented in a minority of states.13

Instead, government responses have centered on programs encouraging the

use of renewable energies that less directly address the social costs of energy

production.14 These tools are implemented to render renewables more competitive

10Interview with Joshua Paradise January 10, 2013. 11Arthur C. Pigou, The Economics of Welfare, (London: Macmillan and Co., 1920). 12There is a substantial literature addressing the role of a carbon a tax or a cap-and-trade system on energy consumption. For instance: William D. Nordhaus, “A Review of the Stern Review on the Economics of Climate Change,” Journal of Economic Literature, Vol. XLV (September, 2007), 686-702. (“in plain English, it is critical to have a harmonized carbon tax or the equivalent both to provide incentives to individual firms and households and to stimulate research and development in low-carbon technologies.”) 13 A minority of states price carbon through cap and trade system. For example, “The New England Governors released an action plan in 2001 that calls for a 10 percent reduction in GHGs below 1990 levels by 2020 (Regional Greenhouse Gas Initiative [RGGI], 2007). New York State’s energy plan requires a 5 percent reduction in GHG levels by 2010 and a 10 percent decrease below 1990 levels by 2020.” (Daniel C. Matisoff, "The Adoption of State Climate Change Policies and Renewable Portfolio Standards: Regional Diffusion or Internal Determinants?," Review of Policy Research 25, no. 6 (2008): p.3, doi:10.1111/j.1541-1338.2008.00360.x.) 14For more information on the concept of the social cost of carbon: Laurie T. Johnson and Chris Hope, "The Social Cost of Carbon in U.S. Regulatory Impact Analyses: An Introduction and Critique," Journal of Environmental Studies and Sciences 2, no. 3 (September 2012), accessed November 07, 2012, http://link.springer.com/article/10.1007%2Fs13412-012-0087-7. /

9

against conventional sources (fossil fuels, nuclear, and hydropower facilities), all of

which were significantly supported by the government in their development stages.15

On a federal, state, and local level, a patchwork of incentives and regulations

promotes grid-connected solar photovoltaic (hereafter PV) electricity. PV

technologies transform sunlight into electricity (refer to “Background Information” at

the end of this introduction) and potentially represent one of the most promising

sources of alternative energy. These policies have been implemented so that PV can

be economically competitive with conventional sources of generation. For the party

investing in PV, cost-competitive means that the cost of the system, or levelized cost

per kWh,16 after inclusion of all state and federal benefits, is at or below the

applicable price of conventional generation.

II. Policy Specifics

Today, American RE policymaking takes place in the context of a

decentralized system. Both states and the national government share responsibility for

approaches to climate change. The prospects of these practices can be determined

from an analysis of the historical experiences of the various American policies

intended to encourage the usage and promote the financial success of PV. It is widely

15According to the Congressional Research Service, “For the 63-year period from 1948 through 2010, nearly 12% [of DOE R&D spending] went to renewables, compared with 9% for efficiency, 25%for fossil, and 50% for nuclear.” Fred Sissine, CRS, “Renewable Energy R&D Funding History: A Comparison with Funding for Nuclear Energy, Fossil Energy, and Energy Efficiency R&D” 16 (January 26, 2011). 16With more description to come in Chapters One and Two, the levelized cost of electricity for a given PV system is the constant (in real terms) price for power that would equate the net present value of revenue from the system’s output with the net present value of the cost of production (Severin Borenstein, "The Private and Public Economics of Renewable Electricity Generation," NBER Working Paper, no. 17695 (December 2011), accessed March 01, 2013, http://www.nber.org/papers/w17695.)

10

accepted that a level of fiscal austerity has been adopted among policymakers.17

Using this budgetary restraint as a point of departure, this thesis focuses on how

regulatory measures, not financial incentives, affect PV’s cost competitiveness and

affect the development of PV markets. It emphasizes the overlooked role that state

regulations play in stimulating PV markets and addressing inefficiencies in electricity

markets. I argue that while financial incentives have served as the sporadic engine of

the U.S.’s PV industry, regulation is the road to long term viability.

Despite the fact that it does not contribute a significant portion to the overall

American Energy System, RE carries tremendous promise. Central to this outlook is

the proactive role that state policymaking has had. Today, almost every state has

adopted one RE policy or another. These policies are often grouped in two categories.

Policies in the first category provide financial incentives to promote PV through

grants, tax incentives, and loans, resembling the policies already established by the

federal government. The second category includes rules and regulations that mandate

certain action promoting RE from obligated entities like utilities.18 Federal financial

incentives have been crucial to PV’s evolution into a rapidly growing industry over

the past decade.19 Regulation, however, carries a more complicated history. Since

there are no federal mandates to accompany state regulations and because state

17Such behavior has been demonstrated in statehouses throughout the U.S. For instance, in his 2013 State of the State Address, New York Governor Andrew Cuomo offered solutions suited for “a time of severe budget conditions.” Governor Andrew Cuomo, NY Rising: 2013 State of the States (Albany, NY: Office of the Governor, 2013), p.29, accessed February 26, 2013, http://www.governor.ny.gov/sites/default/themes/governor/sos2013/2013SOSBook.pd 18Magali A. Delmas and Maria J. Montes-Sancho, "U.S. State Policies for Renewable Energy: Context and Effectiveness," Energy Policy 39, no. 5 (May 2011); Fredric C. Menz and Stephan Vachon, "The Effectiveness of Different Policy Regimes for Promoting Wind Power: Experiences from the States," Energy Policy 34, no. 14 (2006), doi:10.1016/j.enpol.2004.12.018. 19The United States’ net generation of solar electric power grew about 245%, while overall electricity generation increased 8.5%. (Energy Information Administration, "Electric Power Annual 2011.”)

11

financial incentives resemble federal ones, states operate on a voluntary basis. Thus,

regulation has only come from the so-called “laboratory” of the states. As Ford

School of Public Policy’s Barry Rabe points out, the federal government’s political

“gridlock” has meant that, throughout the last decade of the 20th century and

throughout the 21st, the federal government has been relatively absent in climate

change and RE policymaking.20 In turn, the states have adopted a suite of policy

tools, including various forms of standards, mandates, and incentives.21 By analyzing

the role of state policies on the viability of PV, my assessment of the American

regulatory landscape is complementary to Rabe’s on the U.S.’s decentralized

approach to climate change and RE.

Figure 2: Framework for policy stacking22

20Barry G. Rabe, Statehouse and Greenhouse: The Emerging Politics of American Climate Change Policy, (Washington, D.C.: Brookings Institution Press, 2004). 21Table 1 in the Appendix provides a snapshot of government and utility rules, regulations and policies that promote RE in the U.S. It is from DSIRE, the Database of State Incentives for Renewable Energy and Efficiency, and includes public benefit funds, renewable portfolio standards, net metering, interconnection standard, renewable access, construction and design, and required green power policies. 22Elizabeth Dorris, “Policy Building Blocks: Helping Policymakers Determine Policy Staging for the Development of Distributed PV Markets,” report no. NREL/CP-7A30-54801, accessed January 21, 2013, http://www.nrel.gov/docs/fy12osti/54801.pdf.

12

Net metering is a market preparation policy for distributed generation, which allows

system owners who generate their own electricity to receive full retail credit for the

electricity they do not consume but contribute to the grid. Renewable portfolio

standards require that electricity suppliers purchase a growing amount of RE over

time. They are a promotional market mechanism for renewables, as they deliberately

mandate RE deployment. I hope to prove that net metering and renewable portfolio

standards are crucial to growing and competitive PV markets.

In the pages to come, I hope to orient the reader’s perspective on American

RE policymaking to show that PV’s viability depends upon regulation, not incentives.

Cost-competitive PV markets have emerged in states with regulations that take

advantage of federal incentives and establish stable, attractive investment

environments for project financing. In sum, the U.S.’s decentralized approach to RE

promotion has facilitated PV’s gradual emergence as a cost-competitive source in a

minority of electricity markets. In order for PV to compete on a national scale, best-

practice regulatory measures must be implemented on a broader scale.

III. Chapter Roadmaps

My first chapter is a historical survey expanding on the role of the federal

government in the development of PV technologies and markets in the U.S that I

hope will elucidate the issues facing its regulation. Through a qualitative analysis of

the PV industry, I assess the policy and market changes that propelled PV’s

unprecedented growth. Due to the steep drop in solar panel costs, PV is an

increasingly attractive investment in a minority of states with the right blend of

incentives and regulation. However, non-panel expenses that come with

13

implementation now hold the majority share of PV system price and limit PV’s cost-

competitiveness in the majority of states. The end of Chapter One details these softer

costs, leading into the question: can regulation facilitate PV’s cost competitiveness?

Chapter Two identifies several of the market inefficiencies inhibiting PV’s

cost-competitiveness against conventional electricity. It details the historic role that

regulation played in the development of the modern American electricity apparatus.

With the intention of preventing inefficient markets, regulations were implemented to

serve as substitutes for competition in the electricity industry. Beginning with the

“natural monopoly” treatment given to utilities, which have been considered–

correctly or not– incapable of being subject to competition,23 legislators have

recognized that, left alone, the electricity markets may operate inefficiently,

restricting production, offering poor quality, and charging high prices. Almost a

century later, RE policies are meant to solve the same problems created by the

deployment of renewables. Now that there is least one RE regulation in every state,

the question of whether or not policy can successfully promote renewables,

specifically PV, is pertinent. This chapter lays the foundations for the role of

regulation in addressing market barriers and failures to provide context for net

metering and renewable portfolio standards.

The aim of Chapters Three and Four is to exploit the variation in the diversity

of PV policy regulations. I build upon Rabe’s work on decentralized regulatory

23As will be discussed in Chapter Two, natural monopoly mandates were created for utilities to charge “just and reasonable” prices, refrain from discrimination, and provide reliable service. The movement for performance-based rates proceeded from the idea that utilities needed more impetus to satisfy customer demand and become efficient. For almost a century, state governments have regulated electricity through state public utility commissions that make fundamental decisions on pricing, approval of new facilities and technologies, and environmental considerations.

14

climate and RE policymaking to analyze the state net metering and renewable

portfolio standards that have been adopted in the absence of serious action by the

federal government. These chapters attempt to understand which approaches work

well and why. Through qualitative analyses, along with basic quantitative

descriptions that use statistical information on PV capacity provided by Larry

Sherwood, COO of the Interstate Renewable Energy Council and reports jointly

issued by the Solar Energy Industry Association and Greentech Media, I provide

positive details on the policies and draw normative conclusions on the policy’s role in

PV’s cost-competitiveness, which shapes the attractiveness of investments in PV

capacity. Because states have implemented such diverse mechanisms, a comparison

of individual policies allows for valuable analyses and conclusions.

Lastly, the Conclusion brings together the normative conclusions on best

practices from Chapters Three and Four and expands upon their role in improving the

financials of PV federal implementation of net-metering and RPS. The conclusion

brings together the analysis of the preceding chapters. This thesis builds upon the

work of peer-reviewed journals and articles24 with analyses and from PV industry

analysts, executives, and regulators to create a positive analysis and normative

conclusions. The conclusion finishes with a description of the potential for further

analysis brought on by this thesis.

24By peer reviewed, I mean that the articles and journals are assessed for quality by the following criteria provided by the CUNY Library, such as “The author of the article must submit it to the journal editor who forwards the article to experts in the field. Because the reviewers specialize in the same scholarly area as the author, they are considered the author’s peers (hence “peer review”).” ("Evaluating Information Sources," CUNY Library, accessed March 10, 2013, http://guides.lib.jjay.cuny.edu/content.php?pid=209679.)

15

Due to the limited time period and extent to which RE policies have been

implemented, analysis surrounding its implementation has been relatively brief. As a

result, limited evaluation has taken place and the most effective policy designs and

their direct impacts on RE capacity are not always well understood. Of the dozens of

studies that have been conducted regarding the effectiveness of state leadership on

public policy issues, few have specifically examined the U.S.’s decentralized

approach to encouraging the deployment of PV (refer to section below on

technological information). Additionally, in academic literature, the attention paid to

the American climate change policy usually focuses on the failure of Congress to

place a price on carbon. Less effort has been devoted to federal renewable energy

policy, and significantly less effort has been focused on state carbon pricing and

renewable energy efforts.25 This thesis attempts to fill the void in analysis on the role

of regulation in PV’s cost-competitiveness and market development.

General Background Information on PV

The first modern solar cell was invented at the Bell Telephone Laboratories in 1954.

As shown in Figure 3, the Bell researchers discovered that when silicon is specially

treated to form an electric field (positive on one side and negative on the other) light

energy (in the form of photons) is able to knock the electrons loose from the atoms in

the silicon.

Figure 3. Basic Schematic of a PV Module26 25Andrea Sarzynski, Jeremy Larrieu, and Gireesh Shrimali, "The impact of state financial incentives on market deployment of solar technology," Energy Policy, Vol 46, July (2012), p. 550-557 (Motivated by their belief that existing research on state-level financial incentives “has not kept up with the increasing interest in solar from consumers, utilities, and legislators,”). The dearth in financial incentives analysis pales in comparison to that of academic literature on regulation’s impact on solar markets. 26Gil Knier, "How Do Photovoltaics Work?," NASA Science, 2002, accessed January 12, 2013, http://science.nasa.gov/science-news/science-at-nasa/2002/solarcells/.

16

These electrons can then be captured in the form of electric current if conductors are

attached to the positive and negative sides, forming an electric circuit. Under the

general category of PV panels there are several competing sub-technologies relying

on a range of different semiconductor materials and manufacturing processes, with

varying costs ($/Wp) and solar conversion efficiencies.27 Generally, mentions of

“panels” or “modules” refer to crystalline silicon (si) photovoltaic modules, which

represent about 80% to 90% of the PV market and have efficiencies for converting

sunlight into electricity currently range from 14% to 19%.28 Additionally, there are

several non-panel components to a photovoltaic system, as shown in Figure 4.

Figure 4. Example of Standard Residential Photovoltaic System29

27PV sub-technologies are generally classified into two groups: crystalline and thin-film. As will be elaborated in Chapter 1, crystalline panels are composed of silicon and consist of solar wafers that resemble the original Bell Laboratory’s cell. Thin-film panels. The front-runner materials for thin-film modules include amorphous silicon (a- Si), copper indium diselenide (CIS), cadmium telluride (CdTe), and thin-film polycrystalline. Due to the innovations of First Solar, which will be discussed in Chapter 1, CdTe modules have achieved the highest technical efficiency levels in laboratory cells. 28Greentech Media Research and Association, "Solar Market Insight Report 2012 Q3," SEIA, accessed December 01, 2012, http://www.seia.org/research-resources/solar-market-insight-report-2012-q3. 29"Home Owner Ecosoluation," Ecosolargy, accessed December 05, 2012, http://www.ecosolargy.com/solutions/home-owners.

17

The other non-module costs that make up PV system include racking, wires, switches,

inverters, and labor for installing the system.30 Grid-connected solar PV electricity,

whose markets subdivide into large central-station facilities in unused parcels of land

and distributed applications, or “behind the meter,” located near or at the point of use,

is increasing in sophistication, adoption and efficiency. Although other solar

technologies exist such as solar water heating, concentrating solar power (CSP)

systems,31 this report focuses on solar PV electricity generation.

IV. Review of Existing Literature

Existing literature has not, up to this point, addressed the issues I hope to resolve in

my thesis. Studies on decentralized RE policymaking have yet to analyze the direct

impact of policies on PV, specifically the role of regulations in PV’s viability.

Although I draw heavily on the work of Barry Rabe, a leading scholar on state action 30Stephen Smith and MJ Shiao, "Solar PV Balance of System (BOS) Markets: Technologies, Costs and Leading Companies, 2013-2016," GTM Research, accessed January 11, 2013, http://www.greentechmedia.com/research/report/solar-pv-bos-2013. 31CSP systems produce electricity use mirrors to concentrate direct-beam solar radiance onto collecting receivers filled with liquid, solid, or gas to produce heat that is run through a traditional turbine power generator or Stirling engine, producing electricity.

18

in climate change and RE policy,32 and that of his colleagues Victor, House, and Joy

(2005), Carolyn Fischer and Richard G. Newell (2007), 33 their work generally

focuses on the factors encouraging RE policy adoption, not the effects of the policies

concerning PV. When similar studies examine decentralized policymaking’s

influence of PV, they typically focus on financial incentives, not regulation. For

instance, Gouchoe et al. (2002) and Sarzynski et al. (2012) discuss the role of

financial incentives in driving PV, not regulations.34 Additionally, work on

regulation’s role in solving electricity market inefficiencies has yet to extend to PV,

particularly the non-panel costs of a PV system. Alfred Kahn’s work (1998) on

electricity regulation, which is relied upon in Chapter Two, came before the RE and

PV had come to prominence in the U.S. as legitimate alternatives to conventional

electricity.35 More recently, Gillingham and Sweeney (2010) focus on how

regulations address externalities.36 Their work serves as background for claims that

heretofore have not been made on electricity market inefficiencies’ restricting the

32Rabe, Statehouse and Greenhouse: The Emerging Politics of American Climate Change Policy, 2004; Rabe, "The Aversion to Direct Cost Imposition: Selecting Climate Policy Tools in the United States," Governance, Vol. 23, No. 4 (October, 2010), 583-608. Accessed 11/04/12: http://onlinelibrary.wiley.com/doi/10.1111/j.1468-0491.2010.01499.x/ 33David Victor, Joshua C. House, Sarah Joy, "A Madisonian Approach to Climate Policy," Science, Vol. 309, No. 5742 (September, 2005), p. 1820-1821; Carolyn Fischer and Richard G. Newell, "Environmental and Technology Policies for Climate Mitigation," Discussion Paper Prepared for Resources for the Future (April, 2007). Accessed 01/07/2013: http://www.rff.org/Documents/RFF-DP-04-05-REV.pdf 34S. Gouchoe, V. Everette, and R. Haynes, "Case Studies on the Effectiveness of State Financial Incentives for Renewable Energy," NREL/SR-620-32819. Golden, CO: National Renewable Energy Laboratory (June, 2002). Accessed 10/27/12: http://www.nrel.gov/docs/fy02osti/32819.pdf;Andrea Sarzynski, Jeremy Larrieu, Gireesh Shrimali, "The Impact of State Financial Incentives on Market Deployment of Solar Technology," Energy Policy, Vol. 46 (July, 2012), p. 550-557. Accessed January 09, 2013: http://www.sciencedirect.com/science/article/pii/S0301421512003321. 35Alfred E. Kahn, The Economics of Regulation: Principles and Institutions, vol. 1 (Cambridge: Massachusetts Institute of Technology Press, 1998). 36Kenneth Gillingham and James Sweeney, "Market Failure and the Structure of Externalities," in Boaz Moselle, Jorge Padilla, Richard Schmalensee, Harnessing Renewable Energy in Electric Power Systems: Theory, Practice, Policy, (London: Earthscan, 2010). Accessed 3/10/13: http://www.yale.edu/gillingham/Market%20Failure%20and%20the%20Structure%20of%20Externalities.pdf

19

cost-competitiveness of PV. Existing studies on net metering and RPS differ from my

own assessments in several ways. Studies and reports on net metering and RPS,

perhaps because of their infancy, have been limited in both their scope and analysis.

Studies often focus on single states and are not prescriptive. I also aim to depart from

these existing studies by correlating policy analysis to the components of PV’s

financials like non-hardware costs and placing emphasis on PV’s cost-

competitiveness and market development. As such Chapters Three and Four assess

policy specific in terms of effects on PV economics and markets, examine a variety of

state historical experiences, and offer prescriptions regarding best practice parameters

for the regulations. In sum, this thesis hopes to contribute to the field through its

original suggestion of the interrelationship of these important factors.

20

Chapter One

Solar Photovoltaic Technology’s Topsy-Turvy Road To Development

We are like tenant farmers, chopping down the fence around our house for fuel, when we should be using Nature's inexhaustible sources of energy — sun, wind and tide. I'd put my money on the sun and solar energy. What a source of power! I hope we don't wait till oil and coal run out before we tackle that.

-- Thomas Edison in conversation with Henry Ford and Harvey Firestone (1931)37

I. The Federal Government’s Sporadic Support of Solar

The fundamental concern of the viability of solar electricity is its link to

public policy. This is a given for industry leaders, executives, and thinkers, who point

to government’s nurturing other emerging energy technologies as proof of this

assertion. As a recent white paper issued by First Solar states, “no major energy

technology has achieved the necessary cost reduction and scale without sustained

37James Newton, Uncommon Friends: Life with Thomas Edison, Henry Ford, Harvey Firestone, Alexis Carrel & Charles Lindbergh, (New York: Mariner Books, 1989), 31.

Précis: The federal government has been inconsistently supportive of solar photovoltaic technologies (PV). Federal policies have been at times to the benefit and at other times to the detriment of PV’s technological and market development. This chapter assesses the relationship between the federal government and the American PV industry. It begins with a brief survey of the federal government’s RE policymaking, describing the impact of its erratic support on PV’s viability. The chapter then provides a description of recent developments in PV pricing that have enabled its broader affordability and deployment. It concludes with an examination of the components holding back PV’s cost competitiveness, laying the groundwork for the role of regulation in improving PV’s financials.

21

government support, even well after initial maturation.”38 As one one of the leading

American PV companies, First Solar knows this historical reality all too well. In

2004, after its first small manufacturing line became operational, First Solar “started

looking around for markets that would give us the scale that we needed, that would

drive big volumes, so we could get more efficient,” explains former CEO Mike

Ahearn. Founded in Toledo, Ohio, the company wanted to remain in the United

States, so “we came to Washington and then went to many states in the southwest,”

recalls Ahearn “We said to a couple of American utilities, ‘We will lose money to just

get going,’ because we knew that as we scaled, costs would go down. And we still

could not get any takers… We talked to Arizona and Ohio congressmen. They were

all [unsupportive].” The company did not get any traction until they “decided to go to

Germany.”39 The details of First Solar’s story and the influential American and

German policy parameters, of course, need clarification. The intricacies of both

provide material for much of this chapter and will be assessed in the pages to come,

but a significant question begs to be addressed along the way: Have American

policymakers inhibited the growth of PV electricity generation?

The United States hosted the most pivotal breakthroughs in PV technologies.

Nevertheless, the American PV industry is immature, currently contributing mere

basis points to the overall American energy system.40 On page one of its April 26,

38Received from Alan Bernheimer, Public Relations Director, Americas at First Solar, Inc: Solar Institute, Energy Incentives: The Power Behind the Power, The George Washington University, March 12, 2012, p. 3, accessed November 15, 2012, http://solar.gwu.edu/Research/GW_EnergyIncentives.pdf. 39Story and details are borrowed from Thomas Friedman, Hot, Flat, and Crowded: Why we need a green revolution- and how it can renew America, (New York: Farrar, Straus and Giroux, 2008), 386-91. 40In 2011, of the net generation of 4,125,060 thousand megatthours of electricity, solar thermal and photovoltaic accounted for 1,212 thousand megawatthours. (U.S. Department of Energy, Energy

22

1954 issue, The New York Times proclaimed a new technology had the potential to

mark “the beginning of a new era, leading eventually to the realization of one of

mankind’s most cherished dreams -- the harnessing of the almost limitless energy of

the sun for the uses of civilization.”41 With the development of the quantum theory of

light and solid state physics in the early 20th century, PV technologies advanced

significantly in the United States, culminating in the invention of the first modern

silicon solar cell at the Bell Telephone Laboratories in 1954. In order to leave the

laboratory stage, this technology required funding for the development of and

research into the potential of solar for electricity generation.42 Yet, the federal

government made the strategic decision in the 1950s to support nuclear energy as the

alternative of the future,43 despite warnings from J. Robert Oppenheimer, who served

as Chairman of the Atomic Energy Commission’s General Advisory Committee.44 As

a result, the realization of solar energy’s potential as a serious alternative to nuclear

energy or fossil fuels was stymied. Assessing American energy policy through the

Johnson administration, political scientist Frank Laird concludes, “solar never got

serious consideration as a source that might be a major part of the future U.S. energy

Information Administration, Annual Energy Review 2011, 2012, accessed December 01, 2012, http://www.eia.gov/totalenergy/data/annual/pdf/aer.pdf.) 41Unknown, "Vast Power of the Sun Is Tapped by Battery Using Sand Ingredient," New York Times (New York), April 26, 1954, accessed 10/21/12 on: http://www.nytimes.com/packages/pdf/science/TOPICS_SOLAR_TIMELINE/solar1954.pdf 11/07/12 42Darryl Chapin, one of the three Bell engineers that collaborated to invent the modern silicon solar cell, recognized the need for further funding: “we tried to avoid making too much claim for it because we knew it was in the laboratory stage, and there was much to be done before we could speak of lots of power” (Ken Butti and John Perlin, A Golden Thread: 2500 Years of Solar Architecture and Technology, fwd. Amory Lovins (Palo Alto: Cheshire Book, 1980), 231). 43For an elaboration on the influence of Cold War politics on the pursuit of Nuclear Energy from the Presidencies of Dwight D. Eisenhower to George H.W. Bush, please refer to: George A. Gonzalez, Energy and Empire: The Politics of Nuclear and Solar Power in the United States (Albany: State University of New York Press, 2012). 44Ibid, 32.

23

system and so it lacked the support that such a role might have entailed.”45 As a

percentage of inflation-adjusted federal spending, nuclear received more than 1% of

the federal budget over its first 15 years of development, and oil and gas received half

a percent of the total budget,46 while solar received significantly less than a tenth of a

percent: federal support for terrestrial applications of solar energy was only about

$100,000 a year between 1950 and 1970.47

It took the oil crises of the 1970s for the federal government to provide the

research and development (R&D) funding necessary to begin making solar

technologies economically feasible. Although it never matched the funding for fossil

fuels or nuclear technology budgets, the federal solar R&D budget grew to $484

million in 1979, a 12,100 percent increase in just six years. Of the almost $1.2 billion

(in fiscal 1982 dollars) of federal government expenditures on terrestrial photovoltaic

from 1971-91, about 50% of the funding occurred during the Carter administration.48

But during the comparatively oil-rich administration of Ronald Reagan, solar

incentives lapsed. The potential of these nascent initiatives is underscored by their

successes in countries like Germany, where the very same companies started during

the Carter administration were purchased after they lost financial support in the

United States. These firms have contributed effectively to these country’s burgeoning

45Frank Laird, Solar Energy, Technology Policy, and Institutional Values (New York: Cambridge University Press, 2001), 53. 46From the recommendation of Ben Higgins, head of Government Affairs at REC Solar: Nancy Pfund and Ben Healey, Double Bottom Line Investors, report, September 2011, accessed February 17, 2013, http://www.dblinvestors.com/documents/What-Would-Jefferson-Do-Final-Version.pdf. 47Estimate of The United States, Senate, Select Committee on Small Business, Energy Research and Development and Small Business, by John Teem, vol. 1, 94 Congress 1 Sess (Washington D.C.: Government Printing Office, 1975), p. 169-245. 48Linda Cohen and Roger Noll, The Technology Pork Barrel, (Washington: Brookings Institution, 1991), 326.

24

solar electric industries and the restructuring of their energy systems.49 Through the

history of its involvement with solar energy investment, the federal government has

failed to support its homegrown innovations, limiting the development of its PV

industry.

The federal government is responsible for the American PV market’s paradox

of conceiving but not nurturing its innovations. Since spending on R&D technology is

typically framed as a public good, providing widespread benefits such as the

improved quality of life, the government is depended on as the sponsor of basic

research and development in the United States. As MIT economist Robert Solow

emphasized in his Nobel Prize lecture, “stimulation of investment” is crucial to

innovation, transferring a technology “from the laboratory to factory.”50 Unlike its

support of other energies,51 the federal government has been inconsistently committed

to solving PV’s appropriability problems. The funding that Bell Laboratories needed

to fully develop did not occur until a surge in funding in the 70s, but the promises of

these innovations were dulled when the Reagan administration did not consider the

long-term support that is needed for energy innovation, less it fall vulnerable to

volatility, stop-and-go in funding, and uncertainty. With the lone exception of

President Carter, from President Eisenhower to President George H.W. Bush, the

federal government did not provide PV with the support necessary to bridge the gap

49For more information: Osha Gray Davidson, Clean Break: The Story of Germany's Energy Transformation and What Americans Can Learn from It, (InsideClimate News: Amazon Digital Services, 2012) 50Robert M. Solow, "Prize Lecture," The Official Website of the Nobel Prize, accessed February 02, 2013, http://www.nobelprize.org/nobel_prizes/economics/laureates/1987/solow-lecture.html. 51According to the Congressional Research Service, “For the 63-year period from 1948 through 2010, nearly 12% [of DOE R&D spending] went to renewables, compared with 9% for efficiency, 25%for fossil, and 50% for nuclear.” Fred Sissine, CRS Report for Congress, report no. 7-5700, March 07, 2012, accessed February 17, 2013, http://www.fas.org/sgp/crs/misc/RS22858.pdf.

25

from invention and demonstration to adoption and commercialization. Veterans of the

PV industry refer to the funding cuts of 1980s as the Valley of Death, a perhaps

appropriate comparison of the political impasse that was the lack of support to a

spectacular, murderous chasm. Solar advocates were not wrong about what it would

take for their industry to become increasingly cost-competitive. Rather, as Bella

Energy’s Andrew McKenna put it, “we overestimated the political support to

facilitate [it].”52

Germany’s story of political support here offers a useful point of contrast. In

the latter decades of the 20th century, Germany adopted comprehensive solar-

supportive policies that allowed its PV market to mature and scale. Most notable

among these is the German feed-in-tariff (FIT). It requires utility companies to buy

electricity from renewable energy operators at a fixed rate that is guaranteed for 20

years, thereby providing entrepreneurs and lenders with a stable investment

environment. Germany’s FIT put its own spin on American policy: Section 210 of the

Public Utility Regulatory Policies Act of 1978, which authorized utilities to buy

power output from competitive nonutility generators.53 The FIT purchases electricity

from renewable generators at higher fixed rates and then subsidizes those rates by

spreading them across their national electricity market so that the added costs blend

into the mean price of electricity. Such policies facilitated industry growth rates that

averaged 21% per annum between 1982 and 1997,54 providing an outlet for otherwise

52Interview with Andrew McKenna February 22nd, 2013. 53As will be described below, this measure did not stimulate distributed energy production until FERC mandated for electricity market’s restructuring in 1997. 54Tim Jackson and Mark Oliver, "The Viability of Solar Photovoltaics," Energy Policy 28, no. 14 (November 2000): pg. #, doi:10.1016/S0301-4215(00)00085-9.

26

uncompetitive PV energy to be fed into the grid and an opportunity for system owners

to make a profit. Surveying renewable energy (RE) literature from this time, it is clear

that the immense growth in renewable’s share of German electricity consumption,

14% in 2007, was unexpected. As a result of their unexpectedly high rate of RE

deployment, Germany had to establish more aggressive mandates than the ones they

agreed to as part of the European Union, whose target had been to reach 12%

renewable electricity by 2010.55 Germany has led the charge in PV’s international

scaling, significantly influencing the steep decline in the average global price per

Watt of solar panels from $22 in 1980 to under $3 in 2010.56 While the U.S. has yet

to solve many of PV’s scaling and maturation issues, Germany demonstrates that it

has built upon under-appreciated American political and technological developments

to bolster its own solar industry.

German policymakers, however, benefit from a more streamlined process of

regulating RE. In the United States, the federal government and the fifty states share

the responsibilities for government functions in policymaking, administration, and

finance. The lack of precise intergovernmental dividing lines has drawn scholarly

attention towards the expanding and contracting role of the federal government in the

U.S. economy and society (and vice-as-versa with the states).57 States have been

55"European Renewable Energy Council," Renewable Energy Policy Review: Germany, December 27, 2012, pg. #, accessed January 17, 2013, http://www.erec.org/fileadmin/erec_docs/Projcet_Documents/RES2020/GERMANY_RES_Policy_Review_09_Final.pdf 56"2008 Solar Technologies Market Report," National Renewable Energy Laboratory, January 2008, p. 131, accessed November 29, 2013, http://www.nrel.gov/analysis/pdfs/46025.pdf. 57Other scholarly examinations include: Craig Volden, Michael M. Ting, and Daniel P. Carpenter, "A Formal Model of Learning and Policy Diffusion," American Political Science Review 102, no. 03 (2008), doi:10.1017/S0003055408080271; Paul E. Peterson, The Price of Federalism (Washington, D.C.: Brookings Institution, 1995).

27

particularly proactive in making efforts to reduce GHGs, adopting a variety of

policies in recent years. In Statehouse and Greenhouse (2004), Rabe details the

process through which policy entrepreneurs framed various climate policy tools as

advantageous to state economic development while also reducing GHGs. “For

renewable energy, mandates to steadily increase their use on an in-state basis have

commonly been presented as a commitment to new technology that would tap into

“home-grown” energy sources,” Rabe retells. “Under this framing, states would no

longer have to import fuel sources such as coal, natural gas or uranium and instead

could foster ‘high-paying, high-technology’ jobs to take advantage of these more

localized renewable sources.”58 In these cases, states do not view climate change in

terms of its impending environmental challenges but identify it as a problem with

solutions that offer promising economic opportunities.

Much of the impetus for state policy action can be linked to the specific

developments at the federal level. In 1997, under the auspices of the Byrd-Hagel

Resolution, Congress refused to sign the Kyoto Protocol. The resolution forbade the

United States from entering into any global warming treaty that leaves out developing

nations and marked the beginning of a trend of inaction on climate policies. 59 In the

same year, the federal government (through the Federal Energy Regulatory

Commission (FERC)) implemented its only significant regulation to stimulate RE

deployment, FERC 888 and FERC 889. These orders sought to further restructure, or

58Barry G. Rabe, "The Aversion to Direct Cost-Imposition: Selecting Climate Policy Tools in the United States," Governance: An International Journal of Policy, Administrations, and Institutions, Vol. 23, No. 4, (October 2010), p. 589. 59Senator Robert Byrd and Senator Chuck Hagel, “Senate Resolution 98 of the 105th Congress,” Accessed on 11/02/12 on http://www.nationalcenter.org/KyotoSenate.html

28

“deregulate,” electricity markets to allow for more competition in state electricity

provision. While FERC 888 issued guidelines for the implementation of Independent

System Owners to oversee utility-owned transmission lines and ensure no

discrimination would occur against competitive suppliers, FERC 889 created

Regional Transmission Organizations, an extension of sorts of ISOs, to monitor grid

functioning, non-discrimination, security, and other aspects of the electrical

distribution system. The natural monopoly structure of utilities--- controlling

electricity transmission, generation, and distribution assets--- inhibits distributed

electricity generation in the United States, as will be elaborated in Chapter Two.

These orders were implemented to provide oversight and ensure equal access to

transmission services between utilities, competitive suppliers, and prosumers, who

can be defined as distributed generators that produce their own on-site electricity and

consume electricity from the grid when necessary. In sum, along with its widely

publicized rejection of GHG emission restrictions, the federal government spurred the

states to lead on climate change mitigation and RE development through FERC

regulatory measures.60

Since the 1997 FERC measures, state governments have taken a leadership

role on issues with global significance.61 Solar supportive states share the global

priority of increasing PV’s affordability and viability. Figure 5 demonstrates the

spread of state renewable portfolio standards since 1997.

60This topic will be expanded on in Chapter Two. 61William D. Nordhaus, "To Tax or Not to Tax: Alternative Approaches to Slowing Global Warming," Review of Environmental Economics and Policy 26 (2007): 26, 27-28. (State or local governments are thought to regulate small-scale problems (e.g. contaminated properties), the federal government should regulate where interstate spillovers are problematic (e.g. acid rain), and international regimes should be established to deal with global problems (e.g. climate change)).

29

Figure 5. Number of State Renewable Portfolio Standards Policies62

As Figure 1 shows, in the absence of federal leadership, the number of state RPS

policies has risen sharply. States have adopted regulatory measures like RPS and net-

metering in hopes of encouraging renewable energy generation, reducing demand on

an increasingly strained electric grid, facilitating energy self-reliance, reducing GHG

emissions, or promoting in-state economic development. It has been posited by states

as a promising economic opportunity. As Pennsylvania Governor Edward Rendell

said in a 2007 address to his states’ General Assembly, which had endorsed a range of

renewable energy policy initiatives: “I believe renewable energy will dominate the

economy of the next two decades the way information technology and life sciences

have dominated the economy of the last two decades. For too long, Pennsylvania has

been held back because so much of our employment was in industries that were

shrinking. But with renewable energy, we have a chance to be a leader in one of the

62"DSIRE: : Quantitative RPS Data Project Database of Energy Efficiency, Renewable Energy Solar Incentives, Rebates, Programs, Policy," DSIRE USA, accessed April 12, 2013, http://www.dsireusa.org/rpsdata/.

30

fastest-growing segments of this new economy.”63 Emerging from statehouses, policy

entrepreneurs, and pundits around the nation, 64 65 variations on this rhetoric and the

accompanying financial forecasts have compelled states to adopt alternative energy

policies. These statehouses promoted PV policies as a vehicle for economic growth

and the prospect of gaining a “first mover” advantage, by fostering PV innovation and

industries in their jurisdictions.66 Given a lack of federal direction, the states have

taken a more proactive role in shaping their individual energy systems, acting with

virtual free rein in selecting policy tools to improve the viability of their PV markets.

The federal component of the U.S.’ federalist power sharing arrangement in

RE primarily consists of financial incentives. Under the Clinton Administration, the

federal government began its trend of indirectly addressing climate change by

incentivizing RE technologies: from the 15% tax production credit introduced under

President Clinton, to President Bush’s signing the Energy Policy Act of 2005, which

included, amongst other things, an expansion of the federal tax credit to 30%, and

President Obama’s 2009 American Reinvestment and Recovery Act (ARRA) in

which $16.8 billion has been allocated to a wide variety of efficient and renewable

energies. Each of these Presidents has in turn declared renewable energies necessary

investments in the future. Barack Obama, for example, has made a point to mention

63Edward Rendell, “Address to the Special Session of the Pennsylvania General Assembly,” (September 17, 2007) (from Rabe, Ibid). 64This paper is not concerned with the policy development process. For further information on the development process: Barry G. Rabe, Statehouse and Greenhouse: The Emerging Politics of American Climate Change Policy, (Washington, D.C.: Brookings Institution Press, 2004). 65Nor is it concerned with state policy adoption theory: Daniel Judah. Elazar, American Federalism: A View from the States (New York: Harper & Row, 1972); F. Berry & W. Berry, “State lottery adoptions as policy innovations: An event history analysis,” American Political Science Review, Vol. 84, No. 2 (1990), 395–415. 66Maryann Feldman and Roger Martin, "Constructing Jurisdictional Advantage," Research Policy 34, no. 8 (2005), doi:10.1016/j.respol.2005.03.015.

31

this imperative in several of his State of the Union speeches.67 However, these

incentive programs have been insufficient to match the administrations’ very own

promises of the role renewables would play in restructuring the American energy

system to address modern realities like climate change.

The vast majority of federal PV incentive programs suffer from the

unpredictability that comes from the sunset dates and volumetric limits that are often

imposed on them from their beginning. For instance, the federal production tax credit

has been extended seven times since it was first created.68 Figure 2 shows how more

than 70 percent of federal clean technology programs will expire by the end of 2014.

Figure 6. Federal Clean Technology Policy Support is Falling off a Cliff69

Of this policy support from 2009-2014, renewable electricity technologies like wind

67For instance: “We need to encourage American innovation,” Obama told Congress in his 2010 State of the Union Address. “And no area’s more ripe for such innovation than energy.” ("Remarks by the President in State of the Union Address," The White House, accessed March 02, 2013, http://www.whitehouse.gov/the-press-office/remarks-president-state-union-address..) 68Jesse Jenkins, Mark Muro, Ted Nordhaus, Michael Shellenberger, Letha Tawney and Alex Trembath, "Beyond Boom and Bust: Putting Clean Tech On a Path To Subsidy Independence," Brookings Institute (April 2012). Accessed 2/21/13: http://www.brookings.edu/research/papers/2012/04/18-clean-investments-muro) 69Clean Technologies produce energy without the environmental effects of fossil fuels. (Ibid)

32

and solar will have received 32.1%, or 48.4 billion dollars.70 When President Obama

signed ARRA, which contributed $51 billion of the cumulative $150 billion federally

allocated between 2009 and 2014 to clean technologies, he said he hoped that the

clean-technology-related portions of the stimulus would inspire Americans the same

way that President Kennedy's goal to put a man on the moon did in the 1960s.71 At

the time, investors and analysts believed the ARRA stimulus was the start of a more

comprehensive energy policy, marking a more consistent commitment to RE.72 Yet,

federal government’s relationship with renewable energies remains blemished by

inconsistent policy and unrealized market potential. In part, the subsidies exist as a

mere stopgap for more systematic problems brought on by international competition.

As a report recently issued by the Brookings Institute describes: “[RE] markets in

America have lurched from boom to bust for decades, and the root cause remains the

same: the higher costs and risks of emerging US products relative to either incumbent

fossil energy technologies or lower-cost international competitors, which make US

clean tech sectors dependent on subsidy and policy support.”73 Many in the PV

community predicted ARRA as a mark of the beginning of a sustained federal effort

to promote RE, but few could have imagined the budget showdowns occupying

Congress’ time. Now that the federal government has gone over the “fiscal cliff,” the

same predictors are providing more pessimistic forecasts.

70Ibid, 18. 71Martin LaMonica, "Obama Signs Stimulus Plan, Touts Clean Energy," CNET News, February 17, 2009, accessed January 17, 2013, http://news.cnet.com/8301-11128_3-10165605-54.html. ("I hope this investment will ignite our imagination once more in science, medicine, energy and make our economy stronger, our nation more secure, and our planet safer for our children," President Obama said before signing the bill.) 72Ibid. 73Jenkins et al., "Beyond Boom and Bust.”

33

II. The Current Status of the American PV Industry

Despite drastically diminishing federal financial support, America’s PV

market will not be cast back into the Valley of Death. The unprecedented growth

experienced over the last few years by a handful of states, where an effective blend of

incentives and regulations makes PV cost-competitive, offers a hopeful look for PV’s

viability. From a consumer perspective, PV has been increasingly attractive as an

investment over the last decade, driving down prices and injecting new choices into

the marketplace dominated by century old technologies. The United States’ net

generation of solar electric power grew 245% over the first decade of the 21st century,

while overall generation increased 8.5%.74 Figure 7 illustrates this marked increase.

Figure 7. Data Sample Compared to Total U.S. Grid-Connected PV Capacity75

74"U.S. Energy Information Administration - EIA - Independent Statistics and Analysis," Electric Power Annual 2011, accessed October 10, 2012, http://www.eia.gov/electricity/annual/. 75Galen L. Barbose, Naïm Darghouth, Ryan Wiser, Tracking the Sun V An Historical Summary of the Installed Price of Photovoltaics in the United States from 1998 to 2011, (Berkeley: Lawrence Berkeley National Laboratory, 2012), 9 using Larry Sherwood, U.S. Solar Market Trends 2011, (Latham, NY: Interstate Renewable Energy Council Inc., 2012).

34

Inversely, from 1998-2009, wholesale panel, or module, prices dropped by $1.9/W

(40%), while from 1998-2007, implied non-panel costs, including installation labor,

power electronics, permitting and other regulatory costs, and installer profit, fell by

$2.5/W (40%).76 In 2011, installed prices continued to precipitously fall. Over the

course of 2011, the median installed price among projects was $6.1/W for systems

≤10 kW in size, $5.6/W for systems 10-100 kW, and $4.9/W for systems >100 kW.

According to researchers at the Lawrence Berkeley National Laboratory, “this

represent a year over-year decline of $0.7/W (11%) for systems ≤10 kW 10 kW,

$0.9/W (14%) for systems 10-100 kW, and $0.8/W (14%) for systems >100 kW.” As

shown in Figure 8, these price reductions continues a decade long trend of drastically

decreasing system prices in the residential and commercial PV segments.

Figure 8. Installed Price of Residential & Commercial PV over Time77

These trends are also apparent in the utility PV sector,78 in which the Berkeley Lab

76Ibid, Barbose et al., Tracking the Sun. 77Ibid, Barbose et al., Tracking the Sun, p. 12. 78For the sake of terminology clarification: residential PV refers to systems installed at residential customer sites, regardless of size; commercial PV, unless otherwise indicated, includes rooftop systems of any size and ground-mounted systems up to 2 MW in size installed at non- residential

35

approximates “the capacity-weighted average installed price declined from $6.2/W

for projects installed during 2004-2008, to $3.9/W for projects installed during 2009-

2010, and to $3.4/W for projects installed in 2011.”79 The inverse relationship

between the solar industry’s growth and solar system costs is due to the fact that

unlike traditional energy-production technologies that have ongoing consumables

costs, nearly all of the costs for PV systems must be paid at the time of installation.

The nature of the costs involved in adopting solar energy technology positions

it to benefit greatly from government support. Since a solar panel system is almost all

up-front costs and requires very little operations and management expenses after

installation, reducing initial capital costs is crucial to reducing the cost of solar

electricity. As shown in Figure 9, with financial incentives and regulatory measures,

PV system payback times can be relatively short and provide significant cumulative

savings.

Figure 9: Case Studies of Residential Solar Power in Five U.S. cities80

customer sites, regardless of whether the host customer is a for-profit, non-profit, or public-sector entity, and utility-scale PV refers to ground- mounted systems larger than 2 MW.78 Regardless of the sector, PV is an increasingly attractive investment. 79Ibid, Barbose et al., Tracking the Sun, p 1. 80Yuliya Chernova, "The Economics of Installing Solar: Figuring out Whether You save Money Depends on a Lot of Factors—especially Where You Live," Wall Street Journal, September 17, 2012, accessed September 18, 2012, online.wsj.com/article/SB10000872396390444506004577615662289766558.html.

36

Additionally, third party financing offers customers the benefits of a PV

system without the upfront cost, allowing residential and commercial users the ability

to pay a monthly amount for their system rather than an overwhelming upfront cost.

81 This arrangement means that as long as this amount is less than their typical

monthly utility bills, it is in the customer’s best interest to put panels on their roof.

PV’s increasing affordability can be traced to specific developments in solar

panel pricing over the last few years. From 2004 to the third market quarter of 2008,

the price of PV modules remained relatively unchanged at $3.50-$4.00/W. The flat

panel prices were due to two factors. Firstly, German, and then Spanish, tariff

81“A host pays to the third-party financier either a series of payments via a lease ($/month) or PPA payments linked to the system's performance ($/kWh), usually based on a 10– 25 year contract. Effectively, the lease/PPA is a loan agreement between the customer and the third-party financier.” Bloomberg New Energy Finance, "Re-imagining U.S. Solar Financing," National Renewable Energy Laboratory, June 2012, accessed December 04, 2012, https://financere.nrel.gov/finance/content/re-imagining-us-solar-financing.

37

incentives allowed project developers to buy the technology at a standardized price.

Secondly, a worldwide polysilicon shortage constrained effective pricing competition

in the production of the wafers that comprise solar cells. With a global demand

surging and unchanging prices, the 18 largest quoted solar companies followed by

Bloomberg made average operating margins of 14.6%-16.3% from 2005 to 2008.82

As a result, manufacturers and polysilicon companies expanded to meet the demand.

When the global financial crisis hit, however, governments downscaled their

commitments to RE, despite a fixed level of demand. While the availability of

polysilicon increased at least 32%, which is enough to make 8.5 GW of modules,

demand grew only about 1 GW, reaching 7.7 GW in 2009. With a glut of PV

production potential, wafer and module makers suddenly needed to compete on price,

giving up their margins. Panel prices were driven down from a global average of

$4.00/W in 2008 to $2.00 in 2009 (see Figure 10).

Figure 10. The Steady Fall of Solar Panel Prices83

82Morgan Bazilian, Ijeoma Onyeji, Michael Liebreich, Ian MacGill, Jennifer Chase, Jigar Shah, Dolf Gielen, Doug Arent, Doug Landfear, and Shi Zhengrong, "Re-considering the Economics of Photovoltaic Power," Bloomberg New Energy Finance (2012), 3. 83This graph was featured in a variety of presentations by Tom Dinwoodie, CTO and founder of SunPower and Dan Shugar, former president of SunPower and current CEO of Solaria, and Adam Browning, the executive director of the Vote Solar. (Zachary Shahan, "Solar Power Graphs to Make You Smile," CleanTechnica, June 06, 2012, accessed January 13, 2013, http://cleantechnica.com/2011/06/10/solar-power-graphs-to-make-you-smile)

38

The affordability of solar panels can be linked to improvements in the manufacturing

process. Bloomberg News Energy Finance has noted that “The ability of

manufacturers to drop their prices by 50%, and still make a positive operating margin,

was due to the reductions in costs achieved over the previous four years,”84

Companies have made significant advancements in wafer, cell, and module

manufacturing processes, leading to cost evolutions in panel manufacturing. The

adoption of these important improvements by Chinese companies in particular has

created devastating competition for American companies.

The most infamous effect of Chinese companies’ success can be seen in the

story of Solyndra, a California-based solar-panel manufacturing company that went

bankrupt in August 2011. Solyndra, whose design avoided the use of silicon, could 84Bazilian et al., "Re-considering the Economics of Photovoltaic Power," 3.

39

not keep up with the cost decreases in polysilicon panels. Solyndra’s story is perhaps

most effective as a demonstration of the federal government’s inadequacy at

appropriately allocating funds. As a part of ARRA, the Department of Energy gave

Solyndra $528 in federal loan guarantees. Unfortunately, this support came just as

silicon’s glut was about to reshape the manufacturing market. The skepticism

surrounding Solyndra’s failure, which rightfully questions the federal government’s

approach to renewable energy,85 overshadows a significant insight it revealed about

the solar industry. Solyndra’s bankruptcy was caused by the maturation of the

polysilicon solar panel market. With a few exceptions, like First Solar, which also

does not use silicon as its semiconductor but unlike Solyndra had achieved scale,86

American upstream manufacturers cannot keep up with their Chinese rivals’ cost-

innovation. In order to remedy such companies’ woes, the U.S. Commerce

Department instituted tariffs of twenty-four to thirty-six percent on solar panels

imported from China. These tariffs are a punishment for “dumping” solar panels on

the United States market for less than it cost to manufacture and ship them,87

attempting to compensate for the supposedly unfair advantages the Chinese have

gained from their manufacturing and subsidy policies. These measures are intended to

address the market failure of Chinese manufacturer’s learning from the advancements