Public Disclosure Authorized - The World Bank Documents

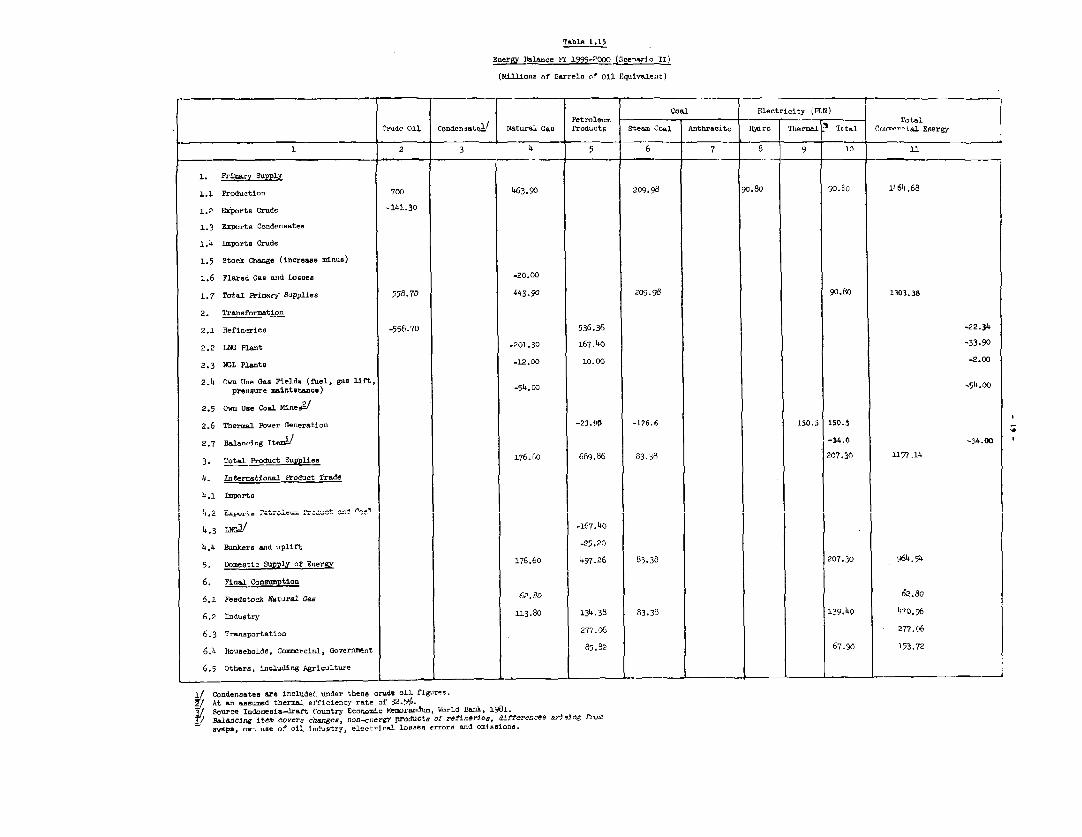

151

zJ -- ;C 0~ _ .. rb~ ~ ^DP r-Y- q~~~~~~~~~~~~~ _S Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized closure Authorized

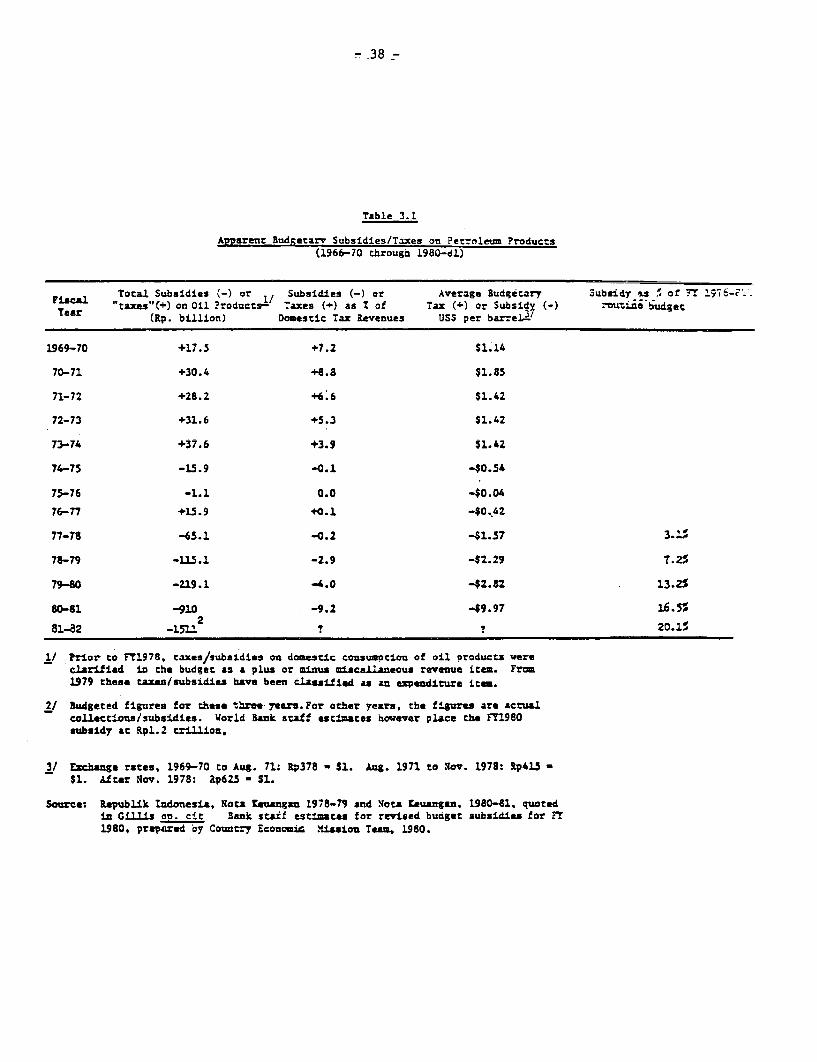

-

Upload

khangminh22 -

Category

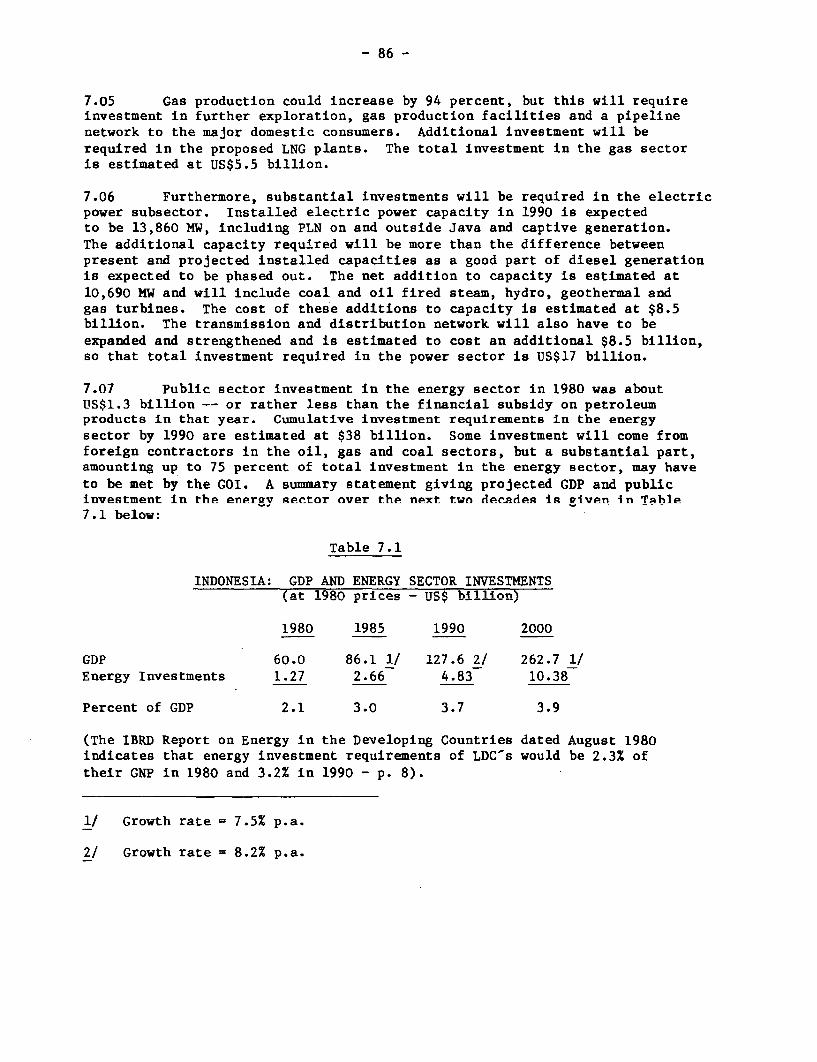

Documents

-

view

1 -

download

0

Transcript of Public Disclosure Authorized - The World Bank Documents

zJ --;C

0~ _ . .

rb~ ~ ^DP

r-Y-

q~~~~~~~~~~~~~ _S

Pub

lic D

iscl

osur

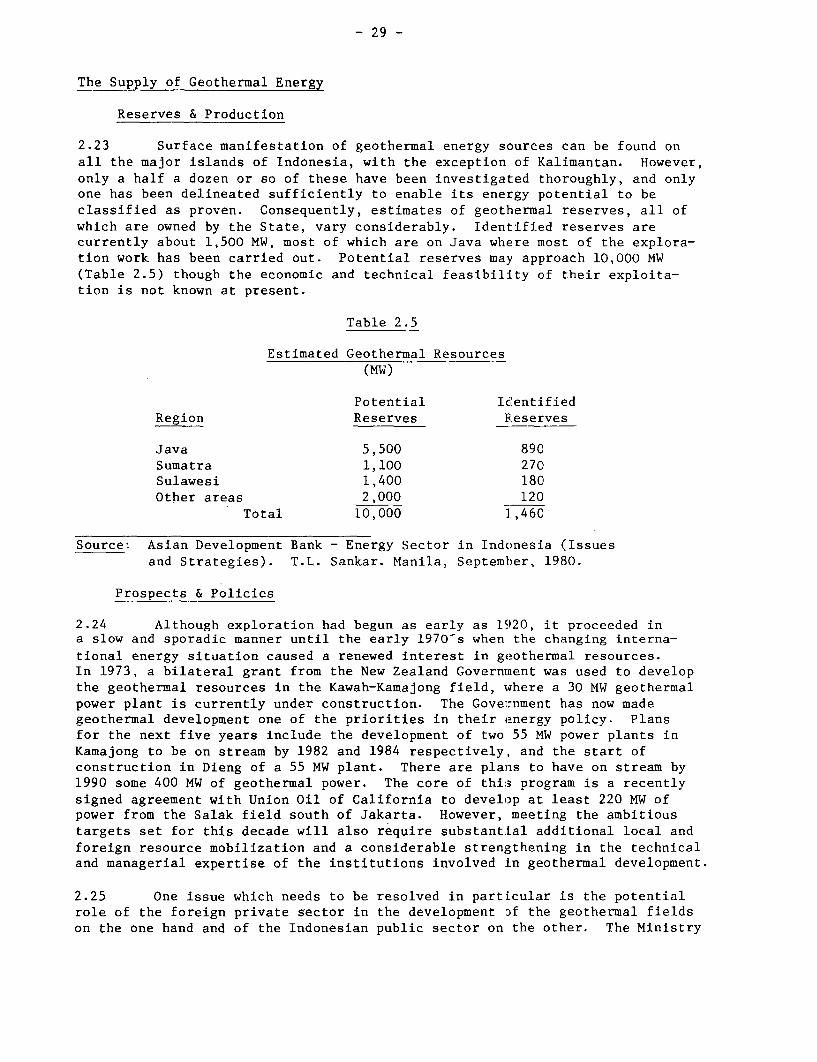

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

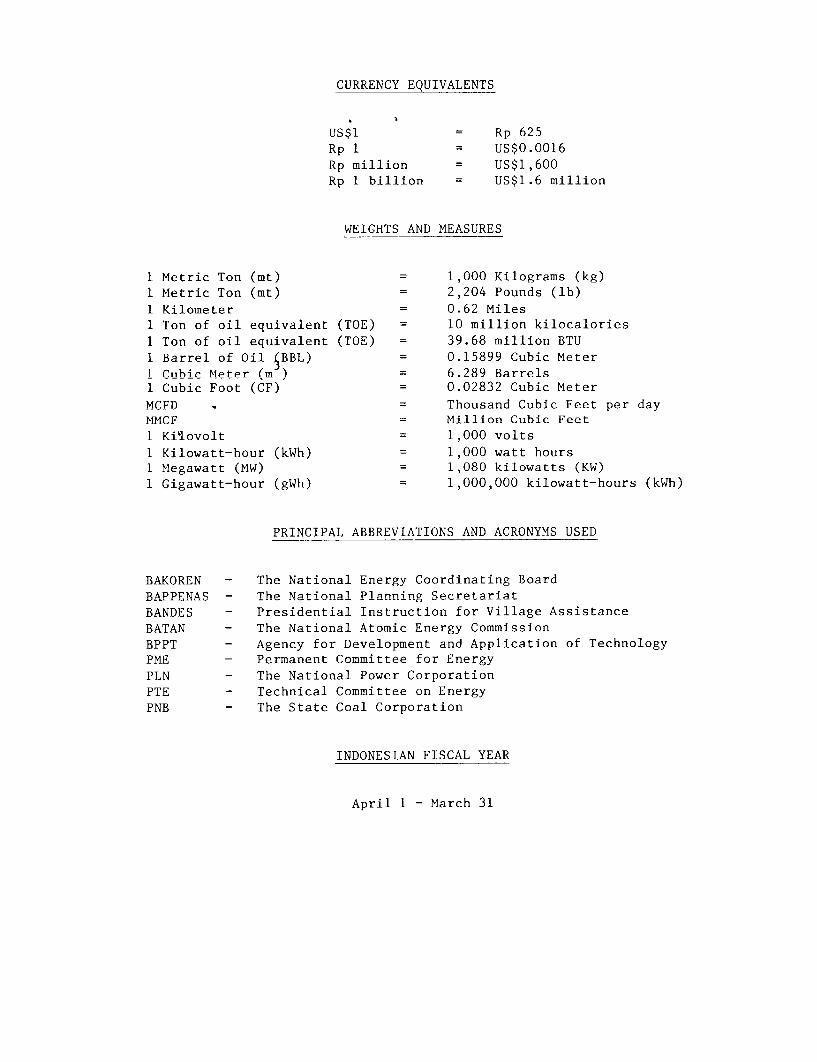

CURRENCY EQUIVALENTS

US$1 = Rp 625

Rp 1 = US$0.0016

Rp million = US$1,600

Rp 1 billion = US$1.6 million

WEIGHTS AND MEASURES

1 Metric Ton (mt) 1,000 Kilograms (kg)1 Metric Ton (mt) = 2,204 Pounds (lb)1 Kilometer = 0.62 Miles

1 Ton of oil equivalent (TOE) = 10 million kilocalories1 Ton of oil equivalent (TOE) 39.68 million BTU1 Barrel of Oil BBL) 0.15899 Cubic Meter1 C2ihir MteIr (m ) = 6.289 Barrels1 Cubic Foot (CF) = 0.02832 Cubic MeterMCFD . = Thousand Cubic Feet per dayMMCF = Million Cubic Feet

1 Ki'lovolt = 1,000 volts

1 Kilowatt-hour (kWh) = 1,000 watt hours1 Megawatt (MW) = 1,080 kilowatts (KW)1 Gigawatt-hour (gWh) = 1,000,000 kilowatt-hours (kWh)

PRINCIPAT. ARRRFVTATIONS AND ACRONYMS USED

BAKOREN - The National Energy Coordinating Board

BAPPENAS - The National Planning Serrptnrint

BANDES - Presidential Instruction for Village AssistanceBATAN - The Nati-nnal Atomicr Pnerau Commfissin

BPPT - Agency for Development and Application of TechnologyPME - Permanent Committee for EnergyPLN - The National Power CorporationPTE - Technical Committee o nEnrgy

PNB - The State Coal Corporation

TMNDONSCTAN FISCAL YEAR

April 1 - March 31

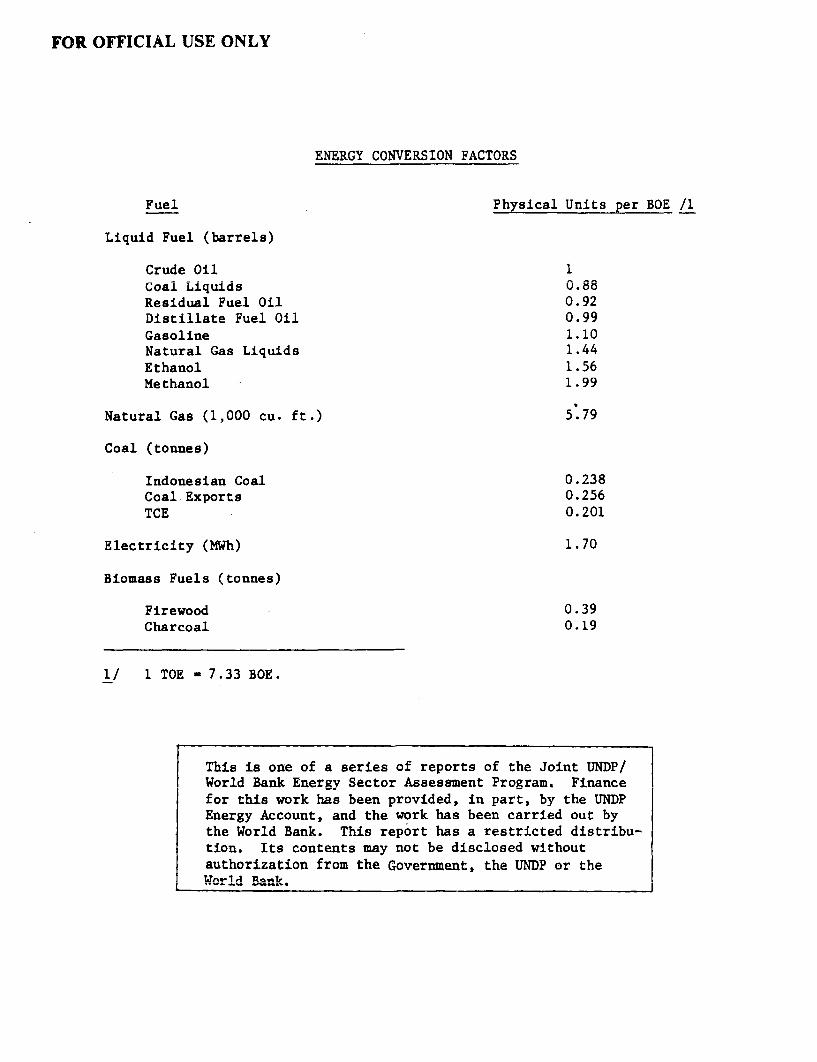

FOR OFFICIAL USE ONLY

VML7(0V r'AUN7VDCTniM VAr1'ADC

Fuel Physical Units per BOE /1

Liquid Fuel (barrels)

Crude Oil 1Coal Liquids 0.88Residual Fuel Oil 0.92Distillate Fuel Oil 0.99Gasoline 1.10Natural Gas Liquids 1.44Ethanol 1.56Methanol 1.99

Natural Gas (1,000 cu. ft.) 5.79

Coal (tonnes)

Indonesian Coal 0.238Coal Exports 0.256TCE 0.201

Electricity (MWh) 1.70

Biomass Fuels (tonnes)

Firewood 0.39ChArtnAl 0.19

1/ 1 TOE - 7.33 BOE.

This is one of a series of reports of the Joint UNDP/World Bank Energy Sector Assessment Program. Financefor this work has been provided, in part, by the UNDPEnergv Account. and the work has been carried out bythe World Bank. This report has a restricted distribu-tion. Tt-s c-o-nteintq may not he diRcloRed without

authorization from the Government, the UNDP or theWorl Ba1n Rk"

INDONESIA

ISSUES AND OPTIONS IN THE ENERGY SECTOR

TrAUTV Av 'nmirMTmC

.LINLR JUC,1 .LO . . . . . . . . . . . . . . . . . . . . . . . . . . . .v

TVQCTTlC' AXTT nDEl IEl.7TT1AqrT'%XPV 1 £).U.J BJ'41J0 il A£.I1WlJV1J.L2J.1IJ L.LSJJ10...V.....J.. .....

flt -- - - I - '.rlPlfl I r.n, TTnrlrrrnnT A ATf 'nnn ClT1y T' rflfl'TTn TflE A ITT 1Chapter 1: ENERGY tU ur.r±JxnI'V ±1u N UoDDlE PUOUSSIB F R r'LuND . . . . . .

Background . . . . . . . . . . . . . . . . . . . . . . . .

Petroleum Products . . . . . . . . . . . . . . . . . . 3,, ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~rKerosene j

Automotive Diesel ... . . . . . . . . . . . . . . . . 5Other Petroleum Products . . . . . . . . . . . . . . . 5

Coal. . . . . . . . . . . . . . . . . . . . . . . . . . 5Natural Gas ... . . . . . . . . . . . . . . . . . . . 6Electricity ... . . . . . . . . . . . . . . . . . . . 6Commercial Energy Balance FY79 . . . . . . . . . . . . 7

Likely Demand to FY89 .7.. . . . . . . . . . . . . .... . 7Background ... . . . . . . . . . . . . . . . . . . . 7The Domestic Demand for Petroleum . . . . . . . . . . . 7The Domestic Demand for Natural Gas . . . . . . . . . . 11The Domestic Demand for Coal . . . . . . . . . . . . . 11The-Domestic Demand for Electricity . . . . . . . . . . 12Commercial Energy Balance, FY89 . . . . . . . . . . . . 13The Outlook for FY99 ... . . . . . . . . . . . . . . 15

Chapter 2: THE SUPPLY OF PRIMARY ENERGY . . . . . . . . . . . . . . . 21

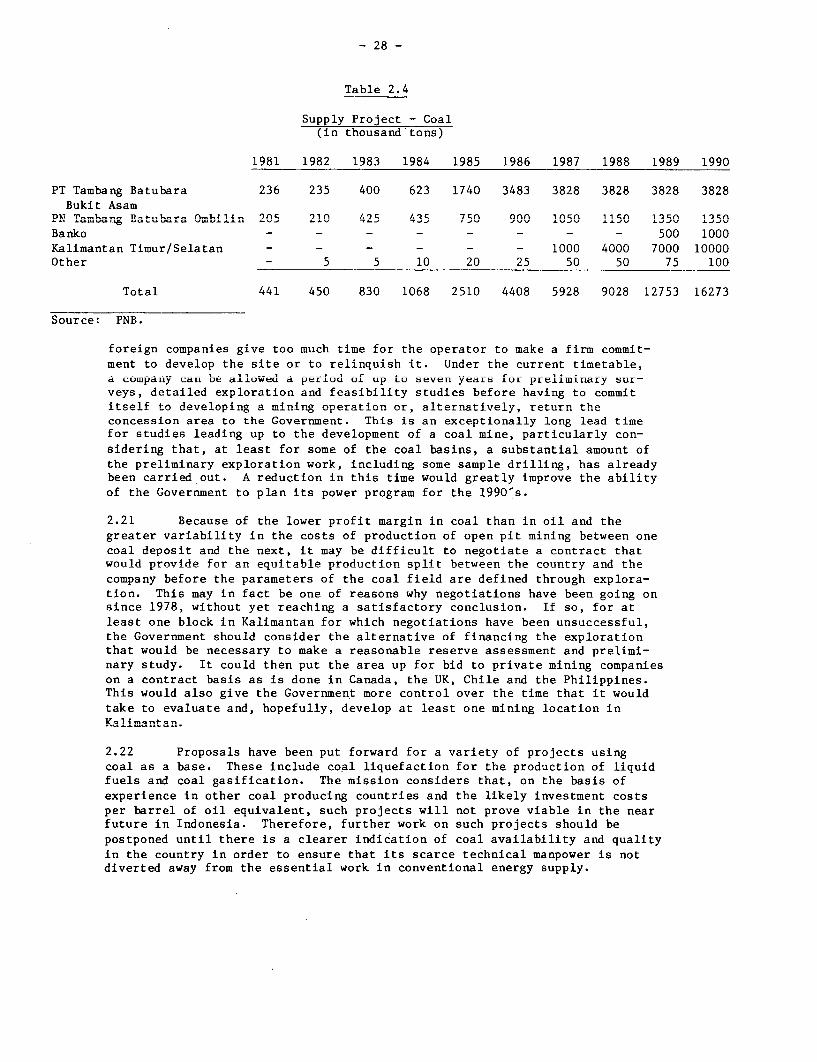

Overview . . . . . . . . . . . . . . . . . . . . . . . . . 21The Supply of Oil . . . . . . . . . . . . . . . . . . . . 21The Supply of Gas ... . . . . . . . . . . . . . . . . . 24The Supply of Coal ... . . . . . . . . . . . . . . . . . 26The Supply of Geothermal Energy . . . . . . . . . . . . . 28The Supply of Hydro ... . . . . . . . . . . . . . . . . 30Traditional Energy Resources . . . . . . . . . . . . . . . 31Other Biomass Resources ... . . . . . . . . . . . . . . 34Conclusion ... . . . . . . . . . . . . . . . . . . . . . 34

Chapter 3: ENERGY PRICING POLICY . . . . . . . . . . . . . . . . . . 35

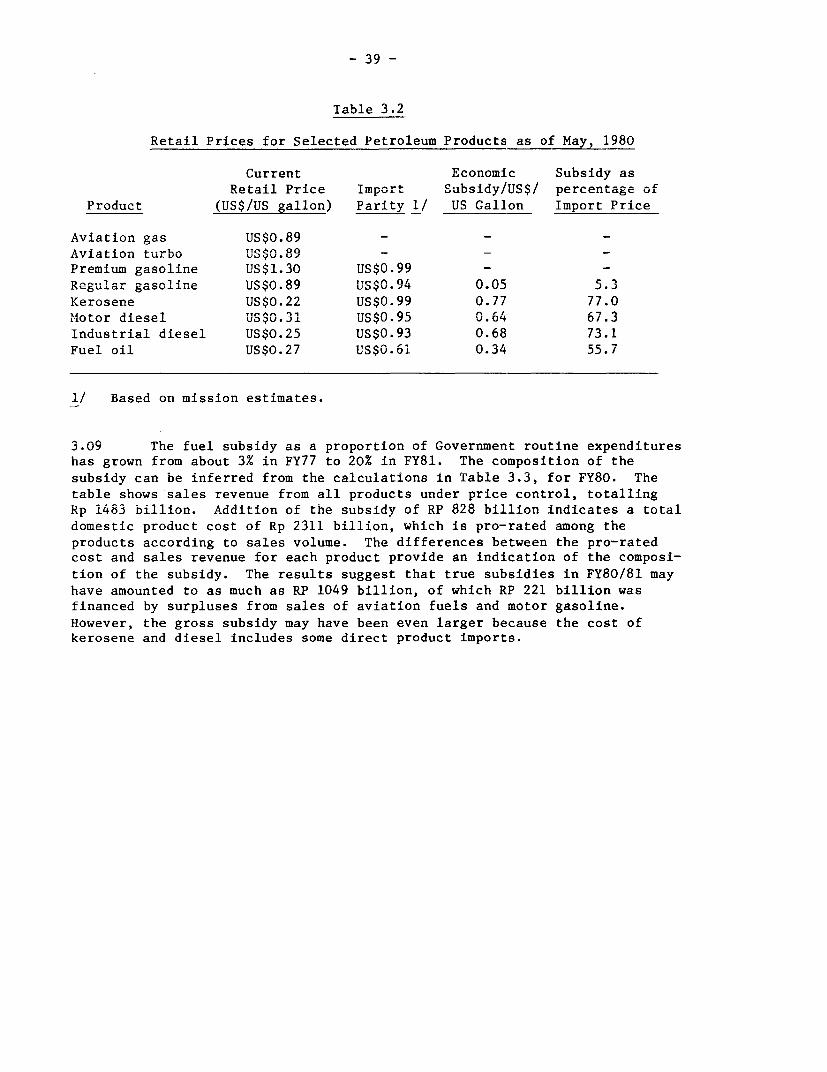

Background ... . . . . . . . . . . . . . . . . . . . . . 35The Pricing of Energy Products . . . . . . . . . . . . . . 37

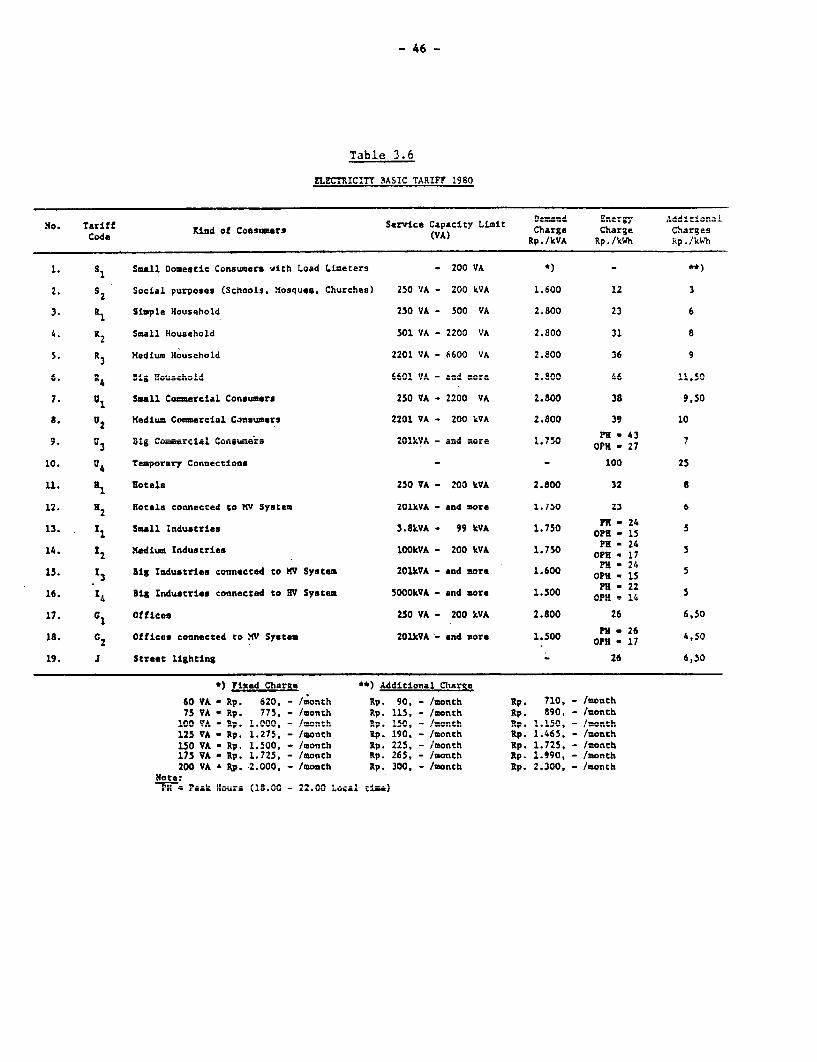

Petroleum . . . . . . . .. . . . . . . . . . . . . . . . 37Natural Gas ... . . . . . . . . . . . . . . . . . . . 41Coal ... . . . . . . . . . . . . . . . . . . . . . . 43Electricity ... . . . . . . . . . . . . . . . . . . . 44

Policy Issues ...................... 47

Page No.

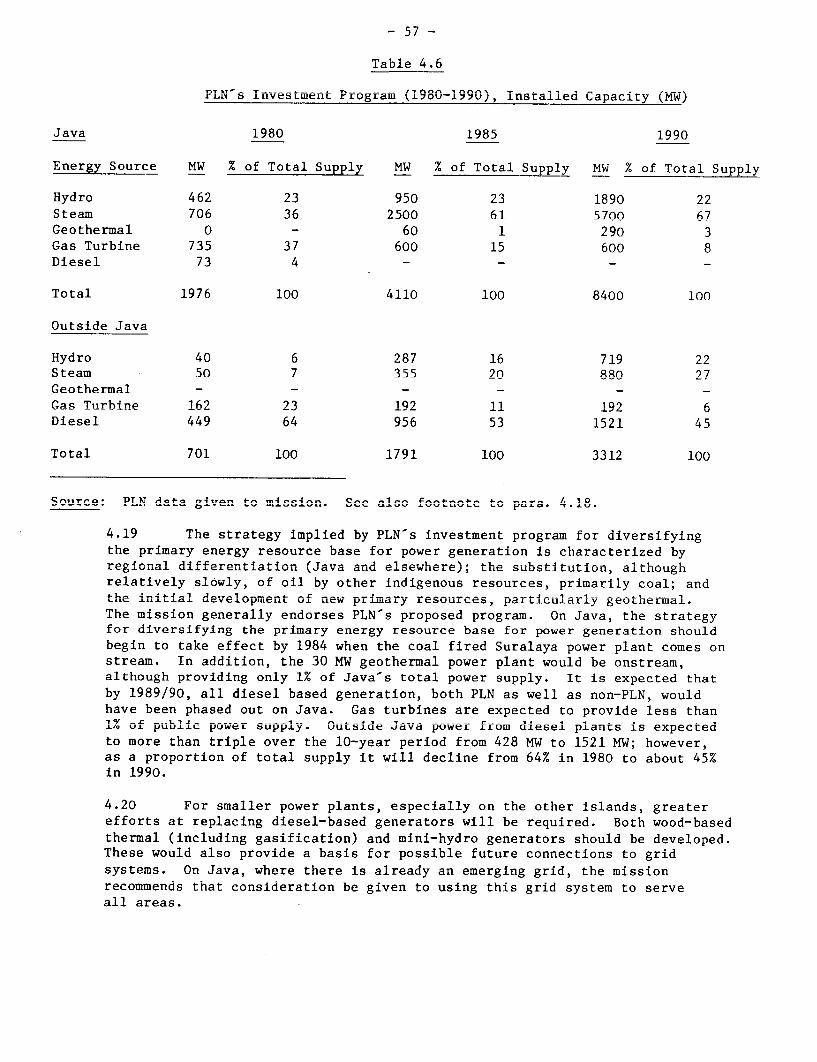

Chapter 4: INTER-FUEL OPTIONS FOR MEETING FUTURE ENERGY NEEDS . . . . 48

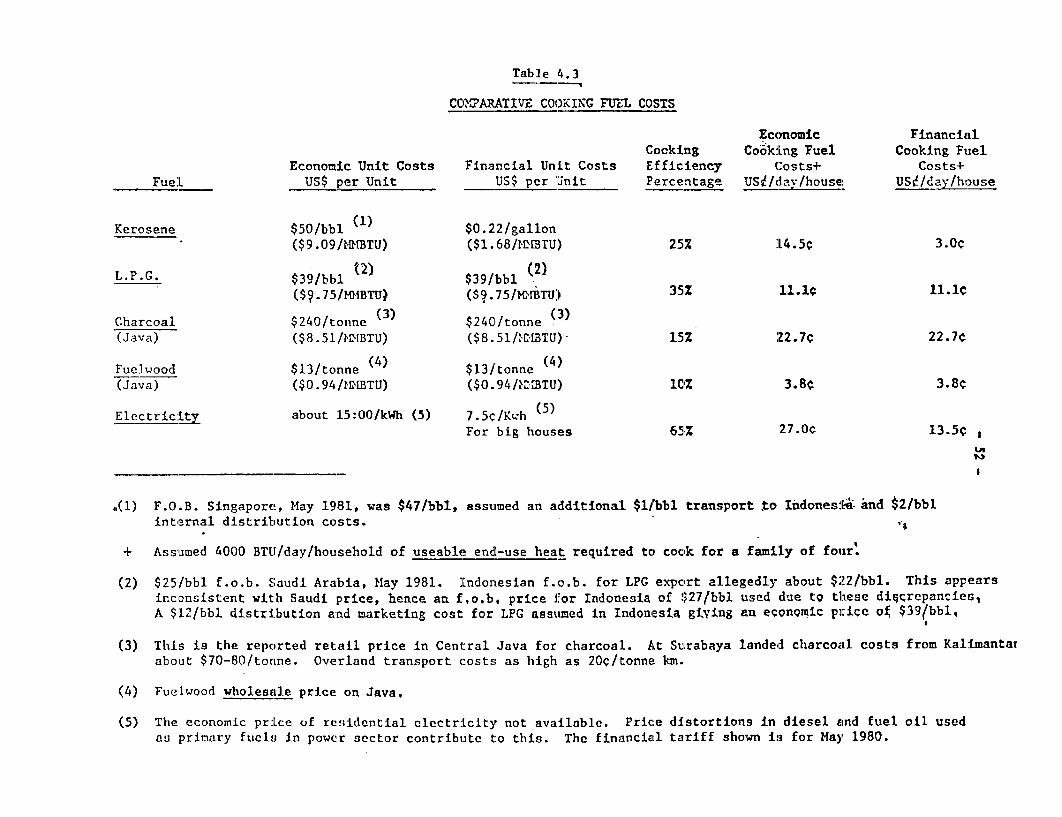

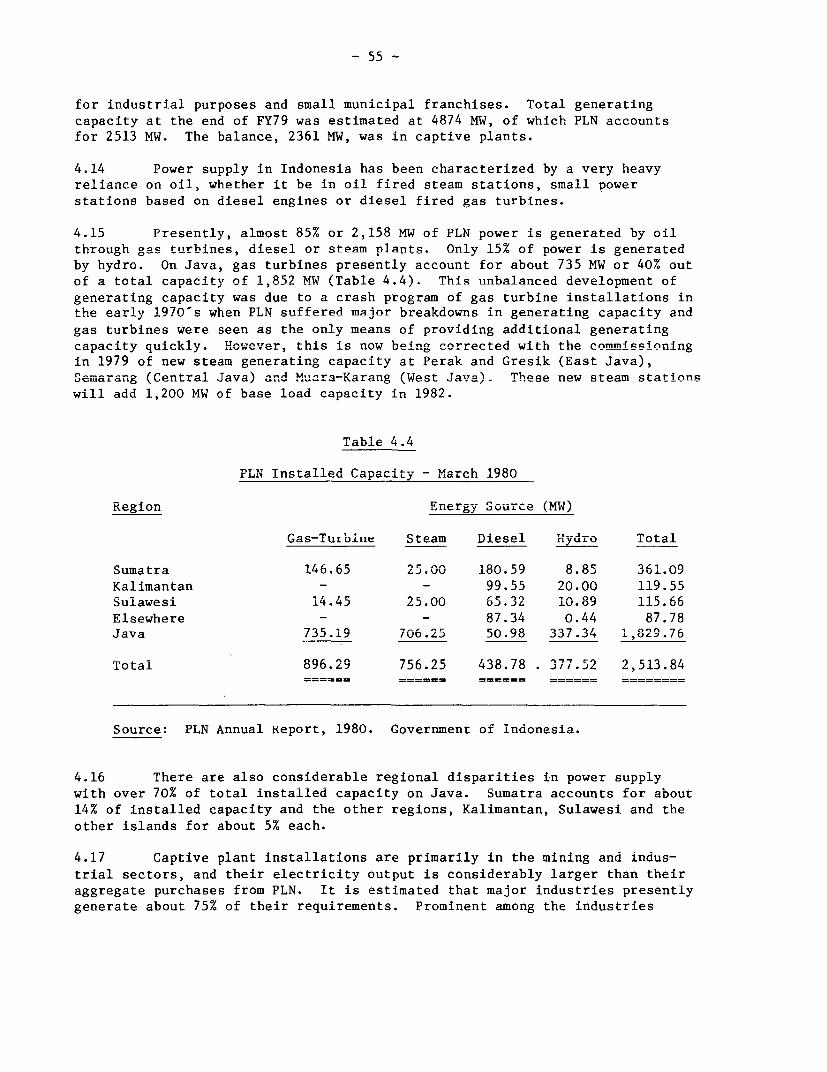

The Household Sector .48Th e TInAustrilal Sector . 53 ..... .The Transport Sector .54The Electric Power Subsector . . . . . . . . . . . . . . . 54

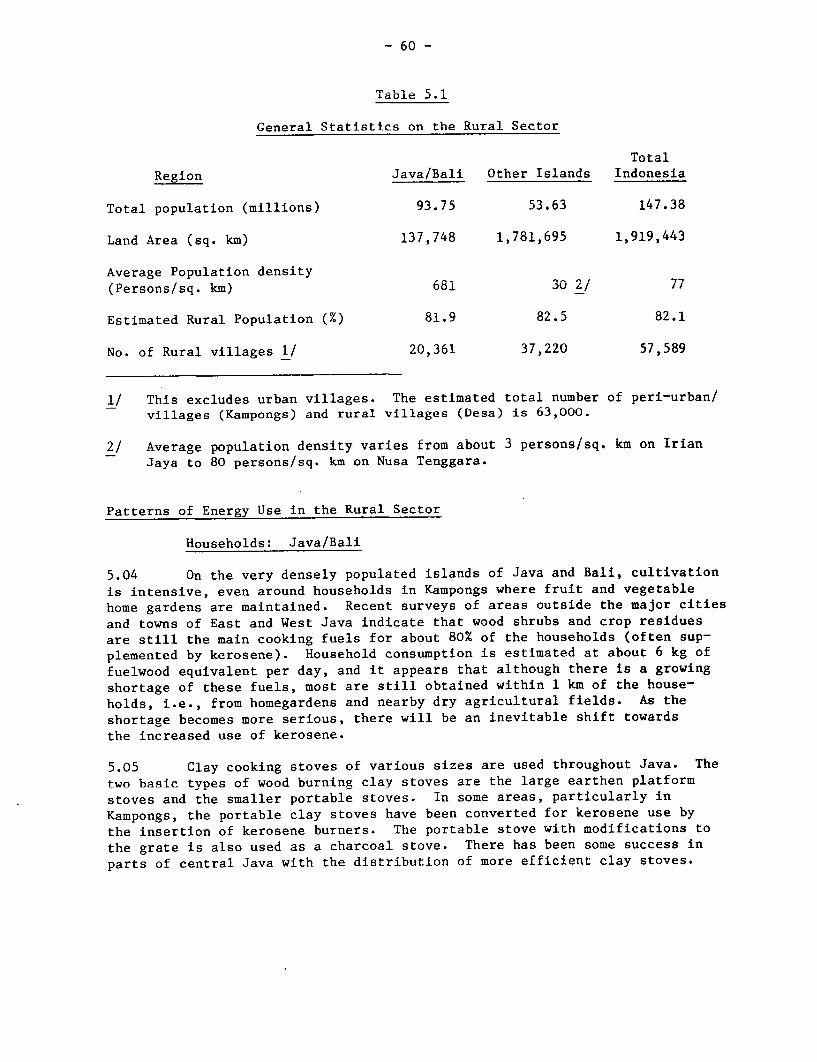

Ch.-apter 5: ?TVD-RG TC'T1TLC ATr f'OPTIONS Th 'rKTY.E DITAT ADVA° I 59

Lnergy Lptlons 'or -le Lural Sector . . . . . . . . . . . 5J2i V~ ' .J L.AJ L . LU . LLII XU .. JO L.L'..

Patterns of Energy Use in the Rural Sector . . . . . . . . 60Households: J ava/ Ba.LL .O. . . . . . . . . . . . . . . UV

Households: Other Islands . . . . . . . . . . . . . . 62cIfRura'l E'Lectric'Lty 'Supp'Ly . . . . . . . . . . . . . . . . . o2

Agriculture ... . . . . . . . . . . . . . . . . . . . . 63Inadustry .... . . . . . . . . . . . . . . . . . . . . . 64

Fuels for Rural Industry . . . . . . . . . . . . . . . 66The Scope for Biomass Gasification . . . . . . . . . . 67

Institutional Considerations for Rural Energy Planning . . 68

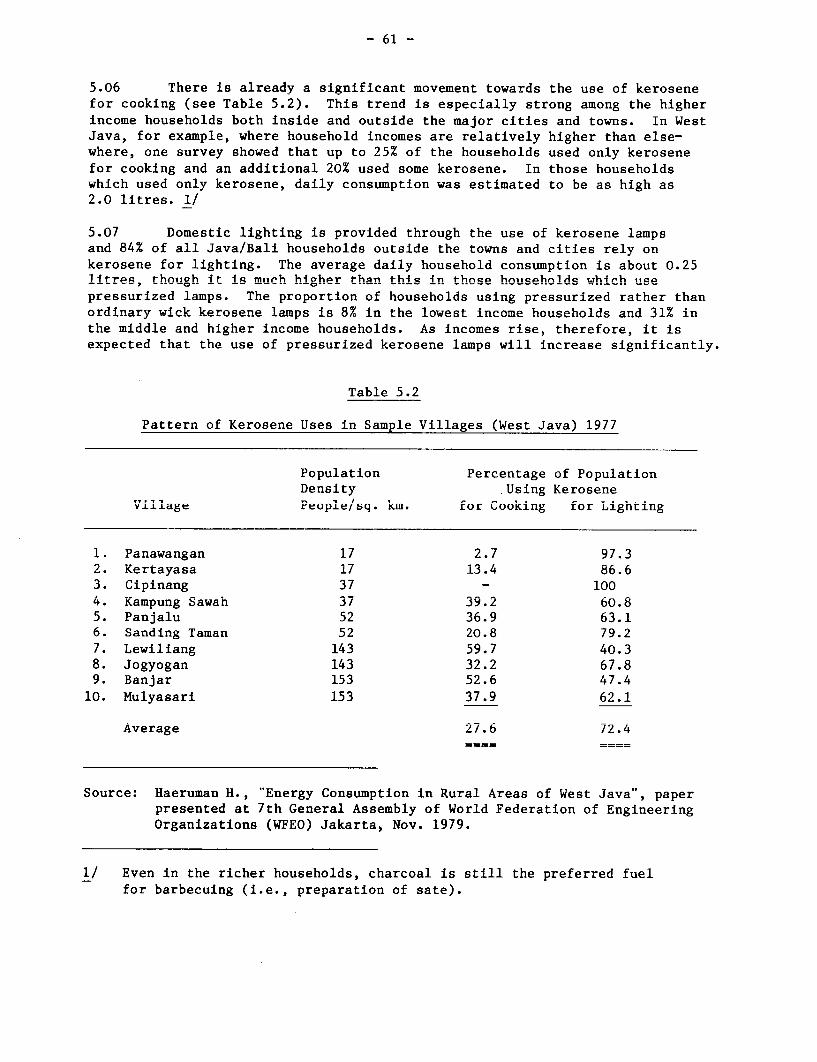

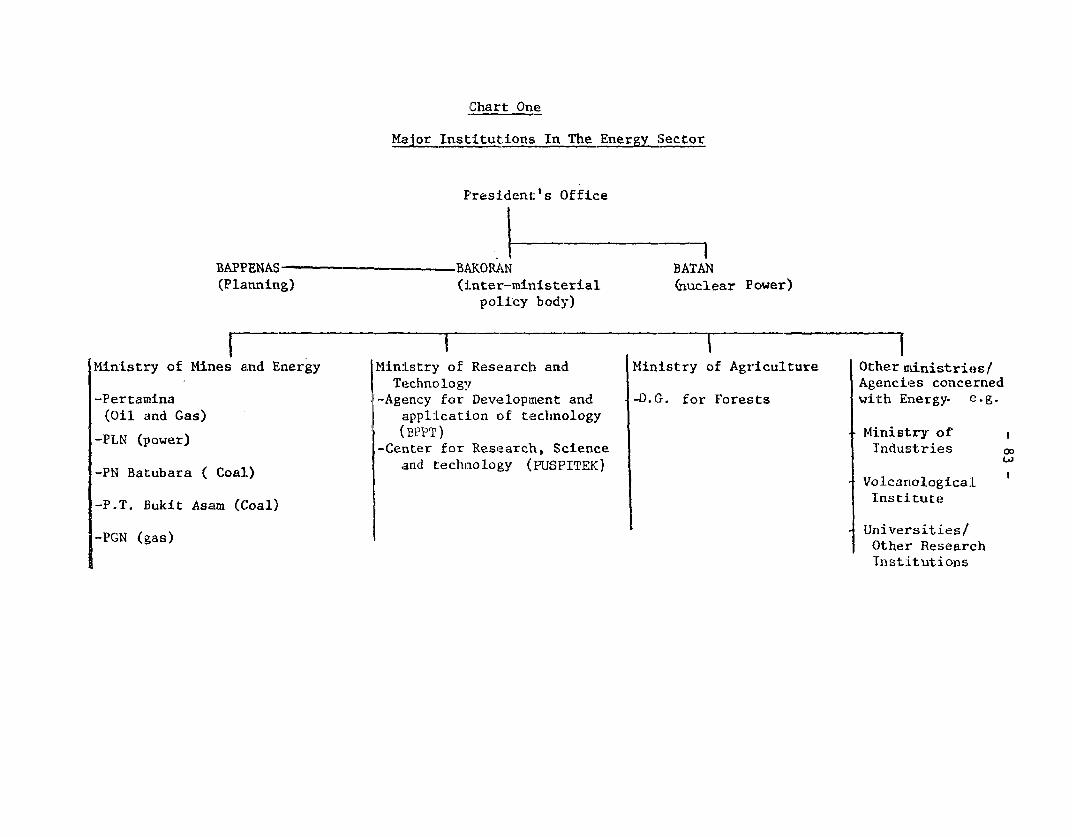

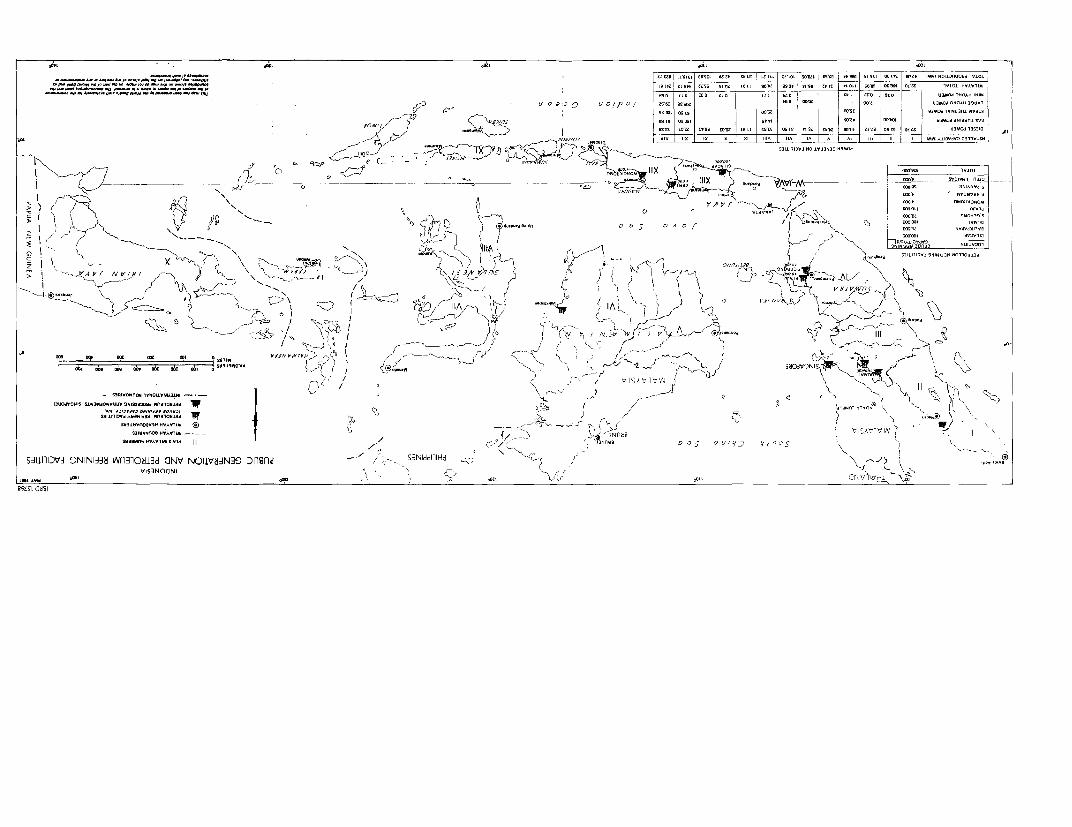

Chapter 6: ENERGY SECTOR ORGANIZATION AND INSTITUTIONS . . . . . . . 70

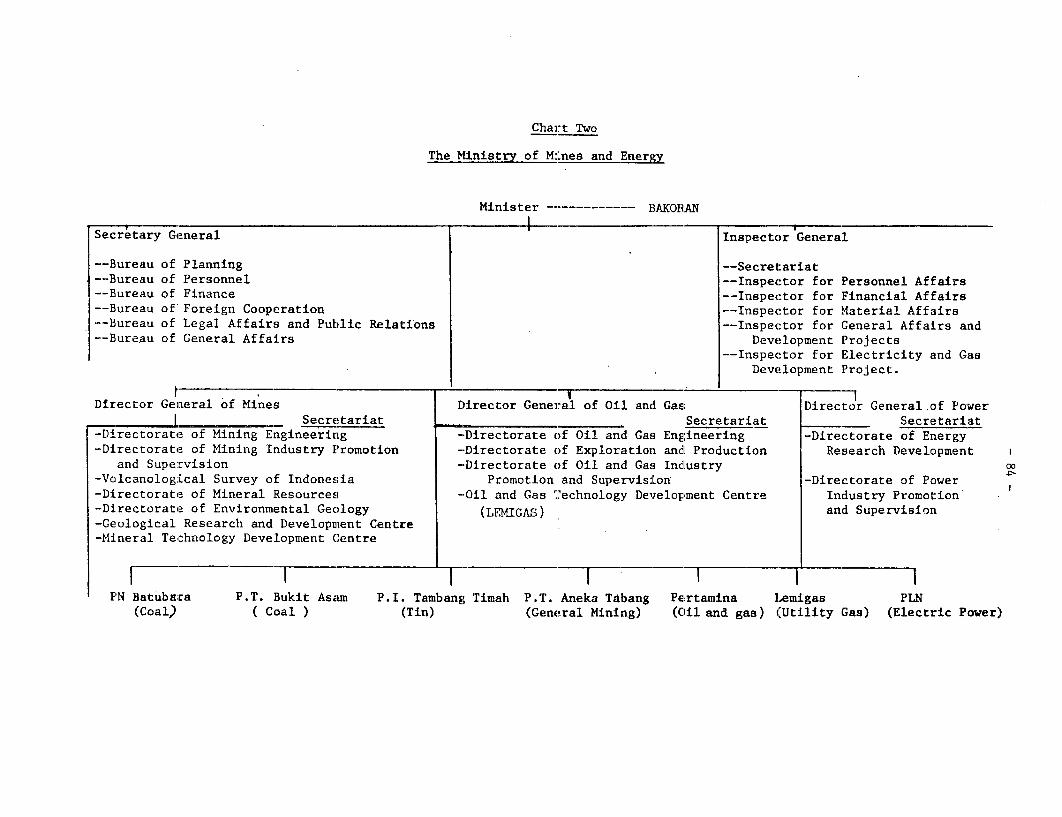

Background .... . . . . . . ..... . . . . . . . . . 70The Ministry of Mines and Energy . .. . . . . . . . . . . 70The Oil and Gas Subsector ... . . . .... . . . . . . 73

PERTAMNA . .. . . . . . . . . . . . . . . . . . . . . 73

The Electric Power Subsector . . . . . . . . . . . . . . 74Perusahaan Umum Listrik Negara (PLN) . . . . . . . . . 74

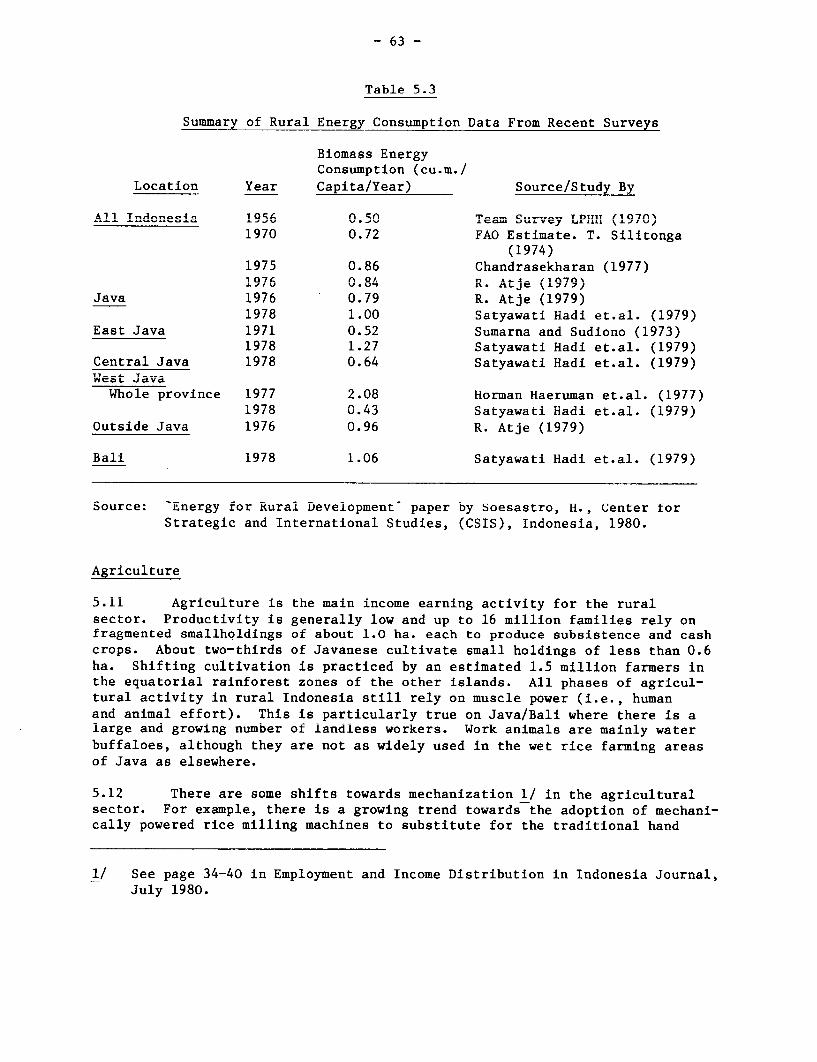

Rural Electrification ... . . . . .... . . . . . . . 76The Coal Subsector ................. . 78Other Institutions ... . . . . . .... . . . . . . . . 80

BATAN . .. . . . . . . . . . . . . . . . . . . . . . . 80Energy Research and Development . . . . . . . . . . . . . 80

Ministry of Research and Technology . . . . . . . . . . 80Other Research Institutes . . . . . . . . . . . . . . . 81

Chapter 7: INVESTMENT IN THE ENERGY SECTOR . . . . . . . . . . . . . 85

ANNEX: ENERGY BALANCES AND PROJECTIONS . . . . . . . . . . . . .

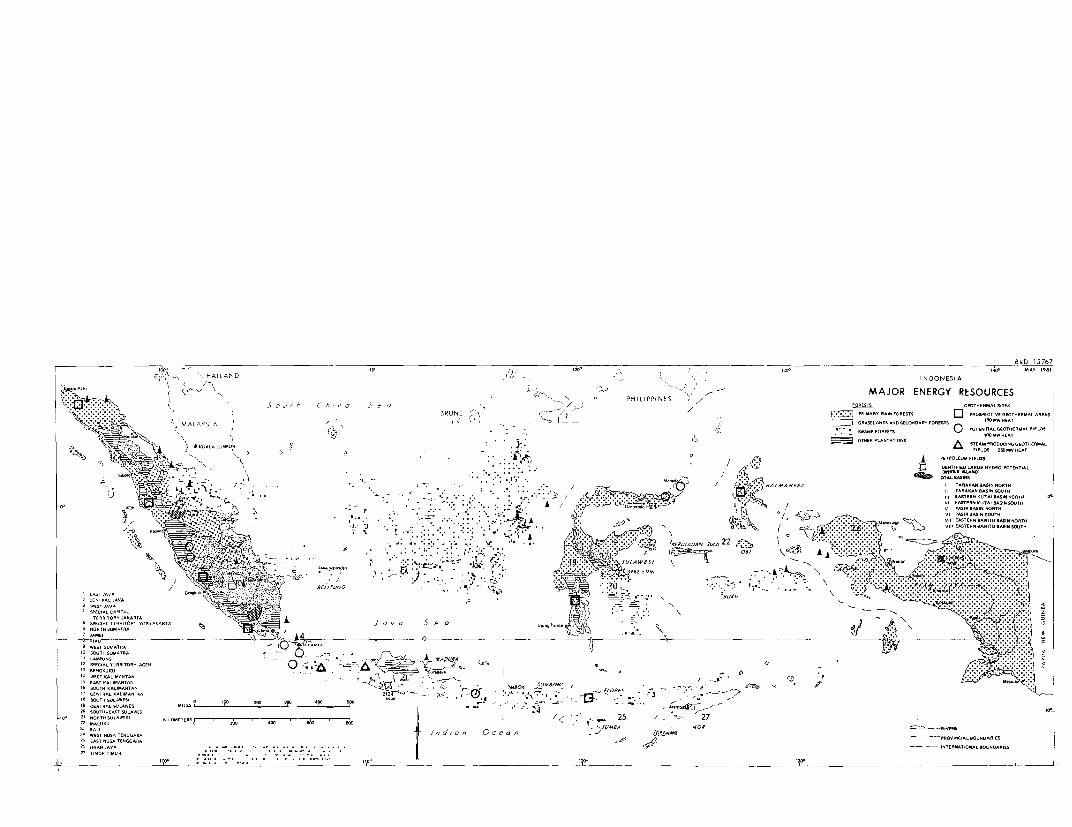

Bibliography .... . . . . . . . . . . . . . . . . . . . . . . . . . 36Maps .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127

This report incorporates the findings of a series of missions toIndonesia between September 1980 and March 1981. The leader of the mainmission was Dr. N.B. Prasad (consultant), who prepared the report. Otherswho contributed to the report were Julian Bharier (leader of the preparatorymission), Ian Johnson, Ion Stancescu (consultant), Richard Berney, EricDaf fern, Amarquay Armar, Max Wilton (consultant), Eric Hassall (consultant},Izzet Zincir, Armeane Choksi, and Julia Tuzun (editor).

TABLES IN TEXT

Page No.

1.1 Energy Consumption, 1960-1978 . . . . . . . . . . . . . . . 21.9 WorArsne -Gonsumto

4n- -a Prr

4,es 196Q-7 A.. . 4

1.3 PLN Sales by Tariff Group, FY79 . . . . . . . . . . . . . . 61.4 Energy Balance, FY 79/80.............81.5 Projected Petroleum Product Consumption . . . . . . . . . . 91.6 Kerosene Consumption ProjectIon, FY79-FY89 .. . 91.7 Consumption of Petroleum Products in the Transport

Sector, FY709-F1Y,89 . . . ........... .......... ........... ........ . 1V1.8 Projected Domestic Consumption of Natural Gas,

FV70-VVQ 0X 1 J L 7 . . . . . . . . . . . . . . . . . . . . . . . . AIA

1.9 Projection of Electrical Energy Sales, FY79-FY2000 . . . . . 121.10 Forecast of Electricity Sales by E=Use... 13

1.11 Energy Balance, FY89/90 . . . . . . . . . . . . . . . . . . 141.12 Commercial Energy Consumption Growth Rates, FY79-FY89

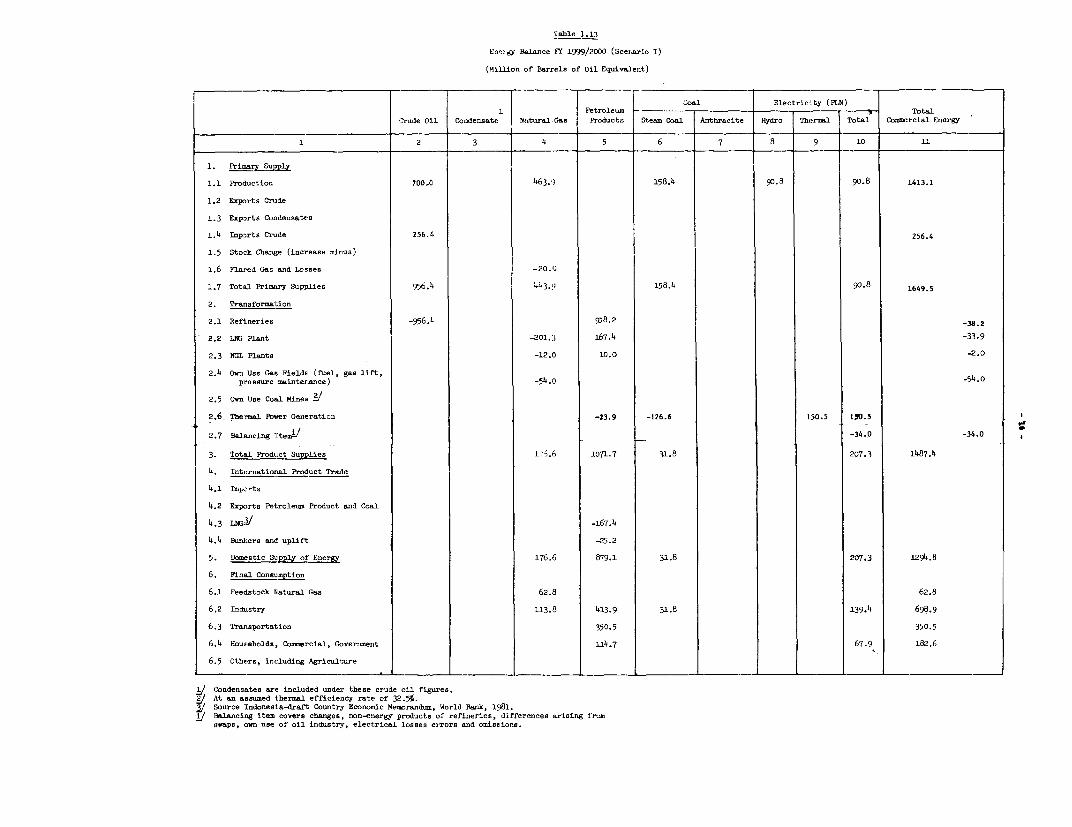

and FY89-FY99 ... . . . . . . . . . . . . . . . . . . . 151.3Energy Balance, FrY99 /2000 (Senr' I)..... 16

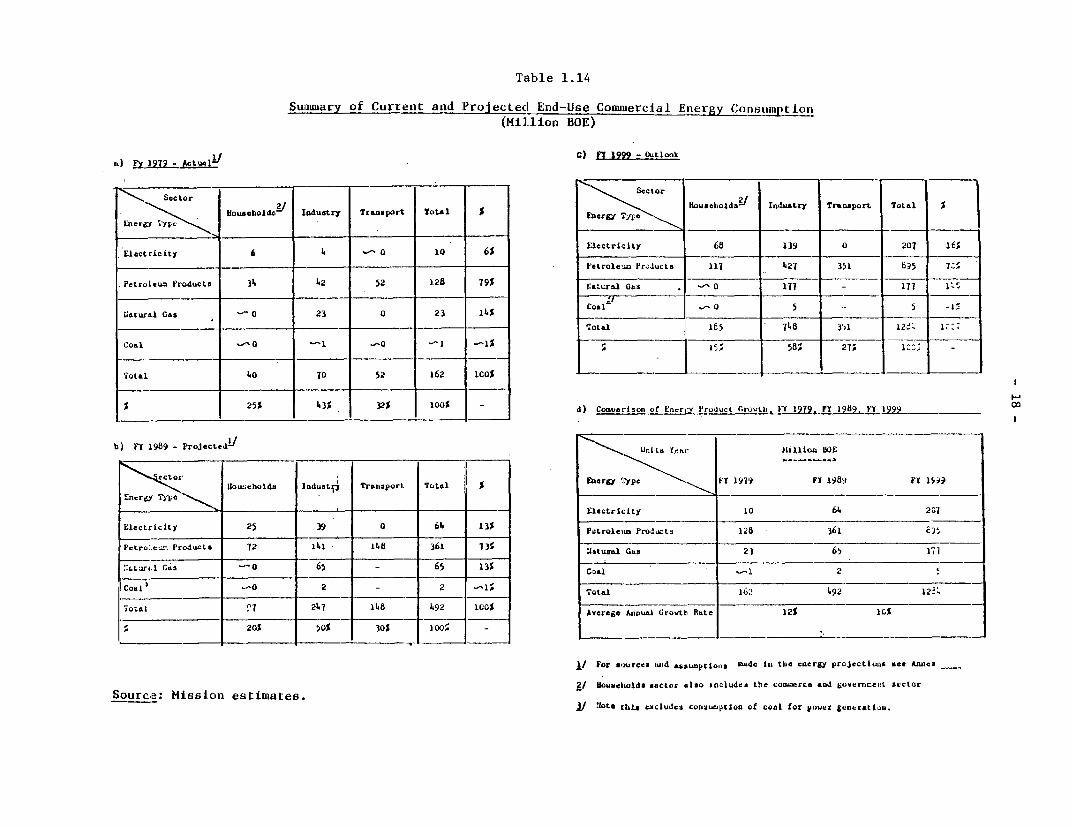

1.14 Summary of Current and Projected End-Use CommercialEnergy Consumption ... . . . . . . . . . . . . . . . . . 18

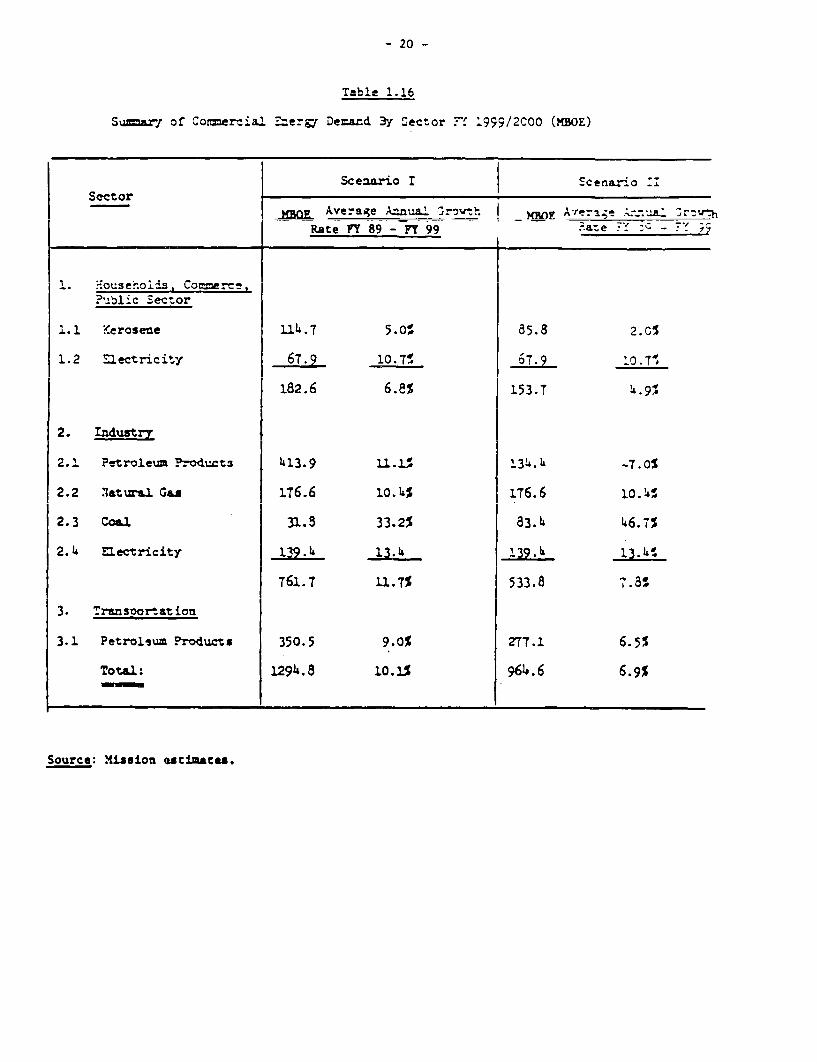

1.15 Energy Balance, FY99-2000 (Scenario II) . . . . . . . . . . 191.16 S-ummary of Commercial Energy Demand Dy Sector,

FY99/2000. ....................... 20

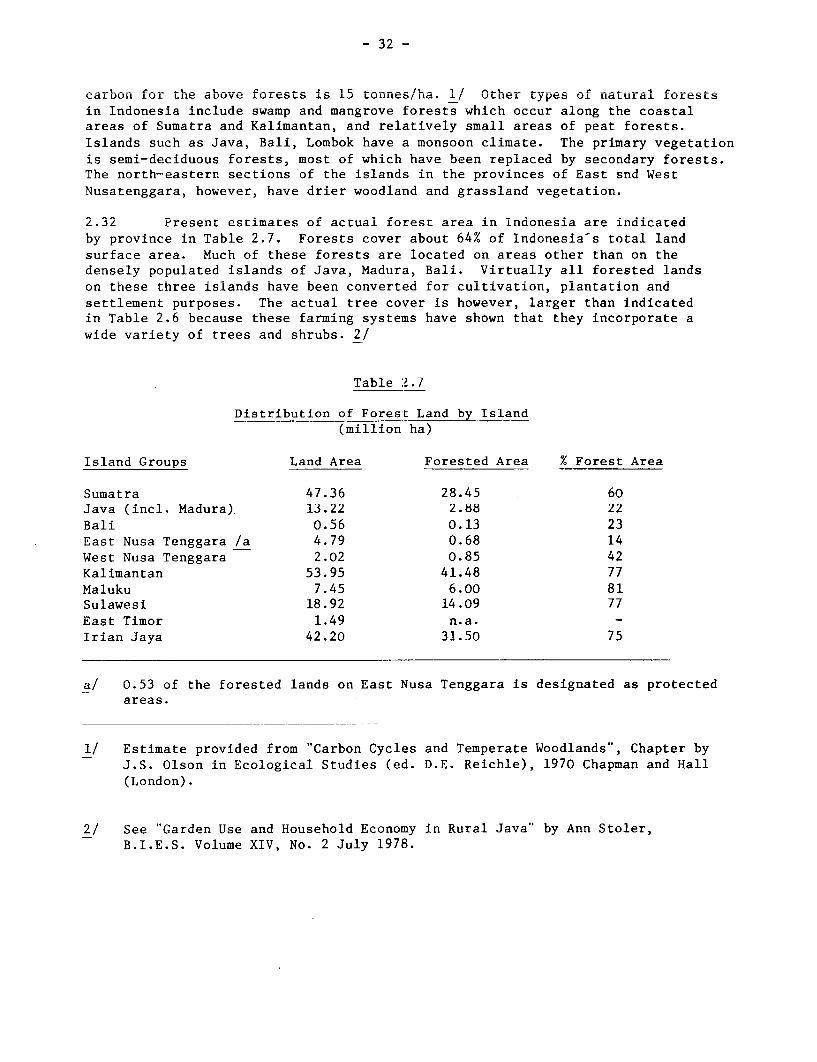

2.1 Total Indonesia Crude Oil Supply . . . . . . . . . . . . . . 222.L indonesian Refineries ... 232.3 Supply Projection - Crude Oil . . . .. . . . . . . . . . . 242.4L Supply Projection - Coal .2.5 Estimated Geothermal Resources . . . .. . . . . . . . . . . 292.6 Supply Projections for Hydro Development . . . .. . . . . . 312.7 Distribution of Forest Land by Island . . . .. . . . . . . 32

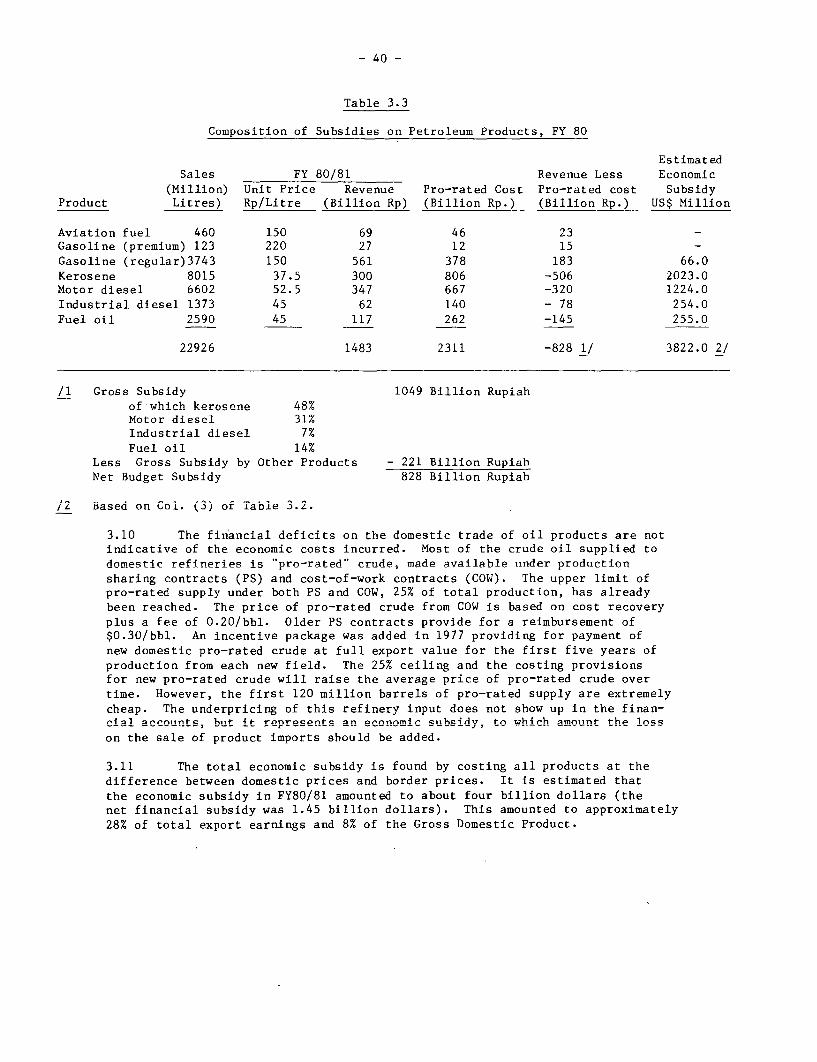

3.1 Apparent Budgeting Subsidies/Taxes on PetroleumProducts ... . . . . . . . . . . . . . ..... . . . . 38

3.2 Retail Prices for Selected Petroleum Productsas of May 1980 . . . . . . . . . . . . . . ...... . . . 39

3.3 Composition of Subsidies on Petroleum Products, FY80 . . . . 403.4 Prices of Natural Gas ... . . . . . . . . . ..... . . 423.5 Domestic Coal Prices, 1980 . . . . . . . . . . . . . . . . . 433.6 Electricity Basic Tariff, 1980 . . . . . . . . . . . . . . . 46

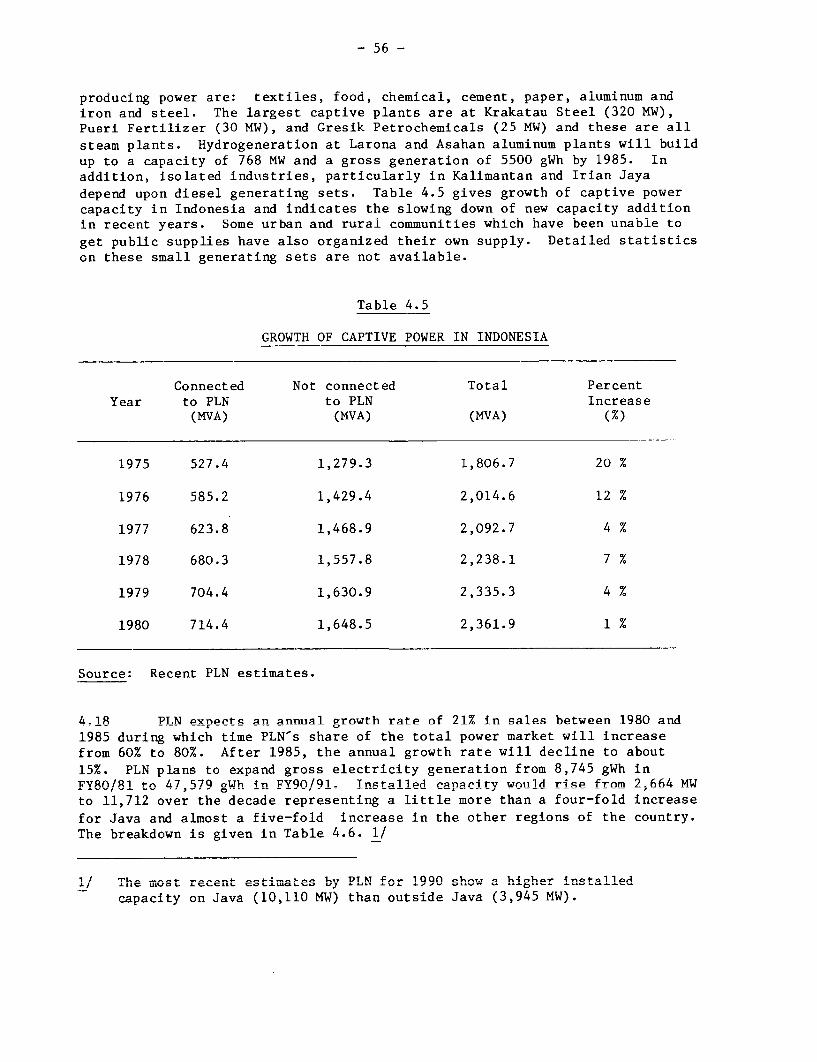

4.1 Household Energy Demand, 1978 . . . . . . . . . . . . . . . 494.2 Comparative Lighting Fuel Costs . . . . . . . . . . . . . . 514.3 Comparative Cooking Fuel Costs . . . . . . . . . . . . . . . 524.4 PLN Installed Capacity - March 1980 . . . . . . . . . . . . 554.5 Growth of Captive Power in Indonesia . . . . . . . . . . . . 564.6 PLN's Investment Program (1980-1990),

Installed Capacity (MW) ............ .... 57

- iv -

P a; g e 1`

5.1 General Statistics on the Rural Sector . . . . . . . . . . . 605.2 Patterr, of Rerose Uses in Sample Villages

(West Java), 1977 . . . . . . . . . . . . . . . . . . . . 61J.J . UUmarLy o'. RU L dL LUII LJfi £LUI AZ L'.LLL

Surveys. . . . . . . . . . . 635.4 Consumption of Petroleum Fuels in Selected

Industries ... . . . . . . . . . . . . . . . . . . . . . 655.5 Relative Fuel Cost as Supplied 'Wholesale to Rural

Industries on Java, 1981 ... . . . . . . . . . . . . . . 67

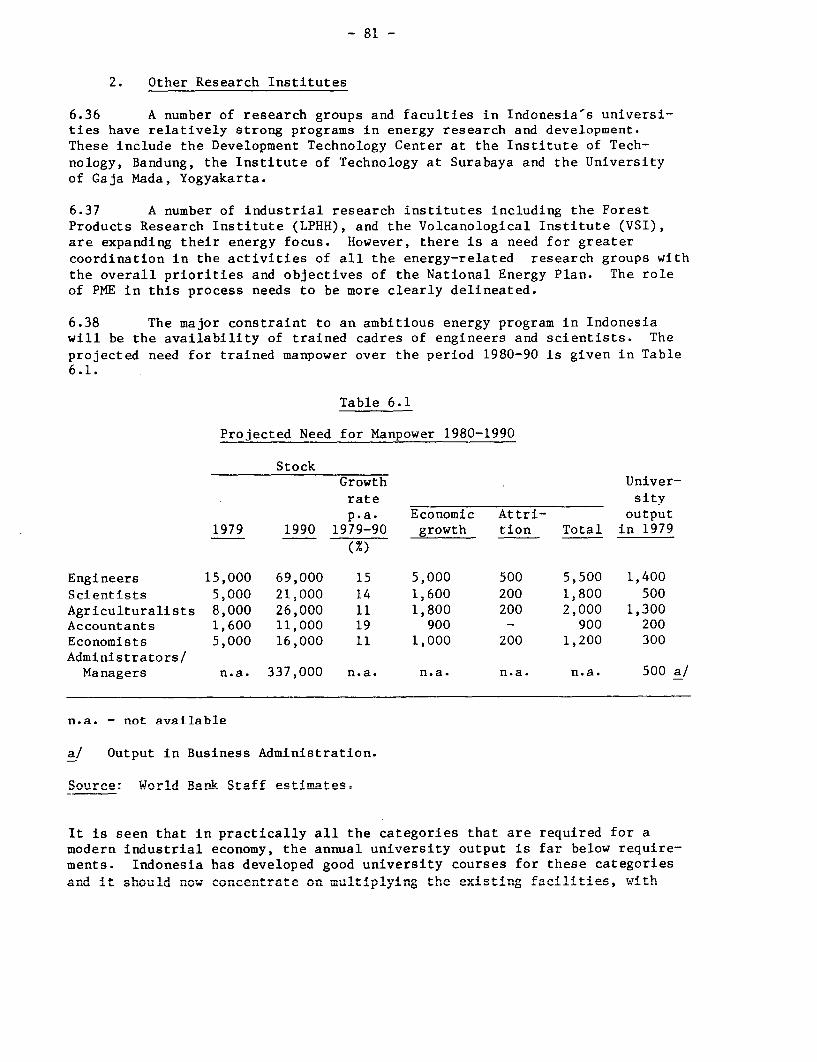

6.1 Projected Need for Manpower, 1980-1990 . . . . . . . . . . . 81

Chart 1 Major Institutions in the Energy Sector . . . . . . . . . 83Chart 2 The Ministry of Mines and Energy . . . . . . . . . . . . 84

7.1 Indonesia: GDP and Energy Sector Investments . . . . . . . 86

INTRODUCTION

i. Indonesia is a major oil producer. Oil meets practically all the

commercial energy needs of the country while oil exports provide the revenues

f 4or most of its current an-d development expeen-ditures. However, the domnestic

demand for oil is accelerating while the oil available for export is declining.Th4o-ut* measures to offs-t this trend, Indonesia could soon find itself

short of the funds that are essential for supporting its economic and social

development. The Governent of Irndonesia (GOI) has already recognized theneed for action in the energy sector and has established an interministerial

group (BAKOREN), headed by the Minister of Mines and Energy, for developing anenergy policy, as well as an Energy Planning Unit for preparing energy plansLor the shILort, medium andu 'long term.

ii. in September 19080, the GOI 'nvited the WorLdU Banl to assess the

problems facing the energy sector; in particular to identify policy options,

analyze investment priorities, provide a framework for technical ass'stancein the energy sector and to advise them on institutional aspects. A recon-naissance misslon visiLteU Inuoesia iLn October/November 1780 anU left an

aide-memoire with the GOI. Following the GOI's response to this aide-memoire,

a follow-up mission visited indonesia in February/March 1981 to study theenergy subsectors and institutions in greater depth.

iii. During the course of this mission, discussions were held withofficials of the various Ministries of the GOT and the institutions/agencies

dealing with the different energy subsectors to ensure that the work of themission was directly focussed on the issues considered most urgent by the GOT.As a result, certain areas of the energy sector have received more attention

than others. The conclusions of the mission were discussed with the GO! in

October 1981, but there are still some areas in which recommendations will notbe possible until further studies are made. This does not in any measure

reflect on the importance or otherwise of the issues which have not beenstudied; it simply reflects the need for additional work. This report is,therefore, just one step in the continuing analysis of the multi-faceted

issues and options facing the energy policy makers in Indonesia.

iv. The major issues and recommendations of the mission are summarized

in the first part of the report. This begins with a statement of the energy

problem, followed by an overview of demand and supply. It concludes with adiscussion of energy pricing policies, the fuel options available to the

country, energy in the rural sector and energy sector institutions.

v. The body of the report starts by reviewing energy consumption trends,

particularly since 1970, and provides a tentative energy balance for FY79/80.Based on these trends and various assumptions about GDP growth, its sectoraldistribution and diversification of the energy base, preliminary indications

of likely future energy demand have been prepared for FY89/90 as well as forFY90/2000 using two scenarios. The first is based on a projection of thehistorical trends and the second on the likely impact of changes in policies

for demand management, conservation and energy export.

- vi -

v' L li r ep r t g s o toe ' u a t e 'L d O L- U -5 i -a - en L-- -- I -e - Ou r C -eV1. LILe LepuLL X gusui LU CVd1UdLt: £LIUU[IIt:id :: Cllt:Lgy L euuLCeS --

particularly oil and gas, coal, geothermal and hydro, and discusses futuresupply poi-cy issues. I't thIlen examies prLicing policy fLor oil prouucts,gas, coal and electricity and continues with a review of the options forinterfuel substitution and for providing enlergy in the rural areas, disLin-guishing between Java/Bali and the other islands. Institutions in the energysector are then discussed, focussing particularly on the need to strengtnensome of these. The final chapter of the report deals with the investmentrequired in the energy sector and the allocation of investment prioritiesamong the different subsectors.

- vii -

ISSUES AND RECOMMENDATIONS

I. The Energy Problem

i. Indonesia is a country richly endowed with energy resources and, as

is well known, a member of the Organization of Petroleum Exporting Countries,

but it is likely to face a severe energy problem in the near future comparable

to the problems faced in most oil-importing developing countries. The problem

arises because only one of its energy resources, oil, has been substantially

developed, and because oil plays such a vital role in the country's social and

economic development. Oil products meet over 80% of the country's commercial

energy needs. Net oil exports are financing practically all non-oil imports,

and oil revenues account for 70% of the Government's total revenues. Since

oil has been relatively cheap to develop, investment in energy has taken only

2% of the Gross Domestic Product which is low compared with other countries at

about the same level of GDP. Moreover, most of this investment has beencarried out by foreign private industry (with its associated technical and

administrative inputs) under production pricing contracts with the Government.

ii. As in most oil-exporting countries, there has, in addition, been a

Icheap oil' policy for domestic energy consumption. This has been implemented

largely by providing heavy subsidies on oil products, especially kerosene,diesel and fuel oil. Together with a GDP growth rate of 7.5%, this policy has

led to a very high growth of demand for oil products. Growth of domestic

demand for oil is now outpacing increases in oil production and oil exports

are showing a declining trend. If unchecked, this will continue to erode the

surplus of oil available for export and, even allowing for the expectedincreases in domestic production and world oil prices, will not only rapidlyreduce the contribution of oil to financing non-oil imports and Government

revenues but could also, within two decades, lead to Indonesia becoming a

substantial oil importer. Further, the subsidies on internally used oil

products, already accounting for 20% of the Government's budget, will increase

the burden. Thus, in a few years, the social and economic development objec-tives of the Government could be seriously jeopardized.

iii. Whereas the problem of most oil-importing developing countries is

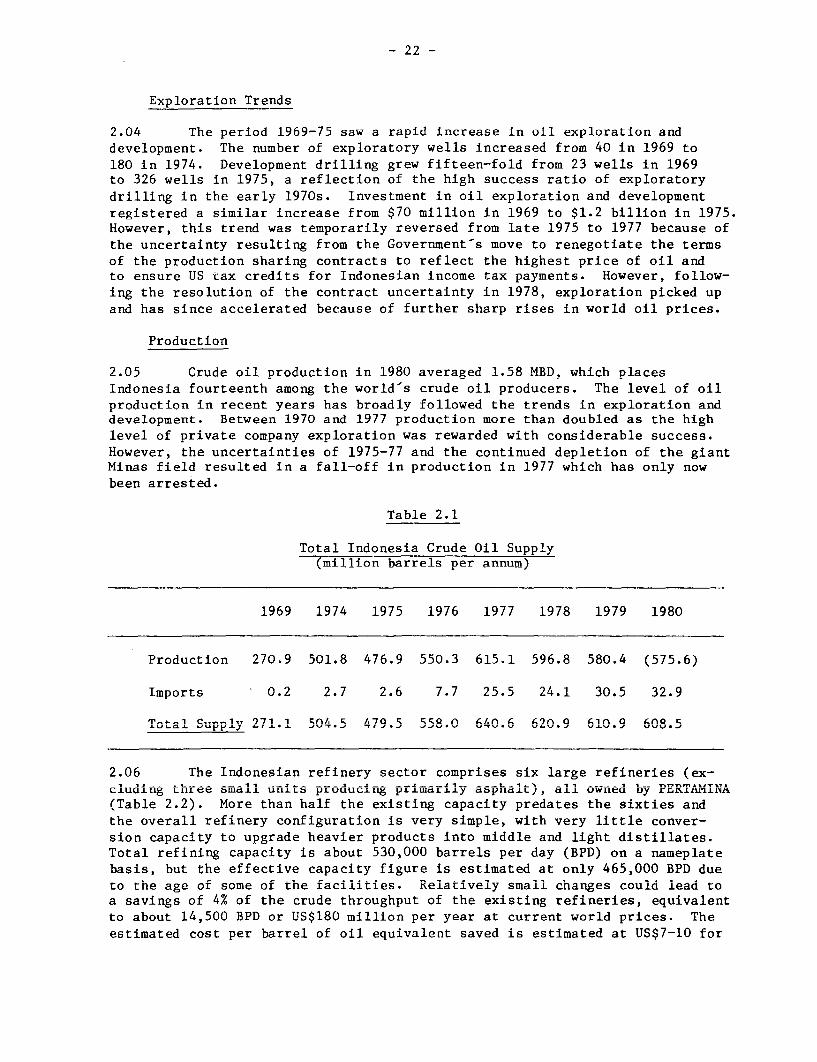

to reduce oil imports, Indonesia's problem is how to ensure a continuationof netroleum exnort earnings. Although the problems differ the remedies in

both cases are remarkably similar in that a major part of the solution lies in

expanding oil nroduction and in develoning other indigenous energy sources in

order to substitute for the oil products used in the country. In the past, a

su1bstantial nart of the investment in the energv sector was devoted to meeting

the needs of the export market which accounted for nearly 62% of the totalenergy produced. Over the next twno decades, domestic energy needs will assume

increasing importance and a substantial part of anticipated investment in the

energy sector will be to meet these needs. While net energy exnort-s-can be

maintained at present levels (about 480 MBOE) during the current decade, witha decline in oil exports being compensated by increased exports of LNG, they

will almost certainly decline over the following decade. Indonesia is in the

early stages of it-s industrial development ar.d will require increasing amounts~aL ~L 0 La5

o 'JL LO .L±U UCUt ~ U V ~~jJUfl~LU aLLwJ~L

- viii -

of energy for meeting domestic needs. It wiii also continue to require theforeign exchange earnings that energy exports provide. Thus, the growth of

the energy sector is the key to tuture economic development. This, in itseif,implies that the level of investment in Indonesia's energy sector will have tobe increased substantially--fourfold in the next decade in real terms and a

further doubling in the following decade. Since much of this increase willhave to be carried out by the public sector, this further implies that majordecisions on national investment allocations will have to be made.

iv. Indonesia has many kinds of energy sources--oil, gas, hydro powersites, coal, geothermal resources and a large biomass potential, but except

for oil and gas, the exploitation of energy resources is in a relatively earlystage of exploration and development. The country has a multitude of options

available for energy development because of this diversified energy base.Indeed, it is the possibility of substitution among primary energy sources,and among individual energy products, that makes the task of the energy

planners in optimizing and achieving a balanced growth of the different energysubsectors a challenging one. Some of the interfuel substitutions can occurrapidly as, for example, a switch from kerosene to LPG in cooking. Otherchanges will occur more slowly as in the case of power generation where leadtimes are long. There are also other policy choices to be made regardingpricing strategies, for example, on the general level of energy prices, on the

relative prices of different fuels to stimulate interfuel substitution, on

prices to encourage production of specific indigenous resources, and on pricesto stimulate more efficient use of energy. There is also the need for conser-vation. For instance, nearly 17% of the energy produced is lost either intransformation or due to flaring; the value of gas flared in FY80 alone is

estimated at US$1.0 billion. These and other policy options need to becontinuously evaluated and appropriate institutional arrangements for nationalenergy planning as well as planning in the energy subsectors is essential.

v. In short, to alleviate its energy problem over the medium to long

term, Indonesia must soon embark on a series of important measures. Themission recognizes that with the country currently exporting substantialquantities of oil and not facing immediate balance of payments problems it maybe difficult to convince some decision-makers and the population at large ofthe need for these measures. However, as it will be several years beforethe necessary investments produce the various fuels in sufficient quantities,there is already an urgency to formulate and to begin to implement a national

energy plan. The mission therefore strongly endorses the recent establishmentof an interministerial group (BAKOREN) for developing an energy policy, and anEnergy Planning Unit for preparing energy plans for the short, medium, and

long term. Furthermore, the mission is impressed by the GOI's commitment, asexnressed in its recent statement of overall energy policy, to developing andimplementing plans to transform the country from an oil-based economy to onein which all Pnprgv rouiirnes are ontimally used in order to support Indonesia's

future economic and social development.

- ix -

II. Energy Demand

vi. Current per capita energy consumption is fairly low, although ithas grown rapidly over the last decade. It is estimated that the per capitaconsumption of total (commercial and non-commercial) energy is only about 2.2BOE, of which nearly 50% is from traditional fuels, namely fuelwood andagricultural wastes, and the rest from commercial energy sources. Oil and gasaccount for 98% of commercial energy consumption; the other 2% comes fromcoal. hvdronower and other resources.

vii. Per ranita ronsumntion of electricity is also low at 76 kWh (1980).Nearly 50% of the generation is in captive power plants, most of it in theindustrIal sector; and the other 50% is generated by the national Dowercorporation, PLN. Of the 57,000 villages in the country, only about 3,000 areplPrt-rified_ reflerting the total lack of access to electricity in most areas

of the country.

viii. The elasticity of commercial energy to GDP is high and was 1.59 forthe period l970-78. It is likely that this will not fall significantly overthe short and medium term, reflecting the growth in population of about 2.3%,the increased substitution of tradition-al fels byr commi a- al fls,l in the

household sector and the growing share of the industrial, transport andservice sectors in the economy. --- t4 14Coerral energy cntion is 1e1,oly tn

increase at an annual rate of about 12% up to 1990 and may increase at 10%subsequently. If so, the probable levels of future demand forn commercial

energy could be about 500 MBOE in 1990 and 1,300 MBOE in 2000, compared toa fi7gure or 1f . Vujr .n loan 16 MEIC.ese tent,at4ve estimates are baseda on currentL

consumption trends and therefore are firmer for 1990. The estimate for 2000£0 OpcLULativE, at-LIU, .Ln LO Lac may never maeLCLalieLCz UCeaUOC loln UCbefULG

demand rises to such a level, Indonesia would have become a net energy importer~LIU Lu[~e4UeI1iy w~y LUL UC a ULt: LU bUPPUL L CL high,1 CkeL1UEUWIUL UW LII La ~LCarldl consequently m1a-y Lr,ot be able to -upr -- hig economi grwt -rate.---

Because of this, the mission presents in Chapter 1 an alternative scenario for2000 which might be feasible if new policies Lor energy UdemandU management an,d

interfuel substitution are successfully implemented and if necessary organiza-t'Lonal an,d 'LnstiLtutLonal changes 'n the energy sector aLe madue. oth scenarios

underscore the need for action to improve energy supplies in the medium termthrough a rapid increase of iLnvestment irn the sector. The impact of demandillustrates the need to improve the data on energy consumption and to introduceformal demand analysis and projections. Indeed, this should be a prioritytask of the recently formed Energy Planning Unit. Chapter 1 provides anexplanation of the mission's tentative estimates and the ways in which thesecan be used to show the need for, and implications of, energy policy decisions.

-x-

III. Primary Energy Resource Development

ix. Indonesia appears to have substantial reserves of oil and gas in,

vast sedimentary basins yet to be explored, signficant deposits of coal with

inferred reserves in the billion of tonnes, and vast geothermal and hydro-

electric potential. In addition, it has a large biomass resource as nearly

64% of the land area is covered with forests. However, while substantialcompared to current levels of consumption, the energy resource base is rela-

tively small on a per capita basis and when compared to likely demand by the

end of the century. Moreover, most of the energy resources are located away

from the main population centers.

x. Before major decisions are made on the best way of moving away from

the massive dependence on oil for commercial energy, it is essential that much

more work be done to prove up the reserves of gas and coal and to firm-up the

potential of geothermal and hydro. Nevertheless, as the discussion in Chapter

2 shows, there are already some indications of the likely pattern of non-oil

primary energy resource development.

xi. Natural gas, though generally located away from the most populated

areas, can play a major role in meeting domestic energy demand not only as a

substitute for oil products, but also as a fuel for power generation. Most of

Indonesia-s natural gas reserves (85%) are not associated with oil production,

and exploitation for uses other than export has been constrained by low

producer prices and poor inter-institutional arrangements. The mission urges that

these policies be changed as they have led to the wasteful flaring of 30% of

the gas associated with oil production. In particular, the mission recom-

mends amendments to the petroleum production-sharing contracts to encourage

the use of gas which is now flared. With these changes the mission considers

that a doubling of production to 353 MBOE is possible by 1990. Inadequate

attention has been paid to natural gas liquids (NGL), which could increasefrom 32 to 80 MBOE by 1985 and there is a clear need for an evaluation of the

relative benefits of using these as a domestic extender for gasoline or as a

spike' for exported crude oil. Furthermore, LPG, which is currently produced

in the refineries and largely exported, and production of which could increase

fourfold by 1988 with the increase in investment in LNG trains, should be used

to replace kerosene in domestic uses because the future world price of LPG is

likely to fall relative to that of kerosene.

xii. Coal has been discovered over large areas in Sumatra and Kalimantan.

but more intensive geological surveys and delineation work is necessary to

upgrade the current figure of only 300 million tonnes for proven recoverable

reserves out of estimated reserves of over 10 billion tonnes. Very little

investment has one into coal expnloration and, given the magnitude of the

reserves likely to be established and the increasing role that coal is expected

to play in industry and power generation, there is a need to accelerate these

programs. While the mission supports the Government's policy of attracting

private industry into co-- exploration ar.d development, it recommends a

reduction in the time period allowed to potential developers either to make

their developmert commitments or to relinquish their concessions= It is

suggested that the Government consider financing the pre-development activities

itself andU tien put tLle areas up for bIs in order to speed up coal develoment

Even if this is done, however, the mission believes that there is likely to be

a shortfall in the domestic coal supply in relation to the future demand for

coal from industry and the electric power subsector.

- xi -

xiii. The mission also recommends that the work on proposals to develop

coal liquefaction and gasification projects be deferred as coal in the required

quantities is not lilkely to be available. Indeed, the mission considers that

not even preliminary studies on these proposals should currently be undertaken

as they will result in the diversion of scarce technical and administrative

manpower away from essential tasks in conventional energy development.

xiv. Geothermal potential is estimated at 10,000 MW but of this only

about 1, r Ml' 'as been i-4entified on a firm basis so far. Althouah a Volcan-

ological Institute has been set up in Bandung and some expertise has been

bult up in geothermal prospecting and evaluation at this Institute and at

PERTAMINA, adequate progress has not been made in prospect identification and

delineation due to irnadequate fundir.g and restrictive operating pr0cedures

Fortunately, over 50% of the potential is in Java, where it is needed most,Dut substantiLal drilling adiU expLoraLory work still has o be carried out to

firm-up the potential and estimate development costs. The mission also recom-

mends the establishment of a public sector agency under the control of the

Directorate-General of Power to encourage geothermal development, to oversee

private sector geothermal contracts, and to expLore for and develop LLLe geo-

thermal resources which do not attract private industry. The mission considers

that if these steps are taken, 400 M of geothermal power could be on stream

by 1990.

xv. The hydroelectric potential of Indonesia is estimated at 31,000

MW. However, only some 2,500 Mw is available on Java, and most of this has

been, or is being, developed. In the rest of the country, development of

hydro potential has received low priority due to the lack oi adequateLy

investigated projects, the long lead time required for construction of hydro

projects and the lack of a long term (15 to 20 years) plan for power uevelop-

ment. A separate hydro survey unit is being established within PLN to carry

out a study on Indonesia½s river basins, to evaluate the nydroelectric poten-

tial on a firmer basis and to build-up a shelf of projects. Once this is

completed it will be possible to assess the potential contribution of hydro

stations for both urban and rural electrification programs outside of Java.

xvi. None of the measures recommended above should detract from the con-

tinuing need to explore for, and develop, new sources of oil, both onshore

and offshore, or to ensure that the country s substantial biomass resources

(especially wood) are used in the most appropriate way. It appears that

recent oil production sharing contract terms have re-established the former

pace of oil exploration activity and should encourage further secondary

recovery activities. However, it is unlikely that annual oil production will

increase beyond about 700 million barrels unless massive new reserves are

discovered. In the areas outside Java/Bali, work is needed on the potential

use of logging and other agricultural residues for use as fuels and, especially,

on the means of transporting these wastes.

IV. Inter-fuel Options

xvii. The energy supply options open to Indonesia are discussed in Chapter

4 largely on the basis of the substitution possibilities of oil products

within the major energy consuming sectors. The key sectors are the household

sector (kerosene), the electric power sector (fuel oil and diesel), the

transport sector (gasoline, diesel and fuel oil), and the industrial sector

(kerosene, diesel and fuel oil).

- xii -

xvJiJ. Energy consumption in the household sector is basicall- for cookingand lighting. For cooking, fuelwood, kerosene and negligible quantities ofLPG are used arld f'or lighting, kerose,e and eLectriLiLty. Current household

use of kerosene is estimated at over 40 million barrels per annum and isexpected to rise rapidly as incomes rise. It is largely Lor this reason thatthe financial (and economic) subsidies on petroleum products have been growingso rapidly.

xix. Preparations should therefore be made, as a matter of urgency, forthe introduction of alternative fuels in the household sector. For cooking, astudy of LPG potential, including marketing and pricing, for replacing kerosenein urban areas and gradual market penetration throughout the whole of Java/Balishould be undertaken. This study should also review the technical and eco-nomic merits of substituting kerosene by methanol for cooking purposesas is being considered elsewhere. Whatever fuelwood is available from privatebackyards should continue to be used since this does not lead to deforestationand it has little or no economic cost. Charcoal is too expensive for useas a basic cooking fuel. For lighting, while LPG can be used in the short tomedium term to replace kerosene, the promotion of electrification of house-holds and specifically in Java/Bali, the longer term development of a nationalpower grid should be given consideration. Outside Java/Bali, while kerosenewould remain the major energy resource for lighting, use of LPG to replacekerosene should be considered as a longer term option.

xx. The industrial sector has three distinct categories of energy re-quirement: feedstock, motive power and heat. The largest use of hydrocarbonenergy in the industrial sector is as feedstock: petroleum products in re-fineries and petrochemicals, and natural gas in fertilizers, methanol andpetrochemicals production. Many of the existing plants in these industriesare not as energy efficient as the plants now being designed and there aresubstantial opportunities to increase energy efficiency by retrofitting. Inthe case of motive power, a vigorous effort is required by the Government toensure that reliable power is supplied by the national agency for power (PLN)and that the small diesel-based private generating plants on Java/Bali areretired. For heat requirements several alternative forms of energy are avail-able: oil products, primarily fuel oil, diesel and kerosene, gas, coal andfuelwood. The most obvious way of reducing the use of oil products in indus-try is the increased use of natural gas, although as long as domestic gasprices are far below the opportunity cost (as feedstock for LNG) there islittle incentive to promote production. As the pricing discrepancies areremedied over time, increased attention should be given to the developmentof a natural gas based industrial sector. This can only occur if gas trans-mission pipelines are developed to meet the needs of the large industrialplants, industrial estates and power stations. A corollary of this is thatattention should be given to locating industries within reasonable proximityof the energy resources used, especially natural gas. In some cases (suchas cement plants) the use of non-oil fuels (such as coal) could be made manda-tory. Attention should also be paid to developing the cogeneration potentialof lumber mills and large industrial plants on the other islands. Specialemphasis should be placed on reducing the diversion of kerosene into indus-trial use and one of the ways this can be achieved is by segregating kerosenemarketing from the marketing of other liquid fuels. In this regard, the Gov-ernment might consider as one option taxes on bulk transport and distributionof kerosene; together with distribution of kerosene only in 10 or 20 litercans for household purposes; this technique has worked well in other countries.

xxi. With the exception of negligible quantities of electricity used intLie ra'.lway subJsector, consufmptioni o0 enCergy 'n1 the transport sector is whollyconfined to petroleum products, principally gasoline and diesel, and some fueloil in inter-islanud shipping. Indeed, the transport sector is the Largestconsumer of oil products and is likely to continue to account for 30% of allcommercial energy consumption. The only possible alternatives to oil proUuctsare NGL, LPG and alcohol. With increasing production of natural gas, therewill be corresponding increases in the amounts of NGL, and, as noted abovethere is a need to assess the economic viability of using NGL as a substitutefor, or extender of, gasoline. LPG is a potential substitute for diesel aswell as for gasoline, but since it requires a spark-ignition engine it canonly be considered as a repiacement for diesei as part of a program forreplacing or adding to bus fleets with new engines. It is unlikely, given thepremium on land and the relatively high cost of producing ethanol, thatalcohol from biomass will prove to be a viable option as an extender of eithergasoline or diesel on a large scale in the near future. The mission considersthat there is no need to replace the fuel oil used in inter-island shippingand some industries, largely because this is probably the most effective wayof utilizing this product which is inevitably produced by the refineries andfor which it is desirable, on technical grounds, to maintain a reasonablelevel of demand. On a broader front, the longer term potential for energydemand management in transport, including widespread railway electrificationand urban public transport systems, as well as changes in transport modesparticularly on Java/Bali, needs to be analyzed. The automobile industry canbe encouraged to concentrate more on the production of fuel efficient vehicles.

xxii. The strategy for the development of the power sector is consistentwith the GOI's energy policy to diversify from oil-based generation and usegeothermal, natural gas, coal and hydro resources. Much emphasis is beingplaced on the development of domestic coal as a fuel for power generation,but, as already mentioned, unless a vigorous exploration effort is initiated,coal may not become the expected backbone of the electric power sector.Indeed, the uncertainties associated with coal development are such thatmulti-fuel-fired plants (coal/gas/oil) should be planned whenever possible.In line with this, feasibility studies should also be done on the alternativesof gas pipelines, coal transport, and electricity transmission from mine-headplants to load centers not only on Java and the other major islands butalso between islands, especially Sumatra and Java. Geothermal and hydrodevelopments have already been mentioned; in the short run the rapid develop-ment of geothermal resources on Java/Bali for base load appears to be essen-tial, while for peak load service hydroelectric power stations should beplanned after the necessary resource identification effort.

xxiii. BATAN, the national agency for atomic energy, had originally consi-dered commissioning a number of nuclear power stations, but given the potentialfor gas, coal, geothermal and hydro in the medium-term and the lower cost ofpower from these sources, the mission agrees that it would be prudent to defercommitment to a large program until more information is available on competingenergy resources. Plans can however be made for the installation of a singlecommercial-size nuclear power plant in order for the country to gain experiencein nuclear technology and have this option available for the longer term.

- xiv -

xxiv. For smaller power plants, especially on the other islands, greaterefforts at supplementing diesel-based generators will be required. Bothwood-based thermal (including gasification) and mini-hydro generators could bedeveloped; these would equally provide a basis for possible future connectionsto grid systems. On Java, where there is already an emerging grid, themission recommends that consideration be given to using this grid system toserve the rural areas in the longer term.

V. Energy in the Rural Sector

xxv. The mission recommends (in Chapter 5) that the special energy needsof the rural areas be met in different ways on different islands. In partic-ular, since it is increasingly difficult to distinguish between the urban andrural areas on the densely-populated islands of Java and Bali, provision ofenergy to rural areas on these islands should be an integral part of the supplysystem to urban areas. This is possible because there is already widespreadcommercialization of energy on Java/Bali, even for traditional fuels such aswood, although the availability of these traditional fuels appears to bediminishing rapidly. Thus, the recommendations made above on the fuel optionsfor households, industry, transport and electric power are appropriate forthe rural areas of Java and Bali. For rural, small-scale industry on theseislands (75% of total small-scale industry) the provision of energy is espe-cially important because, although it accounts for only a small proportion ofmanufacturing activity it represents a substantial proportion of employment.It is estimated that nearly 1.2 million small-scale enterprises are scatteredthroughout the rural areas of Indonesia, providing up to 80% of total employ-ment in the manufacturing sector, but contributing only 12% of gross outputand 14% of total value added to manufacturing. The productivity of theseenterprises could be improved greatly by providing them with easy access toelectricity.

xxvi. Very little commercial energy is being used in agriculture today, butthis is likely to change in the coming years as animate power is replaced bymechanical power in many farming operations for increasing agriculturalyields. While this has not been taken into consideration in the mission'stentative energy demand forecasts, it should certainly be a factor in theforecasting work of the Energy Planning Unit.

xxvii. On the other islands rural energy needs for household cooking andindustry can be largely met by fuelwood. or, possibly, by charcoal and/orgas produced from wood or rice husks. Where kerosene is currently used forlighting it may well continue to be the most economic option unless thetransport and distribution of LPG as a substitute proves to be competitive.It is especially important on the other islands to establish a strong organ-ization for planning and implementing rural energy programs. To this end, themission recommends that a Rural Energy Policy Coordinating Task Force beestablished within the Energy Planning Unit.

VI. Pricing and Subsidies

xxviii. The mission considers that current petroleum product pricing is amajor constraint to the Government's stated policy of replacing oil by otherindigenous energy resources. This pricing policy is characterized by massive

- xv -

financial (and economic) subsidies on almost all petroleum products

which, in addition to the fiscal strain on the Government's budget! is provid-

ing a clear disincentive to potential producers of non-oil resources and is

encouraging the ranidly growing use of netroleum products (sometimes wastefully)

rather than other fuels. The oil products subsidies are dominated by one

product, kerosene, accounting for about 50% of the economic subsidy. As

kerosene can be substituted for diesel in the transport sector and for fuel

oil in the industrial sector, these two fuelLs are also subsidized. Indeed,

if it were politically fea,sible to remove the subsidy on kerosene, many of the

other problems relating to energy product pricing would automatically be

solved.

xxix. The rationale fcor the subsidy on kerosene has been that it replaces

the fuelwood used for cooking and this prevents deforestation and heLps the

poorer households. This cibjective is of relevance only on Java/Bali because of

the ample supply of fuelwood elsewhere. In Tava/Bali, the kerosene subsidy

seems to have been effective in replacing the use of fuelwood except for thepreva'Lence of backyard wocUl.ots which is the most economic way of providin-

cooking fuel, even in comparison with subsidized kerosene. The removal of thekerosene subsidy, if accompanied by measures to further stimulate backyard

woodlots and alternate fuels (as discussed in Chapter 4) would be desirable,especially as the benefit of the present subsidy has gone more to the affluenthouseholds than to the poorer households. There is also evidence that kerosene

is being UdvertedU to industrial use, including thle cement indutry, as the

price differential between kerosene and fuel oil makes it profitable to do this.

xxx. The mission supports the Government's stated policy of eventually

withdrawing subsidies while recognizing the difficulties inherent in this

process. The discussion of energy pricing in Chapter 3 therefore takes into

consideration not only the opportunity costs of different energy ULorms but

also the possibility of lower market prices for some products, particularly

LPG which is a direct substitute for kerosene. If the segregation ofr kerosene

marketing, as suggested earlier, is achieved, there would be little need for

subsidies on other liquid fuels except those designed to help the poor, or

promote specific regions or industries. In such cases, subsidies should be

rearranged so as to ensure that they reach those for whom they are designed.

xxxi. With respect to natural gas, the mission recommends that in all

areas where non-associated gas exists, the producer price should be put at

its opportunity cost as LNG feedstock to stimulate the production of gas for

indigenous use. The government may in some cases consider that a lower

producer price may provide sufficient incentive and therefore tax the differ-

ence between the price and the opportunity cost. To promote the use of gas,

subsidies on the retail price of gas may be required until the subsidies on

competing fuels, especially fuel oil and coal, are removed, but efforts should

be made to shift the subsidies 'downstream' whenever possible (e.g., to the

retail price of fertilizer in the case of gas and the prices of inter-island

shipping in the case of fuel oil). Where gas is associated with oil produc-

tion, and especially where the gas is currently flared, use of the gas can be

encouraged by using a pricing formula based on its marginal cost of production,

transmission and distribution in petroleum production-sharing contracts.

- xvi -

xxx 1i i. In' ' L LILh respectL Lto coalL, the principle of priJc.ing on the bIasUis ofU th.Leopportunity cost of importing an equivalent fuel has been accepted by thegovernment andU the m'issiLon supports this principle.

Xxxiiti. Th1_e m'ssion a'so supports the recenLt adoption byILN feetiA.AAIIL. Lil UIL bLUI.LUb~LL L [Li LCCI UUPL.ULL uy ruN 01 t.!1LCLL1C1LY

tariffs reflecting long-run marginal costs, although regular revisions areessential as tnese costs chRange. Further cnanges are also required in thetariff structure, especially important are increases in the tariffs for mediumand high voltage users. Moreover, the policy of uniform tariffs across thecountry should be reconsidered once the long-run marginal costs of electricitysupplied outside Java can be estimated.

xxxiv. Energy prices and subsidies have to be viewed in the context of aneed for demand management and efficient interfuel choices in the long term.It has to be ensured that the present pricing policies do not distort futureconsumption and demand patterns and become counter-productive to energypolicies. As Indonesia diversifies its energy base, and as opportunities forinterfuel substitution become more and more possible, it is essential thatcomprehensive pricing policies be evolved and that they cover all of theenergy subsectors.

VII. Institutions

xxxv. The GOI has already recognized the need for developing and implement-ing a national energy policy to support Indonesia-s economic and socialdevelopment. As a first step, an Energy Planning Unit has been establishedin the Office of DG of Power. The GOI has also established an interministerialgroup, BAKOREN, headed by the Minister of Mines and Energy for developingan energy policy and ensuring its implementation. There is a need to strengthenthe planning unit and also to place it in the Office of the Minister of Energyand Mines so that it can effectively coordinate with all the Directoratesdealing with energy. Chapter 6 indicates the major terms of reference of thisunit.

xxxvi. Among the many studies recommended in this report, some should becarried out urgently to provide policy options to BAKOREN. These include:

(a) Developing (on the basis of planned GDP growth and its sectoraldistribution) energy demand forecasts and a series of alterna-tive plans over 5, 10 and 15 year periods for meeting this demand;

(b) the feasibility of using LPG to meet the cooking and lightingneeds of the household sector;

(c) alternative transport for energy, including coal shipments, elec-tricity transmission from mine-head plants and natural gas pipe-lines to planned and projected thermal power stations, especiallybetween Sumatra and West Java.

(d) the economics of the complete electrification of Java/Bali as alonger term substitute for kerosene in lighting taking into accountthe income e-lnt-icitv of kerosene in thiq case;

- xvi i -

(e) the feasibility of wood gasification plants on the other islandsto run stationary engines for power generation to meet isolatedloads; and

(f) a marketing strategy for kerosene, especially segregation of itsdistribution system from other petroleum products.

These studies are in addition to studies already proposed for (a) utilizationof flared gas; (b) city gas distribution systems; and (c) LPG marketing. Forthe medium term, studies to assess the potential of geothermal and hydro arerequired, while a similar effort is required for coal in addition to thepreparation of a rational coal policy.

xxxvii. The success of such an ambitious energy program will depend onthe strength of the relevant national agencies or institutions. These arePertamina in the case of oil and gas, PLN in the case of electricity, PNBatubara in the case of coal, and BATAN for nuclear power. The missionconsiders that geothermal development may proceed at a faster pace if aseparate agency is formed for it. Most of the institutions in the energysector still require strengthening, particularly PN Batubara. In view ofthe wide diversity of its operations, some structural changes may be desir-able in the case of Pertamina.

xxxviii. The major constraint for an ambitious energy program, however, isnot the institutions themselves, as the higher echelons of management of theseinstitutions are indeed very competent, but the availability of a cadre oftrained geologists, engineers and scientists for all these energy subsectors.These people are simply not available in sufficient numbers, and steps shouldbe taken to assess the trained manpower needs of the various energy organiza-tions and to increase the enrollment at the universities/technical institutesaccordingly. In the short term, it may be necessary to increase the scope oftechnical assistance schemes in all areas where such shortages are felt.

VIII. Investment

xxxix. The energy requirements of Indonesia will rise rapidly over thenext two decades and will require a maior increase in investment in all theenergy subsectors, most importantly in the power subsector. Public sectorinvestments are expected to rise from a current level of about US$1.25 billionto over US$10 billion by the turn of the century in 1980 prices. As a percent-age of GDP. these investments in the energy sector are expected to rise from2.1% in 1980 to 3.9% in the year 2000. On a cumulative basis, they couldamount to about USA38 billion in the current decade alone. The oil and gassector alone would account for nearly 50% of these investments, and the powersector for nearly 45%. While the mission recognizes that investment in theoil and gas sector should continue to have the highest priority, because oiland gas are exnected to meet most of the demand for commercial energv overthe next two decades, a crucial part of the investment program is the US$350mTillion reqaiire for siurveys and the delinestion of coal, hydro and geothermalresources.

CHAPTER 1

£~LlJ~1xu. L .AJ1AO.Uk1rl I £JN LiJUlu Er ) L.?ij) L~ r'u I r UI\ JEI±11'U4J

Background

1.01 This chapter examines the basis for energy demand forecasts to 1990and provides an 'nitial attempt at tentative estimates for 2000. The import-ance of these estimates is that they indicate the onset of a serious energyproblem in IndonLesia, one which could seriously Jeopardize tne country ssocial and economic development objectives unless important policy and invest-ment decisions are made in the near future. The chapter reviews the reasonsfor the low current demand for energy and explains why this will rise rapidlyin the coming years. Then, from the basis of an energy baiance prepared for1980 it examines the likely demand position in 1990 for the various fuels andthleLr eIIU-uses. The chapter ends with two scenarios for the year 2uuu, onewhich is speculative since it would inevitably lead to a major setback inenergy exports and economic growth (and therefore energy demand) before itactually materializes, and one which may be feasible for the country toachieve if appropriate policy measures are undertaken.

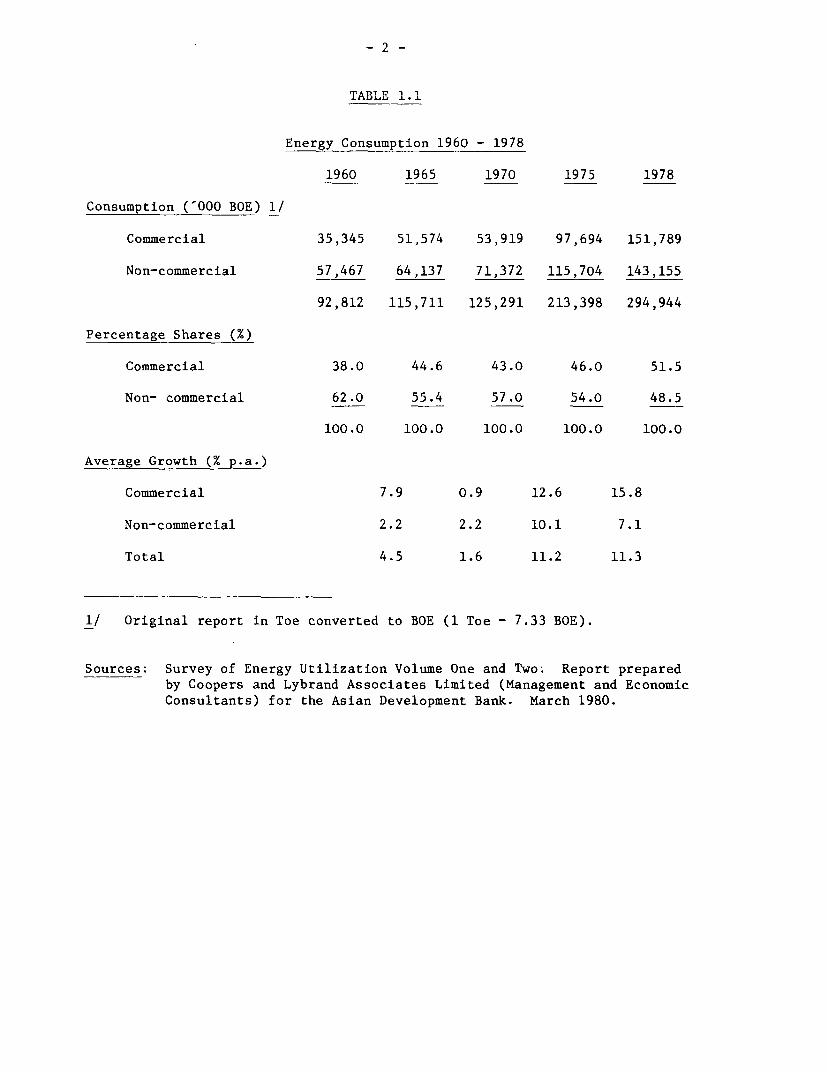

1.02 Commercial energy consumption in FY79/80 is estimated at about 162MBOE. The latest available estimate for non-commercial energy consumption isfor 1978 and is nearly as large, 143 MBOE. Total energy consumption in 1978was somewhat lower on a per capita basis in Indonesia (2.2 BOE) than inThailand (2.7 BOE) or the Philippines (2.8 BOE), but higher on a per - thousanddollar of GDP basis (Indonesia, 6.1 BOE; Thailand and the Philippines, both5.5).

1.03 While declining as a proportion of the total, non-commercial fuels(agricultural residues and fuelwood) accounted for an estimated 48% of 1978energy consumption, compared to 62% in 1960 and 57% in 1970. Petroleumproducts comprised 43% of total supply, having risen considerably in relativeimportance trom 30% in 1960 and 38% in 1970; natural gas (8%) and hydroand coal (0.5% each) contributed the balance. The pattern of consumption ischaracterized by both regional and sectoral variations. Non-commercial energyis used almost entirely in rural areas and commercial energy mainly in urbanareas. Kerosene is used in both.

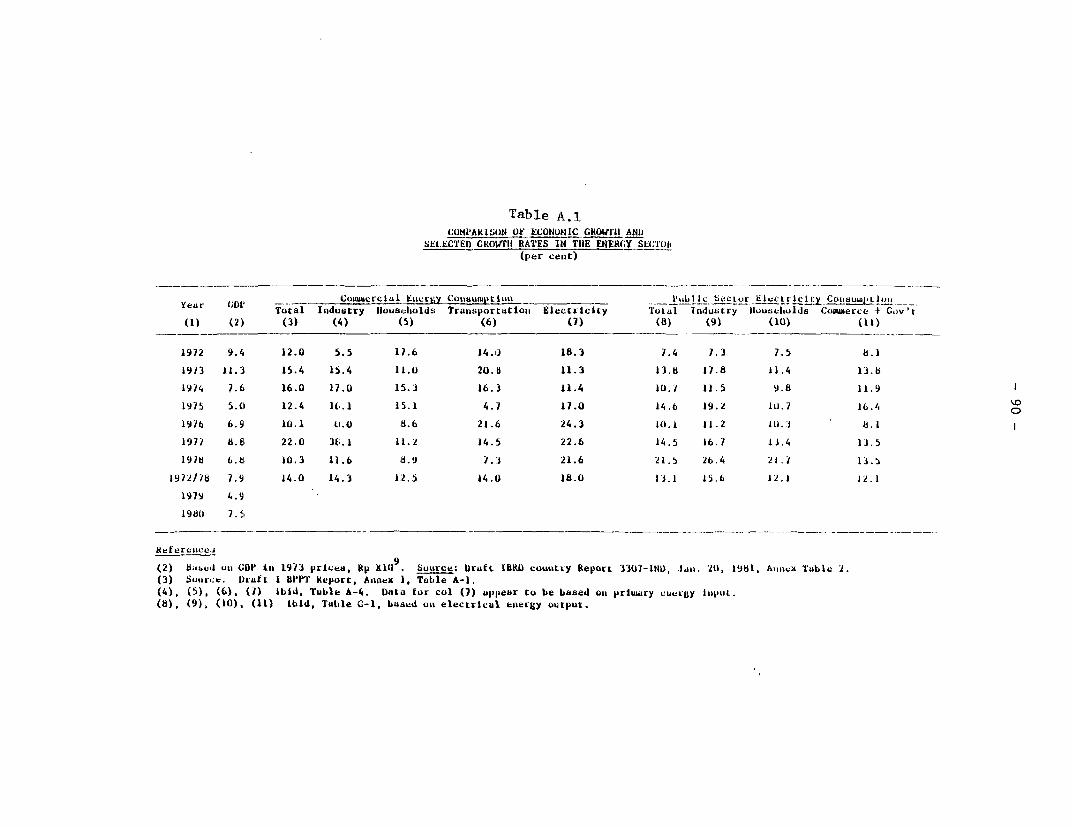

1.04 The growth rate of total energy consumption from 1970 to 1978 wasabout 12.6%, considerably above the average GDP growth rate of 7.9%, givingan average energy/GDP elasticity of 1.59. However, in more recent years,since 1974, the energy/GDP elasticity has been 2.1. This is because until1975, the household sector was the largest consumer of commercial energy.By FY79/80 though the industrial sector had grown to become the largest,consuming approximately 38% of total commercial energy, followed by trans-port (29%), households (25%) and the electricity sector (7%). This isreflected in the particularly rapid growth of commercial energy consumptionin the period 1972-78 in the electric power sector, the industrial sector,and the transport sector, which had annual average growth rates of 18.0%,14.3% and 14.0% respectively compared with the domestic sector growth rateof 7.9%.

-2 -

TABfLI I 1

Energy Consumption 1960 - 1978

1960 1965 1970 1975 1978

Consumption ('000 BOE) 1/

Commercial 35,345 51,574 53,919 97,694 151,789

Non-commercial 57,467 64,137 71,372 115,704 143,155

92,812 115,711 125,291 213,398 294,944

Percentage Shares (%)

Commercial 38.0 44.6 43.0 46.0 51.5

Non- commercial 62.0 55.4 57.0 54.0 48.5

100.0 100.0 100.0 100.0 100.0

Average Growth (% p.a.)

Commercial 7.9 0.9 12.6 15.8

Non-commercial 2.2 2.2 10.1 7.1

Total 4.5 1.6 11.2 11.3

1/ Original report in Toe converted to BOE (1 Toe - 7.33 BOE).

Sources: Survey of Energy Utilization Volume One and Two; Report prepared

by Coopers and Lybrand Associates Limited (Management and Economic

Consultants) for the Asian Development Bank. March 1980.

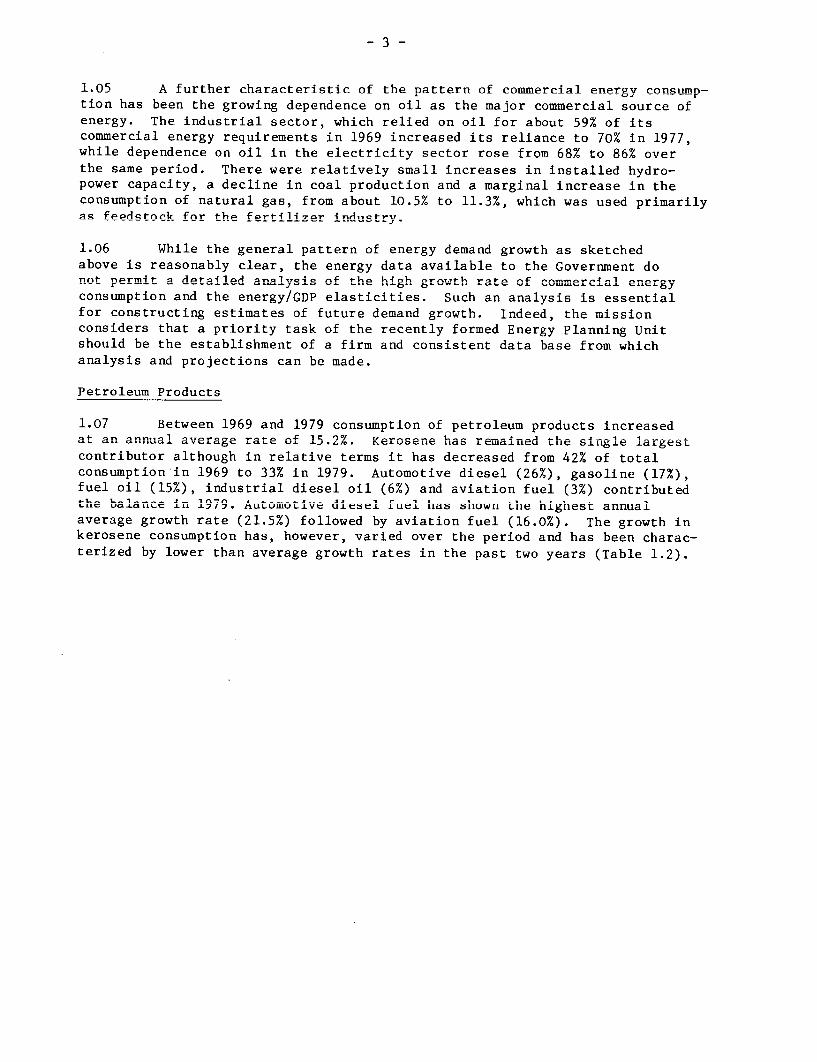

-3-

1.05 A further characteristic of the Dattern of commer^cial energy consnmp-tion has been the growing dependence on oil as the major commercial source ofenergy. The industrial e.ctor- whirh relied on oil for ahouit 5Q9 of its

commercial energy requirements in 1969 increased its reliance to 70% in 1977,while dependence on oil in the ele.tricity se.tor rose from ART to 86%L over

the same period. There were relatively small increases in installed hydro-Dower caDacitv. a decline in rnnl nrodnirtion nnd a marginal inc^rease in theconsumption of natural gas, from about 10.5% to 11.3%, which was used primarilyas feedstork for fhli fert-ili7r 4ndat-ruy.

1=06 While the general pattern of energy demand growth as sketchedabove is reasonably clear, the energy data available to the Government donnt nprmit a dAtailad ar.alysi of the high growth rate of commercial energyconsumption and the energy/GDP elasticities. Such an analysis is essentialfor constructing estImaates of future demand growth. Indeed, the missionconsiders that a priority task of the recently formed Energy Planning Unitshould be the establishment of a firm and consistent data base from whichanalysis and projections can be made.

Petroleum Products

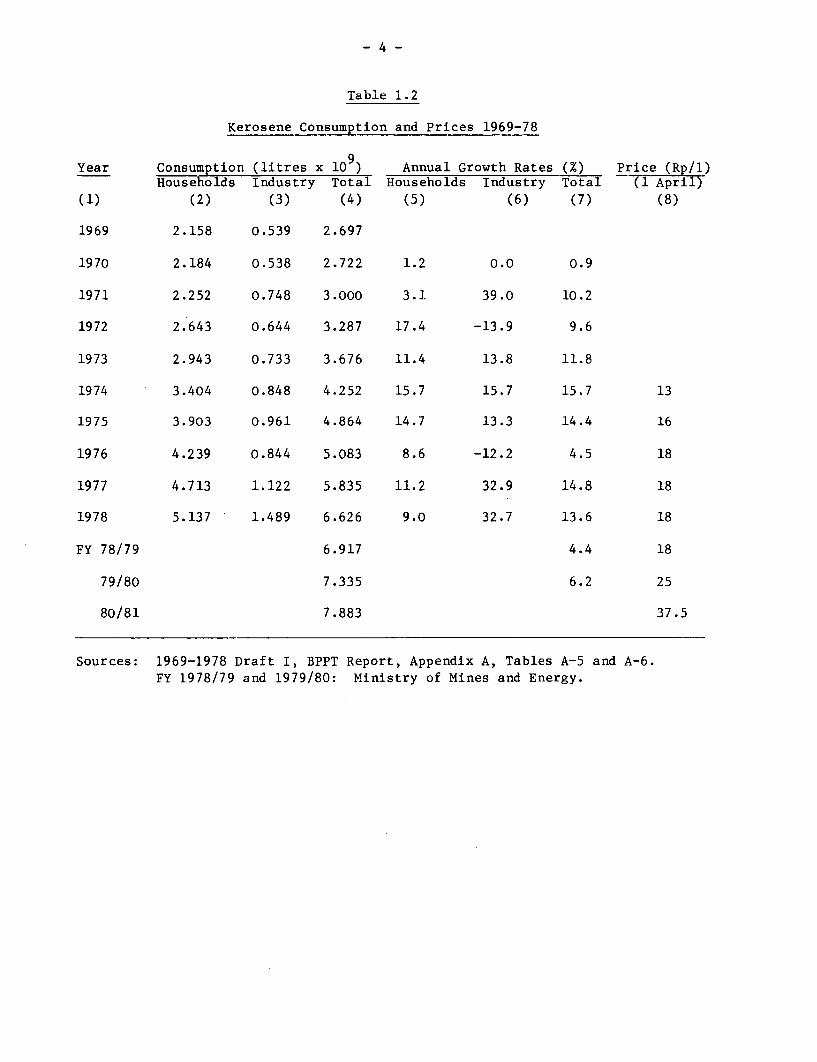

1.07 Between 1969 and 1979 consumption of petroleum products increasedat an annual average rate of 15.2%. Kerosene has remained the sirLgle largestcontributor although in relative terms it has decreased from 42% of totalconsumption in 1969 to 33%O in 1979. Automotive diesel (26%), gasoline (17%/),fuel oil (15%), industrial diesel oil (6%) and aviation fuel (3%) contributedthe balance in 1979. Automotive diesel fuel has shown the highest annualaverage growth rate (21.5%) followed by aviation fuel (16.0%). The growth inkwerosene consumptiOn halas, IhVWUVet, Vdaried UVe Llle perlod ana nas Deen cnarac-terized by lower than average growth rates in the past two years (Table 1.2).

- 4 -

Table i.2

Kerosene Consumption and Prices 1969-78

Year Consumption (litres x 10 ) Annual Growth Rates (%) Price (Rp/1)Households Industry Total Households Industry Total (1 April)

(1) (2) (3) (4) (5) (6) (7) (8)

1969 2.158 0.539 2.697

1970 2.184 0.538 2.722 1.2 0.0 0.9

1971 2.252 0.748 3.000 3.1 39.0 10.2

1972 2.643 0.644 3.287 17.4 -13.9 9.6

1973 2.943 0.733 3.676 11.4 13.8 11.8

1974 3.404 0.848 4.252 15.7 15.7 15.7 13

1975 3.903 0.961 4.864 14.7 13.3 14.4 16

1976 4.239 0.844 5.083 8.6 -12.2 4.5 18

1977 4.713 1.122 5.835 11.2 32.9 14.8 18

1978 5.137 1.489 6.626 9.0 32.7 13.6 18

FY 78/79 6.917 4.4 18

79/80 7.335 6.2 25

80/81 7.883 37.5

80ources: 1969=197t BPT Report, Ap p Adx A s A-5 -.A A-6.

FY 1978/79 and 1979/80: Ministry of Mines and Energy.

1.08 Kerosene: Although the household sector consumes most of the

kerosene, there is also apparently 1l a large and rapidly increasing level of

kerosene consumption in the industrial sector (see Table 1.2). For the period

1971-78, the average annual growth rate of kerosene consumption by households

was 13%, with industrial consumption increasing at a much higher rate in most

years. In-dustrial coLsumptiLon Lhas average approximately t001 of total consump-

tion. A comparison of growth trends and official wholesale prices suggests

that price increases reduce kerosene conusumption significantly-.

1.09 Automotive diesel accounted for approximately 26% of all domesti.

sales of petroleum products. Growth in demand for automotive diesel has

been even greater than kerosene. The high growth rate reflects, in part,

the substitution of gasoline in both the private trucking industry and the

private and public urban and inter-urban passenger transport sector. Of

course, the rapid increases in the consumption of both diesel and kerosene

have been encouraged by the very high subsidies on these commodities, whose

retail prices are currently about 20% to 30% of world prices.

1.10 Other petroleum products including gasoline, fuel oil, industrial

diesel and aviation fuel account for the other 41% of total petroleum productconsumption. Gasoline and aviation fuel are used exclusively in the trans-

port sector, fuel oil in the transport (42o%), industrial (33/o) and electricity(25%) sectors, and industrial diesel in the transport (18%), industrial (80%)

and electricity (2%) sectors.

1.11 The high growth rate in product demand has placed increasing strains

on the present operations of the domestic refinery sector, causing imbalances

which have resulted in the increased import of petroleum products, particularly

for the middle distillates such as kerosene. There are serious structural

problems in the refinery sector which require urgent attention. Due to the

quality of some of the crudes, capacity limitations and the lack of conver-

sion capacity, there is a very substantial imbalance between the domestic

demand for petroleum products and refinery output. In 1980/81, domestic

refineries, which have an effective capacity of 465,000 BPD, could supply only

215,000 BPD of petroleum products for domestic consumption. This is equiv-alent to 53% of total demand. On the other hand, a substantial proportion of

their output was in the form of heavy residues which had to be exported at a

relatively low price.

Coal

1.12 Consumption of coal declined steadily between 1940 and 1973 from

2 million tonnes per annum to 150,000 tonnes per annum. This was largely

due to the switch from coal consumption by the major sectoral consumers,

industry and power, to oil. In the past, low prices for oil products made

it uneconomic to use coal. Thus, by the mid 1970's coal accounted for a

negligible proportion of commercial energy demand. Current domestic consump-

tion of coal is estimated at 130,000 tonnes of which approximately 110,000 is

consumed in the industrial sector and the rest in the transport sector.

1/ The available data are not consistent with respect to kerosene consump-

tion. For example, MOME reports allocate all kerosene consumption to

the household sector, whereas BPPT and BPS (see bibliography) document

consumption in both the household and industrial sectors.

-6-

Naturall Gas

1.1,~~~ ~~~ Dmsi ,smtoof natural gas has been restricted to theL_ D~ tomestLct co)insumptLion'U naua a o,,I .sr~, ~ -O L..S L

industrial sector and in FY79 amounted to 132 billion SCF. The fertilizer and

stee.L L LIUustries were the largest consumers, cwn.Ain..smire RO bl fl u S -a.

34 billion SCF respectively. Use by local industries has grown at an averagean.-,ual rate ofL 22%1 since 19-75 Jrznd in FY-70 was 480 billi1on SCF.

Electricity

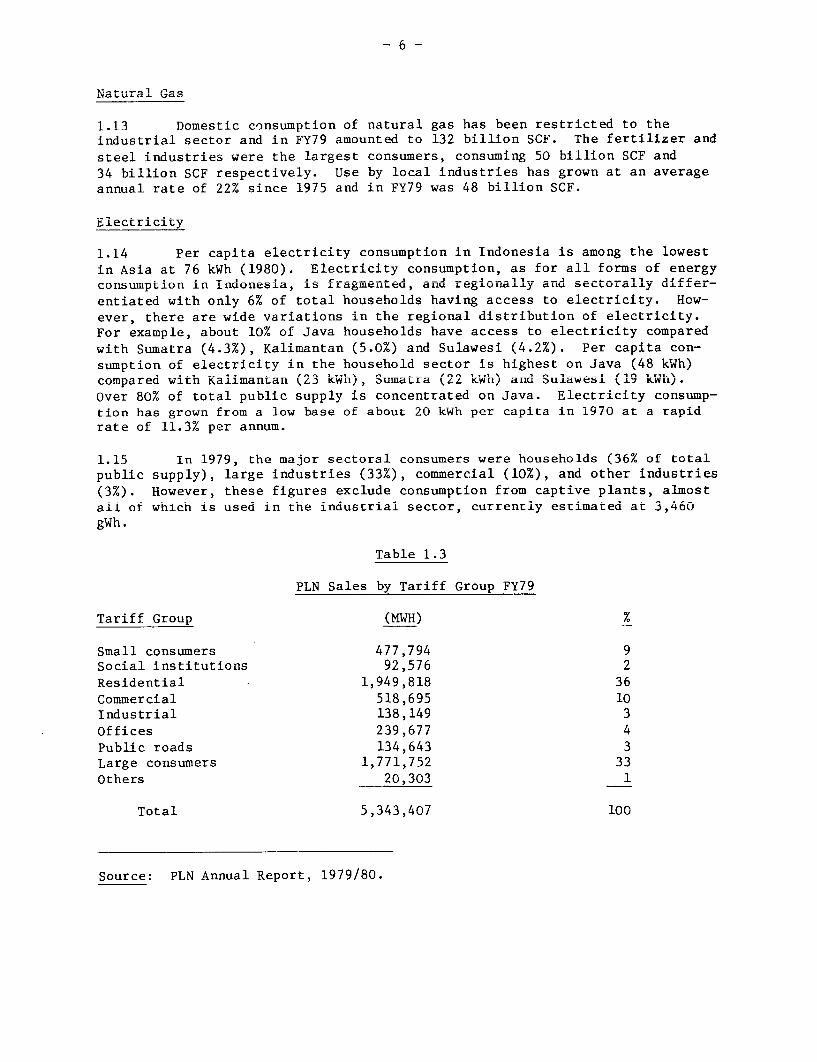

1.14 Per capita e'LectrlL.Cty corsumptLion in LInudonesia is amor,g th Ile 'lowestin Asia at 76 kWh (1980). Electricity consumption, as for all forms of energyconsumption in Indonesia, is fragmented, and regionally a,nd sectorally differ=-entiated with only 6% of total households having access to electricity. How-

ever, there are wide variations in the regional distriDution of eleCtriCity.

For example, about 10% of Java households have access to electricity compared

with Sumatra (4.3%), Kalimantan (5.0%) and Sulawesi (4.2%). Per capita con-sumption of electricity in the household sector is highest on Java (48 kWh)compared with Kalimantan (23 kWh), Sumatra (22 kWh) anrd Sulawesi (19 kWh).

Over 80% of total public supply is concentrated on Java. Electricity consump-tion has grown from a low base of about 20 kWh per capita in 1970 at a rapidrate of 11.3% per annum.

1.15 In 1979, the major sectoral consumers were households (36% of total

public supply), large industries (33%), commercial (10%), a-nd other industries

(3%). However, these figures exclude consumption from captive plants, almostall of which is used in the industrial sector, currently estimated at 3,460gWh.

Table 1.3

PLN Sales by Tariff Group FY79

Tariff Group (MWH) %

Small consumers 477,794 9Social institutions 92,576 2Residential 1,949,818 36

Commercial 518,695 10Industrial 138,149 3

Offices 239,677 4

Public roads 134,643 3Large consumers 1,771,752 33

Others 20,303 1

Total 5,343,407 100

Source: PLN Annual Report, 1979/80.

-7-

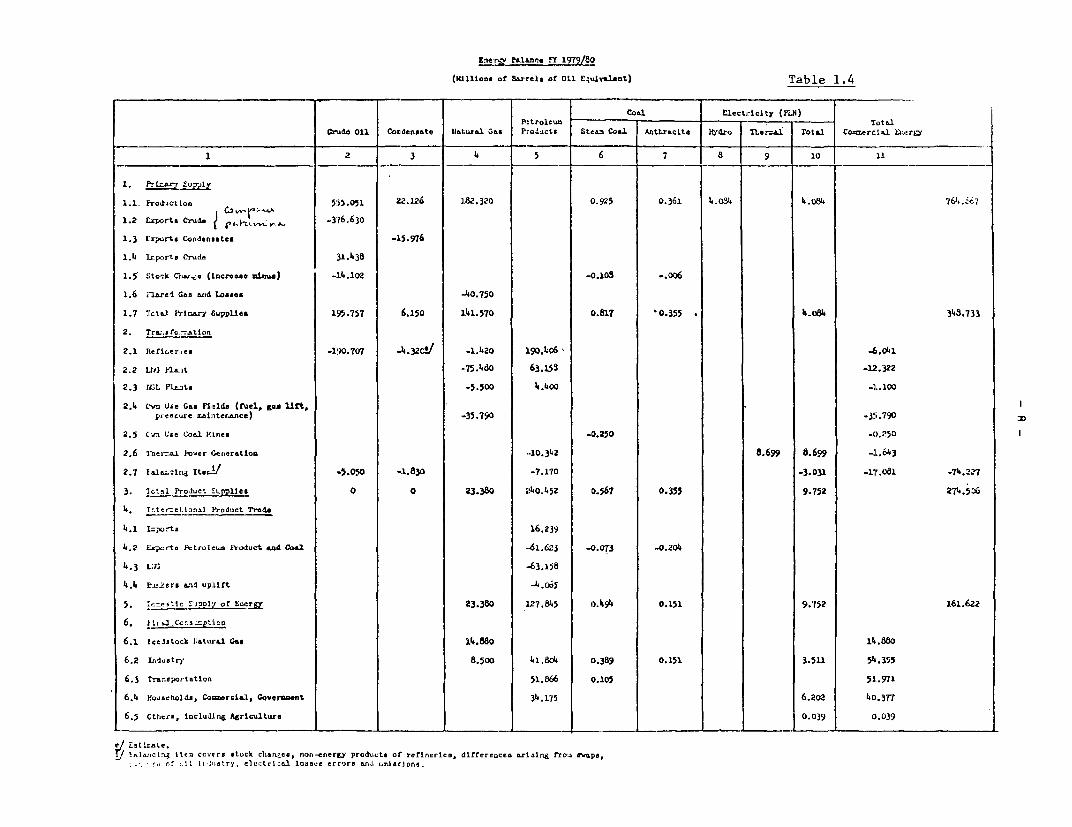

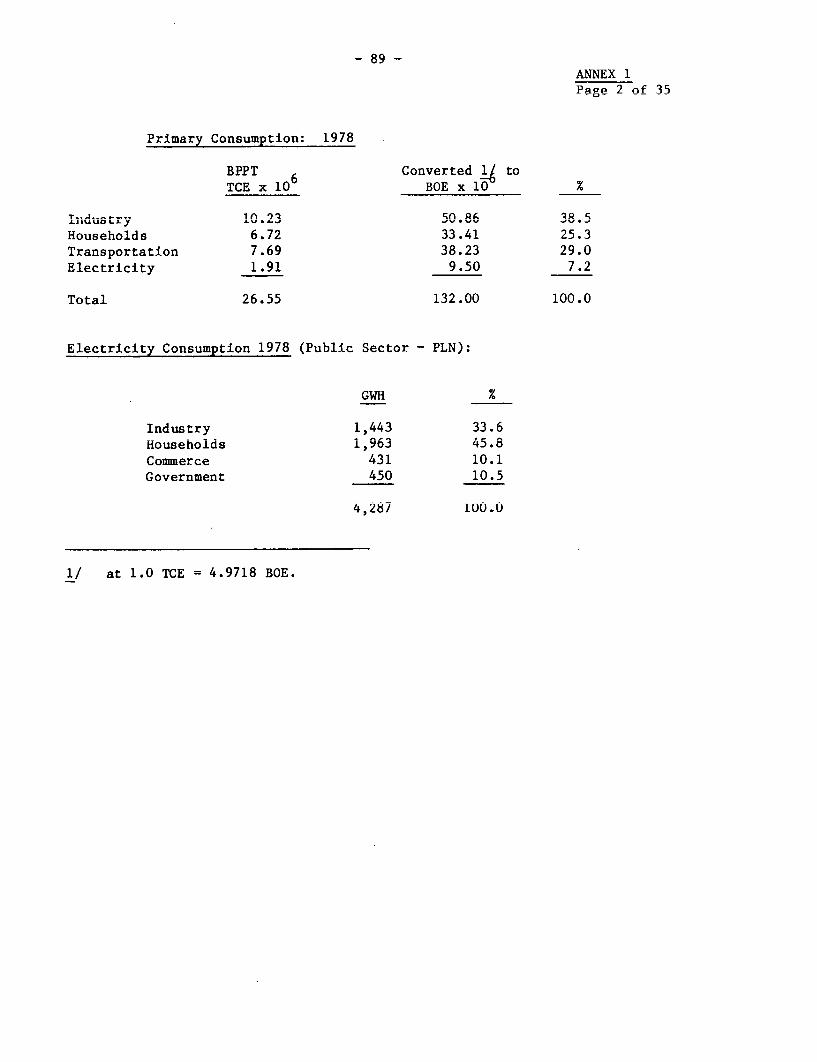

Commercial Energy Balance FY79

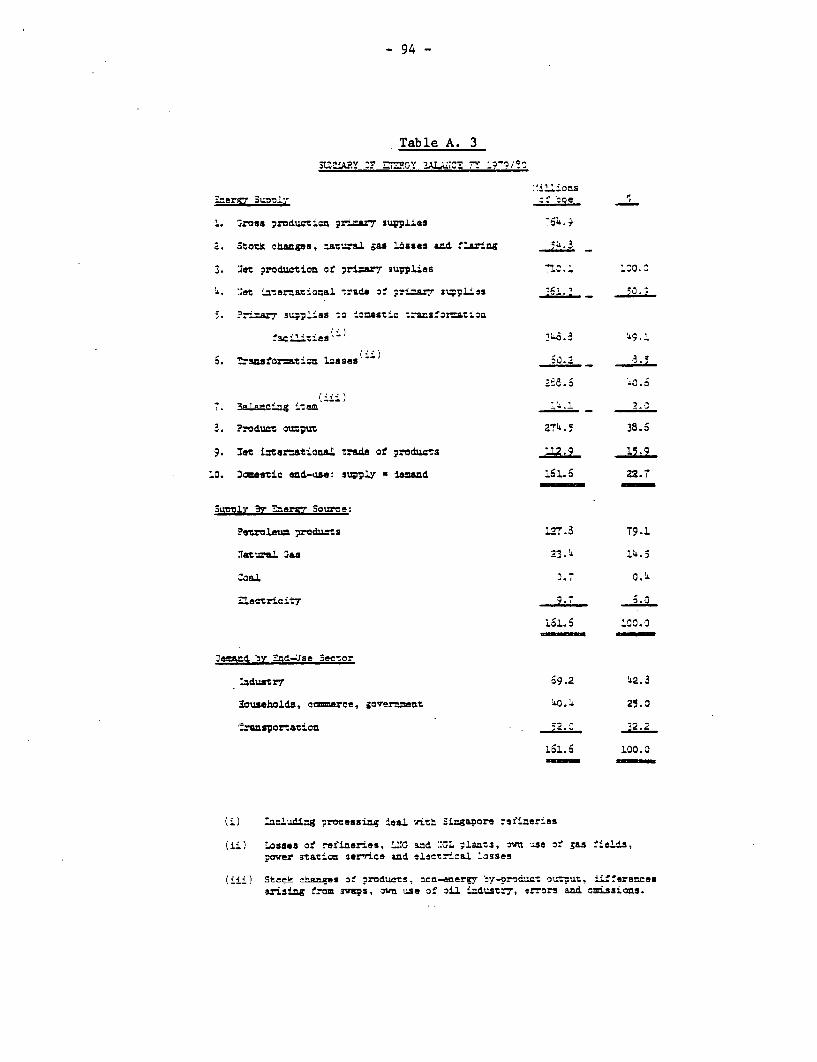

1.16 An energy balance has been prepared for FY79 (Table 1.4). Primaryenergy production for FY79/80 is estimated at 765 MBOE. Energy imports were48 MBOE and exports 522 MBOE (including crude oil, products, LNG and bunkers)with net energy exports at 474 MBOE. The remaining 291 MBOE was used in thedomestic economy: 162 MBOE for end use consumption, 74 MBOE for transformationlosses, 41 MBOE for flared gas and losses, and the other 14 MBOE for "stockchanges". Annex I gives a detailed breakdown of the energy balance togetherwith a commentary on the methodological approach used, the data problemsencountered and the assumptions made.

1.17 Net exports of primary energy supplies and products account for62% of gross energy production. Natural gas losses, flaring, transformationlosses and "unaccounted" account for 17%, leaving 21% (approximately 161MBOE) for domestic consumption. The final demand for energy shows thatindustry is the largest consuming sector (69 MBOE including feedstock) withtransport and households following (52 MBOE and 41 MBOE respectively). Theenergy balance for FY79 has been used as the base for tentative demand projec-tions to 1990 and two alternative and even more tentative projections to 2000.

Likely Demand to FY89

Background

1.18 The projections of commercial energy consumption in Indonesia forFY89 based on sectoral energy demands (which are explained in the Annex) imnlvan overall growth rate of almost 12% during the 1980's. The assumed averagereal GDP growth durinR this period is 8.2% giving a ratio of energy growth toGDP growth of 1.46. The rapid growth assumed in commercial energy consumptionis based on a number of factors: the increases, from low bases, in the growthof the industrial and electric power sectors; increasing demand in the trans-port sector, and, with rising incomes; the continued substitution of commer-cial for non-commercial energy. In these projections, the potential impact ondemand of changes in energy prices has not been taken into account-

The Domestic Demand for Petroleum

1.19 The demand for petroleum nroduicts is likely to grow at an annualrate of 10.9% during the 1980's, with particularly rapid growth in industrialsector consumption (12.9%).

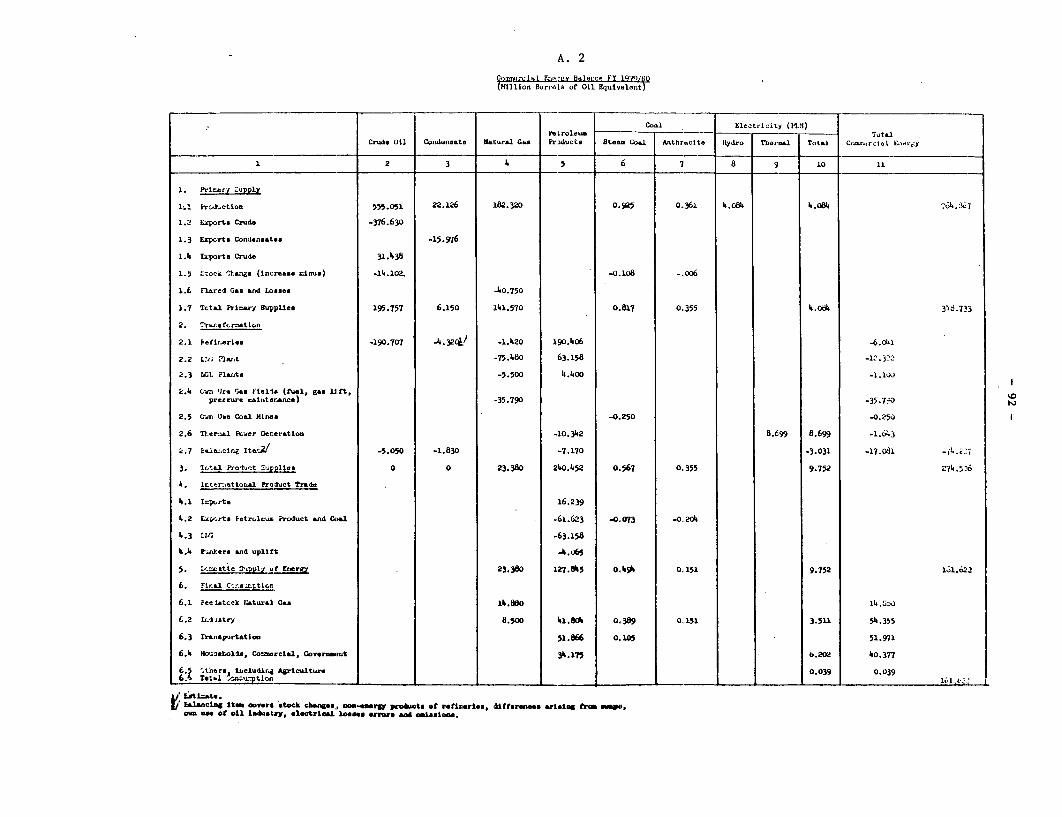

E-neirV?& Lnne FY 1979/80

(4aLmlonm of B&rrels of 011 Equivrlatit) Table 1.4

F:troleur Coa L Elect]ricity (PAN)Petroleum- Total

Crudo Oil Condensatep tlatal c4s Pro4ucts Steac CoMA AntLtrcite iWrdro TLer-&i1 Total Coneercial 1L ,rgy

1 2 3 4 5 6 7 8 9 10 11

1. u;rply .

1.1. iro&ict Lon C.3 555.051 22.126 182.320 O 925 0.361 4.0S4 4.034 764._7

1.2 Ixports Crud. e t -376.630

1.3 Exports Condensates -15.976

1.4 ILrport Crude ii.1438

1.5' ito"k Chw.ue (Lncronoe Wmu -14.102 -0.108 -. 006

1.6 .laret Gas aid Losaes -40.750

1.7 lTct.l PnL ar 7 lpp1aes 195.757 6.150 1141.570 0.817 0.355 *.08i4 343.733

2. T- 1 Aratlon

2.1 RefrLerles -190.707 -4.32C!/ -1.420 L90.k06 .6.041

2.2 11U) k1wit -.75.460 63.153 -1!.322

2.3 lt PIzfts -5.500 14.400 -1. 100

2.4 Cvn Use Gas FlYild. (fuel, gaA Lift,prer u.re aainterance) -35.790 -35.790

2.5 Co.n Uce Coal MInes -0.250 -_.250

2.6 Tber-&l Icuer Gerneration -10.342 8.699 8.699 1.6143

2.7 EL&1"Tin Itce t *-5.050 -1.8330 -7.170 -3.031 -111.o8i -74.2Z7

3. iGtal Proluct ,r cpplleem 0 0 23.380 240.452 O.567 0.355 9.752 2714.536

4. lter-etloaal IProduct Trade

4.1 I=ports 16.239

4.2 Espcrts Btroluu Product &a4d Coal -61.623 -0.073 -o.204

4.3 L:r, .63.158

4.4 E,m>err e.id upLlt -4.065

5. I-cStlc !-jvlr of EnI_ 23.380 127.845 .1)4>94 0.151 9.752 161.622

6. jIr al cs .R.'oO

6.1 Itelutoch I:at.u-l Gas 14.880 lb.d80

6.2 Imm-stry 8.500 41.8oO4 o.389 0.151 3.5 i 54.355

6.3 rarnsportation 51.866 0.105 51.971

6.4 Y!ouseholdi, Cocrnercial, Goverument 34.175 6.202 40.377

6.5 Cthcra, Including Agriculture 0.039 0.039

e/ Lsticate.1/ 1.1-ucl., Item coo.rr itock chantes. non-energy products of refineiriea. differences arialng froo esaps,

.- r (.11 H ,r,mtry, clcctrleal loa.,ce error, anil onmlslono.

Table 1.5

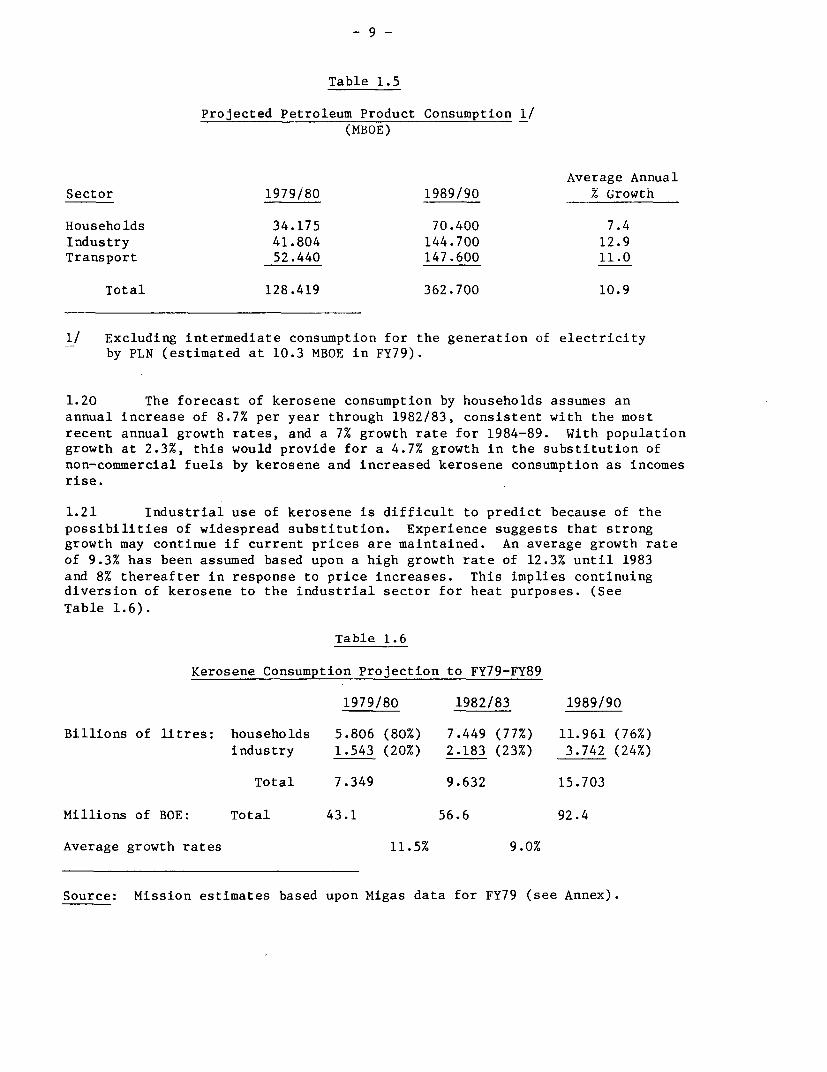

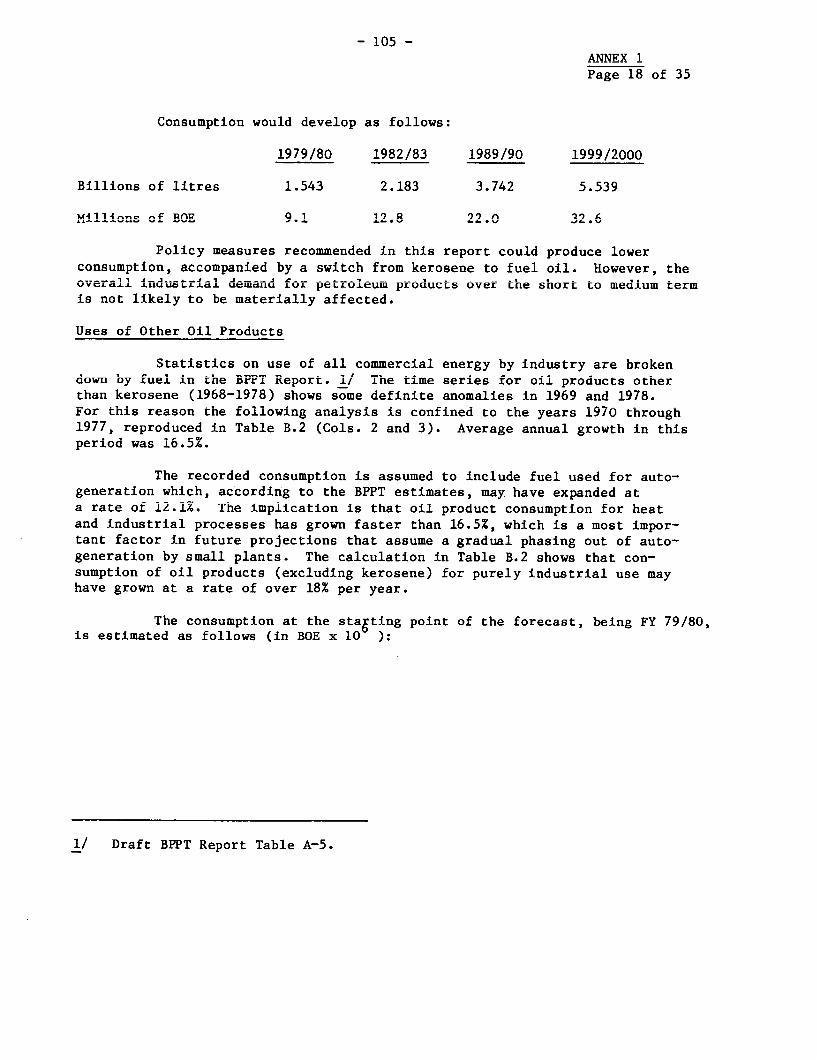

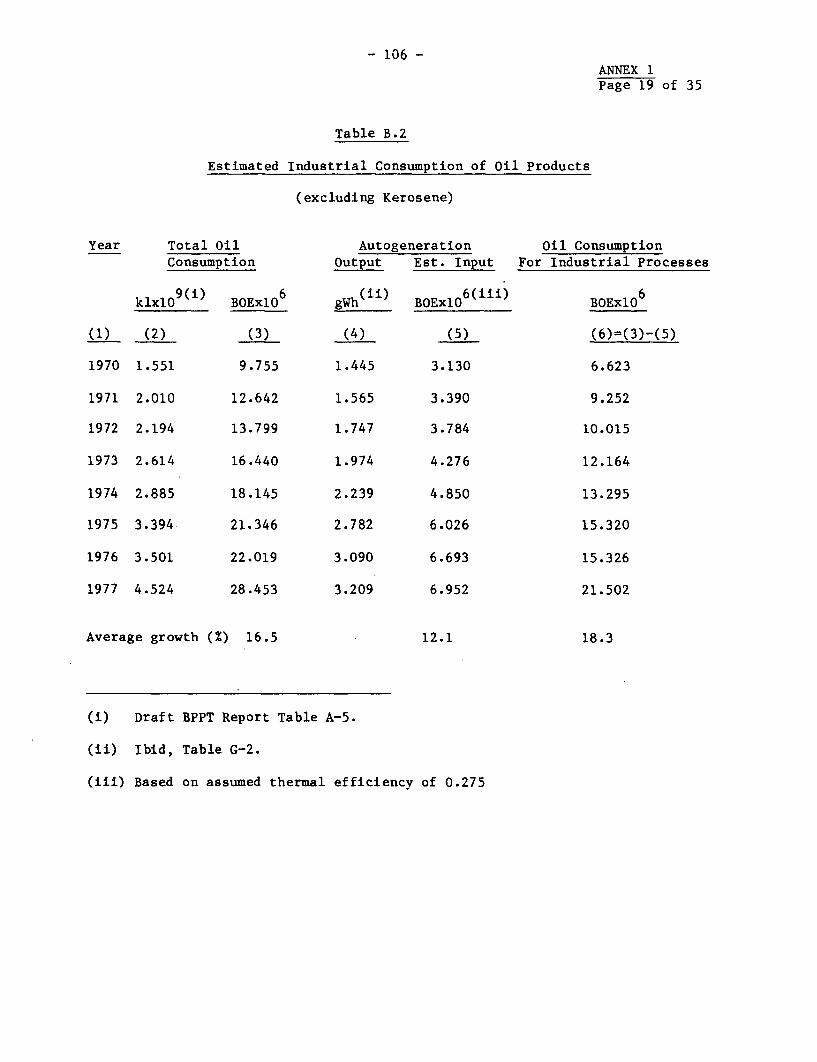

Projected Petroleum Product Consumption _/(MBOE)

Average Annual

Sector 1979/80 1989/90 % Growth

Households 34.175 70.400 7.4

Industry 41.804 144.700 12.9Transport 52.440 147.600 11.0

Total 128.419 362.700 10.9

1/ Excluding intermediate consumption for the generation of electricityby PLN (estimated at 10.3 MBOE in FY79).

1.20 The forecast of kerosene consumption by households assumes an

annual increase of 8.7% per year through 1982/83, consistent with the most

recent annual growth rates, and a 7% growth rate for 1984-89. With populationgrowth at 2.3%, this would provide for a 4.7% growth in the substitution of

non-commercial fuels by kerosene and increased kerosene consumption as incomes

rise.

1.21 Industrial use of kerosene is difficult to predict because of the

possibilities of widespread substitution. Experience suggests that stronggrowth may continue if current prices are maintained. An average growth rate

of 9.3% has been assumed based upon a high growth rate of 12.3% until 1983

and 8% thereafter in response to price increases. This implies continuingdiversion of kerosene to the industrial sector for heat purposes. (See

Table 1.6).

Table 1.6

Kerosene Consumption Projection to FY79-FY89

1979/80 1982/83 1989/90

Billions of litres: households 5.806 (80%) 7.449 (77%) 11.961 (76%)

industry 1.543 (20%) 2.183 (23%) 3.742 (24%)

Total 7.349 9.632 15.703

Millions of BOE: Total 43.1 56.6 92.4

Average growth rates 11.5% 9.0%

Source: Mission estimates based upon Migas data for FY79 (see Annex).

- 10 -

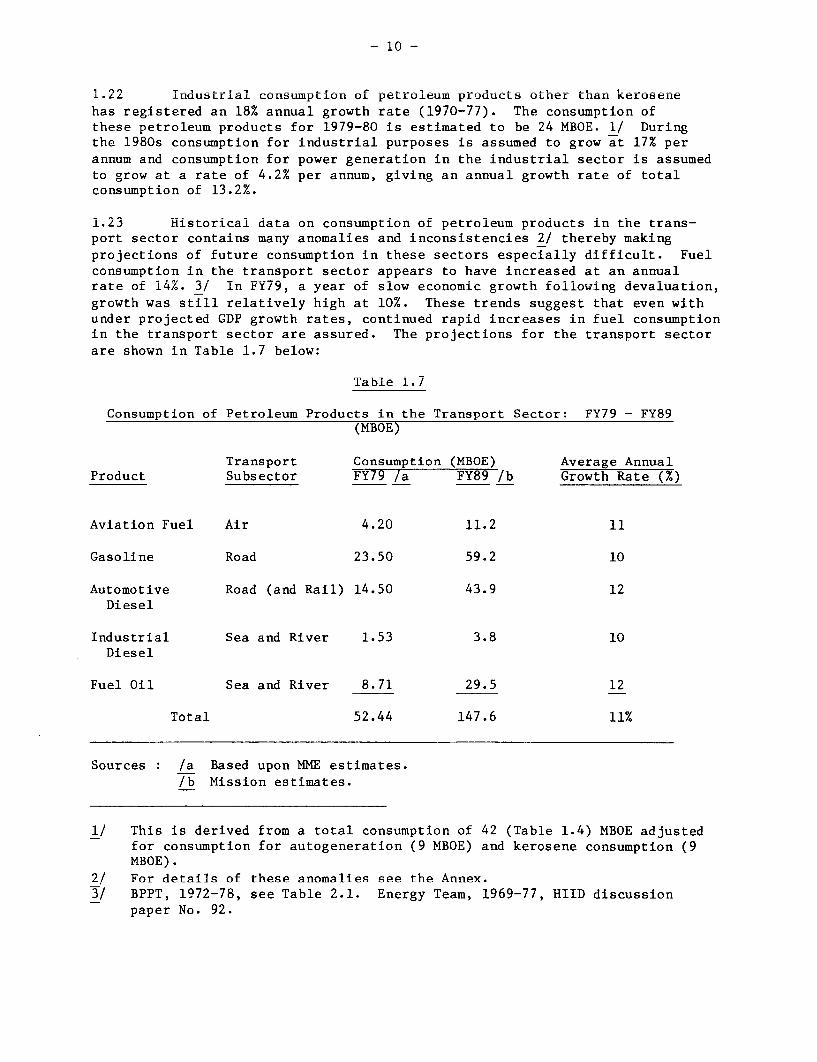

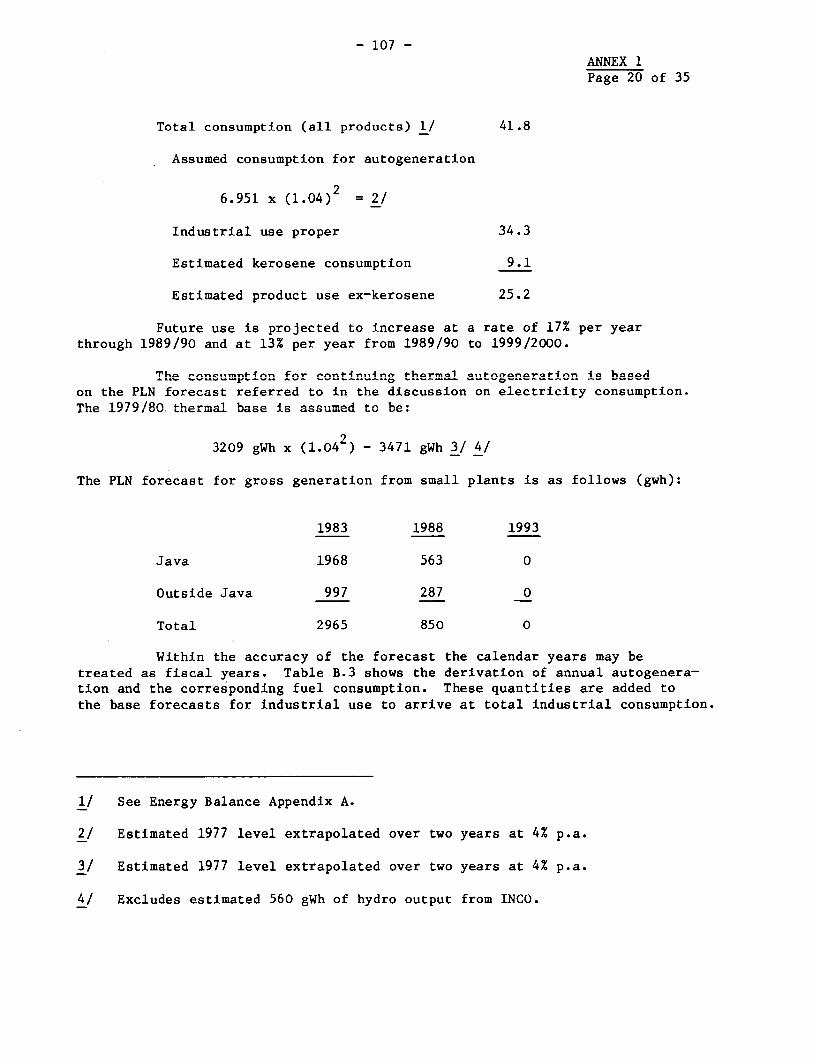

1.22 Industrial consumption o0 petroleum produucts othrer tnan Kerosenehas registered an 18% annual growth rate (1970-77). The consumption ofthese petroleum products for 1979-80 is estimated to be 24 MBOE. 1/ Duringthe 1980s consumption for industrial purposes is assumed to grow at 17% perannum and consumption for power generation in the industrial sector is assumedto grow at a rate of 4.2% per annum, giving an annual growth rate of totalconsumption of 13.l2/.

1.23 Historical data on consumption of petroleum products in the trans-port sector contains many anomalies and inconsistencies 2/ thereby makingprojections of future consumption in these sectors especially difficult. Fuelconsumption in the transport sector appears to have increased at an annualrate of 14%. 3/ In FY79, a year of slow economic growth following devaluation,growth was still relatively high at 10%. These trends suggest that even withunder projected GDP growth rates, continued rapid increases in fuel consumptionin the transport sector are assured. The projections for the transport sectorare shown in Table 1.7 below:

Table 1.7

Consumption of Petroleum Products in the Transport Sector: FY79 - FY89(MBOE)

Transport Consumption (MBOE) Average AnnualProduct Subsector FY79 /a FY89 /b Growth Rate (%)

Aviation Fuel Air 4.20 11.2 11

Gasoline Road 23.50 59.2 10

Automotive Road (and Rail) 14.50 43.9 12Diesel

Industrial Sea and River 1.53 3.8 10Diesel

Fuel Oil Sea and River 8.71 29.5 12

Total 52.44 147.6 11%

Sources : /a Based upon MME estimates./b Mission estimates.

1/ This is derived from a total consumption of 42 (Table 1.4) MBOE adjustedfor consumption for autogeneration (9 MBOE) and kerosene consumption (9MBOE).

2/ For details of these anomalies see the Annex.3/ BPPT, 1972-78, see Table 2.1. Energy Team, 1969-77, HIID discussion

paper No. 92.

- 11 -

Aviation fuel requirements are based upon a continued strong growth in airfreight. The forecast for road transport growth has been used as a proxy forestimating the road and rail subsector requirements since consumption by therail subsector is small. Projected gasoline consumption to FY89 at 10% issomewhat below the trend of automobile registration. The projected highergrowth of automotive diesel (12%) is due to the higher growth rates estimatedfor the registration of trucks and buses and allowances for the possiblefuture expansion of public transportation. The vital role of inter-islandshipping in the Indonesian economy suggests the continued expansion of petro-leum product consumption, particularly fuel oil.

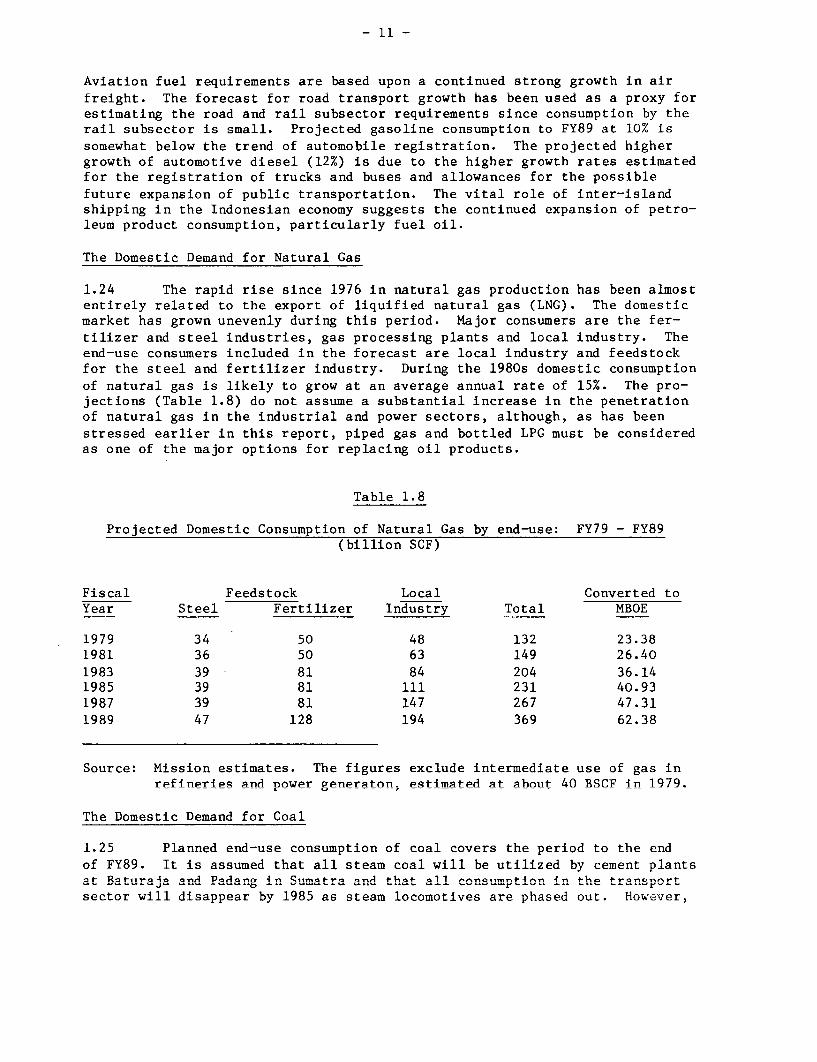

The Domestic Demand for Natural Gas

1.24 The rapid rise since 1976 in natural gas production has been almostentirely related to the export of liquified natural gas (LNG). The domesticmarket has grown unevenly during this period. Major consumers are the fer-tilizer and steel industries, gas processing plants and local industry. Theend-use consumers included in the forecast are local industry and feedstockfor the steel and fertilizer industry. During the 1980s domestic consumptionof natural gas is likely to grow at an average annual rate of 15%. The pro-jections (Table 1.8) do not assume a substantial increase in the penetrationof natural gas in the industrial and power sectors, although, as has beenstressed earlier in this report, piped gas and bottled LPG must be consideredas one of the major options for replacing oil products.

Table 1.8

Projected Domestic Consumption of Natural Gas by end-use: FY79 - FY89(billion SCF)

Fiscal Feedstock Local Converted toYear Steel Fertilizer Industry Total MBOE

1979 34 50 48 132 23.381981 36 50 63 149 26.401983 39 81 84 204 36.141985 39 81 111 231 40.931987 39 81 147 267 47.311989 47 128 194 369 62.38

Source: Mission estimates. The figures exclude intermediate use of gas inrefineries and nower generaton. estimated at about 40 BSCF in 1979.

The nnmpqtir Demnnd fnr Cnnl

1 25 Plannedi Pnd-iusP consuimption of rol covers the neriod to t-he endof FY89. It is assumed that all steam coal will be utilized by cement plantsat Baturaja anrd Padan.g 'ni Sumatra and that all consumption in the transportsector will disappear by 1985 as steam locomotives are phased out. However,

- 12 -

end-use consumption will be negligible compared with the intermediate duemanufor coal by the power sector. With the commissioning of the Suralaya powerplant in 9085, demand will iLncrease from 165,000 tonnes iC n 1i 9 o 2 mitonnes. By 1989, demand by the power sector will reach an estimated 7.5 mil-ilon tonnes per annum anld by thLe LndUustriLaL sector 0.5 million tonnes. Iin

addition, it is likely that up to 0.25 million tonnes could well be used inrural industry if a distribution system were developed.

The Domestic Demand for Electricity

1.26 The projection for electricity demand up to FY89 assumes an averageannual growth rate of 20%. This is based on PLN forecasts (see Table 1.9),together with estimates for auto generation. On Java, other than the expan-sion of the gas fired power plant at the Krakatau steel plant it is assumedthat all small auto generation plants will be phased out by 1990 as PLN is

expected to be able to meet the entire demand by then. Autogeneration will,it is assumed, play a more important role outside Java although by i990 aiismall diesel generating plants will have been phased out. Hydro generation atthe Larona and Asahan Aluminum plants will build up to a net maximum of 5,225gWh by 1985.

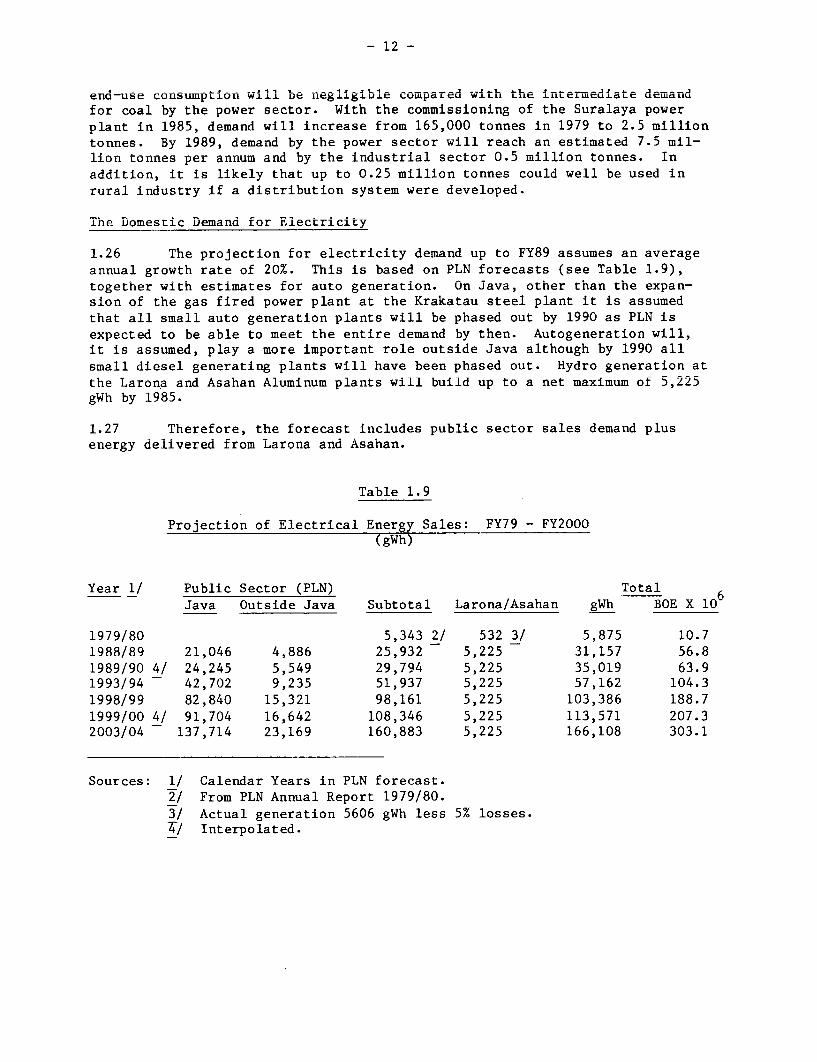

1.27 Therefore, the forecast includes public sector sales demand plusenergy delivered trom Larona and Asahan.

Table 1.9

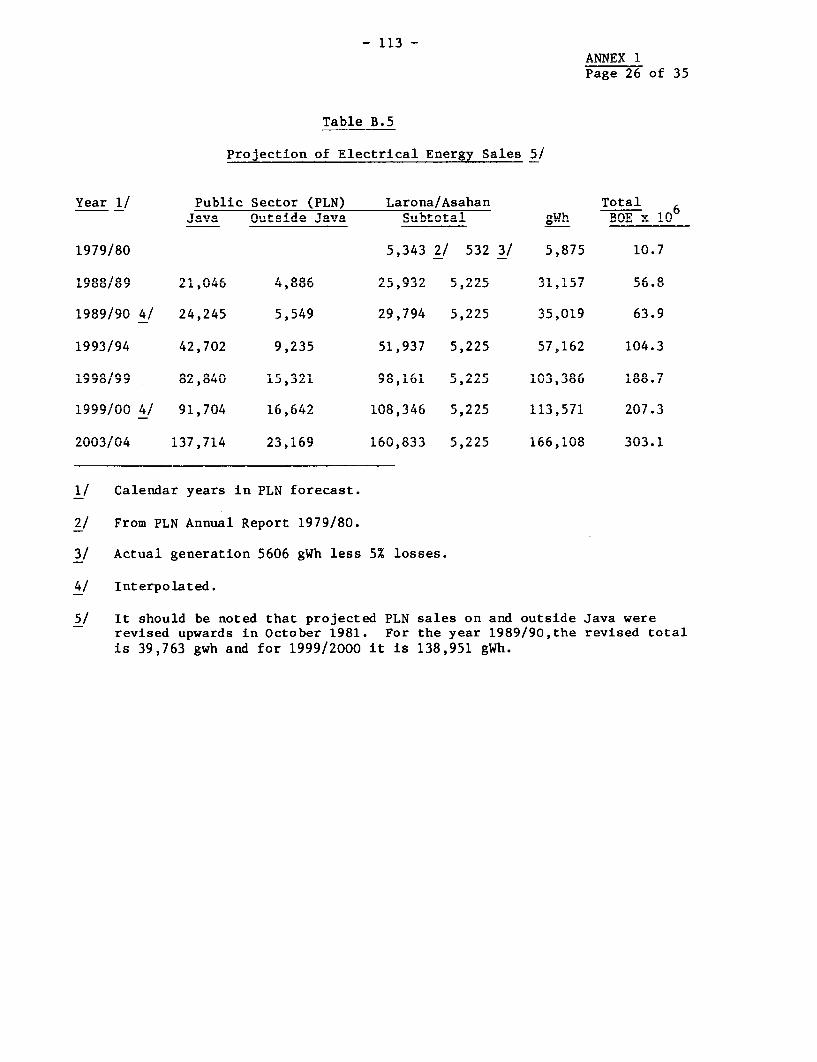

Projection of Electrical Energy Sales: FY79 - FY2000(gWh)

Year 1/ Public Sector (PLN) Total

Java Outside Java Subtotal Larona/Asahan gWh BOE X 10-

1979/80 5,343 2/ 532 3/ 5,875 10.71988/89 21,046 4,886 25,932 5,225 31,157 56.81989/90 4/ 24,245 5,549 29,794 5,225 35,019 63.91993/94 - 42,702 9,235 51,937 5,225 57,162 104.31998/99 82,840 15,321 98,161 5,225 103,386 188.71999/00 4/ 91,704 16,642 108,346 5,225 113,571 207.32003/04 - 137,714 23,169 160,883 5,225 166,108 303.1

Sources: 1/ Calendar Years in PLN forecast.2/ From PLN Annual Report 1979/80.3/ Actual Reneration 5606 RWh less 5% losses.4/ Interpolated.

- 13 -

1.28 Consumption in the industrial sector (as shown in Table 1.9) islikely to grow rapidly and by 1989 could be more than 50% greater than thehousehold sector.

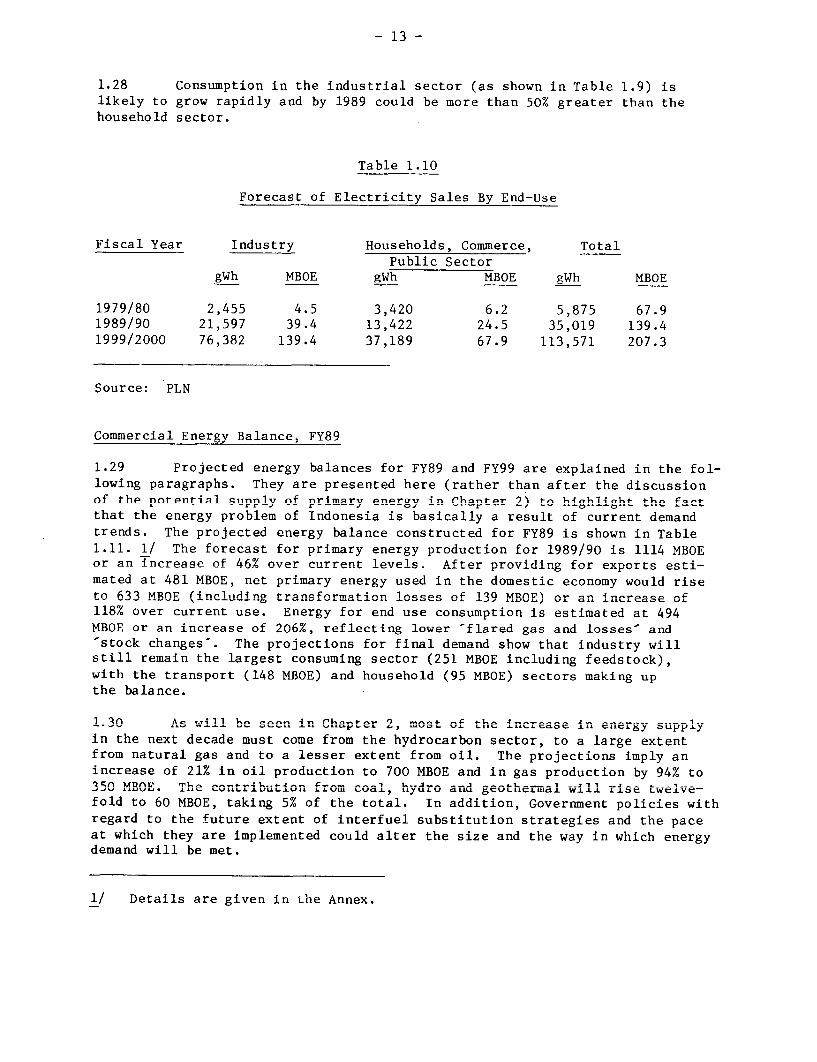

Table 1.10

Forecast of Electricity Sales By End-Use

Fiscal Year Industry Households, Commerce. TotalPublic Sector

gWh MBOE gWh MBOE RWh MBOE

1979/80 2,455 4.5 3,420 6.2 5;875 67.91989/90 21,597 39.4 13,422 24.5 35,019 139.41999/2000 76,382 139.4 37,189 67.9 113,571 207.3

Source: PLN

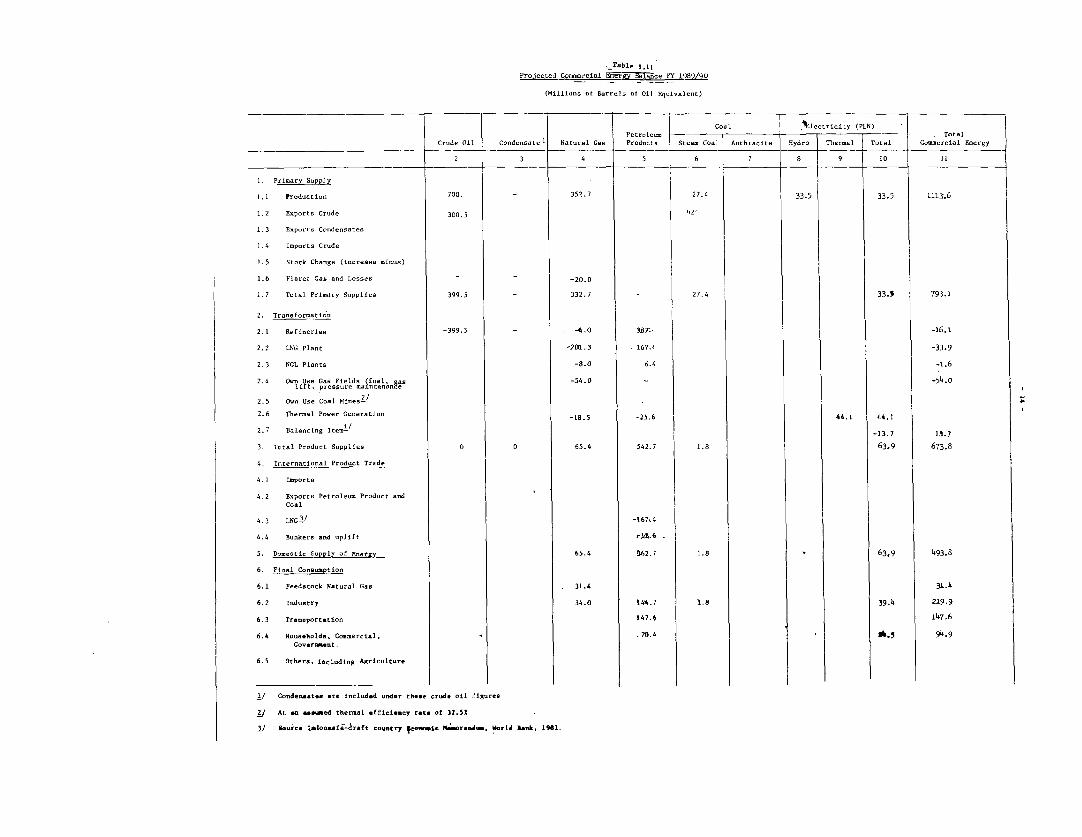

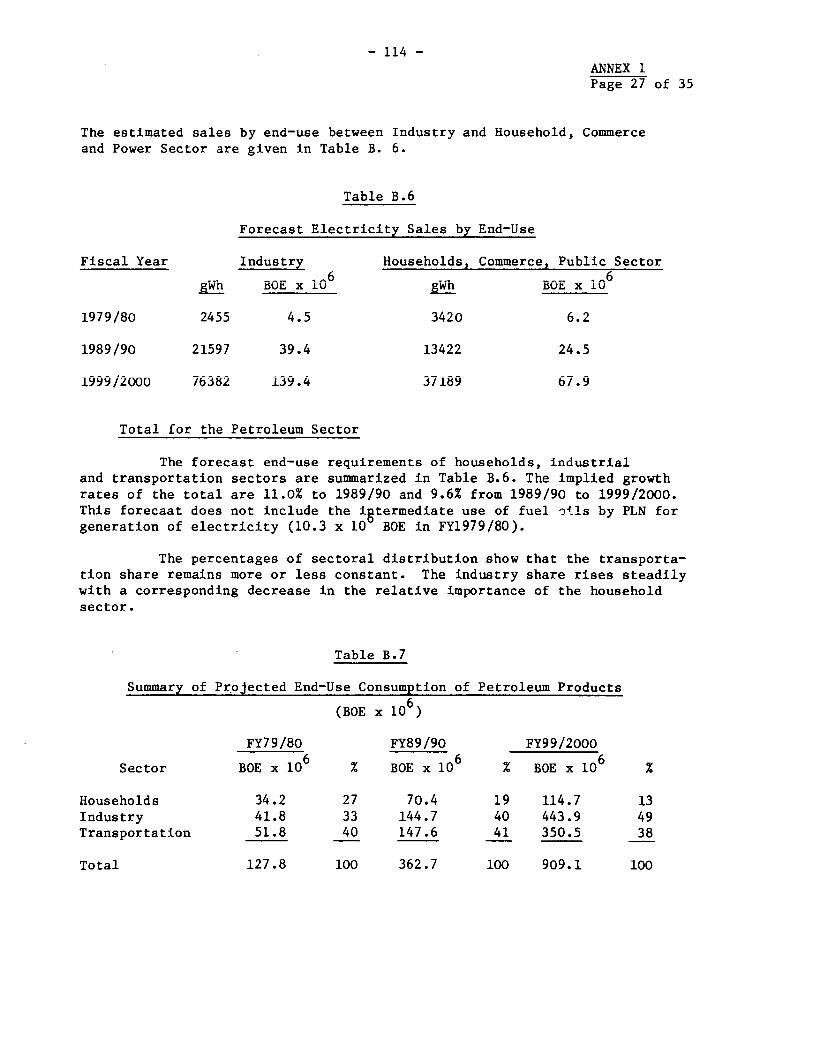

Commercial Energv Balance. FY89