MINISTRY OF EDUCATION FIJI SEVENTH FORM CERTIFICATE EXAMINATION MINISTRY OF EDUCATION FIJI SEVENTH...

22

MINISTRY OF EDUCATION FIJI SEVENTH FORM CERTIFICATE EXAMINATION 2012 ACCOUNTING COPYRIGHT: MINISTRY OF EDUCATION, REPUBLIC OF FIJI, 2012.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of MINISTRY OF EDUCATION FIJI SEVENTH FORM CERTIFICATE EXAMINATION MINISTRY OF EDUCATION FIJI SEVENTH...

MINISTRY OF EDUCATION

FIJI SEVENTH FORM CERTIFICATE EXAMINATION

2012

ACCOUNTING

COPYRIGHT: MINISTRY OF EDUCATION, REPUBLIC OF FIJI, 2012.

2.

MINISTRY OF EDUCATION

FIJI SEVENTH FORM CERTIFICATE EXAMINATION 2012

EXAMINER’S REPORT

ACCOUNTING This year approximately 2138 candidates sat for the Fiji Seventh Form Examination Accounting paper. The paper was of reasonable standard and focused on a variety of competency skills or learning outcomes ranging from recalling facts, comprehension, applications, analysis, synthesis and evaluation. Generally the overall performance of the candidates was below expectation in certain areas of the examination paper and it is once again a reminder for candidates and teachers to note that any areas of the Fiji Seventh Form accounting prescription can be tested by the variety of questions within the examination paper and candidates must be well prepared to handle it. Candidates and teachers are strongly advised not to specialize themselves based on the type of questions that have been presented in previous years. Of concern this year was the number of candidates that did not take enough care when responding to Question 5, Part B- on the general journal entries. It was also noted that majority of the candidates did not attempt this question. The candidates also need to read questions carefully and answer them as asked. It was evident from some of the candidates’ answers that they have learnt accounting through rote learning especially when answering question on accounting theory and lost marks when answering application type questions. Some candidates seem to do selected questions, and wrote partly answers, thus lost valuable marks. Teachers are requested to discourage candidates of accounting from rote – learning and use variety of teaching methods and resources to cope up with the changing trends and demands of the commercial environment. Candidates are also advised that they should not use abbreviation on examinations and avoid excessive use of twink. Teachers are also reminded to teach candidates the correct method as well the presentation of financial statement. On the positive note, teachers and Heads of the Department are commended for their professional support and tireless efforts in ensuring that candidates are able to perform at their level best in the examination. QUESTION 1 REVIEW OF THE FIJI SCHOOL LEAVING CERTIFICATE

COURSEWORK The question was based on Theme One of the FSFE Accounting prescription. Overall this section of the paper was poorly attempted by majority of the candidates. Hardly any candidate scored full mark in this section. It clearly reflected that candidates could not understand the concepts and thus failed to apply the appropriate Accounting procedures to calculate the correct figures. A. BALANCE DAY ADJUSTMENT The performance of the candidates in this section of the paper was below par. It was disappointing to note that hardly any candidate managed to gain full marks. Majority of the candidates were not at all familiar with the balance day adjustments calculation. Teachers are advised once again to give candidates more exercises on balance day adjustments so that performances on this type of question can be improved.

3.

B. INCOMPLETE RECORD This was the well attempted by majority of the candidates. It was a simple straight forward question. However, it was disappointing to note that a few candidates did not attempt this question at all. Common errors observed in the scripts were:

1. Recording of doubtful debts in debtors control account. 2. Candidates posted the entries on the wrong side for example dishonoured cheque and discount

disallowed were posted on the credit side instead of the debit side. 3. Candidates failed to record the cheque received from debtors. They only took into account the

cash amount.

C. BANK RECONCILIATION This section was not handled well by majority of the candidates. Common errors spotted in the scripts were:

1. Candidates were confused on the posting entries on the debit and the credit side of the cash at bank account.

2. Some candidates recorded bank error in cash at bank account. 3. A handful of the candidates were not able to apply the correct formula in the Bank Reconciliation

statement 4. A few candidates added the bank error instead of subtracting it from the Bank Reconciliation

statement 5. Some candidates did not attempt this question at all.

Overall, this section of the exam paper is supposed to be the scoring section for candidates as it is basically a recap of the Fiji School Leaving Certificate prescription. However, looking at the performance of the candidates over the past few years, it seems that this topic is not taken seriously by candidates and teachers. Teachers are once again requested to devise suitable teaching strategies and pay special attention to the review of the FSLC coursework in detail so that all candidates are able to handle this type of questions well and score better marks. QUESTION 2 ACCOUNTING FOR PARTNERSHIP AND LIMITED

LIABILITY COMPANIES The questions were based on Theme Two of the FSFE accounting prescription. The overall performance of the candidates was satisfactory. A. ACCOUNTING FOR PARTNERSHIP This question was well handled by some candidates. However, some candidates misinterpreted the question; for example, they took into account the original or revalued amount instead of taking into account the difference between the two amounts. A handful of candidates did not attempt this question at all.

4.

Common errors identified were:

1. Using the sides wrongly in Capital adjustment account. The items which were supposed to be recorded on the debit side were recorded on the credit side and vice versa. Thus candidates lost valuable marks.

2. Writing wrong entries, e.g. instead of writing accounts receivable, bad debts were written as entries, fixed asset was written instead of accumulated depreciation.

3. Calculating for provision for doubtful debts incorrectly by majority of the candidate. 4. Majority of the candidates were confused with the treatment of Goodwill although the question

clearly stated that goodwill is to be recorded. (b) CAPITAL ACCOUNTS – well attempted question. Few candidates did not attempt this

question at all.

Common errors identified were:

1. Using the sides wrongly. The items which were supposed to be recorded on the debit side were recorded on the credit side and vice versa. Thus candidates lost valuable marks.

2. Failure to record the opening balance on the correct side of the capital account. 3. Failure to transfer Current account balance in the capital account of the retiring partner. 4. Not making an attempt on this question.

(c) This question was not attempted well by majority of the candidates. Most of the candidates

seemed to have misunderstood or did not read the question carefully. Candidates wrote answers which related to events after the admission and not prior to admission of a new partner.

B. ACCOUNTING FOR LIMITED COMPANIES Overall the performance by many candidates has been satisfactory with a few getting full marks. Revenue Statement The performance by many candidates has been good with a few getting full marks. It was also noted that some candidates were careless in writing figures such as having missing zeros. Common errors identified were:

1. Not following a formal layout. Majority of the candidates abbreviated certain accounting. Although no one was penalized on the presentation or use of abbreviations, however it is important for teachers and candidates to use the correct method of presentation as stipulated in the Fiji Accounting standard.

2. Listing all revenues and expenses without proper classification, thus losing valuable marks. 3. Calculating and recording the amount of amortization on patent, profit on gain on sale of land,

separation of the amount for depreciation on motor vehicle, resulted in candidates losing valuable marks.

4. Distinguishing and recording returns inwards and outwards in the financial statement. 5. Failing to identify the opening and closing inventory figures. 6. Recording the assets, liabilities and shareholders equity items in the revenue statement.

5. QUESTION 3 ACCOUNTING THEORY The accounting theory questions were basically based on candidates’ understandings and application of fundamental concepts in accounting. As usual it was noted that the theoretical-type questions continue to be challenging for many candidates. Teachers are requested to expose candidates to different scenarios concerning the application of the accounting concepts to allow them to handle examination questions well. It also seems that candidates are doing rote learning and cramming the concepts and writing the answers anywhere as they feel appropriate. Teachers need to remind candidates that the expectation at Form Seven level is high thus the need to express themselves well. There is a need for teachers to help those candidates who are having difficulties in understanding and interpreting English language and those who might hate wordy question by giving them regular exercise so that candidates are well prepared for this section of the paper. Once again it was noted that few candidates did not attempt this section of the paper. (a) (i) Materiality concept and Matching concept – The definition was handled well by

majority of the candidates. However, some candidates showed lack of understanding and as such did not expressed themselves well as expected at Form Seven level.

(ii) Well answered questions. Most of the candidates were able to explain how materiality

concept assists in determining whether expenditure is classified as capital or revenue. However, majority of the candidates failed to provide an example.

(b) Poor answered questions – Many candidates left this section of the paper blank. Even those who

attempted this question gave definition of the factors rather than discussing how each of the factors poses limitation in the financial statements. It was obvious that candidates could not comprehend the expectation of the question and as such wrote what they knew about the factors rather than what was expected of them.

(c) Some of the candidates answered this part of the question well. However, there were some who

found difficulties in identifying the concept. There were cases where the concepts were correctly identified; however, the justification was wrongly interpreted. The question looked at real life situation and failure of candidates in answering such questions indicated that they were taught with theory questions only. Teachers need to pay heed to accounting concepts both theoretical and practical and use financial report to show and explain the application of accounting concepts.

QUESTION 4 ANALYSIS INTERPRETATIONS OF FINANCIAL STATEMENTS This question is based on Theme Four of the FSFE Prescription. Overal, this question was poorly done by majority of the candidates. This type of questions appear in the exam paper every year, yet candidates were not able to handle such questions well. Majority of the candidates were able to state the formulas correctly yet failed to obtain the correct answer.

This kind of weakness has been highlighted in the previous examiners reports and once again teachers are reminded to teach Analysis and Interpretation of Financial Statement for Companies and NOT only for Sole Trader. This was reflected in the answers the candidates were giving especially with the formulas.

6. Specific comments are as follows: A. FINANCIAL STATEMENT AND POSITION HIGHLIGHTS - 2010 Only a handful of candidates scored full marks in this section of the question. Few candidates did not attempt this question at all. Common errors found in the candidates scripts were: (a) Calculation of Ratios and Percentages

(i) Rate of return on total assets percentage – was well handled by some of the candidates. The formula uses net profit before tax rather than after tax figure so that the ratio is not affected by external tax policies. Moreover, the finance expense (interest) is added back to profit before tax to reflect that efficient use of the resources are not affected by method of financing the acquisition of the assets.

(ii) Debt to equity ratio – was well handled by majority of the candidates. However, some

used owners’ equity in the formula instead of using shareholders equity as the question was based on companies.

(iii) Net Profit percentages – Well attempted by majority of the candidates. (iv) Shareholders equity ratio – Many candidates used the formula for sole – trader which

was marked incorrect but had correct working and final answer which was given the allocated marks .

(v) Accounts receivable turnover (Times) – was well attempted by majority of the

candidates, however, few candidates used 30 and 365 days instead of 300 days as stipulated in the question.

(vi) Stock Turnover in number of times – Well attempted by majority of the candidates.

(b) This question was well answered by majority of the candidates. B. ANALYSING FINANCIAL STATEMENT (a) (i) Current Ratio – Fairly well done by majority of the candidates. However, a handful

of candidates wrote the correct formula but used wrong amounts. It clearly showed that candidates were not able to identify the items into current liabilities and current assets.

(ii) Acid Test Ratio- Few candidates were confused with the formula. Teachers are reminded to emphasise on the correct formula.

(b) Well attempted by majority of the candidates.

7.

(c) Generally, this was poorly attempted by most of the candidates. They were not able to compare and evaluate although these types of question have been tested at form 6 and 7 levels. It was also disappointing to note that candidates were comparing and evaluating the ratios and percentage for the industry against Taylor and Company. Candidates provided all sorts of answers and some did not attempt this question at all.

(d) Well attempted by majority of the candidates. QUESTION 5 COST ACCOUNTING The questions were based on Theme Three of the FSFE accounting prescription. Part B, Job order costing was one of the worst attempted questions. Majority of the candidates lost all 10 marks either because they left this question blank or they failed to provide appropriate journal entries. A. MANUFACTURING STATEMENT This question was reasonably well answered by some candidates. The question was straight forward and similar question has appeared in previous exam papers. However, some candidates were not able to interpret the additional information provided and as a result the calculation was incorrectly stated in the manufacturing statement. A handful of candidates did not attempt this question at all. Common errors identified in the candidates’ scripts were: 1. Not recording Work in progress amounts (opening and closing) in the Manufacturing statement.

2. Balance day adjustment posed lot of difficulties to the candidates. Once again teachers are reminded

to focus more in teaching balance day adjustment as it could be linked to many application problems in financial accounting.

3. Few candidates were confused on the item which needs to be recorded in the Manufacturing Statement. It was seen that candidates simply included all items in the Manufacturing Statement from the given information. Candidates need to develop the expertise to recognize which items should and should not be included in particular accounting reports.

B. JOB ORDER COSTING This question was one of the most poorly attempted questions by majority of the candidates. It was disappointing to note that many candidates left this section blank. The preparations of general journal entries are the first step to the accounting cycle. Majority of the candidates had problems with the general journal entries and the performance here was indicative of candidates not exposed to this kind of teaching and learning. It seems that teachers fail to realise that examinations are prepared from the learning objectives from the prescription and not from selected group of questions from past years exam papers. Teachers need to prepare candidates to tackle all types of questions on cost accounting.

8.

C. COST VOLUME PROFIT ANALYSIS Overall this question was handled well by many candidates. Those who knew the formula and applied it correctly scored full marks. Teachers ought to be commended for this. On the other hand a handful of candidates did not attempt this question at all. Common errors identified in the candidates’ scripts had the following errors: 1. Part (i-ii) Few candidates were not familiar with the formula. 2. Part (iii) was poorly attempted by the candidates as they were not able to calculate the new

breakeven point in dollars. QUESTION 6 INTERNAL CONTROL AND SUBSYSTEMS The questions were merely testing the application of various internal control procedures in a given situation. A number of candidates did not respond well to some of the questions. Few candidates left this section of the paper blank. (a) Well answered by many candidates. Candidates were able to provide logical and sensible answer. (b) Well attempted question. Candidates were able to provide reasonable answers. (c) Poorly attempted question. Majority of the candidates wrote answers prior to granting credit to

customers. (d) Well attempted by many candidates. However, guessing answers seemed to be the norm for some

candidates. (e) Well attempted question. Candidates were able to provide reasonable answers. (f) Well attempted question. Majority of the candidates correctly stated one factor that needs to taken

into account when designing effective accounting system. (g) Poorly attempted question. It seemed that candidates failed to recap and apply what they have

learnt in yesteryears Teachers and candidates need to revise on the different types of source documents used by different businesses in everyday real life situations.

THE END

9.

Index Number: Marking scheme

MINISTRY OF EDUCATION

FIJI SEVENTH FORM CERTIFICATE EXAMINATION 2012

ACCOUNTING

ANSWER BOOK

HAND IN THIS ANSWER BOOK TO THE SUPERVISOR BEFORE YOU LEAVE THE EXAMINATION ROOM.

INSTRUCTIONS 1. Write all your answers in this Answer Book. 2. Write your answer to each question in the appropriate part of this Answer Book. 3. Answer all the questions with a blue or black ballpoint pen or ink pen. Do not use red ink. You

may use a pencil only for drawing. 4. If you use extra sheets of paper, be sure to write clearly the question number(s) being answered

and to tie each sheet securely in this Answer Book in the appropriate places. 5. Before handing in this Answer Book, make sure that your Index Number is at the top

of this page, inside the back flap and on any extra sheet(s) of paper you may have used.

Marks

Gained:

COPYRIGHT: MINISTRY OF EDUCATION, REPUBLIC OF FIJI, 2012.

10.

QUESTION 1 REVIEW OF THE FIJI SCHOOL LEAVING [15 marks] CERTIFICATE COURSEWORK

Part A Balance Day Adjustment

(a) Insurance:

1 800-300=1 500/12=125*3=375. 1 500-375 Answer : $1125

(b) Motor Vehicles:

55 000-6 000

Answer : $49 000

(c) Accumulated Depreciation on Motor Vehicles:

15 000+4 100-3 500

Answer : $15 600

(d) Repairs to Motor Vehicles:

2 500+393 Answer : $2893. (e) Advertising:

5500+300-180

Answer : $5620

(5 marks) Part B Incomplete Record

Debtors Control Account

(5 marks)

Date Particulars $ Date Particulars $

Balance 51 000 Cash 590 000 Dishonoured Cheque 5 100 Discount allowed 24 900 Discount disallowed 20 Bad Debts 4 000 Credit Sales 620 880 Sales return 6500

Contra Purchases account 8 000

Balance 43 600

$677 000 $677 000

Balance 43 600

11.

Part C Bank Reconciliation Statement

(2½ marks)

Bank Reconciliation Statement of Rupa Fashions

Cr Dr

(2½ marks)

Date Particulars $ Date Particulars $

Balance 2 000 Bank charges 120

Direct Deposit -Rent 1 000 Dishonoured Cheque – J.Jenson

520

Cancelled Cheque - 954 1 200 Balance 3 560

$5 200 $5 200

Balance 3 560

$ $ Balance as per Bank Statement 3 160 Add lodgment not yet credited 1 700 4 860 Less Unpresented Cheque

Cheque no. 3015 800

Less Bank Error 500

Balance as per Bank account $3 560

15

(b)

(a) Cash at Bank Account

As at 31 October 2012

12. QUESTION 2 ACCOUNTING FOR PARTNERSHIP AND [23 marks]

LIMITED LIABILITY COMPANIES Part A Accounting for Partnership (a)

Date Particulars $ Date Particulars $ Stock 2 000 Land 10 000 Accumulated Depreciation –

Fixed asset 3 750 Goodwill 25 000

Accounts receivable 100 Building 5 000 Provision for doubtful debts 314 Capital – Amir 11918 Josefa 5959 Seniana 5959 $35 000 $ 35 000

(5 marks) (b) (i)

Date Particulars $ Date Particulars $ Current account /

retained profit 2 000 Balance 60 000

Cash 63 959 Capital adjustment 5 959 $65 959 $65 959

(2 marks) (ii)

Date Particulars $ Date Particulars $ Balance 90 000 Balance 101 918 Capital Adjustment 11 918 $101 918 $101 918 Balance 101 918

(1 mark) (iii)

Date Particulars $ Date Particulars $ Cash 20 000

Balance 30 000 Sundry Accounts 10 000 $30 000 $30 000 Balance 30 000

(1 mark)

Capital Adjustment Account

Capital Account – Seniana

Capital Account – Amir

Capital Account – Jim

13.

(c) It becomes necessary to revalue assets so that it could reflect the fair value of the assets. It is also necessary so that the profit could be distributed to the existing partners.

(1 mark) Part B Accounting for Limited Liability Companies

Lincoln Co Ltd

$ $ Sales 790 000 Less Returns Inwards 5 000 785 000 Less cost of goods sold Inventories 90 000 Purchases 266 000 Less Returns outwards 8 000 258 000 Add Freight Inwards 3 000 261 000 Cost of good available for sales 351 000 Less Closing Stock 220 000 Cost of Goods Sold 131 000 Gross Profit 654 000 Add Operating Gains Discount 4 000 658 000 Less Operating Expenses Selling and Distribution Advertising 12 000 Depreciation on Vehicle 8 000 20 000 General and Administrative Directors Remuneration 55 000 Depreciation on Vehicle 32 000 Depreciation on Building 39 000 Amortization of Patent 10 000 Office Salaries 123 000 Auditors Fees 3 000 262 000 Financial Expenses Bad Debts 1500 Doubtful debts 500 Interest on Debentures 9 600 11 600 Total Operating Expenses 293 600 Net Operating Profit 364 400 Add Non – operating gains

*Gain on Sale of Land 30 000

Investment Income 25 000 55 000

419 400

Less Income Tax 109 320

Less Over-Provision of Income Tax 20 000 89 320

Net Operating profit and Extra-ordinary items after Tax $330 080

(13 marks) * Gain on sale of land – in some textbooks it is treated as operating gain and in some as non-operating gain therefore

both the answers were accepted. This result in having two different amounts for net operating profit, $364 400 and $394 400. These two different amounts also lead to two different amount for income tax. Both the amounts $109320 and $118320 were accepted as income tax .

Revenue Statement for the year ended 31 December 2011

14.

QUESTION 3 ACCOUNTING THEORY [12 marks]

(a)

(i) Materiality concept:

• It refers to the process of summarising information into simple form without losing context.

• It also refers to the relative importance of an item or an event that must be disclosed in the financial statement for the decisions – making process

• If an item or event is material, it is likely to be relevant to the user of the financial statement. • The materially of an item depends on the nature as well as the amount of the item. • Only relevant information must be presented to the very wide range of users of accounting data • It is a concept or convention within auditing and accounting relating to the

importance/significance of an amount, transaction, or discrepancy

Matching concept:

The matching concept is an accounting practice whereby expenses are recognized in the same accounting period when the related revenues are recognized.

(2 marks) Information is material either due to the amount involved or due to the importance of the event. If the amount is insignificant , it is revenue expenditure, if amount is material and makes a difference in decision making it is capital expenditure , Example : The treatment of stationery in a business organization , ignorance of cents in financial reporting , etc

(2 marks)

(b)

(i) Non-financial information Financial accounting does not consider those transactions which are non- monetary in nature, even though such transactions are equally important in business dealings. For example, extent of competition faced by the business, technical innovations possessed by the business, loyalty and efficiency of the employees; changes in the value of money etc. are the important matters in which management of the business is highly interested but accounting is not tailored to take note of such matters. Thus any user of financial information are , naturally, deprived of vital information which is of non-monetary character

(ii) Depreciation • Depreciation figure is subjective – based on estimations and opinions. It is left to the personal

judgment of the accountant

• Additively is a problem- Past years cost is written against current year’s revenue.

• Different methods can result in widely differing depreciation figures , thus comparability is a problem

• Conservatism concept is applied to determine useful life and residual value

15.

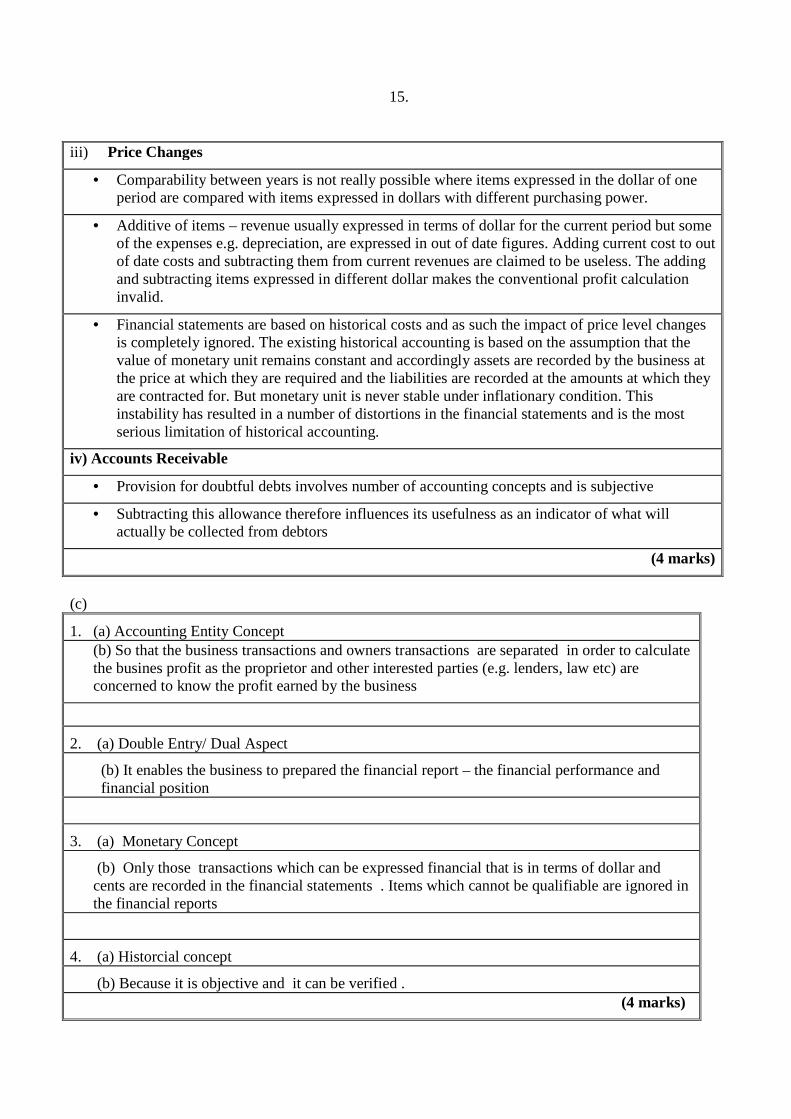

iii) Price Changes

• Comparability between years is not really possible where items expressed in the dollar of one period are compared with items expressed in dollars with different purchasing power.

• Additive of items – revenue usually expressed in terms of dollar for the current period but some of the expenses e.g. depreciation, are expressed in out of date figures. Adding current cost to out of date costs and subtracting them from current revenues are claimed to be useless. The adding and subtracting items expressed in different dollar makes the conventional profit calculation invalid.

• Financial statements are based on historical costs and as such the impact of price level changes is completely ignored. The existing historical accounting is based on the assumption that the value of monetary unit remains constant and accordingly assets are recorded by the business at the price at which they are required and the liabilities are recorded at the amounts at which they are contracted for. But monetary unit is never stable under inflationary condition. This instability has resulted in a number of distortions in the financial statements and is the most serious limitation of historical accounting.

iv) Accounts Receivable

• Provision for doubtful debts involves number of accounting concepts and is subjective

• Subtracting this allowance therefore influences its usefulness as an indicator of what will actually be collected from debtors

(4 marks)

(c)

1. (a) Accounting Entity Concept (b) So that the business transactions and owners transactions are separated in order to calculate the busines profit as the proprietor and other interested parties (e.g. lenders, law etc) are concerned to know the profit earned by the business

2. (a) Double Entry/ Dual Aspect

(b) It enables the business to prepared the financial report – the financial performance and financial position

3. (a) Monetary Concept

(b) Only those transactions which can be expressed financial that is in terms of dollar and cents are recorded in the financial statements . Items which cannot be qualifiable are ignored in the financial reports

4. (a) Historcial concept

(b) Because it is objective and it can be verified . (4 marks)

16. QUESTION 4 ANALYSIS AND INTERPRETATION OF [20 marks] FINANCIAL STATEMENTS

Part A Financial Performance and Position Highlights - 2011

(a) Calculation of Ratios and Percentages

No.

Ratio/Percentage

Formula

Working

Answer : correct to two decimal places

(i) Rate of Return on Total Assets Percentage

Net profit + interest expense Average total assets

253 000 *100 1417 000

17.85 %

(ii) Debt to Equity Ratio

Total liabilities Shareholders Equity

427 000 990 000

0.43: 1.00

(iii) Net Profit Percentage

Net operating profit after tax x 100 Net sales

223 000*100 624 000

35.74 %

(iv) Shareholders Equity Ratio

Shareholders equity Total Assets

990 000 1417 000

0.70 :1.00

(v) Accounts Receivable Turnover in number of days

Average Debtors x time period Net credit sales

41 600 *300 499 200

25 days

(vi) Inventories Turnover in number of times

Cost of goods sold Average stock

274 000 90 000

3.04 Times

(9 marks)

(b) The faster the inventory is sold, the less will be the amount of funds the company will be tied up in inventory ,for example , the storage cost , insurance , security cost etc will be eliminated, (1 mark)

17.

Part B Analysing Financial Data (a)

No.

Ratio/Perce

ntage

Formula

Working

Answer : correct to two decimal places

(i)

Current Ratio

Current Assets Current liabilities

47 600 34 000

1.40: 1.00

(ii)

Acid Test Ratio/ Quick Asset Ratio

Current asset – (inventories prepayments) Current liabilities – Bank Overdraft (secured)

OR Quick asset Quick liability

22 000 34 000 - 8000

0.85 :1.00

(3 marks)

(b) (i) Liquidity Ratio: Liquidity ration measures the solvency and the ability of a business to convert assets to cash. In other words, it is the availability of capital at each and every point of the working capital cycle to ensure the smooth flow of production through the business.

(1 mark)

(ii) Profitability Ratio: Profitability ratio measures the earning capacity of the business. In other words it refers a company's overall efficiency and performance

(1 mark) (c)

Compare and Evaluate:

i) Net Profit percentages

The net profit is 15 % lower compared to the industry level. This is unfavorable and it may be due to company having higher amount of expenses. This indicates that it may not be able to provide satisfactory rate of return to the shareholders

ii) Stock Turnover

The stock turnover is 5 times higher compared to the industry level .This is favorable as it indicates that the inventories are sold at a faster rate and are not being piled up.

18.

(iii) Gross Profit Percentage:

The gross profit is 5 % lower compared to the industry level. The gross profit ratio is 35% which is satisfactory, however it could be further improved.

(iv) Return on Shareholders’ Equity Percentage:

The return on shareholders equity is 9% lower compared to the industry level. This is unfavorable as it indicates that the shareholders are not getting a satisfactory rate of return and instead of investing in this business they may invest somewhere else

(4 marks) (d) Analysis involves extraction of key data from the financial reports and the performance of calculation on this data is done according to predetermined formula whereas interpretation involves making comparison and considering relationship between these data items to determine profitability, financial stability and management efficiency.

(1 mark) QUESTION 5 COST ACCOUNTING [20 marks] Part A Manufacturing Statement

Manufacturing Statement of Honey Limited For the year ended 31 December 2011 $ $ $ $ Direct Materials Purchases 230 000 Less Purchases Return 6 000 224 000 Add Carriage Inwards 3 000 227 000 Less closing Stock 38 000 Direct materials available for use 189 000 Direct Labour Direct Wages 65 000 Factory Overhead Indirect labour 82 000 Indirect materials 45 000 Electricity 22 800 Rent 15 000 Plant and Machinery Repairs 18 000 Depreciation - Plant and Machinery 19 000 201 800 455 800 Less Work In Progress 52 000

Cost of Production $403 800

(7 marks)

19.

Part B Job – Order Costing

Jiveshvil Garments Limited

General Journal Date Particulars Debit ($) Credit ($)

1 Raw materials inventory/ Store control 144 000

Edmond Co.Ltd 144 000

(For purchase of raw materials)

2 Work-in-process 114 000

* Factory (Manufacturing) Overhead 6 000

Raw materials inventory/ Store control 120 000

(Requisition of raw materials)

3 Work-in-process 94 500

* Factory (Manufacturing) Overhead 10 500

Wages Payable 105 000

(labour cost incurred)

4 ** Factory (Manufacturing) overhead control 45 000

Sundry liabilities and accruals 45 000

(To record other manufacturing cost)

Alternative journal entries

* Factory (Manufacturing) Overhead(indirect material and Factory overhead) indirect labour

could be excluded thus the general journal is

1 Work-in-process 114 000

Raw materials inventory/ Store control 114 000

Requisition of Direct materials)

2 Work-in-process 94 500

Wages Payable 94 500

(Direct labour cost incurred)

3 Other Factory (Manufacturing) overhead control 45 000

Factory supplies 6 000

Indirect labour 10500

Sundry liabilities and accruals 61 500

20.

5 Work-in-process 57 760

Factory(Manufacturing) overhead applied 57 760

(To record the applied manufacturing overhead cost)

6 Finished goods 266 260

Work-in-process 266 260

(To record finished goods transferred from WIP)

7 Costs of goods sold 266 260

Finished goods 266 260

(To record finished goods transferred to sales)

8 Aliti 320 000

Sales 320 000

(To record credit sales)

9 Cost of goods sold 3 740

Factory overhead applied 3 740

( To record under applied FOH)

(10 marks)

Part C Cost – Volume – Profit Analysis

(i) Break-Even Point in units

S - VC – FC = NP

(10-2)*S -100 000 =0

8S = 100000

Answer = 12 500 units (1 mark)

(ii) Volume of Sales

Volume

S - VC – FC = NP

10S – 2S -100 000 =20 000

8S = 120 000

Answer: 15 000 units (1 mark)

21.

(iii) Break-Even Point in dollars

S - VC – FC = NP

8S-2S-100000

0.6S = 100 000=16666.67*8

Answer: $ 133 333.33 (1 mark)

QUESTION 6 INTERNAL CONTROLS AND [10 marks] ACCOUNTING SUB-SYSTEMS

(a)

• To prevent fraud, errors, and safeguard assets against misuse and theft

• To make sure the company’s policies is carried out as prescribed

• To produce reliable accounting data

• To promote operational efficiency and to facilitate the breakdown of accounting procedures so

as to avoid bottle neck and encourage even flow of work

• To determine the person responsible for a particular task, or omission by the segregation of

task.

(1 mark)

(b)

i) Loan (Housing , overdraft , education etc ) credit cards, ire purchases

(1 mark)

(c)

1. Past history, by looking at the percentage of debts which have turned bad in past years.

2. Economical factors, by analyzing the state of the economy as to whether it is a boom time or recession.

Knowledge of a particular debtor who may be having financial difficulties

(2 marks)

(d)

(i) Cost of Goods Sold – Overstated

(ii) Closing Stock – Understated

(1 mark)

22.

(e)

1 Provides potential benefits of effectiveness and efficiency for internal control because it enables the entity to:

• Consistently apply predefined rules and perform complex calculations in processing large volumes of transactions or data.

• Enhance the timeliness, availability, and accuracy of information.

• Facilitate the additional analysis of information.

• Enhance the ability to monitor the performance of the entity’s activities and its policies and procedures.

• Reduce the risk that controls will be circumvented.

• Enhance the ability to achieve effective segregation of duties by implementing security controls in applications, databases, and operating

(2 marks)

. (f)

• Nature of the activity and associated product • Size • Location and dispersion • Management polices • Effects of law

(1 mark) (g)

(i) Credit note / Debit note

(ii) Paying –in – counterfoil , Slip, Bank Statement ,

(iii) Bank Statement ,Advice Slip, Electronic Statement

(iv) Tax Invoice

(2 marks)

THE END