Murabaha - Product offerred by BankIslami Pakistan Ltd

15

Syed Salman 1300218 STRUCTURING FINANCIAL REQUIREMENTS March 26 2014 This Project Paper is a partial fulfillment of Module IB-2001 of part II of Chartered Islamic Finance Professional (CIFP) INCEIF – The Global University of Islamic Finance - January 2014 Murabahah Financing Product of BankIslami Pakistan Limited (BIPL)

Transcript of Murabaha - Product offerred by BankIslami Pakistan Ltd

Syed Salman

1300218

STRUCTURING FINANCIAL REQUIREMENTS

March 26

2014 This Project Paper is a partial fulfillment of Module IB-2001 of part II of Chartered Islamic Finance Professional (CIFP) INCEIF – The Global University of Islamic Finance - January 2014

Murabahah Financing Product of BankIslami Pakistan Limited (BIPL)

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 2

Table of Contents

1 Introduction: .............................................................................................................................................................. 3

2 Explanation of the Product: .................................................................................................................................... 3

2.1 Murabahah under Agency Agreement .......................................................................................................... 4

2.2 Documentation ................................................................................................................................................. 7

2.2.1 Master Murabahah Facility Agreement (MMFA): ................................................................................ 7

2.2.2 Agency Agreement (AA): ........................................................................................................................ 7

2.2.3 Purchase Requisition (PR): .................................................................................................................... 7

2.2.4 Confirmation of Goods Purchased: ....................................................................................................... 7

2.2.5 Murabahah Sale Document (MSD): ...................................................................................................... 8

2.2.6 Schedule of Payment (SoP): .................................................................................................................. 8

2.2.7 Demand Promissory Note (DPN): ......................................................................................................... 8

3 The Shariah principle(s) or concept(s) used in the products or package: ...................................................... 9

3.1 Specific & Identifiable ...................................................................................................................................... 9

3.2 Ownership and Possession of Goods ........................................................................................................... 9

3.3 Confirmation of Price ....................................................................................................................................... 9

4 The procedures to offer the products or package ............................................................................................... 9

4.1 Print Media, Website and Phone Banking ................................................................................................. 10

4.2 Through Sales Teams ................................................................................................................................... 10

4.2.1 Corporate Sales Team .......................................................................................................................... 10

4.2.2 Consumer and SME Sales Team ........................................................................................................ 10

5 The comparison between the Intra Bank products ........................................................................................... 10

6 The comparison between the Inter Bank products ........................................................................................... 12

7 The risks and return to the financial institution in offering the product or package: .................................... 12

7.1 Asset Risk ....................................................................................................................................................... 12

7.2 Credit Risk ....................................................................................................................................................... 12

7.3 Risk Return Mechanism ................................................................................................................................ 13

8 The expected performance of the products based on the information from the bank and other external

information ...................................................................................................................................................................... 13

9 Conclusion: ............................................................................................................................................................. 15

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 3

1 Introduction:

Murabahah, one of the most recently used Islamic Banking Product, primarily for

corporate and enterprises is the topic of discussion in this study. We have chosen

BankIslami Pakistan Limited (BIPL) as a reference and will discuss the product detail,

explanation, Shariah contracts indulged in it, process and procedure adopted by the

Bank, its comparison with relevant conventional Banking products, evaluation of the

product with regard to risk return mechanism and its performance. The objective of

the paper is to discuss the Murabahah contracts as practiced in the industry. The

basis of the research is to enlighten the readers with the existing Murabahah contract

and its popularity in the Islamic Finance as well as why the contract is called “Border

Line Transaction” by some shariah scholars. Furthermore the secondary purpose is

also to compare and contrast between the Conventional Banking products to the one

2 Explanation of the Product:

Murabahah Finance is a particular kind of sale where BankIslami (The Seller)

expressly discloses the cost of the sold goods and the profit to the Client (The Buyer).

It can be a spot sale, a credit sale (deferred payment), an advance payment sale or

combination among the three modes of payment. It’s not a loan given on interest

rather, it’s a sale given of goods against cash or on deferred basis. Hence it must

fulfill all the basic principles of a sales contract. BIPL provides assets, raw materials

and goods of certain value upon specific request received from the client. Murabahah

financing is generally used as short term financing this is because there is no option

of price revision during the tenure and the risk lies with the Bank.

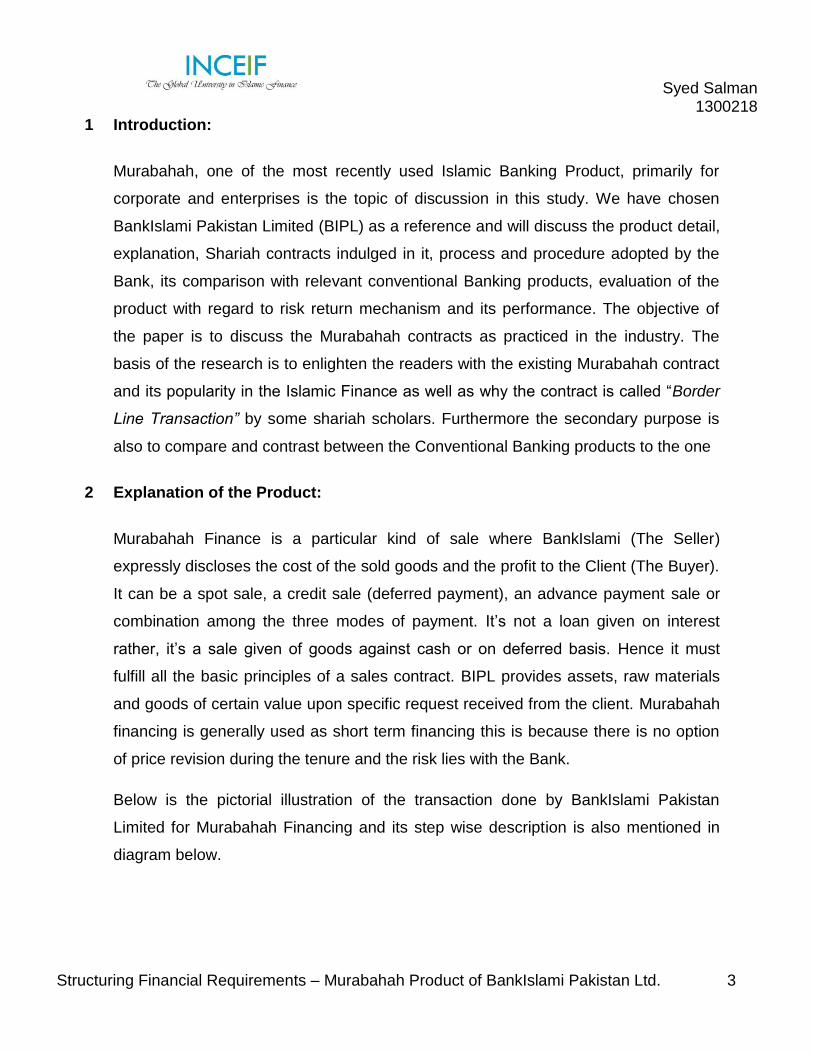

Below is the pictorial illustration of the transaction done by BankIslami Pakistan

Limited for Murabahah Financing and its step wise description is also mentioned in

diagram below.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 4

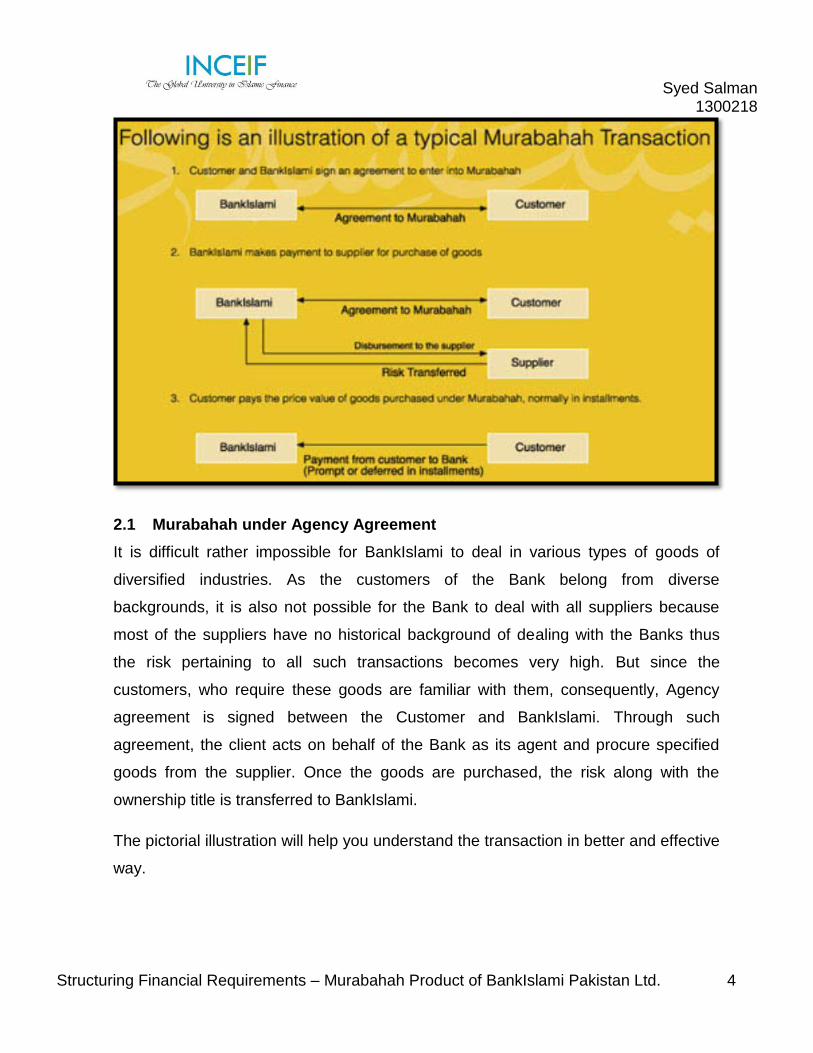

2.1 Murabahah under Agency Agreement

It is difficult rather impossible for BankIslami to deal in various types of goods of

diversified industries. As the customers of the Bank belong from diverse

backgrounds, it is also not possible for the Bank to deal with all suppliers because

most of the suppliers have no historical background of dealing with the Banks thus

the risk pertaining to all such transactions becomes very high. But since the

customers, who require these goods are familiar with them, consequently, Agency

agreement is signed between the Customer and BankIslami. Through such

agreement, the client acts on behalf of the Bank as its agent and procure specified

goods from the supplier. Once the goods are purchased, the risk along with the

ownership title is transferred to BankIslami.

The pictorial illustration will help you understand the transaction in better and effective

way.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 5

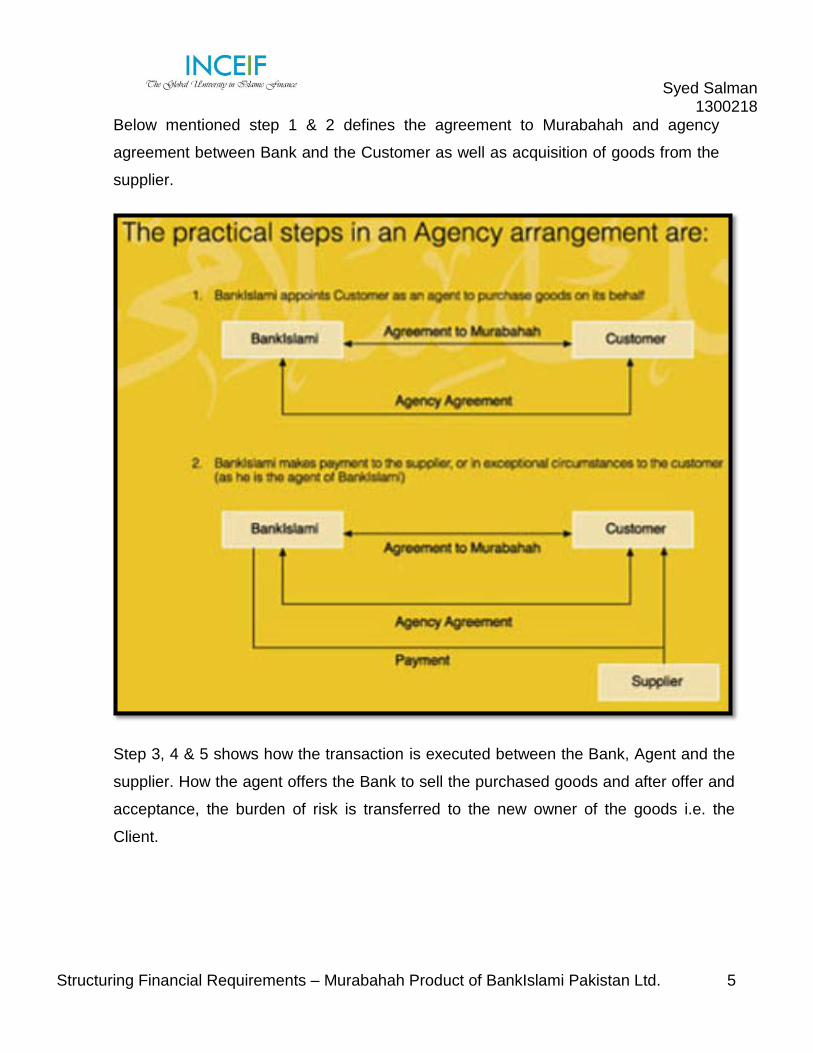

Below mentioned step 1 & 2 defines the agreement to Murabahah and agency

agreement between Bank and the Customer as well as acquisition of goods from the

supplier.

Step 3, 4 & 5 shows how the transaction is executed between the Bank, Agent and the

supplier. How the agent offers the Bank to sell the purchased goods and after offer and

acceptance, the burden of risk is transferred to the new owner of the goods i.e. the

Client.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 6

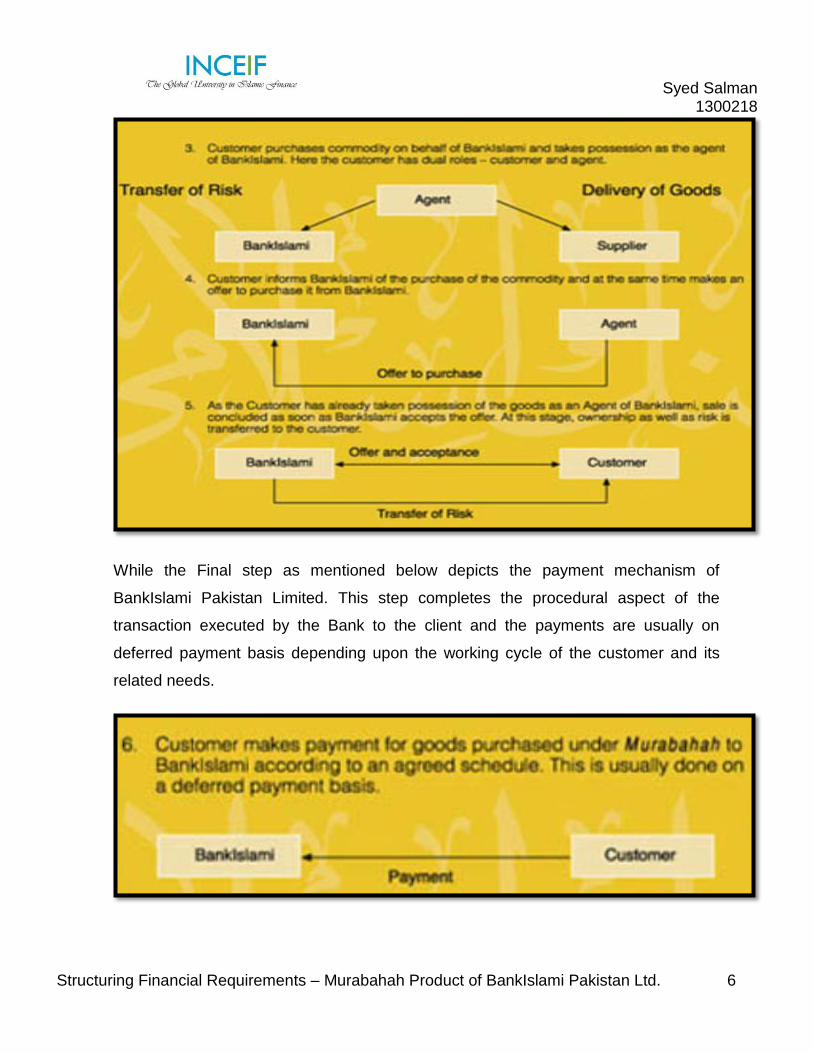

While the Final step as mentioned below depicts the payment mechanism of

BankIslami Pakistan Limited. This step completes the procedural aspect of the

transaction executed by the Bank to the client and the payments are usually on

deferred payment basis depending upon the working cycle of the customer and its

related needs.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 7

2.2 Documentation

The documents signed between the customer and BankIslami are as under.

2.2.1 Master Murabahah Facility Agreement (MMFA):

Since the actual sale at the time of disbursement of funds is not executed, BIPL cannot

enter into sales contract with the customer. Hence BIPL is bound to purchase the goods

first from supplier and then it can sell it to the customer. So BankIslami and the customer

enter into MMFA where the client signs a unilateral promise to purchase from the Bank and

he can also be asked for security deposits (Hamish Jiddeyyah) so that in case of his

refusal of purchasing the asset, the Bank may recover the damages, whatsoever incurred.

This agreement also defines the legal framework between the Bank and the Client through

which business will take place among them.

2.2.2 Agency Agreement (AA):

Through this Agreement, BankIslami appoints the Client as its agent to select and procure

specified goods as mentioned in MMFA for the Bank through the funds disbursed by the

Bank in the name of the identified supplier by the agent.

2.2.3 Purchase Requisition (PR):

This PR document is signed by the client at the time of each sub Murabahah contract i.e.

each time when the client requires Murabahah disbursement for the purchase of goods; he

will send PR to BIPL. In PR, the Client provides the detail of the goods which he wishes to

purchase as well as the details of the cost and the value date. Relevant branch must

ensure that the goods to be purchased are covered in the list of goods mentioned in

MMFA.

* Value date means the date on which cost price will be paid by BIPL for the purchase of goods i.e. the

disbursement date

2.2.4 Confirmation of Goods Purchased:

Upon purchase of goods from supplier, the client being the agent of the bank will provide

this document also called “Declaration”.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 8

2.2.5 Murabahah Sale Document (MSD):

The most critical part of the Murabahah sales contract is MSD. Through this contract the

offer by the client for purchase of goods and acceptance by BIPL against agreed

Murabahah contract price. Through signing this document, BIPL transfers the title of

ownership to the client and he agrees to pay the Bank on deferred payment basis. The

future payment dates are mentioned in the schedule of payments. The most critical thing of

the document is to properly define the subject matter (quality and quantity) and the

purchase evidences of the transaction are also attached with this document

1. It is taken into consideration very prudently that the cost of funds must be equal to

the funds disbursed by BIPL.

2. If the value of the funds is more than the funds disbursed by BIPL which may

happen in case where the client has used his own funds as well, then the cost will

be calculated on BIPL funds plus client’s fund.

3. If the client has paid in full and the goods will be received in tranches then MSD will

also be executed in tranches. Murabahah cost price will be calculated keeping in

view the proportionate cost of the tranches.

2.2.6 Schedule of Payment (SoP):

This document is signed along with the MSD. The payment can be made in Lump sum

amount at one specific date or in installment on different specified dates.

2.2.7 Demand Promissory Note (DPN):

The DPN is used as a security against indebtedness created by executing MSD.

Technically, the DPN must be created after the execution of MSD but this will give rise to

couple of issues such as;

1. Since a fixed tax is imposed by the government on DPN, in case of each sub

Murabahah, the Bank has to impose tax charges with every DPN issuance that will

ultimately increase the cost when compared to conventional Banks.

2. As the asset will be in possession of the client thus he may refuse to pay the price

then non-availability of DPN may create legal issues for BIPL.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 9

3 The Shariah principle(s) or concept(s) used in the products or package:

BankIslami offers financing based on trade. The Shariah principle applied is the concept of

Murabahah where BIPL purchases goods required by the customer and sells the same at

an agreed profit on the cost price under Murabahah transaction. Since it’s a Sale

transaction, the following things are taken into consideration prudently.

3.1 Specific & Identifiable

In Murabahah transaction BankIslami ensure that the goods required by the customer are

specifically identified and known. The goods must also be identifiable and quantifiable as

Murabahah is allowed only for those goods which fulfill this criterion.

3.2 Ownership and Possession of Goods

The basic principle of Islam is religiously followed by BIPL, “what is not owned cannot be

sold”. BankIslami ensure that the goods must remain in the ownership of the Bank at the

time of sale. Ownership may be physical or constructive but the Bank is responsible for the

Risk and reward of the asset before the sale is initiated. BankIslami ensure the compliance

and the payment is directly made to the supplier.

3.3 Confirmation of Price

The price must be agreed at the time of sale to avoid any unnecessary dispute between

the both parties. The price must be mutually agreed upon. The price once fixed cannot be

changed during the tenure. In order to ensure robust compliance mechanism, BankIslami

has drawn manual procedures and agreements which are strictly complied and followed

while executing the Murabahah transaction.

4 The procedures to offer the products or package

The procedure to offer the product is simple and not exceptional. However, the Bank

has crafted a sound strategy to attract the customers. There are two patterns on

which BankIslami Pakistan is working on currently.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 10

4.1 Print Media, Website and Phone Banking

The product is marketed through Print Media i.e. every Friday Newspaper, Sunday

Magazines etc.

BankIslami website is interactive and is convenient for the customer to know about

the product and information. Hence, the website is completely equipped with all the

relevant information.

Phone Banking is another feasible way to communicate the relevant information to

the customers. BankIslami Phone Banking staff is fully trained and skilled to

answer all the queries of the customers and to ensure such perfection, the phone

banking officers are trained and tested on regular basis.

Brochure stands and pamphlets are available in every branch to ensure that the

customer can go through it easily.

4.2 Through Sales Teams

Another approach of offering the product is through two segments of Sales Teams.

Each team is given a target provided by the Management to achieve the roadmap

defined by the BOD. The annual target is thus segregated into monthly targets and is

achieved also through this platform.

4.2.1 Corporate Sales Team

The Corporate Sales Team consist of Relation Officers (RO) and Customer Relation Managers

(CRM) who approach the corporate clients (existing and new) for their requirement regarding the

facility and ensures that the existing facilities are renewed timely with increment or decrement in the

approved limit (if and when necessary)

4.2.2 Consumer and SME Sales Team

The sole proprietorship based consumers and Small and Medium enterprises (SME) are

entertained through another sales team of the BankIslami which consists of Business Executives

(BE) and Wealth Managers (WM). These individuals are responsible for generating business in the

SME and retail sector.

5 The comparison between the Intra Bank products

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 11

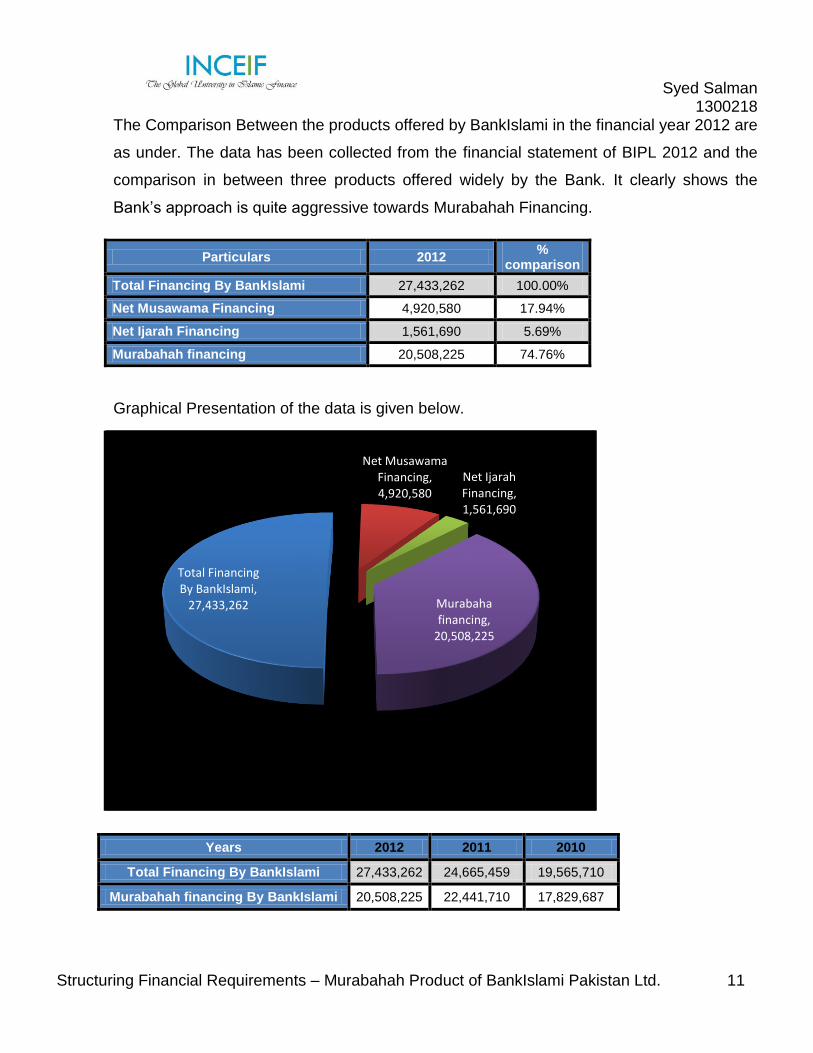

The Comparison Between the products offered by BankIslami in the financial year 2012 are

as under. The data has been collected from the financial statement of BIPL 2012 and the

comparison in between three products offered widely by the Bank. It clearly shows the

Bank’s approach is quite aggressive towards Murabahah Financing.

Particulars 2012 %

comparison

Total Financing By BankIslami 27,433,262 100.00%

Net Musawama Financing 4,920,580 17.94%

Net Ijarah Financing 1,561,690 5.69%

Murabahah financing 20,508,225 74.76%

Graphical Presentation of the data is given below.

Years 2012 2011 2010

Total Financing By BankIslami 27,433,262 24,665,459 19,565,710

Murabahah financing By BankIslami 20,508,225 22,441,710 17,829,687

Total Financing By BankIslami,

27,433,262

Net Musawama Financing, 4,920,580

Net Ijarah Financing, 1,561,690

Murabaha financing,

20,508,225

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 12

6 The comparison between the Inter Bank products

The inter Bank products or the Conventional Products offered for financing like Murabahah

are term financing products. There are three types of working capital financing products

offered by the conventional banks. These products are:

1. Cash Credit / OD facility

2. Term Loan &

3. Letter of Credit

The products offered by Conventional Banks are loans based on interest and has no

element of sale involved in it whereas the Murabahah financing facility involve both the Bank

and the customer to share the risk and reward of the Halal transaction through shariah

compliant contracts.

7 The risks and return to the financial institution in offering the product or

package:

Since Murabahah is a sale based transaction thus the BankIslami is exposed to various

types of Risk(s) but the two major risks that we face are as under

7.1 Asset Risk

Asset risk means the risk of holding the asset after it has been purchased from the supplier

to the time when it has been sold to the client on agreed price. Since the ownership

belongs to the Bank therefore in case there is any loss or damage to the asset before the

sale takes place, such loss is totally borne by the Bank.

7.2 Credit Risk

Another major risk category is the risk of default or the Credit risk where client is unable to

meet its obligation to pay the Bank due to willful or genuine default. In such case Bank is

exposed to the default risk and the procedure for recovering the proceeds is not very easy

as Bank need to enter into litigation matters which require time and cost both.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 13

7.3 Risk Return Mechanism

Although the Bank is exposed to many risks but still the Banks are willing to enter primarily

into the Murabahah contract. The transaction has certain benefits. The transparency factor

is there as the Bank discloses the cost to the Bank, the satisfaction to the customer is

higher as he himself, being as agent of the Bank purchases the product, the transaction is

used generally for short term financing hence in smooth transactions, the Banks earns

higher fixed profit rate in short span of time. So after every successful completion of the

financing term, the Bank can finance to several other customers. As expressed earlier, the

graph and figures at page 9 clearly shows the Banks approach towards Murabahah and

also towards other financing products.

Although Murabahah has been criticized over the past several years due to its border line

nature but it has really helped Islamic Banks to grow in the arena of financial industry.

8 The expected performance of the products based on the information from the

bank and other external information

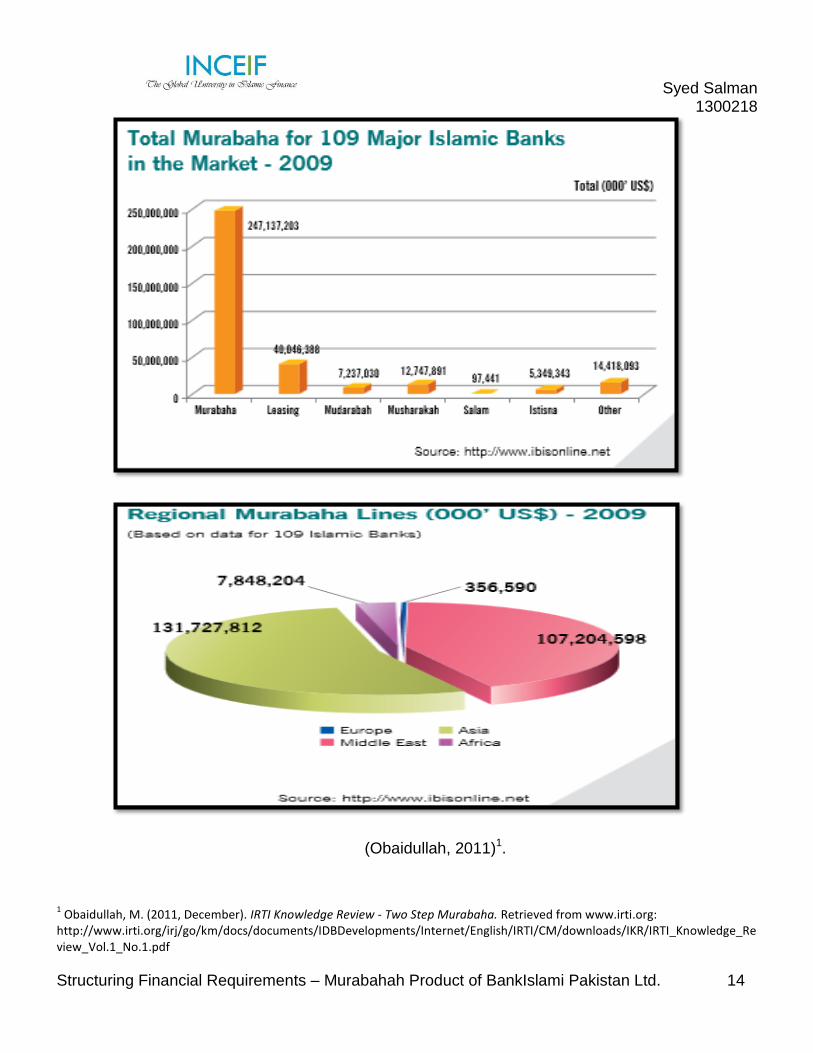

The International fame and popularity of Islamic Finance is can be seen through the below

mentioned data. The below mentioned data stated that the Murabahah has been primarily

focus of Islamic Banking industry and thus the market share against other products are

relatively much lower. The data has been collected from authentic source of IDB (Islamic

Development Bank) which shows the performance of 109 Islamic Banks with reference to

Murabahah financing and their figures according to the same.

BankIslami Pakistan Limited is also striving to expand its financing exposure and thus

Murabahah financing product has shown and proven its viability during the tenure which

has helped the Bank is expansion of its financing portfolio as shown above and the primary

exposure of the Bank was in the Murabahah financing product in terms of their ratio to total

financing.

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 14

(Obaidullah, 2011)1.

1 Obaidullah, M. (2011, December). IRTI Knowledge Review - Two Step Murabaha. Retrieved from www.irti.org:

http://www.irti.org/irj/go/km/docs/documents/IDBDevelopments/Internet/English/IRTI/CM/downloads/IKR/IRTI_Knowledge_Review_Vol.1_No.1.pdf

Syed Salman 1300218

Structuring Financial Requirements – Murabahah Product of BankIslami Pakistan Ltd. 15

9 Conclusion:

The study has concluded the practical aspects of the Murabahah financing product as

adopted by one of the Islamic Banks in Pakistan. The operational procedure, steps,

documentation and other areas are focused as well as the scope of Murabahah financing

across the globe has also been mentioned in the project paper. The study has responded

all the queries of the paper as inquired and has made known the procedure in executing

such transaction.

The purpose of choosing Murabahah financing as mode of discussion was because of its

asset size and its significance in the Islamic financial services industry. As Murabahah is

the most preferred mode of financing for short term needs of the clients, the Banks are

more indulged into such contracts to facilitate the customer as well as to maneuver

accordingly the targets that they can achieve through this product.

It has been criticized by Molana Taqi Usmani and he discouraged the Banks to have mix

asset class in their financing portfolio because of the debt nature of the contract and after

his statement, some Banks have taken step to indulge more in other modes of financing

more but yet in comparison, Murabahah is still the most preferred product in the Islamic

Banks due to its risk return mechanism. But indeed, since it’s a border line transaction, the

Banks must try to focus more on expanding other product portfolios.