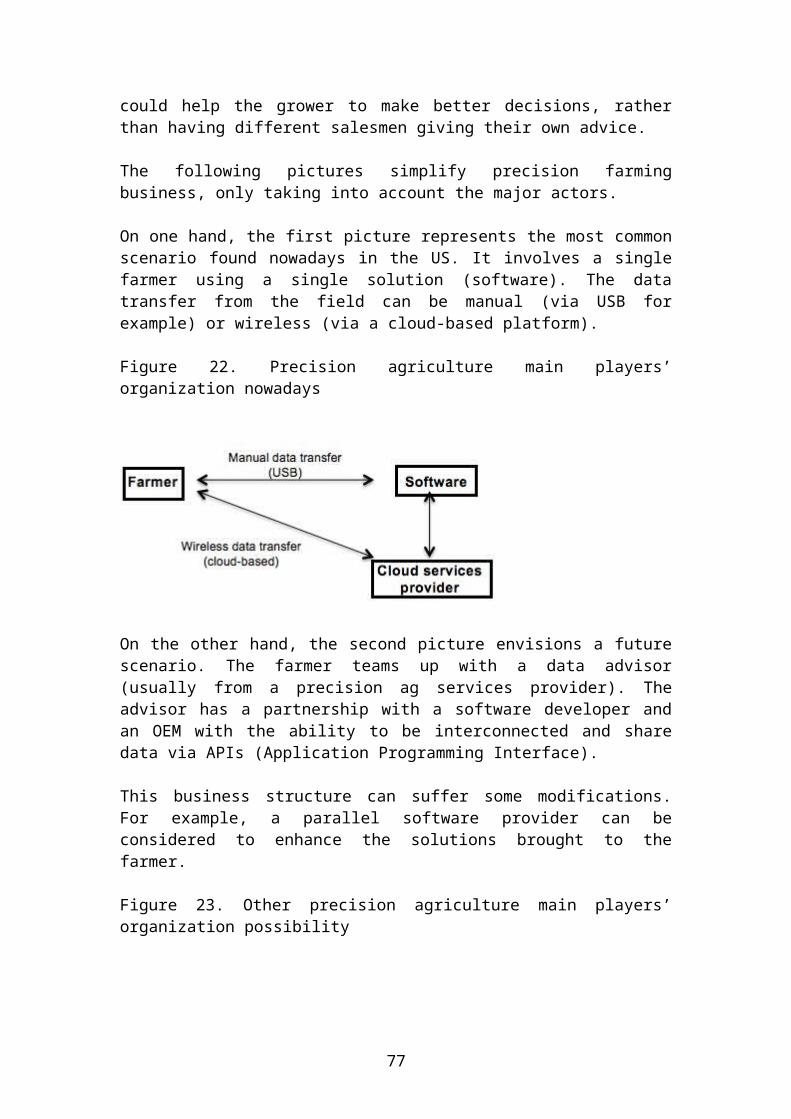

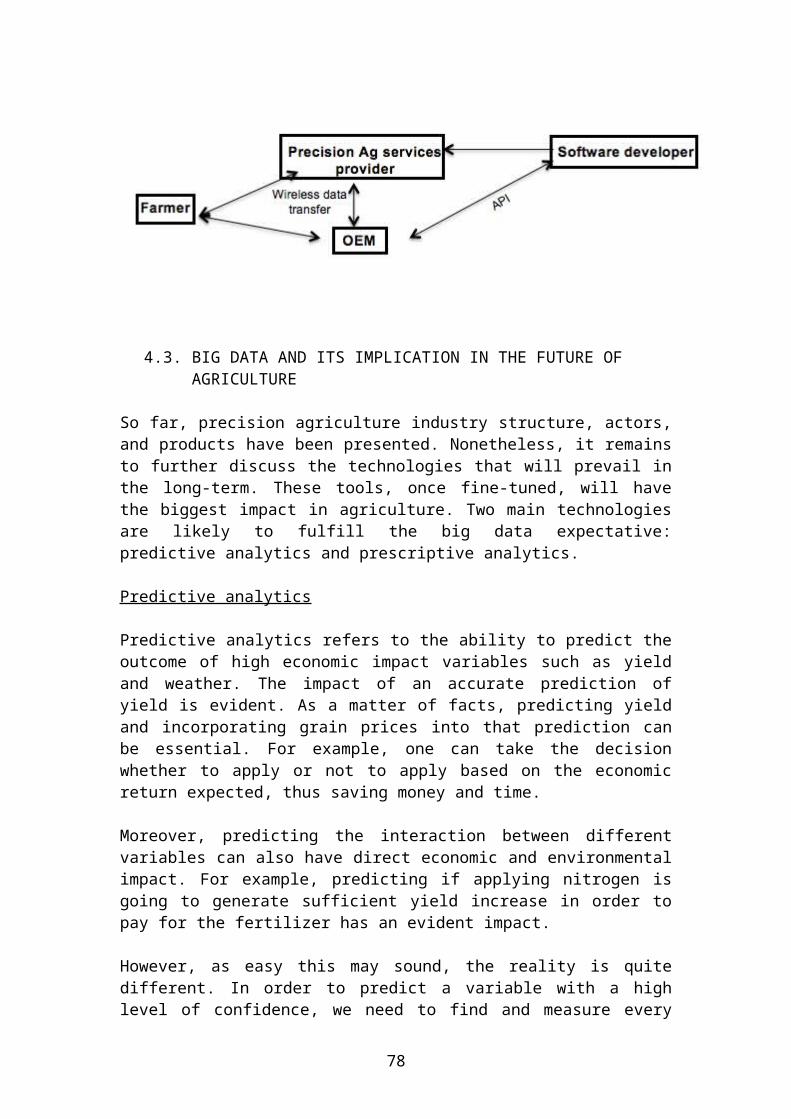

Precision Farming Business

88

Precision Farming Industry Structure Rodrigo Suzacq, Research Assistant Department of Agricultural and Consumer Economics University of Illinois at Urbana-Champaign Mumford Hall 1301 W Gregory Drive Urbana, IL 61801 Mobile: (598) 99 704 604 Email: [email protected] Peter D. Goldsmith, Associate Professor and Interim Director, Food & Agribusiness Management Program Department of Agricultural and Consumer Economics University of Illinois at Urbana-Champaign 318 Mumford Hall 1301 W Gregory Drive Urbana, IL 61801 Office: (217) 333-5131 Email: [email protected] Associate Director Leonardo J. Cristalli, CEO at OKARA LTDA. J. P. Sotura 1268, Dolores, CP75100, Soriano, Uruguay Web: www.okara.com.uy Mobile: (598) 93 381 318 Email: [email protected] 1

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Precision Farming Business

Precision Farming Industry Structure

Rodrigo Suzacq, Research AssistantDepartment of Agricultural and Consumer Economics

University of Illinois at Urbana-ChampaignMumford Hall 1301 W Gregory Drive

Urbana, IL 61801Mobile: (598) 99 704 604

Email: [email protected]

Peter D. Goldsmith, Associate Professor andInterim Director, Food & Agribusiness Management

ProgramDepartment of Agricultural and Consumer Economics

University of Illinois at Urbana-Champaign318 Mumford Hall

1301 W Gregory DriveUrbana, IL 61801

Office: (217) 333-5131Email: [email protected]

Associate DirectorLeonardo J. Cristalli, CEO at OKARA LTDA.

J. P. Sotura 1268, Dolores, CP75100, Soriano,Uruguay

Web: www.okara.com.uy Mobile: (598) 93 381 318

Email: [email protected]

1

Precision Farming Industry Structure

Abstract

Precision farming means collecting data and makingagricultural management decisions based on that data. Thepresent report summarizes literature information foundconcerning precision farming evolutionary phases,profitability, business structure, and data collaborationamong different agents in the agriculture sector for eachof the precision farming technologies. Furthermore, thegaps found concerning precision farming businessstructure is filled analyzing data from semi-structuredinterviews and web-based surveys. Results indicatedifferent scenarios of business structures possible, withdifferent arrangements between farmers, serviceproviders, software developers, machinery manufacturers,sensors providers, input providers, traders, banks, andinsurance agencies. Moreover, survey results provideunprecedented information about the precision farmingindustry companies offering type, market penetration,number of employees, and annual turnover. Finally,insights on the future of precision agriculture arepresented as results of discussion with many leaders ofthis industry.

2

Keywords: precision farming, big data, profitability,adoption, structure

JEL Classification: Q1, O3

1. INTRODUCTION

Several definitions for precision farming are found inthe literature. A definition that includes any otherdescription is that precision farming means collectingdata and making agricultural management decisions basedon that data (Hague, 2014). The objective of precisionfarming is to help farmers to apply the right amounts ofinputs, on the right place, and at right time (Pandit,2012).

The concept of precision farming emerged in the 1980s(Herring, 2001). However, this notion went throughdifferent phases over the last four decades (Hague,2014). To fully understand and precision farming industry

3

structure and taxonomy, it is important to differentiatethese phases one another.

Even though it’s been more than 30 years since precisionfarming emerged, NASA’s specialist Susan Moran statesthat these technologies are still in the experimentalphase (Herring, 2001). Some researchers strengthenMoran’s statement indicating that adoption rates vary alot among the set of technologies known as precisionfarming. Indeed, adoption rates range from 75-80% for GPSand Guidance systems to less than 2% for remote sensing(Griffin et al., 2004; Schimmelpfennig and Ebel, 2011;Cox and Wong, 2013). Thus, the need to differentiatebetween technologies with defined costs benefits ratioand easy-to-measure benefits from those technologies thatdo not have those same characteristics.

In addition to this, during the last five years,precision farming saw an increase in the number oftechnologies, products, companies, investments, andacquisitions (Cox and Wong, 2013; Oganesoff and Howard,2014). Therefore, the business structure of eachtechnology needs to be studied. On one hand, sometechnologies come standard in original equipment, or canbe purchased in the after-market. On the other hand, thedynamics for some technologies have not yet been defined.

What is more, data now plays an increasing role in manybusinesses (Kolb, J. 2012; Mayer-Schonberger, V andCukier, K. 2013). However, in agriculture there is stilla whole unknown space of opportunities. As a matter offact, different agents of the industry can benefit fromthe data. Thus, there is a particular interest incharacterizing the role of data for different agents andat the different levels of the agriculture and foodsupply chain.

4

2. LITERATURE REVIEW

2.1. GLOBAL POSITIONING SYSTEM AND GUIDANCE SYSTEMS

2.1.1. Global Positioning System (GPS)

GPS can be simply defined as a navigation system based ona network of earth-orbiting satellites that lets usersrecord near-instantaneous positional information(latitude, longitude, and elevation) with accuracyranging from 100 m to 0.01 m (Batte, 2000). GPS becameessential in many businesses, and agriculture is becomingmore and more dependent on it. Indeed, GPS is the basisfor many others precision farming technologies.

Standard GPS provides accurate worldwide positioningservices within 10-15 meters, but these systems cannot beany more precise than this because of timing andsatellite orbit errors (Cox and Wong, 2013). For manybusinesses, this kind of accuracy may be enough, but forprecision agriculture, where the idea is to manage eachsquare meter of a farm differently, standard GPS systemsare not accurate enough. There are some ways of improvingstandard accuracy.

Differential Global Positioning System (DGPS):

GPS receivers that are compatible can receive DGPScorrections for free (Cox and Wong, 2013). DGPS is asystem providing a very accurate position (accuracy rangefrom 1 to 10 m), by calculating the difference betweenthe actual locations of a fixed-position ground stationandthe satellite-located position of the station, andproviding a correction signal to a mobile user (HCGA,2009).

Space-based augmentation systems (SBAS):

Another way to improve accuracy is SBAS. These are

5

networks of stations on the ground that correct GPSsignals received from the 24 GPS satellites and send themback up to their proprietary satellites (Cox and Wong,2013).

Privately owned L-band satellite:

The next most accurate technique for GPS correction issubscription to privately owned L-band satellite. Thesesignals virtually cover the whole world and provideaccuracy from eight to two inches (5 – 20 cm) (Cox andWong, 2013).

Real-time kinematic (RTK) positioning:

However, according to the same authors, the most accurate(and expensive) correction solution to date is real-timekinematic (RTK) positioning (accuracy is usually lessthan 1 cm.). RTK is a processor that makes GPS signalcorrections that are transmitted to a satellite andsubsequently stored in real time (Schimmelpfennig andEbel, 2011). Indeed, it is a system that uses a fixedground station to measure satellite drift and send acorrection signal by radio directly to GPS equippedvehicles. The main advantage, besides a better accuracy,is that RTK is not affected by atmospheric interference(HGCA, 2009).

2.1.2. Guidance systems

Guidance systems show a driver where to steer to coverthe field at the spacing required for the implement beingused without overlapping or under lapping (HCGA, 2009).Guidance systems can be as simple as a mechanical markeron a planter or foam marker on a sprayer, and assophisticated as GPS-based auto-steering (Smith et al.,2013). Nowadays, the vast majority of farmers rely onGPS-based guidance systems (

Without guidance systems, every application has highchances of overlap or under lap. Overlapping refers toapplying the product more than once in a certain area,while under lapping means unintentionally not applyingthe product in a certain an area. Overlapping has

6

negative impact in the environment and increasesapplication costs, it can even reduce yield by toxiceffects of the chemical in some cases. On the other hand,under lapping can have negative effects on yield in theareas where fertilizer was not applied, or seed was notplaced.

Auto guidance

Auto guidance systems have an auto steer componentsynchronized with the guidance system to automaticallyand precisely steer the machinery (Smith et al., 2013).By this mean, operators to focus on other tasks such aswatching over seeding monitor or yield variation. Autoguidance systems can be more or less accurate dependingif they rely on standard GPS or in more sophisticatedsystems such as real-time kinematics.

GPS technology has been used in precision industry sinceits origin. Indeed, in the 1980s GPS was used forconnecting grid soil sampling and variable rateapplication of a few inputs. However, the accuracyachieved by GPS technology differs in the differentphases early mentioned. Whereas in the 1980s standard GPSwas the only solution available, in 1990s DGPS wasavailable, and by the 2000s RTK was also available forfarmers. This means that, in the origins of precisionfarming farmers worked with a 15 meters precision,nowadays farmers work with a precision of 1 centimeter.This means that every single process that uses GPStechnology- such as guidance systems, yield monitoring,soil mapping, or VRAs- is more accurate.

Guidance systems have also been through an evolution inthe last decades. In the early 1920s, systems that canfollow furrows guided the machines across the field. Inthe 1970s, wire carrying low current, low frequencysignal was used to guide machines. In the mid-1990s,researchers were studying GPS guidance systems (Reid etal, 2000). In the mid 2000s, auto steering was madecommercially available (Griffin et al, 2004).

7

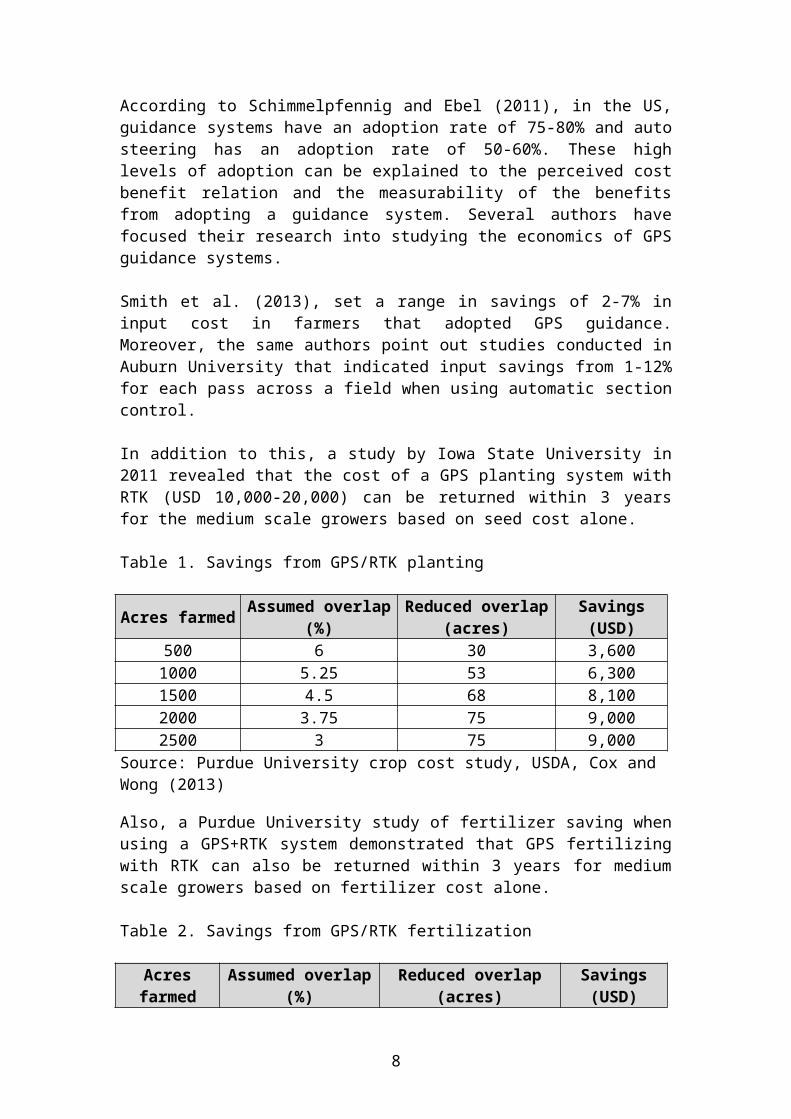

According to Schimmelpfennig and Ebel (2011), in the US,guidance systems have an adoption rate of 75-80% and autosteering has an adoption rate of 50-60%. These highlevels of adoption can be explained to the perceived costbenefit relation and the measurability of the benefitsfrom adopting a guidance system. Several authors havefocused their research into studying the economics of GPSguidance systems.

Smith et al. (2013), set a range in savings of 2-7% ininput cost in farmers that adopted GPS guidance.Moreover, the same authors point out studies conducted inAuburn University that indicated input savings from 1-12%for each pass across a field when using automatic sectioncontrol.

In addition to this, a study by Iowa State University in2011 revealed that the cost of a GPS planting system withRTK (USD 10,000-20,000) can be returned within 3 yearsfor the medium scale growers based on seed cost alone.

Table 1. Savings from GPS/RTK planting

Acres farmed Assumed overlap(%)

Reduced overlap(acres)

Savings(USD)

500 6 30 3,6001000 5.25 53 6,3001500 4.5 68 8,1002000 3.75 75 9,0002500 3 75 9,000

Source: Purdue University crop cost study, USDA, Cox and Wong (2013)

Also, a Purdue University study of fertilizer saving whenusing a GPS+RTK system demonstrated that GPS fertilizingwith RTK can also be returned within 3 years for mediumscale growers based on fertilizer cost alone.

Table 2. Savings from GPS/RTK fertilization

Acresfarmed

Assumed overlap(%)

Reduced overlap(acres)

Savings(USD)

8

500 5 25 4,4001000 4,5 45 7,9201500 4 60 10,5602000 3,5 70 12,3202500 3 75 13,200

Source: Purdue University crop cost study, USDA, Cox and Wong (2013)

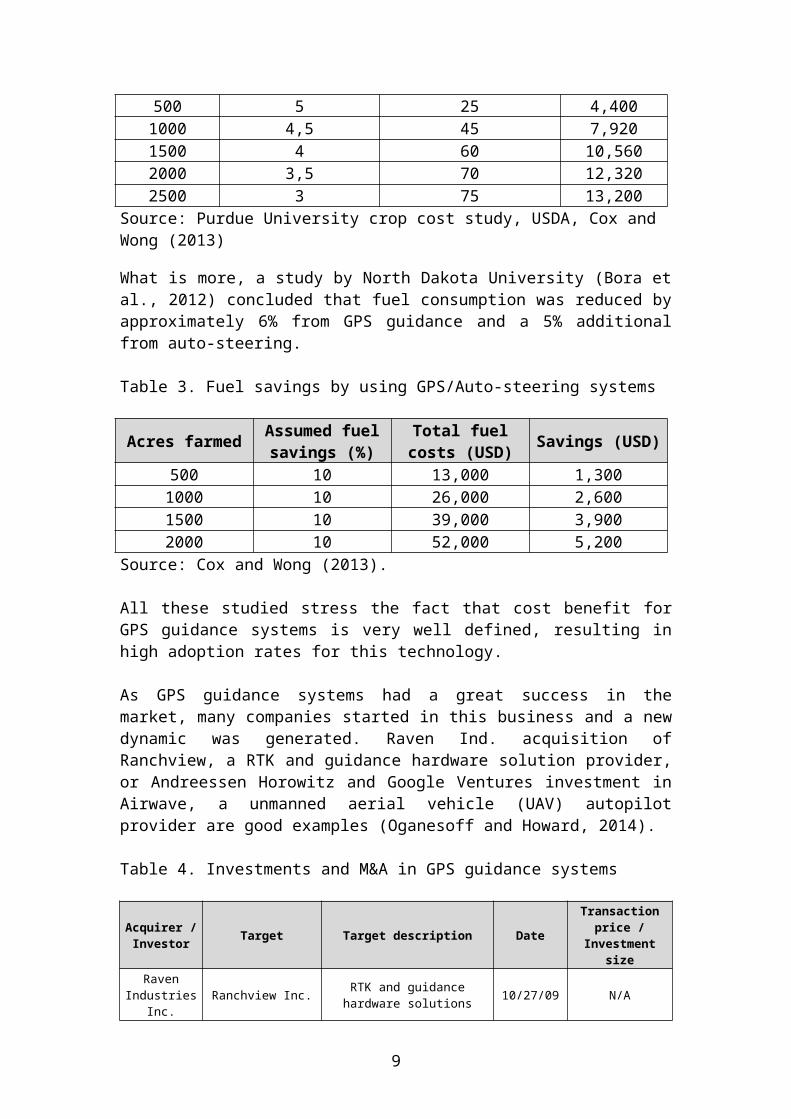

What is more, a study by North Dakota University (Bora etal., 2012) concluded that fuel consumption was reduced byapproximately 6% from GPS guidance and a 5% additionalfrom auto-steering.

Table 3. Fuel savings by using GPS/Auto-steering systems

Acres farmed Assumed fuelsavings (%)

Total fuelcosts (USD) Savings (USD)

500 10 13,000 1,3001000 10 26,000 2,6001500 10 39,000 3,9002000 10 52,000 5,200

Source: Cox and Wong (2013).

All these studied stress the fact that cost benefit forGPS guidance systems is very well defined, resulting inhigh adoption rates for this technology.

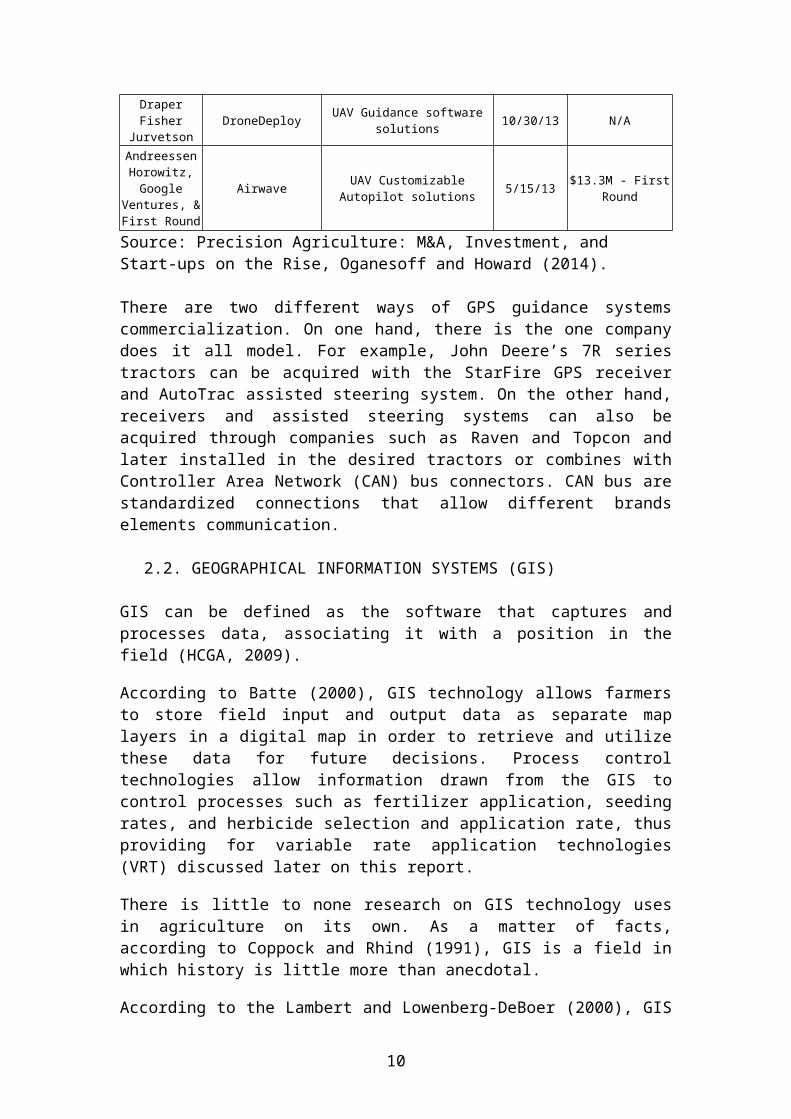

As GPS guidance systems had a great success in themarket, many companies started in this business and a newdynamic was generated. Raven Ind. acquisition ofRanchview, a RTK and guidance hardware solution provider,or Andreessen Horowitz and Google Ventures investment inAirwave, a unmanned aerial vehicle (UAV) autopilotprovider are good examples (Oganesoff and Howard, 2014).

Table 4. Investments and M&A in GPS guidance systems

Acquirer /Investor Target Target description Date

Transactionprice /

Investmentsize

RavenIndustries

Inc.Ranchview Inc. RTK and guidance

hardware solutions 10/27/09 N/A

9

DraperFisher

JurvetsonDroneDeploy UAV Guidance software

solutions 10/30/13 N/A

AndreessenHorowitz,Google

Ventures, &First Round

Airwave UAV CustomizableAutopilot solutions 5/15/13 $13.3M - First

Round

Source: Precision Agriculture: M&A, Investment, and Start-ups on the Rise, Oganesoff and Howard (2014).

There are two different ways of GPS guidance systemscommercialization. On one hand, there is the one companydoes it all model. For example, John Deere’s 7R seriestractors can be acquired with the StarFire GPS receiverand AutoTrac assisted steering system. On the other hand,receivers and assisted steering systems can also beacquired through companies such as Raven and Topcon andlater installed in the desired tractors or combines withController Area Network (CAN) bus connectors. CAN bus arestandardized connections that allow different brandselements communication.

2.2. GEOGRAPHICAL INFORMATION SYSTEMS (GIS) GIS can be defined as the software that captures andprocesses data, associating it with a position in thefield (HCGA, 2009).

According to Batte (2000), GIS technology allows farmersto store field input and output data as separate maplayers in a digital map in order to retrieve and utilizethese data for future decisions. Process controltechnologies allow information drawn from the GIS tocontrol processes such as fertilizer application, seedingrates, and herbicide selection and application rate, thusproviding for variable rate application technologies(VRT) discussed later on this report.

There is little to none research on GIS technology usesin agriculture on its own. As a matter of facts,according to Coppock and Rhind (1991), GIS is a field inwhich history is little more than anecdotal.

According to the Lambert and Lowenberg-DeBoer (2000), GIS

10

is used in combination with other technologies such asvariable rate application (discussed later in thisreport). Thus, examining GIS phases and cost benefitrelation the same way it was analyzed for GPS guidancesystems is not possible with the available literature.

In addition to this, GIS business dynamic has not changedsignificantly over the last years. As a matter of fact,according to the market analysis firm Daratech, onecompany, ESRI, holds approximately 40% of GIS marketshare. This has led users to rely on ESRI’ shapefiles asthe standard file extension for GIS.

2.3. SENSORS AND REMOTE SENSING

Sensors are devices that are capture environmental andnon-environmental factors such as light, temperature,radiation level, pressure, engine use, and transmits asignal to a measuring instrument. Data loggers then storethe data and can wirelessly send that data via cellularor satellite.

Sensors can be mounted on different vehicles for remotesensing, or be stationary such as weather stations.

Remote sensing can be defined as the process of detectinginformation about a field, soil or crop from a distance,using sensors mounted on satellites, aircraft or othermachinery (HGCA, 2009). Remote sensing has been veryuseful over the years, especially for large-scale growersas it isn’t always possible for them to survey all oftheir lands every week (Herring, 2001). Most importantly,according to the same author, remote sensing data cantell the farmers not only where their crops are understress but also why.

Satellite sensing

Landsat TM satellite image data are an alternative toyield monitor data and enable farmers to identify regionsor management zones (Herring, 2001). Satellite imagerycan have many uses, for example:

Oklahoma State University researchers have been able

11

to calibrate these data to wheat yield (Solie, 2000) Creation on false-color images to differentiate bare

fields (blue), while soils that have recently beenleveled in preparation for planting appears whiteand dark red areas show flood irrigation (Herring,2001).

Elaboration of false-color maps representingmeasurements made at thermal infrared wavelengths,to represent surface temperatures. Cool temperatures(blue and green) are associated with vegetation andhot temperatures (yellow and red) with bare soil(Herring, 2001).

Elaboration of maps with color variations determinedby crop density (also referred to as "NormalizedDifference Vegetation Index," or NDVI), where darkblues and greens indicate lush vegetation and redsshow areas of bare soil (Herring, 2001).

Creation of water deficit maps (Herring, 2001).

Aircraft and Unmanned Aerial System (UAS) sensing

Aircraft and UAS can be equipped with many types ofcameras such as visible light, infrared, LIDAR (lightdetection and ranging), multispectral or hyper spectral.The images recovered later can be used to scout the fieldand identify damage and crop stress, create normalizeddifference vegetation index (NDVI) maps, and identifymachine issues among many other tasks (Everaerts, 2008).

NDVI is defined by the following ratio, with VIS and NIRbeing the spectral reflectance measurements acquired fromthe visible and the near infrared. This ratio correlateswith leaf are index, vegetation condition, and biomass(Carlson and Ripley, 1997).

From the three sensing methods described, aircraftsensing is the least used because of its costs. However,satellite and UAS sensing are being used more and moreoften. Nonetheless, the greatest difference betweensatellite and UAS resides in the resolution achieved.

12

Whether satellite imagery such as Landsat has 30 metersper pixel resolution (Solie, 2000), UAS imageryresolution goes from 4 to 10 centimeters per pixel.

The use of sensors varied a lot through the last decades.Sensors were first used for farming in the 1990s whenNASA’s aircraft equipped with sensors started being usedin agriculture (Herring, 2001). Moreover, according tothe same author, in the late 1990s high-resolutionsatellite imagery became commercially available and cropand soil conditions start being diagnosed usingsatellite-based remote sensors. Nevertheless, there islittle information on the literature about the use ofstationary sensors such as soil moisture sensors orweather stations throughout this last three decades.

In addition to this, existing literature has mainlyfocused on the use of sensors for irrigation systems(Hedley et al., 2013; Lichtenberg, 2013; Lichtenberg etal., 2014). However, sensors are being used in many non-irrigated fields. This few information on cost benefits,can be explained to the difficulty on measuring it. As amatter of facts, sensors are used with othertechnologies, such as variable rate application, and itis difficult to separate benefits from one or the othertechnology on its own.

What is more, there is a wide range of market structurein this industry. On one hand, there are companies- suchas Davis Instruments, Spectrum, and Decagon- that providethe whole hardware package (sensors, data loggers, remotecommunication) with specific software to assist in thedecision-making. On the other hand, some companies- suchas Ranch Systems- partner with sensor manufacturers andsoftware makers providing the entire solution to the end-user. Finally, companies- such as AgSense and iLinc-develop software for integrating the sensor’s data whilepartnering with sensors manufacturers.

Finally, there is very no previous research about how touse sensor’s data for different agents and steps of thesupply chain.

2.4. YIELD MONITOR AND YIELD MAPPING

13

Yield monitoring can be defined as "the measurement ofthe harvested portion of a crop over space and time andthe summation of those measurements in graphical form"(Pierce, 1997).

It allows farmers to use GPS maps to pinpoint yieldvariation within their fields (Gebbers and Adamchuck,2010). Yield data from 5-7 years allow growers toelaborate yield maps from a GIS software package. Thesemaps are useful to divide the field into differentmanagement zones according to potential yield, andtherefore chose different crops, varieties, fertilizerrate and any other input according to the zone (Solie,2000).

Yield monitors have been in use since the mid 1990s forsoybeans and corn, and since the late 1990s for cotton(Griffin, 2004; Ping and Dobermann, 2005). Since then,adoption rates grew very fast, reaching more than 65% ofadoption in US grain crop acres (Schimmelpfennig andEbel, 2001; Griffin et al., 2004). Some authors explainthis high level of adoption because yield monitorsprovide an easy mean to develop strategic site-specificmanagement decisions (Ping and Dobermann, 2005).

In addition to this, yield monitors are perceived to havehigh relation between cost and benefits. Many combinescome equipped with yield monitors from factory, providingusers with a technology at virtually no extra cost. Thebenefits are those perceived by site-specific management,which range from seed and fertilizer saving environmentalsustainability (analyzed later in this report).Nonetheless, some authors state that analyzing yield datarequires a level of commitment of time and resources,which can be limiting adoption rate (Lotz, 1997).

What is more, structure for yield monitors business isvery concise. On one hand, companies such as John Deere,AGCO, and CNH provide this technology default fromfactory. On the other hand, companies like LoupElectronics, Trimble, Precision Planting, and AgLeaderprovide the yield monitors straight to the end-user. To

14

differentiate themselves from the OEMs, the lattercompanies usually provide yield analysis softwarepackages as well.

Despite the high adoption rate of yield monitors, noprevious research has focused on the different uses ofthe data gathered with yield monitors. The potential usesfor yield data go from: real-time yield data analysis bytraders when speculating with commodity prices tohistorical yield data for differential land valuemanagement. The business opportunities in this matterneed to be evaluated by the academia.

2.5. SOIL MAPPING

Soil mapping can be simply defined as the production of aplan that defines areas in a field (HGCA, 2009). Thecreation of soil maps is very useful to run site-specificfarming as different soils may be handled separately.There are many ways of creating soil maps.

For example, some soils data are available from the USDANatural Resources Conservation Service’s NationalCartography and Geospatial Center. This information is inthe form of soil boundaries and could be augmented payingonsite sampling services, testing, and detailed study ofspecific sites for intensive cropping uses(Schimmelpfennig and Ebel, 2011). Also, as stressedbefore, different kind of soil maps can be made fromremote sensing.

Logically, the more data a soil map contains, the moreprecise the farm will be managed. For example, combiningyield-variation factors such as topography, pH, and soildepth can be very useful when prescribing inputs rates.These maps can be used as prescription maps for variablerate applications (Grisso et al., 2011).

Soil mapping was one of the first precision technologiesthat emerged. Indeed, according to Herring (2001), in the1980s precision farming meant grid sampling for variablefertilizer input and pH correction. Understanding soiltypes, and its interaction with yield and its variationshas been important throughout the last three decades.

15

According to a dealers survey carried out by Holland etal. (2013), 66% of respondents offered soil-samplingservices.

However, measuring the cost benefit relation from usingsoil samples to perform variable rate applications isvery difficult. It seems difficult to separate thebenefit from a variable rate prescription map that comesfrom soil sample, than a prescription that comes fromyield maps and management zones.

Moreover, there is no previous research on how farmer’saggregated soil maps can benefit different agents in theagribusiness industry. It is a fact, for example, thatinsurance services vary insurance fee according to soiltype. These benefits should be taken into account infuture research.

2.6. VARIABLE RATE APPLICATION (VRAs)

The variable rate technologies (VRTs) are devices thatcan be mounted on tractors and programmed to control thedispersion of seeds and chemicals based upon theinformation gained from the remote sensors orprescription maps (Grisso et al. 2011; Herring, 2001).

First it allows farmers to tailor their input applicationrates to the varying yield response characteristics indifferent parts of a field. Second, it allows forinexpensive gathering of site-specific data, which canprovide the farmer desiring to farm using VRA withvaluable information (Bullock et al., 2002).

Map-based VRA

Map-based VRA can be implemented using a number ofdifferent strategies such as soil type, soil color andtexture, topography, crop yield or field scouting data(Grisso et al., 2011). Whether some strategies are basedon single information, combining the data should performa better prescription map.

These maps can be created by the grid sampling method orzone management method. According to Fleming et al.

16

(2000), grid soil sampling at a density of 1 per ha orlarger has conventionally been used in the US. On theother hand, according to the same authors, a managementzone can be defined as a sub-region of a field thatexpresses a homogeneous combination of yield limitingfactors.

Sensor-based VRA

On the other hand, optical crop sensing requires no mapor positioning system. As a matter of fact, sensor-basedVRA varies the application rate of inputs with no priormapping or data collection. Real-time sensors measure thedesired properties such as soil properties or cropcharacteristics in real time and a control systemcalculates the input needs and transfer the informationto a controller requires no map or positioning systemwhich delivers the input to the location measured by thesensor (Grisso et al., 2011).

VRA sub-technologies

Variable rate technologies can be divided into:fertilizer VRA, seeding VRA, weed control VRA, lime VRAand variable rate irrigation (Grisso et al., 2011; Coxand Wong, 2013).

The objective is the same for all of these subtechnologies. VRA increases growers’ economic return byoptimizing inputs allowing farmers to focus inputs onzones of higher yield potential, while reducing inputs inlower productivity zones or where previous managementresulted in reduced input need (Grisso et al. 2011). Forexample, in variable rate irrigation (VRI), sensors areplaced in the field and the amount of water each nozzlespreads depend on water level in the soil, thus avoidingover-watering (Cox and Wong, 2013).

Variable rate application has been the objective ofprecision farming since the 1980s. As stated before,according to Herring (2001), in the 1980s grid samplingwas used for varied fertilizer input and pH corrections.According to the same author, in the 2000s, variable rate

17

technologies (VRT) start to being used more frequently.According to different researchers, VRT adoption rate is8-12% of US grain crop acres (Schimmelpfennig and Ebel,2011; Griffin et al., 2004).

Previous research has focused a lot on VRT sub-technologies benefits. Table 5 summarizes the percentageof articles that claim that some benefit was found, thepercentage of articles that do not report any benefits,and the percentage of articles that report both.

Consistent with the information presented before, GPSsystem is the technology with more perceivable benefits.As a matter of facts, every revised article reportedbenefit for this technology. As for variable rateseeding, 83% of the articles reported benefits. This isconsistent with the increase in dealership adoptionincrease of this technology reported by Holland et al.(2013). Indeed from 2011 to 2013 VRS dealership adoptiongrew from 24% to 32%.

Concerning VRT fertilizer, 75% percent of the articlesreport benefit in general. However, when separating bynutrient, nitrogen (N) seems to be less profitable thanphosphorus (P) and potassium (K), with 63% versus 71% ofarticles reporting benefits respectively. Nevertheless,the number of articles referring to N stresses theimportance given to this nutrient.

Table 5. Report benefit by the literature for differentprecision farming technologies.

Technology Reported Benefit (%)

Yes No Mixed Base

VRT-N 63 15 22 27VRT-P, K 71 29 0 7VRT-Weeds, Pests 86 14 0 7VRT-pH 75 0 25 4VRT-GPS Systems 100 0 0 3VRT-Irrigation 50 0 50 2VRT-Seeding 83 17 0 6

18

VRT-Yield Monitor Systems*

43 14 43 7

VRT-NPK, General 75 8 16 24Soil Sensing 20 40 40 5PA Technology Summary 77 0 23 14

PA/VRT Technologies combined

63 11 27 108

Source: Lambert and Lowenberg-DeBoer, 2000.

Variable rate technologies business structure is quitediverse as well. There are companies- such as MapShotsand SST - specialized in developing software thatintegrate different factors such as soil type or yieldmaps to create a prescription map. This map is thenuploaded to the on-board computer to perform the task.

Other companies, such as Nozzlework, specialize inhardware by improving chemical delivery methods. Inaddition to this, some companies- such as Trimble andMueller Elektronik- are specialized in variable ratecontrollers that are sold to the end-user. Finally, somecompanies such as JohnDeere and AgLeader offer bothsoftware and variable rate controllers, thus providing afull package for variable rate application.

2.7. FLEET MANAGEMENT TECHNOLOGY

Fleet management technology is commonly known astelematics and includes vehicle-tracking devices andsoftware that pinpoint the exact location of all thevehicles the user owns in real-time (Adrian, Norwood,Mask, 2005). In addition to this, remote diagnosticsystem allows diagnosing a given issue from a distance.

These technologies allow the operator to monitorpotential problems and perform preventative maintenancebefore reaching downtime. Therefore, telematics andremote diagnostic reduce redundancy, cut down labor costsand expand hours of operation (Adrian, Norwood, Mask,2005). For example, if a problem is diagnosed in aplanter, technicians can assist the grower and help him

19

to figure out whether this can be solved the next day orit must be solved immediately (Cox and Wong, 2013).Remote monitoring and diagnostics take significantimportance during short window period such as plantingand harvesting, where machinery must be used in the mosteffective way

Telematics and remote diagnostics are a new technology inagriculture. According to Gartner, these technologieswere first used in automobiles. Professor Kelly Rainerfrom Auburn University states that General Motors firstused telematics in the late 1990s. Even though there isno research analyzing the evolution of these technologiesin agriculture, we can place telematics and remotediagnostic as a technology of the last decade. Indeed,one of the fist companies to offer such technologies wasLeica Geosystems through its Virtual Wrench, which waslaunched in 2007.

Moreover, very little research report cost benefits fromthe adoption of telematics and remote diagnostic. As amatter of facts, Professor Terry Kastens from KansasState University states that it is too early to pretendwe know the economics of telematics. However, Gartnerplaces telematics as entering the plateau of productivityon its hype cycle.

What is more, business structure for telematics is quitesimpler than for most of the already revisedtechnologies. Indeed, telematics devices are installed bydefault or as after-factory boxes that collect andtransmit data (Gartner IT Glossary). Many OEM such asJohn Deere, AGCO and CNHI provide new machinery withtelematics featuring by default. Other companies, such asLeica Geosystems, Trimble, and Raven, provide the servicedirectly to the end-user. Leica Geosystems, for example,added built-in GPS in their displays to providetelematics services. Raven, on the other hand, providetelematics through their Slingshot hub. There is lessinformation on this matter for remote diagnostic. Somecompanies, such as Leica Geosystems, provide this servicethrough their Virtual Wrench portal.

20

In addition to this, there is no previous research on howtelematics in agriculture is changing the way fleet datacan be used among different agents in this business. Forexample, insurance agents could benefit from assettracking but no economic research evaluates its impact.

2.8. FARM MANAGEMENT SYSTEMS (FMS)

FMS are management systems which purpose is to assistagricultural farmers to perform various tasks such asoperational planning, implementation, and documentationin order to evaluate the performed work (Teye, 2011). FMSis part of a wider concept- Decision Support Systems(DSS)- used in many businesses since the 1980s. For somewriters, decision support systems simply mean interactivesystems for use by managers (Keen, 1980). Inagribusiness, DSS rely on: Business Intelligence (BI),Massive Data Management (Big Data), and EnterpriseResource Management (ERM).

Business Intelligence (BI)

BI is defined by Kolb (2012) as the methods and toolsused to analyze and understand important data- both frominternal and external sources. BI uses data analysis tospot patterns, trends, and correlations within data tohelp decision-makers make data-driven decisions.

Massive Data Management (Big Data)

According to Gartner’s IT Glossary, massive datamanagement can be defined as high-volume, high-velocityand high-variety information assets that demand cost-effective, innovative forms of information processing forenhanced insight and decision making.Enterprise Resource Management (ERM)

Al-Mashari et al. (2002) state that Rosemann (1999)defined ERM system as customizable software that includesintegrated business solutions for the core processes(e.g. production planning and control, warehouse

21

management) and the main administrative functions (e.g.accounting, human resource management) of an enterprise.

Moreover, according to Markus et al. (2000), ERP systemswork essentially at integrating inventory data withfinancial, sales, and human resources data, allowingorganizations to price their products, produce financialstatements, and manage effectively their resources ofpeople, materials and money (Al-Mashari et al., 2002).

Figure 1 is a very simple example of the steps requiredto develop a FMS. First, raw data has to be collected-with sensors when possible- and stored. Once the amountof data is significant, it has to be analyzed in order togive sense to all this data (Kolb, 2012). Once the datais analyzed, a decision support system helps the user totake data driven decisions.

Analytics play a key role into transforming raw data intouseful information. Indeed, Kolb (2012) defines analyticsas he collection of technologies and processes that turnsraw data into usable knowledge in order to informdecisions and drive action.

Figure 1. Simplified steps for developing an FMS

Sowing Fertilization Plant height Soil pH DensityGrains/m Grain weight

Soil nutrients Plagues Soil moistureTemperature Humidity yield

DATA

Sensors

Analyt

22

INFORMATION

Source: Mayer-Schonberger et al., 2013; Kolb, 2012.

The data gathered ranges from yield data, maps, soiltests, weather data, insurance policies and taxes toweeds, plagues, nutrients (Cox and Wong, 2013). Sensorssuch as weather stations, soil moisture sensors, or RadioFrequency Identification (RFID) tags for stock controlusually gather this data.

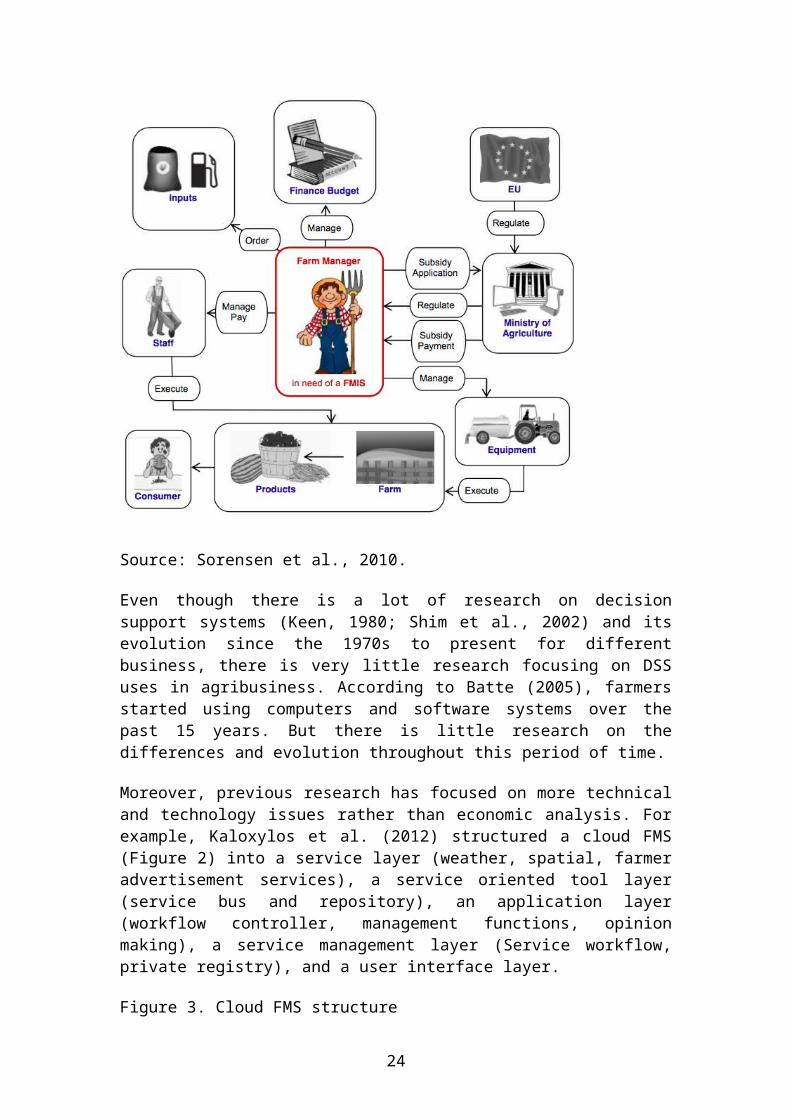

According to Halberg (2001), adoption of FMS aim tobetter undertake managerial demands caused by externalentities (government and public) applying increasingpressure on the agricultural sector to change the methodsof production from a focus on quantity to an alternatefocus on quality and sustainability. This change has beenenforced by restrictions in the use of production input(e.g. fertilizers, agrochemicals). Figure 3 bestdescribes the managerial demands a farmer has toundertake. These range from input ordering and financebudget managing to manage equipment and comply withgovernment.

Figure 2. Activities surrounding farm production and needof an FMS

Decision Support Systems

23

Source: Sorensen et al., 2010.

Even though there is a lot of research on decisionsupport systems (Keen, 1980; Shim et al., 2002) and itsevolution since the 1970s to present for differentbusiness, there is very little research focusing on DSSuses in agribusiness. According to Batte (2005), farmersstarted using computers and software systems over thepast 15 years. But there is little research on thedifferences and evolution throughout this period of time.

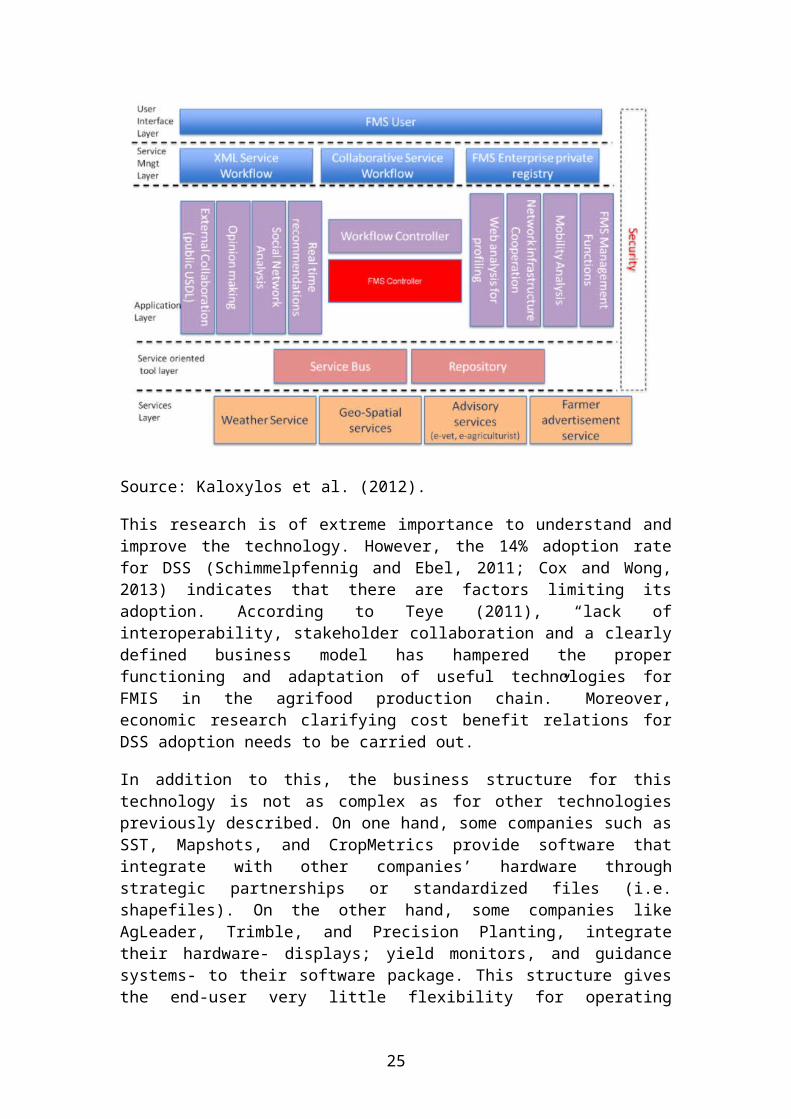

Moreover, previous research has focused on more technicaland technology issues rather than economic analysis. Forexample, Kaloxylos et al. (2012) structured a cloud FMS(Figure 2) into a service layer (weather, spatial, farmeradvertisement services), a service oriented tool layer(service bus and repository), an application layer(workflow controller, management functions, opinionmaking), a service management layer (Service workflow,private registry), and a user interface layer.

Figure 3. Cloud FMS structure

24

Source: Kaloxylos et al. (2012).

This research is of extreme importance to understand andimprove the technology. However, the 14% adoption ratefor DSS (Schimmelpfennig and Ebel, 2011; Cox and Wong,2013) indicates that there are factors limiting itsadoption. According to Teye (2011), “lack ofinteroperability, stakeholder collaboration and a clearlydefined business model has hampered the properfunctioning and adaptation of useful technologies forFMIS in the agrifood production chain.” Moreover,economic research clarifying cost benefit relations forDSS adoption needs to be carried out.

In addition to this, the business structure for thistechnology is not as complex as for other technologiespreviously described. On one hand, some companies such asSST, Mapshots, and CropMetrics provide software thatintegrate with other companies’ hardware throughstrategic partnerships or standardized files (i.e.shapefiles). On the other hand, some companies likeAgLeader, Trimble, and Precision Planting, integratetheir hardware- displays; yield monitors, and guidancesystems- to their software package. This structure givesthe end-user very little flexibility for operating

25

different brands.

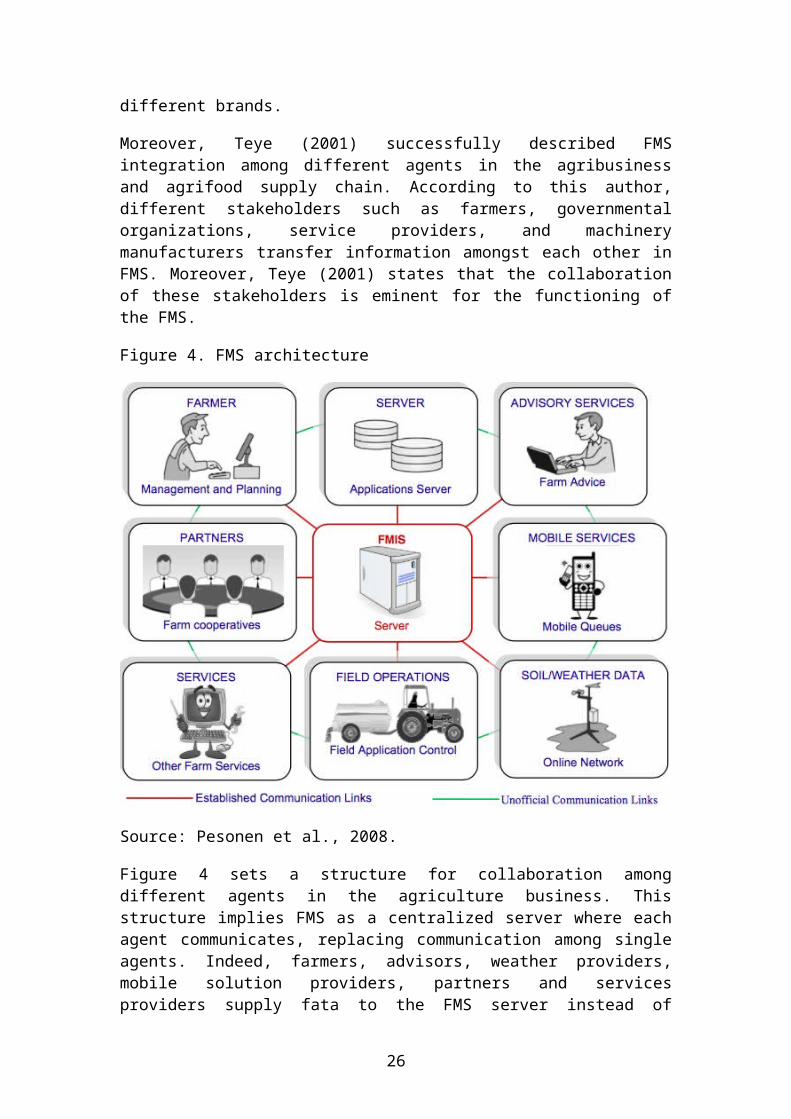

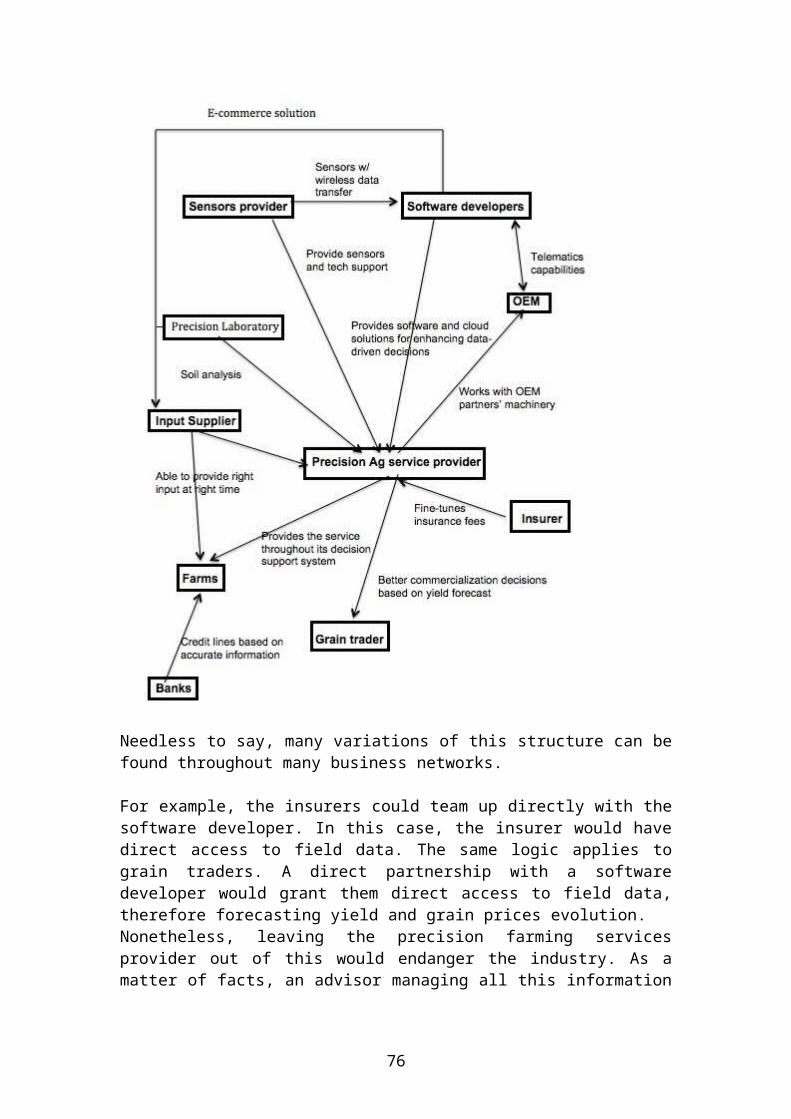

Moreover, Teye (2001) successfully described FMSintegration among different agents in the agribusinessand agrifood supply chain. According to this author,different stakeholders such as farmers, governmentalorganizations, service providers, and machinerymanufacturers transfer information amongst each other inFMS. Moreover, Teye (2001) states that the collaborationof these stakeholders is eminent for the functioning ofthe FMS.

Figure 4. FMS architecture

Source: Pesonen et al., 2008.

Figure 4 sets a structure for collaboration amongdifferent agents in the agriculture business. Thisstructure implies FMS as a centralized server where eachagent communicates, replacing communication among singleagents. Indeed, farmers, advisors, weather providers,mobile solution providers, partners and servicesproviders supply fata to the FMS server instead of

26

sharing data among each other.

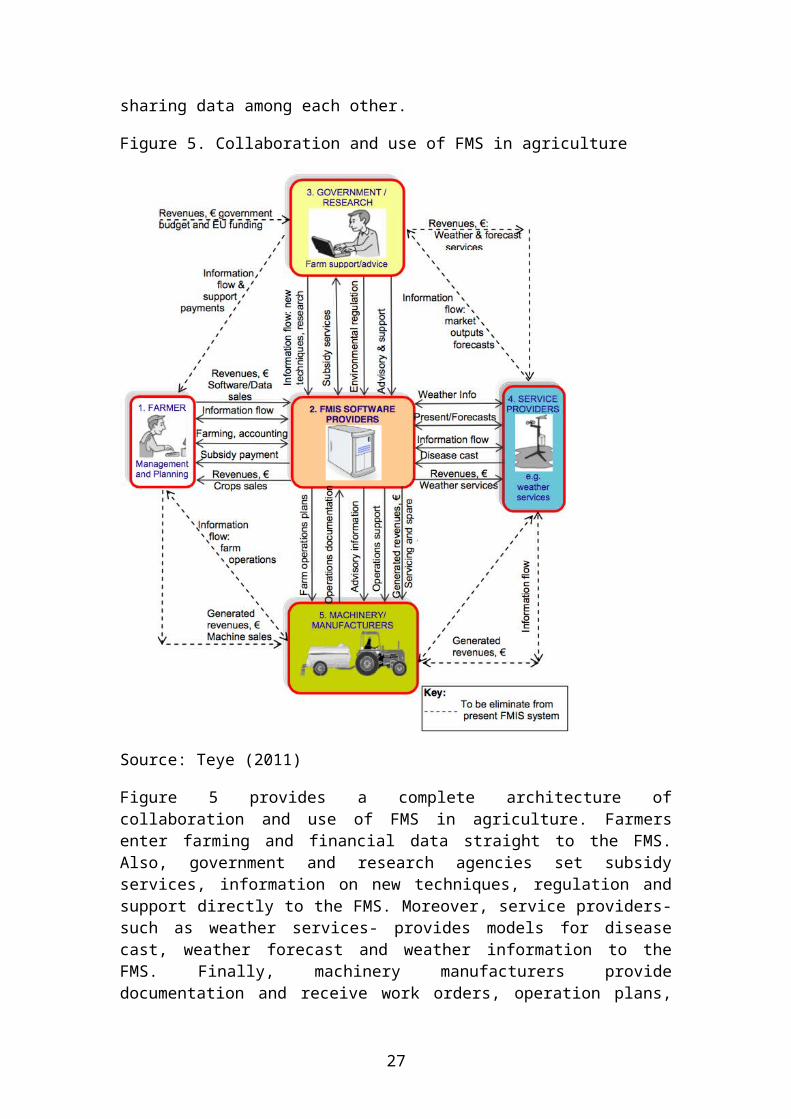

Figure 5. Collaboration and use of FMS in agriculture

Source: Teye (2011)

Figure 5 provides a complete architecture ofcollaboration and use of FMS in agriculture. Farmersenter farming and financial data straight to the FMS.Also, government and research agencies set subsidyservices, information on new techniques, regulation andsupport directly to the FMS. Moreover, service providers-such as weather services- provides models for diseasecast, weather forecast and weather information to theFMS. Finally, machinery manufacturers providedocumentation and receive work orders, operation plans,

27

and operation support straight from the FMS. Figure 5also indicates the steps to be eliminated in the futurefrom adopting FMS. Information flow between farmers,government, service providers and machinery manufacturersis likely to diminish over time, centralizing the data onthe FMS provider.

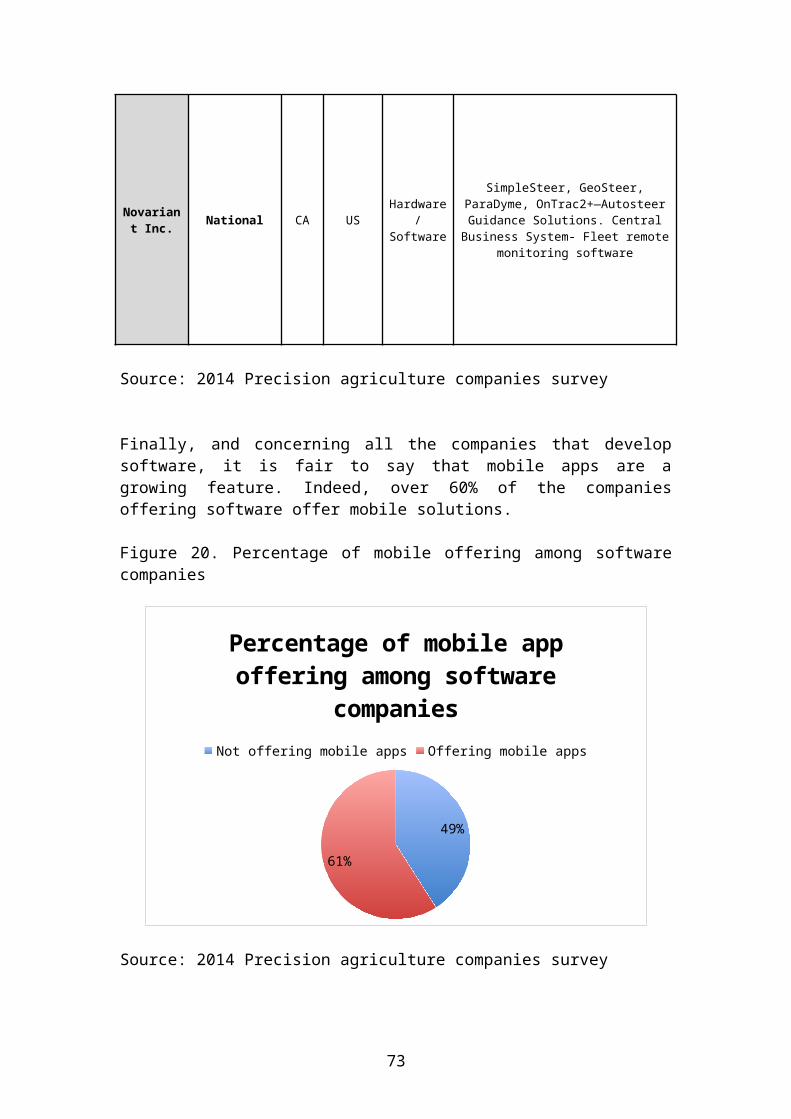

2.9. MOBILE APPLICATIONS AND CLOUB-BASED INFRASTRUCTURE

According to the National Institute of Standards andTechnology, cloud computing can be defined as a “modelfor enabling ubiquitous, convenient, on-demand networkaccess to a shared pool of configurable computingresources (e.g., networks, servers, storage,applications, and services) that can be rapidlyprovisioned and released with minimal management effortor service provider interaction”.

Murazzo and Rodríguez (2010) define mobile solutions asthe cloud computing availability in mobile devices. Thesesolutions create a platform to deploy web-based contentsinto mobile devices in a high-speed and low-cost way.

There are several mobile solutions that allow fieldscouting, boundary mapping, hyper-local weather forecast,and on foot VRA control among many others (Cox and Wong,2013). What is more, mobile solutions allow growers tocontact advisors and technicians everywhere in the field,and show them in site issues concerning their crops ormachinery.

In addition to this, mobile solutions are also startingto grow in the irrigation industry. Growers can monitormultiple irrigation systems from their mobile phones ortablets and make adjustments to application rates andsystem movement as needed (Cox and Wong, 2013).

On the other hand, cloud-based computing connectsmonitors, mobile devices, and office computers. This is ahuge benefit to the growers as they can make changes,record data, take pictures and not worry about having toupload them to each of their systems by physical USBtransfer (Cox and Wong, 2013). Cloud-based computinggenerates more and more data to be analyzed and

28

integrated in farm management software.

Even though there is not much information in theliterature about mobile application adoption inagriculture over the last decades, the InternationalTelecommunication Union (ITU) has monitored the telephoneand broadband subscription rates in industrialized andnon-industrialized countries (Figure 6). On average,since 2012, each inhabitant in the planet is subscribedto a mobile cellular plan, even in non-industrializedcountries. This statistic reveals the potential formobile applications in agriculture. Moreover, mobilebroadband Internet subscriptions support this claim(Figure 7). Some regions in Africa and the Middle East,however, are still far below average of mobile Internetsubscriptions despite the potential and needs in thesezones to adopt the technology (Baumuller, 2013).

Figure 6. Telephone and broadband subscription rates(2000-2012)

Source: International Telecommunication Union website

Figure 7. Mobile broadband Internet subscriptions as apercentage of country population in 2012

29

Source: International Telecommunication Union website

In addition to this, there is still no research foundabout the cost benefit ratio from adopting mobile andcloud-based technologies. This is probably because it issuch a new technology that business structure has not yetbeen defined. Moreover, the apparent lack of easiness tomeasure benefits from adopting a mobile application isprobably contributing as well. For example, there is noliterature on how to measure benefits from adoptingweather or scouting applications. The number of variablesaffecting agriculture is making economists’ work evenharder.

What is more, the business model for mobile applicationsis still being structured. On one hand, many companiesoffer mobile solutions as part as their complete package.This is especially true for software companies such asSST and Mapshots. These companies’ mobile applicationsusually complement their computer-based software withfunctions such as GPS-tagged observations, images, andfield boundary delimitation. On the other hand, companiesnot traditionally involved in mobile offerings haverecently started to develop mobile solutions as well.Some fine examples of this are Cargill’s NextField orDupont’s Encirca, the latter also being developed forwearable technologies such as Google Glass. Moreover,companies allied with sensors developers provide mobileapplications as part of their service package. Some fine

30

examples are AgSense, i-Linc Technologies, andRanchSystems. Finally, machinery manufacturers likeJohnDeere, AGCO, and CNH provide mobile solutions as atool for fleet and data management.

Even though there is no literature on how differentagents of the agriculture sector can benefit from mobileapplications data, it can be expected to suffer a similarstructure as Teye (2011) proposed for FMS. The potentialfor mobile and cloud-based computing data use needs to beexamined for different agents and at different levels ofthe supply chain network.

31

3. METHODOLOGY

To carry out this research, three different steps werefollowed.

First, it was necessary to collect and analyze secondarymarket information and previous research on this subjectin order to formulate and underlie the structure andtaxonomy of precision agriculture market.

Second, semi-structured interviews took place to test thepreviously formulated structure. These interviews werecarried out face to face or by phone call if distanceswere too large.

Finally, a web-based survey was sent to all the companiessomehow involved in one of the precision farming industrykey roles: hardware, software, and sensors developers.The survey was sent to a total of 216, receiving a 17% ofresponses. The results of the “2014 Precision agriculturecompanies survey” are summarized and presented in thisreport.

The next considerations were taken into account whencompiling the companies’ and technologies’ list.

Dealers and services providers that did not developtheir own product were excluded from the list asthis report aims to describe technologies and thecompanies developing those technologies.

In addition to this, the surveys were not sent tocompanies that are directly in the agricultureindustry but are somehow related (i.e. Insurances,Banks, Brokers)

32

4. RESULTS

4.1. PRECISION AG COMPANIES DESCRIPTION

Throughout this section, a brief overall precisionfarming industry characterization will be made. Inaddition to this, precision Ag industry companies will belisted in different categories.

The first distinction to be made is between public andprivates companies. Public companies are, usually, biggercompanies with larger revenues and resources (number ofemployees, R&D investment, facilities). Thus, comparingprivate vs. public companies is not adequate.

In addition to this, private companies will be dividedaccording to their offering type and the marketreached/expected by separating multinational companiesfrom national ones. Within each category, a generalmarket characterization will be made.

4.1.1. General description

33

Precision farming industry has seen over the last fewyears a huge outbreak in the number of companies funded.As stressed in the lit review section, this has led to asignificant business-to-business enhancement throughmergers and acquisitions (M&A) and venture capital (VC)financing.

It is of common knowledge that companies with greatpotential rapidly become VC-backed companies. Thisincludes many private companies such as aWhere,Meteologic, Aquaspy, Farmeron or Granular.

Therefore, it is to be expected that private companieslargely surpass public companies in precision farmingindustry (82% vs. 18%). Moreover, it is likely to see anincrease in this private/public companies ratio over thenext few years as Big Data in agriculture moves towardsthe plateau of productivity on Gartner’s hype cycle.

Figure 8. Public companies / private companies inprecision Ag industry

34

Public companies

18%

Private companies

82%

Public companies / private companies in precision Ag industry

Source: 2014 Precision agriculture companies survey

What is more, around 70% of companies are from the US (orat least headquartered in the US), beating by far thesecond on the list, Canada with 10%.

35

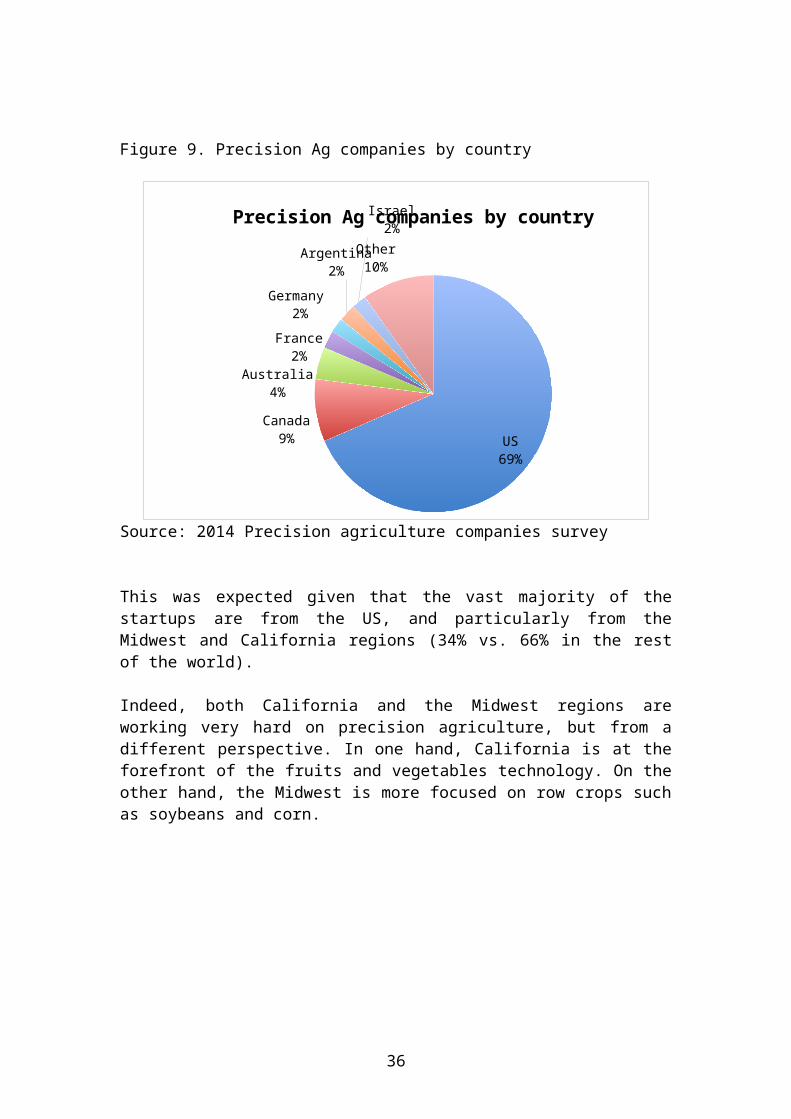

Figure 9. Precision Ag companies by country

US69%

Canada9%

Australia4%

France2%

Germany 2%

Argentina2%

Israel2%

Other10%

Precision Ag companies by country

Source: 2014 Precision agriculture companies survey

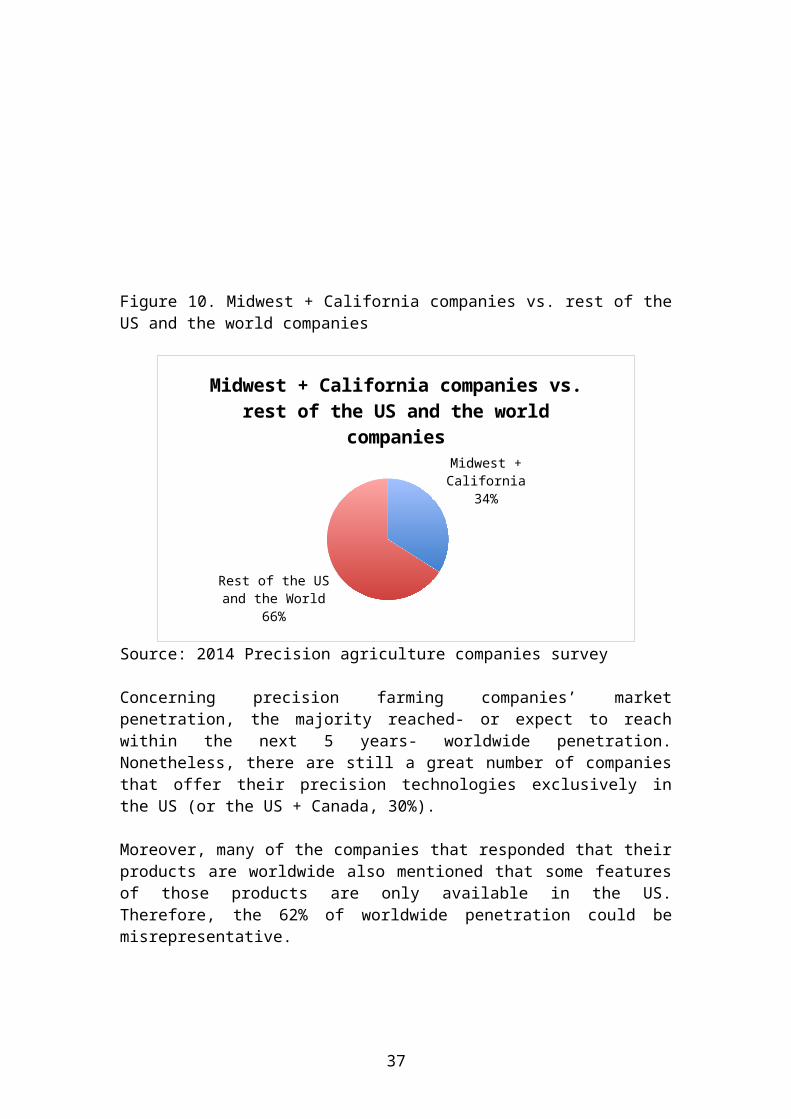

This was expected given that the vast majority of thestartups are from the US, and particularly from theMidwest and California regions (34% vs. 66% in the restof the world).

Indeed, both California and the Midwest regions areworking very hard on precision agriculture, but from adifferent perspective. In one hand, California is at theforefront of the fruits and vegetables technology. On theother hand, the Midwest is more focused on row crops suchas soybeans and corn.

36

Figure 10. Midwest + California companies vs. rest of theUS and the world companies

Midwest + California

34%

Rest of the US and the World

66%

Midwest + California companies vs. rest of the US and the world

companies

Source: 2014 Precision agriculture companies survey

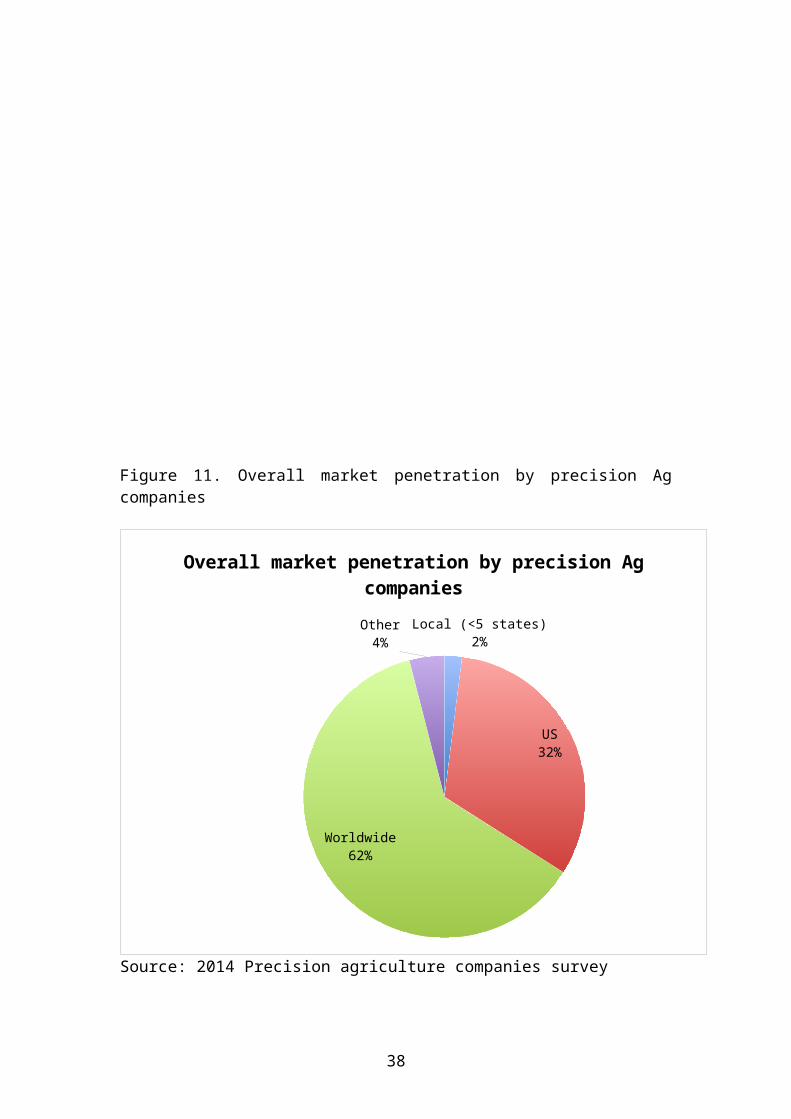

Concerning precision farming companies’ marketpenetration, the majority reached- or expect to reachwithin the next 5 years- worldwide penetration.Nonetheless, there are still a great number of companiesthat offer their precision technologies exclusively inthe US (or the US + Canada, 30%).

Moreover, many of the companies that responded that theirproducts are worldwide also mentioned that some featuresof those products are only available in the US.Therefore, the 62% of worldwide penetration could bemisrepresentative.

37

Figure 11. Overall market penetration by precision Agcompanies

Local (<5 states)2%

US32%

Worldwide62%

Other4%

Overall market penetration by precision Ag companies

Source: 2014 Precision agriculture companies survey

38

4.1.2. Public companies

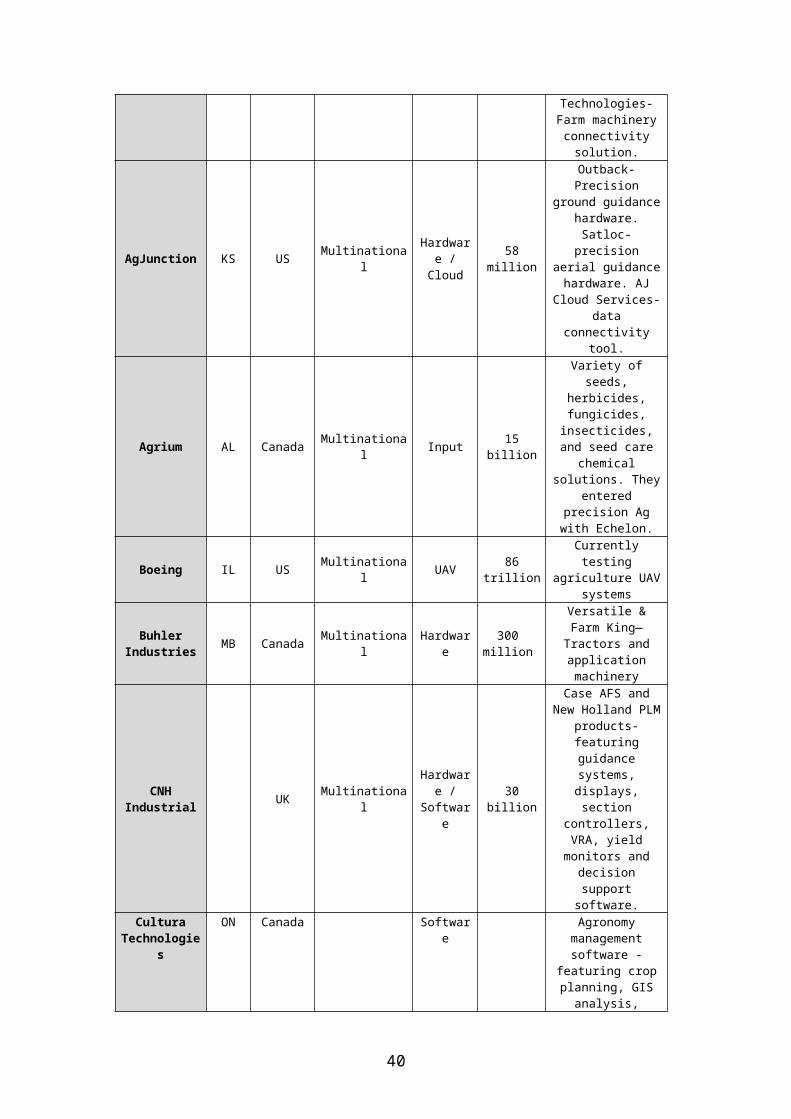

Table 6. Public companies offering precision agriculturetechnologies

CompanyHQState

HQCountr

y

National /Multinatio

nal

Offeringtype

Annualturnover

(USD)

Precision AgProducts

AGCO Corp. GA US Multinational

Hardware

10billion

AgCommand-fleet

management app.VarioDoc,

TaskDoc- fielddocumentationsystems. Auto-Guide 3000-assisted-steeringsolution.VarioGuide-automaticsteering

solution. Fuse

39

Technologies-Farm machineryconnectivitysolution.

AgJunction KS US Multinational

Hardware /Cloud

58million

Outback-Precision

ground guidancehardware.Satloc-

precisionaerial guidancehardware. AJ

Cloud Services-data

connectivitytool.

Agrium AL Canada Multinational Input 15

billion

Variety ofseeds,

herbicides,fungicides,insecticides,and seed care

chemicalsolutions. They

enteredprecision Agwith Echelon.

Boeing IL US Multinational UAV 86

trillion

Currentlytesting

agriculture UAVsystems

BuhlerIndustries MB Canada Multinationa

lHardwar

e 300 million

Versatile &Farm King—Tractors andapplicationmachinery

CNHIndustrial UK Multinationa

l

Hardware /

Software

30billion

Case AFS andNew Holland PLM

products-featuringguidancesystems,displays,section

controllers,VRA, yieldmonitors anddecisionsupport

software.Cultura

Technologies

ON Canada Software

Agronomymanagementsoftware -

featuring cropplanning, GISanalysis,

40

Reporting andfield history

tools.Financial andAccountingsoftware.

Table 6. Public companies offering precision agriculturetechnologies (cont.)

41

42

CompanyHQState

HQCountry

National /Multinationa

l

Offering type

Annualturnover(USD)

PrecisionAg Products

Deere &Co. IL US Multinationa

l

Hardware /

Software /

Cloud /Sensors

37billion

Completeline ofdisplays,reveivers,guidance,controllers, and datamanagementsolutions.

DigiInternatio

nalMN US Multinationa

l

Hardware /

Software /Cloud

Etherios- acloud

solution.Social

machine-software

applicationto connect

everydevice- Canbe usefulfor fleetmanagement

DowAgroScienc

esIN US Multinationa

l

Input /Softwar

e

57billion

Enlist &Enlist app-

weedmanagementcontrol

system andapp.

Dupont DE US Multinational

Software /

Cloud /Sensors

34billion

EncircaView- an

informationrecord/shar

ingsoftwarebetweenusers andhyper-localweatherprovider.EncircaYield

NitrogenManagementService-allows tomanageinput

accordingto datagatheredfrom thefield

(weather,soil, etc.)

E-Markets CO US Software

CINCH &Intellego-agribusines

saccountingsolutions

ExelIndustries France Multinationa

lHardwar

e900

million

Spreaders,tractors,harvesters

andseeders.

Table 6. Public companies offering precision agriculturetechnologies (cont.)

CompanyHQ

State

HQCountry

National /Multinatio

nal

Offering

type

Annualturnov

er(USD)

PrecisionAg

Products

HardiInternatio

nalDenmark Multinationa

l Hardware

VR sprayersand

controllers. Nozzleselectorapp.

HexagonGeospatial AL US Multinationa

l Software 14billion

GeoMedia-GIS

Managementsoftware.ERDAS-remote

sensing andimage

analysis.LiDAR-high-

accuracyelevationdata.

MapWorks-field datacaptureapp.

IBM NY US Multinational

Software/ Cloud

99billion

DeepThunder-hyper-local,

short-term,customizedweatherforecast

foragriculture

.

Iteris CA US Software/ Cloud

> 60Million

ClearPathAG-

hyperlocalcustomizedweather foragribusines

s.

Kuhn France Multinational Hardware > 50

Million

Precisionseeding andfertilizermachinery

Lindsay NE US Multinationa Hardware 400 Zimmatic

43

Corporation l

/Software

/Sensors

Million

IrrigationLine-

VariableRate

Irrigationsystem withsoftware

for remoteirrigationmanagement(FieldNET)

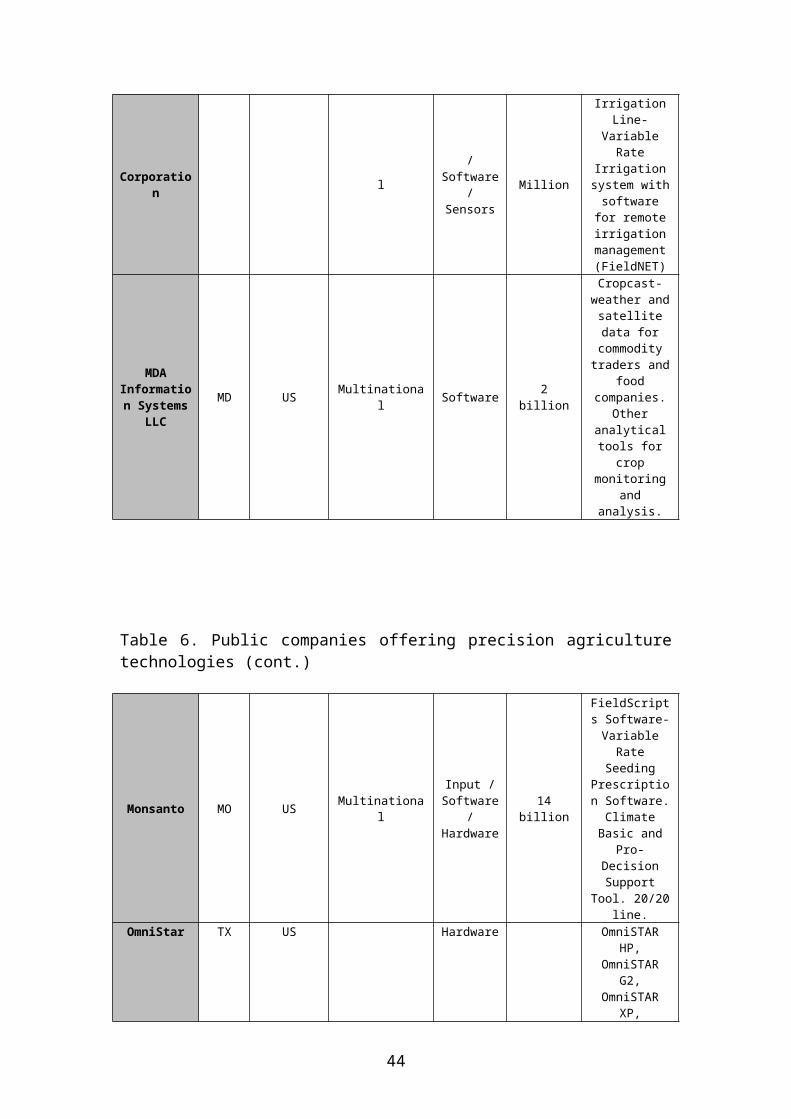

MDAInformation Systems

LLC

MD US Multinational Software 2

billion

Cropcast-weather andsatellitedata forcommoditytraders and

foodcompanies.

Otheranalyticaltools for

cropmonitoring

andanalysis.

Table 6. Public companies offering precision agriculturetechnologies (cont.)

Monsanto MO US Multinational

Input /Software

/Hardware

14billion

FieldScripts Software-VariableRate

SeedingPrescription Software.ClimateBasic and

Pro-DecisionSupport

Tool. 20/20line.

OmniStar TX US Hardware OmniSTARHP,

OmniSTARG2,

OmniSTARXP,

44

OmniSTARVBS-

Satelliteguidancenetworks

andsolutions

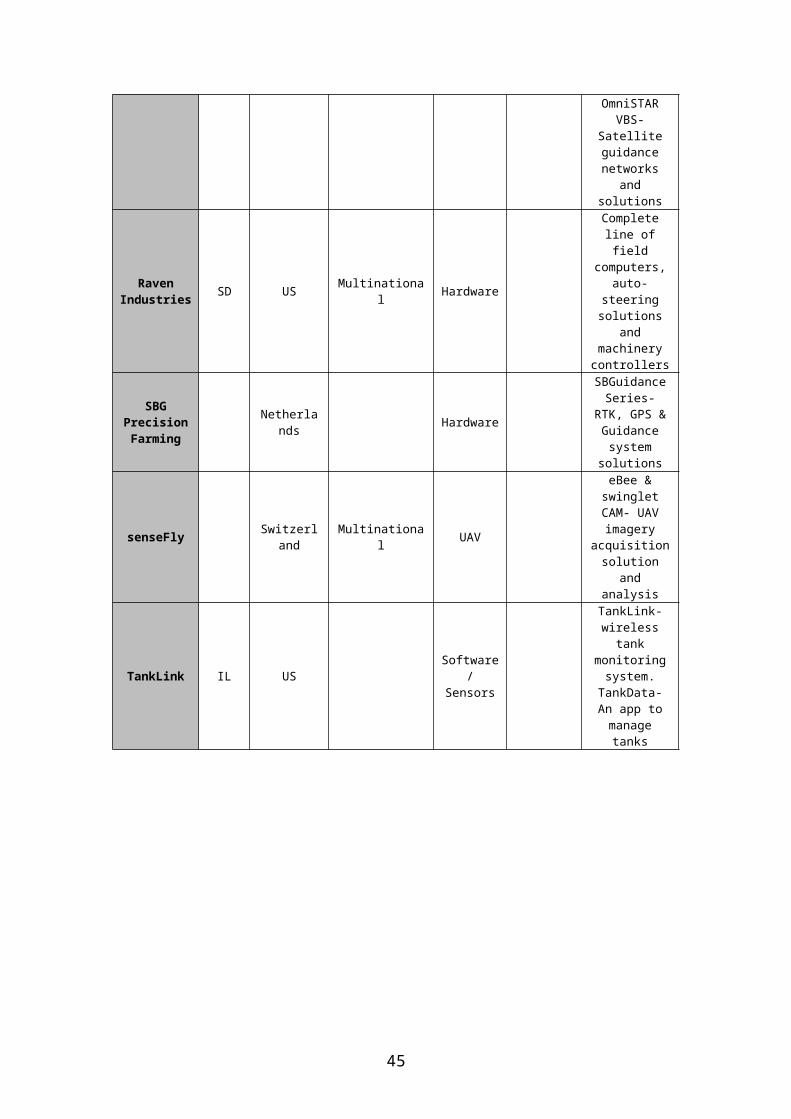

RavenIndustries SD US Multinationa

l Hardware

Completeline offield

computers,auto-

steeringsolutions

andmachinerycontrollers

SBGPrecisionFarming

Netherlands Hardware

SBGuidanceSeries-

RTK, GPS &Guidancesystem

solutions

senseFly Switzerland

Multinational UAV

eBee &swingletCAM- UAVimagery

acquisitionsolution

andanalysis

TankLink IL USSoftware

/Sensors

TankLink-wirelesstank

monitoringsystem.TankData-An app tomanagetanks

45

Table 6. Public companies offering precision agriculturetechnologies (cont.)

CompanyHQ

State

HQCountry

National /Multinational

Offering

type

Annualturnover

(USD)

PrecisionAg

Products

Topcon Japan Multinational

Hardware/

Software/

Cloud /Sensors

6trillion(Toshiba

)

Guidancesystems,

applicationcontrolsystems,field datacollectors,

GPSreceivers,crop canopysensors,SGIS

Farm&Pro-data

managementand analysissoftware

TrimbleNavigation CA US Multinational

Software/

Cloud /Sensors

2billion

GreenSeeker—Crop healthassessmentsensor,

ConnectedFarm—FieldManagementsoftwaresolution &

datamanagement.FarmWorks-mappingsoftware

ublox Switzerland Multinational Hardware 240

million

Positioningdevices &Fastrax

software-positioningsoftware

ValleyIrrigation

NE US Multinational Hardware/

Software

3billion

Variablerate

irrigationequipment.BaseStation

3-Irrigationsystemsremote

46

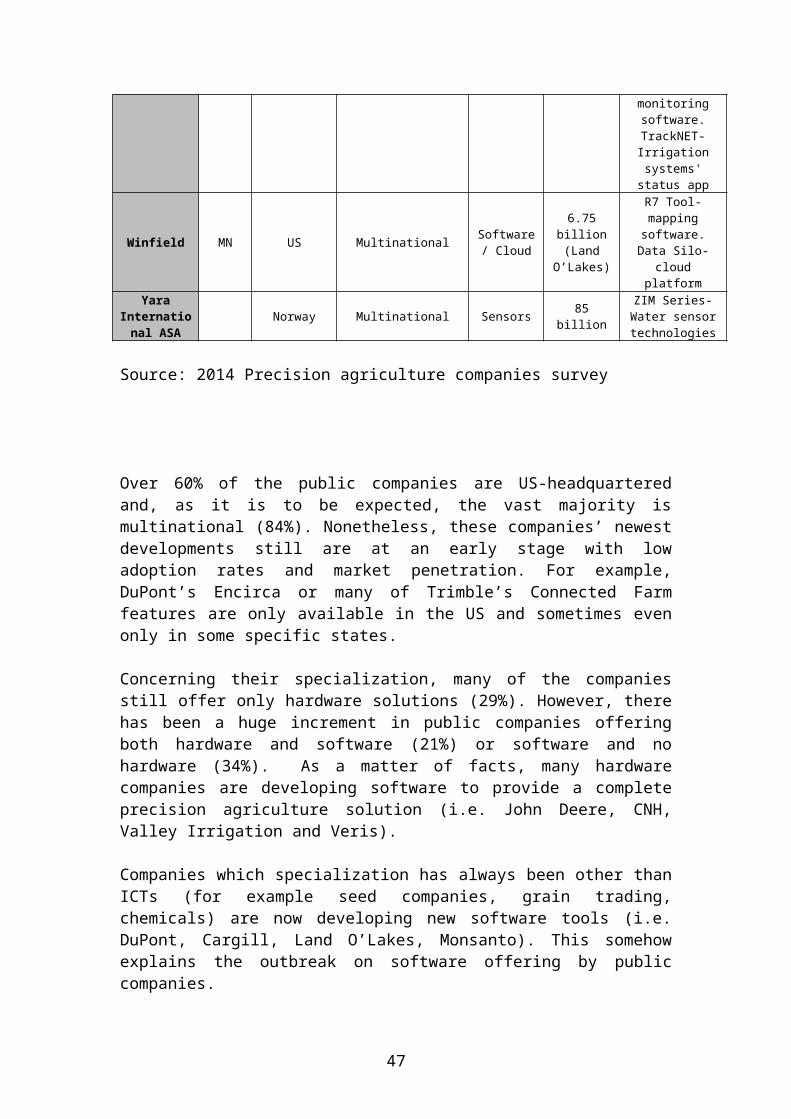

monitoringsoftware.TrackNET-Irrigationsystems'status app

Winfield MN US Multinational Software/ Cloud

6.75billion(Land

O’Lakes)

R7 Tool-mapping

software.Data Silo-

cloudplatform

YaraInternational ASA

Norway Multinational Sensors 85billion

ZIM Series-Water sensortechnologies

Source: 2014 Precision agriculture companies survey

Over 60% of the public companies are US-headquarteredand, as it is to be expected, the vast majority ismultinational (84%). Nonetheless, these companies’ newestdevelopments still are at an early stage with lowadoption rates and market penetration. For example,DuPont’s Encirca or many of Trimble’s Connected Farmfeatures are only available in the US and sometimes evenonly in some specific states.

Concerning their specialization, many of the companiesstill offer only hardware solutions (29%). However, therehas been a huge increment in public companies offeringboth hardware and software (21%) or software and nohardware (34%). As a matter of facts, many hardwarecompanies are developing software to provide a completeprecision agriculture solution (i.e. John Deere, CNH,Valley Irrigation and Veris).

Companies which specialization has always been other thanICTs (for example seed companies, grain trading,chemicals) are now developing new software tools (i.e.DuPont, Cargill, Land O’Lakes, Monsanto). This somehowexplains the outbreak on software offering by publiccompanies.

47

This is a clear example that large companies are enteringthe precision farming software race.

Figure 12. Offering type among public companies

Hardware29%

Hardware / Software

21%

Software*34%

Other (UAV, Sensors)

16%

Offering type among public companies

*These companies do not develop only softwareSource: 2014 Precision agriculture companies survey

4.1.3. Private companies

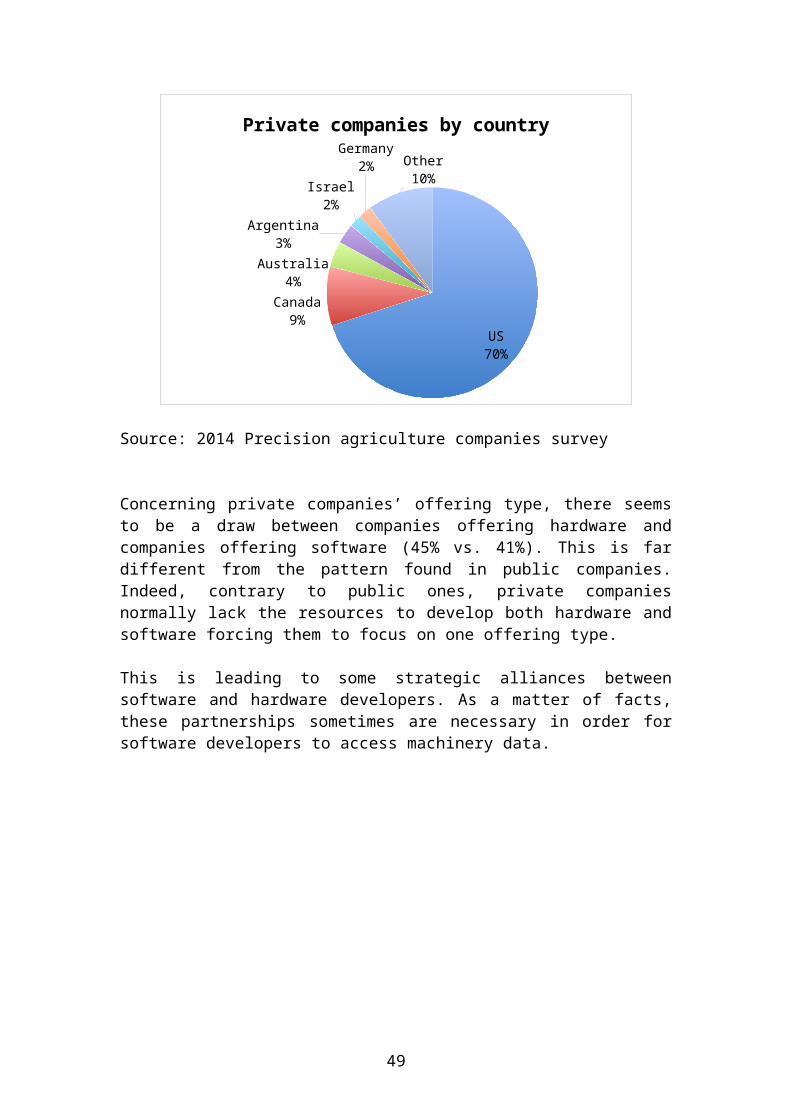

Country ratios’ for private companies is very similar tothe one for total companies (public + private). This is afurther aspect proving that the US is leading inprecision farming industry, with 70% of the privatecompanies, followed by far by Canada with only 9% ofthem. Once again, the Midwest and California regionsconcentration- 30% of private companies in the world-partially explains this ratio.Figure 13. Private companies by country

48

US70%

Canada9%

Australia4%

Argentina3%

Israel2%

Germany2% Other

10%

Private companies by country

Source: 2014 Precision agriculture companies survey

Concerning private companies’ offering type, there seemsto be a draw between companies offering hardware andcompanies offering software (45% vs. 41%). This is fardifferent from the pattern found in public companies.Indeed, contrary to public ones, private companiesnormally lack the resources to develop both hardware andsoftware forcing them to focus on one offering type.

This is leading to some strategic alliances betweensoftware and hardware developers. As a matter of facts,these partnerships sometimes are necessary in order forsoftware developers to access machinery data.

49

Figure 14. Offering type among private companies

Hardware45%

Hardware / Software11%

Software41%

Other3%

Offering type among private companies

Source: 2014 Precision agriculture companies survey

Concerning multinational / national percentages byoffering type, it seems that software companies arecatching up with hardware companies. Indeed, thepercentage of multinational software companies isslightly fewer than that of hardware companies (25% vs.31%).

As for companies offering hardware and software, themulti / national ratio is more equilibrated, near 50 –50. This stresses that these kinds of companies are ingeneral larger companies with more resources.

50

Figure 15. Multinational and national companies byoffering type

Hardware Hardware & Software

Software

31%48%

25%

69%52%

75%

Multinational and national companies by offering type

Multinational National

Source: 2014 Precision agriculture companies survey

The next two figures summarize the respondent annualturnover and number of employees by offering type inorder to have an idea of the different companies’ size inthe precision agriculture industry.

Both charts seem to indicate a tendency where privatesoftware companies are mostly at early stages. As a

51

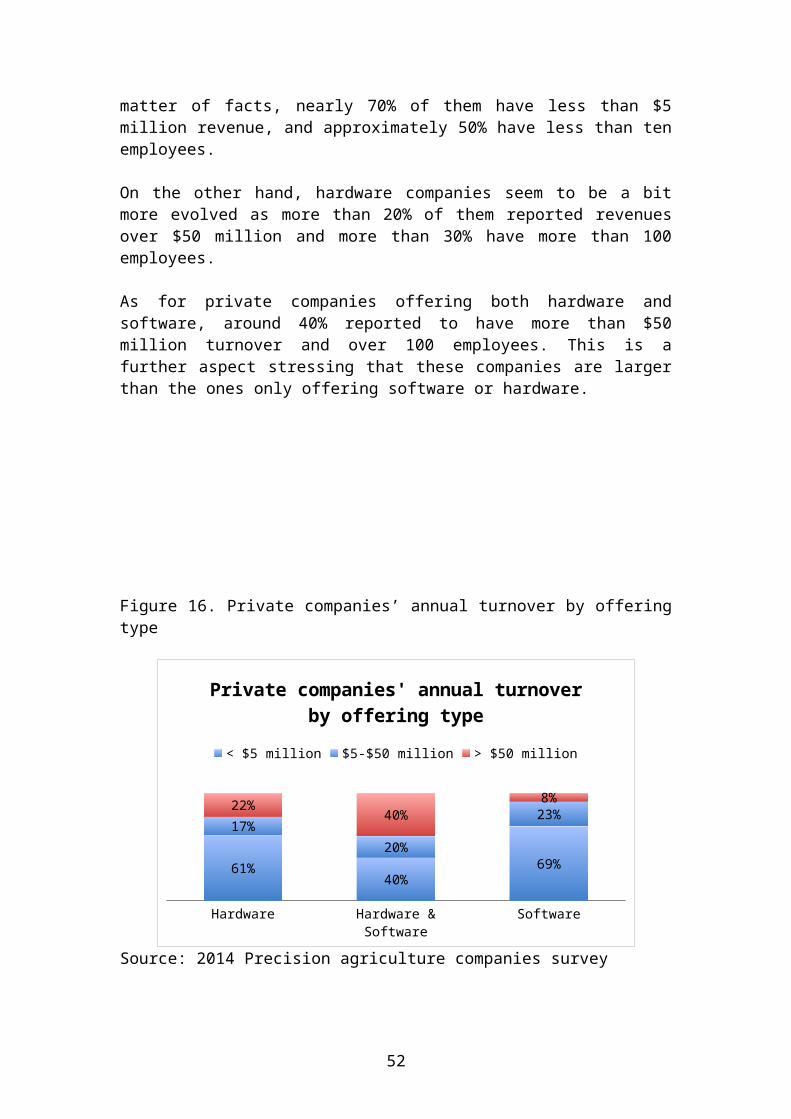

matter of facts, nearly 70% of them have less than $5million revenue, and approximately 50% have less than tenemployees.

On the other hand, hardware companies seem to be a bitmore evolved as more than 20% of them reported revenuesover $50 million and more than 30% have more than 100employees.

As for private companies offering both hardware andsoftware, around 40% reported to have more than $50million turnover and over 100 employees. This is afurther aspect stressing that these companies are largerthan the ones only offering software or hardware.

Figure 16. Private companies’ annual turnover by offeringtype

Hardware Hardware & Software

Software

61%40%

69%

17%20%

23%22% 40%8%

Private companies' annual turnover by offering type

< $5 million $5-$50 million > $50 million

Source: 2014 Precision agriculture companies survey

52

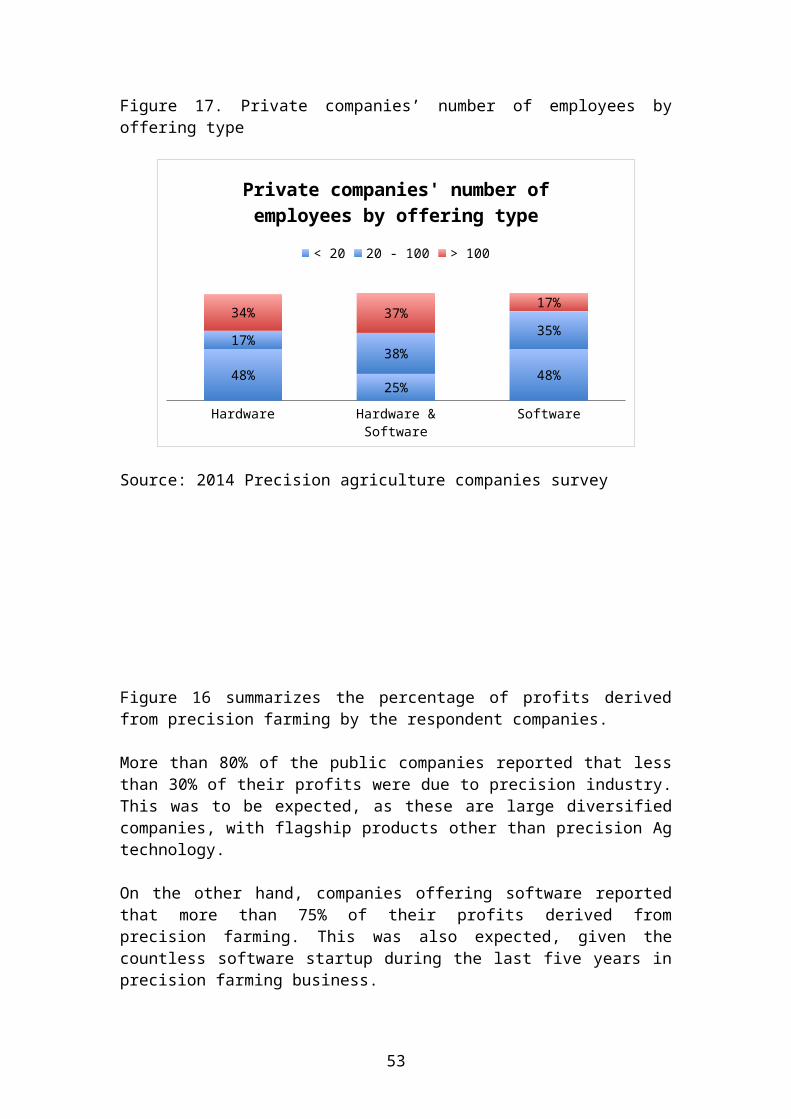

Figure 17. Private companies’ number of employees byoffering type

Hardware Hardware & Software

Software

48%25%

48%

17%38%

35%34% 37% 17%

Private companies' number of employees by offering type

< 20 20 - 100 > 100

Source: 2014 Precision agriculture companies survey

Figure 16 summarizes the percentage of profits derivedfrom precision farming by the respondent companies.

More than 80% of the public companies reported that lessthan 30% of their profits were due to precision industry.This was to be expected, as these are large diversifiedcompanies, with flagship products other than precision Agtechnology.

On the other hand, companies offering software reportedthat more than 75% of their profits derived fromprecision farming. This was also expected, given thecountless software startup during the last five years inprecision farming business.

53

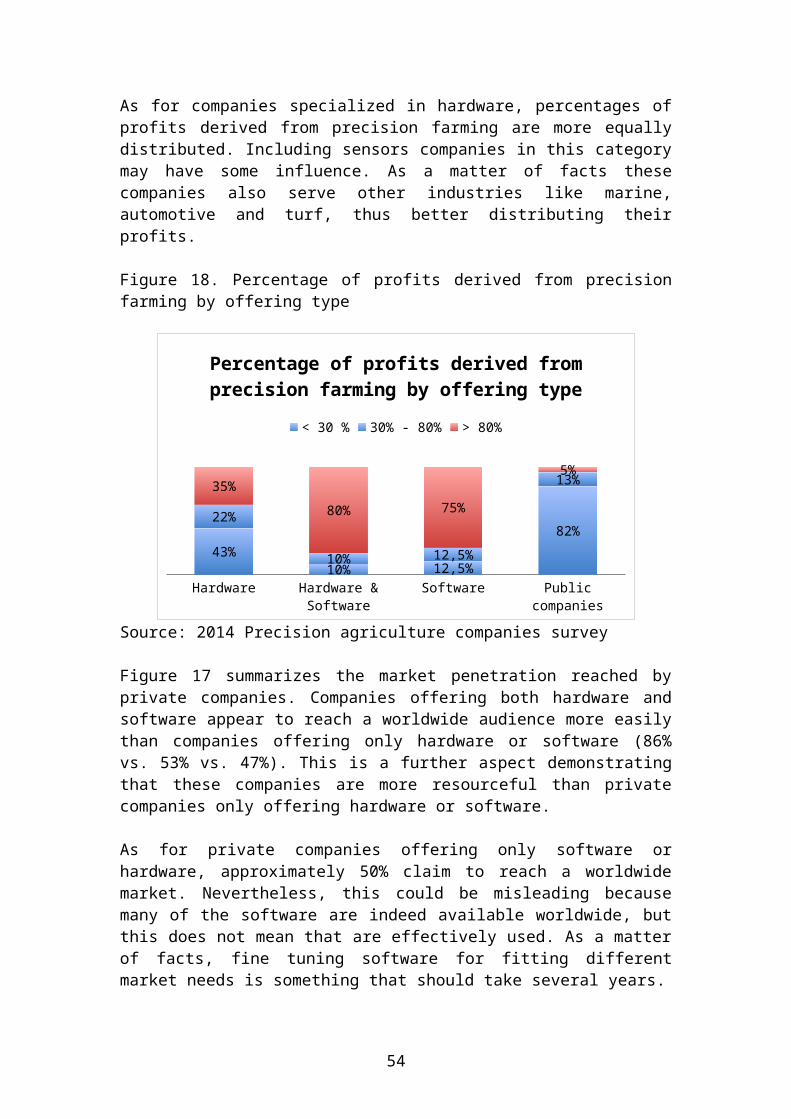

As for companies specialized in hardware, percentages ofprofits derived from precision farming are more equallydistributed. Including sensors companies in this categorymay have some influence. As a matter of facts thesecompanies also serve other industries like marine,automotive and turf, thus better distributing theirprofits.

Figure 18. Percentage of profits derived from precisionfarming by offering type

Hardware Hardware & Software

Software Public companies

43%10% 12,5%

82%22%

10% 12,5%

13%35%80% 75%

5%

Percentage of profits derived from precision farming by offering type

< 30 % 30% - 80% > 80%

Source: 2014 Precision agriculture companies survey

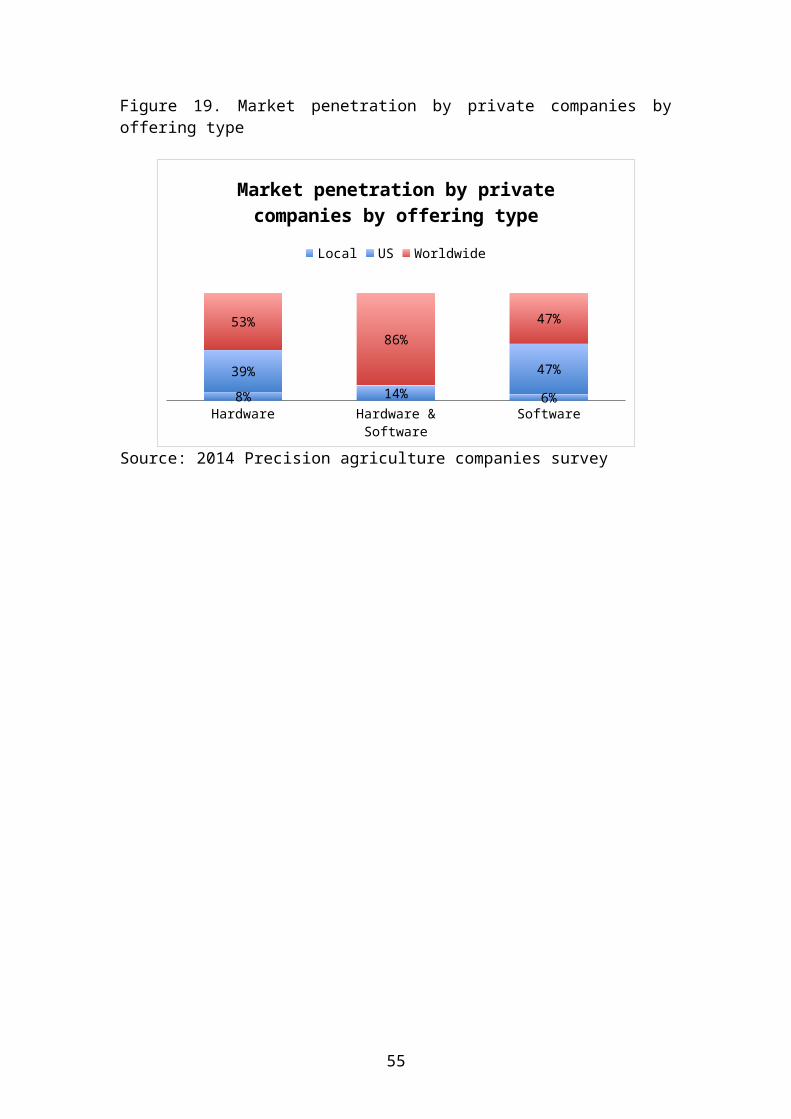

Figure 17 summarizes the market penetration reached byprivate companies. Companies offering both hardware andsoftware appear to reach a worldwide audience more easilythan companies offering only hardware or software (86%vs. 53% vs. 47%). This is a further aspect demonstratingthat these companies are more resourceful than privatecompanies only offering hardware or software.

As for private companies offering only software orhardware, approximately 50% claim to reach a worldwidemarket. Nevertheless, this could be misleading becausemany of the software are indeed available worldwide, butthis does not mean that are effectively used. As a matterof facts, fine tuning software for fitting differentmarket needs is something that should take several years.

54

Figure 19. Market penetration by private companies byoffering type

Hardware Hardware & Software

Software8% 6%39%

14%47%

53%86%

47%

Market penetration by private companies by offering type

Local US Worldwide

Source: 2014 Precision agriculture companies survey

55

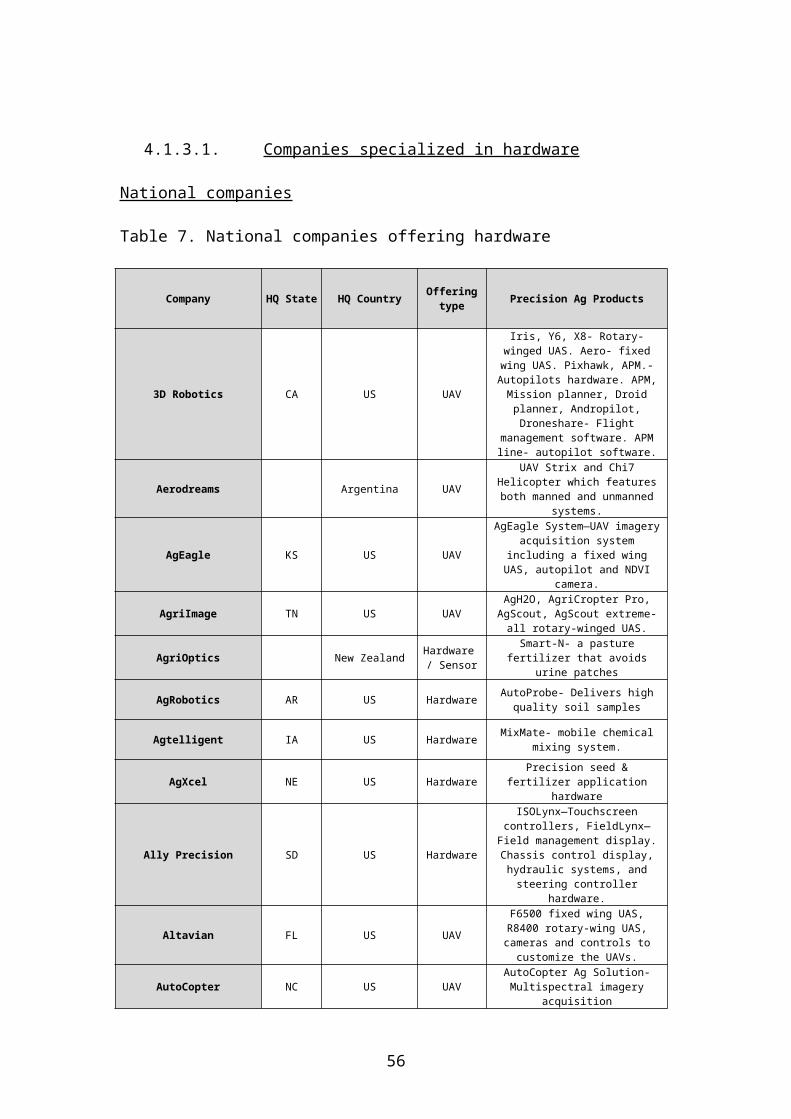

4.1.3.1. Companies specialized in hardware

National companies

Table 7. National companies offering hardware

Company HQ State HQ Country Offeringtype Precision Ag Products

3D Robotics CA US UAV

Iris, Y6, X8- Rotary-winged UAS. Aero- fixedwing UAS. Pixhawk, APM.-Autopilots hardware. APM,Mission planner, Droidplanner, Andropilot,Droneshare- Flight

management software. APMline- autopilot software.

Aerodreams Argentina UAV

UAV Strix and Chi7Helicopter which featuresboth manned and unmanned

systems.

AgEagle KS US UAV

AgEagle System—UAV imageryacquisition system

including a fixed wingUAS, autopilot and NDVI

camera.

AgriImage TN US UAVAgH2O, AgriCropter Pro,

AgScout, AgScout extreme-all rotary-winged UAS.

AgriOptics New Zealand Hardware / Sensor

Smart-N- a pasturefertilizer that avoids

urine patches

AgRobotics AR US Hardware AutoProbe- Delivers highquality soil samples

Agtelligent IA US Hardware MixMate- mobile chemicalmixing system.

AgXcel NE US HardwarePrecision seed &

fertilizer applicationhardware

Ally Precision SD US Hardware

ISOLynx—Touchscreencontrollers, FieldLynx—

Field management display.Chassis control display,hydraulic systems, andsteering controller

hardware.

Altavian FL US UAV

F6500 fixed wing UAS,R8400 rotary-wing UAS,cameras and controls to

customize the UAVs.

AutoCopter NC US UAVAutoCopter Ag Solution-Multispectral imagery

acquisition

56

Back40 Precision IL US Hardware / UAV

GNSS / GPS Receivers withSBAS correction optional.Currently working on an

UAV for agriculture

Barron BrothersInternational GA US Hardware

BBI line of fertilizer andlime spreaders for

Variable Rate Application.Task Command System—New

Guidance system featuringVariable Rate Application

Bestway KS US Hardware / Sensor

AutoGlide—Auto Boom HeightControl System

Blue RiverTechnologies CA US Hardware

/ Sensors

LettuceBot- Automated weedelimination solution inlettuce crops. Currently

working on the samesolution for corn and

soybeans

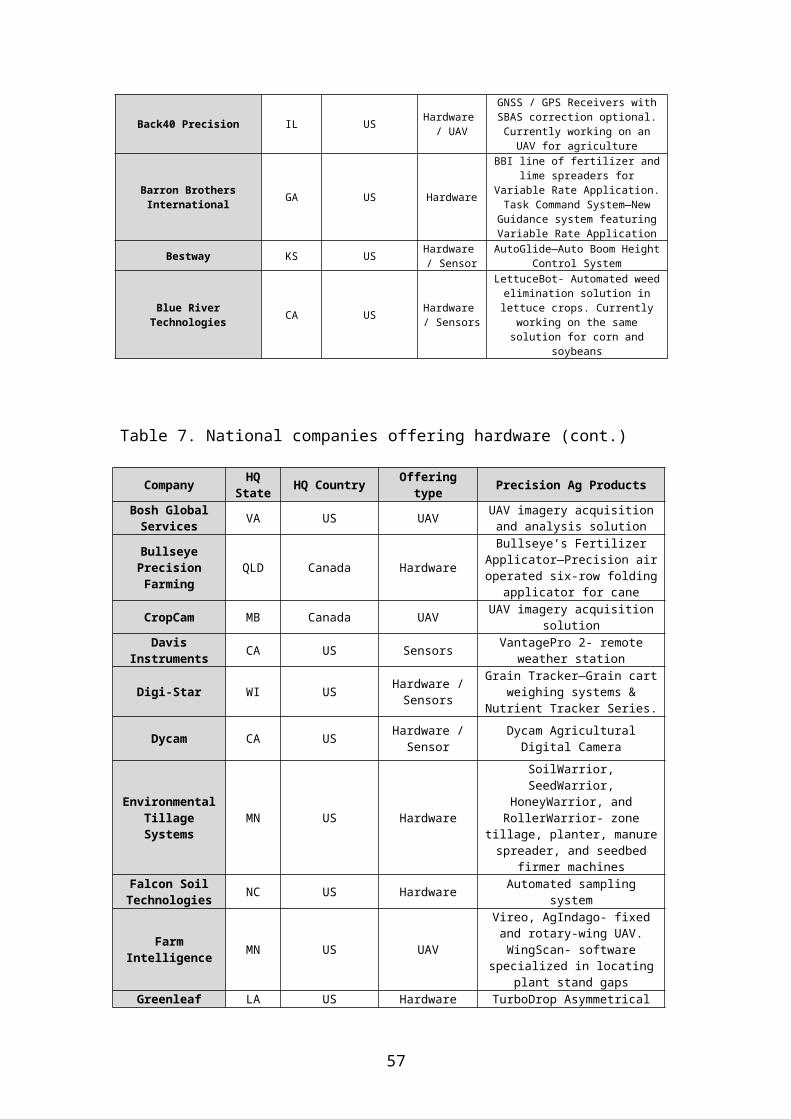

Table 7. National companies offering hardware (cont.)

Company HQState HQ Country Offering

type Precision Ag Products

Bosh GlobalServices VA US UAV UAV imagery acquisition

and analysis solution

BullseyePrecisionFarming

QLD Canada Hardware

Bullseye’s FertilizerApplicator—Precision airoperated six-row folding

applicator for cane

CropCam MB Canada UAV UAV imagery acquisitionsolution

DavisInstruments CA US Sensors VantagePro 2- remote

weather station

Digi-Star WI US Hardware /Sensors

Grain Tracker—Grain cartweighing systems &

Nutrient Tracker Series.

Dycam CA US Hardware /Sensor

Dycam AgriculturalDigital Camera

EnvironmentalTillageSystems

MN US Hardware

SoilWarrior,SeedWarrior,

HoneyWarrior, andRollerWarrior- zone

tillage, planter, manurespreader, and seedbed

firmer machinesFalcon SoilTechnologies NC US Hardware Automated sampling

system

FarmIntelligence MN US UAV

Vireo, AgIndago- fixedand rotary-wing UAV.WingScan- software

specialized in locatingplant stand gaps

Greenleaf LA US Hardware TurboDrop Asymmetrical

57

TechnologiesDualFan- lower drift andmore efficiency in each

pass.

Hawkeye UAV New Zealand UAV

RQ-84Z & RQ-84Z2- fixed-wing UAV with

multispectral cameraoption.

Headsight IN US Hardware /Sensors

Headsight Sensors-Height control systems.Truesight- Row guidance

system.

Honey Comb. OR US UAV AgDrone UAS- a fixedwing drone.

IntelligentAgriculturalSolutions

ND US Hardware /Sensor

Wireless BlockageMonitor & Active Depth

Controller.

ISISGeomatics AB Canada UAV /

Satellite

Pix4D- aerial imageprocessing software.EnsoMOSAIC UAV- readsUAV images. Tetracam-multispectral camera.

Jacto SP Brazil HardwareBoom height & Section

control, Guidancesystems, Ag Cameras

Junge Control IA US Hardware

Automated chemical andfertilizer mixing for

ground and aerialapplication

LoupElectronics NE US Hardware /

SensorsYield & drill monitorsand various sensors

Magictec MI US HardwareAutomatic Soil Probe- a

high accuracy soilsampling system

Metos Austria Sensors iMETOS- Weather stationsMicrodrones

GmbH Germany UAV md4- rotary-wing UAVs

Micro TrakSystems MN US Hardware /

Sensors

DrillMaster—AutomaticRate Controller, Calc-An-Acre II—Speed and

area monitor, Flow- TrakII & FlowMate—Flowmonitors, hydrauliccontrol valves andmotors, and speed

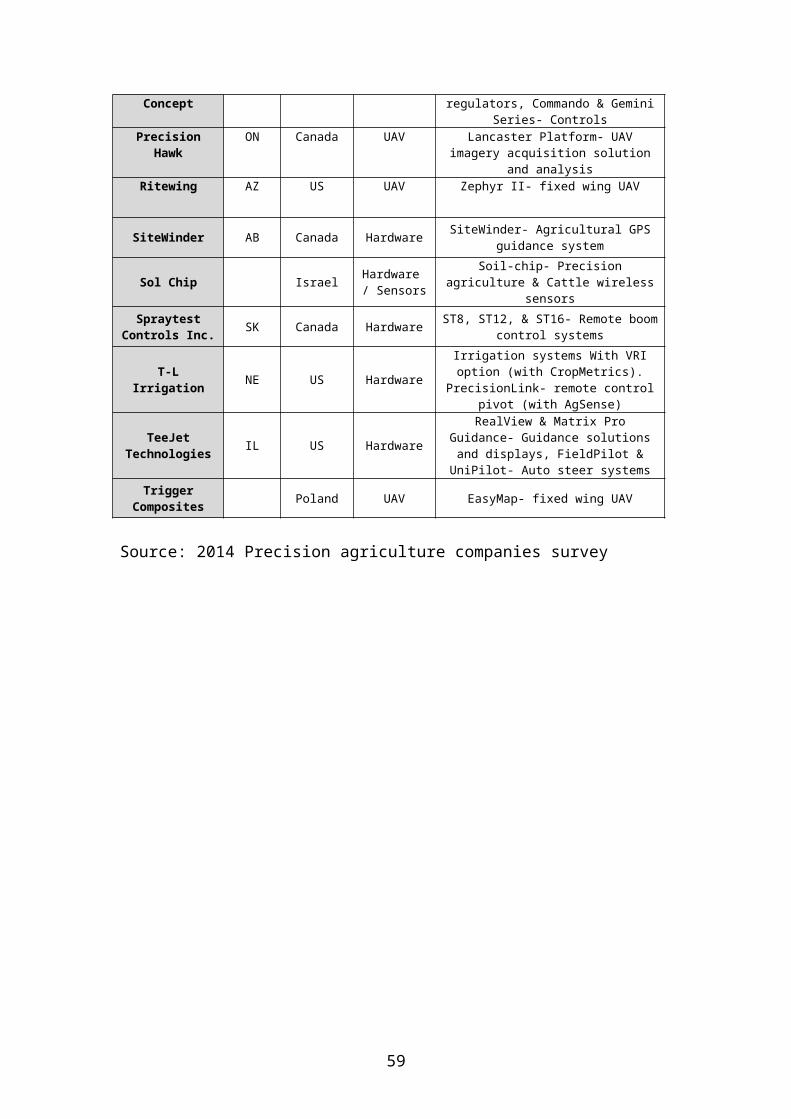

sensorsTable 7. National companies offering hardware (cont.)

Company HQState

HQCountry

Offeringtype Precision Ag Products

MyWay RTK IL US HardwareAgriculture customized RTK

system to assist in auto-steerand field mgmt.

NozzleworksInc. WA US Hardware Variable Orifice Nozzle- VRA

nozzleOptima France Hardware Genius Series- Electronic

58

Concept regulators, Commando & GeminiSeries- Controls

PrecisionHawk

ON Canada UAV Lancaster Platform- UAVimagery acquisition solution

and analysisRitewing AZ US UAV Zephyr II- fixed wing UAV

SiteWinder AB Canada Hardware SiteWinder- Agricultural GPSguidance system

Sol Chip Israel Hardware / Sensors

Soil-chip- Precisionagriculture & Cattle wireless

sensorsSpraytest

Controls Inc. SK Canada Hardware ST8, ST12, & ST16- Remote boomcontrol systems

T-LIrrigation NE US Hardware

Irrigation systems With VRIoption (with CropMetrics).

PrecisionLink- remote controlpivot (with AgSense)

TeeJetTechnologies IL US Hardware

RealView & Matrix ProGuidance- Guidance solutionsand displays, FieldPilot &UniPilot- Auto steer systems

TriggerComposites Poland UAV EasyMap- fixed wing UAV

Source: 2014 Precision agriculture companies survey

59

Multinational companies

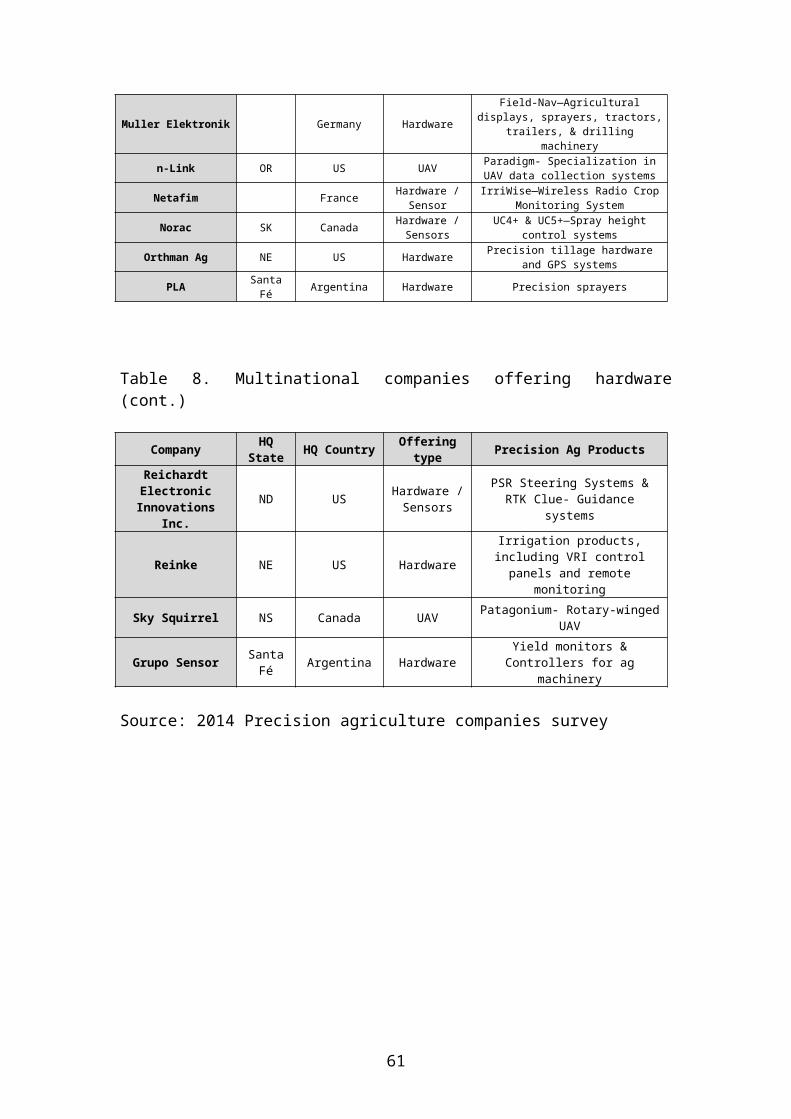

Table 8. Multinational companies offering hardware

Company HQState HQ Country Offering

type Precision Ag Products

Airware CA US UAV

osFlex Pilot—UAV customizableautopilot. In addition,

currently working on a aerialinformation platform

connectingsensors/cloud/software.

Amazone GmbH Germany Hardware

Comprehensive variety ofhardware and heavy equipment,

including precisionspreaders, tillage, rollers,

and seed drills

ARAG Italy Hardware Precision Ag sprayingproducts

Capstan KS US Hardware

Pinpoint, SharpShooter, N-Ject, Synchro- Variable Rate

Application hardware,specialized in liquid

fertilizers.

CLAAS Germany Hardware

Efficient Agriculture Systems(E.A.S.Y) products: auto-steering, guidance systems,remote monitoring and online

telematics systems.

DICKEY-johnCorporation AL US Hardware /

Sensors

Precision plantinghardware/sensors, autosteer,autosection control, groundspeed adapters and sensors

solutions.

Force IA US Hardware VRA hardware

Greentronics ON US Hardware

RiteHeight- Boom spray heighcontrol. RiteDepth- plantingdepth control. Rite yield-

yield monitors.

Hiniker MN US Hardware

Cultivators, Sprayers,Controllers, Shredders, &

Hiniker VOD- Variable orificedistributor.

IDETEC Chile UAV StarDust & Sirol- fixed wingUAV. iMK8- rotary-wing UAV.

Juniper Systems UT US Hardware /Sensors

Mirus- Harvest datacollection software. Field

Research Software- field datacollection software.

Kinze IA US Hardware

Kinze Variable Rate Planters& Currently working on and

electric multi-hybridplanter.

60

Muller Elektronik Germany Hardware

Field-Nav—Agriculturaldisplays, sprayers, tractors,

trailers, & drillingmachinery

n-Link OR US UAV Paradigm- Specialization inUAV data collection systems

Netafim France Hardware /Sensor

IrriWise—Wireless Radio CropMonitoring System

Norac SK Canada Hardware /Sensors

UC4+ & UC5+—Spray heightcontrol systems

Orthman Ag NE US Hardware Precision tillage hardwareand GPS systems

PLA SantaFé Argentina Hardware Precision sprayers

Table 8. Multinational companies offering hardware(cont.)

Company HQState HQ Country Offering

type Precision Ag Products

ReichardtElectronicInnovations

Inc.

ND US Hardware /Sensors

PSR Steering Systems &RTK Clue- Guidance

systems

Reinke NE US Hardware

Irrigation products,including VRI controlpanels and remote

monitoring

Sky Squirrel NS Canada UAV Patagonium- Rotary-wingedUAV

Grupo Sensor SantaFé Argentina Hardware

Yield monitors &Controllers for ag

machinery

Source: 2014 Precision agriculture companies survey

61

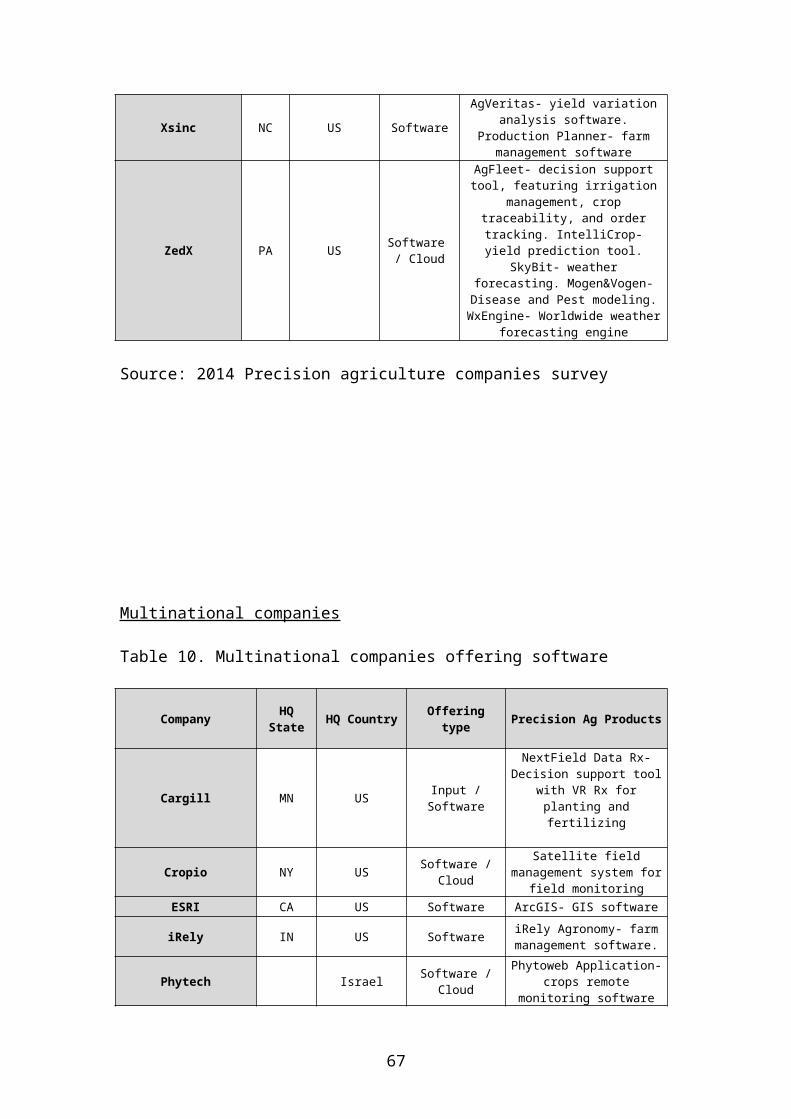

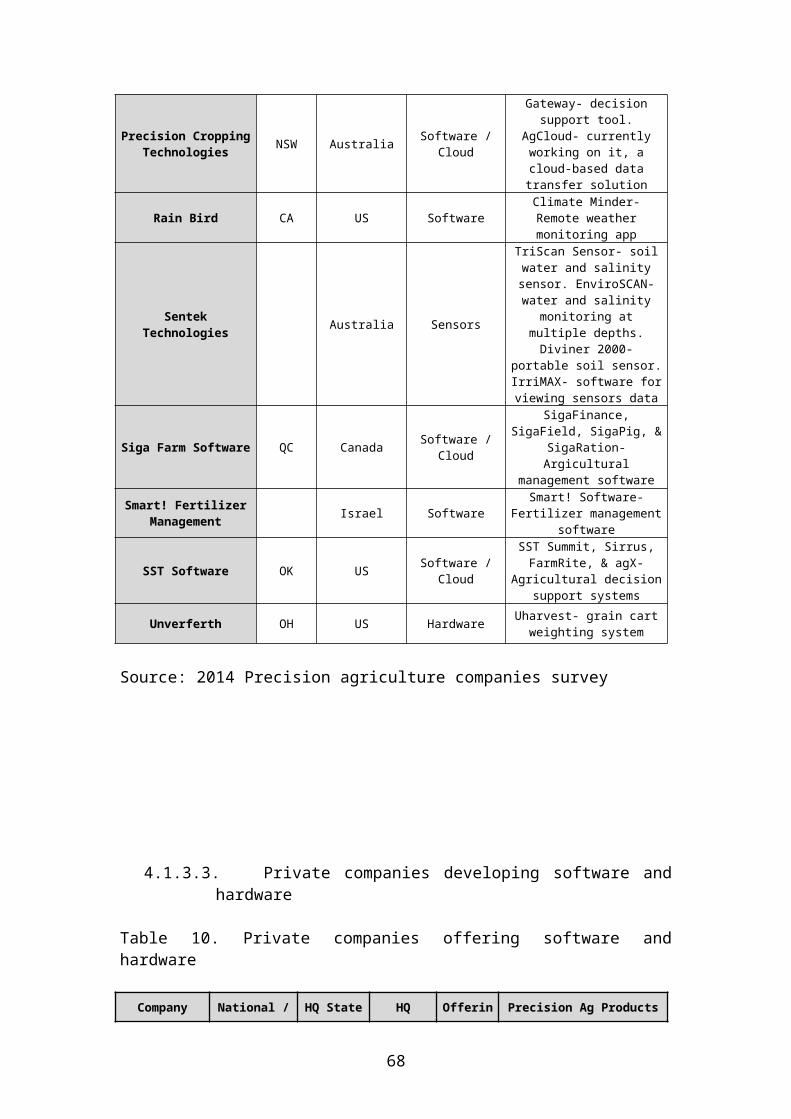

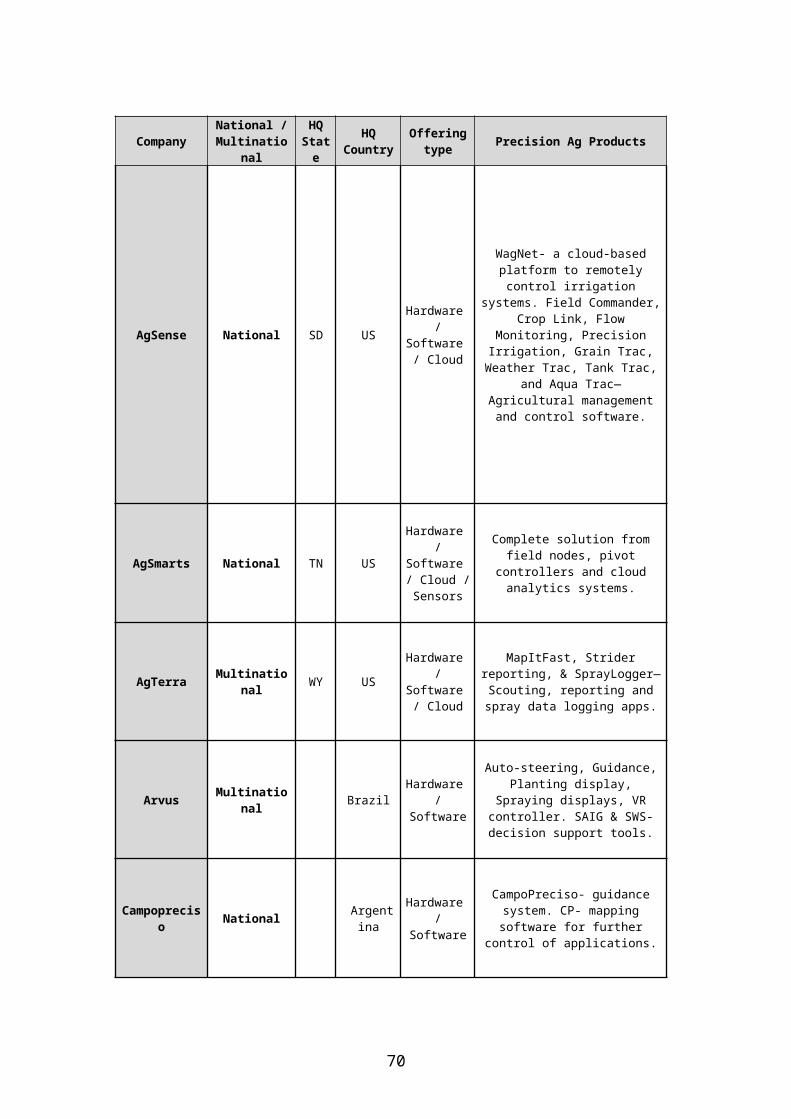

4.1.3.2. Companies specialized in software

National companies

Table 9. National companies offering software

Company HQState HQ Country Offering

type Precision Ag Products

Advanced AgSolutions IN US Software /

Cloud

Optimizer- Decision Supporttool, for creating VR

recommendations, crop scouting,and crop planning.

AdvancedReconnaissance

Corp.NY US Software /

Sensors

Airborne and ground sensorssystems. AgVu- crop analysis &

mapping tool.

Ag Connections KY US Software /Cloud

Land.db- Farm managementsoftware. Land.db Viewer-

Information display software.AgC Mobile- Mobile database

access for Land.db users. Farmby Phone- Remote repportingtool. Map.db- field mapping

application.

62

Ag Integrated PA US Software /Cloud

Onsite App- collection of as-applied and yield files, aswell as prescription filestransfer to major OEMs.

AgData Autralia QLD Australia Software /Cloud

Phoenix Production Software—Suite of modules for

agribusiness management.Phoenix Live—Cloud storagesystem. Phoenix Financials-financial management software

for farmers.

AgDNA QLD Australia Software /Cloud

Mobile Farm Management servicesincluding mobile record

keeping, GPS mapping, Scoutingobservations, Fleet Tracking

AgNition ON Canada Software /Cloud

ScoutDoc—Mobile field scoutingmobile application

Agrian CA US SoftwareAdvisor, Grower, Applicator,Retail and Mobile- Decision

Support Tools.

AgriApps South Africa Software /Cloud

Currently working on FleetManager- a fleet management

software

AgriData ND US SoftwareSurety Online Mapping—Mappingsoftware (with FSA, soil and

topography maps).

Agri-Trend AB Canada Software /Cloud

AgriData- a cloud-basedsolution for field processes

data storage.

AgriculturalInformatics IL US Software It's a startup providing data

for developers (via APIs).

AgriSolutions IL US SoftwareAgManager- A financial

management system. AgIQ- dataaccess software

Agri-vision MO US SoftwareAgVision Grain Software-Accounting and inventory

management suite.

AgSmart UK Software /Cloud

Cloud-based services. Datareports from UK farms. Imagery

for UK.

AgSquared NY US Software /Cloud

AgSquared—Field planning,management and record keepingsoftware for small farms.

Table 9. National companies offering software (cont.)

Company HQState HQ Country Offering

type Precision Ag Products

AgSync IN US Software /Cloud

AgriSite- Scouting application.AgSync Logistics- logisticsoftware. AgSync Operator-employees tracking app.

AgWorks IA US Software /Cloud

AgOS software- featuringscouting, compliancy, mapping,crop planning and precision

63

agronomy tool (w/ VR Rxincluded).

Appareo Hardware /Software

Wireless Blockage Monitor-blockage monitoring system forair-seeding implements. ActiveDepth Controller- for sugar beetharvest. Custom Ag Solutions

aWhere CO US Software /Cloud

aWhere Platform- softwareincorporating weather, long-term

climate scenarios, markets,trials and global research data.

CrescoAg TN US Software Currently working on a suite forfarm data management

Conservis MN US Software /Cloud

Conservis- Farm managementsoftware

Crop DataManagementServices

CA US Software