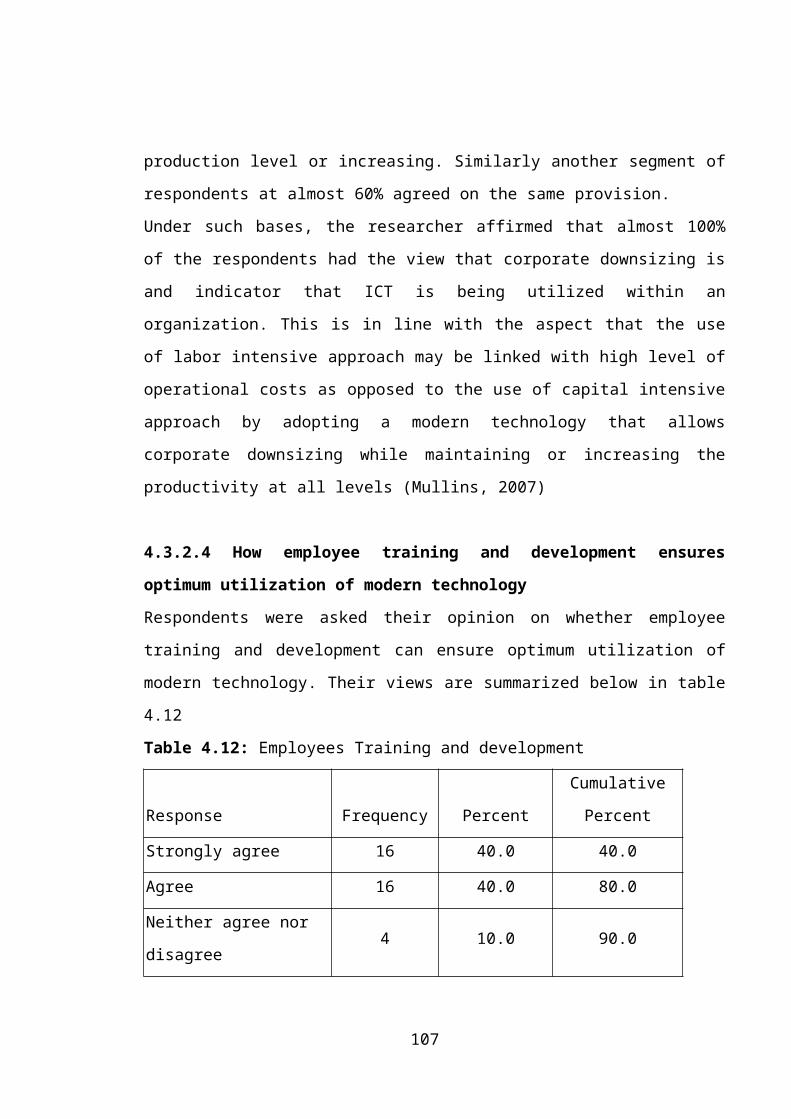

Michael laisser 7 10 2011

175

MODERN TECHNOLOGY AND THE PERFORMANCE OF FINANCIAL SERVICE SECTORS The Case of National Bank of Commerce (NBC) Limited Michael Israel Laisser MBA (Corporate Management) Dissertation 1

Transcript of Michael laisser 7 10 2011

MODERN TECHNOLOGY AND THE PERFORMANCE OF FINANCIAL SERVICE

SECTORS

The Case of National Bank of Commerce (NBC) Limited

Michael Israel Laisser

MBA (Corporate Management) Dissertation

1

Mzumbe University

September 2011

MODERN TECHNOLOGY AND THE PERFORMANCE OF FINANCIAL

The Case of National Bank of Commerce (NBC) Limited

By

Michael Israel Laisser

A Dissertation submitted in (Partial) fulfillment of the

Requirements of the Degree of a Master of Business

Administration (Corporate Management) of the Mzumbe

University.

2

Mzumbe University

September, 2011

`CERTIFICATION

The undersigned certifies that I have read and hereby

recommends for acceptance by the Mzumbe University

(Dar es salaam Business School), a dissertation

titled: The Impact of Modern Technology to the

Performance of Financial Services Sector; The Case of

NBC Limited in partial fulfillment of the

requirements for the degree of Masters of Business

Administration (Corporate Management).

3

……………………………………………………

Mr.Maige Mwakasege Mwasimba

(Supervisor)

Date…………………..

DECLARATION

AND

COPYRIGHT

I, Michael Israel Laisser do hereby declare that this

thesis is my own original work and it has not been

and will not be presented to any other university for

4

a similar or any other degree award.

Signature

----------------------------

This thesis is copyright material protected under the

Berne Convention, the Copyright Act 1999 and other

international and national enactments, in that

behalf. on intellectual property it may not be

reproduced by any means, in full or in part, except

for short extracts in fair dealings, for research or

private study, critical scholarly review or discourse

with an acknowledgement, without the written

permission of the School of Graduate Studies on

behalf of both the author and the Mzumbe

university(Dar es salaam business school)

5

ACKNOWLEDGEMENT

In the setting and conduct of the study, which led to

this research paper and in the course of writing the

final paper, It wouldn’t have been possible if not

for God to whom I can do everything. I also got

assistance and support from different people.

I would like to express my special thanks to Mr

Mwasimba who supervised me throughout my dissertation

process. His criticism, advice and encouragement

helped me to accomplish this study. His kindness,

consultancy and general guidance also played an

important part from first to the final report. I

would like also to express my sincere appreciation to

my family and my friend Zabibu who has given me

support and encouragement to complete my paper.

I would like also to thank those who have helped me

in one way or another in conducting my research and

6

writing the final report

Furthermore, many thanks to my family, relatives,

colleagues at NBC, colleagues in the MBA program and

all other participants for their encouragement and

support.

DEDICATION

This work is dedicated to all business stakeholders

who are always struggling for improved business

performance through technologically sound approach,

to my lovely family who have always been my strength.

7

TABLE OF CONTENT

CHAPTER ONE: INTRODUCTION

1.1 Background to the Study…………………………………………………

1.2 Research Problem………………………………………………………

1.3 Research Objectives………………………………………………………

1.4 Research question…………………………………………………………

1

2

3

4

4

8

1.5 Significance of the study…………………………………………………

1.6 Scope of the study ………………………………………………………

1.7 Limitation of the study…………………………………………………

5

5

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction…………………………………………………………….

2.2 Theoretical Literature Review………………………………………….

2.2.1 Definition of Key Concept……………………………………………..

2.2.2 Basic Motivation Theories……………………………………………..

2.3 Empirical Literature Review……………………………………………

2.3.1 ICT and its Specific Competitive

Factors……………………………..

2.3.2 The Management Information Systems and ICT

Context………………

2.3.3 Globalization Context and the Modern ICT

……………………………

2.3.4 ICT and Organizations’ Cultural

Perspectives………………………….

2.3.5 The Modern ICT and Organization Performance

Context……………..

2.3.6 The Concept of ICT Change Strategies…………………………………

2.3.7 Conceptual Framework…………………………………………………

2.3.8 The Rationale for Selecting an Organization’s

Performance Improvement Model…………………………………………………..

6

6

6

6

8

10

10

10

11

12

13

14

15

16

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction…………………………………………………………….

17

17

9

3.2 Research Paradigm………………………………………………………

3.2.1 Positivism Paradigm………………………………………………………

3.3 Research Design…………………………………………………………

3.3.1 Research Approach………………………………………………………

3.4 Area of Study……………………………………………………………

3.5 Sampling Procedure………………………………………………………

3.6 Study Population……………………………………………………….

3.7 The Sampling Frame……………………………………………………

3.8 Sampling Procedure………………………………………………………

3.9 Sample Size…………………………………………………………….

3.10 Research Variables………………………………………………………

3.11 Data Collection Techniques………………………………………………

3.12 Data Analysis……………………………………………………………..

17

18

19

20

20

20

20

20

21

21

21

22

22CHAPTER FOUR: PRESENTATION OF RESEARCH DATA

4.1 Introduction………………………………………………………………

4.2 Characteristics of the respondents………………………………………

4.2.1 Gender of respondents………………………………………………….

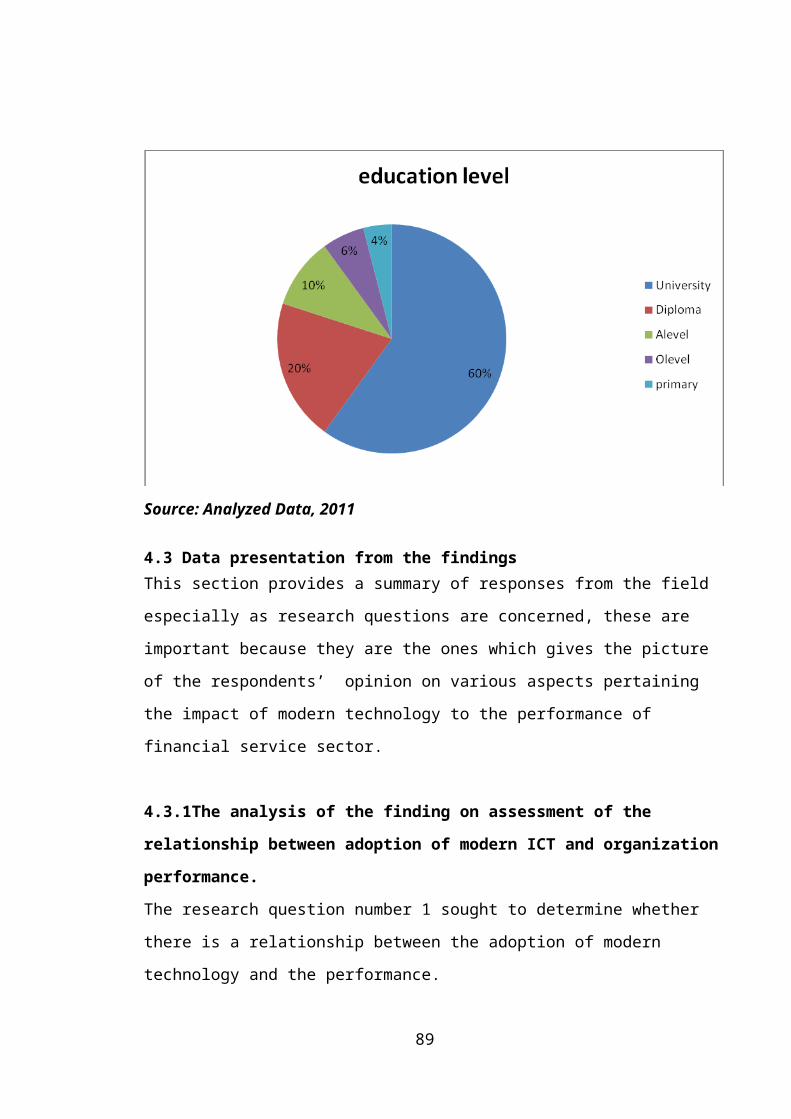

4.2.2 Education of the respondents……………………………………………

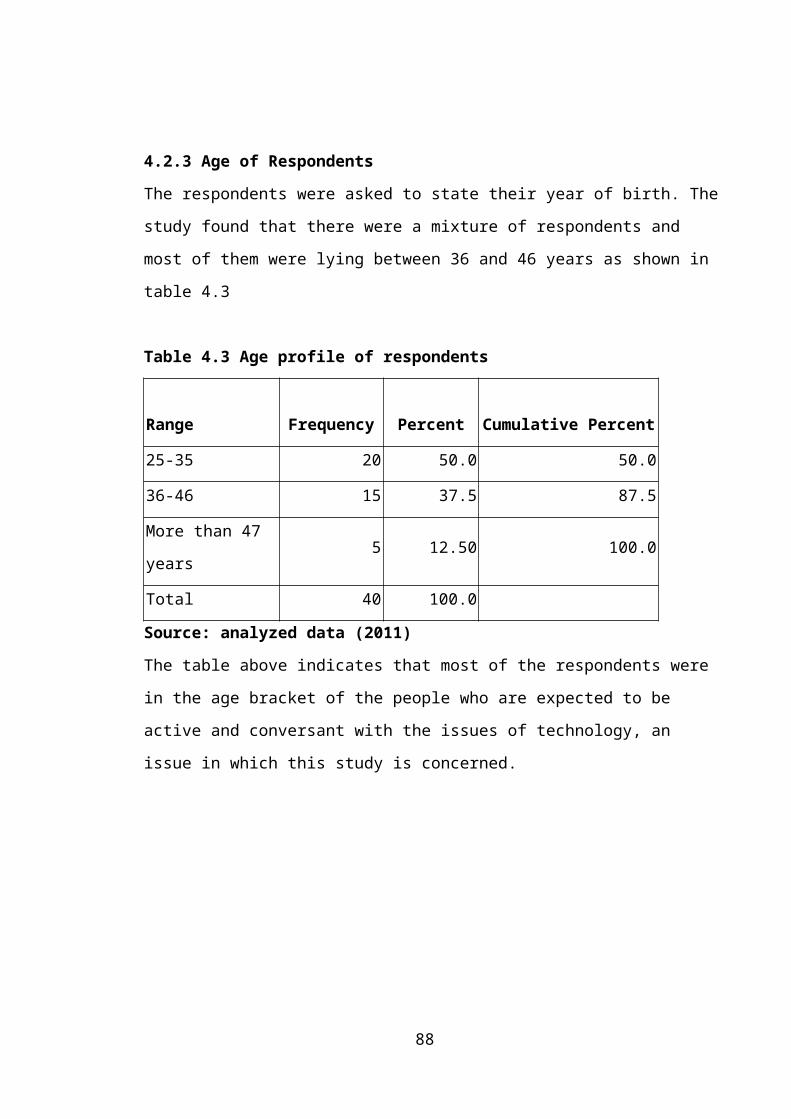

4.2.3 Age profile of the respondents………………….…………………...……

4.3 Findings of the research questions………..

………………………………

4.3.1 The assessment of the relationship between

adoption of modern ICT and organization

performance…………………………………………

4.3.1.1 Customer orientation vs.

performance………………………………….

24

24

24

24

24

25

26

26

26

27

28

10

4.3.1.2 Impact of technology on revenue

growth………………………………

4.3.1.3 Assessment of how modern technology can help

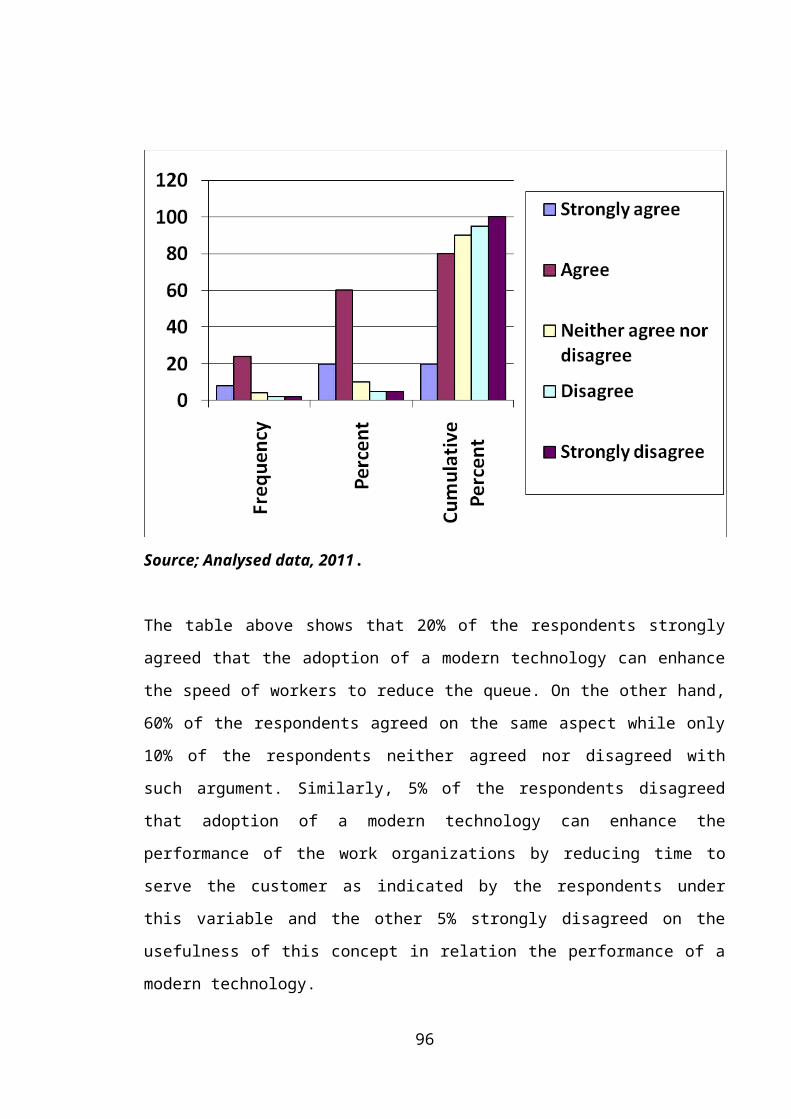

to control queue……

4.3.1.4 Assessment of the improvement of work process

though adoption of modern

technology………………………………………………………

4.3.1.5 Assessment of the relationship between the

working hours and the adoptions of modern

technology…………………………………………

4.3.2 Strategies for Optimum Utilization of the Modern

ICT…………………

4.3.2.1 Assessment of how ATMs ensure optimum

utilization of modern

technology........................................

..................................................

.........

4.3.2.2 Assessment of how research and development

ensure optimum utilization of modern

technology…………………………………………

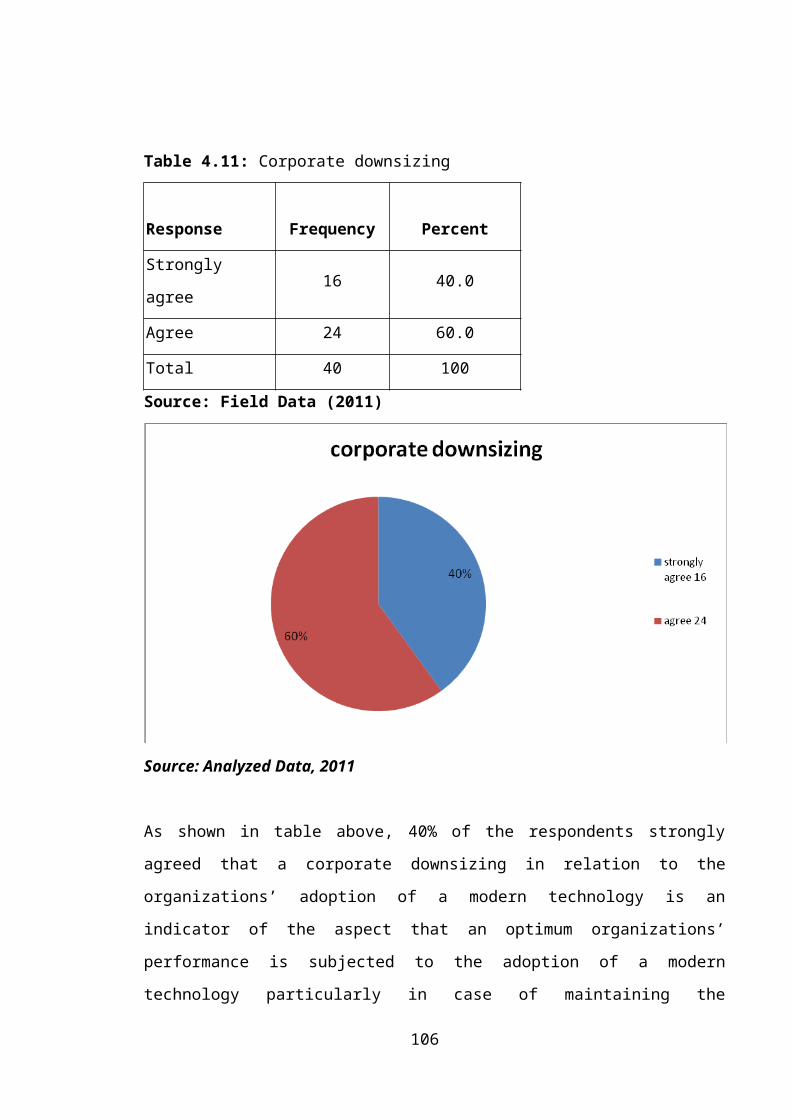

4.3.2.3 Assessment on how corporate downsizing can

enhance optimum utilization of modern

technology…………………………………………

4.3.2.4 The assessment of how employee training and

development ensures optimum utilization of modern

technology……………...……………..

30

31

32

32

33

34

35

36

37

38

39

39

40

41

42

43

11

4.3.2.5 Assessment of how customer training enhances

optimum utilization of modern technology…………………….

………………………………….

4.3.2.6 The usefulness of computers uses in enhancing

utilization of modern

ICT...............................................

..................................................

........

4.3.2.7 Assessment of the relation between

qualification of employee and adoption of modern

ICT………………………………………….……...

4.3.3 Challenges in Implementing the Modern ICT

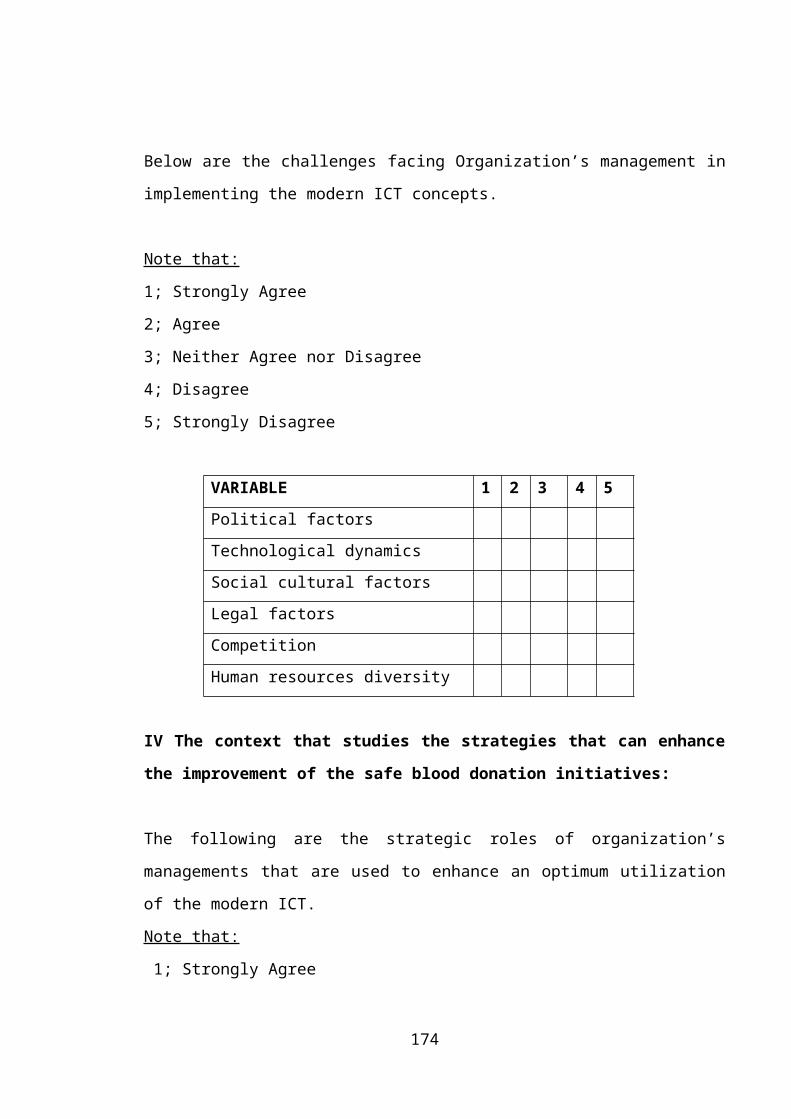

Concept…………………..

4.3.3.1 How political factor can be a challenge in

implanting modern ICT………

4.3.3.2 Technological dynamics as a challenge in

implementing modern

technology………………………………………………………………

4.3.3.3 Social cultural factor as a challenge in

implementing modern

technology………………………………………………………………

4.3.3.4 Legal factor as a challenge in implementation

of modern ICT...................

4.3.3.5 Competition as a challenge in implanting

modern ICT…………………

4.3.3.6 Human resource diversity as challenge when

44

12

implementing modern ICT……………………CHAPTER FIVE:DISCUSSION OF THE FINDINGS

5.1 Discussion of research findings on Impact of

modern technology to

the performance of financial service

sector …………………………

5.1.1 Discussion of research findings on Impact of

technology on revenue growth…………………

5.1.2 Discussion of research findings on how modern

technology can help to control queue…

5.1.3 Discussion of research findings on Strategies for

Optimum Utilization of the Modern ICT……………

5.1.4 Discussion of research findings on Challenges in

Implementing the Modern ICT Concept…………………..

SUMMARY, CONCLUSION AND RECOMMENDATION

6.1 Introduction………………………………………………………………

6.2 Summary………………………………………………………………

6.3 Conclusion………………………………………………………………

6.4 Recommendations………………………………………………………

6.4.1 Relation between the use of modern technology

and organization

performance………………………………………………………….....

6.4.2 Strategies for optimum utilization of Modern

ICT……………………..

6.4.3 Challenges facing organization management in

46

46

46

46

47

48

48

89

90

91

92

102

103

113

114

115

13

implementing the modern

ICT……………………………………………………………..

6.5 Suggestions for the dissertation in Future Research

……………………..

References………………………………………………………………………..

LIST OF TABLESTable 3.1: Criteria for Selection of Research

Paradigms and Research

Methods……………………………………………………

Table: 3.2: Research Sample Selection

Criteria…………………………

Table 3.3: Research Variable Names and

Classifications………………

Table 4.1: Gender of

Respondents…………………………………….

Table 4.2: Education level of

respondents………………………………

Table 4.3: Age profile of

respondents…………………………………

Table 4.4: Customers Orientation………………………………………

Table 4.5: Revenue growth…………………………………………….

Table 4.6: Controlled queue……………………………………………..

Table 4.7: Work process………………………………………………..

Table 4.8: Working hours………………………………………………

18

21

22

24

25

25

26

27

29

30

31

32

33

34

35

36

37

14

Table 4.9: Automated Teller Machines

uses…………………………..

Table 4.10: Research and Development

concept……………………….

Table 4.11: Corporate downsizing……………………………………….

Table 4.12: Employees Training and

development……………………..

Table 4.13: Customers’ training…………………………………………

Table 4.14: Computer uses ………………………………………………

Table 4.15: Qualifications of

employees………………………………..

Table 4.16: Political Factor………………………………………………

Table 4.17: Technological

dynamics…………………………………….

Table 4.18: Social Cultural

Factors……………………………………..

Table 4.19: Legal Factors………………………………………………..

Table 4.20: Competition…………………………………………………

Table 4.21: Human resources

diversity………………………………….

38

40

41

42

43

44

45

LIST OF FIGURES

15

Figure: 2. 1; An Organization’s Performance

Improvement model…………

15

LIST OF ABREVIATIONS

ATMs - Automated Teller Machines

Co - Company

FSSP - Financial Services Sector’s Performance

HRs - Human Resources

ICT - Information Communication and Technology

Ltd - Limited

MBA - Masters of Business Administration

NBC - National Bank of Commerce

PPP - Public Private Partnership

MU - Mzumbe University

URT - United Republic of Tanzania

16

17

ABSTRACT

This study was conducted at the NBC Limited in Dar es

salaam, Tanzania. The general objective was to investigate

the impact of a modern technology to the performance of

financial services sector. Specifically it aimed at

determining the relationships between the adoption of modern

ICT and organization’s performance,the second objective was

to study the current strategic roles of organization’s

managements that are used to enhance an optimum utilization

of the modern ICT.Last the study aimed at exploring the

challenges facing Organization’s management in implementing

the modern ICT concept.

The study was mainly descriptive and cross – sectional. It

was conducted using a case study technique by collecting

primary data at the NBC Dar es Salaam using questionnaires.

It involved a sample of 40 respondents The findings found

that there exists a relationship between the adoption of

modern technology and the performance of the organizations.

The study also indicated the strategies used by the

organization to ensure optimum utilization of technology

through introducing online banking services and the use of

ATMs.Not only had that but the findings also indicated the

challenges faced by Organizations’ when implementing ICT.

The researcher recommends that the adoption of a modern

technology by work organizations have a significant role in

18

influencing the organizations’ performance, thus the

managements of organizations should maintain a state of

innovation in order to attain a competitive scope in

adopting and implementing modern technology for the benefit

of the organization and other stakeholders. It is also

recommended that Organizations should stress on the

strategies that enhance optimum utilization of ICT and

increase the motives for the utilization of the same.Last

the researcher recommends that organization should find ways

to tackle the challenges they face when implementing modern

technology.

19

CHAPTER ONE

AN OVERVIEW OF THE STUDY

1.1INTRODUCTION:

This chapter provides detailed information related to the

introduction of the study. It covers such variables as

background of the study, research problem and research

question. Other aspects included research objectives,

research variables, limitation of the study as well as

significance of the study.

1.2 Background to the Study

The introduction of computing and specifically Information

and Communications Technologies (ICTs) into the workplace

is one of the most significant and dramatic changes in the

realm of office work to be witnessed in recent years

(Wiese, 2001). Today’s business environment is very

dynamic and undergoes rapid changes as a result of

technological innovation, increased awareness and demands

from customers. Business organisations, especially the

banking industry of the 21st century operates in a complex

and competitive environment characterized by these

changing conditions and highly unpredictable economic

climate. The business impacts of information technology

(IT), deregulation and globalisation on the structure and

profitability of the international banking industry is

20

being observed. Information technology creates new

opportunities for the banks in the way they organize

product development, delivery and marketing.

However IT also allows other financial and even non-

financial organisations to start offering bank services.

Information and Communication Technology (ICT) is at the

centre of this global change curve. Laudon and Laudon,

(1991) contend that managers cannot ignore Information

Systems because they play a critical role in contemporary

organisations. They point out that the entire cash flow of

most fortune500 companies is linked to Information System.

The usage of information technology (IT), broadly

referring to computers and peripheral equipment, has seen

tremendous growth in service industries in the recent

past. The most obvious example is perhaps the banking

industry, where through the introduction of IT related

products in internet banking, electronic payments,

security investments, information exchanges (Berger,

2003), banks now can provide more diverse services to

customers with less manpower.

The application of information and communication

technology concepts, techniques, policies and

implementation strategies to banking services has become a

subject of fundamental importance and concerns to all

banks and indeed a prerequisite for local and global

competitiveness. ICT directly affects how managers decide,

21

how they plan and what products and services are offered

in the banking industry. It has continued to change the

way banks and their corporate relationships are organized

worldwide and the variety of innovative devices available

to enhance the speed and quality of service delivery.

Harold and Jeff (1995) contend that financial service

providers should modify their traditional operating

practices to remain viable in the 1990s and the decades

that follow.

The adoption of ICT in banks has improved customer

services, facilitated accurate records, provides for Home

and Office Banking services, ensures convenient business

hour, prompt and fair attention, and enhances faster

services. The adoption of ICT improves the banks’ image

and leads to a wider, faster and more efficient market. It

has also made work easier and more interesting, improves

the competitive edge of banks, improves relationship with

customers and assists in solving basic operational and

planning problems. (DeYoung, Robert 2007) In general,

existing studies have concluded positive effects regarding

the relation between ICT and banks’ performance. First,

ICT can reduce banks’ operational costs (the cost

advantage). For example, internet helps banks to conduct

standardized, low value-added transactions (e.g. bill

payments, balance inquiries, account transfer) through

the online channel, while focusing their resources into

22

specialized, high-value added transactions (e.g. small

business lending, personal trust services, investment

banking) through branches. Furthermore, ICT can facilitate

transactions among customers within the same network (the

network e ect) (see Farrell and Saloner, 1998; Katz andff

Shapiro, 1995; Economides and Salop, 1992). Example the

case of automated teller machines (ATMs) by banks. If

ATMs are largely available over geographically dispersed

areas, the benefit from using an ATM will increase since

customers will be able to access their bank accounts from

any geographic location they want (Milne 2006). This

would imply that the value of an ATM network increases

with the number of available ATM locations, and the

value of a bank’s network to a customer will be

determined in part by the final network size of the bank.

Indeed, Saloner and Shepard (1995), using data for

United States commercial banks for the period 1971-1979,

showed that the concern of network e ect is important inff

the ATM adoption of United States commercial banks (see

also Milne, 2006).

It should be mentioned that as the global reach of the

Internet implies that financial services can

increasingly become borderless and global, a pan-European

initiative for could increase customer confidence, as

certainty for customers that all banks are protected in a

similar fashion may increase the customer’s perception of

23

security.Support the skills development among bank

personnele-Banking and ICT have caused the traditional

branch-based banks to change the service offerings in

their branches. The business model of dual-combination

banking (banks offering internet-banking and branch-based

banking) is emerging, which implies that customers are

increasingly performing basic banking tasks online while

relying on bank branches only for more sophisticated,

advisory tasks. The dual- banking model can give

traditional branch banks the opportunity to adjust their

branch network towards advisory functions and away from

traditional teller services, thus adding value to

their customers from direct and customised bank advisory

services.This development however means that an increasing

number of jobs are being changed from traditional tellers

to branch advisors/counsellors. Bank staff is increasingly

asked to provide highly qualified financial advice

rather than perform simple teller functions. As both the

econometric analysis and the case studies show, bank staff

is being retrained to perform such tasks. From the

econometric analysis it can be seen that ICT usage in

financial services have a significant skill-bias towards

medium-skilled labour, which

The banking industry in Tanzania has witnessed tremendous

changes linked with the developments in ICT over the

years. The quest for survival, global relevance,

24

maintenance of existing market share and sustainable

development has made exploitation of the many advantages

of ICT through the use of automated devices imperative in

the industry. This study evaluates the response of

Tanzania banks to this new trend and examines the extent

to which they have adopted innovative technologies in

their operations and the resultant effects.

1.3 Statement of Research Problem

The role of ICT in banking industry effective use of ICT

is assisting banks to be more customer-centric in their

operations by building a solid foundation for customer

relationship management, to grow the range of

products/services while mitigating fraud levels and

improving risk management, to widen their customer base,

reduce transaction & operational costs and to gain or

retain competitive advantage

A. Khanna (2003) notes that technology has changed the

contours of the three major functions performed by banks

i.e. easy access to liquidity, transformation of assets

and monitoring of risks

Further, IT and the communication networking systems have

a crucial bearing on the efficiency of money, capital and

foreign exchange markets.

25

What are therefore the developments and implications of

ict on banking in Tanzania? Banks in the country are

increasingly gravitating towards digital technology to

create value for their Customers and in competing for

market shares. Still, banking in the country is beset by

long Queues, energy exacting and time-consuming, and on

the whole costly (Appiah and Agyemang 2005). It defeats

the purpose of customer service to see the hard time that

many customers go through to access banking services

around the end of every month when most salaries are paid

through the banks. This has resulted in the loss in

potential exchanges as many people simple keep money

outside the banking system to avoid the ordeal meted out

to them by the banks (William et al 2005; Appiah and

Agyemang 2005).

Physical cash and paperwork still characterize most of the

payment systems in Tanzania and remain popular in spite of

the introduction of digital payment cards.

The main focus of adopting digital technology by the

banks, as it appears to us from our own experiences as

bank customers, is to network customer accounts

information across branches to create business value

(operational excellence) rather than customer value. In

eliminating time, space and distance constraints,

customizing products and services, effecting payment or

26

cross-selling, the internet stands out as the biggest

digital platform for businesses that leverage the

technology.. Ho and Ko (2008) also identify labour cost

for banks as an incentive to introduce technology-based

self-service offer to customers. Most Tanzanian bank

customers also appear to be more comfortable with over-

the-counter banking services than online banking and give

it little or no attention although utilizing ATMs and

other digital services is a way of life for many bank

customers. Indeed, leveraging a new technological platform

is not a guarantee for success as learned the hard way by

many early dotcoms during the internet boom.

Internet banking can boost growth and profits for a bank

but it necessitates considerable resources for both banks

(Williamson 2006, Bauer et al. 2004) and bank customers in

Tanzania. Therefore banks offering online banking need to

continually evaluate the value they offer to their

customers by taking into account customers’ value

perceptions in order to be reactive or proactive (Kotler

and Keller 2006) and to identify factors that affect those

value perceptions to achieve a customer-centric management

strategy. “Customer Value needs to be seen from the

customer’s viewpoint in terms of the value s/he sees in

interacting with the organization” (Customer Value

Foundation 2007).

27

1.4 Research question

1.4.1 General Research question

What is the impact of modern ICT development to the

financial service sector performance (FSSP)?

The researcher answered the following research questions:

(i) What were the relationships between the adoption

of modern ICT concepts and organization’s performance?

(ii) What were the current strategic roles of

organization’s managements that are used to enhance an

optimum utilization of the modern ICT?

(iii) What were the challenges facing Organization’s

management in implementing the modern ICT concept?

1.5 Research Objectives

1.5.1 General Research objective.

The impact of modern ICT development and management to the

FSSP in the URT.

1.5.2. Specific Research objective.

(i) Determined the relationships between the adoption

of modern ICT concepts and organization’s performance

specifically on FSSP.

(ii) Determined the current strategic roles of

organization’s managements that are used to enhance an

optimum utilization of the modern ICT.

28

(iii) Determined the challenges facing Organization’s

management in implementing the modern ICT concept

1.6 Significance of the study

The study was geared toward contributing the following to

the stakeholders at large; It contributed views to general

stakeholders on the impact of modern ICT development and

management to the FSSP and facilitate work organizations in

attaining their performance objectives.

It provided proper means of delivering a result oriented ICT

functions through formulating and re-designing ICT strategy

implementation that can best enhance an operational

efficiency. It also contributed to the existing body of

knowledge and act as reference for other researchers who

will be interested to researching in this area.

1.7 Scope of the study

Geographically the study was conducted in Dar es Salaam in

the URT. Specifically it was conducted at the NBC branches

in Dar es Salaam city.

1.8 Limitation of the study

Based on the prevailing scarcity of research resources

namely; time, financial and human resources, the researcher

conducted the study as a case study at the NBC.

29

1.8 Limitation and scope of the study

However, this study faced many problems and the study

involve the use of sample, generalization will be

made, while the study restrict itself in a case

study approach and thus, it may be difficult to

secure reliable data. Other factors, which are

anticipated to limit the study, include:-

1.8.1 Time constraint

This study has been carried out for a short period of

time because it is the obligation to do so as to

follow the deadline of the academic calendar. Time

constraint affected both, the quality and quantity of

the research study because the researcher had to use

fewer respondents and only one Financial Institution

as a case study which is National Bank of Commerce.

1.8.2 Financial constraint

Lack of adequate finance affects the quality and

quantity of data to be collected during the study.

This hindered the researcher to conduct the study

effectively because the researcher was not able to

interview as many respondents as possible. Not only

that but also funds is not enough to facilitate the

30

conducive environment for the entire study as the

cost of living, transport fare and medical expenses

are very much high.

1.8.3 being new to the respondents.

Some of the respondents create artificial behavior

and become resistant in giving out information on

their free will. In this circumstance it is better

to try the best to get accustomed to the respondents

and narrate clearly the objectives of the study.

1.8.4 Lack of sufficient data.

The researcher faces the problem of data collection

during the fieldwork; this is due to confidentiality

of some documents as well as some respondent’s lack

of co-operation with the researcher during the actual

research. Some documents are not also available in

the area of the study.

1.8.5 Sample size selected

Since the research conducted in Dar es Salaam and at

the offices of NBC Bank the sample size selected

involved only 50 respondents, this may not give a

true representation of the real situation of the

research topic. Thus, a small sample size affects the

reliability of the data to be collected.

31

1.9 Delimitation of the studyThe study faced with many problems such as lack of

sufficient data, fund shortage, time limit, being new

to the respondent, which hinder the accuracy of my

research. But I tried to solve this problem by reduce

the less important expenses so that I can meet with

available amount and complete the research report.

1.9.1 Time constraint

Following the time management, the study carried out

for a short period of time because it is the

obligation to do so as to follow the deadline of the

academic calendar the researcher have to use fewer

respondents and only one Financial Institution as a

case study which is National Microfinance Bank in

order to save the time allocated.

1.9.2 Lack of fund

Due to lack of fund, the researcher tried to solve

this problem by reduce the less important expenses so

that she/he can meet with available amount that can

complete the research report and collect accurate

data for low cost which will not affect the quality

and quantity of the research.

32

1.9.3 Lack of sufficient data.

In case of lack of sufficient data the researcher

tried to target respondents of which will give the

accurate data for the research and try to explain

to the respondent how to fill the questionnaire and

what data expected to get from them according to the

requirement which are in questionnaire.

1.9.4 Sample size selected

Accessibility of some respondents in the sample is

expected to be difficult since these are busy

executive officer. The researcher counter this

limitation by using other data collection approach

such as telephone interview and questionnaires, and

provide for estimated response rate.

33

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This part provides a thorough review of related literature

so as to establish the relationship between variables in the

selected area of study. It established the relationships

that exist between the modern ICT and organizations’

performance. The researcher will present the theoretical as

well as empirical related literature review ad hereunder.

2.1 Theoretical Literature Review

Under the theoretical related literature review the

researcher covers the definition of key terms

2.1.1 Definition of Key Concepts

Information Communication and Technology was defined as the

ways people use resources to meet their wands and needs. For

example people have inverted refrigerators to meet their

need for storing foods (Brian et al (1999), James, (1998)

and Turban et al, 1996).

Human resources management is a set of policies practices

and progress of managing people in organization and

essentially a process of binding people and organization

together (Ngirwa, 2005).

Organization’s Manager is a person responsible for managing

and overseeing the human resources in different department

within a company, organization or agency. This include

posting, advertisement or approving advertisement for new

34

employees, screening, resumes and application, setting

interview appointments and being involved in the hiring

process (Prasad, 2006)

Motivation is the activation or exercitation of goal-

oriented behavior. Motivation is said to be intrinsic or

extrinsic. The term is generally used for humans but,

theoretically, it can also be used to describe the causes

for animal behavior as well. Motivation may be rooted in the

basic need to minimize physical pain and maximize pleasure,

or it may include specific needs such as eating and resting,

or a desired object, hobby, goal, state of being, ideal, or

it may be attributed to less-apparent reasons such as

altruism, selfishness, morality, or avoiding mortality

(Robbins, 2004).

Motivation theories are defined as theories that attempt to

explain the nature of motivation. It explains the behavior

of certain people at certain time (Ngirwa, 2005 and Mullins,

2007).

Employees is defined as any person who has entered into or

works under a contract of services with an employer whether

by way of manual labor, clerical work or other, whether

contract is expressed or implied or is oral or in writing

(Mullins, 2007).

Performance is defined as the achievement of quantified

objectives. It is however not only the matter of what people

achieves but how they achieve it. Performance is both

35

behavior and results (Ruzibuka et al, 1996 and Robbins

2004).

Organization is defined as the ways work is organized and

managed. This includes the following elements: job design,

careers concerns, management style, scheduling and

interpersonal issues (Ruzibuka et al, 1996)

Job is defined as a group of position involving same duties,

responsibilities, knowledge and skills. Each job has

definite title and is different from other jobs. For example

typist, mail clerk, salesman, are jobs (Prasad, 2006)

2.2.2 Basic Organisational Financial Institution Performance

Theories

These are presented as hereunder:

2.2.2.1 Need Theory.

According to Robbins (2005) there are four theories that

focus on human needs that are reflected in the

organizations’ mission. These include Maslow’s Hierarchy of

needs, Two Factors Theory, ERG and McClelland‘s Needs

theory. The strongest of these is the McClelland’s Needs

theory particularly regarding the relationships between

achievements and organizations’ productivity. Furthermore,

the other three have better value in explaining and

predicting satisfaction. Therefore, for the purpose of

creating value of this study the researcher dug deeper on

McClelland’s Needs Theory.

36

37

2.2.2.2 McClelland’s Needs Theory

Achievement, Power and Affiliation are three important needs

that help to explain motivation, for this case motivation

towards modern ICT development and management.

Need for achievement refers to drive to achieve in relation

to the certain set of standards. Some people in

organizations have a strong drive to succeed. They are

striving for personal and organization’s achievement rather

than the reward of achievement per se. They always strive to

attaining a competitive edge by doing their jobs description

and specification better or more efficient than it has been

done before by seeking situations in which they can attain

personal responsibilities for finding solutions to problems

in which they can receive rapid feedback on their

performance and be able to determine easily whether they are

improving or not and in which they can set moderately

challenging goals.

McClelland provided that higher performers (both people and

organizations) dislikes succeeding by chance. They prefer

the challenges of working at problems and accepting the

personal responsibility for success or failure rather than

leaving the outcome to chance or the action of others.

Importantly, they avoid what they perceive to be very

difficult or very easy tasks. They like setting goals that

requires stretching themselves little.

38

On the other hand, needs for power is all about the need to

make others behave in a way that they would not have behaved

otherwise. They have the desire to have impact, to be

influential and to control others. They enjoy being the in

charge and preferring to be placed into competitive and

status oriented situation. They also more concerned with

prestige and gaining influence over others than with

effective performance.

Similarly, need for affiliation is the desire for friendly

and close interpersonal relationships (for this case inters

organization relationships). People under this category of

needs prefer cooperative situation rather than competitive

ones. They desire relationships that involve a high degree

of mutual understanding.

The three components of the motivation theory (need theory)

as propounded by the McClelland’ are also reflected in the

ICT development and management towards attaining the

organization’s predetermined goals. Organizations within

their industry need power, affiliation and achievement in

order to be able to attain a technologically competitive

edge. Success in such context also calls for managers who be

entrepreneur enough to be able to take challenges in

adopting the modern ICT concept that when working in one

system can result in improved performance (Robbins, 2005 and

Laudon et al, 2002).

39

2.2.2.3 Bank theory

Banks, together with other financial intermediaries, are

essential in the allocation of capital in the economy. A

very powerful tool to explain how banks work is provided

by the literature on financial intermediation. This

literature is centred on information

asymmetries, an assumption that “different economic agents

possess different pieces of

Information on relevant economic variables and those

agents will use this information for their own profit”.

The presence of asymmetric information leads to adverse

selection and moral hazard problems. Adverse selection is

an asymmetric information problem that takes place before

the transaction occurs and it is related to the lack of

information about the lenders’ characteristics. Moral

hazard takes place after the transaction occurs. It is

related with incentives by the lenders to behave

opportunistically. The financial intermediation literature

explains that financial intermediaries exist to overcome

the informational asymmetries in markets. Banks, as a

particular type of financial intermediary, perform

different tasks related to these information asymmetries,

among which are the provisions of liquidity through

deposits; and the supply of finance to households and

firms, by the means of loans. Among the different issues

40

analysed by the financial intermediation literature is the

relationship between bank and customers and the monitoring

(including screening) activity that implies that firms and

financial intermediaries develop long-term relationships,

thus mitigating the effects of adverse selection and moral

hazard. Recent developments in ICT, together with new

financial instruments, have lowered informational

asymmetries. In this dissertation we use economic concepts

in the financial intermediation literature to explain the

observed trends in the banking industry.

41

2.2.2.4 ICT and Organizations’ Cultural Perspectives

When organizations become institutionalized, they take on a

life of their own apart from their founder or any of their

stakeholders. They determine their own culture which is a

system of shared meaning held by members that distinguishes

one organization from others. It convey a sense of identity

for organizational members and facilitate the generation of

commitment to something large than one’s individual self –

interest. It also enhance the stability of the social system

by providing appropriate standards for what stakeholders

should say and do and serve as a control mechanism that

guide and shapes the attitude and behavior of stakeholders.

As it guide and shape the attitude and behavior of employees

it calls for strategic roles of organizations’ management to

rely on the same scope and implement their professional

functions focusing on modern ICT development and management

so as to attain their projected performance sustainability

as provided by (Mullins, 2007 and Prasad, 2006)

According to Robbins (2005), researches suggests that there

are seven characteristics that in aggregate captures the

essence of organizations’ culture that may affect the

adoption of the concept of modern ICT development and

management namely; innovation and risk taking, attention to

details, outcome orientation and people orientation. Others

are team orientation, aggressiveness and stability.

42

Innovation and risk taking refers to the degree to which

organizational members are encouraged and to be willing to

be innovative and take risks in developing and managing ICT

functions

Attention to details is the extent to which organizational

members are expected to show precision, analysis and

attention to details.

Outcome orientation is all about the level at which

organizational members are encouraged to be focused on

results or outcomes rather on the techniques and process

used to achieve those outcomes.

People orientation refers to the degree to which

organizational management decisions takes into consideration

the effect of outcomes on people within and outside the

organization.

Team orientation is the extent to which work organizational

activities are organized around teams rather than

individuals.

Aggressiveness is the degree to which organizational members

are aggressive and competitive rather than easygoing.

Stability is the degree to which organizational activities

emphasizes on maintaining the status quo / competitiveness

in contrast to growth using modern ICT.

2.2.2.5 The Concept of ICT Change Strategies

43

As provided by Peter (2005) and Robbins (2005), the multi -

attribute model is a useful guide for devising modern ICT

change strategies. Basically, there are four ICT change

strategies namely adding a new salient belief about the ICT

object, increasing the strength of the existing positive

beliefs, improving the evaluation of the strongly held

beliefs and making an existing favorable belief more

salient.

Adding a new salient belief about the ICT object is probably

the common ICT change strategy. Ideally, it requires adding

a salient belief with a positive image, example, people in

general have positive attitude towards ‘the use of computer

which seem to be linked to such benefits as reduced costs of

operations and simplified work load.

Increasing the strength of the existing positive beliefs

calls for increasing the strength of beliefs about positive

attributes and consequences or they can decrease the

strength of beliefs about the negative attributes and

consequences, example, specialists in ICT works hard to

create strong consumer beliefs that its adoption leads to

organization productivity and apparently many organizations’

managers do believe.

Improving the evaluation of the strongly held beliefs

requires constructing a new mean end chain by linking a more

positive and high ordered consequences to that attribute,

example computer manufacturer such as IBM once tried to

44

enhance customers’ attitude by linking their computer uses

and radioactive rays prevention that leads to assured cancer

prevention. Making an existing favorable belief more salient

usually by convincing the target audience that the

attributes are more self – relevant than it seemed to be. It

attempts to link the attribute to valued consequences.

Through this way, there is increase in both the salience of

customers’ beliefs about the attributes as well as the

evaluation of the beliefs.

Economics of money and banking:

Money and Monetary policy

The definition of money as a means that is generally

accepted in making payment simplies that what constitutes

money depends on the behavior of consumers and firms. New

technology-based payments instruments, if generally

accepted, have the potential to modify what constitutes

money. We are currently moving towards an electronic

payments system. This has the potential to increase

overall efficiency in the economy and also raises new

concerns regarding other essential -besides efficiency-

attributes of payments systems, in particular, their

safety. Both the safety and the efficiency of the payments

systems have become a fundamental concern for policy

makers. Issues that can be examined include changes in the

existing measures of money, the relevance of monetary

45

aggregates in monetary policy making, the potential for e-

money to replace “fiduciary” money, and institutions that

should be allowed to issue e-money. The introduction of

the euro may also have implications on the adoption of new

electronic payments instruments in Europe. ICT

developments have strongly influenced international

capital flows. These developments have prompted a debate

on the role that national and international institutions

should play in the new framework of a globalised economy.

The current international institutional framework has

proved inadequate to deal with the new environment created

by the globalisation of capital flows. Policy options are

required at European and international levels. The volume

and speed of international capital flows and the structure

of international financial system also affect monetary

policy. Exchange rate considerations now play a greater

role in the conduct of monetary policy. Because of the

growing interdependence between economies around the

world, a country’s monetary policy cannot be conducted

without taking international considerations into account.

46

Electronic money. Its characteristics

From Electronic Fund Transfer Systems to Digital cash

From a technical point of view the first system that could

be considered electronic money is the electronic transfer

of funds. This system is used from the late 1960s. It

could also be called electronic checking. It is used by

millions of consumers to pay domestic bills and also by

banks and other institutions when transferring large

amounts of money at the international level. Between the

well-known advantages of Electronic fund transfer we could

mention: saved time, reduced costs for paper handling, no

bounced cheques, flexibility. During the 1990s, and taking

advantage of new information technologies two different

groups of electronic money are being developed and

introduced around the world: prepaid cards and digital

money through Internet. These two kinds of products are

often classified under the generic label of electronic

money or new payment systems. In certain cases they are

labelled as digital cash or electronic cash. By using the

word "cash" one common feature is underlined: the goal is

to be the equivalent of paper cash. Ideally, two main

characteristics of the paper cash should be maintained:

anonymity and liquidity. In the meantime, we are now

seeing the introduction of intermediate products that

coexist with some incipient experiences of pure digital

cash. But, in any case analysts believe that transforming

47

bills into electronics charges on people’s PC electronic

wallet or their intelligent pre-paid card is, without

doubt, a major change since gold became the standard of

payment. Consumers’ viewpoints related to the concepts of

money, cash and value, are probably going to change.

Following Linch and Ludquist (1996): “Digital money is an

electronic replacement for cash. It is storable.

transferrable and unforgeable. Digital money is numbers

that are money”. In general, we can summarise the

advantages and disadvantages of the new electronic payment

systems with respect to the ones currently used as:

Advantages. Increased security, anonymity and preservation

of privacy, reduction of transactions costs, easier

international payments, Consumers have access to much

larger markets (and therefore overall efficiency

improves), better means of control of personal finances by

users directly (instead of financial institutions).

Disadvantages. Everything is fairly new, and therefore

untried. Problems will surely appear and have to be dealt

with. Possibility of losses in case of hardware breakdown.

In general, reliable backup systems have yet to be

developed. Possibility of new criminal activities and

better means to carry out other unlawful ones (tax

evasion, money laundering). About 50m people have access

to the Internet, but this number is expected to reach 200m

within two years2. There are many reasons to vouch for the

48

importance of such a network in the future: the expected

huge markets, the ability to offer 24-hour service across

borders and the potentially enormous savings in

operational costs. Merchants, banks, financial

institutions, credit card companies, and software firms

are, obviously, greatly interested in keeping informed

about the evolution of the Net, and starting to operate in

it.

Pre-paid cards

Smart cards. Technology and purposes

Smart cards consist of a plastic card with an embedded

chip and represent a technological advance in comparison

with cards with magnetic bands. The chip embedded in the

card can hold memory features (as do magnetic bands) and

can as well include a microprocessor. This latter allows

for the use of cards being extended to new applications.

The main use envisaged for smart cards is as a payment

mechanism; with smart cards incorporating electronic cash.

This issue is developed in the next subsection Other

applications for smart cards are covered later in the

report (See section 2.4).The following paragraphs explain

the technological aspects of smart cards systems. The

architecture of a system is the structure of a scheme. The

design of the structure establishes who will be the users

(bank, individuals, and others) and the roles or options

49

available to each user (acquirer, issuer, payee, payer,

and other). It also defines the functional entities (for

instance: purse, till, and reload station) and devices

(for instance: bank terminal and smart card). Finally, it

also establishes the relationships among them The hardware

of smart cards systems is centred on the chips contained

by the card and the several devices related to the card.

Some architectural features of smart cards systems vary

greatly among different schemes. Regarding the types of

microcircuit embedded in the card, four varieties of smart

cards systems can be established: memory cards, shared key

cards, signature-transporting cards and signature creating

cards (See Box .2.1). Schemes currently implemented in

Europe have different levels of technology sophistication.

Among the simplest systems are the single -purpose pre-

paid cards and some multi-purpose cards schemes such as

Dänmont in Denmark. Among the most Sophisticated is

Mondex. The CAFE system is even more sophisticated but its

implementation has been lower. In between, there is a wide

intermediary level range. Although predictions are always

difficult in the technology area there is broad agreement

among experts on the future being based in chip

technology. Predictions also indicate that as chip

technology continues to improve more advanced systems will

become economically feasible and will gradually be

implemented. Considerations on the suitability and

50

consequences of technological innovation for Europe are

drawn latter in the report. Pre-paid smart cards as a new

payment mechanism Pre-paid cards can serve as a payment

mechanism by loading and storing monetary value in the

chip embedded in the card. The value loaded in the card

can later be disbursed when paying for the provision of

goods and services. Pre-paid cards are mainly intended for

some of the usual consumer transactions. When considering

different levels in such transactions, we can establish:

those involving a relative high value (which most

consumers associate with credit cards),

2.3 Empirical Literature Review

The empirical related literature review is linking the

relationships between various variables that are considered

to have significant impact on the enhancing the organization

performance in association with the modern ICT context as

discussed below.

2.3.1 Trends in the development of the banking industry

Since the 1980s, the banking industry has been in a

process of significant transformation that started in the

United States, and moved later on to Europe, where the

single market and the introduction of the Euro have

contributed to accelerate the process of change. The main

forces behind this transformation of the banking industry

51

are deregulation and innovation in information

technologies. Both forces have brought about increased

competition, not only among banks but also from other

financial, and even non-financial, institutions. As a

result of increased competition, the banking business has

changed and, for example, while margins in lending

operations have lowered, banks rely increasingly on income

from fees services rather than interest rate spreads.8

additionally, competition has, in some cases, encouraged

banks towards

taking higher risks (for example, by lending to developing

countries) for which there might not be enough

compensation. This issue, the higher risks9 banks may be

incurring in their operations, matters especially to

regulation authorities, because of the safety net they

intend to provide (which was recently applied widely to

Japanese banks, for instance).On the other hand, the

transformation of the banking industry has contributed to

blurring the differences between retail, wholesale and

investment banking. Yet, banks in America have tended

towards specialisation, while in Europe it is the concept

of universal banking (one bank for all) that prevails. The

developments in information technology that have been

behind the transformation of the banking industry by

providing the means to unbundle risks, diversify assets

internationally (though this practice is only in its

52

infancy), or conducting financial transactions on a multi-

currency, global level. 7 A discussion on the workings of

financial intermediaries and financial markets can be

found in Rogoff (1999).

2.3.2 The Banking Industry of Tanzania

The banking Industry in Tanzania has tremendously changed

its dynamics for the last one decade. Many banks have

joined the industry both local and foreign. Notably, the

nobanks financial institutions have been mushrooming by an

alarming speed. For this very reason the players in the

banking industry need to consider their competitive

positioning and repositioning strategically. In mid 1960s

the industry had only one bank, National Bank of Commerce.

It can therefore be said that in 1960s the industry had a

monopolistic structure. In 1986, Corporate and Rural

Development Bank (CRDB) was established hence to make the

industry to experience a duopolistic market structure. In

any industry, including the banking industry, the nature

of competition is always a function of the market

structure. The trend today is a perfect competition and

the central bank has withdrawn from managing the market

forces. Banks are now working on their own about what are

relevant products and rates to be offered to the market.

In this regard the need for the assessment of the

attractiveness of the industry becomes a necessity.

53

The industry has various key players. These to include;

Fully fledged banks (commercial and non Commercial),

Regional Unit Banks, Financial Institutions, Regional

Financial Institutions, Regional Unit Financial

Institutions and Bureaux de Change. As of December 2005,

the banking supervision of the Bank of Tanzania has

approved and register the key players of the banking

sector of Tanzania as follows: Fully Fledged banks (22),

Regional Unit Banks (5), Financial Institutions (5),

Bureux de Change (102).

2.3.3 Abroad Case

Nigeria

The revolution in ICT has made the banking sector changed

from the traditional mode of operations top resumably

better ways with technological innovation that improves

efficiency. ICT can enhance efficiency via its use and in

recent times banks have been encouraged by the rapid

decline in the price of ICT gadgets. This has perhaps

increased the bank level of ICT usage (Ovia, 2005).The

increase might have also be attributable to business

environment that became relatively flexible to accommodate

new forms of technological change as a result of reforms

in the country .Banking is becoming highly ICT based and

because of its inter-sectoral link, it appears to be

54

reaping mostof the benefits of revolution in technology,

as can be seen by its application to almost all areas of

its activities (Akinuli, 1999). It has broadened the scope

of banking practices and changed the nature of banking as

well as the competitive environment in which they operate.

A broad opening has been experienced around the world for

banks and they are currently taking due advantage of these

innovations to provide improved customer services in the

face of competition and faster services that enhance

productivity (Akinuli, 1999; Ovia,2005).Technological

advancement facilitates payments and creates convenient

alternatives to cash and cheque for making transactions.

Such new practices have led to the development of a truly

global, seamless and Internet enabled 24-hour business of

banking. Technological advance in payments are important

due tothe fact that it will be feasible to outsource quite

a number of the banks’ role in the payments system .Also

banks’ regulation can be more technologically dependent

and better focused rather than focusing on conceptual

guidelines. ICT revolution both in terms of innovation

rate, speedy operation, and cost per unit(portraying

reduction in average total and marginal costs) has made a

good number of banks embrace the use of ICT infrastructure

in their operations (Akinuli, 1999).The technological

innovation that is being witnessed currently in the

Nigerian banking sector is possible of impacting on the

55

banks’ mode of transactions especially in their payment

systems. The payment systems are made feasible by ICT

gadgets such as Automated Teller Machine (ATM), Electronic

Fund Transfer (EFT), Clearing House Automated Payments

(CHAPs), Electronic Purse (E-PURSE),Automated Cheque

Sorter (ACS) and Electronic and Transfer at Point of Sale

(EFTPOS), which have made transactions easy and

convenient. This phenomenon is capable of bringing about

speedy operations and enhanced productivity (Adeoti, 2005;

Ovia, 2005). Though there may be little interruptions at

times due to network failures, which may make customers

unable to carry out transactions at that point in time.

This little shortcoming is not in any way comparable to

the days when banking halls were characterized by long

queues mainly as a result of delays in the traditional

banking operations.

Europe

Continental Europe remains a highly bancarised economy

with the most part of savings and investment in the

economy being channelled through banks10. The

restructuring of the banking industry has gained momentum

after the introduction of the Euro and the single market.

The number of mergers and acquisitions in the sector has

grown, as the consolidation has intensified. Moreover,

56

while up to recently concentration remained mainly

domestic, cross-border operations have begun (for example,

the Portuguese Champalinaud group and the Spanish banking

group Banco Santander Central Hispano), and are expected

to intensify in the near future, in spite of governments’

resilience in some cases. Between 1994 and 1997, the

number of credit institutions in the EU has moved from

10,080 to 9,109, a 10% decrease. Analysts still consider

Europe overbanked, yet the consolidation of European

banking may not go as far as economic considerations might

suggest, because of the differences in languages, cultures

and regulatory environments among EU countries. Today’s

banking markets in Europe, especially retail banking, are

not very homogeneous and, in fact, remain quite

fragmented. In general terms, European banking continues

to be highly regulated. Many banks are owned or

participated by the state, or receive indirect support

from it11. The emphasis on banking policy has been on

stability rather than efficiency. State-owned institutions

and mutual banks are especially significant in France and

Germany. The situation in the peripheral countries such as

Italy, Ireland, Portugal or Spain, is generally different,

and retail banking tends to be a more profitable business.

Because they have been more profitable, banks in these

countries have generally stayed out of investment banking

and emerging-market lending.

57

The United States

In the United States, the banking industry has changed

considerably during the 1990s in a process of growing

competition and specialisation. Restructuring and

consolidation of the sector have occurred to a greater

extent than in continental Europe, with the number of

banks declining from 36,103 to 22,140 during the period

1980 to 1997. Increased competition has contributed to

changing the composition of products in the industry. In

this manner, as margins on corporate lending have been

declining, banks have increased the share of their

revenues coming from non-interest sources such as

commissions on asset management, trading or securities

underwriting. A second tendency in the industry is

securitisation, that is, banks transform their loans to

companies, credit cards or mortgages, into tradeable

securities, instead of keeping them on their balance

sheets. Another feature of the American banking industry

is the increasing disintermediation: companies go directly

to a financial market to raise funds, instead of getting

them from a financial intermediary like a bank. 10 See

White (1999), “The coming transformation of European

Banking”. 11 In Germany, for example, less than one third

of deposits by value are held within the privately owned

banking sector.

58

59

Spain

Within the Spanish banking sector, there are two sets of

institutions -commercial banks and savings banks- which

can, as a generalisation, be identified with two different

business strategies. These distinctive business strategies

have not originated with technology induced changes; they

are rather the continuity of historically different

businesses strategies; widely recognised in the

literature. Until quite recently, commercial and savings

banks were subject to different regulation. Lozano-Vivas

(1998) analyses the effects of deregulation12 in Spanish

banks during the period 1985-1991. She examines frontier

cost efficiency and technical change and finds evidence of

differential response to deregulation of commercial and

savings banks. During the period of the study, commercial

banks focused on adjusting their deposit and loan rates as

a response to increased competition; while savings banks

focused on expanding the size and convenience of their

branch operations and undertook a series of mergers

following the removal of geographical restrictions. The

study shows that, in a sense, commercial banks could be

approximated to wholesale banks, whereas savings banks

could be characterised more like retail banks. We use

these empirical results that show the distinctive features

of commercial and

60

savings banks in the late 1980s, to design our study which

will assess whether the responses to technology

developments during the 1990s, by commercial and savings

banks, have paralleled those observed in the previous

years. Notwithstanding the fact that commercial banks also

engage in the retail services, and that the opposite is

true for savings banks, we will examine whether technology

has affected the two groups of institutions differently,

as could be hypothesised given the differential effects of

changes in information management on wholesale and retail

banking, presented in the previous section. An obvious

caveat is that the differences observed between commercial

and savings banks might not be exclusively attributable to

technology effects. For instance, although 12 some of the

hallmarks of the deregulation process are the following:

On March 1987 started the liberalization of interest

rates. This marked the beginning of increased competition

in short-term bank liabilities. Until then, interest rates

were regulated in the case of demand deposits and time

deposits with maturity less than 6 months, or, for longer

maturities, those of amount less than 1 milion ptas and

maturity under a year. Those deposits represented about

45-55% of savings banks’ liabilities, and 35% of

commercial banks’liabilities.

In 1987, the interbank interest rate increases

significantly. Commercial banks reacted by increasing

61

their intermediation margins, while the savings banks

strategy consisted of reducing margins as a means of

gaining market share.

By the end of 1989, there is another considerable increase

in competition affecting bank liabilities. This starts

with the new ''supercuentas'' launched by Banco Santander.

As a result, margins are reduced further. 92 the main

deregulation phase started in the mid-80s and the most

effects of this process must have been observable by 1992,

some effects may have only appeared later on. Moreover, as

we have already mentioned, the evolution of the banking

industry during the 1990s will also reflect the effects of

EMU. Because retail banking has a more local character, we

would expect that EMU would have affected it to a lesser

extent than wholesale banking. Another consideration is

the legal status of Spanish savings banks. Together with

German savings banks, Spanish savings banks are alone in

the EU in maintaining their traditional status of mutual

banks.13 Other empirical studies are main references in

the literature on the Spanish banking sector. Among the

most relevant are the studies that measure bank

efficiency. Because of the relationship between technology

and efficiency, a common approach to assess technological

impact is through estimating production frontiers. In this

line of research are: Grifell et al. (1992) and Grifell and

Lowell (1996) and Prior and Salas (1994).

62

Japan.

Japanese banks are still facing restructuring plans after

a poor performance record that left them in a difficult

financial situation. Yet the worst of the severe banking

problems in late 1997 and 1998 might be over, as almost

all of the Japanese largest banks obtained profits in the

first half of 1999. However, these results are partially

due to implicit and explicit support from their

government. The biggest banks received public funds of

around 7.45 trillion yens during 1999, a sum equivalent to

half their equity. Also contributing to results are the

cheap costs of obtaining funds: the “zero interest rate

policy” implemented by the Bank of Japan in 1999.

Additional factors that might have contributed to

improvement of results are better management of bad loans

and tighter cost controls. Yet Japanese banks require

further restructuring if they are to become globally

competitive again. During 1999, the Financial Supervisory

Authority took over the Finance Ministry in the regulation

of Japanese banks. The FSA injected funds in the banking

industry that were intended to clearing out bad debts, and

also help in the restructuring process involving a

reduction in costs as well as the closing of some banks.

Concerning the technological challenge, Japanese banks

have been under-investing in technology for several years,

63

as considerable amounts of funds had to be applied to

write down bad debts.

Various empirical studies on information technology and its

impact on sectors in various countries have been conducted

over the years. Various scholars such as Wilson (1993),

Freund, Konig and Roth (1997), Radeck, Wenninger and

Orlow(1997), O’Sullivan (1998, 2000) and others have been

engaged in unending discourse on the positive payoffs

emanating from the utilization of information technology in

various enterprises. Such academic debates have resulted in

the origin of the term ‘information technology productivity

paradox’ which is concerned with appraising the impact of

information technology on operational efficiency and the

productivity of organizations. A cursory look at the

industry level studies of the nineties such as the works

ofWilson (1993), Jordan, John and Katz (1999), Furst, Lang

and Nolle (1998) portray that in many instances a positive

correlation is posited between increased investment in

information technology and productivity. On the contrary,

other works such as those of Strassman (1990), Morrison and

Berndt (1990), Dos-Santos and others (1993) show that

additional investments in information technology does not

necessarily contribute positively to productivity. Such

works argue that the estimated marginal benefits are less

that the estimated marginal costs; that for each additional

64

dollar spent in information technology equipment, the

marginal increase in measured output was only eighty cents.

Brynjolfsson and Hitt (1996) noted that most of such results

from researches account for what he referred to as the

‘economic theory of equilibrium’. This means that increased

profitability is not necessarily a byproduct of increased

spending in information technology. Some other researchers

such as Loveman (1994), Lichtenberg (1995) and others have

worked on ICT impact at the level of firms. Loveman in his

work complied data from the Management Productivity and

Information database (MPIT). He discovered that the

utilization of information technology made no significant

impact to the output of manufacturing firms. Lichtenberg in

his work obtained his data from yearly surveys conducted

from the eighties to the nineties by Computer world

magazines. Empirical reports on impact analysis of

information technology in developing countries especially

Tanzania are quite few. It is upon this premise that this

study is designed to fill this gap in the body of knowledge.

Information Technologies and the banking industry

Information technologies are having a great impact in the

reshaping of the banking industry by leading to the

development of new financial products and of new means of

delivering them. With regards to the delivery of products,

for instance, the last decades have seen the appearance of

65

Automated Tellers Machines (ATMs) and telephone banking,

and are now seeing the spread of Internet banking. These

new channels for the delivery of products have the

advantage for costumers of longer hours of service, but

are also a more efficient, cheaper means of delivering the

products. According to a study by Sybase, a transaction at

a traditional “brick-and-mortar” office costs 1.07 euros,

the same transaction costs 55 eurocents over the

telephone, 27 eurocents at an ATMs, and 1 eurocent only

through the Internet. Quite in accordance with these

figures, many banks already report a majority of

transactions being conducted electronically without

personal contact between client and bank employee. This

assertion is especially true with payments systems, and

above all in Europe, with direct debit systems, than in

the United States. Moreover, further effects from

technology developments are envisaged. For example, with

regards to means of payment, Barclays, a British bank, in

a similar strategy to that carried out by American Express

in the United States, announced in late 1999 that the bank

was considering handing out free smart card readers to

their credit card holders, so that these cards could be

used to pay for transactions over the Internet. It is

expected that, in the near future, all PCs will come with

a slot capable of accepting smart cards, which would

contribute to the expansion of electronic money products

66

such as Mondex or Visa Cash.In Europe, technology