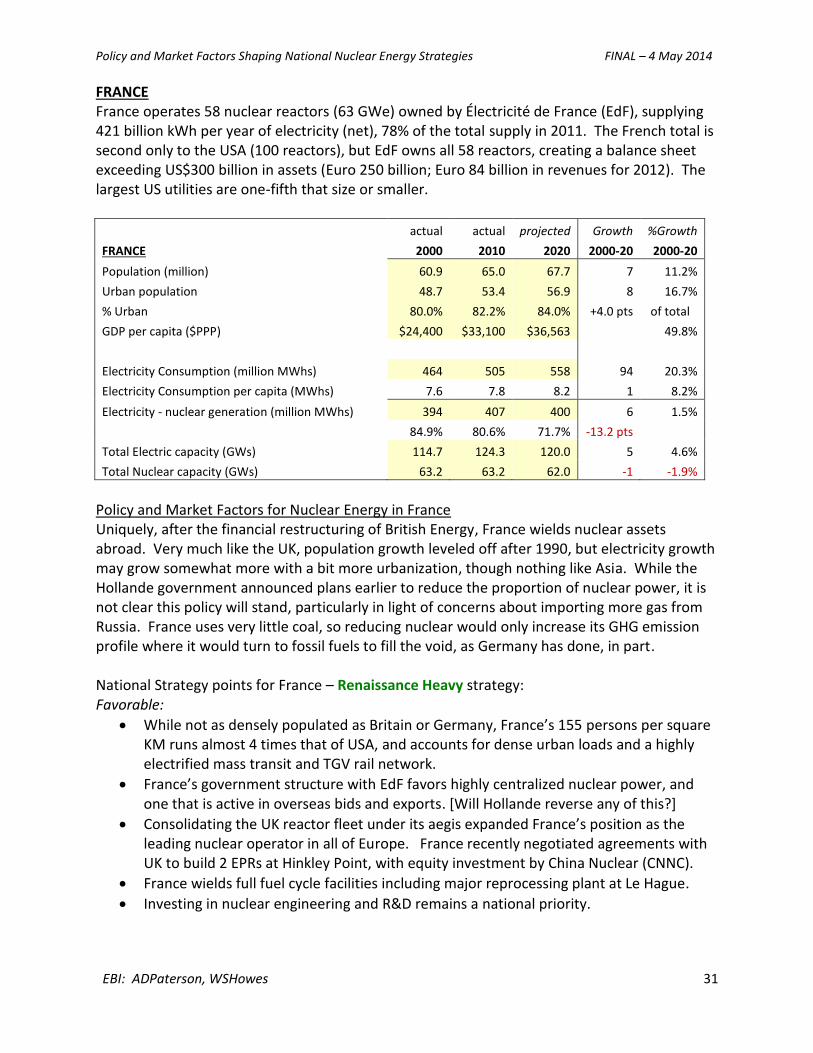

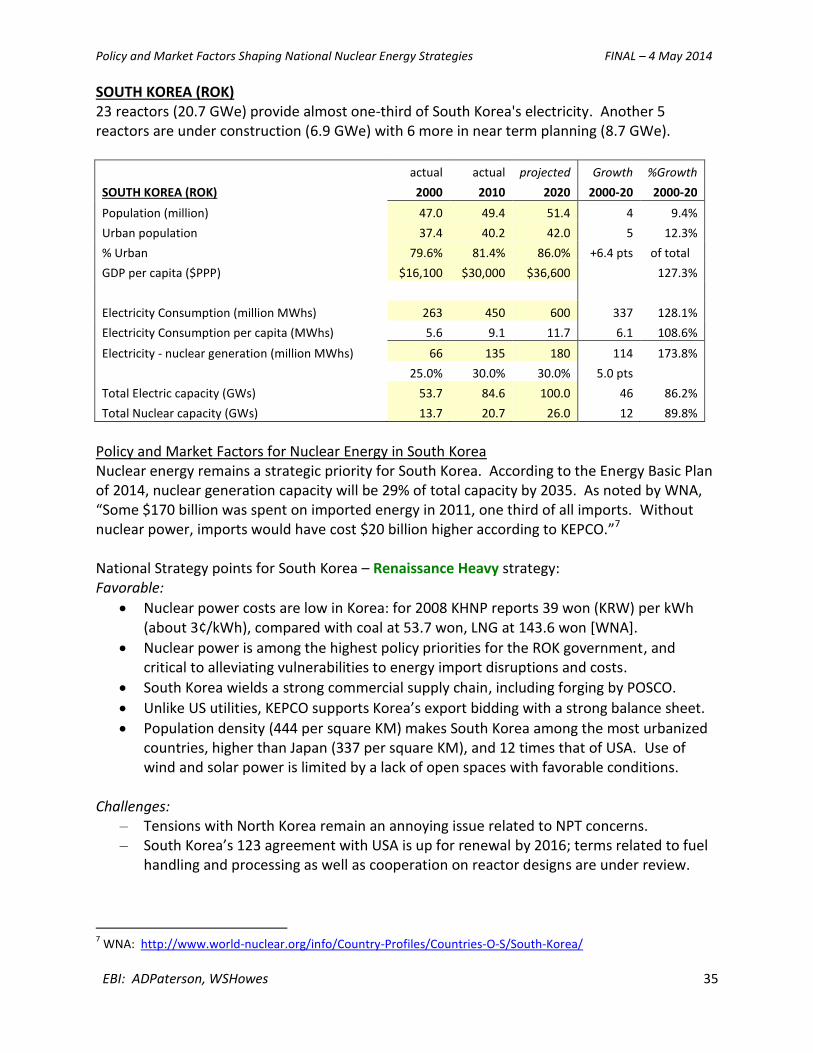

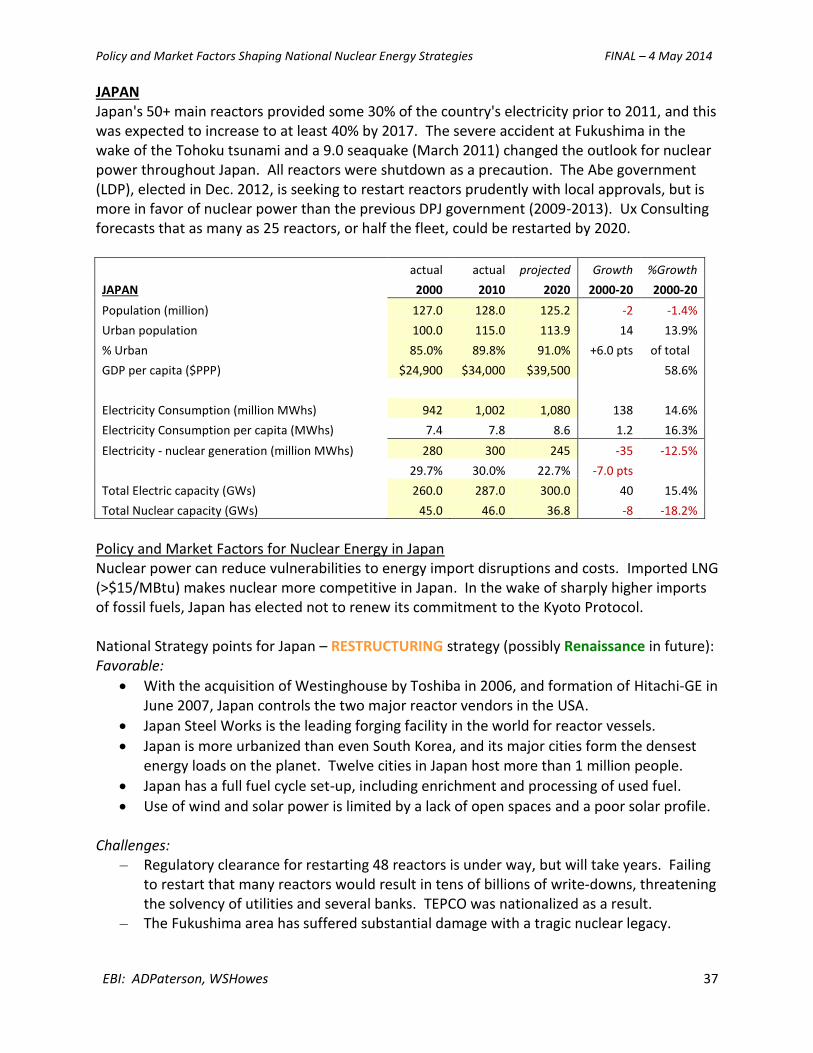

Policy and Market Factors Shaping National Nuclear Energy Strategies

49

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014 EBI: ADPaterson, WSHowes 1 Environmental Business International www.ebiusa.com Policy and Market Factors Shaping National Nuclear Strategies: Part II of “Redefining Leadership in Global Nuclear Energy Markets” AUTHORS Andrew D. Paterson Principal – Environmental Business International [email protected] 571-308-5845 Washington, DC Walter S. Howes Managing Partner – Verdigris Capital, LLC Board member - Environmental Business International [email protected] 202-342-5323 April 2014 Supply-side Enabling Factors for National Nuclear Energy Strategies Demand-side Drivers for National Nuclear Energy Strategies Author’s note: This project was sponsored by the Korea Atomic Energy Research Institute (KAERI). We would like to thank KAERI project coordinator Dr. Lee Byung-Wook for his guidance in developing themes for this manuscript. Florence Lowe-Lee, at the Global America Business Institute, also provided very helpful insights on key issues. Any errors or omissions are the responsibility of the authors.

Transcript of Policy and Market Factors Shaping National Nuclear Energy Strategies

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 1

Environmental Business International www.ebiusa.com

Policy and Market Factors Shaping National Nuclear Strategies:

Part II of “Redefining Leadership in Global Nuclear Energy Markets”

AUTHORS

Andrew D. Paterson Principal – Environmental Business International

[email protected] 571-308-5845 Washington, DC

Walter S. Howes

Managing Partner – Verdigris Capital, LLC Board member - Environmental Business International

[email protected] 202-342-5323

April 2014

Supply-side Enabling Factors for National Nuclear Energy Strategies

Demand-side Drivers for National Nuclear Energy Strategies

Author’s note: This project was sponsored by the Korea Atomic Energy Research Institute (KAERI). We would like to thank KAERI project coordinator Dr. Lee Byung-Wook for his guidance in developing themes for this manuscript. Florence Lowe-Lee, at the Global America Business Institute, also provided very helpful insights on key issues. Any errors or omissions are the responsibility of the authors.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 2

OUTLINE PREFACE – Dr. Gail Marcus, former President - American Nuclear Society (2001-02)

I. EXECUTIVE SUMMARY - Part II: National Nuclear Energy Strategies

Key Supply and Demand Factors for Nuclear Energy going forward

II. Part II: Key Drivers and National Strategies in the Global Nuclear Energy Market

A. Drivers for National Strategy in Nuclear Energy Markets (follow-on from Part I)

1) Supply factors: historical; Cold War era; first wave of reactor construction by P5 nations

2) Demand factors: emerging; 21st Century; future reactor construction for urban demand

3) Economic factors and justification (some factors vary by country)

4) Finance and Policy issues – based on interaction of Supply and Demand factors

B. A Framework for Defining National Strategies: Supply-intensive vs. Demand-driven

1) Specific National Strategies

– “Renaissance” Strategy (“Heavy” and “Light”): Renewal, construction, export-oriented

– “Rollback” Strategy: Phase-out, shutdown, moratoriums

– “Restructuring” Strategy: Open to new construction, but needing policy intervention

2) Observations, and importance of International Partnerships

C. Recommendations; Importance of International Partnerships with Demand in Urban Asia

D. Conclusions

E. Appendix: Individual Country Profiles & National Strategy points

III. SUMMARY – Part I: Redefining Leadership in the Global Nuclear Energy Market REFERENCES Future Report: Part III – Strategies in Industry based on National Strategies with impact on Financing Options

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 3

PREFACE BY DR. GAIL H. MARCUS Dr. Gail H. Marcus, former Deputy Director-General of the OECD Nuclear Energy Agency (Paris), former president of the American Nuclear Society (2001-02), and author of Nuclear Firsts (2010); Sc.D. in Nuclear Engineering, MIT. In the early days of nuclear power, scientists and engineers explored a number of alternative nuclear technologies. The focus in the United States rapidly evolved almost exclusively to light water reactor technology, and led to a large new-build program. The number of reactors built in the US in the 1960s and 1970s far outstripped the number in any other country, and indeed, the total number of reactors built in the US comprised one-quarter of the world's total. Domestic demand in the US and industrial countries rebuilding from World War II fueled construction. There were a handful of other countries that also had significant domestic markets--Canada, the United Kingdom, France, the Soviet Union, and a little later, Japan. France and Japan started their nuclear programs with US technology, but moved to develop their own versions of the US designs. Canada, Britain, and the Soviet Union relied on different reactor technologies. Most of these countries conducted a secondary business selling reactors to other countries. In most cases, the buyers were countries with strong economies and burgeoning demand for electricity. Today, the situation is much different. There are only a few new reactor projects in the countries that traditionally had the strongest “supply-side” nuclear programs, education and infrastructure. Most of their vendors, however, are still active and are seeking projects outside their national borders. At the same time, several vendors from other countries have entered the marketplace. In particular, South Korea and China have emerged as supplier countries. China has a large domestic program, but both China and South Korea have begun to compete against the established vendors from Europe and the USA. Other differences between the past and the present are also important. For example, the market for new reactors, outside China and India, is increasingly in countries with smaller, mainly high-population-growth developing economies, compared to the developed OECD countries, where population growth has crested. For these countries, the multi-billion dollar investment required for a large nuclear reactor is difficult to support. Thus, those countries are increasingly seeking packages that include economic support for the projects, and indeed, that even include management of the facilities once they are operational. Russia offered a "build-own-operate" plan for Turkey, and Korea provided a package of financial incentives to the United Arab Emirates (UAE). Although many people express concern that the 123 nuclear cooperation agreements have hampered some opportunities abroad for US companies, the primary impediment has probably been the ability to finance projects. US vendors do have the Export-Import Bank to help with financing large projects abroad, but they do not have the resources to provide financing packages similar to those offered by Russian, Korean or French companies, which are backed by their governments. And US investor-owned utilities do not participate in these overseas bids the way EDF/Areva, KEPCO, or Rosatom do. Sovereign financing issues are therefore a major theme in this paper. The current market and policy landscape calls for new models for financing and supporting reactor projects in an increasingly diverse marketplace; in essence, “new modes of leadership” are evolving in nuclear energy. This paper (Part I and II, on “Redefining Leadership”) documents some of the key elements that are shaping National Nuclear Strategies, the importance of international alliances, and some of the critical factors that affect how companies might partner to offer services new entrant countries are seeking. In this regard, it may be helpful that many of the vendors are now multi-national companies, having bought each other up or merged over the last couple of decades. For example, both Westinghouse and GE have alliances with Japanese companies. Recent negotiations for UK nuclear projects involving both French and Chinese joint ventures, as well as a US-Japan joint venture, also demonstrate this trend. Thus, if we speak of the competitiveness of "US industry," we need to recognize that with more than 80% of the reactors today being built overseas, and primarily by national enterprises, not investor-owned utilities -- international joint ventures will be essential. As a result, leadership in nuclear energy has been redefined, and new ways of responding in an evolving landscape are needed.

Dr. Gail H. Marcus

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 4

EXECUTIVE SUMMARY – Part II: National Nuclear Energy Strategies

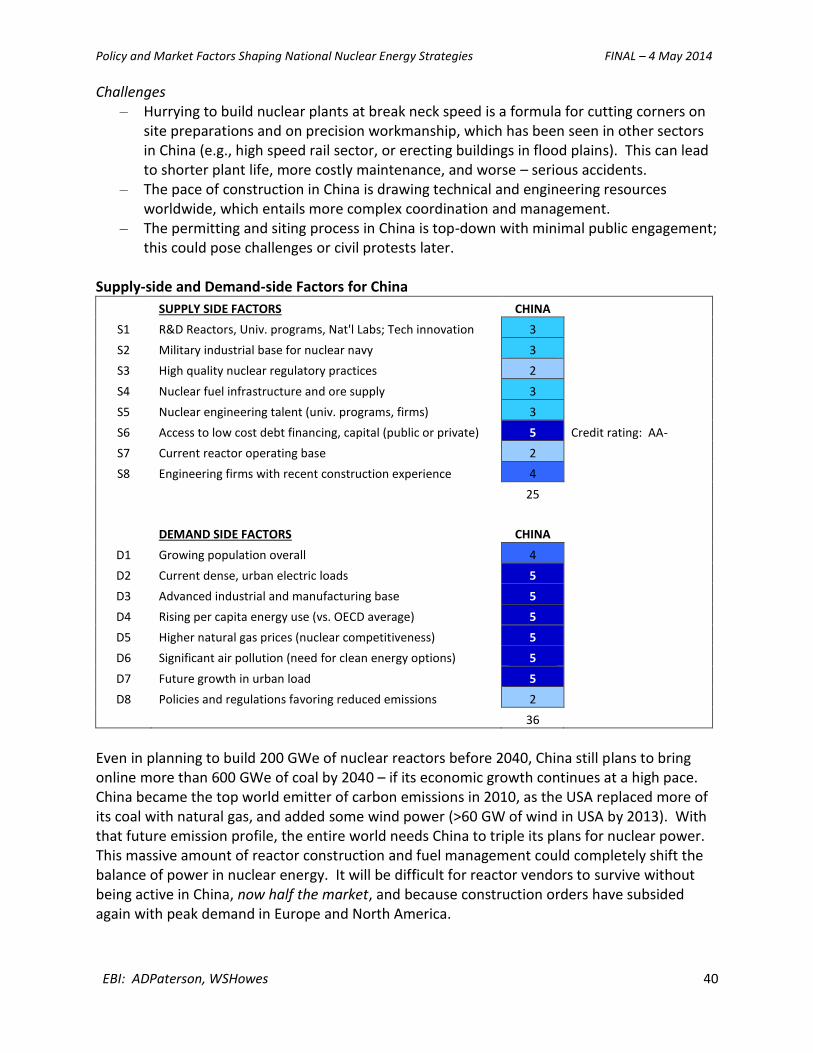

National Nuclear Energy Strategies derived from Supply-side and Demand-side Factors Due to the nature of the shift in factors driving leadership in nuclear energy, it is not possible to “restore” leadership, as if the old Supply-side driven landscape still existed. USA and others must adapt to a new Demand-side driven landscape, via alliances, to exercise leadership. SUPPLY SIDE FACTORS (20th Century) “PUSH” DEMAND SIDE FACTORS (21st Century) “PULL” S1 R&D Reactors, Univ. programs, National Labs S2 Military industrial base for nuclear navy S3 High quality nuclear regulatory practices S4 Nuclear fuel infrastructure and ore supply S5 Nuclear engineering talent (colleges, firms) S6 Access to low cost debt financing, capital S7 Current reactor operating base S8 Engineering firms with construction record

D1 Growing population overall D2 Current dense, urban electric loads D3 Advanced industrial manufacturing base D4 Rising per capita energy use (vs. OECD) D5 Higher natural gas prices (competitiveness) D6 Significant air pollution D7 Future growth in urban load D8 Policies, regulations to reduce emissions

National Nuclear Energy Strategies By plotting this shift from Supply-side factors to Demand-side intensity, a plausible framework emerges, which helps explain the drivers behind National Nuclear Energy Strategies. Based on Supply and Demand factors, the specific National Nuclear Strategies run as follows, and are explained in more detail in Section B: Decommissioning Strategy – “Rollback”, Examples: Germany, Italy, Belgium, Japan (2012) Germany, Italy and Belgium are clear examples of countries that built reactors and then as a policy matter, rather than physical aging, decided to close or are in the process of closing reactors before their approved lives due to social and political pressures rather than mere economics. No countries engaged in a Rollback strategy are elite “P5 nuclear power” members. Exporters – “Restructuring”, Examples: USA, Canada, Japan (2014), Britain (?) Countries with local approval for reactor operation or openings for interveners, in contrast to countries with stronger more centralized governments, experience some delays or friction in promoting a nuclear “renaissance”. Also, these countries use more natural gas for electricity which can lead to volatile electric pricing, rather than stable or regulated rates. Importers – “Renaissance light”, Examples: UAE, Turkey, Jordan, Saudi Arabia, Vietnam, Poland Countries that lack the Supply-side strengths of the traditional nuclear powers seek to import nuclear energy technology because they face higher Demand-side factors with higher population growth, urbanization, and some electricity-intensive desalination demand. These countries cannot afford to invest in building up a supply-side enabling infrastructure. Import and Export – “Renaissance Heavy”, Examples: South Korea, China, India, Russia, France Countries heavily engaged in a renaissance have built up their Supply-side infrastructure (engineering, forging, fuel processing), are building units, and actively engaged in exporting.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 5

SUMMARY: Key Supply and Demand Factors for Nuclear Energy going forward http://www.atlanticcouncil.org/publications/reports/redefining-leadership-in-the-global-nuclear-energy-market

Success Factors for Nuclear Energy: Supply-side and Demand-side Intensity Drivers As previously mentioned a key question going forward will be how to define the best strategic partnership opportunities. In the past, as seen in the Figure below, the United States and Europe had the most favorable supply-side strengths. Summary of Supply and Demand Factors and National Nuclear Strategies Updated from Part I: Redefining Leadership in Global Nuclear Energy Markets” by Andrew Paterson, Walter Howes

During the expansion era of nuclear power construction in the 1960s to 1980s, the United States led the world in many of the key “Supply Side” success factors. The relative strength of each country or mini-region was assessed on a relative basis (on a scale from 1 as a low value to 5 as a high value), and then the combined ratings were indexed to the highest entity in the evaluation. The chart shows how much the demand-side factors have emerged as key drivers in the 21st Century for new reactor construction going forward, compared to the supply-side factors that drove construction among OECD countries in the last Century during the Cold War. On the supply-side, the United States wields superior ratings in (S2) a military industrial base for a nuclear navy; (S3) regulatory practices; (S5) nuclear engineering talent; (S6) access to low cost financing; and (S7) the current reactor base. By contrast, China lacks the operating base of leaders France and the United States; however, China, India, and growing Asia see higher demand side factors associated with rapid population growth and urbanization (D1, D2, D4, D7), as well as higher natural gas prices, which makes nuclear energy more competitive. Each of the Supply and Demand factors are described in more detail in Appendix E.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 6

Part II: Key Drivers and National Strategies in the Global Nuclear Energy Market

A. Drivers for National Strategy in Nuclear Energy Markets (based on Part I)

1. Supply factors: historical; Cold War era; first wave of reactor construction by P5 nations 2. Demand factors: emerging; 21st Century; future reactor construction for urban demand 3. Economic factors and justification (factors vary by country, e.g., gas prices) 4. Finance and Policy issues – based on interaction of Supply and Demand factors 5. Summary of Individual Country Profiles (in Appendix E)

Shift from Supply-side enablers to Demand-side factors drives National Strategies The vast majority of the 435 reactors (370 GW) operating today were built from 1965 to 1985. Factors that accounted for the first wave of reactor construction were concentrated on the “Supply side” of the market arena, built around supporting the US Nuclear Navy, a nuclear weapons complex of DOE laboratories amid the Cold War between a Soviet Union and the NATO alliance, and focused on operational excellence for civilian reactors. Drivers: Supply-side and Demand-side Because of the nature of the shift in factors driving leadership in nuclear energy, it is not possible to “restore” leadership, as if the old “Supply-side push” landscape still existed. Instead, the US must adapt to the new “Demand-side pull” landscape, to exercise leadership in standards and practices via alliances – or even to stay in the game on this pivotal technology.

SUPPLY SIDE FACTORS (20th Century) “PUSH” DEMAND SIDE FACTORS (21st Century) “PULL” S1 R&D Reactors, Univ. programs, National Labs S2 Military industrial base for nuclear navy S3 High quality nuclear regulatory practices S4 Nuclear fuel infrastructure and ore supply S5 Nuclear engineering talent (colleges, firms) S6 Access to low cost debt financing, capital S7 Current reactor operating base S8 Engineering firms with construction record

D1 Growing population overall D2 Current dense, urban electric loads D3 Advanced industrial manufacturing base D4 Rising per capita energy use (vs. OECD) D5 Higher natural gas prices (competitiveness) D6 Significant air pollution D7 Future growth in urban load D8 Policies, regulations to reduce emissions

[Drivers developed for Part I and Part II by the authors; See Appendix E for more detail]

Supply-side factors are driven, in some cases strongly [+++] by governmental policy decisions, or “push”, such as a national commitment to a nuclear Navy, national laboratory funding, and the federal regulatory practices embodied by the Nuclear Regulatory Commission (NRC). In the US, reactors were licensed by the federal government but financed, built and operated by regional utilities and their private sector contractors and reactor vendors, which are driven by market factors, including investment return, reliable supply, and private sector training and management. In most countries, a national entity (e.g., EdF, CNNC, NPCIL, Rosatom) owns, finances, builds, and operates its reactors often with sanction from the sovereign government. Importantly, sovereign entities are now leading bids for new reactors in foreign countries.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 7

A1. Supply-side enabling factors Supply-side factors are driven more by government policy providing high priority and top-down direction to move ahead on nuclear infrastructure under high quality regulation.

PRIMARY DRIVER: Supply Side Enabling Factors Policy Market S1 R&D Reactors, Univ. programs, Nat'l Labs; Technology innovation +++ S2 Military industrial base for nuclear navy +++ S3 High quality nuclear regulatory practices +++ S4 Nuclear fuel infrastructure and ore supply; spent fuel +++ ++ S5 Nuclear engineering talent (university programs, firms) ++ ++ S6 Access to low cost debt financing, capital (public or private) ++ ++ S7 Current reactor operating base + +++ S8 Engineering firms with recent construction experience +++ [Policy versus Market drivers are weighed as Strong (+++), Medium (++), and Weak (+).]

See appendix E for a more detailed description of each Supply and Demand factor, page 21-23.

A reactor fleet and its technical and fueling infrastructure are driven primarily by national policies and even ownership. Many cancellations occurred after 1975, not because of the Three Mile Island accident (March 1979), but because skyrocketing inflation with sharply higher interest rates and stagnant demand killed many capital intensive projects, not just reactors. Construction delays after the TMI accident and lower demand amid a protracted recession (1980-82) curbed new orders, but the US fleet became the largest in the world (104 reactors). A2: Demand-side factors: Dense urban loads drive demand for new reactors in 21st Century An important shift has taken place since 2000, as massive urbanization, especially in Asia, and other demand side or community level end-use factors, such as dense urban loads have emerged as the primary drivers for new nuclear reactor construction going forward. And, Asia sees much higher market prices for natural gas (>$14/Mbtu vs. $4-$5/Mbtu) than do industrial consumers and households in North America. While policy factors, such as permitting of gas supply and distribution to end-users, bear on these demand side factors, market growth in cities is mainly driving the need for large scale, reliable generation that nuclear energy provides: PRIMARY DRIVER: Demand Side “Market pull” Factors Policy Market D1 Growing population overall (native demographics, immigration) + +++ D2 Current dense, urban electric loads (baseload in large cities) + +++ D3 Advanced industrial and manufacturing base (energy intensity) + +++ D4 Rising per capita energy use (vs. flat demand in OECD) + +++ D5 Higher natural gas prices (nuclear is more competitive) ++ +++ D6 Significant air pollution (need for clean energy options) ++ +++ D7 Future growth in urban load (e.g., high rise buildings, mass transit) +++ +++ D8 Policies and regulations favoring reduced emissions +++ + [Policy versus Market drivers are weighed as Strong (+++), Medium (++), and Weak (+).]

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 8

Demand side factors are driven more by the benefits of nuclear power: reliability and “24 hour / 7-day per week” operation independent of weather, no local hazardous air pollutants, a smaller footprint (in the face of land use constraints), and economic development with broader electrification. Satisfying urban demand requires continual attention to public engagement. In addition, Demand-side factors are by their nature, more driven by market phenomenon – population growth, urban uses of energy, market pricing of other energy sources, and land use. The cost of being without electricity in major cities is greater than the cost of electricity. A city dwelling public supports the benefits of nuclear power, not just an abstract fuel source.

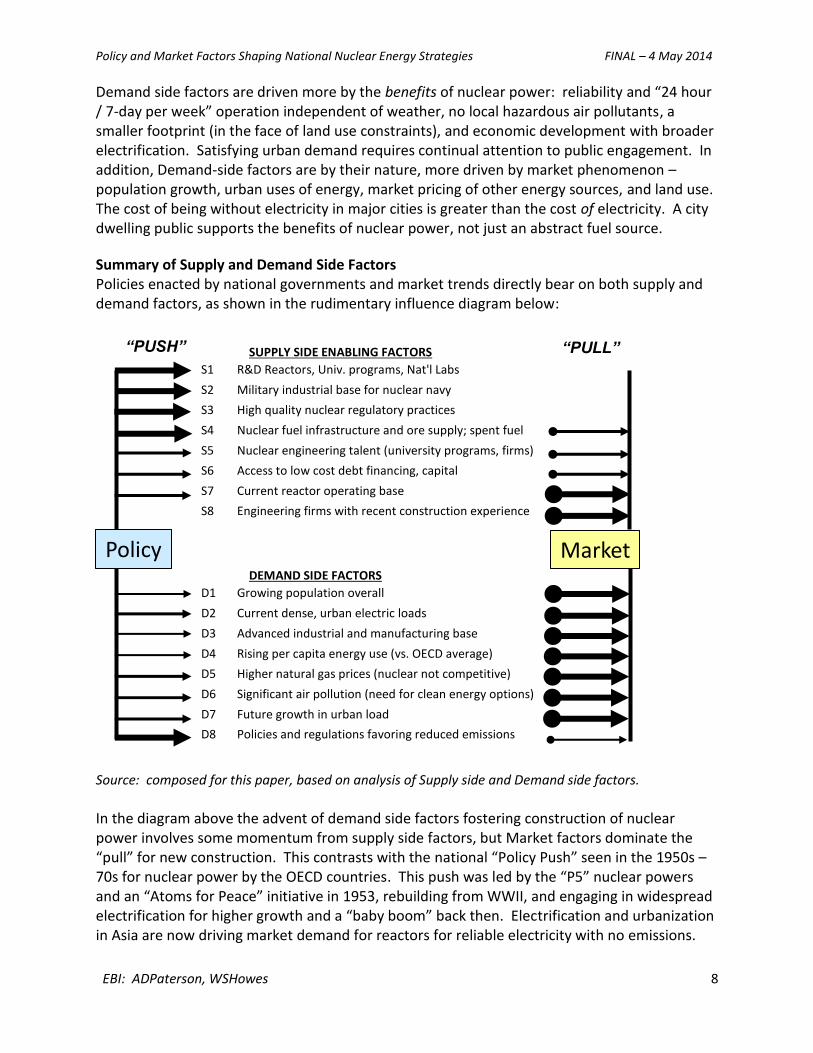

Summary of Supply and Demand Side Factors Policies enacted by national governments and market trends directly bear on both supply and demand factors, as shown in the rudimentary influence diagram below:

Source: composed for this paper, based on analysis of Supply side and Demand side factors.

In the diagram above the advent of demand side factors fostering construction of nuclear power involves some momentum from supply side factors, but Market factors dominate the “pull” for new construction. This contrasts with the national “Policy Push” seen in the 1950s – 70s for nuclear power by the OECD countries. This push was led by the “P5” nuclear powers and an “Atoms for Peace” initiative in 1953, rebuilding from WWII, and engaging in widespread electrification for higher growth and a “baby boom” back then. Electrification and urbanization in Asia are now driving market demand for reactors for reliable electricity with no emissions.

SUPPLY SIDE ENABLING FACTORS

S1 R&D Reactors, Univ. programs, Nat'l Labs

S2 Military industrial base for nuclear navy

S3 High quality nuclear regulatory practices

S4 Nuclear fuel infrastructure and ore supply; spent fuel

S5 Nuclear engineering talent (university programs, firms)

S6 Access to low cost debt financing, capital

S7 Current reactor operating base

S8 Engineering firms with recent construction experience

DEMAND SIDE FACTORS

D1 Growing population overall

D2 Current dense, urban electric loads

D3 Advanced industrial and manufacturing base

D4 Rising per capita energy use (vs. OECD average)

D5 Higher natural gas prices (nuclear not competitive)

D6 Significant air pollution (need for clean energy options)

D7 Future growth in urban load

D8 Policies and regulations favoring reduced emissions

Policy Market

“PUSH” “PULL”

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 9

A3. Economic factors and justification (some factors vary by country) In January 2013, EIA updated its estimated levelized costs for electricity capacity entering

service in the USA after 2018. These estimates importantly include the “game changing”

development of much cheaper gas prices in North America.

(Figures above do not include tax policy incentives, which vary by fuel source, and which expire or expired at

different times.) http://www.eia.gov/forecasts/aeo/er/pdf/electricity_generation.pdf

As shown above, electricity costs for nuclear power would be competitive in regions and countries that lack access to already built hydropower or cheap natural gas, or to old coal units without controls or CCS. In addition, the high reliability capacity factor of >90% is essential for large urban loads, versus the much lower capacity factors (<35%) seen with wind and solar. And wind and solar cost numbers do not include costs of storage or transmission for large scale wind farms, which could add 20%-50% more. Nuclear power remains competitive in Asia.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 10

A4. Finance and Policy issues; Ownership Finance and policy issues must be framed with an understanding of ownership and sovereignty in the nuclear sector. In most countries, nuclear reactors are a sovereign operation. USA and Japan are exceptions with commercial utility ownership. In Germany, E.ON and RWE are also investor-owned utilities, but Germany made a national decision to shut down its nuclear plants by 2022. Canada, Sweden, and South Korea utilize hybrid or blended ownership structures. Major Nuclear Entities The table below summarizes major nuclear utilities in the world, now over $2 trillion in assets. Of note is the heavy involvement of state-owned enterprises. Nuclear energy is a political economy, not decided solely based on economics and the cost of electricity. Reactor licensing is government regulated, and construction and operations are not just “left to the market.” Major Nuclear Operators by Country

Source: Compiled from various sources, company web sites, IAEA.

Recently, the emerging trend is that entities joining the “nuclear renaissance” (renewed construction of reactors since the 1980s-90s) bring a balance sheet in excess of $50 billion. Less than that requires some form of credit support (e.g., federal loan) or reduction of long-term market risk, such as regulated or steady rates with high quality off-takers. Mega-cities make high quality off-takers – they need large amounts of electricity, and for the life of a reactor.

2012 2012

Country Company Govt Ownership Revenues Assets Reactors MWs

P5 France [UK] EDF / British Energy 100% $76,500 $330,000 58 62,400

P5 China China Gen'l Nuclear 100% Government $43,700 12 9,800

P5 China China Gen'l Nuclear 100% Construction Construction 19 19,700

P5 China China Nat'l Nuclear 100% $104,000 $306,000 8 8,330

P5 China China Nat'l Nuclear 100% Construction Construction 14 16,630

P5 Russia Rosatom 100% $12,028 $60,176 31 25,200

S.Korea KEPCO (with KHNP) 51% $46,042 $133,170 23 20,700

P5 USA Exelon 0% $25,000 $78,550 24 18,720

Japan TEPCO (post 2012) . 76% $67,750 $150,000 17 17,300

Japan Kansai Elec 10% . $35,000 $87,000 11 9,770

P5 USA Entergy 0% $10,750 $43,200 11 9,000

P5 USA DUKE 0% $23,600 $113,850 11 8,960

India NPCIL 100% $96,240 $120,000 17 7,300

Spain (Italy) Endesa (ENEL) . 90% $44,070 $78,000 8 7,000

Sweden Vattenfall 100% $26,720 $84,240 7 6,880

P5 USA TVA 100% $11,220 $46,480 6 6,710

Germany E.ON 0% $131,750 $152,600 7 6,700

Canada Ontario Power 100% $6,350 $37,600 10 6,600

Germany RWE 0% $52,200 $75,600 5 6,300

Canada Bruce Power 0% $8,800 $48,500 8 6,300

P5 USA Southern Co 0% $17,000 $63,150 6 5,870

P5 USA Dominion 0% $13,200 $46,800 6 5,350

$808,220 $2,098,616 319 291,520

$million $million

World 468 408,530

of world 68% 71%

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 11

Public vs. Private: Divergence in Ownership for Nuclear Reactor Capacity

In countries other than Japan and the United States, nuclear reactors are more typically owned

wholly or in a majority position by the national government. This mirrors ownership of oil and

gas energy resources worldwide by national energy companies. Only the federally chartered

Tennessee Valley Authority (TVA; with 6,600 MWe of nuclear capacity) resembles ownership

structures seen in many countries where most construction is underway. This chart depicts the

ownership structure for nuclear utilities in different countries versus the capacity operated

currently (GWe). [The size of bubble then shows construction of new reactors in GWs.]

Ownership of Nuclear Entities with Operating Capacity and New Construction

[Updated from Part I: Redefining Leadership in Global Nuclear Energy Markets]

Source: compiled with data from World Nuclear Association, Nuclear Engineering International-UK, EIA [US entities: TVA = Tennessee Valley Authority; DUKE = Duke Energy; DOM = Dominion Power; ETR = Entergy;

EXC = Exelon; SO = Southern Company. EdF = Électricité de France; also owns UK reactor fleet.]

Because of sovereign government dominance in the nuclear arena, there are no privately held “mega-utilities” (lower right quadrant), like an investor-owned version of Électricité de France (EdF; upper right quadrant) or China National Nuclear (CNNC). Bond markets prefer sovereign enterprises with those entities earning higher credit ratings than US utilities, for example. And, some of those entities participate in bids outside their native countries, e.g., EdF’s acquisition of

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 12

British Energy a few years ago, or KEPCO in UAE, or Rosatom in Turkey. New reactors in Britain will be built by foreign groups, principally by Areva (France), with equity now from China. Combined, the “P5” and “Next 5” countries govern 80% of global commercial nuclear reactor capacity (table below). As is characteristic of P5 status, those five countries – the nuclear arsenal powers and victors from WWII now with nearly 2 billion people – account for a majority (57%) of global reactor capacity; the “Next 5” account for about one-quarter of world capacity (23%). Fully half the world’s population lives in just those ten countries, so nuclear power is globally very significant, supplying nearly 14% of electricity worldwide. Those ten countries also produce almost 60% of world GDP (PPP 2011, World Bank data). Notably, with over 50 GWe of the 70 GWe under construction, Asia now accounts for 70% of new reactor build. Summary of Current Commercial Reactors and New Construction: “P5” and “Next 5”

Sources: World Nuclear Association (WNA), DOE Presented at World Nuclear Symposium 2012, London in “The Advent of “Market States: National sovereignty and nuclear strategy after Fukushima -- Renaissance, Rollback, or Restructuring?” by ADPaterson

Only a P5 seat wields political veto power in the UNSC, a concrete form of strategic leverage in a post-Cold War globalized set of power relations, thereby bolstering sovereign impact relative to other nations in an increasingly globalized economy. According to UNCTAD and WTO, the value of global trade in 2011 was four times greater than in 1990, twice that of 2000.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 13

Global Nuclear Entities: A Domination of Sovereigns in Nuclear Energy The chart below was compiled for this paper, depicting in compressed form the universe of operating entities for the vast majority of currently operating reactors and those under construction. Note the dominance of the “P5” nuclear powers. However, with half of the 70 GWe of construction underway in China, leadership within the P5 countries is shifting to Asia and more to China specifically. In addition, China has ordered at least two of nearly every reactor type available and so within 5-10 years they will have built a sampling of the world market within their own borders. Other countries have standardized around one or two models, instead, for operating and maintenance efficiencies. Global Nuclear Operating Entities

[Chart compiled for this paper based on various sources: WNA, NEI, IAEA] Currently, the US prohibits foreign ownership of nuclear reactors for national security reasons, and this was a policy-related factor in the failure of the UniStar joint venture between Constellation and EdF for a third reactor at the Calvert Cliffs site, a French design EPR. However, uncertainties in market pricing of electricity rather than regulated rate-making was also a major factor foiling the financing of the project. In March 2013, the NRC upheld its denial of licensing the $8 billion+ project due to French (foreign) ownership by EdF.1

1 ENS: http://ens-newswire.com/2013/03/13/calvert-cliffs-reactor-license-denied-over-foreign-ownership/

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 14

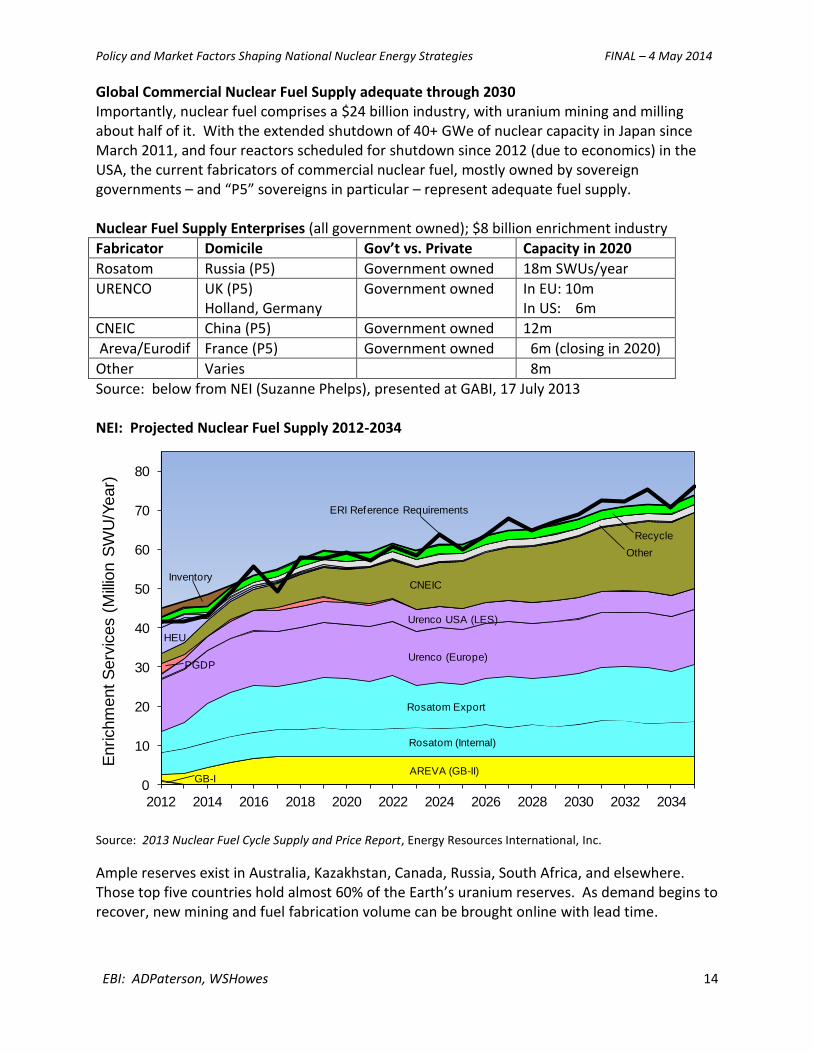

Global Commercial Nuclear Fuel Supply adequate through 2030 Importantly, nuclear fuel comprises a $24 billion industry, with uranium mining and milling about half of it. With the extended shutdown of 40+ GWe of nuclear capacity in Japan since March 2011, and four reactors scheduled for shutdown since 2012 (due to economics) in the USA, the current fabricators of commercial nuclear fuel, mostly owned by sovereign governments – and “P5” sovereigns in particular – represent adequate fuel supply. Nuclear Fuel Supply Enterprises (all government owned); $8 billion enrichment industry

Fabricator Domicile Gov’t vs. Private Capacity in 2020

Rosatom Russia (P5) Government owned 18m SWUs/year

URENCO UK (P5) Holland, Germany

Government owned In EU: 10m In US: 6m

CNEIC China (P5) Government owned 12m

Areva/Eurodif France (P5) Government owned 6m (closing in 2020)

Other Varies 8m

Source: below from NEI (Suzanne Phelps), presented at GABI, 17 July 2013 NEI: Projected Nuclear Fuel Supply 2012-2034

Source: 2013 Nuclear Fuel Cycle Supply and Price Report, Energy Resources International, Inc.

Ample reserves exist in Australia, Kazakhstan, Canada, Russia, South Africa, and elsewhere. Those top five countries hold almost 60% of the Earth’s uranium reserves. As demand begins to recover, new mining and fuel fabrication volume can be brought online with lead time.

GB-IAREVA (GB-II)

Rosatom (Internal)

Rosatom Export

Urenco (Europe)

Urenco USA (LES)

PGDP

CNEIC

HEU

Other

Recycle

Inventory

0

10

20

30

40

50

60

70

80

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2034

Enrichm

ent S

erv

ices (

Mill

ion S

WU

/Year)

R

ERI Reference Requirements

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 15

B. A Framework for Defining National Strategies: Supply-intensive vs. Demand-driven

1. Specific National Strategies – “Renaissance” Strategy (“Heavy” and “Light”): Renewal, construction, growth-driven – “Restructuring” Strategy: Open to new construction, but needing policy intervention – “Rollback” Strategy: Phase-out, shutdown, moratoriums

2. Observations, and importance of International Partnerships

B.1 National Nuclear Energy Strategies derived from Supply-side and Demand-side Factors By plotting this shift from Supply-side factors to Demand-side intensity, a plausible framework emerges, which helps explain the forces shaping National Nuclear Energy Strategies.

Source: ADPaterson; based on presentation Oct. 22 at FAS / GABI / KAIST, Washington, DC. Description of quadrants and Strategies (chart above) “High Supply-side; High Demand-side factors” (upper right) Renaissance Heavy Strategy China and India are the leading examples of rapidly urbanizing countries that must meet growing and massive energy demands for hundreds of millions of people in large cities with low emissions. Reactors are the only clean and reliable source with a small footprint at very large scale for large urban loads. Renewable energy sources (wind, solar, hydro, biomass) are not feasible everywhere, vulnerable to weather events and require large swaths of land to meet the scale of energy needed. Because of the scale of energy demand, and their need to import some forms of energy, China, India, and Japan and South Korea earlier, made the investments on the Supply-side to build a native nuclear engineering sector, so they are high in both sets of factors. Countries in this quadrant will export, and also import some key components to meet demands. France, Japan, South Korea, Russia and USA remain most active in export markets, as domestic demand will not be enough to sustain the engineering and industrial base needed.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 16

“Low Supply-side; High Demand-side” (lower right) Renaissance Light Emerging countries, mostly in the Middle East and Southeast Asia, which face burgeoning urban growth and much larger demand for desalination and water treatment, must meet these demands or they could suffer significant instability or even civil disruptions, as seen with “Arab Spring”. However, these “emerging nuclear power users” lack basic nuclear engineering and operational “supply-side” infrastructure; they must import it via procurement, typically. With a lack of supply factor strengths, these countries will be importers of nuclear technology. “High Supply-side; Low Demand-side” (upper left) Restructuring Countries, like the USA and Canada, operate 117 reactors (100 in USA; 17 in Canada), and nuclear power still provides at least 20% of electricity in North America – much more in Chicago and sub-regions like the mid-Atlantic. Impetus remains to maintain a nuclear “supply-side” infrastructure given this level of supply. Still, North America does not see large urban growth and demand on the scale seen in Asia. A lull in reactor construction from 1985 to 2005 led to industrial restructuring and consolidation among reactor owners (e.g., Unicom merging with ComEd to form Exelon; Duke with Cinergy and Progress). Toshiba bought Westinghouse from BNFL in 2006, and GE merged its nuclear business with Hitachi in 2007. France and Russia are P5 countries, so that status and the prospects for exporting nuclear expertise keeps them committed to maintaining nuclear infrastructure and supply-side factors in “Renaissance” mode. Countries in this quadrant will be exporters because they wield strong supply-side enabling factors, but in the OECD they see less growth in domestic demand. Japan after Fukushima represents a special case, where a massive tsunami in March 2011 from a 9.0+ earthquake killed 19,000 people, and triggered a nuclear disaster at Fukushima. This event led to a “Rollback” (shutdown policy) of its 50 reactors by Prime Minister Noda’s DPJ government. But, a landslide loss (175 seats of a total of 480 in Dec. 2012) by the DPJ, allowed the LDP to recapture a solid majority. LDP is slowly moving Japan back toward prudently restarting plants, with local approval. The largest utility, TEPCO, was nationalized in 2012, a clear sign of “Restructuring”. Prior to the disaster, Japan with major reactor vendors (e.g., Toshiba, Hitachi, Mitsubishi) and construction experience combined with dense urban demand was engaged fully in Renaissance and made plans to expand nuclear from 30% of electricity supply to above 40%. With restarts, Japan could return slowly to a Renaissance strategy. “Low Supply-side; Low Demand-side” (lower left) Rollback Countries, like Germany and Italy, which are fully developed and now face declining population levels, see little influx stressing their cities, and no energy demand growth. Some, like Belgium and Germany, face more vocal anti-nuclear citizenry at the ballot box. They have cut back their investment in nuclear laboratories and are closing reactors rather than building them, in other words, deliberately shrinking their supply-side strengths. None are members of the UNSC “P5” nuclear powers, so they can indulge in Rollback. Countries in Rollback are decommissioning units, and will struggle to replace such baseload with emission free capacity.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 17

Countries may fluctuate between strategies as supply and demand factors shift, or based on a change in political regime – as in Japan with the loss of power by LDP in 2009 after more than 40 years in power, or in Belgium to enable a coalition government. A shift in national strategy can also be triggered by a big event, such as Fukushima or Chernobyl or financial shock (Russian default in 1998; Global financial crisis of 2008-11); but the strength or weakness of factors will directly impact execution of a national strategy. Alliances will be needed to address key gaps. For example, the alliance formed by the UK with France (as in world wars), or Japan with the USA, both via acquisitions, enables these countries to bring more resources to a global market. Hence, based on their Supply and Demand ratings, the most active countries can be plotted relatively to reveal their national strategies, and emphasis for import, export, or both: National Nuclear Energy Strategies derived from Supply-side and Demand-side Factors

Source: ADPaterson; based on presentation Oct. 22 at FAS / GABI / KAIST, Washington, DC. Countries with the highest growth rates and rising urban loads find themselves in the Renaissance mode. More advanced (OECD) countries engaged in Renaissance strategy (e.g., France, Russia) have made top-down national commitments for more reactors and for exports, typically with sovereign financing support. Status as a P5 country bolsters this strategy in favor of nuclear power. Countries ranking lower in both Supply and Demand side factors can consider a Rollback strategy with few consequences to international alliances.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 18

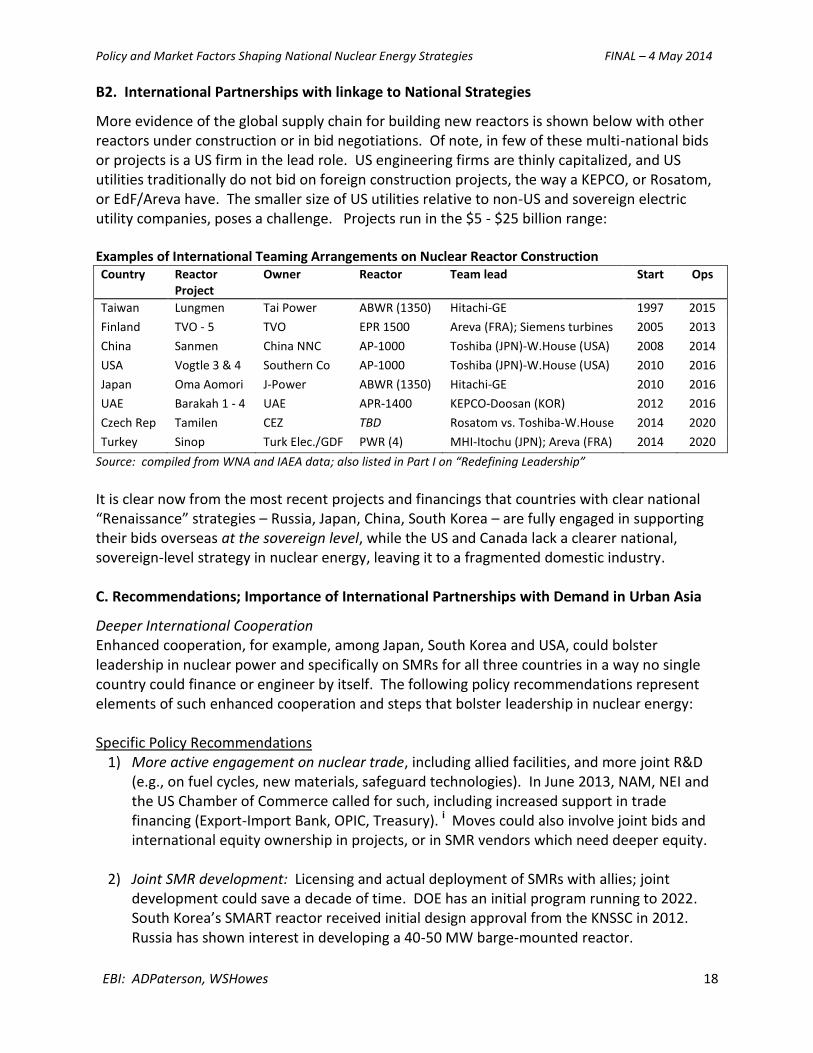

B2. International Partnerships with linkage to National Strategies

More evidence of the global supply chain for building new reactors is shown below with other reactors under construction or in bid negotiations. Of note, in few of these multi-national bids or projects is a US firm in the lead role. US engineering firms are thinly capitalized, and US utilities traditionally do not bid on foreign construction projects, the way a KEPCO, or Rosatom, or EdF/Areva have. The smaller size of US utilities relative to non-US and sovereign electric utility companies, poses a challenge. Projects run in the $5 - $25 billion range: Examples of International Teaming Arrangements on Nuclear Reactor Construction Country Reactor

Project Owner Reactor Team lead Start Ops

Taiwan Lungmen Tai Power ABWR (1350) Hitachi-GE 1997 2015

Finland TVO - 5 TVO EPR 1500 Areva (FRA); Siemens turbines 2005 2013

China Sanmen China NNC AP-1000 Toshiba (JPN)-W.House (USA) 2008 2014

USA Vogtle 3 & 4 Southern Co AP-1000 Toshiba (JPN)-W.House (USA) 2010 2016

Japan Oma Aomori J-Power ABWR (1350) Hitachi-GE 2010 2016

UAE Barakah 1 - 4 UAE APR-1400 KEPCO-Doosan (KOR) 2012 2016

Czech Rep Tamilen CEZ TBD Rosatom vs. Toshiba-W.House 2014 2020

Turkey Sinop Turk Elec./GDF PWR (4) MHI-Itochu (JPN); Areva (FRA) 2014 2020

Source: compiled from WNA and IAEA data; also listed in Part I on “Redefining Leadership”

It is clear now from the most recent projects and financings that countries with clear national “Renaissance” strategies – Russia, Japan, China, South Korea – are fully engaged in supporting their bids overseas at the sovereign level, while the US and Canada lack a clearer national, sovereign-level strategy in nuclear energy, leaving it to a fragmented domestic industry. C. Recommendations; Importance of International Partnerships with Demand in Urban Asia

Deeper International Cooperation Enhanced cooperation, for example, among Japan, South Korea and USA, could bolster leadership in nuclear power and specifically on SMRs for all three countries in a way no single country could finance or engineer by itself. The following policy recommendations represent elements of such enhanced cooperation and steps that bolster leadership in nuclear energy: Specific Policy Recommendations

1) More active engagement on nuclear trade, including allied facilities, and more joint R&D (e.g., on fuel cycles, new materials, safeguard technologies). In June 2013, NAM, NEI and the US Chamber of Commerce called for such, including increased support in trade financing (Export-Import Bank, OPIC, Treasury). i Moves could also involve joint bids and international equity ownership in projects, or in SMR vendors which need deeper equity.

2) Joint SMR development: Licensing and actual deployment of SMRs with allies; joint development could save a decade of time. DOE has an initial program running to 2022. South Korea’s SMART reactor received initial design approval from the KNSSC in 2012. Russia has shown interest in developing a 40-50 MW barge-mounted reactor.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 19

3) Government investment for reactor construction (e.g., federal loans; credit support, such

as mentioned in the White House Climate Action Plan). US Export-Import Bank financing support on the Westinghouse bid in the Czech Republic is a clear example. This could entail a Presidential level agreement, as each named it a top multi-lateral priority. First units will not be bought by investor-owned utilities; as with the first reactors, government orders or financing will be needed to overcome risks on such large plants, or on SMRs.

4) International fuel management: Several experts and IAEA have endorsed multi-lateral fuel governance, with sovereign spent fuel take back, as the US does now on foreign research reactors. ii This would also increase NPT control of nuclear materials and strengthen arguments for less fragmentation of enrichment capability.

Other countries are looking to the US for deeper collaboration, renewal of Section 123 nuclear cooperation agreements, iii and for US leadership in nuclear power to address their own energy security and development. All of these policy recommendations will entail closer coordination (e.g., regular meetings, perhaps joint governance) among State, DOE, NRC, Commerce, and the trade financing units (OPIC, Ex-Im Bank). In her first state visit with President Obama in May 2013 Madame President Park of South Korea directly raised the issue of joint work on nuclear technology deployment as a top priority in their talks at the highest levels.iv Pentagon geo-strategist Thomas Barnett, formerly at the Naval War College, highlighted the importance of engaging in Asia strategically in his latest book: The Great Globalization Build-out “In the Big Push heyday of Western foreign aid the vast majority of infrastructure building was directed by Western public entities using public funds. It was Supply-Push, depending on how the West felt. Today the situation is reversed – the majority of building in emerging economies can be described as Demand-Pull. Asian companies are creating the physical connectivity to access raw materials while back home their governments and national flagship companies engage in massive build outs of road, rail, ports, power generation and distribution. After decades of hand-wringing by the West over ‘who is going to save the world’s poor?’; we find ourselves largely standing on the sidelines while Asians step up to save themselves... And, China accounts for 40% of the total.”

Thomas Barnett, author of The Pentagon’s New Map Great Powers – American and the World after Bush, 2009 [p. 320]

Clean, reliable electricity for major urban areas, particularly in Asia, poses the largest arena for development and deployment of reactors done right. The US will need to team with prominent allies in Asia, particularly Japan and South Korea, and eventually India, to achieve its own geo-political and economic objectives (e.g., trade expansion, lower global pollution levels, retention of nuclear engineering expertise), and to maintain safety and non-proliferation practices in this critical sector. Leadership in nuclear energy, and with SMRs, must now respond to a more intense demand-side landscape via alliances in Asia, where the market is unfolding and where

real progress can be made on global emissions and urban resilience.v

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 20

D. Conclusions

The interaction of these supply and demand factors comprises a dynamic landscape within which trans-national public-private partnerships are becoming more important. Because no single country is self-sufficient, and because the regions with highest demand factors are not those with historically strong supply factors, it appears that the best strategic opportunities for US industry may reside in countries with: – A robust track record of current operations of nuclear reactors (S2) – High quality nuclear regulatory capacity with strong ties to IAEA and US NRC (S3) – Superior engineering, skilled labor, and manufacturing in nuclear supply chain (S4, S5, S7) – Access to low cost capital for financing for capital intensive nuclear plants (S6) – Clear regimes of asset control for nuclear facilities (e.g., military bases, secured sites) – Strong presence in Asia (Japan and Korea are the most obvious allies based on current ties.) An accelerated push for SMRs substantially beyond the small DOE program (<$1 billion over ten years) underway now offers a clear option for US vendors and engineering firms to bring prudent growth and leadership on standards, practices, and regulations to the emerging and replacement market. A smaller, more secure and modular product offering would enable smaller countries with higher population growth and water desalination needs to develop without straining fossil resources further and with much lower emissions. Closing: Letting leadership in nuclear energy wither away… The USA cannot idly let its leadership position wither away in the global nuclear energy landscape, just as Britain did when it discovered “cheap North Sea gas” in the 1980s. Britain used up its cheap gas over three decades and is now dependent once again on imported energy, and faces higher electricity prices. In the nuclear arena, leadership cannot be “restored” based on the old “push” model of Supply-side dominance from the 20th Century. The Demand-side factors now are pulling nuclear power construction forward in the 21st Century to satisfy burgeoning electric demand, primarily in Asian Cities. USA and allies must redefine its leadership role via international partnerships and alliances that are unfolding now. “Energy disparities create dangerous friction between the energy haves and have-nots. Throughout history – both in war and in peace -- poverty and prosperity have been inextricably connected to energy through the enormous power it confers on those who have it and the vulnerability it spells for those who don’t, as well as the tension created by the breach between them. American leadership on energy development and climate change can be an effective means by which we affect world outcomes.” General James L. Jones,

Former National Security Director (2009-10), Supreme Allied Commander Europe (2003-06) Testimony to Senate Foreign Relations Comm., March 13, 2014

Leadership in the global nuclear energy market and in safeguards and regulatory policy no longer means selling or operating more reactors than the next country; instead, it will increasingly be executed through international cooperative agreements and by multinational consortiums and investments, supported by government policies mindful of long-term benefits, such as energy security, urban resilience for large cities, plus vital emissions reductions.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 21

SUMMARY: Key Supply and Demand Factors for Nuclear Energy going forward http://www.atlanticcouncil.org/publications/reports/redefining-leadership-in-the-global-nuclear-energy-market

Success Factors for Nuclear Energy: Supply-side and Demand-side Intensity Drivers As previously mentioned a key question going forward will be how to define the best strategic partnership opportunities. In the past, as seen in the Figure below, the United States and Europe had the most favorable supply-side strengths. Summary of Supply and Demand Factors and National Nuclear Strategies Updated from Part I: Redefining Leadership in Global Nuclear Energy Markets” by Andrew Paterson, Walter Howes

During the expansion era of nuclear power construction in the 1960s to 1980s, the United States led the world in many of the key “Supply Side” success factors. The relative strength of each country or mini-region was assessed on a relative basis (on a scale from 1 as a low value to 5 as a high value), and then the combined ratings were indexed to the highest entity in the evaluation. The chart shows how much the demand-side factors have emerged as key drivers in the 21st Century for new reactor construction going forward, compared to the supply-side factors that drove construction among OECD countries in the last Century during the Cold War. On the supply-side, the United States wields superior ratings in (S2) a military industrial base for a nuclear navy; (S3) regulatory practices; (S5) nuclear engineering talent; (S6) access to low cost financing; and (S7) the current reactor base. By contrast, China lacks the operating base of leaders France and the United States; however, China, India, and growing Asia see higher demand side factors associated with rapid population growth and urbanization (D1, D2, D4, D7), as well as higher natural gas prices, which makes nuclear energy more competitive. A summary of Supply and Demand factors follows:

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 22

S1. R&D Reactors, National Labs and Technology Innovation: The US Department of Energy funds a significant complex of national laboratories with nuclear expertise (weapons, fuel, and reactors). Other P5 countries maintain such R&D infrastructure and programs, but less so than in China, Japan, and in South Korea. Britain’s nuclear engineering establishment has been hollowed out after two decades of inactivity, and now the entire nuclear fleet is owned by EdF (France). S2. Military industrial base for nuclear power: US nuclear power expertise and a commitment to light water reactors (LWRs) started with the construction of the nuclear navy in the 1950s-70s. Today the USA wields ten nuclear-powered aircraft carriers and about 80 nuclear submarines. No other country wields close to this operating base. Early on many retired officers from the US Nuclear Navy were hired as managers at nuclear utilities, bringing reactor management knowledge to the commercial sector. The fueling infrastructure and experience with naval reactors also contributed to US engineering experience. S3. High quality nuclear regulatory practices: The US NRC continues to provide the high benchmark for nuclear regulation. And, national nuclear regulators now meet more often at international forums and via IAEA to share best practices. Regulatory practices for emerging nuclear users are paramount to ensure public engagement, implementation of safeguards, reliable operations, and emissions savings. S4. Nuclear fuel infrastructure and ore supply: Russia and France lead in offering the full slate of fuel cycle services, including enrichment and reprocessing. By law the United States does not reprocess spent fuel, but for the past two decades, the “Megatons to Megawatts” program converted Russian nuclear warheads to reactor fuel (ended in 2013). China and India are developing reprocessing expertise and capacity, and URENCO, a consortium with $2 billion in annual revenues owned by the governments of Germany, Holland, and the UK, provides enriched nuclear fuel worldwide. Southeast Asia (not including China) and the Middle East lack most of the key supply side factors for nuclear power, but are rated quite high on demand side factors, particularly on population growth and urban demand with much faster growth in electricity consumption and demand for fresh water. The profound shift underway in commercial nuclear partnerships, in part, is being driven by demand side factors in rapidly developing urban Asia. Spent fuel will likely require “take back” arrangements because storage in these emerging countries is not and efficient or optimal situation. S5. Nuclear engineering talent and skilled labor (college programs, technical firms, union training): Almost half the US nuclear engineering programs at universities closed in the 1980s when demand slumped after Three Mile Island (1979), and as DOE funding was cutback during the Clinton Administration. In 2010, US colleges graduated more than 450 nuclear engineers (B.S. degrees) with as

many master’s and PhDs awarded; up from below 300 in the late 1990svi

. Skilled labor and union

training plays a major role in precision construction for reactors. Korea, Japan, France, Russia, China and India produce more nuclear engineering graduates now than the USA, and compared to a decade ago. S6. Access to low cost debt financing, capital (public or private): While the Euro currency crisis poses financing challenges in Europe, most of the P5 countries, plus Japan, South Korea, and India retain access to low cost capital, particularly for sovereign entities and national utilities in global bond markets. Still, US utilities garner credit ratings in the BBB to A range, while sovereigns garner AA to AAA ratings. S7. Current reactor operating base: Even with recent shutdowns of four reactors, US reactor capacity leads the world with 100 reactors operating in 2012, with France (58 reactors) and Japan (51) next in line, as the only other countries with more than 50 reactors installed. [See table on page 11]

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 23

S8. Engineering firms with recent construction experience: Since the acquisition in 2006 by Toshiba of Westinghouse Nuclear, and formation of Hitachi-GE Nuclear (2007), engineering firms in Asia (SK, Doosan, Hyundai, Mitsubishi, Shanghai Engineering) are garnering the most construction experience now going forward. Others, such as Fluor, Areva, CB&I/Shaw are seeking work in Asia to keep pace. Going forward, “demand side” market factors will favor construction in markets outside of the US and run much bigger outside North America and Europe. [See table of construction on page 11.] D1. Growing population overall: Unlike Japan or Europe, developing Asia and the Middle East see much higher population growth rates. With Mexico, the North American Free Trade Agreement (NAFTA) region is growing faster than Europe, and will surpass Europe in population before 2030. From 2000, Mexico will add another 30 million people before 2030, creating demand for more energy within the NAFTA bloc. And, Mexico will need alternatives (beyond its two reactors) as its oil production declines further from its peak in 2005. Population growth and urbanization in Asia will drive energy demand growth at higher rates than economic growth. “China’s automobile market will nearly triple in size to 40 million, nearly half of world production by 2020, according to one of the country’s top producers.” [FT] D2. Current dense, urban electric loads: The US and Europe only have 3 or 4 cities with more than 5 million people, whereas, Asia – principally China and India – will see dozens that large by 2030. More than 1,000 cities will top one million residents before 2040 worldwide, about 60 percent of them in Asia. D3. Advanced industrial and manufacturing base: An advanced industrial base requires high quality, reliable electricity and the OECD countries have that. But with more “off-shoring” since 2000, China, India, and Asia have built up their manufacturing capacity considerably with intensified industrialization. Some factory capacity is migrating back to North America because of cheap natural gas feedstock prices and reliable energy. But, those cheap natural gas prices also make nuclear reactors less competitive. D4. Rising per capita energy use (vs. OECD average): OECD countries are developed, so per capita energy use is not rising much, and may even decline. Asia is industrializing, and vehicle use will mushroom over the next decade. By 2025, new car sales in China may double that of US sales. Because oil is priced globally, this demand will raise oil prices unless more electric vehicles are sold. Charging such electric vehicles will increase urban electricity demand further. D5. Higher natural gas prices (nuclear competitiveness): Because natural gas prices in Asia run three or four times more expensive than in North America, nuclear power is more competitive despite the higher construction costs seen in the most recent reactor projects in a globalized nuclear supply chain. D6. Significant air pollution (need for clean energy options): China and India, due to their rising reliance on coal since 2000, are looking to reverse severe air pollution by building more nuclear plants. Large cities will need to reduce emissions to be livable, dramatized by each summer’s heat wave in Asia. D7. Future growth in urban load: The largest cities in North America and Europe are not growing rapidly, or at all. China alone will see 200 cities with more than 1 million people by 2030, and India similarly. D8. Policies and regulations favoring reduced emissions: Where countries have implemented either more regulations on emissions (Europe, North America) or subsidies, nuclear will be more competitive. In some countries, such policies entail a national entity ordering reactors, rather than tax policy.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 24

E. APPENDIX: Country Profiles & National Strategy points Comparative Compilations of Key Demand-side Drivers

actual actual projected Growth %Growth

Population (million) 2000 2010 2020 2000 - 20 2000 - 20

USA 282 308 332 50 17.7%

Canada 30.8 34.1 36.2 5 17.5%

UK - Britain 58.9 62.3 67.2 8 14.1%

France 60.9 65.0 67.7 7 11.2%

Russia 146.3 142.4 149.7 3 2.3%

South Korea 47.0 49.4 51.4 4 9.4%

Japan 127.0 128.0 125.2 -2 -1.4%

China 1,270.0 1,340.0 1,440.0 170 13.4%

India 1,042.0 1,206.0 1,380.0 338 32.4%

Urban population 2000 2010 2020 2000 - 20 2000 - 20

USA 222.0 261.0 285.4 63 28.6%

Canada 24.0 27.3 29.7 6 23.6%

UK - Britain 44.8 49.3 55.1 10 23.1%

France 48.7 53.4 56.9 8 16.7%

Russia 102.4 102.7 110.8 8 8.2%

South Korea 37.4 40.2 42.0 5 12.3%

Japan 100.0 115.0 113.9 14 13.9%

China 533.4 635.0 775.0 242 45.3%

India 286.6 361.8 448.5 162 56.5%

Annual Elec. Consumed (million MWhs) 2000 2010 2020 2000-20 2000-20

USA 3,800 4,125 4,401 601 15.8%

Canada 590 586 634 44 7.5%

UK - Britain 335 329 340 5 1.5%

France 464 505 558 94 20.3%

Russia 751 861 900 149 19.8%

South Korea 263 450 600 337 128.1%

Japan 942 1,002 1,080 138 14.6%

China 1,180 4,100 8,200 7,020 594.9%

India 376.0 700.0 1,400 1,024 272.3%

Electricity Consumed per capita (MWhs) 2000 2010 2020 2000-20 2000-20

USA 13.5 13.4 13.3 -0.2 -1.6%

Canada 19.2 17.2 17.5 -1.6 -8.5%

UK - Britain 5.7 5.3 5.1 -0.6 -11.0%

France 7.6 7.8 8.2 0.6 8.2%

Russia 5.1 6.0 6.0 0.9 17.1%

South Korea 5.6 9.1 11.7 6.1 108.6%

Japan 7.4 7.8 8.6 1.2 16.3%

China 0.9 3.1 5.7 4.8 512.9%

India 0.4 0.6 1.0 0.7 181.1%

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 25

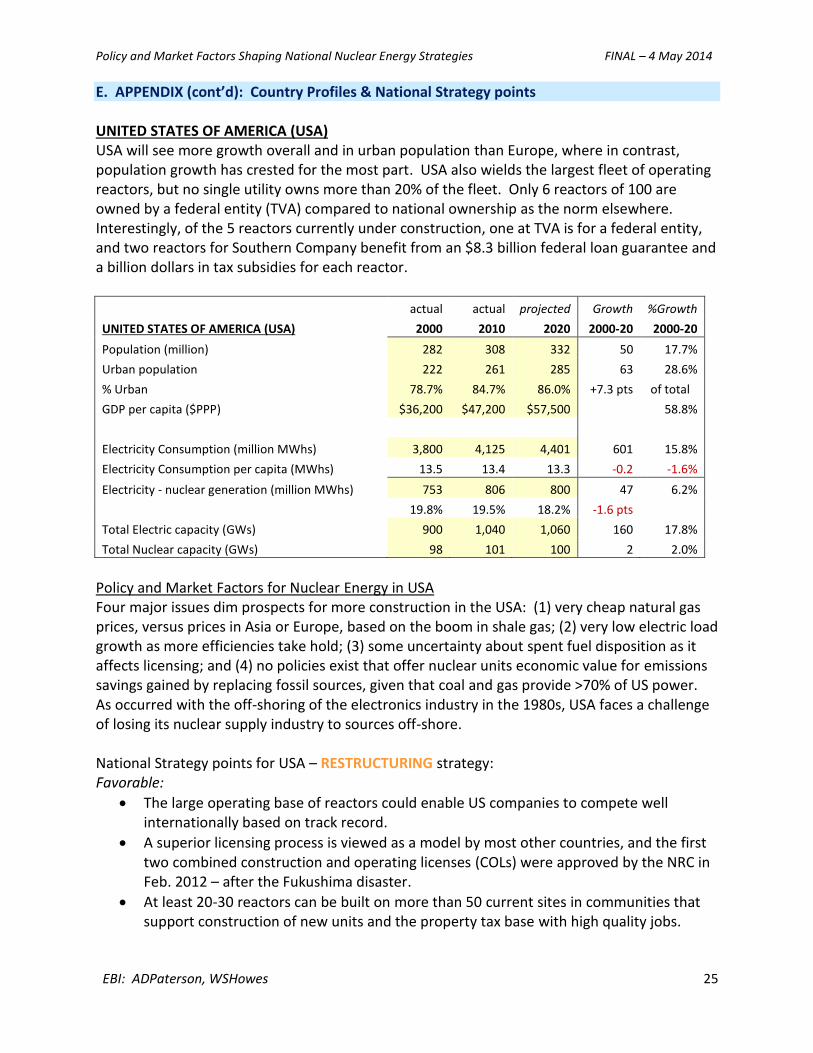

E. APPENDIX (cont’d): Country Profiles & National Strategy points UNITED STATES OF AMERICA (USA) USA will see more growth overall and in urban population than Europe, where in contrast, population growth has crested for the most part. USA also wields the largest fleet of operating reactors, but no single utility owns more than 20% of the fleet. Only 6 reactors of 100 are owned by a federal entity (TVA) compared to national ownership as the norm elsewhere. Interestingly, of the 5 reactors currently under construction, one at TVA is for a federal entity, and two reactors for Southern Company benefit from an $8.3 billion federal loan guarantee and a billion dollars in tax subsidies for each reactor.

actual actual projected Growth %Growth

UNITED STATES OF AMERICA (USA) 2000 2010 2020 2000-20 2000-20

Population (million) 282 308 332 50 17.7%

Urban population 222 261 285 63 28.6%

% Urban 78.7% 84.7% 86.0% +7.3 pts of total

GDP per capita ($PPP) $36,200 $47,200 $57,500 58.8%

Electricity Consumption (million MWhs) 3,800 4,125 4,401 601 15.8%

Electricity Consumption per capita (MWhs) 13.5 13.4 13.3 -0.2 -1.6%

Electricity - nuclear generation (million MWhs) 753 806 800 47 6.2%

19.8% 19.5% 18.2% -1.6 pts

Total Electric capacity (GWs) 900 1,040 1,060 160 17.8%

Total Nuclear capacity (GWs) 98 101 100 2 2.0%

Policy and Market Factors for Nuclear Energy in USA Four major issues dim prospects for more construction in the USA: (1) very cheap natural gas prices, versus prices in Asia or Europe, based on the boom in shale gas; (2) very low electric load growth as more efficiencies take hold; (3) some uncertainty about spent fuel disposition as it affects licensing; and (4) no policies exist that offer nuclear units economic value for emissions savings gained by replacing fossil sources, given that coal and gas provide >70% of US power. As occurred with the off-shoring of the electronics industry in the 1980s, USA faces a challenge of losing its nuclear supply industry to sources off-shore. National Strategy points for USA – RESTRUCTURING strategy: Favorable:

The large operating base of reactors could enable US companies to compete well internationally based on track record.

A superior licensing process is viewed as a model by most other countries, and the first two combined construction and operating licenses (COLs) were approved by the NRC in Feb. 2012 – after the Fukushima disaster.

At least 20-30 reactors can be built on more than 50 current sites in communities that support construction of new units and the property tax base with high quality jobs.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 26

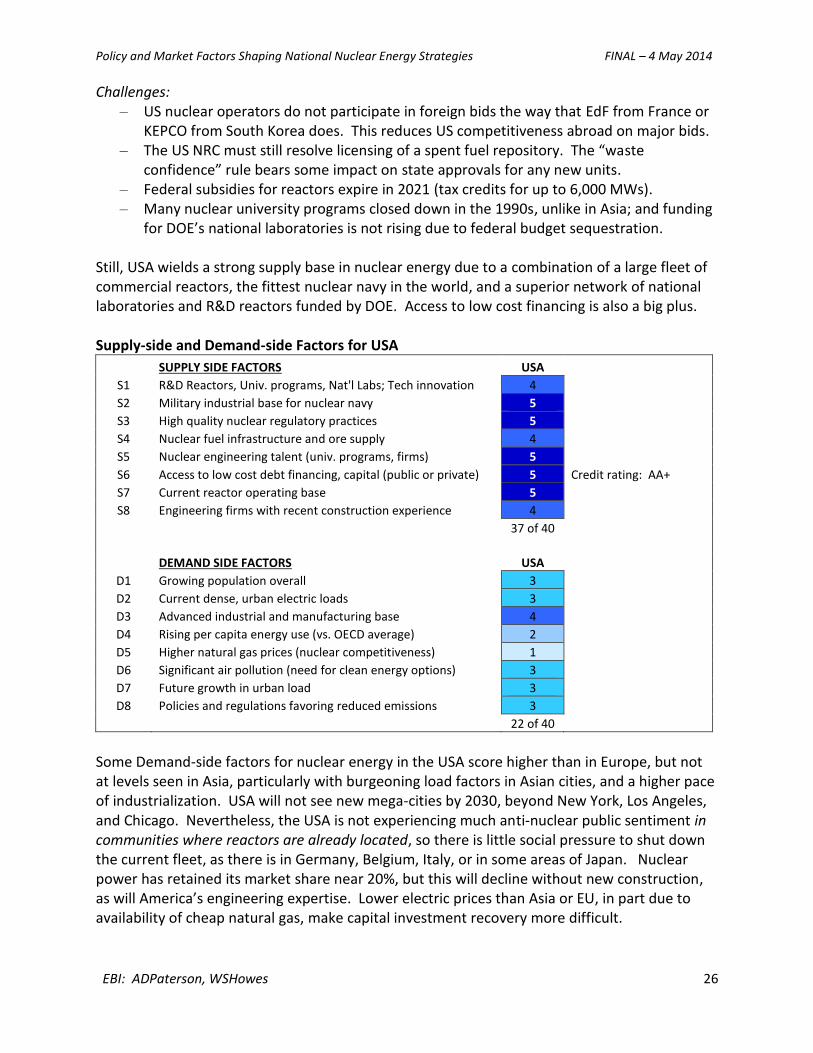

Challenges: ‒ US nuclear operators do not participate in foreign bids the way that EdF from France or

KEPCO from South Korea does. This reduces US competitiveness abroad on major bids. ‒ The US NRC must still resolve licensing of a spent fuel repository. The “waste

confidence” rule bears some impact on state approvals for any new units. ‒ Federal subsidies for reactors expire in 2021 (tax credits for up to 6,000 MWs). ‒ Many nuclear university programs closed down in the 1990s, unlike in Asia; and funding

for DOE’s national laboratories is not rising due to federal budget sequestration. Still, USA wields a strong supply base in nuclear energy due to a combination of a large fleet of commercial reactors, the fittest nuclear navy in the world, and a superior network of national laboratories and R&D reactors funded by DOE. Access to low cost financing is also a big plus. Supply-side and Demand-side Factors for USA

SUPPLY SIDE FACTORS USA

S1 R&D Reactors, Univ. programs, Nat'l Labs; Tech innovation 4 S2 Military industrial base for nuclear navy 5 S3 High quality nuclear regulatory practices 5 S4 Nuclear fuel infrastructure and ore supply 4 S5 Nuclear engineering talent (univ. programs, firms) 5 S6 Access to low cost debt financing, capital (public or private) 5 Credit rating: AA+

S7 Current reactor operating base 5 S8 Engineering firms with recent construction experience 4

37 of 40

DEMAND SIDE FACTORS USA

D1 Growing population overall 3 D2 Current dense, urban electric loads 3 D3 Advanced industrial and manufacturing base 4 D4 Rising per capita energy use (vs. OECD average) 2 D5 Higher natural gas prices (nuclear competitiveness) 1 D6 Significant air pollution (need for clean energy options) 3 D7 Future growth in urban load 3 D8 Policies and regulations favoring reduced emissions 3

22 of 40

Some Demand-side factors for nuclear energy in the USA score higher than in Europe, but not at levels seen in Asia, particularly with burgeoning load factors in Asian cities, and a higher pace of industrialization. USA will not see new mega-cities by 2030, beyond New York, Los Angeles, and Chicago. Nevertheless, the USA is not experiencing much anti-nuclear public sentiment in communities where reactors are already located, so there is little social pressure to shut down the current fleet, as there is in Germany, Belgium, Italy, or in some areas of Japan. Nuclear power has retained its market share near 20%, but this will decline without new construction, as will America’s engineering expertise. Lower electric prices than Asia or EU, in part due to availability of cheap natural gas, make capital investment recovery more difficult.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 27

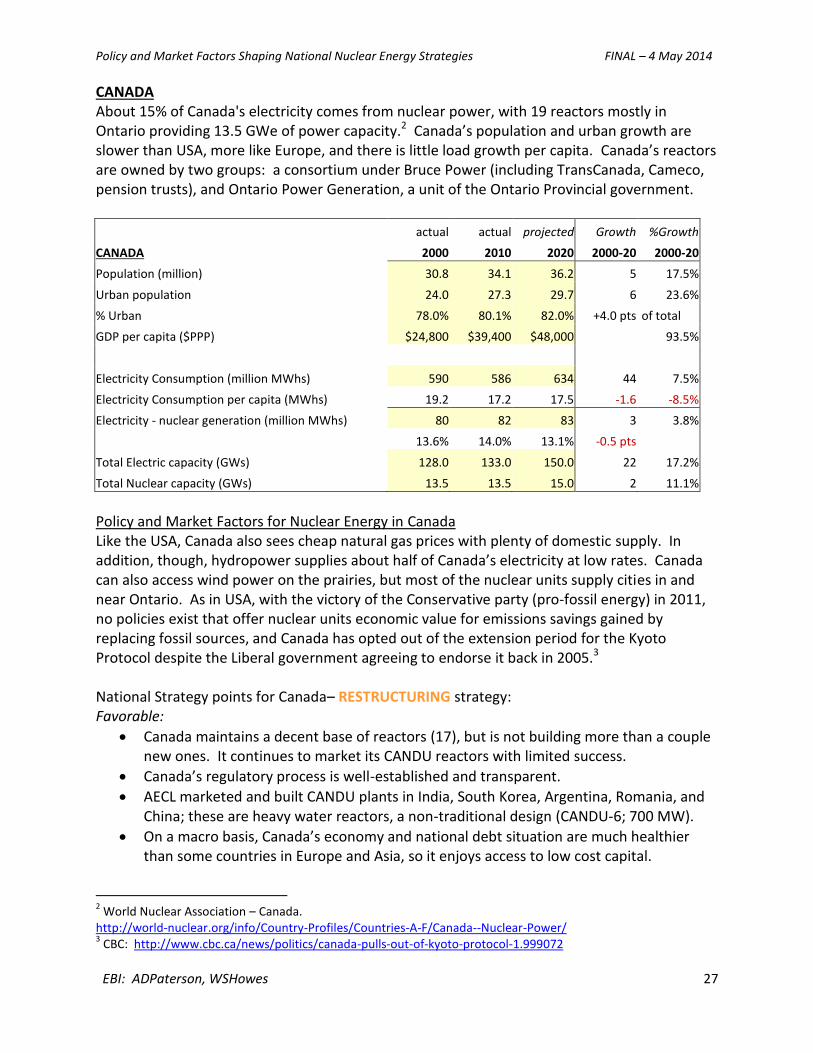

CANADA About 15% of Canada's electricity comes from nuclear power, with 19 reactors mostly in Ontario providing 13.5 GWe of power capacity.2 Canada’s population and urban growth are slower than USA, more like Europe, and there is little load growth per capita. Canada’s reactors are owned by two groups: a consortium under Bruce Power (including TransCanada, Cameco, pension trusts), and Ontario Power Generation, a unit of the Ontario Provincial government.

actual actual projected Growth %Growth

CANADA 2000 2010 2020 2000-20 2000-20

Population (million) 30.8 34.1 36.2 5 17.5%

Urban population 24.0 27.3 29.7 6 23.6%

% Urban 78.0% 80.1% 82.0% +4.0 pts of total

GDP per capita ($PPP) $24,800 $39,400 $48,000 93.5%

Electricity Consumption (million MWhs) 590 586 634 44 7.5%

Electricity Consumption per capita (MWhs) 19.2 17.2 17.5 -1.6 -8.5%

Electricity - nuclear generation (million MWhs) 80 82 83 3 3.8%

13.6% 14.0% 13.1% -0.5 pts

Total Electric capacity (GWs) 128.0 133.0 150.0 22 17.2%

Total Nuclear capacity (GWs) 13.5 13.5 15.0 2 11.1%

Policy and Market Factors for Nuclear Energy in Canada Like the USA, Canada also sees cheap natural gas prices with plenty of domestic supply. In addition, though, hydropower supplies about half of Canada’s electricity at low rates. Canada can also access wind power on the prairies, but most of the nuclear units supply cities in and near Ontario. As in USA, with the victory of the Conservative party (pro-fossil energy) in 2011, no policies exist that offer nuclear units economic value for emissions savings gained by replacing fossil sources, and Canada has opted out of the extension period for the Kyoto Protocol despite the Liberal government agreeing to endorse it back in 2005.3 National Strategy points for Canada– RESTRUCTURING strategy: Favorable:

Canada maintains a decent base of reactors (17), but is not building more than a couple new ones. It continues to market its CANDU reactors with limited success.

Canada’s regulatory process is well-established and transparent.

AECL marketed and built CANDU plants in India, South Korea, Argentina, Romania, and China; these are heavy water reactors, a non-traditional design (CANDU-6; 700 MW).

On a macro basis, Canada’s economy and national debt situation are much healthier than some countries in Europe and Asia, so it enjoys access to low cost capital.

2 World Nuclear Association – Canada.

http://world-nuclear.org/info/Country-Profiles/Countries-A-F/Canada--Nuclear-Power/ 3 CBC: http://www.cbc.ca/news/politics/canada-pulls-out-of-kyoto-protocol-1.999072

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 28

Challenges: ‒ Relatively cheap electricity prices, due primarily to cheap hydropower and low natural

gas prices, make reactors much less competitive for the domestic market. ‒ Unlike the USA, Canada is not a UNSC “P5” nuclear power, and does not maintain much

nuclear infrastructure for a navy or other military “supply-side” applications. Its supply side strength is thinner than that of the USA (a rating of 26 vs 37).

‒ Canada’s smaller size firms lack the balance sheet needed to lead large multiple reactor bids in foreign countries, and neither Bruce Power nor OPG participate in such bids.

‒ Poor sales and cost overruns ($1.2 billion since 2007) led to the Canadian government privatizing AECL in 2011 to engineering firm SNC-Lavalin ($7 billion in revenues).

Supply-side and Demand-side Factors for Canada

SUPPLY SIDE FACTORS CANADA

S1 R&D Reactors, Univ. programs, Nat'l Labs; Tech innovation 3 S2 Military industrial base for nuclear navy 1 S3 High quality nuclear regulatory practices 4 S4 Nuclear fuel infrastructure and ore supply 4 S5 Nuclear engineering talent (univ. programs, firms) 4 S6 Access to low cost debt financing, capital (public or private) 4 Credit rating: AAA

S7 Current reactor operating base 3 S8 Engineering firms with recent construction experience 3

26

DEMAND SIDE FACTORS CANADA

D1 Growing population overall 3 D2 Current dense, urban electric loads 2 D3 Advanced industrial and manufacturing base 4 D4 Rising per capita energy use (vs. OECD average) 4 D5 Higher natural gas prices (nuclear competitiveness) 1 D6 Significant air pollution (need for clean energy options) 1 D7 Future growth in urban load 2 D8 Policies and regulations favoring reduced emissions 2

19

Demand-side factors for nuclear energy in Canada run below even the UK or France, primarily because of inexpensive electricity prices and the lack of very large cities. From 2000 to 2020 Canada will add fewer than 6 million people. As in the USA, there is little social pressure to shut down the current fleet. With coal providing just 13% of electricity, there is a much smaller opportunity to replace coal with nuclear. Nuclear power will likely retain its market share near 15% through 2030, but Canada must amp up a stronger export effort or engage in broader international partnerships to stay competitive in the global nuclear energy market.

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 29

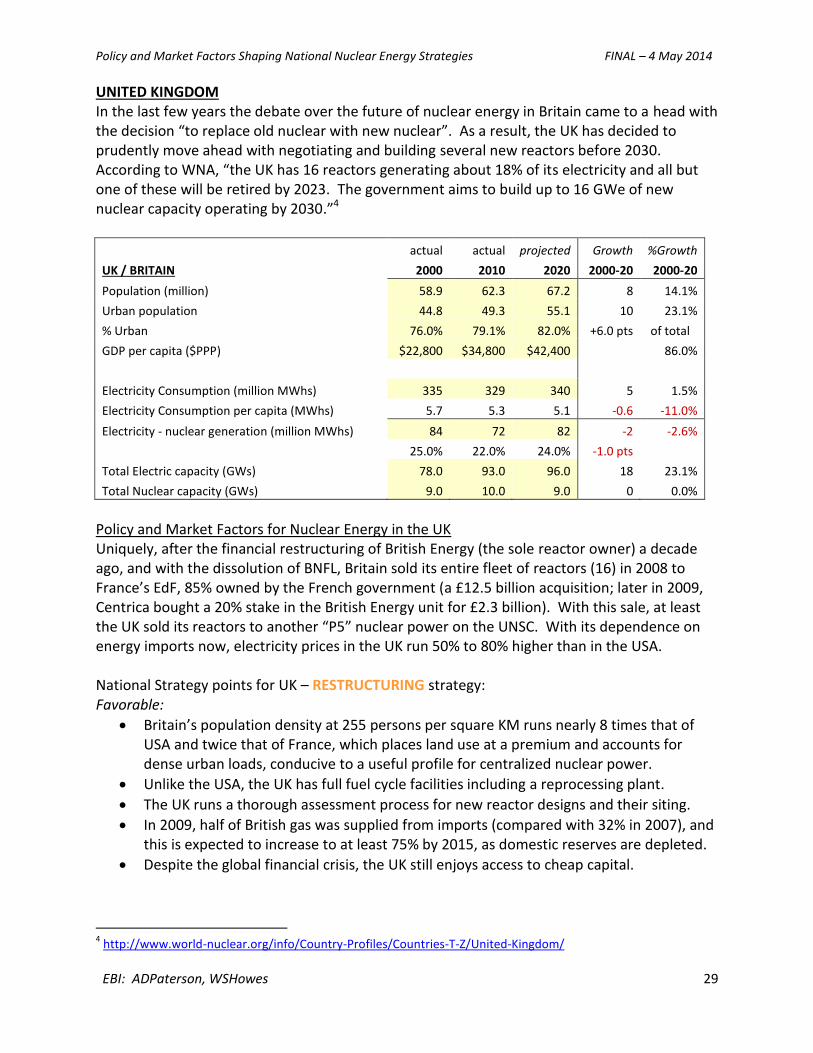

UNITED KINGDOM In the last few years the debate over the future of nuclear energy in Britain came to a head with the decision “to replace old nuclear with new nuclear”. As a result, the UK has decided to prudently move ahead with negotiating and building several new reactors before 2030. According to WNA, “the UK has 16 reactors generating about 18% of its electricity and all but one of these will be retired by 2023. The government aims to build up to 16 GWe of new nuclear capacity operating by 2030.”4

actual actual projected Growth %Growth

UK / BRITAIN 2000 2010 2020 2000-20 2000-20

Population (million) 58.9 62.3 67.2 8 14.1%

Urban population 44.8 49.3 55.1 10 23.1%

% Urban 76.0% 79.1% 82.0% +6.0 pts of total

GDP per capita ($PPP) $22,800 $34,800 $42,400 86.0%

Electricity Consumption (million MWhs) 335 329 340 5 1.5%

Electricity Consumption per capita (MWhs) 5.7 5.3 5.1 -0.6 -11.0%

Electricity - nuclear generation (million MWhs) 84 72 82 -2 -2.6%

25.0% 22.0% 24.0% -1.0 pts

Total Electric capacity (GWs) 78.0 93.0 96.0 18 23.1%

Total Nuclear capacity (GWs) 9.0 10.0 9.0 0 0.0%

Policy and Market Factors for Nuclear Energy in the UK Uniquely, after the financial restructuring of British Energy (the sole reactor owner) a decade ago, and with the dissolution of BNFL, Britain sold its entire fleet of reactors (16) in 2008 to France’s EdF, 85% owned by the French government (a £12.5 billion acquisition; later in 2009, Centrica bought a 20% stake in the British Energy unit for £2.3 billion). With this sale, at least the UK sold its reactors to another “P5” nuclear power on the UNSC. With its dependence on energy imports now, electricity prices in the UK run 50% to 80% higher than in the USA. National Strategy points for UK – RESTRUCTURING strategy: Favorable:

Britain’s population density at 255 persons per square KM runs nearly 8 times that of USA and twice that of France, which places land use at a premium and accounts for dense urban loads, conducive to a useful profile for centralized nuclear power.

Unlike the USA, the UK has full fuel cycle facilities including a reprocessing plant.

The UK runs a thorough assessment process for new reactor designs and their siting.

In 2009, half of British gas was supplied from imports (compared with 32% in 2007), and this is expected to increase to at least 75% by 2015, as domestic reserves are depleted.

Despite the global financial crisis, the UK still enjoys access to cheap capital.

4 http://www.world-nuclear.org/info/Country-Profiles/Countries-T-Z/United-Kingdom/

Policy and Market Factors Shaping National Nuclear Energy Strategies FINAL – 4 May 2014

EBI: ADPaterson, WSHowes 30

Challenges: ‒ While Britain sees some urban growth, its electricity consumption is basically flat. ‒ With little reactor construction the last two decades and the dissolution of BNFL, much

of Britain’s nuclear engineering capacity has withered and retired. It lacks the university or national laboratory infrastructure of the other “P5” nuclear powers.

‒ Now that France owns the UK nuclear fleet, it will be difficult for Britain to formulate an export strategy as it has done traditionally in its mercantile history, except in a subsidiary role to more active foreign partners.

Supply-side and Demand-side Factors for UK

SUPPLY SIDE FACTORS UK