NRG WORKING PAPER SERIES BALANCING THE ROLES OF BUSINESS UNIT CONTROLLERS AN EMPIRICAL INVESTIGATION...

52

NRG WORKING PAPER SERIES BALANCING THE ROLES OF BUSINESS UNIT CONTROLLERS AN EMPIRICAL INVESTIGATION IN THE NETHERLANDS Hans ten Rouwelaar November 2006 no. 06-07 Nyenrode Research Group

Transcript of NRG WORKING PAPER SERIES BALANCING THE ROLES OF BUSINESS UNIT CONTROLLERS AN EMPIRICAL INVESTIGATION...

NRG WORKING PAPER SERIES

BALANCING THE ROLES OF BUSINESS UNITCONTROLLERS

AN EMPIRICAL INVESTIGATION IN THE NETHERLANDS

Hans ten RouwelaarNovember 2006 no. 06-07Nyenrode Research Group

NRG WORKING PAPER SERIES

Balancing the Roles of Business Unit Controllers An empirical investigation in the Netherlands

Hans ten Rouwelaar

November 2006 NRG Working Paper no. 06-07

ISSN 1872-3934

NRG The Nyenrode Research Group (NRG) is a research institute consisting of researchers from Nyenrode Business Universiteit and Hogeschool INHOLLAND, within the domain of Management and Business Administration. Straatweg 25, 3621 BG Breukelen P.O. Box 130, 3620 AC Breukelen The Netherlands Tel: +31 (0) 346 - 291 696 Fax: +31 (0) 346 - 291 250 E-mail: [email protected] NRG working papers can be downloaded at http://www.nyenrode.nl/research/publications

Abstract Business unit-controllers can fulfill two roles in business life: the support role and the control role. The support role is associated with supporting managerial decision-making in the business unit; the control role focuses on providing reliable and timely financial accounting information for the corporate level and ensuring that the financial function complies with relevant regulations. The purpose of this paper is to explain these two roles of business unit-controllers. Survey data from 119 business unit-controllers in Dutch multidivisional organizations indicate that business unit-controllers spend more time on the control role when their organization has a hierarchical or adhocracy culture and fewer employees. On the other hand, controllers spend more time on support activities when their organization is decentralized and when their organization is operating in the service or not-for-profit sector. Finally, controllers who are ‘open to new experiences’ spend less time on their control role, while controllers with a more agreeable personality spend more time on their control role. Please do not quote or distribute without permission of the author Keywords Contingency theory, controllers, culture, performance, support role and control role Address for correspondence Drs J.A. ten Rouwelaar Nyenrode Business Universiteit Straatweg 25, 3621 BG Breukelen, The Netherlands E-mail: [email protected] Phone: (+31) 346 – 291443 This paper has benefited from helpful comments from Jan Bots and Roland Speklé on earlier drafts of this paper, special thanks to Frank Verbeeten for his suggestions. In addition, comments from participants at the 29th congress of the EAA in Dublin (March 2006) are appreciated. I would like to acknowledge the financial support of the Nyenrode Research Group (NRG) of the Nyenrode Business Universiteit.

1 Introduction

Currently the position of the business unit management accountants, or business unit-

controllers1, as the ‘economic conscience of the organization’ has grown in importance.

Changes in reporting requirements, their personal liabilities and the advising of business

unit-managers in decision-making are redefining the roles of business unit (bu)-controllers.

However, we have little information about the current roles of bu-controllers. Until now, the

attention of researchers in this field has been focused on investigating the ways in which the

roles of bu-controllers could be questioned, categorized, and measured (Sathe, 1982). Most

empirical evidence in this area is based upon anecdotic study or case study evidence

(Indjejikian, 2006; Matĕjka, 2002). Roozen and Steens (2006) conclude “after the research of

Vijay Sathe into the controller involvement in 1982, no rigorous research into the

controller’s profession was executed” (Roozen & Steens, 2006, page 6). Empirical studies,

which actually measure and try to explain the roles of the bu-controllers by organizational

characteristics, are not available, except for two working papers by Verstegen et al. (working

paper) and Maas (working paper).

This study contributes to management accounting research by investing empirically the

determinants of the two roles of bu-controllers in large multidivisional organizations in the

Netherlands. According to the accounting literature the ‘position of the bu-controller’

generally consists of two main roles: the support role and the control role. Trends in

management accounting show that controllers spend more time on the support role (by

continuous improvement of operating activities, for example strategic analyses, life cycle

costing, and overhead value analyses) and less time on the control role (Bruin & Van der

Sande, 2005). In addition to the controller’s contribution to business decisions, which calls

for active involvement in management (support role), the bu-controller is also responsible

for the accuracy of financial reporting and for the integrity of internal control. These two

latter responsibilities of accuracy and integrity (control role) are also of growing importance 1 In this paper, I use the term ‘controllers’ to identify management accountants, financial managers, and CFO’s,

who were interviewed as “top-financial representative of the business unit”.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 3 of 50

because of the discussion regarding corporate governance, the public disclosures concerning

corporate illegal payments, and the perception that corporate bribery has been concealed by

falsification of corporate books and records. New legislation, IFRS, and in-control

statements will probably force bu-controllers to pay more attention to their control role.

Three categories of factors are relevant in understanding and explaining variation in the

degree of controller involvement (Sathe, 1982): The first category of factors relates to the

controller’s motivation, personality, and interpersonal relationships with management; The

second set of factors relates to management’s expectations, orientation, and operating

philosophy; Finally, the third category of factors relates to the characteristics of the

company’s environment and business (Roozen & Steens, 2006, page 24).

This exploratory study focuses on the elements of the first category of factors, which I call

“the personal characteristics of the bu-controller”, and on elements of the third category of

factors are selected, which I call the “organizational characteristics”. The second category is

more difficult to study, because you would also have to interview bu-managers to investigate

what their expectations of the roles of the bu-controllers are. I therefore chose to investigate

this second category in a separate research project in 2006. Based upon existing management

accounting literature, I selected several organizational characteristics for my research model.

In this paper I describe the five of these characteristics, which are, from a data point of view,

the most effective in explaining the two roles. These characteristics are: (1) corporate culture;

(2) organizational structure (hierarchical relationships between the bu-controller and the bu-

manager or the corporate controller); (3) interdependencies among the business units; (4)

decentralization; and (5) performance or stress. From a ‘psychological theory’ point of view,

the personal characteristics and personal preferences of the bu-controller affect both roles. It

is interesting to find out what kind of personal characteristics fit to the control role or the

support role of the bu-controller, not only from HRM aspects, but also from educational

point of view (developing competences of future bu-controllers and new accounting process

techniques) (Cooper, 1996a; Helden, 1997; Kroon & Van der Steen, 2005; Maas, 2005). The

goal of this study is to measure these factors and (based upon data-analyses) to investigate

the theoretical framework for studies in examining bu-controllers’ roles.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 4 of 50

The remainder of this paper is structured as follows: Section 2 provides the theoretical basis

for the empirical model in which six hypotheses will be tested. The description of the data

and research model are presented in Section 3. After presenting the results of the test in

Section 4, I provide a discussion and my concluding comments in Section 5.

2 Literature review and development hypotheses

2.1 The roles of the bu-controller

There are several definitions of a controller in the management accounting literature. A

widely used definition is: “A controller is the person in charge of both management

accounting and financial accounting in an organization; usually the chief accountant. Also

called comptroller” (Zimmerman, 2005, page 784). In this paper I will also use this definition

and in order to use Sathe’s conceptional framework and findings on controller involvement,

I confine this study to the bu-controller as “the top-financial representative of the business

unit”.

A controller is a crucial person within an organization. The controller plays key roles in line

management and in the design and operation of a management control system (Merchant &

Van der Stede, 2003, page 493). Bu-controllers are the financial measurement experts within

their business unit and are key members of management teams. As a member of the

management team, he can influence the decisions taken by the managers (act before the

fact). In addition to the bu-controller’s role of contribution in business decisions, the bu-

controller is responsible for the accuracy of financial reporting and for the integrity of

internal control (after the fact reporting).

Traditionally, the controller was at best tolerated as a necessary evil, viewed as a bean

counter or a corporate cop. Nowadays, the controller is welcomed into the halls of

management as a business partner, sought after for business acumen and the strategic

perspectives this professional brings to the table (Colton, 2001; Riedijk et al, 2002). Changes

triggered by a new competitive environment have created enormous new opportunities for

controllers. This new competitive environment demands much more accurate cost and

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 5 of 50

performance information on the organization’s activities, processes, products, services, and

customers. These changes in the environment of the bu-controller do not only have an

impact on the different tasks of the bu-controller, but also will also have influence on the

spread of attention and time between the two different roles of the bu-controller.

An author, who delivered several step stone publications in the seventies and eighties about

the roles of the controller, is Vijay Sathe. He considers two broad questions. First, why is it

that in some companies controllers are involved more actively in the business decision-

making process than in other companies? And the second question concerns the

consequences of controller involvement for company performance. Does active controller

involvement help to improve the company performance? (Sathe, 1982). These two questions

are still relevant today. In this paper I focus on answering the first question. To answer his

questions Sathe defined four ideal types of controllers. If primary emphasis is placed in the

controller’s management-service responsibility, the desired behavior for the controller is to

be actively involved in the business decision-making process (the involved controller). If

primary emphasis is placed on the controller’s financial reporting and internal control

responsibilities, the desired behavior for the controller is to retain objectivity and

independence in dealing with affiliated management (the independent controller). The

potential benefit is a greater assurance of financial reporting and the integrity of internal

control. There are two ways, according to Sathe, of underscoring both controllers’ financial

reporting and their management-service responsibilities. The first is to split the controller’s

role and assign each major responsibility to a different individual (the split controller), the

other way is to retain both major responsibilities in one individual, but than strong emphasis

is placed on both (the strong controller) (Sathe, 1983). But can such “strong controllers”,

who are highly involved as part of the management team, maintain the requisite degree of

independence to fulfill their fiduciary and management oversight responsibilities effectively?

In other words can controllers wear two hats - one role as a member of the management

team and confidant, and the other as a watchdog or police officer? Many people believe that

the control and report responsibilities often conflict with the controller’s management-

service responsibilities (Sathe, 1982; Matĕjka, 2002; Strikwirda, 2002; Indejikian & Matĕjka,

2006).

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 6 of 50

Most researchers define only two different roles for controllers, although they use different

names: One role is the management-service role (support role, or business advocate role),

which involves helping managers with their decision-making and control functions.

The other role is the oversight role, which involves ensuring that the actions of everyone

within the organization, and especially those of the managers, are legally, ethically correct,

and in the best interests of the organizations and its owners (Merchant & Van der Stede,

2003, page 493 or Hopper, 1980, page 402). In other literature there is a distinction between:

‘Corporate Policeman’ (control role), and ‘Business Advocate’ (support role) (Jablonsky et al,

1993; Van Helden, 1999, page 22). Verstegen et al (working paper) have distinguished two

groups of controllers that perform roughly similar activities in practice: the ‘transformers’,

who transform internal and external reports, and the ‘watchmen’, who score high on

prevailing activities that relate to accounting information system and risk management

(Verstegen et al, working paper).

In this paper I also distinguish two roles of the controller, namely: an active involvement in

management (support role) versus responsibilities of accuracy and integrity (control role).

Another reason for this choice, besides the connection to prior management accounting

literature, is the ambiguity of the two extreme points of the spectrum. By choosing both

ends of the spectrum, I can focus on the explanation why these two roles have main

differences.

2.2 Theoretical framework

The controller is responsible for the management accounting control system within an

organization. The applicability of a management accounting control system is contingent on

the circumstances faced by organizations. This approach is known as the contingency theory

approach to management accounting (Otley, 1980; Chehall, 2003).

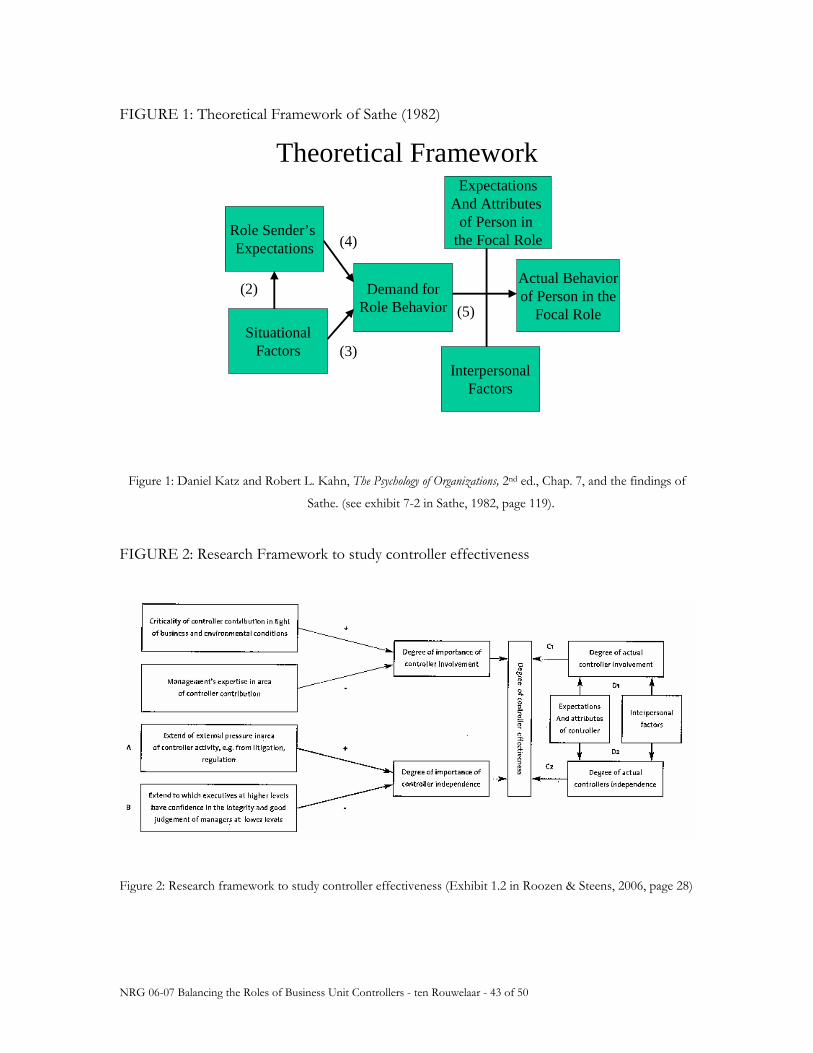

Sathe (1982) developed a theoretical framework, in which it is possible to link situational

variables to role behavior, see figure 1. According to this framework, situational factors not

only influence role behavior indirectly via role sender expectations, as assumed in role theory

(arrow 2), but also directly by generating a demand for role behavior (arrow 3) just as role

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 7 of 50

sender expectations do (arrow 4). The translation of the demand behavior into actual

behavior is moderated by attributes of the person in the focal role and interpersonal factors,

as in role theory (arrow 5). This study investigates what kind of situational (organizational)

factors and what interpersonal (personal) factors influence the actual behavior.

--------------------------------------------------

INSERT FIGURE 1 ABOUT HERE

--------------------------------------------------

Based upon this framework of Sathe (1982), Roozen and Steens (2006) developed their

research framework to study controller effectiveness. The degree of actual controller

involvement (support role) and the degree of actual controller independence (control role)

are affected by “expectations and attributes of controller” and “interpersonal factors” (arrow

D1 and D2). Both have affect upon the Degree of controller effectiveness (arrow C1 and

C2) (Roozen & Steens, 2006, page 28). Besides this part of the research framework, Roozen

and Steens also paid attention to the degree of importance of staff

involvement/independence. This part of the framework is about the managers’ demand for

involvement/independence of their controllers, and is left for future research.

--------------------------------------------------

INSERT FIGURE 2 ABOUT HERE

--------------------------------------------------

Because each organization is unique, the potential range of situations or contingent factors is

enormous, which makes it impossible to study each one separately. To overcome this

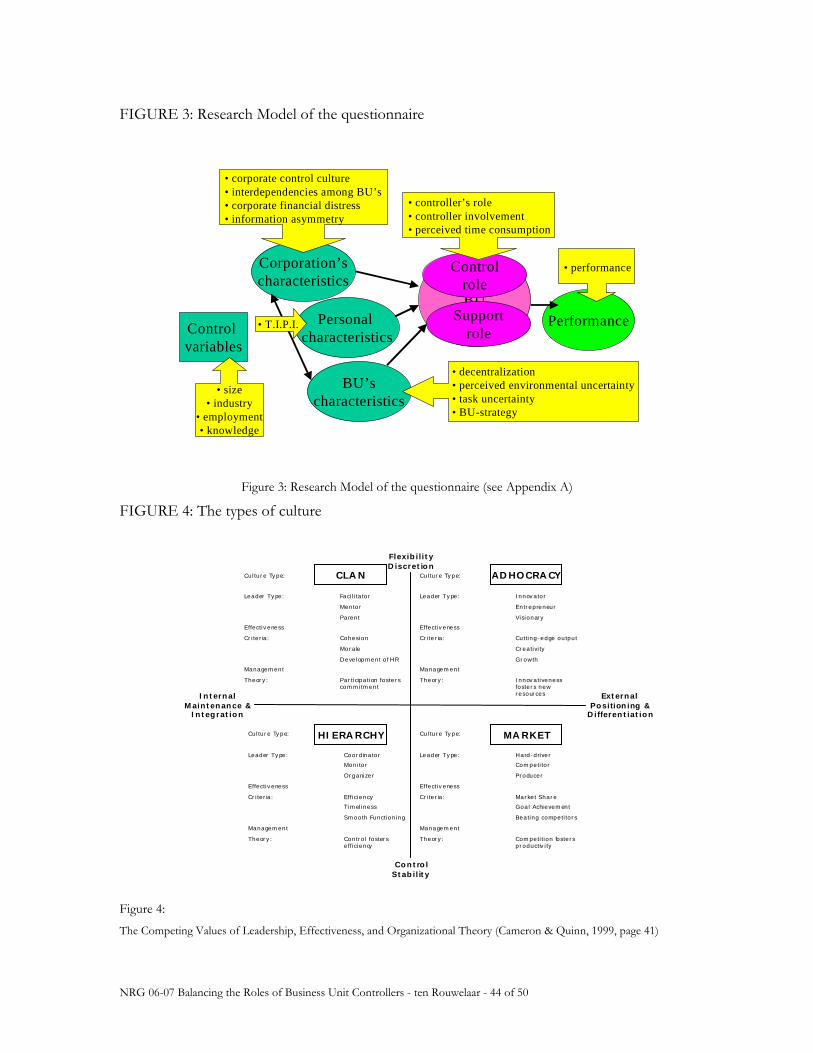

problem I selected those organizational factors in my research model, which are probably

related with the two roles of bu-controllers (see figure 3), a selection based upon both the

findings of Sathe in 1982 and the instruments available in management accounting literature.

--------------------------------------------------

INSERT FIGURE 3 ABOUT HERE

--------------------------------------------------

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 8 of 50

The questionnaire contains four corporation’s characteristics (culture, interdependencies

among business units, corporate financial stress, and information asymmetry), four business

characteristics (decentralization, perceived environmental uncertainty, task uncertainty, and

bu-strategy), five personal characteristic (the Big-Five), and the roles of the bu-controller

were measured in three different ways (controller’s role, controller involvement, and

perceived time consumption). In this paper I will describe only the following five, from data

perspective most effective, organizational factors, namely: (1) corporate culture, (2)

organizational structure (hierarchical relationships), (3) interdependencies, (4)

decentralization, and (5) performance or stress. These kinds of factors are important for

analyzing the roles of bu-controllers, because in 1980 Hopper already stated that:

“accounting systems may be contingent upon organizational circumstances and that it is a

short step from such work to suggest that the role of the accountant is similarly contingent”

(Hopper, 1980, page 401).

2.2.1 Corporate Culture

Organizational/corporate culture has acquired a status similar to structure, strategy, and

control (Hofstede et al, 1990, page 286). Most organizational scholars and observers now

recognize that organizational culture has a powerful effect on the performance and long-

term effectiveness of organizations (Wikins & Ouchi, 1983; Cameron & Quinn, 1999). An

organizational culture depends for its existence on a definable organization, in the sense of a

number of people interacting with each other for the purpose of accomplishing some goal in

their defined environment (Schein, 1983). It was not until the 1980s that organizational

scholars began paying serious attention to the concepts of culture (Cameron & Quinn,

1999).

A useful tool for categorizing corporate cultures is the Organizational Culture Assessment

Instrument (OCAI) as described by Cameron and Quinn in 1999. The four types of

organizations in the OCAI model are based upon a theoretical model entitled the Competing

Values Framework. This framework has four different quadrants, based upon two axes:

Flexibility and Discretion versus Stability and Control (vertical) and Internal Focus and

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 9 of 50

Integration versus External Focus and Differentiation (horizontal). Each of the four

quadrants has been given a label to distinguish the four major culture types: Clan-,

Adhocracy-, Market-, and Hierarchy culture.

--------------------------------------------------

INSERT FIGURE 4 ABOUT HERE

--------------------------------------------------

The use of controls within the organization is likely to depend on the type of culture. In

organizations with different types of culture, the roles of the bu-controller will probably be

different too. Connecting different types of culture to the roles of the bu-controller will lead

to the following hypotheses.

The Hierarchy culture is based on organizations at the beginning of the Industrial Revolution,

which organizations were internally focused and which culture led to stable, efficient, highly

consistent products and services. Clear lines of decision-making authority, standardized rules

and procedures, and control and accountability mechanisms were valued as the keys to

success. In a Hierarchy culture the most highly valued criteria of effectiveness are: efficiency,

timeliness, smooth functioning, and predictability. Bu-controllers, working in a Hierarchy

culture, have more standards and are less frequently affected by changes in type of work.

Therefore, they will have more time for control tasks and less need for putting effort in

support tasks.

It is to be expected that in a Hierarchy culture the control role is more effective than the

support role, which leads to the following hypothesis:

H 1a In case the organization has a Hierarchy culture, the bu-controller will spend more

time on control tasks, and less time on support tasks.

The Market culture refers to a type of organization, that functions as a market in itself. It is

oriented towards the external environment (instead of internal affairs) and operates primarily

through economic market mechanisms, mainly monetary exchange. The major focus is to

conduct transactions with other constituencies to create competitive advantage. Profitability,

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 10 of 50

bottom line results, strength in market niches, stretch targets, and secure customer bases are

primary objectives of the market-organization. In a Market culture specific criteria are highly

valued, for example: achieving goals, outpacing the competition, and increasing market

share. The reason why the bu-controller, working in a business unit or organization with a

Market culture, will spend more time on the support role is probably because the bu-

manager has to react more frequently to changes in the environment of the business unit.

More competition, achieving goals and increasing market share are more dynamic criteria

than the criteria of the other cultures. In a Market culture it is to be expected that the

support role is more effective than the control role, which leads to the following hypothesis:

H 1b In case the organization has a Market culture, the bu-controller will spend more

time on support tasks, and less time on financial rapports (control tasks).

The third ideal form of organization is called Clan culture because of its similarity to a family-

type organization. Instead of rules and procedures of hierarchies or competitive profit

centers, typical characteristics of clan-type organizations are: teamwork, employee

involvement programs, and corporate commitment to employees. The Clan culture is

typified by a friendly place to work where people share a lot of themselves. It is like an

extended family. In the Clan culture rules and regulations are less important than loyalty and

support. It is to be expected that the support role of the bu-controller is more effective than

the control role, which lead to the following hypothesis:

H 1c In case the organization has a Clan culture, the bu-controller will spend more time

on support tasks, and less time on control tasks.

The last type of culture is the Adhocracy Culture. These are organizations in which innovation

and pioneering initiatives are what leads to success. A major goal of an Adhocracy

organization is to foster adaptability, flexibility, and creativity where uncertainty, ambiguity

and/or information-overload are typical. The need for diagnosing and rearranging

organizational culture is growing in importance partly because of an increasing need to

merge and mold different organizations’ cultures as structural changes have occurred (for

instance, when units are consolidated, or when entire organizations merge). In an Adhocracy

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 11 of 50

culture it is to be expected that the control role of the bu-controller is more effective than

the support role, which lead to the following hypothesis:

H 1d In case the organization has an Adhocracy culture, the bu-controller will spend

more time on control tasks, and less time on support tasks.

2.2.2 Organization of the Control function

A bu-controller always has dual responsibilities and provides information both to the bu-

management and the top-management (Simon et al, 1954; Sathe, 1978a; 1978b; Matĕjka,

2002). The bu-controller’s functional responsibility is to ensure that top-management knows

the ‘true’ financial state of the business unit. This includes regular reporting but also

maintaining an informal communication line with the functional superior (the so-called

‘dotted line’). As a part of the local responsibility, the bu-controller is in charge of local

accounting systems and provides reports relevant for decision-making by bu-managers.

Sometimes organizations place bu-controllers under supervision of the corporate controlling

department (the so-called ‘solid line’), which emphasizes the controller’s independency

(Merchant & Van der Stede, 2003, page 496). The bu-controller is than in danger of being

viewed by bu-management as an ‘outsider’, if not a ‘corporate spy’, and the bu-controller

may be denied access to sensitive information or is informed after the relevant decisions and

actions have already been taken (Sathe, 1983; Anthony & Govindarajan, 2004, page 74).

Some firms have found that solid-line reporting in the controller’s organization is effective for

the control of bu-controllers’ activities. Solid-line reporting means that the bu-controller’s

primary reporting relationship is to the corporate controller. The corporate controllers, not

the bu-managers, define the bu-controller’s tasks and priorities and evaluate their

performances. Solid-line reporting is designed to reduce the emotional attachment between

bu-controllers and the operating unit to which they are assigned. The primary cost of solid-

line reporting is a potential reduction in the quality of the controller’s management service

function. The solid-line controller can be viewed as a “corporate spy”, and will be excluded

from sensitive information of the business unit (Merchant, 1998, page 642). In case of a

hierarchical relationship between the bu-controller and the corporate controller (solid line),

the bu-controller (agent) will fulfill the wishes of the corporate controller (principal).

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 12 of 50

In case of a hierarchical relationship between the bu-manager and the bu-controller (dotted

line), the bu-controller (agent) will fulfill the wishes of the bu-manager (principal). The

relationship between the bu-controller and the corporate controller affects the bu-

controller’s roles, which leads to the following hypothesis:

H 2 In case of a hierarchical relationship between bu-controller and corporate controller

(solid line) the bu-controller will spend more time on control tasks, and less time on

support tasks.

2.2.3 Interdependencies among business units

Abernethy, Bouwens, and Van Lent (2004) investigated in their paper two relevant

determinants of the use of divisional summary measures: centralization and

interdependencies (Abernethy et al, 2004). Interdependencies occur when a business unit has

impact on other business units’ activities or performance. There are two types of

interdependencies: (1) when the business unit is influenced by the activities of other business

units (impact on you), and (2) when the business unit influences the performance of other

business units (impact on them) (Abernethy et al, 2004, page 549).

In case of more interdependencies among the business units the corporate controller has to

focus on all relations between the business units, so he will need adequate information of his

business units, and will need more financial rapports from the business units. It is to be

expected that the more impact a business unit has upon other the business units, the more

the bu-manager wants to be supported and the corporate controller will emphasis the

control role of the bu-controller, because of the impact of this business unit on other

business units. On the other hand, in case of influences of other business units upon your

performance, the bu-manager will have less impact on activities of other business units.

Therefore, there is also reason to believe that in case of ‘impact on you’ this bu-manager and

the corporate controller are less interested in the information of the bu-controller, so the

support role of the bu-controller and the control role would decrease. Based upon these

expectations, you might expect that:

H 3a There is a positive relationship between the impact on other business units and

the support role and control role of the bu-controller.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 13 of 50

H 3b There is a negative relationship between the impact by other business units and

the support role and control role of the bu-controller.

2.2.4 Decentralization

The contingency theory suggests that Perceived Environmental Uncertainty (PEU) affects

organizational structure, and that controllers design organizational structures such that the

organization will be able to more effectively respond to the perceived environmental

demands (Gordon & Narayanan, 1984, page 36). According to the contingency theory

decentralization is also caused by knowledge and observability factors. Based upon

differences in information or knowledge about the transformation process and on outcome

(output)- and behavior (effort) observability top-management entrusts tasks to bu-

management since they neither have the time nor the ability to do the task themselves

(Nilakant & Hayagreeva, 1995, page 650). Or corporate management uses decentralization to

encourage the decisions capacity of their bu-managers, in order to increase the value of the

organization (Wruck & Jensen, 1994). Another reason to decentralize the decision rights to

bu-managers is the level of information asymmetry. Information asymmetry occurs when

lower-level managers have specific knowledge about the functioning of the business unit,

which knowledge is either not available to corporate management or is too costly for

corporate management to obtain (Christie et al, 2001). Abernethy et al. (2004) have found

that decentralization is positively related with the level of information asymmetry and

negatively to intra-firm interdependencies (Abernethy et al, 2004, page 547). As a result of

decentralization, bu-managers have opportunities to misrepresent information and divert

resources to their personal use. Decentralization refers to the level of autonomy delegated to

managers (Chenhall & Morris, 1986). By decentralization the bu-manager gets more rights to

take decisions without asking permission of corporate managers. Findings suggest that

attempts by the bu-controllers to improve response time and to assimilate information from

many resources into a broad scope of Management Accounting Systems are of particular

relevance to managers who perceive their operating situation as uncertain (Chenhall &

Morris, 1986). The bu-manager shall demand more adequate information (support) from his

bu-controller, so the support role will increase. On the other hand, the corporate managers

want to get information (reports) from their bu-managers to monitor the managers’ actions,

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 14 of 50

so the corporate controller could ask for more reports (control) as well. In fact the in case of

decentralization both roles will be emphasized:

H 4 There is a positive relationship between decentralization of decision rights to the

local bu-manager and the support role and control role of the bu-controller.

2.2.5 Performance or stress

The most common example of organizational stress influencing the choice of reporting

relationships is poor financial performance. Although there are exceptions, companies using

direct reporting to the corporate controller tend to be those with poorer performance

relative to the industry than those where bu-controllers report directly to bu-management

(Sathe, 1978a, page 102). In case of poor financial performance it is to be expected that the

control role of the bu-controller will be more important. Another form of organizational

stress that bears on reporting relationships for bu-controllers is stress caused by sudden

discovery of serious financial mismanagement in a business unit. These incidents cause top-

management to seriously question the integrity of the company’s reporting and control

system and tend to increase the probability that the corporate controller will be given greater

authority over bu-controllers (Sathe, 1978a, page102).

If the performance of the business unit is really important, not only the corporate controller

will be more focused on the reports, but also the bu-manager will have more stress than in

the situation wherein the performance of the business unit is relatively unimportant. In case

of declining profits, the bu-manager has to react and will need more support of the bu-

controller. Both control and support roles will be more important in case of poor financial

performance within the business unit. Therefore the following hypothesis will be tested:

H 5 There is a positive relationship between financial stress of the business unit and the

support role and the control role of the bu-controller.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 15 of 50

2.3 Psychological theory

Personal Characteristics

According to Roosen and Steens (2006), controllers must take into account the fact that bu-

managers generally score higher than non-executives in terms of intelligence, dominance,

self-confidence, energy, perseverance and knowledge of the task for which they are

responsible. Personal characteristics however, do not make bu-managers effective; it is all

about how these characteristics influence their behavior. Given the fact that bu-controllers

have the same goal, i.e. influencing their bu-managers to ensure that the financial-economic

interest of decisions is adequately taken into account, this aspect of bu-managers makes the

job of bu-controllers especially difficult: the bu-controllers end up taking on experts in

exercising influence! (Roozen & Steens, 2006, page 102). For an effective collaboration and

a smooth working relationship, bu-controllers must be able to adapt their behavior to the

management style of their bu-managers. Besides insights into the management style, bu-

controllers must be aware which part of their own behavior is best suited to the situation.

Bu-controllers find themselves in a somewhat subordinated position vis-à-vis bu-managers

and they continuously have to weigh the pros and cons of being loyal to group control

(control role) on the one hand and to bu-management (support role) on the other. As soon

as a position of trust is achieved, bu-managers will also to a degree be prepared to adapt their

behavior towards their bu-controllers.

The behavior and personal characteristics of the bu-controller affect the effectiveness of bu-

controllers. Van der Ven (2002) found four generic conditions to be met if the bu-controller

has to effectively exercise its responsibilities: (1) substantive knowledge and skills; (2)

personal, intra social (individual instinctive) competences; (3) influencing behavior, by

applying the available tools and instruments bu-controllers have; and (4) a management style

expressing clarity regarding the steering relationship between bu-controllers and bu-

management on the one hand and between bu-controllers themselves on the other hand (in

dealing with ones functional superior: corporate controllers) (Van der Ven, 2002; Roozen &

Steens, 2006).

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 16 of 50

There are a lot of ways to describe the personal characteristics of humans. One of the best

ways (and therefore the most frequently used way) is the Five Factor Model of Howard and

Howard (Howard & Howard, 2001a). The Five Factor Model contains five dimensions: The

Big Five: Neuroticism (also emotional instability), Extraversion, Openness to new

experiences (the Originality Factor), Agreeableness (the Accommodation Factor), and

Conscientiousness (The Consolidation Factor) (Howard & Howard, 2001b; 2001c). Other

researchers have helped to develop this model further (Digman, 1990; Gosling et al, 2003).

In the Five Factor Model, there are five dimensions that all combined give a picture of the

person’s characteristics. These five ‘Big Five dimensions’ are:

1. Neuroticism (Need for Stability): This aspect refers to the degree in which a

person responds to stressful circumstances. More resilient persons (N-) react in a

calm, steady, and secure way. These persons tend to be more rational at work than

most people and they appear rather impervious sometimes to what’s going in around

them. At the other extreme of the Need for Stability continuum, there are the more

reactive persons (N+), who react in an alert, concerned, attentive, or excitable way.

They have high stress sensitiveness and are often unable to deal with stress or

stressful circumstances. In the middle there are the responsive people, who are a

mixture of the characteristics of the resilient and reactive people.

2. Extraversion: This aspect refers to the degree in which a person can tolerate sensory

stimulation from other people or situations. Persons with high scores (E+) are

characterized by their preference of being around other people and by their

involvement in many different activities. These extravert persons have a larger social

sphere in which to acquire the social skills necessary to maintain a larger, more

inclusive number of relationships (Mahony & Stasson, 2005). Persons with a low

degree of extraversion (E-) are characterized by a preference to work alone; they are

often described as quiet, serious, and private persons. These persons for whom

Extraversion is below average (labeled in the vernacular as “Introverts”) presumably

have fewer social interactions with other people (Mahony & Stasson, 2005).

3. Openness (Originality): This aspect refers to the degree in which a person is open

to new experiences or new ways of doing things. People who score high on this

dimension (O+), are called ‘explorers’; they have broader interests, and have a

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 17 of 50

fascination with novelty and innovations. They like to explore their creativity and

dislike repetitive, simple tasks (Tett & Burnett, 2003). The opposite kind of people

(O-), the so-called ‘preservers’, have narrower interests, are perceived as more

conservative, but not necessarily as more authoritarian. They are more comfortable

with the familiar circumstances than the ‘explorers’.

4. Agreeableness (Accommodation): This aspect refers to the social skills

component and the degree in which we defer to others. High accommodation (A+)

describes persons who tend to relate to others in being tolerant, agreeable, and

accepting towards others (so called ‘adapters’). Low accommodating people (A-) may

not accept information without checking; they come across to others as hostile, rude,

self-centered, and not a team player (so called ’challengers’).

5. Conscientiousness (Consolidation): This aspect refers to the degree in which a

person pushes toward reaching goals at work. People with a high consolidation (C+)

tend toward goals in an industrious, disciplined, and dependable fashion (so called

‘focused’). The definition of Conscientiousness includes a number of different

aspects: competence, order, dutifulness, achievement striving, self-discipline and

deliberation (Clarke & Robertson, 2005). A further aspect of Conscientiousness

related to deliberation and order, is reflected in thoroughness in decision-making

style. Low thoroughness is characterized by a lack of forward planning, absence of a

logical or systematic approach to decision making and inadequate cost-benefit

analysis and contingency planning (Clarke & Robertson, 2005). Low consolidation

types (C-) tend to approach goals in a relaxed, spontaneous, and open-ended fashion

(so called ‘flexible’). Towards the middle of the Conscientiousness continuum is the

‘balanced person’, who finds it easier to move from focus to laxity, and providing

just enough of both qualities to keep focus and relax periodically to enjoy life a little.

Bu-controller’s personal preferences and characteristics will affect both roles. For the

support role it is to be expected that bu-controllers are open to new experiences (O+), can

easily relate to others (A+) and have a more extrovert character (E+). For the control role it

is to be expected that bu-controllers have a focused (C+), more resilient character (N-).

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 18 of 50

It will be interesting to know what kind of personal characteristics fit to the control role or

the support role of the bu-controller. Based upon the expectation that bu-controllers have

characteristics that fit to their work and interests, the following hypotheses are interesting to

be tested:

H 6a Bu-controllers with high scores on Extraversion (extravert), Openness (explorer), or

Agreeableness (adapter) are related with the support role of the bu-controller.

H 6b Bu-controllers with low scores on Neuroticism (resilient), or high scores on

Conscientiousness (focused) are related with the control role of the bu-controller.

2.4 Control variables

There are several factors that do not affect the two roles directly, but that could influence the

other factors by enforcing or moderating these direct relationships. Data regarding two of

such factors, that could affect the two roles indirectly, are additionally selected for this paper,

which factors are: firm size and firm industry.

Firm Size

The relation between the two roles of bu-controllers and the size of the organization is

difficult to predict. On the one hand, the larger the organization (size of the organization),

the more business units the corporate organization has. So corporate management wants to

be well informed and they will ask for reports more frequently. But on the other hand, the

larger the company is the more decentralization, which results in more local decisions. So the

bu-manager will also need more support if the organization is larger. It is likely to assume

that there is an enforcing effect of the size of the organization upon the degree in which the

bu-manager will need support or upon the degree in which the corporate management well

need reports.

Firm Industry

The distribution of tasks of a bu-controller over his support - and control roles will depend

upon the type of industry of the organization. I will include a dummy variable for several

industries in order to standardize for the effects of industry.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 19 of 50

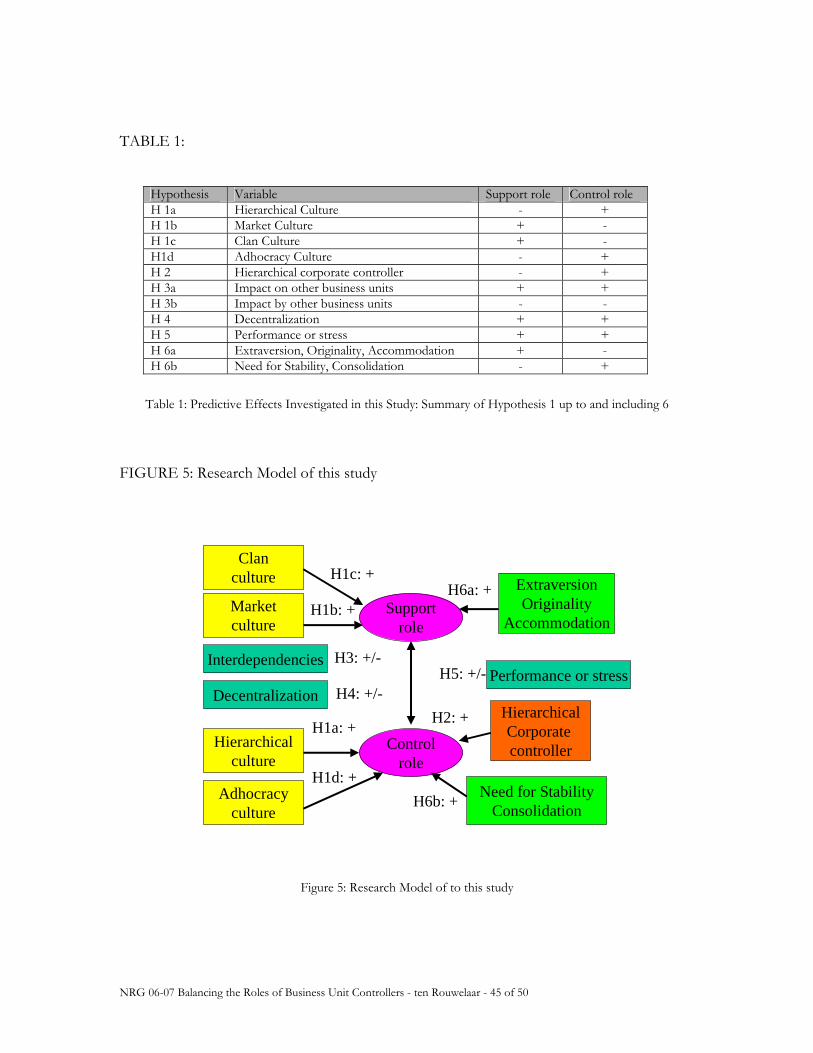

2.5 Summary of hypothesis and Theoretical Framework

Table 1 provides the relations between the selected variables and the two roles, as a summary

of my expectations, hypothesis 1 up to and including 6.

--------------------------------------------------

INSERT TABLE 1 ABOUT HERE

--------------------------------------------------

The research model of this study is shown in Figure 5.

--------------------------------------------------

INSERT FIGURE 5 ABOUT HERE

--------------------------------------------------

3 Research Methodology

3.1 Sample description

The data for this paper were collected through a questionnaire survey, using NIVRA-

Nyenrode students in the Masters of Science in Controlling program to interview bu-

controllers working in practice. Respondents are working as bu-controllers in a business unit

which complies with two conditions: (1) the bu-manager of the business unit has profit- or

result responsibility to corporate headquarters, or division (=organization); and (2) at least 50

Full Time Equivalents (employees) are working within the business unit. In total 119

interviews were held and 119 questionnaires were completed. These 119 different bu-

controllers work within 77 different organizations. A copy of the relevant questions from the

questionnaire is added to this paper in appendix A.

3.2 Variable instruments

In this section I discuss the measurement of the constructs in turn. The numbers (e.g. q110)

refer to the specific questions in Appendix A.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 20 of 50

The roles of the Controller

Measuring the roles of the controller has been done in prior research in several, different

ways. In this paper, the roles of the bu-controller are measured by three different

instruments taken from previous literature: (1) Management accountant’s roles of Sathe

(1982), (2) Involvement instrument of Matjĕka (2002), and (3) Spent Time instrument of

Oude Vrielink & Verbeeten (2004).

Controllers’ roles

This instrument is developed by Sathe e.g. (Sathe, 1982; 1983), who considers the

controller’s management-service responsibility versus the controller’s financial-reporting and

internal-control responsibility. To measure the management-service responsibility the

following questions were used: q108 to q110, and q111 to q116 for the financial-reporting

and control responsibility. This instrument leads to two factors: the first factor is RESPCON

(explaining 24.7% of variance), the second is RESPSUP (explaining 17.5% of variance),

which indicates the controller’s control responsibility and management support

responsibility, respectively. The Cronbach Alpha of RESPSUP (q108 and q110) is 0.5203,

and the Alpha of RESPCON (q111 till q116, except q115) is 0.6580.

Involvement (INVOLV) and Independency (INDEP)

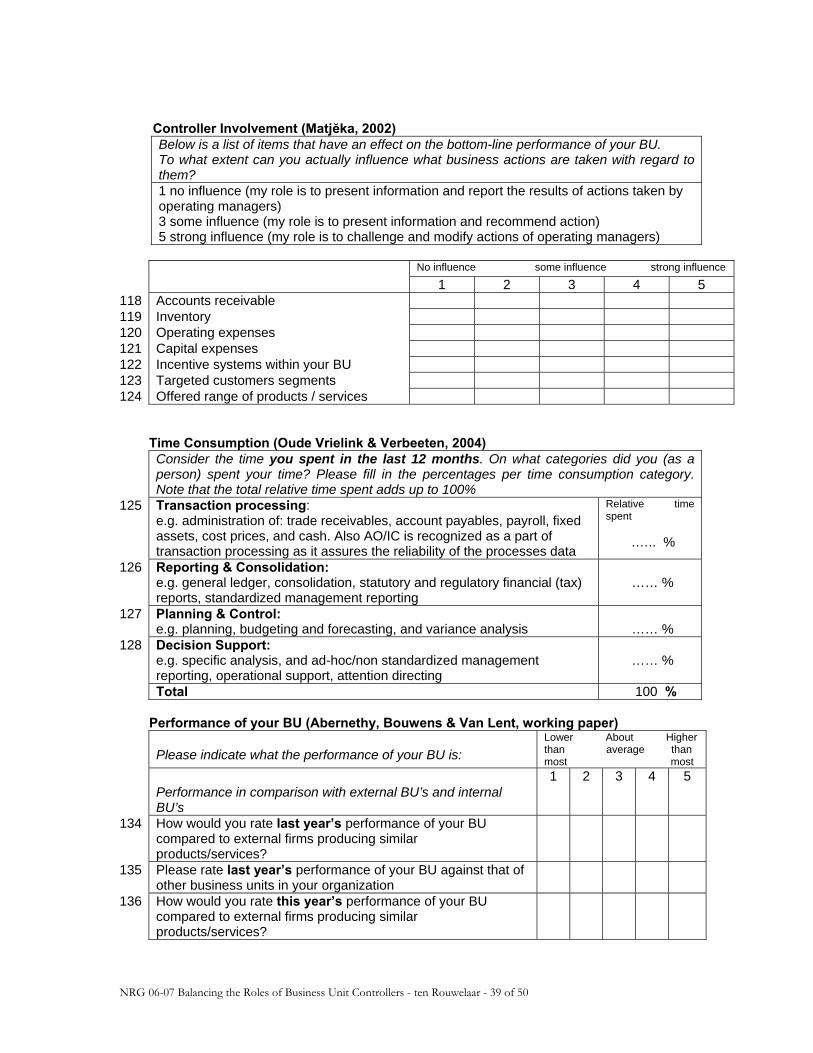

The second instrument to measure the roles of the controller is developed by Matjĕka in his

study, published in Chapter 2 of his Dissertation (Matĕjka, 2002). This instrument, listed in

the questionnaire in questions q118 until q124, measures the influence of the controller on

business actions (1=no influence, 5=strong influence).

My analysis results in two factors; the first factor is positively loaded by all questions q118 to

q124, but the second is negatively loaded by q122 to q124. The first factor I label INVOLV

and the second factor is labeled INDEP, because the first factor, INVOLV, shows that the

bu-controller is concerned with all kinds of tasks, the second factor, INDEP, shows that the

bu-controller doesn’t have any influence on management decisions and acts more

independently. The first factor explained 33.4% and the second factor explains 17.2% of

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 21 of 50

variance. So, both factors together explained 50.6% of variance. The Cronbach Alpha of

INVOLV, capturing all tasks (q118 till q124), is 0.6603.

Control Activities (CONACT) and Support Activities (SUPACT)

Another way in measuring the support role and control role by using the instrument of

Matjĕka (2002) is by defining two variables based upon the scores of the questions q118 to

q124. The variable CONACT is based upon the total score of the control activities: accounts

receivable (q118), inventory (q119), and operating expenses (q120). The variable SUPACT is

based upon the total score of the support activities: incentive systems (q122), target

customers segments (q123), and offered range of products (q124).

Time for Support (TIMESUP) and Time for Control (TIMECON)

The third instrument to measure the different roles is derived from Oude Vrielink and

Verbeeten (2004). They developed questions q125 to q132, which ask controllers how they

spent their time (in %) in the last 12 months to different tasks in four categories: Transaction

processing, Reporting & Consolidation, Planning & Control, and Decision Support,

respectively. CONTIME is based upon the first two categories (= q125 + q126), and

SUPTIME is based upon the third en fourth category (= q127 + q128).

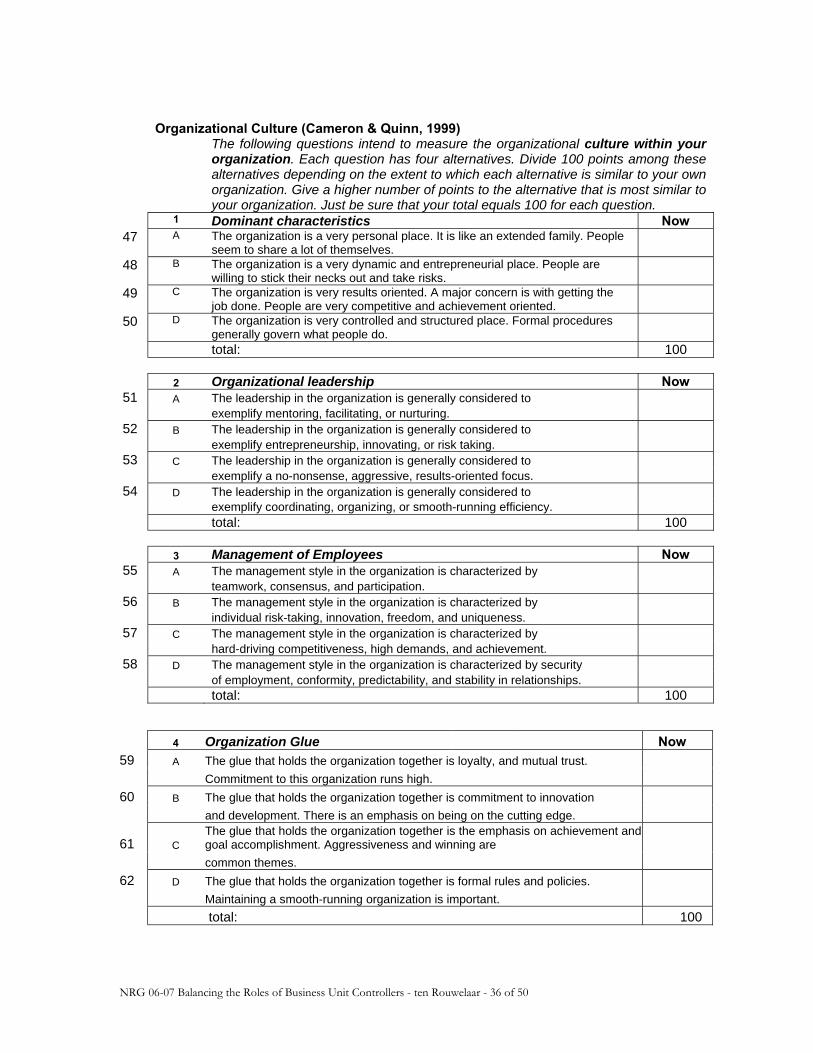

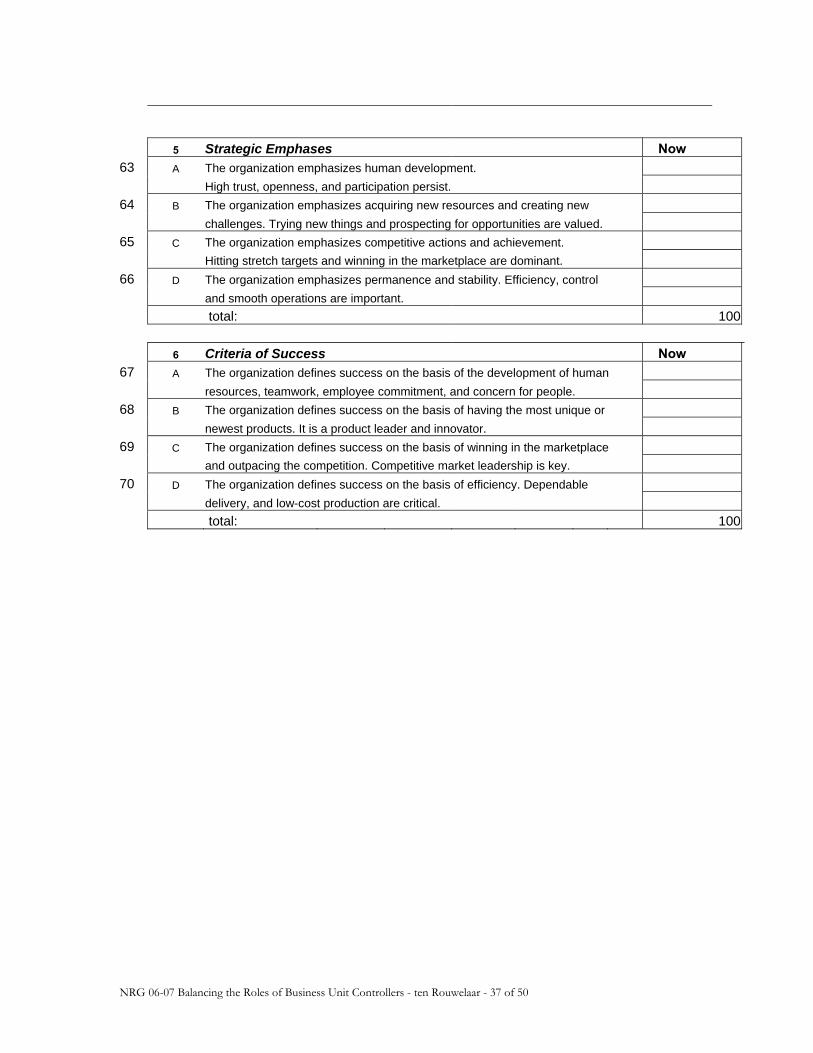

Corporate Culture (CLANCULT, ADHOCULT, MARKCULT, HIERCULT)

To measure the corporate culture I use the Organizational Culture Assessment Instrument

(OCAI). The instrument, that Cameron and Quinn describe, requires individuals to respond

to just six items. Each question has four alternatives. By dividing 100 points over these four

alternatives, a total score is easily calculated. This instrument has been found to be both

useful and accurate in diagnosing important aspects of an organization’s underlying culture

(Cameron & Quinn, 1999, page 20 – 27).

The results of the calculations are four variables measuring the culture of the company:

CLANCULT = (q47 + q51 + q55 + q59 + q63 + q67);

ADHOCULT = (q48 + q52 + q56 + q60 + q64 + q68);

MARKCULT = (q49 + q53 + q57 + q61 + q65 + q69);

HIERCULT = (q50 + q54 + q58 + q62 + q66 + q70).

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 22 of 50

Each of these variables gives an indication on the degree of which the organization has a mix

of each of the four types of culture: Clan- (CLANCULT), Adhocracy- (ADHOCULT),

Market- (MARKCULT), or Hierarchy culture (HIERCULT). The Cronbach Alpha’s are:

0.7959; 0.779; 0.8901, and 0.7593 respectively.

Hierarchical Structure (CORPCNTR)

Respondents have been asked to indicate who their direct principal is: bu-manager or

corporate controller (q21 and q 22). Based upon the answers of these questions I calculated a

Dummy variable, called CORPCNTR, which is a Hierarchy Dummy (i.e. 1 = corporate-

controller is hierarchical principal of the bu-controller, 0 = other is hierarchical principal of

the bu-controller).

Interdependencies (IMPATHEM and IMPAYOU)

This instrument is derived from Abernethy, Bouwens, and Van Lent (2004). The instrument

measures in question q37 “to what extent your BU’s actions impact on work carried out to

other business units” (IMPAYOU) and in question q38 “to what extent other business units’

actions impact on work carried out in your particular business unit” (IMPATHEM) (1= no

impact, 5= a very significant impact). The Spearman’s correlation between both variables is

0.786 (p=0.000), so these variables are strongly correlated with each other.

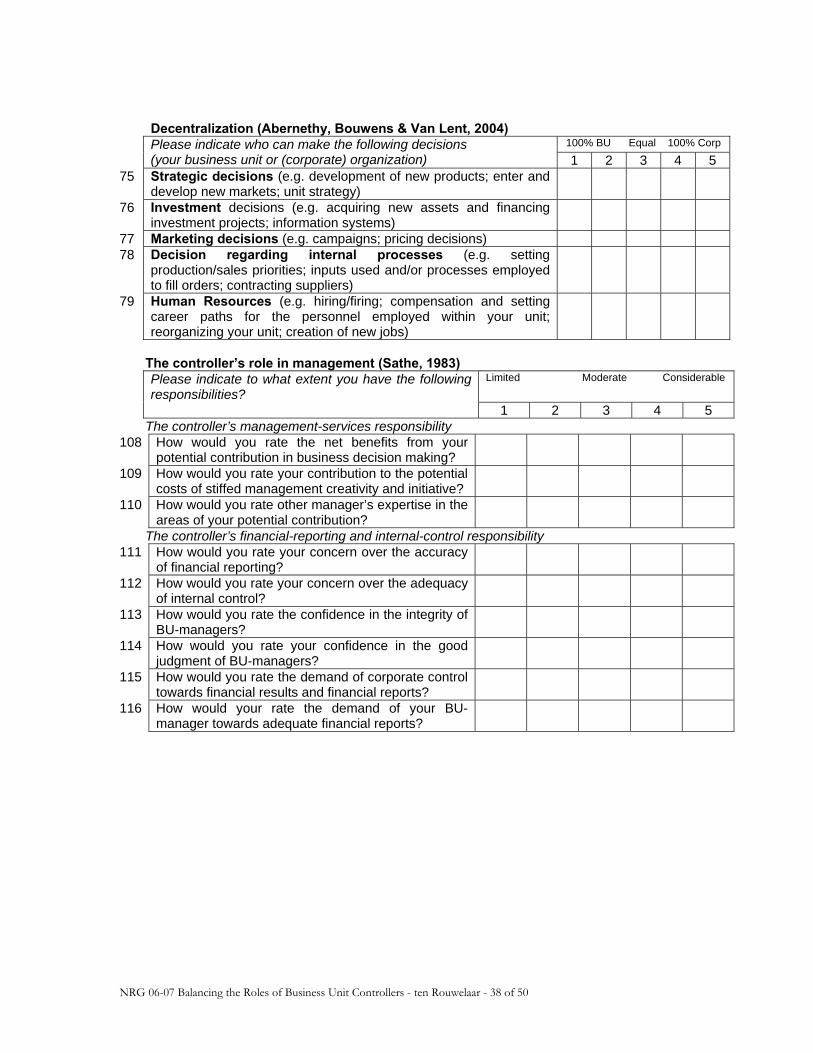

Decentralization (DECENTR)

This instrument is taken from Abernethy, Bouwens, and Van Lent (2004). They measure in

five questions who can make the following decisions in: Strategy, Investment, Marketing,

Internal processes, and Human Resources, ranging 1=100% Business unit to 5=100%

Corporate (see questions q75 to q79 in the questionnaire). These questions are reversed

(reverse code = 6 minus score, makes r75 to r79 out of the questions q75 to q79) and then

factorized. The factor analyses show just one factor: DECENTR, which explains 46.2% of

variance. The Cronbach Alpha of DECENTR is 0.7062.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 23 of 50

Performance (PERFORM)

An instrument of Abernethy, Bouwens and Van Lent (2004) which measures the

performance of the business unit by comparing the performance of the business unit to the

performance of external firms producing similar products or services (Abernethy et al,

working paper). The questions q134 to q139 measure just one factor called: PERFORM,

explaining 56.7% of variance. The Cronbach Alpha of PERFORM is 0.8458.

Personal Characteristics

There are a lot of different ways in measuring the personality characteristics of a person.

Through the years personality theories have tried to reduce the number of personality

characteristics to a small number of predispositions, resulting in the increasingly prominent

Five Factor Model (Mahony & Stasson, 2005).

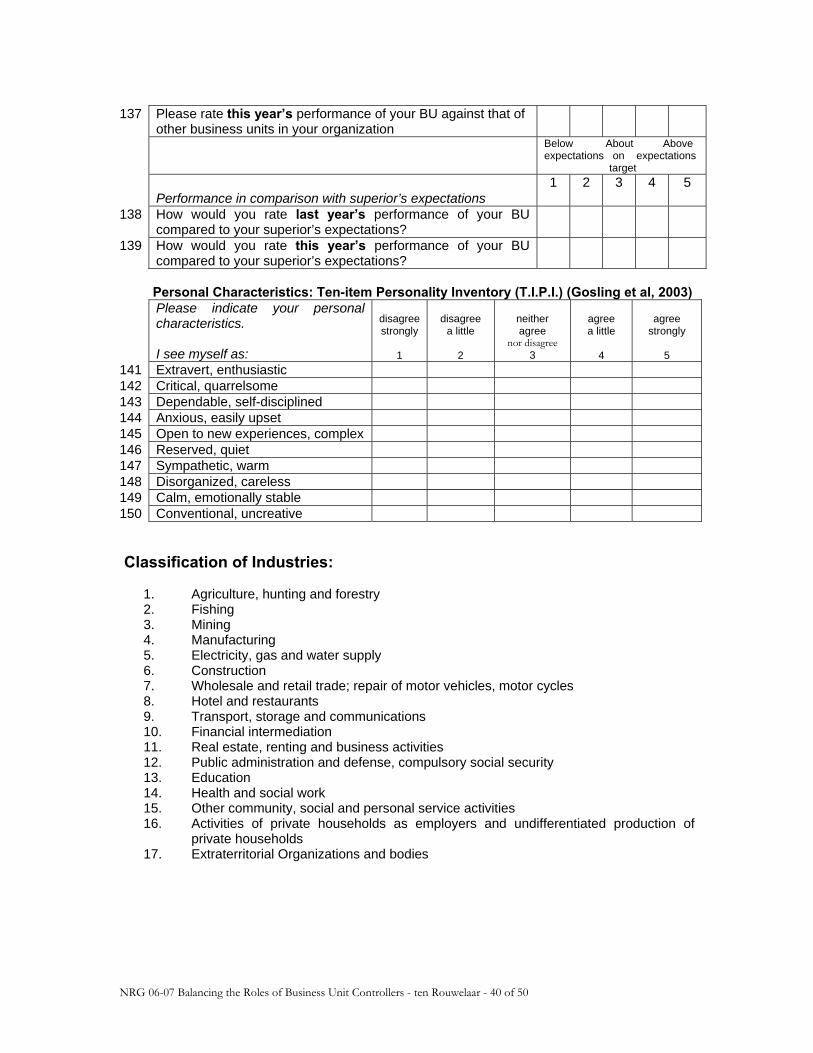

Gosling et al (2003) have developed a small instrument to measure the Five Factor Model:

the Ten-Item Personality Inventory (T.I.P.I.) instrument. This instrument measures the

personal characteristics, with just two questions for each item representing a pole of the five

Big-Five personality dimensions. Gosling et al (2003) have tested this T.I.P.I. instrument and

concluded that the ten questions fit to the Five Factor Model. The instrument, which is

inserted in the questionnaire in q141 to q150, is the “Ten-item Personality Inventory”

(T.I.P.I.). Each item consists of two descriptors, separated by a comma, using the common

stem, “I see myself as:” Each of the five items was rated on a 5-points scale ranging from 1

(disagree strongly) to 5 (agree strongly). The result of the ten measures of T.I.P.I. is a score

on each of the five dimensions of the BIG-Five personality Inventory:

Extraversion (E) = q141 + (6 – q146), Agreeableness (A) = q147 + (6 – q142),

Conscientiousness (C) = q143 + (6 – q148), Neuroticism (N) = q144 + (6 – q149), and

Openness to Experience (O) = q145 + (6 – q150) respectively.

Control Variables

Besides the independent- and dependent variables, I added control variables to the

questionnaire. These control variables are Firm Size, and three indicators for different types

of Industry.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 24 of 50

Firm Size (LOGSIZE)

There are different ways in which the size of the organization can be measured and

implemented in the research model. As proxy for the size of the organization I selected the

logarithm of the number of employees employed within the organization. Matĕjka also used

this variable as a control variable in his Dissertation (Matĕjka, 2002, page 13). The

Spearman’s correlation coefficients of LOGSIZE with Sales and Total Assets are: 0.446

(p<0.001) and 0.230 (p=0.026) respectively.

Industry (SERVICE, FINSERVI, PUBLIC)

Different types of Industry were measured by codes. In the questionnaire the respondents

could indicate in which industry the business unit is working. The number of codes has set

to 17 different codes. Based upon the number of organizations in the data set, I limited the

number of codes to just four different categories: (1) manufacturing organizations, code 4

and 5, (2) financial intermediation, code 10, (3) service organizations in trade, code 7, 8, 9,

and 11, and (4) public sector, code 12 – 15. The codes refer to the list at the end of

Appendix A.

4 Results

4.1. Descriptive Statistics

The bu-controllers who were interviewed, are working in variety of industry: 47.1% is

working in industry, 20.2% in trade, 9.2% in services, 16.0% in financial service, and 5.9% in

not for profit organizations (missing 1.7%). They have on average 9.0 years working

experience, of which 5.4 years as a bu-controller. On average the bu-controllers have worked

for 3.2 years within their current business unit. Of all 119 controllers, 57.2% has university

level education (Master level), 38.7% has a Bachelor level education (the remainder of them

(4.1%) has lower education or is not available in the data).

The bu-controller most frequently has a hierarchical relationship with the bu-manager in 79

business units (66%); in 17 business units (15%) there exists a hierarchical relationship with

the corporate controller. In the remaining 28 business units (19%) both bu-manager and

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 25 of 50

corporate controller have influence on the bu-controller, because of both functional and

hierarchical relationships.

Table 2 and 3 present descriptive statistics for all dependent and independent variables in the

estimation models described in the next sections.

--------------------------------------------------

INSERT TABLE 2 ABOUT HERE

--------------------------------------------------

Table 2 shows that the variables: RESPCON, RESPSUP, INVOLV and INDEP are all

variables, which have been factorized, because they have mean zero and standard deviation

equal to 1. The control time (CONTIME = q125 + q126) and support time (SUPTIME =

q127 + q128) express that the bu-controller on average spends 61.5% of his time on support

tasks and just 38.5% on control tasks. Though when you ask the bu-controller (in the

questions q118 till q124) which of the activities he can actually influence, the bu-controller

answers that he can influence control activities (mean 9.81) more than support activities

(mean 7.26).

--------------------------------------------------

INSERT TABLE 3 ABOUT HERE

--------------------------------------------------

Table 3 shows that almost all 119 respondents filled in all questions. Just two independent

variables, Market culture (MARKCULT) and Decentralization (DECENTR) were missing

one item. The control variables for the types of industry have 117 items. There were 35 (30

%) organizations in the service sector and 19 (16 %) in the financial service sector. There

were 7 (6%) organizations in the public sector in the data set. The remainder of the firms (56

(48%) firms) are active in the manufacturing sector.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 26 of 50

--------------------------------------------------

INSERT TABLE 4 ABOUT HERE

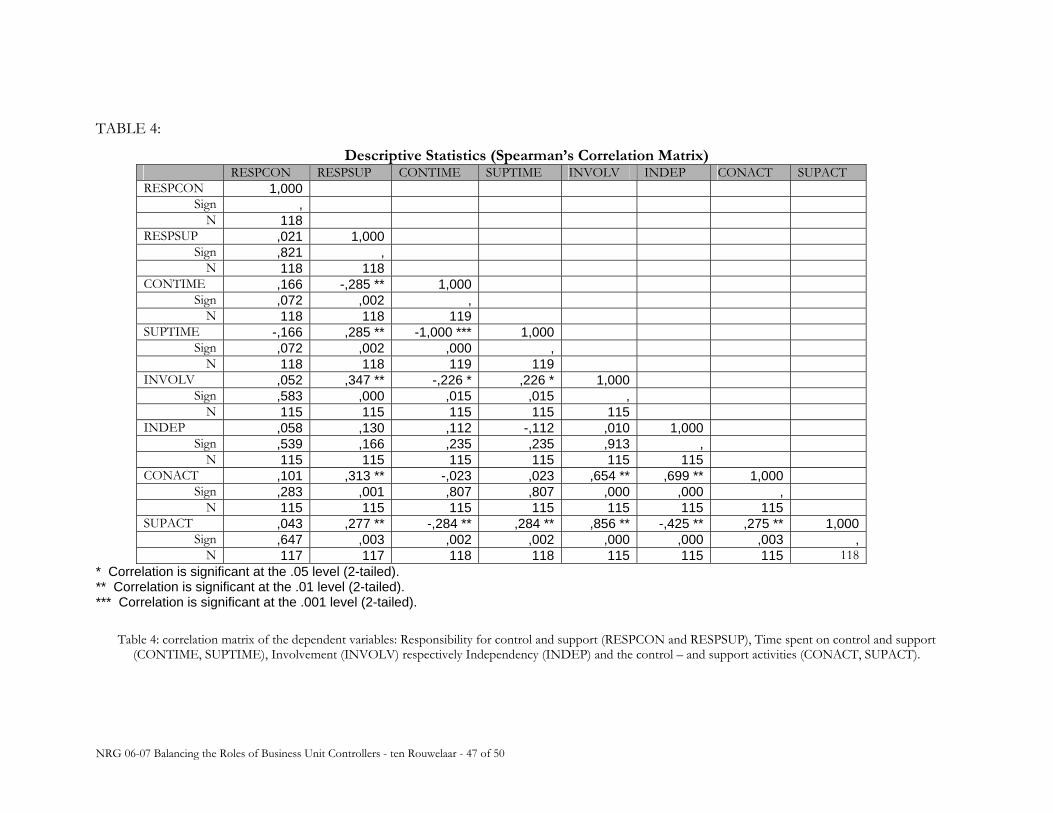

--------------------------------------------------

Table 4, the correlation matrix of the dependent variables, shows that controllers, who

indicate that they are responsible for support tasks (RESPSUP), also spend more time in this

area (SUPTIME, 0.347, p<0.01) and are more involved in management decision-making

(INVOLVE, 0.285, p<0.01). It is strange to notice that RESPSUP is positively correlated

with both Support and Control activities (SUPACT 0.277, p<0.01, and CONACT 0.313,

p<0.01). This means that bu-controllers, who are responsible for support tasks, indicate that

they give more attention to both roles, which is also shown by the fact that INVOLV is

positively related with both CONACT (0.654, p<0.10) and SUPACT (0.856, p<0.10). Bu-

controllers, who indicate that they are more independent, are as expected, more related to

control activities and less related to support activities: INDEP is positively related with

control - and negatively related with support activities (0.699, p<0.01, -0.425, p<0.01). The

variables indicate that the time spend on control (CONTIME) is negatively correlated with

INVOLV (-0.226, p<0.05) and support activities SUPACT (-0.284, p<0.01). The time spent

on support SUPTIME is positively related with support activities SUPACT (0.284, p<0.01).

This is in conformity with the expectations.

--------------------------------------------------

INSERT TABLE 5 ABOUT HERE

--------------------------------------------------

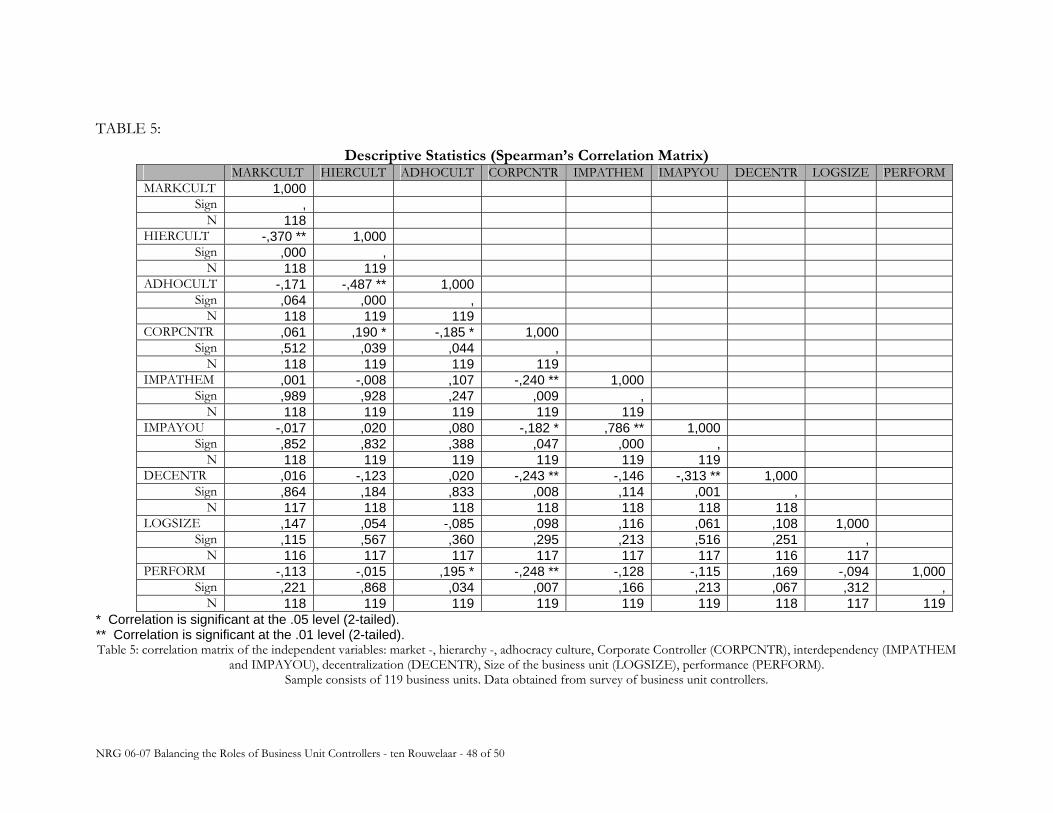

Table 5, the correlation matrix of the independent variables, shows that the independent

variables are hardly correlated among themselves. This indicates that problems with

multicollineairity or biased econometric results are likely to be minimal.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 27 of 50

4.2. Main Findings

Empirical testing of the hypothesis derived earlier involved assessing the impact of the

consistency factors on the support and control roles of the bu-controller. To estimate the

impact of the contextual factors, the following empirical model is defined:

X i = ß 0i + ß 1i * MARKTCULT i + ß 2i * HIERCULT i + ß 3i * ADHOCULT i + ß 4i * CORPCNTR i + ß 5i *

IMPATHEM i + ß 6i * IMPAYOU i + ß 7i * DECENTR i + ß 8i * LOGSIZE i + ß 9i * PERFORM i + ß 10i * N i

+ ß 11i * E i + ß 12i * O i + ß 13i * A i + ß 14i * C i + ß 15i * SERVICE i + ß 16i * FINSERVI i + ß 17i * PUBLIC i +

ε i

Where:

X = One of the following Dependent variables:

RESPCON i = degree of responsibility for control role by bu-controller of

organization i.

RESPSUP i = degree of responsibility for support role by bu-controller of

organization i.

CONTIME i = time spent on control role by bu-controller of organization i.

SUPTIME i = time spent on control role by bu-controller of organization i.

INVOLV i = the degree in which the bu-controller is involved in organization i.

INDEP i = the degree in which the bu-controller is independent in organization

i.

CONTACT i = control activities done by the bu-controller of organization i

SUPACT i = support activities done by the bu-controller of the organization i

And as Independent variables:

MARKTCULT i = Market culture of organization i.

HIERCULT i = Hierarchy culture of organization i.

ADHOCULT i = Adhocracy culture of organization i.

CORPCNTR i = Hierarchy Dummy (i.e. 1 = corporate-controller is hierarchical

principal of the bu-controller, 0 = other is hierarchical principal of

the bu-controller) of organization i.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 28 of 50

IMPATHEM i = the impact of the business unit on other business units of

organization i.

IMPAYOU i = the impact of other business units on the business unit of

organization i.

DECENTR i = Degree of decentralization of activities to the business unit of

organization i.

LOGSIZE i = logarithm of the number of FTE within organization i.

PERFORM i = the degree in which the business units of organization i is successful.

N i = the degree in which the bu-controller is concerned or attentive.

E i = the degree in which the bu-controller is extrovert or social involved.

O i = the degree in which the bu-controller is open to new experiences.

A i = the degree in which the bu-controller is agreeable or tolerant.

C i = the degree in which the bu-controller is conscience or disciplined.

Control variables:

SERVICE i = Industry Dummy (i.e. 1 = service Industry, financial services

excluded, 0 = other industry) for organization i.

FINSERV i = Financial Service Industry Dummy (i.e. 1 = financial service centre, 0

= other industry) for organization i.

PUBLIC i = Public Service Industry Dummy (i.e. 1 = organization in not-for-

profit sector, 0 = other industry) for organization i.

ε i = error term of organization i.

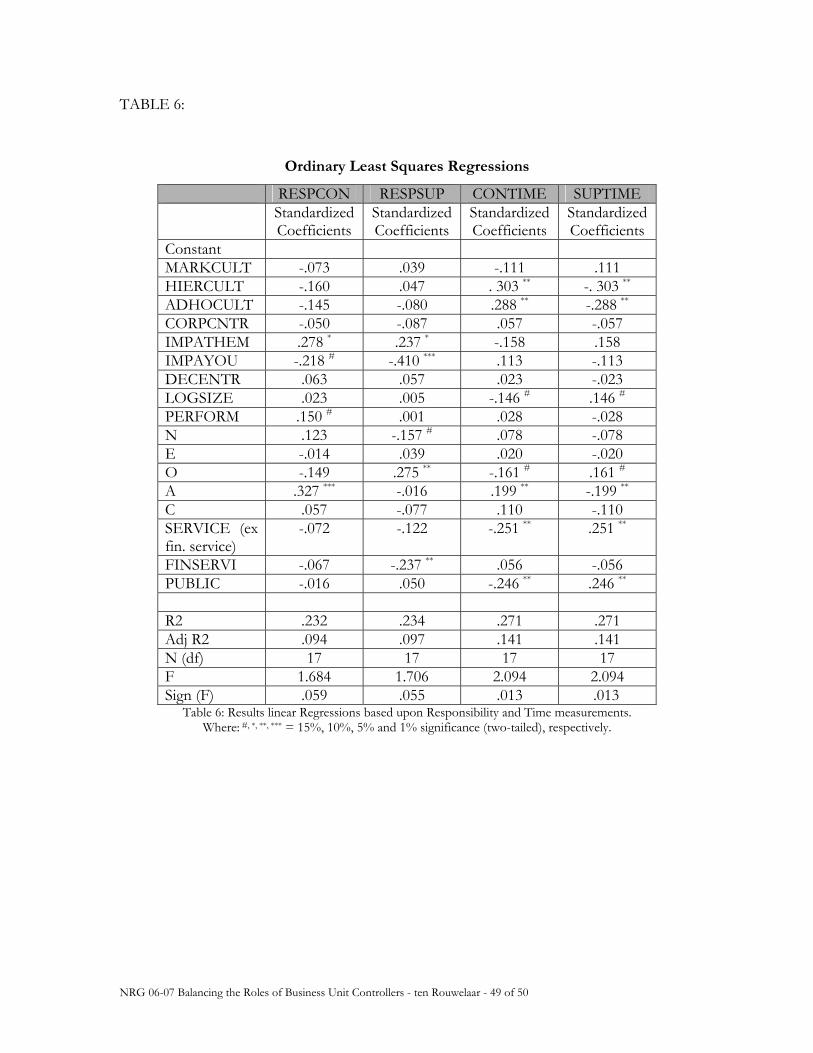

Table 6 presents the results of the bu-controller’s responsibility and time analysis.

--------------------------------------------------

INSERT TABLE 6 ABOUT HERE

--------------------------------------------------

Table 6 indicates that both the support and the control responsibilities were negatively

influenced by the impact of other business units’ activities (IMPAYOU), but positively

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 29 of 50

influenced by influence on other business units (IMPATHEM). In case the organization has

more concern about the results, the control responsibility of the bu-controller will increase,

because more responsibility for control seems to be slightly, positively related with

performance or stress (0.150, p<0.15). Bu-controllers with a character ‘open to new

experiences’ will have more responsibility for support as expected. Bu-controllers with an

accommodating character have more responsibility for control. These findings partly

confirm hypotheses H 6a and H 6b.

Measuring the two roles of the bu-controller based upon the time analyses (CONTIME and

SUPTIME) provides the best results with the highest adjusted R-squared (0.141). Table 6

also indicates, that consistent with the expectations, the time spent by the bu-controller on

the control role is positively related with hierarchical and adhocracy cultures. Bu-controllers

with a character ‘open to new experiences’ are spending less time on control, in contrast to

the bu-controllers with an accommodating character. Bu-controllers with an accommodating

character are more positive toward control tasks. The size of the organization, conform

expectations, indicates that bigger organizations spent more time on support tasks and less

on control tasks. Other factors, like interdependency, decentralization and performance do

not have any effect on the time spent on either control or support tasks. Also, the

hierarchical position of the bu-controller doesn’t seem to have any influence on the way in

which the bu-controllers spend their time. However, organizations in the service- or the

public sector are spending less time on control and more on support than organizations

working in the manufacturing sector.

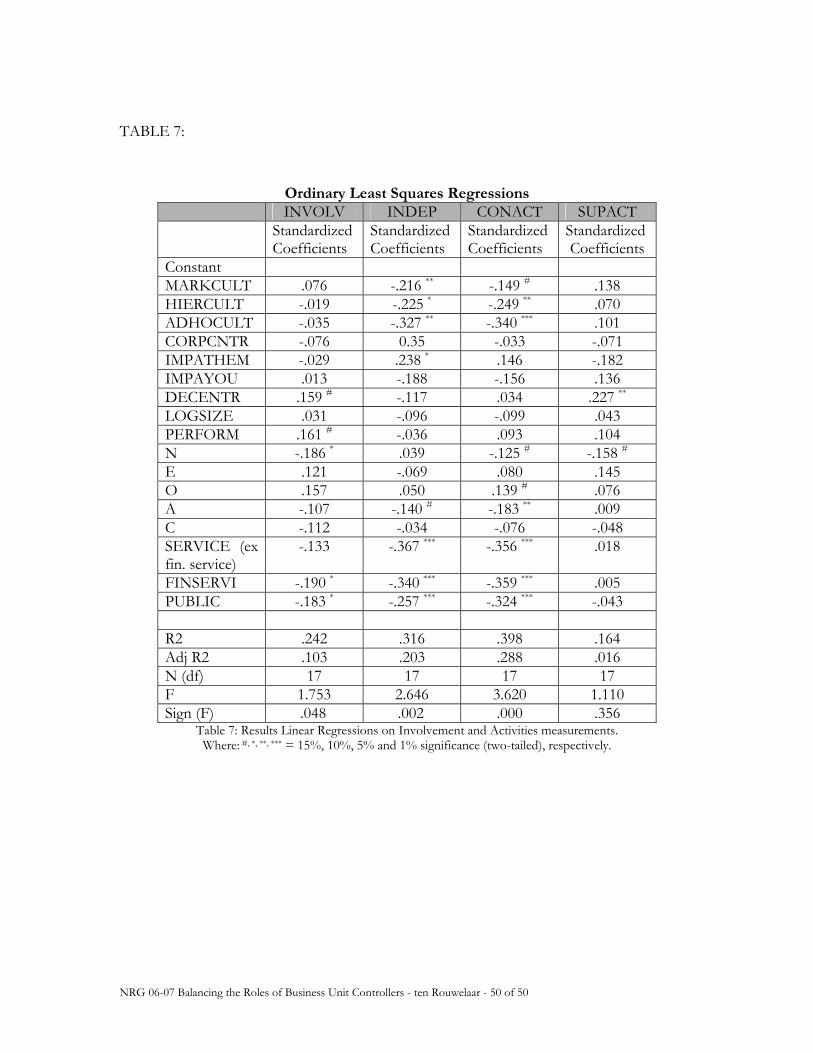

Table 7 presents the results of the analysis of Involvement and Activities.

--------------------------------------------------

INSERT TABLE 7 ABOUT HERE

--------------------------------------------------

Table 7 indicates that, consistent with expectations, the involvement of the bu-controller is

positively related with decentralization (0.159, P<0.15). Giving a bu-manager more

responsibility will increase the involvement of the bu-controller. Bu-controllers with a high

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 30 of 50

score on ‘neuroticism’ (reactive) seem to be less involved than bu-controllers with other

personal characteristics (-0.186, p<0.10). PERFORM, as an indication to the success of the

business unit, indicates to be slightly positively associated to the involvedness of the bu-

controller (0.161, p<0.15). Bu-controllers working in the financial service sector (-0.190,

P<0.10) or the public sector (-0.183, p<0.10) seem to be less involved in management

decisions than bu-controllers working in the manufacturing sector.

The results of the analysis based upon the measurement of control- and support activities,

are quite different in explanation. The regression of the control activities (CONACT) has an

adjusted R-square of 0.398, but the regression of the support activities (SUPACT) has an

adjusted R-square of just 0.164. The control activities of the bu-controller seem to be

negatively associated with all cultural factors and all organizational dummy variables.

Decentralization is positively related with support activities, which is in line with the

expectations (0.227, p<0.10). Bu-controllers with a high score on ‘neuroticism’ (reactive) are

slightly negatively related with control activities and support activities (- 0.125, p<0.15; and -

0.158, p<0.15 respectively). These results are also in line with the expectations (hypothesis

6b). In contrast to the results of the time analysis the relation between bu-controllers with an

agreeable character are now negatively related with control activities (-0.183, p<0.10). Table

7 shows that bu-controllers with these characteristics spend less time on their control tasks.

5 Discussion and Concluding Comments

5.1. Discussion

In this exploratory study the two roles of the bu-controller, support role and control role,

were related with two of the three categories of factors, developed by Sathe 1982: (1) factors

related to the characteristics of the company’s environment and business, and (2) factors

related to the controller’s motivation and personality.

In this paper five characteristics of the company’s environment and business were analyzed.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 31 of 50

First, the relations with four different cultures were examined. When an organization has a

hierarchical or adhocracy culture the bu-controller will spend more time on the control role.

Second, the hierarchical relationship with the corporate controller was tested. The way in

which the bu-controller is supervised did not seem to affect the support or the control role

of the bu-controller.

Third, the relations between two factors of Interdependencies, the impact on other business

units (IMPATHEM) and the impact from other business units on the business units

(IMPAYOU), were tested. Both support and control responsibilities were negatively

influenced by the impact of other business units’ activities (IMPAYOU), but positively

influenced by influence on other business units (IMPATHEM).

Fourth, the involvement of the bu-controller is positively related with decentralization.

Giving a bu-manager more responsibility will in general mean that the involvement of the

bu-controller will increase.

Fifth, performance or financial stress indicates to be slightly positively associated to the

involvedness of the bu-controller, but doesn’t seem to have significantly strong influence on

the two roles of the bu-controller.

The second category of factors is the ‘personal characteristics’-category. In this category

several factors or ‘personal characteristics’ were also measured and interrelated with the two

roles. As expected, bu-controllers with a character ‘open to new experiences’ are spending

more time on support tasks. Bu-controllers with an agreeable or consolidation character are

spending more time to control tasks.

Extra control variables, like the size of the organization and types of industry, do not have

strong effects on the time spent on either control or support tasks. However, there appear to

be some industry effects: Organizations in the service- or the public sector are spending less

time on control tasks than organizations working in the manufacturing sector.

5.2. Limitations

Several steps were taken to limit the scope of this study and to keep the project manageable.

First, only Dutch organizations and their domestic business units are included in this

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 32 of 50

investigation. Second, the study is limited to large, multidivisional organizations. Other data

selected in another country or under other circumstances, could probably lead to other

results. Finally, the third category of factors, developed by Sathe (1982), the factors related to

management’s expectations, orientation, and operating philosophy, was not taken into

account, because it is labour-intensive to interview both bu-controllers and their bu-

managers, so only the bu-controllers were interviewed, and their bu-managers were not

included in this study.

5.3. Future research

Besides the organizational characteristics included in this paper, there are several other

contingency factors, of which it is expected that they have a relation with the roles of the bu-

controllers. For instance: (1) the size of the department the bu-controller: if the department

is very small the bu-controller has to do relatively more executive and reporting tasks, as a

result of which the time spend on the control role will increase; and (2) the degree in which

the bu-controller is relieved with a number of management accounting and ICT-tools, like

Activity Based Costing -, Enterprise Resource Planning (ERP) -, and computerized

Accounting Systems. It is to be expected that if the degree of such ICT-tools is high, the bu-

controller does not have to spend much time on executive (control) tasks, as a result of

which the support role will increase. These other organizational characteristics are interesting

to investigate in the future.

This study investigates bu-controllers only. To measure the effects of the support and

control roles more accurately the bu-managers should also participate in a future study. In

my second study in 2006, I will select data from both bu-controllers and their bu-managers

to explore the third category of factors, developed by Sathe (1982), the factors related to

management’s expectations, orientation, and operating philosophy.

Besides the search for missing organizational factors, other questions are interesting to

investigate in future research. For instance the research of the question whether controllers

are selected for their job based upon their personal characteristics or whether they shape

their job and adjust their tasks to their personal characteristics.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 33 of 50

Future research could probably give better results if the instruments, by which the separate

roles are measured, would improve. Measuring the two roles of bu-controllers by more

adequate questions, that are related with the specific subject, or registration of the time

spend on several control – and support tasks and activities, would certainly improve the

insights of the balancing the roles of bu-controllers.

Despite the limitations, this paper is amongst the first that shed empirical light on the two

roles of bu-controllers and provides a starting-point for further exploring the theoretical

framework to study controller effectiveness, and theorizing the behavioral aspects of the

balance between the two roles of bu-controllers.

NRG 06-07 Balancing the Roles of Business Unit Controllers - ten Rouwelaar - 34 of 50

6. APPENDIX A: Part of the Questionnaire

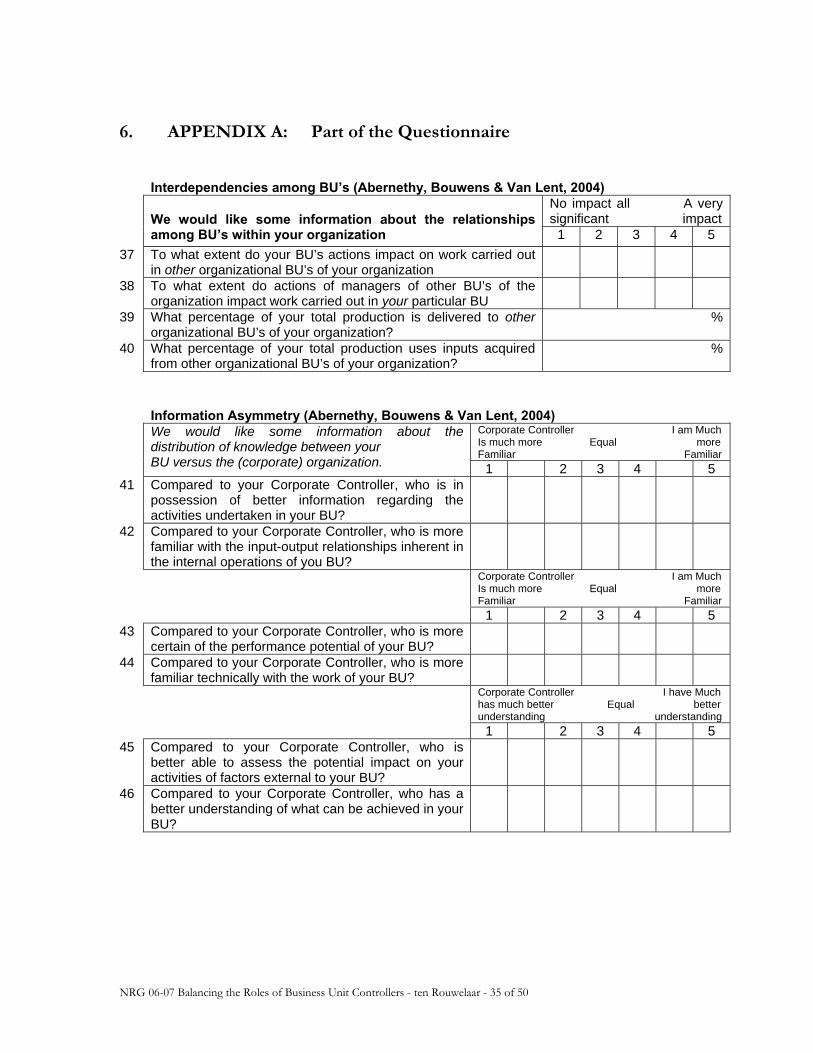

Interdependencies among BU’s (Abernethy, Bouwens & Van Lent, 2004) No impact all A very

significant impact

We would like some information about the relationships among BU’s within your organization 1 2 3 4 5

37 To what extent do your BU’s actions impact on work carried out in other organizational BU’s of your organization

38 To what extent do actions of managers of other BU’s of the organization impact work carried out in your particular BU

39 What percentage of your total production is delivered to other organizational BU’s of your organization?

%

40 What percentage of your total production uses inputs acquired from other organizational BU’s of your organization?

%

Information Asymmetry (Abernethy, Bouwens & Van Lent, 2004)

Corporate Controller I am Much Is much more Equal more Familiar Familiar

We would like some information about the distribution of knowledge between your BU versus the (corporate) organization. 1 2 3 4 5

41 Compared to your Corporate Controller, who is in possession of better information regarding the activities undertaken in your BU?