ot BPo2-22p - Employee Portal - HPSEBL

182

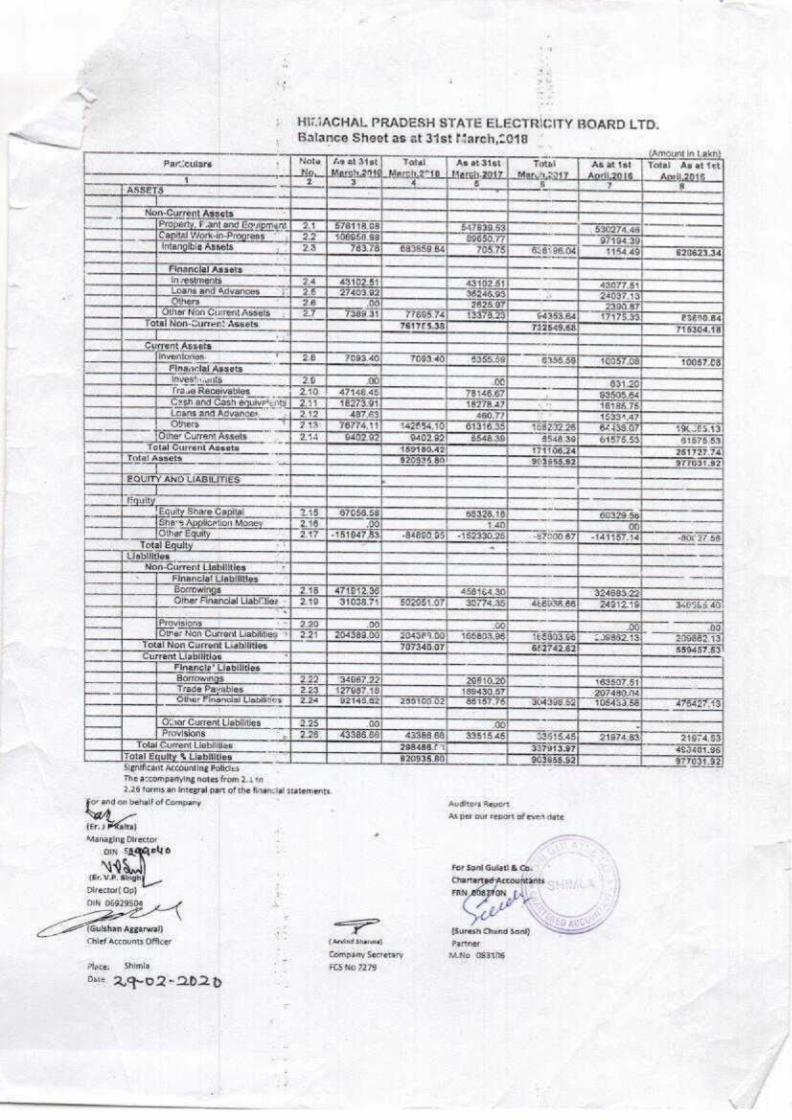

Parcculera: HIGACHAL PRADESH STATE ELECTRICITY BOARD LTD. Balance Sheet as at Jist March,2018 Nota, gat Dtst Tt As atZist Total = 1 atist | Total Asal tet 2 Accounting Policies The accompanying fetes fram 2... tn 2,25 tarms.an Integral part ofthe financial statements a ofCompany fer.) tata) SAanaging Director : =f oN elo (EVP, Singh Director( Op} ON O6929504 LS (GuishanAggarwal) Thief Accounts OFlcer Place; Shimla im — (Andindl Share) Company Secretary FOi-No 7279 ot BPo2-22p Audltord Report Ai Der our report of eves date ForSantGuiatl& Ga. Chartarted Accountants | FRM goayON p41) po | c- i (Sureeh Shand Soni) Partner M.Ne de21N6

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of ot BPo2-22p - Employee Portal - HPSEBL

Parcculera:

HIGACHAL PRADESH STATE ELECTRICITY BOARD LTD. Balance Sheet as at Jist March,2018

Nota, gat Dtst Tt As atZist Total =

1

atist | Total Asal tet

2

Accounting Policies The accompanying fetes fram 2... tn 2,25 tarms.an Integral part of the financial statements

a of Company

fer.) tata) SAanaging Director : =f

oN elo

(EVP, Singh

Director( Op}

ON O6929504

LS (Guishan Aggarwal) Thief Accounts OFlcer

Place; Shimla im

—

( Andindl Share)

Company Secretary

FOi-No 7279

ot BPo2-22p

Audltord Report

Ai Der our report of eves date

For Sant Guiatl& Ga.

Chartarted Accountants |

FRM goayON p41) po |

c- i

(Sureeh Shand Soni)

Partner

M.Ne de21N6

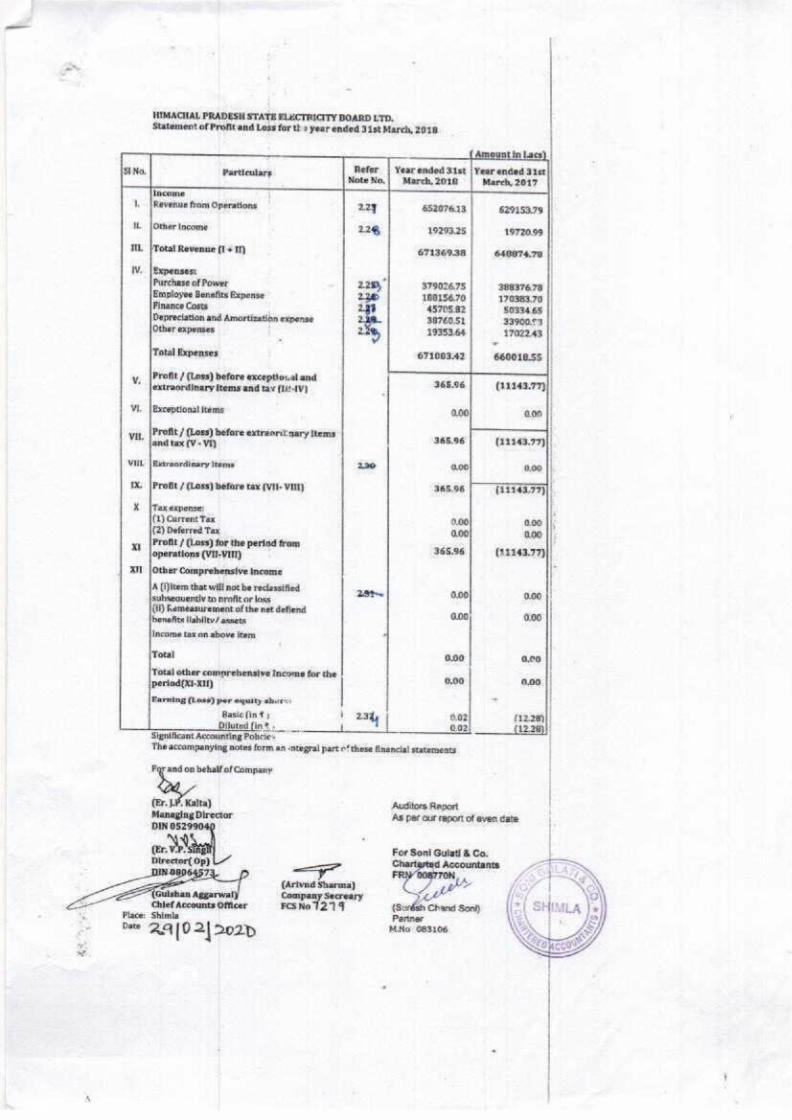

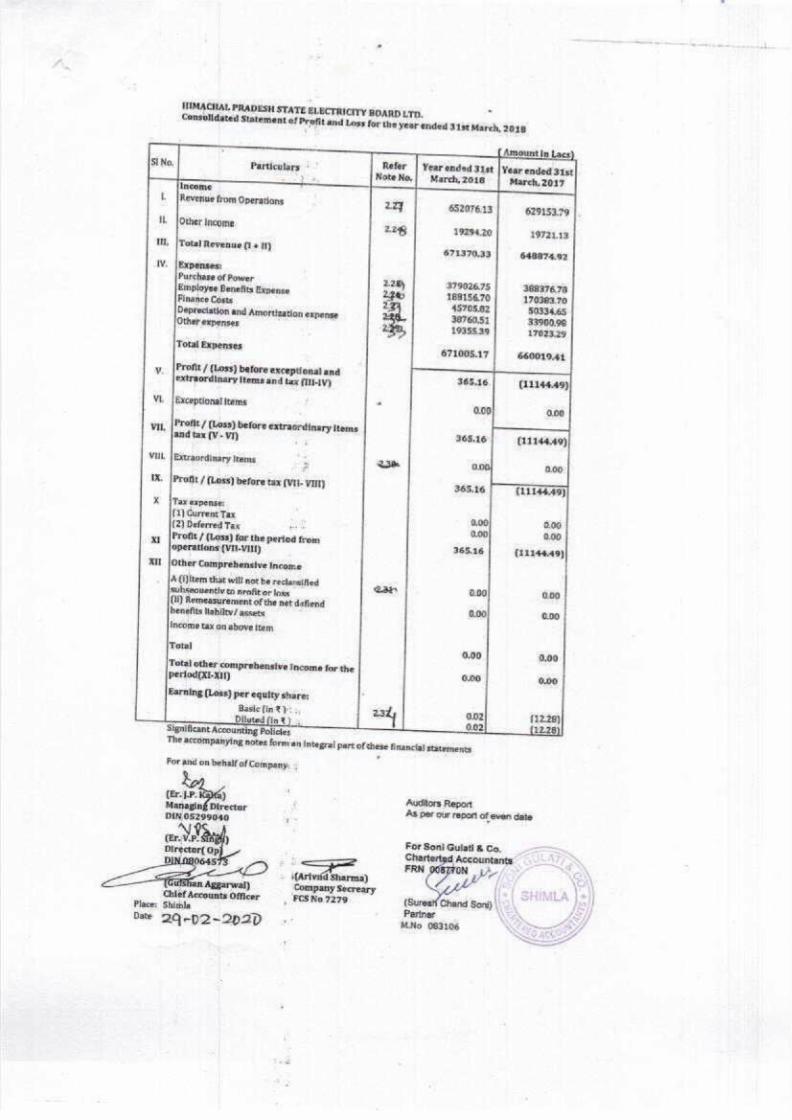

HIMACHAL PRADESH STATE ELECTRICITY BOARD LTD. Statement of Profit and Loss far tha year ended Jist March, 2018

Amount in Lacs

Refer | Yearended 31st | Year ended 31st path arrears NoteNo.| March,2018 | March, 2017 Income ,

1. | Revenue from Operations 229 65207613 629153.79

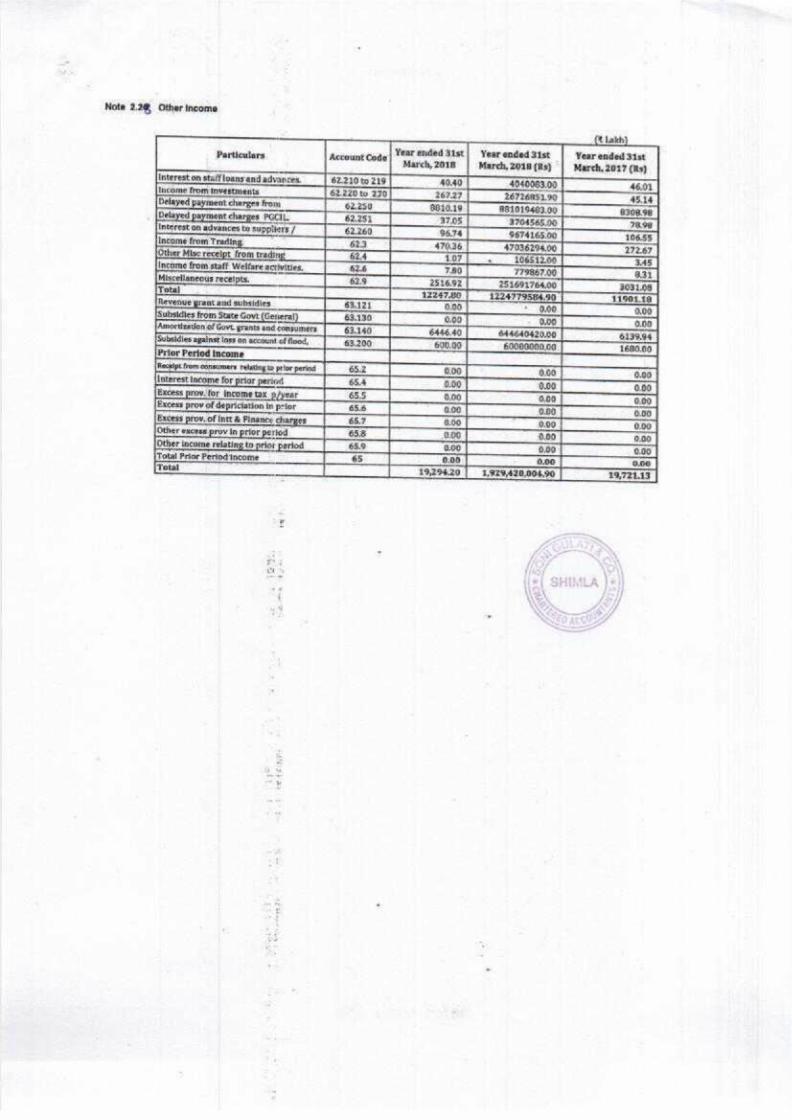

IL | Other Income 228 19293.25 1972099

ML | Total Revense (1+ 11) 671369.38 648074.703

WW. | Expenses: . Purchase of Power 2253, S790Z6,75 3883976.78 Employee Benefits Expense 22 1891546,70 170383,70

Finance Costs 1 45705.82 50334.65 Depreciation and Amortization expanse Sa760.51 3590069 Other expenses » 19953.64 1TAZ2A3

Total Expenses 671003.42 660018.55 |

Profit / (Loss) before excepttoyal and ; v ery ia as TEV) 365.96 (1143.77)

Vi. | Excaiptionat fens 0,00 aan ||

Profit / (Loss) before extraorilnary items j Vil tna tax (V- VI) 365.96 (11143.77)

VIL | Bxtraardinary Iteme 2a 0,00 0.00

IX [Profit / (Loss) before tax (VI- VIII] 965,95 (11343,77)

H |Taxexpense: 3 (1) Current Tax f.00 0.00 ||)

(2) Deferred Tax 0,00 00 Profit / (Loss) for the period from x1 toms (VIl-VUT) 365.96 (41143.77)

XH | Other Comprehensive income |

A (Oltem that will not be reclassified — | subsequently to nrafit or Ioas — a8 (il) Remegnurement of the net defiend aoa coo: benefits lahiltvs aanets . ; Inconm tae dn above iten *

Total o.00 o.c0 Total other comprehensive Income for the | 1.00 n.00 }) period{X1-KI)

i Earning (Loss) per equity shirc: = f

Basle [in t ' 2a 0.02 112.28] | Diluted fine. i 0.02 (12.284)!

Significant Accounting Policie

{

The accompanying notes form an integral part o‘these financial statements

For and on behalf of Company

| (Er. LP. Kalta) Auditors Report Managing Director As per our report of aven date BIND ]

reve For Soni Guiatl & Co; Director( Op) Cha Accountants

Nia

(Gulshan Aggarwal Seereary he Chief Accounts Officer Fes No 712.14 43 Chand Soni)

Place: Shimla Perinar Date Bq hy 2| >202D M.No 083106

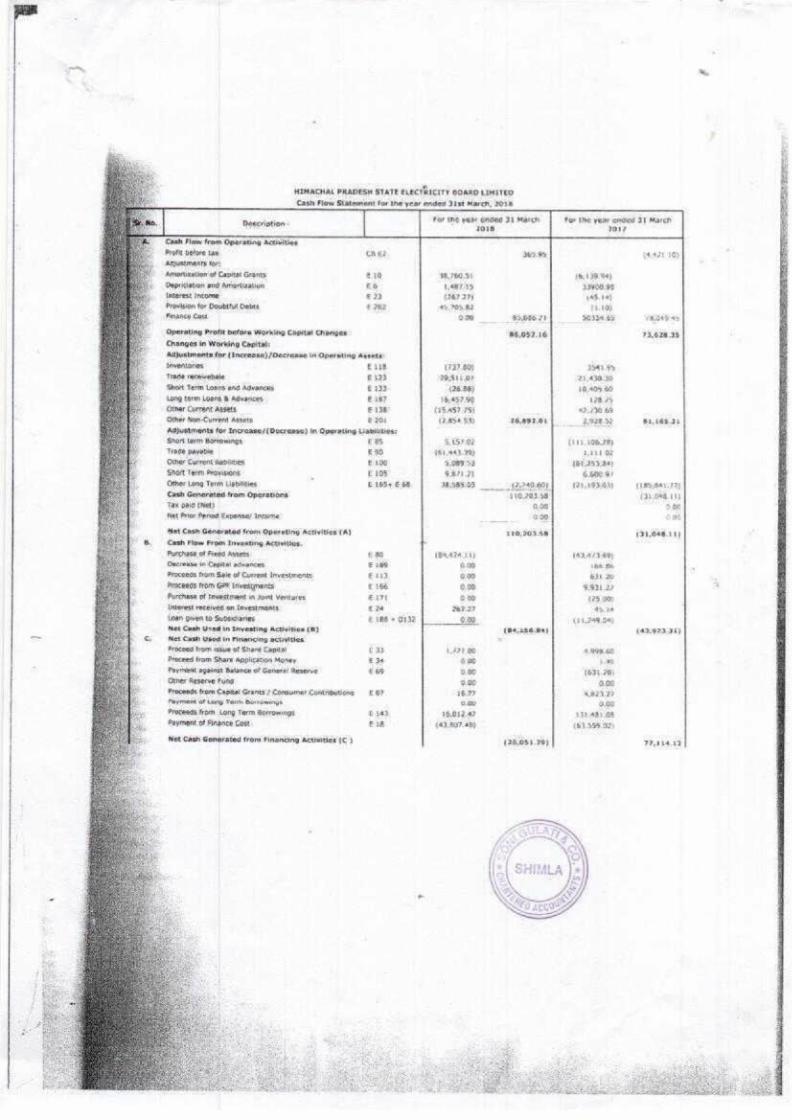

HIMACHAL PRADESH STATE ELECTRICITY BOARD LIMITEO Cash Flow Statement for the year ended Jist March, 2018

Far ing yaar Gnine 34 Maree for (eh pear once 37 March

Beserintion 2078 tony

Cash Flow from Operating Activitigs

Profit before tan: tie? Seu, 35, (ae Tey

Adjumtmannts tors Amortization af Capites! Grants ent 4,750.51 bot eas)

Gepriciaton and Amartiaation E6 1,467 15 Asbags baterest Incocn e}3 (P67 27) 15. bah

(Previion for Doubtful Debrs £202 ah, GH hh BS.

Peancy Coot : eM BSG86. 01 SGADGE FHAE sh

Operating Profit before Working Copite Changes 46,052.16 2a 48 Changes in Working Capitials Adjustments for (Inceease) (Decrease In Operating Assets feenibories ells (737.80) ery Trase recaewahale e423 29,411 OF 2100.30 Short Term Loans and Advancia E133 (26.86) A904 ie

Long ferm Loans & Advances gant MAS? 90 La Gtnar Currant Assets e138 (TRS 7 P5F ad 0.88 Gthde Mon-Current Assets e304 (ainse 54) 26,092.01 202852 84,165.31 Aghsttmanta for Increase/(Decremec) In Qeerating Liabilitiva: |

Short born Batremings as S05 902 (0b 6,27 Traita payabes Fad pik 19} aad ae

Ochar Current then itines E100 S,08g5e ier esagas Shart Term Arowisone £ toe Sara 6,00M),9+ Other Long Teen Liahetities ; i ELBSy E Ge MASADR aa | (a sob Ay LES GAAL Fa

Cash Genorated-from Operations 110,205.38 HOLL CPRR| Uf Tas pale (Met) a.on 00 feet Prise Period Expeneay Income a aon or

Not Cast Génaratad fram Operating Actleitios (A) ro, s0348 134,048,11) Cash Finw From Investing Activia, Purghese of Fined Assets: ER (EAARACL A) WAAL AR Decrtive if Capitel scuarces, Free 6.0 (i! Be

Proceeds from Sale of Cerrent Investimonts €ul2 om 641 20 Proteads from GPE Investments: £454 6.90 ‘932s Purthasa of tnvedtinent in Jowit Vertutes ein oon (75.00) Inberest received on investmants: ena Jer? ab he

Leah Geren to Sebsidiaries (Pt, 20 Day Net Cosh Ured in Investing Activities (B) (a440.89) 7 (ator ay

Net Cash Used in rinnncing activities Proceed hom sue of Share Capital faa a7¢00 908.40) Proneed from Share Application Mosny E34 fi ie

Paymint against Balapew of Gunwrs| Aeserve £69 won i643 Other Agseree Futer oD o.0

Frocends from Capital Grants Consumer Ceathibutions 1 OF 16.97 43.29 Pym OF Long Fann Boridennya oe 3.90

Procebdk from Long term Gorromings, Elta Peaidae Wb A808 Payrnant of Flnsnce Gust: Eis (a Agree) (8) S85 O77

Net Cash Generated fram Fieoneing Activities {C | (20,051.79) FF4i4id

Net Increase/(Decrease) in Cas

| hand Cash Equivatents ( A+B4 (4.56) 2,092.71 Cash end Cash Equivalents as at ist

April (Opening Balance} E197 18,278.47 16185.74 Cash and Cash Equivalents as at 3ist March (Closing Balance) 18,273.91 18,273.46

For and on behalf of Campany Auditors Report { AS par cur report of even date

wus Auditors Report Managiig Director AG per Gur report of even cate

~

For Sont Gulati & pe, Sah Charterted ioe ‘

FRN a Aggarwal)

Chel Amacuaats Officer

(Sure h Chand Moisi (Arei area) Parner = Company Secreary

MNo. 183108 Place: Shimla

Ditte 29|02)282p

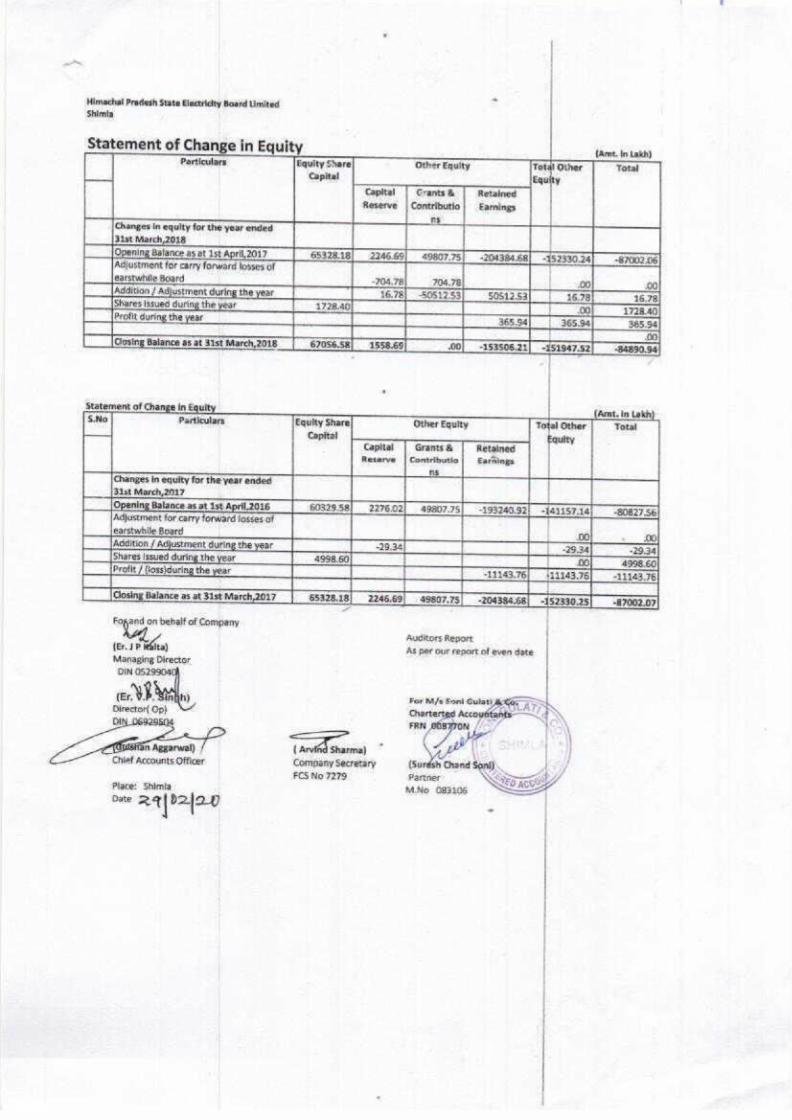

Himachal Pradesh State Elactrichty Board Limited Shimia

Statement of in Particulars Other Equity

Capital Grants & Reserve | Contributla

in equity for the year enced

carry of

Other Equity

Grants & Retained Contributio | Earnings

‘equity for the year ended

as for carry

Balance Foqand on behalf of Company

Auditors Report (er. 1 F iediea) As per our report of even date Managing Director DIN 5.

ete h} For M/s Fonl Gularie: Ar

Birecter| Op) Chart naga = ~N Gilt. . FRN tee -\

ak ee

Aggarwal) ° . | Chief Accounts Officer Company Secretary (Surdsh Chand Sant). if FCS No‘7279 Partner Samal

Place: Shima M.No O83106 pte RAID2IO.p ‘ {°>

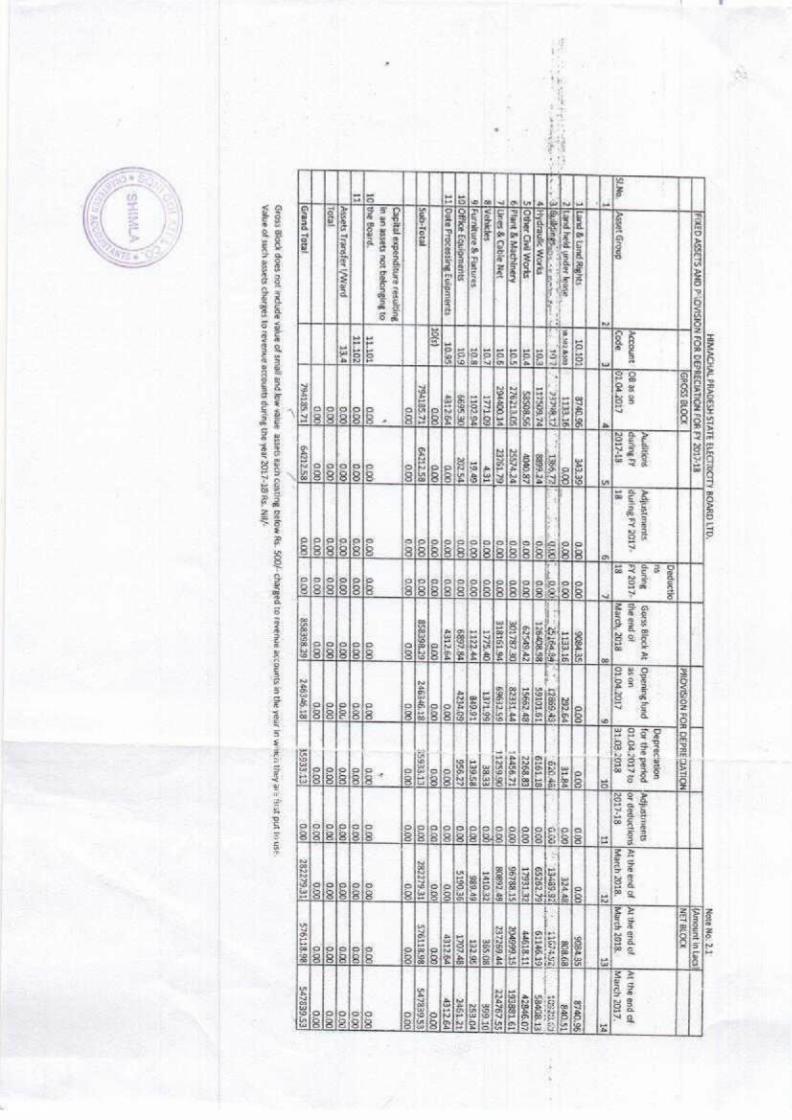

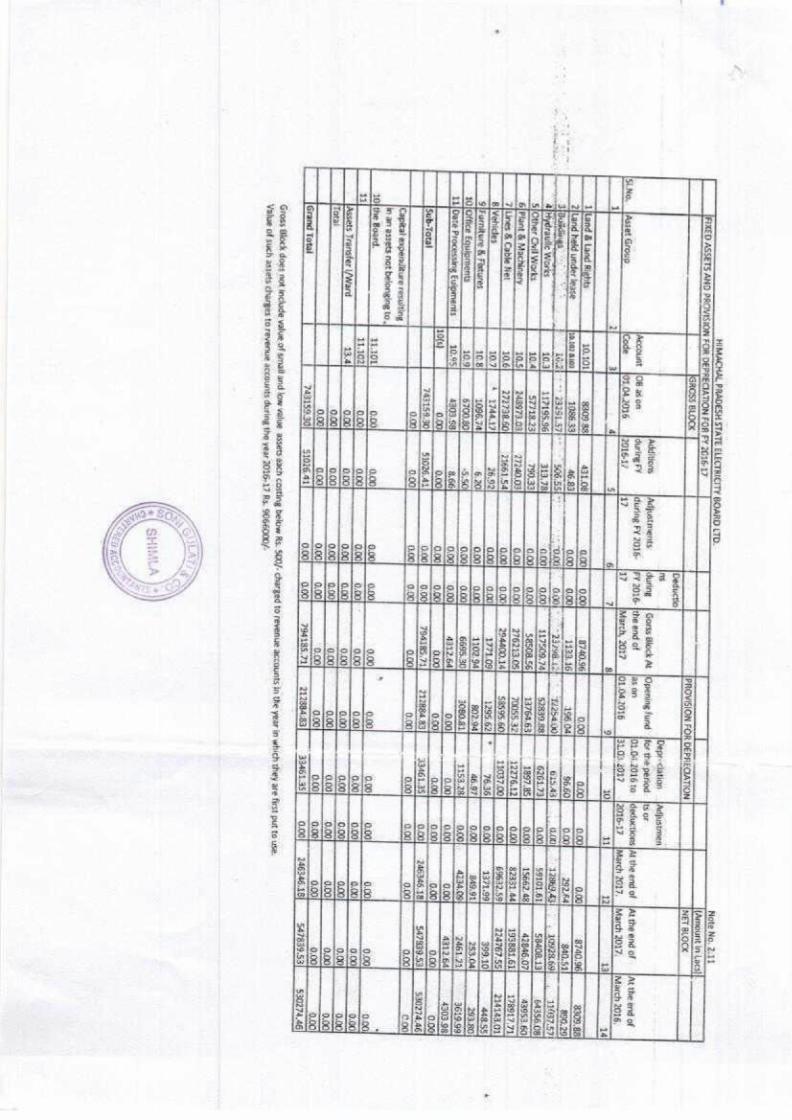

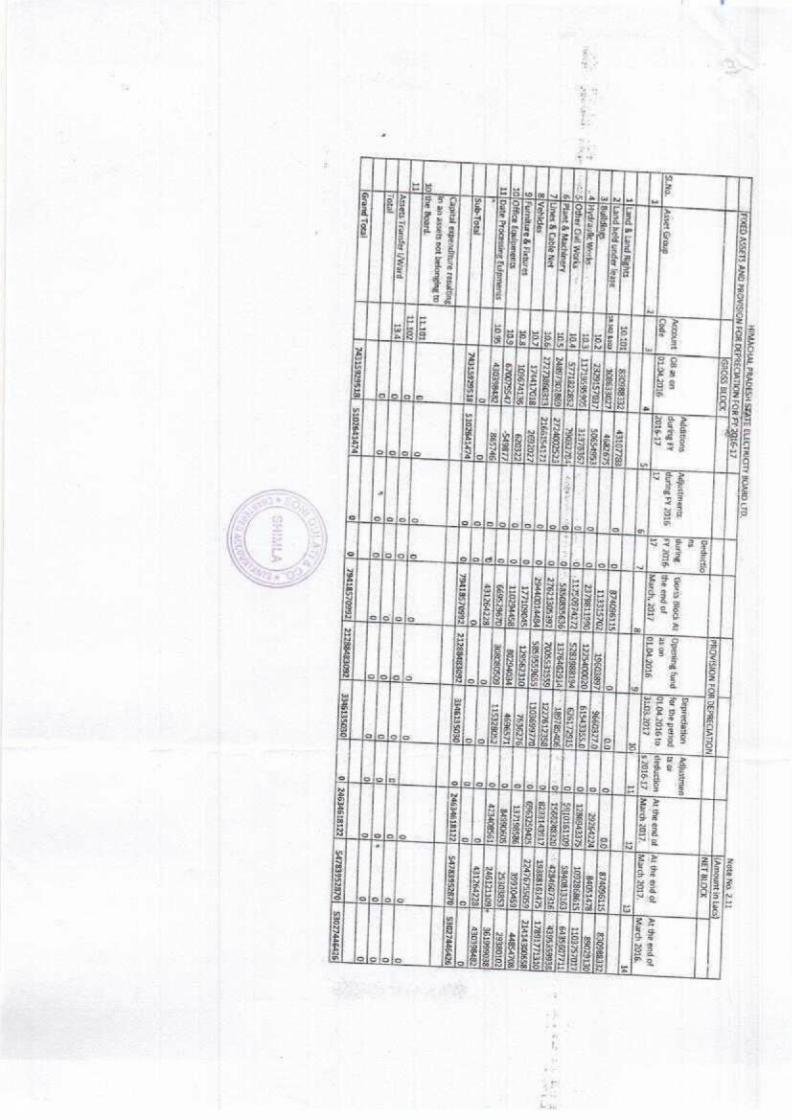

HIMACHAL PRADESH

STATE ELECTRIGTY

BOARD

LTD. Mote

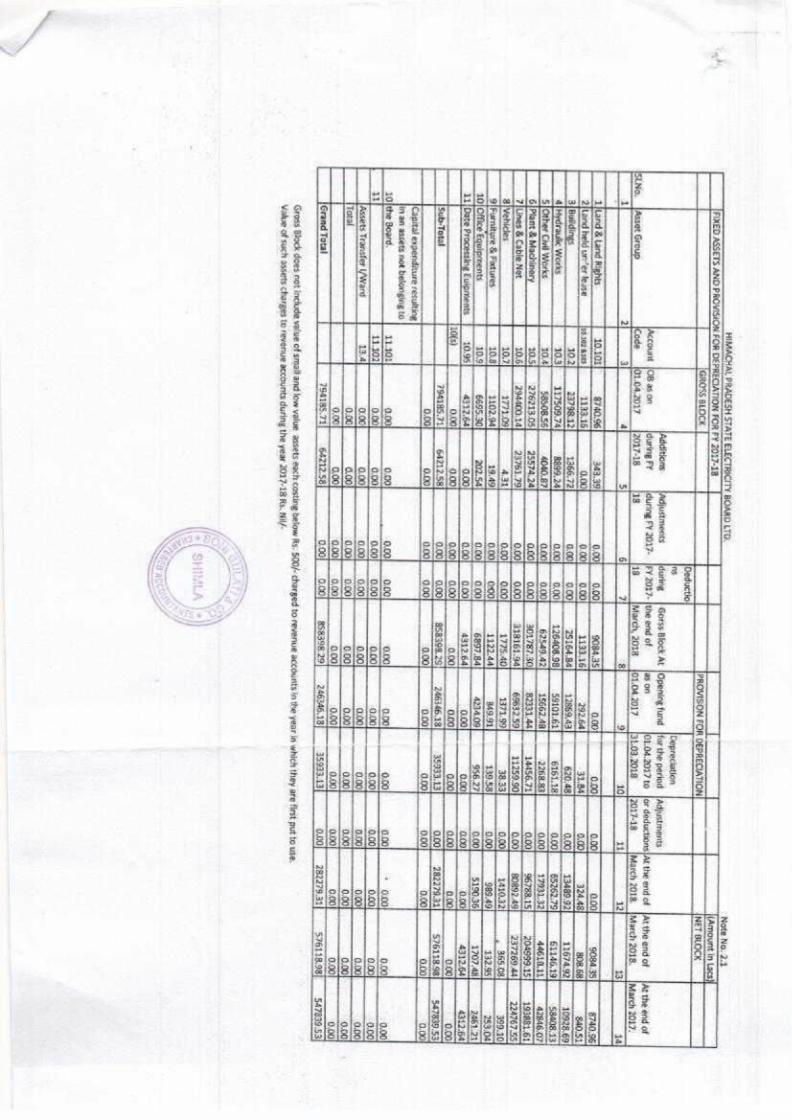

Moc 2.1

FIXED ASSETS AND PAOVISION

FOR DEPRECIATION

FOR FY 2017-48

: L

T[Amount in Lacs

‘AGROSS BLOCK

PROVISION FOR

DEPRECIATION NETBLOCK

Deductio :

ns Depreciation

Auditions =

[Adjustments [during

| Gorss

Block At

|Openingfund for the period

{Adjustments Account:

(OS: as.

on chia roe

EY duting FY

2017: [FY

2027+ [the end

ot aon

OL04 2017 to.

lor deductions|At

the end of

[Attheeandof At

the end

of

SLNo, [Asset

Group Kode

JOLOe20R7 fata y-te

1a 18

IMarch,2018 fOL042017

|31.03.2018 —(12027-18-

March'2028. jMarch2018.

[March 2017. 1

2! 3

4 5

6 7

4 3

10 tl

12 ia

l4

ijland & land

Rights 10,10)

8740.56) 345.39

0.00) 0.00

30435)

ooo

O00 o.00}-

0.00) $084.35)

8740.95 sera

be

2 Land held under lease.

sn.3n3 503

1133.16) _

200). 0.00)

0.00 1153.16

26d 3184)

G00]

#2448) 803.64

640.51) asin

FR SIRs cates

SEH Se aaa

an ata

ag) “aaa

an) aod

(eras tama

a{Hydraulic Works

10.3) 127509.74

‘Ba9.24 0.00]

6.00 125408.98

SO01.51 6161.18

co 6526275]

6114.19) 58408.13

5} Other Civil Works

10.4) 53508,55.

ADAO.BF 0.00)

0.00) 6245.42

TSRS2 Ag 2268.83

0,00 1793132}

4461801 A246.07

6) Plant

& Machinery 10.5

2762U.05 574.24

0.00) 0.00

30178730 3233144

3445671 0.00

86788,15 294999-15

193821.61 Filines

& Cable Net

10.6 29440014

23761,79 0.00)

0,00 318161,54)

6964259 11259.90

0.00) BOBS2.4!

237259.)

‘22476755

8) Vehicles

10.7 1771.09

4,31 0.00)

6.00 1775.40

1371.98) 38.34)

oon 1410.37)

365.08 399.10]

5| Furniture &

Fixtures 10.8

1192.04 19.49)

co] 6.00)

itghad 849.94

13958 oto

989.49 132.95

283,04 10)

Office Equipments 10.9

5695.40 254

0.00] 0.00)

6ao7.84 4224.05]

356.27 a.00

5190.36 1707.48)

2461.21 11/Dste

Processing Euloments

10.55 45th 64)

G00)

0.00) o.08

4312.64 o.o0

O00

0.00 0.00)

4312 64) AF12.64

10{s) oOo)

0.05 OuK)

ocd 6.00

0.00 0.00

2a

0.00 0.00

0,00) Sub-Total

7O4185.71 6A212.58

0.00 0.00)

B52598.29[ —

24Bd46.18 a5933,14

Doo). -FRI27931

57611898 5472399.53

0.00 0.00

0.00) o.00|

ao 0.00)

0.00) 0.00

0,00) 0,00

6.00 Capital

expenditure resulting

i ‘in

an aisets mot

belonging to

. *

10|the Board.

11.101 0.00]

0.00 6.00}

0.00 0.00

a.00 ooo

0.00 0.00

0.00] 9,00

ii 11.102

0.00 0.00)

6.00) O00

0.00) G00

0.00 0.00

O00 0.00}

0.00) Assets

Transfer Ward

iia ono

o.00] o.co]

0.00) 6.00)

0,00 0,00

0,00 oo)

0,00] Ou

Total 600

0:00) 0.00)

0.00 0.00

0.00 0:00)

0,00) 0.00)

0.00 Q.o0;.

0.00) ‘O00

0,00) 0.0

0.00 o.00

oo

0:00 G.00;

000} 0.00

‘Grand Total

7OSEES.71 A712

58 0.00

0.00 358393.29!

266345.18 15533-13

0200 25227931

STOLE;

547839,.53

r ?

Gross Block does not include

value of small

and low

value asseti

each casting

Below As. 500/- charged

to revenue accounts inthe

year In w

ea

they gre

first put to use

Value of such assets charges

to revenue accounts during the year 2017-18

As, Mil

j

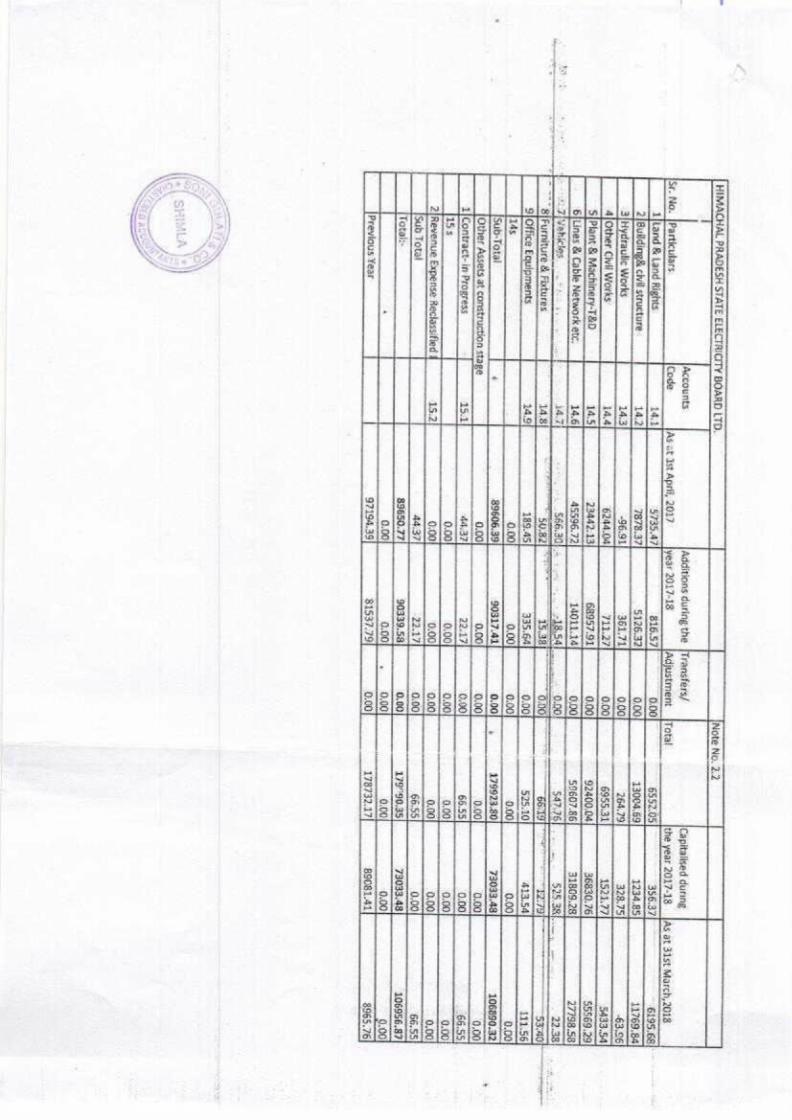

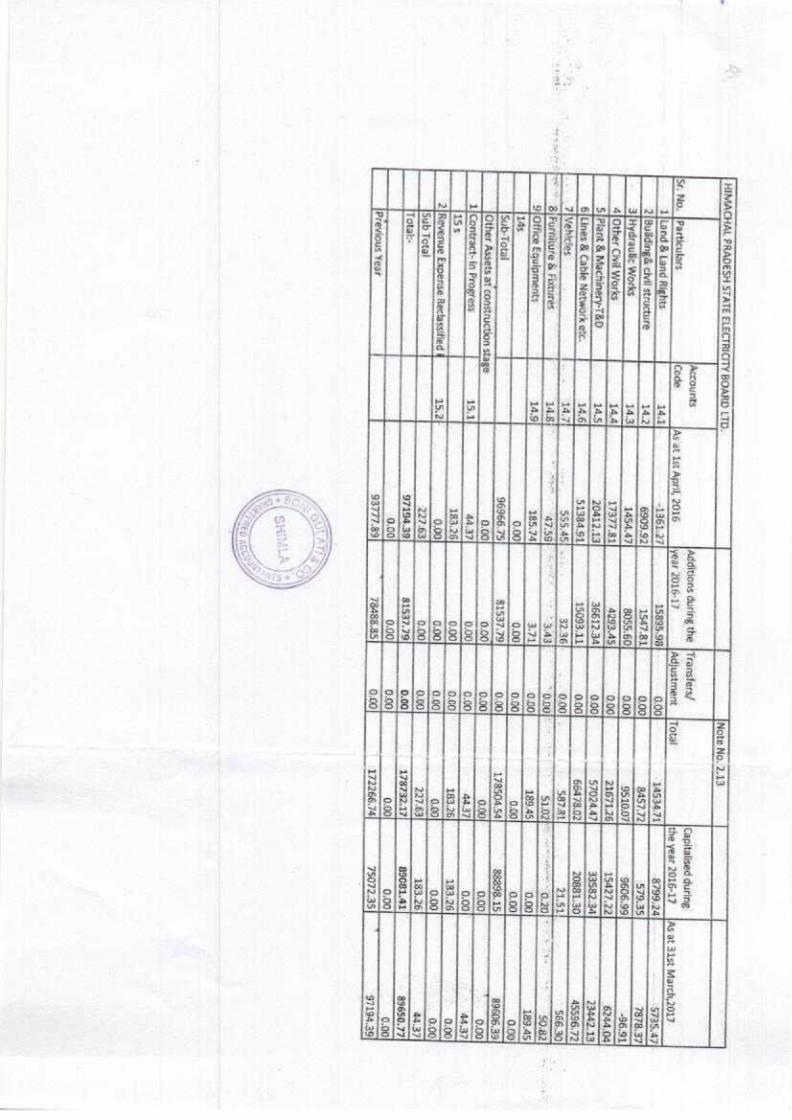

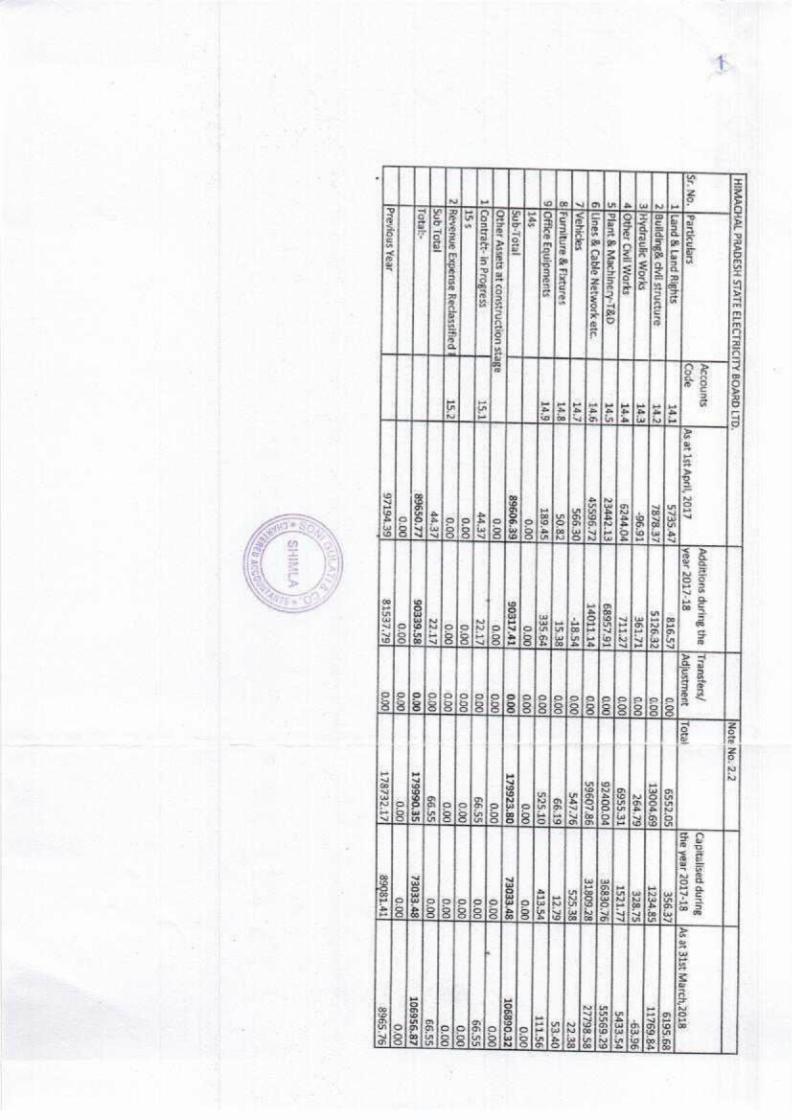

HIMACHAL PRADESH STATE

ELECTRICITY BOARD

LTD. Note

No. 2.2

|

Accounts

Additions during

the |Transfers/

Capitaised during

Sr.No. [Particulars

Code

Agcct Ist

April, 2017

year 2017-18

Adjustment |Total

the year

2017-18 |As

at 31st March, 2018

iftand &

Land Rights

14.1 5735.47

816.57 6.00)

6552.05 356.37]

— 6195.68

2|Building&: civil

structure 1a?

7878.47 5126.32

0.00. 13004.69

1234.85 Liv6s.84

3] Hydraulic

Works 14.3

6.91]. 361,71

G.00 264.79

328.75 -63.96|

4/Other Civil

Works: 14.4,

6244.04 iby

.06 6955.31

1521.77 5433.54

5|Plant &

Machinery-T&0 14.5

23442.13) 68957,91

0.00 92400.04

36830.76 $5569.29

6 {Lines

& Cable

Network ete.

14.6) 45596. 72

14011.14 0.00

59607,86 31809.78)

27798.58 Ay

Wehiclas. =

5 i447

Be

pdBib4t 0.00

SoPT Bl

S2n ete

| ke

22.38 ;

8] Furniture & Fixtures

14.8 “So ea]

15.38] 0.00

pee] Tg

——5 58

9/ Office

Equipments 14.9

189.45 335.64

6.00) 525.10

$13.54) 111.56

145 0.00

(0.00 0.00

0.00, 0.00

0.00 Sub-Total

é 89606,39)

$0317.41 0.00;

, 179923.90

7303348

106890.32 Other Assets.at construction

stage 0.00)

0.00 0.00

0.00 0.00)

0,00 1|Contract-in-Progress

15.1 44,37

22.47, o00

66.55 6.00

66-55) 155

0.00 0.00

0.00) 0.00

0.00 0.00

2]/Revenue Expense

Rectassified 15:2

0.00 0.00

0.00 0.00

0.00 0.00

Sub Total

4437 PAT

0.00 66,55

0.00 66.55

Tatal:- BS650.77

90339.538 0.00

179°90.35 73033.48

106956.87 i

0.00) 0.00

0.00 0.00

0.00 0.00

Previous Year

97194.35 B1S37.79

6.00 178732,17

89081.41 4965.76

;:-

= \

4 —

“n if

A Na

| 1

[HIMACHAL PRADESH

STATE ELECTHNCITY BGARD LTD.

i | Note No. 2.3-

INTANGISLE ASSETS AND PROVISION

FOR DEPRECIATION FOR FY 2017-18

ane [iAmiount in

Lac)

: :

GROSS BLOCK :

: PROVISION FOR DEPRECIATION

[NET BLOCK

Oeprecistion Adtjuisiivine

Additicns Adjustment

|Deductions | Gorss Glock Ar

[Opening forthe period

jntso AL the

end ;

OBason — fduring FY

during F¥ jduring FY

— jthe enc of

furidason- |OL042017

to [deduction jof March

JAR the end of March

Ar the end

of

;No. Asset

Group Account

Code |OLO2017

(2017-18 7-18

[017-18 March,

2018 —

fox.aa.2017..|31.032008 — |s 2007-18

[7078 2008,

March 2017.

2 3

4 3

6 7

a 3

10 it

23 33]

[initiangitile Ascéts tant

man] ar]

oeofaeol~

ae st ee

6.75) Ooh

2045, 7o) = RS

ae

Total 724370]

7a3.78 0.00]

Oo 3027.49

1537.96 70575

O00} 223.70]

7.7

HIMAICHAL PRADESH STATE

ELECTRICITY BOARD

LTD. Note

No, 2.14

[FINED ASSETS AND

PRCIVISION FOR DEPRECIATION

FOR F¥ 201617

| hee.

[Amount

in Lacsl). ;

GROSS BLOCK

PROVISION FOR DEPRECIATION

NET BLOCK Deductic ns

Depr-dation _|Adjustmen

Additions Adjustments

during | Gorss

Glock AL j/Opening

fund’ [for the period.

[ts or Account

(OB-38 on

during FY

durifig

FY 2015- FY

2016- |the

end of

as an

LO

2016 te

fdedwctions|at the endo!

{Attheend of

[At the end of

Sl.No. [Asset Group

Code 0t042036

— frore-17

17 17

arch, 2007

(01.08.2016 —fat.03.4077

2026-17 march

2017, March

3017, [March

2016, 1

z 3

4 5

6 7

8 3

10) ii

12 13

ia

Iland & Land Rights:

10.101 8309.83]

431,08 0.00

o.00) 8740.96

6.00 f.00

0.00 6.00

8740.96 8309.85)

2jLand held under lease

hota Rana

1086:33] 46.83

0.00] G00]

1133.46

196.04) 96.60)

8.00) 29264

240.51 890.29

S]Bundigs dg}

>" @3Sh57)-~

506.55] {[Te0Gh

Gon)” = 2a9se

iF Saasa.oo)

B1543] 0.00]

2B ae)

Ube

0s7.57) _ a[Hydraulic Works

ina] i174195.96

313.78 0.00;

aco) 117508.74

5IR39, 6261.73)

9.00 59101 61

SB408. 13 ES6.08

S[Other Gvil Works 10.4

S7iig.23 790.33

0.00] “ape

$8508.56 1a764.63

1897.85 6.00)

15662.43| 42846,07

43953.60 6] Plant &

Machinery 1035|

248973,08 17240,08

Ooo] —o.o9

276233.05 7005532

12276.12 0.00)

‘82733144 19388161

LPESL7F1 7}Lines

& Cable

Net 10.6]

27273860] 2166154

0,00] _-a.0¢)

2eas00.1d 58895. 60)

11037,00 odo,

6963259) 22476755

214144. 8] Vehicles

TO7] *

174aa7 36.82

O.0G/ 0.00

1771.09 1255.62)

* 76.36

0.00) 1371.99)

399.10 449.55

$/Furniture

& Fixtures 10:8

1096.74 6.20

6.00] o.00

1102.94 802.94

46.97 0.00

849.91 253.04)

293.50 10

[Office Equipments

10.9 a700.80

“5.50 0.00

0.00) 6655.30}

7080.82 1153.28

00 4234.06

2461.24) 3619.99

11 Dete Processing

Euloments 10,85

4303.98 8.66

o.cor oy

4212.64 0.00

o.00| 0.00

0.00 4312.64

4303.08 10s)

6.00 6.00)

coo} o.00)

a.00 0.00

0200 0.09)

0.00 6.00)

0.00 Sub-Total

743159.30| 58026.44

0.00] 0.00)

796185.73/ 1 7RBA Ba

23461,35 0,00]

24634618 547839.53

530274.46 0.09

0,00) 0.00

0.00 0.00

o.08 ooo

0.00 0.00

0.00 C00

Capital expenditure

resulting

in. an assets not

belonging ‘to, 5

. 10|

the Board.

110 0.00)

0.00 00]

0.00 g,00

0.00 o.oo

o.00 0.00

o.00 0,00)

li 11.102]

0.00 0.00)

G00] o.oo}

0.00 0.ca

o.00 0,00

6.00 9.00)

0.60) Assets

Transfer \/Ward “433.4

0.06 0.00

0.00] 0.00

0.00) 0,00)

g,00) 0.00}

6.00) 0.00]

d.06 Total

00 0.00)

0.00] 6.00]

0.00 0.00)

Q.00 0.00

O.co 0.00

0.00 0.00

@.00 ooo}

G00 0.00)

0.00 0.00

a.00 0.00

0.00 0.00

Grand Total

74315930) 5026.41

ono] o.oo)

794198.71| —

212684.83 B2461.35

G00} 24538618

547839,53 530074.46

Gross Ohock

does net

include value of small and

law value assets aach

costing below

Rs. SO0/-

charged to avenue

accounts in the

year in which they

are first put

to use.

Value of such assets charges

to revenue accounts during

the year 2016-17

Rs. S066000/-

Tee ee

[HIMACHAL PRADESH

STATE ELECTRICITY

BOARD LTO.

Hote Nou2d? INTANGISLE

ASSETS AND

PROVISION FOR

DEPRECEATIOM FOR FY 2006-17,

{Amount in Lac}

__|SROS5 BLOG

IM FOR DEPRECIATION MET BLOCK

— /

Depracttion jAdjusime

Additions jAdiustment

|Deductions | Gorss

Bock At

[Opening for the period

|nts or At the

end ,

: O8ason

— fduring Fy. during FY

jduring FY

= [the end of

|fund'as on 02,04,2026

to [deduction jaf March — | At the end

of March

At the end of SiNo.

[Asset Group Account

Code [OCH 2017

[2016-17 20bb-17

|20b-17 March, 2017

GLO 201G

[SLC

fe ue-ty

[2o17. O17,

March 2006.

1 2

a 4

5 5

7 4

5 410

i az

i 14

~ Tlintenigible' Assets ”

~_ 1a30i|

— 2easgo]

oa eet

anol gata

ve| tease]

aaa] >

ouopassnaeboo Gao

705.754- LIS4.49,

Total 2243.70.

0,09 oo

‘1.00 724370)

1089.23] aan

74 2.00

1537.96) 705.75

1154.4)

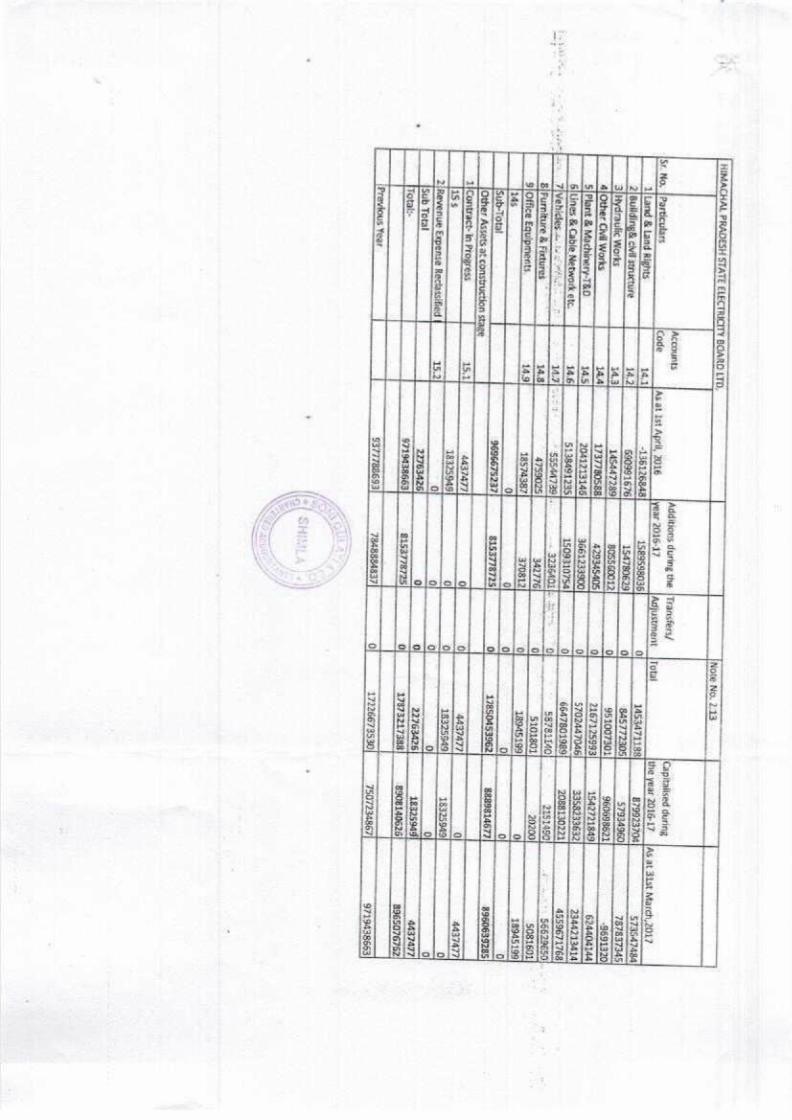

HIMACHAL PRADESH

STATE ELECTRICITY

BOARD LTD.

Note No,

2.13

Accounts Additions during

the |Transfers/

Capltalised during

Sr. No.

[Particulars Code

Asat Ist

April) 2016

year 2016-17

Adjustment [Total

the year

2016-17 |Agat

3st March,2017

1jLand &

Land Rights

14.1 -1361.27

15895.98 0.00

14534.71 8799.24

5735.47) 2 |Building&

civil structure 14.2

6909.92 1547.81

o.00 BAS7.72

579.35 7878.37

aj Hydraulic

Works 143

1454.47 8055.60

0.00 9510.07)

9606.99 -96.:91,

4] Other Civil Works

14.4 1737781

4293.45) 0:00

2167428 15427.22

6244.04) 5}

Plant & Machinery-T&D

14.5 20412,13

36612.34 0.00

5702447 33582.34

7344213 Lines &

Cable Network

etc. 14.6

51984.91 15093,11

0.00 66473.02

20881,30 45596.72

7 {Vehicles ..

ope 555.45!

.- 32.36

. 000

SaT.B1 21.51

566,30 8)

Furniture &

fixtures 14.8)

ie

aa ODOT

BEG gp eS gags

ees

50.82 9)

Office Equipments

14.59 185.74

3.71 o.00

189.45 0.00

189,45 14s

0.00 0.00

0.00 0.00)

0.00 0.00)

Sub-Total 96966,75

81537.79 0.00

178504,54 88898.15

89606.39 Other Assets

at construction stage:

0.00 0.00

0.00 0.00

0.00 =

2.00 1/Contract-

in Progress 15.1

44.37 0.00

0.00 44,37]

0.08 |

84.37) 15s

183.26 0.00

0.00 183.26]

183.26 0:00

2/Revenue Expense

Reclassifind 15.2¢

0,00 6.06

0.00 0.00

0.00 0:00);

Sub Total

227.63 0.00

0.00 227.63)

183.26 84.37

Total: 97194,39

$1537.79, 0.00

178732.17 89081.41

‘89650.77 0.00

0.00) 0.00

0.00) 0.00

0.00 Previous

Year 93777.89

7483.85 0.09

172266.74 75072.35

97194.39

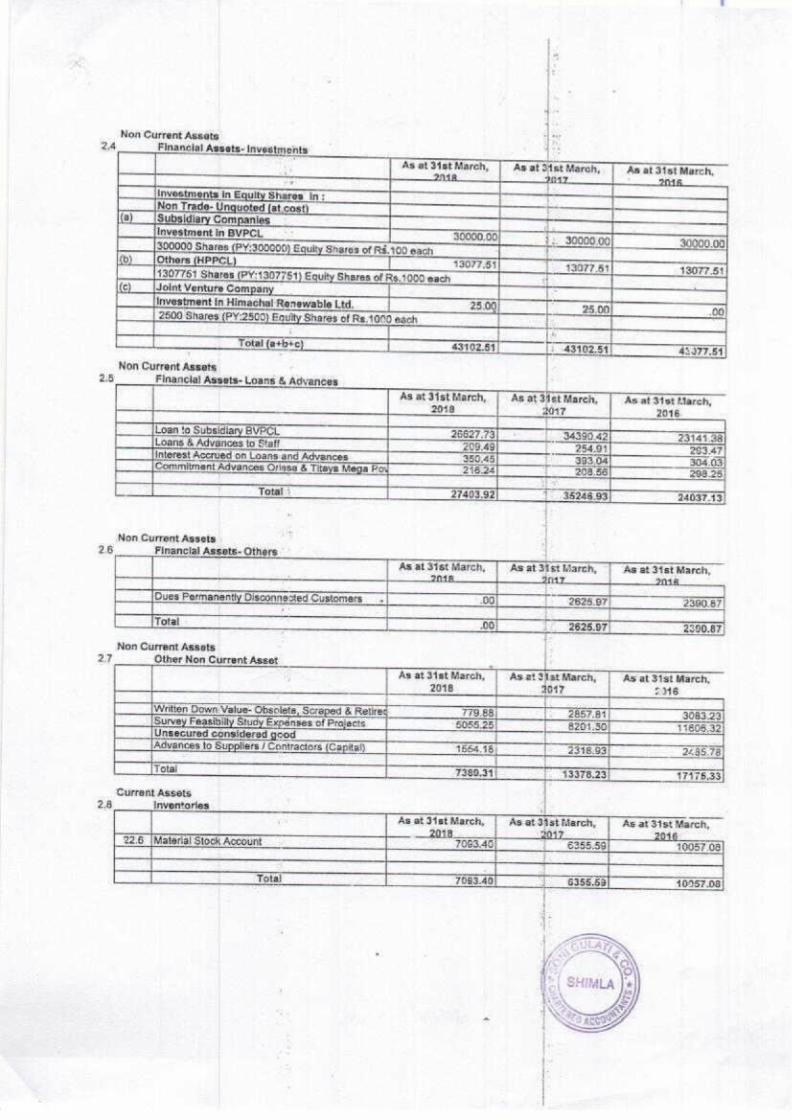

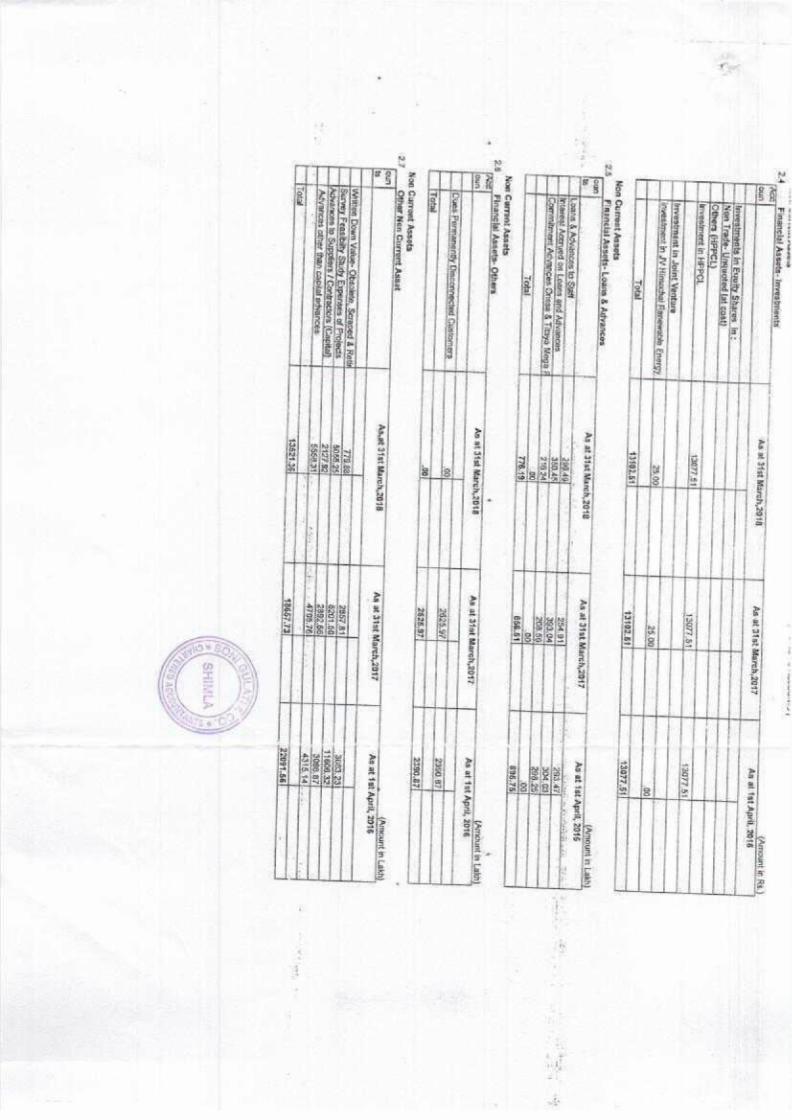

Non Current Assate 2.4 Financial

As at As at 34st March,

Non Current Assets 28

As at 31st March, 2016.

Non Current Assets 26

As al 31st March, Ag at dist March,

Non Current Assets 27 Non

As at 3ist March, As.at 3at'March, ‘As at 31st March, 2018 7 26

Currant Assets 28

As at J1at March, As-atd4st March, at3tst March,

40 1

Current Assets

29 As at 3tst As at dist

Current Assets 2.10

As at 31st March, As at 31st March, 2018 2017

As-at 31st 2076

45

In-opinion of the Company, trade receivable ara valued as stated In accounts, lf realised In the-ordinary course of businads. Current Assets

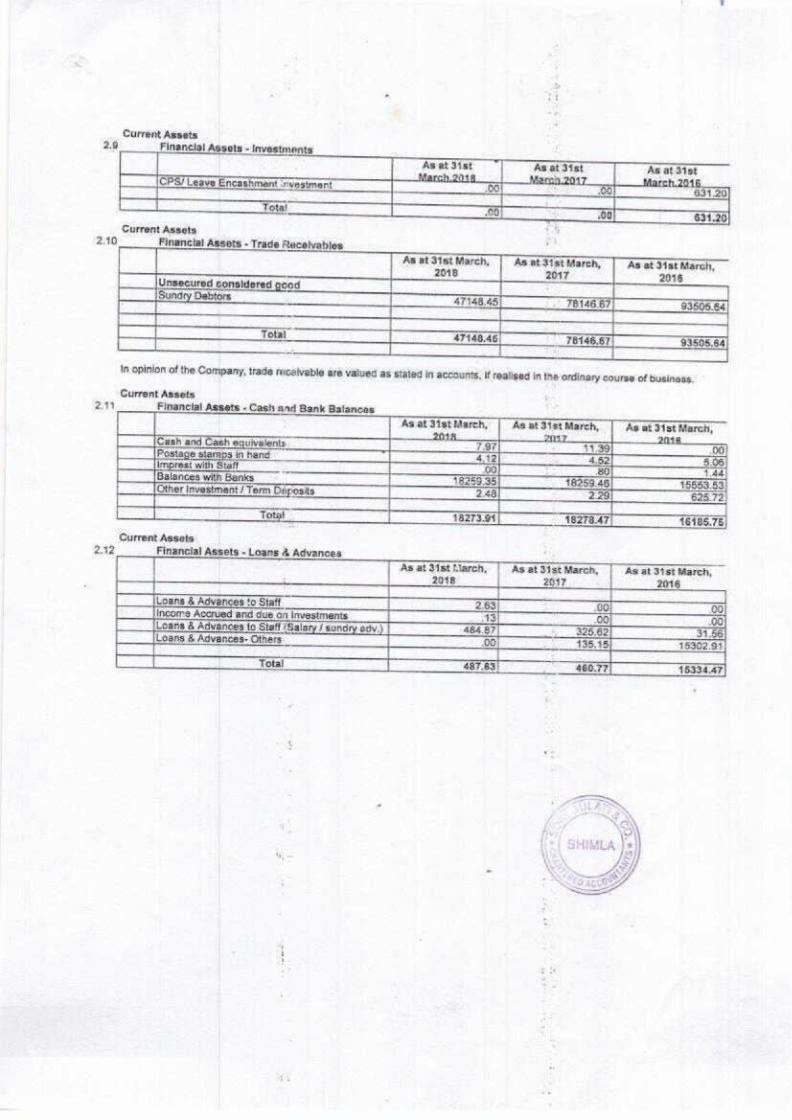

2.17 and Bank Balances

at 31st As at 342t March,

t

Current Assets

St March, As at 31st As-at 31st March, t

aa

15302.94

1

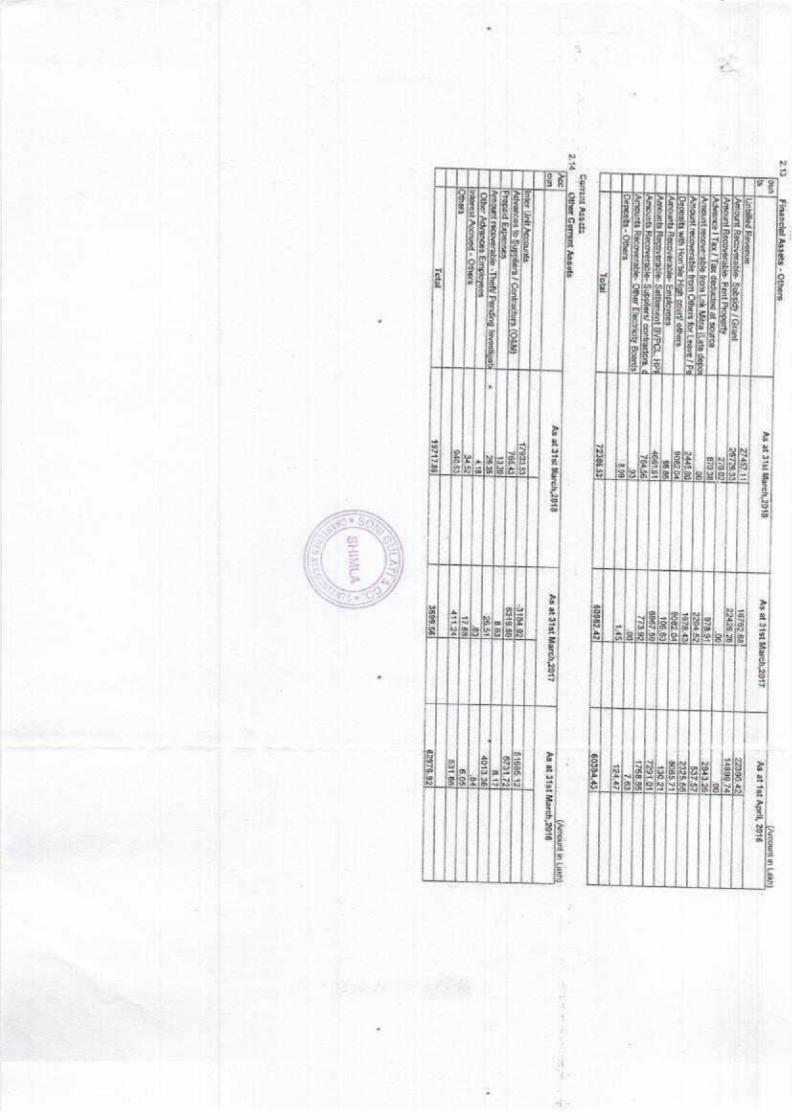

Current Assets: 243

Asat D4st March, As at 31et March, As at 31st 204 17 6

i 68 22990.42

Current Assets 2.14

61575.53

ANNUAL REPORT

2047-18

Notes to Accounts

245 Equity

Share Capital

{Amount’in Lakh)

As at Jist

March, 2018

As at

dist March,

2017 As al

dist March,

2046 No.of

Shares |

Amount No.

of Shares Amount

No, of Shares

Ameuarit Authorised

f Equity

Shares at per valine”

100 each

TiOtooooA 110600.00

T1taO0G00 110000,.00)

i1ooeddda 11G009.06)

EQUITY SUBSCRIBED AND

FULLY PAID UP =

Equity Shares at par value” 100- each fully pad

67058580 ‘7056.58

beazaigo 65928: 15)

‘B02 5R) 60929

58) (

Totat 67 056,58

5328.18 cal

60320.58

Aourethwe soe

hee

Tho reconciliation

of the number

of Shares outstanding is

set out below: '

| ea

ee :

| In Lakh

Peutioufars, As at

3tst March,

2078 As-at3ist

March, 2017

As at3ist March,

2046 No.of

Shares |

Amount

No, of

Shares Amount

No. of Shares Amount

Number of

shares: Outstanding

at the beginning

: B5228

180) 65225,

18) BO320580

Bi

28.55 52203180)

52200, 15) Ni

of shares igsued-during

the year iree4oo

1728.40 aes8600

4596.60 eize4c0

8126.40 Share bought

back during the year

0 lt

5 O01

Nomber of shares outstanding at ihe end, S7055580

87055,50) aaa2e180

6552818 60329590

6029.58 Terms!

Rights attached

to Equity

Shares:-

The Company has only one class of equity shares

having par vue

of Res 100

per-share: Holders of equily shares are

entited to voting figtts

prdpodtionaly to their share halding at the meeting of sharebolders, No tems

and conditions have been mentioned

in investment,

mada by

Gavt in

HPSEBL

As at

34st March, 2047

As at

dist March,

2076

No. of Equity Shares |% of Sharehokding. | Ne. of Equity

Shares /% cf Sharahotting | No,

of Equity Shares |% of Shareholding

_| 1, G

overnor

of Himachal

Pradesh “67056580

100 653,28

100 |

GO320580 100,

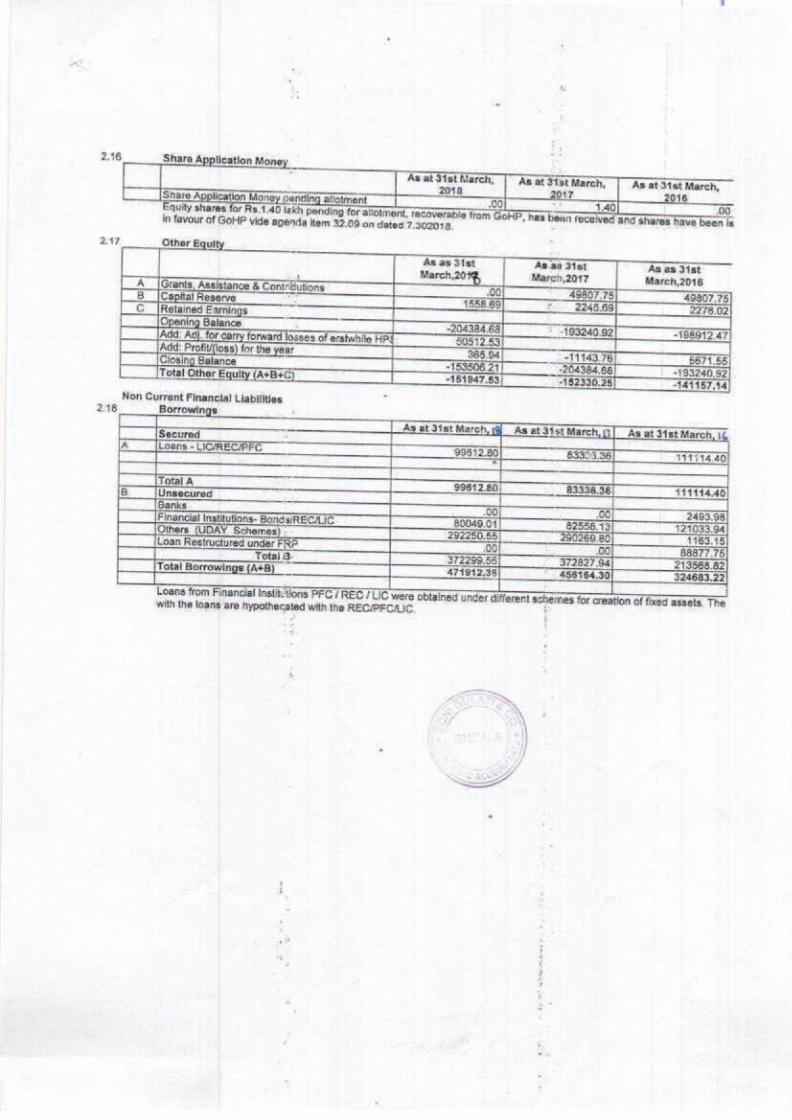

2.16 Shara Application Money

Asal dist March, As at 34st March, As at3tst March, 2018 2017 2076 Share Application Money pending allotment ‘0 1.40 : : 200 Equity shares for Rs.1.40 lekh pending for allotment, recaverable fram GoHP, has bean received and shares have been is in favour of GOHP vide agenda item 32.09 on deted:7,302018. :

ZF

As ag 31st

As an 3ist As as Jist Mare, 2017 Marech,2016

T

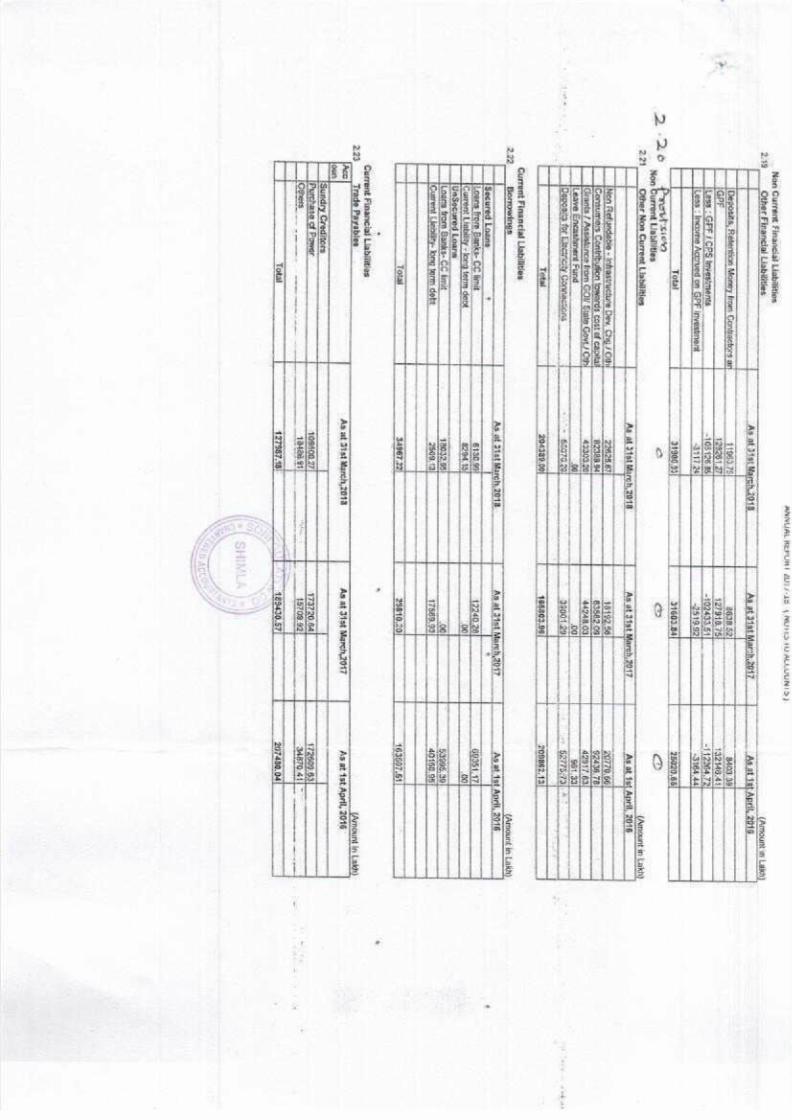

Non Current Financial Liabilities ' 2:18 \

‘otal

from were

with the loans are hypothecated with the REC/PFCILIC. schemes for creation

* There has bean ne defaults In repayiients of apy cf the loan oF Interest thereon at-the-end of the year * The Company had borrowing limit Rs. S000 Cr. which has now been inéreased upto Rs, 6500-Crore during FY 248-49

Non Currant Financial Liabilities 2.49

Non Current Liabilitias 2.21 Non

SY or *| SHIMLA “| 2 S| e ay

ML

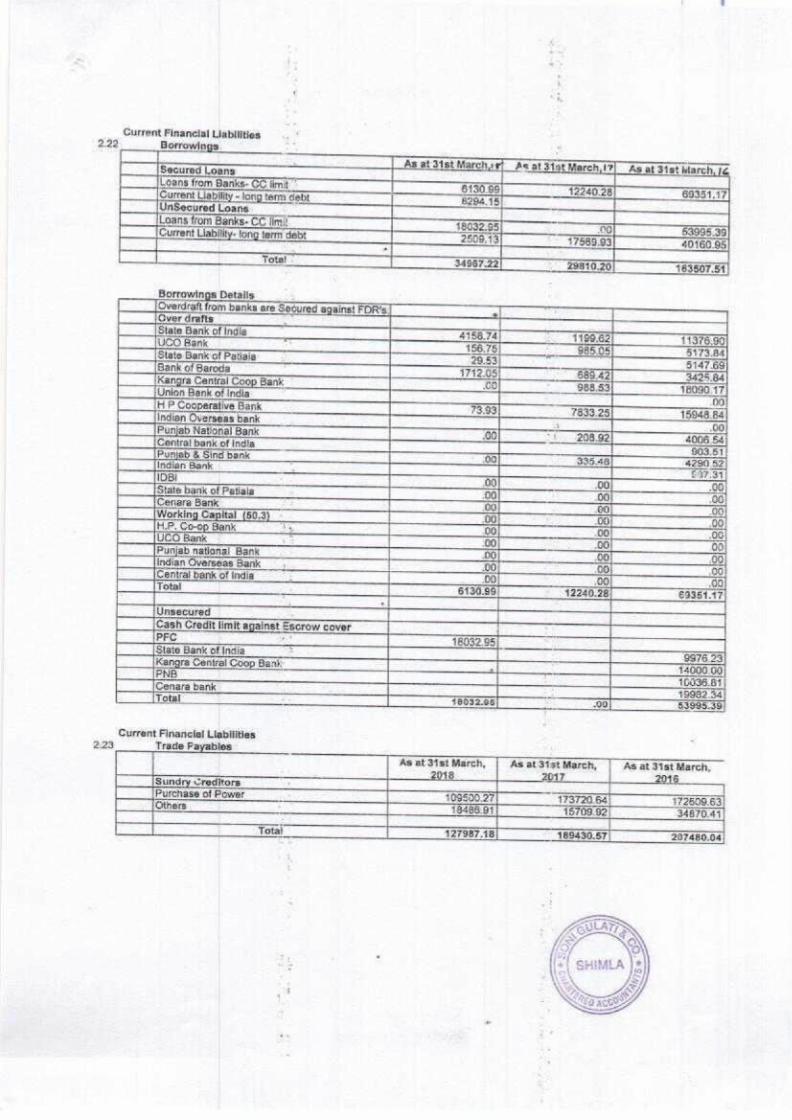

_ Current Financial Liabilities

Current Financial Liabilities

2:23 E AS at 31st Mal As at‘3tst March, AS at 31st March,

7

i}

Current Financtlal Liabilities 2.24

2.25 Other Current Liabilities

00 00 oo Current Uabilities 2.26 T

March, As at dist March,

04

00

80

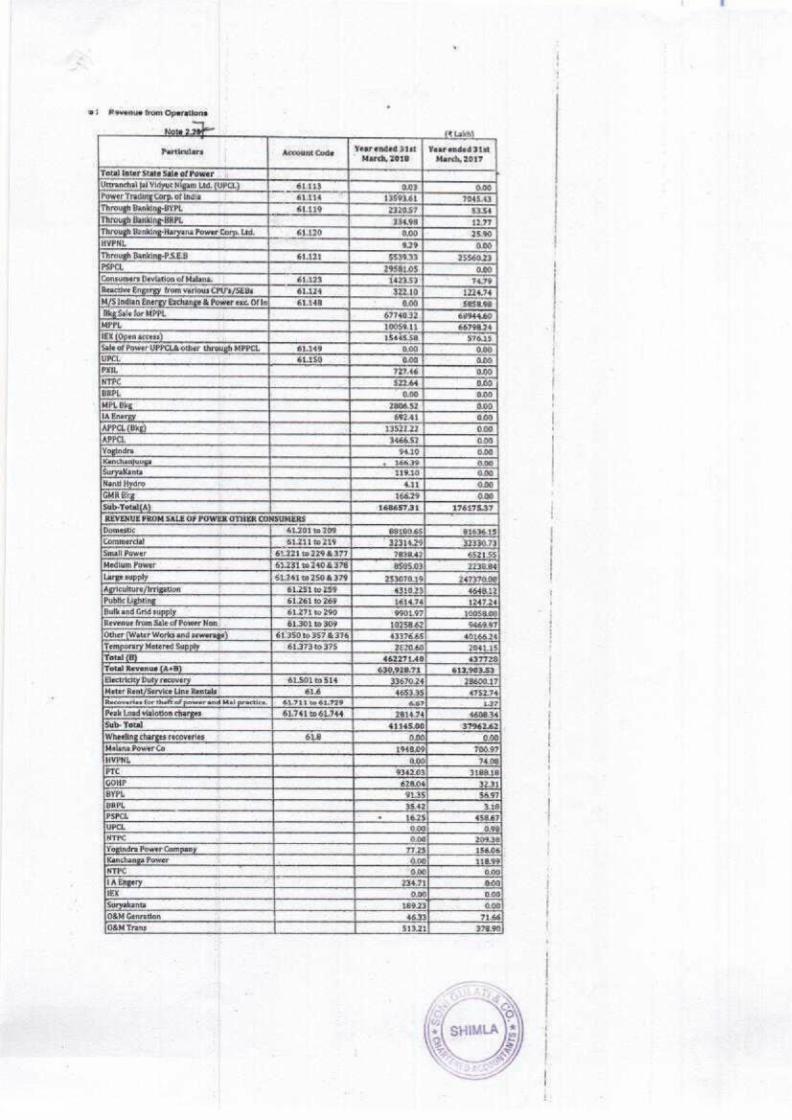

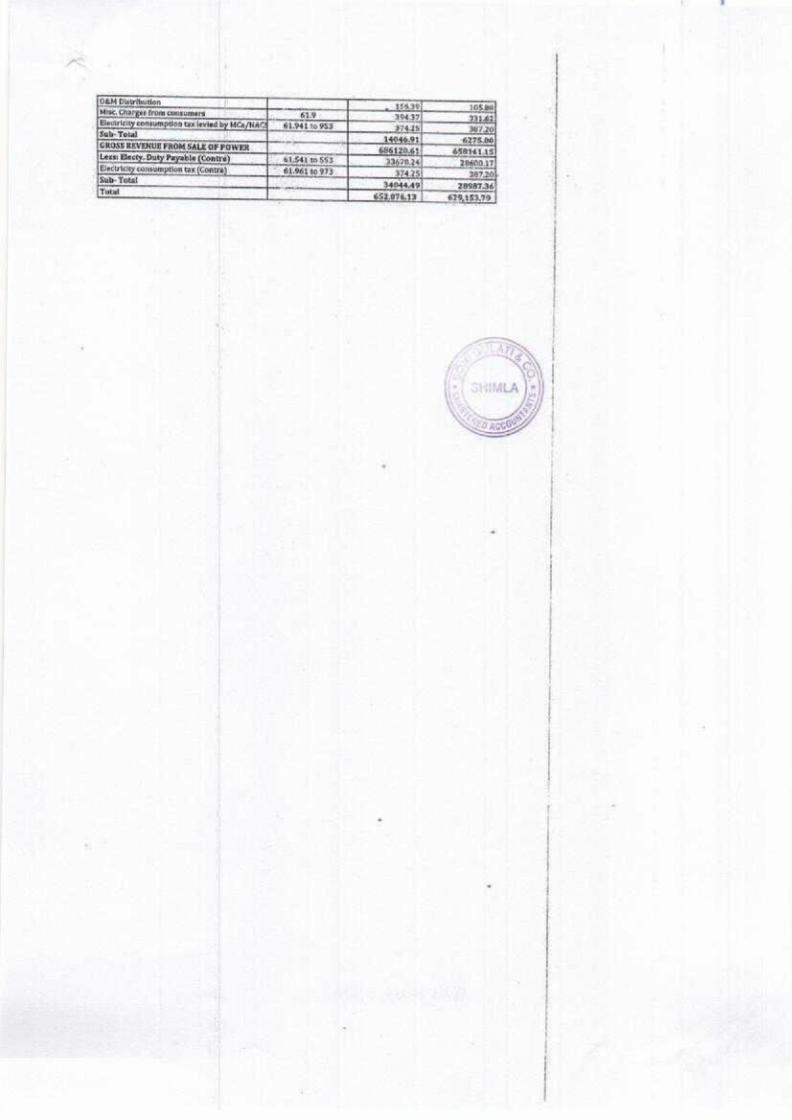

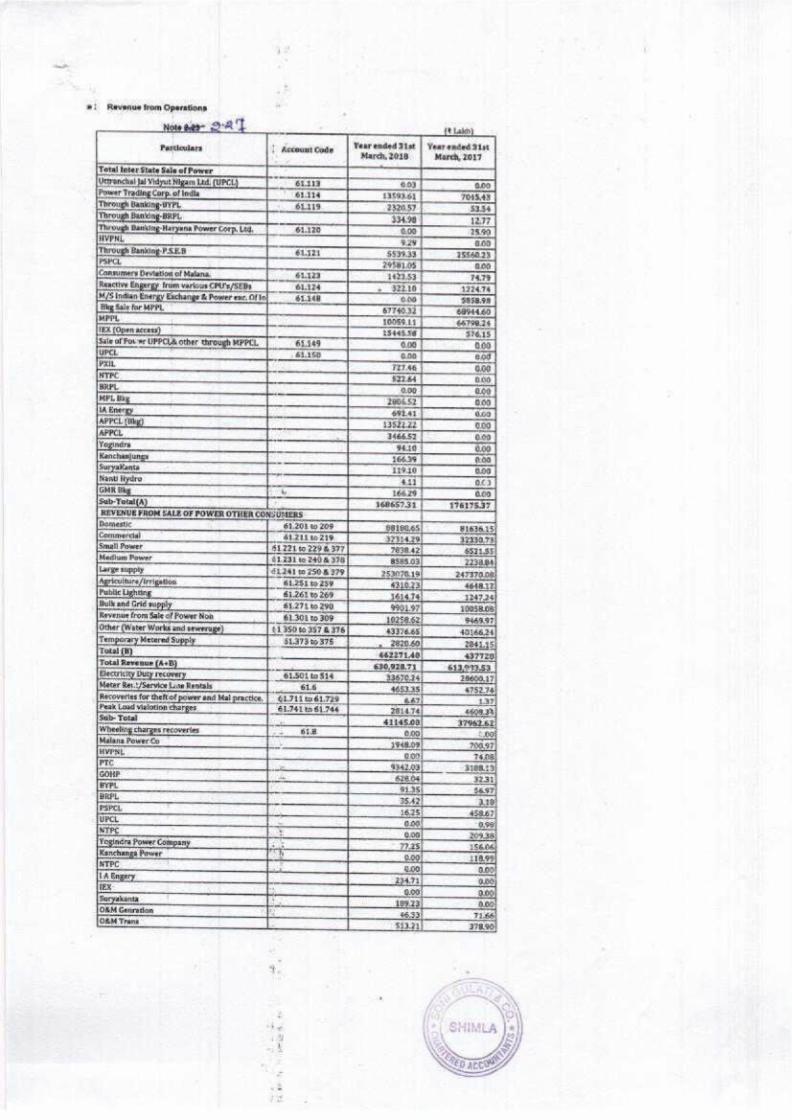

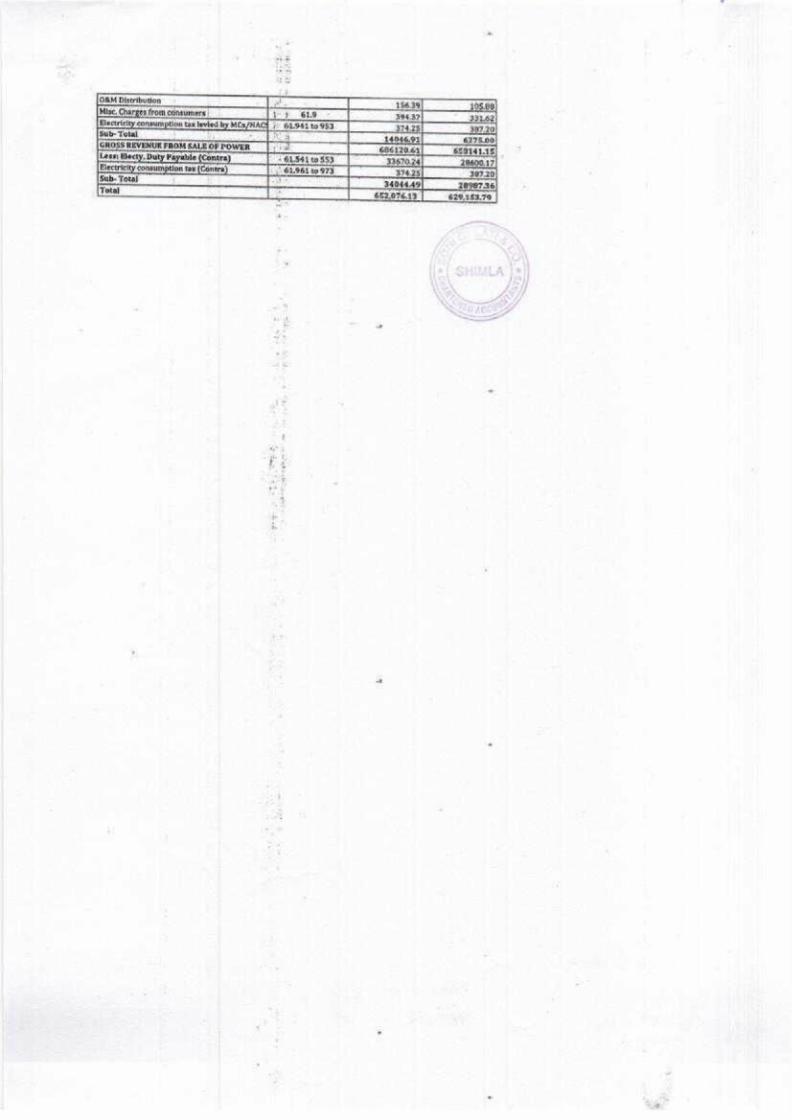

=) Pavitue from Operations

La

ended Fist | Veurended dist March, 2010 March, 2047

OOF 00

13593.61 T4543

Sab4 177

ThLTLAT

lin 219 4377

6 to

S124 to 250.8 379

$1261 to B69

SL27L te

L301 te

to BST,

Year ended Sist March, 2018

40.40

267.

8910.19

3705,

96,74

Accoun? Code

219.

to

780)

251692.

0.00 ooo

4a

Yaar ended Fist March, 2017 (its)

$6M1

a0,

7a.

i

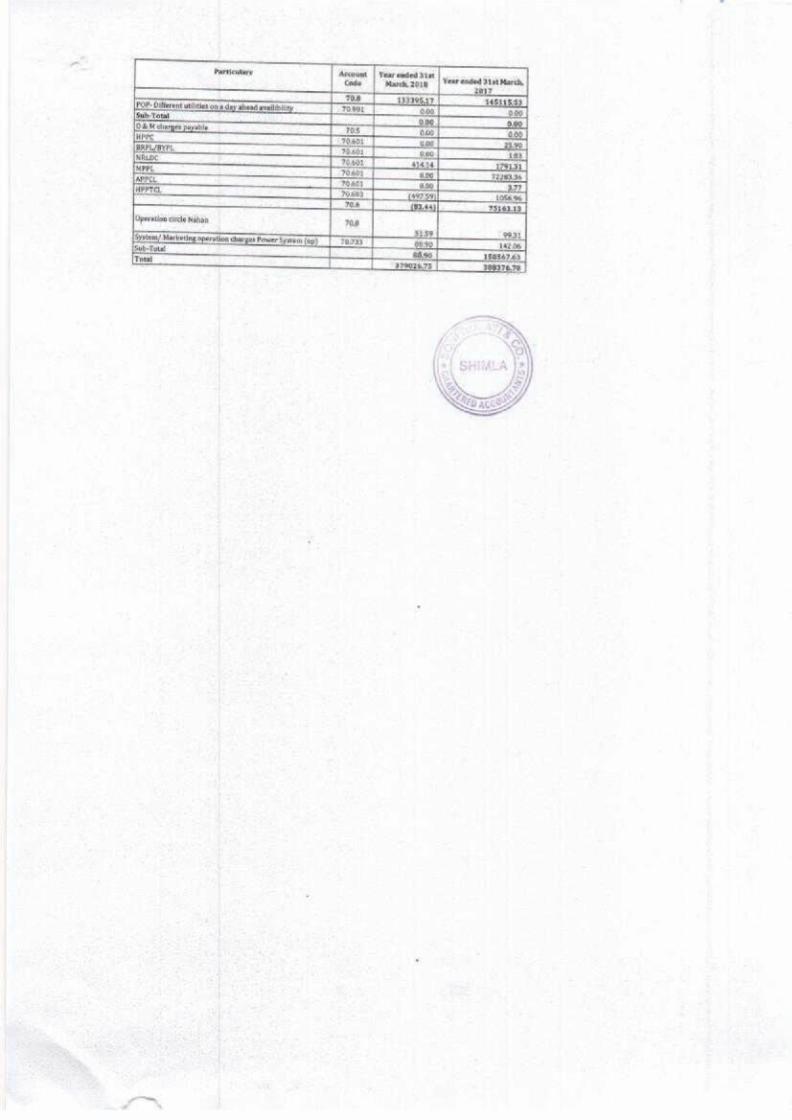

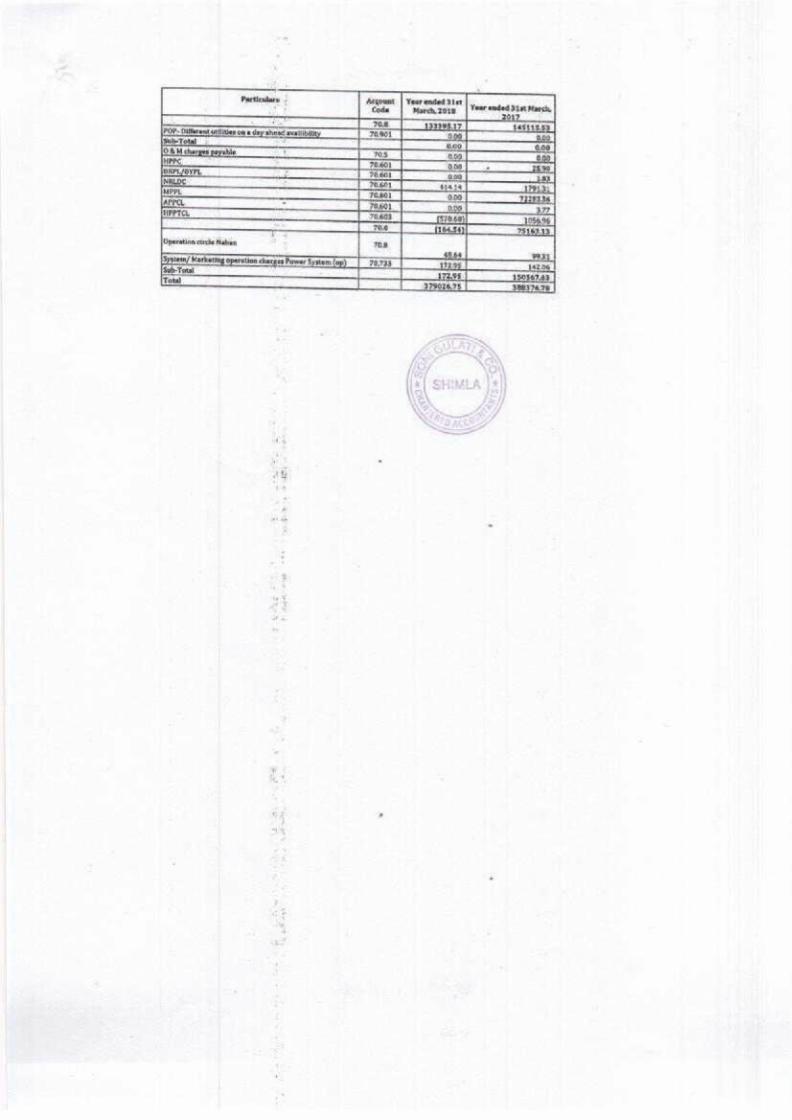

oa Purchase of Pewar

Your ended 34141 Marek, 201g | Yee emiled 54st March,

Account | Yearended Stet |... .. 7 Cndo March 2018 Year ended 314% March,

7

an cicla Nahan

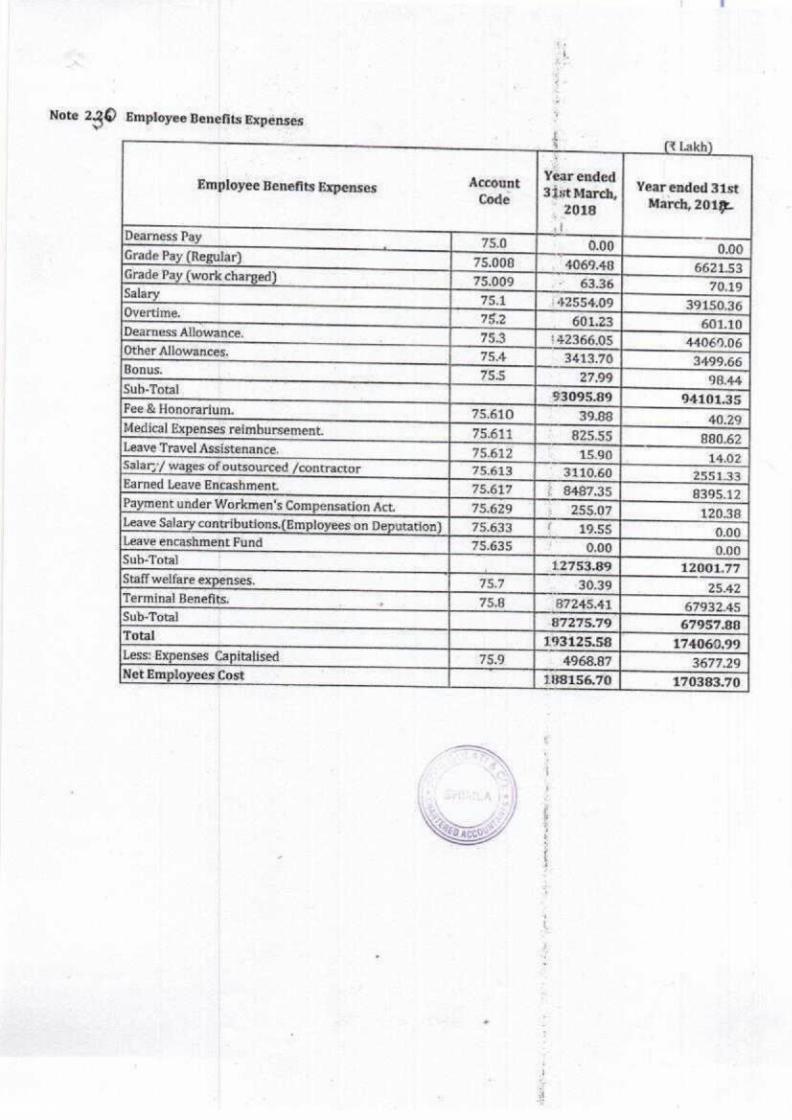

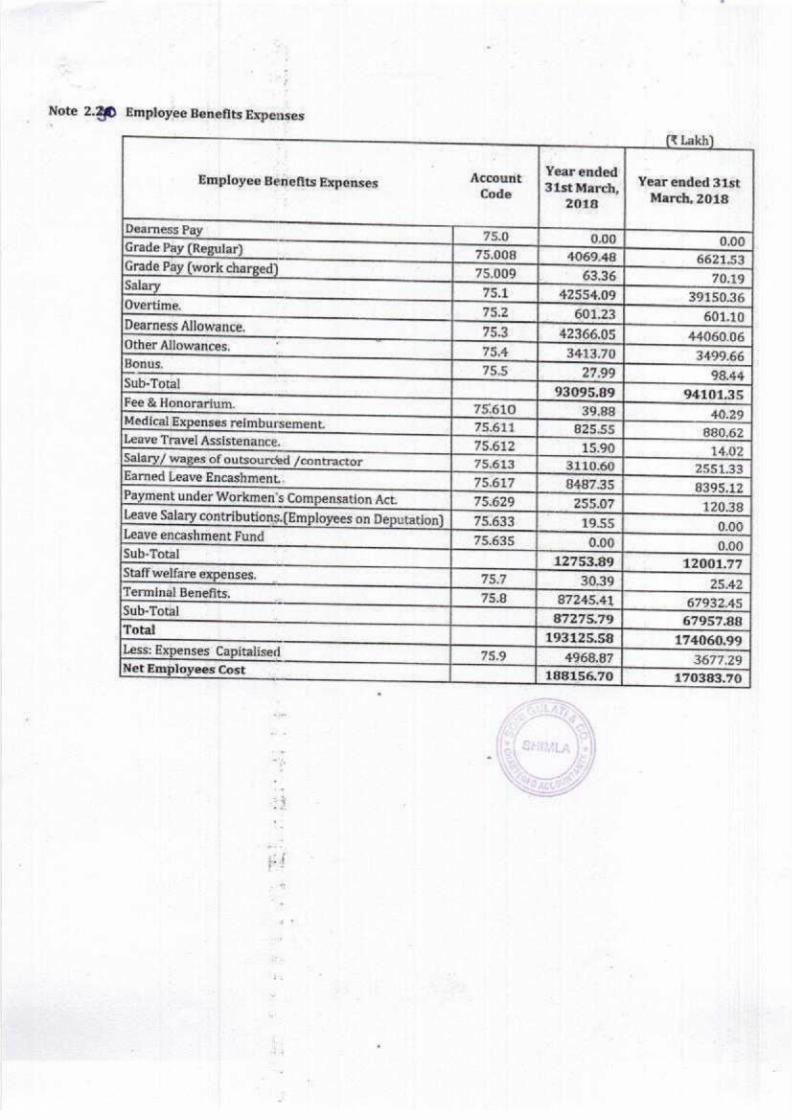

Note 2.20 Employee Benefits Expenses , 4

(% Lakh)

Account Year ended Year ended 3is Employee Benefits Expenses peas 3i mt arch ek ag

_ 2018 af

Dearness Pay . 75.0 0.00 0.00 Grade Pay (Regular) 75.008 4069.48 6621.53 Grade Pay (work charged) 75.009 - 63.36 70.19 Salary

75.1 | 42554.09 39150.36 Overtime,

75.2 601.23 601.10 Dearness Allowance. 75.3 +42366.05 44069.06 Other Allowances. 75.4 3413.70 3499.66 Bonus. 15.5 27,99 98.44

Sub-Total $3095.89 94101.35

Fee.& Honorarium. 75.610 35.88 40.29 Medical Expenses reimbursement. 75.611 825.55 880.62 Leave Travel Assistenance, 75.612 15.90 14.02 Salar;'/ wages of outsourced /contractor 75.613 3110.60 2551.33 Earned Leave Encashment. 75.617 | 8487.35 8395.12 Payment under Workmen's Compensation Act, 75.629 :. 255,07 120,38 Leave Salary contributions.{Employees-on Deputation) 75.633 19.55 0.00 Leave encashment Fund 75.635 0.00 0.00 Sub-Total ; 12753.89 12001,77 Staff welfare expenses. Ta7 20.39 25,42 Terminal Benefits. i 75.8 B7245.41 67932.45 Sub-Total

7275.79 67957.88 Total 193125.58 174069,99 Less: Expenses Capitalised 75.9 4968.87 3677.29 Net Employees Cost 188156.70 170383.70

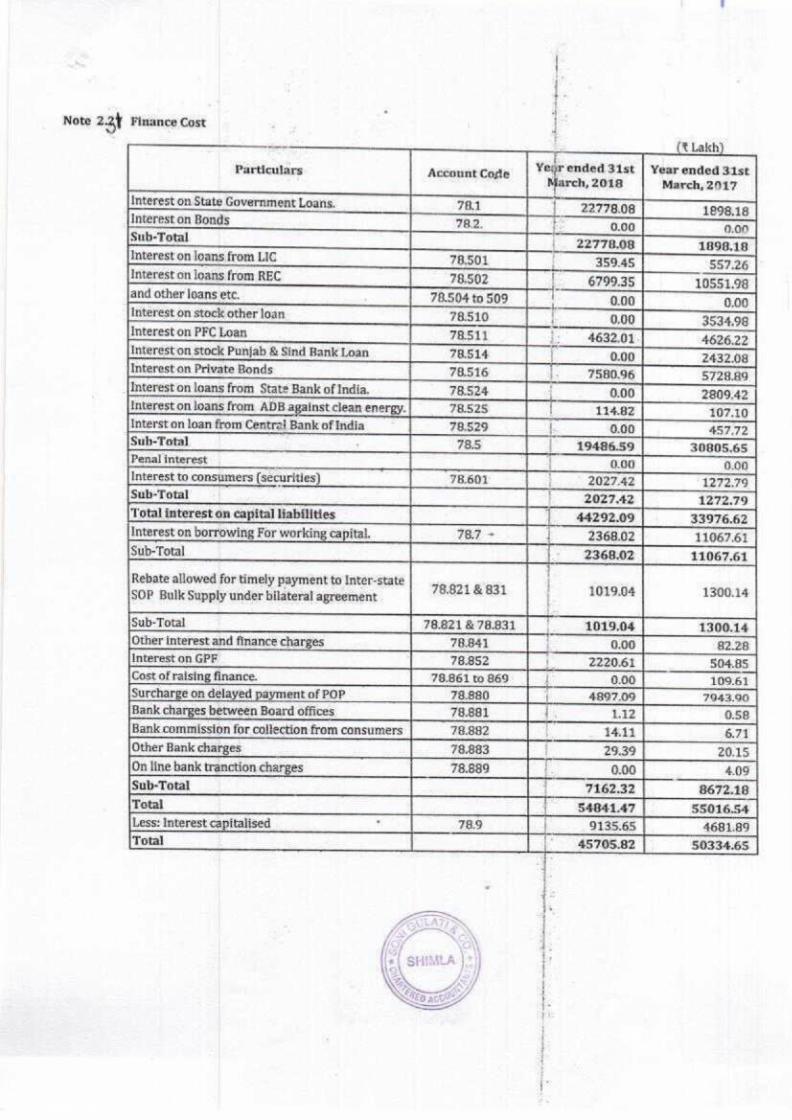

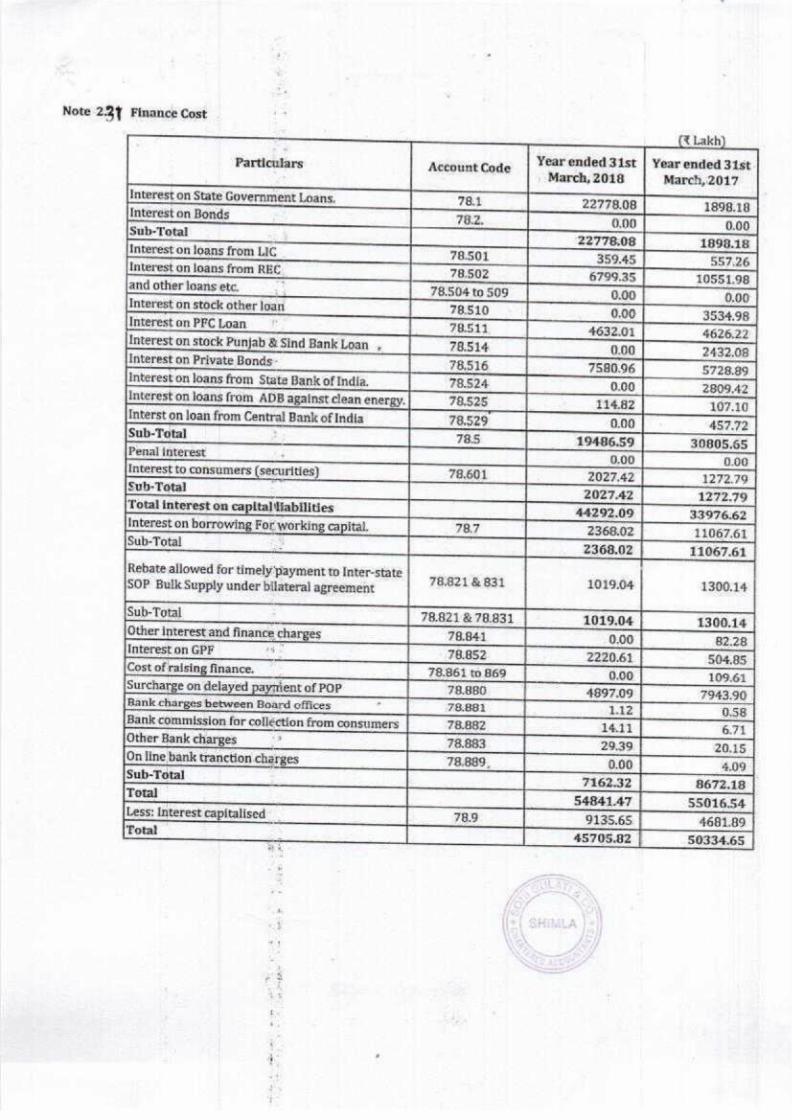

Note 22h Finance Cost

pron

fname A

(Lakh)

Yeur ended 31st | Year ended 31st et Ane aee ‘March, 2018 March, sees

Interest on State Government Loans. 78.1 | 22778.08 1898.18 Interest on Bonds 78.2. i 0,00 0.00 Sub-Total | 22778.08 1898.18 Interest on loans from LIC 78501 i 359.45 557.26 Interest on loans from REC 78,502 | 6799.35 10551.98 and other loans ete. 78.504 to 509 | 0.00 0.00 Interest on stock other loan 78.510 | 0.00 3534.98 Interest-on PFC Loan TES 4632.01, 4626.22 Interest on stock Punjab & Sind Bank Loan 78.514 0.00 2432.08 Interest.on Private Bonds 78.516 1. 7550.96 5728.89 Interest on loans from State Bank of India. 78.524 i 0.00 2809.42 Interest on loans from ADB against clean energy. 78.525 114.82 107.10 Interst on loan from Central Bank of India 78.529 | 0.00 457,72 Sub-Total. 735 19496.59 30805.65 Penal interest 0.00 0.00 Interest to consumers (securities) 7B.601 | 2027.42 1272.79 Sub-Total ; 2027.42 1272.79 Total interest on capital liabilities 44292.09 33976.62 Interest on borrowing For working capital, 73.7 > 2368.02 11067.61 Sub-Total 2368.02 11067.61

Rebate allowed for timely payment to Inter-state | SOP Bulk Supply under bilateral agreement CERLA BST Annas tps

Sub-Total 78.621 & 78.831 1019.04 1300.14 Other interest and finance charges 78.841 0.00 82.28 Interest on GPF 78.852 | 2220.61 504.85 Cost of raising finance. 78,861 to 869 l 0.00 109.61 | Surcharge on delayed payment of POP 73.880 { 4897.09 7943.90 Bank charges between Board offices 78.881 ! 1.12 0.58 Bank commission for collection from consumers 78.882 | 14.14 6.71 Other Bank charges 78,883. 29.39 20.15 On line bank tranction charges 78.889 0.00 4.09 Sub-Total 7162.32 8672.18 Total | 54B44.47 55016.54 Less: Interest capitalised 78.9 | 9135.65 4681.89 ‘Total 45705.82 50334.65

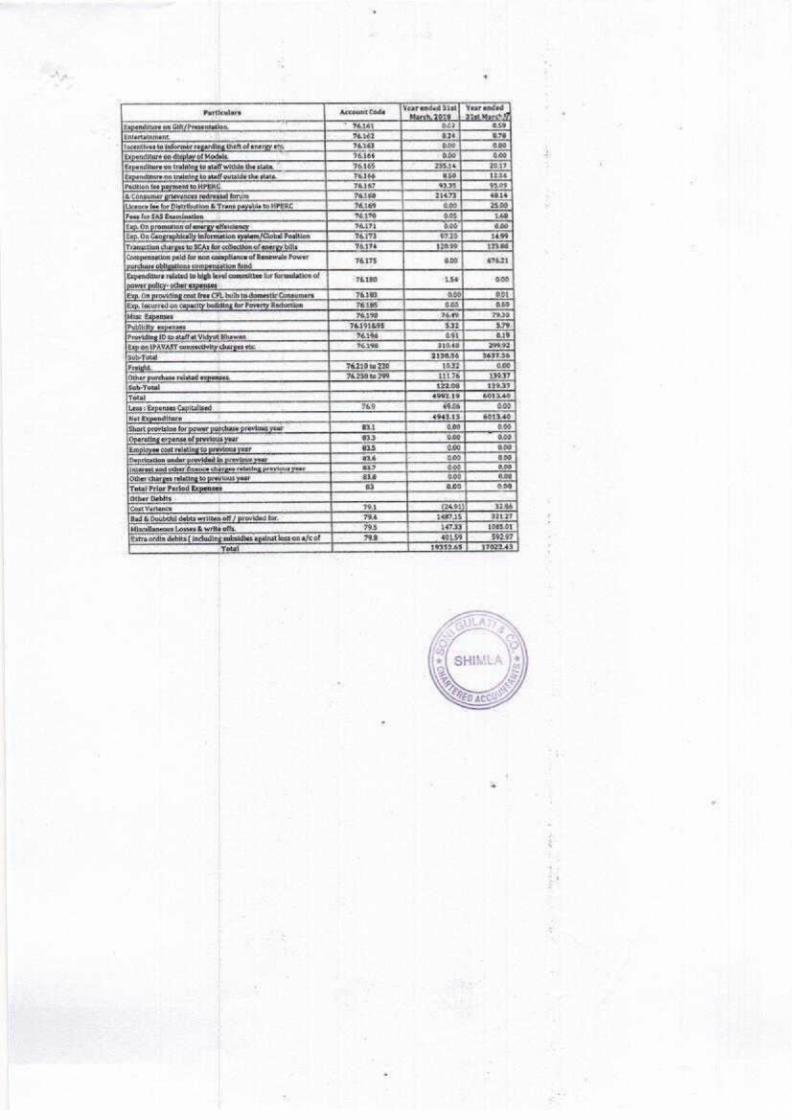

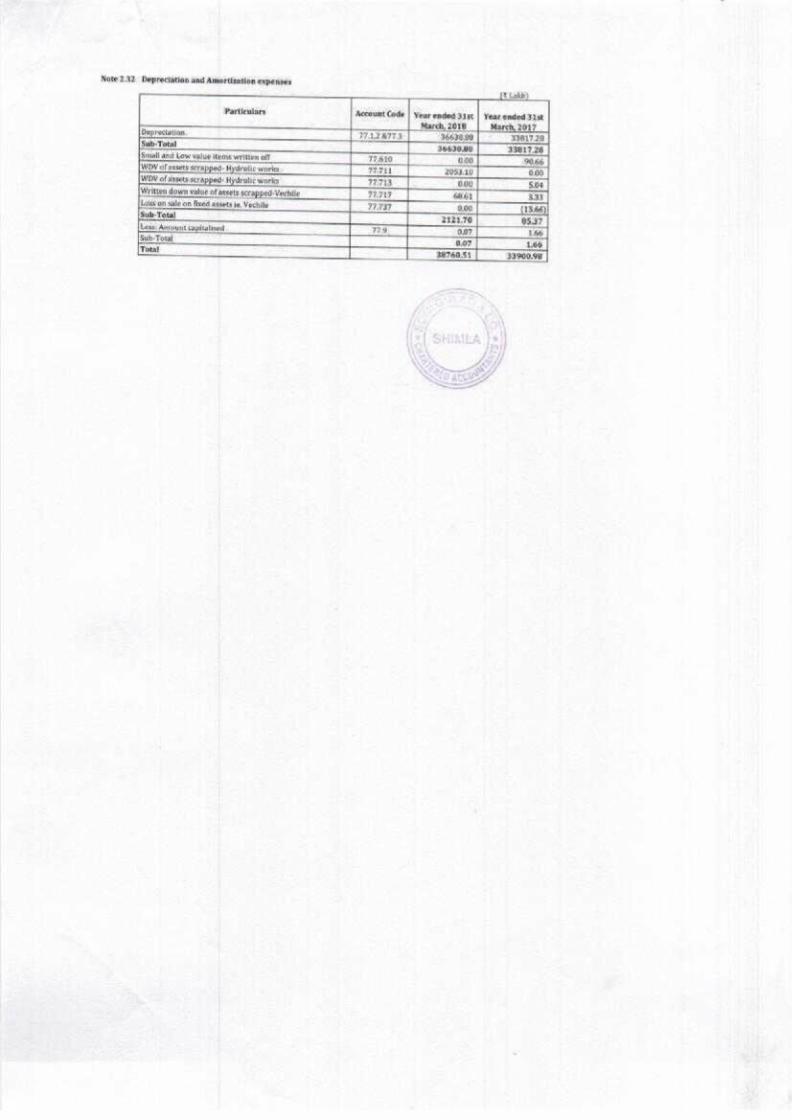

Mote 2.38 Deprectetion and Amortization expences

* Particulars

tt

Account Code | Yearendod dist | Yearended 21st

a7. ed a

‘33817

ey

On a Cel dervics pendared by cence! board keeping

ancien heme

pale for moa compliance of Ruankwie Power

comauitter [nr formulation at

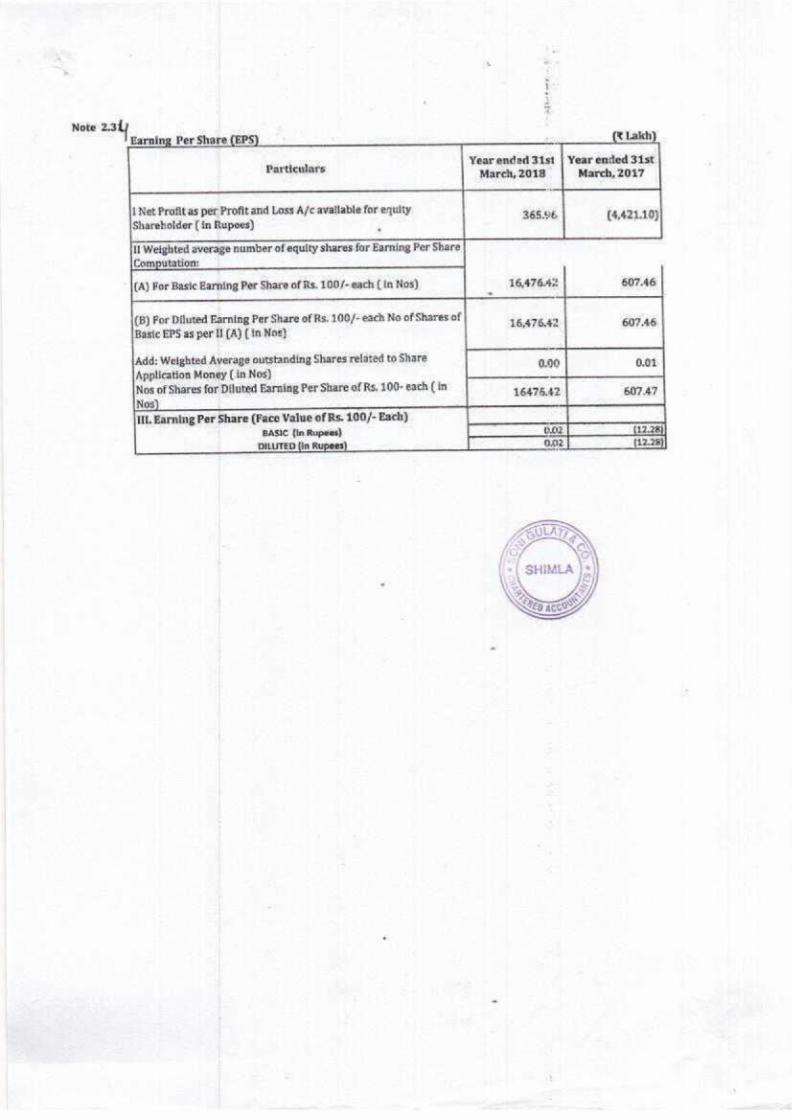

Note asl Earning Per Share (EPS)

(Lakh)

Year ended Jist | Year ended 3ist

Fartouiats March, 2018 | March,2017

I Net Profit as per Profit and Loss A/c avallable for equity

Shareholder ( in Rupees) E 365.96 {4,421.10}

Il Weighted average number of equity shares for Earning Per Share

Computation:

(A) For Basic Earning Per Share of Rs. 100/-each ( In Nos) 16,476.42 607.46

(B) For Diluted Earning Per Share of Rs. 100/- each No of Shares of i :

Basic EPS as per Il (A) (in Nos} AOSPGHE UT AS:

Add: Weighted Average outstanding Shares related to Share o.00 0:01

Application Money (in Nos} ; J

ee for Diluted Earning Per Share of Rs. 100- each (In 1647642 Bay 49

Ill. Earning Per Share (Face Value of Rs. 100/- Each) BASIC (in Rupees) 6,02 (12.28)

DILUTED [in Rupees) Oe {12.23}

Th How much cost has been incurred on abandoned projects and of this how much cost has been written off?

Nil during the year

Is there any system to evaluate the reasonableness of Plant Load Factor including auxiliary consumption and generation loss with reference to norms fixed? Deviations if any may be quantified and commented suitably?

Yes as per HPRC regulation.

In the case of Hydroelectric Projects the water discharge is as per policy/guidelines issued by the State Government to maintain biodiversity, For not maintaining it penalty paid/payable may be reported.

Yes

For Soni Gulati & Co

Suresh Chand (Partner)

FRN: 008770N MRN: 083106

Date: 29.02.2020

2[ Page

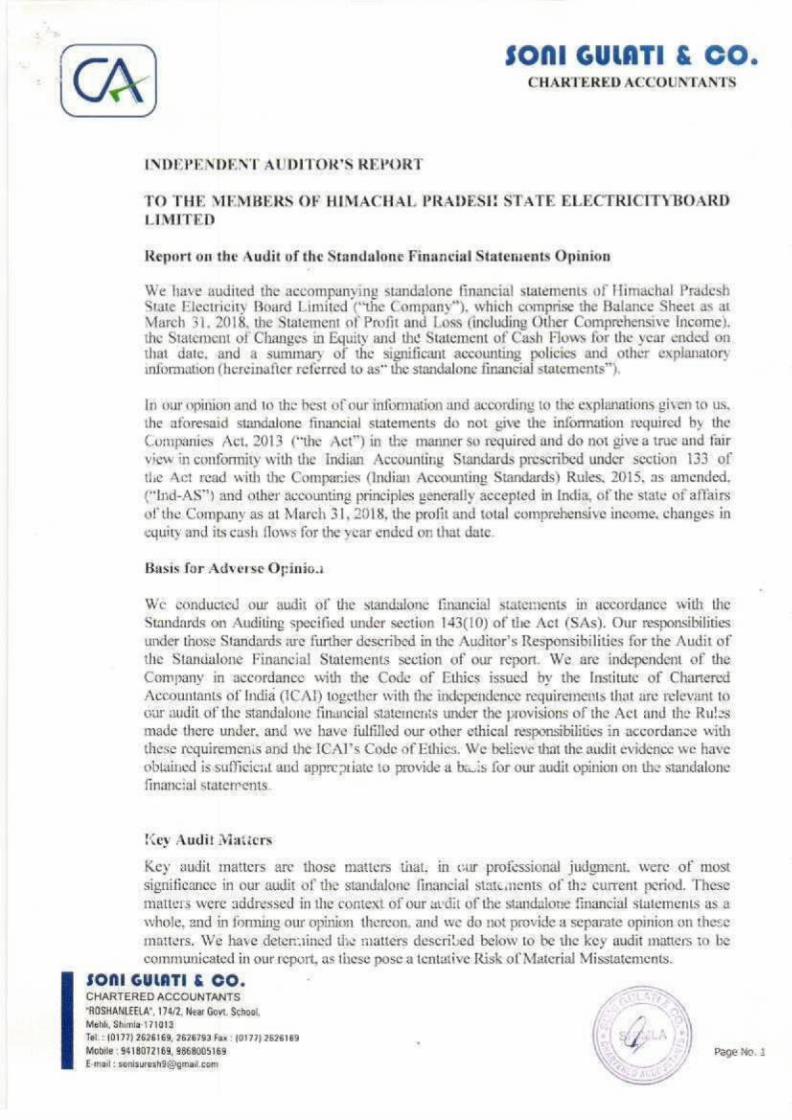

CHARTERED ACCOUNTANTS

OX SONI GULATI & CO.

INDEPENDENT AUDITOR'S REPORT

TO THE MEMBERS OF HIMACHAL PRADESE STATE ELECTRICITYBOARD LIMITED

Report on the Audit of the Standalone Financial Statenvents Opinion

We have audited the accompanying standalone financial statements of Himachal Pradesh State Electricity Board Limited (“the Company”), which comprise the Balance Sheet as at

March 31. 2018, the Statement of Profit and Loss (including Other Comprehensive Income). the Statement of Changes in Equity and the Statement of Cash Flows for the year ended on that date. and a summary of the significant accounting policies and other explanatory information (hereinatier referred to as” the standalone financial statements”),

in our opinion and 16 the best of our information and aceording to the explanations given to us, the aforesaid standalone financial statements do not give the information required by the Companies Act, 2013 (“the Act”) in the manner $0 required and do not givea trae and fair view in conformity with the Indian Accounting Standards prescribed under section 133. of the Act read with the Companies (Indian Aceounting Standards) Rules. 2015. as amended. (Ind-AS") and other accounting principles venerally accepted in India, of the state of affairs

of the Company as at March 31,2018, the profit and total comprehensive income, changes in equity and its cash {lows for the year ended on that date

Basis for Adverse Opinio.

We conducted our audit of the standalone financial statements in accordance with the

Standards on Auditing specified under section 143(10) of the Act (SAs). Our responsibilities

under those Standards are further deseribed in the Auditor's Responsibilities for the Audit of

the Standalone Financial Statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered

Accountants of India (IC.A1) together with the independence requirements that are relevant to

our audit of the standalone financial slatemerits under the provisions of the Act and the Rules made there under. and we have iulfilled our other ethical responsibilities in accordance with these requiremenis and the IGAI’s Cade of Ethics. We believe that the audit evidence we have obtained is-sulficient and apprepiiate to provide a bacis for our audit opinion on the standalone

financial staterrents.

Nev Audit Maticrs

Key audit matters are those matters that: in our professional Judgment. were of most significance in our audit of the standalone financial statuments of the current period, These matters were addressed in the context of our avdit of the standalone financial stulementis asa

whole, and in forming our opinion thereon, and we doe not provide a separate opmion on these inatters, We have detenuined the matters described below to be the key audit matters to be

communicated in our report, as these pose a tentative Risk of Material Misstatements.

sONl GULATI & CO, : = CHARTERED ACCOUNTANTS é ae “ROSHANLEELA", 174/2, Near Goyt, School, j % Mehli, Shien 171013 fi WN Tel. = (0177) 2626169, 2626793 Fax : (0177) 2626169 . \ 4 ee Mobile ; 9418072169, $860005189 a i Page Ma. E-mail : [email protected] X 5 = if

|. Accuracy of recognition, measurement, Presentation and disclosures of revenues and other related balances in view of adoption of IND AS

The Company claimed to have adopted IND AS but we found that only regrouping of amounts in financial statement has been done. We found that the financial statements are not even GAAP compliant not to talk about AS or IND AS compliant . The Companies Act, 2013 gives great importance to the compliance of the accounting standards by the Companies as evident from Section 129(1) wherein it has been stated that financial statements shall comply with the accounting standards , the first proviso tu said section also states that the items contained in financial statements shall be in accordance with the accounting standards, We noticed that the Company has not complied with following accounting standards /IND AS : IND- AS 10] First time adoption only reclassification (not verified by us) of balance sheet & P&L account has been done otherwise there is no compliance j.IND-AS 18 Revenue ,IND-AS 19 Employee benefits , IND-AS 16 — Property Plant and Equipment , IND-AS 17 Leases IND -AS 36 Impairment of Assets IND-AS 37 contingent Liabilities and contingent Assets , IND AS 7 cash management .

After getting report from units that neither access to billing software nor to tenders records was given, we conducted some logistic tests at Head office ¬iced significantly material understatement of revenue. To strengthen the same we performed substantive test through 25 sample bills & found that there was under billing to the tune of Rs.432 Cr. in these samples. Replies of management (dated 25 September 2019) were found to be non sequitur & evasive, as replies has nothing to do with our observations. Based upon these samples & logistic test, we are of the opinion that revenue (income) of the Company is understated by Rs.3082 Cr. This difference is in sales within the state, In reply to other question on revenue understatement the management reply (verbal) was the CMTR sale is only for calculating transmission losses & if we assume the statement of management to be right, the transmission losses declared at 15% will become 45 % .However this is not the case these are not transmission losses but combination of i) under billing ii) reversal of bills due to Court order & iii) accounting of units sold but reversal of amount for open access but non reversal of units sold.

Different sales amount (Assessment fig) are provided by different sources e.gi) Revenue report from SAP Rs.7830 Cr. Similarly Realization fig are i) Revenue CMTR 3 Rs 4684 Cr. il) Notes to Account no 24 Rs 4622 Cr.. iii) Go Live Consolidation Rs.5124 Cr,

We were told at HO that opening balances in SAP were taken wrong at Unit level but how the sale fig could be wrong as it was not opening balance, To strengthen our observation -we noticed that all sales and revenue receipts are booked through K numbers .All statements including CMTR are prepared from K numbers ,how could be there any difference .Of course some differences could be theré due to reversal upon Court order etc., but here the difference is more than 30%.

We understand that in case of all meters with20 KVA sanction load reading is taken through MRI machine but to our surprise in all case we noticed under billing, the reading was manual .In our opinion all this was:a well planned and deliberate act. Replies of the management on revenue during September & December are different from those during February 2020 given after Audit Committee Mecting'¢.g.in case of Anumita Overseas during September & Dec 2019 the Management claimed that the difference in

Page No. 2

billing Rs37,.96 Cr, has been recovered however .during February 2020 it claimed the amount has been billed during January 2020,Thus all bills of major customers will have to be checked during current year i.e. next year audit. The replies of management & Audit committee are itself contrary ,on one side the Audit committee chairman claimed that such fraud is impossible and he again insisted upon number of units which we never disputed and is separate topic latter in reply to our letter under section 143(12) ,on the other side the

Management in its letter & meeting held on 19/02/2019 claimed that under billed amount has been billed during January 2020.It is: worth mentioning that during Dec.2019 the same Management has claimed that amount of Rs 37.96 Cr, short billed to Anumita was billed & recovered during the same month of billing .now on what basis the Management has issued new bill for differential amount. .Only this one bill was discussed during the mecting held

n 15/02/29 as well 19/02/2020. no other bills and the main amount Rs 3082 Cr.was not discussed at all except that such big fraud is not possible thus ail replies are sequitur At evasive. We also understand that there are small cases where amount of bill was reduced by

Court but these were also due to continuous frauds committed by the officers of the Company. In addition in case of Ambuja open access was included in the HPSEBL bills, amount of open access was reduced by not the no of units. There may also be some more

reasons for under billing but still these amounts to frauds as per Companies Act 2013.Qur question on our observations were dodged .

As the company has not disclosed its revenue fully which is substantially under stated .and as per Management it will be reconciled & provided during next year audit (verbally) ,we will assess the Company's process to identify the impact of such billing /under billing &. report accordingly in next year audit report . In the light of our observations on revenue .tenders |Fixéd Assets .sundry debtors &

creditors .inter unit balances ,other assets and liabilities , claim of management to adopt IND AS is false jas the Financial statements are not even AS (GAAP) compliant even there is no arithmetic accuracy...

We notieed that bills of Ambuja contains large amounts of adjustment revised on the claim of ‘open Access” consumption included in‘consumption of HPSEBL but in our opinion this type of mistakes are impossible in SAP environment & will be reported during next year audit report.

After analyzing all aspects of billing, in our opinion, the management has manipulated some aspects/parameters of software e.g, demand / energy charges of billing software just to give benefit to some large customers& also billing of large customers through manual reading instead of MRI. In terms of SE in charge of IT all this is due to faulty software by HCL(verbal Claim) & that Balance Sheet cannot be revised .But in our opinion this is the outcome of manipulation of software as appears from our substantive tests because when same software is giving accurate outcome in other cases how could it provided wrong results in some large consumers. We concluded this under billing and manipulating software alter printing some bills and analyzing the same.

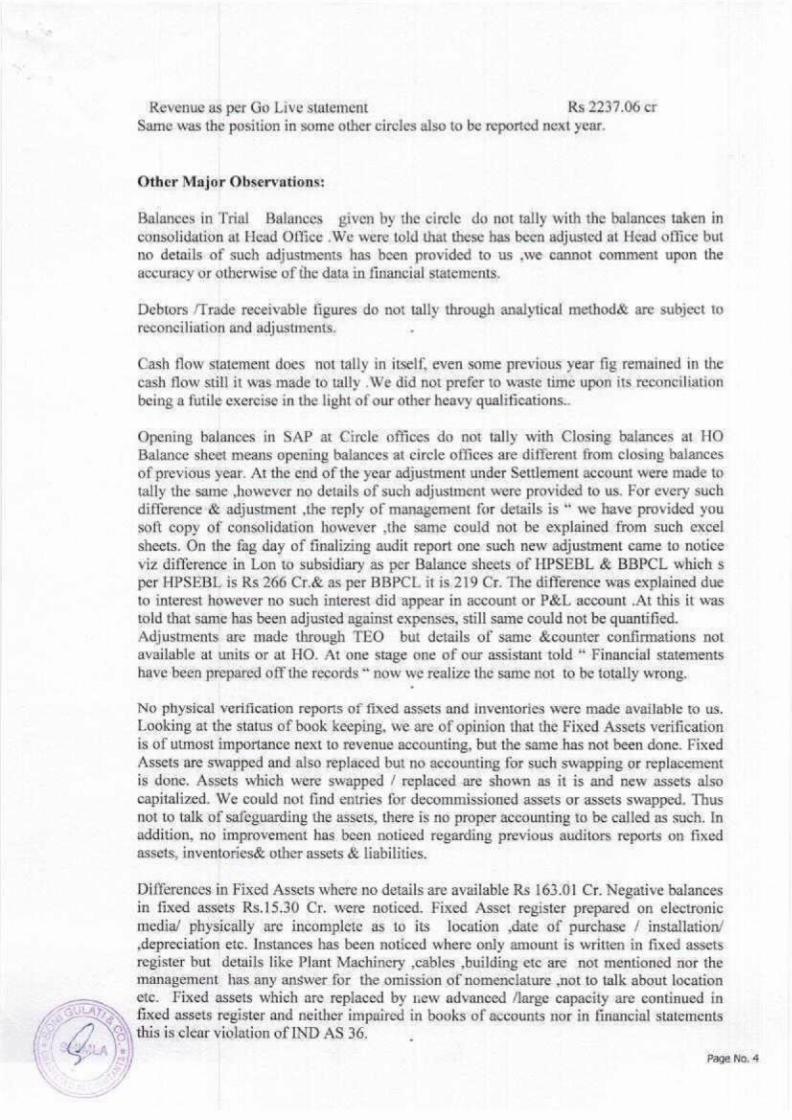

To counter- check such difference we visited Solan Circle again and got 4 sales fig as under:

Revenue billed as per CE (commercial) Rs 3629 .17Cr Revenue as per OP circle Solan A Rs 2512.73 Cr Revenue billed as per manual from divisions Rs 1759.82 er Revenue-as.per CMTR III Rs 1984.44 cr

Page No. 3

Revenue as per Go Live statement Rs 2237.06 cr Same was the position in some other circles also to be reported next year.

Other Major Observations:

Balances in Trial Balances given by the circle do not tally with the balances taken in consolidation at Head Office We were told that these has been adjusted at Head office but

no details-of such adjustments has been provided to us »ve cannot comment upon the accuracy or otherwise of the data in financial statements.

Debtors /Trade receivable figures do not tally through analytical method& are subject to reconciliation and adjustments. ,

Cash flow statement does not tally in itself, even some previous year fig remained in the cash flow still it was made to tally .We did not prefer to waste time upon its reconciliation being a futile exercise in the light of our other heavy qualttications..

Qpening balances in SAP at Circle offices do not tally with Closing balances at HO Balance sheet means opening balances at circle offices are different from closing balances of previous year. At the end of the year adjustment under Settlement account were made to tally the same .however no details of such adjustment were provided to us. For every such difference & adjustment ,the reply of management for details is “ we have provided you soft copy of consolidation however ,he same could not be explained from such excel

sheets. On the fag day of finalizing audit report one-such new adjustment came to notice viz difference in Lon to subsidiary as per Balance sheets of HPSEBL & BBPCL which s per HPSEBL is Rs 266 Cr.& as per BBPCL it is.219 Cr. The difference was explained due

to interest however no such interest did ‘appear in account or P&L account .At this it was told that same has been adjusted against expenses, still same could not be quantified.

Adjustments. are made through TEO but details of same &counter confirmations not available at units or at HO. At one stage one of our assistant told “ Financial statements have been prepared off the records * now we realize the same not to be totally wrong.

No physical verification reports of fixed assets and inventories were made available to us.

Looking at the status of book keeping, we are of opinion that the Fixed Assets verification is of utmost importance next to revenue accounting, but the same has not been done. Fixed Assets are swapped and also replaced but no accounting for such swapping or replacement

is done, Assets which were swapped / replaced are shown as it is and new assets also capitalized. We could not find entries for decommissioned assets or assets swapped. Thus

not to talk of safeguarding the assets, there is no proper accounting to be called as such. In addition, no improvement has been noticed regarding previous auditors reports on fixed assets, inventories& other assets & liabilities.

Differences-in Fixed Assets where no details are available Rs 163.01 Cr. Negative balances in fixed assets Rs.15,30 Cr, were noticed, Fixed Asset register prepared on eléctronic media/ physically are incomplete as to its location ,date of purchase / installation/ depreciation etc. Instances has been noticed where only amount is written in fixed assets register but details like Plant Machinery -cables ,building ete are mot mentioned nor the management has any answer for the omission of nomenclature not to talk about location

ee ete. Fixed assets which are replaced by new advanced /large capacity are continued in Carly aN fixed assets register and neither impaired in books of accounts nor in financial statements

Cg “a\ this is clear violation of IND AS 36, Mn le 3)

Page No.4

Upon test checking at some stores ,significant differences were noticed but remained unexplained ,in reply to our observation the management has replied that specific case not given jin every store such differences were noticed specifically during audit of store at Bhatta kufar management was informed ,that some items like steel ete were there in stores ledger but physically missing , being statutory auditors we cannot afford to conduct physical verification which is a separate assignment for such a large organization .The control records are missing financial statements are prepared from the financial records which can not be compared with physical balances records .For most of our questions the replies of management are” this is as per past & nobody has asked for the same neither Statutory auditors nor internal auditor or CAG auditors’.

Company claimed to have adopted IND AS but actually none has not been adopted, rather

financial statements do not comply even with AS (GAAP)

Tenders :Tenders documents were not provided to us because either the Chief engineer /SE was not available or these were avoided-as we were sent to JE whose records start from

works ‘supply order only .At Dharamshala Ist day CE was on leave ,we conducted audit at

division jnext day initially CE was not thereDy CE informed that he does not have authority to provide the documents and we were asked to wait when CE came at around

2PM .his reply was “his draftsman is on leave this way the records were avoided. At Head office CE MM we were sent to JE whose records start form works order or supply order no tender records available with him. After discussions with management it was decided to check the tender records during next year audit,

Purchase of Power: Note 2.25 —only purchase of power amount is given but quantity of purchase not given, quantity:is given only in table -3.

There are negative amounts in purchase of power and also some purchases shown without name of the seller. This. way and also negative attitude of management checking the purchase of power could

not be concluded, We have decided to chéck purchase of power during next year for both the years & report accordingly.

Thus there could be a risk of material misstatement in Revenue, Téendering& Purchase of

Power some of the same explained above.

Security Deposits: No sub ledger for security deposits has been maintained /provided to us for our verification. No sub ledger maintained/provided for deposits for electrification, service connection ete. made for'acquiring fixed assets.

Ny Ey

wy ’) Information Other than the Standalone Financial Statexaents and Auditor’s Report

i} es Page No. 5

Thereon

The Company's Board of Directors is responsible for the preparation of the other information.

The other information comprises the information included in the Management Discussion and Analysis, Board's Report including Annexure to Board’s Report, Business: Responsibility

Report, Corporate Governance and Shareholder’s Information, but does not include the

standalone financial statements and our auditor’s report thereon.

The standalone financial statements provided to us do not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the standalone financial statements. our responsibility is to

read the other information and, in doing so, consider whether the other information is material ly inconsistent with the standalone financial statements or our knowledge obtained during the course of our audit or otherwise appears lo be materially misstated.

However, no-such other information has been made available to us.

If, based on the work we have performed, we concluded that there is a material misstatement of this other information, we are required te report that fact. We have nothing to report in this

regard, as the statements like Board Report, business Responsibility Report, Corporate

Governance Report &-shareholder’s information has not been verified by us.

Management's Responsibility for the Standalone Financial Statements

‘The Company’s Board of Directors is responsible for the matters stated in section 134(5)

ofthe Act with respect to the preparation of these standalone financial statements that give a true and fair view of the financial position, financial performance, total comprehensive

income, changes in equity and cash flows of the Company in accordance with the IND-AS and other accounting principles generally accepted in India. This responsibility also includes maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments

and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the standalone financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.

In preparing the standalone financial statements, management is responsible for assessing the

Company’s ability to continue-as'a going concern, disclosing, as applicable, matters related to going concern and using the Going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do 80,

The Board of Directors are responsible for overseeing the Company's financial reporting . process.

leat oA 4 Auditor's Responsivilitics for the Audit of the Standalone Financial Statements Was cy Page No. 6

Our objectives are to obtain reasonable assurance about whether the standalone financial

statements as a whole are fice from material misstatement, whether due to fraud or error, and

to issue an auditor's report that includes our opinion. Reasonable assurance is a high level af

assurance, but is nota guarantee that an audit conducted in accordance with SAs will always

detect a material misstatement when itexists. Misstatements can arise from fraud or error and

are considered material if, individually or in the aggregate. they could reasonably be expected

to influence the economic decisions of users taken on the basis of these standalone financial

statements.

As part of an audit in accordance with SAs, we exercise professional judgment and

maintain professional skepticism throughout the audit. We also:

* Identify and assess the risks of material misstatement of the standalone financial

statements, whether due to fraud or error, design and perform audit procedures responsive to

those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for

our opinion. The risk of not detecting a material misstatement resulting from fraud is higher

than for one tesulting from error. as fraud may involve collusion, forgery, intentional

emissions, misrepresentations, or the override of internal control.

* Obtain an understanding of internal financial controls relevant to the audit in order to

design ‘audit procedures that are-appropriate in the circumstances. Under section 143(3){i) of

the Act. we are also responsible for expressing our opinion on whether the Company has

adequate internal financial controls system in place and the operating effectiveness of such

controls,

* Evaluate the appropriateness of accounting policies used and the reasonableness of

accounting estimates and related disclosures made by management.

* Conclude on the appropriateness of management's use of the going concern basis of

accounting and, based on the audit evidence obtained, whether a material uncertainty exists

related to events or conditions that may cast significant doubt on the Company's ability to

continue as a going concern. If we conclude that a material uncertainty exists. we are. required

to draw attention in our auditor’s report to the related disclosures in the standalone financial

statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are

based on the audit evidence obtained up to the date of our auditor's report: However, future events or condilions may cause the Company to cease to continue as a going concern.

« Evaluate the overall presentation, structure and content of the standalone financial statements, including the disclosures; and whether the standalone financial statements

represent the underlying transactions and events in a manner that achieves fair presentation.

Materiality is the magnitude of misstatements in the standalone financial statements. that, individually or in agpregate, makes it probable that the economic decisions of a reasonably knowledgeable user of the financial statements may be influenced. We consider quantitative

materiality and qualitative factors in (i) planning the scope of our audit work and in evaluating the results of our work; and (il) to evaluate the effect of any identified misstatements in the

financial statements,

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant

deficiencies in internal control that we identify during our audit, Page No. 7

4

NY : , of / a

et |

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all

relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the standalone financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor's report unless law or regulation precludes public disclosure about the matter or when,

in-extremely rare circumstances, we determine that-a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication. From the behavior of the Management we concluded that the two key audit matters we selecied, one is of very serious

nature and must be reported viz understatement of revenue on a large scale, as the sales fig disclosed in financial statements is only Rs.6503 Cr. Instead:of Rs9585Cr. Balance Rs.3082 Cr. is

embezzlement /fraud against the Company committed by the management Second Key matter was Tendering ,but records of tenders were not provided to us..the JEs.start the tenders from

Works’/ supply order only , the process before this is foreign to them .However the management has assured (verbally) to provide complete records during next year audit including for this year.

Report on Other Legal and Regulatory Requirements

|. As required by Section 143(3) of the Act, based on our audit we report that:

a) We have sought and obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit except the following

information was partially /not provided to us: i) Tender documents were either not provided or if provided they start from purchase order or works order.

it) Minutes Books of Board Meetings & General Meeting, accounts being in arrear & going through all these records in single year is just impracticable when these are allowed to-aceess at the figure end,

iil) Register of Charges not provided

iv) Register of Investments & Loans/Advances to subsidiaries, joint ventures & other entities.

v) The Company has not complied with the provisions of section 186(5) of the Companies

Act, 2013. Company has.advanced loan to its subsidiary company (BVPCL) form time to

lime and during this year also outstanding on 31.3 2018was Rs 266 crore while outstanding

on 31.3,.2018 was Rs 219 crore. Difference reported to be due to interest but no interest fig

could be seen in books of accounts, One youcher was shown but not entered in books of

account and was claimed to be squared up with expenses no stich squaring could be seen in

books of accounts. This is all bogus clams of management .management is not prepared to

put in writing any such claims .ihis violation of Companies Act 2013 violation of

Accounting standards & Income tax Act.

vi) As reported by previous auditors, Yearend provisions for liabilities / expenses booked at

the close of the year are reversed in the subsequent accounting year by the Company,

vii) The Company has not complied with the provisions of section 188 of the Companies

Page No. 8

Act2013 in making advances to its subsidiary

We further report, that during the year under review Company has made provision for expenses on the basis of budgets approved for particular works irrespective of the fact that actual expense accrued! incurred and same is reversed in the subsequent period on receipt of actual bill / invoice of the vendor / contractor. The same results in overstatement of other current liabilities and revenue expenses / capital work in progress: The sufficient information with regard to quantum of such liabilities provided in financial statements has not been made available to us,

2.As required by Companies (Auditors Report) order 2016 (“the order”) issued by the Govi of India in terms of sub-section (11) of the section 143 of the Act we give in the annexure

“B” a statement on the matters specified in paragraph 3 & 4 of the order to the extent applicable.

3,We-are enclosing our report in terms of section 143(5) of the Act jon the basis of such checks of the books & records of the Company as we considered appropriate & according to the information and explanations given to us in the annexure” A “ on the directions issued by Comptroller & Auditor General of India.

4. we also attach annexure “C” report on the internal controls over financial reporting under

clause (1) of subsection 3 of section 143 of the Companies Act 2013.

5, In view of following, in our opinion, proper books of accounts as required

by Law have not been kept by the company so far as it appears from our examinations of

those statement, registers and related records produced for our verification.

i. The sub divisions prepare CMTR &expenses statement and forward the same to Division & Divisions of the Company has maintained cash & bank book and no

corresponding transactions are recorded in ledger accounts. The adjustment entries were passed in the memorandum statement maintained to compile these financial statements, which is in contrary to the double entry system of recording of transactions as required by the Companies Act 2013.

The Divisions extracts monthly Trial Balance (known as “CS-1") for the purpose of

consolidation of financials by Circle and Wings, The Head Office on the basis of memorandum statements submitted by Circles and Wings compile these financial statements. The adequacy and correciness of memorandum statements and transmission of financial data do not ensure the correctness and sufficiency of accounting and recording of transactions and compilation of Balance Sheet and Profit & Loss account of the Company.

ii. The Divisions do not compile the trial balance with balances of the previous accounting month. The Circles consolidates the Trial Balance provided by the Divisions on monthly basis and Head Office merges the monthly Trial Balance and at the end of year consolidated balances are drawn on the basis of memorandum record for the purpose of preparation of financial statements. The Company does not record balances provided by Divisions at Circle or at Head Office in proper financial books of accounts. These financial

Page No. 9

statements have been compiled on the basis of statements prepared on the basis of merged

Trail Balances provided by Circles and not on the basis of books of accounts.

iii. The consolidated statements / record compiled at Head Office and Circle do not provide complete details of Main Accounting Code and or Sub-Account Code’. The memorandum consolidated record does not provide Circle or Division wise detail of transactions disclosed in these financial statements.

iv. The cash beok maintained at Division is: not balanced on daily basis,

therefore, the cash book do not refleet the cash in hand on daily basis.

(a) The Balance Sheet and Statement of Profit and Loss deait with by this report

are in agreement with the books of statements except our observations in Para,5(i)(ii)

(iii),(iv),

(b) Due to undetermined effects of the matter described in the Basis for Adverse Opinion

paragraph, other qualifications and non compliance of IND AS, in our opinion, the

Balance Sheet. Statement of Profit and Loss does not comply with the accounting standards

referred to in section 133 of Companies Act, 2013 ead with Rule 7 of the

Compantes(Accounts) Rules 2014.As reported in earlier years audit reports the

Company has ‘not complied with most of the AS (GAAP) but claimed to be IND AS

Compliant this year.

(ce) We were informed In terms of Exemption Notification Government of India,

Ministry of Corporate Affairs Notification No 372 dated 05 June2015 Government

companies are exempted from the applicability of section 164 of Companies Act 2013,

therefore, no written representation from Board of Directors have been obtained.

(d) The Company has taken some’ steps to remove the qualifications reported in

earlier year reports while adopting the accounts for the current year, such old qualifications

has been deleted & non complied has been considered in the current year report also,

Other Matters

i) Bank accounts are not reconciled although reconciliation statements are

prepared but are in the nature of formality only as, very old transaction of even cash are appearing in reconciliation statements .In some divisions negative balances shown in CS-1

ii) Capital Work in progress registers are not updated in divisions& on the top of it adjustments in Capital W-I-P are made at Head office .This is not practicable to verify or comment upon the CWIP in any unit. iit) Odd balances noticed in sundry debtors accounts in many units. iv) Details of head44.11,44.120, 44.310. 44.330 not provided nor there is no system of reconciliation of various interconnected heads of account, Actuarial Valuation not available & amount of provisions created is as per Management estimates. v) Details of amounts in ‘CS-1 not provided for many accounting heads, on checking it was noticed that many balances are carried forward from earlier years. v1) We have noticed cases for which neither any provision has been created nor has

GUE St any contingent liability been shown in notes. NSN Vil) No entries has béen passed for Land/ properti¢s acquired by NHAI at unit or Head

Page No. 10

office. We were told this will be done next year.

viii) CWIP remained unverified duc to non availability of work/scheme wise details and

work register,

ix) Large amounts under head 22.810 & 22.830 being stock excess/ short pending

Investigation but units do.not have any details.

x) Debtors/ creditors have adverse balances which remained unexplained.

xi) | Unexplained staff related provisions appearing in units viz 44.110, 44.120, 44.130

xi) Balance of O & M material stock account shown in CS-1 does not mateh with

balance in critical & non critical.

xiii) | Stock shortage pending investigation shown in CS-! remained unexplained amount

are large & significant. xIVv) Receivables as per CS-1 differs from Balances as per manual accounts in many

units. xv) ‘It. was noticed that balance as per books was significant but as per Bank it was NIL.

Differences remained unexplained. Negative bank balances are very common in units.

xvi) Interest payable on consumer deposit shown in CS-1 is odd compared to interest

accrued during the year as interest accrued during the year are adjusted in next year.

xvii) In-some units where stock statements were made available to us stock as per CS-1

do not tally with stock statement. xvili) Differences were noticed in Provision for unbilled Revenue (23.401 to 3.413)

xix) Many balances are carried over from year to year in many units but details are not

available. Some of such balances may be due to wrong entries. xx) Pending ATDs odd balances are shown inCS-1.

xxi} Provision for sundry creditors (46.410) details not available in unit.

xxii) The Company has not disclosed the impact of pending litigation on its financial

position in financial statements.

xxiii) The Conipany has not made provision, as required under applicable law or

accounting standards, for material foreseeable losses. if any. on long term contract

including derivative contracts xiv) No amount has been transferred to investor Education and Protection Fund by the

Company during the -year ended March 31, 2018

a) Loan agreements with various lenders were made available to us at Head office but the

compliance of terms & conditions are to be checked at unit level ,this thing we realized only at Head office .The same will be checked during next year audit.

b) In our opinion, proper books of account as required by law have been kept by the Company so far as it appears from our examination of those books except the following: i) Fixed Assets records are incomplete il) No statements not even Trial balance is prepared at sub-division or division level,

although all primary transactions are entered at subdivision/division level. Trial Balance is prepared at circle level & Financial Statements are prepared at Head office. Due to this reason the financial statements prepared at Head do not tally with the tral balances we got from circle offices. We were informed that differences have been rectified at Head Office but our question like “when the CWIP at subdivisions is X how could HO change it to Y No explanation for this has been provided. iii) Fixed Assets records aré incomplete, neither correct physical verification nor

providing accurate depreciation is possible, under such circumstances how to safeguard the

fa \ fixed assets is also 1 question mark. i Y re iv) Inventories. at stores does not tally with the quantitative records kept at stores. The

Wel SA fa Page No. 11

balance sheet figs are from books of accounts and never tallied with physical/stores records

wAs required by Law no valuation of inventories has been done . v) Negative balances in most type of assets and liabilities are noticed Explanation given

is only eye wash under such circumstances ,balance confirmation from parties are not

possible Means third party confirmation is not practicable. vi) No ledgers are prepared by the company, only excel sheets of transactions are there of course now in online circles it is possibly from HO.

2. Observations of Previous years Auditors to the extent not rectified by the

management :

As reported by previous auditors:

1. It has been observed that expenses approved by Head Office till the year end are only provided in the financial statements. The work completed / services rendered / goods supplied till 31° March. 2018 and not approved by Head Office, has not been provided in the financial Statements, however, the same have been recorded in the subsequent period on receipt of approv al from Head Office. The information with regard to assets / expenses-and liabilities has not been made available to us, therefore, impact of

same on noncurrent assets / current assets/ noncurrent liabilities’ current liabilities / losses

cannot be quantified.

3 Nether the Company has disclosed the facts in- notes nor given any information-as to‘settlement for those casés which were disclosed in earlier years balance

sheet as notes to account / audit report / CAG comments / comments of works audit party/ comments of RA audit /pending court case / settlement where the Company had deposited deposits with various authorities amounts some of them may have been settled

/ awarded by the Court / Govt. / Arbitrator but the status was not disclosed by the

Company. This may.affect the profit & loss account and the balance sheet

4 Old assets (recoverable) and old liabilities (Payables) in all the divisions being time barred mostly remained unconfirmed / un-reconciled. The adjustment required if any may affect the profit & loss account and the balance sheet.

5 The Company has not provided sufficient physical verification records in respect ef Tangible Assets, Capital Work in progress and Contracts in progress at the Division level. The adjustment required if any may affect the profit & loss.account and the balance sheet.

6 The Compary has not taken any reasonable steps to remove the qualifications reported in previous year report and earlier year reports of HPSEB by CAG while adopting the accounts for the current year, therefore old material qualifications has been considered

_ in the current year report where the same is quantifiable as no information for the same has -, been provided by the company.

Page No, 12

7 The Head Office has not provided complete details’ information of the closing balance of sub heads operated by them in respect of respective DDO's except, banks section, loan section, investment section-and Pension Il. The subsidiary records /

register of individual DDO has not been produced for our verification. No sufficient information has been provided in respect of the lability of expenses, other liabilities and provisions at Head Office Level.

8 The reconciliation of the Fixed Assets Register and the Fixed Assets account in the account statement is pending sinée miany years. The pendency is due to non availability of records/ information of earlier years or in some divisions the earlier years records has been burnt. The above pendency has been observed in almost all circles also. The adjustment required if any may affect the profit & loss account and the balance sheet.

9 The reconciliation of the Works register and the Capital Work in progress

account in the account statements is pending since many years. The pendency is due to non availability of reeords/ information of earlier years or in some divisions the earlier year’s records has been burnt. The above pendency has been observed in Solan Circle, Rampur

Cirele, Rohru Circle and other circle also, The adjustment required if any may affect the profit & loss account and the balance sheet.

10 No sufficient information and evidence in support of revenue expenses pending allocation over Capital Works has been provided to us. The adjustment required if any may affect the profit & loss account and the balance sheet.

11 The subsidiary records in relation to consumer ledgers at the end of the year is pending for reconciliation at all divisions of the operation circles The adjustment required if any may affect the profit & loss account and the balance sheet.

12 The Company has not provided any information about those consumers who has gone to the courts on account of disputes’in the bills raised for energy charges.

13 The Company has not settled the old un-reconciled entries in the bank

reconciliations statements. The adjustment required if any may affect the profit & loss account and the balance sheet.

14 The Head office has not supplied to us the employees wise details of loans and advances to staff and interest acerued thereon, The adjustment required if any may affect the profit & loss accaunt.and the balance sheet.

15 The Company has not provided complete details of amount recoverable on account of thelt of property pending investigation (Account Code 28.885). The adjustment required if any may affect the profit & loss account and the balance sheet.

16 The Company has not been able to provide sufficient information/ confirmation from the parties in respect amount payable for purchase of power. The adjustment required if any may affect. the profit & loss account and the balance sheet.

: fay iT The Company has not able to provide reconciliation in respect of deposits and ae Gp \))\ retentions from suppliers and contractars with the subsidiary records maintained.

ies) Serie cn. Val zs it i .

ey Page No, 13

18 The Company has not been able to provide reconciliation in respect of

Deposits for Electrification Services Connections Account Code 47.1 with the subsidiary

records maintained.

19 No sufficient Information has been provided in respect of the Contingent

Liabilities provided in the notes to accounts and further no information for contingent

assets has been provided.

20 The divisions have not provided suffictent information in respect of those assets where the consumer has deposited the departmental charges and executed the work by their own. The adjustment required if any may affect the Value of assets created and the

reserves on the other hand.

21 During the year under review the financial statements are prepared as per

schedule [II of the Companies Act 2013 .The basis for grouping of noncurrent liabilities/

assets and current liabilities and assets as per the requirements of Schedule [II for the. cutrent and previous year has not been produced for our verification. It was also observed

that Figures of previous year was also regrouped in the schedules of balance sheet but the

basis of regrouping was not provided to us.

As per management these 21 paras has been deleted by the previous auditors but did

not have any certificate for the same.

Other observations of previous auditors to the extent not rectified by the

Management:

i) Share Capital: Special Way & Means Advance nonrefundable from H.P. Govt amounting to Rs.49807.75 Lac as per balance sheet dt 13.06.2010 financial year 2010-11 along with other reserves Rs704.78 lakh has been adjusted with carried forward losses of erstwhile Board totaling Rs:50512.53, in response to the audit qualification from

year to year.

ii) Reserves and Surplus (Note 2.2) a) Capital Reserves/Capital Grants from GOHP & GO!

ai) During the year under review the Company has Amortized Rs.6446.40 Lakh on the assets created from Government Grants and Consumer Contribution, The Amount of Amortization has been arrived at after applying the Depreciation Rates on the cost of such assets on yearly basis as per the accounting policy on depreciation refer Note

2.33 (A) 8 .The Company has no system in Place where the assets can be identified as if

these were created from Government Grants / Consumer Contribution. There is no Fixed Assets Register from where the cost of these assets along with date of it being put to use can be verified. The company has arrived at the cost of these assets on Adhoc basis where

it has capitalized the Grant réceived to particular year in which it was received without verifying the actual creation of the assets and without having sufficient records to verify the

actual cost of bringing the asset to use along with the date of it being put to use. It was also observed that in many Divisions the amount of Consumer Deposits was not transferred