Production Budget for each four quarters of 2015

26

PART 1: TASK 1: 1. Sales Budget for each four quarters of 2015 First Quarter Sales Unit : 2,000 Quarterly Unit Increment : 200 Selling Price (RM) : 100 Q1 Q2 Q3 Q4 Year Expected Sales (in units) 2,000 2,200 2,400 2,600 9,200 Selling price (RM) 100.00 100.00 100.00 100.00 100.00 Total sales (RM) 200,000. 00 220,000. 00 240,000 .00 260,000 .00 920,000 .00 2. Production Budget for each four quarters of 2015 Percent of Closing Stock : 10% Q1 Q2 Q3 Q4 Year Expected Sales (in units) 2,000 2,20 0 2,40 0 2,60 0 9,20 0 Add: Desired ending Finished goods (units) 220 240 260 280 1 | BUSINESS MANAGEMENT TECHNIQUE

Transcript of Production Budget for each four quarters of 2015

PART 1:

TASK 1:

1. Sales Budget for each four quarters of 2015

First Quarter Sales Unit : 2,000

Quarterly Unit Increment : 200

Selling Price (RM) : 100

Q1 Q2 Q3 Q4 Year

Expected Sales (inunits)

2,000 2,200 2,400 2,600 9,200

Selling price (RM) 100.00 100.00 100.00 100.00 100.00

Total sales (RM) 200,000.00

220,000.00

240,000.00

260,000.00

920,000.00

2. Production Budget for each four quarters of 2015

Percent of Closing Stock : 10%

Q1 Q2 Q3 Q4 Year

Expected Sales (in units) 2,000 2,200

2,400

2,600

9,200

Add: Desired ending Finished goods (units) 220 240 260 280

1 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Total required units 2,220 2,440

2,660

2,880

Less: Beginning Finished goods (units 0 220 240 260

Required Production Units 2,220 2,220

2,420

2,620

9,480

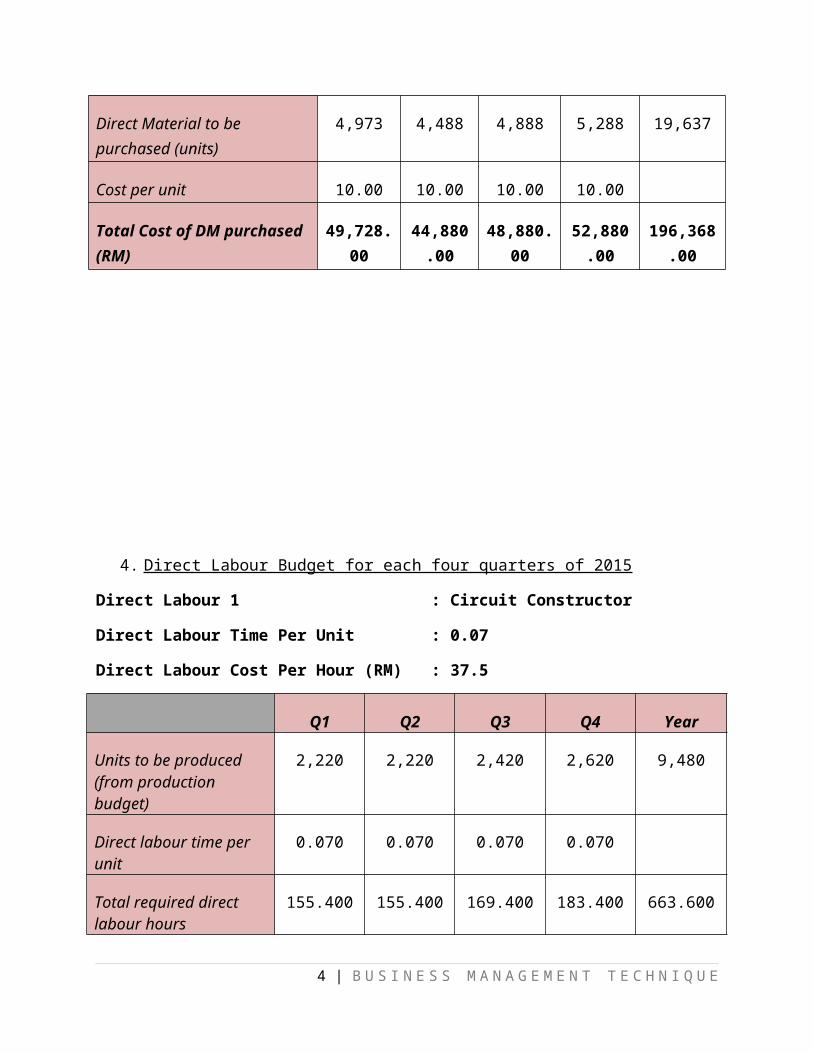

3. Direct Material Budget for each four quarters of 2015

Percent of Closing Stock : 12%

Direct Material 1 : Massage Vibrator

Direct Material Per Unit : 2

Cost Per Unit (RM) : 15

Q1 Q2 Q3 Q4 Year

Units to be produced (from production budget)

2,220 2,220 2,420 2,620 9,480

Direct material per unit 2.000 2.000 2.000 2.000

Total DM required for production (units)

4,440 4,440 4,840 5,240 18,960

Add: Ending DM (units) 533 581 629 677

Total DM required (units) 4,973 5,021 5,469 5,917

Less: Beginning DM (units) 0 533 581 629

Direct Material to be purchased (units)

4,973 4,488 4,888 5,288 19,637

2 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Cost per unit 15.00 15.00 15.00 15.00

Total Cost of DM purchased (RM)

74,592.00

67,320.00

73,320.00

79,320.00

294,552.00

Direct Material 2 : Speaker

Direct Material Per Unit : 2

Cost Per Unit (RM) : 10

Q1 Q2 Q3 Q4 Year

Units to be produced (from production budget)

2,220 2,220 2,420 2,620 9,480

Direct material per unit 2.000 2.000 2.000 2.000

Total DM required for production (units)

4,440 4,440 4,840 5,240 18,960

Add: Ending DM (units) 533 581 629 677

Total DM required (units) 4,973 5,021 5,469 5,917

Less: Beginning DM (units) 0 533 581 629

3 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Direct Material to be purchased (units)

4,973 4,488 4,888 5,288 19,637

Cost per unit 10.00 10.00 10.00 10.00

Total Cost of DM purchased (RM)

49,728.00

44,880.00

48,880.00

52,880.00

196,368.00

4. Direct Labour Budget for each four quarters of 2015

Direct Labour 1 : Circuit Constructor

Direct Labour Time Per Unit : 0.07

Direct Labour Cost Per Hour (RM) : 37.5

Q1 Q2 Q3 Q4 Year

Units to be produced (from production budget)

2,220 2,220 2,420 2,620 9,480

Direct labour time per unit

0.070 0.070 0.070 0.070

Total required direct labour hours

155.400 155.400 169.400 183.400 663.600

4 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Direct labour cost per hour

37.50 37.50 37.50 37.50

Total direct labour cost (RM)

5,827.50

5,827.50

6,352.50

6,877.50

24,885.00

Direct Labour 2 : High Skill Sewer

Direct Labour Time Per Unit : 0.07

Direct Labour Cost Per Hour (RM) : 28.13

Q1 Q2 Q3 Q4 Year

Units to be produced (from production budget)

2,220 2,220 2,420 2,620 9,480

Direct labour time per unit

0.070 0.070 0.070 0.070

Total required direct labour hours

155.400 155.400 169.400 183.400 663.600

Direct labour cost per hour

28.13 28.13 28.13 28.13

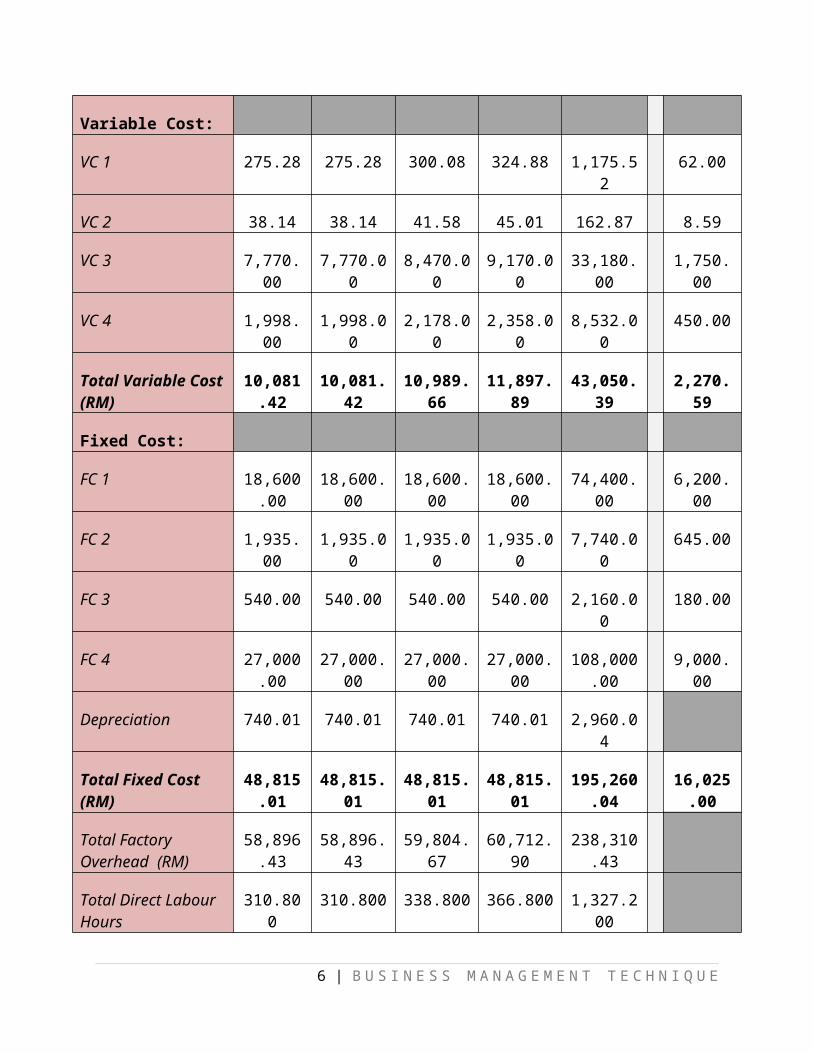

5. Factory Overhead Budget for each four quarters of 2015

Unit Per Month : 500

Depreciation Per Month : 246.67

Q1 Q2 Q3 Q4 Year Cost PerMonth

5 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Variable Cost:

VC 1 275.28 275.28 300.08 324.88 1,175.52

62.00

VC 2 38.14 38.14 41.58 45.01 162.87 8.59

VC 3 7,770.00

7,770.00

8,470.00

9,170.00

33,180.00

1,750.00

VC 4 1,998.00

1,998.00

2,178.00

2,358.00

8,532.00

450.00

Total Variable Cost(RM)

10,081.42

10,081.42

10,989.66

11,897.89

43,050.39

2,270.59

Fixed Cost:

FC 1 18,600.00

18,600.00

18,600.00

18,600.00

74,400.00

6,200.00

FC 2 1,935.00

1,935.00

1,935.00

1,935.00

7,740.00

645.00

FC 3 540.00 540.00 540.00 540.00 2,160.00

180.00

FC 4 27,000.00

27,000.00

27,000.00

27,000.00

108,000.00

9,000.00

Depreciation 740.01 740.01 740.01 740.01 2,960.04

Total Fixed Cost (RM)

48,815.01

48,815.01

48,815.01

48,815.01

195,260.04

16,025.00

Total Factory Overhead (RM)

58,896.43

58,896.43

59,804.67

60,712.90

238,310.43

Total Direct Labour Hours

310.800

310.800 338.800 366.800 1,327.200

6 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

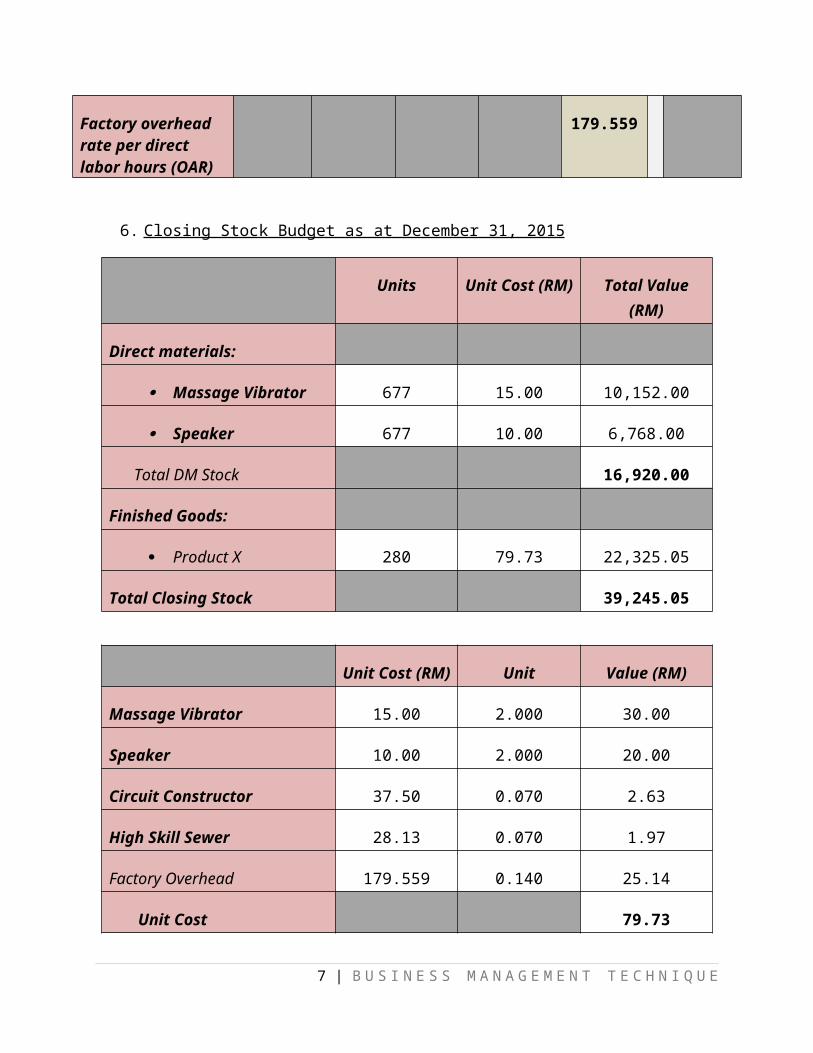

Factory overhead rate per direct labor hours (OAR)

179.559

6. Closing Stock Budget as at December 31, 2015

Units Unit Cost (RM) Total Value(RM)

Direct materials:

Massage Vibrator 677 15.00 10,152.00

Speaker 677 10.00 6,768.00

Total DM Stock 16,920.00

Finished Goods:

Product X 280 79.73 22,325.05

Total Closing Stock 39,245.05

Unit Cost (RM) Unit Value (RM)

Massage Vibrator 15.00 2.000 30.00

Speaker 10.00 2.000 20.00

Circuit Constructor 37.50 0.070 2.63

High Skill Sewer 28.13 0.070 1.97

Factory Overhead 179.559 0.140 25.14

Unit Cost 79.73

7 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

7. Cost of Goods Sold Budget as at December 31,2015

Massage Vibrator 284,400.00

Speaker 189,600.00

Direct Labour 43,552.07

Factory Overhead 238,310.43

Total ProductionCost

755,862.49

Add: Beginning FG 0.00

Less: Ending FG 22,325.05 -22,325.05

Cost of Goods Sold 733,537.44

8 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

8. Selling and Administrative for each four quarters of 2015

Unit Per Month : 500

Depreciation Per Month (Selling) : 0

Depreciation Per Month (Admin) : 115.83

Q1 Q2 Q3 Q4 Year CostPer

Month

Selling Expenses:Variable Cost

VC1 0.00 0.00 0.00 0.00 0.00 0.00VC2 0.00 0.00 0.00 0.00 0.00 0.00

Fixed CostFC1 0.00 0.00 0.00 0.00 0.00 0.00FC2 0.00 0.00 0.00 0.00 0.00 0.00Depreciation 0.00 0.00 0.00 0.00 0.00 Total Selling Expenses 0.00 0.00 0.00 0.00 0.00Administrative Expenses:

Variable Cost

9 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

VC1 1,110.00

1,110.00

1,210.00

1,310.00

4,740.00

250.00

VC2 222.00 222.00 242.00 262.00 948.00 50.00

Fixed Cost

FC1 11,565.00

11,565.00

11,565.00

11,565.00

46,260.00

3,855.00

FC2 6,600.00

6,600.00

6,600.00

6,600.00

26,400.00

2,200.00

FC3 21,600.00

21,600.00

21,600.00

21,600.00

86,400.00

7,200.00

FC4 8,100.00

8,100.00

8,100.00

8,100.00

32,400.00

2,700.00

FC5 3,060.00

3,060.00

3,060.00

3,060.00

12,240.00

1,020.00

Depreciation 347.49 347.49 347.49 347.49 1,389.96

Total Administration 52,604.49

52,604.49

52,724.49

52,844.49

210,777.96

Total Selling & Administrative

expenses

52,604.49

52,604.49

52,724.49

52,844.49

210,777.96

9. Annual Budgeted Profit and Loss Account as at December 31, 2015

Corporate Tax

Q1 Q2 Q3 Q4 YearTax(es) 7.50% 7.50% 7.50% 7.50% 30.00%

10 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Sales 920,000.00

Less: Cost of Goods Sold 733,537.44

Budgeted Gross Profit 186,462.56

Less: Selling & Admin. Expenses 210,777.96

Budgeted Net Profit -24,315.40

Provision for tax (….%) 0.00

Retained Profit -24,315.40

10. Cash Budget for each four quarters of 2015

Expected Cash Collection

% of Cash Collected in Quarter Sold : 75%

% of Cash Collected in following Quarter : 25%

Q1 Q2 Q3 Q4

Q1 Sales 200,000.00 150,000.00

50,000.00

Q2 Sales 220,000.00 165,000.00

55,000.00

Q3 Sales 240,000.00 180,000.00

60,000.00

Q4 Sales 260,000.00 195,000.00

Total CashCollection

150,000.00

215,000.00

235,000.00

255,000.00

11 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Expected Payment of Direct Material

% of Paid in Quarter Purchased : 50%

% of Paid in following Quarter : 50%

Q1 Q2 Q3 Q4

Q1 DM1 Purchase

74,592.00

37,296.00

37,296.00

Q1 DM2 Purchase

49,728.00

24,864.00

24,864.00

Q2 DM1 Purchase

67,320.00

33,660.00

33,660.00

Q2 DM2 Purchase

44,880.00

22,440.00

22,440.00

Q3 DM1 Purchase

73,320.00

36,660.00

36,660.00

Q3 DM2 Purchase

48,880.00

24,440.00

24,440.00

Q4 DM1 Purchase

79,320.00

39,660.00

Q4 DM2 Purchase

52,880.00

26,440.00

Total CashPayments

62,160.00

118,260.00

117,200.00

127,200.00

12 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Cash Budget

Number of Group Member : 5

Common Share from Each Group Member (RM) : 5,000

Opening Cash Balance (RM) : 100,000

Q1 Q2 Q3 Q4 Year

Receipts:

Collection fromcustomer

150,000.00

215,000.00

235,000.00

255,000.00

855,000.00

Common Share 25,000.00

0.00 0.00 0.00 25,000.00

Total Receipts 175,000.00

215,000.00

235,000.00

255,000.00

880,000.00

Payments:

Direct Material 62,160.00

118,260.00

117,200.00

127,200.00

424,820.00

13 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

Direct Labour 10,198.90

10,198.90 11,117.72 12,036.54

43,552.07

Factory Overhead 58,156.42

58,156.42 59,064.66 59,972.89

235,350.39

Selling &Administrative

52,257.00

52,257.00 52,377.00 52,497.00

209,388.00

Income Tax 0.00 0.00 0.00 0.00 0.00

Payment FixedAsset

0.00 0.00 10,000.00 0.00 10,000.00

Total payments 182,772.32

238,872.32

249,759.38

251,706.43

923,110.45

Surplus/Deficit -7,772.32

-23,872.32

-14,759.38

3,293.57 -43,110.4

5

Opening Balance 100,000.00

92,227.68 68,355.36 53,595.98

100,000.00

Closing Balance 92,227.68

68,355.36 53,595.98 56,889.55

56,889.55

TASK 2:

1. Identify and briefly explain TWO(2) potential problem

related to the cash flow in the Cash Budgets.

To success in this field, everyone in this field must faced

any kinds of the problem. Same with my company that are must

faced in our problem.We must smart to solve this problem.If we

14 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

don’t have the patient to solve some problem maybe it will effect

the performance of my company.

-7,772.32 -23,872.32 -14,759.38

In the Quadrant 1 (JAN – MARCH) of this year (2014), my

company have losses. My company have losses RM46, 404.02 for the

first three month Q1 to Q2 in this year.We have to investigate or

find the relevan reason why my company have much losses for the

first three month of this year.We build a special team to

investigate what the main reason of the losses.After a week, we

have decided the reason of the problem that make my company

losses for the first three month.

The main problem is we use the direct material that directly

imported from europe.When we imported directly from europe,the

price will increased dramatically that we are not conscious

exactly.Besides that, when we imported the direct material, the

material that arrived in our factory are little broken.To solve

of the little broken we must take the material that are local

broker that we do no the quality as much as we know the quality

from material that are we imported.When we do our product,we have

many kind of new problem.Thats why we must re doing our product

and when we re doing our product we must add some new budget to

our production department.

The second problem was we use the foreigner for our

industries worker.When we use the foreigner, we muat paid the

15 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

highest salary.We take foreigner for the position engineer and we

must paid the highest salary and we add a some budget to the

Admin department. Besides that, our production budget is over

limit and the output is not archieved the targeted and many of

our product are return back from customers to make a troubleshoot

and many customers are claim for the warranty of our

product.Then, we must the paid high income tax because of our

high year profit in the last year (2013) and we do not archieve

what had been targeted in Quadrant 1 (JAN – MARCH).

That was are problem why we had losses in the Q1 (JAN-

MARCH).From the problem,we solve and we had a quite high profit

in the Q2 untill Q4 which are RM249,759.38.Based on the profit,

we not too happy because our targeted profit from Q2 untill Q4

were RM500,000.00 and above.Then, the team that solve the

problem in Q1 are investigated. After a few weeks,we know that

why we not archieve the targeted profit.The problem is the price

of fuel is increase dramatically.Thats why we cannot archive the

targeted profit.Our production department must add some another

budget because of the increasing of fuel.

16 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

2. For each of the problem indentified above,propose and

briefly explain one possible solution on how the

company can better manage the cash flow.

For solution in our problem was do more research or find

comparison quality between imported and local product.If the

quality of the local broker much better than imported product, we

must use or sign the document that we want the local

product.Besides that, we must use the high class of the Quality

Control worker.This is because we have targeted product of our

output.If we don’t have a high class Quality Control worker,we

are hardly to archieve our targeted output(product).Our customer

17 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

will return back or claim their warranty of our product if the

service or system is not archieved what they want.

Then,we must cut off the budget that are over limit in any

production such as in Admin department.In our company,the

executive position and above are foreigner worker.We must paid

the highest salary to them and this is such a kind reason why we

cannot archieve the targeted profit.We must reduce the executive

position and add some more workers in the production

department.In addition, we must distribute our product to our

distributor in the lamp or much largest number.This is because to

reduce the budget at production department.When we distribute in

the largest number, we automatically reduce the production budget

such as oil fuel and etc.

3. One suggestion on what the company should do with

excess cash.

My suggestion for the excess cash is firstly, the

company must know their company’s strength. This is important

because with the extra cash, the company can use it to make them

more secure. Let say if one day the company facing a financial

problem, they can use the excess money to backup their business.

As we know, all company will not always be in the upper side. So,

it is very important for them to do a long term saving account by

using the excess money that they get in case if something bad

happen to their company.

18 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

PART 2:

SCENARIO:

Direct material 1: Massage Vibrator

(Standard Price = RM 15.00)

(10/100) X RM 15.00 = RM 1.50

RM 15.00 - RM 1.50 = RM 13.50 (Actual Price)

(Standard Quantity = 18 960 Units)

(10/100) X 18 960 = 1896

18960 - 1896 = 17 064 Units (Actual Quantity)

Direct material 2: Speaker

(Standard Price = RM 10.00)

(10/100) X RM 10.00 = RM 1

RM 10.00 + RM 1.00 = RM 11.00 (Actual Price)

(Standard Quantity = 19 637 Units)

(10/100) X 19 637 = 1 963.7

19 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

19 637 + 1 963.7 = 21 600.7 Units (Actual Quantity)

Direct labour 1: Circuit Constructor

Standard Hour = 663.6

(10/100) x 663.6 = 66.36

663.6 + 66.36 = 729.96 (Actual hour)

Standard Rate = RM 37.5

(10/100) x RM 37.5 = RM 3.75

RM 37.5 + RM 3.75 = RM 41.25 (Actual Rate)

Direct labour 2: High Skill Sewer

Standard hour = 663.6

(10/100) X 663.6 = 66.36

663.6 – 66.36 = 597.24 (Actual Hour)

Standard Rate = RM 28.13

20 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

(10/100) X RM 28.13 = RM 2.813

RM 28.13 - RM 2.813 = RM 25.317 (Actual Rate)

TASK 3:

1. Calculate the following variances :

Material Price Variance :

Direct material 1: Massage Vibrator

(Actual Price - Standard Price) x Actual Quantity

= (RM13.50 - RM15.00) x RM 17 064

=RM 25, 596.00 (F)

Therefore it is FAVORABLE because actual price < standard Priceand the company paid less for direct materials than it expected,the variance is Favorable.

Material Usage Variance :

Direct material 2: Speaker

21 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

(Actual Quantity - Standard Quantity) x Standard Price

= (21 600.7 – 19 637) x RM 10.00

= RM 19, 637.00 (A)

Therefore it is ADVERSE because actual quantity > standard

quantity and the company used more for direct materials than it

expected, the variance is Adverse.

Direct Labour Rate Variance :

Direct Labour 1 : Circuit Constructor

(Actual rate - Standard Rate) x Actual Hour

= (RM 41.25 - RM 37.5) x 729.96

= RM 2,737.35 (A)

Therefore it is ADVERSE because actual rate > standard rate and the company paid more per hour for direct labour than it expected, the variance is Adverse.

Direct Labour Efficiency Variance :

Direct Labour 2 : High Skill Sewer

(Actual Hour - Standard Hour) x Standard Rate

= (RM 597.24 – RM 663.6) x RM28.13

= RM 1,866.7068 (F)

Therefore it is FAVORABLE because actual hour < standard hour andthe company used less direct labour hours than it expected, the variance is Favorable.

22 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

2. For each of the above variances, determine and explain why it is Favourable or Adverse.

Material Price Variance : Direct material 1: Massage

Vibrator

Therefore it is FAVORABLE because actual price < standard Price

and the company paid less for direct materials than it expected,

the variance is Favorable.

Material Usage Variance : Direct material 2: Speaker

Therefore it is ADVERSE because actual quantity > standard

quantity and the company used more for direct materials than it

expected, the variance is Adverse.

Direct Labour Rate Variance : Direct Labour 1 : Circuit

Constructor

Therefore it is ADVERSE because actual rate > standard rate and the company paid more per hour for direct labour than it expected, the variance is Adverse.

Direct Labour Efficiency Variance : Direct Labour 2 : High Skill Sewer

Therefore it is FAVORABLE because actual hour < standard hour andthe company used less direct labour hours than it expected, the variance is Favorable.

TASK 4:23 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

1. Investigate the cause of each of the above variances. Identify and explain

each cause.

a) Direct Material Usage for Massage Vibrator is Favorable.

- The direct material usage for massage vibrator becomefavorable because our company get unforeseen discount forelectronics component massage vibrator from electronics suppliercompany that we basically take the component only from thatcompany, and we take a few component , so we get a lot ofdiscount. Our company also used the Greater care taken inpurchasing, we must compare and take the cheapest price of theelectronics component but is high quality. So that, it becomefavorable.

b) Direct Material Usage for Speaker is Adverse.

- The defective material is the main cause effect the speakeris being Adverse. The defective material happen because ourcompany take the industrial training student, so they don’t havean enough experience and they do a lot of mistake when they wantto plug in the speaker, so it become a defective material ofspeaker. Error in allocating material to jobs it will cause toused more to build one product, so it also one of the main cause.When they do a lot of mistake, our company buy more of speaker,sometime when have a lot of the speaker it will become aexcessive waste. it also the cause why it become Adverse.

c) Labour Rate Variance for Circuit Constructor is Adverse.

- The labour rate variance of circuit constructor becomeadverse is because in this quarter 1 we hired a new of circuit

24 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

constructor that have 5years experience, so we have to increase awages rate of this circuit constructor. Besidethat, in quarter 1have a blackout at our factory, so worker cannot do their work,but we still have to pay their wages. It also the cause why itbecome Adverse.

d) Labour Rate Variance for High Skill Sewer is Favorable.

- Labour rate variance for sigh skill sewer is favorablebecause all the high skill sewer in our company have a lotexperience, so our company can produce product more quickly thanexpected for example we target for one month is 200unit, then weget 250unit in the same number of hours working because of workmotivation, better quality of equipment or materials.

2. Propose ONE possible solution for EACH of the abovevariances.

a) Since the variance of massage vibrator is favorable sometimeit can be adverse, so we need to take the right steps toensure that I cant be a adverse. That step is, our companywill not rush negligent in the purchase process. So we canstick with the only one or two wood company for purchasingeverymonth consistently.

b) The variance for speaker is adverse because so many defectivematerial. The step should be taken from my company is toensure the material of speaker is always higher quality thanstandard. The defective material can be reduce if our companyuse speaker quality material and effect for error in

25 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E

allocating material to jobs used less and risk to take morespeaker is low.

c) The variance for circuit constructor result is also adverse,it is because our company pay their wages rate is high due totheir experience, the solution is we have to use theapprentices or trainee that can be pay less than because nothave experience. Other than that we can accept the student forindustrial training, it can do work and our company can payless than the permanent staff.

d) The result for sigh skill sewer is already favorable, so toensure it will stick to favorable we have to do some step.Everymonth we have to ensure the output produces will beincrease or remain same. The output produced more quickly thanexpected in example, actual output produce in excess ofstandard output set for same or more number of hours becauseof work motivation, better quality of equipement or materials.Besidethat we can ensure the error in allocating times to jobis also to reduce.

26 | B U S I N E S S M A N A G E M E N T T E C H N I Q U E