Young Filipino Migrants Working in Sales in Dubai: Does Cultural Capital Help?

Upload

khangminh22Category

view

0download

0

1

PROJECT REPORT

on

A Study On Working Capital Management

BY

Pooja A Nagenhalli

1NZ18MBA58

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BENGALURU

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

Mr. Santosh Kumar S

Assistant Professor2018

2020

2

CERTIFICATE

This is to certify that Pooja A Nagenhalli bearing USN 1NZ18MBA58, is a

bona fide student of Master of Business Administration course of the Institute

2018-2020,autonomous program, affiliated to Visvesvaraya Technological

University, Belgaum. Project report on “A Study on Working Capital

Management” is prepared by her under the guidance of Mr. Santosh Kumar S,

in partial fulfilment of requirements for the award of the degree of Master of

Business Administration of Visvesvaraya Technological University, Belgaum

Karnataka.

Signature of Internal guide Signature of HOD Signature of Principal

Name of the examiners with affiliation Signature with date

1. External Examiner

2. InternalExaminer

3

Date: 01Mar,2020

INTERNSHIP COMPLETION CERTIFICATE

TO WHOMEVER IT MAY CONCERN

This is to certify that MsPooja. A . Nagenhalliof NEW HORIZON COLLEGE OF

ENGINEERING has undertaken internship in our organisation on the topic “WORKING

CAPITAL MANAGEMENT “ Between 14th December 2019 to 13th February 2020. Her

conduct and work ethics were excellent.

During period of her internship program with us she was found to be punctual,

hardworking and sincere. We wish her every success in life and career.

Embizon Technologies www.embizon.com

No.16, Pavan., 31st Main, Chinnappa Naidu Layout Mail:

[email protected] BSK 3rd Stage. Bangalore-560085 09945933211

Layout Design | Gerber Validation | Thermal Analysis | PI & SI Analysis

4

DECLARATION

I, Pooja A Nagenhalli, hereby declare that the project report on “A Study On Working Capital

Management” with reference to “Embizon Technologies” prepared by me under the guidance

of Mr. Santosh Kumar S, faculty of M.B.A Department, New Horizon College of

Engineering.

I also declare that this project report is towards the partial fulfilment of the university

regulations for the award of the degree of Master of Business Administration by

Visvesvaraya Technological University, Belgaum.

I have undergone an industry project for a period of Eight weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the

award of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

5

ACKNOWLEDGEMENT

The successful completion of the project would not have been possible without

the guidance and support of many people. I express my sincere gratitude to

Mr.Sheshadri Joshi, Director, Embizon Technologies, Bengaluru, for allowing

to do my project at Embizon Technologies.

I thank the staff of Embizon Technologies, Bengaluru for their support and

guidance and helping me in completion of the report.

I am thankful to my internal guide Mr. Santosh Kumar S , for his constant

support and inspiration throughout the project and invaluable suggestions,

guidance and also for providing valuable information.

Finally, I express my gratitude towards my parents and family for their

continuous support during the study.

Pooja A Nagenhalli

1NZ18MBA58

6

TABLE OF CONTENTS

SL. NUMBER CONTENTS PAGE NUMBERS

1 Executive Summary 3-7

2 Theoretical Background Of The Study 3-7

3 Industry Profile &Company Profile 8-10

4 Application Of Theoretical Framework 11-47

5 Analysis And Interpretation Of Financial

Statements And Reports 48-51

6 Learning Experience- Findings,

Suggestions And Conclusion 52

7 Bibliography 53

7

INTRODUCTION

The project undertaken is on “WORKING CAPITAL MANAGEMENT IN

EMBIZON TECHNOLOGIES”.

It describes about how the company manages its working capital and the various

steps that are required in the management of working capital.

Cash is the lifeline of a company. If this lifeline deteriorates, so does the

company's ability to fund operations, reinvest and meet capital requirements and

payments. Understanding a company's cash flow health is essential to making

investment decisions. A good way to judge a company's cash flow prospects is

to look at its working capital management (WCM).

Working capital refers to the cash a business requires for day-to-day operations

or, more specifically, for financing the conversion of raw materials into finished

goods, which the company sells for payment. Among the most important items

of working capital are levels of inventory, accounts receivable, and accounts

payable. Analysts look at these items for signs of a company's efficiency and

financial strength

The working capital is an important yardstick to measure the company’s

operational and financial efficiency. Any company should have a right amount

of cash and lines of credit for its business needs at all times.

This project describes how the management of working capital takes place at

Embizon Technologies.

8

THE PROBLEMS

In the management of working capital, the firm is faced with two key problems:

1. First, given the level of sales and the relevant cost considerations, what are the

optimal amounts of cash, accounts receivable and inventories that a firm should

choose to maintain?

2. Second, given these optimal amounts, what is the most economical way to

finance these working capital investments? To produce the best possible

results, firms should keep no unproductive assets and should finance with the

cheapest available sources of funds. Why? In general, it is quite advantageous

for the firm to invest in short term assets and to finance short-term liabilities.

9

PURPOSE OF STUDY

The objectives of this project were mainly to study the inventory, cash and

receivable at Embizon Technologies Ltd., but there are some more and they

are -

➢ The main purpose of our study is to render a better understanding of

the concept “Working Capital Management”.

➢ To understand the planning and management of working capital at

Embizon Technologies Ltd.

➢ To measure the financial soundness of the company by analyzing various

ratios.

➢ To suggest ways for better management and control of working capital at

the concern.

10

RESEARCH METHODOLOGY

➢ This project requires a detailed understanding of the concept –

“Working Capital Management”. Therefore, firstly we need to have a

clear idea of what is working capital, how it is managed in Embizon

Technologies, what are the different ways in which the financing of

working capital is done in the company.

➢ The management of working capital involves managing inventories,

accounts receivable and payable and cash. Therefore one also needs to

have a sound knowledge about cash management, inventory management

and receivables management.

➢ Then comes the financing of working capital requirement, i.e. how the

working capital is financed, what are the various sources through which it

is done.

➢ And, in the end, suggestions and recommendations on ways for better

management and control of working capital are provided.

11

LIMITATIONS OF THE STUDY:

➢ We cannot do comparisons with other companies unless and until we

have the data of other companies on the same subject.

➢ Only the printed data about the company will be available and not the

back–end details.

➢ Future plans of the company will not be disclosed to the trainees.

➢ Lastly, due to shortage of time it is not possible to cover all the factors

and details regarding the subject of study.

➢ The latest financial data could not be reported as the company’s websites

have not been updated.

12

EMBIZON TECHNOLOGIES:

Experienced in providing printed circuit board design and product

consultancy services to companies throughout the India and Abroad. Our clients

appreciate the knowledge, expertise and quality we bring on the table.

We have earned customer appriciation and pat on back for delivering

professionally engineered solutions across many market sectors and

technologies, with a proactive and cost-effective approach.

Embizon Technologies extensive experience in designing PCBs for all types of

applications, including the latest PCI and DDR technologies. We can satisfy all

your requirements for high-speed digital, analog, RF, backplane, flexi-rigid,

high frequency RF Antenna and other high technology designs.

13

EMBIZON TECHNOLOGIES LIMITED

AN OVERVIEW ABOUT THE COMPANY

VISION:

Our vision is to become a recognized leader in delivering highest Quality PCB

Engineering Solutions, Products and Services to our customers. We believe

Happy and Satisfied Customers with the services are the secret to our success

MISSION STATEMENT:

Through human ingenuity and technology, our mission is to provide world-class

engineering solutions, in a timely and cost-effective manner to our clients and

their customers.

CORE VALUES:

• Nothing transforms life like education.

• We shall honor all commitments

• We shall be committed to Quality, Innovation and Growth in every

endeavor

• We shall be responsible corporate citizens

QUALITY POLICY:

"We shall deliver defect-free products, services and solutions to meet the

requirements of our external and internal customers, the first time, every time.

14

OBJECTIVES:

• MANAGEMENT OBJECTIVES –

To fuel initiative and foster activity by allowing individuals, freedom

of action and innovation in attaining defined objectives.

• PEOPLE OBJECTIVES –

To help people in Embizon Technologies Ltd., share company’s

success, which they make possible; to provide job security based on

their performance; to

recognize their individual achievements; and help them gain a sense of

satisfaction and accomplishment from their work.

15

WORKING CAPITAL MANAGEMENT

CONCEPTUAL FRAMEWORK

INTRODUCTION TO WORKING CAPITAL

“Working Capital is the Life-Blood and Controlling Nerve Center of a

business”

The working capital management precisely refers to management of

current assets. A firm’s working capital consists of its investment in

current assets, which include short-term assets such as:

➢ Cash and bank balance,

➢ Inventories,

➢ Receivables (including debtors and bills),

➢ Marketable securities.

Working capital is commonly defined as the difference between current assets

and current liabilities.

WORKING CAPITAL = CURRENT ASSETS-CURRENT LIABILITIES

16

There are two major concepts of working capital:

➢ Gross working capital

➢ Net working capital

Gross working capital:

It refers to firm's investment in current assets. Current assets are the assets,

which can be converted into cash with in a financial year. The gross working

capital points to the need of arranging funds to finance current assets.

Net working capital:

It refers to the difference between current assets and current liabilities. Net

working capital can be positive or negative. A positive net working capital

will arise when current assets exceed current liabilities. And vice-versa for

negative net working capital. Net working capital is a qualitative concept. It

indicates the liquidity position of the firm and suggests the extent to which

working capital needs may be financed by permanent sources of funds. Net

working capital also covers the question of judicious mix of long-term and

short-term funds for financing current assets.

17

Significance Of Working Capital Management

The management of working capital is important for several reasons:

➢ For one thing, the current assets of a typical manufacturing firm account

for half of its total assets. For a distribution company, they account for

even more.

➢ Working capital requires continuous day to day supervision. Working

capital has the effect on company's risk, return and share prices.

➢ There is an inevitable relationship between sales growth and the level of

current assets. The target sales level can be achieved only if supported

by adequate working capital Inefficient working capital management

may lead to insolvency of the firm if it is not in a position to meet its

liabilities and commitments.

18

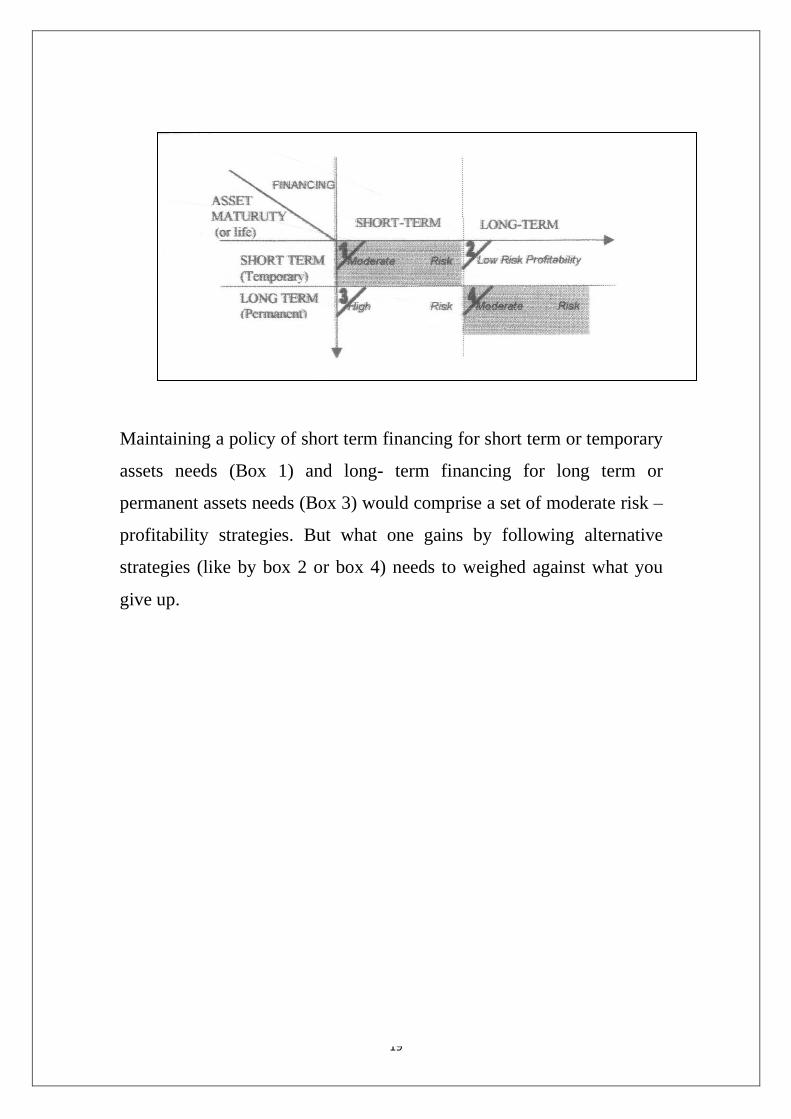

LIQUIDITY VS PROFITABILITY: RISK - RETURN

TRADE OFF

Another important aspect of a working capital policy is to maintain and

provide sufficient liquidity to the firm. Like the most corporate financial

decisions, the decision on how much working capital be maintained

involves a trade off- having a large net working capital may reduce the

liquidity risk faced by a firm, but it can have a negative effect on the

cash flows. Therefore, the net effect on the value of the firm should be

used to determine the optimal amount of working capital.

Sound working capital involves two fundamental decisions for the firm.

They are the determination of:

➢ The optimal level of investments in current assets.

➢ The appropriate mix of short-term and long-term financing used

to support this investment in current assets, a firm should decide

whether or not it should use short-term financing. If short-term

financing has to be used, the firm must determine its portion in

total financing. Short-term financing may be preferred over long-

term financing for two reasons:

➢ The cost advantage

➢ Flexibility

But short-term financing is more risky than long-term financing.

Following table will summarize our discussion of short-term versus

long-term financing.

19

Maintaining a policy of short term financing for short term or temporary

assets needs (Box 1) and long- term financing for long term or

permanent assets needs (Box 3) would comprise a set of moderate risk –

profitability strategies. But what one gains by following alternative

strategies (like by box 2 or box 4) needs to weighed against what you

give up.

20

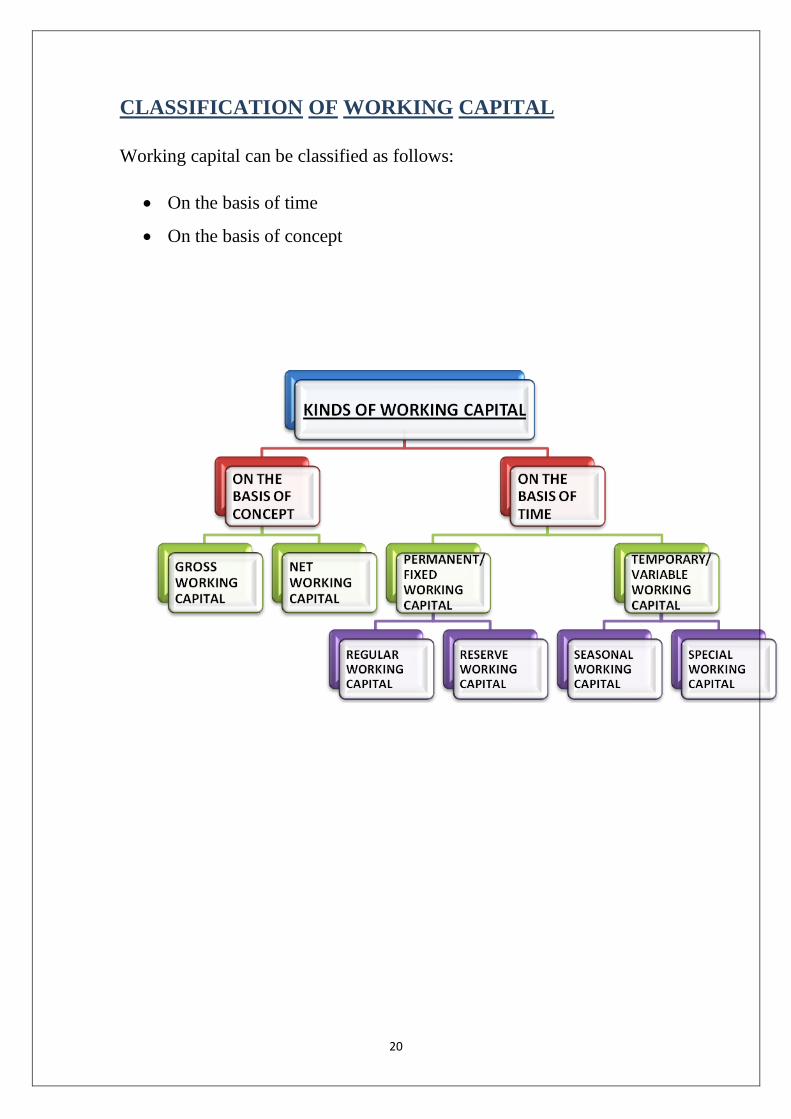

CLASSIFICATION OF WORKING CAPITAL

Working capital can be classified as follows:

• On the basis of time

• On the basis of concept

21

TYPES OF WORKING CAPITAL NEEDS

Another important aspect of working capital management is to analyze

the total working capital needs of the firm in order to find out the

permanent and temporary working capital. Working capital is required

because of existence of operating cycle. The lengthier the operating

cycle, greater would be the need for working capital. The operating

cycle is a continuous process and therefore, the working capital is

needed constantly and regularly. However, the magnitude and quantum

of working capital required will not be same all the times, rather it will

fluctuate.

The need for current assets tends to shift over time. Some of these

changes reflect permanent changes in the firm as is the case when the

inventory and receivables increases as the firm grows and the sales

become higher and higher. Other changes are seasonal, as is the case

with increased inventory required for a particular festival season. Still

others are random reflecting the uncertainty associated with growth in

sales due to firm's specific or general economic factors.

The working capital needs can be bifurcated as:

➢ Permanent working capital

➢ Temporary working capital

22

Permanent working capital:

There is always a minimum level of working capital, which is

continuously required by a firm in order to maintain its activities. Every

firm must have a minimum of cash, stock and other current assets, this

minimum level of current assets, which must be maintained by any firm

all the times, is known as permanent working capital for that firm. This

amount of working capital is constantly and regularly required in the

same way as fixed assets are required. So, it may also be called fixed

working capital.

Temporary working capital:

Any amount over and above the permanent level of working capital is

temporary, fluctuating or variable working capital. The position of the

required working capital is needed to meet fluctuations in demand

consequent upon changes in production and sales as a result of seasonal

changes.

23

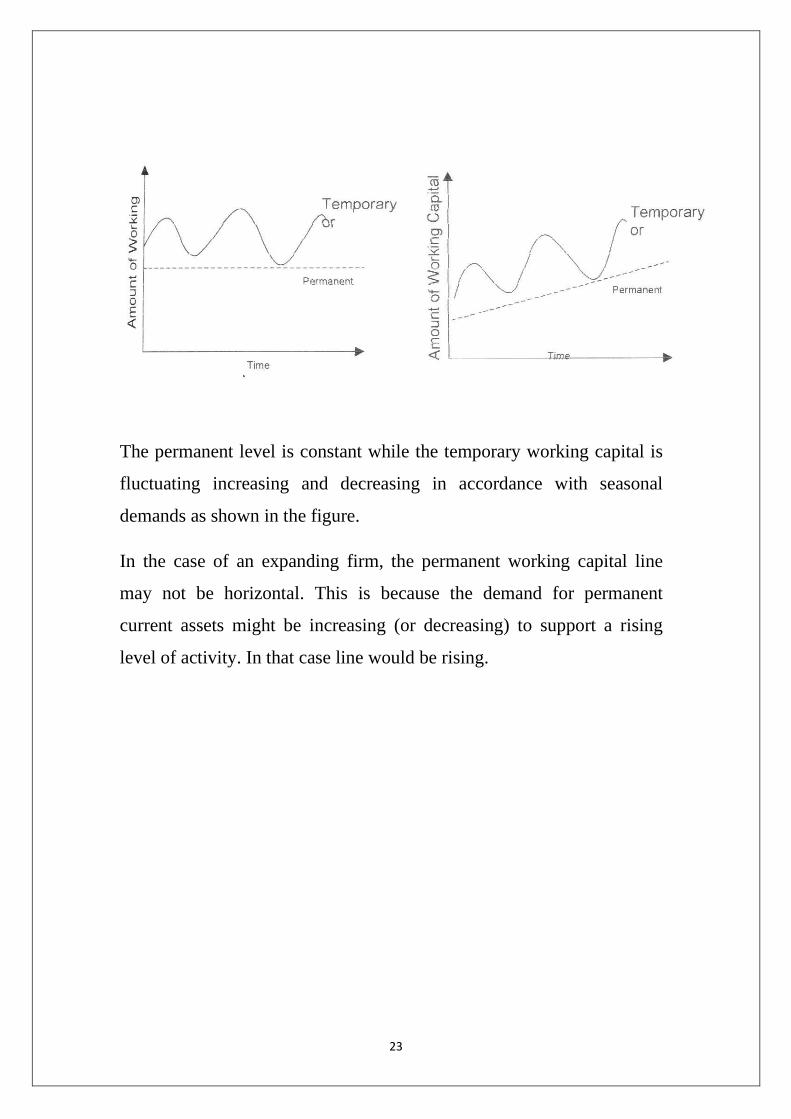

The permanent level is constant while the temporary working capital is

fluctuating increasing and decreasing in accordance with seasonal

demands as shown in the figure.

In the case of an expanding firm, the permanent working capital line

may not be horizontal. This is because the demand for permanent

current assets might be increasing (or decreasing) to support a rising

level of activity. In that case line would be rising.

24

FINANCING OF WORKING CAPITAL

There are types of working capital requirements as discussed above.

They are:

➢ Permanent or Fixed Working Capital requirements

➢ Temporary or Variable Working Capital requirements

➢ Gross and net working capital requirements

➢ Negative working capital requirements

➢ Reserve working capital requirements

➢ Regular working capital requirements

➢ Seasonal working capital requirements

➢ Special working capital requirements

1) PERMANENT WORKING CAPITAL:

It is otherwise called as Fixed Working Capital. Tandon committee

has referred to this type of working capital as Hard Core Working

Capital.

Permanent working capital implies the base investment amount in all

types of current resources which is respected at all times to carry on

business activities. The value of current assets have been increased or

decreased over a period of time. Even though, there is a need of having

minimum level of current assets at all times in order to carry on the

business activities effectively.

2) TEMPORARY WORKING CAPITAL:

It is otherwise called as Fluctuating or Variable Working Capital. There is

a close relationship prevailing between temporary working capital and the

level of production and sales. There is no uniform production and sales

throughout the year. If heavy order is received for production and there is

25

a large amount of credit sales, there is a need of more amount of

temporary working capital. At the same time, if production is carried on

in anticipation of demand in near future, temporary working capital is

required.

In nutshell, temporary working capital is an extra working capital

required to support the changing production and sales activities.

3) GROSS AND NET WORKING CAPITAL:

Gross working capital means an amount of funds invested in the various

forms of current assets in total. Current assets are those assets which are

bought in the ordinary course of business and converted into cash within

a short period which is normally one accounting year.

Net working capital is the excess of current assets over current liabilities.

Again, the net working capital is divided into two types. They are

▪ Positive net working capital and

▪ Negative net working capital.

The positive net working capital exists, whenever the current assets

exceeds current liabilities. The negative net working capital exists

whenever the current liabilities exceeds the current assets. Current

liability means a liability payable within one accounting year in the

ordinary course of business or payable out of the current assets within a

short period normally one year or payable out of the revenue income of

the business

4) NEGATIVE WORKING CAPITAL:

Sometimes, the value of current assets is less than the current liabilities, it

shows negative working capital. If such type of situation arise, the firm is

going to meet the financial crisis very shortly.

26

5) RESERVE WORKING CAPITAL:

It is otherwise called as Cushion Working Capital. It refers to the short

term financial arrangement made by the business units to meet

uncertain changes or to meet uncertainties. A firm is always working

with the expectation of some risks which may be controllable or

uncontrollable. The reserve working capital can be used in order to

meet the uncontrollable risks and sustain in the business world.

6) REGULAR WORKING CAPITAL:

The minimum amount of working capital to be maintained in normal

condition is called Regular Working Capital.

7) SEASONAL WORKING CAPITAL:

Some products have seasonal demand. Seasonal demand arises due to

festival. In this way, seasonal working capital means an amount of

working capital maintained to meet the seasonal demand of the product.

8) SPECIAL WORKING CAPITAL:

Special programmes may be conducted for business development. The

programmes may be advertisement campaign, sales promotion activities,

product development activities, marketing research activities, launching

of new products, expansion of markets and the like. Therefore, special

working capital means an amount of working capital maintained to meet

the expenses of special programmes of the company.

27

FACTORS DETERMINING WORKING CAPITAL

REQUIREMENTS

There are many factors that determine working capital needs of an

enterprise. Some of these factors are explained below:

• Nature or Character of Business.

The working capital requirement of a firm is closely related to the

nature of its business. A service firm, like an electricity

undertaking or a transport corporation, which has a short

operating cycle and which sells predominantly on cash basis, has

a modest working capital requirement. Oh the other hand, a

manufacturing concern like a machine tools unit, which has a long

operating cycle and which sells largely on credit, has a very

substantial working capital requirement.

Sintech is a manufacturing concern so this requires them to keep a

very sizeable amount in working capital.

• Size of Business/Scale of Operations.

Sintech has a good position in its segment and they are also

spending their operations in the domestic market as well as in

foreign market. The scale of operations and the size it holds in the

market makes it a must for them to hold their inventory and

current asset at a huge level.

• Rate of Growth of Business.

The rate of growth of sales indicates a need for increase in the

working capital requirements of the firm. As the firm is projected

to increase their sales by 69% from what it was in 2009, it is

required to guard them against the increasing requirements of the

28

net current asset by way of efficient working capital management.

The sales and projected sales level determine the investment in

inventories and receivables.

• Price Level Changes.

Changes in the price level also affect the working capital

requirements. It was the reduced margins in the price of the raw

materials that had prompted them to go for bulk purchases thus

making on additions to their net current assets. They might have

gone for this large-scale procurement for availing discounts and

anticipating a rise in prices, which would have meant that more

funds are required to maintain the same current assets.

WORKING CAPITAL CYCLE

The upper portion of the diagram above shows in a simplified form the

chain of events in a manufacturing firm. Each of the boxes in the upper

part of the diagram can be seen as a tank through which funds flow.

These tanks, which are concerned with day-to-day activities, have funds

constantly flowing into and out of them.

➢ The chain starts with the firm buying raw materials on credit.

➢ In due course this stock will be used in production, work will be

carried out on the stock, and it will become part of the firm’s work-

in-progress.

➢ Work will continue on the WIP until it eventually emerges as the

finished product.

29

➢ As production progresses, labor costs and overheads need have to

be met.

➢ Of course at some stage trade creditors will need to be paid.

➢ When the finished goods are sold on credit, debtors are increased.

➢ They will eventually pay, so that cash will be injected into the firm.

Each of the areas- Stock (raw materials, WIP, and finished goods), trade

debtors, cash (positive or negative) and trade creditors – can be viewed as

tanks into and from which funds flow.

Working capital is clearly not the only aspect of a business that affects

the amount of cash.

➢ The business will have to make payments to government for

taxation.

➢ Fixed assets will be purchased and sold

➢ Lessors of fixed assets will be paid their rent

➢ Shareholders (existing or new) may provide new funds in the form

of cash

➢ Some shares may be redeemed for cash

➢ Dividends may be paid

➢ Long-term loan creditors (existing or new) may provide loan

finance, loans will need to be repaid from time-to-time, and

➢ Interest obligations will have to be met by the business

Unlike, movements in the working capital items, most of these ‘non-

working capital’ cash transactions are not every day events. Some of

them are annual events (e.g. tax payments, lease payments, dividends,

interest and, possibly, fixed asset purchases and sales). Others (e.g. new

30

equity and loan finance and redemption of old equity and loan finance)

would typically be rarer events.

SOURCES OF WORKING CAPITAL

Embizon Technologies has the following sources available for the

fulfillment of its working capital requirements in order to carry on its

operations smoothly:

➢ Banks:

These include the following banks –

State Bank of India

Canara Bank

HDFC Bank Ltd.

ICICI Bank Ltd.

Societe Generale

Standard Chartered Bank

State Bank of Patiala

State Bank of Saurashtra

➢ Commercial Papers:

Commercial Papers have become an important tool for

financing working capital requirements of a company.

Commercial Paper is an unsecured promissory note issued

by the company to raise short-term funds. The buyers of the

commercial paper include banks, insurance companies, unit

trusts, and companies with surplus funds to invest for a short

period with minimum risk.

31

EMBIZON issues Commercial Papers and had 4000

commercial papers in the year 2006.

INVENTORY MANAGEMENT

Inventories

Inventories constitute the most important part of the current assets of

large majority of companies. On an average the inventories are

approximately 60% of the current assets in public limited companies in

India. Because of the large size of inventories maintained by the firms, a

considerable amount of funds is committed to them. It is therefore,

imperative to manage the inventories efficiently and effectively in order

to avoid unnecessary investment.

Nature of Inventories

Inventories are stock of the product of the company is manufacturing for

sale and components make up of the product. The various forms of the

inventories in the manufacturing companies are:

Raw Material: It is the basic input that is converted into the

finished product through the manufacturing process. Raw materials

are those units which have been purchased and stored for future

production.

Work-in-progress: Inventories are semi-manufactured products.

They represent product that need more work they become finished

products for sale.

Finished Goods: Inventories are those completely manufactured

products which are ready for sale. Stocks of raw materials and

work-in-progress facilitate production, while stock of finished

goods is required for smooth marketing operations. Thus,

32

inventories serve as a link between the production and

consumption of goods.

Inventory Management Techniques

In managing inventories, the firm’s objective should be to be in

consonance with the shareholder wealth maximization principle. To

achieve this, the firm should determine the optimum level of inventory.

Efficiently controlled inventories make the firm flexible. Inefficient

inventory control results in unbalanced inventory and inflexibility-the

firm may sometimes run out of stock and sometimes pile up unnecessary

stocks.

Economic Order Quantity (EOQ):

The major problem to be resolved is how much the inventory should be

added when inventory is replenished. If the firm is buying raw materials,

it has to decide lots in which it has to purchase on replenishment. If the

firm is planning a production run, the issue is how much production to

schedule. These problems are called order quantity problems, and the task

of the firm is to determine the optimum or economic lot size. Determine

an optimum level involves two types of costs:-

• Ordering Costs: This term is used in case of raw material

and includes all the cost of acquiring raw material. They

include the costs incurred in the following activities:

Requisition

Purchase Ordering

Transporting

Receiving

Inspecting

Storing

33

Ordering cost increase with the number of orders placed; thus the more

frequently inventory is acquired, the higher the firm’s ordering costs. On

the other hand, if the firm maintains large inventory’s level, there will be

few orders placed and ordering costs will be relatively small. Thus,

ordering costs decrease with the increasing size of inventory.

• Carrying Costs: Costs are incurred for maintaining a given

level of inventory are called carrying costs. These include

the following activities:

Warehousing Cost

Handling

Administrative cost

Insurance

Deterioration and obsolescence

Carrying costs are varying with inventory size. This behavior is contrary

to that of ordering costs which decline with increase in inventory size.

The economic size of inventory would thus depend on trade-off between

carrying costs and ordering cost.

The increasing component of raw materials in inventory is due to the fact

that the company has gone for bulk purchases and has increased

consumption due to a fall in prices and reduced margins for the year.

Another reason might be the increasing sales, which might have induced

them to purchase more in anticipation of a further increase in demand of

the product. And the low composition of work-in-progress is

understandable as because of the nature of the business firm is involved

in.

34

To the question as to whether the increasing costs in inventory are

justified by the returns from it the answer could be found in the

EMBIZON retail expansion. EMBIZON caters to the need of the two

separate segments:

a) Institutions for which they manufacture against orders and,

b) Retail segment of the market.

They are more into retail than earlier and at present more than 650 retail

outlets branded with EMBIZON sign ages and more are in the pipeline

The company in order to meet its raw materials requirements could have

gone for frequent purchases, which would have resulted in lesser cash

flows for the firm rather than the high expenditure involved when

procuring in at bulk. The reason why the firm has gone for these bulk

purchases because of the lower margins and the discounts it availed

because of procuring in bulk quantities.

A negative growth in WIP could be because:

a) The time taken to convert raw materials to finished goods is

very minimal

b) This is also due to capacity being not utilized at the

optimum.

ABC System:

ABC system of inventory keeping is followed in the factories. Various

items are categorized into three different levels in the order of their

35

importance. For e.g. items such as memory, high capacity processors and

royalty are placed in the ‘A’ category. Large number of firms has to

maintain several types of inventories. It is not desirable the same degree

of control all the items. The firm should pay maximum attention to those

items whose value is highest. The firm should therefore, classify

inventories to identify which items should receive the most effort in

controlling. The firm should be selective in approach to control

investment in various types of inventories. This analytical approach is

called “ABC Analysis”. The high-value items are classified as “A items”

and would be under tightest control. “C items” represent relatively least

value and would require simple control. “ B items” fall in between the

two categories and require reasonable attention of management.

JIT:

The relevance of JIT in EMBIZON Info system can be questioned. This

is because they procure materials on the basis of projections made at least

two or three months before. Even at the time of procurement they ensure

that they procure much more than what actually is required by the firm

that is they hold significant amount of inventory as safety stock. This is

done to counter the threat involved in default and accidental breakdowns.

The levels of safety stock usually vary according to the usage.

36

CASH MANAGEMENT

SOURCES OF CASH:

Sources of additional working capital include the following:

➢ Existing cash reserves

➢ Profits (when you secure it as cash!)

➢ Payables (credit from suppliers)

➢ New equity or loans from shareholders

➢ Bank overdrafts or lines of credit.

➢ Long-term loans

If you have insufficient working capital and try to increase sales, you

can easily over-stretch the financial resources of the business. This is

called overtrading.

Early warning signs include:

❖ Pressure on existing cash

❖ Exceptional cash generating activities e.g. offering high discounts

for early cash payment

❖ Bank overdraft exceeds authorized limit.

❖ Seeking greater overdrafts or lines of credit

❖ Part-paying suppliers or other creditors

❖ Paying bills in cash to secure additional supplies

❖ Management pre-occupation with surviving rather than managing

❖ Frequent short-term emergency requests to the bank (to help pay

wages, pending receipt of a cheque).

37

CASHlMANAGEMENT INEMBIZON TECHNOLOGIES:

The cash management system followed by the Embizon Technologies

is mainly lock box system.

Cash Management System involves the following steps:

1. The branch offices of the company at various locations hold the

collection of cheques of the customers.

2. Those cheques are either handed over to the CMS agencies or bank

of the particular location take charge of whole collection.

3. These CMS agencies or bank send those cheques to the clearing

house to make them realized. These cheques can be local or

outstation.

4. The CMS agencies or bank send information to the central hub of

the company regarding realization/cheque bounced.

5. The central hub passes on the realized funds to the company as per

the agreed agreements.

6. The CMS agencies or concerned bank provides the necessary MIS

to the company as per requirement.

In cash management the collect float taken for the cheques to be realized

into cash is irrelevant and non-interfering because banks such as Standard

Chartered, HDFC and CitiBank who give credit on the basis of these

cheques after charging a very small amount. These credits are given to

immediately and the maximum time taken might be just a day. The

amount they charge is very low and this might cover the threat of the

cheque sent in by two or three customers bouncing. Even otherwise the

time taken for the cheques to be processed is instantaneous. Their Cash

Management System is quite efficient.

38

Cash vs. Marketable Securities

The investment in marketable securities rather than having large cash

balances in something that has been given thought for by the firm. This is

because while a firm gets revenue in the form of interests by investments,

it actually has to pays certain amount money to the banks for maintaining

current accounts and fixed deposits usually have a longer maturity period.

That is, the problem with high investments is that the opportunity to earn

is lost, thus a firm has to maintain an optimal cash balance. But the

investment in mutual funds or other marketable securities might create a

problem of investment, as they might not be readily realizable as say

liquid cash or the amount deposited in the current account. The

investments in say fixed assets say may earn a fixed rate of interest but

they have a maturity period attached to them.

In EMBIZON, Standard Chartered is the concentration bank in which all

the inflows from the deposit banks are concentrated and passed on to the

disbursement banks for further disbursement.

Liquid Cash Balance

The liquid cash maintained in the business is only that much as is

required to satisfy the daily requirements of the firm and not more. The

rest of the cash is invested into mutual funds and also held in fixed

deposits and current accounts.

Instruments Used

The instrument used here are primarily cheques comprising of around

97% of what is used in. The rest 2-3% comprise of the letters of credit.

39

Thus working capital is the lifeline for every business. The main

advantages of sufficient working capital are:

• It helps in prompt payment

• Ensures high solvency in the company and good credit

standing.

• Regular supply of material and continuous production.

• Ensures regular payment of salaries and wages and day to

day commitments.

RECEIVABLES MANAGEMENT

Cash flow can be significantly enhanced if the amounts owing to a

business are collected faster. Every business needs to know.... who owes

them money.... how much is owed.... how long it is owing.... for what it

is owed.

Late payments erode profits and can lead to bad debts.

Slow payment has a crippling effect on business; in particular on small

businesses whom can least afford it. If you don't manage debtors, they

will begin to manage your business as you will gradually lose control

due to reduced cash flow and, of course, you could experience an

increased incidence of bad debt.

The following measures will help manage your debtors:

1. Have the right mental attitude to the control of credit and make sure

that it gets the priority it deserves.

2. Establish clear credit practices as a matter of company policy.

3. Make sure that these practices are clearly understood by staff,

suppliers and customers.

4. Be professional when accepting new accounts, and especially

40

largerones.

5. Check out each customer thoroughly before you offer credit. Use

credit agencies, bank references, industry sources etc.

6. Establish credit limits for each customer and stick to them.

7. Continuously review these limits when you suspect tough times are

coming or if operating in a volatile sector.

8. Keep very close to your larger customers.

9. Invoice promptly and clearly.

10.Consider charging penalties on overdue accounts.

11.Consider accepting credit /debit cards as a payment option.

12.Monitor your debtor balances and aging schedules, and don't let any

debts get too old.

Recognize that the longer someone owes you, the greater the chance you

will never get paid. If the average age of your debtors is getting longer,

or is already very long, you may need to look for the following possible

defects.

• Poor collection procedures.

• Lax enforcement of credit terms.

• Slow issue of invoices or statements.

• Errors in invoices or statements.

• Customer dissatisfaction.

• Weak credit judgement.

41 | P a g e

Debtors due over 90 days (unless within agreed credit terms) should generally

demand immediate attention. Look for the warning signs of a future bad debt.

For example…..

1. Longer credit terms taken with approval, particularly for smaller orders.

2. Use of post-dated checks by debtors who normally settle within agreed

terms.

3. Evidence of customers switching to additional suppliers for the same

goods.

4. New customers who are reluctant to give credit references.

5. Receiving part payments from debtors.

Profits only come from paid sales.

The act of collecting money is one, which most people dislike for many

reasons and therefore put on the long finger because they convince themselves

that there is something more urgent or important that demand their attention

now. There is nothing more important than getting paid for your product or

service. A customer who does not pay is not a customer.

HERE ARE FEW WAYS IN COLLECTING MONEY FROM DEBTORS: -

• Develop appropriate procedures for handling late payments.

• Track and pursue late payers

• Get external help if you own efforts fail.

• Don’t feel guilty asking for money .. its yours and you are entitled to it.

• Make that call now. And keep asking until you get some satisfaction.

• In difficult circumstances, take what you can now and agree terms for the

remainder, it lessens the problem.

42 | P a g e

• When asking for your money, be hard on the issue – but soft on the person.

Don’t give the debtor any excuses for not paying.

• Make that your objective is to get the money, not to score points or get

even.

COLLECTION POLICIES:

It refers to the collection procedures such as letters, phone calls and other follow

up mechanism to recover the amount due from the customers. It is obvious that

costs are incurred towards the collection efforts, but bad debts as well as

average collection period would decrease. Further, a strict collection policy of

the firm is expensive for the firm because of the high cost is required to be

incurred by the firm and it may also result in loss of goodwill. But at the same

time it minimizes the loss on account of bad debts. Therefore, a firm has to

strike a balance between the cost and benefits associated with collection

policies.

The steps usually followed in collection efforts are:

• Sending repeated letters and reminders to the customers

• Personal visits

• Using agencies involved in collection process

• Making telephonic reminders

• Initiating legal actions

• Real Time Gross Settlement (RTGS)

Real Time Gross Settlement as such is a concept new in nature and though the

firm uses the system with all the members of the consortium, it is still in its

primal stage and will take time before all of the clients of the firm are willing to

accept it. The firm has made a proposal to the consortium of the banks during

43 | P a g e

appraisal for faster implementation of internet based banking facility by all the

banks and adoption of RTGS payment system through net.

The debtor’s turnover ratio is completely dependent upon the credit policy

followed by the firm. The credit policy followed by the firm should be such that

the threat of bad debts and the default rate involved should be terminated.

That the creditors turnover ratio has declined and payment period has increased

indicate that the company has got a leeway in making the payment to the

creditors by way of increased time.

With creditors they are having pre-agreements and have undertaken

arrangements with them, which they believe to be the best in the business and

these are fixed.

(NOTE: Acceptances are not included in the computation of creditors turnover)

MANAGING PAYABLES (Creditors)

Creditors are a vital part of effective cash management and should be

managed carefully to enhance the cash position.

Purchasing initiates cash outflows and an over-zealous purchasing function

can create liquidity problems.

Consider the following: -

• Who authorizes purchasing in your company - is it tightly managed or

spread among a number of (junior) people?

• Are purchase quantities geared to demand forecasts?

44 | P a g e

• Do you use order quantities, which take account of stock holding and

purchasing costs?

• Do you know the cost to the company of carrying stock?

• Do you have alternative sources of supply? If not, get quotes from major

suppliers and shop around for the best discounts, credit terms as it reduces

dependence on a single supplier.

• How many of your suppliers have a return policy?

• Are you in a position to pass on cost increases quickly through price

increases to your customers?

• If a supplier of goods or services lets you down can you charge back the

cost of the delay?

• Can you arrange (with confidence!) to have delivery of supplies staggered

or on a just-in-time basis?

There is an old adage in business that "if you can buy well then you can sell

well". Management of your creditors and suppliers is just as important as the

management of your debtors. It is important to look after your creditors- slow

payment by you may create ill feeling and can signal that your company is

inefficient (or in trouble!).

Remember that a good supplier is someone who will work with you to enhance

the future viability and profitability of your company.

Financing Current Assets

The firm has to decide about the sources of funds, which can be availed to

make investment in current assets.

45 | P a g e

Long term financing:

It includes ordinary share capital, preference share capital, debentures, long

term borrowings from financial institutions and reserves and surplus.

Short term financing:

It is for a period less than one year and includes working capital funds from

banks, public deposits, commercial paper etc.

Spontaneous financing:

It refers to automatic sources of short-term funds arising in normal course of

business. There is no explicit cost associated with it. For example, Trade

Credit and Outstanding Expenses etc.

Depending on the mix of short and long term financing, the company can

follow any of the following approaches.

Matching Approach

In this, the firm follows a financial plan, which matches the expected life of

assets with the expected life of source of funds raised to finance assets. When

the firm follows this approach, long term financing will be used to finance

fixed assets and permanent current assets and short term financing to finance

temporary or variable current assets.

46 | P a g e

Conservative Approach

In this, the firm finances its permanent assets and also a part of temporary

current assets with long term financing. In the periods when the firm has no

need for temporary current assets, the long-term funds can be invested in

tradable securities to conserve liquidity. In this the firm has less risk of facing

the problem of shortage of funds.

Aggressive Approach

In this, the firm uses more short term financing than warranted by the

matching plan. Under an aggressive plan, the firm finances a part of its current

assets with short term financing.

Relatively more use of short term financing makes the firm more risky.

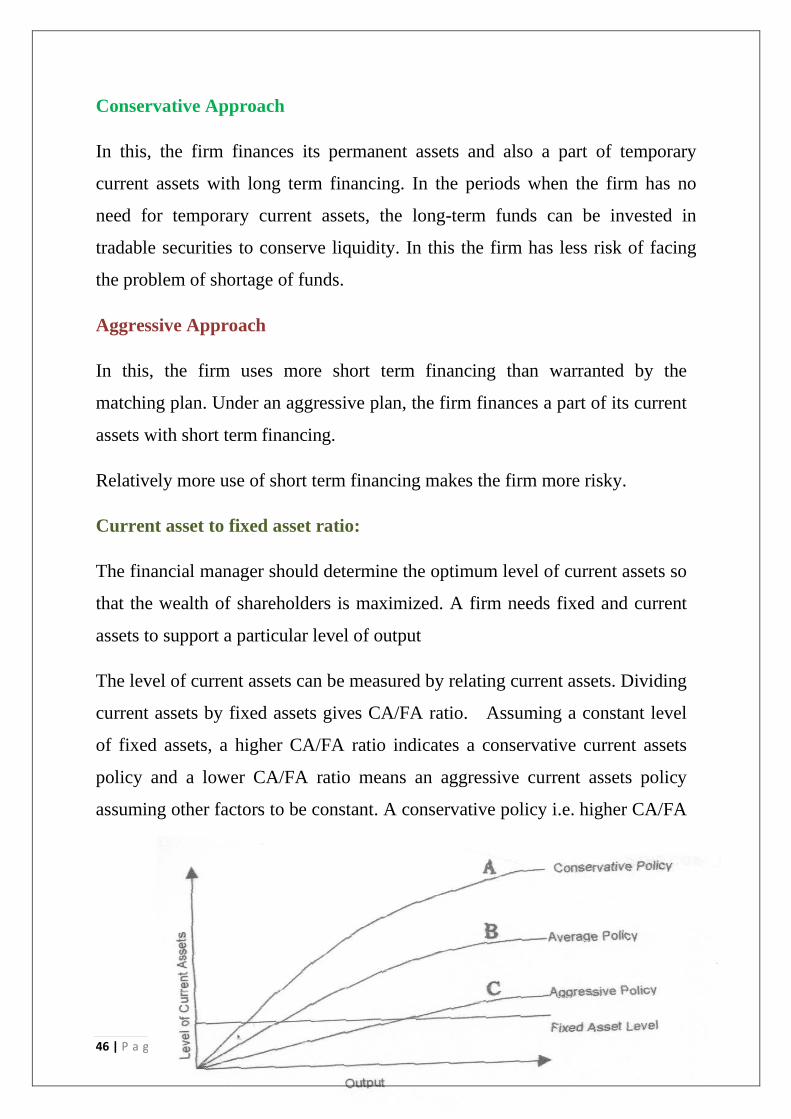

Current asset to fixed asset ratio:

The financial manager should determine the optimum level of current assets so

that the wealth of shareholders is maximized. A firm needs fixed and current

assets to support a particular level of output

The level of current assets can be measured by relating current assets. Dividing

current assets by fixed assets gives CA/FA ratio. Assuming a constant level

of fixed assets, a higher CA/FA ratio indicates a conservative current assets

policy and a lower CA/FA ratio means an aggressive current assets policy

assuming other factors to be constant. A conservative policy i.e. higher CA/FA

47 | P a g e

ratio implies greater liquidity and lower risk; while an aggressive policy i.e.

lower CA/FA ratio indicates higher risk and poor liquidity. The current assets

policy of the most firms may fall between these two extreme policies. The

alternative current assets policies may be shown with the help of the following

figure.

In this figure the most conservative policy is indicated by alternative A, where

as CA/FA ratio is greatest at every level of output. Alternative C is the most

aggressive policy, as CA/FA ratio is lowest at all levels of output. Alternative B

lies between the conservative and aggressive policies and is an average policy.

WORKING CAPITAL & SHORT-TERM FINANCING

SHORT TERM FINANCING

Other than the investment in current assets, the firm also has to be concerned

with short-term to long-term debt as this plays a very important role in

determining the amount of risk undertaken by the firm. That is, the firm not

only has to be concerned about current assets but also the sources through which

they are financed. A firm before financing in either of the two, has to take into

consideration various aspects. While short term might seem the ideal way to

finance your assets than the long term due to shorter maturity period and also

less of costs are involved, there is an inherent risk in short term financing due to

fluctuating interest rates and due to the reason that the firm might be unable to

ready the amount in a shorter span of time.

Under secured loan cash credit, along with non fund based facilities, foreign

currency term loan from banks are secured by way of hypothecation of stock-in-

48 | P a g e

trade, book debts as first charge and by way of second chanrge on all the

immovable and movable assets of the parent company. Term loan in Indian

rupees from a bank is subject to a prior charge in favour of company’s bankers

on book debts and stock in trade for working capital facilities.

Here EMBIZON has a major portion of their financing done through short term

financing than long term financing. The preference of short term financing to

long term as such is not the part of any policy employed by the firm but it was

due to the reason that the interest rates in short term were more investor friendly

and the cost involved in them were also low. At present, we can see that the

firm is moving more towards long term financing as the interest terms in the

long term has reduced compared to the short term.

YEAR- END COMMERCIAL PAPERS

MERITS OF COMMERCIAL PAPERS:

• It is an alternative source of raising short-term finance, and proves to be

handy during periods of tight bank credit.

• It is a cheaper source of finance in comparison to the bank credit.

DEMERITS OF COMMERCIAL PAPERS:

• It is an impersonal method of financing.

• It is always available to the financially sound and highest rated

companies.

• The amount of loanable funds available in the commercial paper market

is limited to the amount of excess liquidity of the various purchasers of

commercial paper.

49 | P a g e

ANALYSIS

INDUSTRY ANALYSIS

INDUSTRY STRUCTURE AND DEVELOPMENTS

Over the past decade, the Information Technology (IT) industry has become one

of the fastest growing industries in India, propelled by exports (the industry

accounted for more than a quarter of India’s services exports in 2004-05). The

key segments that have contributed significantly (96 percent of total) to the

industry’s exports include – Software and services (IT services) and IT enabled

services (ITES) i.e. business services. Over a period of time, India has

established itself

as a preferred global sourcing base in these segments and they are expected to

continue to fuel growth in the future.

CONCLUDING ANAYSIS

• The working capital position of the company is sound and the various

sources through which it is funded are optimal.

• The company has used its dividend policy, purchasing, financing and

investment decisions to good effect can be seen from the inferences made

earlier in the project.

• The debts doubtful have been doubled over the years but their percentage

on the debts has almost become half. This implies a sales and collection

policy that get along with the receivables management of the firm.

• The returns have been affected by a marked growth in working capital

and though a 29.75% in 2006 return on investment is good, but it got

reduced as compared to 39.01% return in 2005.

50 | P a g e

• The various ratios calculated are an indicator as to the fact that the

profitability of the firm and sales are on a rise and also the deletion of the

inefficiencies in the working capital management.

• The firm has not compromised on profitability despite the high liquidity

is commendable.

• Embizon Technologies has reached a position where the default costs are

as low as negligible and where they can readily factor their accounts

receivables for availing finance is noteworthy.

51 | P a g e

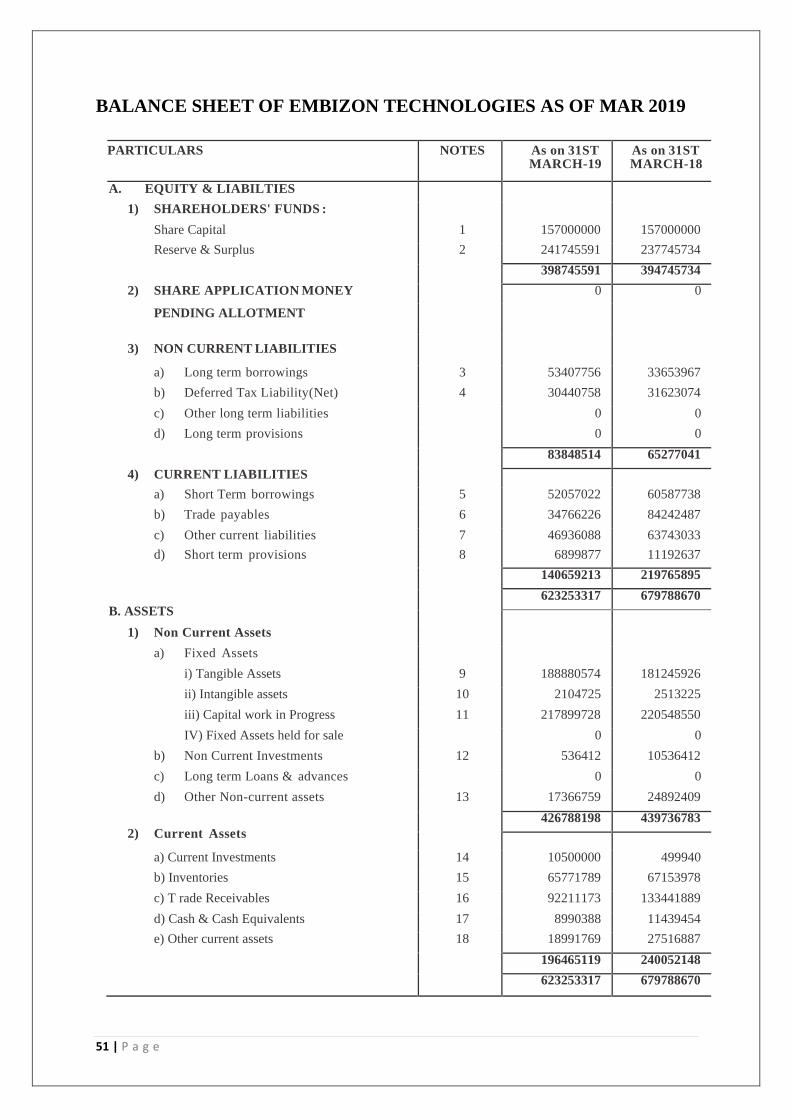

BALANCE SHEET OF EMBIZON TECHNOLOGIES AS OF MAR 2019

PARTICULARS NOTES As on 31ST MARCH-19

As on 31ST MARCH-18

A. EQUITY & LIABILTIES

1) SHAREHOLDERS' FUNDS :

Share Capital 1 157000000 157000000

Reserve & Surplus 2 241745591 237745734

398745591 394745734

2) SHARE APPLICATION MONEY 0 0

PENDING ALLOTMENT

3) NON CURRENT LIABILITIES

a) Long term borrowings 3 53407756 33653967

b) Deferred Tax Liability(Net) 4 30440758 31623074

c) Other long term liabilities 0 0

d) Long term provisions 0 0

83848514 65277041

4) CURRENT LIABILITIES

a) Short Term borrowings 5 52057022 60587738

b) Trade payables 6 34766226 84242487

c) Other current liabilities 7 46936088 63743033

d) Short term provisions 8 6899877 11192637

140659213 219765895

B. ASSETS

623253317 679788670

1) Non Current Assets

a) Fixed Assets

i) Tangible Assets 9 188880574 181245926

ii) Intangible assets 10 2104725 2513225

iii) Capital work in Progress 11 217899728 220548550

IV) Fixed Assets held for sale 0 0

b) Non Current Investments 12 536412 10536412

c) Long term Loans & advances 0 0

d) Other Non-current assets 13 17366759 24892409

2) Current Assets

426788198 439736783

a) Current Investments 14 10500000 499940

b) Inventories 15 65771789 67153978

c) T rade Receivables 16 92211173 133441889

d) Cash & Cash Equivalents 17 8990388 11439454

e) Other current assets 18 18991769 27516887

196465119 240052148

623253317 679788670

52 | P a g e

PROFIT AND LOSS ACCOUNT FOR THE YEAR END 2019

PARTICULARS NOTES As on 31ST MARCH-19

As on 31ST MARCH-18

a) Continuing Operations

i) Revenue from operations Less

: Excise duty Revenue

Operation (Net)

ii) Other Income

iii) Total Revenue

iv) Expenses

a) Cost of materials & stores consumed

b) Purchase of stock in trade

c) Decrease in Inventories

d) Employes benefit expenses

e) Financial cost

f ) Depreciation & amortization expenses

g) Other expenses

Total Expenses

v) Profit before tax, exceptional and

extraordinary items

vi) Exceptional items

vii) Profit before tax and extraordinary items

viii) Extra ordinary items

ix) Profit/(Loss) before tax

x) Tax Expenses

Less : Provision for Taxation

Add : Deferred Tax Assets Add :

Mat credit set off

Net Provision Of Taxation

xi) Profit after tax from contnuing operations

B) Discontinuing Operations

xii) Profit from total operations

(xiii) Earning per share (of Rs.10/- each) ( a)

Basic

(i) Continuing operation

(ii) Total operations

(xiv) Diluted

(i) Contuning operations

(ii) Total operations

19

20

21

22

23

24

25

26

333761535 28933443

405067602 28247569

304828092

7218053

376820033

6405856

312046145 383225889

155492740

0

682442

26478455

15406620

15410401

94307946

215478782

0

1959922

24319930

9642894

17628274

123820785

307778604 392850587

4267541 -9624698

0

0

4267541 -9624698

0 3701473

4267541 -5923225

1450000

1182316

0

1580200

10908479

1369800

-267684 7958479

3999857 0

2035254 0

3999857 2035254

0.25

0.25

0.25

0.25

0.13

0.13

0.13

0.13

53 | P a g e

SUGGESTIONS AND RECOMMENDATIONS

The management of working capital plays a vital role in running of a successful

business. So, things should go with a proper understanding for managing cash,

receivables and inventory.

Embizon Technologies is managing its working capital in a good manner, but

still there is some scope for improvement in its management. This can help the

company in raising its profit level by making less investment in accounts

receivables and stocks etc. This will ultimately improve the efficiency of its

operations. Following are few recommendations given to the company in

achieving its desired objectives:

• The business runs successfully with adequate amount of the working

capital but the company should see to it that the cash should not be tied

up in excessive amount of working capital.

• Though the present collection system is near perfect, the company as due

to the increasing sales should adopt more effective measures so as to

counter the threat of bad debts.

• The over purchasing function should be avoided as it could lead to

liquidity problems.

• The investment of cash in marketable securities should be increased, as it

is very profitable for the company.

• Holding of excessive and insufficient stock must be avoided as it creates

a burden on the cash resources of a business and results in lost sales,

delays for customers, etc respectively.

54 | P a g e

BIBLIOGRAPHY

Following sources have been sought for the preparation of this report:

• Corporate Intranet

• Financial Statements (Annual Reports)

• Direct interaction with the employees of the company

• Internet ----www.embizontechnologies.in

• Textbooks on financial management -

➢ I.M.Pandey

➢ Khan and Jain

➢ Prasanna Chandra

55 | P a g e

Copyright © 2022 FDOKUMEN