Q1 FY 2021-22 JUNE 2021 - Punjab National Bank

49

Follow our Official Page ‘pnbindia’ FINANCIAL RESULTS Q1 FY 2021-22 JUNE 2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Q1 FY 2021-22 JUNE 2021 - Punjab National Bank

Follow our Official Page ‘pnbindia’

FINANCIAL RESULTS

Q1 FY 2021-22

JUNE 2021

Page I

Content

Key Highlights1

Business Performance2

Financial Performance3

Asset Quality4

Share Holding & Capital5

Network, Digitalization & FI6

Group Business & RRBs7

3-4

Slide No

33-35

36-43

44-45

17-24

25-32

5-16

2

Awards & Way Forward8 46-47

Page I

Core Strengths

Improving Operating EfficiencyAcross Key Financial & Productivity Metrics

Strong Distribution NetworkPAN India Presence

Total Delivery Channels: 3685110641 Domestic & 2 International

Branches, 13690 ATMs & 12518 BCs

Synergy realization through rationalization of Branches and ATM

Rationalization of 503 Branches &388 ATMs

Focus on Digitalization and Expanding Digital Footprints

PNB One Mobile App : ‘One for All’‘All for One’

Strong and Granular Low Cost Deposit Base

Domestic CASA Ratio: 45.15%

3

Adequately CapitalizedCRAR % : 15.19%

126 Years of BankingExperience & Resilience

Technology Driven Credit UnderwritingPNB LenS (Lending Solution) –

for Uniform and Efficient Credit Underwriting

Page I

Key Financial Highlights -June’21

2.73%Global NIM %

15.19%

CRAR

45.15%

Domestic CASA Share8.3% YoY Gr

Savings Deposit

15.5% YoY GrOperating Profit

91.2%

43.64%Cost-Income Ratio

Net Profit

4

Net Interest Income6.6% YoY Gr

Retail Term Deposit

10.7% YoY Gr

₹ 8270 Crore

Total Recovery(Incl Up-gradation)

(Retail TD + CASA) Share

53.9%

RAM Share to domestic Advances

232.1 % YoY Gr

Page I

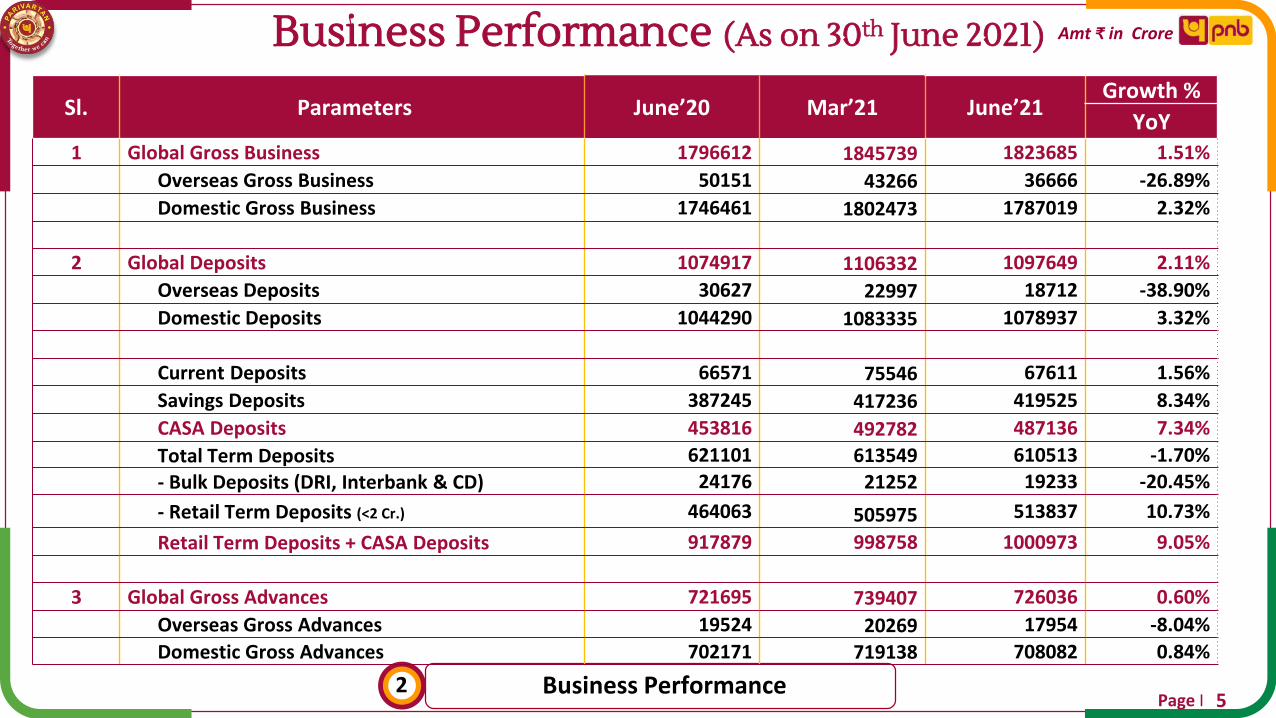

Business Performance (As on 30th June 2021)

Business Performance2

Sl. Parameters June’20 Mar’21 June’21Growth %

YoY1 Global Gross Business 1796612 1845739 1823685 1.51%

Overseas Gross Business 50151 43266 36666 -26.89%

Domestic Gross Business 1746461 1802473 1787019 2.32%

2 Global Deposits 1074917 1106332 1097649 2.11%

Overseas Deposits 30627 22997 18712 -38.90%

Domestic Deposits 1044290 1083335 1078937 3.32%

Current Deposits 66571 75546 67611 1.56%

Savings Deposits 387245 417236 419525 8.34%

CASA Deposits 453816 492782 487136 7.34%

Total Term Deposits 621101 613549 610513 -1.70%

- Bulk Deposits (DRI, Interbank & CD) 24176 21252 19233 -20.45%

- Retail Term Deposits (<2 Cr.) 464063 505975 513837 10.73%

Retail Term Deposits + CASA Deposits 917879 998758 1000973 9.05%

3 Global Gross Advances 721695 739407 726036 0.60%

Overseas Gross Advances 19524 20269 17954 -8.04%

Domestic Gross Advances 702171 719138 708082 0.84%

5

Amt ₹ in Crore

Page I

CASA Performance

Business Performance26

Amt ₹ in Crore

Domestic CASA Share %

66571 67611

Jun'20 June'21

Current Deposits

1.6%

387245 419525

Jun'20 June'21

Savings Deposits

8.3%

6.37% 6.26%

37.08% 38.89%

Jun'20 June'21

Current Deposits % Savings Deposits %

43.45% 45.15%

85.4%

91.2%

Jun'20 Jun'21

(Retail TD < Rs. 2 Cr + CASA) Share %

Page I

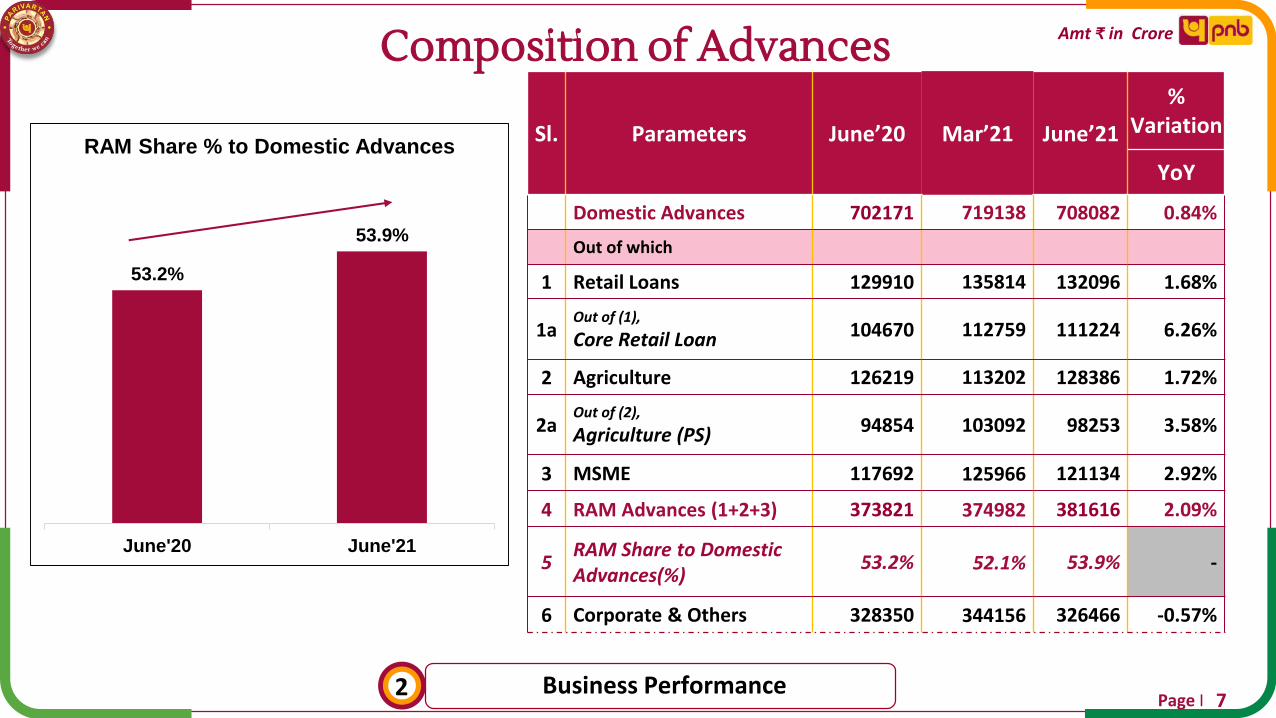

Composition of Advances

Business Performance7

2

Amt ₹ in Crore

Sl. Parameters June’20 Mar’21 June’21

% Variation

YoY

Domestic Advances 702171 719138 708082 0.84%

Out of which

1 Retail Loans 129910 135814 132096 1.68%

1aOut of (1),

Core Retail Loan 104670 112759 111224 6.26%

2 Agriculture 126219 113202 128386 1.72%

2aOut of (2),

Agriculture (PS) 94854 103092 98253 3.58%

3 MSME 117692 125966 121134 2.92%

4 RAM Advances (1+2+3) 373821 374982 381616 2.09%

5RAM Share to Domestic Advances(%)

53.2% 52.1% 53.9% -

6 Corporate & Others 328350 344156 326466 -0.57%

53.2%

53.9%

June'20 June'21

RAM Share % to Domestic Advances

Page I

Composition of Core Retail Advances

Business Performance8

2

Amt ₹ in Crore

Rating profile of Retail Advances

Risk Profiling based on Cibil Scores.

* “-1” Denotes No Credit History.

49.8% 50.9%

10.2% 10.4%

21.2% 19.8%

18.8% 18.9%

June'20 June'21

Abv 725 701-725 upto 700 -1

Above700

(60.0%)

Above700

(61.3%)

8522

10016

June'20 June'21

Vehicle/Car Loan

17.5%7904

10308

June'20 June'21

Personal Loan

30.4%

66761 70848

June'20 June'21

Housing Loan

6.1%104670 111224

June'20 June'21

Core Retail Loan

6.3%

Page I

Priority Sector Achievement

Business Performance2

Sl. ParametersMandated

TargetsJune’20 Mar’21* June’21

ANBC 672161 682197 674350

1 Priority Sector 270558 298140 283935

% to ANBC 40% 40.25% 41.34% 42.10%

2Agriculture - PS(Incl RIDF, IBPC & PSLC)

118527 132185 120658

% to ANBC 18% 17.63% 18.20% 17.89%

3 Small and Marginal Farmers 56943 57392 61900

% to ANBC 9% 8.47% 8.38% 9.17%

4 Weaker Section 73981 82086 85050

% to ANBC 11% 11.01% 11.36% 12.61%

5 Micro Enterprises (PS) 53545 56136 53501

% to ANBC 7.5% 7.97% 7.98% 7.93%

9

Amt ₹ in Crore

*Achievement is on absolute basis;

% to ANBC is on Quarterly average basis.

Page I

MSME Portfolio Mix

Business Performance210

Amt ₹ in Crore

Mudra Loans JUNE’20 JUNE’21

Amount Sanctioned 2362 2179

Amount Disbursed 1283 2046

Performance under PMMY

Upto 30.06.2021 No of Loans Sanctioned - 174460Total Amount Sanctioned - Rs 174 Crore

45.0% 44.3% 44.2%

43.0%36.5% 36.6%

12.0%19.2% 19.2%

JUNE'20 MAR'21 JUNE'21

Segment Mix

Micro Small Medium

Performance under GECL Facility

GECLAs on

June’21

Amount Sanctioned 13512

Amount Disbursed 12008

Page I

External Rating (Standard FB) Portfolio & Advances on Benchmark Rates

Business Performance2

Portfolio > Rs. 100 Crore

Sl Rating GradeJune’21

Amt. % Share

1 AAA 85399 44.0%

2 AA 39500 20.3%

3 A 28687 14.8%

4 BBB 18233 9.4%

Total BBB & Above 171819 88.5%

5 BB 6064 3.1%

6 B 3599 1.9%

7 C 87 0.0%

8 D 7243 3.7%

Total BB & Below 16993 8.7%

9 Unrated 5476 2.8%

Total 194287 100.0%

11

Amt ₹ in Crore

Advances Mix of Benchmark rate

12.3% 10.9% 11.0%

19.3%

10.7% 10.7%

0.4%

0.2% 0.20%

60.0%

50.4% 48.6%

6.0%

14.3% 14.9%

2.0%

13.6% 14.6%

June'20 Mar'21 June'21

Base Rate Fixed BPLR

MCLR RLLR FC & Others

Page I

Diversified Industry Portfolio & Key Sectors

Business Performance2

Sl. Diversified Industry Portfolio(Excl. TWO)

June’20 Mar’21 June’21

O/S O/S O/S% to Total

Industry Adv.1 Infrastructure 89659 103329 99782 45.8%

-Energy 43709 40296 40752 18.7%-Tele-Communication 17555 17774 17540 8.1%-Roads & Ports 23143 34863 35550 16.3%-Other Infra 5252 10396 5940 2.7%

2 Basic Metal & Metal Products 34146 23402 21057 9.7%-Iron & Steel 31539 20386 18059 8.3%

3 Textiles 13199 13592 12817 5.9%4 Food Processing 11895 18086 19166 8.8%5 Chemical & Chemical Products 8079 10806 9009 4.1%6 Other Industries 48336 53179 55840 25.7%

Total 205314 222394 217671 100.0%

12

Amt ₹ in Crore

Sl. Key Sectors June’20 Mar’21 June’21Growth%

YoY1 Capital Market 2194 987 803 -63.4%2 Commercial Real Estate 19748 19681 18338 -7.13%3 NBFC 81165 87538 83601 3.0%4 Aviation 4333 6353 6177 42.6%5 Tourism, Hotel & Restaurant 1501 1690 1671 11.3%

Page I

NBFC & Energy Sector

Business Performance213

Energy Sector

Amt ₹ in Crore

O/s (Funded) as on30-06-2021 : ₹ 83601 Cr

45968, 55.0%22040

26.4%

75489.0%

9911.2% 7054

8.4%

External Rating wise Portfolio

AAA AA A BBB BB & below

NBFC SectorO/s (Funded) as on

30-06-2021 : ₹ 40752 Cr

23568

(28.2%)

60033

(71.8%)

Pvt Sector

Public Sector

33370

(39.9%)

50231

(60.1%)

HFC Others

18933

(46.5%)

21818

(53.5%)

Pvt Sector

Public Sector

21427, 61.3%

1062630.4%

682, 2.0%

21916.3%

External Rating wise Std. Portfolio

A & Above BBB,BB & B C & D Unrated

External Rating Std. Portfolio30-06-2021 : ₹ 34926 Cr

Page I

One Time Restructuring of Advances

Business Performance214

As per RBI's guidelines dated Aug 6, 2020 Amt ₹ in Crore

Sl.Loan and aggregate exposure

category

Restructuring Implemented Provisions Made

No. of accounts Amount involved % of Provision Amt

1 Personal loans 5990 757 10% 76

2 Other Exposures 324 4931 10% 493

3 Total (1+2) 6314 5688 10% 569

4 MSME loans 13955 1099 5% 55

Grand Total (3+4) 20269 6787 - 624

As per RBI's guidelines dated May 5, 2021

Sl.Loan and aggregate exposure

category

Restructuring Implemented Provisions Made

No. of accounts Amount involved % of Provision Amt

1 Individual Borrowers 56523 3396 10% 340

2 Small Business 1530 320 10% 32

3 Total (1+2) 58053 3716 10% 372

4 MSME loans 83852 2886 10% 288

Grand Total (3+4) 141905 6602 10% 660

*Other Exposures includes corporate loans >Rs. 25 Crore as per RBI guidelines.

Page I

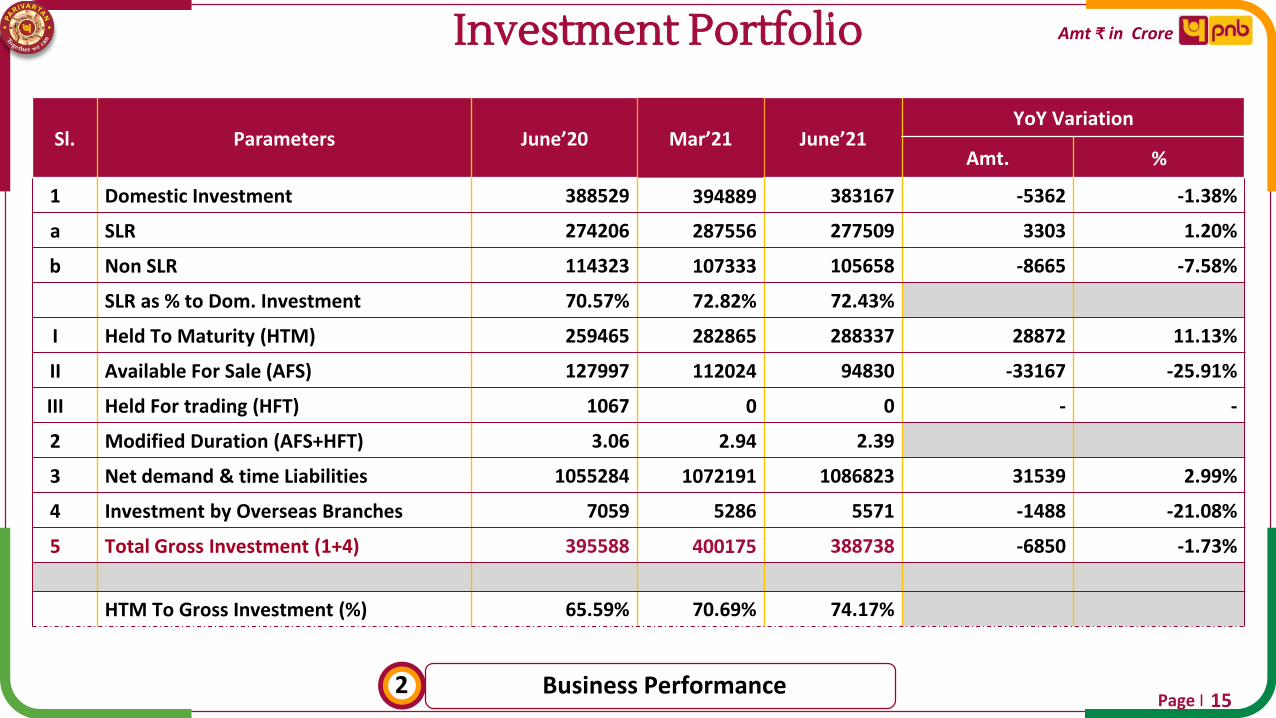

Investment Portfolio

Business Performance215

Sl. Parameters June’20 Mar’21 June’21YoY Variation

Amt. %

1 Domestic Investment 388529 394889 383167 -5362 -1.38%

a SLR 274206 287556 277509 3303 1.20%

b Non SLR 114323 107333 105658 -8665 -7.58%

SLR as % to Dom. Investment 70.57% 72.82% 72.43%

I Held To Maturity (HTM) 259465 282865 288337 28872 11.13%

II Available For Sale (AFS) 127997 112024 94830 -33167 -25.91%

III Held For trading (HFT) 1067 0 0 - -

2 Modified Duration (AFS+HFT) 3.06 2.94 2.39

3 Net demand & time Liabilities 1055284 1072191 1086823 31539 2.99%

4 Investment by Overseas Branches 7059 5286 5571 -1488 -21.08%

5 Total Gross Investment (1+4) 395588 400175 388738 -6850 -1.73%

HTM To Gross Investment (%) 65.59% 70.69% 74.17%

Amt ₹ in Crore

Page I

Non SLR Investment

Business Performance216

Sl. ParametersJune’20 Mar’21 June’21 Y-o-Y Variation

O/S % Share O/S % Share O/S % Share Amt Gr. %

1 PSU Bonds 20164 17.6% 21055 19.6% 20666 19.6% 502 2.49%

2Corporate and Other Bonds & Debentures

12331 10.8% 12407 11.5% 11908 11.3% -423 -3.43%

3 Special Govt. Sec excl. Recap Bonds 1394 1.2% 1253 1.2% 1253 1.2% -141 -10.11%

4 CG Recap. Bond 55274 48.4% 55274 51.5% 55274 52.3% 0 0.00%

5 Share of PSU/Corporate/Others 8935 7.8% 8718 8.1% 8459 8.0% -476 -5.33%

6 Venture Capital Fund 336 0.3% 337 0.3% 356 0.3% 20 5.95%

7 Regional Rural Bank 599 0.5% 814 0.8% 814 0.8% 215 35.89%

8 Security Receipts 2439 2.1% 2050 1.9% 2018 1.9% -421 -17.26%

9 Subsidiaries JV 3196 2.8% 3205 3.0% 3220 3.1% 24 0.75%

10 Other 9656 8.5% 2221 2.1% 1690 1.6% -7966 -82.50%

Total Non SLR Investment 114323 100% 107333 100.00% 105658 100.0% -8665 -7.58%

Amt ₹ in Crore

Page I

Income

Financial Performance3

Sl. Parameters Q1

FY21Q4

FY21Q1

FY22

YoY Variation

Amt. %

1 Interest Income (2+3+4) 20638 18790 18921 -1717 -8.3%

2 Interest on Advances 13919 11869 12322 -1597 -11.5%

3 Interest on Investments 6093 5987 5964 -129 -2.1%

4 Other Interest Income 626 934 635 9 1.5%

5 Other Income (6+7+8+9) 3655 3742 3594 -61 -1.7%

of which

6 Fee Based Income 1604 1551 1635 31 1.9%

7 Recovery in Written off Accounts 719 1150 833 114 15.9%

8 Trading Profit 1324 975 1118 -206 -15.6%

9 Others 8 67 8 - -

10 Total Income (1+5) 24293 22532 22515 -1778 -7.3%

17

Amt ₹ in Crore

Page I

Fee Based Income

Financial Performance3

Sl. Parameters Q1

FY21Q4

FY21Q1

FY22

YoY Variation

Amt. %

Fee Based Income 1604 1551 1635 31 1.9%

1 Processing Fees 520 213 573 53 10.2%

2 LC/BG Income 229 231 104 -125 -54.6%

3 Income from Insurance & MF 69 124 64 -5 -7.2%

4 Govt. Business 31 63 35 4 12.9%

5 Exchange Profit 103 153 131 28 27.2%

6 Miscellaneous Fee Income 652 767 728 76 11.7%

18

Amt ₹ in Crore

Page I

Expenses

Financial Performance3

Sl. Parameters Q1

FY21Q4

FY21Q1

FY22

YoY Variation

Amt. %

1 Total Interest Paid (2+3+4) 13856 11852 11694 -2162 -15.6%

2 Interest Paid on Deposits 13030 11102 10977 -2053 -15.8%

3 Interest Paid on Borrowings 296 163 127 -169 -57.0%

4 Others 530 587 591 61 11.5%

5 Operating Expenses (6+7) 5156 5045 4722 -434 -8.4%

6 Establishment Expenses 3307 2700 2956 -351 -10.6%

Of Which

Employee Benefits (AS-15) 750 16 545 -205 -27.3%

7 Other Operating Expenses 1849 2346 1766 -83 -4.5%

8 Total Expenses (1+5) 19013 16897 16416 -2597 -13.7%

19

Amt ₹ in Crore

Page I

Profit & Provisions

Financial Performance320

Amt ₹ in Crore

Sl. ParametersQ1

FY21Q4

FY21Q1

FY22

YoY Variation

Amt. %

1 Net Interest Income 6781 6938 7227 446 6.6%

2 Other Income 3655 3742 3594 -61 -1.7%

3 Operating Income (1+2) 10436 10680 10821 385 3.7%

4 Operating Expenses 5156 5045 4722 -434 -8.4%

5 Operating Profit 5280 5634 6099 819 15.5%

6 Provisions other than Tax 4686 4686 4679 -7 -0.1%

Of which

a NPAs 4836 5294 3248 -1588 -32.8%

b Standard Advances incl. Standard Restructured 520 -1526 1193 673 129.4%

c Depreciation on Investment -745 478 229 974 -

d Others 74 440 9 -65 -87.8%

7 Profit Before Tax 594 948 1420 826 139.1%

8 Provision for Income Tax 286 362 397 111 38.8%

9 Net Profit 308 586 1023 715 232.1%

Annualized %

Page I

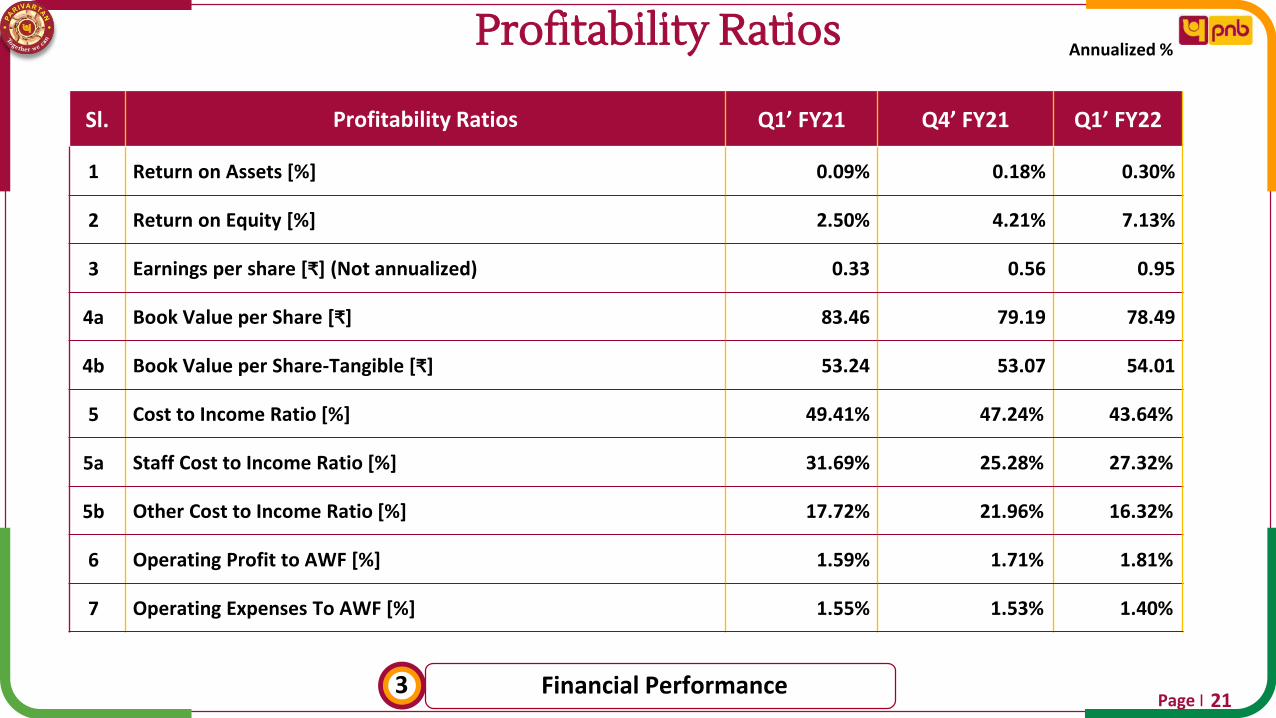

Profitability Ratios

Financial Performance3

Sl. Profitability Ratios Q1’ FY21 Q4’ FY21 Q1’ FY22

1 Return on Assets [%] 0.09% 0.18% 0.30%

2 Return on Equity [%] 2.50% 4.21% 7.13%

3 Earnings per share [₹] (Not annualized) 0.33 0.56 0.95

4a Book Value per Share [₹] 83.46 79.19 78.49

4b Book Value per Share-Tangible [₹] 53.24 53.07 54.01

5 Cost to Income Ratio [%] 49.41% 47.24% 43.64%

5a Staff Cost to Income Ratio [%] 31.69% 25.28% 27.32%

5b Other Cost to Income Ratio [%] 17.72% 21.96% 16.32%

6 Operating Profit to AWF [%] 1.59% 1.71% 1.81%

7 Operating Expenses To AWF [%] 1.55% 1.53% 1.40%

21

Page I

Efficiency Ratios (Quarter)

Financial Performance322

Cost of Deposits [%] Cost of Funds [%] NIM [%]

4.92%

4.22% 4.07%

5.01%

4.31% 4.14%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

4.18%

3.59% 3.47%

4.29%

3.70% 3.56%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

2.50%2.68% 2.73%

2.59%2.83% 2.80%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

7.64%

6.79% 6.91%

7.81%

6.97% 7.07%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

6.21%5.69% 5.61%

6.38%5.90% 5.75%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

6.50% 6.45% 6.28%6.59% 6.49% 6.34%

June'20(Q1)

Mar'21(Q4)

Jun'21(Q1)

Global Domestic

Yield on Advances [%] Yield on Funds [%] Yield on Investment [%]

(Annualised)

Page I

Productivity Ratios

Financial Performance323

in ₹ Lakhs

17631885 1854

Jun’20 Mar’21 Jun'21

Business per Employee

15468

16844 16888

Jun’20 Mar’21 Jun'21

Business per Branch

22.1423.88 25.23

Jun’20 Mar’21 Jun'21

Operating Profit per Employee

193

213230

Jun’20 Mar’21 Jun'21

Operating Profit per Branch

(*Cumulative Annualised)

* *

Page I

Balance Sheet

Financial Performance3

Sl. Parameters 30th June’20 31th March’21 30th June’21

CAPITAL & LIABILITIES

1 Capital 1882 2096 2202

2 Reserves and Surplus 84407 88842 92173

3 Deposits 1074917 1106332 1097649

4 Borrowings 44471 42840 35647

5 Other Liabilities and Provisions 26723 20523 20861

Total Liabilities 1232401 1260633 1248532

ASSETS

1 Cash and Balances with RBI 36174 43959 47030

2 Balances with Banks 71722 67391 74629

3 Investments 389754 392983 381862

4 Loans & Advances 656197 674230 661289

5 Fixed Assets 10987 11021 10887

6 Other Assets 67567 71049 72835

Total Assets 1232401 1260633 1248532

24

Amt ₹ in Crore

Page I

Asset Quality Ratios

Asset Quality425

14.11% 14.12% 14.33%

5.39% 5.73% 5.84%

June'20 Mar’21 June'21

NPA Ratios

Gross NPA% Net NPA%

80.75% 80.14% 80.26%

65.34%63.06% 62.93%

June'20 Mar’21 June'21

Provision Coverage Ratio

PCR%- (Incl. TWO) PCR%- (excl TWO)

2.54%

2.24%1.76%

June'20 Mar’21 June'21

Credit Cost

Credit Cost

1069

5967

3954603

10324316

Jun'20 Mar'21 Jun'21

Total Recovery incl Upgradation(Qtr)

Cash Recovery Up Gradation

1672

69998270

Amt ₹ in Crore

(FY)

Page I

Movement of NPA

Asset Quality4

Sl. Parameters Q1 FY’21 Q4 FY’21 FY 21 Q1 FY’22

1 NPA as at the beginning of Year/Quarter 105165 94479 105165 104423

2 Cash Recovery 1069 5967 11442 3954

3 Up-gradation 603 1032 2363 4316

Cash Recovery & Up-gradation 1672 6999 13805 8270

4a) Consequential Write Off

41202156 3675 676

b) Technical Write Off 5072 12202 1571

5 Total Reduction (2+3+4) 5792 14228 29682 10516

6 Fresh Addition 2476 24172 28940 10168

-Fresh slippages 1917 23185 25001 8241

-Debits in existing NPA A/cs 558 987 3939 1927

7 Gross NPAs at end of the period 101849 104423 104423 104076

8 Eligible Deductions incl. Provisions 66546 65848 65848 65495

9 Net NPAs 35303 38576 38576 38581

10 Recovery in written-off A/cs 719 1150 2498 833

26

Amt ₹ in Crore

Page I

Asset Classification: Global Advances

Asset Quality 4

Sl. Parameters

June’20 Mar’21 June’21 YoY Variation

O/S Share% O/S Share% O/S Share% Amt. Var. %

1 Standard 619846 85.89% 634984 85.88% 621960 85.67% 2114 0.34%

2 Gross NPA 101849 14.11% 104423 14.12% 104076 14.33% 2227 2.19%

2a Sub-Standard 15366 2.13% 22980 3.11% 24792 3.41% 9426 61.34%

2b Doubtful 70619 9.79% 60328 8.16% 57985 7.99% -12634 -17.89%

2c Loss 15864 2.20% 21116 2.86% 21299 2.93% 5435 34.26%

Total Advances(1+2) 721695 100% 739407 100% 726036 100.0% 4341 0.60%

27

Amt ₹ in Crore

Page I

NPA Classification: Sector Wise

Asset Quality428

Amt ₹ in Crore

Sl. ParametersJune’20 Mar’21 June’21

GNPA GNPA% GNPA GNPA% GNPA GNPA%

1 Retail Loans 4458 3.43% 7167 5.26% 7833 5.92%

Out of Which,

1a Housing 2354 2.88% 3767 4.41% 4391 5.24%

1b Car/Vehicle 472 5.49% 575 5.58% 601 5.99%

1c Personal Loan 142 1.83% 260 2.49% 284 2.76%

2 Agriculture (PS+NPS) 19132 15.20% 22201 19.62% 23384 18.21%

3 MSME 17389 14.80% 26859 21.32% 28145 23.23%

4 Corporate & Others 58328 17.80% 46184 13.42% 42730 13.09%

5 Domestic NPA (1+2+3+4) 99307 14.10% 102411 14.24% 102092 14.42%

6 Overseas NPA 2542 13.00% 2013 9.96% 1984 11.05%

7 Global NPA (5+6) 101849 14.11% 104423 14.12% 104076 14.33%

Page I

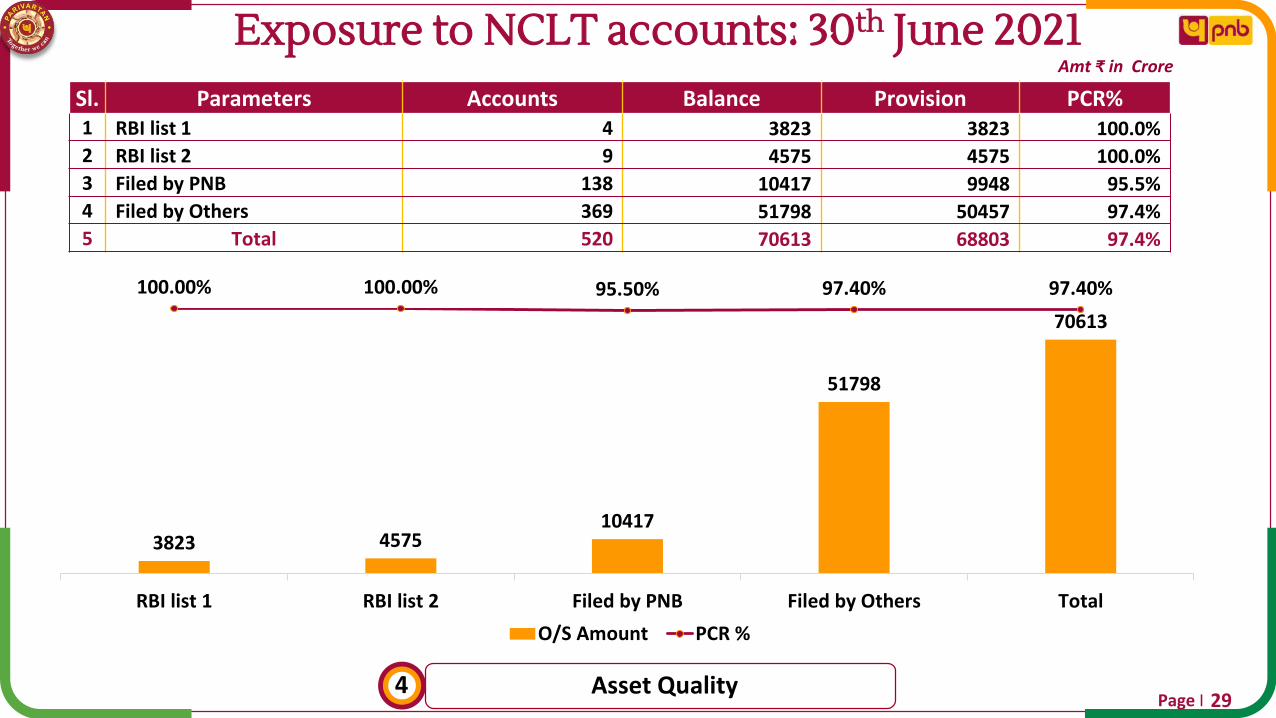

Exposure to NCLT accounts: 30th June 2021

Asset Quality4

Sl. Parameters Accounts Balance Provision PCR%1 RBI list 1 4 3823 3823 100.0%

2 RBI list 2 9 4575 4575 100.0%

3 Filed by PNB 138 10417 9948 95.5%

4 Filed by Others 369 51798 50457 97.4%

5 Total 520 70613 68803 97.4%

29

Amt ₹ in Crore

3823 457510417

51798

70613

100.00% 100.00% 95.50% 97.40% 97.40%

-500.0 0%

-400.0 0%

-300.0 0%

-200.0 0%

-100.0 0%

0.0 0%

100 .00%

0

100 00

200 00

300 00

400 00

500 00

600 00

700 00

800 00

RBI list 1 RBI list 2 Filed by PNB Filed by Others Total

O/S Amount PCR %

Page I

Standard Restructured Advances

Asset Quality4

Sl Movement of Std. Restructured AdvancesJune’20

(Qtr)Mar’21

(FY)June’21

(Qtr)

A Opening Balance 2236 2236 2372

B Total Addition 70 794 33

1 Fresh Restructuring 53 773 33

2 Up-gradation 17 21 0

C Reduction 8 658 49

1 In eligible 5 16 36

2 Down-gradation to NPA 1 19 9

3 Exit/Failure 2 623 4

Closing Balance (A+B-C) 2298 2372 2356

30

Sl. Sector wise Std. Restructured June’ 21

A Agriculture & Allied 1388

B MSME 160

C Corporate & Others 808

Total 2356

Amt ₹ in Crore

Page I

Position of SMA Accounts( > Rs. 5 Crore)

Asset Quality431

Amt ₹ in Crore

As on Gross Global Advances SMA 2SMA 2 as a % of Gross Global

Advances

Mar’21 739407 13708 1.85%

June’21 726036 12524 1.72%

Sector Wise Position – as on 30.06.2021

CATEGORY Domestic Advances SMA 2 SMA 2 as a % of Advances

Agriculture 128386 868 0.68%

MSME 121134 2679 2.21%

Retail 132096 348 0.26%

Corporate & Others 326466 8629 2.64%

Total Domestic Advances 708082 12524 1.77%

Page I

Asset Quality Control – Multi Prong Approach

Asset Quality432

Verticalized Credit Delivery Model

• Large Corporate

Branches (Loans

above Rs. 50 Crore)

• Mid Corporate

Centres (Loans upto

Rs. 50 Crore)

• PNB Loan Points

(RAM Loans upto Rs.

1 Crore)

PNB Lens – The Lending Solution

• Technology Driven

Credit Underwriting

Model

• Uniformity in Process

Across the Bank

• Rolled out for Retail,

Agri and MSME

(Upto Rs. 25 Crore)

Continuous Follow Up for Collections

• Dedicated Credit

Monitoring Vertical

• Use of SMSes and

Out-Bound Call

Centres to Follow up

with Customers

• Mobile app for field

Functionaries to

Monitor SMAs

Strong Recovery Measures

• Sustained Recovery

Efforts

• Special OTS Scheme

• Online Portal for

monitoring of NPA

Accounts

• Mega e- Auctions

Page I

Share holding Pattern – 30th June 2021

Share Holding & Capital533

Amt ₹ in Crore

73.1%

8.9%

2.4%

11.2%

2.5%1.9%

Govt. of India

FIs/Banks/Insurance

Mutual Funds

Resident Individual

FIIs

Others

Raised Rs 1800 Crore under Tier I Equity through Qualified Institutional Placement during Q1 FY’22

Page I

Capital Adequacy

Share Holding & Capital5

Sl. Parameters June’20 Mar’21 June’21

1 Tier I 63745 69713 73330

Common Equity 58697 64351 67955

Additional Tier I 5048 5362 5376

2 Tier II 14781 17145 15970

3 Total (Tier I+II) 78526 86858 89300

4 Risk-weighted Assets 621981 606585 587813

1 Tier I % 10.25% 11.50% 12.47%

Common Equity % 9.44% 10.62% 11.56%

Additional Tier I % 0.81% 0.88% 0.91%

2 Tier II % 2.38% 2.82% 2.72%

3 Total (Tier I+II) % 12.63% 14.32% 15.19%

34

Amt ₹ in Crore

9.44%10.62%

11.56%

0.81%

0.88%

0.91%2.38%

2.82%

2.72%

June'20 Mar'21 June'21

CRAR%

CET AT I Tier II

12.63%

14.32%

15.19%

Page I

Capital Optimization

Share Holding & Capital5

Sl. Parameters June’20 Mar’21 June’21 YoY Variation1 Credit RWA 497376 490310 474391 -4.62%

Of which Credit RWA (Domestic FB) 374105 366545 354699 -5.19%

2 Market RWAs 59052 50722 43795 -25.84%3 Operational RWAs 65553 65553 69628 6.22%4 Total RWAs 621981 606585 587813 -5.49%

5 Global Credit Exposure 842843 905762 889481 5.53%6 Credit Exposure (Domestic FB) 769441 807704 797766 3.68%7 RWA/Advances 74% 67% 66%8 Credit RWA Density (Domestic FB) 49% 46% 44%

9 Total NFB O/S 73401 66631 64730 -11.81%10 NFB RWA 31896 28315 26875 -15.74%

11 Leverage Ratio 4.12 4.37 4.64

35

Amt ₹ in Crore

Sl. Concentration Risk June’20 Mar’21 June’21

1 Exposure to Top 20 Borrowers as % of Total Exposure 17.16% 15.23% 15.31%

2 Exposure to Top 10 Groups as % of Total Exposure 12.96% 12.93% 11.72%

Page I

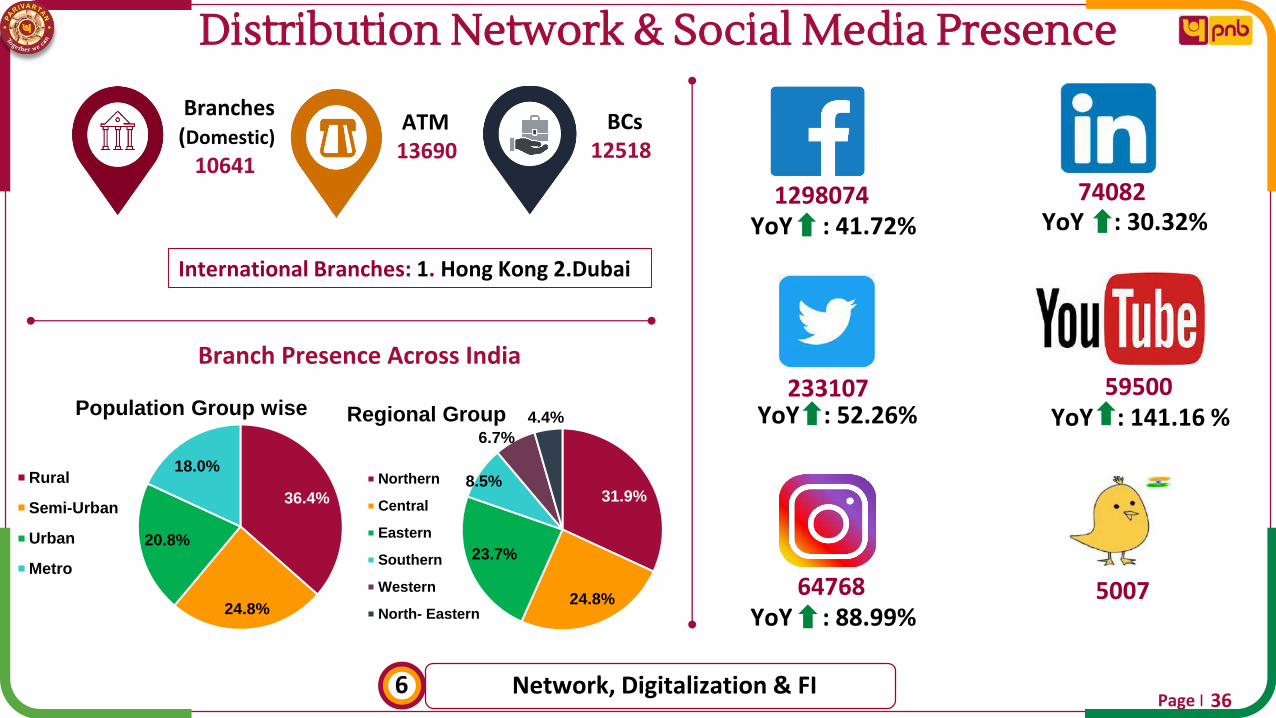

Distribution Network & Social Media Presence

Network, Digitalization & FI636

ATM13690

Branches (Domestic)

10641

BCs12518

International Branches: 1. Hong Kong 2.Dubai

Branch Presence Across India

31.9%

24.8%

23.7%

8.5%

6.7%

4.4%Regional Group

Northern

Central

Eastern

Southern

Western

North- Eastern

36.4%

24.8%

20.8%

18.0%

Population Group wise

Rural

Semi-Urban

Urban

Metro

YoY : 41.72%

74082 YoY : 30.32%

233107 YoY : 52.26% YoY : 141.16 %

5007 YoY : 88.99%

64768

59500

1298074

Page I

Digital Transactions

Network, Digitalization & FI637

19.16

36.45

Q1 FY21 Q1 FY22

90% YOY Increase in UPI Transactions

No. of UPI Txns (Crore)

40%

11%

49%

60%11%

29%

71% ADC Transactions out of Total Transactions

Digital Transactions ATM + BNA

Branches + BC

June’20

June’21

31%

1%1%

2%

65%

75%

1%

2%

4%

18%

Share of Digital Transactions

UPI IMPS IB+MB NEFT Others

June’20

June’21

Page I

Augmenting Digital Base

Network, Digitalization & FI638

233

262

Jun'20 Jun'21

Nu

mb

ers

(in

Lac

s)

12.4% YoY Growth in Internet Banking Users

No. of IBS users (Retail)

169

251

Jun'20 Jun'21

Nu

mb

ers

(in

lacs

)

49% YoY Growth in PNB One (M-Bank) Users

No. of MBS users

1.34

4.00

Jun'20 Jun'21

Nu

mb

ers

(in

Lac

s)

198% YoY Growth in Bharat QR Users

Bharat QR Code

421

447

Jun'20 Jun'21

Nu

mb

ers

(in

lacs

)

6.2% YoY Growth in Debit Card

Debit Card

Page I

Credit Card Business

Network, Digitalization & FI639

PNB Signature PNB Millennial Corporate Credit Card

9% Y-o-Y increase in Credit Card Issuance

27% Y-o-Y increase in No. of Transactions through Credit

Cards

65% Y-o-Y increase in Volume of Transactions through

Credit Cards

Launch of New Credit Cards

Page I

Recent Digital Initiatives

640

Network, Digitalization & FI

Internet Banking Change Home Branch.

Change account variant (for current account customers)

View Senior Citizen Scheme (SCSS)

Password resetting for NRI customers without debit

card

Mobile Banking

Insta-Demat Account opening.

Link of opening online account through video KYC

Others

Bharat bill pay system (BBPS Post log-in) & Positive Pay

System in both IBS and MBS.

Page I6

41Network, Digitalization & FI

– Multifunctional Digital Outlets

Conceptualized on “Banking

on the go” and “Do-it-yourself

@ PNB”

Self-operated machines/kiosks

to facilitate banking operations

An open walk through model –

enables customers to use

paperless and digitally-enabled

services

Being set up at prominent

public places having high foot

falls

New Delhi- Central Secretariat Metro Station

Solan (HP) Chandigarh

Page INetwork, Digitalization & FI6

42

IBBIC shall design, build, implement and commercialize Distributed Ledger Technology (DLT) solutions for the financial services sector with initial focus on Trade Finance

IBBIC is a joint initiative of 18 Scheduled Commercial Banks of India & PNB has subscribed equity share constituting 5.55% of the issued and paid-up capital of IBBIC.

Indian Banks' Blockchain Infrastructure Company (IBBIC)

Fintech Initiatives

Page I

Financial Inclusion : Profitable Business Proposition

Network, Digitalization & FI6

Sl. Jansuraksha Schemes Enrollment Up To June’21

1 Pradhan Mantri Jeevan Jyoti Bima Yojana 22.02 Pradhan Mantri Suraksha Bima Yojana 108.13 Atal Pension Yojana 14.8

Nos. in Lakh

43

385 395

As on June'20 As on June'21

PMJDY Accounts

11291

13487

As on June'20 As on June'21

Deposit Mobilized by BCs

386

536

Q1 FY21 Q1 FY22

Txns done by BCs

4070 3938

As on June'20 As on June'21

PMJDY Avg. BalanceAmt in ₹ Amt ₹ in Crore

Page I

Performance of Subsidiaries, Joint Venture and Associates

44Group Business & RRBs7

Type Name of the entityCountry of

Incorporation

Proportion of

Ownership%

Results

(3/6/9/12 M) Total

Income

Total

Expenses

Gross

ProfitNet Profit

Associates PNB Housing Finance Ltd India 32.59% Mar’21 (12M) 7624 6417 1207 930

Subsidiaries PNB Investment Services Ltd. India 100.00% Mar’21 (12M) 8 6 2 1

Subsidiaries PNB Gilts Ltd. India 74.07% Mar’21 (12M) 1052 438 614 454

Associates PNB MetLife India Insurance Co. Ltd India 30.00% Mar’21 (12M) 9558 9445 113 101

Associates Canara HSBC OBC Life Insurance Co. Ltd India 23.00% June’21 (3M) 1423 1502 -79 -79

SubsidiariesPNB (International) Ltd.(FY : 1st April to 31st March)

UK 100.00% Mar’21 (12M) 177 150 27 -75

Associates India SME Asset Reconstruction Co. Ltd India 20.90% Mar’21 (12M) 11 10 1 0

SubsidiariesDruk PNB Bank Ltd.(FY : 1st January to 31st December)

Bhutan 51.00% Dec’20 (12M) 123 95 28 6

Joint Venture

Everest Bank Ltd.(FY : 16th July to 15th July)

Nepal 20.03% April’21 (9M) 605 471 134 94

(Amount in INR Crore)

Page I

Performance of RRBs

Group Business & RRBs7

Consolidated Position FY 2020 FY 2021

Total Income 10118 11267

Total Expenses 10473 10551

Operating profit 1648 2870

Net Profit -472 481

Capital adequacy ratio 9.41% 9.95%

Business 161918 175191

Loans and advances 57445 62750

Deposits 104472 112440

RRBs: 1.DBGB: Dakshin Bihar Gramin Bank, Patna2.SHGB: Sarva Haryana Gramin Bank, Rohtak3.HPGB: Himachal Pradesh Gramin Bank, Mandi4.PGB: Punjab Gramin Bank, Kapurthala

5. PUPGB: Prathama Uttar Pradesh Gramin Bank, Moradabad6. TGB- Tripura Gramin Bank7. MRB- Manipur Rural Bank8. AGVB- Assam Gramin Vikash Bank9. BGVB- Bangiya Gramin Vikash Bank

45

Amt ₹ in Crore

Page I

Awards for Excellence

Awards & Way Forward846

Finnoviti Awards 2021-

PNB Verify product won the award

“Indian Society for Training & Development Award for Innovative

Training Practices- “2nd Position under

Services (BSFI & IT/ITES Category)

IBA Banking Technology Awards 2021 -Joint Runner up - Cyber Security

Initiatives

Finacle Client Innovation Award by Infosys– Runner Up for PNB’s path breaking “Process Innovations”

Assocham

Runner Up under Digital service under PSB Merged Category

Special Commemorative Award 2021 by NABARD

Best PSU in the fields of Agriculture Credit, Micro Finance, Financial Inclusion and Technology Adoption.

Page I

Way Forward

Awards & Way Forward847

Analytics Driven Approach for Deepening of Customer

Relationship and Pricing

Implementing strong Recovery Measures to improve Asset Quality

Leveraging Digital Credit Underwriting Capabilities for

uniform credit processing standards across the Bank

Sustained profitability and robust capital position

Focus on Cost Optimization

through realization of

synergies in various segments

Differentiated Customer

Experience through

pnb@ease Outlets

Page I

Disclaimer

48

This presentation has been prepared by Punjab National Bank (the “Bank”), solely for general information

purposes, without regard to any specific objectives, financial situations or informational needs of any

particular person.

Except for the historical information contained herein, statements in this presentation which contain words or

phrases such as “is”, “aims”, “will”, “would”, “indicating”, “expected to”, “guidance“, “way forward”, “expected”,

“estimate”, “objective”, “goal”, “strategy”, “philosophy”, “project” etc. and similar expressions or variations of

such expressions may constitute ‘forward-looking statements’. These forward-looking statements involve a

number of risks, uncertainties and other factors that could cause actual results to differ materially from those

suggested by the forward-looking statements. These risks and uncertainties include, dynamic and complex

internal and external environment having bearing on bank’s ability to successfully implement our

strategy, future levels of non-performing loans, our growth and expansion in business, the impact of any

acquisitions, the adequacy of our allowance for credit losses, our provisioning policies, technological

implementation and changes, the actual growth in demand for banking products and services, investment

income, cash flow projections, our exposure to market risks as well as other risks. Punjab National Bank

undertakes no obligation to update the forward-looking statements to reflect events or circumstances after the

date thereof.

Note: All financial numbers in the presentation are from Audited Financials or Limited Reviewed financials or

based on Management estimates.

Page I

Thank You!

49