Protecting Competition from the Postal Monopoly - Criterion ...

Upload

khangminh22Category

view

2download

0

Natural Monopoly Regulation in Platform Markets

by

Francesco Ducci

A thesis submitted in conformity with the requirements for the degree of Doctor of Juridical Science

Graduate Department of the Law School University of Toronto

© Copyright by Francesco Ducci 2019

ii

Natural Monopoly Regulation in Platform Markets

Francesco Ducci

Doctorate of Juridical Studies

Faculty of Law University of Toronto

2019

Abstract

Technological change and digitalization have enabled a wave of multi-sided platform markets

where network externalities, big data and algorithmic matching contribute to concentrated

market structures and monopolistic tendencies. Yet the assessment of conditions under which

such tendencies may be natural and efficient remains underdeveloped, and the consequential

determination of the appropriate regulatory tools and institutions associated with natural

concentration unexplored. This thesis evaluates the applicability of the natural monopoly

framework to three case studies of platform markets: horizontal search engines, e-commerce

marketplaces, and ride-hailing platforms. It demonstrates that technological change and the

increasing predominance of multi-sided platforms overall increase the likelihood of natural

monopolies, although natural concentration is neither inevitable, nor necessarily the consequence

of multi-sided network externalities. On the contrary, natural monopoly conditions are often the

result of a complex interplay between supply side economies of scale, access to data, and the

strength of both direct and indirect network externalities, all factors that vary substantially across

markets and that may be independent of the platform model. The thesis reaches this conclusion

by placing the three case studies along a spectrum of natural concentration. At one extreme, it

characterizes horizontal search as naturally monopolistic, due to high-fixed costs and low

iii

marginal costs, the value of data and direct externalities among users that generate such data. At

the opposite extreme, it concludes that e-commerce marketplaces, while benefiting from scale

economies and network effects, are not natural monopolies and instead benefit from the

competitive advantage offered by efficient logistics. In between, ride-hailing platform markets

are a more ambiguous case that may or may not give rise to natural monopolies depending on the

specific conditions of each local market. Based on this framework, this thesis evaluates

alternative regulatory instruments that can address market power while at the same time

embracing efficient concentration. The dissertation in particular demonstrates how the

institutional dimension of intervention critically affects the trade-offs between imperfect policy

instruments, arguing that policy approaches require more complementarity between regulation

and competition as opposed to clear-cut choices between ex-ante and ex-post approaches to

market power.

iv

Acknowledgments I have accumulated a number of debts throughout the development and completion of this

dissertation. First and foremost, I am indebted to my co-supervisors Professor Michael Trebilcock

and Dean Edward Iacobucci; their guidance and mentorship have been invaluable and without

doubt the most enriching aspects of my doctoral experience at the Faculty of Law. I am equally

indebted to my Committee Member Professor Anthony Niblett, who has been extremely generous

and insightful in guiding me through the various stages of this project. Likewise, my external

examiner professor Roger Ware has contributed to enriching this work with useful comments and

criticisms.

I also would like to thank a number of people whose support and presence has been invaluable: at

the Faculty of Law, Associate Dean Mariana Prado and Professor Ariel Katz for their guidance

and suggestions; in the doctorate program, Eden Sarid, Haim Abraham, and Terry Skolnik for their

precious friendship; at Massey College – my home while at the University of Toronto – a large

number of Junior Fellows to which I am extremely grateful, in particular Claire Jensen, Alexander-

Sarra Davis, Michael Lebenbaum, Amir Reda, Benjamin Gillard, David Sutton, Adrian De Leon,

Michael Bridge, and Floor 2 Lizbeth Ayub, Sharly Chan, and David Gafni. And of course, my

family, which despite the distance has supported me immensely during the four years of the

doctorate.

Finally, I would like to thank the University of Toronto Faculty of Law and the Centre for

International Governance Innovation (CIGI) for their financial support for this doctoral research.

v

Table of Contents

ACKNOWLEDGMENTS.........................................................................................................................................................IV

TABLEOFCONTENTS...........................................................................................................................................................V

LISTOFFIGURESANDTABLES.......................................................................................................................................VII

GENERALINTRODUCTION:NATURALMONOPOLYREGULATIONINPLATFORMMARKETS.........................11. MULTI-SIDEDPLATFORMSANDMARKETCONCENTRATION.....................................................................................................12. THEAPPLICABILITYOFTHENATURALMONOPOLYFRAMEWORK:THREECASESTUDIES..................................................63. STRUCTUREOFTHEDISSERTATION.............................................................................................................................................11

CHAPTER1TECHNOLOGICALANDECONOMICDRIVERSOFINCREASINGCONCENTRATIONINPLATFORMMARKETS........................................................................................................................................................13

TECHNOLOGICALANDECONOMICDRIVERSOFINCREASINGCONCENTRATIONINPLATFORMMARKETS................................................................................................................................................................................141.1 RISINGCONCENTRATIONINTHEWAKEOFTECHNOLOGICALCHANGE.................................................................................141.2 THECONTOURSOFCURRENTTECHNOLOGICALCHANGE........................................................................................................251.2.1 PlatformIntermediationandtheTheoryoftheFirm......................................................................................261.2.2 Data,AlgorithmicPredictionandMatching.........................................................................................................301.2.3 AnExample:TheSharingEconomyPhenomenon............................................................................................34

1.3 THEECONOMICSOFMULTI-SIDEDPLATFORMS:IMPLICATIONSFORTHENATURALMONOPOLYFRAMEWORK...........371.3.1 TheDistinguishingFeaturesofMulti-SidedPlatforms....................................................................................381.3.2 TheImpactofMulti-SidednessonCompetitionPolicyandRegulation...................................................49A. HowMulti-SidednessAffectsEconomicAnalysis..............................................................................................54B. HowMulti-SidednessChangestheRulesthatApplytoPlatforms.............................................................62C. TheRelevanceofMulti-SidednessforNaturalMonopolyRegulation......................................................71

1.4 CONCLUSION....................................................................................................................................................................................72

CHAPTER2APPLYINGTHENATURALMONOPOLYFRAMEWORK......................................................................73

APPLYINGTHENATURALMONOPOLYFRAMEWORK...................................................................................742.1 DETERMINANTSOFNATURALMONOPOLIES..............................................................................................................................762.1.1 TheNaturalMonopolyProblemandJustificationsforRegulation............................................................762.1.2 NaturalMonopoliesinPlatformMarkets..............................................................................................................84

2.2 REGULATINGNATURALMONOPOLYPLATFORMS.....................................................................................................................892.2.1 PriceandEntryRegulation..........................................................................................................................................892.2.2 VerticallyIntegratedNaturalMonopoly................................................................................................................91A. Non-DiscriminatoryAccesstotheNaturalMonopolySegment..................................................................92B. StructuralRemediesandDivestiture......................................................................................................................93

2.3 FRANCHISEBIDDING:AUCTIONINGTHEMARKETTOASINGLEPLATFORM.........................................................................962.4 PUBLICOWNERSHIP....................................................................................................................................................................1002.5 RELIANCEONSCHUMPETERIAN-BASEDCOMPETITIONPOLICYENFORCEMENT..............................................................1022.5.1 PromotingDynamicInter-PlatformCompetitionfortheNaturalMonopolyPosition...................104A. TheLimitsoftheStandardCompetitionPolicyApproach..........................................................................106B. StrategiestoAidPotentialCompetitionandMonopolyDisplacement.................................................1112.5.2 Intra-PlatformCompetitionandDiscriminationbyVerticallyIntegratedHybridPlatforms.....121A. LeveragingCasesandtheEssentialFacilitiesDoctrine...............................................................................122B. TheLimitsofEx-PostInterventionAgainstDiscrimination......................................................................130

2.6 THEINSTITUTIONALDIMENSIONOFINTERVENTION:EXANTEANDEXPOSTRULESASCOMPLEMENTS...................1322.7 CONCLUSION.................................................................................................................................................................................138

INTRODUCTIONTOTHETHREECASESTUDIES.....................................................................................................1401. HORIZONTALSEARCH,E-COMMERCEMARKETPLACES,ANDRIDEHAILINGPLATFORMS..............................................1422. ASPECTRUMOFNATURALCONCENTRATION.........................................................................................................................145

vi

CHAPTER3HORIZONTALSEARCH.............................................................................................................................147

HORIZONTALSEARCH..........................................................................................................................................1483.1 THEEVOLUTIONOFONLINESEARCH:FROMNEUTRALTOUNIVERSALRESULTS............................................................1483.2 ALTERNATIVEBUSINESSMODELS............................................................................................................................................1543.3 HORIZONTALSEARCHASANATURALLYMONOPOLISTICMARKET.....................................................................................1593.3.1 CostStructurewithHighFixedCostsandMarginalCostsClosetoZero..............................................1623.3.2 NetworkExternalitiesandtheValueofDataforHorizontalSearchPredictions.............................1623.3.3 TheConsequencesofNaturalConcentration...................................................................................................165

3.4 REGULATINGMARKETPOWEROFANATURALMONOPOLISTINSEARCH..........................................................................1693.4.1 RegulatingthePriceofSearchesandSearch-Ads...........................................................................................1743.4.2 CompetitionPolicyasaQuasi-StructuralRemedy.........................................................................................1763.4.3 AccesstoHorizontalSearchasanEssentialFacility.....................................................................................1773.4.4 StructuralRemediestoSeparatetheNaturalMonopolySegment..........................................................184

3.5 CONCLUSION.................................................................................................................................................................................187

CHAPTER4E-COMMERCEMARKETPLACES............................................................................................................189

E-COMMERCEMARKETPLACES..........................................................................................................................1914.1 THEEVOLUTIONOFAMAZON:FROMNICHEENTRYTOTHEEVERYTHINGSTORE...........................................................1914.2 CONCERNSABOUTAMAZON’SMARKETPOWER....................................................................................................................1974.3 WHYAMAZONMARKETPLACEISNOTANATURALMONOPOLY..........................................................................................2074.3.1 NetworkEffectsBetweenBuyersandSellers..................................................................................................2084.3.2 TheImportanceofPhysicalInfrastructureforLogistics,StorageandDelivery................................211

4.4 VENUESFORSTRONGERCOMPETITIONPOLICYINTERVENTION.........................................................................................2144.5 CONCLUSION.................................................................................................................................................................................219

CHAPTER5RIDE-HAILINGPLATFORMS...................................................................................................................221

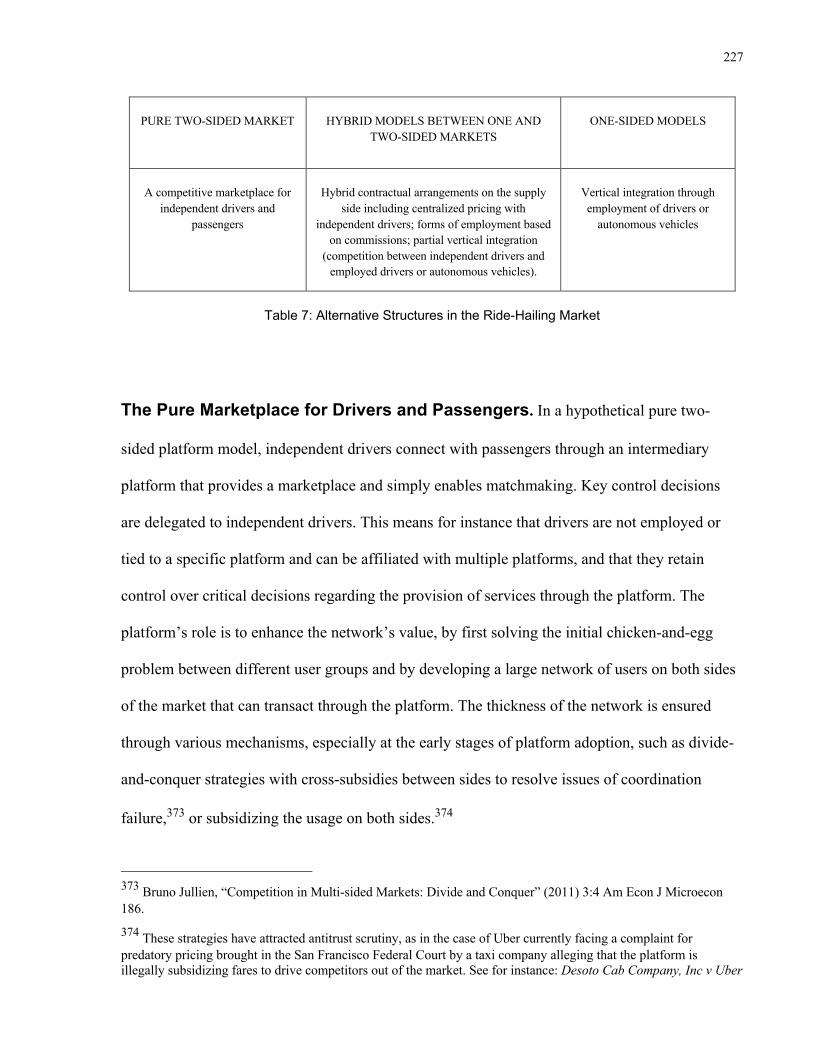

RIDE-HAILINGPLATFORMS................................................................................................................................2255.1 THESTRUCTUREOFSHARINGECONOMYTRANSPORTATIONPLATFORMS........................................................................2255.2 ANTITRUSTCONCERNSOVERINTER-PLATFORMANDINTRA-PLATFORMCOMPETITION...............................................2385.3 ISON-DEMANDTRANSPORTATIONANDRIDE-SHARINGNATURALLYMONOPOLISTIC?.................................................2465.3.1 NetworkExternalities:Availability,WaitingTimes,andRatings............................................................2485.3.2 SupplySideEconomiesofScale..............................................................................................................................2505.3.3 DataandtheEfficiencyofCentralizedAlgorithmicRoutingandPlanning.........................................252

5.4 ARANGEOFPOLICIESBETWEENCOMPETITIONANDNATURALMONOPOLY...................................................................2525.4.1 RegulatingRide-HailingPlatforms........................................................................................................................2545.4.2 AuctioningtheMarkettoaSingleNetwork......................................................................................................2595.4.3 PromotingInter-PlatformCompetition..............................................................................................................260

5.5 CONCLUSION.................................................................................................................................................................................263

CHAPTER6CONCLUSION...............................................................................................................................................266

CONCLUSION............................................................................................................................................................2666.1 NATURALMONOPOLYPLATFORMS:THEHETEROGENEOUSROLEOFNETWORKEXTERNALITIES,DATA,ANDSUPPLY-SIDESCALEECONOMIES..........................................................................................................................................................................2686.2 THEINSTITUTIONALDIMENSIONOFIMPERFECTINTERVENTION:RETHINKINGCOMPETITIONANDREGULATIONASCOMPLEMENTS..........................................................................................................................................................................................277

BIBLIOGRAPHY..................................................................................................................................................................285

vii

List of Figures and Tables

Figure 1: Labor Share of GDP and Inverse Markup .............................................................. 23

Figure 2: Standard Monopoly vs Natural Monopoly .............................................................. 79

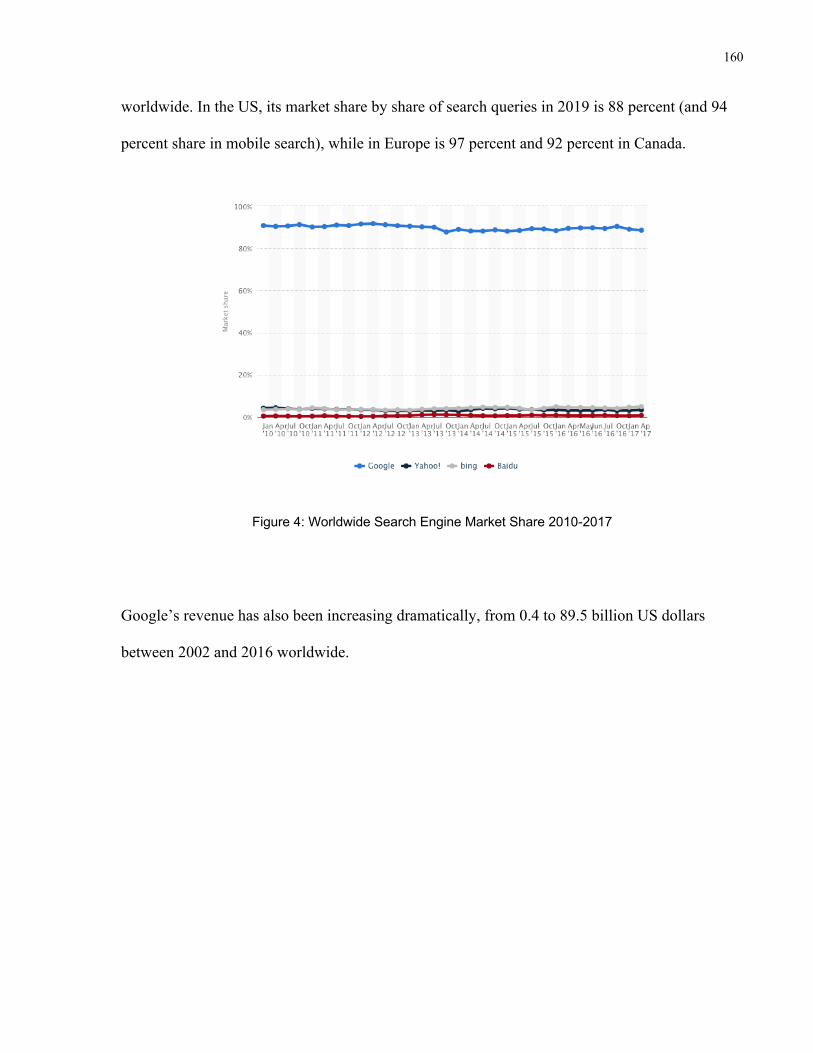

Figure 3: The Structure of Google Search Results ............................................................. 154

Figure 4: Worldwide Search Engine Market Share 2010-2017 ......................................... 160

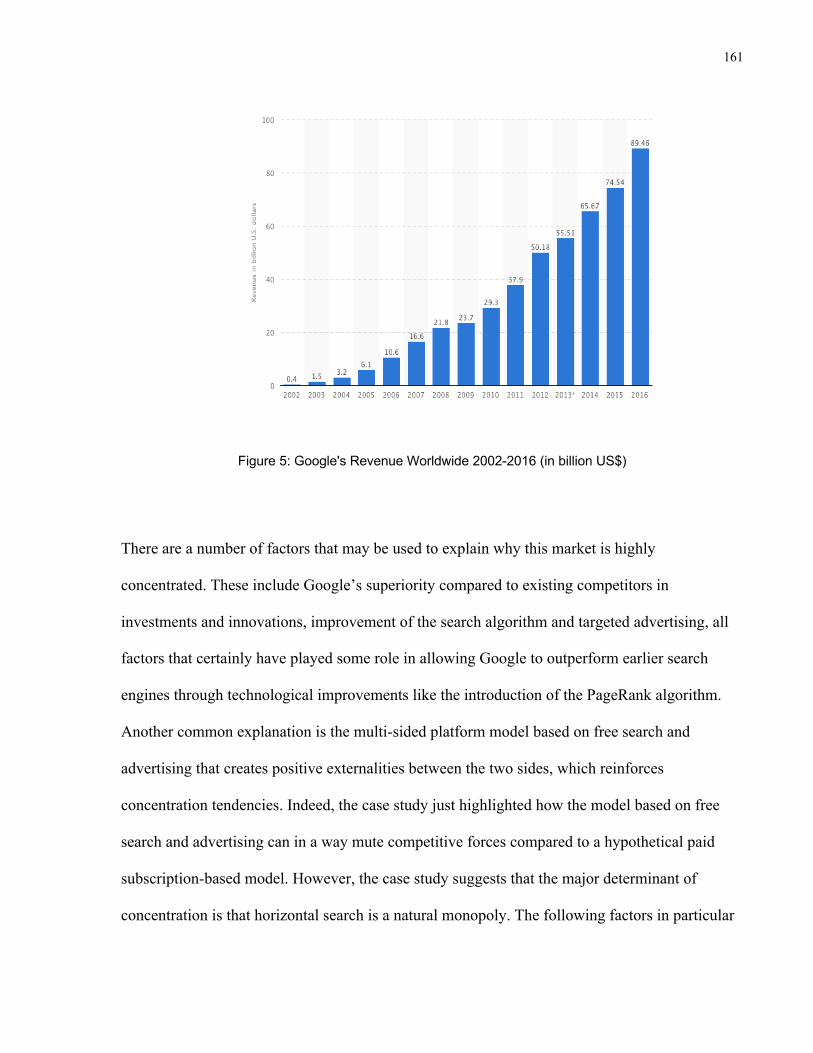

Figure 5: Google's Revenue Worldwide 2002-2016 (in billion US$) ................................ 161

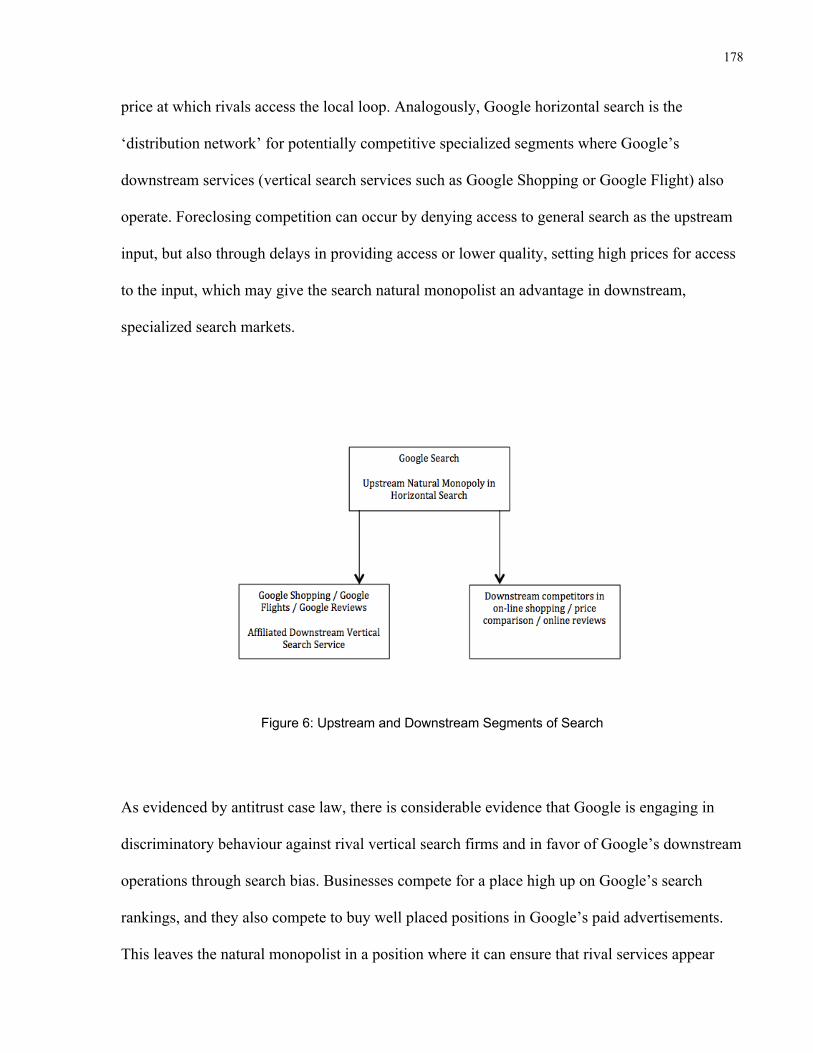

Figure 6: Upstream and Downstream Segments of Search .............................................. 178

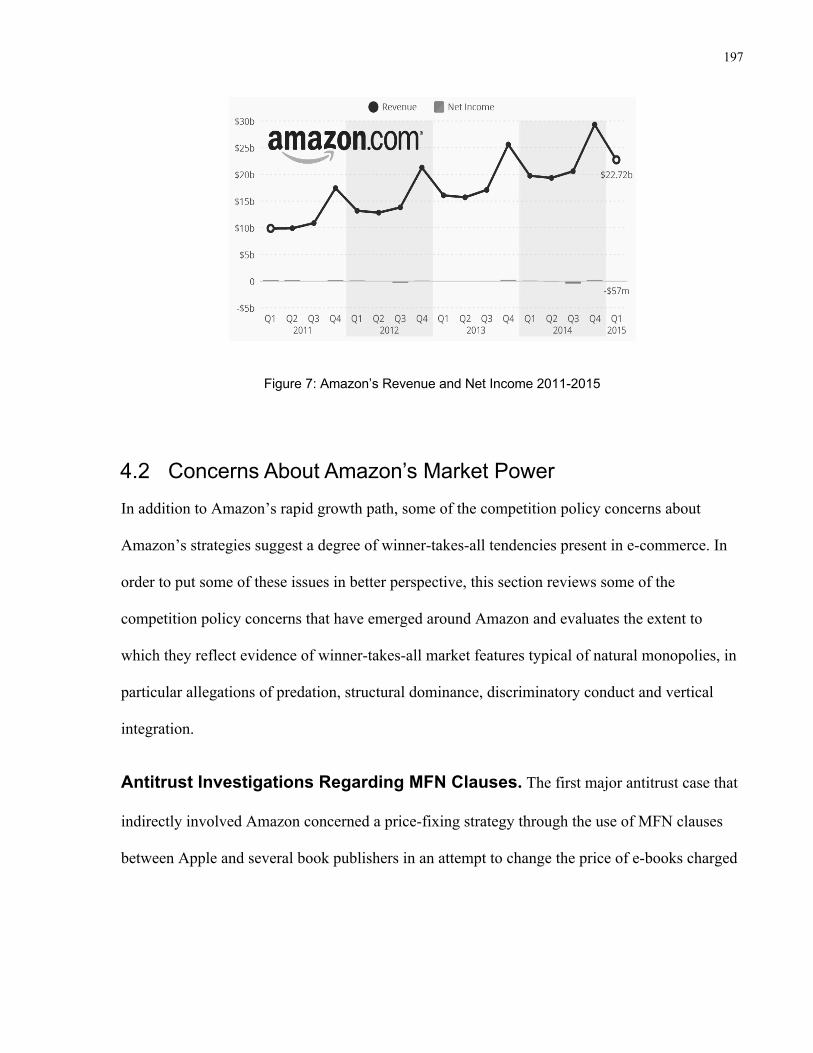

Figure 7: Amazon’s Revenue and Net Income 2011-2015 ................................................ 197

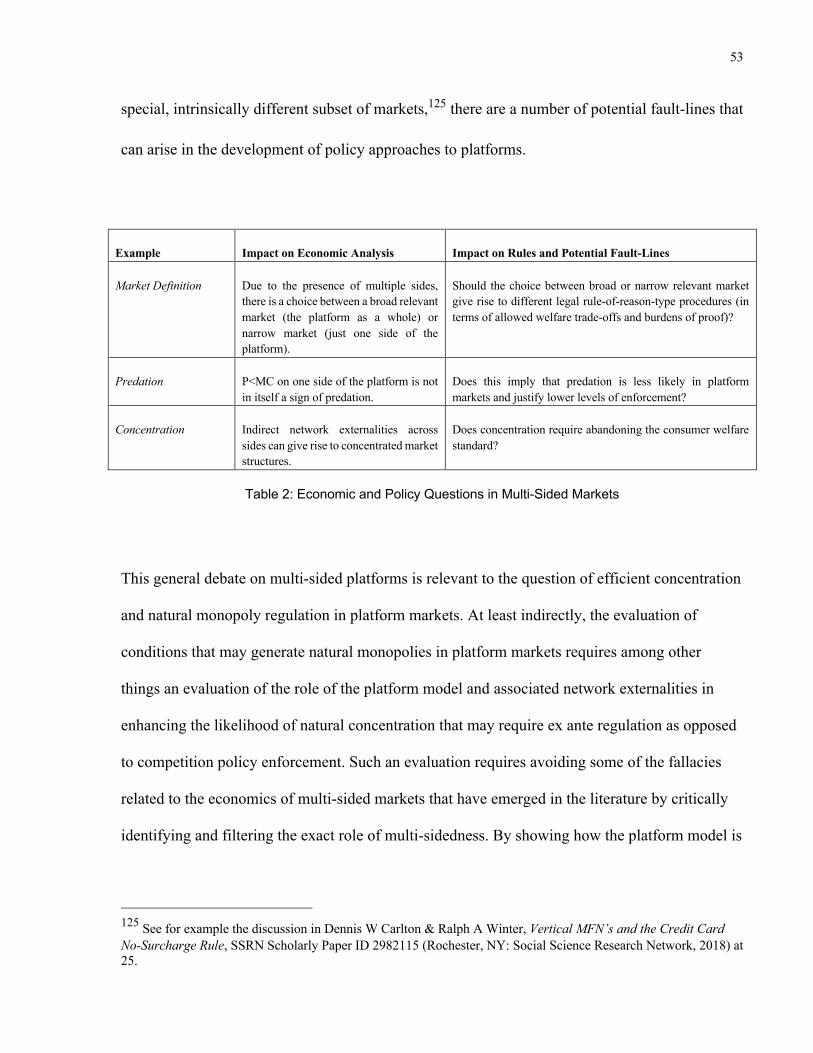

Table 1: Examples of Multi-Sided Platforms .......................................................................... 51

Table 2: Economic and Policy Questions in Multi-Sided Markets ....................................... 53

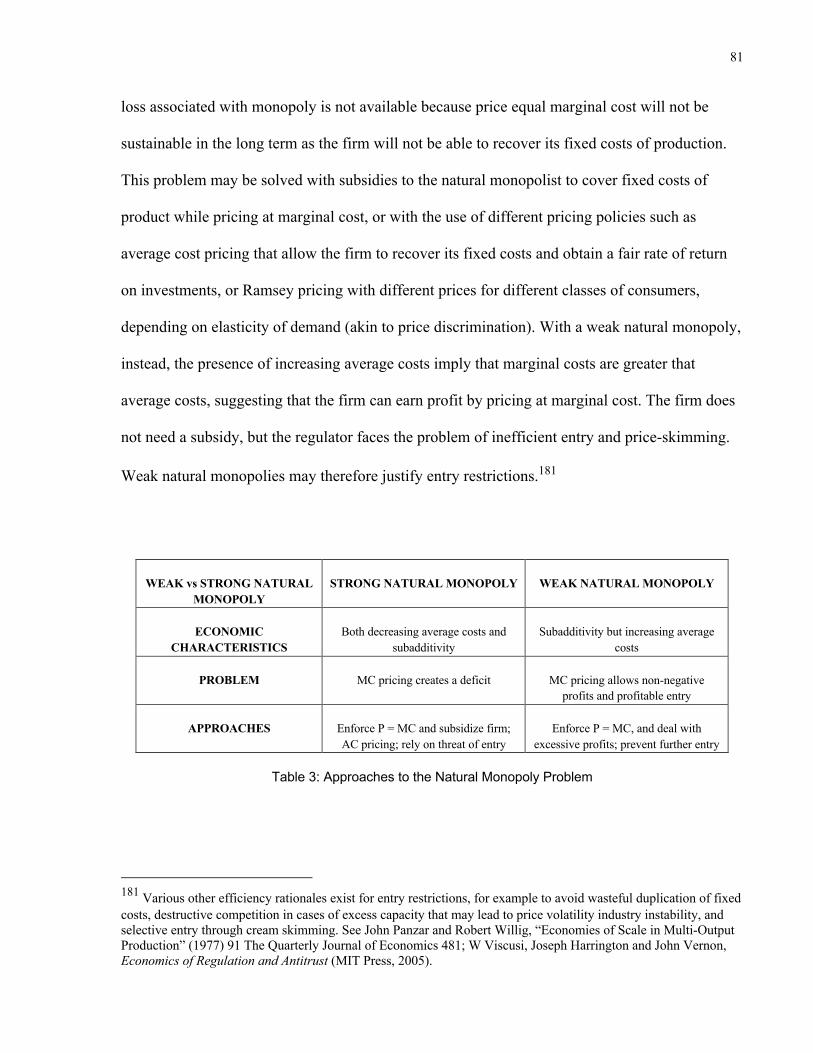

Table 3: Approaches to the Natural Monopoly Problem ....................................................... 81

Table 4: Determinants of Efficient Concentration in Platform Markets .............................. 87

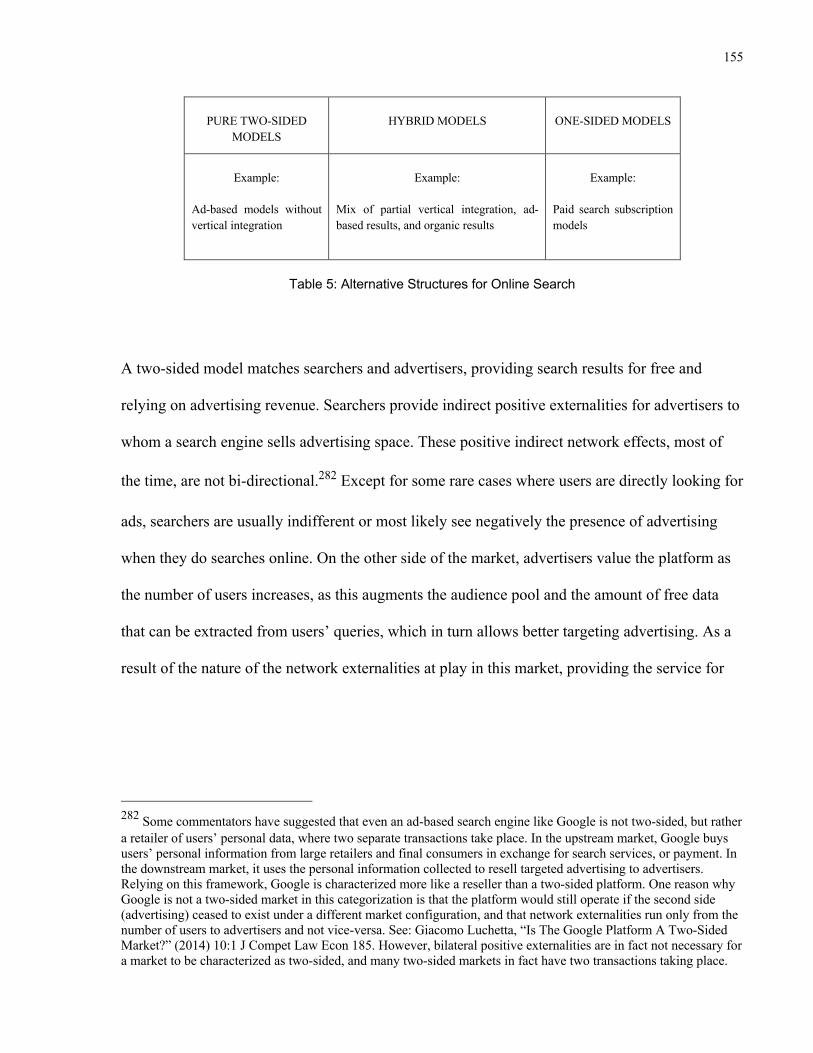

Table 5: Alternative Structures for Online Search ............................................................... 155

Table 6: Alternative Structures for E-Commerce Marketplaces ........................................ 195

Table 7: Alternative Structures in the Ride-Hailing Market ................................................ 227

1

General Introduction: Natural Monopoly Regulation in

Platform Markets

1. Multi-Sided Platforms and Market Concentration Multi-sided platform markets characterized by network externalities have always existed as an

economic paradigm, but in different technological forms. The old village market place, physical

shopping malls, or any traditional fair can be seen as multi-sided platform markets connecting

buyers and sellers. They are all platform-meeting places where different agents that want to

interact and transact with each other are brought together by an intermediary. The traditional

printed ad-based newspaper is also a classic version of a platform connecting advertisers and

eyeballs. More readers increase the value for advertisers that want to reach them, and readers

generally are indifferent to or dislike ads. Due to these externalities across the different sides,

newspapers can often be provided for free to create an audience for advertisers. Payment cards of

various kind, the first two-sided market closely studied in the industrial organization literature,

are also a typical example of platforms, which connect merchant and cardholders concluding

transactions.

The current wave of technological change has created a new generation of multi-sided platforms

that dominate the digital economy: online search engines connecting searchers with advertisers;

social networks connecting users with other users and advertisers; e-commerce online

marketplaces connecting buyers and sellers; sharing economy platforms connecting various kind

of service providers with consumers; price-comparison, reservation, and job search platforms,

and matchmakers for professional services. Due to digitalization, the multi-sided business model

has become one of the predominant forms of organizing economic activity in the age of big data,

2

network effects, and algorithmic-based matching. This new generation of multi-sided platforms

and their widespread growth animate two major debates in the competition policy domain that

are relevant to this dissertation: the first about the economics of multi-sided platforms at large;

the second more narrowly focused on market power and excessive concentration in digital

platform markets.

The Economics of Multi-sided Platforms. There has been a recent surge of interest in the

economics of two-sided markets at large, both in industrial organization research and in the

competition law domain.1 The core of this debate can be summed up in the question of whether

there is something special about the economics of two-sided markets that calls for a different set

of rules, in particular with regard to competition policy doctrines and enforcement policies. The

controversial aspect of this debate stems from the distinction between the economic implications

of multi-sidedness (limited to adjusting standard economic analysis and generally not

controversial) and its legal and regulatory implications (the way multi-sidedness influences not

only economic analysis but also requires changes to standard antitrust rules and forms of

intervention). The latter set of policy implications generally imply treating multi-sided platform

markets as a special sub-set of markets that may deserve a special kind of scrutiny and different

rules compared to standard markets.

Digital Platforms and Market Concentration. The second, narrower, competition policy

debate related to multi-sided platforms deals with the problem of excessive market concentration

in the tech sector. Emerging research points to various forms of increasing concentration and

1 The term ‘multi-sided platform’ is the most accurate way to refer to this economic paradigm, but the dissertation will at times use equivalently other terminology used in the literature, such as two-sided or multi-sided markets.

3

reduced competition in many industrialized economies, including lower levels of new business

creation, higher market shares and firms’ mark ups, evidence of horizontal shareholding, and

indeed winner-takes-all digital markets. The new generation of digital multi-sided platforms, in

particular, has been interpreted as the primary example of excessive levels of concentration and

as the failure of competition policy to deal with increasing monopoly power in the digital

economy. Specific to this subset of platforms is the way in which technological change enhances

the tendencies toward concentration compared to older, physical predecessors of current tech

platforms. First, collection and analysis of big data as the cornerstone of matching and prediction

services through algorithms that improve with larger datasets create important scale and scope

economies that were not available to the same degree to the previous generation of platforms.

Second, the digital, as opposed to physical, dimension of intermediaries can increase the

potential for large supply-side scale economies with low or zero marginal costs, and can enhance

the efficiency of aggregating network externalities due to reduced scarcity constraints and limits

to matching capabilities. Overall, current digital platforms rely on an old economic model of

platform intermediation, but technological change enhances the degree of concentration in the

present generation of platforms. As a result, there are concerns over excessive concentration of

economic and political power which have resulted in a consequential search for effective policy

responses to alleged problems of increasing monopoly power. Many of the prominent proposals

advanced in the policy debates focus on desirable changes to competition policy and seek to

inject more competition by facilitating entry and inducing more market fragmentation – for

example, breaking-up some of the dominant digital platforms or abandoning the consumer

welfare standard.

The unifying theme of these debates (where the first on the economics of platforms at large is of

more general scope compared to the narrower policy debates on technological platforms and

4

market concentration) is an underlying question about the status of multi-sided platforms for the

purpose of competition policy and regulatory intervention; in particular, the way in which the

distinguishing economic or technological features of platforms may potentially warrant a

paradigmatic shift in the regulation of market power. This dissertation contends that this

fundamental question and the resulting debates on platforms, however, are often approached

from the wrong perspective. For one thing, the peculiarities of platform economics often become

a rhetoric argument to treat multi-sided markets a special and distinct from standard single sided

markets – starting point that reverberates in the digital sector as an assumption that the platform

model and multi-sided externalities are the central determinants of concentration and dominance.

For another, policy solutions to market power and concentration in the tech sector are for the

most part addressed from the perspective of competition policy and market fragmentation – for

example, are there desirable substantive changes to antitrust doctrines and goals? How can policy

facilitate entry?

In contrast, the dissertation challenges both perspectives. First, the starting point adopted in the

dissertation is that multi-sidedness belongs to a spectrum of relevance,2 rather than a black-and-

white distinction with single-sided markets, and that the doctrinal and regulatory implications

need to be evaluated accordingly, thereby avoiding the fallacy of treating all platform markets as

special. In the digital platform context, this implies recognizing the highly heterogenous role of

2 The economic literature provides various definitions of two-sided or multi-sided markets but struggles to identify one that is unanimously accepted. As discussed in Chapter 1, generally accepted characteristics of a two-sided platform is the necessary presence of two or multiple user groups with interrelated demand, positive network externalities running at least from one side to the other, and a platform solving a chicken-and-egg problem by coordinating their interaction. Different definitions however point to different elements of two-sided platform markets. Some highlight the non-neutrality of the price-structure, namely that way fees are allocated between sides; other point the necessary presence of indirect network externalities; and others stress a business model perspective, where the platform model of intermediation differs from resellers and other models in the way residual contractual rights are allocated. The lack of a clear definition and distinction from standard markets confirms the fallacy of treating multi-sided platform markets as a special subset of markets.

5

indirect network externalities and the platform model in each market, and accounting for the

much larger range of forces and counterforces possibly related to concentration, such as access to

data for prediction and matching, standard supply-side economies of scale, and production

differentiation.

Second, this dissertation argues that a more fruitful theoretical framework and starting point to

evaluate market power in digital platform markets is one provided by regulation and natural

monopolies rather than competition, entry and market fragmentation. Natural monopolies are

generally associated with infrastructures such as electricity distribution, water supply, or

railroads that entail large fixed costs and high barriers to entry. Due to large economies of scale

relative to the size of demand, the cost structure of a natural monopoly is such that a single firm

will serve a market more efficiently than competing firms. As a result, policy generally

welcomes or encourages concentration toward a natural monopoly while at the same time

regulating the resulting market power. As it is suggested throughout the dissertation, digital

platforms are not necessarily all naturally monopolistic, and regulation is not necessarily the

most desirable institutional approach even in the presence of a natural monopoly platform.

However, the natural monopoly framework becomes a useful theoretical benchmark to evaluate

alternative policy approaches that are consistent with efficient concentration and winner-take-all

markets.

On this basis, this dissertation brings together these related academic debates about multi-sided

platforms by addressing the following research question on the basis of three case studies: What

are the determinants of natural monopoly in multi-sided platform markets that emerged due to

digitalization and technological change, and what are the desirable regulatory responses for

identified natural platform monopolies?

6

2. The Applicability of the Natural Monopoly Framework: Three Case Studies

This dissertation addresses this question by applying the natural monopoly framework to three

case studies, horizontal search engines; e-commerce marketplaces; and on-demand ride-hailing

platforms. The first issue that is confronted in the development of the case studies is whether any

of the evaluated market has in fact the features of a natural monopoly. The dissertation reaches

the following conclusions.

Horizontal Search. The dissertation suggests that horizontal search is a natural monopoly

(where the term ‘horizontal’ or ‘general’ refers to search engines that provide any type of results

covering any search query as opposed to ‘vertical’ or ‘specialized’ search engines that focus only

on specific topics, such as reserving a flight or online shopping). First, horizontal search has a

cost structure with high fixed costs and very low, arguably zero marginal costs on the supply

side. Second, there are strong direct network externalities between users on the demand side,

which are associated with a large degree of positive returns to data collection and analysis. Data

is essential because at the core a horizontal search engine is a general-purpose prediction

technology more than a matching technology. The matchmaking function and indirect network

externalities between advertisers and searchers arising from the multi-sided matching model are

contributing factors to concentration, but play only a limited role and are in fact tangential to the

inevitable tendency toward a single horizontal search monopoly. On the contrary, the value of

data and the economies of scale and scope that arise from larger datasets are critical for the

purpose of improving search algorithm predictions as opposed to matching, where more data

increase the efficiency of search results in terms of quality-adjusted costs. Due to the universal

reach of horizontal search, moreover, specific data can have a positive value not only for a given

narrow search query but also for a larger subset of related queries for which the same data points

7

can be valuable. The predictive and universal nature of horizontal search are such that data can

give rise to a natural monopoly.

E-Commerce Marketplaces. Different conclusions are reached in the second case study on

Amazon and e-commerce marketplaces, for which matching plays a greater role than prediction.

Clearly, there are some network externalities between buyers and sellers joining the same online

shopping marketplace, and important scale economies in developing logistics. Yet the

dissertation suggests that neither is strong enough to generate a natural monopoly. On the

contrary, Amazon’s competitive advantage comes from having combined a large online

marketplace with efficient delivery and storage infrastructure better than any of its competitors.

Amazon faces competition from other online marketplaces, and it is not the only firm providing

delivery, but it is the firm that combines to two aspects in the most efficient and successful way,

which explains its dominance. The fact that the physical infrastructure developed for storage and

logistics plays a major role in e-commerce also shows that dominance has little to do with the

fact that Amazon’s marketplace (in itself a hybrid between marketplace and reseller) can be

described as a multi-sided platform. As in the first case study, any claims that base dominance on

the platform model alone are in themselves inconclusive.

Ride-Hailing Platforms. The third case study on on-demand transportation services provides

more ambiguous results. Ride-hailing platforms benefit from a technological upgrade of the

traditional dispatch mechanism through algorithmic matching that relies on data about riders and

passengers, coupled with the ability to call a ride and pay through an app. Overall, compared to

traditional taxi services this form of matching shifts the point of minimum efficient scale toward

larger networks, suggesting the plausibility of some natural monopoly features. In particular, the

role of network externalities between riders and drivers and the efficiency of aggregating the two

8

sides under a single algorithmic matching, routing, and planning mechanism suggests that a

single network may be more efficient than competition. At the same time, the value of network

externalities and the ability to improve matching tapers off after a critical mass of users is

reached, and the importance of data is weaker than in horizontal search. Similarly, the ratio of

fixed cost-marginal cost on the supply side does not appear to be not as skewed as it is in

horizontal search. These considerations suggest that competition may be possible depending on

the specific conditions of a given geographical market – including the size of demand, density of

population, and availability of alternative methods of transportation. Such a conclusion yields a

less clear determination of natural tendency toward monopoly for platforms like Uber and Lyft.

In sum, the general conclusion that is drawn from the three case studies is that compared to older

examples of platform markets, technological change enhances the likelihood of natural

monopoly in the current wave of platforms, although this means neither that natural monopolies

are inevitable, nor that the possible emergence of a natural monopoly is necessarily the result of

the platform model alone. On the contrary, sources of natural monopoly are much more

heterogeneous and include direct network effects, positive returns to data collection, and scale

economies on the supply side with negligible marginal costs.

Natural Monopoly as a More Promising Theoretical Paradigm: Rethinking

Competition and Regulation as Complements. Based on this framework, the dissertation

evaluates in each case study the desirability of specific regulatory instruments depending on the

strength of natural monopoly features, including ex-ante regulation and structural remedies,

franchise bidding, public ownership, and competition policy enforcement. The central claim of

the dissertation is that policies that seek to constrain market power while at the same time

accepting and embracing the efficiency of concentration are likely more desirable in digital

9

platform markets. Hence, the most promising approach to evaluate issues of market power is to

start by adopting regulation as opposed to competition as a benchmark and theoretical

framework, and then evaluate its concrete merits vis-à-vis second-best instruments that are

consistent with efficient concentration, on the basis of their respective institutional capabilities

and constraints. As the dissertation concludes, this approach reveals a choice of trade-offs

between highly imperfect policy instruments that often imposes a necessary degree of

complementarity between competition policy and regulatory instruments, as opposed to clear-cut

choices between ex ante and ex post intervention.

In theory, perfect economic regulation is a first-best response to some of the problem associated

with natural monopolies in platform markets, for example through the regulation of monopoly

pricing and by addressing issues of discrimination and leveraging by the natural monopolist.

However, its concrete institutional implementation is replete with complexities and limitations,

including the costs of regulation, asymmetric information, rapid technological change, and fears

of regulatory capture. Most importantly, regulation risks undermining or slowing down the

process of technological innovation and dynamic displacement, which is the major source of

competition in these markets. The costs and institutional limitations associated with the concrete

implementation of regulation may ultimately outweigh the magnitude of market imperfections

that it attempts to address.

Because from an institutional perspective regulation may not in practice be a first-best response

to the market failures associated with natural monopoly platforms, second-best approaches that

are consistent with efficient concentration may in specific contexts be more cost-efficient and

incisive than standard ex ante regulation. In some instances, franchise bidding may be a better

tool than ex-ante regulation. This solution, which may be pertinent in a limited set of cases,

10

avoids the need to regulate a natural monopoly by inducing a form of competition for the market

through bidding, although this policy may still not fully mute all concerns associated with

regulatory oversight in so far that it still requires a degree of administrative review and switching

costs (albeit not as substantial as with regulation).

In other instances, competition policy may serve a second-best substitute to regulation. In order

to do so, enforcement must be able to accomplish two necessary objectives: first, competition

policy must be able to preserve a degree of contestability to the natural monopoly position by

encouraging the threat of entry and facilitating the process of displacement by targeting

innovation-based harms; second, competition policy must be able to address issues of

discriminatory access and monopoly leveraging effectively, either through vertical separation or

access rules. A competition policy approach based on this Schumpeterian paradigm and therefore

oriented at contestability may act as a second-best to imperfect regulation, in that it has the virtue

of avoiding the costs and complexities implicit in traditional public utility regulation while

fostering, rather than undermining, incentives to cyclical displacement of monopolies and

innovation. Yet the dissertation argues that this approach also remains affected by critical

limitations imposed by institutional constraints. Addressing some of the central market power

concerns at play with natural monopoly platforms, such as discrimination and leveraging, will be

for example difficult to achieve through antitrust enforcement characterized by slow and

complex procedures, case-by-case adjudication, and remedies such as the application of the

essential facilities doctrine that ultimately require ongoing administration akin to regulatory

oversight. Solutions to these shortcomings will inevitably entail the need to rethink competition

and regulatory solutions as complementary rather than substitute approaches to market power in

digital platform markets.

11

These conclusions differentiate the dissertation from the prevailing positions in favor or against

intervention in digital markets. Laissez-faire arguments generally underplay the ability of

dominant platforms to abuse market power to protect themselves from threats of disruption, to

delay displacement, and to foreclose in adjacent markets, placing excessive emphasis on the role

of market forces alone to erode high profits and market power. On their part, many of the

proposals in favor of stronger antitrust intervention place excessive emphasis on the ability of

competition, entry (conceived in terms of static competition between platforms), and induced

market fragmentation to solve market power concerns in digital markets: proposals that attempt

to fix competition by way of substantive changes to competition laws, for example abandoning

the consumer welfare standard, or by way of horizontal break-up of tech giants to fragment

markets, clash with the contention that technological change makes platform markets overall

more prone to efficient and natural concentration. More refined and nuanced positions that build

on and apply Schumpeterian arguments to the tech sector are closer to the position defended in

the dissertation, in so far as they focus on favoring entry that aims at monopoly displacement and

dynamic competition rather than fragmentation and static competition. However, these positions

often assume away some of the institutional constraints of antitrust enforcement that this

dissertation attempts to highlight, suggesting on the contrary the need for complementary forms

of regulatory oversight.

3. Structure of the Dissertation Chapter 1 of the dissertation outlines the technological and economic drivers of concentration

that differentiate the current wave of digital multi-sided platforms from older traditional

examples of platforms and evaluates what the multi-sidedness of a market implies for the set of

rules that should apply to platforms. Chapter 2 applies the natural monopoly framework and

12

identifies different policy approaches that may be applied to natural platform monopolies, in

particular ex-ante regulation, franchise bidding, public ownership, structural remedies, and

competition policy enforcement. The dissertation then applies this framework to three case

studies of platform markets: online horizontal search (Chapter 3); e-commerce marketplaces

(Chapter 4); on-demand ride-hailing platforms (Chapter 5). Chapter 6 concludes.

13

Chapter 1 Technological and Economic Drivers of Increasing

Concentration in Platform Markets

A central premise of this dissertation is the relationship between technological progress and

competition policy. In this Chapter, the thesis evaluates the ways in which technological change

contributes to increasing market concentration and higher likelihood of natural monopolies in the

current wave of platform markets. It begins by comparing the process of technological progress

that gave birth to modern competition laws in the nineteen-century to the current features of

technological change that affect the structure of firms and markets and fuel concerns about rising

monopoly power – platform intermediation as related to the theory of the firm, big data,

algorithmic prediction and matching, and the sharing economy phenomenon. The Chapter then

shows how technological change increases the likelihood of natural monopolies in the current

wave of multi-sided digital platforms compared to older, physical predecessors of platforms:

first, technological change favors the platform model as the predominant form of intermediation

and firm structure, which benefits from aggregating positive network externalities; second,

technology increases the concentration tendencies at play in the current wave of platforms as

compared to their older physical predecessors, due to digitalization, big data, and algorithmic

prediction. On this basis, the Chapter then overviews the increasingly important literature on the

economics of multi-sided platforms and critically evaluates the doctrinal and regulatory

implications that can be derived from this branch of industrial organization theory. In particular,

it highlights the fallacy of treating platform markets as a special category of markets and using

multi-sidedness as a justification for the creation of different rules for these markets as opposed

14

to standard single-sided markets, showing how analogous fallacies may be relevant in the

evaluation of regulation for natural monopoly platforms.

Technological and Economic Drivers of Increasing Concentration in Platform Markets

1.1 Rising Concentration in the Wake of Technological Change The role of technological change in shaping economic organizations has always been central to

the development of competition policy. Early political economists coming from different

ideological perspectives such as Marx and Schumpeter already saw in capitalism a system

always in the process of revolutionizing itself and constantly shaken by technological progress.

While Marx’s view of capitalist economies necessarily tending toward monopoly contrasted with

the conclusions drawn by Schumpeter based on his insight about market competition as being

driven by a perennial gale of creative destruction, both converged in seeing the instability of

market mechanisms as a force of economic change resulting from the continuous process of

revolutionizing the instruments of productions. 3 As important as the process of selling the best

product at the lowest price, the force of the competitive process driven by the creation of

alternative, better, technologies that generate entirely new markets and destabilize the previous

market equilibrium has shaped many industries and equally influenced the origin and

development of competition policy.

In itself, the emergence of modern competition laws can in fact be read as a response to social

and economic changes created by technological progress. The emergence of the railroad, steam

engines, and changes in telecommunication technologies during the nineteen-century that created

3 Karl Marx, A Contribution to the Critique of Political Economy (1859); Joseph A Schumpeter, Capitalism, socialism, and democracy (London: Harper & Brothers, 1942).

15

the conditions for large-scale production and growth in the scale of manufacturing enterprises

gave rise to drastic economic dislocations.4 Canada was the first country to enact competition

laws in 1889 as a result of the increased concentration of economic power in the aftermath of the

industrial revolution,5 and one year later the Sherman Act was enacted in the United States, as a

result of increasing concerns amongst small producers, farmers, and consumers who perceived

themselves as negatively affected by the forces of such transformations.6 While the history of

various competition law regimes is often unclear and reflect the confluence of heterogeneous

forces and interests affecting the determination of the ultimate goal pursued by antitrust

legislation,7 the opposition to the growth of trusts and the protection of small businesses

succumbing to the emerging large manufacturing enterprises were central to the birth of

competition laws,8 at least partially a by-product of substantial technological changes.

In particular, the increase in economic activity that came with new technologies and expanding

markets gave rise to massive economies of scale in production and to administrative coordination

as the more efficient form of organization, in terms of greater productivity, lower costs, and

higher profits. The emergence of managerial capitalism in large firms through a hierarchy of

middle and top salaried managers did not exist in 1840, but less than a century later the modern

multiunit business enterprise replaced small traditional enterprises. At first, the large enterprise

4 See: Bhu Srinivasan, Americana: A 400-year History of American Capitalism (New York: Penguin Press, 2017).

5 See: Chapter One in Michael J Trebilcock, Ralph A Winter & Edward M Iacobucci, The Law and Economics of Canadian Competition Policy (University of Toronto Press, 2002).

6 See Alfred D Chandler Jr, The Visible Hand (Cambridge: Mass.: Harvard University Press, 1977); William Letwin, Law and Economic Policy in America (New York: Random House, 1956).

7 Henry Rogers Seager & Charles Adams Gulick, Trust and Corporation Problems (New York: Harper, 1929).

8 William Letwin, supra note 6.

16

grew and dominated only a few sectors or industries where technological innovation and market

growth were particularly significant. As technology became more sophisticated and markets

expanded, administrative coordination replaced market coordination in an increasingly larger

portion of the economy. By the middle of the twentieth century, mass production and retail, mass

transportation and distribution dominated major sectors of the American economy.

As noted by Chandler, who traced the birth of the modern enterprise, the organizational changes

which helped create the managerial capitalism of the twentieth century were as significant and as

revolutionary as those that accompanied the rise of commercial capitalism a half a millennium

earlier.9 Where administrative coordination within the firm was the organizational response to

the application of industrial technologies, the passing of antitrust laws was at least in part the

legislative reaction to the same changes in transportation and communication and to the new

processes of production and distribution that gave rise to the increasing number of combinations

that occurred during the 1870s and 1880s. 10

As competition law regimes matured and evolved, the impact of technological progress on

market competition retained its centrality in various areas of competition policy. Among other

things, it remained implicit in the longstanding debates on what market structure – monopoly or

competition – better serves the process of innovation. Many theoretical and empirical studies

have attempted to determine the linkages between technological change, firm size and market

structure. Notably, Schumpeter among others famously emphasized that market power and

concentration are necessary as an incentive for firms to innovate due to economies of scale and

9 Chandler Jr, supra note 6 at 16.

10 Massimo Motta, Competition Policy: Theory and Practice (Cambridge: UK: Cambridge University Press, 2004); Trebilcock, Winter & Iacobucci, supra note 5.

17

the expense and risks involved in carrying out research and development.11 In contrast, Arrow

concluded that competition rather than monopoly creates better conditions for innovation,12 and

others have highlighted the various disadvantages that larger firms can incur in administering

large administrative structures, which undermine rather than facilitative innovative R&D

processes.13

Most recent empirical studies have concluded that innovation presents an inverted U-shaped

relationship with firm size and market concentration,14 where market concentration aids

innovation up to a point, but then concentrated, oligopolistic industries with high barriers to entry

may reduce incentives to innovate. Aghion et al.15 collected empirical evidence about the

relationship between product market concentration and the intensity of innovative activity,

showing that an inverted-U shape pattern16 results from the balance between what they call the

‘Schumpeterian’ and the ‘escaping-competition’ incentive:17 on the one hand, competition can

increase the incremental profits obtained from innovation and therefore encourages R&D

11 Schumpeter, supra note 3.

12 Kenneth Arrow, “Economic Welfare and the Allocation of Resources for Invention” in Rate Dir Econ Act Econ Soc Factors (Princeton: Princeton University Press, 1962).

13 See for instance: Oliver E Williamson, “Economies as an Antitrust Defense: The Welfare Tradeoffs” (1968) 58:1 Am Econ Rev 18.

14 F M Scherer & David Ross, Industrial market structure and economic performance, 3rd ed (Boston Houghton Mifflin, 1990).

15 Philippe Aghion et al, “Competition and Innovation: An Inverted-U Relationship” (2005) 120:2 Q J Econ 701.

16 This pattern was previously hinted at by Scherer. See Scherer & Ross, supra note 14.

17 Flavio Delbono & Luca Lambertini, Innovation and Product Market Concentration: Schumpeter, Arrow and the Inverted-U Shape Curve, SSRN Scholarly Paper ID 2981677 (Rochester, NY: Social Science Research Network, 2017).

18

investments aimed at escaping competition in sectors where incumbent firms are operating at

similar technological levels; on the other hand, in unlevelled sectors where product market

competition may discourage innovation by laggard firms with already low initial profits, the

Schumpeterian effect is at work (even if it does not always necessarily dominate). In sum, the

desirability of competition versus concentration for innovation depends on the technological

state of the sector.18

The different forms and paces of technological change have also been critical in shaping

enforcement policies and intervention in markets characterized by dynamic competition for the

market as opposed to static competition within markets. Technological development is usually

incremental, bringing into markets products or services that are marginally superior to current

ones. At times, and perhaps most critically, it is instead based on more irregular and

unpredictable breakthroughs that bring radical changes to markets and reduce or destroy the

established position of incumbents or create entirely new markets. This radical form of

innovation can either come from an existing firm or from a new market entrant and generally

occurs in markets dominated and occupied by inefficient incumbents that suddenly face

competitive threats from the rapid scaling up of disruptors in niche segments.19 Bower and

Christensen divided the forms of innovation into two types, sustaining and disruptive.20 The

former provides an improvement in something that consumers already value, the latter introduces

a different and new set of features compared to the ones traditionally valued by consumers. In

18 Philippe Aghion et al, supra note 15.

19 “Disruptive innovations and their effect on competition - OECD”, (2015), online: OECD.org <https://www.oecd.org/daf/competition/disruptive-innovations-and-competition.htm>.

20 Joseph Bower & Clayton Christensen, “Disruptive Technologies: Catching the Wave” (1995) 73: January-February Harv Bus Rev 43.

19

The Innovator’s Dilemma, Christensen describes this latter form of disruptive innovation as not

always necessary associated with breakthrough innovation but with a phenomenon that

transforms a product that was previously offered expensively at the high-end of the market and

that is made more affordable and accessible.21 At the start, the new features offered usually

perform worse on many dimensions, but eventually manage to replace older goods or services

due to novelty, lower costs, elimination of middlemen or other inefficiencies. Where sustaining

innovation is usually associated with competition within the market, disruptive innovation is

associated with dynamic forms of winner-takes-all competition for the market. The two different

competitive processes generally call for a different set of enforcement policies: the former

generally based on neo-classical economic assumptions and aiming at fostering competition

through market fragmentation, the latter based on the goal of encouraging ongoing cycles of

monopoly displacement.

The longstanding relationship between technology and the origin of competition policy is

resurrected today due to the current wave of technological change driven by developments in

artificial intelligence, big data, and the growing importance of digital markets, fuelling as a by-

product discontent in many quarters with technology as a visible force of profound economic

change.22Automation has significant effects on labour markets and trends in employment in

many key sectors of the economy. Digitalization is reshaping many traditional professions,23 the

21 “The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail”, online: Clayton Christ <http://www.claytonchristensen.com/books/the-innovators-dilemma/>.

22 Michael J Trebilcock, “The Fracturing of The Post-War Free Trade Consensus: The Challenges of Reconstructing a New Consensus” (2017) Univ Tor Fac Law.

23 Richard Susskind & Daniel Susskind, The Future of the Professions: How Technology Will Transform the Work of Human Experts (Oxford: Oxford University Press, 2016).

20

future of education,24 and the process of lawmaking.25 Artificial intelligence and big data test the

foundations of consumer protection regulation and possibly give rise to new forms of anti-

competitive conduct.26 Perhaps the most relevant consequence of current technological changes

for competition comes from the evidence of increasing levels of market concentration in

industrialized economies, 27 particularly evident in the United States. For instance, the US

Census Bureau data show increases in the revenue share enjoyed by the largest 50 firms in the

timeframe between 1997 and 2012 in a large portion of US industries, with various industry-

specific studies founding similar trends over longer periods of time.28 According to other studies,

more than 75 percent of US industries have experienced an increase in concentration levels over

24 Claudia Goldin & Lawrence F Katz, The Race between Education and Technology (Cambridge: Mass.: Harvard University Press, 2009).

25 Richard Susskind, The Future of Law: Facing the Challenges of Information Technology (Oxford: Clarendon Press, 1998); Benjamin Alarie, Anthony Niblett & Albert H Yoon, “Law in the future” (2016) 66:4 Univ Tor Law J 423; Anthony J Casey & Anthony Niblett, “Self-driving laws” (2016) 66:4 Univ Tor Law J 429.

26 See Ariel Ezrachi & Maurice E Stucke, Virtual Competition: The Promise and Perils of the Algorithm-Driven Economy (Cambridge: Mass.: Harvard University Press, 2016); Ariel Ezrachi & Maurice E Stucke, “Artificial Intelligence & Collusion: When Computers Inhibit Competition” (2017) 2017 Univ Ill Law Rev 1775; Michal Gal & Daniel L Rubinfeld, “The Hidden Costs of Free Goods: Implications for Antitrust Enforcement” (2016) 80:401 Antitrust Law J, online: <https://papers.ssrn.com/abstract=2529425>; Maurice E Stucke & Allen P Grunes, Debunking the Myths Over Big Data and Antitrust, Legal Studies Research Paper Series Research Paper #276 (University of Tennessee, 2015); Darren S Tucker & Hill Wellford, "Big Mistakes Regarding Big Data" SSRN Scholarly Paper ID 2549044 (Rochester, NY: Social Science Research Network, 2014); Cecilia Munoz, Megan Smith & DJ Patil, Big Data: A Report on Algorithmic Systems, Opportunity, and Civil Rights, Obama Administration’s Big Data Working Group (Washington, D.C.: Executive Office of the President, 2016).

27 See for instance: David Autor et al, “Concentrating on the Fall of the Labor Share” (2017) 107:5 Am Econ Rev 180; Joseph Stiglitz, “Toward a Broader View of Competition Policy” in Compet Policy New Era Insights BRICS Ctries (Oxford: Oxford University Press, 2017) 4; Jonathan B Baker, “Market power in the U.S. economy today”, (20 March 2017), online: Wash Cent Equitable Growth <https://equitablegrowth.org/market-power-in-the-u-s-economy-today/>; Luigi Zingales, “Towards a Political Theory of the Firm” (2017) 31:3 J Econ Perspect 113; The University of Chicago Booth School of Business, Is There a Concentration Problem in America? (Gleacher Center, 2017); Council of Economic Advisers, Benefits of Competition and Indicators of Market Power, Issues Brief (Washington, D.C.: Obama White House, 2016); “Too much of a good thing - Business in America”, The Economist (26 March 2016), online: <https://www.economist.com/briefing/2016/03/26/too-much-of-a-good-thing>; Jonathan Tepper, The Myth of Capitalism: Monopolies and the Death of Competition (Hoboken: NJ: John Wiley & Sons, 2018).

28 Council of Economic Advisers, supra note 27.

21

the last two decades,29 with the HHI index increasing by more than 50 percent on average.30

Other evidence points to declining levels of new firm creations each year across sectors31 (with

exit rates of firms remaining fairly stable but entry rates declining over the same timeframe), the

growing problem of horizontal shareholding in concentrated industries,32 and increasing

monopsony power due to excessive concentration in labour markets.33

While not all of these concerns are necessarily or solely linked to technology, the rise of

superstar digital platforms is a particularly prominent manifestation of the role of technological

change in fostering concentrated market structures, and perhaps reflect the strongest concern

about excessive concentration and competition. In this regard, Autor et al for example suggest an

interpretation for the fall in labour’s share of the GDP in the United States based on the rise of

29 Gustavo Grullon, Yelena Larkin & Roni Michaely, Are U.S. Industries Becoming More Concentrated?, SSRN Scholarly Paper ID 2612047 (Rochester, NY: Social Science Research Network, 2018).

30 Ibid. This trend appears to parallel very high levels of merger activity, and a decline in the application of Section 2 of the Sherman Act. There is also evidence that the wave of mergers has improved productivity but has also raised mark-ups from 15 percent to 50 percent above the average mark-ups across U.S. manufacturing industries. See Bruce A Blonigen & Justin R Pierce, Evidence for the Effects of Mergers on Market Power and Efficiency, Finance and Economics Discussion Series 2016–082 (Board of Governors of the Federal Reserve System (US), 2016). In 1980, only 20 percent of small publicly traded firms had negative earnings per share; in 2010, 60 percent did. See: Xiaohui Gao, Jay R Ritter & Zhongyan Zhu, “Where Have All the IPOs Gone?” (2013) 48:6 J Financ Quant Anal 1663.

31 While decreasing rates of entry were identified only in specific sectors during the 1980s and 1990s, this decline affected all sectors in the 2000s. See Ryan Decker et al, “The Role of Entrepreneurship in US Job Creation and Economic Dynamism” (2014) 28:3 J Econ Perspect 3; Ryan Decker et al, The Secular Decline in Business Dynamism in the U.S., Working Paper (Maryland: University of Maryland, 2014).

32José Azar, Martin C Schmalz & Isabel Tecu, Anticompetitive Effects of Common Ownership, SSRN Scholarly Paper ID 2427345 (Rochester, NY: Social Science Research Network, 2018); José Azar, Sahil Raina & Martin C Schmalz, Ultimate Ownership and Bank Competition, SSRN Scholarly Paper ID 2710252 (Rochester, NY: Social Science Research Network, 2016); Einer Elhauge, Horizontal Shareholding, SSRN Scholarly Paper ID 2632024 (Rochester, NY: Social Science Research Network, 2016); Eric A Posner, Fiona M Scott Morton & E Glen Weyl, A Proposal to Limit the Anti-Competitive Power of Institutional Investors, SSRN Scholarly Paper ID 2872754 (Rochester, NY: Social Science Research Network, 2017).

33 See for example Suresh Naidu, Eric A Posner & E Glen Weyl, Antitrust Remedies for Labor Market Power, SSRN Scholarly Paper ID 3129221 (Rochester, NY: Social Science Research Network, 2018).

22

superstar firms in high-tech industries in particular.34 High-tech sectors (and parts of retail and

transportation sector) have increasingly “winner takes all” aspects, suggesting that firms may

initially gain high market shares by legitimately competing on the merits of their innovations or

superior efficiencies, but once they have gained a dominant position, they use their market power

to erect various barriers to entry to protect their position. Similarly, according to the Economist,

the rise of tech titans, often accused in public debates of being too big, engaging in anti-

competitive behaviour, and threatening democracy,35 poses a danger to competition and requires

antitrust policy solutions in a world based on information and networks where digital companies

may use network effects to exclude potential competitors, or implement new ways of exploiting

their dominant position.36 As a result, evidence on the fall in labour share of national income

coinciding with a significant rise in mark-ups37 for incumbent firms is often associated with the

possibility of increasing levels of market power38 – trends that appear especially pronounced in

the tech sector.

34 David Autor et al, The Fall of the Labor Share and the Rise of Superstar Firms, Working Paper 23396 (National Bureau of Economic Research, 2017) at 23.

35 “How to tame the tech titans”, The Economist (18 January 2018), online: <https://www.economist.com/leaders/2018/01/18/how-to-tame-the-tech-titans>; Patrick Foulis, “Across the West powerful firms are becoming even more powerful”, The Economist (15 November 2018), online: <https://www.economist.com/special-report/2018/11/15/across-the-west-powerful-firms-are-becoming-even-more-powerful>; 'Competition, not break-up, is the cure for tech giants' dominance, The Economist (March 13, 2019), online: https://www.economist.com/business/2019/03/13/competition-not-break-up-is-the-cure-for-tech-giants-dominance?fsrc=scn%2Ftw%2Fte%2Fbl%2Fed%2Fauto

36 Adrian Woolridge, “The rise of the superstars”, The Economist (17 September 2016), online: <https://www.economist.com/special-report/2016/09/17/the-rise-of-the-superstars>; “The Superstar Company: A giant problem”, The Economist (17 September 2016), online: <https://www.economist.com/leaders/2016/09/17/a-giant-problem>; Aindrajit Dube et al, “Monopsony in On-line Labor Markets” (2018) Draft Version Pap Prep.

37 The ratio may also be driven by marginal costs going down.

38 Simcha Barkai, “Declining labor and capital shares” (2017) Work Pap, online: <http://www.london.edu/faculty-and-research/academic-research/d/declining-labor-and-capital-shares>. The emerging evidence on common ownership by large institutional investors exacerbates possible concerns over concentration. SeeAzar, Schmalz & Tecu, supra note 32; Azar, Raina & Schmalz, supra note 32; Elhauge, supra note 32; Loukas Karabarbounis & Brent

23

Figure 1: Labor Share of GDP and Inverse Markup

Indeed, various proposals that have been proposed to address the dominance of tech platforms,

driven by concerns over excessive concentration of both economic and political power, evoke an

inevitable parallel between the current discontent with technological change the growth of trusts

and nineteen century robber barons – including radical changes in antitrust law doctrines and

goals with a return to the protection of small businesses and specific market structures, stronger

enforcement against mergers and single firm conduct, or calls to break up digital platforms.39

Neiman, “The Global Decline of the Labor Share” (2014) 129:1 Q J Econ 61; Parijs Philippe Van & Yannick Vanderborght, Basic Income, A Radical Proposal for a Free Society and a Sane Economy (Cambridge: Mass.: Harvard University Press, 2017).

39 See for example Tepper, supra note 27; Lina M Khan, “Amazon’s Antitrust Paradox” (2016) 126 Yale Law J 710. See more generally UK Report of the Digital Competition Expert Panel, Unlocking Digital Competition (March 2019), available at: https://www.gov.uk/government/publications/unlocking-digital-competition-report-of-the-digital-competition-expert-panel; Australian Competition and Consumer Commission, Digital Platform Inquiry (December 2018), available at: https://www.accc.gov.au/system/files/ACCC%20Digital%20Platforms%20Inquiry%20-%20Preliminary%20Report.pdf; The Economist, Competition, Not Break-up, is the Cure for Tech Giants’ Dominance (March 2019), available at: https://www.economist.com/business/2019/03/13/competition-not-break-up-is-the-cure-for-tech-giants-dominance?fsrc=scn%2Ftw%2Fte%2Fbl%2Fed%2Fauto

24

There are however important considerations and distinctions to be considered when evaluating

such parallels.

First, the evidence of alleged decreases in the levels of market competition is not uncontested. In

themselves, data on increases in the revenue share tells little or nothing about trends in

competition and market power in properly defined relevant markets40 and does not provide

informative evidence of concentration as reflecting changes in the levels of competition over

time, nor provide an explanation as to whether economies of scale or network externalities,41

increasing barriers to entry, exclusionary conduct, or lack of effective merger enforcement are

driving these trends. Second, the technological drivers of concentration are different. Where

managerial capitalism was driven by the increasing sophistication of administrative coordination

of large enterprises that exploited supply-side economies of scale, the contemporary form of

organizing economic activity capitalizes on the use of big data and algorithms to perform more

and more efficient prediction and matching functions and relies substantially on demand-side

economies of scale due to network effects. Unlike traditional vertically integrated industrial

enterprises based on a linear value chain, matchmaking platforms sit between users and create a

marketplace for their interaction by reducing information and transaction costs, shifting the focus

from internal production processes to the efficient management of network externalities. As a

result, the nature of the output provided by digital platforms is substantially different: mostly

based on intermediation services and predictive technologies rather than provision of goods;

40Carl Shapiro, Antitrust in a Time of Populism, SSRN Scholarly Paper ID 3058345 (Rochester, NY: Social Science Research Network, 2017).

41 Autor et al, supra note 27; James E Bessen, Information Technology and Industry Concentration, SSRN Scholarly Paper ID 3044730 (Rochester, NY: Social Science Research Network, 2017).

25

often oriented, at least indirectly, at creating the conditions for market entry for smaller

providers;42 usually characterized by very low or zero prices for at least one group of consumers,

which are the result of digitalization driving down marginal and the economics of platforms

often entailing zero prices; generally global in nature.

Therefore, while the similarities between nineteen century monopolies and digital platforms are

evocative of recurrent parallels between waves of technological progress and cycles of increasing

market concentration, proposed policy responses to alleged problem of increasing market power

caused by the current wave of platform markets are often vague and lack a rigorous evaluation of

the following central considerations: what is exactly new about the current wave of platforms

vis-à-vis older generations of platforms that may be causing increasing concentration; what is the

market failure that increasing concentration can cause in terms of market power abuses; what is

the most desirable instrument to address the identified issues. In the next section, the Chapter

discusses some of the distinguishing features of current technological developments associated

with the increasing levels of concentration that are at the root of the present discontent with the

state of competition and that may be potential enablers of natural monopolies – in particular the

platform model based on network externalities, big data, algorithmic matching and prediction

technologies.

1.2 The Contours of Current Technological Change Competition policy has dealt in the past with older, physical predecessors of the online platform

model, or confronted question of competition related to data, matching and prediction. What is

then new in the current wave of technological progress? The Chapter shows how the current

42 As it is the case with platform intermediaries enabling individual drivers to provide taxi services, home owners to offer short-term rentals, or small business to better access consumers online.

26

process of technological change exponentially magnifies the predominance of the platform

model, and the importance of access to data as a central input for algorithmic-based matching

and prediction technologies. These factors generate a tendency that make platforms potentially

more prone to become naturally monopolistic.

1.2.1 Platform Intermediation and the Theory of the Firm

Modern information and communication technologies have scaled up exponentially the viability

and efficiency of the multisided platform business model that have existed for millennia.43 Old

village marketplaces, trade fairs, auction houses, yellow pages,44 bricks-and-mortar shopping

malls, physical newspapers, credit cards are all older analogs to today’s digital platforms and

many of these markets have been under the spotlight of antitrust enforcement in the past.

However, matching capabilities of traditional old physical platforms have been often limited by

the boundary of physical spaces that imposed limits on the extent of markets and the offering of

new goods and services. On the contrary, online platforms can expand, due to digitalization, the

extent of the marketplace both geographically and in terms of increased matching potential

between users, aided by the power of big data and algorithmic matching functions that were not

available to the older physical predecessors of the platform. 45

The increasing predominance of the platform model of intermediation can be explained through

the lens provided by the theory of the firm. Coase’s theory of the firm was based on the idea that

43 SeeDavid Sparks Evans & Richard Schmalensee, Matchmakers: The New Economics of Multisided Platforms (Cambridge: Mass.: Harvard Business Review Press, 2016).

44 Paul Belleflamme & Martin Peitz, Platforms and network effects, Working Papers 16–14 (University of Mannheim, Department of Economics, 2016).

45 Liran Einav, Chiara Farronato & Jonathan Levin, Peer-to-Peer Markets, NBER Working Paper 21496 (Cambridge: Mass.: National Bureau of Economic Research, Inc, 2015).

27

the transaction costs of organizing economic activities determine the boundaries between

markets and within the hierarchy of the firm.46 Coase’s insight was that using the market is

costly: discovering market prices and negotiating contracts for each exchange can be avoided

inside the firm because bargaining is replaced by authority. However, because authority has its

own costs, as the firm gets bigger, the relative cost of authority and the price system is what

determines the boundaries and sizes of firms.

Since then, a voluminous strand of law and economics literature has advanced competing

theories of the firm and why in market economies we have firms at all.47 Building on Coase’s

theory, Williamson made significant progress in understanding the nature of transaction costs in

the market.48 He posited that elements like the frequency and uncertainty of bargaining, and

asset specificity of investments all affect the choice between integration and markets. In

Williamson’s theory, integration is attractive because frequency makes contracting inconvenient

and contracts less important in repeat relations. Similarly, uncertainty makes it more difficult to

predict outcomes in long-term agreements, hence harder to contract. Since any contract will be

incomplete and will have to be renegotiated ex post, vertical integration may be more efficient

for the parties. Integration can avoid socially wasteful haggling and authority becomes a more

46R H Coase, “The Nature of the Firm” (1937) 4:16 Economica 386.