Michigan State Housing Development Authority Agenda

136

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY A G E N D A June 16, 2022 – 10:00 a.m. JUNE 21, 2022 4:00 P.M 735 East Michigan Ave., Lansing, MI 48912 3028 West Grand Blvd., Room 4-602, Detroit, MI 48202 Conference Line: 248-509-0316 | Conference ID: 644 107 820# Roll Call: Public Comments: Remarks: Chairperson Executive Director Voting Issues: Tab A Approval of Agenda CONSENT AGENDA ITEMS Consent Agenda (Tabs B through D are Consent Agenda items. They are considered routine and are to be voted on as a single item by the Authority. There will be no separate discussion of these Tabs; any Authority member, however, may remove any Tab or Tabs from the Consent Agenda prior to the vote by notifying the Chair. The remaining Tabs will then be considered on the Consent Agenda. Tabs removed from the Consent Agenda will be discussed individually.) Tab B Minutes – May 19, 2022 Tab C Resolution Authorizing Professional Services Contract for Auditing Services with Plante Moran, PLLC and Michigan Office of Auditor General Tab D Resolution Authorizing Modification of Workforce Attainable Modular Homes Program aka “MSHDA Mod” REGULAR VOTING ITEMS Tab E Resolution Approving 2022-2023 Budget Tab F Resolution Authorizing Modifications To Mortgage Loan for Field Street III, MSHDA Development No. 3928, City of Detroit, Wayne County Resolution Authorizing Mortgage Resource Fund Loan, Field Street III, MSHDA GOLDENROD TAB A

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Michigan State Housing Development Authority Agenda

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

A G E N D A June 16, 2022 – 10:00 a.m. JUNE 21, 2022 4:00 P.M

735 East Michigan Ave., Lansing, MI 48912 3028 West Grand Blvd., Room 4-602, Detroit, MI 48202

Conference Line: 248-509-0316 | Conference ID: 644 107 820#

Roll Call:

Public Comments:

Remarks:

Chairperson

Executive Director

Voting Issues:

Tab A Approval of Agenda

CONSENT AGENDA ITEMS

Consent Agenda (Tabs B through D are Consent Agenda items. They are considered routine and are to be voted on as a single item by the Authority. There will be no separate discussion of these Tabs; any Authority member, however, may remove any Tab or Tabs from the Consent Agenda prior to the vote by notifying the Chair. The remaining Tabs will then be considered on the Consent Agenda. Tabs removed from the Consent Agenda will be discussed individually.)

Tab B Minutes – May 19, 2022

Tab C Resolution Authorizing Professional Services Contract for Auditing Services with Plante Moran, PLLC and Michigan Office of Auditor General

Tab D Resolution Authorizing Modification of Workforce Attainable Modular Homes Program aka “MSHDA Mod”

REGULAR VOTING ITEMS

Tab E Resolution Approving 2022-2023 Budget

Tab F Resolution Authorizing Modifications To Mortgage Loan for Field Street III, MSHDA Development No. 3928, City of Detroit, Wayne County

Resolution Authorizing Mortgage Resource Fund Loan, Field Street III, MSHDA

GOLDENROD TAB A

WardL10

Cross-Out

Development No. 3928, City of Detroit, Wayne County Tab G Resolution Authorizing Modifications to Mortgage Loans for HOM Flats at Maynard,

MSHDA No. 3955, City of Grand Rapids, Kent County Tab H Resolution Determining Mortgage Loan Feasibility, Clawson Manor, MSHDA

Development No. 4026, City of Clawson, Oakland County Tab I Resolution Determining Mortgage Loan Feasibility, River’s Edge, MSHDA No. 4029,

City of Kalamazoo, Kalamazoo County Resolution Authorizing Mortgage Loan, River’s Edge, MSHDA No. 4029, City of

Kalamazoo, Kalamazoo County Tab J Resolution Authorizing Approval of Delegated Authority to Approve Grants to

Subrecipients Financed Through the Housing Opportunities Promoting Energy Efficiency (“HOPE”)

Tab K Resolution Authorizing Approval of Delegated Authority to Issue Grants from the State and Local Fiscal Recovery Fund to the City of Detroit and The Heat and Warmth

Fund Closed Session None.

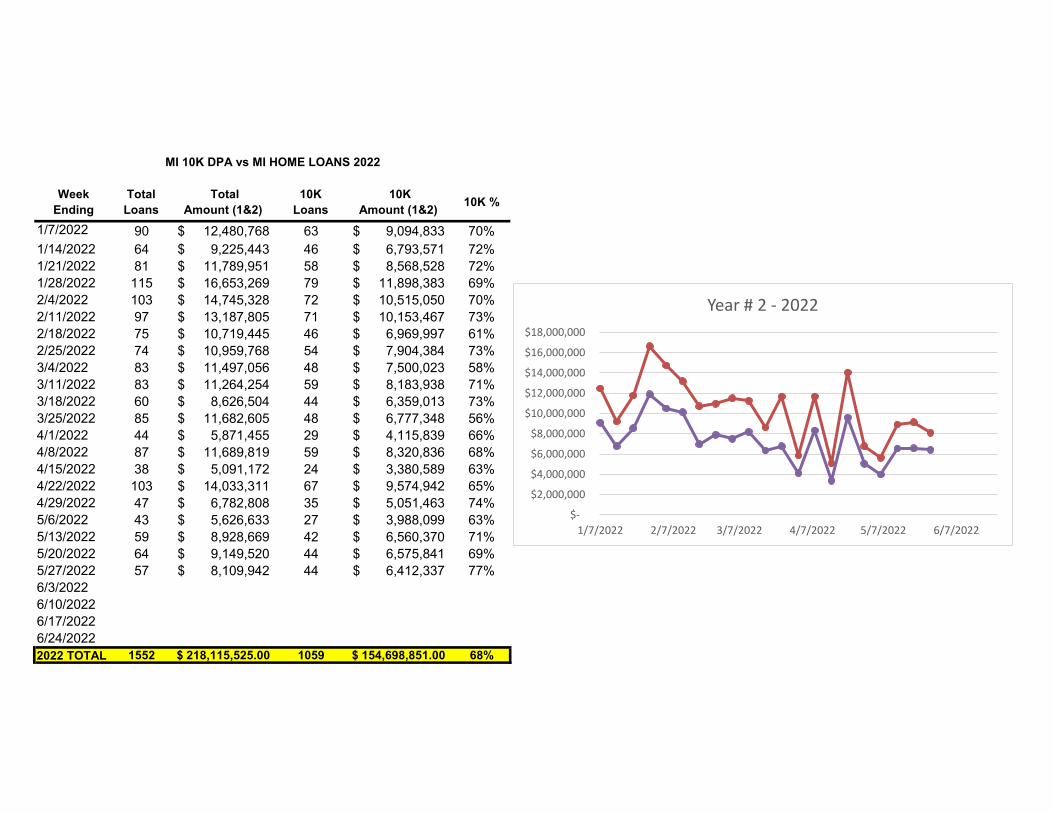

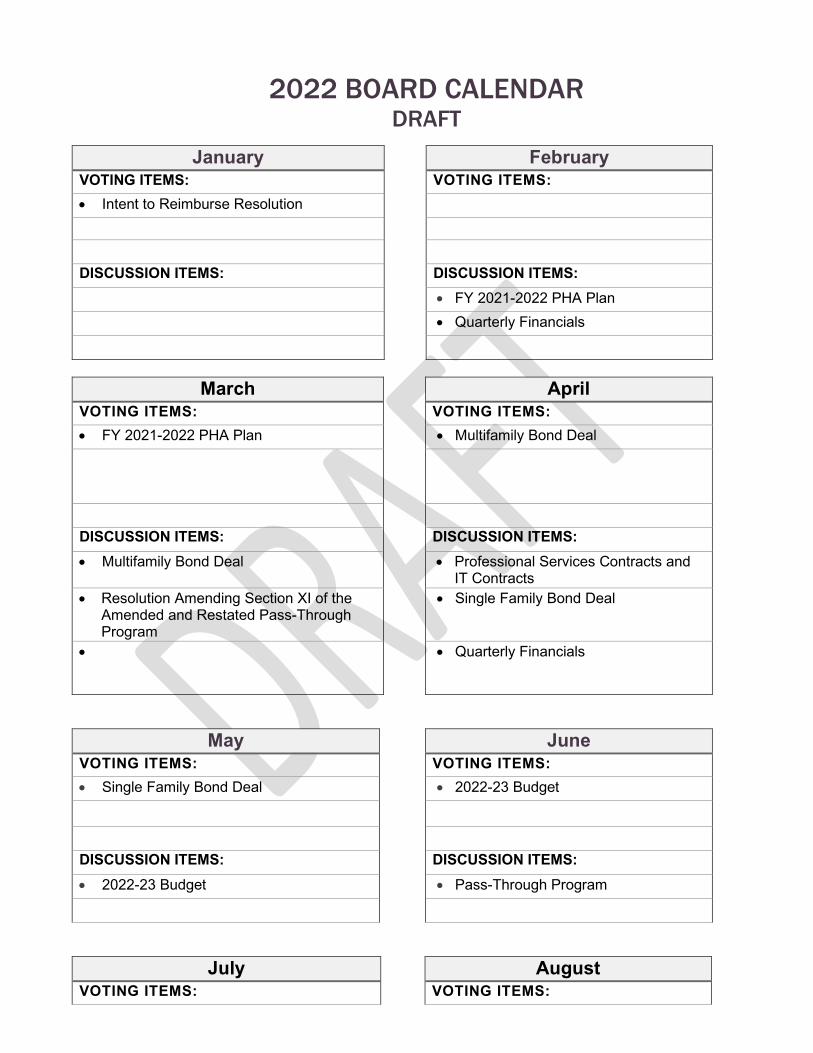

Discussion Issues: None. Reports: Tab 1 Current and Historical Homeownership Data Tab 2 Homeownership Production Report Tab 3 MI 10K DPA Monthly Statistics (Map) Tab 4 MI 10K DPA Weekly Statistics (Graph) Tab 5 2022 Board Calendar Tab 6 Draft - Amended and Restated Pass-Through Bond Program

Michigan State Housing Development Authority Minutes of Regular Authority Meeting

May 19, 2022 – 10:00 a.m.

AUTHORITY MEMBER(S) PRESENT IN LANSING Regina Bell Susan Corbin Carl English Rachael Eubanks Jennifer Grau Deb Muchmore Michele Wildman for Quenton L. Messer, Jr. AUTHORITY MEMBER(S) ABSENT Tyrone Hamilton OTHERS PRESENT IN LANSING Clarence Stone, Legal Affairs Lisa Ward, Legal Affairs Mary Cook, Operations Chris Hall, Information Technology Mark Whitaker, Information Technology Andrew Minegar, MIRS Sandy Pearson, Habitat for Humanity OTHERS PRESENT VIA MICROSOFT TEAMS Gary Heidel, Acting Executive Director Michelle Jenks, Executive Richard Norton, Legal Affairs Jonathan Hilliker, Audit, Compliance and Fraud Investigation Jeff Sykes, Finance Justin Wieber, Asset Management Chad Benson, Rental Development Elizabeth Rademacher, Rental Development John Hundt, Rental Development Sherry Hicks, Operations Mary Townley, Homeownership Katie Bach, Communications Anna Vicari, Communications

Troy Thelen, Asset Management Mark Garcia, Executive Tiffany King, Office of Equity and Engagement Daphne Wells, Operations Carol Brito, Homeownership Joe Kelly, Procurement Amber Martin, Human Resources Lindsey Schmitt, Human Resources Michael Vollick, Environmental Office Matthew Miller, Legal Affairs Bret Bicoy, Legal Affairs Tonya Young, Neighborhood Housing Initiatives Jennifer Bowman, Executive Charles Smith, Rental Development Michael Fobbe, Office of Attorney General John Millhouse, Office of Attorney General Amy Patterson, Office of Attorney General James Kiefer, Dykema Jarrod Smith, Dykema Kris Nied, Miller Canfield Ronald Liscombe, Miller Canfield Seven additional members of the public participated via the Conference Line: 248-509-0316, Conference ID: 644 107 820#. Chairperson Susan Corbin opened the meeting at 10:03 a.m. A quorum was established with the presence of Ms. Corbin, Regina Bell, Carl English, Jennifer Grau, Deb Muchmore and Michele Wildman. Rachael Eubanks joined the meeting at 10:46 a.m. While Authority members were present in Lansing, presenters participated via Microsoft Teams. At Ms. Corbin’s request, Jonathan Hilliker provided instructions for those participating remotely, including guidelines on how to provide public comment via the conference line. Ms. Corbin began the meeting by requesting public comments from participants. Luke Forrest from the Community Economic Development Association of Michigan (CEDAM) thanked the Authority for its support of the Small Town and Rural Development Conference. The conference recently took place in Crystal Mountain, Michigan and was in-person for the first time in three years. Mr. Forrest noted that Authority staff hosted a session on the Statewide Housing Plan and provided information on new funding opportunities available through the American Rescue Plan. He further thanked Authority staff members Tonya Young and Haywood Edwards for their contributions to the event, as well as Authority member Michele Wildman, who served as a judge for the Put Your Town on the Map competition. There being no additional public comment, Ms. Corbin mentioned that there was a goldenrod for the memorandum that covers Tabs E through H. She then provided an update on the Executive Director position by noting there has been ongoing dialogue with the Department of

Housing and Urban Development concerning the exceptions and waivers being sought for Amy Hovey. She is hopeful there will be an update available soon. Following Ms. Corbin’s remarks, Acting Executive Director Gary Heidel provided a brief recap of the Building Michigan Communities Conference (BMCC). He stated that responses to the Statewide Housing Plan have been positive, and the BMCC was a great success. Mr. Heidel further recognized the staff responsible for the event, as well as the Statewide Housing Plan, including Karen Gagnon, Tiffany King, and David Allen. He also recognized the efforts of the Communications Team, including Katie Bach and Molly Ford. To conclude his remarks, Mr. Heidel announced the unveiling of the “We Are MSHDA Wall” during Employee Appreciation Week. The wall celebrates the lives of three former employees—Terrance Duvernay, George Fox, and James Butler--who impacted MSHDA’s culture. Mr. Heidel further noted that the tribute was planned and implemented by staff. Approval of Agenda: Deb Muchmore moved approval of Tab A (Agenda). Michele Wildman supported. The agenda was approved. Voting Items: Consent Agenda (Tabs B through D). Jennifer Grau moved approval of the consent agenda. Regina Bell supported. The Consent Agenda was approved. The Consent Agenda included the following items: Tab B Minutes - April 21, 2022 Tab C Resolution Authorizing Execution of Memorandum of Understanding and Internal

Agency Agreement with Michigan Department of Environment, Great Lakes, and Energy

Tab D Resolution Authorizing Professional Services Contractor for Racial Equity Impact

Assessment Regular Voting Items: Jeff Sykes, Chief Financial Officer, Jarrod Smith, Bond Counsel with Dykema, and Kris Nied, Bond Counsel with Miller Canfield, presented the following items:

• Tab E: Michigan State Housing Development Authority Series Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2022 Series A in an Amount Not to Exceed $300,000,000.

• Tab F: Michigan State Housing Development Authority Series Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2022 Series B in an Amount Not to Exceed $125,000,000.

• Tab G: Michigan State Housing Development Authority Series Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2022 Series C (Federally Taxable) in an Amount Not to Exceed $75,000,000; and

• Tab H: Michigan State Housing Development Authority Resolution Approving Actions Relating to Certain 2017 Swap Transaction for Single-Family Mortgage Revenue Bonds.

Mr. Sykes presented the business terms of Tabs E, F, G and H. Although Rachael Eubanks was not present for this portion of the meeting, Mr. Sykes assured Authority members that he had many discussions with her concerning these items. Following Mr. Sykes’ presentation, Mr. Smith presented the bond resolutions for Tabs E, F, and G. Ms. Nied presented the bond resolution for Tab H. John Millhouse of the Attorney General’s Office confirmed that the documents for Tabs E, F, G and H were acceptable for Board’s action. Clarence Stone, Director of Legal Affairs, confirmed that the documents for Tabs E, F, G and H were acceptable for Board’s action.

Carl English moved approval of Tab E. Jennifer Grau supported. The following Roll Call was taken for Tab E: There were 6 “yes” votes. The resolution was approved. Carl English moved approval of Tab F. Regina Bell supported. The following Roll Call was taken for Tab F:

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

There were 6 “yes” votes. The resolution was approved. Deb Muchmore moved approval of Tab G. Regina Bell supported. The following Roll Call was taken for Tab G: There were 6 “yes” votes. The resolution was approved. Jennifer Grau moved approval of Tab H. Deb Muchmore supported. The following Roll Call was taken for Tab H: There were 6 “yes” votes. The resolution was approved. Jeff Sykes, Chief Financial Officer and Kris Nied, Bond Counsel with Miller Canfield, presented the following items:

• Tab I: Michigan State Housing Development Authority Sixth Resolution Supplementing Se Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2007 Series B in an Amount not to Exceed $215,000,000

• Tab J: Michigan State Housing Development Authority Third Resolution Supplementing Series Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2007 Series F in an Amount Not to Exceed $95,000,000

• Tab K: Michigan State Housing Development Authority Fifth Resolution Supplementing Series Resolution Authorizing the Issuance and Sale of Single-Family Mortgage Revenue Bonds, 2009 Series D in an Amount Not to Exceed $110,000,000

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Mr. Sykes presented the business terms of Tabs, I, J and K. Ms. Nied presented the bond resolutions of Tabs I, J, and K. John Millhouse of the Attorney General’s Office confirmed that the documents for Tabs, I, J and K were acceptable for Board’s action. Clarence Stone, Director of Legal Affairs, confirmed that the documents for Tabs, I, J and K were acceptable for Board’s action. Carl English moved approval of Tab I. Michele Wildman supported. The following Roll Call was taken for Tab I: There were 6 “yes” votes. The resolution was approved. Carl English moved approval of Tab J. Deb Muchmore supported. The following Roll Call was taken for Tab J: There were 6 “yes” votes. The resolution was approved. Carl English moved approval of Tab K. Deb Muchmore supported. The following Roll Call was taken for Tab K: There were 6 “yes” votes. The resolution was approved.

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Regina Bell Yes Jennifer Grau Yes

Susan Corbin Yes Tyrone Hamilton Absent

Carl English Yes Deb Muchmore Yes

Rachael Eubanks Absent Michele Wildman Yes

Rachael Eubanks joined the meeting following the vote on Tab K at 10:46 a.m. Elizabeth Rademacher, Rental Development, presented Tab L: Resolution Adopting the Second Amendment to the 2022-2023 Qualified Allocation Plan for the Housing Tax Credit Program. Ms. Rademacher reviewed the documents as detailed in the board docket. Michele Wildman moved approval of Tab L. Jennifer Grau supported. The resolution was approved. John Hundt, Rental Development, presented Tab M: Resolution Authorizing Modifications to Mortgage Loan for Westchester Village South, MSHDA Development No. 3788, City of Saginaw/Saginaw Township, Saginaw County. Mr. Hundt reviewed the documents as detailed in the board docket. Carl English moved approval of Tab M. Deb Muchmore supported. The resolution was approved. Justin Wieber, Asset Management, presented Tab N: Resolution Authorizing Waiver of Mortgage Loan Prepayment Prohibition, Elmcrest Village, MSHDA No. 3061, City of Flushing, Genesee County. Mr. Wieber reviewed the documents as detailed in the board docket.

Jennifer Grau moved approval of Tab N. Rachael Eubanks supported. The resolution was approved. Justin Wieber, Asset Management, presented Tab O: Resolution Authorizing Waiver of Mortgage Loan Prepayment Prohibition, Valley View III, MSHDA Development No. 1033, Township of Ionia, Ionia County. Mr. Wieber reviewed the documents as detailed in the board docket. Michele Wildman moved approval of Tab O. Regina Bell supported. The resolution was approved. There being no additional discussion, Ms. Corbin announced the following reports were included in the docket for reference: (Tab 1) MSHDA Proposed 2022-2023 Budget; (Tab 2) Current and Historical Homeownership Data; (Tab 3) Homeownership Production Report; (Tab 4) MI 10K DPA Monthly Statistics (Map); (Tab 5) MI 10K DPA Weekly Statistics (Graph); and (Tab 6) 2022 Board Calendar. Ms. Corbin noted that the next regular board meeting would be June 16, 2022. She then requested a motion to adjourn the meeting. Michele Wildman moved to adjourn, and Regina Bell supported. The meeting adjourned at 11:01 a.m.

WardL10

Reviewed

stonec

Reviewed

M E M O R A N D U M

TO:

FROM:

DATE:

RE:

Authority Members

Gary Heidel, Acting Executive Director

June 16, 2022 JUNE 21, 2022

Resolution Authorizing Professional Services Contract with Plante Moran, PLLC as External Auditor

RECOMMENDATION:

I recommend that the Michigan State Housing Development Authority (the “Authority”) authorize a one-year extension of the professional services contract as a third-party beneficiary for external audit services. Principal parties to the contract are the Office of Auditor General (“OAG”) and Plante Moran, PLLC (“Contractor”).

CONTRACT SUMMARY:

Name of Contractor: Plante Moran, PLLC Amount of Contract:

• $160,745 for financial audit of fiscal yearending June 2022, including expenses

• Additional services billed between $112and $223/hour

Length of Contract: 1 year Extension Options: Third-party yearly extensions Request for Start Date: July 1, 2022 Number of Bids Received: 0 MSHDA Division Requesting the Contract: Finance

EXECUTIVE SUMMARY:

Services Requested / Benefit: The Authority requires an independent, third-party contractor to perform certain annual audits. Independent auditing, in accordance with audit-industry standards, benefits the Authority by demonstrating the quality of its financial controls to the public, bond investors, and governmental-oversight authorities.

The Authority is a third-party beneficiary to a contract executed in 2012 between the OAG and the Contractor for performance of an annual end-of-year financial audit of the Authority and an additional single audit of the Authority pursuant to the Single Audit Act Amendments of 1996

GOLDENROD TAB C

WardL10

Reviewed

WardL10

Cross-Out

(“Public Law 104-156”). The OAG has extended the 2012 contract with the Contractor to continue providing auditing and related services in accordance with the terms and conditions of the contract. Following OAG’s periodic extensions of the contract, the Authority has likewise re-authorized engaging in and renewing this contract as a third-party beneficiary. The current third-party beneficiary approval will expire on June 30, 2022.

By renewing as a third-party beneficiary to the contract, the Authority will ensure continuation of the audit and related services with minimal disruption to the Authority, assuring compliance with audit requirements. If approved, the contract will expire on June 30, 2023.

Amount of Contract: Costs of the contract are based on: (a) actual hours spent on the engagements, which shall not exceed $160,745 (previously $150,640 for 2021) for the 2022 financial audit and (b) additional allowances for cap increase if there are major new programs with bond offerings and other services to be billed between $112/hour and $223/hour (previously $107/hour and $213/hour, for 2021, respectively).

Meeting Expectations: The Contractor has consistently met and/or exceeded expectations and has been approved by the OAG to provide the described services.

Milestones and Track Record: Milestones are set in the prior and proposed contract extensions in the form of demonstrated adherence to industry standards and deadlines for production of audit reports. The Contractor has successfully met milestones in performing prior contracts.

Risk to Authority: Preparation of audits involves performing procedures to obtain the auditor’s judgment, including the assessment of the risk of material misstatement of the financial statements, whether due to fraud or error. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. The risk to the Authority of engaging in the proposed contract is similar to that facing the Authority with any other audit-service provider. This Contractor’s positive past performance and approval by the OAG mitigates such risk.

ADVANCING THE AUTHORITY’S MISSION:

• The continued provision of quality audit services by the Contractor will aid the Authority indata-driven decision making.

• Agreement to adopt the contract as approved by the OAG demonstrates partnercollaboration within State government.

COMMUNITY ENGAGEMENT/IMPACT

Not applicable.

ISSUES, POLICY CONSIDERATIONS, AND RELATED ACTIONS:

None.

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

RESOLUTION AUTHORIZING PROFESSIONAL SERVICES CONTRACT FOR AUDITING SERVICES WITH PLANTE MORAN, PLLC AND

MICHIGAN OFFICE OF AUDITOR GENERAL

June 16, 2022 JUNE 21, 2022

WHEREAS, pursuant to Act 346 of the Public Acts of 1966 (“Act”), the Michigan State Housing Development Authority (“Authority) has approximately $3.51 billion in outstanding bonds to assist in the development of affordable housing for low and moderate income Michigan households; and

WHEREAS, to induce the investment community to market and purchase Authority bonds, the Authority has made certain promises including the promise to provide annual financial audits of the Authority prepared by independent, nationally recognized accounting firms; and

WHEREAS, timely preparation of the audited financial statements is required under covenants with bond holders, rating agencies, and credit enhancement providers among others; and

WHEREAS, the Authority’s Act provides the Authority with independent, statutory authority to contract with privately held firms to conduct its financial audits; and

WHEREAS, in 2012, the Authority became a third-party beneficiary to a contract between the Michigan Auditor General’s Office (“OAG”) and Plante Moran, PLLC, following an OAG competitive bid process, to provide independent financial audit, a single audit, and services related to bond offerings and other non-audit services; and

WHEREAS, the OAG has periodically extended the original 2012 contract and the Authority has followed in-kind, periodically extending its approval to continue as a third-party beneficiary to the contract; and

WHEREAS, the Authority’s approval to continue as a third-party beneficiary to the OAG contract is set to expire on June 30, 2022; and

WHEREAS, terms and conditions of the contract include increased costs, including increasing the dollar amount previously authorized by the Authority for the financial audit to an amount not to exceed $160,745; and

WHEREAS, the portion of the contract related to preparation of a single audit will not be renewed at this time; and

WHEREAS, the terms and conditions of the contract include a fee increase for services related to bond offerings and other non-audit services to hourly rates ranging from $112/hour to $223/hour; and

WHEREAS, the Acting Executive Director recommends that the Authority continue as a third-party beneficiary to the OAG contract with Plante Moran, PLLC, to obtain the services described in the accompanying memorandum; and

GOLDENROD TAB C

WardL10

Cross-Out

WHEREAS, the Authority concurs with the recommendations of the Acting Executive Director.

NOW THEREFORE, Be It Resolved by the Michigan State Housing Development Authority, that the Executive Director, the Chief Financial Officer, the Director of Legal Affairs, the Deputy Director of Legal Affairs, or any person duly authorized to act in any of the foregoing capacities, is each hereby authorized to execute, on behalf of the Authority, a third-party beneficiary contract to provide services described in the contract between the Michigan Office of the Auditor General and Plante Moran, PLLC, for the performance of a financial audit, and services related to bond offerings and other non-audit services, as set forth in the accompanying memorandum.

1

M E M O R A N D U M

TO:

FROM:

DATE:

Authority Members

Gary Heidel, Acting Executive Director

June 16, 2022 JUNE 21, 2022

RE: Recommendation to Authorize a Modification of the Workforce Attainable Modular Homes ("MSHDA Mod") Program

RECOMMENDATION:

I recommend the Michigan State Housing Development Authority (the "Authority") adopt a resolution authorizing revisions to the MSHDA Mod Program that was permanently adopted on September 24, 2020, to facilitate implementation of the program by local communities.

The program's primary objective is to enhance opportunities for economic development by providing new affordable single-family housing in areas where there is a housing shortage for moderate income households. The MSHDA Mod Program facilitates and encourages the construction of housing units at an attainable price point.

EXECUTIVE SUMMARY:

MSHDA Mod is designed to encourage building partnerships and increase housing capacity at the local level. It also promotes discussion between community representatives and employers on meeting local workforce housing needs and serves as a catalyst for communities to take an active role in attracting and retaining working families.

The program was developed in response to local officials demonstrating a market need for affordable, workforce single-family housing. Modular homes are typically constructed at the factory, shipped to the site, and assembled by a licensed builder who adds the other site amenities such as a basement, porch, garage, driveway, and landscaping. Modular homes are similar in quality to stick-built homes but typically have a shorter construction timeline, require less local housing capacity, reduce oversight and typically reduce construction waste. Under the pilot program, the Authority provided a repayable grant to the sponsor to acquire and install an initial modular home that could be used as a spec model for up to five (5) years. Once the initial home was sold, the funds received from the sale could be recycled to the grantee to acquire and install additional modular homes for sale in the same community.

Progress to date includes grants awarded to seventeen (17) communities--nine (9) local units of government, six (6) non-profit organizations, and two (2) for-profit developers:

GOLDENROD TAB D

WardL10

Cross-Out

2

• City of Coldwater• Kalamazoo Neighborhood Housing Services (Kalamazoo)• City of Beaverton• Bethany Housing Ministries Community Encompass (Muskegon)• Big Rapids Housing Commission• Northeast Michigan Habitat for Humanity (Harrisville)• Barry County Community Foundation (Hastings)• Northern Michigan Limited Dividend Housing Association, LLC (Grayling)• City of Dowagiac• Marquette County Land Bank Authority (Ishpeming)• Four County Community Foundation (Imlay)• Village of Cassopolis• Detroit Land Bank Authority (Detroit)• City of Albion• Habitat for Humanity of St. Joseph County (Three Rivers)• Jones Construction and Development LDHA, LLC (Detroit)• Genesee County Land Bank Authority (Flint)

PROGRAMMATIC RECOMMENDED MODIFICATIONS TO EXISTING AND FUTURE AWARDS:

• Increase the maximum grant term to thirty-six (36) months.• Increase the maximum grant for eligible costs to $250,000.• Remove the limit on using recycled funds in the same community to allow for the

redistribution of MSHDA Mod grant funds across the state to grantees in othercommunities. Any funds that are repaid to the Authority by the grantee, including intereston the repayable grant, will be eligible for recycling.

The MSHDA Mod program guidelines, policies, and implementing agreements will be revised once the recommended programmatic changes are approved by the Authority.

ADVANCING THE AUTHORITY’S MISSION:

• Workforce housing is an important part of the Authority's housing strategy to expandavailable resources to create and preserve housing that addresses the workforce housingshortage in some Michigan communities.

• The MSHDA Mod Program increases access to housing opportunities in rural communitiesand urban neighborhoods.

MUNICIPAL SUPPORT:

Nine (9) local governments are participating in the program. Other local governments have expressed significant interest or solicited local non-profits to participate.

COMMUNITY ENGAGEMENT/IMPACT:

• One hundred percent (100%) of completed homes have sold (12 of 12 builds).• Thirty-nine (39) occupants are enjoying their new homes.• Three (3) households are first-time homebuyers.

3

• At least four (4) homes are workforce housing (less than 10 miles from buyer’s worklocation).

• A competitive funding round award occurred in spring of 2022, with homes expected to bedelivered in 2023.

• Based on contracts in place, it is anticipated that eight (8) new homes will be constructedin 2023, after adopting the recommended programmatic revisions listed above.

ISSUES, POLICY CONSIDERATIONS, AND RELATED ACTIONS:

Through analysis of the program, it is determined that the proposed revisions are necessary to accommodate local needs and the current economic situation. Approval of these revisions will enable the program to accommodate unforeseen COVID-19-related impacts on construction, including material cost increases, time delays resulting from material shortages/supply chain issues, and labor constraints.

In addition, the program revisions will allow flexibility to redirect the dollars statewide in areas experiencing workforce housing shortages instead of limiting the resources to previous MSHDA Mod communities and grant recipients.

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

RESOLUTION AUTHORIZING MODIFICATION OF WORKFORCE ATTAINABLE MODULAR HOMES PROGRAM aka "MSHDA MOD"

June 16, 2022 JUNE 21, 2022

WHEREAS, the Michigan State Housing Development Authority (the "Authority") is authorized under Public Act No. 346 of the Public Acts of 1966, as amended, to analyze housing conditions and needs in this state and to formulate new and better techniques and methods for increasing the supply of housing; and

WHEREAS, it has been determined that there is a critical need for new affordable housing in areas experiencing job growth in this state, and on September 24, 2020, the Authority adopted the Workforce Attainable Modular Homes ("MSHDA Mod") Program; and

WHEREAS, on April 22, 2021, the Authority adopted modifications to the MSHDA Mod Program; and

WHEREAS, the Acting Executive Director is recommending further modifications to the MSHDA Mod Program, as described in the accompanying memorandum; and

WHEREAS, the Authority concurs in the recommendations of the Acting Executive Director.

NOW, THEREFORE, Be It Resolved by the Michigan State Housing Development Authority as follows:

1. That the modifications to the MSHDA Mod Program, as described in the accompanyingMemorandum dated June 16, 2022, JUNE 21, 2022 are hereby approved.

GOLDENROD TAB D

WardL10

Cross-Out

WardL10

Cross-Out

M E M O R A N D U M

TO: Authority Members

FROM: Gary Heidel, Acting Executive Director

DATE:

RE:

June16, 2022 JUNE 21, 2022

The Michigan State Housing Development Authority’s 2022 – 2023 Proposed Budget

RECOMMENDATION:

I recommend that the Michigan State Housing Development Authority (the “Authority”) review and comment on the Authority’s 2022-2023 Budget (the “Budget”).

EXECUTIVE SUMMARY:

The Budget was developed with input from all divisions within the Authority, the review of prior years’ experience, with consideration of the uncertainty created by the COVID pandemic and the unprecedented amount of Federal Resources to be administered by the Authority. The Authority’s annual budget was developed with consideration given to the Authority’s Strategic and Operational Plans.

A few notable items include:

• Net Interest Income is down as higher rate mortgages are refinancing and being modifiedto lower rate mortgages. This was due to the lower interest rate environment experiencedin the prior fiscal year and single-family mortgages (approximately $85 million) beingmodified into lower rate mortgages, due to an FHA requirement. These reductions will bepartially offset by higher returns on investments. Net Interest Income is generated whilethe Authority is meeting its Mission to provide quality affordable housing.

• Salaries and Fringes have increased ($3.2 million) due to the administration of Federalresources. At the conclusion of these temporary programs, it is expected that Salariesand Fringes will decrease.

• Mortgage Servicing Fees continue to increase, primarily due to increased single-familymortgage balances and the anticipated higher cost of servicing delinquent loans and loanmodifications as borrowers come out of their forbearance agreements.

• The Authority is targeting a 1.00% return on Net Assets, bringing a budgeted increase inNet Assets of $8.5 million.

• By targeting a 1.00% increase in Net Assets, the Authority can provide $10.2 million ingrants for the 2022-23 fiscal year.

GOLDENROD TAB E

WardL10

Cross-Out

Michigan State Housing Development Authority 2022-23 BUDGET(000's Omitted)

PROPOSED ESTIMATED 12 MONTH BUDGETBUDGET 12 MONTH BUDGET ESTIMATED INCREASE

22-23 21-22 21-22 VS. BUDGET (DECREASE)Revenue:

Net interest income $62,957 1 $61,739 $67,606 ($5,867) ($4,649)HCV/FSS fees 17,700 2 17,740 17,500 240 200Fees - Other federal programs 14,053 3 13,425 13,580 (155) 473Preservation fee income 100 4 125 100 25 0LIHTC Fees 4,100 5 4,985 3,900 1,085 200Contract Administration fees 12,500 6 12,500 12,000 500 500Gain (loss) on retirement of bonds 2,500 7 1,775 1,350 425 1,150Gain (loss) on sale of investments 0 8 0 0 0 0Gain on sale of mortgages 950 9 1,096 960 136 (10)Miscellaneous income 7,940 10 14,200 4,084 10,116 3,856

Total Revenue $122,800 $127,585 $121,080 $6,505 $1,720

Expenses:Operating Expenses:

Salaries and fringes $45,996 11 $42,474 $42,754 (280) 3,242Technical service contracts 7,525 12 6,871 7,273 (402) 252General contracts 1,355 13 1,240 1,704 (464) (349)Rent, building depreciation and utilities 1,116 14 1,104 1,092 12 24Buiding maint, equipment purchase & rental 660 19 645 792 (147) (132)Information Technology 8,606 15 4,875 10,042 (5,167) (1,436)State charges for Attorney General, Auditor General, Civil Service and admin 2,657 16 2,861 2,778 83 (121)Travel 156 17 156 204 (48) (48)Telephone 324 17 324 480 (156) (156)Supplies, printing and postage 312 17 312 276 36 36Advertising and publicity 1,950 20 2,065 2,350 (285) (400)HCV contracted agents 9,740 21 9,710 9,755 (45) (15)Memberships, subs., & research mat. 96 17 96 96 0 0Authority sponsored conf. 180 18 180 180 0 0Conference registration fees 108 17 108 108 0 0Temporary support 480 22 135 90 45 390Legal & insurance 450 23 480 480 0 (30)Miscellaneous 840 17 840 372 468 468Deferred loan origination costs (2,625) 24 (2,290) (2,375) 85 (250)

Total Operating expenses 79,926 72,186 78,451 (6,265) 1,475

Single Family & HIP Mortgage servicing/origination/FHA insurance fees 11,152 25 13,750 9,755 3,995 1,397Costs of issuing & paying notes & bonds 3,050 26 2,940 2,900 40 150Bond insurance, LOC & Liquidity fees 1,744 27 1,675 1,693 (18) 51Provision for losses on Mort. loans 7,200 28 10,850 8,700 2,150 (1,500)Rent Subsidies 240 29 (100) 450 (550) (210)Grants (Total $10,188)

Homeless Program (Federal Matching) 5,600 30 5,502 5,502 0 98NEP 2,000 30 2,000 2,000 0 0Key-to-Own 150 30 150 150 0 0Collaborative Grants 2,438 30 2,379 2,379 0 59

Homeownership Counseling 750 31 1,090 700 390 50

Total expenses $114,250 $112,422 $112,680 ($258) $1,570

Net Increase in fund balance $8,550 $15,163 $8,400 $6,763 $150

Notes 1 - 31 - - See pages following

2

NOTES

(1) Net interest income is budgeted at $62,957,000, which is $4,649,000 less than was budgeted in FY 22. Weanticipate lower rates earned on slightly higher average balances for mortgage loans compared to FY 22. Higherinterest rates received on higher average balances for investments are anticipated for FY 23. We anticipate bondinterest expense to increase due to higher interest rates paid on higher bond balances in FY 23 over the budgetedamount in FY 22.

The components of interest income are estimated as follows:

Average Average Budget Balance Rate Amount

Interest income: Mortgage loans $3,856,497,000 4.50 % $173,548,000 Investments $ 904,069,000 1.27 % 11,495,000

Interest expense on bonds $3,767,760,000 3.24 % ( 122,086,000)

Net interest income $ 62,957,000

(2) Housing Choice Voucher and Family Self Sufficiency Administration fees are expected to stay flat compared tothe prior year’s budget.

(3) Represents funds available for administering other federal programs, including the HOME Program ($3,600,000),Hardest-Hit Fund ($300,000)*, the Housing Trust Fund Program ($1,500,000) and new Federal FundingPrograms ($8,653,000).

(4) Budgeted amount includes preservation fees of $0 from anticipated prepayments on multifamily loans and$100,000 of funds received from the required annual payments from projects surplus cash. The amount ofpreservation fee income could vary significantly from the budgeted amount. It is based on large payments from asmall number of projects that are anticipated to prepay their multi-family loan. Actual prepayments may not takeplace or may exceed our expectations.

(5) Fees for administering the Low Income Housing Tax Credit Program.

(6) Fees expected to be received for administering the HUD Section 8 Contract Administration Program.

(7) Whether a bond retirement results in a gain or loss depends on the interest rate of the bond called relative to theaverage rate on the issue from which the bond is being called. We are budgeting a gain of $2,500,000 for 2023.

(8) We have projected no gain from the sale of other long-term investments.

(9) Gain on the sale of securitized single-family loans and REO multi-family loans.

(10) Budget amount of $7,940,000 includes fees expected to be received from administering the Mortgage CreditCertificate program ($100,000), administrative oversight fees to be received from developments that have prepaidtheir mortgage loans ($130,000), late fee/prepayment penalties on mortgages ($1,500,000), amortization of assetmanagement fees ($380,000), fees for the issuance of limited obligation bonds ($1,000,000) and various smallerincome items of ($330,000), BMIR funds ($4,500,000).

3

(11) Budget requests by Division are as follows: Positions Filled Cost

Executive:Director's Office 4.0 $ 434,283 Communications 5.0 376,028

Compliance, Fraud & Internal Audit 8.0 606,272 Equity & Engagement 4.0 372,604 Market Analysis & Research 4.0 324,809 Southeast Michigan Outreach 3.0 281,692 Students & Co-ops 0.0 0

28.0 $2,395,688 Fringes (75%) 1,796,766 TOTAL $4,192,454

Operations: Director’s Office 1.9 $179,445 Technical Support Services 12.0 969,792 Office Services 7.0 520,173 Employee Services 2.0 157,686 Human Resources 3.0 262,399 Students & Co-ops 0.7 24,000

26.6 $2,113,495 Fringes (75%) 1,585,121 TOTAL $3,698,616

Finance: Director's Office 2.0 $ 242,145 Accounting & Investments 6.0 451,300 Single Family Servicing 3.8 227,667 Multi-Family Servicing 3.0 183,264 Audit 4.0 367,008 Operations – HVP 3.0 270,354 Students & Co-ops 0.0 0

21.8 $1,741,738 Fringes (75%) 1,306,304 TOTAL $3,048,042

Legal: Director's Office 6.0 $ 496,986 Staff Attorneys 9.0 1,019,717 Procurement 1.0 86,067 Students & Co-ops 0.7 24,000

16.7 $1,626,770 Fringes (75%) 1,220,078 TOTAL $2,846,848

4

(11) Budget requests by Division (continued) Positions

Filled Cost Neighborhood Housing Initiatives:

Director's Office 1.0 $147,288 Neighborhood Initiatives 9.0 767,611 Students & Co-ops 0.0 0

10.0 $914,899 Fringes (75%) 686,174 TOTAL $1,601,073

Rental Assistance & Housing Solutions: Director's Office* 2.0 $269,081 Rent Assistance* 27.6 1,987,793 Homeless Initiatives 11.0 866,812 CERA* 29.0 1,527,372 Students & Co-ops* 0.7 24,000

70.3 $4,675,058 Fringes (75%) 3,506,294 TOTAL $8,181,352

*Federally Funded

Asset Management: Director's Office 4.0 $339,446 Transactions 6.0 488,655 Small Scale Asset Management 5.0 402,295 Core Properties Intake 8.0 644,378 Operations 4.0 325,749 Contract Administration 9.0 712,718 Compliance Monitoring 9.0 695,763 Students & Co-ops 0.7 24,000

45.7 $3,633,004 Fringes (75%) 2,724,753 TOTAL $6,357,757

5

(11) Budget requests by Division (continued) Positions

Filled Cost Homeownership:

Director's Office 7.0 $ 486,629 Single Family/MCC Operations 14.0 948,975 Business Development 6.0 477,672 MIHAF* 47.0 2,200,439 Students & Co-ops 0.0 0

74.0 $4,113,715 Fringes (75%) 3,085,286 TOTAL $7,199,001

*Federally Funded

Rental Development: Director's Office 4.0 $361,704 Multi-family Development 6.0 512,395 Construction Design & EEO 8.0 753,851 Environmental Quality 2.0 198,172 Low Income Housing Tax Credit 7.0 444,389 Students & Co-ops 0.0 0

27.0 $2,270,511 Fringes (75%) 1,702,883 TOTAL $3,973,394

Total Salaries July 1, 2022 320.1 $23,484,878 Total Fringes July 1, 2022 $17,613,659

General increase effective October 1, 2022 (5% of base wages) 1,541,195 General increase effective April 1, 2023 (1% of base wages) 102,746

$42,742,478 Summary of Costs:

Projected salary cost of positions $42,742,478 Vacant positions salaries (23) 1,936,892 Vacant positions fringes 1,452,668 Unfilled Vacant Positions (40%) (1,355,824) Estimated sick and annual leave accrual 60,000

Total budgeted salaries and fringes 22-23 $44,836,214

Estimating 15 new Federally Funded Positions to be filled 662,730 Fringes for the 15 Federally Funded Positions 497,048

Total budgeted salaries and fringes 22-23 with new Federal Positions $45,995,992

6

(12) Production-related Contracts: 2022-23

Proposed 2021-22 Budget Budget

Multi-Family: Design Review $53,000 105,000

Marketing 21,000 15,000 Environmental and Technical Resources 50,000 70,000

Subtotal $124,000 $190,000

Contract Administration*: Asset Management $4,822,000 $4,745,000 Consulting 55,000 55,000 TRACS Processing 1,224,000 1,214,000

Subtotal $6,101,000 $6,014,000

Single Family Foreclosure Services/Audit 500,000 273,000 Environmental Legal Matters 40,000 40,000 Capital Needs and Project Assessments 200,000 146,000 TRACS Processing 23,000 10,000 Contractual Tenant File Audits/Physical Inspections 537,000 600,000

Total $7,525,000 $7,273,000

*Additional contracts required for HUD Section 8 Contract Administration Program.

(13) General Contracts: 2022-23 Proposed 2021-22

Budget Budget

Operations Contracts $ 55,000 $ 42,000 Executive Contract 575,000 821,000 Legal Contracts 66,000 57,000 Housing Initiatives Contracts 7,000 9,000 Housing Voucher Program Contracts 335,000 590,000

Miscellaneous 317,000 185,000

$1,355,000 $1,704,000

7

(14) Office rent and utility charges by location are as follows:Proposed Budget

Rent: GM Building 395,000

Depreciation on 735 E. Michigan Avenue: $ 525,000

Utilities: 735 E. Michigan Avenue $ 196,000

Total $1,116,000

(15) Information Technology: 2022-23 Proposed 2021-22

Budget Budget

Emphasys system $2,100,000 $1,958,000 Agate 600,000 500,000 DTMB (includes various licenses & equipment) 4,116,000 3,600,000 Ongoing Commitments 940,000 2,304,000

New IT Projects 850,000 1,680,000 $8,606,000 $10,042,000

(16) State Charges include: Proposed Budget Budget

22-23 21-22

Attorney General $1,200,000 $1,200,000 Auditor General 200,000 126,000 Civil Service 732,000 600,000 DTMB Support 225,000 252,000 LEO Admin 300,000 600,000

$2,657,000 $2,778,000

(17) Prior year estimated actual amount.

(18) Amount for Authority sponsored conferences.

(19) Amount includes expense for building maintenance, office equipment and rental.

8

(20) Advertising and publicityProposed Budget

22-23

Advertising Campaign – Media/PR/Creative $1,400,000(1)

Video Creation 250,000

Misc. Advertising, Marketing, Promotion & Outreach Items 300,000

Total $1,950,000

(1) $500,000 of these advertising dollars will promote two Federal programs. The expense will be reimbursed through Federaladministrative fees.

(21) Reflects similar utilization of agents and fees paid to agents.

(22) Temporary clericals and laborers.

(23) Budget amount includes $350,000 of legal fees and $100,000 for insurance premiums. Legal fees and insurancepremiums expected to be higher in FY 21.

(24) Represents the direct costs of originating multi-family loans. Pursuant to generally accepted accountingprinciples, the cost of making loans is deferred and amortized against interest income over the term of the loans.

(25) This is the breakdown of estimated Single Family/ HIP servicing, origination costs and FHA Insurancepremiums. The Authority will assemble a team to investigate cost savings related to servicing fees.

22-23 21-22Budget Budget

Single Family Servicing Fees - $7,800,000 $6,000,000 Cost of Loan Origination (a) - 3,200,000 3,550,000 HUD Risk Sharing - 48,000 50,000 HIP Servicing Fee - 64,000 105,000 HIP Origination Fees - 4,000 5,000 HIP FHA Insurance Premiums - 36,000 45,000

Total $11,152,000 $9,755,000

(a) Amortization of Service release premium, Incentive premium and Origination Fee

(26) Staying flat compared to last year’s estimated actual is budgeted because the number of bonds being issued willbe similar to prior year.

(27) An increase over last year’s estimated actual is budgeted because the number of bonds with liquidity facilitieshas decreased, but the fees have increased.

(28) Assumes $1,000,000 of write-offs and will increase current reserve balance by $6,200,000.

9

(29) Represents estimated expenditures for the Authority's rent subsidy programs that (1) provide up to a $300 perunit per year subsidy for the total number of units in a project under the prior multi-family program ($40,000),(2) provide a subsidy of up to $400 per unit for each unit in a development under our taxable program so thatsome of the units can be afforded by very low income tenants who would otherwise be paying more than 40% oftheir income for rent ($300,000), and (3) ($190,000) for small size and security loans which are being expensedas paid due to the uncertainty of repayment. Excess subsidy repayments are estimated at ($290,000).

(30) Of the $10,188,000, $5,600,000 will be allocated to a number of programs that require a match in order forMSHDA to be eligible for Federal Funds. The remaining $4,588,000 Grant Funds will be allocated throughoutthe FY.

(31) This counseling network is an ongoing responsibility of MSHDA with annual costs estimated at $750,000.

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

RESOLUTION APPROVING 2022-2023 BUDGET

June 16, 2022 JUNE 21, 2022

WHEREAS, the fiscal year of the Michigan State Housing Development Authority (the "Authority") is twelve (12) calendar months commencing with the first day of July and ending the last day of the following June pursuant to Article IV of the Authority’s Bylaws; and

WHEREAS, the Acting Executive Director has recommended that the Authority approve the adoption of the 2022-2023 Budget as described in the accompanying memorandum; and

WHEREAS, the Authority concurs in the recommendation of the Acting Executive Director.

NOW, THEREFORE, Be It Resolved by the Michigan State Housing Development Authority as follows:

1. The Michigan State Housing Development Authority’s 2022-2023 Budget is herebyadopted, subject to the terms of the accompanying memorandum.

2. The Executive Director and the Chief Financial Officer are hereby authorized to implementthe 2022-2023 Budget.

GOLDENROD TAB E

WardL10

Cross-Out

M E M O R A N D U M

TO:

FROM:

DATE:

RE:

Authority Members

Gary Heidel, Acting Executive Director

June 16, 2022 JUNE 21, 2022

Field Street III, MSHDA Development No. 3928

RECOMMENDATION:

I recommend that the Michigan State Housing Development Authority (the “Authority”) adopt a resolution authorizing an increase in the tax-exempt bond mortgage loan and a Mortgage Resource Fund (“MRF”) Loan in the amounts set forth in this memorandum.

PROJECT SUMMARY:

MSHDA No: 3928 Development Name: Field Street III Development Location: City of Detroit, Wayne County Sponsor: Church of the Messiah Housing Corporation Mortgagor: Field Street III Limited Dividend Housing Association, LLC Number of Units: 49 affordable family units – scattered site

November 2020 Board Update Difference Total Development Cost: $8,660,199 $10,566,105 $1,905,906 TE Bond Construction Loan: $0 $6,530,332 $6,530,332 TE Bond Mortgage Loan: $3,590,481 $2,844,718 ($745,763) MSHDA MRF Loan $0 $1,448,201 $1,448,201 City of Detroit ADHP Funds $0 $582,626 $582,626 MSHDA HOME Assumption $677,477 $756,007 $78,530 Detroit HOME Assumption $240,000 $240,000 no change LIHTC Equity: $2,185,615 $3,923,678 $1,738,063 Income from Operations: $164,676 $235,309 $70,633 Seller Note $950,781 $465,192 ($485,589) Transferred Reserves $679,969 $17,752 ($662,217) Deferred Developer Fee: $171,000 $52,422 ($118,578)

GOLDENROD TAB F

WardL10

Cross-Out

EXECUTIVE SUMMARY:

Field Street III (the “Development”) was approved by the Authority Board in November 2020. At that time, the Board approved the financing structure for the Development that included a third-party lender for the construction financing. After receiving Board approval in 2020, the Sponsor decided to have the Authority provide the construction financing in place of the third-party lender.

Since Board approval in 2020, construction pricing has also been extremely volatile, which resulted in an increase of nearly $2 million dollars to the Development’s construction hard costs. Also, due to increased operating expense projections, the first mortgage loan was reduced by an amount of $745,763. To help meet the funding gap caused by the increased construction costs and reduction in the first mortgage loan, the Sponsor secured funds from the City of Detroit to help fund the increase. The Sponsor was also able to take advantage of the 4% fix in the Low Income Housing Tax Credits (“LIHTC”), which will generate an additional $1,738,063 in equity.

I am also recommending the addition of a MRF Loan in the amount of $1,448,201, $634,716 of which is from reserves captured and loaned back out.

The changes described in the attached proforma make the Development feasible and will preserve 49 units of needed affordable family units. Adding an Authority-financed construction loan requires Board approval because it exceeds the Authority’s policy limit, i.e., loan increases greater than 5% percent must be Board approved. The MRF Loan also requires Board approval because it is a new Authority financing source.

I am recommending Board approval for the following reasons:

• The increased costs to be covered are due to the type of unexpected conditions and delays thatthe Loan Increase Policy is intended to address.

• As an existing family development with an excellent occupancy and operational history, thisproposal is low risk to the Authority.

• The Development will remain as an earning asset in the Authority’s portfolio.• All units will be refurbished to meet the physical needs of the Development.

ADVANCING THE AUTHORITY’S MISSION:

• The Development’s affordability will be extended for up to 50 years for all units.• A new Rental Assistance Contract for Section 8 tenants will be executed to continue rental

support for 8 of the units.• Financing the Development results in an earning asset for the Authority.

MUNICIPAL SUPPORT:

• It is anticipated that the City of Detroit will provide a 4% Payment in Lieu of Taxes (“PILOT”) tothe Development.

• The City of Detroit will allow the new ownership to assume a HOME loan in the amount of$240,000.

COMMUNITY ENGAGEMENT/IMPACT:

• The financing of this Development enables rehabilitation to the property that improves the livesof residents as well as the broader community.

• The Sponsor for the Development is the Church of the Messiah Housing Corporation (“CMHC”),a nonprofit corporation that focuses on the development and support of various programs andservices for neighborhood residents.

RESIDENT IMPACT:

• No residents will be displaced as a result of this preservation.• No residents will experience a rent increase that exceeds 5% as a result of this preservation and

a rent subsidy reserve is being established to protect the existing tenants against an increase inrent for an estimated 5-year period.

ISSUES, POLICY CONSIDERATIONS, AND RELATED ACTIONS:

None.

ATTACHMENTS: • Mortgage Modification Proforma

Development Field Street IIIFinancing Tax Exempt

MSHDA No. 3928Step ModificationDate 06/16/2022 06/21/2022 Type Preservation - LIHTC

TOTAL DEVELOPMENT COSTS

Mortgage Mod Per

UnitMortgage Mod Total %

in B

asis

Included in Tax Credit

Basis

Board Approved Per Unit

Board Approved

Total % in

Bas

is

Included in Tax Credit

Basis

Difference Mod vs. Board

AcquisitionLand 5,510 270,000 0% 0 5,918 290,000 0% 0 (20,000)Existing Buildings 37,347 1,830,000 100% 1,812,248 35,918 1,760,000 100% 1,794,496 70,000Other: Transferred Reserves 0 0 0% 0 13,877 679,969 0% 0 (679,969)

Subtotal 42,857 2,100,000 55,714 2,729,969 (629,969)Construction/Rehabilitation

Off Site Improvements 0 0 100% 0 0 0 100% 0 0On-site Improvements 28,263 1,384,871 100% 1,384,871 10,680 523,300 100% 523,300 861,571Landscaping and Irrigation 0 0 100% 0 0 0 100% 0 0Structures 0 0 100% 0 0 0 100% 0 0Community Building and/or Maintenance Facility 57,005 2,793,237 100% 2,793,237 40,622 1,990,500 100% 1,990,500 802,737Construction not in Tax Credit basis (i.e.Carports) 0 0 0% 0 0 0 0% 0 0General Requirements % of Contract 6.00% Within Range 5,116 250,686 100% 250,686 3,078 150,828 100% 150,828 99,858Builder Overhead % of Contract 2.00% Within Range 1,808 88,576 100% 88,576 1,088 53,293 100% 53,293 35,282Builder Profit % of Contract 6.00% Within Range 5,531 271,042 100% 271,042 3,328 163,075 100% 163,075 107,967Bond Premium, Permits, Cost Cert. 2,315 113,440 100% 113,440 2,231 109,341 100% 109,341 4,099Other: 0 0 100% 0 0 0 100% 0 0

Subtotal 100,038 4,901,853 61,027 2,990,337 1,911,51415%/$15,000 test: met 15%/$15,000 test: met

Professional FeesDesign Architect Fees 341 16,720 100% 16,720 341 16,720 100% 16,720 0Supervisory Architect Fees 85 4,180 100% 4,180 85 4,180 100% 4,180 0Engineering/Survey 306 15,000 100% 15,000 306 15,000 100% 15,000 0Legal Fees 2,041 100,000 100% 100,000 1,531 75,000 60% 45,000 25,000

Subtotal 2,773 135,900 2,263 110,900 25,000Interim Construction Costs

Property and Causality Insurance 472 23,128 100% 23,128 284 13,916 100% 13,916 9,212Construction Loan Interest 194,545 3,970 194,545 80% 155,636 2,724 133,457 80% 106,766 61,088Title Work 510 25,000 83% 20,833 612 30,000 83% 25,000 (5,000)Construction Taxes 360 17,636 100% 17,636 353 17,303 100% 17,303 333Other: 0 0 100% 0 807 39,532 100% 39,532 (39,532)

Subtotal 5,312 260,309 4,780 234,208 26,101Permanent Financing

Loan Commitment Fee to MSHDA 2% 3,565 174,691 0% 0 1,742 85,359 0% 0 89,332Other: Pre-pay 327 16,000 0% 0 327 16,000 0% 0 0

Subtotal 3,892 190,691 2,069 101,359 89,332Other Costs (In Basis)

Application Fee 41 2,000 100% 2,000 41 2,000 100% 2,000 0Market Study 133 6,500 100% 6,500 133 6,500 100% 6,500 0Environmental Studies 6,122 300,000 100% 300,000 2,041 100,000 100% 100,000 200,000Cost Certification 306 15,000 0% 0 163 8,000 0% 0 7,000Equipment and Furnishings 204 10,000 100% 10,000 408 20,000 100% 20,000 (10,000)Temporary Tenant Relocation 1,020 50,000 100% 50,000 4,541 222,500 100% 222,500 (172,500)Construction Contingency 10,004 490,185 100% 490,185 6,185 303,045 100% 303,045 187,140Appraisal and C.N.A. 367 18,000 100% 18,000 367 18,000 100% 18,000 0Other: 0 0 100% 0 0 0 100% 0 0

Subtotal 18,198 891,685 13,878 680,045 211,640Other Costs (NOT In Basis)

Start-Up and Organization 1,122 55,000 0% 0 1,122 55,000 0% 0 0Tax Credit Fees (based on 2022 QAP) 31,590 Out of Range 599 29,330 0% 0 348 17,061 0% 0 12,269Compliance Monitoring Fee (based on 2022 QAP) 475 23,275 0% 0 475 23,275 0% 0 0Marketing Expense 204 10,000 0% 0 204 10,000 0% 0 0Syndication Legal Fees 0 0 0% 0 0 0 0% 0 0Rent Up Allowance 0.0 months 0 0 0% 0 0 0 0% 0 0Other: 0 0 0% 0 0 0 0% 0 0

Subtotal 2,400 117,605 2,150 105,336 12,269

Summary of Acquisition Price As of 12/31/20 Construction Loan TermAttributed to Land 270,000 Field St 1 1st mrtg Security 511,428 MonthsAttributed to Existing Structure1,830,000 Field st 2 1st mrtg and HOM 883,380 Construction Contract 12Other: 0 City HOME Loan 240,000 Holding Period (50% Test) 6Fixed Price to Seller 2,100,000 Subordinate Mortgage(s) 0 Rent up Period 0

0 Construction Loan Period 18Premium/(Deficit) vs Existing Debt 465,192

Appraised Value Valuse As of: 11/15/19"Encumbered As-Is" value as determined by appraisal: 2,100,000Plus 5% of Appraised Value: 0 OverrideLESS Fixed Price to the Seller: 2,100,000Surplus/(Gap

Within Range 0

G O L D E N R O D T A B F

WardL10

Cross-Out

Mortgage Mod Per

UnitMortgage Mod Total

Included in Tax Credit

Basis

Board Approved Per Unit

Board Approved

Total

Included in Tax Credit

Basis

Difference Mod vs. Board

Project ReservesOperating Assurance Reserv 4.0 months Funded in Cas 5,093 249,558 0 3,763 184,384 0 65,174 169,129Replacement Reserve Required 700 34,300 0 700 34,300 0 0Operating Deficit Reserve 0 0 0 0 0 0 0Rent Subsidy Reserve 8,761 429,301 0 9,508 465,901 0 (36,600)Syndicator Held Reserve 0 0 0 0 0 0 0Rent Lag Escrow 0 0 0 0 0 0 0Tax and Insurance Escrows 362 17,752 0 567 27,774 0 (10,022)Other: 0 0 0 0 0 0 0Other: Additional OAR per syndicator 0 0 886 43,416 0 (43,416)

Subtotal 14,917 730,911 15,424 755,775 (24,864)MiscellaneousDeposit to Development Operating Account (1MGRRequired 913 44,746 0 905 44,355 0 391Other (Not in Basis): 0 0 0 0 0 0 0Other (In Basis): 0 0 1,020 50,000 50,000 (50,000)Other (In Basis): 0 0 0 0 0 0 0

Subtotal 913 44,746 1,926 94,355 (49,609)

Total Acquisition Costs 42,857 2,100,000 55,714 2,729,969 (629,969)Total Construction Hard Costs 100,038 4,901,853 61,027 2,990,337 1,911,515Total Non-Construction ("Soft") Costs 48,405 2,371,847 42,489 2,081,978 289,869

Developer Overhead and FeeMaximum 1,193,737 24,335 1,192,405 1,192,405 17,508 857,914 857,914 334,491

7.5% of Acquisition/Project Reserves Override 5% Attribution Test15% of All Other Development Costs 1,192,405 met

Total Development Cost 215,635 10,566,105 9,136,324 176,739 8,660,199 8,851,834 1,905,906

TOTAL DEVELOPMENT SOURCES % of TDCMSHDA Permanent Mortgage 26.92% 58,055 2,844,718 73,275 3,590,481 (745,763)Conventional/Other Mortgage 0.00% 0 0 0 0 0 Gap toEquity Contribution from Tax Credit Syndication 37.13% 80,075 3,923,678 # of Units 44,604 2,185,615 # of Units 1,738,063 Hard DebtCity of Detroit ADHP Funds 5.51% 11,890 582,626 2.70 0 0 0.00 582,626 RatioMSHDA HOME 0.00% 0 0 10.00 0 0 0 96%Mortgage Resource Funds 13.71% 29,555 1,448,201 0 0 1,448,201Other MSHDA MSHDA HOME Assumption 7.16% 15,429 756,007 11.00 13,826 677,477 78,530Detroit HOME Assumption 2.27% 4,898 240,000 4,898 240,000 0Income from Operations 2.23% 4,802 235,309 3,361 164,676 70,633Other Equity Seller note 4.40% 9,494 465,192 19,404 950,781 (485,589)Transferred Reserves: 0.17% 362 17,752 13,877 679,969 (662,217)Other: GP cont 0.00% 2 100 2 100 0Other: SPLP cont 0.00% 2 100 2 100 0Deferred Developer Fee 0.50% 1,070 52,422 4.40% 3,490 171,000 19.93% (118,578)Total Permanent Sources 10,566,105 8,660,200 1,905,905

Sources Equal Uses? Balanced SurplusSurplus/(Gap) 0 0 0

61.80% 133,272 6,530,332 80,679 3,953,249 2,577,083 Board LoansConstruction Loan Rate 4.250% 362,768 8,221,207Repaid from equity prior to final closing 3,685,614 Board Test

Eligible Basis for LIHTC/TCAP Value of LIHTC/TCAPAcquisition 1,917,248 Acquisition 76,690 Existing Reserve AnalysisConstruction 9,384,799 Construction 375,392 Override DCE Interes 0 Current Owner's Reserves: 0Acquisition Credit % 4.00% Total Yr Credit 452,082 Insurance: 10,223 634,716Rehab/New Const Credit % 4.00% Equity Price $0.8680 Taxes: 7,529 17,752Qualified Percentage 100.00% Equity Effective Price $0.8680 Override Rep. Reser 588,465QCT/DDA Basis Boost 130% Equity Contribution 3,923,678 ORC: 7,683Historic? No DCE Princip 0

Other: 38,568

Initial Owner's Equity CalculationEquity Contribution from Tax Credit Syndication 3,923,678 Brownfield EquityHistoric Tax Credit EquityGeneral Partner Capitla ContributionsOther Equity Sources

New Owner's Equity 3,923,678

Tax/Ins Escrows transferred to Reserves Transferred in to Proj

4 Month OAR

MSHDA Construction Loan

Deferred Dev Fee

Deferred Dev Fee

LIHTC Basis

LIHTC Basis

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

RESOLUTION AUTHORIZING MODIFICATIONS TO MORTGAGE LOAN FOR FIELD STREET III, MSHDA DEVELOPMENT NO. 3928

CITY OF DETROIT, WAYNE COUNTY

June 16, 2022 JUNE 21, 2022

WHEREAS, on November 19, 2020, the Michigan State Housing Development Authority (the “Authority”) authorized a permanent mortgage loan (the "Mortgage Loan") and assumption of an existing HOME mortgage loan (the “HOME Loan”) for the acquisition and rehabilitation of Field Street III, MSHDA No. 3928 (the “Development”); and

WHEREAS, for a variety of reasons including a change in the construction lender, a global pandemic adversely affecting construction costs, and an increase in operating expense projections, rehabilitation of this 49-unit Development is no longer viable as originally planned; and

WHEREAS, the Authority’s Mortgage Loan Increase Policy dated August 26, 2021, requires Authority approval for loan increases greater than 5% of the original mortgage loan amount or $900,000; and

WHEREAS, for the reasons set forth in the accompanying Memorandum, the Acting Executive Director has recommended a modification of the Mortgage Loan that exceeds 5% of the Mortgage Loan amount or $900,000, and the addition of a Mortgage Resource Fund Loan (the “MRF Loan”); and

WHEREAS, the Authority concurs in the recommendation of the Acting Executive Director.

NOW THEREFORE, the Michigan State Housing Development Authority resolves as follows:

1. The Authority hereby approves the modification of the Mortgage Loan, pursuant and subjectto the terms and conditions set forth in the Memorandum dated June 16, 2022, JUNE21, 2022 and the proforma attached thereto and incorporated herein.

2. The Executive Director, the Director of Legal Affairs, the Deputy Director of Legal Affairs,the Chief Financial Officer, or any person duly appointed and acting in such capacity (each,an Authorized Officer of the Authority), is hereby granted the authority to authorize themodification of the Mortgage Loan as set forth in the Memorandum.

3. The Executive Director or any person duly appointed and acting in such capacity, is herebyauthorized to modify or waive any of the terms and conditions of the Memorandum as maybe deemed necessary to effectuate the ability of the Sponsor to acquire and rehabilitate theDevelopment in a manner that is satisfactory to the Authority.

GOLDENROD TAB F

WardL10

Cross-Out

WardL10

Cross-Out

WHEREAS, on November 19, 2020, the Michigan State Housing Development Authority (the “Authority”) authorized a permanent mortgage loan (the "Mortgage Loan") and assumption of an existing HOME mortgage loan (the “HOME Loan”) for the acquisition and rehabilitation of Field Street III, MSHDA No. 3928 (the “Development”); and

WHEREAS, for a variety of reasons including a change in the construction lender, a global pandemic adversely affecting construction costs, and an increase in operating expense projections, rehabilitation of this 49-unit Development is no longer viable as originally planned; and

WHEREAS, the Mortgagor has sought out and obtained additional financing sources, but a financing gap remains; and

WHEREAS, the Mortgagor has made an application (the "Application") to the Authority for a Mortgage Resource Fund to fund the shortfall on the terms and conditions set forth in the accompanying mortgage modification and proforma dated June 16, 2022 JUNE 21, 2022; and

WHEREAS, the Authority is empowered under Act No. 346 of the Public Acts of 1966, as amended (the "Act") to provide loans in furtherance of the purposes of the Act; and

WHEREAS, the Acting Executive Director has considered the Mortgagor's Application and recommends that the Authority approve a mortgage loan from the Mortgage Resource Fund for the Development as described in the mortgage modification and proforma attached hereto; and

WHEREAS, the Authority has reviewed the Application and the recommendation of the Acting Executive Director and, on the basis of the Application and such recommendation, has made determinations that:

(a) The Mortgagor is an eligible applicant;

(b) The housing project does and will continue to provide housing for persons of lowand moderate income and will serve and improve the residential area in whichAuthority financed housing is located or is planned to be located therebyenhancing the viability of such housing;

(c) The Mortgagor is reasonably expected to be able to achieve successfulcompletion of the housing project;

(d) The housing project does and will continue to meet a social need in the area inwhich it is to be located;

(e) The housing project may reasonably be expected to be marketed successfully;

(f) All elements of the housing project have been established in a manner consistentwith the Authority's evaluation factors, except as otherwise provided herein;

MICHIGAN STATE HOUSING DEVELOPMENT AUTHORITY

RESOLUTION AUTHORIZING MORTAGE RESOURCE FUND LOAN FIELD STREET, MSHDA DEVELOPMENT NO. 3928

CITY OF DETROIT, WAYNE COUNTY

June 16, 2022 JUNE 21, 2022

GOLDENRODTAB F

WardL10

Cross-Out

WardL10

Cross-Out

(g) The construction or rehabilitation will be undertaken in an economical mannerand will not be of elaborate design or materials; and

(h) In light of the total project cost of the housing project, the amount of the mortgageloan authorized hereby is consistent with the requirements of the Act as to themaximum limitation on the ratio of mortgage loan amount to total project cost.

WHEREAS, the Authority has considered the Application in the light of the criteria established for the determination of priorities pursuant to General Rule 125.145 and hereby determines that the proposed Development is consistent therewith.

NOW, THEREFORE, Be It Resolved by the Michigan State Housing Development Authority as follows:

1. The Application be and it hereby is approved, subject to the terms and conditionsof this Resolution, the Act and of the General Rules of the Authority.

2. A Mortgage Resource Fund mortgage loan (the "Mortgage Loan") be and ithereby is authorized for the financing of the Development, with the Mortgage Loan having an initial principal amount of One Million Four Hundred Forty-Eight Thousand Two Hundred One Dollars ($1,448,201), having a term of fifty (50) years and bearing interest at the rate of three percent (3%) per annum. The Executive Director, the Chief Operating Officer, the Chief Housing Investment Officer, the Director of Legal Affairs, the Deputy Director of Legal Affairs, the Director of Finance, the Deputy Director of Finance and any person duly authorized to act in any of the foregoing capacities, or any one of them acting alone (each an "Authorized Officer") is hereby authorized to modify or waive any condition or provision contained in Action Report.

3. This mortgage loan commitment resolution is based on the information obtainedfrom the Mortgagor and the assumption that all factors necessary for the successful construction and operation of the proposed Development shall not change in any materially adverse respect prior to the closing. If the information provided by the Mortgagor is discovered to be materially inaccurate or misleading, or any factors necessary for the successful construction and operation of the proposed Development change in any materially adverse respect, this mortgage loan commitment resolution may, at the option of an Authorized Officer, be rescinded.

4. Notwithstanding passage of this resolution or execution of any documents inanticipation of the closing or the proposed Mortgage Loan, no contractual rights to receive the Mortgage Loan authorized herein shall arise unless and until an Authorized Officer shall have approved disbursement of the proceeds of the Mortgagor Loan, subject to the terms and conditions contained herein.

5. The Mortgage Loan shall further be subject to the conditions set forth in themortgage modification and proforma dated June 16, 2022 JUNE 21, 2022, which conditions are hereby incorporated by reference as if fully set forth herein.

WardL10

Cross-Out

TO:

FROM:

DATE:

RE:

M E M O R A N D U M

Authority Members

Gary Heidel, Acting Executive Director

June 16, 2022 JUNE 21, 2022

HOM Flats at Maynard, MSHDA Development No. 3955

RECOMMENDATION:

I recommend that the Michigan State Housing Development Authority (the “Authority”) adopt a resolution authorizing (i) an increase in the permanent tax-exempt bond mortgage loan, and (ii) an increase in the Mortgage Resource Fund loan to provide construction loan financing in the amounts set forth in this memorandum.

PROJECT SUMMARY:

MSHDA No: 3955 Development Name: HOM Flats at Maynard Development Location: City of Grand Rapids, Kent County Sponsor: Magnus Capital Partners. Mortgagor: Maynard Avenue Limited Dividend Housing

Association Limited Partnership Number of Units: 240 Affordable units

March 17, 2022 Report Update Difference Total Development Cost: $44,034,012 $51,495,257 $7,461,245 TE Bond Construction Loan: $34,069,680 $33,698, 717 $-370,982 TE Bond Mortgage Loan: $28,383,437 $33,698,717 $5,315,280 MSHDA HOME Loan: $1,545,000 $1,545,000 No change MSHDA MRF Loan $967,881 $12,075,868 $11,107,987 LIHTC Equity: $12,081,967 $14,687,677 $2,605,710 Income from Operations: $450,137 $450,137 No change GP Equity: $100 $100 No change Deferred HOME and MRF Interest: $30,126 $24,041 $-6,085 Deferred Developer Fee: $575,364 $315,000 $-260,364

DIFFERENCE

GOLDENROD TAB G

$-370,963

WardL10

Reviewed

WardL10

Cross-Out

WardL10

Cross-Out

WardL10

Cross-Out

EXECUTIVE SUMMARY:

In March of 2022, the Authority approved HOM Flats at Maynard for a mortgage loan commitment. The sponsor was recently informed by the General Contractor that, as the result of global supply shortages and substantial increases in the cost of labor and materials, they were unable to hold the construction costs to those approved by the Authority in March. Construction cost estimates have increased by over $5 million (14% increase) as reflected in the proforma’s Zsources and uses tab.

Since the proposal completed the underwriting process, the 2022 Area Median Income (“AMI”) limits were published by the U.S. Department of Housing and Urban Development (“HUD”) and the Authority’s Marketing Department reviewed and approved substantial increases to the allowable rents. The new rental rates will support an increase to the Authority's permanent tax-exempt bond loan by just over $5 million, effectively keeping the proposal viable.

As part of the tax-exempt bond process, the Authority publishes a Tax Equity and Fiscal Responsibility (“TEFRA”) notice and sets certain bond amounts for the projects within the bond series. In this case, the overall construction loan increase request is above the amount of available bond proceeds from the series, and staff has recommended funding the difference with increased funding from the Mortgage Resource Fund ("MRF"). The additional MRF loan proceeds will be advanced during the construction period only, will require interest only payments, and must be repaid on or before permanent loan conversion.

The $45-million in construction financing requested by the sponsor will cover the increased construction costs as well as allow for an extended LIHTC equity investor pay-in, and will be funded as follows:

The Authority will provide a first priority tax-exempt bond construction Mortgage Loan in the amount $33,698,717 and a second priority MRF Loan in the amount of $12,075,868. The interest rate on both loans will be 3.95%. The MRF Loan will be made pursuant to two notes, a Part A note in the amount of $11,301,283 that will mature at or before permanent loan conversion and require payments of interest only. A Part B MRF note in the amount of $774,585 will be payable from 50% of cash flow beginning in the 13th year or after available cash flow equals the amount of the deferred developer fee, with a maximum 50-year term.

I am recommending Authority approval of the proposed loan increases for the following reasons: • The increased costs to be covered are due to unanticipated supply chain shortages and

increased costs in labor and materials.

ADVANCING THE AUTHORITY’S MISSION:

• HOM Flats at Maynard is a 100% affordable development.• The development will add 240 affordable units to the Authority’s portfolio, including 40 units

targeted to families at or below the 40% MTSP income limit and 60 units targeted to families ator below the 50% MTSP income limit.

MUNICIPAL SUPPORT:

• Community support is evidenced by approval of the site plan, which required a major amendmentto the established Planned Redevelopment District, and approval of the property tax exemptionand a payment in lieu of taxes for the Development.

COMMUNITY ENGAGEMENT/IMPACT:

• This new construction proposal will increase the available housing stock in the Grand Rapidsmarket.

• The Development’s affordability will be maintained for up to 50 years on all units.• The City of Grand Rapids requires community engagement for all developers proposing new

construction developments. The sponsor organized three Google Hangout (virtual meetings)where the proposal was presented to community members. Invitation flyers were handed out toneighbors around the site that described the proposed project and asked that they attend theGoogle Hangout meetings to provide feedback. Feedback from those meetings helped thesponsor in completing their vision for the project.

RESIDENT IMPACT:

• This is a new construction proposal so there are no current residents impacted

ISSUES, POLICY CONSIDERATIONS, AND RELATED ACTIONS:

None.

ATTACHMENTS:

• Mortgage Modification Proforma

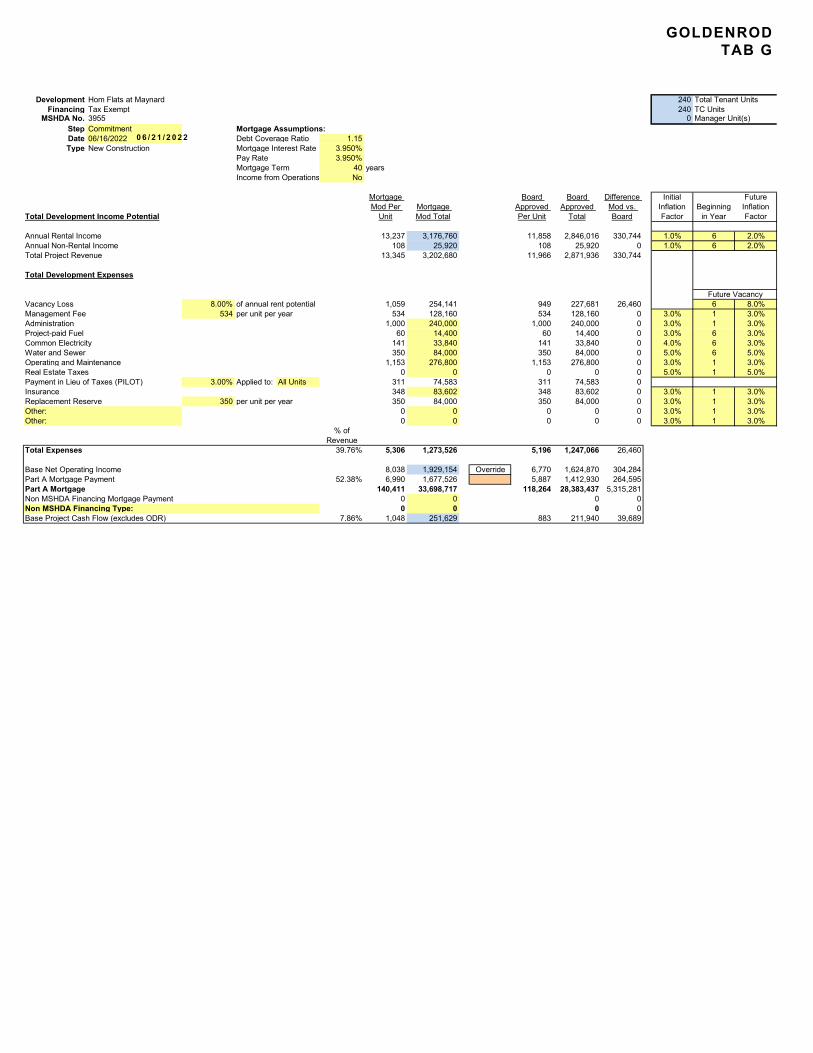

Development Hom Flats at Maynard 240 Total Tenant UnitsFinancing Tax Exempt Z 240 TC Units

MSHDA No. 3955 0 Manager Unit(s)Step Commitment Mortgage Assumptions:Date 06/16/2022 Debt Coverage Ratio 1.15Type New Construction Mortgage Interest Rate 3.950%

Pay Rate 3.950%Mortgage Term 40 yearsIncome from Operations No

Total Development Income Potential

Annual Rental Income 13,237 3,176,760 11,858 2,846,016 330,744 1.0% 6 2.0%Annual Non-Rental Income 108 25,920 108 25,920 0 1.0% 6 2.0%Total Project Revenue 13,345 3,202,680 11,966 2,871,936 330,744

Total Development Expenses

Vacancy Loss 8.00% of annual rent potential 1,059 254,141 949 227,681 26,460 6 8.0%Management Fee 534 per unit per year 534 128,160 534 128,160 0 3.0% 1 3.0%Administration 1,000 240,000 1,000 240,000 0 3.0% 1 3.0%Project-paid Fuel 60 14,400 60 14,400 0 3.0% 6 3.0%Common Electricity 141 33,840 141 33,840 0 4.0% 6 3.0%Water and Sewer 350 84,000 350 84,000 0 5.0% 6 5.0%Operating and Maintenance 1,153 276,800 1,153 276,800 0 3.0% 1 3.0%Real Estate Taxes 0 0 0 0 0 5.0% 1 5.0%Payment in Lieu of Taxes (PILOT) 3.00% Applied to: All Units 311 74,583 311 74,583 0Insurance 348 83,602 348 83,602 0 3.0% 1 3.0%Replacement Reserve 350 per unit per year 350 84,000 350 84,000 0 3.0% 1 3.0%Other: 0 0 0 0 0 3.0% 1 3.0%Other: 0 0 0 0 0 3.0% 1 3.0%

Total Expenses 39.76% 5,306 1,273,526 5,196 1,247,066 26,460

Base Net Operating Income 8,038 1,929,154 Override 6,770 1,624,870 304,284Part A Mortgage Payment 52.38% 6,990 1,677,526 5,887 1,412,930 264,595Part A Mortgage 140,411 33,698,717 118,264 28,383,437 5,315,281Non MSHDA Financing Mortgage Payment 0 0 0 0Non MSHDA Financing Type: 0 0 0 0Base Project Cash Flow (excludes ODR) 7.86% 1,048 251,629 883 211,940 39,689

Beginning in Year

Future Inflation Factor

Future Vacancy

% of Revenue

Board Approved Per Unit

Board Approved

TotalMortgage Mod Total

Mortgage Mod Per

Unit

Difference Mod vs. Board

Initial Inflation Factor

0 6 / 2 1 / 2 0 2 2

GOLDENROD TAB G

WardL10

Cross-Out

Development Hom Flats at Maynard Income Limits for (Effective April 1,2022)Financing Tax Exempt 1 Person 2 Person 3 Person 4 Person 5 Person 6 Person

MSHDA No. 3955 1 2 3 4 5 630% of area median 18,810 21,480 24,180 26,850 29,010 31,17040% of area median 25,080 28,640 32,240 35,800 38,680 41,560

Step Commitment Date ######## 06/21/22 Type New Construction 50% of area median 31,350 35,800 40,300 44,750 48,350 51,950

60% of area median 37,620 42,960 48,360 53,700 58,020 62,340

Rental Income

UnitNo. of Units Unit Type Bedrooms Baths Net Sq. Ft.

Contract Rent Utilities

Total Housing Expense Gross Rent

Section 8 Contract

Rent

% of Gross Rent

% of Total Units