Nine Mile Point Unit 1 and 2, Letter Submitting Leaves Issued by ...

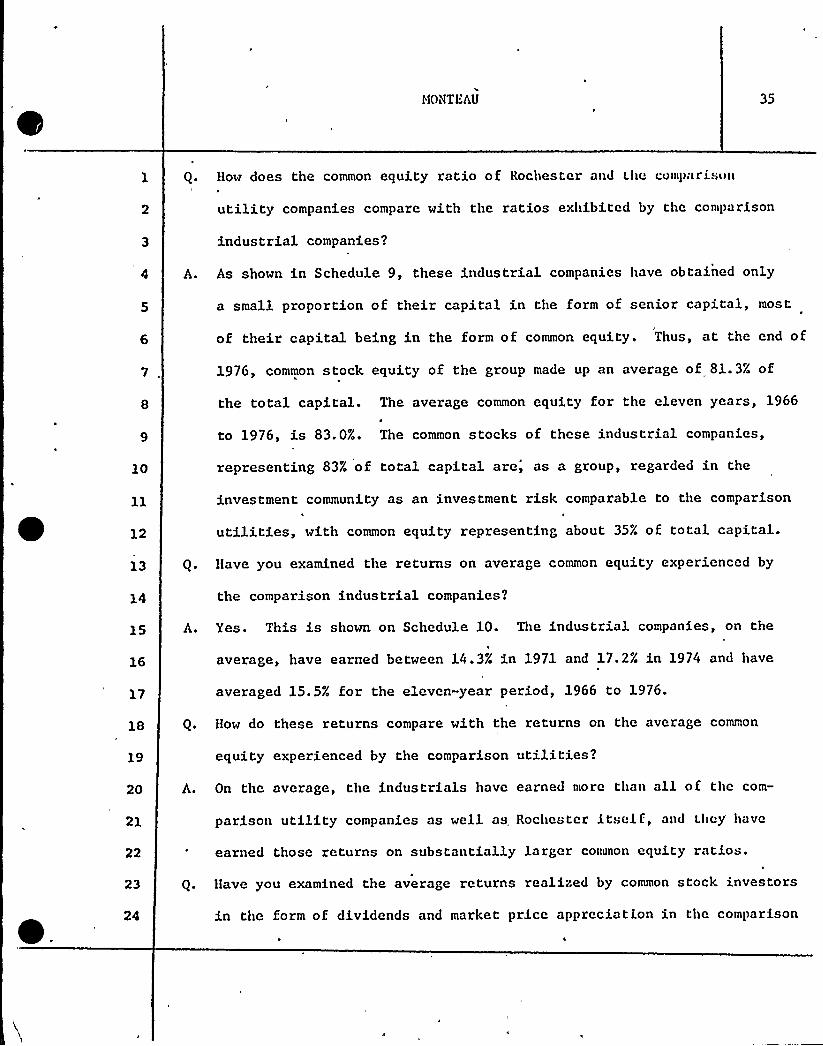

514

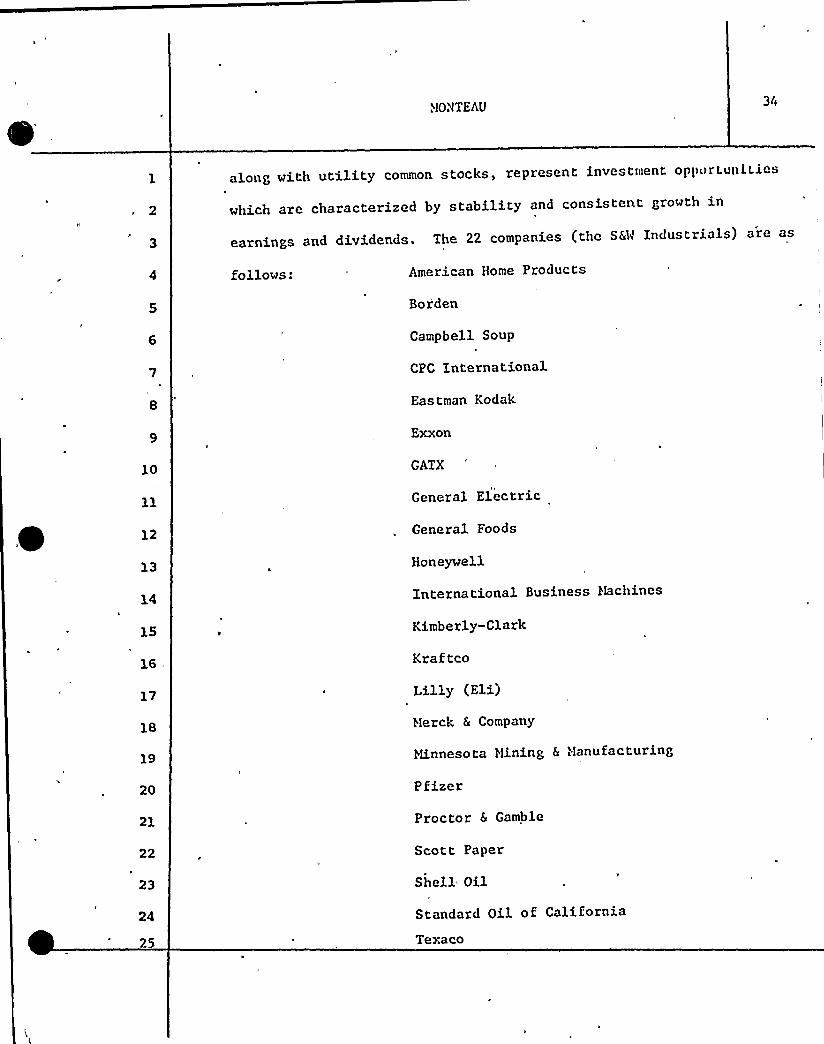

1 ROCVESTER GAS C.HD ELECTRIC CORPORATIOH ~ ~ ~ a a~q 'I PE 'i D ~ lalC ~ ~ 89 Et ST AVEHUE, ROCHESTER, H.Y. )/6/9 J 'O~::i 4 . K + l4iEDY Yltj PRES la)fh ~ ~ May. 26, 1978 ~ ( VCLC><0>t i~c*cooL 7io 5l6 2IOO Hr. 'amuel R. Madison, Secret ary Public Se Tvi ce Commission Zmpire State Plaza Alb any, New. Yor3c 12223 Dear Hr. Madison: The enclosed leaves, issued by Rochester Gas 2nd 'electric Corpora iion, are transmitted for filing in comDliance with The reouiremenis of the 'Public Service Commission of the Siate of New York: P. S. C. No. 9 - El ectrici i P. S. C. No. 13 - elect icitv 2n d. 1 5th 15ih 15 ih 8ih 1 57.h '14th 9ti 9th Revised Revised Revised Revised Revis e.d Revised Revised Revised Revised Leaf No. Leaf No. Leaf No. Leaf No. Leaz No ~ Leaf No. Le2f No Leaf No. Leaf No. 19 31 55 36 38 45 46 47 1 57. Qri 1st. 157. 1s t. 1sT. 1st ls Revise Leaz No. ginal Leaf No. Revised Lea-. No. Revised Leaf No. Revised Lea ~ No. Revised Leaf No. Revised Leaf No. Revise'd'eaf. No. 11-A 21 22 2D 24 25 26 P. S. C. No. 10 - Gas 5in Revise Lea= No. 40 5ih Revised Leaf No. 42 "ect've June 26, 1978 Tne above .revisions a. e being filed or the purpose of increasing revenues approximately $ 34,999,000, or 18.2:, from our electric operaT.ions and $ 9,997',000, or 9. 1:, from our gas operations, based on sales daia or ihe 12-monih period ended December 31, 1977. The average number of customers servec during ine 12-month period endec December 31, 977 ~'as 277,540 electric customers anc 206,479 gas customers. The proDosed'raies would have resulted in increases for all bills rendered during ihat period. Ln 2ccoTd2nce. with 16 w~ ih t'ai'enty" rouT copies Qf Th each ibi7, s whi ch wi 1 1 comp i s e elccTT:c anQ gas 27e f""~ ng. ihai Taie relief is necessary v'able posit'on to provide th expect. NYCRR 2. 3, ihe e prepared writ iis direci case Th's material i — ihe Comp-ny e ouality of se Com'p2ny submiTs here- ten testimony 2nd in suppor i of ihis clearly d emons ira ies i S to rerrlain "n 2 rv 3. Ce OUT CUSTomers

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Nine Mile Point Unit 1 and 2, Letter Submitting Leaves Issued by ...

1

ROCVESTER GAS C.HD ELECTRIC CORPORATIOH

~ ~ ~ a a~q'IPE

'i D~ lalC

~

~ 89 Et ST AVEHUE, ROCHESTER, H.Y. )/6/9J

'O~::i 4 . K + l4iEDYYltj PRES la)fh ~ ~ May. 26, 1978

~ (

VCLC><0>ti~c*cooL 7io 5l6 2IOO

Hr. 'amuel R. Madison, Secret aryPublic Se Tvice CommissionZmpire State PlazaAlbany, New. Yor3c 12223

Dear Hr. Madison:

The enclosed leaves, issued by Rochester Gas 2nd 'electricCorpora iion, are transmitted for filing in comDliance with Thereouiremenis of the 'Public Service Commission of the Siate ofNew York:

P. S. C. No. 9 - El ectrici i P. S. C. No. 13 - elect icitv2n d.

1 5th15ih15 ih

8ih1 57.h'14th

9ti9th

RevisedRevisedRevisedRevisedRevis e.dRevisedRevisedRevisedRevised

Leaf No.Leaf No.Leaf No.Leaf No.Leaz No ~

Leaf No.Le2f NoLeaf No.Leaf No.

1931

553638454647

1 57.Qri1st.157.1s t.1sT.1stls

Revise Leaz No.ginal Leaf No.Revised Lea-. No.Revised Leaf No.Revised Lea ~ No.Revised Leaf No.Revised Leaf No.Revise'd'eaf. No.

11-A21222D242526

P. S. C. No. 10 - Gas5in Revise Lea= No. 405ih Revised Leaf No. 42

"ect've June 26, 1978

Tne above .revisions a. e being filed or the purpose ofincreasing revenues approximately $ 34,999,000, or 18.2:, from ourelectric operaT.ions and $ 9,997',000, or 9. 1:, from our gas operations,based on sales daia or ihe 12-monih period ended December 31, 1977.The average number of customers servec during ine 12-month periodendec December 31, 977 ~'as 277,540 electric customers anc206,479 gas customers. The proDosed'raies would have resulted inincreases for all bills rendered during ihat period.

Ln 2ccoTd2nce. with 16w~ ih t'ai'enty" rouT copies Qf Theach ibi7, s whi ch wi 1 1 comp is eelccTT:c anQ gas 27e f""~ ng.ihai Taie relief is necessaryv'able posit'on to provide thexpect.

NYCRR 2. 3, ihee prepared writiis direci case

Th's materiali— ihe Comp-ny

e ouality of se

Com'p2ny submiTs here-ten testimony 2ndin suppor i of ihisclearly d emons ira iesi S to rerrlain "n 2

rv 3. Ce OUT CUSTomers

li

lROCHESTER CC5 C I'O ELECTRIC CORP.o<TE ~Jay ~6 1S78

~'.r. Samuel R. Madison

SHEET t'O. 2

view of the Commission' Order', issued Harch 8, 1978,in Case 27501, allowing che use of experimental hearing procedures,the Company suDDorts the "concept of using written interrogatoriesand responses', together" v"'iih 'a consolidated h aring procedure, toexDedite the development o a clear 'and. concise record. TheCovii,pany is of the opinion that revised procedures,'uch zs thoseused in. Cases 27094 and. 270SS, will reduce the time required tocomplete the record enabling the Commission to reach a final de-cision more efficiently.'ccordingly, the Company hereby requeststhat the experimental'procedures, including the advance use of ..appropr" aTe daTa reouests and interrogatories, and the filing ofall testimony and exhibits prio~ to any hearings for cross-exam'nation. be used in these proceedings.

A notice to the Dublic regarding these revisions will bemad e in accordance with 16 NYCRR li6. 70 and 6 NYCRR 270. 70.

Very truly yours,ROCHZST"R GAS. Ah'D H.~CHIC CORPORATION

John I. KenneoyVice President

JLk:m)rencl c .

P.S.C. No. 9 — ELE(.TR I(:IIY

ROCHESTER GAS AND ELECTRIC CORPORATION0IIICINALI.EAF hO....,..................

........,2Dd....... REvlsED LEAF N0.........19............

S(II'ERSEDINC ....1.St.............. LEAF NO....'.....l9...........

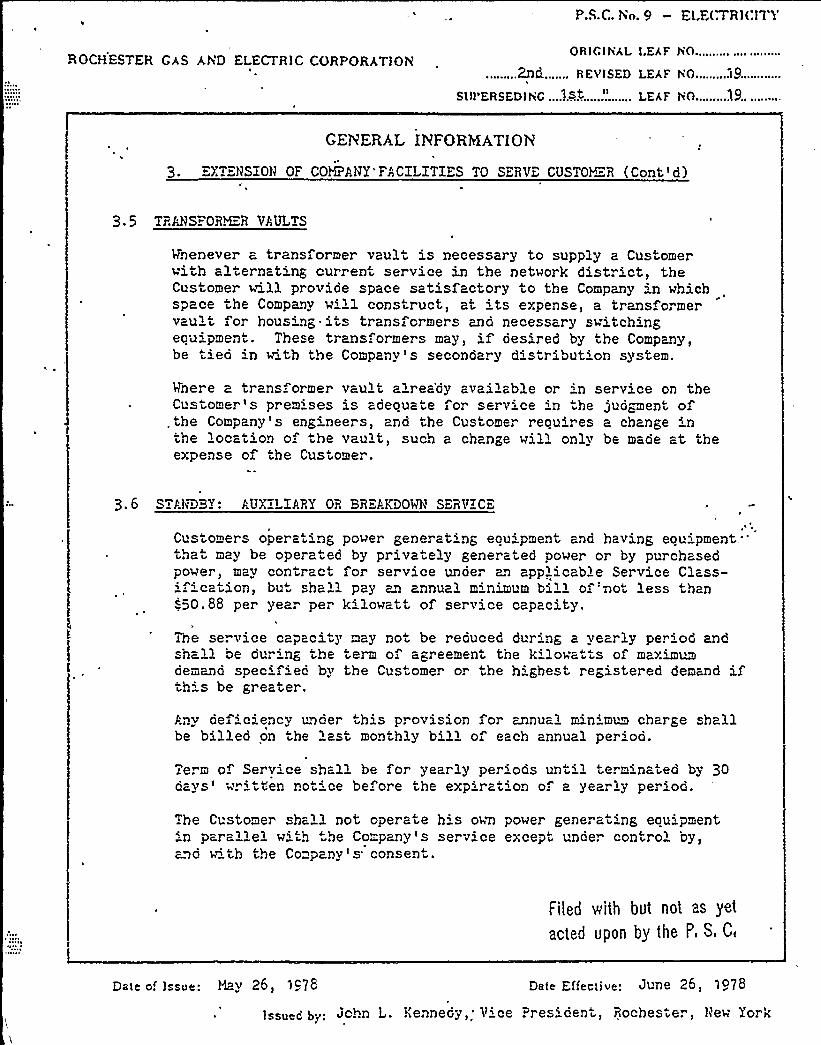

GENERAL INFORMATION

3.:XT".HSION OF COMPANY'FACILITIES TO SERVE CUSTOY:-R (Cont'd)

3.5 Tr".ANS ORMR VAULTS

Vnenever a transformer vault is necessary to supply a Customerwith alternating current service in the network district, theCustomer will provide space satisfactor y to the Company in whichspace the Company will construct, at its expense, a transformervault for housing its transformers and necessary switchingeouipment. These transformers may, if desired by the Company,be t'ed 'n v'th the Company's secondary distribut'on system.

Vnere a trans. ormer vault alrea'dy available or in service on theCustomer's prem'ses is adeouate for service 'n he jud~ment of

, the Company ' engineers, and the Customer reoui. es a change inthe location of the vault, such a change will only be made at theexpense of the Customer.

3.6 STANDBY: AUXILIARY OR BREAKDOWN Sr"RVZCr

Customers operating power generat'ng eouipment and having eouipment."that may be operated by privately generated power or by purchasedpower, may contract for service under an applicable Service Class-if'cation, but shall pay an annual m'nimum bill of'Tarot less than<50.88 per year per kilowatt of service capacity.

The service capacity may no be reduced dur'ng a yearly period andshall be cur'g the term of agreement the k'lowatts of maximm~demand specified by the Cus orner or the h'ghest r egistered demand i.th s be greater.

Anv def'c'ency unoer this provision or z.nual minimum charge shallbe billed on he last monthly bill of each annual period.

Term of Service shall be for yearly periods until terminated by 30c vs w. itten notice before the expiration of a year ly period.

The Customer shall not operate his own power generat'ng eou'pment:n parallel w'th the Co™pany's service except under control by,and v' the Company's consent.

Filed v:ith but not as yet

acted Upon by the P, 8, C

Date of Issue: May 26, lc78 Date Effective: June 26, i/78

Issueo by. John L. Kennedy, V'e Pr es' ent, Rochester, llew Yor k

\

P.S.C. No. 9 — ELECTRICITY

ROCHESTER GAS A.ND ELECTRIC CORPORATIONORIGINAL LEAF HO......................

......1.5.th......... REvlsED I EAF I 0..........3.).......

SUPERSEDINC 13th "I.EAF NO 31

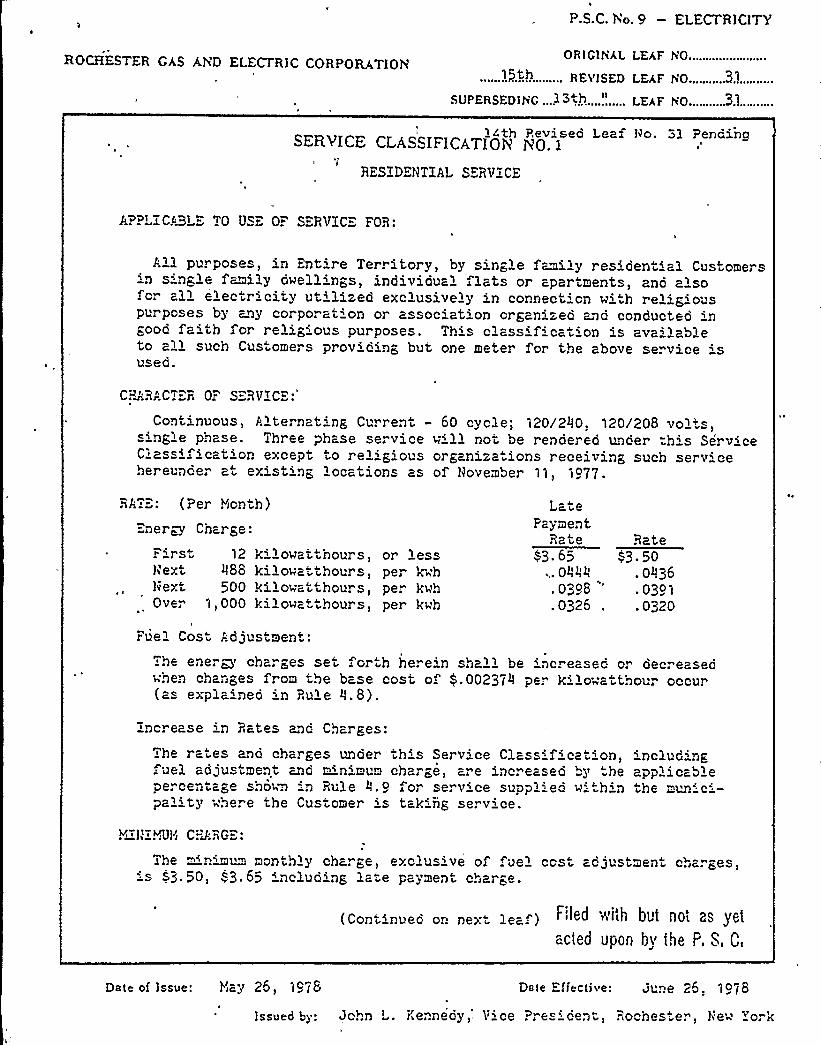

14th Reviseo Leaf Ho. 3l Penc1inaSERVICE CI.ASSIFICATION ÃO. 1

RESZDENTXAL SERVICE

A?PLACABLE TO VS" O." SERVXC FOR:

All purposes, in Entire Territory, by single f~ilty residential Customersin s'ngle family dwellings, individual flats or apartments, ano alsofor all electricity ut'ized exclusively in connection wi h religiouspurposes by ~ay corpo. at'n or association organized and conducted 'ngood faith fo. religious purposes. This classification is ava'lableto all such Customers providing but one meter for the above service 'sused.

CP~.HACT>ER Or SERVICE

Continuous, Alternating Current — 60 cycle; 120/2IIO) 120/208 volts,ingl)e phase. Three phase service w'll not be renoered under th"'s Serv'ce

Ciassification except to rel'ious organizations receiving such serv'ehereuncer at existing 'ocations as of l)ovember 11, 1977.

rirstNextlvextOver

12i88

5001> 000

kilowatthours,kilowatthours,kilowatthou. s,kilowatthours,

RATE: (Per ?')onth)

Energy Char ge

or lessper kwhper kwhper kwh

LatePayment

Rate~3. 65

Orig>I)

. 0398

.0326 .

Bate~e3. 50

. Olt36

. 0391

.0320

ruel Cost Ad„'ustment:

The ener@) charges set forth here'n shall be 'nc. eased cr decreasecwhen chaniges from the base cost o $ .00237'er kilowatthour occur(as expla'neo in Rule l).8).

increase 'n Rates and Charges:

The ra'es and charges under this Serv'ce Classificat'on,uel adjustment and minimum charge, are 'ncreased by he

percen>tage sho'~a in Rule Il.9 fo" serv'ce supplied wi -h'npality where the Customer 's tak'ng se. v'ce.

includ'ngapplicablethe muni c'—

I iI'UI~i C?3;RG

The ~'nimum monthly charge, exclus've o .uel ccs adjustment chiarges,'s 4.50, '3.65 'ncluding late payment charge.

(continued or. nex leaf) r'leu ')t'lttt but not as yetacted upon by the F. S, C,

Date of Isst)e: I'>ay 26, 1978 Date Effective: gute 25. 1o78

Iss))ed by: John L. Kennedy) Vice ?res'ent, Rochester) llew 'York

P.S.C. Yo. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONORIGIhAL LEAF NO..................

......:6.ih......... REVISED LEAF ho........&~......

SUPERSEDlh'C....l3th..."....... LEAF h0........33.;....

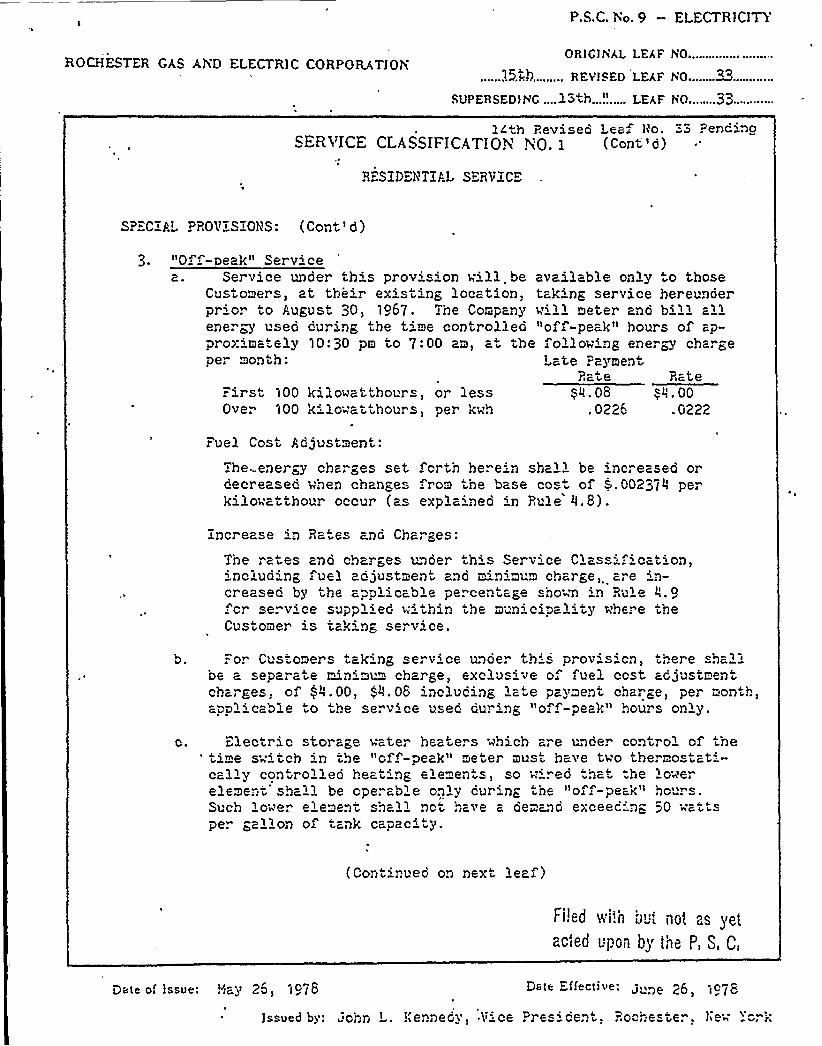

14th Revised Leaf h'o. ".3 PendinoSERVrCE CLASSIFrCATIpy, h;p. y (Cont'd)

RESZDEIiTZAL SERVZCE

SP"CZA'ROV"SZONS: (Cont'd}

~«! . 00.0222

t irst t00 kilowatthours, or lessOver 100 kilowatthours, per kwh

»Of -Deak» Servicea. Service under this prov's'on will be available only to those

Customers, at their existing location, taking ser vice her eunderpr'." to August 30, lo67. The Company w'll meter ano b'll allenergy used dur'ng the t'me controlleo»off-peak» hours of ap-proxima. ely l0:30 pm to 7:00 am, a'he follow'ng energy chargeper month: Late Payment

Rate Rate~~4. 08

~ 0226

r uel Cost C djustment:

The...energy charges set forth herein shall be increased ordecreased when changes rom the base co of >.00237IJ perkilowatthour occur (as explained in Rule JJ.8).

Zncr ease in Ra es and Charges:

The rates ano charges under this Serv'e Class=: ication,'nclud'ng fuel adjustment and minimum charge are in-creasec by the applicable percentage shown 'n Rule «.o

or serv'ce supplied w'thin the mun'cipal'ty t"here theCustomer is tak'ng service.

b..=or Customers tak'ng service unoe. th's prov's'cn, here sha'be a separate minimum charge, exclus've o. fuel ccst adjustmentcharges, of $ IJ.00, <~.08 'ncluding late pavment charge, per month,

vq;c ble to qe se v„ce used du ing»o, P peaI » . ou„s on'ty

Electric storage water heaters which are unoer controlt of'hetime switch in the»off'-peak» eter must have two thermo tati-cally controlled heating elemen s, so w'red tha":he lowerelement sha'l be oDerable onlv dur'ng th~ »off-peak" hours.Such lower element shall nct have a ae and exceed'ng 50 wattsper gallon of ank capacity.

(Contir:ued on next lea.f)

Iried V'I'.ll b~:i rot BS yetacted upon b~ toe p $ Q

Dale of Issue: Y>ay 25, t o78 Date Effective: gune 26 'tc78

Jssoed by: 'ohn. L. !(ennedy ) Vice ~ r6s Gent, Ro hest 6.. Iie ' k

P.S.C. No. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONOR{C{NAL LEAF h0...................

......1.5.~5......... REYlSED LEAF h0........35..."-

SUPERSED)NC ....." "'. 'a......... LEAF Y0........35......

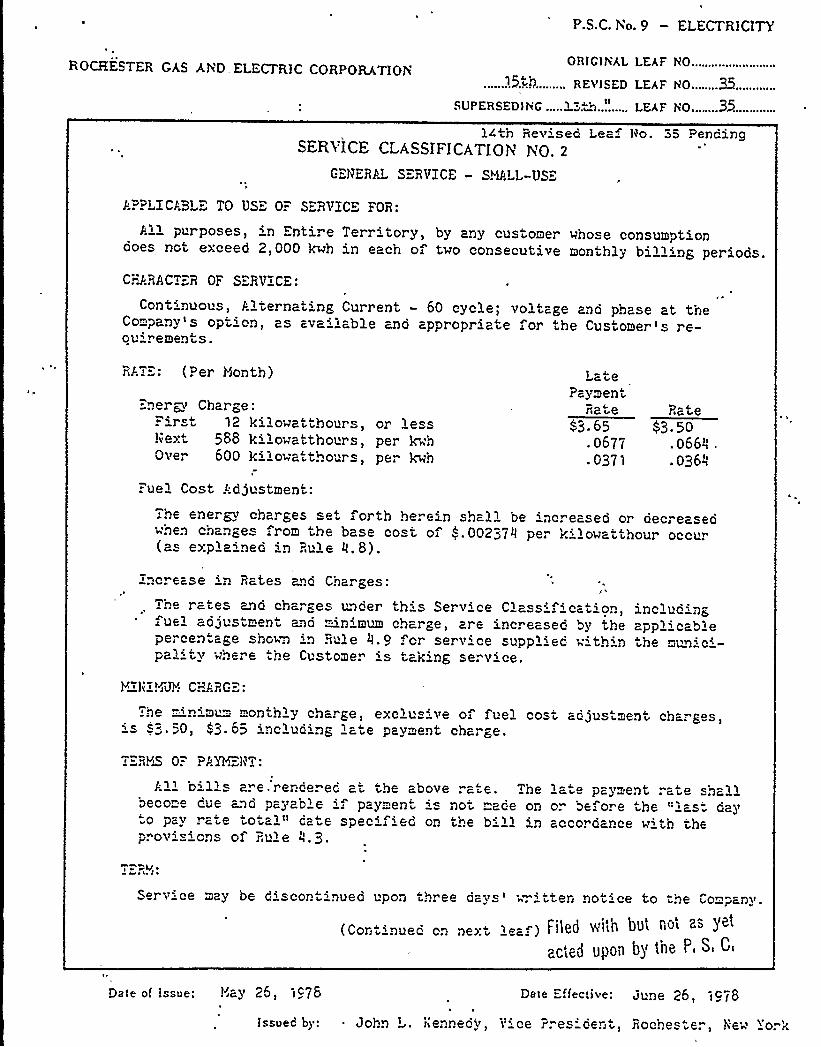

14th Rev'sed Lea~ {<o. 35 PendingSERVICE CLASSIFICATION NO. 2

G:.NERPt SERVICE - SY!ALL-US".

APPLICABL" TO US" 0." S:RVICE FOR:

All purposes, in Enti. e Territory, by any customer whose consumptionooes not exceed 2,000 kwh in each of two consecutive monthly billing per iods.

CATARACT.R OF S:RVICE:

Cont'nuous, A ter nating Current - 60 cyclei voltage and phase at theCompany s option as available aDo appropriate for the Customer's re-ou'rements.

RA!".: (Per Honth)

"=nergy Charge:Fir st 12 kilowa t thours, or lesshe>:t 588 kilowatthours, per kvhOver 600 k'owatthours per kt h

LatePayment

Rate83.65

.067/

. 037'l

Rate$3. 50

066{,.036/,

Fuel Cost P.djustmeni:

The ener~ charges set forth here'n shall be 'Dc. eased or decreaseowhen changes rom the base cost of <.00237{{ per k'owatthour occu.(as expla'ned in Rule !{.8).

Increase 'n Rates and Charges:

The rates and charges under this Service Class''ation~ ue adJustment and minimum charge, are increased by thepercentage shown in Rule i{.o for service supplied withinpa '> where the Customer ' tak'ng serv'e.

lncl ud~ Dgapplicable

he mun'e

Y hI{~iJI. CHJRG=:

:he "'nimu™ monthly charge, exclus've of fuel cost adjustment charges,' 3. 50, 43. 65 including late payment charge.

T" RY!S OF PP.YY~=liT:

b'ls a. e.rercerec at the above ra. e. Thebeco"e cue ano payab e f payment s Dot mace on.o pav rate total<~ cate specifi ed on the billp ovi i oDs of Rul e

la e pay ent rate shallor befo. e he ':l-s: dayaccorcance w'th the

'oM ~2 ~ s

Set ~ri ce may be discontinued upon th. ee days' .'tten not'e to he Company.

p- Vg(Cort'nuec on De> „ leaf) Fll{!0 5'{t{l uut nu

ac'ed upon b~ t'ne P, S, C,

Date of issue: Ya5'6, 1c78 Dale Effective: June 26, to/8

Issued by: John L. i(ennedy, t" ce Pres cent, Roches" er, New York

P.S.C. No. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONORlClNAL LEAF HO...................

......8th........... REviSED LEAF no.........36......

SUPERSED)HC ........tn............ LEAF h0.........3........

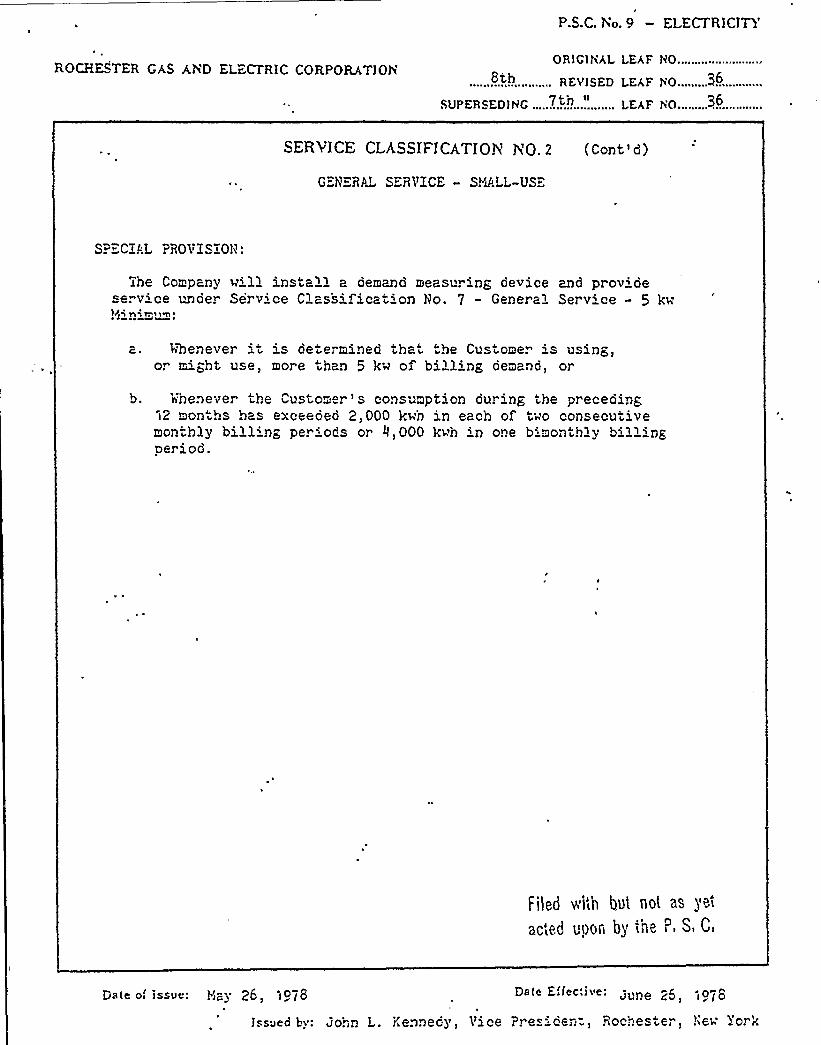

SERVICE CLASSIFICATION YO. 2 (Cont'd)

G"NERAL SERVICE - SHALL-US"-"

SPECIAL PRO'VXSXOH:

The Company vill install a demand measuring device and prov'deserv'ce under Serv'ce Classification No. 7 - General Serv'ce - 5 kt"

a. I henever it is determined that the Customer is using,or might use, more than 5 kw of billing pemand, or

b. whenever the Customer's consumption dur ing the preceding12 months has exceeded 2,000 kt:h in each of t'o consecutivemonthly billing per'ods or II,000 kt"h in one b.:monthly billingpe. iod.

Filed v'ith but not as yet

acted U!)On by the P, S, C,

Date o,'ssue: Hay 2g t p78 Date Elfec',iue: June 25 t p7

o.';. L.: en..edy Vi ce pre~; ce-,- poc'~es e t et,. vork

P.S C. Yo. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONORIGINAL LEAF hO......."..."".

15th REvlsED LEAF Ho 38

SUPERSEDINC ..3.3. N........... LEAF N0.......3%....

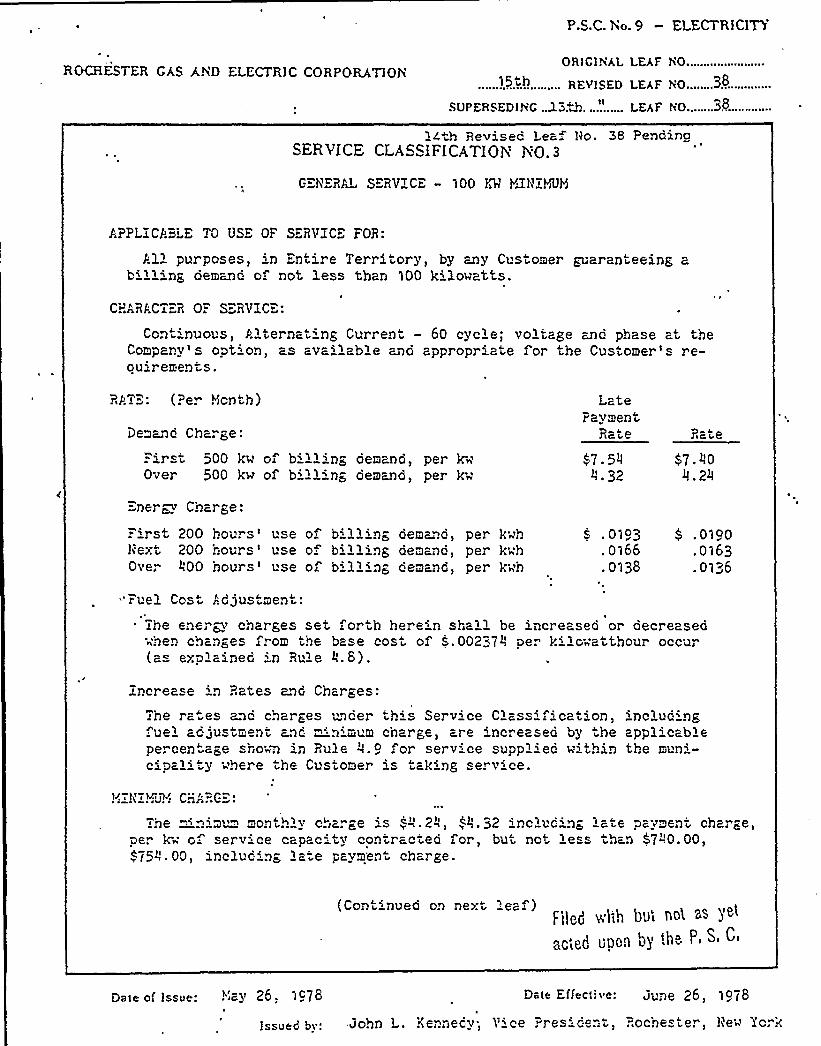

1Cth Revisec Leaf Ho. 38 PendinaSERVICE CLASSIFICATIOY No. 3

GENERAL SERVICE - 100 KM YJliZYUH

APPLiCPiLE TO USE OF SERViCL FOR:

S.'ll purposes, in Entire Territory, by any Customer guaranteeing abilling demand of not less than 100 ki3.ovatts.

cHARrlcTER 0: s. RvIGE:

Con 'nuous, P.lternat ng Current - 60 cycle; voltage ano phase at theCompaDV s option as available ano appropI iate for the CustomeI' re-ou'remen s.

RJIT"": (Per Yionth)

Demand Charge:" i I'st 5QQ kh'f billiDg oemaDG

> perkh'ver

500 k~ of billing demcnd, per kw

LatePaymeDt

Rc.t.e

$7.544. 32

Rcte

Ener~~ Charge:

Firs 200 hours'se o b'lling de"and, per khhNext 200 hours'se o billing demano, per kh'hOVe. ~!00 hOUI S 'Se Of b'' lling demcDd> peI'h'h

S . 0193 $ . 0190. o166 . o163. 0138 . 0136

"Fuel Cost J:djustment.'he

energy charges set, forth here'n shall be increased or decreased"hen changes from the base cost of „'.002374 per kilo"att!lour occu1(a explained 'n Ru'e 4.8).

increase in Rates and Charges:

The ra es and charges under th's Service Classification, includinguel ad Justment and ~'nimum charge, are 'nc. eased by "he applicable

percen"age shohw in Rule 4.9 for service supplied hithin the muni-cipal'ty 'here the Customer is taking service.

l~'Ii:!~u"I C~ARG

lhe "'Dim~ ~ mcnihly Chcrge 'S ~".2~»~~.g2 inc uding 'cte pcVment Charge,per k" o serv'ce capac'ty contracted for, but not less than 57Il0.00,„754. 00, 'nclucing a'e pay" en chaI ge.

(Con 'nueo o.. nex" 'ea. )F'IIgd W'Ith b'J< Ilg SS

)'c'qd

Ilpofl g)'h8 P

Dale of Issue: YIBy 26, 1978 Dale Errecl:ve: June 26, i978

IaaUed bv: John L. Kennedy; V'ce PI esident, Rochester, llew York

P.S.C. No. 9 — EL'ECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONOR)CITAL LEAF VO.....-" "."""""

.......1...th........ REvIsED LEAF 50.........~5........".

SVPERSED)HC ....,.l3.~h..."...... LEAF hO..........(5....,......

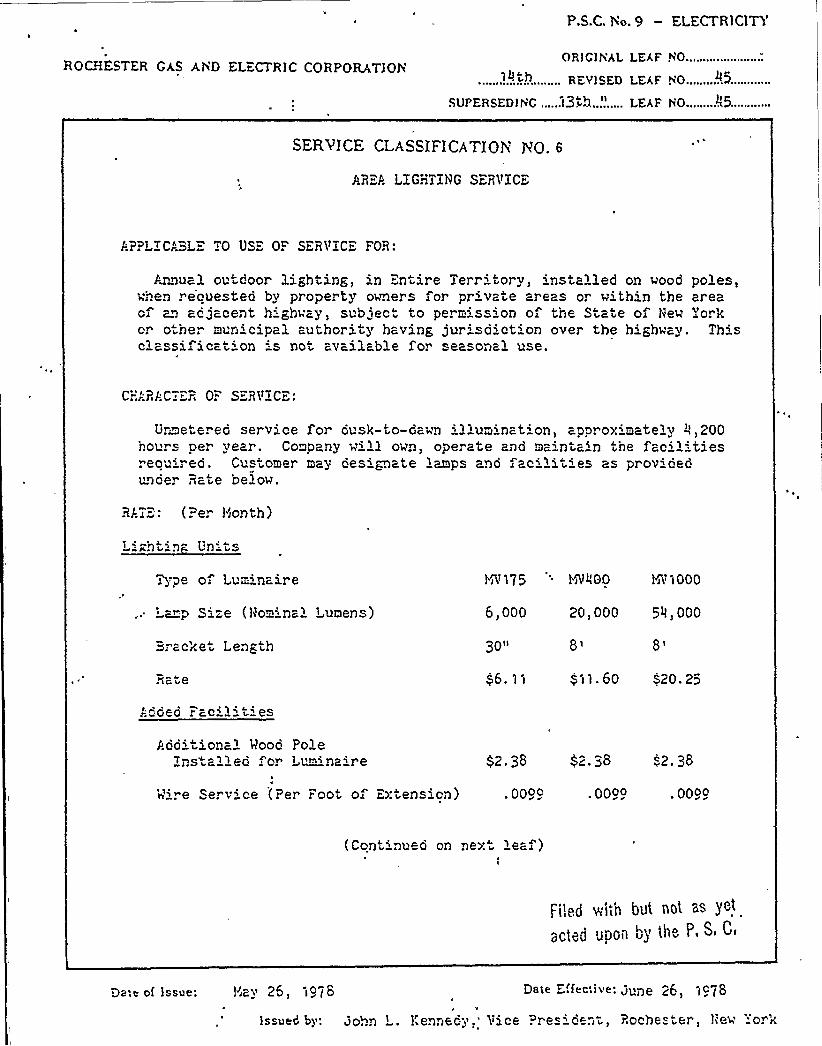

SERVICE CLASSIFICATION NO. 6

AR:A LIGHTING SERVICE

J-;PPLICPZL:" TO US OF SERVICE FOR:

JJ )ual outdoor lighting, in ""ntire Ter ritory, installed on wood poles,when reouested by property owners for private areas or within the areaof an adjacent hi>hway, subject to permis 'on of the State of New Yorkor other muri'cipal authority having jurisdiction over the highway. Thisclassification ":s not available for seasonal use.

C:":ARE.C™"R 0." SERVICE:

Unmetered service for ousk-to-Qahn illumination aporoximately 0 200hours pe. year. Company will own, operate and maintain the facil'iesreouir ed. Customer may designate lamps ano facilities as providedunider Rate below.

RAT=: (Per Yionth)

htin Units

Type of Luminaire

'~p Size (Hominal Lumens)

YrV175

6,000

YiVIlGO YiV1000

20) 000 5Il ) 000

"racke Length 30 Ii 8i

$ 6. 11 ~ i1. 60 $20. 25

Added ..acil't'es

P.dditional Mood PoleIns alled ~ or L~~.'naire $2.38 52. 38 '2. 38

Pire Serv'ce (Per Foot of Extension) .0099 .0099 . 0099

(Continueo on ne>:t le"f)

P~!:.d V,I,h bUt no~ aS

3Ctod UPGil b)'hG P< Si Ci

Dale of issue: Iiay 26 i978~

D'< -' 'Ive: gune 26, 1ct8

Issued bi zo+z» ezaec 3 ace o~e~~ ce Poche e'er Iie o~<

P.S.C. Yo. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIONORIClhAL LEAF YO..............:,....

REvisED LEAF h0.........06.......

SVPERSEDlhC .....l..~h,........,... LEAF h0........%6.......

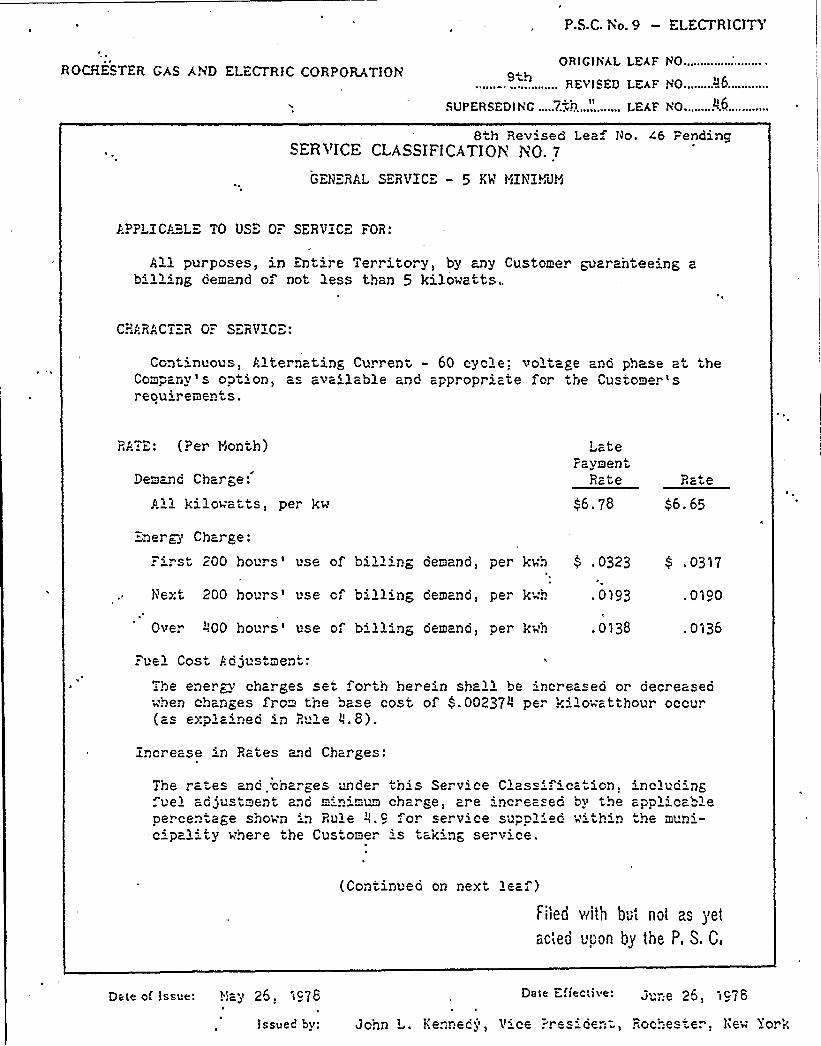

8 h Revisea Leaf Jlo. 46 PendingSERVICE CLASSIFICATIOY, YO. 7

GEH"RAL SERVIC" - 5 KV Y~Ih'IHUH

P.PPLICP.""LE TO USE 0." SERVICE FOR:

All purposes, in Entire Territory, by any Customer guarahtee'ng abilling demand of not less than 5 kilowatts..

C-"fRc'T" R G" S R'PIC":

Continuous, Plternating Current - 60 cycle:. voltage ano phase at theCompanv s opt on) c. avc. lcble and appropri ate fo. the Cu tomel sreouirements.

RATE: (Per I'month)

Demand Charge:

P.ll kilowatts, per kw

LateFayment

Rate

66. 78

Ra e

q6. 65~

~

ner~> Charge:

. 'rst 200 hours'se of billing demand per kwh $ .0323 $ .0317

Next 200 hours'se cf b'lling cemand> per kwh .0)93 . 0 "i 90

Over -".00 hours'se of billing demand) per kwh .oi38 .0~36

Fuel Cos P.cjustment:

'he ener~~ charges se" forth herein shall be increased or decreaseawhen changes from the base cosa of $ .002374 pe k'watthour occur(as explained in R le Il.8).

Increase in Rates and Char ges:

The ra"es and 'charges under th' Service Classi ica ion,.uel adjustment and mini "um charge, are increased by thepercentage shown in Rule ~u. 9 or service suppl'c within-cipality where the Cus'orner 's tak'ng service.

xnclud~ ngappl'ablethe muni-

(Continuea on next leaf)Filed with but not as yet

acted upon by the P, S. C,

Date of Issue: !!ay 25. I978 Da<e E'fecliue: June '25 IQ/8

Issued by: John L. Kennecj, Vice .=resi cen=-, Rochester. hew vork

P.S.C. No. 9 — ELECTRICITY

ROCHESTER GAS AND ELECTRIC CORPORATIOÃORJCI YAL LEAF hO...................

.......9.TIE.......... RFvlSED LEAF hO.........R7......

SUPERSEDlnC ...Z.".:.'.............. LEAF WO.........R7

8 h Revised Leaf ho. L7 .-end'ncSERVICE CLASSIFICATIP>X NP. 7 (Cont')

GEhERAL SERVZCE — 5 KW HZh'ZYiUYi

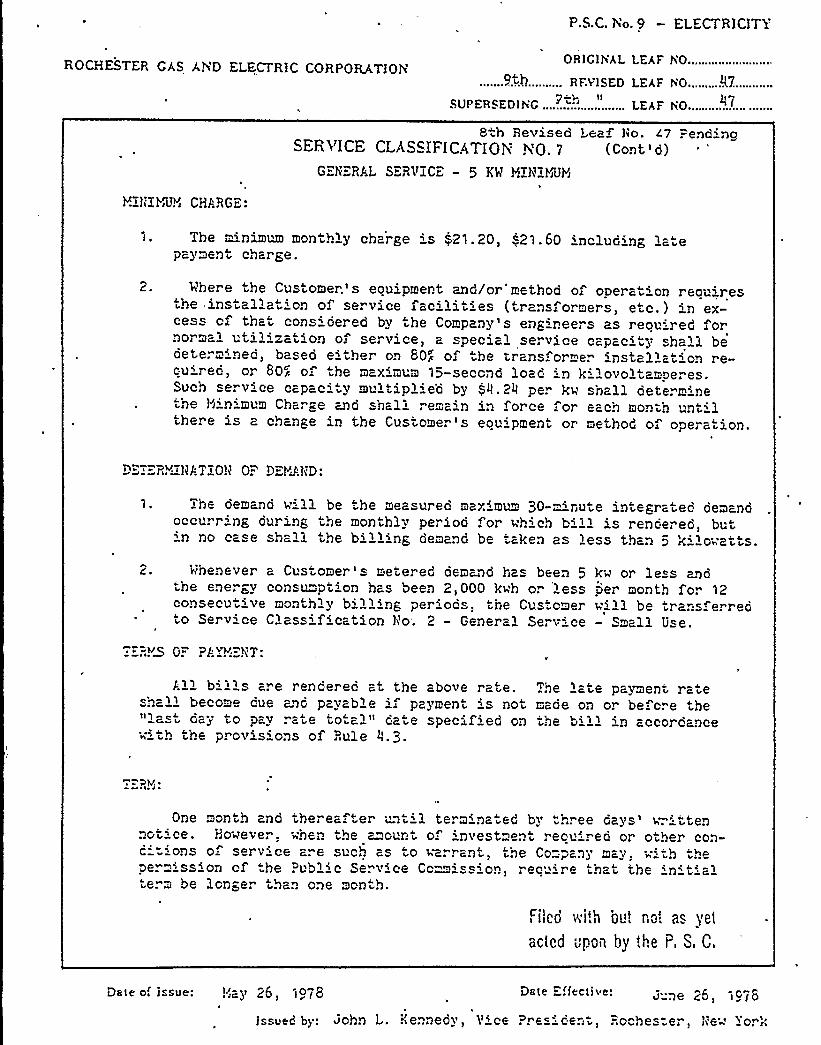

YZhZYiUYi CHARGE:

Tbe minimum monthly charge ' )21. 20, <21 . 60 including latepayment charge.

Mbere the Customer.'s ecuipment, and/or'method of operation reouiresthe installation o se. vice facilities (transformers etc.) in ex-cess c that consioered by the Company's eng'r.eers as reouired fornorma uti ization o. service, a special service capacity shall bedet erm'ed, baseo e'her on 80> of be transfor mer installation re-cu'ed, or 80+ of he maximum 15-second load ' kilovoltamperes.Such se. vice capac' multiplie'a by 54. 24 per kv, shall dete. m'nethe Y!inimum Charge and shall remain in force "or each month untilthere is a change in the Custome. ' eouipment or method of opera" ion.

D".TERY l)A ZOH O." DERED:

1. The Qemand vill be the measured max'mum 30- 'ut 6 integrated demandoccurr'g dur ing the mon hly perioo for vh'b b'l 's renoered but'n no case shall tbe billing demand be taken as less than 5 kilo'~'atts.

2. whenever a Customer's metered demand bas been 5the energy cons~~ ption has been 2,000 kvh o. lessconsecutive monthly b'lling periods, the Custcmerto Serv'e Classification No-. 2 - General Service

k~ or le s andDer month for 12vill be transferred

Small Use.

T"'RYD 0." P '.YY;=!'T:

All b'' l' are renoered at the above rate.shall become cue and payable if payment is notlast Qay tQ pav rate tQtal da e specified on

vith the provisions of Rule 4.3.

Tbe 'te payment ra er'aoe on or be cre thethe bill in accoI Qance

One month and thereafter '-;til termina 6d by .. ec Gays '4 'ennotice. Ho~ever, eben the amount of 'nvestment reouired or other con-c''ns o serv'e are suc.. as ~o varrant, the Company may, v'b th'Qer=ission Qf the Public Serv'e Cc~ission recui re tha" >6 initialterm be longer than one month.

Filed with 0Ut Rot as yet

acted 'pan by the P, S, C,

Dale of I sue:,',ay 26, >Q78 Dele Effective:

IssUed b».. pobn l Kenneov Vicc Presi c nt "0 bes 6.. ice'~'ork

P.S.C. Vo. )3 — ELECTRICITY

ROCHESTER GAS AiD ELECTRIC CORPORATION0 R I G) ~iAL LEAF YO.................

......LIPS........... REvisED LEAF io........3.......

SL:PERSED! iG ......o.r.-'S.-'.JP.l........ LEAF 80.....;..3.......

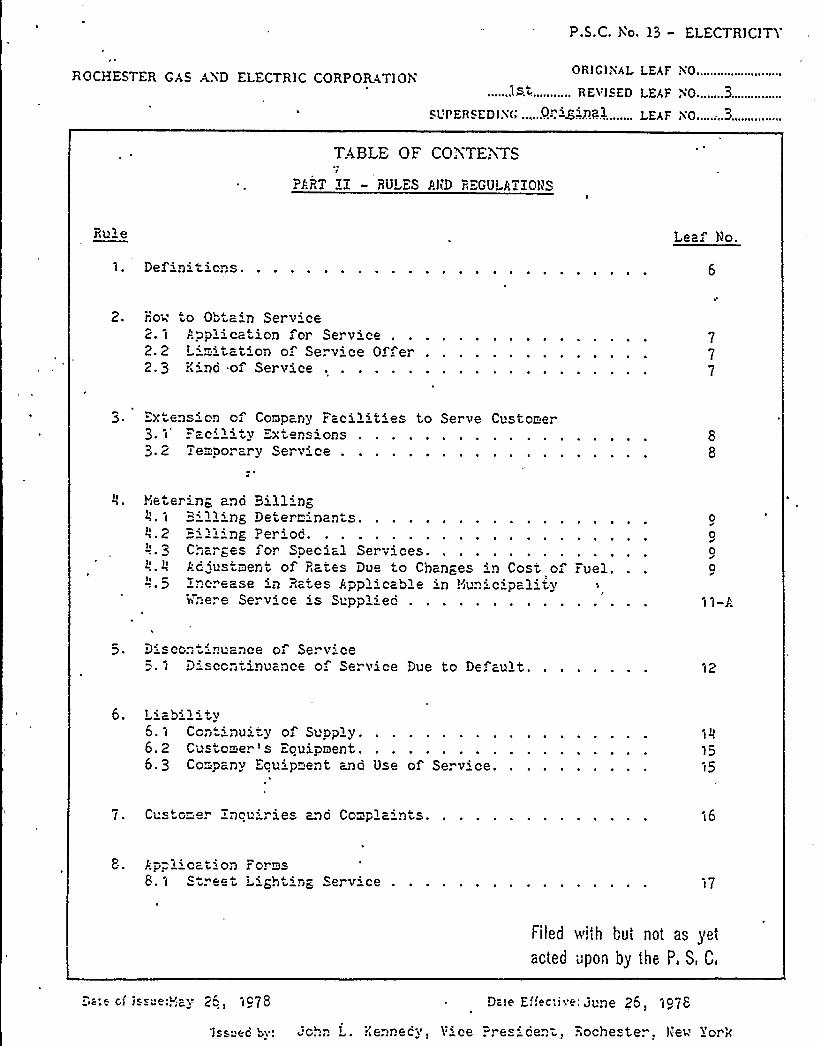

TABLE OF CONTEXTSf

PART ZX — RULES PhD REGULATIOIIS

Pule Leaf No.

1. Def'n'ions.

iso'o Obtain Service2. I Application or Service2. 2 Limitation o Serv'e Of er2.3 Zinc of Service

~ 0 ~ ~ ~

777

3. ="xtens'on of Company Pac3 ~ I "acil itv Extens~ ons3. 2 Temporary Service .

il't'es to Serve Customer

Net erin+ anQ Billing='ll'~ Determinan4.2 "i'l'ng Per'00.

Chas ~es for SpecialAc lustment of Rates

-"..5:ncrease 'n Ra-'es A

4nere Service is S"

Services.Due to Chan~es in Cost of Puel.

pplicabl e in Huni ci pal '.ypp 'ec

000

0

5. D'soon =:nuance of Serv:ce5. I Discontinuance o Service Due to De; ault

6. I iagilitv5. I Cont" nu' of Supply.6.2 Customer's Eouipment.6.3 Co"'pany Ecuip"ent wd Use of Service.

I .

15I5

7. Gusto=e. ncu'rie anc Complaints I6

8.1 S ree L'I",h in< Serv'ce l7

Filed vith but not as yetacted upon by the P, S, C,

Dc'c (I Icc: ~ e lP y 25 I078 D Ie E.';ac;ivy: Ju"Ie 26 I075

'ch.. L. ilennecy, >'ice Pre i cen-, Rochester. he~ For w

ROCHESTER GAS AND ELECTRIC CORPORATION

SL'PERSED) i<'........,

P.S.C. No. 13 — ELECTRICITY

OR!GlYAL LEAF YO........J.l.-.." .......

REVlSED LEAF 40

................ LEAF iO.....

t EYERAL INFOFDIATIQihLp

YiETERING AND BILLIliG (Cont'd)

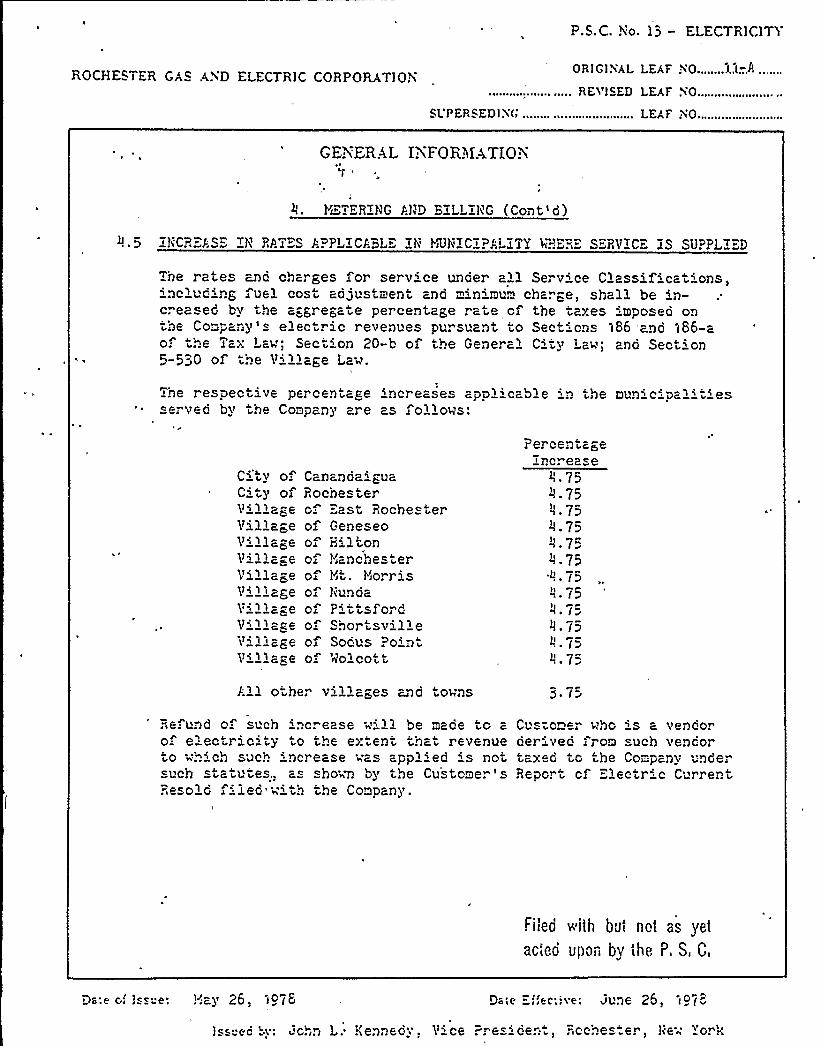

0 ~ 5 I!iCRES.'SE Il'P. ES APPLICA"L IN YUNICIPA'L TY 1"~iER S RVICE IS SUPPLZ" D

The rates md char ges for service under all Service Classifica ''ons,including fuel cost adJustment and minimum charge shall be in-creased by the aggregate percentage rate of the taxes 'mposed onthe Compaiiy's elec ric revenues pursuant to Sections 186 ano 1S6-ao the Tax LavI'Section 20-b of the General City Law; and Sect'on5-530 of the Village La<

The respective percentage increases applicable in the municipalitiesserved by the Company are as follovs:

Citv ofCity of

Village

t" llag

CaDanda"guaRochesterof East Rochesterof Geneseoof till7 onof !'anches erof Nt. Yiorrisof hunQaof PL 7 t sfordof Shor tsvil'of Soous Po~ Dt0-'iiolcot t

PercentageIncrease

4.754.75II

4.75h 7P

!..7SQi

~ IDli P

4. 75li

4.75

All o-her villages and tovns 5 'rRe.unc of such 'ncrease vill be mace to aof e" ectr'ity to the extent that revenueto ih'ch such 'Der ease vas applied is notsuch statutes. as sho~~ by the Custome. 'sResole filed'vith the Company.

Cus-orner hi)o "s a vencorderi. ec :"rom such vencortaxed to the Co pany underReport cf Electric Current

Filed v;ith but riot as yet

acted upon by the P. S, C,

)e;e G )«;e: !;ay 26, lo78 ec'ive'Iu je 25 I

Iss ed 'v: 'chn L. Ilennedyi Vice .. esicen i Rcches.er, !ie" "or<

P.S.C. Yo. 15 - ELECTRlCl7Y

RGCHESTER GAS A4D ELECTRIC CORPORAT10NOR1ClVAL LEAF YO.........................

.......!.s.t........... RES'lSED LEAF 40........2:i.............

SUPERSEDIY(: .....,o. -..g.":.nal........ LEAF ~'O... 2!

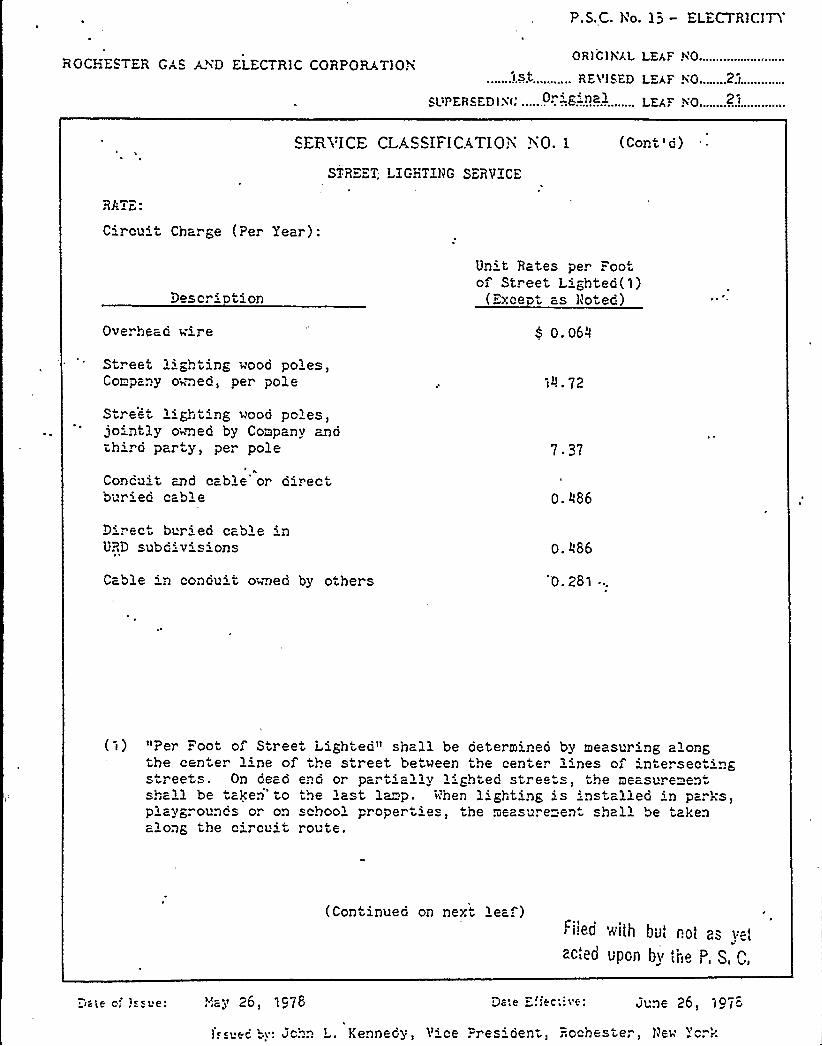

<EBVICE CLA,c:SIFICATIOY 40. 1

STRE" T. LIGHTING SERVICE

(Cont'd)

RATE.'ircu't Charge (Per Year):

Description

Unit Rates per Footof Street Lighted(1)

(Except as Noted)

Overhead wire t o.o6<

St. eet »gh ing wood poles,Company o'~wed, per pole 1>. 72

Stre t lighting wood po'es,jointly o wed by Company ~dthi. d par y, per pole 7 37

Concu't and cable or d'rectbur'ed cable o Ai86

Direc bur'ed cable inURD subd'is'ns o 486

Cable in conduit owned by o hers 'o. 281 ...

"Per ."oot of Street Lighted" shall be determined by measuring alongthe center line o. the street between the center lines of intersectingstreets. On dead enc or part'lly l'hted streets, the measurementshall be takei'o the 'ast lamp. Vhen l'hting is installed 'n pari's,playgrounds or on school properties, the measure=en- shal'e akenalong the c'cu' rou e.

(Continued on nex~ leaf)"i!e.d v;ith bul r.ot as

v=.'Cied

UPG|l bV tlto P, $ , C,

~ g''e@ lg y 26 1078 .)CCi:"6: June 26 ) 1 97

i. ec LF: ichn L. Kennedy, Vice .""resident Rochester, New Yerk

P.S.C. Yo. 15 - ELECTPJCJTY

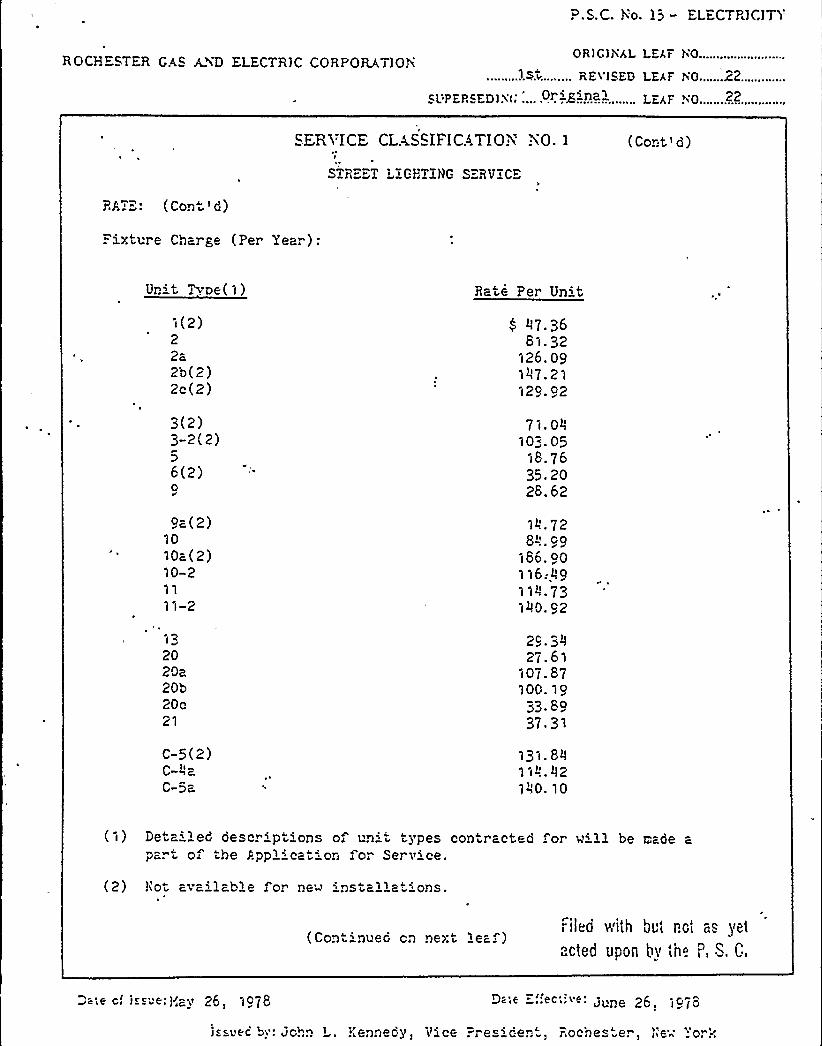

ROCHESTER GAS AND ELECTRJC CORPORATIONORIG) NAL LEAF YO.........................

.........1.%t...,..... REvlSED LEAF NO.......22.............

gg:pEpcEDly~, 'r'g"na LEg,F qO, 22

SERA ICE CLA.SSIFICATIOY'0. I (Cont'd)

STREET LZGJ''TING SERVICE

RAT=": ( Con ')."ixture Charge (Per Year):

Un't Tvoe(1) Rate Per Un't

i(2)22a2b(2)2c(2)

4 II7.3681. 32

'l26. 091ll7. 21129. 92

3(2)3-2(2)56(2)0

71. 04103. 05

18. 7635. 2028. 62

9a(2)1010a(2)10-211

1 l-2

10. 728-':.. 99

(86 90»6:49»4.731>0. 92

l32020a20b20c21

C-5(2)C-IlaC-5a

2c. 3II27. 6'I

107.87100. 19

33. 8937 31

131.8'1-"..42

1~0. 10

(1) Deta'led descr'pt'ons of un't types contracted "or w'll be made apart of the Pppl.'cat=:on for Ser v~ce.

(2) ho ava>lable for ne- 'nstalla 'ns.

(Continued cn ne>:t leaf)""i(ed vrith bl,t net as yet

".cted U".on hy the P, S. C,

DelE ci jK UE'; I,av 26 1978 D '~ ='~c"'~: June 26. 1978

i suec '"y: ~ohn L. !:ennec)>, Vice Pres'cent Roches.e. >ie'; 'o."'~

P.S.C. Yo.. I 3 — ELECTRICIT>

ROCHESTER GAS AND ELECTRIC CORPORATION0 R I G I!lAL LEAr YO.....

.........1.st......... REYIGED LEAr r'Q.......23.....

c.l'PERSEDIN'('.„..Q.—..g-..n.al......... LEAF 4'0..........3.....

SERVlCE CLASSIFICATION NQ. 1

S RE T LZGIiTING SERUZCE

(Cont'd)

RATE: (Cont'd)

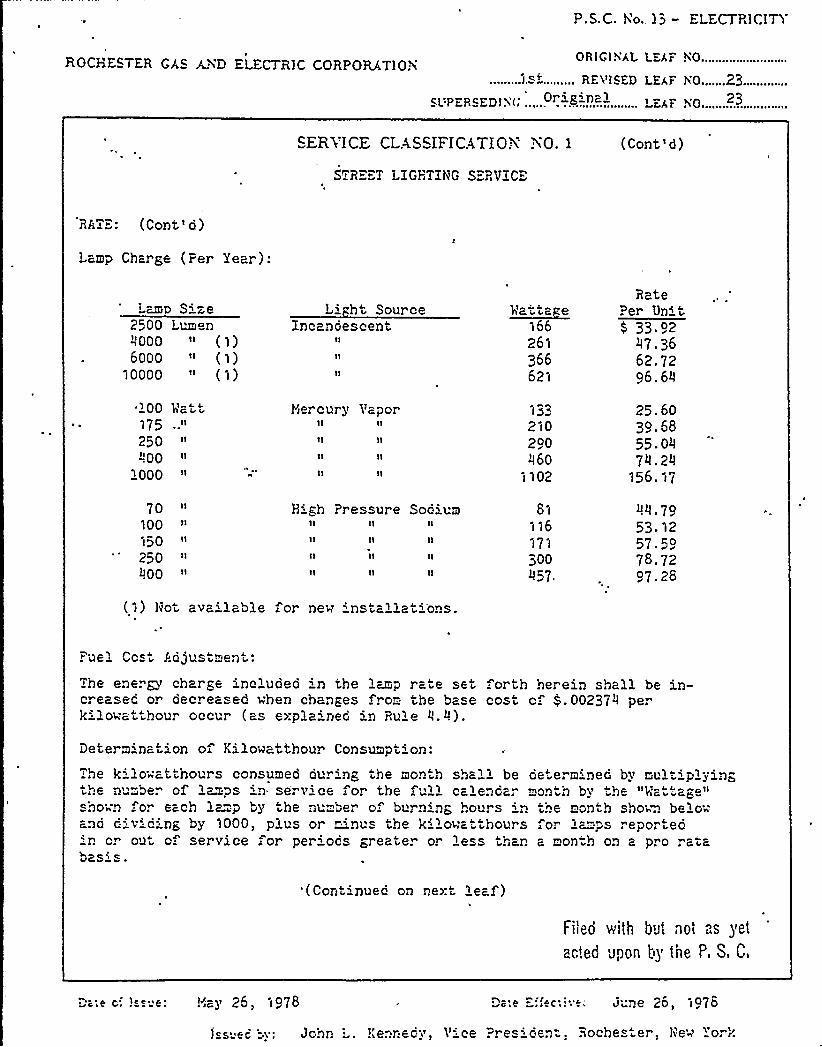

Lamp Charge (Per Year):

Lano Size2500 Lumen"000 'I ( 1)6000 'I (1)

10000 " (1)

Li ht SourceXncandescent

~IlR-:t- e16626I366621

RatePer Unit0 33 92

47.3662.7296.

6I,'oo

Vatt175 II

25Q II

IIQQ

looo

YIercury Vapor11 11

133210290460

1102

25.6039.6855. QII

7II. 2II156. 17

70 Il

10015Q 11

25Q 11

IOQ

Pressure SodiumII II

81116171300457.

I.I!.7953. 12

57.5978.7297.28

(1) Hot ava'lable for new 'nstallat'ons.

Fuel Cost Adjustment

The energy charge included 'n the lamp rate set forth herein shall be in-creasec or oecreased when changes f. on the base cost of $ .00237II perk'lowathour occur (as explained in Rule Il.>).

Determ'nation of Kilowatthour Consumption:~ he kilowatthours consumed dur'ng the month shall be de'erm'ned by multiplyingthe n ~nber of lmvs in serv'ce for the ~ ull calendar mon h bv "Ae "Ma tage"shown for each lamp by he nu ber of burn'ng hours 'n the month sho~~ belowand c'ie'g by 1000, plus or "'us the k' owa "hours ."or lamps reported'n or ou o ser vice or periods greater or less than a month on a prorata

'(Cont'nued on net leaf)

F!)ed vith but not "..s yet

ac!ed JPo!I by the P. 8, C,

cue G: l~~"e'~ay 25, 1978

Jss" ec

D~ e E ''~c;~.'une 26, lG78

Jchn ' !kennedy, Vice 'Pr es'en: I Rochester, hew "ork

P.S.C. Vo. 13 -ELECTR)CITY'OCHESTER

GAS AYD ELECTRIC CORPORATIONOR)CIYAL LEAF YO....

.....,.1.s~.......... REvl&ED LEAF h0..........24....

CL'PERcEDI~'(: .. 0 ig-na-......... I.EAF s'0........2.".....

SERVICE CLAScIFICATIQN YQ

STRE" T LIGHTING S:-RV'|CE

(Con 'd)

RAT"-: {Cont'd)

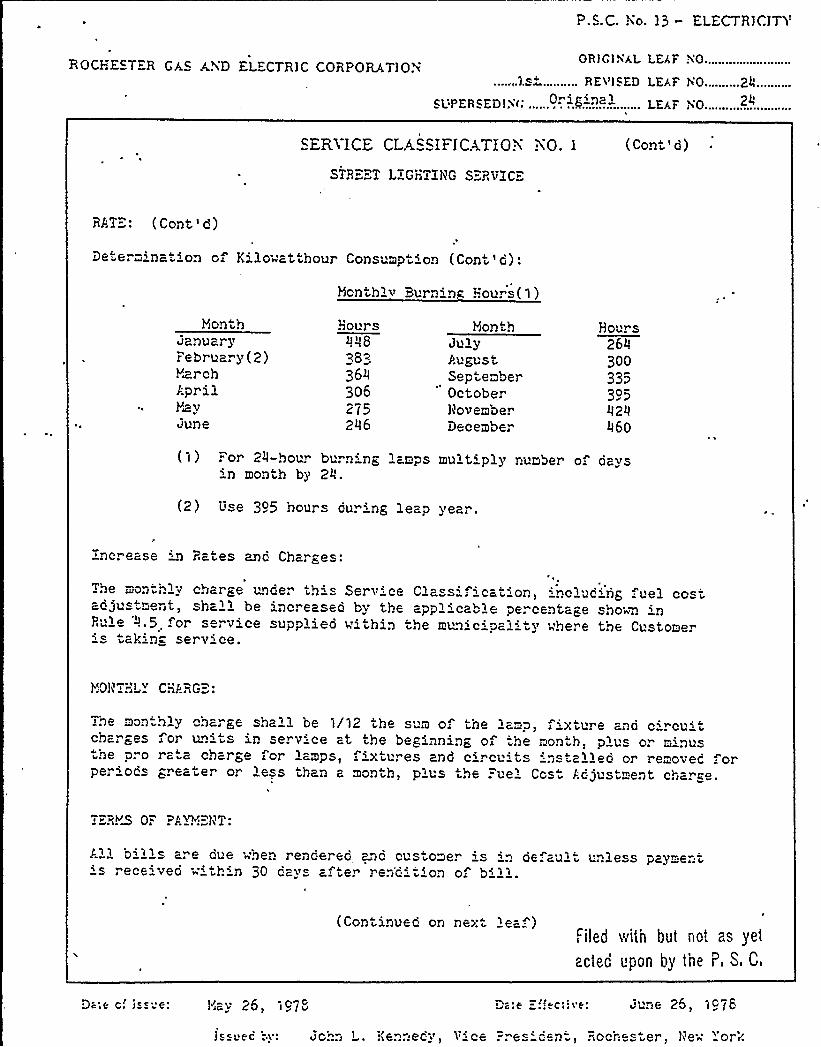

De~e. m nav on of Kilo~atthour Consumption (Cont'o):

Hon hlv Burnin Hours(1)

YionthJanuary".ebruary(2)YwrchaprilYayJune

80UI'S> "83833643062752II6

YiontnJulyPugu stSeptemberOctoberHovemberDecember

Ho'-rs26II30033530502IIII60

{1) .«or 2II-hour bvrn'ng lamps mult'ply number of daysin month by 2'.

(2) Use 395 hours during leap year.

increase Rates anc Cha. ges

The monthlv charge under this Serv'ce Class'f'cation 'nclud'ng .uel costadjustment, shall be increased by the applicable percentage sho'a 'nP~ule '-'!.5 for service supplied within the municipality vhere the Customer' taking se. v'e.

I'.GIANT: L~ CHP.'RG":

The mon.h'y charge shall be 1/12 the sum of the lamp, f'xtvre and c'rcu'tcharges for units in serv'e at the beginning of "he month plus or minusthe pro rata charge for lamps, ixtv.. es and circuits 'nstalled or removed orper'ds greater or ess than a month, pivs the ."-ue'est Adjustment chiarge.

0 '08YMili

Vl bills are oue hen rendered aric customer 's '.. default vnless payment's rece''ved "'thin 30 davs a ter ren'dition of bill.

(Con inueo on next lea )Filed ivith but riot zs yet

acted upoI by the I', S, C,

Yay 25, io78 De 'I c E: i 8 c'a "ne 25, 1o78

Is& 'Pc F: Joh.i L. Kennedy, Vice .. es 'en' .«rochester live„~'or'ii

P.S.C. Yo. 15 - ELECTR)C1TY

ROCHESTER GAS AND ELECTRIC CORPORAT10%ORIGI>4AL LEAF 40...................

......„.1.S>.„....., REVIsED LEAF ~0........2$ ......",-.cI)I ERcEDIi'I: .. O -..G.-:.'-?a.-......... LEAF i0........2$ .............

ER3 ICE CLA.SSII=ICATIQX ~0. 1 (Cont'0)

STREET LXGHTZHG SERVICE,

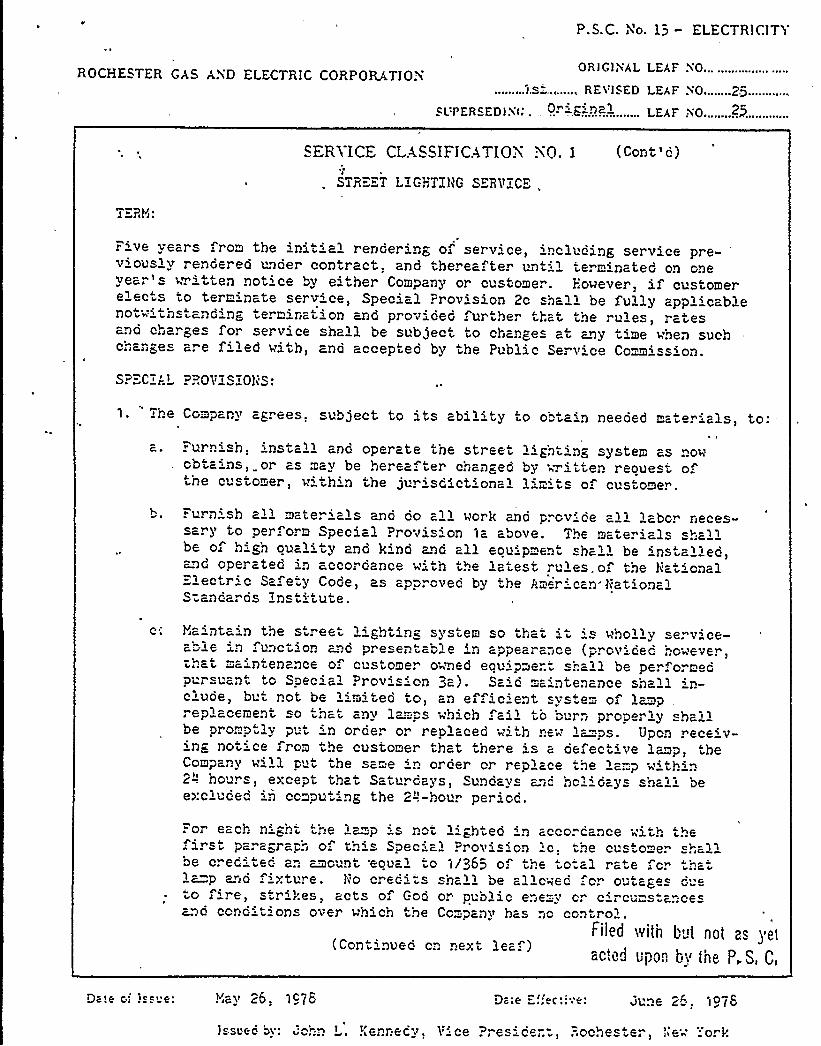

?Y'ive

years from the initial rendering of service, including service pre-'iouslyrendered under contract, and thereafter unt'' terminated on one

year's written Dot'e by either Company or customer. However, i customerelects to terminate serv'ce, Special?rovision 20 shall be fully appl'cableDot« i "ls Da ng t e. Killat" QD cnd provi 060 'l t le that the ules rc tesand charges for service sha~l be subject to chan<es ai any t'me when suchchan>es are f'led with) and accepted by the Public Service Commission.

S?" C:J L ? r,OVZSiOli'S:

Ccmpanv ag. ees, subject to its abil'ty to obtain neeoed materials, to:

c ~ rurnish, install and operate the streetobtains, or a may be herea ter chan<edthe customer ) with'n the jurisd't'nal

-- gh t -Dg sy stem cs Do'n

by n~itten reouest ofli ' of custome..

al 1 mate i al s and OQ cl 1 wor k ana ". Qv'6 al 1 1 aborsary to perform Special?rovis'on 1a above. The materials shallbe. of high puality ana kind ana cll epui pment shell be 'ns all ed~ad operated in accordance "'th the latest ."'les.o. the lpga ional

ectric Safety Code, as approved by the Pmerican'RationalS cnac OS )Ds itui e.

pJ a nta iD t,'

6 s tr6 6 t 1 " $h t i n z $y$ t 6 m s 0 th c t i t, is wh 0 1 1 y s 6 vic 6ab-'6 in -'nCtion end Pl 6Sentcble in cPPec a.)Ce (ProVi Cec ho'«'6V6.

)~hat ma'ntenance of customer o'ned eauipme.".t shall be per;ormed

Special Prov's'n 3a). Sc'd ma'ntenance sh" 11 'D-c'uoe, but r.ot. be limited to, an efficient syste" of 'amp

6p acement so that c Dv lal". s wh ch 'i i 0 burn pl ope ly shalbe promp.lv p)t in oraer or replaced w'th new 1~ps. Upon rece'v-in< notice from the customer that there 's a defect've lamp, theCompany will put the same 'n order or replace the lamp .«" th'n2-"! hours) except that Saturdays, cundays ""c hcl'acys shell beexcluded in computin> the 2-'!-hour perioa.

trQ1Filed with b„)t not ps ~etac!ea UpO.", by tne P,S, C,

(Continuec cn next leaf)

:or ecch ni~ht the l~~p is not lighted 'n accorcance w'th thei. t parae,raph o th'pec=:- Prol'on c) -"he cu tomerbe credi.ec an ~~o nt 'eoucl -o 1/365 o; the ".otal rate ,cr

.ha'p

ana ixture. Ho creci ts shall be allc<ec for outaees d 6to f'e, strikes) acts of Goa or public enemy cr circu stances~ad concitions over which the Company has n)o con

!)av 26 107B Ju )6 2~ 1078

l .suec by: 'chn L. !lennecy, Vice ?res'de;.:) .=.ochester»ew 'ork

P.S.C. Yo. 13 - ELECTR)CITY

ROCHESTER GAS AiD ELECTRIC CORPORATIO>OR IC IiAL LEAF 4 O.........................

......,1.s,~... „... RE> ISED LEAF >O.........~G..........,

FI>PERSEDIs'i: ....,. OriE.-.'.Dal....... LEAF 40.........8..............

SERA ICE CLA.SSIFICATIOi iO. 1 (Con 'd)

STREET LZGHTIh'G S~RVZCE'I

S""C"Ai. P?>OVZSZOÃS: (Cont'd)

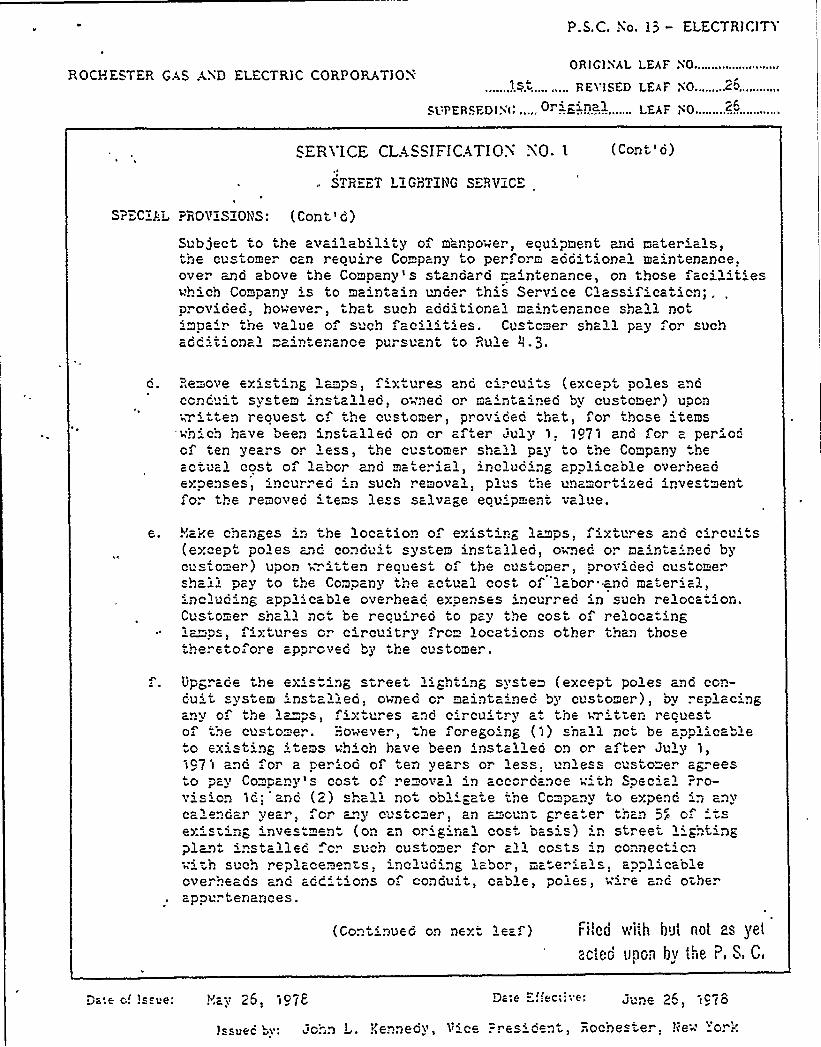

Subject to the avci1 ab''y of manpower> ecuipnent and mater'cls,the customer can reou'e Company to perform aoditional maintenance.over a~d above the Company's standard Laintenance, on those facil't'eshhich Company is to maintain Unde? this Service Classificaticn', .

proviGed, hoiN'ever, that such additiona > ma'r.tenance shall ?30tizpa'r the value o s ch fac'lit'es. Custcmer sha11 pay for suchcccii. Gna ma"'D'ncnCB PU, Suant co, U 6

G. Bzove Gxi s in' cmps>

' Ures aqd ci ~cui t s (except Dol Gs aqdco. >c 'i svctem i mstc 1 1 60 0~"16d or mc. >tc. DGG bv cus'mer) UDGD

ten reouest 0 the customer, pro riced th>at, for those 'tems"h'.ch have been 'nstcllec on cr af er uly 1, 1071 ar.d for a periocof ten years or 'ss, the customer shell pay to the Company .heactual cost of labor and material, 'Deluding applicable overheadGXpen 6-

>DCi'. ~ GG iD SUCh . 620Vc.

> p l'S t..6 Unamol t idled DVB tmeni~ 0 the r6mo'vec t 6ms 1 ess s 1 vc e eouipment val'.

e.."lake changes 'D the 1ocation o. exist'D" lamps fixtures and c'rcv.'( except poles an>c conduit syst em iDst a > 160 0'r nec 0. Ha Dtc'ec bycustomer) upon h-.itten recuest of the c's.orner prov'Ged customershal > pav t0 the Company the cc i l al cost of 1 cbor 'DQ mat Gric1'nc Uding app" c" b1e overheac expenses 'ncvrred in such re1ocat'o? .

CUSi G "6. Shc1 1 DG i be BCuired t0 pav ti16 CGS Of relOCc iDg~ 1~~ps> f'xtures cr circuitry rom locations other than> those

theretofore apprcvec by the customer.

UPe,. cc6 the GX'S in/ Street 'ighting SyS> em (eXCePt POleS c, 3d CGin-cu't system 'ns alled> owned or maintainec by customer) bv replacingcnv 0-'i>6 azPS . 'tl'res c Dc c 'cu 'ry a'he hri tr Bn recuestof the cus orner..-'.Oaeve.

>the foregoing ( >) snail no be app>'cab>e

o existing, 'tems hhich have been installed on or after July 1>

i 71 anQ or a per'od of ten years or 1ess, un1ess custome. agreeso pay Company's cost of re oval 'D accor dance "'th S Gcial ."ro-

vision )c.: 'and (2) sha11 not obli-ate tne Ccmpcny to Gxpenc in anvc cCa G..Gc?'ea;

>i 01" c~y CUSi 0 er, ar> amGUD ~. Ga Br thiaD r> 0' S

Gxis iin~ 'vestmen. (on an ori ginal cos". bas') ' stree-pl~a 'nstallec cr uch cu ~orner or a1'osts in connec 'cn

uch rep1 ccemen '>

s n 1udinhr 1 abQr>

ma" e. ' 'l s>

aggl '. ccbl 6

Gve hec Qs c'1c cQcii 0 .s 0 coDGui ccble po '>

hir6 anc 07 he.appvrtenances.

(Co.>tiDUGG Gn next 16a ' Filed v;i';h hei not as yet

BCICG IIDO;I bV '.:">e I, S, C,

D~:e 0! >Be>!e: !'.Gy 26, >078 Dele E;eci>eel june p6 >c78

1ecl>ee +V: >'Ghn I . l>ennedy 3'iCc, rGSi Gent>

OCDBS er'> J>>G 'r

1).S.(:. Ni). jP — CiAS

ROCHESTER GJ S A4D ELECTR1C CORPORATIO.).......5..ill.......... RE'V')SED LEAF 40.........LO...,

sl:PER<ED)iG .........ro................... LEAF ).0.........~0.....

4 ih Reviseo Lea ho. 40 Pena'no

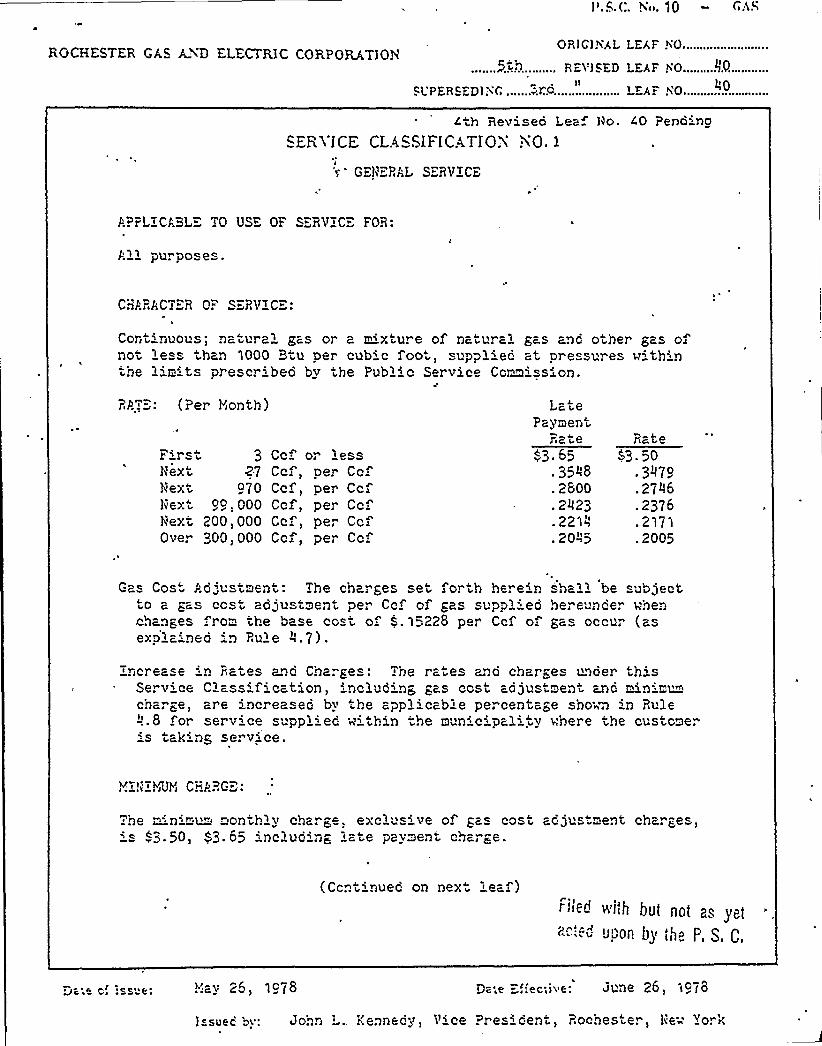

SERi ICE CLA.SSIFICATIOX YQ. 1

GEN.RPL SERViCE

P.PPLiCABLE TO USE OF SEPViCE FOR

P11 purpoc es

CHF.'RPCTER OF SERViCE:

Coritinuous) natur21 gas or 2 mixture of natural gas 2no other gas oinot 'e than 1000 Btu per cub' foo, supplied at pressures vithinthe l'm's prescribed by the Public Service Commission.

RP.! (Per Honth)

First 3Next Z.7

Next G70Next 99)000Next 200)000Over 300) 000

CcCcf)Ccf,Ccf,Ccf)Ccf)

or lessper Ccfper Ccfper Ccfper Cc.per Cc.

1atePaymer t,

Rate:3. 65

. 3548

. 2800

. 2023

. 22 ls20 "5

Rate53. 50

3~79.2706.2376. 2'l7 l

.2005

Gas Cost Pd„'ustment: The charges set forth hereinto a ~as cost adjustment per Cc of gas suppl'dchanEes .rom the base cost of $ . 15228 per Ccf ofexo'lained in Ru1e A.7).

sha" l be subjecthereuncer whengas occur (as

increase 'n Rates ano Charges: .he rates 2nd charades unoer thisSe. vice C ass'ication, includinp, gas cost adjustment 2nd minimumchar~e, are increased by ..he applicable pe. centare sho'n~ 'in Rule>.8 "or service suppliec nithin the municipal::ty where the customeris tak'ng service.

Yi!i'Yii3YiCHPRG

~ he miinimu" month'y charge exc'us'e of gas cost ad)ustment cha. ".es's ~3.50, $3.65 includin< 1a e payment char~e.

(Ccritinued on nex i eaf)Priled v ith but not as yeta..!-:„. u.'on by the P, S C,

Jc16 Ci !SS" ~ ! ..ay 26, i9 ~8 i qc jv~ June 26)

1 suec by: John L., Kennedy, V'ce Presicent, Rochester, Ne 'rr',

RCtCHESTER Ghc AYD ELECTRIC CORPORATION....5 ..'n.

cUPERcED) YG ...~.'.c

OR)GlhhL LEAF hO................

REJOICED LEAF NO, "!Z

...................... LEAF hlO

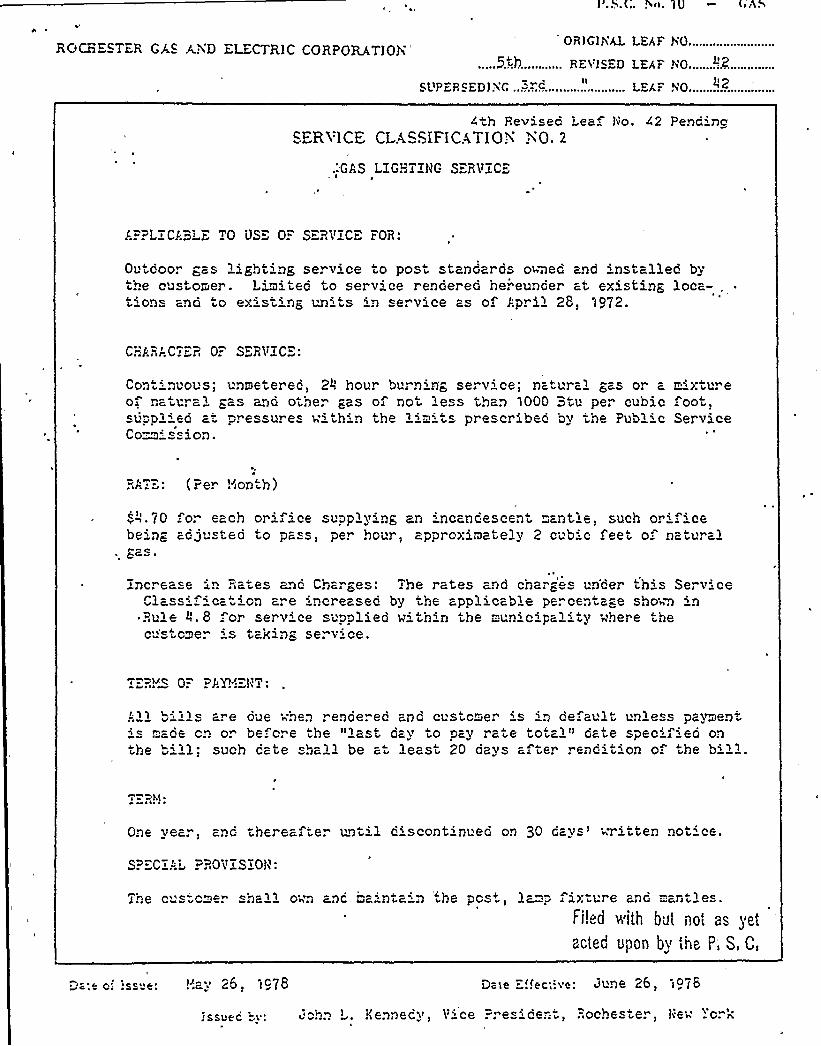

4th Revised Lea IHo. 42 PendincBERVlCE CLACSIFICATIOY YO

.:GAS LXG™ ZHG SERVi'C""

j. PLYCSBLE TO US" 0." SERVICE FOR:

Outcoor gas iight'ng ser vice to post standar ds owned and installed bythe customer. Limited to serv'ce rendered he. eunder at existing loca-t'ons and to existing units in service as of J-'.pril 28, 1972.

C::P.. '.CTiR O.. S"RVTC"

Continuous; unmetered, 2'our burnin'g service; natural gas or aoa natural gas and ot'ie. gas of not less than 'l 000 ~tu per cub'Opplied at p. e res w'thin the lim' prescribed 'oy the Public

C ommi s s ion ~

~'xtureOo~

Ser vice

RAT=-: (Per !'month)

„'~. 70 or each orif'e suppi ying an 'ncancescent -ant le, such orificebeing adq steo to pass, per hour, approximately 2 cub'c feet o natural

inc. ease ' Rates ~ad Charges: The rates and char<es un'der this ServiceClassi ication are increased by the applicable percentage shown inRule ll. 8 or serv'e supplied wi th'n the municipality where thec'ver 's taking serv'ce.

tP& hrc 0 h 'PP+Jw)$ %

!11 b'iis are due when rendered and customer 's in de ault unless paymen-is mace cn o. be o. 6 the "last dav 0 pay rate

total�

'~ Gat 6 specifi 6Q onthe b'll: suc» cate shall be at least 20 oays after renci 'on o. he b'll.

s i 'Ph',

One vear, and thereafter until c'scontinued on 30 days'ritter. not'e.

SP".C:AL:ROV r SZOI'.

Th6 CuS Ome. S "ia" 1 OWn a;iC Lai nta 'e POS r 1c - s ix ure and mant 16S

F'iit'.d with but i~ot ac yetact8d Upoll bv tilB P) S) C<

!';ay 25, 1978

IssUec hy: Yiennecv

D-ie E!~ac;:.ve: dune 26, io78

Vice ."res'en-'., Rochester Iiew 'ork

4

+n '

I

P

I

k\f

Y

jl'

L

I,l

V

N

4 ~I4

I

i

1;

Y =

C

V

V1 p

'+..l~ttg

T

Rochester Gas and Electric Corporation

Direct Testimony

of

WILLIAMW. STODDART

Assistant Division ManagerGeneral Accounting Department

0

Stoddart

Qo

A:

Would you please state your name and business address?

My name is William W. Stoddart. My business address is

Q-

89 East Avenue, Rochester, New York 14649.

Mr. Stoddart, what is your position with Rochester Gas

10

A:

Qe

A:

Q-

and Electric Corporation?

I am Assistant Division Manager of the General Accounting

Department.

How long have you held that position?Since 1970.

What are the duties and responsibilities of thatposition?

12 A: I- am responsible for coordinating the activities of the

13

14

General Accounting Department relative to the collectionand preparation of data utilized to maintain the financial

15 records of the Company. The Property Records, Stores

16 Records, Accounts Payable, Payroll, Accounting Control17

18

19

20

21

22

Q ~

A:

Q ~

and other General Accounting functions come within the

scope of my responsibilities.How long have you been employed by the Company?

Approximately 19 years.

Will you briefly outline your experience .and quali-fications?

23

24

A: I am a graduate of the State University of New York atBuffalo. In 1959 I was employed by the Company as an

J'

Stoddart

10

Q ~

A:

Q ~

accountant in the General Accounting Department.

Subsequently I have held the position of Corporate Tax

Representative and now my present position.Mr. Stoddart, are you generally familiar with the

requests for additional revenue in the Company's

electric and gas filings?Yes, I am.

Have you prepared certain exhibits of a financial and

accounting nature in conjunction with and support ofthese proposed increases?

12

13

14

15

16

17

18

20

21

22

23

24

A:

Q ~

A:

Q-.

Yes. Exhibits l through 7 were prepared by me or under

my supervision and direction utilizing data taken from

the books and records of the Company.

Will you describe Exhibit 1 and state what it purportsto show?

Exhibit l sets forth the comparative balance sheets forthe Company as of December 31, for the yeax;s 1974,

l975, 1976 and 1977, in the form prescribed by the

Commission. These balance sheets are stated on a

corporate basis and include data applicable to all ofthe operating departments of the Company.

Does the Company maintain its accounting records inaccordance with the Uniform System of Accounts prescribed

by the Commission?

I

Stoddart

A: Yes.

Qo Are there any particular accounts upon which you wish

to comment?

A: The balances in account 101, Electric Plant in Service,

10

12

13

14

15

16

17

increased by $ 81<540,839 over We three year period.The majority of the plant additions have been for theCompany's transmission and distribution system to meet

ll

the reliability and growth needs of our system. During

1977 there were also major additions to our nuclearproduction plant.

The balances in account 101, Gas Plant in Service,increased by $ 4,000,985 between December 31, 1974 and

December 31, 1975, decreased by $ 1,499,088 between

December 31, 1975 and December 31, 1976 and then

increased by $ 4,492,009 between December 31, 1976 and

December 31, 1977. Plant additions for the three-yearperiod were for improvement of distribution facilitiesnecessary to assure reliability of service and for

19 continued improvement in safety standards. The decrease

20

21

22

23

24

at, December 31, 1976 reflects the retirement from

service of the Company's gas manufacturing'acilitiestotalling $ 5,350,924.

Account 118.1, Common Utility Plant in Service,consists of office buildings, operations and service

Stoddart

centers and transportation, tools, office,'ommunications

and other equipment. The amounts applicable to the

Electric Department are shown in Exhibit 6 and the

amounts applicable to the Gas Department are shown in

Exhibit 7.

6 The balance in Account 105, Plant Held for Future

10

12

13

Use, is made up of $ 306,365 representing land located

south of the City of Rochester and $ 33,765 representing

land located adjacent to Station 'N5. The current

balance in this account is applicable to the ElectricDepartment.

The Electric Department portion of accounts 107

and 118.1, Construction Work in Progress, at December 31,

14

15

1974, 1975, 1976 and 1977 was $ 36,757,449, $ 77,134,659,

$ 118,228,084 and $ 158,673,781, respectively. The

16 increases 'in this balance through December 31, 1977

18

primarily, reflect the Company's share of expenditures

incurred for three new generating facilities. Expenditures

19

20

21

22

23

24

for licensing and preliminary engineering for its 28%

interest in the 1150 MW nuclear plant to be located inSterling, New York and to be owned by the Company

jointly with Niagara Mohawk Power Corporation, Orange

and Rockland Utilities, Inc. a'nd Central Hudson .Gas and

Electric Corporation amounted to $ 29,054,512 including

0

Stoddart

fuel at December 31, 1977. The Company is also participating

10

in the ownership of two Niagara Mohawk generating

stations: Oswego N6, an 850 MW fossil unit in which

the Company will have a 24% ownership interest and,Nine

Mile Point 42, an 1100 MW nuclear unit in which the

Company will have a 14% ownership interest. Expenditures

on these two units through December 31, 1977, includingfuel, totalled $ 43,589,026 and $ 54,774,342, respectively.

The Gas Department Construction Work in Progress

balance at December 31, 1974, 1975, 1976 and 1977 was

$ 1,645,707, $ 1,228,345, $ 1,255,286 and $ 1,395,385. The

12 lower balances in 1975 through 1977 compared to 1974

13

14

are due primarily to reduced distribution main construction.There are also small balances of Common Utility

15 Plant — Construction Work in Progress applicable to the

17

Electric Department and Gas Department. These amounts

are shown in Exhibits 6 and 7, respectively.18

20

21

22

23

24

Account 114, Plant Acquisition Adjustment, does

not appear in the balance sheet at December 31, 1974.

.At that point in time, $ 3,132,171, representing the

value of certain water rights on the Genesee River

which were acquired on June ll, 1904 in the consoli-dation of Rochester Light and Power Company and Rochester

Gas and Electric Company, was reflected in Account 101,

J

Stoddart

I'Plant in Service. The Commission ordered the Company,

,in a prior Electric rate case, Case 26522," to begin

amortizing these water rights over a forty year period.

The Company transferred the $ 3,132,171 to Account 114,

Plant Acqusition Adjustment, on January 1, 1975 and

commenced amortization in accordance with the order inCase 26522. The balances are applicable to the ElectricDepartment,.

10

The balances in Account 120, Nuclear Fuel, atDecember 31, 1976 and December 31, 1977, represent the

12

original cost of the nuclear fuel components for the

Ginna nuclear plant. The balance at December 31, 1974

includes the Company's share of prepayments for nuclear

14

15

fue'1 applicable to the Sterling nuclear plant in theh

amount of $ 438,167. The balance at December 31, 1975

includes the Company's share of prepayments for nuclear

17 fuel applicable to the Sterling and"'Nine Mile Point

18 nuclear plants in the amounts of $ 736,120 and $ 1,131,017,

19 respectively.

20 The balances in Account 120.'5 reflect the accumulated

21

22

provision for amortization of fuel applicable to Ginna

Station.

23 Qo Turning now to Account 108, Accumulated Provision for24 Depreciation of Electric Plant in Service, will you

Stoddart

A:

comment on the balances shown?

Accumulated Provision for Depreciation of ElectricPlant in Service was $ 109,396,951 at December 31, 1974

and $ 138,106,010 at December 31, 1977. The ratio ofthis provision to Plant in Service at December 31,

10

12

13

14

1974, 1975, 1976 and 1977 was 25.0%, 25.7%, 26.6% and

26.'6%, respectively.Account 108, Accumulated Provision for Depreciation

of Gas Plant in Service was $ 33,663,094 at December 31,

1974 and $ 35,049,799 at December 31, 1977. -The ratioof this provision to Plant in Service at December 31,

1974, 1975, 1976 and 1977 was 23.0%, 23.2%, 21.3% and

22.8%, respectively. The reduction in this account

from December 31, 1975 to December 31, 1976 reflects15

16

the retirement of the Company's gas manufacturing

facilities in the amount of $ 5,350,924.

19

20

Depreciation accruals are provided by applying

1/12 of the annual depreciation rates to the monthly

book balances of the primary plant accounts. The

Company reviews annually its rates used for depreciation21

22

23

24

accruals. Depreciation studies are made each year tohelp the Company gauge the appropriateness of its book

accruals. These studies are based, in part, on an

actuarial analysis of plant history to -determine average

Stoddart

service lives. The annual accrual rates used are based

upon these actuarial studies, salvage studies, theoretical

6

10

12

13

14

A:

reserves and managerial judgment. These studies have

been regularly made available to the staff of the

Commission. The balances shown in Exhibit 1 result

from accrual rates approved by the Commission in several

proceedings, commencing with Case 16510 through, most

recently, the Company's last electric and gas rate

cases, Cases 27108 and 27109.

Would you please continue with your explanations of

this exhibit?

The balances in Account 123.1, Investment in Subsidiary

Companies, represents our investment in Canadea Power

Corporation computed under the equity method of accounting.

The Company adopted the equity method of accounting for

16

18

19.

20

21

22

23

its investment in this wholly-owned subsidiary, effective

January 1, 1973, pursuant to the Federal Power Commission

Order No. 469.

Account 131, Cash, has fluctuated between a high

balance of $ 5,912,089 and a low balance of $ 4,844,109

at the year end dates shown in the exhibit. The variations

in cash balances between balance sheet dates occur forseveral reasons such as cash collections, bill payments

24 and prospective bills due and compensating balance

Stoddart

requirements. These changing conditions are reflectedin the balances shown.

Account 133, Dividend Special Deposits, represents

funds on deposit for payment of dividends on common and

preferred stock. The balance in this account increased

$ 322,079 between December 31, 1974 and December 31,

1975. This increase primarily reflects the increase in

10

dividends due to the October 1975 sale of 220,000

shares of preferred stock. The balance in this account

decreased by $ 1,622,729 at December 31, 1976. This was

12

caused by eliminating a one month lag in reporting ofdisbursements by the disbursing agent which was reflected

13

14

in the prior year balances. The increase in thisbalance of $ 27, 782 at December 31, 1977 primarily

15 reflects the issuance of 1, 000, 000 shares of common

16

17

18

19

20

21

22

stock on September 29, 1977.

The balances in Account 134, Other Special Deposits,

at December 31, 1974 and 1975 reflect funds advanced by

the participants in the Sterling nuclear unit for itsconstruction. The balance at December 31, 1976 representsa deposit in lieu of mortgaged property sold. The

~ large increase at December 31, 1977 represents the par23

24

value, call premium and accrued dividends on the Company's

Series "0" preferred stock which was called for redemption

Stoddart

'subsequent to a request. by the Company and approval by

the Commission in Case 27269. These amounts totalled

$ 28,131,950.

Account 142, Customer Accounts Receivable, decreased

by $ 2,161,285 from December 31, 1974 to December 31,

1975, increased $ 10,485,155 at, December 31, 1976 and

10

then decreased by $ 3,064,937 at December 31, 1977.

These changes were due primarily to the variance insales in the month of December of each year. For

instance, December 1977 sales were approximately $ 3,000,000

lower than December 1976 sales which, in turn, were

12 over $ 10,000,000 higher than December 1975 sales.

13

14

Account 143, Other Accounts Receivable, increased

by $ 1,026,617 to $ 1,119,364 at December 31, 1975 and

15

16

then decreased to $ 318,287 and $ 105,994 at December 31,r

1976 and 1977, respectively. The l975 and 1976 balancesr

primarily related to amounts due from other utilities18 participating in the construction of the Company's

19

20

21

Sterling nuclear generating facility.r

The balances in Account 144, Accumulated Provision

for Uncollectible'ccounts — Credit, have increased by

22

23

24

approximately $ 97,000 in 1976 and $ 250,000 in 1977.

The Company determined that this provision should be

increased due to increases in the amount of customer

10

Stoddart

10

Qe

A:

billings and its history of uncollectibles. Prior to

1976 the Company had maintained the reserve at the

$ 100,000 level for a considerable number of years.

Would you please continue with your explanation of this

exhibit?Account 150, Materials and Supplies, increased by

approximately $ 2,660,000 from December 31, 1974 to

December 31, 1975. This net increase was due primarily

to a $ 3,360,000 increase in fuel stock due to higher

unit costs and a $ 700,000 decrease in other materials

and supplies. The balance in this account decreased- by

12 approximately $ 1,467,'000 at, December 31, 1976 due

13

14

15

16

17

18

20

21

22

primarily to a decrease in fuel stock, while the balance

at December 31, 1977 increased approximately $ 303,000

due primarily to an increase in other materials and

supplies.

The balances in account 165, Prepayments, decreased

approximately $ 200,000 at December 31, 1975 and $ 11,000

at December 31, 1976. The balance increased approximately

,$ 280,000 at December 31, 1977.

The 1975 decrease resulted from the elimination of

a prepayment of $ 262,000 for poles offset by an increase

23

24

in prepayments for insurance under the Employees Welfare .

Association Plan and general insurance. The increase

j

I~ . ~

'

Stoddart

10

12

13

14

15

16

17

19

20

21

22

23

at December 31, 1977 results primarily from increases

in general insurance. Excess public liability insurance

premiums, for instance, doubled during 1977 due to

general premium increases and our recent experience of

claims reserved and paid by our insurance carriers.

Account 181, Unamortized Debt Discount and Expense,

has increased from December 31, 1974 to December 31,

1975 by $ 302,283 reflecting a change in method of

reporting. Prior to the latter date Unamortized

Discount was included in Account 181. However, effective

with that date, it is now reported in Account 226.

Likewise, Unamortized Premium on Debt, previously

reported in Account 251, is now reported in Account 225

as shown on page 2 o'f this exhibit. The further increases

in the balance of this account at December 31, 1976 and

December 31, 1977 reflect $ 514,600 of expense incurred

in the issuance of $ 50,000,000 of Series BB 9 1/4%

bonds in June 1976 and $ 896,700 of expense incurred in

the issuance of $ 50,000,000 of Series CC 8 3/8't bonds

in November 1977.

Account 183, Preliminary Survey and Investigation

Charges, decreased from a balance of $ 1,796,503 at

December 31, 1974 to $ 1,159,495 at December 31, 1975

24 and then increased to $ 1,604,033 at December 31, 1976e

12

4

Stoddart

10

and $ 2,304,943 at December 31, 1977. Expenditures

incurred in obtaining environmental certification of

our proposed 765 KV transmission line comprised a large

portion of the balance in each year shown. The December. 31,

1974 balance also reflects substantial expenditures

incurred to review piping system designs at Ginna Station.

The balance in Account 186, Miscellaneous Deferred

Debits, increased from a balance of $ 3,851,923 at,

December 31, 1974 to $ 3,895,452 at December 31, 1975,

then decreased to $ 3,807,897 at December 31, 1976 and

increased to $ 6,665,154 at December 31, 1977. Of the

12

13

14

15

16

17

19

20

21

$ 3,851,923 balance at December 31, 1974, $ 3,736,605 isapplicable to fuel costs deferred resulting from the

adoption of deferred fuel cost accounting by the Company

in 1974, in accordance with the Statement of Commission

Policy Concerning Fuel Adjustment Clauses of ElectricUtilities. The Order in Case 26547 extended the accounting

provision to Steam Utilities.The balances of $ 3,895,452 at December 31, 1975,

$ 3,807,897 at December 31, 1976 and $ 6,665,154 at

December 31, 1977 further reflect the Commission's

22 ~ Opinion No. 75-10 issued May 1, 1975 together with a

23

24

Resolution adopted April 29, 1975 whereby 16 NYCRR 270

was changed to require a surcharge-refund provision for

P

N

il 4 II

'1

Stoddart

over or under-recoveries of Gas Adjustment Clause

Revenues. Also included in the latter three balances

are Steam Department deferrals arising from a reduction

in fuel cost adjustment revenues which are being amortized

pursuant to the Commission's Order in PSC Case 26766.

These items together with the aforementioned fuel cost

deferrals total $ 3,739,009 at December 31, 1975, $ 3,451,627

10

12

13

14

15

16

17

18

19

20

at December 31, 1976 and $ 6,338,424 at December 31,

1977.

The deferred Federal income taxes applicable to

the deferred steam fuel currently being amortized are

likewise reflected in the December 31, 1975, 1976,and

1977 balances in Account 253, Other Deferred Credits,

in the respective amounts of $ 1,016,200, $ 902,800 and

$ 779,100.

Account 190, Accumulated Deferred Income Taxes,

has a balance only at December 31, 1976 and December 31,

1977. The balance at December 31, 1976 reflects deferred

tax accounting applicable to Contributions in Aid ofConstruction, in accordance with the accounting prescribed

21

22

by the Commission in PSC Case 26848 and 26849, and to

over-recoveries of Gas Adjustment Clause Revenues. The

23 balance at December 31, 1977 increased $ 3,424,600 from

24 December 31, 1976 including a $ 3,346,000 deferral

Stoddart

10

12

13

14

15

16

18

19

20

21

22

23

24

A:

representing the adoption of deferred tax accounting

for nuclear fuel storage costs. This change will be

further described in Exhibit 8. The remainder of the

balance primarily reflects deferred tax accounting

applicable to Contributions in Aid of Construction.

Turning to Page 2 of this exhibit, will you continue

with your comments?

Account 201, Common Stock Issued, has increased from

$ 47,346,950, at December 31, 1974 to $ 54,399,465 at

December 31, 1975, then increased to $ 56,830,555 at

December 31, 1976 and $ 64,448,155 at December 1, 1977.

Credits to this account from common stock issuances

during this period from new offerings and under our

Automatic Dividend Reinvestment Plan were: 1974,

38,511 shares for $ 192,555; 1975, 1,126,457 shares for

$ 5,632,285; 1976, 159,784 shares for $ 798,920 and 1977,

1,182,536 shares for $ 5,912,680.

Stock dividends were issued totalling 274,690

shares in 1974, 284,082 shares in 1975, 326,398 shares

in 1976 and 340,984 sh'ares in 1977. Transfers from

Unappropriated Retained Earnings in connection with the

stock dividends were credited to this account in the

amount of $ 1,373,450, $ 1,420,410, $ 1,631,990 and $ 1,704,920

for the years 1974 through 1977, respectively.

15

Jl

PI I

Stoddart

10

12

13

14

Account 204, Preferred Stock Issued, increased by

$ 22,000,000 from December 31, 1974 to December 31,

1975, increased an additional $ 3, 000, 000 to December 31,

1976 and then decreased $ 24,720,000 at December 31,

1977. These changes reflect the sale of 220,000 shares

of Series 0, 11% preferred stock in October 1975, the

delayed sale of an additional 30,000 shares of Series 0

preferred stock in March 1976 and the announced call ofthe Series 0, 11% preferred stock and sale of 280,000

shares of Series A, 7.60% preference stock, par value

$ 1, in December 1977.

As a result of common stock issuances during thisperiod from new offerings and under our Automatic

Dividend Reinvestment Plan, Account 207, Premium on

15

16

17

19

20

21

22

23

24

Capital Stock, was credited with the following amounts:

1974, $ 301,889; 1975 $ 11,625,384; 1976, $ 1,826,515 and

1977, $ 18,666,651. Transfers from Unappropriated

Retained Earnings in connection with the stock dividends

were credited to this account as follows: 1974, $ 3,570,970;

1975, $ 1,704,492; 1976, $ 3,590,328 and 1977, $ 5,114,760.

An amount totalling $ 27,720,000 was also credited tothis account in 1977 as a result of the issuance ofpreference stock.

The balances in Accounts 211, Miscellaneous Paid

16

t gi" ~

Stoddart

in Capital, and 216.1, Unappropriated Undistributed

Subsidiary Earnings, reflect equity accounting for the

Company's investment in Canadea Power Corporation.

The increase in the debit balance of Account 214,

10

Capital Stock Expense, from December 31, 1974 to December 31,-

1976'reflects the expenses of issuance of common and

preferred stock and for stock dividends during thatperiod. The increase in this balance from December 31,

1976 to December 31, 1977 primarily reflects a $ 2,750,000

call premium on the Series 0, 11%, preferred stock and

12

$ 105,008 issuance cost of the Series A, 7.60% preference

stock. These amounts, totalling $ 2,855,008, will be

13

15

16

17

19

20

amortized in equal'nnual installments to the maturityof the Series A, 7.60% preference stock in 1985 as

authorized by the Commission in Case 27269.

The increases during the past two years in the

balances of 'Account 221, Bonds, have resulted from the

sale of $ 50,000,000 of 9 1/4% Bonds in June 1976 and

$ 50,000,000 of 8 3/8% Bonds in September 1977, offsetby the redemption of $ 333,000 of 10 3/4% Bonds and

21

22

$ 6,000,000 of matured 4 1/2% Bonds in August and September

1977, respectively.23 The balances in Account 224, Other Long Term Debt,

24 represent the non-current liability for deferred purchase

17

yl

Stoddart

contracts for land at Sterling.The balances in Account 225, Unamortized Premium

on Debt, and Account 226, Unamortized Discount on Debt,

reflect a change in the method of reporting as stated

previously in my explanation of Account 181, Unamortized

Debt Discount and Expense. The increase in the balance I

of Account 225 at December 31, 1976 reflects the premium

received from'the sale of bonds in June 1976 in the

10

amount of $ 117,500.

The balance in Account 231; Notes Payable, fluctuates

12

13

14

15

16

18

20

21

22

24

between $ 9,000,000 and $ 21,500,000 at the balance sheet

dates shown. When it is necessary for us to go intothe open market to obtain funds, we first issue eithercommercial paper which generally matures in 30-45 days

or notes to banks which usually mature in 9 months.

Subsequently, we issue long-term securities and use the

proceeds to the extent necessary to extinguish the

outstanding short-term borrowings. This procedure

provides us a degree of flexibility in the timing oflong-term financing.

The balance in Account 232, Accounts Payable, was

$ 9,286,801 at December 31, 1974. The balance increased

by $ 3,469,850-during 1975 with $ 1,756,617 of thatincrease representing the Company's obligations in

18

"F

Stoddart

10

jointly owned generation facilities. The balance

increased an additional $ 3,371,395 during 1976. This

increase was primarily due to an increase of $ 3,077,575

in the balance payable to the Company's natural gas

supplier and an increase of $ 996,399 in the balance

owed for coal, freight and demurrage. During 1977, the

increase of $ 618,517 was caused primarily by an amount

payable of $ 2,997,148, representing a liability forrepayment of nuclear materials to Combustion Engineering

Corporation, coupled with decreases of $ 2,195,443 and

12

$ 597,020 in the balances payable to various coal companies

and to our natural gas supplier, respectively.

13 The balance in Account 236, Taxes Accrued, increased

14 from $ 2,427,741 at, December, 31, 1974 by $ 4,077,033 to

15 $ 6, 504, 774 at December 31, 1975, decreased by $ 3, 545, 499

16

17

19

20

21

22

23

in 1976 and then increased by $ 1,651,680 at year end

1977. The changes in the balances in this account over

the period shown are due primarily to changes in Federal

income tax accrued, which, at December 31, 1974, was

approximately $ 6,700,000 lower than the prior year.

The Company operated at a tax loss for the year 1974

and accrued a negative income tax which, together witha March 1974 payment on the 1973 Federal income tax

24 liability, caused the decrease in this account during

19

Stoddart

4

1974. The balance in this account at December 31, 1975

was approximately $ 4,000,000 higher than 1974 reflectingcurrent year accruals offset by refunds applicable to

the 1974 loss of $ 630,000. The balance at December 31,

1976 was approximately $ 3,750,000 lower than 1975 due

10

12

13

14

17

18

19

20

21

22

23

24

to investment tax credit carrybacks to prior years,

refunds received applicable to 1974 and 1975 and a

March 1976 payment on our 1975 income tax liability.The December 31, 1977 balance in Federal income tax

accrued increased approximately $ 1,650,000 reflecting1977 accruals offset by refunds applicable to previous

years.

Taxes accrued other than Federal income taxes

increased over this period from a balance of $ 1,393,873

at December 31, 1974 to a balance of $ 1,714,594 atDecember 31, 1977. Balances at December 31, 1975 and

1976 were $ 1,509,432 and $ 1,714,542, respectively.Account 237, Interest Accrued, shows a decrease of

$ 667,233 at December 31, 1975 from the balance atDecember 31, 1974, due primarily to a decrease ofinterest accrued on notes payable. The balances inthis account showed increases of $ 205,533 at December 31,

1976 and $ 1,049,498 at December 31, 1977 reflectingaccrued interest on Series BB 9 1/4% Bonds issued in

'20

p 'I

Stoddart

1976 and Series CC, 8 3/8% Bonds issued in 1977.

10

12

13

14

15

16

17

18

Qo

A:

Would you please continue by explaining the changes inthe balances of Account 238, Dividends Declared?

This account represents the balance of dividends

declared but not paid. The increase at December 1975

results from an increase of dividends due to the additional

preferred stock sold in 1975. The large decrease atDecember 31, 1976 was primarily caused by the eliminationof a one month lag in the recording of the bank statement,

as suggested in my testimony concerning Account 133,

Dividend Special Deposits. Prior to 1976, the balances

in these accounts did not reflect dividend checks

presented for payment in the month of December due to

the timing of the receipt of December bank statements.

Commencing in 1976, December activity is reflected inthe year end balances.

The increase in the balance at December 31, 1977

reflects the declaration of a dividend on the Company's

19

20

21

Series "0" preferred stock for the period January 1

through January 19, 1978. The Series "0" preferredstock was called for .redemption on December 20, 1977

22 with a January 20, 1978 redemption date.

23 The balances in Account 241, Tax Collections

24 Payable, have remained relatively constant over this

~ 21

I

s

Stoddart

period. The increase of approximately $ 230,000 from

December 31, 1975 to December 31, 1976 was primarilydue to the New York State Sales and Use Tax payable, as

-was the approximate decrease of $ 120,000 at December 31,

1977.

Q: Would you please explain the large increase in theI

balance of Account 242 at December 31, 1977?

A: The balance in Account 242, Miscellaneous Current and

9

10

Accrued Liabilities, increased by about $ 27,800,000 atDecember 31, 1977. This increase includes $ 27,750,000

reflecting the principal and call premium of the Company's

12

13

,Series "0" preferred stock redeemed January 20, 1978.

Q: Would you please continue by explaining the balance in14

16

A:

Account 255, Accumulated Deferred Investment Tax Credit?

The Company adopted deferred tax accounting for the

increase in investment tax credits arising from the TaxF

Reduction Act of 1975 in accordance with the statements

of policy issued by the Commission. The balance in19 this account of $ 6,247,400 at December 31, 1977 reflects20

21

22

23

Q-.

.the deferrals applicable to these increased investment

tax credits arising from that act.Would you comment on Account 282, Accumulated Deferred

Income Taxes — Liberalized Depreciation and Account

24 283, Accumulated Deferred Income Taxes — Other?

22

'f 1

4

Stoddart

A: The Company adopted. deferred tax accounting for ADR

depreciation in 1971, removal costs in 1972, fuel costs

in 1974 and 1975, and mortgage recording taxes in 1976,

all in accordance with the Commission's statements of

policy for these items. In addition, in 1975 the

10

12

13

14

Public Service Commission approved a Company petitionto adopt deferred tax accounting for liberalized

nuclear fuel depreciation. The balance appearing in

Account 282 for the first time at December 31, 1975

reflects the transfer of deferred taxes relating to ADR

depreciation from Account 283 in accordance with

amendments to the Uniform System of Accounts and also

includes deferred taxes resulting from nuclear fuel

depreciation. At December 31, 1977 the respective

15 deferred tax balances for ADR depreciation and nuclear

17

fuel depreciation were $ 4,918,200 and $ 787,100. The

December 31, 1977 balance in Account 283 includes

19

20

$ 1,475,700 of deferred taxes related to cost of removal,

$ 2',,264,100 of deferred .taxes related to fuel costs,

$ 2,'160,000 of deferred taxes related to the Sterling

22

fossil plant and $ 342,400 of deferred taxes related to

the mortgage recording tax on the Company's 1976 and

23 1977. bond issues.

24

23

Stoddart

Q: Will you please describe Exhibit 2 and state what itpurports to show?

A: Exhibit 2 sets forth Statements of Income for the

twelve months 'ended December 31, 1974, 1975, 1976 and

1977, respectively, in the form prescribed -by the

Commission. This exhibit has been prepared to show

10

12

13

14

15

16

17

18

Q-

A:

Company-wide operating income as well as the operation

of each of the Company's operating departments. Below-

the-line items are shown on a Company-wide basis.

Are details of certain of the accounts shown in Exhibit 2

given in later exhibits as they relate to the Electric

and Gas Departments?

Yes. Account 400, Operating Revenue, Account 401,

Operating Expense, Account 402, Maintenance Expense,

Account 402.1, Joint Expenses and'Account 408.1, Taxes

Other Than Income Taxes are detailed in Exhibit 4 for

the Electric Department and in Exhibit 5 for the Gas

Department. I should point out that certain account

numbers and the format of the Statement of Income

20

21

22

23

24

Q-

,changed throughout the period. However, these changes

are readily apparent and are not commented upon further.

Will you refer now to Accounts 419.1, Allowance for

Other Funds Used During Construction and 432, Allowance

for Borrowed Funds Used During Construction, (Account

'4

p

ll

Stoddart

10

12

13

14

16

19

20

21

22

23

24

A:

419.1, Allowance for Funds Used During Construction)

and indicate the amounts which are applicable to the

Electric and Gas Departments?

Allowance for Funds Used During Construction (AFUDC)

applicable to the Electric Department was $ 1,717,994,

$ 3,549,033, $ 7,512,067 and $ 11,297,104, for the twelve

months ended December 31, 1974, 1975, 1976 and 1977,

respectively. The increases in the amount of AFUDC

over the periods shown primarily reflect AFUDC interestaccrued on the Sterling, Nine Mile Point and Oswego

plants.AFUDC applicable to the Gas Department was $ 24,691,

$ 20,789, $ 13,584 and $ 17,304 for the four periods.

Over the period shown in this exhibit the rateused in AFUDC was 8% through May 31, 1974, 10% effectiveJune 1, 1974, 8.25% effective July 1, 1975 and 8.75%

effective May 1, 1976. Account 419.1, Allowance forFunds Used During Construction, was used for recording

AFUDC in the years 1974 through 1976. Zn 1977, Account

432, Allowance for Borrowed Funds Used During Construction,and Account 419.1, Allowance for Other Funds Used

During Construction, were utilized to record AFUDC.

Also, commencing in December 1977, amounts recorded inAccount 432 reflected AFUDC on the Nine Mile Point

25

Stoddart

and Oswego projects on a net of tax basis as provided

in Case 27108. This rate was 7.04% in that month.

Nuclear fuel for the Sterling and Nine Mile Point

projects is included in the base for determining AFUDC

as provided in Case 26848.

10

12

13

A: