North America Beverages: The Shape of the Future

85

North America Beverages: The Shape of the Future Morgan Stanley Global Consumer & Retail Conference November 20, 2008

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of North America Beverages: The Shape of the Future

North America Beverages: The Shape of the Future

Morgan Stanley Global Consumer & Retail Conference

November 20, 2008

Indra NooyiPepsiCo Chairman & CEO

2

Safe Harbor StatementThis material may contain “forward-looking” statements about our expectations regarding future performance, such as our business outlook. These forward-looking statements are based on currently available information, operating plans and projections about future events and trends. They inherently involve risks and uncertainties that could cause actual results to differ materially from those predicted in any such forward-looking statements. Such risks and uncertainties include, but are not limited to: changes in demand for our products, as a result of shifts in consumer preferences or otherwise; our ability to maintain our reputation; our ability to build and sustain our information technology infrastructure, successfully implement our business process transformation initiative or to outsource certain functions effectively; fluctuations in the cost and availability of raw materials; our ability to compete effectively; disruption of our supply chain; trade consolidation, the loss of any key customer, or failure to maintain good relationships with our bottling partners; changes in the legal or regulatory environment; our ability to hire or retain key employees; unfavorable economic, environmental or political conditions in the countries where we operate; market risks arising from changes in commodity prices, foreign exchange rates and interest rates; and risks that benefits from our Productivity for Growth initiative may not be achieved or may take longer to achieve than expected or may cost more than currently anticipated. For additional information on these and other factors that could cause our actual results to materially differ from those set forth herein, please see our filings with the Securities and Exchange Commission, including our most recent annual report on Form 10-K and subsequent reports on Forms 10-Q and 8-K. Investors are cautioned not to place undue reliance on any such forward-looking statements, which speak only as of the date they are made. We undertake no obligation to update any forward looking statements, whether as a result of new information, future events or otherwise.

3

2008 – The Year In Review

Bright Spots

• Solid North America Foods Performance–Strong net sales management

• Strong Performance in International Markets−Both snacks and beverages performing well

• On track to deliver full year core guidance

4

FLNA: Solid YTD Results

6

8

2

Volume Revenue NOPBT

• Strong top-line growth

• Solid Core salty performance

• Pricing to cover commodity inflation

• Accelerated productivity and cost management

FLNA Q3 YTD %YAGFLNA Q3 YTD %YAG

5

FLNA: Go-Forward Priorities

• Sustain growth of our core salty business

• Balance pricing and value

• Execute Productivity for Growth agenda

• Continue portfolio evolution towards healthier macrosnacking

6

LAF: Outstanding YTD Results

2933

5

Volume Revenue NOPBT

• Balanced top-line growth

• Successful integration of acquisitions

• Accelerated productivity and judicious cost management

LAF Q3 YTD %YAGLAF Q3 YTD %YAG

7

LAF: Go-Forward Priorities

• Sustain growth trends in our key markets– Mexico salty and sweet/baked portfolio– Invest to win in emerging markets

• Stay ahead of inflation – revenue and cost management focus

• Execute Productivity for Growth agenda

• Continue expansion of the Quaker brand and Gamesa sweet/baked portfolio across LAF

8

PI: Solid YTD Results

Volume

1923

128

Snacks Bevs Rev NOPBT

• Balanced top-line growth

• Strong growth across developing markets

• Continued success in China

• Successful expansion of PLI partnership

PI Q3 YTD %YAGPI Q3 YTD %YAG

9

PI: Go-Forward Priorities

• Manage net revenue and profitability

• Successfully integrate Lebedyansky and Marbo

• Execute Productivity for Growth

• Invest to win in key emerging markets

• Continue NCB expansion

Managing for Long Term Growth

• Operating agility to manage through challenging environments− Experience managing through adversity− Focus on consumer value proposition− Leveraging productivity for growth− Selectively investing and making smart trade-offs

• Diverse, consumer-driven product portfolio

• Continuing to invest for the long term− Building brands and innovating− Retaining world class talent− Maintaining focus on Performance with Purpose sustainability agenda

11

Reinvent the consumer proposition

Proactively manage portfolio

Optimize business and asset strategy

Key Elements for Success

We have identified 3 key elements for turnaround success

12

LRB category composition and trends

North America Beverages - Agenda

Our Bottler partnership

Our agenda for growth

Massimo D’Amore

CEO PepsiCo Americas Beverages

14

Consumers are still drinking…

Total beverage occasions increasing…

…but Liquid Refreshment Beverages (LRB) lost share to cheaper in-home alternatives

Continued penetration growth in Non-Carbs (NCBs)- CSDs & bottled water losing occasions

15

% LRB 48.1% 53.4%

Source: Beverage Marketing Corp; 2008 LRB Model v98; internal PAB LRB estimates

LRB

Coffee and Teas

Coffee and Teas

Tap Tap

Alcohol Alcohol

Milks Milks

LRB

1999 2007

34.8 Bn 37.9 Bn

Total US Volume (8oz)Volume

CAGR (99-07)

flat

1%

(4)%

1%

2.4%

1%

Historically LRB sourced share from other beverages

Through 2007 LRB was the fastest Through 2007 LRB was the fastest growing segment within Total Beveragesgrowing segment within Total Beverages

16

Accelerating CSD decline & a halt in bottled water growth were the primary reasons for 2008 fall off

2008F

1. Other NCB — Non-Carbonated Beverages (Juice, Juice Drinks, Sports Drinks, Enhanced Water, Energy, RTD Tea, RTD Coffee, VAD) 2. Water includes bottled water, Jug / bulk and other water (does not include enhanced water)

Source: LRB 2008 Model; Beverage Marketing Corporation; BCG analysis

CSDs45%

Bottled Water2

25%

Other NCBs1

30%

20B 8oz CasesBottled Water2

(5)

0

5

10

15

'00 -'04

'05 -'06

'07 -'08F

'00 -'04

'05 -'06

'07 -'08F

'00 -'04

'05 -'06

'07 -'08F

Volume CAGR (%)

Other NCBs1CSDs

LRB Category Mix

17

• Under-served consumers

• Unfulfilled occasions

• Unmet need intersections

• Advantaged science brings new ways to address needs:

- Nutrition

- Transformation

In-depth consumer analysis identified significant opportunities for LRB growth

18

We expect LRB Will Return to Growth With Economic Recovery

Regain share of occasions from non-LRB

Population Growth

LRB Growth

+

See value-oriented growth through the economic downturn

Returning to volume growth at least in line with population

Positive trends for value-added products over longer term fuelled by:

– Functional benefits

– New occasions

– Leveraging science

19

Over 50% of LRB value remains with CSDs

LRB value % mix

11

31 34 33 35 38

54586065 51

11964

0

25

50

75

100

1990 1995 2000 2005 2008F

CSDs

1. Other NCB — Non-Carbonated Beverages (Juice, Juice Drinks, Sports Drinks, Enhanced Water, Energy, RTD Tea, RTD Coffee, VAD) 2. Water includes bottled water, Jug / bulk and other water (does not include enhanced water)

Source: LRB 2008 Model; Beverage Marketing Corporation; BCG analysis

Other NCBs1

Water2

20

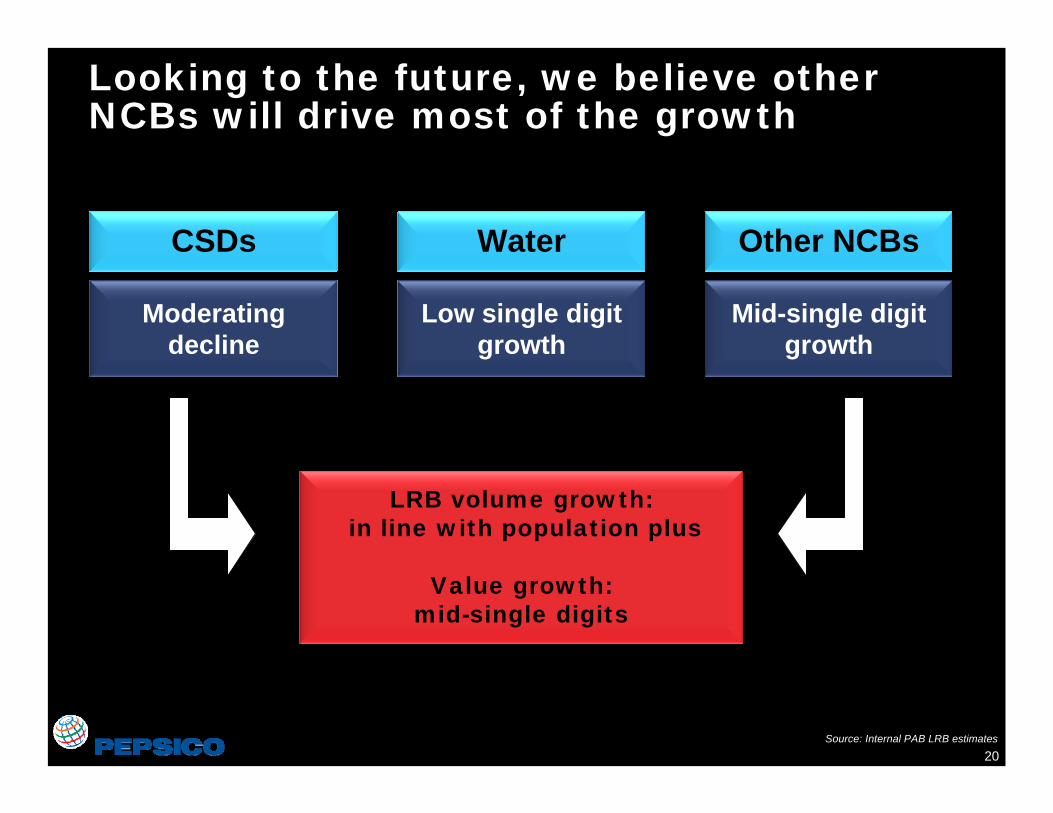

Looking to the future, we believe other NCBs will drive most of the growth

Other NCBsWaterCSDs

Moderating decline

Low single digit growth

Mid-single digit growth

LRB volume growth:in line with population plus

Value growth: mid-single digits

Source: Internal PAB LRB estimates

21

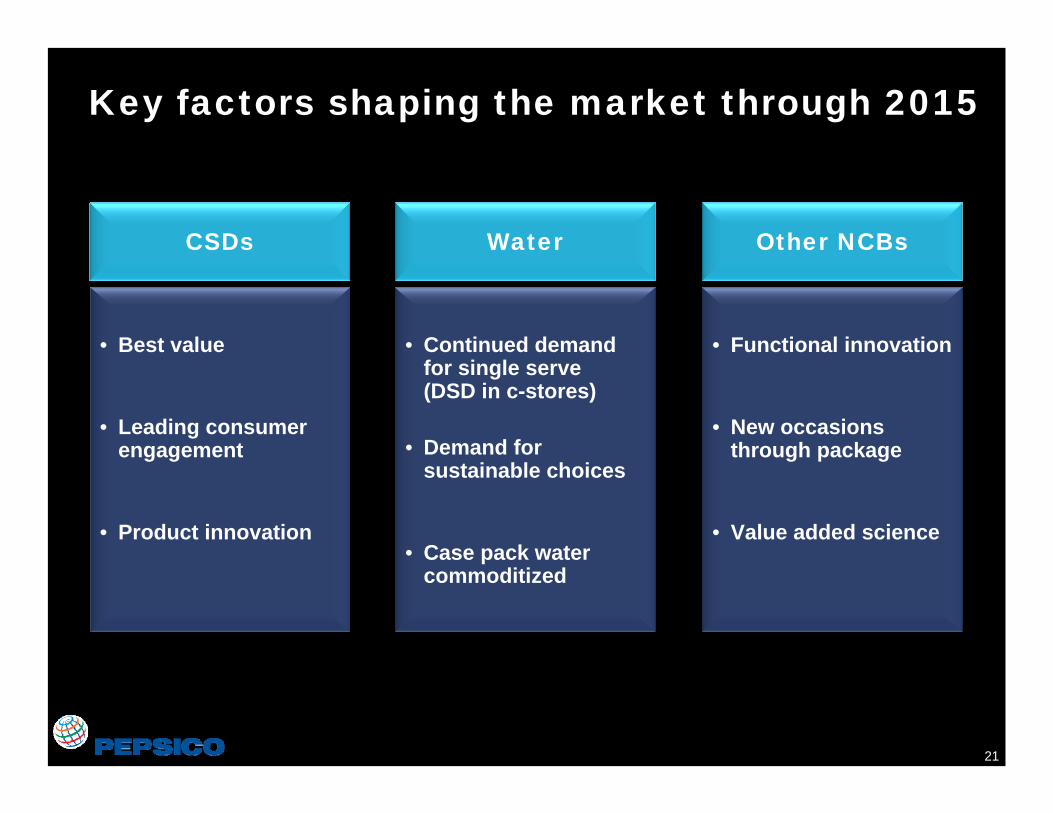

Key factors shaping the market through 2015

Other NCBsWaterCSDs

• Best value

• Leading consumer engagement

• Product innovation

• Continued demand for single serve (DSD in c-stores)

• Demand for sustainable choices

• Case pack water commoditized

• Functional innovation

• New occasions through package

• Value added science

22

LRB category composition and trends

North America Beverages - Agenda

Our Bottler partnership

Our agenda for growth

23

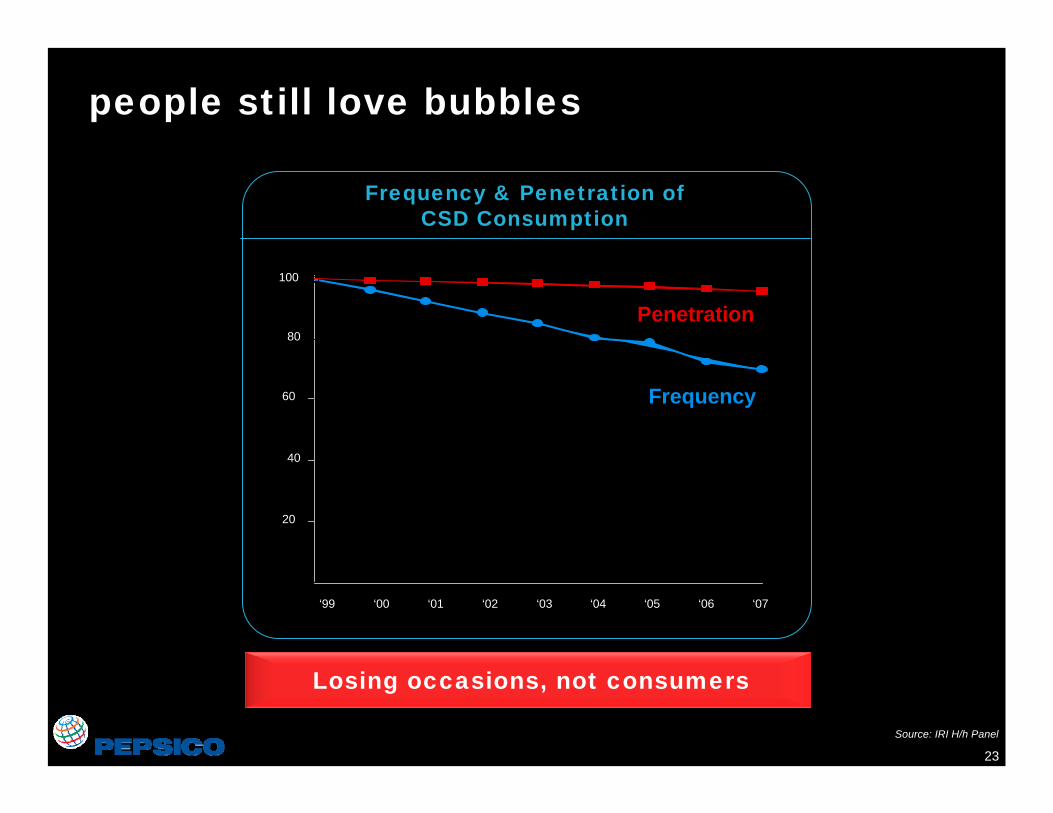

people still love bubbles

Index (1999 = 100)

Penetration

‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07

80

100

40

60

20

Frequency

Frequency & Penetration of CSD Consumption

Source: IRI H/h Panel

Losing occasions, not consumers

24

Regaining CSD momentum requires removing frequency barriers

Natural sweetener

Less “artificial” ingredients

Reinvent the consumer proposition

We’re making focused bets against all of these

25

With Mt Dew we have proven our ability to deliver despite category headwinds

Mt Dew Succeeding Despite CSD Headwinds

#1 Flavored CSD brand

#1 C&G CSD SKU

Extremely Loyal &

Passionate Consumers

0%

1% 1%

(3%)

CSD Mt Dew

’99-’06Vol CAGR

’07-’08FVol CAGR

Source: PAB LRB Model, IRI GDMxC YTD Nov 2, 2008

26

Dew succeeding with deep consumer connection

Beyond flavored line extension to “experiences”

Harnessing the power of the

masses

Leveraging an open source model for

creativity

Driving affinity via compelling content

27

Sierra mist video

28

1920s 1940s 1960s 1980s 2000s

Timeline

Culture

Double Ounces‘Jingle’ that united

Spirit of Victory

First Moverto Embrace

Diversity

PepsiGeneration

SuperstarsNew Generation

GenerationNextYouth identity

PEPSI

At its best, Pepsi was a catalyst for change in popular culture

29

• A catalyst for positive change

• Leading rather than mirroring culture

• A true challenger

We have a history of being…

30

Humanity

Simplicity Modern, iconic

Optimism and energy

Heritage Sign of the times

… And Renewed Our Brand Identity

31

DesignHeritage

Sign of the Times

Simplicity

Modern,simple, iconic

Humanity

Humanity, Optimism,Energy

32

Smile

Wink

Laugh

:-)

;-)

:-D

33

34

Our New Icon

PEPSIDIET PEPSI

SmileSavor theOriginal

GrinIndulgence

Without Regret

PEPSI MAX

LaughMaximumEnjoyment

35

Arnell Video

36

Bharat

37

Bharat

38

39

40

41

42

43

44

Water and Non-Carbs…

1. NCB — Non-Carbonated Beverages (eg, sports drinks, RTD tea, etc) 2. Water includes bottled water, Jug / bulk and other waterSource: LRB 2008 Model; Beverage Marketing Corporation; BCG analysis

2008F LRB Category Mix

3038

5145

1125

0

25

50

75

100

Volume Value

CSDs

Other NCBs1

Water2

• Energy• RTD CoffeeTransform

Nourish

Hydrate• Bottled Water• Enhanced Water• Sports Drinks

• Chilled Juice• Shelf Stable Juice• RTD Tea• Value Added Protein

Fulfill three consumer needs

1. Other NCB — Non-Carbonated Beverages (Juice, Juice Drinks, Sports Drinks, Enhanced Water, Energy, RTD Tea, RTD Coffee, VAD) 2. Water includes bottled water, Jug / bulk and other water (does not include enhanced water)

Source: LRB 2008 Model; Beverage Marketing Corporation; BCG analysis

45

PepsiCo is the #1 player in hydration with top brand positions

Share of 04-08F Category Vol CAGR

Bottled Water 14% 10%

Sports Drinks 78% 7%

Enhanced Water 34% 26%

Total Hydration* 30% 10%

PEP Hydration Portfolio

* Excludes jug waterSource: YTD Nov 2, 08 GDMxC IRI, PAB LRB Model

Rank

#1 Aquafina

#1 Gatorade

#2 Propel#3 Aquafina Flavor Splash#4 SoBe Lifewater

46

Hydration is a big category serving broad needs

Transform

Nourish

Hydrate

• Simple hydration

• Body wellness

• Performance hydration

• Bottled Water

• Enhanced Water

• Sports Drinks

47

Consumers have clearly segmented hydration needs

PepsiCo hydration portfolio designed to address unique consumer needs

Simple Hydration Body WellnessPerformance

Hydration

48

48

49

Aquafina – Flavor Splash

50

Body wellness – Propel was #1 brand and will be reasserted in 2009

51

52

53

54

55

56

Performance Hydration: Gatorade

Source: PepsiCo Market Research

Heritage

Opportunity

57

“G” will become the essence of Gatorade

58

jimmy video

59

‘G’ comes to life in our 2009 product line-up

60

Gatorade sizzle video

61

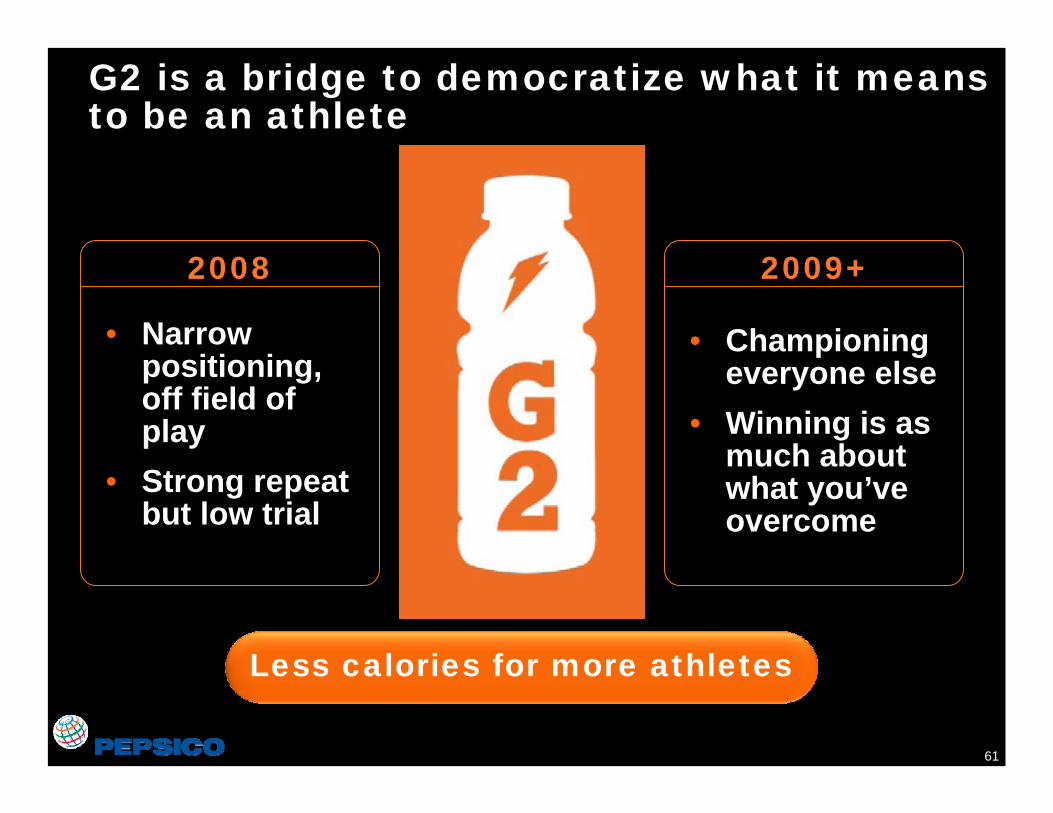

G2 is a bridge to democratize what it means to be an athlete

• Narrow positioning, off field of play

• Strong repeat but low trial

2008

Less calories for more athletes

• Championing everyone else

• Winning is as much about what you’ve overcome

2009+

62

PepsiCo’s right to succeed in Hydration

# 1 share, leading portfolio of brands

Know consumer segments well

Portfolio aligned to consumer needs

Source: YTD Nov 2, 08 GDMxC IRI, PAB LRB Model

63

Nourishment: a growing category

Transform

Hydrate

Nourish

Sustain My

Health

Tide Me

Over

Manage My

Weight

64

We are re-positioning Tropicana to own the breakfast occasion

Great Start To The Day

Emotional Connection

Positive Nutrition 100% Goodness

65

TPP Morning video

66

For lapsed OJ drinkers concerned about calories

Great Start To The Day

Positive Nutrition 100% Goodness

50% Less Sugar

67

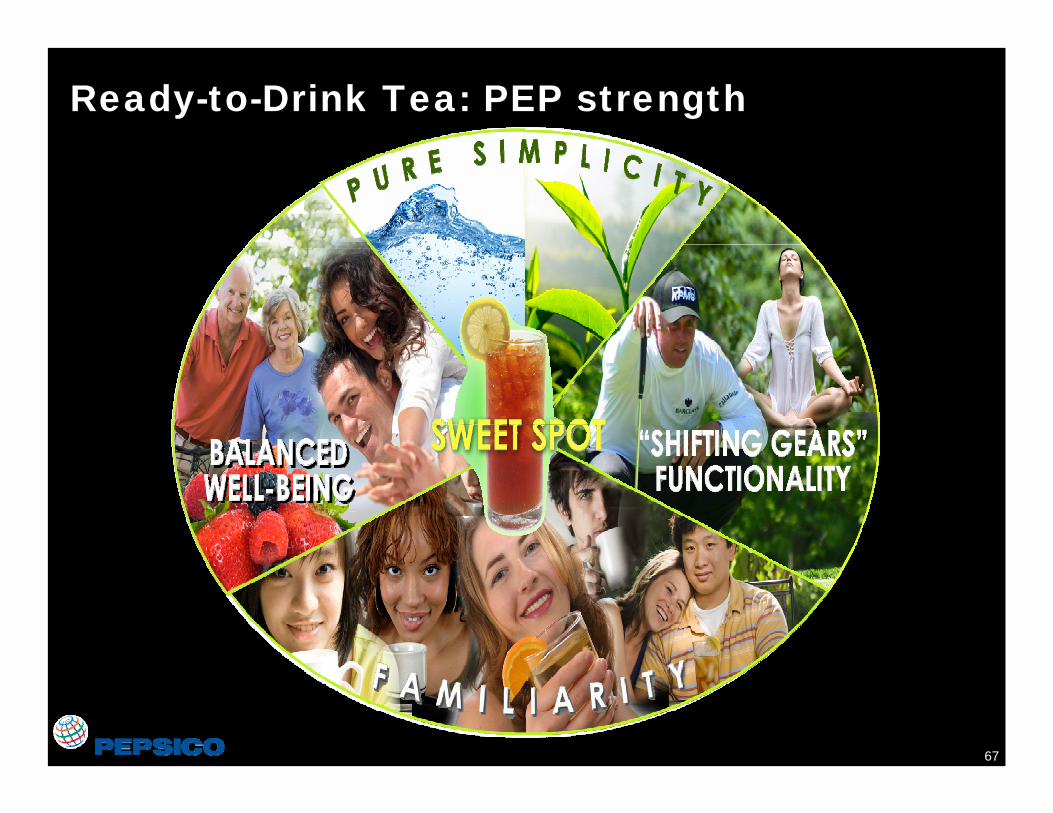

Ready-to-Drink Tea: PEP strength

68

Terrific partnership and portfolio

Demographic

Need

Benefit

69

Leadership growth with roll-out of Green Tea

$950MM

$115MM05-08F CAGR

LIT +99%RTD Tea +15%

PAB estimates

70

Sparkling Tea with the joy of bubbles

71

Magnify the benefits of tea with Alpha…

• Goodness from the Leaf

• Breakthrough Beverage

• Improved Focus & Concentration

72

Creating new occasions with Jug

73

Attract the super-premium tea purist with TazoAttract the super-premium tea purist with Tazo

• Artfully crafted teas

• Highest quality plants & botanical

• Super-premium

• Available nationwide via our distribution reach

74

Transformation

Nourish

Hydrate

Transform

75

We are targeting AMP growth at expanding light users

Significant number of light users in category

Reasons For NotDrinking/Drinking More

Unfamiliar Ingredients: 51%

Bad Taste: 47%

Not Thirst Quenching: 44%

14%

43% 16%

21%

70%

36%

% Users % Volume

Heavy

Medium

Light

Source: Itrac March 2008 Source: 2008 Energy A&U

76

Hybrids fuse Energy with familiar LRB segments

GREEN and BLACK TEA LEMONADE

77

Grassroots

Programs

Media

Value

Dale Jr. has been a Big Win engaging consumers

78

NA BeveragesGrowth

Transforming our portfolio

Other NCBsWaterCSDs

Stem Declinein CSDs

Grow NCBs• Functional benefits• Natural sweeteners• Increase occasions

Source: Internal PAB LRB estimates

Re-inventing the consumer proposition for many key brands

Pro-actively managing the portfolio

ProfitableGrowth

79

Optimizing our business and asset strategy

75% of US PEP Volume

Source: 2007 internal volume estimates (PBUS)

Bottling System Warehouse System

25% of US PEP Volume

PepsiCo Advantaged with Flexible GTM system

80

We view our bottling partners as essential to our joint success

• Healthy relationship, constructive dialogue

• Win-win partnership for margin expansion– Joint supply chain productivity– Cold fill manufacturing consolidation

• Robust joint business planning process– 4% concentrate price increase

• Aligned, integrated plans for 2009 innovation

81

Reinvent the consumer proposition

Proactively manage portfolio

Optimize business and asset strategy

Key Elements for Success

Our beverage plan addresses all 3 key elements for turnaround success

82

PepsiCo NA Beverages long-term prospects

• PepsiCo re-architecting portfolio to achieve growth– Gatorade re-positioning for

profitable growth– Re-energizing CSDs to

moderate declines– Focused efforts on key

NCBs for targeted growth bets

NA Beverageslong-term goal

• At least 1+%volume growth

• Mid-single digitNOPBT growth

83

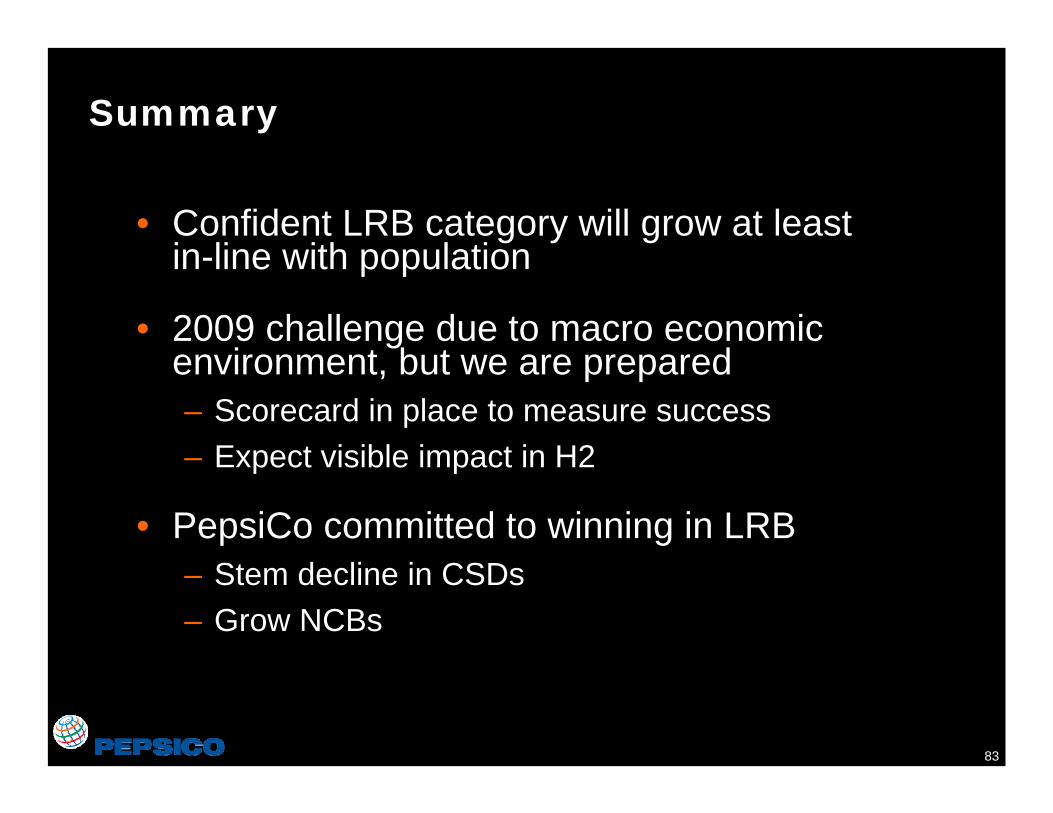

Summary

• Confident LRB category will grow at least in-line with population

• 2009 challenge due to macro economic environment, but we are prepared– Scorecard in place to measure success– Expect visible impact in H2

• PepsiCo committed to winning in LRB– Stem decline in CSDs– Grow NCBs

84