Post-Keynesian Theories of the Firm under Financialization

22

1 Post-Keynesian Theories of the Firm under Financialization Thomas DALLERY * Université de Lille 1 – Clersé (CNRS) (Second draft of a paper initially presented at the workshop “Financialization: Post- Keynesian Approaches” in Lille, April 2008). Abstract : Financialization is studied here from a microeconomic viewpoint. Following Stockhammer (2004a), the theory of the firm is amended by introducing agency problems and class analysis between shareholders and managers. We propose two alternative configurations: the first one incorporates financialization as a constraint for a managerial firm, whereas the second one discusses shareholders’ interests and integrates it as an objective in itself for a finance- dominated firm. Our conclusions underline finance-oppressed accumulation, financial fragility and macroeconomic instability. Keywords: financialization, theory of the firm, Post-Keynesian economics, investment JEL Classification: D21, E12, G30 * Cité Scientifique, Faculté des Sciences Economiques et Sociales, bâtiment SH2, 59655 Villeneuve d’Ascq cedex, France. E-mail : [email protected]

-

Upload

univ-littoral -

Category

Documents

-

view

0 -

download

0

Transcript of Post-Keynesian Theories of the Firm under Financialization

1

Post-Keynesian Theories of the Firm under Financialization

Thomas DALLERY∗

Université de Lille 1 – Clersé (CNRS)

(Second draft of a paper initially presented at the workshop “Financialization: Post-Keynesian Approaches” in Lille, April 2008).

Abstract:

Financialization is studied here from a microeconomic viewpoint. Following Stockhammer (2004a), the theory of the firm is amended by introducing agency problems and class analysis between shareholders and managers. We propose two alternative configurations: the first one incorporates financialization as a constraint for a managerial firm, whereas the second one discusses shareholders’ interests and integrates it as an objective in itself for a finance-dominated firm. Our conclusions underline finance-oppressed accumulation, financial fragility and macroeconomic instability. Keywords: financialization, theory of the firm, Post-Keynesian economics, investment JEL Classification: D21, E12, G30

∗ Cité Scientifique, Faculté des Sciences Economiques et Sociales, bâtiment SH2, 59655 Villeneuve d’Ascq cedex, France. E-mail: [email protected]

2

I – Introduction

The aim of this contribution is to question to which extent financialization modifies the Post-Keynesian theory of the firm. Lavoie (1992) offers a synthesis of firm’s representation among Post-Keynesians. Nevertheless, financialization is tackled as a minor issue, which does not affect the core of the theory of the firm. As far as we know, Stockhammer (2004a) and Crotty (1990, 1992) are the only Post-Keynesians who propose a framework for the analysis of financialization’s microeconomic implications.

At the macroeconomic level, much has been done to deal with changes involved by financialization. Most of this literature put forward the existence’s possibility of a broadly defined finance-led growth regime1. If it seems to be some dissensions about which channel is appropriate to capture financialization’s effects, there are more agreements on the opportunity to finance-pushed growth. When looking at the three basic components of aggregate demand – investment, consumption and public spending2 – we could expect contrasted results about theoretical impacts of financialization on these components3. First, financialization may be assumed to depress accumulation4, but it may also be assumed that financialization fosters investment thanks to a profitability increase that encourages firms to invest5. Second, financialization is also assumed to potentially boost consumption through either a credit-fuelled consumption, or a wealth effect (Boyer [2000], Maki et Palumbo [1990]), or the real consumption of financial enrichment on stock market6, or the consumption of increased distributed dividends (Cordonnier [2006]). Once again, one can find the opposite, traditionally Keynesian arguments according to which financialization would slow down consumption, through the channel of wage moderation. Third, and probably the most undisputed point, public spending is expected to be drown out by financialization and the advocators of state withdrawal. Putting all these potential effects end to end, the conclusions of financialization literature often assess the possibility of a finance-led growth regime depending on which of the positive and negative effects overcome the other ones. Indeed, some stylized facts about OECD countries over the last thirty years tend to recognize a declining trend in capital investment, but it is also empirically recorded that consumption fed by finance keeps being the last support for a low growth process, which is punctually helped by the recovery of other components of aggregate demand within cyclical fluctuations. It is quite astonishing that a so prolific literature never came to interrogate the microeconomic implications of financialization. We relieve Stockhammer’s attempt to rebuild the Post-Keynesian theory of the firm in the new context of financialization. Our study of the Post-Keynesian theory of the firm will especially focus on the financialization’s implications on investment decisions within the firm. We let aside macroeconomic considerations about finance-driven, credit-fuelled consumption or downsized public spending. Before setting up a macroeconomic theory of accumulation under financialization, we want to establish the

1 Finance-led growth comes from Boyer (2000) and it is a larger concept than the concept of profit-led growth one can find in Bhaduri et Marglin (1990). 2 We do not study here financialization effects on international exchanges. 3 See Stockhammer (2007) for complete stylised facts on these different components. 4 See Stockhammer (2005-2006), who presents both microeconomic and macroeconomic implications, and concludes to a decline in investment due to financialization. See also Hein et Van Treeck (2007). 5 It refers to the specification of investment function in Bhaduri et Marglin (1990). 6 Bhaduri et al. (2006) argue that at the macroeconomic level, financial wealth cannot be converted to real wealth because the previous increase in equity’s prices would vanish if the prevailing winds turn to “sell” on the stock market.

3

microeconomic theory of how financialization concretely affects the accumulation process within the firm. We do not want to choose a specific and definitive representation of corporate governance and agency problems between managers and shareholders7. So we will expose the two extreme cases of the shareholder-manager power struggle. First, we present the case for a managerial firm with strong autonomy of managers over shareholders. Second, we present the case for fully-dominated managers in a shareholder-ruled firm. Following Stockhammer (2004a) and the works of James Crotty in several contributions (Crotty, 1990, 1992 and Crotty and Goldstein, 1992), we try to put further here the analysis of what the shareholders’ and managers’ respective logic is, and of how it affects the accumulation decision of the firm. The contribution is structured as follows. Section Two presents the Post-Keynesian theory of the firm and the framework proposed by Stockhammer (2004a). Section Three offers an integration of financialization within the Post-Keynesian theory of the firm where managers keep the effective control of firms’ objectives while facing an additional constraint due to shareholders’ pressure. This would be consistent with a Galbraithian theory of the firm, and it would be very similar with the representation supplied by Lavoie (1992). Section Four outlines the opposite case in terms of power struggle. Firms are managed in the exclusive sense of shareholders’ interest pursuit with a purely passive manager. Section Five concludes on the potential macroeconomic implications of the microeconomic theorizing of financialization. II – Accumulation decision inside the Post-Keynesian theory of the firm This Section is based on diverse contributions of Stockhammer, who addresses the Post-Keynesian theory of the firm from a financialization’s outlook8. His work tries to improve the Post-Keynesian theory of the firm one can find in Lavoie (1992), by introducing financialization concerns more broadly. In this Section, we first present the initial spirit of the Post-Keynesian theory of the firm. Then, we present the general framework. Finally, we survey financialization as introduced by Stockhammer. II-1. The general framework: a Galbraithian theory of the firm

Lavoie (1992) develops a seminal presentation of the Post-Keynesian theory of the firm, originally presented by Wood (1975). Post-Keynesians are not interested in the study of small firms in a perfectly competitive market, and they prefer the study of big businesses on oligopolistic markets. Firms are price-maker in Post-Keynesian economics. Prices are set up in long term perspectives, and they are supposed to allow firms to achieve their objectives (in terms of profitability and market share) through a difficult balance seeking between making high margins to finance investment and making low margins to capture demand9. In Post-Keynesian economics, firms are not assumed to maximize profits, as it is clear in Lavoie (1992, p. 105):

7 Two reasons for this choice: first, the empirical evidence cannot conclude on this point because managers’ autonomy is not observable, and second, managers’ autonomy may be different in different firms depending on the structure and concentration of shareholding. 8 See Stockhammer (2003), (2004a), (2004b) or (2005-6). 9 Firms increase their addressed demand either at the expense of competitors or as an outcome of a growing market.

4

“The standard critique of the neoclassical theory of the firm is that profit maximization is not possible because of the lack of pertinent knowledge due to an uncertain environment. Profit maximization is then replaced by profit satisficing. Firms are assumed to set themselves threshold levels of profits; that is, minimum levels of profits or of rates of return.”

Furthermore, profits are not the ultimate objective for firms. Profits are pursued for the achievement of the final objective which is firm’s survival and firm’s power increase. Firms strive for ensuring their own existence. To survive in a competitive world, one has to be powerful and to monitor one’s environment. The best way to do this remains growth. By means of growth objectives, firms spread their sphere of influence and they reduce uncertainty which weighs on their future. Profits are a prerequisite for growth because they release the financial constraint on accumulation. Wood (1975) linked the accumulation decision of the firm to its pricing decision through the determination of the profit margin. In this frame, firms have a profit margin target which permits to grow at a certain speed, provided the retention ratio and the debt-to-capital ratio judged safe. Firms seek profits because it will allow them to grow10. There is a bridge often built between this view of the firm and the view developed by Galbraith (1967). It is commonly admitted since the seminal works of Berle et Means (1933) that firms are places of conflicts between managers in charge of effective directions and shareholders who effective own firms. These conflicts between control and property have already given rise to a huge literature related to principal-agent problems or more recently to debates about the new rules of corporate governance. Lavoie (1992, p. 107) neglects the capacity of shareholders to influence the strategic orientation of firms:

“In the Galbraithian and Post-Keynesian firm, shareholders play a purely passive role.”

This conception is inherited from a specific institutional configuration where shareholders were dispersed. They were not in such a place that they could put forward their interest and reclaim their demand to be fulfilled. It was the era of the technostructure described by Galbraith. Firms were managed in the spirit of growth seeking: control overcame property. This theory of the firm seems to have stopped in the nearly eighties. Since then, financialization has changed this rule of the game, and nowadays shareholders are able to reclaim their demand to be fulfilled. This point of view is defended by some authors for whom capitalism has evolved from a managerial capitalism to a patrimonial one11. If the theory of the firm by Lavoie (1992) was a priori perfectly relevant with the managerial capitalism, it seems that major changes need to be incorporated into it when trying to fit better the evolution of institutional configurations. II-2. The two pillars of the model of accumulation

The model presented here is a very basic model. It assumes away many complications. It is devoted to clearly expose the question at stake: how investment decisions are made. The model insists on two limits to investment plans. The first limit is a finance constraint on

10 Lavoie (1992, p. 106) tells us that: “Put briefly, growth is the objective, and profits are the means to realize this objective”. In the new institutional configuration, it is often assessed that profits are no longer a mean to an end, but they become an end in itself. 11 See Aglietta (1999) for example.

5

investment, and the second one is a limit on the profitability of investment. The key structure of the Post-Keynesian theory of the firm can be found in Lavoie (1992). It can be pedagogically sketched out within a simple two-curve diagram which links profit rates and accumulation rates. The first component of the traditional theory of the firm, the finance frontier, brings back to a finance constraint curve. It means that profits are a prerequisite for firm desiring to invest. Profits are needed because it is a mean to internally finance investment, and as far as external finance is concerned, profits are a signal for bankers to grant loans, and also a tool necessary to raise more funds when new equities are issued. The more profits you made, the more investment you will be able to undertake. Here is an expression of this finance constraint close to Lavoie (1992, p. 111). Investment is lower or just equal to the amount of internal finance plus the amount of external finance:

( ) ( )llssllss KiKiKiKiI

EFIFI

−−Π+−−Π≤⇔+≤

ρ (1)

The first parenthesis gives the amount of investment financed by retained earnings, which are profits minus dividend payments to shareholders and/or interest payments to loaners. The second parenthesis, that is external finance, is a multiple of retained earnings accordingly to Kalecki’s principle of increasing risk12. Building on this, we could formulate a linear expression of the finance frontier that gives the necessary profit rate r which allows the firm to grow at the rate g. But, here, we will follow a different path, which is more faithful to the pioneered work of Wood (1975). Originally, Wood (1975) expressed the finance frontier in terms of the minimum profit margin necessary to finance any given investment pace. Starting with the equality between sources of funds and uses of funds, we simply assert that the individual firm has to decide its productive investment and its financial investment spendings, given its retained earnings and the funds stemming from new net borrowings and new net share issues:

IxIIxIxiDs

iDsIxIIxIxiD

fdsf

ffds

+=++−Π⇔

−Π−++=++−Π

)(

))(1()( (2)

with sf being the retention ratio, ∏ firm’s profits, i the interest rate, D the stock of debt, I physical investment. In the previous equation, xs, xd and xf stand for respectively new net share issues, new net debt and financial investment, each time as a ratio of physical investment. We can rearrange this equation in order to have the minimum profit margin (π) necessary to finance any growth rate of the capital stock (g):

idu

v

s

xxx

u

gv

K

Di

Y

Y

Y

K

s

xxx

Y

Y

Y

K

K

I

Y

f

dsf

f

dsf

+

−−+

=⇔

+

−−+

=Π=

1

1 *

*

*

*

π

π

(3)

12 The more profits are made by the firm, the more money the firm will be able to receive from banks. Profits are a signal that reduces their risk to grant money to this firm.

6

where v is the ratio between the capital stock and the full-capacity output, u is the rate of utilization of the firm’s productive capacity and d is the ratio between the amount of debt and the capital stock. The more the firm desires to invest, the higher the profit margin necessary to finance its accumulation goal. Moreover, the firm will need a high profit margin if it invests a lot on financial markets, if the interest rate is high or if the debt-to-capital ratio is high. Conversely, the firm will be able to secure its investment more easily, if it has a high retention ratio, if it finances an important part of investment either through new net borrowings or new net share issues. The profit margin is a key determinant of the pricing policy for the firm. Since the Post-Keynesian firm is supposed to set prices according to a cost-plus pricing procedure, one can derive the general formula for the mark-up pricing behavior of the firm:

µw

mp )1( += (4)

where m is the mark-up rate, w labor costs and µ labor productivity. In the absence of overhead labor, it is possible to draw a simple relation between the mark-up rate and the profit margin:

m

m

+=

1π (5)

It follows that the finance frontier can be associated with the pricing behavior of the firm. It gives the minimum profit margin necessary to secure investment, but in the same time, it is incorporated into pricing decisions. From this perspective, the need to secure investment with high margins and the need to boost sales with low prices reappear conflictive. In the remainder of the paper, we will express the finance frontier in terms of profit rates in order to place it in the same plan as the expansion frontier, so that the finance frontier in (3) becomes:

ids

xxxgr

f

dsf +

−−+=

1 (6)

The finance constraint now gives the minimum rate of profit necessary to implement any rate of accumulation. Graphically, on the right of the finance constraint, one can find the unsustainable area, where firms are going to face a drying up of means to externally finance investment (see Figure 1). It can be suggested that firms in these positions will be forced to sell liquid financial assets to balance their spendings: xf becomes negative (Wood, 1975). On the contrary, firms located on the left side preserve themselves finance opportunities for additional spendings. The second curve of the theory of the firm is called by Lavoie (1992) the expansion frontier13. It gives the maximum level of profitability that can be reached for each rate of investment. There is a concave relation between accumulation and profit expectations. When firm grows, there are positive effects on profitability and negative effects due to the difficulties to assimilate profitable effects at a larger scale14. At the end, it emerges an increasing relation 13 Wood (1975) called it the opportunity frontier. 14 It relies on a Penrosean effect. As it is clearly mentioned in Lavoie (1992, p. 115): “There are no managerial diseconomies of scale, but there are increasing costs to growth. The negative segment of the expansion frontier […] is thus due in part to the inherent difficulties of management in coping efficiently with change and expansion”. More convincingly, Wood (1975) explained this negative relationship with the need for the firm to

7

between accumulation rate and profit rate up to the accumulation rate that maximizes the foreseen profit rate, and beyond this point accumulation rate and profit rate are negatively related (see Figure 1). On the expansion frontier, firms take advantage of their investments the best they could have expected. Below this frontier, firms are in a situation of inefficiency due to the misevaluation of investments, which revealed to be less profitable than they could have been. Excess capacity and over-investment may therefore be represented by the area below the expansion frontier where the firm operates below its standard rate of utilization, with a relatively high level of potential production compared to the effective level of demand. Formally, the expansion frontier can be illustrated through the usual accounting decomposition of the profit rate:

v

u

K

Y

Y

Y

YKr

π=Π=Π=*

* (7)

On the expansion frontier, production efficiency is assured and it means that the firm operates at its standard rate of utilization with a profit margin given by the competitive advantage of the firm and influenced by the conflict with workers about wage bargaining15. What explains the shape of the expansion frontier is thus the comparative strength of contradictory forces of accumulation on the microeconomic profit margin. For low accumulation rates, the firm is able to incorporate efficiency gains thanks to the implementation of new production technologies. The increase in productivity allows the firm to improve its profit margin without raising its price (see equations 4 and 5), so that the profit rate goes up. For high accumulation rates, the firm is obliged to reduce its price and therefore its profit margin if it wants to increase its sales fast enough in order to remain at standard utilization. The position of the expansion frontier is explained by either the different rates of standard utilization or the different macroeconomic influences on the profit margin stemming from conflicts with workers or the intensity of competition on the market. Moreover, a firm with better technology benefits from a competitive advantage over its competitors, and it means that its expansion frontier will be located above the one of its competitors. This firm will be able, for each rate of accumulation, to implement a higher profit margin compared to its competitors. When combining the finance frontier with the expansion frontier, one can get the thereafter diagram, which was first exposed in a slightly different manner in Wood (1975, p. 83) and which is taken from Lavoie (1992, p.117). In a managerial capitalism, firms invest as much as allowed by the finance constraint and the realization of their profit expectations. Hence, the individual firm decides to accumulate at the rate g*, with a profit rate r* which finances and legitimates this accumulation goal. This representation of the Post-Keynesian firm in the historical context of its birth constitutes the referential work on which every further developments will be based.

reduce its profit margin if it desires to grow at a faster rate, because of market share’s competition with other firms and increasing selling costs like advertising costs. 15 Wage bargaining determines a macroeconomic component of the profit margin, and so, we will not deal with it in this paper. See Dallery et van Treeck (2008) for a more complete analysis of conflict inflation.

8

II-3. Stockhammer’s model After this presentation of the Post-Keynesian theory of the firm and its application to managerial capitalism, the second part of this Section tackles the issue of financialization within the framework proposed by Stockhammer (2004a). Stockhammer keeps many characteristics of the previous theory of the firm, and he adds a firm utility function which depends on power struggles between shareholders and managers. He assumes, for the sake of simplicity, that shareholders only target profit rate while managers are only interested in growth rate. In a second time, he builds a utility function for the firm which depends on these two objectives, and of the respective ability of each class to impose to the other one its interests as firm’s goal:

βα RIrguu ff == ),( (8)

Firm’s utility is then a function of growth rate (g) and profit rate (r) so as to take into account the two orientations desired by the two different actors of the firm. In other words, if managers were in a powerful situation towards shareholders, α would be high and firm’s policy would be based on a growth strategy. At the opposite, if shareholders were in a better position, β would be higher16 and firm’s strategy would be more profit-seeking biased. According to the evolution of power struggle between managers and shareholders, the policy conducted by firm would be more profit- or growth-oriented, that is they would be more shareholders-satisfying or managers-satisfying. In this framework, financialization leads to a change in power struggle. Starting from a situation with powerful managers and growth policies by the firm, financialization implies a change in power relation in support of shareholders and profit-seeking policies (increase in β). Shareholders are now in a situation that allows their interests to be satisfied. Graphically, the

16 α would be lower because here it is assumed that α = 1 – β, that is no place is made for the other stakeholders (workers for example) to influence firm’s orientations.

g*

Expansion frontier

Finance frontier

Accumulation rate (g)

Profit rate (r)

Figure 1: The representation of the traditional Post-Keynesian firm

r*

9

firm’s utility function is moving upward (see Figure 2). If shareholders became powerful, they would be able to force managers to implement g** , the accumulation rate maximizing the profit rate. Due to the balance of power between the two classes, the firm’s investment decision will be located somewhere between g* and g** . The more powerful the shareholders are, the nearer g** the firm’s investment decision will be.

This integration of financialization leads to a decline in accumulation by construction, since shareholders are only interested in profitability at the expense of growth. A reinforcement of shareholders’ power exhibits unavoidably a drop in accumulation. For us, it seems that this is more an assumption than a result. Actually, the drop in accumulation appears to be the outcome one has to arrive at. The theory is built to produce this outcome, because what is at stake is the macroeconomic study and one has to match with some stylized facts about accumulation’s slowdown. Microeconomic theory arises in order to fit macroeconomic trends. Instead of going from macroeconomic laws to microeconomic theorizing, we prefer to build first a microeconomic theory of financialization, and then see what happen at the macroeconomic level when applying the theoretical framework. Stockhammer takes for granted that shareholders are only interested in profitability maximization. Yet, shareholders’ objectives are no longer so obvious for us. It seems that the trade-off is not between profits and investment, or between profit rate and accumulation rate. The trade-off under study may be one between today’s profitability and tomorrow’s profitability. Considering this trade-off brings back to the puzzling question of shareholders’ preferences in terms of accumulation, because tomorrow’s profitability depends on today’s accumulation (see Section IV for more). In the rest of this contribution, we try to develop two alternative ways to introduce financialization into the Post-Keynesian theory of the firm. The first one interrogates the theoretical effects of financialization if managers keep the direction of the firm and face an additional constraint through shareholders’ demand. The second one deals with the opposite case where shareholders run the firm in their only interests. We do not want to assess the effective division of power between shareholders and managers. We simply hint at the possible theoretical effects on accumulation of two different cases: the case for semi-autonomous managers, and the case for total domination of shareholders.

r**

g** g* Accumulation rate (g)

Profit rate (r)

uf1 : utility function for managerial preferences

Figure 2: The Post-Keynesian firm under financialization (Stockhammer’s case)

r*

uf2 : utility function for shareholders’ preferences

10

III – Financialization and the persistence of the Galbraithian firm This Third Section studies the impact of financialization in the Galbraithian firm, which is a firm in which managers still govern the strategic orientations. For the purpose of this Section, financialization will be seen as a constraint on firm’s orientation. Managers do not want to inflect their policy in support of shareholders’ interests, but they have to run their firm by taking into account this new constraint. This configuration is quite different from the one to be analyzed further in this article where shareholders will reign on firm’s policy. We first interpret financialization as a new constraint, and in the next Section we will take it as the emergence of a new objective in itself. III-1. Financialization and the increase in dividend payments

Financialization has numerous implications for the firm. Looking back at (2), financialization implies both changes in the sources of funds and changes in the uses of funds. Due to the new financial environment, firms may face an increase pressure to distribute dividends (sf drops), an injunction not to issue new equities (xs drops) in order to preserve shares’ value on the market, an increase in indebtedness (d) consecutive to debt-financing spendings (increase in xd). Amongst all these potential effects, we will focus here, essentially, on the increase in dividends payments.

Financialization as a constraint brings back to firm’s finance structure. Shareholder

value orientation implies that dividends payments increase, and the firm has to experience a lower retention ratio (see equation 3). This new convention17 arises from the new institutional context. In order to wheedle shareholders and to keep them quiet, managers have to distribute more dividends. This tendency is an undoubted fact on financialization. The ratio dividend payments divided by profits has undergone a huge surge for the last twenty years. According to Cordonnier (2006), in France, the ratio between dividends payments and net operating surplus18 has jumped from around 30% until the end of the eighties to more than 80% at the very end of the nineties. For the USA, the boom was similar but it came earlier, since the ratio between dividends payments and after-tax profits went from nearly 40% during the 1960-1980 period to an average of 70% on the period from 1982 to 2003. Cordonnier (2006) also witnesses a puzzling case where this ratio became superior to unity in the very first years of the 2000s in the United States. One has to bear in mind that in several cases firms had to borrow funds in order to distribute dividends. More widely, Crotty (2005, p. 99) shows that total payments to financial markets19 as a percentage of cash flows for non-financial companies strongly increased since the beginning of the eighties. Whereas these payments as a percentage of cash flows used to fluctuate around 25-30% from the end of the Second World War to the end of the seventies, this ratio has undergone an outstanding increase, since it has often reached 60% during the next period (1980-2001). These income redistributions led to a new sharing of wealth in support of profits, and especially of rentiers (see van Treeck

17 As it has been widely said, dividends payments are a “convention” for J. Robinson (1964, p. 38). 18 It can be associated to (1 – sf) in our framework. 19 Total payments to financial markets are the sum of net interest, net dividends and net share purchases. This measurement of financial redistribution of income deals with dividends payments, but it also takes into account share buybacks by firms. Crotty (2005) also shows that non financial companies decided to deeply buyback their own shares (xs becomes negative in the model).

11

[2007a, pp. 4-5]). In France, the profit share in value added of the business sector20 goes from 30.2% between 1975 and 1984 to 38.3% between 1985 and nowadays. In the same time, the rentiers’ income share in GDP goes from 6.24% on the period 1970-1979 to more than 20% between 1990 and 1999.

Managers have to face this increased shareholders’ pressure. In particular, they have to distribute more dividends if they want to preserve their autonomy in an environment that can threaten their decision-making, and even their job (Crotty, 1990). Indeed, disappointed shareholders may lead financial raids in order to settle a new management more willing to provide them for their demands. This threat leads managers to accept the increase payments of dividends. III-2. Financialization as a constraint for managers

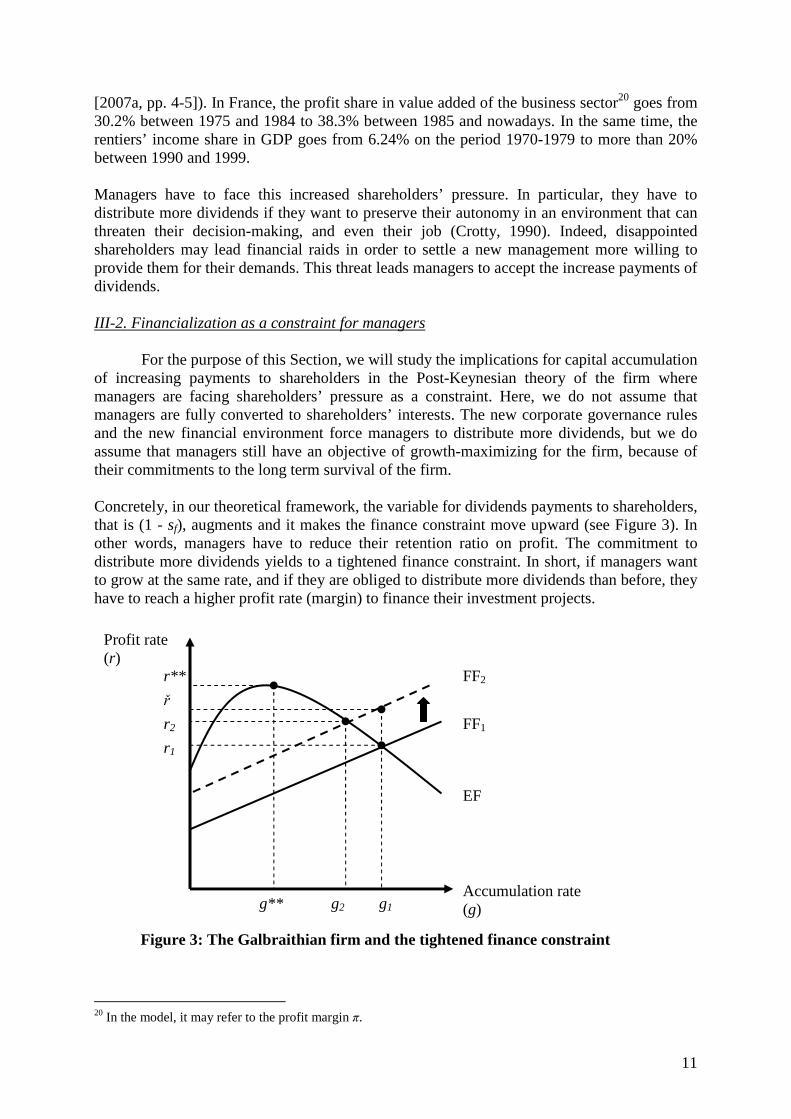

For the purpose of this Section, we will study the implications for capital accumulation of increasing payments to shareholders in the Post-Keynesian theory of the firm where managers are facing shareholders’ pressure as a constraint. Here, we do not assume that managers are fully converted to shareholders’ interests. The new corporate governance rules and the new financial environment force managers to distribute more dividends, but we do assume that managers still have an objective of growth-maximizing for the firm, because of their commitments to the long term survival of the firm. Concretely, in our theoretical framework, the variable for dividends payments to shareholders, that is (1 - sf), augments and it makes the finance constraint move upward (see Figure 3). In other words, managers have to reduce their retention ratio on profit. The commitment to distribute more dividends yields to a tightened finance constraint. In short, if managers want to grow at the same rate, and if they are obliged to distribute more dividends than before, they have to reach a higher profit rate (margin) to finance their investment projects.

20 In the model, it may refer to the profit margin π.

ř

r1

FF2 r**

g** g1 Accumulation rate (g)

Profit rate (r)

Figure 3: The Galbraithian firm and the tightened finance constraint

EF

FF1 r2

g2

12

In this case, managers do want to go on growing at a rate g1. But for this accumulation rate, the profit rate allowing the firm to get finance for investment goes from r1 to ř, due to the enforcement of the finance constraint. The problem is that this rate of profit couldn’t be reached since it is beyond the expansion frontier21. In brief, the demand for an increased profit margin to finance investment enters in conflict with the possibility for the firm to sell its product on a competitive market with an increase in prices. The new profit rate necessary to finance investment exceeds firm’s productive efficiency. Even though managers are reluctant to modify their investment policy inserted into long term perspectives, they have to resign themselves to change their mind. Managers maximize growth under a harsher finance constraint. In other words, they choose to locate their policy at the intersection of the new finance frontier and the expansion one. Therefore the new policy run by managers will induce lower accumulation (g2) and it will still require higher profit rate (r2). If one desires to reach it, this higher required profit rate (r2) implies either a higher mark-up rate on prices, or a drop in costs, and/or an increase in the utilization of productive capacity (see equation 7). This way of theorizing financialization conducts just as before to a decline in accumulation. But this time, this is a constraint’s slackness, while it was previously a desired decline in Stockhammer (2004a). Facing the new financial constraint of increased dividend distribution, managers have been obliged to reduce their growth objective in order to preserve their decision-making autonomy. A temporary solution may have been to sell financial assets (xf becomes negative in equation 6) in order to release the finance constraint. But, this solution is not sustainable, and the coming back downward of the finance frontier would have been only temporary. III-3. Risk transfers as a solution

For now, the reasoning was made at a constant expansion frontier. This assumption could be release if we authorize managers to reorganize their firm, so as to become more efficient and to improve the possibility of opportunity expansion. Two types of policies may lead to an increase in the expansion frontier, correspondingly to the increase of the profit rate either through an increase in the profit margin, or through an increase in the utilization rate, each time for all rate of accumulation. The first type of policy refers to the transfer of shareholders’ pressure from managers to workers. The second type of policy implies an acceptation by managers of an increased real fragility: they transfer a financial risk into a real risk (Dallery et van Treeck, 2008). Under the first discourse, one can find productivity’s policies or wage pressure. According to this hypothesis, expansion frontier can shift upward, so that managers may keep their first accumulation policy unchanged (see Figure 4). This story brings back to risk transfer theory22. Facing a new constraint, managers try to transfer the weight of change on workers, so that shareholders’ pressure appears as the workers’ burden before being the managers’ problem. Here, labor market flexibility and financialization could be linked within the theory of the firm. The increased distribution of dividends prevent managers to lead the accumulation policy they previously decided, but by means of flexibility managers succeed in realizing higher profit rate allowing them to finance their initial accumulation goal. In practice, managers will try to increase their profit margin at the expense of labor costs, thanks to externalization or productivity enhancing working conditions23. This increase in the profit

21 See Cordonnier et Van de Velde (2008) for a study of the “profitability’s glass ceiling”. 22 Cf. Aglietta et Réberioux (2004). 23 This profit margin increase is done for a given level of prices, in order not to loose market shares.

13

margin with constant prices is only possible under the conditions of either productivity gains and/or wage reductions (see equations 4 and 5)24. The second mean for managers to improve their expansion frontier is associated with an increased real fragility. Referring to the decomposition of the profit rate, we can notice three different ways of increasing the profit rate: it necessarily comes either from a higher profit margin, or an increased utilization rate, or a better capital coefficient, or a combination of the three ones. When facing shareholders’ claims, managers may try to provide this improved profit rate thanks to a more intensive use of their productive capacities. It means that managers will accept to operate above their desired rate of capacity utilization, if it allows them to reach a better profit rate. Managers have to trade-off between shareholders’ profitability target and their own utilization rate target (Dallery et van Treeck, 2008). Consequently, the firm will be exposed to an increased risk of default in case of an unexpected rise in demand. In turn, it could lead to a loss in the firm’s market shares. This result seems consistent with the profitability-safety trade-off used by Crotty (1990, 1992) or Crotty and Goldstein (1992). But here, what is at stake is not a financial security. Managers are not involved in an autonomy-seeking policy. They do not try only to meet their financial commitments to creditors and shareholders in order to preserve the autonomy of their decision making. At the difference of Crotty’s trade-off, managers also try to balance their real security with their growth objective and the profitability requirements stemming from shareholders. All these different objectives cannot be met in the same time, and managers will choose which one of these different objectives should prevail and which one has to be violated. Among these objectives, we assume that managers will choose their growth objective, and they will also reach the shareholders’ requirements through the increased real fragility.

24 At this point, it is worth noticing that this way of thinking is valid only at the microeconomic level. When all the firms implement this type of policy by pressuring their workers, the macroeconomic effects of increased workers’ insecurity and constrained demand are no longer certain compared to the expected benefits of firms’ reorganizations. Therefore it is difficult to predict the moving of the expansion frontier. The moral lesson of this story is that an individual firm may fully benefit from flexibility, but at the condition that the other firms do not apply these new organizational methods.

ř

r1

FF2 r**

g** g1 Accumulation rate (g)

Profit rate (r)

Figure 4: Risk transfers inside the Galbraithian firm

EF1

FF1 r2

g2

EF2

14

This last story explains a different case of a Post-Keynesian firm under financialization. Accumulation does not slow down, profitability increases, but the price to be paid is a higher pauperization of workers and/or a production process in tense stream with an increased risk of default to demand. IV – Financialization and the shareholders-ruled firm In this Section, we explore financialization’s implications for firm’s orientation regarding capital accumulation, if the firm is managed in the exclusive interests of shareholders. The former Section studied the case of Galbraithian firms in which managers keep being at the head of strategic orientations, in spite of financialization and moving frontiers. Shareholder value orientation was only a constraint, but here it will become a prism guiding firm’s orientation. Whatever shareholders effectively manage firms or succeed in imposing their objectives as managers’ ones25, the purpose of this Section is to see what would happen if firms are ruled in shareholders’ exclusive interests. Financialization is now seen as a move in objectives for the firm, not as changing constraints. But we now have to wonder what precisely shareholders’ objectives are, and what the implications for investment are. IV-1. Profit rate maximization or cash flow maximization?

Stockhammer (2004a) assumes for the sake of simplicity that shareholders are motivated by profits seeking only. Thanks to this abstraction, Stockhammer is capable of drawing his diagram and to model shareholder value orientation through a move towards profitability. In this context, a shareholders-ruled firm would undertake the accumulation rate which would generate the maximum rate of profit. Coming back to Figure 2, it means that a shareholders-ruled firm would invest so as to grow at a rate g** , hoping for a profit rate r** . Shareholders only care about the expansion frontier, and they choose the maximum on it. They are not interested in the finance frontier, and the financial structure of the firm. But, in reality, it does not seem to work that way. Shareholders express claims regarding the financial structure of the firm. Concretely, they will encourage a reduction of new equity issuance (xs drops in equation 3) or they will advocate indebtedness beyond cautious limits to permit leverage effect (increase in both xd and d equation in 3). Hence, viewing shareholders only as profit-seekers seems to us a too strong hypothesis. In order to match precisely what could be the objectives of a shareholders-ruled firm, one has to enter in a sort of role-playing by adopting shareholders’ viewpoint. One has to establish what defines the best decision to be made in order to meet one’s interests. From this, it arises that shareholders are not interested in profit maximization as assumed by Stockhammer (2004a). A first approach to shareholders’ objectives assumes that shareholders are rather interested in cash-flows maximizing. Actually, shareholders own the firm, the firm owns the productive capital, but shareholders do not own the productive capital. So, shareholders do not want to maximize the whole amount of profits, and instead they want to maximize the amount of profits they could demand back, that is to say profits minus interest payments to 25 The specific class nature of managers, as well as the nature of their objectives and the ability to impose them, vanishes in this Section.

15

creditors and minus self-financed investment. Moreover, as already noticed, shareholders advocate firm’s indebtedness so as to benefit from leverage effect, and increase their profitability. One can argue that this objectives’ discrepancy refers to the discrepancy between Return On Capital Engaged (ROCE) and Return On Equity (ROE)26.

DK

Dirr

DK

iDROE

KrROCE

−−+=

−−Π=⇔

Π==

)( (9)

Here, it is clear that the firm may increase the financial profitability for its shareholders if it is willing to increase debt. As long as there is a positive gap between the economic profit rate and the interest rate, shareholders could encourage the firm to go more and more into debt, in order to benefit from leverage effects which increase the financial profitability. Indebtedness does not only play through the numerator, but it is also at stake on the denominator. Indeed, shareholders may advocate, for a given capital stock, a reduction of owners’ equity (total capital minus total debt) thanks to share buybacks (negative xs in equation 3). It means that increasing the debt-to-capital ratio will reduce the denominator of (9) and augments financial profitability. Whereas the maximization of ROCE refers to profit rate maximization (r** ), the maximization of ROE refers here to the maximization of cash flows, that is the gap between the finance frontier27 and the expansion one. Shareholders are thus trying to maximize cash flows as expressed in equation (10):

( )( )

)1(

)1(1

)1()(

dsf

ff

dsff

xxxgidrK

CF

ROEsDK

iDs

DK

CF

xxxIiDiDsiDCF

−−+−−=⇔

−=−

−Π−=

−⇔

−−+−−Π=−Π−−Π=

(10)

If we refer to the ratio between the amount of cash flows and owners’ equity, we can state that shareholders claim both high financial profitability through leverage effects and high rate of distribution of dividends. If we refer to the ratio between cash flows and total capital, we notice that the cash-flows-to-capital ratio is consistent with its definition as the difference between the expansion frontier profit rate and the finance frontier one. On the Figure 5, one can see that the accumulation rate which maximizes the profit rate (g** ) is different from the accumulation rate which maximizes the gap between the finance frontier and the expansion one, which is the accumulation rate that maximizes cash-flows-to-capital ratio (gCF):

26 The distinction is then between an economic and a financial profitability. See Batsch (2002, p. 81) for more about this point. 27 In the case of a shareholder-ruled firm, the finance frontier changes by the simple fact that shareholders cannot be a constraint for themselves. So, the retention ratio disappears from the finance constraint.

16

If shareholders effectively run the firm in order to maximize the cash flows that will be claimed back through dividends payments or share buybacks, the accumulation rate undertaken by the firm would be below the one that maximizes the gross profit rate. Compared to the situation where managers effectively run the firm via growth-seeking policies (g*), the drop in accumulation is then even larger than the one given by shareholder value orientation policies in Stockhammer’s framework (g** ). If one agrees with the maximization of cash flows being the absolute shareholders’ objectives, one has to expect a huge slowdown of accumulation. IV-2. Shareholders’ wealth maximization

When looking at injunctions issued from new corporate governance, one can find out another way to describe the theoretical objectives of shareholders-ruled firms. A widely spread assertion brings back to the need to “create shareholder value”. Here, the assumption will be that a shareholders-ruled firm tries to maximize the creation of value for its shareholders through the maximization of firm’s value on the market. For the purpose of this Section, we will adopt the purest theory of shareholders’ value creation. We assume the general efficiency of market in equilibrium inside the Capital Asset Pricing Model (CAPM), and we try to find out what the best policy for shareholders would be. Thanks to this traditional theory of equity market, one can derive the equation giving the value of the firm:

( )∑∞

+=

0: 1tt

s

t

r

CFV (11)

The value of the firm (V) is nothing else than the sum of actualized future cash flows (CFt). The actualization rate (rs) is equal to the rate of return claimed at market equilibrium. Thanks to the definition of cash flows as the difference between gross profit rate and finance constrained profit rate, and if we assume that cash flows grow at the same rate than the capital

r**

g** g* Accumulation rate (g)

Profit rate (r)

Figure 5: Cash flows maximizing

r*

EF

FF

gCF

17

stock (g)28, and that the growth rate (g) is inferior to the actualization rate (rs), the previous equation can be restated as a function of today’s cash flows only:

gr

iDxxxIV

s

dsf

−−−−+−Π

=)1(

(12)

Dividing (12) by the total capital of the firm K, one gets the unit share’s value of the firm:

gr

idxxxgrv

s

dsf

−−−−+−

=)1(

(13)

In this equation, it becomes clearer why shareholders shouldn’t be only interested in the firm’s profit rate (r) when attempting to maximize the unit share’s value of the firm. The usual assessments advanced by shareholder value creation tend to be limited to numerator’s maximization: the requirements are either a high firm’s profit rate, or a low firm’s growth rate, or a low interest rate. This view neglects the role of the denominator in determining share’s price. By looking closely to the denominator of (13), the striking point is that the firm’s growth rate has a positive effect on share’s value. As a consequence, shareholders who try to maximize firm’s value shouldn’t focus on the profit rate at the expense of accumulation. In other words, if shareholders target firm’s value maximization, they wouldn’t escape the profit-growth trade-off in spite of what has been assessed by Stockhammer (2004a). A shareholders-ruled firm will undertake neither the accumulation rate that maximizes the profit rate (g** ), nor the accumulation rate that maximizes the cash flows (gCF). It will instead attempt at choosing the accumulation rate that maximizes firm’s value. This outcome emerges from a very specific set of assumptions. Here shareholders are supposed to maximize firm’s value on the market in an infinite time horizon. That’s why they need to take into account the growth rate for the firm. But if we assume that shareholders try to maximize firm’s value on the market on a shorter time horizon, growth rate may be neglected, as it was the case when shareholders only wanted to maximize today’s cash flows. IV-3. The absence of a relevant knowledge

Nevertheless, the growth rate that maximizes firm’s market value is far more uncertain than the other ones. It fluctuates a lot for little changes in the value of parameters entering in (13), and especially the value of the standard rate of return at markets equilibrium (rs)

29. This equilibrium rate of return serves to the definition of the rate of return on equity for a firm (ROE) given by a function of the rate of return of a non-risked asset (i)30 plus a risk bonus (ψ) specific to the firm. We have to bear in mind that this formula stems from market equilibrium.

)( iriROE s −×+= ψ (7)

At the end, the maximization of firm’s market value is extremely sensitive and dependent on several variables totally exterior to firm’s monitoring, so that it becomes almost unfeasible to 28 In this case, the sum of cash flows is the sum of a geometric series. 29 For a definition of rs, see the Capital Asset Pricing Model (CAPM) as exposed in Aglietta et Rebérioux (2004, p. 25). 30 Here the non-risked asset may be public bounds, and the interest rate on public bounds is expected to be the same one of the one prevailing on credit market.

18

determine a rate of accumulation that would maximize firm’s market value. Instead of this, one may assume that firms act conventionally by following rules of thumb. This type of rationality suggests a satisfying behavior rather than a maximizing one. By adopting threshold level established as standard by a market convention, firms attempt at lifting the veil of shareholder-value-maximization governance. When firms target the well-known 15% of ROE, they do not maximize shareholder value creation, but they choose this intermediate objective to reach, or more precisely to get nearer from the final objective of maximizing shareholder value creation. Firms do not really know how to maximize shareholder wealth, but they know that displaying the 15% or more of ROE will send the signal that they are willing to maximize it. This policy does not effectively maximize shareholder wealth, but it has emerged as the convention that points the firm’s approach towards shareholder value maximization. Graphically (see Figure 6), one can observe this proximity between the accumulation rate that maximizes cash flows (gCF), and the accumulation rate that tries to maximize shareholder wealth through targeting the standard conventional level of ROE (gsw).

The objective of firm’s market value maximization requires taking into account growth: although one deals with the purest shareholders’ theory of the firm, one needs growth. When shareholders act in order to maximize their wealth, they do not maximize cash flows31, but they try to be easy with firm’s growth, because growth also matters when considering firm’s financial valuation32. Today’s growth keeps being a prerequisite for tomorrow’s profitability, which in turn determines today’s firm valuation on the market. The implementation of shareholders’ maxims is not a sort of clearance sale of managerial corporate governance principles, since growth is still needed for shareholders’ interests. When trying to reach their objectives, shareholders have to rely on managers who are the best skilled to implement growth policies. In brief, considering shareholders-ruled firm, one faces two different configurations where shareholders target either cash flows maximizing or share’s value maximizing. The first case

31 In other words, they do not try to maximize only the numerator of (13). 32 This appears on the denominator of (13).

r**

g** g* Accumulation rate (g)

Profit rate (r)

Figure 6: Shareholder wealth maximizing

r*

EF

FF

gCF gsw

rsw 15% of ROE

19

seems to treat shareholders as short-term rent-seekers who are involved in several firms and who do not care about long term survival of these firms. They are only interested by short term financial performance. The second case is characterized by shareholders who are more implied in firm’s long term interest. It brings back to shareholders’ activism. Actually, one can draw an opposition among shareholders between those interested in the valorization of their income through dividend payments (cash flows), and those interested in the valorization of their asset through share’s value increases. V – Conclusion What has been done in this article is trying to make sense of financialization’s implications for the investment decision inside the Post-Keynesian theory of the firm. The concern wasn’t to assess the most accurate configuration of firm’s theory in the context of financialization. It was rather to provide the two polar cases of possible theoretical implications of financialization for the purpose at hand. Depending on different corporate governance rules and depending on shareholders’ target, financialization will have different effects for the individual firm. Our conclusion also suggests that the Post-Keynesian theory of the firm is resistant to institutional transformations, since we have showed that it is possible to introduce financialization within the frame of the Post-Keynesian theory of the firm. The introduction of financialization within the Post-Keynesian framework of the theory of the firm has been first considered by Stockhammer (2004a) who derived his theory from the seminal work of Lavoie (1992). Stockhammer’s contributions enlightened power struggles within the firm and their consequences for firm’s accumulation policies. Then, Stockhammer built a macroeconomic closure where the slowdown of capital accumulation explained by the changing power struggles within firms meets some stylized facts about financialization. For Stockhammer, capital accumulation at the macroeconomic level has decreased, because firms at the microeconomic level have desired to invest less. In this paper, we tried to tell different stories about why firms at the microeconomic level have decided to invest less. Whether firm’s orientation is decided by managers under shareholders’ pressure or by shareholders themselves, financialization effectively leads to a decreasing trend in accumulation. In this, we agree with Stockhammer’s outcome. But we have attempted to detail the process that produced this outcome. What we have showed is that financialization taken as a constraint for managers implies a relatively low drop in accumulation, and it could even lead to a constant accumulation by means of increasing pressure on workers and/or increasing real fragility. Considering the opposite case where shareholders preside over firm’s fates, we find out that the decrease in accumulation is far higher, but the scale of this reduction is dependent on what is assumed to be shareholders’ objectives. The way financialization has been introduced here offers a theoretical representation of corporate governance evolution “from an orientation towards retention of corporate earnings and reinvestment in corporate growth through the 1970s to one of downsizing of corporate labor forces and distribution of corporate earnings to shareholders over the past two decades” (Lazonick et O’Sullivan [2000], p. 13). The microeconomic implications of financialization for the theory of the firm need to rejoin the macroeconomic story of financialization. Our results suggest a drop in accumulation that confirms usual macroeconomic assumption towards financialization’s effects. Aggregate investment is expected to decrease due to financialization, and other things being equal, this would lead to economic growth contraction. But as far as financialization is concerned, other

20

things are not equal. Consumption may be fuelled by financialization and credit expansion, but consumption may also be affected by wage pressure as noted earlier in this paper. At the end, we need to assess the potential boom in consumption with the potential decrease in accumulation at the macroeconomic level. Another point to be mentioned about macroeconomic closure is that the situations presented here could occur only under the implicit condition that firms would experience the higher profit rate they expected when they decided to decrease their accumulation rate33. In fact, the microeconomic profit rate of a firm depends on the macroeconomic accumulation rate of the other firms. If other firms decided to cut their investment outlays, the individual firm would experience difficulties to reach the profit rate that legitimated its accumulation drop, because the expansion frontier would be moving downward. Then, it opens the way both to real instability with ever decreasing expansion frontiers and ever depressing investment decisions, as well as financial instability with ever increasing financial risk of default. Moreover, what should be kept in mind is that the position of the two frontiers are based on subjective factors, such as managers’ optimism about investment profitability for the expansion frontier and managers’ sensitivity to financial risk for the finance frontier. It goes without saying that both factors are likely to generate cyclical real as well as financial fluctuations, depending on optimism and caution. Regarding financialization at the macroeconomic level, the question to be asked is whether the positive effects on consumption through dividend payments, credit and financial wealth overwhelm the negative effects on investment. If the answer is no, there will be no room for finance-led capitalism and the economy will experience instability. If the answer is yes, finance-led capitalism could emerge. Several studies notice the divorce between accumulation and profitability that has been witnessed in many countries34. In brief, these considerations can be explained by what Cordonnier (2006, p. 89) calls “the extended Kalecki’s law”. Accumulation may slow down simultaneously with profitability increases, if the distribution of profits through dividend payments increases and if the propensity to consume out of dividends also increases. These key features of Post-Keynesian economics give a solid theoretical explanation of recent stylized facts of finance-led capitalism at the macroeconomic level. And they can also provide a rational for persistent investment slackness without global depression. Financialization’s literature often tackles the theoretical conditions of finance-driven consumption allowing to profitability recovery. Our work tends to offer a reappraisal of the theoretical background for finance-oppressed investment. The finance-led capitalism debates have to relay on this confrontation of financialization’s two sides. In this perspective, the present contribution has filled in an under-studied field in the way financialization is approached. References: AGLIETTA M. (1999): “Les transformations du capitalisme contemporain”, pp. 275-292, in CHAVANCE B., MAGNIN E., MOTAMED-NEJAD R. et SAPIR J. (1999): Capitalisme et

33 This ex post confirmation of ex ante expectation is no longer certain when, as it seems to be the case, financial claims are above the “glass ceiling” of profitability. See Cordonnier et Van de Velde (2008). 34 See Van Treeck (2007a) and (2007b) or Hein et Van Treeck (2007).

21

socialisme en perspective. Evolutions et transformations des systèmes économiques, La Découverte, Paris, 382 p. AGLIETTA M. et REBERIOUX A. (2004): Dérives du Capitalisme financier, Éditions Albin Michel, 394 p. BATSCH L. (2002): Le Capitalisme financier, Editions La Découverte et Syros, coll. Repères, Paris, 120 p. BERLE A. et MEANS G. (1933): The Modern Corporation and Private Property, The Macmillan Company, New York, 396 p. BHADURI A. et MARGLIN S. (1990): “Unemployment and the real wage: the economic basis for contesting political ideologies”, Cambridge Journal of Economics, vol. 14, n°4, pp. 375-393. BHADURI A., LASKI K. et RIESE M. (2006): “A model of interaction between the virtual and the real economy”, Metroeconomica, vol. 57, n°3, pp. 412-427. BOYER R. (2000): “Is a finance-led growth regime a viable alternative to Fordism? A preliminary analysis”, Economy and Society, vol. 29, n°1, pp. 111-145. CORDONNIER L. (2006): “Le profit sans l’accumulation : la recette du capitalisme gouverné par la finance”, Innovations, Cahiers d’économie de l’innovation, n°23, pp.79-108. CORDONNIER L. et VAN DE VELDE F. (2008): “Financial Claims and the Glass Ceiling of Profitability”, Mimeo, Université de Lille 1. CROTTY J. (1990): “Owner-Manager Conflict and Financial Theories of Investment Instability: a critical assessment of Keynes, Tobin, and Minsky”, Journal of Post Keynesian Economics, vol. 12, n°4, pp. 519-542. CROTTY J. (1992): “Neoclassical and Keynesian Approaches to the Theory of Investment”, Journal of Post Keynesian Economics, vol. 14, n°4, pp. 483-496. CROTTY J. (2005): “The Neoliberal Paradox: the Impact of Destructive Product Market Competition and ‘Modern’ Financial Markets on Nonfinancial Corporation Performance in the Neoliberal Era”, pp. 77-110, in EPSTEIN G. A. (2005): Financialization and the World Economy, Edward Elgar, Cheltenham, 440 p. CROTTY J. et GOLDSTEIN J. (1992): “The Investment Decision of the Post Keynesian Firm: a Suggested Microfoundation for Minsky’s Investment Instability Thesis”, The Levy Economics Institute Working Paper n°79. DALLERY T. et VAN TREECK T. (2008): “Conflicting Claims and Equilibrium Macroeconomic Adjustment Processes in a Stock-Flow Consistent Macromodel”, IMK Working Paper, n°9/2008, 31 p. GALBRAITH J.K. (1967): The New Industrial State, Houghton Mifflin, Boston, 443 p.

22

HEIN E. et VAN TREECK T. (2007): “‘Financialisation’ in Kaleckian / Post-Kaleckian models of distribution and growth”, IMK Working Paper, n°7/2007, 33 p. LAVOIE M. (1992): Foundations of Post Keynesian Analysis, Edward Elgar, Aldershot, 464 p. LAZONICK W. et O’SULLIVAN M. (2000): “Maximizing shareholder value: a new ideology for corporate governance”, Economy and Society, vol. 29, n°1, pp. 13-35. MAKI D. et PALUMBO M. (2001): “Disentangling the Wealth Effect: A Cohort Analysis of Household Saving in the 1990s”, Federal Reserve Board. ROBINSON J. (1964): Essays in the Theory of Economic Growth, Macmillan and Co Ltd, London, 137 p. STOCKHAMMER E. (2004a): “Financialization and the slowdown of accumulation”, Cambridge Journal of Economics, vol. 28, n°5, pp. 719-741. STOCKHAMMER E. (2004b): The Rise of Unemployment in Europe: a Keynesian Approach, Edward Elgar, Cheltenham, 232 p. STOCKHAMMER E. (2005-6): “Shareholder value orientation and the investment – profit puzzle”, Journal of Post Keynesian Economics, vol. 28, n°2, pp. 193-215. STOCKHAMMER E. (2007): “Some stylized facts on the finance-dominated accumulation regime”, Communication at the 11th conference of the Research Network Macroeconomic Policies, Finance-led capitalism? Macroeconomic Effects of Changes in the Financial Sector, Berlin, 26 and 27 October. VAN TREECK T. (2007a): “Reconsidering the investment-profit nexus in finance-led economies: an ARDL-based approach”, IMK Working Paper, n°1/2007, 1/2007, 32 p. VAN TREECK T. (2007b): “A synthetic, stock-flow consistent macroeconomic model of financialisation”, IMK Working Paper, n°6/2007, 28 p. WOOD A. (1975): A Theory of Profits, Cambridge University Press, Cambridge, 184 p.