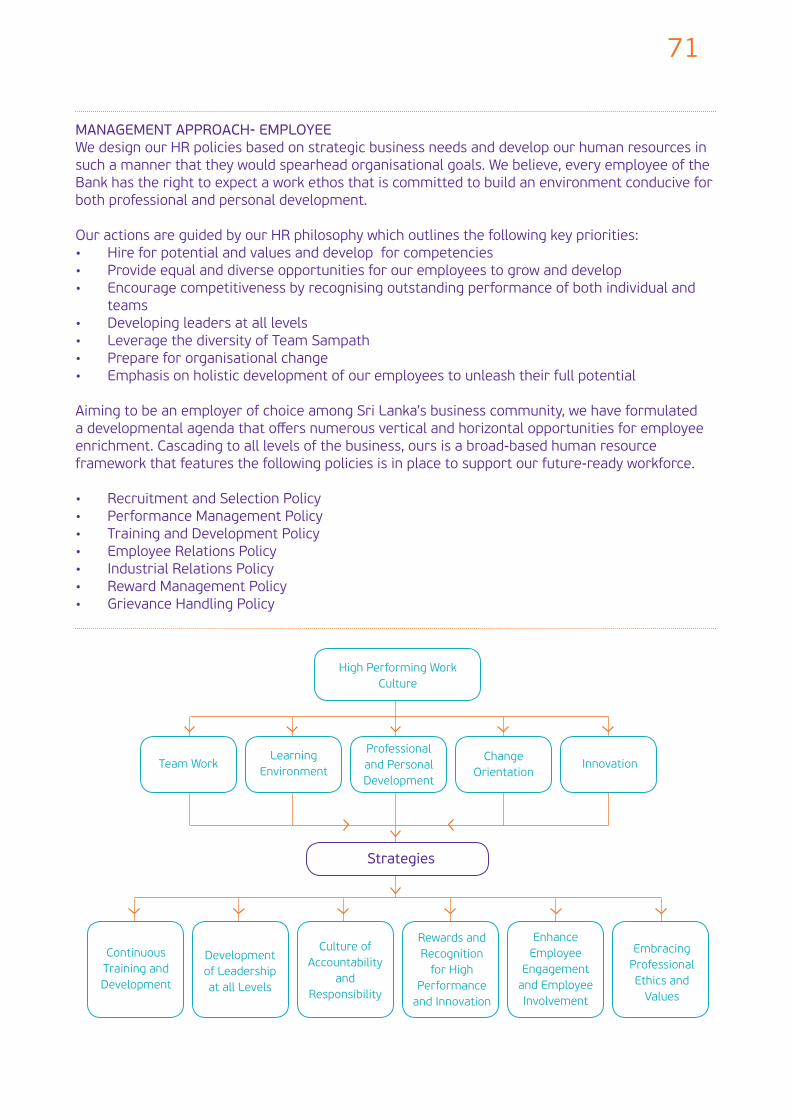

OUR STAKEHOLDERS - Sampath Bank PLC

472

JUST ASK OUR STAKEHOLDERS ANNUAL REPORT 2014 FINANCIAL, SOCIAL AND ENVIRONMENTAL PERFORMANCE

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of OUR STAKEHOLDERS - Sampath Bank PLC

JUST ASK

OUR STAKEHOLDERS

ANNUAL REPORT 2014FINANCIAL, SOCIAL AND ENVIRONMENTAL PERFORMANCE

At Sampath Bank, we’re very proud of the many ways in which we create value for everyone we work with; through our innovative banking products and services, our principled business practices and ethical approach and the prudent and far-sighted strategies that have driven our trajectory of growth for over 27 years.

a comprehensive analysis of how we generate real

levels, for the thousands of stakeholders we serve.

But you don’t have to take our word for it.

Just ask our stakeholders.

JUST ASK

OUR STAKEHOLDERS

READ THIS REPORT ONLINE

http://www.sampath.lk/images/annual_reports/ar2014.pdf

Content

3 7

Board of Directors 10Corporate Management 16Chief Managers 21Senior Managers 24Vision & Values 28

29 30

Highlights 32Awards and Accolades for the Year 36

38 40

42

Integrated Management Discussion and Analysis 50

Stakeholder Value Creation Blueprint 56 Getting to Know Our Stakeholders and Their Expectations 57 Stakeholder Engagement 58 Stakeholder Strategies 61

Stakeholders Customers 62 Employees 70 84 Society 85 Environment 99 Shareholders 109

Business Pillars 111 113 116 119 121 123 125 127 Corporate Banking: Corporate Credit 129 Corporate Banking: Commercial Credit 131 132 Corporate Banking: Development Banking - MSME Development 134 136 138 139 140 Corporate Finance 141 Treasury 142 144

Support Services 145 Call Centre Operation 148 149

Subsidiaries 150 151 152 153

154 160

Correspondent Banks and Exchange Companies 162 168

Stewardship178204

Corporate Governance 206252256257259262264265267268

Financial Information Financial Calendar 271

272

283

285

286287

289290291292

Statement of Cash Flow 293 Statement of Changes in Equity 295

297

Supplementary Information422423424425

Value Addition 426 Ten Years at a Glance 427 Quarterly Statistics 428 Capital Adequacy 430

436446447

Glossary of Financial and Banking Terms 448 Abbreviations 455

457463465

Stakeholder Feedback Form 467

3

aspects of our business and forms part of a comprehensive suite of

for the year 2014.

Report Profile

SCOPE AND BOUNDARY

subsidiaries for the period 1st January 2014 to 31st December 2014. This report demonstrates the Bank’s commitment to adopt a competent reporting framework that would allow a true representation of the activities

has been prepared in full compliance with all mandatory

banking industry.

transparent disclosure channel that seeks to clarify the Bank’s actions vis-à-vis various stakeholder

environmental and social performance for the reporting period.

A special section has also been incorporated to highlight the Bank’s strategic focus and management approach in relation to all key stakeholders, moreover, material aspects deemed relevant to each stakeholder cluster have been evaluated to establish their relevance to the stakeholder alongside the potential impact on

documented account of this process.

To record how well the Bank has performed with regard

G4 guidelines for sustainability reporting and is prepared in accordance with the “Comprehensive” application level.

unique to the banking business.

and service innovations. This template has been used

to its intended recipients in a manner that would convey meaningful change to the community and society as a whole.

performance for the year has been summarised in the

the directives laid out under the Customer Charter issued

with global best practices for sustainability reporting, the report also carries voluntary disclosures on the following;

OECD guidelines for Multinational Enterprises

G4 - 14, 15, 28, 30, 32

4 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Report Profile

MATERIALITY ASSESSMENT

impact of each area. Thereby, evaluating the degree to

stakeholders but also the degree to which it is relevant

and determining materiality, we observe each aspect in the light of the management ethos pertaining to the particular stakeholder group. Accordingly, a number of quantitative and qualitative tools are used to obtain a deeper understanding of the large volume of information. Materiality is then measured using the following aspects.

No Aspect BoundarySustainability

Sampath Bank

Sustainability

Stakeholders

Economic

1 Sampath Bank High High

2 Sampath Bank High Medium

3 Sampath Bank / Community

High High

4 Supplier High Medium

Environmental

5 Materials Sampath Bank High

6 Energy Sampath Bank High High

7 Water Sampath Bank High High

8 Biodiversity Sampath Bank High High

9 Emissions Sampath Bank High High

10 Community Medium High

11 Sampath Bank High High

12 Compliance - Environmental Sampath Bank High High

13 Transport Community Medium Medium

14 Overall Sampath Bank High High

15 Supplier Environment Assessment Suppliers Medium Medium

16 Environment Grievance Mechanisms Sampath Bank Medium Medium

Social - Labour Practices and Decent Work

17 Employment Sampath Bank High Medium

18 Employee High High

19 Occupational Health and Safety Employee High High

20 Training and Education Employee High High

21 Diversity and Equal Opportunity Sampath Bank High Medium

22 Sampath Bank High Medium

23 Supplier Medium Medium

24 Employee High Medium

Human Rights

25 Sampath Bank High Medium

26 Sampath Bank High Medium

27 Freedom of Association & Collective Bargaining

Employee High Medium

28 Sampath Bank High High

G4 - 18, 19, 20, 21

5

H

M

M H

Sus

tain

abili

ty S

igni

fica

nce

to

Sam

path

Ban

k

Sustainability Significance to Stakeholders

2, 4, 17, 21, 22,

24, 25, 26, 27, 33 46

40, 44

31, 41

13, 15, 16, 23,

38, 4310

532

1, 3, 6, 7, 8, 9, 11, 12, 14, 18, 19, 20, 28, 29, 30, 34, 35, 36, 37, 39,

42, 45

No Aspect BoundarySustainability

Sampath Bank

Sustainability

Stakeholders

29 Sampath Bank High High

30 Sampath Bank High High

31 Sampath Bank

32 Sampath Bank Medium

33 Sampath Bank High Medium

34 Sampath Bank High High

Society

35 Community High High

36 Anti-Corruption Sampath Bank High High

37 Sampath Bank High High

38 Anti-Competitive Behaviour Sampath Bank Medium Medium

39 Compliance - Society Sampath Bank High High

40 Supplier Medium

41 Grievance Mechanism for impact on Society

Sampath Bank

Product Responsibility

42 Customer Health and Safety Customer High High

43 Sampath Bank Medium Medium

44 Marketing Communications Sampath Bank Medium

45 Sampath Bank High High

46 Supplier High

H

M

High

Medium

6 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Report Profile

A Snapshot of Our Progress Towards Sustainability Reporting

Year GRI Application Level Declaration StatusExternal

Assurance Provided

2011 Self-declared Yes

2012 Self-declared Yes

2013 - Yes

2014 - Yes

ASSURANCETo determine the credibility of our reporting framework

that Messrs Ernst and Young have no involvement or

interest in the scope of activities conducted by Sampath

independent assurance report for our sustainability

comprehensive assurance report issued by Messrs Ernst and Young.

G4-29, 33

Information Source

Compliance Department

ServicesMarketing DepartmentCorporate Credit DepartmentCommercial Credit DepartmentCorporate Finance DepartmentDevelopment Banking UnitForeign Currency Banking UnitTrade Services DepartmentElectronic Banking UnitData Warehouse UnitCard CentreCall Centre All Branches

Marketing DepartmentDevelopment Banking Department

All Branches / Departments

Development Banking UnitOperations DepartmentMarketing Department

Finance Department

Operations Department

Bank’s triple bottom line performance for the reporting period, information has been sought out from the following sources:

7

Corporate Profile

December 2014.

South Asia in 1997.

the prestigious, global Business Magazine "The Euromoney", for the second consecutive year. The Bank has also been adjudged both the Best Commercial

operate with a fully computerised database and related technologies in 1987.

terms of total assets, since 2009. The Bank now operates 220 branches and

G4 - 9

8 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Corporate Profile

BOARD OF DIRECTORS OF SAMPATH BANK PLC

pages 10 to 15.

SUBSIDIARY COMPANIES OF THE BANKDetails of Subsidiaries as of 31st December 2014 are tabulated below.

Subsidiary Principal ActivitiesOwnership as at 31st

December 2014

Siyapatha Finance PLC 100.00%

Names of Board of Directors

Chairman

Mr M A Abeynaike Deputy Chairman

Mr S G Wijesinha Director

Director

Dr H S D Soysa Director

Director

Director

Director

Subsidiary Principal ActivitiesOwnership as at 31st

December 2014

Sampath Centre Ltd 97.14%

Names of Board of Directors

Chairman

Mr S G Wijesinha Director

Director

Mr Wije Dambawinne Director

Subsidiary Principal ActivitiesOwnership as at 31st

December 2014

S C Securities (Pvt) Ltd Share Broking 100.00%

Names of Board of Directors

Mr D J Gunarathne Chairman

CEO / Director

Dr S Kelegama Director

Mr Deshal de Mel Director

Director

Director

9

Subsidiary Principal ActivitiesOwnership as at 31st

December 2014

Sampath Information Technology Solutions Ltd Hardware

100.00%

Names of Board of Directors

Chairman

Mr D J Gunaratne Director

Director

Director

MEMBERSHIP OF ASSOCIATIONS

Name of the Association Membership Status

Member

Member

Member & Treasurer

Member

Member

Member

Member

Member

Member

Member

Member

The Ceylon Chamber of Commerce

Member

Member

Member

Member

Member

Clearing Association of Bankers Member

Member

G4-16, 17

10 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Board of Directors

Mr Sanjiva Senanayake (Senior Independent Director)

Mr Dhammika Perera (Chairman)

Mr Channa Palansuriya (Deputy Chairman)

Mr Deepal Sooriyaarachchi

Mr Ranil Pathirana

Mr Deshal De Mel

Mr Ranjith Samaranayake

Mrs Dhara Wijayatilake

Mrs Saumya Amarasekera

11

Mr S Sudarshan (Group Company Secretary)

Mr Aravinda Perera (Managing Director)

Prof Malik Ranasinghe

Miss Annika Senanayake

12 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

MR DHAMMIKA PERERASkills & Experience: quintessential business leader, with interests in a variety of key industries including Hydropower Generation, Manufacturing, Hospitality, Entertainment, Banking and Finance. He enriches the Board with over 25 years of experience in building formidable businesses through unmatched strategic foresight.

Appointed to the Board: 1st August 2007. Appointed as

Membership of Board Sub Committees: Chairman of

Current appointments:

Former appointments: Chairman and Director General,

MR ARAVINDA PERERASkills & Experience: Counts over 30 years in the Banking

Management Accountants, UK; Chartered Engineer and

from the University of Sri Jayewardenepura; Bachelor of Science degree in Engineering from the University of Moratuwa.

Appointed to the Board:Executive Director and appointed as Managing Director

Membership of Board Sub Committees: Member

Board of Directors

Board Treasury Committee

Current Appointments: Managing Director Sampath

Colombo Stock Exchange.

Former Appointments: Deputy Managing Director, Chief

roles spanning a career of 27 years at Sampath Bank

Manager and Service Engineer at Ceylon Tobacco

MR CHANNA PALANSURIYASkills & Experience: Over 30 years of vast experience in the Apparel sector by heading Orit Group of Companies and continuous leadership given to other companies in

Government Administration by being a Board Member

category in 2012.

Appointed to the Board: Executive Director and appointed as Deputy Chairman on 26th January 2012.

Membership of Board Sub Committees: Chairman of

Board Credit Committee.

Current Appointments: Deputy Chairman Sampath

Managing Director of Orit Group comprising of Orit

Committee Member of Joint Apparel Association Forum

Exporters Association and Executive Committee Member

13

Former Appointments:

Exporters’ Association 200gfp during 2006-2008,

2005 to January 2015.

MR SANJIVA SENANAYAKESkills & Experience: Extensive local and overseas

institutions and as an independent consultant.

Appointed to the Board: 1st January 2012 as

Membership of Board Sub Committees: Chairman of Board Treasury Committee, Member of the Board Audit

Current Appointments:

Former Appointments:

Brunei, various positions including Treasurer and Head of

MR DEEPAL SOORIYAARACHCHISkills & Experience: Counts over 30 years experience

Development & Strategy with extensive experience

Marketer. Holds an MBA from the University of Sri

development consultant and Author.

Appointed to the Board: 5th August 2010 as an

Membership of Board Sub Committees: Chairman

Marketing Committee. Member of Board Audit Committee

Current Appointments:

Member of Council, University of Moratuwa, Consulting

Former Appointments:

Marketing.

PROF MALIK RANASINGHESkills & Experience: Extensive governance experience

Vancouver, Canada in Civil Engineering as a Canadian Commonwealth Scholar; published extensively on

Excellence Award for 2012 for the Most Outstanding

the Award for Outstanding Contribution to Education 2012 at World Education Congress and the Education

Awards, Singapore.

Appointed to the Board: 30th August 2011 as an

Membership of Board Sub Committees: Chairman of Board Credit Committee, Member of Board Audit

Management Committee

Current Appointments:

Former Appointments: Vice-Chancellor of the University of Moratuwa, Chairman of the Committee of Vice Chancellors

Association of Commonwealth Universities, Fellow of the

14 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

MRS DHARA WIJAYATILAKESkills & Experience:

Secretary to a Cabinet Ministry.

Appointed to the Board: 30th August 2011 as

Membership of Board Sub Committees: Chairperson of

Committee

Current Appointments:

Former Appointments: Secretary to the Ministry of

MISS ANNIKA SENANAYAKESkills & Experience: Bachelor of Arts in Management

media & broadcast, automobiles, aviation, warehousing, food & beverage processing and packaging.

Appointed to the Board: 1st January 2012 as an

Membership of Board Sub Committees: Chairperson of

Committee, Member of Board Marketing Committee,

Committee

Current Appointments:

Former Appointments :

Board of Directors

MR DESHAL DE MELSkills & Experience: Master of Science degree in

of Economics, Bachelor of Arts degree with Honours

University of Oxford.

Appointed to the Board: Executive Director

Membership of Board Sub Committees: Member of

Committee and Board Marketing Committee,

Current Appointments:

Committee of the Ceylon Chamber of Commerce

Former Appointments:

MR RANIL PATHIRANASkills & Experience:

Bachelor of Commerce degree from the University of Sri Jayawardenapura.

Appointed to the Board: Executive Director

Membership of Board Sub Committees: Chairman of Board Audit Committee, Member of Board Strategic

Current Appointments:

Former Appointments:

15

MRS SAUMYA AMARASEKERASkills & Experience: Counts over 27 years in active legal

services sector clients and has specialised in local and international arbitrations.

Appointed to the Board: 1st June 2012 as an

Membership of Board Sub Committees: Chairperson

Current Appointments:

Former Appointments: Member of Supreme Court Complex Board of Management

MR RANJITH SAMARANAYAKESkills & Experience: Extensive experience as Head

Appointed to the Board: 1st January 2009 as an Executive Director.

Membership of Board Sub Committees: Member

Committee and Board Treasury Committee

Current Appointments:

Former Appointments: Senior Deputy General Manager,

16 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

1 Mr Aravinda Perera Managing Director

2 Mr Ranjith Samaranayake

3 Mr Nanda Fernando Senior Deputy General Manager

4 Mr Saman Herath

Branch Credit

5 Mr Wije Dambawinne Deputy General Manager - Treasury

6 Mr Tharaka Ranwala Deputy General Manager - Marketing & Business

Development

Corporate Management

17

7 Mr Aruna Jayasekera

8 Mr Ajantha de Vas Gunasekara Deputy General Manager - Finance

9 Mrs Hiranthi De Silva Deputy General Manager - Corporate Credit

10 Mr Dinusha Ihalalanda Deputy General Manager - Operations

18 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Corporate Management

11 Mr S Sudarshan Group Company Secretary

12 Mr Amanda Abeyweera Assistant General Manager - Administration

13 Mr Upali Dharmasiri

14 Mrs Nimali Abeyratne Assistant General Manager - Branch Banking

15 Mrs Shashi Jassim Assistant General Manager - Corporate Finance &

FCBU

16 Mr Pradeep Perera

19

17 Mrs Anuja Goonetilleke

18 Mrs Nirosha De Silva Assistant General Manager - Card Centre

19 Mr Manoj Akmeemana Assistant General Manager - Branch Banking

20 Mr Ajith Salgado

20 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

21 Mr Rajendra Ranasinghe

Development

22 Mr Pununuwan Wickremasekera

23 Mr Sanath Abhayaratne Assistant General Manager - Global Business

24 Mr Sanjaya Gunawardena

25 Mrs Ayodya Iddawela Perera Assistant General Manager - Corporate Credit

Corporate Management

21

1 Mr Maheel Kuragama

2 Mr H B Keerthiratne

3 Mr Amal Kirihena

Chief Managers

4 Mr Thusitha Nakandala

5 Mr Prasantha De Silva Chief Dealer

22 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

6 Mr Dushyantha Dassanayake

7 Mr Asoka Manikgoda

8 Mr Ananda Wijitha

9 Mr Thilak Abeysinghe Head of Deposits

10 Mr Sisira Dabare

11 Mr Saman De Silva

12 Mrs Achala Wickramaratne

13 Mrs Chamila Bandara

Chief Managers

23

14 Mr Hemantha Marasinghe

15 Mr Lalith Weragoda

24 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Senior Managers

1 Mr Vijith Peiris

2 Mr Priam Kasturiratna

3 Mr Prasada Gooneratne

4 Mr Chatura Rudesh

5 Mr Nalaka Gunawardena

6 Mr Prasanna Mullegama

7 Mr Janaka Jayasuriya

8 Mr Lasantha Senaratne Assistant Company Secretary

25

9 Mrs Kumari Jayasuriya

10 Mr Pasan Manukith Senior Manager - Systems Development

11 Mr Deepal De Silva

12 Mr Halin Hettigoda

13 Mr Gayan Ranaweera

26 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Senior Managers

14 Ms Dulsiri Jayasinghe

15 Mrs Aloka Ekanayake

16 Mr Lakmal Munasinghe

17 Mr Sumie Mithrapala

18 Mr Senaka Hewavitharana

19 Mrs Champika Nanayakkara

20 Mr Kasun Ratnayake

21 Mr Shiran Kossinna

27

22 Mr Kasun Fernando

23 Mr Janaka Karunaratne

24 Mr Thushantha Sumithraarachchi

25 Mr Udara Suraweera

26 Mr Kusal De Silva

28 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

“The Growing Force

Our Values Create a learning culture that promotes individual

and organisational development as well as promoting innovation and value for customers.

Treat all internal and external customers the way we would like to be treated.

Encourage and promote teamwork in all aspects of behaviour.

Open to feedback and demonstrate an eagerness for personal development.

Monitor and demonstrate an impressive commitment to results.

Uncompromising ethical and professional standards of behaviour.

Vision & Values

Our Vision

29

Sustainability Philosophy

OUR SUSTAINABILITY VISIONFocus: 3600 Approach to SustainabilityOur sustainability vision is aligned to our strategic goal to

so, it has always been our aim to create competitive advantages that would spearhead the accomplishment

of corporate goals in sync with national priorities. As

a philanthropic focus to a more strategic approach. We have since embraced a 3600 approach towards sustainability to embody the promise of a sustainable future for all those associated with the business.

3600 Approach to

Sustainability

Sustainability Trends

Corporate Objectives

Strategic

Opportunities and Threats

Management

Sustainability Stewardship

Stakeholder

Framework

30 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Our product portfolio is geared to support the needs of diverse customers. We provide customized solutions that complement our mainstream

empower our customers and help them map out their path to success.

Product Portfolio

Housing Loan Solutions

G4-4

Sampath App

31

41 OFF SITE ATMs

12 Super Branches (365 Days Banking)

1,565Interbank ATM Network 220

326Branches

ATMs

presents a range of delivery channels that aim to strike a balance between traditional values and advances in modern technology.

32 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Highlights

FINANCIAL HIGHLIGHTS

BANK GROUP

2014 2013 Change 2014 2013 Change Rs Mn Rs Mn % Rs Mn Rs Mn %

Gross income 45,469 47,334Total operating income 22,863 20,757 10.15 24,143 21,606 11.74Operating expenses, impairment losses and

16,136 16,896 16,817 0.486,727 4,491 49.79 7,247 4,789 51.331,813 1,061 70.88 1,979 1,151 71.944,914 3,430 43.27 5,268 3,638 44.80

Assets & LiabilitiesDue to banks and other

341,946 302,429 13.07 341,655 302,261 13.03

impairment losses 302,370 260,040 16.28 310,504 266,548 16.49Total equity 30,912 28,418 8.78 34,604 31,760 8.95Total assets 432,026 382,042 13.08 442,790 391,304 13.16

Investor Information184.10 169.37 8.70 205.53 188.75 8.89236.30 171.90 37.46

29.27 20.45 43.13 31.35 21.67 44.6729.26 20.44 43.15 31.34 21.66 44.69

4.66 4.65 0.2211.00 8.00 37.50

2.66 2.56 3.911,847 1,343 37.53

39,677 28,843 37.56

Key Indicators

2.27 2.31

- before tax 1.69 1.29 31.01 1.78 1.34 32.841.23 0.98 25.51 1.29 1.02 26.47

16.35 12.88 26.94 15.68 12.47 25.74

53.95 51.23 5.31 53.24 51.22 3.94

60.67 55.54 9.24 59.86 55.53 7.8024.54

Capital adequacy ratios (%)-Tier 1 8.83 8.96-Tier 1 &11 13.62 13.72

LRA rating Fitch rating

33

SAMPATH APP DOWNLOADED

VISHWA LOGINS

SMS ALERTS REGISTRATIONS

CUSTOMERS

GROWTH IN NUMBER OF ATMS

GROWTH IN NUMBER OF BRANCHES

3.8%

11.4%

9.7%

19%

2014

2014

2014

2014

2014CUSTOMER COMPLAINTS SOLVED

100%2014

51.3%

58.5%

40.5%

23.5%

GROWTH IN CUSTOMER BASE

GROWTH IN NUMBER OF DEPOSITACCOUNTS

GROWTH IN NUMBER OF LOANACCOUNTS

9.3%

Sampath App

34 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Highlights

EMPLOYEES

GROWTH IN WORK FORCE

EMPLOYEE RETENTION

TOTAL NUMBER OF TRAINING HOURS

NUMBER OF INDUSTRIAL DISPUTES

MALE : FEMALE RATIO

AVERAGE TRAINING HOURS PER EMPLOYEE PER ANNUM

8.5%

1.2

1.9 : 1

47.8

3.05 1.24

97%

191,261

NIl

2014

2014

2014

2014

2014

2014

2014 2014

2014

0.9 2013

2013

GOVERNMENT

TAXES PAID TO THE GOVERNMENT TAXES COLLECTED ON BEHALF OF THE GOVERNMENT

1.7 : 1

Bn BnRs Rs

35

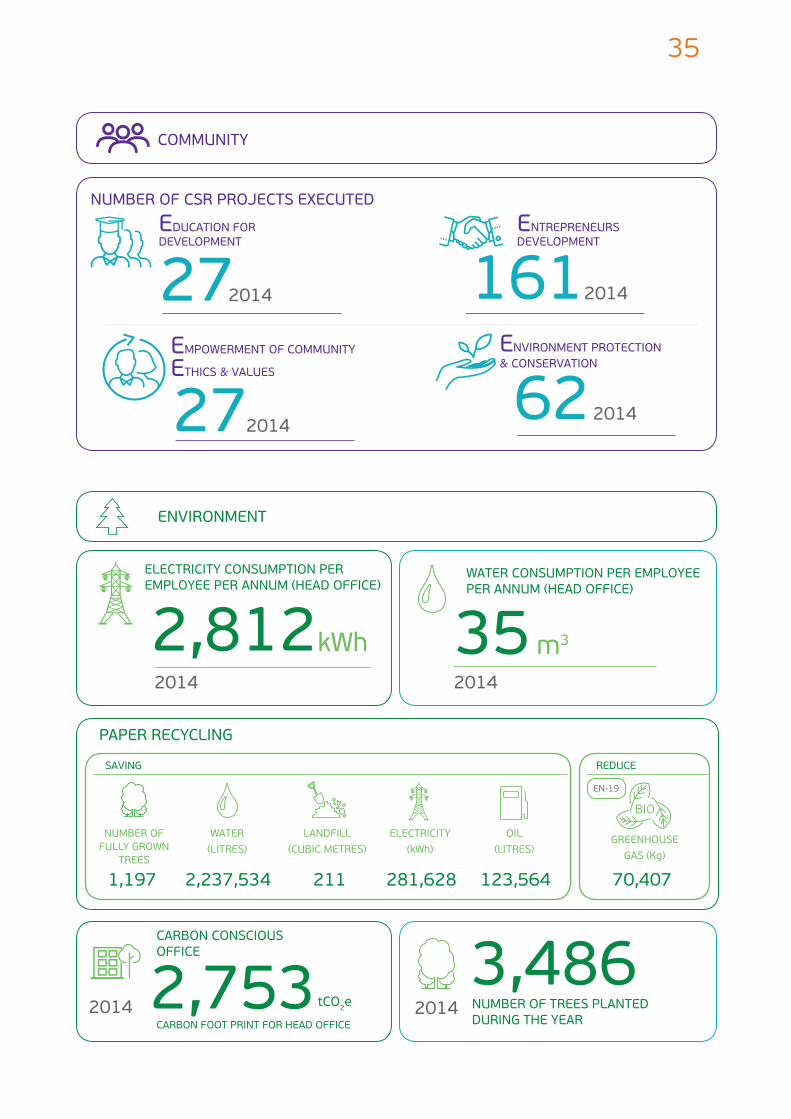

ENVIRONMENT

COMMUNITY

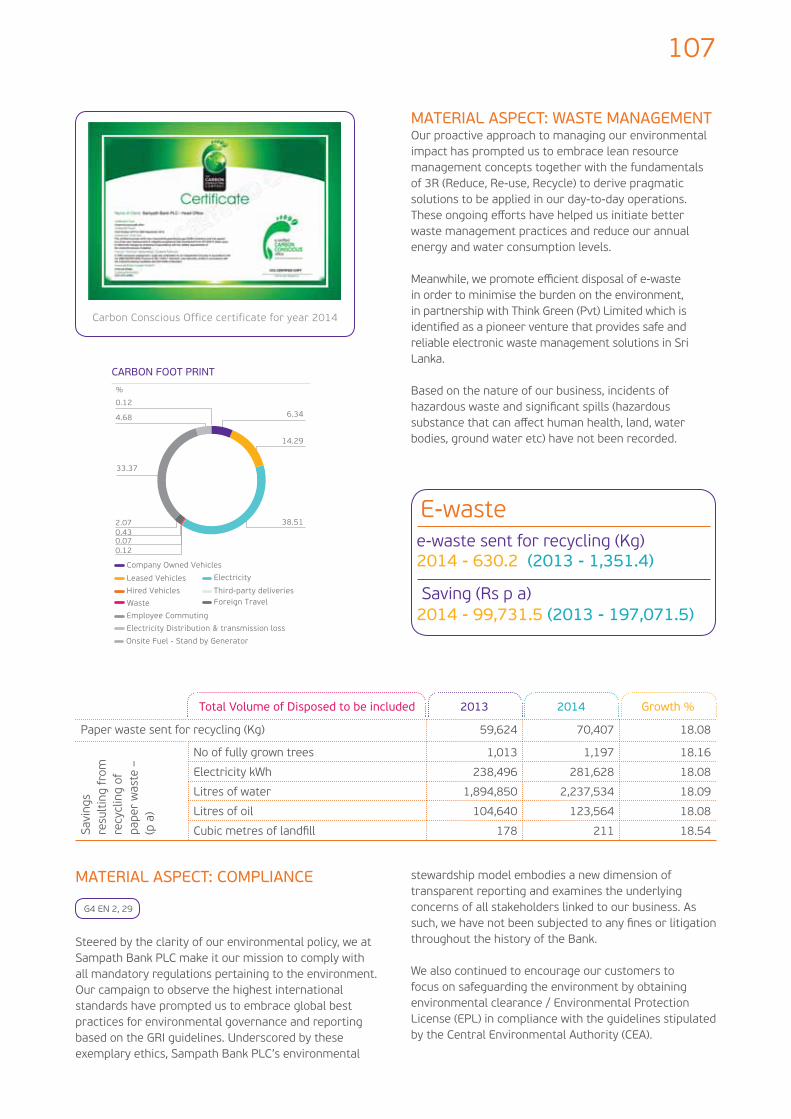

CARBON FOOT PRINT FOR HEAD OFFICE

CARBON CONSCIOUS OFFICE

NUMBER OF TREES PLANTED DURING THE YEAR

2,753 3,486

NUMBER OF CSR PROJECTS EXECUTED

EDUCATION FOR DEVELOPMENT

ELECTRICITY CONSUMPTION PER

PAPER RECYCLING

SAVING REDUCE

WATER CONSUMPTION PER EMPLOYEE

EMPOWERMENT OF COMMUNITY

ETHICS & VALUES

27

2,812 35

161

27

1,197 2,237,534 211 281,628 123,564 70,407

m3

2014

2014

2014 2014

2014

2014

2014

ENVIRONMENT PROTECTION & CONSERVATION

622014

NUMBER OF FULLY GROWN

TREES

WATER LANDFILL OIL GREENHOUSE

GAS (Kg)

ENTREPRENEURS DEVELOPMENT

kWh

tCO2e

ELECTRICITY

(kWh)

36 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Best Community Program Leadership Award 2014Sampath Bank was awarded with the prestigious Best

Excellence Awards - 2014 held in Singapore

Best Corporate Citizen Sustainability Awards 2014Sampath Bank won prestigious awards in Best Corporate Citizen Sustainability Awards 2014 - the country’s top most Corporate Social

organized by the Ceylon Chamber of Commerce.

National Best Quality ICT Awards 2014Sampath Bank won the Gold Award for Commercial Applications and a Bronze

Awards and Accolades for the Year

CA Sri Lanka Annual Report Awards 2014Bronze award in Overall Excellence

CA Sri Lanka Annual Report Awards 2014Gold award in the Banking

HR Excellence Awards 2014Sampath Bank, Human

Conference 2014

37

Silver Award at the BestWeb.LK 2014Sampath Bank Website has

in the Corporate, Banking,

Best Bank in Sri Lanka – 2014Sampath Bank has been selected

2014" by the prestigious Business Magazine "The Euromoney" for the second consecutive year

Sri Lanka’s Best Commercial and Retail Bank in 2014Sampath Bank is Sri

awarded at the World Finance Banking Awards.

Sumathi Awards 2014Sampath Bank Television Commercial on Sampath Sevana was awarded as the Best Television Commercial

at the Sumathi Awards 2014

CSR Brand of the Year Silver Award 2014Sampath Bank has won The Silver Award in the category

Ceremony

38 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Macro-economic Review

THE GLOBAL PERSPECTIVE

economy expecting to expand only by 3.3% in 2014, as the pace of growth fell below forecasts for the second consecutive year. Although emerging economies did account for a major portion of this growth, a noticeable deceleration of economic activity in these economies meant a lower than expected result. On the other hand, a gradual recovery was observed among the advanced economies, which allowed these economies to register moderately improved growth rates for 2014. While this

cumulative down-side risks associated with low growth,

together with the sharp drop in oil prices, also impacted the global economic performance for the year.

SRI LANKA AT A GLANCE

economy is estimated to record 7.8% growth for the year 2014, more or less on par with the 7.3% registered

construction sector throughout the year, largely driven by the growing number of condominium projects and infrastructure development across the country. The leisure sector too, continued to expand strongly linked to the rapid increase in tourist arrivals in the country, which surpassed 1.5 Mn tourists as at 31st December 2014.

in large part due to prudent demand management,

expectations.

in 2014.

The currency platform too remained strong throughout

Dollar, while depreciating marginally against the US Dollar by December 2014.

As the leading contributor to the country’s foreign exchange earning’s, worker remittances are expected to grow yet again by 9.2% adding USD 592 Mn to the

are also expected to reach USD 8,200 Mn by the end of the year 2014.

INDUSTRY OVERVIEW

licensed commercial banks, 12 foreign commercial banks and 9 licensed specialised banks, with a collective branch network of 6,531 branches and 2,599 ATMs as at

the Banking Sector accounts for approximately 70% of

decision to maintain a low interest rate regime was the

systematic rate reductions, were followed by a steady

and 12 month Treasury Bill yields.

Amidst this backdrop, total banking sector assets grew

compared to December 2013, aided by a growth of

anticipated private sector credit momentum and the industry continued to be trapped in a credit slump for the second consecutive year. With the private sector

industry found itself weighed down by excess liquidity throughout the year. Consequently most key players were seen resorting to low-yielding Treasury Bills and other Government Securities as a means of mopping up the excess liquidity situation. On a positive note, the excess liquidity helped to maintain a healthy Capital Adequacy

Meanwhile, with the industry embracing stricter credit control measures to curb the volume of bad loans,

resulted in an increase in the overall provision coverage for the year.

On the other hand, the low interest rates had an unhealthy impact on deposits, which demonstrated only a

39

previous year 2013.

excess liquidity and the slow deposit growth caused an

the corresponding period in 2013. This was mainly due to timely re-pricing and other fund management strategies adopted by Banks.

Underscored by the prospect of continuous drop in

streamline their operational parametres and derive a

produce an acceptable level of performance in 2014.

2011 2012 2013

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

4,2

52 5,0

98 5,9

41

6,7

80

INDUSTRY TREND IN ASSETS

Rs Bn

Nov 2014

2011 2012 2013

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

LKR Loans FCY Loans

451

559

623

791

3,0

12

2,8

03

2,5

90

2,1

50

INDUSTRY TREND IN LOANS

Rs Bn

Nov 2014

2011 2012 2013 Nov 2014

0

1,000

2,000

3,000

4,000

5,000

LKR Deposits FCY Deposits

496

615680

730

3,8

71

3,4

90

3,0

10

2,5

77

INDUSTRY TREND IN DEPOSITS

Rs Bn

INDUSTRY TREND IN NPL

(%)

2011 2012 2013

0

50

100

150

200

Gross NPL

Rs Bn

Nov 2014

0

2

4

6

8

Gross NPL Ratio

3.83.7

5.6

4.8

99

11

7

19

1

18

1

40 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Chairman’s Report

41

Dear Stakeholders,

year 2014. Despite the many challenges, the intense

indeed the interplay of global pressures, your Bank continued to maintain its momentum of growth.

theme “Ask our Stakeholders” all the more relevant,

growth stories around the country of our multiple

business partners to the communities around us and the environment.

we have continued to deliver consistent value for our

the value that we will present to the future that makes us unique.

With a clear vision and purpose based on solid values, Sampath Bank has worked with resolve to meet its strategic priorities. As a sustainable business that integrates sustainable practice to how we do business, we have utilised a focused strategy-driven approach that leverages our core competencies. With a sustainable business strategy that is fully aligned to the national strategy, we have consistently catalysed socio-economic change. Underpinned by our sustainability philosophy, we have formulated a sustainable business blueprint that addresses key national priorities alongside corporate objectives. You, our shareholders and stakeholders will be pleased to note that at Sampath Bank, our interpretation

performance alone but the collective impact on the triple

We remain committed to the principles of the United

business ethic, while the Customer Charter of The Central

we have re-asserted our commitment to sustainability

reporting format that is representative of and facilitates sustainable business agendas.

just to shareholders, but to all stakeholders especially the

achieved this by better abiding to our strategy, focusing on the basics of good banking, with clients and customers with whom we have deep, and in many cases long, relationships. We endeavour to create value and take a long-term view of our obligations to our shareholders, our clients and customers and the communities in which we operate.

and cost controls, provide our shareholders with a basis

seen. A stable bank over time provides shareholders with the greatest appreciation in value. At the same time the Board understands that it is the employees through their day-to day work to build good customer relations and to run the Bank well, which creates this value and results.

remuneration programme that helps to produce positive results and sound risk-taking. This cyclical movement of

We believe that strong governance is crucial to our long-term success. The complexity of operations in the

corporate governance necessary, and has necessitated that we establish clear goals, strategies, values and good risk controls. Governance remains the Board’s highest priority, duty and responsibility.

performance for Sampath Bank. Today we are a stronger bank in many respects thanks to a consistent strategy, a stable management team, supportive clients, customers and shareholders, and, above all, our great

markets develop. A bank like yours, which wants to gives stakeholders the opportunity to grow in a sustainable

My appreciation to the Board of Directors, the Management and the entire Sampath Bank team for their dedication and resolve.

Dhammika PereraChairman

19th February 2015

G4-1

42 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Managing Director’s Review

43

We continue to uphold the promise to deliver consistent value for all stakeholders as we believe that our success is measured not only in terms of our ability to produce shareholder value, but also our accountability to all stakeholders associated with our business.

People Planet

Profit

Symbolic of our vision to present a promising future for all citizens

remain committed to engender meaningful change for the nation.

We have embraced the triple bottom line model as a template to convey tangible value to all those impacted by our work.

Symbolic of our vision to present a promising future for

committed to engender meaningful change for the nation.

country’s business landscape or navigating through socio-environmental undercurrents, we have always remained true to our fundamental values. We continue to uphold the promise to deliver consistent value to all stakeholders as we believe that our success is measured not only in terms of our ability to produce shareholder value, but also our accountability to all stakeholders associated with our business. Underscored by this rationale we have embraced the triple bottom line model as a template to convey tangible value to all

integrated report, we seek to illustrate our long-term commitment to foster sustainable progress along a

2014 was yet another trying one not only for Sampath

industry, where industry-wide advance growth remained

factors were responsible for this restrained performance, among them was the visible slump in the private sector

credit demand. An alarming trend observed throughout the year, saw many private institutions moving away from the banking system and seeking alternative funding through listed debentures and foreign direct

create a competitive credit culture, by a reduction in policy rates also failed to trigger the desired credit momentum. Beleaguered by the lack of an adequate credit demand, the industry struggled with the problem

of excess liquidity throughout the year, arguably the most disturbing aspect that marred the performance of the industry.

For our part, we continued to respond with strategies that would rationalise market sentiments in tandem

mortar banking ideology towards a more vibrant banking blueprint that advocates a new level of quality assurance

drawn on the stability of our banking legacy. To further strengthen our core competencies, during the year we made investments in developing our infrastructure network and worked on repositioning our brand identity

We continued with our expansion agenda to increase the number of touch points across the country, albeit at a slower pace than in the past few years. While 8 new branches were added to the network in 2014, we also sought to further expand our footprint, mainly through

44 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

get together of trade customers

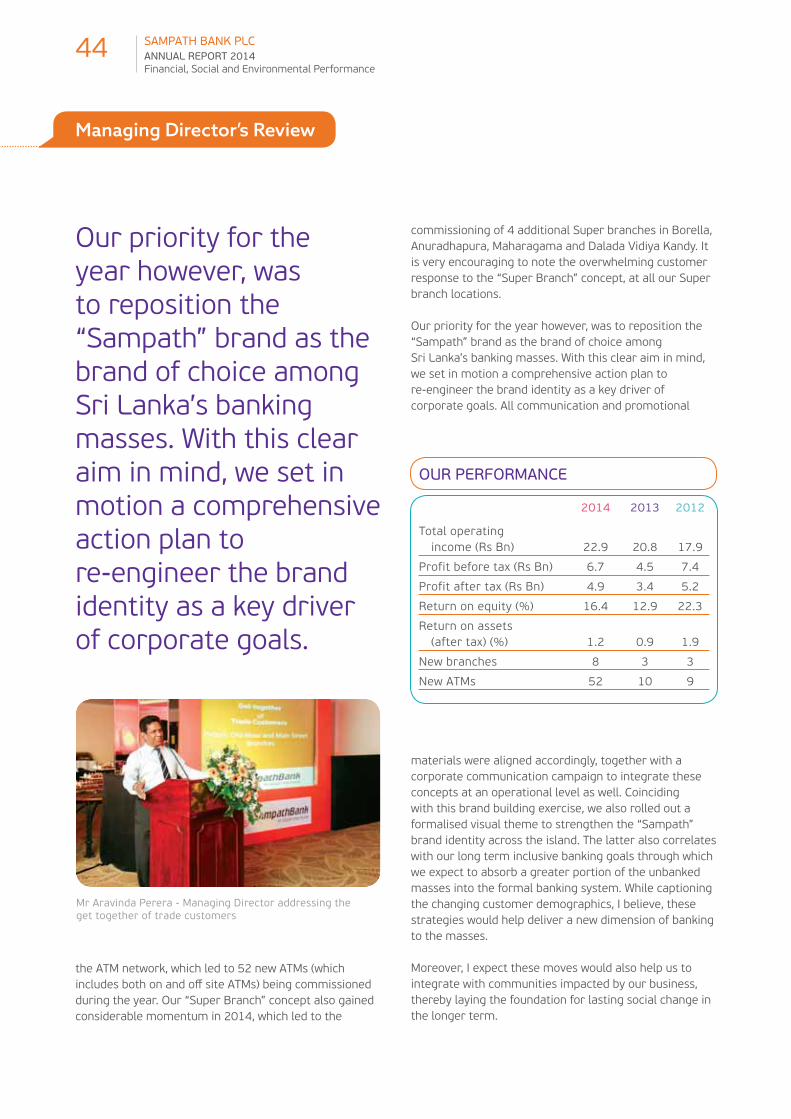

OUR PERFORMANCE

2014 2013 2012

Total operating

Our priority for the year however, was to reposition the “Sampath” brand as the brand of choice among

masses. With this clear aim in mind, we set in motion a comprehensive action plan to re-engineer the brand identity as a key driver of corporate goals.

Managing Director’s Review

commissioning of 4 additional Super branches in Borella,

is very encouraging to note the overwhelming customer response to the “Super Branch” concept, at all our Super branch locations.

Our priority for the year however, was to reposition the “Sampath” brand as the brand of choice among

we set in motion a comprehensive action plan to re-engineer the brand identity as a key driver of corporate goals. All communication and promotional

materials were aligned accordingly, together with a corporate communication campaign to integrate these concepts at an operational level as well. Coinciding with this brand building exercise, we also rolled out a formalised visual theme to strengthen the “Sampath” brand identity across the island. The latter also correlates with our long term inclusive banking goals through which we expect to absorb a greater portion of the unbanked masses into the formal banking system. While captioning

strategies would help deliver a new dimension of banking to the masses.

integrate with communities impacted by our business, thereby laying the foundation for lasting social change in the longer term.

during the year. Our “Super Branch” concept also gained considerable momentum in 2014, which led to the

45

focus on commercial and personal lending, including leasing. Meanwhile, despite the inevitable negative

in the pawning space. Thus, our loan portfolio, excluding

this is indeed a commendable achievement given the intense competition in the market and near stagnant

strategies were also initiated in a bid to maintain the

space, we also aggressively promoted the Credit cards. To meet our growth objectives we formulated a campaign that would target both organic and non-organic growth of our cards customer base. With service enhancements and value additions being the crux of our platform, we were able to record a YoY growth of 16.4%. Sampath cards

celebrating its 25th anniversary in 2014. Celebrations to

event held in the Maldives to coincide with the launch

remained the key determinant of performance in the corporate banking arm. Our strategic focus was therefore to develop sound business fundamentals that would support the stability of our corporate banking model and ensure consistent performance in the long term. Despite

Despite the drop in margins, the portfolio has continued to perform consistently with a satisfactory contribution to the Bank’s overall bottom line in 2014.

alternatives to halt any further erosion of the bottom line. While serving the mainstream banking needs of the

develop dynamic business solutions and gear ourselves to facilitate the emerging needs of modern commerce. Hence the strong emphasis on fee-based activities

we launched an aggressive campaign to promote our

our trade services platform, with greater emphasis on servicing the export sector.

Meanwhile, considerable resources were channelled towards research and new product development to help us understand the complexities of the modern customer. By leveraging on our competitive advantage, extensive infrastructure and superior technological platform, we were able to produce pragmatic solutions

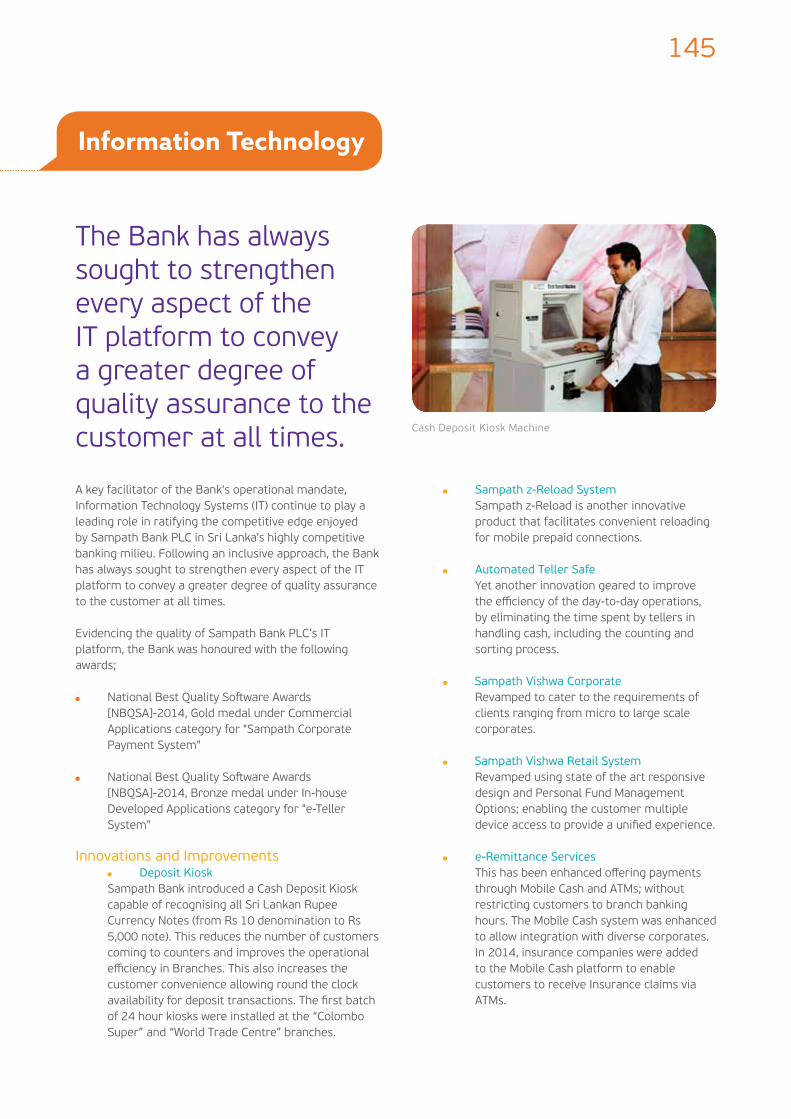

“Deposit Kiosks” introduced by us in two locations is one of the many initiatives launched during the year. Having a well-established ATM presence across the country, we were assured of being able to support customer cash withdrawals, without the need to visit the Bank. This prompted us to look at the deposit aspect as well, which spearheaded the introduction of the Deposit

was critical in ensuring customer retention amid the underlying challenges that characterised the banking industry in 2014.

we revisited our personal banking model in order to arrest any further decline in the bottom line. Altering the deposit mix in a bid to capture current market movements, we took a conscious decision to ease high-cost term deposits and focused on growing our Current

also aimed at curtailing any further escalation of our liquid assets. We embarked on an aggressive volume driven agenda to generate organic growth, particularly in

13.1%, with CASA accounting for over 47.0% of the total deposits as at the end of 2014.

burdened by excess liquidity as we faced with the

To curb the negative impact on the bottom line we

CASA

%

2011 2012 2013 20140

10

20

30

40

50

41

35

34

47

46 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

To diversify our corporate banking platform, during the year we took steps to capture a larger segment of the Micro, Small and Medium Scale Entrepreneur

to our goal to develop the country’s non-conventional

promoting clean energy projects that would safeguard

responsibility to the environment, as the direct impact from our operations are decidedly limited.

However, our consciousness of the issue has led us to develop a framework of environmental reporting that

who are the driving force behind everything that we do.

aspirations regardless of the challenges of 2014. As in the past, in this year too, we have remained steadfast in the commitment to our employees as we continue to provide a nurturing environment that would stimulate the desire to succeed.

LOOKING AHEAD

prospects for the future to be more conducive for sustainable growth for all stakeholders of Sampath Bank

strategies that would ensure consistent performance in line with medium term corporate goals.

As the level of market competition continues to heighten,

model to escalate considerably in the near term. We would thus need to look at altering the conventional

concepts that represents the diversity of the market needs while at the same time corresponding to a more sustainable cost structure. Further, as customer demographics continue to change, we are likely have to deal with lifestyle banking as opposed to the conventional

explore alternate delivery channels that feature solution-

At the same time, it is also important that we strike the right balance between innovation and feasibility. This would undoubtedly depend on a strong product development and research platform, where data analytics

Euromoney Award for excellence 2014

Managing Director’s Review

TOTAL ASSETS

(Rs Mn)432,000Over

NET FEE AND COMMISSION INCOME & NIM

Rs Mn (%)

2011 2012 2013 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Net Fee & Commission Income

0

1

2

3

4

5

6

8

NIM

3.99 4.05 4.39

3.95

1,8

11

2,1

49

2,5

43

3,0

87

47

as an environmental

Supported by this invaluable business framework, we also expect to connect with communities through our work and help manifest truly meaningful societal change that will ensure the betterment of the nation as a whole.

As we strive to translate these strategies into reality, we

developing our people. Given our corporate ambitions,

workforce capable of ensuring progress for all

Aravinda PereraManaging Director

19th February 2015

INTEGRATED MANAGEMENT

DISCUSSION AND ANALYSIS

a trajectory of growth

Content

Stakeholder Value Creation Blueprint 56Getting to Know Our Stakeholders and Their Expectations 57Stakeholder Engagement 58Stakeholder Strategies 61

StakeholdersCustomers 62Employees 70

84Society 85Environment 99Shareholders 109

111113116

119121123125

127Corporate Banking: Corporate Credit 129Corporate Banking: Commercial Credit 131Corporate Banking: Development Banking -

132Corporate Banking: Development Banking - MSME Development 134

136138139140

Corporate Finance 141Treasury 142

144

Support Services145

Call Centre Operation 148149

Subsidiaries150151152153

Correspondent Banks and Exchange Companies 162

50 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Financial Performance Review

Despite the stable performance recorded by Sampath

whole. Of the key challenges, the policy decision by the

crucial factor in determining the performance of the Bank and the banking industry in 2014.

ASSETSFollowing the sluggish credit appetite seen towards the end of 2013, the demand for credit continued to slow

interest rates at the start of the year also failed to spark the anticipated credit momentum, with the industry experiencing negative credit growth in 1st quarter,

the marginal credit growth seen in the second half

movement and consequently the industry ended the year with a moderate credit growth of 11%. Sampath Bank

movements of the industry credit growth, with the asset portfolio recording only a marginal 13.1% YoY growth for the year. Meanwhile, as a direct consequence of the low credit growth, excess liquidity was yet another crucial

The Bank also settled a foreign currency borrowing which

quarter in order to reduce the excess liquidity it had at that time and this too contributed towards slowing down

Sampath Bank’s total assets crossed the

at the year end.

Faced with the uphill task of lending amidst the stubborn lack of demand for credit, the Bank sought to alter the lending mix to keep pace with market sentiments and improve returns. Accordingly, the Bank initiated

much as possible, parallel to facilitating the existing

branch network accounting for 57.4% of the advances for 2014, with corporate lending responsible for 42.6%.

strategies across the loan book to achieve maximum

made, Sampath Bank managed to post a credit growth of 14.6% as at the year end.

drop in global gold prices, in 2013, the Bank continued

Meanwhile, as stability continued to elude the gold

to be a challenge in this year too. On a positive note, due to the substantial and adequate impairment provisions made in 2013, impairment charge on pawning was only

charge booked against the same product in 2013.

settlement options. Moreover, an auction process was initiated to dispose articles of hardcore defaulters. As a result the exposure to this product was reduced to 7.9% of the total loan book as at 31st December 2014 compared to 19.7% of the total loan book as at the previous year end. On the other hand, while the funds so released due to the reduced exposure to pawning were used for other

ASSETS

Rs Bn

0

50

100

150

200

250

300

350

2011 2012 2013 2014

16

9.7

23

.1 54

.9

20

8.2

35

.2 66

.0

25

9.4

46

.9 75

.7

30

1.4

17

.01

13

.6

Loans to & Receivable from Other Customers

Financial Assets Held for Trading

Other Assets

retail lending as much as possible, parallel to facilitating the existing corporate lending model.

51

appetite meant that the Bank was yet again faced with an excess liquidity situation.

Financial Assets held for Trading which consists of Government Treasury Bills and quoted equity securities

in Government Treasury Bills as at 31st December 2014

LIABILITIESThe low interest rate regime, continued to undermine

model as the Bank was forced to cut interest rates in an

customer perspective, as the earning capacity of term deposits continued to diminish, some customers were seen moving away from term deposits in pursuit of more

throughout the year.

Aggressive steps taken to boost Current Accounts and

on the widespread island-wide branch network to capture a larger share of the provincial and rural markets in the

the Bank was able to yet again pioneer a number of value added solutions and service enhancements that enrich

CASA portfolio reaching a commendable 47% of the total deposit base as at 31st December 2014, notwithstanding the re-pricing strategies initiated by competitors.

Debt issued and other borrowed funds decreased from

31st December 2014 due to the settlement of USD 100

based operations and representing over 69% of the total

3.95% in 2014, aided by the growth of 15.2% recorded in the Bank’s fund base. The main reasons for achieving

to reduction in net interest margin due to downward pressure on interest rates, lower credit growth in customer advances and the Bank being compelled by the

income securities.

LIABILITIESRs Bn

0

50

100

150

200

250

300

350

2011 2012 2013 2014

19

5.2

19

.81

1.2

24

3.3

28

.8

11

.7

30

0.5

38

.91

4.2

33

9.9

36

.32

4.9

Due to Other Customers Debt Issued & Other Borrowed Funds

Other Liabilities

NET INTEREST INCOME & NIM

Rs Bn

2011 2012 2013 2014

0

4

8

12

16

20

Net Interest Income

8.9

11

.6

15

.3

15

.7

0

1

2

3

4

5

NIM

3.99 4.054.39

3.95

%

INTEREST INCOME & INTEREST EXPENSE

Rs Bn

2011 2012 2013 2014

0

10

20

30

40

50

Interest Income Interest Expense

21

.1

12

.2

31

.9

20

.3

41

.9

26

.6

38

.1

22

.3

NET FEE AND COMMISSION INCOME & NIM

Rs Mn (%)

2011 2012 2013 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Net Fee & Commission Income

0

1

2

3

4

5

6

8

NIM

3.99 4.05 4.39

3.95

1,8

11

2,1

49

2,5

43

3,0

87

52 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Financial Performance Review

NET FEE AND COMMISSION INCOME Although the net interest income recorded only a moderate growth, net fee and commission income of the

growth. This was mainly in line with the growth of business volumes in the card operations, inward remittances and commission income from other banking services.

NET TRADING AND OTHER OPERATING INCOME

accounts for 17.7% of the total operating income have recorded a 40.9% increase over the previous year. The major contributory factors to this increase were higher bad debt recoveries and exchange income generated from foreign exchange related transactions.

IMPAIRMENT OF LOANS AND OTHER LOSSES Total impairment losses decreased during the year

reduction in impairment losses against pawning. The Bank managed to auction the articles that were not redeemed recovering the capital and even a portion of the interest in some instances. The impairment charge

63.3% over the previous year’s charge mainly due to

products discussed above.

OPERATING EXPENSES

growth in operating expenses was due to general price

opening of new branches and ATMs and an island wide programme to upgrade branches to a consistent standard over the last few years. Cost to income ratio of Sampath Bank tends to be high due to a relatively young branch network. The Bank almost doubled its network since 2008. As a result, the contribution from the new members in the network is lower compared to their more mature counterparts. However it is encouraging to note that the new branches are improving rapidly and it is expected that their contribution towards improving cost to income ratio

monitoring its cost structure and continues to reduce

specialised functions. Though the operating expenses grew by 16%, this was very much lower than the growth of 28.6% in the Bank’s net operating income.

NET FEE & COMMISSION INCOME

2011 2012 2013 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1,8

11 2,1

49 2,5

43 3

,08

7

Rs Mn

OPERATING EXPENSES & GROWTH IN OPERATING EXPENSES

Rs Mn (%)

2011 2012 2013 2014

0

3,000

6,000

9,000

12,000

15,000

Operating Expenses

8,0

59

9,2

48

10

,63

4

12

,33

5

0

6

12

18

24

30

Growth in Operating Expenses

25.8

14.8 14.916.0

53

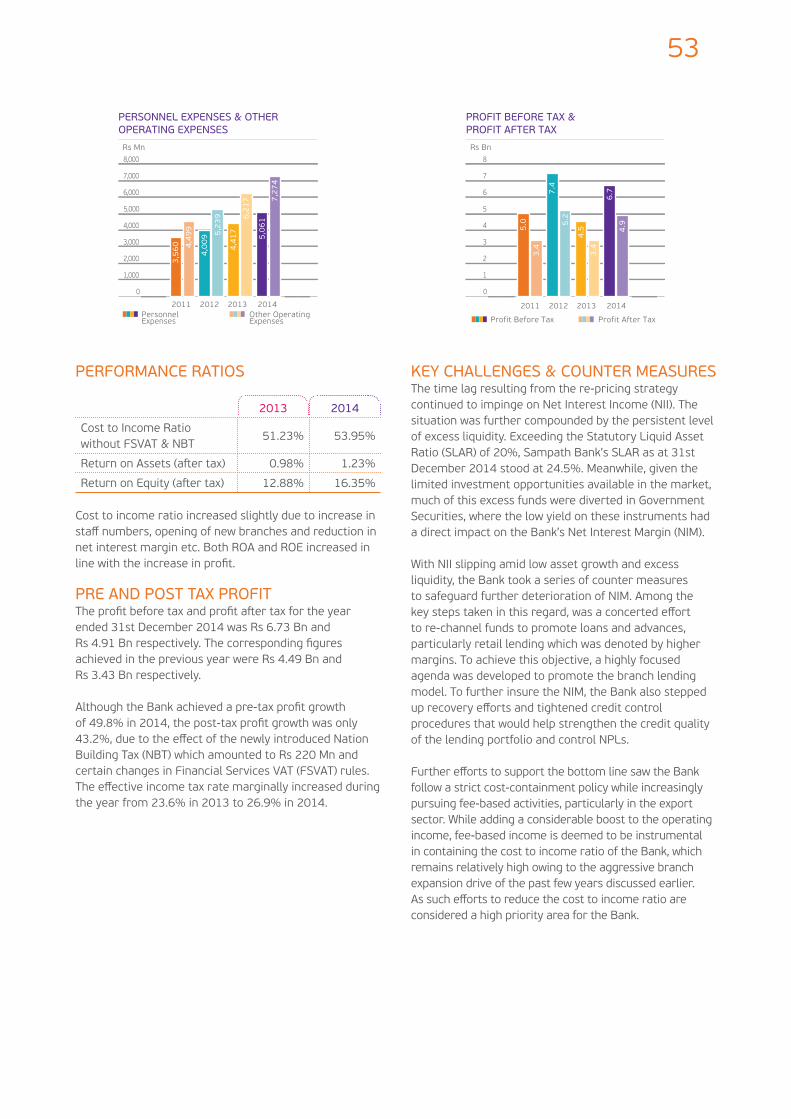

PERFORMANCE RATIOS

2013 2014

51.23% 53.95%

0.98% 1.23%

12.88% 16.35%

Cost to income ratio increased slightly due to increase in

PRE AND POST TAX PROFIT

the year from 23.6% in 2013 to 26.9% in 2014.

KEY CHALLENGES & COUNTER MEASURES The time lag resulting from the re-pricing strategy

situation was further compounded by the persistent level

December 2014 stood at 24.5%. Meanwhile, given the limited investment opportunities available in the market, much of this excess funds were diverted in Government Securities, where the low yield on these instruments had

liquidity, the Bank took a series of counter measures

to re-channel funds to promote loans and advances, particularly retail lending which was denoted by higher margins. To achieve this objective, a highly focused agenda was developed to promote the branch lending

procedures that would help strengthen the credit quality

follow a strict cost-containment policy while increasingly pursuing fee-based activities, particularly in the export sector. While adding a considerable boost to the operating income, fee-based income is deemed to be instrumental in containing the cost to income ratio of the Bank, which remains relatively high owing to the aggressive branch expansion drive of the past few years discussed earlier.

considered a high priority area for the Bank.

PERSONNEL EXPENSES & OTHER OPERATING EXPENSES

Rs Mn

2011 2012 2013 2014

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Personnel Expenses

Other Operating Expenses

3,5

60 4,4

99

4,0

09 5

,23

9

4,4

17

6,2

17

5,0

61

7,2

74

PROFIT BEFORE TAX & PROFIT AFTER TAX

Rs Bn

2011 2012 2013 2014

0

1

2

3

4

5

6

7

8

Profit Before Tax Profit After Tax

5.0

3.4

7.4

5.2

4.5

3.4

6.7

4.9

54 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

SHAREHOLDERS' FUNDS

at 31st December 2014 which was a 8.8% growth. Stated

options exercisable period ended on 30th June 2014 and

The maintenance of the investment fund was a mandatory requirement and comprised retentions of

of income tax as per the relevant direction issued by

October 2014. Consequently the Bank transferred the investment fund account balance that prevailed as at

The net impact due to other comprehensive income on

Financial Performance Review

CAPITAL ADEQUACY AND LIQUID ASSETS RATIOS

2013 2014 Statutory Requirement

27.62% 24.54% 20.00%

10.08% 8.83% 5.00%

14.22% 13.62% 10.00%

due to excess liquidity in the market. However the Bank managed to reduce it compared to 2013 as shown in table above.

compared to 2013, due to several factors. A decision was taken in 2014 to pay the dividend for 2013 exclusively

in cash without any scrip element being included therein, to minimise the excess liquidity that prevailed.

in products other than pawning which attracted higher capital allocation. Furthermore, the other comprehensive

which arose from the Actuarial Valuation as at 31st

DIVIDEND PAY OUT RATIO

201437.59%

2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

21

,34

4

25

,64

5

28

,41

8

30

,91

2

SHAREHOLDERS FUND

Rs Mn

55

subordinated redeemable debentures at the face value

These debentures were subsequently listed in the Colombo Stock Exchange.

result of the increase in the risk-weighted value of assets.

DIVIDEND

in the form of scrip dividend.

AWARDS

Sampath Bank has been selected as the "Best Bank in

Magazine "The Euromoney", for the second consecutive year. Also the Bank has been adjudged the Best

World Finance Banking Magazine.

EXTERNAL RATINGS

asset quality, better compliance, transparency, capital adequacy, internal control systems and processes of the

56 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Stakeholder Value Creation Blueprint

we believe it is our duty to convey tangible value to all People of the Planet in addition to ensuring the stability and

of our institution. Capturing the essence

strength and structured risk mapping to help deliver measurable change to all stakeholders associated with the business.

STRATEGIC MANAGEMENT

APPROACH

FINANCIAL STABILITY & RISK

MANAGEMENT

TRIPLE BOTTOM LINE IMPACTS

traditional philanthropic focus, towards a more strategic approach that creates competitive advantages for all our stakeholders

Wealth creation for all stakeholders of

corporate strategies, while assessing the relative market risk

Ensure the value creation

through a sustainable banking platform

G4-2, 24, 25

57

Getting to Know Our Stakeholders and Their Expectations

IDENTIFICATION OF ISSUE

No

No

Customers Society Employees

Setting Goals and Objectives Evaluating Alternatives

EnvironmentRegulators

Evaluation & Getting Feedback from Stakeholders

Shareholders Suppliers & Service Providers

Categorisation of Issues

Implementation and Monitoring

Review

Acceptable

Reporting and Record Keeping

Material Aspect

Stakeholder Engagement

Materiality Testing

Stakeholder Engagement

Yes

Yes

58 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

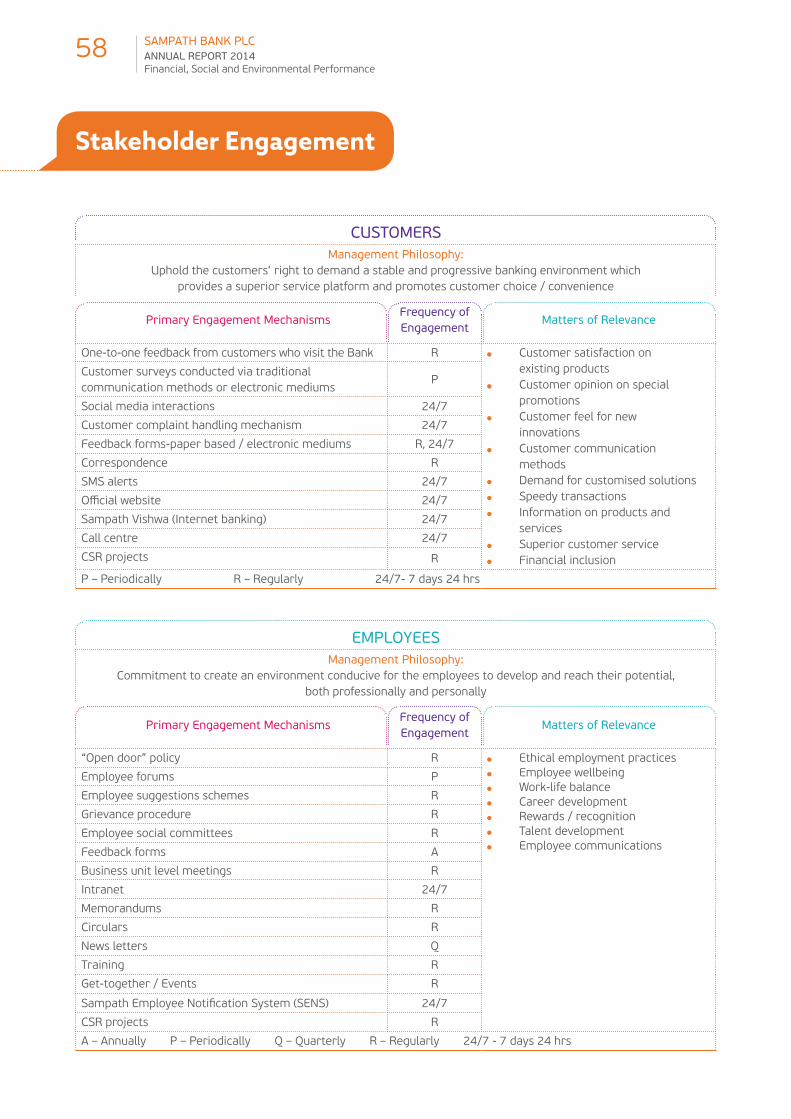

Stakeholder Engagement

CUSTOMERSManagement Philosophy:

Uphold the customers’ right to demand a stable and progressive banking environment which provides a superior service platform and promotes customer choice / convenience

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

One-to-one feedback from customers who visit the Bank Customer satisfaction on existing products

Customer opinion on special promotions

Customer feel for new innovations

Customer communication methods

Demand for customised solutions Speedy transactions

services Superior customer service Financial inclusion

Customer surveys conducted via traditional communication methods or electronic mediums

Social media interactions 24/7

Customer complaint handling mechanism 24/7

Feedback forms-paper based / electronic mediums

Correspondence

SMS alerts 24/7

24/7

24/7

Call centre 24/7

EMPLOYEESManagement Philosophy:

Commitment to create an environment conducive for the employees to develop and reach their potential, both professionally and personally

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

“Open door” policy Ethical employment practices Employee wellbeing Work-life balance Career development

Talent development Employee communications

Employee forums

Employee suggestions schemes

Grievance procedure

Employee social committees

Feedback forms A

Business unit level meetings

24/7

Memorandums

Circulars

Q

Training

Get-together / Events

24/7

59

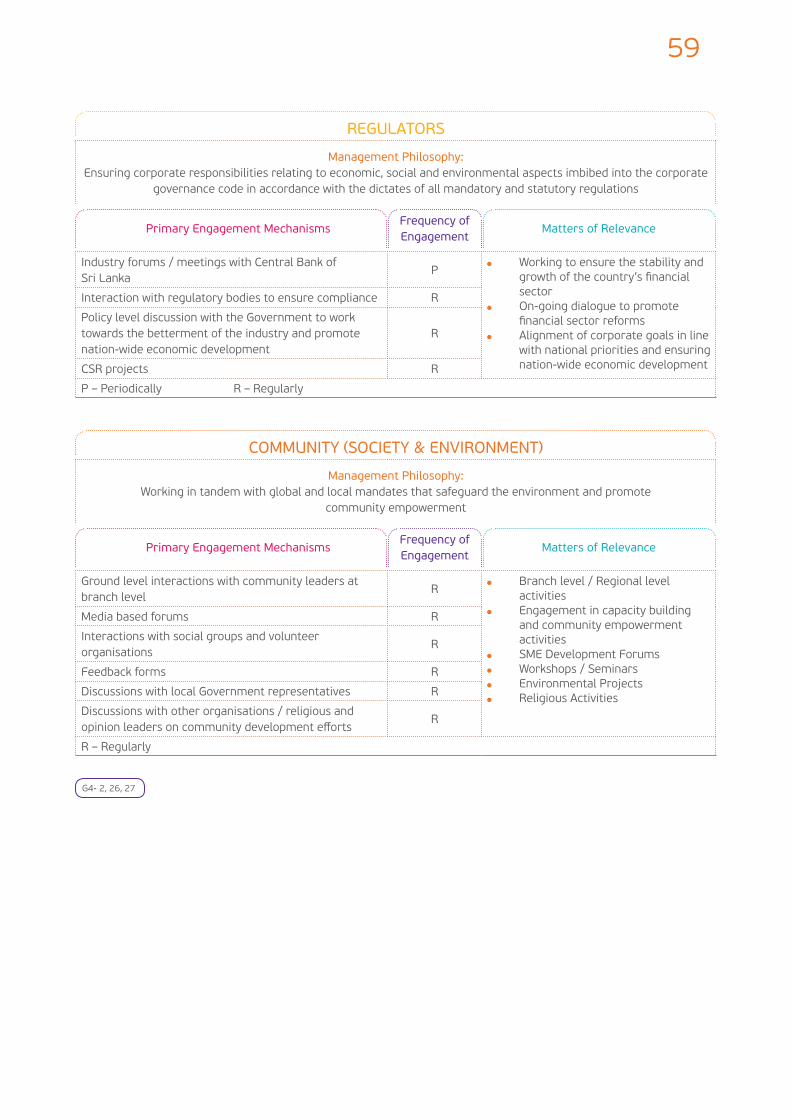

REGULATORS

Management Philosophy: Ensuring corporate responsibilities relating to economic, social and environmental aspects imbibed into the corporate

governance code in accordance with the dictates of all mandatory and statutory regulations

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

Working to ensure the stability and

sector On-going dialogue to promote

Alignment of corporate goals in line with national priorities and ensuring nation-wide economic development

towards the betterment of the industry and promote nation-wide economic development

Management Philosophy: Working in tandem with global and local mandates that safeguard the environment and promote

community empowerment

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

Ground level interactions with community leaders at branch level activities

Engagement in capacity building and community empowerment activities

SME Development Forums Workshops / Seminars

Media based forums

organisations

Feedback forms

Discussions with local Government representatives

Discussions with other organisations / religious and

G4- 2, 26, 27

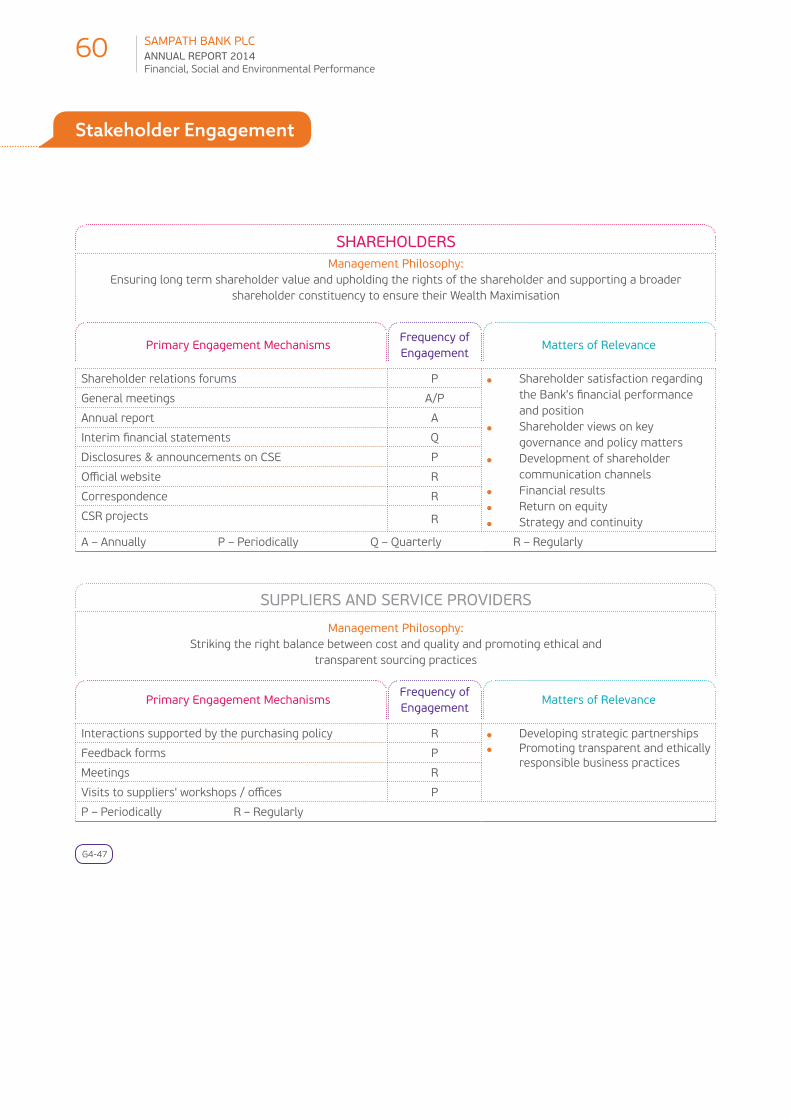

60 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

SUPPLIERS AND SERVICE PROVIDERS

Management Philosophy: Striking the right balance between cost and quality and promoting ethical and

transparent sourcing practices

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

Developing strategic partnerships

responsible business practices Feedback forms

Meetings

Stakeholder Engagement

SHAREHOLDERSManagement Philosophy:

Ensuring long term shareholder value and upholding the rights of the shareholder and supporting a broader shareholder constituency to ensure their Wealth Maximisation

Primary Engagement MechanismsFrequency of Engagement

Matters of Relevance

Shareholder relations forums Shareholder satisfaction regarding

and position Shareholder views on key

governance and policy matters Development of shareholder

communication channels Financial results Strategy and continuity

General meetings

Annual report A

Q

Disclosures & announcements on CSE

Correspondence

G4-47

61

Stakeholder Strategies

STR

ATEG

Y EX

ECU

TIO

N P

LATF

OR

M

PLA

NM

AN

AG

EIM

PR

OV

E

CUSTOMERS GOAL: Create a stable and progressive banking environment, which renders high quality banking solutions together with adequate information for the customer to make an informed decision

Strategies

Service excellence Technology-driven banking solutions

customer network Establishing of a broader based nationwide SME

lending across the country Ethical lending practices

customer Complaint resolution Maintaining customer privacy

SHAREHOLDERS GOAL: Support shareholder wealth creation and generate sustainable growth

Strategies Consistent bottom line Ensuring sustainable return on investment Transparency and responsible stewardship

Safeguard asset quality

EMPLOYEESGOAL: Develop a culture where people can

and as a team

Strategies Attraction of best talents from the market Development within through training & development Employee engagement

Grievance Handling Occupational health & safety and employee welfare

REGULATORS GOAL: Developing a voluntary reporting code that integrates all aspects of economic, environmental, social, labour and human rights practices in line with global best practices for sustainability

Strategies Adherence to all mandatory regulations

ENVIRONMENT GOAL: Adopt green management practices and operational procedures to mitigate the environmental impact of the business

Strategies

Managing the impact on the environment

SOCIETY GOAL:

community-based socio-economic issues in line with national priorities

Strategies Community development and capacity building Education and literacy Health and nutritional development of society Ethical sourcing

SUPPLIERSGOAL: To adopt a transparent sourcing mechanism that would ensure fair and equitable purchasing practices

Strategies

Tender procedure that optimises the level of competition throughout the supplier selection process

Ethical sourcing practices

G4-2, EC 1

62 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

Stakeholder: Customers

The rapidly changing business environment of today has resulted in an unprecedented level of competition in Sri

pursuing a broader share of the market.

customer needs through unique and innovative solutions

most sustainable manner possible. Working with a clear purpose, we have thus aligned our strategic vision in tandem with the needs of our customers and corporate clients. Moreover, as pioneers in the country’s banking

structure is well equipped to articulate a meaningful value proposition for both mainstream and niche markets in the country.

PRESENTING A MEANINGFUL VALUE PROPOSITION FOR ALL

technology and professionalism are the hallmarks of our customer service paradigm. Our customer-centric strategy helps to create sustainable relationships with all our customers and enhances our commitment towards product responsibility.

We believe that every customer has the right to expect a stable and progressive environment which renders sound and superior banking solutions, backed by the latest

our dedication towards achieving exceptional customer service and operational excellence.

As we expand our presence across the nation, we continue to transform our approach in cognisance with the needs of the customer,

these diverse expectations.

Priyanga GunasekaraManaging Director

Sampath Bank came forward with an innovative

to expand our operation. Sampath Bank has always responded quickly to our banking requirements. When the Development Banking Unit of Sampath Bank

have truly understood our business and has been a partner rather than a banker to us.

G4-DMA

63

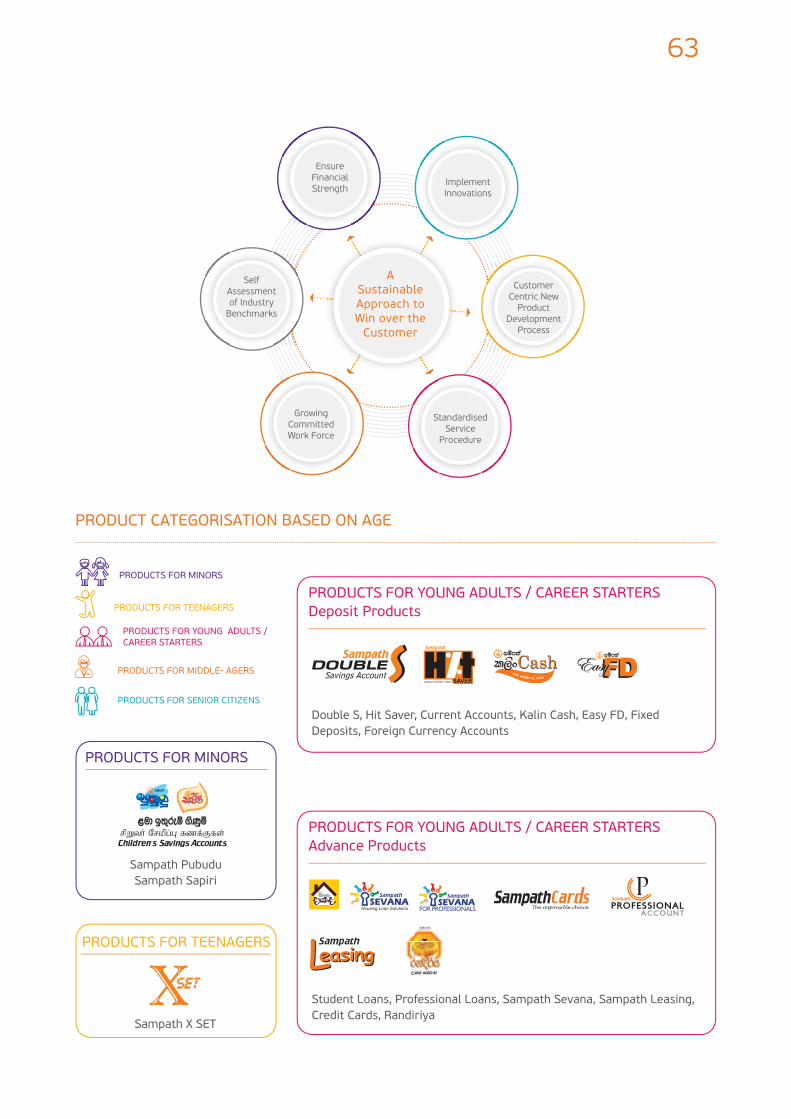

PRODUCTS FOR TEENAGERS

A Sustainable Approach to Win over the

Customer

Ensure Financial Strength

Customer

Development

Standardised Service

Growing Committed Work Force

Self Assessment

Benchmarks

PRODUCTS FOR MINORS

PRODUCTS FOR MINORS

PRODUCTS FOR TEENAGERS

PRODUCTS FOR YOUNG ADULTS / CAREER STARTERS

PRODUCTS FOR SENIOR CITIZENS

PRODUCTS FOR YOUNG ADULTS / CAREER STARTERSDeposit Products

PRODUCTS FOR YOUNG ADULTS / CAREER STARTERSAdvance Products

PRODUCT CATEGORISATION BASED ON AGE

Housing Loan Solutions

Sampath PubuduSampath Sapiri

Sampath X SET

Double S, Hit Saver, Current Accounts, Kalin Cash, Easy FD, Fixed Deposits, Foreign Currency Accounts

Student Loans, Professional Loans, Sampath Sevana, Sampath Leasing, Credit Cards, Randiriya

64 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

PRODUCT CATEGORISATION BASED ON AGE CONTD.

Stakeholder: Customers

PRODUCTS FOR YOUNG ADULTS / CAREER STARTERSAlternate Channel Products

Alternate Channel Products

Deposit Products

Advance Products

ATM Banking, Telebanking, Sampath Vishwa, Payeasy, Sampath Z – reload, SMS Alertz, SMS Banking, Mobile Cash, Sampath Bank APP, Cardless Cash

ATM Banking, Telebanking, Sampath Viswa, Payeasy, Sampath Z – reload, SMS Alertz, SMS Banking, Mobile Cash, Sampath Bank APP, Cardless Cash

Double S, Hit Saver, Current Accounts, Sampath Supreme, Kalin Cash, Easy FD, Fixed Deposits, Foreign Currency Accounts

Professional Loans, Sampath Sevana, Sampath Leasing, Credit Cards, Randiriya, Bizcash

Housing Loan Solutions

Sampath App

Sampath App

65

CUSTOMER ENGAGEMENT

and deciding on how best to respond to the evolving needs of our customers, has prompted us to map the degree of change needed to derive a sustainable customer service channel. Customer engagement thus forms an integral part of our day-to-day business processes, where we encourage all employees to “Go the extra mile” on behalf of the customer. Moreover, gauging the pulse of the customer, through regular feedback and special customer gatherings, we are able to catalogue progressive industry trends that are likely to impact our

PRODUCTS FOR SENIOR CITIZENSAdvance Products

PRODUCTS FOR SENIOR CITIZENSAlternate Channel Products

PRODUCTS FOR SENIOR CITIZENSDeposit Products

Sampath Sevana Dayada, Randiriya, Bizcash

ATM Banking, Telebanking, Sampath Vishwa, Payeasy, Sampath Z – reload, SMS Alertz, SMS Banking, Mobile Cash, Sampath Bank APP, Cardless Cash

Sampath Sanhinda Saver, Sampath Sanhinda FD, Double S, Hit Saver, Current Accounts, Sampath Supreme, Kalin Cash, Easy FD, Fixed Deposits, Foreign Currency Accounts

Sampath App

66 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

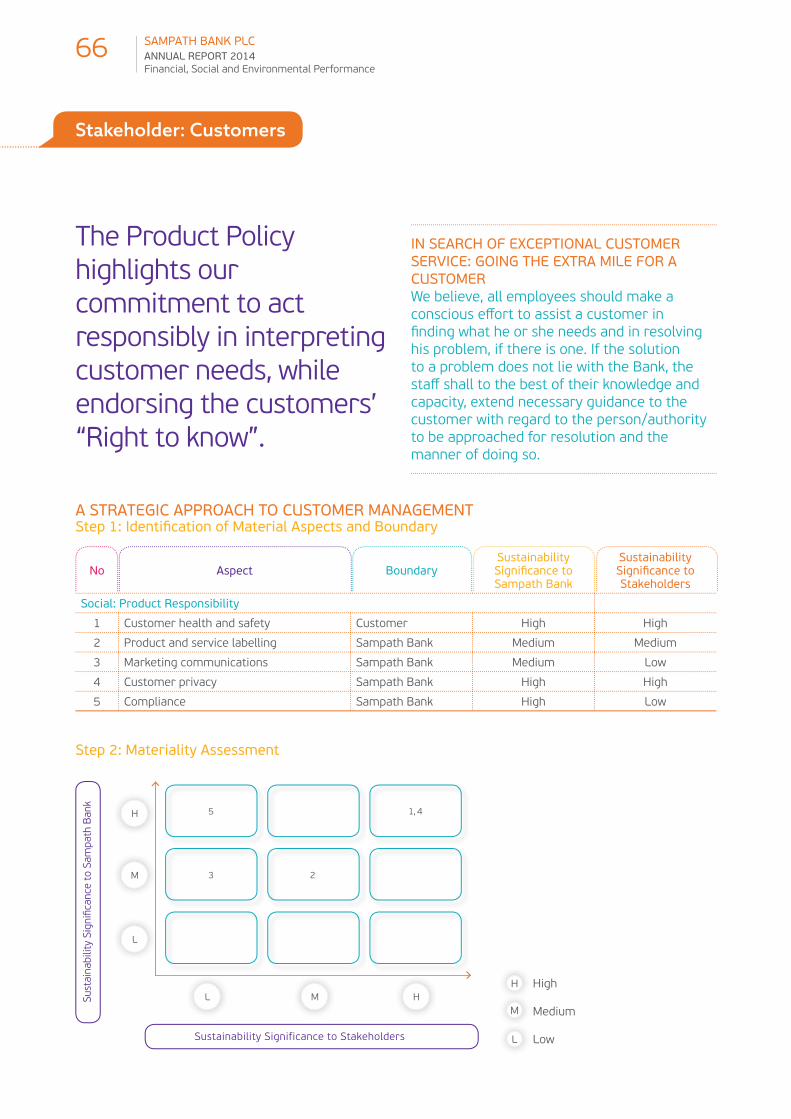

IN SEARCH OF EXCEPTIONAL CUSTOMER SERVICE: GOING THE EXTRA MILE FOR A CUSTOMER We believe, all employees should make a

to a problem does not lie with the Bank, the

capacity, extend necessary guidance to the customer with regard to the person/authority to be approached for resolution and the manner of doing so.

highlights our commitment to act responsibly in interpreting customer needs, while endorsing the customers’

A STRATEGIC APPROACH TO CUSTOMER MANAGEMENT

Step 2: Materiality Assessment

No Aspect BoundarySustainability

Sampath Bank

Sustainability

Stakeholders

Social: Product Responsibility

1 Customer health and safety Customer High High

2 Sampath Bank Medium Medium

3 Marketing communications Sampath Bank Medium

4 Customer privacy Sampath Bank High High

5 Compliance Sampath Bank High

H

M

M H

5

3 2

1, 4

Sustainability Significance to Stakeholders

Stakeholder: Customers

H

M

High

Medium

67

Type of research - Quantitative

Sample Size - 1,000 per quarterCoverage - Colombo, Galle, Kandy and Kurunegala

During the year, a comprehensive brand tracking exercise was initiated to measure the success of our advertising and branding

ASPECT: MARKETING COMMUNICATIONSRaising the Bar - Customer Communication While working to enhance customer convenience, as keen advocates of customer rights, we also strive to ensure adequate information is made available to assist the customer to make an informed decision at all times.

guidelines on how our products are conveyed to the end consumer. Developed in cognizance with all mandatory

accordance with the guidelines applicable to banking

commitment to act responsibly in interpreting customer

Moreover, our campaign to establish the Sampath brand

prompted a trilingual format for all communications. Meanwhile, a voluntary code of ethics governs the transparency of our actions and ensures that all our communications are free from social, cultural and

for all citizens of the country, our above-the-line and below-the-line communication mediums seek to convey

remains a critical aspect of our publicity framework, we have also sought to embrace the new developments in electronic, digital and social media platforms that have

Mr H D De SilvaChairman - HDDES Group

As a leading bank currently in the forefront of Sri

been associated with the Bank for the past two

instrumental in promoting our company as a leading

unstinted support extended to us by the Bank which has helped us make a name for ourselves in the global marketplace.

campaigns vis-à-vis the success of the corporate brand as perceived by the customer. An island-wide exercise to table the health of the “Sampath” brand, the undertaking also aims to ascertain the general perception of brand strength from the general public.

Outsourced to an independent third party research consultant, the project entails quarterly brand tracking for a one year period.

communication platform, the insights obtained from this process would help us align our brand strategies and derive a more sustainable blueprint for future growth.

past. Our marketing communications are aligned to

violation of these laws have been recorded.

68 SAMPATH BANK PLCANNUAL REPORT 2014Financial, Social and Environmental Performance

ASPECT: PRODUCT AND SERVICE LABELLING

As a service organisation, our operations have no impact or potential impact on the following: The sourcing of components of the product or

service Content, particularly with regard to substance that

might produce an environmental or social impact Safe use of the product or service Disposal of the product and environmental/social

impact

and banking solutions have been developed in

Sampath Bank Product

Information and Accessibility

Brochures and

Traditional Advertising

24 Hour Call Centre

Branch Merchandising

Accompanied by Application

Forms

CorporateWebsite

E-Channels

Social Media

Marketing Communication Status

product and service policies which mirror the national regulations for banking products. As such there have been no reports of regulatory violations nor any incidents of non-compliance with voluntary codes in relation to disclosure of product information and labelling of our products or services.

ASPECT: CUSTOMER PRIVACYAs a responsible banking institution in the country, we have always upheld the customers’ right to privacy and

this regard, the following measures have been integrated into our day-to-day operations in order to ensure that customer privacy is upheld at all times.

Stakeholder: Customers

69

Measures adopted in order to ensure customer privacy

located islandwide with the intention to prevent risk of counterfeit credit card

Additional security to credit card holders via added encryption for chip enabled cards

SMS alerts to notify each transaction Direct calls to customer prior to performing high

value transaction

operation.

Mr R D PremasiriChairman / Managing Director