Micro-economics I BCM -121

117

Micro-economics I BCM - 121 Prepared by: Yordanos Gebremeskel

Transcript of Micro-economics I BCM -121

Micro-economics I BCM - 121

Prepared by: Yordanos Gebremeskel

Contents ------------------------------------------------------------ Page

UNIT ONE -------------------------------------------------------------------------------------------------------------------------- 2

FOUNDATION OF ECONOMICS------------------------------------------------------------------------------------------------ 2

INTRODUCTION ------------------------------------------------------------------------------------------------------------------- 2 1.1 Economics and Economic System --------------------------------------------------------------------------------- 3

1.1.1 What you study in Economics? ----------------------------------------------------------------------------------------- 3 1.1.2 Distinction between Macroeconomics and Microeconomics ---------------------------------------------------- 4 1.1.3 Microeconomics and Choice -------------------------------------------------------------------------------------------- 5 1.1.4 Economic Systems -------------------------------------------------------------------------------------------------------- 6 1.1.5 Kinds of economic system ----------------------------------------------------------------------------------------------- 6

1.2 Using Diagrams and models in Economics --------------------------------------------------------------------- 8 1.3 Scarcity, Choice and Opportunity cost --------------------------------------------------------------------------- 8 1.4 Rational choices ---------------------------------------------------------------------------------------------------- 10 1.5 The Production Possibility Curve -------------------------------------------------------------------------------- 11

Unit Summary ---------------------------------------------------------------------------------------------------------- 14 Unit Assignment-------------------------------------------------------------------------------------------------------- 15

UNIT TWO ------------------------------------------------------------------------------------------------------------------------ 16

MARKET, SUPPLY AND DEMAND ------------------------------------------------------------------------------------------- 16

INTRODUCTION ----------------------------------------------------------------------------------------------------------------- 16 2.1 Markets and Prices ------------------------------------------------------------------------------------------------ 17

2.1.1 Basic features of a market --------------------------------------------------------------------------------------------- 17 2.1.2 Addressing economic problems in a market system ------------------------------------------------------------- 18

2.2 Demand -------------------------------------------------------------------------------------------------------------- 19 2.2.1 Individual and Market Demand -------------------------------------------------------------------------------------- 19 2.2.2 The Law of Demand----------------------------------------------------------------------------------------------------- 19 2.2.3 The Demand Schedule ------------------------------------------------------------------------------------------------- 20 2.2.4 The Demand Curve------------------------------------------------------------------------------------------------------ 21 2.2.5 Exceptions to the Law of Demand ----------------------------------------------------------------------------------- 22 2.2.6 Determinants of Market Demand------------------------------------------------------------------------------------ 23 2.2.7 Movements along and shifts in the demand curve --------------------------------------------------------------- 25

2.3 Supply ----------------------------------------------------------------------------------------------------------------- 26 2.3.1 Market Supply ----------------------------------------------------------------------------------------------------------- 26 2.3.2 The Law of Supply ------------------------------------------------------------------------------------------------------- 27 2.3.3 The Supply Schedule ---------------------------------------------------------------------------------------------------- 28 2.3.4 The supply curve -------------------------------------------------------------------------------------------------------- 28 2.3.5 Other Determinants of Supply ---------------------------------------------------------------------------------------- 29 2.3.6 Movements along and shifts in the supply curve ----------------------------------------------------------------- 31

2.3 Equilibrium of Demand and Supply ---------------------------------------------------------------------------- 31 2.3.1 The Concept of Equilibrium ------------------------------------------------------------------------------------------- 32 2.3.2 Determination of market price --------------------------------------------------------------------------------------- 32 2.3.3 Shift in Demand or Supply Curve and Market Equilibrium ------------------------------------------------------ 33

2.3.3.1 Shift in Demand Curve and Market Equilibrium ------------------------------------------------------------ 34 2.3.3.2 Shift in the Supply Curve and Market Equilibrium --------------------------------------------------------- 34

2.3.4 Algebra of Demand, Supply and Equilibrium ---------------------------------------------------------------------- 35 2.3.4.1 Demand Function ------------------------------------------------------------------------------------------------- 35 2.3.4. 2 Supply function --------------------------------------------------------------------------------------------------- 36 2.3.4.3 Demand – Supply Equilibrium ---------------------------------------------------------------------------------- 37

Unit Summary ---------------------------------------------------------------------------------------------------------- 39 Unit Assignment-------------------------------------------------------------------------------------------------------- 40

Unit One

Foundation of economics

Introduction

Unit one of this module is an introductory unit to the study of

economics. Microeconomics being one branch of economics, it is useful

to start first by introducing what economics is all about. In this unit,

emphasis is also given to basic concepts and methodologies that are

significantly useful in the whole learning of economics.

Upon completion of this unit, you will be able to answer basic questions

like:

What is economics?

What is an economic system?

What is microeconomics and macroeconomics?

What is scarcity, choice and opportunity cost?

1.1 Economics and Economic System

1.1.1What you study in Economics?

Economics is concerned with addressing different economic questions that relate with

individuals, households, society and the economy in general. For instance, why students

like you decide to pursue additional education by paying fees? How does a given firm

(factory) decide what to produce, how much to produce and how to produce? How the

prices of copper and other minerals are determined in national and international markets?

How is the value of 1 Kwacha expressed with other currencies like Euro or USD? What

is the reason behind the 2008/2009 economic recession in most developed countries and

its impact on other developing countries? Economics addresses these and other questions

systematically and logically by analyzing economic units’ behavior.

Definitions of Economics

There is no universally accepted single definition of economics. Different

economists defined economics in different ways. Let us look at some of

the definitions made by prominent economists.

Economics is “an inquiry into the nature and causes of the wealth

of nations”

Adam Smith

“Economics is the science which studies human behavior as a

relationship between ends and scarce means which have

alternative uses”

Lionel Robbins

“Economics is the study of humankind in the ordinary business of

life; it examines that part of individual and social action which is

most closely connected with the attainment and with the use of the

material requisites of well being”

Alfred Marshall

“Economics is the study of how men and society choose, with or

without the use of money, to employ the scarce productive

resources which could have alternative uses, to produce various

commodities over time and distribute them for consumption now

and in the future amongst various people and groups of society”

Paul A. Samuelson

In general, economics is the study of the process and technique of

making choices and making allocation of resources aimed at maximizing

the gains. Economics also studies:

The total outcome of the economic activities of the people

participating in the economy.

The determination of national income, saving, investment and

growth of national income.

Trends in general price level, supply and demand of money and

their impact on the economy, public revenue and public

expenditure, economic policies and financial transactions, and

economic transactions among countries.

1.1.2 Distinction between Macroeconomics and Microeconomics

Economics is traditionally divided into two main branches called

Microeconomics and Macroeconomics. The prefixes, „micro‟ and „macro‟

have been derived from Greek words where „mikros = micro‟ means small

and „makros = macro‟ means big.

When an economic study deals with economic behavior of an individual

decision making unit (consumer and producer) or and economic variable

(price and quantity of a good) it is Microeconomics. And, when an

economic study deals with economic aggregates like national income,

general employment, aggregate consumption, savings and investment,

general price level and balance of payments position, etc is called

Macroeconomics.

There are a number of branches of economics under the umbrella of

microeconomics or macroeconomics. Some of these are Welfare

Economics, Resource Economics, Health Economics, Labor Economics

and International Economics.

1.1.3 Microeconomics and Choice

Because resources are scarce, choices have to be made by individuals,

groups or the government in order to address what is called the three

basic economic questions. Choices must be made in any society

regarding:

What and how much to produce. That is, what goods and services

are going to be produced and in what quantities, since there are

not enough resources to produce all the things people desire?

How to produce. That is, how are things going to be produced,

given that there is normally more than one way of producing

things? What resources are going to be used and in what

quantities? What techniques of production are going to be

adopted?

For whom to produce. That is, for whom are things going to be

produced? In other words, how will the nation‟s income be

distributed?

These three economic problems can be solved differently by the type of

economic system a given nation has.

1.1.4 Economic Systems

An economic system is a social organization through which people make

their living. It is constituted of all those individuals, households, farms,

firms, factories, banks and government which act and interact to

produce and consume goods and services.

1.1.5 Kinds of economic system

Depending on the degree of government control of the economy,

economies are generally classified as:

i. planned or command economy

ii. free-market economy

iii. mixed economy

(i) Planned or command economy

In this type of economic system all the economic decisions are taken by

the government. These economies are largely controlled, regulated and

managed by government agencies. It is usually associated with a socialist

or communist economic system, where land and capital are collectively

owned. The three basic economic questions are addressed by the state.

The state plans the allocation of resources between current

consumption and investment for the future.

At a micro level, it plans the output of each industry and firm, the

techniques that will be used, and the labor and other resources

required by each industry and firm.

It plans the distribution of output between consumers.

(ii)The free-market economy

In a free market, individuals are free to make their own economic

decisions. In this type of economy there is less government intervention

at all.

Consumers are free to decide what to buy with their incomes: free

to make demand decisions.

Firms are free to choose what to sell and what production methods

to use: free to make supply decision.

The demand and supply decisions of consumers and firms are

transmitted to each other through their effect on prices: through

price mechanism.

The prices that result are the prices that firms and consumers

have to accept.

(iii) The mixed economy

In practice, all economies are a mixture of both planned and free-

market system. Therefore, we can say it is the degree of government

intervention that distinguishes different economic systems in the

world.

In mixed market economies, the government may be involved in

affecting:

Relative prices of goods and inputs, by taxing or subsidizing

them or by direct price controls.

Relative incomes, by the use of income taxes, welfare payments

or direct controls over wages, profits etc.

The pattern of production and consumption, by the use of

legislation (e.g. making illegal the production of drugs (cocaine,

heroin), by direct provision of goods and services (e.g. education

and defense), by taxes and subsidies or by nationalization.

The macroeconomic problems of unemployment, inflation,

tradebalance (Import-Export), foreign exchange rate, by the use

of taxes and government expenditure, the control of bank

lendingand interest rates, the direct control of prices and the

control of the foreign exchange rate.

1.2 Using Diagrams and models in Economics

Economics discussion frequently uses diagrams. The reasons are:

- Diagrams are very useful for illustrating economic relationships.

- They show simplified pictures of reality.

- Ideas and arguments that might take long time to explain in words

can often be expressed clearly and simply in a diagram.

Economics also use models to make quantitative predictions. A model is

a mathematical representation, based on economic theory, of a firm, a

market or some other entity.

1.3 Scarcity, Choice and Opportunity cost

‘You can’t always get what you want’

Individuals, society and government have to make choices because of

certain basic facts of human life. These facts are related to human

beings‟ endless wants and the reality of there are only limited resources

in the world at any given time.

Human wants and desires are unlimited. The poor people as well as the

wealthiest people desire to consume more and better of different goods

and services. In general human wants are virtually unlimited.

The endless human wants are attributable to:

People have insatiable desire to raise their standard of living to a

level as high as possible.

Human nature is accumulative, i.e., people accumulate things

beyond their present need.

Human wants multiply with growth of human knowledge, science

and technology, which lead to production of new goods through

inventions and innovations.

Human wants are multiplicative. Introduction of a new commodity

create need for many others. For example, purchase of a car

creates demand for petrol, driver, parking place, spare parts,

insurance, etc.

Since resources (income) are not sufficient to satisfy all the wants

simultaneously, consumers have to make choice among their wants –

which wants to fulfill now and which want to fulfill later.

Resources are limited and scarce. While human wants are unlimited,

resources that are available to satisfy human wants are limited. At any

one time the world can only produce a limited amount of goods and

services. – The world only has limited amount of resources. These

resources (factors of production) are broadly classified as:

Human resource: the labor available both in number and skill at

any point of time is limited. Labor is limited by the size of

population.

Natural resource: land and raw materials are limited by the area of

a country.

Manufactured resource: The man-made resources like capital and

technology are limited by the scarcity of inputs that go into their

production, such as, Limited supplies of factories, machines,

transportation, telecommunication and other equipment. The

productivity of capital is also limited by the state of technology.

Furthermore, choice involves sacrifice. The more food you choose to buy,

the less money you will have to spend on other goods like fees for

education or buying a house. The more food a nation produces the fewer

resources will there be for producing other goods.

→The production and consumption of one thing involves the

sacrifice/ trade-off of other alternatives.

This sacrifice/ trade-off of alternatives in consumption or production of a

good or service is known as its opportunity cost.

→ The opportunity cost of any activity is the sacrifice made to do it.

It is the best thing that could have been done as an alternative.

→ It is the cost of the explicit and implicit resources that are

forgone when a decision is made.

Example: Assume the farmer can produce either 10,000 kgs of

wheat or 15,000 kgs of maize on his land. Thus, the opportunity

cost of producing 1 kg of wheat is 1.5 kgs of maize forgone. The

opportunity cost of overtime work could be the leisure (social affair)

you have sacrificed.

1.4 Rational choices

The assumption of rational choice is central for studying behavior of

economic units (individuals, firms, society and government). It simply

means, economic units weigh-up costs and benefits when they make

whatever economic decisions. For instance:

- Firms calculate costs and benefits when choosing what and how

much to produce

- Workers consider costs and benefits when choosing whether to

take a particular job or to work extra hours.

- Consumers do the same when they decide what to buy.

Particularly for consumers, a rational decision making refers choosing

those items that give you the best value for money, that is, the greatest

benefit relative to cost.

1.5The Production Possibility Curve

Production possibility curve is a curve that shows all the possible

combinations of two goods that a firm or for that matter a country can

produce within a specified time period with all its resources fully and

efficiently employed.

Example: Assume Zambia allocates all its resources (land, labor

and capital) for producing two goods, i.e., food and clothing.

Table 1.1 Maximum possible combinations of maize and copper that can

be produced in a given time period

From the above table you can see that, Zambia by allocating all its

resources for producing maize could produce 8 metric tons of maize but

no copper. Alternatively, by producing 6 metric tons of maize it could

release enough resources to produce 4 metric tons of copper in addition.

The information in the table can be translated into the following graph.

Units of maize

(in metric tons)

Units of copper

(in metric tons)

8 0

7 2

6 4

5 5

4 5.6

3 6

2 6.4

1 6.7

0 7

Figure 1.1 Production possibility curve for copper and maize

The above production possibilities curve (PPC) shows the maximum

combinations of output that the economy can produce using all

available resources. The curve displays a trade-off, that is, more of

maize production implies less of copper production (example point A).

The PPC shows the points at which the economy is producing

efficiently using the available resources and technologies. Points

above the PPC are unattainable points (example point D, because it

requires more resource than the economy has available).

Whereas, points inside the PPC (example point E) are attainable but

inefficient – since it indicates there are idle resources which can

increase production of both goods if used efficiently.

E

A

B

C

D

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7 8 9

Co

pp

er

in m

etr

ic t

on

es

Maize (in metric tones)

production possibility curve

Unit Summary Economics is the study of the process and technique of making

choices and making allocation of resources aimed at maximizing

the gains among individuals, households, firms, societies,

countries and so forth.

Economics is divided into two main branches. These are

microeconomics and macroeconomics.

The study of microeconomics deals with economic behavior of an

individual decision making unit (consumer and producer) or and

economic variable (price and quantity of a good).

The study of macroeconomics deals with economic aggregates like

national income, general employment, aggregate consumption,

savings and investment, general price level and balance of

payments position, etc is called Macroeconomics.

Any economic system must address the three basic economic

questions of what to produce, how to produce and for whom to

produce.

Since resources are scarce every human being is forced to make

choices for every economic activity. Every choice entails

opportunity cost.

The assumption of rational choice is central for studying behavior

of economic units or economic agents.

Production possibility curve shows all the possible combinations of

two goods that a country can produce within a specified time

period with all its resources fully and efficiently employed.

Unit Review Questions 1. The study of economics generally lies in the endless wants and

scarcity of resources. Explain

2. Do you think the study of microeconomics and macroeconomics

are exclusively separated studies? Why?

3. What is the relationship between scarcity, rational choice and

opportunity cost?

4. How do you interpret the economic difference between developed

countries and resource abundant poor countries using the PPF

model?

Unit Two

Market, Supply and Demand

Introduction

In this unit you will learn about the functioning of a market economic

system and its basic problems. How the three economic problems are

addressed in the market economic system and the role of price in this

system will be discussed. Mathematical application of theory of demand

and supply is also attached as an annex. This will give you a chance to

refresh your high school mathematics knowledge and to alert you, there

will be some mathematical applications of microeconomics in subsequent

chapters.

Upon completion of this unit you will be able to:

Understand and discuss the meaning and features of a market

Understand and discuss the role of price in a market economic

system

Understand and define the concepts of demand, supply and

market equilibrium

Familiarize and discuss different factors that affect demand,

supply and market equilibrium

2.1 Markets and Prices

In economics a market means a system in which sellers and buyers of a

commodity interact to settle the price and the quantity to be bought and

sold. The sellers and buyers may be individuals, firms, factories, dealers

and agents.

2.1.1 Basic features of a market

A market need not be situated in a particular place or locality. The

size of the market stretches from a local fish or vegetable market to

a worldwide market for automobiles, copper or medicines.

Buyers and sellers need not always come in personal contact with

each other. The transaction can be conducted through agents,

telephone, fax, postal services and internet.

The word „market‟ refers to either a commodity or service (e.g., fish

market, automobile market, money market, entertainment market)

or a geographical area (e.g., Lusaka market, London market,

Europe market).

In economics markets are further distinguished on the basis of

(1) On the nature of goods and services, e.g., factor market and

commodity market / input market and output market.

(2) Number of firms and degree of competition, e.g., competitive

market, monopoly market, Oligopolistic market and monopolistic

competitive market.

In unit one you recall that, the way the three basic economic problems

are addressed depends on the nature of the economic system. There we

said, in a free market system, the problems are solved by the market

(price) mechanism. Now let us see how the price mechanism solves the

basic economic problems in a free market economy system.

2.1.2 Addressing economic problems in a market system

What to produce?

The goods and services that are produced in a market economy are

determined by consumer demand. Only those goods and services which

are demanded by the consumers or users are produced by the producers.

Therefore, every kwacha a consumer spends on a commodity is treated

as a vote for producing that commodity. Continuing demand is a

continuous process of voting.

How to produce?

It is the question of choice of technology, that is, the proportion of labor,

capital and raw material used to produce a commodity. The choice of

resource combination is also determined by the market forces of supply

and demand.

For whom to produce?

The market rule for this problem is – produce for those who have ability

and willingness to pay. That is, in a free market mechanism, goods and

services are produced for those who possess the ability to pay.

Market (price) mechanism is a process through which the market

economy functions. The market economy functions through the market

forces of demand and supply. The demand and supply forces interact to

determine the price of goods and services. Therefore, a price system is

generated. The system is operated by, what Adam Smith called „invisible

hands’, i.e., the market forces of demand and supply.

Prices perform two functions in the market system.

1. Prices serve as signals for the producers to decide „what to

produce‟ and for the consumers to decide „what to consume‟.

2. Prices force the demand and supply conditions to adjust

themselves to the prevailing prices.

2.2 Demand

Demand can be defined as the desire for a good for whose fulfillment a

person has sufficient resources and willingness to pay for the good. A

desire without sufficient money income is a simple desire, not demand. A

desire with resources but without willingness to pay is a potential

demand.

→ A desire accompanied by ability and willingness to pay makes

the Real or Effective Demand.

2.2.1 Individual and Market Demand

Individual Demand can be defined as the quantity of a commodity that a

person is willing to buy at a given price over a specified period of time –

per day, per week or per month. On the other hand, Market Demand is

the total quantity that all consumers of a commodity are willing to buy at

given price over a specific period of time.

→ Market demand is the sum of individual demands.

2.2.2 The Law of Demand

The Law of Demand states the relationship between the quantity

demanded and price of a commodity. The law of demand is generally

associated with price. This is because, price is the most and often the

only determinant in the short-run period. In fact, we have other factors

which also affect the quantity demand and we will discuss them shortly.

→ Law of demand:All other things remaining constant, the quantity

demanded of a commodity increases when its price decreases and it

decreases when its price increases.

The law implies that quantity and price changes are inversely related.

The law of demand can be easily discussed by using a demand schedule

and demand curve.

2.2.3 The Demand Schedule

Demand Schedule is a tabular presentation of a series of prices of a

commodity with the corresponding quantities demanded. Let us consider

the following example.

Table 2.1 Demand schedule for maize

Price per kg (in

kwacha)

2,000 1,800 1,600 1,400 1,200 1,000

Quantity demanded (in

kgs)

100 150 200 300 400 500

Table 2.1 clearly illustrates the law of demand. As the price of maize

decreases, we can see that the demand for maize increases. For instance,

when price of maize is 2,000k, 100 kgs of maize is demanded per day.

When price decreases by half, i.e., to 1,000k, the demand for maize

increases to 500 kgs per day.

2.2.4 The Demand Curve

A Demand Curve is a graphical representation of the law of demand. The

demand curve can be obtained by plotting the demand schedule on a two

dimension graph.

Figure 2.1 Demand curve for maize

The curve DD is the Demand curve. The curve reflects the law of demand

and it is a downward curve to the right. It has a negative slope. The

negative slope of a demand curve shows the inverse relationship between

D

B

A

D

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0 20 40 60 80 100

Pri

ce o

f m

aiz

e (

in k

wach

a)

Quantity of maize (in kgs)

quantity demanded of maize and price of maize. It shows that demand

for maize increases as the price decreases and vice versa.

Why Demand Curve Slopes Downward to the Right?

The reasons behind the downward sloping demand curve or law of

demand are:

A. Income Effect: when the price of a commodity falls, the real income of

its consumers increases in terms of this commodity. In other words,

consumers‟ purchasing power increases since they are required to pay

less for the same quantity. Furthermore, increase in real income (or

purchasing power) increases demand for goods and services in general

and for the good with reduced price in particular. The increase in

demand due to an increase in income is called income effect.

B. Substitution Effect: when price of a commodity falls, it becomes

cheaper compared to its substitutes, other prices remaining constant, or,

the substitute becomes more costly. In general, consumers tend to

substitute cheaper goods for costly ones. The increase in demand on

account of this factor is called substitution effect.

2.2.5 Exceptions to the Law of Demand

The law of demand does not apply to the following cases:

I. Expectations regarding future prices: when consumers expect a

continuous increase in the price of a durable commodity, they buy

more of it despite increase in its price to avoid the burden of still

higher price in future. Similarly, sometimes consumers anticipate

a considerable decrease in the price in the future and they

postpone their purchases by waiting for the price to fall further.

II. Prestigious goods: the law of demand also does not apply to the

commodities which serve as a „status symbol‟ or display wealth

and richness. Example, gold, diamond, paintings and antiques.

These goods are still demanded by rich people despite their prices

increasing.

III. Giffen goods:the other exception to this law is the case of Giffen

goods named after Robert Giffen (1837 – 1910). A Giffen goods

does not mean any specific commodity. It may be any essential

commodity much cheaper than its substitutes, consumed mostly

by the poor households claiming a large part of their incomes. If

price of such goods increases (price of its substitute remaining

constant), its demand increases instead of decreasing.

2.2.6 Determinants of Market Demand

Until now we have discussed demand by holding everything constant

other than the price. But there are other factors than the price of a good

which influence demand. The following are the major demand affecting

factors in addition to price.

(i)Income

The consumer‟s income is the basic determinant of the quantity

demanded of a product. Because income affects the ability of consumers

to purchase a good, changes in income affect how much consumers will

buy at any price. That is why the people with higher disposable income

spend a larger amount of money on goods and services than those with

lower income.

In graphical terms, a change in income shifts the entire demand curve.

Whether an increase in income shifts the demand curve to the right or to

the left depends on the nature of consumer consumption pattern.

Accordingly, economists distinguish between two types of goods: normal

and inferior goods.

Normal goods

A good whose demand increases (a right shift in the demand curve)

when consumers‟ incomes rise is called a normal good. Food,

clothes, household furniture are some of the examples of this

category. As income goes up, consumers typically buy more of

these goods at any given price. Conversely, when consumers suffer

a decline in income, the demand for a normal good will decrease

(shift to the left).

Inferior goods

Sometimes, an increase in income reduces the demand for a good.

As income goes up, consumers typically consume less of these

goods at each price. But, you need to be careful for not interpreting

inferior goods as goods of poor quality. We use this term simply to

define products that consumers purchase less of it when their

incomes rise, and purchase more of it when their incomes fall.

(ii)The number and price of substitute goods (competitive goods)

Two commodities are considered to be substitutes for each other if a

change in the price of one affects the demand for the other in the same

direction. For example, tea and coffee, Pepsi and Coca cola, hamburger

and hot dog are common substitutes. The relation between demand for a

product and the price of its substitute is positive. When price of product

(say, tea) falls, then demand for its substitute (coffee) falls.

(iii) The number and price of complementary goods

Complementary goods are those that are consumed together. For

example, car and petrol, shoe and polish are common complimentary.

Technically, two goods are complement for one another if an increase in

the price of one causes a decrease in the demand for another. There is

aninverse relationship between the demand for a good and the price of its

complement. An increase in the price of petrol causes a decrease in the

demand for car, other things remaining the same.

(iv) Consumer‟s taste and preference

Consumer‟s taste and preferences play an important role in determining

the demand for a product. The more desirable people find the good, the

more they will demand. Taste and preferences depend, generally on the

social customs, values attached to a commodity, habits of the people, age

and sex of the consumers. For example, Zambians are highly attached to

their staple food Nshima. In today‟s modern world, tastes are also

affected by advertising, by fashion, by observing other consumers and by

considerations of health.

2.2.7 Movements along and shifts in the demand curve

The effect of a change in price on quantity demanded is simply a

movement along the demand curve. For example, in figure 2.1, a move

from point A to point B is caused by a change in price. In general we call

this change (move) a change in quantity demanded. In other words, any

change that arises from change in price is change in quantity demanded

and it is explained by movement along the same demand curve. Whereas

a change in other demand affecting factors than price leads to a change

in demand. If a change in one of the other determinants causes demand

to rise – say, income rises – the whole curve will shift to the right.

Generally, a change in demand is explained by a shift in the entire

demand curve.

A rightward shift in the demand curve is called an increase in demand,

since more of the good is demanded at each price. A leftward shift in the

demand curve is called a decreasein demand.

Figure 2.2 Movements along and shifts in demand curve

2.3 Supply

In a market economy, while buyers of a product constitute the demand

side of the market, sellers of that product make the supply side of the

market.

2.3.1 Market Supply

Supply means the quantity of a commodity which its producers or sellers

offer to sell at a given price, per unit of time. Market supply, like market

demand, is the sum of supplies of a commodity made by individual firms.

2.3.2 The Law of Supply

The supply of a commodity depends on its price and cost of production.

That is, supply is the function of price and production cost. The law of

supply is, however, expressed generally in terms of price-quantity

relationship. The law of supply can be stated as:

→ The supply of a product increases with the increase in its price

and decreases with decrease in its price, other things remaining

constant.

There are three reasons for this:

The higher the price of the good, the more profitable it becomes to

produce. That is, firms will be encouraged to produce more.

Given time, if the price of good remains high, new producers will

be encouraged to participate in production. Thus, total market

supply will increase.

As producers supply more, they are likely to find that beyond a

certain level of output, costs rise more and more rapidly. For

instance, costs are likely to rise as production increases because it

requires employing more workers, more payment for over time and

utilizing the machines to their maximum working capacity. If

higher output involves higher costs of producing each unit,

producers will need to get a higher price if they are to produce

additional output.

2.3.3 The Supply Schedule

The supply schedule is a tabular presentation of the law of supply. It

shows alternative price of a commodity and the corresponding quantity

that suppliers are willing to supply. Let us consider the following

example.

Table 2.2 Supply schedule for canned beef

Price

(in kwacha)

10,000 20,000 30,000 40,000 55,000 75,000

Supply (canned

beef in pcs)

10,000 35,000 50,000 60,000 75,000 80,000

From the table you can see that at price level of 10,000k per canned beef,

only 10 thousand canned beef are supplied per month. When prices

increase to 20,000, suppliers offer 35,000 canned beef and, when price

increased as much as 75,000 per canned beef, supply rises to 80

thousand canned beef.

2.3.4 The supply curve

The supply schedule can be represented graphically as a supply curve. In

figure 2.3 the curve SS is the Supply curve. The curve reflects the law of

supply and it is an upward curve to the right. In contrast to a demand

curve, a supply curve has a positive slope.

Figure 2.3 Supply curve for canned beefs

2.3.5 Other Determinants of Supply

Although price of a commodity is the most important determinant of

supply, there are also other factors that influence the supply of a

commodity.

(i) The costs of production

The higher the costs of production, the less profit will be made at any

price. As costs rise, firms will reduce production. The main reasons for a

change in costs are as follows:

S

A

B

C

S

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

0 20,000 40,000 60,000 80,000 100,000

Pri

ce (

in k

wach

a)

Quantity supplied (canned beef)

Change in input prices: costs of production will increase if payment

for labor, raw materials and capital increase.

Change in technology: Technological changes that reduce cost of

production or increase efficiency increase the product supply.

Organizational changes: A lot of cost can be saved by reorganizing

the production system.

Government policy: Firm‟s cost may increase (example due to

higher tax) or decrease (example by getting subsidy).

Labor productivity: Firms could enjoy efficiency in cost

minimization as they recruit the required proportionate amount of

skilled labor with other inputs (such as capital).

(ii)Price of alternative products (substitutes in supply)

In many kinds of production activities, it is possible to produce a

substitute product. If a product which is a substitute in supply becomes

more profitable to supply than before, producers are likely to switch from

the first good to this alternative. For example if a refrigerator price goes

up the company may decide to reduce the production of Air conditioners‟

production in order to produce more refrigerators.

(iii)Expectation of future price changes

If price is expected to rise, producers may temporarily reduce the amount

they sell. In order to gain more from future higher price, they tend to

keep the stocks.

(iv) Number of Suppliers.

If size of the industry increases due to new firms joining the industry, the

total supply will increase.

2.3.6 Movements along and shifts in the supply curve

The effect of a change in price on quantity supplied is simply a movement

along the supply curve. For example, in figure 2.3, a move from point A to

point B or from B to C is caused by a change in price. In general we call

this change (move) a change in quantity supplied. In other words, any

change that arises from change in price is change in quantity supplied

and it is explained by movement along the same supply curve. Whereas,

a change in other supply affecting factors than price leads to a change in

supply. Generally, a change in supply is explained by a shift in the entire

supply curve.

A rightward shift in the supply curve illustrates an increase in supply,

since more of the good is supplied at each price. A leftward shift in the

demand curve on the other hand illustrates a decreasein supply.

2.3 Equilibrium of Demand and Supply

In the previous sections, you have seen the demand and supply sides of

the market and how demand and supply behave in response to a change

in price and other factors. Now, we can combine the analysis of demand

and supply and see how they form a balance, how market attains

equilibrium, and how equilibrium price is determined in a free market

and competitive market.

2.3.1 The Concept of Equilibrium

The term equilibrium means the „state of rest‟ – a point where conflicting

interests are balanced. It indicates the condition where forces working in

opposite direction are in balance. In market context:

→ Equilibrium refers to a state of market in which the quantity

demanded of a commodity equals the quantity supplied of the

commodity. The equality of demand and supply produces an

equilibrium price and output.

In general, at equilibrium price, demand and supply are in equilibrium.

And, the equilibrium price is called market-clearing price because at this

point a market clears when supply matches demand, leaving no shortage

or surplus.

2.3.2 Determination of market price

The equilibrium price in a free market is determined by the market forces

of demand and supply. Let us consider the following example to

understand how the market forces bring the suppliers‟ plan in balance

with the buyers‟ plan.

Table 2.3 Demand and supply schedule for maize

Price

(per kg)

Demand

for maize

(in kgs)

Supply

of maize

(in kgs)

Market

position

Effect on

price

1,200 400 100 Shortage Rise

1,400 300 150 Shortage Rise

1,600 200 200 Equilibrium Stable

1,800 150 250 Surplus Fall

2,000 100 300 Surplus Fall

As the above table shows you, there is a single price, 1,600K, at which

the market is in equilibrium. At this point the quantity demanded and

the quantity supplied is equal at 200 kgs of maize. Other price levels

than this indicatedisequilibrium in the market price. That is, there is

either an excess of demand over supply or an excess of supply over

demand. At all prices below 1,600 K, demand exceeds supply showing

shortage of maize in the market. Again, at all prices above 1,600 K

supply exceeds demand showing surplus supply.

Figure 2.4 Market equilibrium

Price

D S

Pe

S D

Qe Quantity

Graphically, market equilibrium is attained at the intersection point of

the demand curve (DD) and the supply curve (SS) as shown above in

figure 2.4. At the point of intersection the market clears out at a price

level of Pe and quantity level of Qe.

2.3.3 Shift in Demand or Supply Curve and Market Equilibrium

The equilibrium price will remain unchanged as long as the demand and

supply curves remain unchanged. But, a shift in either demand or

supply curves (due to other factors than price), will cause for a new

equilibrium to be formed.

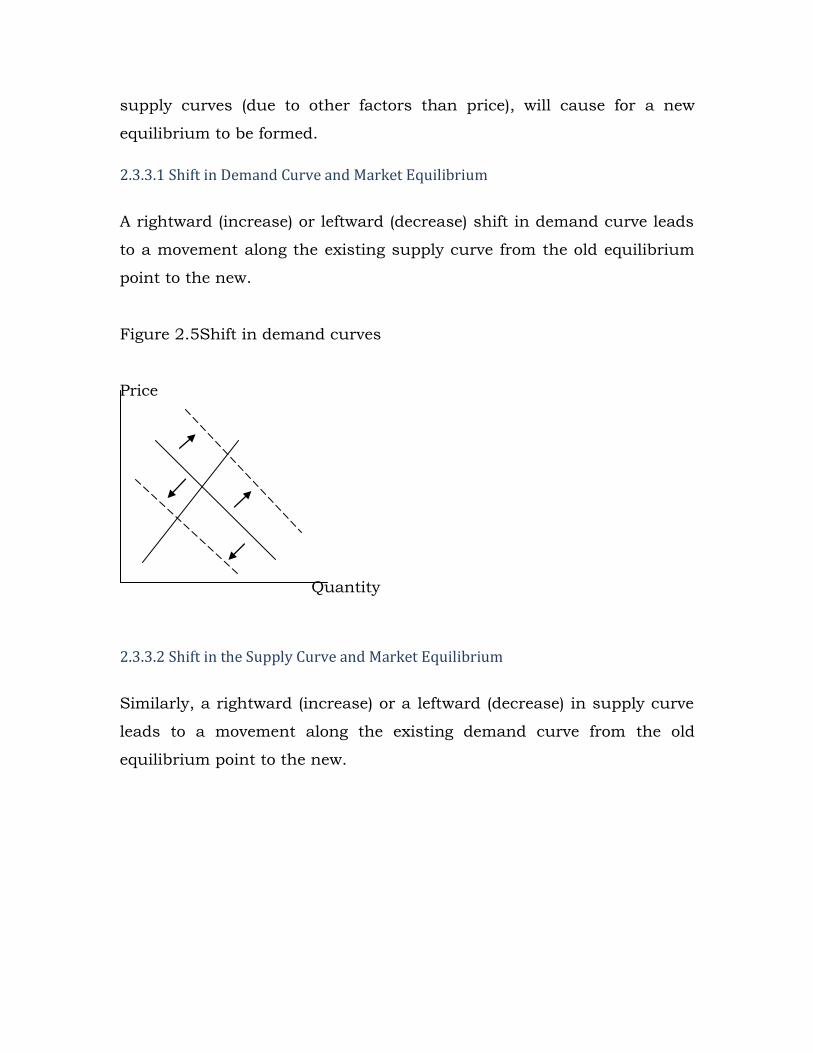

2.3.3.1 Shift in Demand Curve and Market Equilibrium

A rightward (increase) or leftward (decrease) shift in demand curve leads

to a movement along the existing supply curve from the old equilibrium

point to the new.

Figure 2.5Shift in demand curves

Price

Quantity

2.3.3.2 Shift in the Supply Curve and Market Equilibrium

Similarly, a rightward (increase) or a leftward (decrease) in supply curve

leads to a movement along the existing demand curve from the old

equilibrium point to the new.

Figure 2.6Shift in supply curves

Price

Quantity

2.3.4Algebra of Demand, Supply and Equilibrium

Beside graphical representation of demand, supply and equilibrium

analysis, economics often use algebraic representation for better clarity

and precision.

2.3.4.1Demand Function

Demand function represents the market demand for a good and the

determinants of demand in the form of equation.

The demand function for a commodity can take an equation form:

Qd = a – bP

Where, Qd is quantity demanded

P is price of the good

-b is slope of the demand curve (recall that quantity demand

and price are negatively related)

a is the constant term, which equals the quantity demanded

if price is zero.

This equation relates quantity demanded to price. In other words, the

equation assumed that all the other determinants of demand remain

constant (ceteris paribus). For example, the actual equation might be:

Qd = 100 – 5P

Now from this you can easily calculate a complete demand schedule and

demand curve by assigning a hypothetical price levels.

This simple equation can be expanded by incorporating other demand

affecting factors. For example demand function of the form:

Qd = a – bP + cY + dPs

describes that, the quantity demanded (Qd) is determined by price (P)

which is negatively related; level of consumer income(Y) which is

positively related; and price of the substitute good (Ps) which is positively

related.

2.3.4. 2Supply function

Likewise, supply function represents the market supply for a good and

the determinants of supply in the form of equation.

A supply function can take a form:

Qs = c + dP

Where, Qs is quantity supplied

P is the price f the good

d is slope of the supply curve (recall that quantity supplied

and price are positively related)

c is the constant term, which equals quantity supplied if

price is zero

This equation relates quantity supplied to price. In other words, the

equation assumed that all the other determinants of supply remain

constant (ceteris paribus). For example the actual equation might be:

Qs = 25P

Again by taking hypothetical values for price it is easy to construct both

supply schedule and supply curve.

More complex supply equations would relate supply to more than one

determinant. For instance:

Qs = 4 + 8P – 5Ps + 12Pc

This supply equation shows that, the quantity supplied (Qs) is

determined by price (P) which is positively related; price of substitute

goods(Ps) which is negatively related; and price of the complementary

good (Pc) which is positively related.

2.3.4.3Demand – Supply Equilibrium

Once we have the demand and supply functions it is easy to calculate

equilibrium price and equilibrium output levels.

Let us consider that supply and demand equation for a given market is

as follows:

Qd = a – bP (1)

Qs = c + dP (2)

Now we can find the market equilibrium price by setting the two

equations equal to each other – taking the fact that, equilibrium is a

situation where demand and supply are equal in the market.

c + dP = a – bP

Subtracting c form the left side and adding bP to both sides will give us:

dP + bP = a – c

(d + b)P = a – c

P = a – c

d + b (3)

For calculating equilibrium quantity (Q𝜖), we need to substitute equation

(3) in either the demand function - (1) or the supply function - (2).

Therefore, from equation (1)

Q𝜖 = a – b (a – c)

(d + b)

= a (d + b) – b(a – c)

d + b

= ad + ab – ba + bc

d + b

= ad + bc

d + b

or from equation (2)

Q𝜖= c + d (a – c)

(d + b)

= cd + cb + da − dc

d + b

= cb + da

d + b

Unit Summary Market is a system in which sellers and buyers of a commodity

interact to settle the price and the quantity to be bought and sold.

A market can be defined as a commodity or service, as a

geographical area, by the nature of goods and services or by the

number of firms and degree of competition.

While, Individual Demand refers to the quantity of a commodity

that a person is willing to buy at a given price over a specified

period of time; Market Demand is the total quantity that all

consumers of a commodity are willing to buy at given price over a

specific period of time.

The law of demand states that, the quantity demanded of a

commodity increases when its price decreases and it decreases

when its price increases holding other factors constant.

While Supply refers to the quantity of a commodity which its

producers or sellers offer to sell at a given price, per unit of time;

Market supply is the sum of supplies of a commodity made by

individual firms.

The law of supply states that, a product‟s supply increases with

the increase in its price and decreases with decrease in its price,

other factors remaining constant.

Equilibrium refers to a state of market in which the quantity

demanded of a commodity equals the quantity supplied of the

commodity.

Unit Review Questions 1. What is the difference among desire, effective demand and

potential demand?

2. What is the relationship between law of demand and the slope of a

demand curve?

3. Which demand factors cause a shift in the demand and supply

curves from their original positions?

4. Given the demand function Q= 30 – 5P, develop a demand

schedule and derive a demand curve?

5. From the demand function Qd = 100 – 15P and a supply function

Qs = 10P calculate,

(a) Equilibrium price

(b) Equilibrium quantity

(c) The gap between demand and supply at P=2 and P=6

Unit Three

Elasticity of Demand

Introduction

In this unit you will extend your knowledge of theory of demand to

understand a new concept known as elasticity of demand. As you recall,

the laws of demand and supply simply states the nature (not the extent)

of relationship between the changes in price and quantity demanded and

supplied respectively, at different price levels. But in most cases we want

to know by how much the quantity demanded or quantity supplied

changed for a given change in price.

Upon completion of this unit you will be able to

Define the concept of elasticity, price elasticity of demand and

income elasticity of demand.

Measure demand elasticity for changes in market price and

consumer‟s income.

Discuss the different uses of the concept of elasticity in economic

activities.

3.1 Price Elasticity of Demand

For certain types of goods, a given percentage change in price brings

about a small change in quantity demanded (quantity supplied),

whereas, for another good it will result in a big change. So, how much

are these small and big changes? This problem is addressed by the

measure of responsiveness of demand and supplyto change in price.

The price elasticity of demand is generally defined as the degree of

responsiveness or sensitiveness of demand for a commodity to the

changes in its price. That is, elasticity of demand is the percentage change

in the quantity demanded of a commodity as a result of a certain

percentage change in its price. We use percentage or proportionate

changes since price and quantity are measured in different units.

Price elasticity of demand is one of the most important concepts in

economics. For example, if we know the price elasticity of demand for a

product, we can easily predict the effect on price and quantity of a

change for an increase or decrease of supply.

3.1.1 Measuring the price elasticity of demand

In measuring price elasticity of demand our interest is in knowing the

size of change in quantity demanded with the size of the change in price.

The formula for the price elasticity of demand for a product is percentage

(or proportionate) change in quantity demanded divided by the

percentage (or proportionate) change in price.

A general formula for calculating coefficient of price-elasticity (PϵD) is:

PϵD = Percentage change in quantity demanded

Percentage change in price

=

𝑄1−𝑄0𝑄0

𝑃1−𝑃0𝑃0

= ∆Q

Qo÷

∆P

Po

We use the absolute value sign to avoid negative elasticity results

= ∆Q

Qo×

Po

∆P

Where Qo = original quantity demanded, Po = original price, ∆Q = change

in quantity demanded, and ∆P = change in price. We use the symbol 𝜖for

elasticity, and ∆ for a „change in‟.

Example: given original price (Po) = 10, new price (P1) = 20, original

quantity demanded (Qo) = 40, and new quantity (Q1) = 20

Thus, ∆P = (P1) − (Po) = 20 – 10 = 10 and

∆Q = (Q1) − (Qo) = 20 – 40 = −20

P𝜖D = ∆Q

Qo×

Po

∆P =

−20

40×

10

10 = −0.5 = 0.5

(Recall that the absolute value of any number is positive)

3.1.2 Interpreting elasticity figures

(i) The sign (positive or negative)

Demand curves are generally downward sloping. This means price and

quantity change in opposite direction. A rise in price (a positive figure)

will cause a fall in the quantity demanded (a negative figure). Likewise, a

fall in price will cause a rise in the quantity demanded. Therefore, our

final elasticity figure is negative and for convenience as we said above we

consider it as a positive value (but keeping in mind the inverse

relationship between price and quantity demanded).

(ii) The value (greater or less than 1)

As we have said, if we ignore the negative sign and concentrate on the

value of the figure, it tells us whether demand is elastic, inelastic or unit

elastic.

Elastic (𝜖> 1): This is where a change in price causes a

proportionately larger change in the quantity demanded. That is, a

case when 1 percentage change in price will brings about a more

than 1 percentage change in quantity demanded. The value of

elasticity will be greater than 1 since we are dividing a larger figure

by a smaller figure.

Inelastic (𝜖< 1): This is where a change in a price causes a

proportionately smaller change in the quantity demanded. That is,

a case when 1 percentage change in price will brings about a less

than 1 percentage change in quantity demanded. The value of

elasticity will be less than 1 since we are dividing a smaller figure

by a larger figure.

Unit elastic (𝜖 = 1): Unitary elasticity of demand occurs where price

and quantity demanded change by the same proportion. That is, a

case when 1 percentage change in price will brings about an equal

1 percentage change in quantity demanded. The value of elasticity

will be equal to 1 since we are dividing equal figures.

3.1.3 Determinants of price elasticity of demand

The elasticity of demand varies from commodity to commodity. While the

demand for some commodities is highly elastic, for some it is highly

inelastic. What determines price elasticity of demand?

i. Number and closeness of substitute goods: this is the most

important determinant. The more substitutes there are for a good,

and the closer they are, the greater will be the elasticity of demand

for a commodity. For instance, consider coffee and tea as close

substitutes for one another. If price of coffee increases, then tea

becomes relatively cheaper and consumers switch to the

consumption of more tea.

Beside closeness, the wider the range of the substitutes, the

greater will be the elasticity. For instance, soaps, toothpastes,

cigarettes are available in different brands, each brand being a

close substitute for the other.

ii. Nature of commodity: commodities can be in general grouped as

luxuries and necessities. Demand for luxury goods (cars, costly TV

sets, decoration items etc) is more elastic because consumption of

these goods can be postponed when their prices rise. On the other

hand demand for necessity goods (food, cloths, electricity, water

etc) cannot be postponed, and hence their demand is inelastic.

iii. The proportion of income spent on the good: if proportion of income

spent on a commodity is very small, its demand will be less elastic,

and vice versa. For instance salt and matches have a very low price

elasticity of demand. Part of the reason is that there are no close

substitutes. But part is that we spend a small fraction of our

income on these goods that we would find little difficulty in paying

a relatively large percentage increase in prices. On the other hand,

the higher the proportion of our income we spend on a good, the

more we will be forced to cut consumption when its price rises.

iv. Time factor: price elasticity of demand also depends on the time

consumers take to adjust to a new price – the longer the time

taken, the greater will be the elasticity. When price rises, people

may take time to adjust their consumption patterns and find

alternatives. For instance, if price of cars is decreased demand will

not immediately increase unless people possess strong purchasing

power.

3.1.4 Special cases in price elasticity of demand

i. Totally inelastic demand (P𝜖D = 0): No matter what happens to

price, quantity demanded remains the same.

ii. Infinitely elastic demand (P𝜖D = ∞): At any price above P1 demand is

zero. But at P1 (or any price below) demand is infinitely large.

iii. Unit elastic demand (P𝜖D = 1): this is where price and quantity

change in exactly the same proportion. Any rise in price will be

exactly offset by a fall in quantity.

3.2 Arc and point elasticities

The measure of elasticity of demand between two finite points on a

demand curve is known as arc elasticity. We use the name arc elasticity

when change in price is significantly high (different from zero). For

instance, when a price changes by 5%, 15% or more. It shows a

movement from one point on the demand curve to another point. The

formula we developed earlier is basically for measuring arc elasticity.

Note, however that, in most cases the elasticity will vary along the length

of a given demand curve. That is, the measurement refers to the

elasticity of a portion of the demand curve, not of the whole curve.

Sometimes, rather than measuring elasticity between two points on a

demand curve, we may want to measure it at a single point. In this case,

the point elasticity measure of elasticity at a finite point on a demand

curve will be an appropriate tool. Point elasticity may be defined as the

proportionate change in quantity demanded in response a very small

proportionate change in price.

The point elasticity (an infinitesimally small change) may be symbolically

expressed as:

dQ

dP×

P

Q

Where, dQ dP is the differential calculus term for the rate of change of

quantity with respect to a change in price. Conversely, dP/dQ is the rate

of change of price with respect to a change n quantity demanded. In fact,

at any point on the demand curve, dP/dQ is given by the slope of the

curve (its rate of change).

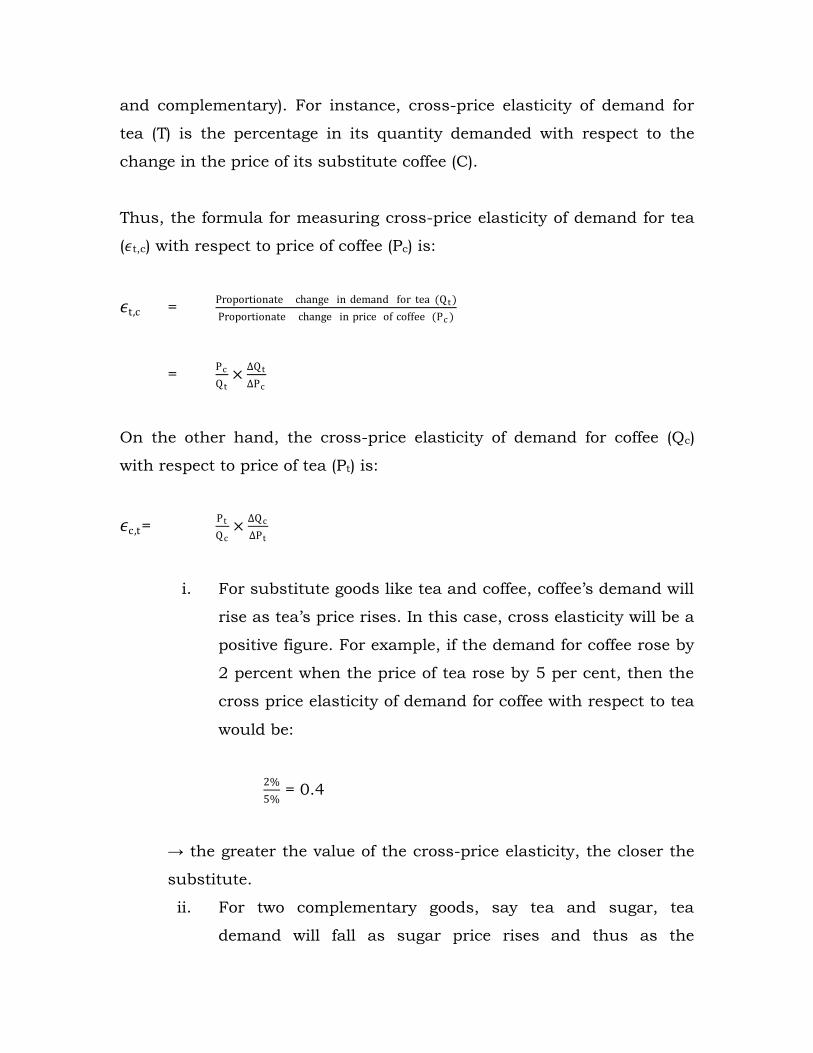

3.3 Cross-price elasticity of demand

The cross-price elasticity of demand measures the responsiveness of the

demand for a good to changes in the price of a related good (substitutes

and complementary). For instance, cross-price elasticity of demand for

tea (T) is the percentage in its quantity demanded with respect to the

change in the price of its substitute coffee (C).

Thus, the formula for measuring cross-price elasticity of demand for tea

(𝜖t,c) with respect to price of coffee (Pc) is:

𝜖t,c = Proportionate change in demand for tea (Q t )

Proportionate change in price of coffee (Pc )

= Pc

Q t×

∆Q t

∆Pc

On the other hand, the cross-price elasticity of demand for coffee (Qc)

with respect to price of tea (Pt) is:

𝜖c,t= Pt

Qc×

∆Qc

∆Pt

i. For substitute goods like tea and coffee, coffee‟s demand will

rise as tea‟s price rises. In this case, cross elasticity will be a

positive figure. For example, if the demand for coffee rose by

2 percent when the price of tea rose by 5 per cent, then the

cross price elasticity of demand for coffee with respect to tea

would be:

2%

5% = 0.4

→ the greater the value of the cross-price elasticity, the closer the

substitute.

ii. For two complementary goods, say tea and sugar, tea

demand will fall as sugar price rises and thus as the

quantity of sugar demanded falls. In this case, cross price

elasticity of demand will be a negative figure. For example, if

a 4% rise in the price of sugar led to a 2% percent fall in

demand for tea, the cross elasticity of demand for tea with

respect to sugar would be:

2%

4% = - 0.5

→ the greater the value of negative cross-price elasticity, the higher

the degree of complementarity.

Some applications of cross-price elasticity For a given firm knowing the cross-price elasticity

of demand for its product is important during production plan. The firm must know the cross price elasticity of demand for their product when considering the effect on the demand for their product of a change in the price of rival’s product (substitute) or of a complementary good.

The other important application of this concept is

international trade. A nation must address the question, how does a change in the price of domestic goods affect the demand for imports? In most of the cases, if there is a high cross elasticity of demand for imports, and if prices at home rise due to inflation or other reasons, the demand for imports will rise substantially, and this will have a negative impact on the nation’s trade balance.

3.4 Income elasticity of demand

Apart from price of a product and related goods, another important

determinant of demand for a product is consumer‟s income. Thus,

income elasticity of demand (Y𝜖D) measures the responsiveness of

demand to a change in consumer incomes (Y). This measurement helps

us to predict how much the demand curve will shift for a given change in

income.

As you recall from earlier discussions, we said that, the relationship

between demand for normal goods and consumer‟s income is of positive

nature, unlike the negative price – demand relationship. That is, the

demand for normal goods and services increases with increase in

consumer‟s income and vice versa.

The formula for income-elasticity of demand for a product is: the

percentage (or proportionate) change in demand divided by the

percentage (or proportionate) change in income.

Y𝜖D = % ∆ QD

% ∆ Y

Thus, if a 2 percent rise in income caused a 5 percent rise in a product‟s

demand, then its income elasticity of demand would be:

5%

2% = 2.5

The major determinant of income elasticity of demand is the degree of

„necessity‟ of the good. When an economy develops, like the case for

developed countries, the demand for luxury goods expands rapidly as

people‟s incomes rise, whereas the demand for basic goods rises only a

little.

For instance, in most cases demand for vehicles, recreation and

entertainment have a high income elasticity of demand, whereas

items like vegetables have a low income elasticity of demand.

The other fact is, demand for some goods decreases as people‟s incomes

rise beyond a certain level. These are inferior goods. As people earn more,

they switch to a better quality of such inferior goods.

Some applications of income-elasticity The concept of income-elasticity can be used to

estimate future demand provided the rate of increase in income and income-elasticity of demand for the products are known. – Useful for firms in forecasting demand when changes in personal incomes are expected, holding other things constant.

It also can be used to define the ‘normal and ‘inferior’ goods. The goods whose income-elasticity is positive for all levels of income are termed as ‘normal goods’. On the other hand, the goods for which income elasticities are negative, beyond a certain level of income, are termed as ‘inferior goods’.

Unit Summary Elasticity describes the responsiveness of demand to changes in

price, income or other variables.

The value of the elasticity measure tells us whether the change is

elastic, unitary elastic or inelastic.

Number and closeness of substitute goods, nature of the

commodity, proportion of income spent on the good and time are

the major determinant factors of price elasticity of demand.

The cross-price elasticity of demand measures the responsiveness

of the demand for a good to changes in the price of a related good –

substitute or complementary good.

For substitute goods, demand will rise as price rises; but for

complementary goods demand will decrease as price rises.

Unit Review Questions 1. In a given demand curve there are different elasticity values

between different points. Explain.

2. Give an example of a good or a service that you know will have

totally elastic or infinitely inelastic demand nature.

3. Given the demand function Q= 30 – 2P,

(a) Calculate the elasticity and interpret the result for the fall in

price from 6 to 4

(b) Calculate the elasticity and interpret the result for the increase

in price from 8 to 10

Unit Four

Theory of Consumer Behavior

Introduction

This unit illustrates basic tools to understand the behavior of individuals

as consumers and the impact of alternative incentives on their decision.

The major focus will be on understanding how consumers behave in

market place. Again we use unit two‟s discussion of demand theory to

further analyze how a consumer decides how much of a good to buy at a

given price and why he/she buys more/less of a good when the price

changes. In general, you will understand how consumers respond to the

alternative choices that confront them.

Upon completion of this unit you will be able to

Discuss the different approaches to consumer behavior analysis.

Familiarize yourselves to different measurements of consumer

satisfaction (utility).

Understand and discuss consumer equilibrium in terms of utility

and indifference curve analysis.

4.1 Consumer Behavior

A consumer is an individual who purchases goods and services from

firms for the purpose of consumption. And, consumer behavior is about

how consumers decide on the basket of goods and services they

consume. It is essentially a decision-making behavior.

4.1.1 Approaches to consumer behavior analysis

We begin with an important axiom (assumption) that a consumer is a

utility maximizing entity. As a utility maximizing entity, the consumer

buys goods and services in such a way that he will generate maximum

utility from consumption. Utility refers to the power or property of a

commodity to satisfy human needs – a feeling of pleasure or a feeling of

satisfaction. A consumer who attempts to get the best value for the

money from his or her purchases is referred by economists as a rational

consumer.

4.1.2 Measuring utility

The question of measurability of utility is not a resolved concept among

economists. In one hand, economists hold that utility is quantitatively

measurable in absolute terms like weight and height of a person. On the

other hand, other groups of economists hold that utility is only ordinal

measurement – like high, higher, highest etc.

For our discussion we will ignore this unresolved problem and assume

that a person‟s utility can be measured in utils, where a util is one unit of

satisfaction.

4.2 Total and marginal utility

In order to understand more on the concept of utility we need to look at

the distinction between total utility and marginal utility.

4.2.1 Total utility (TU)

Total utility from a single commodity, may be defined as the sum of the

satisfaction derived from all the units consumed of the commodity within

a given time period. If a consumer consumes 4 units of apple a day, her

daily total utility from apple would be the satisfaction derived from those

apples. That is:

TU = U1 + U2 + U3 + U4

If she consumes n units, then total utility (TU) from n units is expressed

as:

TU𝑛 = U1 + U2 + U3 + … + U𝑛

And in case the number of commodities consumed is greater than one:

TU = Ua + Ub + Uc + … + U𝑛

Where subscripts a, b, c and n represent the consumption of different

commodities in a given period, say within a day.

4.2.2 Marginal utility (MU)

The marginal utility is the additional satisfaction gained from consuming

one extra unit within a given period of time. Thus from our example, we

might refer to the marginal utility that the consumer gains from her

second or fourth apple within a day.

→ Marginal utility is the change in the total utility resulting from

the change in the consumption. That is:

MU = ∆ TU

∆ C

Where ∆ TU = change in total utility, and ∆ C = change in consumption

Marginal utility (MU) can be also expressed as:

MU = MUn – (MUn−1)

4.3Law of diminishing marginal utility

This law states that as the quantity consumed of a commodity increase,

over a unit of time, the utility derived by the consumer from the successive

units goes on decreasing. Up to a certain level, the more of a commodity a

consumer consumes, the greater will be the total utility. However, as one

becomes more satisfied, each extra unit that the consumer consumes

will probably give a lesser additional utility than previous units. –

marginal utility falls, the more we consume a commodity within a given

time period.

For example, the second apple gives the consumer less additional

satisfaction than the first. The third and the fourth give less satisfaction

still. At some level of consumption, consumers‟ total utility will be at a

maximum. It will become hard to generate extra satisfaction by

consuming of further units within a given period of time. The sixth or

seventh unit of eating apple within an hour may result in zero marginal

utility. The tenth or eleventh unit of apple may give displeasure –

negative marginal utility.

The next table represents a numerical illustration of the law of

diminishing marginal utility. As you can see from the table, total utility

increases with increased in consumption of sausage, but at a decreasing

rate. This means, marginal utility decreases with increase in

consumption.

Table 4.1 Consumer‟s utility from consuming sausages per day

Units of sausage

consumed TU in utils MU in utils

0 0 0 – 0 = 0

1 15 15 – 0 = 15

2 25 25 – 15 = 10

3 30 30 – 25 = 5

4 32 32 – 30 = 2

5 30 30 – 32 = - 2

6 20 20 – 30 = - 10

The law of diminishing marginal utility is graphically illustrated in figure

4.1 and 4.2. The total utility and marginal utility curves have been

obtained by plotting the data given in table 4.1 above.

Figure 4.1 Total utility curve for sausage consumption

Figure 4.2 Marginal utility curve for sausage consumption

Note the following points from the total and marginal utility curves.

TU

0

5

10

15

20

25

30

35

0 2 4 6 8

To

tal u

tili

ty

Sausage consumed per unit of time

MU

-15

-10

-5

0

5

10

15

20

0 1 2 3 4 5 6 7

Marg

inal u

tili

ty

Sausages consumed per unit of time

The MU curve slopes downwards. This is due to the law of

diminishing marginal utility.

The TU curve starts at the origin. Zero consumption yields zero

utility.

TU reaches a peak when MU is zero. MU can be derived from the

TU curve since, MU = ∆ TU

∆ C

4.4 Consumer Equilibrium

As we said earlier, a consumer is assumed as a utility maximizer. A

consumer reaches equilibrium position, when she maximizes her total

utility given her income and prices of commodities she consumes.

Considering the consumer‟s money (payment to the commodity) will help

us to resolve the problem of measuring utils that we mentioned earlier.

Measuring utility with money means, utility becomes the value that a

rational consumer places on her consumption.

Marginal utility therefore becomes the amount of money a consumer

would pay to obtain one more unit, that is, what the extra unit is worth

to the consumer. Generally, analyzing consumer‟s equilibrium requires

answering the question as to how a consumer allocates her money

income among the various goods and services she consumes.

4.4.1 Consumer equilibrium – one commodity case

A utility maximizing consumer reaches her equilibrium position when

allocation of her expenditure is such that the last Kwacha spent on each

commodity yields the same utility. How does the consumer reach this

position?

Suppose that a consumer with a given level of money income consumes

only one commodity, X. Both money income and commodity X have

utility for the consumer. She has an option of either spend her money

income on commodity X or retain it with her.