Online Video Industry China 2018

70

Online Video Industry China 2018

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Online Video Industry China 2018

Online Video Industry

China 2018

Online Video Industry – China 2018

Page 1 of 68

Table of Contents PREFACE .................................................................................................................................................... 4

1. EXECUTIVE SUMMARY ....................................................................................................................... 5

1.1. CHINA TV MARKET OVERVIEW ...................................................................................................................... 5 1.2. CHINA PAY TV MARKET OVERVIEW ................................................................................................................ 5 1.3. CHINA TELECOM INDUSTRY OVERVIEW ............................................................................................................ 6 1.4. CHINA’S ONLINE VIDEO LANDSCAPE ................................................................................................................ 6 1.5. NEW DEVELOPMENTS IN CHINA’S ONLINE VIDEO INDUSTRY ................................................................................ 7 1.6. VIDEO CONTENT PIRACY IN CHINA .................................................................................................................. 7 1.7. REGULATORY ENVIRONMENT ......................................................................................................................... 8

2. CHINA TV MARKET OVERVIEW.......................................................................................................... 11

2.1. TV MARKET OVERVIEW ..............................................................................................................................11 2.2. FREE-TO-AIR TV IN CHINA ..........................................................................................................................11 2.3. TV ADVERTISING .......................................................................................................................................12 2.4. SMART TV OWNERSHIP ..............................................................................................................................13 2.5. GENERAL TV AND ONLINE VIEWING BEHAVIOR IN CHINA ..................................................................................13 2.5.1. VIEWING HABITS AND CONTENT PREFERENCES ...........................................................................................14 2.5.2. TRENDS IN DIGITAL VIDEO CONTENT VIEWING ...........................................................................................15

3. CHINA’S PAY TV INDUSTRY ............................................................................................................... 19

3.1. PAY TV MARKET OVERVIEW ........................................................................................................................19 3.1.1. TYPES OF CHANNELS IN CHINA .................................................................................................................20 3.1.2. PROVINCIAL SATELLITE TV BROADCASTERS (“PSTVS”) ................................................................................21 3.1.3. CITY SATELLITE TV BROADCASTERS (”CSTVS”)...........................................................................................23

4. OVERVIEW OF CHINA’S TELECOMS INDUSTRY ................................................................................... 24

4.1. CHINA’S MOBILE INDUSTRY OVERVIEW .........................................................................................................24 4.1.1. MOBILE SUBSCRIBER NUMBERS ...............................................................................................................24 4.1.2. MOBILE INDUSTRY REVENUES ..................................................................................................................26 4.1.3. MOBILE OPERATORS’ NEAR-TERM STRATEGIC PRIORITIES ............................................................................27 4.2. CHINA’S FIXED BROADBAND INDUSTRY OVERVIEW ..........................................................................................28 4.2.1. FIXED BROADBAND SUBSCRIBERS .............................................................................................................28 4.2.2. FIXED BROADBAND INDUSTRY REVENUES...................................................................................................30 4.3. CHINA’S TELECOM OPERATORS’ ONLINE VIDEO INITIATIVES ..............................................................................31

5. CHINA’S ONLINE VIDEO LANDSCAPE ................................................................................................. 33

5.1. ONLINE VIDEO LANDSCAPE - OVERVIEW ........................................................................................................33 5.2. MAJOR ONLINE VIDEO PLAYERS IN CHINA ......................................................................................................35 5.2.1. IQIYI ...................................................................................................................................................37 5.2.2. TENCENT .............................................................................................................................................39 5.2.3. YOUKU ................................................................................................................................................39 5.3. OTHER ESTABLISHED ONLINE VIDEO PLATFORMS IN CHINA ...............................................................................40

6. NEW DEVELOPMENTS IN CHINA’S ONLINE VIDEO INDUSTRY .............................................................. 45

6.1. LIVE STREAMING IN CHINA ..........................................................................................................................45 6.2. DESCRIPTION OF MAJOR LIVE STREAMING PLATFORMS ....................................................................................47 6.3. ESPORTS IN CHINA .....................................................................................................................................49 6.4. SHORT VIDEO PLATFORMS IN CHINA .............................................................................................................51

Online Video Industry – China 2018

Page 2 of 68

7. VIDEO CONTENT PIRACY IN CHINA .................................................................................................... 55

7.1. SUMMARY OF KEY FINDINGS ON PIRACY IN CHINA ...........................................................................................55 7.2. CONSUMER VIDEO CONTENT PIRACY IN CHINA ...............................................................................................55 7.3. CLOUD PIRACY IN CHINA .............................................................................................................................56 7.4. ACTIONS TAKEN TO STOP PIRACY BY REGULATORS ...........................................................................................57

8. REGULATION OF THE CHINESE ONLINE VIDEO INDUSTRY ................................................................... 60

8.1. KEY STAKEHOLDERS IN CHINESE TV REGULATION ............................................................................................60 8.2. LICENSING REQUIREMENTS ..........................................................................................................................62 8.2.1. LICENSES NEEDED FOR OPERATING ONLINE VIDEO SERVICES .........................................................................62 8.2.2. INTERNET AUDIO-VIDEO PROGRAM TRANSMISSION LICENSE REQUIREMENTS ...................................................63 8.2.3. THREE-WAY CONVERGENCE PROGRAM .....................................................................................................65 8.2.4. REGULATOR INTERVENTIONS ON ONLINE VIDEO PLATFORMS.........................................................................65 8.3. REGULATIONS ON FOREIGN CONTENT............................................................................................................65 8.3.1. APPLICATION PROCESS FOR FOREIGN CONTENT PERMITS ..............................................................................66 8.4. LIVE STREAMING REGULATIONS ....................................................................................................................67 8.4.1. REGULATOR INTERVENTIONS ON LIVE STREAMING PLATFORMS ......................................................................68

Online Video Industry – China 2018

Page 3 of 68

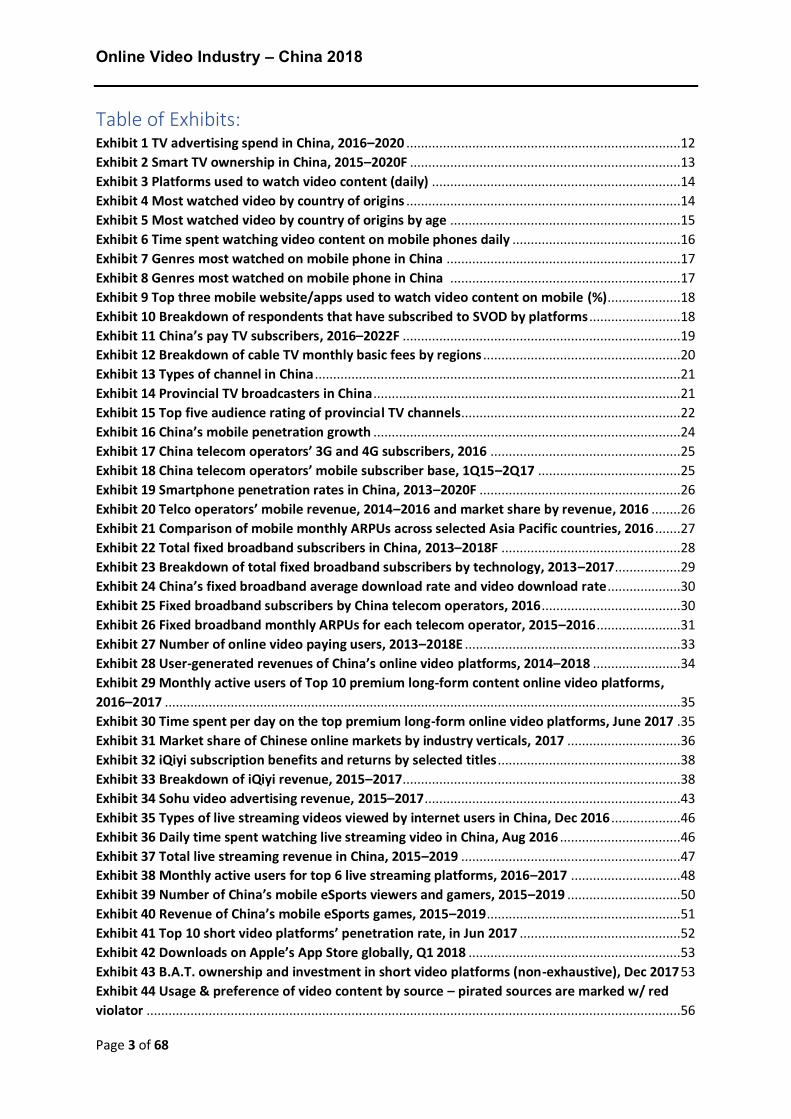

Table of Exhibits: Exhibit 1 TV advertising spend in China, 2016–2020 ...........................................................................12 Exhibit 2 Smart TV ownership in China, 2015–2020F ..........................................................................13 Exhibit 3 Platforms used to watch video content (daily) ....................................................................14 Exhibit 4 Most watched video by country of origins ...........................................................................14 Exhibit 5 Most watched video by country of origins by age ...............................................................15 Exhibit 6 Time spent watching video content on mobile phones daily ..............................................16 Exhibit 7 Genres most watched on mobile phone in China ................................................................17 Exhibit 8 Genres most watched on mobile phone in China ...............................................................17 Exhibit 9 Top three mobile website/apps used to watch video content on mobile (%) ....................18 Exhibit 10 Breakdown of respondents that have subscribed to SVOD by platforms .........................18 Exhibit 11 China’s pay TV subscribers, 2016–2022F ............................................................................19 Exhibit 12 Breakdown of cable TV monthly basic fees by regions ......................................................20 Exhibit 13 Types of channel in China ....................................................................................................21 Exhibit 14 Provincial TV broadcasters in China ....................................................................................21 Exhibit 15 Top five audience rating of provincial TV channels ............................................................22 Exhibit 16 China’s mobile penetration growth ....................................................................................24 Exhibit 17 China telecom operators’ 3G and 4G subscribers, 2016 ....................................................25 Exhibit 18 China telecom operators’ mobile subscriber base, 1Q15–2Q17 .......................................25 Exhibit 19 Smartphone penetration rates in China, 2013–2020F .......................................................26 Exhibit 20 Telco operators’ mobile revenue, 2014–2016 and market share by revenue, 2016 ........26 Exhibit 21 Comparison of mobile monthly ARPUs across selected Asia Pacific countries, 2016 .......27 Exhibit 22 Total fixed broadband subscribers in China, 2013–2018F .................................................28 Exhibit 23 Breakdown of total fixed broadband subscribers by technology, 2013–2017..................29 Exhibit 24 China’s fixed broadband average download rate and video download rate ....................30 Exhibit 25 Fixed broadband subscribers by China telecom operators, 2016 ......................................30 Exhibit 26 Fixed broadband monthly ARPUs for each telecom operator, 2015–2016 .......................31 Exhibit 27 Number of online video paying users, 2013–2018E ...........................................................33 Exhibit 28 User-generated revenues of China’s online video platforms, 2014–2018 ........................34 Exhibit 29 Monthly active users of Top 10 premium long-form content online video platforms, 2016–2017 .............................................................................................................................................35 Exhibit 30 Time spent per day on the top premium long-form online video platforms, June 2017 .35 Exhibit 31 Market share of Chinese online markets by industry verticals, 2017 ...............................36 Exhibit 32 iQiyi subscription benefits and returns by selected titles ..................................................38 Exhibit 33 Breakdown of iQiyi revenue, 2015–2017............................................................................38 Exhibit 34 Sohu video advertising revenue, 2015–2017 ......................................................................43 Exhibit 35 Types of live streaming videos viewed by internet users in China, Dec 2016 ...................46 Exhibit 36 Daily time spent watching live streaming video in China, Aug 2016 .................................46 Exhibit 37 Total live streaming revenue in China, 2015–2019 ............................................................47 Exhibit 38 Monthly active users for top 6 live streaming platforms, 2016–2017 ..............................48 Exhibit 39 Number of China’s mobile eSports viewers and gamers, 2015–2019 ...............................50 Exhibit 40 Revenue of China’s mobile eSports games, 2015–2019 .....................................................51 Exhibit 41 Top 10 short video platforms’ penetration rate, in Jun 2017 ............................................52 Exhibit 42 Downloads on Apple’s App Store globally, Q1 2018 ..........................................................53 Exhibit 43 B.A.T. ownership and investment in short video platforms (non-exhaustive), Dec 2017 53 Exhibit 44 Usage & preference of video content by source – pirated sources are marked w/ red violator ..................................................................................................................................................56

Online Video Industry – China 2018

Page 4 of 68

Preface

Information Validity The information contained in this report is prepared from data gathered in the first half of 2018 and believed to be correct and reliable at the time of writing. Whilst Pioneer Consulting Asia has exercised all reasonable endeavors to ensure that the contents of the report are accurate and up to date, it does not accept liability for any information which may not be accurate. Our Approach This report focuses on China’s online video market. Descriptions of Free-to-Air (FTA) TV and pay TV are brief and intended to provide context to the reader. It should be understood that some information contained in the accompanying report was obtained verbally from third parties without written documentation. In certain cases, publicly available sources were not available for independent verification. Where possible, Pioneer Consulting Asia has sought to verify the information supplied by checking multiple sources. Pioneer Consulting Asia agreed to provide results of its own primary research in this report. The study was conducted in urban areas across China and only included respondents who had access to the internet via a mobile or fixed line connection. The study comprised of a quantitative online survey as well as qualitative interviews with selected online survey respondents to provide a more in-depth understanding of their video viewing behaviors. Use of Information The report has been prepared for information purposes only and is intended for the Asia Video Industry Association (AVIA) and its members. The report must not be acted on or relied upon for any investment decisions or other specific actions without further study.

Online Video Industry – China 2018

Page 5 of 68

1. Executive Summary

1.1. China TV Market Overview Broadcast television has long played an important role in China both as a medium for entertainment and the spread of government approved ideology thanks to its wide reach. According to the latest official government statistics, the percentage of households in China that owned a TV set was 99% in 2014. That is equivalent to 455 million households at the end of 2014 and 495 million at the end of 2017 assuming the penetration rate held steady. Currently, there are more than 2000 television stations in China including FTA and pay TV stations. Advertising on FTA channels is estimated to have generated US$12.5 billion in 2016 and is forecast to shrink slightly to US$12.3 billion by 2020. Parallel to the preparation of this report, Pioneer Consulting Asia (PCA) conducted a consumer study on the topic of general audience trends/preferences in China and agreed to share with AVIA and its members some of the findings in this report. Below is a summary of consumer viewing trends in China from this research:

• High daily incidence (91%) of urban online consumers viewing video on their mobiles

• Significant amounts of time spent watching video on mobile devices with over 60% of respondents watching over 30 minutes of video per day on their mobiles

• Content preferences of respondents to watch both short-form and long-form content on their mobiles

• Dominance of iQiyi, Tencent and Youku respectively both in terms of online viewers and paying subscribers

1.2. China Pay TV Market Overview The overall size of the pay TV market across all technologies was estimated to be 325 million subscribers at the end 2017, roughly equivalent to 65% household penetration which makes it the largest pay TV market in Asia Pacific by subscriber numbers. This number was up 3.8% from 313 million households in 2016. By 2022, the number is expected to grow to 353 million, representing a CAGR of 2.4%. Cable TV is the most widely adopted pay TV distribution technology in China. It is estimated that around 160 million households were subscribed to cable pay TV services in June 2017 representing a household penetration rate of 35%. Licensed IPTV has been growing rapidly in recent years and reportedly reached 102 million households in June 2017, a household penetration rate of 22%. To be a licensed IPTV provider in China with permission to provide domestic subscription television, platforms must obtain an “Information Network Audio-visual Program Broadcast Permit” which requires the platform to have a private ecosystem that is not linked to websites on the public internet.

Online Video Industry – China 2018

Page 6 of 68

Household penetration of any form of pay TV reaches over 90% for urban areas in China. However, in rural areas, licensed Satellite TV is more widely used and overall reaches an estimated 63 million households. It should be noted that the size of the unlicensed satellite TV market in China is estimated to be comparable in size to that of the licensed market. Unlicensed satellite TVs in China receive channel signals that are officially being targeted at foreign countries such as Taiwan and Thailand, hence the content is not censored by regulators and fees for the content do not get distributed to the rightful IP holders. Advertising on pay TV platforms generated revenues of US$5 billion in 2016 and represented 29% of total TV advertising in that year.

1.3. China Telecom Industry Overview Our overview of China’s telecom industry covers two major services:

• Mobile • Fixed broadband

China’s mobile penetration rate was 76% of the total population in 2016 and is expected to grow to 86% of the total population by 2020. It’s worth noting that penetration at end-2014 was only 48% but by the end of 2015, this had increased by almost 52% to reach 73%. This fast increase in penetration can primarily be attributed to the construction of an extensive 4G network and heavy promotions of 4G-compatible handsets. In 2017, it was estimated that 73% of mobile subscribers were on a 4G network and China’s smartphone penetration was 71% of all phone users in 2016. This latter figure is expected to grow to 74% by 2020. With widely available 4G and smartphone devices, all three major mobile operators in China have built their own online video & entertainment platforms to capitalize on the digital lifestyle of Chinese consumers but take up of these services has been limited. China’s fixed broadband growth has been driven by a national strategic initiative known as “Broadband China” which has set a 2020 target for fixed broadband to reach 70% of households with broadband speeds in cities and rural area of 50 megabits (“Mbps”) and 12Mbps respectively. China’s fixed broadband subscriber numbers experienced annual growth of 9% between 2013 and 2016, growing from 185 million subscribers to 241 million. By the end of 2018, fixed broadband subscriber numbers are forecast to reach 268 million, representing an annual growth rate of 6% from 2016.

1.4. China’s Online Video Landscape China’s online video market size by number of active users was estimated to be 596 million at the end of June 2017. This represented roughly 76% of the online population, highlighting that online video viewing is one the most common online activities in China. Revenues for the online video sector have grown by a factor of five over the last three years, from RMB 10 billion in June 2014 to an estimated RMB 50 billion in June 2017.

Online Video Industry – China 2018

Page 7 of 68

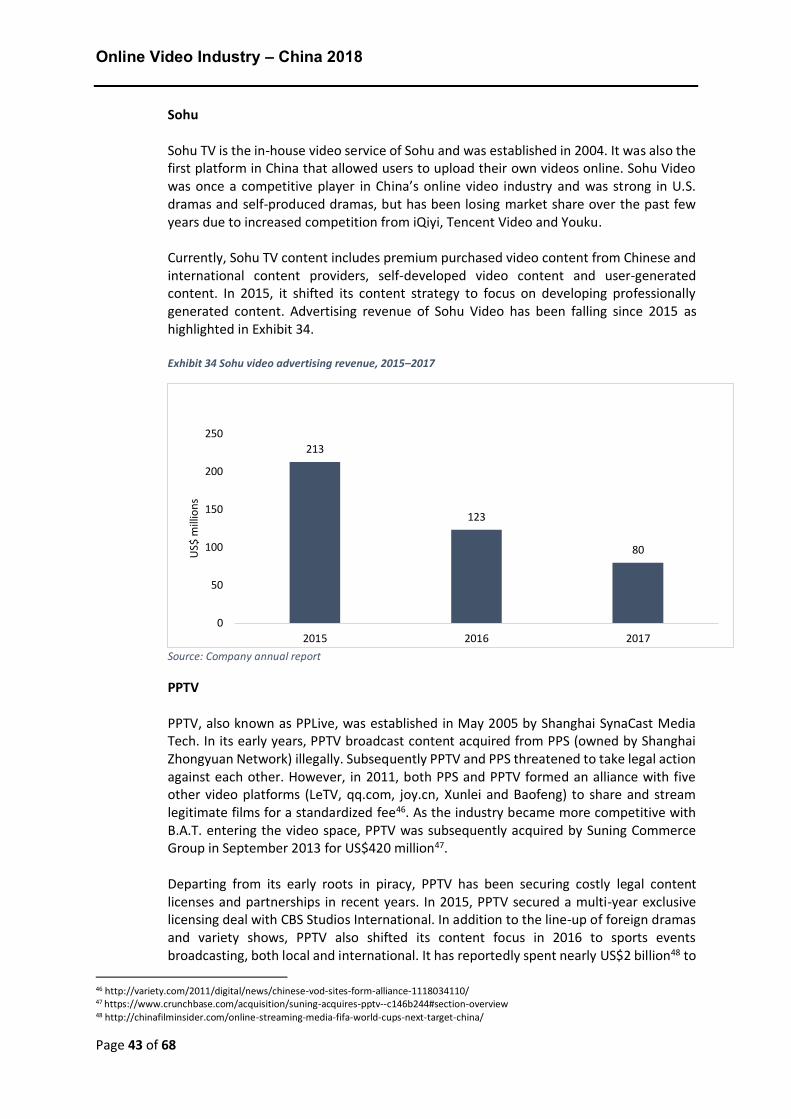

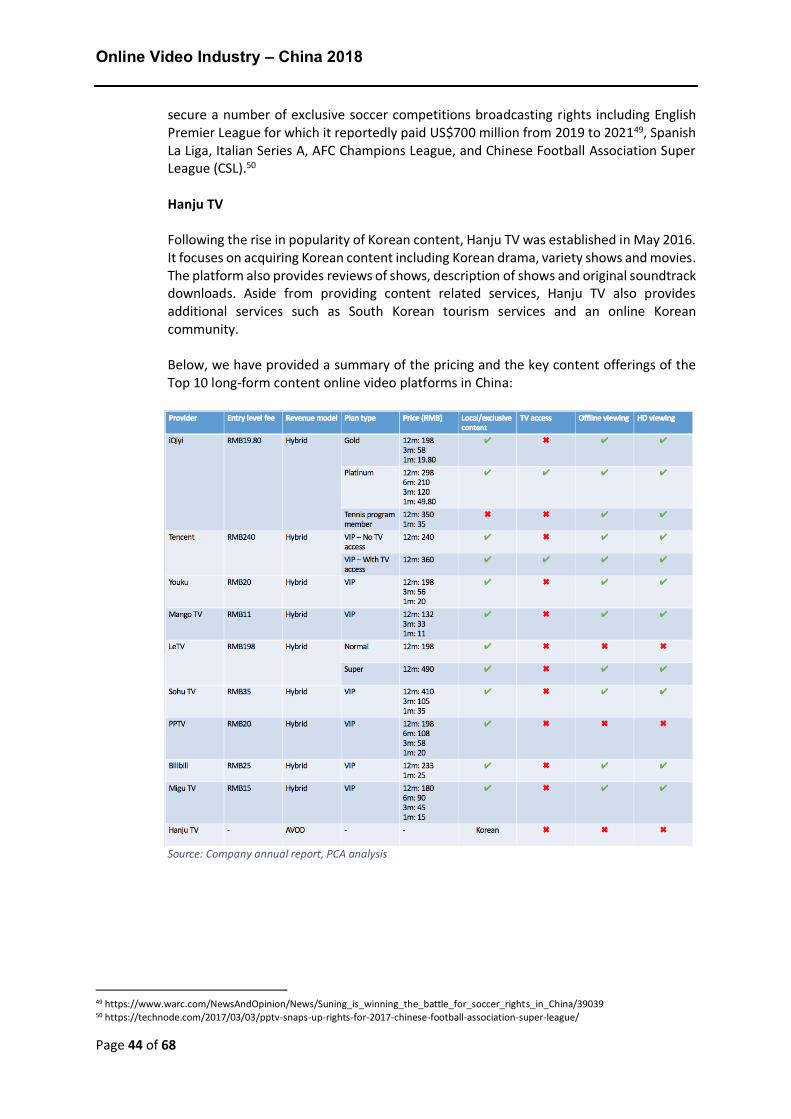

The evolution of China’s online video market has seen it transition from services with links to piracy, to legitimate services driven by advertising and, more recently, to subscription driven services. At the end of 2017, there were an estimated 74 million paying video users, up from only 8 million in 2014. The 2017 figure represents approximately 12% of the entire online video user base, up from 2% in 2014. A one-month subscription to an online service in China ranges between RMB 20 to RMB 40 depending on the platform and type of package selected. While the online video space is made up of more than 200 players, the premium long-form content space is dominated by just three players: iQiyi, Youku and Tencent Video. These players are owned by the three largest internet companies in China, Baidu, Alibaba and Tencent respectively (commonly referred to as B.A.T.), who aggressively compete head-to-head across a range of digital businesses. Other established online video platforms in China include both native online players and the online platforms of traditional FTA broadcasters. Rounding out the Top 10 premium long-form content video platforms in terms of monthly active users (MAUs) are MangoTV, LeTV, Bilibili, Sohu, PPTV, Hanju TV, and Migu TV.

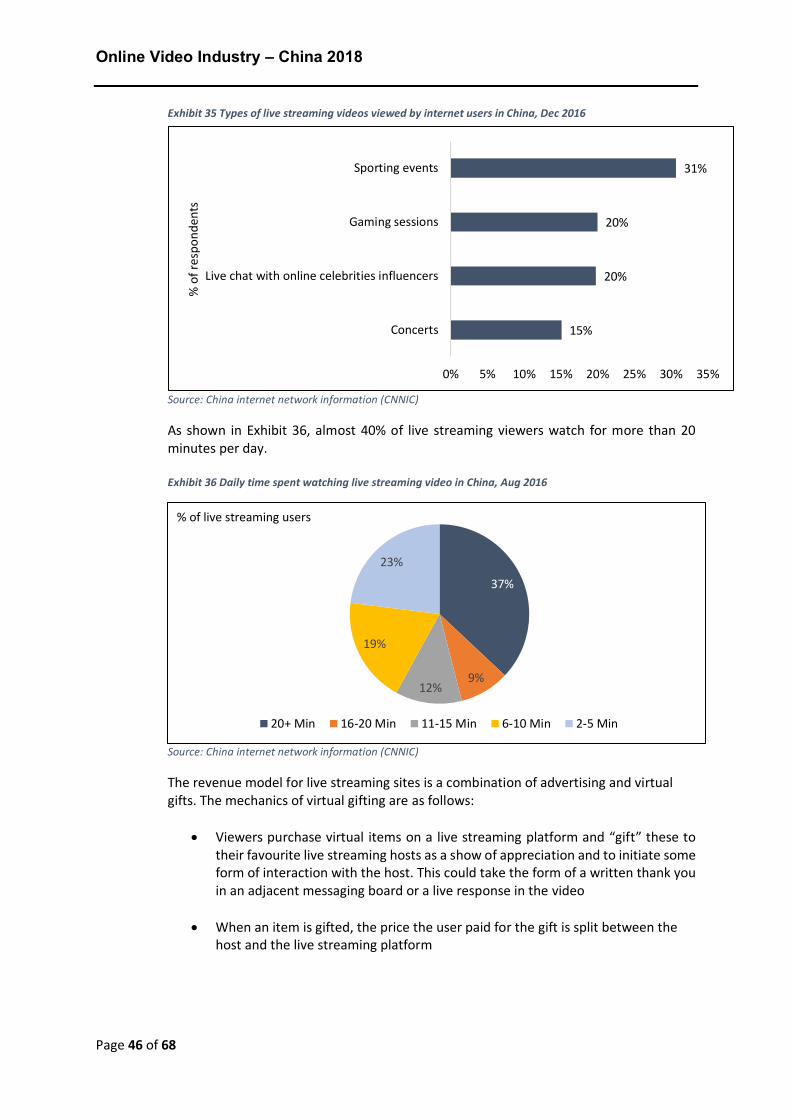

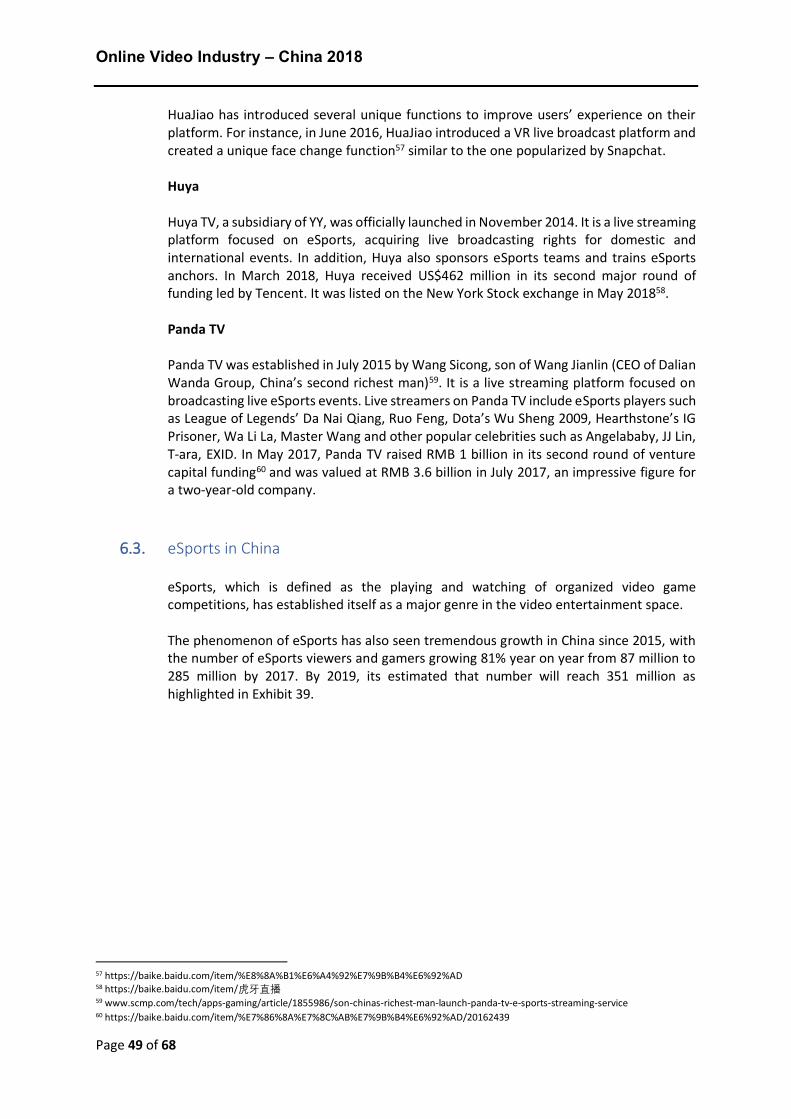

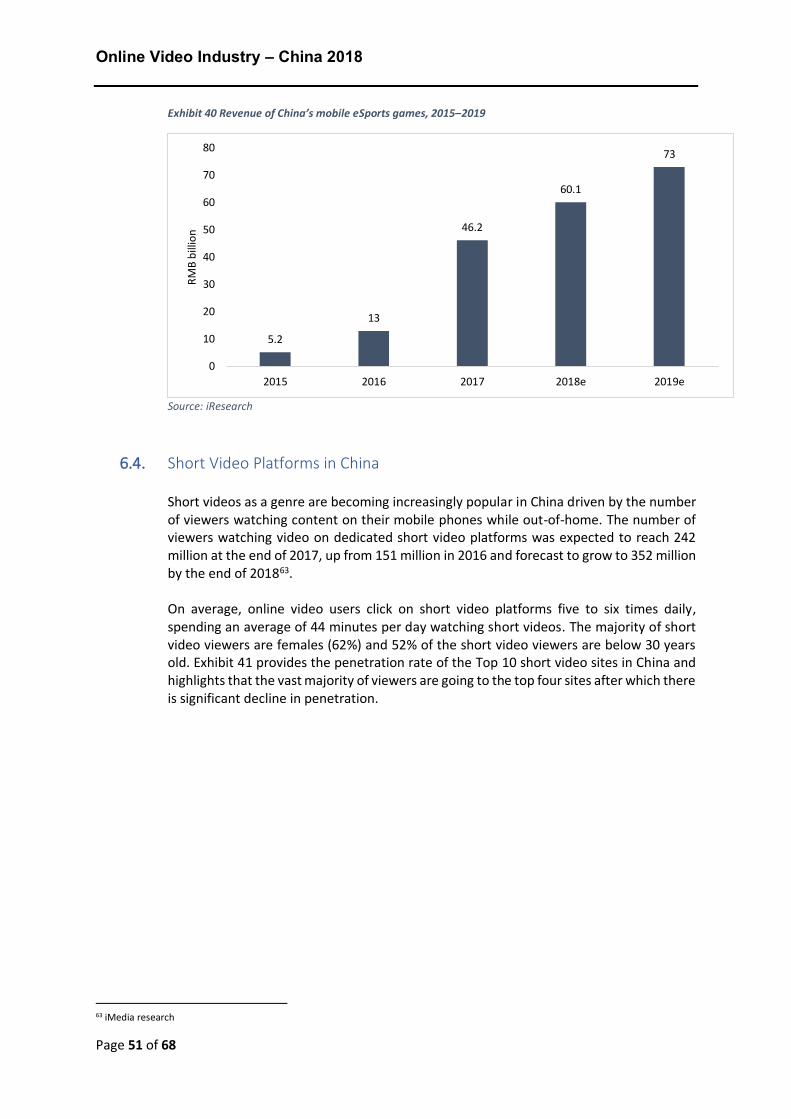

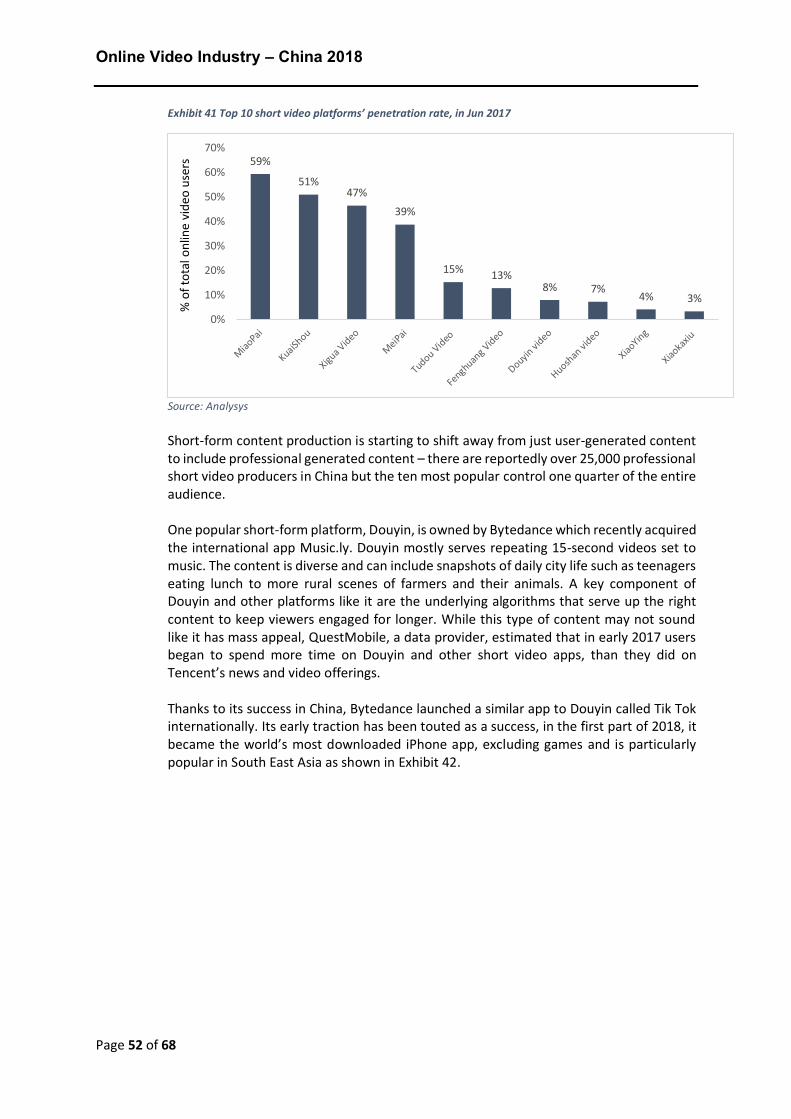

1.5. New Developments in China’s Online Video Industry Three emerging developments in the online video industry are live streaming, eSports and short video. The live streaming user base in China grew 60% from 194 million in 2015 to 310 million in 2016. However, growth forecasts for the next three years have dropped to 12% largely due to stricter regulatory enforcements which have severely reduced the amount of live streaming content that is considered too risqué. The phenomenon of eSports has also seen tremendous growth in China since 2015, with the number of eSports viewers and gamers growing 81% year on year from 87 million to 285 million by 2017. By 2019, it is estimated that number will reach 351 million. Industry revenues have also expanded quickly, increasing 198% per annum from RMB 5.2 billion in 2015 to RMB 46.2 billion in 2017. Short videos as a genre are becoming increasingly popular in China driven by the number of viewers watching content on their mobile phones while out-of-home. The number of viewers watching video on dedicated short video platforms was expected to reach 242 million at the end of 2017, up from 151 million in 2016, and forecast to grow to 352 million by the end of 2018. A key success driver for platforms offering short-form content is the algorithms they use to serve the right content to each individual user in order to keep them engaged for longer periods of time. On average, online video users click on short video platforms five to six times daily, spending an average of 44 minutes per day watching short videos.

1.6. Video Content Piracy in China According to one estimate, revenue losses in China due to video piracy will increase from US$5.5 billion in 2016 to US$9.8 billion in 2022. (Figures only take into account TV episodes and films and do not include sports). This accounts for roughly 17% and 19% respectively of the estimated global cost of piracy in those years. Based on our research

Online Video Industry – China 2018

Page 8 of 68

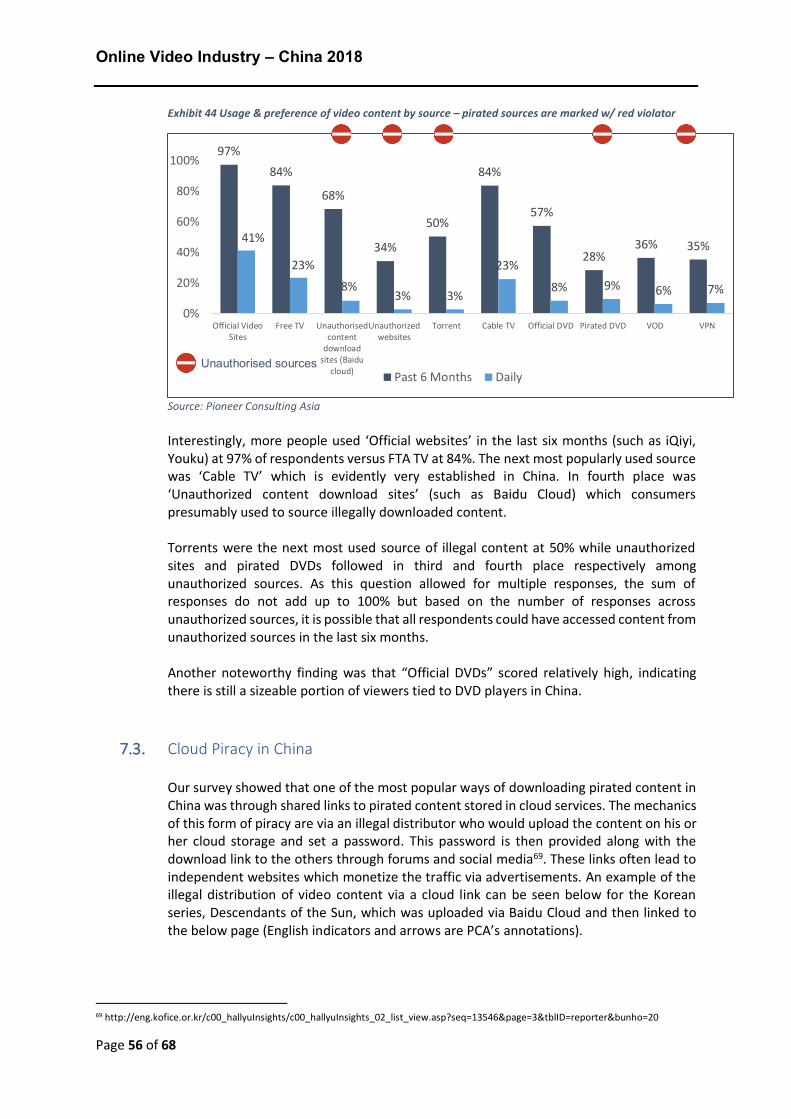

it was reported that the most frequently used sources of pirated content in order of usage are cloud site downloads, unauthorized streaming sites and torrents. While these pirated sources were used in the past six months by 50%–68% of total survey respondents, Free Official Websites (iQiyi, Tencent, Youku) were the most cited source for video usage on a daily basis at 41% of respondents. Given the size of the piracy issue in China, regulators have started to take a more active approach to enforcement. In 2009, the regulator released a provision that requires operators to enhance their processes for protecting copyrights and to take appropriate measures to protect the rights and interest of copyright holders. In November 2016, an anti-piracy campaign known as the Jianwang Operation resulted in a seizure of 1.5 million pirated publications, the shutdown of 1,655 websites containing pirated content and the removal of 274,800 pirated links. In May 2017, the Beijing court awarded one of the highest fines ever issued (US$1 million) for a case of copyright infringement against an online platform. Below is a summary of the findings on piracy from our research:

• 68% of respondents said they used cloud downloads to access pirated content in the last six months, making this the most commonly used source of piracy in China

• The highest proportion of respondents using pirated sources on a daily basis drops to 9% for pirated DVDs, followed by 8% of respondents for cloud downloads, indicating that most viewers are not visiting pirated sources on a daily basis

• Based on our interviews, respondents aged 18-24 were more likely to watch pirated content than other age segments, reporting incidences of 2-3 times per week

• While both males and females reported using pirated sources, males reported higher incidences overall across age groups

• The primary reasons given for watching pirated content were: o It was difficult to find legitimate versions of western shows and movies o Pirated content was easy to use and find online as it is very prominent in

search listings o Pirated content is free

• In terms of respondents’ views on piracy, our respondents who watched pirated content fell into two camps:

o The first camp expressed support for copyright laws saying they should be observed but said pirated sources were the only way to obtain a lot of content that they could not find on legitimate websites

o The second camp expressed the sentiment that everyone watches pirated content and that they do not really care if it is illegal and therefore were not concerned whether the content was available legally or not

1.7. Regulatory Environment Our overview of the regulatory environment in China related to digital content focuses on four areas: 1. Key stakeholders in Chinese TV regulation 2. Licensing requirements for online platforms

Online Video Industry – China 2018

Page 9 of 68

3. Regulations on foreign content 4. Live streaming regulations Below we have provided a summary of each of these areas: 1. Key Stakeholders in Chinese TV Regulation

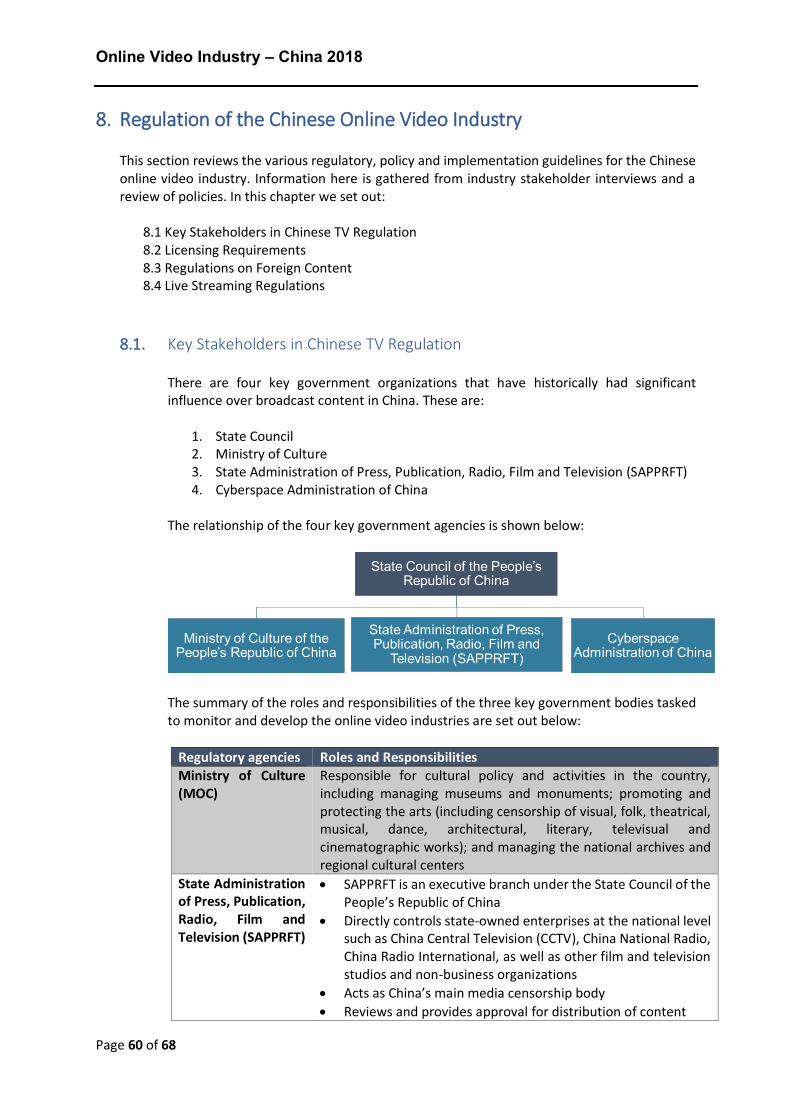

There are four key government organizations that oversee broadcast content in China:

i. State Council ii. Ministry of Culture iii. State Administration of Press, Publication, Radio, Film and Television (“SAPPRFT”) iv. Cyberspace Administration of China

Content censorship in China has historically been primarily overseen by SAPPRFT. Oversight of TV content in particular, is viewed as vital to the government’s efforts to communicate key messages and influence public opinion as TV’s reach spans the entire nation and is hence tightly regulated. As a relatively new medium, professionally produced online content has had less comprehensive censorship guidelines applied to it with lax enforcement in the past, but the government has undertaken a number of enforcement campaigns over the last two years. This more active approach to enforcement is likely to continue as online video viewing becomes more pervasive in the country making it a greater threat to the country’s social fabric in the government’s eyes. In another move widely seen as further tightening the government’s control over the media sector, it was announced in March 2018 that SAPPRFT would be abolished and replaced by three new bodies that would report directly to the State Council:

1. The State Administration of Radio and Television (“SART”) 2. The State Bureau of Film (Film Bureau) 3. The State Administration of Press and Publication (“SAPP”)

2. Licensing requirements for Online platforms In December 2007, SAPPRFT issued the Administrative Provision of the Internet Audio-Video Program service or the Audio-Video Program Provision, which came into effect in January 2008 and was later amended in August 2015. The Audio-Video Program Provision defines “internet audio-video program services” as the producing, editing and integrating of audio-video programs, supplying audio-video programs to the public via the internet, and providing audio-video programs uploading and transmission services to a third party. Providers of internet audio-visual program services must obtain an Internet Audio-Video Program Transmission License to provide their services.

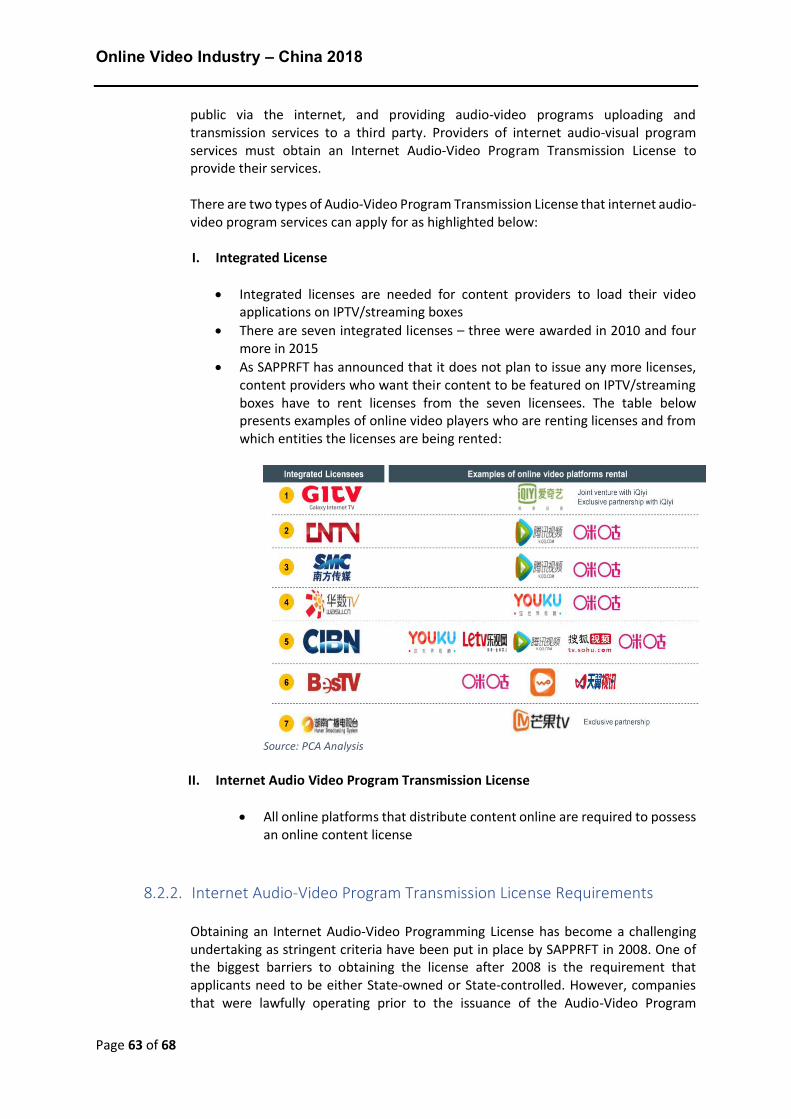

There are two types of Audio-Video Program Transmission Licenses that internet audio-video program services can apply for as highlighted below:

I. Integrated license • Integrated licenses are needed for content providers to load their video

applications on IPTV/streaming boxes • There are seven integrated licenses – three were awarded in 2010 and

four more in 2015

Online Video Industry – China 2018

Page 10 of 68

II. Internet Audio Video Program Transmission License

• All online platforms that distribute content online are required to possess an Internet Audio Video Program Transmission License

As a result of the stringent criteria for an Internet Audio-Visual Programming License, many platforms are either forming partnerships with existing licensees or acquiring companies who have the license. 3. Regulations on foreign content Another key regulation affecting online platforms in China is the restriction on foreign content which requires operators of online video platforms to obtain permits for all foreign and TV dramas per title before they are transmitted via internet. To obtain approval for a serialized show, applicants must submit the full season to the regulator for review. The impact of this is that the release date of legitimate content significantly lags the release date in the country of origin which inevitably leads to a higher incidence of piracy. In addition, online video platforms must import foreign films and television dramas for use on their own websites and not exclusively to resell to others. Finally, the annual import quantity of foreign films and television dramas may not exceed 30% of the total hours of content an online video platform purchased in the previous year. 4. Live Streaming Regulations In a bid to regulate the live streaming industry, SAPPRFT issued the notice on Strengthening the Management of Live Services of Internet Audio-Visual Program Services in September 2016. This ultimately resulted in 19 articles specifying the regulations and codes of conduct for operating a live streaming platform in China which were designed to restrict popular live streaming content that was seen as not promoting desired social values. In May 2017, the Ministry of Culture launched inspections of live streaming sites that were operating without a license or allowing restricted content to be streamed on their platforms. This enforcement campaign resulted in ten live streaming platforms being closed. In addition, 48 live streaming operators were subject to administrative punishments. The following month, in June 2017, the Ministry of Culture reviewed 10,562 mobile live broadcast applications and required another 12 of them to be closed down.

Online Video Industry – China 2018

Page 11 of 68

2. China TV Market Overview

In this chapter, we set out

2.1 TV Market Overview 2.2 Free-to-Air TV in China 2.3 TV Advertising 2.4 Smart TV Ownership 2.5 General TV and Online Viewing Behaviour

2.1. TV Market Overview

Broadcast television has long played an important role in China both as a medium for entertainment and the spread of government approved ideology thanks to its wide reach. According to the latest official government statistics available, the percentage of households in China that own a TV set was 99%1 in 2014. That is equivalent to 455 million2 households at the end of 2014 and 495 million 3 at the end of 2017 assuming the penetration rate held steady. Currently, there are more than 2000 television stations in China including FTA and pay TV stations. The exact number of broadcasters varies from source to source as stations are consolidated, merged, separated or even reopened following a closure. In almost all cases, these stations are linked to government entities through their shareholding structure. The three categories of broadcasters in China are:

• National TV Broadcaster (e.g. CCTV) • Provincial Satellite TV Broadcaster (e.g. Hunan TV, Jiangsu TV, Zhejiang TV) • City Satellite TV Broadcaster (e.g. Nanjing TV, Hangzhou TV)

While the National TV Broadcaster channels are available free-to-air, all other channels in China require a subscription. Approximately 65% of households4 in China subscribe to what amount to pay TV services which offer both Provincial Satellite TV and City Satellite TV channels.

2.2. Free-to-Air TV in China

CCTV is the only national FTA TV broadcaster in China. Known as Beijing TV prior to May 1978, it was officially launched in September 1958. Thanks to its ubiquitous availability, CCTV is the most watched channel in the country and over the years, has expanded the number of channels it operates. Today, it broadcasts a total of 15 free public channels each focusing on a specific theme:

• CCTV1 – General

1 http://www.stats.gov.cn/tjsj/ndsj/2016/indexeh.htm 2 http://www.stats.gov.cn/tjsj/ndsj/2015/indexeh.htm 3 https://www.ceicdata.com/en/china/population-no-of-person-per-household/population-average-household-size 4 All View Cloud(AVC),"2017 China OTT Big Screen Industry Trends Analysis," March 31, 2017

Online Video Industry – China 2018

Page 12 of 68

• CCTV2 – Finance • CCTV3 – Variety • CCTV4 – Asia, Europe, US • CCTV5 – Sports • CCTV6 – Movies • CCTV7 – Military and agriculture • CCTV8 – TV series • CCTV9 – Documentary • CCTV10 – Education • CCTV11 – Opera • CCTV12 – Society and law • CCTV13 – News • CCTV14 – Kids • CCTV15 – Music

In March 2018, the Chinese government announced that CCTV will merge with two state radio platforms, China Radio International (CRI) and China National Radio (CNR) to form one entity called the “Voice of China”. The new entity will be under the direct supervision of the State Council and will be led by the Publicity Department of the Communist Party China. This is widely seen as a move to tighten government control on public sentiment and to expand efforts to improve China’s global image.

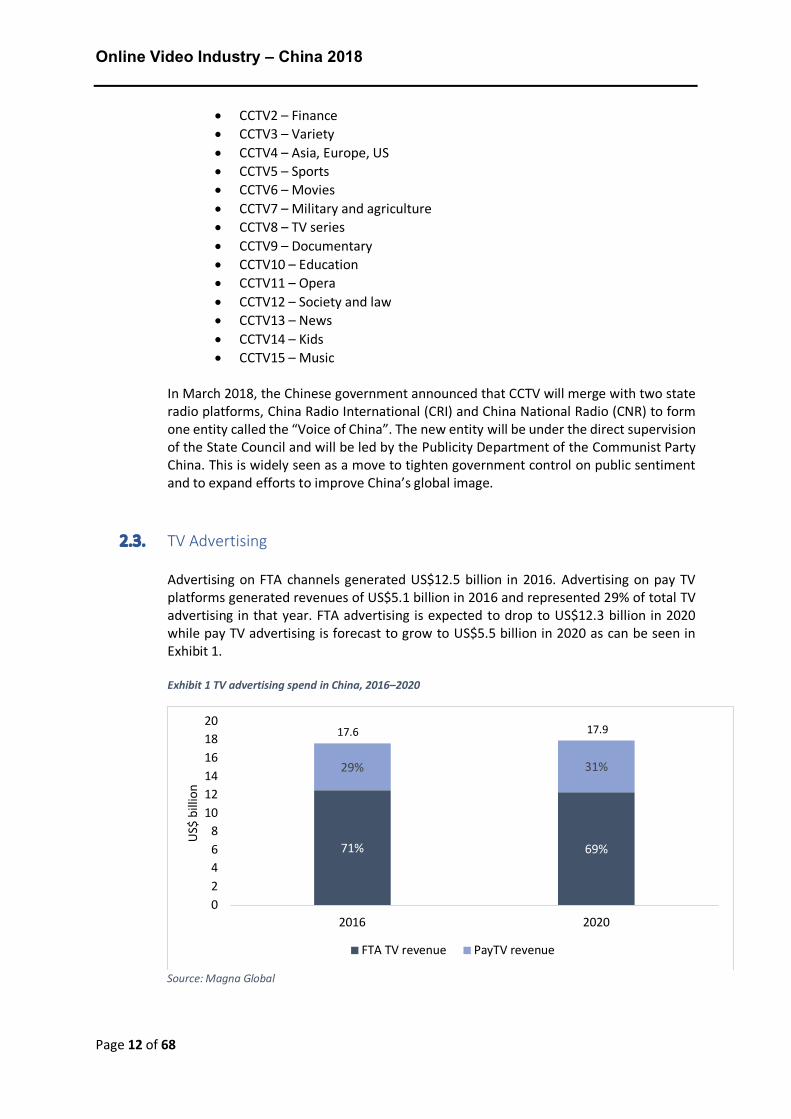

2.3. TV Advertising Advertising on FTA channels generated US$12.5 billion in 2016. Advertising on pay TV platforms generated revenues of US$5.1 billion in 2016 and represented 29% of total TV advertising in that year. FTA advertising is expected to drop to US$12.3 billion in 2020 while pay TV advertising is forecast to grow to US$5.5 billion in 2020 as can be seen in Exhibit 1. Exhibit 1 TV advertising spend in China, 2016–2020

Source: Magna Global

71% 69%

29% 31%

02468

101214161820

2016 2020

US$

bill

ion

FTA TV revenue PayTV revenue

17.6 17.9

Online Video Industry – China 2018

Page 13 of 68

2.4. Smart TV Ownership

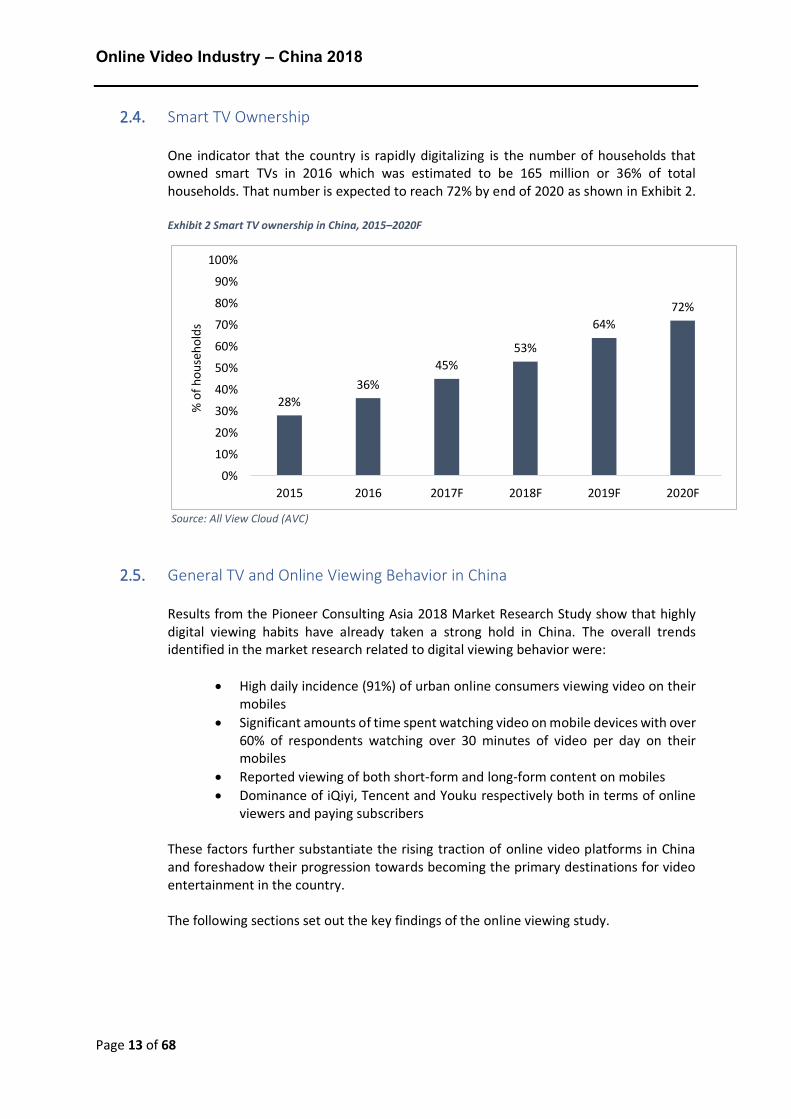

One indicator that the country is rapidly digitalizing is the number of households that owned smart TVs in 2016 which was estimated to be 165 million or 36% of total households. That number is expected to reach 72% by end of 2020 as shown in Exhibit 2. Exhibit 2 Smart TV ownership in China, 2015–2020F

Source: All View Cloud (AVC)

2.5. General TV and Online Viewing Behavior in China Results from the Pioneer Consulting Asia 2018 Market Research Study show that highly digital viewing habits have already taken a strong hold in China. The overall trends identified in the market research related to digital viewing behavior were:

• High daily incidence (91%) of urban online consumers viewing video on their

mobiles • Significant amounts of time spent watching video on mobile devices with over

60% of respondents watching over 30 minutes of video per day on their mobiles

• Reported viewing of both short-form and long-form content on mobiles • Dominance of iQiyi, Tencent and Youku respectively both in terms of online

viewers and paying subscribers

These factors further substantiate the rising traction of online video platforms in China and foreshadow their progression towards becoming the primary destinations for video entertainment in the country. The following sections set out the key findings of the online viewing study.

28%36%

45%53%

64%72%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017F 2018F 2019F 2020F

% o

f hou

seho

lds

Online Video Industry – China 2018

Page 14 of 68

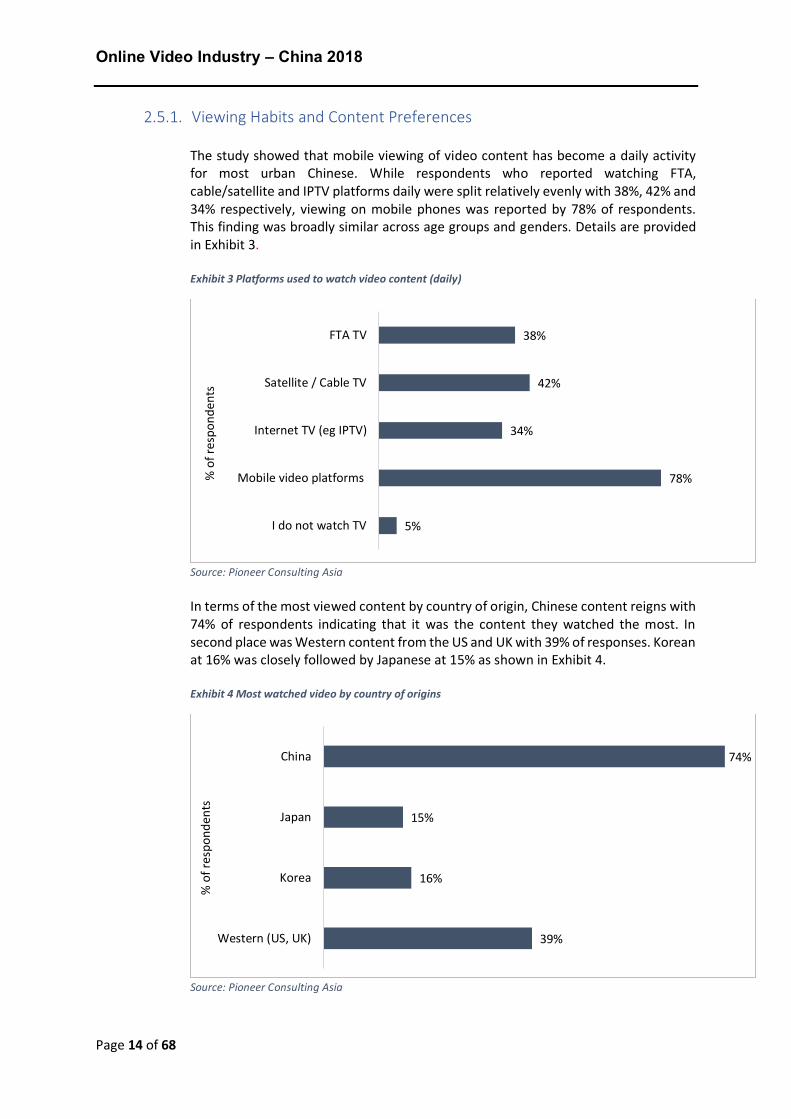

2.5.1. Viewing Habits and Content Preferences The study showed that mobile viewing of video content has become a daily activity for most urban Chinese. While respondents who reported watching FTA, cable/satellite and IPTV platforms daily were split relatively evenly with 38%, 42% and 34% respectively, viewing on mobile phones was reported by 78% of respondents. This finding was broadly similar across age groups and genders. Details are provided in Exhibit 3. Exhibit 3 Platforms used to watch video content (daily)

Source: Pioneer Consulting Asia In terms of the most viewed content by country of origin, Chinese content reigns with 74% of respondents indicating that it was the content they watched the most. In second place was Western content from the US and UK with 39% of responses. Korean at 16% was closely followed by Japanese at 15% as shown in Exhibit 4. Exhibit 4 Most watched video by country of origins

Source: Pioneer Consulting Asia

5%

78%

34%

42%

38%

I do not watch TV

Mobile video platforms

Internet TV (eg IPTV)

Satellite / Cable TV

FTA TV

% o

f res

pond

ents

39%

16%

15%

74%

Western (US, UK)

Korea

Japan

China

% o

f res

pond

ents

Online Video Industry – China 2018

Page 15 of 68

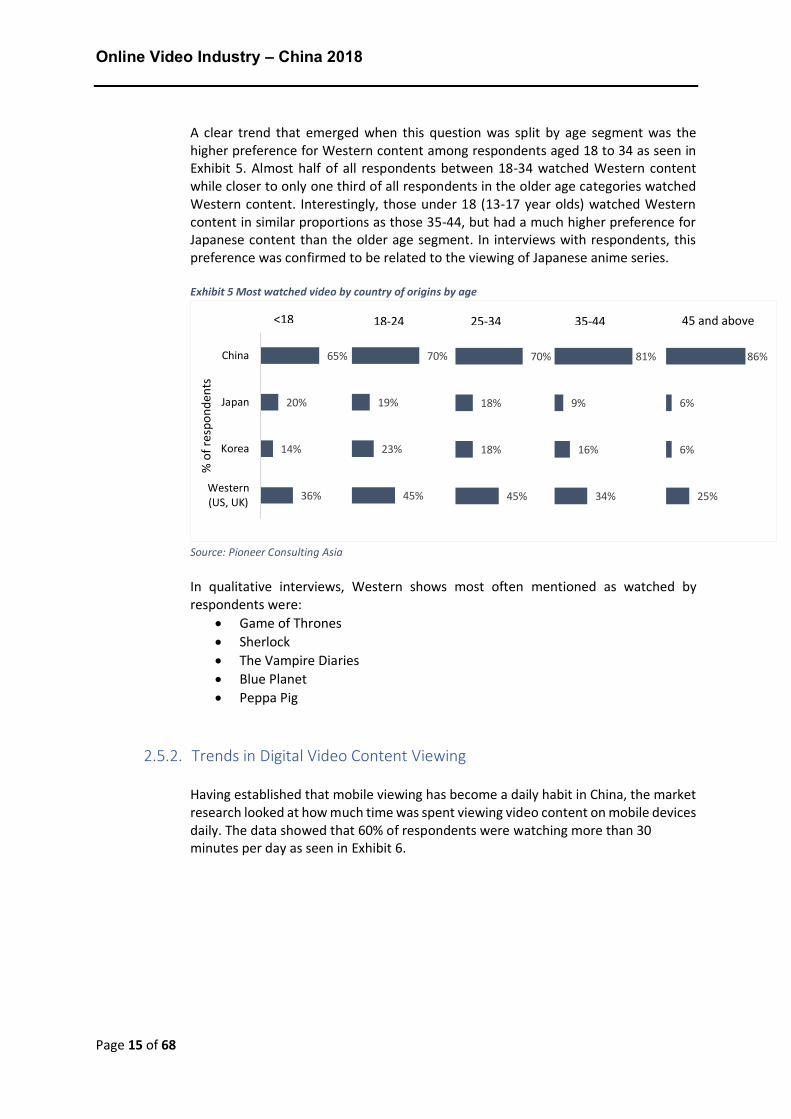

A clear trend that emerged when this question was split by age segment was the higher preference for Western content among respondents aged 18 to 34 as seen in Exhibit 5. Almost half of all respondents between 18-34 watched Western content while closer to only one third of all respondents in the older age categories watched Western content. Interestingly, those under 18 (13-17 year olds) watched Western content in similar proportions as those 35-44, but had a much higher preference for Japanese content than the older age segment. In interviews with respondents, this preference was confirmed to be related to the viewing of Japanese anime series. Exhibit 5 Most watched video by country of origins by age

Source: Pioneer Consulting Asia In qualitative interviews, Western shows most often mentioned as watched by respondents were:

• Game of Thrones • Sherlock • The Vampire Diaries • Blue Planet • Peppa Pig

2.5.2. Trends in Digital Video Content Viewing

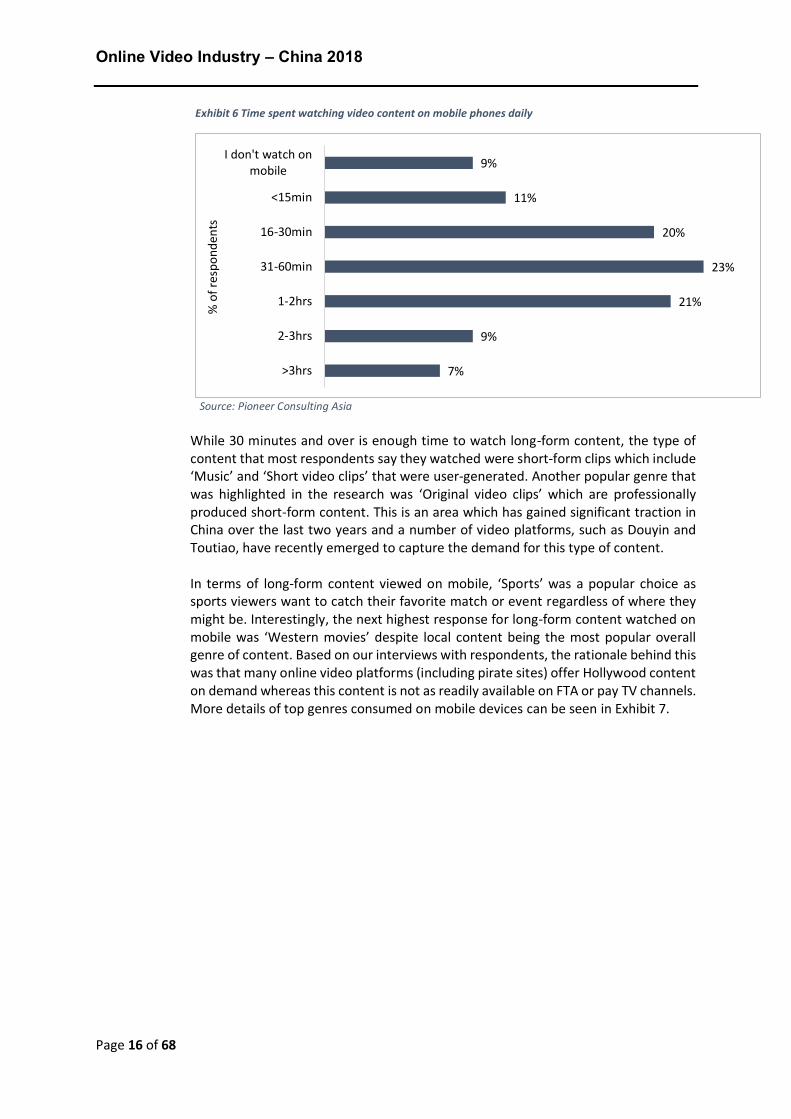

Having established that mobile viewing has become a daily habit in China, the market research looked at how much time was spent viewing video content on mobile devices daily. The data showed that 60% of respondents were watching more than 30 minutes per day as seen in Exhibit 6.

<18

45%

23%

19%

70%

45%

18%

18%

70%

34%

16%

9%

81%

25%

6%

6%

86%

18-24 25-34 35-44 45 and above

36%

14%

20%

65%

Western(US, UK)

Korea

Japan

China

% o

f res

pond

ents

Online Video Industry – China 2018

Page 16 of 68

Exhibit 6 Time spent watching video content on mobile phones daily

Source: Pioneer Consulting Asia

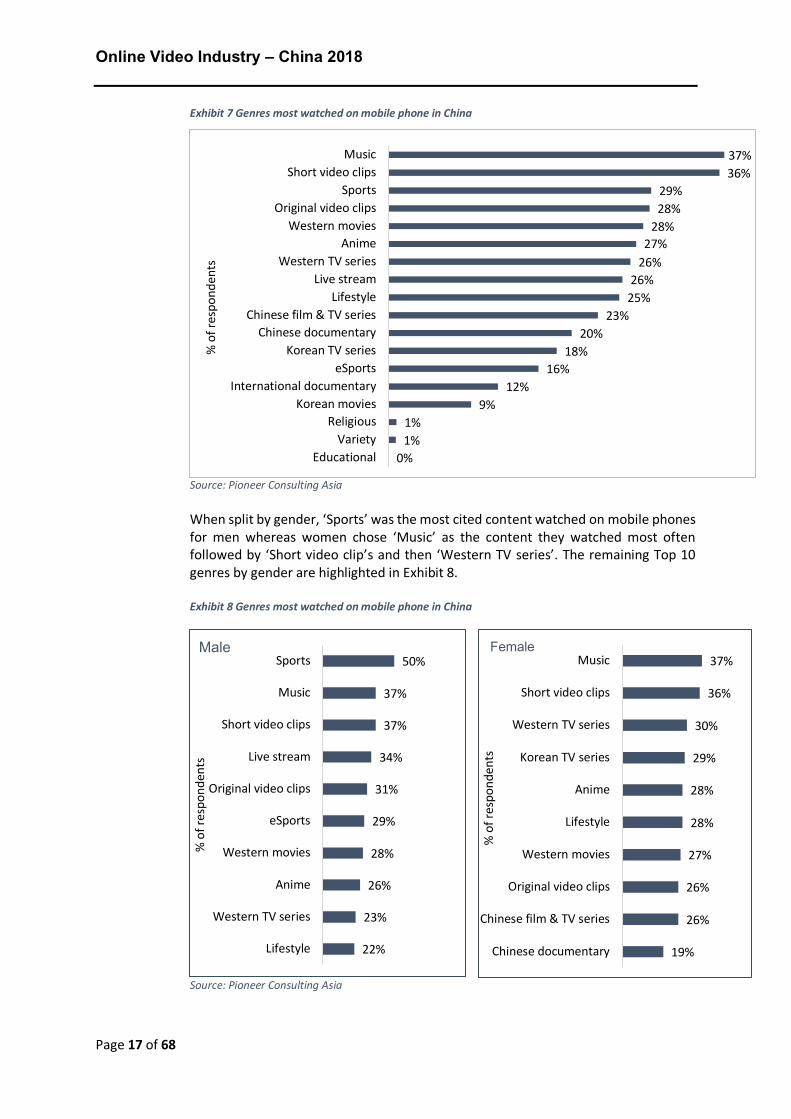

While 30 minutes and over is enough time to watch long-form content, the type of content that most respondents say they watched were short-form clips which include ‘Music’ and ‘Short video clips’ that were user-generated. Another popular genre that was highlighted in the research was ‘Original video clips’ which are professionally produced short-form content. This is an area which has gained significant traction in China over the last two years and a number of video platforms, such as Douyin and Toutiao, have recently emerged to capture the demand for this type of content. In terms of long-form content viewed on mobile, ‘Sports’ was a popular choice as sports viewers want to catch their favorite match or event regardless of where they might be. Interestingly, the next highest response for long-form content watched on mobile was ‘Western movies’ despite local content being the most popular overall genre of content. Based on our interviews with respondents, the rationale behind this was that many online video platforms (including pirate sites) offer Hollywood content on demand whereas this content is not as readily available on FTA or pay TV channels. More details of top genres consumed on mobile devices can be seen in Exhibit 7.

7%

9%

21%

23%

20%

11%

9%

>3hrs

2-3hrs

1-2hrs

31-60min

16-30min

<15min

I don't watch onmobile

% o

f res

pond

ents

Online Video Industry – China 2018

Page 17 of 68

Exhibit 7 Genres most watched on mobile phone in China

Source: Pioneer Consulting Asia When split by gender, ‘Sports’ was the most cited content watched on mobile phones for men whereas women chose ‘Music’ as the content they watched most often followed by ‘Short video clip’s and then ‘Western TV series’. The remaining Top 10 genres by gender are highlighted in Exhibit 8. Exhibit 8 Genres most watched on mobile phone in China

Source: Pioneer Consulting Asia

0%1%1%

9%12%

16%18%

20%23%

25%26%

26%27%

28%28%29%

36%37%

EducationalVariety

ReligiousKorean movies

International documentaryeSports

Korean TV seriesChinese documentary

Chinese film & TV seriesLifestyle

Live streamWestern TV series

AnimeWestern movies

Original video clipsSports

Short video clipsMusic

% o

f res

pond

ents

22%

23%

26%

28%

29%

31%

34%

37%

37%

50%

Lifestyle

Western TV series

Anime

Western movies

eSports

Original video clips

Live stream

Short video clips

Music

Sports

% o

f res

pond

ents

Male

19%

26%

26%

27%

28%

28%

29%

30%

36%

37%

Chinese documentary

Chinese film & TV series

Original video clips

Western movies

Lifestyle

Anime

Korean TV series

Western TV series

Short video clips

Music

% o

f res

pond

ents

Female

Online Video Industry – China 2018

Page 18 of 68

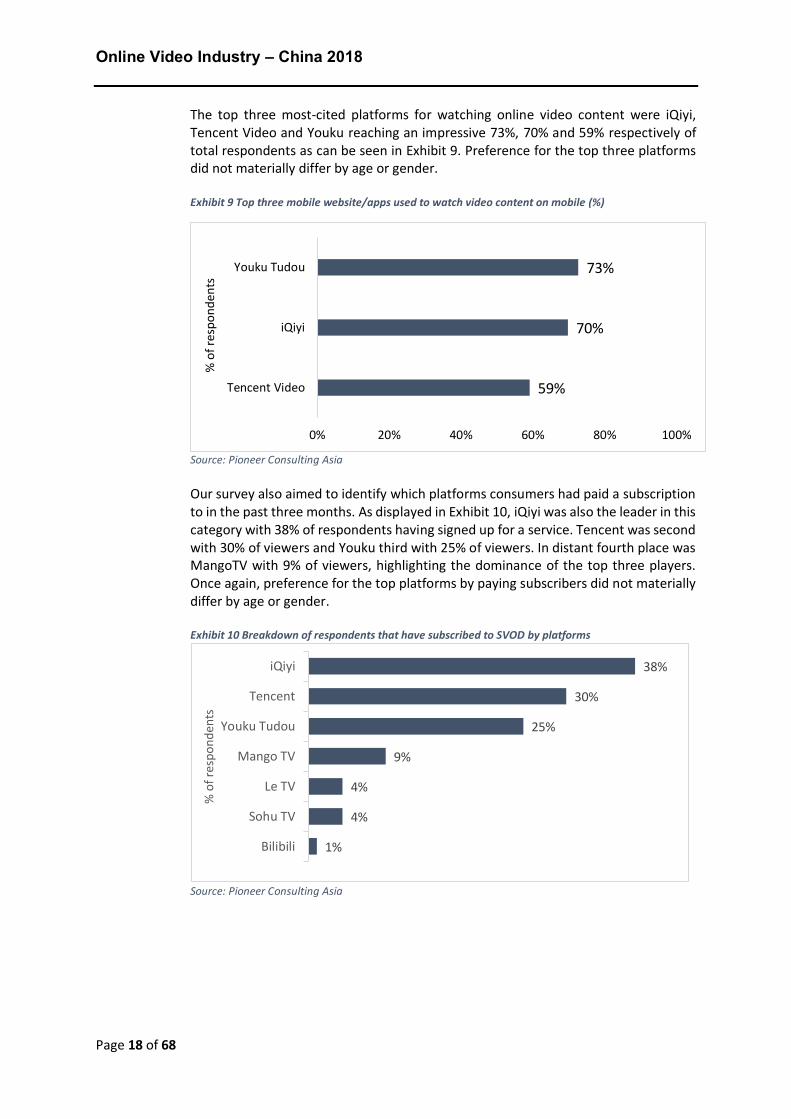

The top three most-cited platforms for watching online video content were iQiyi, Tencent Video and Youku reaching an impressive 73%, 70% and 59% respectively of total respondents as can be seen in Exhibit 9. Preference for the top three platforms did not materially differ by age or gender. Exhibit 9 Top three mobile website/apps used to watch video content on mobile (%)

Source: Pioneer Consulting Asia Our survey also aimed to identify which platforms consumers had paid a subscription to in the past three months. As displayed in Exhibit 10, iQiyi was also the leader in this category with 38% of respondents having signed up for a service. Tencent was second with 30% of viewers and Youku third with 25% of viewers. In distant fourth place was MangoTV with 9% of viewers, highlighting the dominance of the top three players. Once again, preference for the top platforms by paying subscribers did not materially differ by age or gender. Exhibit 10 Breakdown of respondents that have subscribed to SVOD by platforms

Source: Pioneer Consulting Asia

59%

70%

73%

0% 20% 40% 60% 80% 100%

Tencent Video

iQiyi

Youku Tudou

% o

f res

pond

ents

1%

4%

4%

9%

25%

30%

38%

Bilibili

Sohu TV

Le TV

Mango TV

Youku Tudou

Tencent

iQiyi

% o

f res

pond

ents

Online Video Industry – China 2018

Page 19 of 68

3. China’s Pay TV Industry In this chapter, we set out

3.1 Pay TV Market Overview 3.1. Pay TV Market Overview

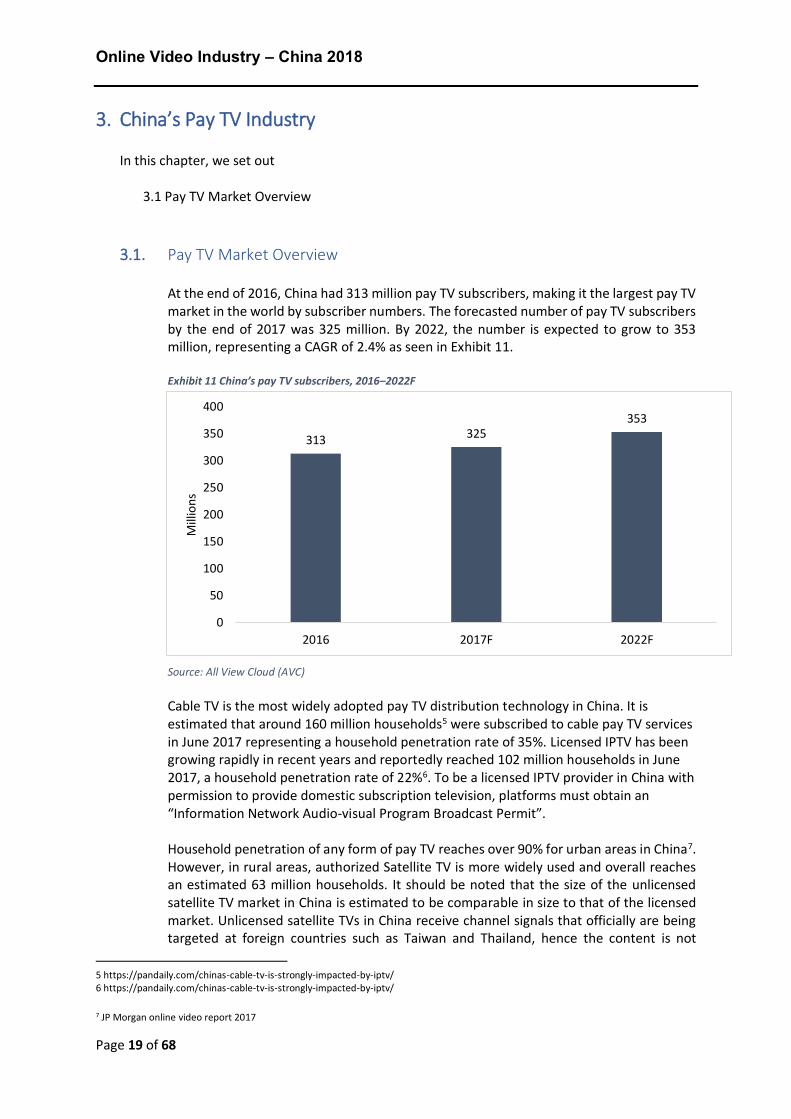

At the end of 2016, China had 313 million pay TV subscribers, making it the largest pay TV market in the world by subscriber numbers. The forecasted number of pay TV subscribers by the end of 2017 was 325 million. By 2022, the number is expected to grow to 353 million, representing a CAGR of 2.4% as seen in Exhibit 11. Exhibit 11 China’s pay TV subscribers, 2016–2022F

Source: All View Cloud (AVC)

Cable TV is the most widely adopted pay TV distribution technology in China. It is estimated that around 160 million households5 were subscribed to cable pay TV services in June 2017 representing a household penetration rate of 35%. Licensed IPTV has been growing rapidly in recent years and reportedly reached 102 million households in June 2017, a household penetration rate of 22%6. To be a licensed IPTV provider in China with permission to provide domestic subscription television, platforms must obtain an “Information Network Audio-visual Program Broadcast Permit”. Household penetration of any form of pay TV reaches over 90% for urban areas in China7. However, in rural areas, authorized Satellite TV is more widely used and overall reaches an estimated 63 million households. It should be noted that the size of the unlicensed satellite TV market in China is estimated to be comparable in size to that of the licensed market. Unlicensed satellite TVs in China receive channel signals that officially are being targeted at foreign countries such as Taiwan and Thailand, hence the content is not

5 https://pandaily.com/chinas-cable-tv-is-strongly-impacted-by-iptv/ 6 https://pandaily.com/chinas-cable-tv-is-strongly-impacted-by-iptv/ 7 JP Morgan online video report 2017

313 325353

0

50

100

150

200

250

300

350

400

2016 2017F 2022F

Mill

ions

Online Video Industry – China 2018

Page 20 of 68

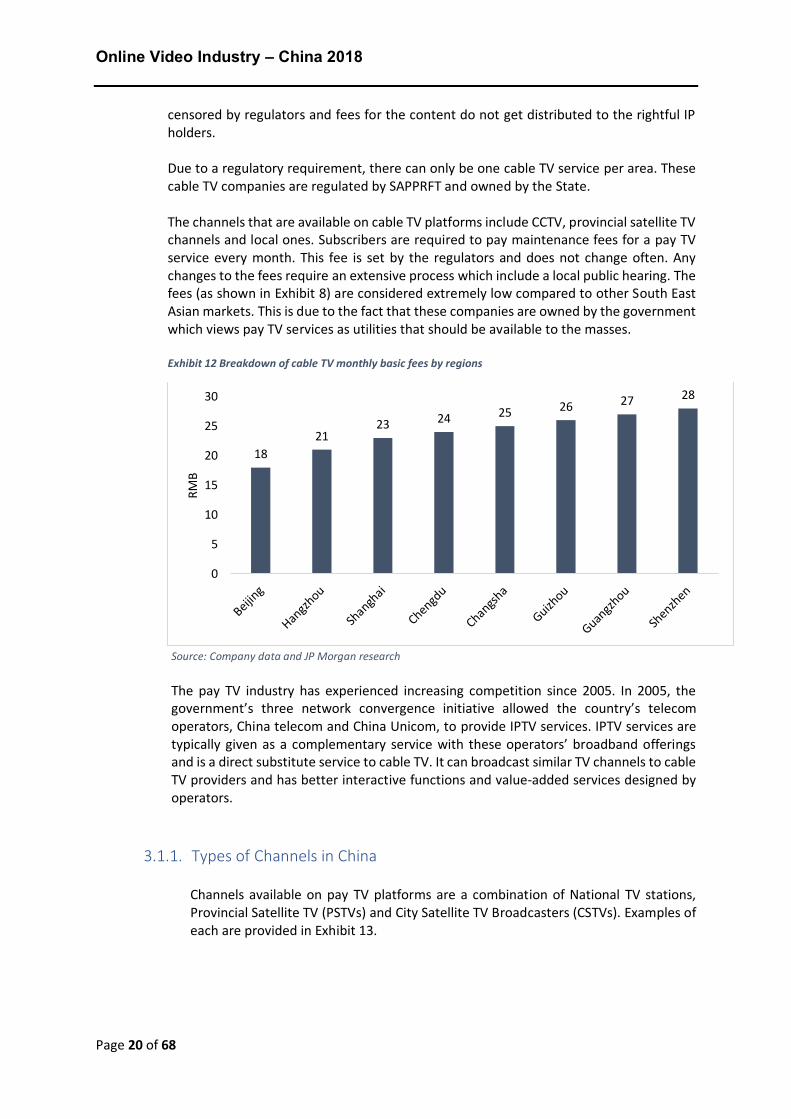

censored by regulators and fees for the content do not get distributed to the rightful IP holders. Due to a regulatory requirement, there can only be one cable TV service per area. These cable TV companies are regulated by SAPPRFT and owned by the State. The channels that are available on cable TV platforms include CCTV, provincial satellite TV channels and local ones. Subscribers are required to pay maintenance fees for a pay TV service every month. This fee is set by the regulators and does not change often. Any changes to the fees require an extensive process which include a local public hearing. The fees (as shown in Exhibit 8) are considered extremely low compared to other South East Asian markets. This is due to the fact that these companies are owned by the government which views pay TV services as utilities that should be available to the masses. Exhibit 12 Breakdown of cable TV monthly basic fees by regions

Source: Company data and JP Morgan research

The pay TV industry has experienced increasing competition since 2005. In 2005, the government’s three network convergence initiative allowed the country’s telecom operators, China telecom and China Unicom, to provide IPTV services. IPTV services are typically given as a complementary service with these operators’ broadband offerings and is a direct substitute service to cable TV. It can broadcast similar TV channels to cable TV providers and has better interactive functions and value-added services designed by operators.

3.1.1. Types of Channels in China

Channels available on pay TV platforms are a combination of National TV stations, Provincial Satellite TV (PSTVs) and City Satellite TV Broadcasters (CSTVs). Examples of each are provided in Exhibit 13.

1821

23 24 25 26 27 28

0

5

10

15

20

25

30

RMB

Online Video Industry – China 2018

Page 21 of 68

Exhibit 13 Types of channel in China

Source: IHS Technology

3.1.2. Provincial Satellite TV Broadcasters (“PSTVs”)

PSTVs are defined as television stations owned and operated by Chinese provincial governments but available to Chinese audiences nationwide. There is a total of 24 provincial operators in China as per the following list in Exhibit 14: Exhibit 14 Provincial TV broadcasters in China

Source: IHS Technology In Exhibit 15, we have provided the top five Provincial Satellite TV broadcasters by audience rating from 2014–2017.

Type of channels Channels

National TV station CCTV, China education television

Provincial Satellite TV Beijing TV, Hunan TV, Dragon TV, Jiangsu TV, Zhejiang TV

City Satellite TV Shenzhen, Amoystar, Sansha, Yanbian

Other terrestrial channels All others

Online Video Industry – China 2018

Page 22 of 68

Exhibit 15 Top five audience rating of provincial TV channels

Source: CMS Media Research Below we provide more details on the top five key PSTV channels by TV audience rating: Hunan TV, ZhejiangTV, Shanghai (Dragon) TV, Jiangsu TV and Beijing TV.

Hunan TV

Zhejiang TV

Dragon TV

Hunan TV is the most popular provincial TV station in China. It is China’s second most watched channel after CCTV. The channel, formerly known as Golden Broadcasting System, launched in January 1997. Hunan TV focuses on targeting youth and has produced a number of popular original TV dramas and variety shows. Examples of notable programs include “Happy Camp” (one of China’s first variety shows), “Super Girl” and the drama series, “In the Name of the People”, which received the highest audience rating (7.3%) in China in 2017.

Zhejiang TV was launched on October 1960 and started broadcasting nationwide in January 1994. Zhejiang TV was initially focused on producing news content but over the years has shifted its focus to variety shows. The channel also frequently purchases format rights and broadcasting rights from foreign players. Some of the notable variety programs it has acquired and produced include “Running Man China” and “The Voice of China”.

Dragon (Shanghai) TV, previously known as Shanghai Metropolitan TV, was launched in October 1998 and renamed Dragon TV in October 2003. The channel focuses mainly on all day news and includes a number of live news programs presented at standard times across the day.

Online Video Industry – China 2018

Page 23 of 68

Jiangsu TV

Beijing TV

3.1.3. City Satellite TV Broadcasters (”CSTVs”)

City Satellite TV Broadcasters (CSTVs) are owned by city governments across China. The total number of operating channels is hard to keep track of due to a continuous stream of corporate actions such as acquisitions, mergers, closures, and re-openings. It is estimated that there are approximately 2000 CSTVs in China. These are also available on pay TV platforms but only in the cities and nearby suburbs where they originate from.

Jiangsu TV, a provincial channel based in Nanjing city, was launched in December 1997. It is very active in producing news content on the social media platform known as Weibo, China’s equivalent to Twitter. However, the channel’s main focus is on producing variety shows. One of the most popular variety shows produced by Jiangsu channel is a dating show called “If You Are the One”.

Beijing TV, a provincial channel based in Beijing city, was launched in May 1979. One of the oldest provincial TV channels in China focused mainly on news, educational and variety shows.

Online Video Industry – China 2018

Page 24 of 68

4. Overview of China’s Telecoms industry The following chapter gives an overview of China’s telecoms landscape and its key players. It provides a summary of business scope, descriptions of strategies, and key financial highlights. In this chapter, we set out:

4.1 China’s Mobile Industry Overview 4.2 China’s Fixed Broadband Industry Overview 4.3 China’s Telecom Operators’ Online Video Initiatives

4.1. China’s Mobile Industry Overview

4.1.1. Mobile Subscriber Numbers

China’s mobile penetration rate was 76% of the total population in 2016 and is expected to grow to 86% of the total population by 2020. It is worth noting that penetration at end-2014 was only 48% but by the end of 2015, this had increased by almost 52% to reach 73%. The rapid increase in penetration can primarily be attributed to the construction of an extensive 4G network and heavy promotions of 4G-compatible handsets by mobile operators. In 2017, it was estimated that 73% of mobile subscribers were on a 4G network and China’s smartphone penetration was 71% of all phone users in 2016. Exhibit 16 highlights the growth in China’s overall mobile penetration as well as the forecast penetration rate by 2020.

Exhibit 16 China’s mobile penetration growth

Source: GSMA Thanks to the wide availability of broadband capable networks (3G and above) and the wide adoption of smartphones, China boasts the largest online population in the world with an estimated 772 million internet users at the end of 2017, equating to 56% of the population.

46% 48%

73% 76% 78% 81% 83% 86%

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017 2018F 2019F 2020F

% o

f tot

al p

opul

atio

n

Online Video Industry – China 2018

Page 25 of 68

There are three nationwide mobile telecoms operators in China:

1. China Mobile 2. China Unicom 3. China Telecom

The largest mobile operator by total number of mobile subscribers is China Mobile, which had 638 million customers as at the end of 2016. China Unicom followed with 264 million subscribers and China Telecom trailed with 215 million subscribers at end-2016. As China Mobile was the biggest investor in the nation’s 4G networks, it currently has 70% of the 4G subscriber market share in the country. China Unicom has the biggest 3G subscriber base in the country with 45% market share. A detailed breakdown by subscriber numbers is provided in Exhibits 17 and 18.

Exhibit 17 China telecom operators’ 3G and 4G subscribers, 2016

Source: Company annual reports

Exhibit 18 China telecom operators’ mobile subscriber base, 1Q15–2Q17

Source: Company annual reports

815 817 823 826 834 837 844 849 856 867

295 289 288 287 259 261 262 264 266 269190 191 194 198 203 207 212 215 222 230

0100200300400500600700800900

1000

1Q2015 2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Mill

ions

China Mobile China Unicom China Telecom

535

105 122

103

159 93

0

100

200

300

400

500

600

700

China Mobile China Unicom China Telecom

Mill

ions

4G 3G

264215

638

Online Video Industry – China 2018

Page 26 of 68

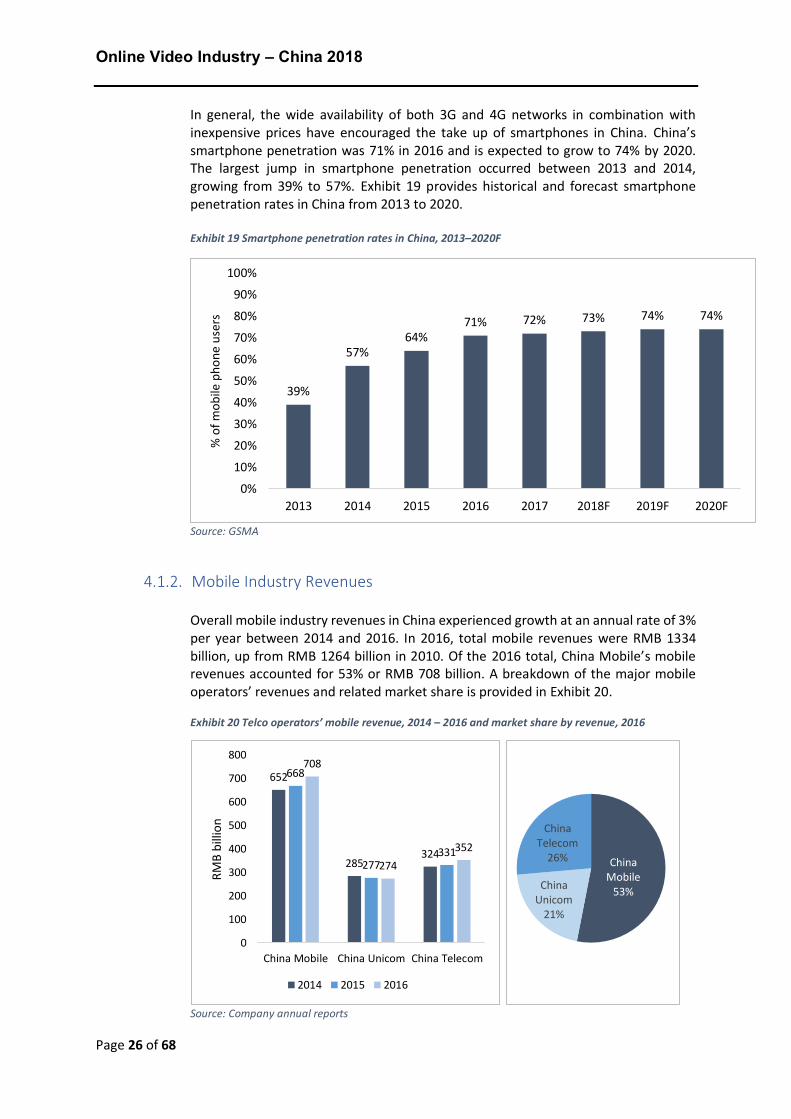

In general, the wide availability of both 3G and 4G networks in combination with inexpensive prices have encouraged the take up of smartphones in China. China’s smartphone penetration was 71% in 2016 and is expected to grow to 74% by 2020. The largest jump in smartphone penetration occurred between 2013 and 2014, growing from 39% to 57%. Exhibit 19 provides historical and forecast smartphone penetration rates in China from 2013 to 2020. Exhibit 19 Smartphone penetration rates in China, 2013–2020F

Source: GSMA

4.1.2. Mobile Industry Revenues

Overall mobile industry revenues in China experienced growth at an annual rate of 3% per year between 2014 and 2016. In 2016, total mobile revenues were RMB 1334 billion, up from RMB 1264 billion in 2010. Of the 2016 total, China Mobile’s mobile revenues accounted for 53% or RMB 708 billion. A breakdown of the major mobile operators’ revenues and related market share is provided in Exhibit 20. Exhibit 20 Telco operators’ mobile revenue, 2014 – 2016 and market share by revenue, 2016

Source: Company annual reports

39%

57%64%

71% 72% 73% 74% 74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015 2016 2017 2018F 2019F 2020F

% o

f mob

ile p

hone

use

rs

652

285 324

668

277 331

708

274 352

0

100

200

300

400

500

600

700

800

China Mobile China Unicom China Telecom

RMB

billi

on

2014 2015 2016

China Mobile

53%China Unicom

21%

China Telecom

26%

Online Video Industry – China 2018

Page 27 of 68

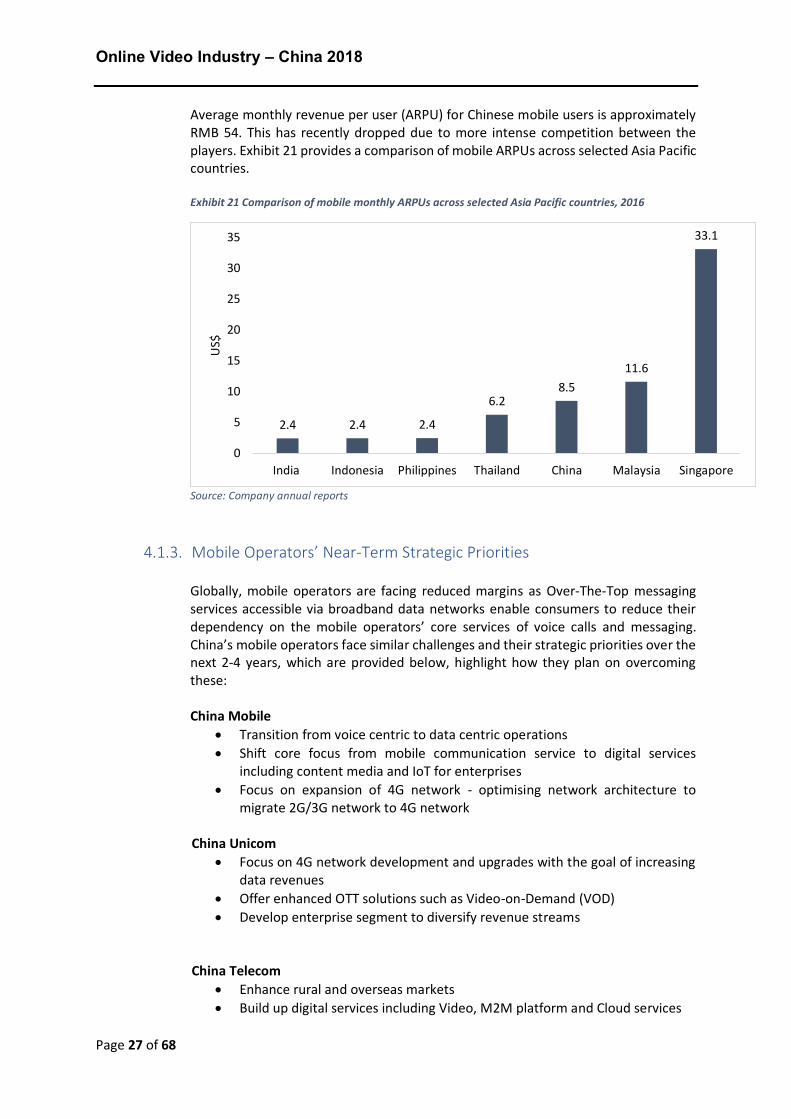

Average monthly revenue per user (ARPU) for Chinese mobile users is approximately RMB 54. This has recently dropped due to more intense competition between the players. Exhibit 21 provides a comparison of mobile ARPUs across selected Asia Pacific countries.

Exhibit 21 Comparison of mobile monthly ARPUs across selected Asia Pacific countries, 2016

Source: Company annual reports

4.1.3. Mobile Operators’ Near-Term Strategic Priorities

Globally, mobile operators are facing reduced margins as Over-The-Top messaging services accessible via broadband data networks enable consumers to reduce their dependency on the mobile operators’ core services of voice calls and messaging. China’s mobile operators face similar challenges and their strategic priorities over the next 2-4 years, which are provided below, highlight how they plan on overcoming these:

China Mobile

• Transition from voice centric to data centric operations • Shift core focus from mobile communication service to digital services

including content media and IoT for enterprises • Focus on expansion of 4G network - optimising network architecture to

migrate 2G/3G network to 4G network

China Unicom • Focus on 4G network development and upgrades with the goal of increasing

data revenues • Offer enhanced OTT solutions such as Video-on-Demand (VOD) • Develop enterprise segment to diversify revenue streams

China Telecom

• Enhance rural and overseas markets • Build up digital services including Video, M2M platform and Cloud services

2.4 2.4 2.4

6.28.5

11.6

33.1

0

5

10

15

20

25

30

35

India Indonesia Philippines Thailand China Malaysia Singapore

US$

Online Video Industry – China 2018

Page 28 of 68

Shared themes amongst at least two of the operators are improving 4G networks to drive data revenues, offering digital services such as content, and developing new enterprise opportunities. The former two bode well for the video industry:

• Enhanced data networks will provide a better user experience which encourages more video usage

• Focus on digital services has already manifested itself in the form of multiple partnerships with video platforms to provide less expensive access via promotional data rates.

It should also be noted that all three telcos have launched their own OTT video services in the country, although to date, none has gained significant traction in the market. More details are provided in Section 4.3.

4.2. China’s Fixed Broadband Industry Overview

4.2.1. Fixed Broadband Subscribers

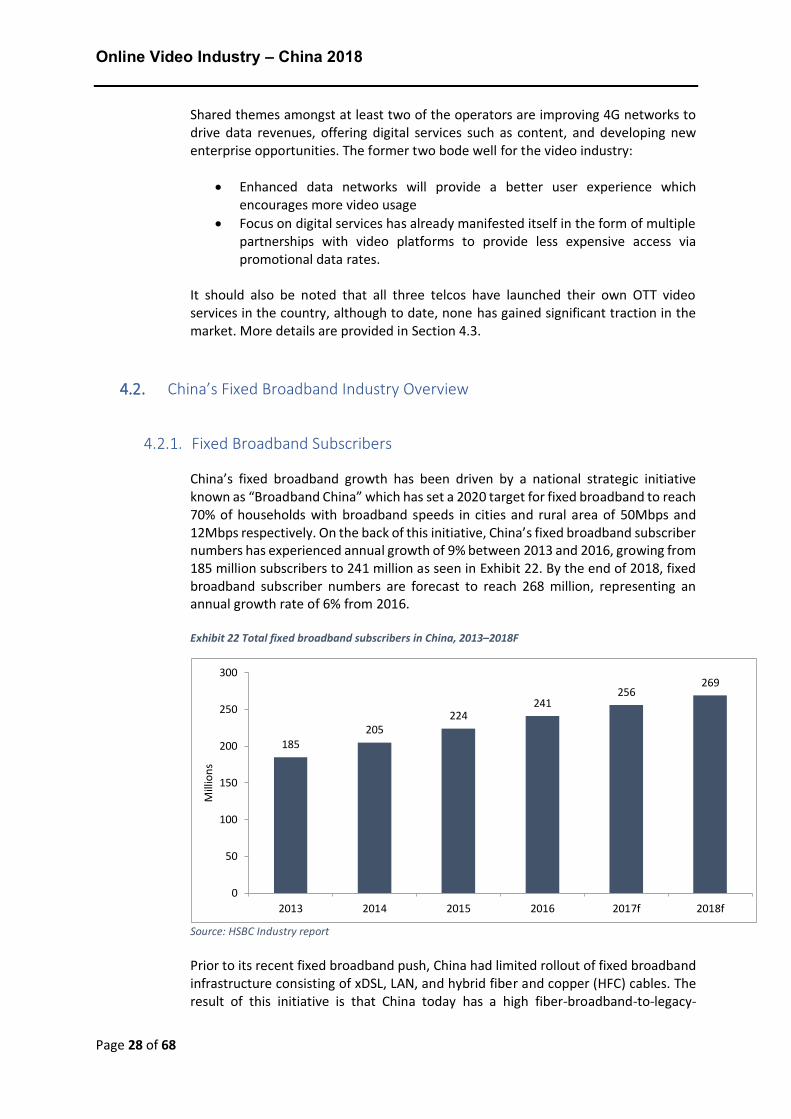

China’s fixed broadband growth has been driven by a national strategic initiative known as “Broadband China” which has set a 2020 target for fixed broadband to reach 70% of households with broadband speeds in cities and rural area of 50Mbps and 12Mbps respectively. On the back of this initiative, China’s fixed broadband subscriber numbers has experienced annual growth of 9% between 2013 and 2016, growing from 185 million subscribers to 241 million as seen in Exhibit 22. By the end of 2018, fixed broadband subscriber numbers are forecast to reach 268 million, representing an annual growth rate of 6% from 2016. Exhibit 22 Total fixed broadband subscribers in China, 2013–2018F

Source: HSBC Industry report Prior to its recent fixed broadband push, China had limited rollout of fixed broadband infrastructure consisting of xDSL, LAN, and hybrid fiber and copper (HFC) cables. The result of this initiative is that China today has a high fiber-broadband-to-legacy-

185205

224241

256269

0

50

100

150

200

250

300

2013 2014 2015 2016 2017f 2018f

Mill

ions

Online Video Industry – China 2018

Page 29 of 68

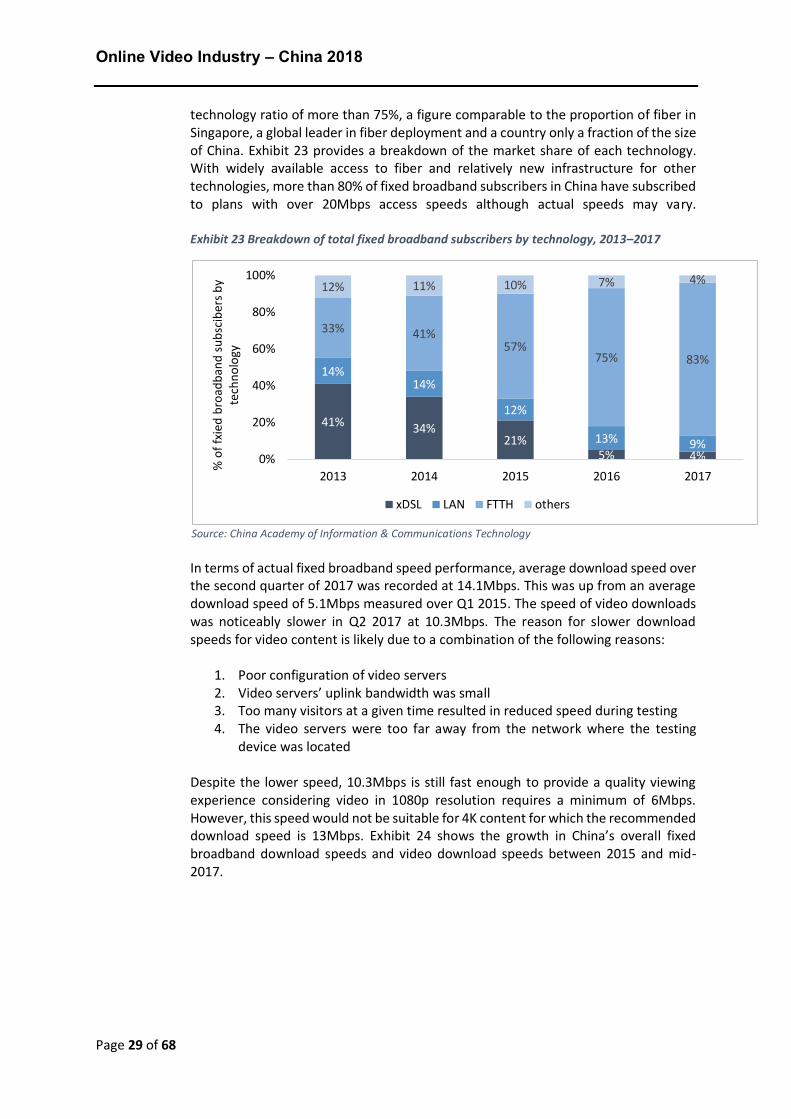

technology ratio of more than 75%, a figure comparable to the proportion of fiber in Singapore, a global leader in fiber deployment and a country only a fraction of the size of China. Exhibit 23 provides a breakdown of the market share of each technology. With widely available access to fiber and relatively new infrastructure for other technologies, more than 80% of fixed broadband subscribers in China have subscribed to plans with over 20Mbps access speeds although actual speeds may vary. Exhibit 23 Breakdown of total fixed broadband subscribers by technology, 2013–2017

Source: China Academy of Information & Communications Technology In terms of actual fixed broadband speed performance, average download speed over the second quarter of 2017 was recorded at 14.1Mbps. This was up from an average download speed of 5.1Mbps measured over Q1 2015. The speed of video downloads was noticeably slower in Q2 2017 at 10.3Mbps. The reason for slower download speeds for video content is likely due to a combination of the following reasons:

1. Poor configuration of video servers 2. Video servers’ uplink bandwidth was small 3. Too many visitors at a given time resulted in reduced speed during testing 4. The video servers were too far away from the network where the testing

device was located

Despite the lower speed, 10.3Mbps is still fast enough to provide a quality viewing experience considering video in 1080p resolution requires a minimum of 6Mbps. However, this speed would not be suitable for 4K content for which the recommended download speed is 13Mbps. Exhibit 24 shows the growth in China’s overall fixed broadband download speeds and video download speeds between 2015 and mid-2017.

41% 34%21%

5% 4%

14%14%

12%

13% 9%

33% 41%57%

75% 83%

12% 11% 10% 7% 4%

0%

20%

40%

60%

80%

100%

2013 2014 2015 2016 2017

% o

f fxi

ed b

road

band

subs

cibe

rs b

y te

chno

logy

xDSL LAN FTTH others

Online Video Industry – China 2018

Page 30 of 68

Exhibit 24 China’s fixed broadband average download rate and video download rate

Source: China Statistical Yearbook In 2016, China Telecom was the market leader in fixed broadband with 127 million fixed broadband subscribers as displayed in Exhibit 25. Exhibit 25 Fixed broadband subscribers by China telecom operators, 2016

Source: HSBC Industry Report

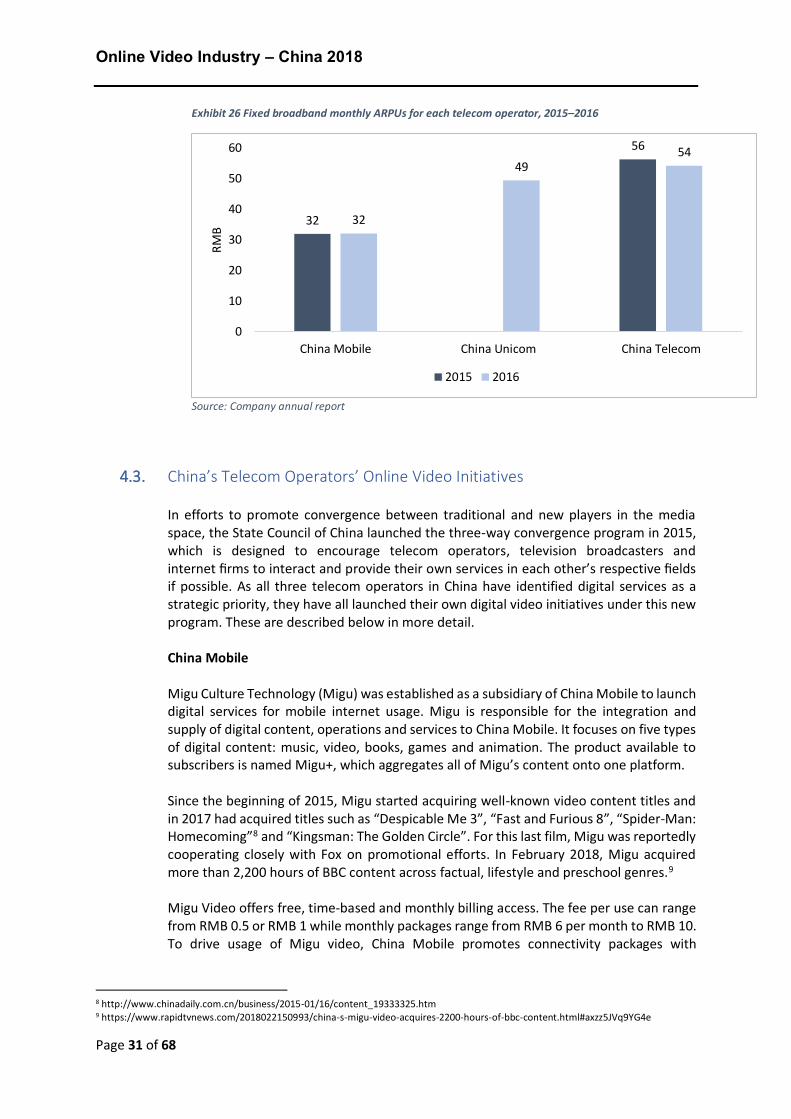

4.2.2. Fixed Broadband Industry Revenues

China Telecom also had the highest fixed broadband ARPU in 2016, which was RMB 54, while China Mobile had the smallest fixed broadband ARPU in 2016 as seen in Exhibit 26.

5.1 6.1

7.9 8.3 9.5

10.5 11.0 11.9

13.0 14.1

4.8 6.0 6.4 6.9 7.5 8.1 8.5

9.3 9.9 10.3

0

2

4

6

8

10

12

14

16

1Q2015 2Q2015 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 4Q2016 1Q2017 2Q2017

Meg

abits

per

seco

nd (M

bps)

download video download

9077

127

0

20

40

60

80

100

120

140

China Mobile China Unicom China Telecom

Mill

ions

Online Video Industry – China 2018

Page 31 of 68

Exhibit 26 Fixed broadband monthly ARPUs for each telecom operator, 2015–2016

Source: Company annual report

4.3. China’s Telecom Operators’ Online Video Initiatives

In efforts to promote convergence between traditional and new players in the media space, the State Council of China launched the three-way convergence program in 2015, which is designed to encourage telecom operators, television broadcasters and internet firms to interact and provide their own services in each other’s respective fields if possible. As all three telecom operators in China have identified digital services as a strategic priority, they have all launched their own digital video initiatives under this new program. These are described below in more detail. China Mobile Migu Culture Technology (Migu) was established as a subsidiary of China Mobile to launch digital services for mobile internet usage. Migu is responsible for the integration and supply of digital content, operations and services to China Mobile. It focuses on five types of digital content: music, video, books, games and animation. The product available to subscribers is named Migu+, which aggregates all of Migu’s content onto one platform. Since the beginning of 2015, Migu started acquiring well-known video content titles and in 2017 had acquired titles such as “Despicable Me 3”, “Fast and Furious 8”, “Spider-Man: Homecoming”8 and “Kingsman: The Golden Circle”. For this last film, Migu was reportedly cooperating closely with Fox on promotional efforts. In February 2018, Migu acquired more than 2,200 hours of BBC content across factual, lifestyle and preschool genres.9 Migu Video offers free, time-based and monthly billing access. The fee per use can range from RMB 0.5 or RMB 1 while monthly packages range from RMB 6 per month to RMB 10. To drive usage of Migu video, China Mobile promotes connectivity packages with

8 http://www.chinadaily.com.cn/business/2015-01/16/content_19333325.htm 9 https://www.rapidtvnews.com/2018022150993/china-s-migu-video-acquires-2200-hours-of-bbc-content.html#axzz5JVq9YG4e

32

56

32

49 54

0

10

20

30

40

50

60

China Mobile China Unicom China Telecom

RMB

2015 2016

Online Video Industry – China 2018

Page 32 of 68

exclusive perks for Migu products through its sales channels. These include bonus data quotas for customers who sign up to Migu monthly packages for Migu Video usage.

China Mobile has also leveraged Migu to launch an overseas video business in October 2017 which translated to English is called “Watch Freely Overseas”. By subscribing to this service, China Mobile subscribers who travel abroad can enjoy a variety of video content from domestic TV broadcasts to news and popular short videos by paying RMB 1 per day for access to the content. Users of “Watch Freely Overseas” websites will not be charged extra content fees and can enjoy the same benefits as Migu Video members. Despite its acquisition of popular Hollywood titles, Migu’s overall library is described by users as small compared to other mainstream video services in the country and traction of the service remains limited with an estimated viewership share of only 0.45% of online viewers. Migu’s market share is widely viewed as the highest among all the telecom operators’ video platforms. While traction for Migu has been low, China mobile views Migu as its priority for long-form content and has not formed any major partnerships with other long-form platforms. However, they have issued requests for proposals for partnerships with live streaming and short video platforms.

China Unicom China Unicom launched a promotional offer specifically around “Unlimited Video Enjoyment” to promote its transition to a “data + content” business model. The offer relates to data quotas for usage on video services China Unicom has partnered with which include Tencent, iQIYI, Youku, LeTV, BesTV, Mango TV, Huashu and others. Once a user subscribes to any of these services through China Unicom’s direct carrier billing option, the user can watch videos (at 480p resolution) without paying data usage fees.

At the same time, China Unicom has also launched its own service, “WO Video”, a mobile video platform independently developed and operated by China Unicom. In May 2017, the number of users of WO Video had reportedly reached 12 million, of which active monthly users constituted 30%. Similar to Migu, Wo Video purchased and promoted big Western titles but their overall library remains relatively small compared to other native video services. China Telecom China Telecom has partnered with a host of online video services to offer unlimited video streaming with purchase of data bundles of a certain size. Examples of their online video service partners include iQiyi, Youku, LeTV, PPTV 10, Douyu TV11 and Hujiao TV 12. The impact of these bundles on revenue or acquisition is not yet clear. China Telecom also established its mobile online video platform business, Tianyi Video Media, in March 2011. The service’s traction is generally seen as limited and trailing that of China Mobile’s Migu although official numbers are not released.

10 http://www.chinaz.com/mobile/2017/0426/692411.shtml 11 http://cservice.client.189.cn:9092/douyucard/douyucard_index.html?ct=0 12 http://news.qudong.com/article/428413.shtml

Online Video Industry – China 2018

Page 33 of 68

5. China’s Online Video Landscape

The following section provides information on China’s online video landscape and covers overall market size and growth trends, key players, revenues, business models and content offerings. The online video initiatives of telcos in China have been covered in a separate chapter. In this chapter we set out:

5.1 Online Video Landscape Overview 5.2 Major Online Video Players in China 5.3 Other Established Online Video Platforms in China

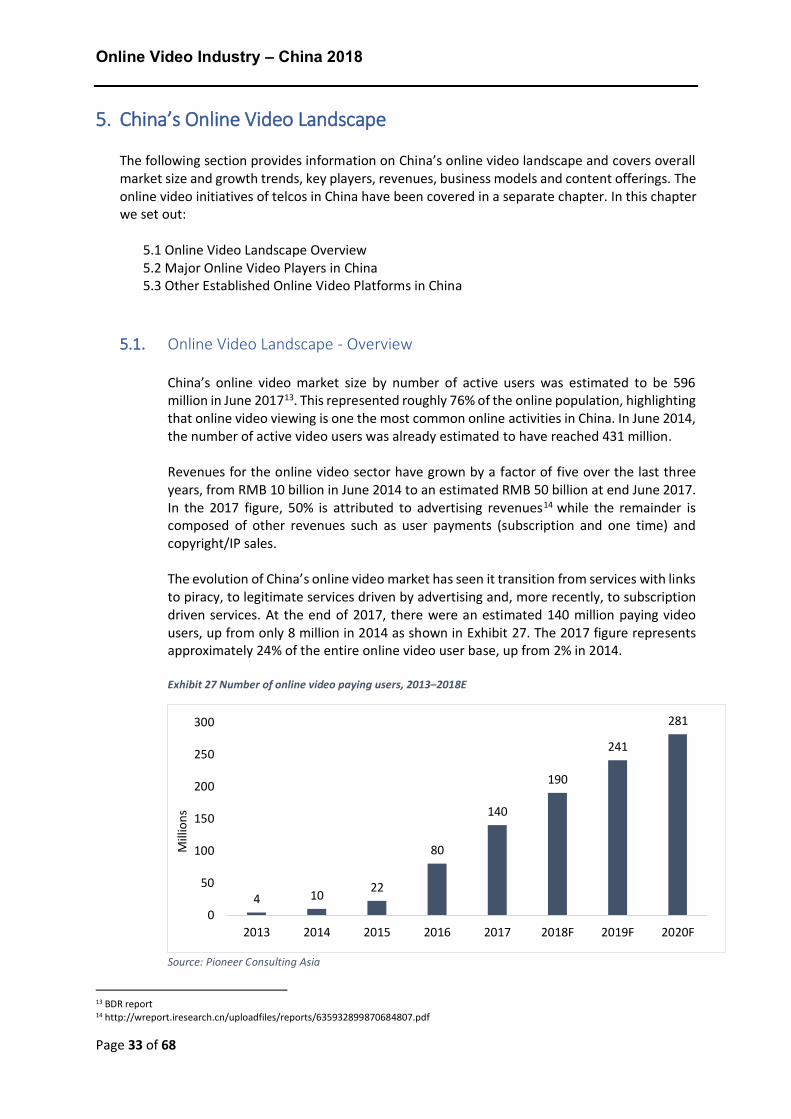

5.1. Online Video Landscape - Overview China’s online video market size by number of active users was estimated to be 596 million in June 201713. This represented roughly 76% of the online population, highlighting that online video viewing is one the most common online activities in China. In June 2014, the number of active video users was already estimated to have reached 431 million. Revenues for the online video sector have grown by a factor of five over the last three years, from RMB 10 billion in June 2014 to an estimated RMB 50 billion at end June 2017. In the 2017 figure, 50% is attributed to advertising revenues14 while the remainder is composed of other revenues such as user payments (subscription and one time) and copyright/IP sales. The evolution of China’s online video market has seen it transition from services with links to piracy, to legitimate services driven by advertising and, more recently, to subscription driven services. At the end of 2017, there were an estimated 140 million paying video users, up from only 8 million in 2014 as shown in Exhibit 27. The 2017 figure represents approximately 24% of the entire online video user base, up from 2% in 2014. Exhibit 27 Number of online video paying users, 2013–2018E

Source: Pioneer Consulting Asia

13 BDR report 14 http://wreport.iresearch.cn/uploadfiles/reports/635932899870684807.pdf

4 10 22

80

140

190

241

281

0

50

100

150

200

250

300

2013 2014 2015 2016 2017 2018F 2019F 2020F

Mill

ions

Online Video Industry – China 2018

Page 34 of 68

In 2017, the size of user-generated revenue (subscription or one-time transactions) in the online video market was estimated to be RMB 14 billion, up by a factor of ten from 2014’s revenue of only RMB 1.4 billion as highlighted in Exhibit 28. Despite paying users only accounting for just over one tenth of overall online video users, the proportion of revenue they generate already accounts for close to 28% of the market, highlighting the strategic importance of user-generated revenue in the online video space. Exhibit 28 User-generated revenues of China’s online video platforms, 2014–2018

Source: BDR

Mirroring initiatives seen in the global online video market, Chinese video platforms have shifted content budgets towards original productions as they believe there is a high correlation between original content and subscription revenue growth. There is also the added benefit that original content can generate additional revenue through distribution rights. As such, the market is likely to see growing investments in original production in the coming years as online players seek to differentiate themselves and cultivate their paying subscriber bases. The online video player space is made up of more than 200 players, with many serving targeted niches or offering specific types of content such as live streaming or short videos. Some recent entrants have leveraged new technology, such as virtual reality (VR) to differentiate their offerings from the competition. In the premium long-form content space, despite the wide array of choices, the market is dominated by three key players: iQiyi, Tencent and Youku. Together, the number of active users on these sites make up 83% of the users across the Top 10 platforms in the country. Exhibit 29 provides a breakdown of users and year-on-year growth by site for the ten most visited premium long-form content video sites in China.

1

5

10

14

19

2014 2015 2016 2017E 2018E0

2

4

6

8

10

12

14

16

18

20

RM

B b

illion

Online Video Industry – China 2018

Page 35 of 68

Exhibit 29 Monthly active users of Top 10 premium long-form content online video platforms, 2016–2017

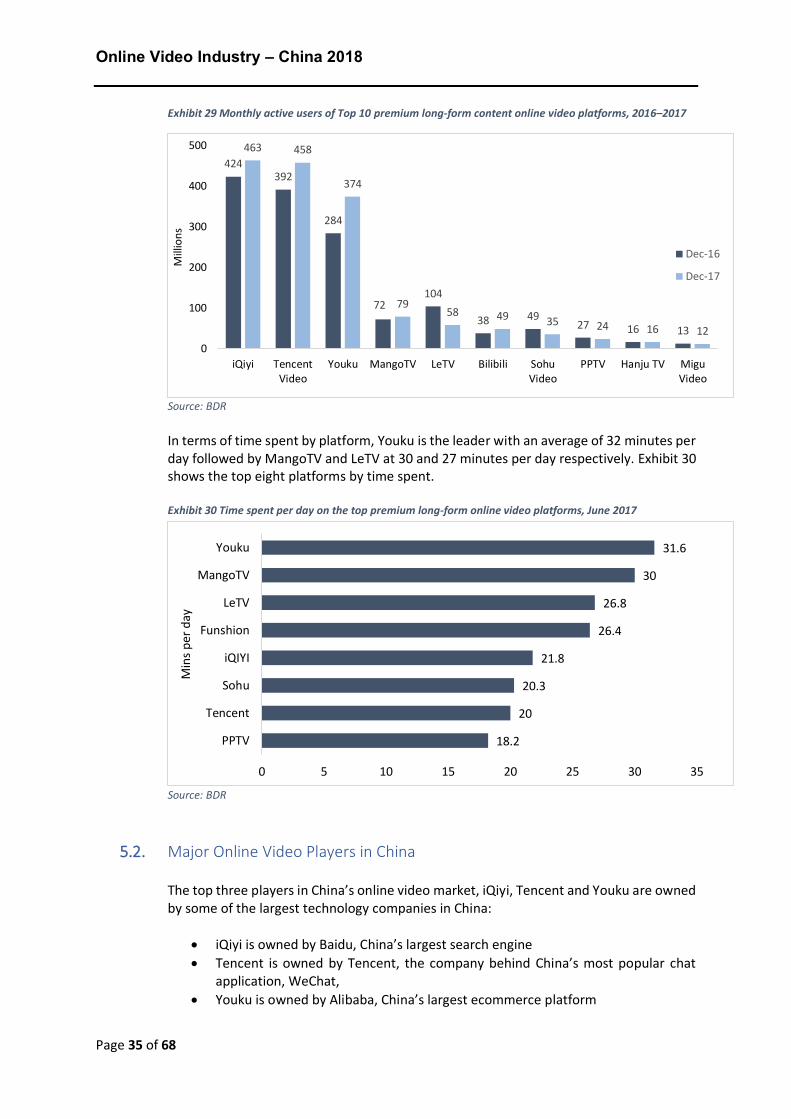

Source: BDR

In terms of time spent by platform, Youku is the leader with an average of 32 minutes per day followed by MangoTV and LeTV at 30 and 27 minutes per day respectively. Exhibit 30 shows the top eight platforms by time spent. Exhibit 30 Time spent per day on the top premium long-form online video platforms, June 2017

Source: BDR

5.2. Major Online Video Players in China The top three players in China’s online video market, iQiyi, Tencent and Youku are owned by some of the largest technology companies in China:

• iQiyi is owned by Baidu, China’s largest search engine • Tencent is owned by Tencent, the company behind China’s most popular chat

application, WeChat, • Youku is owned by Alibaba, China’s largest ecommerce platform

424392

284

72104

38 4927 16 13

463 458

374

7958 49 35 24 16 12

0

100

200

300

400

500

iQiyi TencentVideo

Youku MangoTV LeTV Bilibili SohuVideo

PPTV Hanju TV MiguVideo

Mill

ions

Dec-16

Dec-17

18.2

20

20.3

21.8

26.4

26.8

30

31.6

0 5 10 15 20 25 30 35

PPTV

Tencent

Sohu

iQIYI

Funshion

LeTV

MangoTV

Youku

Min

s per

day

Online Video Industry – China 2018

Page 36 of 68

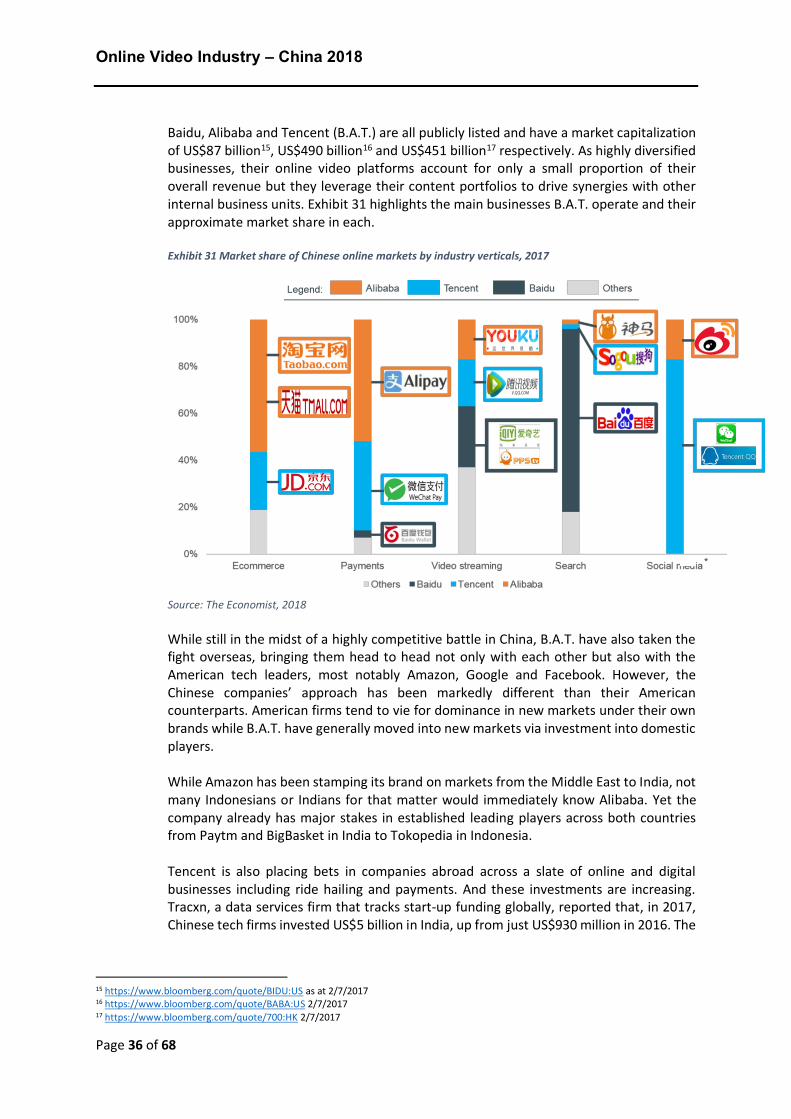

Baidu, Alibaba and Tencent (B.A.T.) are all publicly listed and have a market capitalization of US$87 billion15, US$490 billion16 and US$451 billion17 respectively. As highly diversified businesses, their online video platforms account for only a small proportion of their overall revenue but they leverage their content portfolios to drive synergies with other internal business units. Exhibit 31 highlights the main businesses B.A.T. operate and their approximate market share in each. Exhibit 31 Market share of Chinese online markets by industry verticals, 2017

Source: The Economist, 2018 While still in the midst of a highly competitive battle in China, B.A.T. have also taken the fight overseas, bringing them head to head not only with each other but also with the American tech leaders, most notably Amazon, Google and Facebook. However, the Chinese companies’ approach has been markedly different than their American counterparts. American firms tend to vie for dominance in new markets under their own brands while B.A.T. have generally moved into new markets via investment into domestic players. While Amazon has been stamping its brand on markets from the Middle East to India, not many Indonesians or Indians for that matter would immediately know Alibaba. Yet the company already has major stakes in established leading players across both countries from Paytm and BigBasket in India to Tokopedia in Indonesia. Tencent is also placing bets in companies abroad across a slate of online and digital businesses including ride hailing and payments. And these investments are increasing. Tracxn, a data services firm that tracks start-up funding globally, reported that, in 2017, Chinese tech firms invested US$5 billion in India, up from just US$930 million in 2016. The