Mr Krishan - ENC Software Solutions (P) Limited - PhillipCapital

103

Vol 8. Issue 2. 1 - 31 MAY 2021 | For Private Circulation Only pg 4. From MAKE-IN-INDIA to MAKE-FOR-THE-WORLD pg 95. Indian Economy: Trend Indicators pg 60, 62, 78, 90. Interviews: Mr Krishan Sachdev, Mr Nipun Singhal, Mr Saurabh Gupta, Mr Maulesh Chhaya pg 97. PhillipCapital Coverage Universe

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Mr Krishan - ENC Software Solutions (P) Limited - PhillipCapital

Vol 8. Issue 2. 1 - 31 MAY 2021 | For Private Circulation Only

pg 4. From MAKE-IN-INDIA to MAKE-FOR-THE-WORLD

pg 95. Indian Economy: Trend Indicators

pg 60, 62, 78, 90. Interviews: Mr Krishan Sachdev, Mr Nipun Singhal, Mr Saurabh Gupta, Mr Maulesh Chhaya

pg 97. PhillipCapital Coverage Universe

3GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 2

1st Mar 2021 Vol 8. Issue 1 1st Nov 2020 Vol 7. Issue 4

1st Sep 2020 Vol 7. Issue 3 1st Jul 2020 Vol 7. Issue 2

1st Feb 2020 Vol 7. Issue 1 1st Oct 2019 Vol 6. Issue 6

Ground View - Previous Issues

GROUND VIEW Vol 8. Issue 2. 1 - 31 MAY 2021

FOR EDITORIAL QUERIESPhillipCapital (India) Private Limited. No. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400 013

MANAGING DIRECTOR & CEO Vineet Bhatnagar

EDITORIAL BOARDManish AgarwallaKinshuk Bharti Tiwari

DESIGN & ILLUSTRATION Chaitanya Modakwww.inhousedesign.co.in

EDITORRoshan Sony

HEAD- INSTITUTIONAL EQUITIES Kinshuk Bharti Tiwari

RESEARCHAUTOMOBILESSaksham KaushalAmar Kant Gaur

AGRI INPUTSDeepak Chitroda

BANKING, NBFCsManish AgarwallaSujal Kumar Pradeep Agrawal

CONSUMERVishal GutkaBinay Shukla

CEMENTVaibhav Agarwal

ECONOMICS Anjali VermaNavneeth Vijayan

ENGINEERING, CAPITAL GOODS Jonas BhuttaSandesh Shetty

HEALTHCARE, SPECIALTY CHEMICALS Surya PatraHrishikesh PatoleRishita Raja

IT SERVICESVibhor SinghalKaran Uppal

INFRASTRUCTUREVibhor SinghalDeepika Bhandari

LOGISTICS, TRANSPORTATIONVikram Suryavanshi

MEDIA, CONSUMER DISCRETIONARY Ankit Kedia Rahul Jain

METALS Vikash Singh

MIDCAPS Deepak AgarwalVineet ShankerKeshav Bharadia

REAL-ESTATEVaibhav Agarwal

STRATEGYAnjali VermaManoj Rawat

TECHNICALSSubodh Gupta

PRODUCTION MANAGERGanesh Deorukhkar

EQUITY SALES & EVENTSRosie Ferns

SALES & DISTRIBUTION Archan VyasAshka GulatiJignesh KananiSneha BaxiAmarinder Sabharwal

CORPORATE COMMUNICATIONS Zarine DamaniaMrunal Pawar

3GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 2

4. COVER STORY

From MAKE-IN-INDIA to MAKE-FOR-THE-WORLDBy Deepak Agarwal, Vineet Shanker &

Keshav Bharadia

78. INTERVIEW

Mr Saurabh Gupta, CFO, Dixon Technologies

62. INTERVIEW

Mr Nipun Singhal, MD and CEO, Amstrad (OVOT Pvt. Ltd

60. INTERVIEW

Mr Krishan Sachdev, Chairman, Carrier Midea India

90. INTERVIEW

Mr Maulesh Chhaya, Industry Expert, Mentor

CONTENTSLetter from the MD I want to express my sincere gratitude to all the frontline COVID-19

warriors who continue to manage and fight the crisis, especially in this

second wave. I am also proud to see how our country has successfully

rolled out its vaccination strategy and hope that most of our people

are vaccinated by the end of June, bringing an end to this dreaded

second wave. Although the vaccination drive is in full swing, the threat

is very real, so we need to take ample care of ourselves and our fellow

human beings. There is no doubt that fighting and overcoming the

pandemic is going to take collective effort.

The pandemic has caused an economic fallout across sectors.

However, the consumer electronics industry has shown its resilience

and has performed better than anticipated. As people were working

from home, demand for products that offer convenience and provide

a better life (such as washing machines, dryers, air conditioners, TVs,

and other home appliances) increased significantly. Traditionally, the

Indian electronics industry, especially consumer electronics, has been

largely dependent on imports. However, our government’s strong

emphasis is on becoming self-reliant ‘Atmanirbhar’ and promoting

domestic manufacturing (by bringing in schemes like Production

Linked Incentives (PLI) and imposing import restrictions) – which has

started leading to reduction in imports.

The pandemic has exposed the frailties of the supply chain and the

importance of de-risking it at a global scale; the world is keen to adopt

a China +1 strategy in preparation of more challenging times. This, our

midcaps team believes, can lead to an unprecedented opportunity

for the Indian consumer electronics industry, especially for Electronic

Manufacturing Services (EMS). Deepak Agarwal, Vineet Shanker, and

Keshav Bharadia, our midcaps team members, dug deep into the

electronics manufacturing industry from the perspective of its current

very-low global market share, and how India is likely to be a major

electronics manufacturing hub in the future.

In addition to this, the team interviewed Mr Krishan Sachdev, Chairman,

Carrier Midea India, Mr Saurabh Gupta, CFO, Dixon Technologies, Mr

Nipun Singhal, MD & CEO, Amstrad (OVOT Pvt. Ltd) and some other

industry leaders and experts – to understand how well electronics

manufacturing is positioned to capture domestic demand and increase

value addition, and to gauge the global exports opportunity.

Cheers and Best Wishes, Vineet Bhatnagar

95. Indian Economy: Trend Indicators

97. PhillipCapital Coverage Universe Valuation Summary

INTERVIEWS

5GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 4

COVER STORY

BY DEEPAK AGARWAL, VINEET SHANKER, KESHAV BHARADIA

COVER STORY

BY DEEPAK AGARWAL, VINEET SHANKER, KESHAV BHARADIA

India will see an increase in domestic value-addition across product segments (currently quite below the global average). With the setting up of a

components ecosystem, and scaling up of large-scale electronics manufacturing capabilities in the country, this industry should see tremendous growth.

Manufacturing is the next big theme

From MAKE-IN-INDIA to MAKE-FOR-THE-WORLD

5GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 4

The Indian electronics industry is in a sweet spot because of the government’s initiatives such as Make-in-India, Aatmanirbhar Bharat, and the de-risking of the global supply chain coupled with an increased adoption of the China+1 strategy worldwide. India has essentially been a net importer of electronics goods and components in the past, due to drawbacks and challenges in local manufacturing. However, this is changing rapidly and experts believe that various government incentives such as PLI, EMC 2.0, SPECS, NPE, along with reformed labour laws, will prove conducive to manufacturing in India for the world.

As a result, There is likely to be huge capex over the next 3-5 years in the electronics industry. India has already seen an influx of investments coming in to scale up manufacturing, from both domestic and international companies.

The global supply chain disruption arising out of China last year has increased awareness amongst companies worldwide about the consequences of doing most of their manufacturing in China. This has led to companies relocating to other countries. India has the lowest penetration rates across consumer durables, a large domestic market, supportive government policies, lower tax rates and the lowest wages, making it a lucrative destination for many global giants and domestic companies.

India will see an increase in domestic value-addition across product segments (currently quite below the global average). With the setting up of a components ecosystem, and scaling up of large-scale electronics manufacturing capabilities in the country, this industry should see tremendous growth.

pg. 6 INDIA’S ELECTRONICS INDUSTRY

Eyeing a bigger share of the global supply chain

_______________________________________ pg. 17 GOVERNMENT’S INCENTIVES FOR INDIA INC

Government is the catalyst that is driving growth

_______________________________________pg. 31 CHINA + 1 STRATEGY

De-risking the global supply chain

_______________________________________ pg. 46 PRODUCTS

Lower penetration and a large domestic market = huge growth

_______________________________________ pg. 91 OUTLOOK

Make in India! But how soon will India make for the world?

_______________________________________

7GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 6

INDIA’S ELECTRONICS INDUSTRY

Eyeing a bigger share of the global supply chain Contract manufacturers will support growth

Electronics: The fastest growing industry in the worldExperts believe that the electronics industry will surpass the

US$ 7.3tn mark by 2025. In fact, the Indian market is likely to

be second only to China’s, followed by Vietnam, Thailand,

and Indonesia. India’s electronics industry has undergone

drastic changes in the last 20 years, mostly in products, the

retail environment, and in terms of an evolving administrative

landscape. Of late, innovation and technology changes have

been rising, because of a shift in consumer behaviour and

changing business requirements.

These five factors will push the industry’s growth to the next

level:

1. Low penetration of products; much lower than the global

average.

2. Positive GDP growth outlook.

3. Huge push from the government to become self-reliant

(reduce import dependency) and to increase exports by

introducing various schemes (EMS is a big part of this).

4. Rising discretionary incomes.

5. Evolving of physical and social infrastructure, better

logistics, and an expanding e-commerce industry.

India’s electronics market size

• India’s electronics hardware production has increased

from Rs 1.9tn in FY15 to touch an estimated Rs 5.46tn in

FY20. This includes production of consumer electronics,

electronics components, computers, strategic and

industrial electronics (Source: MEITY Annual Report

FY20).

• The Indian consumer electronics and consumer durables

market is likely to become the fifth-largest globally by

2025.

• Despite disruption due to covid, smartphone shipments

saw a decline of only 1.7% in CY20. The production worth

of mobile phones in India reached US$ 30bn in FY20

from US$ 3bn in FY15, which should only increase from

here. India is focussing on manufacturing and becoming a

global manufacturing hub.

• Under EMS, there is ESDM (Electronics System and

Design Manufacturing), which has two sub sections –

electronics systems and electronics design.

• In consumer durables, LCD/LED TVs grew more than two

times in terms of volumes – from 5.2mn units in FY15 to

12mn units in FY19.

7GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 6

Work-from home culture is driving growth in electronics

After the government lifted the lockdown in India, the

consumer durables sector saw healthy growth, led by a

strong surge in online sales across product categories.

Restrictions and paranoia caused a drastic shift in the

working style – which is now firmly work-from-home (WFH)

for many job profiles. Compared to metros, consumer

durables sales saw a sharper rise in non-metros due to lower

penetration of appliances, combined with lower intensity of

lockdowns, which resulted in many first-time buyers. Sales

of laptops and tablets saw a sharp uptick due to schooling

from home and WFH. TVs also saw robust sales, as majority

houses had only one TV and found the need for a spare

one, with more members spending most of their time at

home. The need for washing machines, air conditioners,

dishwashers, microwaves increased for the same reasons.

The fact that India’s nationwide penetration for consumer

durables is less than 10%, provides massive headroom for

growth. With an increasing shift towards work-from-home

and bans on imports of ACs with refrigerants and ban on LED

TV imports, domestic companies are set to gain. The uptrend

in growth of the consumer durables sector could continue,

with increase in GDP per capita as shown in the figure given

below, which could lead to higher consumption and higher

consumer spending.

India can use this moment to emerge as a leading electronics

and components manufacturer. COVID-19, along with the

anti-China sentiment is leading to a seismic shift in global

supply chains. Some of the factors that support India are as

follows:

• A post pandemic reality: There has been a change in

global supply chains due to the pandemic. Companies

have realised the drawbacks of being dependant on

only one nation (China) as a single source of supply,

as they faced disruptions to the flow of materials from

there. Trade tensions between the US and China have

added to diversification in supply chains. As multinational

companies look for alternate destinations to set up their

manufacturing bases, they view India as an attractive

option.

• Anti-China sentiment: The US-China trade and tariff

war and increasing anti-China sentiment offer India

an ideal base to leverage the strong push by the

Indian government for manufacturing and to attract

multinational companies looking to set up new bases and

to diversify their supply chains.

• Ease of doing business and policy support: India has

made significant progress in its ‘ease of doing business’

parameters in recent years. This, coupled with many

new government initiatives towards boosting domestic

manufacturing (PLI, SPECS. EMC (2.0), M-SIPS, NPE, PMP,

Make in India, Digital India and Start-up India) should

increase FDI inflows into electronics manufacturing.

Sales of laptops and tablets saw a sharp uptick due to schooling from home and WFH

Companies have realised the drawbacks of being dependant on only one nation (China) as a single source of supply, as they faced disruptions to the flow of materials from there

The government expects PLI schemes for mobile phone manufacturing, AC components, and LEDs to generate total revenues of around Rs 12tn

Trend showing an increase in GDP per capita over the years

Sour

ce: W

orld

ban

k

9GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 8

• PLI scheme for mobile manufacturing, AC, LED

lighting, laptops, tablets, etc.: The government

has cleared 16 proposals, both from domestic and

international companies, constituting an investment of Rs

110bn under the PLI scheme for mobile manufacturing

worth Rs 10.5tn over the next five years. In the PLI

scheme for AC components and LED lights, the

government has approved an outlay of Rs 62.4bn and

in the PLI for laptops, tablets, and for all-in-one PCs, it

has approved Rs 73.2bn. The government expects PLI

schemes for mobile phone manufacturing to bring in tax

revenues of around Rs 800bn over the next five years,

apart from making India a destination for manufacturing

electronic goods (exports hub) for global giants such as

Apple and Samsung. It expects GST revenues of around

Rs 720bn from Rs 4tn worth of domestically produced

mobile phones. It believes it can generate exports of c.Rs

6.5tn through the PLI scheme over the next five years.

Recent PLI is looking to create component ecosystem in

India.

• Electronics is at the heart of world trade: Electronics

will always remain an integral part of the global

manufacturing processes. India has given electronics and

component manufacturing special attention through its

progressive policies and regulatory frameworks.

• New labour codes: The Indian parliament has passed

four codes on wages, industrial relations, social security,

and occupational safety and health (OSH), which will

ultimately rationalize 44 central labour laws. The code on

wages was passed in 2019, while the three other codes

got clearance from both the Houses in 2020. These

codes are favourable for both employers and employees;

some of the provisions like 14 days of notice prior to

strikes remove the uncertainty in day-to-day operations,

and give some time to employers to come up with an

alternate plan of action, which was not there in previous

labour laws. Experts highlighted that with an increasing

share of contract-labour under the new labour code,

contract manufacturers can scale up manufacturing.

9GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 8

Structure of the industry

The Indian electronics industry consists of consumer

electronics, industrial electronics, electronic components,

LED products, strategic electronics, computer hardware, and

broadcasting electronics. Communication and broadcasting

devices along with consumer electronics constitute c.40%

of the revenues of the Indian electronics industry; industrial

electronics make up 20.5% and electrical components 22%.

In domestic electronics production, mobiles have seen highest 64% CAGR over FY15-20

Consumer electronics constitute 31% of the electronics industry

Communication and broadcasting devices along with consumer electronics constitute c.40% of the revenues of the Indian electronics industry

Source: meity.gov.in, PhillipCapital Estimates

Sour

ce: m

eity

.gov

.in

11GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 10

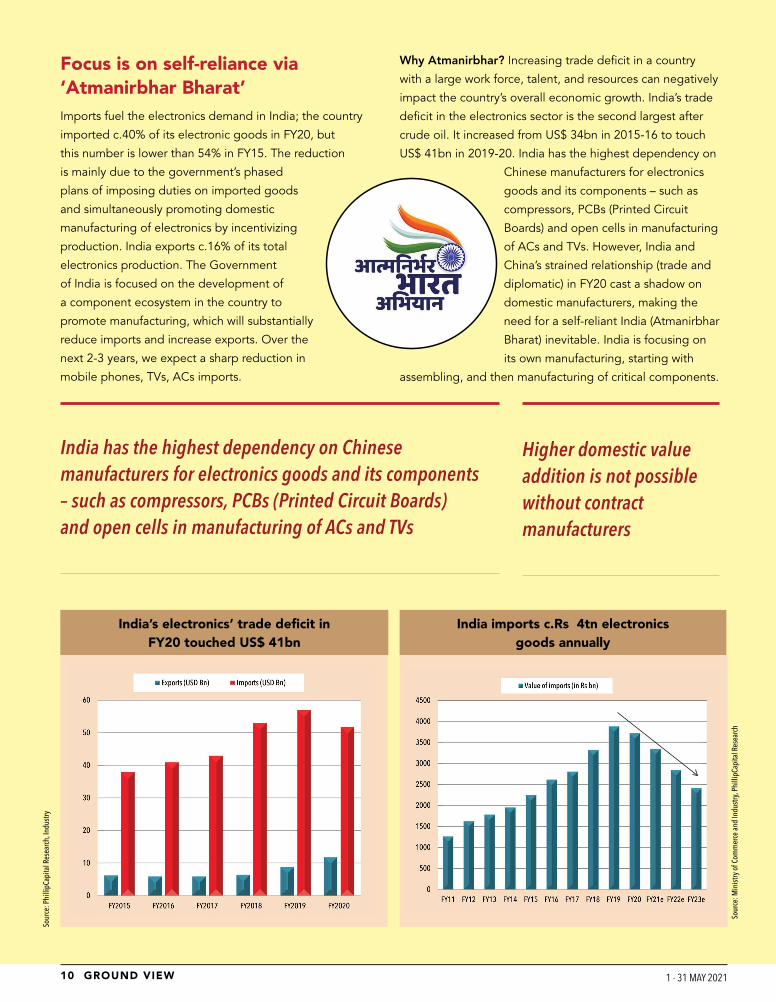

Focus is on self-reliance via ‘Atmanirbhar Bharat’Imports fuel the electronics demand in India; the country

imported c.40% of its electronic goods in FY20, but

this number is lower than 54% in FY15. The reduction

is mainly due to the government’s phased

plans of imposing duties on imported goods

and simultaneously promoting domestic

manufacturing of electronics by incentivizing

production. India exports c.16% of its total

electronics production. The Government

of India is focused on the development of

a component ecosystem in the country to

promote manufacturing, which will substantially

reduce imports and increase exports. Over the

next 2-3 years, we expect a sharp reduction in

mobile phones, TVs, ACs imports.

Why Atmanirbhar? Increasing trade deficit in a country

with a large work force, talent, and resources can negatively

impact the country’s overall economic growth. India’s trade

deficit in the electronics sector is the second largest after

crude oil. It increased from US$ 34bn in 2015-16 to touch

US$ 41bn in 2019-20. India has the highest dependency on

Chinese manufacturers for electronics

goods and its components – such as

compressors, PCBs (Printed Circuit

Boards) and open cells in manufacturing

of ACs and TVs. However, India and

China’s strained relationship (trade and

diplomatic) in FY20 cast a shadow on

domestic manufacturers, making the

need for a self-reliant India (Atmanirbhar

Bharat) inevitable. India is focusing on

its own manufacturing, starting with

assembling, and then manufacturing of critical components.

India has the highest dependency on Chinese manufacturers for electronics goods and its components – such as compressors, PCBs (Printed Circuit Boards) and open cells in manufacturing of ACs and TVs

Higher domestic value addition is not possible without contract manufacturers

India’s electronics’ trade deficit in FY20 touched US$ 41bn

India imports c.Rs 4tn electronics goods annually

Sour

ce: M

inist

ry o

f Com

mer

ce a

nd In

dust

ry, P

hilli

pCap

ital R

esea

rch

Sour

ce: P

hilli

pCap

ital R

esea

rch,

Indu

stry

11GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 10

Due to the Atmanirbhar initiative, over next two years, imports of products like air conditioners, LED TVs, and mobile phones will significantly fall

Product Domestic growth % (last 5 year CAGR)

Current domestic value addition (%)

Domestic manufac-turing can increase

to %

Domestic Market size (in Rs bn)

Current India import %

Mobile 47% 12-15% 30-35% 3165 50-60%

TV 17% 12-15% 25-30% 694 70-80%

RAC 16% 25-30% 70-75% 112 34%

WM 15% 50%-70% 90% 104 15%

Ref 15% 50%-70% 90% 120 35%

LED Lighting 15% 70% 90% 201 22%

Other Small Appliances* 16% 70-90% 90% 100 20-30%

Domestic value addition to increase across product segments over the next 5-7 years

Source: PhillipCapital Estimates

• OEM (original equipment manufacturer): Produces parts and equipment that may be marketed and retailed by

another manufacturer. Could also focus on product innovation and development, and outsource manufacturing to

partners.

• ODM (original design manufacturer): Designs and manufactures a product that is subsequently rebranded and

retailed by other companies that do not carry out their own manufacturing.

• EMS (electronics manufacturing services): Contract electronics manufacturer that makes products for OEMs; could

also aid in design, software development, supply chain management, testing, distribution, and repairs. EMS is a

generally an accepted term for contract manufacturers in the electronics field.

How does the government plan to reduce trade deficit in electronics?

The government wants to increase domestic value addition in electronics

manufacturing. To develop a robust manufacturing base, it has started making

the following moves – providing fiscal incentives to set up local manufacturing

facilities, large-scale cluster development, world-class testing facilities,

and skilling ecosystems – to name a few. Higher domestic value addition is

not possible without contract manufacturers. This is because, for OEMs it

becomes difficult to scale or integrate production of its components. Contract

manufacturers offer skills beyond just manufacturing – in terms of design

and other value-added services. Thus, a big part of the domestic electronics

industry is likely to be in the form of Electronic Manufacturing Service (EMS) or

contract manufacturing.

13GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 12

Contract manufacturing is projected to grow at a rapid pace, outperforming the entire electronics industry

History of EMS (Electronics Manufacturing Services)

The shift in manufacturing – from in-house to outsourced

– began decades ago. Today, companies are extending

their outsourcing to almost every aspect of production,

from design manufacturing to final product assembly. They

have extended the array of outsourcing activities, beyond

just component manufacturing, to complete production

of a branded product. EMS players have become active

partners in product designing and development, including

extension of the companies they service. In fact, top EMS

executives say that the sustained growth of their companies

depends on the ability to extend their responsibilities to

running the complete supply chain for global players. At

present, domestic EMS companies play a key role in reducing

shipments into India.

However, it was not always like this. Initially, EMS providers

started providing services for PCBA (printed control board

assembly) and consignment work, where they did not own

any material and just executed simple assembly operations.

This industry saw substantial growth in the 1990s due to

downsizing by many OEMs in the economic recession early in

that decade. During the recession, companies were strapped

for capital and were hence loath to invest in new equipment.

However, cash-rich EMS providers were able to enhance

and increase their production capabilities. They continued

investments in latest technologies and expanded their

services within the industry. OEMs, starved of capital, started

focusing on becoming asset-light, which gave agility to their

business models, leading to high profitability and return on

capital employed.

Many OEMs soon realized that hiring contract manufacturers

for producing most of their components was viable, because

with their large client bases, EMS providers were able to

leverage the benefits of year-long full-volume productions

and provide cheaper services. As a result, even after the

economic recovery, global companies continued to shift

their business models towards more contract manufacturing,

instead of ramping up their in-house manufacturing

Contract manufacturing is projected to grow at a rapid pace,

outperforming the entire electronics industry. Companies

have now started focusing more on new, smaller, and online

brands. They focus more on marketing, and outsource

manufacturing to EMS companies. This is likely to benefit

OEM/ODM players of all sizes.

EMS companies are no longer just vendors, but assume full responsibility for the engineering, production, and distribution of products

EMS industry is becoming more difficult

Getting a pie of the rapidly growing contract manufacturing

industry is more difficult than it seems, as economies of

scale, purchasing power, and global logistics are making

the business an increasingly concentrated one. Here,

one must either be a big player or serve a niche market.

Historically, the preferred path in contract manufacturing

was to grow with a major global client, but today, the capital

investment required by an EMS provider is enormous. In

fact, the introduction of surface-mount technology in PCB

(printed control boards) assembly has increased the capital

expenditure. Short product life cycles and declining prices

have prompted contract manufacturers to launch their

own products across geographies and to indulge in a

broad range of services, not just manufacturing.

Electronics System Design and Manufacturing (ESDM)

Electronics hardware manufacturing is an integral part of

the government’s Make in India, Digital India, and Start Up

India initiatives. ESDM plays an imperative role, and has

high weightage, in the government’s vision of garnering US$

1tn economic value from the digital economy by 2025. The

demand for electronics products has been rising in recent

years, mainly due to the surge in the internet penetration

rate in India. Manufacturing has gained traction in this

segment, with increased production and product assembly

taking place across consumer electronics.

13GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 12

Outlook of ESDM in India

IBEF (Indian Brand Equity Foundation) predicts India’s

ESDM sector reaching US$ 220bn by 2025 expanding at a

16% CAGR between 2019 and 2025, fuelled by a pickup in

public and private investments, rising demand for electronic

products, and a strong policy framework in place. Currently

electronics manufacturing in India contributes to 1.7%

of the GDP, while in China, Taiwan, and South Korea,

the sector’s contribution is significantly large at 12-15%;

as India’s consumption increases, and the dependency on

India has been one of the largest consumers of electronics goods in the past decade

India will see an increase in domestic value-addition across product segments (currently quite below the global average). With the setting up of a components ecosystem, and scaling up of large-scale electronics manufacturing capabilities in the country, this industry should see tremendous growth.

India has just 2% market share in EMS globally; China has the largest share

Sour

ce: I

ndus

try, P

hilli

pCap

ital R

esea

rch

imports decreases, its electronics industry’s contribution to

GDP will also be in a similar range as these countries (over

the next 7-8 years). Industry watchers attribute the growth

in the domestic consumption of electronics mainly to rising

disposable incomes, an increasing middle-class population,

and a drop in prices of need-based electronics in the country.

The Indian electronics industry has the lowest contribution to GDP at 1.7% vs. 12.7% for China

Sour

ce: I

ndus

try, P

hilli

pCap

ital R

esea

rch

15GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 14

Name HQ Manufacturing locations Revenue (US $mn)

HonHai Precision (Foxconn) Taiwan China, India, Japan, Vietnam, Malaysia, US 1,78,600

Pegatron Taiwan China, Indonesia, US, Europe, India 45672

Wistron Taiwan US, Europe, China, Taiwan, India 29358

Jabil Inc US US, China, Malaysia, India, Europe 25282

Flex Singapore US, China, India, Malaysia, Indonesia 24210

Sanmina US China, Canada, Europe, India, Malaysia, Thailand, US 8234

BYD Electronics China China 7616

Celestica Canada Canada, US, China, Malaysia, Europe, Thailand 5888

Universal Scientific Industrial China China, Taiwan, Mexico, Poland 5343

New Kinpo Group Taiwan US, China, Thailand, Malaysia, Brazil, Mexico, Philippines 4598

Kaga Electronics Japan Japan 4123

Plexus Corp US US, China, Malaysia, UK 3164

Venture Corporations Singapore Singapore, US, China, Malaysia 2702

Benchmark Electronics US US, China, Malaysia, Netherlands, Romania 2268

SIIX Corp Japan Japan, China, Thailand, Indonesia 2052

Shenzhen Kaifa China China, Malaysia, Philippines 1899

Fabrinet Cayman Islands China, Thailand, Japan, US 1584

UMC Electronics Japan Japan, China, Vietnam, Thailand 1310

Integrated Micro Electronics Philippines Philippines, China, Europe, Japan US 1250

Kimball Electronics US US Thailand, China and Poland 1182

Top EMS companies of the world

Government measures to increase local ESDM

manufacturing

The Government of India has allowed 100% FDI in the

ESDM segment under the automatic route even for

Original equipment manufacturers (OEMs) and Integrated

Device Manufacturers (IDMs). PLI will also boost domestic

manufacturing.

Increasing localisation in supply chain and miniaturisation of electronic products have been the two main trends in Indian electronics market

Sour

ce: I

ndus

try, P

hilli

pCap

ital R

esea

rch

Domestic EMS market share in India

Phill

ipca

pita

l res

earc

h

*Note: we have taken only domestic contract manufacturing companies.

15GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 14

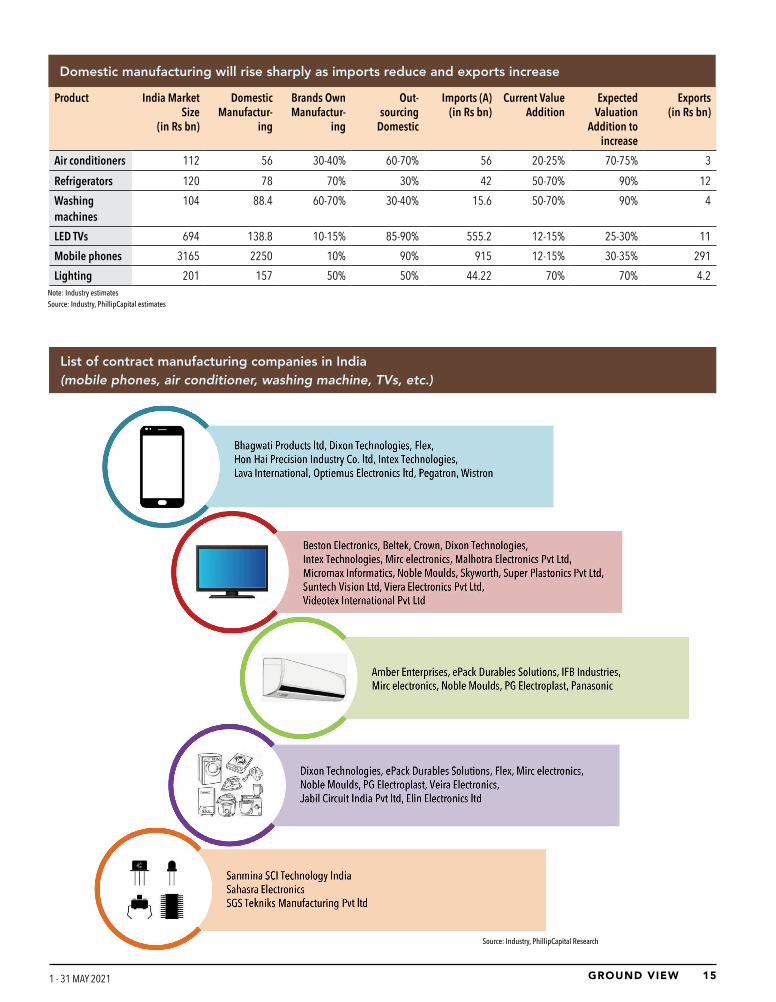

Product India Market Size

(in Rs bn)

Domestic Manufactur-

ing

Brands Own Manufactur-

ing

Out- sourcing

Domestic

Imports (A) (in Rs bn)

Current Value Addition

Expected Valuation

Addition to increase

Exports (in Rs bn)

Air conditioners 112 56 30-40% 60-70% 56 20-25% 70-75% 3

Refrigerators 120 78 70% 30% 42 50-70% 90% 12

Washing machines

104 88.4 60-70% 30-40% 15.6 50-70% 90% 4

LED TVs 694 138.8 10-15% 85-90% 555.2 12-15% 25-30% 11

Mobile phones 3165 2250 10% 90% 915 12-15% 30-35% 291

Lighting 201 157 50% 50% 44.22 70% 70% 4.2Note: Industry estimatesSource: Industry, PhillipCapital estimates

Domestic manufacturing will rise sharply as imports reduce and exports increase

List of contract manufacturing companies in India (mobile phones, air conditioner, washing machine, TVs, etc.)

Source: Industry, PhillipCapital Research

17GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 16

Major contract manufacturers companies in India Mobile phone and component manufacturing ecosystem on the Indian map. A large numbers of contract manufacturers are located in and around the national capital region

Source: Industry, PhillipCapital Research

Many global companies (Wistron, Foxconn, etc.) have started coming to India. Domestic manufacturers have increased their capacity significantly and are focusing on contract manufacturing

17GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 16

Source: Company, PhillipCapital Research

GOVERNMENT’S INCENTIVES FOR INDIA INC

Government is the catalyst that is driving growthIt has implemented several policy measures to kick-start electronic manufacturing in India

List of GoI schemes, funds, and cluster programs over the years

Government’s push for domestic manufacturing

Electronics Development Fund (EDF)

The Government of India set

up EDF as a Fund of Fund

(FOF), through which it has

invested into several other

funds (also known as Daughter

Funds”). These daughter

funds then invest in companies

that have business around

electronics. EDF enables

creation of an ecosystem

for providing risk capital to

companies developing new

technologies in the areas of

electronics, nano-electronics,

and IT. This fund fosters

R&D and innovation in these

technology sectors. This was

one of the most important

strategies to enable creating an

electronics industry ecosystem

in India.

19GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 18

Name of the daugh-ter fund

Amount in-vested by EDF

(in Rs mn)

Total amount invested by the daughter fund

start-up/ companies (in Rs mn.)

No of investee start-ups/ Compa-nies of Daughter

fund

Portfolio Companies (Investee)

Endiya Seed Co-cre-ation fund

243.3 1158.8 12 Steradian Semi, AiCS Advance AI Compute, Cell Propulsion

KARSEMVEN Fund 131.1 441.5 10 Graphene, Prodigy Technoventions, SenseGiz, Pinaka, Greendzine, Remido, CNB Technologies, Aptener Mechatronics, Open Appliances, Bellatrix Aerospace and Bionic Yantra

YourNest India VC Fund II

117.1 434 14 Argoid, Koinearth, Uptime AI, Xpedize, Lightspeed Labs, Dozee, Mauna.ai, Miko, Cron AI, Practically, Lavelle Networks, Trezi, CredRight, Orbo

PI Venture Fund-1 70.1 872.3 10 Sigtuple, Ten3T Health (Cicer), Zenatix, Niramai, Customer Suc-cess Box, Locus, OweMe, True Lark, SwitchOn, Wysa, Agnikul, Pyxis

Unicorn India Venture Fund

128.6 494.8 17 Boxx.ai, ChitMonks, Clootrack, Fedo, Finin, Finsall, Fund Our-selves, GamerJi, Genrobotics, GrabonRent, Goldex, Inc42, inntot, iDefigo, Libryo, Moteefe, SmartCoin, supplyCompass, Sascan, Sequretek, Probus, Perfit 3D

Aaruha Technology Fund-I

40.2 134.9 8 Aus, Aibono, Singularity, CloudSEK, Bellatrix, Anlyz, Aics, Steradi-anSemi, SmarterBiz

Venture East Proac-tive Fund II

448.4 2073.5 11 Infinite uptime, Acko, Moengage, Portea, Kissht, Sresta's 24 Mantra, Edge Networks, Seclore, Mardil Medical, Perpetual, Ben Franklin, iNurture, Boonbox, Indus OS, Orca System, ekincare, Iqlect, Bog Orchid, Orion Edutech, E2E Retail, Richcore, CPO, Diabetomics, iMedX, Onebreath

Total 1178.8 5609.8 75

Daughter funds, funded by Electronics Development Fund (EDF), set up by the GoI

Source: MEITY Annual Report

Preference given to domestic manufacturers over importers

To promote ‘Make-in India’, the

government issued a public

procurement order, where it gives

preference to ‘Class 1 local suppliers’

in procurement of all goods, services

or works; the government defines

these supplier or service providers as

those whose goods, services, or work

offered for procurement have local

content equal to or more than 50%.

19GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 18

National Policy on Electronics, 2019

NPE, 2019 envisages India as a global hub for ESDM, with

a thrust on exports, by encouraging and driving capabilities

in the country for developing core components, including

chipsets, and creating an enabling environment for the

industry to compete globally. The NPE aims to create a

competitive electronic manufacturing sector and to achieve

a turnover of about US$ 400bn by 2025, and targets a

production of 1bn mobile handsets for export. It also aims

to create 10mn employment opportunities in the country by

2025.

NPE aims for a turnover of about US$ 400bn by 2025, and production of 1bn mobile handsets for exports

Phased manufacturing plans

Phased manufacturing plans first introduced basic custom

duty in products that can be easily sourced domestically

and then in products that are difficult to source, and are

high in terms of domestic value addition. Under this, in

the near term, products like display assemblies and PCBs

(printed circuit boards) that have lower domestic output,

large domestic opportunity, and high value addition – offer

the most obvious investment opportunities for domestic

manufacturers. Although PCB manufacturing has already

begun in India, it still needs to undergo changes to happen

at a larger scale.

India has been investing in capabilities in the manufacturing

of cells and antennas over a longer period; these products

could be the high value adding components and a realistic

long-term goal for the country. Manufacturers could

consider these products for sub-assembly in India. With the

announcement of levies on imports of display units, India

should witness a rise in domestic manufacturing. However,

components such as camera modules, ICs, semiconductors

require substantial investments and would most likely

continue to be imported. Domestic manufacturing in these

components would take time and would need to develop

gradually over time.

Year Sub-assembly Value addition

Basic Cus-tom Duty

(BCD)

2016-17 (i) Charger/ Adapter, (ii) Battery Pack, (iii) Wired Headset

Low 15%

2017-18 (iv) Mechanics, (v) Die Cut Parts, (vi) Microphone and Receiver, (vii) Key Pad, (viii) USB Cable

Moderate 15%

2018-19 (ix) Printed Circuit Board Assem-bly (PCBA)

High 20%

2018-19 (x) Camera Module, (xi) Connectors

High 10%

2019-20 (xii) Display Assembly, (xiii) Touch Panel/ Cover Glass Assembly (xiv) Vibrator Motor / Ringer

High 10%

Phased manufacturing plans in cell phones

Source: meity.gov.in

Tariff rationalization

Rationalization of tariff structures is an ongoing process. The

government rationalised tariff structures to promote domestic

manufacturing of electronic goods (such as cellular mobile

handsets, televisions, LED products). It started a phased

manufacturing programme (PMP) to promote domestic value

addition in mobile handsets and air conditioners (including

parts and components), manufacturing of mobile handsets

and their parts/ components has been steadily moving from

semi-knocked down (SKD) to completely-knocked down

(CKD), increasing value addition.

Item BCD up to 13.12.17 BCD w.e.f 14.12.17

Cellular Mobile Handsets

10% 15% (Further increased to 20% in FY19 budget)

Set top box TV 10% 20%

Colour TV 10% 20%

Microwave ovens 10% 20%

DVR/ Network Video Recorder

10% 15% (further increased to 20% in FY20 budget)

CCTV Camera/ IP Camera

10% 20%

LED Lamps 10% 20%

Smart meters 10% 15%

Power banks* 10% 20%

Increase in BCD (Basic custom duty) in products, which can be sourced/ assembled in India

*w.e.f 30.01.2019, BCD on power banks has increased from 10% to 20%

21GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 20

Rate of Duty

Appliances From To

Electronic goods, parts thereof

Copper and articles thereof used in manu-facturing of specified electronic items

Nil Applicable BCD

PCBA of cellular mobile phones (with effect from 01.04.2020)

10% 20%

Fingerprint readers for use in cellular mobile phones

nil 15%

Vibrator/ringer of cellular mobile phones (with effect from 01.04.2020)

nil 10%

Display panel and touch assembly of cellular mobile phones (with effect from 01.10.2020)

nil 10%

Headphones and earphones Applicable BCD

15%

Following parts of microphone for use in manufacture of microphone namely

10% nil

Government of India announced an increase in duty on electronics goods in the Annual Budget FY22

Electronic Manufacturing Cluster (EMC 2.0)

Purpose: To create and strengthen the infrastructure

ecosystem for electronics manufacturing and provide

support for creating world-class infrastructure – for attracting

investments in the ESDM sector

• The scheme was notified in October 2012.

• It helps with projects in ‘greenfield electronics

manufacturing clusters’ – here, aid is available up to 50%

of the project cost, subject to a ceiling of Rs 500mn for

every 100acres of land.

• For brownfield EMC (common facility centre), it offers aid

(as a grant) up to 75% of the cost of infrastructure, subject

to a ceiling of Rs 500mn.

• EMCs are poised to attract an investment of over Rs

548bn over the next 5-7 years, and are likely to generate

employment opportunities for about 640,000 people

once fully operational.

EMCs are poised to attract an investment of over Rs 548bn over the next 5-7 years

Production Linked Incentives (PLI) scheme – a game changer

The domestic electronics manufacturing sector in India is

not at par with competing nations, as it faces a ‘disability’

of around 8.5-11.0% due to the following – lack of proper

infrastructure, logistics framework and domestic supply chain,

high finance cost, lack of good quality power, insufficient

training in required skills, limited design capabilities, and

insufficient focus on R&D by the industry.

To alleviate its debility, the government introduced the

PLI (Production Linked Incentive) scheme on 1 April

2020, to boost manufacturing of electronics in India,

especially attracting large-scale investments in smartphone

manufacturing. PLI entails not just manufacturing, but also

assembly, testing, marking, and packaging units. The scheme

has the potential to boost the domestic manufacturing

of electronics in India and make the country globally

competitive. The scheme entails an incentive of 4-6% on

incremental sales of goods manufactured (over the base

year) under target segments, to eligible companies, for a

duration of five years after the base year. Base year for the

PLI scheme is 2019-2020 and the target segments covered

under the scheme include mobile phones, ACs, LED lighting,

laptops/notebooks, computer hardware, and IoT devices. PLI

schemes could extend to other electronics categories with

high import dependency, if the response is encouraging.

Sector Total outlay (in Rs bn)

Advanced cell chemistry battery storage 181

High efficiency solar PV modules 45

Large scale electronics manufacturing 410

Electronics (Laptops/Notebooks, Server, IoT devices, Computer Hardware)

50

Automobiles & Auto components 570

Pharmaceutical drugs APIs and KSMs 56

Medical devices 34

Pharmaceutical drugs (Specialised pharma prod-ucts, APIs/KSMs/Dis etc)

300

Telecom & Networking products 152

Textiles 107

Food processing 154

Specialty steel 63

White goods (Air conditioners & LED) 62

Total 2185

Outlay for PLI - 5-year period

Sour

ce: m

eity

.gov

.in

Sour

ce: m

eity

.gov

.in

21GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 20

Electronics manufacturing cluster (EMC) sites approved by GoI

Source: meity.gov.in

Tamil Nadu: Electronics and Hardware Manufacturing Policy aims at an output of US$ 100bn by 2025

Uttar Pradesh government: In August 2020, the UP government unveiled a new electronics manufacturing policy to attract foreign investors willing to shift their production base to India, aiming to garner US$ 540bn in the next five years

23GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 22

Mobile PLI

• Incentive: 4-6% PLI for 5 years.

• Outlay: Rs 409.95bn (US$ 5.5bn).

• Tenure: 5 years. Base year FY19-20. Incentives applicable

from 1 August 2020.

• Despite recent challenging times, mobile PLI will lead

to production worth Rs 350bn and investments worth Rs

130bn by applicant companies.

• Additional employment generation is 22,000 jobs.

AC / LED PLI

• Incentives are 4-6% on incremental sales for 5 years.

• Effective 1 April 2021.

• Open for applications for 6 months.

• Expected incremental investment from AC / LED PLI is Rs

79.2bn for an incremental production of Rs 1.68tn over

five years.

• The export opportunity due to AC / LED PLI is of

Rs 644bn over five years; it can create additional

employment of 100,000 jobs.

• Tax revenue likely at Rs 113bn in direct taxes and Rs

380bn through GST over the next five years

Domestic companies International com-panies

Electronic component companies

Lava Hon Hai Precision Industry Co Ltd

AT&S

Bhagwati Products Ltd

Rising Star Ascent circuits

Padget Electronics Samsung Visicon

UTL Neolyncs Wistron Walsin

Optiemus Electronics Pegatron Sahasra Electronics

NeoLync

PLI highlights Benefits

Incentives for ACs & LED 4-6% on incremental sales for 5 years

W.e. f 1/4/2021

Incremental investment Rs 79.2bn

Incremental production Rs 1.7tn

Exports Rs 644bn

Incremental employment 1lakh jobs

Direct tax revenue Rs 113bn

GST Rs 380bn

Companies approved under PLI for mobile phone manufacturing

Production-linked incentives scheme’s benefits over the next 5 years

Source: meity.gov.in, media reportsSource: meity.gov.in

Mobile PLI will lead to production worth Rs 350bn and investments worth Rs 130bn by applicant companies

The export opportunity due to AC / LED PLI is of Rs 644bn over five years

Modified special incentive package scheme (M-SIPS)

To promote large-scale manufacturing in the country, the Government of India’s M-SIPS scheme will offset disability and

attract investments in ESDM. The scheme entails incentives for investments on capital expenditure, of which 20% is for

investments in Special Economic Zones (SEZs) and 25% for non-SEZs. The scheme provides incentives for both new and

expanding units. For some high-capital-investment projects like fabrications, it reimburses central taxes and duties. The

goal of this scheme is to reach net zero imports in electronics by creating an indigenous manufacturing ecosystem for

electronics in India.

23GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 22

The key objective of the PLI scheme is to increase the

domestic value addition in ACs to 75% from the current 25%

in the next five years, and in LED lighting to 75% from the

current 40%.

• This will lead to an increase in manufacturing of

components of Air Conditioners:

n Components include High Value / Low Value

Intermediates or sub-assemblies or a combination

thereof.

n High Value Intermediates: namely Copper Tubes,

Aluminium Foil and Compressors.

n Low Value Intermediates: namely PCB assembly for

controllers, BLDC motors, Service Valves and Cross

Flow fans for AC and other components.

• Components of LED lighting will see higher

manufacturing in India:

n LED lighting products (core components like LED

chip packaging, resisters, ICs, fuses and large-scale

investments in other components, etc.)

n Components of LED lighting products (like LED

chips, LED drivers, LED engines, mechanicals,

packaging, modules, wire wound inductors and other

components).

Overall, with this PLI, the industry will see a capex of more

than Rs 80bn over the next 5-6 years in ACs and LED

lighting.

Large Investment Normal Investments

Segment & % of BOM

Total Invest-

ment (Rs mn)

-A

Total Reve-

nue (Rs mn) -B

Total Incen-

tive (Rs mn) -C

Avg. In-centive

(%)

Invest-ment/Incen-

tive (x) (A/C)

Sales/Asset

(x)

Total Invest-

ment (Rs mn)

Total Reve-

nue (Rs mn)

Total Incen-

tive (Rs mn)

Avg. In-centive

(%)

Invest-ment/Incen-

tive (x) (A/C)

Sales/Asset

(x)

AC

ACs (Components)* 6,000 97,500 4,800 4.9% 1.3 3.82 3,000 41,250 1,988 4.8% 1.5 3.67

High Value inter-mediates of ACs**

40%-50% % of BOM

4,000 53,750 2,575 4.8% 1.6 3.64 2,500 37,500 1,825 4.9% 1.4 3.75

Lower Value intermediates of ACs***

20% of BOM 1,000 15,000 730 4.9% 1.4 3.75 500 7,500 365 4.9% 1.4 3.75

LED light

LED Lights # 3,000 60,000 2,970 5.0% 1.0 4.62 1,000 18,000 876 4.9% 1.1 4.50

Components of LED Lights ##

250 4,500 219 4.9% 1.1 4.50 100 1,800 88 4.9% 1.1 4.50

Source: DPIIT, Ministry of Commerce and Industry, PhillipCapital India Research

Note:AC: * High Value Intermediates or Low Value intermediates or sub-assemblies or a combination thereof. **Aluminum Foil, Cu tube, Compressor. ***PCB Assembly for Controllers, BLDC Motors, Service Valves for ACs, Cross Flow Fans and other components. LED light: # (Core Components like LED Chip Packaging, Resisters, ICs, Fuses and large scale investments in other components etc.) ## LED Chips, LED Drivers, LED Engines, Mechanicals, Packaging, Modules, Wire Wound Inductors and other components.

PLI Scheme: Details of the next five years

25GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 24

PLI for solar PV modules

The government has extended the PLI scheme to the

manufacturing of solar PV modules, with a budgetary outlay

of Rs 45bn. The PLI scheme for solar photo voltaic modules

is expected to add 10,000 MW capacity of integrated solar

PV manufacturing plants and bring direct investment of

around Rs 172bn, thus creating 30,000 direct jobs. The

scheme comes in the backdrop of India’s decision to impose

40% BCD on solar modules and 25% on solar cells from 1st

April 2022, a move that would make imports costlier and

encourage local manufacturing.

PLI Segment (in Rs mn) PC: est. no of Players each investment

segment* Incentive

Large Invest-ment

Normal Invest-ment

Total

ACs (Components) 4 4,800 1,988 6,788

High Value intermediates of Acs 3 2,575 1,825 4,400

Lower value intermediates of Acs 9 730 365 1,095

LED Lights 3 2,970 876 3,846

Components of LED Lights 8 219 88 307

Total (A) 27 11,294 5,141 16,435

Government has approved the PLI for AC and LED Lights (B) 62,380

Average. No. of Players each segment & investment size (B/A =C)

4

Total Approx. players can apply (C*Segment*Investment type) 38

PC Estimates: In AC- Major Players in Lower Value intermedi-ates & In Components of LEDs

53

Revised PLI: c.40+ applications should come in if all segments receive applications

Source: DPIIT, Ministry of Commerce and Industry, PhillipCapital EstimatesThrough this PLI we expect 40+ applications, companies globally will come to set up manufacturing for lower value intermediaries and components in AC and LED components. Indian manufacturers will form JVs with global companies to set up manufacturing for high value AC intermediaries.

PLI for IT hardware

• Incentive: 4-1% on net incremental sales over base year

of FY20

• Outlay: Rs 73.25bn

• Duration: 4 years

• 15 companies will benefit; 5 global players, 10 domestic

• PLI for IT hardware incentives will generate additional

investments of Rs 27bn and incremental production of Rs

3.26tn, of which 75% would be exported

PLI for IT hardware incentives will generate additional investments of Rs 27bn and incremental production of Rs 3.26tn

Making India a global hub of electronics (Production linked incentive (PLI) scheme for IT hardware approved)

• The government expects this PLI to reduce import

dependency for IT hardware, which is currently at 80%.

• It expects domestic value addition to rise from 5-10% at

present to 20-25% by 2025.

• The scheme could generate 180,000 direct and indirect

jobs over the 4-year period.

Sour

ce: I

ndus

try, m

eity

.gov

.in

25GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 24

Ince

ntiv

eAn

dhra

Pra

desh

Utta

r Pra

desh

Tela

ngan

aM

ahar

asht

raTa

mil

Nadu

Karn

atak

a

Capi

tal

Subs

idy

10%

of t

otal

inve

stmen

t up

to

Rs 5

0mn

• 15

% o

r Rs 1

00m

n (m

axi-

mum

) for

inve

stmen

ts up

to

Rs 2

bn.

• 15

% o

r Rs 1

.5bn

max

imum

fo

r inv

estm

ents

from

Rs

2-10

bn.

• Ad

ditio

nal s

ubsid

y of 1

0%

or R

s 1bn

on

FCI e

xcee

ding

Rs

10b

n.

Capi

tal s

ubsid

y of 2

0% w

ith

a cei

ling

of R

s 100

mn

per

com

pany

in ca

se o

f mob

ile

man

ufac

turin

g un

its

Fo

r lar

ge e

nter

prise

s, 15

%

for A

, 20%

for B

, 25%

for C

wi

th e

mpl

oym

ent o

f ove

r 500

pe

ople

. For

meg

a ent

erpr

ises,

18%

for A

, 24%

for B

and

30%

fo

r C w

ith e

mpl

oym

ent o

f ove

r 2,

000

peop

le

10%

up

to a

max

of R

s 10

0mn

for r

egist

ered

KES

DM

com

pani

es

Powe

r Su

bsid

y50

% to

micr

o, 4

0% to

smal

l, 25

% to

med

ium

and

10%

to

larg

e sc

ale

indu

stry l

imite

d to

Rs

5m

n fo

r a p

erio

d of

5 ye

ars

from

the

date

of C

oCO

Ex

empt

ion

of e

lectr

icity

dut

y fo

r a p

erio

d of

10

year

sEl

igib

le n

ew E

SDM

uni

ts ex

empt

from

pay

ing

elec

tric-

ity d

uty f

or 1

5 ye

ars.

Powe

r su

bsid

y to

the

tune

of R

s 1 p

er

unit

for a

per

iod

of 3

year

s in

cate

gory

A &

B an

d 5

year

s in

othe

rs su

bjec

t to

ceili

ng.

Exem

ptio

n of

ele

ctrici

ty co

st fo

r 5 ye

ars

Powe

r sub

sidy i

s app

licab

le

for a

ll KE

SDM

regi

stere

d co

mpa

nies

Land

25%

reba

te o

n la

nd co

st lim

ited

to R

s 1m

n pe

r acr

e25

% re

bate

on

land

cost

25%

reba

te o

n la

nd co

st fo

r a

perio

d of

10

year

s

Re

bate

on

land

cost

Tax R

e-im

burs

e-m

ent

100%

tax r

eim

burs

emen

t for

a p

erio

d of

10

year

s sub

ject

to a

max

of 1

00%

FCI o

ther

th

an la

nd

100%

stat

e GS

T rei

mbu

rse-

men

t up

to a

max

FCI o

f 100

%

(exc

ept l

and)

100%

tax r

eim

burs

emen

t for

a pe

riod

of 5

year

s for

micr

o an

d sm

all c

ompa

nies

or m

ax o

f Rs

50m

n. R

eim

burs

emen

t is

appl

icabl

e fo

r 7 ye

ars f

or la

rge

com

pani

es

Reim

burs

emen

t for

GST

Skill

Up

grad

a-tio

n

Skill

upg

rada

tion

train

ing

50%

re

imbu

rsem

ents

with

a ca

pSk

ill u

pgra

datio

n up

to 5

%

of FC

ISk

ill u

pgra

datio

n by

pro

visio

n of

75%

of t

rain

ing

fee

for

train

ing

cour

ses

Stam

p du

ty e

x-em

ptio

n

100%

reim

burs

emen

t of

stam

p du

ty o

n sa

le/le

ase

of

deed

s on

first

trans

actio

n an

d 50

% th

ereo

f on

the

seco

nd

trans

actio

n

100%

reim

burs

emen

t on

stam

p du

ty fo

r ind

ividu

al

ESDM

uni

ts

100%

reim

burs

emen

t of

stam

p du

ty

Elig

ible

uni

ts ex

empt

ed

from

pay

ing

stam

p du

ty fo

r ac

quiri

ng la

nd an

d fo

r loa

n te

rm p

urpo

ses

50%

exe

mpt

ion

for A

&B

distr

ict. 1

00%

exe

mpt

ion

for

C di

strict

100%

for s

tartu

ps an

d M

SMEs

75

% fo

r lar

ge an

d m

ega

ente

rpris

es

Inve

st-m

ent

subs

idy

20%

lim

ited

to R

s 2m

n fo

r M

SME,

and

addi

tiona

l 5%

in-

vestm

ent s

ubsid

y for

wom

en/

SC/S

T ent

repr

eneu

r

20

% o

r a m

ax o

f Rs 2

0mn

for

first

25 e

ligib

le la

rge

com

pa-

nies

. Rs 5

mn

for fi

rst 5

0 sm

all

and

micr

o co

mpa

nies

Stat

e p

olic

ies

for

man

ufac

turi

ng o

f el

ectr

oni

cs a

nd e

lect

roni

c co

mp

one

nts

Note

: Diff

eren

t dist

ricts

in Ta

mil

Nadu

are

segr

egat

ed in

to d

iffer

ent c

ateg

orie

s nam

ely A

, B a

nd C

Sou

rce:

Sta

te g

ovt.,

Indu

stry

. Phi

llipC

apita

l res

earc

h

27GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 26

Impact of government policies

• Private investment: The electronics sector has attracted

US$ 14bn investment in the past five years for capacity

expansion. The higher import percentage provides

business opportunity to manufacture goods locally, which

can attract even more investment from Indian players.

• Employment opportunity: The sector employs close to

300,000 people, across product categories, including air

conditioners, refrigerators, mobile phones and washing

machines. With an increase in localisation, it has the

potential to employ additional 200,000 people in the

next five years. India has a competitive advantage over

other emerging market countries in Asia due to its wide

availability of cheap labour.

• Positive impact on component manufacturers and

adjacent sectors: Localisation of components for air

conditioners, mobile phones, refrigerators, etc, at scale,

can help reduce the cost gap with China and can also

help galvanize the micro, small, and medium enterprise

(MSME) sector.

• Operational efficiencies: The Indian consumer durables

industry has seen supply-chain disruption in all major

product categories due to heightened supply chain

localization. However, dependency on external factors

can be reduced, achieving efficiencies in supply chain,

operational procedures, inventory volumes, and logistics.

• Economies of scale and automation: With more

investments coming in, India’s economies of scale have

the potential to mirror that of China’s, which is where

the world’s largest home-appliances manufacturing

takes place. China is also the source of imports across

the world, driven by its large domestic market and early

investments in scale. The number of units sold of ACs/

washing machines/refrigerators in China are 19x/65x/9x

those in India. China has the largest AC compressor

manufacturing hub, with a total installed capacity of 86%

of the world. It has emerged as a low-cost manufacturing

spot for consumer durables, and is responsible for 33.5%

of the global AC exports and 23% of global refrigerator

exports. However, India will eventually secure a decent

portion of the total global exports market for air

conditioners and other consumer durables. In the current

environment, when the world is looking for an alternate

hub, India is amongst the top countries that stand to

benefit. The opportunity is ripe for Indian manufacturers

to step up and make a dent at the global level in the

consumer durable industry.

• Becoming competitive in products like washing

machines, refrigerators, etc., and mobile phones. With

the government’s initiatives, Indian manufacturers have

a strong chance of becoming cost competitive in some

products. Although, washing machines and refrigerators

have no direct schemes (such as PLI), a robust electronics

components ecosystem due to PLI in large-scale

electronics manufacturing will lead to the already

indigenised product category, i.e., semi-automatic

washing machines and refrigerators (of capacity below

300 litres) becoming competitive in terms of exports.

India aims to become a strong electronics component manufacturing base

The number of units sold of ACs/washing machines/refrigerators in China are 19x/65x/9x those in India

27GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 26

Mechanism Impact on disability Remarks

Production linked incentives scheme 4%-6% Financial incentives on large scale production

SPECS 0-1.6% 20% capex subsidy annualised on 8% capital cost

EMC 2.0 1% Logistics, Plug and Play infrastructure

RoDTEP 0.2%-0.7% In lieu of MEIS as a duty-free scrip administered by DGFT

Concessional Rate of Income Tax 0.2%-0.9%

Ease of doing business measure 0.50% Custom bonded warehouse, Port logistics, ECB reforms

Total 5.9%-10.7%

Impact of new and existing schemes

Recent investments in EMS in India The impact of the government’s policies has led to an

increase in global interest, which in turn has boosted

investments in the country. According to DPIIT (Department

for Promotion of Industry and Internal Trade), FDI inflows into

the electronics sector between FY01 and FY20 stood at US$

2.91bn.

Some key investments and developments in the Indian

ESDM and electronics segment are as follows:

• Apple’s contract manufacturers: In September 2020,

Wistron, Pegatron, and Foxconn announced investments

of +US$ 900mn over the next five years. The investments

are mainly for capacity expansions and ramping up of

domestic production of mobile phones.

• Samsung Electronics and Apple Inc.’s assembly

partners: Announced investments worth US$ 110bn to

establish mobile-phone manufacturing units in August

2020.

• Hon Hai Precision Industry Co Ltd: Plans to invest US$

1bn to ramp up production at its Sriperumbudur plant

in Tamil Nadu over the next three years and hopes to

generate 6,000 additional jobs.

• Aequs: In October 2020, it committed to an investment

of Rs 35bn towards setting up of a consumer electronics

cluster in Karnataka.

• Tata Group: Announced its plan to invest Rs 50bn in

October 2020 to set up an Apple phone component

plant in Hosur, Tamil Nadu.

• Sahasra Electronics: In October 2020, it announced

plans to invest Rs 3.5bn in assembling mobile phone

memory chipsets, laptop hard drives, and motherboards

in India over the next four years. The company also set up

two manufacturing facilities in UP and Rajasthan.

• PG Electroplast: Started production at its AC ODU

(outdoor unit) assembly line in 2020; the complete

ODU plant will begin manufacturing in 2021. The plant

is at Ahmednagar in Maharashtra and should generate

revenue of Rs 1bn for the company in the first year.

• Phillips: In May 2020, it announced investments worth Rs

2.5-3.0bn to boost its manufacturing and R&D facilities in

India.

• Nokia: It partnered with Flipkart in November 2019 to

enter the consumer durables market in India.

• Godrej Appliances: In January 2020, it announced plans

to foray into the air cooler segment with a target of

acquiring 15% market share in the next five years.

Source: Industry, PhillipCapital research

Key Segments (USD Bn)

Global Market Size

India

Market Size ExportsTargeted Produc-

tion in FY25Targeted Value

Addition by FY25

2019 2025 CAGR % 2019 2025 CAGR % 2019 2025 CAGR %

Mobile Phone 495 640 4% 24 80 22% 0.16 110.0 197% 190 34%

Personal Comput-ers & Monitors

237 237 0% 5.53 5.5 0% 0.04 41.9 218% 47.4 25%

Network Equip-ment*

49.7 112.27 15% 1.3 2.87 14% 0.01 13.8 229% 15.6 18%

Note: * Ethernet Switches, WLAN & Routers. Source: IT, Industry, PhillipCapital estimates

Government policies will lead to better in value addition, domestic production, and strong exports growth

29GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 28

Company name CAPEX ( in Rs

mn.)

For PLI*

State Comments Capacity Date of Announce-

ment

Haier Appliances 30,690 Noida, NCR Refrigerators, washers, ACs are expected to start 1st phase by June'21

2019

HP Ltd 36,000 South India Capex over the next 5 years for computers and laptops 2019

Godrej Appliances 11,000 Shirwal and Mohali

Will invest till 2022; with this will be increasing capacity by 33% for premium products

6.5mn units p.a

2019

Xiaomi India 35,000 Noida, UP Xiaomi Corp (still on)* 2019

Jaina Group 10,000 Manufacturing hub for Sansui brand products; will export to other geographies, including the neighbouring South East Asian markets. Capex will be over the next 3 years.

2019

VIVO India 35,000 Smart phone (120mn annual capacity) 2019

Amber Enterprises 3,000 PLI Pune & South India

Greenfield facilities 3mn units p.a 2020

Samsung India 48,250 NCR, Uttar Pradesh

Mobile and IT display production unit 2020

Lava International 8,000 Shifting operation from China to India, capex will be over the next 5 years.

2020

Dixon Technologies 2,500 PLI South India Padget Electronics 2020

Thomson 10,000 Will invest in the next 5 year for home appliances. 2020

Daikin* 500 R&D 2020

GMCC 8,000 Compressor plants 2020

Highly* 500 Increasing the capacity of compressor plant 2020

TCL 24,000 Capex for TV plants 2020

ABAJ 1,000 For a manufacturing unit with a capacity of 2.5mn TVs and 0.6mn ACs

2020

Voltas* 5,000 PLI Planning to set up an AC plant in South India 2020

Realme 3,000 Eight new SMT lines for TVs in Noida 2020

Tata Group 70,000 For mobile phones in south India 2020

Micromax 5,000 PLI For mobile phones, 2mn/month current capacity; increasing it to 3mn/month.

2021

Pegatron Corporation 11,000 PLI Chennai Leased 500,000 sq. ft. of land 2021

Hon Hai Precision Industry Co Ltd

39,000 PLI Tamil Nadu Expanding manufacturing capacity 2021

Sahasra Semiconductors 1,500 ELCINA, Bhiwadi ELCINA 2021

ePack Durables Solution 1,000 PLI ELCINA, Bhiwadi ELCINA 2021

Havells India 2,500 PLI Sri city, Chittoor AC plant 0.56mn units p.a.

2021

PG Electroplast 1,000 PLI Ahmednagar AC plant AC: 0.9mn p.a. -IDU + 0.4mn

-ODU

2021

Panasonic 3,000 Jhajjar Panasonic Technopark 2021

Super Plastronics 3,000 Building IOT capabilities 2021

SPPL - Kodak TV 3,000 Expanding capacity for TV assembly 2021

Bosch 8,000 Dishwashers, washers, refrigerators 2021

Blue Star 1,350 PLI Wada Capacity expansion 2021

Burly Home Appliances 500 Set up a manufacturing plant in Telangana for air coolers 2021

Total 394,600

Total Ex. Of Expected PLI

349,940

India will see total capex of Rs 323bn over the next 3-4 years in the electronics industry

Note

: * e

stim

ates

. So

urce

: med

ia re

ports

, Phi

llipC

apita

l Res

earc

h

29GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 28

Some industry views

“ICEA welcomes the new UP Electronics

Manufacturing Policy 2020, which is aligned

towards the fulfilment of the NPE 2019 goals.

On the basis of such policies, India should

be able to focus its efforts on capturing the

investment opportunities from global as well

as domestic stakeholders to establish itself

as the world’s number one mobile phone

manufacturing destination. UP is already home to

60% of the total manufacturing units related to

mobile phones and components, and with such

policy support the state would further witness

accelerated establishment of units in the short

to medium periods. These policy interventions

would pave the way for shifting of production

bases from China and elsewhere to UP and

India.”

Pankaj Mohindroo, Chairman,

Indian Cellular & Electronics Association (ICEA)

“Over the next five years, the PLI scheme is likely to

lead to production of mobiles and components worth

Rs 11.5 lakh crore (Rs 11.5tn). Of these over 7 lakh

crore (7tn) worth of products will be exported. This

scheme is also expected to generate 3 lakh (300,000)

direct jobs and over 9 lakh (900,000) indirect jobs in

the country.”

Ravi Shankar Prasad,

Minister for Electronics and Information Technology

(MeitY), Government of India

“Electronics manufacturing in India has registered 23

percent cumulative annual rate of growth over past

5 years. The growth is likely to be 30% yoy for the

next 5 years. Mobile manufacturing in the country

has grown from 6 crore (60mn) handsets five years

ago to 33 crore (330mn) handsets at present, with

90% of the mobile phone requirements being met

through domestic production. In next 5 years, growth

in exports could be 40-50% at a bare minimum.”

Ajay Prakash Sawhney, Secretary,

Electronics and Information technology (MeitY)

Currently, planned capex

amount is Rs 349.9bn*

Total expected capex is Rs 565bn

Mobile PLI capex

amount is Rs 110bn

AC and AC components,

LED PLI capex is Rs 99bn

Laptop and tablet

capex is Rs 33bn

+

+

31GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 30

31GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 30

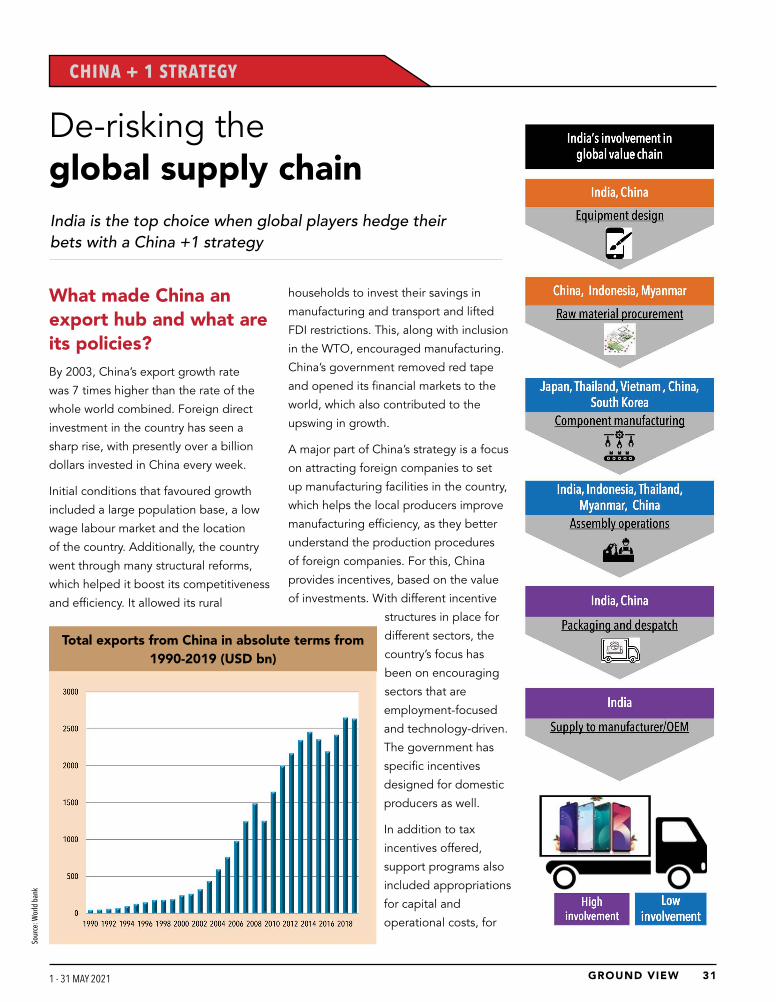

De-risking the global supply chainIndia is the top choice when global players hedge their bets with a China +1 strategy

CHINA + 1 STRATEGY

What made China an export hub and what are its policies?By 2003, China’s export growth rate

was 7 times higher than the rate of the

whole world combined. Foreign direct

investment in the country has seen a

sharp rise, with presently over a billion

dollars invested in China every week.

Initial conditions that favoured growth

included a large population base, a low

wage labour market and the location

of the country. Additionally, the country

went through many structural reforms,

which helped it boost its competitiveness

and efficiency. It allowed its rural

households to invest their savings in

manufacturing and transport and lifted

FDI restrictions. This, along with inclusion

in the WTO, encouraged manufacturing.

China’s government removed red tape

and opened its financial markets to the

world, which also contributed to the

upswing in growth.

A major part of China’s strategy is a focus

on attracting foreign companies to set

up manufacturing facilities in the country,

which helps the local producers improve

manufacturing efficiency, as they better

understand the production procedures

of foreign companies. For this, China

provides incentives, based on the value

of investments. With different incentive

structures in place for

different sectors, the

country’s focus has

been on encouraging

sectors that are

employment-focused

and technology-driven.

The government has

specific incentives

designed for domestic

producers as well.

In addition to tax

incentives offered,

support programs also

included appropriations

for capital and

operational costs, for

Total exports from China in absolute terms from 1990-2019 (USD bn)

Sour

ce: W

orld

ban

k

33GROUND VIEW GROUND VIEW 1 - 31 MAY 2021 1 - 31 MAY 2021 32

e.g., financial aid for R&D, transport of

labour and workforce training, exemption

in costs for construction of dormitories,

etc. The Chinese government made sure

that the working conditions were safe,

infrastructure facilities were improved,

land was easily available, good quality

and reasonably priced power supply was

ensured, and that the location of the SEZs was usually close

to the airports. The government conducted periodic reviews

to examine the impact of its policies.

Factors that helped China become an exports hub

Chinese people from Hong Kong and Taiwan were the first

to open factories in China. They gradually learned and

conquered mass manufacturing. They had a large domestic

workforce, many of whom aspired to jobs in foreign factories.

The Chinese government became involved in motivating its

citizens to work in factories and loosened controls on them,

allowing them to move around the country and find their

own jobs.

American corporations that were pro-outsourcing moved

their manufacturing bases to China in the early 1990s.

Wall Street fostered globalization and outsourcing as

captivating world trends – which further helped the

country achieve great export growth. China attracted a

lot of foreign investment from the US, Japan, and other

developed economies through Hong Kong or Taiwan. In

exchange for paying lower wages, these companies trained